| UNITED STATES | ||

| SECURITIES AND EXCHANGE COMMISSION | ||

| Washington, D.C. 20549 | ||

| FORM N-CSR | ||

| CERTIFIED SHAREHOLDER REPORT OF REGISTERED | ||

| MANAGEMENT INVESTMENT COMPANIES | ||

| Investment Company Act file number | 811-06247 | |

| AMERICAN CENTURY WORLD MUTUAL FUNDS, INC. | ||

| (Exact name of registrant as specified in charter) | ||

| 4500 MAIN STREET, KANSAS CITY, MISSOURI | 64111 | |

| (Address of principal executive offices) | (Zip Code) | |

| CHARLES A. ETHERINGTON | ||

| 4500 MAIN STREET, KANSAS CITY, MISSOURI 64111 | ||

| (Name and address of agent for service) | ||

| Registrant’s telephone number, including area code: | 816-531-5575 | |

| Date of fiscal year end: | 11-30 | |

| Date of reporting period: | 11-30-2009 | |

| ITEM 1. REPORTS TO STOCKHOLDERS. | |

| Annual Report | |

| November 30, 2009 | |

![]()

| American Century Investments |

International Growth Fund

Global Growth Fund

Emerging Markets Fund

International Value Fund

| Table of Contents |

| President’s Letter | 2 |

| Independent Chairman’s Letter | 3 |

| Market Perspective | 4 |

| International Equity Total Returns | 4 |

| International Growth | |

| Performance | 5 |

| Portfolio Commentary | 7 |

| Top Ten Holdings, Types of Investments in Portfolio | |

| and Investments by Country | 9 |

| Global Growth | |

| Performance | 10 |

| Portfolio Commentary | 12 |

| Top Ten Holdings, Types of Investments in Portfolio | |

| and Investments by Country | 14 |

| Emerging Markets | |

| Performance | 15 |

| Portfolio Commentary | 17 |

| Top Ten Holdings, Types of Investments in Portfolio | |

| and Investments by Country | 19 |

| International Value | |

| Performance | 20 |

| Portfolio Commentary | 22 |

| Top Ten Holdings, Types of Investments in Portfolio | |

| and Investments by Country | 24 |

| Shareholder Fee Examples | 25 |

| Financial Statements | |

| Schedule of Investments | 28 |

| Statement of Assets and Liabilities | 41 |

| Statement of Operations | 43 |

| Statement of Changes in Net Assets | 44 |

| Notes to Financial Statements | 46 |

| Financial Highlights | 59 |

| Report of Independent Registered Public Accounting Firm | 83 |

| Other Information | |

| Management | 84 |

| Approval of Management Agreements | 87 |

| Additional Information | 93 |

| Index Definitions | 94 |

The opinions expressed in the Market Perspective and each of the Portfolio Commentaries reflect those of the portfolio management team as of the date of the report, and do not necessarily represent the opinions of American Century Investments or any other person in the American Century Investments organization. Any such opinions are subject to change at any time based upon market or other conditions and American Century Investments disclaims any responsibility to update such opinions. These opinions may not be relied upon as investment advice and, because investment decisions made by American Century Investments funds are based on numerous factors, may not be relied upon as an indication of trading intent on behalf of any American Century Investments fund. Security examples are used for representational purposes only and are not intended as recommendations to purchase or sell securities. Performance information for com parative indices and securities is provided to American Century Investments by third party vendors. To the best of American Century Investments’ knowledge, such information is accurate at the time of printing.

| President’s Letter |

Dear Investor:

Thank you for taking time to review the following pages, which provide the performance of your investment along with the perspectives of our experienced portfolio management team for the financial reporting period ended November 30, 2009. We appreciate your trust in American Century Investments® at this volatile, transitional time in the economy and investment markets.

As the upheavals associated with the “Great Recession” gradually subside, our senior management team has put considerable thought into how the investment environment has changed and what new challenges and opportunities await us. Critical factors that we are anticipating in 2010 include marked shifts in investment and spending behavior, along with consolidation in our industry.

Most importantly, we think the U.S. economic recovery will be slow and extended. The economy and capital markets have come a long way since Lehman Brothers collapsed in the third quarter of 2008, but 2010 will likely bring continuing challenges. The U.S. stock market’s rebound since last March and the second-half economic surge in 2009 were fueled largely by corporate cost-cutting and unprecedented monetary and fiscal stimulus, including some key programs that have since expired or been scaled back.

Meanwhile, the resilient but struggling consumer sector still faces double-digit unemployment, heavy debt burdens, tight credit conditions, and a housing market that is starting to stabilize, but remains vulnerable. Much of our investment positioning in 2009 cautiously reflected these still unstable economic fundamentals, leading to underperformance, in some cases, versus market benchmarks buoyed by the rally of riskier assets. We still support our fundamentally based positioning because we believe strongly that some markets—driven more by technical factors than fundamentals—have advanced further than underlying economic conditions warrant, and remain susceptible to the possibility of more volatility ahead.

Thank you for your continued confidence in us.

Sincerely,

Jonathan Thomas

President and Chief Executive Officer

American Century Investments

2

| Independent Chairman’s Letter |

In my first letter to shareholders of the American Century Investments funds, I invited you to contact me with your questions. I have been gratified with your response. Most shareholder inquiries to date have related to specific fund performance issues. As I noted in my individual responses, your board through the Fund Performance Committee continues to stress improved performance in our quarterly meetings with chief investment officers and fund managers.

An important part of our fund performance review process is a face-to-face meeting with portfolio managers. The board traveled during the second quarter to the American Century Investments office in Mountain View, California to meet with the fund of funds and asset allocation portfolio management teams. These meetings validated the importance of thorough reviews of investment opportunities by the credit management personnel resident in that office. As a result of their efforts, American Century Investments funds were able to avoid the “toxic assets” that plagued many other fund families in 2008.

From April through June 2009, the board conducted its annual review of the advisory contracts between American Century Investments and each fund. Our efforts involved a review of fund information, including assets under management; total expense ratio compared to peers; economies of scale; fee breakpoints that reduce shareholder costs as assets increase; performance compared to peers and benchmarks; and the quality of services provided to fund shareholders. A detailed discussion of board considerations in connection with advisory contract renewal is included annually in each fund’s shareholder reports. During this review, the board focuses on a detailed comparison of the competitive position of each fund and has negotiated more than 60 breakpoints or fee reductions in the past five years.

The board looks forward to another year of work on your behalf and your comments are appreciated. You are invited to email me at dhpratt@fundboardchair.com.

3

| Market Perspective |

By Mark Kopinski, Chief Investment Officer, Global and Non-U.S. Equity

Stocks Shook Off Early Declines

The near-collapse of the global financial system in the fall of 2008 fueled the worldwide recession and credit crisis and sent investors fleeing stocks and other risky assets. In this environment, international equity markets plunged to multi-year lows on sharp double-digit losses.

By mid-March, investor confidence and stock market performance showed an abrupt and surprising turnaround, triggered by a belief that the global financial system was no longer on the verge of collapse. Optimistic investors focused on early signs suggesting the global recession was easing, favoring lower-quality stocks that had been battered the most in the prior months. By the third quarter of 2009, gross domestic product returned to positive territory in Germany, France, and Japan, while industrial production and global trade levels improved in China. Meanwhile, consumer confidence improved throughout Europe, and in the United Kingdom the troubled housing market showed signs of stabilizing.

After bottoming on March 9, global stock markets rallied sharply to finish the 12-month period with strong gains. With renewed confidence in equities, investors shifted funds toward riskier assets, which, combined with rising commodity prices, bolstered performance among emerging markets.

Recovery’s Sustainability Remained in Question

Despite improving conditions, central bankers worldwide voiced concerns about the overall stability and sustainability of the economic recovery. The Bank of Japan stated downside risks remain, and European Central Bank officials stressed a recovery likely would be uneven. At the same time, officials mulled plans to reduce market liquidity, as the massive and widespread government stimulus efforts neared expiration. Meanwhile, rising unemployment dampened consumer spending, pricing data failed to support inflationary or deflationary expectations, and the Chinese government repeated concerns about overcapacity in the materials sector.

If, in the coming months, consumers worldwide do not increase spending, either due to prolonged unemployment or the need to repair their net worth, additional stimulus packages may become necessary. We expect continued easy monetary and fiscal policies globally, as most central banks seek to avoid fostering a “double dip” recession.

| International Equity Total Returns | ||||

| For the 12 months ended November 30, 2009 (in U.S. dollars) | ||||

| MSCI EAFE Index | 37.72% | MSCI Europe Index | 40.83% | |

| MSCI EAFE Growth Index | 34.93% | MSCI World Free Index | 31.79% | |

| MSCI EAFE Value Index | 40.54% | MSCI Japan Index | 14.01% | |

| MSCI EM Growth Index | 83.97% | |||

4

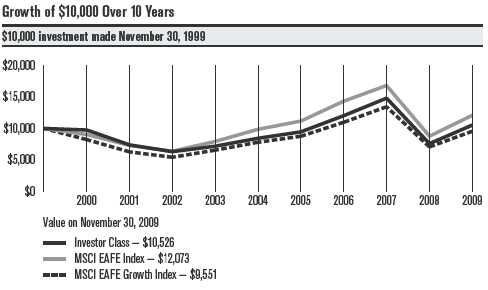

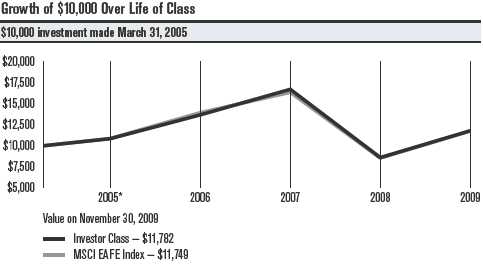

| Performance |

| International Growth | ||||||

| Total Returns as of November 30, 2009 | ||||||

| Average Annual Returns | ||||||

| Since | Inception | |||||

| 1 year | 5 years | 10 years | Inception | Date | ||

| Investor Class | 38.66% | 4.52% | 0.51% | 7.88% | 5/9/91 | |

| MSCI EAFE Index | 37.72% | 4.13% | 1.90% | 5.34%(1) | — | |

| MSCI EAFE Growth Index | 34.93% | 4.10% | -0.46% | 3.55%(1) | — | |

| Institutional Class | 38.96% | 4.72% | 0.72% | 4.99% | 11/20/97 | |

| A Class(2) | 10/2/96 | |||||

| No sales charge* | 38.30% | 4.26% | 0.26% | 5.76% | ||

| With sales charge* | 30.43% | 3.04% | -0.33% | 5.28% | ||

| B Class | 1/31/03 | |||||

| No sales charge* | 37.36% | 3.49% | — | 8.01% | ||

| With sales charge* | 33.36% | 3.32% | — | 8.01% | ||

| C Class | 37.29% | 3.47% | — | 1.36% | 6/4/01 | |

| R Class | 37.97% | 4.01% | — | 6.99% | 8/29/03 | |

| * Sales charges include initial sales charges and contingent deferred sales charges (CDSCs), as applicable. A Class shares have a 5.75% | ||||||

| maximum initial sales charge for equity funds and may be subject to a maximum CDSC of 1.00%. B Class shares redeemed within six | ||||||

| years of purchase are subject to a CDSC that declines from 5.00% during the first year after purchase to 0.00% the sixth year after | ||||||

| purchase. C Class shares redeemed within 12 months of purchase are subject to a maximum CDSC of 1.00%. The SEC requires that | ||||||

| mutual funds provide performance information net of maximum sales charges in all cases where charges could be applied. | ||||||

| (1) | Since 4/30/91, the date nearest the Investor Class’s inception for which data are available. | |||||

| (2) | Prior to December 3, 2007, the A Class was referred to as the Advisor Class. Performance, with sales charge, prior to that date has been adjusted | |||||

| to reflect the A Class’s current sales charge. | ||||||

Data presented reflect past performance. Past performance is no guarantee of future results. Current performance may be higher or lower than the performance shown. Investment return and principal value will fluctuate, and redemption value may be more or less than original cost. To obtain performance data current to the most recent month end, please call 1-800-345-2021 or visit americancentury.com. International investing involves special risks, such as political instability and currency fluctuations. Investing in emerging markets may accentuate these risks.

Unless otherwise indicated, performance reflects Investor Class shares; performance for other share classes will vary due to differences in fee structure. For information about other share classes available, please consult the prospectus. Data assumes reinvestment of dividends and capital gains, and none of the charts reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Returns for the indices are provided for comparison. The fund’s total returns include operating expenses (such as transaction costs and management fees) that reduce returns, while the total returns of the indices do not.

5

International Growth

| One-Year Returns Over 10 Years | ||||||||||

| Periods ended November 30 | ||||||||||

| 2000 | 2001 | 2002 | 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | |

| Investor Class | -2.47% | -24.18% | -14.54% | 13.70% | 17.45% | 12.09% | 27.03% | 23.09% | -48.67% | 38.66% |

| MSCI EAFE Index | -9.67% | -19.13% | -12.50% | 24.22% | 24.19% | 13.25% | 28.20% | 17.30% | -47.79% | 37.72% |

| MSCI EAFE | ||||||||||

| Growth Index | -17.66% | -23.61% | -13.53% | 20.63% | 19.07% | 12.14% | 25.29% | 22.32% | -47.28% | 34.93% |

| Total Annual Fund Operating Expenses | |||||

| Institutional | |||||

| Investor Class | Class | A Class | B Class | C Class | R Class |

| 1.41% | 1.21% | 1.66% | 2.41% | 2.41% | 1.91% |

The total annual fund operating expenses shown is as stated in the fund’s prospectus current as of the date of this report. The prospectus may vary from the expense ratio shown elsewhere in this report because it is based on a different time period, includes acquired fund fees and expenses, and, if applicable, does not include fee waivers or expense reimbursements.

Data presented reflect past performance. Past performance is no guarantee of future results. Current performance may be higher or lower than the performance shown. Investment return chart and principal value will fluctuate, and redemption value may be more or less than original cost. To obtain performance data current to the most recent month end, please call 1-800-345-2021 or visit americancentury.com. International investing involves special risks, such as political instability and currency fluctuations. Investing in emerging markets may accentuate these risks.

Unless otherwise indicated, performance reflects Investor Class shares; performance for other share classes will vary due to differences in fee structure. For information about other share classes available, please consult the prospectus. Data assumes reinvestment of dividends and capital gains, and none of the charts reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Returns for the indices are provided for comparison. The fund’s total returns include operating expenses (such as transaction costs and management fees) that reduce returns, while the total returns of the indices do not.

6

| Portfolio Commentary |

International Growth

Portfolio Managers: Alex Tedder and Raj Gandhi

Performance Summary

The International Growth portfolio advanced 38.66%* for the 12 months ended November 30, 2009, outperforming its benchmark, the MSCI EAFE Index, which gained 37.72%.

Despite the severe global recession, credit-market meltdown, and financial-sector crisis, international stocks finished the 12-month period with sharp gains. Initially, stocks plunged, as rising unemployment, shrinking industrial output, and negative economic growth rates sent investor confidence tumbling. But, by mid-March, market sentiment and stock performance reversed course quickly, as massive stimulus efforts from global central banks and governments generated optimism among investors.

On an absolute basis, all sectors and nearly every country represented in the portfolio and benchmark posted positive returns for the 12-month period. Stock selection, primarily in the information technology and financial sectors, accounted for the portfolio’s outperformance relative to the benchmark.

Japan, South Korea Were Top Countries

From a regional perspective, the portfolio’s holdings in Japan contributed the most to relative performance, due to favorable stock selection combined with an underweight position. South Korea, a non-benchmark country, also contributed strongly to portfolio results, as the country’s economy benefited from low interest rates and government stimulus efforts at home and abroad. In particular, Hyundai Motor Co. was among the portfolio’s leading contributors, benefiting from the United States’ “cash for clunkers” incentive program, which helped boost sales figures for the automaker.

At the opposite end of the spectrum, an underweight position in Australia and poor stock selection in Germany hurt the portfolio’s performance.

Technology, Utilities Drove Sector Results

Information technology was the portfolio’s top-performing sector, with stock selection driving the solid results. Our stock selection was particularly effective in the communications equipment segment, where Canadian-based Research In Motion (RIM) was the top-contributing stock. The portfolio’s out-of-benchmark position in RIM, the developer of the BlackBerry wireless device, was among the leading contributors for the period. Sales of the company’s touch-screen Storm device, RIM’s answer to Apple’s iPhone, gained traction after RIM resolved several software issues that emerged after the product’s initial launch.

The portfolio’s utilities sector, which ended the period as the smallest weighting in the fund, also contributed strongly to relative performance, driven primarily by our underweight position. In addition, the portfolio’s consumer discretionary sector, among the largest-weighted segments in

*All fund returns referenced in this commentary are for Investor Class shares.

7

International Growth

the fund, contributed positively, with stock selection and an overweight helping performance. In addition to the positive contribution from Hyundai Motor Co., an overweight to specialty retailers boosted results. In the challenging economic environment, consumers “traded down” for value. Portfolio holdings such as the U.K.’s Kingfisher (home improvement) and Japan’s FAST RETAILING (lower-priced clothing) and Nitori (the “Japanese IKEA”) benefited from these consumer spending trends.

Industrials, Health Care Sectors Lagged

The industrials sector represented the portfolio’s largest performance detractor. Our underweight in industrial conglomerates combined with negative stock selection in the building products, commercial services and supplies, and transportation infrastructure industries accounted for the bulk of the sector’s underperformance.

The portfolio’s health care sector also detracted from performance, primarily due to an overweight in the biotechnology industry and in the health care providers and services segment. In particular, our overweight positions in Switzerland-based Actelion Ltd., a biopharmaceutical company, and Germany’s Fresenius Medical Care, a provider of dialysis products and services, hurt results.

Outlook

Signs of improvement in corporate earnings have surfaced throughout the world. While most of the improvements have come from cost cutting and restructuring, we remain encouraged and believe any revenue growth may immediately affect the bottom line. We will closely monitor the upcoming corporate earnings reporting season, which could provide more clarity on the sustainability of recent improvements. International Growth continues to primarily invest in companies located in developed countries around the world (excluding the United States).

8

| International Growth | ||

| Top Ten Holdings as of November 30, 2009 | ||

| % of net assets | % of net assets | |

| as of 11/30/09 | as of 5/31/09 | |

| BHP Billiton Ltd. | 2.4% | 1.7% |

| HSBC Holdings plc (Hong Kong) | 2.1% | 1.2% |

| Banco Santander SA | 1.9% | 1.8% |

| Saipem SpA | 1.8% | 1.6% |

| BG Group plc | 1.8% | 1.8% |

| Roche Holding AG | 1.7% | 1.2% |

| Nestle SA | 1.7% | 1.8% |

| Vale SA Preference Shares | 1.7% | 1.5% |

| Telefonica SA | 1.7% | 1.1% |

| BNP Paribas | 1.6% | 1.2% |

| Types of Investments in Portfolio | ||

| % of net assets | % of net assets | |

| as of 11/30/09 | as of 5/31/09 | |

| Foreign Common Stocks | 99.7% | 99.5% |

| Temporary Cash Investments | 0.2% | 0.5% |

| Other Assets and Liabilities | 0.1% | —(1) |

| (1) Category is less than 0.05% of total net assets. | ||

| Investments by Country as of November 30, 2009 | ||

| % of net assets | % of net assets | |

| as of 11/30/09 | as of 5/31/09 | |

| United Kingdom | 18.8% | 17.6% |

| Japan | 15.2% | 14.2% |

| Switzerland | 8.1% | 9.9% |

| Germany | 6.3% | 6.9% |

| France | 6.0% | 6.1% |

| Australia | 4.6% | 4.8% |

| Brazil | 4.0% | 2.7% |

| People’s Republic of China | 3.8% | 3.3% |

| Spain | 3.6% | 3.4% |

| Sweden | 3.4% | 0.6% |

| Netherlands | 3.3% | 2.0% |

| South Korea | 3.1% | 2.9% |

| Italy | 2.9% | 5.1% |

| Other Countries | 16.6% | 20.0% |

| Cash and Equivalents(2) | 0.3% | 0.5% |

| (2) Includes temporary cash investments and other assets and liabilities. | ||

9

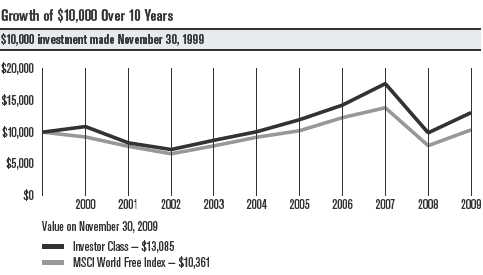

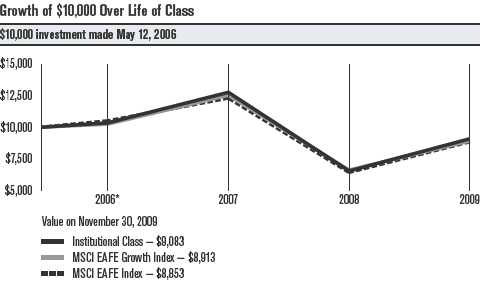

| Performance |

| Global Growth | ||||||

| Total Returns as of November 30, 2009 | ||||||

| Average Annual Returns | ||||||

| Since | Inception | |||||

| 1 year | 5 years | 10 years | Inception | Date | ||

| Investor Class | 32.24% | 5.37% | 2.72% | 7.34% | 12/1/98 | |

| MSCI World Free Index | 31.79% | 2.41% | 0.36% | 2.09%(1) | — | |

| Institutional Class | 32.61% | 5.62% | — | 1.04% | 8/1/00 | |

| A Class(2) | 2/5/99 | |||||

| No sales charge* | 32.01% | 5.13% | 2.48% | 6.12% | ||

| With sales charge* | 24.51% | 3.89% | 1.87% | 5.55% | ||

| B Class | 12/1/05 | |||||

| No sales charge* | 31.06% | — | — | 0.84% | ||

| With sales charge* | 27.06% | — | — | 0.10% | ||

| C Class | 31.23% | 4.37% | — | 5.10% | 3/1/02 | |

| R Class | 31.79% | — | — | 2.94% | 7/29/05 | |

| * Sales charges include initial sales charges and contingent deferred sales charges (CDSCs), as applicable. A Class shares have a 5.75% | ||||||

| maximum initial sales charge for equity funds and may be subject to a maximum CDSC of 1.00%. B Class shares redeemed within six | ||||||

| years of purchase are subject to a CDSC that declines from 5.00% during the first year after purchase to 0.00% the sixth year after | ||||||

| purchase. C Class shares redeemed within 12 months of purchase are subject to a maximum CDSC of 1.00%. The SEC requires that | ||||||

| mutual funds provide performance information net of maximum sales charges in all cases where charges could be applied. | ||||||

| (1) | Since 11/30/98, the date nearest the Investor Class’s inception for which data are available. | |||||

| (2) | Prior to September 4, 2007, the A Class was referred to as the Advisor Class. Performance, with sales charge, prior to that date has been | |||||

| adjusted to reflect the A Class’s current sales charge. | ||||||

Data presented reflect past performance. Past performance is no guarantee of future results. Current performance may be higher or lower than the performance shown. Investment return and principal value will fluctuate, and redemption value may be more or less than original cost. To obtain performance data current to the most recent month end, please call 1-800-345-2021 or visit americancentury.com. International investing involves special risks, such as political instability and currency fluctuations. Investing in emerging markets may accentuate these risks.

Unless otherwise indicated, performance reflects Investor Class shares; performance for other share classes will vary due to differences in fee structure. For information about other share classes available, please consult the prospectus. Data assumes reinvestment of dividends and capital gains, and none of the charts reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Returns for the index are provided for comparison. The fund’s total returns include operating expenses (such as transaction costs and management fees) that reduce returns, while the total returns of the index do not.

10

Global Growth

| One-Year Returns Over 10 Years | ||||||||||

| Periods ended November 30 | ||||||||||

| 2000 | 2001 | 2002 | 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | |

| Investor Class | 8.81% | -23.62% | -12.78% | 20.22% | 15.59% | 18.87% | 19.30% | 23.73% | -44.01% | 32.24% |

| MSCI World | ||||||||||

| Free Index | -7.64% | -16.01% | -15.27% | 19.17% | 17.43% | 11.20% | 20.28% | 12.71% | -43.30% | 31.79% |

| Total Annual Fund Operating Expenses | |||||

| Institutional | |||||

| Investor Class | Class | A Class | B Class | C Class | R Class |

| 1.26% | 1.06% | 1.51% | 2.26% | 2.26% | 1.76% |

The total annual fund operating expenses shown is as stated in the fund’s prospectus current as of the date of this report. The prospectus may vary from the expense ratio shown elsewhere in this report because it is based on a different time period, includes acquired fund fees and expenses, and, if applicable, does not include fee waivers or expense reimbursements.

Data presented reflect past performance. Past performance is no guarantee of future results. Current performance may be higher or lower than the performance shown. Investment return and principal value will fluctuate, and redemption value may be more or less than original cost. To obtain performance data current to the most recent month end, please call 1-800-345-2021 or visit americancentury.com. International investing involves special risks, such as political instability and currency fluctuations. Investing in emerging markets may accentuate these risks.

Unless otherwise indicated, performance reflects Investor Class shares; performance for other share classes will vary due to differences in fee structure. For information about other share classes available, please consult the prospectus. Data assumes reinvestment of dividends and capital gains, and none of the charts reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Returns for the index are provided for comparison. The fund’s total returns include operating expenses (such as transaction costs and management fees) that reduce returns, while the total returns of the index do not.

11

| Portfolio Commentary |

Global Growth

Portfolio Managers: Keith Creveling and Brent Puff

Performance Summary

The Global Growth portfolio advanced 32.24%* for the 12 months ended November 30, 2009, outperforming its benchmark, the MSCI World Free Index, which gained 31.79%.

Despite the severe worldwide recession, credit-market meltdown, and financial-sector crisis, global stocks finished the 12-month period with sharp gains. Initially, stocks plunged, as rising unemployment, shrinking industrial output, and negative economic growth rates sent investor confidence tumbling. But, by mid-March, market sentiment and stock performance reversed course quickly, as massive stimulus efforts from global central banks and governments generated optimism among investors.

Overall, good stock selection combined with favorable sector allocations accounted for the portfolio’s outperformance relative to the benchmark. Our stock selection was particularly strong in the energy and financials sectors, while an overweight in the top-performing information technology segment and an underweight in the benchmark-trailing utilities sector contributed positively.

U.S. Was Top Contributor

The United States, which comprised approximately half the portfolio as of November 30, led all country contributors in the fund, followed by Japan and China. Performance in the United States was driven by an overweight position in American Express, the top-performing stock in the portfolio for the period. The credit card issuer reported firming fundamentals within its customer base, as delinquency and loan charge-off rates steadily improved.

Favorable stock selection combined with an underweight led to outperforming results for the portfolio in Japan. In China, our small, out-of-benchmark allocation generated favorable results, as China’s economy benefited from infrastructure spending and stimulus efforts designed to boost domestic consumption.

The largest laggards from a regional perspective included Canada and Spain, where underweights and negative stock selection detracted from results. Spain was home to one of the portfolio’s leading detractors, toll road operator Cintra Concesiones de Infraestructuras de Transporte. The company reported traffic declines on its roads in the U.S. and Spain and experienced funding and shareholder challenges when it explored a potential merger with its parent, Grupo Ferrovial of Spain.

*All fund returns referenced in this commentary are for Investor Class shares.

12

Global Growth

Technology Led All Sectors

Information technology stocks were among the benchmark leaders, and our overweight combined with good stock selection enhanced the portfolio’s performance. In particular, U.S.-based computer and electronic device maker Apple drove the portfolio’s results. Better-than-expected revenues and strong market enthusiasm for the company’s iPhone helped push the stock price higher. Tencent Holdings, China’s leading Internet service provider, also generated strong results for the portfolio.

A sharp upswing in oil prices throughout most of 2009 helped generate strong returns in the energy sector. Stock selection was key, as our overweight positions in Saipem, an Italian oil and gas services company, and Occidental Petroleum, U.S.-based oil and natural gas exploration companies, helped the portfolio’s outperformance.

Materials, Consumer Discretionary Stocks Lagged

The portfolio’s performance was negatively affected by stock selection and an underweight position in the materials sector, which was the top-performing sector in the benchmark.

In the consumer discretionary sector, our overweight had a positive influence on performance, but disappointing stock selection dragged down the sector’s overall contribution compared with the benchmark. U.S.-based Apollo Group, an educational services company, was the portfolio’s largest individual detractor. Apollo’s stock tumbled on concerns about potential regulatory and legal changes from the U.S. Department of Education.

Outlook

Global Growth continues to invest primarily in companies located in developed countries throughout the world, including the United States. Recently, corporate earnings have shown signs of improvement throughout the world. While most of the improvements have come from better cost management and restructuring, we remain encouraged by the progress and believe even a moderate improvement in underlying demand will drive sharply improved profit performance. We will closely monitor the upcoming corporate earnings reporting season, which should provide more clarity on the sustainability of earnings improvements.

13

| Global Growth | ||

| Top Ten Holdings as of November 30, 2009 | ||

| % of net assets | % of net assets | |

| as of 11/30/09 | as of 5/31/09 | |

| BHP Billiton Ltd. | 2.6% | 1.8% |

| Apple, Inc. | 2.4% | 2.0% |

| American Express Co. | 2.3% | 1.5% |

| Google, Inc., Class A | 2.2% | 1.5% |

| Colgate-Palmolive Co. | 2.1% | 1.8% |

| 3M Co. | 2.0% | 1.3% |

| MasterCard, Inc., Class A | 2.0% | 1.0% |

| Occidental Petroleum Corp. | 2.0% | 1.8% |

| priceline.com, Inc. | 1.9% | 1.0% |

| Banco Santander SA | 1.9% | — |

| Types of Investments in Portfolio | ||

| % of net assets | % of net assets | |

| as of 11/30/09 | as of 5/31/09 | |

| Domestic Common Stocks | 51.8% | 50.4% |

| Foreign Common Stocks | 47.3% | 48.5% |

| Total Equity Exposure | 99.1% | 98.9% |

| Temporary Cash Investments | 0.8% | 0.5% |

| Other Assets and Liabilities | 0.1% | 0.6% |

| Investments by Country as of November 30, 2009 | ||

| % of net assets | % of net assets | |

| as of 11/30/09 | as of 5/31/09 | |

| United States | 51.8% | 50.4% |

| United Kingdom | 8.7% | 9.7% |

| Japan | 8.0% | 6.3% |

| Switzerland | 5.6% | 4.5% |

| Australia | 4.3% | 3.3% |

| Ireland | 3.0% | 2.2% |

| Brazil | 2.7% | 1.5% |

| South Korea | 2.0% | 0.6% |

| Spain | 1.9% | — |

| Other Countries | 11.1% | 20.4% |

| Cash and Equivalents* | 0.9% | 1.1% |

| * Includes temporary cash investments and other assets and liabilities. | ||

14

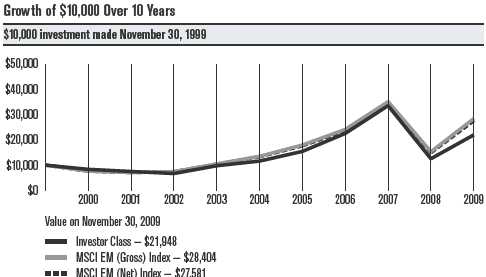

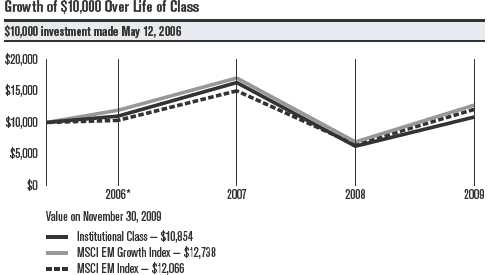

| Performance |

| Emerging Markets | ||||||

| Total Returns as of November 30, 2009 | ||||||

| Average Annual Returns | ||||||

| Since | Inception | |||||

| 1 year | 5 years | 10 years | Inception | Date | ||

| Investor Class | 75.36% | 13.62% | 8.17% | 7.70% | 9/30/97 | |

| MSCI EM Growth Index(1)(2) | 83.97% | 13.90% | — | — | — | |

| MSCI EM (Net) Index(1)(2) | 85.12% | 15.70% | 10.68% | — | — | |

| MSCI EM (Gross) Index(2) | 85.68% | 16.07% | 11.00% | 8.11% | — | |

| Institutional Class | 75.92% | 13.86% | 8.38% | 12.87% | 1/28/99 | |

| A Class(3) | 5/12/99 | |||||

| No sales charge* | 75.24% | 13.37% | 7.92% | 9.89% | ||

| With sales charge* | 65.10% | 12.03% | 7.28% | 9.28% | ||

| B Class | 9/28/07 | |||||

| No sales charge* | 74.10% | — | — | -16.81% | ||

| With sales charge* | 70.10% | — | — | -18.54% | ||

| C Class | 73.99% | 12.49% | — | 12.77% | 12/18/01 | |

| R Class | 74.94% | — | — | -16.42% | 9/28/07 | |

| * Sales charges include initial sales charges and contingent deferred sales charges (CDSCs), as applicable. A Class shares have a 5.75% | ||||||

| maximum initial sales charge for equity funds and may be subject to a maximum CDSC of 1.00%. B Class shares redeemed within six | ||||||

| years of purchase are subject to a CDSC that declines from 5.00% during the first year after purchase to 0.00% the sixth year after | ||||||

| purchase. C Class shares redeemed within 12 months of purchase are subject to a maximum CDSC of 1.00%. The SEC requires that | ||||||

| mutual funds provide performance information net of maximum sales charges in all cases where charges could be applied. | ||||||

| (1) | MSCI EM Growth Index data first available 2/1/01. MSCI EM (Net) Index data first available 12/31/98. | |||||

| (2) | From September of 1997 through December 2008, the fund’s benchmark was the MSCI EM (Gross) Index. From January 2009 through | |||||

| March 2009, the fund’s benchmark was the MSCI EM (Net) Index. In April of 2009, the fund’s benchmark changed from the MSCI EM (Net) | ||||||

| Index to the MSCI EM Growth Index. The fund’s investment advisor believes this index better represents the fund’s portfolio composition. | ||||||

| (3) | Prior to September 4, 2007, the A Class was referred to as the Advisor Class. Performance, with sales charge, prior to that date has been | |||||

| adjusted to reflect the A Class’s current sales charge. | ||||||

Data presented reflect past performance. Past performance is no guarantee of future results. Current performance may be higher or lower than the performance shown. Investment return and principal value will fluctuate, and redemption value may be more or less than original cost. To obtain performance data current to the most recent month end, please call 1-800-345-2021 or visit americancentury.com. International investing involves special risks, such as political instability and currency fluctuations. Investing in emerging markets may accentuate these risks.

Unless otherwise indicated, performance reflects Investor Class shares; performance for other share classes will vary due to differences in fee structure. For information about other share classes available, please consult the prospectus. Data assumes reinvestment of dividends and capital gains, and none of the charts reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Returns for the indices are provided for comparison. The fund’s total returns include operating expenses (such as transaction costs and management fees) that reduce returns, while the total returns of the indices do not.

15

Emerging Markets

| One-Year Returns Over 10 Years | ||||||||||

| Periods ended November 30 | ||||||||||

| 2000 | 2001 | 2002 | 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | |

| Investor Class | -16.73% | -10.28% | -10.86% | 46.26% | 18.94% | 33.10% | 46.10% | 48.81% | -62.66% | 75.36% |

| MSCI EM | ||||||||||

| Growth Index* | — | -25.19%** | 5.63% | 35.32% | 21.59% | 33.59% | 34.42% | 42.79% | -59.37% | 83.97% |

| MSCI EM | ||||||||||

| (Net) Index | -23.84% | -7.60% | 4.75% | 40.46% | 28.47% | 32.60% | 33.95% | 45.15% | -56.56% | 85.12% |

| MSCI EM | ||||||||||

| (Gross) Index | -23.63% | -7.37% | 4.95% | 40.87% | 28.88% | 33.13% | 34.38% | 45.57% | -56.42% | 85.68% |

| * Since benchmark data is only available from 2/1/01, it is not included in the line chart. One year data is listed for all periods available. | ||||||||||

| **Benchmark return from 2/1/01 to 11/30/01. Not annualized. | ||||||||||

| Total Annual Fund Operating Expenses | ||||||||||

| Institutional | ||||||||||

| Investor Class | Class | A Class | B Class | C Class | R Class | |||||

| 1.82% | 1.62% | 2.07% | 2.82% | 2.82% | 2.32% | |||||

The total annual fund operating expenses shown is as stated in the fund’s prospectus current as of the date of this report. The prospectus may vary from the expense ratio shown elsewhere in this report because it is based on a different time period, includes acquired fund fees and expenses, and, if applicable, does not include fee waivers or expense reimbursements.

Data presented reflect past performance. Past performance is no guarantee of future results. Current performance may be higher or lower than the performance shown. Investment return and principal value will fluctuate, and redemption value may be more or less than original cost. To obtain performance data current to the most recent month end, please call 1-800-345-2021 or visit americancentury.com. International investing involves special risks, such as political instability and currency fluctuations. Investing in emerging markets may accentuate these risks.

Unless otherwise indicated, performance reflects Investor Class shares; performance for other share classes will vary due to differences in fee structure. For information about other share classes available, please consult the prospectus. Data assumes reinvestment of dividends and capital gains, and none of the charts reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Returns for the indices are provided for comparison. The fund’s total returns include operating expenses (such as transaction costs and management fees) that reduce returns, while the total returns of the indices do not.

16

| Portfolio Commentary |

Emerging Markets

Portfolio Managers: Patricia Ribeiro and Anthony Han

Performance Summary

The Emerging Markets portfolio advanced 75.36%* for the 12 months ended November 30, 2009, underperforming its benchmark, the MSCI EM Growth Index,** which gained 83.97%.

Emerging markets stocks surged in 2009, as investors seeking to recoup the losses of 2008 sought higher-yielding assets perceived to have fewer links with the battered developed economies that had been negatively affected by the global economic crisis and subprime market debacle. The fallout in global markets left few economies unscathed, but sound macroeconomic fundamentals and stimulus measures helped emerging market countries cope better than other nations. Furthermore, emerging markets remained shielded from the problems of the developed world due to years of conservative fiscal policy, which resulted in higher savings rates and employment growth and increases in business and infrastructure investment. Unlike consumers in the U.S. and other developed countries, consumers in emerging economies did not take on huge amounts of debt, and financial institutions did not have exposure to toxic assets such as subprime mortgages.

The portfolio’s underperformance relative to the benchmark primarily was due to sector allocations and the impact of currency exchange rates. Overall, our stock selection was a positive contributor, but it was not sufficient to offset the currency and allocation influences.

Israel Led Detractors; Mexico Led Contributors

From a regional perspective, the portfolio’s largest detractors to performance included Israel, India, and South Korea. In each country, our allocation decisions were effective, but stock selection primarily accounted for the poor relative performance. On the positive side, Mexico, Turkey, and Russia represented the portfolio’s leading country contributors, primarily due to positive stock selection.

All Sectors Showed Strong Returns

On an absolute basis, all of the portfolio’s 10 sectors posted strong gains for the 12-month period, with returns in the utilities and materials sectors topping 100%. Relative to the benchmark, the portfolio’s information technology, energy, and materials sectors detracted from results, while its telecommunication services, utilities and industrials sectors contributed positively to relative performance.

* All fund returns referenced in this commentary are for Investor Class shares.

**In April 2009, the fund’s benchmark changed from the MSCI EM (Net) Index to the MSCI EM Growth Index. The fund’s investment advisor believes

this index better represents the fund’s portfolio composition.

17

Emerging Markets

Our poor relative performance in the information technology sector was primarily due to portfolio-only holding Rolta India, the fund’s leading detractor for the period. Stock in the India-based geospatial mapping systems company plummeted in the wake of a financial scandal involving Indian technology outsourcing company Satyam. Subsequent rumors implicated Rolta, which denied any wrongdoing.

In the energy sector, our stock selection and overweight position generally were favorable, but currency exchange rates detracted from results. In the materials sector, our strategies in the chemicals and metals and mining industries accounted for the bulk of the lagging results. In particular, our underweight position in Brazilian iron ore miner Companhia Vale do Rio Doce detracted from performance.

The portfolio’s outperformance in the telecommunication services sector was largely due to stock selection and our underweight position in the wireless industry. Specifically, Mexico’s America Movil SAB, a wireless telecom services provider doing business in Mexico and Latin America, was a leading contributor. Stock selection drove the strong overall performance in the portfolio’s utilities sector. In particular, the portfolio benefited from our overweight position in India’s state-owned Power Grid Corp. In the industrials sector, our overweight position in China High Speed Transmission Equipment Group, a manufacturer of gear boxes for wind turbines, drove results. With an absolute total return of nearly 200%, the stock finished the 12-month period as the leading contributor to the portfolio’s performance.

Outlook

Emerging markets have been able to withstand the greatest economic crisis since the Great Depression, primarily because they have managed their economies well throughout the past several years. While challenges remain, we expect emerging markets may continue to offer above-average earnings growth in the short and long term. We believe the global economy should start growing again in 2010, and the emerging markets may accelerate at a much faster rate than the U.S. and Europe, due in part to continued frugality among Western consumers.

18

| Emerging Markets | ||

| Top Ten Holdings as of November 30, 2009 | ||

| % of net assets | % of net assets | |

| as of 11/30/09 | as of 5/31/09 | |

| Samsung Electronics Co. Ltd. | 5.3% | 3.5% |

| Vale SA Preference Shares | 5.0% | 4.3% |

| Petroleo Brasileiro SA-Petrobras ADR | 3.7% | 4.9% |

| Itau Unibanco Holding SA Preference Shares | 3.0% | 2.0% |

| Hon Hai Precision Industry Co. Ltd. | 2.8% | 1.9% |

| Taiwan Semiconductor Manufacturing Co. Ltd. | 2.7% | 2.4% |

| China Life Insurance Co. Ltd. H Shares | 2.5% | 1.8% |

| Infosys Technologies Ltd. | 2.3% | 0.8% |

| Sberbank of Russian Federation | 2.3% | 1.2% |

| America Movil SAB de CV, Series L ADR | 2.2% | 2.3% |

| Types of Investments in Portfolio | ||

| % of net assets | % of net assets | |

| as of 11/30/09 | as of 5/31/09 | |

| Foreign Common Stocks | 98.0% | 98.1% |

| Temporary Cash Investments | 2.2% | 0.8% |

| Other Assets and Liabilities | (0.2)% | 1.1% |

| Investments by Country as of November 30, 2009 | ||

| % of net assets | % of net assets | |

| as of 11/30/09 | as of 5/31/09 | |

| Brazil | 16.3% | 16.8% |

| People’s Republic of China | 14.0% | 13.7% |

| South Korea | 13.0% | 11.6% |

| Russian Federation | 9.4% | 6.7% |

| Taiwan (Republic of China) | 8.5% | 13.9% |

| India | 8.0% | 8.5% |

| Hong Kong | 5.9% | 5.2% |

| South Africa | 5.4% | 6.7% |

| Mexico | 4.1% | 2.9% |

| Indonesia | 3.3% | 2.3% |

| Turkey | 2.3% | 1.9% |

| Thailand | 2.0% | 0.9% |

| Other Countries | 5.8% | 7.0% |

| Cash and Equivalents* | 2.0% | 1.9% |

| * Includes temporary cash investments and other assets and liabilities. | ||

19

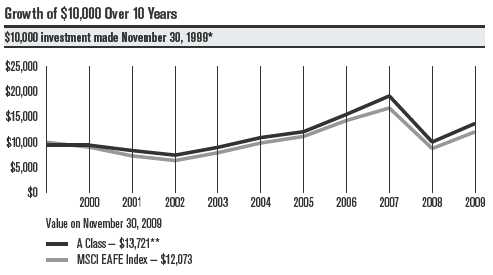

| Performance |

| International Value | |||||

| Total Returns as of November 30, 2009 | |||||

| Average Annual Returns | |||||

| Since | Inception | ||||

| 1 year | 5 years | 10 years | Inception | Date | |

| A Class | 3/31/97 | ||||

| No sales charge* | 36.40% | 4.65%(1) | 3.82%(1) | 3.70%(1) | |

| With sales charge* | 28.65% | 3.41%(1) | 3.21%(1) | 3.22%(1) | |

| MSCI EAFE Index | 37.72% | 4.13% | 1.90% | 4.49% | — |

| Investor Class | 36.98% | — | — | -0.16% | 4/3/06 |

| Institutional Class | 37.18% | — | — | 0.03% | 4/3/06 |

| B Class | 3/31/97 | ||||

| No sales charge* | 35.36% | 3.90%(1) | 3.11%(1) | 3.01%(1) | |

| With sales charge* | 31.36% | 3.73%(1) | 3.11%(1) | 3.01%(1) | |

| C Class | 35.44% | — | — | -1.17% | 4/3/06 |

| R Class | 35.90% | — | — | -0.70% | 4/3/06 |

| * Sales charges include initial sales charges and contingent deferred sales charges (CDSCs), as applicable. A Class shares have a 5.75% | |||||

| maximum initial sales charge for equity funds and may be subject to a maximum CDSC of 1.00%. B Class shares redeemed within six | |||||

| years of purchase are subject to a CDSC that declines from 5.00% during the first year after purchase to 0.00% the sixth year after | |||||

| purchase. C Class shares redeemed within 12 months of purchase are subject to a maximum CDSC of 1.00%. The SEC requires that | |||||

| mutual funds provide performance information net of maximum sales charges in all cases where charges could be applied. | |||||

International Value acquired all the net assets of the Mason Street International Equity Fund on March 31, 2006, pursuant to a plan of reorganization approved by the acquired fund’s shareholders on March 15, 2006. Performance information prior to April 1, 2006, is that of the Mason Street International Equity Fund.

(1) Class returns would have been lower if fees had not been waived.

Data presented reflect past performance. Past performance is no guarantee of future results. Current performance may be higher or lower than the performance shown. Investment return and principal value will fluctuate, and redemption value may be more or less than original cost. To obtain performance data current to the most recent month end, please call 1-800-345-2021 or visit americancentury.com. International investing involves special risks, such as political instability and currency fluctuations. Investing in emerging markets may accentuate these risks.

Unless otherwise indicated, performance reflects A Class shares; performance for other share classes will vary due to differences in fee structure. For information about other share classes available, please consult the prospectus. Data assumes reinvestment of dividends and capital gains, and none of the charts reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Returns for the index are provided for comparison. The fund’s total returns include operating expenses (such as transaction costs and management fees) that reduce returns, while the total returns of the index do not.

20

International Value

| One-Year Returns Over 10 Years | ||||||||||

| Periods ended November 30 | ||||||||||

| 2000 | 2001 | 2002 | 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | |

| A Class | ||||||||||

| (no sales charge)** | 0.00% | -11.24% | -10.87% | 20.77% | 21.40% | 10.68% | 28.36% | 23.44% | -47.53% | 36.40% |

| MSCI EAFE Index | -9.67% | -19.13% | -12.50% | 24.22% | 24.19% | 13.25% | 28.20% | 17.30% | -47.79% | 37.72% |

| * International Value A Class’s initial investment is $9,425 to reflect the maximum 5.75% initial sales charge. | ||||||||||

| **Class returns would have been lower if fees had not been waived. | ||||||||||

| Total Annual Fund Operating Expenses | |||||

| Institutional | |||||

| Investor Class | Class | A Class | B Class | C Class | R Class |

| 1.31% | 1.11% | 1.56% | 2.31% | 2.31% | 1.81% |

The total annual fund operating expenses shown is as stated in the fund’s prospectus current as of the date of this report. The prospectus may vary from the expense ratio shown elsewhere in this report because it is based on a different time period, includes acquired fund fees and expenses, and, if applicable, does not include fee waivers or expense reimbursements.

Data presented reflect past performance. Past performance is no guarantee of future results. Current performance may be higher or lower than the performance shown. Investment return and principal value will fluctuate, and redemption value may be more or less than original cost. To obtain performance data current to the most recent month end, please call 1-800-345-2021 or visit americancentury.com. International investing involves special risks, such as political instability and currency fluctuations. Investing in emerging markets may accentuate these risks.

Unless otherwise indicated, performance reflects A Class shares; performance for other share classes will vary due to differences in fee structure. For information about other share classes available, please consult the prospectus. Data assumes reinvestment of dividends and capital gains, and none of the charts reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Returns for the index are provided for comparison. The fund’s total returns include operating expenses (such as transaction costs and management fees) that reduce returns, while the total returns of the index do not.

21

| Portfolio Commentary |

International Value

Portfolio Managers: Gary Motyl and Guang Yang

Performance Summary

International Value returned 36.40%* for the 12 months ended November 30, 2009. By comparison, its benchmark, the MSCI EAFE Index, returned 37.72%. (Please see pages 20 and 21 for additional performance comparisons.)

The portfolio’s strong absolute return reflects the ongoing rebound of global financial markets from the depths of the credit crisis, as well as the decline in the value of the U.S. dollar. (A weaker greenback is beneficial because overseas investments are worth more when translated back into dollars.) No sector had negative results in dollar terms.

Relative to the benchmark, performance was led by some of the most economically sensitive segments of the market, including consumer discretionary, industrial, and information technology shares. Positioning in three sectors detracted from relative results: financials, materials, and health care.

Financials, Materials Detracted Most

The portfolio’s financial and materials shares were the leading detractors from relative performance because of negative currency effects and underweight positions. While these two sectors were the poorest-performing portions of the MSCI EAFE Index in 2008, they rebounded dramatically to become the two best-performing segments of the benchmark for the last 12 months.

The largest individual detractor in these sectors was global property and casualty insurer ACE Limited. We see it as a conservatively managed, high-quality company trading at very attractive valuations, but the stock did not participate in the recent rally, when traders favored higher-flying, riskier names. In addition, it hurt to be underrepresented in the commercial banks and capital markets stocks that rebounded sharply since March 2009, including HSBC Holdings, Banco Santander, Commonwealth Bank of Australia, and Deutsche Bank.

With respect to materials shares, it hurt to be underrepresented in metals and mining stocks in favor of paper and forest product companies. The portfolio had no exposure to natural resources giants BHP Billiton and Rio Tinto, which rallied sharply on signs of economic stabilization in 2009. At the same time, stakes in Finnish paper-products companies UPM-Kymmene and Stora Enso Oyj underperformed because of ongoing concern about excess capacity, high input costs, and poor demand.

In the health care sector, the primary source of weakness was an overweight position in the defensive-oriented pharmaceutical industry. These stocks lagged in the rally, making Merck KGaA (“German Merck,” as opposed to U.S.-based pharma giant Merck & Co.), Takeda Pharmaceutical, and Novartis notable detractors.

* All fund returns referenced in this commentary are for A Class shares and are not reduced by sales charges. A Class shares are subject to a

maximum sales charge of 5.75%. Had the sales charge been applied, returns would be lower than those shown.

22

International Value

Key Contributors

The leading contribution to the portfolio’s outperformance came from stock selection among consumer discretionary shares. One theme evident in this space was the portfolio’s effective positioning among auto makers and auto component companies. Among the leading contributors for the year were Korean car maker Hyundai Motor Co., Chinese battery and auto manufacturer BYD (an industrial conglomerate that’s actually categorized in the information technology sector), German automobile manufacturer Bayerische Motoren Werke (BMW), and France-based tire manufacturer Michelin. Hyundai’s relatively low-cost, fuel-efficient lineup saw it gain market share in the U.S. and, along with BYD, the company benefited from exposure to the growing Chinese market.

Industrials a Source of Strength

Stock picks among industrial shares proved another source of strength, led by positioning across a wide range of industries. For example, it helped to favor commercial services, electrical equipment, and airlines stocks, while avoiding poor-performing road and rail shares. Vestas Wind Systems was the leading contributor in the sector thanks to strong demand for alternative energy sources. British Airways benefited from a decline in 2008 record oil price levels, improvement in the global economy, and the prospect of better margins thanks to fee increases and cost cuts. Global business services provider Rentokil Initial and Shanghai Electric were other notable contributors in the sector.

Other Contributors

Stock picks in information technology (IT) and telecommunication services also helped relative results. The top contributors in the IT sector were Samsung Electronics, Compal Electronics, and Taiwan Semiconductor. Meanwhile, the number-one contributor to relative return was diversified telecommunication firm Telenor. The Norwegian-based telecom provider rebounded sharply beginning in late 2008 on the strength of cost cuts, stronger-than-expected margins, and exposure to desirable east European and Asian markets.

Outlook

“The portfolio’s positioning in terms of its sector and industry weightings, as well as country allocations, typically reflect where we are finding what we believe to be the most attractive securities at a given time,” said portfolio manager Guang Yang. “This follows from our value-oriented investment approach, which seeks to build a portfolio of high-quality companies trading at attractive valuations. As of November 30, 2009, we found opportunity in the telecommunication services sector. Information technology, energy, and consumer discretionary shares were other notable overweight positions,” he added. “And as we’ve been reporting to shareholders for some time now, we continue to hold underweight positions in the financials, consumer staples, and materials sectors.”

23

| International Value | ||

| Top Ten Holdings as of November 30, 2009 | ||

| % of net assets | % of net assets | |

| as of 11/30/09 | as of 5/31/09 | |

| Telefonica SA ADR | 3.9% | 1.8% |

| France Telecom SA | 2.9% | 1.7% |

| Vodafone Group plc | 2.9% | 1.2% |

| Telenor ASA | 2.9% | 1.1% |

| E.ON AG | 2.8% | 1.5% |

| Deutsche Post AG | 2.7% | 1.2% |

| Merck KGaA | 2.2% | 1.4% |

| AXA SA | 2.1% | 0.9% |

| Roche Holding AG | 2.1% | 0.8% |

| Cie Generale des Etablissements Michelin, Class B | 2.1% | 1.0% |

| Types of Investments in Portfolio | ||

| % of net assets | % of net assets | |

| as of 11/30/09 | as of 5/31/09 | |

| Foreign Common Stocks & Rights | 93.5% | 92.9% |

| Temporary Cash Investments | 5.3% | 6.4% |

| Other Assets and Liabilities | 1.2% | 0.7% |

| Investments by Country as of November 30, 2009 | ||

| % of net assets | % of net assets | |

| as of 11/30/09 | as of 5/31/09 | |

| United Kingdom | 17.7% | 16.5% |

| France | 13.2% | 9.0% |

| Germany | 12.2% | 8.2% |

| Switzerland | 8.7% | 7.9% |

| Spain | 6.9% | 4.5% |

| Netherlands | 5.5% | 5.4% |

| South Korea | 4.9% | 4.6% |

| Brazil | 3.9% | 3.2% |

| Japan | 3.0% | 6.8% |

| Norway | 2.9% | 1.1% |

| Hong Kong | 2.1% | 4.5% |

| Other Countries | 12.5% | 21.2% |

| Cash and Equivalents* | 6.5% | 7.1% |

| * Includes temporary cash investments and other assets and liabilities. | ||

24

| Shareholder Fee Examples (Unaudited) |

Fund shareholders may incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments and redemption/ exchange fees; and (2) ongoing costs, including management fees; distribution and service (12b-1) fees; and other fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in your fund and to compare these costs with the ongoing cost of investing in other mutual funds.

The example is based on an investment of $1,000 made at the beginning of the period and held for the entire period from June 1, 2009 to November 30, 2009.

Actual Expenses

The table provides information about actual account values and actual expenses for each class. You may use the information, together with the amount you invested, to estimate the expenses that you paid over the period. First, identify the share class you own. Then simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number under the heading “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

If you hold Investor Class shares of any American Century Investments fund, or Institutional Class shares of the American Century Diversified Bond Fund, in an American Century Investments account (i.e., not a financial intermediary or retirement plan account), American Century Investments may charge you a $12.50 semiannual account maintenance fee if the value of those shares is less than $10,000. We will redeem shares automatically in one of your accounts to pay the $12.50 fee. In determining your total eligible investment amount, we will include your investments in all personal accounts (including American Century Investments Brokerage accounts) registered under your Social Security number. Personal accounts include individual accounts, joint accounts, UGMA/UTMA accounts, personal trusts, Coverdell Education Savings Accounts and IRAs (including traditional, Roth, Rollover, SEP-, SARSEP- and SIMPLE-IRAs), and certain other retirement accounts. If you have only business, business retirement, employer-sponsored or American Century Investments Brokerage accounts, you are currently not subject to this fee. We will not charge the fee as long as you choose to manage your accounts exclusively online. If you are subject to the Account Maintenance Fee, your account value could be reduced by the fee amount.

Hypothetical Example for Comparison Purposes

The table also provides information about hypothetical account values and hypothetical expenses based on the actual expense ratio of each class of your fund and an assumed rate of return of 5% per year before expenses, which is not the actual return of a fund’s share class. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in your fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

25

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads) or redemption/exchange fees. Therefore, the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| Beginning | Ending | Expenses Paid | ||

| Account Value | Account Value | During Period* | Annualized | |

| 6/1/09 | 11/30/09 | 6/1/09 – 11/30/09 | Expense Ratio* | |

| International Growth | ||||

| Actual | ||||

| Investor Class | $1,000 | $1,205.20 | $7.52 | 1.36% |

| Institutional Class | $1,000 | $1,207.40 | $6.42 | 1.16% |

| A Class | $1,000 | $1,204.50 | $8.90 | 1.61% |

| B Class | $1,000 | $1,200.00 | $13.03 | 2.36% |

| C Class | $1,000 | $1,200.00 | $13.03 | 2.36% |

| R Class | $1,000 | $1,201.50 | $10.27 | 1.86% |

| Hypothetical | ||||

| Investor Class | $1,000 | $1,018.25 | $6.88 | 1.36% |

| Institutional Class | $1,000 | $1,019.25 | $5.87 | 1.16% |

| A Class | $1,000 | $1,017.00 | $8.14 | 1.61% |

| B Class | $1,000 | $1,013.22 | $11.93 | 2.36% |

| C Class | $1,000 | $1,013.22 | $11.93 | 2.36% |

| R Class | $1,000 | $1,015.74 | $9.40 | 1.86% |

| Global Growth | ||||

| Actual | ||||

| Investor Class | $1,000 | $1,211.20 | $6.60 | 1.19% |

| Institutional Class | $1,000 | $1,213.50 | $5.49 | 0.99% |

| A Class | $1,000 | $1,209.80 | $7.98 | 1.44% |

| B Class | $1,000 | $1,205.50 | $12.11 | 2.19% |

| C Class | $1,000 | $1,205.60 | $12.11 | 2.19% |

| R Class | $1,000 | $1,207.90 | $9.35 | 1.69% |

| Hypothetical | ||||

| Investor Class | $1,000 | $1,019.10 | $6.02 | 1.19% |

| Institutional Class | $1,000 | $1,020.10 | $5.01 | 0.99% |

| A Class | $1,000 | $1,017.85 | $7.28 | 1.44% |

| B Class | $1,000 | $1,014.09 | $11.06 | 2.19% |

| C Class | $1,000 | $1,014.09 | $11.06 | 2.19% |

| R Class | $1,000 | $1,016.60 | $8.54 | 1.69% |

| * Expenses are equal to the class’s annualized expense ratio listed in the table above, multiplied by the average account value over the period | ||||

| multiplied by 183, the number of days in the most recent fiscal half-year, divided by 365, to reflect the one-half year period. | ||||

26

| Beginning | Ending | Expenses Paid | ||

| Account Value | Account Value | During Period* | Annualized | |

| 6/1/09 | 11/30/09 | 6/1/09 – 11/30/09 | Expense Ratio* | |

| Emerging Markets | ||||

| Actual | ||||

| Investor Class | $1,000 | $1,266.10 | $9.94 | 1.75% |

| Institutional Class | $1,000 | $1,267.90 | $8.81 | 1.55% |

| A Class | $1,000 | $1,263.30 | $11.35 | 2.00% |

| B Class | $1,000 | $1,260.40 | $15.58 | 2.75% |

| C Class | $1,000 | $1,259.60 | $15.58 | 2.75% |

| R Class | $1,000 | $1,263.90 | $12.77 | 2.25% |

| Hypothetical | ||||

| Investor Class | $1,000 | $1,016.29 | $8.85 | 1.75% |

| Institutional Class | $1,000 | $1,017.30 | $7.84 | 1.55% |

| A Class | $1,000 | $1,015.04 | $10.10 | 2.00% |

| B Class | $1,000 | $1,011.28 | $13.87 | 2.75% |

| C Class | $1,000 | $1,011.28 | $13.87 | 2.75% |

| R Class | $1,000 | $1,013.79 | $11.36 | 2.25% |

| International Value | ||||

| Actual | ||||

| Investor Class | $1,000 | $1,197.70 | $7.22 | 1.31% |

| Institutional Class | $1,000 | $1,199.30 | $6.12 | 1.11% |

| A Class | $1,000 | $1,195.80 | $8.59 | 1.56% |

| B Class | $1,000 | $1,193.00 | $12.70 | 2.31% |

| C Class | $1,000 | $1,192.40 | $12.70 | 2.31% |

| R Class | $1,000 | $1,193.40 | $9.95 | 1.81% |

| Hypothetical | ||||

| Investor Class | $1,000 | $1,018.50 | $6.63 | 1.31% |

| Institutional Class | $1,000 | $1,019.50 | $5.62 | 1.11% |

| A Class | $1,000 | $1,017.25 | $7.89 | 1.56% |

| B Class | $1,000 | $1,013.49 | $11.66 | 2.31% |

| C Class | $1,000 | $1,013.49 | $11.66 | 2.31% |

| R Class | $1,000 | $1,015.99 | $9.15 | 1.81% |

| * Expenses are equal to the class’s annualized expense ratio listed in the table above, multiplied by the average account value over the period | ||||

| multiplied by 183, the number of days in the most recent fiscal half-year, divided by 365, to reflect the one-half year period. | ||||

27

| Schedule of Investments |

| International Growth | ||||||

| NOVEMBER 30, 2009 | ||||||

| Shares | Value | Shares | Value | |||

| Common Stocks — 99.7% | LVMH Moet Hennessy | |||||

| Louis Vuitton SA | 90,980 | $ 9,475,340 | ||||

| AUSTRALIA — 4.6% | Pernod-Ricard SA | 110,747 | 9,443,732 | |||

| BHP Billiton Ltd. | 957,604 | $ 36,222,971 | Publicis Groupe SA | 196,300 | 7,557,499 | |

| Commonwealth Bank | Societe Television Francaise 1 | 263,074 | 4,684,922 | |||

| of Australia | 304,800 | 14,739,982 | ||||

| QBE Insurance Group Ltd. | 184,530 | 3,758,805 | Total SA | 248,796 | 15,395,217 | |

| Wesfarmers Ltd. | 602,879 | 16,443,827 | 92,812,518 | |||

| 71,165,585 | GERMANY — 6.3% | |||||

| BELGIUM — 1.1% | Allianz SE | 140,570 | 17,269,983 | |||

| Anheuser-Busch InBev NV | 226,597 | 11,309,801 | BASF SE | 243,700 | 14,695,658 | |

| KBC Groep NV(1) | 122,130 | 5,435,511 | Bayer AG | 154,740 | 11,847,519 | |

| 16,745,312 | Daimler AG | 245,500 | 12,430,221 | |||

| BERMUDA — 0.8% | Deutsche Boerse AG | 44,220 | 3,684,455 | |||

| Seadrill Ltd. | 537,600 | 12,428,087 | E.ON AG | 138,600 | 5,481,744 | |

| Fresenius Medical Care | ||||||

| BRAZIL — 4.0% | AG & Co. KGaA | 160,843 | 8,552,004 | |||

| Banco Santander | HeidelbergCement AG | 162,733 | 10,800,347 | |||

| Brasil SA ADR(1) | 406,810 | 5,552,956 | ||||

| Companhia Brasileira de | Metro AG | 83,380 | 5,239,588 | |||

| Meios de Pagamento | 689,459 | 6,460,610 | Muenchener | |||

| Rueckversicherungs- | ||||||

| Itau Unibanco Holding SA | Gesellschaft AG | 39,910 | 6,258,162 | |||

| Preference Shares | 526,290 | 11,377,218 | ||||

| Petroleo Brasileiro | 96,259,681 | |||||

| SA-Petrobras ADR | 231,460 | 11,869,269 | GREECE — 1.2% | |||

| Vale SA Preference Shares | 1,090,100 | 26,310,189 | National Bank of Greece SA(1) | 632,125 | 18,603,679 | |

| 61,570,242 | HONG KONG — 1.1% | |||||

| CANADA — 1.1% | Li & Fung Ltd. | 3,730,000 | 15,016,161 | |||

| Canadian National | Melco Crown | |||||

| Railway Co. | 178,870 | 9,372,286 | Entertainment Ltd. ADR(1) | 367,697 | 1,555,358 | |

| EnCana Corp. | 73,924 | 3,983,025 | 16,571,519 | |||

| Research In Motion Ltd.(1) | 51,510 | 2,981,914 | INDIA — 1.2% | |||

| 16,337,225 | Housing Development | |||||

| CZECH REPUBLIC — 0.5% | Finance Corp. Ltd. | 91,978 | 5,470,926 | |||

| CEZ AS | 157,570 | 7,884,073 | Infosys Technologies Ltd. | 82,530 | 4,221,601 | |

| Infrastructure Development | ||||||

| DENMARK — 1.7% | Finance Co. Ltd. | 450,170 | 1,605,572 | |||

| Novo Nordisk A/S B Shares | 263,979 | 17,709,920 | Larsen & Toubro Ltd. | 219,410 | 7,616,025 | |

| Vestas Wind Systems A/S(1) | 119,580 | 8,396,404 | 18,914,124 | |||

| 26,106,324 | INDONESIA — 0.1% | |||||

| FRANCE — 6.0% | PT Bank Rakyat Indonesia | 2,904,500 | 2,273,221 | |||

| BNP Paribas | 300,208 | 24,792,753 | IRELAND — 1.2% | |||

| Cie Generale des | CRH plc | 339,344 | 8,550,114 | |||

| Etablissements Michelin, | ||||||

| Class B | 59,780 | 4,533,014 | Experian plc | 510,380 | 4,811,058 | |

| Danone SA | 101,354 | 6,058,608 | Ryanair Holdings plc ADR(1) | 183,782 | 4,816,926 | |

| GDF Suez | 123,620 | 5,162,137 | 18,178,098 | |||

| Legrand SA | 207,831 | 5,709,296 | ||||

28

| International Growth | ||||||

| Shares | Value | Shares | Value | |||

| ITALY — 2.9% | NETHERLANDS — 3.3% | |||||

| ENI SpA | 285,819 | $ 7,081,330 | Akzo Nobel NV | 73,550 | $ 4,663,839 | |

| Luxottica Group SpA | 119,400 | 2,972,547 | ASML Holding NV | 496,050 | 15,239,506 | |

| Saipem SpA | 860,534 | 27,677,528 | Koninklijke KPN NV | 414,920 | 7,364,133 | |

| UniCredit SpA(1) | 1,789,280 | 6,112,227 | TNT NV | 486,870 | 14,124,073 | |

| 43,843,632 | Unilever NV CVA | 285,660 | 8,752,373 | |||

| JAPAN — 15.2% | 50,143,924 | |||||

| Asahi Glass Co. Ltd. | 474,000 | 4,140,097 | NORWAY — 0.3% | |||

| Canon, Inc. | 81,500 | 3,139,692 | Yara International ASA | 126,880 | 5,439,343 | |

| FAST RETAILING CO. LTD. | 79,200 | 14,366,682 | PEOPLE’S REPUBLIC OF CHINA — 3.8% | |||

| Hitachi Construction | Baidu, Inc. ADR(1) | 14,360 | 6,228,506 | |||

| Machinery Co. Ltd. | 586,600 | 13,708,144 | Ctrip.com International | |||

| Honda Motor Co. Ltd. | 734,100 | 22,930,009 | Ltd. ADR(1) | 158,821 | 11,649,520 | |

| HOYA Corp. | 577,700 | 14,736,563 | Industrial & Commercial | |||

| Ibiden Co., Ltd. | 278,000 | 9,391,023 | Bank of China Ltd. H Shares | 13,913,000 | 11,758,653 | |

| iShares MSCI Japan | Mindray Medical | |||||

| Index Fund | 335,270 | 3,201,828 | International Ltd. ADR | 160,020 | 4,845,406 | |

| JGC Corp. | 395,000 | 7,389,114 | Sino-Ocean Land | |||

| Kubota Corp. | 275,000 | 2,421,043 | Holdings Ltd. | 3,693,500 | 3,683,945 | |

| Mitsubishi Corp. | 887,400 | 20,018,857 | Tencent Holdings Ltd. | 749,800 | 13,863,955 | |

| Mitsubishi UFJ | ZTE Corp. H Shares | 1,142,800 | 6,473,367 | |||

| Financial Group, Inc. | 1,684,500 | 9,392,978 | 58,503,352 | |||

| Nidec Corp. | 200,000 | 17,561,314 | POLAND — 1.0% | |||

| Nitori Co. Ltd. | 180,000 | 15,076,354 | Powszechna Kasa | |||

| Nomura ETF - Nikkei 225 | 102,205 | 11,138,028 | Oszczednosci Bank Polski SA | 1,127,610 | 15,307,844 | |

| ORIX Corp. | 260,340 | 18,010,565 | RUSSIAN FEDERATION — 0.3% | |||

| Rakuten, Inc. | 21,620 | 17,458,075 | Mechel ADR | 7,675 | 149,279 | |

| SOFTBANK CORP. | 497,900 | 11,923,334 | Vimpel-Communications ADR | 230,470 | 4,399,672 | |

| Toshiba Corp.(1) | 1,599,000 | 8,472,258 | 4,548,951 | |||

| SINGAPORE — 0.4% | ||||||

| Unicharm Corp. | 79,400 | 8,101,666 | ||||

| United Overseas Bank Ltd. | 401,000 | 5,458,699 | ||||

| 232,577,624 | ||||||

| SOUTH KOREA — 3.1% | ||||||

| LUXEMBOURG — 0.6% | ||||||

| Hyundai Motor Co. | 160,432 | 13,659,071 | ||||

| Millicom International | ||||||

| Cellular SA(1) | 97,527 | 7,295,020 | POSCO | 37,730 | 18,105,727 | |

| SES SA Fiduciary | Samsung Electronics Co. Ltd. | 24,680 | 15,281,734 | |||

| Depositary Receipt | 70,220 | 1,493,541 | 47,046,532 | |||

| 8,788,561 | SPAIN — 3.6% | |||||

| MEXICO — 0.2% | Banco Santander SA | 1,686,864 | 28,900,510 | |||

| Grupo Financiero Banorte | Telefonica SA | 893,090 | 25,640,289 | |||

| SAB de CV, Series O | 1,000,960 | 3,444,580 | 54,540,799 | |||

| MULTI-NATIONAL — 1.4% | SWEDEN — 3.4% | |||||

| iShares MSCI EAFE | Atlas Copco AB A Shares | 1,207,060 | 17,106,315 | |||

| Growth Index Fund | 55,810 | 3,062,853 | Autoliv, Inc. | 66,008 | 2,680,585 | |

| iShares MSCI EAFE | Electrolux AB B Shares(1) | 416,180 | 10,184,293 | |||

| Index Fund | 140,250 | 7,772,655 | ||||

| iShares MSCI Emerging | Getinge AB B Shares | 238,760 | 4,852,908 | |||

| Markets Index Fund | 284,210 | 11,516,189 | H & M Hennes & Mauritz AB | |||

| 22,351,697 | B Shares | 118,780 | 7,024,692 | |||

| Volvo AB B Shares | 1,128,400 | 10,723,082 | ||||

| 52,571,875 | ||||||

29

| International Growth | ||||||

| Shares | Value | Shares | Value | |||

| SWITZERLAND — 8.1% | HSBC Holdings plc | |||||

| Adecco SA | 140,230 | $ 6,994,398 | (Hong Kong) | 2,730,751 | $ 31,958,389 | |

| Credit Suisse Group AG | 333,770 | 17,279,148 | Intercontinental | |||

| Julius Baer Group Ltd. | 108,840 | 3,592,061 | Hotels Group plc | 571,140 | 7,906,586 | |

| Nestle SA | 562,560 | 26,592,015 | Kingfisher plc | 2,875,426 | 11,220,422 | |

| Novartis AG | 442,000 | 24,532,331 | Man Group plc | 1,065,119 | 5,579,092 | |

| Roche Holding AG | 162,619 | 26,599,932 | Next plc | 284,900 | 9,261,295 | |

| Sonova Holding AG | 45,800 | 5,439,733 | Reckitt Benckiser Group plc | 265,113 | 13,520,259 | |

| Rolls-Royce Group plc(1) | 998,950 | 7,797,803 | ||||

| Syngenta AG | 49,812 | 13,206,168 | ||||

| 124,235,786 | Rolls-Royce Group plc | |||||

| C Shares(1) | 56,410,200 | 92,800 | ||||

| TAIWAN (REPUBLIC OF CHINA) — 1.5% | Smiths Group plc | 468,490 | 7,352,601 | |||

| Hon Hai Precision | ||||||

| Industry Co. Ltd. | 2,843,000 | 12,015,538 | Standard Chartered plc | 151,888 | 3,708,085 | |

| Taiwan Semiconductor | Tesco plc | 3,174,943 | 22,093,708 | |||

| Manufacturing Co. Ltd. ADR | 459,908 | 4,778,444 | Tullow Oil plc | 400,290 | 8,126,101 | |

| Wistron Corp. | 3,558,773 | 6,536,048 | Vodafone Group plc | 3,457,650 | 7,798,495 | |

| 23,330,030 | 288,194,980 | |||||

| TURKEY — 0.9% | TOTAL COMMON STOCKS | |||||

| Turkiye Garanti Bankasi AS | 3,958,540 | 13,557,044 | (Cost $1,163,149,920) | 1,529,734,941 | ||

| UNITED KINGDOM — 18.8% | Temporary Cash Investments — 0.2% | |||||

| Admiral Group plc | 550,657 | 9,611,449 | JPMorgan U.S. Treasury | |||

| Antofagasta plc | 776,150 | 11,497,984 | Plus Money Market Fund | |||

| ARM Holdings plc | 2,427,630 | 6,178,245 | Agency Shares | 21,645 | 21,645 | |

| Repurchase Agreement, Bank of America | ||||||

| AstraZeneca plc | 196,270 | 8,772,752 | Securities, LLC, (collateralized by various | |||

| Autonomy Corp. plc(1) | 97,680 | 2,289,881 | U.S. Treasury obligations, 4.125%-4.50%, | |||

| Barclays plc | 4,237,187 | 20,378,538 | 5/15/15-11/15/15, valued at $2,552,155), | |||

| BG Group plc | 1,508,799 | 27,377,842 | in a joint trading account at 0.12%, | |||

| dated 11/30/09, due 12/1/09 | ||||||

| BP plc | 1,266,710 | 11,973,886 | (Delivery value $2,500,008) | 2,500,000 | ||

| British Airways plc(1) | 1,745,240 | 5,607,247 | TOTAL TEMPORARY | |||

| British American Tobacco plc | 283,238 | 8,606,186 | CASH INVESTMENTS | |||

| British Sky Broadcasting | (Cost $2,521,645) | 2,521,645 | ||||