Table of Contents

As Filed Electronically with the Securities and Exchange Commission on October 18, 2004.

Securities Act File No. 333-117809

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-14

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933 x |

Pre-Effective Amendment No. 1 x |

Post-Effective Amendment No. ¨ |

SCUDDER TAX FREE TRUST

(Exact Name of Registrant as Specified in Charter)

Two International Place Boston, Massachusetts 02110-4103

(Address of Principal Executive Offices) (Zip Code)

617-295-2572

(Registrant’s Area Code and Telephone Number)

John Millette

Deutsche Investment Management Americas Inc.

Two International Place

Boston, Massachusetts 02110-4103

(Name and Address of Agent for Service)

With copies to:

John W. Gerstmayr, Esq. Thomas R. Hiller, Esq. Ropes & Gray LLP One International Place Boston, Massachusetts 02110-2624 | Burton M. Leibert, Esq. Mary C. Carty, Esq. Willkie Farr & Gallagher LLP 787 Seventh Avenue New York, New York 10019-6099 |

TITLE OF SECURITIES BEING REGISTERED:

Shares of the Scudder Intermediate Tax/AMT Free Series of the Registrant

Approximate date of proposed public offering: As soon as practicable after the effective date of this Registration Statement.

No filing fee is required because an indefinite number of shares have previously been registered pursuant to Rule 24f-2 under the Investment Company Act of 1940.

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

Questions & Answers

Scudder Municipal Bond Fund

Scudder MG Investments Trust

Q&A

Q What is happening?

A Deutsche Asset Management has initiated a program to reorganize and combine selected funds within the Scudder fund family, expand product offerings across more share classes, and adjust or eliminate share classes as necessary to increase potential economies of scale for the funds’ shareholders.

Q What issue am I being asked to vote on?

A You are being asked to vote on a proposal to combine Scudder Municipal Bond Fund with and into Scudder Intermediate Tax/AMT Free Fund. Both funds are managed by the same portfolio management team and seek to achieve substantially the same investment objective through similar types of investments. Combining the two funds offers the potential to create greater economies of scale for the combined fund and its shareholders.

After carefully reviewing the proposal, your fund’s Board has determined that this action is in the best interest of the fund. The Board unanimously recommends that you vote for this proposal.

Q Why has this proposal been made for my fund?

A As discussed in the enclosed prospectus/proxy statement, the combination of the two funds is intended to create greater cost efficiencies and the potential for greater economies of scale for the combined fund and its shareholders. Although there can be no guarantee, it is expected that the combined fund will have lower total operating expenses than Scudder Municipal Bond Fund. Fund shareholders who are subject to the federal alternative minimum tax are expected to be protected from such tax liability by the investment strategies of Scudder Intermediate Tax/AMT Free Fund, which currently does not invest in bonds subject to this tax.

Table of Contents

Q&A continued

Q Will the combination of my fund be a taxable event?

A The combination is expected to be a tax-free transaction for federal income tax purposes and will not take place unless special tax counsel provides an opinion to that effect. As a result of the combination, however, your fund may lose the benefit of certain tax losses that could have been used to offset or defer future gains. If you choose to redeem or exchange your shares before or after the combination, the redemption or exchange will generate taxable gain or loss; therefore, you may wish to consult a tax advisor before doing so. Of course, you may also be subject to capital gains as a result of the normal operations of your fund whether or not the combination occurs.

Q After the combination, will I own the same number of shares?

A The value of your shares will not change as a result of the combination. It is likely that the number of shares you own will change as a result of the combination. Your shares will be exchanged at the net asset value of Scudder Intermediate Tax/AMT Free Fund, which will probably be higher or lower than the net asset value of Scudder Municipal Bond Fund.

Q What impact will the combination have on the portfolio managers who currently manage the assets of Scudder Municipal Bond Fund?

A None. The portfolio managers who currently manage the assets of Scudder Municipal Bond Fund also manage the assets of Scudder Intermediate Tax/AMT Free Fund.

Q Will my fund pay for the proxy solicitation and legal costs associated with this solicitation?

A No. Deutsche Asset Management will bear these costs.

Q When would the combination take place?

A If approved by shareholders of Scudder Municipal Bond Fund, the combination would occur on or about December 20, 2004 or as soon as reasonably practicable after shareholder approval is obtained. Shortly after completion of the combination, shareholders whose accounts are affected by the combination will receive a confirmation statement reflecting their new account number and number of shares owned.

Table of Contents

Q&A continued

Q How can I vote?

A You can vote in any one of four ways:

| n | Through the Internet by going to the website listed on your proxy card; |

| n | By telephone, with a toll-free call to the number listed on your proxy card; |

| n | By mail, by sending the enclosed proxy card, signed and dated, to us in the enclosed envelope; or |

| n | In person, by attending the special meeting. |

We encourage you to vote over the Internet or by telephone, following the instructions that appear on your proxy card. Whichever method you choose, please take the time to read the full text of the proxy statement before you vote.

Q If I send my proxy in now as requested, can I change my vote later?

A You may revoke your proxy at any time before it is voted by: (1) sending a written revocation to the Secretary of the fund as explained in the proxy statement; or (2) forwarding a later-dated proxy that is received by the fund at or prior to the special meeting; or (3) attending the special meeting and voting in person. Even if you plan to attend the special meeting, we ask that you return the enclosed proxy. This will help us ensure that an adequate number of shares are present for the special meeting to be held.

Q Will I be able to continue to track my fund’s performance in the newspaper, on the Internet or through the voice response system (Scudder ACCESS or SAIL, as applicable)?

A Yes. You will be able to continue to track your fund’s performance through all these means.

Q Whom should I call for additional information about this proxy statement?

A Please call Georgeson Shareholder, your fund's proxy solicitor, at 1-888-288-5518.

Table of Contents

A Message from the Fund’s Chief Executive Officer

November [_], 2004

Dear Scudder Municipal Bond Fund Shareholder:

I am writing to you to ask for your vote on an important matter that affects your investment in Scudder Municipal Bond Fund (“Municipal Bond Fund”). While you are, of course, welcome to join us at Municipal Bond Fund’s special meeting, most shareholders cast their vote by filling out and signing the enclosed proxy card, or by voting by telephone or through the Internet.

We are asking for your vote on the following matter:

| Approval of a proposed combination of Municipal Bond Fund into Scudder Intermediate Tax/AMT Free Fund (“Intermediate Tax/AMT Free Fund”). In this combination, your shares of Municipal Bond Fund would, in effect, be exchanged, on a tax-free basis, for shares of Intermediate Tax/AMT Free Fund with an equal net asset value. | ||

The proposed combination is part of a program initiated by Deutsche Asset Management. This program is intended to provide a more streamlined selection of investment options that is consistent with the changing needs of investors. If approved by fund shareholders, this program will enable Deutsche Asset Management to:

| • | Eliminate redundancies within the Scudder fund family by reorganizing and combining certain funds; |

| • | Adjust or eliminate share classes as necessary to maximize potential economies of scale; and |

| • | Focus its investment resources on core products that best meet investor needs. |

The Trustees of Municipal Bond Fund recommend approval of the combination because they believe it offers fund shareholders the following benefits:

| • | A similar investment opportunity in a larger asset pool that offers greater economies of scale; |

| • | Alternative minimum tax protection for those shareholders who are subject to this tax; |

| • | A lower expense ratio; and |

| • | Potential for a more predictable income stream. |

Except for the extent to which Intermediate Tax/AMT Free Fund does not currently invest in bonds subject to the alternative minimum tax, the investment objectives and policies of Intermediate Tax/AMT Free Fund are substantially similar to those of Municipal Bond Fund. If the combination is approved, the Board expects that the proposed changes will take effect during the fourth calendar quarter of this year.

Included in this booklet is information about the upcoming shareholders’ special meeting:

| • | A Notice of a Special Meeting of Shareholders, which summarizes the issue for which you are being asked to provide voting instructions; and |

Table of Contents

| • | A Prospectus/Proxy Statement, which provides detailed information on Intermediate Tax/AMT Free Fund, the specific proposal being considered at the shareholders’ special meeting, and why the proposal is being made. |

Although we would like very much to have each shareholder attend the special meeting, we realize this may not be possible. Whether or not you plan to be present, however, we need your vote. We urge you to review the enclosed materials thoroughly. Once you’ve determined how you would like your interests to be represented, please promptly complete, sign, date and return the enclosed proxy card, vote by telephone or record your voting instructions on the Internet. A postage-paid envelope is enclosed for mailing, and telephone and Internet voting instructions are listed at the top of your proxy card. You may receive more than one proxy card. If so, please vote each one.

I’m sure that you, like most people, lead a busy life and are tempted to put this proxy aside for another day. Please don’t. Your prompt return of the enclosed proxy card (or your voting by telephone or through the Internet) may save the necessity and expense of further solicitations.

Your vote is important to us. We appreciate the time and consideration I am sure you will give this important matter. If you have questions about the proposal, please call Georgeson Shareholder, Municipal Bond Fund’s proxy solicitor, at 1-888-288-5518, or contact your financial advisor. Thank you for your continued support of Scudder Investments.

Sincerely yours,

Julian F. Sluyters

Chief Executive Officer

Scudder Municipal Bond Fund

Table of Contents

Notice of a Special Meeting of Shareholders

This is the formal agenda for your fund’s shareholder special meeting. It tells you what matter will be voted on and the time and place of the special meeting, in the event you choose to attend in person.

To the Shareholders of Scudder Municipal Bond Fund:

A Special Meeting of Shareholders of Scudder Municipal Bond Fund (“Municipal Bond Fund”) will be held December 10, 2004 at 4:00 p.m. Eastern time, at the offices of Deutsche Asset Management, Inc., One South Street, Baltimore, Maryland 21202 (the “Meeting”), to consider the following:

| Proposal: | Approving an Agreement and Plan of Reorganization and the transactions it contemplates, including the transfer of all of the assets of Municipal Bond Fund to Scudder Intermediate Tax/AMT Free Fund (“Intermediate Tax/AMT Free Fund”), in exchange for shares of Intermediate Tax/AMT Free Fund and the assumption by Intermediate Tax/AMT Free Fund of all liabilities of Municipal Bond Fund, and the distribution of such shares, on a tax-free basis, to the shareholders of Municipal Bond Fund in complete liquidation of Municipal Bond Fund. |

The persons named as proxies will vote in their discretion on any other business that may properly come before the Meeting or any adjournments or postponements thereof.

Holders of record of shares of Municipal Bond Fund at the close of business on September 16, 2004 are entitled to vote at the Meeting and at any adjournments or postponements thereof.

In the event that the necessary quorum to transact business or the vote required to approve the combination is not obtained at the Meeting, the persons named as proxies may propose one or more adjournments of the Meeting in accordance with applicable law to permit such further solicitation of proxies as may be deemed necessary or advisable. Any adjournment will require the affirmative vote of a majority of the votes cast on the question in person or by proxy at the session of the Meeting to be adjourned. The persons named as proxies will vote FOR any such adjournment those proxies which they are entitled to vote in favor of the proposal and will vote AGAINST any such adjournment those proxies to be voted against the proposal.

By order of the Trustees

[Insert graphic]

Joseph R. Hardiman, Chairman

Richard R. Burt

S. Leland Dill

Martin J. Gruber

Richard J. Herring

Graham E. Jones

Rebecca W. Rimel

Phillip Saunders, Jr.

William N. Searcy

William Shiebler

Robert H. Wadsworth

WE URGE YOU TO MARK, SIGN, DATE AND MAIL THE ENCLOSED PROXY IN THE POSTAGE-PAID ENVELOPE PROVIDED OR RECORD YOUR VOTING INSTRUCTIONS BY TELEPHONE OR THROUGH THE INTERNET SO THAT YOU WILL BE REPRESENTED AT THE MEETING.

November [_], 2004

Table of Contents

INSTRUCTIONS FOR SIGNING PROXY CARDS

The following general rules for signing proxy cards may be of assistance to you and avoid the time and expense involved in validating your vote if you fail to sign your proxy card properly.

1. Individual Accounts: Sign your name exactly as it appears in the registration on the proxy card.

2. Joint Accounts: Either party may sign, but the name of the party signing should conform exactly to the name shown in the registration on the proxy card.

3. All Other Accounts: The capacity of the individual signing the proxy card should be indicated unless it is reflected in the form of registration. For example:

Registration | Valid Signature | |

Corporate Accounts | ||

(1) ABC Corp. | ABC Corp. John Doe, Treasurer | |

(2) ABC Corp. | John Doe, Treasurer | |

(3) ABC Corp. c/o John Doe, Treasurer | John Doe | |

(4) ABC Corp. Profit Sharing Plan | John Doe, Trustee | |

Partnership Accounts | ||

(1) The XYZ Partnership | Jane B. Smith, Partner | |

(2) Smith and Jones, Limited Partnership | Jane B. Smith, General Partner | |

Trust Accounts | ||

(1) ABC Trust Account | Jane B. Doe, Trustee | |

(2) Jane B. Doe, Trustee u/t/d 12/28/78 | Jane B. Doe | |

Custodial or Estate Accounts | ||

(1) John B. Smith, Cust. f/b/o John B. Smith Jr. | John B. Smith | |

(2) Estate of John B. Smith | John B. Smith, Jr., Executor | |

Table of Contents

IMPORTANT INFORMATION

FOR SHAREHOLDERS OF

SCUDDER MUNICIPAL BOND FUND

This document contains a prospectus/proxy statement and a proxy card. A proxy card is, in essence, a ballot. When you vote your proxy, it tells us how to vote on your behalf on an important issue relating to your fund. If you complete and sign the proxy (or tell us how you want to vote by voting by telephone or through the Internet), we’ll vote exactly as you tell us. If you simply sign the proxy, we’ll vote it in accordance with the Trustees’ recommendation on page 8.

We urge you to review the prospectus/proxy statement carefully and either fill out your proxy card and return it to us by mail, vote by telephone or record your voting instructions via the Internet. You may receive more than one proxy card since several shareholder special meetings are being held as part of the broader restructuring program of the Scudder fund family. If so, please vote each one. Your prompt return of the enclosed proxy card (or your voting by telephone or through the Internet) may save the necessity and expense of further solicitations.

We want to know how you would like to vote and welcome your comments. Please take a few minutes to read these materials and return your proxy to us. If you have any questions, please call Georgeson Shareholder, Municipal Bond Fund’s proxy solicitor, at the special toll-free number we have set up for you (1-888-288-5518) or contact your financial advisor.

Table of Contents

October [_], 2004

Acquisition of the assets of: | By and in exchange for shares of: | |

Scudder Municipal Bond Fund | Scudder Intermediate Tax/AMT Free Fund | |

a series of Scudder MG Investments Trust One South Street Baltimore, MD 21202 (410) 895-5000 | a series of Scudder Tax Free Trust Two International Place Boston, MA 02110 (617) 295-2572 | |

This Prospectus/Proxy Statement is being furnished in connection with the proposed combination of Scudder Municipal Bond Fund (“Municipal Bond Fund”) into Scudder Intermediate Tax/AMT Free Fund (“Intermediate Tax/AMT Free Fund”). Intermediate Tax/AMT Free Fund and Municipal Bond Fund are referred to herein collectively as the “Funds,” and each is referred to herein individually as a “Fund.” As a result of the proposed combination, each shareholder of Municipal Bond Fund will receive a number of full and fractional shares of the corresponding class of Intermediate Tax/AMT Free Fund equal in value as of the date of the exchange to the total value of such shareholder’s Municipal Bond Fund shares.

This Prospectus/Proxy Statement is being mailed on or about November [_], 2004. It explains concisely what you should know before voting on the matter described in this Prospectus/Proxy Statement or investing in Intermediate Tax/AMT Free Fund, a diversified series of an open-end, management investment company. Please read it carefully and keep it for future reference.

The securities offered by this Prospectus/Proxy Statement have not been approved or disapproved by the SEC, nor has the SEC passed upon the accuracy or adequacy of this Prospectus/Proxy Statement. Any representation to the contrary is a criminal offense.

The following documents have been filed with the Securities and Exchange Commission (“SEC”) and are incorporated into this Prospectus/Proxy Statement by reference:

| (i) | the prospectuses of Intermediate Tax/AMT Free Fund, dated October 1, 2004, as supplemented from time to time, relating to Institutional Class and Investment Class shares, the applicable copy of which is included with this Prospectus/Proxy Statement; |

| (ii) | the prospectuses of Municipal Bond Fund, dated March 1, 2004, as supplemented from time to time, relating to Institutional Class and Investment Class shares; |

| (iii) | the statement of additional information of Municipal Bond Fund, dated March 1, 2004, as supplemented from time to time, relating to Institutional Class and Investment Class shares; |

1

Table of Contents

| (iv) | the statement of additional information relating to the proposed combination, dated October [ ], 2004 (the “Merger SAI”); and |

| (v) | the financial statements and related Independent Registered Public Accounting Firm’s report included in Municipal Bond Fund’s Annual Report to Shareholders for the fiscal year ended October 31, 2003 and the financial statements included in Municipal Bond Fund’s Semi-Annual Report to Shareholders for the period ended April 30, 2004. |

Shareholders may receive free copies of the Funds’ annual reports, semi-annual reports, prospectuses, statements of additional information or the Merger SAI, request other information about a Fund, or make shareholder inquiries, by contacting their financial advisor or by calling the corresponding Fund at the phone number listed above.

Like shares of Municipal Bond Fund, shares of Intermediate Tax/AMT Free Fund are not deposits or obligations of, or guaranteed or endorsed by, any financial institution, are not insured by the Federal Deposit Insurance Corporation, the Federal Reserve Board or any other agency, and involve risk, including the possible loss of the principal amount invested.

This document is designed to give you the information you need to vote on the proposal. Much of the information is required disclosure under rules of the SEC; some of it is technical. If there is anything you don’t understand, please contact Georgeson Shareholder, Municipal Bond’s Fund’s proxy solicitor, at 1-888-288-5518, or contact your financial advisor.

Intermediate Tax/AMT Free Fund is subject to the informational requirements of the Securities Exchange Act of 1934, as amended, and in accordance therewith files reports and other information with the SEC. You may review and copy information about the Funds, including the prospectuses and the statements of additional information, at the SEC’s public reference room at 450 Fifth Street, NW, Washington, D.C. You may call the SEC at 1-202-942-8090 for information about the operation of the public reference room. You may obtain copies of this information, with payment of a duplication fee, by electronic request at the following e-mail address: publicinfo@sec.gov, or by writing the SEC’s Public Reference Branch, Office of Consumer Affairs and Information Services, Securities and Exchange Commission, Washington, D.C. 20549-0102. You may also access reports and other information about the Funds on the EDGAR database on the SEC’s Internet site at http://www.sec.gov.

2

Table of Contents

The responses to the questions that follow provide an overview of key points typically of concern to shareholders considering a proposed combination between mutual funds. These responses are qualified in their entirety by the remainder of this Prospectus/Proxy Statement, which you should read carefully because it contains additional information and further details regarding the proposed combination.

| 1. | What is being proposed? |

The Trustees of Municipal Bond Fund are recommending that shareholders approve the transactions contemplated by the Agreement and Plan of Reorganization (as described below in Part IV and a form of which is attached hereto as Exhibit A), which we refer to as a combination of Municipal Bond Fund with and into Intermediate Tax/AMT Free Fund. If approved by shareholders, all of the assets of Municipal Bond Fund will be transferred to Intermediate Tax/AMT Free Fund solely in exchange for (a) the issuance and delivery to Municipal Bond Fund of Institutional Class and Investment Class shares of Intermediate Tax/AMT Free Fund (“Merger Shares”) with a value equal to the value of Municipal Bond Fund’s assets net of liabilities, and (b) the assumption by Intermediate Tax/AMT Free Fund of all liabilities of Municipal Bond Fund. Immediately following the transfer, the appropriate class of Merger Shares received by Municipal Bond Fund will be distributed to each of its shareholders, pro rata.

| 2. | What will happen to my shares of Municipal Bond Fund as a result of the combination? |

Your shares of Municipal Bond Fund will, in effect, be exchanged on a tax-free basis for shares of the same class of Intermediate Tax/AMT Free Fund with an equal aggregate net asset value on the date of the combination.

| 3. | Why have the Trustees of Municipal Bond Fund recommended that I approve the combination? |

The Trustees of Municipal Bond Fund believe that the combination may provide shareholders of Municipal Bond Fund with the following benefits:

| • | Compatible Investment Opportunity in a Larger Fund. The combination offers shareholders of Municipal Bond Fund the opportunity to invest in a substantially larger combined fund with similar investment policies. The larger asset pool of the combined fund is expected to result in more efficient portfolio management, although there can be no guarantee. Deutsche Asset Management, Inc. (“DeAM, Inc.”), Municipal Bond Fund’s investment advisor, has advised the Trustees that Municipal Bond Fund and Intermediate Tax/AMT Free Fund have generally similar investment objectives and policies. In addition, DeAM, Inc. has advised the Trustees that the Funds have the same management team and similar investment styles and processes, except that Municipal Bond Fund may invest in bonds that are subject to the federal alternative minimum tax (“AMT”) while Intermediate Tax/AMT Free Fund does not currently make such investments. |

| • | Alternative Minimum Tax Protection. The combined fund will continue to pursue the investment objectives, policies and restrictions of Intermediate Tax/AMT Free Fund. This means, among other things, that the combined fund is not |

3

Table of Contents

expected to invest in obligations the interest on which is a preference item for purposes of the federal AMT. As a result, the combination is expected to provide AMT protection for those Municipal Bond Fund shareholders who are subject to this tax. |

| • | Lower Total Fund Operating Expenses in the Combined Fund. |

| • | Potential for More Predictable Income Stream Through Investments in Certain Fixed Income Investments. |

The Trustees of Municipal Bond Fund have concluded that: (1) the combination is in the best interests of Municipal Bond Fund, and (2) the interests of the existing shareholders of Municipal Bond Fund will not be diluted as a result of the combination. Accordingly, the Trustees of the Municipal Bond Fund unanimously recommend approval of the Agreement and Plan of Reorganization (as defined below) and the combination as contemplated thereby.

| 4. | How do the investment goals, policies and restrictions of the two Funds compare? |

While not identical, the investment objectives, policies and restrictions of the Funds are substantially similar. Municipal Bond Fund seeks a high level of income exempt from regular federal income tax, consistent with the preservation of capital. Intermediate Tax/AMT Free Fund seeks to provide a high level of income exempt from regular federal income taxes and seeks to limit principal fluctuation. Under normal market conditions, Municipal Bond Fund invests at least 80% of its assets, determined at the time of purchase, in municipal securities that pay interest exempt from regular federal income tax. Under normal circumstances, Intermediate Tax/AMT Free Fund invests at least 80% of net assets, plus the amount of any borrowings for investment purposes, in securities of municipalities across the United States and in other securities whose income is free from regular federal income tax and the federal AMT. Either fund may purchase investment grade municipal bonds of any maturity. Municipal Bond Fund may invest no more than 5% of total fund assets in below investment grade issues, while Intermediate Tax/AMT Free Fund may not invest at all in such issues. However, while Municipal Bond Fund may invest up to 15% of its assets in investment grade bonds that are rated in the fourth highest rating category, Intermediate Tax/AMT Free Fund may invest up to 35% of net assets in bonds rated in the fourth credit grade. In addition, Intermediate Tax/AMT Free Fund does not currently invest in securities whose income is subject to the federal AMT, whereas Municipal Bond Fund does not limit the percentage of assets that may be invested in obligations of this type. The Trustees of Municipal Bond Fund anticipate a pre-combination liquidation by Municipal Bond Fund of all investments that are not consistent with the current investment objective, policies and restrictions of Intermediate Tax/AMT Free Fund, or whose income is subject to the federal AMT. After the combination is complete, the proceeds of the liquidation would be used to invest in instruments that are appropriate investments for Intermediate Tax/AMT Free Fund. Please also see Part II—Investment Strategies and Risk Factors—below for a more detailed comparison of the Funds’ investment policies and restrictions.

4

Table of Contents

The following table sets forth a summary of the composition of the investment portfolio of each Fund as of May 31, 2004, and of Intermediate Tax/AMT Free Fund on a pro forma combined basis, giving effect to the proposed combination:

Portfolio Composition

(as a % of Fund)

(excludes cash equivalents)

Quality | Municipal Bond Fund | Intermediate Tax/AMT Free Fund | Intermediate Tax/AMT | |||

AAA | 67% | 78% | 74% | |||

AA | 9% | 13% | 12% | |||

A | 12% | 7% | 9% | |||

BBB | 6% | 2% | 3% | |||

Not Rated | 6% | — | 2% | |||

| 100% | 100% | 100% |

| (1) | Reflects the blended characteristics of Municipal Bond Fund and Intermediate Tax/AMT Free Fund as of May 31, 2004. The portfolio composition and characteristics of the combined fund will change consistent with its stated investment objective and policies. |

| 5. | How do the management fees and other expenses of the two Funds compare, and what are they estimated to be following the combination? |

The following tables summarize the fees and expenses you may pay when investing in the Funds, the expenses that each of the Funds incurred for the year ended May 31, 2004, and the pro forma estimated expenses of Intermediate Tax/AMT Free Fund assuming consummation of the combination as of that date.

Shareholder Fees

(fees that are paid directly from your investment)

| Institutional Class | Investment Class | |||

Maximum Sales Charge (Load) Imposed on Purchases (as a percentage of the offering price) | ||||

Municipal Bond Fund | None | None | ||

Intermediate Tax/AMT Free Fund | None | None | ||

Intermediate Tax/AMT Free Fund (Pro forma combined) | None | None | ||

Maximum Contingent Deferred Sales Charge (Load) | ||||

Municipal Bond Fund | None | None | ||

Intermediate Tax/AMT Free Fund | None | None | ||

Intermediate Tax/AMT Free Fund (Pro forma combined) | None | None | ||

Redemption Fee (as a percentage of total redemption proceeds) | ||||

Municipal Bond Fund | None | None | ||

Intermediate Tax/AMT Free Fund | None | None | ||

Intermediate Tax/AMT Free Fund (Pro forma combined) | None | None | ||

5

Table of Contents

The table below compares the annual management fee schedules of the Funds, expressed as a percentage of net assets. As of May 31, 2004, Intermediate Tax/AMT Free Fund and Municipal Bond Fund had net assets of $612,739,252 and $296,647,075, respectively.

Intermediate Tax/AMT Free Fund | Municipal Bond Fund | |||

Average Daily Net Assets | Management Fee | Management Fee | ||

$0—$250 million | 0.55% | 0.40% | ||

$250 million—$1 billion | 0.52% | |||

$1 billion—$2.5 billion | 0.49% | |||

$2.5 billion—$5 billion | 0.47% | |||

$5 billion—$7.5 billion | 0.45% | |||

$7.5 billion—$10 billion | 0.43% | |||

$10 billion—$12.5 billion | 0.41% | |||

Over $12.5 billion | 0.40% | |||

As shown below, the combination is expected to result in a lower total expense ratio for shareholders of Municipal Bond Fund. However, there can be no assurance that the combination will result in expense savings.

Annual Fund Operating Expenses

(expenses that are deducted from Fund assets)

| Management Fees | Distribution/ Service (12b-1) Fees | Other Expenses | Total Annual Fund Operating Expenses | Less Expense Waiver/ Reimburse- ments | Net Annual Fund Operating Expenses (after Waiver) | ||||||||||||

Municipal Bond Fund | |||||||||||||||||

Institutional Class | 0.40 | % | None | 0.16 | % | 0.56 | % | 0.01 | %(1) | 0.55 | % | ||||||

Investment Class | 0.40 | % | None | 0.36 | %(2) | 0.76 | %(2) | None | 0.76 | % | |||||||

Intermediate Tax/AMT Free Fund | |||||||||||||||||

Institutional Class | 0.53 | % | None | 0.08 | %(3) | 0.61 | % | None | 0.61 | % | |||||||

Investment Class | 0.53 | % | None | 0.28 | %(2),(3) | 0.81 | %(2) | None | 0.81 | % | |||||||

Intermediate Tax/AMT Free Fund (Pro forma combined)(4) | |||||||||||||||||

Institutional Class | 0.40 | % | None | 0.08 | %(3),(5) | 0.48 | % | None | 0.48 | % | |||||||

Investment Class | 0.40 | % | None | 0.28 | %(2),(3),(5) | 0.68 | %(2) | None | 0.68 | % |

| (1) | Through February 28, 2005, the investment advisor and administrator of Municipal Bond Fund have contractually agreed to waive their fees and/or reimburse expenses so that total operating expenses will not exceed 0.55% for the Institutional Class. |

| (2) | Includes a shareholder servicing fee of up to 0.25%. |

| (3) | The Institutional and Investment share classes of Intermediate Tax/AMT Free Fund were not operational during the prior fiscal year as they are being created in connection with the proposed combination. Therefore, the other expenses listed in the table for that Fund are based on estimates for the coming fiscal year. |

| (4) | Through December 19, 2006, the investment advisor of Intermediate Tax/AMT Free Fund has contractually agreed to waive all or a portion of its management fee and/or reimburse or pay operating expenses of the combined fund to the extent necessary to maintain the combined fund’s total operating expenses at 0.55% for Institutional Class shares and Investment Class shares excluding certain expenses such as extraordinary expenses, taxes, brokerage, interest, Rule 12b-1 and/or service fees, trustee and trustee counsel fees. |

| (5) | Other expenses are estimated, accounting for the effect of the merger. |

6

Table of Contents

The tables are provided to help you understand the expenses of investing in the Funds and your share of the operating expenses that each Fund incurs and that Deutsche Asset Management expects the combined Fund to incur in the first year following the combination.

Examples:

The following examples translate the expenses shown in the preceding table into dollar amounts. By doing this, you can more easily compare the costs of investing in the Funds. The examples make certain assumptions. They assume that you invest $10,000 in a Fund for the time periods shown and reinvest all dividends and distributions. They also assume a 5% return on your investment each year and that a Fund’s operating expenses remain the same. This is only an example; actual expenses will be different.

| 1 Year | 3 Years | 5 Years | 10 Years | |||||||||

Municipal Bond Fund | ||||||||||||

Institutional Class1 | $ | 56 | $ | 178 | $ | 312 | $ | 700 | ||||

Investment Class | $ | 78 | $ | 243 | $ | 422 | $ | 942 | ||||

Intermediate Tax/AMT Free Fund | ||||||||||||

Institutional Class | $ | 62 | $ | 195 | $ | 340 | $ | 762 | ||||

Investment Class | $ | 83 | $ | 259 | $ | 450 | $ | 1,002 | ||||

Intermediate Tax/AMT Free Fund (Pro forma combined) | ||||||||||||

Institutional Class | $ | 49 | $ | 154 | $ | 269 | $ | 604 | ||||

Investment Class | $ | 69 | $ | 218 | $ | 379 | $ | 847 | ||||

| (1) | Includes one year of capped expenses in each period. |

| 6. | What are the federal income tax consequences of the proposed combination? |

For federal income tax purposes, no gain or loss is expected to be recognized by Municipal Bond Fund or its shareholders as a direct result of the combination. For a discussion of taxes that you may incur indirectly as a result of the combination (e.g., due to differences in the Funds’ portfolio turnover rates and net investment income), please see “Information about the Proposed Combination—Federal Income Tax Consequences,” below.

| 7. | Will my dividends be affected by the combination? |

The combination will not result in a change in dividend policy.

| 8. | Do the procedures for purchasing, redeeming and exchanging shares of the two Funds differ? |

No. The procedures for purchasing and redeeming shares of each Fund, and for exchanging shares of each Fund for shares of other Scudder funds, are identical.

| 9. | How will I be notified of the outcome of the combination? |

If the proposed combination is approved by shareholders, you will receive confirmation after the reorganization is completed, indicating your new account number and the number of Merger Shares you are receiving. Otherwise, you will be notified in the next annual report of Municipal Bond Fund.

7

Table of Contents

| 10. | Will the number of shares I own change? |

Yes, the number of shares you own will most likely change. However, the total value of the shares of Intermediate Tax/AMT Free Fund you receive will equal the total value of the shares of Municipal Bond Fund that you hold at the time of the combination. Even though the net asset value per share of each Fund is likely to be different, the total value of each shareholder’s holdings will not change as a result of the combination.

| 11. | What percentage of shareholders’ votes is required to approve the combination? |

Approval of the combination will require the “yes” vote of a majority of the outstanding voting securities of Municipal Bond Fund entitled to vote at the special meeting.

The Trustees of Municipal Bond Fund believe that the proposed combination is in the best interest of Municipal Bond Fund and its shareholders. Accordingly, the Trustees unanimously recommend that shareholders vote FOR approval of the proposed combination.

II. INVESTMENT STRATEGIES AND RISK FACTORS

What are the main investment strategies and related risks of Intermediate Tax/AMT Free Fund and how do they compare with those of Municipal Bond Fund?

Investment Objectives and Strategies. As noted above, the Funds have similar investment objectives and are managed by the same portfolio management team. Municipal Bond Fund seeks a high level of income exempt from regular federal income tax, consistent with the preservation of capital. Intermediate Tax/AMT Free Fund seeks to provide a high level of income exempt from regular federal income taxes and seeks to limit principal fluctuation. Under normal market conditions, Municipal Bond Fund invests at least 80% of its assets, determined at the time of purchase, in municipal securities that pay interest exempt from regular federal income tax. Under normal circumstances, Intermediate Tax/AMT Free Fund invests at least 80% of net assets, plus the amount of any borrowings for investment purposes, in securities of municipalities across the United States and in other securities whose income is free from regular federal income tax and the federal AMT.

Municipal Bond Fund invests primarily in higher quality investment grade municipal securities. The Fund may invest no more than 15% of its assets in investment grade bonds that are rated in the fourth highest rating category. The Fund may also invest a significant portion of its total assets (i.e., 25% or more) in private activity and industrial development bonds if the interest paid on them is exempt from regular federal income tax. The Fund’s portfolio managers typically maintain a dollar-weighted effective average portfolio maturity of five to ten years. Subject to its portfolio maturity policy, the Fund may purchase individual securities with any stated maturity. The dollar-weighted average portfolio maturity may be shorter than the stated maturity. There is no restriction on the percentage of the Fund’s assets that may be invested in obligations the interest on which is a preference item for purposes of the federal AMT.

8

Table of Contents

In selecting individual securities for investment, the Fund’s portfolio managers (i) use credit research conducted by full time in-house analysts to determine the issuer’s current and future potential ability to pay principal and interest; (ii) look to exploit any inefficiencies between intrinsic value and trading price; and (iii) subordinate sector weightings to individual bonds that may add above-market value.

Intermediate Tax/AMT Free Fund normally invests at least 65% of net assets in municipal securities of the top three grades of credit quality, but is permitted to put up to 35% of net assets in bonds rated in the fourth credit grade, which is still considered investment grade. Although the managers can buy municipal securities of all maturities and may adjust the maturity of the Fund’s portfolio between three and ten years, they generally intend to keep it between five and ten years. The Fund does not currently invest in securities whose income is subject to the federal AMT. The portfolio managers look for securities that appear to offer the best total return potential and often seek those that cannot be called in before maturity.

Like Municipal Bond Fund, Intermediate Tax/AMT Free Fund may use various types of derivative instruments for hedging purposes and to enhance return. However, only Intermediate Tax/AMT Free Fund uses derivatives as a significant part of its hedging strategy.

Deutsche Asset Management believes that Intermediate Tax/AMT Free Fund should provide a comparable investment opportunity for shareholders of Municipal Bond Fund, although it should be noted that, unlike Municipal Bond Fund, Intermediate Tax/AMT Free Fund does not currently invest any of its assets in securities whose income is subject to the federal AMT. It is anticipated that there will be a pre-combination liquidation by Municipal Bond Fund of all investments that are not consistent with the current investment objective, policies and restrictions of Intermediate Tax/AMT Free Fund, or whose income is subject to the federal AMT.

For a more detailed description of the investment techniques used by Municipal Bond Fund and Intermediate Tax/AMT Free Fund, please see the applicable Fund’s Prospectus(es), statement of additional information and the Merger SAI.

Primary Risks. As with any mutual fund, you may lose money by investing in Intermediate Tax/AMT Free Fund. Certain risks associated with an investment in Intermediate Tax/AMT Free Fund are summarized below. Subject to limited exceptions, the risks of an investment in Intermediate Tax/AMT Free Fund are substantially similar to the risks of an investment in Municipal Bond Fund. More detailed descriptions of the risks associated with an investment in Intermediate Tax/AMT Free Fund can be found in the current Prospectus and SAI for Intermediate Tax/AMT Free Fund.

The value of your investment in Intermediate Tax/AMT Free Fund will change with changes in the values of the investments held by Intermediate Tax/AMT Free Fund. A wide array of factors can affect those values. In this summary, we describe the principal risks that may affect Intermediate Tax/AMT Free Fund’s investments as a whole. Intermediate Tax/AMT Free Fund could be subject to additional principal risks because the types of investments it makes can change over time.

9

Table of Contents

There are several risk factors that could hurt the performance of Intermediate Tax/AMT Free Fund, cause you to lose money, or cause the performance of Intermediate Tax/AMT Free Fund to trail that of other investments.

Interest Rate Risk. Generally, fixed income securities will decrease in value when interest rates rise. The longer the effective maturity of the Fund’s securities, the more sensitive it will be to interest rate changes. (As a general rule, a 1% rise in interest rates means a 1% fall in value for every year of duration.) In addition to the general risks associated with changing interest rates, the Fund may also be subject to additional, specific risks. As interest rates decline, the issuers of securities held by the Fund may prepay principal earlier than scheduled, forcing the Fund to reinvest in lower yielding securities. Prepayment may reduce the Fund’s income. As interest rates increase, fewer issuers tend to prepay, which may extend the average life of fixed income securities and have the effect of locking in a below-market interest rate, increasing the Fund��s effective duration and reducing the value of the security. An investment in Municipal Bond Fund is also subject to this risk; in addition, because Municipal Bond Fund may invest in mortgage-related securities, it is more vulnerable to the specific risks discussed above.

Credit Risk. A fund purchasing bonds faces the risk that the creditworthiness of the issuer may decline, causing the value of its bonds to decline. In addition, an issuer may be unable or unwilling to make timely payments on the interest and principal on the bonds it has issued. An investment in Municipal Bond Fund is also subject to this risk.

In addition, Municipal Bond Fund may invest up to 5% of total Fund assets in high yield bonds. Because the issuers of high yield bonds (rated below the fourth highest category) may be in uncertain financial health, the prices of their bonds are generally more vulnerable to bad economic news or even the expectation of bad news, than those of investment grade bonds. High yield bonds are also more illiquid and more difficult to value than investment grade bonds. In some cases, bonds, particularly junk bonds, may decline in credit quality or go into default.

Focused Investing Risk. The fact that the Fund may focus on investments from a single state or sector of the municipal securities market increases risk, because factors affecting the state or region, such as economic or fiscal problems, could affect a large portion of the Fund’s securities in a similar manner. For example, a state’s technology or biotech industries could experience a downturn or fail to develop as expected, hurting the local economy. While an investment in Municipal Bond Fund is also subject to focused investing risk, the fact that Intermediate Tax/AMT Free Fund does not intend to invest in AMT issues may cause the investments of this Fund to be more focused and may leave the Fund somewhat more susceptible to this risk.

Market Risk. Deteriorating conditions might cause a general weakness in the municipal securities market that reduces the overall level of securities prices in that market. Developments in a particular class of bonds or the stock market could also adversely affect the Fund by reducing the relative attractiveness of bonds as an investment. Also, to the extent that the Fund emphasizes bonds from any given industry, it could be hurt if that industry does not do well. An investment in Municipal Bond Fund is also subject to this risk.

10

Table of Contents

Derivatives Risk. Risks associated with derivatives include: the risk that the derivative is not well correlated with the security, index or currency to which it relates; the risk that derivatives used for risk management may not have the intended effects and may result in losses or missed opportunities; the risk that the Fund will be unable to sell the derivative because of an illiquid secondary market; and the risk that the derivatives transaction could expose the Fund to the effects of leverage, which could increase the Fund’s exposure to the market and magnify potential losses. There is no guarantee that these derivatives activities will be employed or that they will work, and their use could cause lower returns or even losses to the Fund. An investment in Municipal Bond Fund is also subject to this risk.

Tax Liability Risk. Distributions by the Fund that are derived from income from taxable securities held by the Fund will generally be taxable to shareholders as ordinary income. Other distributions such as capital gains are also subject to federal taxation. New federal or state legislation could adversely affect the tax-exempt status of securities held by the Fund, resulting in higher tax liability for shareholders. In addition, distribution of the Fund’s income and gains will generally be subject to state taxation. An investment in Municipal Bond Fund is also subject to this risk.

Other factors that could affect performance include:

| • | the managers could be incorrect in their analysis of interest rate trends, credit quality or other factors or in their municipal securities selections generally |

| • | political or legal actions could change the way the Fund’s dividends are treated for tax purposes |

| • | at times, market conditions might make it hard to value some investments or to get an attractive price for them. |

III. OTHER COMPARISONS BETWEEN THE FUNDS

Investment Advisors. DeAM, Inc. is the investment advisor for Municipal Bond Fund and Deutsche Investment Management Americas Inc. (“DeIM”) is the investment advisor for Intermediate Tax/AMT Free Fund. Each advisor makes investment decisions for the applicable Fund, buys and sells securities for the Fund and conducts the research that leads to the purchase and sale decisions. Each advisor is a part of Deutsche Asset Management and an indirect wholly owned subsidiary of Deutsche Bank AG. Deutsche Asset Management is the marketing name in the U.S. for the asset management activities of Deutsche Bank AG, DeAM, Inc., DeIM, Deutsche Asset Management Investment Services Limited, Deutsche Bank Trust Company Americas and Scudder Trust Company. Deutsche Bank AG is a major global banking institution that is engaged in a wide range of financial services, including investment management, mutual fund, retail, private and commercial banking, investment banking and insurance. Both Funds are managed by the same portfolio management team.

Distributor. Pursuant to separate Underwriting and Distribution Services Agreements, Scudder Distributors, Inc. (“SDI”), 222 South Riverside Plaza, Chicago, Illinois 60606, an affiliate of Deutsche Asset Management, is the principal underwriter and distributor of the Institutional Class and Investment Class shares of both Municipal Bond Fund and Intermediate Tax/AMT Free Fund, and acts as agent of each Fund in the continuing offer of such shares.

11

Table of Contents

Administrator. SDI is also the administrator of the Institutional Class and Investment Class shares of Intermediate Tax/AMT Free Fund, pursuant to the Fund’s above-referenced Underwriting and Distribution Services Agreement. DeAM, Inc. serves as the administrator for Municipal Bond Fund, pursuant to its Administrative Agreement.

Trustees and Officers. The Trustees of Scudder Tax Free Trust (of which Intermediate Tax/AMT Free Fund is a series) are different from those of Scudder MG Investments Trust (of which Municipal Bond Fund is a series). As more fully described in the statement of additional information for Intermediate Tax/AMT Free Fund, which is available upon request, the following individuals comprise the Board of Trustees of Scudder Tax Free Trust: Dawn-Marie Driscoll (Chair), Henry P. Becton, Jr., Keith R. Fox, Louis E. Levy, Jean Gleason Stromberg, Jean C. Tempel, and Carl W. Vogt. In addition, the officers of Scudder Tax Free Trust are different from those of Scudder MG Investments Trust. Please see the Merger SAI for further details.

Independent Registered Public Accounting Firm (“Auditors”). PricewaterhouseCoopers LLP serves as Auditors for both Municipal Bond Fund and Intermediate Tax/AMT Free Fund.

Charter Documents. Municipal Bond Fund is a series of Scudder MG Investments Trust, a Delaware business trust governed by Delaware law. Intermediate Tax/AMT Free Fund is a series of Scudder Tax Free Trust, a Massachusetts business trust governed by Massachusetts law. Municipal Bond Fund is governed by an Agreement and Declaration of Trust dated September 13, 1993, as amended from time to time. Intermediate Tax/AMT Free Fund is governed by an Amended and Restated Declaration of Trust dated December 8, 1987, as amended from time to time. Each charter document is referred to herein as a Declaration of Trust. These charter documents are similar but not identical to one another, and therefore shareholders of the Funds may have different rights. Additional information about each Fund’s Declaration of Trust is provided below.

Shareholders of Municipal Bond Fund and Intermediate Tax/AMT Free Fund have a number of rights in common. Shares of each Fund entitle their holders to one vote per share, with fractional shares voting proportionally; however, a separate vote will be taken by the applicable Fund or class of shares on matters affecting the particular Fund or class, as determined by its Trustees. For example, a change in a fundamental investment policy for a particular Fund would be voted upon only by shareholders of that Fund and adoption of a distribution plan relating to a particular class and requiring shareholder approval would be voted upon only by shareholders of that class. Shares of each Fund have noncumulative voting rights with respect to the election of Trustees. Neither trust is required to hold annual meetings of their shareholders. However, meetings of the shareholders may be called for the purpose of electing Trustees and for such other purposes as may be prescribed by law, by the applicable Declaration of Trust, or by the applicable By-Laws. Shares of both Funds have no preemptive, conversion or subscription rights, and are fully-paid, non-assessable (except as set forth below) and transferable. Shares of both Funds are entitled to dividends as declared by its Trustees, and if a Fund were liquidated, each class of shares of that Fund would receive the net assets of the Fund attributable to said class.

Under Massachusetts law, shareholders of a Massachusetts business trust could, under certain circumstances, be held personally liable for the obligations of a fund. The Declaration of Trust for Scudder Tax Free Trust, however, disclaims shareholder liability for the acts or obligations of Intermediate Tax/AMT Free Fund and permits notice of

12

Table of Contents

such disclaimer to be given in each agreement, obligation or instrument entered into or executed by the Fund or the Trust’s Trustees. Moreover, the Declaration of Trust provides for indemnification out of Fund property for all loss and expense of any shareholder held personally liable for the obligations of the Fund, and the Fund will be covered by insurance which the Trustees consider adequate to cover foreseeable tort claims. Thus, the risk of a shareholder incurring financial loss on account of shareholder liability is considered by Deutsche Asset Management remote and not material, since it is limited to circumstances in which a disclaimer is inoperative and the Fund itself is unable to meet its obligations. Under Delaware law, shareholders of a Delaware business trust also could, under certain circumstances, be held liable for the obligations of a fund. The Declaration of Trust for Scudder MG Investments Trust, of which Municipal Bond Fund is a series, contains substantially similar provisions regarding the disclaimer of liability and indemnification of shareholders as the Declaration of Trust for Scudder Tax Free Trust.

All consideration received by a trust for the issue or sale of shares of the applicable Fund, together with all assets in which such consideration is invested or reinvested, and all income, earnings, profits and proceeds, including proceeds from sale, exchange or liquidation of assets, are held and accounted for separately from the other assets of the trust and belong irrevocably to the Fund for all purposes, subject only to the rights of creditors.

Either trust or any series thereof (including the Funds) may be terminated by vote of its Trustees, or at a meeting of its shareholders by vote of the holders of a majority of the shares of the trust or series outstanding and entitled to vote. The Declaration of Trust governing Municipal Bond Fund may be amended and/or restated at any time by an instrument in writing signed by a majority of the then Trustees and, if required, by approval of such amendment by a majority of the shares voted when a quorum is present. The Declaration of Trust governing Intermediate Tax/AMT Free Fund may be amended by a vote of the holders of a majority of the shares outstanding and entitled to vote. The Declaration of Trust governing Intermediate Tax/AMT Free Fund may also be amended by the Trustees without shareholder consent if the Trustees deem it necessary to conform the Declaration of Trust to the requirements of applicable federal or state laws or regulations of the Internal Revenue Code, or if they determine that such a change does not materially adversely affect the rights of the shareholders.

The voting powers of shareholders of each Fund are substantially similar. However, the Declaration of Trust governing Intermediate Tax/AMT Free Fund provides expressly that shareholders have the power to vote to the same extent as the stockholders of a Massachusetts business corporation as to whether a court action, proceeding or claim should be brought or maintained derivatively or as a class action on behalf of the trust or the shareholders.

Quorum for a shareholder meeting of Scudder MG Investments Trust is 40% of the shares entitled to vote in person or by proxy, except that, where the vote is by series or class, then the quorum is 40% of the aggregate number of shares of that series or class entitled to vote. Quorum for a shareholder meeting of Scudder Tax Free Trust is one-third of the shares entitled to vote in person or by proxy, and, where the vote is by series or by class, the quorum is one-third of the aggregate number of shares of that series or class entitled to vote.

13

Table of Contents

The foregoing is a very general summary of certain provisions of the Declarations of Trust governing Municipal Bond Fund and Intermediate Tax/AMT Free Fund. It is qualified in its entirety by reference to the charter documents themselves.

IV. INFORMATION ABOUT THE PROPOSED COMBINATION

General. The shareholders of Municipal Bond Fund are being asked to approve a combination between Municipal Bond Fund and Intermediate Tax/AMT Free Fund pursuant to an Agreement and Plan of Reorganization between the Funds (the “Agreement”), a form of which is attached to this Prospectus/Proxy Statement as Exhibit A.

The combination is structured as a transfer of all of the assets of Municipal Bond Fund to Intermediate Tax/AMT Free Fund in exchange for the assumption by Intermediate Tax/AMT Free Fund of all of the liabilities of Municipal Bond Fund and for the issuance and delivery to Municipal Bond Fund of Merger Shares of Intermediate Tax/AMT Free Fund equal in aggregate value to the net value of the assets transferred to Intermediate Tax/AMT Free Fund.

After receipt of the Merger Shares, Municipal Bond Fund will distribute the Merger Shares to its shareholders, in proportion to their existing shareholdings, in complete liquidation of Municipal Bond Fund, and the legal existence of Municipal Bond Fund as a series of Scudder MG Investments Trust will be terminated. Each shareholder of Municipal Bond Fund will receive a number of full and fractional Merger Shares of the same class(es) as, and equal in value at the date of the exchange to, the aggregate value of the shareholder’s Municipal Bond Fund shares.

Prior to the date of the combination, Municipal Bond Fund will sell all investments that are not consistent with the current investment objective, policies and restrictions of Intermediate Tax/AMT Free Fund, or whose income is subject to the federal AMT, and declare a taxable distribution which, together with all previous distributions, will have the effect of distributing to shareholders all of its net investment income and net realized capital gains, if any, through the date of the combination. The sale of such investments may increase the taxable distribution to shareholders of the Municipal Bond Fund occurring prior to the combination above that which they would have received absent the combination.

The Trustees of Municipal Bond Fund have voted unanimously to approve the Agreement and the proposed combination and to recommend that shareholders also approve the combination. The actions contemplated by the Agreement and the related matters described therein will be consummated only if approved by the affirmative vote of a majority of the outstanding voting securities of Municipal Bond Fund entitled to vote at the special meeting.

In the event that the combination does not receive the required shareholder approval, each Fund will continue to be managed as a separate Fund in accordance with its current investment objectives and policies, and the Trustees of each Fund may consider such alternatives as may be in the best interests of each Fund’s respective shareholders.

14

Table of Contents

Background and Trustees’ Considerations Relating to the Proposed Combination. Deutsche Asset Management first proposed the combination to the Trustees of Municipal Bond Fund at a meeting held in February 2004. The combination was presented to the Trustees and considered by them as part of a broader program initiated by Deutsche Asset Management to consolidate its mutual fund lineup. This initiative is intended to:

| • | Eliminate redundancies within the Scudder fund family by reorganizing and combining certain funds; and |

| • | Adjust or eliminate share classes as necessary to maximize potential economies of scale. |

The Trustees of Municipal Bond Fund, including all Trustees who are not “interested persons” of the Fund (as defined by the 1940 Act), conducted a thorough review of the potential implications of this program for Municipal Bond Fund as well as the various other funds for which they serve as trustees or directors. They were assisted in this review by their independent legal counsel. Following the February 2004 meeting, the Trustees met on several occasions to review and discuss this program, including the proposed combination, both among themselves and with representatives of Deutsche Asset Management. In the course of their review, the Trustees requested and received substantial additional information and suggested numerous changes to Deutsche Asset Management’s program, many of which were accepted.

On September 16, 2004, the Trustees of Municipal Bond Fund, including all Trustees who are not “interested persons” of the Fund (as defined by the 1940 Act), approved the terms of the combination. The Trustees have also unanimously agreed to recommend that the combination be approved by shareholders.

In determining to recommend that the shareholders of Municipal Bond Fund approve the combination, the Trustees considered, among other factors:

| • | The fees and expense ratios of each Fund, including comparisons between the expenses of Municipal Bond Fund and the estimated operating expenses of the combined fund, and between the estimated operating expenses of the combined fund and other mutual funds with similar investment objectives; |

| • | That DeIM had agreed to cap the combined fund’s operating expenses for a two-year period at levels below Municipal Bond Fund’s current operating expenses; |

| • | The terms and conditions of the combination and whether the combination would result in the dilution of shareholder interests; |

| • | Similarities between Municipal Bond Fund’s and Intermediate Tax/AMT Free Fund’s investment objectives, policies, restrictions and portfolios; |

| • | The service features available to shareholders of Municipal Bond Fund and Intermediate Tax/AMT Free Fund; |

| • | That the costs of the combination would be borne by Deutsche Asset Management; |

| • | Prospects for the combined fund to attract additional assets; |

15

Table of Contents

| • | The tax consequences of the combination on Municipal Bond Fund, Intermediate Tax/AMT Free Fund and their respective shareholders, including, in particular, the historical and pro forma tax attributes of Municipal Bond Fund and Intermediate Tax/AMT Free Fund and the effect of the combination on certain tax losses of the Funds (see “Federal Income Tax Consequences” below). The Trustees concluded that lower fund operating expenses and other benefits to shareholders resulting from the combination outweighed the potentially less favorable tax attributes of the combined fund.; and |

| • | The investment performance of Municipal Bond Fund and Intermediate Tax/AMT Free Fund. |

The Trustees also gave extensive consideration to possible economies of scale that might be realized by Deutsche Asset Management in connection with the combination, as well as the other fund combinations included in the Deutsche Asset Management restructuring proposal. The Trustees concluded that these economies were appropriately reflected in the fee and expense arrangements of Intermediate Tax/AMT Free Fund, as proposed to be revised upon completion of the combination.

The Trustees considered the impact of the combination on the total expenses to be borne by shareholders of the Fund. The Trustees also considered that the combination would permit the shareholders of the Fund to pursue similar investment goals in a larger fund.

Based on all of the foregoing, the Trustees concluded that Municipal Bond Fund’s participation in the combination would be in the best interests of the Fund and would not dilute the interests of the Fund’s existing shareholders. The Trustees of Municipal Bond Fund, including all of the Trustees who are not “interested persons” of the Fund (as defined in the 1940 Act), unanimously recommend that shareholders of the Fund approve the combination.

Agreement and Plan of Reorganization. The proposed combination will be governed by the Agreement, a form of which is attached as Exhibit A. The Agreement provides that Intermediate Tax/AMT Free Fund will acquire all of the assets of Municipal Bond Fund solely in exchange for the assumption by Intermediate Tax/AMT Free Fund of all liabilities of Municipal Bond Fund and for the issuance of Merger Shares equal in value to the value of the transferred assets net of assumed liabilities. The Merger Shares will be issued on the next full business day (the “Exchange Date”) following the time as of which the Funds’ shares are valued for determining net asset value for the combination (4:00 p.m. Eastern time on December 17, 2004, or such other date and time as may be agreed upon by the parties (the “Valuation Time”)). The following discussion of the Agreement is qualified in its entirety by the full text of the Agreement.

Municipal Bond Fund will transfer all of its assets to Intermediate Tax/AMT Free Fund, and in exchange, Intermediate Tax/AMT Free Fund will assume all liabilities of Municipal Bond Fund and deliver to Municipal Bond Fund a number of full and fractional Merger Shares of each class having an aggregate net asset value equal to the value of the assets of Municipal Bond Fund attributable to shares of the corresponding class of Municipal Bond Fund, less the value of the liabilities of Municipal Bond Fund assumed by Intermediate Tax/AMT Free Fund attributable to shares of such class of Municipal Bond Fund. Immediately following the transfer of assets on the Exchange Date, Municipal Bond Fund will distribute pro rata to its shareholders of record as of the

16

Table of Contents

Valuation Time the full and fractional Merger Shares received by Municipal Bond Fund, with Merger Shares of each class being distributed to holders of shares of the corresponding class of Municipal Bond Fund. As a result of the proposed combination, each shareholder of Municipal Bond Fund will receive a number of Merger Shares of each class equal in aggregate value at the Valuation Time to the value of the Municipal Bond Fund shares of the corresponding class surrendered by the shareholder. This distribution will be accomplished by the establishment of accounts on the share records of Intermediate Tax/AMT Free Fund in the name of such Municipal Bond Fund shareholders, each account representing the respective number of full and fractional Merger Shares of each class due to the respective shareholder. New certificates for Merger Shares will not be issued.

The Trustees of each Fund have determined that the proposed combination is in the best interests of their respective Fund and that the interests of their respective Fund’s shareholders will not be diluted as a result of the transactions contemplated by the Agreement.

The consummation of the combination is subject to the conditions set forth in the Agreement. The Agreement may be terminated and the combination abandoned (i) by mutual consent of Intermediate Tax/AMT Free Fund and Municipal Bond Fund, (ii) by either party if the combination shall not be consummated by February 28, 2005 or (iii) if any condition set forth in the Agreement has not been fulfilled and has not been waived by the party entitled to its benefits, by such party.

If shareholders of Municipal Bond Fund approve the combination, both Funds agree to coordinate their respective portfolios, subject to each Fund’s respective investment objective and any investment restrictions, from the date of the Agreement up to and including the Exchange Date in order that, when the assets of Municipal Bond Fund are added to the portfolio of Intermediate Tax/AMT Free Fund, the resulting portfolio will meet the investment objective, policies and restrictions of Intermediate Tax/AMT Free Fund.

Except for the trading costs associated with the coordination described above, the fees and expenses for the combination and related transactions are estimated to be $227,828. All fees and expenses, including legal and accounting expenses, portfolio transfer taxes (if any), the trading costs described above and any other expenses incurred in connection with the consummation of the combination and related transactions contemplated by the Agreement, will be borne by Deutsche Asset Management.

Description of the Merger Shares. Merger Shares will be issued to Municipal Bond Fund’s shareholders in accordance with the Agreement as described above. The Merger Shares will be Institutional Class and Investment Class shares of Intermediate Tax/AMT Free Fund. (Institutional Class and Investment Class shares of Intermediate Tax/AMT Free Fund are not currently offered and are being offered for the first time in connection with the combination.) Each class of Merger Shares has the same characteristics as shares of the corresponding class of Municipal Bond Fund. Your Merger Shares will be treated as having been purchased on the date you purchased your Municipal Bond Fund shares and for the price you originally paid. For more information on the characteristics of each class of Merger Shares, please see the Intermediate Tax/AMT Free Fund Prospectus, a copy of which is included with this Prospectus/Proxy Statement.

17

Table of Contents

Federal Income Tax Consequences. As a condition to each Fund’s obligation to consummate the reorganization, each Fund will receive a tax opinion, from Willkie Farr & Gallagher LLP (which opinion would be based on certain factual representations and certain customary assumptions), to the effect that, on the basis of the existing provisions of the U.S. Internal Revenue Code of 1986, as amended (the “Code”), current administrative rules and court decisions, for federal income tax purposes:

| (i) | the acquisition by Intermediate Tax/AMT Free Fund of all of the assets of Municipal Bond Fund solely in exchange for Merger Shares and the assumption by Intermediate Tax/AMT Free Fund of all of Municipal Bond Fund liabilities followed by the distribution by Municipal Bond Fund to its shareholders of Merger Shares in complete liquidation of Municipal Bond Fund, all pursuant to the plan of reorganization, constitutes a reorganization within the meaning of Section 368(a) of the Code, and Municipal Bond Fund and Intermediate Tax/AMT Free Fund will each be a “party to a reorganization” within the meaning of Section 368(b) of the Code; |

| (ii) | under Section 361 of the Code, no gain or loss will be recognized by Municipal Bond Fund upon the transfer of Municipal Bond Fund’s assets to and the assumption of the Municipal Bond Fund liabilities by Intermediate Tax/AMT Free Fund or upon the distribution of the Merger Shares to Municipal Bond Fund’s shareholders in liquidation of Municipal Bond Fund; |

| (iii) | under Section 354 of the Code, no gain or loss will be recognized by shareholders of Municipal Bond Fund on the exchange of their shares of Municipal Bond Fund for Merger Shares; |

| (iv) | under Section 358 of the Code, the aggregate basis of the Merger Shares received by Municipal Bond Fund’s shareholders will be the same as the aggregate basis of Municipal Bond Fund shares exchanged therefor; |

| (v) | under Section 1223(1) of the Code, the holding periods of the Merger Shares received by the shareholders of Municipal Bond Fund will include the holding periods of Municipal Bond Fund shares exchanged therefor, provided that at the time of the reorganization Municipal Bond Fund shares are held by such shareholders as a capital asset; |

| (vi) | under Section 1032 of the Code, no gain or loss will be recognized by Intermediate Tax/AMT Free Fund upon the receipt of assets of Municipal Bond Fund in exchange for Merger Shares and the assumption by Intermediate Tax/AMT Free Fund of the liabilities of Municipal Bond Fund; |

| (vii) | under Section 362(b) of the Code, the basis in the hands of Intermediate Tax/AMT Free Fund of the assets of Municipal Bond Fund transferred to Intermediate Tax/AMT Free Fund will be the same as the basis of such assets in the hands of Municipal Bond Fund immediately prior to the transfer; and |

| (viii) | under Section 1223(2) of the Code, the holding periods of the assets of Municipal Bond Fund in the hands of Intermediate Tax/AMT Free Fund will include the periods during which such assets were held by Municipal Bond Fund. |

Intermediate Tax/AMT Free Fund’s ability to carry forward the pre-combination losses of Municipal Bond Fund technically will be limited as a result of the combination. The effect of this limitation, however, will depend on the amount of losses

18

Table of Contents

in each fund at the time of the combination. For example, if the combination were to have occurred on April 30, 2004, the effects of such limitation would have had no impact due to the size of Municipal Bond Fund’s pre-combination losses, which equaled approximately 1% of its net asset value.

This description of the federal income tax consequences of the combination is made without regard to the particular facts and circumstances of any shareholder. Shareholders are urged to consult their own tax advisors as to the specific consequences to them of the combination, including the applicability and effect of state, local, non-U.S. and other tax laws.

While as noted above, no tax liability for shareholders is expected to arise directly from the combination, differences in the Funds’ portfolio turnover rates, and net investment income and net realized capital gains may result in future taxable distributions to shareholders arising indirectly from the combination.

The portfolio turnover rate for Intermediate Tax/AMT Free Fund, i.e. the ratio of the lesser of annual sales or purchases to the monthly average value of the portfolio (excluding from both the numerator and the denominator securities with maturities at the time of acquisition of one year or less), for the fiscal year ended May 31, 2004 was 23%. The portfolio turnover rate for Municipal Bond Fund for the fiscal year ended October 31, 2003 was 18%. While these figures do not reflect a significant difference between the Funds, a higher portfolio turnover rate involves greater brokerage and transaction expenses to a fund and may result in the realization of net capital gains, which would be taxable to shareholders when distributed (and, in the case of net short-term capital gains, would be taxed as ordinary income).

Each Fund intends to declare dividends daily and distribute dividends monthly from its net investment income and distribute net realized capital gains after utilization of capital loss carryforwards, if any, in December of each year. An additional distribution may be made if necessary. Shareholders of each Fund can have their dividends and distributions automatically invested in additional shares of the same class of that Fund, or a different fund in the same family of funds, at net asset value and credited to the shareholder’s account on the payment date or, at the shareholder’s election, sent to the shareholder by check. If the Agreement is approved by Municipal Bond Fund’s shareholders, the Fund will pay its shareholders a distribution of all undistributed net investment income and undistributed realized net capital gains (after reduction by any capital loss carryforwards) immediately prior to the Closing (as defined in the Agreement).

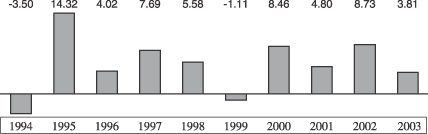

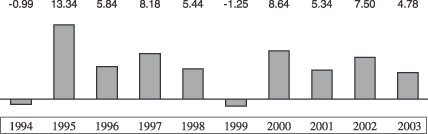

Performance Information. The following information provides some indication of the risks of investing in the Funds. The bar charts show year-to-year changes in Fund performance. The table following the charts shows how each Fund’s performance compares to that of a broad-based market index (which, unlike a Fund, does not have any fees or expenses). Because the inception date for Institutional Class and Investment Class shares of Intermediate Tax/AMT Free Fund is August 31, 2004, performance figures for these classes are not available for periods prior to that date. The bar chart and table reflect the performance of the Fund’s original share class, Class S. Class S shares

19

Table of Contents