UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-05201

| Thornburg Investment Trust |

(Exact name of registrant as specified in charter)

c/o Thornburg Investment Management, Inc. 2300 North Ridgetop Road, Santa Fe, New Mexico 87506 |

(Address of principal executive offices) (Zip code)

| Garrett Thornburg, 2300 North Ridgetop Road, Santa Fe, New Mexico 87506 |

(Name and address of agent for service)

Registrant’s telephone number, including area code: 505-984-0200

Date of fiscal year end: September 30, 2011

Date of reporting period: September 30, 2011

Item 1. Reports to Stockholders

The following annual reports are attached hereto, in order:

Thornburg Limited Term Municipal Fund

Thornburg Intermediate Municipal Fund

Thornburg Strategic Municipal Income Fund

Thornburg California Limited Term Municipal Fund

Thornburg New Mexico Intermediate Municipal Fund

Thornburg New York Intermediate Municipal Fund

Thornburg Limited Term Income Funds

Thornburg Strategic Income Fund

Thornburg Value Fund

Thornburg International Value Fund

Thornburg Core Growth Fund

Thornburg International Growth Fund

Thornburg Investment Income Builder Fund

Thornburg Global Opportunities Fund

Thornburg Developing World Fund

Important Information

The information presented on the following pages is current as of September 30, 2011. The managers’ views, portfolio holdings, and sector diversification are provided for the general information of the Fund’s shareholders; to the extent this information is historical, it should not be considered predictive of future circumstances. This material should not be deemed a recommendation to buy or sell any of the securities mentioned.

Investments in the Fund carry risks, including possible loss of principal. Bond funds have the same interest rate, inflation, and credit risks that are associated with the underlying bonds. The principal value of bonds will fluctuate relative to changes in interest rates, decreasing when interest rates rise. Unlike bonds, bond funds have ongoing fees and expenses. Please see the Fund’s Prospectus for a discussion of the risks associated with an investment in the Fund. Investments in the Fund are not FDIC insured, nor are they deposits of or guaranteed by a bank or any other entity. There is no guarantee that the Fund will meet its investment objectives. The laddering strategy does not assure or guarantee better performance and cannot eliminate the risk of investment losses.

Performance data given at net asset value (NAV) does not take into account applicable sales charges. If the sales charges had been included, the performance would have been lower.

Minimum investments for Class I shares are higher than those for other classes. Class I shares may not be available to all investors.

Share Class | NASDAQ Symbol | Cusip | ||

Class A | LTMFX | 885-215-459 | ||

Class C | LTMCX | 885-215-442 | ||

Class I | LTMIX | 885-215-434 |

Lipper Fund Award 2011

Thornburg Limited Term Municipal Fund, Class I Shares, was granted a Lipper Fund Award for the ten-year period ended 12/31/10, among 22 Short-Intermediate Municipal Debt Funds. Lipper Fund Awards are granted annually to the fund in each Lipper classification that consistently delivered the strongest risk-adjusted performance (calculated with dividends reinvested). Awards are given for three-year, five-year, and ten-year periods. The fund did not win the award for other time periods. Past performance does not guarantee future results.

Glossary

Barclays Capital Five-Year Municipal Bond Index – A rules-based, market-value-weighted index of the tax-exempt bond market. To be included in the index, bonds must have a minimum credit rating of Baa. The approximate maturity of the municipal bonds in the index is five years.

Barclays Capital Municipal Bond Index – The Municipal Index covers the USD-denominated, investment-grade, long-term, tax-exempt bond market. The index has four main sectors: state and local general obligation bonds, revenue bonds, insured bonds, and prerefunded bonds.

BofA Merrill Lynch 1-10 Year U.S. Municipal Securities Index – A subset of the BofA Merrill Lynch U.S. Municipal Securities Index including all securities with a remaining term to final maturity less than 10 years.

Unless otherwise noted, index returns reflect the reinvestment of income dividends and capital gains, if any, but do not reflect fees, brokerage commissions or other expenses of investing. Investors may not make direct investments into any index.

Alternative Minimum Tax (AMT) – A federal tax aimed at ensuring that high-income individuals, estates, trusts, and corporations pay a minimal level income tax. For individuals, the AMT is calculated by adding tax preference items to regular taxable income.

Annualized Distribution Yield – The distribution yield is calculated by taking the sum of the month’s total distribution factors and dividing this sum by a 30-day period and annualizing to a 360-day year. The value is then divided by the ending maximum offering price per share to arrive at the annualized distribution yield. The yield is calculated on a periodic basis and is subject to change.

Basis Point (bps) – A unit equal to 1/100th of 1%. 1% = 100 basis points (bps).

Bond Credit Ratings – A bond credit rating assesses the financial ability of a debt issuer to make timely payments of principal and interest. Ratings of AAA (the highest), AA, A, and BBB are investment-grade quality. Ratings of BB, B, CCC, CC, C, and D (the lowest) are considered below investment grade, speculative grade, or junk bonds. Unless otherwise noted, the ratings listed are from Municipal Market Data and are a combination of ratings from Standard and Poor’s, Moody’s Investors Service, and Fitch Ratings.

Build America Bonds (BAB) – Taxable municipal bonds that feature tax credits and/or federal subsidies for bondholders and state and local government bond issuers. Build America Bonds (BABs) were introduced in 2009 as part of President Obama’s American Recovery and Reinvestment Act to create jobs and stimulate the economy. BABs attempt to achieve this by lowering the cost of borrowing for state and local governments in financing new projects.

Consumer Price Index (CPI) – An index that measures prices of a fixed basket of goods bought by a typical consumer, including food, transportation, shelter, utilities, clothing, medical care, entertainment and other items. The CPI, published by the Bureau of Labor Statistics in the Department of Labor, is based at 100 in 1982 and is released monthly. It is widely used as a cost-of-living benchmark to adjust Social Security payments and other payment schedules, union contracts and tax brackets. The CPI is also known as the cost-of-living index.

This page is not part of the Annual Report. 3

| Important Information, | ||

Continued | ||

Core CPI – Consumer Price Index minus the energy and food components.

Duration – A bond’s sensitivity to interest rates. Bonds with longer durations experience greater price volatility than bonds with shorter durations.

Effective Duration – A bond’s sensitivity to interest rates, incorporating the embedded option features, such as call provisions. Bonds with longer durations experience greater price volatility than bonds with shorter durations.

Fed Funds Rate – The interest rate at which a depository institution lends immediately available funds (balances at the Federal Reserve) to another depository institution overnight.

General Obligation Bond – A municipal bond backed by the credit and “taxing power” of the issuing jurisdiction rather than the revenue from a given project.

M2 – The amount of money in circulation in notes and coin plus non-interest-bearing bank deposits, building-society deposits, and National Savings accounts.

Operation Twist – A monetary policy where, in an attempt to lower long-term interest rates, the Fed sold short-term Treasury bonds and bought long-term Treasury bonds, which pressured the long-term bond yields downward.

Quantitative Easing – The Federal Reserve’s monetary policy used to stimulate the U.S. economy following the recession that began in 2007/08.

SEC Yield – SEC Yield is computed in accordance with SEC standards measuring the net investment income per share over a specified 30-day period expressed as a percentage of the maximum offering price of the Fund’s shares at the end of the period.

Treasuries – U.S. Treasury securities, such as bills, notes and bonds, are negotiable debt obligations of the U.S. government. These debt obligations are backed by the “full faith and credit” of the government and issued at various schedules and maturities. Income from Treasury securities is exempt from state and local, but not federal, taxes.

4 This page is not part of the Annual Report.

Thornburg Limited Term Municipal Fund

At Thornburg, our approach to management of the Fund is based on the premise that investors in the Fund seek preservation of capital along with an attractive, relatively stable yield. While aggressive bond strategies may generate stronger returns when the market is turning a blind eye towards risk, they often fail to stack up over longer periods of time.

We apply time-tested techniques to manage risk and provide attractive returns. These include:

| • | Building a laddered portfolio. Laddering has been shown over time to mitigate reinvestment and interest rate risk. |

| • | Investing on a cash-only basis without using leverage. While leveraged strategies may enhance returns when market conditions are favorable, they can quickly compound losses when sentiment shifts. |

| • | Conducting in-depth fundamental research on each issue and actively monitoring positions for subsequent credit events. |

| • | Diversifying among a large number of generally high-quality bonds. |

CO-PORTFOLIO MANAGERS

Josh Gonze, Chris Ryon,CFA, and Chris Ihlefeld

IMPORTANT

PERFORMANCE INFORMATION

Performance data shown represents past performance and is no guarantee of future results. Investment return and principal value will fluctuate so shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than quoted. For performance current to the most recent month end, visit thornburg.com or call 800.847.0200.

The maximum sales charge for the Fund’s Class A shares is 1.50% . The total annual fund operating expense of Class A shares is 0.78%, as disclosed in the most recent Prospectus.

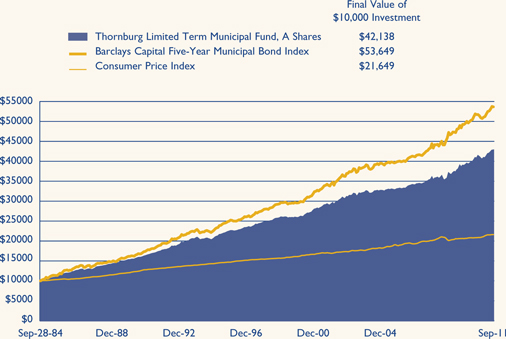

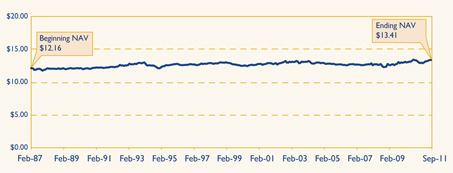

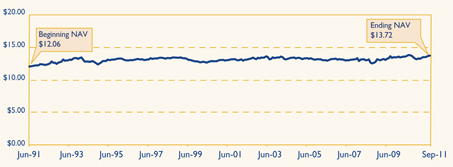

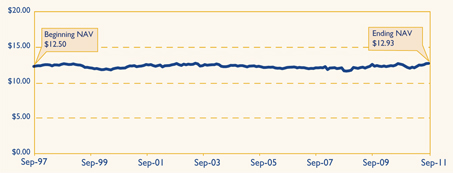

LONG-TERM STABILITY OF PRINCIPAL

Net asset value history of A shares from September 28, 1984 through September 30, 2011

AVERAGE ANNUAL TOTAL RETURNS

For periods ended September 30, 2011

| 1 Yr | 3 Yrs | 5 Yrs | 10 Yrs | Since Inception | ||||||||||||||||

A Shares (Incep: 9/28/84) | ||||||||||||||||||||

Without sales charge | 3.43 | % | 5.90 | % | 4.47 | % | 3.78 | % | 5.53 | % | ||||||||||

With sales charge | 1.86 | % | 5.37 | % | 4.15 | % | 3.62 | % | 5.47 | % | ||||||||||

30-DAY YIELDS, A SHARES

As of September 30, 2011

Annualized Distribution Yield | SEC Yield | |||

2.39% | 1.39 | % | ||

KEY PORTFOLIO ATTRIBUTES

As of September 30, 2011

Number of Bonds | 1,235 | |||

Effective Duration | 3.7 Yrs | |||

Average Maturity | 4.4 Yrs | |||

See the entire portfolio in the Schedule of Investments beginning on page 11.

This page is not part of the Annual Report. 5

Thornburg Limited Term Municipal Fund

September 30, 2011

Table of Contents | ||||

| 7 | ||||

| 11 | ||||

| 42 | ||||

| 43 | ||||

| 44 | ||||

| 45 | ||||

| 50 | ||||

| 52 | ||||

| 53 | ||||

| 54 | ||||

| 55 | ||||

| 58 |

This report is certified under the Sarbanes-Oxley Act of 2002, which requires that public companies, including mutual funds, affirm that the information provided in their annual and semiannual shareholder reports fully and fairly represents their financial position.

6 Certified Annual Report

Christopher Ihlefeld Co-Portfolio Manager

Christopher Ryon,CFA Co-Portfolio Manager

Josh Gonze Co-Portfolio Manager | October 14, 2011

Dear Fellow Shareholder:

We are pleased to present the annual report for the Thornburg Limited Term Municipal Fund. The net asset value (NAV) of the Class A shares increased by 12 cents to $14.39 per share for the fiscal year ended September 30, 2011. If you were with us for the entire period, you received dividends of 35.8 cents per share. If you reinvested your dividends, you received 36.2 cents per share. Dividends per share were lower for Class C shares and higher for Class I shares to account for varying class-specific expenses. The Class A shares of your Fund produced a total return of 3.43% at NAV over the fiscal year ended September 30, 2011, compared to 3.75% for the Barclays Capital Five-Year Municipal Bond Index. The main contributor to the difference in performance is that the Barclays Capital Five-Year Municipal Bond Index has all of its holdings in four- to six-year maturities. The Thornburg Limited Term Municipal Fund has holdings that span one- to ten-year maturities in a laddered structure.

The Economy and the Federal Reserve (the Fed)

As we started the fiscal year, beginning in October 2010, the Federal Reserve Board announced a new wrinkle to its already accommodative stance toward monetary policy. “Quantitative Easing” is a policy of buying bonds and other assets to boost demand and fight off deflation. As we close this fiscal year, the Fed has announced another extraordinary measure known as “Operation Twist.” This policy enhancement calls for the Fed to purchase, by the end of June 2012, $400 billion of Treasury securities with remaining maturities from 6 to 30 years and to sell an equal amount of Treasury securities with remaining maturities of 3 years or less. This is intended to cause the yield curve (a representation of the prevailing yields of Treasury securities by maturity) to flatten, reducing the yield difference between long-term and short-term Treasury securities. A typical measure of this phenomenon is the difference between the yield of a 10-year Treasury security and the yield of a 30-year Treasury security. The difference in yield between these two securities was 1.38% on September 1, 2011 (30-year Treasury securities yielded 1.38% more than 10-year Treasury securities). The formal announcement of the Fed’s new policy directive was on September 21, 2011, and by September 30, 2011, the difference had narrowed to 1.02%. The above change in the relationship between 10-year and 30-year Treasury securities means that longer maturity Treasury securities outperformed shorter maturity Treasury securities.

The Federal Open Market Committee, in its September 21, 2011 release, stated that “economic growth remains slow” and that there are “significant downside risks to the economic outlook, including strains in global financial markets.” These concerns explain why Treasury yields are lower by 0.17% to 1.59% since March 31, 2011. Longer maturity Treasury securities have |

Certified Annual Report 7

| Letter to Shareholders, | ||

Continued | ||

decreased in yield more than shorter maturity Treasury securities. The “strains in the global financial markets,” have led the Treasury market to experience a “flight to quality” in spite of a downgrade to AA+ by Standard and Poor’s on August 5, 2011. As one of our colleagues has stated, “the world views Treasury securities as the best house in a bad neighborhood.”

We share the Fed’s view that “economic growth remains low,” but there are some reasons for hope. June 2011 gross domestic product (GDP), a measure of a country’s overall economic output, recorded a 1.3% increase, higher than the 0.4% increase recorded in March of 2011. Capacity utilization, a measure of an economy’s usage of its productive resources, was running at 77.4% for the month ended August 31, 2011, slightly higher than the 75.7% recorded on September 30, 2011. Money supply as measured by M2, a broad measure of money and money substitutes, remains elevated. The velocity of M2, a measure of the rate at which money in circulation is used in transactions, continues to decline. Typically rising money supply is viewed as an inflationary threat, as long as velocity remains constant or increases. The combination of rising money supply and decreasing velocity is not inflationary. The one significant difference between this fiscal year end and last fiscal year end is that commercial and industrial loans and leases (loans to corporations, commercial enterprises, and joint ventures) have begun to increase, from a very low base. These loans have increased 7.98% over the 12 months ended September 30, 2011 versus a 10.57% decline for the 12 months ended September 30, 2010. These increases in loans to businesses may be laying the groundwork for a more robust expansion.

The employment picture is still a major concern; with so many Americans either unemployed or underemployed, it’s hard to fathom where demand for goods and services will come from. The unemployment rate is 9.1%, lower than the 9.8% registered in November 2010. In the 12 months ended September 2011, 1.49 million jobs have been created versus the 118,000 lost in the prior 12 months.

The economic picture is not as bleak as some in the media would paint it. The risks of a double-dip recession seem low, but so do the probabilities of a robust recovery. Our outlook for interest rates is much the same as it was last year with one exception; over the next 6–12 months, we believe the Fed will keep short-term interest rates low but long-term interest rates have and may continue to benefit from Operation Twist. Investors should ready themselves for increased periods of volatility as some of the exogenous forces impacting the United States play themselves out.

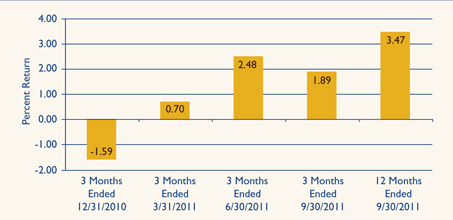

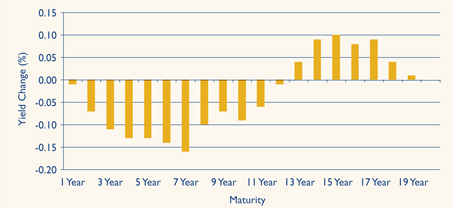

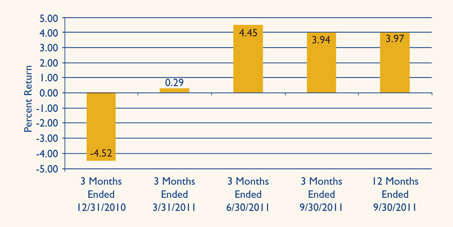

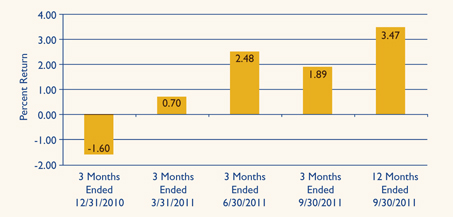

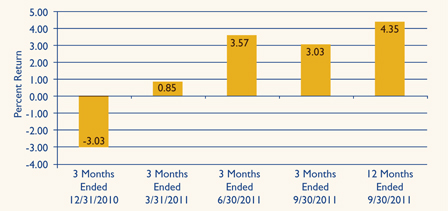

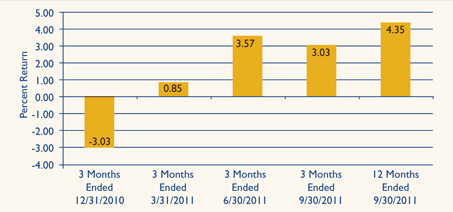

CHART I: BofA MERRILL LYNCH 1-10 YEAR MUNICIPAL INDEX

Periodic Returns During the Period from 9/30/2010 through 9/30/2011

Source: Bloomberg

Past performance does not guarantee future results.

The Municipal Market

The calendar year began with various predictions of numerous defaults in the municipal bond market; the term “hundreds of billions of dollars” was used. For the nine

8 Certified Annual Report

months ended September 30, 2011, the municipal bond market experienced $1.1 billion in defaults, a relatively small amount. This means, if one uses $200 billion as the low end of the estimate, we have only $198.9 billion to go by December 31, 2011 for these dire predictions to be achieved. These estimates were overly dramatic but they did add to the volatility of returns experienced throughout fiscal 2011. Chart I shows the volatility of returns generated by the BofA Merrill Lynch 1–10 Year Municipal Index for the 12 months ended September 30, 2011.

Most, if not all, of the other predictions of doom proved equally false. Supply of new issue municipal bonds did not expand as the Build America Bond program expired on December 31, 2010. In fact, the supply of newly issued municipal debt is down 35% through September 30, 2011 versus the same period in 2010. On the credit side, the revenue picture for state and local governments is improving. Revenues are increasing, although they are still below peak levels. Also expenditures are being cut. One example of this is that state and local employment payrolls have been cut by in excess of 500,000 jobs nationwide since August 2008.

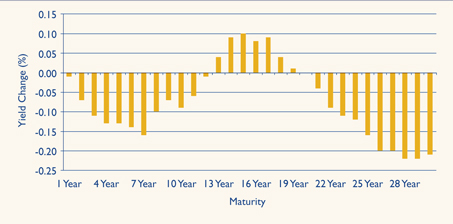

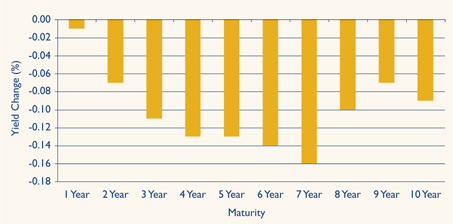

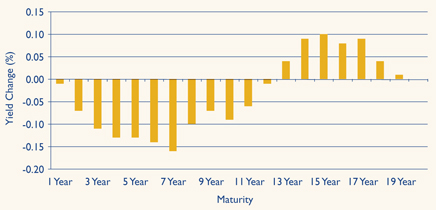

Chart II illustrates how yields have changed over the last 12 months. The largest declines occurred in the mid-range of Limited Term Fund’s investable universe. The general level of municipal bond yields appear to be moving in sympathy with the yields on Treasury securities, albeit at a different pace.

The major drivers of returns for the fiscal year have been duration (longer is better than shorter as rates declined) and yield curve exposure (allocation of assets to mid-range maturities versus shorter and longer maturities is better). The discipline of the laddered portfolio structure seeks to ensure that investors benefit from these opportunities.

Conclusion

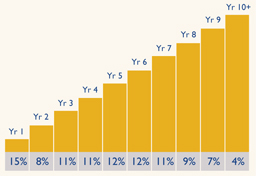

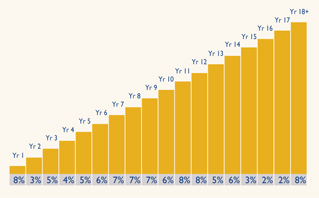

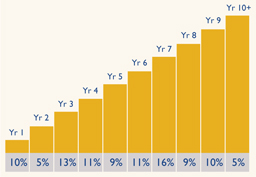

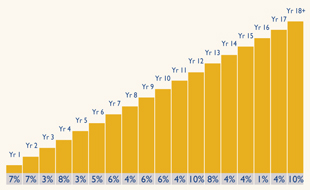

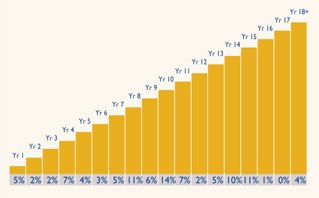

Your Thornburg Limited Term Municipal Fund is a laddered portfolio of 1,235 municipal obligations from 49 states and territories. We ladder the maturity dates of the bonds in your portfolio so that some of the bonds are scheduled to mature during each of the coming years. Laddering short and intermediate bonds accomplishes two goals. First, the staggered bond maturities contained in a ladder reduce interest-rate risk and dampen the Fund’s price volatility. Second, laddering reduces reinvestment risk by giving the Fund a steady cash flow stream from maturing bonds to reinvest

CHART II: CHANGES IN AAA GENERAL OBLIGATION BOND YIELDS

9/30/2010 through 9/30/2011

Source: Standard and Poor’s 09/30/2011

Past performance does not guarantee future results.

Certified Annual Report 9

| Letter to Shareholders, | ||

Continued | ||

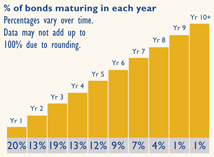

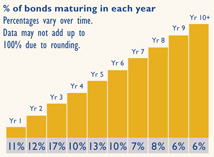

toward the top of the ladder where yields are typically higher. Chart III describes the percentages of your Fund’s bond portfolio maturing in each of the coming years. The Fund’s adherence to the discipline of the laddered structure served investors well.

We plan to continue to search for opportunities in the municipal market, using our fundamental, bottom-up approach to portfolio management, and the discipline of the laddered structure. In closing, we would like to thank you for the trust you have placed with us. We continue to keep that foremost in our minds as we go forward into a new year.

CHART III: % OF PORTFOLIO MATURING

As of 9/30/11. Percentages vary over time.

Data may not add up to 100% due to rounding.

Sincerely,

|  |  | ||

| Christopher Ihlefeld | Christopher Ryon,CFA | Josh Gonze | ||

| Co-Portfolio Manager | Co-Portfolio Manager | Co-Portfolio Manager | ||

| Managing Director | Managing Director | Managing Director |

The matters discussed in this report may constitute forward-looking statements made pursuant to the safe harbor provisions of the Securities Litigation Reform Act of 1995. These include any advisor or portfolio manager prediction, assessment, analysis or outlook for individual securities, industries, investment styles, market sectors and/or markets. These statements involve risks and uncertainties. In addition to the general risks described for each fund in its current prospectus, other factors bearing on these reports include the accuracy of the advisor’s or portfolio manager’s forecasts and predictions, the appropriateness of the investment strategies designed by the advisor or portfolio manager and the ability of the advisor or portfolio manager to implement their strategies efficiently and successfully. Any one or more of these factors, as well as other risks affecting the securities markets generally, could cause the actual results of any fund to differ materially as compared to its benchmarks.

10 Certified Annual Report

| SCHEDULE OF INVESTMENTS | ||

| Thornburg Limited Term Municipal Fund | September 30, 2011 | |

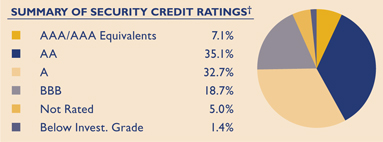

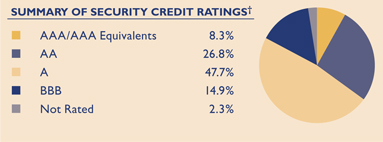

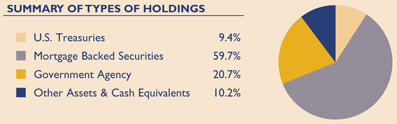

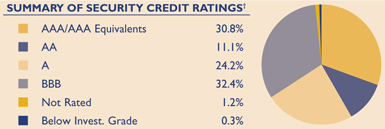

We have used ratings from Standard & Poor’s (S&P). Where S&P ratings are not available, we have used Moody’s Investors Service. Where neither rating is available, we have used ratings from Fitch Ratings. The category of investments identified as “AAA” in this graph includes investments which are pre-refunded or escrowed to maturity. Such investments are backed by an escrow or trust containing sufficient U.S. Government or U.S. Government agency securities to satisfy the timely payment of principal and interest and, therefore, are normally deemed to be equivalent to AAA-rated securities.

Issuer-Description | Credit Rating† S&P/ Moody’s | Principal Amount | Value | |||||||

ALABAMA — 1.91% | ||||||||||

Alabama State Public School & College Authority, 5.00% due 5/1/2012 | AA/Aa1 | $ | 2,000,000 | $ | 2,055,240 | |||||

Alabama State Public School & College Authority, 5.00% due 5/1/2013 | AA/Aa1 | 5,000,000 | 5,354,150 | |||||||

Alabama State Public School & College Authority, 5.00% due 5/1/2015 | NR/Aa1 | 8,530,000 | 9,775,721 | |||||||

Alabama State Public School & College Authority, 5.00% due 5/1/2016 | AA/Aa1 | 5,000,000 | 5,843,600 | |||||||

Birmingham GO, 5.00% due 10/1/2013 (Insured: Natl-Re) | AA/Aa2 | 2,500,000 | 2,705,600 | |||||||

Birmingham GO, 5.00% due 2/1/2015 | AA/Aa2 | 4,240,000 | 4,738,539 | |||||||

Birmingham GO, 4.00% due 8/1/2015 | AA/Aa2 | 3,005,000 | 3,290,355 | |||||||

Birmingham GO, 5.00% due 2/1/2016 | AA/Aa2 | 3,775,000 | 4,291,344 | |||||||

Birmingham GO, 4.00% due 8/1/2016 | AA/Aa2 | 3,645,000 | 3,977,971 | |||||||

Birmingham GO, 5.00% due 2/1/2017 | AA/Aa2 | 2,045,000 | 2,349,521 | |||||||

Birmingham GO, 4.00% due 8/1/2017 | AA/Aa2 | 2,760,000 | 2,997,526 | |||||||

Birmingham GO, 5.00% due 2/1/2018 | AA/Aa2 | 2,000,000 | 2,321,620 | |||||||

Courtland Solid Waste Disposal Revenue, 4.75% due 5/1/2017 (International Paper Company) | BBB/NR | 5,000,000 | 5,090,950 | |||||||

Huntsville GO, 5.50% due 11/1/2014 pre-refunded 5/1/2012 | AAA/Aaa | 3,425,000 | 3,599,058 | |||||||

Lake Martin Area IDA, 5.00% due 11/1/2011 | NR/NR | 3,000,000 | 3,006,720 | |||||||

Mobile GO Warrants, 5.25% due 8/1/2012 (Insured: AGM) | AA+/Aa2 | 1,025,000 | 1,067,230 | |||||||

Mobile GO Warrants, 4.50% due 8/15/2016 | NR/NR | 1,735,000 | 1,808,096 | |||||||

Mobile GO Warrants, 5.00% due 2/15/2019 | AA-/Aa2 | 2,000,000 | 2,274,460 | |||||||

Mobile Industrial Development PCR, 5.00% due 6/1/2034 put 3/19/2015 (Alabama Power Co.) | A/A2 | 6,000,000 | 6,733,080 | |||||||

Montgomery Waterworks & Sanitation, 5.00% due 9/1/2016 | AAA/Aa2 | 2,080,000 | 2,441,878 | |||||||

Montgomery Waterworks & Sanitation, 5.00% due 9/1/2019 | AAA/Aa2 | 3,375,000 | 3,939,030 | |||||||

University of Alabama at Birmingham Hospital Revenue, 5.25% due 9/1/2017 | A+/A1 | 2,500,000 | 2,831,475 | |||||||

University of Alabama at Birmingham Hospital Revenue, 5.00% due 9/1/2018 | A+/A1 | 1,500,000 | 1,679,205 | |||||||

ALASKA — 0.78% | ||||||||||

Alaska Energy Power Authority, 6.00% due 7/1/2013 (Bradley Lake Hydroelectric; Insured: AGM) | AA+/Aa2 | 1,600,000 | 1,728,992 | |||||||

Alaska Housing Finance Corp. GO, 5.00% due 12/1/2018 (Insured: Natl-Re) | AA+/Aa2 | 2,000,000 | 2,306,520 | |||||||

Alaska Industrial Development & Export Authority GO, 5.00% due 4/1/2014 | AA-/Aa3 | 2,000,000 | 2,184,900 | |||||||

Alaska Industrial Development & Export Authority GO, 5.00% due 4/1/2015 | AA-/Aa3 | 1,900,000 | 2,132,883 | |||||||

Alaska Industrial Development & Export Authority GO, 5.00% due 4/1/2016 | AA-/Aa3 | 1,000,000 | 1,140,740 | |||||||

Alaska Industrial Development & Export Authority GO, 5.00% due 4/1/2017 | AA-/Aa3 | 3,000,000 | 3,456,630 | |||||||

Alaska Industrial Development & Export Authority GO, 5.00% due 4/1/2018 | AA-/Aa3 | 2,455,000 | 2,848,095 | |||||||

Alaska Municipal Bond Bank, 5.00% due 6/1/2014 (Insured: Natl-Re) (State Aid Withholding) | A+/Aa2 | �� | 1,175,000 | 1,291,419 | ||||||

Alaska Student Loan Corp., 5.25% due 1/1/2012 (Insured: AGM) | AA+/NR | 3,000,000 | 3,034,230 | |||||||

North Slope Boro GO, 5.00% due 6/30/2015 (Insured: Natl-Re) | AA-/Aa3 | 3,250,000 | 3,740,230 | |||||||

North Slope Boro GO, 5.00% due 6/30/2017 (Insured: Natl-Re) | AA-/Aa3 | 8,800,000 | 10,427,032 | |||||||

ARIZONA — 3.45% | ||||||||||

Arizona Board of Regents COP, 5.00% due 7/1/2018 (Arizona State University; Insured: Natl-Re) | AA-/A1 | 1,285,000 | 1,439,637 | |||||||

Certified Annual Report 11

| SCHEDULE OF INVESTMENTS, CONTINUED | ||

| Thornburg Limited Term Municipal Fund | September 30, 2011 | |

Issuer-Description | Credit Rating† S&P/ Moody’s | Principal Amount | Value | |||||||

Arizona Board of Regents COP, 5.00% due 7/1/2019 (Arizona State University; Insured: Natl-Re) | AA-/A1 | $ | 3,735,000 | $ | 4,145,588 | |||||

Arizona HFA, 5.25% due 1/1/2018 (Banner Health) | AA-/NR | 3,500,000 | 4,069,205 | |||||||

Arizona HFA, 5.00% due 7/1/2018 (Catholic Health Care West) | A/A2 | 1,470,000 | 1,633,729 | |||||||

Arizona HFA, 5.00% due 7/1/2019 (Catholic Health Care West) | A/A2 | 1,365,000 | 1,509,731 | |||||||

Arizona HFA, 5.00% due 7/1/2020 (Catholic Health Care West) | A/A2 | 1,290,000 | 1,416,652 | |||||||

Arizona Lottery Revenue, 5.00% due 7/1/2018 (Insured: AGM) | AA+/Aa3 | 8,370,000 | 9,738,746 | |||||||

Arizona Lottery Revenue, 5.00% due 7/1/2020 (Insured: AGM) | AA+/Aa3 | 8,000,000 | 9,246,640 | |||||||

Arizona Transportation Board Highway Revenue, 5.25% due 7/1/2015 | AAA/Aa1 | 3,860,000 | 4,072,339 | |||||||

Chandler Street & Highway User Revenue, 3.00% due 7/1/2013 | AA/Aa2 | 1,905,000 | 1,984,248 | |||||||

Chandler Street & Highway User Revenue, 3.00% due 7/1/2014 | AA/Aa2 | 2,790,000 | 2,954,415 | |||||||

Gilbert Public Facilities Municipal Property Refunding, 3.00% due 7/1/2015 | AA/Aa2 | 1,080,000 | 1,148,245 | |||||||

Glendale IDA, 5.00% due 5/15/2015 (Midwestern University) | A-/NR | 1,000,000 | 1,100,800 | |||||||

Glendale IDA, 5.00% due 5/15/2016 (Midwestern University) | A-/NR | 1,325,000 | 1,480,462 | |||||||

Glendale IDA, 5.00% due 5/15/2017 (Midwestern University) | A-/NR | 1,440,000 | 1,618,920 | |||||||

Glendale Western Loop 101 Public Facilities Corp., 6.00% due 7/1/2019 | AA/A2 | 2,200,000 | 2,330,262 | |||||||

Maricopa County IDA Health Facilities Revenue, 4.125% due 7/1/2015 (Catholic Health Care West) | A/A2 | 1,000,000 | 1,064,490 | |||||||

Maricopa County IDA Health Facilities Revenue, 5.00% due 7/1/2038 put 7/1/2014 (Catholic Health Care West) | A/A2 | 7,500,000 | 8,190,225 | |||||||

Maricopa County Pollution Control Corp. PCR, 5.50% due 5/1/2029 put 5/1/2012 (Arizona Public Service Co.) | BBB/Baa2 | 10,000,000 | 10,227,800 | |||||||

Mesa Highway GO, 3.25% due 7/1/2016 | AA+/Aa3 | 10,000,000 | 10,493,600 | |||||||

Mohave County IDA, 5.00% due 4/1/2014 (Mohave Prison LLC) (ETM) | AA+/NR | 3,135,000 | 3,480,446 | |||||||

Mohave County IDA, 7.25% due 5/1/2015 (Mohave Prison LLC) | BBB+/NR | 12,100,000 | 12,530,276 | |||||||

Navajo County PCR, 5.50% due 6/1/2034 put 6/1/2014 (Arizona Public Service Co.) | BBB/Baa2 | 1,600,000 | 1,733,856 | |||||||

Navajo County PCR, 5.50% due 6/1/2034 put 6/1/2014 (Arizona Public Service Co.) | BBB/Baa2 | 2,600,000 | 2,817,516 | |||||||

Navajo County PCR, 5.75% due 6/1/2034 put 6/1/2016 (Arizona Public Service Co.) | BBB/Baa2 | 5,600,000 | 6,338,584 | |||||||

Northern Arizona University COP, 5.00% due 9/1/2019 (Insured: AMBAC) | A/A2 | 3,500,000 | 3,651,305 | |||||||

Pima County IDA, 6.40% due 7/1/2013 (Arizona Charter Schools) | NR/Baa3 | 410,000 | 411,591 | |||||||

Pima County IDA, 5.00% due 7/1/2016 (Metro Police Facility) | AA/Aa3 | 2,500,000 | 2,792,600 | |||||||

Pima County IDA, 5.00% due 7/1/2017 (Metro Police Facility) | AA/Aa3 | 3,000,000 | 3,366,960 | |||||||

Pima County IDA, 5.00% due 7/1/2018 (Metro Police Facility) | AA/Aa3 | 3,285,000 | 3,688,037 | |||||||

Pima County IDA, 5.00% due 7/1/2019 (Metro Police Facility) | AA/Aa3 | 2,000,000 | 2,232,260 | |||||||

Pima County Sewer Revenue, 4.50% due 7/1/2017 (Insured: AGM) | AA+/Aa3 | 5,000,000 | 5,708,050 | |||||||

Pima County Sewer Revenue, 5.00% due 7/1/2018 (Insured: AGM) | AA+/Aa3 | 5,000,000 | 5,870,450 | |||||||

Salt River Agricultural Improvement & Power District, 3.00% due 1/1/2014 | AA/Aa1 | 11,275,000 | 11,895,125 | |||||||

University Arizona Medical Center Corp. GO, 5.00% due 7/1/2014 | BBB+/Baa1 | 1,000,000 | 1,064,420 | |||||||

Yuma Property Corp. Utility Systems Revenue, 5.00% due 7/1/2016 (Insured: Syncora) | A+/A1 | 2,000,000 | 2,254,700 | |||||||

Yuma Property Corp. Utility Systems Revenue, 5.00% due 7/1/2018 (Insured: Syncora) | A+/A1 | 2,130,000 | 2,381,510 | |||||||

CALIFORNIA — 7.92% | ||||||||||

Alameda County COP, 5.00% due 12/1/2017 (Santa Rita Jail; Insured: AMBAC) | AA/NR | 1,000,000 | 1,157,550 | |||||||

Anaheim Public Financing Authority, 5.25% due 10/1/2018 (Electric Systems Generation; Insured: AGM) | AA+/Aa3 | 1,560,000 | 1,624,709 | |||||||

Calexico USD COP, 5.75% due 9/1/2013 | A-/NR | 1,155,000 | 1,214,598 | |||||||

California Educational Facilities, 5.00% due 4/1/2017 (Pitzer College) | NR/A3 | 1,460,000 | 1,643,361 | |||||||

aCalifornia Educational Facilities, 5.00% due 4/1/2021 (Chapman | NR/A2 | 4,870,000 | 5,433,264 | |||||||

California GO, 4.75% due 4/1/2018 | A-/A1 | 1,250,000 | 1,424,513 | |||||||

California GO, 5.00% due 9/1/2020 | NR/NR | 10,000,000 | 11,534,500 | |||||||

California GO, 5.00% due 9/1/2021 | A-/A1 | 5,000,000 | 5,756,450 | |||||||

California GO, 0.13% due 5/1/2034 put 10/3/2011 (LOC: Citibank N.A./California State Teachers’ Retirement System) (daily demand notes) | A+/Aa3 | 2,970,000 | 2,970,000 | |||||||

California HFA, 5.50% due 2/1/2017 (Community Program; Insured: California Mtg Insurance) | A-/NR | 2,575,000 | 2,867,031 | |||||||

12 Certified Annual Report

| SCHEDULE OF INVESTMENTS, CONTINUED | ||

| Thornburg Limited Term Municipal Fund | September 30, 2011 | |

Issuer-Description | Credit Rating† S&P/ Moody’s | Principal Amount | Value | |||||||

California HFA, 5.50% due 2/1/2019 (Community Program; Insured: California Mtg Insurance) | A-/NR | $ | 2,865,000 | $ | 3,192,756 | |||||

California HFA, 5.75% due 2/1/2020 (Community Program; Insured: California Mtg Insurance) | A-/NR | 1,975,000 | 2,232,342 | |||||||

California HFA, 5.75% due 2/1/2021 (Community Program; Insured: California Mtg Insurance) | A-/NR | 1,695,000 | 1,913,825 | |||||||

California HFA, 5.00% due 7/1/2027 put 7/1/2014 (Catholic Health Care West) | A/A2 | 3,500,000 | 3,804,325 | |||||||

California HFA, 5.00% due 7/1/2028 put 7/1/2014 (Catholic Health Care West) | A/A2 | 2,000,000 | 2,173,900 | |||||||

California State Department of Transportation COP, 5.25% due 3/1/2016 (Insured: Natl-Re) | BBB/A2 | 1,000,000 | 1,003,810 | |||||||

California State Department of Water Resources Power Supply, 5.50% due 5/1/2012 | AA-/Aa3 | 2,600,000 | 2,679,638 | |||||||

California State Department of Water Resources Power Supply, 6.00% due 5/1/2013 pre-refunded 5/1/2012 | AA-/Aa3 | 2,550,000 | 2,661,435 | |||||||

California State Department of Water Resources Power Supply, 5.00% due 5/1/2015 | AA-/Aa3 | 5,000,000 | 5,727,500 | |||||||

California State Department of Water Resources Power Supply, 5.00% due 5/1/2016 | AA-/Aa3 | 5,000,000 | 5,807,450 | |||||||

California State Economic Recovery GO, 5.00% due 7/1/2020 | A+/Aa3 | 4,200,000 | 4,884,264 | |||||||

California State Economic Recovery GO, 5.00% due 7/1/2016 | A+/Aa3 | 10,350,000 | 10,387,260 | |||||||

California State Economic Recovery GO, 5.00% due 7/1/2018 | A+/Aa3 | 4,000,000 | 4,710,360 | |||||||

California State Public Works Board, 5.00% due 9/1/2016 (Regents of University of California; Insured: Natl-Re/FGIC) | AA-/Aa2 | 3,000,000 | 3,472,950 | |||||||

California State Public Works Board, 5.00% due 9/1/2017 (Regents of University of California; Insured: Natl-Re/FGIC) | AA-/Aa2 | 3,000,000 | 3,512,820 | |||||||

California State Public Works Board, 5.00% due 11/1/2017 (California State University Trustees) | BBB+/Aa3 | 3,000,000 | 3,406,410 | |||||||

California State Public Works Board, 5.00% due 11/1/2018 (California State University Trustees) | BBB+/Aa3 | 2,700,000 | 3,058,560 | |||||||

California Statewide Community Development Authority, 5.00% due 6/15/2013 | A-/A1 | 9,500,000 | 10,157,495 | |||||||

California Statewide Community Development Authority, 5.00% due 5/15/2017 (Irvine LLC- UCI East Campus) | NR/Baa2 | 2,200,000 | 2,318,800 | |||||||

California Statewide Community Development Authority, 5.00% due 4/1/2019 (Kaiser Credit Group) | A+/NR | 27,000,000 | 31,491,180 | |||||||

California Statewide Community Development Authority, 5.00% due 7/1/2020 (Aspire Public Schools; Insured: College for Certain LLC) | NR/NR | 2,000,000 | 1,972,000 | |||||||

California Statewide Community Development Authority PCR, 4.10% due 4/1/2028 put 4/1/2013 (Southern California Edison Co.; Insured: Syncora) | A/A1 | 1,000,000 | 1,044,970 | |||||||

Castaic USD GO, 0% due 5/1/2018 (Insured: Natl-Re/FGIC) | A+/NR | 7,000,000 | 5,320,420 | |||||||

Centinela Valley Unified High School District GO, 4.00% due 12/1/2013 | SP-1+/NR | 5,665,000 | 5,950,573 | |||||||

Central Valley Financing Authority, 5.00% due 7/1/2017 (Carson Ice) | A+/A1 | 600,000 | 682,644 | |||||||

Central Valley Financing Authority, 5.00% due 7/1/2019 (Carson Ice) | A+/A1 | 1,750,000 | 1,995,612 | |||||||

Chula Vista COP, 5.25% due 3/1/2018 | A-/NR | 1,170,000 | 1,302,842 | |||||||

Chula Vista COP, 5.25% due 3/1/2019 | A-/NR | 1,235,000 | 1,369,245 | |||||||

Clovis USD GO, 0% due 8/1/2019 (Insured: Natl-Re/FGIC) | AA/NR | 2,685,000 | 1,978,174 | |||||||

Golden State Tobacco Securitization Corp., 5.50% due 6/1/2043 pre-refunded 6/1/2013 | AA+/Aaa | 2,000,000 | 2,168,380 | |||||||

Inland Valley Development Agency, 5.25% due 4/1/2013 (ETM) | A/NR | 2,000,000 | 2,143,000 | |||||||

Inland Valley Development Agency, 5.50% due 4/1/2014 (ETM) | A/NR | 2,000,000 | 2,245,200 | |||||||

Inland Valley Development Agency, 4.50% due 3/1/2041 put 3/1/2016 | A/NR | 8,000,000 | 8,415,120 | |||||||

Irvine USD, 5.25% due 9/1/2017 (Community Facilities District 86; | AA+/NR | 5,000,000 | 5,710,700 | |||||||

Irvine USD, 5.25% due 9/1/2018 (Community Facilities District 86; Insured: AGM) | AA+/NR | 3,000,000 | 3,432,990 | |||||||

Irvine USD, 5.25% due 9/1/2019 (Community Facilities District 86; Insured: AGM) | AA+/NR | 3,000,000 | 3,413,670 | |||||||

Kern Community College District COP, 4.00% due 4/1/2014 | SP-1+/NR | 2,000,000 | 2,074,820 | |||||||

Los Angeles Convention & Exhibition Center Authority, 5.00% due 8/15/2018 | A+/A2 | 2,095,000 | 2,334,060 | |||||||

Los Angeles County Public Works Financing Authority, 5.00% due 8/1/2019 (Multiple Capital Projects) | A+/A1 | 8,260,000 | 9,574,414 | |||||||

Los Angeles County Public Works Financing Authority, 5.00% due 8/1/2018 (Multiple Capital Projects) | A+/A1 | 4,000,000 | 4,647,600 | |||||||

Los Angeles USD COP, 5.00% due 10/1/2017 (Insured: AMBAC) | A+/A1 | 2,445,000 | 2,716,468 | |||||||

Los Angeles USD COP, 5.50% due 12/1/2018 (Capital Projects) | A+/A1 | 4,600,000 | 5,238,664 | |||||||

Los Angeles USD COP, 5.50% due 12/1/2019 | A+/A1 | 7,040,000 | 7,989,766 | |||||||

Los Angeles USD GO, 5.00% due 7/1/2018 (Insured: AGM) | AA+/Aa2 | 4,000,000 | 4,650,080 | |||||||

Monterey County COP, 5.00% due 8/1/2016 (Insured: AGM) | AA+/Aa3 | 1,435,000 | 1,614,963 | |||||||

Certified Annual Report 13

| SCHEDULE OF INVESTMENTS, CONTINUED | ||

| Thornburg Limited Term Municipal Fund | September 30, 2011 | |

Issuer-Description | Credit Rating† S&P/ Moody’s | Principal Amount | Value | |||||||

Monterey County COP, 5.00% due 8/1/2018 (Insured: AGM) | AA+/Aa3 | $ | 2,260,000 | $ | 2,558,297 | |||||

Mount San Antonio Community College GO, 0% due 8/1/2017 (Insured: Natl-Re) | AA/Aa2 | 5,000,000 | 4,216,900 | |||||||

Newport Beach Revenue, 5.00% due 12/1/2038 put 2/7/2013 (Hoag Memorial Hospital) | AA/Aa3 | 3,000,000 | 3,177,810 | |||||||

Northern California Power Agency Revenue, 5.00% due 7/1/2017 | A/A2 | 1,000,000 | 1,171,120 | |||||||

Northern California Power Agency Revenue, 5.00% due 6/1/2018 (Lodi Energy Center) | A-/A3 | 4,480,000 | 5,207,552 | |||||||

Northern California Power Agency Revenue, 5.00% due 7/1/2019 | A/A2 | 1,000,000 | 1,177,480 | |||||||

Northern California Power Agency Revenue, 5.00% due 7/1/2020 | A/A2 | 1,325,000 | 1,528,321 | |||||||

Orange County Public Financing Authority, 5.00% due 7/1/2017 (Insured: Natl-Re) | A+/Aa3 | 1,245,000 | 1,452,131 | |||||||

Palo Alto USD GO, 0% due 8/1/2019 | AAA/Aa1 | 1,000,000 | 773,950 | |||||||

Palomar Community College Capital Appreciation GO, 0% due 8/1/2021 | AA-/Aa2 | 2,560,000 | 1,630,080 | |||||||

Pittsburgh Redevelopment Agency, 5.00% due 8/1/2012 (Los Medanos Community Development; Insured: Natl-Re) | A+/Baa1 | 1,255,000 | 1,281,468 | |||||||

Pittsburgh Redevelopment Agency, 5.00% due 8/1/2018 (Los Medanos Community Development; Insured: Natl-Re) | A+/Baa1 | 5,150,000 | 5,276,999 | |||||||

Redding Electrical Systems Revenue COP, 5.00% due 6/1/2020 (Insured: AGM) | NR/Aa3 | 3,955,000 | 4,404,446 | |||||||

Sacramento Cogeneration Authority, 5.00% due 7/1/2017 (Procter & Gamble) | A+/A1 | 750,000 | 869,018 | |||||||

Sacramento Cogeneration Authority, 5.00% due 7/1/2017 (Insured: AMBAC) | BBB/NR | 8,290,000 | 8,846,591 | |||||||

Sacramento Municipal Utility District, 5.00% due 7/1/2016 (Cosumnes Project; Insured: Natl-Re) | BBB/Baa1 | 4,870,000 | 5,334,403 | |||||||

Sacramento Municipal Utility District, 5.00% due 7/1/2019 (Cosumnes Project; Insured: Natl-Re) | BBB/Baa1 | 5,000,000 | 5,260,600 | |||||||

Sacramento Municipal Utility District, 5.00% due 7/1/2020 (Cosumnes Project; Insured: Natl-Re) | BBB/Baa1 | 8,675,000 | 9,052,276 | |||||||

San Diego Redevelopment Agency, 4.50% due 9/1/2019 (Centre City Redevelopment; Insured: AMBAC) | NR/A2 | 1,240,000 | 1,265,184 | |||||||

San Diego USD GO, 5.50% due 7/1/2020 (Election 1998; Insured: Natl-Re) | AA/Aa1 | 10,000,000 | 11,822,800 | |||||||

San Joaquin Delta Community College District GO, 0% due 8/1/2019 (Insured: AGM) | AA+/Aa2 | 7,600,000 | 5,501,640 | |||||||

San Jose Redevelopment Agency Tax Allocation, 6.00% due 8/1/2015 (Insured: Natl-Re) | BBB/Baa1 | 2,780,000 | 3,038,373 | |||||||

San Luis & Delta-Mendota Water Authority, 4.50% due 3/1/2014 (Water Utility Improvements) | A+/NR | 3,900,000 | 4,181,970 | |||||||

Santa Ana USD GO, 0% due 8/1/2019 (Insured: Natl-Re/FGIC) | A+/NR | 3,425,000 | 2,523,369 | |||||||

Santa Clara County Financing Authority Lease Revenue, 4.00% due 5/15/2014 (Multiple Facilities) | AA/Aa2 | 4,245,000 | 4,531,835 | |||||||

Solano County COP, 5.00% due 11/15/2017 | AA-/A1 | 1,580,000 | 1,782,414 | |||||||

Southeast Resource Recovery Facilities Authority, 5.25% due 12/1/2017 (Insured: AMBAC) | A+/A1 | 2,000,000 | 2,112,320 | |||||||

Tuolumne Wind Project Authority, 5.00% due 1/1/2018 (Tuolumne Co.) | A+/A2 | 2,000,000 | 2,298,940 | |||||||

Tuolumne Wind Project Authority, 5.00% due 1/1/2019 (Tuolumne Co.) | A+/A2 | 2,000,000 | 2,299,660 | |||||||

Tustin Community Redevelopment Agency, 4.00% due 9/1/2017 (Tustin Redevelopment) | A/NR | 935,000 | 952,260 | |||||||

Tustin Community Redevelopment Agency, 4.00% due 9/1/2019 (Tustin Redevelopment) | A/NR | 1,010,000 | 993,143 | |||||||

Tustin Community Redevelopment Agency, 4.00% due 9/1/2020 | A/NR | 1,050,000 | 1,014,972 | |||||||

Twin Rivers USD GO, 0% due 4/1/2014 | SP-1+/NR | 3,490,000 | 3,281,228 | |||||||

Ventura County COP, 5.00% due 8/15/2016 | AA/Aa3 | 1,520,000 | 1,732,815 | |||||||

Ventura County COP, 5.25% due 8/15/2017 | AA/Aa3 | 1,635,000 | 1,893,248 | |||||||

COLORADO — 2.50% | ||||||||||

Adams County Platte Valley Medical Center, 5.00% due 2/1/2015 (Brighton Community Hospital Association; Insured: FHA/Natl-Re) | BBB/NR | 1,530,000 | 1,678,838 | |||||||

Adams County Platte Valley Medical Center, 5.00% due 8/1/2015 (Brighton Community Hospital Association; Insured: FHA/Natl-Re) | BBB/NR | 1,565,000 | 1,734,928 | |||||||

Beacon Point Metropolitan District, 4.375% due 12/1/2015 (LOC: Compass Bank) | A/NR | 1,335,000 | 1,335,254 | |||||||

Broomfield Water Activity Enterprise, 5.30% due 12/1/2014 (Insured: Natl-Re) | NR/Aa3 | 1,620,000 | 1,641,643 | |||||||

Colorado COP, 3.00% due 3/1/2013 (Colorado Penitentiary) | AA-/Aa2 | 1,205,000 | 1,230,920 | |||||||

Colorado COP, 4.00% due 3/1/2014 (Colorado Penitentiary) | AA-/Aa2 | 1,285,000 | 1,354,506 | |||||||

Colorado COP, 5.00% due 3/1/2016 (Colorado Penitentiary) | AA-/Aa2 | 2,000,000 | 2,229,660 | |||||||

Colorado COP, 5.00% due 3/1/2017 (Colorado Penitentiary) | AA-/Aa2 | 2,000,000 | 2,241,240 | |||||||

Colorado COP, 5.00% due 3/1/2018 (Colorado Penitentiary) | AA-/Aa2 | 1,500,000 | 1,688,790 | |||||||

Colorado Educational & Cultural Facilities, 4.00% due 6/1/2014 (NCSL) | A/A3 | 1,300,000 | 1,381,926 | |||||||

Colorado Educational & Cultural Facilities, 5.00% due 6/1/2016 (NCSL) | A/A3 | 1,475,000 | 1,652,959 | |||||||

14 Certified Annual Report

| SCHEDULE OF INVESTMENTS, CONTINUED | ||

| Thornburg Limited Term Municipal Fund | September 30, 2011 | |

Issuer-Description | Credit Rating† S&P/ Moody’s | Principal Amount | Value | |||||||

Colorado Educational & Cultural Facilities, 5.00% due 6/1/2018 (NCSL) | A/A3 | $ | 1,625,000 | $ | 1,846,991 | |||||

Colorado Educational & Cultural Facilities, 5.00% due 6/1/2020 (NCSL) | A/A3 | 1,805,000 | 2,041,906 | |||||||

Colorado Educational & Cultural Facilities, 5.00% due 6/1/2021 (NCSL) | A/A3 | 1,000,000 | 1,121,670 | |||||||

Colorado HFA, 5.00% due 11/15/2013 (Adventist Health/Sunbelt Group) | AA-/Aa3 | 2,840,000 | 3,088,926 | |||||||

Colorado HFA, 5.00% due 11/15/2015 (Adventist Health/Sunbelt Group) | AA-/Aa3 | 2,365,000 | 2,693,830 | |||||||

Colorado HFA, 5.25% due 5/15/2017 (Northern Colorado Medical Center; Insured: AGM) | AA+/NR | 1,185,000 | 1,359,124 | |||||||

Colorado HFA, 5.25% due 5/15/2019 (Northern Colorado Medical Center; Insured: AGM) | AA+/NR | 2,225,000 | 2,559,951 | |||||||

Colorado HFA, 5.50% due 10/1/2038 put 11/12/2015 (Catholic Health Initiatives) | AA/Aa2 | 1,000,000 | 1,170,620 | |||||||

Colorado HFA, 5.00% due 7/1/2039 put 11/8/2012 (Catholic Health Initiatives) | AA/Aa2 | 3,500,000 | 3,674,300 | |||||||

Colorado HFA, 5.00% due 7/1/2039 put 11/12/2013 (Catholic Health Initiatives) | AA/Aa2 | 7,255,000 | 7,905,266 | |||||||

Colorado HFA, 5.00% due 7/1/2039 put 11/11/2014 (Catholic Health Initiatives) | AA/Aa2 | 3,000,000 | 3,373,470 | |||||||

Colorado Higher Education COP, 5.00% due 11/1/2013 | AA-/Aa2 | 1,025,000 | 1,112,166 | |||||||

Denver City & County Airport System, 5.00% due 11/15/2016 (Insured: Natl-Re) | A+/A1 | 1,725,000 | 1,999,465 | |||||||

Denver City & County Airport System, 5.00% due 11/15/2017 (Insured: Natl-Re) | A+/A1 | 1,000,000 | 1,166,780 | |||||||

Denver City & County COP, 5.00% due 5/1/2013 (Insured: Natl-Re) | AA+/Aa1 | 3,890,000 | 4,145,923 | |||||||

Denver City & County COP, 5.00% due 5/1/2014 (Insured: Natl-Re) | AA+/Aa1 | 4,000,000 | 4,391,680 | |||||||

Denver City & County COP, 5.00% due 12/1/2016 (Buell Theatre/Jail Dormitory; Insured: Natl-Re) | AA+/Aa1 | 3,025,000 | 3,245,190 | |||||||

Denver City & County COP, 0.14% due 12/1/2029 put 10/3/2011 (SPA: JPMorgan Chase Bank) (daily demand notes) | AA+/Aa2 | 9,880,000 | 9,880,000 | |||||||

Denver Convention Center Hotel Authority, 5.25% due 12/1/2014 (Insured: Syncora) | BBB-/Baa3 | 3,450,000 | 3,624,190 | |||||||

Denver Convention Center Hotel Authority, 5.00% due 12/1/2019 pre-refunded 12/1/2013 (Insured: Syncora) | NR/NR | 5,000,000 | 5,448,100 | |||||||

Denver Convention Center Hotel Authority, 5.00% due 12/1/2022 pre-refunded 12/1/2013 (Insured: Syncora) | NR/NR | 2,000,000 | 2,179,240 | |||||||

E-470 Public Highway Authority Capital Appreciation, 0% due 9/1/2014 (Insured: Natl-Re) | BBB/Baa1 | 1,910,000 | 1,695,622 | |||||||

Longmont Sales & Use Tax, 6.00% due 5/15/2019 | AA+/NR | 3,215,000 | 3,934,646 | |||||||

Mesa County Residual Revenue, 0% due 12/1/2011 (ETM) | NR/Aaa | 1,250,000 | 1,249,425 | |||||||

Park Creek Metropolitan District, 5.00% due 12/1/2015 (Insured: AGM) | AA+/NR | 1,000,000 | 1,131,360 | |||||||

Park Creek Metropolitan District, 5.00% due 12/1/2016 (Insured: AGM) | AA+/NR | 1,035,000 | 1,182,477 | |||||||

Park Creek Metropolitan District, 5.00% due 12/1/2017 (Insured: AGM) | AA+/NR | 1,525,000 | 1,752,011 | |||||||

Park Creek Metropolitan District, 5.50% due 12/1/2018 (Insured: AGM) | AA+/NR | 1,200,000 | 1,420,980 | |||||||

Park Creek Metropolitan District, 5.50% due 12/1/2019 (Insured: AGM) | AA+/NR | 1,000,000 | 1,183,880 | |||||||

Regional Transportation District COP, 5.00% due 6/1/2018 | A-/Aa3 | 1,750,000 | 1,989,522 | |||||||

Regional Transportation District COP, 5.00% due 6/1/2019 | A-/Aa3 | 1,750,000 | 1,984,290 | |||||||

Regional Transportation District COP, 5.00% due 6/1/2020 | A-/Aa3 | 3,655,000 | 4,132,964 | |||||||

Regional Transportation District COP, 5.50% due 6/1/2021 | A-/Aa3 | 1,000,000 | 1,157,220 | |||||||

Southlands Metropolitan District GO, 6.75% due 12/1/2016 pre-refunded 12/1/2014 | AA+/NR | 840,000 | 952,358 | |||||||

CONNECTICUT — 0.07% | ||||||||||

Connecticut Development Authority PCR, 5.75% due 6/1/2026 put 2/1/2012 (United Illuminating Co.) | NR/Baa2 | 1,000,000 | 1,013,810 | |||||||

Connecticut Health & Educational Facilities, 3.50% due 11/15/2029 put 2/1/2012 (Ascension Health) | AA+/Aa1 | 1,860,000 | 1,879,939 | |||||||

DELAWARE — 0.02% | ||||||||||

Delaware EDA, 6.375% due 5/1/2027 pre-refunded 5/1/2012 (Peninsula | NR/NR | 1,000,000 | 1,044,430 | |||||||

DISTRICT OF COLUMBIA — 1.01% | ||||||||||

District of Columbia Convention Center Authority, 5.00% due 10/1/2013 (Washington Convention Center; Insured: AMBAC) | A/A1 | 3,000,000 | 3,213,060 | |||||||

District of Columbia COP, 5.25% due 1/1/2013 (Insured: AMBAC) | A/NR | 4,065,000 | 4,171,462 | |||||||

District of Columbia COP, 5.25% due 1/1/2015 (Insured: Natl-Re/FGIC) | A/Aa3 | 2,875,000 | 3,206,258 | |||||||

Certified Annual Report 15

| SCHEDULE OF INVESTMENTS, CONTINUED | ||

| Thornburg Limited Term Municipal Fund | September 30, 2011 | |

Issuer-Description | Credit Rating† S&P/ Moody’s | Principal Amount | Value | |||||||

District of Columbia COP, 5.25% due 1/1/2016 (Insured: Natl-Re/FGIC) | A/Aa3 | $ | 4,625,000 | $ | 5,224,677 | |||||

District of Columbia COP, 5.00% due 1/1/2019 (Insured: Natl-Re) | A/Aa3 | 5,000,000 | 5,383,800 | |||||||

District of Columbia GO, 6.00% due 6/1/2018 (Insured: Natl-Re) | A+/Aa2 | 5,000,000 | 6,093,400 | |||||||

District of Columbia Housing Finance Agency, 5.00% due 7/1/2014 (Insured: AGM HUD Loan) | AA+/Aa3 | 1,195,000 | 1,299,073 | |||||||

District of Columbia Housing Finance Agency, 5.00% due 7/1/2015 (Insured: AGM HUD Loan) | AA+/Aa3 | 1,480,000 | 1,640,565 | |||||||

District of Columbia Revenue, 4.00% due 4/1/2015 (National Public Radio) | AA-/Aa3 | 1,000,000 | 1,089,220 | |||||||

District of Columbia Revenue, 5.00% due 4/1/2016 (National Public Radio) | AA-/Aa3 | 500,000 | 571,535 | |||||||

District of Columbia Revenue, 4.00% due 4/1/2017 (National Public Radio) | AA-/Aa3 | 1,830,000 | 2,021,821 | |||||||

District of Columbia Revenue, 5.00% due 4/1/2018 (National Public Radio) | AA-/Aa3 | 1,195,000 | 1,392,605 | |||||||

District of Columbia Revenue, 5.00% due 4/1/2019 (National Public Radio) | AA-/Aa3 | 805,000 | 937,712 | |||||||

District of Columbia Revenue, 5.00% due 4/1/2020 (National Public Radio) | AA-/Aa3 | 1,250,000 | 1,453,000 | |||||||

District of Columbia Tax Increment, 0% due 7/1/2012 (Mandarin Oriental; Insured: AGM) | AA+/Aa3 | 1,580,000 | 1,568,419 | |||||||

Metropolitan Washington Airports Authority, 0% due 10/1/2014 (Dulles Toll Road; Insured: AGM) | AA+/Aa3 | 2,000,000 | 1,841,700 | |||||||

Metropolitan Washington Airports Authority, 0% due 10/1/2016 (Dulles Toll Road; Insured: AGM) | AA+/Aa3 | 4,000,000 | 3,379,520 | |||||||

FLORIDA — 9.23% | ||||||||||

Broward County Airport Systems, 5.00% due 10/1/2014 (Insured: AMBAC) | A+/A1 | 4,000,000 | 4,407,960 | |||||||

Broward County Port Facilities, 5.00% due 9/1/2013 | A-/A2 | 2,000,000 | 2,131,260 | |||||||

Broward County Port Facilities, 5.00% due 9/1/2017 | A-/A2 | 2,820,000 | 3,187,390 | |||||||

Broward County Port Facilities, 5.50% due 9/1/2018 | A-/A2 | 3,500,000 | 4,069,100 | |||||||

Broward County Port Facilities, 5.50% due 9/1/2019 | A-/A2 | 2,800,000 | 3,249,428 | |||||||

Broward County School Board COP, 5.25% due 7/1/2015 (Insured: AGM) | AA+/Aa3 | 3,035,000 | 3,401,507 | |||||||

Broward County School Board COP, 5.00% due 7/1/2016 (Insured: AGM) | AA+/Aa3 | 1,495,000 | 1,679,633 | |||||||

Broward County School Board COP, 5.25% due 7/1/2016 (Insured: AGM) | AA+/Aa3 | 7,630,000 | 8,657,837 | |||||||

Broward County School Board COP, 5.25% due 7/1/2016 (Insured: AGM) | AA+/Aa3 | 3,715,000 | 4,215,448 | |||||||

Broward County School Board COP, 5.00% due 7/1/2017 (Insured: Natl-Re/FGIC) | A/Aa3 | 1,000,000 | 1,125,150 | |||||||

Capital Projects Finance Authority, 5.50% due 10/1/2012 (Insured: Natl-Re) | BBB/Baa1 | 1,820,000 | 1,809,881 | |||||||

Capital Projects Finance Authority, 5.50% due 10/1/2015 (Insured: Natl-Re) | BBB/Baa1 | 2,660,000 | 2,596,719 | |||||||

Collier County Special Obligation Revenue, 4.00% due 10/1/2014 | AA/Aa2 | 1,410,000 | 1,523,801 | |||||||

Dade County Florida GO, 7.125% due 10/1/2011 (Insured: AMBAC) | NR/Aa2 | 1,000,000 | 1,000,190 | |||||||

Escambia County HFA, 5.25% due 11/15/2014 (Ascension Health Credit) | AA+/Aa1 | 1,650,000 | 1,869,021 | |||||||

Escambia County Utilities Authority, 6.25% due 1/1/2012 (Insured: Natl-Re/FGIC) | BBB/NR | 5,235,000 | 5,307,034 | |||||||

Flagler County School Board COP, 5.00% due 8/1/2014 (Insured: AGM) | AA+/Aa3 | 1,605,000 | 1,755,035 | |||||||

Flagler County School Board COP, 5.00% due 8/1/2015 (Insured: AGM) | AA+/Aa3 | 1,500,000 | 1,677,345 | |||||||

Florida Atlantic University Financing Corp. Capital Improvements Revenue, 5.00% due 7/1/2014 (Innovation Village) | A/A2 | 1,950,000 | 2,123,121 | |||||||

Florida Atlantic University Financing Corp. Capital Improvements Revenue, 5.00% due 7/1/2015 (Innovation Village) | A/A2 | 2,395,000 | 2,661,252 | |||||||

Florida Atlantic University Financing Corp. Capital Improvements Revenue, 5.00% due 7/1/2016 (Innovation Village) | A/A2 | 2,275,000 | 2,548,341 | |||||||

Florida Board of Education Lottery Revenue, 5.25% due 7/1/2016 (Insured: Natl-Re/FGIC) | AAA/A1 | 1,000,000 | 1,045,760 | |||||||

Florida Department of Management Services, 5.25% due 9/1/2016 (Insured: AGM) | AA+/Aa2 | 3,500,000 | 4,087,545 | |||||||

Florida Higher Educational Facilities Financing, 4.00% due 4/1/2013 (Nova Southeastern University) | BBB/Baa2 | 1,100,000 | 1,128,127 | |||||||

Florida Higher Educational Facilities Financing, 5.00% due 4/1/2014 (Nova Southeastern University) | BBB/Baa2 | 2,365,000 | 2,498,717 | |||||||

Florida Higher Educational Facilities Financing, 5.00% due 4/1/2015 (Nova Southeastern University) | BBB/Baa2 | 2,350,000 | 2,507,591 | |||||||

Florida Higher Educational Facilities Financing, 5.00% due 4/1/2016 (Nova Southeastern University) | BBB/Baa2 | 2,345,000 | 2,516,631 | |||||||

Florida Higher Educational Facilities Financing, 5.25% due 4/1/2017 (Nova Southeastern University) | BBB/Baa2 | 1,325,000 | 1,431,888 | |||||||

16 Certified Annual Report

| SCHEDULE OF INVESTMENTS, CONTINUED | ||

| Thornburg Limited Term Municipal Fund | September 30, 2011 | |

Issuer-Description | Credit Rating† S&P/ Moody’s | Principal Amount | Value | |||||||

Florida Higher Educational Facilities Financing, 5.25% due 4/1/2018 (Nova Southeastern University) | BBB/Baa2 | $ | 2,630,000 | $ | 2,840,032 | |||||

Florida Higher Educational Facilities Financing, 5.50% due 4/1/2019 (Nova Southeastern University) | BBB/Baa2 | 1,705,000 | 1,857,836 | |||||||

Florida Hurricane Catastrophe, 5.00% due 7/1/2014 | AA-/Aa3 | 11,000,000 | 11,965,690 | |||||||

Florida State Correctional Privatization Commission COP, 5.00% due 8/1/2015 (Insured: AMBAC) | AA+/Aa2 | 2,000,000 | 2,192,100 | |||||||

Florida State Department of Children & Families COP, 5.00% due 10/1/2012 | AA+/NR | 770,000 | 799,121 | |||||||

Florida State Department of Children & Families COP, 5.00% due 10/1/2014 | AA+/NR | 905,000 | 995,138 | |||||||

Florida State Department of Children & Families COP, 5.00% due 10/1/2015 | AA+/NR | 925,000 | 1,037,684 | |||||||

Florida State Department of Transportation GO, 5.375% due 7/1/2017 | AAA/Aa1 | 4,675,000 | 4,899,166 | |||||||

Florida State Department of Transportation GO, 5.00% due 7/1/2018 | AAA/Aa1 | 3,000,000 | 3,544,860 | |||||||

Florida Turnpike Authority, 5.00% due 7/1/2013 (Department of Transportation) | AA-/Aa3 | 4,875,000 | 5,251,984 | |||||||

Fort Myers Florida Improvement Revenue, 5.00% due 12/1/2018 (Insured: Natl-Re) | A+/Aa3 | 2,195,000 | 2,450,959 | |||||||

Gainesville Utilities Systems Revenue, 6.50% due 10/1/2013 | AA/Aa2 | 4,800,000 | 5,304,960 | |||||||

Gainesville Utilities Systems Revenue, 0.20% due 10/1/2026 put 10/3/2011 (SPA: Suntrust Bank) (daily demand notes) | AA/Aa2 | 6,315,000 | 6,315,000 | |||||||

Gainesville Utilities Systems Revenue, 0.22% due 10/1/2026 put 10/3/2011 (SPA: Suntrust Bank) (daily demand notes) | AA/Aa2 | 13,715,000 | 13,715,000 | |||||||

Highlands County HFA, 5.00% due 11/15/2015 (Adventist Health) | AA-/Aa3 | 1,000,000 | 1,137,030 | |||||||

Highlands County HFA, 5.00% due 11/15/2016 (Adventist Health) | AA-/Aa3 | 1,000,000 | 1,148,570 | |||||||

Highlands County HFA, 5.00% due 11/15/2017 (Adventist Health) | AA-/Aa3 | 3,200,000 | 3,710,720 | |||||||

Highlands County HFA, 5.00% due 11/15/2017 (Adventist Health) | AA-/Aa3 | 1,000,000 | 1,109,810 | |||||||

Highlands County HFA, 5.00% due 11/15/2019 (Adventist Health) | AA-/Aa3 | 3,000,000 | 3,488,400 | |||||||

Highlands County HFA, 3.95% due 11/15/2032 put 9/1/2012 (Adventist Health) | AA-/Aa3 | 2,500,000 | 2,577,375 | |||||||

Hillsborough County Assessment, 5.00% due 3/1/2015 (Insured: Natl-Re/FGIC) | A+/A1 | 5,000,000 | 5,468,850 | |||||||

Hillsborough County IDA PCR, 5.10% due 10/1/2013 (Tampa Electric Co.) | BBB+/Baa1 | 7,410,000 | 7,657,939 | |||||||

bHillsborough County IDA PCR, 5.00% due 12/1/2034 put 3/15/2012 (Tampa Electric Co.; Insured: AMBAC) | BBB+/Baa1 | 6,650,000 | 6,777,746 | |||||||

Hillsborough County Investment Tax Revenue, 5.00% due 11/1/2016 (Insured: AMBAC) | AA/Aa2 | 1,000,000 | 1,149,230 | |||||||

Hillsborough County School Board COP, 5.25% due 7/1/2017 (Insured: Natl-Re) | AA-/Aa2 | 1,000,000 | 1,154,570 | |||||||

Hollywood Community Redevelopment Agency, 5.00% due 3/1/2016 (Insured: Syncora) | NR/A3 | 2,000,000 | 2,187,240 | |||||||

Hollywood Community Redevelopment Agency, 5.00% due 3/1/2017 (Insured: Syncora) | NR/A3 | 2,000,000 | 2,191,000 | |||||||

Hollywood Water & Sewer Revenue, 5.00% due 10/1/2014 (Insured: AGM) | NR/Aa2 | 1,300,000 | 1,402,180 | |||||||

Jacksonville Economic Development Commission, 6.00% due 9/1/2017 (Florida Proton Therapy Institute) | NR/NR | 5,235,000 | 5,519,313 | |||||||

JEA, 5.25% due 10/1/2012 (St. John’s River Park Systems) | AA-/Aa2 | 5,500,000 | 5,522,110 | |||||||

JEA, 5.00% due 10/1/2014 (Electric Systems) | A+/Aa3 | 7,165,000 | 7,852,553 | |||||||

JEA, 4.00% due 10/1/2016 (Electric Systems) | A+/Aa3 | 3,540,000 | 3,912,231 | |||||||

JEA, 5.00% due 10/1/2017 (St. John’s River Park Systems) | AA-/Aa2 | 8,385,000 | 8,414,599 | |||||||

JEA Water & Sewer Systems Revenue, 3.50% due 10/1/2013 | AA-/Aa2 | 5,565,000 | 5,889,273 | |||||||

JEA Water & Sewer Systems Revenue, 5.00% due | AA-/Aa2 | 1,500,000 | 1,781,160 | |||||||

Kissimmee Utilities Authority Electrical Systems Revenue, 5.25% due 10/1/2016 (Insured: AGM) | NR/Aa3 | 1,700,000 | 1,977,355 | |||||||

Lakeland Florida Energy System Revenue, 5.00% due 10/1/2016 (Insured: AGM) | AA+/Aa3 | 9,780,000 | 11,304,800 | |||||||

Lakeland Florida Energy System Revenue, 5.00% due 10/1/2017 (Insured: AGM) | AA+/Aa3 | 7,105,000 | 8,287,556 | |||||||

Lakeland Florida Energy System Revenue, 5.00% due 10/1/2019 (Insured: AGM) | AA+/Aa3 | 5,000,000 | 5,850,150 | |||||||

Lakeland Florida Energy System Revenue, 5.00% due 10/1/2020 (Insured: AGM) | AA+/Aa3 | 1,695,000 | 1,976,285 | |||||||

Lakeland Florida Hospital System Revenue, 3.00% due 11/15/2013 (Lakeland Regional Health) | NR/NR | 1,000,000 | 1,027,750 | |||||||

Lakeland Florida Hospital System Revenue, 4.00% due 11/15/2014 (Lakeland Regional Health) | NR/NR | 1,000,000 | 1,058,810 | |||||||

Lakeland Florida Hospital System Revenue, 5.00% due 11/15/2019 (Lakeland Regional Health) | NR/A2 | 4,950,000 | 5,302,687 | |||||||

Marion County Hospital District, 5.00% due 10/1/2015 (Munroe Regional Health Systems) | NR/A3 | 1,000,000 | 1,084,340 | |||||||

Miami Dade County Educational Facilities Authority GO, 5.00% due 4/1/2016 (University of Miami; Insured: AMBAC) | A-/A3 | 3,000,000 | 3,321,960 | |||||||

Miami Dade County Expressway Authority, 5.00% due 7/1/2019 (Insured: Assured Guaranty) | AA+/Aa3 | 6,530,000 | 7,427,091 | |||||||

Certified Annual Report 17

| SCHEDULE OF INVESTMENTS, CONTINUED | ||

| Thornburg Limited Term Municipal Fund | September 30, 2011 | |

Issuer-Description | Credit Rating† S&P/ Moody’s | Principal Amount | Value | |||||||

Miami Dade County GO, 5.25% due 7/1/2018 (Building Better Communities) | AA-/Aa2 | $ | 4,540,000 | $ | 5,300,405 | |||||

Miami Dade County Professional Sports Franchise Facilities Tax, 0% due 10/1/2015 (Insured: AGM) | AA+/Aa3 | 3,845,000 | 3,420,397 | |||||||

Miami Dade County Professional Sports Franchise Facilities Tax, 0% due 10/1/2016 (Insured: AGM) | AA+/Aa3 | 3,535,000 | 3,002,841 | |||||||

Miami Dade County Professional Sports Franchise Facilities Tax, 0% due 10/1/2017 (Insured: AGM) | AA+/Aa3 | 2,435,000 | 1,963,219 | |||||||

Miami Dade County Professional Sports Franchise Facilities Tax, 0% due 10/1/2018 (Insured: AGM) | AA+/Aa3 | 5,385,000 | 4,124,964 | |||||||

Miami Dade County Professional Sports Franchise Facilities Tax, 0% due 10/1/2019 (Insured: AGM) | AA+/Aa3 | 2,170,000 | 1,567,955 | |||||||

Miami Dade County School Board COP, 5.00% due 5/1/2014 (Insured: Natl-Re) | A/A1 | 1,000,000 | 1,076,200 | |||||||

Miami Dade County School Board COP, 5.00% due 10/1/2015 (Insured: AMBAC) | A/A1 | 1,000,000 | 1,106,040 | |||||||

Miami Dade County School Board COP, 5.00% due 5/1/2016 (Insured: Natl-Re) | A/A1 | 4,015,000 | 4,447,295 | |||||||

Miami Dade County School Board COP, 5.00% due 10/1/2016 (Insured: AMBAC) | A/A1 | 1,000,000 | 1,113,740 | |||||||

Miami Dade County School Board COP, 5.00% due 5/1/2032 put 5/1/2016 | A/A1 | 6,000,000 | 6,604,200 | |||||||

Miami Dade County School District GO, 5.375% due 8/1/2015 (Insured: AGM) | AA+/Aa3 | 5,000,000 | 5,742,500 | |||||||

Miami Dade County Special Housing, 5.80% due 10/1/2012 (HUD Section 8) | NR/Baa3 | 625,000 | 636,075 | |||||||

Miami GO, 5.00% due 1/1/2017 (Homeland Defense/Neighborhood Capital Improvements) | BBB-/A3 | 1,245,000 | 1,315,467 | |||||||

Miami GO, 5.00% due 1/1/2018 (Homeland Defense/Neighborhood Capital Improvements) | BBB-/A3 | 2,040,000 | 2,139,083 | |||||||

Miami GO, 5.00% due 1/1/2019 (Homeland Defense/Neighborhood Capital Improvements) | BBB-/A3 | 1,325,000 | 1,376,317 | |||||||

Miami Special Obligation, 5.00% due 1/1/2018 (Insured: Natl-Re) | A-/A2 | 1,970,000 | 2,246,036 | |||||||

North Miami Educational Facilities Revenue, 5.00% due 4/1/2013 (Johnston & Wales University; Insured: Syncora) | NR/NR | 1,530,000 | 1,594,719 | |||||||

Orange County HFA, 5.00% due 10/1/2014 (Orlando Health) | A/A2 | 2,790,000 | 3,007,787 | |||||||

Orange County HFA, 5.00% due 10/1/2017 (Orlando Health) | A/A2 | 1,980,000 | 2,179,485 | |||||||

Orange County HFA, 5.25% due 10/1/2019 (Orlando Health) | A/A2 | 4,000,000 | 4,432,520 | |||||||

Orange County HFA, 6.25% due 10/1/2021 (Orlando Health; Insured: Natl-Re) | A/A2 | 1,870,000 | 2,196,857 | |||||||

Orlando & Orange County Expressway Authority, 5.00% due 7/1/2013 (Insured: AMBAC) | A/A1 | 5,845,000 | 6,272,445 | |||||||

Palm Beach County Public Improvement, 5.00% due 11/1/2030 put 11/1/2011 (Convention Center; Insured: Natl-Re/FGIC) | AA+/Aa1 | 3,000,000 | 3,011,790 | |||||||

Port Everglades Authority, 5.00% due 9/1/2016 (Insured: AGM) | AA+/Aa3 | 9,990,000 | 10,358,531 | |||||||

Putnam County Development Authority PCR, 5.35% due 3/15/2042 put 5/1/2018 (Seminole Project; Insured: AMBAC) | A-/A3 | 10,000,000 | 11,442,200 | |||||||

Putnam County Development Authority PCR, 5.35% due 3/15/2042 put 5/1/2018 (Seminole Project; Insured: AMBAC) | A-/A3 | 3,125,000 | 3,575,687 | |||||||

South Florida Water Management District COP, 5.00% due 10/1/2015 (Insured: AMBAC) | AA/Aa2 | 1,000,000 | 1,129,740 | |||||||

South Miami HFA, 5.00% due 8/15/2016 (Baptist Health) | AA/Aa2 | 1,560,000 | 1,792,752 | |||||||

South Miami HFA, 5.00% due 8/15/2017 (Baptist Health) | AA/Aa2 | 4,610,000 | 5,364,565 | |||||||

St. John’s County IDA, 5.50% due 8/1/2014 (Presbyterian Retirement) | NR/NR | 2,120,000 | 2,199,924 | |||||||

St. Petersburg HFA, 5.50% due 11/15/2016 (All Children’s Hospital; | NR/A1 | 1,980,000 | 2,050,250 | |||||||

Tampa Bay Regional Water Supply Authority, 5.00% due 10/1/2017 | AA+/Aa2 | 5,615,000 | 6,703,524 | |||||||

Tampa Bay Regional Water Supply Authority, 5.00% due 10/1/2018 | AA+/Aa2 | 2,890,000 | 3,477,566 | |||||||

Tampa Bay Regional Water Supply Authority, 5.00% due 10/1/2019 | AA+/Aa2 | 3,000,000 | 3,615,750 | |||||||

Tampa Baycare Health Systems, 5.00% due 11/15/2016 | NR/Aa3 | 2,855,000 | 3,258,954 | |||||||

Tampa Baycare Health Systems, 5.00% due 11/15/2017 | NR/Aa3 | 1,215,000 | 1,402,146 | |||||||

Tampa Sports Authority Revenue, 5.75% due 10/1/2015 (Tampa Bay Arena; Insured: Natl-Re) | BBB/ Baa1 | 1,235,000 | 1,286,043 | |||||||

University of Central Florida Athletics Association Inc. COP, 5.00% due 10/1/2016 (Insured: Natl-Re/FGIC) | BBB/NR | 1,640,000 | 1,762,852 | |||||||

Volusia County Educational Facility Authority, 4.00% due 10/15/2013 (Embry-Riddle; Insured: AGM) | AA+/Aa3 | 675,000 | 702,783 | |||||||

Volusia County Educational Facility Authority, 5.00% due 10/15/2016 (Embry-Riddle; Insured: AGM) | AA+/Aa3 | 2,320,000 | 2,575,919 | |||||||

Volusia County Educational Facility Authority, 4.00% due 10/15/2017 (Embry-Riddle; Insured: AGM) | AA+/Aa3 | 1,030,000 | 1,089,318 | |||||||

Volusia County Educational Facility Authority, 5.00% due 10/15/2018 (Embry-Riddle; Insured: AGM) | AA+/Aa3 | 2,075,000 | 2,299,411 | |||||||

18 Certified Annual Report

| SCHEDULE OF INVESTMENTS, CONTINUED | ||

| Thornburg Limited Term Municipal Fund | September 30, 2011 | |

Issuer-Description | Credit Rating† S&P/ Moody’s | Principal Amount | Value | |||||||

Volusia County Educational Facility Authority, 5.00% due 10/15/2019 (Embry-Riddle; Insured: AGM) | AA+/Aa3 | $ | 2,245,000 | $ | 2,468,490 | |||||

GEORGIA — 2.66% | ||||||||||

Atlanta Airport Passenger Facility Charge Revenue, 5.00% due 1/1/2018 | NR/A1 | 2,100,000 | 2,404,689 | |||||||

Atlanta Airport Passenger Facility Charge Revenue, 5.00% due 1/1/2020 | NR/A1 | 6,000,000 | 6,885,420 | |||||||

Atlanta Airport Passenger Facility Charge Revenue, 5.00% due 1/1/2021 | NR/A1 | 7,000,000 | 7,950,670 | |||||||

Atlanta Airport Revenue, 5.00% due 1/1/2019 | NR/A1 | 3,145,000 | 3,618,448 | |||||||

b Atlanta Airport Revenue, 5.25% due 1/1/2020 | NR/A1 | 5,000,000 | 5,832,700 | |||||||

Atlanta Airport Revenue, 5.50% due 1/1/2021 | NR/A1 | 3,525,000 | 4,197,711 | |||||||

Atlanta Tax Allocation, 5.25% due 12/1/2016 (Atlantic Station; Insured: AGM) | AA+/Aa3 | 3,850,000 | 4,319,007 | |||||||

Atlanta Water & Wastewater Revenue, 5.50% due 11/1/2014 (Insured: Natl-Re/FGIC) | A/A1 | 3,000,000 | 3,373,410 | |||||||

Atlanta Water & Wastewater Revenue, 5.50% due 11/1/2015 (Insured: Natl-Re/FGIC) | A/A1 | 4,000,000 | 4,615,960 | |||||||

Atlanta Water & Wastewater Revenue, 5.00% due 11/1/2016 (Insured: AGM) | AA+/Aa3 | 3,215,000 | 3,671,659 | |||||||

Atlanta Water & Wastewater Revenue, 5.50% due 11/1/2016 (Insured: Natl-Re/FGIC) | A/A1 | 8,215,000 | 9,618,286 | |||||||

Atlanta Water & Wastewater Revenue, 5.00% due 11/1/2017 (Insured: AGM) | AA+/Aa3 | 4,745,000 | 5,451,198 | |||||||

Atlanta Water & Wastewater Revenue, 6.00% due 11/1/2019 | A/A1 | 5,650,000 | 6,940,855 | |||||||

Burke County Development Authority PCR, 2.50% due 1/1/2040 put 3/1/2013 (Oglethorpe Power) | A/Baa1 | 7,000,000 | 7,119,420 | |||||||

Fulton County Facilities COP, 5.00% due 11/1/2017 | AA-/Aa3 | 8,400,000 | 9,609,180 | |||||||

Fulton County Facilities COP, 5.00% due 11/1/2019 | AA-/Aa3 | 6,600,000 | 7,521,558 | |||||||

Gainesville Water & Sewer Revenue, 6.00% due 11/15/2012 (Insured: Natl-Re/FGIC) | AA-/Aa3 | 1,160,000 | 1,188,838 | |||||||

Lagrange Troup County Hospital Authority, 5.00% due 7/1/2018 (West Georgia Health Foundation Inc.) | A+/Aa2 | 2,500,000 | 2,761,800 | |||||||

Main Street Natural Gas, Inc., 5.00% due 3/15/2013 (Georgia Gas) | A/Baa1 | 1,500,000 | 1,559,970 | |||||||

Main Street Natural Gas, Inc., 5.00% due 3/15/2014 (Georgia Gas) | A+/Aa3 | 3,000,000 | 3,207,000 | |||||||

Main Street Natural Gas, Inc., 5.00% due 3/15/2014 (Georgia Gas) | A/Baa1 | 3,590,000 | 3,781,455 | |||||||

Main Street Natural Gas, Inc., 5.00% due 3/15/2015 (Georgia Gas) | A/Baa1 | 2,000,000 | 2,116,460 | |||||||

Main Street Natural Gas, Inc., 5.00% due 3/15/2018 (Georgia Gas) | A/Baa1 | 5,000,000 | 5,054,900 | |||||||

Monroe County Development Authority PCR, 6.80% due 1/1/2012 (Oglethorpe Power; Insured: Natl-Re) | BBB/Baa1 | 1,000,000 | 1,015,490 | |||||||

Municipal Electric Authority of Georgia, 6.60% due 1/1/2018 (Insured: Natl-Re) | BBB/A1 | 2,990,000 | 3,429,859 | |||||||

GUAM — 0.31% | ||||||||||

Guam Government Limited Obligation Revenue, 5.25% due 12/1/2016 | BBB-/NR | 5,610,000 | 6,101,268 | |||||||

Guam Government Limited Obligation Revenue, 5.25% due 12/1/2017 | BBB-/NR | 2,000,000 | 2,185,520 | |||||||

Guam Government Limited Obligation Revenue, 5.50% due 12/1/2018 | BBB-/NR | 3,000,000 | 3,294,570 | |||||||

Guam Government Limited Obligation Revenue, 5.50% due 12/1/2019 | BBB-/NR | 2,000,000 | 2,182,440 | |||||||

HAWAII — 0.15% | ||||||||||

Hawaii Department of Budget & Finance, 6.40% due 7/1/2013 (Kapiolani Health Care; Insured: Natl-Re) | BBB/A3 | 610,000 | 627,422 | |||||||

Hawaii State Department of Budget & Finance, 4.95% due 4/1/2012 (Hawaiian Electric Company; Insured: Natl-Re) | BBB/Baa1 | 5,850,000 | 5,899,257 | |||||||

IDAHO — 0.35% | ||||||||||

Twin Falls Urban Renewal Agency, 4.95% due 8/1/2014 | NR/NR | 1,260,000 | 1,290,101 | |||||||

Twin Falls Urban Renewal Agency, 5.15% due 8/1/2017 | NR/NR | 1,455,000 | 1,472,547 | |||||||

University of Idaho, 5.25% due 4/1/2041 put 4/1/2021 | A+/Aa3 | 10,805,000 | 12,610,516 | |||||||

ILLINOIS — 7.59% | ||||||||||

Aurora GO, 4.25% due 12/30/2015 (Insured: AMBAC) | AA+/NR | 1,030,000 | 1,037,694 | |||||||

Certified Annual Report 19

| SCHEDULE OF INVESTMENTS, CONTINUED | ||

| Thornburg Limited Term Municipal Fund | September 30, 2011 | |

Issuer-Description | Credit Rating† S&P/ Moody’s | Principal Amount | Value | |||||||

Bolingbrook GO, 0% due 1/1/2016 (Insured: Natl-Re) | NR/Aa3 | $ | 1,500,000 | $ | 1,276,830 | |||||

Bolingbrook GO, 0% due 1/1/2017 (Insured: Natl-Re) | NR/Aa3 | 2,000,000 | 1,605,960 | |||||||

Broadview Tax Increment Revenue, 5.375% due 7/1/2015 | NR/NR | 3,400,000 | 3,401,292 | |||||||

Chicago Board of Education GO, 6.25% due 1/1/2015 (Insured: Natl-Re) | BBB/Aa2 | 1,700,000 | 1,811,775 | |||||||

Chicago Board of Education GO, 5.25% due 12/1/2017 (Chicago School Reform Board; Insured: Natl-Re/FGIC) | AA-/Aa2 | 4,100,000 | 4,680,314 | |||||||

Chicago Board of Education GO, 5.00% due 12/1/2018 (Insured: Natl-Re) | AA-/Aa2 | 1,000,000 | 1,116,560 | |||||||

Chicago GO, 6.125% due 1/1/2012 (Insured: AMBAC) (ETM) | A+/Aa3 | 775,000 | 786,656 | |||||||

Chicago GO, 6.125% due 1/1/2012 (Insured: AMBAC) | A+/Aa3 | 225,000 | 228,148 | |||||||

Chicago GO, 5.375% due 1/1/2013 (Insured: Natl-Re) | A+/Aa3 | 2,130,000 | 2,180,374 | |||||||

Chicago GO, 0% due 1/1/2016 (City Colleges; Insured: Natl-Re/FGIC) | A+/Aa3 | 2,670,000 | 2,357,343 | |||||||

Chicago GO, 5.40% due 1/1/2018 (Insured: AGM) | AA+/Aa3 | 3,000,000 | 3,010,530 | |||||||

Chicago GO, 5.44% due 1/1/2018 (Capital Appreciation; Insured: Natl-Re) | A+/Aa3 | 3,050,000 | 3,396,388 | |||||||

Chicago Housing Authority Capital Program, 5.00% due 7/1/2015 (Insured: AGM) | AA+/Aa3 | 8,460,000 | 9,355,153 | |||||||

Chicago Housing Authority Capital Program, 5.00% due 7/1/2016 (Insured: AGM) | AA+/Aa3 | 2,000,000 | 2,233,620 | |||||||

Chicago Illinois Board of Education GO, 5.00% due 12/1/2018 | AA-/Aa2 | 3,000,000 | 3,349,680 | |||||||

Chicago Illinois Board of Education GO, 5.00% due 12/1/2019 | AA-/Aa2 | 2,000,000 | 2,217,460 | |||||||

Chicago Illinois Board of Education GO, 0% due 12/1/2020 (Insured: BHAC/FGIC) | AA+/Aa1 | 12,000,000 | 8,242,080 | |||||||

Chicago Illinois Board of Education GO, 5.00% due 12/1/2020 | AA-/Aa2 | 2,500,000 | 2,756,575 | |||||||

Chicago Illinois Park District GO, 5.00% due 1/1/2018 (Personal Property Replacement) | AA+/Aa2 | 1,150,000 | 1,304,031 | |||||||

Chicago Illinois Public Building Commerce Building, 4.00% due 1/1/2012 | NR/Aa2 | 1,660,000 | 1,675,156 | |||||||

Chicago Illinois Public Building Commerce Building, 4.00% due 1/1/2013 | NR/Aa2 | 3,275,000 | 3,394,898 | |||||||

Chicago Illinois Transit Authority Capital Grant, 5.50% due 6/1/2018 (Federal Transit Administration) | A/A1 | 2,500,000 | 2,780,525 | |||||||

Chicago Midway Airport, 5.50% due 1/1/2013 (Insured: Natl-Re) | A/A2 | 1,180,000 | 1,239,850 | |||||||

Chicago Sales Tax Revenue, 0.14% due 1/1/2034 put 10/3/2011 (SPA: JPMorgan Chase Bank) (daily demand notes) | AAA/Aa2 | 2,735,000 | 2,735,000 | |||||||

Chicago Tax Increment, 6.75% due 6/1/2022 (Pilsen Redevelopment) | NR/NR | 5,000,000 | 5,090,700 | |||||||

Chicago Wastewater Transmission Revenue, 4.00% due 1/1/2018 | A+/Aa3 | 1,475,000 | 1,542,186 | |||||||

Chicago Water Revenue, 2.00% due 11/1/2011 | AA-/Aa3 | 2,360,000 | 2,362,690 | |||||||

Cicero Illinois GO, 5.25% due 1/1/2019 (Insured: Syncora) | NR/NR | 6,140,000 | 6,297,982 | |||||||

Cook County Community Consolidated School District GO, 0% due 12/1/2011 (Insured: AGM) (ETM) | NR/Aa3 | 2,370,000 | 2,369,005 | |||||||

Cook County Community Consolidated School District GO, 9.00% due 12/1/2016 (Tinley Park; Insured: Natl-Re/FGIC) | NR/Aa2 | 2,500,000 | 3,232,250 | |||||||

Cook County Community High School District, 5.00% due 12/15/2012 (Insured: Assured Guaranty) | AA+/NR | 3,180,000 | 3,340,876 | |||||||

Cook County Community High School District, 5.00% due 12/15/2013 (Insured: Assured Guaranty) | AA+/NR | 6,875,000 | 7,444,869 | |||||||

Cook County Community School District GO, 9.00% due 12/1/2013 (Oak Park; Insured: Natl-Re/FGIC) | NR/Aa2 | 2,250,000 | 2,599,177 | |||||||

Cook County GO, 3.25% due 11/15/2011 (ETM) | NR/NR | 220,000 | 220,849 | |||||||

Cook County GO, 3.25% due 11/15/2011 | AA/Aa3 | 1,030,000 | 1,033,533 | |||||||

Cook County GO, 5.00% due 11/15/2012 | AA/Aa3 | 6,000,000 | 6,277,380 | |||||||

Cook County GO, 6.25% due 11/15/2013 (Insured: Natl-Re) | AA/Aa3 | 3,995,000 | 4,414,315 | |||||||

De Kalb County USD GO, 0% due 1/1/2021 (Capital Appreciation) | AA-/Aa2 | 6,140,000 | 3,997,140 | |||||||

Illinois Educational Facilities, 4.75% due 3/1/2030 put 3/1/2017 (Art | A+/A1 | 3,030,000 | 3,364,876 | |||||||

Illinois Educational Facilities, 5.00% due 3/1/2030 put 3/1/2017 (Art Institute of Chicago) | NR/A1 | 3,000,000 | 3,356,400 | |||||||

Illinois Educational Facilities, 5.25% due 3/1/2034 put 3/1/2018 (Art Institute of Chicago) | NR/NR | 3,500,000 | 3,978,975 | |||||||

Illinois Educational Facilities, 3.40% due 11/1/2036 put 11/1/2017 (Medical Terminal Field Museum) | A/NR | 1,300,000 | 1,354,678 | |||||||

Illinois Educational Facilities, 4.15% due 11/1/2036 put 11/1/2012 (Field Museum) | A/A2 | 5,250,000 | 5,409,810 | |||||||

Illinois Educational Facilities, 4.30% due 11/1/2036 put 11/1/2013 (Field Museum) | A/A2 | 3,100,000 | 3,270,562 | |||||||

Illinois Finance Authority, 5.00% due 12/1/2012 (Columbia College) | BBB+/NR | 1,000,000 | 1,036,580 | |||||||

20 Certified Annual Report

| SCHEDULE OF INVESTMENTS, CONTINUED | ||

| Thornburg Limited Term Municipal Fund | September 30, 2011 | |

Issuer-Description | Credit Rating† S&P/ Moody’s | Principal Amount | Value | |||||||

Illinois Finance Authority, 4.00% due 2/15/2013 (Alexian Brothers Health Systems) | NR/A3 | $ | 1,500,000 | $ | 1,538,145 | |||||

Illinois Finance Authority, 5.00% due 2/15/2014 (Alexian Brothers Health Systems) | NR/A3 | 3,000,000 | 3,173,940 | |||||||

Illinois Finance Authority, 5.00% due 5/1/2014 | NR/Baa3 | 3,895,000 | 4,049,904 | |||||||

Illinois Finance Authority, 5.00% due 11/1/2014 (Central DuPage Health) | AA/NR | 5,000,000 | 5,524,650 | |||||||

Illinois Finance Authority, 4.00% due 4/1/2015 (Advocate Health Care) | AA/Aa2 | 3,000,000 | 3,233,130 | |||||||