Exhibit 99.1

|

Welcome to

Microsemi’s Analyst Day

New York, NY March 18, 2015

|

Disclaimer

This presentation contains projections or other forward-looking statements regarding future events or the future financial performance of Microsemi Corporation.

We wish to caution you that these statements are only predictions and that actual events or results may differ materially. We refer you to all of the documents that the company filed with the Securities and Exchange

Commission. Please pay special attention to the Company’s most recent Form 10-K and subsequent Form 10-Qs.

These documents contain and identify important factors that could cause the actual results to differ materially from those contained in our projections or forward-looking statements.

2

© 2015 Microsemi Corporation

|

Introduction

Rob Adams

VP Corporate Development

|

Today’s Agenda

9:05-9:15 Analyst Highlights

Jim Peterson, Chairman & CEO

9:15-9:35 60/30: How do we get there?

John Hohener, EVP & CFO

9:35-9:55 FPGA Growth and Opportunity

Esam Elashmawi, Corporate VP & GM, SoC Product Group

9:55-10:15 Timing Growth and Opportunity

Roger Holliday, Senior VP & General Manager, Communications Product Group

Maamoun Seido, VP & Business Unit Manager, Timing and Optical Products

10:15-10:25 Small Cell/Backhaul

Maamoun Seido, VP & Business Unit Manager, Timing and Optical Products

10:25-10:35 Residential Gateway

Roger Holliday, Senior VP & General Manager, Communications Product Group

4

|

Today’s Agenda

10:35-10:45 Aerospace

Siobhan Dolan Clancy, VP, Worldwide Business Development, Aerospace

10:45-10:55 Space/Satellite

Siobhan Dolan Clancy, VP, Worldwide Business Development, Aerospace

10:55-11:00 Acquisition Overview

Steve Litchfield, EVP & Chief Strategy Officer

11:00-11:15 Executive Summary

Paul Pickle, President & COO

11:15-11:30 Q&A

11:30-1:00 Management Luncheon

5

|

Investor Highlights

James J. Peterson

Chairman & CEO

|

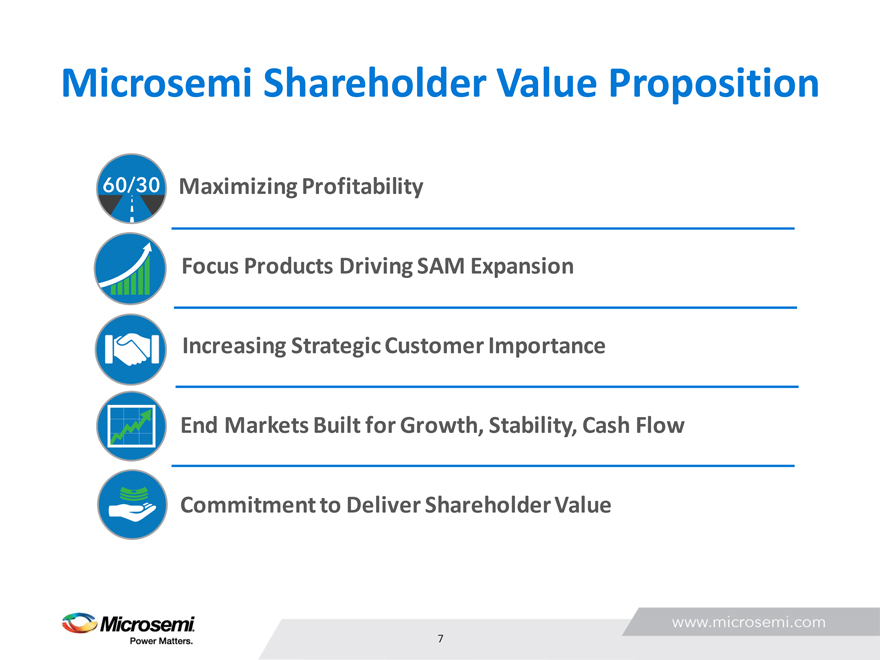

Microsemi Shareholder Value Proposition

Maximizing Profitability

Focus Products Driving SAM Expansion Increasing Strategic Customer Importance End Markets Built for Growth, Stability, Cash Flow Commitment to Deliver Shareholder Value

7

|

60/30: How do we get there?

John Hohener

EVP & CFO

|

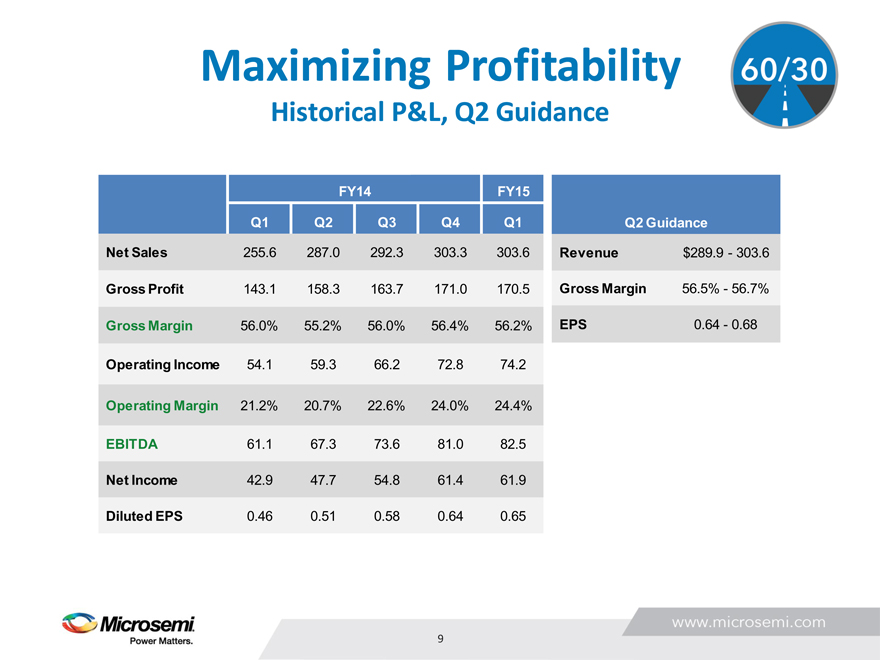

Maximizing Profitability

Historical P&L, Q2 Guidance

FY14 FY15

Q1 Q2 Q3 Q4 Q1 Q2 Guidance

Net Sales 255.6 287.0 292.3 303.3 303.6 Revenue $289.9—303.6 Gross Profit 143.1 158.3 163.7 171.0 170.5 Gross Margin 56.5%—56.7% Gross Margin 56.0% 55.2% 56.0% 56.4% 56.2% EPS 0.64—0.68 Operating Income 54.1 59.3 66.2 72.8 74.2

Operating Margin 21.2% 20.7% 22.6% 24.0% 24.4%

EBITDA 61.1 67.3 73.6 81.0 82.5

Net Income 42.9 47.7 54.8 61.4 61.9

Diluted EPS 0.46 0.51 0.58 0.64 0.65

9

|

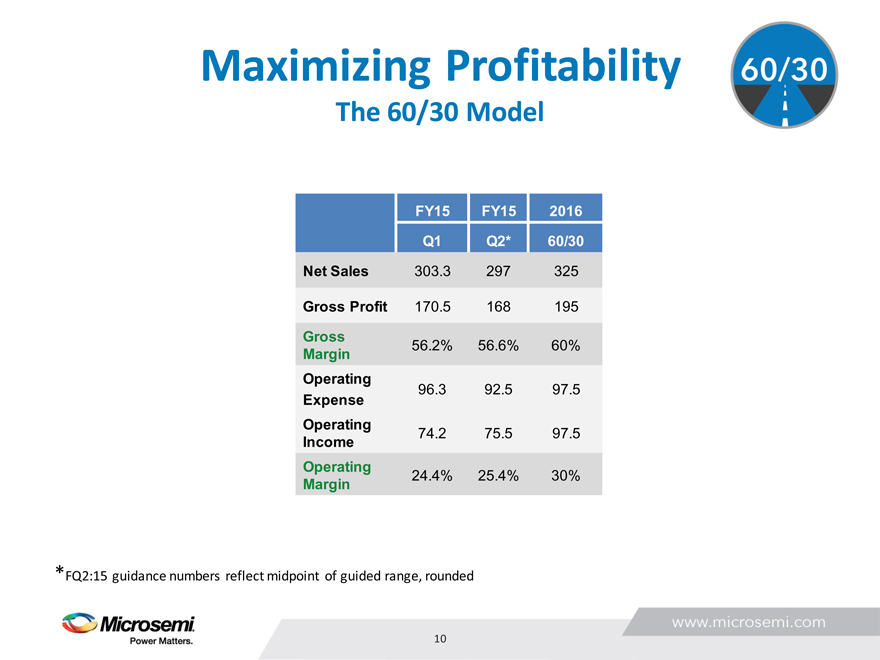

Maximizing Profitability

The 60/30 Model

FY15 FY15 2016

Q1 Q2* 60/30

Net Sales 303.3 297 325

Gross Profit 170.5 168 195

Gross

Margin 56.2% 56.6% 60%

Operating

96.3 92.5 97.5

Expense

Operating

Income 74.2 75.5 97.5

Operating

Margin 24.4% 25.4% 30%

*FQ2:15 guidance numbers reflect midpoint of guided range, rounded

10

|

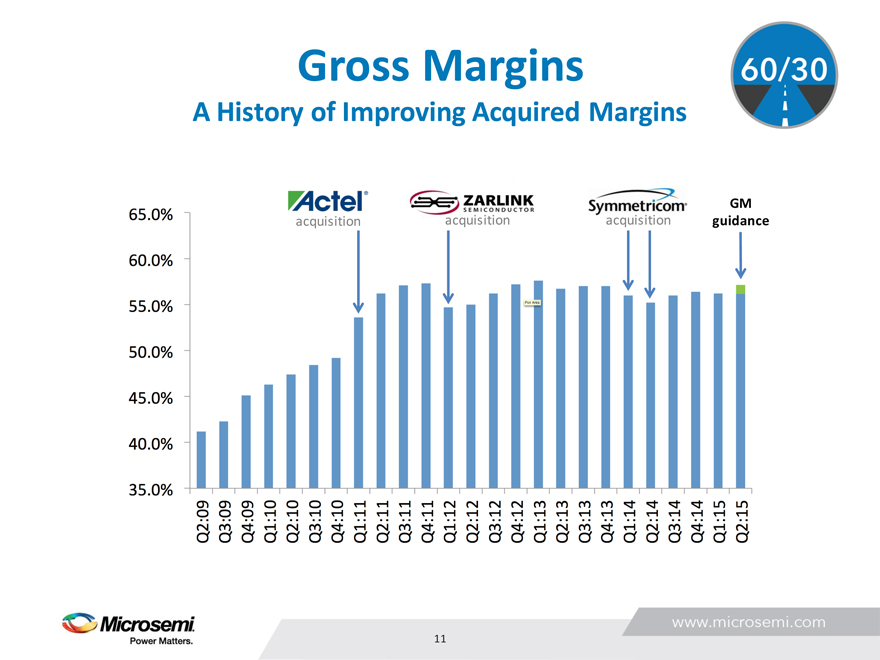

Gross Margins

A History of Improving Acquired Margins

GM acquisition acquisition acquisition guidance

11

|

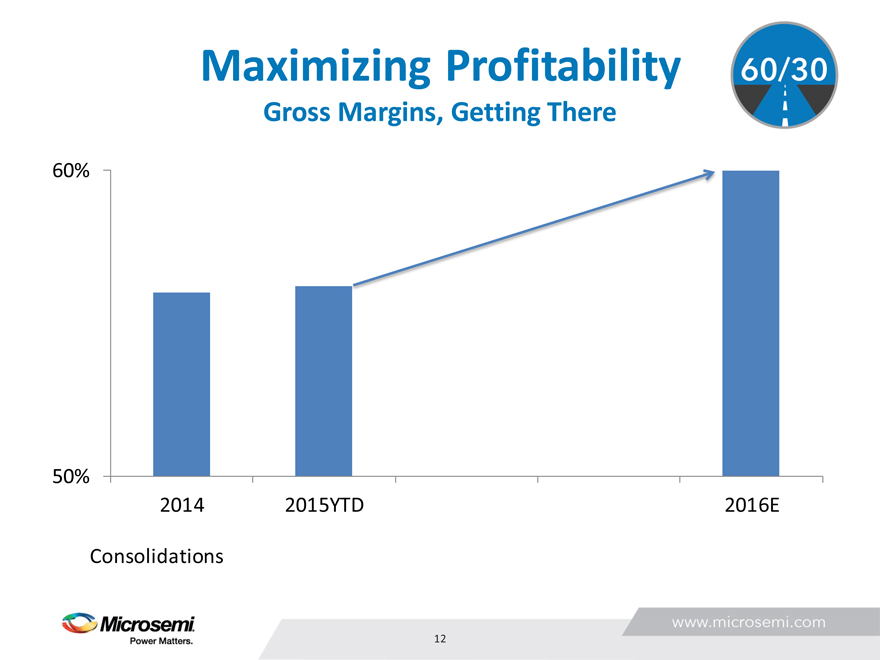

Maximizing Profitability

Gross Margins, Getting There

60%

50%

2014 2015YTD 2016E

Consolidations

12

|

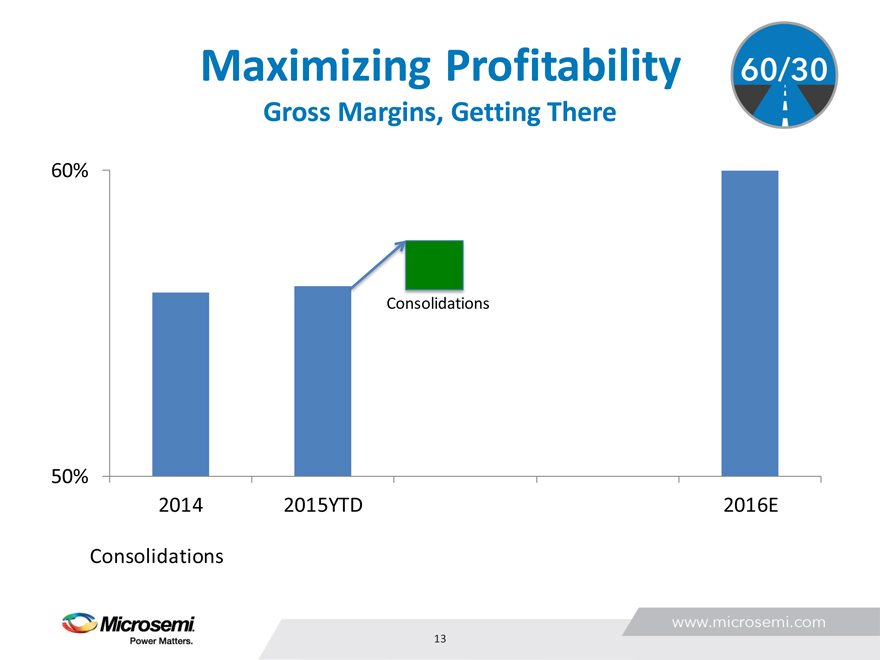

Maximizing Profitability

Gross Margins, Getting There

60%

Consolidations

50%

2014 2015YTD 2016E

Consolidations

13

|

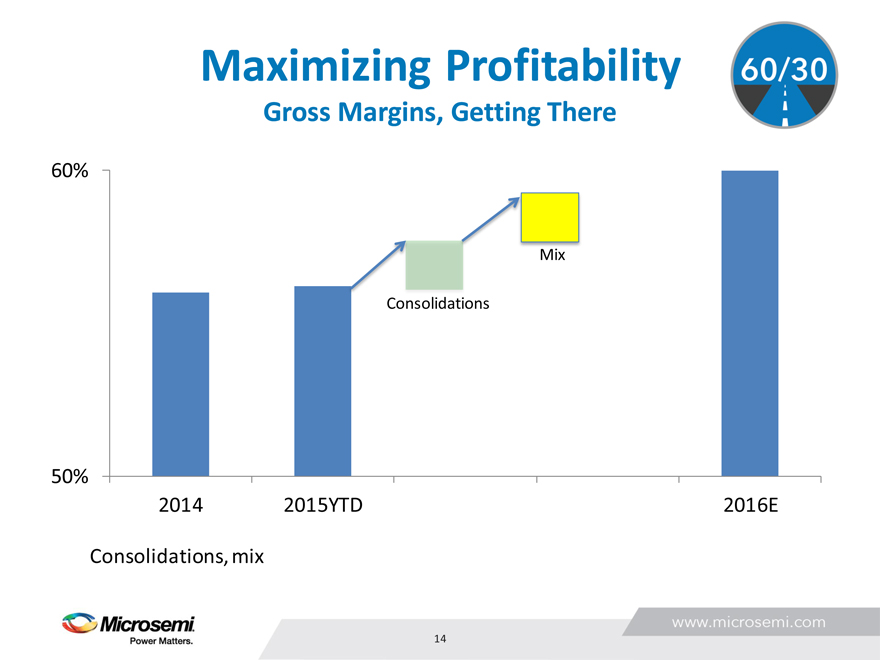

Maximizing Profitability

Gross Margins, Getting There

60%

Mix

Consolidations

50%

2014 2015YTD 2016E

Consolidations, mix

14

|

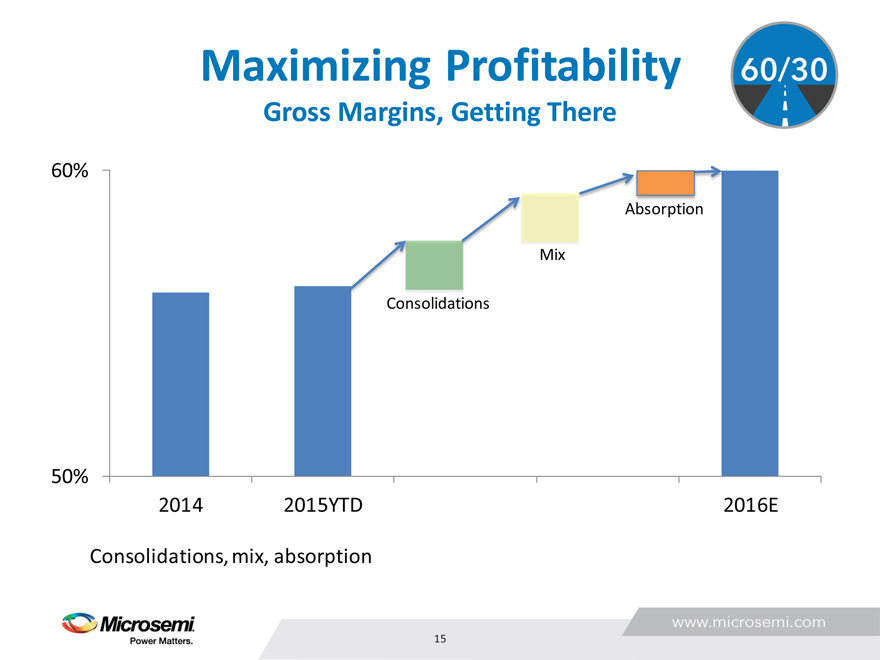

Maximizing Profitability

Gross Margins, Getting There

60%

Absorption

Mix

Consolidations

50%

2014 2015YTD 2016E

Consolidations, mix, absorption

15

|

Maximizing Profitability

Operating Margins

Majority GM fall through

– Infrastructure already in place

Targeted R&D reductions, redeployment

– Focus groups: FPGA, timing, MS/RF

Ongoing back end transfer offshore

Real estate consolidations

Strategic customer focus

16

|

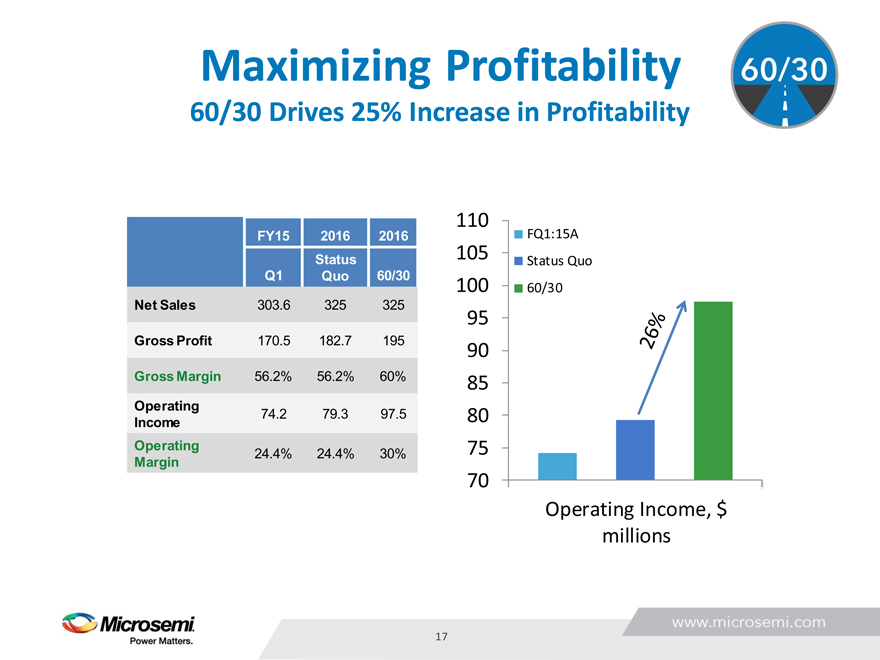

Maximizing Profitability

60/30 Drives 25% Increase in Profitability

FY15 2016 2016 Status Q1 Quo 60/30

Net Sales 303.6 325 325 Gross Profit 170.5 182.7 195 Gross Margin 56.2% 56.2% 60%

Operating

74.2 79.3 97.5

Income Operating

24.4% 24.4% 30%

Margin

110 FQ1:15A

105

Status Quo 100 60/30

95 90 85 80 75 70

Operating Income, $ millions

17

|

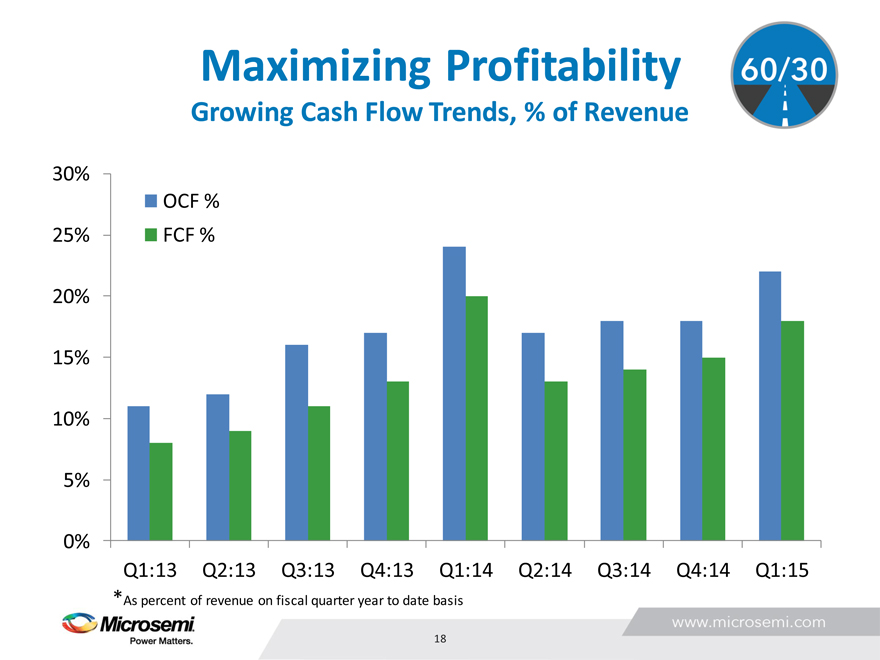

Maximizing Profitability

Growing Cash Flow Trends, % of Revenue

30%

OCF % 25% FCF %

20% 15% 10% 5%

0%

Q1:13 Q2:13 Q3:13 Q4:13 Q1:14 Q2:14 Q3:14 Q4:14 Q1:15

*As percent of revenue on fiscal quarter year to date basis

18

|

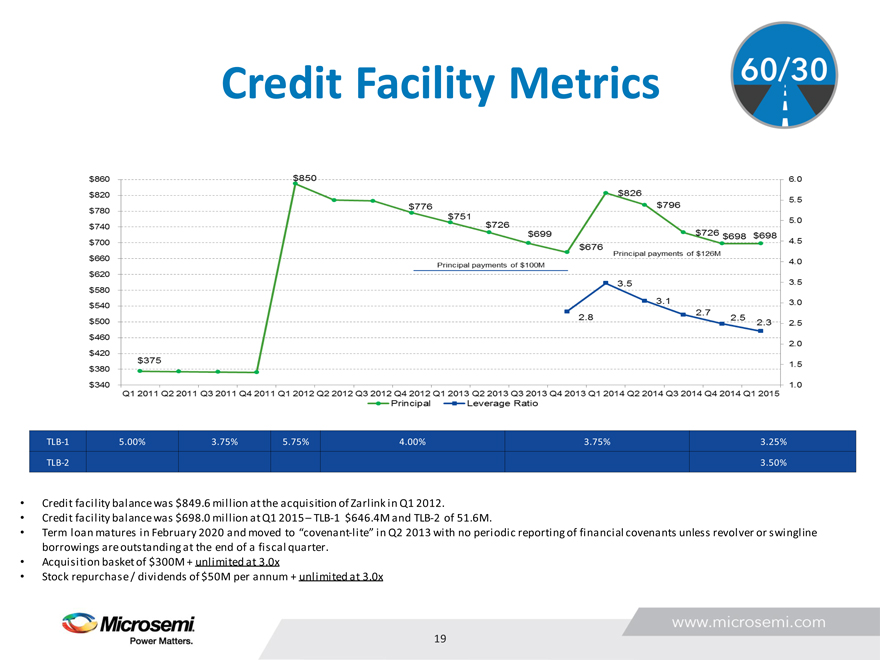

Credit Facility Metrics

TLB-1 5.00% 3.75% 5.75% 4.00% 3.75% 3.25%

TLB-2 3.50%

Credit facility balance was $849.6 million at the acquisition of Zarlink in Q1 2012.

Credit facility balance was $698.0 million at Q1 2015 – TLB-1 $646.4M and TLB-2 of 51.6M.

Term loan matures in February 2020 and moved to “covenant-lite” in Q2 2013 with no periodic reporting of financial covenants unless revolver or swingline borrowings are outstanding at the end of a fiscal quarter.

Acquisition basket of $300M + unlimited at 3.0x

Stock repurchase / dividends of $50M per annum + unlimited at 3.0x

19

|

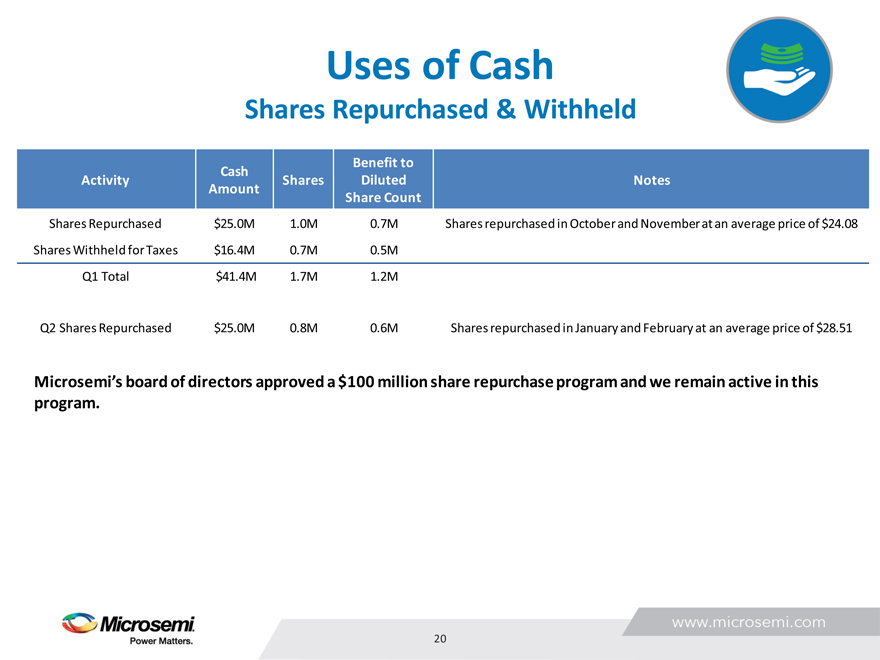

Uses of Cash

Shares Repurchased & Withheld

Benefit to

Cash

Activity Shares Diluted Notes

Amount

Share Count

Shares Repurchased $25.0M 1.0M 0.7M Shares repurchased in October and November at an average price of $24.08

Shares Withheld for Taxes $16.4M 0.7M 0.5M

Q1 Total $41.4M 1.7M 1.2M

Q2 Shares Repurchased $25.0M 0.8M 0.6M Shares repurchased in January and February at an average price of $28.51

Microsemi’s board of directors approved a $100 million share repurchase program and we remain active in this program.

20

|

FPGA Growth and Opportunity

Esam Elashmawi

Corporate VP & General Manager

|

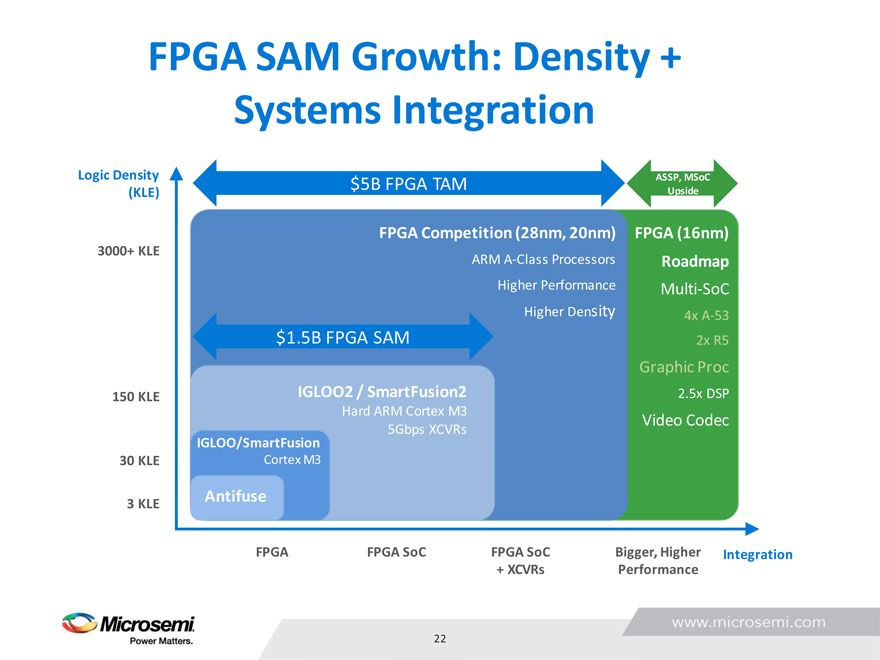

FPGA SAM Growth: Density + Systems Integration

Logic Density ASSP, MSoC

$5B FPGA TAM

(KLE) Upside

FPGA Competition (28nm, 20nm) FPGA (16nm)

3000+ KLE

ARM A-Class Processors Roadmap Higher Performance Multi-SoC

Higher Density 4x A-53

$1.5B FPGA SAM 2x R5

Graphic Proc

150 KLE IGLOO2 / SmartFusion2 2.5x DSP

Hard ARM Cortex M3

Video Codec

5Gbps XCVRs

IGLOO/SmartFusion

30 KLE Cortex M3

Antifuse

3 KLE

FPGA FPGA SoC FPGA SoC Bigger, Higher Integration

+ XCVRs Performance

22

|

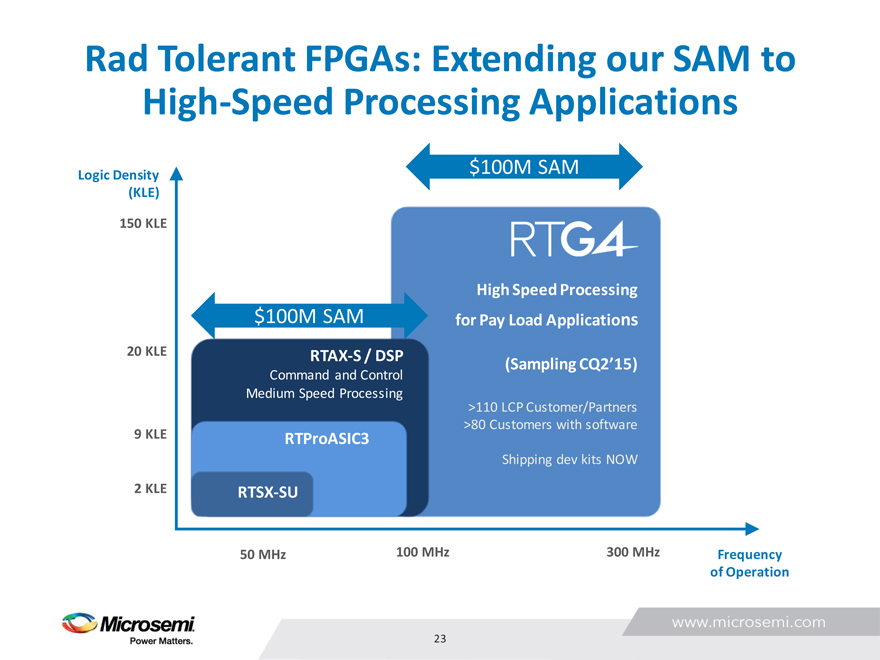

Rad Tolerant FPGAs: Extending our SAM to High-Speed Processing Applications

$100M SAM

Logic Density (KLE)

150 KLE

High Speed Processing $100M SAM for Pay Load Applications

20 KLE RTAX-S / DSP (Sampling CQ2’15)

Command and Control

Medium Speed Processing >110 LCP Customer/Partners

>80 Customers with software

9 KLE RTProASIC3

Shipping dev kits NOW

2 KLE

RTSX-SU

50 MHz 100 MHz 300 MHz Frequency of Operation

23

|

Customers Engaged on Roadmap

Communications

Aerospace & Defense

Industrial

24

|

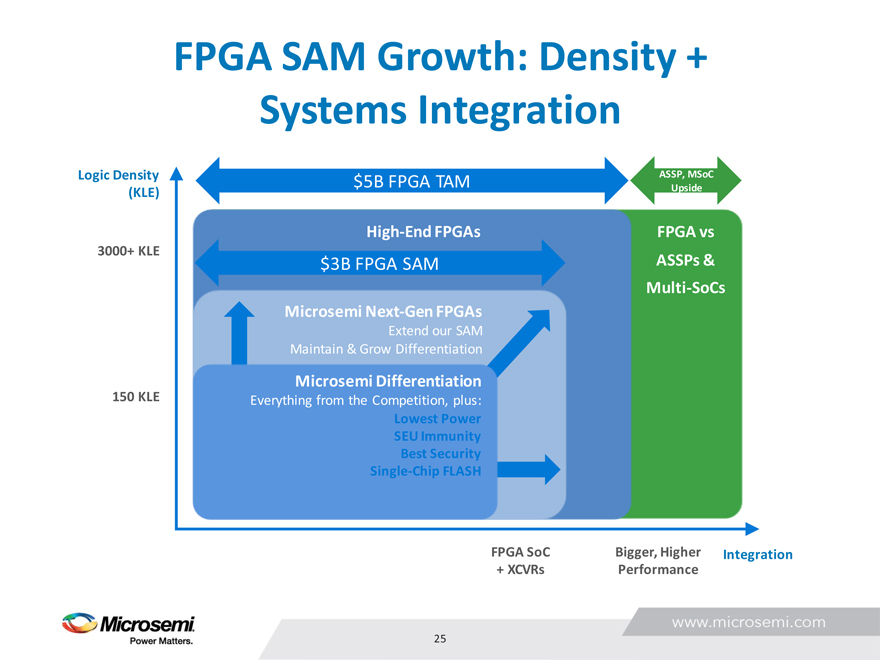

FPGA SAM Growth: Density + Systems Integration

Logic Density $5B FPGA TAM ASSP, MSoC

(KLE) Upside

High-End FPGAs FPGA vs

3000+ KLE

$3B FPGA SAM ASSPs &

Multi-SoCs

Microsemi Next-Gen FPGAs

Extend our SAM

Maintain & Grow Differentiation

Microsemi Differentiation

150 KLE Everything from the Competition, plus:

Lowest Power

SEU Immunity Best Security Single-Chip FLASH

FPGA SoC Bigger, Higher Integration

+ XCVRs Performance

25

|

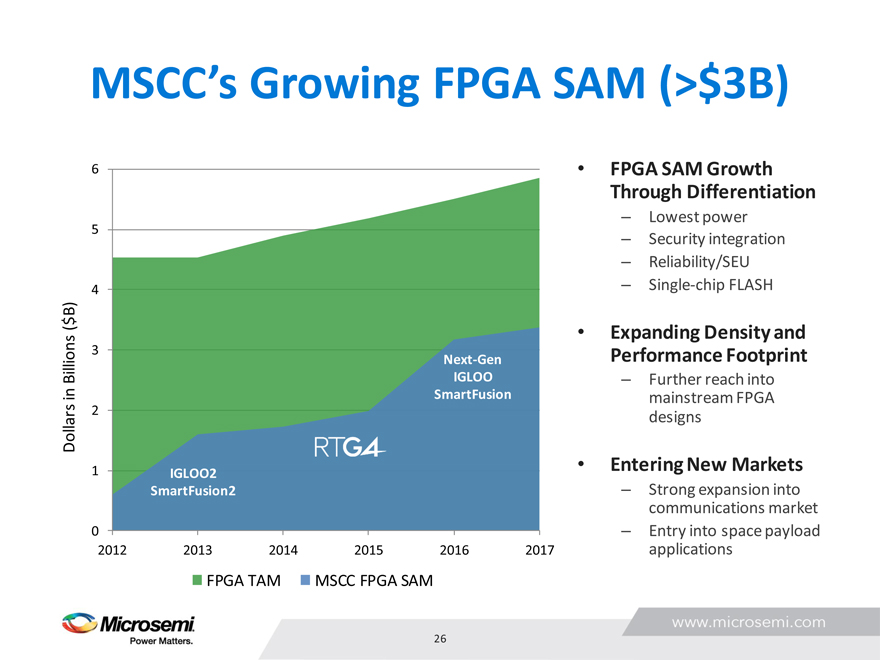

MSCC’s Growing FPGA SAM (>$3B)

6

5

4

B) ( $

3

Next-Gen

Billions IGLOO

in SmartFusion

Dollars 2

1 IGLOO2 SmartFusion2

0

2012 2013 2014 2015 2016 2017

FPGA TAM MSCC FPGA SAM

26

FPGA SAM Growth Through Differentiation

– Lowest power

– Security integration

– Reliability/SEU

– Single-chip FLASH

Expanding Density and Performance Footprint

– Further reach into mainstream FPGA designs

Entering New Markets

– Strong expansion into communications market

– Entry into space payload applications

|

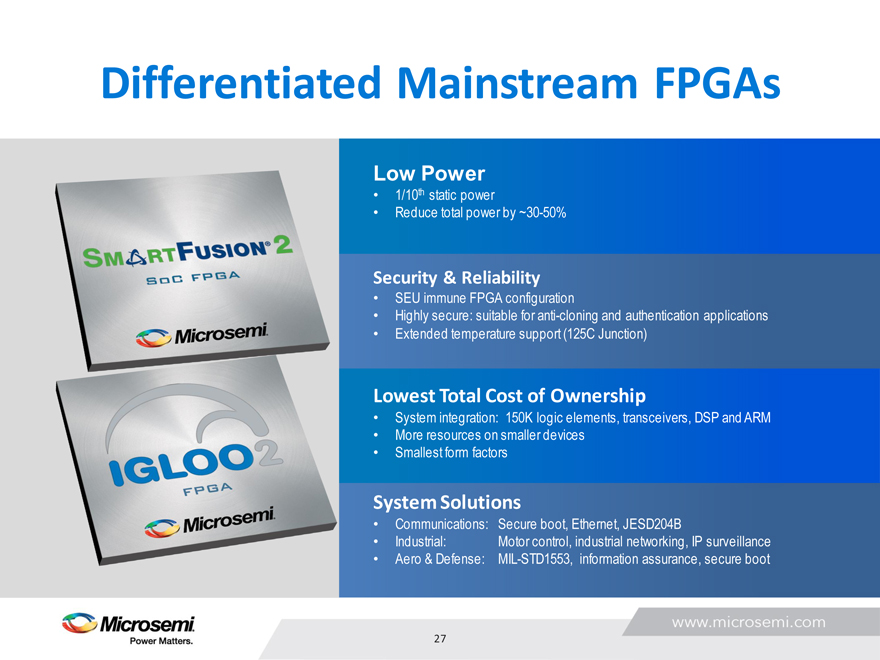

Differentiated Mainstream FPGAs

Low Power

1/10th static power

Reduce total power by ~30-50%

Security & Reliability

SEU immune FPGA configuration

Highly secure: suitable for anti-cloning and authentication applications

Extended temperature support (125C Junction)

Lowest Total Cost of Ownership

System integration: 150K logic elements, transceivers, DSP and ARM

More resources on smaller devices

Smallest form factors

System Solutions

Communications: Secure boot, Ethernet, JESD204B

Industrial: Motor control, industrial networking, IP surveillance

Aero & Defense: MIL-STD1553, information assurance, secure boot

27

|

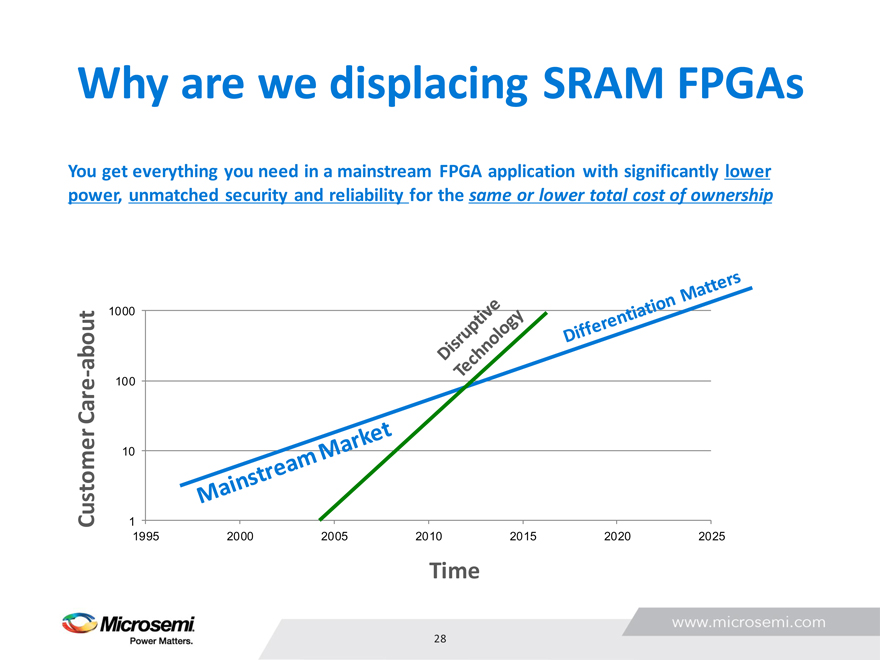

Why are we displacing SRAM FPGAs

You get everything you need in a mainstream FPGA application with significantly lower power, unmatched security and reliability for the same or lower total cost of ownership

about 1000 -Care 100

10

Customer 1

1995 2000 2005 2010 2015 2020 2025

Time

28

|

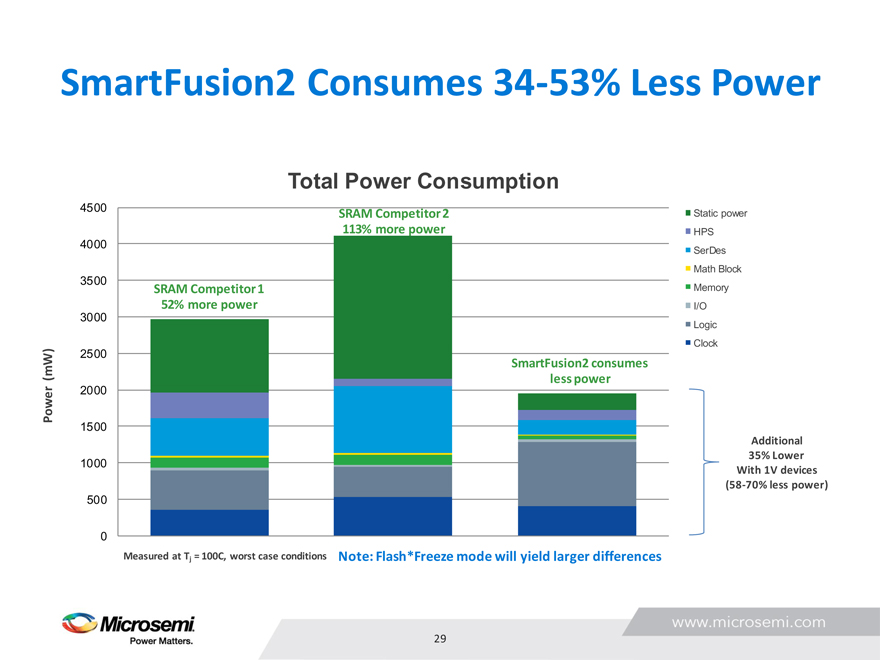

SmartFusion2 Consumes 34-53% Less Power

Total Power Consumption

4500

SRAM Competitor 2 Static power 113% more power HPS

4000

SerDes

Math Block

3500

SRAM Competitor 1 Memory 52% more power I/O

3000

Logic

Clock

2500

(mW) SmartFusion2 consumes less power Power 2000 1500

Additional 35% Lower

1000

With 1V devices (58-70% less power)

500

0

Measured at Tj = 100C, worst case conditions Note: Flash*Freeze mode will yield larger differences

29

|

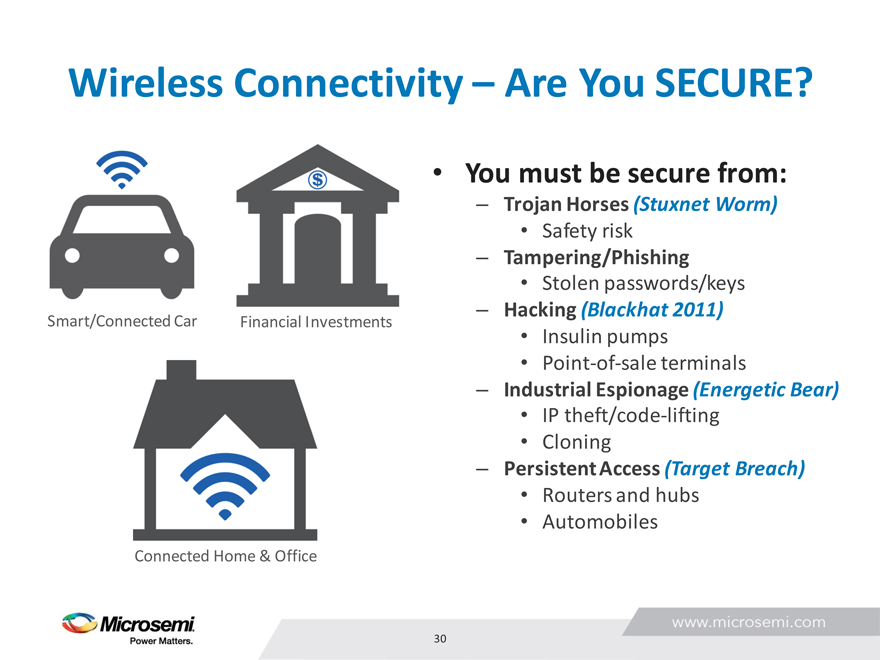

Wireless Connectivity – Are You SECURE?

You must be secure from:

– Trojan Horses (Stuxnet Worm)

Safety risk

– Tampering/Phishing

Stolen passwords/keys

– Hacking (Blackhat 2011)

Smart/Connected Car Financial Investments

Insulin pumps

Point-of-sale terminals

– Industrial Espionage (Energetic Bear)

IP theft/code-lifting

Cloning

– Persistent Access (Target Breach)

Routers and hubs

Automobiles

Connected Home & Office

30

|

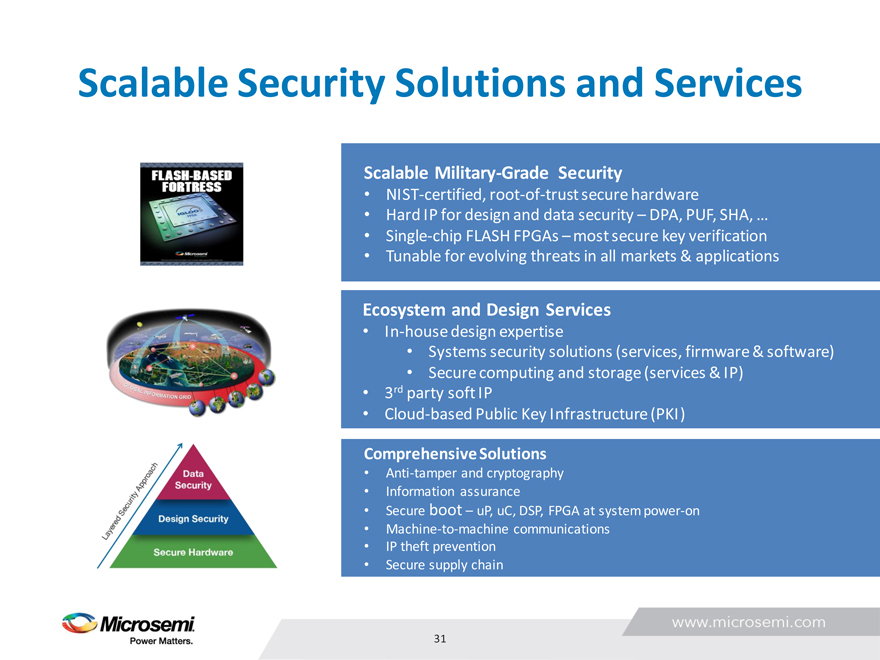

Scalable Security Solutions and Services

Scalable Military-Grade Security

NIST-certified, root-of-trust secure hardware

Hard IP for design and data security – DPA, PUF, SHA, …

Single-chip FLASH FPGAs – most secure key verification

Tunable for evolving threats in all markets & applications

Ecosystem and Design Services

In-house design expertise

Systems security solutions (services, firmware & software)

Secure computing and storage (services & IP)

3rd party soft IP

Cloud-based Public Key Infrastructure (PKI)

Comprehensive Solutions

Anti-tamper and cryptography

Information assurance

Secure boot – uP, uC, DSP, FPGA at system power-on

Machine-to-machine communications

IP theft prevention

Secure supply chain

31

|

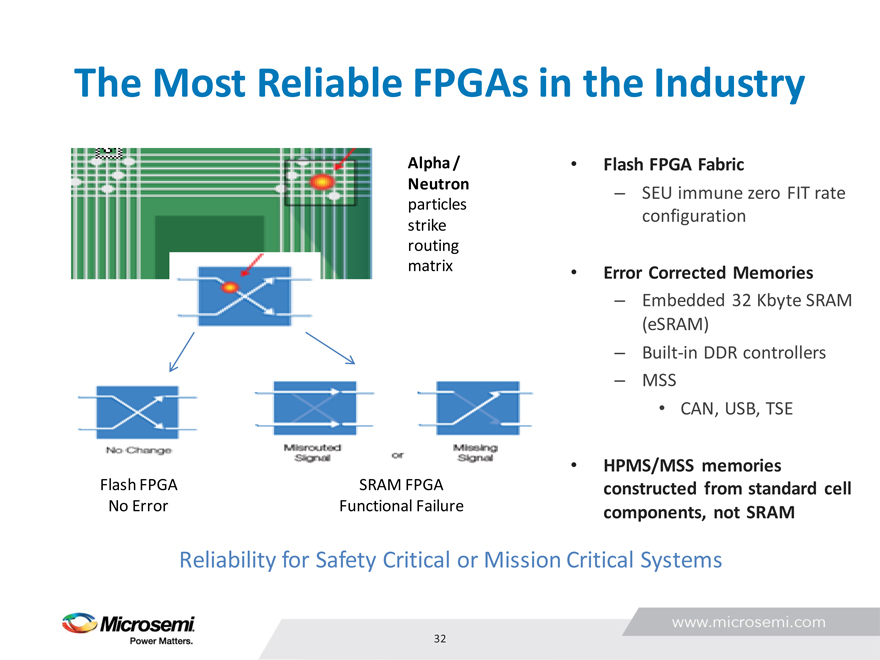

The Most Reliable FPGAs in the Industry

Alpha / • Flash FPGA Fabric

Neutron

– SEU immune zero FIT rate particles configuration strike routing matrix • Error Corrected Memories

Embedded 32 Kbyte SRAM

–

(eSRAM)

– Built-in DDR controllers

– MSS

CAN, USB, TSE

HPMS/MSS memories Flash FPGA SRAM FPGA constructed from standard cell

No Error Functional Failure components, not SRAM

Reliability for Safety Critical or Mission Critical Systems

32

|

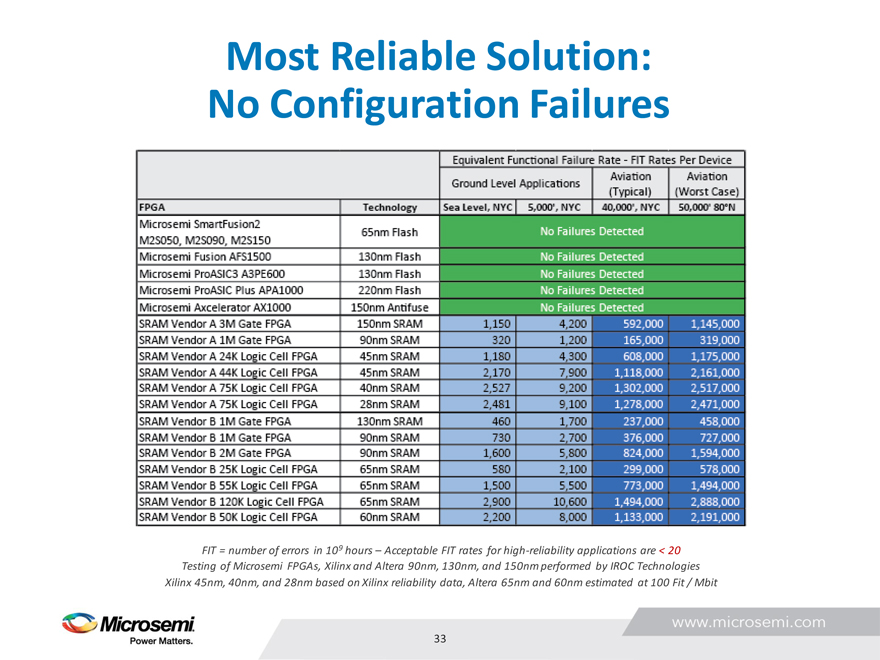

Most Reliable Solution: No Configuration Failures

FIT = number of errors in 109 hours – Acceptable FIT rates for high-reliability applications are < 20 Testing of Microsemi FPGAs, Xilinx and Altera 90nm, 130nm, and 150nm performed by IROC Technologies Xilinx 45nm, 40nm, and 28nm based on Xilinx reliability data, Altera 65nm and 60nm estimated at 100 Fit / Mbit

33

|

Many Reasons Why Customers Engage, Many Reasons Why We Win

Geography Market Segment Primary Reason for Secondary Reasons for Win

Engagement

Americas Communications (Router) SEU More PCIe

More I/O

Americas Communications (Secure Router) Security Small parts with mainstream features

Small footprint

China Communications (SFP) SEU Low power

Small footprint

China Communications Low power 1588

Americas Automotive (ECM) Reliability SEU

China Automotive (Cloud based control) Security Small parts with mainstream features

Americas Defense (Secure Communications) Low power Small footprint

Multi PCIe end points (090)

Europe Defense (Secure Communications) Low power Security

China Industrial Security Small parts with MCU and PCIe

Japan Industrial (POS) PCIe @ 10K LE Lower cost than ASIC

Europe Industrial (Networking) Single chip ASIC Security

replacement

Americas Consumer (Mobile Platform) Security Security

Europe Consumer (Gaming) Small chip with Security

transceiver Small parts with MCU and XCVR

VQ package

34

|

SmartFusion2 / IGLOO2 Design Win Rate

FY13-FY15 ($) Opportunities Design Ins Design Wins

Grand Total $337,001,918 $92,682,687 $40,626,274

3000

Cumulative Design Opportunities

2500 2000 1500 1000 500 0

Growing Opportunities

– >2500 count

– $337M in value

>$90M of Design Ins

– Customers have chosen MSCC over competitors

>$40M of Design Wins

– Customers have purchased >$1K silicon

35

|

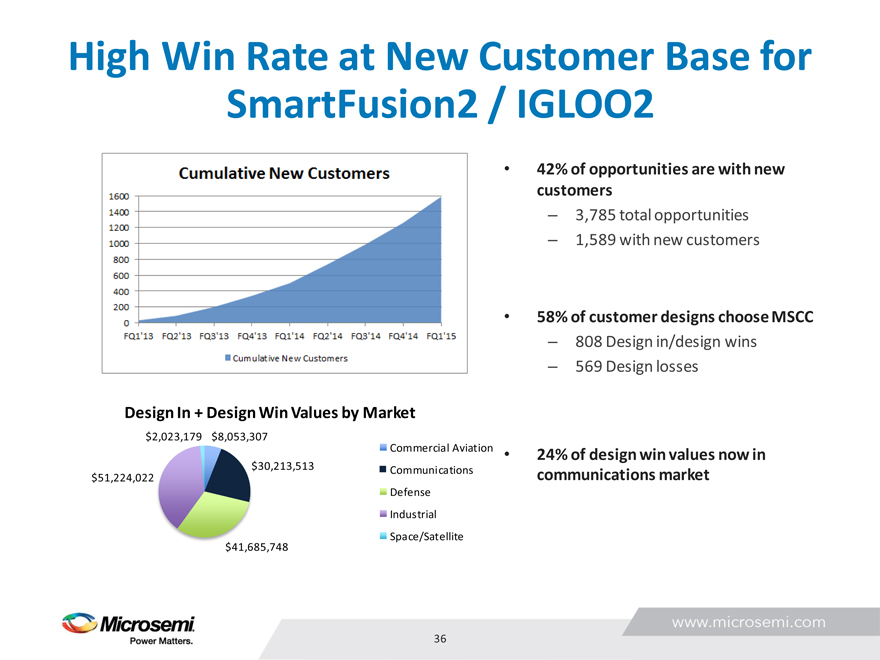

High Win Rate at New Customer Base for SmartFusion2 / IGLOO2

Design In + Design Win Values by Market

$2,023,179 $8,053,307

Commercial Aviation $30,213,513 Communications $51,224,022 Defense

Industrial

Space/Satellite $41,685,748

42% of opportunities are with new customers

– 3,785 total opportunities

– 1,589 with new customers

58% of customer designs choose MSCC

– 808 Design in/design wins

– 569 Design losses

24% of design win values now in communications market

36

|

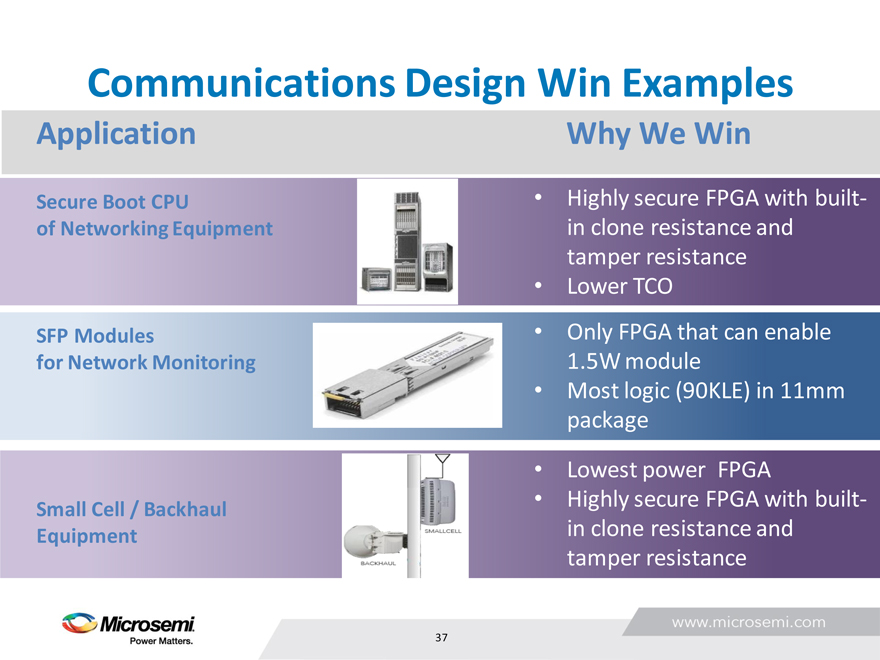

Communications Design Win Examples

Application

Secure Boot CPU of Networking Equipment

SFP Modules for Network Monitoring

Small Cell / Backhaul Equipment

Why We Win

Highly secure FPGA with builtin clone resistance and tamper resistance Lower TCO

Only FPGA that can enable 1.5W module Most logic (90KLE) in 11mm package

Lowest power FPGA Highly secure FPGA with builtin clone resistance and tamper resistance

37

|

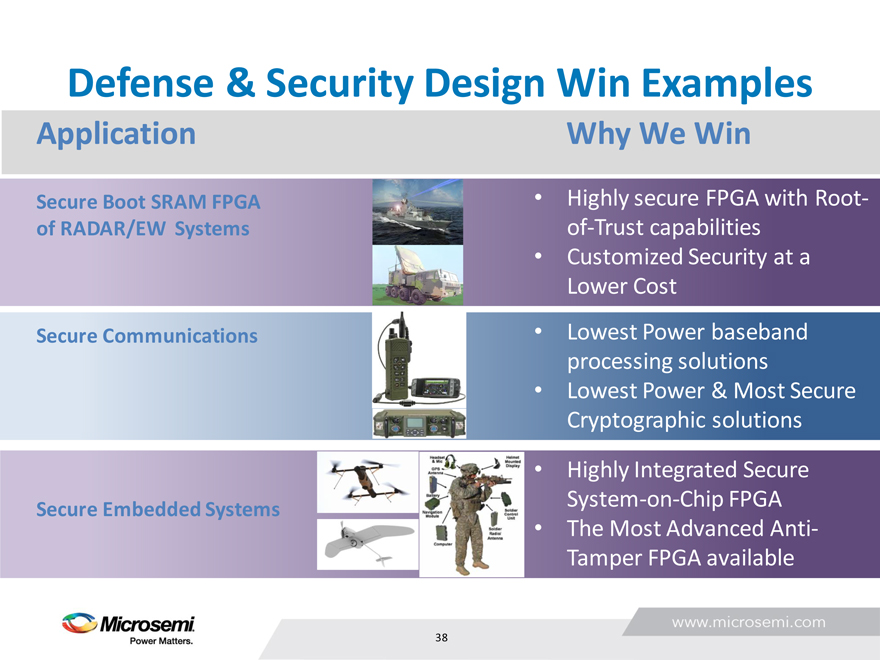

Defense & Security Design Win Examples

Application

Secure Boot SRAM FPGA of RADAR/EW Systems

Secure Communications

Secure Embedded Systems

Why We Win

Highly secure FPGA with Root-of-Trust capabilities

Customized Security at a Lower Cost

Lowest Power baseband processing solutions

Lowest Power & Most Secure Cryptographic solutions

Highly Integrated Secure System-on-Chip FPGA

The Most Advanced Anti-Tamper FPGA available

38

|

Timing Growth and Opportunity

Roger Holliday & Maamoun Seido

Senior VP & General VP & Business Unit Manager, Manager, Communications Timing and Optical Products Product Group

|

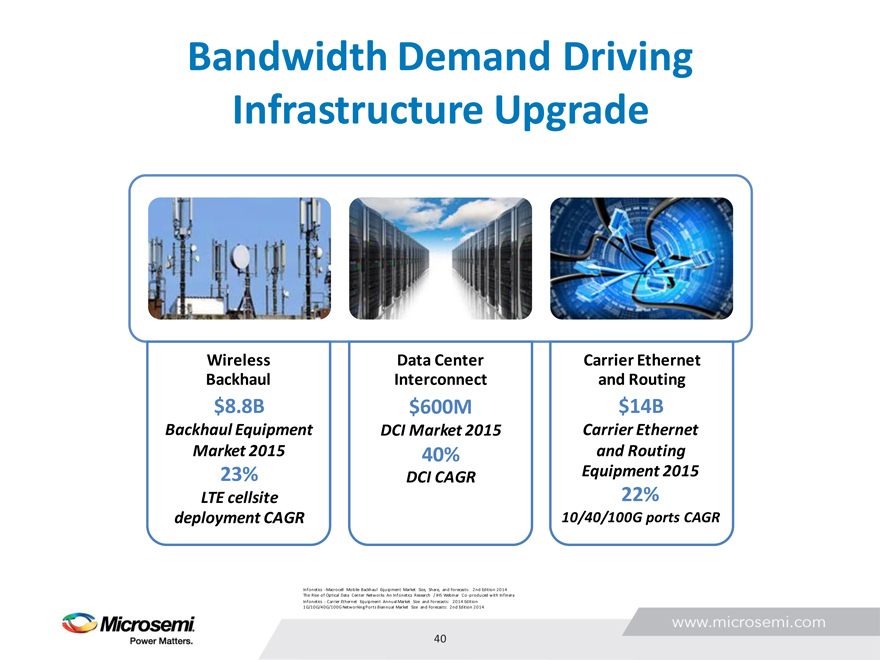

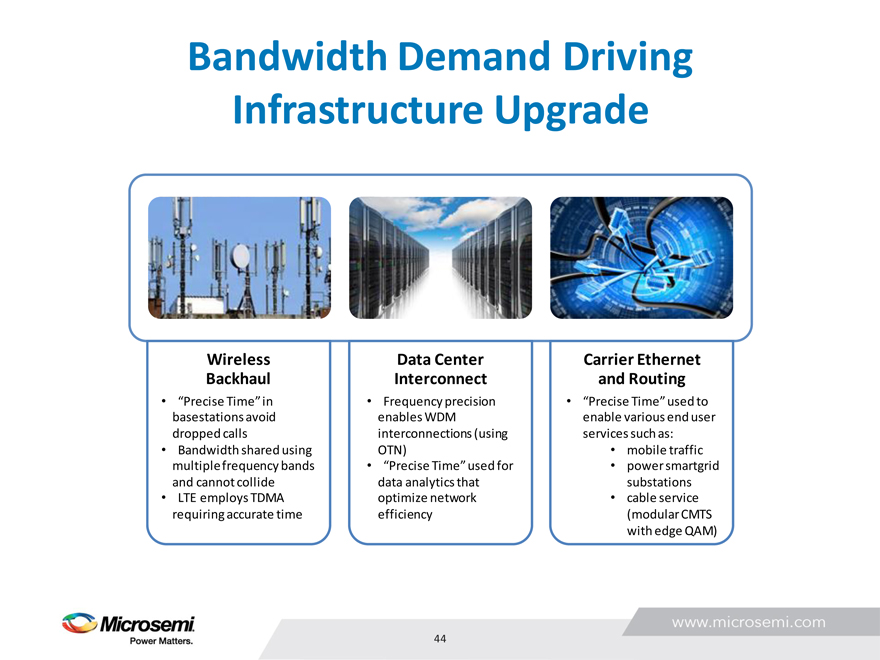

Bandwidth Demand Driving Infrastructure Upgrade

Wireless Backhaul

$8.8B

Backhaul Equipment Market 2015

23%

LTE cellsite deployment CAGR

Data Center Interconnect

$600M

DCI Market 2015

40%

DCI CAGR

Carrier Ethernet and Routing

$14B

Carrier Ethernet and Routing Equipment 2015

22%

10/40/100G ports CAGR

Infonetics -Macrocell Mobile Backhaul Equipment Market Size, Share, and Forecasts: 2nd Edition 2014 The Rise of Optical Data Center Networks An Infonetics Research / IHS Webinar Co-produced with Infinera Infonetics—Carrier Ethernet Equipment Annual Market Size and Forecasts: 2014 Edition 1G/10G/40G/100G Networking Ports Biannual Market Size and Forecasts: 2nd Edition 2014

40

|

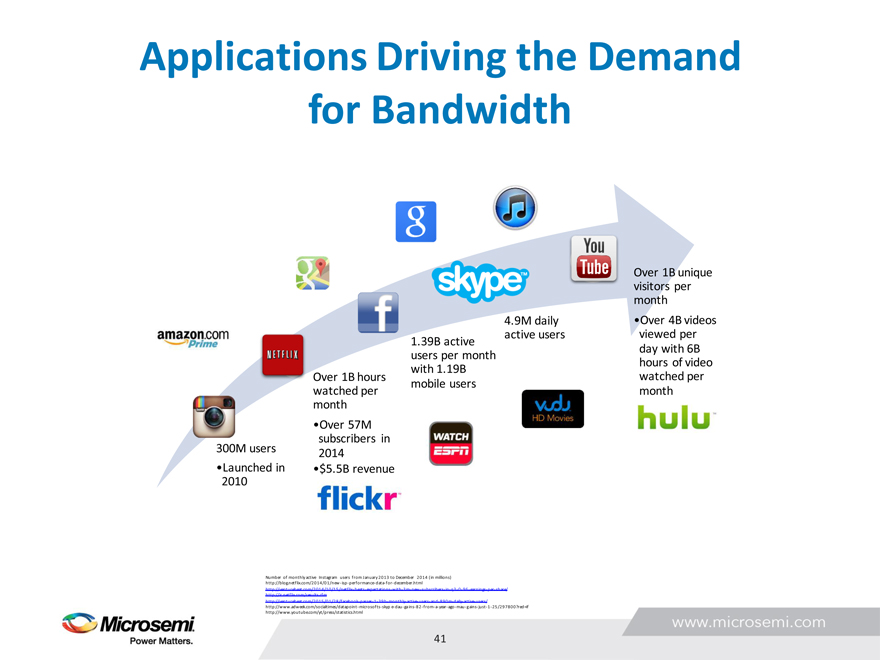

Applications Driving the Demand for Bandwidth

Over 1B unique visitors per month

4.9M daily •Over 4B videos active users viewed per

1.39B active day with 6B users per month hours of video with 1.19B

Over 1B hours watched per mobile users watched per month month

Over 57M 300M users subscribers in 2014 Launched in $5.5B revenue 2010

Number of monthly active Instagram users from January 2013 to December 2014 (in millions) http://blog.netflix.com/2014/01/new-isp-performance-data-for-december.html http://venturebeat.com/2014/10/15/netflix-beats-expectations-with-3m-new-subscribers-in-q3-0-96-earnings-per-share/ http://ir.netflix.com/results.cfm http://venturebeat.com/2015/01/28/facebook-passes-1-39b-monthly-active-users-and-890m-daily-active-users/ http://www.adweek.com/socialtimes/datapoint-microsofts-skyp e-dau-gains-82-from-a-year-ago-mau-gains-just-1-25/297800red=if http://www.youtube.com/yt/press/statistics.html

41

|

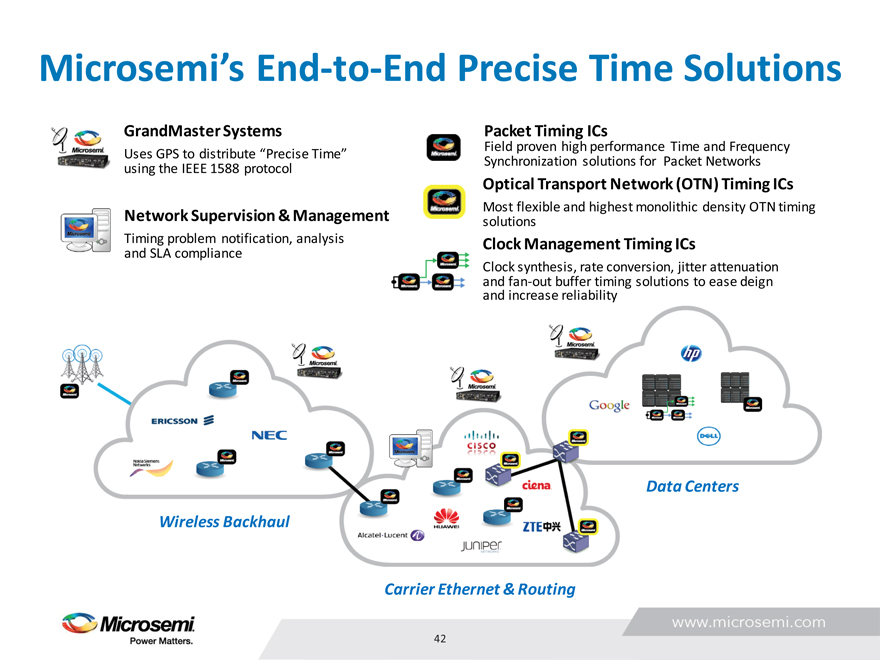

Microsemi’s End-to-End Precise Time Solutions

GrandMaster Systems

Uses GPS to distribute “Precise Time” using the IEEE 1588 protocol

Network Supervision & Management

Timing problem notification, analysis and SLA compliance

Packet Timing ICs

Field proven high performance Time and Frequency

Synchronization solutions for Packet Networks

Optical Transport Network (OTN) Timing ICs

Most flexible and highest monolithic density OTN timing solutions

Clock Management Timing ICs

Clock synthesis, rate conversion, jitter attenuation and fan-out buffer timing solutions to ease deign and increase reliability

Data Centers

Wireless Backhaul

Carrier Ethernet & Routing

42

|

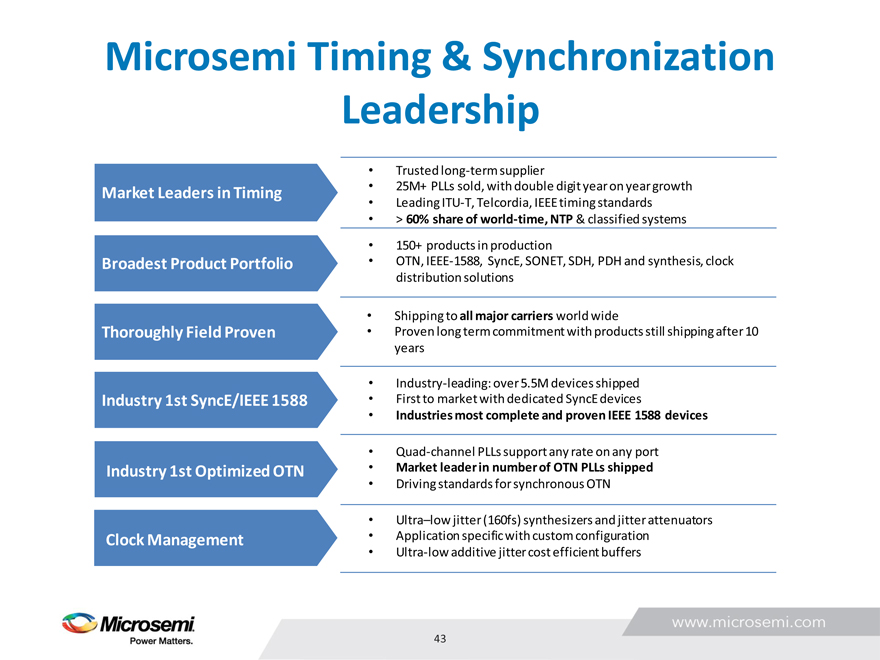

Microsemi Timing & Synchronization Leadership

Market Leaders in Timing

Broadest Product Portfolio

Thoroughly Field Proven

Industry 1st SyncE/IEEE 1588

Industry 1st Optimized OTN

Clock Management

Trusted long-term supplier

25M+ PLLs sold, with double digit year on year growth

Leading ITU-T, Telcordia, IEEE timing standards

> 60% share of world-time, NTP & classified systems

150+ products in production

OTN, IEEE-1588, SyncE, SONET, SDH, PDH and synthesis, clock distribution solutions

Shipping to all major carriers world wide

Proven long term commitment with products still shipping after 10 years

Industry-leading: over 5.5M devices shipped

First to market with dedicated SyncE devices

Industries most complete and proven IEEE 1588 devices

Quad-channel PLLs support any rate on any port

Market leader in number of OTN PLLs shipped

Driving standards for synchronous OTN

Ultra–low jitter (160fs) synthesizers and jitter attenuators

Application specific with custom configuration

Ultra-low additive jitter cost efficient buffers

43

|

Bandwidth Demand Driving Infrastructure Upgrade

Wireless

Backhaul

“Precise Time” in basestations avoid dropped calls

Bandwidth shared using multiple frequency bands and cannot collide

LTE employs TDMA requiring accurate time

Data Center

Interconnect

Frequency precision enables WDM interconnections (using OTN)

“Precise Time” used for data analytics that optimize network efficiency

Carrier Ethernet and Routing

“Precise Time” used to enable various end user services such as: mobile traffic power smartgrid substations cable service (modular CMTS with edge QAM)

|

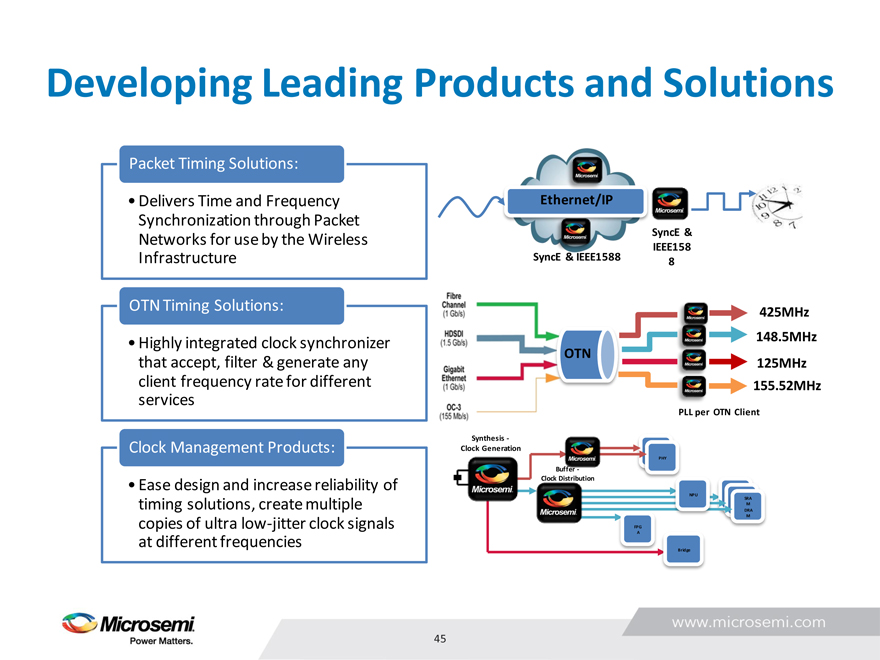

Developing Leading Products and Solutions

Packet Timing Solutions:

Delivers Time and Frequency Synchronization through Packet Networks for use by the Wireless Infrastructure

OTN Timing Solutions:

Highly integrated clock synchronizer that accept, filter & generate any client frequency rate for different services

Clock Management Products:

Ease design and increase reliability of timing solutions, create multiple copies of ultra low-jitter clock signals at different frequencies

Ethernet/IP

SyncE & IEEE158 SyncE & IEEE1588 8

425MHz

148.5MHz OTN

125MHz

155.52MHz

PLL per OTN Client

Synthesis—Clock Generation

PHY

Buffer—

Clock Distribution

NPU SRA M

DRA M

FPG A

Bridge

45

|

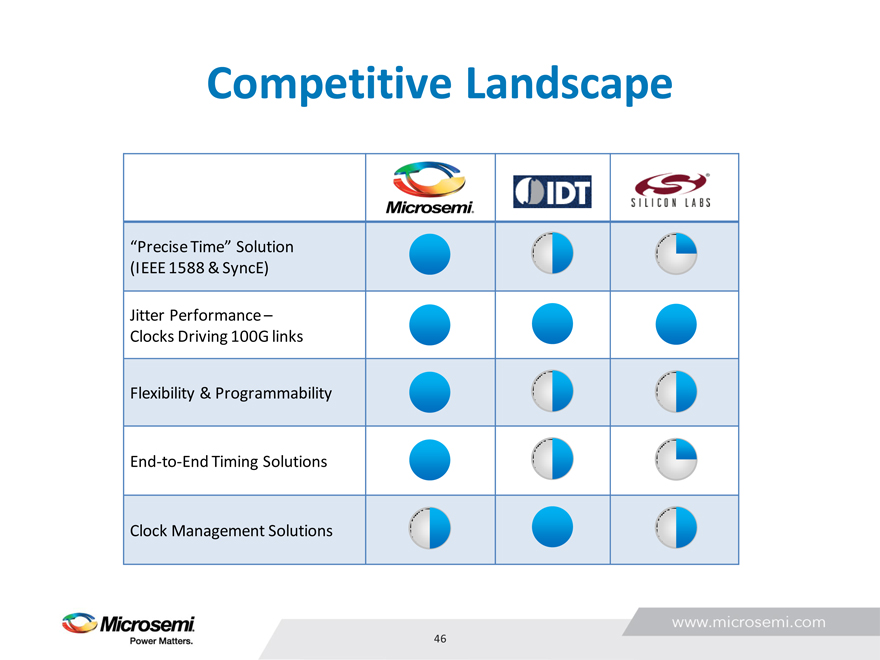

Competitive Landscape

“Precise Time” Solution

(IEEE 1588 & SyncE)

Jitter Performance – Clocks Driving 100G links

Flexibility & Programmability

End-to-End Timing Solutions

Clock Management Solutions

46

|

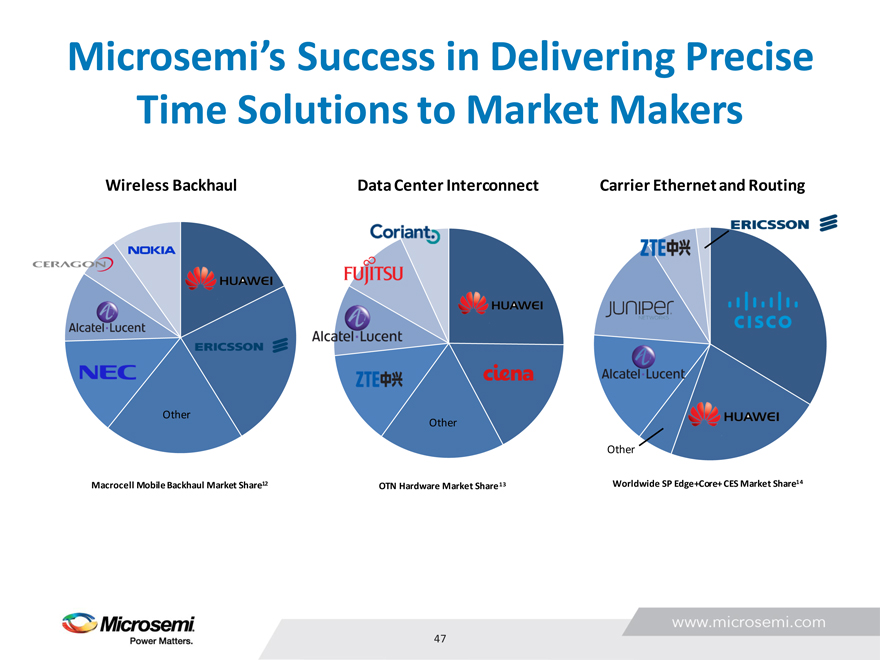

Microsemi’s Success in Delivering Precise Time Solutions to Market Makers

Wireless Backhaul Data Center Interconnect Carrier Ethernet and Routing

Other

Other

Other

Macrocell Mobile Backhaul Market Share12 OTN Hardware Market Share13 Worldwide SP Edge+Core+ CES Market Share14

47

|

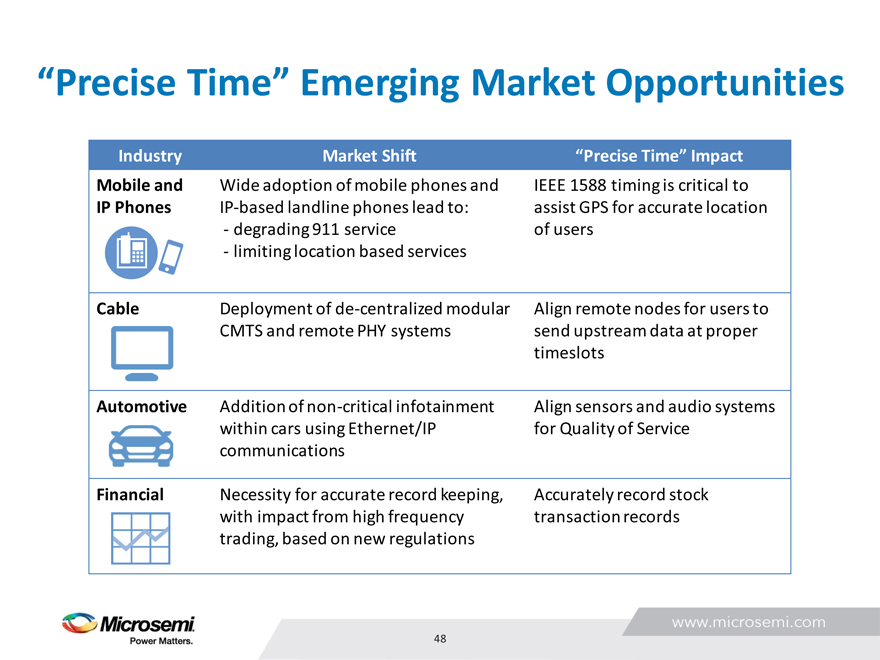

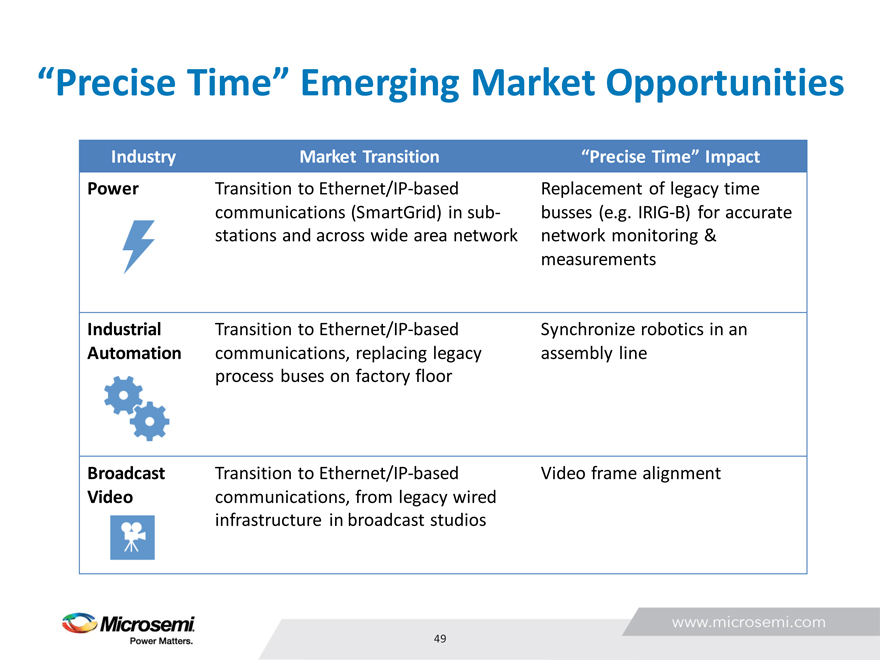

“Precise Time” Emerging Market Opportunities

Industry Mobile and IP Phones

Cable Automotive Financial

Market Shift

Wide adoption of mobile phones and IP-based landline phones lead to: —degrading 911 service —limiting location based services

Deployment of de-centralized modular CMTS and remote PHY systems

Addition of non-critical infotainment within cars using Ethernet/IP communications

Necessity for accurate record keeping, with impact from high frequency trading, based on new regulations

“Precise Time” Impact

IEEE 1588 timing is critical to assist GPS for accurate location of users

Align remote nodes for users to send upstream data at proper timeslots

Align sensors and audio systems for Quality of Service

Accurately record stock transaction records

48

|

“Precise Time” Emerging Market Opportunities

Industry Power

Industrial Automation

Broadcast Video

Market Transition

Transition to Ethernet/IP-based communications (SmartGrid) in substations and across wide area network

Transition to Ethernet/IP-based communications, replacing legacy process buses on factory floor

Transition to Ethernet/IP-based communications, from legacy wired infrastructure in broadcast studios

“Precise Time” Impact

Replacement of legacy time busses (e.g. IRIG-B) for accurate network monitoring & measurements

Synchronize robotics in an assembly line

Video frame alignment

49

|

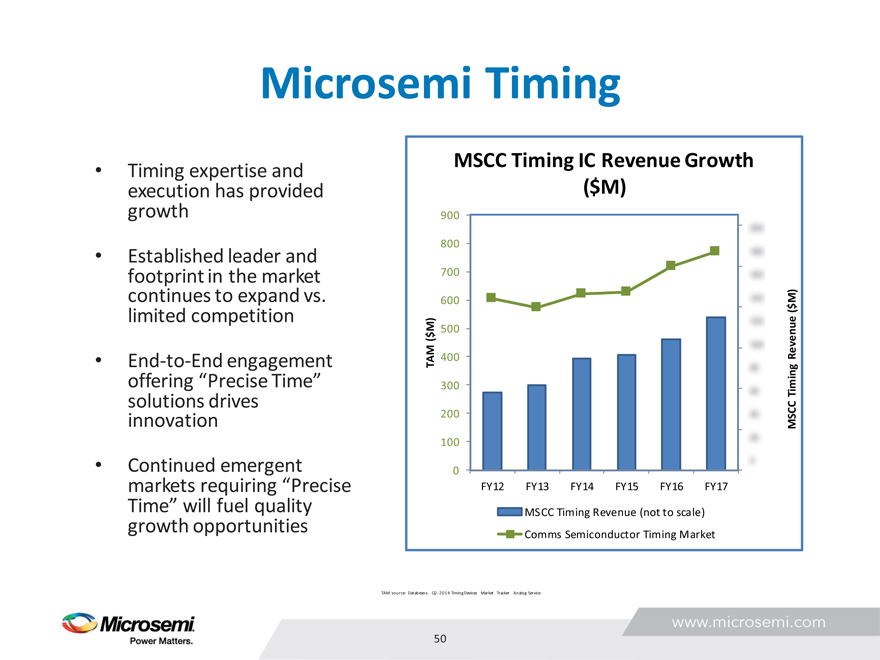

Microsemi Timing

Timing expertise and

execution has provided

growth

Established leader and

footprint in the market

continues to expand vs.

limited competition

End-to-End engagement

offering “Precise Time”

solutions drives

innovation

Continued emergent

markets requiring “Precise

Time” will fuel quality

growth opportunities

MSCC Timing IC Revenue Growth

($M)

900

800

700

M)

600

( $ M)

500

( $

Revenue TAM 400 300 Timing 200 MSCC

100

0 0 FY12 FY13 FY14 FY15 FY16 FY17

MSCC Timing Revenue (not to scale)

Comms Semiconductor Timing Market

TAM source: Databeans- Q2-2014 Timing Devices Market Tracker Analog Service

50

|

Driving Growth in Key Applications: Small Cell/Backhaul

Maamoun Seido

VP & Business Unit Manager, Timing and Optical Products

|

Small Cells – Integral to Future Deployments

The existing macrocell infrastructure is not easily scalable for future 4G/LTE deployments Small Cells offer a way to complement the macrocell architectures providing cost effective, heterogeneous solutions for high user locations Small cells are defined (by the SmallCellForum): number of users and location

Urban Enterprise Home Rural

www.microsemi.com

52

|

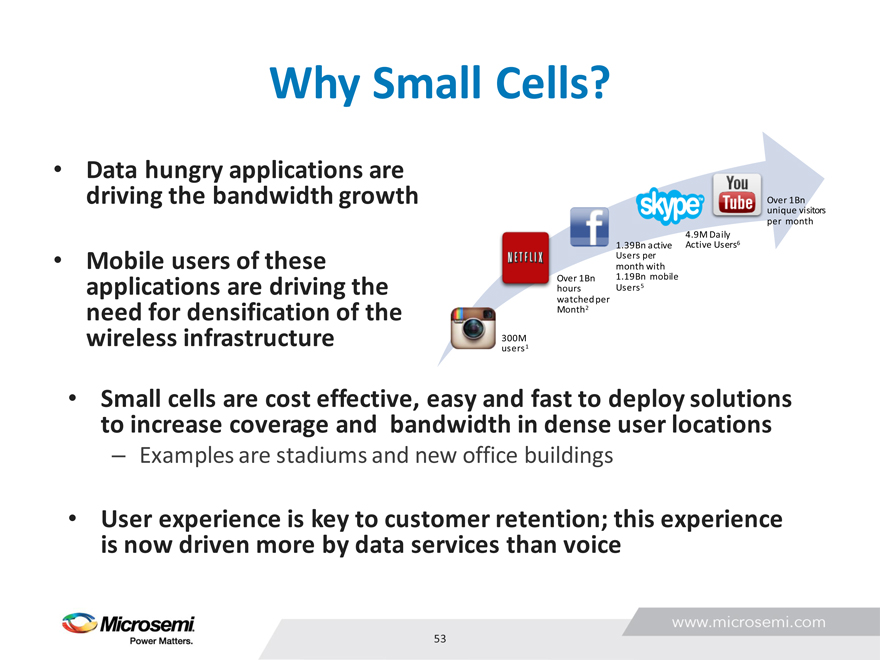

Why Small Cells

Data hungry applications are driving the bandwidth growth

Mobile users of these applications are driving the need for densification of the wireless infrastructure

Over 1Bn

unique visitors

per month

4.9M Daily

1.39Bn active Active Users6

Users per

month with

Over 1Bn 1.19Bn mobile

hours Users5

watched per

Month2

300M

users1

Small cells are cost effective, easy and fast to deploy solutions to increase coverage and bandwidth in dense user locations

– Examples are stadiums and new office buildings

User experience is key to customer retention; this experience is now driven more by data services than voice

www.microsemi.com

53

|

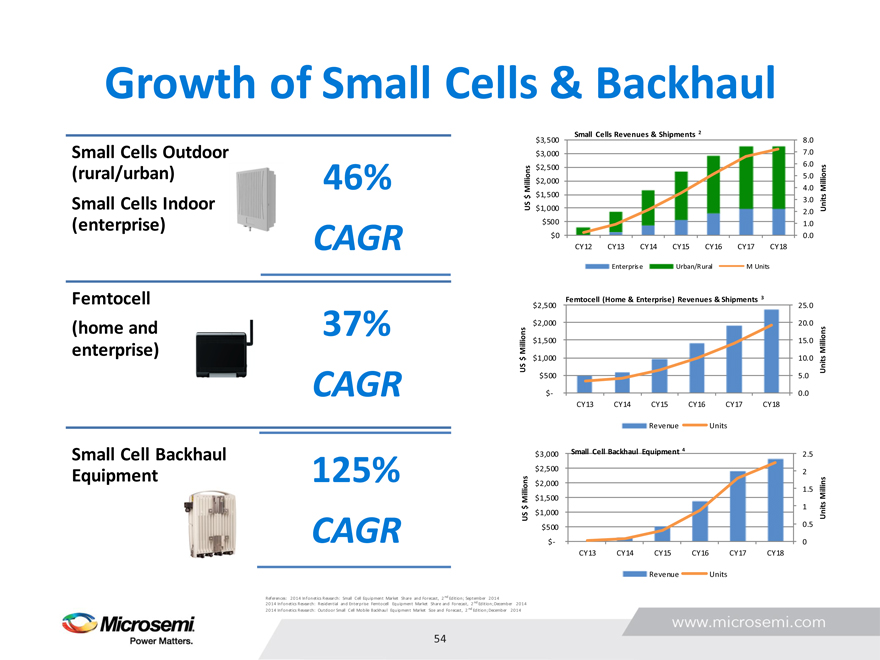

Growth of Small Cells & Backhaul

Small Cells Outdoor

(rural/urban) 46%

Small Cells Indoor

(enterprise) CAGR

Femtocell

(home and 37%

enterprise)

CAGR

Small Cell Backhaul

Equipment 125%

CAGR

References: 2014 Infonetics Research: Small Cell Equipment Market Share and Forecast, 2 nd Edition; September 2014

2014 Infonetics Research: Residential and Enterprise Femtocell Equipment Market Share and Forecast, 2 nd Edition; December 2014 2014 Infonetics Research: Outdoor Small Cell Mobile Backhaul Equipment Market Size and Forecast, 2 nd Edition; December 2014

Small Cells Revenues & Shipments 2

$3,500 8.0

$3,000 7.0

$2,500 6.0

5.0

$2,000

Millions 4.0 Millions

$1,500

$ 3.0

US $1,000 Units

2.0

$500 1.0

$0 0.0

CY12 CY13 CY14 CY15 CY16 CY17 CY18

Enterprise Urban/Rural M Units

Femtocell (Home & Enterprise) Revenues & Shipments 3

$2,500 25.0

$2,000 20.0

Millions $1,500 15.0 Millions

US $ $1,000 10.0 Units

$500 5.0

$- 0.0

CY13 CY14 CY15 CY16 CY17 CY18

Revenue Units

$3,000 Small Cell Backhaul Equipment 4 2.5

$2,500 2

$2,000

1.5

Millions $1,500 Millins

$ 1

US $1,000 Units

$500 0.5

$- 0

CY13 CY14 CY15 CY16 CY17 CY18

Revenue Units

www.microsemi.com

54

|

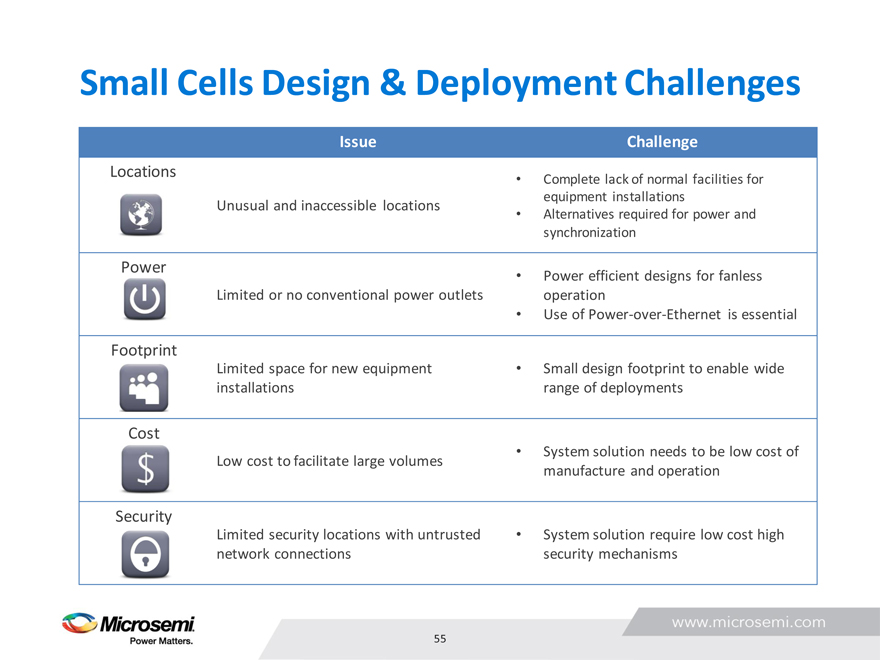

Small Cells Design & Deployment Challenges

Issue Challenge

Locations • Complete lack of normal facilities for

equipment installations

Unusual and inaccessible locations • Alternatives required for power and

synchronization

Power • Power efficient designs for fanless

Limited or no conventional power outlets operation

• Use of Power-over-Ethernet is essential

Footprint

Limited space for new equipment • Small design footprint to enable wide

installations range of deployments

Cost

• System solution needs to be low cost of

Low cost to facilitate large volumes

manufacture and operation

Security

Limited security locations with untrusted • System solution require low cost high

network connections security mechanisms

www.microsemi.com

55

|

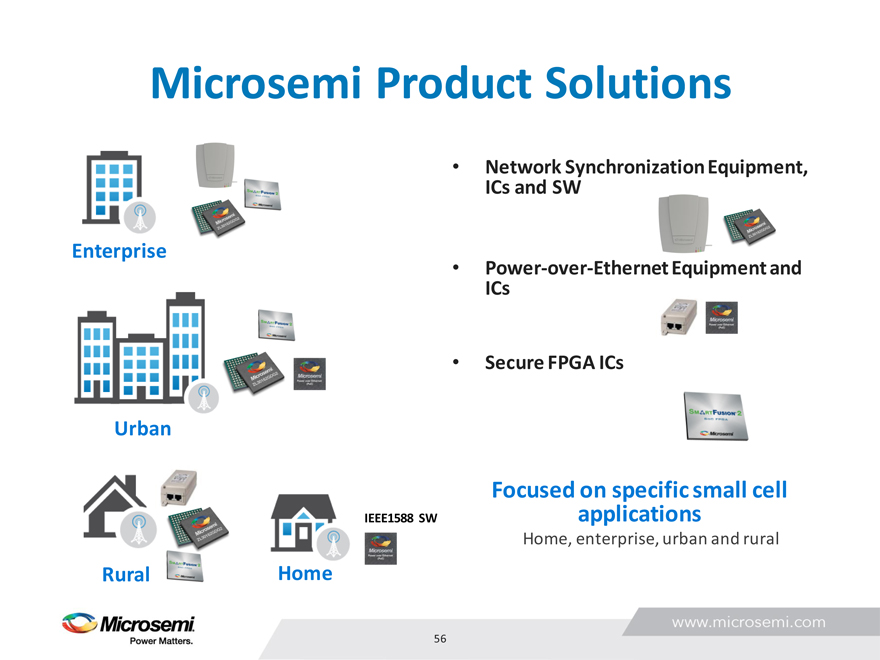

Microsemi Product Solutions

Enterprise

Urban

IEEE1588 SW

Rural Home

Network Synchronization Equipment, ICs and SW

Power-over-Ethernet Equipment and ICs

Secure FPGA ICs

Focused on specific small cell applications

Home, enterprise, urban and rural

www.microsemi.com

56

|

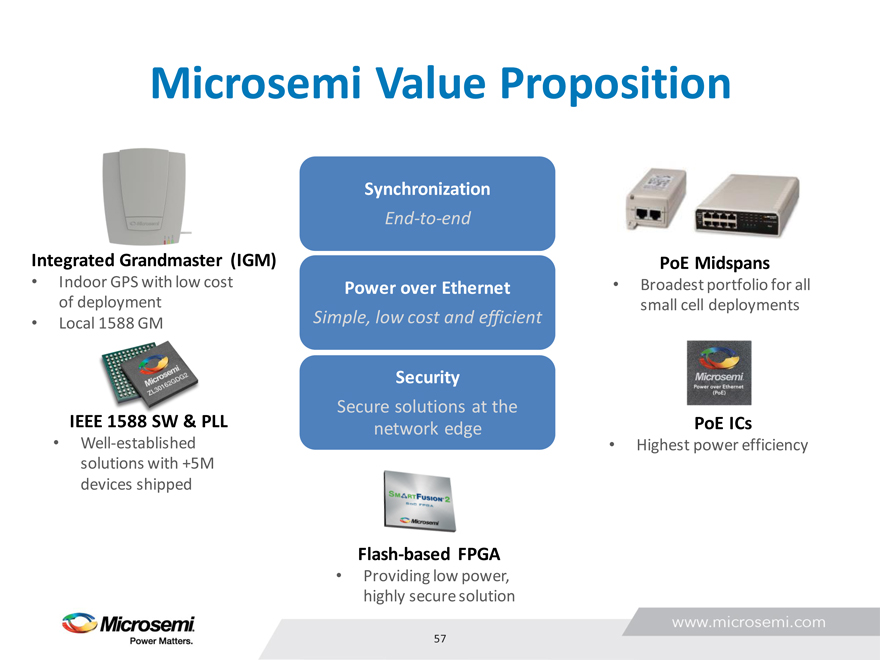

Microsemi Value Proposition

Integrated Grandmaster (IGM)

Indoor GPS with low cost of deployment Local 1588 GM

IEEE 1588 SW & PLL

Well-established solutions with +5M devices shipped

Synchronization

End-to-end

Power over Ethernet

Simple, low cost and efficient

Security

Secure solutions at the

network edge

Flash-based FPGA

Providing low power, highly secure solution

PoE Midspans

Broadest portfolio for all

small cell deployments

PoE ICs

Highest power efficiency

www.microsemi.com

57

|

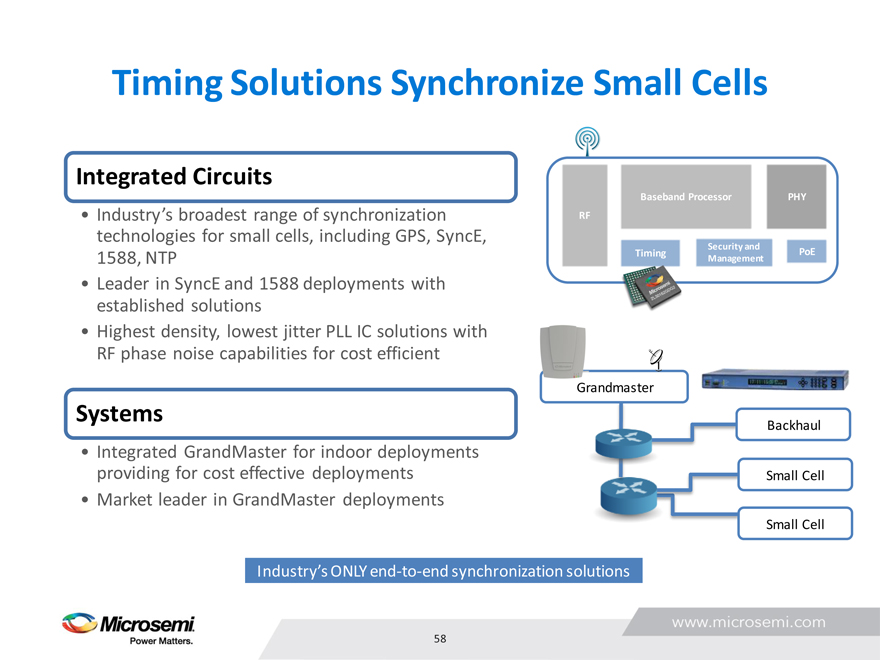

Timing Solutions Synchronize Small Cells

Integrated Circuits

Industry’s broadest range of synchronization

technologies for small cells, including GPS, SyncE,

1588, NTP

Leader in SyncE and 1588 deployments with

established solutions

Highest density, lowest jitter PLL IC solutions with

RF phase noise capabilities for cost efficient

Systems

Integrated GrandMaster for indoor deployments

providing for cost effective deployments

Market leader in GrandMaster deployments

Baseband Processor PHY

RF

Security and

Timing PoE

Management

Grandmaster

Backhaul

Small Cell

Small Cell

Industry’s ONLY end-to-end synchronization solutions

www.microsemi.com

58

|

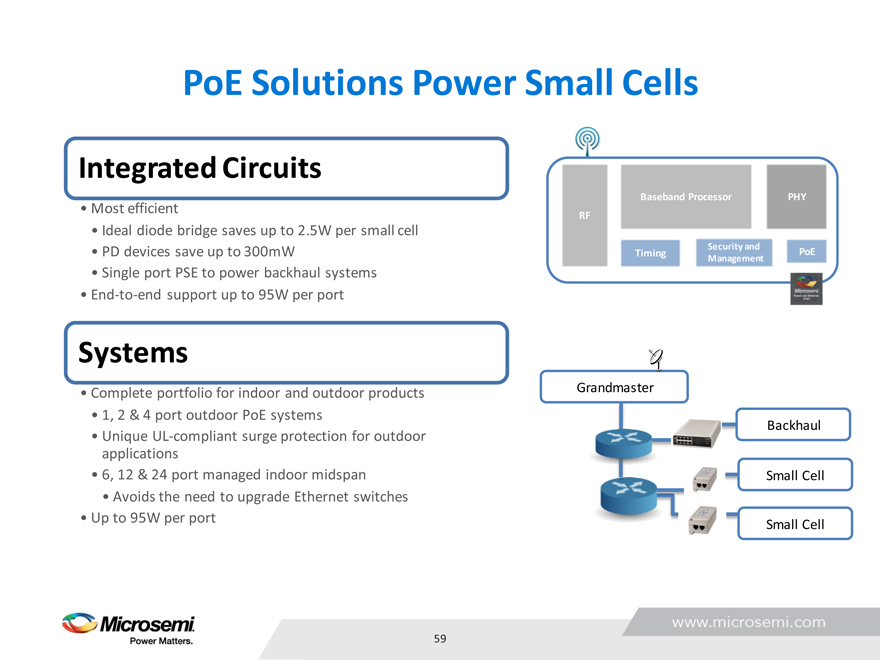

PoE Solutions Power Small Cells

Integrated Circuits

Most efficient

Ideal diode bridge saves up to 2.5W per small cell

PD devices save up to 300mW

Single port PSE to power backhaul systems

End-to-end support up to 95W per port

Systems

Complete portfolio for indoor and outdoor products

1, 2 & 4 port outdoor PoE systems

Unique UL-compliant surge protection for outdoor

applications

6, 12 & 24 port managed indoor midspan

Avoids the need to upgrade Ethernet switches

Up to 95W per port

Baseband Processor PHY

RF

Security and

Timing PoE

Management

Grandmaster

Backhaul

Small Cell

Small Cell

www.microsemi.com

59

|

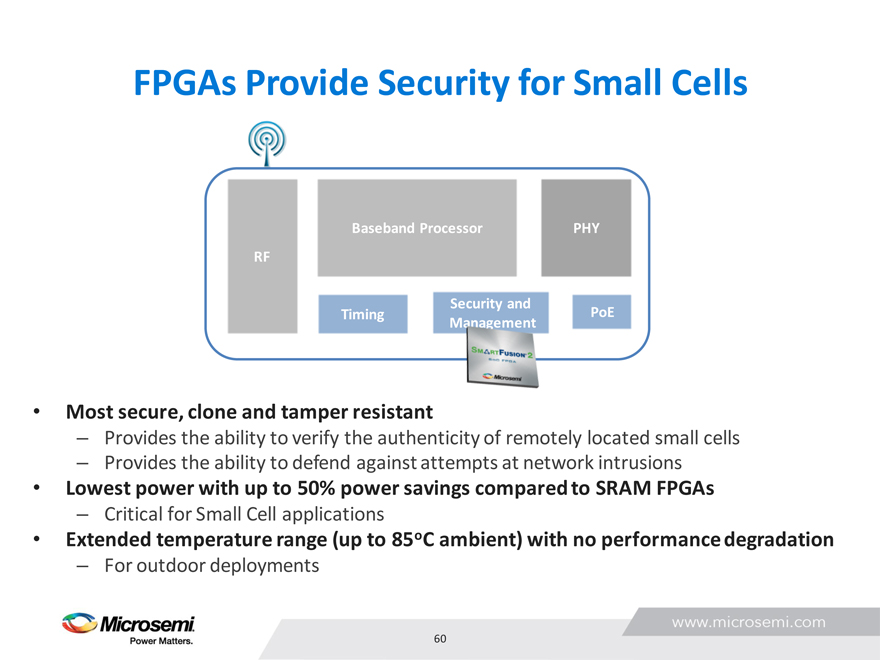

FPGAs Provide Security for Small Cells

Baseband Processor PHY

RF

Security and Management

Timing PoE

Most secure, clone and tamper resistant

– Provides the ability to verify the authenticity of remotely located small cells

– Provides the ability to defend against attempts at network intrusions

Lowest power with up to 50% power savings compared to SRAM FPGAs

– Critical for Small Cell applications

Extended temperature range (up to 85oC ambient) with no performance degradation

– For outdoor deployments

www.microsemi.com

60

|

Driving Growth in Key Applications: Residential Gateway

Roger Holliday

Senior VP & General Manager, Communications Product Group

|

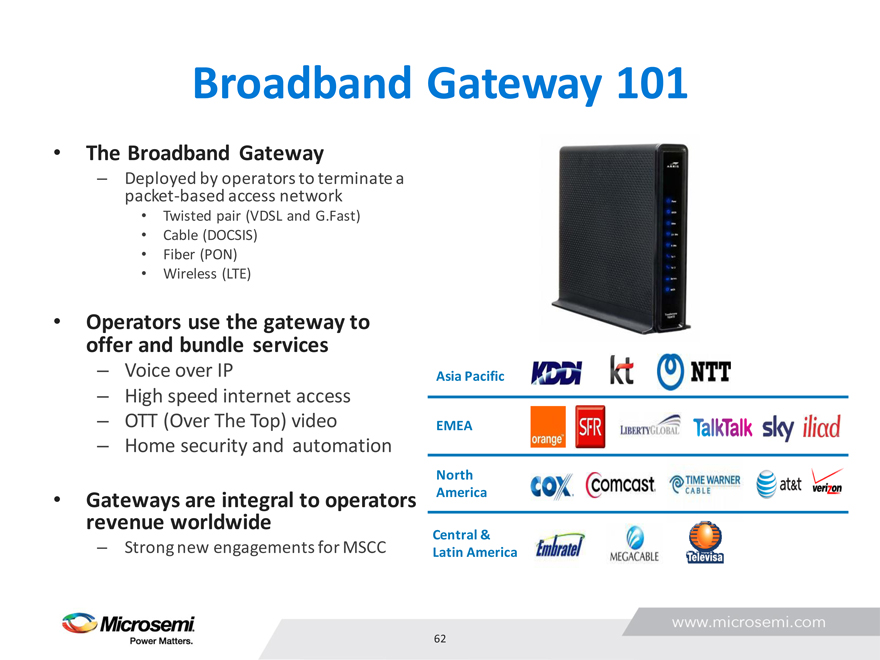

Broadband Gateway 101

The Broadband Gateway

– Deployed by operators to terminate a packet-based access network

Twisted pair (VDSL and G.Fast)

Cable (DOCSIS)

Fiber (PON)

Wireless (LTE)

Operators use the gateway to offer and bundle services

– Voice over IP

– High speed internet access

– OTT (Over The Top) video

– Home security and automation

Gateways are integral to operators revenue worldwide

– Strong new engagements for MSCC

Asia Pacific

EMEA

North

America

Central &

Latin America

www.microsemi.com

62

|

Why Gateways?

Broadband Subscriptions

1,000 747 782 816 847

800 707

144 167 191 217

Millions 600 123

117 120 122 124 126 PON

400 CABLE

Subscribers 200 467 483 494 501 504 DSL

0

2014* 2015* 2016* 2017* 2018*

Operators transitioning from TDM to packet-based infrastructure New features to drive new services

– Home security, home automation

In addition, massive new upgrade cycles started in CY14 and will continue over the next few years

– DSL ? G.FAST or GPON

– Cable ? DOCSIS 3.0 to DOCSIS 3.1

– Fiber ? EPON to GPON

Replacement boxes to existing subscribers

Connectivity targets from megabits to gigabits and demand for enhanced wireless

www.microsemi.com

63

|

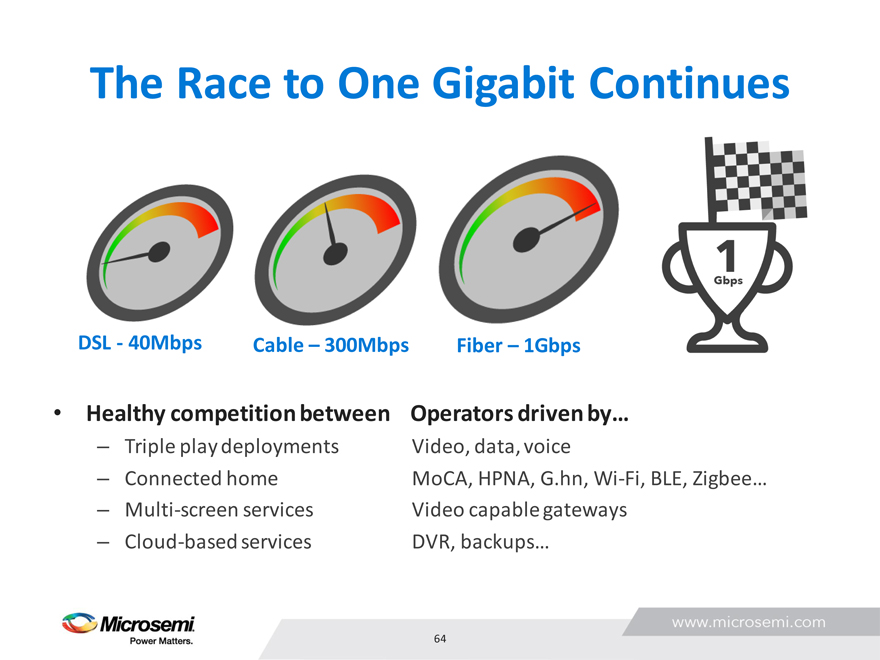

The Race to One Gigabit Continues

DSL—40Mbps Cable – 300Mbps Fiber – 1Gbps

Healthy competition between Operators driven by…

– Triple play deployments Video, data, voice

– Connected home MoCA, HPNA, G.hn, Wi-Fi, BLE, Zigbee…

– Multi-screen services Video capable gateways

– Cloud-based services DVR, backups…

www.microsemi.com

64

|

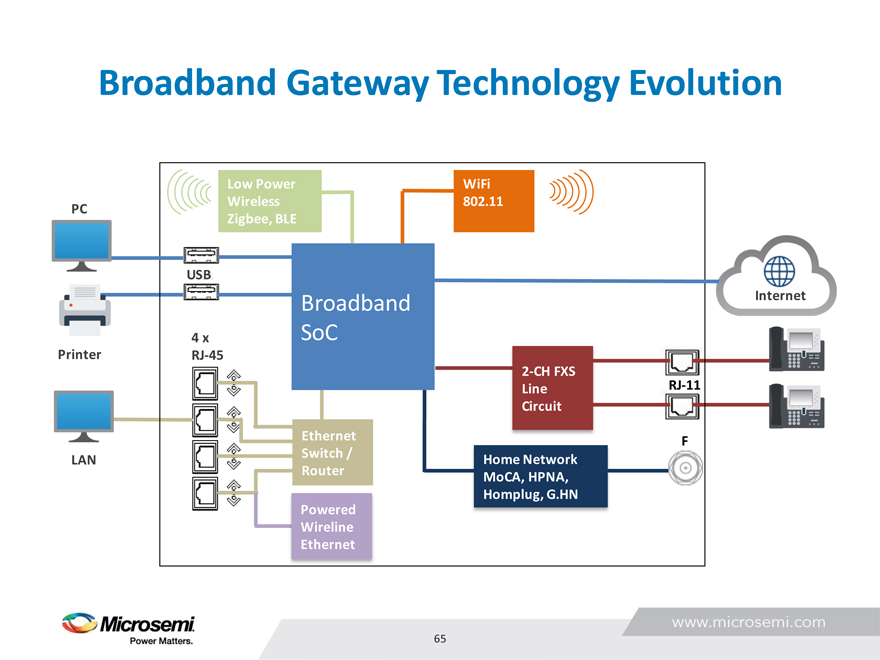

Broadband Gateway Technology Evolution

Low Power WiFi

PC Wireless 802.11

Zigbee, BLE

USB

Broadband Internet

4 x SoC

Printer RJ-45

2-CH FXS

Line RJ-11

Circuit

Ethernet F

Switch /

LAN Home Network

Router MoCA, HPNA,

Homplug, G.HN

Powered

Wireline

Ethernet

www.microsemi.com

65

|

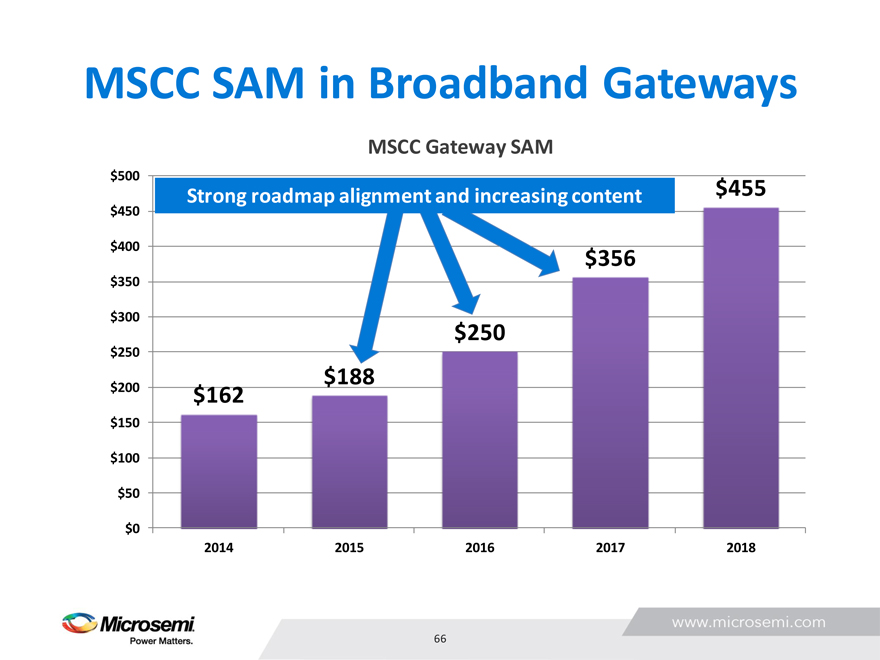

MSCC SAM in Broadband Gateways

MSCC Gateway SAM

$500

Strong roadmap alignment and increasing content $455

$450

$400

$356

$350

$300

$250

$250

$188

$200 $162

$150

$100

$50

$0

2014 2015 2016 2017 2018

www.microsemi.com

66

|

MSCC Solutions for Broadband Gateways

Voice:

– Dominant market share leader

– Demand upside across all geographies

WiFi PA/LNA:

– Strong offering in high power, high efficiency, high integration

Line Drivers:

– VDSL and G.Fast

– PLC – HomePlug® AV2, G.HN

Powered Wireline Ethernet (PoE):

– Pioneer and market leader for PoE

Reverse Power Feed (RPF):

– Leader in innovative powering mechanism enabling FTTdp

The Connected Home

www.microsemi.com

67

|

Solidifying Microsemi’s Market Leadership

Microsemi provides world class broadband gateway solutions

Strong engagement with leading gateway suppliers

Delivering voice solutions today

– Over 1 billion lines shipped

High performance Wi-Fi and 802.11AC

Providing line driver and power solutions for tomorrows enhanced DSL services

PoE for “2-Box” gateway architectures

www.microsemi.com

68

|

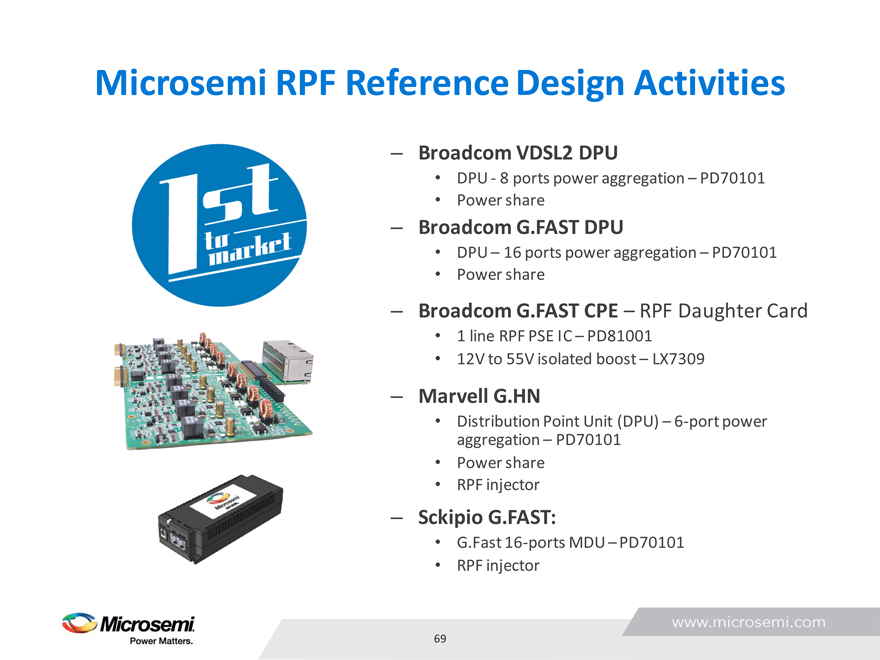

Microsemi RPF Reference Design Activities

Broadcom VDSL2 DPU

DPU—8 ports power aggregation – PD70101

Power share

Broadcom G.FAST DPU

DPU – 16 ports power aggregation – PD70101

Power share

Broadcom G.FAST CPE – RPF Daughter Card

1 line RPF PSE IC – PD81001

12V to 55V isolated boost – LX7309

Marvell G.HN

Distribution Point Unit (DPU) – 6-port power aggregation – PD70101

Power share

RPF injector

Sckipio G.FAST:

G.Fast 16-ports MDU – PD70101

RPF injector

69

www.microsemi.com

|

Strong Partnership Program and Go To Market

70

www.microsemi.com

|

Microsemi Gateway Leadership

Growing market

– New subscribers

– Existing subscriber hardware replacement needs

– Increasing silicon content

Systems engineering brings substantial value to operators.

Roadmap and trends provide strong growth for the second half of the year and beyond

71

www.microsemi.com

|

Driving Growth in Key Applications: Aerospace

Siobhan Dolan Clancy

VP, Worldwide Business Development, Aerospace

|

Commercial Aviation Market Dynamics

Market Demand

World traffic annual growth predicted at 4.7% (Airbus GMF 2014-2033)

Demand for 30K + new aircraft by 2033

Single-aisle aircraft represents 70% demand in units

Fuel efficiency will continue to drive profitability

Technology Drivers for “More Electric” Aircraft

Environmental impact

Weight

Reliability, safety, cost

Operational efficiencies

Supply Chain Efficiency

Manufacturability – 10 year OEM backlog

Traceability

73

www.microsemi.com

|

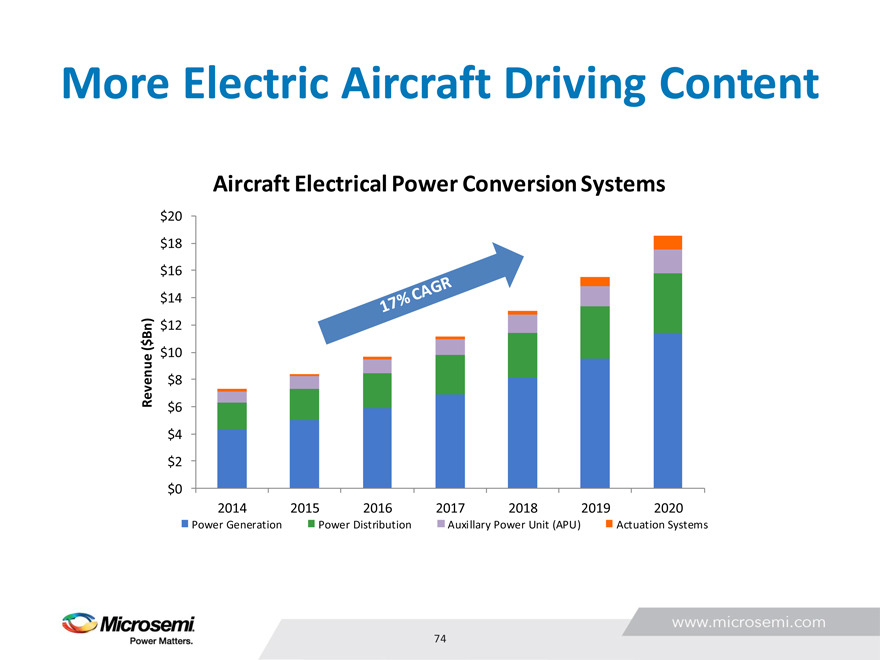

More Electric Aircraft Driving Content

Aircraft Electrical Power Conversion Systems

$20

$18

$16

$14

Bn) $12

$

( $10

Revenue $8

$6

$4

$2

$0

2014 2015 2016 2017 2018 2019 2020

Power Generation Power Distribution Auxillary Power Unit (APU) Actuation Systems

74

www.microsemi.com

|

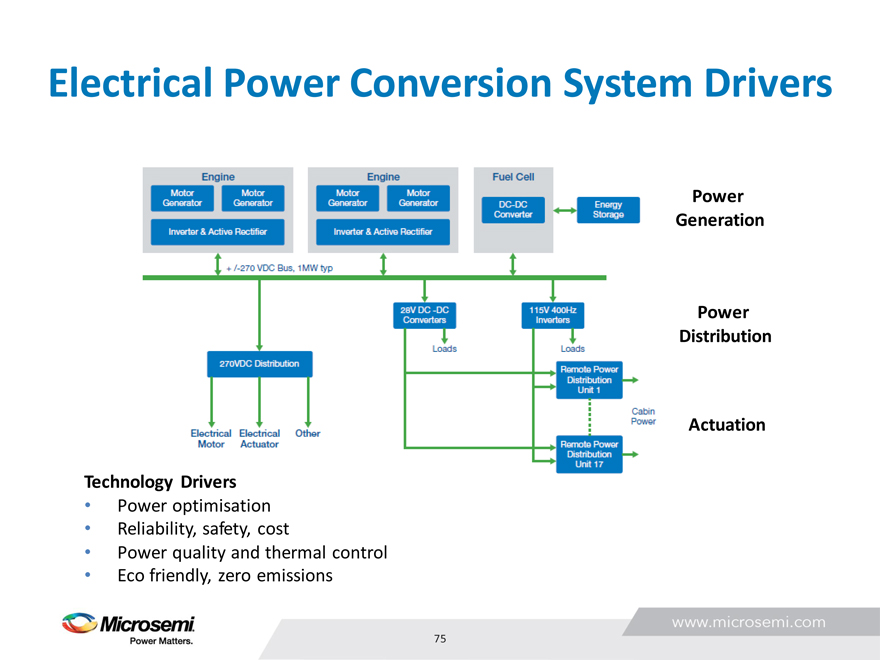

Electrical Power Conversion System Drivers

Power

Generation

Power

Distribution

Actuation

Technology Drivers

Power optimisation

Reliability, safety, cost

Power quality and thermal control

Eco friendly, zero emissions

75

www.microsemi.com

|

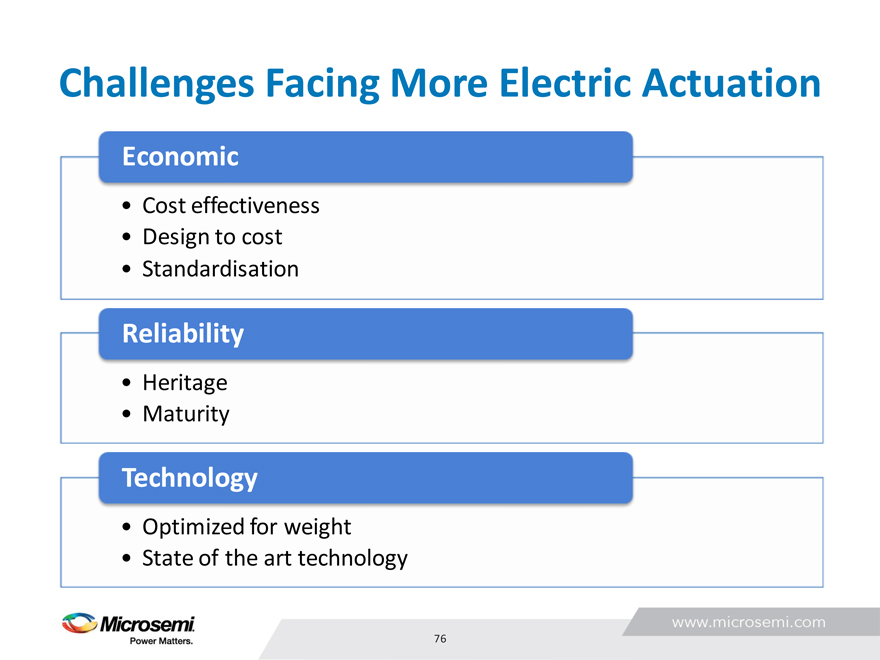

Challenges Facing More Electric Actuation

Economic

Cost effectiveness

Design to cost

Standardisation

Reliability

Heritage

Maturity

Technology

Optimized for weight

State of the art technology

76

www.microsemi.com

|

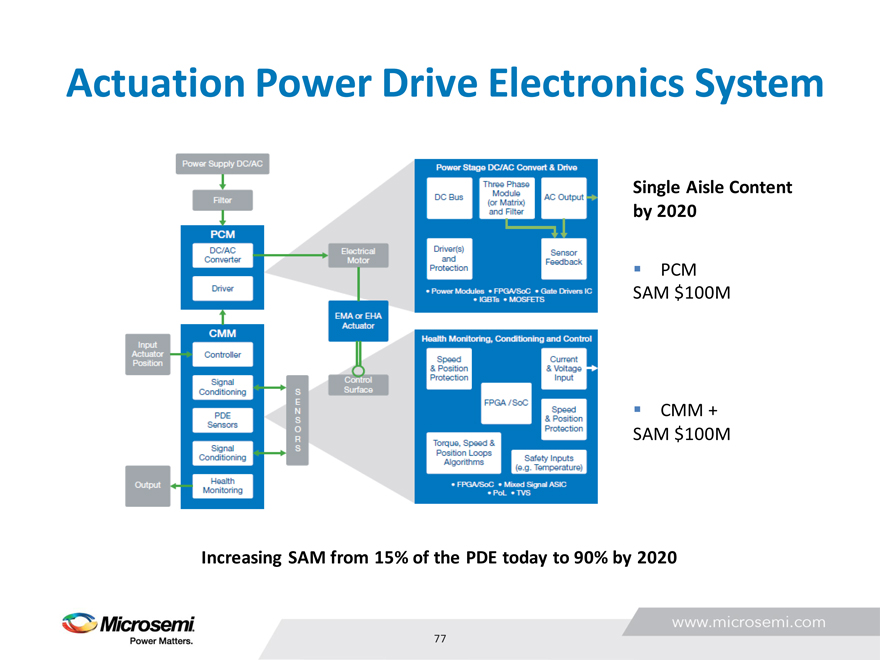

Actuation Power Drive Electronics System

Single Aisle Content by 2020

PCM SAM $100M

CMM + SAM $100M

Increasing SAM from 15% of the PDE today to 90% by 2020

77

www.microsemi.com

|

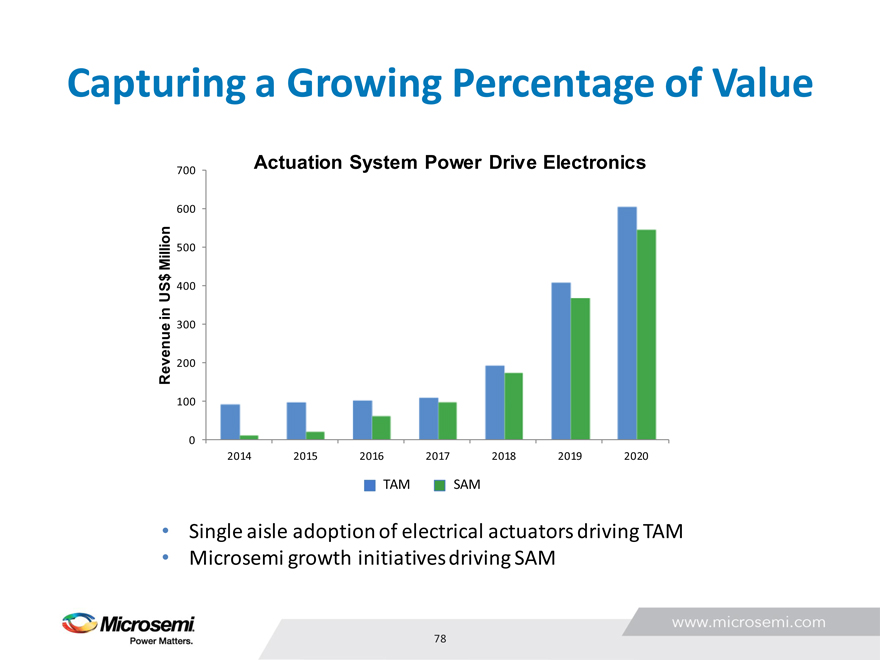

Capturing a Growing Percentage of Value

700 Actuation System Power Drive Electronics

600

Million 500

$

US 400

in 300

Revenue 200

100

0

2014 2015 2016 2017 2018 2019 2020

TAM SAM

Single aisle adoption of electrical actuators driving TAM Microsemi growth initiatives driving SAM

78

www.microsemi.com

|

Technology Leadership Driving Content

FPGA

Integration, power, reliability and security

SEU immune

Motor control IP and development platform

Power Discretes

SiC technology, extended temperature range

Broadest portfolio of TVS technology

Higher Level Integration

ASIC/SoC

Power core modules (PCM) & sub-systems

Potential to offer full PDE

79

www.microsemi.com

|

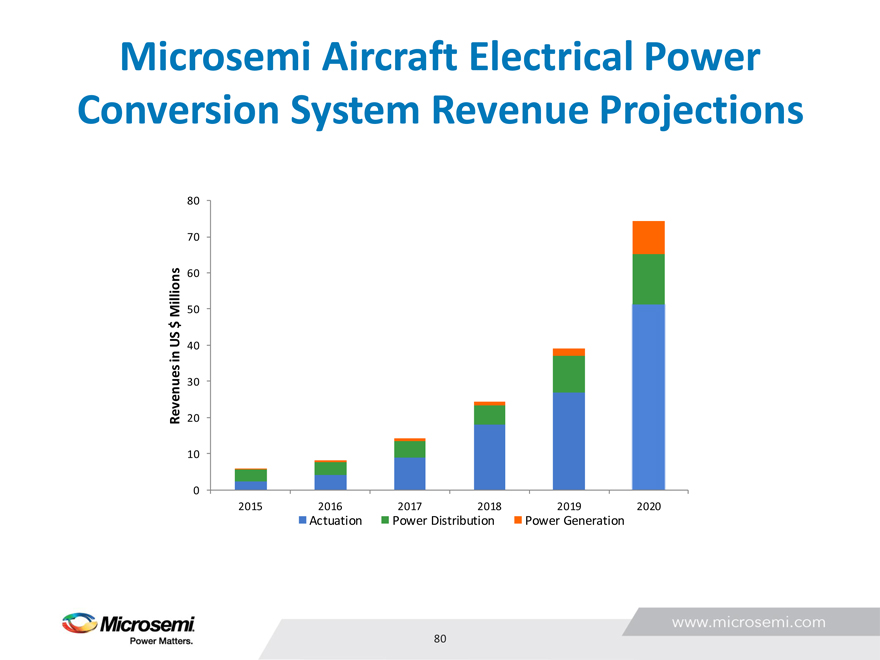

Microsemi Aircraft Electrical Power Conversion System Revenue Projections

80

70

60

Millions 50

$

US 40

in

30

Revenues 20

10

0

2015 2016 2017 2018 2019 2020

Actuation Power Distribution Power Generation

80

www.microsemi.com

|

Solid Engagements with Market Leaders

Airframers Electrical Power Actuation

81

www.microsemi.com

|

Competitive Landscape

Industry Competitors

FPGA Xilinx, Altera

ASICs BAE, Raytheon, Aeroflex

TVS Vishay, Sensitron

Power devices, MOSFETs, IGBTs Infineon, IXYS, Rohm

Modules Semelab, Powerex, Fuji

Customers

Make or Buy Decision

Microsemi Differentiation

Building “solutions” capability based on core competencies (PCM/PDE)

Scale and breadth of product line

Significant footprint with market leaders

Reliability

Technology leadership

Aviation heritage

82

www.microsemi.com

|

Summary

Microsemi is well positioned to be a key partner for aircraft electric power conversion systems

Key growth initiatives based on double digit growth applications

Microsemi a “solutions partner”

Impressive technology and capabilities roadmap from semiconductor material to packaging, integration and test

Scale and breadth to drive the best “cost of ownership”

83

www.microsemi.com

|

Driving Growth in Key Applications: Space/Satellite

Siobhan Dolan Clancy

VP, Worldwide Business Development, Aerospace

|

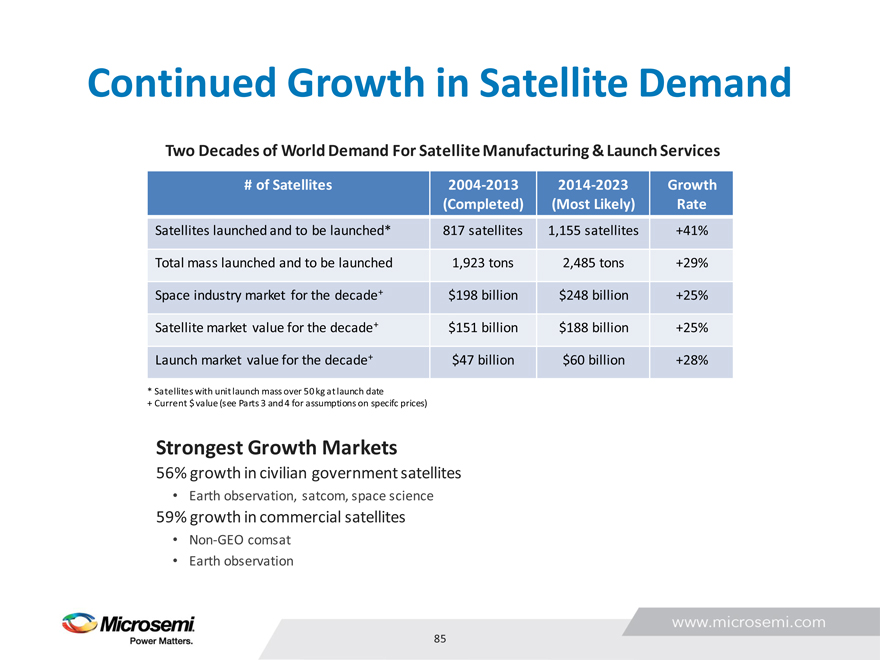

Continued Growth in Satellite Demand

Two Decades of World Demand For Satellite Manufacturing & Launch Services

# of Satellites 2004-2013 2014-2023 Growth

(Completed) (Most Likely) Rate

Satellites launched and to be launched* 817 satellites 1,155 satellites +41%

Total mass launched and to be launched 1,923 tons 2,485 tons +29%

Space industry market for the decade+ $198 billion $248 billion +25%

Satellite market value for the decade+ $151 billion $188 billion +25%

Launch market value for the decade+ $47 billion $60 billion +28%

* Satellites with unit launch mass over 50 kg at launch date

+ Current $ value (see Parts 3 and 4 for assumptions on specifc prices)

Strongest Growth Markets

56% growth in civilian government satellites

Earth observation, satcom, space science

59% growth in commercial satellites

Non-GEO comsat

Earth observation

85

www.microsemi.com

|

Capitalizing on Growth Drivers in Space

Remote Sensing

Growing requirements for imaging for commercial and government purposes ? Increasingly complex sensor data processing on board the spacecraft

Commercial Satellites

Redesigns of GEO communications platforms to support larger payloads and greater versatility

Digital Communications

Flexible reconfigurable repeaters

LEO constellations and GEO platforms

86

|

www.microsemi.com

Microsemi Technology Leader in Space

87

www.microsemi.com

|

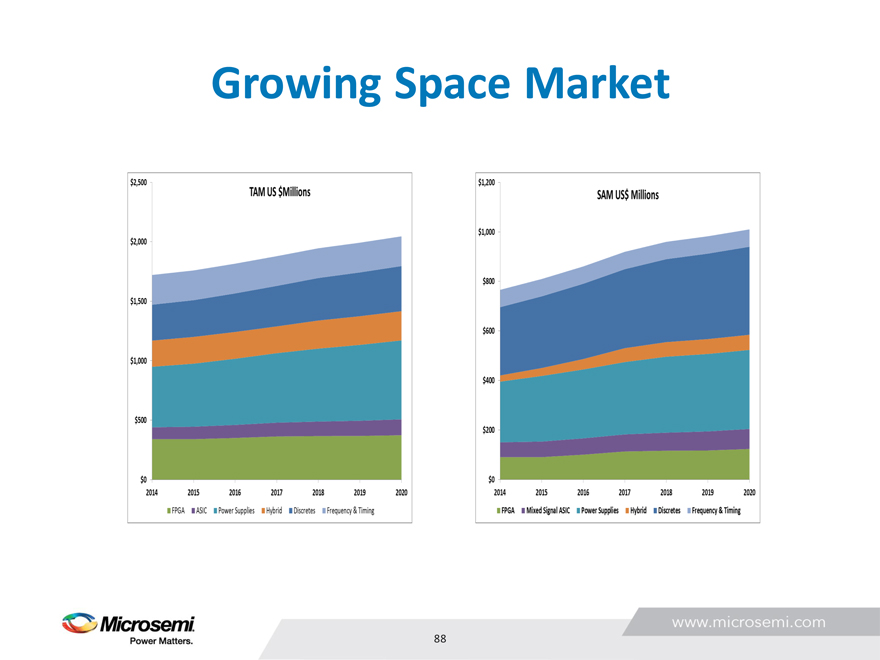

Growing Space Market

88

www.microsemi.com

|

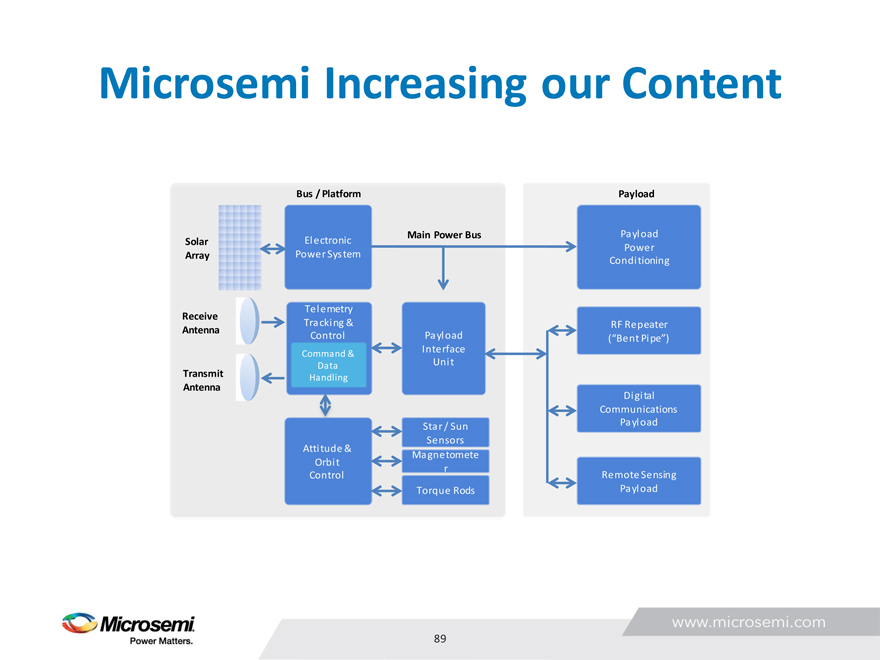

Microsemi Increasing our Content

Bus / Platform Payload

Solar Electronic Main Power Bus Payload

Power

Array Power System Conditioning

Telemetry

Receive

Tracking & RF Repeater

Antenna Control Payload (“Bent Pipe”)

Command & Interface

Data Unit

Transmit Handling

Antenna

Digital

Communications

Star / Sun Payload

Sensors

Attitude &

Magnetomete

Orbit r

Control Remote Sensing

Torque Rods Payload

89

www.microsemi.com

|

Growth Initiatives Driving Content

Introducing High Speed Processing Radiation Tolerant FPGA

Best-in-Class FPGA for Space

– Size, performance, power

– Radiation effects

– Microsemi heritage in space

Targeting Remote Sensing Payload Applications

– Sensor resolution increasing, downlink bandwidth not keeping pace

– Operators require on-board processing, satellites send information not raw data

Market Opportunity

– Potential up to $100M revenue per annum

TM

GOES-R Program:

4 satellites, each with 6 instruments

90

|

Growth Initiatives Driving Content

Radiation Tolerant Telemetry Controller IC

Provides key functions for sensor monitoring, attitude and payload control

Weight reduction, board space savings, reliability

Interfaces with a radiation tolerant FPGA

Precise Timing and Frequency Solutions

Crystal oscillators provide accurate frequency and time required for timing, radar and communication functions

Power Solutions Provider

Extending our range of complementary power solutions including DC-DC converters, relays, hybrid and discrete technology

91

www.microsemi.com

|

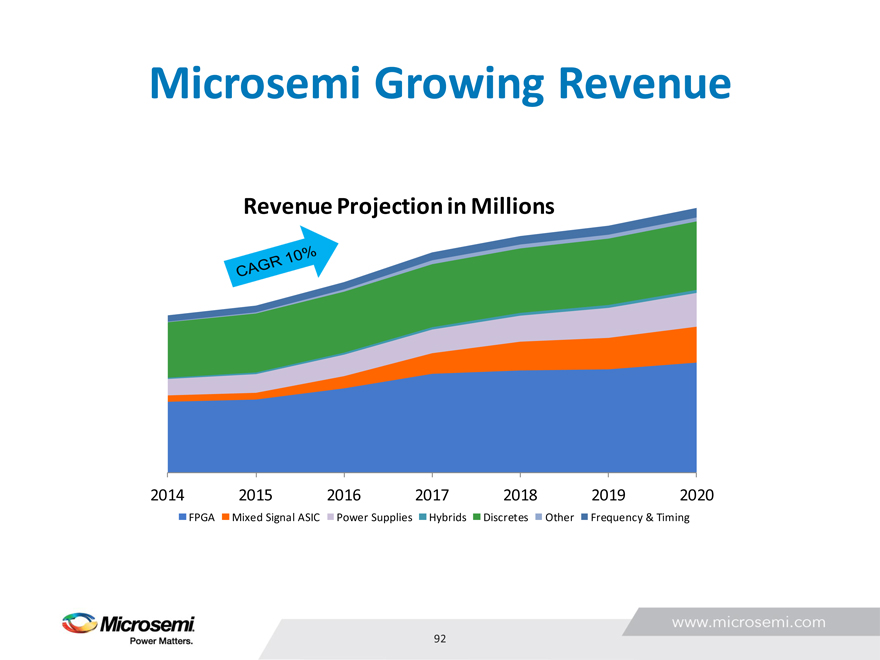

Microsemi Growing Revenue

Revenue Projection in Millions

2014 2015 2016 2017 2018 2019 2020

FPGA Mixed Signal ASIC Power Supplies Hybrids Discretes Other Frequency & Timing

92

www.microsemi.com

|

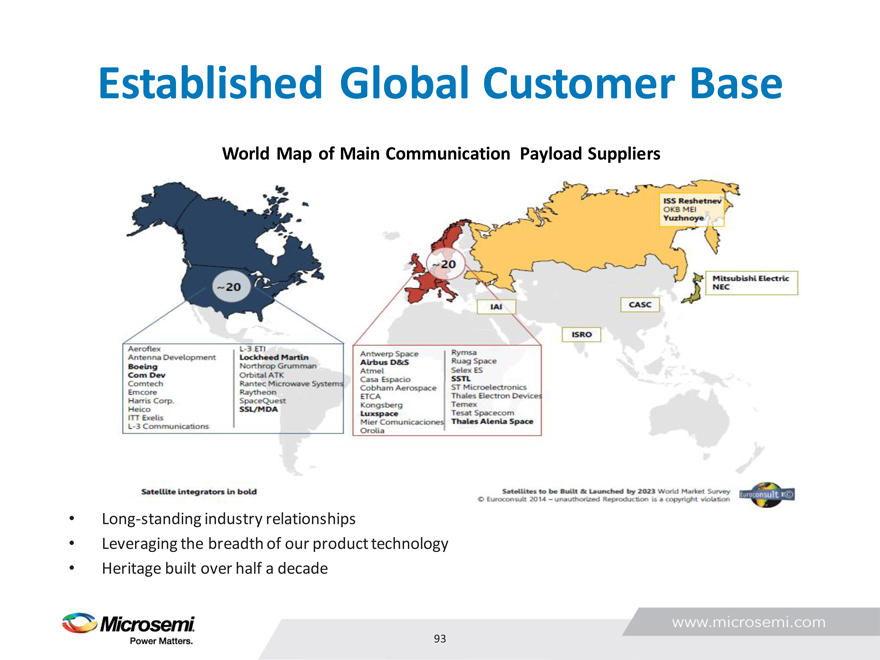

Established Global Customer Base

World Map of Main Communication Payload Suppliers

Long-standing industry relationships

Leveraging the breadth of our product technology Heritage built over half a decade

93

www.microsemi.com

|

Competitive Environment

Microsemi positioning to capture an increasing share of payload signal processing applications

– Replacing ASICs, SRAM FPGAs

Higher levels of integration for telemetry applications

– Replacing inefficient and expensive discrete and hybrid solutions

Positioning as a credible “solutions” provider replacing in-house solutions at a higher level in the system

—Oscillators, DC-DC converters, space system managers

94

www.microsemi.com

|

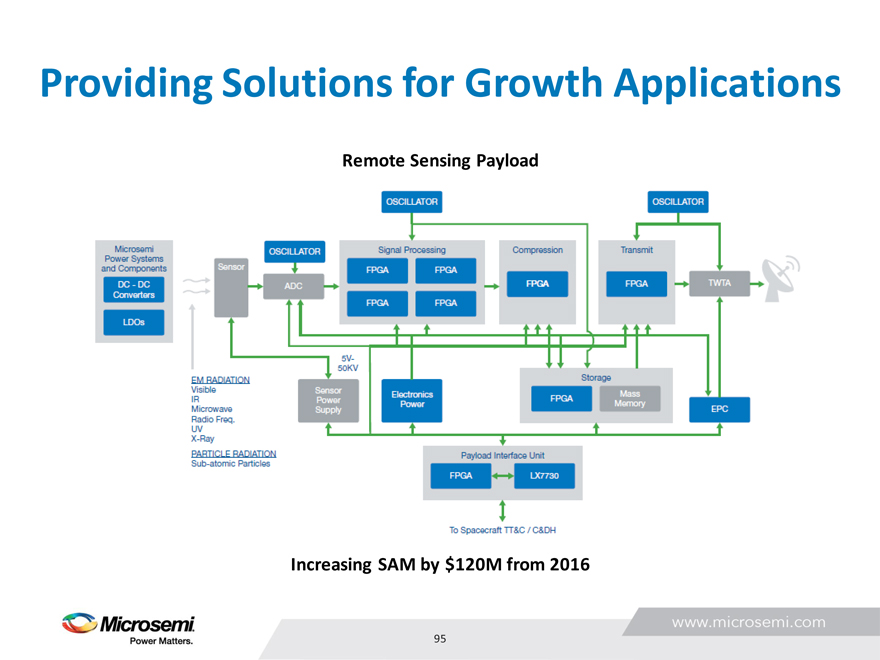

Providing Solutions for Growth Applications

Remote Sensing Payload

Increasing SAM by $120M from 2016

95

www.microsemi.com

|

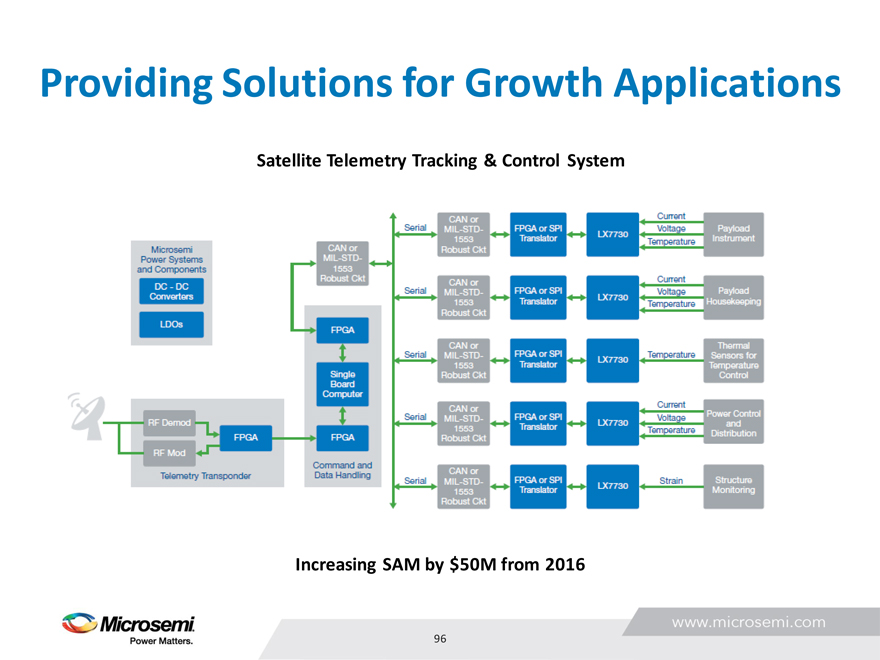

Providing Solutions for Growth Applications

Satellite Telemetry Tracking & Control System

Increasing SAM by $50M from 2016

96

www.microsemi.com

|

Space Satellite Summary

Leadership in space

Leveraging our product breadth

Innovative new product introductions

Focused on growth applications

97

www.microsemi.com

|

Acquisition Overview

Steve Litchfield

EVP & Chief Strategy Officer

|

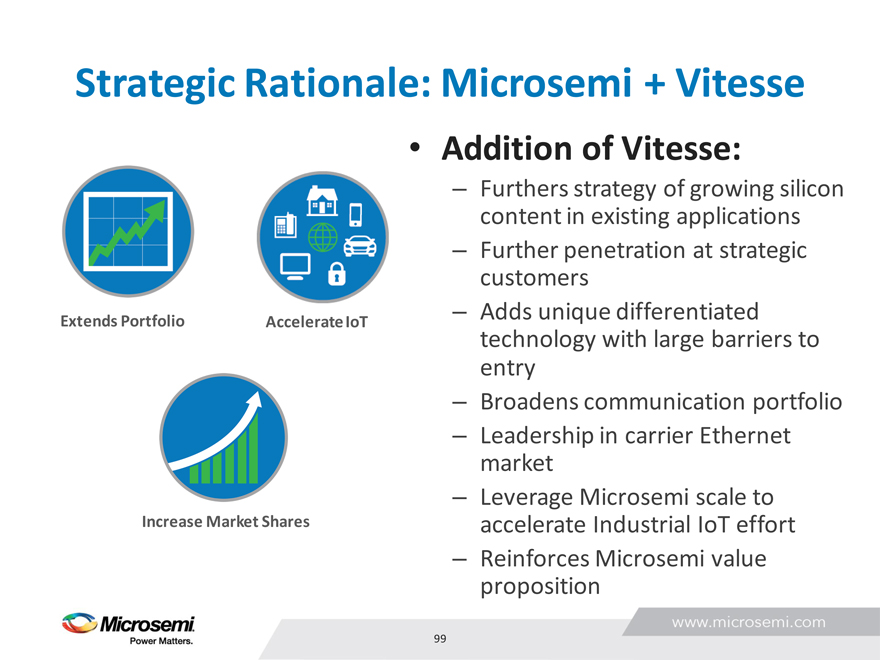

Strategic Rationale: Microsemi + Vitesse

Addition of Vitesse:

– Furthers strategy of growing silicon content in existing applications

– Further penetration at strategic customers

– Adds unique differentiated technology with large barriers to entry

– Broadens communication portfolio

– Leadership in carrier Ethernet market

– Leverage Microsemi scale to accelerate Industrial IoT effort

– Reinforces Microsemi value proposition

Extends Portfolio Accelerate IoT

Increase Market Shares

99

www.microsemi.com

|

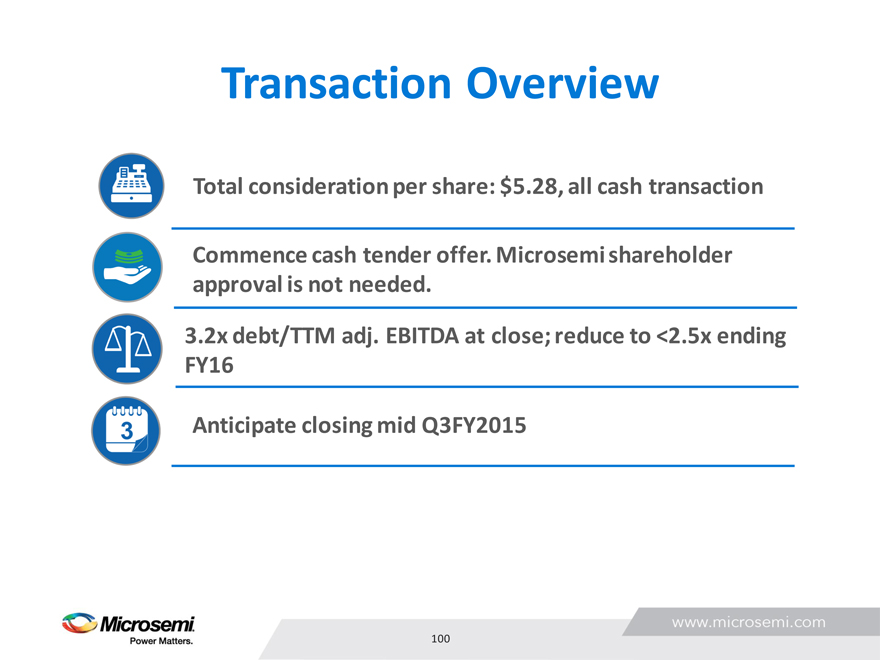

Transaction Overview

Total consideration per share: $5.28, all cash transaction

Commence cash tender offer. Microsemi shareholder approval is not needed.

3.2x debt/TTM adj. EBITDA at close; reduce to <2.5x ending FY16

Anticipate closing mid Q3FY2015

www.microsemi.com

|

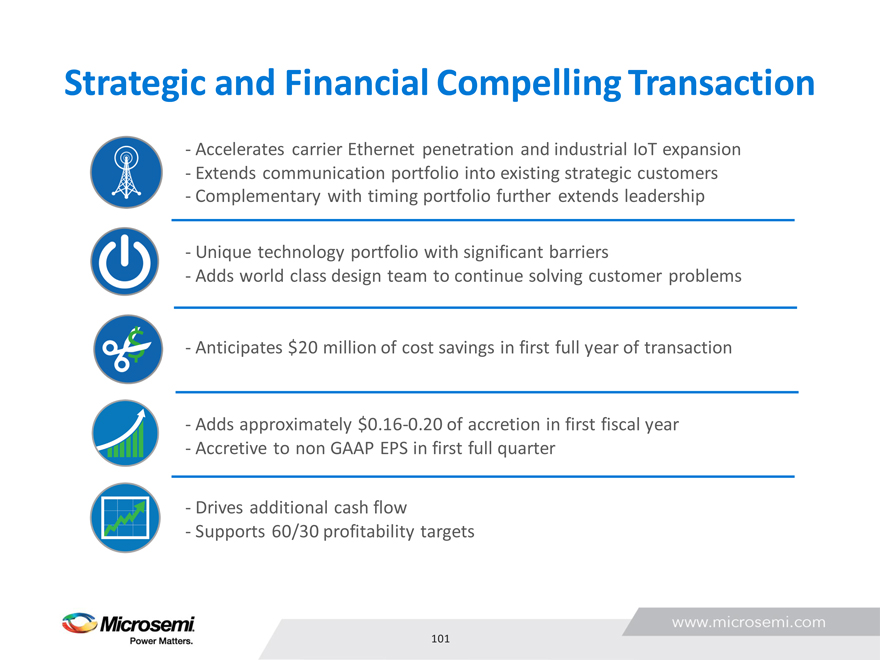

Strategic and Financial Compelling Transaction

- Accelerates carrier Ethernet penetration and industrial IoT expansion

- Extends communication portfolio into existing strategic customers

- Complementary with timing portfolio further extends leadership

- Unique technology portfolio with significant barriers

- Adds world class design team to continue solving customer problems

- Anticipates $20 million of cost savings in first full year of transaction

- Adds approximately $0.16-0.20 of accretion in first fiscal year

- Accretive to non GAAP EPS in first full quarter

- Drives additional cash flow

- Supports 60/30 profitability targets

101

www.microsemi.com

|

Executive Summary

Paul Pickle

President & COO

|

Microsemi Shareholder Value Proposition

Maximizing Profitability

103

www.microsemi.com

|

Focus Products Driving SAM Expansion

Microsemi offers tailored feature sets for targeted applications

104

www.microsemi.com

|

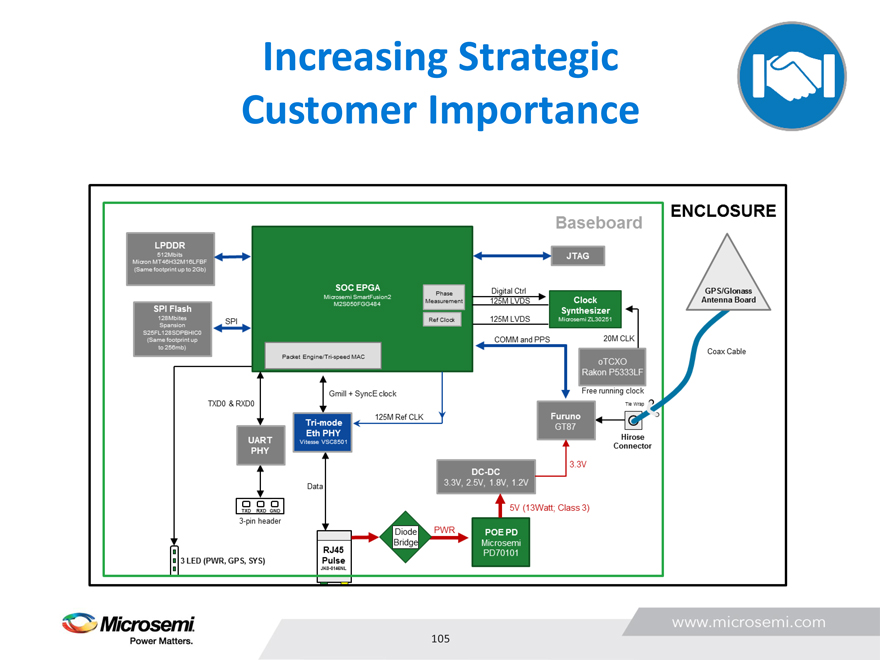

Increasing Strategic Customer Importance

105

www.microsemi.com

|

Microsemi Shareholder Value Proposition

Maximizing Profitability

Focus Products Driving SAM Expansion Increasing Strategic Customer Importance End Markets Built for Growth, Stability, Cash Flow Commitment to Deliver Shareholder Value

106

www.microsemi.com

|

Q&A

Management Luncheon