UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-8104 | |||||||

| ||||||||

Touchstone Funds Group Trust | ||||||||

(Exact name of registrant as specified in charter) | ||||||||

| ||||||||

303 Broadway, Suite 1100, Cincinnati, Ohio |

| 45202 | ||||||

(Address of principal executive offices) |

| (Zip code) | ||||||

| ||||||||

Jill T. McGruder, 303 Broadway, Suite 1100, Cincinnati, Ohio 45202 | ||||||||

(Name and address of agent for service) | ||||||||

| ||||||||

Registrant’s telephone number, including area code: | (513) 878-4066 |

| ||||||

| ||||||||

Date of fiscal year end: | 09/30 |

| ||||||

| ||||||||

Date of reporting period: | 9/30/10 |

| ||||||

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

September 30, 2010

Annual Report

Touchstone Funds Group Trust

Touchstone Capital Appreciation Fund

Touchstone Core Plus Fixed Income Fund

Touchstone Emerging Markets Equity Fund

Touchstone Focused Equity Fund

Touchstone Global Equity Fund

Touchstone Global Real Estate Fund

Touchstone Healthcare and Biotechnology Fund

Touchstone Intermediate Fixed Income Fund

Touchstone International Fixed Income Fund

Touchstone Large Cap Relative Value Fund

Touchstone Market Neutral Equity Fund

(formerly Touchstone Long/Short Equity Fund)

Touchstone Mid Cap Fund

Touchstone Mid Cap Value Fund

Touchstone Premium Yield Equity Fund

Touchstone Sands Capital Select Growth Fund

Touchstone Short Duration Fixed Income Fund

Touchstone Small Cap Core Fund

Touchstone Small Cap Value Opportunities Fund

Touchstone Ultra Short Duration Fixed Income Fund

Table of Contents

| Page | |||||||

| Letter from the President | 3 | ||||||

| Management's Discussion of Fund Performance (Unaudited) | 4-53 | ||||||

| Tabular Presentation of Portfolios of Investments (Unaudited) | 54-57 | ||||||

| Statements of Assets and Liabilities | 58-67 | ||||||

| Statements of Operations | 68-72 | ||||||

| Statements of Changes in Net Assets | 73-79 | ||||||

| Financial Highlights | 80-111 | ||||||

| Notes to Financial Statements | 112-137 | ||||||

| Portfolios of Investments: | |||||||

| Touchstone Capital Appreciation Fund | 138 | ||||||

| Touchstone Core Plus Fixed Income Fund | 139-144 | ||||||

| Touchstone Emerging Markets Equity Fund | 145-146 | ||||||

| Touchstone Focused Equity Fund | 147 | ||||||

| Touchstone Global Equity Fund | 148-149 | ||||||

| Touchstone Global Real Estate Fund | 150-152 | ||||||

| Touchstone Healthcare and Biotechnology Fund | 153 | ||||||

| Touchstone Intermediate Fixed Income Fund | 154-157 | ||||||

| Touchstone International Fixed Income | 158-159 | ||||||

| Touchstone Large Cap Relative Value Fund | 160 | ||||||

| Touchstone Market Neutral Equity Fund | 161-166 | ||||||

| Touchstone Mid Cap Fund | 167-168 | ||||||

| Touchstone Mid Cap Value Fund | 169-170 | ||||||

| Touchstone Premium Yield Equity Fund | 171 | ||||||

| Touchstone Sands Capital Select Growth Fund | 172 | ||||||

| Touchstone Short Duration Fixed Income Fund | 173-177 | ||||||

| Touchstone Small Cap Core Fund | 178 | ||||||

| Touchstone Small Cap Value Opportunities Fund | 179-180 | ||||||

| Touchstone Ultra Short Duration Fixed Income Fund | 181-186 | ||||||

| Report of Independent Registered Public Accounting Firm | 187 | ||||||

| Other Items (Unaudited) | 188-193 | ||||||

| Management of the Trust (Unaudited) | 194-196 | ||||||

| Privacy Protection Policy | 197 | ||||||

2

Letter from the President

Dear Shareholder:

We are pleased to provide you with the Touchstone Funds Group Trust Annual Report. Inside you will find key financial information, as well as manager commentaries for the Funds, for the twelve months ended September 30, 2010.

All traditional asset classes posted strong positive absolute returns regardless of style or geographic region during the year. The U.S. equity markets had a solid year, despite continued anxiety about the economy and capital markets. For the one-year period ending September 30, 2010, the U.S. stock market outperformed the international equity market. From an investment style and market capitalization perspective, U.S. growth equities outpaced their value counterparts, with mid cap leading the way. Over the last year, broad investment grade bonds and Treasuries exhibited solid returns.

The U.S. equity market is currently considered to be reasonably valued-to-undervalued, with a powerful rebound in corporate profits providing the main support. It is thought that given the current state of the economy, earnings growth should moderate somewhat during the balance of this year and into 2011. It is generally believed that the economy will continue to recover, albeit at a sub-par pace. Even though forecasters believe bond yields are expected to increase from current low levels over the coming year, it is recognized that interest rates could stay unusually low for a while longer.

One year ago we diversified our portfolio offerings and launched ten funds to provide greater investment breadth and depth to our chosen distribution partners. We selected 10 institutional asset managers who were carefully screened and selected for their considerable capabilities and strong track records to act in a sub-advisory capacity for each of the ten funds. Based on Lipper Analytical Services' rankings, five of the ten funds posted returns in the top quintile of their respective categories for the one-year period when ranked amongst their peers.

The Touchstone Sands Capital Select Growth Fund reached its 10-year milestone this past quarter; it proudly boasts top quartile performance across all time periods; year-to-date, as well as 1-, 3-, 5- and 10-years, according to Lipper Analytical Services' rankings amongst their peers. Sands Capital Management's strategy of investing in a concentrated portfolio of leading companies, also known as fortress franchises, has helped it achieve these strong, hard-earned results.

We continue to believe that diversification is essential to balancing risk and return. We recommend that you continue to work with your financial professional to employ a sound asset allocation strategy that invests in a combination of stock, bond, and money market mutual funds to help keep your financial strategy on course. It is critical to maintain a long-term approach to gain the full potential benefits of investing.

Touchstone is committed to helping investors achieve their financial goals by providing access to a distinctive selection of institutional asset managers who are known and respected for proficiency in their specific area of expertise. We hope that you will find the enclosed commentaries helpful.

We greatly appreciate your continued support. Thank you for including Touchstone as part of your investment plan.

Sincerely,

Jill T. McGruder

President

Touchstone Funds Group Trust

3

Management's Discussion of Fund Performance (Unaudited)

Touchstone Capital Appreciation Fund

Sub-Advised by Farr, Miller & Washington

Investment Philosophy and Process

The Touchstone Capital Appreciation Fund seeks long-term capital appreciation. The Fund invests, under normal market conditions, at least 80 percent of its net assets (including borrowings for investment purposes) in common stocks of large capitalization U.S. companies that are believed to be trading at attractive valuations.

Fund Performance and Positioning

The total return of the Touchstone Capital Appreciation Fund was 6.10% for the twelve month period ended September 30, 2010 which was calculated excluding the maximum sales charge. The total return of the Russell 1000® Growth Index was 12.65% and the total return of the S&P 500 Index was 10.16% for the same period. The Fund underperformed both of its benchmarks over the past 12-month period.

The majority of the Fund's underperformance occurred during the market's sharp rally in the third quarter. Despite signs that the U.S. economy had begun to weaken again, the market was up sharply on news that the Federal Reserve would be ready to stabilize things with a second round of quantitative easing (QE2). Needless to say, the Fund's portfolio of large-cap, stable growth companies did not keep up during a rally that generally favored higher beta sectors and stocks. The recent underperformance has left the stocks in the Fund trading at reasonable relative valuations, as there continues to be little to no premium being awarded for quality at this point.

The Fund's performance was hurt by its conservative stance over the past 12 months. Underperformance in the Information Technology, Financials and Consumer Staples sectors stood out over this time period. Stocks contributing to underperformance in the Fund were Cisco Systems Inc., Microsoft Corp., Dell Inc., Nokia Corp., Google Inc., and Paychex Inc. With the exception of Nokia, each of these companies produced solid results over this time period but were not rewarded with a higher P/E multiple by the market. Nokia underperformed due to its continuing struggle in the high-end smart phone market. Within the Energy sector, Exxon Mobil Corp., and Schlumberger Ltd., both hurt performance. Other underperformers for the year included Monsanto Co., Bank of America Corp., JPMorgan Chase & Co., Goldman Sachs Group Inc., and CVS Caremark Corp. The general trend has been that large, blue chip companies with stable growth prospects have not kept up with the market over the past 12 months. This trend was especially pronounced during the third quarter of 2010.

During the past 12 months, strong stock selection in the Consumer Discretionary and Industrial sectors contributed to the Fund's performance. O'Reilly Automotive Inc., and PetSmart Inc., both performed well during the downturn and continued to generate solid same-store sales growth and expense control as the economy recovered. Danaher Corp., United Technologies Corp., Donaldson Co. Inc., and Rockwell Collins Inc., each continued to recover nicely from the downturn and drove the outperformance in the Industrials sector. Genzyme Corp. and Waters Corp. also stood out as outperformers during this recovery period. However, contributions from these positions were not enough to overcome the underperformance.

Strategy and Outlook

We believe that the Fund continues to be conservatively postured vs. its benchmark, the Russell 1000® Growth Index. Roughly, 40 percent of the Fund is currently invested in the less economically sensitive Consumer Staples and Health Care sectors. We continue to add to positions in large-cap, blue-chip companies trading at what appear to be very attractive relative valuations. Proceeds for these purchases are generally coming from stocks that have outperformed and are now trading at rich valuations.

4

Management's Discussion of Fund Performance (Continued)

The economic rebound appears to have hit a bump in the road. However, the market has responded positively to the potential for more quantitative easing. We are not optimistic that more quantitative easing is a long-term solution to this country's problems. As such, we continue to favor global companies trading at reasonable valuations. We believe that the Fund is well positioned for this uncertain environment. If our stance is too cautious, it seems reasonable to believe that the Fund's stocks would continue to benefit from earnings growth and P/E multiple expansions.

Comparison of the Change in Value of a $10,000 Investment in the Touchstone Capital Appreciation Fund - Class A*, the Russell 1000® Growth Index and the S&P 500 Index

* The chart above represents performance for Class A shares only, which will vary from the performance of Class C shares, Class Y shares and Institutional Class shares based on the differences in loads and fees paid by shareholders in the different classes. The Fund commenced operations on September 30, 2009.

** The total returns shown above are adjusted for maximum applicable sales charges.

The performance of the above Fund does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

5

Management's Discussion of Fund Performance (Continued)

Touchstone Core Plus Fixed Income Fund

Sub-Advised by Bradford & Marzec LLC

Investment Philosophy and Process

The Fund seeks to provide current income. Capital appreciation is a secondary goal. It seeks to add excess return by capturing relative value between fixed income sectors and securities through economic cycles using a traditional, long-only investment style.

Fund Performance and Positioning

The total return of the Touchstone Core Plus Fixed Income Fund was 7.46% for the twelve month period ended September 30, 2010 which was calculated excluding the maximum sales charge. The total return of the Barclays Capital Aggregate Bond Index was 8.16% for the same period. During the past 12 months, the Fund underperformed its benchmark.

During the first month the Fund was invested, it underperformed its benchmark by 112 basis points. This was partly due to initial investment costs as well as market timing. From the end of that initial month through the end of September 2010, the Fund outperformed its benchmark by 114 basis points. Sector rotation was the primary source of positive returns, due in large part to overweighting the spread sectors, High Yield and CMBS (Commercial Mortgage-Backed Securities) – both of which performed very well. Security selection detracted from performance, particularly within High Yield and CMBS. The duration and yield curve strategies were positive performers. Underweighting MBS (Mortgage-Backed Securities) also had a positive effect on performance. Finally, the Fund's currency positioning detracted from performance. Non-dollar bonds were used as surrogate treasuries which underperformed the benchmark.

Strategy and Outlook

Globally, European spending cuts continue to hurt; however, global growth is forecast to be resilient in the face of a possible U.S. slowdown. The global economic focus is increasingly on Europe and the strains appearing across the board as fiscally responsible governments address burgeoning budget deficits by introducing tax increases and painful spending cuts. France is expected to grow at about +1.0% for 2010 with Germany only slightly higher. Despite 2Q growth of 4.0%, recent data shows Germany to be slowing. The new conservative U.K. government cut child subsidy payments to the wealthy and reduced unemployment benefits as part of its ongoing effort to save $135 billion from the budget over the next 5 years. As a result, U.K. growth will likely slow along with the rest of core Europe. The effects of these Pan-European cuts are being felt across the Eurozone with strikes and demonstrations on the rise. Last month sizeable demonstrations o ccurred in Brussels, the home of the European Parliament, in protest to the cuts. Strikes in France, the U.K. and Greece also occurred. Although Greece continues to struggle it appears to be on target to meet its Gross Domestic Product (GDP) target of -8.1% for 2010, although in the first half of the year tax receipts were lower than expected. Ireland continues to take difficult action to reduce its budget deficit which presently stands at $12.1 billion (as of 08/10) down from $18.7 billion the previous year. Italy, Portugal and Spain are generally making headway toward meeting budget deficit targets. Further cuts, however, will need to be implemented.

The bifurcation of global recovery continues as Asian and South American growth outstrips Europe and the U.S. Although growth in Brazil is expected to slow, second quarter growth came in above expectations at a surprising +8.8%. This follows +9.0% in first quarter 2010. Chinese growth still underpins Asia with little signs of slowing. Major Wall Street economists are also predicting that world growth will only slow slightly to 4.6% despite a significant slowdown in U.S. growth in 2011. Japan's economy remains sluggish in the face of an overvalued Yen.

6

Management's Discussion of Fund Performance (Continued)

Domestically, the prospect of further quantitative easing is keeping rates low. Growth signals remain mixed with activity subpar. Outside of slightly disappointing economic data, the U.S. focus remains on the likelihood of further quantitative easing (QE2) by the Federal Reserve. On the surface, it is a win-win situation for the authorities. Excessive treasury supply will be met, interest rates should stay low, which should help the economy, stocks and commodities should rise, and the dollar will fall — boosting exports. At the end of the day, however, the action is nothing more than debt monetization that could ultimately lead to out-of-control inflation. For the time being, the markets are likely to view QE2 positively. U.S. data continues to be mixed with the U.S. economy struggling to grow. Although there are no immediate signs of a double dip, the lack of any clear recovery is causing concern as 2011 approaches, especially if no po litical agreement is reached on extending the Bush tax cuts. Regardless, other tax increases are in the pipeline.

The stock market's strong September was likely in response to the upcoming U.S. elections. Whether this helps consumer confidence is still a moot point as unemployment continues to remain high and is forecast to get worse before it gets better. On a more positive note, lower long-term U.S. yields are ultimately expected to provide significant stimulus to the slowing U.S. economy. The 30-year bond yield remains below 4%. Longer term, there is a close correlation between house prices and nominal GDP in the U.S. Therefore, housing needs to recover before any meaningful growth momentum is likely. Further quantitative easing, if enacted, will ensure that long-term rates remain low, at least for the time being.

Portfolio Strategy — Duration & Yield Curve

The possibility of further quantitative easing is keeping U.S. interest rates low as the Fed indicates concern over disinflation in its post FOMC meeting statement. Further yield curve flattening is possible. At the Fed's most recent meeting, concern was expressed over the continuing decline of U.S. inflation, raising the possibility of further quantitative easing. This is where the Fed simply buys U.S. treasuries issued by the U.S. Treasury. The action has three short-term positive effects; it absorbs treasury supply, pumps dollars into the system and keeps downward pressure on interest rates. As a result, long-term interest rates remain in a clearly defined, downward trend spurred on by declining inflation, in addition to the possibility of further quantitative easing by the Federal Reserve. With the U.S. economy slowing, the Fed is unlikely to begin tightening until well into 2011, at the earliest. Inflation continues to be of little conc ern. Long-term interest rates are likely to fall, further flattening the yield curve. Under this scenario, returns for bonds should be favorable. Looking farther ahead, massive fiscal imbalances in the U.S. will ultimately push long-term interest rates higher. The market could inevitably become saturated with U.S. treasuries as government spending as a percent of GDP grows, although the outcome of U.S. elections could have a beneficial impact on spending. Eventually investors' appetite for risk will direct capital away from (safe) low yielding assets. In that event, a strategic short duration position would be considered. Our stated philosophical range is +/- 25% of the index.

Portfolio Strategy — Investment Grade Credit

The Fund's overweight in Investment Grade Credit will be maintained. We expect Investment Grade Credit to continue to outperform higher rated asset classes as fundamentals and market technicals support further gains. Conservatively positioned corporate balance sheets, improved corporate earnings and attractive relative valuations will keep corporate bonds a favored investment alternative in the current low interest rate and sluggish macro-economic environment. Fundamentally, strong corporate balance sheets and healthy earnings momentum support corporate credit quality, even in the current soft patch of U.S. economic activity. Balance sheets have strengthened as companies have reduced financial leverage, meaningfully improved their liquidity, and continued to term-out their debt maturities. Furthermore, we expect tight expense controls to lead to further expansion of corporate profit margins. Importantly, financial institution profitability s hould continue to recover, irrespective of the new financial regulations, as credit losses have begun to moderate. Technicals remain strong as greater transparency regarding U.S. financial regulation, European banking system risk, and

7

Management's Discussion of Fund Performance (Continued)

second quarter earnings have encouraged investors to continue to put money into corporate bonds. Wall Street bond inventory remains relatively low despite the continued heavy new issue calendar. While new corporate bond issuance will remain high as companies refinance and extend debt maturities, we expect investor demand to absorb this issuance rather easily. Valuations are attractive. Corporate spreads are still well wide of long-term averages and are in-line with spread ranges of the prior two recessionary periods (1991 and 2001). We favor companies with improving operating trends, solid balance sheets, and that show a commitment to reducing leverage. We favor Financials as current valuations do not seem to reflect greater regulatory transparency and improvements in earnings, asset quality, and capital ratios. We continue to favor cross-over credits and BBB-rated bonds, as we believe quality spreads will continue to compress. The Fund is o verweight Banks, Insurance, Non-Captive Finance, Electric Utility Holding Companies, and Real Estate Investment Trusts (REITs). It is underweight Single-A Industrials, Consumer Discretionary, Pharmaceuticals, and Yankee Sovereign-related securities.

Portfolio Strategy — High Yield

We believe strong credit fundamentals and attractive yields position high yield relatively well for the remainder of 2010. Corporate earnings remained impressive in the second quarter despite slower overall economic growth, with top line revenue growth and profits beating estimates again. Strong cash flows continue to enhance balance sheet strength as corporations reduce debt and build cash balances. Corporate executives are becoming somewhat more upbeat, but remain reluctant to increase their leverage given numerous macro uncertainties. High yield mutual fund inflows in September were an impressive $3.6 billion, bringing year-to-date inflows to approximately $8.9 billion. High yield inflows have picked up significantly since the market correction in April/May, and we believe that strong underlying credit fundamentals and attractive relative yields will keep demand strong in the coming months. Global high yield default rates (Moody's 12 mont h trailing) fell again in August to 5% from their peak of 13.5% last November. Rating agencies are responding to the positive news with upgrades significantly outpacing downgrades in 2010. These trends support further gains in high yield. High yield new issuance remained historically high in September, with a near record $32 billion issued over the month. Year-to-date issuance stands at over $200 billion, already exceeding last year's record of $180 billion. Refinancing remains the key driver of issuance, accounting for over 75% of new deals year-to-date. Corporations continue to focus on maintaining balance sheet strength by reducing leverage and extending debt maturities through these refinancings. We continue to take advantage of recent strong performance to selectively swap into higher yielding credits possessing solid fundamentals. Smaller issuers that tend to fly below the radar of larger managers remain an attractive way to conservatively add yield. Given our outlook for subpar U.S. economic growth, w e remain underweight most consumer cyclical industries. We do find value in a few cyclical industries such as airlines, gaming/lodging and paper. We still anticipate yield/income to be the key driver of performance in 2010. Merger and Acquisition (M&A) activity should increase going forward, but we believe that most deals will be smaller in nature, conservatively financed and driven by larger/higher rated companies looking to grow revenues. The Fund is overweight Banking/Finance, Energy, Gaming/Lodging, Insurance, Paper/Packaging, Railroads, REITs, Technology and Transports and underweight Autos, Building Materials/Housing, Chemicals, Electric, Food/Beverage/Tobacco, Health Care, Non-captive Finance and Supermarkets.

Portfolio Strategy — Governments & TIPS

The Fund remains underweight Governments in both the U.S. Treasury and Agency debenture sectors given better relative value in other higher-yielding sectors. Treasuries gain support from the Fed's purchases with proceeds from their mortgage portfolio and in anticipation of a second round of quantitative easing, and domestic banks and foreign buyers continue to add to U.S. Treasury holdings. Agency debentures remain fully valued with a meager yield advantage to treasuries. Government Sponsored Enterprise (GSE) reform should

8

Management's Discussion of Fund Performance (Continued)

continue to make headlines, but resolution will wait until 2011. The Fund has no allocation to TIPS as this sector is out of favor as we believe deflation will be a larger concern than inflation in the next six months. Breakeven inflation rates have collapsed following modest inflation releases and a strong rally in nominal U.S. treasuries. The latest Federal Reserve policy statement cites "substantial resource slack" and that "inflation is likely to remain subdued for some time."

Portfolio Strategy — Structured Products

The Fund continues to be underweight agency mortgages given better upside potential in other risk sectors. Agency MBS remain vulnerable to elevated refinancing fears and potential GSE reforms. Recent underperformance has returned mortgage spreads to fair value. To increase portfolio yield, the Fund is currently overweight conventional 30-year mortgages rather than 15-year mortgages. Higher coupon mortgages, typically comprised of credit-impaired borrowers, provide an attractive yield with very muted refinancing response. We recommend non-agency mortgages which are supported by strong supply and demand and stabilizing fundamentals with focus on prime non-agency securities that provide 5% to 6% yields and attractive relative value versus other sectors. The Fund is underweight in Asset Backed Securities (ABS) as current ABS valuations leave little upside potential, but should remain firm given strong investor support. We believe fundamentals in consumer-related finance are showing early signs of reaching a bottom and weakness in the labor markets will continue to weigh on credit card, auto, and student loan ABS. The Fund remains overweight CMBS despite Europe; however, we recently reduced allocation from 10% to 7% following the strong recent performance. The CMBS sector continues to benefit from attractive yields and positive supply and demand technicals. Commercial real estate fundamentals are reaching a bottom — early signs include improved transaction volume and stabilizing prices.

Portfolio Strategy — Non-Dollar

Risk is back despite a weak U.S. economy/mixed Euro economy. Asia/emerging markets outpace the West and the U.K. is starting to fade. The Yen is selling off with huge government intervention, but pressure remains with strong Chinese buying. Despite economic vulnerabilities in the U.S. and Europe, risk products are well-supported, as Asia and emerging markets economies remain solid. Government intervention by the Japanese kept the Yen from further appreciation. Hints from the Fed for further quantitative easing kept treasuries bid in the face of a risk rally. While Asia doesn't appear as bullet-proof as before, strength remains, particularly in exports, with the powerhouse China retaining solid growth. This Asian/emerging market strength continues to benefit Australia and New Zealand, with increasingly stronger export and terms of trade figures being registered by the former. Aussie markets ignored the victory by the ruling labor party, despi te their support for increased resource taxes. The Reserve Bank of Australia (RBA) is poised to raise rates, possibly at the next meeting, unless an unexpected global event appears. New Zealand's economy is less robust than Australia's, with housing particularly precarious. This has pushed back rate hike expectations from the Reserve Bank of New England (RBNZ) to 2011. Government bonds are still attractive to global investors, but the unprecedented rally in U.S. rates widened spreads.

Canada has seen some softening in economic releases, but is still much stronger than its neighbor to the south. Canadian sovereign bonds continue to share the safe haven category with the U.S. and attract a record volume of foreign purchases. The attractiveness of its resource companies keeps the currency within a range, with current levels depending on M&A activity and the price of oil. The BHP Billiton attempt to pay $40 billion for Canada's prized Potash Corporation rocketed the CAD to recent highs versus the dollar, but the corporation's rebuff and Saskatchewan Province's efforts to thwart the transaction have pushed the currency backward. The Bank of Canada, also data-dependent, is expected to continue to be in rate-hike mode, albeit at a much slower pace than previously thought, especially after Governor Carney's recent dovish comments. Due to a budget-friendly U.K. electoral outcome, bond buying continues in gilts, leading to outp erformance

9

Management's Discussion of Fund Performance (Continued)

versus both U.S. and European sovereigns. Dovish comments by Bank of England officials regarding deflationary fears further support gilts. Talk about quantitative easing has grown, especially after heightened expectations of a U.S. move. Spreads remain attractive given the U.K. absence from the bailout packages and affirmation of the country's 'AAA' sovereign rating by the rating agencies. After "tranquility" imparted to the market by the bank stress tests, turmoil returned with concerns about Spain, Portugal and Ireland; however, at month-end, these concerns were assuaged by more concrete estimates regarding the Irish bank bailout and the elimination of any further debt issuance in 2010, assignment of a "stable outlook" by S&P for Spain after their expected downgrade, and stern austerity budget measures by Portugal. While European economic conditions remain mixed, there are some bright spots and the feared return-to-recession doesn't ap pear imminent. The euro remains buoyed by low yielding U.S. dollar assets, however the European Central Bank (ECB) is still reluctant to raise rates due to growth concerns.

Comparison of the Change in Value of a $10,000 Investment in the Touchstone Core Plus Fixed Income Fund - Class A* and the Barclays Capital Aggregate Bond Index

* The chart above represents performance for Class A shares only, which will vary from the performance of Class C shares, Class Y shares and Institutional Class shares based on the differences in loads and fees paid by shareholders in the different classes. The Fund commenced operations on September 30, 2009.

** The total returns shown above are adjusted for maximum applicable sales charges.

The performance of the above Fund does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

10

Management's Discussion of Fund Performance (Continued)

Touchstone Emerging Markets Equity Fund

Sub-Advised by AGF Investments America, Inc.

Investment Philosophy and Process

The Touchstone Emerging Markets Equity Fund seeks capital appreciation by primarily investing in equity securities of companies in emerging markets. It seeks to invest in businesses believed to be mispriced by the market and that are expected to generate positive and sustainable earnings growth.

Fund Performance and Positioning

The total return of the Touchstone Emerging Markets Equity Fund was 26.80% for the twelve month period ended September 30, 2010 which was calculated excluding the maximum sales charge. The total return of the MSCI Emerging Markets Index was 20.54% for the same period. For the year, the Fund outperformed its benchmark.

Financials, Consumer Discretionary, Consumer Staples, Energy and Information Technology sectors represented the most significant positive contribution to relative return. The Health Care sector was the largest detractor during the period. Financials advanced amid positive domestic economic news and exposure to regional banks. Bank Mandiri, Indonesia's largest bank by assets, was a contributor, as the Indonesian stock market rose on expectations that faster economic growth and record-low interest rates will boost earnings. The central bank in Indonesia raised its growth forecast, citing rising consumer spending. The nation's sovereign debt rating was upgraded based on positive structural reforms, contributing to further appreciation in the rupiah, the second-best-performing currency in Asia. Optimism was also fueled by the finance ministry's efforts to improve governance and implement tax reforms to lure investment. Kasikornbank Public Compan y Ltd., Thailand's third-largest lender by assets, jumped to a 13-year high after lending climbed in February to 905.1 billion baht. Despite the implementation of tightening policies in China, Singapore property developers such as Keppel Land, reported encouraging news for the sector as sales activities remained robust. Also contributing to Fund performance was First Pacific Company, an investment and management company based in Hong Kong whose principal operations and business interests has exposure to Asia's growth in industries such as telecommunications, consumer food products, infrastructure and natural resources. Shares of the Hong Kong-listed company rose following an announcement to sell $300 million worth of bonds to pay down debt.

One of the main investment themes within the Fund focused on rising domestic income and consumption growth, and an overweight exposure in the Consumer Discretionary sector was positive. Lojas Renner, Brazil's largest publicly traded retailer was a positive performance contributor as quarterly profits rose while the company continued to focus on its growth strategy. Daphne International Holdings, a leading retailer of ladies footwear in China contributed as the company's operating profit rose 27 percent amid a challenging environment in 2009. Hankook Tire, South Korea's largest tire maker, was also a contributor following an announcement of plans to expand manufacturing capacity in China.

The Consumer Staples sector added to the Fund's relative return following an announcement that Wal-Mart planned to buy Massmart Holdings Ltd., in a transaction worth approximately U.S. $4.6 billion, to gain access into South Africa, the largest deal in more than a decade. Massmart is one of the Fund's top ten holdings and South Africa's largest food and general-goods wholesaler. Another top contributor was India-listed ITC Ltd., Asia's second-largest cigarette maker by market value, whose earnings continued to rise as price increases from higher taxes failed to deter smokers. Revenue from ITC's hotel business also rose as business travel gained momentum after the global recession and Mumbai terrorist attacks in November 2008. The Energy sector contributed positively from a relative underweight allocation and security selection. Oil prices remained volatile amid concerns that economic growth was slowing down in the U.S. and China, the world's two largest energy consumers. Oil and natural gas producer Petroleo Brasileiro S.A. added to positive performance as the company announced an aggressive five-year, $224 billion investment plan to double current oil production,

11

Management's Discussion of Fund Performance (Continued)

which included a stock offering worth a record U.S. $70 billion. No exposure to Russian natural gas producer Gazprom was also positive as the company's board approved a 13 percent increase in investments despite a decline in revenues. Tupras Turkiye Petrol Rafinerileri AS of Turkey contributed as the company reported a rise in total sales volume and in output, but first-half profit declined by 3 percent due to higher idle capacity costs.

A relative underweight exposure to the Information Technology sector, combined with positive security selection, was additive to Fund performance. Top holdings included VTech Holdings, a Hong Kong-based manufacturer of consumer electronics which recently announced new investment in factory equipment to reduce labor reliance and increase efficiency, and Infosys Technologies Limited, a provider of IT consulting and software services, whose revenue growth is expected to reach 20 percent this year.

The Health Care sector rose during the quarter, but detracted from Fund performance on company specific news. Teva Pharmaceutical was the primary detractor, as the world's largest generic drug manufacturer was in the midst of a legal dispute over existing patents which included a treatment for Alzheimer's. Exposure to Piramal Health Care was positive within the Fund, however, the position was trimmed following the sale of one of its largest operating business units to Abbott Laboratories.

Regionally, a relative underweight allocation to China/Hong Kong, Taiwan, and South Korea, and an overweight to Thailand and Singapore drove positive relative returns in Asia. Overweight exposure to Turkey and South Africa, and no exposure to Russia was beneficial in the EMEA region. In Latin America, an underweight allocation to Brazil and overweight Mexico was positive.

During the year, a number of holdings were added to the Fund. MTN Group Limited, a dominant wireless operator in Africa with exposure in the Middle East, has exhibited excellent fundamentals in terms of balance sheet quality, and a proven track record of positive EVA (Economic Value Added) creation. Fresnillo PLC, a silver mining company based in Mexico with an experienced management team, is a superior low cost producer with an attractive multi-year production growth profile from a high quality asset base. Bharti Airtel is the dominant wireless operator in India, and is well positioned in the growing wireless market. Enersis is a Chilean holding company whose main operating assets are in electricity generation, and is positioned to leverage increased electricity demand due to strong GDP growth. Southern Copper Corporation owns and operates mining operations in Peru and Mexico, and is a producer of copper and zinc. The company's earnings out look is expected to improve as capital requirements decline, and a strong production growth profile should provide positive exposure to the expected long-term secular growth in copper prices.

The Fund exited the following positions over the year: Johnson Health Tech Company, a manufacturer and global distributor of physical fitness equipment, was removed due to deterioration in the operating environment and a decline in demand across key Western markets. Gamuda Berhad, a Malaysian investment holding and civil engineering construction company was removed as recent valuation was becoming expensive against a backdrop of deteriorating fundamentals. Banco Compartamos SA, a Mexican bank that offers financial services to individuals within the lower economic segments, faced sustainability challenges of its current growth rate from increasing competition and regulation. Piramal Health Care Limited of India was also sold as the business model fundamentally changed when it sold its largest operating division, Health Care Solutions, which represented 49 percent of consolidated sales, to Abbott Laboratories. Genting Malaysia Berhad was sold following an aggressive acquisition in the U.K., resulting in a fundamental change in the capital structure of the company and we became concerned about management's ability to create value. Fibria Celulose SA was also removed, as declining profitability ratios for the pulp and paper company indicated a deteriorating business environment.

By the end of the period, the Fund remains overweight the Consumer Discretionary, Consumer Staples, and Materials sectors, and underweight Financials, Telecommunication Services, and Energy sectors.

12

Management's Discussion of Fund Performance (Continued)

Strategy and Outlook

Growth in emerging markets continues to be robust, supported by positive macroeconomic fundamentals, rising domestic consumption and infrastructure spending. Traditional growth economies like China, India and Brazil, are now joined by peripheral economies like Indonesia, Thailand, Turkey and South Africa. Domestic currencies are expected to appreciate further, reflecting optimism in the outlook. Policy reforms in emerging economies continue to translate into long-term structural improvements and long-term productivity advancements which should be positive for domestic economic growth.

As the risk of a double-dip scenario in the broader global economy gradually dissipates, there is support for further upside in EM valuations as long as corporate earnings remain strong. The key challenge for policymakers now rests in taming inflationary pressure as food and commodity prices recover from 2009 trough levels. In China, the government's determination to stabilize the property sector will likely result in further tightening on credit and financing, taxation and ownership. But as leading indicators have shown, growth in China remains unimpeded, largely attributable to supportive monetary and fiscal policies. Earlier fears of a slowdown now appear to be unwarranted. We continue to implement a disciplined investment approach to uncovering the best companies across all regions that have demonstrated a proven track record of generating sustainable and positive economic profits, to provide consistent long-term risk-adjusted returns fo r the Fund's shareholders.

Comparison of the Change in Value of a $10,000 Investment in the Touchstone Emerging Markets Equity Fund - Class A* and the MSCI Emerging Markets Index

* The chart above represents performance for Class A shares only, which will vary from the performance of Class C shares, Class Y shares and Institutional Class shares based on the differences in loads and fees paid by shareholders in the different classes. The Fund commenced operations on September 30, 2009.

** The total returns shown above are adjusted for maximum applicable sales charges.

The performance of the above Fund does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

13

Management's Discussion of Fund Performance (Continued)

Touchstone Focused Equity Fund

Sub-Advised by Fort Washington Investment Advisors Inc.

Investment Philosophy and Process

The Touchstone Focused Equity Fund seeks capital appreciation by investing in equity securities of companies of any size.

Fund Performance and Positioning

The total return of the Touchstone Focused Equity Fund was 9.40% for the nine months ended September 30, 2010 which was calculated excluding the maximum sales charge. The Fund was launched on December 31, 2009. The total return of the Russell 3000® Index was 4.78% for the same period. The Fund outperformed its benchmark.

We are encouraged by the fact that the outperformance for this year has been broad based as six out of the nine sectors in which we were invested added value to the Fund. The key driver was significant outperformance in the Health Care, Consumer Discretionary, and Industrial sectors. Other sectors adding value to the Fund included Energy, Financials, and Telecommunication Services. Underperforming sectors included Information Technology, Consumer Staples, and Materials. Segmenting the Fund by market capitalization, companies under $10 billion increased in value more than 16% on average while the Fund's large capitalization companies also outperformed the Russell 3000® Index. Finally, the Fund's domestic holdings which made up 83% of the Fund, increased in value by more than 14%, dramatically outperforming its international holdings.

The companies that made the most positive contribution to performance in the past nine months included Time Warner Cable Inc. (Consumer Discretionary sector), Genzyme Corp. (Health Care sector), CORNELL COS. and AGCO Corp. (Industrials sector ). Detractors from performance included Nokia Corp. (Information Technology sector), Dean Foods Co. (Consumer Staples sector), Bank of America Corp. (Financials sector), and Cemex S.A.B. de C.V. (Materials sector). Over the course of 2010, we have increased exposure to the Information Technology, Telecommunication Services, Financials, and Materials sectors and decreased exposure to the Industrials and Consumer Staples sectors. While the Fund's weight in the Health Care sector remained generally the same throughout the course of 2010, we have made several changes within the sector as we emphasized names that are more attractive from a risk/reward basis. We were also able to take advantage of opportuniti es that arose from the decline in the Energy sector following the BP oil spill. The Fund is currently tilted to more non-defensive sectors as it has overweight positions in the Consumer Discretionary, Information Technology, and Financials sectors. Underweight sectors include Consumer Staples, Energy, and Industrials and no exposure to the Utilities sector.

Strategy and Outlook

What we are seeing is re-levering. Key segments of bank loans have stopped contracting (even standards for commercial & industrial loans to small businesses are starting to ease for the first time since late 2006); bank credit, the commercial-paper market, corporate-bond financing by non-financials and broad money (i.e. M3) are also growing. The commercial paper market is important to the shadow banking system. Notably, non-financial corporations access three times more credit from commercial paper and corporate bonds than they do from bank loans or said another way, the banking system provides only about 22% of private-sector credit in the U.S. In our opinion, these data points are providing evidence that deleveraging in the U.S. is ending; and when stocks are this cheap versus bonds then equities will move up and they should move up quickly (and that may be what is starting to happen in the equity market today). Moreover, we believe th e consumer is in better shape than most think and companies are still spending at depreciation which can't continue for a long period of time. Corporations cannot retain $2.4 trillion in liquidity while non-financial

14

Management's Discussion of Fund Performance (Continued)

corporations' accumulate an additional $1.7 trillion in cash flow this year. Listed companies cannot continue to keep this cash as the demand for the return of this cash to shareholders is inevitable; this will likely drive an increase in Merger & Acquisition activities and share buybacks hopefully at prices that create value for shareholders.

The several items mentioned previously give us comfort that we will reflate as a country. Think about the fact that real wages in the U.S. over the last several years have grown (versus in past recessions real wages declined); this country just came through one of the worst job cycles since the Great Depression and employee earnings held up remarkably well. This suggests wages are unlikely to be a source of deflationary pressure. Also, you have to ask yourself the question: if there is no demand for a strong exchange rate, how can the U.S. have deflation? If Japan, the U.S. and other countries cannot devalue their currencies against each other, then they must inevitably devalue them against goods and services. Lastly, on the inflation versus deflation argument, post World War II, it was the end of the gold standard which allowed central bankers to have a monetary response to all recessions and as a result post WWII recessions were started by inflation rather than deflation (which happened pre-WWII). We believe that inflation is of greater concern than deflation; and as you go from no inflation to 4%, equities tend to do well. As a result, we believe the Fund is positioned for a relatively solid equity market.

Comparison of the Change in Value of a $10,000 Investment in the Touchstone Focused Equity Fund - Class A* and the Russell 3000® Index

* The chart above represents performance for Class A shares only, which will vary from the performance of Class C shares, Class Y shares and Institutional Class shares based on the differences in loads and fees paid by shareholders in the different classes. The Fund commenced operations on December 31, 2009.

** The total returns shown above are adjusted for maximum applicable sales charges.

The performance of the above Fund does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

15

Management's Discussion of Fund Performance (Continued)

Touchstone Global Equity Fund

Sub-Advised by Bedlam Asset Management plc

Investment Philosophy and Process

The Touchstone Global Equity Fund seeks capital appreciation by primarily investing in U.S. and foreign equity securities including those of emerging market countries without regard to market capitalizations.

Fund Performance and Positioning

The total return of the Touchstone Global Equity Fund was 6.50% for the twelve month period ended September 30, 2010 which was calculated excluding the maximum sales charge. The total return of the MSCI All Country World Index was 8.95% for the same period.

Although the Fund's performance lagged the Index, it was significantly less volatile in absolute terms. Thus, the Fund generated a positive return in each of the three months prior to September, in contrast to the Index's decline in August. This is a result of the Fund's valuation bias, as it seeks to buy undervalued growth companies and, in the process, provide downside protection. Performance was boosted towards year-end by the biggest September rally in 71 years for U.S. equities, together with a steady stream of positive announcements across the Fund's holdings. The cause for the recent market euphoria was the prospect of a second round of quantitative easing (QE2), which should benefit emerging market currencies and cheap equities (particularly companies geared to emerging market demand) as well as precious metals.

The largest contributors to performance were the Fund's agriculture and gold (Materials sector) weight, with corn and gold prices up by 26% and 30% respectively, over the year. Other notable performers at the stock level were the emerging market companies Genting Berhad, TVB (Television Broadcasts Ltd.) and Hutchison Telecommunications Hong Kong Holdings Ltd. However, it was not exclusively the cyclical stocks that drove performance. The Health Care sector in particular posted strong gains, most notably from Bristol-Myers Squibb Co., as management raised their estimate for trough earnings in 2013. The Consumer Staples sector also contributed strongly over the period; they continue to benefit from pricing power and sector consolidation, as exemplified by Sara Lee Corp., recently reported to have received two separate private equity bids. The lag in performance relative to the Index was mainly due to the underweight in the Information Technolo gy sector, together with the overweight in the Telecommunication Services sector. The latter position will be maintained, as the telecoms are virtually all high-yielding emerging market companies, profiting from the demand for smartphones and the growth in data.

In other sector themes, the Fund's 10% agricultural weight soared as the corn price jumped sharply, with the sector's attractive valuations and growth prospects starting to receive the market's attention. This followed the weight being sharply increased in June/July of 2010, with the best performers being fertilizer producers CF Industries Holdings Inc., and Yara International ASA. The leap in grain prices arose from the supply shock of droughts in Russia, floods in Canada and Pakistan and storage problems in India. Grain prices have continued their rise as the USDA announced that demand was higher than expected and corn inventories are set to hit their lowest level since 1998. The other overweight for the Fund is gold and silver miners. Given the prospect for increasingly aggressive money printing from the world's central banks, the long-term structural story for precious metals remains intact. Even so, following the strong rally in the sha re prices of the miners, the weight was reduced in early October, from 14% to 10%.

16

Management's Discussion of Fund Performance (Continued)

A top stock performer for the Fund, Genting Berhad, a leading Asian gambling conglomerate, announced strong numbers thanks to its 52%-owned Singaporean casino business. The new casino complex opened in Singapore (one of only two permitted there) in January and the ramp-up in volume and margins far exceeded expectations. In the space of mere months Singapore has become a regional gambling hub for South East Asia and the Indian subcontinent. Gaming revenue has reached $4 billion (more than a fifth of Macau's) and is forecast to surpass the $6 billion of the Las Vegas strip, to reach $7 billion in 2012. Hutchison Telecomm prospered on the back of a 5% increase in sales growth and 7% rise in mobile revenue. The market awoke to the realization that it is a prime beneficiary of the explosion in smartphone demand and the surge in data revenue. Thus, we believe revenue growth and margins should expand further in 2011. Late in the year both TVB and F osters Group Ltd., received bids for parts of their business, following two separate take-over bids for Lihir Gold Ltd., and Allegheny Energy Inc., earlier in the year.

Stocks that detracted from performance over the past twelve months included Tom Tom N.V. (Information Technology sector), Koninklijke KPN N.V., France Telecom (Telecommunication Services), and Japan Steel Works Ltd. (Industrials sector). Sectors that detracted for the same period were Telecommunication Services, Industrials and Financials.

Strategy and Outlook

The Fund is well positioned to prosper from the two long-term structural trends of continued corporate consolidation and faster economic growth (and appreciating currencies) across the developing world. Currently, 65% of the Fund is weighted to small and mid-sized companies (market capitalization of less than $10 billion). As always, the weight of the Fund to small and mid-sized companies is purely a consequence of the bottom-up stock picking process, being a factor of valuations and the business cycle. One of the key drivers of sector consolidation is the fact that corporate cash levels are at all-time highs. To add to this, corporate bond yields are now at record lows, providing inexpensive finance. We believe that consolidation is in fact, bad for corporate bonds as it means gearing levels rise. Investors now face the dilemma of having to take on more risk to obtain a higher yield and we feel that, for equities, it is exactly the opposite . Quality companies such as Sara Lee and Kimberly Clark appear to offer some of the better yields. The return prospects for equities look more appealing than either government or corporate bonds.

Emerging market currencies are the long-term structural winners from the increasingly aggressive monetary policy actions - not only in the U.S., but also in Japan and, most likely, the U.K. and euro-zone. Faced with ballooning foreign reserves, the central banks of the developing world have to choose between currency appreciation and asset inflation. Either way, we believe investors in emerging economies are set to benefit. At year-end the Fund was 23% exposed to emerging markets by company domicile, but 44% based on where companies generate their profits.

At the sector level, Fund overweights remain Materials, Industrials, Consumer Staples, Health Care and Telecommunication Services. Sector underweights are Information Technology and Financials, due to rich valuations and the expectation of slowing earnings growth. The Materials sector exposure is to gold/silver miners and agriculture. As noted above, we continue to be positive on both the soft commodities and precious metals sectors. The Industrials sector companies are heavily weighted to infrastructure spending across both developed and emerging markets. Finally, many of the Health Care sector stocks remain undervalued and are posting solid growth; this comes at a time when the sector is in the midst of major consolidation.

17

Management's Discussion of Fund Performance (Continued)

Comparison of the Change in Value of a $10,000 Investment in the Touchstone Global Equity Fund - Class A* and the MSCI All Country World Index

* The chart above represents performance for Class A shares only, which will vary from the performance of Class C shares, Class Y shares and Institutional Class shares based on the differences in loads and fees paid by shareholders in the different classes. The Fund commenced operations on September 30, 2009.

** The total returns shown above are adjusted for maximum applicable sales charges.

The performance of the above Fund does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

18

Management's Discussion of Fund Performance (Continued)

Touchstone Global Real Estate Fund

Sub-Advised by Cornerstone Real Estate Advisers LLC

Investment Philosophy and Process

The Touchstone Global Real Estate Fund seeks capital appreciation by primarily investing in common stocks and other equity securities of U.S. and foreign real estate companies. Fund management utilizes a core research approach that combines top-down macroeconomic, capital and property market analysis with bottom-up understanding of local real estate and operational capacity to evaluate both property sectors and individual companies.

Fund Performance and Positioning

Global equity markets were volatile but ended on a strong upward trend during the twelve month period ending September 30, 2010. Throughout the year, investors were constantly re-adjusting views on the global economic outlook and implications on valuations, particularly as this twelve month period came on the heels of two quarters of very strong equity market performance. The market was also impacted by credit events in Dubai and southern European countries, including Greece. Government policy was another main theme during the year. In general, it has had a negative overall impact in emerging and commodities-based countries because of their tightening bias. On the other hand, it has mostly been a positive factor especially recently in some of the larger economies, such as the U.S. and Japan where the government is aggressive in providing liquidity to the market.

The total return of the Touchstone Global Real Estate Fund was 18.54% for the twelve month period ended September 30, 2010 which was calculated excluding the maximum sales charge. The total return of the FTSE EPRA/NAREIT Developed Index was 18.41% for the same period. The Fund outperformed its benchmark and other major global equity indices during the period.

While the MSCI World Index did not reach the recent twelve month high reached in April, the Fund's benchmark FTSE EPRA/NAREIT Developed Index (Index) surpassed this mark in September 2010 and continues to move higher. Real estate fundamentals continued to improve throughout the year, with a bottoming in real estate values and improvements in market fundamentals seen in many markets around the globe. The low interest rate environment has supported the real estate sector in multiple ways, such as the reduction of cost of capital for real estate companies, compression of cap rates and increasing fund flow from yield starved investors due to real estate's reasonably attractive yield spreads and inflation protection features. These positive factors should remain intact as the leading economies continue to promote accommodative monetary policy.

Within the Index, North America was the strongest region with a total return of 30.62%. Canada and the U.S. both contributed positively to this performance with total returns of 41.91% and 29.46%, respectively. Asia and Europe underperformed the Index with a total return of 11.77% and 7.98%, respectively. Within Asia, Singapore was the lone outperformer registering a total return of 28.00%. In Europe, while none of the major countries outperformed, two smaller Index weights Sweden and Switzerland, recorded strong total return performance of 51.53% and 31.66%, respectively.

The Fund benefited from strong security selection during the period, particularly in the U.S., Hong Kong, and Germany. The largest contributors to performance in the U.S. were Glimcher Realty Trust, ProLogis, AvalonBay Communities and BRE Properties.

Glimcher Realty Trust, a "B" quality Regional Mall REIT, was trading at an extremely discounted valuation relative to its peers due to concerns about its ability to refinance its balance sheet. Our analysis indicated that

19

Management's Discussion of Fund Performance (Continued)

the balance sheet issues were not as great as the market was pricing, in leading us to take a position in the company. When the company was able to alleviate its balance sheet problems through the sale of some assets into a joint venture early in 2010, the gap in valuation quickly began to close. We decided to underweight ProLogis, a global industrial REIT, based on our belief that the company would need to issue additional equity to strengthen its balance sheet and the recovery in fundamentals for industrial real estate would be slow due to weak global trade. Our belief that demand for apartments would recover faster than many were expecting due to positive demographics and a shift from homeownership to renting, drove our decision to overweight apartment REITs AvalonBay Communities and BRE Properties.

In Hong Kong, the Fund was generally overweight large cap developers and underweight REITs. Although Hong Kong property prices rose strongly during the period, the Hong Kong government was reluctant to impose harsh measures to contain the potential bubble. As developers sold projects at higher prices and paid record prices at land auctions, developer stocks performed well, which contributed positively to Fund performance during the period. Recently however, the Hong Kong government has begun to announce various measures addressing rising property prices and deteriorating affordability. As a result, we believe developer stocks may have hit a plateau and we have shifted some weights to retail-focused landlords.

During most of the period, the Fund held a position in what we perceive is one of the few quality companies in Germany, Alstria Office REIT, which had strong alpha contribution. This company invests in offices throughout Germany with its largest exposure to Hamburg. The company owns high quality, centrally located assets that are leased on long contracts to strong tenants like the City of Hamburg. On top of the quality of the company and the solid growth prospects, we saw two triggers for the share price. One is that the company was in danger of breaching a LTV covenant, but could not issue equity because the majority shareholder would not cooperate. Secondly, they had to arrange the refinancing of the major part of their debt maturing in 2014. We anticipated that these two problems would be solved, and after they were, the company performed very well.

Securities detracting from relative performance during the period were positions in the U.S., France, Norway, and Singapore. During the period, the Fund's performance was adversely impacted by our decision to underweight the U.S. region. This decision was predicated upon the belief that Asian economies would post greater economic growth than a still struggling U.S. economy and therefore fundamentals for U.S. commercial real estate would be slower to recover. Unfortunately, low borrowing costs and signs that fundamentals were beginning to improve were enough to drive investors seeking the predictable cash flows back into commercial real estate, boosting asset prices and spurring a rally in the U.S. REIT market. We were able to offset the impact of the Fund's underweight position during the year with strong security selection in the region.

The Fund's overweight position during the period in France did not work in its favor, although this was compensated by the positive security selection within the country. The U.S. Dollar denominated French EPRA Index underperformed the Index, while the Euro denominated French EPRA Index underperformed the Global EPRA/NAREIT Index. Hence, most of this underperformance was due to volatility in the U.S. Dollar to Euro exchange rate.

During the period, the Fund held a position in one stock in Norway, Norwegian Properties, which underperformed the benchmark during the period on two fronts. First, rental growth in the Oslo office market has turned out not to be as strong as expected given the general macroeconomic strength of the country. Secondly, we had expected Norwegian Properties to profit significantly from the disposal of the Norgani Hotel portfolio, making the company a more focused office play and taking down the gearing by paying off

20

Management's Discussion of Fund Performance (Continued)

debt with the sales proceeds. However, the sales price had been slightly disappointing and the share price reaction was negative. In Singapore, the government was proactive in trying to contain residential prices by announcing a number of measures addressing both supply and demand. As a result, we underweighted the developers and overweighted SREITs and diversified players for both defensiveness and yield. However, due to strong liquidity in the region, the Singapore residential market held up well and developer stocks had solid performance, contributing negatively to Fund performance during the period.

Strategy and Outlook

Cornerstone's expectations are for a slowly improving U.S. economy in 2011 with employment growth accelerating late in the year. Several factors support the slower-growth forecast, including sturdy corporate balance sheets and profits, aggressive austerity measures and stress tests that have eased Eurozone debt concerns for now, and relatively robust growth in Asia. While we are cognizant of the threats to this thesis, we believe modest growth should support continued improvement in the underlying real estate fundamentals and limit new development activity, positioning REITs for a period of moderate internal growth over the next few years. Interest rates will likely remain low for the foreseeable future, which supports real estate fundamentals and fund flows into real estate.

In Europe, we will begin to see the impact of the government austerity programs being implemented over the next few quarters. While the austerity programs will provide more certainty to corporations and individuals and may stimulate investment and demand, they could also increase unemployment and impact growth. Although Europe has made progress in economic recovery efforts, risk remains for growth to stall as a result of budget restructuring that needs to take place in Southern Europe. Northern Italy, French and Swedish retail markets are still among the most attractive in Europe. There is also rising investor interest in Spanish shopping centers in the healthier, more stable regions. The most attractive office markets are London, Paris and Stockholm.

In Asia, we generally have a positive macro fundamental outlook on the region, with the exception of Japan. Policy risk will continue to be a key theme in Asia and needs to be monitored closely. To that end, we are still cautious in China where central and local governments continue to have a tightening stance and have announced various measures targeted at both increasing supply and controlling demand since April. Hong Kong residential and commercial markets are tight and continue to perform extremely well. Policy is a risk in Hong Kong as well since surging home prices are politically disruptive. Although the RBA in Australia is biased towards further interest rate hikes, we have a favorable view on the country with a focus on careful stock selection. Valuations and return expectations are attractive based on strong fundamental underpinnings and positive currency trends. With a deteriorating macroeconomic outlook, which is exacerbated by t he strengthening Yen, and unfavorable supply-demand fundamentals in the Tokyo office market, it is difficult to take a positive view on Japan. Policy risk in the form of BOJ's newfound aggressive easing stance and asset purchase program and the resulting increase in real estate transactions are risks to our view.

We are grounded in fundamental research with the ability to adapt to changing market conditions. Our philosophy and process are focused on understanding management's business and financial strategies; and their ability to unlock value and growth from their properties and markets given where we are in the economic, property market, and capital market cycles. Our process is managed using a proprietary multifactor ranking model that considers quantitative and qualitative rankings for top-down and bottom-up factors which drive potential returns. The model allows appropriate adaptation to dynamic market conditions.

21

Management's Discussion of Fund Performance (Continued)

Comparison of the Change in Value of a $10,000 Investment in the Touchstone Global Real Estate Fund - Class A* and the FTSE EPRA/NAREIT Developed Index

* The chart above represents performance for Class A shares only, which will vary from the performance of Class C shares, Class Y shares and Institutional Class shares based on the differences in loads and fees paid by shareholders in the different classes. The Fund commenced operations on September 30, 2009.

** The total returns shown above are adjusted for maximum applicable sales charges.

The performance of the above Fund does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

22

Management's Discussion of Fund Performance (Continued)

Touchstone Healthcare and Biotechnology Fund

Sub-advised by Turner Investment Partners

Investment Philosophy and Process

The Touchstone Healthcare and Biotechnology Fund invests primarily in common stocks of Health Care and biotechnology companies. The Fund employs rigorous fundamental research with supporting qualitative and technical analysis. Its bottom-up strategy emphasizes fundamental analysis. The Fund seeks companies with improving fundamentals, superior earnings prospects, reasonable valuations, and favorable trading-volume and price patterns.

Fund Performance and Positioning

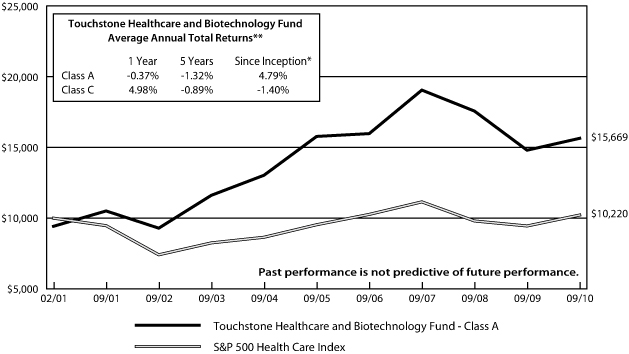

The total return of the Touchstone Healthcare and Biotechnology Fund was 5.74% for the twelve month period ended September 30, 2010 which was calculated excluding the maximum sales charge. The total return of the S&P 500 Healthcare Index was 8.31% for the same period. The Fund underperformed its benchmark.

The Fund's relative performance was hurt by holdings held in the Health Care Providers & Services industry. Although these service holdings in the Fund's portfolio posted a positive return for the one-year period, it was not enough to overcome the return generated by these holdings held in the Index.

Strong stock selection in the Fund's Health Care Equipment & Supplies' holdings added to relative outperformance. These holdings traded higher for the period, whereas these holdings held in the Index posted a loss.

Within the Health Care Providers & Services industry, Tenet Healthcare Corp. and McKesson Corp. detracted from results. Hospital operator Tenet Healthcare Corp. traded lower after the company's attempt to buy an Australian hospital failed. Investors reacted negatively to this news as Tenet Healthcare Corp. is seen as a de-leveraging story. Additionally, hospitals are currently in a weakened state as a result of stagnant unemployment and a more cautious consumer along with the government not extending COBRA benefits to the unemployed. We sold the security from the Fund's portfolio. The performance of McKesson Corp., a pharmaceutical distribution and healthcare information technology company, was also a drag on relative results for the quarter. There is a short-term concern of an absence of new generics entering the market. This could potentially have an adverse impact on operating margins for McKesson Corp., as generic drugs have much hig her margins for Mckesson when compared to branded drugs. We believe these concerns are overblown, and we were pleased to see the recent launches of generic Lovenox and generic Taxotere, all within the past month. We continue to own the security in the Fund.

Merck & Co. Inc. (Pharmaceuticals industry) was the largest detractor in the Fund over the one year period ending September 30, 2010. The underperformance here had more to do with our timing of owning this security. We do own the security currently as Merck & Co. Inc. is the second largest company held in the Index.

Within the Health Care Equipment & Supplies industry, Fund holding ev3 Inc., a global endovascular company, traded substantially higher after the company was acquired by drug and medical device maker Covidien at a sizeable premium. We expect more deals to take shape in the medical technology space throughout the remainder of 2010 as large pharmaceutical companies have excess cash on hand to acquire smaller boutique companies. Edwards Lifesciences Corp., the developer of products and technologies to treat advanced cardiovascular disease, also advanced on the news of the buyout for ev3 Inc. We believe Edwards Lifesciences Corp. is likely a near-term takeout candidate.

23

Management's Discussion of Fund Performance (Continued)

Other outperformers included Valeant Pharmaceuticals International Inc. and Human Genome Sciences Inc. Within the Pharmaceuticals space, Valeant Pharmaceuticals International Inc. traded significantly higher as the U.S. based drug maker agreed to purchase Toronto based drug maker Biovail Laboratories Inc. Valeant Pharmaceuticals International Inc. benefits in many ways from this transaction in that they will be able to take advantage of Biovail Laboratories Inc.'s low tax base in Barbados and benefit from greater efficiencies as the new company will shed roughly 25% of its employee headcount, which will be accretive to earnings. Biotechnology company Human Genome Sciences Inc. spiked higher after the FDA gave a priority review for Human Genome Sciences Inc.'s and GlaxoSmithKline's joint drug Benlysta, their new drug aimed at treating systemic lupus. A decision for drug approval could be as early as December of this year and investors flocked to the stock anticipating good news from the FDA. If approved, Benlysta would be the first new lupus drug to reach the market in more than 50 years. Additionally, we believe that Human Genome Sciences Inc. could at some point be an acquisition target of GlaxoSmithKline, fueling the upside stock price potential.

Although the Fund underweight position in large capitalization pharmaceuticals detracted from performance, strong stock selection in this industry more than made up for the lack of exposure. Large cap pharmaceuticals stocks make up 52% of the Index and the Fund has typically been underweight this group. More recently, we have added to the Fund's exposure in large Pharmaceuticals companies as we have begun to witness a trade up for companies that pay a healthy dividend.

In general, the Fund has a higher weight in Health Care Technology companies as we believe this space is primed for Merger & Acquisition activity. We did slightly reduce the Fund's exposure to Health Care Providers & Services providers during the quarter but it still holds an overweight position compared to the benchmark.

Strategy and Outlook

We continue to find companies with compelling fundamentals. Balance sheets in the Health Care sector remain flush with cash, keeping open the possibility of stock buybacks, mergers and acquisitions in the sector. The November elections could play a role in healthcare reform if Republicans gain seats in Congress as they will look to lock down healthcare programs by limiting spending. Actual reversal of the reform initiatives is unlikely, but lack of funding could stall implementation indefinitely.

24