UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM 10-K

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2006

OR

o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

FOR THE TRANSITION PERIOD FROM _____________ TO _____________

Commission file number: 0-21202

Firstwave Technologies, Inc.

(Exact name of Registrant as Specified in its Charter)

Georgia | 58-1588291 |

(I.R.S. Employer | |

Incorporation or Organization) | Identification No.) |

5775 Glenridge Drive, Building E,

Suite 400, Atlanta, Georgia, 30328

(Address of Principal Executive Offices including Zip Code)

(770) 250-0360

(Registrant’s Telephone Number, Including Area Code)

Securities registered pursuant to Section 12(b) of the Act: None

Securities registered pursuant to Section 12(g) of the Act:

COMMON STOCK, $.0019 PAR VALUE

(Title of Class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer or a non-accelerated filer.

Large accelerated filer o Accelerated filer o Non-accelerated filer x

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No x

Aggregate market value of the Common Stock held by non-affiliates of the Registrant, based on the closing price as quoted on the NASDAQ Small Cap Market on June 30, 2006: $5,666,709

Number of shares of Common Stock outstanding as of March 20, 2007: 2,868,302

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Company’s definitive Proxy Statement for its 2007 Annual Meeting of Shareholders to be held are incorporated by reference into Part III of this Report.

FIRSTWAVE TECHNOLOGIES, INC.

ANNUAL REPORT ON FORM 10-K

FOR THE YEAR ENDED DECEMBER 31, 2006

TABLE OF CONTENTS

Part I | Page | |||

| 1 | ||||

| 5 | ||||

| 11 | ||||

| 11 | ||||

| 11 | ||||

Part II | ||||

| 12 | ||||

| 14 | ||||

| 14 | ||||

| 25 | ||||

| 25 | ||||

| 43 | ||||

| 44 | ||||

| 44 | ||||

Part III | ||||

| 45 | ||||

| 45 | ||||

| 45 | ||||

| 45 | ||||

| 45 | ||||

Part IV | ||||

| 46 | ||||

| 50 |

PART I

| ITEM 1. | BUSINESS |

Safe Harbor for Forward Looking Statements

Except for historical information contained herein, this section and other parts of this Form 10-K contain “forward-looking statements” within the meaning of various provisions of the Securities Act of 1933 and the Securities Exchange Act of 1934. Such forward-looking statements can generally be identified by words such as “will”, “expect”, “intends”, “believes”, “anticipates”, “should” and words of similar meaning. Firstwave Technologies, Inc. (“Firstwave” or “the Company”) notes that the forward-looking statements involve a number of risks and uncertainties that could cause actual results to differ materially from any such statement, such as potential fluctuations in quarterly results due to factors including delays in purchase decisions and other adverse market conditions, whether the Company will be able to continue diversification of its revenues, competition and technological developments, the Company’s capital requirements and other liquidity concerns, the Company’s ability to continue to comply with NASDAQ listing requirements, and the size, timing, and contractual terms of orders, and also the risks and uncertainties discussed under the caption “Risk Factors” in this Annual Report on Form 10-K. The information set forth herein is provided as of the date hereof.

General

Headquartered in Atlanta, Georgia, Firstwave is a provider of lead generation, lead nurturing and customer management and tracking solutions built upon a suite of Customer Relationship Management (CRM) products. Firstwave’s solutions help customers find new prospects, continuously engage these prospects throughout the sales cycle and maintain contact with customers throughout their lifecycle. Firstwave’s modular internet marketing, sales lead, and customer management solutions help customers achieve results. The Company was incorporated in October of 1984 in the State of Georgia, and has one subsidiary, Connect-Care, Inc., acquired in March of 2003, which is incorporated under the laws of the State of Georgia. Our product solutions include client-server based CRM products, web-based (on demand or behind the firewall) CRM products and a series of marketing products and services integrated with our CRM product suite.

Firstwave CRM Solutions

Firstwave CRM

Firstwave provides enterprise-wide CRM software solutions in both client/server and web-based architectures. This allows our customers tremendous flexibility in determining how they would like to purchase, implement and support their CRM system. By embracing a customer-focused business strategy, Firstwave’s CRM solutions help improve an organization’s efficiency enabling revenue growth, cost containment and customer retention.

Firstwave CRM handles the collaboration and interaction between workforce, customers and prospects. Through the use of Firstwave CRM, companies have the ability to increase revenue growth, customer retention and employee productivity.

Firstwave offers a variety of tools, applications and access options designed to enhance the customer experience across the entire enterprise. Firstwave client-server CRM consists of the following modules:

First-Sales™ – Manage sales cycle for increased revenue and efficiency

First-Market™ – Marketing campaign and content management

First-Support™ – Increase customer satisfaction, retention and loyalty

First-Survey™ – Keep a pulse on customer preferences through poll and survey management

First-Project™ – Streamline service delivery and project management

First-Quality™ – Close the customer feedback loop and quickly identify product issues

1

First-Web™ – Reduce customer support costs and improve communication through customized web portal

DataWave – Help maintain a quality database

Firstwave’s web-based (.NET architecture) CRM consists of the following modules:

Sales - Manage sales cycles for increased revenue and efficiency

Marketing – Marketing campaign tracking and management

Customer Support – Increase customer satisfaction, retention and loyalty

Quality – Close the customer feedback loop and quickly identify product issues

Customer Portal – Reduce customer support costs and improve communication through customer web portal

Firstwave Marketing services and products:

Email Marketing Service

Firstwave’s technology delivers a very high percentage of email to decision makers’ in-boxes. With Firstwave, it is not just about the list, or the delivery mechanism or the tracking, it is about results. Through technology, process and expertise, Firstwave is able to help our customers deliver the most effective message to the right buyer.

Features include:

| · | Real-time metric dashboard |

| · | Behavioral Tracking |

| · | Real-time lead quality scoring on each prospect |

| · | Automatic unsubscribe accumulation and management |

| · | Integration with Firstwave sales and marketing modules or third party tools |

Lead Nurturing email module

Our lead nurturing email module consists of the following components:

| · | Newsletters: Email-based publications, custom communications and promotional announcements |

| · | Surveys: Instant, online market research into customer satisfaction, member interests, or employee preference |

| · | Invitations: RSVP tracking and event management for trade shows, meetings, or other events |

Together, these modules make “coordinated contact” possible. Our customers can touch their target audiences multiple times, in multiple ways because Firstwave provides a vehicle for recurring, meaningful contact with prospects or customers.

Personalization solutions: These solutions allow marketers to send out personalized emails or post cards to prospects with a complete loop to a personal URL.

PURL (Personal URLs) – These dynamically derived web pages are personal to the prospect and provide a connection to the outbound direct mail post card or email that was received. As well, full tracking allows the customer to track interest for all outbound marketing campaigns including direct mail. Additionally, prospects’ interests are scored based on their behavior on the website.

Variable Data Printing – through a web-based interface, a marketing person can put together a fully integrated campaign targeted at specific prospects catering to their specific interests and printing post cards with personalized information, including the prospect’s name.

2

Firstwave Technology™

Firstwave Technology is an enterprise-wide CRM solution specifically designed for today’s fast-paced software and hardware companies. Maintaining our customer-first commitment, Firstwave Technology gives high technology companies the tools to improve operational efficiency, maximize revenue and legacy investments, and increase customer satisfaction, loyalty and retention.

Firstwave Technology handles the collaboration and interaction between a company’s workforce, customers and prospects.

Firstwave’s CRM product suite is built on Microsoft technologies and includes support for multiple databases, including Oracle and Microsoft SQL. The web-based CRM suite is built on .NET technologies allowing for strong web-based functionality. In addition to offering support for multiple database technologies, Firstwave offers a plug-in based architecture allowing for a flexible approach to changing business logic and new data sources.

TakeControl™

The TakeControl suite consists of CRM systems designed to optimize sales, marketing and customer service operations through delivering highly functional solutions.

TakeControl Sales creates a virtual sales environment through linking field and office personnel into a powerful sales team by automating account and opportunity management procedures. Management tools include a report writing facility, scheduling features, full account and contact details, and graphical analysis tools.

TakeControl Marketing pinpoints marketing opportunities to support and enhance differing marketing campaigns. Specializing on capturing the information required from prospects and customers, it delivers key facilities such as call scripting, mail merge, order taking, and activity scheduling to provide a compilation of simplified, yet precise, information.

TakeControl Customer Support establishes a support center that builds customer satisfaction and loyalty by providing support team members with instant access to customer information to quickly log and trouble-shoot problems while shortening response times. It also identifies the trends of calls received within the support center to enable future improvements based on customer feedback.

Leveraging Strategic Alliances

We market and support our CRM solutions through a combination of limited direct sales channels and the efforts of our strategic alliance partners, including M1 Global Solutions, Inc. (“M1 Global”). Our relationship with M1 Global is based on a three-year OEM/Outsourcing Agreement and a Licensing Agreement. M1 Global has licensed the Firstwave CRM database schema to develop its future products, and is a non-exclusive reseller of Firstwave products. During the first six months of 2006, M1 Global handled most of the professional services and paid a commission of 20% of services revenues to Firstwave. Commissions received from M1 Global for professional services for 2006 were $72,259. As we have increased our professional services staff since July of 2006, the amount of professional services provided by M1 Global to our customers, and the commissions received from M1 Global, have declined. In addition, during the first six months of 2006, M1 Global provided most of the maintenance services for our customers in exchange for a quarterly fee of $154,315 per quarter. Since July of 2006, we have hired additional personnel for customer support and the support services provided by M1 Global have also been reduced. The quarterly fees to M1 Global were approximately $90,000 in the third quarter and $78,000 in the fourth quarter of 2006. For 2007, there have been no fees paid or payable to M1Global through March 31, 2007.

On June 3, 2005, Firstwave entered into a Stock Purchase Agreement with AllAboutTickets LLC, now operating as First Sports International (“First Sports”). Under the terms of the Agreement, the Company sold all of the issued share capital of Firstwave Technologies U.K., Ltd., a subsidiary of the Company, to First Sports. The total purchase price was $2,214,000, of which $256,000 was paid at closing, $1,620,000 was agreed to be paid pursuant to a Promissory Note, and $338,000 was agreed to be paid as software revenues are achieved to reimburse the Company for certain prepaid royalties. As of December 31, 2006, the Company has received $445,000 in payments on the promissory note and $104,051 as payments against the prepaid royalties.

3

On July 1, 2005, we entered into a consulting arrangement with First Sports to provide service and maintenance to our existing U.K. CRM customers. These CRM customers remain customers of Firstwave, but First Sports provides the services to support these customers. If First Sports were not to provide the services, we would either provide the support services ourselves or would contract with another third party in the U.K. to provide such services. These customers are not associated with the sports customers acquired by First Sports as part of the sale of the U.K. Subsidiary on June 3, 2005, and they are part of the continuing operations of Firstwave described in this Form 10-K. Under the terms of this outsourcing arrangement, we pay First Sports a fee of 20% of the maintenance revenues upon collection, for providing local support. The agreement was renewed for one year under the same terms and conditions in July of 2006, except that Firstwave now pays First Sports a fee of 15% of the maintenance revenues upon collection.

Sources of Revenues, Pricing and Material Terms for Licensing Agreements

The first component of revenue is software license revenues. The Company’s technology solutions are generally licensed on a per-user model, except for hosting services. Customers generally pay a license fee for the software based upon the number of licensed users for the application as well as for the tool set. Hosting allows organizations to deploy the applications without the need for internal hardware infrastructure, system administrative capabilities or large capital outlays. All license fees are fixed and determinable, whether under the per-user model or hosting model. On sales made by M1 Global, Firstwave receives 33% of the license fees.

The second component of revenue is services revenues, including hosting revenues, which consist of professional consulting, technical services, email services, and training services. Consulting and technical services are charged on an hourly basis and may be billed in advance or weekly, pursuant to customer work orders. Email services are charged by volume of contacts that are sent emails, pursuant to customer order forms. Training services are charged on a per training session charge. For classes conducted at customer sites, we charge a per-day rate for a set number of attendees. Actual travel expenses are billed as incurred. Hosting services are priced as a monthly or yearly amount based upon the number of users and are recognized as services revenues ratably by month over the period of services. During the first six months of 2006, M1 Global handled most of the professional services for our customers and paid Firstwave a commission of 20% on professional services revenues received. Commissions received from M1 Global for 2006 were $72,259. As we have increased our professional services staff since July of 2006, the amount of professional services provided by M1 Global to our customers, and the commissions received from M1 Global, have declined.

The third component of revenue is maintenance revenues, which are derived from the provision of: (1) customer support in the form of customer services via communication channels, and (2) updates and enhancements of products and related documentation provided on a when and if available basis. Customers are provided maintenance and support for an annual fee. This fee is billed monthly, quarterly, or annually and is subject to changes in pricing upon 90 days’ written notice to the customer. During the first six months of 2006, M1 Global handled most of the maintenance services for our customers in exchange for a quarterly fee of $154,315 per quarter. Since July of 2006, we have hired additional personnel for customer support and the services provided by M1 Global have been reduced. The quarterly fees to M1 Global were approximately $90,000 in the third quarter and $78,000 in the fourth quarter of 2006. For 2007, there have been no fees paid or payable to M1Global through March 31, 2007.

Customers

Firstwave’s customers operate in many industries. We have an industry-focused solution developed specifically for companies in the technology industry, taking into consideration their unique needs, revenue sources and customer demands. During 2006, we continued to pursue strategies to transition our revenue stream to a more diverse customer base.

The table below identifies the customer who contributed more than 10% of total revenue in 2006, 2005, or 2004.

Year ended December 31, | ||||||||||

2006 | 2005 | 2004 | ||||||||

| Electronic Data Systems, Ltd | 4.3 | % | 6.2 | % | 11.8 | % | ||||

| Galactus Software | 18.8 | % | 0.0 | % | 0.0 | % | ||||

4

Competition

The competition in our high technology vertical comes from a multitude of software vendors, including existing CRM vendors, new web-based CRM vendors and ERP vendors who have penetrated the CRM industry through acquisitions or product development. Firstwave’s solutions help customers find new prospects, continuously engage these prospects throughout the sales cycle and maintain contact with customers throughout their lifecycle. Firstwave’s modular internet marketing, sales lead, and customer management solutions help customers achieve results.

Companies that offer competing products include Salesforce.com, Peoplesoft, Epiphany, Onyx, Microsoft, Seibel On Demand (now part of Oracle), Pivotal, SAP, and SalesLogix. These companies offer comprehensive packages, which include marketing, sales, and service. These companies also have integrated some Internet technology into their products and have customization capabilities within their product sets. In our new market spaces, we compete with Eloqua Corporation, Genius.com, Inc., iCentera Corporation, Market2Lead, Inc., and Vtrenz, Inc. There are also hundreds of vendors addressing the needs evident in this industry, including specialists who provide cross-industry solutions and vertically focused solutions, such as for pharmaceutical companies or financial institutions.

Our biggest competitive advantage is our demonstrated expertise in modular internet marketing, sales lead, and customer management solutions, our interactive web-based marketing capabilities, and high customer satisfaction, as well as providing a unique combination of list, delivery, and metrics capability. Although we frequently compete favorably with respect to these factors, there can be no assurance that we will be able to achieve the innovation, product development and market share necessary to maintain competitive advantage. Associated risks and uncertainties are discussed under the caption “Risk Factors” in this Annual Report on Form 10-K.

Proprietary Rights and Licenses

We depend upon a combination of trade secrets, copyright and trademark laws, license agreements, non-disclosure and other contractual provisions with customers and employees to protect our proprietary rights in our products. We also maintain confidentiality agreements with our employees. Because our solutions allow customers to customize their applications without altering the source code, the source code for our products is neither licensed nor provided to customers, although we have contractually agreed in certain instances to have our source code held in escrow by a third party. Notwithstanding these precautions, it may be possible for unauthorized persons to copy aspects of the products or to obtain information that we regard as proprietary. There can be no assurance that these protections will be adequate or that competitors will not independently develop technologies that are substantially equivalent or superior to our technology.

Employees

As of March 1, 2007, the Company employed 16 individuals, including 3 executive and administrative personnel, 2 sales and marketing personnel, 4 professional services personnel, 2 customer support personnel, and 5 persons involved in product innovation and development.

| ITEM 1A. | RISK FACTORS |

An investment in our common stock involves a significant degree of risk. Prospective investors should carefully consider the following factors that may affect our current and future operations and prospects. If any of the following risks actually occur, our business, financial condition or results of operations could be materially adversely affected, the trading price of our common stock could decline, and you may lose all or part of your investment.

Negative cash flow and the difficulty of raising additional capital may adversely affect our operations and the price of our common stock.

In the past, we have experienced negative cash flows and may experience negative cash flow in the future. Our ability to maintain and develop our revenue sources will directly impact our ability to raise capital needed to grow our business. We do not expect to incur any material capital costs in connection with the subleasing of new furnished office space in June of 2007.

5

In the past, we have funded our operating losses and working capital needs through existing cash balances and cash flows from operations and from the proceeds of equity offerings and debt financings. If we raise additional funds through the issuance of equity, equity-linked or debt securities, those securities may have rights, preferences or privileges senior to those of the rights of our common stock and, in light of our current market capitalization, our shareholders may experience substantial dilution.

We are reliant upon our new lead generation and web-based marketing solutions, expertise in the CRM software market, and future business strategy, the loss of which could affect our ability to successfully grow or maintain our business.

We depend upon not only our existing CRM products but also our lead generation and web-based products and our ability to successfully market, sell, service and support these products. The loss of key personnel or an inability to penetrate the web-based marketing industry would likely harm our operations significantly. Our revenues could suffer, and we may experience a material adverse impact on our business, operating results, and financial condition.

We are reliant upon First Sports’ expertise in the CRM software market and with our U.K. customers; the loss of which could affect our ability to successfully support our U.K. customers and retain the maintenance revenues associated therewith.

Outside of the discontinued operations associated with the sale of the U.K. Subsidiary to First Sports on June 3, 2005, we depend upon First Sports and its ability to successfully support and maintain our U.K. CRM customers. If First Sports were to no longer provide such local support, we would need to support these customers ourselves or contract with another third party to provide the support services, or our maintenance revenues from the U.K. CRM customers would suffer, and we may experience an adverse impact on our revenues, operating results, and financial condition.

We have in the past and may in the future experience significant fluctuations in our operating results and rate of growth, and the price of our common stock may be adversely affected by these fluctuations.

Our quarterly and annual operating results have in the past and may in the future vary or decrease significantly depending on factors such as:

| · | the effect of past and future acquisitions, |

| · | the dependence on the efforts of others, such as ListK and First Sports, |

| · | changes in operating expenses, |

| · | changes in our strategy, |

| · | key personnel departures, |

| · | the size and timing of significant orders, |

| · | the impact of estimates of our future operating results published by third parties, |

| · | the timing of revenue from software sales and professional services, |

| · | the timing of new product and service announcements, |

| · | changes in pricing policies by us and our competitors, |

| · | market acceptance of new and enhanced versions of our products, |

| · | the introduction of alternative technologies, and |

| · | general economic factors. |

We have limited or no control over many of these factors. Investors are cautioned that as a matter of policy we do not provide earnings projections or guidance to any financial analysts or other publishers of financial reports. If we change this policy, which we do not anticipate, we will make a public announcement regarding such change. Until such time, if it occurs, you should not rely upon any such information, reports, statements, estimates or projections of financial analysts, publishers of financial reports or others as having been provided or endorsed by us. We expressly do not adopt or endorse, and expressly disclaim, any and all such independent third party information, reports, statements, estimates and projections.

6

We believe that period-to-period comparisons of our results of operations are not necessarily meaningful and should not be relied upon as indications of future performance. Due to all these factors, it is likely that in some future quarter our operating results will be below the expectations of investors. In that event, the price of our common stock will likely be adversely affected.

Our stock price has been and may continue to be highly volatile, and our stock is thinly traded.

The trading price of our common stock fluctuates significantly for a variety of reasons, including the fact that on a typical day, less than 10,000 shares of stock are traded. Trading prices of our common stock may fluctuate in response to a number of events and factors such as:

| · | general economic conditions, |

| · | conditions or trends in the CRM industry, |

| · | fluctuations in the stock market in general, and |

| · | quarterly variations in operating results. |

Decreases or delays in our target customers’ information technology spending and other circumstances that result from poor economic conditions may harm our revenues; if general economic conditions do not improve or if they worsen, our revenues may be materially harmed.

Some of our customers and prospective customers have indicated that they have reduced their budgets available for spending on outsourced technology applications or have delayed purchase decisions for information technology products like ours due, in part, to difficult economic conditions. If the economy does not improve or if it worsens, our customers may continue to delay or reduce their spending on CRM software and customization. When economic conditions weaken, sales cycles for sales of software products tend to lengthen and companies’ information technology budgets tend to be reduced. Accordingly, our business has suffered and could continue to suffer. The impact of these reduced budgets and delays in purchase decisions is not possible to measure or quantify.

The market for our CRM software and services is subject to rapid change stemming from customer requirements and changes in related technologies, including hardware, operating systems and telecommunications; if we fail to improve our products in response to these changes, our sales may decline.

The market for our CRM software and services is subject to rapid change, including technological advances, changes in customer requirements and frequent new product introductions and enhancements. Our future success depends upon our ability to enhance our current products and continue to develop and market new products that address the increasingly sophisticated needs of customers and achieve market acceptance. In particular, we believe that we must continue to respond quickly to customer needs for additional functionality and to ongoing advances in hardware, operating systems and telecommunications. Any failure by us to anticipate or respond rapidly to technological advances, new products and enhancements and changes in customer requirements could have a material adverse effect on our competitive position or render some of our products obsolete or less desirable than available alternatives.

With any new product release, we are subject to the risks generally associated with new product introductions and applications, including lack of market acceptance, delays in development and implementation, and failure of products to perform as expected. In order to introduce and market new or enhanced products successfully with minimal disruption in customer purchasing patterns, we must manage the transition from existing products. There can be no assurance that we will be successful in developing and marketing, on a timely basis, product enhancements or products that respond to technological advances by others, that our new products will adequately address the changing needs of the market or that we will successfully manage product transitions. Further, failure to generate sufficient cash from operations or financing activities to develop or obtain improved products and technologies could have a material adverse effect on our results of operations and financial condition.

7

To grow our business, we may acquire additional companies, including by issuing shares of our stock, which may subject us to additional risks and may dilute your ownership.

To initiate our growth strategies, we acquired Connect-Care, Inc. in March 2003, and we may acquire other businesses. An inability to identify, acquire and integrate businesses, products or services that complement our business may negatively affect our ability to grow. We cannot guarantee that we will be able to identify and acquire suitable candidates on acceptable terms. We also cannot provide any assurance that we will be able to arrange adequate financing, complete additional transactions or successfully integrate the acquired businesses. As in the case of the Connect-Care merger, we may issue shares of stock in future acquisitions or in financing transactions, which would dilute the ownership percentages of our existing shareholders. Acquisitions and stock offerings may also distract management and result in the incurrence of debt, expenses and unforeseen liabilities, all of which could have a material adverse effect on our business and financial condition. In addition, we may not be able to successfully compete with other companies for acquisition candidates. In order for any acquisition to be successful, we would have to successfully and quickly integrate the new business with our business, including:

| · | cross-market and sell our services and products to the new business’ customers; |

| · | minimize duplicative managerial, sales and marketing efforts and eliminate redundant costs of our operations; and |

| · | make the new business’ personnel operate together with our personnel in a cost-effective manner. |

If we do not integrate our operations successfully, we may fail to achieve our business goals. This would likely cause a slow-down in our growth rate that may result in a decrease in the value of your investment.

Our software products, like most software products of a complex nature, may contain undetected errors; as a result, we could experience delays, additional expenses or lost revenues.

Software products as complex as those we offer may contain undetected errors. We could experience delays or lost revenues during the period required to correct those errors. There can be no assurance that, despite testing by us and by current and potential customers, errors will not be found in our software. If our products are found to contain errors, the result to us could be:

| · | a loss of or delay in market acceptance, |

| · | additional and unexpected expenses to fund further product development, |

| · | additional and unexpected expenses to add programming personnel to complete a development project, |

| · | loss of revenue because of the inability to sell the new product on a timely basis, and |

| · | loss of revenue due to adverse effect on our reputation, |

any one or more of which could have a material adverse effect on us.

Like most providers of complex software, our most valuable asset is an intangible, intellectual property; protection of our proprietary rights can be difficult, complex and expensive; if we are unable to protect our proprietary rights, then our competitive position could be weakened, which may reduce our revenues.

We derive a significant portion of our revenues from license, service and maintenance fees generated from our software. We do not have any patents on our software; rather we rely on a combination of trade secrets, copyright and trademark laws, non-disclosure and other contractual provisions and technical measures to protect our proprietary rights. We may be required to spend significant resources to monitor and police our proprietary rights. There can be no assurance that these protections will be adequate or that our competitors will not independently develop technologies that are substantially equivalent or superior to our technologies.

Other software providers could copy or otherwise obtain and use our products or technology without authorization. We may not be able to detect infringement and may lose a competitive position in the market before we do so. In addition, competitors may design around our technology or develop competing technologies. The laws of some foreign countries do not protect proprietary rights to the same extent as the laws of the United States. If we fail to successfully enforce our proprietary rights, our competitive position may be harmed.

8

Because it is not difficult to enter our industry, we expect increased competition from the introduction of superior products or by pricing pressure from competitors, all of which could harm our business.

The market for our products is characterized by significant price competition, and we expect that we will face increasing pricing pressures from our current competitors. In addition, some of our competitors may have significant advantages including the ability to adapt quickly to new technologies and changes in customer demands, and substantially greater resources and market presence. Moreover, because there are low barriers to entry into the software market, we believe that competition will increase in the future. Accordingly, there can be no assurance that we will be able to provide products that compare favorably with the products of our competitors or that competitive pressures will not require us to reduce our prices. Any material reduction in the price of our products would negatively affect gross margins as a percentage of new revenue and would require us to increase software unit sales in order to maintain net revenues.

The terms of our preferred stock include dividend payments, preferences over our common stock, and anti-dilution provisions that may have a material adverse effect on the market value of our common stock.

Our board of directors has the authority to issue up to 1,000,000 shares of preferred stock and to fix the rights, preferences, privileges and restrictions, including voting rights, of these shares without any further vote or action by our shareholders. At December 31, 2006, shares of outstanding preferred stock were as follows:

| · | 10,000 shares of Series A Convertible Preferred Stock |

| · | 7,020 shares of Series B Convertible Preferred Stock |

| · | 10,000 shares of Series C Convertible Preferred Stock |

| · | 6,700 shares of Series D Convertible Preferred Stock |

The rights of the holders of the common stock are subject to, and may be adversely affected by, the rights of the holders of Series A, Series B, Series C and Series D Convertible Preferred Stock and any other preferred stock that may be issued in the future. The issuance of the Series A, Series B, Series C and Series D Convertible Preferred Stock and any future issuances of other classes of preferred stock, while providing desirable flexibility in connection with possible acquisitions and other corporate purposes, could have the effect of making it more difficult for a third party to acquire a majority of our outstanding voting stock, thereby delaying, deferring or preventing a change in control of our company. Furthermore, the Series A, Series B, Series C and Series D Convertible Preferred Stock have other rights, including dividend rights and economic rights, senior to the common stock and, as a result, the existence of our preferred stock may have a material adverse effect on the market value of our common stock. Any future issuances of other classes of preferred stock may have other rights, including dividend rights and economic rights, senior to the common stock, and as a result, the issuance of new preferred stock could have a material adverse effect on the market value of our common stock. We may, in the future, adopt other measures that may have the effect of delaying, deferring or preventing a change in control of our company. Some of these measures may be adopted without any further vote or action by our shareholders. We have no present plans to adopt any of those types of measures.

We are reliant upon certain key personnel for expertise in the CRM software market and in the technical aspects of the CRM software product; the loss of such key personnel could affect our ability to successfully grow our business.

We depend in large part upon the continued service of our chief executive officer and key engineering and technical staff with expertise in our industry and products. The loss of the services of our executive officer and/or key personnel could harm our operations. Currently, none of our personnel are bound by an employment agreement, and we do not maintain key person insurance on any of our employees. We would also be harmed if one or more of our key employees decided to join a competitor or otherwise compete with us.

The market for CRM software has fluctuated over the past several years, and we are uncertain as to its future; if the market for CRM software does not grow, our revenues may be reduced.

9

The CRM software market is fluctuating, and our success depends on its growth. If the market for CRM software does not grow as quickly or become as large as anticipated, our revenues may be reduced. Our potential customers may:

| · | not understand or see the benefits of using these products, |

| · | not achieve favorable results using these products, |

| · | experience technical difficulty in implementing or using these products, or |

| · | use alternative methods to solve the same business problems. |

Our products can have long sales cycles which make it difficult to plan expenses and forecast results.

It takes between three and six months to complete the majority of our sales, and some sales take longer to complete. Therefore, it is difficult to predict the quarter in which a particular sale will occur and to plan expenditures accordingly. The length of the period between initial contact with a potential customer and their purchase of products and services is due to several factors, including:

| · | the complex nature of our products, |

| · | our need to educate potential customers about the uses and benefits of our products, |

| · | the purchase of our products may require a significant investment of resources by a customer, |

| · | customer budget cycles which affect the timing of purchases, |

| · | uncertainty regarding future economic conditions, |

| · | customer requirements for competitive evaluation and internal approval before purchasing our products, |

| · | customer delay of purchases due to announcements or planned introductions of new products by us or our competitors, and |

| · | large customer purchasing procedures, which may require a longer time to make decisions. |

The delay or failure to complete sales in a particular quarter could reduce our revenues in that quarter, as well as subsequent quarters over which revenues for the sale would likely be recognized. If our sales cycle unexpectedly lengthens in general or for one or more large orders, it would adversely affect the timing of our revenues.

Because our business involves the electronic transmission and storage of data, privacy and security concerns, particularly related to the use of our software on the internet, may limit the effectiveness of and reduce the demand for our products.

The effectiveness of our software products relies on the storage and use of customer data collected from various sources, including information collected on web sites, as well as other data derived from customer registrations, billings, purchase transactions and surveys. Our collection and use of that data for customer profiling may raise privacy and security concerns. Our customers generally have implemented security measures to protect customer data from disclosure or interception by third parties. However, these security measures may not be effective against all potential security threats. If a well-publicized breach of customer data security were to occur, our software products may be perceived as less desirable, impacting our future sales and profitability.

In addition, due to privacy concerns, some internet commentators, consumer advocates, and governmental or legislative bodies have suggested legislation to limit the use of customer profiling technologies. The European Union and some European countries have already adopted some restrictions on the use of customer profiling data. In addition, internet users can, if they choose, configure their web browsers to limit the collection of user data for customer profiling. Should many internet users choose to limit the use of customer profiling technologies, or if major countries or regions adopt legislation or other restrictions on the use of customer profiling data, our software would be less useful to customers, our sales could decrease and our results of operations could be materially adversely affected.

The requirements of Section 404 of the Sarbanes-Oxley Act of 2002 require that we undertake an evaluation of our internal controls that may identify internal control weaknesses.

The Sarbanes-Oxley Act of 2002 imposes new duties on us and our executives, directors, attorneys and independent registered public accounting firm. In order to comply with the Sarbanes-Oxley Act, we are evaluating our internal controls systems to allow management to report on, and our independent auditors to attest to, our internal controls. We have initiated establishing the procedures for performing the system and process evaluation and testing required in an effort to comply with the management certification and auditor attestation requirements of Section 404 of the Sarbanes-Oxley Act. As the Securities and Exchange Commission has extended the deadline for non-accelerated filers, such as Firstwave, until December 31, 2007, we anticipate being able to fully implement the requirements relating to reporting on internal controls and all other aspects of Section 404 in a timely fashion. If we are not able to implement the reporting requirements of Section 404 in a timely manner or with adequate compliance, our management and/or our auditors may not be able to render the required certification and/or attestation concerning the effectiveness of the internal controls over financial reporting, we may be subject to investigation and/or sanctions by regulatory authorities, such as the Securities and Exchange Commission or The NASDAQ Stock Market, and our reputation may be harmed. Any such action could adversely affect our financial results and the market price of our common stock.

10

| ITEM 2. | PROPERTIES |

As of December 31, 2006, the Company’s headquarters and principal operations were located in approximately 5,000 square feet of office space sublet from M1 Global in metropolitan Atlanta, Georgia. The sublease expires on June 30, 2007. The total amount of base rent ($10.00 per square foot) is being charged to rent expense. As of April 1, 2007, the Company will move its headquarters to 7000 Central Parkway, Suite 330, Atlanta, GA 30328, in approximately 4,200 square feet of furnished subleased office space at a rate of $16.50 per square foot. The term of the new subleased office space expires in June of 2009.

| ITEM 3. | LEGAL PROCEEDINGS |

From time to time, the Company may be involved in litigation relating to claims arising out of its operations in the normal course of business. As of the date of this Report, the Company was not engaged in any legal proceedings that are expected, individually or in the aggregate, to have a material adverse effect on the Company.

| ITEM 4. | SUBMISSION OF MATTERS TO A VOTE OF SECURITY HOLDERS |

None

11

PART II

| ITEM 5. | MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS, AND ISSUER PURCHASES OF EQUITY SECURITIES |

Our common stock is traded on the NASDAQ SmallCap Market under the symbol “FSTW”. The following table sets forth, for the calendar quarters indicated, the high and low close prices of the Company’s common stock. Note that prices set forth below reflect inter-dealer prices without retail mark-ups, markdowns, or commissions and may not necessarily reflect actual transactions.

Period | High | Low | |||||

| Fiscal 2006: | |||||||

| First Quarter | $ | 2.18 | $ | 1.65 | |||

| Second Quarter | $ | 2.15 | $ | 1.66 | |||

| Third Quarter | $ | 2.29 | $ | 2.00 | |||

| Fourth Quarter | $ | 2.47 | $ | 2.08 | |||

| Fiscal 2005: | |||||||

| First Quarter | $ | 2.57 | $ | 1.55 | |||

| Second Quarter | $ | 3.07 | $ | 1.62 | |||

| Third Quarter | $ | 1.99 | $ | 1.57 | |||

| Fourth Quarter | $ | 2.45 | $ | 1.23 | |||

As of March 20, 2007, there were approximately 75 shareholders of record and approximately 1700 persons or entities that hold common stock in nominee name. There were no common stock dividends declared during 2006 or 2005. The Company does not plan to pay dividends on its common stock in the future. Pursuant to a merger agreement, on March 3, 2003. Firstwave issued 200,000 shares of common stock to the shareholders of Connect-Care, Inc. in exchange for all outstanding shares of Connect-Care stock. These 200,000 shares, valued at $2,630,000, were registered effective July 25, 2003. On August 12, 2004, the Company filed a Post-Effective Amendment No 1 to Registration Statement on Form S-3, File No. 333-103903, to remove from registration 198,925 shares originally registered related to the Connect-Care acquisition that remained unsold by the former Connect-Care shareholders at the termination of the offering.

12

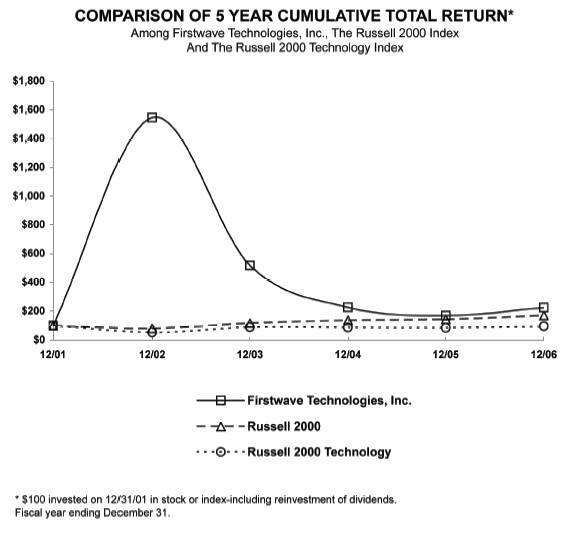

STOCK PERFORMANCE GRAPH

The following indexed line graph indicates the Company’s total return to shareholders from December 31, 2001 to December 31, 2006, as compared to total return for the Russell 2000 and Russell 2000-Technology indices for the same period. The Russell 2000 index is comprised of the 2,000 publicly traded companies with market capitalizations (in terms of number of shares outstanding) ranked immediately below the 1,000 companies with the highest market capitalizations. The Russell 2000-Technology index is comprised of the 2,000 publicly traded companies in the high-technology industry with market capitalizations (in terms of number of shares outstanding) ranked immediately below the 1,000 companies in the high-technology industry with the highest market capitalizations.

13

| ITEM 6. | SELECTED FINANCIAL DATA |

For the Year Ended December 31, | ||||||||||||||||

(in thousands, except per share amounts) | ||||||||||||||||

2006 | 2005** | 2004*** | 2003**** | 2002 | ||||||||||||

| Net revenues from continuing operations | $ | 2,694 | $ | 3,224 | $ | 4,526 | $ | 11,169 | $ | 13,200 | ||||||

| Income/(loss) from continuing operations | ||||||||||||||||

| before income tax | 172 | (1,578 | ) | (5,048 | ) | (1,212 | ) | 2,679 | ||||||||

| Income tax | — | — | — | — | — | |||||||||||

| Net income/(loss) from continuing operations | 172 | (1,578 | ) | (5,048 | ) | (1,212 | ) | 2,679 | ||||||||

| Income/(loss) from discontinued operations | — | (457 | ) | 410 | 437 | 346 | ||||||||||

| Gain/(loss) on sale of discontinued operations | — | 327 | — | — | — | |||||||||||

| Net income/(loss) applicable to common | ||||||||||||||||

| shareholders | (111 | ) | (1,992 | ) | (4,893 | ) | (996 | ) | 2,773 | |||||||

| Basic & diluted earnings per share | ||||||||||||||||

| Earnings/(loss) from continuing operations | (0.04 | ) | (0.69 | ) | (1.98 | ) | (0.56 | ) | 1.13 | |||||||

| Earnings/(loss) from discontinued operations | — | (0.05 | ) | 0.15 | 0.17 | 0.16 | ||||||||||

| Net income/(loss) per common share | (0.04 | ) | (0.74 | ) | (1.82 | ) | (0.39 | ) | 1.29 | |||||||

| Total assets | 3,824 | 4,259 | 6,273 | 11,807 | 9,803 | |||||||||||

| Basic and diluted weighted average shares | ||||||||||||||||

| outstanding* | 2,792 | 2,709 | 2,682 | 2,572 | 2,150 | |||||||||||

| * | Stock options and convertible preferred stock are not included in the diluted earnings per share if they are antidilutive. |

| ** | 2005 includes a charge for Goodwill Impairment of $528,000, the gain on sale of discontinued operations was reduced by an allocation of Goodwill totaling $488,000. |

| *** | 2004 includes the one-time write-off of certain amounts of capitalized software and a charge for Goodwill Impairment of $750,000. |

| **** | 2003 includes the acquisition of Connect-Care in March of 2003. |

| ITEM 7. | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

The following discussion should be read in conjunction with the Financial Statements and Notes thereto presented elsewhere herein. This section contains forward-looking statements that reflect the Company’s management’s expectations, estimates, and projections for future periods. These statements may be identified by the use of forward-looking words such as “may”, “will”, “believe”, “anticipate”, “estimate”, “expect”, “projects”, or “intends”. Actual events and results may differ from the results anticipated by the forward-looking statements. Factors that might cause such differences include, but are not limited to, those items discussed previously under the caption “Risk Factors” and the discussion below in “Management’s Discussion and Analysis of Financial Condition and Results of Operations”.

Overview

Headquartered in Atlanta, Georgia, Firstwave is a provider of lead generation, lead nurturing and customer management and tracking solutions built upon a suite of Customer Relationship Management (CRM) products. Firstwave’s solutions help customers find new prospects, continuously engage these prospects throughout the sales cycle and maintain contact with customers throughout their lifecycle. Firstwave’s modular internet marketing, sales lead, and customer management solutions help customers achieve results.

On October 10, 2005, the Company entered into a three-year OEM/Outsourcing Agreement and a Licensing Agreement with M1 Global, an Atlanta-based technology company. Under the terms of the agreements, M1 Global has licensed the Firstwave CRM database schema to develop its future products, and is a non-exclusive reseller of Firstwave products. Although the agreements included the outsourcing of Firstwave’s Professional Services and Support functions to M1 Global, Firstwave is currently providing its own coverage in those areas and no longer pays M1 Global for these services. The agreements provide that M1 Global also pays royalty commissions to Firstwave as follows: 33% on licenses and 20% on services. During the first six months of 2006, M1 Global handled most of the professional services and paid a commission of 20% of services revenues to Firstwave. Commissions received from M1 Global for professional services for 2006 were $72,259. As we have increased our professional services staff since July of 2006, the amount of professional services provided by M1 Global to our customers, and the commissions received from M1 Global, have declined. In addition, during the first six months of 2006, M1 Global provided most of the maintenance services for our customers in exchange for a quarterly fee of $154,315 per quarter. Since July of 2006, we have hired additional personnel for customer support and the support services provided by M1 Global have also been reduced. The quarterly fees to M1 Global were approximately $90,000 in the third quarter and $78,000 in the fourth quarter of 2006. For 2007, there have been no fees paid or payable to M1Global through March 31, 2007.

14

On May 5, 2006, the Company entered into an Intellectual Property Assignment Agreement with Galactus Software LLP (“Galactus”), a Florida-based software application company. Under the terms of the agreement, Galactus assumes ownership of the .Net Integrated Development Environment (IDE) that Firstwave developed to use in writing applications in the CRM Market. Firstwave retains exclusive use of the technology in the CRM Market, and Galactus will use the technology in the software application marketplace. The purchase price for the assignment was Five Hundred Thousand Dollars ($500,000.00) and, as directed by the agreement, paid by cashier’s check on the Assignment Effective Date, May 2, 2006, when Galactus gave notice to Firstwave that it had accepted the software.

Results of Continuing Operations

On June 3, 2005, Firstwave entered into a Stock Purchase Agreement (the “Agreement”) with AllAboutTickets LLC, now doing business as First Sports International (“First Sports”). Pursuant to the Agreement, the Company sold to First Sports all of the issued share capital of Firstwave Technologies U.K., Ltd., a subsidiary of the Company. The Company sold its U.K. Subsidiary to re-focus on the high technology market and to direct its efforts away from the Sports business that was concentrated in the U.K. market. This Management’s Discussion and Analysis of Financial Condition compares the Company’s results from continuing operations, not including the operations from the discontinued business.

15

The following table sets forth for the periods indicated selected financial data and the percentages of our net revenues represented by each line item presented. It also sets forth the percentage change in each line item presented from 2005 to 2006. Certain percentage columns do not add to 100% due to rounding.

Year Ended | Year Ended | % Change | ||||||||||||||

December 31, 2006 | December 31, 2005 | 2005 to 2006 | ||||||||||||||

| Revenues: | ||||||||||||||||

| Software | $ | 743 | 27.6 | % | $ | 551 | 17.1 | % | 34.8 | |||||||

| Services | 291 | 10.8 | 623 | 19.3 | (53.3 | ) | ||||||||||

| Maintenance | 1,651 | 61.3 | 2,002 | 62.1 | (17.5 | ) | ||||||||||

| Other | 9 | 0.3 | 48 | 1.5 | (81.2 | ) | ||||||||||

| Net revenues | 2,694 | 100.0 | 3,224 | 100.0 | (16.4 | ) | ||||||||||

| Costs and expenses: | ||||||||||||||||

| Cost of revenues | ||||||||||||||||

| Software | 411 | 15.3 | 803 | 24.9 | (48.8 | ) | ||||||||||

| Services | 159 | 5.9 | 578 | 17.9 | (72.5 | ) | ||||||||||

| Maintenance | 563 | 20.9 | 422 | 13.1 | 33.4 | |||||||||||

| Other | 14 | 0.5 | 32 | 1.0 | (56.3 | ) | ||||||||||

| Sales and marketing | 339 | 12.6 | 506 | 15.7 | (33.0 | ) | ||||||||||

| Product development | 317 | 11.8 | 631 | 19.6 | (49.8 | ) | ||||||||||

| General and administrative | 768 | 28.5 | 1,410 | 43.7 | (45.5 | ) | ||||||||||

| Goodwill impairment | — | — | 528 | 16.4 | (100.0 | ) | ||||||||||

| Total operating cost and expenses | 2,571 | 95.4 | 4,910 | 152.3 | (47.6 | ) | ||||||||||

| Operating income/(loss) | 123 | 4.6 | (1,686 | ) | (52.3 | ) | (107.3 | ) | ||||||||

| Gain/(loss) on investment | (57 | ) | (2.1 | ) | ||||||||||||

| Interest income, net | 106 | 3.9 | 108 | 3.3 | (1.9 | ) | ||||||||||

| Income/(loss) from continuing operations | $ | 172 | 6.4 | $ | (1,578 | ) | (48.9 | ) | (110.9 | ) | ||||||

| Loss from discontinued operations | — | — | (457 | ) | (14.2 | ) | (100.0 | ) | ||||||||

| Gain on sale of discontinued operations | — | — | 327 | 10.1 | ||||||||||||

| Net loss from discontinued operations | — | — | (130 | ) | (4.0 | ) | (100.0 | ) | ||||||||

| Net income/(loss) before/after income taxes | $ | 172 | 6.4 | $ | (1,708 | ) | (53.0 | ) | (110.1 | ) | ||||||

In general, competition in the software industry has increasingly been characterized by shortening product cycles, and we are not immune to this trend. If the product cycle for our systems proves to be shorter than management anticipates, our pricing structure and revenues could be impaired. In addition, in order to remain competitive, we may be required to expend a greater percentage of our revenues on product innovation and development than has historically been the case. In either case, our gross profit margins and results of operations could be materially adversely affected. See “Risk Factors” in Part I, Item 1A of this Annual Report.

2006 COMPARED TO 2005

The information presented below compares the Company’s results from continuing operations, after consideration of discontinued operations from the sale of the U.K. Subsidiary on June 3, 2005.

Revenue

Total revenues, which include software license fees, services, and maintenance revenues, decreased 16.4% from $3,224,000 in 2005 to $2,694,000 in 2006 due to decreases in services and maintenance revenues, offset by an increase in software license revenues. Software revenues increased 34.8% from $551,000 in 2005 to $743,000 in 2006, primarily due to the assignment of the Company’s .Net Integrated Development Environment to Galactus Software in the second quarter of fiscal 2006. Our software revenues are significantly dependent upon the timing of closing of license agreements. Total revenues from international sources decreased from 24% of total revenues in 2005 to 16% in 2006 primarily due to decreased maintenance revenue from our U.K. CRM customers.

16

Services revenues decreased 53.3% from $623,000 in 2005 to $291,000 in 2006. Our services revenues are subject to fluctuations based on variations in the length of and number of active service engagements in a given quarter. Professional services revenues from the M1 Global relationship were lower than anticipated in 2006. We have, therefore, increased our professional services staff in an effort to expand those services ourselves.

Maintenance revenues decreased 17.5% from $2,002,000 in 2005 to $1,651,000 in 2006. The decrease is due to cancellations of $240,000 from existing customers and reductions of $105,000 in maintenance for existing customers, offset by additional maintenance revenues of $9,000 associated with new and existing customers. Maintenance revenues are primarily the result of renewal agreements from previous software license agreements as well as new license agreements.

Cost of Revenue

Cost of software revenues decreased 48.8% from $803,000 in 2005 to $411,000 in 2006. Cost of software revenues includes amortization of capitalized software costs, costs of third party software, media costs, and documentation materials. The decrease is due to a decrease in amortization expense related to the assignment of the .Net Integrated Development Environment technology to Galactus and final amortization of the remaining capitalized software. Cost of software revenues as a percentage of software revenues decreased from 145.7% in 2005 to 55.3% in 2006, primarily due to a decrease in amortization expense.

Cost of revenues for services decreased 72.5% from $578,000 in 2005 to $159,000 in 2006. The decrease is primarily due to decreases in payroll, resulting from a reduction in the number of services personnel, and payroll related costs, including travel expenses, consistent with decreased services revenues. As we reduced the services outsourced to M1 Global after July of 2006 and increased our personnel providing these services, costs of revenues for services increased. The cost of revenues for services as a percentage of services revenues decreased from 92.8% in 2005 to 54.6% in 2006, due to reduction in personnel and personnel-related expenses.

Cost of revenues for maintenance increased 33.4% from $422,000 in 2005 to $563,000 in 2006. The increase is primarily due to the outsourcing arrangement with M1 Global as to which we paid $476,925 in 2006 and the fees paid to First Sports of $68,908 for the support of our U.K. CRM customers. The reduction of the maintenance and support services outsourced to M1 Global after July of 2006 reduced our quarterly fees to M1 Global and increased our personnel related expenses. Costs of revenues for maintenance as a percentage of maintenance revenues increased from 21.1% in 2005 to 34.1% in 2006, primarily due to the outsourcing of personnel to M1 Global.

Sales and Marketing Expense

Sales and marketing expense decreased 33.0% from $506,000 in 2005 to $339,000 in 2006, and decreased as a percentage of total revenues from 15.7% in 2005 to 12.6% in 2006. The decreases are the result of lower payroll expenses associated with a reduction in the number of personnel and lower marketing expenses. However, we added a Chief Sales and Marketing Officer in August of 2006 and other sales personnel to focus on lead generation and to begin our new marketing efforts.

Product Development Expense

The Company’s product innovation and development expenditures decreased 49.8% from $631,000 in 2005 to $317,000 in 2006. The decrease is primarily related to decreases in payroll costs associated with staff reductions, and reductions associated with fewer outside contractors. There were no software development costs capitalized during either 2005 or 2006. We have added to our personnel in product development in late 2006.

General and Administrative Expense

General and administrative expenses decreased 45.5% from $1,410,000 in 2005 to $768,000 in 2006. These changes were primarily due to $791,000 in reduced payroll costs associated with a reduction in personnel and $183,806 of decreased rent expense. Management anticipates that general and administrative expenses will not increase materially with the new facilities in April 2007.

17

Goodwill Impairment

In accordance with SFAS No. 142 “Goodwill and Other Intangible Assets”, intangible assets with indefinite useful lives must be tested periodically for impairment. Examples of Management’s judgment regarding the existence of impairment of an intangible asset and the resulting fair value, would include management’s estimates of future net cash flows and assessment of adverse changes in legal factors, market conditions, or loss of key personnel. If the fair value of the intangible asset is determined to be less than the carrying value, the Company would record an impairment loss. SFAS No. 142 prescribes a two-phase approach for impairment testing of goodwill. The first phase screens for impairment; while the second phase (if necessary) measures the amount of the impairment.

Goodwill was evaluated for impairment quarterly throughout 2006 and 2005 in accordance with SFAS No. 142. The fair value was estimated using the expected net present value of future cash flows. The analysis for the third quarter of 2005 identified lower-than-expected operating results, and the Company revised the anticipated future earnings projections. As a result of these reviews, it was determined that there was an impairment of goodwill, and the second phase was required. The second phase resulted in the Company recording a non-cash impairment charge of $528,000 during the third quarter of 2005 to write-off a portion of the carrying value of goodwill. Additionally, as a result of the sale of the U.K. Subsidiary, goodwill was written down by $488,000 in June of 2005 to account for the allocation of goodwill to the U.K. Subsidiary. Based on the quarterly analyses conducted in 2006, it was determined that there was no further instance of impairment of the remaining recorded goodwill. Therefore, the second phase of the testing was not required.

Net Interest Income

Interest income decreased 1.9% from $108,000 in 2005 to $106,000 in 2006 primarily from imputed interest recognized on the note receivable from First Sports, explained in “Discontinued Operations.” In 2006 and 2005, there was no interest expense, as the Company carried no debt during those years.

Income Tax Expense

There was no income tax expense in either 2006 or 2005. As of December 31, 2006, the Company had a net operating loss carryforward in the United States of approximately $25,600,000, which expires in years 2009 through 2019. A valuation allowance has been established for all deferred tax assets as of December 31, 2006 and 2005, respectively.

2005 COMPARED TO 2004

The information presented below compares the Company’s results from continuing operations, after consideration of discontinued operations from the sale of the U.K. Subsidiary on June 3, 2005.

Revenue

Total revenues, which include software license fees, services, and maintenance revenues, decreased 29% from $4,526,000 in 2004 to $3,224,000 in 2005 due to decreases in software license, services and maintenance revenues. The decrease in total revenues was primarily attributable to lower revenues from our relationship with Electronic Data Systems, Ltd. (“EDS”), which contributed 12%, or $874,000, of total revenues during 2004, compared to 6%, or $222,000, of total revenues for 2005.

Software revenues decreased 37% from $876,000 in 2004 to $551,000 in 2005. During 2004, we recognized three large software license agreements with Manhattan Associates, Inc., SmartMail, LLC, and Northrop Grumman; while in 2005 we recognized just one large software license with M1 Global Solutions.

Total revenues from international sources decreased from 33% of total revenues in 2004 to 24% in 2005 primarily due to decreased services revenue from our U.K. CRM customers, including revenue from the EDS relationship that decreased from $874,000 in 2004 to $222,000 in 2005.

Services revenues decreased 46% from $1,145,000 in 2004 to $623,000 in 2005, primarily due to decreased services revenue from EDS. The service revenues from EDS were $358,000 in 2004 compared to only $11,000 in 2005. Our services revenues decreased from 2004 levels because the services revenues we derived from the multi-year contract with EDS have not been replaced with other customer accounts.

18

Maintenance revenues decreased 19% from $2,457,000 in 2004 to $2,002,000 in 2005. The decrease was due to cancellations from existing customers offset by additional maintenance revenues associated with new and expansion customers.

Cost of Revenue

Cost of software revenues decreased 61% from $2,032,000 in 2004 to $803,000 in 2005. The decrease was primarily due to a decrease in amortization expense related to the write-off of two product lines in the fourth quarter of 2004, resulting in lower amortization expense in 2005. Cost of software revenues as a percentage of software revenues decreased from 232% in 2004 to 146% in 2005, primarily due to a decrease in amortization expense. Amortization of capitalized software represented 97% of total cost of software revenues during 2004, compared to 91% in 2005.

Cost of revenues for services decreased 52% from $1,193,000 in 2004 to $578,000 in 2005. The decrease was primarily due to decreases in payroll, resulting from a reduction in the number of services personnel, and payroll related costs, including travel expenses, consistent with decreased services revenues. The cost of revenues for services as a percentage of services revenues decreased from 104% in 2004 to 93% in 2005.

Cost of revenues for maintenance increased 4% from $405,000 in 2004 to $422,000 in 2005. The increase was primarily due to the launch of our outsourcing arrangement with M1 Global Solutions, Inc. and the fees paid to First Sports for the support of our U.K. CRM customers. Costs of revenues for maintenance as a percentage of maintenance revenues increased from 16% in 2004 to 21% in 2005.

Sales and Marketing Expense

Sales and marketing expense decreased 73% from $1,903,000 in 2004 to $506,000 in 2005, and decreased as a percentage of total revenues from 42% in 2004 to 16% in 2005. The decreases were the result of decreases in payroll expenses associated with a reduction in the number of personnel, telemarketing costs, and costs relating to sports sponsorships in the U.S.

Product Development Expense

The Company’s product innovation and development expenditures, which includes amounts capitalized, decreased 47% from $1,188,000 in 2004 to $631,000 in 2005. The decrease was primarily related to decreases in payroll costs associated with staff reductions, and reductions associated with fewer outside contractors. Software development costs capitalized during 2004 were $94,000; there were no software development costs capitalized during 2005.

A net realizable analysis of capitalized software development costs was performed as of December 31, 2005 in accordance with SFAS 86 “Accounting for the Costs of Computer Software to be Sold, Leased, or Otherwise Marketed.” Based on the results of the analysis, a determination was made that the carrying amount of the unamortized capitalized software costs does not exceed their net realizable value; therefore, no impairment loss was recorded.

General and Administrative Expense

General and administrative expenses decreased 32% from $2,082,000 in 2004 to $1,410,000 in 2005. These changes were primarily due to reduced payroll costs associated with a reduction in personnel and decreased rent expense.

Goodwill Impairment

In accordance with SFAS No. 142 “Goodwill and Other Intangible Assets”, intangible assets with indefinite useful lives must be tested periodically for impairment. Examples of Management’s judgment regarding the existence of impairment of an intangible asset and the resulting fair value, would include management’s estimates of future net cash flows and assessment of adverse changes in legal factors, market conditions, or loss of key personnel. If the fair value of the intangible asset is determined to be less than the carrying value, the Company would record an impairment loss. SFAS No. 142 prescribes a two-phase approach for impairment testing of goodwill. The first phase screens for impairment; while the second phase (if necessary) measures the impairment.

19

Goodwill was evaluated for impairment quarterly throughout 2005 and 2004 in accordance with SFAS No. 142. The fair value was estimated using the expected net present value of future cash flows. The analysis for the third quarter of 2005 and the fourth quarter of 2004, identified lower than previously expected operating results, and the Company revised the anticipated future earnings projections at the end of each of those quarters. As a result of these reviews, it was determined that there was an impairment of goodwill, and the second phase was required. The second phase resulted in the Company recording non-cash impairment charges of $528,000 at September 30, 2005, and $750,000 at December 31, 2004, to write-off a portion of the carrying value of goodwill. Additionally, as a result of the sale of the U.K. Subsidiary, goodwill was written down by $488,000 in the second quarter of 2005 to account for the allocation of goodwill to the U.K. Subsidiary. From the analysis conducted at December 31, 2005, it was determined that there was no further instance of impairment of the remaining recorded goodwill. Therefore, the second phase of the testing was not required.

Net Interest Income

Interest income increased 151% from $43,000 in 2004 to $108,000 in 2005 primarily from imputed interest recognized on the note receivable from First Sports, explained in “Discontinued Operations.” Interest expense of $26,000 in 2004 was related to the Company’s line of credit with RBC Centura that was paid off December 30, 2004. In 2005, there was no interest expense, as the Company carried no debt during the year. The above factors resulted in a net increase in net interest income of 535.0% from $17,000 in 2004 to $108,000 in 2005.

Income Tax Expense

There was no income tax expense in either 2005 or 2004. As of December 31, 2005, the Company had a net operating loss carryforward in the United States of approximately $25,600,000, which expires in years 2009 through 2019. A valuation allowance has been established for all deferred tax assets as of December 31, 2005 and 2004, respectively.

BALANCE SHEET

Net accounts receivable decreased 37.8% from $399,000 at December 31, 2005 to $248,000 at December 31, 2006 consistent with lower total revenues. The allowance for doubtful accounts decreased 53.5% from $43,000 at December 31, 2005 to $20,000 at December 31, 2006 consistent with the decrease in accounts receivable. As a result of the sale of the U.K. Subsidiary explained below in “Discontinued Operations,” a note receivable in the amount of $1,620,000 was received. At December 31, 2006, the portion of the note receivable due within twelve months is $500,000 and is classified as a current asset on the Balance Sheet. Other assets decreased 10.5% from $475,000 at December 31, 2005 to $425,000 at December 31, 2006, primarily due to reimbursement of prepaid royalty expenses by First Sports International. Property and equipment decreased 32.9% from $82,000 at December 31, 2005 to $55,000 at December 31, 2006 due to fixed asset purchases of $20,000 offset by year-to-date depreciation and disposals totaling $47,000.

Goodwill remained at $593,000 at December 31, 2005 and December 31, 2006. Other intangible assets decreased 26.9% from $572,000 at December 31, 2005 to $418,000 at December 31, 2006, as a result of amortization expense of $154,000. There was no capitalized software at December 31, 2006, as compared to $363,000 at December 31, 2005, as a result of amortization expense of $363,000.

As a result of the sale of the U.K. Subsidiary, a note receivable in the amount of $1,620,000 was received in June of 2005. The initial long-term portion of the note was $1,250,000, payable in installments, and is classified as a non-current asset on the Balance Sheet. In accordance with APB 21 “Interest on Receivables and Payables,” imputed interest, which was calculated at 8%, resulted in an unamortized discount at May 31, 2005 totaling $233,000 and recorded as a direct reduction from the face amount of the note. Through December of 2006, $137,000 was amortized, resulting in a balance of $96,000 in imputed interest and a net non-current note receivable of $580,000 as of December 31, 2006.

20

Accounts payable decreased 54.3% from $302,000 at December 31, 2005 to $138,000 at December 31, 2006 due to certain expense reductions and the timing of payment of certain payables. Deferred revenue decreased 37.1% from $1,117,000 at December 31, 2005 to $703,000 at December 31, 2006 primarily due to customer cancellations and customer prepayments prior to 2006 recognized as revenue in 2006 Accrued employee compensation and benefits decreased 40.4% from $99,000 at December 31, 2005 to $59,000 at December 31, 2006 due to reduced vacation expense and employee incentives, consistent with reduced revenues and staff reductions. Other accrued liabilities decreased 6.3% from $32,000 at December 31, 2005 to $30,000 at December 31, 2006 primarily due to reduced sales tax.

LIQUIDITY AND CAPITAL RESOURCES