UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-05201

Thornburg Investment Trust

(Exact name of registrant as specified in charter)

c/o Thornburg Investment Management, Inc.

2300 North Ridgetop Road, Santa Fe, New Mexico 87506

(Address of principal executive offices) (Zip code)

Garrett Thornburg, 2300 North Ridgetop Road, Santa Fe, New Mexico 87506

(Name and address of agent for service)

Registrant’s telephone number, including area code: 505-984-0200

Date of fiscal year end: September 30, 2012

Date of reporting period: September 30, 2012

Explanatory Note: The Registrant is filing this amendment to its Form N-CSR for the period ended September 30, 2012, originally filed with the Securities and Exchange Commission on November 28, 2012, to correct information about the NASDAQ symbols and CUSIP numbers for the share classes of Thornburg Strategic Municipal Income Fund. This amendment does not modify in any way information for any other Fund of the Registrant

Item 1. Reports to Stockholders

The following annual report is attached hereto:

Thornburg Strategic Municipal Income Fund

IMPORTANT INFORMATION

The information presented on the following pages is current as of September 30, 2012. The managers’ views, portfolio holdings, and sector diversification are provided for the general information of the Fund’s shareholders; to the extent this information is historical, it should not be considered predictive of future circumstances. This material should not be deemed a recommendation to buy or sell any of the securities mentioned.

Investments in the Fund carry risks, including possible loss of principal. Bond funds have the same interest rate, inflation, and credit risks that are associated with the underlying bonds. The principal value of bonds will fluctuate relative to changes in interest rates, decreasing when interest rates rise. This effect is more pronounced for longer-term bonds. Unlike bonds, bond funds have ongoing fees and expenses. Investments in lower-rated and unrated bonds may be more sensitive to default, downgrades, and market volatility; these investments may also be less liquid than higher-rated bonds. Investments in derivatives are subject to counterparty risk and the risks associated with the securities or other assets underlying the pool of securities, including illiquidity and difficulty in valuation. Please see the Fund’s Prospectus for a discussion of the risks associated with an investment in the Fund. Investments in the Fund are not FDIC insured, nor are they deposits of or guaranteed by a bank or any other entity. There is no guarantee that the Fund will meet its investment objectives.

Performance data given at net asset value (NAV) does not take into account applicable sales charges. If the sales charges had been included, the performance would have been lower.

Minimum investments for Class I shares are higher than those for other classes. Class I shares may not be available to all investors.

Share Class | NASDAQ Symbol | CUSIP | ||

Class A | TSSAX | 885-216-101 | ||

Class C | TSSCX | 885-216-200 | ||

Class I | TSSIX | 885-216-309 |

Lipper’s 2012 Best Fixed Income Funds Manager

Thornburg Investment Management ranked #1 out of 41 eligible firms in Lipper, Inc.’s fixed income Large Company universe for the three-year period ended 11/30/11, based on risk-adjusted returns. Lipper’s Large Company universe is comprised of fund families with more than $40 billion in total net assets. Only fund families with at least five bond funds were eligible for the fixed income funds manager award. Asset Class Group Awards are given for the three-year period only.

Glossary

BofA Merrill Lynch Municipal Master Index – This index tracks the performance of the investment-grade U.S. tax-exempt bond market. Qualifying bonds must have at least one year remaining term to maturity, a fixed coupon schedule, and an investment grade rating (based on an average of Moody’s, S&P, and Fitch).

Unless otherwise noted, index returns reflect the reinvestment of income dividends and capital gains, if any, but do not reflect fees, brokerage commissions or other expenses of investing. Investors may not make direct investments into any index.

Alternative Minimum Tax (AMT) – A federal tax aimed at ensuring that high-income individuals, estates, trusts, and corporations pay a minimal level income tax. For individuals, the AMT is calculated by adding tax preference items to regular taxable income.

Annualized Distribution Yield – The distribution yield reflects actual distributions made to shareholders. The annualized distribution yield is calculated by summing the last 30 days of income at a given month end and annualizing to a 360-day year. The result is divided by the ending maximum offering price.

Basis Point (bps) – A unit equal to 1/100th of 1%. 1% = 100 basis points (bps).

Bond Credit Ratings – A bond credit rating assesses the financial ability of a debt issuer to make timely payments of principal and interest. Ratings of AAA (the highest), AA, A, and BBB are investment-grade quality. Ratings of BB, B, CCC, CC, C, and D (the lowest) are considered below investment grade, speculative grade, or junk bonds. Unless otherwise noted, the ratings listed are from Municipal Market Data and are a combination of ratings from Standard and Poor’s, Moody’s Investors Service, and Fitch Ratings.

Consumer Price Index (CPI) – Index that measures prices of a fixed basket of goods bought by a typical consumer, including food, transportation, shelter, utilities, clothing, medical care, entertainment and other items. The CPI, published by the Bureau of Labor Statistics in the Department of Labor, is based at 100 in 1982 and is released monthly. It is widely used as a cost-of-living benchmark to adjust Social Security payments and other payment schedules, union contracts and tax brackets. Also known as the cost-of-living index.

This page is not part of the Annual Report. 3

IMPORTANT INFORMATION, CONTINUED

Core CPI – Consumer Price Index minus the energy and food components.

Core PCE Price Index – Personal Consumption Expenditures (PCE) prices excluding food and energy.

Duration – A bond’s sensitivity to interest rates. Bonds with longer durations experience greater price volatility than bonds with shorter durations.

Effective Duration – A bond’s sensitivity to interest rates, incorporating the embedded option features, such as call provisions. Bonds with longer durations experience greater price volatility than bonds with shorter durations.

Fed Funds Rate – The interest rate at which a depository institution lends immediately available funds (balances at the Federal Reserve) to another depository institution overnight.

General Obligation Bond – A municipal bond backed by the credit and “taxing power” of the issuing jurisdiction rather than the revenue from a given project.

Gross Domestic Product (GDP) – A country’s income minus foreign investments: the total value of all goods and services produced within a country in a year, minus net income from investments in other countries.

Quantitative Easing – The Federal Reserve’s monetary policy used to stimulate the U.S. economy following the recession that began in 2007/08.

SEC Yield – SEC yield is computed in accordance with SEC standards measuring the net investment income per share over a specified 30-day period expressed as a percentage of the maximum offering price of the Fund’s shares at the end of the period.

4 This page is not part of the Annual Report.

THORNBURG STRATEGIC MUNICIPAL INCOME FUND

The Thornburg Strategic Municipal Income Fund differentiates itself in four ways from other high-yield municipal funds.

| Ÿ | First, it has a more flexible mandate; we go where we perceive value. This allows us to search various sectors, issuers, credit qualities, geographic areas, and segments of the yield curve. |

| Ÿ | Second, we don’t have a legacy of bonds purchased prior to the credit meltdown of 2007–2008. |

| Ÿ | Third, the Fund does not use leverage, as do many other high-yield muni funds. |

| Ÿ | Finally, we believe that we can apply some of the risk-management skills we have demonstrated in our investment grade funds. Our portfolio managers have over 55 years of combined experience in the municipal market. |

Portfolio Managers

Josh Gonze, Chris Ryon, CFA, and Chris Ihlefeld

Average Annual Total Returns

For Periods Ended September 30, 2012

| 1 Yr | 3 Yrs | Since Inception | ||||||||||

A Shares (Incep: 4/1/09) | ||||||||||||

Without sales charge | 11.71 | % | 7.74 | % | 11.94 | % | ||||||

With sales charge | 9.45 | % | 7.02 | % | 11.31 | % | ||||||

Important

Performance Information

Performance data shown represents past performance and is no guarantee of future results. Investment return and principal value will fluctuate so shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than quoted. For performance current to the most recent month end, visit thorn-burg.com or call 800.847.0200.

The maximum sales charge for the Fund’s Class A shares is 2.00%. The total annual fund operating expense of Class A shares is 1.38%, as disclosed in the most recent Prospectus. Thornburg Investment Management and Thornburg Securities Corporation have contractually agreed to waive fees and reimburse expenses through at least February 1, 2013, so that actual expenses for Class A shares do not exceed 1.25%.

30-Day Yields, A Shares

As of September 30, 2012

| Annualized | SEC | |

Distribution Yield | Yield | |

2.80% | 2.09% |

Without fee waivers and expense reimbursements, the 30-day SEC Yield would have been 1.98% and the Annualized Distribution Yield would have been 2.69%.

Key Portfolio Attributes

As of September 30, 2012

Number of Bonds | 180 | |||

Effective Duration | 7.6 Yrs | |||

Average Maturity | 14.1 Yrs |

See the entire portfolio in the Schedule of Investments beginning on page 13.

This page is not part of the Annual Report 5

Thornburg Strategic Municipal Income Fund — September 30, 2012

Table of Contents | ||||

| 7 | ||||

| 13 | ||||

| 20 | ||||

| 21 | ||||

| 22 | ||||

| 23 | ||||

| 28 | ||||

| 30 | ||||

| 31 | ||||

| 32 | ||||

| 33 | ||||

| 36 |

This report is certified under the Sarbanes-Oxley Act of 2002, which requires that public companies, including mutual funds, affirm that the information provided in their annual and semiannual shareholder reports fully and fairly represents their financial position.

6 Certified Annual Report

October 18, 2012

Dear Fellow Shareholder:

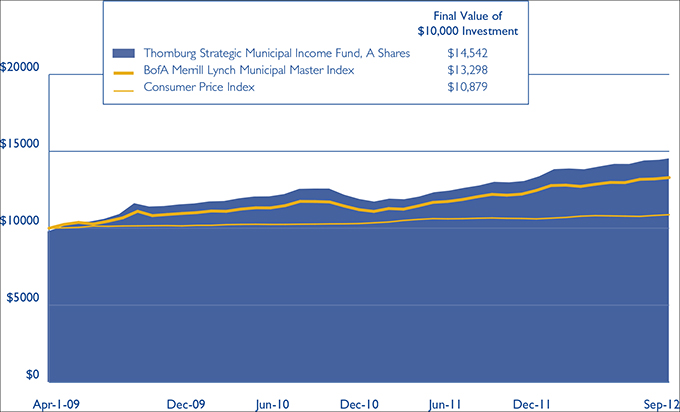

We are pleased to present the annual report for the Thornburg Strategic Municipal Income Fund. The net asset value (NAV) of the Class A shares increased by $1.11 to $15.17 per share during the fiscal year ended September 30, 2012. If you were with us for the entire period, you received dividends of 49.7 cents per share. If you reinvested your dividends, you received 50.5 cents per share. Dividends per share were lower for Class C shares and higher for Class I shares to account for varying class-specific expenses. The Class A shares of your Fund outperformed the index with a total return of 11.71% at NAV for the fiscal year ended September 30, 2012, compared to the 8.96% for the BofA Merrill Lynch Municipal Master Index. The Fund generated 3.73% more price appreciation, but 0.98% less income.

The markets’ positive returns were primarily due to declining interest rates and narrowing credit spreads. Interest rates declined more for longer maturities and consequently longer maturity bonds outperformed shorter maturity bonds. As credit spreads compressed, lower-quality bonds outperformed higher-quality bonds. The Fund’s additional price appreciation is due to several factors. Our interest rate sensitivity as measured by the Fund’s duration and differing allocations along the yield curve added 0.79% of relative price appreciation. Our overweight to the insured and revenue sectors added 2.08%. We underweighted the general obligation and pre-refunded sectors, which added 0.50% of relative price performance. Our overweight to lower credit quality securities added 1.35% of performance relative to its benchmark. Our allocations to bonds of varying dollars prices cost the Fund 1.33% of relative price performance. Other risk factors accounted for an additional 0.34%.

The Economy and the Federal Reserve

During the first quarter of the fiscal year, economic activity looked to be picking up. The December 2011 gross domestic product (GDP) reading was a strong 4.1%. The pickup in activity proved to be an illusion as the March and June 2012 GDP readings were 2.0% and 1.3% respectively. Non-farm payrolls continued to grow, but at rather anemic rates. The unemployment rate began the fiscal year at 9.0% and decreased to 7.8% by the end of the fiscal year.

Inflation as measured by the Consumer Price Index (CPI) is running in the 2.0% range. If one takes out the food and energy components (Core CPI), the trend is declining with the last reading of 2.0%. Inflation as measured by the Personal Consumption Expenditure Index (PCE), the Federal Reserve Board’s (the Fed) favorite inflation measure, is running at a core level of 1.6%. All of these economic indicators and others point to an economy that is on shaky footing.

In addition to these fundamental factors, many investors are concerned about the impact of the “fiscal cliff”, which The Washington Post described as follows:

The “ fiscal cliff” is a term coined by Federal Reserve Chairman Ben S. Bernanke. It refers to a collection of changes in current law that are all set to strike in January, triggering the sharpest reduction in the federal budget deficit in more than 40 years.

Certified Annual Report 7

LETTER TO SHAREHOLDERS,

CONTINUED

The Washington Post goes on to say that taxes would also increase:

For most taxpayers, the bulk of the increase would be triggered by the expiration of tax cuts enacted in 2001 and 2003 during the George W. Bush administration. The expiration of President Obama’s payroll tax holiday, which shaved two percentage points off the 6.2 percent Social Security tax, comes in a close second. If these issues are not addressed many analysts think the United States will be pushed into another recession.

On top of all this, Europe is still a mess but the fixed income markets seem not to be as headline sensitive to news coming out of Europe as they were last year. The Fed, at its last meeting, decided to enter into its third round of quantitative easing, known as QE3. In this round, the Fed will concentrate its security purchases to the mortgage market in an effort to lower borrowing costs for homebuyers, which should spur the housing market. As anyone who has recently applied for a mortgage knows, it is not the interest cost of the product that stands as a borrower’s major roadblock. The fixed income market’s initial reaction to the latest Fed move was an increase in inflation expectations and a decrease in bond prices, though this fear has subsided in recent weeks.

The Presidential Election and Tax Policy

Tax policy and the federal deficit have proven to be key election season issues. Both candidates have put forward their respective plans for deficit reduction; both could influence the municipal bond market. Below, in Table I is a side-by-side analysis based on a recent article in the Bond Buyer, a leading publication about the municipal bond market.

Table I

| Obama | Romney | |

| Extends the 2001 and 2003 tax cuts for individuals earning under $200,000 and families earning under $250,000. | Permanently extend all the 2001 and 2003 tax cuts. Eliminate taxation of investment income for individuals earning less than $200,000. | |

Returns to the Clinton Era highest marginal tax rate of 39.6%. | Lowers marginal rates across the board by 20%, eliminates the alternative minimum tax. | |

| In a jobs bill he floated last October and his 2013 budget, Obama proposed to place a 28% cap on the value of tax-exempt interest for the wealthy. | Announced he would cap individual tax deductions at $17,000. Not clear if he would cap exclusions, like tax exemption, as well as deductions. | |

| Bruce Bartlett, former policy adviser to President Ronald Reagan and Treasury official under President George H. W. Bush, said without a doubt Obama’s tax proposals would be more beneficial to the municipal market primarily because he wants to impose higher tax rates on the wealthy, which would make tax-exempt bonds more attractive. | While Romney has not specifically mentioned capping tax exemption, in a Wall Street Journal editorial in August, Glenn Hubbard, his senior economic adviser, said the exclusion of interest on tax-exempt municipal bonds is “on the table” for the Republican candidate. | |

8 Certified Annual Report

One can see that both candidates’ potential tax policies, as known today, could influence the municipal bond market. However, as with most election rhetoric the eventual legislation may look nothing like the original thoughts. There are two things that people should never watch being made, sausage and legislation!

The Municipal Market

The demand picture in the municipal market improved during the fiscal year. Investors poured $56 billion into municipal bond mutual funds over the last twelve months. The total assets in municipal bond mutual funds were $562 billion according to the Investment Company Institute, a mutual fund industry advocacy group. Assets in municipal bond mutual funds on November 30, 2010, just before the six-month period of investor exodus, were $497 billion. On the other side of the ledger, the supply picture improved. The supply of new issue municipal bonds was $379 billion for the 12 months ending September 30, 2012. This exceeded the $329 billion for the twelve months ending September 30, 2011, by $50 billion, or a 15% increase.

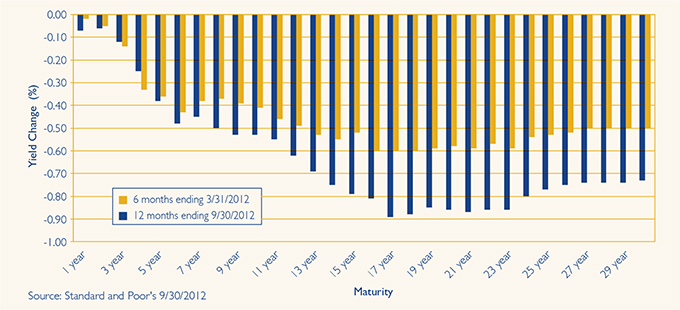

The trend towards lower interest rates continued throughout this fiscal year. With short-term yields anchored near zero, investors moved out along the yield curve in search of more income. This caused long-term maturities to decrease in yield much more than short-term maturities. The average change in yield for the Thornburg Strategic Municipal Income Fund’s investment universe (1-30 years) as measured by the average change in yield of a AAA general obligation bond, was negative 0.17% for the first half of the fiscal year. In the second half of the fiscal year the same measure of average yield change decreased 0.45%. This change in average yields was almost double that of the 1-10 year maturity range of the municipal market. See Graph I.

Graph I: AAA General Obligation Municipal Yield Changes for 9/30/2011 through 9/30/2012

Past performance does not guarantee future results.

Certified Annual Report 9

LETTER TO SHAREHOLDERS,

CONTINUED

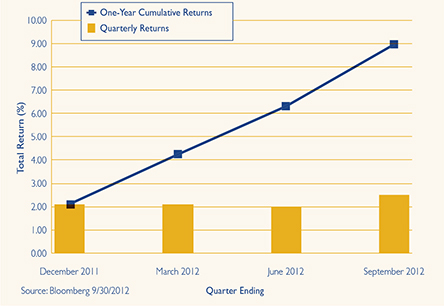

Graph II: BofA Merrill Lynch Municipal Master Index

Quarterly and Cumulative Total Returns

Past performance does not guarantee future results.

Investors, again in a search for income, have been willing to pay much more for lower quality securities than any time since 2008. This caused quality spreads to narrow and lower quality securities to out-perform higher quality securities. On December 30, 2011, the incremental yield an investor picked up for buying a BBB security versus an AAA security with a 10-year maturity was 3.00%. On September 30, 2012, that incremental yield equaled 2.08%, a 0.92% decrease. Graph II shows the quarter by quarter and cumulative total return performance of the BofA Merrill Lynch Municipal Master Index for the fiscal year.

The credit picture in the municipal market is still mixed. At the state level, revenues continue to increase. At the local level, which has a heavy reliance on real estate taxes, the continued decline of assessed values has put pressure on local finances. Pension funding levels continue to decline due to poor investment returns and cutbacks in annual pension contributions. Several state and local pension plans, recognizing the folly of this condition, have begun to reform their pension system calling for higher participant contributions, higher retirement ages or both. These measures and others have caused us to forsake investments in the state of Illinois and Puerto Rico general obligation debt.

In the last semi-annual letter to shareholders, we noted the risks of rising interest rates. As bond portfolio managers, we are always worried. If bonds are doing well, the economy is probably doing poorly, and we worry. If the economy is doing well, we worry because yields are probably rising and bond prices are declining. This is the life we chose.

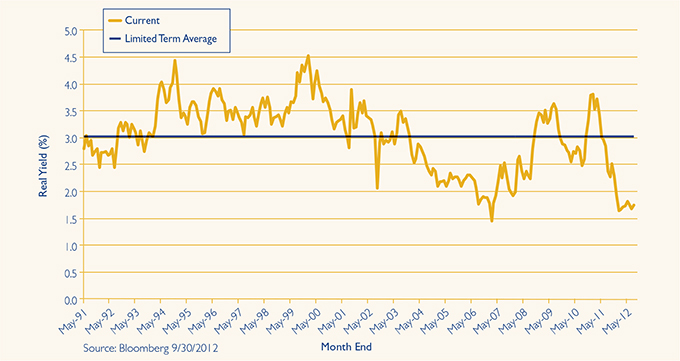

The level of real yields (yield less inflation) is a measure of value for fixed income products. Real yield levels are at record lows across all fixed income products. Relative to other fixed income products, municipal bonds appear to be attractive. Graph III illustrates this measure.

Real yield levels for a 30-year AAA general obligation municipal bond using Core PCE as an inflation measure are near 20-year lows, and we worry. At the same time, we are reminded of a famous quote by John Maynard Keynes, “The market can stay irrational longer than you can stay solvent.” Not that solvency is an issue but Graph III would suggest rationality is. This state of affairs can continue for some time, but it is still a risk.

10 Certified Annual Report

Graph III: 30 Year AAA Muni Real Yield Using Core PCE

Past performance does not guarantee future results.

The long-term average real yield for a 30-year AAA municipal general obligation bond is 3.03%. This means that since May 1991, investors have demanded 3.03% above the Core PCE inflation rate to invest in 30-year AAA general obligation bonds. The current yield on a 30-year AAA municipal general obligation bond is 3.35% and Core PCE inflation is 1.60% as of August 31, 2012 (last data point available). If this relationship were to return back to the average long-term real yield level one of three things must happen. First, 30-year interest rates need to increase approximately 1.25%. Second, inflation must decrease by 1.25%. Neither of these two outcomes will be pleasant. Third, some combination of the two prior outcomes could occur, which also promises to be unpleasant. Investors should use this information to recognize the risk inherent in fixed income products at these historically low yield levels. They should take this opportunity to review their portfolios and determine if these portfolios are properly diversified. In addition, they should ask themselves if they have an appropriate time horizon in mind for their investments; we suggest two to three years from the point you ask yourself that question.

Conclusion

Your Thornburg Strategic Municipal Income Fund continues to traverse the municipal market looking for undervalued securities. We do not maintain a laddered portfolio structure for this Fund as we do for the “core” funds (Limited and Intermediate). This Fund strives to offer its shareholders a durable income stream and as such purchases securities with longer durations (market risk) and lower credit quality when valuations are attractive. We would like to thank you for the trust you have placed with us and will continue to keep that foremost in our minds.

Certified Annual Report 11

LETTER TO SHAREHOLDERS,

CONTINUED

Sincerely, | ||||

|

|

| ||

Christopher Ihlefeld | Christopher Ryon, CFA | Josh Gonze | ||

Portfolio Manager | Portfolio Manager | Portfolio Manager | ||

Managing Director | Managing Director | Managing Director | ||

The matters discussed in this report may constitute forward-looking statements made pursuant to the safe harbor provisions of the Securities Litigation Reform Act of 1995. These include any advisor or portfolio manager prediction, assessment, analysis or outlook for individual securities, industries, investment styles, market sectors and/or markets. These statements involve risks and uncertainties. In addition to the general risks described for each fund in its current prospectus, other factors bearing on these reports include the accuracy of the advisor’s or portfolio manager’s forecasts and predictions, the appropriateness of the investment strategies designed by the advisor or portfolio manager and the ability of the advisor or portfolio manager to implement their strategies efficiently and successfully. Any one or more of these factors, as well as other risks affecting the securities markets generally, could cause the actual results of any fund to differ materially as compared to its benchmarks.

12 Certified Annual Report

| SCHEDULE OF INVESTMENTS | ||

| Thornburg Strategic Municipal Income Fund | September 30, 2012 | |

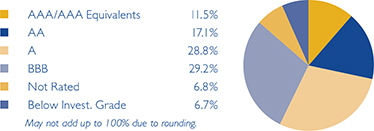

SUMMARY OF SECURITY CREDIT RATINGS†

We have used ratings from Standard & Poor’s (S&P). Where S&P ratings are not available, we have used Moody’s Investors Service. Where neither rating is available, we have used ratings from Fitch Ratings. The category of investments identified as “AAA” in this graph includes investments which are pre-refunded or escrowed to maturity. Such investments are backed by an escrow or trust containing sufficient U.S. Government or U.S. Government agency securities to satisfy the timely payment of principal and interest and, therefore, are normally deemed to be equivalent to AAA-rated securities.

Issuer-Description | Credit Rating† S&P/ Moody’s | Principal Amount | Value | |||||||

ALABAMA — 0.56% | ||||||||||

City of Mobile Industrial Development Board PCR, 1.65% due 6/1/2034 put 3/20/2017 (Alabama Power Company Barry Plant Project) | A/A2 | $ | 1,000,000 | $ | 1,021,650 | |||||

ARIZONA — 1.04% | ||||||||||

Maricopa County PCR, 6.00% due 5/1/2029 put 5/1/2014 (Arizona Public Service Co.) | BBB/Baa1 | 500,000 | 534,815 | |||||||

Pima County IDA, 6.25% due 7/1/2013 (Arizona Charter Schools) | NR/Baa3 | 185,000 | 185,736 | |||||||

Pima County IDA, 5.875% due 4/1/2022 (Cambridge Academy) | NR/NR | 435,000 | 454,706 | |||||||

Pima County IDA, 5.125% due 12/1/2040 (Providence Day School) | BBB+/NR | 710,000 | 716,319 | |||||||

CALIFORNIA — 21.30% | ||||||||||

Brea Redevelopment Agency, 0% due 8/1/2032 (Redevelopment Project AB) | AA-/NR | 1,370,000 | 372,613 | |||||||

Brea Redevelopment Agency, 0% due 8/1/2034 (Redevelopment Project AB) | AA-/NR | 5,000,000 | 1,141,700 | |||||||

California HFFA, 6.25% due 2/1/2026 (Community Program Developmental Disabilities; Insured: California Mtg Insurance) | A-/NR | 1,500,000 | 1,766,400 | |||||||

California HFFA, 5.00% due 11/15/2034 (Children’s Hospital Los Angeles) | BBB+/Baa2 | 420,000 | 451,781 | |||||||

California Housing Finance Agency, 4.625% due 8/1/2016 (Low-Moderate Income Housing Loans; Insured: FGIC) (AMT) | BBB/Baa2 | 1,175,000 | 1,222,576 | |||||||

California Housing Finance Agency, 4.625% due 8/1/2026 (Low-Moderate Income Housing Loans; Insured: FGIC) (AMT) | BBB/Baa2 | 560,000 | 544,846 | |||||||

California Municipal Finance Authority, 8.50% due 11/1/2039 (Harbor Regional Center) | NR/Baa1 | 1,000,000 | 1,205,420 | |||||||

California State Public Works Board, 5.00% due 4/1/2028 (Corrections & Rehabilitation and Judicial Council) | BBB+/A2 | 1,000,000 | 1,137,770 | |||||||

California State Public Works Board, 6.25% due 4/1/2034 (Department of General Services-Offices Renovation) | BBB+/A2 | 100,000 | 118,825 | |||||||

California Statewide Communities Development Authority, 5.00% due 8/15/2039 (Children’s Hospital of Los Angeles; Insured: Natl-Re) | BBB/Baa2 | 1,185,000 | 1,217,433 | |||||||

California Statewide Communities Development Authority, 6.125% due 7/1/2046 (Aspire Public Schools) | NR/NR | 1,000,000 | 1,033,150 | |||||||

Calipatria USD, 0% due 8/1/2025 (Educational Facilities Improvements; Insured: ACA) | NR/NR | 2,425,000 | 1,120,980 | |||||||

Carson Redevelopment Agency, 7.00% due 10/1/2036 (Project Area 1) | A-/NR | 500,000 | 586,885 | |||||||

Chico Redevelopment Agency, 5.00% due 4/1/2030 (Chico Amended & Merged Redevelopment; Insured: AMBAC) | A+/NR | 1,000,000 | 1,032,430 | |||||||

City of Los Angeles, 5.00% due 6/1/2027 (Insured: MBIA) (Wastewater System) | AA/Aa3 | 600,000 | 616,686 | |||||||

Corona-Norco USD COP, 5.00% due 4/15/2031 (Insured: AGM) | AA-/Aa3 | 1,750,000 | 1,937,442 | |||||||

County of El Dorado, 5.00% due 9/1/2026 (El Dorado Hills Development-Community Facilities) | A/NR | 630,000 | 706,583 | |||||||

Daly County Housing Development Finance Agency, 5.25% due 12/15/2023 (Franciscan Mobile Park) | A/NR | 650,000 | 701,174 | |||||||

Kern Community College District COP, 4.00% due 4/1/2014 | SP-1+/NR | 2,500,000 | 2,612,000 | |||||||

M-S-R Energy Authority, 6.50% due 11/1/2039 | A-/NR | 1,000,000 | 1,318,890 | |||||||

Merced Redevelopment Agency, 6.50% due 9/1/2039 (Merced Gateways Redevelopment) | BB+/NR | 300,000 | 320,445 | |||||||

Certified Annual Report 13

| SCHEDULE OF INVESTMENTS, CONTINUED | ||

| Thornburg Strategic Municipal Income Fund | September 30, 2012 | |

Issuer-Description | Credit Rating† S&P/ Moody’s | Principal Amount | Value | |||||||

Moorpark Mobile Home Park, 6.15% due 5/15/2031 (Villa Del Arroyo) | BBB/NR | $ | 1,000,000 | $ | 1,099,600 | |||||

Newport-Mesa USD, 0% due 8/1/2034 (Orange County District Schools) | AA/Aa1 | 5,000,000 | 1,882,450 | |||||||

Oak Park USD GO, 0% due 8/1/2030 (Insured: AGM) | AA-/Aa3 | 500,000 | 206,080 | |||||||

Pittsburg Redevelopment Agency, 0% due 8/1/2027 (Los Medanos Community Development; Insured: AMBAC) | BBB+/NR | 1,275,000 | 548,097 | |||||||

Pittsburg Redevelopment Agency, 0% due 8/1/2028 (Los Medanos Community Development; Insured: AMBAC) | BBB+/NR | 5,000,000 | 2,011,900 | |||||||

Placentia-Yorba Linda USD COP, 5.00% due 10/1/2030 (Educational Facilities Construction; Insured: Natl-Re/FGIC) | A+/A1 | 1,500,000 | 1,567,635 | |||||||

Redwood City Redevelopment Agency, 0% due 7/15/2021 (Redevelopment Project Area 2; Insured: AMBAC) | A-/NR | 1,285,000 | 839,825 | |||||||

Riverside County Asset Leasing Corp., 0% due 6/1/2021 (Riverside County Hospital; Insured: Natl-Re) | BBB/A2 | 535,000 | 350,602 | |||||||

San Diego USD, 0% due 7/1/2035 | AA-/Aa2 | 1,700,000 | 569,551 | |||||||

San Francisco City & County Redevelopment Financing Authority, 0% due 8/1/2023 (Redevelopment Project; Insured: Natl-Re) | A/Baa2 | 925,000 | 564,898 | |||||||

San Francisco City & County Redevelopment Financing Authority, 6.50% due 8/1/2039 (Mission Bay North Redevelopment) | A-/NR | 250,000 | 290,643 | |||||||

San Francisco City & County Redevelopment Financing Authority, 6.75% due 8/1/2041 (Mission Bay North Redevelopment) | A-/NR | 500,000 | 585,610 | |||||||

San Jose Redevelopment Agency, 5.50% due 8/1/2035 (Merged Area Redevelopment) | A/Ba1 | 1,000,000 | 1,017,110 | |||||||

Sonoma County Community Redevelopment Agency, 6.50% due 8/1/2034 (The Springs Redevelopment; Insured: AGM) | AA-/NR | 100,000 | 104,206 | |||||||

State of California, 2.50% due 6/20/2013 (General Fund Cash Management) | SP-1+/Mig1 | 1,050,000 | 1,066,873 | |||||||

State of California GO, 0.17% due 5/1/2034 put 10/1/2012 (Kindergarten University Facilities; LOC: Citibank N.A.) (daily demand notes) | AAA/Aa2 | 400,000 | 400,000 | |||||||

State of California GO, 0.20% due 5/1/2034 put 10/1/2012 (Kindergarten University Facilities; LOC: Citibank N.A./California State Teachers’ Retirement System) (daily demand notes) | A/Aa3 | 1,430,000 | 1,430,000 | |||||||

State of California GO, 0.22% due 5/1/2034 put 10/1/2012(Kindergarten University Facilities; LOC: Citibank N.A./California State Teachers’ Retirement System) (daily demand notes) | A/Aa3 | 1,000,000 | 1,000,000 | |||||||

Union Elementary School District, 0% due 9/1/2027 (Santa Clara County District Schools; Insured: Natl-Re) | AA+/NR | 905,000 | 490,239 | |||||||

Whittier Public Financing Authority, 5.00% due 11/1/2030 (Whittier Boulevard Redevelopment Project; Insured: AMBAC) | A-/NR | 1,425,000 | 1,438,951 | |||||||

COLORADO — 4.90% | ||||||||||

Denver City & County COP, 0.20% due 12/1/2029 put 10/1/2012 (Wellington E. Webb Municipal Office Building; SPA: JPMorgan Chase Bank) (daily demand notes) | AA+/Aa2 | 3,225,000 | 3,225,000 | |||||||

Denver Convention Center Hotel Authority, 5.125% due 12/1/2026 (Insured: Syncora) | BBB-/Baa3 | 1,000,000 | 1,034,780 | |||||||

Denver Convention Center Hotel Authority, 5.00% due 12/1/2030 (Insured: Syncora) | BBB-/Baa3 | 450,000 | 466,128 | |||||||

Denver Convention Center Hotel Authority, 5.00% due 12/1/2035 (Insured: Syncora) | BBB-/Baa3 | 605,000 | 621,625 | |||||||

Eagle Bend Metropolitan District GO, 5.00% due 12/1/2020 (Insured: Radian) | A-/NR | 1,010,000 | 1,053,814 | |||||||

Eagle River Fire District, 6.625% due 12/1/2024 | NR/NR | 225,000 | 249,118 | |||||||

Eagle River Fire District, 6.875% due 12/1/2030 | NR/NR | 400,000 | 443,192 | |||||||

Public Authority for Colorado Energy, 5.75% due 11/15/2018 (Natural Gas Purchase) | A-/Baa2 | 770,000 | 885,092 | |||||||

Public Authority for Colorado Energy, 6.50% due 11/15/2038 (Natural Gas Purchase) | A-/Baa2 | 260,000 | 331,835 | |||||||

Regional Transportation District COP, 5.375% due 6/1/2031 | A-/Aa3 | 500,000 | 573,280 | |||||||

CONNECTICUT — 1.16% | ||||||||||

Connecticut Health & Educational Facilities Authority, 6.00% due 7/1/2039 (Ethel Walker School) | BBB-/NR | 1,000,000 | 1,096,870 | |||||||

a State of Connecticut GO, 0.68% due 9/15/2017 (Public Improvements) Floating Rate Note | AA/Aa3 | 1,000,000 | 1,003,600 | |||||||

14 Certified Annual Report

| SCHEDULE OF INVESTMENTS, CONTINUED | ||

| Thornburg Strategic Municipal Income Fund | September 30, 2012 | |

Issuer-Description | Credit Rating† | Principal Amount | Value | |||||||

DISTRICT OF COLUMBIA — 0.42% | ||||||||||

Metropolitan Washington Airports Authority, 0% due 10/1/2027 (Dulles Toll Road; Insured: AGM) | AA-/Aa3 | $ | 1,500,000 | $ | 755,760 | |||||

FLORIDA — 7.26% | ||||||||||

Florida Higher Educational Facilities Financing Authority, 5.00% due 4/1/2027 (Nova Southeastern University) | BBB/Baa2 | 1,000,000 | 1,098,780 | |||||||

Gainesville Utilities Systems, 0.21% due 10/1/2026 put 10/1/2012 (SPA: SunTrust Bank) (daily demand notes) | AA/Aa2 | 865,000 | 865,000 | |||||||

Hollywood Community Redevelopment Agency, 5.625% due 3/1/2024 | NR/A3 | 340,000 | 351,893 | |||||||

Lakeland Energy System, 5.25% due 10/1/2036 | AA/A1 | 2,000,000 | 2,623,420 | |||||||

Miami GO, 5.00% due 1/1/2017 (Homeland Defense/Neighborhood Capital Improvements) | BBB-/A3 | 1,245,000 | 1,355,743 | |||||||

Miami GO, 5.00% due 1/1/2018 (Homeland Defense/Neighborhood Capital Improvements) | BBB-/A3 | 1,790,000 | 1,959,226 | |||||||

Miami-Dade County School Board COP, 5.00% due 8/1/2027 (District School Facilities and Infrastructure) | A/A1 | 1,100,000 | 1,232,275 | |||||||

Pinellas County Educational Facilities Authority, 5.25% due 10/1/2030 (Barry University) | BBB/NR | 500,000 | 547,245 | |||||||

Sarasota County Public Hospital Board, 4.202% due 10/1/2021 (Sarasota Memorial Hospital; Insured: Natl-Re) | BBB/A1 | 1,000,000 | 993,530 | |||||||

Sarasota County Public Hospital Board, 5.50% due 7/1/2028 (Sarasota Memorial Hospital; Insured: Natl-Re) | BBB/A1 | 665,000 | 792,820 | |||||||

St. Johns County IDA, 5.625% due 8/1/2034 (Presbyterian Retirement) | NR/NR | 230,000 | 238,324 | |||||||

Tampa Sports Authority, 5.75% due 10/1/2020 (Tampa Bay Arena; Insured: Natl-Re) | BBB/Baa2 | 1,000,000 | 1,115,740 | |||||||

GEORGIA — 1.55% | ||||||||||

City of Atlanta, 6.25% due 11/1/2034 (Water and Wastewater Capital Improvement Program) | A/A1 | 500,000 | 608,265 | |||||||

Fulton County Development Authority, 5.00% due 10/1/2019 (Georgia Tech Athletic Association) | NR/A2 | 1,000,000 | 1,213,850 | |||||||

Main Street Natural Gas, Inc., 5.00% due 3/15/2018 (Georgia Gas) | A/A2 | 515,000 | 590,679 | |||||||

Main Street Natural Gas, Inc., 5.50% due 9/15/2023 (Georgia Gas) | A-/Baa2 | 350,000 | 404,303 | |||||||

GUAM — 1.24% | ||||||||||

Guam Government, 5.75% due 12/1/2034 (Layon Solid Waste Disposal Facility) | BBB+/NR | 500,000 | 562,370 | |||||||

Guam Government Department of Education COP, 6.875% due 12/1/2040 (John F. Kennedy High School) | B/NR | 1,000,000 | 1,098,950 | |||||||

Guam Government GO, 7.00% due 11/15/2039 | B+/NR | 520,000 | 587,850 | |||||||

ILLINOIS — 5.70% | ||||||||||

City of Chicago, 4.70% due 11/15/2013 (Near South Redevelopment; Insured: AMBAC) | NR/NR | 800,000 | 802,336 | |||||||

City of Chicago, 6.75% due 6/1/2022 (Pilsen Redevelopment) | NR/NR | 1,000,000 | 1,043,230 | |||||||

City of Chicago, 5.00% due 1/1/2035 (Midway Airport Development Plan; Insured: Natl-Re) | A/A2 | 1,055,000 | 1,057,996 | |||||||

Cook County GO, 5.25% due 11/15/2033 | AA/Aa3 | 1,000,000 | 1,139,560 | |||||||

Illinois Civic Center, 5.375% due 12/15/2012 (Insured: AGM) | NR/Aa3 | 505,000 | 507,086 | |||||||

Illinois Finance Authority, 5.75% due 11/15/2037 (OSF Healthcare System) | A/A3 | 330,000 | 361,010 | |||||||

Illinois Finance Authority, 6.00% due 5/15/2039 (OSF Healthcare System) | A/A3 | 1,565,000 | 1,815,854 | |||||||

Metropolitan Pier & Exposition Authority, 5.00% due 6/15/2050 (McCormick Place) | AAA/A3 | 1,500,000 | 1,632,885 | |||||||

Railsplitter Tobacco Settlement Authority, 6.00% due 6/1/2028 | A-/NR | 1,000,000 | 1,178,220 | |||||||

Village of Melrose Park GO, 6.75% due 12/15/2016 (Redevelopment Project Costs; Insured: Natl-Re) | NR/Baa2 | 250,000 | 279,685 | |||||||

Village of Melrose Park GO, 6.75% due 12/15/2021 (Redevelopment Project Costs; Insured: Natl-Re) | NR/Baa2 | 410,000 | 519,913 | |||||||

Certified Annual Report 15

| SCHEDULE OF INVESTMENTS, CONTINUED | ||

| Thornburg Strategic Municipal Income Fund | September 30, 2012 | |

Issuer-Description | Credit Rating† | Principal Amount | Value | |||||||

INDIANA — 5.66% | ||||||||||

Carmel Redevelopment District COP, 6.50% due 7/15/2035 (Performing Arts Center) | NR/NR | $ | 1,000,000 | $ | 1,065,800 | |||||

Indiana Finance Authority, 6.00% due 12/1/2019 (U.S. Steel Corp.) | BB/B1 | 2,500,000 | 2,789,225 | |||||||

Indiana Finance Authority, 0.23% due 2/1/2035 put 10/1/2012 (Lease Appropriation; SPA: | ||||||||||

JPMorgan Chase Bank) (daily demand notes) | AA+/NR | 2,800,000 | 2,800,000 | |||||||

Indiana Finance Authority, 0.20% due 2/1/2037 put 10/1/2012 (Lease Appropriation; SPA: JPMorgan Chase Bank) (daily demand notes) | AA+/Aa2 | 2,500,000 | 2,500,000 | |||||||

b Indiana Finance Authority, 6.375% due 9/15/2041 (Marian University) | BBB-/NR | 1,000,000 | 1,108,630 | |||||||

KANSAS — 2.76% | ||||||||||

City of Wichita GO, 0.30% due 8/15/2013 (Norris Training Systems) | SP-1+/Mig1 | 3,900,000 | 3,900,390 | |||||||

City of Wichita MFR, 5.90% due 12/1/2016 (Brentwood Apartments) | B/NR | 400,000 | 379,556 | |||||||

City of Wichita MFR, 5.85% due 12/1/2025 (Brentwood Apartments) | B/NR | 895,000 | 732,352 | |||||||

KENTUCKY — 1.49% | ||||||||||

Kentucky EDA, 0% due 10/1/2021 (Norton Healthcare, Inc.; Insured: Natl-Re) | BBB/Baa2 | 715,000 | 496,703 | |||||||

Kentucky EDA, 0% due 10/1/2022 (Norton Healthcare, Inc.; Insured: Natl-Re) | BBB/Baa2 | 2,490,000 | 1,636,578 | |||||||

Owen County Waterworks Systems, 6.25% due 6/1/2039 (American Water Co.) | BBB+/Baa2 | 500,000 | 564,055 | |||||||

LOUISIANA — 1.56% | ||||||||||

Louisiana Public Facilities Authority, 5.00% due 7/1/2032 (Black & Gold Facilities; Insured: CIFG) | AA-/Aa3 | 120,000 | 126,101 | |||||||

Louisiana Public Facilities Authority, 5.375% due 5/15/2043 (Ochsner Clinic Foundation) | NR/Baa1 | 500,000 | 523,390 | |||||||

Parish of St. Charles, 4.00% due 12/1/2040 put 6/1/2022 (Valero Energy Corp. Refinery) | BBB/Baa2 | 2,000,000 | 2,172,060 | |||||||

MASSACHUSETTS — 0.27% | ||||||||||

Massachusetts Educational Financing Authority, 6.00% due 1/1/2028 | AA/NR | 420,000 | 490,573 | |||||||

MICHIGAN — 7.72% | ||||||||||

Charter County of Wayne, 5.00% due 12/1/2030 (Airport Hotel; Insured: Natl-Re) | BBB+/Baa2 | 805,000 | 805,354 | |||||||

Detroit School District, 5.00% due 5/1/2025 (School Building & Site; Insured: Q-SBLF) | AA-/Aa2 | 1,000,000 | 1,159,890 | |||||||

Detroit School District, 5.25% due 5/1/2027 (School Building & Site; Insured: AGM) | AA-/Aa2 | 1,000,000 | 1,234,840 | |||||||

Detroit Water and Sewerage Department, 5.25% due 7/1/2039 (Sewage Disposal System; Insured: AGM) | A+/Baa2 | 1,250,000 | 1,337,575 | |||||||

Detroit Water Supply Systems, 5.00% due 7/1/2018 (Insured: Natl-Re) | BBB/Baa2 | 350,000 | 384,090 | |||||||

Kalamazoo Hospital Finance Authority, 5.00% due 5/15/2036 (Bronson Methodist Hospital) | NR/A2 | 1,000,000 | 1,072,630 | |||||||

Kalamazoo Hospital Finance Authority, 5.25% due 5/15/2041 (Bronson Healthcare Group) | NR/A2 | 1,000,000 | 1,102,700 | |||||||

Michigan Finance Authority, 5.00% due 4/1/2031 (Local Government Loan Program) | A+/NR | 1,000,000 | 1,090,020 | |||||||

Michigan Finance Authority, 8.125% due 4/1/2041 (Hope Academy) | NR/NR | 1,000,000 | 1,170,900 | |||||||

Michigan Hospital Finance Authority, 5.00% due 7/15/2025 (Oakwood Southshore Medical Center) | A/A2 | 650,000 | 700,102 | |||||||

Michigan Hospital Finance Authority, 5.75% due 4/1/2032 pre-refunded 4/1/2013 (Various Hospital Facility Improvements) | AA+/A2 | 150,000 | 154,205 | |||||||

Michigan Hospital Finance Authority, 5.75% due 11/15/2039 (Henry Ford Health) | A/A1 | 1,000,000 | 1,151,750 | |||||||

Michigan Housing Development Authority, 3.375% due 11/1/2016 (AMT) | AA/NR | 865,000 | 891,607 | |||||||

Michigan Public School Academy, 8.00% due 8/1/2035 (Will Carleton Charter School) | NR/NR | 1,070,000 | 1,115,903 | |||||||

Michigan Strategic Fund, 5.00% due 8/1/2013 (NSF International) | A-/NR | 300,000 | 308,457 | |||||||

Michigan Strategic Fund, 7.00% due 5/1/2021 (The Detroit Edison Company; Insured: Natl- Re/AMBAC) | NR/NR | 250,000 | 326,717 | |||||||

MINNESOTA — 0.29% | ||||||||||

St. Paul Housing & Redevelopment Authority, 5.25% due 5/15/2023 | A-/A3 | 100,000 | 106,797 | |||||||

16 Certified Annual Report

| SCHEDULE OF INVESTMENTS, CONTINUED | ||

| Thornburg Strategic Municipal Income Fund | September 30, 2012 | |

Issuer-Description | Credit Rating† | Principal Amount | Value | |||||||

Washington County Housing Redevelopment Authority, 5.625% due 6/1/2037 (Birchwood & Woodbury) | NR/NR | $ | 415,000 | $ | 422,462 | |||||

MISSOURI — 1.23% | ||||||||||

Kansas City Tax Increment Financing Commission, 5.25% due 3/1/2018 (Maincor Project- Public Improvements) | NR/NR | 1,265,000 | 1,331,311 | |||||||

Missouri Development Finance Board, 0.20% due 12/1/2033 put 10/1/2012 (Nelson Gallery Foundation; SPA: JPMorgan Chase Bank) (daily demand notes) | AAA/Aaa | 900,000 | 900,000 | |||||||

NEVADA — 1.61% | ||||||||||

Carson City, 5.00% due 9/1/2033 (Carson Tahoe Regional Healthcare Project) | BBB+/NR | 1,250,000 | 1,345,162 | |||||||

Redevelopment Agency of the City of Mesquite, 7.00% due 6/1/2019 (Public Facility and Redevelopment Projects) | BBB+/NR | 700,000 | 733,229 | |||||||

Redevelopment Agency of the City of Mesquite, 7.125% due 6/1/2021 (Public Facility and Redevelopment Projects) | BBB+/NR | 300,000 | 312,738 | |||||||

Redevelopment Agency of the City of Mesquite, 7.375% due 6/1/2024 (Public Facility and Redevelopment Projects) | BBB+/NR | 500,000 | 520,610 | |||||||

NEW JERSEY — 0.43% | ||||||||||

Higher Education Student Assistance Authority, 5.75% due 12/1/2039 (NJCLASS Student Loan Program) (AMT) | A/A2 | 750,000 | 775,672 | |||||||

NEW MEXICO — 0.61% | ||||||||||

City of Farmington PCR, 4.70% due 9/1/2024 (Arizona Public Service Co.) | BBB/Baa1 | 1,000,000 | 1,113,940 | |||||||

NEW YORK — 2.62% | ||||||||||

New York State Dormitory Authority, 5.00% due 6/15/2031 (Metropolitan Transportation Authority and Urban Development Corp.) | AAA/NR | 3,000,000 | 3,621,150 | |||||||

New York Thruway Authority, 5.00% due 1/1/2037 (Governor Thomas E. Dewey Thruway) | A+/A1 | 1,000,000 | 1,135,480 | |||||||

OHIO — 2.83% | ||||||||||

American Municipal Power, Inc., 5.00% due 2/15/2037 (AMP Fremont Energy Center) | A/A1 | 1,000,000 | 1,114,790 | |||||||

Cleveland Cuyahoga County Port Authority, 6.25% due 5/15/2016 (LOC: FifthThird Bank) | BBB/NR | 345,000 | 348,981 | |||||||

Cleveland Cuyahoga County Port Authority, 7.00% due 5/15/2040 (Insured: City Appropriations) | BBB/NR | 1,000,000 | 1,131,840 | |||||||

Ohio State Water Development Authority PCR, 5.875% due 6/1/2033 put 6/1/2016 (FirstEnergy Nuclear Generation Corp.) | BBB-/Baa2 | 1,000,000 | 1,131,920 | |||||||

Ohio State Water Development Authority PCR, 3.375% due 7/1/2033 put 7/1/2015 (FirstEnergy Nuclear Generation Corp.) | BBB-/Baa3 | 1,350,000 | 1,396,238 | |||||||

OREGON — 0.84% | ||||||||||

Oregon MFR Pass-Through Certificates, 6.05% due 11/1/2034 (AMT) | NR/Baa1 | 500,000 | 500,490 | |||||||

Western Generation Agency, 5.00% due 1/1/2016 (Wauna Cogeneration; Insured: ACA) | NR/NR | 1,000,000 | 1,027,900 | |||||||

PENNSYLVANIA — 5.33% | ||||||||||

Allegheny County IDA, 6.75% due 8/15/2035 (Propel Charter School) | BBB-/NR | 950,000 | 1,056,542 | |||||||

Hospitals and Higher Educational Facilities Authority of Philadelphia, 0.20% due 7/1/2025 put 10/1/2012 (The Children’s Hospital of Philadelphia; SPA: JPMorgan Chase Bank) (daily demand notes) | AA/Aa2 | 1,000,000 | 1,000,000 | |||||||

Pennsylvania Economic Development Financing Authority, 5.00% due 12/1/2014 (Colver Project; Insured: AMBAC) (AMT) | BBB-/Ba1 | 450,000 | 459,261 | |||||||

Certified Annual Report 17

| SCHEDULE OF INVESTMENTS, CONTINUED | ||

| Thornburg Strategic Municipal Income Fund | September 30, 2012 | |

Issuer-Description | Credit Rating† | Principal Amount | Value | |||||||

Pennsylvania Economic Development Financing Authority, 4.625% due 12/1/2018 (Colver Project; Insured: AMBAC) (AMT) | BBB-/Ba1 | $ | 1,800,000 | $ | 1,826,694 | |||||

Pennsylvania Turnpike Commission, 0% due 12/1/2030 (Convertible Capital Appreciation) | A-/A3 | 2,000,000 | 1,959,800 | |||||||

Philadelphia Airport, 5.00% due 6/15/2027 (AMT) | A+/A2 | 2,000,000 | 2,238,040 | |||||||

Philadelphia IDA, 6.00% due 8/1/2035 (Mast Charter School) | BBB+/NR | 1,000,000 | 1,132,700 | |||||||

RHODE ISLAND — 0.45% | ||||||||||

Housing Authority of the City of Pawtucket, 5.50% due 9/1/2022 (Public Housing Development) | AA-/NR | 315,000 | 384,502 | |||||||

Housing Authority of the City of Pawtucket, 5.50% due 9/1/2024 (Public Housing Development) | AA-/NR | 350,000 | 421,438 | |||||||

SOUTH DAKOTA — 0.47% | ||||||||||

South Dakota Health & Educational Facilities Authority, 5.50% due 11/1/2040 (Sanford Health) | A+/A1 | 750,000 | 845,460 | |||||||

TENNESSEE — 0.37% | ||||||||||

Tennessee Energy Acquisition Corp., 5.00% due 2/1/2015 | BBB/Baa3 | 100,000 | 106,621 | |||||||

Tennessee Energy Acquisition Corp., 5.25% due 9/1/2024 | A-/Baa2 | 500,000 | 554,790 | |||||||

TEXAS — 11.13% | ||||||||||

Austin Convention Enterprises, Inc., 5.25% due 1/1/2024 (Austin Convention Center; Insured: Syncora) | BB+/Ba1 | 720,000 | 769,111 | |||||||

Austin Convention Enterprises, Inc., 5.00% due 1/1/2034 (Austin Convention Center; Insured: Syncora) | BB+/Ba1 | 665,000 | 687,863 | |||||||

Clifton Higher Education Finance Corp., 9.00% due 2/15/2038 (Tejano Center for Community Concerns, Inc.) | BBB-/NR | 1,000,000 | 1,194,380 | |||||||

Gulf Coast Waste Disposal Authority, 6.10% due 8/1/2024 (International Paper Co.) (AMT) | BBB/Baa3 | 100,000 | 100,351 | |||||||

Houston Higher Education Finance Corp., 0.18% due 5/15/2048 put 10/1/2012 (William Marsh Rice University) (daily demand notes) | AAA/Aaa | 780,000 | 780,000 | |||||||

Kimble County Hospital District, 6.25% due 8/15/2033 | NR/NR | 500,000 | 555,000 | |||||||

La Vernia Higher Education Finance Corp., 6.25% due 8/15/2039 (Kipp, Inc.) | BBB/NR | 1,000,000 | 1,166,150 | |||||||

San Antonio Energy Acquisition Public Facilities Corp., 5.50% due 8/1/2021 | A-/Baa3 | 40,000 | 45,392 | |||||||

San Juan Higher Education Finance Authority, 6.70% due 8/15/2040 (IDEA Public School) | BBB/NR | 1,000,000 | 1,161,830 | |||||||

State of Texas, 2.50% due 8/30/2013 (General Revenue Fund Cash Management) | SP-1+/Mig1 | 3,500,000 | 3,572,765 | |||||||

Tarrant County Cultural Educational Facilities Finance Corp., 0.20% due 10/1/2041 put 10/1/2012 (Methodist Hospitals of Dallas; LOC: JPMorgan Chase Bank) (daily demand notes) | AAA/Aa1 | 1,955,000 | 1,955,000 | |||||||

Texas City Industrial Development Corp., 7.375% due 10/1/2020 (BP Pipelines N.A., Inc.) | A/A2 | 1,000,000 | 1,370,350 | |||||||

Texas Multi-Family Housing Corp., 7.00% due 7/1/2043 (HDSA Affordable Housing Pool) | BB/NR | 3,000,000 | 3,022,950 | |||||||

Texas Public Finance Authority Charter School Finance Corp., 4.15% due 8/15/2016 (IDEA Public Schools; Insured: ACA) | BBB/NR | 100,000 | 107,097 | |||||||

Texas Public Finance Authority Charter School Finance Corp., 5.00% due 2/15/2018 (Cosmos Foundation, Inc.) | BBB/NR | 785,000 | 826,895 | |||||||

Texas Public Finance Authority Charter School Finance Corp., 5.00% due 8/15/2023 (IDEA Public Schools; Insured: ACA) | BBB/NR | 155,000 | 164,912 | |||||||

Texas Public Finance Authority Charter School Finance Corp., 5.00% due 8/15/2030 (IDEA Public Schools; Insured: ACA) | BBB/NR | 1,500,000 | 1,562,460 | |||||||

Texas Public Finance Authority Charter School Finance Corp., 6.20% due 2/15/2040 (Cosmos Foundation, Inc.) | BBB/NR | 1,000,000 | 1,148,990 | |||||||

U.S. VIRGIN ISLANDS — 0.41% | ||||||||||

Virgin Islands Public Finance Authority, 6.75% due 10/1/2037 | NR/Baa3 | 500,000 | 591,625 | |||||||

Virgin Islands Water & Power Authority, 5.50% due 7/1/2017 | NR/NR | 150,000 | 150,360 | |||||||

UTAH — 1.06% | ||||||||||

Herriman City, 4.75% due 11/1/2022 (Towne Center Access and Utility Improvements) | A/NR | 1,000,000 | 1,115,710 | |||||||

18 Certified Annual Report

| SCHEDULE OF INVESTMENTS, CONTINUED | ||

| Thornburg Strategic Municipal Income Fund | September 30, 2012 | |

Issuer-Description | Credit Rating† | Principal Amount | Value | |||||||

Murray City, 0.20% due 5/15/2037 put 10/1/2012 (IHC Health Services, Inc.; SPA: JPMorgan Chase Bank) (daily demand notes) | AA+/Aa1 | $ | 800,000 | $ | 800,000 | |||||

VERMONT — 0.44% | ||||||||||

Vermont Student Assistance Corp., 5.10% due 6/15/2032 (Student Loan Program) (AMT) | A/NR | 760,000 | 789,184 | |||||||

VIRGINIA — 0.86% | ||||||||||

Lexington IDA Residential Care Facility, 5.375% due 1/1/2028 (Kendal at Lexington) | NR/NR | 1,000,000 | 1,018,750 | |||||||

Virginia Small Business Financing Authority, 9.00% due 7/1/2039 (Hampton RDS Proton) | NR/NR | 500,000 | 540,250 | |||||||

WASHINGTON — 0.61% | ||||||||||

Washington Health Care Facilities Authority, 5.70% due 7/1/2038 (Overlake Hospital Medical Center) | A-/A3 | 1,000,000 | 1,111,240 | |||||||

WISCONSIN — 2.01% | ||||||||||

Wisconsin Health & Educational Facilities Authority, 5.00% due 8/15/2027 (ProHealth Care, Inc.) | A+/A1 | 3,300,000 | 3,644,091 | |||||||

|

| |||||||||

TOTAL INVESTMENTS — 98.19% (Cost $163,320,885) | $ | 178,063,074 | ||||||||

OTHER ASSETS LESS LIABILITIES — 1.81% | 3,290,248 | |||||||||

|

| |||||||||

NET ASSETS — 100.00% | $ | 181,353,322 | ||||||||

|

| |||||||||

Footnote Legend

| † | Credit ratings are unaudited. Rating changes may have occurred subsequent to the reporting period end. Bonds issued with a maturity of one year or less are assigned Moody’s ratings from MIG-1 to MIG-4 and Standard and Poor’s ratings from SP-1+ to SP-3 with MIG-1 and SP-1+ being the strongest ratings. |

| a | When-issued security. |

| b | Segregated as collateral for a when-issued security. |

Portfolio Abbreviations

To simplify the listings of securities, abbreviations are used per the table below:

| ACA | Insured by American Capital Access | |

| AGM | Insured by Assured Guaranty Municipal Corp. | |

| AMBAC | Insured by American Municipal Bond Assurance Corp. | |

| AMT | Alternative Minimum Tax | |

| CIFG | CIFG Assurance North America Inc. | |

| COP | Certificates of Participation | |

| EDA | Economic Development Authority | |

| FGIC | Insured by Financial Guaranty Insurance Co. | |

| GO | General Obligation | |

| HFFA | Health Facilities Financing Authority | |

| IDA | Industrial Development Authority | |

| LOC | Letter of Credit | |

| MBIA | Insured by Municipal Bond Investors Assurance | |

| Mtg | Mortgage | |

| MFR | Multi-Family Revenue | |

| Natl-Re | Insured by National Public Finance Guarantee Corp. | |

| PCR | Pollution Control Revenue Bond | |

| Q-SBLF | Qualified School Bond Loan Fund | |

| Radian | Insured by Radian Asset Assurance | |

| SPA | Stand-by Purchase Agreement | |

| Syncora | Insured by Syncora Guarantee Inc. | |

| USD | Unified School District |

See notes to financial statements.

Certified Annual Report 19

| STATEMENT OF ASSETS AND LIABILITIES | ||

| Thornburg Strategic Municipal Income Fund | September 30, 2012 | |

ASSETS | ||||

Investments at value (cost $163,320,885) (Note 2) | $ | 178,063,074 | ||

Cash | 254,611 | |||

Receivable for investments sold | 1,165,000 | |||

Receivable for fund shares sold | 1,096,312 | |||

Interest receivable | 2,098,131 | |||

Prepaid expenses and other assets | 23,003 | |||

|

| |||

Total Assets | 182,700,131 | |||

|

| |||

LIABILITIES | ||||

Payable for investments purchased | 1,000,000 | |||

Payable for fund shares redeemed | 80,743 | |||

Payable to investment advisor and other affiliates (Note 3) | 136,215 | |||

Accounts payable and accrued expenses | 49,516 | |||

Dividends payable | 80,335 | |||

|

| |||

Total Liabilities | 1,346,809 | |||

|

| |||

NET ASSETS | $ | 181,353,322 | ||

|

| |||

NET ASSETS CONSIST OF: | ||||

Undistributed net investment income | $ | 3,622 | ||

Net unrealized appreciation on investments | 14,742,189 | |||

Accumulated net realized gain (loss) | 431,429 | |||

Net capital paid in on shares of beneficial interest | 166,176,082 | |||

|

| |||

| $ | 181,353,322 | |||

|

| |||

NET ASSET VALUE: | ||||

Class A Shares: | ||||

Net asset value and redemption price per share ($65,445,781 applicable to 4,315,010 shares of beneficial interest outstanding—Note 4) | $ | 15.17 | ||

Maximum sales charge, 2.00% of offering price | 0.31 | |||

|

| |||

Maximum offering price per share | $ | 15.48 | ||

|

| |||

Class C Shares: | ||||

Net asset value and offering price per share* ($23,521,020 applicable to 1,549,180 shares of beneficial interest outstanding—Note 4) | $ | 15.18 | ||

|

| |||

Class I Shares: | ||||

Net asset value, offering and redemption price per share ($92,386,521 applicable to 6,085,721 shares of beneficial interest outstanding—Note 4) | $ | 15.18 | ||

|

| |||

| * | Redemption price per share is equal to net asset value less any applicable contingent deferred sales charge. |

See notes to financial statements.

20 Certified Annual Report

| STATEMENT OF OPERATIONS | ||

| Thornburg Strategic Municipal Income Fund | Year Ended September 30, 2012 | |

INVESTMENT INCOME: | ||||

Interest income (net of premium amortized of $280,708) | $ | 6,586,471 | ||

|

| |||

EXPENSES: | ||||

Investment advisory fees (Note 3) | 1,078,438 | |||

Administration fees (Note 3) | ||||

Class A Shares | 68,243 | |||

Class C Shares | 23,706 | |||

Class I Shares | 35,116 | |||

Distribution and service fees (Note 3) | ||||

Class A Shares | 136,486 | |||

Class C Shares | 113,792 | |||

Transfer agent fees | ||||

Class A Shares | 29,199 | |||

Class C Shares | 14,637 | |||

Class I Shares | 25,065 | |||

Registration and filing fees | ||||

Class A Shares | 22,370 | |||

Class C Shares | 27,495 | |||

Class I Shares | 22,278 | |||

Custodian fees (Note 3) | 55,880 | |||

Professional fees | 41,068 | |||

Accounting fees | 3,108 | |||

Trustee fees | 4,008 | |||

Other expenses | 21,700 | |||

|

| |||

Total Expenses | 1,722,589 | |||

Less: | ||||

Expenses reimbursed by investment advisor (Note 3) | (76,228 | ) | ||

Fees paid indirectly (Note 3) | (357 | ) | ||

|

| |||

Net Expenses | 1,646,004 | |||

|

| |||

Net Investment Income | 4,940,467 | |||

|

| |||

REALIZED AND UNREALIZED GAIN (LOSS) | ||||

Net realized gain (loss) on investments | 431,431 | |||

Net change in unrealized appreciation (depreciation) on investments | 10,241,692 | |||

|

| |||

Net Realized and Unrealized Gain | 10,673,123 | |||

|

| |||

Net Increase in Net Assets Resulting from Operations | $ | 15,613,590 | ||

|

| |||

See notes to financial statements.

Certified Annual Report 21

| STATEMENTS OF CHANGES IN NET ASSETS |

| Thornburg Strategic Municipal Income Fund |

| Year Ended September 30, 2012 | Year Ended September 30, 2011 | |||||||

INCREASE (DECREASE) IN NET ASSETS FROM | ||||||||

OPERATIONS: | ||||||||

Net investment income | $ | 4,940,467 | $ | 3,933,277 | ||||

Net realized gain (loss) on investments | 431,431 | 98,722 | ||||||

Net unrealized appreciation (depreciation) on investments | 10,241,692 | (464,465 | ) | |||||

|

|

|

| |||||

Net Increase (Decrease) in Net Assets Resulting from Operations | 15,613,590 | 3,567,534 | ||||||

DIVIDENDS TO SHAREHOLDERS: | ||||||||

From net investment income | ||||||||

Class A Shares | (1,821,624 | ) | (1,443,523 | ) | ||||

Class C Shares | (577,455 | ) | (599,513 | ) | ||||

Class I Shares | (2,541,388 | ) | (1,887,215 | ) | ||||

From realized gains | ||||||||

Class A Shares | (35,959 | ) | (48,451 | ) | ||||

Class C Shares | (13,233 | ) | (26,448 | ) | ||||

Class I Shares | (48,816 | ) | (67,868 | ) | ||||

FUND SHARE TRANSACTIONS (NOTE 4): | ||||||||

Class A Shares | 21,540,065 | 11,532,230 | ||||||

Class C Shares | 6,778,829 | 401,837 | ||||||

Class I Shares | 32,570,889 | 12,899,113 | ||||||

|

|

|

| |||||

Net Increase in Net Assets | 71,464,898 | 24,327,696 | ||||||

NET ASSETS: | ||||||||

Beginning of Year | 109,888,424 | 85,560,728 | ||||||

|

|

|

| |||||

End of Year | $ | 181,353,322 | $ | 109,888,424 | ||||

|

|

|

| |||||

Undistributed net investment income | $ | 3,622 | $ | 3,622 | ||||

See notes to financial statements.

22 Certified Annual Report

| NOTES TO FINANCIAL STATEMENTS, | ||

| Thornburg Strategic Municipal Income Fund | September 30, 2012 | |

NOTE 1 – ORGANIZATION

Thornburg Strategic Municipal Income Fund (the “Fund”) is a diversified series of Thornburg Investment Trust (the “Trust”). The Trust is organized as a Massachusetts business trust under a Declaration of Trust dated June 3, 1987 and is registered as a diversified, open-end management investment company under the Investment Company Act of 1940, as amended. The Fund is currently one of sixteen separate series of the Trust. Each series is considered to be a separate entity for financial reporting and tax purposes and bears expenses directly attributable to it. The Fund’s primary investment objective is to seek a high level of current income exempt from federal individual income tax.

The Fund currently has three classes of shares of beneficial interest outstanding: Class A, Class C, and Institutional Class (Class I). Each class of shares of the Fund represents an interest in the same portfolio of investments, except that (i) Class A shares are sold subject to a front-end sales charge collected at the time the shares are purchased and bear a service fee, (ii) Class C shares are sold at net asset value without a sales charge at the time of purchase, but are subject to a contingent deferred sales charge upon redemption within one year of purchase, and bear both a service fee and a distribution fee, (iii) Class I shares are sold at net asset value without a sales charge at the time of purchase and may be subject to a service fee, and (iv) the respective classes may have different reinvestment privileges and conversion rights. Additionally, the Fund may allocate among its classes certain expenses, to the extent allowable to specific classes, including transfer agent fees, government registration fees, certain printing and postage costs, and administrative and legal expenses. Currently, class specific expenses of the Fund are limited to service and distribution fees, administration fees, and certain registration and transfer agent expenses.

NOTE 2 – SIGNIFICANT ACCOUNTING POLICIES

Significant accounting policies of the Trust are as follows:

Valuation Policy and Procedures: The Fund’s Trustees of the Trust (the “Trustees”) have authorized employees of the Fund’s investment advisor, acting as the Valuation and Pricing Committee (the “Committee”), to make certain valuation determinations, subject to oversight and review by the Trustees and the Audit Committee of the Trustees. The Committee and other employees of the Fund’s investment advisor administer and implement the valuation process and make fair value decisions. The Committee regularly reviews its own fair value decisions, as well as valuations, valuation techniques and services furnished by pricing services, considers circumstances in the markets which may require valuation determinations by the Committee and reviews previous valuation determinations. The Committee also reports on its activities, the performance of the pricing services, and other matters to the Trustees and the Audit Committee of the Trustees.

In determining a fair value for a portfolio investment, the Committee seeks to determine the price that the Fund would reasonably expect to receive upon a sale of the investment in an orderly transaction between market participants at the measurement date. Typically, the fair value process employs standing instructions to use quoted prices in active markets or the use of independent pricing services. Less frequently, the Committee may make a fair value determination using other methods. However, because fair value prices are estimated prices, the determination of fair value for an investment may differ from the value that would be realized by the Fund upon a sale of the investment, and that difference could be material to the Fund’s financial statements. The Committee’s determination of fair value for an investment may also differ from the prices obtained by other persons (including other mutual funds) for the investment.

Valuation of Investments: Debt obligations held by the Fund have a primary market over-the-counter and are valued by an independent pricing service approved by the Trustees. The pricing service ordinarily values debt obligations at quoted bid prices. When quotations are not available, debt obligations held by the Fund are valued at evaluated prices determined by the pricing service using methods which include consideration of yields or prices of debt obligations of comparable quality, type of issue, coupon, maturity, and rating, and indications as to value from dealers and general market conditions. Short-term obligations having remaining maturities of 60 days or less are ordinarily valued at amortized cost, which approximates market value.

In any case where the market value of a debt obligation held by the Fund is not readily available, a determination of a fair value for the investment is made by the Committee. In any case where a pricing service fails to provide a price for a debt obligation held by the Fund, the Committee determines a fair value for the debt obligation using procedures in accordance with a policy approved by the Trustees, which may include the use of a price obtained from a different independent pricing service. Additionally, in any case where management believes that a price provided by a pricing service for a debt obligation held by the Fund may be unreliable, the Committee decides whether or not to use the pricing service’s valuation or to use an alternative method to determine a fair value for the debt obligation.

Certified Annual Report 23

| NOTES TO FINANCIAL STATEMENTS, CONTINUED | ||

| Thornburg Strategic Municipal Income Fund | September 30, 2012 | |

Valuation Measurements: The Fund categorizes its investments based upon the inputs used in valuing those investments, according to a three-level hierarchy established by guidance by the Financial Accounting Standards Board (the “FASB”). Categorization of investments using this hierarchy is intended by the FASB to maximize the use of observable inputs and minimize the use of unobservable inputs by prioritizing that the most observable input be used when available. Observable inputs are those that market participants would use in valuing an investment based on available market data. Unobservable inputs are those that reflect assumptions about the information market participants would use in valuing an investment. An investment’s level within the hierarchy is based on the lowest level input that is deemed significant to the fair value measurement. The methodologies and relative inputs used to value investments are not necessarily indications of the risk or liquidity associated with investing in those investments.

Various inputs are used in determining the fair value measurement of the Fund’s investments. These inputs are generally summarized according to the three-level hierarchy below:

Level 1: Quoted prices in active markets for identical investments.

Level 2: Other direct or indirect significant observable inputs (including quoted prices for similar investments in active markets and other observable inputs, such as interest rates, prepayment rates, credit risk, etc.).

Level 3: Significant unobservable inputs, (including the Committee’s own assumptions in determining the fair value of investments), are generally applicable to investments fair valued with single broker quotes and other investments.

Portfolio investments with minimal, if any, market activity are characterized as Level 3 and are valued using significant unobservable inputs, typically including single broker quotes, which may be adjusted or unadjusted, related or comparable investments, recent transactions, and other relevant information. Valuations may also be based upon current market prices of investments that are comparable in coupon, rating, maturity and industry, as applicable. An income based valuation approach would consider discounted anticipated future cash flows of the investment. Discounts may also be applied due to the nature or duration of any restrictions on the disposition of the investment. The derived value of a Level 3 investment may not represent the value which is received upon disposition.

The following table displays a summary of the fair value hierarchy measurements of the Fund’s investments as of September 30, 2012. In any instance when valuation inputs from more than one level are used to determine the fair value of a specific investment, the investment is placed in the level of the table based upon the lowest level input that is significant in determining the fair value of the investment:

| Fair Value Measurements at September 30, 2012 | ||||||||||||||||

| Total | Level 1 | Level 2 | Level 3 | |||||||||||||

Assets | ||||||||||||||||

Investments in Securities Municipal Bonds | $ | 178,063,074 | $ | — | $ | 178,063,074 | $ | — | ||||||||

Total Investments in Securities | $ | 178,063,074 | $ | — | $ | 178,063,074 | $ | — | ||||||||

In accordance with the guidance prescribed in Accounting Standards Update No. 2011-04, amending Topic 820 Fair Value Measurements and Disclosures, it is the policy of the Fund to recognize transfers between Levels 1, 2 and 3 and to disclose those transfers due to the underlying event which caused the movement. The Fund recognized no transfers between levels for the year ended September 30, 2012.

24 Certified Annual Report

| NOTES TO FINANCIAL STATEMENTS, CONTINUED | ||

| Thornburg Strategic Municipal Income Fund | September 30, 2012 | |

Federal Income Taxes: It is the policy of the Trust to comply with the provisions of the Internal Revenue Code applicable to “regulated investment companies” and to distribute to shareholders substantially all taxable (if any) and tax exempt income of the Fund. Therefore, no provision for federal income tax is required.

Management reviews each uncertain tax position believed to be material to the preparation of the Fund’s financial statements, to assess if it is more likely than not that the position would be sustained upon examination, based upon the technical merits of the position. As of September 30, 2012, management has not identified any such position for which a liability must be reflected in the Statement of Assets and Liabilities. The Fund’s tax returns remain subject to examination for three years after filing.

When-Issued and Delayed Delivery Transactions: The Fund may engage in when-issued or delayed delivery transactions. To the extent the Fund engages in such transactions, it will do so for the purpose of acquiring portfolio investments consistent with the Fund’s investment objectives and not for the purpose of investment leverage or to speculate on interest rate and/or market changes. At the time the Fund makes a commitment to purchase an investment on a when-issued or delayed delivery basis, the Fund will record the transaction and reflect the value in determining its net asset value. When effecting such transactions, assets of an amount sufficient to make payment for the portfolio investments to be purchased will be segregated on the Fund’s records on the trade date. Investments purchased on a when-issued or delayed delivery basis do not earn interest until the settlement date.

Dividends: Net investment income of the Fund is declared daily as a dividend on shares for which the Fund has received payment. Dividends are paid monthly and are reinvested in additional shares of the Fund at net asset value per share at the close of business on the dividend payment date, or at the shareholder’s option, paid in cash. Net realized capital gains, to the extent available, will be distributed at least annually.

General: Investment transactions are accounted for on a trade date basis. Interest income is accrued as earned. Premiums and discounts on investments purchased are amortized to call dates or maturity dates of the respective investments. Realized gains and losses from the sale of investments are recorded on an identified cost basis. Net investment income (other than class specific expenses) and realized and unrealized gains and losses are allocated daily to each class of shares based upon the relative net asset value of outstanding shares (or the value of the dividend-eligible shares, as appropriate) of each class of shares at the beginning of the day (after adjusting for the current capital shares activity of the respective class). Expenses common to all Funds are allocated among the Funds comprising the Trust based upon their relative net asset values or other appropriate allocation methods.

Guarantees and Indemnifications: Under the Trust’s organizational documents (and under a separate agreement with the Trustees), its officers and Trustees are indemnified against certain liabilities arising out of the performance of their duties to the Fund. Additionally, in the normal course of business the Trust enters into contracts with service providers that contain general indemnification clauses. The Trust’s maximum exposure under these arrangements is unknown. However, based on experience, the Trust expects the risk of loss to be remote.

Use of Estimates: The preparation of financial statements, in conformity with United States generally accepted accounting principles, requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and the disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of increases and decreases in net assets from operations during the reporting period. Actual amounts could differ from those estimates.

NOTE 3 – INVESTMENT ADVISORY FEE AND OTHER TRANSACTIONS WITH AFFILIATES

Pursuant to an investment advisory agreement, Thornburg Investment Management, Inc. (the “Advisor”) serves as the investment advisor and performs services to the Fund for which the fees are payable at the end of each month. For the year ended September 30, 2012, these fees were payable at annual rates ranging from .75 of 1% to .50 of 1% per annum of the average daily net assets of the Fund depending on the Fund’s asset size. The Trust also has entered into administrative services agreements with the Advisor, whereby the Advisor will perform certain administrative services for the shareholders of each class of the Fund’s shares, and for which fees will be payable at an annual rate of up to .125 of 1% per annum of the average daily net assets attributable to each class of shares. For the year ended September 30, 2012, the Advisor contractually reimbursed certain class specific expenses and administrative fees of $31,039 for Class A shares and $45,189 for Class C shares.

Certified Annual Report 25

| NOTES TO FINANCIAL STATEMENTS, CONTINUED | ||

| Thornburg Strategic Municipal Income Fund | September 30, 2012 | |

The Trust has an underwriting agreement with Thornburg Securities Corporation (the “Distributor,” an affiliate of the Advisor), which acts as the distributor of the Fund’s shares. For the year ended September 30, 2012, the Distributor has advised the Fund that it earned net commissions aggregating $1,085 from the sale of Class A shares, and collected contingent deferred sales charges aggregating $1,384 from redemptions of Class C shares of the Fund.

Pursuant to a service plan under Rule 12b-1 of the Investment Company Act of 1940, the Fund may reimburse to the Advisor an amount not to exceed .25 of 1% per annum of the average daily net assets attributable to each class of shares of the Fund for payments made by the Advisor to securities dealers and other financial institutions to obtain various shareholder and distribution related services. For the year ended September 30, 2012, there were no 12b-1 service plan fees charged for Class I shares. The Advisor may pay out of its own resources additional expenses for distribution of the Fund’s shares.

The Trust has also adopted a distribution plan pursuant to Rule 12b-1, applicable only to the Fund’s Class C shares, under which the Fund compensates the Distributor for services in promoting the sale of Class C shares of the Fund at an annual rate of up to .35 of 1% per annum of the average daily net assets attributable to Class C shares. Total fees incurred by each class of shares of the Fund under their respective Service and Distribution Plans for the year ended September 30, 2012, are set forth in the Statement of Operations.

The Trust has an agreement with the custodian bank to indirectly pay a portion of the custodian’s fees through credits earned by the Fund’s cash on deposit with the bank. This deposit agreement is an alternative to overnight investments. Custodial fees are adjusted to reflect amounts that would have been paid without this agreement, with a corresponding adjustment reflected as fees paid indirectly in the Statement of Operations. For the year ended September 30, 2012, fees paid indirectly were $357.

Certain officers and Trustees of the Trust are also officers or directors of the Advisor and Distributor. The compensation of independent Trustees is borne by the Trust.

NOTE 4 – SHARES OF BENEFICIAL INTEREST

At September 30, 2012, there were an unlimited number of shares of beneficial interest authorized. Transactions in shares of beneficial interest were as follows:

| Year Ended September 30, 2012 | Year Ended September 30, 2011 | |||||||||||||||

| Shares | Amount | Shares | Amount | |||||||||||||

Class A Shares | ||||||||||||||||

Shares sold | 2,136,532 | $ | 31,110,750 | 1,515,491 | $ | 20,437,728 | ||||||||||

Shares issued to shareholders in reinvestment of dividends | 97,853 | 1,436,857 | 83,263 | 1,126,525 | ||||||||||||

Shares repurchased | (750,631 | ) | (11,007,542 | ) | (748,444 | ) | (10,032,023 | ) | ||||||||

|

|

|

|

|

|

|

| |||||||||

Net increase (decrease) | 1,483,754 | $ | 21,540,065 | 850,310 | $ | 11,532,230 | ||||||||||

|

|

|

|

|

|

|

| |||||||||

Class C Shares | ||||||||||||||||