SECURITIES AND EXCHANGE COMMISSION

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT

OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-03599

Name of Registrant: The Royce Fund

Address of Registrant: 745 Fifth Avenue

New York, NY 10151

| Name and address of agent for service: | John E. Denneen, Esq. | |

| 745 Fifth Avenue | ||

| New York, NY 10151 |

Registrant’s telephone number, including area code: (212) 508-4500

Date of fiscal year end: December 31, 2013

Date of reporting period: January 1, 2014 – June 30, 2014

Item 1. Reports to Shareholders.

|

SEMIANNUAL

REVIEW AND REPORT

TO SHAREHOLDERS

Royce Pennsylvania Mutual Fund Royce Micro-Cap Fund Royce Premier Fund Royce Low-Priced Stock Fund Royce Total Return Fund Royce Heritage Fund Royce Opportunity Fund Royce Special Equity Fund Royce Value Fund Royce Value Plus Fund Royce 100 Fund Royce Dividend Value Fund Royce Global Value Fund Royce International Smaller-Companies Fund Royce Special Equity Multi-Cap Fund | ||

www.roycefunds.com |  | |

| www.roycefunds.com |

|

eDelivery Saves! Sign Up Now. eDelivery saves paper, time, and fund expenses.1 Sign up now to view statements, prospectuses, financial reports, and tax forms online. > www.roycefunds.com/edelivery 1 Any direct Royce Funds IRA investor who chooses eDelivery of prospectuses, financial reports, and RWord will be exempt from the $15 annual IRA maintenance fee. (We will continue to also waive the fee for investors with more than $20,000 invested in Royce IRAs at the time the fee is charged, and for new transfer and rollover accounts in their first year.) Stay Informed Follow us on Twitter, connect with us on LinkedIn, watch us on YouTube, subscribe to our RSS feed, and sign up for our monthly eWord newsletter to stay up to date on the latest from The Royce Funds.  www.twitter.com/roycefunds www.twitter.com/roycefunds www.linkedin.com/roycefunds www.linkedin.com/roycefunds www.youtube.com/roycefunds www.youtube.com/roycefunds www.roycefunds.com/eword www.roycefunds.com/eword |

| This page is not part of the 2014 Semiannual Report to Shareholders |

| Table of Contents | |

| Semiannual Review | |

| Royce Featured Fund Guide | 2 |

| Portfolio Characteristics | 4 |

| Performance and Expenses | 5 |

| U.S. Small-Cap Market Cycle and Risk Adjusted Performance | 6 |

| Letter to Our Shareholders | 7 |

| Fund Focus | 14 |

| 2014 In Quotes | 135 |

| Postscript: There’s No Such Thing as a Sure Thing | Inside Back Cover |

| Semiannual Report to Shareholders | 15 |

| |

| This page is not part of the 2014 Semiannual Report to Shareholders | 1 |

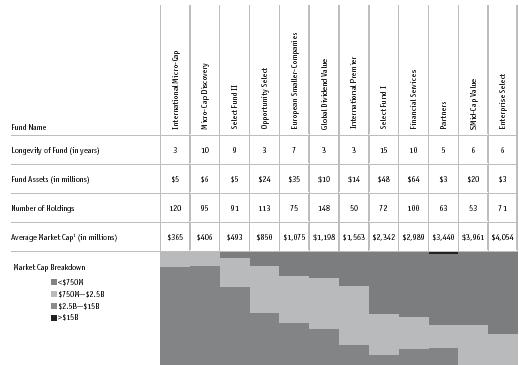

| Royce Fund Guide |

| VALUE-ORIENTED SMALL-CAP OFFERINGS TAILORED TO SPECIFIC INVESTOR NEEDS |

The size and diversity of the small-company universe make it a unique and fertile area for investment. For more than 40 years, it has been our primary area of focus. Over that time, this universe has evolved into an established asset class used by a wide range of investors, including institutions, consultants, advisors, and individuals. Today, there are numerous small-cap and micro-cap indexes and ETFs. Importantly, the continuous regeneration of the asset class, through the entrance of new companies, spin-offs, and IPOs, makes it an evergreen source of investment opportunities. This is why we have elected to focus on the smaller-company universe and believe it is ideally suited for a variety of distinct offerings. |

| INVESTMENT UNIVERSE BREAKDOWN1 |

Market Cap |

| The Royce Funds, other than Royce Special Equity Multi-Cap Fund, invest primarily in micro-cap, small-cap, and/or mid-cap stocks, which may involve considerably more risk than investing in larger-cap stocks (please see “Primary Risks for Fund Investors” in the prospectus). Each Fund may invest a portion of its net assets in foreign securities, which may involve political, economic, currency, and other risks not encountered in U.S. investments (please see “Investing in Foreign Securities” in the prospectus). |

| 2 | This page is not part of the 2014 Semiannual Report to Shareholders |

This guide is designed to help investors better understand both the different approaches and the common ground among our portfolios. Looking closely at our Featured Funds allows investors to see other important differences—in levels of volatility, sector orientation, and investment themes. We think that understanding these differences can inform asset allocation decisions, especially when investors incorporate more than one Royce offering within their portfolios. Listed below are our Funds arranged by average market cap. For a complete listing of our Funds and their attributes please visit our website at www.roycefunds.com. |

| Fund Tools Go online for more tools to help you better understand our Funds. Compare Funds > www.roycefunds.com/compare Prices & Performance > www.roycefunds.com/prices |

|

1 Only available to existing investors and relationships. |

2 Geometric Average. This weighted calculation uses each portfolio holding’s market cap in a way designed to not skew the effect of very large or small holdings; instead, it aims to better identify the portfolio’s center, which Royce believes offers a more accurate measure of average market cap than a simple mean or median. |

| This page is not part of the 2014 Semiannual Report to Shareholders | 3 |

| Portfolio Characteristics | Through June 30, 2014 |

| Longevity | Average | 2013 | % of | ||||||||||||||||||||||||

| of Fund | Market | Number of | Turnover | Non-U.S. | |||||||||||||||||||||||

| Fund | Portfolio Manager(s) | (in years) | Cap1 | Holdings | Rate | Securities | |||||||||||||||||||||

| Royce Pennsylvania Mutual Fund | Chuck Royce | 41 | $ | 1,922 | 461 | 26 | % | 9.6 | % | ||||||||||||||||||

| Royce Micro-Cap Fund | Jenifer Taylor | 22 | 433 | 205 | 22 | 14.6 | |||||||||||||||||||||

| Royce Premier Fund | Chuck Royce, Whitney George | 22 | 2,895 | 71 | 11 | 12.3 | |||||||||||||||||||||

| Royce Low-Priced Stock Fund | Whitney George | 20 | 1,299 | 100 | 16 | 37.5 | |||||||||||||||||||||

| Royce Total Return Fund | Chuck Royce, Jay Kaplan | 20 | 2,306 | 510 | 21 | 12.2 | |||||||||||||||||||||

| Royce Heritage Fund | Chuck Royce, Jim Harvey, Steven McBoyle | 18 | 3,000 | 206 | 79 | 24.1 | |||||||||||||||||||||

| Royce Opportunity Fund | Buzz Zaino, Bill Hench | 17 | 833 | 323 | 39 | 4.2 | |||||||||||||||||||||

| Royce Special Equity Fund | Charlie Dreifus | 16 | 1,846 | 43 | 28 | 0.0 | |||||||||||||||||||||

| Royce Value Fund | Jay Kaplan | 13 | 2,706 | 63 | 51 | 8.7 | |||||||||||||||||||||

| Royce Value Plus Fund | Chip Skinner | 13 | 1,830 | 97 | 45 | 13.6 | |||||||||||||||||||||

| Royce 100 Fund | Chuck Royce, Lauren Romeo | 11 | 1,828 | 97 | 31 | 7.6 | |||||||||||||||||||||

| Royce Dividend Value Fund | Chuck Royce, Jay Kaplan | 10 | 3,366 | 269 | 36 | 24.9 | |||||||||||||||||||||

| Royce Global Value Fund | Whitney George | 7 | 1,773 | 61 | 41 | 71.8 | |||||||||||||||||||||

| Royce International Smaller-Companies Fund | David Nadel | 6 | 1,013 | 100 | 64 | 95.5 | |||||||||||||||||||||

| Royce Special Equity Multi-Cap Fund | Charlie Dreifus | 3 | 26,524 | 28 | 44 | 0.0 | |||||||||||||||||||||

| 4 | This page is not part of the 2014 Semiannual Report to Shareholders |

| Performance and Expenses | Through June 30, 2014 |

| Average Annual Total Returns | ||||||||||||||||||||||||||||||||||||

| Gross Annual | Net Annual | |||||||||||||||||||||||||||||||||||

| 40-Year or Since | Inception | Operating | Operating | |||||||||||||||||||||||||||||||||

| Fund | Year-to-Date1 | 1-Year | 5-Year | 10-Year | 20-Year | Inception | Date | Expenses | Expenses | |||||||||||||||||||||||||||

| Royce Pennsylvania Mutual Fund | 2.04 | % | 23.70 | % | 18.77 | % | 9.41 | % | 11.61 | % | 15.18 | % | n.a. | 0.93 | % | 0.93 | % | |||||||||||||||||||

| Royce Micro-Cap Fund | 1.02 | 18.91 | 14.13 | 8.24 | 11.49 | 12.43 | 12/31/91 | 1.56 | 1.56 | |||||||||||||||||||||||||||

| Royce Premier Fund | 7.33 | 27.08 | 18.57 | 11.07 | 12.62 | 12.73 | 12/31/91 | 1.09 | 1.09 | |||||||||||||||||||||||||||

| Royce Low-Priced Stock Fund | 9.03 | 24.64 | 13.69 | 7.38 | 12.36 | 11.82 | 12/15/93 | 1.51 | 1.49 | |||||||||||||||||||||||||||

| Royce Total Return Fund | 2.74 | 20.87 | 18.28 | 8.72 | 11.92 | 11.57 | 12/15/93 | 1.18 | 1.18 | |||||||||||||||||||||||||||

| Royce Heritage Fund | 2.90 | 18.49 | 16.91 | 9.43 | n.a. | 13.78 | 12/27/95 | 1.49 | 1.49 | |||||||||||||||||||||||||||

| Royce Opportunity Fund | 3.02 | 24.76 | 23.48 | 9.53 | n.a. | 13.62 | 11/19/96 | 1.17 | 1.17 | |||||||||||||||||||||||||||

| Royce Special Equity Fund | 0.16 | 15.27 | 16.16 | 8.61 | n.a. | 10.03 | 5/1/98 | 1.13 | 1.13 | |||||||||||||||||||||||||||

| Royce Value Fund | 3.41 | 21.81 | 16.02 | 10.08 | n.a. | 11.57 | 6/14/01 | 1.48 | 1.48 | |||||||||||||||||||||||||||

| Royce Value Plus Fund | 4.08 | 22.74 | 15.84 | 8.42 | n.a. | 12.69 | 6/14/01 | 1.49 | 1.49 | |||||||||||||||||||||||||||

| Royce 100 Fund | 2.79 | 21.66 | 16.64 | 10.39 | n.a. | 11.70 | 6/30/03 | 1.51 | 1.51 | |||||||||||||||||||||||||||

| Royce Dividend Value Fund | 3.35 | 21.85 | 19.38 | 10.34 | n.a. | 10.24 | 5/3/04 | 1.52 | 1.52 | |||||||||||||||||||||||||||

| Royce Global Value Fund | 11.04 | 23.93 | 13.76 | n.a. | n.a. | 6.53 | 12/29/06 | 1.84 | 1.70 | |||||||||||||||||||||||||||

| Royce International Smaller-Companies Fund | 6.59 | 21.02 | 13.15 | n.a. | n.a. | 7.56 | 6/30/08 | 2.08 | 1.70 | |||||||||||||||||||||||||||

| Royce Special Equity Multi-Cap Fund | 5.35 | 21.85 | n.a. | n.a. | n.a. | 16.73 | 12/31/10 | 1.46 | 1.24 | |||||||||||||||||||||||||||

| INDEX | ||||||||||||||||||||||||||||||||||||

| Russell 2000 Index | 3.19 | 23.64 | 20.21 | 8.70 | 9.81 | n.a. | n.a. | n.a. | n.a. | |||||||||||||||||||||||||||

| Russell Microcap Index | 1.56 | 24.98 | 20.03 | 6.67 | n.a. | n.a. | n.a. | n.a. | n.a. | |||||||||||||||||||||||||||

| Russell Global Small Cap Index | 5.72 | 23.60 | 15.93 | 9.02 | n.a. | n.a. | n.a. | n.a. | n.a. | |||||||||||||||||||||||||||

| Russell Global ex-U.S. Small Cap Index | 7.54 | 23.86 | 13.88 | 9.67 | n.a. | n.a. | n.a. | n.a. | n.a. | |||||||||||||||||||||||||||

| Russell 1000 Index | 7.27 | 25.35 | 19.25 | 8.19 | 10.00 | n.a. | n.a. | n.a. | n.a. | |||||||||||||||||||||||||||

| 1 Not Annualized | ||||||||||||||||||||||||||||||||||||

Important Performance, Expense, and Risk Information

All performance information in this Review and Report reflects past performance, is presented on a total return basis, reflects the reinvestment of distributions, and does not reflect the deduction of taxes a shareholder would pay on fund distributions or the redemption of fund shares. Past performance is no guarantee of future results. Investment return and principal value of an investment will fluctuate, so that shares may be worth more or less than their original cost when redeemed. Shares of Royce Global Value and International Smaller-Companies Funds redeemed within 180 days of purchase may be subject to a 2% redemption fee payable to The Royce Funds. Shares of all other Funds redeemed within 180 days of purchase may be subject to a 1% redemption fee payable to the Fund. Redemption fees are not reflected in the performance shown above; if they were, performance would be lower. Current performance may be higher or lower than performance quoted. Current month-end performance may be obtained at www.roycefunds.com. All performance and expense information reflects results of the Fund’s oldest share Class (Investment Class or Service Class, as the case may be). Price and total return information is based on net asset values calculated for shareholder transactions. Price and total return information is based on net asset values calculated for shareholder transactions. Gross annual operating expenses reflect the Fund’s gross total annual operating expenses and include management fees, any 12b-1 distribution and service fees, other expenses, and any applicable acquired fund fees and expenses. Net annual operating expenses reflect contractual fee waivers and/or reimbursements. All expense information is reported as of the Fund’s most current prospectus. Royce & Associates has contractually agreed to waive fees and/or reimburse operating expenses, (excluding brokerage commissions, taxes, interest litigation expenses, acquired fund fees and expenses, and other expenses not borne in the ordinary course of business), and to the extent necessary to maintain net operating expenses at or below: 1.24% for Royce Special Equity Multi-Cap Fund; 1.49% for Royce Low-Priced Stock Fund; 1.69% for Royce Global Value and International Smaller-Companies Funds through April 30, 2015; and at or below 1.99% for Royce International Smaller-Companies Fund through April 30, 2024. Acquired fund fees and expenses reflect the estimated amount of fees and expenses incurred indirectly by the Fund through its investments in mutual funds, hedge funds, private equity funds, and other investment companies. Shares of the Funds’ Service, Consultant, R, and K Classes bear an annual distribution expense that is not borne by the Funds’ Investment Class. Investments in securities of micro-cap, small-cap, and/or mid-cap companies may involve considerably more risk than investments in securities of larger-cap companies. (Please see “Primary Risks for Fund Investors” in the prospectus.) Royce Global Value and International Smaller-Companies Funds invest a significant portion of their respective assets in foreign companies which may be subject to different risks than investments in securities of U.S. companies, including adverse political, social, economic, or other developments that are unique to a particular country or region. (Please see “Investing in foreign securities” in the prospectus.) Therefore, the prices of securities of foreign companies in particular countries or regions may, at times, move in a different direction than those of securities of U.S. companies. (Please see “Primary Risk of Fund Investors” in the prospectus.) Please read the prospectus carefully before investing or sending money. Russell Investment Group is the source and owner of the trademarks, service marks, and copyrights related to the Russell Indexes. Russell® is a trademark of Russell Investment Group. The Russell 2000 Index is an unmanaged, capitalization-weighted index of domestic small-cap stocks. It measures the performance of the 2,000 smallest publicly traded U.S. companies in the Russell 3000 Index. The Russell Microcap Index includes 1,000 of the smallest securities in the Russell 2000 Index, along with the next smallest eligible securities as determined by Russell. The Russell Global Small Cap Index is an index of global small-cap stocks. The Russell Global ex-U.S. Small Cap Index is an index of global small-cap stocks, excluding the United States. The Russell 1000 is an unmanaged, capitalization-weighted index of domestic large-cap stocks. It measures the performance of the 1,000 largest publicly traded U.S. companies in the Russell 3,000 Index. The performance of an index does not represent exactly any particular investment, as you cannot invest directly in an index. Distributor: Royce Fund Services, Inc. |

| This page is not part of the 2014 Semiannual Report to Shareholders | 5 |

| U.S. Small-Cap Market Cycle and Risk Adjusted Performance |

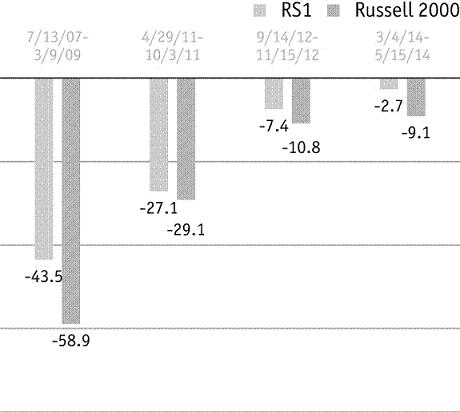

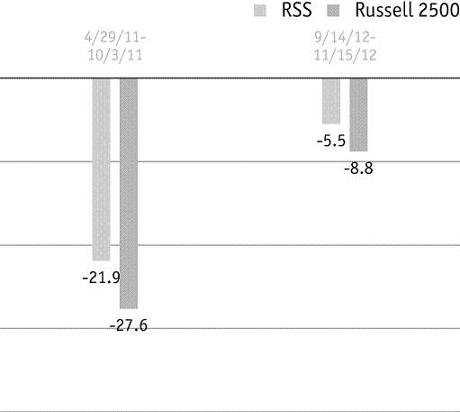

We believe strongly in the idea that a long-term investment perspective is crucial for determining the success of a particular investment approach. While flourishing in an up market is wonderful, surviving a bear market by losing less (or not at all) is at least as good. However, the true test of a portfolio’s mettle is performance over full market cycle periods, which include both an up and down market periods. |

| Since the inception of the Russell 2000 index on 12/31/78, there have been 10 full market cycles, with the most recent peaking on 4/29/11. Market cycles are defined as those that have retreated at least 15% from a previous market peak and have rebounded to establish a new peak above the previous one. Each market cycle contains a peak-to-trough and a trough-to-peak period. Interestingly, over the small-cap index’s 30+ year history, each style index—the Russell 2000 Value Index and the Russell 2000 Growth Index—outperformed in five of the 10 full market cycles. In fact, leadership has alternated between growth and value over the last six cycles. If history were to adhere to this pattern, value would lead in the current cycle that began on 4/29/11. |

RISK / RETURN PROFILE 10-YEAR PERIOD ENDED JUNE 30, 2014 |

|

| For the 10-year period ended 6/30/14, eight out of 12 Royce Funds with 10 years of history outperformed the Russell 2000, while eight of the 12 did so with better risk-adjusted returns and Sharpe ratios. | |

| In addition, for the 10-year period ended 6/30/14, five of the 12 Royce Funds outperformed the Russell 2000 with lower volatility. |

SMALL-CAP MARKET CYCLE: RUSSELL 2000 INDEXES TOTAL RETURNS |

|

| ROYCE U.S. EQUITY FUNDS VS. RUSSELL 2000 INDEX: | ||||||||||||

| MARKET CYCLE RESULTS | ||||||||||||

| Peak-to- | Peak-to- | Peak-to- | ||||||||||

| Peak | Peak | Current | ||||||||||

| 3/9/00– | 7/13/07– | 4/29/11 | ||||||||||

| Fund | 7/13/07 | 4/29/11 | 6/30/14 | |||||||||

| Royce Pennsylvania Mutual Fund | 207.1 | % | 11.6 | % | 35.8 | % | ||||||

| Royce Micro-Cap Fund | 197.4 | 24.9 | 5.9 | |||||||||

| Royce Premier Fund | 198.1 | 29.9 | 34.3 | |||||||||

| Royce Low-Priced Stock Fund | 198.9 | 27.2 | 0.7 | |||||||||

| Royce Total Return Fund | 193.9 | 6.8 | 41.3 | |||||||||

| Royce Heritage Fund | 150.4 | 25.3 | 21.7 | |||||||||

| Royce Opportunity Fund | 191.8 | 6.9 | 46.3 | |||||||||

| Royce Special Equity Fund | 227.4 | 20.8 | 39.4 | |||||||||

| Royce Value Fund | n.a. | 17.4 | 19.8 | |||||||||

| Royce Value Plus Fund | n.a. | -3.0 | 30.4 | |||||||||

| Royce 100 Fund | n.a. | 27.6 | 27.1 | |||||||||

| Royce Dividend Value Fund | n.a. | 21.6 | 39.4 | |||||||||

| INDEX | ||||||||||||

| Russell 2000 | 54.8 | 6.6 | 44.2 | |||||||||

| Russell 2000 Value | 189.4 | -1.4 | 44.4 | |||||||||

| Russell 2000 Growth | -14.8 | 14.3 | 44.0 | |||||||||

| All performance information above reflects past performance, is presented on a total return basis, reflects the reinvestment of distributions, and does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Past performance is no guarantee of future results. Please see page 5 for 1-, 5-, and 10-year average annual total return information. |

| 6 | This page is not part of the 2014 Semiannual Report to Shareholders |

| Letter to Our Shareholders |

|

No Drama |

Whatever other opinions we may all hold about the stock market’s behavior over the last six years, we think everyone can agree that it has certainly been dramatic. The action began in earnest in the fall of 2008, although it is important to recall that small-cap stock prices had actually been falling for more than a year prior to that—the peak for the Russell 2000 Index having been established on July 13, 2007. Yet the full effects of the bear were unleashed by the events of the Financial Crisis, which keyed the dangerously precipitous nosedive of share prices in the fall of 2008. The tumult lasted until small-caps finally hit a bottom on March 9, 2009. The fear and anxiety the descent created, however, reached into the next several years. The feeling of extraordinary fragility that characterized the early days of the recovery in the spring of 2009 did not magically evaporate when markets began to find their feet again. In fact, one could argue that these emotions dominated the behavior of investors at least until the end of 2012. The three years from 2010 through 2012 were eventful, even if the stress and excitement they generated did not equal that of the first six months of 2009. In fact, much of the market’s most extreme moves in that entire four-year span (2009-2012) took place in the first six months of those years, driven in large part by events both actual and potential. The recession in the U.S., debt issues in Europe, and slow growth in China were all very real, while a double-dip recession here at home, default in Europe, and implosion in China fortunately failed to materialize. By the end of 2012, with the stock market climbing and the economy expanding, investors seemed to recognize that, in spite of high volatility and political uncertainty, equity returns had been solidly positive since the March 2009 bottom. This improved confidence helped to spur a different kind of dramatic arc. The long, slow recovery entered a new phase in 2013—a heady, and |

| This page is not part of the 2014 Semiannual Report to Shareholders | 7 |

Charles M. Royce, President The long-running, and probably unresolvable, debate about active versus passive investment strategies has taken on new life in the years since the onset of the Financial Crisis, often to the detriment of active approaches. To take one example, Morningstar compiled data showing that inflows into equity mutual funds have been dwarfed by those into equity ETFs (exchange traded funds) measuring from the momentous year of 2008. For the six calendar years from 2008-2013, traditional equity funds have taken in $5.52 billion while ETFs have attracted $389.08 billion. That’s quite a disparity. It seems to be no secret that many active managers have struggled to keep pace with their respective equity indexes in these often eventful years. These years have also seen a raft of studies purporting to show that most investment managers are unable to consistently beat the market, i.e., regularly outperform a relevant index such as the Russell 2000 or S&P 500 Indexes. Perhaps unsurprisingly, we would offer two caveats before one embraces uncritically the notion that passive Continued on page 10... | Letter to Our Shareholders virtually correction-free, bull run in which returns for each of the major domestic stock indexes topped 30%. The curtain opened on 2014, then, on the heels of one of the better calendar-year performances in the history of domestic equities, which followed four consecutive years of mostly rising stock prices in an uncertain economy. So the question now is, what is the next act for equities? Some argue that the economy is not strong enough to really take flight. They worry about the rich valuations sported by large numbers of stocks. Others see the relative absence of volatility as a sign of complacency and fret that stocks are about to enter a destructive bear phase. There are those who point to increasingly unsettled international situations, such as in Ukraine, Syria, and Iraq, and argue that the market cannot continue to pretend that events in these nations take place far offstage, not in an increasingly intertwined global economy. We, however, are in accord with the more widespread consensus that sees the U.S. economy as gradually normalizing. As evidence we would point to the following: The deficit continues to fall, the Fed continues to wind down the rate of its monthly bond purchases, and interest rates, though they remain close to zero, look likely to rise again in the near future as they did last year between May and December. Inflation is tame, commodity prices stable. Volatility, as measured by the VIX, finished the first half of 2014 at low levels not seen since 2007. Add an increasingly robust M&A market, and it seems to us that the recipe for ongoing growth—and bullishness, however mild, at least compared to last year—seems almost complete. And this process of normalization looks likely to accelerate as the Fed’s role recedes further and further into the background, setting the stage for a more dynamic pace of growth. So while there remain voices who insist that stocks are overvalued, we think the case for additional gains, which could include a correction along the way, remains persuasive. It seems to us that the relatively lower returns of the first half of 2014 indicate not an end to a bull phase, but a chance for the market to catch its breath and assess its surroundings. It may be that investors need a break from all the drama, a respite from the unrelenting pace of the last six years. So the desire to stand back for a moment and evaluate what is happening seems eminently reasonable. How many investors have enjoyed more than a few moments of true calm since before the recession began back in 2007? Ultimately, we suspect that both the expanding economy and slower pace of returns will result in more fundamentally focused investors. Indeed, the indications that the strength of companies and the businesses they manage are beginning to matter more than indexes and the macro events that move them go back to the spring of 2012, when quality stocks—those with high returns on invested capital—enjoyed a brief run of outperformance. This nascent phenomenon re-started—again, briefly—in May 2013 when the 10-year Treasury rate reached a bottom. Quality companies, particularly those in our chosen small-cap space, have not yet emerged as leaders, but they have inched closer over the last two years. Correlation levels throughout the market are falling. These are excellent conditions, in our view, for disciplined active management approaches, especially those with a long-term investment horizon. | ||

| 8 | This page is not part of the 2014 Semiannual Report to Shareholders |

| No Direction Home |

U.S. stocks turned in a respectable performance in the first half of 2014. If results were not as lofty as they were in the first half of 2013 (and they were not), they were achieved in a more tranquil domestic environment than in the first halves of 2010, 2011, or 2012. One consequence of the more relaxed atmosphere of the first half was that stocks did not seem to know quite what to do with themselves. While the overvalued/not-quite-overvalued-yet argument goes on, the market has not established a clear direction so far in 2014. The bull has so far remained in place during the current cycle; he simply slowed his run to a brisk walk in the first half. For the year-to-date period ended June 30, 2014, the major domestic indexes remained in the black. The small-cap Russell 2000 Index gained 3.2%, taking a back seat to the more tech-oriented Nasdaq Composite, which advanced 5.5% in the first half, and the large-cap S&P 500 and Russell 1000 Indexes, which scored respective gains of 7.1% and 7.3% for the year-to-date period ended June 30, 2014. The year began on a more moderate note following a red-hot second half of 2013. Nevertheless, 2014’s opening quarter was the seventh consecutive quarter of positive performance for the Russell 2000, which rose 1.1%. Large-caps led for the quarter—the S&P 500 and Russell 1000 gained 1.8% and 2.0%, respectively, while the Nasdaq Composite rose 0.5%. Small-caps reached a first-half high on March 4, and the only correction so far this year was the 9.1% drop for the Russell 2000 from that date through May 15, 2014. April was thus the cruelest month, but a series of mini-rallies from mid-May through the end of June made the second quarter mostly positive. The Russell 2000 posted its eighth consecutive positive quarter, up 2.0%. Once again, large-cap outperformed, with the S&P 500 advancing 5.2% and the Russell 1000 up 5.1% for the second quarter. The Nasdaq bounced back strong as well, climbing 5.0% in the second quarter and leaving only the small-cap index out of the five-percent club. Small-cap held onto leadership outside the U.S. In the first quarter, the Russell Global ex-U.S. Small Cap Index was up 3.2% while the Russell Global ex-U.S. Large Cap Index rose 0.8%. Results were stronger in the second quarter and, as in the first, closer to their domestic counterparts than we have seen in a while. For the second quarter, the Russell Global ex-U.S. Small Cap was up 4.2% versus 5.0% for the Russell Global ex-U.S. Large Cap. Year-to-date, non-U.S. small-caps had the edge, with the Russell Global ex-U.S. Small Cap returning 7.5% versus a gain of 5.8% for the Russell Global ex-U.S. Large Cap. After a challenging first quarter, many Asian equities bounced back in the second and finished closer to the European indexes, most of which had been on a tear prior to cooling off in the second quarter. Moving back to the U.S., mid-cap and micro-caps were equally solid in the first quarter. The Russell Midcap Index was up 3.5% versus a gain of 3.0% for the Russell Microcap Index in 2014’s first three months. This pattern broke down around the time of the March 4 small-cap high and can be seen in the second-quarter results for each index. | Quality companies, particularly those in our chosen small-cap space, have not yet emerged as leaders, but they have inched closer over the last two years. Correlation levels throughout the market are falling. These are excellent conditions, in our view, for disciplined active management approaches, especially those with a long-term investment horizon. U.S. stocks turned in a respectable performance in the first half of 2014. If results were not as lofty as they were in the first half of 2013 (and they were not), they were achieved in a more tranquil domestic environment than in the first halves of 2010, 2011, or 2012. | |||

| This page is not part of the 2014 Semiannual Report to Shareholders | 9 |

| investing is always better: First, a number of managers have consistently outperformed the market over long-term periods and especially within the small-cap asset category. In fact, we believe strongly in the idea that it is not necessary for all managers to beat the market in order for active management to be validated as an approach. Our second note of caution relates to time periods. While it would be nice to outperform an index every year, it is just as unrealistic to expect that as it would be to expect an index to outperform active management every year. It is also unrealistic to expect a high degree of outperformance in the long term without experiencing some short-term underperformance periods. A willingness to stick to one’s approach, regardless of market movements and trends, is critical to long-term outperformance in our opinion. This is especially important during market extremes because there are active managers who exhibit style drift or other changes in their discipline when their investment style falls out of favor or is stressed, such as during the tech bubble. Successful active management also entails a willingness to think independently in terms of sector and industry weightings. It is not unusual for the most successful managers to be significantly out of sync relative to a Continued on page 12... | |||

| Letter to Our Shareholders | ||

The Russell Midcap continued its notable 2014 performance, rising 5.0% in the second quarter. This gave mid-caps an impressive 8.7% advance on a year-to-date basis. In contrast, micro-caps struggled in the second quarter, suffering more in the brief downturn than their larger cousins. The Russell Microcap Index fell 1.4% for the quarter and was up only 1.6% for the year-to-date period ended June 30, 2014. Many mid-cap stocks have demonstrated strong records of growth over the last few years, and their success throughout the entire post-Financial Crisis cycle has not been a surprise to us. In fact, mid-caps have been an area of significant interest to us for years now. The small- and micro-cap spaces have, by contrast, high numbers of very speculative companies and are typically more volatile—sometimes much more so in the case of micro-caps. They have also enjoyed very strong results over the last several years. The three- and five-year annualized returns through the end of June for the Russell 2000 and Russell Microcap Indexes were terrific on an absolute basis. With equity investors acting more cautiously, if not always consistently, so far in 2014, the relative breather for small- and micro-cap stocks—and we do not think it’s any more than a breather—was also not a surprise. | ||

No Excuses Each of our Featured Funds enjoyed strong absolute performance in the first half. We were also pleased with both the year-to-date and one-year results for several portfolios, though we recognize fully that more needs to be done with regard to relative performance, especially over more intermediate-term periods. Six portfolios outpaced their respective benchmarks for the year-to-date period ended June 30, 2014—Royce Premier, Low-Priced Stock, Value Plus, Dividend Value, Value, and Global Value Funds. In addition, Royce Pennsylvania Mutual, Premier, Low-Priced Stock, Opportunity, and Global Value Funds beat their respective benchmarks for the one-year period ended June 30, 2014. This was welcome news because, with a few exceptions, shorter-term performance advantages have been elusive over the last few years. Of course short-term outperformance must always be kept in perspective as exactly that—short term. We are hopeful, however, having seen many of our Featured Funds narrow the gap in their respective one-, three-, and five-year results versus their respective benchmarks over the last three to four quarters. Featured Funds with more than 10 years of history have also generally held their relative edge for periods of a decade or longer. Yet we still have work to do. As encouraged as we have been about the recent short spates of leadership for quality stocks and the likelihood that a strengthening, less Fed-dependent economy will benefit active small-cap approaches, lower quality small-caps again assumed leadership when prices were rallying in June. Investors are still working out their preferences. Profitable companies—as well those with high returns on invested capital—led through the downturn before falling behind in the up phase. The market thus remained a peculiar place in the first half. This may be because we still have a very active Fed at work in an economy that arguably has not needed the extra help in at least a year. | ||

| 10 | This page is not part of the 2014 Semiannual Report to Shareholders |

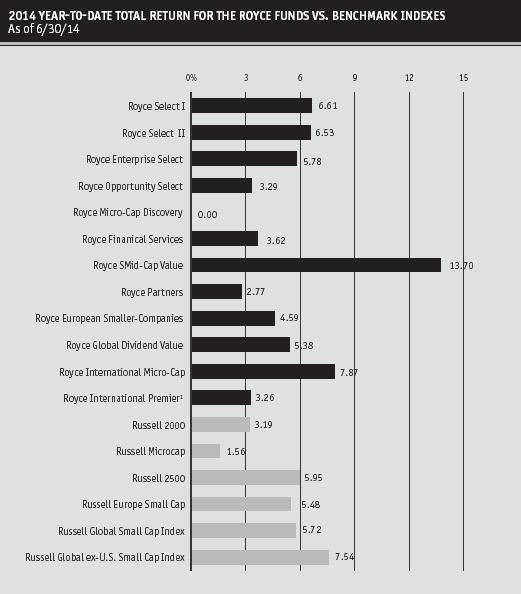

| 2014 YEAR-TO-DATE TOTAL RETURN FOR THE ROYCE FUNDS VS. BENCHMARK INDEXES As of 6/30/14 | ||

| ||

No Worries We are very bullish about the prospects for active small-cap management. We have an obvious bias in favor of active approaches here at Royce, but we think that over the last 14 months—dating back to the low for the 10-year Treasury in May of last year—we have reached a point at which active management in small-cap stocks simply makes more sense, especially for long-term investors. Since that May 2013 low, company fundamentals have gradually become more important as drivers of share-price success. Rather than invest in a small-cap index vehicle in which approximately 25% of the companies are losing money (as was the case for the Russell 2000 for the 12 months ended May 31, 2014), we think it is smarter for investors to consider portfolios that look for well-run, financially strong companies with attractive long-term prospects. So while quality has not yet seized small-cap leadership, we suspect that the reign of low-quality stocks is coming to an end. In our view, the next phase will be one in which companies with attractive characteristics such as strong balance sheets and high returns on invested capital should begin to lead. In spite of not showing as much strength when the market was recovering in May and June, many | We are very bullish about the prospects for active small-cap management... we have reached a point at which active management in small-cap stocks simply makes more sense, especially for long-term investors. | |

| This page is not part of the 2014 Semiannual Report to Shareholders | 11 |

| benchmark index with respect to industry and sector weightings (commonly referred to as tracking error). In addition, active managers are not required to invest cash inflows at the time of receipt when market conditions or prices may not be conducive. They may screen for quality and use buy/sell triggers as a means of reducing risk. While a passive manager must own everything, an active manager has the freedom to look for attractive stocks across a targeted universe. All of this helps to explain why we remain so fond of small-caps and so confident in the effectiveness and value of active approaches in the asset class. Active small-cap managers can capture valuation opportunities beyond their respective indexes—an opportunity that would be lost if one were limited to owning only the constituents that make up an index. For example, the Russell 2000, while quite broad, only includes about 2,000 of the more than 4,100 companies1 that make up the domestic small-cap universe (those with market caps up to $2.5 billion). While self-serving, we nevertheless think that the small-cap asset class is ideally suited for active management given its enormous size, lack of institutional focus, and limited research availability. 1 Source: Reuters as of 6/30/14 | |

| Letter to Our Shareholders |

|

did well enough to lead the small-cap pack from the 2014 high in March through the end of the first half. We would expect something like this pattern to continue at least through the end of the year as the market continues to adjust to the growing normalization of the economy. With diverse small-cap sectors such as Consumer Discretionary, Health Care, and Information Technology showing sizable declines since the end of February, we have been looking closely there (and elsewhere) for what we think are attractively priced, fundamentally strong small-cap businesses. As always, volatility in the small-cap market is something that we seek to use to our advantage, even when it is in short supply. Know This We feel somewhat fortunate in that we do not need to choose a side in the “overvalued versus ongoing bull market” debate. Rather than trying to make a correct market call, our attention has been focused on those potential opportunities that can materialize even in a widespread bull market. Corrections can arrive at any time, of course, and it has been a while since we have seen one of any significance. The last downturn of more than 10% for the Russell 2000 occurred in the fall of 2012. And share prices recovered so quickly from the 9.1% March-May decline this year that the down phase barely registered. This might lead one to argue that the market is being set up for at least a decent-sized pullback. Our sense, however, is that we are more likely to see smaller ones in the 5-10% range as part of the ongoing bull phase. Against the backdrop of an economy that looks poised for faster growth, a Fed tapering at a healthy clip, and an interest-rate environment in which a steady rate of increase is much more of a “when” than an “if,” less severe downturns look more likely. Small-cap valuations on the whole are above average, though not unreasonably so given near-zero interest rates and low inflation. A number of anomalies remain in the market, and in many cases we see a wide disparity between what look to us like expensive stocks |

| 12 | This page is not part of the 2014 Semiannual Report to Shareholders |

and those that look inexpensive on an absolute basis. The market seems to be in the process of sorting that out—certainly those areas of the market that do not interest us, and that did well in 2012 and 2013, have been more volatile so far in 2014. In addition, we are still seeing companies that look attractively valued to us based on their fundamentals. All in all, it is looking more and more like a stock-picker’s market to us. We could see the second half of the year being pretty similar to the first in terms of the overall returns for stocks. More important, we think there are still enough opportunities out there to keep returns in positive territory through the end of 2014. This could make the market’s next act a very happy one for active small-cap managers. | |||||

Sincerely, | |||||

|  |  | |||

| Charles M. Royce | Christopher D. Clark | Francis D. Gannon | |||

| President | Co-Chief Investment Officer, Royce & Associates | Co-Chief Investment Officer, Royce & Associates | |||

| July 31, 2014 | |||||

| This page is not part of the 2014 Semiannual Report to Shareholders | 13 |

| Fund Focus | |

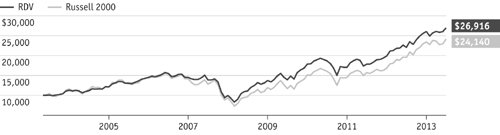

Here at Royce, we are happily contrarian. We look for what we deem to be high-quality companies trading at a discount to our estimate of their intrinsic worth as businesses. Quality, of course, can take many forms. For us, it generally consists of a suite of attributes that includes a strong balance sheet, high returns on invested capital, and the ability to generate free cash flow. There is another ingredient that we also see as an excellent measure of a business’s underlying quality—the practice of paying dividends. (A whitepaper detailing performance and volatility history for small-cap dividend payers is available on our website, roycefunds.com/dividends.) While there is no guarantee that companies that pay them will continue to do so in the future, dividends offer a number of potential portfolio merits, most crucially as a potentially mitigating factor against market volatility. To our way of thinking, a steady stream of income is always a good thing, but it can be particularly helpful for investors trying to more comfortably navigate market extremes. This opinion is not always widely shared in the small-cap world. Many investors tend to think of “dividend-paying small-cap company” as an oxymoron, if they think of it at all. This fact is borne out by Morningstar data. Of the 516 small-cap objective funds identified by Morningstar as of June 30, 2014, only six funds have dividend, income, or total return in their respective names—and two of them are Royce Funds. Royce Dividend Value Fund (RDV), which debuted in May 2004, is one of those portfolios. It seeks long-term growth of capital and current income. In its security selection criteria, we first look for what we think are fundamentally strong, high-quality companies trading at attractive discounts to our estimate of their intrinsic worth. We then add the additional criteria that the bulk of the portfolio selections must also pay a dividend. Royce Dividend Value Fund ranges a little higher in market capitalization than many other Royce Funds. RDV may invest in small-cap and mid-cap companies with market caps up to $15 billion. The Fund may also invest up to 25% of its net assets in foreign securities because we like the opportunity presented by non-U.S. dividend-paying companies. We are pleased with the Fund’s absolute performance and its historically low volatility. (For more information on RDV’s historical volatility scores, please see page 39.) We think the Fund offers an attractive option for a risk-conscious investor seeking exposure to smaller companies, especially those that pay dividends. | |

| |

| Jay Kaplan Portfolio Manager since 2007 | Chuck Royce Lead Portfolio Manager since 2004 |

| Royce Dividend Value Fund—Measuring for Quality: Performance and Expense Information Through June 30, 2014 |

| Average Annual Total Returns | Royce Dividend Value Fund | Russell 2000 | ||

| Year-to-Date1 | 3.35% | 3.19% | ||

| One-Year | 21.85 | 23.64 | ||

| Three-Year | 12.97 | 14.57 | ||

| Five-Year | 19.38 | 20.21 | ||

| Ten-Year | 10.34 | 8.70 | ||

| Since Inception (5/3/2004) | 10.24 | 9.06 | ||

| Annual Operating Expenses | 1.52 | n.a. | ||

| Important Performance and Expense Information All performance information reflects past performance, is presented on a total return basis and reflects the reinvestment of distributions. Past performance is no guarantee of future results. Investment return and principal value of an investment will fluctuate, so that shares may be worth more or less than their original cost when redeemed. Shares redeemed within 180 days of purchase may be subject to a 1% redemption fee payable to the Fund, which is not reflected in the performance shown above; if it were, performance would be lower. Current performance may be higher or lower than performance quoted. Current month-end performance may be obtained at www.roycefunds.com. Operating expenses reflect Royce Dividend Value Fund’s total annual operating expenses for the Service Class as of the Fund’s most current prospectus and include management fees, other expenses, and acquired fund fees and expenses. Acquired fund fees and expenses are those incurred indirectly as a result of investment in one or more acquired funds, including mutual funds, hedge funds, private equity funds, and other pooled investment vehicles. The Fund invests primarily in small-cap and/or mid-cap stocks, which may involve considerably more risk than investing in larger-cap stocks (Please see “Primary Risks for Fund Investors” in the prospectus). The Fund may invest up to 25% of its net assets (at the time of investment) in foreign securities, which may involve political, economic, currency, and other risks not encountered in U.S. investments (Please see “Investing in Foreign Securities” in the prospectus). |

| 14 | This page is not part of the 2014 Semiannual Report to Shareholders |

| Table of Contents |

| Semiannual Report to Shareholders | ||||||||||

| Managers’ Discussions of Fund Performance | ||||||||||

| Royce Pennsylvania Mutual Fund | 16 | |||||||||

| Royce Micro-Cap Fund | 18 | |||||||||

| Royce Premier Fund | 20 | |||||||||

| Royce Low-Priced Stock Fund | 22 | |||||||||

| Royce Total Return Fund | 24 | |||||||||

| Royce Heritage Fund | 26 | |||||||||

| Royce Opportunity Fund | 28 | |||||||||

| Royce Special Equity Fund | 30 | |||||||||

| Royce Value Fund | 32 | |||||||||

| Royce Value Plus Fund | 34 | |||||||||

| Royce 100 Fund | 36 | |||||||||

| Royce Dividend Value Fund | 38 | |||||||||

| Royce Global Value Fund | 40 | |||||||||

| Royce International Smaller-Companies Fund | 42 | |||||||||

| Royce Special Equity Multi-Cap Fund | 44 | |||||||||

| Schedules of Investments and Financial Statements | 46 | |||||||||

| Notes to Financial Statements | 114 | |||||||||

| Understanding Your Fund’s Expenses | 127 | |||||||||

| Trustees and Officers | 130 | |||||||||

| Board Approval of Investment Advisory Agreements | 131 | |||||||||

| Notes to Performance and Other Important Information | 134 | |||||||||

| The Royce Funds 2014 Semiannual Report to Shareholders | 15 |

| Royce Pennsylvania Mutual Fund |

| ||||||||||||

| AVERAGE ANNUAL TOTAL RETURNS Through 6/30/14 | ||||||||||||

| January–June 20141 | 2.04 | % | ||||||||||

| One-Year | 23.70 | |||||||||||

| Three-Year | 12.25 | |||||||||||

| Five-Year | 18.77 | |||||||||||

| 10-Year | 9.41 | |||||||||||

| 15-Year | 11.00 | |||||||||||

| 20-Year | 11.61 | |||||||||||

| 25-Year | 10.98 | |||||||||||

| 30-Year | 11.93 | |||||||||||

| 35-Year | 13.08 | |||||||||||

| 40-Year | 15.18 | |||||||||||

| ANNUAL EXPENSE RATIO | ||||||||||||

| Operating Expenses | 0.93 | % | ||||||||||

| 1 Not Annualized | ||||||||||||

| CALENDAR YEAR TOTAL RETURNS | ||||||||||||

| Year | PMF | Year | PMF | |||||||||

| 2013 | 35.3 | % | 2005 | 12.5 | % | |||||||

| 2012 | 14.6 | 2004 | 20.2 | |||||||||

| 2011 | -4.2 | 2003 | 40.3 | |||||||||

| 2010 | 23.9 | 2002 | -9.2 | |||||||||

| 2009 | 36.3 | 2001 | 18.4 | |||||||||

| 2008 | -34.8 | 2000 | 18.3 | |||||||||

| 2007 | 2.8 | 1999 | 6.0 | |||||||||

| 2006 | 14.8 | 1998 | 4.2 | |||||||||

| TOP 10 POSITIONS % of Net Assets | ||||||||||||

| Reliance Steel & Aluminum | 1.1 | % | ||||||||||

| NVR | 1.0 | |||||||||||

| Unit Corporation | 1.0 | |||||||||||

| Federated Investors Cl. B | 0.9 | |||||||||||

| Pason Systems | 0.8 | |||||||||||

| Genesco | 0.8 | |||||||||||

| Nu Skin Enterprises Cl. A | 0.7 | |||||||||||

| Thor Industries | 0.7 | |||||||||||

| Tennant Company | 0.7 | |||||||||||

| Helmerich & Payne | 0.7 | |||||||||||

| PORTFOLIO SECTOR BREAKDOWN % of Net Assets | ||||||||||||

| Industrials | 23.8 | % | ||||||||||

| Information Technology | 20.7 | |||||||||||

| Consumer Discretionary | 14.9 | |||||||||||

| Materials | 10.8 | |||||||||||

| Financials | 10.7 | |||||||||||

| Energy | 7.2 | |||||||||||

| Health Care | 6.6 | |||||||||||

| Consumer Staples | 2.1 | |||||||||||

| Diversified Investment Companies | 0.4 | |||||||||||

| Telecommunication Services | 0.2 | |||||||||||

| Utilities | 0.0 | |||||||||||

| Miscellaneous | 1.4 | |||||||||||

| Cash and Cash Equivalents | 1.2 | |||||||||||

|

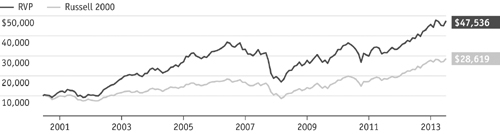

Manager’s Discussion Our flagship, Royce Pennsylvania Mutual Fund (PMF), was up 2.0% for the year-to-date period ended June 30, 2014, finishing the first half behind its small-cap benchmark, the Russell 2000 Index, which gained 3.2% for the same period. This was somewhat disappointing because the market has at times been more hospitable to disciplined and active investment approaches over the last 14 months, dating back to the May 2, 2013 low for the 10-Year Treasury. This occasional strength could be seen in PMF’s results from the second half of 2013, when it outperformed its benchmark. Unlike the previous four years, 2014 got off to a slow, though still positive, start. This was not terribly surprising in the context of a highly bullish 2013, a year that saw no major corrections and enjoyed a particularly dynamic second half. The result was a nondescript opening quarter in which the Fund was up 0.3% versus a gain of 1.1% for the Russell 2000. The second quarter seemed similarly uninspired, though it was more volatile. Equities failed to establish any clear direction as the economy continued to grow slowly and a still-unresolved debate went on about whether or not stocks are overvalued or still have some room to run. This argument has so far been a low-intensity dispute, at least insofar as it has affected share prices. The same could be said for volatility, which has been low. Small-caps reached a first-half high on March 4, declining 9.1% through May 15. This was as close to a correction as stocks have come so far in 2014. Markets began to rally in May and continued doing so through the end of June. For the second quarter, PMF rose 1.7% while the Russell 2000 was up 2.0%. We have been very pleased to see value-oriented styles such as our own gradually narrow the performance gap over the last several months with their respective benchmarks and the passively managed portfolios and ETFs that mirror the indexes. While the Fund’s first-half results did not show this growing strength to the degree that we would like, results over the one-year period ended June 30, 2014 were more encouraging. We therefore remain resolute about PMF’s approach and optimistic about its long-term prospects. We were also happy that its longer-term performance advantages remained in place. The Fund outpaced the Russell 2000 for the one-, 10-, 15-, 20-, 25-, 30-, and 35-year periods ended June 30, 2014. PMF’s average annual total return for the 40-year period—all under the management of Chuck Royce—was 15.2%. We take great pride in this four-decade result. |

| GOOD IDEAS THAT WORKED Top Contributors to Performance Year-to-Date through 6/30/141 | ||

| Helmerich & Payne | 0.33% | |

| Unit Corporation | 0.29 | |

| Pason Systems | 0.22 | |

| Myriad Genetics | 0.19 | |

| Westlake Chemical | 0.18 | |

| 1 Includes dividends. | ||

Important Performance and Expense Information All performance information in this Report reflects past performance, is presented on a total return basis, reflects the reinvestment of distributions, and does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Past performance is no guarantee of future results. Investment return and principal value of an investment will fluctuate, so that shares may be worth more or less than their original cost when redeemed. Shares redeemed within 180 days of purchase may be subject to a 1% redemption fee payable to the Fund, which is not reflected in the performance shown above; if it were, performance would be lower. Current month-end performance may be higher or lower than performance quoted and may be obtained at www.roycefunds.com. All performance and risk information reflects results of the Investment Class (its oldest class). Operating expenses reflect the Fund’s total annual operating expenses for the Investment Class as of the Fund’s most current prospectus and include management fees, other expenses, and acquired fund fees and expenses. Acquired fund fees and expenses reflect the estimated amount of the fees and expenses incurred indirectly by the Fund through its investment in mutual funds, hedge funds, private equity funds, and other investment companies. Shares of PMF’s Service, Consultant, R, and K Classes bear an annual distribution expense that is not borne by the Investment Class. Regarding the two “Good Ideas” tables shown above, the sum of all contributors to, and all detractors from, performance for all securities in the portfolio would approximate the Fund’s year-to-date performance for 2014. |

16 | The Royce Funds 2014 Semiannual Report to Shareholders

Performance and Portfolio Review Although net losses were relatively light, the portfolio held a number of detractors clustered in the Industrials sector, a cyclical area that has seen some recovery in the small-cap market and where the Fund was overweight in the first half compared to the Russell 2000. Global supply chain logistics services and solutions company UTi Worldwide suffered from weaker freight-forwarding volumes and pricing. Combined with delays collecting receivables due to the implementation of a major new IT system in the U.S., this caused the company to violate its debt covenants, forcing an expensive and dilutive recapitalization. Liking its chances for a turnaround, we built our position in the first half. KBR, a Houston-based engineering and construction firm with global operations, saw its fiscal 2014 outlook reduced by cancellations and losses on some engineering and construction bids, as well as on pushed out start dates for certain LNG (liquefied natural gas) projects. We also liked its prospects for reversing its fortunes and added shares as its price slipped. As for those sectors that made a positive contribution in the first half, Energy stocks led by a wide margin, followed by solid net gains for Materials, Health Care, and Financials. Holdings in the Energy sector accounted for three of PMF’s five, five of its 10, and eight of its 20 top contributors. Helmerich & Payne, Unit Corporation, and Pason Systems are all long-term holdings. Along with other strong performers in the sector, they benefited from a revival of interest in energy stocks. Helmerich & Payne saw growth in demand for new rigs, confirming that its technologically superior offerings are driving market share gains for companies eager to reduce drilling costs by upgrading to its more efficient rigs. Unit Corporation operates as a contract driller and exploration and production company, among other energy-related businesses. Double-digit production growth, the introduction of a new advanced drilling rig, and continued strong performance from its midstream operations all helped to draw investors to its stock. | |||

| Along with Industrials, Consumer Discretionary also had a small net loss in the first half. We increased our position in multiline women’s fashion business Ascena Retail Group as it endured a generally awful market for retail businesses. The company was more specifically challenged by depressed holiday results that did not improve as the year went on, particularly at Justice, a brand in the promotion-driven teen fashion space. The company is aiming for better results in the second half with revamped products for, and reduced inventory lead times at, Justice, increasing profitability from their plus-size brands, and cost reduction realizations. | |||

GOOD IDEAS AT THE TIME | |

| UTi Worldwide | -0.17% |

| Ascena Retail Group | -0.14 |

| Advisory Board (The) | -0.12 |

| KBR | -0.12 |

| Barrett Business Services | -0.11 |

| 1 Net of dividends. | |

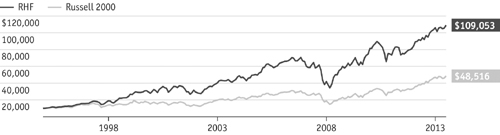

| ROYCE PENNSYLVANIA MUTUAL FUND VS. RUSSELL 2000 Value of $10,000 Invested on 12/31/78 (Russell 2000 Inception) | |

|

| Includes reinvestment of distributions. | |||

| PORTFOLIO DIAGNOSTICS | |||

| Fund Net Assets | $6,813 million | ||

| Number of Holdings | 461 | ||

| Turnover Rate | 13% | ||

| Average Market Capitalization1 | $1,922 million | ||

| Weighted Average P/E Ratio2,3 | 20.7x | ||

| Weighted Average P/B Ratio2 | 2.2x | ||

| U.S. Investments (% of Net Assets) | 89.2% | ||

| Non-U.S. Investments (% of Net Assets) | 9.6% | ||

| Symbol | |||

| Investment Class | PENNX | ||

| Service Class | RYPFX | ||

| Consultant Class | RYPCX | ||

| Institutional Class | RPMIX | ||

| R Class | RPMRX | ||

| K Class | RPMKX | ||

1 Geometric Average. This weighted calculation uses each portfolio holding’s market cap in a way designed to not skew the effect of very large or small holdings; instead, it aims to better identify the portfolio’s center, which Royce believes offers a more accurate measure of average market cap than a simple mean or median. | |||

| MORNINGSTAR STATISTICAL MEASURES1 | |||

| Sharpe Ratio | Standard Deviation | ||

| PMF | 1.09 | 17.16 | |

| Russell 2000 | 1.10 | 18.23 | |

| Category Median | 1.13 | 17.71 | |

| Best Quartile Breakpoint | 1.20 | 16.80 | |

1Five years ended 6/30/14. Category Median and Best Quartile Breakpoint based on 357 small-cap objective funds (oldest class only) with at least five years of history. | |||

The Fund produced lower volatility than the Russell 2000 and 50% of small-cap objective funds, as shown by its standard deviation. | |||

DOWN MARKET PERFORMANCE COMPARISON | |||

| |||

The Royce Funds 2014 Semiannual Report to Shareholders | 17

| Royce Micro-Cap Fund |

| AVERAGE ANNUAL TOTAL RETURNS Through 6/30/14 | ||||||||||

| January–June 20141 | 1.02 | % | ||||||||

| One-Year | 18.91 | |||||||||

| Three-Year | 4.17 | |||||||||

| Five-Year | 14.13 | |||||||||

| 10-Year | 8.24 | |||||||||

| 15-Year | 11.23 | |||||||||

| 20-Year | 11.49 | |||||||||

| Since Inception (12/31/91) | 12.43 | |||||||||

| ANNUAL EXPENSE RATIO | ||||||||||

| Operating Expenses | 1.56 | % | ||||||||

| 1 Not Annualized | ||||||||||

| CALENDAR YEAR TOTAL RETURNS | ||||||||||

| Year | RMC | Year | RMC | |||||||

| 2013 | 21.3 | % | 2005 | 11.5 | % | |||||

| 2012 | 8.0 | 2004 | 15.8 | |||||||

| 2011 | -12.1 | 2003 | 52.6 | |||||||

| 2010 | 30.1 | 2002 | -13.4 | |||||||

| 2009 | 55.7 | 2001 | 23.1 | |||||||

| 2008 | -40.9 | 2000 | 16.7 | |||||||

| 2007 | 7.1 | 1999 | 13.7 | |||||||

| 2006 | 22.3 | 1998 | -3.3 | |||||||

| TOP 10 POSITIONS % of Net Assets | ||||||||||

| Total Energy Services | 1.4 | % | ||||||||

| Patriot Transportation Holding | 1.4 | |||||||||

| Kennedy-Wilson Holdings | 1.3 | |||||||||

| Foster (L.B.) Company | 1.2 | |||||||||

| Resources Connection | 1.2 | |||||||||

| Universal Stainless & Alloy Products | 1.1 | |||||||||

| Tesco Corporation | 1.1 | |||||||||

| Stein Mart | 1.1 | |||||||||

| Marten Transport | 1.1 | |||||||||

| Gulf Island Fabrication | 1.1 | |||||||||

| PORTFOLIO SECTOR BREAKDOWN % of Net Assets | ||||||||||

| Industrials | 25.5 | % | ||||||||

| Consumer Discretionary | 14.9 | |||||||||

| Information Technology | 14.4 | |||||||||

| Health Care | 9.8 | |||||||||

| Materials | 9.1 | |||||||||

| Energy | 8.9 | |||||||||

| Financials | 8.3 | |||||||||

| Consumer Staples | 1.0 | |||||||||

| Utilities | 0.1 | |||||||||

| Miscellaneous | 4.8 | |||||||||

| Cash and Cash Equivalents | 3.2 | |||||||||

|

Manager’s Discussion Royce Micro-Cap Fund (RMC) finished the year-to-date period ended June 30, 2014 with an advance of 1.0% versus respective gains of 1.6% for its benchmark, the Russell Microcap Index, and 3.2% for the small-cap Russell 2000 Index for the same period. Following a wonderfully bullish 2013, stocks as a group cooled down in the opening months of 2014, though returns for the most part remained solidly in the black. The Fund’s participation was more limited than we would prefer. The year began with many share prices accelerating at a slower pace than they did in the torrid second half of 2013. The Fund, however, fell out of step with the market as a whole—and micro-caps more specifically—during both that highly bullish phase and the more moderate market that ushered in 2014. The Fund was down 0.8% in the first quarter versus a gain of 3.0% for the Russell Microcap and 1.1% for the Russell 2000. The Fund’s results improved in the second quarter, which saw the year’s only correction so far. In fact, its performance from the interim small-cap high on March 4 through the end of June was better than both the micro-cap and small-cap indexes. This relative edge over the indexes played a major role in giving a boost to quarterly results. For the second quarter, RMC advanced 1.8% compared to a decline of 1.4% for the Russell Microcap and an increase of 2.0% for the Russell 2000. A look at longer-term periods showed a healthier advantage. The Fund outpaced the Russell Microcap for the 10-year period ended June 30, 2014. (Data for this index only goes back to June 30, 2000.) RMC also beat the Russell 2000 for the 15-, 20-year, and since inception (12/31/91) periods ended June 30, 2014. The Fund’s average annual total return since inception was 12.4%. We remain proud of RMC’s long-term performance record. The Fund’s overweight in Energy was a factor as 2014 wore on—the sector’s strong second-quarter results made it the portfolio’s top-performing sector for the year-to-date period ended June 30, 2014. In the micro-cap space we have invested in a larger number of E&P (exploration & production) companies and energy services businesses. While the former are often more volatile, we have found a number of conservatively capitalized services companies that we think are well-managed businesses. We believe that Triangle Petroleum offers an interesting high risk/high reward example in the E&P space. A Denver-based E&P business, its share price was volatile through much of the first half, |

| GOOD IDEAS THAT WORKED Top Contributors to Performance Year-to-Date through 6/30/141 | |||||||||||

| Furiex Pharmaceuticals | 0.43% | ||||||||||

| VASCO Data Security International | 0.40 | ||||||||||

| Super Micro Computer | 0.33 | ||||||||||

| Triangle Petroleum | 0.32 | ||||||||||

| Kennedy-Wilson Holdings | 0.27 | ||||||||||

| 1 Includes dividends. | |||||||||||

Important Performance and Expense Information All performance information in this Report reflects past performance, is presented on a total return basis, reflects the reinvestment of distributions, and does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Past performance is no guarantee of future results. Investment return and principal value of an investment will fluctuate, so that shares may be worth more or less than their original cost when redeemed. Shares redeemed within 180 days of purchase may be subject to a 1% redemption fee payable to the Fund, which is not reflected in the performance shown above; if it were, performance would be lower. Current month-end performance may be higher or lower than performance quoted and may be obtained at www.roycefunds.com. All performance and risk information reflects results of the Investment Class (its oldest class). Price and total return information is based on net asset values calculated for shareholder transactions. Certain immaterial adjustments were made to the net assets of Royce Micro-Cap Fund at 12/30/11 for financial reporting purposes, and as a result the net asset values for shareholder transactions on that date and the calendar year total returns based on those net asset values differ from the adjusted net asset values and calendar year total returns reported in the Financial Highlights. Operating expenses reflect the Fund’s total annual operating expenses for the Investment Class as of the Fund’s most current prospectus and include management fees, other expenses, and acquired fund fees and expenses. Acquired fund fees and expenses reflect the estimated amount of the fees and expenses incurred indirectly by the fund through its investments in mutual funds, hedge funds, private equity funds, and other investment companies. Shares of RMC’s Service and Consultant Classes bear an annual distribution expense that is not borne by the Investment Class. Regarding the two “Good Ideas” tables shown above, the sum of all contributors to, and all detractors from, performance for all securities in the portfolio would approximate the Fund’s year-to-date performance for 2014. | |||||||||||

18 | The Royce Funds 2014 Semiannual Report to Shareholders

Performance and Portfolio Review |

| though its overall direction was up. Moving quickly, in just two years, from exploration to production helped attract interest in the stock. We liked its prospects going forward, modestly trimming our shares in the first half. The Fund’s top performer was Furiex Pharmaceuticals, which was acquired by Forest Laboratories at a healthy premium. The announcement came in April, when we sold our position. We were drawn first to its royalty and revenues on two approved drugs and to promising results for an IBS (irritable bowel syndrome) drug. VASCO Data Security International specializes in bank security and develops security systems to secure and manage access to user digital assets. Its stock made two significant upticks in the first half. In February, its shares rose on better-than-expected fourth quarter of 2013 earnings and a strong outlook for fiscal 2014. Increased revenues and ongoing earnings strength saw the shares getting another major boost late in April, especially with HSBC, USA, its customer, offering VASCO authentication solutions to its retail customers. A disappointing holiday season and a miserably cold winter spelled tough times for many consumer stocks in both the Discretionary and Staples sectors. Seeing better times ahead, we held onto our shares of Shoe Carnival, a family footwear retailer based in Indiana. The company has a history of strong top-line growth and what we think are reasonable and intelligent plans to both grow and improve its business. It was RMC’s eleventh-largest holding at the end of June. After a very successful 2013, we were not shocked to see some pullback for transportation and real estate business Patriot Transportation Holding. The stock is thinly traded and tightly held, so transactions tend to have an outsized effect on its shares. Earnings cooled down a bit during the first half, but we think its core strategic business realignment remains on track. Over the past several years, we have been finding some of the most attractive micro-cap valuations in more economically sensitive sectors. Two of the Fund’s three larger sector weightings at the end of the period reflected this, with Industrials at 25.5% and Information Technology at 14.4%. The portfolio also remained overweight versus the Russell Microcap in other cyclical sectors, most notably Energy and Materials. Our view is that many portfolio holdings in these (and other) sectors can benefit from a faster-growing economy in which the Fed’s quantitative easing program comes to a close and interest rates are rising. Such an environment is likely to reward disciplined active approaches that focus on fundamentals such as strong balance sheets and high returns on invested capital. So while we remain frustrated by the Fund’s recent performance record, we are confident in its prospects going forward. |

| GOOD IDEAS AT THE TIME Top Detractors from Performance Year-to-Date through 6/30/141 | |

| Shoe Carnival | -0.39% |

| Patriot Transportation Holding | -0.25 |

| Destination Maternity | -0.24 |

| TGC Industries | -0.24 |

| Global Power Equipment Group | -0.23 |

| 1 Net of dividends. | |

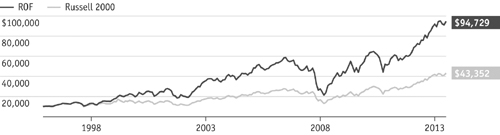

| ROYCE MICRO-CAP FUND VS. RUSSELL MICROCAP AND RUSSELL 2000 Value of $10,000 Invested on 6/30/00 (Russell Microcap Inception) | |

|

| Includes reinvestment of distributions. |

| PORTFOLIO DIAGNOSTICS | ||||

| Fund Net Assets | $736 million | |||

| Number of Holdings | 205 | |||

| Turnover Rate | 10% | |||

| Average Market Capitalization1 | $433 million | |||

| Weighted Average P/E Ratio2,3 | 22.0x | |||

| Weighted Average P/B Ratio2 | 1.7x | |||

| U.S. Investments (% of Net Assets) | 82.2% | |||

| Non-U.S. Investments (% of Net Assets) | 14.6% | |||

| Symbol | ||||

| Investment Class | RYOTX | |||

| Service Class | RMCFX | |||

| Consultant Class | RYMCX | |||

1 Geometric Average. This weighted calculation uses each portfolio holding’s market cap in a way designed to not skew the effect of very large or small holdings; instead, it aims to better identify the portfolio’s center, which Royce believes offers a more accurate measure of average market cap than a simple mean or median. | ||||

2 Harmonic Average. This weighted calculation evaluates a portfolio as if it were a single stock and measures it overall. It compares the total market value of the portfolio to the portfolio’s share in the earnings or book value, as the case may be, of its underlying stocks. | ||||

3 The Fund’s P/E ratio calculation excludes companies with zero or negative earnings (25% of portfolio holdings as of 6/30/14). | ||||

| MORNINGSTAR STATISTICAL MEASURES1 | ||||

| Sharpe Ratio | Standard Deviation | |||

| RMC | 0.83 | 17.86 | ||

| Russell Microcap | 1.04 | 19.40 | ||

| Category Median | 1.07 | 18.88 | ||

| Best Quartile Breakpoint | 1.19 | 17.24 | ||

1Five years ended 6/30/14. Category Median and Best Quartile Breakpoint based on 18 micro-cap objective funds (oldest class only) with at least five years of history. | ||||

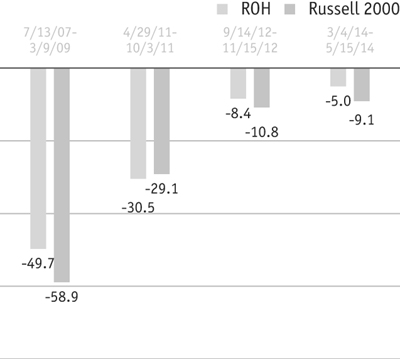

DOWN MARKET PERFORMANCE COMPARISON All Down Periods of 7.5% or Greater Over the Last 7 Years, in Percentages(%)  | ||||

The Royce Funds 2014 Semiannual Report to Shareholders | 19

| Royce Premier Fund |

| AVERAGE ANNUAL TOTAL RETURNS Through 6/30/14 | ||||||||||

| January–June 20141 | 7.33 | % | ||||||||

| One-Year | 27.08 | |||||||||

| Three-Year | 11.63 | |||||||||

| Five-Year | 18.57 | |||||||||

| 10-Year | 11.07 | |||||||||

| 15-Year | 12.07 | |||||||||

| 20-Year | 12.62 | |||||||||

| Since Inception (12/31/91) | 12.73 | |||||||||

| ANNUAL EXPENSE RATIO | ||||||||||

| Operating Expenses | 1.09 | % | ||||||||

| 1 Not Annualized | ||||||||||

| CALENDAR YEAR TOTAL RETURNS | ||||||||||

| Year | RPR | Year | RPR | |||||||

| 2013 | 27.7 | % | 2005 | 17.1 | % | |||||

| 2012 | 11.4 | 2004 | 22.8 | |||||||

| 2011 | -0.9 | 2003 | 38.7 | |||||||

| 2010 | 26.5 | 2002 | -7.8 | |||||||

| 2009 | 33.3 | 2001 | 9.6 | |||||||

| 2008 | -28.3 | 2000 | 17.1 | |||||||

| 2007 | 12.7 | 1999 | 11.5 | |||||||

| 2006 | 8.8 | 1998 | 6.7 | |||||||

| TOP 10 POSITIONS % of Net Assets | ||||||||||

| Myriad Genetics | 3.6 | % | ||||||||

| Thor Industries | 3.4 | |||||||||

| Alleghany Corporation | 2.9 | |||||||||

| Lincoln Electric Holdings | 2.8 | |||||||||

| Woodward | 2.8 | |||||||||

| Unit Corporation | 2.6 | |||||||||

| Kennedy-Wilson Holdings | 2.1 | |||||||||

| Westlake Chemical | 2.0 | |||||||||

| Trican Well Service | 2.0 | |||||||||

| Cirrus Logic | 2.0 | |||||||||

| PORTFOLIO SECTOR BREAKDOWN % of Net Assets | ||||||||||

| Industrials | 24.2 | % | ||||||||

| Information Technology | 18.2 | |||||||||

| Materials | 11.0 | |||||||||

| Consumer Discretionary | 10.6 | |||||||||

| Financials | 10.3 | |||||||||

| Energy | 9.8 | |||||||||

| Health Care | 8.0 | |||||||||

| Consumer Staples | 4.8 | |||||||||

| Miscellaneous | 0.9 | |||||||||

| Cash and Cash Equivalents | 2.2 | |||||||||

| ||||||

Managers’ Discussion The kind of well-run, fundamentally solid, and profitable companies that we typically seek for the portfolio of Royce Premier Fund (RPR) have not been consistent market leaders over the last several years. But you wouldn’t know that by looking at the Fund’s first-half results. For the year-to-date period ended June 30, 2014, RPR increased 7.3%, more than doubling the 3.2% gain of its small-cap benchmark, the Russell 2000 Index, over the same period. We refer to stocks with the characteristics listed above as quality companies, and they have been performing better by fits and starts dating back to the spring of 2012. Most rallies over that same period, however, have generally been better for lower-quality, faster-growing stocks or those with high yields. That held true for the small-cap market through 2014’s first six months, though RPR’s first-quarter advantage and, more important, its strong showing through the year’s only correction allowed it to cruise past its benchmark. The first quarter saw an extension of the bull run that made 2013 such a terrific year for equities in general, though the pace was much slower. The Fund beat the small-cap index in the year’s opening quarter, up 1.8% compared to a 1.1% gain for the benchmark. The Russell 2000 reached its year-to-date high on March 4, falling 9.1% through May 15. This made April a bearish month for the index, but the Fund escaped 2014’s cruelest month with a small gain. When small-caps began to reverse course in mid-May, RPR continued to advance. Although it slightly trailed the index in May and June, the Fund easily outpaced the Russell 2000 in the second quarter, gaining 5.5% versus 2.0% for the benchmark. RPR’s strong first half helped to create an advantage over the small-cap index for the one-year period ended June 30, 2014 (+27.1% versus +23.6%). While the Fund lagged the Russell 2000 through recent market cycles as well as for the three- and five-year periods ended June 30, 2014, we are confident that this pattern is beginning to shift. Based on the normalization and expansion of the economy, we believe stocks are entering a more congenial phase for active managers who focus on quality companies and have a long-term investment horizon. RPR outperformed the Russell 2000 for the 10-, 15-, 20-year, and since inception (12/31/91) periods ended June 30, 2014. The Fund’s average annual total return for the since inception period was 12.7%, a long-term record in which we take great pride. | ||||||

| GOOD IDEAS THAT WORKED Top Contributors to Performance Year-to-Date through 6/30/141 | |||||||||||

| Myriad Genetics | 1.80% | ||||||||||

| Zebra Technologies Cl. A | 0.78 | ||||||||||

| Westlake Chemical | 0.77 | ||||||||||

| Unit Corporation | 0.75 | ||||||||||

| Trican Well Service | 0.57 | ||||||||||

| 1 Includes dividends. | |||||||||||

Important Performance and Expense Information All performance information in this Report reflects past performance, is presented on a total return basis, reflects the reinvestment of distributions, and does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Past performance is no guarantee of future results. Investment return and principal value of an investment will fluctuate, so that shares may be worth more or less than their original cost when redeemed. Shares redeemed within 180 days of purchase may be subject to a 1% redemption fee payable to the Fund, which is not reflected in the performance shown above; if it were, performance would be lower. Current month-end performance may be higher or lower than performance quoted and may be obtained at www.roycefunds.com. All performance and risk information reflects results of the Investment Class (its oldest class). Operating expenses reflect the Fund’s total annual operating expenses for the Investment Class as of the Fund’s most current prospectus and include management fees and other expenses. Shares of RPR’s Service, Consultant, R, and K Classes bear an annual distribution expense that is not borne by the Investment Class. Regarding the two “Good Ideas” tables shown above, the sum of all contributors to, and all detractors from, performance for all securities in the portfolio would approximate the Fund’s year-to-date performance for 2014. | |||||||||||

20 | The Royce Funds 2014 Semiannual Report to Shareholders

Performance and Portfolio Review |