Table of Contents

As filed with the Securities and Exchange Commission on April 15, 2021

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 20-F

| ☐ | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| ☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2020

OR

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| ☐ | SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission file number: 001-12568

BANCO BBVA ARGENTINA S.A.

(Exact name of Registrant as specified in its charter)

BBVA ARGENTINE BANK

(Translation of Registrant’s name into English)

Republic of Argentina

(Jurisdiction of incorporation or organization)

Av. Córdoba 111, C1054AAA

Ciudad Autónoma de Buenos Aires, Argentina

(Address of principal executive offices)

Eduardo González Correas – 011-54-11-4348-0000 (ext. 14483) – egonzalezcorreas@bbva.com – Av. Córdoba 111 31° (C1054AAA)

Ciudad Autónoma de Buenos Aires, Republic of Argentina

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

Title of each class | Name of each exchange on which registered | |

| American Depositary Shares, each representing the right to receive three ordinary shares, par value Ps.1.00 per share | New York Stock Exchange | |

| Ordinary shares, par value Ps.1.00 per share | New York Stock Exchange* |

| * | The ordinary shares are not listed for trading, but are listed only in connection with the registration of the American Depositary Shares, pursuant to requirements of the New York Stock Exchange. |

Securities registered or to be registered pursuant to Section 12(g) of the Act: None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock

as of the close of the period covered by the annual report:

Title of class | Number of shares outstanding | |

| Ordinary Shares, par value Ps.1.00 per share | 612,710,079 |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ☐ Yes ☒ No

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. ☐ Yes ☒ No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days: ☒ Yes ☐ No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). ☒ Yes ☐ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or an emerging growth company. See definition of “large accelerated filer”, “accelerated filer” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer | ☐ | Accelerated filer | ☒ | |||

| Non-accelerated filer | ☐ | Emerging growth company | ☐ | |||

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☐

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| U.S. GAAP | ☐ | International Financial Reporting Standards by the International Accounting Standards Board as issued | ☒ | Other | ☐ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow. ☐ Item 17 ☐ Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). ☐ Yes ☒ No

Table of Contents

| Page | ||||||

| 1 | ||||||

| 1 | ||||||

| 3 | ||||||

| PART I | ||||||

ITEM 1. | 3 | |||||

ITEM 2. | 3 | |||||

ITEM 3. | 3 | |||||

ITEM 4. | 34 | |||||

ITEM 4A. | 119 | |||||

ITEM 5. | 119 | |||||

ITEM 6. | 154 | |||||

ITEM 7. | 168 | |||||

ITEM 8. | 171 | |||||

ITEM 9. | 172 | |||||

ITEM 10. | 176 | |||||

ITEM 11. | 187 | |||||

ITEM 12. | 196 | |||||

| PART II | ||||||

ITEM 13. | 198 | |||||

ITEM 14. | MATERIAL MODIFICATIONS TO THE RIGHTS OF SECURITY HOLDERS AND USE OF PROCEEDS | 198 | ||||

ITEM 15. | 198 | |||||

ITEM 16A. | 200 | |||||

ITEM 16B. | 200 | |||||

ITEM 16C. | 200 | |||||

ITEM 16D. | 201 | |||||

ITEM 16E. | PURCHASES OF EQUITY SECURITIES BY ONE ISSUER AND AFFILIATED PERSONS | 201 | ||||

ITEM 16F. | 201 | |||||

ITEM 16G. | 201 | |||||

| PART III | ||||||

ITEM 17. | 205 | |||||

ITEM 18. | 205 | |||||

ITEM 19. | 205 | |||||

Table of Contents

This Form 20-F contains words, such as “believe”, “expect”, “estimate”, “intend”, “plan”, “may” and “anticipate” and similar expressions that identify forward-looking statements, which reflect our views about future events and financial performance. Actual results could differ materially as a result of factors beyond our control, including but not limited to:

| • | changes in general economic, business or political or other conditions in the Republic of Argentina (“Argentina” or “the Republic”) or changes in general economic or business conditions in Latin America; |

| • | effects of the Covid-19 pandemic; |

| • | changes in exchange rates or capital markets in general that may affect policies towards or lending to Argentina or Argentine companies; |

| • | increased costs and decreased income related to macroeconomic variables such as exchange rates and the Consumer Price Index in Argentina (“CPI”); |

| • | unanticipated increases in financing and other costs or the inability to obtain additional debt, equity or wholesale financing on attractive terms or at all; and |

| • | the factors discussed under “Item 3. Key Information—D. Risk Factors”. |

Accordingly, readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date hereof. Banco BBVA Argentina S.A. (“BBVA Argentina” or the “Bank”), formerly BBVA Banco Francés S.A. undertakes no obligation to update or revise these forward-looking statements or to publicly release the results of any revisions to these forward-looking statements. The accompanying information in this annual report, including, without limitation, the information under “Item 4. Information on the Company”, “Item 5. Operating and Financial Review and Prospects” and “Item 11. Quantitative and Qualitative Disclosures About Market Risk” identifies important factors that could cause material differences between any forward-looking statements and actual results.

PRESENTATION OF FINANCIAL INFORMATION

General

The Bank’s audited consolidated financial statements as of December 31, 2020 and 2019 and for the years ended December 31, 2020, 2019 and 2018 (the “Consolidated Financial Statements”) are prepared in accordance with International Financial Reporting Standards as issued by the International Accounting Standards Board (“IFRS-IASB”).

All 2020, 2019 and 2018 data included in this report have been prepared in accordance with IFRS-IASB for the sole purpose of filing this annual report on Form 20-F with the U.S. Securities and Exchange Commission (“SEC”).

The statutory consolidated annual financial statements that the Bank prepares to comply with the requirements of the Argentine Central Bank (the “Central Bank” or “BCRA”) are prepared pursuant to the reporting framework established by the Central Bank requiring supervised entities to submit financial statements prepared pursuant to IFRS-IASB except for:

| (i) | temporary exceptions from the application of the expected loss model set forth under paragraph 5.5. of IFRS 9 for debt instruments issued by the non-financial government sector. In addition, the BCRA issued Communication “A” 6938, extended by Communication “A” 7181, deferring the application of the impairment model set forth in paragraph 5.5 of IFRS 9 to fiscal years beginning on or after January 1, 2022 for Group “C” institutions (institutions consolidated by the Bank), which would remain subject to the impairment model established by the BCRA that requires financial institutions recognize an allowance for loan losses based on the minimum guidelines set forth by the BCRA; |

| (ii) | the treatment to be applied to uncertain tax positions, which follows the guidance prescribed by Memorandum No. 6/2017 Financial Reporting Framework Established by the BCRA issued on May 29, 2017; |

| (iii) | the accounting treatment to be applied to the remaining investment held by the Bank in Prisma Medios de Pago S.A.,by applying the instructions provided in Memorandum No. 7/2019 issued by the BCRA dated April 29, 2019; and |

| (iv) | the debt securities issued by the government sector received in exchange for other instruments, which are measured at the carrying value of the instruments delivered in replacement on such date, in accordance with Communication “A” 7014 issued by the BCRA. According to the IFRS-IASB, these instruments should be accounted for at fair value, recognizing in profit or loss the difference with the carrying value of the instruments delivered. |

Because of such differences, our statutory consolidated annual financial statements for the fiscal year ended December 31, 2020 are not comparable with the Consolidated Financial Statements included herein. In addition, we will continue to have differences during the year 2021 between our statutory consolidated financial statements and the financial statements required by IFRS-IASB. We do not intend to report in accordance with IFRS-IASB on an interim basis during 2021. Consequently, our interim financial information for 2021 will not be comparable with the Consolidated Financial Statements and other information contained in this annual report on Form 20-F. We refer in this annual report on Form 20-F to IFRS-IASB as adjusted by the regulations of the BCRA as “IFRS-BCRA”.

1

Table of Contents

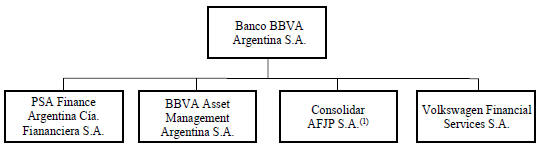

The Consolidated Financial Statements consolidate all the subsidiaries of the Bank in which the Bank holds direct or indirect control. See “Item 4. Information on the Company—C. Organizational Structure” for an organizational chart of BBVA Argentina and its subsidiaries.

In this annual report, references to “$”, “US$”, “U.S. dollars”, “US dollars” and “dollars” are to United States dollars and references to “Ps.”, “Pesos” and “pesos” are to Argentine pesos. Percentages and certain dollar and peso amounts have been rounded for ease of presentation. Unless otherwise stated, all market share and other industry information has been derived from information published by the Central Bank.

Unless otherwise indicated, financial information contained in this annual report reflects the consolidation of the following subsidiaries at the year end and for the fiscal years indicated below:

| As of December 31, | ||||||

Entity | 2020 | 2019 | 2018 | |||

Volkswagen Financial Services Compañía Financiera S.A. | X | X | ||||

Consolidar AFJP S.A. (undergoing liquidation proceedings) | X | X | X | |||

BBVA Francés Valores S.A. (1) | X | |||||

BBVA Asset Management Argentina S.A. | X | X | X | |||

PSA Finance Argentina Compañía Financiera S.A. | X | X | ||||

| (1) | Merged into the Bank as from October 1, 2019. |

On September 25, 2018, BBVA Francés lost control of Volkswagen Financial Services Compañia Financiera S.A. (“VWFS”) due to the termination of the two year commitment by the Bank to provide financing to VWFS if it were unable to diversify its sources of funding. According to IAS 28 Investments in Associates and Joint Ventures, VWFS qualified thereafter as a joint venture and, as such, it was deconsolidated in 2018 as of the date of loss of control.

Pursuant to certain amendments to the relevant shareholders’ agreements, effective since July 1, 2019, the Bank has assumed the power to direct the relevant activities of VWFS and PSA Finance Argentina Compañía Financiera S.A. Pursuant to International Financial Reporting Standard (“IFRS”) 10, the Bank concluded that it controls such companies effective since July 1, 2019. Therefore, the Consolidated Financial Statements consolidate financial information for these companies since the date on which the Bank gained control over them.

Also on October 9, 2019 the Argentine National Securities Commission (“CNV”) issued Resolution No. 20484/2019 approving the merger by absorption of the Bank with BBVA Francés Valores S.A.

IAS 29 Financial Reporting in Hyperinflationary Economies requires that an entity whose functional currency is the currency of a hyperinflationary economy must state its assets, liabilities, income and expenses in terms of the measuring unit current at the end of the reporting period (December 31, 2020). The Bank has applied IAS 29 as follows for purposes of the Consolidated Financial Statements:

| • | Restated the consolidated statement of profit or loss, the consolidated statement of comprehensive income, the consolidated statement of changes in equity and consolidated statements of cash flow for the years ended December 31, 2019 and 2018, including the calculation and separate disclosure of the gain or loss on the net monetary position. |

| • | Restated the consolidated statement of financial position as of December 31, 2019. |

| • | Adjusted the consolidated statement of financial position as of December 31, 2020. |

| • | Adjusted the consolidated statement of profit or loss, the consolidated statement of comprehensive income, the consolidated statement of changes in equity and consolidated statements of cash flow for the year ended December 31, 2020, including the calculation and separate disclosure of the gain or loss on the net monetary position. |

2

Table of Contents

For further information regarding the methodology and criteria applied see Note 5.22 to the Consolidated Financial Statements.

See “Item 3. Key Information—A. Selected Financial Data—Exchange Rates” for information regarding the evolution of rates of exchange since 2012.

All figures and percentages of variations in this annual report on Form 20-F, unless otherwise stated, are presented in the measuring unit current at December 31, 2020. All comparisons of the financial system contained in this annual report on Form 20-F are presented in nominal terms.

The terms below are used as follows throughout this report:

| • | “BBVA Argentina”, the “Bank” or the “Company” and terms such as “we”, “us” and “our” mean Banco BBVA Argentina S.A. and its consolidated subsidiaries unless otherwise indicated or the context otherwise requires. |

| • | “BBVA” or the “BBVA Group” means Banco Bilbao Vizcaya Argentaria, S.A. and its consolidated subsidiaries unless otherwise indicated or the context otherwise requires. |

| • | “Consolidated Financial Statements” means our audited consolidated financial statements as of December 31, 2020 and 2019 and for the years ended December 31, 2020, 2019 and 2018, prepared in accordance with IFRS-IASB and included in this Form 20-F. |

- PART I -

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not applicable.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not applicable.

| A. | Selected Financial Data |

The financial information set forth below as of and for the years ended December 31, 2020, 2019, 2018 and 2017 has been selected from, and should be read together with, the Consolidated Financial Statements included herein.

For information concerning the preparation and presentation of the Consolidated Financial Statements, see “Presentation of Financial Information”. See also “D. Risk Factors—Risks Relating to Argentina”, and “D. Risk Factors—Risks Relating to the Argentine Financial System and to BBVA Argentina” below.

3

Table of Contents

| For the year ended December 31, | ||||||||||||||||

| 2020 | 2019 | 2018 | 2017 | |||||||||||||

| (in thousands of pesos) (1) | ||||||||||||||||

CONSOLIDATED STATEMENT OF PROFIT OR LOSS | ||||||||||||||||

Interest income | 118,522,759 | 156,367,921 | 118,269,467 | 74,795,581 | ||||||||||||

Interest expenses | (41,471,892 | ) | (66,123,069 | ) | (51,808,825 | ) | (25,046,199 | ) | ||||||||

|

|

|

|

|

|

|

| |||||||||

NET INTEREST INCOME | 77,050,867 | 90,244,852 | 66,460,642 | 49,749,382 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Fee and commission income | 23,663,181 | 23,976,155 | 26,334,964 | 22,560,248 | ||||||||||||

Fee and commission expense | (11,423,234 | ) | (12,841,847 | ) | (11,521,703 | ) | (10,225,068 | ) | ||||||||

Gains on financial assets and liabilities at fair value through profit or loss, net | 11,239,112 | 15,604,469 | 242,608 | 9,133,787 | ||||||||||||

(Losses) gains on derecognition of financial assets not measured at fair value through profit or loss, net | (2,309,858 | ) | (80,874 | ) | (286,372 | ) | 25,096 | |||||||||

Exchange differences, net | 6,227,725 | 14,026,409 | 13,589,850 | 7,072,763 | ||||||||||||

Other operating income | 6,322,980 | 11,982,201 | 4,412,604 | 4,069,562 | ||||||||||||

Other operating expenses | (15,590,218 | ) | (22,028,412 | ) | (16,720,831 | ) | (15,384,948 | ) | ||||||||

|

|

|

|

|

|

|

| |||||||||

GROSS INCOME | 95,180,555 | 120,882,953 | 82,511,762 | 67,000,822 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Administration costs | (39,138,572 | ) | (41,728,066 | ) | (40,920,004 | ) | (41,114,132 | ) | ||||||||

|

|

|

|

|

|

|

| |||||||||

Personnel benefits | (20,379,135 | ) | (22,698,425 | ) | (22,801,895 | ) | (23,501,740 | ) | ||||||||

Other administrative expenses | (18,759,437 | ) | (19,029,641 | ) | (18,118,109 | ) | (17,612,392 | ) | ||||||||

Depreciation and amortization | (4,065,981 | ) | (5,728,534 | ) | (4,025,755 | ) | (2,993,487 | ) | ||||||||

Impairment of financial assets | (11,864,861 | ) | (21,445,415 | ) | (8,029,553 | ) | (5,293,972 | ) | ||||||||

Loss on net monetary position | (22,274,824 | ) | (27,518,847 | ) | (24,407,251 | ) | (12,900,314 | ) | ||||||||

|

|

|

|

|

|

|

| |||||||||

NET OPERATING INCOME | 17,836,317 | 24,462,091 | 5,129,199 | 4,698,917 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Share of profit of equity accounted investees | 266,572 | 174,422 | 664,982 | 708,523 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

PROFIT BEFORE TAX | 18,102,889 | 24,636,513 | 5,794,181 | 5,407,440 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Income tax expense | (8,034,094 | ) | (2,821,059 | ) | (9,081,582 | ) | (1,513,102 | ) | ||||||||

|

|

|

|

|

|

|

| |||||||||

PROFIT (LOSS) FOR THE YEAR | 10,068,795 | 21,815,454 | (3,287,401 | ) | 3,894,338 | |||||||||||

|

|

|

|

|

|

|

| |||||||||

Attributable to owners of the Bank | 10,051,035 | 21,819,964 | (3,119,918 | ) | 3,987,136 | |||||||||||

Attributable to non-controlling interest | 17,760 | (4,510 | ) | (167,483 | ) | (92,797 | ) | |||||||||

Profit (Loss) for the year attributable to owners of the Bank per ordinary share (2)(3) | 16.41 | 35.61 | (5.09 | ) | 7.00 | |||||||||||

Profit (Loss) for the year attributable to owners of the Bank per ADS (2)(3)(5) | 49.23 | 106.83 | (15.27 | ) | 21.00 | |||||||||||

Diluted profit (loss) for the year attributable to owners of the Bank per ordinary share (2)(3) | 16.41 | 35.61 | (5.09 | ) | 7.00 | |||||||||||

Diluted profit (loss) for the year attributable to owners of the Bank per ADS (2)(3)(5) | 49.23 | 106.83 | (15.27 | ) | 21.00 | |||||||||||

Declared dividends per ordinary share (2)(3)(4) | 11.42465 | 25.36946 | 8.22796 | 4.80275 | ||||||||||||

Declared dividends per ADS (2)(3)(4)(5) | 34.27396 | 76.10830 | 24.68388 | 14.40825 | ||||||||||||

Net operating income per ordinary share (2)(3) | 29.11 | 39.93 | 8.37 | 8.25 | ||||||||||||

Net operating income per ADS (2)(3)(5) | 87.33 | 119.79 | 25.11 | 24.75 | ||||||||||||

Average ordinary shares outstanding (000s) (3) | 612,671 | 612,671 | 612,660 | 569,910 | ||||||||||||

4

Table of Contents

| As of December 31, | ||||||||||||||||

| 2020 | 2019 | 2018 | 2017 | |||||||||||||

| (in thousands of pesos) (1) | ||||||||||||||||

CONSOLIDATED STATEMENT OF FINANCIAL POSITION | ||||||||||||||||

Cash and cash equivalents | 152,040,070 | 212,733,025 | 207,554,781 | 118,229,933 | ||||||||||||

Financial assets at fair value through profit or loss | 12,616,460 | 15,424,483 | 18,068,509 | 19,884,259 | ||||||||||||

Financial assets at amortized cost | 349,113,843 | 280,486,554 | 433,864,823 | 421,056,810 | ||||||||||||

Financial assets at fair value through Other Comprehensive Income (“OCI”) | 127,572,351 | 61,543,514 | 51,443,863 | 52,818,795 | ||||||||||||

Tangible assets | 35,658,422 | 37,423,357 | 35,730,974 | 37,216,974 | ||||||||||||

All other assets | 16,023,379 | 10,699,766 | 10,508,885 | 16,895,704 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

TOTAL ASSETS | 693,024,525 | 618,310,699 | 757,171,835 | 666,102,475 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Financial liabilities at fair value through profit or loss | 188,694 | 4,974,233 | 4,334,178 | 710,491 | ||||||||||||

Financial liabilities at amortized cost | 528,244,795 | 457,814,875 | 619,308,479 | 528,647,214 | ||||||||||||

All other liabilities | 50,047,642 | 40,704,682 | 38,151,095 | 34,562,143 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

TOTAL LIABILITIES | 578,481,131 | 503,493,790 | 661,793,752 | 563,919,848 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Share capital | 612,710 | 612,710 | 612,660 | 612,660 | ||||||||||||

Share premium | 26,386,953 | 26,386,953 | 26,373,705 | 26,373,705 | ||||||||||||

Inflation adjustment to share capital | 18,640,670 | 18,640,670 | 18,640,578 | 18,640,578 | ||||||||||||

Reserves | 119,196,249 | 92,525,638 | 63,613,039 | 55,406,542 | ||||||||||||

Accumulated (loss) gains | (58,285,838 | ) | (26,122,154 | ) | (13,988,581 | ) | 74,965 | |||||||||

Accumulated other comprehensive income | 5,830,351 | 626,581 | 63,619 | 121,729 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Equity attributable to owners of the Bank | 112,381,095 | 112,670,398 | 95,315,020 | 101,230,179 | ||||||||||||

Non-controlling interests | 2,162,299 | 2,146,511 | 63,063 | 952,448 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

TOTAL EQUITY | 114,543,394 | 114,816,909 | 95,378,083 | 102,182,627 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

SELECTED RATIOS | ||||||||||||||||

Profitability and Performance | ||||||||||||||||

Return on average total assets (6) | 1.53 | % | 3.17 | % | (0.44 | )% | 1.19 | % | ||||||||

Return on average total equity (7) | 8.93 | % | 20,98 | % | (3.17 | )% | 7.88 | % | ||||||||

Capital | ||||||||||||||||

Total equity as a percentage of total assets | 16.53 | % | 18.57 | % | 12.60 | % | 15.31 | % | ||||||||

Total liabilities as a multiple of total equity | 5.05x | 4.39x | 6.94x | 5.52x | ||||||||||||

Credit Quality | ||||||||||||||||

Allowances for loan losses as a percentage of financial assets at amortized cost (loans and advances) | 3.82 | % | 5.60 | % | 1.98 | % | 1.37 | % | ||||||||

Non-performing loans ratio (8) | 1.50 | % | 3.58 | % | 1.78 | % | 0.65 | % | ||||||||

Coverage ratio (9) | 245.53 | % | 148.30 | % | 109.17 | % | 207.61 | % | ||||||||

| (1) | Except net income per ordinary share and net income per ADS data and financial ratios. |

| (2) | Based on the average number of ordinary shares outstanding during the year. |

| (3) | The average number of ordinary shares outstanding during a year was computed as the average number of shares outstanding during the twelve months taking into account the outstanding amounts as of the end of each month. |

| (4) | On March 9, 2021, the Board of Directors resolved to propose for shareholder approval at the next ordinary and extraordinary shareholders’ meeting, to be held on April 20, 2021, a distribution of cash dividends in the amount of Ps.7,000 million, subject to the prior authorization of the BCRA. For the fiscal year ended December 31, 2019, the dividends in cash declared at the ordinary and extraordinary shareholders’ meetings held on May 15, 2020 and November 20, 2020 were Ps.2,500 million (nominal value) and Ps.12,000 million (nominal value), respectively. For the year ended December 31, 2018, the dividends in cash declared at the ordinary and extraordinary shareholders’ meeting on April 24, 2019 were Ps.2,407 million (nominal value). For the fiscal year ended December 31, 2017, the dividends in cash declared at the ordinary and extraordinary shareholders’ meeting on April 10, 2018 were Ps.970 million (nominal value). Dividends per ordinary share for each year are calculated taking into account dividends declared in such year and the number of outstanding shares at the end of such year. BCRA Communication “A” 6886, in force since January 31, 2020, provides that financial institutions must have the prior authorization of the Central Bank for the distribution of their results. Subsequently, BCRA issued Communication “A” 7181 whereby [financial institutions] may not distribute dividends until at least June 30, 2021. |

| (5) | Each ADS represents three ordinary shares. |

| (6) | Profit or loss for the year attributable to owners of the Bank as a percentage of average total assets, computed as the average of fiscal-year-beginning and fiscal-year-ending balances. |

| (7) | Profit or loss for the year attributable to owners of the Bank as a percentage of average shareholders’ equity, computed as the average of fiscal-year-beginning and fiscal-year-ending balances. |

| (8) | Non-performing loans and advances as a percentage of loans and advances before allowances. |

5

Table of Contents

| (9) | Allowances for loan losses as a percentage of non-performing loans and advances. Non-performing loans and advances include all loans and advances to borrowers classified as Stage 3 in accordance with IFRS 9. |

Dividends

The table below sets forth the dividends declared with respect to the years ended December 31, 2020, 2019, 2018, 2017 and 2016 on each ordinary share and the equivalent of those dividends expressed in terms of dividends per American Depositary Share, each representing three ordinary shares (the “ADSs”), in each case adjusted for all stock dividends during the relevant periods. For the year ended December 31, 2020, this table sets forth the dividends that have been approved by the Bank’s Board of Directors but which are pending shareholder approval. The Central Bank requires that we maintain 20% of our net income (according to IFRS-BCRA) in legal reserves.

| Declared Dividends Per Ordinary Share (2) | Declared Dividends Per ADS (2) | |||||||||||||||

| Ps. | US$ | Ps. | US$ | |||||||||||||

December 31, 2020 (1)(3) | 11.42465 | 0.12340 | 34.27396 | 0.37020 | ||||||||||||

December 31, 2019 (2)(4) | 25.36946 | 0.17227 | 76.10830 | 1.68986 | ||||||||||||

December 31, 2018 (2) (5) | 8.22796 | 0.56329 | 24.68388 | 1.22253 | ||||||||||||

December 31, 2017 (2) (6) | 4.46762 | 0.40751 | 13.40287 | 0.87259 | ||||||||||||

December 31, 2016 (2) (7) | 6.54784 | 0.29086 | 19.64352 | 1.36388 | ||||||||||||

| (1) | On March 9, 2021, the Board of Directors resolved to propose for shareholder approval at the next ordinary and extraordinary shareholders’ meeting, to be held on April 20, 2021, a distribution of cash dividends in the amount of Ps.7,000 million, subject to the prior authorization of the BCRA. BCRA issued Communication “A” 6768, in force since August 30, 2019, which provides that financial institutions must have the prior authorization of the Central Bank for the distribution of their results. Subsequently, BCRA issued Communication “A” 7181 whereby financial institutions may not distribute dividends until at least June 30, 2021. |

| (2) | For the fiscal year ended December 31, 2019, the dividends in cash declared at the ordinary and extraordinary shareholders’ meetings held on May 15, 2020 and November 20, 2020 were Ps.2,500 million (nominal value) and Ps.12,000 million (nominal value), respectively. For the fiscal year ended December 31, 2018, the dividends in cash declared at the ordinary and extraordinary shareholders’ meeting on April 24, 2019 were Ps.2,407 million (nominal value). For the fiscal year ended December 31, 2017, the dividends in cash declared at the ordinary and extraordinary shareholders’ meeting on April 10, 2018 were Ps.970 million (nominal value). For the fiscal year ended December 31, 2016, the dividends in cash declared at the ordinary and extraordinary shareholders’ meeting on March 30, 2017 were Ps.911 million (nominal value). As of December 31, 2019 the number of outstanding shares was 612,710,079. As of both December 31, 2018 and 2017 the number of outstanding shares was 612,659,638. During the fiscal year ended December 31, 2016 the number of outstanding shares was 536,877,850. Dividends per ordinary share for each year are calculated taking into account dividends declared in such year and the number of outstanding shares at the end of such year. |

| (3) | Dollar amounts are based upon the reference exchange rate quoted by the Central Bank at April 12, 2021. |

| (4) | Dollar amounts are based upon the reference exchange rate quoted by the Central Bank at April 21, 2020. |

| (5) | Dollar amounts are based upon the reference exchange rate quoted by the Central Bank at May 8, 2019. |

| (6) | Dollar amounts are based upon the reference exchange rate quoted by the Central Bank at April 26, 2018. |

| (7) | Dollar amounts are based upon the reference exchange rate quoted by the Central Bank at April 12, 2017. |

Exchange Rates

The following tables show the annual high, low, average and period-end exchange rate for US$1.00 for the periods indicated. The exchange rate is calculated by the Central Bank based on the information provided by financial institutions on the exchange rate for trading of U.S. dollars for settled transactions in Argentine pesos and U.S. dollars. Such information must be representative of the prevailing market conditions. After gathering this information, the Central Bank calculates the daily exchange rate using the formula set out in Annex I of Communication “A” 3500.

The Federal Reserve Bank of New York does not report a noon buying rate for pesos.

Year /Period | High (1) | Low (1) | Average (2) | Period-end | ||||||||||||

| (in pesos per US$1.00) | ||||||||||||||||

2016 | 16.0392 | 13.0692 | 14.7738 | 15.8502 | ||||||||||||

2017 | 18.8300 | 15.1742 | 16.5665 | 18.7742 | ||||||||||||

2018 | 40.8967 | 18.4158 | 28.0937 | 37.8083 | ||||||||||||

2019 | 60.0033 | 37.0350 | 48.2423 | 59.8950 | ||||||||||||

October 2020 | 78.3283 | 76.2450 | 77.5693 | 78.3283 | ||||||||||||

November 2020 | 81.2967 | 78.6900 | 79.9332 | 81.2967 | ||||||||||||

December 2020 | 84.1450 | 81.3950 | 82.6379 | 84.1450 | ||||||||||||

2020 | 84.1450 | 59.8152 | 70.5941 | 84.1450 | ||||||||||||

January 2021 | 87.2983 | 84.7033 | 85.9708 | 87.2983 | ||||||||||||

February 2021 | 89.8250 | 87.6050 | 88.6746 | 89.8250 | ||||||||||||

March 2021 | 91.9850 | 90.0850 | 91.0664 | 91.9850 | ||||||||||||

April 2021 (through April 12, 2021) | 92.5817 | 92.2367 | 92.3770 | 92.5817 | ||||||||||||

| (1) | Source: BCRA. |

| (2) | For annual averages, this is the average of monthly average rates during the period. |

6

Table of Contents

Fluctuations in the exchange rate between pesos and dollars affect the dollar equivalent of the peso price of the ordinary shares on the Bolsa y Mercados Argentinos S.A. (“BYMA”) and as a result, would most likely affect the market price of the ADSs. Fluctuations in exchange rates also affect dividend income measured in dollars. The Bank of New York Mellon, as depositary for the ADSs, is required, subject to the terms of the deposit agreement, to convert pesos to dollars at the prevailing exchange rate at the time of making any dividend payments or other distributions. The following table shows the rate of devaluation of the peso compared with the dollar at year end, the rate of exchange (number of pesos per dollar prevailing in the Argentine foreign exchange market at year end) and the rate of inflation for consumer price for the fiscal years ended December 31, 2020, 2019, 2018, 2017 and 2016.

Since the repeal of the Convertibility Law in January 2002, the peso has devalued 9,158.2% compared with the dollar.

|

| As at December 31, | ||||||||||||||||||

| 2020 | 2019 | 2018 | 2017 | 2016 | ||||||||||||||||

Devaluation Rate(1) | 40.49 | % | 58.42 | % | 101.38 | % | 18.45 | % | 21.88 | % | ||||||||||

Exchange Rate(2) | 84.1450 | 59.8950 | 37.8083 | 18.7742 | 15.8502 | |||||||||||||||

Inflation Rate(3) | 36.14 | % | 53.83 | % | 47.65 | % | 24.80 | % | 34.59 | % | ||||||||||

| (1) | For the twelve-month period then ending according to the Argentine Central Bank. |

| (2) | Pesos per dollar according to the Argentine Central Bank. |

| (3) | The inflation rate presented is for the Consumer Price Index published by the Argentine National Statistics and Censuses Institute (“INDEC”) and is calculated over the prior twelve months. |

| B. | Capitalization and indebtedness |

Not applicable.

| C. | Reasons for the offer and use of proceeds |

Not applicable.

| D. | Risk Factors |

The following summarizes some, but not all, of the risks provided below. Please carefully consider all of the information discussed in this Item 3.D. “Risk Factors” in this annual report for a more thorough description of these and other risks:

| • | Risks Relating to Argentina |

| • | economic and political instability in Argentina; |

| • | current levels of inflation; |

| • | high levels of public spending; |

| • | the effects on the Argentine economy of economic events in other markets; |

| • | a decline in international prices for Argentina’s principal commodity exports; |

| • | exchange controls and restrictions on capital inflows and outflows; |

| • | the insufficiency of the measures adopted to resolve the crisis in the energy sector; |

| • | any failure to adequately address actual and perceived risks of institutional deterioration and corruption; |

| • | fluctuations in the value of the peso; |

| • | the inability of the Republic to obtain financing on satisfactory terms; |

| • | salary increases or additional employments benefits as a resut of government measures or pressure from union sectors; |

| • | government intervention in the Argentine economy; |

| • | amendments to the Central Bank’s Charter and the Convertibility Law; and |

| • | the Covid-19 pandemic. |

7

Table of Contents

| • | Risks Relating to the Argentine Financial System and to BBVA Argentina |

| • | the short-term structure of the deposit base of the Argentine financial system, including the deposit base of the Bank, could lead to a reduction in liquidity levels and limit the long-term expansion of financial intermediation; |

| • | reduced spreads between interest rates received on loans and those paid on deposits; |

| • | volatility in interest rates; |

| • | a mismatch between UVA (“Unidad de Valor Adquisitivo”, in Spanish) loans and UVA deposits; |

| • | the inaccuracy and/or insufficiency of our estimates and established reserves for credit risk and potential credit losses; |

| • | increased competition in the banking industry; |

| • | the dependency of our credit ratings on Argentine sovereign credit ratings; |

| • | the increasing dependency of the financial industry on information technology systems; |

| • | security risks; |

| • | an increase in fraud or transaction errors; |

| • | any insolvency proceeding against us that could subject us to the powers of, and intervention by, the Central Bank; |

| • | lawsuits brought against us outside Argentina; |

| • | class actions against financial institutions for an indeterminate amount; |

| • | the ability of BBVA, our controlling shareholder, to direct our business; |

| • | our ability to grow our business is dependent on our ability to manage our relationships with partners and grow our deposit base; |

| • | acquisitions that could adversely affect the value of the Bank; |

| • | any adverse consequences related to our calculation of income tax for the years ended December 31, 2018 and 2017; |

| • | the application of IAS 29 to our Consolidated Financial Statements; and |

| • | restrictions on our ability to pay dividends. |

| • | Legal, Regulatory and Compliance Risks |

| • | material weaknesses in our internal control over financial reporting; |

| • | our operations are conducted in a highly regulated environment; |

| • | the instability of the regulatory framework, in particular the regulatory framework affecting financial institutions; |

| • | our exposure to multiple provincial and municipal legislation and regulations; |

| • | limitations arising from the Consumer Protection Law and the Credit Card Law; |

| • | compliance risks; |

| • | differences between U.S. and Argentine corporate disclosure, governance and accounting standards; |

| • | special rules that govern the priority of different stakeholders of financial institutions in Argentina; and |

| • | uncertainty regarding the possible effects that tax reform could have in the Argentine economy. |

8

Table of Contents

Risks Relating to Argentina

Overview

We are an Argentine corporation (sociedad anónima), and the vast majority of our operations, properties and customers are located in Argentina. Accordingly, the quality of our assets, our financial condition and our results of operations are significantly affected by macroeconomic and political conditions prevailing in Argentina.

Economic and political instability in Argentina may adversely and materially affect our business, results of operations and financial condition.

The Argentine economy has experienced significant volatility in recent decades, characterized by periods of low or negative growth, high levels of inflation and currency devaluation. As a consequence, our business and operations have been, and could in the future be, affected from time to time to varying degrees by economic and political developments and other material events affecting the Argentine economy, such as inflation, price controls, foreign exchange controls, fluctuations in foreign currency exchange rates and interest rates, governmental policies regarding spending and investment, national, provincial or municipal tax increases and other initiatives increasing government involvement in business activities, and civil unrest and local security concerns.

In 2001 and 2002, the Argentine economy suffered a severe economic and political crisis. Among other consequences, the Argentine Crisis resulted in Argentina defaulting on its foreign debt obligations and introducing emergency measures and numerous changes in economic policies that affected utilities, financial institutions and many other sectors of the economy. Argentina also suffered a significant real devaluation of the peso, which in turn caused numerous Argentine private sector debtors with foreign currency exposure to default on their outstanding debt. Restrictions on deposit withdrawals from the banking system were implemented, as dollar denominated loans and deposits were “pesified” (reclassified as peso denominated) and maturities reprogrammed. Although following that crisis, Argentina substantially increased its real gross domestic product (“GDP”), growing 8.9% in 2005, 8.0% in 2006, 9.0% in 2007 and 4.1% in 2008, in 2009 it was affected by an extended drought, which reduced agricultural production, and the effects of the global economic crisis which led to a contraction of the economy of 5.9% during that year. Real GDP growth was strong in 2010 and 2011, increasing to 10.1% and 6.0%, respectively, but economic performance was erratic in subsequent years and after another recession in 2014, GDP contracted by 2.5%, leading to a GDP level below that of 2011 in constant prices. The economy grew again by 2.7% in 2015, primarily driven by an increase in public expenditures and investment.

The economic and financial environment in Argentina was significantly influenced by the presidential elections held on November 22, 2015, which resulted in Mr. Mauricio Macri being elected President of Argentina. Mr. Macri’s administration (the “Macri administration”) assumed office on December 10, 2015 and launched a wide array of measures intended to correct the longstanding fiscal and monetary policies that had resulted in recurrent public sector deficits, high inflation, pervasive foreign exchange controls and limited foreign investment. In 2016, the elimination of foreign exchange restrictions and rebalancing of utility rates led to an increase in inflation to 41% year-on-year according to the City of Buenos Aires index at year end and a considerable decline in consumption. As a result, GDP fell by 1.8% in 2016. Once the main imbalances were eliminated, the economy picked up again in 2017, with GDP growing 2.9% and inflation slowing to 24.8% year-on-year, though higher than the goal defined by the Central Bank. The Macri administration’s Cambiemos political party triumphed in the midterm elections of 2017, obtaining the necessary support to implement certain gradual tax and pension reforms, as well as a fiscal agreement with the provinces aimed at normalizing the finances of the provincial administrations.

The Macri administration carried out a gradual approach intended to reduce the significant fiscal and current account deficit and to correct the macroeconomic imbalances received from the previous administration. This gradual approach ended abruptly in the second quarter of 2018 due to a combination of domestic impacts (mainly a severe drought), a deterioration of the global financial environment (including an increase in US interest rates and the US-China trade war) coupled with policy errors (including a change to BCRA inflation targets and a capital gains tax), which brought about significant capital outflows from Argentina and the closing of global credit markets for Argentine issuers. From April 30 to July 31, 2018, the Argentine peso (based on the reference exchange rate of the Central Bank) depreciated 32.1% despite frequent exchange market interventions. Even after a strong adjustment of monetary policy and assistance from the International Monetary Fund (“IMF”) in the form of a stand-by high-access agreement of US$50 billion signed in mid-June 2018, tensions in the foreign exchange market reemerged in August, and the peso devalued 35.8% during that month in a strong sell-off of Argentine assets. Between April and September 2018, nearly US$14 billion of international reserves were lost due to sales of U.S. dollars by the Central Bank in the foreign exchange market.

9

Table of Contents

Monetary policy was highly influenced by the IMF plan, and by the end of September 2018, a new monetary and foreign exchange scheme was announced. It was adopted in order to control exchange rate volatility by absorbing all excess liquidity in pesos, holding the nominal monetary base constant until December 2018. It also set wide bands within which the foreign exchange rate could float. It allowed currency to be stabilized until February 2019. The peso appreciated 5% between September 30, 2018 and February 28, 2019 (from Ps.40.89/US$ to Ps.39.00/US$) and interest rates of Central Bank Liquidity Bills (Leliq) fell in that period more than 2,900 basis points from the peak. By the end of April 2019, the Central Bank changed its exchange rate scheme by eliminating intervention bands, which became exchange reference bands since intervention of the Central Bank in the exchange market was allowed at any level of the exchange rate of the peso, which led to the stability of the peso until the primary elections of August 11, 2019 (on August 9, 2019 the exchange rate closed at Ps.45.40/US$, 1.6% above the value as of April 29, 2019). However, the unexpected loss by 15 points gap of President Macri to Alberto Fernández in those elections caused the exchange market to react negatively, and the reference exchange rate rose 10.3 pesos on Monday, August 12, 2019, a 22.8% increase over the value recorded the prior Friday, and finished 2019 at Ps.59.89/US$ with high volatility. On August 28, 2019, Argentina announced a new schedule of payment on its short term local debt, including instruments like Lecap, Letes, Lecer and Lelink, where original dates of payment were postponed between three and six months.

During 2019 the IMF advanced disbursements planned to be made in 2020 and 2021 within the framework of a revised agreement that required an additional fiscal adjustment in 2019, including reaching the goal of a primary deficit of 0% of GDP, the strengthening of Central Bank reserves with the support of official creditors and the continuity of orthodox monetary and fiscal policies. This was part of a new program established in October 2018.

In October 2019, Alberto Fernández was elected president of Argentina and took office on December 10, 2019. Since then, his government (the “Fernandez administration”) has implemented a wide range of economic and political reforms, including limiting access to the exchange market for natural persons (seeking to contain the exchange rate without losing reserves) and the adoption of Law No. 27,541 on Social Solidarity and Productive Reactivation (the “Solidarity Law”), which covers a wide range of political and economic areas and adopts measures that have had, and continue to have, a significant impact on the Argentine economy, including the declaration of a public emergency in economic, financial, fiscal, administrative, pensions, utility rates and energy issues, as well as health and social services. The Solidarity Law also increased taxes, while providing incentives for production and benefits for the poorest and most vulnerable sectors. Moreover, the Solidarity Law also set up the “Tax for an Inclusive and Solidary Argentina” (the “PAIS Tax”) which will be in force for a five year period since its enactment, which applies a 30% rate on banknotes purchases in foreign currency for hoarding purposes, the acquisition of foreign services, and cross-border transportation services.

The Fernández administration has also undertaken a sovereign debt restructuring, designed to make Argentina’s debt sustainable, including through the reschedulement of maturities of sovereign securities, some of which were held by the Bank. As of December 31, 2020, sovereign debt securities affected by these measures and held by the Bank represented 2.67% of the Bank’s total assets. Pursuant to such debt restructuring, investors agreed to exchange their defaulted bonds by new bonds. The “Net Present Value” paid for such securities was around US$53.5 for every US$100 of nominal value, discounted at an exit rate of 10%, for those securities issued during 2015-2019 and around US$59.5 for those previously issued in 2005 and 2010.

Additionally, the Fernandez administration has also undertaken a restructuring of domestic debt that resulted in a 130% foreign exchange premium and a loss of US$1,300 million international reserves to smooth the official exchange rate depreciation. Initially, foreign exchange controls were partially eased and the market responded positively, the foreign exchange premium was reduced to 85% and the international reserves loss was drastically reduced.

As of the date of this annual report, it is not possible to predict the impact that these measures and any future measures that the Fernandez administration will have on the Argentine economy as a whole and on the financial system in particular. The Fernandez administration’s attempt to stabilize the economy and reduce the fiscal deficit, the trade deficit, inflation, poverty, and country risk, have to date proved unsuccessful. Any further measures could be detrimental to the economy and adversely affect our business, results of operations and financial condition.

Additionally, the Covid-19 crisis has adversely affected the Argentine economy. The Metropolitan Area of Buenos Aires was under Preventive and Mandatory Social Isolation (PMSA) from March, 20, 2020 to November, 8, 2020. Meanwhile, the rest of the country has suffered a significant increase in the number of Covid-19 positive cases since September and has, since then, also been subject to PMSA measures. This context has significantly affected the ability to function normally, mainly those that are more labor intensive which has significantly adversely affected the country’s economic performance. For example, GDP for the second quarter of 2020 fell 19.1% compared to GDP for the second quarter of 2019. As a result, our business, results of operations and financial condition could be significantly adversely affected. See “ —The Covid-19 pandemic is affecting the Bank.”.

10

Table of Contents

If current levels of inflation continue, the Argentine economy and the Bank’s business, results of operations and financial condition could be adversely affected.

Argentina has faced price increases since 2007. According to information published by the National Institute of Statistics and Censuses (“INDEC”), the consumer price index (“CPI”) increased 9.5% in 2011, 10.8% in 2012, 10.9% in 2013, 24% in 2014 and 11.9% in the ten-month period ended on October 31, 2015. INDEC stopped publishing the CPI in the period between November 2015 and April 2016, and resumed the publication of inflation rates with its new methodology for calculating the CPI as of June 2016, reflecting a cumulative increase of 16.9% from May to December 2016. The INDEC reported an annual variation of the CPI of 24.8%, 47.6%,53.8% and 36.1% in 2017, 2018, 2019 and 2020, respectively.

The efforts made by the government to contain and lower inflation have not obtained the desired results and inflation continues to be a significant problem for the Argentine economy. During the first two months of 2020, the freezing of public utility rates and fuels, as well as the controlled exchange rate slide (due to foreign exchange restrictions and the usage of international reserves), resulted in lower-than-expected monthly inflation levels, being 2.3% in January and 2.0% in February. This downward trend was reversed in March with a 3.3% inflation and then rejoined in April and May, when inflation fell to 1.5%. However, this initial disinflationary effect of the social isolation was compensated with an increasing money issuance (Ps.1,640 billion) to cope with the expenditures derived from the pandemic (mainly direct transfers to the most affected sectors). Inflation started a timid acceleration in June (2.2% month on month), which was partially reversed in July (1.9%) when the government retightened the mobility restrictions. However, once the contagion curve started to flatten, mobility restrictions were partially eased and the monetary overhang (resulting from the money issuance) began to take the scene. Inflation levels started to accelerate, being 2.7% in August, 2.8% in September, 3.8% in October, 3.2% in November and 4.0% in December (representing the maximum monthly variation of 2020), thus reaching a 36.1% year-on-year inflation rate in 2020. According to the Central Bank consensus, high inflation levels are expected to persist in 2021. The aforementioned expansive monetary policy carried out by the government since December imposes severe risks for the acceleration of inflation in the future. Moreover, if the value of the Argentine peso cannot be stabilized through fiscal and monetary policies, a further increase in inflation rates could be expected.

As a result of the devaluation of the exchange rate and the continuity of the process of adjustment of public service rates, as well as an unfavorable international context in terms of financing, the three-year accumulated inflation as of July 2018 ranked above 100%. Consequently, the Bank applied International Accounting Standard N° 29 (“IAS 29”) “Financial Reporting in Hyperinflationary Economies”, as from July 1, 2018 in the preparation of its financial statements accompanying this annual report, which requires the financial statements of any entity whose functional currency is the currency of a hyperinflationary economy, either based on the historical cost method or on the current cost method, be expressed in terms of the unit of measure that is in effect at the end of the reporting period. IAS 29 does not establish an absolute inflation rate above which hyperinflation is presumed.

Likewise since January 1, 2020, financial entities supervised by the BCRA, such as the Bank, are required to prepare their statutory financial statements in accordance with IAS 29 in the preparation of their financial statements as established by Communication “A” 6651.

We cannot predict whether any measures to be implemented by the Fernandez administration to control inflation will have the desired effect. Currently and in the past, inflation has adversely affected the Argentine economy and the government’s ability to create conditions conducive to growth. An environment of high inflation rates also negatively affects Argentina’s international competitiveness, real wages, employment rates, the consumption rate, and interest rates. High levels of inflation and the high level of uncertainty regarding economic variables such as inflation has in the past, and may in the future, adversely affect economic activity, which could materially and adversely affect our business, results of operations and financial condition.

A high level of public spending could negatively affect the Argentine economy and its access to international financial markets.

During the last years of the mandate of Fernández de Kirchner (the “Kirchner administration”), the government significantly increased public spending, turning to the BCRA and Argentine Social Security Office (“ANSES”) to cover part of the funding requirements of the public administration, generated in part by the policy of subsidies to certain public services such as electricity, gas, water and transportation, which together with an expansionary monetary policy led to a greater increase in prices all of which adversely affected consumer purchasing power and economic activity levels.

However, the Macri administration adopted measures to mitigate the increase in the fiscal deficit and reduce its current level. For 2017 and 2018, the Macri government set a fiscal deficit target of 4.2% and 2.7% of GDP, respectively, achieving a fiscal deficit of 3.9% and 2.4% of GDP, respectively. Although the objective of the Macri administration was to achieve a primary fiscal deficit equivalent to 1.3% of GDP in 2019, by virtue of negotiations with the IMF and in accordance with the National Budget Law for 2019, the fiscal deficit target was reduced to 0% of GDP in 2019 with a surplus of 1% in 2020. Subsequently, this target was increased to 0.5% of GDP. The deficit in 2019 finally amounted to Ps.95,121 million, equivalent to 0.4% of GDP.

11

Table of Contents

In 2020, in the face of the crisis caused by the health emergency caused by Covid-19, the Fernandez administration announced a package of fiscal stimulus measures to alleviate the effects of the recession, focused on sustaining the income of the most vulnerable families and companies most affected by the PSMA. The combined effect of the increase in spending and the fall in revenue (due to the economic recession) has produced a significant increase in the fiscal deficit in 2020. The 2020 primary fiscal deficit was 6.5% of GDP, the highest in more than 40 years. Although the Treasury showed signs of fiscal austerity by the end of 2020, the inaccessibility to debt markets forced the government to finance the fiscal needs exclusively with monetary issuance from the Central Bank. This dynamic is leading to inflationary and exchange rate disruptions. In addition, any deterioration in the government’s fiscal position negatively affects its ability to access debt markets in the future and could result in greater restrictions on accessing those markets by Argentine companies, including BBVA.

A weaker fiscal position could have a material adverse effect on the government’s ability to obtain long-term financing and adversely affect economic conditions in Argentina, which could adversely affect the business, results of operations and financial condition of the Bank.

The Argentine economy could be adversely affected by economic events in other markets.

Weak or no economic growth or recession or adverse situations that affect any of Argentina’s main trading partners could negatively affect the balance of payments and, therefore, the economic growth of Argentina. In recent years, several Argentine trading partners (such as Brazil, Europe and China) have experienced significant slowdowns or periods of recession in their economies. If these slowdowns or recessions were to occur again, this could impact the demand for products that come from Argentina and thus affect its economy. Furthermore, there is uncertainty about how the commercial relationship will develop between the Mercosur member states, especially between Argentina and Brazil.

Furthermore, the global economy faces significant challenges. There is considerable uncertainty regarding the long-term effects of expansive monetary and fiscal policies adopted by the central banks and financial authorities of some of the world’s major economies, including the United States and China. There have been concerns about unrest and terrorist threats in the Middle East, Europe and Africa and conflicts involving Iran, Ukraine, Syria and North Korea. Likewise, economic and social crises emerged in several Latin American countries during 2019, as the economy in most of the region has slowed down after almost a decade of sustained growth, among other factors. There has also been concern about the relationship between China and other Asian countries, which can result in or intensify potential conflicts in relation to territorial disputes, and the possibility of a trade war between the United States and China. Furthermore, the UK withdrew from the European Union (“Brexit”) on January 31, 2020, and recently completed a transition period ending on December 31, 2020, the long-term effects of which are uncertain. The medium and long-term implications of Brexit could adversely affect European and global market and economic conditions and could contribute to instability in global financial and currency markets. The UK withdrew from the European Union (“Brexit”) on January 31, 2020. The medium and long-term implications of Brexit could adversely affect European and global market and economic conditions and could contribute to instability in global financial and currency markets.

The Covid-19 pandemic has led to economic contractions in most of the world’s economies, both developed and emerging. This has affected the Argentine economy mainly through trade, since the demand for its exports (mainly from Brazil and Europe) has dropped substantially. Argentina accumulated a trade balance surplus of Ps.12,528 million in 2020. The Brazilian economy is showing signs of a sharp recovery since 3Q20, which could turn out to be positive for Argentina, given the fact that the country is one of its main importers. Moreover, the current excess of liquidity could mean more and cheaper credit for emerging markets, a fact that could also be facilitated by the result of the recent US Presidential election. The Argentine economy could also benefit from the fact that the new IMF board is willing to reach a new agreement that allows Argentina to postpone its current maturities while giving a couple of years to retake the sustained growth path.

If international and local economic conditions fail to improve or deteriorate even more, the Argentine economy could be negatively affected as a result of lower international demand and lower prices for its products and services, higher international interest rates, less capital inflow and greater aversion to risk. Any of the foregoing could also adversely affect the Bank’s business, results of operations and financial condition.

12

Table of Contents

A decline in international prices for Argentina’s principal commodity exports could have a material adverse effect on Argentina’s economy and public finances, and, as a result, on our business.

Historically, the commodities market has been characterized by high volatility. Despite the volatility of prices of most of Argentina’s commodities exports, commodities have significantly contributed to the government’s revenues during the 2000s due to the imposition of export duties on agricultural products in 2002. Although most duties were eliminated and the export tax on soy was reduced from 35% to 30% by the Macri administration in 2016, and was further reduced in 2018 by 0.5% per month, the Argentine economy is still relatively dependent on the price of its main agricultural exports, primarily soy. This dependence, in turn, renders the Argentine economy vulnerable to commodity prices fluctuations. International soybean prices decreased slightly during 2017 and further in 2018 due to growing trade tensions between the United States and China. During 2019, soybean prices reached their lowest prices over the prior five years, but recovered from US$305.5 per ton in May 2019 to US$335.0 per ton in December 2019. The average price for soybeans was US$326.9 per ton in 2019, down from US$345.0 per ton in 2018. During the last months of 2020 prices have demonstrated an upward trend (due to recent purchases from China and the promising news regarding the Covid-19 vaccine) reaching US$444.0 per ton.

Declines in commodity prices may adversely affect the Argentine economy and the government’s fiscal revenues, which could in turn adversely impact the business, results of operations and financial condition of the Bank.

Exchange controls and restrictions on capital inflows and outflows could have a material adverse effect on Argentine public sector activity, and, as a result, on our business.

From 2011 to 2015, the Argentine government introduced exchange controls and restrictions on the transfer and entry of foreign currency that significantly limited the ability of companies to hold foreign currency in Argentina or make payments abroad.

After taking office in 2015, the Macri administration substantially eliminated all exchange restrictions that had been implemented under the previous administration. Nevertheless, on September 1, 2019, due to the economic instability and the significant devaluation of the peso that took place in August 2019 after the primary elections, the government and the BCRA adopted a series of measures reinstating certain exchange controls limiting the access to the local exchange market in order to reduce the purchases of foreign currency. The payment of external financial debt, dividends in foreign currency and the payment of imports of goods and services were severely restricted and the obligation to enter and settle in pesos the funds from the export of goods and services, was reinstated, among other measures. Other financial transactions such as derivatives and transactions in securities are also limited by the new exchange regime.

The Fernandez administration extended the period during which these measures would apply and established additional measures through the Solidarity Law, including a tax on certain transactions that imply the acquisition of foreign currency by individuals and companies. During 2020, foreign exchange market regulations have been strengthened and made increasingly more complex. Towards the end of May 2020, the BCRA issued Communication “A” 7030 by means of which access to foreign currency to pay for imports was severely limited. As of the date of this annual report this measure is still in effect. After that, on September 15, 2020, the Central Bank tightened the foreign exchange market controls. First of all, companies with external financial maturities of more than US$1 million due before March, 31, 2021 had to present a restructuring plan of at least 60% of the capital payment. Secondly, a 35% tax was added to individuals who buy dollars in the official market (already limited to US$200 per month, and on top of a 30% tax on the official exchange rate) and finally, communication “A” 7106 banned non-residents from selling bonds for foreign currency. These decisions resulted in a notorious sell off of sovereign bonds, which led to a 7% daily fall. The Central Bank sold US$1,318 million the following five weeks, in order to keep the exchange rate depreciation at desirable levels. Due to this unsustainable situation, the Government decided to partially ease the restrictions by reducing the interval between bond transactions and the resulting currency exchange between pesos and dollars from fifteen to three days, and also by repealing the aforementioned prohibition for non-residents. The Central Bank purchased US$608 million in the spot market in December 2020.

Any changes in the policies of the current government concerning economic, exchange and financial matters in order to preserve the balance of payments, the Central Bank’s reserves, a capital outflow or a significant depreciation of the Peso, such as the mandatory conversion into Pesos of obligations assumed by legal entities resident in Argentina in US Dollars which could be due to a period of crisis and political, economic and social instability affecting Argentina, or otherwise, any of which could be exacerbated as a result of the Covid-19 pandemic, could have an adverse effect on Argentina’s economic activity, and the Bank’s business, results of operations and financial condition.

13

Table of Contents

The measures adopted to resolve the crisis in the energy sector may not be sufficient, which could affect the business, the results of operations and the financial condition of the Bank.

The economic policies applied since the Argentine crisis of 2001-2002 have had an adverse effect on the Argentine energy sector. The failure to reverse the freeze on electricity and natural gas rates imposed during the crisis became a barrier to investment in the energy sector. The government tried to encourage investment by subsidizing energy consumption but the policy proved ineffective and served to further discourage investment in the energy sector, causing oil and gas production and electricity generation, transmission and distribution to stagnate while consumption continued to rise. To address the power supply shortage that began in 2011, the government attempted to increase imports of electrical power, with adverse consequences for the trade balance and international reserves.

In response to the growing energy crisis, the Macri administration declared a state of emergency for the national electricity system, which ended on December 31, 2017. The state of emergency allowed the government to take measures to stabilize the supply of electricity to the country. In this context, subsidy policies were re-examined and new electricity rates were adopted.

Additionally, the Macri administration eliminated part of the subsidies for natural gas consumption and the adjustment of rates. As a result, average prices for electricity and gas increased. However, some of the government initiatives related to the energy and gas sectors were challenged in Argentine courts and resulted in adverse court rulings, which were subsequently lifted as legal challenges were resolved.

Although actions have been carried out to attempt to address the crisis in the energy sector, the lack of a definitive resolution of the negative effects on the generation, transport and distribution of electricity in Argentina with respect to residential and industrial supply could undermine confidence and produce an adverse effect on Argentine’s economic and financial condition, generating political instability, and adversely affecting the Bank’s business and results of operations.

Likewise, the elimination of subsidies and the progressive increase in prices could continue to generate social unrest and be challenged in local courts. We can give no assurance that the measures adopted by the government to deal with the energy crisis will be sufficient to restore energy production in Argentina in the short or medium term. Since the Fernandez administration took office, the rates of public services have been frozen, so a rise in energy demand is expected to generate deficit pressures on the trade balance due to the need to import gas to maintain the levels of domestic production and prevent it from declining as a result of the lack of investment driven by the capped prices.

The current lack of resolution on tariffs results in uncertainty regarding the future situation of the energy market in Argentina and constitutes a source of potential risk for the country’s economy and could lead to exchange rate volatility, either of which could adversely affect the Bank’s business, results of operations and financial condition.

Any failure to adequately address actual and perceived risks of institutional deterioration and corruption may adversely affect Argentina’s economy and financial condition.

The lack of a sound institutional framework and corruption have been identified as, and continue to be, serious problems for Argentina. Argentina ranked 65 out of 180 countries in the 2019 Corruption Perceptions Index published by Transparency International. In the World Bank’s Doing Business 2020 report, Argentina ranked 126 out of 190 countries, as compared with 119 in 2019.

Recognizing that the failure to address these issues could increase the risk of political instability, distort decision-making processes and adversely affect Argentina’s international reputation and ability to attract foreign investment, the Macri administration announced several measures aimed at strengthening Argentina’s institutions and reducing corruption. These measures included reducing criminal sentences in exchange for cooperation with the government in corruption investigations, increasing access to public information, seizing assets from corrupt officials, increasing the powers of the Anticorruption Office (Oficina Anticorrupción) and the passing of a new public ethics law, among others. The government’s ability to implement these initiatives is uncertain as it requires the involvement of the judicial branch, which is independent, as well as legislative support from opposition parties. In 2018, a thorough investigation of a corruption scandal linked to a public works bribery scheme implemented by the previous administration led to the arrest of several prominent individuals. Public perception of the independence of the judicial system has been strengthened by these actions, but we cannot assure that the implementation of these measures will be successful.

14

Table of Contents

If the actual and perceived risks of institutional deterioration and corruption are not adequately addressed, Argentina’s economy and financial situation might be adversely affected, which could have a material adverse effect on the business, the results of operations and the financial condition of the Bank.

Fluctuations in the value of the peso could adversely affect the Argentine economy and Argentine’s ability to service its debt obligations.

Fluctuations in the value of the peso may adversely affect the Argentine economy. A devaluation of the peso may adversely affect the government’s revenues (measured in U.S. dollars), fuel inflation and significantly reduce real wages. After several years of moderate variations in the nominal exchange rate, the peso lost 35.3% of its value in 2014 and 33.7% in 2015. Persistent high inflation during this period, with formal and “de facto” exchange controls, resulted in an increasingly overvalued real official exchange rate. Compounded by the effects of foreign exchange controls and restrictions on foreign trade, these highly distorted relative prices resulted in a loss of competitiveness of Argentine production, impeded investment and resulted in economic stagnation during this period.

After the foreign exchange controls were lifted at the end of 2015, the peso depreciated by 38.5% in 2016 considering the average foreign exchange rate in December of 2016 compared with the average foreign exchange rate in December of 2015. In 2017, the depreciation of the peso fell to 11.8%, well below inflation, raising doubts about potential appreciation of the peso in real terms once again. In this scenario, the vulnerability of the Argentine economy to a tightening of international financial conditions was reflected in a current account deficit of 4.9% of GDP in 2017 and a low level of international reserves compared to other countries in the region. When ten-year U.S. treasury rates began to rise and the U.S. dollar strengthened, these vulnerabilities resulted in a negative differentiation of Argentina compared with other emerging countries, which led to a prolonged run on the currency despite frequent interventions by the Central Bank and a sizeable loan from the IMF signed in June 2018. Finally, after another sell-off of Argentine assets in August 2018 and a strong depreciation, in early October 2018 a revised program with the IMF which further tightened fiscal and monetary policy managed to stabilize the foreign exchange market and the peso appreciated by 7.5% in the last quarter of 2018. Considering the full year, the peso depreciated by 50.3% in nominal terms in 2018. Together with the decline in economic activity, the real depreciation of the peso resulted in a strong reduction in imports and a correction of the external deficit in the fourth quarter of 2018.

According to the revised IMF agreement, the Argentine peso floated freely within an accepted band of exchange rates, but the Central Bank may intervene to a limited extent in the foreign exchange market selling reserves if the exchange rate rises above a certain level, defined initially at Ps.44/US$ (and subsequently adjusted by inflation) which is the upper threshold of the accepted band in which the peso floats freely without intervention of the Central Bank. Conversely the Central Bank was charged with purchasing reserves if the foreign exchange rate fell below the lower threshold of the non-intervention band.

In early 2019, the peso crossed the lower threshold, prompting purchases by the Central Bank and a strong decline in interest rates pursuant to the monetary program. As the level of inflation has remained high, a stronger nominal appreciation of the peso could lead to renewed doubts regarding the appreciation of the peso against the U.S. dollar in real terms. This presents risks for the Argentine economy, including the possibility of a reduction in exports as a consequence of the loss of external competitiveness and deterioration of the current account deficit. Any such appreciation could also have a negative effect on economic growth and employment, reduce tax revenues in real terms and also raise fears regarding the impact of a sudden stop in capital flows