UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-05601

SEI Institutional International Trust

(Exact name of registrant as specified in charter)

SEI Investments

One Freedom Valley Drive

Oaks, PA 19456

(Address of principal executive offices) (Zip code)

Timothy D. Barto, Esq.

SEI Investments

One Freedom Valley Drive

Oaks, PA 19456

(Name and address of agent for service)

Registrant’s telephone number, including area code: 610-676-1000

Date of fiscal year end: September 30, 2021

Date of reporting period: September 30, 2021

| Item 1. | Reports to Stockholders. |

September 30, 2021

ANNUAL REPORT

SEI Institutional International Trust

| International Equity Fund

| |

| Emerging Markets Equity Fund

| |

| International Fixed Income Fund

| |

| Emerging Markets Debt Fund |

Paper copies of the Funds’ shareholder reports are no longer sent by mail, unless you specifically request them from the Funds or from your financial intermediary, such as a broker-dealer or bank. Shareholder reports are available online and you will be notified by mail each time a report is posted on the Funds’ website and provided with a link to access the report online.

You may elect to receive all future reports in paper free of charge. If you invest through a financial intermediary, you can contact your financial intermediary to inform it that you wish to continue receiving paper copies of your shareholder reports. If you invest directly with the Funds, you can inform the Funds that you wish to continue receiving paper copies of your shareholder reports by calling 1-800-DIAL-SEI. Your election to receive reports in paper will apply to all funds held with the SEI Funds or your financial intermediary.

The Trust files its complete schedule of portfolio holdings with the Securities and Exchange Commission for the first and third quarters of each fiscal year as an exhibit to its reports on Form N-PORT. The Trust’s Form N-PORT reports are available on the Commission’s website at http://www.sec.gov.

A description of the policies and procedures that the Trust uses to determine how to vote proxies relating to portfolio securities, as well as information relating to how a Fund voted proxies relating to portfolio securities during the most recent 12-month period ended June 30, is available (i) without charge, upon request, by calling 1-800-DIAL-SEI; and (ii) on the Commission’s website at http://www.sec.gov.

September 30, 2021 (Unaudited)

To Our Shareholders:

The fiscal year ending September 30, 2021, saw strong returns for U.S. equities as investors gained exposure to businesses they believed would benefit from the improving economy and a “return to normal” enabled by the widespread availability of COVID-19 vaccines. Financial markets anticipated increased volatility around the U.S. presidential election, but with Joe Biden winning a close election for U.S. president, markets advanced higher and volatility generally declined. Expectations of further, but less expansive, fiscal stimulus from Congress and a less likely reversal of the corporate tax cuts under the Trump administration helped fuel this appreciation. Investor exuberance was also driven by a series of positive vaccine clinical trial results in November; the enthusiasm was sustained by subsequent emergency use authorizations by the FDA.

Work-from-home and mega-cap stocks gave up ground to cyclical and “go-out” names before a slight reversal later in the period. Market observers attributed this to the FOMC deciding to increase its projection for the federal-funds rate in 2023. Meanwhile, for the first time since April this year, the seven-day moving average of new COVID-19 cases reported in the U.S. stopped falling in mid-June after an impressive period of declines that had brought cases to their lowest levels since March 2020.

Tightening supply chain dynamics contributed to higher prices for both consumers and producers; this caused input prices for a wide variety of goods to increase, resulting in higher prices for consumers as well. Intermediate- and long-term interest rates increased from historically low levels due to evidence of rising global inflation. The U.S. Treasury yield curve steepened over the course of the fiscal year, especially as future expectations for a rebound in economic growth increased with the rising inflation expectations. U.S. Treasury yields further out the curve rose considerably as the yield on 10-year Treasurys rose by roughly 80 basis points. Government-bond yields (which had been rising slowly since the fall) began to spike further in February. The specter of a sharp increase in borrowing costs sent chills through markets during the second half of February, leading to selloffs of varying intensity before equity markets resumed their climb again in March.

The Federal Reserve’s (Fed) federal-funds rate target continued to range between 0.0% and 0.25% through the reporting period. Over the course of the third quarter, the Federal Open Market Committee (FOMC) moved incrementally closer to declaring a start date for tapering (reducing) asset purchases. The FOMC currently purchases $80 billion in Treasurys and $40 billion in agency mortgage-backed securities per month; Federal Reserve (Fed) Chairman Jerome Powell indicated that the tapering timeline could be determined at the November FOMC meeting. The central bank noted in its latest quarterly Summary of Economic Projections that the projected timing of the next fed-funds interest-rate hike has moved up to 2022 from 2023 (as projected in June).

Geopolitical events

In the U.S. general election in November, Joe Biden was declared the winner of the presidential race in early November. Most candidates from the Republican Party performed better in their races for state- and national-level offices compared to President Trump’s quest for a second term; in January, a violent security breach of the U.S. Capitol by a mob of protesters delayed—but did not stop—the counting of electoral votes in the U.S. Congress. Trump was impeached by the House of Representatives for inciting an insurrection—the first president in U.S. history to be impeached twice. Two weeks later, Joe Biden was inaugurated as president under heavy security provided by 25,000 National Guard troops.

In September 2020, the millionth victim of the COVID-19 outbreak was claimed globally, a figure that would climb to almost 5 million by the end of the fiscal year. The Delta wave of new COVID-19 cases drove U.S. infection and hospitalization counts to a peak at the beginning of September, just two weeks ahead of the country’s mid-September top in daily deaths. U.K. cases peaked during mid-July, and had a smaller resurgence in early September. Both episodes roughly coincided with high points in the hospitalization rate, while the number of daily deaths crested along with the early September infections surge. There were contrasting takes among global regions on how to approach the pandemic, with Asia broadly taking a zero-tolerance approach, Eastern Europe’s approach closer to Western Europe (to accept and live with it), and Latin America initially being dismissive (particularly in Brazil and Mexico), before moving to a more proactive stance.

SEI Institutional International Trust / Annual Report / September 30, 2021 |

1 |

LETTER TO SHAREHOLDERS (Continued)

September 30, 2021 (Unaudited)

President Joe Biden’s administration proposed a $6 trillion budget for the 2022 fiscal year that would serve as a starting point from which Congress can decide how to appropriate the country’s economic funding. The president incorporated his two major economic initiatives into the budget, infrastructure and families programs.

In August, the U.S. Senate approved a bipartisan infrastructure plan, which awaited approval in the House of Representatives at the end of the reporting period. Formally called the Infrastructure Investment and Jobs Act, the plan includes roughly $1 trillion with $550 billion in new spending over a five-year period. It is projected to add approximately two million jobs per year for a decade as the nation undertakes modernizing roads, railways, ports, public transit, airports and power grids; improving water quality and broadband access; and cleaning abandoned environmentally hazardous sites.

In a push to re-establish tourism ahead of the traditionally busy summer season, the EU approved a proposal made by the European Commission in May to ease travel restrictions within the bloc for vaccinated foreigners. Tensions between the EU and China—which have flared over the last six months as the EU condemned China’s record on human rights and China imposed retaliatory economic sanctions—remained unsettled. In May, the European Parliament suspended ratification of the Comprehensive Agreement on Investment that EU and Chinese leaders had finalized in December 2020. As for U.S.-EU trade relations, friction smoothed as the European Commission delayed an increase to tariffs on the U.S. that had been planned in response to the Trump administration’s tariffs on European metals; existing tariffs will remain as the two sides negotiate a long-term solution.

Finance ministers and central bank leaders from the Group of 20 (G-20), representing the world’s 20 largest economies, unanimously agreed to endorse the major components of a tax plan that would establish a global minimum corporate tax of at least 15%. The agreement was finalized just after the end of the reporting period and was expected to crack down on tax havens used by companies to avoid paying income tax in their countries of residence.

Economic performance

A 4.0% gain in U.S. gross domestic product (GDP) in the fourth quarter of 2020 resulted in a decline of 3.5% for the full year, the worst figure since at least the end of World War II. The U.S. economy expanded at a robust annualized rate of 6.3% in the first quarter of 2021; consumer spending (which accounts for nearly 70% of U.S. economic activity) spiked by 11.3% as Americans put their stimulus payments to work, providing a much-needed boost to restaurants, hotels and airlines. Overall U.S. economic growth measured an annualized 6.7% during the second quarter, just above the first-quarter pace, as service-oriented businesses anticipated saw continued gains from the rise in vaccinations and reopenings. A widely followed tracking estimate from the Federal Reserve Bank of Atlanta put third-quarter growth at 0.5% as supply-chain issues and the Delta variant again challenged economic growth.

After touching a 50-year low of 3.5% early in 2020 and then jumping as high as 14.8% at the beginning of the pandemic (prior to the start of the fiscal year), the U.S. unemployment rate remained over 6.0% through April, with the final figure settling at 4.8% in September 2021, down from 7.8% a year earlier. The labor-force participation rate ended at 61.6%, up from 61.4% a year earlier. Average hourly earnings gained 4.6% over the fiscal year, as the leisure and hospitality industry continued to reopen and looked to boost pay in order to fill vacant positions.

Two off-cycle moves before the start of the fiscal year brought the federal-funds rate to near zero and were designed to bolster the economy in response to the economic threat posed by the coronavirus outbreak; the emergency actions were the first since the global financial crisis. Additionally, the Fed committed to purchasing unlimited amounts of Treasurys and established or renewed multiple facilities designed to support the economy. The FOMC held the federal-funds rate near zero throughout the third quarter and continued its asset purchases apace ($80 billion in Treasurys and $40 billion in agency mortgage-backed securities per month). In its September statement, it indicated that the U.S. economy had made progress toward its employment and price stability goals, and that if progress continues as expected, a moderation in the pace of asset purchases may soon be warranted. Its latest Summary of Economic Projections (SEP), released in mid-September, featured a projected increase in the federal-funds rate to 1.0% in 2023 (up from 0.6% in its June projection). The SEP also depicted higher real gross domestic product (GDP) and inflation projections for 2021, although out-year projections were only modestly higher.

2 |

SEI Institutional International Trust / Annual Report / September 30, 2021 |

Market developments

The S&P 500 Index returned 30.00% during the fiscal year. Large-cap value stocks (as measured by the Russell 1000® Value Index) gained 35.01% and led large-cap growth stocks (as measured by the Russell 1000® Growth Index), which rose 27.32%. At the sector level, energy, financials and capital goods stocks led, while utilities, consumer staples and consumer discretionary lagged. Overall, U.S. equities outpaced major developed markets during the fiscal year.

Small-cap stocks, which tend to be value-oriented and sensitive to the success or decline in a local economy, outperformed large caps overall. U.S. large-cap stocks (Russell 1000® Index) finished the reporting period up 30.96%, while small-cap stocks (Russell 2000® Index) finished the period ahead 47.68%. The reason for this difference in performance was a shift in investor preference toward companies with smaller market caps and lower valuation ratios. These companies were viewed as able to benefit from the post-pandemic economic recovery and primed for a rebound following a prolonged period of prior underperformance.

Developed markets, as measured by the MSCI World Index (Net), finished up 28.82% for the year, outperforming emerging markets. The MSCI Emerging Markets Index (Net) finished the reporting period up 18.20% in U.S. dollar terms. Emerging-market equities were on a tear in the first quarter of the reporting period (after bottoming early in the pandemic) but gave up some ground over the remainder of the fiscal year. The best-performing region was EM EMEA, which was lifted by strong performance from Russia and the Gulf countries as they benefited from tightness in oil supply and rising oil prices. EM Asia was a relative benchmark laggard as pandemic restrictions continued to disrupt the area’s consumption and services sector.

The MSCI Europe Index (Net) advanced 27.25% in U.S. dollar terms. The MSCI ACWI Index (Net), a proxy for global equities in both developed and emerging markets, rose 27.44% in U.S. dollar terms. The FTSE UK Series All-Share Index recorded a 33.39% gain in U.S. dollar terms over the full reporting period.

U.S. investment-grade corporate debt, as represented by the Bloomberg US Corporate Investment Grade Index, returned 1.74%, while the U.S. high-yield market, as measured by the ICE BofA US High Yield Constrained Index, benefited from a broad reopening of the U.S. economy and was up 11.46% during the reporting period. Within the high-yield market, energy remained the largest sector, and it easily outperformed the broader market. Lower-quality issues also outperformed, as CCC rated securities led, followed by B and BB rated. U.S. asset-backed securities managed a small gain as the health of U.S. consumers improved during the fiscal year; mortgage-backed securities were down slightly, as elevated supply and fast prepayment speeds offset the Fed adding around $40 billion of MBS to its balance sheet each month.

Inflation-sensitive assets, such as commodities and Treasury inflation-protected securities (TIPS), were higher. The Bloomberg Commodity Total Return Index (which represents the broad commodity market) finished up 42.29% over the full one-year period due to increased demand expectations, as well as constrained supply in certain markets; the Bloomberg 1-10 Year US TIPS Index (USD) moved 5.75% higher during the reporting period as it benefited from higher inflation expectations in the U.S.

Global fixed income, as measured by the Bloomberg Global Aggregate Index, was down 0.91%. Emerging-market debt (EMD) delivered positive performance due to an improving growth outlook in the region relative to developed markets. The JP Morgan Global Bond Index-Emerging Markets (GBI-EM) Global Diversified Index, which tracks local-currency-denominated EM bonds, gained 2.63% in U.S. dollar terms. The JP Morgan Emerging Markets Bond Index (EMBI) Global Diversified Index, which tracks EMD denominated in external currencies (such as the U.S. dollar), was up 4.36%.

After the U.S. dollar initially rebounded from its January low (relative to a trade-weighted basket of foreign currencies), it resumed an overall downward trend and neared its earlier low again in May before recovering some in the final quarter of the fiscal year. After hitting an all-time low in 2020 before the start of the reporting period, the West Texas Intermediate crude-oil price reached a 7-year high in the final month of the fiscal year due to optimistic forecasts for global economic growth and increased demand for crude.

SEI Institutional International Trust / Annual Report / September 30, 2021 |

3 |

LETTER TO SHAREHOLDERS (Continued)

September 30, 2021 (Unaudited)

Our view

In a natural reaction to the prospect of more lockdowns and delayed returns to normal life given the surge in COVID-19 infections that began this past May, investors revisited stocks that benefited the most during 2020—namely the work-at-home, big technology companies and other large-cap stocks that do well when interest rates fall (lower interest rates make future cash flows of these types of stocks more attractive). However, the subsequent bounce-back in growth- and momentum-oriented large-cap stocks at the expense of value and cyclical stocks has already shown signs of deteriorating as rates spiked at the end of the third quarter.

We expect economic growth—in the U.S. and globally—to continue over the next year or two at a pace that meaningfully exceeds the sluggishness of the years that followed the 2007-to-2009 global financial crisis; the recent gloom about flagging economic growth is likely a bit overdone.

Household wealth is at an all-time high, owing to booming stock and home prices. A big decline in the saving rate has helped cushion the blow to consumer spending; still, saving as a percentage of disposable income remains elevated compared to pre-pandemic levels. We think households generally can adjust to a decline in pandemic relief payments without necessitating a sharp contraction in their expenditures.

The impact of COVID-19 on global supply chains has been a more significant impediment. Vendor deliveries have seldom been as slow in the 74-year history of the Institute for Supply Management’s (ISM) survey as they are now, even with the situation having eased slightly since May. Inventories remain exceedingly low relative to demand.

Input costs have been rising rapidly, but companies have been able to compensate by passing along their increased costs to customers. After-tax corporate margins an economy-wide basis hit a new all-time high in the second quarter, rising to 14.9% of sales.

Corporate pricing power is the good news. The bad news is that inflation keeps exceeding consensus expectations. We still expect inflation to run at higher rate for a longer period than has been commonly assumed, not just over the next one or two years, but well into the decade.

Growth in unit labor costs typically plummets when the economy emerges from recession. Now, however, unit labor costs are running near a 2.7% rate—the fastest pace since the peak of the 2002-to-2007 expansion.

While commodity inflation and parts shortages may indeed prove transitory, it isn’t clear whether the labor shortage and resultant pressure on compensation growth will be as quick to revert to lower levels. The tax and regulatory initiatives of the Biden administration will likely add to the cost pressures facing businesses in the years immediately ahead.

Since U.S. demand is expected to remain robust as economic growth normalizes, it would not be surprising to see companies continue passing along their increased costs. Inflation over the long haul could thus be closer to 3% than the 2% or so currently expected by the Fed and most investors.

If that turns out to be the case, the Fed may be forced to raise interest rates higher and faster over the next three years than anticipated.

A concern that is much nearer in timeframe is the fight in Washington over infrastructure spending and the debt limit. We assume President Biden will get about half of what he is seeking, but the devil will be in the details. Investors are probably right not to react too dramatically to every development. The debt-limit drama, however, could elicit a more significant disruption as the deadline for must-pass legislation nears. Although the debt ceiling will be raised, the wrangling over it will almost certainly come down to the wire.

We suggest focusing on longer-term considerations: The latest COVID-19 wave will eventually pass. Economic growth should stay relatively strong in 2022. Households are in solid financial shape and will benefit as employment and wages continue to move higher. Companies are still able to pass along increased costs and maintain high profit margins. Fed policy is still biased toward easing, allowing the economy to run hot at the risk of higher inflation. This should all create a favorable backdrop for risk assets and support a resumption in the coming months of the cyclical/ financial/value trend versus growth/technology.

Other developed countries are broadly on the same path as the U.S., and are reacting to the same catalysts.

4 |

SEI Institutional International Trust / Annual Report / September 30, 2021 |

Purchasing managers’ surveys from recent months show that U.S. economic growth is cooling, yet still strong versus pre-pandemic levels. Activity in Europe, led by Germany, appears to be on the upswing—boosted by a decline in Delta (which has allowed for more travel and tourism in Europe) and an increase in EU fiscal support.

The major outlier is Japan, which has been rather weak so far this year versus its industrial-country peers. Inflation-adjusted GDP fell in the first quarter and posted only a tepid gain in the second quarter. Economists blame COVID-19-related restrictions. The global shortage in the supply of semiconductor chips, meanwhile, has impeded auto production. Citizens nonetheless blamed Prime Minister Yoshihide Suga. In response, he pledged to cede leadership of the Liberal Democratic Party to former foreign minister Fumio Kishida, who is expected to also succeed Suga as prime minister following the November elections.

U.S. inflation may be near a peak, but a further acceleration appears in store for Europe. The immediate concern for households in the region is the cost of energy. Even without energy-production shortages, electricity prices across Europe tend to be much higher than in North America—especially for households, particularly in Germany. The U.K. is in the midst of a petrol crisis due to an inability to make deliveries to gas stations amid a severe truck-driver shortage.

Europe’s energy woes probably won’t cause the region’s governments to deviate from the climate-change agenda they have put in place. The German election underscores this point. Although it will take a couple of months to cobble together a coalition, all political parties are committed to reducing carbon admissions.

Beyond energy, Europe’s reopening should cause the price of services to rise as they have in the U.S., albeit to far less of an extent. The overwhelming assumption is that any pickup in inflation will be short-lived.

China is dominating investor perceptions of emerging markets. The Xi government’s push to enforce “common prosperity” has had far-reaching effects on corporate China. The country’s 20-year boom has exacerbated social inequality. Crackdowns on for-profit tutoring companies, major gig employers, and individuals (notably, Jack Ma) is a brutal but effective way of addressing disparities in wealth and income.

Although some of these moves have hurt foreign equity investors, it’s unclear whether the economy itself will be severely constrained. China is a huge country with tremendous internal capital upon which to draw. Foreign companies probably won’t cut and run, but they will certainly be forced to play by Beijing’s rules if they stay.

We expect diversification of supply chains away from China at the margin, but this has been happening anyway. It is in advanced countries’ interests to be more self-sufficient in producing critical products. But China is too big, too efficient and too important a manufacturer for the world to turn its back on.

China’s economic growth rate should nevertheless slow as a result of the government’s actions. Property development has been the driving force behind its rapid expansion over the past 15 years. Critics of China’s economic model have wondered for years if the bill would ever come due. It might be coming due now.

We are watching the trend in commodity prices for hints that pressure on China’s construction activity is beginning to reverberate beyond its borders. So far, there has been little sign of that occurring. Iron ore prices have plunged, but that appears to have been caused primarily by government-mandated closures of steel plants in an effort to curb pollution.

Even within China itself, investors seem to be taking the Evergrande debacle in stride. The effective yield on the country’s high-yield bonds has been rising sharply since May, but it is nowhere near the 40% yield reached in 2008. It also remains some six percentage points below the high reached in 2011, when the government clamped down on excessive credit growth and rampant speculation in the property and stock markets.

In contrast to high yield, the yield on Chinese investment-grade bonds is currently at its lowest level in the past 20 years—indicating no sign of contagion.

One explanation for the resiliency of the MSCI Emerging Markets Index is the strength of the global economy outside China. The U.S. has been leading the way, but other advanced countries—notably Europe—continue to post improved economic activity.

If history is any guide, however, upside inflation surprises in the G-10 countries suggest that emerging economies will follow suit over the next few months. Unlike advanced countries, where inflation expectations tend to better

SEI Institutional International Trust / Annual Report / September 30, 2021 |

5 |

LETTER TO SHAREHOLDERS (Concluded)

September 30, 2021 (Unaudited)

anchored, central banks in vulnerable emerging economies are forced to raise interest rates sooner than they would prefer in order to dampen inflation pressures and defend their currencies.

Given these concerns, investors might be tempted to avoid emerging-market equities. We believe that would be a mistake. Valuations, particularly relative to the developed world, look especially cheap.

Sincerely,

James Smigiel

Head and Chief Investment Officer of Non-Traditional Asset Management

6 |

SEI Institutional International Trust / Annual Report / September 30, 2021 |

Index Definitions

Bloomberg Global Aggregate Index: is a broad-based benchmark that is considered representative of global investment-grade, fixed-income markets.

Bloomberg US Corporate Investment Grade Index: is a broad-based benchmark that measures the investment-grade, fixed-rate, taxable corporate bond market.

Bloomberg US Aggregate Bond Index: The Bloomberg Barclays U.S. Aggregate Bond Index is a benchmark index composed of U.S. securities in Treasury, government-related, corporate and securitized sectors. It includes securities that are of investment-grade quality or better, have at least one year to maturity and have an outstanding par value of at least $250 million.

Dow Jones Industrial Average: The Index measures the stock performance of 30 large companies listed on stock exchanges in the United States.

FTSE UK Series All-Share Index: is a capitalization-weighted index, comprising around 600 of more than 2,000 companies traded on the London Stock Exchange.

ICE BofA US High Yield Constrained Index: tracks the performance of below-investment-grade, U.S. dollar-denominated corporate bonds publicly issued in the U.S. domestic market; exposure to individual issuers is capped at 2%.

JP Morgan EMBI Global Diversified Index: tracks the performance of external debt instruments (including U.S.-dollar-denominated and other external-currency-denominated Brady bonds, loans, eurobonds and local-market instruments) in emerging markets.

JP Morgan GBI-EM Global Diversified Index: tracks the performance of debt instruments issued in local currencies by emerging-market governments.

MSCI EAFE Index: is a free float-adjusted market capitalization index that is designed to measure the equity market performance of developed markets, excluding the US & Canada.

MSCI Europe Index: is a free float-adjusted market-capitalization-weighted index designed to measure the performance of large- and mid-capitalization stocks across developed-market countries in Europe.

MSCI Emerging Markets Index: is a free float-adjusted market-capitalization-weighted index designed to measure the performance of global emerging-market equities.

MSCI World Index: is a free float-adjusted market-capitalization-weighted index that is designed to measure the equity-market performance of developed markets.

Russell 1000® Index: includes 1,000 of the largest U.S. stocks based on market cap and current index membership; it is used to measure the activity of the U.S. large-cap equity market.

Russell 2000® Index: The Russell 2000 Index measures the performance of the 2,000 smallest companies in the Russell 3000 Index, which represents approximately 8% of the total market capitalization of the Russell 3000 Index.

S&P 500 Index: is an unmanaged, market-weighted index that consists of approximately 500 of the largest publicly-traded U.S. companies and is considered representative of the broad U.S. stock market.

SEI Institutional International Trust / Annual Report / September 30, 2021 |

7 |

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FUND PERFORMANCE

September 30, 2021 (Unaudited)

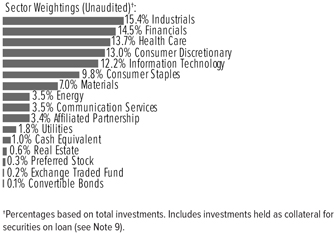

International Equity Fund

I. Objective

The International Equity Fund (the “Fund”) seeks long-term capital appreciation.

II. Multi-Manager Approach Statement

The Fund uses a multi-manager approach, relying on a number of sub-advisors with differing investment approaches to manage portions of the Fund’s portfolio, under the general supervision of SEI Investments Management Corporation (“SIMC”). The Fund utilized the following sub-advisors as of September 30, 2021: Acadian Asset Management LLC (“Acadian”), Causeway Capital Management LLC (“Causeway”), INTECH Investment Management LLC (“INTECH”), JO Hambro Capital Management Limited (“JO Hambro”), Lazard Asset Management LLC (“Lazard”), Delaware Investments Fund Advisers, a series of Macquarie Investment Management Business Trust (“Macquarie”) and WCM Investment Management LLC (“WCM”).

During the period, NWQ Investment Management Company, LLC (NWQ), was removed from the Fund, while Macquarie was added to the Fund.

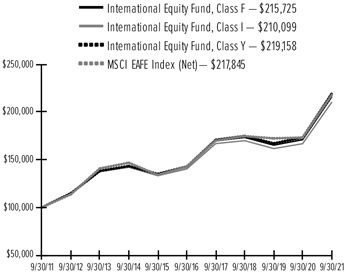

III. Return vs. Benchmark

For the year ended September 30, 2021, the Fund’s Class F shares outperformed the MSCI EAFE Index (Net)—which tracks the performance of developed-market equities outside North America—returning 26.18% versus the Index return of 25.73%.

IV. Fund Attribution

Markets rose steadily throughout the fiscal year. As noted in the shareholder letter, the announcement of Pfizer’s COVID-19 vaccine led to a strong yearend rally in 2020 that continued for most of the reporting period. U.K. stocks led other regional markets during the 12 months, lifted by strong performance of vaccine progress and a reopening of the economy. Despite Delta variant concerns during the summer of 2021, U.K. equities maintained their lead as a shortage in energy supply lifted many of the region’s energy producers. Europe was also strong and initially lagged the U.K. due to slower vaccination rollouts. However, as the region caught up, and lockdown measures across the continent were lifted, cyclical sectors, such as energy and metals & mining, benefited from a sharp increase in pent-up consumer demand that drove prices higher. Cyclicals helped lift equities in the Pacific ex-Japan region. Japan was the only area to lag the benchmark as

slow vaccination progress and supply chain disruptions weighed on the country’s equity performance.

Cyclical sectors led the market as pent-up consumer and manufacturer demand drove up commodity prices. Energy and materials were the best performers, followed by financials and industrials. Information technology stocks also posted strong gains due to the strong performance of semiconductor stocks as a global semiconductor shortage emerged. Chips became scarce as supply was limited, while demand rose in the form of increased usage among autos and consumer devices. Defensive sectors lagged the market, with utilities and consumer staples posting the biggest losses. Rising rates presented a headwind for these rate-sensitive sectors, while investors preferred sectors offering faster growth.

The information technology sector was the biggest contributor to relative Fund performance due to strong results from the hardware group and an overweight to semiconductors. Consumer staples also contributed due to the Fund’s underweight to the underperforming sector. The Fund was underweight due to the sector’s expensive valuations, and the sector underperformed as higher rates decreased the sector’s appeal. Industrials benefited from positive gains among transportation stocks held by value managers. Materials was helped by positive results across metals & mining stocks, which rallied on higher commodity demand. Consumer discretionary detracted due to weak security selection across the entire sector. Energy was the only other detractor due to the Fund’s underweight. The underweight was driven by a negative outlook on volatile energy prices.

Causeway was the best-performing manager during the period and was helped by tailwinds to its value style, which resulted in strong gains from the industrials and financials sectors. NWQ was terminated from the Fund during the period but also benefited from value tailwinds, in addition to strong gains within the information technology and telecommunication services sectors. Despite headwinds to its quality style, WCM contributed through strong stock selection and bottom-up results from the information technology and health-care sectors, especially from semiconductors, which experienced a strong tailwind from rising demand. Lazard saw strong tailwinds to value offset losses from exposure to Asian consumer names, which failed to experience a strong reopening rally. Acadian outperformed on strong quant model results within the materials and utilities sectors, which offset losses in consumer discretionary and an underweight to energy.

8 |

SEI Institutional International Trust / Annual Report / September 30, 2021 |

JO Hambro was the biggest detractor during the period due to a partial headwind to momentum as momentum stocks suffered during the market rotation into “stay at home” names. JO Hambro lagged the momentum rotation into value and suffered even more losses due to stock specifics. INTECH also detracted due to a similar momentum headwind. Macquarie was added to the Fund during the fiscal year and was the smallest detractor due to headwinds to low-volatility and quality stocks, which lagged the market due to rising rates.

Investing is subject to risk, including the possible loss of principal. Past performance is no indication of future results.

AVERAGE ANNUAL TOTAL RETURN1

| 1 Year Return | Annualized 3 Year Return | Annualized 5 Year Return | Annualized 10 Year Return | Annualized Inception to Date | ||||||||||||||||

| International Equity Fund, Class F | 26.18% | 7.57% | 8.67% | 7.99% | 4.08% | |||||||||||||||

| International Equity Fund, Class I | 25.91% | 7.31% | 8.41% | 7.71% | 3.82% | |||||||||||||||

| International Equity Fund, Class Y | 26.45%2 | 7.81% | 8.94% | 8.16% | 4.13% | |||||||||||||||

| MSCI EAFE Index (Net) | 25.73% | 7.62% | 8.81% | 8.10% | 4.79% | |||||||||||||||

Comparison of Change in the Value of a $100,000 Investment in the International Equity Fund, Class F, Class I and Class Y, versus the MSCI EAFE Index (Net)

| 1 | For the year ended September 30, 2021. Past performance is no indication of future performance. Class F shares were offered beginning December 20, 1989. Class I shares were offered beginning January 4, 2002. The performance of Class I shares prior to January 4, 2002 is calculated using the performance of Class F shares adjusted for the higher expenses of the Class I shares. Returns for Class I shares are substantially similar to those of Class F shares and differ only to the extent that Class I shares have higher total annual fund operating expenses than Class F shares. The Fund’s Class Y shares commenced |

| operations on December 31, 2014. For periods prior to December 31, 2014, the performance of the Fund’s Class F Shares has been used. Returns for Class Y Shares would have been substantially similar to those of Class F shares and would have differed only to the extent that Class Y shares have lower total annual fund operating expenses than Class F shares. Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. The returns for the period reflect fee waivers and/or reimbursements in effect for the period; absent fee waivers and reimbursements, performance would have been lower. |

| 2 | Total returns disclosed in the Financial Highlights of the Annual Report may reflect adjustments to conform to generally accepted accounting principles. |

SEI Institutional International Trust / Annual Report / September 30, 2021 |

9 |

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FUND PERFORMANCE

September 30, 2021 (Unaudited)

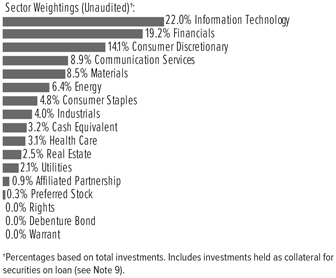

Emerging Market Equity Fund

I. Objective

The Emerging Markets Equity Fund (the “Fund”) seeks capital appreciation.

II. Multi-Manager Approach Statement

The Fund uses a multi-manager approach, relying on a number of sub-advisors with differing investment approaches to manage portions of the Fund’s portfolio, under the general supervision of SEI Investments Management Corp. (“SIMC”). The Fund utilized the following sub-advisors as of September 30, 2021: JO Hambro Capital Management Limited (“JO Hambro”), KBI Global Investors (North America) Ltd. (“KBI”), Neuberger Berman Investment Advisers LLC (“Neuberger Berman”), Qtron Investments LLC (“Qtron”), Robeco Institutional Asset Management US Inc. (“Robeco”) and RWC Asset Advisors (US) LLC (“RWC”).

During the period, Lazard Asset Management LLC (“Lazard”) was removed from the Fund, while Robeco was added to the Fund.

III. Return vs. Benchmark

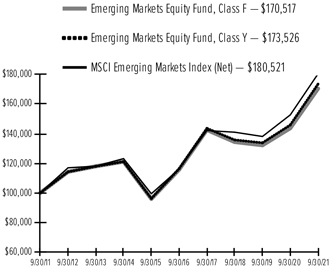

For the year ended September 30, 2021, the Fund’s Class F shares outperformed the MSCI Emerging Markets Index (Net)—which tracks the performance of global emerging market equities—returning 18.63% versus the Index return of 18.20%.

IV. Fund Attribution

As noted in the shareholder letter, emerging markets experienced positive returns during the fiscal year, although gains were concentrated within the first quarter of the reporting period. The announcement of Pfizer’s COVID-19 vaccine led to a strong yearend rally in 2020. Value stocks and smaller emerging-market countries that had lagged during the “stay at home” trade led the rally as the vaccine improved the prospects of an economic recovery in less-developed economies. The rally was short-lived, as the Chinese government’s crackdown on Alibaba’s ANT Financial IPO intensified and spread to other parts of the Chinese economy. What began as a curb on Alibaba’s dominance led to increasing regulatory focus on other dominant Chinese e-commerce and internet companies as the government began a renewed push for social equality and common prosperity. The crackdown spread to other sectors, including private education companies, while the country’s push toward deleveraging and decreasing loan issuance rattled property developers dependent on debt as funding. The default of large real-estate developer,

Evergrande, created major headlines and added to selling pressure that intensified over the summer. As a result of these regulatory pressures, the broader emerging markets fell throughout the rest of the period as the underperformance of the largest companies in China had an outsized effect on the index given their large weight. Outside of China, Taiwan benefited from higher semiconductor prices, while India had a rough time before Delta variant infections stabilized and India rebounded.

EMEA region was the best-performing region throughout the period, led by rising crude and other commodity prices. News of a vaccine, alongside expectations for further fiscal stimulus in the U.S. and pent-up consumer demand, contributed sharply to rising global yields and outperformance for stocks that would benefit most from a reopening of the global economy. This helped commodity stocks as demand for commodities surged. Outperformance continued throughout the rest of the fiscal period despite the effects that the Delta variant had on the global supply chain. Russia and the Gulf countries benefited from tightness in oil supply and rising oil prices, helping to lift the region’s equity prices to new highs. Latin America outperformed Asia but lagged EMEA throughout the period. Brazil led the regional rally in the fourth quarter of 2020, but the country fell in the first and third quarter of 2021 due to growth fears around the Delta variant, as well as concerns around political issues and the economic outlook. Mexico outperformed the region and the benchmark as Mexican consumer and industrial stocks held up better in the face of pressure from the Delta variant.

The best-performing sectors were materials and energy due to strong demand for commodities as pent-up demand from both consumers and industrials drove prices higher. Utilities and financials were also strong as the energy shortage lifted utilities over the summer of 2021 and banks benefited from prospects of an economic rebound from the pandemic lows. Consumer discretionary and real estate were the two biggest laggards. Consumer discretionary was dragged down by the underperformance of large e-commerce heavyweights in China due to government regulatory crackdowns. Real estate suffered from China’s efforts to deleverage, as fears of default and slower loan issuance weighed on the sector.

From a sector perspective, consumer discretionary was the biggest contributor due to bottom-up driven results in China’s e-commerce sector, partially driven by lower exposure to the country’s underperforming e-commerce companies. Materials also contributed due to the Fund’s

10 |

SEI Institutional International Trust / Annual Report / September 30, 2021 |

overweight. Strong bottom-up results in utilities and financials were also beneficial. Industrials and health-care were the only two sector detractors due to poor security selection.

RWC was the biggest contributor as the manager was able to navigate China’s e-commerce stocks, as well as an overweight to the metals & mining sector. JO Hambro benefitted from a tailwind to momentum stocks that lifted companies with positive earnings revisions in both the consumer and information technology spaces. KBI benefited from a tailwind to value stocks that rewarded the manager’s dividend yield investment philosophy. Qtron’s quantitative model-driven bottom-up results in the consumer discretionary, industrials and telecommunication services sectors were also beneficial. Robeco was added to the Fund during the fiscal year, and the Fund benefited from tailwinds to the manager’s value-based philosophy. Prior to its termination from the Fund during the fiscal year, Lazard contributed due to selection within the financials and telecommunication services sectors.

Neuberger Berman was the only detractor as the manager’s quality investment style faced headwinds during the period in the form of rising rates, which resulted in losses across most benchmark sectors.

Investing is subject to risk, including the possible loss of principal. Past performance is no indication of future results.

AVERAGE ANNUAL TOTAL RETURN1

| 1 Year Return | Annualized 3 Year Return | Annualized 5 Year Return | Annualized 10 Year Return | Annualized Inception to Date | ||||||||||||||||

| Emerging Markets Equity Fund, Class F | 18.63% | 8.26% | 8.05% | 5.48% | 4.84% | |||||||||||||||

| Emerging Markets Equity Fund, Class Y | 18.96% | 8.52% | 8.33% | 5.67% | 4.91% | |||||||||||||||

| MSCI Emerging Markets Index (Net) | 18.20% | 8.58% | 9.23% | 6.09% | 6.57% | |||||||||||||||

Comparison of Change in the Value of a $100,000 Investment in the Emerging Markets Equity Fund, Class F and Class Y, versus the MSCI Emerging Markets Index (Net)

| 1 | For the year ended September 30, 2021. Past performance is no indication of future performance. Class F shares were offered beginning January 17, 1995. The Fund’s Class Y shares commenced operations on December 31, 2014. For periods prior to December 31, 2014, the performance of the Fund’s Class F Shares has been used. Returns for Class Y Shares would have been substantially similar to those of Class F shares and would have differed only to the extent that Class Y shares have lower total annual fund operating expenses than Class F shares. Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. The returns for the period reflect fee waivers and/or reimbursements in effect for the period; absent fee waivers and reimbursements, performance would have been lower. |

SEI Institutional International Trust / Annual Report / September 30, 2021 |

11 |

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FUND PERFORMANCE

September 30, 2021 (Unaudited)

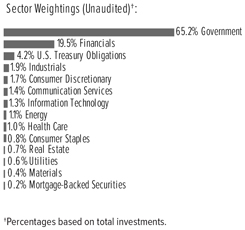

International Fixed Income Fund

I. Objective

The International Fixed Income Fund (the Fund) seeks capital appreciation and current income.

II. Multi-Manager Approach Statement

The Fund uses a multi-manager approach, relying on a number of sub-advisors with differing investment approaches to manage portions of the Fund’s portfolio, under the general supervision of SEI Investments Management Corporation (“SIMC”). The Fund utilized the following sub-advisors as of September 30, 2021: AllianceBernstein L.P. (“AllianceBernstein”), Colchester Global Investors Limited (“Colchester”) and Wellington Management Company LLP (“Wellington”).

No manager changes were made during the Fund’s fiscal year.

III. Return vs. Benchmark

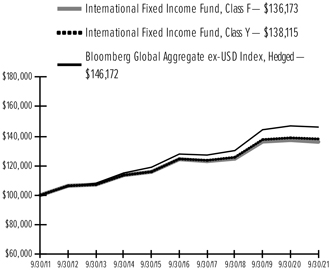

For the year ended September 30, 2021, the Fund’s Class F shares underperformed the Bloomberg Global Aggregate ex-USD Index, Hedged (the “Index”)—which tracks the performance of the global investment-grade fixed-rate debt markets outside of the U.S.—returning -0.83% versus the Index return of -0.54%.

IV. Fund Attribution

Core fixed-income indexes delivered negative returns over the fiscal year against a backdrop of rising government yields and inflation concerns. Long duration assets suffered the largest losses, while the more credit-sensitive sectors of the bond market were able to absorb the adverse rates impact through spread compression and record positive absolute performance. As noted in the shareholder letter, inflation-linked bonds outperformed nominal bonds on rising inflation expectations and falling real yields. High-yield corporates (an out-of-index sector) registered the strongest absolute returns over the period. The local-currency emerging-market debt complex also enjoyed positive performance, led by China, Mexico, South Africa, Indonesia and Russia. In the currency space, the Japanese yen, euro and Swiss franc all lost ground to the U.S. dollar, although most other G10 currencies strengthened against the greenback over the period.

The Fund underperformed during the reporting period and was challenged by its overweights to Australia and Mexican local rates. Short currency positions in the New Zealand dollar and South African rand also detracted. Positive contributors included duration underweights in the U.K., core Europe and South Korea.

An overweight to corporate credit, including off-index USD-denominated securities and high yield, also helped relative performance as spread sectors generated excess returns versus duration-matched government bonds. Positive currency trades included long positions in the Mexican peso, Chinese yuan, Norwegian krone, Swedish krona, Russian ruble and British pound, and a short position in Thai baht.

Wellington detracted during the period and was challenged by its currency positioning, while duration underweights in the UK and South Korea, a short currency position in JPY and out-of-index exposure to corporate credit benefited.

AllianceBernstein outperformed and was helped by its overweight to corporate credit and underweights to government-related and European covered bonds. Off-index exposure to high yield also boosted relative performance. Colchester outperformed and benefited from duration underweights in core Europe and the U.K., as well as an overweight to Indonesian local-currency bonds. Active currency positioning further added value, courtesy of long positons in the Norwegian krone, Mexican peso, British pound and Swedish krona, and a short position in Thai baht.

The Fund used FX forwards, financial futures, interest-rate swaps and over-the-counter options during the reporting period to hedge existing exposures and gain exposure to particular areas of the market. The use of derivatives did not have a material impact on relative performance.

Investing is subject to risk, including the possible loss of principal. Past performance is no indication of future results.

AVERAGE ANNUAL TOTAL RETURN1

| 1 Year Return | Annualized 3 Year Return | Annualized 5 Year Return | Annualized 10 Year Return | Annualized Inception to Date | ||||||||||||||||

| International Fixed Income Fund, Class F | -0.83% | 2.96% | 1.84% | 3.14% | 4.03% | |||||||||||||||

| International Fixed Income Fund, Class Y | -0.54% | 3.20% | 2.09% | 3.28% | 4.09% | |||||||||||||||

| Bloomberg Global Aggregate ex-USD Index, Hedged | -0.54% | 3.93% | 2.71% | 3.87% | 4.81% | |||||||||||||||

12 |

SEI Institutional International Trust / Annual Report / September 30, 2021 |

Comparison of Change in the Value of a $100,000 Investment in the International Fixed Income Fund, Class F and Class Y, versus the Bloomberg Global Aggregate ex-USD Index, Hedged

| ¹ | For the year ended September 30, 2021. Past performance is no indication of future performance. Class F shares were offered beginning September 1, 1993. The Fund’s Class Y shares commenced operations on October 30, 2015. For periods prior to October 30, 2015, the performance of the Fund’s Class F Shares has been used. Returns for Class Y Shares would have been substantially similar to those of Class F shares and would have differed only to the extent that Class Y shares have lower total annual fund operating expenses than Class F shares. Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. The returns for the period reflect fee waivers and/or reimbursements in effect for the period; absent fee waivers and reimbursements, performance would have been lower. |

SEI Institutional International Trust / Annual Report / September 30, 2021 |

13 |

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FUND PERFORMANCE

September 30, 2021 (Unaudited)

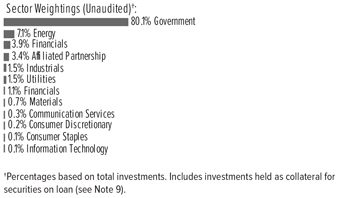

Emerging Markets Debt Fund

I. Objective

The Emerging Markets Debt Fund (the “Fund”) seeks to maximize total return.

II. Multi-Manager Approach

The Fund uses a multi-manager approach, relying on a number of sub-advisors with differing investment approaches to manage portions of the Fund’s portfolio, under the general supervision of SEI Investments Management Corp. (“SIMC”). The Fund utilized the following sub-advisors as of September 30, 2021: Colchester Global Investors Limited (“Colchester”), Marathon Asset Management, L.P. (“Marathon”), Neuberger Berman Investment Advisers LLC (“Neuberger Berman”), Ninety One UK Ltd. (“Ninety One”) and Stone Harbor Investment Partners LP (“Stone Harbor”).

No manager changes were made during the Fund’s fiscal year.

III. Return vs. Benchmark

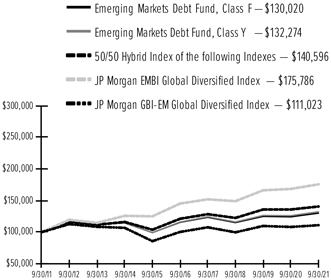

For the year ended September 30, 2021, the Fund’s Class F shares outperformed a hybrid of 50% JP Morgan EMBI Global Diversified Index (“JPM EMBI GD”) (which tracks the performance of external debt instruments in the emerging markets) and 50% JP Morgan GBI Emerging Markets Global Diversified Index (“JPM GBI-EM GD”) (which tracks the performance of debt instruments issued in domestic currencies by emerging-market governments), returning 4.71% versus the Index return of 3.51%.

IV. Fund Attribution

Emerging markets (EM) began the reporting period strong, with both hard- and local-currency indexes posting positive returns in the fourth quarter of 2020. EM foreign exchange (FX) led the way during the first three months of the period, followed by spreads, the majority of which came through in November 2020. EM FX would go on to have mixed fortunes in the following nine months of the fiscal year as risk markets coped with a series of spikes in COVID-19 cases and repeat lockdowns. As noted in the shareholder letter, there were contrasting takes among regions on how to approach the pandemic, with Asia broadly taking a zero-tolerance approach, Eastern Europe’s approach closer to Western Europe (to accept and live with it), and Latin America initially being dismissive (particularly in Brazil and Mexico), before moving to a more proactive stance. Emerging markets reacted with modest fiscal

support comparatively to the scope and depth of developed markets. Financial conditions were eased through central bank policy rates early in 2020, although the trend began to reverse in 2021, led by the Latin American and Eastern European regions, in comparison to the markets not pricing the first U.S. Federal Reserve policy move until 2023.

Though growth remains vulnerable, higher EM central bank policy rates, positive current account balances and steeper yield curves stemmed the weaker returns of local-currency markets, as measured by the JPM GBI-EM GD Index. While the total return of the local-currency index was 2.63% for the fiscal year, the nine months to September 2021 saw a return of -6.38%, highlighting the contrasting periods.

The hard-currency market, as measured by the JPM EMBI-GD Index, returned 4.36% for the fiscal year, with a milder -1.36% over the nine months to September 2021. The headwind for returns for the hard-currency market did not come from spread compression, but from linkage to the Treasury curve. The first quarter of 2021, and again in September, represented periods when U.S. Treasury rates rose rapidly. Given the high starting level, spread returns have been positive, contributing high single-digit returns that were offset by losses from the move in Treasury prices.

The Fund outperformed its blended benchmark during the fiscal year. An overweight to Mexico (in MXN-issued Pemex bonds) benefited from a recovery in oil prices, while positioning in South Africa (biased long ZAR and short duration) and Zambia (as the ZMW recovered along with copper prices) also added to performance. As the Fund was tilted toward higher-yielding spread names, underweights in the Gulf Cooperation Council countries, where spreads were already perceived to be tight but tightened further, detracted.

Stone Harbor’s hard-currency mandate outperformed the blended benchmark and benefited from overweights to Venezuela, Ghana and Brazil; exposure to Panama and Argentina and an underweight to Bahrain detracted. Ninety One’s local-currency mandate also outperformed the blended benchmark; South Africa was a notable detractor from performance, but it was more than offset by longs in Mexico, Zambia, Egypt and Ukraine, as well as underweight to Thailand. Neuberger Berman outperformed thanks to an overweight to Ukraine in USD bonds and Mexico in MXN-issued bonds; a Czech Republic overweight and underweight to Hungary both detracted from performance. Colchester outperformed due to its exposure to Mexico and South

14 |

SEI Institutional International Trust / Annual Report / September 30, 2021 |

African currency; underweights in Thailand and Chile also benefited contributed strongly. An underweight to Chinese yuan and long exposure in South Korean won both detracted. Marathon underperformed its hard-currency benchmark but outperformed the blended benchmark; performance was held back by exposure to long duration investment-grade assets in Israel and exposure in Peru. Underweights to Mexico and Oman and longs in Dominican Republic and Venezuela partially offset the detractors.

Currency forwards and swap contracts were used in the Fund for the one-year period ending September 30, 2021, as a way to either hedge particular positions or gain exposure to additional areas of the market. Currency forwards had a material impact on the Fund during the period as 50% of the Index is directly affected by foreign currencies. Positive and negative impacts differed on a country-to-country basis, depending on whether the forward increased or decreased currency exposure and whether the currency strengthened or weakened relative to the U.S. dollar.

Investing is subject to risk, including the possible loss of principal. Past performance is no indication of future results.

AVERAGE ANNUAL TOTAL RETURN1

| 1 Year Return | Annualized 3 Year | Annualized 5 Year Return | Annualized 10 Year Return | Annualized Inception to Date | ||||||||||||||||

| Emerging Markets Debt Fund, Class F | 4.71% | 4.16% | 2.40% | 2.66% | 7.06% | |||||||||||||||

| Emerging Markets Debt Fund, Class Y | 4.98% | 4.43% | 2.66% | 2.84% | 7.13% | |||||||||||||||

| JP Morgan EMBI Global Diversified Index | 4.36% | 5.65% | 3.89% | 5.80% | 5.17% | |||||||||||||||

| JP Morgan GBI-EM Global Diversified Index | 2.63% | 3.66% | 2.06% | 1.05% | 1.50% | |||||||||||||||

| 50/50 Hybrid of the JP Morgan EMBI Global Diversified Index and the JP Morgan GBI-EM Global Diversified Index | 3.51% | 4.70% | 3.02% | 3.67% | 6.85% | |||||||||||||||

Comparison of Change in the Value of a $100,000 Investment in the Emerging Markets Debt Fund, Class F and Class Y, versus a 50/50 Hybrid of the Following Indexes: the JP Morgan EMBI Global Diversified Index and the JP Morgan GBI-EM Global Diversified Index

| ¹ | For the year ended September 30, 2021. Past performance is no indication of future performance. Class F shares were offered beginning June 26, 1997. The Fund’s Class Y shares commenced operations on December 31, 2014. For periods prior to December 31, 2014, the performance of the Fund’s Class F Shares has been used. Returns for Class Y Shares would have been substantially similar to those of Class F shares and would have differed only to the extent that Class Y shares have lower total annual fund operating expenses than Class F shares. Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. The returns for the period reflect fee waivers and/or reimbursements in effect for the period; absent fee waivers and reimbursements, performance would have been lower. |

SEI Institutional International Trust / Annual Report / September 30, 2021 |

15 |

September 30, 2021

International Equity Fund

| Description | Shares | Market Value ($ Thousands) | ||||||

COMMON STOCK — 96.5% | ||||||||

Argentina — 0.2% | ||||||||

MercadoLibre Inc * | 6,127 | $ | 10,290 | |||||

Ternium SA ADR | 16,990 | 718 | ||||||

|

|

| ||||||

| 11,008 | ||||||||

|

|

| ||||||

Australia — 2.2% | ||||||||

Australia & New Zealand Banking Group Ltd | 382,365 | 7,682 | ||||||

BHP Group Ltd (A) | 219,271 | 5,938 | ||||||

BlueScope Steel Ltd | 896,249 | 13,207 | ||||||

Champion Iron Ltd * | 598,702 | 2,070 | ||||||

CSL Ltd | 49,712 | 10,439 | ||||||

CSR Ltd | 807,866 | 3,228 | ||||||

Fortescue Metals Group Ltd | 636,358 | 6,845 | ||||||

IGO Ltd | 306,173 | 1,964 | ||||||

James Hardie Industries PLC ADR *(A) | 15,047 | 537 | ||||||

Lynas Rare Earths Ltd * | 137,584 | 656 | ||||||

Orora Ltd | 1,270,565 | 2,814 | ||||||

OZ Minerals Ltd | 398,158 | 6,444 | ||||||

South32 Ltd | 8,526,015 | 21,608 | ||||||

Westpac Banking Corp | 447,956 | 8,310 | ||||||

Whitehaven Coal Ltd * | 3,132,371 | 7,255 | ||||||

WiseTech Global Ltd | 46,419 | 1,768 | ||||||

|

|

| ||||||

| 100,765 | ||||||||

|

|

| ||||||

Austria — 0.5% | ||||||||

ANDRITZ AG | 72,724 | 3,982 | ||||||

OMV AG | 119,948 | 7,252 | ||||||

Verbund AG, Cl A | 58,369 | 5,917 | ||||||

voestalpine AG | 111,336 | 4,180 | ||||||

|

|

| ||||||

| 21,331 | ||||||||

|

|

| ||||||

Belgium — 0.0% | ||||||||

Ackermans & van Haaren NV | 3,554 | 612 | ||||||

Umicore SA | 19,349 | 1,144 | ||||||

|

|

| ||||||

| 1,756 | ||||||||

|

|

| ||||||

Brazil — 0.2% | ||||||||

JBS SA | 670,000 | 4,547 | ||||||

| Description | Shares | Market Value ($ Thousands) | ||||||

COMMON STOCK (continued) | ||||||||

Magazine Luiza SA * | 1,292,000 | $ | 3,405 | |||||

|

|

| ||||||

| 7,952 | ||||||||

|

|

| ||||||

Canada — 2.3% | ||||||||

Advantage Energy Ltd * | 224,783 | 1,136 | ||||||

Air Canada, Cl A * | 781,200 | 14,263 | ||||||

Alimentation Couche-Tard Inc, Cl B | 462,400 | 17,688 | ||||||

Birchcliff Energy Ltd | 269,560 | 1,492 | ||||||

BRP Inc | 19,300 | 1,786 | ||||||

Canadian Pacific Railway Ltd (A) | 159,857 | 10,402 | ||||||

Canfor Corp * | 120,381 | 2,644 | ||||||

Cascades Inc | 149,184 | 1,845 | ||||||

CI Financial Corp | 167,200 | 3,393 | ||||||

Empire Co Ltd, Cl A | 210,700 | 6,420 | ||||||

Fairfax Financial Holdings Ltd | 3,700 | 1,493 | ||||||

George Weston Ltd | 10,000 | 1,078 | ||||||

Intertape Polymer Group Inc | 98,500 | 2,142 | ||||||

Magna International Inc, Cl A | 212,234 | 15,969 | ||||||

MEG Energy Corp * | 225,200 | 1,758 | ||||||

Onex Corp | 206,460 | 14,592 | ||||||

Russel Metals Inc | 31,084 | 745 | ||||||

Stelco Holdings Inc | 44,300 | 1,298 | ||||||

Stella-Jones Inc | 26,800 | 902 | ||||||

Tourmaline Oil Corp | 85,100 | 2,973 | ||||||

Transcontinental Inc, Cl A | 45,473 | 722 | ||||||

Viemed Healthcare Inc * | 43,126 | 240 | ||||||

|

|

| ||||||

| 104,981 | ||||||||

|

|

| ||||||

China — 0.4% | ||||||||

Beijing Capital International Airport Co Ltd, Cl H * | 7,930,000 | 4,653 | ||||||

Shenzhou International Group Holdings Ltd | 291,400 | 6,180 | ||||||

STMicroelectronics NV | 169,785 | 7,424 | ||||||

|

|

| ||||||

| 18,257 | ||||||||

|

|

| ||||||

Denmark — 3.0% | ||||||||

Ambu A/S, Cl B | 150,825 | 4,459 | ||||||

AP Moller - Maersk A/S, Cl B | 7,452 | 20,136 | ||||||

Carlsberg AS, Cl B | 31,574 | 5,159 | ||||||

Demant A/S * | 79,944 | 4,026 | ||||||

DSV A/S | 109,462 | 26,234 | ||||||

Genmab A/S * | 7,943 | 3,478 | ||||||

GN Store Nord AS | 48,367 | 3,344 | ||||||

H Lundbeck A/S | 5,011 | 136 | ||||||

Novo Nordisk A/S, Cl B | 438,998 | 42,388 | ||||||

Novozymes A/S, Cl B | 4,874 | 334 | ||||||

Orsted AS | 67,697 | 8,975 | ||||||

Pandora A/S * | 82,175 | 9,949 | ||||||

ROCKWOOL International A/S, Cl B | 4,004 | 1,716 | ||||||

Vestas Wind Systems A/S | 263,222 | 10,558 | ||||||

|

|

| ||||||

| 140,892 | ||||||||

|

|

| ||||||

Finland — 0.9% | ||||||||

Fortum Oyj | 24,474 | 744 | ||||||

Kesko Oyj, Cl B | 417,376 | 14,409 | ||||||

Kone Oyj, Cl B | 92,018 | 6,464 | ||||||

16 |

SEI Institutional International Trust / Annual Report / September 30, 2021 |

| Description | Shares | Market Value ($ Thousands) | ||||||

COMMON STOCK (continued) | ||||||||

Neste Oyj | 146,007 | $ | 8,274 | |||||

Nokia Oyj * | 151,574 | 835 | ||||||

Orion Oyj, Cl B | 248,353 | 9,858 | ||||||

|

|

| ||||||

| 40,584 | ||||||||

|

|

| ||||||

France — 12.0% | ||||||||

Air Liquide SA | 136,420 | 21,889 | ||||||

Airbus SE * | 105,981 | 14,011 | ||||||

Alstom SA | 354,590 | 13,463 | ||||||

AXA SA | 1,687,339 | 46,867 | ||||||

BNP Paribas SA (A) | 36,165 | 2,310 | ||||||

Bollore SA | 3,938,473 | 22,829 | ||||||

Carrefour SA | 1,423,771 | 25,603 | ||||||

Cie de Saint-Gobain | 47,788 | 3,220 | ||||||

Cie Generale des Etablissements Michelin SCA, Cl B | 13,356 | 2,048 | ||||||

Criteo SA ADR * | 60,571 | 2,220 | ||||||

Danone SA | 535,335 | 36,577 | ||||||

Engie SA | 1,863,765 | 24,476 | ||||||

Eurazeo SE | 21,824 | 2,052 | ||||||

Eurofins Scientific SE | 166,682 | 21,392 | ||||||

Ipsen SA | 62,682 | 5,995 | ||||||

IPSOS | 18,645 | 849 | ||||||

L’Oreal SA | 20,274 | 8,370 | ||||||

LVMH Moet Hennessy Louis Vuitton SE | 13,414 | 9,589 | ||||||

Orange SA | 1,073,500 | 11,616 | ||||||

Orpea SA | 4,250 | 495 | ||||||

Pernod Ricard SA | 72,365 | 15,967 | ||||||

Publicis Groupe SA | 505,882 | 34,032 | ||||||

Rexel SA * | 312,272 | 6,035 | ||||||

Sanofi | 612,204 | 58,878 | ||||||

Sartorius Stedim Biotech | 43,901 | 24,605 | ||||||

Schneider Electric SE | 59,545 | 9,905 | ||||||

Societe Generale SA | 486,175 | 15,234 | ||||||

Sodexo SA * | 166,500 | 14,564 | ||||||

Stellantis NV | 1,250,527 | 23,787 | ||||||

Thales SA | 247,999 | 24,100 | ||||||

TotalEnergies SE (A) | 577,822 | 27,584 | ||||||

Valeo | 268,474 | 7,507 | ||||||

Vinci SA | 104,076 | 10,818 | ||||||

Vivendi SE (A) | 238,120 | 2,994 | ||||||

Wendel SE | 19,831 | 2,740 | ||||||

|

|

| ||||||

| 554,621 | ||||||||

|

|

| ||||||

Germany — 8.2% |

| |||||||

adidas AG | 71,242 | 22,386 | ||||||

Aroundtown SA | 58,392 | 403 | ||||||

BASF SE | 335,315 | 25,516 | ||||||

Bayer AG | 153,318 | 8,333 | ||||||

Bayerische Motoren Werke AG | 11,915 | 1,148 | ||||||

BioNTech SE ADR * | 57,825 | 15,786 | ||||||

Carl Zeiss Meditec AG | 76,144 | 14,587 | ||||||

Continental AG * | 61,690 | 6,734 | ||||||

Daimler AG | 100,123 | 8,856 | ||||||

| Description | Shares | Market Value ($ Thousands) | ||||||

COMMON STOCK (continued) | ||||||||

Deutsche Bank AG * | 1,051,721 | $ | 13,369 | |||||

Deutsche Boerse AG | 56,709 | 9,210 | ||||||

Deutsche Post AG | 387,445 | 24,377 | ||||||

E.ON SE | 60,242 | 738 | ||||||

Fresenius Medical Care AG & Co KGaA | 326,130 | 22,937 | ||||||

GEA Group AG | 88,914 | 4,063 | ||||||

Hannover Rueck SE | 3,886 | 678 | ||||||

HeidelbergCement AG | 31,040 | 2,319 | ||||||

Infineon Technologies AG | 286,237 | 11,753 | ||||||

KION Group AG | 208,559 | 19,466 | ||||||

Knorr-Bremse AG | 68,500 | 7,340 | ||||||

Linde PLC | 33,762 | 9,969 | ||||||

Merck KGaA | 139,181 | 30,222 | ||||||

Rheinmetall AG | 42,432 | 4,149 | ||||||

RTL Group SA | 20,818 | 1,249 | ||||||

RWE AG | 701,152 | 24,780 | ||||||

SAP SE | 331,362 | 44,872 | ||||||

Scout24 AG | 4,824 | 335 | ||||||

Siemens AG | 261,713 | 42,806 | ||||||

Vitesco Technologies Group AG * | 12,338 | 729 | ||||||

Wacker Chemie AG | 9,909 | 1,853 | ||||||

|

|

| ||||||

| 380,963 | ||||||||

|

|

| ||||||

Hong Kong — 2.0% | ||||||||

AIA Group Ltd | 863,800 | 9,981 | ||||||

ASM Pacific Technology Ltd | 49,000 | 538 | ||||||

Chaoda Modern Agriculture Holdings Ltd * | 2,440,000 | 15 | ||||||

Chow Tai Fook Jewellery Group Ltd | 991,400 | 1,899 | ||||||

CK Asset Holdings Ltd | 273,500 | 1,577 | ||||||

Hong Kong & China Gas Co Ltd | 1,068,650 | 1,616 | ||||||

Hong Kong Exchanges & Clearing Ltd | 272,694 | 16,775 | ||||||

Li Ning Co Ltd | 568,500 | 6,619 | ||||||

Link REIT ‡ | 143,600 | 1,229 | ||||||

Orient Overseas International Ltd | 68,500 | 1,194 | ||||||

Sands China Ltd * | 4,841,600 | 9,898 | ||||||

SJM Holdings Ltd * | 24,807,340 | 16,881 | ||||||

Techtronic Industries Co Ltd | 502,500 | 9,882 | ||||||

WH Group Ltd | 6,457,333 | 4,584 | ||||||

Wuxi Biologics Cayman Inc * | 518,598 | 8,487 | ||||||

|

|

| ||||||

| 91,175 | ||||||||

|

|

| ||||||

India — 0.1% | ||||||||

HDFC Bank Ltd ADR | 61,127 | 4,468 | ||||||

|

|

| ||||||

Indonesia — 0.1% | ||||||||

Bank Mandiri Persero Tbk PT | 13,318,100 | 5,703 | ||||||

|

|

| ||||||

Ireland — 1.8% | ||||||||

Accenture PLC, Cl A | 59,985 | 19,190 | ||||||

Experian PLC | 242,829 | 10,197 | ||||||

ICON PLC * | 148,054 | 38,793 | ||||||

Ryanair Holdings PLC ADR * | 138,759 | 15,272 | ||||||

|

|

| ||||||

| 83,452 | ||||||||

|

|

| ||||||

Israel — 1.4% | ||||||||

Bank Hapoalim BM | 2,378,928 | 20,902 | ||||||

Bank Leumi Le-Israel BM | 2,855,202 | 24,329 | ||||||

SEI Institutional International Trust / Annual Report / September 30, 2021 |

17 |

SCHEDULE OF INVESTMENTS

September 30, 2021

International Equity Fund (Continued)

| Description | Shares | Market Value ($ Thousands) | ||||||

COMMON STOCK (continued) | ||||||||

Check Point Software Technologies Ltd * | 53,327 | $ | 6,028 | |||||

FIBI Holdings Ltd | 17,608 | 744 | ||||||

First International Bank Of Israel Ltd/The | 50,557 | 1,846 | ||||||

ICL Group Ltd | 175,057 | 1,272 | ||||||

Isracard Ltd | – | – | ||||||

Israel Discount Bank Ltd, Cl A * | 882,543 | 4,684 | ||||||

Mizrahi Tefahot Bank Ltd | 198,719 | 6,714 | ||||||

|

|

| ||||||

| 66,519 | ||||||||

|

|

| ||||||

Italy — 4.0% | ||||||||

Assicurazioni Generali SpA | 397,365 | 8,430 | ||||||

Azimut Holding SpA | 141,983 | 3,895 | ||||||

Banca Mediolanum SpA | 299,871 | 3,235 | ||||||

CNH Industrial NV | 1,622,525 | 27,214 | ||||||

Davide Campari-Milano NV | 99,767 | 1,404 | ||||||

DiaSorin SpA | 34,057 | 7,140 | ||||||

Enel SpA | 3,043,494 | 23,364 | ||||||

Eni SpA | 856,773 | 11,400 | ||||||

EXOR NV | 128,476 | 10,798 | ||||||

Ferrari NV | 39,811 | 8,316 | ||||||

FinecoBank Banca Fineco SpA | 570,224 | 10,325 | ||||||

La Doria SpA | 11,734 | 229 | ||||||

Mediaset NV * | 360,579 | 1,034 | ||||||

Moncler SpA | 57,521 | 3,516 | ||||||

Nexi SpA * | 443,631 | 8,282 | ||||||

Stellantis NV | 218,617 | 4,185 | ||||||

UniCredit SpA | 4,142,965 | 54,894 | ||||||

|

|

| ||||||

| 187,661 | ||||||||

|

|

| ||||||

Japan — 16.8% | ||||||||

77 Bank Ltd/The | 86,064 | 981 | ||||||

Advantest Corp | 172,800 | 15,448 | ||||||

AEON Financial Service Co Ltd | 223,700 | 2,818 | ||||||

AGC Inc | 16,400 | 844 | ||||||

Ajinomoto Co Inc | 129,700 | 3,819 | ||||||

Asahi Group Holdings Ltd | 205,800 | 9,900 | ||||||

ASKUL Corp | 101,000 | 1,478 | ||||||

Bandai Namco Holdings Inc | 149,902 | 11,207 | ||||||

BayCurrent Consulting Inc | 9,800 | 4,920 | ||||||

Bridgestone Corp | 495,654 | 23,347 | ||||||

Brother Industries Ltd | 62,600 | 1,376 | ||||||

Canon Inc | 313,500 | 7,652 | ||||||

Canon Marketing Japan Inc | 94,900 | 2,199 | ||||||

Capcom Co Ltd | 371,000 | 10,172 | ||||||

Credit Saison Co Ltd | 55,000 | 722 | ||||||

CyberAgent Inc | 474,500 | 9,116 | ||||||

Dai-ichi Life Holdings Inc | 114,200 | 2,510 | ||||||

Daito Trust Construction Co Ltd (A) | 62,100 | 7,192 | ||||||

Daiwa House Industry Co Ltd | 110,100 | 3,668 | ||||||

DeNA Co Ltd * | 24,000 | 444 | ||||||

Disco Corp | 18,100 | 5,043 | ||||||

FANUC Corp | 102,000 | 22,220 | ||||||

FUJIFILM Holdings Corp | 11,300 | 972 | ||||||

Fujitsu Ltd | 224,005 | 40,528 | ||||||

| Description | Shares | Market Value ($ Thousands) | ||||||

COMMON STOCK (continued) | ||||||||

Glory Ltd | 93,100 | $ | 2,074 | |||||

GungHo Online Entertainment Inc * | 63,600 | 1,167 | ||||||

H.U. Group Holdings Inc (A) | 34,300 | 932 | ||||||

Hakuhodo DY Holdings Inc | 117,100 | 2,011 | ||||||

Hitachi Ltd | 497,267 | 29,333 | ||||||

Ibiden Co Ltd | 14,000 | 770 | ||||||

Iida Group Holdings Co Ltd (A) | 92,600 | 2,375 | ||||||

Inpex Corp | 153,200 | 1,195 | ||||||

Isuzu Motors Ltd | 105,300 | 1,374 | ||||||

ITOCHU Corp (A) | 245,400 | 7,137 | ||||||

Japan Exchange Group Inc | 412,542 | 10,211 | ||||||

Japan Post Insurance Co Ltd (A) | 113,300 | 2,054 | ||||||

Japan Tobacco Inc | 78,300 | 1,532 | ||||||

Kao Corp | 260,000 | 15,448 | ||||||

Kawasaki Heavy Industries Ltd | 15,700 | 361 | ||||||

KDDI Corp (A) | 428,700 | 14,110 | ||||||

Keyence Corp | 16,700 | 9,948 | ||||||

Kirin Holdings Co Ltd | 240,000 | 4,433 | ||||||

Kokuyo Co Ltd | 221,300 | 3,736 | ||||||

Konami Holdings Corp | 6,800 | 425 | ||||||

Konica Minolta Inc (A) | 417,800 | 2,245 | ||||||

K’s Holdings Corp (A) | 171,240 | 1,770 | ||||||

Lasertec Corp | 52,600 | 12,010 | ||||||

Lawson Inc | 183,700 | 8,991 | ||||||

Lixil Corp | 11,100 | 320 | ||||||

Mazda Motor Corp | 467,500 | 4,027 | ||||||

Mitsubishi Chemical Holdings Corp | 36,500 | 332 | ||||||

Mitsubishi Electric Corp | 1,332,500 | 18,482 | ||||||

Mixi Inc (A) | 127,100 | 2,854 | ||||||

Mizuno Corp | 41,500 | 991 | ||||||

MS&AD Insurance Group Holdings Inc (A) | 67,500 | 2,251 | ||||||

Murata Manufacturing Co Ltd | 244,500 | 21,743 | ||||||

Nihon Kohden Corp | 11,400 | 387 | ||||||

Nihon Unisys Ltd | 156,700 | 4,046 | ||||||

Nikon Corp (A) | 609,700 | 6,773 | ||||||

Nippon Steel Corp | 150,600 | 2,727 | ||||||

Nippon Telegraph & Telephone Corp (A) | 433,100 | 11,939 | ||||||

Nissan Motor Co Ltd * | 207,800 | 1,032 | ||||||

Nitto Denko Corp | 57,100 | 4,048 | ||||||

Nomura Holdings Inc | 1,685,000 | 8,236 | ||||||

Okuwa Co Ltd | 63,100 | 668 | ||||||

Olympus Corp | 118,100 | 2,585 | ||||||

ORIX Corp | 546,266 | 10,153 | ||||||

Otsuka Corp | 83,300 | 4,261 | ||||||

Panasonic Corp | 1,659,200 | 20,532 | ||||||

PeptiDream Inc * | 101,400 | 3,279 | ||||||

Persol Holdings Co Ltd | 168,100 | 4,181 | ||||||

Recruit Holdings Co Ltd | 362,193 | 21,994 | ||||||

Rinnai Corp | 5,600 | 612 | ||||||

Ryohin Keikaku Co Ltd | 1,036,900 | 23,082 | ||||||

Sankyo Co Ltd (A) | 129,500 | 3,221 | ||||||

Sanwa Holdings Corp | 186,100 | 2,410 | ||||||

18 |

SEI Institutional International Trust / Annual Report / September 30, 2021 |

| Description | Shares | Market Value ($ Thousands) | ||||||

COMMON STOCK (continued) | ||||||||

SBI Holdings Inc/Japan | 390,931 | $ | 9,555 | |||||

Seiko Epson Corp (A) | 46,900 | 942 | ||||||

Seven & i Holdings Co Ltd | 431,200 | 19,541 | ||||||

Shimamura Co Ltd | 67,900 | 6,365 | ||||||

Shimano Inc | 2,500 | 733 | ||||||

Shiseido Co Ltd | 44,600 | 2,995 | ||||||

SoftBank Group Corp | 20,300 | 1,168 | ||||||

Sompo Holdings Inc | 183,100 | 7,924 | ||||||

Sony Group Corp | 92,300 | 10,216 | ||||||

Sony Group Corp ADR | 284,298 | 31,438 | ||||||

Sumitomo Dainippon Pharma Co Ltd (A) | 118,900 | 2,119 | ||||||

Sumitomo Mitsui Financial Group Inc | 1,184,200 | 41,488 | ||||||

Sumitomo Rubber Industries Ltd | 221,200 | 2,797 | ||||||

Sundrug Co Ltd | 18,400 | 556 | ||||||

Sysmex Corp | 44,000 | 5,435 | ||||||

T&D Holdings Inc | 387,200 | 5,324 | ||||||

Takeda Pharmaceutical Co Ltd | 810,500 | 26,784 | ||||||

Teijin Ltd | 45,100 | 639 | ||||||

Terumo Corp | 45,100 | 2,121 | ||||||

TIS Inc | 144,900 | 3,939 | ||||||

Tokio Marine Holdings Inc | 29,500 | 1,577 | ||||||

Tokyo Electron Ltd | 44,353 | 19,671 | ||||||

Tokyo Seimitsu Co Ltd | 10,600 | 435 | ||||||

Tomy Co Ltd | 122,200 | 1,245 | ||||||

Toshiba Corp | 216,700 | 9,116 | ||||||

Toyota Industries Corp | 277,978 | 22,708 | ||||||

Toyota Tsusho Corp | 12,100 | 510 | ||||||

Universal Entertainment * | 396,253 | 8,921 | ||||||

Yamada Holdings Co Ltd | 944,200 | 3,967 | ||||||

Yamaha Motor Co Ltd | 133,300 | 3,709 | ||||||

Z Holdings Corp | 2,012,019 | 12,822 | ||||||

ZOZO Inc | 44,700 | 1,668 | ||||||

|

|

| ||||||

| 779,812 | ||||||||

|

|

| ||||||

Jordan — 0.0% | ||||||||

Hikma Pharmaceuticals PLC | 58,461 | 1,926 | ||||||

|

|

| ||||||

Luxembourg — 0.0% | ||||||||

APERAM SA | 6,874 | 379 | ||||||

|

|

| ||||||

Malta — 0.0% | ||||||||

BGP Holdings *(B) | 198,683 | – | ||||||

|

|

| ||||||

Mexico — 0.9% | ||||||||

Arca Continental SAB de CV | 2,744,250 | 16,788 | ||||||