Item 1: Report to Shareholders| Total Equity Market Index Fund | June 30, 2005 |

The views and opinions in this report were current as of June 30, 2005. They are not guarantees of performance or investment results and should not be taken as investment advice. Investment decisions reflect a variety of factors, and the managers reserve the right to change their views about individual stocks, sectors, and the markets at any time. As a result, the views expressed should not be relied upon as a forecast of the fund’s future investment intent. The report is certified under the Sarbanes-Oxley Act of 2002, which requires mutual funds and other public companies to affirm that, to the best of their knowledge, the information in their financial reports is fairly and accurately stated in all material respects.

REPORTS ON THE WEB

Sign up for our E-mail Program, and you can begin to receive updated fund reports and prospectuses online rather than through the mail. Log in to your account at troweprice.com for more information.

Fellow ShareholdersLarge-cap U.S. stocks generally declined in the first half of 2005, as modest second-quarter gains were not enough to offset first-quarter losses. Some small- and mid-cap indexes fared better than large-cap benchmarks and produced slight gains for the six-month period. Nevertheless, the market’s attempts to advance were hindered by concerns about the pace of economic growth amid surging oil prices—which reached $60 per barrel in late June—and rising short-term interest rates.

MARKET ENVIRONMENT

Economic conditions were mostly favorable in the first half of 2005. Although the manufacturing sector decelerated somewhat, the economy expanded at a steady pace. New job growth continued at a reasonable rate, the unemployment rate hovered slightly above 5%, and inflation remained contained, despite skyrocketing oil prices.

Relatively low interest rates continued to provide a helpful stimulus to the economy. Although money market and short-term bond yields increased as the Federal Reserve raised the fed funds target rate, long-term interest rates unexpectedly declined. The result was a flattening of the Treasury yield curve, which currently indicates that long-term Treasury yields are not much higher than short-term yields.

Large-cap U.S. stocks generally declined through April amid fears of slower economic growth accompanied by higher inflation. However, Federal Reserve officials assuaged investor worries by asserting that the economy was on a “reasonably firm footing” and that “underlying inflation remains contained.” Brisk merger activity and generally favorable corporate earnings news helped lift stocks in the second quarter, though a late-June spike in oil prices and prospects for the central bank to continue raising the overnight federal funds target rate—which has already risen from 1.00% to 3.25% over the last 12 months—capped the market’s advance.

Large-cap shares, as measured by the S&P 500 Stock Index, returned -0.81% versus 2.19% for the Dow Jones Wilshire 4500 Completion Index, a broad benchmark for small- and mid-cap stocks. As measured by various Russell indexes, value stocks outperformed their growth counterparts across all market capitalizations.| WILSHIRE 5000 RETURNS BY SECTOR |

| | |

| Periods Ended 6/30/05 | 6 Months | 12 Months |

| Consumer Discretionary | -3.81% | 8.26% |

| Consumer Staples | 0.27 | 2.59 |

| Energy | 20.63 | 40.82 |

| Financials | -1.60 | 8.82 |

| Health Care | 4.53 | 5.18 |

| Industrials and Business Services | -3.52 | 6.68 |

| Information Technology | -5.13 | -2.28 |

| Materials | -7.48 | 6.41 |

| Telecommunication Services | -2.81 | 11.89 |

| Utilities | 14.36 | 35.68 |

The market for initial public offerings (IPOs) was relatively quiet in the first half of the year, though activity picked up in recent months. Fewer than 100 companies went public in the last six months, according to data from Dealogic and Thomson Financial. Nevertheless, the universe of publicly traded companies based in the U.S., as measured by the Dow Jones Wilshire 5000 Composite Index, continued to shrink in the last six months. One likely reason is brisk merger and acquisition activity; another may be insufficient trading activity involving shares of some of the smallest companies. As of June 30, there were 4,905 companies in the index versus 4,971 at the end of 2004.

SECTOR PERFORMANCE

In the U.S. stock market, as measured by the Wilshire 5000, energy stocks and utilities produced vigorous gains and far surpassed other sectors in the last six months. Health care was also modestly higher. The materials and information technology sectors performed worst, but stocks in the consumer discretionary and industrials and business services sectors also struggled.

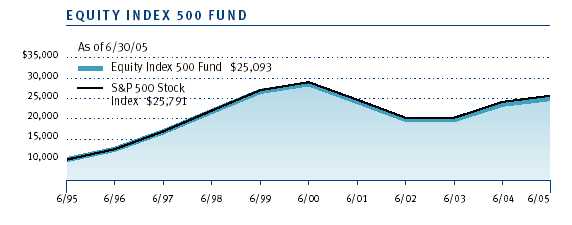

EQUITY INDEX 500 FUND

| PERFORMANCE COMPARISON |

| | |

| Periods Ended 6/30/05 | 6 Months | 12 Months |

| Equity Index 500 Fund | -0.95% | 6.02% |

| S&P 500 Stock Index | -0.81 | 6.32 |

Your fund returned -0.95% in the last six months and 6.02% for the 12-month period ended June 30, 2005. As shown in the table, the fund closely tracked the performance of its benchmark, the S&P 500 Stock Index, in both periods. The fund usually lags slightly due to annual operating and management expenses.

Energy stocks (8.8% of equities as of June 30) produced outstanding results as oil prices extended last year’s ascent into the first half of 2005. Nearly every energy holding appreciated in value, and many were among our largest contributors to performance. The largest was ExxonMobil, which gained 13% amid rising oil prices and following better-than-expected earnings in the fourth quarter of 2004. (Please refer to the fund’s portfolio of investments for a complete listing of the fund’s holdings and the amount each represents in the portfolio.)

Utility stocks (3.5% of equities) also extended last year’s brisk performance, led by electric utilities. One of our top contributors in this segment was Exelon, which advanced 18%. Independent power producers also performed well, especially TXU Corporation, whose shares surged 30% as its energy division benefited from rising natural gas prices. Gas utility companies trailed.

In the health care sector (13.4% of equities), gains were driven by providers and service companies. UnitedHealth Group, a high-quality, diversified, national managed care provider, was our best holding in the sector. Shares of WellPoint, HCA, and Aetna also performed very well. Pharmaceutical stocks were mixed, as weakness in Merck and Schering-Plough offset gains in Pfizer and Johnson & Johnson. Biotechnology and health care equipment and supply companies generally declined, though Gilead Sciences and Medtronic contributed to our results.

On the downside, information technology shares (15.2% of equities) detracted the most in the last six months. Nearly every underlying industry declined, but semiconductor-related stocks produced gains, thanks primarily to strength in Intel and Texas Instruments. Software stocks were dragged lower by weakness in industry giant Microsoft, but makers of computers and peripherals performed worst, led by IBM, which reported lower-than-expected first-quarter earnings and which tumbled more than 24% in the first half. Hewlett-Packard, however, bucked the negative trend as the company replaced CEO Carly Fiorina and began focusing on increasing its profitability.Consumer discretionary stocks (11.4% of equities) generally fell, though multi-line retailers J.C. Penney, May Department Stores, and Nordstrom performed very well. Media stocks continued to struggle across the board, especially Time Warner and Viacom, while automobile stocks Ford Motor and GM suffered from weakening sales and credit rating downgrades. Specialty retailers were mixed, as gains in Best Buy and Office Depot were offset by weak performance of Home Depot. Toys R Us performed well, however, after the company received a buy-out offer from two private equity firms and a real estate developer.

| PORTFOLIO CHARACTERISTICS |

|

| | | | Extended |

| | Equity | Total Equity | Equity |

| As of 6/30/05 | Index 500 | Market Index | Market Index |

| Market Cap | | | |

| (Investment- | | | |

| Weighted Median) | $48.8 billion | $25.0 billion | $2.6 billion |

| |

| Earnings Growth | | | |

| Rate Estimated | | | |

| Next 5 Years * | 11.2% | 11.3% | 14.4% |

| |

| P/E Ratio (Based | | | |

| on Next 12 Months’ | | | |

| Estimated Earnings) * | 15.4X | 15.8X | 17.5X |

| | | |

| * Source data: IBES. Forecasts are in no way indicative of future investment returns. |

Most major underlying industries in the financial sector (20.3% of equities) declined in the last six months. Real estate-related companies outperformed, however, especially Simon Property Group and Equity Office Properties, which benefited from the booming real estate market. Insurance stocks also held up well, with Prudential and Allstate producing good returns, though shares of American International Group suffered amid regulatory scrutiny of its accounting practices. Commercial banks did worst, especially Bank of America and Wachovia. Brokerage stocks and asset managers also struggled, though Lehman Brothers and Franklin Resources traded higher.The industrials and business services sector (11.2% of equities) also detracted substantially from our performance. Industrial conglomerates GE, 3M, and Tyco International were responsible for a large portion of the sector’s weakness. Machinery stocks also struggled amid fears that slower economic growth would hurt the earnings of these cyclical companies. On the plus side, aerospace and defense firms gained altitude, led by Boeing and Lockheed Martin.

Standard & Poor’s authorized only three changes to the composition of the S&P 500 in the last six months, two of which stemmed from mergers. Adolph Coors, which was acquired by Canadian brewer Molson, was replaced by Molson Coors Brewing; Sears, Roebuck & Co., which merged with K-Mart, was replaced by Sears Holdings; and Power-One was supplanted by National Oilwell Varco.

TOTAL EQUITY MARKET INDEX FUND

| PERFORMANCE COMPARISON |

| | |

| Periods Ended 6/30/05 | 6 Months | 12 Months |

| Total Equity Market Index Fund | -0.08% | 8.11% |

| Dow Jones Wilshire 5000 | | |

| Composite Index * | 0.02 | 8.39 |

|

| * Dow Jones Wilshire 5000 returns through 6/30/05, calculated as of 7/11/05. |

Your fund returned -0.08% in the last six months and 8.11% for the 12-month period ended June 30, 2005. The fund closely tracked the performance of the Dow Jones Wilshire 5000 Composite Index in both periods, as shown in the table, but slightly lagged due to annual operating and management expenses.Because the Wilshire 5000 includes more than 4,900 publicly traded companies, it is impractical for us to buy shares of each. Instead, we use sampling strategies in an attempt to match the performance of the index. We manage the portfolio so that its characteristics—including sector allocations and price/earnings ratio—closely resemble those of the index. At the end of June, the fund owned stocks of approximately 2,000 companies.

| SECTOR DIVERSIFICATION |

| | | |

| Percent of | | | Extended |

| Equities | Equity | Total Equity | Equity |

| As of 6/30/05 | Index 500 | Market Index | Market Index |

| Consumer | | | |

| Discretionary | 11.4% | 13.4% | 18.5% |

| Consumer Staples | 10.1 | 9.1 | 4.9 |

| Energy | 8.8 | 8.3 | 6.9 |

| Financials | 20.3 | 21.3 | 24.9 |

| Health Care | 13.4 | 13.0 | 12.3 |

| Industrials and Business | | | |

| Services | 11.2 | 10.3 | 9.2 |

| Information | | | |

| Technology | 15.2 | 15.3 | 14.5 |

| Materials | 2.9 | 3.1 | 3.7 |

| Telecommunication | | | |

| Services | 3.2 | 2.8 | 2.0 |

| Utilities | 3.5 | 3.4 | 3.1 |

| | | |

| Note: The numbers in this table may not match the sector percentages in each fund’s portfolio of |

| investments, which are calculated as a percentage of net assets. |

| | | | |

In general, what was true about the performance of the Equity Index 500 Fund in the last six months was also true for this fund: energy, health care, and utilities were the sectors that contributed the most to fund performance, while the information technology, financial, consumer discretionary, and industrials and business services sectors detracted the most. The Wilshire 5000, which represents the entire U.S. stock market, includes all S&P 500 companies. In fact, the S&P 500 represents about 74% of the Wilshire 5000’s total market value. The largest components of the Wilshire index—as with the S&P 500—have the greatest influence on performance. In addition, the percentage weightings of the major sectors are similar, as shown in the Sector Diversification table above.

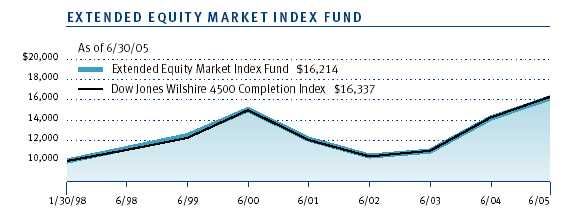

EXTENDED EQUITY MARKET INDEX FUND

| PERFORMANCE COMPARISON |

| | |

| Periods Ended 6/30/05 | 6 Months | 12 Months |

| Extended Equity Market | | |

| Index Fund | 2.11% | 14.10% |

| Dow Jones Wilshire 4500 | | |

| Completion Index * | 2.19 | 14.49 |

| | |

| * Dow Jones Wilshire 4500 returns through 6/30/05, calculated as of 7/11/05. |

Your fund returned 2.11% in the last six months and 14.10% for the 12-month period ended June 30, 2005. The fund closely tracked the performance of the Dow Jones Wilshire 4500 Completion Index in both periods, as shown in the table, but lagged slightly due to annual operating and management expenses.The index includes more than 4,400 small- and mid-cap companies, so it is impractical for us to buy shares of each. Instead, we use sampling strategies (just as we do with the Total Equity Market Index Fund) in an attempt to match the performance of the index. At the end of June, the fund held nearly 2,500 names.

The energy sector (6.9% of equities as of June 30) contributed the most to fund performance in the last six months. Most of our holdings produced gains. Premcor and Murphy Oil led the oil and gas industry, while GlobalSantaFe and Diamond Offshore Drilling were our top contributors in the energy equipment and services industry. Utilities (3.1% of equities) also advanced in the last six months. Gas and electric utilities fared best; water utilities trailed, though Aqua America performed fairly well. (Please refer to the fund’s portfolio of investments for a complete listing of the fund’s holdings and the amount each represents in the portfolio.)

Health care stocks (12.3% of equities) performed very well. Providers and services companies paced the sector’s advance, especially Coventry Health Care, Triad Hospitals, and WellChoice. Biotechnology stocks were fairly lackluster, but Genentech and Celgene were exceptions. Health care equipment and supply companies and pharmaceutical shares were mostly flat.

Consumer discretionary shares (18.5% of equities) made a small contribution to our results in the first half of the year. Specialty retailers did best, led by Chico’s and Abercrombie & Fitch, but PETsMART and Petco were disappointing. In the household durables industry, homebuilders were some of our top contributors to performance, especially Toll Brothers and D.R. Horton, but audio equipment maker Harman International Industries performed poorly. Media stocks struggled, particularly Liberty Media and DIRECTV, though Cablevision Systems and Fox Entertainment Group were two of our largest contributors.

Information technology shares (14.5% of equities) detracted the most from our results in the last six months. Most underlying industries declined, with communications equipment, electronics equipment, and semiconductor stocks among the weakest segments. Internet software and services stocks did best, primarily because of stellar performance of Google, a provider of Web search and online advertising services.

Stocks in the materials sector (3.7% of equities), which produced good returns in 2004, faltered in the first half of 2005 amid concerns that a slowing economy would dent the earnings of these cyclical companies. Chemical companies fared worst. Metals and mining stocks also stumbled, with AK Steel and Steel Dynamics among our worst performers. Construction materials companies held up best, benefiting from the robust real estate market.

Financial stocks (24.9% of equities) generally declined in the last six months. Commercial banks paced the sector’s decline. Thrifts and mortgage finance companies also detracted from our performance. On the plus side, real estate investment trusts (REITs) outperformed, as the real estate market remained hot and investors found REIT yields appealing in an environment of relatively low interest rates. Companies tied to the capital markets also outperformed other financial industries, led by Legg Mason. Online brokerage firm AmeriTrade also performed well: E*Trade initially sought to acquire the company, but AmeriTrade chose instead to purchase TD Waterhouse from Toronto-Dominion Bank.

Industrial and business services stocks (9.2% of equities) also detracted from our performance. Electrical equipment companies faltered, and airline stocks were grounded by record oil prices. Air freight and logistics companies, as well as road and rail stocks, also struggled amid high fuel costs, and machinery stocks were disabled by fears of slower economic growth. Favorable performance of aerospace and defense names helped to limit the losses in the sector, with United Defense Industries among the fund’s largest contributors to performance.

OUTLOOK

The economy is likely to continue expanding this year, despite elevated oil prices, and short-term interest rates are likely to keep rising. Fundamentals in corporate America are generally sound, but unless corporate profit growth remains vigorous, stocks could have difficulty making progress until the Fed signals that rates are at or near a neutral level that neither stimulates nor stifles economic growth.

Although macroeconomic factors are a major influence on the stock market, we are not preoccupied with discerning how individual stocks, sectors, or the market as a whole will react to the latest economic data, interest rate trends, or corporate developments. Our goal is to closely track the broad equity market indexes with the assets you have entrusted to us. Thank you for your support in this endeavor.

Respectfully submitted,

E. Frederick Bair

Chairman of the Investment Advisory Committee,

Equity Index 500 Fund and Extended Equity Market Index Fund

Co-chairman of the Investment Advisory Committee,

Total Equity Market Index Fund

Ken D. Uematsu

Co-chairman of the Investment Advisory Committee,

Total Equity Market Index Fund

July 14, 2005

The committee chairmen have day-to-day responsibility for managing the portfolios and work with committee members in developing and executing the funds’ investment programs.

PROSPECTUS UPDATE

This updates the Total Equity Market Index Fund’s prospectus dated May 1, 2005. The Portfolio Management paragraph in Section 3 of the prospectus is amended to reflect the following change:

Effective May 2005, Ken D. Uematsu became co-chairman of the Total Equity Market Index Fund’s Investment Advisory Committee. Mr. Uematsu, who joined T. Rowe Price in 1997, is an assistant vice president of T. Rowe Price Associates, Inc., a quantitative analyst in the Systematic Equity Group, and a vice president and Investment Advisory Committee member for the Equity Index 500 and Extended Equity Market Index Funds.

RISKS OF INVESTING

As with all stock mutual funds, the fund’s share price can fall because of weakness in the stock market, a particular industry, or specific holdings. Stock markets can decline for many reasons, including adverse political or economic developments, changes in investor psychology, or heavy institutional selling. The prospects for an industry or company may deteriorate because of a variety of factors, including disappointing earnings or changes in the competitive environment.

GLOSSARY

Fed funds target rate: An overnight lending rate set by the Federal Reserve and used by banks to meet reserve requirements. Banks also use the fed funds rate as a benchmark for their prime lending rates.

S&P 500 Stock Index: Tracks the stocks of 500 mostly large U.S. companies.

Dow Jones Wilshire 5000 Composite Index: Tracks the performance of the most active stocks in the broad U.S. market.

Dow Jones Wilshire 4500 Completion Index: Tracks the performance of all stocks in the Dow Jones Wilshire 5000 Composite Index, excluding those in the S&P 500 Stock Index.

| THE EVOLVING S&P 500 STOCK INDEX |

| |

| Changes in the index in 2005 | |

| Additions | Deletions |

| Sears Holdings Corp. | Sears, Roebuck & Co. |

| National Oilwell Varco | Power-One |

| Molson Coors Brewing | Adolph Coors |

| PORTFOLIO HIGHLIGHTS |

| |

| TWENTY-FIVE LARGEST HOLDINGS | |

| | Percent of |

| | Net Assets |

| | 6/30/05 |

| Equity Index 500 Fund | |

| GE | 3.2 |

| ExxonMobil | 3.2 |

| Microsoft | 2.2 |

| Citigroup | 2.1 |

| Pfizer | 1.8 |

| Johnson & Johnson | 1.7 |

| Bank of America | 1.6 |

| Intel | 1.4 |

| Wal-Mart | 1.4 |

| American International Group | 1.3 |

| Altria Group | 1.2 |

| Procter & Gamble | 1.1 |

| J.P. Morgan Chase | 1.1 |

| Cisco Systems | 1.1 |

| IBM | 1.1 |

| Chevron | 1.0 |

| Wells Fargo | 0.9 |

| Dell | 0.8 |

| Verizon Communications | 0.8 |

| Coca-Cola | 0.8 |

| PepsiCo | 0.8 |

| Home Depot | 0.7 |

| ConocoPhillips | 0.7 |

| SBC Communications | 0.7 |

| Time Warner | 0.7 |

| Total | 33.4% |

| |

| Note: Table excludes investments in the T. Rowe Price Reserve Investment Fund. | |

| Total Equity Market Index Fund | |

| ExxonMobil | 2.4% |

| GE | 2.4 |

| Microsoft | 1.8 |

| Citigroup | 1.6 |

| Pfizer | 1.4 |

| Wal-Mart | 1.3 |

| Johnson & Johnson | 1.3 |

| Bank of America | 1.2 |

| Intel | 1.1 |

| American International Group | 1.0 |

| Procter & Gamble | 0.9 |

| Altria Group | 0.9 |

| Berkshire Hathaway | 0.8 |

| Cisco Systems | 0.8 |

| J.P. Morgan Chase | 0.8 |

| IBM | 0.8 |

| Chevron | 0.8 |

| Wells Fargo | 0.7 |

| Coca-Cola | 0.7 |

| Dell | 0.6 |

| Verizon Communications | 0.6 |

| PepsiCo | 0.6 |

| Home Depot | 0.6 |

| Genentech | 0.5 |

| Google | 0.5 |

| Total | 26.1% |

| |

| Note: Table excludes investments in the T. Rowe Price Reserve Investment Fund. | |

| Extended Equity Market Index Fund | |

| Berkshire Hathaway | 3.2% |

| Genentech | 2.1 |

| Google | 2.1 |

| Kraft Foods | 1.4 |

| Liberty Media | 0.7 |

| DIRECTV | 0.5 |

| IAC/InterActiveCorp | 0.4 |

| Genworth Financial | 0.4 |

| Juniper Networks | 0.3 |

| Amazon.com | 0.3 |

| Las Vegas Sands | 0.3 |

| Liberty Global | 0.3 |

| MGM Mirage | 0.3 |

| Legg Mason | 0.3 |

| Vornado Realty Trust | 0.3 |

| UnionBancal | 0.2 |

| Murphy Oil | 0.2 |

| Enterprise Products Partners | 0.2 |

| Chicago Mercantile Exchange Holdings | 0.2 |

| Cablevision Systems | 0.2 |

| Lennar | 0.2 |

| GlobalSantaFe | 0.2 |

| Royal Caribbean Cruises | 0.2 |

| General Growth Properties | 0.2 |

| MCI | 0.2 |

| Total | 14.9% |

| |

| Note: Table excludes investments in the T. Rowe Price Reserve Investment Fund. | |

This chart shows the value of a hypothetical $10,000 investment in the fund over the past 10 fiscal year periods or since inception (for funds lacking 10-year records). The result is compared with benchmarks, which may include a broad-based market index and a peer group average or index. Market indexes do not include expenses, which are deducted from fund returns as well as mutual fund averages and indexes.

| AVERAGE ANNUAL COMPOUND TOTAL RETURN |

This table shows how the fund and its benchmark would have performed if their actual (or cumulative) returns for the periods shown had been earned at a constant rate.

| Periods Ended 6/30/05 | 1 Year | 5 Years | 10 Years |

| |

| Equity Index 500 Fund | 6.02% | -2.64% | 9.64% |

| |

| S&P 500 Stock Index | 6.32 | -2.37 | 9.94 |

| |

| Current performance may be higher or lower than the quoted past performance, which can- |

| not guarantee future results. Share price, principal value, and return will vary, and you may |

| have a gain or loss when you sell your shares. For the most recent month-end performance |

| information, please visit our Web site (troweprice.com) or contact a T. Rowe Price repre- |

| sentative at 1-800-225-5132. The fund charges a redemption fee of 0.5% on shares held |

| for three months or less. The performance information shown does not reflect the deduc- |

| tion of the redemption fee. If it did, the performance would be lower. | |

| | | |

| Average annual total return figures include changes in principal value, reinvested dividends, and capital |

| gain distributions. Returns do not reflect taxes that the shareholder may pay on fund distributions or the |

| redemption of fund shares. When assessing performance, investors should consider both short- and |

| long-term returns. | | | |

This chart shows the value of a hypothetical $10,000 investment in the fund over the past 10 fiscal year periods or since inception (for funds lacking 10-year records). The result is compared with benchmarks, which may include a broad-based market index and a peer group average or index. Market indexes do not include expenses, which are deducted from fund returns as well as mutual fund averages and indexes.

| AVERAGE ANNUAL COMPOUND TOTAL RETURN |

This table shows how the fund and its benchmark would have performed if their actual (or cumulative) returns for the periods shown had been earned at a constant rate.

| | | | Since |

| | | | Inception |

| Periods Ended 6/30/05 | 1 Year | 5 Years | 1/30/98 |

| Total Equity Market Index Fund | 8.11% | -1.47% | 4.65% |

| Dow Jones Wilshire 5000 Composite Index | 8.39 | -1.25 | 4.77 |

Dow Jones Wilshire 5000 returns through 6/30/05, calculated as of 7/11/05. | | |

| | | |

| Current performance may be higher or lower than the quoted past performance, which can- |

| not guarantee future results. Share price, principal value, and return will vary, and you may |

| have a gain or loss when you sell your shares. For the most recent month-end performance |

| information, please visit our Web site (troweprice.com) or contact a T. Rowe Price represen- |

| tative at 1-800-225-5132. The fund charges a redemption fee of 0.5% on shares held for |

| three months or less. The performance information shown does not reflect the deduction |

| of the redemption fee. If it did, the performance would be lower. | | |

| | | |

| Average annual total return figures include changes in principal value, reinvested dividends, and capital |

| gain distributions. Returns do not reflect taxes that the shareholder may pay on fund distributions or the |

| redemption of fund shares. When assessing performance, investors should consider both short- and long- |

| term returns. | | | |

This chart shows the value of a hypothetical $10,000 investment in the fund over the past 10 fiscal year periods or since inception (for funds lacking 10-year records). The result is compared with benchmarks, which may include a broad-based market index and a peer group average or index. Market indexes do not include expenses, which are deducted from fund returns as well as mutual fund averages and indexes.

| AVERAGE ANNUAL COMPOUND TOTAL RETURN |

This table shows how the fund and its benchmark would have performed if their actual (or cumulative) returns for the periods shown had been earned at a constant rate.

| | | | Since |

| | | | Inception |

| Periods Ended 6/30/05 | 1 Year | 5 Years | 1/30/98 |

| Extended Equity Market Index Fund | 14.10% | 1.52% | 6.74% |

| Dow Jones Wilshire 4500 Completion Index | 14.49 | 1.75 | 6.85 |

Dow Jones Wilshire 4500 returns through 6/30/05, calculated as of 7/11/05. | | |

Current performance may be higher or lower than the quoted past performance, which can- |

| not guarantee future results. Share price, principal value, and return will vary, and you may |

| have a gain or loss when you sell your shares. For the most recent month-end performance |

| information, please visit our Web site (troweprice.com) or contact a T. Rowe Price represen- |

| tative at 1-800-225-5132. The fund charges a redemption fee of 0.5% on shares held for |

| three months or less. The performance information shown does not reflect the deduc- |

| tion of the redemption fee. If it did, the performance would be lower. | |

Average annual total return figures include changes in principal value, reinvested dividends, and capital |

| gain distributions. Returns do not reflect taxes that the shareholder may pay on fund distributions or the |

| redemption of fund shares. When assessing performance, investors should consider both short- and long- |

| term returns. | | | |

As a mutual fund shareholder, you may incur two types of costs: (1) transaction costs such as redemption fees or sales loads and (2) ongoing costs, including management fees, distribution and service (12b-1) fees, and other fund expenses. The following example is intended to help you understand your ongoing costs (in dollars) of investing in the fund and to compare these costs with the ongoing costs of investing in other mutual funds. The example is based on an investment of $1,000 invested at the beginning of the most recent six-month period and held for the entire period.Actual Expenses

The first line of the following table (“Actual”) provides information about actual account values and actual expenses. You may use the information in this line, together with your account balance, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The information on the second line of the table (“Hypothetical”) is based on hypothetical account values and expenses derived from the fund’s actual expense ratio and an assumed 5% per year rate of return before expenses (not the fund’s actual return). You may compare the ongoing costs of investing in the fund with other funds by contrasting this 5% hypothetical example and the 5% hypothetical examples that appear in the shareholder reports of the other funds. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period.

Note: T. Rowe Price charges an account maintenance fee that is not included in the accompanying table. The account maintenance fee is charged on a quarterly basis, usually during the last week of a calendar quarter, and applies to accounts with balances below $10,000 on the day of the assessment. The fee is charged to accounts that fall below $10,000 for any reason, including market fluctuations, redemptions, or exchanges. When an account with less than $10,000 is closed either through redemption or exchange, the fee is charged and deducted from the proceeds. The fee applies to IRA accounts but not to retirement plans directly registered with T. Rowe Price Services or accounts maintained by intermediaries through NSCC® Networking. If you are subject to the fee, keep it in mind when you are estimating the ongoing expenses of investing in the fund and when comparing the expenses of this fund with other funds.

You should also be aware that the expenses shown in the table highlight only your ongoing costs and do not reflect any transaction costs, such as redemption fees or sales loads. Therefore, the second line of the table is useful in comparing ongoing costs only and will not help you determine the relative total costs of owning different funds. To the extent a fund charges transaction costs, however, the total cost of owning that fund is higher.

| T. ROWE PRICE EQUITY INDEX 500 FUND |

| |

| | Beginning | Ending | Expenses Paid |

| | Account Value | Account Value | During Period* |

| | 1/1/05 | 6/30/05 | 1/1/05 to 6/30/05 |

| Actual | $1,000.00 | $990.50 | $1.73 |

| Hypothetical (assumes 5% | | | |

| return before expenses) | 1,000.00 | 1,023.06 | 1.76 |

| * Expenses are equal to the fund’s annualized expense ratio for the six-month period (0.35%), multiplied |

| by the average account value over the period, multiplied by the number of days in the most recent fiscal |

| half year (181) divided by the days in the year (365) to reflect the half-year period. |

| |

| |

| T. ROWE PRICE TOTAL EQUITY MARKET INDEX FUND |

| |

| | Beginning | Ending | Expenses Paid |

| | Account Value | Account Value | During Period* |

| | 1/1/05 | 6/30/05 | 1/1/05 to 6/30/05 |

| Actual | $1,000.00 | $999.20 | $1.98 |

| Hypothetical (assumes 5% | | | |

| return before expenses) | 1,000.00 | 1,022.81 | 2.01 |

| * Expenses are equal to the fund’s annualized expense ratio for the six-month period (0.40%), multiplied |

| by the average account value over the period, multiplied by the number of days in the most recent fiscal |

| half year (181) divided by the days in the year (365) to reflect the half-year period. |

| |

| |

| T. ROWE PRICE EXTENDED EQUITY MARKET INDEX FUND |

| |

| | Beginning | Ending | Expenses Paid |

| | Account Value | Account Value | During Period* |

| | 1/1/05 | 6/30/05 | 1/1/05 to 6/30/05 |

| Actual | $1,000.00 | $1,021.10 | $2.00 |

| Hypothetical (assumes 5% | | | |

| return before expenses) | 1,000.00 | 1,022.81 | 2.01 |

| * Expenses are equal to the fund’s annualized expense ratio for the six-month period (0.40%), multiplied |

| by the average account value over the period, multiplied by the number of days in the most recent fiscal |

| half year (181) divided by the days in the year (365) to reflect the half year-period. |

Unaudited

| FINANCIAL HIGHLIGHTS | For a share outstanding throughout each period |

| | | 6 Months | | Year | | | | | | | | |

| | | Ended | | Ended | | | | | | | | |

| | | 6/30/05** | | 12/31/04 | | 12/31/03 | | 12/31/02 | | 12/31/01 | | 12/31/00 |

| NET ASSET VALUE | | | | | | | | | | | | |

| Beginning of period | $ | 12.80 | $ | 11.55 | $ | 8.91 | $ | 11.44 | $ | 13.02 | $ | 14.77 |

|

|

| |

| Investment activities | | | | | | | | | | | | |

| Net investment | | | | | | | | | | | | |

| income (loss) | | 0.08 | | 0.17 | | 0.12 | | 0.11 | | 0.11 | | 0.12 |

| Net realized and | | | | | | | | | | | | |

| unrealized gain (loss) | | (0.09) | | 1.24 | | 2.64 | | (2.53) | | (1.57) | | (1.64) |

|

|

| Total from | | | | | | | | | | | | |

| investment activities | | (0.01) | | 1.41 | | 2.76 | | (2.42) | | (1.46) | | (1.52) |

|

|

| |

| Distributions | | | | | | | | | | | | |

| Net investment income | | – | | (0.16) | | (0.12) | | (0.11) | | (0.11) | | (0.11) |

| Net realized gain | | – | | – | | – | | – | | (0.01) | | (0.12) |

|

|

| Total distributions | | – | | (0.16) | | (0.12) | | (0.11) | | (0.12) | | (0.23) |

|

|

| |

| NET ASSET VALUE | | | | | | | | | | | | |

| End of period | $ | 12.79 | $ | 12.80 | $ | 11.55 | $ | 8.91 | $ | 11.44 | $ | 13.02 |

|

|

| |

| |

| Ratios/Supplemental Data | | | | | | | | | | |

| Total return^ | | (0.08)% | | 12.22% | | 31.02% | | (21.16)% | | (11.20)% | | (10.33)% |

| Ratio of total expenses to | | | | | | | | | | | | |

| average net assets | | 0.40%† | | 0.40% | | 0.40% | | 0.40% | | 0.40% | | 0.40% |

| Ratio of net investment | | | | | | | | | | | | |

| income (loss) to average | | | | | | | | | | | | |

| net assets | | 0.63%† | | 1.44%+ | | 1.28% | | 1.13% | | 0.98% | | 0.85% |

| Portfolio turnover rate | | 4.3%† | | 5.2% | | 2.3% | | 5.6% | | 8.6% | | 7.6% |

| Net assets, end of period | | | | | | | | | | | | |

| (in thousands) | $ | 357,858 | $ | 356,015 | $ | 293,967 | $ | 167,680 | $ | 197,775 | $ | 206,058 |

| ^ | Total return reflects the rate that an investor would have earned on an investment in the fund during each period, |

| | assuming reinvestment of all distributions and payment of no redemption or account fees. |

| † | Annualized |

| ** Per share amounts calculated using average shares outstanding method. |

| + | Includes the effect of a one-time special dividend (0.24% of average net assets) that is not expected to recur. |

The accompanying notes are an integral part of these financial statements.

Unaudited

| PORTFOLIO OF INVESTMENTS (1) | Shares/$ Par | Value |

| (Cost and value in $ 000s) | | |

| COMMON STOCKS 97.5% | | |

| |

| CONSUMER DISCRETIONARY 13.1% | | |

| Auto Components 0.3% | | |

| American Axle & Manufacturing Holdings § | 2,300 | 58 |

| Arvinmeritor | 1,700 | 30 |

| Bandag § | 800 | 37 |

| Borg-Warner | 1,500 | 81 |

| Cooper Tire § | 2,500 | 46 |

| Dana | 3,400 | 51 |

| Delphi | 13,514 | 63 |

| Gentex § | 3,600 | 66 |

| Goodyear Tire & Rubber *§ | 5,100 | 76 |

| Johnson Controls | 4,500 | 254 |

| Lear | 1,600 | 58 |

| Modine Manufacturing | 1,500 | 49 |

| Standard Motor Products § | 2,000 | 26 |

| TRW * | 2,300 | 56 |

| Visteon § | 8,286 | 50 |

| | | 1,001 |

| Automobiles 0.4% | | |

| Fleetwood *§ | 3,800 | 38 |

| Ford Motor § | 42,561 | 436 |

| GM § | 13,052 | 444 |

| Harley-Davidson | 7,000 | 347 |

| Thor Industries | 1,800 | 57 |

| Winnebago § | 1,800 | 59 |

| | | 1,381 |

| Distributors 0.1% | | |

| Genuine Parts | 4,300 | 177 |

| Handleman | 2,500 | 41 |

| | | 218 |

| Diversified Consumer Services 0.4% | | |

| Apollo Group, Class A * | 4,025 | 315 |

| Bright Horizons Family Solutions *§ | 1,600 | 65 |

| Career Education * | 2,400 | 88 |

| Corinthian Colleges *§ | 2,000 | 25 |

| Devry * | 1,700 | 34 |

| Education Management * | 1,900 | 64 |

| H&R Block | 4,300 | 251 |

| ITT Educational Services * | 1,400 | 75 |

| Laureate * | 1,168 | 56 |

| Matthews International, Class A | 1,300 | 51 |

| Regis | 1,200 | 47 |

| Service Corp. International | 8,800 | 70 |

| ServiceMaster | 6,700 | 90 |

| Sotheby's, Class A * | 2,500 | 34 |

| Stewart Enterprises, Class A | 7,000 | 46 |

| Strayer Education | 300 | 26 |

| Weight Watchers *§ | 2,500 | 129 |

| | | 1,466 |

| Hotels, Restaurants & Leisure 2.0% | | |

| Applebee's | 2,037 | 54 |

| Bob Evans Farms | 1,700 | 40 |

| Brinker * | 2,050 | 82 |

| Carnival | 15,100 | 824 |

| CEC Entertainment * | 1,300 | 55 |

| Cedar Fair § | 1,300 | 42 |

| Choice Hotels International | 1,700 | 112 |

| Cracker Barrel § | 1,100 | 43 |

| Darden Restaurants | 4,300 | 142 |

| Gaylord Entertainment *§ | 1,500 | 70 |

| Great Wolf Resorts *§ | 1,700 | 35 |

| GTECH | 3,500 | 102 |

| Harrah's Entertainment | 4,590 | 331 |

| Hilton | 8,372 | 200 |

| International Game Technology | 8,300 | 234 |

| International Speedway, Class A | 1,200 | 67 |

| Jack In The Box * | 1,700 | 64 |

| John Q Hammons Hotels * | 3,500 | 82 |

| Krispy Kreme *§ | 3,000 | 21 |

| Landry's Seafood Restaurant § | 1,100 | 33 |

| Las Vegas Sands *§ | 8,800 | 315 |

| Lone Star Steakhouse & Saloon | 1,700 | 52 |

| Marriott, Class A | 5,500 | 375 |

| McDonald's | 29,300 | 813 |

| MGM Mirage * | 7,600 | 301 |

| MTR Gaming Group * | 1,900 | 22 |

| Multimedia Games *§ | 3,300 | 36 |

| Outback Steakhouse | 1,600 | 72 |

| Panera Bread, Class A *§ | 1,200 | 74 |

| Papa John's International *§ | 1,000 | 40 |

| Penn National Gaming * | 900 | 33 |

| PF Chang's China Bistro *§ | 1,100 | 65 |

| Rare Hospitality International * | 1,400 | 43 |

| Royal Caribbean Cruises § | 4,500 | 218 |

| Ruby Tuesday § | 1,400 | 36 |

| Ryan's Restaurant Group * | 2,000 | 28 |

| Six Flags *§ | 5,100 | 24 |

| Sonic *§ | 1,400 | 43 |

| Speedway Motorsports | 1,200 | 44 |

| Starbucks * | 9,400 | 486 |

| Starwood Hotels & Resorts Worldwide, Equity Units | 5,200 | 304 |

| Station Casinos | 2,100 | 139 |

| The Cheesecake Factory *§ | 2,100 | 73 |

| Triarc, Class B § | 3,000 | 45 |

| Vail Resorts * | 1,800 | 50 |

| Wendy's | 2,900 | 138 |

| WMS Industries *§ | 900 | 30 |

| Wynn Resorts * | 2,800 | 132 |

| Yum! Brands | 7,400 | 385 |

| | | 7,049 |

| Household Durables 1.1% | | |

| American Greetings, Class A | 1,500 | 40 |

| Black & Decker | 1,900 | 171 |

| Blyth Industries | 1,500 | 42 |

| Brillian Corp *§ | 750 | 2 |

| Cavco Industries * | 1,540 | 43 |

| Centex | 3,300 | 233 |

| Champion Enterprises * | 4,500 | 45 |

| D. R. Horton | 8,360 | 314 |

| Ethan Allen Interiors § | 1,400 | 47 |

| Fortune Brands | 3,300 | 293 |

| Furniture Brands International § | 2,900 | 63 |

| Harman International | 1,700 | 138 |

| Helen of Troy Limited *§ | 1,300 | 33 |

| Hovnanian Enterprises *§ | 1,700 | 111 |

| KB Home | 2,500 | 191 |

| Kimball International, Class B § | 2,400 | 32 |

| Knape & Vogt Manufacturing | 1,600 | 19 |

| La-Z-Boy § | 2,600 | 38 |

| Leggett & Platt | 4,400 | 117 |

| Lennar, Class A | 3,900 | 247 |

| Levitt, Class A § | 1,475 | 44 |

| Maytag § | 2,700 | 42 |

| MDC Holdings | 945 | 78 |

| Meritage * | 800 | 64 |

| Mohawk Industries * | 1,531 | 126 |

| Newell Rubbermaid § | 6,976 | 166 |

| NVR * | 180 | 146 |

| Pulte | 3,400 | 286 |

| Rockford Corporation *§ | 2,100 | 8 |

| Russ Berrie § | 1,900 | 24 |

| Ryland Group | 1,100 | 83 |

| Skyline | 600 | 24 |

| Snap-On | 1,400 | 48 |

| Standard Pacific | 1,000 | 88 |

| Stanley Furniture § | 1,200 | 30 |

| Stanley Works | 1,900 | 87 |

| Toll Brothers * | 1,900 | 193 |

| Tupperware § | 3,100 | 72 |

| Whirlpool | 1,500 | 105 |

| | | 3,933 |

| Internet & Catalog Retail 0.4% | | |

| Amazon.com *§ | 9,300 | 308 |

| Blue Nile *§ | 1,400 | 46 |

| eBay * | 30,600 | 1,010 |

| Insight Enterprises *§ | 1,350 | 27 |

| J. Jill Group *§ | 1,100 | 15 |

| Netflix *§ | 1,400 | 23 |

| priceline.com *§ | 1,450 | 34 |

| ValueVision International *§ | 3,200 | 38 |

| | | 1,501 |

| Leisure Equipment & Products 0.3% | | |

| Action Performance Cos § | 1,900 | 17 |

| Arctic Cat § | 1,000 | 21 |

| Brunswick | 2,000 | 87 |

| Callaway Golf § | 1,900 | 29 |

| Eastman Kodak | 7,500 | 201 |

| Hasbro | 4,000 | 83 |

| K2 * | 2,834 | 36 |

| MarineMax *§ | 900 | 28 |

| Marvel Enterprises *§ | 3,300 | 65 |

| Mattel | 10,700 | 196 |

| Nautilus Group § | 1,475 | 42 |

| Oakley § | 2,900 | 49 |

| Polaris Industries § | 1,100 | 60 |

| SCP Pool | 2,305 | 81 |

| The Boyds Collection *§ | 4,000 | 7 |

| | | 1,002 |

| Media 3.9% | | |

| 4Kids Entertainment *§ | 800 | 16 |

| ADVO | 1,450 | 46 |

| Arbitron | 680 | 29 |

| Belo Corporation, Class A | 1,900 | 46 |

| Cablevision Systems, Class A *§ | 5,700 | 184 |

| Catalina Marketing | 1,200 | 31 |

| Charter Communications, Class A *§ | 7,700 | 9 |

| Citadel Broadcasting * | 3,100 | 36 |

| Clear Channel Communications | 13,401 | 415 |

| Comcast, Class A * | 52,494 | 1,612 |

| Cox Radio, Class A * | 900 | 14 |

| Cumulus Media, Class A * | 1,406 | 17 |

| Directv * | 31,750 | 492 |

| Disney | 47,700 | 1,201 |

| Dow Jones | 1,700 | 60 |

| Dreamworks Animation, Class A * | 3,000 | 79 |

| EchoStar Communications, Class A | 5,100 | 154 |

| Emmis Communications *§ | 1,200 | 21 |

| Entercom Communications * | 1,200 | 40 |

| Entravision Communications, Class A *§ | 4,000 | 31 |

| Gannett | 5,900 | 420 |

| Gemstar TV Guide * | 10,100 | 36 |

| Getty Images *§ | 1,600 | 119 |

| Gray Communications Systems | 1,900 | 23 |

| Harte-Hanks | 1,900 | 56 |

| Hearst-Argyle Television § | 1,700 | 42 |

| Hollinger International § | 3,900 | 39 |

| Insight Communications *§ | 3,400 | 38 |

| Interactive Data | 2,900 | 60 |

| Interpublic Group * | 9,912 | 121 |

| John Wiley & Sons | 1,900 | 76 |

| Journal Register * | 1,600 | 28 |

| Knight-Ridder | 1,700 | 104 |

| Lamar Advertising * | 1,900 | 81 |

| Lee Enterprises | 1,100 | 44 |

| Liberty | 500 | 18 |

| Liberty Global * | 3,280 | 153 |

| Liberty Media, Class A * | 68,000 | 693 |

| McClatchy | 1,200 | 79 |

| McGraw-Hill | 9,200 | 407 |

| Media General, Class A | 700 | 45 |

| Mediacom Communications *§ | 5,000 | 34 |

| Meredith | 1,200 | 59 |

| New York Times, Class A § | 3,400 | 106 |

| News Corp., Class A | 55,584 | 899 |

| News Corp., Class B § | 33,100 | 558 |

| Omnicom | 4,200 | 335 |

| Paxson Communications * | 9,300 | 6 |

| Pixar * | 2,200 | 110 |

| Primedia *§ | 13,700 | 55 |

| ProQuest *§ | 1,000 | 33 |

| R.H. Donnelley * | 940 | 58 |

| Radio One *§ | 3,400 | 43 |

| Reader's Digest | 3,800 | 63 |

| Regal Entertainment Group, Class A § | 3,700 | 70 |

| Regent Communications *§ | 6,500 | 38 |

| Scholastic * | 1,100 | 42 |

| Scripps, Class A | 3,800 | 185 |

| Sirius Satellite Radio *§ | 32,900 | 213 |

| Spanish Broadcasting, Class A * | 4,100 | 41 |

| Time Warner * | 103,320 | 1,726 |

| TiVo *§ | 2,800 | 19 |

| Tribune | 7,422 | 261 |

| Univision Communications, Class A * | 7,640 | 210 |

| Valassis Communications * | 1,200 | 44 |

| Viacom, Class B | 40,258 | 1,289 |

| Washington Post, Class B | 220 | 184 |

| Westwood One | 2,200 | 45 |

| WPP Group ADR | 681 | 35 |

| XM Satellite Radio Holdings, Class A *§ | 4,800 | 162 |

| | | 14,138 |

| Multiline Retail 1.1% | | |

| 99 Cents Only Stores *§ | 1,600 | 20 |

| Big Lots * | 3,700 | 49 |

| Dillards, Class A § | 2,700 | 63 |

| Dollar General § | 7,450 | 152 |

| Dollar Tree Stores * | 2,500 | 60 |

| Family Dollar Stores | 4,200 | 110 |

| Federated Department Stores | 4,000 | 293 |

| J.C. Penney | 6,200 | 326 |

| Kohl's * | 7,900 | 442 |

| May Department Stores | 6,350 | 255 |

| Neiman Marcus, Class A | 1,200 | 116 |

| Nordstrom | 3,200 | 218 |

| Saks * | 4,175 | 79 |

| Sears Holding * | 3,531 | 529 |

| Shopko Stores * | 700 | 17 |

| Target | 21,400 | 1,164 |

| Tuesday Morning § | 2,000 | 63 |

| | | 3,956 |

| Specialty Retail 2.6% | | |

| Abercrombie & Fitch | 2,016 | 139 |

| Advance Auto Parts * | 1,600 | 103 |

| American Eagle Outfitters | 3,300 | 101 |

| Autonation * | 6,300 | 129 |

| AutoZone * | 2,100 | 194 |

| Barnes & Noble * | 1,600 | 62 |

| bebe stores § | 4,087 | 108 |

| Bed Bath & Beyond * | 7,000 | 293 |

| Best Buy | 7,700 | 528 |

| Blockbuster, Class A § | 6,600 | 60 |

| Borders Group | 1,900 | 48 |

| Burlington Coat Factory | 1,100 | 47 |

| CarMax * | 2,429 | 65 |

| Charming Shoppes * | 4,000 | 37 |

| Chico's * | 5,300 | 182 |

| Christopher & Banks § | 1,700 | 31 |

| Circuit City | 4,800 | 83 |

| Claire's Stores | 2,600 | 63 |

| Cost Plus *§ | 900 | 22 |

| Deb Shops § | 600 | 17 |

| Electronics Boutique Holdings *§ | 700 | 44 |

| Foot Locker | 3,600 | 98 |

| Franklin Covey * | 1,800 | 14 |

| GameStop, Class B * | 934 | 28 |

| GAP | 21,050 | 416 |

| Genesco *§ | 900 | 33 |

| Group One Automotive * | 1,600 | 39 |

| Guitar Center * | 800 | 47 |

| Gymboree * | 600 | 8 |

| Harvey Electronics, * | 10,500 | 12 |

| Hibbett Sporting Goods * | 1,575 | 60 |

| Home Depot | 52,450 | 2,040 |

| Hot Topic *§ | 1,050 | 20 |

| Linens 'n Things * | 1,000 | 24 |

| Lowes | 18,600 | 1,083 |

| Men's Wearhouse * | 1,500 | 52 |

| Michaels Stores | 3,000 | 124 |

| Movie Gallery § | 1,800 | 48 |

| O'Reilly Automotive * | 3,100 | 92 |

| Office Depot * | 8,400 | 192 |

| OfficeMax § | 2,022 | 60 |

| Pacific Sunwear * | 2,325 | 53 |

| Pantry * | 1,400 | 54 |

| Payless Shoesource * | 2,806 | 54 |

| Pep Boys § | 1,700 | 23 |

| Petco * | 1,300 | 38 |

| PETsMART | 3,700 | 112 |

| Pier 1 Imports § | 2,000 | 28 |

| RadioShack | 3,700 | 86 |

| Rent-A-Center * | 1,700 | 40 |

| Ross Stores | 3,400 | 98 |

| Select Comfort *§ | 900 | 19 |

| Sherwin-Williams | 3,700 | 174 |

| Shoe Pavilion * | 2,100 | 10 |

| Staples | 17,775 | 379 |

| Talbots | 1,300 | 42 |

| The Children's Place *§ | 800 | 37 |

| The Limited | 10,755 | 230 |

| The Sports Authority *§ | 1,392 | 44 |

| Tiffany | 3,300 | 108 |

| TJX | 11,600 | 283 |

| Too * | 1,657 | 39 |

| Toys "R" Us * | 5,600 | 148 |

| Tweeter Home Entertainment Group *§ | 3,600 | 9 |

| Ultimate Electronics * | 1,000 | 0 |

| United Retail Group *§ | 3,500 | 27 |

| Urban Outfitters * | 2,300 | 130 |

| West Marine *§ | 1,300 | 24 |

| Williams-Sonoma * | 2,700 | 107 |

| Zale * | 1,600 | 51 |

| | | 9,293 |

| Textiles, Apparel, & Luxury Goods 0.5% | | |

| Coach * | 9,800 | 329 |

| Columbia Sportswear *§ | 1,000 | 50 |

| Culp *§ | 600 | 3 |

| Deckers Outdoor *§ | 1,300 | 32 |

| Forward Industries *§ | 1,200 | 19 |

| Fossil * | 1,600 | 36 |

| Jones Apparel Group | 3,100 | 96 |

| K-Swiss, Class A | 2,000 | 65 |

| Kellwood § | 800 | 22 |

| Liz Claiborne | 2,600 | 103 |

| Movado Group | 2,000 | 38 |

| Nike, Class B | 6,400 | 554 |

| Polo Ralph Lauren | 2,300 | 99 |

| Quiksilver * | 3,700 | 59 |

| Reebok | 1,800 | 75 |

| Rocky Shoes & Boots *§ | 1,100 | 34 |

| Russell | 1,600 | 33 |

| Superior Uniform Group § | 200 | 3 |

| Tarrant Apparel *§ | 3,100 | 9 |

| Timberland, Class A * | 2,100 | 81 |

| Unifi * | 7,500 | 32 |

| V. F. | 3,200 | 183 |

| | | 1,955 |

| Total Consumer Discretionary | | 46,893 |

| CONSUMER STAPLES 8.9% | | |

| Beverages 1.8% | | |

| Anheuser-Busch | 19,100 | 874 |

| Brown-Forman, Class B | 2,800 | 169 |

| Coca-Cola | 56,700 | 2,367 |

| Coca-Cola Enterprises | 10,900 | 240 |

| Constellation Brands, Class A * | 5,400 | 159 |

| Cruzan International *§ | 980 | 25 |

| Molson Coors Brewing, Class B § | 1,900 | 118 |

| Pepsi Bottling Group | 5,900 | 169 |

| PepsiAmericas | 4,500 | 116 |

| PepsiCo | 39,670 | 2,139 |

| | | 6,376 |

| Food & Staples Retailing 2.5% | | |

| Albertsons § | 8,590 | 178 |

| BJ's Wholesale Club * | 2,000 | 65 |

| Costco Wholesale | 10,600 | 475 |

| CVS | 18,800 | 547 |

| Great Atlantic & Pacific Tea *§ | 1,200 | 35 |

| Kroger * | 17,000 | 323 |

| Longs Drug Stores § | 1,200 | 52 |

| Marsh Supermarkets § | 1,600 | 23 |

| Performance Food Group * | 2,100 | 63 |

| Rite Aid *§ | 14,500 | 61 |

| Ruddick | 1,700 | 43 |

| Safeway § | 9,600 | 217 |

| Supervalu | 2,700 | 88 |

| Sysco | 14,500 | 525 |

| Topps § | 4,300 | 43 |

| United Natural Foods * | 2,200 | 67 |

| Wal-Mart | 99,800 | 4,810 |

| Walgreen | 24,100 | 1,108 |

| Weis Markets § | 1,500 | 58 |

| Whole Foods Market | 1,600 | 189 |

| | | 8,970 |

| Food Products 1.6% | | |

| Alico § | 1,000 | 51 |

| American Italian Pasta, Class A § | 1,500 | 32 |

| Archer-Daniels-Midland | 15,672 | 335 |

| Bunge Limited § | 2,900 | 184 |

| Campbell Soup | 10,500 | 323 |

| ConAgra | 12,308 | 285 |

| Corn Products International | 2,000 | 48 |

| Dean Foods * | 3,379 | 119 |

| Del Monte Foods * | 4,911 | 53 |

| Delta Pine & Land | 1,400 | 35 |

| Flowers Foods | 1,785 | 63 |

| Fresh Del Monte Produce § | 2,100 | 57 |

| Galaxy Nutritional Foods * | 1,800 | 4 |

| General Mills | 8,800 | 412 |

| Hain Celestial Group * | 2,100 | 41 |

| Heinz | 8,200 | 290 |

| Hershey Foods | 6,400 | 397 |

| Hormel Foods | 3,900 | 114 |

| J.M. Smucker § | 1,316 | 62 |

| Kellogg | 9,500 | 422 |

| Kraft Foods, Class A | 39,700 | 1,263 |

| Lancaster Colony | 1,200 | 52 |

| Lance | 2,000 | 34 |

| McCormick | 3,400 | 111 |

| Pilgrim's Pride § | 1,700 | 58 |

| Sara Lee | 18,900 | 374 |

| Smithfield Foods * | 2,400 | 66 |

| Tasty Baking § | 1,000 | 8 |

| Tootsie Roll Industries § | 1,745 | 51 |

| Treehouse Foods * | 675 | 19 |

| Tyson Foods, Class A | 8,154 | 145 |

| Wrigley | 5,300 | 365 |

| | | 5,873 |

| Household Products 1.4% | | |

| Clorox | 5,200 | 290 |

| Colgate-Palmolive | 12,300 | 614 |

| Energizer * | 1,700 | 106 |

| Kimberly-Clark | 11,900 | 745 |

| Procter & Gamble | 59,700 | 3,149 |

| | | 4,904 |

| Personal Products 0.6% | | |

| Alberto Culver, Class B | 2,300 | 100 |

| Avon | 11,300 | 428 |

| Chattem *§ | 1,000 | 41 |

| Elizabeth Arden *§ | 1,600 | 37 |

| Estee Lauder, Class A | 2,800 | 110 |

| Gillette | 23,500 | 1,190 |

| NBTY * | 1,600 | 41 |

| Playtex Products *§ | 5,400 | 58 |

| | | 2,005 |

| Tobacco 1.0% | | |

| Alliance One International | 6,800 | 41 |

| Altria Group | 47,600 | 3,078 |

| Reynolds American § | 3,433 | 270 |

| Universal Corporation | 500 | 22 |

| UST | 4,100 | 187 |

| Vector Group § | 3,281 | 61 |

| | | 3,659 |

| Total Consumer Staples | | 31,787 |

| |

| ENERGY 8.1% | | |

| Energy Equipment & Services 1.5% | | |

| Atwood Oceanics * | 700 | 43 |

| Baker Hughes | 7,400 | 379 |

| BJ Services | 4,300 | 226 |

| Carbo Ceramics | 800 | 63 |

| Cooper Cameron * | 1,600 | 99 |

| Diamond Offshore Drilling § | 3,200 | 171 |

| ENSCO International | 3,700 | 132 |

| FMC Technologies * | 1,487 | 47 |

| Global Industries * | 2,300 | 20 |

| GlobalSantaFe | 5,496 | 224 |

| Grant Prideco * | 3,100 | 82 |

| Halliburton | 10,300 | 492 |

| Hanover Compressor * | 1,900 | 22 |

| Helmerich & Payne | 1,600 | 75 |

| Input/Output *§ | 6,200 | 39 |

| Nabors Industries * | 3,130 | 190 |

| National Oilwell Varco * | 3,984 | 189 |

| Newpark Resources *§ | 4,300 | 32 |

| Noble Drilling | 3,200 | 197 |

| Oceaneering International * | 1,200 | 46 |

| Offshore Logistics * | 1,200 | 39 |

| Parker Drilling * | 6,800 | 48 |

| Patterson-UTI Energy | 4,800 | 134 |

| Pride International * | 3,300 | 85 |

| Rowan | 3,100 | 92 |

| Schlumberger | 13,772 | 1,046 |

| Smith International | 2,500 | 159 |

| Superior Energy * | 2,900 | 52 |

| TETRA Technologies * | 650 | 21 |

| Tidewater | 1,300 | 50 |

| Todco, Class A * | 2,400 | 62 |

| Transocean * | 7,625 | 411 |

| Unit * | 1,700 | 75 |

| Universal Compression Holdings * | 1,400 | 51 |

| Veritas DGC * | 1,700 | 47 |

| W-H Energy Services * | 1,800 | 45 |

| Weatherford International * | 3,000 | 174 |

| | | 5,359 |

| Oil, Gas & Consumable Fuels 6.6% | | |

| Alliance Resource Partners *§ | 600 | 44 |

| Amerada Hess | 2,100 | 224 |

| Anadarko Petroleum | 5,629 | 462 |

| Apache | 8,086 | 522 |

| Arch Coal § | 1,446 | 79 |

| Ashland | 1,500 | 108 |

| Bill Barrett *§ | 1,600 | 47 |

| BP Prudhoe Bay Royalty Trust | 1,500 | 107 |

| Buckeye Partners, Equity Units *§ | 1,200 | 55 |

| Burlington Resources | 9,600 | 530 |

| Cabot Oil & Gas | 1,950 | 68 |

| Callon Petroleum *§ | 1,400 | 21 |

| Chesapeake Energy | 6,308 | 144 |

| Chevron | 50,028 | 2,798 |

| Cimarex Energy *§ | 3,244 | 126 |

| ConocoPhillips | 32,668 | 1,878 |

| CONSOL Energy | 3,000 | 161 |

| Cross Timbers Royalty Trust § | 928 | 38 |

| Denbury Resources * | 1,800 | 72 |

| Devon Energy | 10,932 | 554 |

| El Paso Corporation § | 16,244 | 187 |

| Encore Acquisition * | 1,200 | 49 |

| Energy Partners *§ | 2,200 | 58 |

| Enterprise Products Partners, Equity Units *§ | 8,300 | 222 |

| EOG Resources | 6,200 | 352 |

| ExxonMobil | 151,162 | 8,687 |

| Forest Oil * | 1,200 | 50 |

| General Maritime § | 900 | 38 |

| Houston Exploration * | 1,200 | 64 |

| Hugoton Royalty Trust § | 2,400 | 73 |

| Kerr-McGee | 2,343 | 179 |

| KFX *§ | 3,900 | 56 |

| Kinder Morgan | 3,100 | 258 |

| Magellan Midstream Partners § | 1,800 | 59 |

| Marathon Oil | 8,000 | 427 |

| Massey | 2,300 | 87 |

| Murphy Oil | 4,600 | 240 |

| Newfield Exploration * | 3,600 | 144 |

| Noble Energy | 1,500 | 113 |

| Occidental Petroleum | 9,200 | 708 |

| Peabody Energy | 3,400 | 177 |

| Penn Virginia § | 1,000 | 45 |

| Petroleum Development * | 1,300 | 41 |

| Pioneer Natural Resources | 3,100 | 130 |

| Plains All American Pipeline *§ | 1,900 | 83 |

| Plains Exploration & Production * | 2,100 | 75 |

| Pogo Producing § | 1,900 | 99 |

| Premcor | 2,400 | 178 |

| Quicksilver Resources *§ | 1,900 | 121 |

| Remington Oil & Gas * | 1,200 | 43 |

| Southwestern Energy * | 2,600 | 122 |

| Spinnaker Exploration *§ | 1,300 | 46 |

| Stone Energy *§ | 1,200 | 59 |

| Sunoco | 1,900 | 216 |

| Syntroleum *§ | 4,300 | 44 |

| Tel Offshore Trust § | 63 | 1 |

| Teppco Partners * | 1,500 | 62 |

| Tesoro Petroleum | 2,500 | 116 |

| Ultra Petroleum * | 3,600 | 109 |

| Unocal | 5,814 | 378 |

| Valero Energy | 6,400 | 506 |

| Vintage Petroleum | 2,500 | 76 |

| Western Gas Resources § | 2,600 | 91 |

| Whiting Petroleum * | 1,200 | 44 |

| Williams Companies | 13,585 | 258 |

| World Fuel Services § | 2,400 | 56 |

| XTO Energy | 8,842 | 301 |

| | | 23,566 |

| Total Energy | | 28,925 |

| |

| FINANCIALS 20.8% | | |

| Capital Markets 2.4% | | |

| A.G. Edwards | 2,100 | 95 |

| Aether Systems *§ | 1,250 | 4 |

| Affiliated Managers Group *§ | 1,150 | 79 |

| AmeriTrade * | 12,400 | 230 |

| Bank of New York | 17,900 | 515 |

| Bear Stearns | 2,327 | 242 |

| Charles Schwab | 34,006 | 384 |

| E*TRADE Financial * | 10,500 | 147 |

| Eaton Vance | 3,800 | 91 |

| Federated Investors, Class B | 2,950 | 88 |

| Franklin Resources | 5,800 | 446 |

| Goldman Sachs | 11,200 | 1,143 |

| Greenhill § | 1,300 | 53 |

| Investment Technology Group * | 2,600 | 55 |

| Investors Financial Services § | 1,800 | 68 |

| Janus Capital Group | 5,700 | 86 |

| Jefferies Group | 1,700 | 64 |

| John Nuveen § | 2,800 | 105 |

| Knight Capital Group *§ | 6,500 | 50 |

| LaBranche & Co. *§ | 3,900 | 25 |

| Ladenburg Thalmann Financial Services *§ | 787 | 0 |

| Legg Mason | 2,550 | 265 |

| Lehman Brothers | 6,634 | 659 |

| Mellon Financial | 9,800 | 281 |

| Merrill Lynch | 22,000 | 1,210 |

| Morgan Stanley | 25,600 | 1,343 |

| Northern Trust | 5,700 | 260 |

| Piper Jaffray * | 1,215 | 37 |

| Raymond James Financial | 2,150 | 61 |

| SEI | 2,600 | 97 |

| State Street | 8,500 | 410 |

| Stifel Financial *§ | 2,000 | 48 |

| Waddell & Reed Financial, Class A | 2,951 | 55 |

| Westwood Holdings Group | 1,300 | 23 |

| | | 8,719 |

| Commercial Banks 5.5% | | |

| 1st Source | 1,830 | 42 |

| Amcore Financial | 1,200 | 36 |

| Amegy Bancorp § | 1,600 | 36 |

| AmSouth | 8,767 | 228 |

| Associated Banc Corp | 3,167 | 107 |

| BanCorpSouth § | 2,700 | 64 |

| Bank of America | 94,754 | 4,322 |

| Bank of Hawaii | 1,200 | 61 |

| Bank of the Ozarks § | 900 | 30 |

| Bay View Capital | 1,310 | 20 |

| BB&T | 13,320 | 532 |

| BOK Financial | 1,315 | 61 |

| Boston Private Financial § | 1,300 | 33 |

| BWC Financial § | 1,115 | 29 |

| Capital Corp of the West § | 1,800 | 50 |

| Capitol Bancorp Limited § | 1,247 | 42 |

| Chittenden | 1,068 | 29 |

| Citizens Banking | 1,000 | 30 |

| City National | 1,100 | 79 |

| Colonial BancGroup | 2,500 | 55 |

| Comerica | 3,900 | 225 |

| Commerce Bancorp § | 3,800 | 115 |

| Commerce Bancshares § | 1,510 | 76 |

| Community Banks § | 1,083 | 28 |

| Community Bankshares of Indiana | 1,340 | 31 |

| Community Capital | 1,500 | 33 |

| Compass Bancshares | 2,800 | 126 |

| Cullen/Frost Bankers | 1,300 | 62 |

| CVB Financial § | 2,792 | 55 |

| East West Bancorp | 1,600 | 54 |

| Fidelity Southern | 2,300 | 36 |

| Fifth Third Bancorp § | 13,609 | 561 |

| First Charter § | 1,200 | 26 |

| First Financial Bancorp § | 1,670 | 32 |

| First Horizon National | 2,800 | 118 |

| First M & F Corporation § | 700 | 24 |

| First Merchants § | 1,630 | 41 |

| First Midwest Bancorp § | 1,350 | 47 |

| FirstBank Puerto Rico § | 1,200 | 48 |

| FirstMerit | 2,000 | 52 |

| FNB § | 2,492 | 49 |

| Frontier Financial § | 1,200 | 30 |

| Fulton Financial § | 3,786 | 68 |

| German American Bancorp § | 1,874 | 26 |

| Gold Banc § | 3,400 | 49 |

| Greater Bay Bancorp § | 2,200 | 58 |

| Hancock Holding | 1,300 | 45 |

| Hibernia, Class A | 3,400 | 113 |

| Hudson United Bancorp § | 970 | 35 |

| Huntington Bancshares | 5,366 | 130 |

| IBERIABANK § | 600 | 37 |

| Integra Bank § | 1,071 | 24 |

| International Bancshares | 1,366 | 39 |

| KeyCorp | 9,400 | 312 |

| M & T Bank | 2,700 | 284 |

| Main Street Banks § | 1,200 | 31 |

| Marshall & Ilsley | 5,278 | 235 |

| Mercantile Bankshares | 1,700 | 88 |

| Merrill Merchants Bancorp | 938 | 21 |

| Metrocorp Bancshares § | 1,500 | 32 |

| Mid-State Bancshares § | 900 | 25 |

| Midwest Banc Holdings § | 1,200 | 23 |

| National City | 14,688 | 501 |

| NBT Bancorp | 1,400 | 33 |

| North Fork Bancorporation | 11,718 | 329 |

| Old National Bancorp § | 2,112 | 45 |

| Omega Financial § | 1,300 | 40 |

| Oriental Financial Group § | 1,527 | 23 |

| Pacific Capital Bancorp | 1,710 | 63 |

| Park National § | 315 | 35 |

| Peoples Bancorp | 1,345 | 36 |

| Peoples Financial | 1,500 | 27 |

| PNC Financial Services Group | 6,200 | 338 |

| Popular | 6,200 | 156 |

| Prosperity Bancshares | 1,200 | 34 |

| Provident Bankshares | 999 | 32 |

| Regions Financial | 11,366 | 385 |

| Renasant § | 1,250 | 38 |

| Republic Bancorp § | 3,497 | 52 |

| S&T Bancorp § | 1,100 | 40 |

| Sandy Spring Bancorp § | 900 | 32 |

| Santander Bancorp § | 1,703 | 43 |

| Signature Bank *§ | 1,300 | 32 |

| Sky Financial | 3,133 | 88 |

| South Financial Group | 1,265 | 36 |

| Southwest Bancorp of Oklahoma § | 1,800 | 37 |

| Sterling Bancshares | 1,750 | 27 |

| SunTrust | 8,270 | 597 |

| Susquehanna Bancshares § | 2,000 | 49 |

| SVB Financial Group *§ | 900 | 43 |

| Synovus Financial | 7,600 | 218 |

| TCF Financial | 3,700 | 96 |

| TD Banknorth | 4,341 | 129 |

| Texas Capital Bancshares *§ | 1,700 | 34 |

| Texas Regional Bancshares, Class A | 1,717 | 52 |

| The Savannah Bancorp | 750 | 22 |

| Toronto Dominion Bank § | 835 | 37 |

| Trustmark | 1,500 | 44 |

| U.S. Bancorp | 43,955 | 1,283 |

| U.S.B. Holding Company § | 1,651 | 39 |

| UCBH Holdings § | 3,400 | 55 |

| UMB Financial | 598 | 34 |

| UnionBancal | 3,300 | 221 |

| United Bankshares § | 900 | 32 |

| Unity Bancorp § | 3,819 | 46 |

| Valley National Bancorp § | 2,948 | 69 |

| Wachovia | 37,201 | 1,845 |

| Wells Fargo | 39,252 | 2,417 |

| WesBanco § | 1,100 | 33 |

| WestAmerica | 1,100 | 58 |

| Whitney Holding | 1,425 | 46 |

| Wilmington Trust | 1,500 | 54 |

| Wintrust Financial § | 1,050 | 55 |

| Zions Bancorp | 2,400 | 176 |

| | | 19,716 |

| Consumer Finance 1.2% | | |

| Advance America Cash Advance Centers § | 3,500 | 56 |

| Advanta, Class A § | 2,155 | 55 |

| American Express | 29,500 | 1,570 |

| AmeriCredit * | 4,300 | 110 |

| Capital One Financial | 5,700 | 456 |

| CompuCredit *§ | 2,100 | 72 |

| First Marblehead *§ | 2,200 | 77 |

| MBNA | 29,375 | 768 |

| Metris Companies *§ | 2,300 | 33 |

| Moneygram International | 2,200 | 42 |

| Providian Financial * | 6,900 | 122 |

| SLM Corporation | 10,600 | 539 |

| Student Loan | 500 | 110 |

| WFS Financial | 900 | 46 |

| World Acceptance * | 1,100 | 33 |

| | | 4,089 |

| Diversified Financial Services 2.8% | | |

| Alliance Capital | 1,700 | 79 |

| CapitalSource *§ | 2,700 | 53 |

| Chicago Mercantile Exchange Holdings | 900 | 266 |

| CIT Group | 5,200 | 223 |

| Citigroup | 121,214 | 5,604 |

| eSpeed, Class A *§ | 3,400 | 30 |

| Instinet Group * | 9,900 | 52 |

| J.P. Morgan Chase | 83,577 | 2,952 |

| Leucadia National § | 3,381 | 131 |

| Moody's | 7,400 | 333 |

| Principal Financial Group | 7,700 | 323 |

| | | 10,046 |

| Insurance 4.9% | | |

| 21st Century Insurance Group § | 4,200 | 62 |

| AFLAC | 11,700 | 506 |

| Alfa § | 2,100 | 31 |

| Allmerica Financial * | 1,500 | 56 |

| Allstate | 16,700 | 998 |

| Ambac | 2,550 | 178 |

| American Financial Group | 1,500 | 50 |

| American International Group | 60,718 | 3,528 |

| American National Insurance | 500 | 57 |

| AmerUs Life § | 900 | 43 |

| Aon | 7,050 | 177 |

| Arch Capital Group * | 1,500 | 68 |

| Arthur J. Gallagher § | 2,000 | 54 |

| Assurant | 2,400 | 87 |

| Berkshire Hathaway, Class A * | 36 | 3,006 |

| Bristol West Holdings | 1,500 | 28 |

| Brown & Brown | 1,800 | 81 |

| Chubb | 4,700 | 402 |

| Cincinnati Financial | 3,969 | 157 |

| Citizens Financial *§ | 600 | 5 |

| CNA Financial *§ | 4,800 | 136 |

| Commerce Group | 1,100 | 68 |

| Conseco * | 3,500 | 76 |

| Delphi Financial, Class A | 1,050 | 46 |

| Erie Indemnity, Class A § | 1,400 | 76 |

| FBL Financial Group, Class A § | 1,432 | 40 |

| Fidelity National Financial | 4,562 | 163 |

| First American Financial | 1,685 | 68 |

| FPIC Insurance Group *§ | 1,300 | 38 |

| Genworth Financial, Class A | 12,000 | 363 |

| Great American Financial Resources § | 2,000 | 40 |

| Hartford Financial Services | 6,700 | 501 |

| HCC Insurance Holdings | 1,500 | 57 |

| Hilb Rogal and Hobbs § | 1,400 | 48 |

| Horace Mann Educators | 1,800 | 34 |

| Infinity Property & Casualty | 1,200 | 42 |

| Jefferson Pilot | 3,100 | 156 |

| LandAmerica Financial Group § | 900 | 53 |

| Lincoln National | 4,000 | 188 |

| Loews | 4,200 | 326 |

| Markel * | 260 | 88 |

| Marsh & McLennan | 12,200 | 338 |

| MBIA | 3,200 | 190 |

| Mercury General | 1,400 | 76 |

| MetLife | 18,200 | 818 |

| Midland | 1,200 | 42 |

| Nationwide Financial Services, Class A | 1,400 | 53 |

| Navigators Group * | 900 | 31 |

| Odyssey Re Holdings § | 1,600 | 40 |

| Ohio Casualty | 2,200 | 53 |

| Old Republic International | 4,150 | 105 |

| Phoenix Companies § | 4,000 | 48 |

| Presidential Life § | 1,700 | 29 |

| ProAssurance * | 824 | 34 |

| Progressive Corporation | 4,950 | 489 |

| Protective Life | 1,500 | 63 |

| Prudential | 12,000 | 788 |

| Reinsurance Group of America | 1,700 | 79 |

| RLI § | 700 | 31 |

| SAFECO | 3,100 | 169 |

| St. Paul Companies | 15,923 | 629 |

| StanCorp Financial Group | 800 | 61 |

| Torchmark | 2,600 | 136 |

| Transatlantic Holdings § | 1,437 | 80 |

| UICI | 1,400 | 42 |

| United America Indemnity * | 1,939 | 33 |

| United Fire & Casualty § | 900 | 40 |

| Unitrin | 1,800 | 88 |

| UnumProvident § | 6,376 | 117 |

| Vesta Insurance § | 3,300 | 9 |

| W. R. Berkley | 2,925 | 104 |

| Wesco Financial | 150 | 54 |

| White Mountains Insurance Group § | 300 | 189 |

| Zenith National § | 1,100 | 75 |

| | | 17,314 |

| Real Estate 2.2% | | |

| Agree Realty, REIT § | 1,300 | 39 |

| AMB Property, REIT | 1,900 | 83 |

| American Mortgage Acceptance, REIT § | 1,600 | 24 |

| AmeriVest Properties, REIT § | 4,900 | 20 |

| Annaly Mortgage Management, REIT § | 4,100 | 74 |

| Apartment Investment & Management, Class A, REIT | 2,900 | 119 |

| Archstone-Smith Trust, REIT | 4,900 | 189 |

| Arden Realty, REIT | 2,100 | 76 |

| Avalonbay Communities, REIT | 2,007 | 162 |

| Bedford Property Investors, REIT § | 1,200 | 28 |

| Boston Properties, REIT | 2,400 | 168 |

| Brandywine Realty Trust, REIT | 1,900 | 58 |

| BRE Properties, REIT, Class A | 1,700 | 71 |

| Camden Property Trust, REIT | 1,500 | 81 |

| CarrAmerica Realty, REIT | 2,100 | 76 |

| Catellus Development, REIT | 3,378 | 111 |

| CBL & Associates Properties, REIT | 2,200 | 95 |

| Centerpoint Properties, REIT | 1,600 | 68 |

| Consolidated-Tomoka Land | 700 | 60 |

| Cousins Properties, REIT | 1,850 | 55 |

| Crescent Real Estate Equities, REIT § | 4,000 | 75 |

| CRT Properties, REIT | 1,700 | 46 |

| Developers Diversified Realty, REIT | 3,100 | 142 |

| Duke Realty, REIT | 3,800 | 120 |

| EastGroup Properties, REIT § | 1,000 | 42 |

| Equity Lifestyle Properties, REIT | 1,000 | 40 |

| Equity Office Properties, REIT | 10,461 | 346 |

| Equity Residential, REIT | 7,400 | 272 |

| Federal Realty Investment Trust, REIT | 1,500 | 89 |

| FelCor Lodging Trust, REIT * | 3,748 | 54 |

| First Industrial Realty, REIT § | 1,800 | 72 |

| Forest City Enterprises, Class A | 1,100 | 78 |

| Friedman, Billings, Ramsey Group, REIT, Class A § | 4,900 | 70 |

| General Growth Properties, REIT | 5,900 | 242 |

| Getty Realty, REIT § | 1,200 | 33 |

| Health Care Property Investors, REIT | 3,900 | 105 |

| Heritage Property Investment Trust, REIT | 1,900 | 67 |

| Highwoods Properties, REIT | 1,500 | 45 |

| Home Properties of New York, REIT | 1,400 | 60 |

| Hospital Properties Trust, REIT | 2,000 | 88 |

| Host Marriott, REIT | 8,200 | 144 |

| Innkeepers USA, REIT | 3,100 | 46 |

| IStar Financial, REIT | 3,017 | 126 |

| Kilroy Realty, REIT | 1,300 | 62 |

| Kimco Realty, REIT | 2,850 | 168 |

| Liberty Property Trust, REIT § | 2,100 | 93 |

| Macerich Company, REIT | 1,900 | 127 |

| Mack-Cali Realty, REIT | 1,700 | 77 |

| Maguire Properties, REIT | 1,700 | 48 |

| MeriStar Hospitality, REIT * | 6,000 | 52 |

| Mid-America Apartment Communities, REIT | 1,000 | 45 |

| Mills, REIT | 1,800 | 109 |

| Mission West Properties, REIT § | 3,200 | 33 |

| Monmouth Real Estate Investment, REIT, Class A § | 3,100 | 26 |

| Nationwide Health Properties, REIT § | 2,500 | 59 |

| New Plan Excel Realty, REIT | 3,200 | 87 |

| NovaStar Financial, REIT § | 1,200 | 47 |

| One Liberty Properties, REIT § | 1,700 | 35 |

| Pan Pacific Retail Properties, REIT | 1,200 | 80 |

| Parkway Properties, REIT | 1,000 | 50 |

| Pennsylvania, REIT | 1,630 | 77 |

| Plum Creek Timber, REIT | 4,944 | 179 |

| PMC Commercial Trust, REIT | 1,591 | 21 |

| Post Properties, REIT | 1,800 | 65 |

| ProLogis, REIT | 4,576 | 184 |

| Public Storage, REIT | 3,200 | 202 |

| Rayonier, REIT § | 1,596 | 85 |

| Realty Income, REIT § | 2,400 | 60 |

| Reckson Associates Realty, REIT | 2,600 | 87 |

| Regency Centers, REIT | 1,600 | 92 |

| Shurgard Storage Centers, REIT § | 1,700 | 78 |

| Simon Property Group, REIT | 5,681 | 412 |

| SL Green Realty, REIT § | 1,500 | 97 |

| St. Joe | 1,700 | 139 |

| Strategic Hotel Capital, REIT | 1,600 | 29 |

| Taubman Centers, REIT | 2,200 | 75 |

| Thornburg Mortgage, REIT § | 2,900 | 84 |

| Trizec Properties, REIT | 4,500 | 93 |

| United Dominion Realty Trust, REIT | 3,800 | 91 |

| Vencor, REIT | 3,000 | 91 |

| Vornado Realty Trust, REIT | 3,200 | 257 |

| Weingarten Realty Investors, REIT | 2,575 | 101 |

| Wellsford Real Properties * | 1,200 | 21 |

| WP Carey & Co § | 1,600 | 47 |

| | | 7,924 |

| Thrifts & Mortgage Finance 1.8% | | |

| Alliance Bank | 800 | 18 |

| Anchor Bancorp Wisconsin § | 1,200 | 36 |

| Astoria Financial | 3,625 | 103 |

| BankAtlantic, Class A § | 2,700 | 51 |

| Berkshire Hills Bancorp § | 500 | 17 |

| Brookline Bancorp § | 2,693 | 44 |

| Capitol Federal Financial § | 1,900 | 65 |

| Commercial Capital Bancorp § | 2,800 | 47 |

| Commercial Federal | 1,300 | 44 |

| Corus Bankshares § | 1,000 | 55 |

| Countrywide Credit | 13,098 | 506 |

| Doral Financial § | 2,350 | 39 |

| Downey Financial | 1,200 | 88 |

| Fannie Mae | 22,300 | 1,302 |

| First Busey § | 1,450 | 28 |

| First Niagra Financial | 3,405 | 50 |

| FirstFed Financial * | 800 | 48 |

| Flushing Financial § | 1,350 | 25 |

| Freddie Mac | 16,300 | 1,063 |

| Fremont General § | 2,300 | 56 |

| Golden West Financial | 7,600 | 489 |

| Horizon Financial § | 1,200 | 27 |

| Hudson City Bancorp | 15,709 | 179 |

| Independence Community Bank | 2,754 | 102 |

| IndyMac Mortgage Holdings | 1,900 | 77 |

| MAF Bancorp § | 1,411 | 60 |

| MGIC Investment | 2,400 | 157 |

| Net Bank | 3,921 | 37 |

| New York Community Bancorp § | 6,953 | 126 |

| Northwest Bancorp § | 1,800 | 38 |

| People's Bank § | 3,975 | 120 |

| PMI Group § | 2,000 | 78 |

| Radian | 2,100 | 99 |

| Sovereign Bancorp | 8,983 | 201 |

| Triad Guaranty * | 600 | 30 |

| Washington Federal | 2,842 | 67 |

| Washington Mutual | 21,006 | 855 |

| Webster Financial | 2,103 | 98 |

| | | 6,525 |

| Total Financials | | 74,333 |

| |

| HEALTH CARE 12.6% | | |

| Biotechnology 2.0% | | |

| Abgenix *§ | 2,900 | 25 |

| Affymetrix *§ | 1,900 | 102 |

| Albany Molecular Research * | 1,300 | 18 |

| Alexion Pharmaceutical *§ | 700 | 16 |

| Alkermes *§ | 3,900 | 52 |

| Amgen * | 29,360 | 1,775 |

| Amylin Pharmaceuticals *§ | 2,900 | 61 |

| Aphton *§ | 7,000 | 5 |

| Applera | 4,600 | 91 |

| Arena Pharmaceuticals *§ | 2,500 | 17 |

| Ariad Pharmaceuticals *§ | 4,600 | 31 |

| Array BioPharma * | 2,100 | 13 |

| AVI BioPharma *§ | 1,200 | 3 |

| Avigen *§ | 700 | 2 |

| Biogen Idec * | 7,610 | 262 |

| BioMarin Pharmaceutical *§ | 4,300 | 32 |

| Biopure *§ | 433 | 1 |

| Caliper Life Sciences * | 2,200 | 12 |

| Celera Genomics * | 1,500 | 16 |

| Celgene *§ | 3,800 | 155 |

| Cell Genesys *§ | 1,300 | 7 |

| Cell Therapeutics *§ | 3,900 | 11 |

| Cephalon * | 1,800 | 72 |

| Charles River Laboratories International * | 1,968 | 95 |

| Chiron *§ | 4,800 | 167 |

| Cubist Pharmaceuticals *§ | 1,000 | 13 |

| CuraGen *§ | 6,100 | 31 |

| CV Therapeutics *§ | 1,600 | 36 |

| Cytrx *§ | 6,400 | 6 |

| Digene *§ | 400 | 11 |

| Discovery Partners * | 3,900 | 11 |

| Diversa *§ | 2,400 | 13 |

| Encysive Pharmaceuticals *§ | 2,700 | 29 |

| Enzo Biochem § | 770 | 14 |

| Enzon Pharmaceuticals * | 2,000 | 13 |

| Exelixis * | 1,800 | 13 |

| Eyetech Pharmaceuticals *§ | 2,700 | 34 |

| Gene Logic *§ | 1,500 | 5 |

| Genentech * | 24,400 | 1,959 |

| Genta *§ | 2,600 | 3 |

| Genzyme * | 5,949 | 357 |

| Gilead Sciences * | 9,880 | 435 |

| Human Genome Sciences *§ | 4,600 | 53 |

| ICOS *§ | 2,000 | 42 |

| ImClone Systems *§ | 2,307 | 71 |

| ImmunoGen *§ | 4,700 | 27 |