Exhibit 13

Commission File No. 0-15261

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF

THE SECURITIES AND EXCHANGE ACT OF 1934

For the Year Ended December 31, 2005

BRYN MAWR BANK CORPORATION

ANNUAL MEETING

The Annual Meeting of Shareholders of Bryn Mawr Bank Corporation will be held in The Gregg Conference Center at The American College, Bryn Mawr, Pennsylvania, on Tuesday, April 25, 2006, at 2:00 p.m.

STOCK LISTING

Bryn Mawr Bank Corporation common stock is traded over-the-counter and is listed on the NASDAQ National Market System under the symbol BMTC.

FORM 10-K

A copy of the Corporation’s Form 10-K, including financial statement schedules as filed with the Securities and Exchange Commission, is available without charge to shareholders upon written request to Robert J. Ricciardi, Secretary, Bryn Mawr Bank Corporation, 801 Lancaster Avenue, Bryn Mawr, Pennsylvania 19010-3396, or via e-mail to bricciardi@bmtc.com.

EQUAL EMPLOYMENT OPPORTUNITY

The Corporation continues its commitment to equal opportunity employment and does not discriminate against minorities or women with respect to recruitment, hiring, training, or promotion. It is the policy of the Corporation to comply voluntarily with the practices of Affirmative Action.

BRYN MAWR BANK CORPORATION

By expanding our network of branches and reaching out to new markets, our goal is to position Bryn MawrTrust as the dominant community bank and wealth management group in the region.

LETTER FROM THE CHAIRMAN

Dear Fellow Shareholders:

It is a pleasure to write to you this year and to report on the excellent progress of the Corporation in 2005. Earnings were up 29.4%, when adjusted for the one-time sale of “mortgage servicing rights” in 2004, and our return-on-equity and return-on-assets ratios of 15.44% and 1.66% respectively, put us among the top banks in the nation in terms of financial performance.

Leading the way was a tremendous performance by our Wealth Management Group, which in 2005 increased its assets under management and administration to $2.25 billion, up 16.0% over 2004. Similarly, our Business Banking group, led by Marty Gallagher, had another strong year as we continued to attract clients who are tired of the large, out-of-town banks that unfortunately dominate the Philadelphia banking scene.

Our strategy of concentrating on our core competencies is working.

Our strategy of sticking to the basics, on executing our straightforward and uncomplicated business plan, and of concentrating on our core competencies is working!

In March of 2005, we opened our eighth full-service office in Exton, which is in the heart of fast-growing Chester County. Annette McNee is heading up our efforts in that region and we are on target to meet our initial year’s projections. In addition, we are currently negotiating the construction of a regional Chester County office in the West Chester area. This large facility would house a Business Banking team as well as Wealth Management personnel, along with a full-service retail branch. To be successful in Chester County, we must have a meaningful presence there.

Furthermore, we will be building a new facility in Ardmore at a superb site providing good access and egress, excellent visibility, and a very high traffic-count. The projected completion date is November 2006. The full-service banking operation that we conduct from our Wynnewood office, which suffers from poor visibility and access, will be relocated to the Ardmore facility.

Accompanying all this good news are some serious challenges for 2006 and beyond. Attracting quality deposits to fund our loan growth is becoming more and more difficult. This is my 30th year in the banking industry and I have never seen deposit generation as competitive as it is now. A second serious challenge is protecting our balance sheet against the time when interest rates begin to fall. As our balance sheet is currently structured, rising interest rates benefit Bryn Mawr Trust because we re-price loans upward at a faster pace than we re-price deposits. In a falling rate environment, the opposite is true, resulting in a decline in net interest income. Not

PAGE TWO

BRYN MAWR BANK CORPORATION

only are we attempting to book more fixed rate loans to help correct this imbalance, but we are also examining other solutions such as interest rate swaps and floors.

Like you, I have been disappointed that despite our outstanding results, we have not seen a commensurate increase in the price of our shares. While the value of the stock has gone up 105% over the past five years, it has not done much of anything the last two years. To help address this problem, we have engaged an investor relations firm, Gregory FCA Communications, to enable us to tell our story better to the investment community. This is the same firm that has given our Wealth Management Group national visibility on television and in the print media.

I would like to note the retirement of Bill Harral from the Board of Directors after a decade of extraordinary service. Bill has been a major contributor to the success of this institution in many ways, but especially in the areas of corporate governance and organizational effectiveness. He will be missed.

As always, thank you for being a shareholder of the Corporation. Please call me on my direct line at 610-581-4800 if I can help you in any way.

Sincerely, |

|

Ted Peters |

Chairman and Chief Executive Officer |

PAGE THREE

FINANCIAL HIGHLIGHTS 2005

Consolidated Financial Highlights

(Dollars in thousands, except per share amounts)

| 2005 | 2004 | CHANGE | |||||||||||||

FOR THE YEAR | |||||||||||||||

Net interest income | $ | 31,368 | $ | 26,828 | $ | 4,540 | 16.9 | % | |||||||

Net interest income after loan loss provision | 30,606 | 25,928 | 4,678 | 18.0 | |||||||||||

Other income | 18,245 | 19,794 | (1,549 | ) | -7.8 | ||||||||||

Other expenses | 31,573 | 31,625 | (52 | ) | -0.2 | ||||||||||

Income taxes | 5,928 | 4,752 | 1,176 | 24.7 | |||||||||||

Net income | 11,350 | 9,345 | 2,005 | 21.5 | |||||||||||

AT YEAR-END | |||||||||||||||

Total assets | $ | 727,226 | $ | 682,946 | $ | 44,280 | 6.5 | % | |||||||

Total loans | 597,930 | 564,597 | 33,333 | 5.9 | |||||||||||

Total deposits | 636,260 | 600,965 | 35,295 | 5.9 | |||||||||||

Shareholders’ equity | 77,513 | 71,238 | 6,275 | 8.8 | |||||||||||

Wealth assets under management and administration | 2,248,000 | 1,938,000 | 310,000 | 16.0 | |||||||||||

PER COMMON SHARE | |||||||||||||||

Basic earnings per common share | $ | 1.33 | $ | 1.09 | $ | 0.24 | 22.0 | % | |||||||

Diluted earnings per common share | 1.31 | 1.07 | 0.24 | 22.4 | |||||||||||

Dividends declared | 0.42 | 0.40 | 0.02 | 5.0 | |||||||||||

Book value | 9.06 | 8.29 | 0.77 | 9.3 | |||||||||||

Closing price | 21.66 | 21.99 | (0.33 | ) | -1.5 | ||||||||||

SELECTED RATIOS | |||||||||||||||

Return on average assets | 1.66 | % | 1.45 | % | |||||||||||

Return on average shareholders’ equity | 15.44 | 13.67 | |||||||||||||

Net interest margin | 5.00 | 4.57 | |||||||||||||

Efficiency ratio | 63.64 | 64.97 | |||||||||||||

Note: Net income, earnings per share and selected ratios are from net income from continuing operations.

See Note 14, earnings per share, in the Notes to the Consolidated Financial Statements.

Primary Corporate Strategies

| • | Expand our footprint in targeted communities |

| • | Concentrate on our core competencies: business banking, wealth management, mortgage services and value-added retail banking |

| • | Maintain obsessive client service |

| • | Cultivate aggressive sales culture |

| • | Exercise diligent control of expenses |

PAGE FOUR

BRYN MAWR BANK CORPORATION

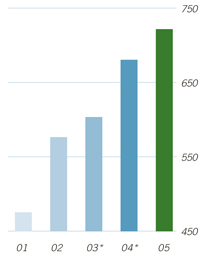

SHAREHOLDERS’ EQUITY | DILUTED EARNINGS PER SHARE FROM CONTINUING OPERATIONS | ASSETS UNDER MANAGEMENT AND ADMINISTRATION | ||

| (Dollars in millions) | (Dollars) | (Dollars in billions) | ||

|  |  | ||

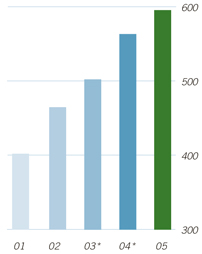

| TOTAL ASSETS | TOTAL LOANS | TOTAL DEPOSITS | ||

| (Dollars in millions) | (Dollars in millions) | (Dollars in millions) | ||

|  |  | ||

| * | Reclassified for comparative purposes |

PAGE FIVE

THE YEAR IN REVIEW 2005

Repositioning for Growth Based on a Foundation of Superior Client Service

Bryn Mawr Bank Corporation’s principal subsidiary, The Bryn Mawr Trust Company, was founded in 1889. Its eight full-service branches serve residents and businesses in the affluent

Executive Vice President and Chief Financial Officer

J. Duncan Smith oversees the Corporation’s financial well-being.

Net Interest Income shows a 16.9% increase in 2005.

“Main Line” suburbs of Philadelphia. It also maintains seven limited service offices located in upscale adult communities throughout the region. Bryn Mawr Trust has an extremely attractive clientele, including high-net-worth individuals, successful small businesses, and active adults who value the Bank’s long-standing tradition of providing excellent personal service.

In an effort to maximize the effectiveness of the organization, the responsibilities of the executive management team were realigned.

Community Banking now reports to Alison Gers in order to leverage her extensive retail and marketing experience. Marketing, Information Services and Banking & Trust Operations continue to report to her. Loan Operations now reports to Chief Financial Officer Duncan Smith to consolidate accounting resources, streamline processes, and to enable Chief Lending Officer Joe Keefer to concentrate all his efforts on developing new credit business. Bob Ricciardi continues as Corporate Secretary and Chief Credit Policy Officer. In addition, Human Resources and Facilities now report to him as well as Risk Management and Insurance Counsellors, the Corporation’s full-service insurance agency. His special focus is on managing new branch construction.

PAGE SIX

BRYN MAWR BANK CORPORATION

Growth Strategies Identified for Expanding the Footprint of our Branch Network

The Corporation’s growth strategy, which guides the selection of potential branch sites, targets two entirely different types of neighborhoods:

| • | Older, established neighborhoods that share similar demographic characteristics as established Bryn Mawr Trust branches. A good example of this type of target market is Newtown Square, where we opened a branch in 2004. |

| • | Newer neighborhoods that provide exposure to growing communities with a high concentration of businesses. Our Exton Office, which opened in 2005, fits this profile. |

Executive Vice President Robert J. Ricciardi focuses on managing

new branch construction for the Corporation.

New Exton branch deposits and loans are on target.

There are two branch initiatives expected to be announced in 2006. A handsome new building is to be constructed in Ardmore, which will be the new home for our Wynnewood office. Estimated completion date for this project is November of 2006. The other new branch location will involve a site in Chester County.

Construction of our new Exton Branch on Route 100 was completed in early 2005. The Branch began doing business in March with an official ribbon-cutting ceremony and a public grand opening in April. A reception for the business community followed in May. All these activities were well attended.

PAGE SEVEN

THE YEAR IN REVIEW 2005

A Myriad of Promotional Initiatives Foster the Development of an Aggressive Sales Culture

Throughout 2005, many initiatives were held to promote the Exton Branch. There were several direct mail campaigns supported by media blitzes, sweepstakes drawings, and special product offers. The Bank sponsored a free public summer concert, had free ice cream Saturdays, gave away bottled water at the train station, participated in Exton’s Little League Opening Day, and exhibited at the Exton Chamber of Commerce’s Business Expo.

Senior Vice President June M. Falcone discusses bank operations

with Executive Vice President Alison E. Gers who is responsible for

Community Banking, including Operations.

Positioning to meet the challenge of attracting quality deposits.

All of these efforts are designed to spotlight Bryn Mawr Trust as an integral part of the community. Special public events are planned for 2006. First on the docket is an open house to introduce our Wealth Management professionals and the services they provide to the Chester County business community.

Proven to be a successful initiative, the Share-the-Client Program started in 2001 is still going strong. This program rewards the efforts of staff members for making referrals to services provided by business units other than the one where they work. During 2005, there were 2,336 employee referrals generated — about the same number of referrals that were generated in 2004. The amount of revenue produced by the referrals in 2005 showed a 38% increase over revenues resulting from 2004 referrals.

PAGE EIGHT

BRYN MAWR BANK CORPORATION

High-touch Lending Services: the Hallmark of a Bryn Mawr Trust Lender

Our lending professionals continue to base all business development efforts on building banking relationships with privately-owned businesses, non-profits, quality residential builders and owners of commercial real estate. In addition, Bryn Mawr Trust continues to provide high-touch retail lending services to individuals throughout the Delaware Valley. For our lenders, whether commercial or retail, their ultimate overriding goal is establishing long-lasting relationships with individuals and businesses.

Executive Vice President and Chief Lending Officer Joseph G. Keefer

with Senior Vice President Martin F. Gallagher, Jr., who is in charge of

Commercial Lending.

Average loans increase by 8.1% in 2005.

The small business package of services, which was introduced in 2004, still gaining acceptance in the small business community. It has also provided our team small business lenders with a perfect entrée into the Exton Area business community.

Our Residential Mortgage business is still an important segment of the financial services that we provide for our customers, despite the effect of rising mortgage interest rates and the possible impending slowdown of residential construction. There are many efforts in place to heighten the awareness for this part of our business, primarily via newspaper and other forms of print advertising.

Based on the theory that an educated consumer is an excellent prospect for future business, plans were set in motion to present free homeownership seminars to the public. These seminars will provide, firsthand: information concerning real estate financing, homeowners insurance, home warranties, inspections and other important aspects of the ever-changing real estate market. The first program in this series is scheduled to be held in March of 2006.

PAGE NINE

THE YEAR IN REVIEW 2005

Wealth Management Professionals Continue to Gain Prominence in Financial Industry

Our Wealth Management Division provides comprehensive trust & estate services, investment management, retirement planning, brokerage, custody and philanthropic services, and tax planning & preparation. During the year 2005, the assets managed and administered by this Division surpassed the two billion-dollar mark.

Gilbert B. Mateer, Senior Vice President Wealth Management and

President of Retirement Services, with John Pickering, Executive

Vice President and Head of Wealth Management.

2005 Wealth Management assets up 16%.

Wealth Management staff members belong to a variety of professional, civic and philanthropic organizations. Many serve as board members. By doing so, they come in contact with many community leaders and high-net-worth individuals. The group sponsored special events and seminars to win referrals from financial intermediaries and sources of influence. The topics addressed in 2005 included:A New Framework for Tax Advisors, What’s New in Tax Planning, Enhancing the Advisor/Client Relationship, and Intervention Tips for Families in Crisis.

In September 2005, Gilbert B. Mateer joined Bryn Mawr Trust Wealth Management Group as President of Bryn Mawr Retirement Services and Senior Vice President of Business Development. He is responsible for acquiring new business with an emphasis on corporate executives, and family business owners with complex wealth management requirements.

Retirement Services manages 401k and qualified retirement plans on behalf of corporations and other entities. The demand for these services is expected to rise as more companies discontinue traditional pension plans.

PAGE TEN

BRYN MAWR BANK CORPORATION

Our Investment Managers and Wealth Consultants are Nationally Recognized for Their Expertise

During 2005, Bryn Mawr Trust wealth management professionals continued to be sought after for their opinions on current and future market conditions. Their views have been aired on CNBC, Bloomberg Radio and Television, and Fox News. They have been quoted inBarron’s, Forbes, SmartMoney, Buyside Magazine,theNew York Times,theChicago Tribuneand other publications.

Miguel L. Biamon, Vice President and Chief Fixed Income Manager with

F. Peter Brodie, Senior Vice President and Director of Investments.

John M. Grib, Senior Vice President and Portfolio Manager, has been heard on KYW NewsRadio Market Reports for over five years. With his holiday stock report, broadcast on January 2, 2006, he achieved the milestone of having provided 1,000 market updates to KYW listeners.

Wealth professionals gain nationwide visibility.

In addition to its comprehensive menu of financial services, Wealth Management also brings the latest in financial information to our clients, referral sources, prospects and the public at large.The Economic Forecast & Market Reviewis issued quarterly and provides a handy synopsis of current market conditions.BMT in The Newsis a quarterly newsletter providing highlights of media appearances by our Wealth Management professionals.Wealth Watch,issued twice a year, provides general financial information, industry updates and the latest developments and news from the Wealth Management Division.

PAGE ELEVEN

THE YEAR IN REVIEW 2005

Corporate Information

CORPORATE HEADQUARTERS

801 Lancaster Avenue

Bryn Mawr, Pennsylvania 19010-3396

610-525-1700

www.bmtc.com

DIRECTORS

Andrea F. Gilbert

President, Bryn Mawr Hospital

William Harral, III

Chairman, C&D Technologies, Inc.; President,

The Barra Foundation

Wendell F. Holland

Chairman, Pennsylvania Public Utilities Commission

David E. Lees

Senior Partner, myCIO Wealth Partners

Francis J. Leto

Partner, Celli and Leto, LLP, Attorneys at Law;

President, The Brandywine Abstract Companies

Frederick C. “Ted” Peters II

Chairman, President and Chief Executive Officer,

Bryn Mawr Bank Corporation and

The Bryn Mawr Trust Company

B. Loyall Taylor, Jr.

President, Taylor Gifts, Inc.

Nancy J. Vickers

President, Bryn Mawr College

Thomas A. Williams

Retired, formerly Vice President,

Secretary/Treasurer,

Houghton International, Inc.

MARKET MAKERS

Boenning & Scattergood

Citigroup Global Markets

Goldman, Sachs & Co.

Janney Montgomery LLC

Keefe, Bruyette & Woods Inc.

Knight Equity Markets, L.P.

Lehman Brothers Inc.

McConnell Budd & Romano, Inc.

Morgan Stanley & Co., Inc.

Ryan Beck &Co., Inc.

UBS Capital Markets L.P.

UBS Securities LLC

AUDITORS

KPMG LLP

1601 Market Street

Philadelphia, Pennsylvania 19103-2499

REGISTRAR & TRANSFER AGENT

Mellon Investor Services L.L.C.

P.O. Box 3315

South Hackensack, NJ 07606

www.mellon-investor.com

PRINCIPAL SUBSIDIARY

The Bryn Mawr Trust Company

A Subsidiary of Bryn Mawr Bank Corporation

EXECUTIVE MANAGEMENT

Frederick C. “Ted” Peters II*

Chairman, President and Chief Executive Officer

Alison E. Gers

Executive Vice President, Retail Banking,

Marketing, Information Systems & Operations

Joseph G. Keefer

Executive Vice President and Chief Lending Officer

John Pickering

Executive Vice President, Wealth Management

Robert J. Ricciardi*

Executive Vice President, Chief Credit Policy Officer and Corporate Secretary

J. Duncan Smith*

Executive Vice President and Chief Financial Officer

| * | Also officer of the Corporation |

BRANCH OFFICES

801 Lancaster Avenue

Bryn Mawr, Pennsylvania 19010

237 North Pottstown Pike

Exton, Pennsylvania 19341

18 West Eagle Road

Havertown, Pennsylvania 19083

3601 West Chester Pike

Newtown Square, PA 19073

39 West Lancaster Avenue

Paoli, Pennsylvania 19301

330 East Lancaster Avenue

Wayne, Pennsylvania 19087

One Tower Bridge

West Conshohocken,

Pennsylvania 19428

312 East Lancaster Avenue

Wynnewood, Pennsylvania 19096

WEALTH MANAGEMENT DIVISION

10 South Bryn Mawr Avenue

Bryn Mawr, Pennsylvania 19010

LIMITED SERVICE OFFICES

Beaumont at Bryn Mawr Retirement Community

Bryn Mawr, Pennsylvania

Bellingham Retirement Living

West Chester, Pennsylvania

Martins Run Life Care Community

Media, Pennsylvania

Rosemont Presbyterian Village

Rosemont, Pennsylvania

The Quadrangle

Haverford, Pennsylvania

Waverly Heights

Gladwyne, Pennsylvania

White Horse Village

Newtown Square, Pennsylvania

OTHER SUBSIDIARIES AND FINANCIAL SERVICES

BMT Mortgage Company

A Department of The Bryn Mawr Trust Company

Bryn Mawr, Pennsylvania

Myron H. Headen, President

BMT Mortgage Services, Inc.

A Subsidiary of The Bryn Mawr Trust Company

Bryn Mawr, Pennsylvania

Joseph G. Keefer, Chairman

Myron H. Headen, President

Bryn Mawr Retirement Services

A Department of The Bryn Mawr Trust

Company’s Wealth Management Division

Bryn Mawr, Pennsylvania

Gilbert B. Mateer, President

BMT Settlement Services, Inc.

A Subsidiary of The Bryn Mawr Trust Company

Bryn Mawr, Pennsylvania

Joseph G. Keefer, Chairman

Myron H. Headen, President

Insurance Counsellors of Bryn Mawr, Inc.

A Subsidiary of The Bryn Mawr Trust Company

Bryn Mawr, Pennsylvania

Thomas F. Drennan, President

LEGAL COUNSEL

Monteverde, McAlee & Hurd,P.C.

One Penn Center at Suburban Station

1617 John F. Kennedy Boulevard Suite 1500

Philadelnhia Pennsylvania 19103-1815

PAGE TWELVE

BRYN MAWR BANK CORPORATION ANNUAL REPORT 2005

Selected Financial Data 1

Management’s Discussion and Analysis of Financial Condition and Results of Operations 2

Management’s Report on Internal Control over Financial Reporting 15

Report of Independent Registered Public Accounting Firm on Management’s Report on Internal Control over Financial Reporting 16

Report of Independent Registered Public Accounting Firm 17

Consolidated Balance Sheets 18

Consolidated Statements of Income 19

Consolidated Statements of Cash Flows 20

Consolidated Statements of Changes in Shareholders’ Equity 21

Consolidated Statement of Comprehensive Income 21

Notes to Consolidated Financial Statements 22

Price Range of Shares 37

Selected Financial Data

| For the years ended December 31, | 2005 | 2004 | 2003 | 2002 | 2001 | |||||||||||||||

| (dollars in thousands, except for share and per share data) | ||||||||||||||||||||

Interest income | $ | 37,968 | $ | 31,381 | $ | 29,261 | $ | 29,412 | 30,311 | |||||||||||

Interest expense | 6,600 | 4,553 | 4,330 | 4,484 | 6,302 | |||||||||||||||

Net interest income | 31,368 | 26,828 | 24,931 | 24,928 | 24,009 | |||||||||||||||

Loan loss provision | 762 | 900 | 750 | 1,000 | 1,200 | |||||||||||||||

Net interest income after loan loss provision | 30,606 | 25,928 | 24,181 | 23,928 | 22,809 | |||||||||||||||

Non-interest income | 18,245 | 19,794 | 26,577 | 23,899 | 18,846 | |||||||||||||||

Non-interest expense | 31,573 | 31,625 | 33,437 | 31,642 | 28,199 | |||||||||||||||

Income before income taxes and discontinued operations | 17,278 | 14,097 | 17,321 | 16,185 | 13,456 | |||||||||||||||

Applicable income taxes | 5,928 | 4,752 | 6,049 | 5,543 | 4,524 | |||||||||||||||

Income from continuing operations | 11,350 | 9,345 | 11,272 | 10,642 | 8,932 | |||||||||||||||

(Loss) income from discontinued operations | — | — | (1,916 | ) | (435 | ) | 194 | |||||||||||||

Net Income | $ | 11,350 | $ | 9,345 | $ | 9,356 | $ | 10,207 | $ | 9,126 | ||||||||||

Per share data | ||||||||||||||||||||

Earnings per common share from continuing operations: | ||||||||||||||||||||

Basic | $ | 1.33 | $ | 1.09 | $ | 1.30 | $ | 1.22 | $ | 1.03 | ||||||||||

Diluted * | $ | 1.31 | $ | 1.07 | $ | 1.29 | $ | 1.21 | $ | 1.01 | ||||||||||

Earnings per common share | ||||||||||||||||||||

Basic | $ | 1.33 | $ | 1.09 | $ | 1.08 | $ | 1.17 | $ | 1.05 | ||||||||||

Diluted * | $ | 1.31 | $ | 1.07 | $ | 1.07 | $ | 1.16 | $ | 1.04 | ||||||||||

Dividends declared | $ | .42 | $ | 0.40 | $ | 0.40 | $ | 0.38 | $ | 0.36 | ||||||||||

Weighted-average shares outstanding | 8,563,027 | 8,610,171 | 8,657,527 | 8,706,390 | 8,651,040 | |||||||||||||||

Dilutive potential common shares * | 101,200 | 110,854 | 103,107 | 84,606 | 165,216 | |||||||||||||||

Adjusted weighted-average shares | 8,664,227 | 8,721,025 | 8,760,634 | 8,790,996 | 8,816,256 | |||||||||||||||

| At December 31, | 2005 | 2004 | 2003 | 2002 | 2001 | |||||||||||||||

| (dollars in thousands) | ||||||||||||||||||||

Total assets | $ | 727,226 | $ | 682,946 | $ | 604,848 | $ | 577,242 | $ | 476,823 | ||||||||||

Earning assets | 665,667 | 628,754 | 547,637 | 520,562 | 427,805 | |||||||||||||||

Total loans | 597,930 | 564,597 | 502,416 | 466,975 | 400,849 | |||||||||||||||

Deposits | 636,260 | 600,965 | 527,139 | 483,620 | 391,059 | |||||||||||||||

Shareholders’ equity | 77,513 | 71,238 | 67,382 | 62,607 | 57,307 | |||||||||||||||

Ratio of equity to assets | 10.66 | % | 10.43 | % | 11.14 | % | 10.85 | % | 12.02 | % | ||||||||||

Loans serviced for others | 417,649 | 507,421 | 797,326 | 631,105 | 442,373 | |||||||||||||||

Wealth assets under management & administration | 2,248,000 | 1,938,000 | 1,752,000 | 1,551,000 | 1,708,000 | |||||||||||||||

| For the years ended December 31, | 2005 | 2004 | 2003 | 2002 | 2001 | |||||||||||||||

Selected financial ratios: | ||||||||||||||||||||

Net interest margin | 5.00 | % | 4.57 | % | 4.83 | % | 5.47 | % | 5.99 | % | ||||||||||

Income from continuing operations to: | ||||||||||||||||||||

Average total assets | 1.66 | % | 1.45 | % | 1.98 | % | 2.01 | % | 2.05 | % | ||||||||||

Average shareholders’ equity | 15.44 | % | 13.67 | % | 17.76 | % | 17.26 | % | 16.95 | % | ||||||||||

Average shareholders’ equity to average total assets | 10.76 | % | 10.64 | % | 11.13 | % | 11.67 | % | 12.09 | % | ||||||||||

Dividends declared per share to net income per basic common share | 31.58 | % | 36.70 | % | 37.04 | % | 32.48 | % | 34.29 | % | ||||||||||

| * | See Note 14, Earnings Per Share, in the Notes to the Consolidated Financial Statements. |

1

Management’s Discussion and Analysis of Financial Condition and Results of Operations

SPECIAL CAUTIONARY NOTICE REGARDING FORWARD LOOKING STATEMENTS

Certain of the statements contained in this report and the documents incorporated by reference herein, may constitute forward-looking statements for the purposes of the Securities Act of 1933, as amended and the Securities Exchange Act of 1934, as amended, and may involve known and unknown risks, uncertainties and other factors which may cause actual results, performance or achievements of the Corporation to be materially different from future results, performance or achievements expressed or implied by such forward-looking statements. These forward-looking statements include statements with respect to the Corporation’s financial goals, business plans, business prospects, credit quality, credit risk, reserve adequacy, liquidity, origination and sale of residential mortgage loans, impairment of goodwill, the effect of changes in accounting standards, and market and pricing trends. The words “expect,” “anticipate,” “intended,” “plan,” “believe,” “seek,” “estimate,” and similar expressions are intended to identify such forward-looking statements. The Corporation’s actual results may differ materially from the results anticipated by the forward-looking statement due to a variety of factors, including without limitation:

| • | the effect of future economic conditions on the Corporation and its customers, including economic factors which affect consumer confidence in the securities markets, wealth creation, investment and savings patterns, and the Corporation’s interest rate risk exposure and credit risk; |

| • | changes in the securities markets with respect to the market values of financial assets and the stability of particular securities markets; |

| • | governmental monetary and fiscal policies, as well as legislation and regulatory changes; |

| • | changes in accounting requirements or interpretations; |

| • | the risks of changes in interest rates on the level and composition of deposits, loan demand, and the value of loan collateral and securities, as well as interest rate risk; |

| • | the effects of competition from other commercial banks, thrifts, mortgage companies, finance companies, credit unions, securities brokerage firms, insurance companies, money-market and mutual funds and other institutions operating in the Corporation’s trade market area and elsewhere including institutions operating locally, regionally, nationally and internationally together with such competitors offering banking products and services by mail, telephone, computer and the Internet; |

| • | any extraordinary event (such as the September 11, 2001 events, the war on terrorism and the U.S. Government’s response to those events including the war in Iraq); |

| • | the Corporation’s success in continuing to generate new business in its existing markets, as well as its success in identifying and penetrating targeted markets and generating a profit in those markets in a reasonable time; |

| • | the Corporation’s ability to continue to generate investment results for customers and the ability to continue to develop investment products in a manner that meets customer’s needs; |

| • | the Corporation’s timely development of competitive new products and services in a changing environment and the acceptance of such products and services by customers; |

| • | the Corporation’s ability to originate, sell and service residential mortgage loans; |

| • | the accuracy of assumptions underlying the establishment of reserves for loan losses and estimates in the value of collateral, the market value of mortgage servicing rights and various financial assets and liabilities; |

| • | technological changes being more difficult or expensive than anticipated; |

| • | the Corporation’s success in managing the risks involved in the foregoing. |

All written or oral forward-looking statements attributed to the Corporation are expressly qualified in their entirety by use of the foregoing cautionary statements. All forward-looking statements included in this Report are based upon information presently available, and the Corporation assumes no obligation to update any forward-looking statement.

2

BRIEF HISTORYOFTHE CORPORATION

The Bryn Mawr Trust Company (the “Bank”) received its Pennsylvania banking charter in 1889 and is a member of the Federal Reserve System. In 1986, Bryn Mawr Bank Corporation (the “Corporation”) was formed and on January 2, 1987, the Bank became a wholly-owned subsidiary of the Corporation. The Bank and Corporation are headquartered in Bryn Mawr, PA, a western suburb of Philadelphia, PA. The Corporation and its subsidiaries provide wealth management, community banking, residential mortgage lending, insurance and business banking services to its customers through eight full service branches and seven retirement community offices throughout Montgomery, Delaware and Chester counties. The Corporation trades on the NASDAQ National Market under the symbol BMTC.

The goal of the Corporation is to become the preeminent community bank and wealth management organization in the Philadelphia area.

The Corporation operates in a highly competitive market area that includes local, national and regional banks as competitors along with savings banks, credit unions, insurance companies, trust companies, registered investment advisors and mutual fund families. The Corporation and its subsidiaries are regulated by many regulatory agencies including the SEC, NASD, FDIC, the Federal Reserve and the Pennsylvania Department of Banking.

RESULTSOF OPERATIONS

The following is Management’s discussion and analysis of the significant changes in the results of operations, capital resources and liquidity presented in its accompanying consolidated financial statements for the Corporation. The Corporation’s consolidated financial condition and results of operations consist almost entirely of the Bank’s financial condition and results of operations. Current performance does not guarantee, and may not be indicative of similar performance in the future.

CRITICAL ACCOUNTING POLICIES, JUDGMENTSAND ESTIMATES

The accounting and reporting policies of the Corporation and its subsidiaries conform with accounting principles generally accepted in the United States of America applicable to the financial services industry. All significant inter-company transactions are eliminated in consolidation and certain reclassifications are made when necessary to conform the previous year’s financial statements to the current year’s presentation. In preparing the consolidated financial statements, Management is required to make estimates and assumptions that affect the reported amount of assets and liabilities as of the dates of the balance sheets and revenues and expenditures for the periods presented. Therefore, actual results could differ from these estimates.

The allowance for loan losses involves a higher degree of judgment and complexity than other significant accounting policies. The allowance for loan losses is calculated with the objective of maintaining a reserve level believed by Management to be sufficient to absorb estimated probable credit losses. Management’s determination of the adequacy of the allowance is based on periodic evaluations of the loan portfolio and other relevant factors. However, this evaluation is inherently subjective as it requires significant estimates by Management. Consideration is given to a variety of factors in establishing these estimates, including, specific terms and conditions of loans, underwriting standards, delinquency statistics, industry concentration, overall exposure to a single customer, adequacy of collateral, the dependence on collateral, and results of internal loan review, including borrowers perceived financial and management strengths, the amounts and timing of the present value of future cash flows, and access to additional funds. The evaluation process also considers the impact of competition, current and expected economic conditions, national and international events, the regulatory and legislative environment and inherent risks in the loan portfolio. All of these factors may be susceptible to significant change. To the extent actual outcomes differ from Management estimates, additional provisions for loan losses may be required that might adversely affect the Corporation’s results of operations in future periods.

The Corporation recognizes deferred tax assets and liabilities for the future tax effects of temporary differences, net of operating loss carry forwards and tax credits. Deferred tax assets are subject to Management’s judgment based upon available evidence that future realization is more likely than not. If Management determines that the Corporation may be unable to realize all or part of net deferred tax assets in the future, a direct charge to income tax expense may be required to reduce the recorded value of the net deferred tax asset to the expected realizable amount.

The valuation of mortgage servicing rights (“MSRs”) is a critical accounting policy due to the complexity of the quarterly valuation process which is performed by an outside consultant based on data provided by Management. Changes in market interest rates, consumer behavior, demographic trends and other factors influence the value of MSRs. See Note 6 in the accompanying financial statements for additional information.

Other significant accounting policies are presented in Note 1 in the accompanying financial statements. The Corporation has not substantively changed any aspect of its overall approach in the application of the foregoing policies. There have been no material changes in assumptions or estimation techniques utilized as compared to prior periods.

3

EXECUTIVE OVERVIEW

2005 Compared to 2004

The Corporation had net income of $11.350 million for the year ended December 31, 2005, an increase of 21.5% or $2.005 million compared with $9.345 million in 2004. Diluted earnings per share for 2005 were $1.31, an increase of $0.24 or 22.4% compared with $1.07 in 2004. Return on Average Equity (ROE) and Return on Average Assets (ROA) for 2005 were 15.44% and 1.66%, respectively. ROE was 13.67% and ROA was 1.45% in 2004. Management attributes part of this year’s success to a focus on the Corporation’s core competencies which include Wealth, Business Banking, “High Touch” Retail Banking and Mortgage Banking, along with an obsession on client service, close control over expenses and the development of a more assertive sales culture.

The major factor contributing to the increase in earnings for 2005 compared to 2004 was a 43 basis point or 9.4% increase in the Corporation’s net interest margin to 5.00% from 4.57% as the Corporation’s asset sensitive loan portfolio continued to benefit from a series of Federal Reserve interest rate increases. Net interest income for 2005 increased $4.540 million or 16.9%, to $31.368 million from $26.828 million in the same period last year. Additionally, fees for Wealth Management services increased 12.0% or $1.236 million to $11.539 million in 2005 versus $10.303 million in 2004, partially offsetting declines in residential mortgage-related revenues.

In 2004, the Corporation sold mortgage-servicing rights (“MSRs”) that contributed $572 thousand to after tax income and increased diluted earnings per share $0.07. There were no sales of MSRs in 2005. Net income and diluted earnings per share for 2004, excluding the after tax impact of the MSRs sale, would have been $8.773 million and $1.01 per share, respectively. Excluding the impact of the MSRs sale, 2005 net income increased $2.577 million or 29.4% and diluted earnings per share increased $0.30 or 29.7% over the same period last year. (See accompanying reconcilement of GAAP net income and diluted earnings per share to net income and diluted earnings per share that exclude the MSRs sale).

Total loans increased $33.3 million or 5.9% to $597.9 million from $564.6 million over the past 12 months and average loans for 2005 increased $43.6 million or 8.1% to $582.4 million compared to $538.8 million in 2004. The Corporation’s asset quality remains strong as non-performing loans as a percent of total loans was 0.07% at December 31, 2005. The Corporation continues its business development efforts on building banking relationships with privately held businesses, non-profits, quality residential builders and owners of commercial real estate. In addition, the Corporation continues to provide high-touch retail lending services to consumers in the Philadelphia area.

Total deposits grew $35.3 million or 5.9% over the past 12 months to $636.3 million at December 31, 2005 from $601.0 million at December 31, 2004. Average deposits for 2005 increased $32.7 million or 5.8% to $596.4 million compared to $563.7 million in 2004. Deposit balances typically spike near year end as evidenced by an increase in deposits of $31.6 million at December 31, 2005 compared to September 30, 2005. Average deposits for the fourth quarter of 2005 were $600.6 million compared to third quarter 2005 average deposits of $603.3 million reflecting the competitive nature of the deposit gathering business in our market area.

The Corporation will continue with the expansion of its retail banking footprint with controlledde novo expansion in the suburban Philadelphia market. Management anticipates relocating the Wynnewood, PA branch to a new branch in Ardmore, PA in late 2006. Management also plans a new regional office in West Chester, PA some time in 2007 to complement the recently opened Exton, PA and Newtown Square, PA retail branch locations.

Non-interest income for 2005, excluding the $1.145 million gain on MSR sales in 2004, decreased $404 thousand or 2.2% to $18.245 million from $18.649 million in the same period last year. Non-interest income was negatively impacted by the slowdown in residential mortgage activity, as residential mortgage originations and sales declined 7.2% or $15.0 million and $13.3 million or 9.1%, respectively in 2005 compared to 2004. This decline in residential mortgage activity along with very competitive pricing resulted in a reduction in the gain on sale of loans of 44.5% or $1.298 million to $1.622 million in 2005 from $2.920 million in 2004. Non-interest income was also negatively impacted by a $234 thousand or 12.8% decrease in service charges on deposit accounts reflecting the impact of higher earnings credits on commercial checking accounts and the industry’s trend toward “free” checking.

Partially offsetting this decrease in non-interest income was a 2005 increase of $1.236 million or 12.0% in fees for Wealth Management services compared to 2004. Wealth assets under management and administration increased $310 million or 16.0% to $2.248 billion at December 31, 2005, compared to $1.938 billion at December 31, 2004. The increase in assets under management and administration is partly a result of a business acquisition by a significant client in the third quarter of 2005.

Non-interest expense for 2005, excluding $266 thousand of expenses related to the sale of the MSRs, increased $214 thousand or 0.7% to $31.573 million when compared to $31.359 million in the same period last year. The increase is a combination of many factors including increased medical benefit costs, staff merit raises, incentive compensation, and occupancy and furniture and fixture expenses related to the

4

new Exton, PA branch. Partially offsetting these increases were reduced levels of professional fees, lower amortization of mortgage servicing rights, and reduced residential mortgage staffing levels.

2004 Compared to 2003

The Corporation had net income from continuing operations of $9.345 million for the year ended December 31, 2004, a decrease of 17.1% or $1.927 million compared with $11.272 million in 2003. Diluted earnings per share from continuing operations for 2004 were $1.07, a decrease of $0.22 or 17.1% from $1.29 in 2003. ROE and ROA for 2004 on continuing operations were 13.67% and 1.45%, respectively. ROE and ROA for continuing operations in 2003 were 17.76% and 1.98%, respectively.

The major factors contributing to the decline in earnings from continuing operations in 2004 compared to 2003 were a significant drop in residential mortgage related activity, a decline in the Corporation’s net interest margin and compliance costs associated with the implementation of Sarbanes Oxley legislation. Partially offsetting these declines was a gain on the sale of mortgage servicing rights (there were no such sales in 2003) and improved Wealth Division performance (revenues and expense control).

During 2003, the Corporation sold the assets of its family office subsidiary, Joseph W. Roskos & Company (“JWR & Co.”) to its former owners. In accordance with SFAS No. 144 – Accounting for the Impairment or Disposal of Long Lived Assets, the Corporation classified all revenues, expenses, goodwill writedowns, related disposal expenses and applicable income taxes as a loss from discontinued operations. The disposal of the JWR & Co. subsidiary resulted in a loss, net of applicable income taxes, of $1.916 million or $0.22 per share (basic and diluted) in 2003. Additional details related to the disposal of JWR & Co.’s assets are included in Note 20 in the Notes to the Consolidated Financial Statements.

Key Performance Ratios

Key financial performance ratios for the years and years ended December 31, 2005, 2004 and 2003 are shown in the tables below. Ratios are from continuing operations unless noted otherwise.

| 2005 | 2004 | 2003 | ||||||||||

Return on Average Equity (ROE) | 15.44 | % | 13.67 | % | 17.76 | % | ||||||

Return on Average Assets (ROA) | 1.66 | % | 1.45 | % | 1.98 | % | ||||||

Efficiency Ratio* | 63.64 | % | 67.83 | % | 64.34 | % | ||||||

Net Interest Margin | 5.00 | % | 4.57 | % | 4.83 | % | ||||||

Total Diluted Earnings Per Share (including discontinued operations) | $ | 1.31 | $ | 1.07 | $ | 1.07 | ||||||

Dividend Per Share | $ | .42 | $ | 0.40 | $ | 0.40 | ||||||

Diluted Earnings Per Share** | $ | 1.31 | $ | 1.07 | $ | 1.29 | ||||||

| December 31, | ||||||||||||

| 2005 | 2004 | 2003 | ||||||||||

Book Value Per Share | $ | 9.06 | $ | 8.29 | $ | 7.77 | ||||||

Allowance for Loan Losses as a Percentage of Loans | 1.24 | % | 1.23 | % | 1.25 | % | ||||||

Wealth assets under management and administration (in billions) | $ | 2.248 | $ | 1.938 | $ | 1.752 | ||||||

| * | Efficiency ratio is calculated by dividing non-interest expense by the sum of net interest income and non-interest income. |

| ** | See Note 14, Earnings Per Share, in the Notes to Consolidated Financial Statements |

Reconcilement of Non-GAAP Information

See the table below for a reconcilement of GAAP net income, diluted earnings per share, non-interest income and non-interest expense to comparable data that excludes the MSRs sale. Management believes that the presentation excluding the impact of the sale of MSRs in 2004 provides useful supplemental information essential to the proper understanding of the operating results of the Corporation’s core business. These disclosures should not be viewed as a substitute for operating results determined in accordance with GAAP, nor are they necessarily comparable to non-GAAP performance measures, which may be presented by other companies.

Net Income From Continuing Operations | Diluted Earnings Per Share From Continuing Operations | |||||||||||||||||||

| Year Ended December 31, | ||||||||||||||||||||

| 2005 | 2004 | 2003 | 2005 | 2004 | 2003 | |||||||||||||||

| (dollars in thousands except per share data) | ||||||||||||||||||||

As reported2 | $ | 11,350 | $ | 9,345 | $ | 11,272 | 1.31 | $ | 1.07 | 1.29 | ||||||||||

After tax effect of MSR sale1,2 | — | (572 | ) | — | — | (0.07 | ) | |||||||||||||

Adjusted for sale2 | $ | 11,350 | $ | 8,773 | $ | 11,272 | 1.31 | $ | 1.01 | 1.29 | ||||||||||

| Non-Interest Income | Non-Interest Expense | |||||||||||||||||||

| 2005 | 2004 | 2003 | 2005 | 2004 | 2003 | |||||||||||||||

As reported | $ | 18,245 | $ | 19,794 | $ | 26,577 | $ | 31,573 | $ | 31,625 | $ | 33,437 | ||||||||

MSR sale income | — | 1,145 | — | — | — | — | ||||||||||||||

MSR sale expenses | — | — | — | — | 266 | — | ||||||||||||||

Adjusted for sale | $ | 18,245 | $ | 18,649 | $ | 26,577 | $ | 31,573 | $ | 31,359 | $ | 33,437 | ||||||||

| 1 | MSR gain consists of revenues of $1.145 million, direct expenses of $266 thousand and allocated income taxes of $307 thousand netting to $572 thousand of net income. |

| 2 | Dilutive potential shares have been adjusted to reflect the tax benefit of non-qualified stock options. This resulted in an increase to diluted earnings per share from continuing operations for the year 2004 and year 2003 of $0.01 per share. The difference in diluted earnings per share from continuing operations adjusted for the MSR sale is due to rounding. |

5

COMPONENTSOF NET INCOME

Net income is affected by five major elements:Net Interest Income, or the difference between interest income and loan fees earned on loans and investments and interest expense paid on deposits and borrowed funds; The Provision For Loan Losses, or the amount added to the allowance for loan losses to provide reserves for estimated inherent losses on loans;Non-Interest Income which is made up primarily of certain fees, wealth revenue, residential mortgage activities and gains and losses from the sale of securities;Non-Interest Expense, which consists primarily of salaries, employee benefits and other operating expenses; andIncome Taxes. Each of these major elements will be reviewed in more detail in the following discussion.

NET INTEREST INCOME

Rate/Volume Analyses

The rate volume analysis in the table below analyzes changes in net interest income for the year ended December 31, 2005 over December 31, 2004 and December 31, 2004 over December 31, 2003 by its rate and volume components. The change in interest income/expense due to both volume and rate has been allocated to changes in volume.

| Year Ended December 31, | ||||||||||||||||||||||

| (dollars in thousands) | 2005 Compared to 2004 | 2004 Compared to 2003 | ||||||||||||||||||||

| Increase/(decrease) | Volume | Rate | Total | Volume | Rate | Total | ||||||||||||||||

Interest Income: | ||||||||||||||||||||||

Interest-bearing deposits with other banks | $ | (11 | ) | $ | 39 | $ | 28 | $ | (8 | ) | $ | 19 | $ | 11 | ||||||||

Federal funds sold | (99 | ) | 118 | 19 | 25 | 56 | 81 | |||||||||||||||

Investment securities available for sale, taxable | 122 | 42 | 164 | 209 | (135 | ) | 74 | |||||||||||||||

Investment securities available for sale, tax-exempt | — | — | — | 82 | (3 | ) | 79 | |||||||||||||||

Loans | 2,729 | 3,647 | 6,376 | 3,383 | (1,508 | ) | 1,875 | |||||||||||||||

Total interest income | 2,741 | 3,846 | 6,587 | 3,691 | (1,571 | ) | 2,120 | |||||||||||||||

Interest expense: | ||||||||||||||||||||||

Savings, NOW and market rate | (59 | ) | 804 | 745 | 341 | 0 | 341 | |||||||||||||||

Time deposits | 825 | 430 | 1,255 | 115 | (235 | ) | (120 | ) | ||||||||||||||

Short term borrowings | 29 | 18 | 47 | 4 | (2 | ) | 2 | |||||||||||||||

Total interest expense | 795 | 1,252 | 2,047 | 460 | (237 | ) | 223 | |||||||||||||||

Interest differential | $ | 1,946 | $ | 2,594 | $ | 4,540 | $ | 3,231 | $ | (1,334 | ) | $ | 1,897 | |||||||||

Analyses of Interest Rates and Interest Differential

The table below presents the major asset and liability categories on an average daily basis for the periods presented, along with interest income and expense and key rates and yields. The following table shows an analysis of the composition of net interest income for each of the last three years. Interest income on loans includes fees on loans of $645,000, $677,000 and $620,000 in 2004, 2003 and 2002 respectively. The average loan balances include non-accrual loans. All average balances are calculated on a daily basis. Yields on investment securities are not calculated on a tax-equivalent basis.

| For the Year Ended December 31 | 2005 | 2004 | 2003 | |||||||||||||||||||||||||||

| (dollars in thousands) | Average Balance | Interest Income/ Expense | Average Rates Earned/ Paid | Average Balance | Interest Income/ Expense | Average Rates Earned/ Paid | Average Balance | Interest Income/ Expense | Average Rates Earned/ Paid | |||||||||||||||||||||

Assets: | ||||||||||||||||||||||||||||||

Interest-bearing deposits with other banks | $ | 2,398 | $ | 76 | 3.17 | % | $ | 3,079 | $ | 48 | 1.56 | % | $ | 3,737 | $ | 37 | 0.99 | % | ||||||||||||

Federal funds sold | 6,281 | 210 | 3.34 | % | 13,052 | 191 | 1.46 | % | 10,638 | 110 | 1.03 | % | ||||||||||||||||||

Investment securities available for sale: | ||||||||||||||||||||||||||||||

Taxable | 30,848 | 1,018 | 3.30 | % | 27,173 | 854 | 3.14 | % | 21,087 | 780 | 3.70 | % | ||||||||||||||||||

Tax –Exempt | 5,069 | 165 | 3.26 | % | 5,071 | 165 | 3.25 | % | 2,499 | 86 | 3.44 | % | ||||||||||||||||||

Total investment securities | 35,917 | 1,183 | 3.29 | % | 32,244 | 1,019 | 3.16 | % | 23,586 | 866 | 3.67 | % | ||||||||||||||||||

Loans(1) | 582,386 | 36,499 | 6.27 | % | 538,775 | 30,123 | 5.59 | % | 478,397 | 28,248 | 5.90 | % | ||||||||||||||||||

Total interest earning assets | 626,982 | 37,968 | 6.06 | % | 587,150 | 31,381 | 5.34 | % | 516,358 | 29,261 | 5.67 | % | ||||||||||||||||||

Cash and due from banks | 29,918 | 32,774 | 33,005 | |||||||||||||||||||||||||||

Allowance for loan losses | (7,283 | ) | (6,957 | ) | (6,519 | ) | ||||||||||||||||||||||||

Other assets | 33,312 | 29,827 | 27,557 | |||||||||||||||||||||||||||

Total assets | $ | 682,929 | $ | 642,794 | $ | 570,401 | ||||||||||||||||||||||||

Liabilities: | ||||||||||||||||||||||||||||||

Savings, NOW and market rate | $ | 317,205 | $ | 2,744 | .87 | % | $ | 323,972 | $ | 1,999 | 0.62 | % | $ | 263,646 | $ | 1,658 | 0.63 | % | ||||||||||||

Time deposits | 130,667 | 3,799 | 2.91 | % | 102,369 | 2,544 | 2.49 | % | 96,996 | 2,664 | 2.75 | % | ||||||||||||||||||

Total interest-bearing deposits | 447,872 | 6,543 | 1.46 | % | 426,341 | 4,543 | 1.07 | % | 360,642 | 4,322 | 1.20 | % | ||||||||||||||||||

Short term borrowings | 1,700 | 57 | 3.35 | % | 850 | 10 | 1.18 | % | 496 | 8 | 1.61 | % | ||||||||||||||||||

Total interest-bearing liabilities | 449,572 | 6,600 | 1.47 | % | 427,190 | 4,553 | 1.07 | % | 361,138 | 4,330 | 1.20 | % | ||||||||||||||||||

Demand deposits, non-interest-bearing | 148,495 | 137,336 | 135,335 | |||||||||||||||||||||||||||

Other liabilities | 11,370 | 9,900 | 10,454 | |||||||||||||||||||||||||||

Total non-interest-bearing liabilities | 159,865 | 147,236 | 145,789 | |||||||||||||||||||||||||||

Total liabilities | 609,437 | 574,426 | 506,927 | |||||||||||||||||||||||||||

Shareholder’s equity | 73,492 | 68,367 | 63,474 | |||||||||||||||||||||||||||

Total liabilities and shareholders’ equity | $ | 682,929 | $ | 642,794 | $ | 570,401 | ||||||||||||||||||||||||

Net interest spread | 4.59 | % | 4.27 | % | 4.47 | % | ||||||||||||||||||||||||

Effect of non-interest-bearing sources | .41 | % | 0.30 | % | 0.36 | % | ||||||||||||||||||||||||

Net interest income/margin on earning assets | $ | 31,368 | 5.00 | % | $ | 26,828 | 4.57 | % | $ | 24,931 | 4.83 | % | ||||||||||||||||||

| (1) | Non-accrual loans have been included in average loan balances, but interest on non-accrual loans has not been included for purposes of determining interest income. |

6

Net Interest Margin 2005 Compared to 2004 Commentary

Net interest income for the year ended December 31, 2005 of $31.368 million was $4.540 million or 16.9% higher than the net interest income for the same period in 2004 of $26.828 million. The analyses above indicate that both increased loan volume and an increase in rates contributed to the increase in net interest income. Average earning assets increased $39.8 million or 6.8% in 2005 compared to the same period in 2004. Average total loans grew $43.6 million or 8.1% in 2005 compared to 2004.

The average earning asset yield during 2005 of 6.06% was 72 basis points higher than the 5.34% during the same period in 2004. The rate paid on average interest bearing liabilities of 1.47% in 2005 was 40 basis points higher than the 1.07% in 2004. Average non-interest-bearing demand deposits grew 8.1%, while savings decreased 2.1% and time deposits increased 27.6% in 2005 compared to 2004.

Net Interest Margin 2004 Compared to 2003 Commentary

Net interest income for the year ended December 31, 2004 of $26.828 million was $1.897 million or 7.6% higher than the net interest income for the same period in 2003 of $24.931 million. The rate volume analysis and average balance sheet data above clearly show that the increase in interest earning assets, particularly loans, more than offset the decline in interest rates. Average earning assets increased $70.792 million or 13.7% for 2004 compared to the same period in 2003. Average total loans grew $60.378 million or 12.6% while investments increased $8.658 million or 36.7% in 2004 over 2003.

The average earning asset yield during 2004 of 5.34% was 33 basis points lower than the 5.67% in 2003. The rate paid on average interest bearing liabilities of 1.07% in 2004 was 13 basis points lower than the 1.20% in 2003. Average non-interest-bearing demand deposits grew 1.5%, while savings and time deposits increased 22.9% and 5.5%, respectively, in 2004 compared to 2003.

Net Interest Margin

The Corporation’s net interest margin increased 51 basis points to 5.15% in the fourth quarter of 2005 from 4.64% in the same period last year. The net interest margin and related components for the past five linked quarters are shown in the table below. The Corporation anticipates that continued increases in interest rates will have a positive effect on the Corporation’s net interest margin in the first half of 2006. However, factors such as competitive market conditions for deposits and competitive share driven loan pricing could impact the net interest margin in the second half of 2006 and beyond. The Corporation’s net interest margin was 5.00% in 2005 compared with 4.57% in 2004 and 4.83% in 2003. These results reflect the decline in interest rates during 2003 and the first half of 2004. Rates started to rise in 2004 as reflected in the five quarter and three year analyses below.

| Year | Earning Asset Yield | Interest Bearing Liability Cost | Net Interest Spread | Effect of Non-Interest Bearing Sources | Net Interest Margin | ||||||||||||

Net Interest Margin Last Five Quarters |

| ||||||||||||||||

4thQuarter | 2005 | 6.37 | % | 1.73 | % | 4.64 | % | 0.51 | % | 5.15 | % | ||||||

3rdQuarter | 2005 | 6.13 | % | 1.57 | % | 4.56 | % | 0.45 | % | 5.01 | % | ||||||

2ndQuarter | 2005 | 5.94 | % | 1.37 | % | 4.57 | % | 0.37 | % | 4.94 | % | ||||||

1stQuarter | 2005 | 5.76 | % | 1.19 | % | 4.57 | % | 0.32 | % | 4.89 | % | ||||||

4thQuarter | 2004 | 5.45 | % | 1.10 | % | 4.35 | % | 0.29 | % | 4.64 | % | ||||||

Net Interest Margin Last Three Years | |||||||||||||||||

| 2005 | 6.06 | % | 1.47 | % | 4.59 | % | 0.41 | % | 5.00 | % | |||||||

| 2004 | 5.34 | % | 1.07 | % | 4.27 | % | 0.30 | % | 4.57 | % | |||||||

| 2003 | 5.67 | % | 1.20 | % | 4.47 | % | 0.36 | % | 4.83 | % | |||||||

Interest Rate Sensitivity

The Corporation actively manages its interest rate sensitivity position. The objectives of interest rate risk management are to control exposure of net interest income to risks associated with interest rate movements and to achieve sustainable growth in net interest income. Management’s Asset Liability Committee (“ALCO”), using policies and procedures approved by the Corporation’s Board of Directors, is responsible for managing the interest rate sensitivity position. The Corporation manages interest rate sensitivity by changing the mix, pricing and repricing characteristics of its assets and liabilities, through the management of its investment portfolio, its offering of loan and selected deposit terms and through borrowings from the Federal Home Loan Bank of Pittsburgh (“FHLB”). The ALCO is presently evaluating various strategies including interest rate swaps and floors to mitigate the impact of future changes in interest rates on its net interest income.

The Corporation uses several tools to manage its interest rate risk including interest rate sensitivity analysis (aka “GAP Analysis”), market value of portfolio equity analysis, interest rate simulations under various rate scenarios and net interest margin reports. The results of these reports are compared to limits established by the Corporation’s Asset Liability Management Policies and appropriate adjustments are made if the results are outside of established limits.

7

The following table demonstrates the annualized result of an interest rate simulation and the estimated effect that a parallel interest rate shift in the yield curve and subjective adjustments in deposit pricing might have on the Corporation’s projected net interest income over the next 12 months.

Summary of Interest Rate Simulation

| December 31, 2005 | |||||||

| (dollars in thousands) | Estimated Change Next 12 Months | ||||||

Change in Interest Rates | |||||||

+200 basis points | $ | 2,086 | 6.10 | % | |||

+100 basis points | $ | 1,235 | 3.61 | % | |||

-100 basis points | $ | (1,496 | ) | (4.37 | )% | ||

-200 basis points | $ | (3,684 | ) | (10.76 | )% | ||

The interest rate simulation above indicates that the Corporation’s balance sheet as of December 31, 2005 is asset sensitive meaning that an increase in interest rates should increase net interest income and a decline in interest rates will cause a decline in net interest income over the next 12 months when compared to projected net income under a flat or stable rate scenario.

GAP Report

The following table presents the Corporation’s interest rate sensitivity position or GAP Analysis as of December 31, 2005:

| (dollars in thousands) | 0 to 90 Days | 90 to 365 Days | 1 - 5 Years | Over 5 Years | Non- Rate | Total | ||||||||||||||||

Assets: | ||||||||||||||||||||||

Interest-bearing deposits with other banks | $ | 405 | $ | — | $ | — | $ | — | $ | — | $ | 405 | ||||||||||

Federal Funds Sold | 32,341 | — | — | — | — | 32,341 | ||||||||||||||||

Investment securities | 221 | 13,052 | 16,434 | 5,284 | 34,991 | |||||||||||||||||

Loans, net of allowance | 265,199 | 36,961 | 210,559 | 77,809 | 590,528 | |||||||||||||||||

Cash and due from banks | — | — | — | — | 33,896 | 33,896 | ||||||||||||||||

Other assets | — | — | — | — | 35,065 | 35,065 | ||||||||||||||||

Total assets | $ | 298,166 | $ | 50,013 | $ | 226,993 | $ | 83,093 | $ | 68,961 | $ | 727,226 | ||||||||||

Liabilities and shareholders’ equity: | ||||||||||||||||||||||

Non-interest- bearing demand | $ | 47,707 | $ | 18,429 | $ | 98,290 | $ | — | $ | 3,616 | $ | 168,042 | ||||||||||

Savings, NOW and market rate | 51,318 | 43,222 | 166,806 | 51,550 | — | 312,896 | ||||||||||||||||

Time deposits | 74,302 | 55,651 | 25,233 | 136 | — | 155,322 | ||||||||||||||||

Other liabilities | — | — | — | — | 13,453 | 13,453 | ||||||||||||||||

Shareholders’ equity | 2,768 | 8,305 | 44,294 | 22,146 | — | 77,513 | ||||||||||||||||

Total liabilities and shareholders’ equity | $ | 176,095 | $ | 125,607 | $ | 334,623 | $ | 73,832 | $ | 17,069 | $ | 727,226 | ||||||||||

GAP | $ | 122,071 | $ | (75,594 | ) | $ | (107,630 | ) | $ | 9,261 | $ | 51,892 | $ | — | ||||||||

Cumulative GAP | $ | 122,071 | $ | 46,477 | $ | (61,153 | ) | $ | (51,892 | ) | $ | — | $ | — | ||||||||

Cumulative earning assets as a % of cumulative interest bearing liabilities | 238 | % | 155 | % | 138 | % | 141 | % | — | — | ||||||||||||

The table above indicates that the Corporation is asset sensitive in the immediate to 90 day time frame and should experience an increase in net interest income in the near term if interest rates rise. The converse is also true.

Maturity of Certificates of Deposit of $100,000 or Greater

| (dollars in thousands) | |||

Three months or less | $ | 61,148 | |

Three to six months | 8,424 | ||

Six to twelve months | 12,567 | ||

Greater than twelve months | 5,642 | ||

Total | $ | 87,781 | |

PROVISIONFOR LOAN LOSSES

General Discussion of the Allowance for Loan Losses

The Corporation uses the allowance method of accounting for credit losses. The balance in the allowance for loan losses is determined based on Management’s review and evaluation of the loan portfolio in relation to past loss experience, the size and composition of the portfolio, current economic events and conditions, and other pertinent factors, including Management’s assumptions as to future delinquencies, recoveries and losses.

Increases to the allowance for loan losses are implemented through a corresponding provision (expense) in the Corporation’s statement of income. Loans deemed uncollectible are charged against the allowance for loan losses. Recoveries of previously charged-off amounts are credited to the allowance for loan losses.

While Management considers the allowance for loan losses to be adequate based on information currently available, future additions to the allowance may be necessary due to changes in economic conditions or Management’s assumptions as to future delinquencies, recoveries and losses and Management’s intent with regard to the disposition of loans. In addition, the Pennsylvania Department of Banking and the Federal Reserve Bank of Philadelphia, as an integral part of their examination process, periodically review the Corporation’s allowance for loan losses.

The Corporation’s allowance for loan losses is the accumulation of four components that are calculated based on various independent methodologies. All components of the allowance for loan losses are estimations. Management discusses these estimates earlier in this document under the heading of “Critical Accounting Policies, Judgments and Estimates”. The four components are as follows:

| • | Specific Loan Evaluation Component – Includes the specific evaluation of larger classified loans |

8

| • | Historical Charge-Off Component – Applies a five year historical charge-off rate to pools of non-classified loans |

| • | Additional Factors Component – The loan portfolio is broken down into multiple homogenous subclassifications upon which multiple factors (such as delinquency trends, economic conditions, loan terms, and regulatory environment) are evaluated resulting in an allowance amount for each of the subclassifications. The sum of these amounts equals the Additional Factors Component. |

| • | Unallocated Component – This amount represents a general reserve against all loans. |

The Corporation has a material portion of its loans in real estate related loans. A predominant percentage of the Corporation’s real estate exposure, both commercial and residential, is in the Corporation’s primary trade area which includes portions of Delaware, Chester, Montgomery and Philadelphia counties in Southeastern Pennsylvania.

Management is aware of this concentration and mitigates this risk to the extent possible in many ways, including the underwriting and assessment of the borrower’s capacity to repay.

Asset Quality and Analysis of Credit Risk

Asset quality remains strong at December 31, 2005 as non-performing loans as a percentage of total loans were 7 basis points. This compares with 24 basis points at December 31, 2004 and 9 basis points at December 31, 2003. The allowance for loan losses as a percentage of total loans was 1.24% at December 31, 2005 compared with 1.23% at December 31, 2004 and 1.33% at December 31, 2003. The provision for loan losses in 2005 was $762 thousand compared to $900 thousand in 2004. The lower provision is reflective of the high credit quality of the Corporation’s loan portfolio. The provision of $900 thousand in 2004 was higher than the $750 thousand in 2003 due to strong loan growth in 2004 and net charge-offs of $643 thousand. See table below for additional details.

Non-Performing Assets and Related Ratios

| December 31, | ||||||||||||||||||||

| (dollars in thousands) | 2005 | 2004 | 2003 | 2002 | 2001 | |||||||||||||||

Non-accrual loans | $ | 261 | $ | 1,353 | $ | 371 | $ | 209 | $ | 21 | ||||||||||

Loans 90 days or more past due | 129 | 22 | 62 | 45 | 43 | |||||||||||||||

Total non-performing loans | 390 | 1,375 | 433 | 254 | 64 | |||||||||||||||

Other real estate owned (“OREO”) | 25 | 357 | — | — | — | |||||||||||||||

Total non-performing assets | $ | 415 | $ | 1,732 | $ | 433 | $ | 254 | $ | 64 | ||||||||||

Allowance for loan losses to non-performing assets | 1,783.6 | % | 399.9 | % | 1,540.4 | % | 2,407.1 | % | 7,700.0 | % | ||||||||||

Allowance for loan losses to non-performing loans | 1,897.9 | % | 503.8 | % | 1,540.4 | % | 2,407.1 | % | 7,700.0 | % | ||||||||||

Non-performing loans to total loans | 0.07 | % | 0.24 | % | 0.09 | % | 0.05 | % | 0.02 | % | ||||||||||

Allowance for loan losses to total loans | 1.24 | % | 1.23 | % | 1.33 | % | 1.31 | % | 1.23 | % | ||||||||||

Non-performing assets to total assets | 0.06 | % | 0.25 | % | 0.07 | % | 0.04 | % | 0.01 | % | ||||||||||

Period end loans | $ | 597,930 | $ | 564,597 | $ | 502,416 | $ | 466,975 | $ | 400,868 | ||||||||||

Average loans (average for year) | $ | 582,386 | $ | 538,775 | $ | 478,397 | $ | 421,904 | $ | 367,571 | ||||||||||

Allowance for loan losses | $ | 7,402 | $ | 6,927 | $ | 6,670 | $ | 6,114 | $ | 4,928 | ||||||||||

Summary of Changes in the Allowance for Loan Losses

| (dollars in thousands) | 2005 | 2004 | 2003 | 2002 | 2001 | |||||||||||||||

Balance, beginning of period | $ | 6,927 | $ | 6,670 | $ | 6,114 | $ | 4,928 | $ | 4,320 | ||||||||||

Charge-offs: | ||||||||||||||||||||

Consumer | (158 | ) | (94 | ) | (102 | ) | (68 | ) | (178 | ) | ||||||||||

Commercial and industrial | — | (167 | ) | (112 | ) | — | (940 | ) | ||||||||||||

Real estate | (156 | ) | (431 | ) | (13 | ) | — | (51 | ) | |||||||||||

Total charge-offs | (314 | ) | (692 | ) | (227 | ) | (68 | ) | (1,169 | ) | ||||||||||

Recoveries: | ||||||||||||||||||||

Consumer | 11 | 47 | 32 | 24 | 38 | |||||||||||||||

Commercial and industrial | 12 | 2 | — | 220 | 63 | |||||||||||||||

Real estate | 4 | — | 1 | 10 | 476 | |||||||||||||||

Total Recoveries | 27 | 49 | 33 | 254 | 577 | |||||||||||||||

Net (charge-offs) / recoveries | (287 | ) | (643 | ) | (194 | ) | 186 | (592 | ) | |||||||||||

Provision for loan losses | 762 | 900 | 750 | 1,000 | 1,200 | |||||||||||||||

Balance, end of period | $ | 7,402 | $ | 6,927 | $ | 6,670 | $ | 6,114 | $ | 4,928 | ||||||||||

9

Allocation of Allowance for Loan Losses

The following table sets forth an allocation of the allowance for loan losses by loan category. The specific allocations in any particular category may be changed in the future to reflect then current conditions. Accordingly, Management considers the entire allowance to be available to absorb losses in any category.

| December 31, | ||||||||||||||||||||||||||||||

| 2005 | 2004 | 2003 | 2002 | 2001 | ||||||||||||||||||||||||||

| (dollars in thousands) | % Loans to Total Loans | % Loans to Total Loans | % Loans to Total Loans | % Loans to Total Loans | % Loans to Total Loans | |||||||||||||||||||||||||

Balance at end of period applicable to: | ||||||||||||||||||||||||||||||

Commercial and industrial | $ | 2,191 | 28.5 | % | $ | 3,575 | 33.1 | % | $ | 3,656 | 35.7 | % | $ | 2,940 | 36.4 | % | $ | 2,729 | 39.1 | % | ||||||||||

Real estate – construction | 569 | 7.6 | % | 741 | 6.6 | 558 | 7.2 | 494 | 5.9 | 214 | 5.1 | |||||||||||||||||||

Real estate – mortgage | 4,141 | 62.3 | % | 806 | 58.5 | 1,089 | 53.4 | 1,107 | 52.4 | 1,019 | 45.0 | |||||||||||||||||||

Consumer | 143 | 1.6 | % | 1,174 | 1.8 | 906 | 3.7 | 907 | 5.3 | 316 | 10.8 | |||||||||||||||||||

Unallocated | 358 | — | 631 | — | 461 | — | 666 | — | 650 | — | ||||||||||||||||||||

Total | $ | 7,402 | 100.0 | % | $ | 6,927 | 100.0 | % | $ | 6,670 | 100.0 | % | $ | 6,114 | 100.0 | % | $ | 4,928 | 100.0 | % | ||||||||||

NON-INTEREST INCOME

2005 Compared to 2004

Non-Interest Income for 2005 was down $1.549 million or 7.8% compared to 2004 which included a gain related to the sale of mortgage servicing rights (MSR’s) in March 2004. Exclusive of the gain on the sale of MSR’s, Total Non-Interest Income decreased $404 thousand or 2.2%. The most significant decline was in gain on sale of loans, down $1.298 million or 44.5% compared to 2004 as a result of the slow down in the mortgage refinance activity compounded by very competitive pricing pressures which also contributed to the reduction in the gain from year to year. Other fees and service charges were down $337 thousand or 17.9% also as a result of the MSR sale in March 2004 and a decline in volume of loans sold servicing retained from year to year. Service charges on deposit accounts decreased $234 thousand or 12.8% compared to 2004 as a result of higher earnings credits on commercial checking accounts and the industry trend toward “free” checking. Partially offsetting these decreases was an increase in fees for Wealth Management services of $1.236 million or 12.0% compared to the same time last year. The growth in Wealth Management services revenue was primarily the result of new business development, estate revenue and a fee increase in the second quarter of 2005. Wealth Management assets under management and administration increased $310 million or 16.0% to $2.248 billion at December 31, 2005 compared to $1.938 billion at December 31, 2004, partly a result of a business acquisition by a significant client in the third quarter of 2005.

2004 Compared to 2003

Non-Interest Income for 2004 was down $6.783 million or 25.5% compared to 2003. The largest decline was in gain on loan sales, down $7.730 million or 72.6% as a result of the slow down in the mortgage refinance market from 2003 to 2004. Loan sale volume was down $483.136 million or 76.9% to $144.916 million in 2004 from $628.052 million in 2003. Partially offsetting this decrease was an increase of $1.145 million in 2004 related to the sale of MSR’s in 2004. Also contributing to the overall decrease in Total Non-Interest Income in 2004 were other fees and service charges, down $541 thousand or 22.4% directly related to the decline in mortgage activity. Fees for Wealth Management services increased $567 thousand or 5.8% in 2004 compared to 2003. The growth in Wealth Management services revenue was primarily the result of new business fees and an increase in the market value of assets under management and administration in 2004. Wealth assets under management and administration increased $186 million or 10.6% from $1.752 billion at December 31, 2003 to $1.938 billion at December 31, 2004.

NON-INTEREST EXPENSE

2005 Compared to 2004

Non-Interest Expense for 2005 remained level compared to 2004, down $52 thousand or 0.2%. Exclusive of expenses associated with the sale of MSR’s in March 2004, Total Non-Interest Expenses increased $214 thousand or 0.7%. The largest growth was in salaries, up $849 thousand or 56.6% as a result of increased incentive compensation based on overall corporate profitability. Other increases included occupancy expense, up $111 thousand and furniture, fixtures and equipment expense, up $156 thousand both related to the Newtown Square branch added in 2004 and the new Exton branch added in 2005. Partially offsetting these increases were decreases in employee benefits primarily related to pension and post-retirement medical benefit expenses, professional fees, lower amortization of MSR’s and reduced residential mortgage staffing levels.

10

2004 Compared to 2003

Non-Interest Expense decreased $1.812 million or 5.4% in 2004 compared to 2003. The most significant decline was in amortization of MSR’s, down $1.975 million or 70.2% as well as other operating expenses, down $995 thousand or 17.0%. These decreases were both directly attributable to the 76.9% decline in volume of residential mortgage loans sold from year to year discussed above. The largest increase, partially offsetting these decreases, was professional fees, up $862 thousand in 2004 compared to 2003 as a result of increased fees associated with the required Sarbanes Oxley Act Section 404 compliance. Other significant increases included advertising expense, up $205 thousand or 30.4% and occupancy expense, up $200 thousand or 10.2% as a result of the new Newtown Square branch opened in 2004.

INCOME TAXES

Income taxes from operations for the year ended December 31, 2005 were $5.928 million compared to $4.752 million for the same period in 2004. This represents an effective tax rate for the year ended December 31, 2005 of 34.3% and an effective tax rate of 33.7% for the same period in 2004.

Income taxes from continuing operations for 2004 were $4.752 million compared to $6.049 million in 2003. This represents an effective tax rate of 33.7% for the year ended December 31, 2004 and an effective tax rate of 34.9% for the same period in 2003.

BALANCE SHEET ANALYSIS

Total assets increased $44.3 million or 6.5% from $682.9 million as of December 31, 2004 to $727.2 million as December 31, 2005. Total loans increased $33.3 million or 5.9% over the same time period from $564.6 million at December 31, 2004 to $597.9 million at December 31, 2005. Average assets increased $40.1 million or 6.2% to $682.9 million and average loans increased $43.6 million or 8.1% to $582.4 million, in 2005 compared to 2004. Although not reflected in quarter end totals (during the 2nd half of 2005), loan balances grew steadily during the year, as average quarterly loans outstanding was $549.2, $567.8, $578.1, $588.7 and $594.4 million during the 4th quarter of 2004, and the 1st, 2nd, 3rd and 4th quarters of 2005, respectively.