June 25, 2009

Mr. Kevin L. Vaughn

Accounting Branch Chief

Division of Corporation Finance

U.S. Securities and Exchange Commission

450 Fifth Street, N.W.

Washington, DC 20549

| Re: | Theragenics Corporation |

| Form 10-K for the Fiscal Year Ended December 31, 2008 | |

| Filed March 13, 2009 | |

| File No. 001-14339 |

Dear Mr. Vaughn:

We offer the following information in response to the comments and questions raised in your letter dated May 29, 2009 related to our above referenced filing. Our responses are keyed to your comments.

Form 10-K for the year ended December 31, 2008

Cover Page

| 1. | You indicate on the cover page of the Form 10-K that your Commission file number is “0-15443.” It appears, however, that you are actually filing under the file number 001-14339. In applicable future filings, please use your correct Commission file number. |

Response

We will include our correct Commission file number on all future filings.

Item 1. Business, Page 1

| 2. | We see from the transcript of your earnings call that occurred on February 19, 2009 that your backlog increased by 15% from the third to fourth quarter and your Chief Executive Officer’s statements that although such backlog is subject to cancellation or delay, the backlog is still an indicator of the company’s prospects. In your applicable future filings, please disclose the information required by Item 101(c)(1)(vii) with respect to each segment in which you operate and include any appropriate disclosure regarding cancellations or delays. |

Response

In applicable future filings we will disclose the information required by Item 101(c)(1)(vii) with respect to each segment in which we operate and include any appropriate disclosure regarding cancellations or delays.

Item 6. Selected Financial Data, page II-2

| 3. | Please revise future filings to describe, or cross-reference to a discussion thereof, factors that affect comparability of the information reflected in your selected financial data. In this regard we note you consummated several business combinations during the 5 year period ended December 31, 2008. For reference, see Item 301 of Regulation S-K. |

U.S. Securities and Exchange Commission

June 25, 2009

Page 2

Response

We will revise future filings to describe, or cross-reference to a discussion thereof, factors that affect comparability of the information reflected in our selected financial data.

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations, page II-3

Operating income (loss) and costs and expenses, page II-5

| 4. | We note your presentation of the non-GAAP measure operating income, excluding special items. In order to fully comply with the guidance in Item 10(e) of Regulation S-K and the guidance in our related Frequently Asked Questions Regarding the Use of Non-GAAP Financial Measures, please revise your disclosure in future filings to discuss the following items: | |

| o | the manner in which management uses the non-GAAP measure to conduct or evaluate its business; | |

| o | the economic substance behind management’s decision to use such a measure; | |

| o | the material limitations associated with use of the non-GAAP financial measure as compared to the use of the most directly comparable GAAP financial measure; | |

| o | the manner in which management compensates for these limitations when using the non-GAAP financial measure; and | |

| o | the substantive reasons why management believes the non-GAAP financial measure provides useful information to investors. | |

| Please provide us with a sample of the proposed revised disclosure to be included in future filings. | ||

Response

We believe we provided the information required by Item 10(e) of Regulation S-K in the first full paragraph following the tabular presentation of Operating Income (Loss) and Costs and Expenses on page II-5. However, to enhance this disclosure and to more fully address the concerns raised in bullet point five in your comment, we will revise the disclosure in applicable future filings regarding this non-GAAP measure as provided in the following paragraph:

“In addition to calculations measuring operating income (loss) as calculated and presented in accordance with accounting principles generally accepted in the United States of America (“GAAP”), we utilize operating income excluding special items to make operational decisions, evaluate performance, prepare internal forecasts and allocate resources. Operating income excluding special items is a non-GAAP financial measure which, when compared with operating income calculated in accordance with GAAP, allows us to more accurately determine whether a given increase or decrease in operations for a given segment is a result of an event that is non-recurring in nature or is reflective of an on-going performance issue. We believe presentation of these non-GAAP financial measures provides supplemental information that is helpful to an understanding of the operating results of our businesses and period-to-period comparisons of performance. However, non-GAAP financial measures should be considered in addition to, but not as a substitute for, the comparable measure calculated and presented in accordance with GAAP.”

U.S. Securities and Exchange Commission

June 25, 2009

Page 3

| 5. | As a related matter, please note that Item 10(e) of Regulation S-K prohibits adjusting a non-GAAP financial performance measure to eliminate items when the nature of the charge is such that it is reasonably likely to recur within two years or there was a similar charge or gain within the prior two years. Please explain to us why you believe that your presentation of the non-GAAP financial measure complies with this guidance. |

Response

We believe that our disclosure of “operating income excluding special items” complies with Item 10(e) of Regulation S-K. Our disclosure includes a presentation of operating income (loss) in accordance with GAAP with equal or greater prominence than our non-GAAP operating income excluding special items. We also note that Question 8 of the Frequently Asked Questions Regarding the Use of Non-GAAP Financial Measures states that “such measures more likely would be permissible if management reasonably believes it is probable that the financial impact of the item will disappear or become immaterial within a near-term finite period.” Our decision to disclose “operating income excluding special items” is based on the significant impact on our segment operating results of four items: goodwill and tradename impairment charges recorded in the fourth quarter of 2008; changes in the estimated fair value of an asset held for sale in 2007 and 2008 (this asset was sold in 2008); one-time license fees in 2006; and restructuring related expenses in 2006.

We have not had a pattern or history of items of these types and do not expect such items to be material going forward. In particular, we note that in 2008 we fully impaired all of our previously recorded goodwill, so there is no remaining goodwill subject to future impairment. We believe the presentation of “operating income excluding special items,” when taken together with the corresponding GAAP results, presents a more useful measure of our core operating results. Indeed, these identical non-GAAP measures are utilized by our executive management to make operational decisions, evaluate performance, prepare internal forecasts and allocate resources. These non-GAAP measures are also reported to our board of directors who use them, along with the corresponding GAAP measures, to evaluate performance.

| 6. | We note your disclosures here and on pages II-6 through II-7 and page F-22 regarding the impairment of your goodwill and intangible assets. You state on page II-7 that “these impairment charges are not expected to affect [y]our liquidity, cash flows from operating activities, or future operations.” However, you state that the impairment charges were based in part on a discounted cash flow model. As such, it appears that the impairment charges are based in part on an expected decline in cash flows in future periods which will also impact your liquidity. Please revise future filings to provide enhanced disclosure of how the impairment charge relates to your expectations for your results of operations in future periods. In this regard, please specifically discuss any known trends or uncertainties that have had or that you reasonably expect will have a material favorable or unfavorable impact on revenues or income from continuing operations. Refer to Item 303(A)(3)(ii) of Regulation S-K. |

Response

In estimating the fair value of our reporting units for purposes of assessing impairment of goodwill and other intangible assets, the significant increases in the discount rates used in our discounted cash flow models and the significant decreases in the comparable company market multiples (rather than our gross forecasted cash flows), had a material effect on our impairment testing. Please also refer to our responses to item numbers 7 and 8 below.

U.S. Securities and Exchange Commission

June 25, 2009

Page 4

With regard to our expectations for results of operations in future periods, we do specifically discuss known trends or uncertainties that have had or that we reasonably expect will have a material favorable or unfavorable impact on revenues or income from continuing operations. For example, we refer to the first paragraph under “Revenue” on page II-4 which contains the following disclosure related to our surgical products segment:

“A significant portion of the products in our surgical business is sold to OEMs and a network of distributors. Ordering patterns of these customers vary and are difficult to predict. Accordingly, surgical products revenue is subject to fluctuation, especially on a quarter-to-quarter basis. In addition, the volatility and disruptions in the U.S. and global economies and credit markets, and other uncertainties due to the economic slowdown in the U.S. and around the world, have had a negative effect on our surgical product revenue, especially as general economic conditions worsened in the fourth quarter of 2008. Scheduled shipping dates for orders were farther out than we have typically experienced. We believe the lengthening lead times have been, at least in part, our customers’ response to hospitals’ efforts to reduce inventories and conserve cash. We believe this has affected all companies in the supply chain, including ours. Looking forward, we expect that the difficult economic climate and macroeconomic uncertainties generally will continue to affect our surgical products business at least through 2009, and perhaps make the fluctuations in our results even more volatile from period to period.”

We will continue to specifically discuss any known trends or uncertainties that have had or that we reasonably expect will have a material favorable or unfavorable impact on revenues or income from continuing operations in our future filings.

| 7. | Further to the above, you stated that “[y]our estimates of fair value of [y]our reporting units were severely limited by [y]our market capitalization.” Please tell us and revise future filings to explain in greater detail how your market capitalization “limited” your fair value estimates. |

Response

Our market capitalization declined significantly in the fourth quarter of 2008, along with the significant declines in the overall market value of all of the major stock markets in the United States and around the world. We considered our market capitalization when we developed the appropriate discount rates and comparable company market multiples for purposes of estimating the fair value of our reporting units. The significant decline in our market capitalization resulted in discount rates that were considerably higher, and comparable company market multiples that were considerably lower, than the discount rates and comparable company market multiples we previously considered appropriate. We attempted to identify the underlying reasons for this circumstance. However, we were not aware of any underlying fundamental reason directly related to our businesses operations or results for the decline in our market capitalization; indeed, the long-term expectations for our reporting units did not materially change during this period. We considered many factors, including: the conditions of the companies in our sectors; unusual short selling or other unusual activity in the trading of our common stock; and whether the overall general economic outlook and stock market declines could be considered as “temporary.” We were unable to identify any of these factors as directly affecting the decline in our market capitalization. We concluded that the significant increase in our discount rates and decrease in our comparable company market multiples was a result of the increased risk associated with the distressed equity and credit markets generally, especially as these factors relate to a small company such as ours. We are smaller than companies that are generally considered as “micro cap” companies. In the current environment, we believe investors demand higher returns and have a desire to conserve cash. In addition, the scarcity of capital, especially for a very small company, affects the risks associated with investments in its common stock and its share price. Indeed, through the date of this letter our market capitalization has remained significantly lower than the levels of the previous several years.

U.S. Securities and Exchange Commission

June 25, 2009

Page 5

The intent of our disclosure that our market capitalization “limited” our estimates of fair value was intended to describe the above circumstances. We will clarify and more fully explain the above circumstances in applicable future filings.

| 8. | Please provide us with additional information regarding your evaluation of goodwill for impairment. Discuss in greater detail the valuation methodologies you used. To the extent you used more than one methodology; explain how you weighted each of the methodologies. Disclose the specific assumptions used, including discount rates, growth rates, market multiples, etc. Please also revise the critical accounting policies and estimates section on pages II-9 through II-11 in future filings to provide more specific disclosure of the significant management judgments and estimates. |

Response

We prepared discounted cash flow analyses (“income approach”) and comparable company market multiples analyses (“market approach”) to determine the fair values of our reporting units.

For the income approach we projected future cash flows for each reporting unit. This approach requires significant judgments including the projected net cash flows, the weighted average cost of capital (“WACC”) used to discount the cash flows and terminal value assumptions. We derived the assumptions related to cash flows primarily from our internal budgets and forecasts. These budgets and forecasts include information related to our current and future products, revenues, capacity, operating costs, and other information. All such information is derived in the context of our long-term operational strategies. The WACC and terminal value assumptions were based on the capital structure, cost of capital, inherent business risk profiles, and industry outlooks for each of our reporting units, and for our company on a consolidated basis. Please also refer to our response to item 7 above for additional considerations related to our WACC.

For the market approach we identified reasonably similar public companies for each of our reporting units, analyzed the financial and operating performance of these similar companies relative to our financial and operating performance, calculated market multiples primarily based on the ratio of Business Enterprise Value (“BEV”) to revenue and BEV to earnings before interest, taxes, depreciation and amortization (“EBITDA”), adjusted such multiples for differences between the similar companies and our reporting units, and applied the resulting multiples to the fundamentals of our reporting units to arrive at an indication of fair value. Please also refer to our response to item 7 above for additional considerations related to our comparable company market multiples.

To assess the reasonableness of our valuations under each method, we reconciled the aggregate fair values of our reporting units to our market capitalization, relying primarily on the market approach. Indeed, the market approach was utilized for all reporting units within our surgical products segment. Impairment of goodwill in our surgical products segment was $65.3 million, representing 100% of the recorded goodwill in that segment and 96% of our total consolidated goodwill impairment. We also note that substantially all of our goodwill would have been impaired had we utilized the income approach to determine the fair value of our reporting units.

We note that 100% of our recorded goodwill was impaired, and we had no goodwill recorded on our consolidated balance sheet at December 31, 2008. Accordingly, we do not believe it would be meaningful to disclose specific assumptions, such as the revenue and EBITDA multiples, growth rates and discount rates utilized in our modeling.

We will revise applicable future filings, including the critical accounting policies and estimates section on pages II-9 through II-11, to provide more specific disclosure related to our significant judgments and estimates, as discussed above.

U.S. Securities and Exchange Commission

June 25, 2009

Page 6

| 9. | We note your disclosure that in connection with your evaluation of your tradename intangible assets, you determined that these assets no longer had an indefinite life but instead had a remaining useful life of 10 years. Please tell us and revise future filings to explain what changed in relation to these assets that caused you to conclude they no longer had an indefinite life. |

Response

In accordance with SFAS 142, an entity should evaluate all of its indefinite-lived intangible assets each reporting period to determine whether facts and circumstances continue to support an indefinite life. Accordingly, we reviewed the facts and circumstances surrounding our tradenames intangible assets. We performed this review in the context of our evaluation of goodwill impairment. We also considered the updated estimate of fair value of our tradenames intangible assets, which was performed in accordance with step 2 of our SFAS 142 assessment. In considering all of the facts and circumstances, including the increased risk associated with our businesses as perceived by investors, the distressed general equity and credit markets, especially as these factors relate to a small company such as ours, and the significant economic uncertainties caused by the worsening overall economic conditions, we concluded that an indefinite life for our tradenames intangible assets was no longer supportable. We also considered changes to our terminal value assumptions in our estimate of fair value based upon the income approach (please also see our response to item 8 above) for each reporting unit, which affected assumptions beyond year 10 in our cash flow forecasts. We note that we included the following disclosure on page II-7:

“Our tradenames were intangible assets with indefinite lives and accordingly were not subject to amortization. Pursuant to SFAS No. 142 the recorded value of our tradenames intangible asset is tested for impairment annually or more frequently if changes in circumstances indicate that impairment may exist. The determination of fair value used in the impairment evaluation is based on discounted estimates of future sales projections attributable to ownership of the tradenames. Significant judgments inherent in this analysis include assumptions about appropriate sales growth rates, royalty rates, discount rates and the amount of expected future cash flows. The judgments and assumptions used in the estimate of fair value are consistent with the projections and assumptions that are used in our internal budgeting and forecasting process. They are also consistent with the judgments and assumptions used in our goodwill impairment testing. The determination of fair value is highly sensitive to changes in the related discount rate used to evaluate the fair value of our tradenames. We estimated the current fair value of our tradenames, as determined using discount rates reflective of current economic conditions and our market capitalization. We compared these estimated fair values to the recorded amounts of our tradenames and determined that there was impairment of $2.5 million, all related to reporting units in our surgical products segment. In connection with our review of tradename impairment, we determined that current facts and circumstances no longer supported an indefinite life. We estimated that the remaining useful life of our tradenames was 10 years. Accordingly, we will amortize our tradenames over 10 years beginning in 2009; and amortization expense in 2009 is expected to be $324,000 higher than it would be if tradenames were not subject to amortization.”

We believe this disclosure adequately described what changed in relation to our tradenames intangible asset to cause us to conclude that they no longer had an indefinite life, especially in the context of the in depth disclosures related to goodwill impairment that immediately preceded the above disclosure. However, we will expand this disclosure in future filings as appropriate to more fully explain what changed in relation to our tradenames to cause us to conclude that they no longer had an indefinite life.

U.S. Securities and Exchange Commission

June 25, 2009

Page 7

Item 11. Executive Compensation, page III-1

| 10. | The Compensation Discussion and Analysis section should be a narrative at the beginning of your compensation disclosure, putting into perspective the tables that follow. Your current format includes a list of your executive officers between your Compensation Discussion and Analysis and the required compensation tables for your named executive officers. Please revise your future filings, as applicable, so that your Compensation Discussion and Analysis immediately precedes these tables. |

Response

In future filings we will locate our Compensation Discussion and Analysis immediately preceding the compensation tables.

| 11. | We note from your discussion on pages 11 and 12 of the proxy statement that you have incorporated by reference into your Form 10-K that you have not disclosed the specific targets to be achieved in order for your named executive officers to earn their respective short-term cash incentive payments for 2008. We also note similar disclosures on page 13 regarding your 2009 short-term incentive compensation program and on pages 13 and 14 regarding your long-term incentive compensation program. Please disclose those targets in your future filings, as applicable. To the extent you believe that disclosure of such information, on a historical basis, would result in competitive harm such that the information could be excluded under Instruction 4 to Item 402(b) of Regulation S-K, please provide us with a detailed explanation supporting your conclusion. To the extent that it is appropriate to omit specific targets or performance objectives, you are required to provide appropriate disclosure pursuant to Instruction 4 to Item 402(b) of Regulation S-K. Refer also to Question 118.04 of the Regulation S-K Compliance and Disclosure Interpretations available on our website at http://www.sec.gov/divisions/corpfin/guidance/regs-kinterp.htm. In discussing how difficult or likely it will be to achieve the target levels or other factors, you should provide as much detail as necessary without disclosing information that poses a reasonable risk of competitive harm. |

Response

We believe that the disclosure of individual performance goals would result in competitive harm to us. Each of these goals relate to the named executive officers’ achievement of specific objectives outlined in our strategy and also relate to financial targets such as product plans, sales projections and other projections based on commercial and financial information available to management and the Board that is confidential. More specifically, as we discuss on pages 11 and 12 of our proxy statement,

“Revenue, profitability, and EBITDA targets are taken from the Company’s annual operating budget for the year, which has been reviewed and approved by Theragenics’ Board of Directors. These operating budget numbers represent what the Board views to be an appropriate result when Theragenics’ strategic business plan is well executed within the current industry business climate.”

U.S. Securities and Exchange Commission

June 25, 2009

Page 8

We believe encouraging our named executive officers to achieve personally-tailored goals motivates the named executive officers to better execute on our strategy. To give effect to such encouragement, the performance goals are designed to be individually specific and detailed. The individual performance goals for all named executive officers, except the Chief Executive Officer, are developed through confidential discussions between the Chief Executive Officer and the Compensation Committee and are approved by the Board upon recommendation by the Compensation Committee. The individual goals for the Chief Executive Officer are developed through confidential discussions between the members of the Compensation Committee and are approved by the Company’s independent directors. Therefore, we believe that these targets and the information relating to their establishment constitutes confidential commercial and financial information. This information is not publicly known or available to the general public, and we have carefully kept all of this information confidential because we believe disclosure would cause substantial harm to our competitive position.

Instruction 4 to Item 402(b) of Regulation S-K instructs that the standard for determining whether the disclosure of certain information would lead to competitive harm to a registrant is the same as the standard in determining a request for confidential treatment pursuant to Rule 24b-2 under the Securities Exchange Act of 1934 (incorporating certain criteria from the Freedom of Information Act (5 U.S.C. 552(b)(4)) and the parallel Commission regulation (17 C.F.R. 200.80(b)(4)) known as the “(b)(4) Exemption.”). The Commission’s rule adopted under the Freedom of Information Act allows for confidential protection for information which, if made public, would reveal “commercial or financial information” from the registrant that is “privileged or confidential.” In applying this standard, the federal courts have formulated a two-pronged test which considers information to be confidential if disclosure would either: (1) impair the government’s ability to obtain necessary information in the future or (2) cause substantial harm to the competitive position of the person from whom the information was obtained. (See, e.g. Contract Freighters, Inc. v. Sec’y of United States Dep’t of Transp., 260 F.3d 858 (8th Cir. 2001)).

In applying this test to us, the information would be confidential under the second prong given the substantial harm to our competitive position for several reasons:

| 1. | Competitors may have more resources than we do which will allow them to exploit competitive information quickly, such that we would face a severe disadvantage. Although competitors vary in size, many competitors are large corporations with substantial financial, marketing and product development resources. Disclosure of this information will provide our competitors with clear information about our corporate strategies and approach to business that is not otherwise available to the public. | |

| 2. | This information could disclose parts of our internal business plans and targets, leading to a significant competitive disadvantage for us. This information contains performance targets and financial goals which, if disclosed, would reveal specific information about our current and future goals, anticipated corporate actions and resource allocation, as well as give our competitors insight into our efforts to exploit identified opportunities in the industry and its specific strategic objectives for increasing market share and attaining other strategic goals identified by us. This information contains highly sensitive and specific Company plans for success in the industry. Disclosure of this information is tantamount to disclosure of our strategies to execute our strategic plan and could compromise our ability to compete successfully. |

U.S. Securities and Exchange Commission

June 25, 2009

Page 9

| 3. | This information will allow competitors to increase their competitive advantage by giving them the opportunity to alter their strategic vision based on knowledge of our anticipated actions. For example, as part of this information, we consider product development and launch plans which have not been announced to the public or our customers. This could allow our competitors to divert resources to their own departments in order to usurp our market share or to launch specific marketing efforts meant to derail our efforts with our current or potential customers, especially considering the small size of our company relative to many of our competitors. Similarly, sales projections are considered in these performance targets, and a competitor would be given unfair insight into our expectations regarding customer response, costs for production and marketing, expected profit margins and industry reaction. Furthermore, individual performance goals may provide time-related information which, if provided to a competitor prior to the launch of a product, could cause a competitor to bring a similar product to market sooner or to contact suppliers who have reached an arrangement with us in order to gain a competitive advantage. | |

| 4. | This information will allow competitors to use our individual targets in soliciting our named executive officers. Our success depends to a significant extent upon the abilities of our executive officers. Disclosure of the individual performance goals of our executive officers will identify “high-performers” to our competitors and grant them an unfair advantage in soliciting and negotiating potential agreements with our executive officers. This could allow our competitors to solicit key members of management by structuring a more attractive compensation plan utilizing different goals or financial targets which may increase the likelihood of a cash bonus payout and thereby make an alternative employer more attractive than us. Competition for highly-skilled senior management in our industries is intense, and we may not be successful in attracting or retaining them on terms acceptable to us, or at all, if this information were made available to our competitors. If we are not able to attract and retain talented senior management then our ability to execute on our strategy is compromised. An increase in the costs necessary to attract and retain skilled management and any delays resulting from such search or departures could also have an adverse effect on our business, results of operations and financial condition. |

The foregoing are just a few examples of the substantial competitive harm that disclosure of this information could cause. Any of these consequences would significantly harm our business, results of operations and financial condition. Therefore, we believe this information constitutes confidential commercial and financial information that, if disclosed, would cause substantial competitive harm. For these reasons, we respectfully submit to the Staff that our non-disclosure of this information is justified in light of the competitive harm that such disclosure may cause.

Our Compensation Discussion and Analysis disclosure addresses how difficult or likely it will be to achieve the targeted level of performance as follows:

“Short-term Incentive Compensation – General Guidelines. Revenue, profitability, and EBITDA targets are taken from the Company’s annual operating budget for the year, which has been reviewed and approved by Theragenics’ Board of Directors. These operating budget numbers represent what the Board views to be an appropriate result when Theragenics’ strategic business plan is well executed within the current industry business climate. Threshold goals for revenue, profitability, and EBITDA represent the minimally acceptable financial results in order for a Named Executive Officer to receive any portion of the short-term incentive compensation based on these financial metrics…. Maximum goals related to financial metrics represent attainable financial results but achievement of Maximum goals will require results significantly above those thought to be reasonably achievable under Theragenics business plan given the current business climate.”

U.S. Securities and Exchange Commission

June 25, 2009

Page 10

Similarly, our Compensation Discussion and Analysis indicates that the performance goals for the cash portion of our long-term incentives (the only portion for which there are confidential performance metrics) are “based on the achievement of Board approved revenue and EBITDA goals based on the Company’s three-year strategic plan” for the applicable performance cycle. Accordingly, the financial metric performance goals for both our short-term incentives and long-term incentives are directly taken from our Board approved strategic plan. With respect to discretionary components and individual performance goals, these are generally discussed under the heading “Performance” at the beginning of our Compensation Discussion and Analysis.

Item 15. Exhibits and Financial Statement Schedules, page IV-1

| 12. | It appears you have not filed as an exhibit the distribution agreement with C.R. Bard that is mentioned on page I-8. Since this agreement accounts for a substantial portion of your revenues, please provide us your analysis as to whether that agreement is required to be filed pursuant to Regulations S-K Item 601(b)(10). If that agreement should be filed as an exhibit, please include that agreement in your next available filing. |

Response

Our distribution agreement with C.R. Bard (“Bard”) is in the ordinary course of our business. Item 601(b)(10)(ii)(B) of Regulation S-K provides that contracts in the ordinary course of business, other than contracts “upon which the registrant’s business is substantially dependent, as in the case of continuing contracts to sell the major part of the registrant’s products and services” need not be filed.

It may be helpful to review the background of our distribution strategy and agreements. From 1997 to 2000, we marketed and sold TheraSeed pursuant to an exclusive Sales and Marketing Agreement (which we filed as a material contract at the time) with a subsidiary of Johnson and Johnson. In 2000, we shifted from this exclusive arrangement to a combination of direct sales and non-exclusive distribution agreements, entering into at least four separate non-exclusive distribution agreements including the Bard Agreement. These non-exclusive distribution agreements were not filed because they were in the ordinary course of our business as a manufacturer selling through non-exclusive distributors.

While the number of our distributors has decreased over time due to, among our things, consolidation in the industry, non-exclusive distribution agreements are in the ordinary course of our business, and we are not “substantially dependent” on the Bard Agreement for several reasons. The Bard Agreement is not a “continuing contract to sell the major part of” our products because it does not obligate Bard to purchase any minimum volume and does not obligate us to deliver any specified volume; it merely provides pricing and delivery terms for orders placed. In that regard, the Bard Agreement is an “ordinary purchase and sales agency” agreement which is excluded from the definition of a material contract by paragraph (iii)(C) of Item 601(b)(10). Moreover, the Bard Agreement is not a “continuing contract” because either party may give notice to terminate the agreement as of December 31 of the following year.

U.S. Securities and Exchange Commission

June 25, 2009

Page 11

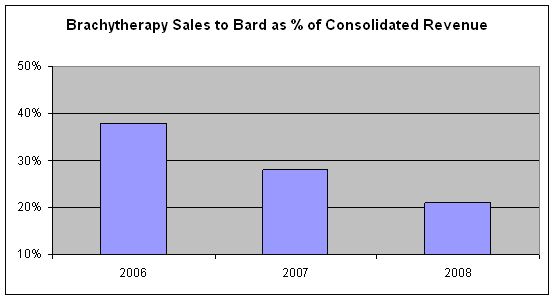

The following chart demonstrates the declining significance of brachytherapy sales to Bard to our consolidated revenue:

We note that brachytherapy segment sales to Bard totaled 18% of pro forma consolidated revenue in 2008 (i.e. – assuming the NeedleTech acquisition occurred on January 1, 2008). While we do not believe that that the Bard Agreement is material, we note that Item 601(b)(10)(ii) sets a higher threshold than ordinary materiality, referring instead to “substantial dependence” and “contracts to sell the major portion,” not just a material portion, of the registrant’s sales.

As we have noted in our filings for some time, Bard’s sales have been consistently declining, and the relative significance of direct sales has increased over time. We expect these trends to continue.

We have a strong direct sales force and the ability to directly serve accounts currently ordering TheraSeed through Bard. Historically, we have converted a substantial portion of former distributor accounts to direct accounts when distribution agreements have been terminated because our customers prefer TheraSeed to competing products. Accordingly, we are not substantially dependent on the Bard Agreement.

Given the declining significance of the Bard Agreement and that no additional meaningful information would be provided to investors by filing it, we do not view the Bard Agreement as a material contract under S-K Item 601(b)(10).

U.S. Securities and Exchange Commission

June 25, 2009

Page 12

Financial Statements, page F-1

Note B – Summary of Significant Accounting Policies, page F-13

Revenue Recognition, page F-13

| 13. | We note that your product sales are recognized upon shipment and are “generally” not returnable. Please tell us and revise future filings to disclose the material terms of your revenue generating agreements. Explain how you apply to the criteria set forth in SAB 104 and any other relevant literature to your sales agreements, including a discussion of why recognition of revenue upon shipment is appropriate. Describe the circumstances where product sales are returnable including how those return provisions impact your revenue recognition. |

Response

SAB 104 establishes the following criteria for revenue recognition:

| ● | Pervasive evidence of an arrangement exists, | |

| ● | Delivery has occurred or services have been rendered, | |

| ● | The seller’s price to the buyer is fixed or determinable, and | |

| ● | Collectibility is reasonably assured. |

We ship our products upon receipt of a firm order from our customers and do not engage in “bill and hold” sales; we ship our products FOB shipping point, at which point the risk of loss has transferred to the customer; selling prices are always fixed; there are no further obligations on our behalf after shipment from our facilities; and our credit policies and procedures ensure that collectibility is reasonably assured. Accordingly, we recognize product revenue upon shipment.

Charges for returns and allowances are recognized as a deduction from revenue on an accrual basis in the period in which the related revenue is recorded. The accrual for product returns and allowances is based on our history. We allow customers to return defective products. In our brachytherapy segment, we also allow customers to return products in cases where the attending physician or hospital has certified that the brachytherapy procedure was unable to be performed as scheduled due to the patient’s health or other valid reason. Historically, product returns and allowances have not been material.

We will clarify our revenue recognition policy in applicable future filings.

Note C – Acquisitions, page F-17

NeedleTech, page F-18

| 14. | Please tell us and revise future filings to disclose the factors that contributed to a purchase price that resulted in the recognition of a significant amount of goodwill in accordance with paragraph 51(b) of SFAS 141. In this regard, please also tell us and revise future filings to explain in greater detail the factors that led to the goodwill recognized in connection with the July 28, 2008 acquisition to be deemed to be fully impaired as of December 31, 2008. |

U.S. Securities and Exchange Commission

June 25, 2009

Page 13

Response

In footnote C on page F-18, we disclose the following:

“This transaction further diversifies Theragenics’ surgical products business and leverages the Company’s existing strengths within these markets. The acquisition of NeedleTech is designed to forward the Company’s stated strategy of becoming a diversified medical device manufacturer, increase its breadth of offerings to existing customers, and expand its customer base of large leading-edge original equipment manufacturers.”

We believe this adequately describes the factors that contributed to a purchase price that resulted in the recognition of a significant amount of goodwill, as required by paragraph 51(b) of SFAS 141. We also note that this acquisition was negotiated, executed and accounted for (including the determination of the fair value of the assets acquired, liabilities assumed and resulting goodwill) in an economic environment that was substantially different than the economic environment experienced near the end of 2008. This transaction and the resulting accounting reflected the economic environment that existed at that time.

As to the factors that led to this goodwill to be deemed fully impaired as of December 31, 2008, we refer to our responses to comment numbers 7 and 8 above.

Note E – Fair Value, page F-20

| 15. | If your cash equivalents or outstanding borrowings are material in future periods, please revise this note to provide the disclosures required by paragraphs 32-35 of SFAS 157 for all of your financial assets and liabilities. |

Response

If our cash equivalents or outstanding borrowings are material in future periods, we will revise this note to provide the disclosures required by generally accepted accounting principles.

Note I – Credit Facility, page F-24

| 16. | We note that your credit facility requires you to maintain credit financial ratios. To the extent you are subject to material financial debt covenants in future filings, please revise future filings to disclose your most significant debt covenants and ratios. |

Response

We will disclose our most significant debt covenants and ratios in our future filings.

U.S. Securities and Exchange Commission

June 25, 2009

Page 14

Other

As your letter requested, we also acknowledge that:

| ● | the Company is responsible for the adequacy and accuracy of the disclosure in the filing; | |

| ● | staff comments or changes to disclosure in response to staff comments do not foreclose the Commission from taking any action with respect to the filing; and | |

| ● | the Company may not assert staff comments as a defense in any proceedings initiated by the Commission or any person under the federal securities laws of the United States. |

Do not hesitate to contact us if you have questions or comments regarding our responses.

Sincerely,

| /s/ Francis J. Tarallo | |

| Francis J. Tarallo | |

| Chief Financial Officer and Treasurer |

cc: M. Christine Jacobs, Chief Executive Officer, Theragenics Corporation