Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-4096

MFS MUNICIPAL SERIES TRUST

(Exact name of registrant as specified in charter)

500 Boylston Street, Boston, Massachusetts 02116

(Address of principal executive offices) (Zip code)

Susan S. Newton

Massachusetts Financial Services Company

500 Boylston Street

Boston, Massachusetts 02116

(Name and address of agents for service)

Registrant’s telephone number, including area code: (617) 954-5000

Date of fiscal year end: March 31

Date of reporting period: September 30, 2012

Table of Contents

| ITEM 1. | REPORTS TO STOCKHOLDERS. |

Table of Contents

SEMIANNUAL REPORT

September 30, 2012

MFS® MUNICIPAL INCOME FUND

LMB-SEM

Table of Contents

MFS® MUNICIPAL INCOME FUND

The report is prepared for the general information of shareholders. It is authorized for distribution to prospective investors only when preceded or accompanied by a current prospectus.

NOT FDIC INSURED Ÿ MAY LOSE VALUE Ÿ NO BANK GUARANTEE

Table of Contents

LETTER FROM THE CHAIRMAN AND CEO

Dear Shareholders:

World financial markets face major economic and political challenges. While the European debt crisis continues, there are signs of improvement given the European Central Bank's willingness to backstop troubled sovereigns and the agreement to provide direct financial aid to struggling banks. Economic activity in China, until

recently the world’s growth engine, appears to be bottoming. Even the relatively strong and stable US economy has been affected by uncertainty over the presidential election and the threat of a “fiscal cliff” at year-end. At the same time, global consumer and producer confidence is weak. And a search for safe havens by nervous investors has kept yields historically low on highly rated government bonds, including those issued by Germany and the United States.

But there is also good news: Global economic data have modestly improved, performing slightly better than expected. However, the improvement is too short-lived to be

called a trend. Equity markets have been largely range bound since the Fed extended its quantitative easing program. Equity markets have started to build in expectations of further stimulus activity by the US, European and Chinese central banks. It is hard to know how much of the recent gain in financial markets has been the result of actual economic improvements versus expectations that renewed central bank action will soon lead to an economic rebound.

Through all this uncertainty, managing risk remains a top priority for investors and their advisors. At MFS®, our emphasis on global research is designed to keep our investment process functioning smoothly at all times. Close collaboration among colleagues around the world is vital in periods of uncertainty and heightened volatility. We share ideas and evaluate opportunities across continents and across all investment disciplines and types of investments. We employ this uniquely collaborative approach to build better insights — and better results — for our clients.

Like our investors, we are mindful of the many economic challenges we face at the local, national and international levels. In times like these, it is more important than ever to maintain a long-term view, adhere to time-tested investing principles such as asset allocation and diversification and work closely with investment advisors to research and identify the most suitable opportunities.

Respectfully,

Robert J. Manning

Chairman and Chief Executive Officer

MFS Investment Management®

November 15, 2012

The opinions expressed in this letter are subject to change, may not be relied upon for investment advice, and no forecasts can be guaranteed.

1

Table of Contents

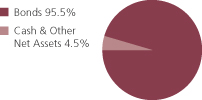

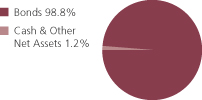

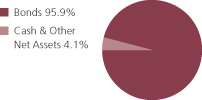

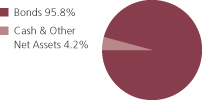

Portfolio structure (i)

| Top five industries (i) | ||||

| Healthcare Revenue-Hospitals | 15.6% | |||

| Universities-Colleges | 8.8% | |||

| Water & Sewer Utility Revenue | 8.1% | |||

| Utilities-Municipal Owned | 7.6% | |||

| General Obligations-General Purpose | 6.7% |

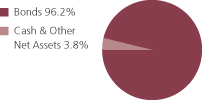

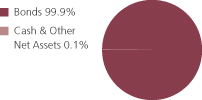

| Composition including fixed income credit quality (a)(i) | ||||

| AAA | 9.5% | |||

| AA | 31.9% | |||

| A | 25.9% | |||

| BBB | 22.7% | |||

| BB | 2.2% | |||

| B | 2.0% | |||

| CCC | 0.1% | |||

| CC (o) | 0.0% | |||

| C | 0.1% | |||

| Not Rated | 2.5% | |||

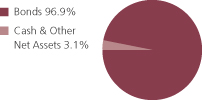

| Cash & Other | 3.1% | |||

| Portfolio facts (i) | ||||

| Average Duration (d) | 8.6 | |||

| Average Effective Maturity (m) | 17.6 yrs. | |||

| (a) | For all securities other than those specifically described below, ratings are assigned to underlying securities utilizing ratings from Moody’s, Fitch, and Standard & Poor’s rating agencies and applying the following hierarchy: If all three agencies provide a rating, the middle rating (after dropping the highest and lowest ratings) is assigned; if two of the three agencies rate a security, the lower of the two is assigned. Ratings are shown in the S&P and Fitch scale (e.g., AAA). Securities rated BBB or higher are considered investment grade. All ratings are subject to change. Not Rated includes fixed income securities, including fixed income futures contracts, which have not been rated by any rating agency. Cash & Other includes cash, other assets less liabilities, offsets to derivative positions, and short-term securities. The fund may not hold all of these instruments. The fund is not rated by these agencies. |

| (d) | Duration is a measure of how much a bond’s price is likely to fluctuate with general changes in interest rates, e.g., if rates rise 1.00%, a bond with a 5-year duration is likely to lose about 5.00% of its value due to the interest rate move. |

| (i) | For purposes of this presentation, the components include the market value of securities, and reflect the impact of the equivalent exposure of derivative positions, if any. These amounts may be negative from time to time. The bond component will include any accrued interest amounts. Equivalent exposure is a calculated amount that translates the derivative position into a reasonable approximation of the amount of the underlying asset that the portfolio would have to hold at a given point in time to have the same price sensitivity that results from the portfolio’s ownership of the derivative contract. When dealing with derivatives, equivalent exposure is a more representative measure of the potential impact of a position on portfolio performance than market value. Where the fund holds convertible bonds, these are treated as part of the equity portion of the portfolio. |

2

Table of Contents

Portfolio Composition – continued

| (m) | In determining an instrument’s effective maturity for purposes of calculating the fund’s dollar-weighted average effective maturity, MFS uses the instrument’s stated maturity or, if applicable, an earlier date on which MFS believes it is probable that a maturity-shortening device (such as a put, pre-refunding or prepayment) will cause the instrument to be repaid. Such an earlier date can be substantially shorter than the instrument’s stated maturity. |

| (o) | Less than 0.1%. |

Percentages are based on net assets as of 9/30/12.

The portfolio is actively managed and current holdings may be different.

3

Table of Contents

Fund expenses borne by the shareholders during the period,

April 1, 2012 through September 30, 2012

As a shareholder of the fund, you incur two types of costs: (1) transaction costs, including sales charges (loads) on certain purchase or redemption payments, and (2) ongoing costs, including management fees; distribution and service (12b-1) fees; and other fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period April 1, 2012 through September 30, 2012.

Actual Expenses

The first line for each share class in the following table provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second line for each share class in the following table provides information about hypothetical account values and hypothetical expenses based on the fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads). Therefore, the second line for each share class in the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

4

Table of Contents

Expense Table – continued

| Share Class | Annualized Ratio | Beginning Account Value 4/01/12 | Ending Account Value | Expenses Paid During 4/01/12-9/30/12 | ||||||||||||||

| A | Actual | 0.77% | $1,000.00 | $1,057.20 | $3.97 | |||||||||||||

| Hypothetical (h) | 0.77% | $1,000.00 | $1,021.21 | $3.90 | ||||||||||||||

| B | Actual | 1.51% | $1,000.00 | $1,051.98 | $7.77 | |||||||||||||

| Hypothetical (h) | 1.51% | $1,000.00 | $1,017.50 | $7.64 | ||||||||||||||

| C | Actual | 1.51% | $1,000.00 | $1,053.07 | $7.77 | |||||||||||||

| Hypothetical (h) | 1.51% | $1,000.00 | $1,017.50 | $7.64 | ||||||||||||||

| I | Actual | 0.52% | $1,000.00 | $1,058.59 | $2.68 | |||||||||||||

| Hypothetical (h) | 0.52% | $1,000.00 | $1,022.46 | $2.64 | ||||||||||||||

| A1 | Actual | 0.52% | $1,000.00 | $1,057.33 | $2.68 | |||||||||||||

| Hypothetical (h) | 0.52% | $1,000.00 | $1,022.46 | $2.64 | ||||||||||||||

| B1 | Actual | 1.28% | $1,000.00 | $1,054.53 | $6.59 | |||||||||||||

| Hypothetical (h) | 1.28% | $1,000.00 | $1,018.65 | $6.48 | ||||||||||||||

| (h) | 5% class return per year before expenses. |

| (p) | Expenses paid are equal to each class’ annualized expense ratio, as shown above, multiplied by the average account value over the period, multiplied by the number of days in the period, divided by the number of days in the year. Expenses paid do not include any applicable sales charges (loads). If these transaction costs had been included, your costs would have been higher. |

Expenses Impacting the Table

Expense ratios include 0.03% of investment related expenses from inverse floaters that are outside of the expense cap arrangement (See Note 3 of the Notes to Financial Statements).

5

Table of Contents

9/30/12 (unaudited)

The Portfolio of Investments is a complete list of all securities owned by your fund. It is categorized by broad-based asset classes.

| Municipal Bonds - 95.6% | ||||||||

| Issuer | Shares/Par | Value ($) | ||||||

| Airport Revenue - 2.9% | ||||||||

| Atlanta, GA, Airport Rev., “B”, 5%, 2025 | $ | 1,415,000 | $ | 1,680,853 | ||||

| Atlanta, GA, Airport Rev., “B”, 5%, 2026 | 800,000 | 950,328 | ||||||

| Chicago, IL, O’Hare International Airport Rev., Third Lien, “A”, 5.625%, 2035 | 7,125,000 | 8,368,028 | ||||||

| Cleveland, OH, Airport System Rev., “A”, AGM, 5%, 2030 | 1,640,000 | 1,831,404 | ||||||

| Cleveland, OH, Airport System Rev., “A”, AGM, 5%, 2031 | 1,095,000 | 1,221,878 | ||||||

| Dallas Fort Worth, TX, International Airport Rev., “D”, 5%, 2038 | 12,440,000 | 13,427,985 | ||||||

| Houston, TX, Airport System Rev., “B”, 5%, 2026 | 1,855,000 | 2,164,804 | ||||||

| Houston, TX, Airport System Rev., Subordinate Lien, “A”, 5%, 2031 | 2,345,000 | 2,641,431 | ||||||

| Los Angeles, CA, Department of Airports Rev. (Los Angeles International), “A”, 5%, 2029 | 2,990,000 | 3,503,144 | ||||||

| Massachusetts Port Authority Rev., “A”, 5%, 2037 | 470,000 | 525,291 | ||||||

| Miami-Dade County, FL, Aviation Rev., “B”, AGM, 5%, 2035 | 5,885,000 | 6,561,069 | ||||||

| Niagara, NY, Frontier Transportation Authority Rev. (Buffalo-Niagara International Airport), NATL, 5.875%, 2013 | 1,485,000 | 1,487,331 | ||||||

| Port Authority of NY & NJ, Special Obligation Rev. (JFK International Air Terminal LLC), 6%, 2036 | 2,315,000 | 2,706,536 | ||||||

| San Francisco, CA, City & County Airports Commission, International Airport Rev., “A”, 5%, 2028 | 6,000,000 | 6,821,040 | ||||||

| San Jose, CA, Airport Rev., “A-2”, 5.25%, 2034 | 7,570,000 | 8,480,898 | ||||||

|

| |||||||

| $ | 62,372,020 | |||||||

| General Obligations - General Purpose - 6.6% | ||||||||

| Allegheny County, PA, “C-70”, 5%, 2037 | $ | 2,010,000 | $ | 2,218,397 | ||||

| Chicago, IL, Greater Chicago Metropolitan Water Reclamation District, “C”, 5%, 2029 | 9,145,000 | 10,800,977 | ||||||

| Commonwealth of Massachusetts, “A”, AMBAC, 5.5%, 2030 | 5,000,000 | 6,987,800 | ||||||

| Commonwealth of Puerto Rico, “A”, ETM, FGIC, 5.5%, 2015 (c) | 5,585,000 | 6,358,355 | ||||||

| Commonwealth of Puerto Rico, Public Improvement, “A”, 5.5%, 2039 | 2,000,000 | 2,063,760 | ||||||

| Commonwealth of Puerto Rico, Public Improvement, “B”, 6.5%, 2037 | 2,180,000 | 2,418,972 | ||||||

| Detroit, MI, 5.25%, 2035 | 5,000,000 | 5,496,450 | ||||||

| Las Vegas Valley, NV, Water District, “C”, 5%, 2029 | 8,145,000 | 9,493,893 | ||||||

| Luzerne County, PA, AGM, 6.75%, 2023 | 1,200,000 | 1,421,928 | ||||||

| New York, NY, “B”, 5%, 2020 | 10,730,000 | 13,341,360 | ||||||

| Palm Beach County, FL, Public Improvement Rev. “2”, 5.375%, 2028 | 1,000,000 | 1,182,800 | ||||||

| State of California, 5%, 2024 | 4,365,000 | 5,245,421 | ||||||

6

Table of Contents

Portfolio of Investments (unaudited) – continued

| Issuer | Shares/Par | Value ($) | ||||||

| Municipal Bonds - continued | ||||||||

| General Obligations - General Purpose - continued | ||||||||

| State of California, 5.25%, 2028 | $ | 2,965,000 | $ | 3,539,054 | ||||

| State of California, 5.125%, 2033 | 2,155,000 | 2,408,514 | ||||||

| State of California, 6.5%, 2033 | 4,000,000 | 5,054,960 | ||||||

| State of California, 6%, 2039 | 3,000,000 | 3,618,840 | ||||||

| State of Hawaii, “DZ”, 5%, 2031 | 2,230,000 | 2,681,843 | ||||||

| State of Illinois, 5%, 2025 | 1,060,000 | 1,190,274 | ||||||

| State of Louisiana, “C”, 5%, 2026 | 4,380,000 | 5,427,959 | ||||||

| State of Maryland, “C”, 5%, 2019 | 6,890,000 | 8,725,565 | ||||||

| State of Tennessee, “A”, 5%, 2029 | 1,000,000 | 1,224,620 | ||||||

| State of Washington, “A”, 4%, 2030 | 7,585,000 | 8,300,569 | ||||||

| State of Washington, “A”, 5%, 2033 | 5,000,000 | 5,878,300 | ||||||

| Washington Motor Vehicle Fuel Tax, “B”, NATL, 5%, 2032 (u) | 25,010,000 | 28,706,728 | ||||||

|

| |||||||

| $ | 143,787,339 | |||||||

| General Obligations - Improvement - 1.8% | ||||||||

| Columbus, OH, ”A”, 4%, 2028 | $ | 19,075,000 | $ | 21,332,526 | ||||

| Guam Government, “A”, 7%, 2039 | 910,000 | 1,025,333 | ||||||

| Massachusetts Bay Transportation Authority, “A”, ETM, 7%, 2021 (c) | 4,700,000 | 5,436,866 | ||||||

| Massachusetts Bay Transportation Authority, “A”, 7%, 2021 | 3,800,000 | 5,109,176 | ||||||

| Massachusetts Bay Transportation Authority, “C”, ETM, 6.1%, 2013 (c) | 3,640,000 | 3,728,052 | ||||||

| New Orleans, LA, 5%, 2030 | 660,000 | 745,820 | ||||||

| New Orleans, LA, 5%, 2031 | 790,000 | 887,684 | ||||||

|

| |||||||

| $ | 38,265,457 | |||||||

| General Obligations - Schools - 4.5% | ||||||||

| Beverly Hills, CA, Unified School District (Election of 2008), Capital Appreciation, 0%, 2031 | $ | 2,010,000 | $ | 962,408 | ||||

| Beverly Hills, CA, Unified School District (Election of 2008), Capital Appreciation, 0%, 2032 | 2,035,000 | 924,338 | ||||||

| Beverly Hills, CA, Unified School District (Election of 2008), Capital Appreciation, 0%, 2033 | 4,070,000 | 1,751,321 | ||||||

| Chesterfield County, SC, School District, 5%, 2025 | 2,250,000 | 2,750,738 | ||||||

| Chicago, IL, Board of Education, NATL, 6.25%, 2015 | 15,670,000 | 16,172,380 | ||||||

| Chicago, IL, Board of Education, “A”, 5%, 2041 | 2,700,000 | 2,944,188 | ||||||

| Denver, CO, City & County School District No. 1, 5%, 2024 | 10,000,000 | 12,302,100 | ||||||

| Escondido, CA, Union High School District (Election of 2008), Capital Appreciation, “A”, ASSD GTY, 0%, 2030 | 4,495,000 | 2,090,714 | ||||||

| Escondido, CA, Union High School District (Election of 2008), Capital Appreciation, “A”, ASSD GTY, 0%, 2031 | 4,015,000 | 1,759,574 | ||||||

| Escondido, CA, Union High School District (Election of 2008), Capital Appreciation, “A”, ASSD GTY, 0%, 2032 | 2,825,000 | 1,166,725 | ||||||

7

Table of Contents

Portfolio of Investments (unaudited) – continued

| Issuer | Shares/Par | Value ($) | ||||||

| Municipal Bonds - continued | ||||||||

| General Obligations - Schools - continued | ||||||||

| Escondido, CA, Union High School District (Election of 2008), Capital Appreciation, “A”, ASSD GTY, 0%, 2033 | $ | 2,785,000 | $ | 1,077,879 | ||||

| Florence, AL, Board of Education, Tax Anticipation School Warrants, 4%, 2025 | 1,225,000 | 1,366,255 | ||||||

| Florida Board of Education, Capital Outlay, 9.125%, 2014 | 795,000 | 841,905 | ||||||

| Florida Board of Education, Capital Outlay, “E”, 5%, 2023 | 250,000 | 305,925 | ||||||

| Florida Board of Education, Capital Outlay, ETM, 9.125%, 2014 (c) | 665,000 | 742,632 | ||||||

| Florida Board of Education, Public Education, “J”, 5%, 2033 | 1,000,000 | 1,041,820 | ||||||

| Fresno, CA, Unified School District, “A”, NATL, 6.55%, 2020 | 1,225,000 | 1,287,242 | ||||||

| Hartnell, CA, Community College District (Election of 2002), Capital Appreciation, “D”, 0%, 2039 | 9,645,000 | 1,691,251 | ||||||

| Knox County, KY, SYNCORA, 5.5%, 2014 (c) | 640,000 | 709,722 | ||||||

| Knox County, KY, SYNCORA, 5.625%, 2014 (c) | 1,150,000 | 1,278,363 | ||||||

| Lancaster, TX, Independent School District, Capital Appreciation, AGM, 0%, 2014 (c) | 2,250,000 | 1,083,195 | ||||||

| Lancaster, TX, Independent School District, Capital Appreciation, AGM, 0%, 2014 (c) | 2,000,000 | 905,360 | ||||||

| Los Angeles, CA, Community College District (Election of 2008), “C”, 5.25%, 2039 | 5,000,000 | 5,802,150 | ||||||

| Los Angeles, CA, Unified School District, “D”, 5%, 2034 | 825,000 | 934,181 | ||||||

| Merced, CA, Union High School District, Capital Appreciation, “A”, ASSD GTY, 0%, 2030 | 580,000 | 245,120 | ||||||

| Monongalia County, WV, Board of Education, 5%, 2029 | 2,445,000 | 2,882,851 | ||||||

| Monongalia County, WV, Board of Education, 5%, 2031 | 675,000 | 787,867 | ||||||

| Monongalia County, WV, Board of Education, 5%, 2033 | 965,000 | 1,114,179 | ||||||

| Oceanside, CA, Unified School District, Capital Appreciation, ASSD GTY, 0%, 2024 | 2,900,000 | 1,777,845 | ||||||

| Oceanside, CA, Unified School District, Capital Appreciation, ASSD GTY, 0%, 2027 | 1,930,000 | 1,002,017 | ||||||

| Oceanside, CA, Unified School District, Capital Appreciation, ASSD GTY, 0%, 2029 | 3,915,000 | 1,824,233 | ||||||

| Oceanside, CA, Unified School District, Capital Appreciation, ASSD GTY, 0%, 2030 | 4,335,000 | 1,910,218 | ||||||

| Reading, PA, School District, “A”, 5%, 2020 | 1,000,000 | 1,154,370 | ||||||

| San Marcos, TX, Independent School District, PSF, 5.625%, 2014 (c) | 2,000,000 | 2,194,740 | ||||||

| San Marcos, TX, Independent School District, PSF, 5.625%, 2014 (c) | 2,000,000 | 2,194,740 | ||||||

| San Mateo County, CA, Community College District (2005 Election), Capital Appreciation, “A”, NATL, 0%, 2026 | 5,100,000 | 3,004,512 | ||||||

| Schertz-Cibolo-Universal City, TX, Independent School District, PSF, 5%, 2036 | 10,000,000 | 10,906,900 | ||||||

| Sunnyvale, TX, Independent School District, PSF, 5.25%, 2028 | 1,900,000 | 2,029,257 | ||||||

| Wattsburg, PA, Public School Building Authority Rev., Capital Appreciation, NATL, 0%, 2029 | 2,150,000 | 1,038,085 | ||||||

8

Table of Contents

Portfolio of Investments (unaudited) – continued

| Issuer | Shares/Par | Value ($) | ||||||

| Municipal Bonds - continued | ||||||||

| General Obligations - Schools - continued | ||||||||

| West Contra Costa, CA, Unified School District (Election of 2005), Capital Appreciation, “C”, ASSD GTY, 0%, 2029 | $ | 3,440,000 | $ | 1,600,254 | ||||

| Whittier, CA, Union High School District, Capital Appreciation, 0%, 2034 | 2,005,000 | 548,107 | ||||||

|

| |||||||

| $ | 98,107,661 | |||||||

| Healthcare Revenue - Hospitals - 15.3% | ||||||||

| Allegheny County, PA, Hospital Development Authority Rev. (West Penn Allegheny Health), “A”, 5%, 2028 | $ | 255,000 | $ | 194,489 | ||||

| Allegheny County, PA, Hospital Development Authority Rev. (West Penn Allegheny Health), “A”, 5.375%, 2040 | 3,995,000 | 3,029,888 | ||||||

| Baxter County, AR, Hospital Rev., 5.375%, 2014 | 10,000 | 10,032 | ||||||

| Brunswick, GA, Hospital Authority Rev. (Glynn-Brunswick Memorial Hospital), 5.625%, 2034 | 1,320,000 | 1,476,974 | ||||||

| California Health Facilities Financing Authority Rev. (St. Joseph Health System), “A”, 5.75%, 2039 | 2,580,000 | 2,950,875 | ||||||

| California Health Facilities Financing Authority Rev. (Sutter Health), “D”, 5.25%, 2031 | 5,000,000 | 5,870,000 | ||||||

| California Statewide Communities Development Authority Rev. (Enloe Medical Center), CALHF, 5.75%, 2038 | 2,640,000 | 2,869,258 | ||||||

| California Statewide Communities Development Authority Rev. (Kaiser Permanente), “A”, 5%, 2042 | 8,170,000 | 8,979,484 | ||||||

| Citrus County, FL, Hospital Development Authority Rev. (Citrus Memorial Hospital), 6.25%, 2023 | 350,000 | 351,810 | ||||||

| Cullman County, AL, Health Care Authority (Cullman Regional Medical Center), “A”, 6.75%, 2029 | 3,550,000 | 3,845,147 | ||||||

| DeKalb County, GA, Hospital Authority Rev. (DeKalb Medical Center, Inc.), 6.125%, 2040 | 4,850,000 | 5,610,480 | ||||||

| Florence County, SC, Hospital Rev. (McLeod Regional Medical Center), “A”, AGM, 5.25%, 2034 | 5,000,000 | 5,185,950 | ||||||

| Grundy County, MO, Industrial Development Authority, Health Facilities Rev. (Wright Memorial Hospital), 6.75%, 2034 | 1,410,000 | 1,601,055 | ||||||

| Harris County, TX, Health Facilities Development Corp., Hospital Rev. (Memorial Hermann Healthcare Systems), “B”, 7%, 2027 | 1,795,000 | 2,211,961 | ||||||

| Harris County, TX, Health Facilities Development Corp., Hospital Rev. (Memorial Hermann Healthcare Systems), “B”, 7.25%, 2035 | 2,050,000 | 2,562,849 | ||||||

| Harris County, TX, Health Facilities Development Corp., Hospital Rev. (Texas Children’s Hospital Project), “A”, ETM, 5.375%, 2015 (c) | 4,300,000 | 4,314,792 | ||||||

| Harrison County, TX, Health Facilities Development Corp., Hospital Rev. (Good Shepherd Health System), 5.25%, 2028 | 5,000,000 | 5,388,250 | ||||||

| Henrico County, VA, Industrial Development Authority Rev. (Bon Secours Health Systems, Inc.), RIBS, FRN, AGM, 11.171%, 2027 (p) | 4,700,000 | 6,495,306 | ||||||

9

Table of Contents

Portfolio of Investments (unaudited) – continued

| Issuer | Shares/Par | Value ($) | ||||||

| Municipal Bonds - continued | ||||||||

| Healthcare Revenue - Hospitals - continued | ||||||||

| Hillsborough County, FL, Industrial Development Authority Rev. (University Community Hospital), NATL, ETM, 6.5%, 2019 (c) | $ | 1,000,000 | $ | 1,239,260 | ||||

| Hillsborough County, FL, Industrial Development Authority Rev. (University Community Hospital), “A”, 5.625%, 2018 (c) | 300,000 | 382,200 | ||||||

| Illinois Finance Authority Rev. (Edward Hospital), “A”, AMBAC, 5.5%, 2040 | 3,040,000 | 3,244,653 | ||||||

| Illinois Finance Authority Rev. (KishHealth Systems Obligated Group), 5.75%, 2028 | 2,990,000 | 3,402,889 | ||||||

| Illinois Finance Authority Rev. (O.S.F. Healthcare Systems) “A”, 7%, 2029 | 2,975,000 | 3,571,488 | ||||||

| Illinois Finance Authority Rev. (O.S.F. Healthcare Systems) “A”, 7.125%, 2037 | 2,445,000 | 2,953,095 | ||||||

| Illinois Finance Authority Rev. (Provena Health), “A”, 7.75%, 2034 | 3,685,000 | 4,766,400 | ||||||

| Illinois Finance Authority Rev. (Resurrection Health), 6.125%, 2025 | 6,900,000 | 8,005,380 | ||||||

| Illinois Finance Authority Rev. (Silver Cross Hospital & Medical Centers), 6.875%, 2038 | 1,500,000 | 1,798,455 | ||||||

| Illinois Finance Authority Rev. (Silver Cross Hospital & Medical Centers), 7%, 2044 | 2,455,000 | 2,945,460 | ||||||

| Illinois Finance Authority Rev. (Silver Cross Hospital & Medical Centers), “A”, 5.5%, 2030 | 2,975,000 | 3,230,434 | ||||||

| Illinois Health Facilities Authority Rev. (Riverside Health Systems), 5.75%, 2012 (c) | 2,625,000 | 2,641,433 | ||||||

| Indiana Finance Authority, Hospital Rev. (Deaconess Hospital, Inc.), “A”, 6.75%, 2039 | 3,000,000 | 3,547,920 | ||||||

| Indiana Finance Authority, Hospital Rev. (Parkview Health System), 5%, 2029 | 1,585,000 | 1,804,681 | ||||||

| Indiana Health & Educational Facilities Authority, Hospital Rev. (Clarian Hospital), “B”, 5%, 2033 | 2,490,000 | 2,636,786 | ||||||

| Indiana Health & Educational Facilities Authority, Hospital Rev. (Deaconess Hospital), “A”, AMBAC, 5.375%, 2034 | 2,640,000 | 2,711,887 | ||||||

| Jacksonville, FL, Health Facilities Rev. (Ascension Health), “A”, 5.25%, 2032 | 1,000,000 | 1,014,250 | ||||||

| Jefferson Parish, LA, Hospital Rev., Hospital Service District No. 1 (West Jefferson Medical Center), “B”, AGM, 5.25%, 2028 | 1,980,000 | 2,206,393 | ||||||

| Jefferson Parish, LA, Hospital Service District No. 2 (East Jefferson General Hospital), 6.25%, 2031 | 3,355,000 | 3,896,396 | ||||||

| Kentucky Economic Development Finance Authority, Hospital Facilities Rev. (Baptist Healthcare System), “A”, 5.375%, 2024 | 2,305,000 | 2,648,168 | ||||||

| Kentucky Economic Development Finance Authority, Hospital Facilities Rev. (Baptist Healthcare System), “A”, 5.625%, 2027 | 770,000 | 891,414 | ||||||

| Kentucky Economic Development Finance Authority, Hospital Facilities Rev. (Owensboro Medical Health System), “A”, 6%, 2030 | 640,000 | 745,267 | ||||||

10

Table of Contents

Portfolio of Investments (unaudited) – continued

| Issuer | Shares/Par | Value ($) | ||||||

| Municipal Bonds - continued | ||||||||

| Healthcare Revenue - Hospitals - continued | ||||||||

| Kentucky Economic Development Finance Authority, Hospital Facilities Rev. (Owensboro Medical Health System), “A”, 6.375%, 2040 | $ | 4,445,000 | $ | 5,270,748 | ||||

| Knox County, IN, Economic Development Rev. (Good Samaritan Hospital), “A”, 5%, 2037 | 585,000 | 627,968 | ||||||

| Knox County, IN, Economic Development Rev. (Good Samaritan Hospital), “A”, 5%, 2042 | 1,170,000 | 1,250,227 | ||||||

| Knox County, TN, Health, Educational, Hospital & Housing Facilities Board Rev. (Covenant Health), Capital Appreciation, “A”, 0%, 2035 | 3,205,000 | 1,082,104 | ||||||

| Knox County, TN, Health, Educational, Hospital & Housing Facilities Board Rev. (Covenant Health), Capital Appreciation, “A”, 0%, 2036 | 2,010,000 | 642,818 | ||||||

| Laramie County, WY, Hospital Rev. (Cheyenne Regional Medical Center Project), 5%, 2032 | 440,000 | 489,562 | ||||||

| Laramie County, WY, Hospital Rev. (Cheyenne Regional Medical Center Project), 5%, 2037 | 1,005,000 | 1,100,244 | ||||||

| Laramie County, WY, Hospital Rev. (Cheyenne Regional Medical Center Project), 5%, 2042 | 2,205,000 | 2,393,726 | ||||||

| Lebanon County, PA, Health Facilities Authority Rev. (Good Samaritan Hospital), 5.9%, 2028 | 1,700,000 | 1,715,759 | ||||||

| Louisiana Public Facilities Authority Hospital Rev. (Lake Charles Memorial Hospital), 6.375%, 2034 | 3,990,000 | 4,299,824 | ||||||

| Louisiana Public Facilities Authority, Hospital Rev. (Lafayette General Medical Center), 5.5%, 2040 | 5,000,000 | 5,438,250 | ||||||

| Louisville & Jefferson County, KY, Metropolitan Government Healthcare Systems Rev. (Norton Healthcare, Inc.), 5.25%, 2036 | 5,850,000 | 6,130,683 | ||||||

| Lufkin, TX, Health Facilities Development Corp. Rev. (Memorial Health System), 5.5%, 2037 | 310,000 | 319,421 | ||||||

| Macomb County, MI, Hospital Finance Authority Rev. (Mount Clemens General Hospital), 5.75%, 2013 (c) | 1,000,000 | 1,060,940 | ||||||

| Martin County, FL, Health Facilities Authority Rev. (Martin Memorial Medical Center), “A”, 5.75%, 2012 (c) | 850,000 | 863,821 | ||||||

| Martin County, FL, Health Facilities Authority Rev. (Martin Memorial Medical Center), “B”, 5.875%, 2012 (c) | 2,200,000 | 2,236,102 | ||||||

| Maryland Health & Higher Educational Facilities Authority Rev. (Anne Arundel Health System, Inc.), “A”, 6.75%, 2039 | 1,510,000 | 1,835,843 | ||||||

| Massachusetts Development Finance Agency Rev. (Partners Healthcare), “L”, 5%, 2031 | 2,780,000 | 3,220,964 | ||||||

| Massachusetts Development Finance Agency Rev. (Partners Healthcare), “L”, 5%, 2036 | 1,670,000 | 1,889,455 | ||||||

| Mecosta County, MI, General Hospital Rev., 6%, 2018 | 220,000 | 220,275 | ||||||

| Miami-Dade County, FL, Health Facilities Authority, Hospital Rev. (Variety Children’s Hospital), “A”, 6.125%, 2042 | 2,240,000 | 2,632,739 | ||||||

| Michigan Finance Authority Rev. (Trinity Health Corp.), 5%, 2035 | 3,195,000 | 3,597,059 | ||||||

11

Table of Contents

Portfolio of Investments (unaudited) – continued

| Issuer | Shares/Par | Value ($) | ||||||

| Municipal Bonds - continued | ||||||||

| Healthcare Revenue - Hospitals - continued | ||||||||

| Michigan Hospital Finance Authority Rev. (Henry Ford Health System), 5.625%, 2029 | $ | 1,270,000 | $ | 1,457,617 | ||||

| Michigan Hospital Finance Authority Rev. (Henry Ford Health System), 5.75%, 2039 | 7,165,000 | 8,024,012 | ||||||

| Monroe County, PA, Hospital Authority Rev. (Pocono Medical Center), 6%, 2014 (c) | 750,000 | 801,983 | ||||||

| Monroe County, PA, Hospital Authority Rev. (Pocono Medical Center), “A”, 5%, 2032 | 610,000 | 658,184 | ||||||

| Monroe County, PA, Hospital Authority Rev. (Pocono Medical Center), “A”, 5%, 2041 | 440,000 | 464,636 | ||||||

| Montgomery, AL, Medical Clinic Board Health Care Facility Rev. (Jackson Hospital & Clinic), 5.25%, 2031 | 585,000 | 602,246 | ||||||

| New Hampshire Business Finance Authority Rev. (Elliot Hospital Obligated Group), “A”, 6%, 2027 | 4,610,000 | 5,388,030 | ||||||

| New Hampshire Business Finance Authority Rev. (Huggins Hospital), 6.875%, 2039 | 490,000 | 540,632 | ||||||

| New Hampshire Health & Education Facilities Authority Rev. (Memorial Hospital at Conway), 5.25%, 2036 | 565,000 | 569,633 | ||||||

| New Jersey Health Care Facilities, Financing Authority Rev. (Palisades Medical Center), 6.5%, 2021 | 500,000 | 505,530 | ||||||

| New York Dormitory Authority Rev., Non-State Supported Debt (Bronx-Lebanon Hospital Center), LOC, 6.5%, 2030 | 1,475,000 | 1,789,249 | ||||||

| New York Dormitory Authority Rev., Non-State Supported Debt (Bronx-Lebanon Hospital Center), LOC, 6.25%, 2035 | 1,395,000 | 1,634,745 | ||||||

| North Texas Health Facilities Development Corp. Rev. (United Regional Health Care System, Inc.), 6%, 2013 (c) | 5,000,000 | 5,252,950 | ||||||

| Ohio Higher Educational Facility Commission (University Hospital Health System), “A”, 6.75%, 2015 (c) | 6,000,000 | 6,868,020 | ||||||

| Oklahoma Development Finance Authority Rev. (Comanche County Hospital), “B”, 6.6%, 2031 | 255,000 | 260,416 | ||||||

| Orange County, FL, Health Facilities Authority Hospital Rev. (Orlando Regional Healthcare), 5.75%, 2012 (c) | 2,230,000 | 2,249,847 | ||||||

| Orange County, FL, Health Facilities Authority Rev. (Adventist Health System), 5.625%, 2012 (c) | 1,490,000 | 1,514,198 | ||||||

| Orange County, FL, Health Facilities Authority Rev. (Orlando Health, Inc.), “A”, 5%, 2042 | 4,455,000 | 4,796,743 | ||||||

| Orange County, FL, Health Facilities Authority, Hospital Rev. (Orlando Regional Healthcare), “C”, 5.25%, 2035 | 1,000,000 | 1,071,540 | ||||||

| Palomar Pomerado Health Care District, CA, COP, 6.75%, 2039 | 2,210,000 | 2,481,410 | ||||||

| Rhode Island Health & Educational Building Corp. Rev., Hospital Financing (Lifespan Obligated Group), “A”, ASSD GTY, 7%, 2039 | 7,645,000 | 9,039,448 | ||||||

| Richmond, IN, Hospital Authority Rev. (Reid Hospital & Health Center Services), “A”, 6.625%, 2039 | 4,715,000 | 5,477,321 | ||||||

12

Table of Contents

Portfolio of Investments (unaudited) – continued

| Issuer | Shares/Par | Value ($) | ||||||

| Municipal Bonds - continued | ||||||||

| Healthcare Revenue - Hospitals - continued | ||||||||

| Royal Oak, MI, Hospital Finance Authority Rev. (William Beaumont Hospital), 8.25%, 2039 | $ | 2,325,000 | $ | 2,993,228 | ||||

| Scioto County, OH, Hospital Facilities Rev. (Southern Ohio Medical Center), 5.625%, 2031 | 1,095,000 | 1,204,522 | ||||||

| Scioto County, OH, Hospital Facilities Rev. (Southern Ohio Medical Center), 5.75%, 2038 | 4,195,000 | 4,599,230 | ||||||

| Shelby County, TN, Health, Educational & Housing Facilities Board Rev. (Methodist Le Bonheur Healthcare), 5%, 2042 | 2,290,000 | 2,497,314 | ||||||

| Skagit County, WA, Public Hospital District No. 001 Rev. (Skagit Valley Hospital), 5.625%, 2025 | 1,000,000 | 1,104,460 | ||||||

| South Broward, FL, Hospital District Rev., 5%, 2036 | 500,000 | 535,075 | ||||||

| South Carolina Jobs & Economic Development Authority (Bon Secours - St. Francis Medical Center, Inc.), 5.625%, 2012 (c) | 430,000 | 432,709 | ||||||

| South Carolina Jobs & Economic Development Authority (Bon Secours - St. Francis Medical Center, Inc.), 5.625%, 2030 | 1,625,000 | 1,634,523 | ||||||

| South Dakota Health & Educational Facilities Authority Rev. (Avera Health), “A”, 5%, 2042 | 1,205,000 | 1,305,136 | ||||||

| South Dakota Health & Educational Facilities Authority Rev. (Prairie Lakes Health Care System, Inc.), 5.625%, 2013 (c) | 500,000 | 513,375 | ||||||

| South Lake County, FL, Hospital District Rev. (South Lake Hospital), “A”, 6%, 2029 | 1,025,000 | 1,177,838 | ||||||

| St. Louis Park, MN, Health Care Facilities Rev. (Nicollet Health Services), 5.75%, 2039 | 6,445,000 | 7,214,597 | ||||||

| Sullivan County, TN, Health, Educational & Housing Facilities Board Hospital Rev. (Wellmont Health Systems Project), “C”, 5.25%, 2026 | 3,135,000 | 3,349,183 | ||||||

| Sumner County, TN, Health, Educational & Housing Facilities Board Rev. (Sumner Regional Health Systems, Inc.), “A”, 5.5%, 2046 (a)(d) | 2,000,000 | 25,000 | ||||||

| Tallahassee, FL, Health Facilities Rev. (Tallahassee Memorial Healthcare, Inc.), 6.25%, 2020 | 3,300,000 | 3,306,831 | ||||||

| Tallahassee, FL, Health Facilities Rev. (Tallahassee Memorial Regional Medical Center), NATL, 6.625%, 2013 | 330,000 | 331,521 | ||||||

| Tyler, TX, Health Facilities Development Corp. (East Texas Medical Center), “A”, 5.25%, 2032 | 1,715,000 | 1,816,614 | ||||||

| Tyler, TX, Health Facilities Development Corp. (East Texas Medical Center), “A”, 5.375%, 2037 | 1,410,000 | 1,472,548 | ||||||

| Tyler, TX, Health Facilities Development Corp. (Mother Frances Hospital), 5.5%, 2027 | 5,360,000 | 6,011,026 | ||||||

| Upland, CA, COP (San Antonio Community Hospital), 6.375%, 2032 | 2,075,000 | 2,498,902 | ||||||

| Upland, CA, COP (San Antonio Community Hospital), 6.5%, 2041 | 915,000 | 1,089,820 | ||||||

| Upper Illinois River Valley Development, Health Facilities Rev. (Morris Hospital), 6.625%, 2031 | 500,000 | 505,705 | ||||||

13

Table of Contents

Portfolio of Investments (unaudited) – continued

| Issuer | Shares/Par | Value ($) | ||||||

| Municipal Bonds - continued | ||||||||

| Healthcare Revenue - Hospitals - continued | ||||||||

| Washington Health Care Facilities Authority Rev. (Central Washington Health Services), 6.75%, 2029 | $ | 1,450,000 | $ | 1,726,022 | ||||

| Washington Health Care Facilities Authority Rev. (Central Washington Health Services), 7%, 2039 | 3,690,000 | 4,291,064 | ||||||

| Washington Health Care Facilities Authority Rev. (Highline Medical Center), FHA, 6.25%, 2036 | 5,285,000 | 6,221,608 | ||||||

| Washington Health Care Facilities Authority Rev. (Providence Health & Services), “A”, 5%, 2027 | 14,095,000 | 16,237,581 | ||||||

| Washington Health Care Facilities Authority Rev. (Virginia Mason Medical Center), “A”, 6.25%, 2042 | 3,955,000 | 4,370,512 | ||||||

| West Virginia Hospital Finance Authority, Hospital Rev. (Thomas Health System), 6.5%, 2038 | 2,110,000 | 2,190,370 | ||||||

| Wisconsin Health & Educational Facilities Authority Rev. (Aurora Health Care, Inc.), 6.875%, 2030 | 2,750,000 | 2,818,365 | ||||||

| Wisconsin Health & Educational Facilities Authority Rev. (Aurora Health Care, Inc.), “A”, 5%, 2026 | 2,215,000 | 2,505,387 | ||||||

| Wisconsin Health & Educational Facilities Authority Rev. (Aurora Health Care, Inc.), “A”, 5%, 2028 | 665,000 | 738,243 | ||||||

| Wisconsin Health & Educational Facilities Authority Rev. (Mercy Alliance), 5%, 2039 | 3,115,000 | 3,334,047 | ||||||

| Wisconsin Health & Educational Facilities Authority Rev. (ProHealth Care, Inc. Obligated Group), 6.625%, 2032 | 1,730,000 | 1,879,766 | ||||||

| Wisconsin Health & Educational Facilities Authority Rev. (ProHealth Care, Inc. Obligated Group), 6.625%, 2039 | 1,220,000 | 1,446,542 | ||||||

| Wisconsin Health & Educational Facilities Authority Rev. (Wheaton Franciscan Healthcare), 5.25%, 2018 | 1,500,000 | 1,668,060 | ||||||

| Wisconsin Health & Educational Facilities Authority Rev. (Wheaton Franciscan Healthcare), 5.25%, 2031 | 4,155,000 | 4,345,216 | ||||||

| Wisconsin Health & Educational Facilities Authority Rev. (Wheaton Franciscan Services), 5.25%, 2034 | 1,360,000 | 1,421,268 | ||||||

|

| |||||||

| $ | 333,813,039 | |||||||

| Healthcare Revenue - Long Term Care - 2.4% | ||||||||

| Bell County, TX, Health Facility Development Corp. (Advanced Living Technologies, Inc.), 8%, 2036 | $ | 1,595,000 | $ | 1,444,257 | ||||

| Bucks County, PA, Industrial Development Authority Retirement Community Rev. (Ann’s Choice, Inc.), “A”, 6.25%, 2035 | 1,120,000 | 1,131,189 | ||||||

| California Statewide Communities Development Authority Rev. (American Baptist Homes of the West), 6.25%, 2039 | 1,050,000 | 1,143,450 | ||||||

| Cumberland County, PA, Municipal Authority Retirement Community Rev. (Wesley), “A”, 7.25%, 2013 (c) | 270,000 | 277,306 | ||||||

| Cumberland County, PA, Municipal Authority Retirement Community Rev. (Wesley), “A”, 7.25%, 2013 (c) | 105,000 | 107,841 | ||||||

14

Table of Contents

Portfolio of Investments (unaudited) – continued

| Issuer | Shares/Par | Value ($) | ||||||

| Municipal Bonds - continued | ||||||||

| Healthcare Revenue - Long Term Care - continued | ||||||||

| Cumberland County, PA, Municipal Authority Rev. (Asbury Atlantic, Inc.), 6%, 2030 | $ | 715,000 | $ | 760,174 | ||||

| Cumberland County, PA, Municipal Authority Rev. (Asbury Atlantic, Inc.), 6%, 2040 | 505,000 | 531,568 | ||||||

| Cumberland County, PA, Municipal Authority Rev. (Diakon Lutheran Social Ministries), 6.125%, 2029 | 830,000 | 929,957 | ||||||

| Cumberland County, PA, Municipal Authority Rev. (Diakon Lutheran Social Ministries), 6.375%, 2039 | 5,045,000 | 5,621,341 | ||||||

| Hawaii Department of Budget & Finance, Special Purpose Rev. (15 Craigside Project), “A”, 8.75%, 2029 | 375,000 | 446,426 | ||||||

| Hawaii Department of Budget & Finance, Special Purpose Rev. (15 Craigside Project), “A”, 9%, 2044 | 1,100,000 | 1,314,797 | ||||||

| Illinois Finance Authority Rev. (Christian Homes, Inc.), 5.5%, 2023 | 3,355,000 | 3,479,538 | ||||||

| Indiana Health Facilities Financing Authority Rev. (Hoosier Care, Inc.), “A”, 7.125%, 2034 | 730,000 | 730,212 | ||||||

| Iowa Finance Authority, Health Care Facilities Rev. (Care Initiatives), “A”, 5.5%, 2025 | 1,205,000 | 1,295,833 | ||||||

| Maryland Health & Higher Educational Facilities Authority Rev. (Charlestown Community), 6.25%, 2041 | 2,225,000 | 2,541,573 | ||||||

| Montgomery County, OH, Health Care & Multifamily Housing Rev. (St. Leonard), 6.375%, 2030 | 1,915,000 | 2,091,640 | ||||||

| Montgomery County, OH, Health Care & Multifamily Housing Rev. (St. Leonard), 6.625%, 2040 | 2,770,000 | 3,001,683 | ||||||

| Pell City, AL, Special Care Facilities, Financing Authority Rev. (Noland Health Services, Inc.), 5%, 2039 | 1,750,000 | 1,863,680 | ||||||

| St. John’s County, FL, Industrial Development Authority (Bayview Project), “A”, 5.2%, 2027 | 150,000 | 133,740 | ||||||

| St. John’s County, FL, Industrial Development Authority Rev. (Presbyterian Retirement), “A”, 6%, 2045 | 6,795,000 | 7,598,509 | ||||||

| Tarrant County, TX, Cultural Education Facilities Finance Corp. Retirement Facility (Air Force Village), 6.125%, 2029 | 395,000 | 439,027 | ||||||

| Tarrant County, TX, Cultural Education Facilities Finance Corp. Retirement Facility (Air Force Village), 6.375%, 2044 | 3,100,000 | 3,393,167 | ||||||

| Tarrant County, TX, Cultural Education Facilities Finance Corp. Retirement Facility (Stayton at Museum Way), 8.25%, 2044 | 4,500,000 | 5,037,615 | ||||||

| Travis County, TX, Health Facilities Development Corp. Rev. (Westminster Manor Health), 7%, 2030 | 735,000 | 864,250 | ||||||

| Travis County, TX, Health Facilities Development Corp. Rev. (Westminster Manor Health), 7.125%, 2040 | 2,575,000 | 3,009,428 | ||||||

| Wisconsin Health & Educational Facilities Authority Rev. (St. John’s Community, Inc.), “A”, 7.25%, 2029 | 430,000 | 500,447 | ||||||

| Wisconsin Health & Educational Facilities Authority Rev. (St. John’s Community, Inc.), “A”, 7.625%, 2039 | 1,390,000 | 1,612,567 | ||||||

|

| |||||||

| $ | 51,301,215 | |||||||

15

Table of Contents

Portfolio of Investments (unaudited) – continued

| Issuer | Shares/Par | Value ($) | ||||||

| Municipal Bonds - continued | ||||||||

| Human Services - 0.1% | ||||||||

| Orange County, FL, Health Facilities Authority Rev. (GF/Orlando Healthcare Facilities), 8.875%, 2021 | $ | 280,000 | $ | 281,355 | ||||

| Orange County, FL, Health Facilities Authority Rev. (GF/Orlando Healthcare Facilities), 9%, 2031 | 890,000 | 891,860 | ||||||

|

| |||||||

| $ | 1,173,215 | |||||||

| Industrial Revenue - Airlines - 0.3% | ||||||||

| Clayton County, GA, Development Authority Special Facilities Rev. (Delta Airlines, Inc.), “A”, 8.75%, 2029 | $ | 1,295,000 | $ | 1,599,869 | ||||

| Clayton County, GA, Development Authority Special Facilities Rev. (Delta Airlines, Inc.), “B”, 9%, 2035 | 970,000 | 1,087,021 | ||||||

| Denver, CO, City & County Airport Rev. (United Airlines), 5.25%, 2032 | 720,000 | 728,503 | ||||||

| Denver, CO, City & County Airport Rev. (United Airlines), 5.75%, 2032 | 615,000 | 637,909 | ||||||

| Houston, TX, Airport Systems Rev., Special Facilities (Continental Airlines, Inc. Terminal E project), 6.75%, 2029 | 570,000 | 572,075 | ||||||

| Los Angeles, CA, Regional Airport Lease Rev. (American Airlines), “C”, 7.5%, 2024 (a)(d) | 1,435,000 | 1,421,726 | ||||||

| New York, NY, City Industrial Development Agency Special Facility Rev. (American Airlines, Inc. - JFK International Airport), 7.75%, 2031 (d)(q) | 1,190,000 | 1,255,902 | ||||||

|

| |||||||

| $ | 7,303,005 | |||||||

| Industrial Revenue - Chemicals - 1.1% | ||||||||

| Brazos River, TX, Brazoria County Environmental Rev. (Dow Chemical, Co.), “A-7”, 6.625%, 2033 | $ | 500,000 | $ | 505,800 | ||||

| Brazos River, TX, Harbor Navigation District (Dow Chemical Co.), “A”, 5.95%, 2033 | 7,310,000 | 8,279,818 | ||||||

| Louisiana Environmental Facilities & Community Development Authority Rev. (Westlake Chemical), 6.75%, 2032 | 1,600,000 | 1,796,416 | ||||||

| Louisiana Environmental Facilities & Community Development Authority Rev. (Westlake Chemical), “A”, 6.5%, 2029 | 1,400,000 | 1,635,200 | ||||||

| Louisiana Environmental Facilities & Community Development Authority Rev. (Westlake Chemical), “A-2”, 6.5%, 2035 | 6,000,000 | 6,990,420 | ||||||

| Michigan Strategic Fund Ltd. Obligation Rev. (Dow Chemical Co.), 6.25%, 2014 | 2,870,000 | 3,127,554 | ||||||

| Red River Authority, TX, Pollution Control Rev. (Celanese Project) “B”, 6.7%, 2030 | 1,200,000 | 1,213,260 | ||||||

|

| |||||||

| $ | 23,548,468 | |||||||

16

Table of Contents

Portfolio of Investments (unaudited) – continued

| Issuer | Shares/Par | Value ($) | ||||||

| Municipal Bonds - continued | ||||||||

| Industrial Revenue - Environmental Services - 0.2% | ||||||||

| California Pollution Control Financing Authority, Solid Waste Disposal Rev. (Republic Services, Inc.), “B”, 5.25%, 2023 (b) | $ | 950,000 | $ | 1,093,612 | ||||

| California Pollution Control Financing Authority, Solid Waste Disposal Rev. (Waste Management, Inc.), “C”, 5.125%, 2023 | 1,665,000 | 1,806,508 | ||||||

| Colorado Housing & Finance Authority, Solid Waste Rev. (Waste Management, Inc.), 5.7%, 2018 | 1,960,000 | 2,359,899 | ||||||

| Gulf Coast Waste Disposal Authority (Waste Management, Inc.), 5.2%, 2028 | 300,000 | 320,487 | ||||||

|

| |||||||

| $ | 5,580,506 | |||||||

| Industrial Revenue - Other - 0.7% | ||||||||

| California Statewide Communities, Development Authority Environmental Facilities (Microgy Holdings), 9%, 2038 (a)(d) | $ | 126,224 | $ | 1,262 | ||||

| Gulf Coast, TX, Industrial Development Authority Rev. (Microgy Holdings LLC Project), 7%, 2036 (a)(d) | 116,013 | 1,160 | ||||||

| Hardeman County, TN, Correctional Facilities Corp. (Corrections Corp. of America), 7.375%, 2017 | 430,000 | 430,280 | ||||||

| Houston, TX, Industrial Development Corp. (United Parcel Service, Inc.), 6%, 2023 | 265,000 | 254,684 | ||||||

| Massachusetts Development Finance Agency Rev., Resource Recovery (Fluor Corp.), 5.625%, 2019 | 11,545,000 | 11,567,975 | ||||||

| Massachusetts Industrial Finance Agency Rev. (Welch Foods, Inc.), 5.6%, 2017 | 1,300,000 | 1,304,225 | ||||||

| Park Creek Metropolitan District, CO, Rev. (Custodial Receipts), “CR-2”, 7.875%, 2032 (b)(n) | 560,000 | 573,681 | ||||||

| Peninsula Ports Authority, VA, Coal Terminal Rev. (Dominion Terminal Associates), 6%, 2033 | 470,000 | 478,122 | ||||||

|

| |||||||

| $ | 14,611,389 | |||||||

| Industrial Revenue - Paper - 0.3% | ||||||||

| Butler, AL, Industrial Development Board, Solid Waste Disposal Rev. (Georgia-Pacific Corp.), 5.75%, 2028 | $ | 1,760,000 | $ | 1,832,195 | ||||

| Jay, ME, Solid Waste Disposal Rev. (International Paper Co.), “A”, 5.125%, 2018 | 1,500,000 | 1,526,205 | ||||||

| Rockdale County, GA, Development Authority Project Rev. (Visy Paper Project), “A”, 6.125%, 2034 | 2,055,000 | 2,141,454 | ||||||

| Sabine River, LA, Water Facilities Authority Rev. (International Paper Co.), 6.2%, 2025 | 1,250,000 | 1,261,713 | ||||||

| West Point, VA, Industrial Development Authority, Solid Waste Disposal Rev. (Chesapeake Corp.), “A”, 6.375%, 2019 (a)(d) | 550,000 | 11,550 | ||||||

|

| |||||||

| $ | 6,773,117 | |||||||

17

Table of Contents

Portfolio of Investments (unaudited) – continued

| Issuer | Shares/Par | Value ($) | ||||||

| Municipal Bonds - continued | ||||||||

| Miscellaneous Revenue - Entertainment & Tourism - 0.7% | ||||||||

| Brooklyn, NY, Arena Local Development Corp. (Barclays Center Project), 6%, 2030 | $ | 2,015,000 | $ | 2,363,132 | ||||

| Brooklyn, NY, Arena Local Development Corp. (Barclays Center Project), 6.25%, 2040 | 3,205,000 | 3,693,666 | ||||||

| Harris County, Houston, TX, Sports Authority, Special Rev., “A”, NATL, 5%, 2025 | 2,460,000 | 2,460,221 | ||||||

| Seminole Tribe, FL, Special Obligation Rev., “A”, 5.75%, 2022 (n) | 2,850,000 | 3,146,999 | ||||||

| Seminole Tribe, FL, Special Obligation Rev., “A”, 5.5%, 2024 (n) | 2,000,000 | 2,159,960 | ||||||

| Seneca Nation Indians, NY, Capital Improvements Authority, Special Obligation, 5%, 2023 (n) | 670,000 | 678,844 | ||||||

|

| |||||||

| $ | 14,502,822 | |||||||

| Miscellaneous Revenue - Other - 1.5% | ||||||||

| Austin, TX, Convention Center (Convention Enterprises, Inc.), “A”, SYNCORA, 5.25%, 2017 | $ | 845,000 | $ | 929,407 | ||||

| Austin, TX, Convention Center (Convention Enterprises, Inc.), “A”, SYNCORA, 5.25%, 2019 | 1,375,000 | 1,501,390 | ||||||

| Austin, TX, Convention Center (Convention Enterprises, Inc.), “A”, SYNCORA, 5.25%, 2020 | 1,120,000 | 1,219,680 | ||||||

| Austin, TX, Convention Center (Convention Enterprises, Inc.), “A”, SYNCORA, 5.25%, 2024 | 2,230,000 | 2,358,203 | ||||||

| Capital Trust Agency Rev. (Aero Miami FX LLC), “A”, 5.35%, 2029 | 3,900,000 | 4,060,095 | ||||||

| Citizens Property Insurance Corp., “A-1”, 5.25%, 2017 | 750,000 | 868,080 | ||||||

| Citizens Property Insurance Corp., FL, “A-1”, 5%, 2019 | 505,000 | 591,128 | ||||||

| Citizens Property Insurance Corp., FL, “A-1”, 5%, 2020 | 2,770,000 | 3,252,119 | ||||||

| Cleveland-Cuyahoga County, OH, Port Authority Rev., 7%, 2040 | 1,105,000 | 1,227,147 | ||||||

| District of Columbia Rev. (American Society Hematology), 5%, 2036 | 760,000 | 827,192 | ||||||

| District of Columbia Rev. (American Society Hematology), 5%, 2042 | 985,000 | 1,065,435 | ||||||

| Fulton County, GA, Development Authority Rev. (Georgia Tech Athletic Association), “A”, 5%, 2042 | 2,320,000 | 2,605,105 | ||||||

| Massachusetts Port Authority Facilities Rev. (Conrac Project), “A”, 5.125%, 2041 | 465,000 | 509,724 | ||||||

| Miami-Dade County, FL, Special Obligation, Capital Appreciation, “A”, NATL, 0%, 2032 | 2,000,000 | 720,140 | ||||||

| New Orleans, LA, Aviation Board Gulf Opportunity Zone CFC Rev. (Consolidated Rental Car), “A”, 6.25%, 2030 | 1,810,000 | 2,048,956 | ||||||

| New York Liberty Development Corp., Liberty Rev. (World Trade Center Project), 5%, 2031 | 2,300,000 | 2,632,879 | ||||||

| Oklahoma Industries Authority Rev. (Oklahoma Medical Research Foundation Project), 5.5%, 2029 | 4,400,000 | 4,944,148 | ||||||

| Summit County, OH, Port Authority Building Rev. (Flats East Development Recovery Zone Facility Bonds), 6.875%, 2040 | 415,000 | 460,866 | ||||||

18

Table of Contents

Portfolio of Investments (unaudited) – continued

| Issuer | Shares/Par | Value ($) | ||||||

| Municipal Bonds - continued | ||||||||

| Miscellaneous Revenue - Other - continued | ||||||||

| Summit County, OH, Port Authority Building Rev. (Seville Project), “A”, 5.1%, 2025 | $ | 160,000 | $ | 160,042 | ||||

|

| |||||||

| $ | 31,981,736 | |||||||

| Multi-Family Housing Revenue - 0.3% | ||||||||

| Bay County, FL, Housing Finance Authority, Multi-Family Rev. (Andrews Place II Apartments), AGM, 5%, 2035 | $ | 1,045,000 | $ | 1,057,247 | ||||

| Eden Prairie, MN, Multi-Family Housing Rev. (Rolling Hills), “A”, GNMA, 6%, 2021 | 200,000 | 208,452 | ||||||

| Indianapolis, IN, Multi-Family Rev. (Cambridge Station Apartments II), FNMA, 5.25%, 2039 (b) | 1,375,000 | 1,401,139 | ||||||

| Michigan Housing Development Authority, GNMA, 5.2%, 2038 | 1,200,000 | 1,232,556 | ||||||

| MuniMae TE Bond Subsidiary LLC, “A-2”, 4.9%, 2049 (z) | 2,000,000 | 1,820,020 | ||||||

|

| |||||||

| $ | 5,719,414 | |||||||

| Parking - 0.2% | ||||||||

| Boston, MA, Metropolitan Transit Parking Corp., Systemwide Parking Rev., 5.25%, 2036 | $ | 3,250,000 | $ | 3,659,435 | ||||

| Port Revenue - 1.2% | ||||||||

| Louisiana Offshore Terminal Authority Deepwater Port Rev. (Loop LLC), “B-1A”, 1.375%, 2037 (b) | $ | 1,885,000 | $ | 1,886,828 | ||||

| Maryland Economic Development Corp. Rev. (Port America Chesapeake Terminal Project), “B”, 5.375%, 2025 | 795,000 | 870,867 | ||||||

| Maryland Economic Development Corp. Rev. (Port America Chesapeake Terminal Project), “B”, 5.75%, 2035 | 1,535,000 | 1,665,322 | ||||||

| Massachusetts Port Authority Rev., ETM, 13%, 2013 (c) | 545,000 | 596,513 | ||||||

| Port Authority of NY & NJ, “173”, 4%, 2027 | 15,000,000 | 16,688,550 | ||||||

| Port of Oakland, CA, Rev., “P”, 5%, 2033 | 1,000,000 | 1,116,830 | ||||||

| Seattle, WA, Port Rev., “B”, 5%, 2024 | 3,000,000 | 3,518,460 | ||||||

|

| |||||||

| $ | 26,343,370 | |||||||

| Sales & Excise Tax Revenue - 6.4% | ||||||||

| Chicago, IL, Transit Authority Sales Tax Receipts Rev., 5.25%, 2029 | $ | 1,755,000 | $ | 2,072,269 | ||||

| Chicago, IL, Transit Authority Sales Tax Receipts Rev., 5.25%, 2030 | 3,505,000 | 4,120,198 | ||||||

| Chicago, IL, Transit Authority Sales Tax Receipts Rev., 5.25%, 2031 | 655,000 | 767,103 | ||||||

| Chicago, IL, Transit Authority Sales Tax Receipts Rev., 5.25%, 2040 | 4,685,000 | 5,346,288 | ||||||

| Colorado Regional Transportation District, Private Activity Rev. (Denver Transportation Partners), 6.5%, 2030 | 6,150,000 | 7,439,102 | ||||||

| Colorado Regional Transportation District, Private Activity Rev. (Denver Transportation Partners), 6%, 2034 | 5,000,000 | 5,841,200 | ||||||

| Illinois Sales Tax Rev., “P”, 6.5%, 2022 | 5,000,000 | 6,118,250 | ||||||

| Massachusetts Bay Transportation Authority, Sales Tax Rev., “A”, 5%, 2024 | 9,445,000 | 12,271,038 | ||||||

19

Table of Contents

Portfolio of Investments (unaudited) – continued

| Issuer | Shares/Par | Value ($) | ||||||

| Municipal Bonds - continued | ||||||||

| Sales & Excise Tax Revenue - continued | ||||||||

| Massachusetts Bay Transportation Authority, Sales Tax Rev., “A-1”, 5.25%, 2031 | $ | 3,615,000 | $ | 4,925,221 | ||||

| Massachusetts Bay Transportation Authority, Sales Tax Rev., Capital Appreciation, “A-2”, 0%, 2028 | 6,930,000 | 3,567,425 | ||||||

| Massachusetts School Building Authority, Dedicated Sales Tax Rev., “B”, 5%, 2032 (u) | 10,730,000 | 12,810,332 | ||||||

| Massachusetts School Building Authority, Sales Tax Rev., “A”, 5%, 2026 | 12,500,000 | 15,538,625 | ||||||

| Metropolitan Atlanta, GA, Rapid Transit Authority Rev., 6.25%, 2018 | 3,640,000 | 4,157,098 | ||||||

| Metropolitan Pier & Exposition Authority, Dedicated State Tax Rev. (McCormick Place), “B”, AGM, 5%, 2050 (u) | 20,000,000 | 21,519,000 | ||||||

| Miami-Dade County, FL, Transit Sales Surtax Rev., 5%, 2037 | 3,435,000 | 3,890,515 | ||||||

| Puerto Rico Sales Tax Financing Corp., Sales Tax Rev., “A”, 5.5%, 2019 (c) | 45,000 | 58,470 | ||||||

| Puerto Rico Sales Tax Financing Corp., Sales Tax Rev., “A”, 5.5%, 2028 | 5,855,000 | 6,609,710 | ||||||

| Puerto Rico Sales Tax Financing Corp., Sales Tax Rev., “A”, 5.5%, 2037 | 1,105,000 | 1,191,842 | ||||||

| Puerto Rico Sales Tax Financing Corp., Sales Tax Rev., “A”, 5.375%, 2039 | 1,745,000 | 1,863,992 | ||||||

| Puerto Rico Sales Tax Financing Corp., Sales Tax Rev., “A”, 5.5%, 2042 | 1,530,000 | 1,638,309 | ||||||

| Puerto Rico Sales Tax Financing Corp., Sales Tax Rev., “A”, 6%, 2042 | 3,460,000 | 3,845,652 | ||||||

| Puerto Rico Sales Tax Financing Corp., Sales Tax Rev., “C”, 5.375%, 2038 | 605,000 | 647,386 | ||||||

| Puerto Rico Sales Tax Financing Corp., Sales Tax Rev., Capital Appreciation, “A”, 0% to 2016, 6.75% to 2032 | 4,190,000 | 4,272,878 | ||||||

| Puerto Rico Sales Tax Financing Corp., Sales Tax Rev., Capital Appreciation, “A”, 0%, 2033 | 2,345,000 | 2,014,988 | ||||||

| Puerto Rico Sales Tax Financing Corp., Sales Tax Rev., Capital Appreciation, “A”, 0%, 2033 | 280,000 | 87,914 | ||||||

| State of Illinois, “B”, 5.25%, 2034 | 1,275,000 | 1,462,055 | ||||||

| Utah Transit Authority Sales Tax Rev., Capital Appreciation, “A”, NATL, 0%, 2028 | 2,225,000 | 1,099,128 | ||||||

| Volusia County, FL, Tourist Development Tax Rev., AGM, 5%, 2034 | 815,000 | 841,911 | ||||||

| Wyandotte County/Kansas City, KS, Unified Government Special Obligation Rev., Capital Appreciation, “B”, 0%, 2021 | 3,970,000 | 2,807,624 | ||||||

|

| |||||||

| $ | 138,825,523 | |||||||

20

Table of Contents

Portfolio of Investments (unaudited) – continued

| Issuer | Shares/Par | Value ($) | ||||||

| Municipal Bonds - continued | ||||||||

| Single Family Housing - Local - 0.7% | ||||||||

| Chicago, IL, Single Family Mortgage Rev., “C”, GNMA, 5.5%, 2038 | $ | 990,000 | $ | 1,036,738 | ||||

| Chicago, IL, Single Family Mortgage Rev., “C”, GNMA, 5.75%, 2042 | 1,525,000 | 1,560,487 | ||||||

| Denver, CO, Single Family Mortgage Rev., GNMA, 7.3%, 2031 | 40,000 | 40,528 | ||||||

| Manatee County, FL, Housing Finance Mortgage Rev., Single Family, Sub-Series 2, GNMA, 6.5%, 2023 | 35,000 | 37,460 | ||||||

| Manatee County, FL, Housing Finance Mortgage Rev., Single Family, Sub-Series 3, GNMA, 5.3%, 2028 | 225,000 | 230,963 | ||||||

| Manatee County, FL, Housing Finance Mortgage Rev., Single Family, Sub-Series 3, GNMA, 5.4%, 2029 | 180,000 | 181,813 | ||||||

| Nortex, TX, Housing Finance Corp., Single Family Mortgage Rev., “A”, GNMA, 5.5%, 2038 | 1,790,000 | 1,863,157 | ||||||

| Oklahoma County, OK, Home Finance Authority, Single Family Mortgage Rev., “A”, GNMA, 5.4%, 2038 | 1,060,000 | 1,079,281 | ||||||

| Permian Basin Housing Finance Corp., TX, Single Family Mortgage Backed Securities (Mortgage Backed Project) “A”, GNMA, 5.65%, 2038 | 1,180,000 | 1,236,640 | ||||||

| Sedgwick & Shawnee Counties, KS, Single Family Housing Rev., “A”, GNMA, 5.9%, 2035 | 345,000 | 367,263 | ||||||

| Sedgwick & Shawnee Counties, KS, Single Family Housing Rev., “A”, GNMA, 6.25%, 2035 | 130,000 | 137,847 | ||||||

| Sedgwick & Shawnee Counties, KS, Single Family Housing Rev., “A”, GNMA, 5.8%, 2036 | 1,460,000 | 1,544,738 | ||||||

| Sedgwick & Shawnee Counties, KS, Single Family Housing Rev., “A-1”, GNMA, 5.75%, 2037 | 95,000 | 101,462 | ||||||

| Sedgwick & Shawnee Counties, KS, Single Family Housing Rev., “A-3”, GNMA, 6%, 2035 | 475,000 | 512,554 | ||||||

| Sedgwick & Shawnee Counties, KS, Single Family Housing Rev., “A-3”, GNMA, 5.5%, 2037 | 620,000 | 668,527 | ||||||

| Sedgwick & Shawnee Counties, KS, Single Family Housing Rev., “A-4”, GNMA, 5.85%, 2037 | 110,000 | 113,930 | ||||||

| Sedgwick & Shawnee Counties, KS, Single Family Housing Rev., “A-5”, GNMA, 5.8%, 2027 | 425,000 | 438,681 | ||||||

| Sedgwick & Shawnee Counties, KS, Single Family Housing Rev., “A-5”, GNMA, 5.7%, 2036 | 1,270,000 | 1,354,226 | ||||||

| Sedgwick & Shawnee Counties, KS, Single Family Housing Rev., “A-5”, GNMA, 5.9%, 2037 | 200,000 | 209,986 | ||||||

| Sedgwick & Shawnee Counties, KS, Single Family Mortgage Rev., “A”, GNMA, 5.45%, 2038 | 1,525,000 | 1,620,206 | ||||||

|

| |||||||

| $ | 14,336,487 | |||||||

21

Table of Contents

Portfolio of Investments (unaudited) – continued

| Issuer | Shares/Par | Value ($) | ||||||

| Municipal Bonds - continued | ||||||||

| Single Family Housing - State - 1.0% | ||||||||

| California Housing Finance Agency Rev. (Home Mortgage), “G”, 4.95%, 2023 | $ | 4,595,000 | $ | 4,712,816 | ||||

| California Housing Finance Agency Rev. (Home Mortgage), “G”, 5.5%, 2042 | 1,935,000 | 2,029,389 | ||||||

| California Housing Finance Agency Rev. (Home Mortgage), “L”, 5.45%, 2033 | 6,600,000 | 6,771,006 | ||||||

| California Housing Finance Agency Rev. (Home Mortgage), “L”, FNMA, 5.5%, 2038 | 2,220,000 | 2,271,193 | ||||||

| Colorado Housing & Finance Authority Rev., 6.05%, 2016 | 25,000 | 25,526 | ||||||

| Colorado Housing & Finance Authority Rev., “B-2”, 6.1%, 2023 | 45,000 | 45,933 | ||||||

| Colorado Housing & Finance Authority Rev., “B-3”, 6.55%, 2033 | 50,000 | 51,711 | ||||||

| Colorado Housing & Finance Authority Rev., “C-2”, 5.9%, 2023 | 305,000 | 320,576 | ||||||

| Colorado Housing & Finance Authority Rev., “C-2”, FHA, 6.6%, 2032 | 255,000 | 267,255 | ||||||

| Colorado Housing & Finance Authority Rev., “C-3”, FHA, 6.375%, 2033 | 25,000 | 25,937 | ||||||

| Delaware Housing Authority Rev. (Single Family), “C”, 6.25%, 2037 | 665,000 | 720,740 | ||||||

| Florida Housing Finance Corp. Rev. (Homeowner Mortgage), “1”, GNMA, 4.8%, 2031 | 525,000 | 536,057 | ||||||

| Iowa Finance Authority Single Family Mortgage Rev. (Mortgage Backed Securities), “A”, GNMA, 5.3%, 2033 | 500,000 | 530,750 | ||||||

| Louisiana Housing Finance Agency, Single Family Mortgage Rev., GNMA, 6.375%, 2033 | 100,000 | 100,276 | ||||||

| Mississippi Home Corp., Single Family Rev., “A”, GNMA, 6.1%, 2034 | 820,000 | 849,389 | ||||||

| New Hampshire Housing Finance Authority Rev., 6.85%, 2030 | 180,000 | 180,302 | ||||||

| New Hampshire Housing Finance Authority Rev., “B”, 6.5%, 2035 | 85,000 | 85,886 | ||||||

| New Mexico Mortgage Finance Authority Rev., GNMA, 5.95%, 2037 | 685,000 | 733,142 | ||||||

| New Mexico Mortgage Finance Authority Rev., “I”, GNMA, 5.75%, 2038 | 935,000 | 988,407 | ||||||

| Oregon Health & Community Services (Single Family Mortgage), “B”, 6.25%, 2031 | 660,000 | 698,386 | ||||||

| Texas Affordable Housing Corp. (Single Family Mortgage), “B”, GNMA, 5.25%, 2039 | 455,000 | 476,740 | ||||||

|

| |||||||

| $ | 22,421,417 | |||||||

| Solid Waste Revenue - 0.2% | ||||||||

| Delaware County, PA, Industrial Development Authority, Resource Recovery Facilities Rev. (American Ref-Fuel Co.), “A”, 6.2%, 2019 | $ | 1,950,000 | $ | 1,951,463 | ||||

| Massachusetts Development Finance Agency, Resource Recovery Rev. (Ogden Haverhill Associates), “A”, 6.7%, 2014 | 355,000 | 355,880 | ||||||

| Massachusetts Development Finance Agency, Resource Recovery Rev. (Ogden Haverhill Associates), “A”, 5.6%, 2019 | 1,000,000 | 1,003,010 | ||||||

22

Table of Contents

Portfolio of Investments (unaudited) – continued

| Issuer | Shares/Par | Value ($) | ||||||

| Municipal Bonds - continued | ||||||||

| Solid Waste Revenue - continued | ||||||||

| Palm Beach County, FL, Solid Waste Authority Rev. Improvement, BHAC, 5%, 2027 | $ | 295,000 | $ | 347,858 | ||||

| Pennsylvania Economic Development Financing Authority, Sewer Sludge Disposal Rev. (Philadelphia Biosolids Facility), 6.25%, 2032 | 575,000 | 656,794 | ||||||

|

| |||||||

| $ | 4,315,005 | |||||||

| State & Agency - Other - 0.1% | ||||||||

| Commonwealth of Puerto Rico (Mepsi Campus), “A”, 6.5%, 2037 | $ | 1,200,000 | $ | 1,240,164 | ||||

| Massachusetts Development Finance Agency (Visual & Performing Arts), 6%, 2021 | 1,000,000 | 1,223,920 | ||||||

|

| |||||||

| $ | 2,464,084 | |||||||

| State & Local Agencies - 3.7% | ||||||||

| California Public Works Board Lease Rev. (Various Capital Projects), “G-1”, 5.75%, 2030 | $ | 2,950,000 | $ | 3,410,082 | ||||

| Cape Coral, FL, Special Obligation Rev., NATL, 5%, 2030 | 500,000 | 544,060 | ||||||

| Colorado State University Board of Governors, System Enterprise Rev., “B”, 5%, 2025 | 3,000,000 | 3,821,730 | ||||||

| Delaware Valley, PA, Regional Finance Authority, AMBAC, 5.5%, 2018 | 7,840,000 | 9,112,510 | ||||||

| Delaware Valley, PA, Regional Finance Authority, “B”, FRN, AMBAC, 0.781%, 2018 | 250,000 | 250,000 | ||||||

| Delaware Valley, PA, Regional Finance Authority, “C”, FRN, 1.032%, 2037 | 7,000,000 | 4,718,490 | ||||||

| Delaware Valley, PA, Regional Finance Authority, RITES, FRN, AMBAC, 9.944%, 2018 (p) | 900,000 | 1,192,158 | ||||||

| Florida Municipal Loan Council Rev., “C”, NATL, 5.25%, 2022 | 1,000,000 | 1,012,210 | ||||||

| FYI Properties Lease Rev. (Washington State Project), 5.5%, 2034 | 2,255,000 | 2,559,470 | ||||||

| Golden State, CA, Tobacco Securitization Corp., Tobacco Settlement Rev., “A”, AGM, 4.55%, 2022 | 3,415,000 | 3,710,841 | ||||||

| Golden State, CA, Tobacco Securitization Corp., Tobacco Settlement Rev., Enhanced, “A”, FGIC, 5%, 2035 | 1,000,000 | 1,025,970 | ||||||

| Golden State, CA, Tobacco Securitization Corp., Tobacco Settlement Rev., Enhanced, “A-1”, AMBAC, 4.6%, 2023 | 995,000 | 1,075,127 | ||||||

| Golden State, CA, Tobacco Securitization Corp., Tobacco Settlement Rev., Enhanced, “B”, 5.5%, 2013 (c) | 5,000,000 | 5,174,650 | ||||||

| Los Angeles, CA, Municipal Improvement Corp. Lease Rev. (Real Property), “E”, 6%, 2039 | 2,580,000 | 2,952,397 | ||||||

| Manassas Park, VA, Economic Development Authority Lease Rev., “A”, 6%, 2035 | 845,000 | 909,000 | ||||||

| Miami-Dade County, FL, School Board, COP, “B”, ASSD GTY, 5%, 2033 | 500,000 | 544,830 | ||||||

| Mississippi Development Bank (Harrison County Coliseum), “A”, 5.25%, 2034 | 3,755,000 | 4,814,623 | ||||||

23

Table of Contents

Portfolio of Investments (unaudited) – continued

| Issuer | Shares/Par | Value ($) | ||||||

| Municipal Bonds - continued | ||||||||

| State & Local Agencies - continued | ||||||||

| New York Dormitory Authority Rev. (City University), 5.75%, 2013 | $ | 1,355,000 | $ | 1,409,349 | ||||

| Pennsylvania Convention Center Authority Rev., ETM, FGIC, 6.7%, 2016 (c) | 14,765,000 | 16,860,892 | ||||||

| Philadelphia, PA, Municipal Authority Rev., 6.5%, 2034 | 1,020,000 | 1,179,722 | ||||||

| Puerto Rico Public Finance Corp., Commonwealth Appropriations, “B”, 6%, 2026 | 2,455,000 | 2,797,423 | ||||||

| Puerto Rico Public Finance Corp., Commonwealth Appropriations, “B”, 5.5%, 2031 | 3,565,000 | 3,726,922 | ||||||

| San Bernardino, CA, Joint Powers Financing Authority Lease Rev. (California Department of Transportation), 5.5%, 2014 | 6,320,000 | 6,342,878 | ||||||

| Tennessee School Bond Authority, “B”, 5.125%, 2033 | 1,500,000 | 1,728,240 | ||||||

|

| |||||||

| $ | 80,873,574 | |||||||

| Student Loan Revenue - 0.9% | ||||||||

| Access to Loans for Learning, CA, Student Loan Rev., 7.95%, 2030 | $ | 650,000 | $ | 650,241 | ||||

| Iowa Student Loan Liquidity Corp., “A-2”, 5.5%, 2025 | 2,240,000 | 2,503,379 | ||||||

| Iowa Student Loan Liquidity Corp., “A-2”, 5.6%, 2026 | 2,240,000 | 2,511,286 | ||||||

| Iowa Student Loan Liquidity Corp., “A-2”, 5.7%, 2027 | 185,000 | 207,809 | ||||||

| Iowa Student Loan Liquidity Corp., “A-2”, 5.75%, 2028 | 3,795,000 | 4,256,852 | ||||||

| Massachusetts Educational Financing Authority, “J”, 4.7%, 2026 | 2,600,000 | 2,682,628 | ||||||

| Massachusetts Educational Financing Authority, “J”, 4.9%, 2028 | 2,705,000 | 2,814,066 | ||||||

| Massachusetts Educational Financing Authority, Education Loan Rev., “H”, ASSD GTY, 6.35%, 2030 | 2,650,000 | 2,944,442 | ||||||

| Massachusetts Educational Financing Authority, Education Loan Rev., “I-A”, 5.5%, 2022 | 225,000 | 260,577 | ||||||

|

| |||||||

| $ | 18,831,280 | |||||||

| Tax - Other - 0.6% | ||||||||

| Hudson Yards, NY, Infrastructure Corp. Rev., “A”, 5.75%, 2047 | $ | 3,950,000 | $ | 4,664,990 | ||||

| New York Dormitory Authority, State Personal Income Tax Rev., “A”, 5%, 2025 | 5,000,000 | 6,231,300 | ||||||

| Virgin Islands Public Finance Authority Rev. (Diageo Project), “A”, 6.75%, 2037 | 2,200,000 | 2,567,422 | ||||||

| Virgin Islands Public Finance Authority Rev., “A”, 5.25%, 2024 | 130,000 | 137,277 | ||||||

|

| |||||||

| $ | 13,600,989 | |||||||

| Tax Assessment - 0.6% | ||||||||

| Arborwood Community Development District, FL, Special Assessment (Master Infrastructure Projects), “B”, 5.1%, 2014 | $ | 160,000 | $ | 134,549 | ||||

| Baltimore, MD, Special Obligation, (East Baltimore Research Park Project), “A”, 7%, 2038 | 1,285,000 | 1,387,106 | ||||||

| Capital Region Community Development District, FL, Capital Improvement Rev., “A”, 7%, 2039 | 890,000 | 831,830 | ||||||

24

Table of Contents

Portfolio of Investments (unaudited) – continued

| Issuer | Shares/Par | Value ($) | ||||||

| Municipal Bonds - continued | ||||||||

| Tax Assessment - continued | ||||||||

| Concord Station Community Development District, FL, Special Assessment, 5%, 2015 | $ | 75,000 | $ | 74,584 | ||||

| Fishhawk Community Development District, FL, 7.04%, 2014 | 10,000 | 10,101 | ||||||

| Glendale, CA, Redevelopment Agency, Tax Allocation Rev. (Central Glendale Redevelopment Project), 5.5%, 2024 | 2,250,000 | 2,359,598 | ||||||

| Heritage Harbour North Community Development District, FL, Capital Improvement Rev., 6.375%, 2038 | 835,000 | 805,900 | ||||||

| Homestead 50, FL, Community Development District, Special Assessment, “A”, 6%, 2037 | 1,665,000 | 1,186,662 | ||||||

| Homestead 50, FL, Community Development District, Special Assessment, “B”, 5.9%, 2013 | 700,000 | 494,004 | ||||||

| Killarney Community Development District, FL, Special Assessment, “B”, 5.125%, 2009 (a)(d) | 190,000 | 85,500 | ||||||

| Lancaster County, SC, Assessment Rev. (Sun City Carolina Lakes), 5.45%, 2037 | 40,000 | 37,802 | ||||||

| Main Street Community Development District, FL, “A”, 6.8%, 2038 | 540,000 | 520,295 | ||||||

| Massachusetts Bay Transportation Authority Rev., “A”, 5.25%, 2034 | 2,000,000 | 2,336,820 | ||||||

| Middle Village Community Development District, FL, Special Assessment, “A”, 5.8%, 2022 | 70,000 | 56,024 | ||||||

| New Port Tampa Bay Community Development District, FL, Special Assessment, “B”, 5.3%, 2012 (a)(d) | 200,000 | 78,500 | ||||||

| Noblesville, IN, Redevelopment Authority Lease Rental, 5.25%, 2025 | 2,000,000 | 2,221,140 | ||||||

| Old Palm Community Development District, FL, Special Assessment (Palm Beach Gardens), “B”, 5.375%, 2014 | 70,000 | 69,231 | ||||||

| Parkway Center Community Development District, FL, Special Assessment, “B”, 5.625%, 2014 | 585,000 | 540,295 | ||||||

| Sterling Hill Community Development District, FL, Capital Improvement Rev., “B”, 5.5%, 2010 (d) | 55,000 | 38,504 | ||||||

| Tuscany Reserve Community Development District, FL, Special Assessment, “B”, 5.25%, 2016 | 375,000 | 341,048 | ||||||

| Washington County, PA, Redevelopment Authority (Victory Centre Project), “A”, 5.45%, 2035 | 120,000 | 122,806 | ||||||

| Watergrass Community Development District, FL, Special Assessment, “B”, 6.96%, 2017 | 75,000 | 72,506 | ||||||

|

| |||||||

| $ | 13,804,805 | |||||||

| Tobacco - 3.4% | ||||||||

| Buckeye, OH, Tobacco Settlement Financing Authority, “A-2”, 5.125%, 2024 | $ | 8,605,000 | $ | 7,241,280 | ||||

| Buckeye, OH, Tobacco Settlement Financing Authority, “A-2”, 5.75%, 2034 | 5,000,000 | 3,979,650 | ||||||

25

Table of Contents

Portfolio of Investments (unaudited) – continued

| Issuer | Shares/Par | Value ($) | ||||||

| Municipal Bonds - continued | ||||||||

| Tobacco - continued | ||||||||

| Buckeye, OH, Tobacco Settlement Financing Authority, Capital Appreciation, “A-3”, 0% to 2012, 6.25% to 2037 | $ | 8,900,000 | $ | 7,499,140 | ||||

| District of Columbia, Tobacco Settlement, 6.25%, 2024 | 855,000 | 874,306 | ||||||

| Golden State, CA, Tobacco Securitization Corp., Tobacco Settlement Rev., “A-1”, 6.25%, 2013 (c) | 1,405,000 | 1,460,554 | ||||||

| Golden State, CA, Tobacco Securitization Corp., Tobacco Settlement Rev., “A-1”, 5.75%, 2047 | 4,760,000 | 4,041,716 | ||||||

| Golden State, CA, Tobacco Securitization Corp., Tobacco Settlement Rev., Asset Backed, “A-1”, 5%, 2033 | 475,000 | 386,232 | ||||||

| Illinois Railsplitter Tobacco Settlement Authority, 5.5%, 2023 | 3,970,000 | 4,639,421 | ||||||

| Illinois Railsplitter Tobacco Settlement Authority, 6.25%, 2024 | 2,610,000 | 2,904,773 | ||||||

| Illinois Railsplitter Tobacco Settlement Authority, 6%, 2028 | 8,750,000 | 10,243,363 | ||||||

| Iowa Tobacco Settlement Authority, Tobacco Settlement Rev., Asset Backed, “B”, 5.6%, 2034 | 3,070,000 | 2,844,908 | ||||||

| Louisiana Tobacco Settlement Authority Rev., “2001-B”, 5.5%, 2030 | 955,000 | 978,197 | ||||||

| Louisiana Tobacco Settlement Authority Rev., “2001-B”, 5.875%, 2039 | 2,835,000 | 2,899,298 | ||||||

| New Jersey Tobacco Settlement Financing Corp., “1-A”, 5%, 2041 | 12,095,000 | 10,019,982 | ||||||

| Suffolk, NY, Tobacco Asset Securitization Corp., Tobacco Settlement, “B”, 5.25%, 2037 | 765,000 | 815,062 | ||||||

| Tobacco Securitization Authority, Minnesota Tobacco Settlement Rev., “B”, 5.25%, 2031 | 7,965,000 | 8,911,481 | ||||||

| Washington Tobacco Settlement Authority Rev., 6.5%, 2026 | 180,000 | 187,450 | ||||||

| Washington Tobacco Settlement Authority Rev., 6.625%, 2032 | 4,485,000 | 4,659,915 | ||||||

|

| |||||||

| $ | 74,586,728 | |||||||

| Toll Roads - 2.3% | ||||||||

| E-470 Public Highway Authority Rev., CO, “C”, 5.375%, 2026 | $ | 1,495,000 | $ | 1,651,302 | ||||

| Illinois Toll Highway Authority Rev., “B”, 5.5%, 2033 | 5,645,000 | 6,284,296 | ||||||

| Mid-Bay Bridge Authority, FL, Springing Lien Rev., “A”, 7.25%, 2040 | 6,920,000 | 8,724,459 | ||||||

| North Texas Tollway Authority Rev. (Special Projects System), “D”, 5%, 2029 | 15,000,000 | 17,586,150 | ||||||

| Northwest Parkway, CO, Public Highway Authority Rev., “C”, ETM, AGM, 5.35%, 2016 (c) | 1,000,000 | 1,173,550 | ||||||

| Oklahoma Turnpike Authority, “B”, 5%, 2027 | 3,835,000 | 4,586,161 | ||||||

| Oklahoma Turnpike Authority, “B”, 5%, 2028 | 745,000 | 887,854 | ||||||

| Oklahoma Turnpike Authority, “B”, 5%, 2030 | 500,000 | 590,955 | ||||||

| Oklahoma Turnpike Authority, “B”, 5%, 2031 | 750,000 | 882,165 | ||||||

| Orlando & Orange County, FL, Expressway Authority Rev., “A”, 5%, 2040 | 1,000,000 | 1,102,360 | ||||||

| Triborough Bridge & Tunnel Authority Rev., NY, “A”, 5%, 2025 | 2,675,000 | 3,278,293 | ||||||

26

Table of Contents

Portfolio of Investments (unaudited) – continued

| Issuer | Shares/Par | Value ($) | ||||||

| Municipal Bonds - continued | ||||||||

| Toll Roads - continued | ||||||||

| Virginia Small Business Financing Authority Rev. (Elizabeth River Crossings Opco LLC Project), 5.25%, 2032 | $ | 1,310,000 | $ | 1,428,830 | ||||

| Virginia Small Business Financing Authority Rev. (Elizabeth River Crossings Opco LLC Project), 6%, 2037 | 2,180,000 | 2,502,269 | ||||||

|

| |||||||

| $ | 50,678,644 | |||||||

| Transportation - Special Tax - 2.3% | ||||||||

| Commonwealth of Virginia, Transportation Board Rev., “A”, 4%, 2026 | $ | 8,180,000 | $ | 9,155,792 | ||||

| Commonwealth of Virginia, Transportation Board Rev., Capital Projects, 5%, 2020 | 4,870,000 | 6,084,481 | ||||||

| Jacksonville, FL, Transportation Authority Rev., ETM, 9.2%, 2015 (c) | 1,120,000 | 1,237,298 | ||||||

| New Jersey Transportation Trust Fund Authority Rev., “D”, 5.25%, 2023 | 7,500,000 | 9,411,825 | ||||||

| New York Metropolitan Transportation Authority Rev., ETM, 5.75%, 2013 (c) | 330,000 | 343,589 | ||||||

| Pennsylvania Turnpike Commission Oil Franchise Tax Rev., “A”, ETM, AMBAC, 5.25%, 2018 (c) | 1,150,000 | 1,275,592 | ||||||

| State of Connecticut, Special Tax Obligation Rev., “A”, 5%, 2028 | 4,595,000 | 5,542,765 | ||||||

| State of Connecticut, Special Tax Obligation Rev., “A”, 5%, 2029 | 4,595,000 | 5,517,722 | ||||||

| State of Connecticut, Special Tax Obligation Rev., “A”, 5%, 2030 | 4,615,000 | 5,516,725 | ||||||

| State of Hawaii, Highway Rev., “A”, 5%, 2030 | 3,695,000 | 4,422,767 | ||||||

| State of Hawaii, Highway Rev., “A”, 5%, 2031 | 1,380,000 | 1,643,056 | ||||||

| State of Hawaii, Highway Rev., “A”, 5%, 2032 | 920,000 | 1,089,574 | ||||||

|

| |||||||

| $ | 51,241,186 | |||||||

| Universities - Colleges - 8.7% | ||||||||

| Alcorn State University, MS, Educational Building Corp. Rev. (Student Housing Project), “A”, 5.125%, 2034 | $ | 2,500,000 | $ | 2,804,425 | ||||

| Alcorn State University, MS, Educational Building Corp. Rev. (Student Housing Project), “A”, 5.25%, 2039 | 1,625,000 | 1,818,278 | ||||||

| Allegheny County, PA, Higher Education Building Authority Rev. (Robert Morris University), “A”, 5.9%, 2028 | 1,195,000 | 1,315,623 | ||||||