| UNITED STATES | ||

| SECURITIES AND EXCHANGE COMMISSION | ||

| Washington, D.C. 20549 | ||

| FORM N-CSR | ||

| CERTIFIED SHAREHOLDER REPORT OF REGISTERED | ||

| MANAGEMENT INVESTMENT COMPANIES | ||

| Investment Company Act file number | 811-07820 | |

| AMERICAN CENTURY CAPITAL PORTFOLIOS, INC. | ||

| (Exact name of registrant as specified in charter) | ||

| 4500 MAIN STREET, KANSAS CITY, MISSOURI | 64111 | |

| (Address of principal executive offices) | (Zip Code) | |

| CHARLES A. ETHERINGTON | ||

| 4500 MAIN STREET, KANSAS CITY, MISSOURI 64111 | ||

| (Name and address of agent for service) | ||

| Registrant’s telephone number, including area code: | 816-531-5575 | |

| Date of fiscal year end: | 03-31 | |

| Date of reporting period: | 09-30-09 | |

| ITEM 1. REPORTS TO STOCKHOLDERS. |

| Provided under separate cover. |

| Semiannual Report |

| September 30, 2009 |

![]()

| American Century Investments |

Mid Cap Value Fund

Small Cap Value Fund

| President’s Letter |

Dear Investor:

Thank you for your investment with us during the financial reporting period ended September 30, 2009. We appreciate your trust in American Century Investments® at this volatile, transitional time in the economy and investment markets.

As the upheavals associated with the “Great Recession” gradually subside, our senior management team has put considerable thought into how the investment environment has changed and what new challenges and opportunities await us. Critical factors that we are anticipating in the coming year include marked shifts in investment and spending behavior, along with consolidation in our industry.

Most importantly, we think the economic recovery will be slow and extended. The economy and capital markets have come a long way since Lehman Brothers collapsed over a year ago, but 2010 will likely bring continuing challenges. The stock market’s rebound since last March and the third-quarter economic surge this year were fueled largely by corporate cost-cutting and unprecedented monetary and fiscal stimulus, including some key programs that have since expired or been scaled back.

Meanwhile, the resilient but struggling consumer sector still faces rising unemployment, heavy debt burdens, tight credit conditions, and a housing market that is starting to stabilize, but remains vulnerable. Much of our investment positioning in 2009 has cautiously reflected these still unstable economic fundamentals, leading to underperformance, in some cases, versus market benchmarks buoyed by the rally of riskier assets. We still support our fundamentally based positioning because we believe strongly that some markets—driven more by technical factors than fundamentals—have advanced further than underlying economic conditions warrant, and remain susceptible to the possibility of more volatility ahead.

For more detailed information from our portfolio management team about the performance and positioning of your investment, please review the following pages, or visit our website, americancentury.com.

Thank you for your continued confidence in us.

Sincerely,

Jonathan Thomas

President and Chief Executive Officer

American Century Investments

| Independent Chairman’s Letter |

I am Don Pratt, an independent director and chairman of the mutual fund board responsible for the U.S. Growth Equity, U.S. Value Equity, Global and Non-U.S. Equity and Asset Allocation funds managed by American Century Investments. The board consists of seven independent directors and two directors who are affiliated with the investment advisor.

As one of your independent shareholder representatives on the fund board, I plan to write you from time to time with updates on board activities and news about your funds. My co-independent directors and I are committed to putting your interests first. We work closely with American Century Investments on maintaining strong fund performance, providing quality service to shareholders at competitive fees and ensuring ethical business practices and compliance with all applicable fund regulations.

Last year, the board welcomed its newest independent director, John R. Whitten. He is a great addition to an experienced board where, collectively, the independent directors have served the funds for more than 76 years. This continuity served shareholders well as the investment advisor initiated a successful management transition, creating a strong senior leadership team consisting of well-tenured company executives and experienced industry veterans. Under the leadership of President and Chief Executive Officer Jonathan Thomas and Chief Investment Officer Enrique Chang, the firm has made the achievement of superior investment performance its primary focus and the key driver of its success going forward. This focus helped the company generate strong relative performance against the backdrop of 2008’s unprecedented market volatility.

As investors in the American Century funds, my fellow directors and I share your investing experience. We know firsthand how decisions made at the board level affect all shareholders. To further guide our efforts on your behalf, I invite you to send me your comments, questions or suggestions by email to dhpratt@fundboardchair.com. Thank you for allowing me to serve as your advocate on our board.

| Table of Contents |

| Market Perspective | 2 |

| U.S. Stock Index Returns | 2 |

| Mid Cap Value | |

| Performance | 3 |

| Portfolio Commentary | 5 |

| Top Ten Holdings | 7 |

| Top Five Industries | 7 |

| Types of Investments in Portfolio | 7 |

| Small Cap Value | |

| Performance | 8 |

| Portfolio Commentary | 10 |

| Top Ten Holdings | 12 |

| Top Five Industries | 12 |

| Types of Investments in Portfolio | 12 |

| Shareholder Fee Examples | 13 |

| Financial Statements | |

| Schedule of Investments | 15 |

| Statement of Assets and Liabilities | 25 |

| Statement of Operations | 27 |

| Statement of Changes in Net Assets | 28 |

| Notes to Financial Statements | 29 |

| Financial Highlights | 38 |

| Other Information | |

| Approval of Management Agreements | 45 |

| Additional Information | 50 |

| Index Definitions | 51 |

The opinions expressed in the Market Perspective and each of the Portfolio Commentaries reflect those of the portfolio management team as of the date of the report, and do not necessarily represent the opinions of American Century Investments or any other person in the American Century Investments organization. Any such opinions are subject to change at any time based upon market or other conditions and American Century Investments disclaims any responsibility to update such opinions. These opinions may not be relied upon as investment advice and, because investment decisions made by American Century Investments funds are based on numerous factors, may not be relied upon as an indication of trading intent on behalf of any American Century Investments fund. Security examples are used for representational purposes only and are not intended as recommendations to purchase or sell securities. Performance information for com parative indices and securities is provided to American Century Investments by third party vendors. To the best of American Century Investments’ knowledge, such information is accurate at the time of printing.

| Market Perspective |

By Phil Davidson, Chief Investment Officer, U.S. Value Equity

A Value-Led Market Recovery

The U.S. stock market enjoyed an extraordinary rally during the six months ended September 30, 2009. The 35% advance in the broad equity indices—representing the market’s best six-month gain since 1938—reflected investors’ renewed confidence in an economic recovery following the deep recession and credit crisis that occurred in 2008.

As the table below indicates, value stocks led the market’s advance, outperforming growth issues across all market capitalizations. One factor behind the outperformance of value shares was a recovery in the financial sector, which comprises a significant portion of the value universe. Financial stocks were priced for failure amid the economic and credit turmoil in late 2008 and early 2009. Since then, the credit environment has improved considerably, helped in part by a series of federal government programs, and financial companies have taken steps to raise capital and reduce debt. As a result, financial stocks rebounded sharply during the six-month period, posting the best returns in the stock market.

Another factor supporting value shares was a renewed emphasis on cost management and deleveraging. As the economic downturn deepened, many businesses quickly implemented aggressive cost-cutting measures, which helped sustain profits despite declining revenues. In addition, companies that focused on growth (often using debt to do so) were hit the hardest during the recession, while those that concentrated on strengthening their balance sheets and improving cash flows held up the best.

The New Reality

Despite signs of economic improvement, particularly in housing and manufacturing, we still expect a slow, gradual recovery. Consumer spending, which accounts for 70% of the economy, is likely to remain weak as consumers continue to reduce debt and increase savings. In this environment, we believe that higher-quality companies with self-funding business models and whose strategies emphasize higher returns on capital will outperform over time. These companies will be in the best position to gain market share from weaker competitors and generate cash flows regardless of the pace of economic recovery.

| U.S. Stock Index Returns | ||||

| For the six months ended September 30, 2009* | ||||

| Russell 1000 Index (Large-Cap) | 35.22% | Russell 2000 Index (Small-Cap) | 43.95% | |

| Russell 1000 Value Index | 37.99% | Russell 2000 Value Index | 44.79% | |

| Russell 1000 Growth Index | 32.58% | Russell 2000 Growth Index | 43.06% | |

| Russell Midcap Index | 45.71% | *Total returns for periods less than one year are not annualized. | ||

| Russell Midcap Value Index | 49.51% | |||

| Russell Midcap Growth Index | 41.89% | |||

2

| Performance |

| Mid Cap Value | ||||||

| Total Returns as of September 30, 2009 | ||||||

| Average Annual Returns | ||||||

| Since | Inception | |||||

| 6 months(1) | 1 year | 5 years | Inception | Date | ||

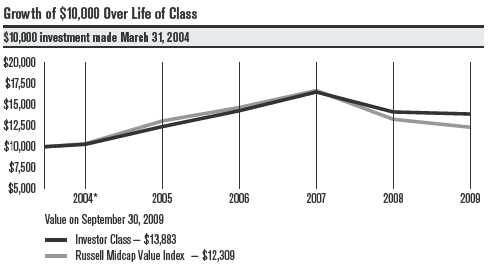

| Investor Class | 37.79% | -1.72% | 6.19% | 6.14% | 3/31/04 | |

| Russell Midcap Value Index(2) | 49.51% | -7.12% | 3.53% | 3.85% | — | |

| Institutional Class | 37.92% | -1.52% | 6.40% | 6.58% | 8/2/04 | |

| Advisor Class | 37.61% | -1.96% | — | 4.18% | 1/13/05 | |

| R Class | 37.44% | -2.20% | — | 1.65% | 7/29/05 | |

| (1) | Total returns for periods less than one year are not annualized. | |||||

| (2) | Data provided by Lipper Inc. – A Reuters Company. © 2009 Reuters. All rights reserved. Any copying, republication or redistribution of Lipper | |||||

| content, including by caching, framing or similar means, is expressly prohibited without the prior written consent of Lipper. Lipper shall not be | ||||||

| liable for any errors or delays in the content, or for any actions taken in reliance thereon. | ||||||

| The data contained herein has been obtained from company reports, financial reporting services, periodicals and other resources believed to be | ||||||

| reliable. Although carefully verified, data on compilations is not guaranteed by Lipper and may be incomplete. No offer or solicitations to buy or | ||||||

| sell any of the securities herein is being made by Lipper. | ||||||

Data presented reflect past performance. Past performance is no guarantee of future results. Current performance may be higher or lower than the performance shown. Investment return and principal value will fluctuate, and redemption value may be more or less than original cost. To obtain performance data current to the most recent month end, please call 1-800-345-2021 or visit americancentury.com.

Unless otherwise indicated, performance reflects Investor Class shares; performance for other share classes will vary due to differences in fee structure. For information about other share classes available, please consult the prospectus. Data assumes reinvestment of dividends and capital gains, and none of the charts reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Returns for the index are provided for comparison. The fund’s total returns include operating expenses (such as transaction costs and management fees) that reduce returns, while the total returns of the index do not.

3

Mid Cap Value

| One-Year Returns Over Life of Class | ||||||

| Periods ended September 30 | ||||||

| 2004* | 2005 | 2006 | 2007 | 2008 | 2009 | |

| Investor Class | 2.80% | 20.48% | 15.22% | 15.59% | -14.36% | -1.72% |

| Russell Midcap Value Index | 3.50% | 26.13% | 12.28% | 13.75% | -20.50% | -7.12% |

| *From 3/31/04, the Investor Class’s inception date. Not annualized. | ||||||

| Total Annual Fund Operating Expenses | ||||||

| Investor Class | Institutional Class | Advisor Class | R Class | |||

| 1.01% | 0.81% | 1.26% | 1.51% | |||

The total annual fund operating expenses shown is as stated in the fund’s prospectus current as of the date of this report. The prospectus may vary from the expense ratio shown elsewhere in this report because it is based on a different time period, includes acquired fund fees and expenses, and, if applicable, does not include fee waivers or expense reimbursements.

Data presented reflect past performance. Past performance is no guarantee of future results. Current performance may be higher or lower than the performance shown. Investment return and principal value will fluctuate, and redemption value may be more or less than original cost. To obtain performance data current to the most recent month end, please call 1-800-345-2021 or visit americancentury.com.

Unless otherwise indicated, performance reflects Investor Class shares; performance for other share classes will vary due to differences in fee structure. For information about other share classes available, please consult the prospectus. Data assumes reinvestment of dividends and capital gains, and none of the charts reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Returns for the index are provided for comparison. The fund’s total returns include operating expenses (such as transaction costs and management fees) that reduce returns, while the total returns of the index do not.

4

| Portfolio Commentary |

Mid Cap Value

Portfolio Managers: Kevin Toney, Michael Liss, and Phil Davidson

Performance Summary

Mid Cap Value returned 37.79%* for the six months ended September 30, 2009. By comparison, the average return for Morningstar’s Mid Cap Value category** (whose performance, like Mid Cap Value’s, reflects operating expenses) was 43.97%. The fund’s benchmark, the Russell Midcap Value Index (which does not include operating expenses), was up 49.51%.

The stock market rally, which began in March, persisted through the end of the reporting period. The U.S. economy continued to show signs of improvement in response to government stimulus programs, while corporate earnings were better than anticipated. Improving conditions in the capital markets were also favorable for the more highly leveraged companies. These factors led many investors to shift into riskier assets, and many of the period’s largest gains were made by lower-quality companies. That situation was at odds with Mid Cap Value’s investment approach, which emphasizes higher-quality businesses with sound balance sheets. Nonetheless, the portfolio received positive contributions in absolute terms from all 10 of the sectors in which it was invested. On a relative basis, Mid Cap Value’s positions in the consumer discretionary and financials sectors detracted. Investments among information technology compani es contributed.

Since its inception on March 31, 2004, Mid Cap Value has produced an average annual return of 6.14%, topping the returns for that period for Morningstar’s Mid Cap Value category average** and the Russell Midcap Value Index (see the performance information on pages 3-4).

Consumer Discretionary Detracted

Relative performance was hampered by the combination of an underweight position and security selection in the consumer discretionary sector, the strongest in the benchmark. Many of these stocks, which suffered steep declines as the recession took hold, rallied on optimism about a possible economic recovery and improving consumer sentiment.

Generally speaking, the portfolio’s performance was a result of what it didn’t own rather than what it did. For example, Mid Cap Value did not hold shares of Ford Motor, which nearly tripled during the period. The car maker has been able to restructure its business without the help of the U.S. government, unlike competitors General Motors and Chrysler, and has steadily gained market share.

| * | All fund returns referenced in this commentary are for Investor Class shares. Total returns for periods less than one year are not annualized. |

| ** The one-, five-year and since inception average returns as of September 30, 2009, for Morningstar’s Mid Cap Value category were -2.80%, 2.83% | |

| and 2.86%, respectively. © 2009 Morningstar, Inc. All Rights Reserved. The information contained herein: (1) is proprietary to Morningstar and/ | |

| or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor | |

| its content providers are responsible for any damages or losses arising from any use of this information. | |

5

Mid Cap Value

The consumer discretionary sector also provided a top detractor, Lowe’s. The home-improvement retailer experienced weak demand for the big-ticket products in its stores, but expects to gain additional market share in 2010. We also believe investors punished Lowe’s for failing to cut costs and reduce capital expenditures as meaningfully as its competitors.

Financials Slowed Results

Mid Cap Value’s underweight in financials stocks, which had been advantageous during the turmoil that roiled the sector, acted as a restraint as companies with stressed balance sheets, many of which had been staring at bankruptcy only months earlier, rallied from historic lows, outperforming stronger, higher-quality businesses. For some time, we have approached the financials sector with caution and conservatism. During the reporting period, Mid Cap Value’s investments were concentrated in the less-volatile insurance and thrifts names. However, many of these companies underperformed during the low-quality rally, including portfolio holding People’s United Financial, a conservatively run and well-capitalized thrift.

The insurance industry was the source of a notable detractor. Aon Corp., one of the world’s largest insurance brokers, lagged due to continued softness in property and casualty insurance pricing and because of weak results in its consulting segment.

Information Technology Enhanced Performance

The portfolio’s holdings in the information technology sector added to relative results. A top contributor was Emulex Corp., a maker of storage-networking equipment. Its share price rose dramatically on news of an unsolicited takeover bid from chipmaker Broadcom Corp. The stock remained elevated as Emulex resisted the takeover, urging shareholders to reject Broadcom’s offer on the grounds that it materially undervalued the company. Ultimately, Broadcom withdrew the offer.

Another notable contributor was Littelfuse Inc., a leading supplier of circuit protection components for the consumer electronics, telecommunications, and automotive markets. The company benefited from its restructuring initiatives and an improved outlook for the automotive sector.

Outlook

We continue to follow our disciplined, bottom-up process, selecting companies one at a time for the portfolio. As of September 30, 2009, we see opportunities in consumer staples, industrials, and health care stocks, reflected by overweight positions in these sectors, relative to the benchmark. Our fundamental analysis and valuation work are also directing us toward smaller relative weightings in financials, materials, and consumer discretionary stocks.

6

| Mid Cap Value | ||

| Top Ten Holdings as of September 30, 2009 | ||

| % of net assets | % of net assets | |

| as of 9/30/09 | as of 3/31/09 | |

| Marsh & McLennan Cos., Inc. | 3.5% | 3.3% |

| Wisconsin Energy Corp. | 2.6% | 2.8% |

| Kimberly-Clark Corp. | 2.6% | 3.5% |

| Aon Corp. | 2.5% | 2.3% |

| iShares Russell Midcap Value Index Fund | 2.3% | 2.8% |

| Northern Trust Corp. | 2.1% | — |

| Commerce Bancshares, Inc. | 2.0% | 0.8% |

| Lowe’s Cos., Inc. | 2.0% | 0.7% |

| People’s United Financial, Inc. | 2.0% | 1.2% |

| Waste Management, Inc. | 2.0% | 2.0% |

| Top Five Industries as of September 30, 2009 | ||

| % of net assets | % of net assets | |

| as of 9/30/09 | as of 3/31/09 | |

| Insurance | 9.8% | 10.0% |

| Commercial Services & Supplies | 6.3% | 3.7% |

| Food Products | 6.3% | 7.5% |

| Oil, Gas & Consumable Fuels | 6.2% | 4.2% |

| Electric Utilities | 5.2% | 6.0% |

| Types of Investments in Portfolio | ||

| % of net assets | % of net assets | |

| as of 9/30/09 | as of 3/31/09 | |

| Domestic Common Stocks | 93.3% | 96.3% |

| Foreign Common Stocks(1) | 5.3% | 2.7% |

| Total Common Stocks | 98.6% | 99.0% |

| Temporary Cash Investments | 2.0% | 1.2% |

| Other Assets and Liabilities | (0.6)% | (0.2)% |

| (1) Includes depositary shares, dual listed securities and foreign ordinary shares. | ||

7

| Performance |

| Small Cap Value | |||||||

| Total Returns as of September 30, 2009 | |||||||

| Average Annual Returns | |||||||

| Since | Inception | ||||||

| 6 months(1) | 1 year | 5 years | 10 years | Inception | Date | ||

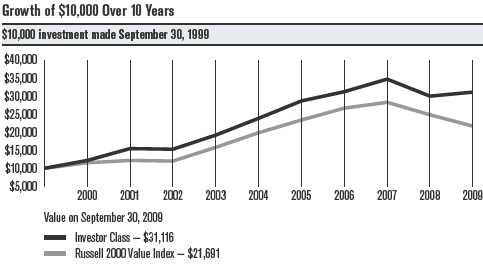

| Investor Class | 50.46% | 3.72% | 5.46% | 12.01% | 10.90% | 7/31/98 | |

| Russell 2000 Value Index(2) | 44.79% | -12.61% | 1.78% | 8.05% | 6.62% | — | |

| Institutional Class | 50.71% | 3.88% | 5.65% | 12.23% | 11.73% | 10/26/98 | |

| Advisor Class | 50.17% | 3.53% | 5.18% | — | 12.04% | 12/31/99 | |

| (1) | Total returns for periods less than one year are not annualized. | ||||||

| (2) | Data provided by Lipper Inc. – A Reuters Company. © 2009 Reuters. All rights reserved. Any copying, republication or redistribution of Lipper | ||||||

| content, including by caching, framing or similar means, is expressly prohibited without the prior written consent of Lipper. Lipper shall not be | |||||||

| liable for any errors or delays in the content, or for any actions taken in reliance thereon. | |||||||

| The data contained herein has been obtained from company reports, financial reporting services, periodicals and other resources believed to be | |||||||

| reliable. Although carefully verified, data on compilations is not guaranteed by Lipper and may be incomplete. No offer or solicitations to buy or | |||||||

| sell any of the securities herein is being made by Lipper. | |||||||

Data presented reflect past performance. Past performance is no guarantee of future results. Current performance may be higher or lower than the performance shown. Investment return and principal value will fluctuate, and redemption value may be more or less than original cost. To obtain performance data current to the most recent month end, please call 1-800-345-2021 or visit americancentury.com. Historically, small company stocks have been more volatile than the stocks of larger, more established companies.

Unless otherwise indicated, performance reflects Investor Class shares; performance for other share classes will vary due to differences in fee structure. For information about other share classes available, please consult the prospectus. Data assumes reinvestment of dividends and capital gains, and none of the charts reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Returns for the index are provided for comparison. The fund’s total returns include operating expenses (such as transaction costs and management fees) that reduce returns, while the total returns of the index do not.

8

Small Cap Value

| One-Year Returns Over 10 Years | |||||||||||

| Periods ended September 30 | |||||||||||

| 2000 | 2001 | 2002 | 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | ||

| Investor Class | 21.76% | 27.06% | -1.21% | 25.63% | 24.21% | 20.19% | 8.94% | 11.13% | -13.57% | 3.72% | |

| Russell 2000 | |||||||||||

| Value Index | 15.36% | 5.61% | -1.47% | 31.66% | 25.66% | 17.75% | 14.01% | 6.09% | -12.25% | -12.61% | |

| Total Annual Fund Operating Expenses | |||||||||||

| Investor Class | Institutional Class | Advisor Class | |||||||||

| 1.49% | 1.29% | 1.74% | |||||||||

The total annual fund operating expenses shown is as stated in the fund’s prospectus current as of the date of this report. The prospectus may vary from the expense ratio shown elsewhere in this report because it is based on a different time period, includes acquired fund fees and expenses, and, if applicable, does not include fee waivers or expense reimbursements.

Data presented reflect past performance. Past performance is no guarantee of future results. Current performance may be higher or lower than the performance shown. Investment return and principal value will fluctuate, and redemption value may be more or less than original cost. To obtain performance data current to the most recent month end, please call 1-800-345-2021 or visit americancentury.com. Historically, small company stocks have been more volatile than the stocks of larger, more established companies.

Unless otherwise indicated, performance reflects Investor Class shares; performance for other share classes will vary due to differences in fee structure. For information about other share classes available, please consult the prospectus. Data assumes reinvestment of dividends and capital gains, and none of the charts reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Returns for the index are provided for comparison. The fund’s total returns include operating expenses (such as transaction costs and management fees) that reduce returns, while the total returns of the index do not.

9

| Portfolio Commentary |

Small Cap Value

Portfolio Managers: Ben Giele and James Pitman

Performance Summary

Small Cap Value returned 50.46%* for the six months ended September 30, 2009. By comparison, its benchmark, the Russell 2000 Value Index, returned 44.79%. The portfolio’s returns reflect operating expenses while the index’s returns do not. The Lipper Small-Cap Value Funds Index, which includes operating expenses, returned 48.06%.**

The stock market rally, which began in March, persisted through the end of the reporting period. The U.S. economy continued to show signs of improvement in response to government stimulus programs, while corporate earnings were better than anticipated. Small-company stocks posted significant gains, outperforming all other parts of the capitalization spectrum except mid-cap stocks. In this environment, Small Cap Value received positive contributions in absolute terms from all 10 of the sectors in which it was invested. On a relative basis, the portfolio outperformed largely because of effective security selection. Contributing the most were investments in the financials, utilities, and energy sectors. The portfolio’s position in the health care sector detracted.

Since Small Cap Value’s inception on July 31, 1998, the portfolio has produced an average annual return of 10.90%, outpacing the returns of the Russell 2000 Value Index and the Lipper Small-Cap Value Funds Index** for the same period (see performance information on pages 8-9).

Financials Enhanced Results

Security selection among financials stocks added significantly to relative performance. The rally in financials was primarily among large banks and financial institutions, some of which had seemed on the brink of bankruptcy just months before. Although small-cap financials advanced, their shares tended to lag their large-cap counterparts.

The portfolio benefited from its investments in well-capitalized commercial banks. A notable contributor was Webster Financial Corp., a regional bank serving customers in southern New England and eastern New York State. Webster Financial has successfully raised capital to cover credit concerns and support its expansion plans.

Small Cap Value’s mix of capital markets firms was also advantageous. A top performer was Calamos Asset Management. During the market turmoil, Calamos’ share price had suffered in sympathy with other asset managers. As the environment improved, the company earned a profit, helped by investment gains.

| * | All fund returns referenced in this commentary are for Investor Class shares. Total returns for periods less than one year are not annualized. |

| ** The Lipper Small-Cap Value Funds Index returned -4.42%, 3.02%, 8.72% and 7.16% for the one-, five-, ten-year and since inception periods | |

| ended September 30, 2009, respectively. | |

10

Small Cap Value

Utilities Contributed

The portfolio’s underweight in the utilities sector contributed to relative results. During difficult economic times, utilities stocks tend to be viewed as defensive investments. However, when the market rallied during the period, utilities did not gain as much as other sectors and turned in the weakest performance of the benchmark index.

Energy Powered Performance

An overweight in energy stocks was beneficial as oil prices rose and improving economic conditions sparked renewed demand for oil in the U.S., Europe, and emerging markets such as China and India. Security selection was also a plus. A key contributor was W&T Offshore, an oil and natural gas exploration and production company with primary activities in the Gulf of Mexico, which benefited from the rise in oil prices. W&T Offshore reported an increase in production and continued success in its drilling program.

Health Care Detracted

In health care, the portfolio’s overweight position hindered relative progress. Health care stocks gained, but their performance was constrained as investors priced in worst-case scenarios for health care reform. Although the health care sector rebounded from its lows by the end of the period, it remained one of the weakest performers in the benchmark. Two health care providers were notable detractors—specialty health care manager Magellan Health Services and National Healthcare Corp., which operates long-term health care centers. Shares of both companies declined with the sector as a whole.

Outlook

We continue to be bottom-up investment managers, evaluating each company individually and building the portfolio one stock at a time. In our search for companies that are undervalued, we will structure exposure to market segments based on the attractiveness of individual companies. As of September 30, 2009, the portfolio is broadly diversified, with larger positions than the benchmark in consumer discretionary, health care, and information technology. Our fundamental analysis and valuation work is also directing us toward a smaller relative weighting in financials and utilities stocks.

11

| Small Cap Value | ||

| Top Ten Holdings as of September 30, 2009 | ||

| % of net assets | % of net assets | |

| as of 9/30/09 | as of 3/31/09 | |

| Aspen Insurance Holdings Ltd., Series AHL, | ||

| 5.625%, 2/6/13 (Conv. Pref.) | 2.6% | 3.2% |

| iShares Russell 2000 Value Index Fund | 2.2% | 1.5% |

| iShares Russell 2000 Index Fund | 1.1% | 1.6% |

| Young Innovations, Inc. | 1.1% | 1.3% |

| Parametric Technology Corp. | 0.9% | 1.4% |

| HCC Insurance Holdings, Inc. | 0.9% | 0.6% |

| Ares Capital Corp. | 0.8% | 0.7% |

| IESI-BFC Ltd. | 0.8% | — |

| Fulton Financial Corp. | 0.7% | 0.8% |

| Sybase, Inc. | 0.7% | 0.6% |

| Top Five Industries as of September 30, 2009 | ||

| % of net assets | % of net assets | |

| as of 9/30/09 | as of 3/31/09 | |

| Insurance | 8.1% | 9.2% |

| Commercial Banks | 6.6% | 8.8% |

| Real Estate Investment Trusts (REITs) | 5.0% | 6.5% |

| Specialty Retail | 4.7% | 3.4% |

| Machinery | 3.8% | 3.6% |

| Types of Investments in Portfolio | ||

| % of net assets | % of net assets | |

| as of 9/30/09 | as of 3/31/09 | |

| Common Stocks | 90.9% | 92.2% |

| Convertible Preferred Stocks | 4.5% | 4.6% |

| Preferred Stocks | 1.0% | 1.4% |

| Total Equity Exposure | 96.4% | 98.2% |

| Temporary Cash Investments | 2.3% | 2.3% |

| Other Assets and Liabilities | 1.3% | (0.5)% |

12

| Shareholder Fee Examples (Unaudited) |

Fund shareholders may incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments and redemption/ exchange fees; and (2) ongoing costs, including management fees; distribution and service (12b-1) fees; and other fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in your fund and to compare these costs with the ongoing cost of investing in other mutual funds.

The example is based on an investment of $1,000 made at the beginning of the period and held for the entire period from April 1, 2009 to September 30, 2009.

Actual Expenses

The table provides information about actual account values and actual expenses for each class. You may use the information, together with the amount you invested, to estimate the expenses that you paid over the period. First, identify the share class you own. Then simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number under the heading “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

If you hold Investor Class shares of any American Century Investments fund, or Institutional Class shares of the American Century Diversified Bond Fund, in an American Century Investments account (i.e., not a financial intermediary or retirement plan account), American Century Investments may charge you a $12.50 semiannual account maintenance fee if the value of those shares is less than $10,000. We will redeem shares automatically in one of your accounts to pay the $12.50 fee. In determining your total eligible investment amount, we will include your investments in all personal accounts (including American Century Investments Brokerage accounts) registered under your Social Security number. Personal accounts include individual accounts, joint accounts, UGMA/UTMA accounts, personal trusts, Coverdell Education Savings Accounts and IRAs (including traditional, Roth, Rollover, SEP-, SARSEP- and SIMPLE-IRAs), and certain other retirement accounts. If you have only business, business retirement, employer-sponsored or American Century Investments Brokerage accounts, you are currently not subject to this fee. We will not charge the fee as long as you choose to manage your accounts exclusively online. If you are subject to the Account Maintenance Fee, your account value could be reduced by the fee amount.

Hypothetical Example for Comparison Purposes

The table also provides information about hypothetical account values and hypothetical expenses based on the actual expense ratio of each class of your fund and an assumed rate of return of 5% per year before expenses, which is not the actual return of a fund’s share class. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in your fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

13

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads) or redemption/exchange fees. Therefore, the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| Beginning | Ending | Expenses Paid | ||

| Account Value | Account Value | During Period* | Annualized | |

| 4/1/09 | 9/30/09 | 4/1/09 - 9/30/09 | Expense Ratio* | |

| Mid Cap Value | ||||

| Actual | ||||

| Investor Class | $1,000 | $1,377.90 | $5.96 | 1.00% |

| Institutional Class | $1,000 | $1,379.20 | $4.77 | 0.80% |

| Advisor Class | $1,000 | $1,376.10 | $7.45 | 1.25% |

| R Class | $1,000 | $1,374.40 | $8.93 | 1.50% |

| Hypothetical | ||||

| Investor Class | $1,000 | $1,020.05 | $5.06 | 1.00% |

| Institutional Class | $1,000 | $1,021.06 | $4.05 | 0.80% |

| Advisor Class | $1,000 | $1,018.80 | $6.33 | 1.25% |

| R Class | $1,000 | $1,017.55 | $7.59 | 1.50% |

| Small Cap Value | ||||

| Actual | ||||

| Investor Class | $1,000 | $1,504.60 | $7.85 | 1.25% |

| Institutional Class | $1,000 | $1,507.10 | $6.60 | 1.05% |

| Advisor Class | $1,000 | $1,501.70 | $9.41 | 1.50% |

| Hypothetical | ||||

| Investor Class | $1,000 | $1,018.80 | $6.33 | 1.25% |

| Institutional Class | $1,000 | $1,019.80 | $5.32 | 1.05% |

| Advisor Class | $1,000 | $1,017.55 | $7.59 | 1.50% |

| *Expenses are equal to the class’s annualized expense ratio listed in the table above, multiplied by the average account value over the period, | ||||

| multiplied by 183, the number of days in the most recent fiscal half-year, divided by 365, to reflect the one-half year period. The class’s annualized | ||||

| expense ratio does not include any acquired fund fees and expenses. | ||||

14

| Schedule of Investments |

| Mid Cap Value | ||||||

| SEPTEMBER 30, 2009 (UNAUDITED) | ||||||

| Shares | Value | Shares | Value | |||

| Common Stocks — 98.6% | DIVERSIFIED FINANCIAL SERVICES — 0.1% | |||||

| AEROSPACE & DEFENSE — 0.6% | McGraw-Hill Cos., Inc. (The) | 13,100 | $ 329,334 | |||

| DIVERSIFIED TELECOMMUNICATION | ||||||

| Northrop Grumman Corp. | 52,300 | $ 2,706,525 | SERVICES — 2.8% | |||

| AIRLINES — 0.5% | BCE, Inc. | 159,527 | 3,932,114 | |||

| Southwest Airlines Co. | 239,203 | 2,296,349 | CenturyTel, Inc. | 176,253 | 5,922,101 | |

| BEVERAGES — 0.7% | Iowa Telecommunications | |||||

| Coca-Cola Enterprises, Inc. | 83,600 | 1,789,876 | Services, Inc. | 173,089 | 2,180,921 | |

| Pepsi Bottling Group, Inc. | 38,000 | 1,384,720 | 12,035,136 | |||

| 3,174,596 | ELECTRIC UTILITIES — 5.2% | |||||

| CAPITAL MARKETS — 4.6% | American Electric Power | |||||

| AllianceBernstein Holding LP | 78,800 | 2,149,664 | Co., Inc. | 46,755 | 1,448,937 | |

| Ameriprise Financial, Inc. | 157,901 | 5,736,543 | Great Plains Energy, Inc. | 35,759 | 641,874 | |

| Invesco Ltd. | 75,140 | 1,710,187 | IDACORP, Inc. | 275,868 | 7,942,240 | |

| Legg Mason, Inc. | 29,700 | 921,591 | Northeast Utilities | 82,983 | 1,970,016 | |

| Northern Trust Corp. | 155,900 | 9,067,144 | Portland General Electric Co. | 189,236 | 3,731,734 | |

| 19,585,129 | Westar Energy, Inc. | 334,741 | 6,530,797 | |||

| CHEMICALS — 1.2% | 22,265,598 | |||||

| International Flavors & | ELECTRICAL EQUIPMENT — 2.0% | |||||

| Fragrances, Inc. | 86,639 | 3,286,217 | Cooper Industries plc, | |||

| Minerals Technologies, Inc. | 40,801 | 1,940,496 | Class A | 76,300 | 2,866,591 | |

| 5,226,713 | Emerson Electric Co. | 53,200 | 2,132,256 | |||

| COMMERCIAL BANKS — 2.4% | Hubbell, Inc., Class A | 4,672 | 189,169 | |||

| City National Corp. | 34,100 | 1,327,513 | Hubbell, Inc., Class B | 76,400 | 3,208,800 | |

| Commerce Bancshares, Inc. | 235,671 | 8,776,388 | 8,396,816 | |||

| 10,103,901 | ELECTRONIC EQUIPMENT, INSTRUMENTS | |||||

| COMMERCIAL SERVICES & SUPPLIES — 6.3% | & COMPONENTS — 1.6% | |||||

| IESI-BFC Ltd. | 378,088 | 4,884,897 | AVX Corp. | 141,301 | 1,685,721 | |

| Pitney Bowes, Inc. | 249,100 | 6,190,135 | Littelfuse, Inc.(1) | 15,391 | 403,860 | |

| Republic Services, Inc. | 283,498 | 7,532,542 | Molex, Inc. | 229,484 | 4,791,626 | |

| Waste Management, Inc. | 288,444 | 8,601,400 | 6,881,207 | |||

| 27,208,974 | ENERGY EQUIPMENT & SERVICES — 1.8% | |||||

| COMMUNICATIONS EQUIPMENT — 0.8% | Baker Hughes, Inc. | 38,600 | 1,646,676 | |||

| Emulex Corp.(1) | 341,100 | 3,509,919 | BJ Services Co. | 66,300 | 1,288,209 | |

| COMPUTERS & PERIPHERALS — 1.3% | Cameron | |||||

| International Corp.(1) | 70,100 | 2,651,182 | ||||

| Diebold, Inc. | 110,651 | 3,643,737 | ||||

| Helmerich & Payne, Inc. | 53,900 | 2,130,667 | ||||

| QLogic Corp.(1) | 105,000 | 1,806,000 | ||||

| 7,716,734 | ||||||

| 5,449,737 | FOOD & STAPLES RETAILING — 0.5% | |||||

| CONTAINERS & PACKAGING — 1.1% | Costco Wholesale Corp. | 36,600 | 2,066,436 | |||

| Bemis Co., Inc. | 184,768 | 4,787,339 | FOOD PRODUCTS — 6.3% | |||

| DISTRIBUTORS — 1.5% | Campbell Soup Co. | 237,200 | 7,737,464 | |||

| Genuine Parts Co. | 173,794 | 6,614,600 | ConAgra Foods, Inc. | 375,890 | 8,149,295 | |

| DIVERSIFIED — 2.3% | General Mills, Inc. | 14,900 | 959,262 | |||

| iShares Russell Midcap | ||||||

| Value Index Fund | 278,400 | 9,860,928 | H.J. Heinz Co. | 171,300 | 6,809,175 | |

| Kellogg Co. | 64,700 | 3,185,181 | ||||

| 26,840,377 | ||||||

15

| Mid Cap Value | ||||||

| Shares | Value | Shares | Value | |||

| GAS UTILITIES — 1.9% | LEISURE EQUIPMENT & PRODUCTS — 0.9% | |||||

| AGL Resources, Inc. | 29,300 | $ 1,033,411 | Mattel, Inc. | 198,800 | $ 3,669,848 | |

| Southwest Gas Corp. | 283,003 | 7,239,217 | MACHINERY — 2.7% | |||

| 8,272,628 | Altra Holdings, Inc.(1) | 491,879 | 5,504,126 | |||

| HEALTH CARE EQUIPMENT & SUPPLIES — 3.6% | Dover Corp. | 50,500 | 1,957,380 | |||

| Beckman Coulter, Inc. | 52,756 | 3,636,999 | Kaydon Corp. | 131,776 | 4,272,178 | |

| Boston Scientific Corp.(1) | 106,000 | 1,122,540 | 11,733,684 | |||

| CareFusion Corp.(1) | 69,200 | 1,508,560 | METALS & MINING — 1.6% | |||

| Covidien plc | 32,700 | 1,414,602 | Barrick Gold Corp. | 51,083 | 1,936,045 | |

| Symmetry Medical, Inc.(1) | 330,841 | 3,430,821 | Newmont Mining Corp. | 110,938 | 4,883,491 | |

| Zimmer Holdings, Inc.(1) | 83,300 | 4,452,385 | 6,819,536 | |||

| 15,565,907 | MULTI-UTILITIES — 4.1% | |||||

| HEALTH CARE PROVIDERS & SERVICES — 2.5% | Ameren Corp. | 49,503 | 1,251,436 | |||

| Cardinal Health, Inc. | 96,200 | 2,578,160 | PG&E Corp. | 35,000 | 1,417,150 | |

| LifePoint Hospitals, Inc.(1) | 189,800 | 5,135,988 | Wisconsin Energy Corp. | 244,300 | 11,035,031 | |

| Patterson Cos., Inc.(1) | 49,000 | 1,335,250 | Xcel Energy, Inc. | 211,959 | 4,078,091 | |

| Select Medical | 17,781,708 | |||||

| Holdings Corp.(1) | 128,378 | 1,292,767 | OIL, GAS & CONSUMABLE FUELS — 6.2% | |||

| Universal Health Services, | Apache Corp. | 53,751 | 4,935,954 | |||

| Inc., Class B | 3,937 | 243,818 | EOG Resources, Inc. | 40,600 | 3,390,506 | |

| 10,585,983 | EQT Corp. | 166,252 | 7,082,335 | |||

| HEALTH CARE TECHNOLOGY — 0.8% | Imperial Oil Ltd. | 122,500 | 4,662,472 | |||

| IMS Health, Inc. | 220,900 | 3,390,815 | Murphy Oil Corp. | 48,300 | 2,780,631 | |

| HOTELS, RESTAURANTS & LEISURE — 3.1% | Noble Energy, Inc. | 57,500 | 3,792,700 | |||

| CEC Entertainment, Inc.(1) | 148,700 | 3,845,382 | 26,644,598 | |||

| International Speedway | PAPER & FOREST PRODUCTS — 0.7% | |||||

| Corp., Class A | 201,807 | 5,563,819 | MeadWestvaco Corp. | 49,385 | 1,101,779 | |

| Speedway Motorsports, Inc. | 280,143 | 4,031,258 | Weyerhaeuser Co. | 57,436 | 2,105,030 | |

| 13,440,459 | 3,206,809 | |||||

| HOUSEHOLD DURABLES — 1.0% | PERSONAL PRODUCTS — 0.8% | |||||

| Fortune Brands, Inc. | 100,100 | 4,302,298 | Estee Lauder Cos., Inc. | |||

| Whirlpool Corp. | 2,400 | 167,904 | (The), Class A | 91,700 | 3,400,236 | |

| 4,470,202 | REAL ESTATE INVESTMENT TRUSTS (REITs) — 2.5% | |||||

| HOUSEHOLD PRODUCTS — 2.6% | Boston Properties, Inc. | 41,599 | 2,726,814 | |||

| Kimberly-Clark Corp. | 186,223 | 10,983,432 | Federal Realty | |||

| INSURANCE — 9.8% | Investment Trust | 7,038 | 431,922 | |||

| Aon Corp. | 263,200 | 10,709,608 | Government Properties | |||

| Income Trust(1) | 150,167 | 3,605,510 | ||||

| Chubb Corp. (The) | 154,500 | 7,788,345 | ||||

| HCC Insurance | HCP, Inc. | 8,483 | 243,801 | |||

| Holdings, Inc. | 94,332 | 2,579,980 | Host Hotels & Resorts, Inc. | 272,976 | 3,212,928 | |

| Marsh & McLennan | Public Storage | 4,300 | 323,532 | |||

| Cos., Inc. | 607,237 | 15,016,971 | 10,544,507 | |||

| Transatlantic Holdings, Inc. | 33,549 | 1,683,153 | ROAD & RAIL — 0.4% | |||

| Travelers Cos., Inc. (The) | 87,500 | 4,307,625 | Heartland Express, Inc. | 133,800 | 1,926,720 | |

| 42,085,682 | ||||||

| IT SERVICES — 0.7% | ||||||

| Accenture plc, Class A | 80,100 | 2,985,327 | ||||

16

| Mid Cap Value | ||||||

| Shares | Value | Shares | Value | |||

| SEMICONDUCTORS & SEMICONDUCTOR | ||||||

| EQUIPMENT — 2.5% | Temporary Cash Investments — 2.0% | |||||

| Applied Materials, Inc. | 321,500 | $ 4,308,100 | JPMorgan U.S. Treasury | |||

| Plus Money Market Fund | ||||||

| KLA-Tencor Corp. | 45,700 | 1,638,802 | Agency Shares | 57,984 | $ 57,984 | |

| Teradyne, Inc.(1) | 170,000 | 1,572,500 | Repurchase Agreement, Credit Suisse First | |||

| Verigy Ltd.(1) | 258,500 | 3,003,770 | Boston, Inc., (collateralized by various | |||

| 10,523,172 | U.S. Treasury obligations, 0.24%, 6/10/10, | |||||

| valued at $8,466,648), in a joint trading | ||||||

| SOFTWARE — 0.4% | account at 0.01%, dated 9/30/09, due | |||||

| Synopsys, Inc.(1) | 72,658 | 1,628,992 | 10/1/09 (Delivery value $8,300,002) | 8,300,000 | ||

| SPECIALTY RETAIL — 3.8% | TOTAL TEMPORARY | |||||

| Lowe’s Cos., Inc. | 419,100 | 8,775,954 | CASH INVESTMENTS | |||

| PetSmart, Inc. | 355,300 | 7,727,775 | (Cost $8,357,984) | 8,357,984 | ||

| 16,503,729 | TOTAL INVESTMENT | |||||

| THRIFTS & MORTGAGE FINANCE — 2.4% | SECURITIES — 100.6% | |||||

| Hudson City Bancorp., Inc. | 81,600 | 1,073,040 | (Cost $374,599,828) | 431,857,733 | ||

| People’s United | OTHER ASSETS | |||||

| Financial, Inc. | 553,189 | 8,607,621 | AND LIABILITIES — (0.6)% | (2,376,774) | ||

| Washington Federal, Inc. | 35,514 | 598,766 | TOTAL NET ASSETS — 100.0% | $429,480,959 | ||

| 10,279,427 | ||||||

| TOTAL COMMON STOCKS | ||||||

| (Cost $366,241,844) | 423,499,749 | |||||

| Forward Foreign Currency Exchange Contracts | ||||||

| Contracts to Sell | Settlement Date | Value | Unrealized Gain (Loss) | |||

| 12,943,298 CAD for USD | 10/30/09 | $12,089,197 | $(184,606) | |||

| (Value on Settlement Date $11,904,591) | ||||||

| Notes to Schedule of Investments | ||||||

| CAD = Canadian Dollar | ||||||

| USD = United States Dollar | ||||||

| (1) Non-income producing. | ||||||

| See Notes to Financial Statements. | ||||||

17

| Small Cap Value | ||||||

| SEPTEMBER 30, 2009 (UNAUDITED) | ||||||

| Shares | Value | Shares | Value | |||

| Common Stocks — 90.9% | PennantPark | |||||

| Investment Corp. | 405,000 | $ 3,284,550 | ||||

| AEROSPACE & DEFENSE — 1.8% | Prospect Capital Corp. | 210,000 | 2,249,100 | |||

| AAR Corp.(1) | 120,000 | $ 2,632,800 | ||||

| Pzena Investment | ||||||

| Ceradyne, Inc.(1) | 145,000 | 2,657,850 | Management, Inc., Class A(1) | 275,000 | 2,246,750 | |

| Curtiss-Wright Corp. | 130,000 | 4,436,900 | TradeStation Group, Inc.(1) | 505,000 | 4,115,750 | |

| Esterline | 50,091,750 | |||||

| Technologies Corp.(1) | 90,000 | 3,528,900 | ||||

| CHEMICALS — 2.3% | ||||||

| Moog, Inc., Class A(1) | 205,000 | 6,047,500 | A. Schulman, Inc. | 105,000 | 2,092,650 | |

| Orbital Sciences Corp.(1) | 150,000 | 2,245,500 | Arch Chemicals, Inc. | 140,000 | 4,198,600 | |

| Triumph Group, Inc. | 115,000 | 5,518,850 | Cytec Industries, Inc. | 175,000 | 5,682,250 | |

| 27,068,300 | H.B. Fuller Co. | 150,000 | 3,135,000 | |||

| AIR FREIGHT & LOGISTICS — 0.5% | Innophos Holdings, Inc. | 100,000 | 1,850,000 | |||

| Hub Group, Inc., Class A(1) | 165,000 | 3,770,250 | Intrepid Potash, Inc.(1) | 125,000 | 2,948,750 | |

| UTi Worldwide, Inc. | 285,000 | 4,126,800 | Minerals Technologies, Inc. | 80,000 | 3,804,800 | |

| 7,897,050 | Olin Corp. | 290,000 | 5,057,600 | |||

| AIRLINES — 0.6% | OM Group, Inc.(1) | 100,000 | 3,039,000 | |||

| Alaska Air Group, Inc.(1) | 110,000 | 2,946,900 | Sensient Technologies Corp. | 110,000 | 3,054,700 | |

| JetBlue Airways Corp.(1) | 545,000 | 3,259,100 | 34,863,350 | |||

| SkyWest, Inc. | 165,000 | 2,735,700 | COMMERCIAL BANKS — 6.4% | |||

| 8,941,700 | American National | |||||

| AUTO COMPONENTS — 0.4% | Bankshares, Inc. | 100,000 | 2,182,000 | |||

| Cooper Tire & Rubber Co. | 210,000 | 3,691,800 | Associated Banc-Corp. | 270,000 | 3,083,400 | |

| Dana Holding Corp.(1) | 325,000 | 2,213,250 | Boston Private Financial | |||

| 5,905,050 | Holdings, Inc. | 475,000 | 3,092,250 | |||

| BEVERAGES — 0.3% | Central Pacific | |||||

| Financial Corp. | 425,000 | 1,071,000 | ||||

| Boston Beer Co., Inc., | ||||||

| Class A(1) | 140,000 | 5,191,200 | CVB Financial Corp. | 270,000 | 2,049,300 | |

| BIOTECHNOLOGY — 0.1% | East West Bancorp, Inc. | 340,000 | 2,822,000 | |||

| Martek Biosciences Corp.(1) | 80,000 | 1,807,200 | First Citizens BancShares, | |||

| Inc., Class A | 20,000 | 3,182,000 | ||||

| BUILDING PRODUCTS — 0.6% | First Midwest Bancorp., Inc. | 130,000 | 1,465,100 | |||

| Apogee Enterprises, Inc. | 170,000 | 2,553,400 | FirstMerit Corp. | 165,000 | 3,139,950 | |

| Griffon Corp.(1) | 270,000 | 2,718,900 | ||||

| FNB Corp. | 265,000 | 1,884,150 | ||||

| Simpson Manufacturing | Fulton Financial Corp. | 1,460,000 | 10,745,600 | |||

| Co., Inc. | 165,000 | 4,167,900 | ||||

| Hampton Roads | ||||||

| 9,440,200 | Bankshares, Inc. | 350,000 | 1,008,000 | |||

| CAPITAL MARKETS — 3.3% | Heritage Financial Corp. | 320,000 | 4,208,000 | |||

| Apollo Investment Corp. | 545,000 | 5,204,750 | Huntington Bancshares, Inc. | 460,000 | 2,166,600 | |

| Ares Capital Corp. | 1,150,000 | 12,673,000 | IBERIABANK Corp. | 50,000 | 2,278,000 | |

| Artio Global Investors, Inc.(1) | 110,000 | 2,876,500 | KeyCorp | 910,000 | 5,915,000 | |

| Calamos Asset Management, | Marshall & Ilsley Corp. | 1,100,000 | 8,877,000 | |||

| Inc., Class A | 310,000 | 4,048,600 | MB Financial, Inc. | 135,000 | 2,830,950 | |

| HFF, Inc., Class A(1) | 440,000 | 2,965,600 | ||||

| National Bankshares, Inc. | 85,000 | 2,163,250 | ||||

| Investment Technology | ||||||

| Group, Inc.(1) | 140,000 | 3,908,800 | Old National Bancorp. | 281,292 | 3,150,470 | |

| MCG Capital Corp.(1) | 1,025,000 | 4,294,750 | Sterling Bancshares, Inc. | 305,000 | 2,229,550 | |

| Patriot Capital Funding, Inc. | 545,000 | 2,223,600 | Synovus Financial Corp. | 975,000 | 3,656,250 | |

18

| Small Cap Value | ||||||

| Shares | Value | Shares | Value | |||

| TCF Financial Corp. | 300,000 | $ 3,912,000 | CONTAINERS & PACKAGING — 0.5% | |||

| United Bankshares, Inc. | 135,000 | 2,644,650 | Bemis Co., Inc. | 75,000 | $ 1,943,250 | |

| Washington Banking Co. | 272,795 | 2,526,082 | Sonoco Products Co. | 220,000 | 6,058,800 | |

| Webster Financial Corp. | 170,000 | 2,119,900 | 8,002,050 | |||

| Whitney Holding Corp. | 650,000 | 6,201,000 | DISTRIBUTORS — 0.2% | |||

| Wilmington Trust Corp. | 225,000 | 3,195,000 | Core-Mark Holding Co., Inc.(1) | 85,000 | 2,431,000 | |

| Zions Bancorp. | 125,000 | 2,246,250 | DIVERSIFIED — 3.3% | |||

| 96,044,702 | iShares Russell 2000 | |||||

| COMMERCIAL SERVICES & SUPPLIES — 2.3% | Index Fund | 285,000 | 17,165,550 | |||

| ABM Industries, Inc. | 100,000 | 2,104,000 | iShares Russell 2000 Value | |||

| American Ecology Corp. | 395,000 | 7,386,500 | Index Fund | 585,000 | 33,070,050 | |

| ATC Technology Corp.(1) | 155,000 | 3,062,800 | 50,235,600 | |||

| Brink’s Co. (The) | 225,000 | 6,054,750 | DIVERSIFIED CONSUMER SERVICES — 1.1% | |||

| Corinthian Colleges, Inc.(1) | 345,000 | 6,403,200 | ||||

| Consolidated | ||||||

| Graphics, Inc.(1) | 90,000 | 2,245,500 | Lincoln Educational | |||

| Services Corp.(1) | 280,000 | 6,406,400 | ||||

| G&K Services, Inc., Class A | 1,920 | 42,547 | ||||

| IESI-BFC Ltd. | 925,000 | 11,951,000 | Regis Corp. | 195,000 | 3,022,500 | |

| SYKES Enterprises, Inc.(1) | 100,000 | 2,082,000 | 15,832,100 | |||

| 34,929,097 | DIVERSIFIED FINANCIAL SERVICES — 0.2% | |||||

| COMMUNICATIONS EQUIPMENT — 1.0% | Fifth Street Finance Corp. | 210,000 | 2,295,300 | |||

| Avocent Corp.(1) | 145,000 | 2,939,150 | DIVERSIFIED TELECOMMUNICATION | |||

| SERVICES — 0.2% | ||||||

| Bel Fuse, Inc., Class B | 170,000 | 3,235,100 | Atlantic Tele-Network, Inc. | 30,000 | 1,602,600 | |

| Black Box Corp. | 80,000 | 2,007,200 | Iowa Telecommunications | |||

| Emulex Corp.(1) | 280,000 | 2,881,200 | Services, Inc. | 135,000 | 1,701,000 | |

| Opnext, Inc.(1) | 825,000 | 2,417,250 | 3,303,600 | |||

| Plantronics, Inc. | 80,000 | 2,144,800 | ELECTRIC UTILITIES — 2.0% | |||

| 15,624,700 | Central Vermont Public | |||||

| COMPUTERS & PERIPHERALS — 0.9% | Service Corp. | 134,458 | 2,595,039 | |||

| Electronics for | Cleco Corp. | 80,000 | 2,006,400 | |||

| Imaging, Inc.(1) | 390,000 | 4,395,300 | Empire District Electric | |||

| Lexmark International, Inc., | Co. (The) | 100,000 | 1,809,000 | |||

| Class A(1) | 130,000 | 2,800,200 | Great Plains Energy, Inc. | 460,000 | 8,257,000 | |

| NCR Corp.(1) | 230,000 | 3,178,600 | Portland General Electric Co. | 440,000 | 8,676,800 | |

| QLogic Corp.(1) | 140,000 | 2,408,000 | Unitil Corp. | 115,000 | 2,581,750 | |

| Silicon Graphics | Westar Energy, Inc. | 220,000 | 4,292,200 | |||

| International Corp.(1) | 200,000 | 1,342,000 | 30,218,189 | |||

| 14,124,100 | ELECTRICAL EQUIPMENT — 2.0% | |||||

| CONSTRUCTION & ENGINEERING — 1.9% | Acuity Brands, Inc. | 60,000 | 1,932,600 | |||

| Comfort Systems USA, Inc. | 360,000 | 4,172,400 | Belden, Inc. | 195,000 | 4,504,500 | |

| EMCOR Group, Inc.(1) | 235,000 | 5,950,200 | Brady Corp., Class A | 120,000 | 3,446,400 | |

| Granite Construction, Inc. | 255,000 | 7,889,700 | Encore Wire Corp. | 160,000 | 3,574,400 | |

| KBR, Inc. | 130,000 | 3,027,700 | General Cable Corp.(1) | 55,000 | 2,153,250 | |

| KHD Humboldt Wedag | Hubbell, Inc., Class B | 60,000 | 2,520,000 | |||

| International Ltd.(1) | 375,000 | 3,892,500 | ||||

| II-VI, Inc.(1) | 115,000 | 2,925,600 | ||||

| Pike Electric Corp.(1) | 246,957 | 2,958,545 | LSI Industries, Inc. | 570,000 | 3,790,500 | |

| 27,891,045 | Regal-Beloit Corp. | 45,000 | 2,056,950 | |||

| CONSTRUCTION MATERIALS — 0.2% | Thomas & Betts Corp.(1) | 100,000 | 3,008,000 | |||

| Texas Industries, Inc. | 70,000 | 2,939,300 | 29,912,200 | |||

19

| Small Cap Value | ||||||

| Shares | Value | Shares | Value | |||

| ELECTRONIC EQUIPMENT, INSTRUMENTS | GAS UTILITIES — 0.8% | |||||

| & COMPONENTS — 2.8% | Nicor, Inc. | 145,000 | $ 5,305,550 | |||

| Anixter International, Inc.(1) | 75,000 $ | $ 3,008,250 | Southwest Gas Corp. | 130,000 | 3,325,400 | |

| Benchmark | WGL Holdings, Inc. | 120,000 | 3,976,800 | |||

| Electronics, Inc.(1) | 300,000 | 5,400,000 | ||||

| 12,607,750 | ||||||

| Coherent, Inc.(1) | 125,000 | 2,915,000 | ||||

| HEALTH CARE EQUIPMENT & SUPPLIES — 2.5% | ||||||

| Electro Scientific | Analogic Corp. | 100,000 | 3,702,000 | |||

| Industries, Inc.(1) | 330,000 | 4,418,700 | ||||

| CONMED Corp.(1) | 120,000 | 2,300,400 | ||||

| FLIR Systems, Inc.(1) | 85,000 | 2,377,450 | ||||

| Cutera, Inc.(1)(2) | 730,000 | 6,314,500 | ||||

| Littelfuse, Inc.(1) | 70,000 | 1,836,800 | ||||

| Molex, Inc. | 190,000 | 3,967,200 | Utah Medical Products, Inc. | 150,000 | 4,398,000 | |

| Young Innovations, Inc.(2) | 635,000 | 16,706,850 | ||||

| Park Electrochemical Corp. | 125,000 | 3,081,250 | ||||

| Zoll Medical Corp.(1) | 215,000 | 4,626,800 | ||||

| PC Connection, Inc.(1) | 440,000 | 2,393,600 | ||||

| Rogers Corp.(1) | 215,000 | 6,443,550 | 38,048,550 | |||

| HEALTH CARE PROVIDERS & SERVICES — 3.0% | ||||||

| Tech Data Corp.(1) | 55,000 | 2,288,550 | ||||

| Alliance HealthCare | ||||||

| TTM Technologies, Inc.(1) | 160,000 | 1,835,200 | Services, Inc.(1) | 545,000 | 3,084,700 | |

| Vishay | Almost Family, Inc.(1) | 100,000 | 2,975,000 | |||

| Intertechnology, Inc.(1) | 280,000 | 2,212,000 | ||||

| AMERIGROUP Corp.(1) | 135,000 | 2,992,950 | ||||

| 42,177,550 | ||||||

| Amsurg Corp.(1) | 270,000 | 5,732,100 | ||||

| ENERGY EQUIPMENT & SERVICES — 1.4% | ||||||

| Bristow Group, Inc.(1) | 75,000 | 2,226,750 | Assisted Living Concepts, | |||

| Inc., Class A(1) | 185,000 | 3,833,200 | ||||

| Global Industries Ltd.(1) | 210,000 | 1,995,000 | ||||

| Kindred Healthcare, Inc.(1) | 180,000 | 2,921,400 | ||||

| Helix Energy Solutions | LifePoint Hospitals, Inc.(1) | 120,000 | 3,247,200 | |||

| Group, Inc.(1) | 150,000 | 2,247,000 | ||||

| Key Energy Services, Inc.(1) | 370,000 | 3,219,000 | Magellan Health | |||

| Services, Inc.(1) | 340,000 | 10,560,400 | ||||

| Lufkin Industries, Inc. | 45,000 | 2,393,100 | National Healthcare Corp. | 165,000 | 6,152,850 | |

| North American Energy | U.S. Physical Therapy, Inc.(1) | 280,735 | 4,230,677 | |||

| Partners, Inc.(1) | 275,000 | 1,650,000 | ||||

| Superior Energy | 45,730,477 | |||||

| Services, Inc.(1) | 100,000 | 2,252,000 | HOTELS, RESTAURANTS & LEISURE — 1.5% | |||

| Unit Corp.(1) | 105,000 | 4,331,250 | Bally Technologies, Inc.(1) | 100,000 | 3,837,000 | |

| 20,314,100 | Bob Evans Farms, Inc. | 110,000 | 3,196,600 | |||

| FOOD & STAPLES RETAILING — 0.9% | Burger King Holdings, Inc. | 175,000 | 3,078,250 | |||

| BJ’s Wholesale Club, Inc.(1) | 65,000 | 2,354,300 | Jack in the Box, Inc.(1) | 175,000 | 3,585,750 | |

| Casey’s General Stores, Inc. | 65,000 | 2,039,700 | Red Robin Gourmet | |||

| Burgers, Inc.(1) | 320,000 | 6,534,400 | ||||

| Ruddick Corp. | 105,000 | 2,795,100 | ||||

| Ruby Tuesday, Inc.(1) | 275,000 | 2,315,500 | ||||

| Weis Markets, Inc. | 175,572 | 5,609,525 | ||||

| 12,798,625 | 22,547,500 | |||||

| FOOD PRODUCTS — 0.5% | HOUSEHOLD DURABLES — 0.6% | |||||

| B&G Foods, Inc., Class A | 265,000 | 2,170,350 | CSS Industries, Inc | 15,000 | 296,550 | |

| Corn Products | Helen of Troy Ltd.(1) | 95,000 | 1,845,850 | |||

| International, Inc. | 65,000 | 1,853,800 | Jarden Corp. | 75,000 | 2,105,250 | |

| Farmer Bros. Co. | 35,000 | 724,500 | M.D.C. Holdings, Inc. | 60,000 | 2,084,400 | |

| Seneca Foods Corp., | M/I Homes, Inc.(1) | 175,000 | 2,378,250 | |||

| Class A(1) | 80,000 | 2,192,000 | 8,710,300 | |||

| 6,940,650 | HOUSEHOLD PRODUCTS — 0.2% | |||||

| WD-40 Co. | 105,000 | 2,982,000 | ||||

20

| Small Cap Value | ||||||

| Shares | Value | Shares | Value | |||

| INDUSTRIAL CONGLOMERATES — 0.2% | LIFE SCIENCES TOOLS & SERVICES — 0.5% | |||||

| Tredegar Corp. | 170,000 | $ 2,465,000 | Pharmaceutical Product | |||

| INSURANCE — 5.2% | Development, Inc. | 375,000 | $ 8,227,500 | |||

| American Equity Investment | MACHINERY — 3.8% | |||||

| Life Holding Co. | 335,000 | 2,351,700 | Actuant Corp., Class A | 370,000 | 5,942,200 | |

| Assured Guaranty Ltd. | 185,000 | 3,592,700 | Barnes Group, Inc. | 265,000 | 4,528,850 | |

| Baldwin & Lyons, Inc., | FreightCar America, Inc. | 115,000 | 2,794,500 | |||

| Class B | 265,000 | 6,214,250 | IDEX Corp. | 120,000 | 3,354,000 | |

| Delphi Financial Group, Inc., | Kadant, Inc.(1) | 165,000 | 2,001,450 | |||

| Class A | 120,000 | 2,715,600 | ||||

| Kaydon Corp. | 65,000 | 2,107,300 | ||||

| Erie Indemnity Co., Class A | 260,000 | 9,739,600 | ||||

| Kennametal, Inc. | 220,000 | 5,414,200 | ||||

| Hanover Insurance | ||||||

| Group, Inc. (The) | 125,000 | 5,166,250 | Lincoln Electric | |||

| Holdings, Inc. | 115,000 | 5,456,750 | ||||

| HCC Insurance | ||||||

| Holdings, Inc. | 500,000 | 13,675,000 | Mueller Industries, Inc. | 425,000 | 10,144,750 | |

| Max Capital Group Ltd. | 145,000 | 3,098,650 | Mueller Water Products, | |||

| Inc., Class A | 930,000 | 5,096,400 | ||||

| Mercer Insurance | ||||||

| Group, Inc.(2) | 300,000 | 5,421,000 | Pentair, Inc. | 75,000 | 2,214,000 | |

| Platinum Underwriters | RBC Bearings, Inc.(1) | 130,000 | 3,032,900 | |||

| Holdings Ltd. | 180,000 | 6,451,200 | Robbins & Myers, Inc. | 135,000 | 3,169,800 | |

| ProAssurance Corp.(1) | 105,000 | 5,479,950 | Wabtec Corp. | 60,000 | 2,251,800 | |

| United Fire & Casualty Co. | 125,000 | 2,237,500 | 57,508,900 | |||

| Unitrin, Inc. | 175,000 | 3,410,750 | MARINE — 0.5% | |||

| Validus Holdings Ltd. | 145,905 | 3,764,349 | Diana Shipping, Inc. | 375,000 | 4,875,000 | |

| Zenith National | Genco Shipping | |||||

| Insurance Corp. | 145,000 | 4,480,500 | & Trading Ltd. | 140,000 | 2,909,200 | |

| 77,798,999 | 7,784,200 | |||||

| INTERNET SOFTWARE & SERVICES — 0.7% | MEDIA — 3.1% | |||||

| Akamai Technologies, Inc.(1) | 160,000 | 3,148,800 | Belo Corp., Class A | 625,000 | 3,381,250 | |

| IAC/InterActiveCorp(1) | 170,000 | 3,432,300 | E.W. Scripps Co. (The), | |||

| Class A(1) | 735,000 | 5,512,500 | ||||

| RealNetworks, Inc.(1) | 1,175,000 | 4,371,000 | ||||

| Entercom Communications | ||||||

| 10,952,100 | Corp., Class A(1) | 1,028,191 | 5,243,774 | |||

| IT SERVICES — 1.5% | Entravision Communications | |||||

| CACI International, Inc., | Corp., Class A(1) | 3,194,902 | 5,527,181 | |||

| Class A(1) | 75,000 | 3,545,250 | ||||

| Gannett Co., Inc. | 185,000 | 2,314,350 | ||||

| Cass Information | Harte-Hanks, Inc. | 325,000 | 4,494,750 | |||

| Systems, Inc. | 85,000 | 2,538,100 | ||||

| Heartland Payment | Interactive Data Corp. | 115,000 | 3,014,150 | |||

| Systems, Inc. | 150,000 | 2,176,500 | Journal Communications, | |||

| MAXIMUS, Inc. | 45,000 | 2,097,000 | Inc., Class A | 984,500 | 3,622,960 | |

| McClatchy Co. (The), | ||||||

| NeuStar, Inc., Class A(1) | 80,000 | 1,808,000 | Class A | 2,725,000 | 6,976,000 | |

| Perot Systems Corp., | Sinclair Broadcast Group, | |||||

| Class A(1) | 210,000 | 6,237,000 | Inc., Class A, Class A | 1,175,000 | 4,206,500 | |

| Total System Services, Inc. | 230,000 | 3,705,300 | Value Line, Inc. | 90,000 | 2,778,300 | |

| 22,107,150 | 47,071,715 | |||||

| LEISURE EQUIPMENT & PRODUCTS — 0.5% | METALS & MINING — 2.0% | |||||

| JAKKS Pacific, Inc.(1) | 165,000 | 2,362,800 | Brush Engineered | |||

| RC2 Corp.(1) | 130,000 | 1,852,500 | Materials, Inc.(1) | 120,000 | 2,935,200 | |

| Sport Supply Group, Inc. | 275,000 | 2,802,250 | Carpenter Technology Corp. | 155,000 | 3,625,450 | |

| 7,017,550 | Commercial Metals Co. | 200,000 | 3,580,000 | |||

21

| Small Cap Value | ||||||

| Shares | Value | Shares | Value | |||

| Globe Specialty | PHARMACEUTICALS — 1.0% | |||||

| Metals, Inc.(1) | 270,000 | $ 2,435,400 | Biovail Corp. | 160,000 | $ 2,468,800 | |

| Haynes International, Inc.(1) | 180,000 | 5,727,600 | Endo Pharmaceuticals | |||

| Kaiser Aluminum Corp. | 45,000 | 1,636,200 | Holdings, Inc.(1) | 185,000 | 4,186,550 | |

| Mesabi Trust | 270,000 | 2,740,500 | Obagi Medical | |||

| Royal Gold, Inc. | 85,000 | 3,876,000 | Products, Inc.(1) | 145,000 | 1,682,000 | |

| RTI International | Par Pharmaceutical | |||||

| Metals, Inc.(1) | 125,000 | 3,113,750 | Cos., Inc.(1) | 95,000 | 2,043,450 | |

| 29,670,100 | Perrigo Co. | 90,000 | 3,059,100 | |||

| MULTILINE RETAIL — 0.5% | Sepracor, Inc.(1) | 90,000 | 2,061,000 | |||

| Big Lots, Inc.(1) | 190,000 | 4,753,800 | 15,500,900 | |||

| Fred’s, Inc., Class A | 185,000 | 2,355,050 | PROFESSIONAL SERVICES — 0.9% | |||

| 7,108,850 | CDI Corp. | 190,000 | 2,669,500 | |||

| MULTI-UTILITIES — 0.8% | Heidrick & Struggles | |||||

| International, Inc. | 110,000 | 2,558,600 | ||||

| Avista Corp. | 165,000 | 3,336,300 | ||||

| Korn/Ferry International(1) | 120,000 | 1,750,800 | ||||

| Black Hills Corp. | 140,000 | 3,523,800 | ||||

| MPS Group, Inc.(1) | 195,000 | 2,051,400 | ||||

| MDU Resources Group, Inc. | 155,000 | 3,231,750 | ||||

| TrueBlue, Inc.(1) | 150,000 | 2,110,500 | ||||

| NorthWestern Corp. | 105,000 | 2,565,150 | ||||

| 12,657,000 | Watson Wyatt Worldwide, | |||||

| Inc., Class A | 60,000 | 2,613,600 | ||||

| OFFICE ELECTRONICS — 0.1% | 13,754,400 | |||||

| Zebra Technologies Corp., | ||||||

| Class A(1) | 80,000 | 2,074,400 | REAL ESTATE INVESTMENT TRUSTS (REITs) — 3.4% | |||

| OIL, GAS & CONSUMABLE FUELS — 3.5% | BioMed Realty Trust, Inc. | 150,000 | 2,070,000 | |||

| Berry Petroleum Co., Class A | 75,000 | 2,008,500 | Capstead Mortgage Corp. | 195,000 | 2,712,450 | |

| Bill Barrett Corp.(1) | 185,000 | 6,066,150 | Chimera Investment Corp. | 985,000 | 3,762,700 | |

| DHT Maritime, Inc. | 1,700,000 | 6,392,000 | DCT Industrial Trust, Inc. | 585,000 | 2,989,350 | |

| Forest Oil Corp.(1) | 520,000 | 10,176,400 | Getty Realty Corp. | 85,000 | 2,085,900 | |

| Frontier Oil Corp. | 255,000 | 3,549,600 | Hatteras Financial Corp. | 90,000 | 2,698,200 | |

| Goodrich Petroleum Corp.(1) | 85,000 | 2,193,850 | Healthcare Realty Trust, Inc. | 160,000 | 3,380,800 | |

| Highwoods Properties, Inc. | 195,000 | 6,132,750 | ||||

| Mariner Energy, Inc.(1) | 360,000 | 5,104,800 | ||||

| Inland Real Estate Corp. | 170,000 | 1,489,200 | ||||

| Nordic American | ||||||

| Tanker Shipping | 70,000 | 2,070,600 | Medical Properties | |||

| Trust, Inc. | 290,000 | 2,264,900 | ||||

| Penn Virginia Corp. | 135,000 | 3,092,850 | MFA Financial, Inc. | 800,000 | 6,368,000 | |

| St. Mary Land | ||||||

| & Exploration Co. | 75,000 | 2,434,500 | National Health | |||

| Investors, Inc. | 110,000 | 3,481,500 | ||||

| W&T Offshore, Inc. | 860,000 | 10,070,600 | National Retail | |||

| 53,159,850 | Properties, Inc. | 100,000 | 2,147,000 | |||

| PAPER & FOREST PRODUCTS — 0.4% | Omega Healthcare | |||||

| Louisiana-Pacific Corp.(1) | 475,013 | 3,168,337 | Investors, Inc. | 140,000 | 2,242,800 | |

| P.H. Glatfelter Co. | 185,000 | 2,123,800 | Redwood Trust, Inc. | 120,000 | 1,860,000 | |

| 5,292,137 | Senior Housing | |||||

| PERSONAL PRODUCTS — 0.7% | Properties Trust | 115,000 | 2,197,650 | |||

| Alberto-Culver Co. | 65,000 | 1,799,200 | Sunstone Hotel | |||

| Investors, Inc.(1) | 205,000 | 1,455,500 | ||||

| Inter Parfums, Inc. | 305,000 | 3,724,050 | ||||

| Washington Real Estate | ||||||

| Prestige Brands | Investment Trust | 80,000 | 2,304,000 | |||

| Holdings, Inc.(1) | 345,000 | 2,428,800 | ||||

| Schiff Nutrition | 51,642,700 | |||||

| International, Inc. | 460,000 | 2,396,600 | ||||

| 10,348,650 | ||||||

22

| Small Cap Value | ||||||

| Shares | Value | Shares | Value | |||

| ROAD & RAIL — 0.5% | Children’s Place Retail | |||||

| Arkansas Best Corp. | 90,000 | $ 2,694,600 | Stores, Inc. (The)(1) | 175,000 | $ 5,243,000 | |

| Old Dominion Freight | Christopher & Banks Corp. | 680,000 | 4,603,600 | |||

| Line, Inc.(1) | 65,000 | 1,977,950 | Dress Barn, Inc. (The)(1) | 245,000 | 4,392,850 | |

| Werner Enterprises, Inc. | 120,000 | 2,235,600 | DSW, Inc., Class A(1) | 130,000 | 2,076,100 | |

| 6,908,150 | Finish Line, Inc. (The), | |||||

| SEMICONDUCTORS & SEMICONDUCTOR | Class A | 590,000 | 5,994,400 | |||

| EQUIPMENT — 2.5% | Foot Locker, Inc. | 200,000 | 2,390,000 | |||

| Cohu, Inc. | 165,000 | 2,237,400 | Genesco, Inc.(1) | 235,000 | 5,656,450 | |

| Cymer, Inc.(1) | 65,000 | 2,525,900 | Hot Topic, Inc.(1) | 400,000 | 2,996,000 | |

| Integrated Device | Men’s Wearhouse, Inc. (The) | 105,000 | 2,593,500 | |||

| Technology, Inc.(1) | 475,000 | 3,211,000 | ||||

| PEP Boys-Manny | ||||||

| Intellon Corp.(1) | 615,000 | 4,360,350 | Moe & Jack | 310,000 | 3,028,700 | |

| Intersil Corp., Class A | 195,000 | 2,985,450 | RadioShack Corp. | 140,000 | 2,319,800 | |

| Mattson Technology, Inc.(1) | 800,000 | 2,256,000 | Rent-A-Center, Inc., | |||

| MEMC Electronic | Class A(1) | 240,000 | 4,531,200 | |||

| Materials, Inc.(1) | 175,000 | 2,910,250 | Stage Stores, Inc. | 180,000 | 2,332,800 | |

| MKS Instruments, Inc.(1) | 135,000 | 2,604,150 | Wet Seal, Inc. (The), | |||

| Rudolph Technologies, Inc.(1) | 283,718 | 2,099,513 | Class A(1) | 1,225,000 | 4,630,500 | |

| Sigma Designs, Inc.(1) | 195,000 | 2,833,350 | 71,462,400 | |||

| Varian Semiconductor | TEXTILES, APPAREL & LUXURY GOODS — 1.2% | |||||

| Equipment Associates, Inc.(1) | 90,000 | 2,955,600 | Crocs, Inc.(1) | 300,000 | 1,995,000 | |

| Verigy Ltd.(1) | 375,000 | 4,357,500 | Deckers Outdoor Corp.(1) | 65,000 | 5,515,250 | |

| Zoran Corp.(1) | 190,000 | 2,188,800 | Skechers U.S.A., Inc., | |||

| Class A(1) | 105,000 | 1,799,700 | ||||

| 37,525,263 | ||||||

| SOFTWARE — 3.5% | Volcom, Inc.(1) | 145,000 | 2,389,600 | |||

| Aspen Technology, Inc.(1) | 290,000 | 2,958,000 | Weyco Group, Inc. | 100,000 | 2,290,000 | |

| Cadence Design | Wolverine World Wide, Inc. | 150,000 | 3,726,000 | |||

| Systems, Inc.(1) | 300,000 | 2,202,000 | 17,715,550 | |||

| Compuware Corp.(1) | 400,000 | 2,932,000 | THRIFTS & MORTGAGE FINANCE — 1.7% | |||

| Parametric | Brookline Bancorp., Inc. | 300,000 | 2,916,000 | |||

| Technology Corp.(1) | 1,025,000 | 14,165,500 | First Financial | |||

| Radiant Systems, Inc.(1) | 205,000 | 2,201,700 | Northwest, Inc. | 385,000 | 2,240,700 | |

| Sybase, Inc.(1) | 275,000 | 10,697,500 | First Niagara Financial | |||

| Group, Inc. | 520,000 | 6,411,600 | ||||

| Synopsys, Inc.(1) | 150,000 | 3,363,000 | ||||

| Flushing Financial Corp. | 185,000 | 2,109,000 | ||||

| THQ, Inc.(1) | 710,000 | 4,856,400 | ||||

| K-Fed Bancorp. | 260,000 | 2,345,200 | ||||

| TIBCO Software, Inc.(1) | 370,000 | 3,511,300 | ||||

| PMI Group, Inc. (The) | 475,000 | 2,018,750 | ||||

| Ulticom, Inc.(2) | 2,112,830 | 6,127,207 | Provident Financial | |||

| 53,014,607 | Services, Inc. | 215,000 | 2,212,350 | |||

| SPECIALTY RETAIL — 4.7% | Washington Federal, Inc. | 270,000 | 4,552,200 | |||

| Aaron’s, Inc. | 115,000 | 3,036,000 | 24,805,800 | |||

| American Eagle | TRADING COMPANIES & DISTRIBUTORS — 1.0% | |||||

| Outfitters, Inc. | 175,000 | 2,950,500 | GATX Corp. | 80,000 | 2,236,000 | |

| Barnes & Noble, Inc. | 165,000 | 3,666,300 | Kaman Corp. | 260,000 | 5,714,800 | |

| Bebe Stores, Inc. | 305,000 | 2,244,800 | Lawson Products, Inc. | 180,000 | 3,133,800 | |

| Cabela’s, Inc.(1) | 295,000 | 3,935,300 | WESCO International, Inc.(1) | 125,000 | 3,600,000 | |

| Cato Corp. (The), Class A | 140,000 | 2,840,600 | 14,684,600 | |||

23

| Small Cap Value | |||||||

| Shares | Value | Shares | Value | ||||

| WATER UTILITIES — 0.2% | Temporary Cash Investments — 2.3% | ||||||

| Artesian Resources Corp., | |||||||

| Class A | 175,000 | $ 2,943,500 | JPMorgan U.S. Treasury | ||||

| Plus Money Market Fund | |||||||

| TOTAL COMMON STOCKS | Agency Shares | 27,332 | $ 27,332 | ||||

| (Cost $1,158,592,345) | 1,369,048,256 | ||||||

| Repurchase Agreement, Credit Suisse First | |||||||

| Convertible Preferred Stocks — 4.5% | Boston, Inc., (collateralized by various | ||||||

| U.S. Treasury obligations, 0.24%, 6/10/10, | |||||||

| COMMERCIAL BANKS — 0.2% | valued at $35,498,718), in a joint trading | ||||||

| Huntington Bancshares, Inc., | account at 0.01%, dated 9/30/09, due | ||||||

| Series A, 8.50%, 4/15/13(3) | 2,200 | 1,914,000 | 10/1/09 (Delivery value $34,800,010) | 34,800,000 | |||

| Midwest Banc Holdings, Inc., | TOTAL TEMPORARY | ||||||

| Series A, 7.75%, 12/10/12(3) | 140,000 | 448,000 | CASH INVESTMENTS | ||||

| 2,362,000 | (Cost $34,827,332) | 34,827,332 | |||||

| INSURANCE — 2.6% | TOTAL INVESTMENT | ||||||

| Aspen Insurance Holdings | SECURITIES — 98.7% | ||||||

| Ltd., Series AHL, | (Cost $1,270,927,050) | 1,487,300,115 | |||||

| 5.625%, 2/6/13(3) | 770,000 | 39,077,500 | OTHER ASSETS | ||||

| LEISURE EQUIPMENT & PRODUCTS — 0.3% | AND LIABILITIES — 1.3% | 19,059,836 | |||||

| Callaway Golf Co., Series B, | TOTAL NET ASSETS — 100.0% | $1,506,359,951 | |||||

| 7.50%, 6/15/12(3)(4) | 40,000 | 5,030,000 | |||||

| MEDIA — 0.2% | Notes to Schedule of Investments | ||||||

| LodgeNet Interactive Corp., | (1) | Non-income producing. | |||||

| 10.00%, 12/31/49(1)(3)(4) | 1,669 | 3,509,073 | (2) | Affiliated Company: the fund’s holding represents ownership of | |||

| REAL ESTATE INVESTMENT TRUSTS (REITs) — 0.9% | 5% or more of the voting securities of the company; therefore, the | ||||||

| Digital Realty Trust, Inc., | company is affiliated as defined in the Investment Company Act of | ||||||

| Series D, 5.50%, 2/6/13(3) | 305,000 | 8,555,250 | 1940. | ||||

| Entertainment Properties | (3) | Perpetual security. These securities do not have a predetermined | |||||

| Trust, Series E, | maturity date. The coupon rates are fixed for a period of time and | ||||||

| 9.00%, 4/20/13(3) | 125,000 | 2,696,250 | may be structured to adjust thereafter. Interest reset or next call | ||||

| date is indicated, as applicable. | |||||||

| Lexington Realty Trust, | |||||||

| Series C, 6.50%, 11/16/09(3) | 70,000 | 2,088,100 | (4) | Security was purchased under Rule 144A or Section 4(2) of | |||

| the Securities Act of 1933 or is a private placement and, unless | |||||||

| 13,339,600 | registered under the Act or exempted from registration, may only | ||||||

| TOBACCO — 0.3% | be sold to qualified institutional investors. The aggregate value | ||||||

| Universal Corp., | of these securities at the period end was $8,539,073, which | ||||||

| 6.75%, 3/15/18(3) | 4,900 | 5,145,000 | represented 0.6% of total net assets. | ||||

| TOTAL CONVERTIBLE | |||||||

| PREFERRED STOCKS | |||||||

| (Cost $63,186,360) | 68,463,173 | See Notes to Financial Statements. | |||||

| Preferred Stocks — 1.0% | |||||||

| INSURANCE — 0.3% | |||||||

| Odyssey Re Holdings | |||||||

| Corp., Series A, | |||||||

| 8.125%, 10/20/10(3) | 150,000 | 3,753,000 | |||||

| REAL ESTATE INVESTMENT TRUSTS (REITs) — 0.7% | |||||||

| National Retail Properties, | |||||||

| Inc., Series C, | |||||||

| 7.375%, 10/12/11(3) | 275,000 | 6,294,750 | |||||

| PS Business Parks, Inc., | |||||||

| Series K, 7.95%, 11/9/09(3) | 205,000 | 4,913,604 | |||||

| 11,208,354 | |||||||

| TOTAL PREFERRED STOCKS | |||||||

| (Cost $14,321,013) | 14,961,354 | ||||||

24

| Statement of Assets and Liabilities |

| SEPTEMBER 30, 2009 (UNAUDITED) | ||

| Mid Cap Value | Small Cap Value | |

| Assets | ||

| Investment securities — unaffiliated, at value (cost of $374,599,828 | ||

| and $1,228,597,570, respectively) | $431,857,733 | $1,452,730,558 |

| Investment securities — affiliated, at value (cost of $– and | ||

| $42,329,480, respectively) | — | 34,569,557 |

| Total investment securities, at value (cost of $374,599,828 | ||

| and $1,270,927,050, respectively) | 431,857,733 | 1,487,300,115 |

| Receivable for investments sold | 6,022,754 | 25,684,593 |

| Receivable for capital shares sold | 743,223 | 13,497,104 |

| Dividends and interest receivable | 903,500 | 2,765,274 |

| 439,527,210 | 1,529,247,086 | |

| Liabilities | ||

| Payable for investments purchased | 9,331,364 | 19,247,573 |

| Payable for capital shares redeemed | 189,393 | 2,160,720 |

| Payable for forward foreign currency exchange contracts | 184,606 | — |

| Accrued management fees | 327,920 | 1,412,353 |

| Distribution and service fees payable | 12,968 | 66,489 |

| 10,046,251 | 22,887,135 | |

| Net Assets | $429,480,959 | $1,506,359,951 |