UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act File Number 811-07102

The Advisors’ Inner Circle Fund II

(Exact name of registrant as specified in charter)

SEI Investments

One Freedom Valley Drive

Oaks, PA 19456

(Address of principal executive offices) (Zip code)

SEI Investments

One Freedom Valley Drive

Oaks, PA 19456

(Name and address of agent for service)

Registrant’s telephone number, including area code: (877) 446-3863

Date of fiscal year end: July 31, 2022

Date of reporting period: July 31, 2022

| Item 1. | Reports to Stockholders. |

A copy of the report transmitted to stockholders pursuant to Rule 30e-1 under the Investment Company Act of 1940, as amended (the “Act”) (17 CFR § 270.30e-1) is attached hereto.

The Advisors’ Inner Circle Fund II

Reaves Infrastructure Fund

(Formerly, Reaves Utilities and Energy Infrastructure Fund)

| Annual Report | July 31, 2022 |

| THE ADVISORS’ INNER CIRCLE FUND II | REAVES INFRASTRUCTURE FUND | |

| JULY 31, 2022 | ||

| ||||

| 1 | ||||

| 8 | ||||

| 11 | ||||

| 12 | ||||

| 13 | ||||

| 14 | ||||

| 15 | ||||

| 23 | ||||

| 24 | ||||

| 32 | ||||

| 34 | ||||

| 35 | ||||

The Fund files its complete schedule of investments with the Securities and Exchange Commission (“SEC”) for the first and third quarters of each fiscal year as an exhibit to its reports on Form N-PORT within sixty days after period end. The Fund’s Form N-PORT reports are available on the SEC’s website at http://www.sec.gov, and may be reviewed and copied at the SEC’s Public Reference Room in Washington, D.C. Information the operation of the Public Reference Room may be obtained by calling 1-800-SEC-0330.

A description of the policies and procedures that the Fund uses to determine how to vote proxies relating to fund securities, as well as information relating to how the Fund voted proxies relating to fund securities during the most recent 12-month period ended June 30, is available (i) without charge, upon request, by calling 1-844-755-3863; and (ii) on the SEC’s website at http:// www.sec.gov.

| THE ADVISORS’ INNER CIRCLE FUND II | REAVES INFRASTRUCTURE FUND | |

| JULY 31, 2022 | ||

July 31, 2022

Dear Shareholder:

As you know, we invest primarily in infrastructure sectors such as utilities, telecommunications, and transportation selecting companies from the bottom up via a rigorous and independent research process. The following review includes perspective segregated by sector with performance estimates on a consolidated basis, gross of fees.

Portfolio Review

In the twelve months ended July 31, 2022, the Reaves Infrastructure Fund generated the following net-of-fee returns:

Reaves Infrastructure Fund | -6.01% | |||

This compares to the following: | ||||

MSCI USA Infrastructure Indexi | 7.58% | |||

S&P 500 Indexii | -4.64% | |||

Over the past year, broader markets declined as inflation and global central bank monetary tightening became the principal drivers of returns. Higher interest rates were especially negative for long duration growth companies. This backdrop generally favors the Fund’s defensive positioning. Stocks in the utility transportation and Real Estate Investment Trust (“REIT”) sectors outperformed broader markets. However, this was offset by weakness in our communications investments where growth rates slowed after accelerating during the pandemic.

We discuss these trends in more detail below.

The Fund invests primarily in infrastructure sectors such as utilities, telecommunications, and transportation. Companies are selected based on a rigorous and independent research effort. The Fund’s largest investments tend to be businesses with high barriers to entry, predictable business models, and the consistent ability to grow cash flow. The following review includes perspective segregated by sector with performance estimates on a consolidated basis, gross of fees.

1

| THE ADVISORS’ INNER CIRCLE FUND II | REAVES INFRASTRUCTURE FUND | |

| JULY 31, 2022 | ||

Utilities (40.4% weighting as of 7/31/2022)

Our utility investments proved safe havens as markets transitioned from favoring high beta to favoring safety. Utilities generally pass-on fuel costs and are relatively insulated from some of the worst of inflationary forces. In fact, higher fuel prices can create greater financial incentive for electricity producers to accelerate development of renewable generation, helping drive further earnings growth. The combination of business stability and earnings growth acceleration created strong demand for utility equity in the period.

Our strongest contributor to performance was Exelon Corp. The company spun out its merchant generating company (Constellation Energy Corp), creating the nation’s largest pure play nuclear power operator. We believe that since nuclear power, despite historical challenges, is the only source of carbon-free baseload power generation, that legislation/regulation will become increasingly supportive and the sector will enjoy greater investor acceptance over time.

During the period we increased our exposure to the utility sector by adding Entergy Corp and Atmos Energy. Both companies have strong growth potential and are reasonably valued. Entergy should benefit from favorable infrastructure renewal legislation in Louisiana and Atmos, a key Texas utility, should benefit from serving communities with some of the fastest growing population in the country.

Overall, we remain confident that the long-term outlook for the industry is robust. This is driven by spending associated with transitioning away from fossil fuels. The industry provides essential, non-discretionary services, with consistent growth underwritten by the need for safety and reliability.

Communications Infrastructure (35.9% weighting as of 7/31/2022)

This segment of the portfolio had been a source of strong profit contribution in recent years, but the past twelve months was somewhat challenging for some of the Fund’s communications infrastructure stocks.

Most notably, cable experienced a slowdown in broadband subscriber growth that weighed on performance. There were a variety of contributing factors including 1) a pull-forward of demand for residential broadband during the early months of the pandemic; 2) high product penetration / market saturation; 3) lower levels of new household formation, and 4) increased competition from fixed wireless and fiber-to-the-home services. We would note that despite this lower rate of subscriber growth, earnings and cash flow growth remained robust.

REITs within the communications infrastructure space provided a positive contribution during the year. Our tower investments demonstrated their durability by outperforming the broader market. CoreSite, a data center business built on powerful

2

| THE ADVISORS’ INNER CIRCLE FUND II | REAVES INFRASTRUCTURE FUND | |

| JULY 31, 2022 | ||

network effects, was the standout performer. We had long admired the business and often wish to come across more management teams like that of CoreSite. American Tower seemingly shared our admiration, as it paid a significant premium to acquire CoreSite at the end of calendar 2021.

During the past twelve months we have repositioned the communications infrastructure portfolio to better reflect a long-term goal of balancing growth with risk. Specifically, we reduced our cable weighting by exiting positions in both Altice USA and Comcast. We also exited positions in Liberty Latin America and Warner Brothers Discovery. In their place, we reallocated assets to other sectors and initiated positions in Cogent Communications and Telus Corp. Cogent is a competitively differentiated provider of internet service to corporate customers. Its shares have come under pressure due to the delay in return-to-office dynamics and we think the valuation is compelling. We believe Canadian operator Telus is among the best-run telecom businesses in the world. A reasonably benign competitive environment and large dividend make it especially attractive. We believe these adjustments have reduced future portfolio volatility while maintaining favorable exposure to the secular tailwinds in communications infrastructure.

Transportation, Logistics and Other (23.7% weighting as of 7/31/2022)

Extreme supply chain tightness and strong pricing drove our investment performance. Several factors coalesced to create this condition: the post-Covid economic recovery proved robust, ecommerce continued to take share from traditional retail, and there was widespread recognition that inventories need to be structurally higher to meet increasingly stringent delivery timetables. These factors emerged at a time when many logistics companies were still unwinding Covid-era capacity curtailments. The result was very strong pricing for shippers like rail and truck as demand outpaced supply. Additionally, there was unprecedented demand for warehouse space, particularly for space close to end markets. Going forward, some of cyclical drivers of recent strength should ebb, but the long-term shift towards ecommerce and structurally higher inventories should remain supportive for the sector.

Our best performers were Rexford Industrial Realty and Canadian National Rail.

During the period we swapped out of Canadian National Rail into Canadian Pacific. Canadian Pacific is merging with Kansas City Southern, a deal we expect to close early in 2023 at which time we expect better than industry growth due to merger synergies. We also purchased shares of Old Dominion Freight Line, a less than truckload (LTL) carrier that has been an industry leader in margin enhancement and operational best practices.

3

| THE ADVISORS’ INNER CIRCLE FUND II | REAVES INFRASTRUCTURE FUND | |

| JULY 31, 2022 | ||

Outlook

Our utility sector investments are focused on subsectors that have above-average organic growth. In particular, the outlook for companies with renewable development opportunities that they can put into rate base remains very healthy. These companies should be able to raise their dividends at a measured pace and continue to provide stability to the portfolio in the event of unforeseen volatility.

In communications, we prefer infrastructure businesses with high barriers to entry, predictable business models, and the consistent ability to grow cash flow and return capital to shareholders. We think communications REITs, such as towers and interconnection-focused data centers, have particularly challenging assets to replicate and very high switching costs. These dynamics are buttressed by underlying secular growth drivers such as mobile broadband and cloud computing. We are more selective with traditional telecommunications businesses, where we look for favorable valuations, unique competitive advantages, and benign competitive dynamics.

In other infrastructure investments, we prefer businesses that have strategic advantages that translate into above average growth prospects. We are particularly excited about the long-term prospects for pricing gains and high free cash yields in the rail business and ecommerce opportunities in our logistics and industrial REIT investments.

We remain committed to providing you with a portfolio of well-researched, high-quality companies in vital industries that have the ability to grow earnings and dividends while providing substantial defensive characteristics.

Sincerely,

|

| |

Tim Porter | Brian Weeks | |

Chief Investment Officer | Portfolio Manager | |

Performance data represents past performance which is no guarantee of future results. Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. Mutual fund performance changes over time and current performance may be lower or higher than what is stated.

4

| THE ADVISORS’ INNER CIRCLE FUND II | REAVES INFRASTRUCTURE FUND | |

| JULY 31, 2022 | ||

For performance current to the most recent month-end and after tax returns, please call 1.866.342.7058.

The above commentary represents management’s assessment of the Fund and the market environment at a specific point in time and should not be relied upon by the reader as research or investment advice. This information should not be relied upon by the reader as research or investment advice regarding the Fund or any stock in particular, nor should it be construed as a recommendation to purchase or sell a security.

Mutual fund investing involves risk, including possible loss of principal. In addition to the normal risks associated with investing, narrowly focused investments typically exhibit higher volatility. There can be no assurance that the Fund will achieve its stated objective.

5

| THE ADVISORS’ INNER CIRCLE FUND II | REAVES INFRASTRUCTURE FUND | |

| JULY 31, 2022 | ||

Definition of the Comparative Indices

| i | The MSCI USA Infrastructure Index captures the opportunity set of U.S. companies that are owners or operators of infrastructure assets. Constituents are selected from the equity universe of the MSCI USA Index, the parent index, which covers large and mid-cap securities in the U.S. All index constituents are categorized in one of thirteen sub-industries, which MSCI aggregates and groups into five infrastructure sectors: Telecommunications, Utilities, Energy, Transportation and Social. Reaves’ portfolios may at times be more diversified by including companies classified as operating in the Real Estate and Industrials sectors. The MSCI USA Infrastructure Index was launched on Jan 22, 2008. Data prior to the launch date is back-tested data (i.e., calculations of how the index might have performed over that time period had the index existed). There are frequently material differences between back-tested performance and actual results. Past performance, whether actual or back-tested, is no indication or guarantee of future performance. |

| ii | The S&P 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries. The typical Reaves portfolio includes a significant percentage of assets that are also found in the S&P 500. However, Reaves’ portfolios are far less diversified, resulting in higher sector concentrations than found in the broad-based S&P 500 Index. |

6

| THE ADVISORS’ INNER CIRCLE FUND II | REAVES INFRASTRUCTURE FUND | |

| JULY 31, 2022 | ||

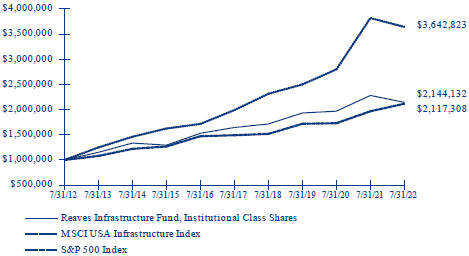

Growth of a $1,000,000 Investment (Unaudited)

| ANNUALIZED TOTAL RETURN FOR PERIODS ENDED JULY 31, 2022 | ||||||||

| 1 Year Return | 3 Year Return | 5 Year Return | 10 Year Return | |||||

Reaves Infrastructure Fund, Institutional Class Shares | -6.01% | 3.50% | 5.44% | 7.93% | ||||

MSCI USA Infrastructure Index (i) | 7.58% | 7.20% | 7.26% | 7.79% | ||||

S&P 500 Index (ii) | -4.64% | 13.36% | 12.83% | 13.80% | ||||

The performance data quoted herein represents past performance and the return and value of an investment in the Fund will fluctuate so that, when redeemed, may be worth less than its original cost. Past performance is no guarantee of future performance and should not be considered a representation of the future results of the Fund.

The Fund’s performance assumes the reinvestment of dividends and capital gains. Index returns assume reinvestment of dividends and, unlike a fund’s returns, do not reflect any fees or expenses. If such fees and expenses were included in the index returns, the performance would have been lower. Please note that one cannot invest directly in an unmanaged index.

There are no assurances that the Fund will meet its stated objectives. The Fund’s holdings and allocations are subject to change because it is actively managed and should not be considered recommendations to buy individual securities.

Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. If the Adviser had not limited certain expenses, the Fund’s total return would have been lower.

See definition of comparative indices on page 6.

7

| THE ADVISORS’ INNER CIRCLE FUND II | REAVES INFRASTRUCTURE FUND | |

| JULY 31, 2022 | ||

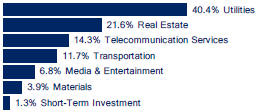

SECTOR WEIGHTINGS†(Unaudited): |

† Percentages are based on total investments. More narrow industries are utilized for compliance purposes, whereas broad sectors are utilized for reporting purposes.

COMMON STOCK — 98.7% | ||||||||

| Shares | Value | |||||||

COMMUNICATION SERVICES — 21.1% | ||||||||

Alphabet, Cl A * | 16,120 | $ | 1,875,078 | |||||

Charter Communications, Cl A * | 3,555 | 1,536,116 | ||||||

Cogent Communications Holdings | 21,000 | 1,340,010 | ||||||

Rogers Communications, Cl B | 38,625 | 1,775,205 | ||||||

TELUS | 75,000 | 1,725,000 | ||||||

T-Mobile US * | 16,140 | 2,308,988 | ||||||

|

|

| ||||||

| 10,560,397 | ||||||||

|

|

| ||||||

ELECTRIC UTILITIES — 13.3% | ||||||||

Entergy | 18,758 | 2,159,609 | ||||||

Exelon | 37,716 | 1,753,417 | ||||||

NextEra Energy | 32,233 | 2,723,366 | ||||||

|

|

| ||||||

| 6,636,392 | ||||||||

|

|

| ||||||

GAS UTILITIES — 3.3% | ||||||||

Atmos Energy | 13,400 | 1,626,626 | ||||||

|

|

| ||||||

INDEPENDENT POWER AND RENEWABLE ELECTRICITY PRODUCERS — 2.8% | ||||||||

Constellation Energy | 21,387 | 1,413,681 | ||||||

|

|

| ||||||

INDUSTRIALS — 11.7% | ||||||||

Canadian Pacific Railway | 24,947 | 1,967,570 | ||||||

Old Dominion Freight Line | 6,068 | 1,841,699 | ||||||

Union Pacific | 9,024 | 2,051,155 | ||||||

|

|

| ||||||

| 5,860,424 | ||||||||

|

|

| ||||||

The accompanying notes are an integral part of the financial statements.

8

| THE ADVISORS’ INNER CIRCLE FUND II | REAVES INFRASTRUCTURE FUND | |

| JULY 31, 2022 | ||

COMMON STOCK — continued | ||||||||

| Shares | Value | |||||||

MATERIALS — 3.9% | ||||||||

Linde | 6,529 | $ | 1,971,758 | |||||

|

|

| ||||||

MULTI-UTILITIES — 17.1% | ||||||||

Alliant Energy | 35,424 | 2,158,384 | ||||||

Ameren | 21,948 | 2,043,798 | ||||||

CMS Energy | 31,752 | 2,182,315 | ||||||

Xcel Energy | 29,491 | 2,158,151 | ||||||

|

|

| ||||||

| 8,542,648 | ||||||||

|

|

| ||||||

REAL ESTATE — 21.6% | ||||||||

Crown Castle International REIT † | 10,378 | 1,874,890 | ||||||

Equinix REIT † | 3,087 | 2,172,445 | ||||||

Prologis REIT † | 15,295 | 2,027,505 | ||||||

Rexford Industrial Realty REIT † | 30,647 | 2,004,620 | ||||||

SBA Communications REIT, Cl A † | 8,185 | 2,748,441 | ||||||

|

|

| ||||||

| 10,827,901 | ||||||||

|

|

| ||||||

WATER UTILITIES — 3.9% | ||||||||

American Water Works | 12,711 | 1,975,798 | ||||||

|

|

| ||||||

TOTAL COMMON STOCK | 49,415,625 | |||||||

|

|

| ||||||

| ||||||||

SHORT-TERM INVESTMENT (A) — 1.3% | ||||||||

SEI Daily Income Trust Treasury II Fund, Cl F, 1.460% | 633,641 | 633,641 | ||||||

|

|

| ||||||

TOTAL INVESTMENTS— 100.0% | $ | 50,049,266 | ||||||

|

|

| ||||||

Percentages are based on Net Assets of $50,032,052. |

| * | Non-income producing security. |

| (A) | The rate reported is the 7-day effective yield as of July 31, 2022. |

Cl — Class

REIT — Real Estate Investment Trust

As of July 31, 2022, all of the Fund’s investments in securities were considered Level 1, in accordance with the authoritative guidance on fair value measurements and disclosure under U.S. GAAP.

The accompanying notes are an integral part of the financial statements.

9

| THE ADVISORS’ INNER CIRCLE FUND II | REAVES INFRASTRUCTURE FUND | |

| JULY 31, 2022 | ||

For more information on valuation inputs, see Note 2 — Significant Accounting Policies in the Notes to Financial Statements.

The accompanying notes are an integral part of the financial statements.

10

| THE ADVISORS’ INNER CIRCLE FUND II | REAVES INFRASTRUCTURE FUND | |

| JULY 31, 2022 | ||

Assets: | ||||

Investments at Value (Cost $39,141,635) | $ | 50,049,266 | ||

Receivable for Investment Securities Sold | 1,728,086 | |||

Dividends Receivable | 17,281 | |||

Receivable for Capital Shares Sold | 12,286 | |||

Prepaid Expenses | 11,027 | |||

Receivable from Investment Adviser | 1,629 | |||

|

|

| ||

Total Assets | 51,819,575 | |||

|

|

| ||

Liabilities: | ||||

Payable for Investment Securities Purchased | 1,725,120 | |||

Payable due to Trustees | 7,670 | |||

Payable due to Administrator | 7,219 | |||

Chief Compliance Officer Fees Payable | 3,282 | |||

Payable for Capital Shares Redeemed | 978 | |||

Other Accrued Expenses | 43,254 | |||

|

|

| ||

Total Liabilities | 1,787,523 | |||

|

|

| ||

Net Assets | $ | 50,032,052 | ||

|

|

| ||

Net Assets Consist of: | ||||

Paid-in-Capital | $ | 37,975,008 | ||

Total Distributable Earnings | 12,057,044 | |||

|

|

| ||

Net Assets | $ | 50,032,052 | ||

|

|

| ||

Net Asset Value, Offering and Redemption Price Per Share | ||||

Institutional Class Shares ($50,032,052 ÷ 4,857,017) | $ | 10.30 | ||

|

|

| ||

The accompanying notes are an integral part of the financial statements.

11

| THE ADVISORS’ INNER CIRCLE FUND II | REAVES INFRASTRUCTURE FUND | |

FOR THE YEAR ENDED | ||

| JULY 31, 2022 | ||

Investment Income | ||||

Dividend Income | $ | 759,387 | ||

Less: Foreign Taxes Withheld | (13,891 | ) | ||

|

|

| ||

Total Investment Income | 745,496 | |||

|

|

| ||

Expenses: | ||||

Investment Advisory Fees | 412,304 | |||

Administration Fees | 98,371 | |||

Professional Fees | 85,973 | |||

Transfer Agent Fees | 64,840 | |||

Trustees’ Fees | 30,239 | |||

Registration Fees | 25,984 | |||

Printing Fees | 25,000 | |||

Chief Compliance Officer Fees | 8,998 | |||

Custodian Fees | 5,523 | |||

Insurance and Other Expenses | 23,068 | |||

|

|

| ||

Total Expenses | 780,300 | |||

|

|

| ||

Less: Investment Advisory Fees Waived | (175,324 | ) | ||

Less: Fees Paid Indirectly(1) | (165 | ) | ||

|

|

| ||

Net Expenses | 604,811 | |||

|

|

| ||

Net Investment Income | 140,685 | |||

|

|

| ||

Net Realized Gain on Investments | 1,251,525 | |||

Net Change in Unrealized Depreciation on Investments | (4,774,353 | ) | ||

|

|

| ||

Net Realized and Unrealized Loss on Investments | (3,522,828 | ) | ||

|

|

| ||

Net Decrease in Net Assets Resulting from Operations | $ | (3,382,143 | ) | |

|

|

| ||

| (1) | See Note 4 in the Notes to Financial Statements. |

The accompanying notes are an integral part of the financial statements.

12

| THE ADVISORS’ INNER CIRCLE FUND II | REAVES INFRASTRUCTURE FUND | |

| Year Ended July 31, 2022 | Year Ended July 31, 2021 | |||||||

Operations: | ||||||||

Net Investment Income | $ | 140,685 | $ | 135,831 | ||||

Net Realized Gain on Investments | 1,251,525 | 5,201,705 | ||||||

Net Change in Unrealized Appreciation/(Depreciation) on Investments | (4,774,353 | ) | 2,591,861 | |||||

|

|

|

|

|

| |||

Net Increase/(Decrease) in Net Assets Resulting from | ||||||||

Operations | (3,382,143 | ) | 7,929,397 | |||||

|

|

|

|

|

| |||

Distributions | (3,081,114 | ) | (201,376 | ) | ||||

|

|

|

|

|

| |||

Capital Share Transactions:(1) | ||||||||

Issued | 3,970,215 | 8,004,694 | ||||||

Reinvestment of Distributions | 2,925,578 | 182,239 | ||||||

Redeemed | (8,108,114 | ) | (10,503,216 | ) | ||||

|

|

|

|

|

| |||

Net Decrease from Capital Share Transactions | (1,212,321 | ) | (2,316,283 | ) | ||||

|

|

|

|

|

| |||

Total Increase/(Decrease) in Net Assets | (7,675,578 | ) | 5,411,738 | |||||

|

|

|

|

|

| |||

Net Assets: | ||||||||

Beginning of Year | 57,707,630 | 52,295,892 | ||||||

|

|

|

|

|

| |||

End of Year | $ | 50,032,052 | $ | 57,707,630 | ||||

|

|

|

|

|

| |||

| (1) | For share transactions, see Note 6 in the Notes to Financial Statements. |

The accompanying notes are an integral part of the financial statements.

13

| THE ADVISORS’ INNER CIRCLE FUND II | REAVES INFRASTRUCTURE FUND | |

Selected Per Share Data & Ratios For a Share Outstanding Throughout the Years | ||

| Institutional Class Shares | ||||||||||||||||||||||||||||||

| Year Ended July 31, 2022 | Year Ended July 31, 2021 | Year Ended July 31, 2020 | Year Ended July 31, 2019 | Year Ended July 31, 2018 | ||||||||||||||||||||||||||

Net Asset Value, Beginning of Year | $ | 11.56 | $ | 10.02 | $ | 10.58 | $ | 10.34 | $ | 10.59 | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||||

Income from Operations: | ||||||||||||||||||||||||||||||

Net Investment Income(1) | 0.03 | 0.03 | 0.07 | 0.06 | 0.11 | |||||||||||||||||||||||||

Net Realized and Unrealized Gain/(Loss) on Investments | (0.68 | ) | 1.55 | 0.14 | 1.07 | 0.32 | ||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||||

Total from Operations | (0.65 | ) | 1.58 | 0.21 | 1.13 | 0.43 | ||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||||

Dividends and Distributions from: | ||||||||||||||||||||||||||||||

Net Investment Income | (0.05 | ) | (0.04 | ) | (0.13 | ) | (0.13 | ) | (0.13 | ) | ||||||||||||||||||||

Net Realized Gains | (0.56 | ) | — | (0.64 | ) | (0.76 | ) | (0.55 | ) | |||||||||||||||||||||

Total Dividends and | ||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||||

Distributions | (0.61 | ) | (0.04 | ) | (0.77 | ) | (0.89 | ) | (0.68 | ) | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||||

Net Asset Value, End of Year | $ | 10.30 | $ | 11.56 | $ | 10.02 | $ | 10.58 | $ | 10.34 | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||

Total Return † | (6.01 | )% | 15.80 | % | 1.87 | % | 12.76 | % | 4.24 | % | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||

Ratios and Supplemental Data | ||||||||||||||||||||||||||||||

Net Assets, End of Year (Thousands) | $ | 50,032 | $ | 57,708 | $ | 52,296 | $ | 43,129 | $ | 46,951 | ||||||||||||||||||||

Ratio of Expenses to Average Net Assets (including waivers and reimbursements/ excluding fees paid indirectly) | 1.10% | 1.30% | 1.30% | 1.30% | 1.30% | |||||||||||||||||||||||||

Ratio of Expenses to Average Net Assets (excluding waivers, reimbursements and fees paid indirectly) | 1.42% | 1.38% | 1.46% | 1.49% | 1.47% | |||||||||||||||||||||||||

Ratio of Net Investment Income to Average Net Assets | 0.26% | 0.25% | 0.68% | 0.63% | 1.07% | |||||||||||||||||||||||||

Portfolio Turnover Rate | 46% | 42% | 36% | 31% | 66% | |||||||||||||||||||||||||

| (1) | Per share data calculated using average shares method. |

| † | Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Total return would have been lower had certain fees not been waived and expenses assumed by the Adviser during the period. |

Amounts designated as “—” are $0.

The accompanying notes are an integral part of the financial statements.

14

| THE ADVISORS’ INNER CIRCLE FUND II | REAVES INFRASTRUCTURE FUND | |

| JULY 31, 2022 | ||

| 1. | Organization: |

The Advisors’ Inner Circle Fund II (the “Trust”) is organized as a Massachusetts business trust under an Amended and Restated Agreement and Declaration of Trust dated July 24, 1992. The Trust is registered under the Investment Company Act of 1940, as amended, as an open-end management investment company with 9 funds. The financial statements herein are those of the Reaves Infrastructure Fund (the “Fund”). The financial statements of the remaining funds of the Trust are presented separately. The investment objective of the Fund is total return from income and capital growth. The Fund is a diversified fund, and invests primarily in securities of domestic and foreign public utility and energy companies, with a concentration (at least 80% of its assets) in companies involved to a significant extent in the Utilities and Energy Industries. The assets of each fund of the Trust are segregated, and a shareholder’s interest is limited to the fund of the Trust in which shares are held.

| 2. | Significant Accounting Policies: |

The following are significant accounting policies, which are consistently followed in the preparation of the financial statements of the Fund. The Fund is an investment company that applies the accounting and reporting guidance issued in Topic 946 by the U.S. Financial Accounting Standards Board (“FASB”).

Use of Estimates — The preparation of financial statements, in conformity with U.S. GAAP requires management to make estimates and assumptions that affect the reported amount of assets and liabilities and disclosure of contingent assets and liabilities as of the date of the financial statements and the reported amounts of increases and decreases in net assets from operations during the reporting period. Actual results could differ from those estimates and such differences could be material.

Security Valuation —Securities listed on a securities exchange, market or automated quotation system for which quotations are readily available (except for securities traded on the NASDAQ Stock Market (the “NASDAQ”)), including securities traded over the counter, are valued at the last quoted sale price on an exchange or market (foreign or domestic) on which they are traded on the valuation date (or at approximately 4:00 pm ET if a security’s primary exchange is normally open at that time), or, if there is no such reported sale on the valuation date, at the most recent quoted bid price. For securities traded on NASDAQ, the NASDAQ Official Closing Price will be used. All investment companies held in the Fund’s portfolio are valued at the published net asset value.

15

| THE ADVISORS’ INNER CIRCLE FUND II | REAVES INFRASTRUCTURE FUND | |

| JULY 31, 2022 | ||

Securities for which market prices are not “readily available” are valued in accordance with Fair Value Procedures established by the Trust’s Board of Trustees (the “Board”). The Trust’s Fair Value Procedures are implemented through a Fair Value Committee (the “Committee”) designated by the Board. Some of the more common reasons that may necessitate that a security be valued using Fair Value Procedures include: the security’s trading has been halted or suspended; the security has been de-listed from a national exchange; the security’s primary trading market is temporarily closed at a time when under normal conditions it would be open; the security has not been traded for an extended period of time; the security’s primary pricing source is not able or willing to provide a price; or trading of the security is subject to local government-imposed restrictions. When a security is valued in accordance with the Fair Value Procedures, the Committee will determine the value after taking into consideration relevant information reasonably available to the Committee. As of July 31, 2022, there were no securities valued in accordance with the Fair Value Procedures.

In accordance with the authoritative guidance on fair value measurements and disclosures under U.S. GAAP, the Fund discloses the fair value of its investments in a hierarchy that prioritizes the inputs to valuation techniques used to measure the fair value. The objective of a fair value measurement is to determine the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date (an exit price). Accordingly, the fair value hierarchy gives the highest priority to quoted prices (unadjusted) in active markets for identical assets or liabilities (Level 1) and the lowest priority to unobservable inputs (Level 3). The guidance establishes three levels of the fair value hierarchy as follows:

| ● | Level 1 — quoted prices in active markets for identical securities. |

| ● | Level 2 — other significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds, credit risk, etc.). |

| ● | Level 3 — significant unobservable inputs (including the Fund’s own assumptions in determining the fair value of investments). |

During the year ended July 31, 2022, there have been no changes to the Fund’s fair value methodologies.

Federal Income Taxes — It is the Fund’s intention to continue to qualify as a regulated investment company under Subchapter M of the Internal Revenue Code and to distribute all of its taxable income. Accordingly, no provision for Federal income taxes has been made in the financial statements.

The Fund evaluates tax positions taken or expected to be taken in the course of preparing the Fund’s tax returns to determine whether it is “more-likely-than-

16

| THE ADVISORS’ INNER CIRCLE FUND II | REAVES INFRASTRUCTURE FUND | |

| JULY 31, 2022 | ||

not” (i.e., greater than 50-percent) that each tax position will be sustained upon examination by a taxing authority based on the technical merits of the position. Tax positions not deemed to meet the more-likely-than-not threshold are recorded as a tax benefit or expense in the current year. The Fund did not record any tax provision in the current year. However, management’s conclusions regarding tax positions taken may be subject to review and adjustment at a later date based on factors including, but not limited to, examination by tax authorities (i.e., the last 3 tax year ends, as applicable), on-going analysis of and changes to tax laws, regulations and interpretations thereof.

As of and during the year ended July 31, 2022, the Fund did not have a liability for any unrecognized tax benefits. The Fund recognizes interest and penalties, if any, related to unrecognized tax benefits as income tax expense in the Statement of Operations. During the year ended July 31, 2022, the Fund did not incur any interest or penalties relating to unrecognized tax benefits.

Security Transactions and Investment Income — Security transactions are accounted for on the trade date for financial reporting purposes. Costs used in determining realized gains and losses on the sales of investment securities are based on specific identification. Dividend income is recognized on the ex-dividend date and interest income is recognized on an accrual basis.

Investments in Real Estate Investment Trusts (“REITs”) — With respect to the Fund, dividend income is recorded based on the income included in distributions received from REIT investments using published REIT reclassifications including some management estimates when actual amounts are not available. Distributions received in excess of any estimated amount are recorded as a reduction of the cost of investments or reclassified to capital gains. The actual amounts of income, return of capital, and capital gains are only determined by each REIT after its fiscal year-end, and may differ from estimated amounts.

Expenses — Most expenses of the Trust can be directly attributed to a particular fund. Expenses that cannot be directly attributed to a fund are apportioned among the funds of the Trust based on the number of funds and/ or relative net assets.

Dividends and Distributions to Shareholders — The Fund seeks to declare quarterly dividends at fixed rates approved by the Board. To the extent that the amount of the Fund’s net investment income and short-term capital gains is less than the approved fixed rate, some of its dividends may be paid from net capital gains or as a return of shareholder capital. To the extent the amount of the Fund’s net investment income and short-term capital gains exceeds the approved fixed rate, the Fund may pay additional dividends. An additional distribution of net

17

| THE ADVISORS’ INNER CIRCLE FUND II | REAVES INFRASTRUCTURE FUND | |

| JULY 31, 2022 | ||

capital gains realized by the Fund, if any, may be made annually; provided, however, that no more than one distribution of net capital gains shall be made with respect to any one taxable year of the Fund (other than a permitted, supplemental distribution which does not exceed 10% of the aggregate amount distributed for such taxable year).

| 3. | Transactions with Affiliates: |

Certain officers and trustees of the Trust are also officers of SEI Investments Global Funds Services (the “Administrator”), a wholly owned subsidiary of SEI Investments Company, and/or SEI Investments Distribution Co. (the “Distributor”). Such officers and trustees are paid no fees by the Trust for serving as officers and trustees of the Trust.

The services provided by the Chief Compliance Officer (“CCO”) and his staff, who are employees of the Administrator, are paid for by the Trust, as incurred. The services include regulatory oversight of the Trust’s advisers and service providers as required by SEC regulations. The CCO’s services and fees have been approved by and are reviewed by the Board.

| 4. | Administration, Transfer Agent and Custodian Agreements: |

The Fund and the Administrator are parties to an administration agreement under which the Administrator provides management and administrative services to the Fund. For these services, the Administrator is paid an asset-based fee (subject to certain minimums), which will vary depending on the number of share classes and the average daily net assets of the Fund. For the year ended July 31, 2022, the Fund was charged $98,371 for these services.

DST Systems, Inc. serves as the transfer agent and dividend disbursing agent for the Fund under a transfer agency agreement with the Trust. The Fund may earn cash management credits which can be used to offset transfer agent expenses. During the year ended July 31, 2022, the Fund earned credits of $165, which were used to offset transfer agent expenses. This amount is listed as “Fees Paid Indirectly” on the Statement of Operations.

U.S. Bank, N.A. acts as custodian (the “Custodian”) for the Fund. The Custodian plays no role in determining the investment policies of the Fund or which securities are to be purchased or sold by the Fund.

18

| THE ADVISORS’ INNER CIRCLE FUND II | REAVES INFRASTRUCTURE FUND | |

| JULY 31, 2022 | ||

| 5. | Investment Advisory Agreement: |

Under the terms of an investment advisory agreement, Reaves Asset Management (the “Adviser”) provides investment advisory services to the Fund at a fee, which is calculated daily and paid monthly at an annual rate of 0.75% of the Fund’s average daily net assets. The Adviser has voluntarily agreed to waive a portion of its advisory fees and to assume expenses, if necessary, in order to keep the Fund’s total annual operating expenses from exceeding 0.99% of the Institutional Class Share average daily net assets. The expense limitation changed from 1.30% to 0.99% on November 28, 2021. The Adviser may discontinue the expense limitation at any time. In addition, if at any point it becomes unnecessary for the Adviser to reduce fees or make expense reimbursements, the Adviser may retain the difference between the “Total Annual Fund Operating Expenses” and the aforementioned expense limitations to recapture all or a portion of its prior expense limitation reimbursements made during the preceding three-year period up to the expense cap in place at the time the expenses were waived. As of July 31, 2022, fees which were previously waived and reimbursed by the Adviser which may be subject to possible future reimbursement to the Adviser were $69,899 expiring in 2023, $45,520 expiring in 2024, and $175,324 expiring in 2025. During the year ended July 31, 2022, there has been no recoupment of previously waived and reimbursed fees.

| 6. | Share Transactions: |

| Year Ended July 31, 2022 | Year Ended July 31, 2021 | |||||||

Share Transactions: | ||||||||

Institutional Class Shares | ||||||||

Issued | 364,809 | 753,399 | ||||||

Reinvestment of Distributions | 263,421 | 17,067 | ||||||

Redeemed | (764,512 | ) | (994,469 | ) | ||||

|

|

|

|

|

| |||

Net Decrease in Shares Outstanding | (136,282 | ) | (224,003 | ) | ||||

|

|

|

|

|

| |||

| 7. | Investment Transactions: |

The cost of security purchases and the proceeds from security sales, other than long-term U.S. Government and short-term investments, for the year ended July 31, 2022 were $24,835,943, and $28,793,662, respectively. There were no purchases or sales of long-term U.S. Government securities.

19

| THE ADVISORS’ INNER CIRCLE FUND II | REAVES INFRASTRUCTURE FUND | |

| JULY 31, 2022 | ||

| 8. | Federal Tax Information: |

The amount and character of income and capital gain distributions, if any, to be paid are determined in accordance with Federal income tax regulations, which may differ from U.S. GAAP. As a result, net investment income (loss) and net realized gain (loss) on investment transactions for a reporting period may differ significantly from distributions during such period. These book/tax differences may be temporary or permanent. The permanent differences primarily consist of reclassification of long term capital gain distribution on REITs and reclassification of distribution of ordinary income. There are no permanent differences that are credited or charged to Paid-in Capital and Distributable Earnings as of July 31, 2022.

The tax character of dividends and distributions declared during the fiscal year ended July 31, 2022 and 2021 was as follows:

| Long-Term | ||||||||||||||||

| Ordinary Income | Capital Gain | Distributions | Total | |||||||||||||

| 2022 | $ | 150,543 | $ | 2,930,571 | $ | — | $ | 3,081,114 | ||||||||

| 2021 | 149,493 | 51,883 | — | 201,376 | ||||||||||||

As of July 31, 2022, the components of Distributable Earnings on a tax basis were as follows:

Undistributed Long-Term Capital Gains | 1,149,413 | |||

Net Unrealized Appreciation | 10,907,631 | |||

|

| |||

Total Distributable Earnings | $ | 12,057,044 | ||

|

| |||

The Federal tax cost and aggregate gross unrealized appreciation and depreciation on investments held by the Fund at July 31, 2022 were as follows:

Federal Tax Cost | Aggregate Gross Unrealized Appreciation | Aggregate Gross Unrealized Depreciation | Net Unrealized Appreciation | |||

| $39,141,635 | $11,279,637 | $(372,006) | $10,907,631 |

| 9. | Concentration/Risks: |

The Fund has adopted a policy to concentrate its investments (at least 80% of its assets) in companies involved to a significant extent in the Utilities and Energy Industries. To the extent that the Fund’s investments are focused in issuers conducting business in the Utilities Industry and/or Energy Industry, the Fund is subject to

20

| THE ADVISORS’ INNER CIRCLE FUND II | REAVES INFRASTRUCTURE FUND | |

| JULY 31, 2022 | ||

the risk that legislative or regulatory changes, adverse market conditions and/or increased competition will negatively affect these industries.

Equity Risk – Equity securities include publicly and privately issued equity securities, common and preferred stocks, warrants, rights to subscribe to common stock and convertible securities, as well as instruments that attempt to track the price movement of equity indices. Investments in equity securities and equity derivatives in general are subject to market risks that may cause their prices to fluctuate over time. The value of securities convertible into equity securities, such as warrants or convertible debt, is also affected by prevailing interest rates, the credit quality of the issuer and any call provision. Fluctuations in the value of equity securities in which a mutual fund invests will cause the fund’s net asset value (“NAV”) to fluctuate. An investment in a portfolio of equity securities may be more suitable for long-term investors who can bear the risk of these share price fluctuations. In addition, the impact of any epidemic, pandemic or natural disaster, or widespread fear that such events may occur, could negatively affect the global economy, as well as the economies of individual countries, the financial performance of individual companies and sectors, and the markets in general in significant and unforeseen ways. Any such impact could adversely affect the prices and liquidity of the securities and other instruments in which the Fund invests, which in turn could negatively impact the Fund’s performance and cause losses.

Foreign Security Risk – Investments in securities of foreign companies or governments can be more volatile than investments in U.S. companies or governments. Diplomatic, political, or economic developments, including nationalization or appropriation, could affect investments in foreign companies. Foreign securities markets generally have less trading volume and less liquidity than U.S. markets. In addition, the value of securities denominated in foreign currencies, and of dividends from such securities, can change significantly when foreign currencies strengthen or weaken relative to the U.S. dollar. Financial statements of foreign issuers are governed by different accounting, auditing, and financial reporting standards than the financial statements of U.S. issuers and may be less transparent and uniform than in the United States. Thus, there may be less information publicly available about foreign issuers than about most U.S. issuers. Transaction costs are generally higher than those in the United States and expenses for custodial arrangements of foreign securities may be somewhat greater than typical expenses for custodial arrangements of similar U.S. securities. Some foreign governments levy withholding taxes against dividend and interest income. Although in some countries a portion of these taxes are recoverable, the non-recovered portion will reduce the income received from the securities comprising the portfolio.

21

| THE ADVISORS’ INNER CIRCLE FUND II | REAVES INFRASTRUCTURE FUND | |

| JULY 31, 2022 | ||

| 10. | Other: |

At July 31, 2022, 40% of Institutional Class Shares outstanding were held by two record shareholders each owning 10% or greater of the aggregate total shares outstanding. These shareholders are comprised of individual shareholders and omnibus accounts that were held on behalf of various individual shareholders.

In the normal course of business, the Fund enters into contracts that provide general indemnifications. The Fund’s maximum exposure under these arrangements is dependent on future claims that may be made against the Fund and, therefore, cannot be established; however, based on experience, the risk of loss from such claims is considered remote.

| 11. | Subsequent Events: |

Management has evaluated the need for disclosures and/or adjustments resulting from subsequent events through the date the financial statements were issued. Based on this evaluation, no disclosures and/or adjustments were required to the financial statements as of July 31, 2022.

22

| THE ADVISORS’ INNER CIRCLE FUND II | REAVES INFRASTRUCTURE FUND | |

| JULY 31, 2022 | ||

To the Board of Trustees of The Advisors’ Inner Circle Fund II and

Shareholders of Reaves Infrastructure Fund (formerly, Reaves Utilities and Energy Infrastructure Fund)

Opinion on the Financial Statements

We have audited the accompanying statement of assets and liabilities of Reaves Infrastructure Fund (formerly, Reaves Utilities and Energy Infrastructure Fund) (the “Fund”) (one of the series constituting The Advisors’ Inner Circle Fund II (the “Trust”)), including the schedule of investments, as of July 31, 2022, and the related statement of operations for the year then ended, the statements of changes in net assets for each of the two years in the period then ended, the financial highlights for each of the five years in the period then ended and the related notes (collectively referred to as the “financial statements”). In our opinion, the financial statements present fairly, in all material respects, the financial position of the Fund (one of the series constituting The Advisors’ Inner Circle Fund II) at July 31, 2022, the results of its operations for the year then ended, the changes in its net assets for each of the two years in the period then ended and its financial highlights for each of the five years in the period then ended, in conformity with U.S. generally accepted accounting principles.

Basis for Opinion

These financial statements are the responsibility of the Trust’s management. Our responsibility is to express an opinion on the Fund’s financial statements based on our audits. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (“PCAOB”) and are required to be independent with respect to the Trust in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement, whether due to error or fraud. The Trust is not required to have, nor were we engaged to perform, an audit of the Trust’s internal control over financial reporting. As part of our audits we are required to obtain an understanding of internal control over financial reporting but not for the purpose of expressing an opinion on the effectiveness of the Trust’s internal control over financial reporting. Accordingly, we express no such opinion.

Our audits included performing procedures to assess the risks of material misstatement of the financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of July 31, 2022, by correspondence with the custodian and brokers. Our audits also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that our audits provide a reasonable basis for our opinion.

We have served as the auditor of one or more Reaves Asset Management investment companies since 2005.

Philadelphia, Pennsylvania

September 29, 2022

23

| THE ADVISORS’ INNER CIRCLE FUND II | REAVES INFRASTRUCTURE FUND | |

| JULY 31, 2022 | ||

TRUSTEES AND OFFICERS OF THE ADVISORS’ INNER CIRCLE FUND II (UNAUDITED) |

Set forth below are the names, years of birth, positions with the Trust, length of term of office, and the principal occupations for the last five years of each of the persons currently serving as Trustees and Officers of the Trust. Unless otherwise noted, the business address of each Trustee is SEI Investments Company, One Freedom Valley Drive, Oaks, Pennsylvania 19456. Trustees who are deemed not to be “interested persons” of the Trust are referred to as “Independent Trustees.” Messrs.

| Position with Trust | ||||

| and Length of Time | Principal Occupations | |||

| Name and Year of Birth | Served1 | In the Past Five Years | ||

INTERESTED TRUSTEES 3 4 | ||||

Robert Nesher (Born: 1946) | Chairman of the Board of Trustees (since 1991) | SEI employee 1974 to present; currently performs various services on behalf of SEI Investments for which Mr. Nesher is compensated. President, Chief Executive Officer and Trustee of SEI Daily Income Trust, SEI Tax Exempt Trust, SEI Institutional Managed Trust, SEI Institutional International Trust, SEI Institutional Investments Trust, SEI Asset Allocation Trust, Adviser Managed Trust, New Covenant Funds, SEI Insurance Products Trust and SEI Catholic Values Trust. President and Director of SEI Structured Credit Fund, LP. Vice Chairman of O’Connor EQUUS (closed-end investment company) to 2016. President, Chief Executive Officer and Trustee of SEI Liquid Asset Trust to 2016. Vice Chairman of Winton Series Trust to 2017. Vice Chairman of Winton Diversified Opportunities Fund (closed-end investment company), The Advisors’ Inner Circle Fund III, Gallery Trust, Schroder Series Trust and Schroder Global Series Trust to 2018. | ||

N. Jeffrey Klauder (Born: 1952) | Trustee (since 2018) | Senior Advisor of SEI Investments since 2018. Executive Vice President and General Counsel of SEI Investments, 2004 to 2018. | ||

| 1 | Each Trustee shall hold office during the lifetime of this Trust until the election and qualification of his or her successor, or until he or she sooner dies, resigns, or is removed in accordance with the Trust’s Declaration of Trust. |

| 2 | Directorships of Companies required to report to the Securities and Exchange Commission under the Securities Exchange Act of 1934 (i.e., “public companies”) or other investment companies under the 1940 Act. |

| 3 | Denotes Trustees who may be deemed to be “interested” persons of the Fund as that term is defined in the 1940 Act by virtue of their affiliation with the Distributor and/or its affiliates. |

| 4 | Trustees oversee 9 funds in The Advisors’ Inner Circle Fund II. |

24

| THE ADVISORS’ INNER CIRCLE FUND II | REAVES INFRASTRUCTURE FUND | |

| JULY 31, 2022 | ||

Nesher and Klauder are Trustees who may be deemed to be “interested” persons of the Trust as that term is defined in the 1940 Act by virtue of their affiliation with the Trust’s Distributor. The Trust’s Statement of Additional Information (“SAI”) includes additional information about the Trustees and Officers. The SAI may be obtained without charge by calling 1-866-342-7058. The following chart lists Trustees and Officers as of July 31, 2022.

Other Directorships

Held in the Past Five Years2

Current Directorships: Trustee of The Advisors’ Inner Circle Fund, Bishop Street Funds, Frost Family of Funds, Catholic Responsible Investments Funds, SEI Daily Income Trust, SEI Institutional International Trust, SEI Institutional Investments Trust, SEI Institutional Managed Trust, SEI Asset Allocation Trust, SEI Tax Exempt Trust, Adviser Managed Trust, New Covenant Funds, SEI Insurance Products Trust and SEI Catholic Values Trust. Director of SEI Structured Credit Fund, LP, SEI Global Master Fund plc, SEI Global Assets Fund plc, SEI Global Investments Fund plc, SEI Investments—Global Funds Services, Limited, SEI Investments Global, Limited, SEI Investments (Europe) Ltd., SEI Investments—Unit Trust Management (UK) Limited, SEI Multi-Strategy Funds PLC and SEI Global Nominee Ltd.

Former Directorships: Trustee of The KP Funds to 2021. Trustee of SEI Liquid Asset Trust to 2016.

Current Directorships: Trustee of The Advisors’ Inner Circle Fund, Bishop Street Funds and Catholic Responsible Investments Funds. Director of SEI Private Trust Company, SEI Global Fund Services Ltd., SEI Investments Global Limited, SEI Global Master Fund, SEI Global Investments Fund, SEI Global Assets Fund and SEI Investments - Guernsey Limited.

Former Directorships: Trustee of The KP Funds to 2021. Trustee of SEI Investments Management Corporation, SEI Trust Company, SEI Investments (South Africa), Limited and SEI Investments (Canada) Company to 2018.

25

| THE ADVISORS’ INNER CIRCLE FUND II | REAVES INFRASTRUCTURE FUND | |

| JULY 31, 2022 | ||

TRUSTEES AND OFFICERS OF THE ADVISORS’ INNER CIRCLE FUND II (UNAUDITED) |

| Name and Year of Birth | Position(s) with Trust and Length of Time Served1 | Principal Occupation(s) in the Past Five Years | ||

INDEPENDENT TRUSTEES3 | ||||

Joseph T. Grause, Jr. (Born: 1952) | Trustee (since 2011) Lead Independent Trustee (since 2018) | Consultant since 2012. Director of Endowments and Foundations, Morningstar Investment Management, Morningstar, Inc., 2010 to 2011. Director of International Consulting and Chief Executive Officer of Morningstar Associates Europe Limited, Morningstar, Inc., 2007 to 2010. Country Manager – Morningstar UK Limited, Morningstar, Inc., 2005 to 2007. | ||

Mitchell A. Johnson (Born: 1942) | Trustee (since 2005) | Retired. Private Investor since 1994. | ||

Betty L. Krikorian (Born: 1943) | Trustee (since 2005) | Vice President, Compliance, AARP Financial Inc., from 2008 to 2010. Self-Employed Legal and Financial Services Consultant since 2003. Counsel (in-house) for State Street Bank from 1995 to 2003. | ||

Robert Mulhall (Born: 1958) | Trustee (since 2019) | Partner, Ernst & Young LLP, from 1998 to 2018. | ||

Bruce Speca (Born: 1956) | Trustee (since 2011) | Global Head of Asset Allocation, Manulife Asset Management (subsidiary of Manulife Financial), 2010 to 2011. Executive Vice President – Investment Management Services, John Hancock Financial Services (subsidiary of Manulife Financial), 2003 to 2010.

| ||

| 1 | Each Trustee shall hold office during the lifetime of this Trust until the election and qualification of his or her successor, or until he or she sooner dies, resigns, or is removed in accordance with the Trust’s Declaration of Trust. |

| 2 | Directorships of Companies required to report to the Securities and Exchange Commission under the Securities Exchange Act of 1934 (i.e., “public companies”) or other investment companies under the 1940 Act. |

| 3 | Trustees oversee 9 funds in The Advisors’ Inner Circle Fund II. |

26

| THE ADVISORS’ INNER CIRCLE FUND II | REAVES INFRASTRUCTURE FUND | |

| JULY 31, 2022 | ||

Other Directorships

Held in the Past Five Years2

Current Directorships: Trustee of The Advisors’ Inner Circle Fund, Bishop Street Funds, Frost Family of Funds and Catholic Responsible Investments Funds. Director of RQSI GAA Systematic Global Macro Fund, Ltd.

Former Directorships: Trustee of The KP Funds to 2021. Director of The Korea Fund, Inc. to 2019.

Current Directorships: Trustee of The Advisors’ Inner Circle Fund, Bishop Street Funds, Catholic Responsible Investments Funds, SEI Asset Allocation Trust, SEI Daily Income Trust, SEI Institutional International Trust, SEI Institutional Managed Trust, SEI Institutional Investments Trust, SEI Tax Exempt Trust, Adviser Managed Trust, New Covenant Funds, SEI Insurance Products Trust and SEI Catholic Values Trust. Director of Federal Agricultural Mortgage Corporation (Farmer Mac) since 1997 and RQSI GAA Systematic Global Macro Fund, Ltd.

Former Directorships: Trustee of the KP Funds to 2021. Trustee of SEI Liquid Asset Trust to 2016.

Current Directorships: Trustee of The Advisors’ Inner Circle Fund, Bishop Street Funds and Catholic Responsible Investments Funds. Director of RQSI GAA Systematic Global Macro Fund, Ltd.

Former Directorships: Trustee of The KP Funds to 2021.

Current Directorships: Trustee of The Advisors’ Inner Circle Fund, Bishop Street Funds, Frost Family of Funds and Catholic Responsible Investments Funds. Director of RQSI GAA Systematic Global Macro Fund, Ltd.

Former Directorships: Trustee of The KP Funds to 2021. Trustee of Villanova University Alumni Board of Directors to 2018.

Current Directorships: Trustee of The Advisors’ Inner Circle Fund, Bishop Street Funds, Frost Family of Funds and Catholic Responsible Investments Funds. Director of Stone Harbor Investments Funds (8 Portfolios), Stone Harbor Emerging Markets Income Fund (closed-end fund) and Stone Harbor Emerging Markets Total Income Fund (closed-end fund). Director of RQSI GAA Systematic Global Macro Fund, Ltd.

Former Directorships: Trustee of The KP Funds to 2021.

27

| THE ADVISORS’ INNER CIRCLE FUND II | REAVES INFRASTRUCTURE FUND | |

| JULY 31, 2022 | ||

TRUSTEES AND OFFICERS OF THE ADVISORS’ INNER CIRCLE FUND II (UNAUDITED) | ||

| Name and Year of Birth | Position(s) with Trust and Length of Time Served | Principal Occupation(s) in the Past Five Years | ||

OFFICERS | ||||

Michael Beattie (Born: 1965) | President (since 2011)

| Director of Client Service, SEI Investments, since 2004. | ||

James Bernstein (Born: 1962) | Vice President and Assistant Secretary (since 2017) | Attorney, SEI Investments, since 2017.

Prior Positions: Self-employed consultant, 2017. Associate General Counsel & Vice President, Nationwide Funds Group and Nationwide Mutual Insurance Company, from 2002 to 2016. Assistant General Counsel & Vice President, Market Street Funds and Provident Mutual Insurance Company, from 1999 to 2002.

| ||

John Bourgeois (Born: 1973) | Assistant Treasurer (since 2017)

| Fund Accounting Manager, SEI Investments, since 2000. | ||

Russell Emery (Born: 1962) | Chief Compliance Officer (since 2006) | Chief Compliance Officer of SEI Structured Credit Fund, LP since 2007. Chief Compliance Officer of The Advisors’ Inner Circle Fund, Bishop Street Funds, Frost Family of Funds, Catholic Responsible Investments Funds, The Advisors’ Inner Circle Fund III, Gallery Trust, Schroder Series Trust, Schroder Global Series Trust, Delaware Wilshire Private Markets Master Fund, Delaware Wilshire Private Markets Fund, Delaware Wilshire Private Markets Tender Fund, SEI Institutional Managed Trust, SEI Asset Allocation Trust, SEI Institutional International Trust, SEI Institutional Investments Trust, SEI Daily Income Trust, SEI Tax Exempt Trust, Adviser Managed Trust, New Covenant Funds, SEI Insurance Products Trust and SEI Catholic Values Trust. Chief Compliance Officer of O’Connor EQUUS (closed-end investment company) to 2016. Chief Compliance Officer of SEI Liquid Asset Trust to 2016. Chief Compliance Officer of Winton Series Trust to 2017. Chief Compliance Officer of Winton Diversified Opportunities Fund (closed-end investment company) to 2018. Chief Compliance Officer of The KP Funds to 2021. | ||

28

| THE ADVISORS’ INNER CIRCLE FUND II | REAVES INFRASTRUCTURE FUND | |

| JULY 31, 2022 | ||

Other Directorships

Held in the Past Five Years

None.

None.

None.

None.

29

| THE ADVISORS’ INNER CIRCLE FUND II | REAVES INFRASTRUCTURE FUND | |

| JULY 31, 2022 | ||

TRUSTEES AND OFFICERS OF THE ADVISORS’ INNER CIRCLE FUND II (UNAUDITED) |

| Name and Year of Birth | Position(s) with Trust and Length of Time Served | Principal Occupation(s) in the Past Five Years | ||

OFFICERS (continued) | ||||

Eric C. Griffith (Born: 1969) | Vice President and Assistant Secretary (since 2019)

| Counsel at SEI Investments since 2019. Vice President and Assistant General Counsel, JPMorgan Chase & Co., from 2012 to 2018. | ||

Matthew M. Maher (Born: 1975) | Vice President (since 2018) Secretary (since 2020)

| Counsel at SEI Investments since 2018. Attorney, Blank Rome LLP, from 2015 to 2018. Assistant Counsel & Vice President, Bank of New York Mellon, from 2013 to 2014. Attorney, Dilworth Paxson LLP, from 2006 to 2013. | ||

Andrew Metzger (Born: 1980) | Treasurer, Controller and Chief Financial Officer (since 2021)

| Director of Fund Accounting, SEI Investments, since 2020. Senior Director, Embark, from 2019 to 2020. Senior Manager, PricewaterhouseCoopers LLP, from 2002 to 2019. | ||

Robert Morrow (Born: 1968) | Vice President (since 2017)

| Account Manager, SEI Investments, since 2007. | ||

Alexander F. Smith (Born: 1977) | Vice President and Assistant Secretary (since 2020)

| Counsel at SEI Investments since 2020. Associate Counsel & Manager, Vanguard, 2012 to 2020. Attorney, Stradley Ronon Stevens & Young, LLP, 2008 to 2012. | ||

Bridget E. Sudall (Born: 1980) | Anti-Money Laundering Compliance Officer and Privacy Officer (since 2015)

| Senior Associate and AML Officer, Morgan Stanley Alternative Investment Partners, from 2011 to 2015. Investor Services Team Lead, Morgan Stanley Alternative Investment Partners, from 2007 to 2011. | ||

30

| THE ADVISORS’ INNER CIRCLE FUND II | REAVES INFRASTRUCTURE FUND | |

| JULY 31, 2022 | ||

| Other Directorships |

| Held in the Past Five Years |

| None. |

| None. |

| None. |

| None. |

| None. |

| None. |

31

| THE ADVISORS’ INNER CIRCLE FUND II | REAVES INFRASTRUCTURE FUND | |

| JULY 31, 2022 | ||

All mutual funds have operating expenses. As a shareholder of a mutual fund, your investment is affected by these ongoing costs, which include (among others) costs for portfolio management, administrative services, and shareholder reports like this one. It is important for you to understand the impact of these costs on your investment returns.

Operating expenses such as these are deducted from a mutual fund’s gross income and directly reduce its final investment return. These expenses are expressed as a percentage of a mutual fund’s average net assets; this percentage is known as a mutual fund’s expense ratio.

The following examples use the expense ratio and are intended to help you understand the ongoing costs (in dollars) of investing in your Fund and to compare these costs with those of other mutual funds. The examples are based on an investment of $1,000 made at the beginning of the period shown and held for the entire period (February 1, 2022 to July 31, 2022).

The table on the following page illustrates your Fund’s costs in two ways.

| ● | Actual Fund Return. This section helps you to estimate the actual expenses after fee waivers that your Fund incurred over the period. The “Expenses Paid During Period” column shows the actual dollar value expense cost incurred by a $1,000 investment in the Fund, and the “Ending Account Value” number is derived from deducting that expense cost from the Fund’s gross investment return. |

You can use this information, together with the actual amount you invested in the Fund, to estimate the expenses you paid over that period. Simply divide your actual account value by $1,000 to arrive at a ratio (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply that ratio by the number shown for your Fund under “Expenses Paid During Period.”

| ● | Hypothetical 5% Return. This section helps you compare your Fund’s costs with those of other mutual funds. It assumes that the Fund had an annual 5% return before expenses during the year, but that the expense ratio (Column 3) for the period is unchanged. This example is useful in making comparisons because the Securities and Exchange Commission requires all mutual funds to make this 5% calculation. You can assess your Fund’s comparative cost by comparing the hypothetical result for your Fund in the “Expenses Paid During Period” column with those that appear in the same charts in the shareholder reports for other mutual funds. |

32

| THE ADVISORS’ INNER CIRCLE FUND II | REAVES INFRASTRUCTURE FUND | |

| JULY 31, 2022 | ||

DISCLOSURE OF FUND EXPENSES (UNAUDITED) |

Note: Because the hypothetical return is set at 5% for comparison purposes —NOT your Fund’s actual return — the account values shown may not apply to your specific investment.

Beginning Account Value 2/1/2022 | Ending Account Value 7/31/2022 | Annualized Expense Ratios | Expenses Paid During Period* | |||||||||||||

Actual Fund Return | ||||||||||||||||

Institutional Class Shares | $1,000.00 | $966.30 | 0.99% | $4.83 | ||||||||||||

Hypothetical Fund Return | ||||||||||||||||

Institutional Class Shares | $1,000.00 | $1,019.89 | 0.99% | $4.96 | ||||||||||||

| * | Expenses are equal to the Fund’s annualized expense ratio multiplied by the average account value over the period, multiplied by 181/365 (to reflect the one half year period). |

33

| THE ADVISORS’ INNER CIRCLE FUND II | REAVES INFRASTRUCTURE FUND | |

| JULY 31, 2022 | ||

Pursuant to Rule 22e-4 under the 1940 Act, the Fund’s investment adviser has adopted, and the Board has approved, a liquidity risk management program (the “Program”) to govern the Fund’s approach to managing liquidity risk. The Program is overseen by the Fund’s Liquidity Risk Management Program Administrator (the “Program Administrator”), and the Program’s principal objectives include assessing, managing and periodically reviewing the Fund’s liquidity risk, based on factors specific to the circumstances of the Fund.

At a meeting of the Board held on May 24, 2022, the Trustees received a report from the Program Administrator addressing the operations of the Program and assessing its adequacy and effectiveness of implementation for the period from January 1, 2021 through December 31, 2021. The Program Administrator’s report included an assessment of how market conditions caused by the COVID-19 pandemic impacted the Fund’s liquidity risk during the period covered by the report. The Program Administrator’s report noted that the Program Administrator had determined that the Program is reasonably designed to assess and manage the Fund’s liquidity risk and has operated adequately and effectively to manage the Fund’s liquidity risk during the period covered by the report. The Program Administrator’s report noted that during the period covered by the report, there were no liquidity events that impacted the Fund or its ability to timely meet redemptions without dilution to existing shareholders. The Program Administrator’s report further noted that no material changes have been made to the Program during the period covered by the report.

There can be no assurance that the Program will achieve its objectives in the future. Please refer to the prospectus for more information regarding the Fund’s exposure to liquidity risk and other principal risks to which an investment in the Fund may be subject.

34

| THE ADVISORS’ INNER CIRCLE FUND II | REAVES INFRASTRUCTURE FUND | |

| JULY 31, 2022 | ||

For shareholders who do not have a July 31, 2022 taxable year end, this notice is for informational purposes only. For shareholders with a July 31, 2022 taxable year end, please consult your tax adviser as to the pertinence of this notice. For the fiscal year ended July 31, 2022, the Fund is designating the following items with regard to distributions paid during the year.

| Return of Capital | Long-Term Capital Distributions | Ordinary Income Distributions | Total Distributions | Qualifying for Corporate Dividends Received Deduction (1) | Qualifying Dividend Income (2) | Qualifying Business Income (3) | Interest Related Dividend (4) | Short-Term Capital Gains Dividends (5) | ||||||||

| 0.00% | 95.11% | 4.89% | 100.00% | 100.00% | 100.00% | 0.00% | 0.00% | 0.00% |

| (1) | Qualifying dividends represent dividends which qualify for the corporate dividends received deduction and is reflected as a percentage of ordinary income distributions (the total of short-term capital gain and net investment income distributions). |

| (2) | The percentage in this column represents the amount of “Qualifying Dividend Income” as created by the Jobs and Growth Tax Relief Reconciliation Act of 2003 and is reflected as a percentage of ordinary income distributions (the total of short-term capital gain and net investment income distributions). It is the intention of the Fund to designate the maximum amount permitted by law. |

| (3) | The percentage of this column represents that amount of ordinary dividend income that qualified for 20% Business Income Deduction. |

| (4) | The percentage in this column represents the amount of “Interest Related Dividend” and is reflected as a percentage of ordinary income distribution. Interest related dividends are exempted from U.S. withholding tax when paid to foreign investors. |

| (5) | The percentage in this column represents the amount of “Short-Term Capital Gain Dividends” and is reflected as a percentage of short-term capital gain distributions that are exempted from U.S. withholding tax when paid to foreign investors. |

35

NOTES

NOTES

Reaves Infrastructure Fund

P.O. Box 219009

Kansas City, MO 64121-9009

1-866-342-7058

Investment Adviser:

Reaves Asset Management

10 Exchange Place

18th Floor

Jersey City, NJ 07302

Distributor:

SEI Investments Distribution Co.

One Freedom Valley Drive

Oaks, PA 19456

Administrator:

SEI Investments Global Funds Services

One Freedom Valley Drive

Oaks, PA 19456

Legal Counsel:

Morgan, Lewis & Bockius LLP

1701 Market Street

Philadelphia, PA 19103-2921

Independent Registered Public Accounting Firm:

Ernst & Young LLP

2005 Market Street, Suite 700

Philadelphia, PA 19103

This information must be preceded or accompanied by a current prospectus for the Portfolio described.

WHR-AR-001-1800

| Item 2. | Code of Ethics. |

The Registrant has adopted a code of ethics that applies to the Registrant’s principal executive officer, principal financial officer, controller or principal accounting officer, and any person who performs a similar function. There have been no amendments to or waivers granted to this code of ethics during the period covered by this report.

| Item 3. | Audit Committee Financial Expert. |

(a)(1) The Registrant’s board of trustees has determined that the Registrant has at least one audit committee financial expert serving on the audit committee.

(a)(2) The Registrant’s audit committee financial expert is Robert Mulhall. Mr Mulhall is considered to be “independent”, as that term is defined in Form N-CSR Item 3(a)(2).

| Item 4. | Principal Accountant Fees and Services. |

Fees billed by Ernst & Young LLP (“E&Y”) relate to The Advisors’ Inner Circle Fund II (the “Trust”).

E&Y billed the Trust aggregate fees for services rendered to the Trust for the last two fiscal years as follows:

| FYE July 31, 2022 | FYE July 31, 2021 | |||||||||||||

| All fees and services to the Trust that were pre-approved | All fees and services to service affiliates that were pre-approved | All other fees and services to service affiliates that did not require pre-approval | All fees and services to the Trust that were pre-approved | All fees and services to service affiliates that were pre-approved | All other fees and services to service affiliates that did not require pre-approval | |||||||||

| (a) | Audit Fees(1) | $24,030 | None | None | $23,330 | None | None | |||||||

| (b) | Audit-Related Fees | None | None | None | None | None | None | |||||||

| (c) | Tax Fees | None | None | None | None | None | None | |||||||

| (d) | All Other Fees | None | None | None | None | None | None | |||||||

Notes:

| (1) | Audit fees include amounts related to the audit of the Trust’s annual financial statements and services normally provided by the accountant in connection with statutory and regulatory filings. |

(e)(1) The Trust’s Audit Committee has adopted and the Board of Trustees has ratified an Audit and Non-Audit Services Pre-Approval Policy (the “Policy”), which sets forth the procedures and the conditions pursuant to which services proposed to be performed by the independent auditor of the Funds may be pre-approved.

The Policy provides that all requests or applications for proposed services to be provided by the independent auditor must be submitted to the Registrant’s Chief Financial Officer (“CFO”) and must include a detailed description of the services proposed to be rendered. The CFO will determine whether such services:

| 1. | require specific pre-approval; |

| 2. | are included within the list of services that have received the general pre-approval of the Audit Committee pursuant to the Policy; or |

| 3. | have been previously pre-approved in connection with the independent auditor’s annual engagement letter for the applicable year or otherwise. In any instance where services require pre-approval, the Audit Committee will consider whether such services are consistent with SEC’s rules and whether the provision of such services would impair the auditor’s independence. |