Investor Presentation

First Quarter 2009

Forward-Looking Statements

and Non-GAAP Financial Information

The forward-looking statements, as defined in the applicable federal securities laws, being made today are subject to risks

and uncertainties. TSFG’s actual results may differ materially from those set forth in such forward-looking statements.

These statements include, but are not limited to, factors that may affect TSFG’s return goals, loan growth, loan sales,

customer funding growth, expense control, income tax rate, expected financial results for acquisitions, noninterest income,

adequacy of capital and future capital levels, factors that will affect credit quality and the net interest margin, effectiveness

of hedging strategies, risks and effects of changes in interest rates, effects of general economic and financial market

conditions, and market performance. Reference is made to TSFG’s reports filed with the Securities and Exchange

Commission for a discussion of factors that may cause such differences to occur. TSFG undertakes no obligation to release

revisions to these forward-looking statements or reflect events or circumstances after today’s presentation.

This presentation contains certain non-GAAP measures that exclude the impact of certain nonoperating items. TSFG

management uses these non-GAAP, or operating measures, in its analysis of TSFG’s performance. TSFG believes

presentations of financial measures excluding the impact of certain items provide useful supplemental information and

better reflect its core operating activities. Management uses operating measures, in particular, to analyze on a consistent

basis and over a longer period of time, the performance of which it considers to be its core operations.

Operating measures adjust GAAP information to exclude the effects of nonoperating items, such as gains or losses on

certain asset sales, early extinguishment of debt, employment contract buyouts, impairment charges, and other

nonoperating expenses. The limitations associated with utilizing operating measures are the risk that persons might

disagree as to the appropriateness of items comprising these measures and different companies might calculate these

measures differently. Management compensates for these limitations by providing detailed reconciliations between GAAP

and operating measures. These disclosures should not be considered an alternative to GAAP results. A reconciliation of

GAAP results and non-GAAP measures is provided in the Quarterly Financial Data Supplement on our web site,

www.thesouthgroup.com, in the Investor Relations section under Quarterly Earnings.

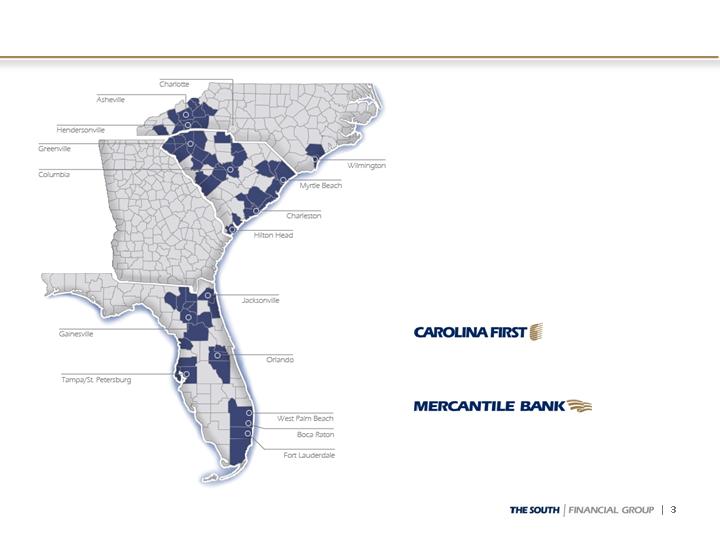

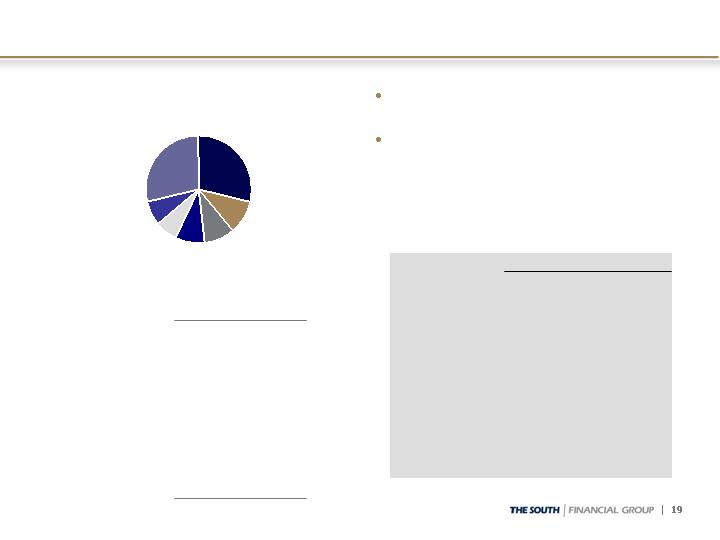

Total assets $13.6

Loans held for investment $10.2

Customer funding* $8.0

Tangible shareholders’ equity $1.4

Tangible equity to tangible

assets

Branch offices:

NC 27

SC 82

FL 71

TSFG AT A GLANCE

$ in billions, as of 12/31/08

Company Overview

* Customer funding includes total deposits less brokered deposits plus customer sweeps.

** Mercantile Bank is a division of Carolina First Bank.

10.29%

Goal: Relationship Bank of Choice

Building core banking relationships

Focused on customer relationships with local decision-making

Accessible and responsive

Involved in our communities

Target small businesses, middle market, and retail customers

Built through multi-product relationships

Located in attractive Southeastern markets with long-term growth

potential

Led by local Market Presidents in 12 markets

Average of 24 years banking experience

Local market and customer knowledge

Local authority to make customer decisions

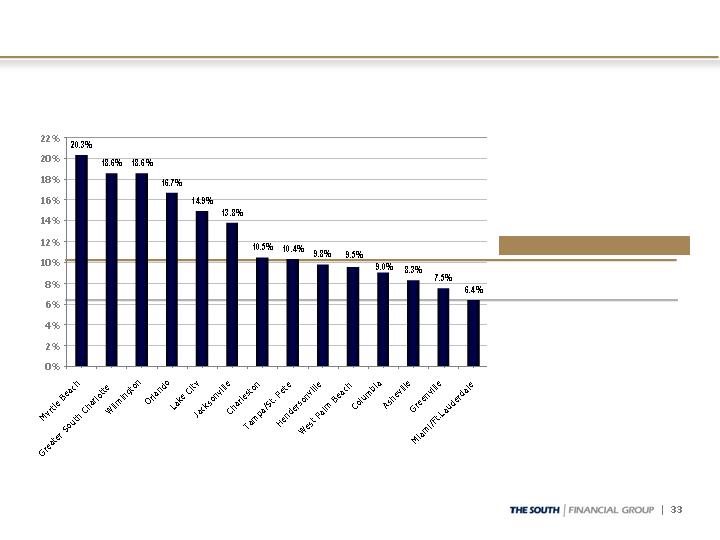

PROJECTED HOUSEHOLD GROWTH (2008-2013)

Growth estimates deposit weighted by county as of 6/30/08

SOURCE: SNL Financial

Footprint: Long-term Growth Potential

6.3

Trustmark

6.4

Regions

6.5

Operating Peer Median

6.5

U.S. Median

7.0

Whitney

6.7

BOK Financial

10.5

Colonial BancGroup

10.5

SunTrust Banks

11.1

Zions Bancorporation

11.8

Cullen/Frost

8.3

BB&T

10.2

The South Financial Group

%

14.2

United Community Banks

5.5

8.8

Household Growth

(%)

Synovus

Company Name

First Horizon

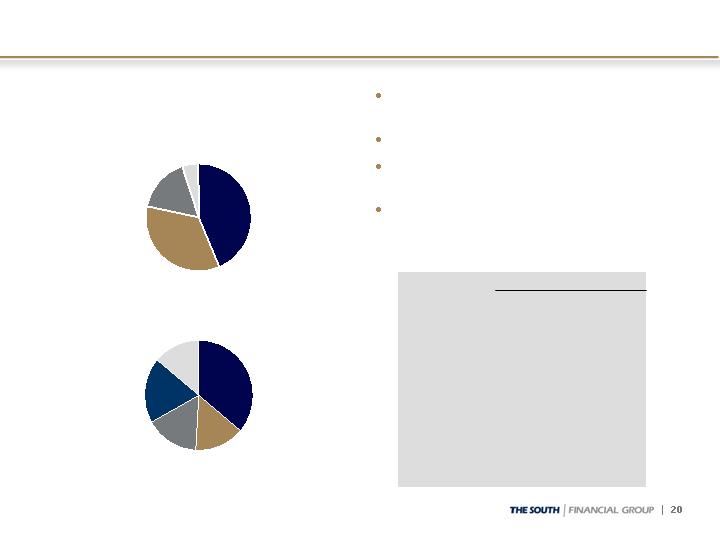

DEPOSITS BY STATE*

*Percent of total deposits by state as of December 31; reflects customer deposits after 12/31/04

As of December 31, 2008

Footprint: Geographic Diversification

Proactive and Realistic Approach to Cycle

$250 million Capital Raise in May 2008

Attracted sophisticated large investors

Reduced quarterly common cash dividend to $0.01 per share;

preserves $52 million annually in retained capital

Strengthened overall Liquidity Position

$4.4 billion unused secured capacity at 12/31/08

In May 2008, suspended indirect automobile lending in Florida

Parent company has $210 million in cash at 12/31/08 to cover

expected cash flow needs, debt service and existing dividends

through 2012 with no support from banking subsidiary

New Risk Management team

Lynn Harton (former Chief Credit Officer of Regions/Union

Planters) hired in June 2007; now President & CEO

Significant number of senior leadership level hires from same

team

Large bank experience in turnaround situations

Proactive and Realistic Approach (continued)

Resulted in Early Identification of real estate credit issues

New management processes reflected in risk grades identified

growing level of problems

Disclosed rising levels of nonaccruals in 1Q08, ahead of

Southeastern Peers

Increased loan loss reserve in 1Q08 to one of the highest levels in

the Southeast; built to 2.45% at 12/31/08

Began loan sales (2Q08) earlier than peers

Recognized by analysts as having a realistic and aggressive

posture in managing credit risk

$347 million of U.S. Treasury CPP Capital in December 2008

Lynn Harton named President & CEO in February 2009

Served as Interim since 11/13/08

New Leadership - Initial Actions

Organizational leadership changes

New Florida leadership

Executive Mgmt structure modified to clarify responsibilities/ownership

Director of Commercial Banking Strategy created to drive support and

strategy for largest business line

All line bankers now reporting to the State Bank Presidents instead of

operating in “silo” lines of business

Intense focus on communication to clarify ONE Bank strategy

Clarify target customers and methods of delivering value

Changed incentive plans to support relationship bank strategy

Created internal segmentation of “core/non-core” product segments to

measure success of each piece of the business

Quick moves to begin streamlining cost structure

December 2008 staff reductions

No 2008 bonus or 2009 merit increases for Executive Mgmt Team

Corporate campus evaluation

Initiated Phase 1 of Project NOW

8 workstreams, each with a full-time employee “owner” supported by

outside project management experts

Anticipated annual pre-tax operating benefits of $18-$20 million

Citizens/Southern Bank

1988

45

President, North and South Carolina

Scott M. Frierson

Colonial/Chase Manhattan

Mortgage/HomeSide Lending

2006

50

EVP, Chief Operations and

Technology Officer

Tanya A. Butts

AmSouth/Wells Fargo

2005

49

EVP, Director Commercial Strategy

Christopher S. Gompper

BB&T/Regions

2007

44

EVP, Chief Credit Officer

Robert A. Edwards

PwC/Union Planters/National

Commerce

2007

43

Sr. EVP, Chief Financial Officer

James R. Gordon

National Commerce/Trustmark

2006

45

Sr. EVP, Director Retail Strategy

Christopher T. Holmes

Wyche, Burgess, Freeman &

Parham

2002

46

EVP, Chief Legal and Risk Officer

William P. Crawford, Jr.

Barnett Bank/NationsBank

2002

58

EVP, Chief Human Resources Officer

Mary A. Jeffrey

Regions/Terrabank/Southeast

Bank

2007

43

President, Florida

J. Ernesto “Ernie” Diaz

BB&T/Union Planters/Regions

2007

47

President and CEO

H. Lynn Harton

First Horizon

2005

54

EVP, General Auditor

Keith D. Williamson

Prior Experience

Year

Joined

TSFG

Age

Position

Name

Executive Management Team

NOTE: Shading indicates new role or added responsibilities effective in 4Q08.

Control operating noninterest expenses, excluding

environmental costs

Launched Phase 1 of efficiency project with focus on

both expense management and revenue

opportunities

Expense Control

Increase through growth in deposits and wealth

management revenues

Noninterest Income

Continue to manage tangible equity ratio

Maintain strong regulatory capital ratios

Capital Management

Aggressively identify and resolve stressed portfolios

Improve longer-term performance relative to peers

Credit Quality

Focus on liquidity in near-term with longer-term

view of improving NIM

Lower funding costs longer-term by improving

volume, mix, and cost of deposits

Funding

Focus on relationship-based lending to small and

family-owned businesses in market

Deemphasize noncore portfolios: indirect, lot loans,

residential construction, shared national credits

Loan Growth

OBJECTIVES

EXECUTION POINTS

Strategic Objectives

Diversified Loan Portfolio

Loan Mix

As of December 31, 2008

($ in millions)

Total Loans Held for

Investment $10,192

C&I

Commercial

Development

Mortgage*

Diversified portfolio

By product and customer

By geography

In-footprint focus

Customers we know; markets

we understand

No broker mortgage/HE loans

Minimal subprime exposure

Suspended Florida indirect

Disciplined approval and portfolio

management processes

Local credit officers

Executive credit committee

approval for largest

relationships

Special assets department for

high risk loans

Centralized consumer

approval and collections

Specialized credit support for our

largest businesses

CRE; Corporate Banking/SNC

Owner-

Occupied

Indirect -

Sales Finance

Income

Property

Residential

Construction

Home Equity

* Mortgage includes Consumer Lot Loans and Other (Direct Retail and Unsecured Lines).

Credit Quality Results

Residential construction and housing-related loans continue to be primary

stress across entire footprint

Reduced residential construction portfolio by $365 million, or 22%, since

3/31/08

Recession showing signs of impacting C&I and consumer loan categories

NCOs $76.1 million, or 2.93% of average loans annualized (YTD 2.16%)

Provision of $122.9 million, a $38.3 million increase from 3Q08

Exceeds NCOs by $46.9 million; reserve build of $121.2 million in 2008

Built reserve to 2.45% (from 1.97% at 9/30/08 and 1.26% at

12/31/07)

NPAs increased to 4.10% of loans and foreclosed property

NPLs held for investment increased to $355.6 million, up from $240.1

million at 9/30/08

Commercial NALs carried at 67% after deducting specific reserves

Inflows reflect migration of existing watch loans (NAL inflows: $195

million for 4Q08, $104 million for 3Q08, $74 million for 2Q08, and $175

million for 1Q08)

Gaining control of assets through foreclosure process

Limited loan sale activity in 4Q08 due to less liquidity for buyers and

continuing uncertainty regarding market outlook

Loan and Credit Quality Composition

1.16%

$75.4

2.30%

$238

$10,300

9/30/08

0.84%

$47.0

2.09%

$219

$10,476

6/30/08

2.22%

$223.4

$76.1

3.42%

$349

100%

$10,192

Total Loans HFI

9.46%

24.1

12.1

10.17%

59

6%

580

Mortgage**

2.21%

14.1

5.0

0.11%

1

6%

636

Indirect – sales

finance

1.42%

6.1

2.4

1.01%

8

8%

813

Home equity

2.16%

0.26%

11.24%

4.85%

2.67%

1.17%

1.32%

NAL % of

O/S

Balance

1.0

102.6

15.1

15.2

3.5

$42.1

YTD Net

Charge-

offs

$25.0

0.0

24.5

2.6

10.3

1.8

$17.6

QTD Net

Charge-

offs

1.14%

3.04%

4.93%

1.45%

1.32%

1.19%

1.01%

30-day

past due

%

59

22%

2,203

Completed

income property

29

6%

608

Commercial

development

$10,276

95

1,263

1,271

$ 2,723

Outstanding

Balance

1%

12%

12%

27%

% of

O/S

Balance

--

Other**

15

Owner-occupied

CRE

$36

C&I

142

Residential

construction

$222

Nonaccrual

Loans

HFI*

3/31/08

As of December 31, 2008, $ in millions

HFI = Held for Investment; 30-day past due % of outstanding balance excludes nonaccrual loans. See page 9 of the Quarterly Financial Data Supplement

for Commercial Real Estate loans by product type and by geography. Commercial Development includes Commercial A&D and Commercial Construction.

Residential Construction includes Residential A&D, Residential Construction, Residential Condo, and Undeveloped Land.

* Nonaccrual loans exclude nonaccrual loans held for sale of $16.5 million.

** Mortgage includes Consumer Lot Loans. Other includes Direct Retail and Unsecured Lines.

Credit Quality Trends - Commercial

1.76%

$44.6

9.03%

$127

$1,410

3Q08

1.33%

$22.3

8.47%

$131

$1,550

2Q08

0.27%

$2.5

1.87%

$11

$601

3Q08

0.86%

$8.7

0.57%

$3

$575

2Q08

1.15%

$1.9

1.05%

$22

$2,084

3Q08

0.21%

$2.6

0.84%

$17

$2,037

2Q08

0.79%

$0.8

0.58%

$7

$1,207

3Q08

0.43%

$0.4

0.43%

$5

$1,184

2Q08

0.44%

$12.7

0.97%

$28

$2,824

3Q08

0.50%

$4.4

0.98%

$28

$2,891

2Q08

4Q08

4Q08

4Q08

4Q08

4Q08

11.24%

4.85%

2.67%

1.17%

1.32%

NAL % of

O/S Balance

$24.5

$2.6

$10.3

$1.8

$17.6

QTD Net

Charge-offs

4.93%

1.45%

1.32%

1.19%

1.01%

30-day past

due %

$59

$2,203

Completed income

$29

$608

Commercial

development

$1,263

$1,271

$ 2,723

Outstanding

Balance

$15

Owner-occupied CRE

$36

C&I

$142

Residential

construction

Nonaccrual

Loans HFI

$ in millions

HFI = Held for Investment; 30-day past due % of outstanding balance excludes nonaccrual loans.

Credit Quality Trends - Consumer

3.04%

$0.0

0.26%

$ --

$95

4Q08

Other**

1.84%

$0.0

0.94%

$1

$100

3Q08

4.64%

$6.9

5.92%

$36

$610

3Q08

3.21%

$3.8

4.51%

$28

$629

2Q08

0.71%

$2.6

0.68%

$5

$784

3Q08

0.74%

$0.8

0.60%

$5

$781

2Q08

1.69%

$3.4

0.10%

$1

$680

3Q08

1.46%

$3.3

0.07%

$1

$729

2Q08

2Q08

4Q08

4Q08

4Q08

9.46%

$12.1

10.17%

$59

$580

Mortgage**

2.21%

$5.0

0.11%

$1

$636

Indirect–sales finance

1.42%

$2.4

1.01%

$8

$813

Home equity

0.20%

NAL % of

O/S Balance

$1.0

QTD Net

Charge-offs

1.95%

30-day past

due %

$100

Outstanding

Balance

$ --

Nonaccrual

Loans HFI

$ in millions

HFI = Held for Investment; 30-day past due % of outstanding balance excludes nonaccrual loans.

** Mortgage includes Consumer Lot Loans. Other includes Direct Retail and Unsecured Lines.

Residential Construction by Geography

1.76%

$44.6

9.03%

$127

$1,410

9/30/08

1.33%

$22.3

8.47%

$131

$1,550

6/30/08

5.35%

$5.5

$2.0

4.85%

$22

35%

$439

Total SC, 12/31/08

0.45%

$2.5

2.14%

$10

34%

$485

9/30/08

3.63%

$2.7

6.93%

$21

22%

$306

9/30/08

6.13%

$88.8

$18.6

16.94%

$90

42%

$534

Total FL, 12/31/08

1.87%

$39.4

15.47%

$96

44%

$619

9/30/08

4.93%

$102.6

$24.5

11.24%

$142

100%

$1,263

Overall Total,

12/31/08

1.58%

$11.2

8.23%

$134

$1,628

3/31/08

2.10%

$8.3

$3.9

10.45%

$30

23%

$290

Total NC,12/31/08

17.61%

16.16%

11.21%

20.20%

NAL %

of O/S

Balance

28.0

5.5

35.6

$19.7

YTD Net

Charge-

offs

6.2

2.1

7.9

$2.4

QTD Net

Charge-

offs

0.00%

1.46%

1.29%

11.88%

30-day

past due

%

16

11%

145

FL residential A&D

9

5%

59

FL residential

construction

78

$252

Outstanding

Balance

6%

20%

% of

Resid.

Constr.

14

FL residential

condo

$51

FL undeveloped

land

Residential Construction:

Nonaccrual

Loans HFI

As of December 31, 2008, $ in millions

30-day past due % of outstanding balance excludes nonaccrual loans.

See page 9 of the Quarterly Financial Data Supplement for detail for NC and SC.

Commercial Nonaccruals – Net Balance

$281

142

29

59

15

$36

12/31/08

Nonaccrual

Loan

Balance

$237

122

22

54

11

$28

Net

Balance

Less

Specific

Reserve

67%

$44

$71

$352

Total

Commercial

69%

57%

76%

65%

57%

Net

Balance

as % of

Unpaid

Principal

5

12

71

Completed

income property

8

9

38

Commercial

development

177

17

$49

Unpaid

Principal

(1)

35

2

$13

Cumulative

Net Charge-

offs (2)

19

Residential

construction

4

Owner-occupied

CRE

$8

C&I

12/31/08

Specific

Reserve(3)

$ in millions

-

=

-

=

(1) Outstanding balance at default

(2) Typically charge-down at nonaccrual to approximately 80% of most recent appraised value

(3) Additional specific reserves are established as necessary based on estimated disposal costs, estimated holding period and current market

and economic conditions; recognized as charge-offs when realized. However, these amounts do not include the qualitative components within

the overall allowance for credit loans.

Consistent

with

9/30/08

Indirect – Sales Finance

As of December 31, 2008, $ in millions

In 5/08, ceased production in

Florida

Effective 1/09, offered only

through full relationship

dealerships in NC and SC

Toyota

29%

Summary Statistics

66%

70%

61%

New %

34%

30%

39%

Used %

$699

$464

$235

12/07 Balance

59%

41%

695

722

$636

Total

66%

48%

Foreign %

34%

52%

Domestic %

686

710

Jan 09 FICO

716

729

Orig FICO

$381

$255

12/08 Balance

FL

NC/SC

30-day Past Dues, By Auto Make (Top 10)

Total, $636 million or 6% of loans

By Auto Make

2.35%

18

Chrysler

2.55%

18

Hyundai

2.16%

$530

Top 10

0.98%

19

Jeep

2.20%

25

Nissan

2.78%

42

Dodge

2.10%

47

Ford

1.77%

56

Kia

2.94%

60

Chevrolet

2.09%

62

Honda

1.99%

$183

Toyota

30-day %

O/S$

Honda

10%

Ford

7%

Other

29%

Chevrolet

9%

Dodge

7%

Kia

9%

Home Equity Lines/Loans

SC, $354

43%

FL, $283

35%

NC, $135

17%

As of December 31, 2008, $ in millions

Originated by TSFG sales force

in-market; no broker loans

Strong FICO scores

Conservative LTV position and

usage amounts

Not pushed as a growth product

Home Equity Portfolio = HE Line and HE Loan portfolios

Geography based on customer address

Other, $41

5%

Summary Statistics

NA

NA

70%

WAvg Util %

69%

56%

44%

718

727

$812

Total

66%

70%

Orig WAvg

LTV %

19%

67%

2ndLien %

81%

33%

1stLien %

701

724

Jan 09 FICO

711

730

Orig FICO

$185

$627

Balance $

Loans

Lines

2008, $112

14%

2007, $155

19%

2006, $131

16%

2004 or before

$294, 36%

2005, $121

15%

By Vintage

Total, $813 million or 8% of loans

By Geography

Mortgage Banking Portfolio

Remains a small portion of

entire portfolio

$580 million

6% of total loans HFI

NAL increase of $23 million

from Q3 to Q4

Increases from higher risk

portions of the portfolio

(Lot Loans and

Construction Perm)

Reduced balances in Lot

Loans and Construction

Perm products by $136

million in 2008

Consumer restructured

loans of $3.6 million

(included in NPLs) from

working with borrowers to

do loan modifications

As of December 31, 2008, $ in millions

$12.6

15.98%

0.00%

1.70%

$78.8

$15.2

6.12%

2.34%

3.84%

$249.1

$8.3

2.94%

2.21%

1.89%

$282.3

3Q08

$4.7

4.11%

0.00%

2.91%

$113.3

$8.4

2.89%

1.03%

5.34%

$291.4

$3.9

1.56%

1.87%

6.22%

$251.8

1Q08

Construction Perm:

$95.7

$64.0

Balance

5.86%

5.22%

30-89 DPD

0.00%

0.00%

90+ DPD

9.85%

20.02%

NAL %

$9.4

$12.8

NAL $

Lot Loans:

$266.2

$225.5

Balance

2.09%

6.34%

30-89 DPD

2.00%

1.84%

90+ DPD

4.07%

13.20%

NAL %

$10.8

$29.9

NAL $

SIVA* Alt-A:

$8.1

$16.3

NAL $

3.04%

5.59%

NAL %

0.69%

3.41%

90+ DPD

0.90%

7.90%

30-89 DPD

$267.9

$290.7

Balance

2Q08

4Q08

Mortgage Portfolio = Mortgage, Consumer Lot Loans, and Construction Perm products (excludes HE Loan)

* SIVA = Stated Income Verified Assets

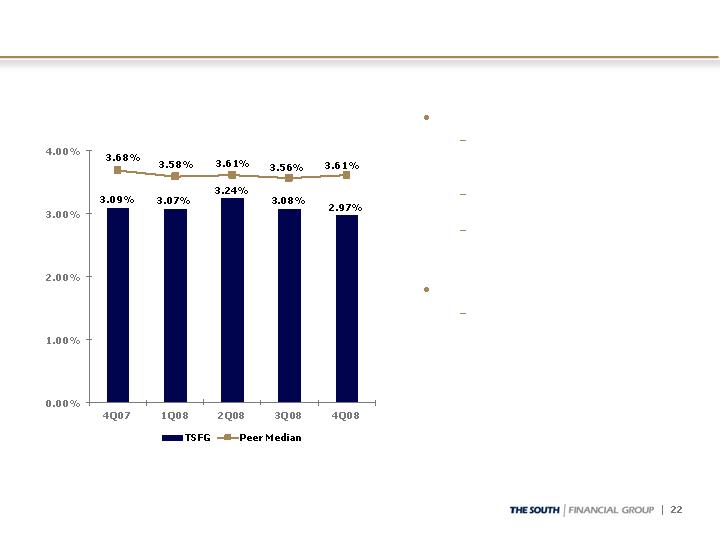

Net Interest Margin

Net Interest Margin (FTE)

Decrease 4Q08 vs. 3Q08

Increase in nonaccrual

interest reversals:

-4 bp

Maturing prime-based

swaps: -4 bp

Balance sheet mix:

-3 bp

1Q09 Headwind

Limitations for passing-

through the recent

sharp Federal funds

rate cuts given the low

absolute level of

interest rates on non-

maturity deposits and

impact from credit

issues

+5

-5

+3

-10

-3

Peer

-11

-16

+17

-2

-3

TSFG

Basis Point Change:

Customer Funding

1.3%

24

1,840

1,864

Time deposits < $100,000

(1.6)%

28

1,806

1,834

Money market

0.8%

62

7,435

7,497

Customer deposits

(10.7)%

(59)

552

493

Customer sweep accounts

Customer deposits:

-- %

(2.4)%

26.7%

(1.1)%

1.8%

LQ %

Change

(12)

1,091

1,079

Interest-bearing

40

150

190

Savings accounts

(36)

1,525

1,489

Time deposits $100,000 or

more

$3

$7,987

$7,990

Total customer funding

$18

$ Change

$1,023

9/30/08

Balance

$1,041

12/31/08

Balance

Noninterest-bearing

$ in millions

Customer funding reflects total deposits excluding brokered deposits plus customer

sweeps. Customer deposits reflect seasonal increase in public funds.

Wholesale Borrowings

By Maturity

$4,385

$3,750

$1,396

$2,354

Total wholesale

borrowings

--

1,909

719

1,190

Brokered CDs

--

13

--

13

Commercial paper

864

233

203

30

FHLB advances

274

200

--

$ --

> 1

year

274

200

1,054

$67

Total

--

851

2,670

$ --

Unused

Secured

capacity

--

Repurchase

agreements

--

1,054

$ 67

1 year

or less

Other*

Fed Reserve and

T,T&L

Fed funds

purchased

As of December 31, 2008, $ in millions

* No bank ($68 million) exposure to capital markets rollover risk for debt obligations

until 2012

$4.7 billion

at 9/30/08

Strong parent company

liquidity position

Parent company cash of

$210 million at

12/31/08

No debt maturities until

2033

Expected annual

dividends of $43 million

(preferred and common)

Cash sufficient to satisfy

all fixed obligations over

the next 4 years

Parent Company Liquidity

Capital Position

Capital Purchase Program (U.S. Treasury Investment)

Received $347 million on December 5, 2008

Issued warrant to purchase 10.1 million shares at $5.15 per share

($19.6 million allocated value)

Effective dividend yield of 6.3%

Utilized $260 million for capital injection into Carolina First Bank

Kept $87 at parent company for liquidity

Temporary use of proceeds to enhance liquidity (increase cash reserves

and pay-down wholesale borrowings) pending opportunity to lend

Tangible common equity to tangible assets of 6.05%

Down 56 bp from 12/31/07 while absorbing $344.6 million of credit

losses in 2008

Does not include Mandatorily Convertible Preferred Stock (MCPS) of

$238.7 million, or 179 basis points reflecting conversion

Believe MCPS should be viewed as key component of common equity

since automatically converts on May 1, 2011; conversion is assumed

when looking at common tangible book value per share

Approximately $60 million has already converted to date, including

$48.7 million subsequent to year-end (which includes conversion

involving issuance of 2.5 million common shares as inducement to

convert)

Capital Position

7.84%

7.94%

Tangible common equity to tangible

assets

$9.40

$9.42

Common tangible book value per

share

Assuming conversion of Mandatorily Convertible Preferred:***

8.54%

11.55%

9.82%

9.70%

12.68%

11.18%

6.06%

9/30/08

Actual

$604

$304

$573

$839

$512

$808

Capital in Excess of

Well Capitalized

Minimum

After-tax $

5%

10%

6%

5%

10%

6%

Well

Capitalized

Minimum

9.49%

12.59%

10.88%

11.22%

14.35%

12.86%

6.05%

12/31/08

Actual*

Total risk-based

Leverage

CAROLINA FIRST BANK

Tier 1 risk-based

Total risk-based

Leverage

Tier 1 risk-based

Tangible common equity to

tangible assets

THE SOUTH FINANCIAL GROUP

$ in millions

* Estimated

** For illustrative purposes only

*** Assumes full conversion of $239 million of Mandatorily Convertible Preferred at $6.50 per common share fixed conversion ratio (automatically

converts into common stock on May 1, 2011) and excludes CPP Preferred

Noninterest Expenses

3.1

0.1

1.5

4.5

4.6

Loan and foreclosed asset*

1.9

0.4

1.5

3.0

3.4

FDIC insurance*

1.6

0.3

(3.6)

(2.3)

(2.0)

FAS 91 Salary Deferral (included in Salaries)*

237.6

237.6

--

--

237.6

Goodwill impairment

1.0

0.2

3.8

4.6

4.8

Professional fees

2.0

0.6

15.4

16.8

17.4

Occupancy and FF&E

$ Change

$341.8

2.8

9.6

91.8

15.7

$45.9

4Q08

1.5

2.9

1.3

(0.1)

Other

$261.1

$247.6

$80.7

$94.2

Total noninterest expenses

9.6

12.4

0.9

$3.5

4Q08 vs.

4Q07

1.8

14.8

13.9

Other

2.1

79.4

89.7

Operating noninterest expenses

5.0

--

4.6

Employment contracts

$(1.0)

4Q08 vs.

3Q08

$42.4

4Q07

$46.9

3Q08

Salaries and employee benefits

$ in millions

Note: Other includes (gain) loss on early extinguishment of debt ($1.7 million for 4Q08, $(125,000) for 3Q08, and $499,000 for 4Q07), loss on

derivative collateral ($1.1 million for 4Q08), and Visa-related litigation ($881,000 for 4Q07).

*Approximately half of the $12.4 million year-over-year increase relates to the current

environment – higher loan and foreclosed asset and FDIC insurance expense and lower

loan origination salary deferrals. For 2009, expect higher FDIC insurance, loan and

foreclosed asset expense, and non-operating charges related to the corporate campus

under construction (evaluation of alternatives underway).

Noninterest Income

(0.2)

0.2

1.3

0.9

1.1

Mortgage banking income

$ Change

$1.0

2.3

(1.3)

0.3

(0.1)

1.0

(0.2)

(0.9)

$(1.6)

4Q08 vs.

3Q08

(0.1)

0.8

0.9

0.7

Merchant processing income, net

$29.7

1.6

28.1

3.2

(0.3)

3.9

6.3

$13.2

4Q08

Non-operating items:

(0.3)

--

(0.2)

Gain/(loss) on certain derivative

activities

0.8

3.1

2.9

Bank-owned life insurance**

2.9

(1.3)

(0.7)

Gain/(loss) on securities

$0.7

$29.0

$28.7

Total noninterest income

(1.2)

7.5

7.2

Wealth management income*

0.4

2.8

2.9

Other

(2.2)

30.3

29.4

Operating noninterest income

$(1.6)

4Q08 vs.

4Q07

$14.8

4Q07

$14.8

3Q08

Customer fee income*

$ in millions

*Together, approximately 70% of operating noninterest income. Reflect impacts from

economic downturn, such as fewer customer transactions and lower asset valuations.

**4Q08 includes $1.3 million for death proceeds partially offset by $645,000 in related

compensation expense (included in operating noninterest expenses).

Expectations for 2009

Operating environment and results will remain challenging for all of 2009

Credit losses for first half of 2009 similar to last half of 2008; provisioning

depends on continuing economic developments

Continued headwinds from loan collection costs and FDIC insurance

Potential one-time charges arising from ultimate corporate campus decision

and continuing evaluation of small level of other investments for

impairment

Continue to evaluate the realizability of the net deferred tax asset

throughout 2009 for both book and regulatory purposes

Near-term pressure on margin in first half of year, followed by expansion of

margin as pricing initiatives on both the loan and deposit side begin to show

results

Positive impact from Project NOW and other expense initiatives

Potential for FDIC deposit transactions if market overlap promotes

efficiency and product set improves customer funding measures

Focus on cross sell; customer satisfaction; other measures that support our

strategic positioning

Positioned to Emerge Stronger

Mission to be best relationship bank in each of our markets

Leverage strategic footprint and its long-term growth

potential

Deep and experienced management team

Risk management talent and processes

Maintain strong balance sheet throughout credit environment

Capital position

Liquidity management

Higher loan loss reserves

Relationship lending with focus on deposit balances

Appendix – List of Operating Peers

Associated (ASBC)

BOK Financial (BOKF)

Colonial (CNB)

Commerce (CBSH)

Cullen/Frost (CFR)

Fulton (FULT)

Synovus (SNV)

Trustmark (TRMK)

United Community (UCBI)

Valley National (VLY)

U.S. Median 6.5%

TSFG Weighted Average* 10.2%

*Deposit weighted by county based on

TSFG deposits in each market

SOURCE: SNL Financial

PROJECTED HOUSEHOLD GROWTH (2008-2013)

NOTE: The regions highlighted are complete MSAs except for Greater South Charlotte, which is York County, SC (Rock Hill), Hendersonville, NC, which is

Henderson County, and West Palm Beach, which is Palm Beach County.

TSFG’s Footprint: Household Growth

Current as of 2/19/09