| | OMB APPROVAL |

| | OMB Number: 3235-0570 |

| | Expires: November 30, 2005 |

| | Estimated average burden

hours per response. . . . 5.0 |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-05309

First American Investment Funds, Inc.

(Exact name of registrant as specified in charter)

800 Nicollet Mall, Minneapolis, MN | | 55402 |

(Address of principal executive offices) | | (Zip code) |

Charles D. Gariboldi 800 Nicollet Mall, Minneapolis, MN 55402

(Name and address of agent for service)

Registrant’s telephone number, including area code: 800-677-3863

Date of fiscal year end: September 30

Date of reporting period: September 30, 2005

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. Section 3507.

Item 1. Report to Shareholders

| 2005

Annual Report |

First American Index Funds

An index fund is a mutual fund that seeks to mirror, as closely as possible, the returns of a market index. It does so by purchasing almost all of the holdings in the index in roughly the same percentages. An equity index measures the collective value of a group of stocks in a specific segment of the marketplace. The most commonly known market index is the S&P 500 Index.

TABLE OF CONTENTS

Message to Shareholders | 1 |

Report of Independent Registered Public Accounting Firm | 11 |

Schedule of Investments | 12 |

Statements of Assets and Liabilities | 42 |

Statements of Operations | 43 |

Statements of Changes in Net Assets | 44 |

Financial Highlights | 46 |

Notes to Financial Statements | 52 |

Notice to Shareholders | 60 |

| Mutual fund investing involves risk; principal loss is possible. |

| |

| NOT FDIC INSURED NO BANK GUARANTEE MAY LOSE VALUE |

Message to SHAREHOLDERS November 14, 2005

Dear Shareholders:

We invite you to take a few minutes to review the results of the fiscal year ended September 30, 2005.

This report includes comparative performance graphs and tables, portfolio commentaries, complete listings of portfolio holdings, and additional fund information. We hope you will find this helpful in monitoring your investment portfolio.

Also, through our website, firstamericanfunds.com, we provide quarterly performance fact sheets on all First American Funds, the economic outlook as viewed by our senior investment officers, and other information about fund investments and portfolio strategies.

Please contact your financial professional if you have questions about First American Funds or contact First American Investor Services at 800.677.FUND.

We appreciate your investment with First American Funds and look forward to serving your financial needs in the future.

Sincerely,

/s/ Virginia L. Stringer | | /s/ Thomas S. Schreier, Jr. | |

| |

Virginia L. Stringer | Thomas S. Schreier, Jr. |

Chairperson of the Board | President |

First American Investment Funds, Inc. | First American Investment Funds, Inc. |

FIRST AMERICAN FUNDS Annual Report 2004

1

Equity Index fund

Investment Objective: to provide investment results that correspond to the performance of the Standard & Poor's 500 Composite Index ("S&P 500 Composite Index")

How did the fund perform for the fiscal year ended September 30, 2005?

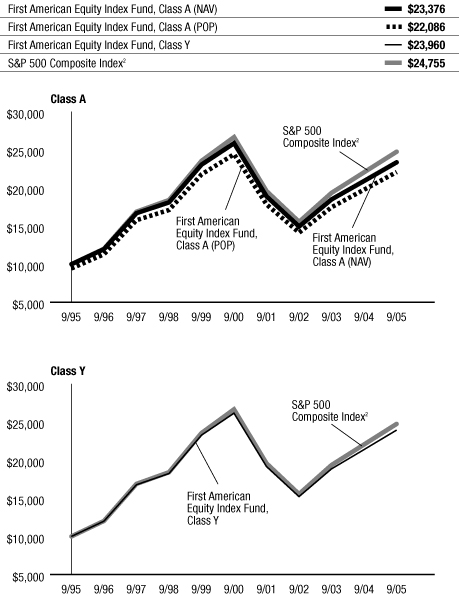

The First American Equity Index Fund (the "fund"), Class Y shares, returned 11.92% for the fiscal year ended September 30, 2005 (Class A shares returned 11.69% without taking the sales charge into account). By comparison, the fund's benchmark, the S&P 500 Composite Index*, returned 12.25% for the same period.

How did general economic and market conditions affect performance?

Economic growth moderated but nevertheless continued at a solid pace over the course of the fiscal year. Solid economic growth, in turn, improved labor market conditions. While core inflation has been basically stable at a relatively low level, overall inflation has risen with the continuing climb of energy prices during the past year. The combination of solid growth, lower unemployment, and the potential for higher energy prices to be reflected by broader inflation measures has kept the Fed incrementally raising the Fed Funds Rate at each Federal Open Market Committee meeting since June 2004. The corporate sector of the economy has performed very well in this economic environment, with operating earnings up sharply through the third quarter of 2005. The energy sector proved a standout, making the most substantial contribution to the fund's performance.

While stocks in general were up in excess of their long-term historical averages, mid- and small-capitalization stocks generally outperformed large-capitalization stocks as they were more leveraged to the growing economy. The S&P 500 Composite Index, constructed of large-cap stocks, lagged somewhat behind the mid- and small- cap indices but still experienced positive returns of more than 12%.

Underlying economic conditions remain generally favorable for the financial markets, although risks have risen with energy prices and the widespread disruption to activity from Hurricanes Katrina and Rita.

Fund Overview

The fund is invested to replicate the S&P 500 Composite Index as closely as possible with consideration to turnover costs and fees. As a result, the fund performed very similarly to the index. The index includes 500 leading companies in the leading industries of the U.S. economy and covers about 75% of the dollar value of all traded stocks in the U.S. market.

During the fiscal year, Standard & Poor's modified its methodology: rather than counting all shares outstanding of a particular stock, the index now counts only the freely traded "float" shares outstanding. Since insiders often have significant impediments to trading even if the stock appears over or undervalued, tracking holdings of independent investors (i.e., noninsiders) allows the index to better reflect the consensus judgment of the potential benefit of holding a specific company's stock.

Like the index, the fund benefited from strong performance by the energy sector, which had a total return of 48%. Of the 29 company stocks currently in the energy sector, seven more than doubled in price and none had a total return of less than 24%. In keeping with the developments in the energy market, the small utilities sector rose 39%, primarily on the performance of independent power producers.

Last year's top performer, the consumer discretionary sector, proved the largest detractor from performance during this fiscal period, with a total return of 5% for the year. Although the economy was growing steadily and consumer spending remained robust, the sector was weakened chiefly because it contained two of the three worst performing industries, automobiles and auto components (the third was leisure equipment and products).

*Unlike mutual funds, index returns do not reflect any expenses, transaction costs, or cash flow effects.

| Top 10 Holdings as of September 30, 20051 (% of net assets) | |

| Exxon Mobil | | | 3.6 | % | |

| General Electric | | | 3.2 | % | |

| Microsoft | | | 2.1 | % | |

| Citigroup | | | 2.1 | % | |

| Pfizer | | | 1.7 | % | |

| Johnson & Johnson | | | 1.7 | % | |

| Bank of America | | | 1.5 | % | |

| American International Group | | | 1.4 | % | |

| Intel | | | 1.4 | % | |

| Altria Group | | | 1.4 | % | |

| Sector Allocation as of September 30, 20051 (% of net assets) | |

| Financials | | | 19.7 | % | |

| Information Technology | | | 15.6 | % | |

| Heath Care | | | 13.0 | % | |

| Industrials | | | 11.1 | % | |

| Consumer Discretionary | | | 10.1 | % | |

| Energy | | | 10.1 | % | |

| Consumer Staples | | | 9.6 | % | |

| Utilities | | | 3.5 | % | |

| Telecommunication Services | | | 3.0 | % | |

| Materials | | | 2.9 | % | |

| Short Term Investments | | | 1.5 | % | |

| Other Assets and Liabilities, Net | | | (0.1 | )% | |

| | | | 100.0 | % | |

1Fund holdings and sector allocations are subject to change at any time and are not recommendations to buy or sell any security.

FIRST AMERICAN FUNDS Annual Report 2005

2

Equity Index fund continued

Annual Performance1 as of September 30, 2005

| | | | | | | | | Since Inception | |

| | | 1 year | | 5 years | | 10 years | | 2/01/1999 | | 9/24/2001 | |

| Average annual return with sales charge (POP) | | | |

| Class A | | | 5.54 | % | | | (3.11 | )% | | | 8.25 | % | | | - | | | | - | | |

| Class B | | | 5.86 | % | | | (3.10 | )% | | | 8.06 | % | | | - | | | | - | | |

| Class C | | | 9.84 | % | | | (2.75 | )% | | | - | | | | (0.37 | )% | | | - | | |

| Average annual return without sales charge (NAV) | | | |

| Class A | | | 11.69 | % | | | (2.00 | )% | | | 8.86 | % | | | - | | | | - | | |

| Class B | | | 10.86 | % | | | (2.73 | )% | | | 8.06 | % | | | - | | | | - | | |

| Class C | | | 10.84 | % | | | (2.75 | )% | | | - | | | | (0.37 | )% | | | - | | |

| Class R | | | 11.38 | % | | | - | | | | - | | | | - | | | | 6.31 | % | |

| Class Y | | | 11.92 | % | | | (1.76 | )% | | | 9.13 | % | | | - | | | | - | | |

| S&P 500 Composite Index2 | | | 12.25 | % | | | (1.49 | )% | | | 9.49 | % | | | 1.00 | % | | | 7.00 | % | |

Value of $10,000 Investment1, 3 as of September 30, 2005

The performance data quoted on this page represents past performance and does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance data quoted. Performance data current to the most recent month-end may be obtained by calling 800.677.FUND.

1 Performance does not reflect the deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares. Investment performance reflects fee waivers that are or were in effect. In the absence of such fee waivers, total returns would be reduced. Index performance is for illustrative purposes only and does not reflect any expenses, transaction costs, or cash flow effects. Direct investment in the index is not available.

Total returns at net asset value ("NAV") reflect performance over the time period indicated without including the fund's maximum sales charge and assume reinvestment of all distributions at NAV.

Total returns at public offering price ("POP") reflect performance over the time period indicated including a maximum front-end sales charge of 5.50% for Class A shares and the maximum contingent deferred sales charge ("CDSC") for Class B and Class C shares for the relevant period. Maximum CDSC is 5.00% for Class B shares, decreasing annually to 0% in the seventh year following purchase, and 1.00% for Class C shares. Total returns assume reinvestment of all distributions at NAV.

2 An unmanaged index of large-capitalization stocks that includes a representative sample of 500 leading companies in leading industries of the U.S. economy. Although the S&P 500 focuses on the large-cap segment of the market, with over 80% coverage of U.S. equities, it also serves as a proxy for the total market.

3 Performance for Class B, Class C, and Class R shares is not presented. Performance for these classes will vary due to different expense structures.

The charts above illustrate the total value of an assumed $10,000 investment in the fund's Class A and Class Y shares (from 9/30/1995 to 9/30/2005) as compared to the S&P 500 Composite Index.2

FIRST AMERICAN FUNDS Annual Report 2005

3

Equity Index fund continued

Expense Example

As a shareholder of the Equity Index Fund (the "fund"), you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments; and (2) ongoing costs, including advisory fees; distribution and/or service (12b-1) fees; and other fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the fund and to compare these costs with the ongoing costs of investing in other mutual funds. The example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period from April 1, 2005, to September 30, 2005.

Actual Expenses

For each class, the first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled "Expenses Paid During Period" to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

For each class, the second line of the table below provides information about hypothetical account values and hypothetical expenses based on the fund's actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the fund's actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads). Therefore, the second line of the table for each class is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

Expense Examples

| | | Beginning Account

Value (4/01/05) | | Ending Account

Value (9/30/05) | | Expenses Paid During

Period1 (4/01/05 to

9/30/05) | |

| Class A Actual2 | | $ | 1,000.00 | | | $ | 1,047.60 | | | $ | 3.18 | | |

| Class A Hypothetical (5% return before expenses) | | $ | 1,000.00 | | | $ | 1,021.96 | | | $ | 3.14 | | |

| Class B Actual2 | | $ | 1,000.00 | | | $ | 1,043.80 | | | $ | 7.02 | | |

| Class B Hypothetical (5% return before expenses) | | $ | 1,000.00 | | | $ | 1,018.20 | | | $ | 6.93 | | |

| Class C Actual2 | | $ | 1,000.00 | | | $ | 1,043.60 | | | $ | 7.02 | | |

| Class C Hypothetical (5% return before expenses) | | $ | 1,000.00 | | | $ | 1,018.20 | | | $ | 6.93 | | |

| Class R Actual2 | | $ | 1,000.00 | | | $ | 1,046.00 | | | $ | 4.46 | | |

| Class R Hypothetical (5% return before expenses) | | $ | 1,000.00 | | | $ | 1,020.71 | | | $ | 4.41 | | |

| Class Y Actual2 | | $ | 1,000.00 | | | $ | 1,048.40 | | | $ | 1.90 | | |

| Class Y Hypothetical (5% return before expenses) | | $ | 1,000.00 | | | $ | 1,023.21 | | | $ | 1.88 | | |

1 Expenses are equal to the fund's annualized expense ratio for the most recent six-month period of 0.62%, 1.37%, 1.37%, 0.87% and 0.37% for Class A, Class B, Class C, Class R and Class Y, respectively, multiplied by the average account value over the period, multiplied by the number of days in the most recent half-year/365 days (to reflect the one-half year period).

2 Based on the actual returns for the six months ended September 30, 2005: 4.76% for Class A, 4.38% for Class B, 4.36% for Class C, 4.60% for Class R, and 4.84% for Class Y.

FIRST AMERICAN FUNDS Annual Report 2005

4

Mid Cap Index fund

Investment Objective: to provide investment results that correspond to the performance of the Standard & Poor's MidCap 400 Composite Index ("S&P MidCap 400 Index")

How did the fund perform for the fiscal year ended September 30, 2005?

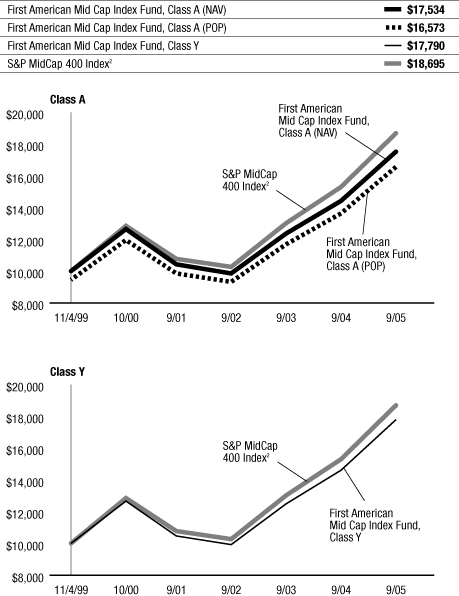

The First American Mid Cap Index Fund (the "fund"), Class Y shares, returned 21.82% for the fiscal year ended September 30, 2005 (Class A shares returned 21.43% without taking the sales charge into account). By comparison, the fund's benchmark, the S&P MidCap 400 Index*, returned 22.16% for the same period.

How did general economic and market conditions affect performance?

Economic growth moderated but nevertheless continued at a solid pace over the course of the fiscal year. Solid economic growth, in turn, improved labor market conditions. While core inflation has been basically stable at a relatively low level, overall inflation has risen with the continuing climb of energy prices during the past year. The combination of solid growth, lower unemployment, and the potential for higher energy prices to be reflected by broader inflation measures has kept the Fed incrementally raising the Fed Funds Rate at each Federal Open Market Committee meeting since June 2004. The corporate sector of the economy has performed very well in this economic environment, with operating earnings up sharply through the third quarter of 2005. The energy sector proved a standout, making the most substantial contribution to the fund's performance.

While stocks in general were up in excess of their long-term historical averages, the fund benefited from the fact that mid- and small-capitalization stocks generally outperformed large-capitalization stocks as they were more leveraged to the growing economy. The S&P MidCap 400 Index, constructed of stocks in the middle range of company size (companies with market capitalizations between $1.5 billion to $5 billion) reflected this performance, returning more than 22% for the fiscal year.

Underlying economic conditions remain generally favorable for the financial markets, although risks have risen with energy prices and the widespread disruption to activity from Hurricanes Katrina and Rita.

Fund Overview

The fund is invested to replicate the S&P MidCap 400 Index closely before fees, while attempting to reduce turnover costs. As a result, the fund performed very similarly to that index. The index includes stocks that reflect the risk and return characteristics of the broader mid-cap universe. Mid-cap stocks are now being recognized as an independent asset class and the capitalization range of this index covers about 10% of the U.S. equities market.

During the fiscal year, the largest contributor to performance for the fund was the energy sector, which had, on an average, a weighting of 9% and a total return of 61%. Other contributors to the fund's performance were the consumer staples and utilities sectors, which performed better than the overall index.

The telecommunications sector, in which the fund had a small position, experienced the worst overall performance, falling 2.5% during the fiscal year.

*Unlike mutual funds, index returns do not reflect any expenses, transaction costs, or cash flow effects.

| Top 10 Holdings as of September 30, 20051 (% of net assets) | |

| Legg Mason | | | 1.1 | % | |

| Peabody Energy | | | 1.0 | % | |

| Whole Foods Market | | | 0.8 | % | |

| SanDisk | | | 0.8 | % | |

| Noble Energy | | | 0.8 | % | |

| Lennar | | | 0.7 | % | |

| Pioneer Natural Resources | | | 0.7 | % | |

| Fidelity National Financial | | | 0.7 | % | |

| Questar | | | 0.7 | % | |

| ENSCO International | | | 0.7 | % | |

| Sector Allocation as of September 30, 20051 (% of net assets) | |

| Financials | | | 17.9 | % | |

| Consumer Discretionary | | | 15.6 | % | |

| Information Technology | | | 14.6 | % | |

| Industrials | | | 13.4 | % | |

| Health Care | | | 12.0 | % | |

| Utilities | | | 8.0 | % | |

| Energy | | | 7.7 | % | |

| Materials | | | 5.7 | % | |

| Consumer Staples | | | 3.3 | % | |

| Short Term Investments | | | 1.6 | % | |

| Telecommunication Services | | | 0.5 | % | |

| Other Assets and Liabilities, Net | | | (0.3 | )% | |

| | | | 100.0 | % | |

1Fund holdings and sector allocations are subject to change at any time and are not recommendations to buy or sell any security.

FIRST AMERICAN FUNDS Annual Report 2005

5

Mid Cap Index fund continued

Annual Performance1 as of September 30, 2005

| | | | | | | Since Inception | |

| | | 1 year | | 5 year | | 11/04/1999 | | 11/27/2000 | | 9/24/2001 | |

| Average annual return with sales charge (POP) | | | |

| Class A | | | 14.75 | % | | | 4.79 | % | | | 8.93 | % | | | - | | | | - | | |

| Class B | | | 15.57 | % | | | 4.92 | % | | | 9.09 | % | | | - | | | | - | | |

| Class C | | | 19.60 | % | | | - | | | | - | | | | - | | | | 13.91 | % | |

| Average annual return without sales charge (NAV) | | | |

| Class A | | | 21.43 | % | | | 5.99 | % | | | 9.97 | % | | | - | | | | - | | |

| Class B | | | 20.57 | % | | | 5.25 | % | | | 9.20 | % | | | - | | | | - | | |

| Class C | | | 20.60 | % | | | - | | | | - | | | | - | | | | 13.91 | % | |

| Class R | | | 21.09 | % | | | - | | | | - | | | | 7.63 | % | | | - | | |

| Class Y | | | 21.82 | % | | | 6.27 | % | | | 10.24 | % | | | - | | | | - | | |

| S&P MidCap 400 Index2 | | | 22.16 | % | | | 7.05 | % | | | 11.17 | % | | | 8.73 | % | | | 15.69 | % | |

Value of $10,000 Investment1, 3 as of September 30, 2005

The charts above illustrate the total value of an assumed $10,000 investment in the fund's Class A and Class Y shares (from 11/4/1999 to 9/30/2005) as compared to the S&P MidCap 400 Index.2

The performance data quoted on this page represents past performance and does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance of the fund may be lower or higher than the performance data quoted. Performance data current to the most recent month-end may be obtained by calling 800.677.FUND.

1 Performance does not reflect the deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares. Investment performance reflects fee waivers that are or were in effect. In the absence of such fee waivers, total returns would be reduced. Index performance is for illustrative purposes only and does not reflect any expenses, transaction costs, or cash flow effects. Direct investment in the index is not available.

Stocks of mid-capitalization companies may be slightly less volatile than those of small-capitalization companies, but they still involve substantial risk and may be subject to increased volatility and more price fluctuation than large-capitalization companies.

Total returns at net asset value ("NAV") reflect performance over the time period indicated without including the fund's maximum sales charge and assume reinvestment of all distributions at NAV.

Total returns at public offering price ("POP") reflect performance over the time period indicated including a maximum front-end sales charge of 5.50% for Class A shares and the maximum contingent deferred sales charge ("CDSC") for Class B and Class C shares for the relevant period. Maximum CDSC is 5.00% for Class B shares, decreasing annually to 0% in the seventh year following purchase, and 1.00% for Class C shares. Total returns assume reinvestment of all distributions at NAV.

On September 24, 2001, the Mid Cap Index Fund became the successor by merger to the Firstar MidCap Index Fund, a series of the Firstar Funds, Inc. Prior to the merger, the First American Fund had no assets or liabilities. Performance presented prior to September 24, 2001, represents that of the Firstar MidCap Index Fund.

2 An unmanaged, capitalization-weighted index that represents the aggregate market value of the common equity of 400 companies chosen by Standard & Poor's with a median capitalization of approximately $700 million to measure the performance of the mid-range sector of the U.S. stock market.

3 Performance for Class B, Class C, and Class R shares is not presented. Performance for these classes will vary due to different expense structures.

FIRST AMERICAN FUNDS Annual Report 2005

6

Mid Cap Index fund continued

Expense Example

As a shareholder of the Mid Cap Index Fund (the "fund"), you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments; and (2) ongoing costs, including advisory fees; distribution and/or service (12b-1) fees; and other fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the fund and to compare these costs with the ongoing costs of investing in other mutual funds. The example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period from April 1, 2005, to September 30, 2005.

Actual Expenses

For each class, the first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled "Expenses Paid During Period" to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

For each class, the second line of the table below provides information about hypothetical account values and hypothetical expenses based on the fund's actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the fund's actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads). Therefore, the second line of the table for each class is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

Expense Examples

| | | Beginning Account

Value (4/01/05) | | Ending Account

Value (9/30/05) | | Expenses Paid During

Period1 (4/01/05 to

9/30/05) | |

| Class A Actual2 | | $ | 1,000.00 | | | $ | 1,091.20 | | | $ | 3.93 | | |

| Class A Hypothetical (5% return before expenses) | | $ | 1,000.00 | | | $ | 1,021.31 | | | $ | 3.80 | | |

| Class B Actual2 | | $ | 1,000.00 | | | $ | 1,087.60 | | | $ | 7.85 | | |

| Class B Hypothetical (5% return before expenses) | | $ | 1,000.00 | | | $ | 1,017.55 | | | $ | 7.59 | | |

| Class C Actual2 | | $ | 1,000.00 | | | $ | 1,087.30 | | | $ | 7.85 | | |

| Class C Hypothetical (5% return before expenses) | | $ | 1,000.00 | | | $ | 1,017.55 | | | $ | 7.59 | | |

| Class R Actual2 | | $ | 1,000.00 | | | $ | 1,089.60 | | | $ | 5.24 | | |

| Class R Hypothetical (5% return before expenses) | | $ | 1,000.00 | | | $ | 1,020.05 | | | $ | 5.05 | | |

| Class Y Actual2 | | $ | 1,000.00 | | | $ | 1,092.40 | | | $ | 2.62 | | |

| Class Y Hypothetical (5% return before expenses) | | $ | 1,000.00 | | | $ | 1,022.56 | | | $ | 2.54 | | |

1 Expenses are equal to the fund's annualized expense ratio for the most recent six-month period of 0.75%, 1.50%, 1.50%, 1.00% and 0.50% for Class A, Class B, Class C, Class R and Class Y, respectively, multiplied by the average account value over the period, multiplied by the number of days in the most recent half-year/365 days (to reflect the one-half year period).

2 Based on the actual returns for the six months ended September 30, 2005: 9.12% for Class A, 8.76% for Class B, 8.73% for Class C, 8.96% for Class R, and 9.24% for Class Y.

FIRST AMERICAN FUNDS Annual Report 2005

7

Small Cap Index fund

Investment Objective: to provide investment results that correspond to the performance of the Russell 2000 Index

How did the fund perform for the fiscal year ended September 30, 2005?

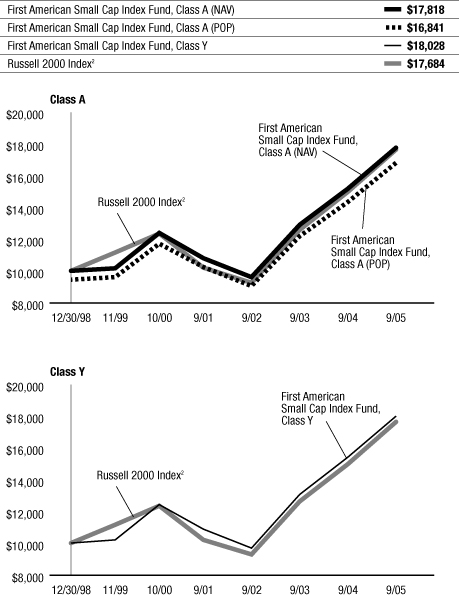

The First American Small Cap Index Fund (the "fund"), Class Y shares, returned 16.93% for the fiscal year ended September 30, 2005 (Class A shares returned 17.08% without taking the sales charge into account). By comparison, the fund's benchmark, the Russell 2000 Index*, returned 17.95% for the same period.

How did general economic and market conditions affect performance?

Economic growth moderated but nevertheless continued at a solid pace over the course of the fiscal year. Solid economic growth, in turn, improved labor market conditions. While core inflation has been basically stable at a relatively low level, overall inflation has risen with the continuing climb of energy prices during the past year. The combination of solid growth, lower unemployment, and the potential for higher energy prices to be reflected by broader inflation measures has kept the Fed incrementally raising the Fed Funds Rate at each Federal Open Market Committee meeting since June 2004. The corporate sector of the economy has performed very well in this economic environment, with operating earnings up sharply through the third quarter of 2005. The energy sector proved a standout, making the most substantial contribution to the fund's performance.

While stocks in general were up in excess of their long-term historical averages, the fund benefited from the fact that mid- and small-capitalization stocks generally outperformed large-capitalization stocks as they were more leveraged to the growing economy. The Russell 2000 Index, constructed of small-cap stocks, reflected this performance, returning more than 17% for the fiscal year.

Underlying economic conditions remain generally favorable for the financial markets, although risks have risen with energy prices and the widespread disruption to activity from Hurricanes Katrina and Rita.

Fund Overview

The fund is invested to replicate the Russell 2000 Index as closely as possible with consideration to turnover costs and fees. The index includes the traded shares of U.S. companies ranked 1,001 through 3,000 in size, thereby skipping large- and mid-capitalization names in the list of investable companies. When Russell "re-constitutes" its list to reflect changes in company size (in late June of each year), the index incurs turnover in excess of 25%.

Unlike the index, the fund must pay transactions costs to adjust its holdings. From these costs – and from management's efforts to reduce them by updating holdings at slightly different dates than other index managers were selling and buying the same names – the fund's performance lagged slightly behind the index.

The fund's 6% weighting in the energy sector helped it take advantage of a very strong performance in that area. During the fiscal year, the sector rose 74%, with many of the smaller, independent producers more than doubling in price. The fund also benefited from exposure to industrials, with a 14% weighting, mainly due to the strong performance of the construction and engineering industries.

Last year's top performer, the consumer discretionary sector, proved the largest detractor from performance during this fiscal period, with a total return of 10.5% for the year. Although the economy was growing steadily and consumer spending remained robust, the sector was weakened chiefly because it contained two of the three worst performing industries, automobiles and auto components (the third was leisure equipment and products).

*Unlike mutual funds, index returns do not reflect any expenses, transaction costs, or cash flow effects.

| Top 10 Holdings as of September 30, 20051 (% of net assets) | |

| Cimarex Energy | | | 0.3 | % | |

| Amylin Pharmaceuticals | | | 0.3 | % | |

| Cabot Oil & Gas | | | 0.2 | % | |

| Intuitive Surgical | | | 0.2 | % | |

| Cal Dive International | | | 0.2 | % | |

| Frontier Oil | | | 0.2 | % | |

| York International | | | 0.2 | % | |

| Eagle Materials | | | 0.2 | % | |

| Vertex Pharmaceuticals | | | 0.2 | % | |

| Jarden | | | 0.2 | % | |

| Sector Allocation as of September 30, 20051 (% of net assets) | |

| Financials | | | 21.4 | % | |

| Information Technology | | | 17.9 | % | |

| Industrials | | | 14.9 | % | |

| Consumer Discretionary | | | 14.1 | % | |

| Heath Care | | | 12.8 | % | |

| Energy | | | 6.6 | % | |

| Materials | | | 4.7 | % | |

| Consumer Staples | | | 2.8 | % | |

| Utilities | | | 2.7 | % | |

| Telecommunication Services | | | 1.3 | % | |

| Short Term Investments | | | 0.7 | % | |

| Other Assets and Liabilities, Net | | | 0.1 | % | |

| | | | 100.0 | % | |

1Fund holdings and sector allocations are subject to change at any time and are not recommendations to buy or sell any security.

FIRST AMERICAN FUNDS Annual Report 2005

8

Small Cap Index fund continued

Annual Performance1 as of September 30, 2005

| | | | | | | Since Inception | |

| | | 1 year | | 5 years | | 12/30/1998 | | 12/11/2000 | | 9/24/2001 | |

| Average annual return with sales charge (POP) | |

| Class A | | | 10.63 | % | | | 6.40 | % | | | 8.03 | % | | | - | | | | - | | |

| Class B | | | 10.82 | % | | | - | | | | - | | | | 6.92 | % | | | - | | |

| Class C | | | 14.84 | % | | | - | | | | - | | | | - | | | | 12.96 | % | |

| Average annual return without sales charge (NAV) | |

| Class A | | | 17.08 | % | | | 7.61 | % | | | 8.93 | % | | | - | | | | - | | |

| Class B | | | 15.82 | % | | | - | | | | - | | | | 7.24 | % | | | - | | |

| Class C | | | 15.84 | % | | | - | | | | - | | | | - | | | | 12.96 | % | |

| Class R | | | 16.45 | % | | | 7.44 | % | | | 8.75 | % | | | - | | | | - | | |

| Class Y | | | 16.93 | % | | | 7.81 | % | | | 9.12 | % | | | - | | | | - | | |

| Russell 2000 Index2 | | | 17.95 | % | | | 6.44 | % | | | 8.81 | % | | | 8.18 | % | | | 15.51 | % | |

Value of $10,000 Investment1, 3 as of September 30, 2005

The charts above illustrate the total value of an assumed $10,000 investment in the funds Class A and Class Y shares (from 12/30/1998 to 9/30/2005) as compared to the Russell 2000 Index.2

The performance data quoted on this page represents past performance and does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance of the fund may be lower or higher than the performance data quoted. Performance data current to the most recent month-end may be obtained by calling 800.677.FUND.

1 Performance does not reflect the deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares. Investment performance reflects fee waivers that are or were in effect. In the absence of such fee waivers, total returns would be reduced. Index performance is for illustrative purposes only and does not reflect any expenses, transaction costs, or cash flow effects. Direct investment in the index is not available.

Stocks of small-capitalization companies involve substantial risk. These stocks historically have experienced greater price volatility than stocks of larger companies, and they may be expected to do so in the future.

Total returns at net asset value ("NAV") reflect performance over the time period indicated without including the fund's maximum sales charge and assume reinvestment of all distributions at NAV.

Total returns at public offering price ("POP") reflect performance over the time period indicated including a maximum front-end sales charge of 5.50% for Class A shares and the maximum contingent deferred sales charge ("CDSC") for Class B and Class C shares for the relevant period. Maximum CDSC is 5.00% for Class B shares, decreasing annually to 0% in the seventh year following purchase, and 1.00% for Class C shares. Total returns assume reinvestment of all distributions at NAV.

On September 24, 2001, the Small Cap Index Fund became the successor by merger to the Firstar Small Cap Index Fund, a series of the Firstar Funds, Inc. Prior to the merger, the First American Fund had no assets or liabilities. Performance presented prior to September 24, 2001, represents that of the Firstar Small Cap Index Fund. The Firstar Small Cap Index Fund was organized on December 11, 2000, and, prior to that, was a separate series of Mercantile Mutual Funds, Inc.

2 An unmanaged index that measures the performance of the 2,000 smallest companies in the Russell 3000 Index. The Russell 3000 Index measures the performance of the 3,000 largest U.S. companies based on total market capitalization, which represents approximately 98% of the investable U.S. equity market.

3 Performance for Class B, Class C, and Class R shares is not presented. Performance for these classes will vary due to different expense structures.

FIRST AMERICAN FUNDS Annual Report 2005

9

Small Cap Index fund continued

Expense Example

As a shareholder of the Small Cap Index Fund, you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments; and (2) ongoing costs, including advisory fees; distribution and/or service (12b-1) fees; and other fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the fund and to compare these costs with the ongoing costs of investing in other mutual funds. The example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period from April 1, 2005, to September 30, 2005.

Actual Expenses

For each class, the first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled "Expenses Paid During Period" to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

For each class, the second line of the table below provides information about hypothetical account values and hypothetical expenses based on the fund's actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the fund's actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads). Therefore, the second line of the table for each class is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

Expense Examples

| | | Beginning Account

Value (4/01/05) | | Ending Account

Value (9/30/05) | | Expenses Paid During

Period1 (4/01/05 to

9/30/05) | |

| Class A Actual2,3 | | $ | 1,000.00 | | | $ | 1,085.70 | | | $ | 4.60 | | |

| Class A Hypothetical (5% return before expenses) | | $ | 1,000.00 | | | $ | 1,020.66 | | | $ | 4.46 | | |

| Class B Actual2,3 | | $ | 1,000.00 | | | $ | 1,081.40 | | | $ | 8.50 | | |

| Class B Hypothetical (5% return before expenses) | | $ | 1,000.00 | | | $ | 1,016.90 | | | $ | 8.24 | | |

| Class C Actual2,3 | | $ | 1,000.00 | | | $ | 1,081.50 | | | $ | 8.50 | | |

| Class C Hypothetical (5% return before expenses) | | $ | 1,000.00 | | | $ | 1,016.90 | | | $ | 8.24 | | |

| Class R Actual2,3 | | $ | 1,000.00 | | | $ | 1,085.20 | | | $ | 5.91 | | |

| Class R Hypothetical (5% return before expenses) | | $ | 1,000.00 | | | $ | 1,019.40 | | | $ | 5.72 | | |

| Class Y Actual2,3 | | $ | 1,000.00 | | | $ | 1,087.00 | | | $ | 3.29 | | |

| Class Y Hypothetical (5% return before expenses) | | $ | 1,000.00 | | | $ | 1,021.91 | | | $ | 3.19 | | |

1 Expenses are equal to the fund's annualized expense ratio for the most recent six-month period of 0.88%, 1.63%, 1.63%, 1.13% and 0.63% for Class A, Class B, Class C, Class R and Class Y, respectively, multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year/365 (to reflect the one-half year period).

2 Based on the actual returns for the six months ended September 30, 2005: 8.57% Class A, 8.14% Class B, 8.15% Class C, 8.52% Class R, and 8.70% for Class Y, respectively.

3 Prior to July 1, 2005 the contractual limitation on annual expenses was 0.93%, 1.68%, 1.68%, 1.18%, and 0.68% for Class A, Class B, Class C, Class R, and Class Y, respectively. Effective July 1, 2005, the contractual limitation on annual expenses for Class A, Class B, Class C, Class R, and Class Y was lowered to 0.83%, 1.58%, 1.58%, 1.08%, and 0.58%, respectively. If this new limitation had been in place during the entire period, actual and hypothetical ending account balances would hav e been $1,085.96 and $1,020.91 for Class A, $1,081.66 and $1,017.15 for Class B, $1,081.76 and $1,017.15 for Class C, $1,085.46 and $1,019.65 for Class R, and $1,087.26 and $1,022.16 for Class Y, and the actual and hypothetical expenses paid during the period would have been approximately $4.34 and $4.20 for Class A, $8.24 and $7.99 for Class B, $8.24 and $7.99 for Class C, $5.65 and $5.47 for Class R, and $3.03 and $2.94 for Class Y.

FIRST AMERICAN FUNDS Annual Report 2005

10

Report of Independent Registered Public Accounting Firm

To the Shareholders and Board of Directors

First American Investment Funds, Inc.

We have audited the accompanying statements of assets and liabilities, including the schedules of investments, of the Equity Index, Mid Cap Index, and Small Cap Index Funds (series of First American Investment Funds, Inc.) (the "funds") as of September 30, 2005, and the related statements of operations, statements of changes in net assets and the financial highlights for each of the periods indicated therein, except as noted below. These financial statements and financial highlights are the responsibility of the funds' management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits. The financial highlights of the Mid Cap Index and Small Cap Index Funds for the periods presented through October 31, 2000, were audited by other auditors whose report dated December 29, 2000 expressed an unqualified opinion on those financial highlights.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. We were not engaged to perform an audit of the funds' internal control over financial reporting. Our audits included consideration of internal control over financial reporting as a basis for designating audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the funds' internal control over financial reporting. Accordingly, we express no such opinion. An audit also includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements and financial highlights, assessing the ac counting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. Our procedures included confirmation of securities owned as of September 30, 2005, by correspondence with the custodian and brokers or by other appropriate auditing procedures where replies from brokers were not received. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights audited by us as referred to above present fairly, in all material respects, the financial position of the funds listed above of the First American Investment Funds, Inc. at September 30, 2005, the results of their operations for the year then ended, the changes in their net assets for each of the two years in the period then ended and their financial highlights for each of the periods indicated herein in conformity with U.S. generally accepted accounting principles.

Minneapolis, Minnesota

November 18, 2005

FIRST AMERICAN FUNDS Annual Report 2005

11

Schedule of Investments September 30, 2005

Equity Index Fund

| DESCRIPTION | | SHARES | | VALUE (000) | |

| Common Stocks – 98.6% | |

| Consumer Discretionary – 10.1% | |

| AutoNation* (a) | | | 36,590 | | | $ | 731 | | |

| Autozone* | | | 13,254 | | | | 1,103 | | |

| Bed Bath & Beyond* | | | 59,503 | | | | 2,391 | | |

| Best Buy | | | 86,529 | | | | 3,767 | | |

| Big Lots* (a) | | | 23,098 | | | | 254 | | |

| Black & Decker | | | 15,719 | | | | 1,290 | | |

| Brunswick | | | 18,613 | | | | 702 | | |

| Carnival (a) | | | 101,533 | | | | 5,075 | | |

| Centex (a) | | | 25,324 | | | | 1,635 | | |

| Circuit City Stores | | | 41,375 | | | | 710 | | |

| Clear Channel Communications | | | 95,365 | | | | 3,137 | | |

| Coach* | | | 75,306 | | | | 2,362 | | |

| Comcast, Class A* (a) | | | 445,645 | | | | 13,093 | | |

| Cooper Tire & Rubber | | | 12,929 | | | | 197 | | |

| D.R. Horton | | | 53,920 | | | | 1,953 | | |

| Dana (a) | | | 30,366 | | | | 286 | | |

| Darden Restaurants | | | 27,909 | | | | 848 | | |

| Delphi | | | 114,633 | | | | 316 | | |

| Dillards, Class A | | | 14,252 | | | | 298 | | |

| Dollar General (a) | | | 60,055 | | | | 1,101 | | |

| Dow Jones & Company | | | 14,122 | | | | 539 | | |

| Eastman Kodak (a) | | | 56,661 | | | | 1,379 | | |

| Family Dollar Stores | | | 33,838 | | | | 672 | | |

| Federated Department Stores | | | 53,514 | | | | 3,578 | | |

| Ford Motor (a) | | | 371,866 | | | | 3,667 | | |

| Fortune Brands | | | 28,725 | | | | 2,336 | | |

| Gannett (a) | | | 50,184 | | | | 3,454 | | |

| Gap | | | 123,951 | | | | 2,160 | | |

| General Motors (a) | | | 114,260 | | | | 3,497 | | |

| Genuine Parts | | | 34,608 | | | | 1,485 | | |

| Goodyear Tire & Rubber* (a) | | | 35,553 | | | | 554 | | |

| Harley-Davidson | | | 58,672 | | | | 2,842 | | |

| Harrah's Entertainment | | | 31,512 | | | | 2,054 | | |

| Hasbro | | | 31,797 | | | | 625 | | |

| Hilton Hotels | | | 75,458 | | | | 1,684 | | |

| Home Depot (a) | | | 437,526 | | | | 16,687 | | |

| International Game Technology (a) | | | 69,000 | | | | 1,863 | | |

| Interpublic Group of Companies* (a) | | | 84,361 | | | | 982 | | |

| J.C. Penney | | | 53,312 | | | | 2,528 | | |

| Johnson Controls | | | 37,496 | | | | 2,327 | | |

| Jones Apparel Group | | | 24,349 | | | | 694 | | |

| KB HOME (a) | | | 15,656 | | | | 1,146 | | |

| Knight-Ridder (a) | | | 13,733 | | | | 806 | | |

| Kohl's* (a) | | | 62,453 | | | | 3,134 | | |

| Leggett & Platt | | | 37,737 | | | | 762 | | |

| Limited | | | 71,922 | | | | 1,469 | | |

| Liz Claiborne (a) | | | 21,714 | | | | 854 | | |

| Lowe's (a) | | | 153,891 | | | | 9,911 | | |

| Marriott International, Class A (a) | | | 40,271 | | | | 2,537 | | |

| Mattel (a) | | | 81,925 | | | | 1,367 | | |

| Maytag (a) | | | 16,242 | | | | 297 | | |

| McDonald's (a) | | | 252,258 | | | | 8,448 | | |

| McGraw-Hill (a) | | | 75,652 | | | | 3,634 | | |

| New York Times, Class A | | | 29,575 | | | | 880 | | |

| Newell Rubbermaid (a) | | | 54,258 | | | | 1,229 | | |

| News | | | 523,110 | | | | 8,155 | | |

| Nike, Class B (a) | | | 41,949 | | | | 3,426 | | |

| Nordstrom | | | 43,596 | | | | 1,496 | | |

| Office Depot* (a) | | | 61,244 | | | | 1,819 | | |

| Officemax | | | 13,316 | | | | 422 | | |

| Omnicom Group (a) | | | 37,431 | | | | 3,130 | | |

| Pulte | | | 47,080 | | | | 2,021 | | |

| RadioShack | | | 28,263 | | | | 701 | | |

| Reebok International | | | 11,933 | | | | 675 | | |

Equity Index Fund (continued)

| DESCRIPTION | | SHARES | | VALUE (000) | |

| Sears* (a) | | | 20,660 | | | $ | 2,571 | | |

| Sherwin Williams (a) | | | 30,372 | | | | 1,338 | | |

| Snap-On | | | 11,538 | | | | 417 | | |

| Stanley Works (a) | | | 16,419 | | | | 766 | | |

| Staples (a) | | | 149,051 | | | | 3,178 | | |

| Starbucks* (a) | | | 79,976 | | | | 4,007 | | |

| Starwood Hotels & Resorts Worldwide (a) | | | 40,820 | | | | 2,334 | | |

| Target (a) | | | 178,575 | | | | 9,273 | | |

| Tiffany & Company | | | 29,181 | | | | 1,161 | | |

| Time Warner (a) | | | 931,138 | | | | 16,863 | | |

| TJX | | | 95,054 | | | | 1,947 | | |

| Tribune (a) | | | 59,311 | | | | 2,010 | | |

| Univision Communications, Class A* (a) | | | 51,773 | | | | 1,374 | | |

| V.F. (a) | | | 17,498 | | | | 1,014 | | |

| Viacom, Class B (a) | | | 327,178 | | | | 10,800 | | |

| Visteon* | | | 26,057 | | | | 255 | | |

| Walt Disney (a) | | | 404,173 | | | | 9,753 | | |

| Wendy's International | | | 22,437 | | | | 1,013 | | |

| Whirlpool (a) | | | 13,258 | | | | 1,005 | | |

| Yum! Brands | | | 57,664 | | | | 2,792 | | |

| | | | 229,046 | | |

| Consumer Staples – 9.6% | | | |

| Alberto-Culver, Class B | | | 16,946 | | | | 758 | | |

| Albertson's | | | 74,582 | | | | 1,913 | | |

| Altria Group | | | 413,621 | | | | 30,488 | | |

| Anheuser-Busch (a) | | | 158,300 | | | | 6,813 | | |

| Archer-Daniels-Midland | | | 123,753 | | | | 3,052 | | |

| Avon Products | | | 93,416 | | | | 2,522 | | |

| Brown-Forman, Class B | | | 9,846 | | | | 586 | | |

| Campbell Soup | | | 55,814 | | | | 1,660 | | |

| Clorox (a) | | | 30,623 | | | | 1,701 | | |

| Coca-Cola | | | 432,631 | | | | 18,685 | | |

| Coca-Cola Enterprises | | | 47,507 | | | | 926 | | |

| Colgate-Palmolive (a) | | | 105,732 | | | | 5,582 | | |

| ConAgra Foods (a) | | | 104,873 | | | | 2,596 | | |

| Constellation Brands, Class A* (a) | | | 33,200 | | | | 863 | | |

| Costco Wholesale (a) | | | 99,260 | | | | 4,277 | | |

| CVS (a) | | | 158,520 | | | | 4,599 | | |

| General Mills (a) | | | 66,015 | | | | 3,182 | | |

| Gillette | | | 191,880 | | | | 11,167 | | |

| H.J. Heinz | | | 69,550 | | | | 2,541 | | |

| Hershey Foods (a) | | | 43,274 | | | | 2,437 | | |

| Kellogg | | | 57,352 | | | | 2,646 | | |

| Kimberly-Clark | | | 95,057 | | | | 5,659 | | |

| Kroger* | | | 146,178 | | | | 3,010 | | |

| McCormick | | | 27,600 | | | | 901 | | |

| Molson Coors Brewing (a) | | | 15,666 | | | | 1,003 | | |

| Pepsi Bottling (a) | | | 38,883 | | | | 1,110 | | |

| PepsiCo | | | 336,660 | | | | 19,092 | | |

| Procter & Gamble (a) | | | 492,488 | | | | 29,283 | | |

| Reynolds American (a) | | | 17,150 | | | | 1,424 | | |

| Safeway (a) | | | 90,595 | | | | 2,319 | | |

| Sara Lee (a) | | | 156,284 | | | | 2,962 | | |

| SUPERVALU | | | 26,471 | | | | 824 | | |

| Sysco (a) | | | 132,130 | | | | 4,145 | | |

| Tyson Foods, Class A | | | 50,150 | | | | 905 | | |

| UST (a) | | | 33,476 | | | | 1,401 | | |

| Walgreen (a) | | | 203,512 | | | | 8,843 | | |

| Wal-Mart Stores (a) | | | 520,667 | | | | 22,816 | | |

| Wrigley, William Jr. | | | 33,203 | | | | 2,387 | | |

| | | | 217,078 | | |

| Energy – 10.1% | | | |

| Amerada Hess (a) | | | 16,049 | | | | 2,207 | | |

| Anadarko Petroleum (a) | | | 47,624 | | | | 4,560 | | |

| Apache | | | 66,318 | | | | 4,988 | | |

The accompanying notes are an integral part of the financial statements.

FIRST AMERICAN FUNDS Annual Report 2005

12

Equity Index Fund (continued)

| DESCRIPTION | | SHARES | | VALUE (000) | |

| Baker Hughes (a) | | | 68,876 | | | $ | 4,111 | | |

| BJ Services (a) | | | 65,436 | | | | 2,355 | | |

| Burlington Resources | | | 77,894 | | | | 6,334 | | |

| ChevronTexaco (a) | | | 453,961 | | | | 29,385 | | |

| ConocoPhillips | | | 281,328 | | | | 19,668 | | |

| Devon Energy (a) | | | 95,722 | | | | 6,570 | | |

| El Paso (a) | | | 130,237 | | | | 1,810 | | |

| EOG Resources (a) | | | 48,442 | | | | 3,628 | | |

| Exxon Mobil (a) | | | 1,279,042 | | | | 81,270 | | |

| Halliburton (a) | | | 102,195 | | | | 7,002 | | |

| Kerr-McGee | | | 23,525 | | | | 2,285 | | |

| Kinder Morgan (a) | | | 19,226 | | | | 1,849 | | |

| Marathon Oil | | | 70,678 | | | | 4,872 | | |

| Murphy Oil | | | 31,340 | | | | 1,563 | | |

| Nabors Industries* | | | 29,560 | | | | 2,123 | | |

| National-Oilwell Varco* (a) | | | 34,765 | | | | 2,288 | | |

| Noble | | | 27,453 | | | | 1,879 | | |

| Occidental Petroleum | | | 80,474 | | | | 6,875 | | |

| Rowan* (a) | | | 21,883 | | | | 777 | | |

| Schlumberger (a) | | | 119,054 | | | | 10,046 | | |

| Sunoco | | | 27,314 | | | | 2,136 | | |

| Transocean* | | | 69,462 | | | | 4,259 | | |

| Valero Energy (a) | | | 60,810 | | | | 6,875 | | |

| Weatherford International* (a) | | | 28,960 | | | | 1,988 | | |

| Williams (a) | | | 115,342 | | | | 2,889 | | |

| XTO Energy | | | 72,930 | | | | 3,305 | | |

| | | | 229,897 | | |

| Financials – 19.7% | | | |

| ACE | | | 55,940 | | | | 2,633 | | |

| AFLAC (a) | | | 101,587 | | | | 4,602 | | |

| Allstate | | | 138,567 | | | | 7,661 | | |

| Ambac Financial Group (a) | | | 21,529 | | | | 1,551 | | |

| American Express | | | 232,347 | | | | 13,346 | | |

| American International Group | | | 524,330 | | | | 32,487 | | |

| AmSouth Bancorp (a) | | | 69,346 | | | | 1,752 | | |

| AON | | | 64,217 | | | | 2,060 | | |

| Apartment Investment & Management (a) | | | 19,538 | | | | 758 | | |

| Archstone-Smith Trust (a) | | | 40,210 | | | | 1,603 | | |

| Bank of America (a) | | | 814,452 | | | | 34,288 | | |

| Bank of New York | | | 153,539 | | | | 4,516 | | |

| BB&T (a) | | | 107,976 | | | | 4,216 | | |

| Bear Stearns (a) | | | 21,591 | | | | 2,370 | | |

| Capital One Financial (a) | | | 58,293 | | | | 4,635 | | |

| Charles Schwab (a) | | | 202,294 | | | | 2,919 | | |

| Chubb (a) | | | 37,048 | | | | 3,318 | | |

| Cincinnati Financial | | | 31,632 | | | | 1,325 | | |

| CIT Group | | | 40,732 | | | | 1,840 | | |

| Citigroup (a) | | | 1,039,734 | | | | 47,329 | | |

| Comerica (a) | | | 34,690 | | | | 2,043 | | |

| Compass Bancshares | | | 9,660 | | | | 443 | | |

| Countrywide Financial (a) | | | 113,318 | | | | 3,737 | | |

| E*TRADE Financial* | | | 74,620 | | | | 1,313 | | |

| Equity Office Properties Trust (REIT) | | | 82,897 | | | | 2,712 | | |

| Equity Residential Properties Trust (REIT) (a) | | | 57,246 | | | | 2,167 | | |

| Fannie Mae | | | 193,852 | | | | 8,688 | | |

| Federated Investors, Class B | | | 19,160 | | | | 637 | | |

| Fifth Third Bancorp | | | 111,395 | | | | 4,092 | | |

| First Horizon National | | | 24,885 | | | | 905 | | |

| Franklin Resources | | | 35,645 | | | | 2,993 | | |

| Freddie Mac (a) | | | 136,757 | | | | 7,721 | | |

| Golden West Financial (a) | | | 53,464 | | | | 3,175 | | |

| Goldman Sachs Group (a) | | | 89,898 | | | | 10,930 | | |

| Hartford Financial Services Group (a) | | | 57,939 | | | | 4,471 | | |

| Huntington Bancshares | | | 45,212 | | | | 1,016 | | |

| J.P. Morgan Chase | | | 711,001 | | | | 24,124 | | |

Equity Index Fund (continued)

| DESCRIPTION | | SHARES | | VALUE (000) | |

| Janus Capital Group | | | 47,381 | | | $ | 685 | | |

| Jefferson-Pilot (a) | | | 26,933 | | | | 1,378 | | |

| KeyCorp (a) | | | 81,886 | | | | 2,641 | | |

| Lehman Brothers Holdings (a) | | | 55,047 | | | | 6,412 | | |

| Lincoln National | | | 35,165 | | | | 1,829 | | |

| Loew's | | | 29,676 | | | | 2,742 | | |

| M & T Bank | | | 16,540 | | | | 1,748 | | |

| Marsh & McLennan (a) | | | 105,272 | | | | 3,199 | | |

| Marshall & Ilsley | | | 42,377 | | | | 1,844 | | |

| MBIA (a) | | | 28,709 | | | | 1,740 | | |

| MBNA | | | 256,143 | | | | 6,311 | | |

| Mellon Financial | | | 85,196 | | | | 2,724 | | |

| Merrill Lynch | | | 187,616 | | | | 11,510 | | |

| Metlife (a) | | | 152,013 | | | | 7,575 | | |

| MGIC Investment (a) | | | 19,638 | | | | 1,261 | | |

| Moody's (a) | | | 53,748 | | | | 2,745 | | |

| Morgan Stanley | | | 218,423 | | | | 11,782 | | |

| National City | | | 118,265 | | | | 3,955 | | |

| North Fork Bancorp | | | 94,017 | | | | 2,397 | | |

| Northern Trust (a) | | | 43,746 | | | | 2,211 | | |

| Plum Creek Timber (REIT) (a) | | | 36,766 | | | | 1,394 | | |

| PNC Financial Services (a) | | | 55,381 | | | | 3,213 | | |

| Principal Financial Group (a) | | | 64,140 | | | | 3,038 | | |

| Progressive (a) | | | 39,718 | | | | 4,161 | | |

| Prologis (a) | | | 36,820 | | | | 1,631 | | |

| Providian Financial* (a) | | | 59,519 | | | | 1,052 | | |

| Prudential Financial (a) | | | 102,120 | | | | 6,899 | | |

| Public Storage (a) | | | 17,960 | | | | 1,203 | | |

| Regions Financial (a) | | | 92,982 | | | | 2,894 | | |

| SAFECO | | | 24,785 | | | | 1,323 | | |

| Simon Property Group (REIT) (a) | | | 44,306 | | | | 3,284 | | |

| SLM | | | 83,370 | | | | 4,472 | | |

| Sovereign Bancorp | | | 69,222 | | | | 1,526 | | |

| St. Paul Travelers Companies | | | 136,146 | | | | 6,109 | | |

| State Street | | | 70,435 | | | | 3,446 | | |

| SunTrust Banks | | | 64,764 | | | | 4,498 | | |

| Synovus Financial | | | 59,559 | | | | 1,651 | | |

| T. Rowe Price Group | | | 25,046 | | | | 1,636 | | |

| Torchmark | | | 20,727 | | | | 1,095 | | |

| U.S. Bancorp (b) | | | 371,914 | | | | 10,443 | | |

| UnumProvident (a) | | | 60,147 | | | | 1,233 | | |

| Vornado Realty Trust (a) | | | 19,380 | | | | 1,679 | | |

| Wachovia | | | 319,897 | | | | 15,224 | | |

| Washington Mutual (a) | | | 173,846 | | | | 6,818 | | |

| Wells Fargo | | | 335,648 | | | | 19,659 | | |

| XL Capital Limited, Class A | | | 26,999 | | | | 1,837 | | |

| Zions Bancorporation (a) | | | 17,740 | | | | 1,263 | | |

| | | | 445,746 | | |

| Health Care – 13.0% | | | |

| Abbott Laboratories | | | 310,178 | | | | 13,152 | | |

| Aetna | | | 58,714 | | | | 5,058 | | |

| Allergan (a) | | | 25,816 | | | | 2,365 | | |

| AmerisourceBergen (a) | | | 20,944 | | | | 1,619 | | |

| Amgen* (a) | | | 250,553 | | | | 19,962 | | |

| Applied Biosystems Group – Applera | | | 39,038 | | | | 907 | | |

| Bausch & Lomb (a) | | | 10,292 | | | | 830 | | |

| Baxter International | | | 121,373 | | | | 4,839 | | |

| Becton, Dickinson & Company | | | 50,223 | | | | 2,633 | | |

| Biogen IDEC* (a) | | | 68,592 | | | | 2,708 | | |

| Biomet | | | 49,957 | | | | 1,734 | | |

| Boston Scientific* (a) | | | 142,904 | | | | 3,340 | | |

| Bristol-Myers Squibb (a) | | | 386,084 | | | | 9,289 | | |

| C.R. Bard | | | 19,100 | | | | 1,261 | | |

| Cardinal Health | | | 88,083 | | | | 5,588 | | |

| Caremark Rx* (a) | | | 89,340 | | | | 4,461 | | |

FIRST AMERICAN FUNDS Annual Report 2005

13

Schedule of Investments September 30, 2005

Equity Index Fund (continued)

| DESCRIPTION | | SHARES | | VALUE (000) | |

| Chiron* (a) | | | 23,560 | | | $ | 1,028 | | |

| CIGNA (a) | | | 26,668 | | | | 3,143 | | |

| Coventry Health Care* | | | 21,260 | | | | 1,829 | | |

| Eli Lilly (a) | | | 224,064 | | | | 11,992 | | |

| Express Scripts* (a) | | | 30,500 | | | | 1,897 | | |

| Fisher Scientific International* (a) | | | 23,673 | | | | 1,469 | | |

| Forest Laboratories, Class A* | | | 69,093 | | | | 2,693 | | |

| Genzyme* (a) | | | 49,547 | | | | 3,550 | | |

| Gilead Sciences* (a) | | | 86,010 | | | | 4,194 | | |

| Guidant | | | 63,694 | | | | 4,388 | | |

| HCA | | | 83,147 | | | | 3,984 | | |

| Health Management Associates, Class A (a) | | | 47,401 | | | | 1,113 | | |

| Hospira* | | | 30,890 | | | | 1,266 | | |

| Humana* (a) | | | 31,968 | | | | 1,531 | | |

| IMS Health | | | 46,223 | | | | 1,163 | | |

| Johnson & Johnson (a) | | | 590,899 | | | | 37,392 | | |

| King Pharmaceuticals* | | | 48,849 | | | | 751 | | |

| Laboratory Corporation of America Holdings* (a) | | | 27,581 | | | | 1,343 | | |

| Manor Care (a) | | | 17,628 | | | | 677 | | |

| McKesson HBOC | | | 58,528 | | | | 2,777 | | |

| Medco Health Solutions* | | | 60,923 | | | | 3,340 | | |

| MedImmune* | | | 49,418 | | | | 1,663 | | |

| Medtronic | | | 241,558 | | | | 12,952 | | |

| Merck | | | 445,173 | | | | 12,113 | | |

| Millipore* | | | 9,917 | | | | 624 | | |

| Mylan Laboratories | | | 43,327 | | | | 834 | | |

| PerkinElmer | | | 24,388 | | | | 497 | | |

| Pfizer | | | 1,500,955 | | | | 37,479 | | |

| Quest Diagnostics | | | 36,186 | | | | 1,829 | | |

| Schering-Plough (a) | | | 292,463 | | | | 6,156 | | |

| St. Jude Medical* | | | 71,998 | | | | 3,370 | | |

| Stryker (a) | | | 76,228 | | | | 3,768 | | |

| Tenet Healthcare* (a) | | | 91,708 | | | | 1,030 | | |

| Thermo Electron* (a) | | | 32,105 | | | | 992 | | |

| UnitedHealth Group (a) | | | 256,938 | | | | 14,440 | | |

| Watson Pharmaceuticals* (a) | | | 21,647 | | | | 792 | | |

| WellPoint Health Networks* | | | 118,772 | | | | 9,005 | | |

| Wyeth Pharmaceuticals | | | 265,222 | | | | 12,272 | | |

| Zimmer Holdings* (a) | | | 49,926 | | | | 3,439 | | |

| | | | 294,521 | | |

| Industrials – 11.1% | | | |

| 3M (a) | | | 156,270 | | | | 11,464 | | |

| Allied Waste Industries* | | | 42,805 | | | | 362 | | |

| American Power Conversion | | | 34,401 | | | | 891 | | |

| American Standard | | | 35,557 | | | | 1,655 | | |

| Apollo Group, Class A* (a) | | | 28,993 | | | | 1,925 | | |

| Avery Dennison (a) | | | 21,315 | | | | 1,117 | | |

| Boeing (a) | | | 167,985 | | | | 11,415 | | |

| Burlington Northern Santa Fe | | | 74,948 | | | | 4,482 | | |

| Caterpillar (a) | | | 135,834 | | | | 7,980 | | |

| Cendant (a) | | | 210,578 | | | | 4,346 | | |

| Cintas (a) | | | 27,356 | | | | 1,123 | | |

| Cooper Industries (a) | | | 18,480 | | | | 1,278 | | |

| CSX | | | 42,294 | | | | 1,966 | | |

| Cummins (a) | | | 8,270 | | | | 728 | | |

| Danaher | | | 54,762 | | | | 2,948 | | |

| Deere & Company | | | 48,695 | | | | 2,980 | | |

| Dover | | | 34,462 | | | | 1,406 | | |

| Eaton | | | 29,706 | | | | 1,888 | | |

| Emerson Electric | | | 83,601 | | | | 6,003 | | |

| Equifax | | | 27,797 | | | | 971 | | |

| FedEx (a) | | | 60,031 | | | | 5,230 | | |

| Fluor (a) | | | 16,131 | | | | 1,039 | | |

| General Dynamics | | | 38,983 | | | | 4,660 | | |

| General Electric (a) | | | 2,136,791 | | | | 71,946 | | |

Equity Index Fund (continued)

| DESCRIPTION | | SHARES | | VALUE (000) | |

| Goodrich | | | 23,775 | | | $ | 1,054 | | |

| H & R Block (a) | | | 71,186 | | | | 1,707 | | |

| Honeywell International | | | 170,122 | | | | 6,380 | | |

| Illinois Tool Works | | | 55,803 | | | | 4,594 | | |

| Ingersoll-Rand, Class A | | | 68,608 | | | | 2,623 | | |

| ITT Industries | | | 18,266 | | | | 2,075 | | |

| L-3 Communications Holdings (a) | | | 20,661 | | | | 1,634 | | |

| Lockheed Martin (a) | | | 79,543 | | | | 4,855 | | |

| Masco | | | 92,656 | | | | 2,843 | | |

| Monster Worldwide* (a) | | | 23,505 | | | | 722 | | |

| Navistar International* | | | 13,242 | | | | 429 | | |

| Norfolk Southern | | | 79,588 | | | | 3,228 | | |

| Northrop Grumman | | | 71,304 | | | | 3,875 | | |

| Paccar | | | 35,132 | | | | 2,385 | | |

| Pall | | | 24,545 | | | | 675 | | |

| Parker Hannifin | | | 23,353 | | | | 1,502 | | |

| Pitney Bowes | | | 38,637 | | | | 1,613 | | |

| R.R. Donnelley & Sons (a) | | | 42,381 | | | | 1,571 | | |

| Raytheon | | | 88,211 | | | | 3,354 | | |

| Robert Half International | | | 31,640 | | | | 1,126 | | |

| Rockwell Automation | | | 34,136 | | | | 1,806 | | |

| Rockwell Collins (a) | | | 35,139 | | | | 1,698 | | |

| Ryder System | | | 12,511 | | | | 428 | | |

| Southwest Airlines | | | 154,416 | | | | 2,293 | | |

| Textron | | | 27,086 | | | | 1,943 | | |

| Tyco International | | | 408,075 | | | | 11,365 | | |

| Union Pacific | | | 52,176 | | | | 3,741 | | |

| United Parcel Service, Class B (a) | | | 222,341 | | | | 15,370 | | |

| United Technologies | | | 209,726 | | | | 10,872 | | |

| W.W. Grainger | | | 18,043 | | | | 1,135 | | |

| Waste Management | | | 114,010 | | | | 3,262 | | |

| | | | 251,961 | | |

| Information Technology – 15.6% | | | |

| ADC Telecommunications* (a) | | | 23,486 | | | | 537 | | |

| Adobe Systems (a) | | | 99,234 | | | | 2,962 | | |

| Advanced Micro Devices* (a) | | | 77,076 | | | | 1,942 | | |

| Affiliated Computer Services, Class A* (a) | | | 26,030 | | | | 1,421 | | |

| Agilent Technologies* | | | 97,467 | | | | 3,192 | | |

| Altera* (a) | | | 75,682 | | | | 1,446 | | |

| Analog Devices (a) | | | 74,903 | | | | 2,782 | | |

| Andrew* (a) | | | 31,575 | | | | 352 | | |

| Apple Computer* (a) | | | 167,554 | | | | 8,983 | | |

| Applied Materials | | | 333,598 | | | | 5,658 | | |

| Applied Micro Circuits* | | | 62,612 | | | | 188 | | |

| Autodesk | | | 46,392 | | | | 2,154 | | |

| Automatic Data Processing (a) | | | 118,331 | | | | 5,093 | | |

| Avaya* (a) | | | 96,388 | | | | 993 | | |

| BMC Software* (a) | | | 45,204 | | | | 954 | | |

| Broadcom, Class A* (a) | | | 57,080 | | | | 2,678 | | |

| CIENA* | | | 116,869 | | | | 309 | | |

| Cisco Systems* (a) | | | 1,293,939 | | | | 23,200 | | |

| Citrix Systems* | | | 34,343 | | | | 863 | | |

| Computer Associates International (a) | | | 94,402 | | | | 2,625 | | |

| Computer Sciences* (a) | | | 37,021 | | | | 1,751 | | |

| Compuware* | | | 78,826 | | | | 749 | | |

| Comverse Technology* (a) | | | 38,829 | | | | 1,020 | | |

| Convergys* (a) | | | 32,160 | | | | 462 | | |

| Corning* | | | 292,843 | | | | 5,661 | | |

| Dell * | | | 483,990 | | | | 16,552 | | |

| eBay* (a) | | | 220,886 | | | | 9,101 | | |

| Electronic Arts* (a) | | | 62,208 | | | | 3,539 | | |

| Electronic Data Systems | | | 97,618 | | | | 2,191 | | |

| EMC* (a) | | | 486,080 | | | | 6,290 | | |

| First Data | | | 161,559 | | | | 6,462 | | |

| Fiserv* (a) | | | 38,286 | | | | 1,756 | | |

The accompanying notes are an integral part of the financial statements.

FIRST AMERICAN FUNDS Annual Report 2005

14

Equity Index Fund (continued)

| DESCRIPTION | | SHARES | | VALUE (000) | |

| Freescale Semiconductor* (a) | | | 79,367 | | | $ | 1,871 | | |

| Gateway* | | | 58,921 | | | | 159 | | |

| Hewlett-Packard (a) | | | 575,934 | | | | 16,817 | | |

| IBM | | | 330,319 | | | | 26,498 | | |

| Intel | | | 1,247,330 | | | | 30,747 | | |

| Intuit* (a) | | | 37,463 | | | | 1,679 | | |

| Jabil Circuit* (a) | | | 38,647 | | | | 1,195 | | |

| JDS Uniphase* (a) | | | 333,029 | | | | 739 | | |

| KLA-Tencor (a) | | | 38,504 | | | | 1,877 | | |

| Lexmark International Group, Class A* (a) | | | 25,305 | | | | 1,545 | | |

| Linear Technology (a) | | | 60,899 | | | | 2,289 | | |

| LSI Logic* (a) | | | 76,908 | | | | 758 | | |

| Lucent Technologies* (a) | | | 895,173 | | | | 2,909 | | |

| Maxim Integrated Products (a) | | | 64,998 | | | | 2,772 | | |

| Mercury Interactive* (a) | | | 17,932 | | | | 710 | | |

| Micron Technology* (a) | | | 120,591 | | | | 1,604 | | |

| Microsoft | | | 1,878,122 | | | | 48,324 | | |

| Molex | | | 29,406 | | | | 785 | | |

| Motorola (a) | | | 485,448 | | | | 10,724 | | |

| National Semiconductor (a) | | | 70,678 | | | | 1,859 | | |

| NCR* (a) | | | 37,856 | | | | 1,208 | | |

| Network Appliance* | | | 71,815 | | | | 1,705 | | |

| Novell* (a) | | | 77,299 | | | | 576 | | |

| Novellus Systems* (a) | | | 29,810 | | | | 748 | | |

| NVIDIA* (a) | | | 33,151 | | | | 1,136 | | |

| Oracle* | | | 747,999 | | | | 9,268 | | |

| Parametric Technology* (a) | | | 55,129 | | | | 384 | | |

| Paychex (a) | | | 74,605 | | | | 2,766 | | |

| PMC-Sierra* (a) | | | 35,351 | | | | 311 | | |

| QLogic* (a) | | | 18,653 | | | | 638 | | |

| QUALCOMM (a) | | | 326,434 | | | | 14,608 | | |

| Sabre Holdings, Class A (a) | | | 28,450 | | | | 577 | | |

| Sanmina – SCI* | | | 106,912 | | | | 459 | | |

| Scientific-Atlanta (a) | | | 30,345 | | | | 1,138 | | |

| Seagate Escrow Security (c) (d) | | | 44,886 | | | | - | | |

| Siebel Systems (a) | | | 104,855 | | | | 1,083 | | |

| Solectron* | | | 194,533 | | | | 761 | | |

| Sun Microsystems* (a) | | | 673,374 | | | | 2,640 | | |

| Symantec* (a) | | | 241,856 | | | | 5,480 | | |

| Symbol Technologies | | | 48,163 | | | | 466 | | |

| Tektronix | | | 16,770 | | | | 423 | | |

| Tellabs* | | | 90,766 | | | | 955 | | |

| Teradyne* (a) | | | 38,636 | | | | 637 | | |

| Texas Instruments (a) | | | 336,540 | | | | 11,409 | | |

| Unisys* | | | 65,967 | | | | 438 | | |

| Waters* | | | 24,009 | | | | 999 | | |

| Xerox* (a) | | | 190,531 | | | | 2,601 | | |

| Xilinx (a) | | | 68,801 | | | | 1,916 | | |

| Yahoo!* (a) | | | 245,486 | | | | 8,307 | | |

| | | | 353,364 | | |

| Materials – 2.9% | | | |

| Air Products and Chemicals | | | 44,936 | | | | 2,478 | | |

| Alcoa | | | 176,144 | | | | 4,301 | | |

| Allegheny Technologies | | | 17,586 | | | | 545 | | |

| Ashland | | | 13,339 | | | | 737 | | |

| Ball (a) | | | 22,032 | | | | 809 | | |

| Bemis (a) | | | 21,140 | | | | 522 | | |

| Dow Chemical | | | 194,230 | | | | 8,094 | | |

| E.I. DuPont de Nemours (a) | | | 201,269 | | | | 7,884 | | |

| Eastman Chemical | �� | | 15,047 | | | | 707 | | |

| Ecolab | | | 44,396 | | | | 1,418 | | |

| Engelhard | | | 24,383 | | | | 681 | | |

| Freeport-McMoran Copper & Gold, Class B (a) | | | 36,311 | | | | 1,764 | | |

| Georgia-Pacific | | | 52,566 | | | | 1,790 | | |

| Hercules* (a) | | | 21,918 | | | | 268 | | |

Equity Index Fund (continued)

| DESCRIPTION | | SHARES | | VALUE (000) | |

| International Flavors & Fragrances | | | 14,319 | | | $ | 510 | | |

| International Paper (a) | | | 99,310 | | | | 2,959 | | |

| Louisiana Pacific (a) | | | 21,635 | | | | 599 | | |

| MeadWestvaco | | | 36,401 | | | | 1,005 | | |

| Monsanto | | | 54,193 | | | | 3,401 | | |

| Newmont Mining (a) | | | 89,973 | | | | 4,244 | | |

| NuCor | | | 32,380 | | | | 1,910 | | |

| Pactiv* | | | 31,179 | | | | 546 | | |

| Phelps Dodge (a) | | | 19,106 | | | | 2,482 | | |

| PPG Industries (a) | | | 34,067 | | | | 2,016 | | |

| Praxair (a) | | | 65,360 | | | | 3,133 | | |

| Rohm & Haas (a) | | | 38,413 | | | | 1,580 | | |

| Sealed Air* (a) | | | 16,796 | | | | 797 | | |

| Sigma-Aldrich | | | 14,013 | | | | 898 | | |

| Temple-Inland | | | 23,108 | | | | 944 | | |

| United States Steel (a) | | | 23,074 | | | | 977 | | |

| Vulcan Materials (a) | | | 20,092 | | | | 1,491 | | |

| Weyerhaeuser | | | 47,008 | | | | 3,232 | | |

| | | | 64,722 | | |

| Telecommunication Services – 3.0% | | | |

| ALLTEL (a) | | | 66,232 | | | | 4,312 | | |

| AT&T | | | 161,892 | | | | 3,205 | | |

| BellSouth (a) | | | 367,574 | | | | 9,667 | | |

| CenturyTel (a) | | | 26,583 | | | | 930 | | |

| Citizens Communications (a) | | | 69,291 | | | | 939 | | |

| Qwest Communications International* | | | 332,798 | | | | 1,364 | | |

| SBC Communications (a) | | | 667,096 | | | | 15,990 | | |

| Sprint (a) | | | 580,114 | | | | 13,795 | | |

| Verizon Communications | | | 550,387 | | | | 17,992 | | |

| | | | 68,194 | | |

| Utilities – 3.5% | | | |

| AES* (a) | | | 131,984 | | | | 2,168 | | |

| Allegheny Energy* (a) | | | 32,350 | | | | 994 | | |

| Ameren (a) | | | 38,137 | | | | 2,040 | | |

| American Electric Power (a) | | | 78,161 | | | | 3,103 | | |

| Calpine* (a) | | | 130,493 | | | | 338 | | |

| CenterPoint Energy (a) | | | 60,543 | | | | 900 | | |

| Cinergy | | | 36,004 | | | | 1,599 | | |

| CMS Energy* (a) | | | 44,209 | | | | 727 | | |

| Consolidated Edison (a) | | | 45,475 | | | | 2,208 | | |

| Constellation Energy | | | 32,968 | | | | 2,031 | | |

| Dominion Resources (a) | | | 68,803 | | | | 5,927 | | |

| DTE Energy (a) | | | 33,250 | | | | 1,525 | | |

| Duke Energy (a) | | | 191,727 | | | | 5,593 | | |

| Dynegy* (a) | | | 65,856 | | | | 310 | | |

| Edison International | | | 64,437 | | | | 3,047 | | |

| Entergy (a) | | | 45,143 | | | | 3,355 | | |

| Exelon (a) | | | 135,204 | | | | 7,225 | | |

| FirstEnergy (a) | | | 65,238 | | | | 3,400 | | |

| FPL Group (a) | | | 78,570 | | | | 3,740 | | |

| KeySpan | | | 34,056 | | | | 1,253 | | |

| NICOR | | | 8,938 | | | | 376 | | |

| NiSource (a) | | | 51,937 | | | | 1,259 | | |

| People's Energy (a) | | | 3,070 | | | | 121 | | |

| PG&E | | | 83,534 | | | | 3,279 | | |

| Pinnacle West Capital | | | 18,032 | | | | 795 | | |

| PPL (a) | | | 72,468 | | | | 2,343 | | |

| Progress Energy (a) | | | 48,731 | | | | 2,181 | | |

| Progress Energy-CVO* | | | 7,906 | | | | 1 | | |

| Public Service Enterprises | | | 46,971 | | | | 3,023 | | |

| Sempra Energy | | | 48,095 | | | | 2,263 | | |

| Southern (a) | | | 148,122 | | | | 5,297 | | |

| TECO Energy (a) | | | 39,562 | | | | 713 | | |

FIRST AMERICAN FUNDS Annual Report 2005

15

Schedule of Investments September 30, 2005

Equity Index Fund (concluded)

| DESCRIPTION | | SHARES/PAR (000) | | VALUE (000) | |

| TXU (a) | | | 51,152 | | | $ | 5,774 | | |

| Xcel Energy (a) | | | 77,960 | | | | 1,529 | | |

| | | | 80,437 | | |

Total Common Stocks

(Cost $1,626,578) | | | | | | | 2,234,966 | | |

| Short Term Investments – 1.5% | | | |

| Affiliated Money Market Fund – 1.3% | | | |

First American Prime

Obligations Fund, Class Z (b) (e) | | | 28,481,314 | | | | 28,481 | | |

| U.S. Treasury Obligation – 0.2% | | | |

U.S. Treasury Bill

3.735%, 03/02/06 (f) | | $ | 4,600 | | | | 4,528 | | |

Total Short-Term Investments

(Cost $33,013) | | | | | | | 33,009 | | |

Investments Purchased with Proceeds

from Securities Lending (g) – 31.4% | | | |

| | | | (Cost $712,377) | | | | 712,377 | | |

Total Investments – 131.5%

(Cost $2,371,968) | | | | | | | 2,980,352 | | |

| Other Assets and Liabilities, Net – (31.5)% | | | | | | | (714,628 | ) | |

| Total Net Assets – 100.0% | | | | | | $ | 2,265,724 | | |

* Non-income producing security