UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

Proxy Statement Pursuant to Section 14(a)

of the Securities Exchange Act of 1934 (Amendment No. 2)

Filed by the Registrant ý

Filed by a Party other than the Registrant o

Check the appropriate box:

ý Preliminary Proxy Statement

o Confidential, For Use of the Commission Only (as permitted by Rule 14a-6(e)(2))

o Definitive Proxy Statement

o Definitive Additional Materials

o Soliciting Material Under Rule 14a-12

STRATFORD AMERICAN CORPORATION

(Name of Registrant as Specified in Its Charter)

(Name of Person(s) Filing Proxy Statement, if Other Than the Registrant)

Payment of Filing Fee (Check the appropriate box):

| o | No fee required. |

| ý | Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. |

| (1) | Title of each class of securities to which transaction applies: Common Stock, $0.01 par value. |

| (2) | Aggregate number of securities to which transaction applies: 7,790,807. |

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): The proposed maximum aggregate value of the transaction for purposes of calculating the filing fee is $7,011,726.30. The transaction value is based upon 7,790,807 shares of Common Stock to be exchanged for cash in the merger multiplied by the $0.90 per share merger consideration. The filing fee, calculated in accordance with Exchange Act Rule 0-11(c), was calculated by multiplying the transaction valuation by .000107. |

| (4) | Proposed maximum aggregate value of transaction: $7,011,726.30 |

| (5) | Total fee paid: $750.25 |

| o | Fee paid previously with preliminary materials. |

| ý | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the form or schedule and the date of its filing. |

| (1) | Amount Previously Paid: $666.89 |

| (2) | Form, Schedule or Registration Statement No.: Schedule 14A |

| (3) | Filing Party: Stratford American Corporation |

| (4) | Date Filed: February 10, 2006 |

STRATFORD AMERICAN CORPORATION

2400 EAST ARIZONA BILTMORE CIRCLE

BUILDING 2, SUITE 1270

PHOENIX, ARIZONA 85016

[_______], 2006

Dear Shareholder,

A special meeting of shareholders of Stratford American Corporation, an Arizona corporation (“Stratford”), will be held at Stratford’s executive offices located at 2400 East Arizona Biltmore Circle, Building 2, Suite 1270, Phoenix, Arizona 85016, on ______, 2006 at 9:00 a.m., local time.

At the special meeting, you will be asked to consider and vote upon a proposal to approve and adopt the Agreement and Plan of Merger dated as of January 31, 2006, as amended, by and among Stratford, Stratford Holdings Investment, L.L.C., an Arizona limited liability company (“Stratford Holdings”), Stratford Acquisition, L.L.C., an Arizona limited liability company (“Stratford Acquisition”), and JDMD Investments, L.L.C., an Arizona limited liability company (“JDMD”), and approve the merger contemplated by the merger agreement. Pursuant to the merger, Stratford Acquisition will merge with and into Stratford, and each outstanding share of Stratford’s common stock will be converted into the right to receive $0.90 in cash (other than shares held by JDMD, which will be cancelled without payment, and shares held by shareholders who properly exercise dissenters rights under Arizona law).

Stratford Acquisition is a wholly-owned subsidiary of Stratford Holdings, which itself is wholly-owned by JDMD. As of April 21, 2006, the record date, JDMD owned 3,287,298 shares of Stratford’s common stock, which represented approximately 29.7% of the shares outstanding as of that date. If the merger is completed, Stratford will survive as a wholly-owned subsidiary of Stratford Holdings and will cease to be a publicly traded company.

Stratford’s board of directors has unanimously approved and adopted the merger and the merger agreement and has determined that approval of the merger agreement is advisable and the proposed merger is fair to, and in the best interests of, all Stratford shareholders (other than JDMD). Accordingly, the board of directors unanimously recommends that shareholders vote FOR approval and adoption of the merger agreement and the merger and FOR the approval of the adjournment or postponement of the special meeting, if necessary or appropriate, to solicit additional proxies.

In the materials accompanying this letter, you will find a notice of special meeting of shareholders, a proxy statement relating to the action to be taken by Stratford’s shareholders at the special meeting, and a proxy. The proxy statement describes the merger and the principal terms of the merger agreement. To ensure your representation at the special meeting, please complete, sign, and date the enclosed proxy and return it in the envelope provided. If you attend the special meeting, you may vote in person if you wish, even though you have previously turned in your proxy.

Thank you for your attention to this important matter.

| [___________________] | ||

| David H. Eaton | ||

| Chairman of the Board of Directors | ||

NEITHER THE SECURITIES AND EXCHANGE COMMISSION NOR ANY STATE SECURITIES COMMISSION HAS APPROVED OR DISAPPROVED OF THE MERGER, PASSED UPON THE MERITS OR FAIRNESS OF THE MERGER AGREEMENT OR THE TRANSACTIONS CONTEMPLATED THEREBY OR PASSED UPON THE ADEQUACY OR ACCURACY OF THE ENCLOSED PROXY STATEMENT. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE.

The proxy statement, dated [______], 2006, is first being mailed to shareholders on or about [_____], 2006.

STRATFORD AMERICAN CORPORATION

2400 EAST ARIZONA BILTMORE CIRCLE

BUILDING 2, SUITE 1270

PHOENIX, ARIZONA 85016

NOTICE OF SPECIAL MEETING OF SHAREHOLDERS

TO BE HELD ______, 2006

To the Shareholders of Stratford American Corporation:

A special meeting of shareholders of Stratford American Corporation, an Arizona corporation (“Stratford”), will be held at Stratford’s executive offices located at 2400 East Arizona Biltmore Circle, Building 2, Suite 1270, Phoenix, Arizona 85016, on ______, 2006 at 9:00 a.m., local time, for the following purposes:

| 1. | To consider and vote upon a proposal to approve and adopt the Agreement and Plan of Merger dated as of January 31, 2006, as amended, by and among Stratford, Stratford Holdings Investment, L.L.C., an Arizona limited liability company (“Stratford Holdings”), Stratford Acquisition, L.L.C., an Arizona limited liability company (“Stratford Acquisition”), and JDMD Investments, L.L.C., an Arizona limited liability company (“JDMD”), and to approve the merger contemplated by the merger agreement. Pursuant to the merger, Stratford Acquisition will merge with and into Stratford, and each outstanding share of Stratford’s common stock will be converted into the right to receive $0.90 in cash (other than shares held by JDMD, which will be cancelled without payment, and shares held by shareholders who properly exercise dissenters rights under Arizona law). |

| 2. | To consider and vote upon a proposal to approve the adjournment or postponement of the special meeting, if necessary or appropriate, to solicit additional proxies if there are insufficient votes at the time of the special meeting to adopt the Agreement and Plan of Merger. |

| 3. | To transact such other business as may properly come before the meeting. |

Only shareholders of record at the close of business on April 21, 2006 are entitled to notice of, and to vote at, the special meeting. Holders of common stock as of such date are entitled to vote on the above proposals. Shares can be voted at the meeting only if the holder is present or represented by proxy. A list of shareholders entitled to vote at the special meeting will be open for inspection at the special meeting and at Stratford’s executive offices at 2400 East Arizona Biltmore Circle, Building 2, Suite 1270, Phoenix, Arizona 85016, during ordinary business hours, for 10 days prior to the special meeting.

YOUR VOTE IS VERY IMPORTANT. THE MERGER WILL NOT OCCUR UNLESS THE MERGER AGREEMENT AND THE MERGER ARE APPROVED BY THE AFFIRMATIVE VOTE OF (A) THE HOLDERS OF A MAJORITY OF THE ISSUED AND OUTSTANDING UNAFFILIATED SHARES OF STRATFORD’S COMMON STOCK (THOSE NOT OWNED, DIRECTLY OR INDIRECTLY, BY JDMD AND THE EATON FAMILY TRUST), AND (B) THE HOLDERS OF A MAJORITY OF ALL OF STRATFORD’S OUTSTANDING SHARES OF COMMON STOCK (INCLUDING THOSE SHARES OWNED, DIRECTLY OR INDIRECTLY, BY JDMD AND THE EATON FAMILY TRUST). TO ASSURE YOUR REPRESENTATION AT THE MEETING, PLEASE COMPLETE, DATE, SIGN, AND PROMPTLY MAIL THE ENCLOSED PROXY CARD IN THE ACCOMPANYING ENVELOPE, WHICH REQUIRES NO POSTAGE IF MAILED IN THE UNITED STATES.

The merger and the principal terms of the merger agreement are described in the accompanying proxy statement, which we urge you to read carefully. A copy of the merger agreement and amendment thereto is included as Exhibit A to the accompanying proxy statement.

| By Order of the Board of Directors, | ||

| | ||

| [___________________] | ||

| David H. Eaton | ||

| Phoenix, Arizona | Chairman of the Board of Directors | |

| [ ], 2006 | ||

| 1 | |

| 1 | |

| 1 | |

| 1 | |

| 1 | |

| 2 | |

| 3 | |

| 3 | |

| 3 | |

| 3 | |

| 4 | |

| 4 | |

| 4 | |

| 5 | |

| 5 | |

| 5 | |

| 5 | |

| 6 | |

| 6 | |

| 7 | |

| 7 | |

| 7 | |

| 7 | |

| 8 | |

| 8 | |

| 10 | |

| 10 | |

| 10 | |

| 10 | |

| 11 | |

| 11 | |

| 11 | |

| 12 | |

| 12 | |

| 12 | |

| 13 | |

| 13 | |

| 14 | |

| 14 | |

| 14 | |

| 14 | |

| 14 | |

| 15 | |

| 15 | |

| 15 | |

| 17 | |

| 17 | |

| 22 | |

| 24 |

TABLE OF CONTENTS

(Continued)

| 25 | |

| 29 | |

| 34 | |

| 35 | |

| 36 | |

| 37 | |

| 37 | |

| 37 | |

| 37 | |

| 37 | |

| 37 | |

| 38 | |

| 38 | |

| 38 | |

| 39 | |

| 40 | |

| 41 | |

| 41 | |

| 43 | |

| 43 | |

| 43 | |

| 43 | |

| 44 | |

| 44 | |

| 45 | |

| 45 | |

| 46 | |

| 47 | |

| 47 | |

| 48 | |

| 48 | |

| 48 | |

| 48 | |

| 49 | |

| 49 | |

| 50 | |

| 50 | |

| 51 | |

| 51 | |

| 51 | |

| 51 | |

| 53 | |

| 53 | |

| Exhibit A: Agreement and Plan of Merger and Amendment to Agreement and Plan of Merger | |

| Exhibit B: Arizona Dissenters’ Rights Statutes | |

This summary highlights selected information presented in this proxy statement and may not contain all of the information that is important to you. To understand the transactions fully and for a more complete description of the terms of the transactions, you should read this document and the documents we have referred you to carefully, including the merger agreement and amendment thereto attached as Exhibit A to this proxy statement. Whenever the merger agreement is referred to in this proxy statement, it includes the amendment thereto.

The Participants (page [ _ ])

| · | Stratford American Corporation. Stratford is an Arizona corporation that was incorporated on May 13, 1988. Stratford, through its subsidiaries, is engaged principally in the business of natural resource exploration and development. Stratford employs four employees, one of whom works full time. |

| · | JDMD Investments, L.L.C. JDMD is an Arizona limited liability company whose principal business is (i) making investments in businesses, companies, and properties by means of acquisitions of stock, partnership interests, limited liability company memberships, and direct acquisitions of property and assets, and (ii) holding and managing such investments. JDMD currently owns 29.7% of the outstanding common stock of Stratford. The managers of JDMD are Gerald Colangelo, David Eaton, Mel Shultz and Dale Jensen, all of whom are also directors of Stratford. Mr. Eaton is also the Chairman and Chief Executive Officer of Stratford and Mr. Shultz is Stratford’s President. The members of JDMD are Mr. Jensen and affiliates of Messrs. Colangelo, Eaton and Shultz. |

| · | Stratford Holdings Investment, L.L.C. Stratford Holdings is an Arizona limited liability company formed in January 2006 by JDMD to hold all of the outstanding common stock of Stratford effective upon completion of the merger. |

| · | Stratford Acquisition, L.L.C. Stratford Acquisition is an Arizona limited liability company formed in January 2006 and is a wholly-owned subsidiary of Stratford Holdings. The sole purpose of Stratford Acquisition is to merge with and into Stratford pursuant to the merger described in this proxy statement, with Stratford as the surviving corporation. |

Date, Time, Place and Matters to be Considered (page [ _ ])

Date, Time and Place. The special meeting of the shareholders will be held on ______, 2006 at 9:00 a.m., local time, at Stratford’s executive offices located at 2400 East Arizona Biltmore Circle, Building 2, Suite 1270, Phoenix, Arizona 85016.

Proposals. At the special meeting, you will be asked to consider and vote in favor of proposals to approve and adopt the merger agreement and the merger, and to approve the adjournment or postponement of the special meeting, if necessary or appropriate, to solicit additional proxies if there are insufficient votes at the time of the special meeting to approve the adoption of the merger agreement and the merger. The merger and the principal terms of the merger agreement are explained in greater detail elsewhere in this proxy statement.

Record Date, Quorum and Required Vote (page [ _ ])

Record Date. Stratford’s board of directors set the close of business on April 21, 2006, as the record date for determining the holders of shares of Stratford’s common stock entitled to notice of and to vote at the special meeting. On the record date, there were 11,078,105 shares of common stock outstanding, of which 7,725,807 shares were held by unaffiliated shareholders (that is, those shareholders other than JDMD and The Eaton Family Trust (“Eaton Trust”)). Each holder of record of Stratford’s common stock on the record date is entitled to one vote for each share held.

Quorum Requirement. A majority of the outstanding shares of common stock will constitute a quorum for the transaction of business related to the proposals and for the transaction of all other business at the special meeting.

Vote Required for Approval. Approval and adoption of the merger agreement and the merger requires:

| · | the affirmative vote of holders of a majority of the outstanding unaffiliated shares of Stratford’s common stock (those not owned, directly or indirectly, by JDMD and Eaton Trust); and |

| · | the affirmative vote of holders of a majority of the outstanding shares of Stratford’s common stock (including those shares owned, directly or indirectly, by JDMD and Eaton Trust). |

If holders of a majority of the outstanding unaffiliated shares (those not owned, directly or indirectly, by JDMD and Eaton Trust) vote to approve and adopt the merger agreement and the merger, the holders of the interested shares (those owned, directly or indirectly, by JDMD and Eaton Trust, which in the aggregate constitute approximately 30.3% of the total outstanding shares of common stock) are required under the merger agreement to vote their shares in favor of the approval and adoption of the merger agreement and the merger.

The board of directors of Stratford also has been informed that The DRD 97 Trust expects to vote its shares in favor of the approval and adoption of the merger agreement and the merger. The shares held by The DRD 97 Trust represent approximately 23.0% of the total outstanding shares of Stratford’s common stock and approximately 33.0% of the unaffiliated shares of Stratford’s common stock.

Approval and adoption of any adjournment or postponement of the special meeting, if necessary or appropriate, requires the affirmative vote of holders of a majority of the outstanding shares of Stratford’s common stock (including those shares owned, directly or indirectly, by JDMD and Eaton Trust).

Withheld Votes, Abstentions and Broker Non-Votes. Votes that are withheld will have the same effect as a negative vote. Abstentions and broker non-votes will be counted as present for purposes of determining a quorum, and will have the same effect as a negative vote.

Completion of Merger. In the event the shareholders vote in favor of the approval and adoption of the merger agreement and the merger, the board of directors of Stratford anticipates completing the merger promptly after the special meeting and after all the conditions to the merger are satisfied or waived. If the merger is completed, you will receive written instructions for exchanging your shares of Stratford common stock for a cash payment of $0.90 per share.

After carefully reading and considering the information contained in the proxy statement, you should complete, date and sign the enclosed proxy card and mail the proxy card in the enclosed return envelope as soon as possible, but in any event prior to the time that the special meeting is called to order, so that your shares of common stock will be represented at the special meeting, even if you plan to attend the special meeting in person. Stratford will not accept proxies to be voted by telephone or internet. You may revoke your proxy at any time before the special meeting is called to order by:

| · | attending the special meeting and giving oral notice of your intention to vote in person; or |

| · | delivering a written notice of revocation or a duly executed proxy bearing a later date to the following address: Stratford American Corporation Attn: Secretary (Proxy Vote) 2400 East Arizona Biltmore Circle Building 2, Suite 1270 Phoenix, Arizona 85016 |

Your attendance at the meeting will not by itself constitute a revocation of your proxy. You must also vote your shares in person at the meeting. Furthermore, if your shares are held of record by a broker, bank or other nominee and you wish to vote at the meeting, you must obtain a “legal proxy” from the record holder. You must bring this legal proxy to the meeting in order to vote in person. If your shares are held in “street name” by a broker, your broker will not be able to vote your shares without instructions from you. If you wish to have your broker vote your shares, you should instruct your broker to vote your shares by following the procedures provided to you by your broker. If you fail to return your proxy card, and do not attend the meeting in person, your shares will not be counted towards the quorum; however, there will be no effect on the number of votes required for approval of the merger proposal.

What You Will Receive in the Merger (page [ _ ])

If the merger is completed, holders of Stratford’s common stock (other than JDMD and shareholders who validly exercise dissenters’ rights under the Arizona law) will be entitled to receive $0.90 per share in cash, without interest, in exchange for each share of Stratford’s common stock that they own. Shares of Stratford’s common stock that are owned by JDMD will be automatically cancelled in the merger and no consideration will be delivered in exchange for its shares.

Effects of the Merger (page [ _ ])

This is a “going private” transaction. The merger will extinguish all equity interests in Stratford held by its public shareholders and will result in Stratford being a wholly-owned subsidiary of Stratford Holdings. JDMD, as sole owner of Stratford Holdings, will be the beneficiary of the earnings and growth of Stratford, if any, following the merger and will bear the risks of any decrease in the value of Stratford following the merger.

Following the merger, Stratford’s common stock will no longer be publicly traded, and Stratford will no longer file periodic reports with the Securities and Exchange Commission (the “SEC”).

Background of the Merger (pages [ _ ] - [ _ ])

For a description of the events leading to the approval and adoption of the merger agreement and the merger by Stratford’s board of directors, you should refer to “SPECIAL FACTORS — Background of the Merger,” “— Recommendations of the Board of Directors; Reasons for Recommending the Approval and Adoption of the Merger Agreement and the Merger,” and “—Interests of Certain Persons in the Merger.”

Recommendations of the Board of Directors (pages [ _ ] - [ _ ])

Our board of directors has unanimously determined that the proposed merger and the terms of the merger agreement are advisable and fair to, and in the best interests of, Stratford and its unaffiliated shareholders (those other than JDMD and Eaton Trust). Accordingly, the members of the board approved the merger agreement and resolved to recommend that the shareholders vote “FOR” approval and adoption of the merger agreement and the merger and “FOR” approval of the adjournment or postponement of the special meeting, if necessary or appropriate, to solicit additional proxies. For a description of the factors considered by the board of directors in making their recommendations, see “SPECIAL FACTORS — Background of the Merger,” “— Recommendations of the Board of Directors; Reasons for Recommending the Approval and Adoption of the Merger Agreement and the Merger,” and “—Interests of Certain Persons in the Merger.”

Position of the Buyout Parties and the Other Filers Regarding the Fairness of the Merger (pages [ _ ] - [ _ ])

JDMD, Stratford Holdings and Stratford Acquisition (collectively, the “Buyout Parties”), and each of the members of JDMD and Messrs. Colangelo, Jensen, Eaton and Shultz (collectively, the “Other Filers”) believes that the merger is fair to Stratford’s unaffiliated shareholders (those shareholders other than JDMD and Eaton Trust). See “SPECIAL FACTORS - Position of Buyout Parties and the Other Filers Regarding the Fairness of the Merger.”

Interests of Certain Persons in the Merger (page [ _ ])

In considering the board of directors’ recommendation that you vote in favor of the merger, you should be aware that certain of Stratford’s directors and executive officers have interests in the merger that are different from your interests as a shareholder, including the following:

| · | Each of Mr. Colangelo, Mr. Eaton, Mr. Shultz and Mr. Jensen are directors of Stratford Acquisition and the merger agreement provides that the directors of Stratford Acquisition immediately prior to the effective time of the merger will comprise Stratford’s board of directors immediately after the effective time of the merger; |

| · | Each of Mr. Eaton and Mr. Shultz are executive officers of Stratford, and the merger agreement provides that Stratford’s current executive officers will remain executive officers of the surviving corporation following the merger; |

| · | Each of Mr. Colangelo, Mr. Eaton, Mr. Shultz and Mr. Jensen are beneficial owners of JDMD. After the consummation of the merger, Stratford Holdings will be wholly-owned by JDMD, and Stratford will be wholly-owned by Stratford Holdings. Accordingly, after the merger is completed, Mr. Colangelo, Mr. Eaton, Mr. Shultz and Mr. Jensen will be the ultimate owners of Stratford; |

| · | Eaton Trust will receive aggregate merger consideration of $58,500 for the Stratford shares that it owns on the same basis as the other shareholders. Mr. Eaton, a co-trustee of Eaton Trust, is the Chief Executive Officer and a director of Stratford; and |

| · | Richard H. Dozer, a director of Stratford, will receive aggregate merger consideration of approximately $3,000 for the Stratford shares that he owns on the same basis as the other shareholders. |

The board of directors was aware of these interests and considered them in making their recommendations. For a more detailed discussion of these interests, see page [__] of this proxy statement.

Merger Financing (pages [ _ ])

The total amount of funds required to consummate the merger and to pay related fees and expenses is estimated to be approximately $7,157,476. JDMD intends to finance the merger through use of:

| · | the cash reserves of Stratford, which will become available immediately upon the effectiveness of the merger; and |

| · | $900,000 of cash on hand available to JDMD from its business activities unrelated to Stratford. |

As of the date of this proxy statement, Stratford had approximately $6,260,000 in cash and cash equivalents. Because Stratford and JDMD have sufficient funds to finance the merger, the merger is not conditioned upon any third party financing arrangements. Pending the closing and subject to the conditions of closing, JDMD has deposited $900,000 of its own cash on hand on a non-refundable basis in a segregated account to cover the estimated shortfall in anticipated funds necessary to consummate the merger over Stratford’s cash reserves.

In general, you will be taxed on the cash you receive in the merger to the extent that the cash exceeds your tax basis in your shares, or, conversely, you will recognize a loss to the extent that your tax basis exceeds the cash you receive. Because JDMD will have a continuing interest in Stratford following the merger, it will have no immediate tax consequence as a result of the merger. We recommend that you consult your tax advisor regarding your individual tax consequences as a result of the merger.

Conditions to the Merger (page [ _ ])

Each party’s obligation to complete the merger is subject to the following conditions:

| · | the merger agreement must have been approved by the holders of (a) a majority of the outstanding shares of Stratford’s common stock (including those owned, directly or indirectly, by JDMD and Eaton Trust) and (b) a majority of the unaffiliated shares of Stratford’s common stock (those not owned, directly or indirectly, by JDMD or Eaton Trust); and |

| · | the absence of any statute, rule, regulation, executive order, decree, injunction or other order that materially restricts, prevents or prohibits the consummation of the merger. |

Stratford Acquisition’s obligation to complete the merger is subject to the following additional conditions:

| · | shareholders, if any. who exercise their dissenter’s rights under Arizona law hold not more than 5% of the outstanding shares of common stock; |

| · | the board of directors must not have withheld or withdrawn and shall not have modified or amended in a manner adverse to Stratford Acquisition, the approval, adoption or recommendation of the merger or the merger agreement; |

| · | Stratford will have obtained all of the third party consents and made all of the required filings, except where the failure to obtain such consents or make such filings would not have a material adverse effect on Stratford and its subsidiaries, taken as a whole; and |

| · | since the date of the merger agreement there will not have been any state of facts, event, change, effect, development, condition or occurrence that, individually or in the aggregate, has had or would reasonably be expected to have a material adverse effect on Stratford and its subsidiaries, taken as a whole. |

None of these conditions has yet been satisfied. However, as of the date of this proxy statement, Stratford does not believe that any third party consents or filings will be required (other than filings with the SEC, which Stratford has undertaken, and filings with the Arizona Corporation Commission and the OTC Bulletin Board that will be required only if and after the merger is approved). Further, no statutes, rules, regulations, orders or the like have been issued, and no material adverse effect on Stratford has occurred as of the date of this proxy statement. At this point it is not anticipated that any closing conditions will need to be or will be waived. We will re-circulate revised proxy materials and re-solicit proxies in the event of any material changes in the terms of the merger, including material changes that result in a waiver of any condition of Stratford described above which would adversely affect the unaffiliated shareholders.

Prior to the date that Stratford’s shareholders approve and adopt the merger agreement and the merger at the special meeting, the board of directors is permitted to engage in discussions and negotiations with a third party regarding a competing acquisition offer if:

| · | the board determines in good faith, after consultation with and taking into account the advice of its outside legal counsel and any outside financial advisor retained by Stratford, that any such competing offer is a superior alternative to the merger; |

| · | the board reasonably determines in good faith, after consultation with and taking into account the advice of its outside legal counsel, that board’s fiduciary duties under Arizona law require discussions to be conducted with the third party; and |

| · | Stratford provides Stratford Holdings with written notice of the competing offer and the material terms of such offer. |

The board of directors is permitted by the merger agreement to withdraw its recommendation of the merger agreement and the merger only if it:

| · | reasonably determines in good faith, after consultation with and taking into account the advice of its outside legal counsel, that such action is necessary in order for the board to comply with its fiduciary duties under Arizona law; and |

| · | has given notice of its intention to withdraw its recommendation, and has not received an offer from Stratford Holdings within five business days which matches or exceeds the competing acquisition offer. |

Termination of the Merger Agreement (page [ _ ])

Stratford Acquisition may terminate the merger agreement prior to the completion of the merger if:

| · | Stratford’s board of directors withdraws, modifies or changes its recommendation regarding the merger in accordance with the merger agreement; or |

| · | there has been a material adverse effect on the business, assets, results of operations or financial condition of Stratford and its subsidiaries, taken as a whole. |

Stratford may terminate the merger agreement prior to the completion of the merger to accept a competing acquisition offer from a third party that Stratford Holdings fails to match or exceed.

The merger agreement may also be terminated prior to the completion of the merger under other circumstances that are described in the merger agreement, including an uncured material breach, the failure of the parties to consummate the merger before May 31, 2006, or a final governmental order prohibiting the merger.

Fees and Expenses (page [ _ ])

Each party to the merger agreement has agreed to pay its own costs and expenses in connection with the merger agreement and the transactions contemplated thereby. If, however, Stratford terminates the merger agreement to accept a competing third party offer, Stratford is required to pay all of the costs and expenses incurred by Stratford Holdings in connection with the merger, in an amount not to exceed $200,000. The merger agreement does not require a “break fee” under any circumstances.

Regulatory Approvals and Requirements (page [ _ ])

In connection with the merger, Stratford will be required to make certain filings with, and comply with certain laws of, various federal and state governmental agencies. Nevertheless, it is currently expected that no regulatory approvals will be required in order to complete the merger.

Certain Risks in the Event of Bankruptcy (page [ _ ])

If Stratford is insolvent at the time of the merger or becomes insolvent because of the merger, the funds paid to shareholders upon completion of the merger may be deemed to be a “fraudulent conveyance” under applicable law and therefore may be subject to the claims of Stratford’s creditors. If such claims are asserted by Stratford’s creditors, there is a risk that persons who were shareholders at the effective time of the merger would be ordered by a court to return to Stratford’s trustee in bankruptcy all or a portion of the funds received upon the completion of the merger. Stratford’s board of directors has no reason to believe that Stratford and its subsidiaries, on a consolidated basis, will be insolvent immediately after giving effect to the merger.

Appraisal Rights (page [ _ ])

If the merger agreement and the merger are properly approved by Stratford’s shareholders and the merger is actually consummated, you have the right under Arizona law to dissent and to receive payment equal to the “fair value” of your shares if you do not wish to exchange your shares of Stratford common stock for the merger consideration. This “right of appraisal” is subject to a number of restrictions and technical requirements. Generally, in order to exercise appraisal rights, you must:

| · | before the shareholder vote related to the merger is taken at the special meeting, deliver written notice to Stratford of your intent to demand payment for your shares if the merger is completed; |

| · | not vote for approval and adoption of the merger agreement and the merger; and |

| · | upon receipt of a dissenters’ notice from Stratford, demand payment, certify the date that you acquired beneficial ownership of your shares, and deposit your stock certificates in accordance with the terms of the notice. |

You will not protect your right of appraisal by merely voting against the merger agreement and the merger. A copy of the relevant section of the Arizona Business Corporation Act addressing appraisal rights is attached to this proxy statement as Exhibit B.

This proxy statement contains certain forward-looking statements regarding Stratford that are based on the beliefs of Stratford’s management as well as assumptions made by, and information currently available to, Stratford’s management. Such statements are subject to risks and uncertainties that could cause actual results to differ materially from those contemplated in such forward-looking statements. Certain factors that could cause actual results to differ materially from Stratford’s expectations include, but are not limited to, general business conditions, competition and other factors which are described from time to time in Stratford’s public filings with the SEC, news releases and other communications. Also, when Stratford uses the words “believes,” “expects,” “anticipates,” “estimates,” “plans,” “intends,” “objectives,” “goals,” “aims,” “projects,” or similar words or expressions, Stratford is making forward-looking statements. Readers are cautioned not to place undue reliance on these forward-looking statements to reflect events or circumstances after the date hereof or to reflect the occurrence of unanticipated events. All forward-looking statements contained in this proxy statement speak only as of the date of this proxy statement or as of such earlier date that those statements were made and are based on current expectations or expectations as of such earlier date and involve a number of assumptions, risks and uncertainties that could cause the actual results to differ materially from such forward-looking statements. Stratford will update or amend this proxy statement to further reflect any material changes to the forward-looking information disclosed herein as required by law.

The following table summarizes certain selected consolidated financial data, which should be read in conjunction with our Annual Report on Form 10-KSB for the fiscal year ended December 31, 2005, which is attached as Exhibit C to this proxy statement. The selected consolidated financial data set forth below as of and for each of the years in the two-year period ended December 31, 2005, have been derived from our consolidated financial statements which have been audited by KPMG LLP, who was our independent registered public accounting firm for those periods.

Year Ended December 31, | |||||||

2005 | 2004 | ||||||

REVENUES: | |||||||

| Oil and gas revenues | $ | 1,605,000 | $ | 1,002,000 | |||

| Gain on restructuring of payables | 0 | 0 | |||||

| Interest and other income | 194,000 | 25,000 | |||||

| 1,799,000 | 1,027,000 | ||||||

EXPENSES: | |||||||

| General and administrative | 625,000 | 631,000 | |||||

| Depreciation, depletion and amortization | 337,000 | 306,000 | |||||

| Oil and gas operations | 339,000 | 229,000 | |||||

| Interest | 0 | 0 | |||||

| 1,301,000 | 1,166,000 | ||||||

| Income (loss) from continuing operations before income taxes | 498,000 | (139,000 | ) | ||||

| Income tax expense | 22,000 | 17,000 | |||||

| Income (loss) from continuing operations | 476,000 | (156,000 | ) | ||||

Year Ended December 31, | |||||||

2005 | 2004 | ||||||

DISCONTINUED OPERATIONS: | |||||||

| Income (loss) from operations | (6,000 | ) | 423,000 | ||||

| Gain on sale of building, net of tax benefit of $49,000 for the year ended December 31, 2005 and net of tax expense of $430,000 for the year ended December 31, 2004 | 69,000 | 5,326,000 | |||||

| Minority interest | (3,000 | ) | (1,269,000 | ) | |||

| Income from discontinued operations | 60,000 | 4,480,000 | |||||

Net income | $ | 536,000 | $ | 4,324,000 | |||

| Basic and diluted net income (loss) per share: | |||||||

| Income (loss) from continuing operations | $ | 0.04 | $ | (0.01 | ) | ||

| Income from discontinued operations | 0.01 | 0.40 | |||||

Basic and diluted net income per share | $ | 0.05 | $ | 0.39 | |||

Shares used to compute income (loss) per share | |||||||

| Basic | 11,078,105 | 11,078,105 | |||||

| Diluted | – | – | |||||

Year Ended December 31, | |||||||

2005 | 2004 | ||||||

Balance Sheet Data | |||||||

| Working capital | $ | 6,487,000 | $ | 6,392,000 | |||

| Total current assets | $ | 6,728,000 | $ | 7,029,000 | |||

| Total current liabilities | $ | 241,000 | $ | 637,000 | |||

| Total shareholders’ equity | $ | 8,023,000 | $ | 7,487,000 | |||

| Book value per share | $ | 0.72 | $ | 0.68 | |||

| Ratio of earnings to fixed charges | 20.14 | 4.32 | |||||

We have not provided any pro forma data giving effect to the merger as we do not believe that such information is material to our shareholders in evaluating the merger and the merger agreement. The merger consideration consists solely of cash and, if the merger is consummated, our common stock will cease to be publicly traded. As a result, we do not believe that the changes to our financial condition resulting from the merger would provide meaningful or relevant information in evaluating the merger and the merger agreement since our shareholders (other than JDMD) will not be shareholders of, and will have no direct interest in, Stratford following the merger.

Stratford’s common stock is listed on the OTC Bulletin Board under the symbol “STFA.OB” The table below sets forth the range of high and low closing bid prices on the OTC Bulletin Board for fiscal years 2004, 2005, and 2006 to date.

High | Low | ||||||

| Fiscal Year Ending December 31, 2004 | |||||||

First Quarter | $ | 0.60 | $ | 0.20 | |||

Second Quarter | $ | 0.45 | $ | 0.29 | |||

Third Quarter | $ | 0.41 | $ | 0.32 | |||

Fourth Quarter | $ | 0.55 | $ | 0.38 | |||

| Fiscal Year Ending December 31, 2005 | |||||||

First Quarter | $ | 0.61 | $ | 0.41 | |||

Second Quarter | $ | 0.64 | $ | 0.40 | |||

Third Quarter | $ | 0.70 | $ | 0.54 | |||

Fourth Quarter | $ | 0.75 | $ | 0.58 | |||

| Fiscal Year Ending December 31, 2006 | |||||||

First Quarter (through April 21, 2006) | $ | 0.82 | $ | 0.68 | |||

The closing sale price, and the high and low sale prices for shares of Stratford’s common stock on the OTC Bulletin Board on January 30, 2006, the last trading day before Stratford announced the proposed merger and the signing of the merger agreement, was $0.80 per share. On [_______], 2006, the last trading day for which information was practicably available prior to the date of the first mailing of this proxy statement, the closing price per share of Stratford’s common stock as reported on the OTC Bulletin Board was $[____]. We recommend that shareholders obtain a current market quotation for Stratford’s common stock before making any decision with respect to the merger.

As of April 21, 2006, 261 record owners and approximately 460 beneficial owners owned 11,078,105 issued and outstanding shares of Stratford’s common stock.

Stratford has not paid any dividend with respect to shares of its common stock in the past two years. Under the merger agreement, Stratford has agreed not to pay any dividends on its shares of common stock prior to the completion of the merger.

The enclosed proxy is solicited on behalf of our board of directors for use at a special meeting of shareholders to be held on ______, 2006 at 9:00 a.m., local time, or at any adjournments or postponements of the special meeting, for the purposes set forth in this proxy statement and in the accompanying notice of special meeting. The special meeting will be held at Stratford’s executive offices located at 2400 East Arizona Biltmore Circle, Building 2, Suite 1270, Phoenix, Arizona 85016. Stratford intends to mail this proxy statement and the accompanying proxy card on or about [________], 2006 to all shareholders entitled to vote at the special meeting.

The special meeting of the shareholders will be held on ______, 2006 at 9:00 a.m., local time, at Stratford’s executive offices located at 2400 East Arizona Biltmore Circle, Building 2, Suite 1270, Phoenix, Arizona 85016. At the special meeting, you will be asked to consider and vote in favor of proposals to approve and adopt the merger agreement and the merger and to approve the adjournment or postponement of the special meeting, if necessary or appropriate, to solicit additional proxies if there are insufficient votes at the time of the special meeting to adopt the merger agreement and the merger.

Pursuant to the merger, Stratford Acquisition will be merged with and into Stratford, with Stratford as the surviving corporation and becoming a wholly-owned subsidiary of Stratford Holdings. At the effective time of the merger, each share of Stratford’s common stock issued and outstanding immediately prior to the filing of articles of merger with the Arizona Corporation Commission will be converted into the right to receive $0.90 in cash, without interest, except for:

| · | shares for which appraisal rights have been perfected properly under the Arizona Business Corporation Act, which will be entitled to receive the consideration provided for by Arizona law; |

| · | shares held by Stratford in treasury and shares held by Stratford’s wholly-owned subsidiaries, which will be cancelled without payment; and |

| · | shares held by JDMD prior to the merger, which will be cancelled without payment. |

Like all other Stratford shareholders, Stratford’s executive officers and directors (other than Messrs. Colangelo, Eaton, Shultz and Jensen, with respect to their ownership interest in JDMD) will be entitled to receive $0.90 per share in cash, without interest, for each share of Stratford common stock held by them at the time of the merger.

Stratford does not expect a vote to be taken at the special meeting on any matter other than the proposals to approve and adopt the merger agreement and the merger and to approve the adjournment or postponement of the special meeting, if necessary or appropriate, to solicit additional proxies if there are insufficient votes at the time of the special meeting to adopt the merger agreement and the merger. However, if any other matters are properly presented at the special meeting for consideration, the holders of the proxies will have discretion to vote on these matters in accordance with their best judgment. The proxies Stratford is soliciting will grant discretionary authority to vote in favor of adjournment or postponement of the special meeting to the extent the proxy holders may deem such actions appropriate in their discretion.

Only holders of record of Stratford’s common stock at the close of business on April 21, 2006, the record date for the special meeting, are entitled to notice of, and to vote at, the special meeting and any adjournments or postponements thereof. At the close of business on the record date, 11,078,105 shares of Stratford’s common stock were outstanding and entitled to vote at the special meeting. A list of shareholders will be available for review at Stratford’s executive offices during regular business hours beginning two business days after notice of the special meeting is given and continuing to the date of the special meeting and will be available for review at the special meeting or any adjournment thereof. Each holder of record of Stratford’s common stock on the record date will be entitled to one vote for each share held. If you sell or transfer your shares of Stratford’s common stock after the record date, but before the special meeting, you will transfer the right to receive the $0.90 in cash per share, without interest, if the merger is consummated to the person to whom you sell or transfer your shares, but you will retain your right to vote at the special meeting.

All votes will be tabulated by the inspector of elections appointed for the special meeting, who will separately tabulate affirmative and negative votes, abstentions and broker non-votes. Brokers who hold shares in “street name” for clients typically have the authority to vote on “routine” proposals when they have not received instructions from beneficial owners. Absent specific instructions from the beneficial owner of the shares, however, brokers are not allowed to exercise their voting discretion with respect to the approval of non-routine matters, such as the approval and adoption of the merger agreement and the merger. Proxies submitted without a vote by brokers on these matters are referred to as “broker non-votes.”

A majority of the outstanding shares of common stock will constitute a quorum for the transaction of business related to the proposals and for the transaction of all other business at the special meeting. If a share is represented for any purpose at the special meeting it will be deemed present for purposes of determining whether a quorum exists.

Any shares of common stock held in treasury by Stratford are not considered to be outstanding on the record date or otherwise entitled to vote at the special meeting for purposes of determining a quorum.

Shares represented by proxies reflecting abstentions and properly executed broker non-votes are counted for purposes of determining whether a quorum exists at the special meeting.

Approval and adoption of the merger agreement and the merger requires (a) the affirmative vote of holders of a majority of the outstanding unaffiliated shares of Stratford’s common stock (those not owned, directly or indirectly, by JDMD and Eaton Trust), and (b) the affirmative vote of holders of a majority of the outstanding shares of Stratford’s common stock (including those shares owned, directly or indirectly, by JDMD and Eaton Trust). If holders of a majority of the outstanding unaffiliated shares (those not owned, directly or indirectly, by JDMD and Eaton Trust) vote to approve and adopt the merger agreement and the merger, the holders of the interested shares (those owned, directly or indirectly, by JDMD and Eaton Trust, which in the aggregate constitute approximately 30.3% of the total outstanding shares of common stock) are required under the merger agreement to vote their shares in favor of the approval and adoption of the merger agreement and the merger.

The board of directors of Stratford also has been informed that The DRD 97 Trust expects to vote its shares in favor of the approval and adoption of the merger agreement and the merger. The shares held by The DRD 97 Trust represent approximately 23.0% of the total outstanding shares of Stratford’s common stock and approximately 33.0% of the unaffiliated shares of Stratford’s common stock.

Approval and adoption of any adjournment or postponement of the special meeting, if necessary or appropriate, requires the affirmative vote of holders of a majority of the outstanding shares of Stratford’s common stock (including those shares owned, directly or indirectly, by JDMD and Eaton Trust).

Proxies that reflect abstentions and broker non-votes, as well as proxies that are not returned, will have the same effect as a vote against both proposals.

If the special meeting is adjourned or postponed for any reason, at any subsequent reconvening of the special meeting, all proxies will be voted in the same manner as they would have been voted at the original convening of the meeting, except for any proxies that have been revoked or withdrawn.

Shareholders of record may submit proxies by mail. We will not accept proxies to be voted by telephone or internet. After carefully reading and considering the information contained in this proxy statement, you should complete, date and sign your proxy card and mail the proxy card in the enclosed postage paid return envelope as soon as possible so that your shares may be voted at the special meeting, even if you plan to attend the special meeting in person. Submitting a proxy now will not limit your right to vote at the special meeting if you decide to attend in person. If your shares are held of record in “street name” by a broker or other nominee and you wish to vote in person at the special meeting, you must obtain from the record holder a proxy issued in your name.

Proxies received at any time before the special meeting is called to order and not revoked or superseded before being voted will be voted at the special meeting. If the proxy indicates specific voting instructions, it will be voted in accordance with the voting instructions. If no voting instructions are indicated, the proxy will be voted “FOR” approval and adoption of the merger agreement and the merger.

Please do not send in stock certificates at this time. If the merger is consummated, you will receive instructions regarding the procedures for exchanging your existing Stratford stock certificates for the $0.90 per share cash payment, without interest.

Any person giving a proxy pursuant to this solicitation has the power to revoke and change it at any time before the meeting is called to order. It may be revoked and changed by filing a written notice of revocation with Stratford’s Secretary at Stratford’s executive offices located at 2400 East Arizona Biltmore Circle, Building 2, Suite 1270, Phoenix, Arizona 85016, by submitting in writing a proxy bearing a later date, or by attending the special meeting and voting in person. Attendance at the special meeting will not, by itself, revoke a proxy. If you have given voting instructions to a broker or other nominee that holds your shares in “street name,” you may revoke those instructions by following the directions given by the broker or other nominee.

This proxy statement is being furnished in connection with the solicitation of proxies by our board of directors. Stratford will bear the entire cost of soliciting, including costs relating to preparation, assembly, printing and mailing of this proxy statement, the notice of the special meeting of shareholders, the enclosed proxy and any additional information furnished to shareholders. Copies of solicitation materials will also be furnished to banks, brokerage houses, fiduciaries and custodians holding in their names shares of Stratford’s common stock beneficially owned by others to forward to these beneficial owners. Stratford may, upon request, reimburse brokers, bankers and other nominees representing beneficial owners of Stratford’s common stock for their costs of forwarding solicitation materials to the beneficial owners. Original solicitation of proxies by mail may be supplemented by telephone or personal solicitation by directors, officers or other regular employees of Stratford. No additional compensation will be paid to directors, officers or other regular employees for their services.

Although it is not currently expected, the special meeting may be adjourned or postponed for the purpose of soliciting additional proxies. If the special meeting is adjourned to a different place, date or time, Stratford need not give notice of the new place, date or time if the new place, date or time is announced at the meeting before adjournment or postponement, unless a new record date is or must be set for the adjourned meeting. Stratford’s board of directors must fix a new record date if the meeting is adjourned to a date more than 120 days after the date fixed for the original meeting. Any adjournment or postponement of the special meeting for the purpose of soliciting additional proxies will allow Stratford’s shareholders who have already sent in their proxies to revoke them at any time prior to their use at the special meeting as adjourned or postponed.

In order to attend the special meeting in person, you must be a shareholder of record on the record date, hold a valid proxy from a record holder or be an invited guest of Stratford. You will be asked to provide proper identification at the registration desk on the day of the meeting or any adjournment or postponement of the meeting.

Shareholders who do not vote in favor of approval and adoption of the merger agreement and the merger, and who otherwise comply with the applicable statutory procedures of Arizona law summarized elsewhere in this proxy statement, will be entitled to seek appraisal of the value of their Stratford common stock as set forth in the Arizona Business Corporation Act. See “SPECIAL FACTORS — Appraisal Rights.”

2400 East Arizona Biltmore Circle

Building 2, Suite 1270

Phoenix, Arizona 85016

(602) 956-7809

Stratford is an Arizona corporation that was incorporated on May 13, 1988. Stratford, through its subsidiaries, is engaged principally in the business of natural resource exploration and development. Stratford has the following wholly-owned subsidiaries: Stratford American Car Rental Systems, Stratford American Energy Corporation, Stratford American Gold Venture Corporation, Stratford American Oil and Gas Corporation, Stratford American Properties Corporation, Stratford American Resource Corporation, and SA Oil and Gas Corporation. All of Stratford’s wholly-owned subsidiaries are Arizona corporations, except Stratford American Energy Corporation, which is an Oklahoma corporation, and Stratford American Resource Corporation, which is a Texas corporation. Stratford employs four employees, one of whom works full time.

2400 East Arizona Biltmore Circle

Building 2, Suite 1270

Phoenix, Arizona 85016

(602) 224-2312

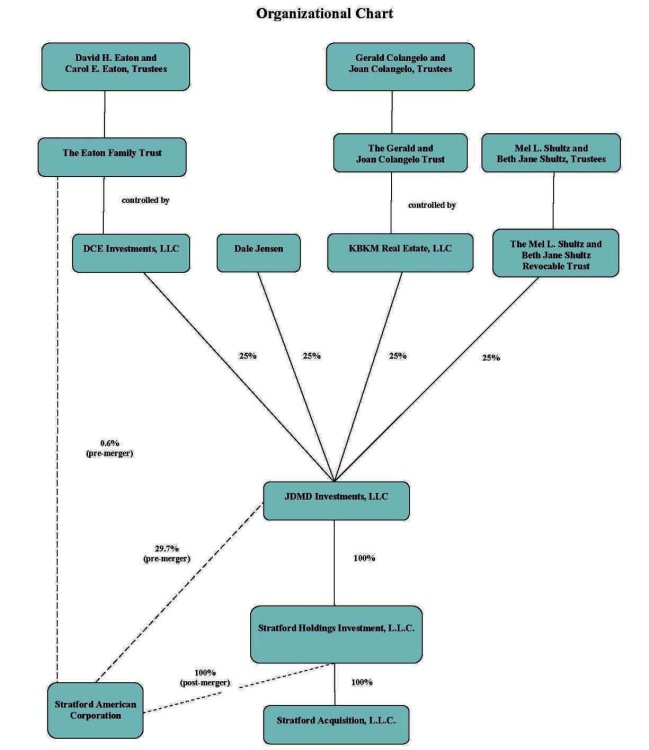

JDMD is an Arizona limited liability company formed in 1996 whose principal business is (i) making investments in businesses, companies, and properties by means of acquisitions of stock, partnership interests, limited liability company memberships, and direct acquisitions of property and assets, and (ii) holding and managing such investments. The managers of JDMD are Gerald Colangelo, a director of Stratford, David Eaton, the Chief Executive Officer and a director of Stratford, Mel Shultz, the President and a director of Stratford, and Dale Jensen, a director of Stratford. The members of JDMD are: (a) the Mel L. Shultz and Beth Jane Shultz Revocable Trust, of which Mr. and Mrs. Shultz are co-trustees; (b) DCE Investments, LLC, which is majority-owned by The Eaton Family Trust, of which David Eaton and Carol Eaton are co-trustees; (c) KBKM Real Estate, LLC, which is majority-owned by The Gerald and Joan Colangelo Family Trust, of which Gerald Colangelo and Joan Colangelo are co-trustees; and (d) Dale Jensen. JDMD currently owns 29.7% of the outstanding common stock of Stratford, and also has significant business interests unrelated to Stratford.

2400 East Arizona Biltmore Circle

Building 2, Suite 1270

Phoenix, Arizona 85016

(602) 224-2312

Stratford Holdings is an Arizona limited liability company formed in January 2006 by JDMD to hold all of the outstanding common stock of Stratford effective upon completion of the merger.

2400 East Arizona Biltmore Circle

Building 2, Suite 1270

Phoenix, Arizona 85016

(602) 224-2312

Stratford Acquisition is an Arizona limited liability company formed in January 2006 and is a wholly-owned subsidiary of Stratford Holdings. The sole purpose of Stratford Acquisition is to merge with and into Stratford pursuant to the merger described in this proxy statement, with Stratford as the surviving corporation.

The following diagram depicts the organizational structure of JDMD and the other Buyout Parties, as well as the structure of Stratford after giving effect to the merger:

SPECIAL FACTORS

Stratford sold its major real estate asset in November 2004, and since that time its sole assets have consisted primarily of the cash proceeds from the sale and minority working interests in various oil and gas properties primarily located in Oklahoma and Texas. In connection with and beginning around the time of the sale, the board of directors and management of Stratford began discussing in general terms the future direction of Stratford’s business, including specifically whether to invest in additional income-producing real estate or oil and gas ventures, or to liquidate Stratford and distribute its assets to the shareholders. These discussions included the disadvantages faced by Stratford as a smaller-sized publicly-traded company. In particular, the directors noted:

• | Stratford’s difficulty in attracting analyst coverage, market attention and institutional shareholder investment due to its small size, low market capitalization and low share price; |

| • | the common stock’s small public float, extremely limited trading volume, and bid-asked trading price spread, all of which have: |

| • | limited Stratford’s ability to use its common stock as acquisition currency, |

| • | significantly limited the ability of shareholders to sell their shares without also reducing the trading price of the common stock, and |

| • | impaired Stratford’s ability to use equity-based incentives to successfully attract and retain employees; |

| • | the existence of competitors in Stratford’s industry with greater resources at their disposal; and | |

| • | the costs and associated burdens of being a public company, including: |

| • | the actual out-of-pocket costs of SEC compliance; |

| • | the burden on management of compliance efforts; |

| • | the distraction of investor relations and the focus on short-term goals such as quarterly results per share occasioned by periodic public reporting; |

| • | the compliance and competitive costs associated with requirements to publicly disclose detailed information regarding Stratford’s business, operations and results; and |

| • | the enactment of the Sarbanes-Oxley Act of 2002, which has led to increased compliance costs and additional burdens on management. |

As a result of these discussions, management engaged Meagher Oil & Gas Properties, Inc. (“Meagher”) on November 8, 2004 to evaluate Stratford’s oil and gas properties and to assist in offering them for sale. Meagher is a nationally recognized acquisition and divestiture firm that specializes in the oil and gas industry, and had been recommended to Stratford by several of its partners in the oil and gas properties. Stratford had no previous relationship with Meagher. Pursuant to the exclusive Services Agreement with Meagher, Stratford paid an initial retainer of $25,000 and is obligated to pay a commission equal to the sum of: (a) 5% of the cumulative sales price of the oil and gas properties from $1.00 to $1,000,000; plus (b) 4% of the cumulative sales price of the properties from $1,000,001 to $2,000,000; plus (c) 3% of the cumulative sales price of the properties from $2,000,001 to $3,000,000; plus (d) 2% of the cumulative sales price of the properties from $3,000,001 to $4,000,000; plus (e) 1% of the cumulative sales price of the properties from $4,000,001 and above, but in no event will the commission exceed $200,000.

Between November 2004 and early February 2005 the Stratford board did not meet formally, but officers and directors of Stratford worked with Meagher to compile the package of marketing information concerning the oil and gas properties that would be delivered to potential buyers. The package consisted of engineering reports compiled by Meagher based on information provided by management and information publicly available on the Dwight’s databases about oil and gas wells. In early February 2005, Meagher sent solicitations of interest to approximately 3,500 potential buyers, and received requests for information from 61 companies. The marketing information indicated that the oil and gas properties were for sale by state or as a total package, with preference to be given by Stratford to a single buyer.

During February and March, 2005, Meagher engaged in discussions with each of the 61 companies that requested the marketing information, and received eight bids, five of which were for the entire package of oil and gas properties and three of which were for partial packages of properties. The bids for the entire package of properties generally ranged from $1.75 million to $2.925 million, or approximately $0.62 to $0.71 per share based upon the value of Stratford reflected in its financial statements as of March 31, 2005, with one bid management did not believe was legitimate at $750,000. The per share value of the bids was determined using a liquidation analysis, assuming the assets were sold at the bid price and the sales proceeds plus Stratford’s cash and cash equivalents on the relevant date (in this case, March 31, 2005) were distributed to the shareholders in liquidation, after payment of transaction costs, including the Meagher commission, all liabilities of Stratford and taxes as a result of the sale. The liabilities to be satisfied included the liabilities reflected on the balance sheet plus $947,000 for committed drilling costs, professional fees and expenses and employee severance. This same per share determination was used by the board in calculating the various per share amounts which follow in this discussion.

Meagher had ongoing negotiations with each of the bidders in an effort to increase their bids, but none of the bids were increased and ultimately none of the bids was acceptable to or pursued by management because in light of increasing oil and gas prices, Mr. Eaton and Mr. Shultz, representing Stratford as management and directors, did not believe that any of the bids would provide Stratford with fair market value. Meagher’s engineering studies in December 2004 indicated a probable market value of the properties of $2.4 million (or $0.67 per share based upon the value of Stratford reflected in its financial statements as of March 31, 2005) using a 10% discount rate, but using a cash flow multiple the probable market value according to Meagher was $3.3 million (or $0.74 per share based upon the value of Stratford reflected in its financial statements as of March 31, 2005). The engineering studies prepared by Meagher assumed (a) oil prices are $41.85/bbl NYMEX from December 2004 to November 2005, $40.31/bbl NYMEX from December 2005 to November 2006, $38.91/bbl NYMEX from December 2006 to November 2007, $37.98/bbl NYMEX from December 2007 to November 2008, and beginning December 1, 2008 oil prices will be escalated 2% to a cap (or drop) of $30.00 NYMEX, (b) gas prices are $6.53/mmbtu NYMEX from December 2004 to November 2005, $6.34/mmbtu NYMEX from December 2005 to November 2006, $5.99/mmbtu NYMEX from December 2006 to November 2007, $5.67/mmbtu NYMEX from December 2007 to November 2008, and beginning December 1, 2008, gas prices will escalate (or drop) at 4% to a cap of $4.50 NYMEX price, and (c) operating expenses will escalate at 3% per annum starting immediately and running for five years. Accordingly, management decided not to pursue a sale transaction with any of the bidders. While no formal board meetings were held during this time period, management communicated regularly with the individual members of the board during this process and received their support as to strategy and direction.

Meagher continued to market the properties. On June 20, 2005, a new bidder submitted a bid of $4 million (or $0.79 per share based upon the value of Stratford reflected in its financial statements as of March 31, 2005) for Stratford’s entire package of oil and gas properties, subject to due diligence, and with an effective date of March 1, 2005 (so that the buyer would get the benefit of the income derived from the properties from and after that date, thereby effectively reducing the purchase price). During this time period, however, the prices of natural gas and oil had increased dramatically and were continuing to increase. Meagher re-ran the engineering studies to determine what impact the higher prices would have on the value of the properties over time. The new analysis indicated a value of $4,895,000 at September 1, 2005 (or $0.86 per share based upon the value of Stratford reflected in its financial statements as of June 30, 2005). The increase in value was due solely to the increase in the prices of natural gas and oil. Meagher sent the new engineering studies to the new bidder and the previous bidders but none responded with an increased bid. Management rejected the new bid as too low (including the fact that the new bidder was requiring all income after March 1st) and so informed the individual board members. Meagher’s new engineering studies assumed (a) oil prices average $67.35/bbl for the remainder of 2005, NYMEX strip data was used for the remaining years out to 2008 and thereafter the price was held fixed for life at $61.16/bbl, (b) gas prices average $9.87/mmbtu for the remainder of 2005, NYMEX strip data was used for the remaining years out to 2008 and thereafter the price was held fixed for life at $8.73/mmbtu, and (c) direct operating expenses were escalated by 3% per year.

In early November, 2005, JDMD had purchased 467,774 shares of Stratford common stock from a shareholder for $0.75 per share, which price was requested by the shareholder and not negotiated. This transaction was not part of the buyout proposal ultimately presented by JDMD. However, the purchase was reflected in an amendment to JDMD’s Schedule 13D, wherein JDMD publicly announced that it was exploring the possibility of taking Stratford private. Messrs. Eaton and Shultz, who are officers and directors of Stratford as well as principals of JDMD, were frustrated by the lack of acceptable bids for the oil and gas properties, and, along with the other principals of JDMD, were working on developing a buyout proposal as an alternative for Stratford if Meagher was unable to secure a bid for the oil and gas properties that approximated their market value as determined by the engineering reports. On December 29, 2005, Mel Shultz and David Eaton, on behalf of JDMD, submitted the buyout proposal to the board of directors of Stratford.

Under JDMD’s proposal, Stratford would be merged with and into a newly formed entity owned by JDMD, with Stratford being the surviving corporation and becoming wholly-owned by JDMD. Pursuant to the merger, each outstanding share of Stratford’s common stock would be converted into the right to receive $0.75 in cash (other than shares held by JDMD and shareholders who validly exercise dissenters’ right under Arizona law). This price was the same price that JDMD paid to acquire the 467,774 shares in a private purchase in November 2005. At the time the buyout proposal was submitted to Stratford’s board of directors, the market price for Stratford’s stock was $0.68 per share. The current market price is $0.89 per share. The original offer by JDMD was substantially identical to the merger described in this proxy statement, except that (a) the merger consideration was $0.75 per share, (b) Stratford’s right to consider a competing offer was limited to offers that were unsolicited, (c) the surviving corporation was obligated to maintain directors’ and officers’ liability insurance for six years following the closing, (d) Stratford was obligated to take the merger to a vote of shareholders even if there was a competing offer that the board desired to accept, and (e) a competing offer was to be considered by the full board of directors. The total price to be paid by JDMD to the non-JDMD shareholders pursuant to the proposal was $5,843,105.

The board engaged Fennemore Craig, P.C. as legal counsel to evaluate the JDMD proposal. At a meeting of the board held on January 18, 2006, with all members present in person or telephonically, the board reviewed the proposal with counsel, including the terms thereof, the pros and cons of the proposal, alternatives to the proposal and the directors’ fiduciary obligations in evaluating the proposal. For a detailed discussion of the alternatives to the merger considered by the board, see “SPECIAL FACTORS - Alternatives to the Merger.” At the conclusion of the meeting, counsel for Stratford was authorized to negotiate the proposal with counsel for JDMD. At this meeting, the board also endorsed an extension of Meagher’s services agreement, and directed management to work with Meagher to continue to offer the oil and gas properties for sale to obtain, if possible, an offer that exceeded the price offered by JDMD.

Counsel for Stratford and JDMD negotiated the terms of the buyout proposal, and then provided drafts of the merger agreement, this proxy statement and Stratford’s Schedule 13E-3 filing to the board for review. As a result of the negotiations, (a) Stratford’s right to consider a competing offer was no longer limited to offers that were unsolicited, so that Stratford could continue marketing the oil and gas properties in an effort to obtain a better price for the shareholders, (b) the time period that the surviving corporation was obligated to maintain directors’ and officers’ liability insurance was shortened from six years to two years following the closing, (c) Stratford was no longer obligated to take the merger to a vote of shareholders if there was a competing offer that the board desired to accept, and (d) a competing offer was to be considered by those members of the board of directors who are not members of the buyout group. JDMD’s original proposal allowed Stratford to consider competing offers, subject to JDMD’s right to match any offer so received that the board considered a superior offer, without Stratford being required to pay JDMD a break-up fee. Stratford would, however, reimburse JDMD for its out-of-pocket expenses not to exceed $200,000. Stratford did not negotiate a similar payment from JDMD if JDMD failed to close the transaction because JDMD did not ask for a financing contingency and because every closing condition was beyond JDMD’s control. If for any reason JDMD failed to close in breach of the agreement, Stratford would have customary legal rights for damages.

In connection with the negotiations and otherwise during the course of this transaction, no material, non-public information, including projections or potential synergies, were exchanged by Stratford and JDMD as JDMD never asked Stratford to prepare or provide any such information. That being said, all of the principals of JDMD are members of the board of Stratford, and in discussing the buyout proposal the board considered the Meagher engineering studies and liquidation value analyses as part of its evaluation process.

On January 30, 2006, a meeting of the board of directors of Stratford was convened, with all members except Gerald Colangelo attending either in person or telephonically, together with representatives of Fennemore Craig. The board and counsel reviewed the proposed definitive draft of the merger agreement and discussed the proposed merger consideration. JDMD agreed, after extensive negotiation with the board, to increase the merger consideration offered by JDMD to $0.80 per share. All other terms and conditions of the merger were as described in this proxy statement. With the increase in the price to $0.80 per share, the total price to be paid by JDMD to the non-JDMD shareholders increased to $6,232,646. The price increase was negotiated based on two primary factors. First, there had been a few sales of Stratford common stock in the days before the meeting at $0.80 per share, compared to $0.68 per share at the time the proposal was submitted and the surrounding time period. While the board did not believe that the limited trading volume established a true fair market value for Stratford’s common stock, the board did believe that it was some evidence of market value and was not willing to proceed at a price less than $0.80 per share. Second, $0.80 per share is the amount the shareholders would have received if Stratford were liquidated following the sale of the oil and gas properties for $4 million, which was the highest price it had ever been offered (although the true price was less than $4 million due to the buyer’s demand for a back-dated effective date for the transaction). Even though the engineering studies indicated a value in excess of $4 million, oil and gas buyers to date had not been willing to pay the full engineering value for Stratford’s oil and gas properties, and the board did not know if they would ever be so willing.

On January 31, 2006, Mr. Colangelo and counsel reviewed the proposed definitive draft of the merger agreement. The meeting of the board of directors was reconvened on January 31, 2006, with all members attending telephonically, together with representatives of Fennemore Craig. The board of directors then unanimously adopted resolutions approving and adopting the merger agreement and the transactions contemplated by the merger agreement, including the merger, determining that the merger agreement and the transactions contemplated by the merger agreement, including the merger, are advisable and fair to, and in the best interests of, the unaffiliated holders of Stratford’s common stock (those other than JDMD and Eaton Trust) and recommending that the holders of Stratford’s common stock vote for the approval of the merger agreement and the transactions contemplated by the merger agreement, including the merger.

On January 31, 2006, in accordance with the authorizations of their respective boards of directors, the parties finalized and thereafter executed the merger agreement.

On the evening of January 31, 2006, Stratford issued a press release announcing the execution of the merger agreement. On February 1, 2006, Stratford filed a Current Report on Form 8-K announcing the execution of the merger agreement and filed both the press release and the merger agreement as exhibits.

Pursuant to the board’s directive, Meagher has continued to market the oil and gas properties. They were featured on Meagher’s website in January and February, 2006, and at an industry convention in February. In light of continuing volatility in the oil and gas markets, Meagher re-ran the engineering studies using statistical information as of January 1, 2006, which resulted in the properties having a value of $4,283,000 (or $0.82 per share based upon the value of Stratford reflected in its financial statements as of June 30, 2005). The differences in value in this analysis compared to the prior analyses are attributable solely to fluctuating prices of natural gas and oil during the relevant time period. Meagher’s new engineering studies assumed (a) oil prices average $65.82/bbl for the remainder of 2006, NYMEX strip data was used for the remaining years out to 2008 and thereafter the price was held fixed for life at $65.42/bbl, (b) gas prices average $9.24/mmbtu for the remainder of 2006, NYMEX strip data was used for the remaining years out to 2008 and thereafter the price was held fixed for life at $9.23/mmbtu, and (c) direct operating expenses were escalated by 3% per year for three years and thereafter were held fixed for life.

Following the February convention, 60 prospective purchasers asked for information about Stratford’s properties, and on March 17, 2006, Meagher received four bids ranging from $1,625,000 to $3,555,000, and two bids in excess of $4,000,000 at $4,100,000 and $4,325,000, respectively. These latter two bids correlate to per share values of $0.81 and $0.83, respectively, based on the value of Stratford reflected in its financial statements as of December 31, 2005. Then on March 21, 2006, Meagher received a bid to purchase Stratford (as opposed to the oil and gas properties) for $4,500,000 plus the amount of Stratford’s cash in excess of its liabilities at the closing, which correlates to a per share value of approximately $0.85 based on the number of shares currently outstanding and assuming cash and liabilities remain constant from the date of this proxy statement to the closing date. This bidder spoke with Meagher and Mr. Shultz on March 21, 2006 to discuss this bid. All of the foregoing bids were extremely preliminary. None of the bids included any details of the proposed transaction, including whether the buyer would assume any liabilities, timing, conditions to closing, required representations and warranties, escrow or hold back provisions, required indemnities or the like, all of which have economic consequences to Stratford and its shareholders and may reduce the proceeds ultimately available to the shareholders. Further, none of the bidders provided financial statements or references that would support their ability to pay the purchase price.