North American Palladium Ltd.

TABLE OF CONTENTS

| | Page |

| | |

| Management’s Discussion and Analysis | |

| | |

| INTRODUCTION | 1 |

| | |

| FORWARD-LOOKING INFORMATION | 1 |

| | |

| CAUTIONARY NOTE TO U.S. INVESTORS CONCERNING MINERAL RESERVES AND RESOURCES | 2 |

| | |

| OUR BUSINESS | 2 |

| | |

| KEY HIGHLIGHTS | 3 |

| | |

| EXECUTIVE SUMMARY | 4 |

| | |

| FINANCIAL REVIEW | 9 |

| | |

| FINANCIAL CONDITION, CASH FLOWS, LIQUIDITY AND CAPITAL RESOURCES | 15 |

| | |

| OUTSTANDING SHARE DATA | 18 |

| | |

| REVIEW OF OPERATIONS | 18 |

| | |

| EXPLORATION UPDATE | 21 |

| | |

| FUTURE ACCOUNTING STANDARDS | 28 |

| | |

| RISKS AND UNCERTAINTIES | 31 |

| | |

| INTERNAL CONTROLS | 31 |

| | |

| OTHER INFORMATION | 32 |

| | |

| NON-IFRS MEASURES | 32 |

North American Palladium Ltd.

Management’s Discussion and Analysis

Unless the context suggests otherwise, references to “NAP” or the “Company” or similar terms refer to North American Palladium Ltd. and its subsidiaries. “LDI” refers to Lac des Iles Mines Ltd., and “Cadiscor” refers to Cadiscor Resources Inc. On March 4, 2011, the name Cadiscor Resources Inc., was changed to NAP Quebec Mines Ltd.

The following is management’s discussion and analysis (“MD&A”) of the financial condition and results of operations to enable readers of the Company’s consolidated financial statements and related notes to assess material changes in financial condition and results of operations for the three and nine months ended September 30, 2011, compared to those of the respective periods in the prior year. This MD&A has been prepared as of November 2, 2011 and is intended to supplement and complement the unaudited consolidated financial statements and notes thereto for the three and nine months ended September 30, 2011 (collectively, the “Financial Statements”). Readers are encouraged to review the Financial Statements in conjunction with their review of this MD&A and the most recent Form 40-F/Annual Information Form on file with the U.S. Securities and Exchange Commission (“SEC”) and Canadian provincial securities regulatory authorities, available at www.sec.gov and www.sedar.com, respectively.

All amounts are in Canadian dollars unless otherwise noted and all references to production ounces refer to payable production.

| FORWARD-LOOKING INFORMATION |

Certain information included in this MD&A constitutes ‘forward-looking statements’ within the meaning of the ‘safe harbor’ provisions of the United States Private Securities Litigation Reform Act of 1995 and Canadian securities laws. The words ‘expect’, ‘believe’, ‘will’, ‘intend’, ‘estimate’ and similar expressions identify forward-looking statements. Such statements include without limitation: any information as to our future exploration, financial or operating performance, including the Company’s forward looking production guidance, operating cost estimates, project timelines, the methods by which ore will be extracted, projected capital expenditures and other statements that express management's expectations or estimates of future performance. Forward-looking statements are necessarily based upon a number of factors and assumptions that, while considered reasonable by management, are inherently subject to significant business, economic and competitive uncertainties and contingencies. The factors and assumptions contained in this MD&A, which may prove to be incorrect, include, but are not limited to: that metal prices will be consistent with the Company’s expectations, that the exchange rate between the Canadian dollar and the United States dollar will be approximately consistent with current levels, that there will be no significant disruptions affecting operations, that prices for key mining and construction supplies, including labour costs, will remain consistent with the Company’s expectations, that the Company’s current estimates of mineral reserves and resources are accurate and that there are no material delays in the timing of ongoing development projects. The forward-looking statements are not guarantees of future performance. The Company cautions the reader that such forward-looking statements involve known and unknown risks that may cause the actual results to be materially different from those expressed or implied by the forward-looking statements. Such risks include, but are not limited to: the possibility that metal prices, foreign exchange assumptions and operating costs may differ from management’s expectations, uncertainty of mineral reserves and resources, inherent risks associated with mining and processing, uncertainty of the ability of the Company to obtain financing, that the Lac des Iles and Sleeping Giant mines and may not perform as planned, and that the Offset Zone, Vezza project and other properties may not be successfully developed. For more details on the factors, assumptions and risks see the Company’s most recent Form 40-F/Annual Information Form on file with the U.S. Securities and Exchange Commission and Canadian provincial securities regulatory authorities. The Company disclaims any obligation to update or revise any forward-looking statements, whether as a result of new information, events or otherwise, except as expressly required by law. Readers are cautioned not to put undue reliance on these forward-looking statements.

THIRD QUARTER REPORT 2011

North American Palladium Ltd.

CAUTIONARY NOTE TO U.S. INVESTORS CONCERNING MINERAL RESERVES AND RESOURCES |

Mineral reserve and mineral resource information contained herein has been calculated in accordance with National Instrument 43-101 – Standards of Disclosure for Mineral Projects, as required by Canadian provincial securities regulatory authorities. Canadian standards differ significantly from the requirements of the SEC, and mineral reserve and mineral resource information contained herein is not comparable to similar information disclosed in accordance with the requirements of the SEC. While the terms “measured”, “indicated” and “inferred” mineral resources are required pursuant to National Instrument 43-101, the SEC does not recognize such terms. U.S. investors should understand that “inferred” mineral resources have a great amount of uncertainty as to their existence and great uncertainty as to their economic and legal feasibility. In addition, U.S. investors are cautioned not to assume that any part or all of NAP’s mineral resources constitute or will be converted into reserves. For a more detailed description of the key assumptions, parametres and methods used in calculating NAP’s mineral reserves and mineral resources, see NAP’s most recent Annual Information Form/Form 40-F on file with Canadian provincial securities regulatory authorities and the SEC.

North American Palladium Ltd. is a Canadian precious metals company focused on growing its production of palladium and gold in mining-friendly jurisdictions. As an established producer, the Company operates its two 100%-owned mines in Canada and has a pipeline of growth projects near its mine sites where both mills have excess capacity available for production growth.

Lac des Iles (“LDI”), the Company's flagship mine, is one of the world’s two primary palladium producers. Located approximately 85 kilometres northwest of Thunder Bay, Ontario, LDI started producing palladium in 1993. The Company is expanding the LDI mine to transition from mining via ramp access to mining via shaft while utilizing a high volume bulk mining method. The mine expansion is currently underway, with commercial production from the shaft at an increased mining rate targeted for the fourth quarter of 2012. It is expected that this expansion will transform LDI into a long life, low cost producer of palladium.

NAP also owns and operates the Sleeping Giant gold mine located in the Abitibi region of Quebec, north of Val d’Or. The Company is also currently advancing the Vezza gold project towards a production decision expected at the end of 2011.

The Company has a strong portfolio of development and exploration assets near the LDI and Sleeping Giant mines, and is engaged in a significant exploration program in 2011 aimed at increasing its reserves and resources.

With an experienced senior management team, a strong balance sheet of over $96 million in working capital (including $37 million in cash) as at September 30, 2011, and a recently completed $72 million term debt financing, NAP is well positioned to pursue its growth strategy.

NAP trades on the TSX under the symbol PDL and on the NYSE Amex under the symbol PAL. The Company’s common shares are included in the S&P/TSX Composite Index.

THIRD QUARTER REPORT 2011

North American Palladium Ltd.

KEY HIGHLIGHTS

(expressed in thousands of dollars except cash cost and per share amounts) | | Three months ended September 30 | | | Nine months ended September 30 | |

| | | 2011 | | | 2010 | | | 2011 | | | 2010 | |

| FINANCIAL HIGHLIGHTS | | | | | | | | | | | | |

| Revenue | | | | | | | | | | | | |

| Revenue after pricing adjustments | | $ | 38,310 | | | $ | 38,451 | | | $ | 126,422 | | | $ | 67,596 | |

| | | | | | | | | | | | | | | | | |

| Unit sales | | | | | | | | | | | | | | | | |

| Palladium (oz) | | | 34,524 | | | | 38,122 | | | | 111,341 | | | | 62,211 | |

| Gold (oz) | | | 4,977 | | | | 5,295 | | | | 17,877 | | | | 17,067 | |

| Platinum (oz) | | | 2,278 | | | | 2,013 | | | | 6,570 | | | | 3,100 | |

| Nickel (lb) | | | 159,476 | | | | 146,496 | | | | 464,924 | | | | 236,129 | |

| Copper (lb) | | | 380,287 | | | | 238,698 | | | | 944,778 | | | | 412,184 | |

| | | | | | | | | | | | | | | | | |

| Earnings | | | | | | | | | | | | | | | | |

| Net income (loss) | | $ | (2,816 | ) | | $ | 2,804 | | | $ | (7,757 | ) | | $ | (27,396 | ) |

| Net income (loss) per share | | $ | (0.02 | ) | | $ | 0.02 | | | $ | (0.05 | ) | | $ | (0.20 | ) |

Adjusted net income (loss)1 | | $ | (1,751 | ) | | $ | 9,898 | | | $ | 3,039 | | | $ | (3,696 | ) |

EBITDA 1 | | $ | 1,727 | | | $ | 5,432 | | | $ | 7,475 | | | $ | (16,366 | ) |

Adjusted EBITDA 1 | | $ | 2,792 | | | $ | 12,526 | | | $ | 18,271 | | | $ | 7,334 | |

| | | | | | | | | | | | | | | | | |

| Cash flow provided by (used in) operations | | | | | | | | | | | | | | | | |

| Cash flow provided by (used in) operations before changes in non-cash working capital | | $ | 3,061 | | | | 6,092 | | | $ | 7,850 | | | $ | (11,792 | ) |

Cash flow provided by (used in) operations before changes in non-cash working capital per share 1 | | $ | 0.02 | | | $ | 0.04 | | | $ | 0.05 | | | $ | (0.08 | ) |

| | | | | | | | | | | | | | | | | |

| Capital spending | | $ | 50,561 | | | $ | 14,589 | | | $ | 133,068 | | | $ | 29,222 | |

| | | | | | | | | | | | | | | | | |

| OPERATING HIGHLIGHTS | | | | | | | | | | | | | | | | |

| Production | | | | | | | | | | | | | | | | |

| Palladium (oz) | | | 34,871 | | | | 34,420 | | | | 112,503 | | | | 62,259 | |

| Gold (oz) | | | 4,747 | | | | 5,287 | | | | 16,287 | | | | 15,505 | |

| Platinum (oz) | | | 2,309 | | | | 1,830 | | | | 6,639 | | | | 3,103 | |

| Nickel (lb) | | | 164,126 | | | | 131,154 | | | | 472,606 | | | | 236,297 | |

| Copper (lb) | | | 390,800 | | | | 214,853 | | | | 960,385 | | | | 412,464 | |

| | | | | | | | | | | | | | | | | |

| Realized metal prices | | | | | | | | | | | | | | | | |

| Palladium | | $ | 769 | | | | - | | | $ | 721 | | | | - | |

| Gold | | $ | 1,597 | | | $ | 1,231 | | | $ | 1,479 | | | $ | 1,172 | |

| | | | | | | | | | | | | | | | | |

Cash costs 1 | | | | | | | | | | | | | | | | |

| Palladium (US$) | | $ | 496 | | | $ | 219 | | | $ | 436 | | | $ | 253 | |

| Gold (US$) | | $ | 1,869 | | | $ | 1,660 | | | $ | 1,835 | | | $ | 1,527 | |

| | | | | | | |

| FINANCIAL CONDITION | | | | | | |

| | | As at September 30 | | | As at December 31 | |

| (expressed in thousands of dollars) | | 2011 | | | 2010 | |

| Net working capital | | $ | 95,663 | | | $ | 169,559 | |

| Cash balance | | $ | 37,479 | | | $ | 75,159 | |

| Shareholders’ equity | | $ | 325,996 | | | $ | 290,450 | |

1 Non-IFRS measure. Please refer to Non-IFRS Measures on pages 32-34.

THIRD QUARTER REPORT 2011

North American Palladium Ltd.

Financial Highlights

Revenue for the quarter ended September 30, 2011 was $38.3 million. Net loss for the third quarter was $2.8 million or $0.02 per share and adjusted net loss1 for the quarter was $1.8 million. NAP provided cash from operating activities of $3.1 million, before changes in non-cash working capital, or $0.02 per share.1 EBITDA1 was $1.7 million and adjusted EBITDA1 was $2.8 million.

Strong Balance Sheet

As at September 30, 2011, the Company had approximately $95.7 million in working capital, including $37.5 million cash on hand. Subsequent to the quarter end, the Company closed a $72.0 million term debt financing which included the sale of senior secured notes by way of a private placement with Sprott Resource Lending Corp. as the lead investor. The notes mature on October 4, 2014 (subject to a one year extension at the option of the Company) and bear interest at a rate of 9.25%. With the debt financing completed, combined with the Company’s cash, operating line of credit, and cash flow from operations, NAP has the financial resources to accomplish its current mine expansion objectives.

Investment in Growth

For the quarter ended September 30, 2011, the Company invested $2.0 million in exploration activities ($1.8 million at its palladium operations and $0.2 million at its gold operations) and $50.6 million in development expenditures ($39.7 million at its palladium operations and $10.9 million at its gold operations).

LDI Mine Palladium Production

During a very active development period, LDI achieved steady results in the third quarter, producing 34,871 ounces of payable palladium (at an average palladium head grade at the mill of 3.46 grams per tonne), at a cash cost1 (net of byproduct credits) of US$496 per ounce.

LDI’s cash costs1 in the third quarter were higher than the Company’s 2011 annual forecast of US$450 per ounce due primarily to lower grades processed by the mill, and due in part to higher spending on contractor costs on surface to process stockpiles of oversized ore. The cash costs1 were also adversely affected by the precipitous decline in September in the value of LDI’s provisionally priced by-product metals, which increased cash costs1 by approximately US$35 per ounce.

Third quarter production at the LDI mine included the blending of higher grade underground ore with lower grade surface stockpiles. The decreased head grade during the third quarter resulted from processing more lower grade surface stockpiles than in past quarters. For the nine months ended September 30, 2011, the milled head grade was 4.1 grams per tonne, which is in line with the Company’s guidance of 4.2 grams per tonne for 2011. Quarterly variability in LDI’s production metrics is to be expected during the Company’s mine expansion transition phase, and reflects the planned mining sequence to mitigate logistical congestion between operations and the underground development activities.

LDI Mine Expansion Update

The Company is currently expanding the LDI mine to transition from mining via ramp access to mining via shaft to increase future production at lower cash costs1 per ounce. During the third quarter, the Company made significant progress in advancing the critical aspects of the mine expansion and remains on schedule for commercial production from Phase I of the new production shaft in the fourth quarter of 2012 at an increased mining rate of 3,500 tonnes per day. Phase II entails sinking the shaft deeper and further increasing the mining rate to 5,500 tonnes per day in the first quarter of 2015. This is expected to increase production to over 250,000 ounces of palladium, at cash costs1 of approximately US$200 per ounce using current metal price assumptions.

1 Non-IFRS measure. Please refer to Non-IFRS Measures on pages 32-34.

THIRD QUARTER REPORT 2011

North American Palladium Ltd.

Recent mine expansion development highlights include:

| | · | Completed an updated mine expansion plan that capitalizes on the significant growth of the Offset Zone and various scope changes to further enhance the expansion; |

| | · | Surface construction activities continued to progress to a scheduled completion date at the end of the first quarter of 2012; |

| | · | Completed the 2.4-metre diametre Phase I shaft pilot raise to surface; |

| | · | Awarded the Phase I shaft sinking contract and began mobilization activities for a start to shaft sinking activities in the fourth quarter of 2011; |

| | · | Completed over 50% of the 456-metre long primary ventilation raise; |

| | · | Exceeded internal lateral development forecast by 20% year to date; |

| | · | Advanced ramp development to just below the 4740 mine level, approximately 715 metres from surface; and |

| | · | Began an engineering scoping study for the future underground backfill system. |

In the nine month period ended September 30, 2011, $99.1 million was invested in the mine expansion (of which $38.5 million was spent during the third quarter). Capital expenditures for mine expansion activities in 2011 are estimated at $175 million.

Sleeping Giant Mine Gold Production

During the third quarter, Sleeping Giant produced 2,976 ounces of gold (at an average head grade at the mill of 6.68 grams per tonne), at a cash cost1 of US$1,869 per ounce. While development of higher grade zones at depth continues, mining was focused above the 975-metre elevation – mining the lower grade remnant reserves left behind by the previous operator. As the Company completes the development work and refines its mining plan to reflect the labour-related challenges it faces, the goal is to reduce operating costs to achieve break-even cash flow for the balance of 2011. Profitability from Sleeping Giant is expected to improve in 2012 when the Company will be mining from new deeper mine levels and continues to rationalize the overall cost structure.

In July, mining operations shut down for a two-week maintenance period to allow the development team to re-rope the hoist for the new shaft depth (1,275 metres). During that period, the Company also implemented a new shift schedule and restructuring plan aimed at optimizing operations, which came into effect when the mining crews returned after the maintenance shutdown. Along with the shift schedule change, a detailed operational review was initiated through a third party consultant to look for operational improvements in productivity to reduce operating costs per tonne. Despite mining in the remnant areas above the 975 level and at overall lower grade than initially expected, the operations have made some improvement in reducing the cost profile from the beginning of the year.

Sleeping Giant Mine Development Update

The Company also made progress during the quarter in the development work at depth which will be integral for improved profitability in 2012. With the 200-metre mine shaft deepening and commissioning completed, underground development of the new mining levels is in progress. Accessing the higher grade zone extensions in 2012 will be integral to improving Sleeping Giant’s operating results next year.

Vezza Gold Project Development Update

During the quarter, the Company made good progress in the development work at its advanced-stage Vezza gold project which is currently being advanced through exploration and development towards a production decision at year-end.

1 Non-IFRS measure. Please refer to Non-IFRS Measures on pages 32-34.

THIRD QUARTER REPORT 2011

North American Palladium Ltd.

Recent highlights include:

| | · | Advanced permitting (obtained Certificate of Authorization for 40,000-tonne bulk sample, and milling permit applied for and expected in the fourth quarter); |

| | · | Secured contract with Promec Mining Inc., a local Val d’Or mining contractor, to provide the mining workforce at Vezza (total workforce including contractors is expected to be in the range of 150 people); |

| | · | Progressed lateral development on levels 100, 200, 300, 450 and 550 and 650; |

| | · | Completed excavation related to the ventilation raise and ore pass raise; |

| | · | Completed 6,418 metres of underground diamond drilling in the third quarter (year to date, 6,258 metres were drilled from surface, and 12,285 metres from underground); |

| | · | Completed an engineering study on the crown pillars and commenced the update of the Sleeping Giant mill tailings storage facilities expansion; and |

| | · | Commenced studies on backfill requirements and initiated the design of a cement slurry plant. |

The capital budget to advance Vezza to be production ready in 2012 is estimated at $34 million. Management expects that the total spend will be reduced by estimated pre-production revenue of $9 million from the bulk sample.

Exploration Updates

During the third quarter, the 2011 drill program at LDI was increased from 52,000 metres to 78,000 metres. Since the start of 2011 until September 14, 2011 (the date of the LDI exploration update press release), a total of 28,000 metres have been drilled from the underground and 40,000 metres from surface, for a total of 68,000 metres at LDI.

During the third quarter on September 14, 2011, the Company released the second tranche of drilling results from its 2011 exploration program at LDI. Highlights included:

| | · | Positive infill drill results in the Offset Zone, including 26 metres at 6.0 grams per tonne palladium (“g/t Pd”) in the upper part of the zone; |

| | · | Surface drilling on the Offset Zone intersected significant mineralization close to the deepest limit of the current resource wireframe, supporting further exploration potential; and |

| | · | Exploration drilling following the possible extension of the upper north Roby Zone encountered palladium mineralization to be followed up with additional drilling. |

As previously disclosed, NAP is investigating the upper north and south resource extensions of the Roby Zone, which have the potential to provide an additional source of production ore in 2012. During the third quarter the Company completed its definition drilling program on the upper north Roby Zone extension (to allow development planning to begin for this area of the Roby Zone resource), and has recently completed the access development extension drift in the upper south Roby Zone resource to conduct definition drilling during the fourth quarter.

From the beginning of the year until July 12, 2011 (the date of the most recent gold exploration update press release), a total of 11,234 metres have been drilled at Vezza, and 24,477 metres at Sleeping Giant. Highlights of the most recent update included:

| | · | Surface and underground drilling at Vezza advanced the project towards bulk sampling and confirmed the grades, continuity, and widths of the gold zones (which were similar or better than the last resource estimate dated December 31, 2010; and |

| | · | Sleeping Giant’s gold zones continue to extend at depth below the proposed three new mine levels and announced the discovery of new zones in the lower part of the mine, along with a number of other significant gold intersections. |

THIRD QUARTER REPORT 2011

North American Palladium Ltd.

Outlook

Despite the recent volatility in the price of palladium arising from global macroeconomic concerns, the supply and demand fundamentals of palladium remain strong, and most forecasters continue to have a positive outlook. A supporting factor behind the positive outlook for the metal’s future performance is the resilient industrial demand, increasing investment demand and constrained global supply.

For the balance of 2011, the Company plans to focus on:

| | · | Progressing the LDI mine expansion; |

| | · | Progressing the development work at depth at Sleeping Giant; |

| | · | Advancing the Vezza gold project towards a production decision by year-end; and |

| | · | Continuing exploration programs aimed at increasing reserves and resources at LDI and in the gold division. |

The Company expects to release detailed guidance for its 2012 production and cash costs1, capital expenditures, and exploration budget in January 2012.

Selected Quarterly Information

(expressed in thousands of dollars, except per share amounts) | | | Three months ended September 30 | | | Nine months ended September 30 | |

| | | 2011 | | | 2010 | | | 2011 | | | 2010 | |

| Revenue | | $ | 38,310 | | | $ | 38,451 | | | $ | 126,422 | | | $ | 67,596 | |

| Income (loss) from mining operations | | | 2,534 | | | | 11,389 | | | | 15,973 | | | | (2,735 | ) |

| Net income (loss) | | | (2,816 | ) | | | 2,804 | | | | (7,757 | ) | | | (27,396 | ) |

| Net income (loss) per share – Basic and diluted | | | (0.02 | ) | | | 0.02 | | | | (0.05 | ) | | | (0.20 | ) |

| Cash flow provided by (used in) operations prior to changes in non-cash working capital | | | 3,061 | | | | 6,092 | | | | 7,850 | | | | (11,792 | ) |

| Total assets | | | 390,295 | | | | 308,584 | | | | 390,295 | | | | 308,584 | |

| Obligations under finance leases | | | 2,051 | | | | 2,575 | | | | 2,051 | | | | 2,575 | |

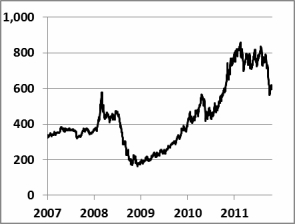

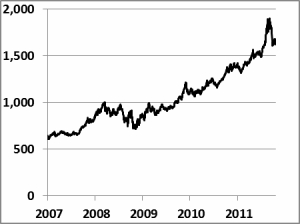

Metal Prices

| Palladium Price (US$/ Troy oz) | Gold Price (US$/ Troy oz) |

| |

In 2008, the price of palladium declined significantly by 69% to US$183 per ounce prompting the Company to put the LDI mine on temporary care and maintenance. As the price of palladium began to recover, the Company restarted the LDI mine in April 2010, ahead of schedule and under budget.

THIRD QUARTER REPORT 2011

North American Palladium Ltd.

During the third quarter of 2011, the palladium price averaged US$752 per ounce, ranging from a low of US$612 to a high of US$836 per ounce. During the first part of the quarter, palladium benefited from positive automotive news and rising investment demand. In September, palladium price came under heavy selling pressure as the global economic outlook appeared increasingly dim and as concerns of a new worldwide recession grew. This led to ETF selling which further exacerbated the fall in price. Amid global economic uncertainty in Europe and U.S., the price of palladium still showed strong support above US$550 per ounce level. As of November 1, 2011, the price of palladium was US$637 per ounce.

Despite the recent volatility in the price of palladium arising from global macroeconomic concerns, the supply and demand fundamentals of palladium remain strong. Most forecasters continue to have an optimistic outlook for the price of palladium. A supporting factor behind the positive outlook for the metal’s future performance is the resilient industrial demand, increasing investment demand, and constrained global supply.

During the third quarter of 2011, the average price of gold was US$1,706 per ounce, with gold trading in a range of US$1,488 to US$1,900 per ounce. The price of gold rallied during the first part of the quarter and reached an all time high of $1,920. Worries over a slowing global economy and fear that the European debt crisis might drive sovereign defaults caused a significant retracement in the price of gold in September. The price of gold was US$1,720 as of November 1, 2011.

At the end of the third quarter, the U.S. dollar rallied as investors sought out safe-haven assets like U.S. treasury bills. The Canadian dollar closed at $0.96 cents to the U.S. dollar, compared to $1.04 at the end of the second quarter of 2011. As of November 1, 2011, the Canadian dollar exchange rate was $1.02.

Realized Metal Prices and Exchange Rates | | | Three months ended September 30 | | | Nine months ended September 30 | |

| | | 2011 | | | 2010 | | | 2011 | | | 2010 | |

Palladium – US$/oz1 | | $ | 769 | | | | - | | | $ | 721 | | | | - | |

| Platinum – US$/oz | | $ | 1,773 | | | | - | | | $ | 1,769 | | | | - | |

| Gold – US$/oz | | $ | 1,597 | | | $ | 1,231 | | | $ | 1,479 | | | $ | 1,172 | |

| Nickel – US$/lb | | $ | 10.12 | | | $ | 9.35 | | | $ | 10.98 | | | $ | 9.35 | |

| Copper – US$/lb | | $ | 4.18 | | | $ | 3.23 | | | $ | 4.23 | | | $ | 3.23 | |

| Average exchange rate (Bank of Canada) – CDN$1 = US$ | | $ | 1.02 | | | $ | 0.96 | | | $ | 1.02 | | | $ | 0.97 | |

| 1 | Includes adjustments for financial contracts. |

Under LDI’s smelter agreement, metal prices are not finalized until three months after delivery to the smelter for base metals and six months for precious metals. Prior to final pricing and settlement, LDI’s metals are provisionally priced at month end forward prices. The Company enters into financial contracts to mitigate this provisional pricing exposure to rising or declining palladium prices for past production already delivered and sold to the smelters. For further details, see the Financial Review section.

THIRD QUARTER REPORT 2011

North American Palladium Ltd.

Spot Metal Prices* and Exchange Rates

For comparison purposes, the following table details recorded spot metal prices and exchange rates.

| | | Sep-30 | | | Jun-30 | | | Mar-31 | | | Dec-31 | | | Sep-30 | | | Jun-30 | | | Mar 31 | | | Dec 31 | |

| | | 2011 | | | 2011 | | | 2011 | | | 2010 | | | 2010 | | | 2010 | | | 2010 | | | 2009 | |

| Palladium – US$/oz | | $ | 614 | | | $ | 761 | | | $ | 766 | | | $ | 791 | | | $ | 573 | | | $ | 446 | | | $ | 479 | | | $ | 393 | |

| Gold – US$/oz | | $ | 1,620 | | | $ | 1,506 | | | $ | 1,439 | | | $ | 1,410 | | | $ | 1,307 | | | $ | 1,244 | | | $ | 1,116 | | | $ | 1,104 | |

| Platinum – US$/oz | | $ | 1,511 | | | $ | 1,722 | | | $ | 1,773 | | | $ | 1,731 | | | $ | 1,662 | | | $ | 1,532 | | | $ | 1,649 | | | $ | 1,461 | |

| Nickel – US$/lb | | $ | 8.30 | | | $ | 10.48 | | | $ | 11.83 | | | $ | 11.32 | | | $ | 10.57 | | | $ | 8.78 | | | $ | 11.33 | | | $ | 8.38 | |

| Copper – US$/lb | | $ | 3.24 | | | $ | 4.22 | | | $ | 4.26 | | | $ | 4.38 | | | $ | 3.65 | | | $ | 2.95 | | | $ | 3.56 | | | $ | 3.33 | |

| Exchange rate (Bank of Canada) – CDN$1 = US$ | | $ | 0.96 | | | US$ | 1.04 | | | US$ | 1.03 | | | US$ | 1.01 | | | US$ | 0.97 | | | US$ | 0.94 | | | US$ | 0.98 | | | US$ | 0.96 | |

* Based on the London Metal Exchange

LDI Palladium Mine

Income from mining operations for the LDI palladium mine are summarized in the following table.

| | | Three months ended September 30 | | | Nine months ended September 30 | |

| | | 2011 | | | 2010 | | | 2011 | | | 2010 | |

| Revenue after pricing adjustments | | $ | 32,689 | | | $ | 33,394 | | | $ | 106,454 | | | $ | 49,462 | |

| Operating expenses | | | | | | | | | | | | | | | | |

| Production costs | | $ | 22,497 | | | $ | 13,700 | | | $ | 63,667 | | | $ | 29,834 | |

| Smelting, refining and freight costs | | | 2,425 | | | | 1,940 | | | | 5,970 | | | | 3,103 | |

| Royalty expense | | | 1,106 | | | | 1,439 | | | | 4,131 | | | | 2,184 | |

| Inventory pricing adjustment | | | - | | | | (388 | ) | | | - | | | | - | |

| Depreciation and amortization | | | 2,693 | | | | 677 | | | | 7,042 | | | | 3,874 | |

| Loss (gain) on disposal of equipment | | | (891 | ) | | | 84 | | | | (1,133 | ) | | | 105 | |

| Total operating expenses | | $ | 27,830 | | | $ | 17,452 | | | $ | 79,677 | | | $ | 39,100 | |

| Income (loss) from mining operations | | $ | 4,859 | | | $ | 15,942 | | | $ | 26,777 | | | $ | 10,362 | |

Revenue – LDI Mine

Revenue is affected by sales volumes, commodity prices and currency exchange rates. Metal sales for LDI are recognized in revenue at provisional prices when delivered to a smelter for treatment or designated shipping point. On a substantial amount of sales, final pricing is not determined until the refined metal is sold by the smelter, which in the case of LDI base metals is three months and precious metals is six months after delivery to the smelter. These final pricing adjustments can result in additional revenues in a rising commodity price environment and reductions to revenue in a declining commodity price environment. Similarly, a weakening in the Canadian dollar relative to the U.S. dollar will result in additional revenues and a strengthening in the Canadian dollar will result in reduced revenues. The Corporation enters into financial contracts to mitigate the smelter agreements’ provisional pricing exposure to rising or declining palladium prices and an appreciating Canadian dollar for past production delivered to the smelter. The total of these financial contracts represent 76,500 ounces of palladium as at September 30, 2011. These contracts mature from October 2011 through March 2012 at an average price of $743 per ounce of palladium. The amounts specified in the financial contracts substantially match final pricing settlement periods of palladium delivered to the customer under the smelter agreement. The palladium financial contracts are being recognized on a mark-to-market basis as an adjustment to revenue. The fair value of these contracts at September 30, 2011 was an asset of $7.5 million, included in accounts receivable (December 31, 2010 - $11.1 million liability).

THIRD QUARTER REPORT 2011

North American Palladium Ltd.

Sales volumes of LDI’s major commodities are set out in the table below.

| | | Three months ended September 30 | | | Nine months ended September 30 | |

| | | 2011 | | | 2010 | | | 2011 | | | 2010 | |

| Sales volumes | | | | | | | | | | | | |

| Palladium (oz) | | | 34,524 | | | | 38,122 | | | | 111,341 | | | | 62,211 | |

| Gold (oz) | | | 1,736 | | | | 1,553 | | | | 4,726 | | | | 2,525 | |

| Platinum (oz) | | | 2,278 | | | | 2,013 | | | | 6,570 | | | | 3,100 | |

| Nickel (lbs) | | | 159,476 | | | | 146,496 | | | | 464,924 | | | | 236,129 | |

| Copper (lbs) | | | 380,287 | | | | 238,698 | | | | 944,778 | | | | 412,184 | |

| Cobalt (lbs) | | | 4,588 | | | | 3,622 | | | | 12,295 | | | | 5,941 | |

| Silver (oz) | | | 1,519 | | | | - | | | | 2,364 | | | | - | |

Revenue from metal sales from the LDI palladium mine are set out below.

| | | Three months ended September 30 | | | Nine months ended September 30 | |

| | | 2011 | | | 2010 | | | 2011 | | | 2010 | |

| Revenue before pricing adjustments | | $ | 34,417 | | | $ | 28,667 | | | $ | 110,735 | | | $ | 45,200 | |

| Pricing adjustments | | | (1,728 | ) | | | 4,727 | | | | (4,281 | ) | | | 4,262 | |

| Revenue after pricing adjustments | | $ | 32,689 | | | $ | 33,394 | | | $ | 106,454 | | | $ | 49,462 | |

| Revenue by metal | | | | | | | | | | | | | | | | |

| Palladium | | $ | 23,423 | | | $ | 24,989 | | | $ | 80,187 | | | $ | 36,568 | |

| Gold | | | 3,568 | | | | 2,141 | | | | 7,903 | | | | 3,425 | |

| Platinum | | | 3,413 | | | | 3,503 | | | | 10,363 | | | | 5,296 | |

| Nickel | | | 1,085 | | | | 1,984 | | | | 4,385 | | | | 2,524 | |

| Copper | | | 1,101 | | | | 701 | | | | 3,345 | | | | 1,524 | |

| Cobalt | | | 68 | | | | 61 | | | | 186 | | | | 106 | |

| Silver | | | 31 | | | | 15 | | | | 85 | | | | 19 | |

| | | $ | 32,689 | | | $ | 33,394 | | | $ | 106,454 | | | $ | 49,462 | |

For the three months ended September 30, 2011, revenue before pricing adjustments was $34.4 million, compared to $28.7 million for the same comparative period last year, reflecting higher realized palladium prices in the current year, partially offset by fewer ounces of palladium sold. For the nine months ended September 30, 2011, revenue before pricing adjustments was $110.7 million, compared to $45.2 million for the same comparative period last year. Due to the recovery of metal prices, the Company recommenced operations in April 2010 after being on care and maintenance since October 2008.

Revenue after pricing adjustments from metal settlements for the three months ended September 30, 2011 was $32.7 million, reflecting a $3.0 million negative commodity price adjustment partially offset by a $1.3 million positive foreign exchange adjustment. For the nine months ended September 30, 2011, revenue after pricing adjustments from metal settlements was $106.5 million, including a $6.7 million negative commodity price adjustment partially offset by a $2.4 million positive foreign exchange adjustment.

THIRD QUARTER REPORT 2011

North American Palladium Ltd.

Operating Expenses – LDI Mine

For the three months ended September 30, 2011, operating expenses were $27.8 million compared to $17.5 million in the same period last year. Operating expenses for the nine months ended September 30, 2011 were $79.7 million compared to $39.1 million in the same period last year. The three and nine months ended September 30, 2010 included costs related to restarting the LDI mine and mill, which occurred in April 2010. Cash costs1 per ounce of palladium sold, net of by product credits1, were US$496 for the three months ended September 30, 2011 (2010 – US$219) and US$436 for the nine months ended September 30, 2011 (2010 - US$253). The increase in operating expenses in 2011 result from processing lower grade stockpiles blended with the higher grade underground ore.

Smelting, refining and freight costs for the three months ended September 30, 2011 were $2.4 million compared to $1.9 million in the same period last year and $6.0 million compared to $3.1 million for the nine months ended September 30, 2011 and 2010, respectively. The increase over the prior year is due to the LDI mine and mill restart in April 2010 as well as increased production volume in the nine months ended September 30, 2011.

For the three months ended September 30, 2011, the royalty expense was $1.1 million compared to $1.4 million in the same period last year. Royalty expense was $4.1 million for the nine months ended September 30, 2011 compared to $2.2 million for the same period last year. Royalty expense was lower in the current year quarter as a result of lower sales volume in the current year. Royalty expense was higher in the current year to date period as revenue increased in 2011 as well as the mine was restarted in April 2010.

Depreciation and amortization at the LDI mine for the three months ended September 30, 2011 was $2.7 million, compared to $0.7 million for the three months ended September 30, 2010. For the nine months ended September 30, 2011, depreciation and amortization was $7.0 million compared to $3.9 million in the same period last year. The increase over the prior year is due to the LDI mine and mill restart in April 2010.

During the second quarter, the Company was advised of its inclusion in the Ontario government’s Northern Industrial Electricity Rate (“NIER”) program to receive electricity price rebates of two cents per kilowatt hour. The NIER program is a three-year initiative designed to help large industries in Northern Ontario improve energy efficiency and sustainability. It is available to industrial facilities that consume greater than 50,000 megawatt hours of electricity per year. The Company’s commitment to the preparation and implementation of comprehensive energy management plans qualified the Company to participate, which resulted in a rebate of $1.4 million for the three months ended September 30, 2011, representing a rebate for the period April 1, 2011 through September 30, 2011. The rebate was treated as a reduction of third quarter operating expenses. For the nine months ended September 30, 2011, a rebate of $3.3 million was received, including a retroactive rebate of $1.9 million for LDI’s electricity costs for the period of April 1, 2010 through March 31, 2011, reflected in the second quarter of 2011. LDI will be entitled to receive additional quarterly rebates over the next two years if it continues to meet eligibility criteria, which the Company anticipates will be the case.

| 1 | Non-IFRS measure. Please refer to Non-IFRS Measures on pages 32-34. |

THIRD QUARTER REPORT 2011

North American Palladium Ltd.

Income from mining operations for the Sleeping Giant gold mine is summarized in the following table.

| | | Three months ended September 30 | | | Nine months ended September 30 | |

| | | 2011 | | | 2010 | | | 2011 | | | 2010 | |

| Revenue | | $ | 5,621 | | | $ | 5,057 | | | $ | 19,968 | | | $ | 18,134 | |

| Operating expenses | | | | | | | | | | | | | | | | |

| Production costs | | $ | 6,431 | | | $ | 6,752 | | | $ | 24,471 | | | $ | 23,319 | |

| Smelting, refining and freight costs | | | 7 | | | | 13 | | | | 37 | | | | 44 | |

| Depreciation and amortization | | | 1,464 | | | | 2,815 | | | | 6,126 | | | | 7,784 | |

| Loss (gain) on disposal of equipment | | | - | | | | 2 | | | | - | | | | (2 | ) |

| Total operating expenses | | $ | 7,902 | | | $ | 9,582 | | | $ | 30,634 | | | $ | 31,145 | |

| Loss from mining operations | | $ | (2,281 | ) | | $ | (4,525 | ) | | $ | (10,666 | ) | | $ | (13,011 | ) |

Revenue – Sleeping Giant Mine

Metal sales for the Sleeping Giant gold mine are recognized at the time the title is transferred to a third party. Sales volumes are set out in the table below.

Revenue from metal sales from the Sleeping Giant gold mine is set out below.

| | | Three months ended September 30 | | | Nine months ended September 30 | |

| | | 2011 | | | 2010 | | | 2011 | | | 2010 | |

| Revenue | | $ | 5,621 | | | $ | 5,057 | | | $ | 19,968 | | | $ | 18,134 | |

| Revenue by metal | | | | | | | | | | | | | | | | |

| Gold | | $ | 5,122 | | | $ | 4,763 | | | $ | 19,123 | | | $ | 17,661 | |

| Silver | | | 499 | | | $ | 294 | | | | 845 | | | $ | 473 | |

| | | $ | 5,621 | | | $ | 5,057 | | | $ | 19,968 | | | $ | 18,134 | |

For the three months ended September 30, 2011, revenue was $5.6 million, reflecting gold sales of 3,241 ounces with a realized price of US$1,596 per ounce, compared to $5.1 million in the prior year with gold sales of 3,742 ounces with a realized price of US$1,231 per ounce. Revenue was $20.0 million for the nine months ended September 30, 2011, compared to $18.1 million in the prior year, reflecting gold sales of 13,151 ounces with a realized price of US$1,482 per ounce (2010 – 14,542 ounces at US$1,172 per ounce).

Operating Expenses – Sleeping Giant Mine

For the three months ended September 30, 2011, total production costs at the Sleeping Giant gold mine were $6.4 million as compared to $6.8 million in the same period in 2010 due to fewer ounces produced in the current year period. Total production costs were $24.5 million for the nine months ended September 30, 2011, compared to $23.3 million in 2010. Cash costs1 were US$1,869 per ounce for the quarter ended September 30, 2011, compared to US$1,660 per ounce for the three months ended September 30, 2010 and US$1,835 per ounce for the nine months ended September 30, 2011 compared to US$1,527 per ounce for the same period in the prior year due to higher labour costs.

Depreciation and amortization at the Sleeping Giant gold mine was $1.5 million for the three months ended September 30, 2011, compared to $2.8 million in the prior year due to fewer ounces produced in the current year period. For the nine months ended September 30, 2011, depreciation and amortization was $6.1 million compared to $7.8 million in the prior year.

| 1 | Non-IFRS measure. Please refer to Non-IFRS Measures on pages 32-34. |

THIRD QUARTER REPORT 2011

North American Palladium Ltd.

General and administrationThe Company’s general and administration expenses for the three months ended September 30, 2011 were $2.9 million, compared to $2.5 million, an increase of $0.4 million. For the nine months ended September 30, 2011, general and administration costs were $9.5 million compared to $7.8 million in the prior year, an increase of $1.7 million. The increase is due to additional administration costs from increased activities at the LDI palladium mine and at the Corporate head quarters.

Exploration

Exploration expenditures for the three months ended September 30, 2011 were $2.0 million compared to $7.0 million in the prior year period and $11.9 million for the nine months ended September 30, 2011 compared to $17.6 million in the same period in the prior year. The decrease reflects $1.9 million of exploration costs capitalized to the mine expansion for the three months ended September 30, 2011 ($8.3 million for the nine months ended September 30, 2010), compared to $1.1 million in the prior year quarter ($1.1 million for the nine months ended September 30, 2010). Exploration expenditures are comprised as follows:

| | | Three months ended September 30 | | | Nine months ended September 30 | |

| | | 2011 | | | 2010 | | | 2011 | | | 2010 | |

| Ontario exploration projects* | | | 1,742 | | | | 3,764 | | | | 7,549 | | | | 10,792 | |

| Sleeping Giant mine property | | | 669 | | | | 796 | | | | 2,647 | | | | 2,265 | |

| Other Quebec exploration projects** | | | 737 | | | | 2,448 | | | | 2,925 | | | | 4,537 | |

| Exploration tax credits | | | (1,192 | ) | | | - | | | | (1,192 | ) | | | - | |

| Total exploration expenditures | | $ | 1,956 | | | $ | 7,008 | | | $ | 11,929 | | | $ | 17,594 | |

| * | Ontario exploration projects are comprised of LDI exploration projects, including the Cowboy, Outlaw and Sheriff zones, West LDI, North VT Rim, and the Legris Lake option and Shebandowan. |

| ** | Other Quebec exploration projects are comprised of the Vezza, Flordin, Discovery, Dormex, Montbray, Harricana, Cameron Shear, Laflamme, and Florence properties. |

On February 18, 2011, the Company completed a flow-through share offering of 2,667,000 flow-through common shares. The Company is required to spend gross proceeds of $22.0 million on Canadian exploration expenses prior to December 31, 2012. For the three months ended September 30, 2011, $3.2 million was spent ($18.8 million for the nine months ended September 30, 2011.

Interest and other costs (income)

Interest and other income for the three months ended September 30, 2011 was $0.3 million compared to a nominal amount in the prior year. The current year balance includes a gain on renouncement of flow-through expenditures of $0.5 million and $0.2 million of interest income. For the nine months ended September 30, 2011, interest and other income was $1.7 million compared to $2.0 million in the prior year. The current year balance includes a gain on renouncement of flow-through expenditures of $1.8 million and interest income of $0.8 million and the prior year balance consists primarily of interest income, partially offset by interest expense and accretion. Interest and other income also include interest on capital leases, accretion expense, interest income and interest expense in the current and prior year period.

THIRD QUARTER REPORT 2011

North American Palladium Ltd.

Income and Mining Tax Recovery (Expense)

The income and mining tax recovery (expense) for the three and nine months ended September 30, are provided in the table below.

| | | Three months ended September 30 | | | Nine months ended September 30 | |

| | | 2011 | | | 2010 | | | 2011 | | | 2010 | |

| LDI palladium mine | | | | | | | | | | | | |

| Ontario transitional tax (debit) credit | | $ | - | | | $ | - | | | $ | (2,387 | ) | | $ | 280 | |

| Corporate minimum tax credit | | | - | | | | - | | | | - | | | | 75 | |

| Ontario resource allowance recovery | | | - | | | | - | | | | - | | | | 315 | |

| | | $ | - | | | | - | | | $ | (2,387 | ) | | $ | 670 | |

| Sleeping Giant gold mine | | | | | | | | | | | | | | | | |

| Quebec mining duties (expense) recovery | | $ | 925 | | | | - | | | $ | 833 | | | $ | 110 | |

| Quebec income tax recovery | | | - | | | | - | | | | 107 | | | | 26 | |

| Mining interests temporary difference expense | | | (1,555 | ) | | | (456 | ) | | | (2,219 | ) | | | (273 | ) |

| | | $ | (630 | ) | | $ | (456 | ) | | $ | (1,279 | ) | | $ | (137 | ) |

| Corporate and other | | | | | | | | | | | | | | | | |

| Expiration of warrants | | | - | | | | - | | | $ | 3 | | | $ | 542 | |

| Renunciation of exploration expenditures | | | - | | | | 1,322 | | | | - | | | | (2,404 | ) |

| | | | - | | | $ | 1,322 | | | $ | 3 | | | $ | (1,862 | ) |

| | | $ | (630 | ) | | $ | 866 | | | $ | (3,663 | ) | | $ | (1,329 | ) |

For the three months ended September 30, 2011, income and mining tax expense was $0.6 million compared to a $0.9 million recovery in the same period in 2010, primarily due to mining interest temporary differences in Quebec ($1.6 million), partially offset by Quebec mining duties recovery ($0.9 million) in the current year, as compared to renunciation of exploration expenditures ($1.3 million), partially offset by mining interest temporary differences in Quebec ($0.5 million) in the prior year period. Income and mining tax expense for the nine months ended September 30, 2011 was $3.7 million compared to $1.3 million in the same period in the prior year. In the current year, income and mining tax expense includes Ontario transitional tax debits ($2.4 million) and mining interest temporary differences ($2.2 million), partially offset by Quebec mining duties recovery ($0.8 million). The prior year balance includes renunciation of exploration expenditures ($2.4 million), partially offset by the expiration of warrants ($0.5 million).

Net Income (loss)

For the three months ended September 30, 2011, the Company reported a net loss of $2.8 million or $0.02 per share compared to net income of $2.8 million or $0.02 per share in the prior year. For the nine months ended September 30, 2011, net loss was $7.8 million or $0.05 per share compared to a net loss of $27.4 million or $0.20 per share in 2010.

THIRD QUARTER REPORT 2011

North American Palladium Ltd.

Summary of Quarterly Results

(expressed in thousands of Canadian dollars except per share amounts)

| | | 2011 | | | 2010 | | | 2009* | |

| | | Q3 | | | Q2 | | | Q1 | | | Q4 | | | Q3 | | | Q2 | | | Q1 | | | Q4 | |

| Revenue | | $ | 38,310 | | | $ | 51,398 | | | $ | 36,714 | | | $ | 39,502 | | | $ | 38,451 | | | $ | 21,215 | | | $ | 7,930 | | | $ | 1 | |

| Exploration expense | | | 1,956 | | | | 6,134 | | | | 3,839 | | | | 12,532 | | | | 7,008 | | | | 6,421 | | | | 4,165 | | | | 4,287 | |

| Cash provided by (used in) operations | | | 15,883 | | | | 4,121 | | | | 24,647 | | | | (25,234 | ) | | | (20,053 | ) | | | (18,433 | ) | | | (10,172 | ) | | | (12,186 | ) |

Cash provided by (used in) operations prior to changes in non-cash working capital per share1 | | | 0.02 | | | | 0.07 | | | | (0.04 | ) | | | - | | | | 0.04 | | | | (0.04 | ) | | | (0.11 | ) | | | (0.11 | ) |

| Capital expenditures | | | 50,561 | | | | 41,363 | | | | 41,144 | | | | 20,142 | | | | 14,589 | | | | 10,146 | | | | 4,487 | | | | 4,450 | |

| Net income (loss) | | | (2,816 | ) | | | 5,380 | | | | (10,321 | ) | | | (260 | ) | | | 3,185 | | | | (11,560 | ) | | | (14,624 | ) | | | (14,361 | ) |

| Net income (loss) per share – basic and diluted | | $ | (0.02 | ) | | $ | 0.03 | | | $ | (0.06 | ) | | | - | | | $ | 0.02 | | | $ | (0.08 | ) | | $ | (0.11 | ) | | $ | (0.11 | ) |

| * | Certain prior period amounts, prepared under Canadian GAAP, have been reclassified to conform to the current period’s classification. |

| 1 | Non-IFRS measure. Please refer to Non-IFRS Measures on pages 32-34. |

| FINANCIAL CONDITION, CASH FLOWS, LIQUIDITY AND CAPITAL RESOURCES |

| | | Three months ended September 30 | | | Nine months ended September 30 | |

| | | 2011 | | | 2010 | | | 2011 | | | 2010 | |

| Cash provided by (used in) operations prior to changes in non-cash working capital | | $ | 3,061 | | | $ | 6,092 | | | $ | 7,850 | | | $ | (11,792 | ) |

| Changes in non-cash working capital | | | 12,822 | | | | (26,099 | ) | | | 36,801 | | | | (36,762 | ) |

| Cash provided by (used in) operations | | | 15,883 | | | | (20,007 | ) | | | 44,651 | | | | (48,554 | ) |

| Cash provided by (used in) financing | | | 67 | | | | (724 | ) | | | 49,434 | | | | 92,700 | |

| Cash provided by (used in) investing | | | (49,710 | ) | | | (14,185 | ) | | | (131,765 | ) | | | (28,787 | ) |

| Increase (decrease) in cash and cash equivalents | | $ | (33,760 | ) | | $ | (34,916 | ) | | $ | (37,680 | ) | | $ | 15,359 | |

Operating Activities

For the three months ended September 30, 2011, cash provided by operations prior to changes in non-cash working capital was $3.1 million, compared to cash provided by operations of $6.1 million in the prior year, a decrease of $3.0 million. This decrease is due primarily to lower net income of $4.9 million (including $0.7 million increased depreciation and amortization) and an increase in gains on disposal of equipment ($1.0 million), partially offset by an increase of deferred income and mining tax expense ($2.4 million). Cash provided by operations prior to changes in non-cash working capital was $7.9 million for the nine months ended September 30, 2011, compared to cash used in operations of $11.8 million in the prior year, an increase of $19.7 million. This increase is primarily due to higher net income of $21.2 million (including $1.6 million increased depreciation and amortization) partially offset by lower deferred income and mining tax expense of $1.8 million.

For the three months ended September 30, 2011, changes in non-cash working capital resulted in a source of cash of $12.8 million compared to a use of cash of $26.1 million in the prior year. The current quarter balance of $12.8 million is substantially due to a decrease in accounts receivable ($11.3 million), a decrease in inventories ($2.3 million) and an increase in accounts payable and accrued liabilities ($2.4 million), partially offset by an increase in other assets ($1.1 million) and a decrease in taxes payable ($2.0 million). Changes in non-cash working capital for the nine months ended September 30, 2011 provided cash of $36.8 million compared to a use of cash of $36.8 million in the prior year. The 2011 balance is primarily due to a decrease in other assets ($21.1 million) representing proceeds received from the exercise of warrants, a decrease in accounts receivable ($11.7 million) and a decrease in inventories ($7.1 million), partially offset by an increase in accounts payable and accrued liabilities ($3.3 million).

THIRD QUARTER REPORT 2011

North American Palladium Ltd.

For the three months ended September 30, 2011, cash provided by operations was $15.9 million compared to cash used in operations of $20.0 million in the comparative period in 2010. Cash provided by operations for the nine months ended September 30, 2011 was $44.7 million compared to cash used in operations of $48.6 million in the prior year period.

Financing Activities

For the three months ended September 30, 2011, financing activities provided cash of $0.1 million consisting of $0.5 million related to the issuance of common shares, partially offset by the scheduled repayment of capital leases of $0.4 million. This compared to cash used in financing activities of $0.7 million in the corresponding period last year. For the nine months ended September 30, 2011, financing activities provided cash of $49.4 million of which $19.8 million was related to the exercise of warrants. This compared to cash provided by financing activities in the prior year of $92.7 million. Net proceeds of $94.2 million were received from the April 2010 equity offering discussed below.

In October 2009, the Company completed an equity offering of 18.4 million units for net proceeds of $53.6 million. Each unit consisted of one common share and one-half of one common share purchase warrant of the Company. Each whole warrant (Series A warrants) entitled the holder to purchase an additional common share at a price of $4.25 per share, subject to adjustment, at any time prior to September 30, 2011. Since the 20-day volume weighted average price of the common shares on the TSX was equal to or greater than C$5.75 per share (as per the acceleration event in the warrant indenture), on December 8, 2010 the Company announced the acceleration of the expiry of the Series A warrants to January 14, 2011. During the first quarter of 2011, $21.3 million of proceeds were received from the exercise of 5,009,986 Series A warrants. Total proceeds of $38.8 million were received from the exercise of Series A warrants and 67,938 Series A warrants were not exercised prior to expiry.

On April 28, 2010, the Company completed an equity offering of 20 million units at a price of $5.00 per unit for total net proceeds of $94.2 million (issue costs $5.8 million), which included the exercise of an over-allotment option in the amount of 2,600,000 units at a price of $5.00 per unit. Each unit consists of one common share and one-half of one common share purchase warrant of the Company. Each whole warrant (Series B warrants) entitled the holder to purchase an additional common share at a price of $6.50, subject to adjustment, at any time prior to October 28, 2011. In the event that the 20-day volume weighted average price of the common shares on the TSX was greater than $7.50 per share, the Company had the option to accelerate the expiry date of the warrants by giving notice to the holders thereof and in such case the warrants would have expired on the 30th day after the date on which such notice would have been given by the Company. In 2010, 1,240,000 Series B warrants were exercised for total proceeds of $8.1 million. No additional warrants were exercised in 2011. Subsequent to the third quarter ended September 30, 2011, on October 28, 2011, the Series B warrants expired.

Investing Activities

For the three months ended September 30, 2011, investing activities required cash of $49.7 million, relating to additions to mining interests and proceeds on disposal of equipment of $0.9 million. For the three months ended September 30, 2010, investing activities required cash of $14.2 million, relating to additions to mining interests. Investing activities required cash of $131.8 million for the nine months ended September 30, 2011, compared to $28.8 million cash required by investing activities for the nine months ended September 30, 2011. The majority of the additions to mining interests were attributable to LDI’s mine expansion project as well as the Sleeping Giant gold mine.

THIRD QUARTER REPORT 2011

North American Palladium Ltd.

Additions to mining interests

| | | Three months ended September 30 | | | Nine months ended September 30 | |

| | | 2011 | | | 2010 | | | 2011 | | | 2010 | |

| Palladium operations | | | | | | | | | | | | |

| Offset Zone development | | $ | 36,622 | | | $ | 3,979 | | | $ | 90,821 | | | $ | 9,951 | |

| Roby Zone development | | | 82 | | | | 1,443 | | | | 149 | | | | 2,425 | |

| Offset Zone exploration costs | | | 1,893 | | | | 1,127 | | | | 8,260 | | | | 1,127 | |

| Roby Zone exploration costs | | | - | | | | 639 | | | | 45 | | | | 639 | |

| Jaw crusher | | | - | | | | 90 | | | | - | | | | 1,132 | |

| Mill flotation redesign | | | - | | | | 2 | | | | - | | | | 798 | |

| Tailings management facility | | | 391 | | | | 227 | | | | 584 | | | | 524 | |

| Other equipment and betterments | | | 685 | | | | 805 | | | | 4,004 | | | | 1,545 | |

| | | $ | 39,673 | | | $ | 8,312 | | | $ | 103,863 | | | $ | 18,141 | |

| Gold operations | | | | | | | | | | | | | | | | |

| Vezza project | | $ | 8,333 | | | $ | 3,779 | | | $ | 20,941 | | | $ | 3,779 | |

| Sleeping Giant Shaft deepening | | | 1,209 | | | | 1,504 | | | | 4,603 | | | | 4,162 | |

| Sleeping Giant Mill expansion | | | 805 | | | | - | | | | 1,639 | | | | - | |

| Sleeping Giant Underground and deferred development | | | 472 | | | | 892 | | | | 1,733 | | | | 2,406 | |

| Other equipment and betterments | | | 69 | | | | 102 | | | | 289 | | | | 734 | |

| | | $ | 10,888 | | | $ | 6,277 | | | $ | 29,205 | | | $ | 11,081 | |

| | | $ | 50,561 | | | $ | 14,589 | | | $ | 133,068 | | | $ | 29,222 | |

In addition to the mining interests acquired by cash reflected in the above table, the Company also acquired by means of finance leases, equipment in the amount $0.1 million for the three months ended September 30, 2011 and $1.0 million for the nine months ended September 30, 2011.

Capital Resources

As at September 30, 2011, the Company had cash and cash equivalents of $37.5 million compared to $75.2 million as at December 31, 2010. The funds are invested in short term interest bearing deposits at a major Canadian chartered bank.

In July 2011, the Company increased its operating line of credit with the Bank of Nova Scotia from $30 million to $60 million. The credit facility is secured by the Company's accounts receivables and inventory and may be used for working capital liquidity and general corporate purposes. At September 30, 2011, the Company had $50.0 million available to be drawn from the credit facility and $10.0 million was utilized for letters of credit primarily for reclamation deposits.

During the quarter, the Company received an advanced payment under its smelter agreement for $11.3 million.

Subsequent to the third quarter end, on October 4, 2011, the Company sold $72.0 million of senior secured notes by way of a private placement for net proceeds of $69.6 million. The notes which mature on October 4, 2014, were issued in $1,000 denominations and bear interest at a rate of 9.25% per year, payable semi-annually. The Company also issued a palladium warrant with each note. Each warrant entitles the holder to purchase 0.35 ounces of palladium at a purchase price of US$620 per ounce, anytime up to October 4, 2014. If the palladium warrants are exercised, the Company has the option to pay the amount owing to the warrant holder in either cash or common shares priced at a 7% discount. At the Company’s option, notes may be extended for one additional year.

The Company’s operating cash flow and capital resources provide the Company with the financial flexibility to advance its development projects.

THIRD QUARTER REPORT 2011

North American Palladium Ltd.

Contractual Obligations

| As at September 30, 2011 | | Payments Due by Period | |

| (expressed in thousands of Canadian dollars) | | Total | | | Less than 1 year | | | 2-5 Years | | | >5 years | |

| Capital lease obligations | | $ | 2,173 | | | $ | 1,448 | | | $ | 725 | | | | - | |

| Operating leases | | | 8,673 | | | | 5,760 | | | | 2,643 | | | | 270 | |

| Purchase obligations | | | 122,938 | | | | 122,938 | | | | - | | | | - | |

| | | $ | 133,784 | | | $ | 130,146 | | | $ | 3,368 | | | $ | 270 | |

In addition to the above, the Company also has asset retirement obligations at September 30, 2011 in the amount of $19.9 million that would become payable at the time of the closures of the LDI and Sleeping Giant mines. Deposits established by the Company to offset these future outlays amount to $2.1 million. In addition, the Company obtained a letter of credit of $8.5 million to offset these future outlays. As a result, $9.3 million of funding is required prior to closure of the mines.

Related Party Transactions

There were no related party transactions for the quarter ended September 30, 2011.

As of November 1, 2011, there were 162,851,432 common shares of the Company outstanding. In addition, there were options outstanding pursuant to the Amended and Restated 2010 Corporate Stock Option Plan entitling holders thereof to acquire 3,769,582 common shares of the Company at a weighted average exercise price of $4.47 per share.

LDI Palladium Mine

The key operating results for the LDI palladium mine are set out in the following table.

| | | Three months ended September 30 | | | Nine months ended September 30 | |

| | | 2011 | | | 2010 | | | 2011 | | | 2010 | |

| Tonnes of ore milled | | | 442,253 | | | | 198,907 | | | | 1,157,956 | | | | 401,910 | |

| Production | | | | | | | | | | | | | | | | |

| Palladium (oz) | | | 34,871 | | | | 34,420 | | | | 112,503 | | | | 62,259 | |

| Gold (oz) | | | 1,771 | | | | 1,408 | | | | 4,791 | | | | 2,526 | |

| Platinum (oz) | | | 2,309 | | | | 1,830 | | | | 6,639 | | | | 3,103 | |

| Nickel (lbs) | | | 164,126 | | | | 131,154 | | | | 472,606 | | | | 236,297 | |

| Copper (lbs) | | | 390,800 | | | | 214,853 | | | | 960,385 | | | | 412,464 | |

| Palladium head grade (g/t) | | | 3.46 | | | | 7.05 | | | | 4.07 | | | | 6.41 | |

| Palladium recoveries (%) | | | 76.38 | | | | 82.10 | | | | 79.74 | | | | 80.90 | |

| Tonnes of ore mined | | | 477,923 | | | | 225,960 | | | | 1,239,138 | | | | 405,194 | |

| Total cost per tonne milled | | $ | 51 | | | $ | 69 | | | $ | 55 | | | $ | 59 | |

Cash cost ($USD)1 | | $ | 496 | | | $ | 218 | | | $ | 436 | | | $ | 253 | |

The LDI mine consists of a previously mined open pit, an operating underground mine, and a mill with a design capacity of approximately 15,000 tonnes per day. The primary deposits on the property are the Roby Zone and the Offset Zone, both disseminated magmatic palladium-platinum group metal (“PGM”) deposits. The other identified underground mineralized zones include the Cowboy, Outlaw and Sheriff zones, which are not included in the Company’s current mine expansion plan due to insufficient drilling at this time.

| 1 | Non-IFRS measure. Please refer to Non-IFRS Measures on pages 32-34. |

THIRD QUARTER REPORT 2011

North American Palladium Ltd.

Third quarter production at the LDI mine included the blending of underground ore with lower-grade surface stockpiles. During the three months ended September 30, 2011, 477,923 tonnes of ore was extracted from underground and from the surface stockpiles (2010 – 225,960 tonnes). For the nine months ended September 30, 2011, 1,239,138 tonnes of ore was extracted (2010 – 405,194 tonnes).

Ore production from the Roby Zone at the LDI mine is operating at approximately 2,600 tonnes per day, seven days a week, on two 12-hour shifts per day. The Company has a workforce of approximately 270 people at LDI and its collective agreement with the United Steelworkers is effective until May 31, 2012.

LDI Mill

For the three months ended September 30, 2011, the LDI mill processed 442,253 tonnes of ore at an average of 10,352 tonnes per operating day, producing 34,871 ounces of payable palladium at an average palladium head grade of 3.46 grams per tonne, with a palladium recovery of 76.4%, and mill availability of 99.0% (2010 – 198,907 tonnes processed, producing 34,420 ounces at an average grade of 7.05 grams per tonne). LDI’s cash costs1, net of byproduct credits, were US$496 per ounce (2010 – US$219 per ounce, when production consisted of only higher-grade underground ore). Production costs, per tonne of ore milled, were $51 for the quarter ended September 30, 2011. The mill is operating on a batch basis, with a two-week operating and a two-week planned non-operating schedule.

For the nine months ended September 30, 2011, the LDI mill processed 1,157,956 tonnes of ore at an average of 9,891 tonnes per operating day, producing 112,503 ounces of payable palladium at an average palladium head grade of 4.07 grams per tonne, palladium recovery of 79.7% and mill availability of 97.3% (2010 – 401,910 tonnes processed, producing 62,259 ounces at an average grade of 6.41 grams per tonne). LDI’s cash costs1, net of byproduct credits, were US$436 per ounce (2010 – US$253 per ounce, when production consisted of only higher-grade underground ore).

LDI’s cash costs1 in the third quarter were higher than the Company’s calendar year 2011 forecast of US$450 per ounce due primarily to lower grades processed by the mill, and due in part to higher spending on contractor costs on surface to process stockpiles of oversized ore. The cash costs1 were also adversely affected by the precipitous decline in September in the value of LDI’s provisionally priced by-product metals, which increased costs by approximately $35 per ounce.

The average palladium head grade at the mill during the third quarter was 3.46 grams per tonne. The decreased head grade during the third quarter resulted from processing more lower grade surface stockpiles than in past quarters. For the nine months ended September 30, 2011, the milled head grade was 4.1 grams per tonne, which is in line with the Company’s guidance of 4.2 grams per tonne for 2011.

Quarterly variability in LDI’s production metrics is to be expected during the Company’s mine expansion transition phase, and reflects the planned mining sequence to mitigate logistical congestion between operations and the underground development activities.

LDI Mine Expansion Update

The Company is currently expanding the LDI mine to transition from mining via ramp access to mining via shaft to increase future production at lower cash costs1 per ounce. During the third quarter, the Company made significant progress in advancing the critical aspects of the mine expansion and remains on schedule for commercial production from Phase I of the new production shaft in the fourth quarter of 2012 at an increased mining rate of 3,500 tonnes per day. Phase II entails sinking the shaft deeper and further increasing the mining rate to 5,500 tonnes per day in the first quarter of 2015. This is expected to increase production to over 250,000 ounces of palladium, at cash costs1 of approximately US$200 per ounce using current metal price assumptions.

| 1 | Non-IFRS measure. Please refer to Non-IFRS Measures on pages 32-34. |

THIRD QUARTER REPORT 2011

North American Palladium Ltd.

Recent mine expansion development highlights include:

| | · | Completed an updated mine expansion plan that capitalizes on the significant growth of the Offset Zone and various scope changes to further enhance the expansion; |

| | · | Surface construction activities continued to progress to a scheduled completion date at the end of Q1, 2012; |

| | · | Completed the 2.4-metre diametre Phase I shaft pilot raise to surface; |

| | · | Awarded the Phase I shaft sinking contract and began mobilization activities for start to shaft sinking activities in the fourth quarter of 2011; |

| | · | Completed over 50% of the 456-metre long primary ventilation raise; |

| | · | Exceeded internal lateral development forecast by 20% year to date; |

| | · | Advanced ramp development to just below the 4740 mine level, approximately 715 metres from surface; and |

| | · | Began an engineering scoping study for the future underground backfill system. |

In the nine month period ended September 30, 2011, $99.1 million was invested in the mine expansion (of which $38.5 million was spent during the third quarter). Capital expenditures for 2011 are estimated at $175 million.

Sleeping Giant Gold Mine

The key operating results for the Sleeping Giant gold mine are set out in the following table.

| | | Three months ended September 30 | | | Nine months ended September 30 | |

| | | 2011 | | | 2010 | | | 2011 | | | 2010 | |

| Tonnes of ore milled | | | 14,322 | | | | 21,645 | | | | 57,661 | | | | 71,546 | |

| Production | | | | | | | | | | | | | | | | |

| Gold (oz) | | | 2,976 | | | | 3,879 | | | | 11,496 | | | | 12,979 | |

| Gold head grade (g/t) | | | 6.68 | | | | 5.84 | | | | 6.43 | | | | 5.54 | |

| Gold recoveries (%) | | | 96.74 | | | | 95.50 | | | | 96.35 | | | | 95.40 | |

| Tonnes of ore hoisted | | | 14,322 | | | | 22,494 | | | | 57,208 | | | | 73,076 | |

| Total cost per tonne milled | | $ | 449 | | | $ | 312 | | | $ | 424 | | | $ | 326 | |

Cash cost ($USD)1 | | $ | 1,869 | | | $ | 1,660 | | | $ | 1,835 | | | $ | 1,527 | |

The Sleeping Giant gold mine consists of a narrow vein underground mine and a mill with a capacity of 900 tonnes per operating day that can be easily expanded. For the three months ended September 30, 2011, 14,322 tonnes of ore were hoisted from the underground mine with an average gold grade of 6.68 grams per tonne (2010 – 22,494 tonnes hoisted with average grade of 5.84 grams per tonne). For the nine months ended September 30, 2011, 57,208 tonnes of ore were hoisted with an average gold grade of 6.43 grams per tonne (2010 – 73,076 tonnes hoisted with average grade of 5.54 grams per tonne).

While development of higher grade zones at depth continues, mining was focused above the 975-metre elevation – mining the lower grade remnant reserves left behind by the previous operator. As the Company completes the development work and refines its mining plan to reflect the labour-related challenges it faces, the goal is to reduce operating costs to achieve break-even cash flow for the balance of 2011. Profitability from Sleeping Giant is expected to improve in 2012 when the Company will be mining from new deeper mine levels and continues to rationalize the overall cost structure.

| 1 | Non-IFRS measure. Please refer to Non-IFRS Measures on pages 32-34. |

THIRD QUARTER REPORT 2011

North American Palladium Ltd.

In July, mining operations shut down for a two-week maintenance period to allow the development team to re-rope the hoist for the new shaft depth (1,275 metres). During that period, the Company also implemented a new shift schedule and restructuring plan aimed at optimizing operations, which came into effect when the mining crews returned after the maintenance shutdown. Along with the shift schedule change, a detailed operational review was initiated through a third party consultant to look for operational improvements in productivity to reduce operating costs per tonne. Despite mining in the remnant areas above the 975 level and at overall lower grade than initially expected, the operations have made some improvements in reducing the cost profile from the beginning of the year.

The Company made good progress during the quarter in the development work at depth which will be integral for improved profitability in 2012. With the 200-metre mine shaft deepening and commissioning completed, underground development of the new mining levels is in progress. Accessing the higher grade zone extensions in 2012 will be integral to improving Sleeping Giant’s operating results next year.

Sleeping Giant Mill

For the three months ended September 30, 2011, the mill processed 14,322 tonnes of ore, producing 2,976 ounces of gold at an average gold head grade of 6.68 grams per tonne, with a gold recovery of 96.7% and mill availability of 100.0% (2010 – 21,645 tonnes processed, producing 3,879 ounces at an average grade of 5.84 grams per tonne). For the nine months ended September 30, 2011, 57,661 tonnes of ore were processed, producing 11,496 ounces of gold at an average gold head grade of 6.43 grams per tonne, gold recovery of 96.4% and mill availability of 98.5% (2010 – 71,546 tonnes processed, producing 12,979 ounces at an average grade of 5.54 grams per tonne).

Sleeping Giant’s cash costs1 were US$1,869 per ounce for the three months ended September 30, 2011 and US$1,835 per ounce for the nine months ended September 30, 2011, compared to US$1,660 per ounce and US$1,527 per ounce for the three and nine months ended September 30, 2010, respectively. Production costs per tonne of ore milled were $449 for the three months ended September 30, 2011 (2010 - $312 per tonne) and $424 per tonne of ore milled for the nine months ended September 30, 2011 (2010 - $326 per tonne).

At September 30, 2011, the mill contained approximately 1,656 ounces of gold that was included in inventory and valued at net realizable value, as it had not been sold by the end of the period.

The Sleeping Giant mill has a rated capacity of 900 tonnes per day and was operating at approximately 715 tonnes per operating day, for the three months ended September 30, 2011 and 789 tonnes per operating day for the nine months ended September 30, 2011.

The expansion of Sleeping Giant’s mill to either 1,250 or 1,750 tonnes per day has been deferred to 2012 to give the Company the flexibility to do a one-step increase depending on the Company’s other gold projects development timelines. In 2011, the Company will spend approximately $2.0 million on the expansion, which includes the detailed engineering work, the geotechnical tests, building and foundation designs, receiving the required construction permits, materials procurement, and refurbishing the rod mill and jaw crusher.

NAP’s future growth will come from its significant exploration upside and through the continued exploration and development of the Company’s projects. With permits, mine infrastructure and excess capacity at both of its mills, NAP can move from exploration success to production on an accelerated timeline.

LDI Mine & Property

Exploration is central to LDI’s future and will represent an important part of future growth for the mine and for the Company. Situated in unique geology, LDI’s substantial +33,000-acre land package offers exploration upside that is further complimented by the underutilized, large 15,000-tonnes per day mill. Beyond the mine site, most of the land has had minimal historic exploration. The exploration success achieved during the past few years gives management great encouragement that there is strong potential to continue to grow the Company’s palladium reserve and resource base through exploration.

THIRD QUARTER REPORT 2011

North American Palladium Ltd.

The LDI mine consists of the following underground zones:

| | · | Roby Zone: currently being mined. |

| | · | Offset Zone: discovered in 2001, located below and approximately 250 metres south west of the Roby Zone. The Offset Zone remains open in all directions and continues to expand through exploration. LDI mine expansion is currently underway to access Offset Zone ore. |