EXHIBIT 99.5

MANAGEMENT’S DISCUSSION & ANALYSIS

FOR THE PERIOD ENDED DECEMBER 31, 2004

Management’s Discussion and Analysis (MD&A) is intended to help you understand the dynamics of our business and the key factors underlying our financial results. It explains trends in our financial condition and results of our operations for the year ended December 31, 2004 compared with our operating results for the year ended December 31, 2003. It also compares our balance sheet as at December 31, 2004 to our balance sheet as at December 31, 2003. This MD&A should be read in conjunction with our Audited Consolidated Financial Statements for December 31, 2004.

‘The information in this MD&A is as of February 21, 2005 and in this MD&A ‘we’, ‘us’, and ‘our’ refers to Call-Net Enterprises Inc. (Call-Net). Additional information relating to our company, including our Annual Information Form (AIF), is available on SEDAR atwww.sedar.com.

FORWARD-LOOKING STATEMENTS

Securities laws encourage companies to disclose forward-looking information so that investors can get a better understanding of the company’s future prospects and make informed investment decisions. Statements that are not historical fact and are based on current expectations, estimates and assumptions are forward-looking statements.

This MD&A contains forward-looking statements about our business. Inherent in these statements are known and unknown risks, uncertainties, and other factors that may cause the results, performance or achievements of our Company to differ materially from those expressed or implied by such statements. Such factors include, among others, general economic and business conditions, demographic changes, regulation, major technology changes, timing of product introductions, competition and our ability to attract and retain key employees.

NON GAAP FINANCIAL MEASURES

Certain financial measures used in this MD&A do not have any standardized meaning under Canadian generally accepted accounting principles (GAAP). Below is a definition of each of the non-GAAP financial measures used in this MD&A. At the point where each non-GAAP financial measure is first discussed, a table has been provided to reconcile that financial information to the most directly comparable GAAP measure.

| | EBITDA |

| | Earnings before interest, taxes, depreciation and amortization (EBITDA) is a financial metric used to analyze operating results. We define EBITDA as revenue less carrier charges and operating costs. We use EBITDA as a benchmark of operating performance and as a performance threshold in the management incentive plan. We caution you that EBITDA as calculated by us may not be comparable to similarly titled amounts reported by other companies. |

| | |

| | FREE CASH FLOW |

| | We define free cash flow as EBITDA less financing costs (including interest expense on long-term debt, servicing fees, bank charges and any late payment charges), cash income taxes paid, net capital expenditures and the cash component of changes in deferred costs. We use free cash flow as a measure of our ability to maintain operations and service debt. |

| Call-Net Enterprises Inc. | Page 1 | 2004 & Q4 Managements Discussion & Analysis |

OVERVIEW

CALL-NET’S BUSINESS

We are a national, full-service, facilities-based telecommunications alternative to the long-established telephone companies, known as incumbent local exchange carriers, or ILECs. Primarily through our wholly-owned subsidiary Sprint Canada Inc. (Sprint Canada), we offer home phone, long distance, wireless, and dial-up Internet access services to residential customers targeting Canada’s largest metropolitan areas. We also offer local, long distance, data and Internet Protocol (IP) solutions (including access) to Canadian businesses and governments of all sizes.

We provide services to three types of customers: consumers, businesses and other telecommunications companies. Services to the first two are offered largely under the Sprint Canada brand, while services to the third group, sometimes called carriers, are delivered under the Call-Net brand.

BUSINESS STRATEGY

Our mission is to leverage proven technologies and outstanding people to deliver telecommunications services in a smart and simple way.

In order to deliver on that mission, our business plan identifies five areas of focus:

| | 1. | Identify, develop, and exploit profitable segments within the Canadian telecommunications marketplace |

| | 2. | Provide competitive services and solutions that optimize partner relationships, internal capabilities and the regulatory environment |

| | 3. | Hire, train and recognize outstanding people that exemplify our values |

| | 4. | Differentiate through superior sales and customer service |

| | 5. | Be financially prudent with respect to cash flow, capital expenditure and acquisitions. |

KEY PERFORMANCE DRIVERS

Our business success and financial performance will be driven principally by our success at identifying and managing the following performance drivers in our industry.

CUSTOMER DEMAND

Customer demand for telecommunications services is generally growing, although the growth rate varies, sometimes substantially, by product. For example, we believe that long distance usage, as measured by the number of long distance minutes, is growing despite the fact that industry long distance revenues are generally declining. In addition, the number of local lines in service in Canada has been growing, albeit quite modestly. Wireless service and high speed Internet services are currently growing at more substantial rates, generally greater than 10 per cent per year. Our company is less sensitive to the growth rate of any given telecommunications product or service because we have a very small share of the markets in which we operate. Underlying growth in demand for the products we sell helps, but we do not currently need to rely on industry growth to drive revenue growth.

COMPETITIVE INTENSITY AND INDUSTRY PRICING

The Canadian telecommunications industry is very competitive. The industry is dominated by a small number of very large incumbent firms that have benefited from historical advantages of scale resulting from the fact that they were able to build their networks and capital and customer bases while under protection as statutory monopolies. In spite of the steps taken over the past several years to deregulate the market for telecommunication services and the investments made by competitors in infrastructure to compete, the incumbent advantage has proven to be very difficult to overcome, with most competitors having failed over the past five years. Competition continues to be based primarily on price, although we are establishing ourselves based on our service capabilities as well. However, because of this price competition and because of technological changes discussed later, per-unit pricing in the telecommunications industry has been falling for several years in many product categories. We have been successful at bringing costs down at a rate that exceeds the rate of decline in per-unit pricing and so our profitability has been improving, and we must be careful to maintain profitability in the face of continued competition.

OPERATIONAL EFFICIENCY

In part because of falling prices, we must become ever more operationally efficient. Each year, we set objectives for reducing our carrier charges and improving operational efficiencies. We have generally met these objectives, improving our gross margins over the past two years while growing business volumes and keeping our network operations and corporate costs stable. We must continue to improve efficiencies in the future to be assured of having a successful, long-term enterprise.

| Call-Net Enterprises Inc. | Page 2 | 2004 & Q4 Managements Discussion & Analysis |

FAIR REGULATION

We continue to pursue regulatory reforms to lower carrier costs and remove operational barriers to competition in the telecommunications industry. While, in general, we are satisfied with the regulatory regime as currently constructed by the Canadian Radio-television and Telecommunications Commission (CRTC), we are engaged in a number of follow-up proceedings resulting from the price cap decisions to lower our access costs. Our business strategy does not depend on additional relief from the CRTC on access costs, but we do depend on the regulator to ensure that incumbents are implementing and respecting the decisions it makes.

QUARTERLY SUMMARY INFORMATION

In order to track our financial performance and condition, we pay particular attention to the measures summarized in the following table of quarterly information.

2004 Quarterly Information

| (in millions Canadian $) | | Q4 | | Q3 | | Q2 | | Q1 | |

| Revenue | | | 211.1 | | | 204.2 | | | 200.8 | | | 202.5 | |

| Gross profit | | | 109.2 | | | 101.1 | | | 100.3 | | | 107.4 | |

| Operating income | | | (11.5 | ) | | (7.8 | ) | | (13.3 | ) | | (10.3 | ) |

| Net income | | | (13.8 | ) | | (1.6 | ) | | (33.1 | ) | | (29.9 | ) |

| Earnings per share (EPS) | | | (0.39 | ) | | (0.05 | ) | | (0.93 | ) | | (0.84 | ) |

| EBITDA (1) | | | 31.9 | | | 24.1 | | | 22.4 | | | 26.5 | |

| Net capital expenditures | | | 14.9 | | | 15.9 | | | 10.2 | | | 14.0 | |

| Free cash flow (1) | | | 8.4 | | | (1.6 | ) | | 2.6 | | | 1.4 | |

| Local equivalent line count (2) | | | 464,900 | | | 371,300 | | | 336,800 | | | 301,600 | |

| Churn (3) | | | 2.1 | % | | 2.7 | % | | 2.1 | % | | 2.2 | % |

| (1) | See reconciliation in the ‘MD&A Summary Information’ table found on the final page of this document. |

| (2) | Includes primary rate interfaces (PRIs) quantified as 23 individual business lines (IBLs) |

| (3) | Equals monthly disconnections divided by the average number of lines per month. |

2003 Quarterly Information

| (in millions Canadian $) | | Q4 | | Q3 | | Q2 | | Q1 | |

| Revenue | | | 204.1 | | | 204.9 | | | 194.1 | | | 202.2 | |

| Gross profit | | | 107.3 | | | 96.4 | | | 95.7 | | | 96.0 | |

| Operating income | | | (13.7 | ) | | (15.8 | ) | | (23.0 | ) | | (15.7 | ) |

| Net income | | | (16.9 | ) | | (30.2 | ) | | 2.0 | | | 7.6 | |

| Earnings per share (EPS) | | | (0.48 | ) | | (1.15 | ) | | 0.08 | | | 0.32 | |

| EBITDA | | | 24.9 | | | 23.0 | | | 23.7 | | | 24.5 | |

| Net capital expenditures | | | 13.3 | | | 12.8 | | | 4.8 | | | 5.4 | |

| Free cash flow | | | 0.9 | | | (1.7 | ) | | 6.5 | | | 6.3 | |

| Local equivalent line count | | | 267,600 | | | 234,900 | | | 208,600 | | | 188,500 | |

| Churn | | | 2.7 | % | | 3.3 | % | | 3.6 | % | | 3.2 | % |

The factors affecting these metrics over the past eight quarters are discussed throughout this MD&A.

| Call-Net Enterprises Inc. | Page 3 | 2004 & Q4 Managements Discussion & Analysis |

CALL-NET’S 2004 RESULTS

2004 IN REVIEW

In 2004, we set out to return Call-Net to growth. After several years of declining revenue, brought about by persistent industry-wide declines in the per-unit pricing of the products and services we sell, as well as unprecedented changes in the structure of our industry, we hoped to be able to return to year-over-year growth in both revenue and EBITDA. We are pleased to report success on this front in 2004; marking another turning point in the evolution of our business.

Selected Financial Information | | For the years ended December 31 | |

| (in millions Canadian $) | | 2004 | | 2003 | | 2002 | |

| Revenue | | | 818.6 | | | 805.3 | | | 800.7 | |

Netincome (loss) | | | (78.4 | ) | | (37.5 | ) | | (151.1 | ) |

| Earnings (loss) per share (EPS) - basic | | | (2.20 | ) | | (1.36 | ) | | (N/A | ) |

| Total assets | | | 648.9 | | | 839.1 | | | 921.6 | |

| Long-term financial liabilities | | | 321.8 | | | 436.2 | | | 518.6 | |

| EBITDA | | | 104.9 | | | 96.1 | | | 46.6 | |

| Net capital expenditures | | | (55.0 | ) | | (36.3 | ) | | (71.7 | ) |

| Free cash flow | | | 10.8 | | | 12.0 | | | (105.7 | ) |

REVENUE IS GROWING

Revenue in 2004 was $818.6 million and includes the results of our acquisition of the Bell/360 customer base. Prior to the inclusion of the Bell/360 acquisition, our revenue was $811.0 million, up by $5.7 million, or approximately one per cent from 2003.

| • | Acquisitions have accelerated revenue growth and product diversification |

On May 25, 2004, we entered into an agreement with Bell Canada to acquire certain assets of 360networks Corporation including significant portions of its business customer base and specific network facilities in Ontario, Quebec and Atlantic Canada (the ’Bell/360 acquisition’). The closing of this transaction occurred on November 20, 2004, at which time more than 50 former employees of 360networks joined our company.

At closing, we entered into a two-year transitional services agreement with Bell Canada under which it will provide technical and operational services to the newly acquired customer base and in exchange be paid approximately 70 per cent of the total revenue subject to a minimum monthly amount of approximately $2.0 million. We will have an option at the end of the term of the agreement to acquire certain CLEC network assets used to service these customers. This CLEC network is one of the most significant telecommunications networks in Central and Atlantic Canada connecting over 1,000 office buildings.

The acquisition price for the business customer base totaled $17.6 million, representing three months of acquired revenue plus acquisition costs, and will be paid in four installments over the life of the transition services agreement. The $17.6 million was recorded as a customer relationship intangible asset and is being amortized over 30 months.

In the fourth quarter, revenue from the Bell/360 customer base accounted for approximately $7.6 million of our consolidated revenue and contributed approximately $1.2 million of recurring EBITDA. The Bell/360 customer base and the employees we acquired to support and grow this base are in the process of being integrated into our company. In December, the acquired customer base received its first invoices from Sprint Canada.

In 2005, we expect to be able to grow both the number of customers on this network and the total revenue on the network without compromising any of our other Business Services activities. Already, significant work is underway on a number of strong business opportunities.

| Call-Net Enterprises Inc. | Page 4 | 2004 & Q4 Managements Discussion & Analysis |

| • | Consumer and business services revenue continues to grow |

We operate two growth businesses; Consumer Services and Business Services. The revenues in each of these businesses grew in 2004; Consumer Services by 10 per cent and Business Services by six per cent. Growth was fueled by our ongoing migration into new products and services. In Consumer Services, this means bundled home phone service, while in Business Services, it means local and IP-enabled data services. Our Carrier Services business declined by 16 per cent in 2004 reflecting industry-wide weakness in this market.

| • | We continue to diversify our revenue base |

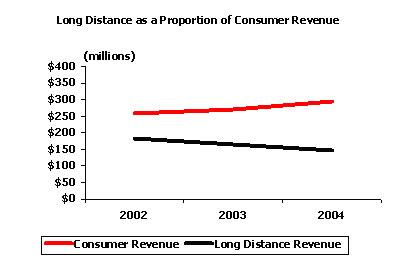

We have historically been a long distance services company and long distance services have been a very profitable product for us to sell. But several years ago we realized that being a long distance only company was not a viable long term strategy. Accordingly, we began to diversify our revenue base. In 2004, we saw our growth businesses - business and consumer - add significantly to the local and data services we offer, more than offsetting the decline in long distance revenues. In 2004, 52 per cent of our revenue came from long distance while 48 per cent came from these other products and services. The effects of this diversification are more dramatic at the divisional level, where in both Consumer Services and Business Services, long distance is no longer our largest product by revenue.

OUR NETWORK AND OPERATIONS ARE MORE EFFICIENTLY MANAGED

In 2004 we realized significant improvements in the efficiency of our network and in our various processes supporting both the provisioning and servicing of our customers. Our aim has been to create operational efficiencies with the dollar savings being reinvested to create growth.

| • | Carrier charges were less than 50 per cent of revenue |

In 2004, we were successful at keeping carrier charges below 50 per cent of revenue. As our local business grows, we are able to take advantage of scale economies in co-location operations and in back-haul. A co-location site and the associated back-haul is generally a fixed cost. As we add more customers in a co-location the per customer cost drops. Our increased scale also gives us the opportunity to make small changes in our network to replace leased with owned facilities. In 2004, we constructed Metro Area Networks (MANs) in Toronto and Ottawa, complementing MANs already existing in Montreal and Vancouver. These MANs allow us to bring our traffic to our switch sites over fibre that we own, rather than fibre leased from other telecommunications companies, reducing our carrier charges as a result. In addition, the cost of terminating calls in Canada, the United States and internationally continues to drop reflecting the overall decline in the costs of operating telecommunications companies world-wide. For example, in 2004 we had an 40 per cent increase in international traffic, but our total costs for terminating international traffic dropped by nine per cent.

| Call-Net Enterprises Inc. | Page 5 | 2004 & Q4 Managements Discussion & Analysis |

| • | Provisioning efficiency improved |

We have made significant investments in becoming smarter in our provisioning operations. Because of the growth rate of our local business, and because we are the only telecommunications company in Canada that has been significantly growing its local customer base, we have established a provisioning operation that rivals those of ILECs that may be 10 or 20 times our size. Because of our smaller size, however, it is important, that we become ever more efficient in provisioning so that this cost does not grow in step with our local revenues. In 2004 our total expenditures in provisioning were essentially unchanged from 2003. This despite the fact that we activated 40 per cent more customers in 2004 than 2003, and processed more than 150,000 moves, adds, and changes in the year. During business hours in 2004, our provisioning operation successfully completed an average of one provisioning order every 15 seconds.

| • | Network operating expenses remain stable |

While operating costs grew from $299.3 million in 2003 to $313.1 million in 2004, this growth was deliberate and limited to the ongoing investment in the growth of our Business Services and Consumer Services customer base. Expenses related to network operations and corporate services actually declined despite a 10 per cent increase in long distance minutes from 2003 to 2004 and a 76 per cent increase in the number of local line equivalents in service on the Call-Net network.

CONSUMER SERVICES IS GROWING AND DIVERSIFYING

Our revenue diversification has come in part from our successful penetration of the home phone service business in Canada. As we grow the number of customers in this part of our business, we also expect to grow the revenue per customer as we bundle home phone service with long distance, wireless and, in 2005, DSL service. In addition to providing top line revenue growth, this strategy allows us to diversify our consumer revenue stream so that we are less dependent on any one product.

| • | Continued profitable growth in local service lines |

We continued our success in adding local and home phone service customers, adding 92,500 net consumer lines and 98,500 net equivalent business lines for a total of 197,300 lines in the year. This brings our total number of local line equivalents to 464,900. Of the increase in net business local equivalent lines, 61,900 comes from the inclusion of the Bell/360 acquisition in the fourth quarter.

| Selected Key Performance Indicators | | For the years ended December 31 | |

| | 2004 | | 2003 | | 2002 | |

| Net local line additions | | | | | | | | | | |

| | Consumer home phone service | | | 104,800 | | | 65,000 | | | 79,900 | |

| | Business local line equivalents | | | 92,500 | | | 31,400 | | | 33,100 | |

| Total net additions | | | 197,300 | | | 96,400 | | | 113,000 | |

| Local lines | | | | | | | | | | |

| | Consumer home phone service lines | | | 310,800 | | | 206,000 | | | 141,000 | |

| | Business local line equivalents* | | | 154,100 | | | 61,600 | | | 30,200 | |

| Total local lines | | | 464,900 | | | 267,600 | | | 171,200 | |

| Average monthly churn** | | | 2.2 | % | | 3.0 | % | | 4.3 | % |

| Consumer customers | | | 578,000 | | | 645,125 | | | 584,536 | |

| Business customers | | | 20,000 | | | 11,400 | | | 6,300 | |

| * | Includes primary rate interfaces (PRIs) quantified as 23 individual business lines (IBLs) |

| ** | Equals monthly disconnections divided by the average number of lines per month. |

| • | Home phone service bundles continue to grow |

We have focused on selling product bundles to our consumer customers using home phone service as the foundation product, as a means of increasing customer loyalty, increasing our share of our customers’ monthly communications spend, and reducing customer churn. In the fourth quarter of 2004, 69 per cent of consumer services revenue came from customers who purchase more than one product from us, as compared to 50 per cent in the fourth quarter of 2003. Most of these customers purchase a bundle of home phone and long distance services with some taking a third product such as a wireless second line or dial-up Internet access.

Average revenue per line (ARPL) includes revenue from home phone and long distance services together with additional bundled revenues from services such as Fido® wireless and dial-up Internet, all divided by the average number of lines. The additional products and services added to the home phone bundle in 2004 have allowed us to offset declines in long distance revenue per line per month.

| Call-Net Enterprises Inc. | Page 6 | 2004 & Q4 Managements Discussion & Analysis |

We believe that our bundled home phone service business has many characteristics desirable in consumer telecommunications including: a relatively stable monthly spend consisting of basic service, features and long distance service, a healthy contribution to margin,; low churn, a reliable cost of acquisition and the potential for significant growth to the customer base.

Finally, our cost of acquisition and provisioning continues to fall. In the fourth quarter, we spent an average of $269 to acquire and provision a home phone service line, down from $315 in the fourth quarter of 2003. For the full year, 2004, our cost of acquisition averaged $304 per line. We have seen efficiency improvements in both selling and marketing and in provisioning new customers.

After a modest run up in the third quarter of 2004, fourth quarter overall churn returned to the levels of earlier in the year - about 2.1 per cent. Overall churn for the year was 2.2 per cent, down from 3.0 per cent last year.

Customer churn in home phone service in the quarter averaged 2.5 per cent, and allowed us to average 2.6 per cent consumer churn for the year. Over the past year, we have been able to reduce churn by focusing on customer retention and improving the credit profile of customers. In addition, two CRTC decisions, have helped. The extension of the ’no-winback’ period from three months to 12 months (Telelcom Decision CRTC 2004-04), and the direction that ILECs unbundle home phone service from their offerings (Telelcom Decision CRTC 2003-49). According to customer surveys done at the time of disconnect, the principal element of voluntary churn continues to be a desire to have high-speed Internet (via DSL) and home phone service provided by one supplier. We will address this with the launch of our own facilities-based high-speed Internet product in the second half of 2005.

| • | VoIP - planning for tomorrow, without sacrificing today |

In 2004, we launched a voice over Internet protocol (VoIP) service under the name Sprint Canada Internet Phone Service. Customer take-up of this offering is modest - consistent with our expectations. We have committed to try to deliver the highest quality VoIP service available because we believe that consumers buy service first and technology second. VoIP is an important investment for the future because we believe that consumer adoption of Internet phone services will continue to grow as the reliability of the service improves.

BUSINESS SERVICES ENHANCES FOCUS ON NEXT- GENERATION DATA AND LOCAL SERVICES

| • | IP Enabled Solutions continues to win converts |

After the launch ofIP Enabled Solutions in late 2003, we saw revenue growth in excess of 40 per cent in Internet protocol (IP) based services in 2004 as we began to focus on IP as a dominant networking solution. Our IP solution allows our customers to leverage the benefits of this technology through hybrid networks and has several advantages:

| | • | A single flexible network that encompasses a range of access types from xDSL to Ethernet allowing a customer to tailor a solution to precisely match the requirements of each site |

| | • | A migration path from legacy frame relay services that delivers more bandwidth, more flexibility and a platform for emerging converged IP applications |

| | • | An opportunity to simplify customers’ data solutions, moving from disparate services to a single IP platform. |

| • | Cross-border services are an important source of growth and profits |

We continue to succeed in our initiative with Sprint to win a greater share of the cross-border market. Our revenue from cross border initiatives grew by 32 per cent in 2004 and is now 15 percent of our Business Services revenue. Sprint and Sprint Canada offer a unique value proposition to North American business in the provision of seamless North American telecommunications services. We expect continued success in 2005.

| • | Local service bundles are attractive in the business market |

The small and medium enterprise (SME) market in Canada has been an important source of growth in local service bundles. Not only do we offer SMEs the benefits of local access and long distance services at reduced rates, but we also provide high-speed Internet access. In 2004, business local services revenue increased by $14.6 million, or 47 per cent and contributed to average churn levels of less than one per cent.

| Call-Net Enterprises Inc. | Page 7 | 2004 & Q4 Managements Discussion & Analysis |

FOURTH QUARTER 2004 OPERATING HIGHLIGHTS

Fourth Quarter Revenue by Product

| | | | For the three months ended December 31 | |

| (in millions Canadian $) | | 2004 | | 2003 | | Change | | % Change | |

| | Long distance services | | | 101.7 | | | 119.9 | | | (18.2 | ) | | (15.2 | )% |

| | Data services | | | 53.5 | | | 48.6 | | | 4.9 | | | 10.1 | % |

| | Local services | | | 52.8 | | | 34.1 | | | 18.7 | | | 54.8 | % |

| | Wireless services | | | 3.1 | | | 1.5 | | | 1.6 | | | 106.7 | % |

| Total revenue | | | 211.1 | | | 204.1 | | | 7.0 | | | 3.4 | % |

In the fourth quarter of 2004, our total revenue grew by $7.0 million, or three per cent, from the fourth quarter of 2003 to $211.1 million. Fourth quarter revenue includes the impact of the Bell/360 acquisition from the date of closing, which contributed approximately $7.6 million of revenue in the quarter.

Fourth Quarter Revenue by Business

| | | For the three months ended December 31, 2004 | |

| (in millions Canadian $) | | Total | | Consumer | | Business | | Carrier | |

| Long distance services | | | 101.7 | | | 33.7 | | | 37.7 | | | 30.3 | |

| Data services | | | 53.5 | | | 2.9 | | | 39.5 | | | 11.1 | |

| Local services | | | 52.8 | | | 35.9 | | | 14.7 | | | 2.2 | |

| Wireless services | | | 3.1 | | | 3.1 | | | - | | | - | |

Total revenue | | | 211.1 | | | 75.6 | | | 91.9 | | | 43.6 | |

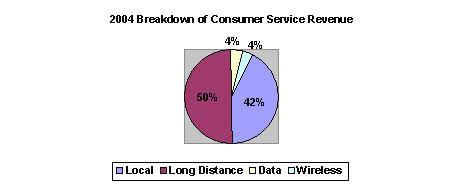

We continue to grow non-long distance services, including local and home phone service as well as IP-based data offerings. As a result, the proportion of local, wireless and data revenue in our business mix continues to increase as long distance declines. Long distance comprised 48 per cent of total revenue in the quarter, down from 59 per cent in the fourth quarter of 2003.

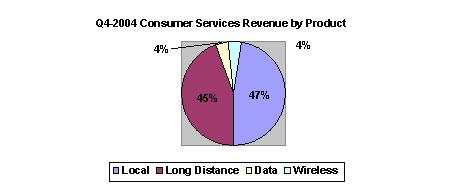

In our consumer services division, local or home phone service is now our biggest single product segment at 47 per cent of consumer revenue. Long distance services comprise 45 per cent of revenues, while the remaining eight per cent of revenue comes from dial-up and wireless services.

In the fourth quarter, we made a change to the allocation of the system access fee (SAF) charged to our consumer customers. Historically, 100 percent of this SAF had been allocated to long distance revenue. The SAF charge is more properly described as a customer charge, rather than a product charge, so we have changed the allocation of the SAF to one based on revenues from each product. We have applied this change retroactively in our consumer services division. As a result, in the fourth quarter $3.9 million long distance revenue was reallocated to local services ($3.3 million), data services ($0.3 million) and wireless services ($0.3 million).

| Call-Net Enterprises Inc. | Page 8 | 2004 & Q4 Managements Discussion & Analysis |

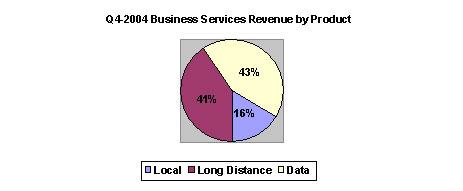

In our business services group, data service is our biggest single product segment at 43 per cent of business revenue. Long distance services comprise 41 per cent of revenues, while the remaining 16 per cent of revenue comes from local services.

In our carrier services division, long distance continues to be our biggest single product segment at 70 per cent of revenue. Data services comprise 25 per cent of revenues, while the remaining five per cent of revenue comes from local services.

Fourth Quarter Carrier Charges & Gross Margin

| | | | For the three months ended December 31 | |

| (in millions Canadian $) | | 2004 | | 2003 | | Change | | % Change | |

| Carrier charges | | | 101.9 | | | 96.8 | | | 5.1 | | | 5.3 | % |

| | % of revenue | | | 48.3 | % | | 47.4 | % | | 0.9 | % | | | |

| Gross margin | | | 109.2 | | | 107.3 | | | 1.9 | | | 1.8 | % |

| | % of revenue | | | 51.7 | % | | 52.6 | % | | (0.9 | )% | | | |

Carrier charges in the fourth quarter were $101.9 million, or 48 per cent of revenue. This is up by $5.1 million from the same quarter last year. The growth in carrier charges primarily reflects costs associated with growth in revenue.

In the fourth quarter we received a beneficial decision from the CRTC (Telecom Decision CRTC 2004-72) reducing primary inter-exchange carrier (PIC) charges by up to 90 per cent in some cases. This decision also has a retroactive component totaling $1.7 million that has been included in the fourth quarter as a credit against carrier charges.

Fourth Quarter Operating Costs

| | | | For the three months ended December 31 | |

| (in millions Canadian$) | | 2004 | | 2003 | | Change | | % Change | |

| | Consumer Services | | | 28.0 | | | 28.0 | | | - | | | 0.0 | % |

| | Business Services | | | 23.2 | | | 16.6 | | | 6.6 | | | 39.8 | % |

| | Carrier Services | | | 2.7 | | | 0.3 | | | 2.4 | | | 800.0 | % |

| | Network operations & corporate | | | 23.4 | | | 37.5 | | | (14.1 | ) | | (37.6 | )% |

| Total operating costs | | | 77.3 | | | 82.4 | | | (5.1 | ) | | (6.2 | )% |

| Call-Net Enterprises Inc. | Page 9 | 2004 & Q4 Managements Discussion & Analysis |

Operating costs fell in the quarter, reflecting the positive impact of our organizational realignment. We undertook the realignment in order to consolidate and streamline provisioning, reduce the number of levels of management and consolidate marketing and development activities across divisions. As a result of corporate reorganizations over the past year, changes in operating costs in business services and network operations reflect the movement of personnel between these divisions, rather than a significant change in the costs associated with these personnel. As a result, operating costs for these groups are not directly comparable across quarters. An apparent increase in the operating costs in carrier services in the fourth quarter reflects the reversal of a portion of our bad debt reserve in 2003.

Fourth Quarter EBITDA & Operating Profit (Loss)

| | | | For the three months ended December 31 | |

| (in millions Canadian $) | | 2004 | | 2003 | | Change | | % Change | |

| EBITDA | | | 31.9 | | | 24.9 | | | 7.0 | | | 28.1 | % |

| Depreciation & amortization | | | (36.9 | ) | | (38.6 | ) | | 1.7 | | | (4.4 | )% |

| Realignment & other charges | | | (6.5 | ) | | - | | | (6.5 | ) | | - | |

| Operating profit (loss) | | | (11.5 | ) | | (13.7 | ) | | 2.2 | | | (16.1 | )% |

| | EBITDA as a % of revenue | | | 15.1 | % | | 12.2 | % | | 2.9 | % | | | |

Fourth quarter EBITDA was $31.9 million. This is $7.0 million above the level of the same period in 2003, and is equivalent to approximately 15 per cent of revenue. Much of the increase in EBITDA reflects the positive impact of our realignment and the effect of the PIC decision referred to above. We recorded a charge of $6.5 million in the fourth quarter reflecting the severance costs associated with our realignment, announced on September 29, 2004. The realignment directly affected approximately 135 of our employees.

Home Phone Service Bundles

| | | | For the three months ended December 31 | |

| | | | 2004 | | 2003 | | Change | |

| Consumer home phone service lines | | | | | | | | | | |

| | Gross additions | | | 48,000 | | | 46,600 | | | 1,400 | |

| | Net additions | | | 25,500 | | | 30,600 | | | (5,100 | ) |

| | Churn | | | 2.5 | % | | 2.8 | % | | (0.3 | )% |

| | Average monthly revenue per line | | $ | 60.28 | | $ | 60.45 | | | ($0.17 | ) |

| Cost of acquisition (millions) | | | | | | | | | | |

| | Selling and marketing costs | | $ | 7.9 | | $ | 9.3 | | | ($1.4 | ) |

| | Activation costs | | | 5.0 | | | 5.4 | | | (0.4 | ) |

| Total cost of acquisition | | $ | 12.9 | | $ | 14.7 | | | ($1.8 | ) |

| | Cost of acquisition per line | | $ | 269 | | $ | 315 | | | ($46 | ) |

We had another good quarter in our home phone business in consumer services. We added 48,000 gross and 25,500 net new home phone service lines at a cost of acquisition of $269 per line. Our net line additions dropped by 5,100 from the level of the fourth quarter of 2003 as a result of higher disconnects in the home phone customer base. As our base of home phone service grows, a similar percentage churn level will result in a higher number of disconnects just as a result of the larger customer base. Churn in the quarter returned to the level we have been targeting of 2.5 per cent as a result of refocusing certain of our customer retention strategies and activities.

| Call-Net Enterprises Inc. | Page 10 | 2004 & Q4 Managements Discussion & Analysis |

2004 OPERATING RESULTS

For the full year, 2004, our total revenue grew by $13.3 million, or two per cent, to $818.6 million. 2004 revenue includes the impact of the Bell/360 acquisition from the date of closing, and contributed approximately $7.6 million of revenue in the fourth quarter and full year.

2004 Revenue by Product

| | | | For the 12 months ended December 31 | |

| (in millions Canadian $) | | 2004 | | 2003 | | Change | | % Change | |

| | Long distance services | | | 427.8 | | | 482.2 | | | (54.4 | ) | | (11.3 | )% |

| | Data services | | | 202.8 | | | 201.1 | | | 1.7 | | | 0.8 | % |

| | Local services | | | 177.7 | | | 120.4 | | | 57.3 | | | 47.6 | % |

| | Wireless services | | | 10.3 | | | 1.6 | | | 8.7 | | | 543.8 | % |

| Total revenue | | | 818.6 | | | 805.3 | | | 13.3 | | | 1.7 | % |

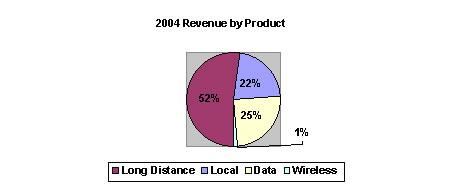

We continue to grow non-long distance services, including local, home phone and wireless service as well as IP-based data offerings. As a result, the proportion of long distance revenue in our business mix continues to decline. However, local, wireless and data services revenue grew by $67.7 million, or 21 per cent over 2003, more than offsetting the $54.4 million, or 11 per cent decline in long distance revenue. For the full year, long distance services revenue comprised 52 per cent of revenue.

2004 Revenue by Business

| | | | For the 12 months ended December 31, 2004 | |

| (in millions Canadian $) | | Total | | Consumer | | Business | | Carrier | |

| | Long distance services | | | 427.8 | | | 147.4 | | | 150.9 | | | 129.5 | |

| | Data services | | | 202.8 | | | 13.1 | | | 142.5 | | | 47.2 | |

| | Local services | | | 177.7 | | | 124.8 | | | 45.6 | | | 7.3 | |

| | Wireless services | | | 10.3 | | | 10.3 | | | - | | | - | |

| Total revenue | | | 818.6 | | | 295.6 | | | 339.0 | | | 184.0 | |

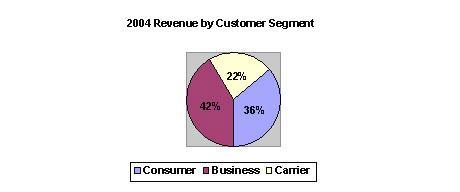

Our revenue is also well diversified by customer segment, with $295.6 million, or 36 per cent of our revenue coming from consumer services and 41 per cent and 23 percent coming from each of business and carrier services. Consistent with the recent past, year-over-year growth in our consumer and business services revenue has offset declines in carrier services revenue.

CONSUMER SERVICES

In the consumer segment, we provide home phone, long distance, dial-up Internet access and wireless services to residences and small office home office (SOHO) customers targeting five major urban areas that incorporates more than 33 different municipalities.

Over the past year, consumer revenue has grown by $26.6 million or 10 per cent to $295.6 million. In general, growth has been driven by our success in selling home phone and wireless service.

| Call-Net Enterprises Inc. | Page 11 | 2004 & Q4 Managements Discussion & Analysis |

2004 Consumer Services Revenue

| | | For the 12 months ended December 31 | |

| (in millions Canadian $) | | 2004 | | 2003 | | Change | | % Change | |

| Long distance services | | | 147.4 | | | 165.8 | | | (18.4 | ) | | (11.1 | )% |

| Data services | | | 13.1 | | | 17.0 | | | (3.9 | ) | | (22.9 | )% |

| Home phone services | | | 124.8 | | | 84.6 | | | 40.2 | | | 47.5 | % |

| Wireless services | | | 10.3 | | | 1.6 | | | 8.7 | | | 543.8 | % |

Consumer services revenue | | | 295.6 | | | 269.0 | | | 26.6 | | | 9.9 | % |

| Consumer services operating costs | | | 119.3 | | | 98.3 | | | 21.0 | | | 21.4 | % |

CONSUMER SERVICES LONG DISTANCE SERVICES REVENUE

In 2004, we made a change to the allocation of the system access fee charged to our consumer customers. Historically, 100 per cent of this SAF had been allocated to long distance revenue. This charge is more properly described as a customer charge, rather than a product charge, so we have changed the allocation of the SAF to one based on revenues from each product. We have applied this change retroactively in our consumer services division. In 2004, this change resulted in $13.8 million of revenue being reallocated from long distance services to local services ($11.6 million), data services ($1.2 million) and wireless services ($1.0 million). Historical periods have also been restated to reflect this change.

After changes relating to the allocation of SAF revenue, consumer long distance revenue was $147.4 million, down $18.4 million from last year. This decline is a result of declines in the average per minute charge for long distance services. The total volume of long distance minutes grew by approximately 16 per cent during 2004, driven by a large increase in North American calling under our North American unlimited plan. In 2004, long distance revenue now accounted for approximately 50 per cent of our total consumer services revenue; however, most of this revenue comes from customers who also buy home phone service from us. Sprint Canada-branded long distance only customers account for 15 per cent of our consumer revenue, while indirect long distance programs, including affinity programs, and alternative long distance products, comprise another 12 per cent.

The average revenue per minute (ARPM) of our per-minute long distance plans fell by almost 10 per cent in 2004. However, the growth in popularity in unlimited plans caused a significant increase in the number of minutes in these plans. For example, our consumer U.S. bound minute volumes grew by 38 per cent in 2004, driven by the popularity of the North American Unlimited Plan. The popularity of these unlimited plans caused our overall consumer ARPM to decline by 23 per cent in 2004. Due to continued improvements in the cost structure of our business and our on-going efforts at cost reduction, average cost per minute for consumer services declined by 34 per cent.

CONSUMER SERVICES HOME PHONE SERVICE REVENUE

Home phone, service revenue was $124.8 million in the year, an increase of 48 per cent or $40.2 million from 2003. The growth in customer count has been consistent and the average monthly home phone service revenue per customer has been stable. This stability has resulted from a number of factors offsetting one another, including the mix of wireless in the bundle, revenue promotions, as well as changes in revenue from features such as voice mail and calling line identification.

| Call-Net Enterprises Inc. | Page 12 | 2004 & Q4 Managements Discussion & Analysis |

CONSUMER SERVICES DATA REVENUE

Revenue from dial-up customers was $13.1 million for the year, a decline of $3.9 million, or 23 per cent from 2003. The number of subscribers stood at 51,700 at year-end, down 21 per cent from last year. We activated more than 26,000 new dial-up customers during the year, but this was offset by the continued migration of Canadian households to high-speed Internet services. We expect to begin to offset the decline in consumer data revenues in 2005 with the deployment of our own consumer high-speed Internet offering using DSL technology.

CONSUMER SERVICES WIRELESS REVENUE

Under our bundled wireless service offering using the Fido® brand, we activated 17,800 net new lines in the year and ended the year with 28,900 customers and 30,600 lines. Revenue from wireless services was $10.3 million, in this first full year of offering the service. Churn in wireless services was stable throughout the year at approximately 2.4 per cent.

CONSUMER SERVICES OPERATING COSTS

Operating costs in consumer services were $119.3 million, up $21.0 million, or 21 per cent from last year. The increase in operating costs year-over-year is primarily the result of the transfer of certain provisioning operations amounting to $11.1 million into consumer services. After adjusting for this change, Consumer Services operating costs were up by $9.9 million from last year. This increase resulted from an increase in marketing programs and investments in customer care.

BUSINESS SERVICES

We continue to focus on four initiatives in the business market in Canada:

| • | Maintaining and developing our working relationship with Sprint to offer multi-national corporations (MNCs) single-service, single-invoice, seamless North American network services; |

| | |

| • | Delivering ourIP Enabled Solutionsat substantial cost savings and time efficiencies to Canadian customers allowing them to integrate legacy systems with next-generation services in an efficient and cost-effective manner; |

| | |

| • | Continuing our Enhanced Voice Services (EVS) initiative by penetrating the call centre sector with complex interactive voice response (IVR) and advanced voice recognition (AVR) applications; and |

| | |

| • | Bundling long distance, local, and high-speed access for small and medium-sized enterprises (SME). |

To these four initiatives we have added a fifth; maximizing the value of the Bell/360 acquisition by fully integrating the people, products, and new customers, and by making the best possible use of the future opportunities afforded by the acquisition.

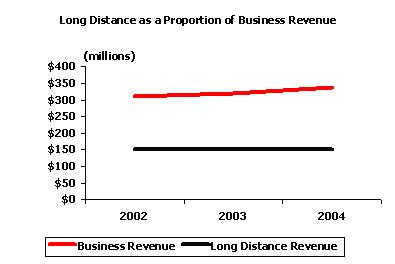

BUSINESS SERVICES REVENUE

In 2004, our Business Services revenue was $339.0 million, up $20.4 million from last year. The Bell/360 acquisition contributed approximately $7.6 million to growth, while the remaining $12.8 million was organic growth, split between local and data services.

2004 Business Services Revenue

| | | For the 12 months ended December 31 | |

| (in millions Canadian $) | | 2004 | | 2003 | | Change | | % Change | |

| Long distance services | | | 150.9 | | | 153.6 | | | (2.7 | ) | | (1.8 | )% |

| Data services | | | 142.5 | | | 134.0 | | | 8.5 | | | 6.3 | % |

| Local services | | | 45.6 | | | 31.0 | | | 14.6 | | | 47.1 | % |

Business Services revenue | | | 339.0 | | | 318.6 | | | 20.4 | | | 6.4 | % |

| Business Services operating costs | | | 78.2 | | | 63.2 | | | 15.0 | | | 23.7 | % |

BUSINESS SERVICES LONG DISTANCE REVENUE

Business Services long distance revenue declined by two per cent compared to last year. Revenue decline was the result of a nine per cent decrease in ARPM, partially offset by an eight per cent increase in minute volumes.

| Call-Net Enterprises Inc. | Page 13 | 2004 & Q4 Managements Discussion & Analysis |

Long distance, as a percentage of business services revenue, continues to decline from a level of 48 per cent of business services revenue in 2003 to 45 per cent of revenue in this year.

BUSINESS SERVICES LOCAL REVENUE

Business local line equivalents grew by 92,500 lines, or 150 per cent, in 2004. Most of that growth came from the addition of the Bell/360 business customers who used approximately 61,900 local line equivalents at year-end. Revenue from business local services grew by 47 per cent from last year and contributed $14.6 million of the increase in revenue during the year.

BUSINESS SERVICES DATA REVENUE

Business data revenue also grew in the year 2004. We continue to have success in sellingIP Enabled Solutions and the growth of this offering has generally compensated for the decline in legacy data revenues. In 2004, we recorded $142.5 million of data revenue, up 6 per cent from 2003. The growth in data revenue in the year caused this product category in the fourth quarter to surpass long distance as the dominant product sold to our business customers.

BUSINESS SERVICES OPERATING COSTS

Business services operating costs totaled $78.2 million in 2004, an increase of $15.0 million over 2003. This increase is primarily the result of the transfer of certain provisioning operations, amounting to $7.0 million, into Business Services. This coupled with the Bell/360 acquisition, contributed approximately $3.0 million to operating costs. Adjusting for this transfer and acquisition, operating costs in Business Services grew by $5.0 million, reflecting an increase in people and marketing costs necessary to support increased volumes.

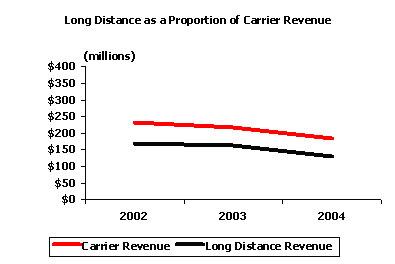

CARRIER SERVICES

Our strategy is to optimize the contribution from carrier services by focusing on profitability rather than revenue growth. The wholesale market has been under substantial pricing pressure for the past several years and the ongoing results of this division reflect this industry trend.

CARRIER SERVICES REVENUE

2004 Carrier Services Revenue

| | | For the 12 months ended December 31 | |

| (in millions Canadian $) | | 2004 | | 2003 | | Change | | % Change | |

| Long distance services | | | 129.5 | | | 162.8 | | | (33.3 | ) | | (20.5 | )% |

| Data services | | | 47.2 | | | 50.1 | | | (2.9 | ) | | (5.8 | )% |

| Local services | | | 7.3 | | | 4.8 | | | 2.5 | | | 52.1 | % |

Carrier services revenue | | | 184.0 | | | 217.7 | | | (33.7 | ) | | (15.5 | )% |

| Carrier services operating costs | | | 9.7 | | | 6.9 | | | 2.8 | | | 40.6 | % |

| Call-Net Enterprises Inc. | Page 14 | 2004 & Q4 Managements Discussion & Analysis |

Carrier Services revenue in the year totaled $184.0 million; a 16 per cent decline from 2003. Long distance services led the decline, down 21 per cent from 2003. Minute volumes grew by 10 per cent in the year while ARPMs were down significantly, 27 per cent. Much of this ARPM decline can be attributed to changes in the mix of minutes. For example, in international traffic, where rates and costs are declining the fastest, we saw a 47 per cent increase in minute volume and a 45 per cent reduction in ARPM. In 2004, Carrier Services revenue comprised approximately 22 per cent of consolidated revenue and was 70 per cent long distance. Average costs per minute (ACPM), especially for international traffic, has been declining at similar rates to ARPMs.

CARRIER SERVICES OPERATING COSTS

Carrier Services operating costs were $9.7 million, up in the year relative to the $6.9 million recorded in the last year. The apparent increase in costs was largely a result of changes in 2003 to the provision for bad debt. Excluding this factor, operating costs were $0.6 million higher in 2004, the result of increased people costs.

CARRIER CHARGES & GROSS PROFIT

Carrier charges were $400.6 million in 2004, or 49 per cent of revenue, down from $409.9 million or 51 per cent of revenue in 2003. This $9.3 million improvement reflects, in part, targeted efforts at carrier cost reduction - a focus on network efficiencies and maximizing the benefits of the regulatory environment. In 2004, we set targets for savings from operational efficiencies and targets for regulatory cost savings based on our run rate at the beginning of the year. The success of these programs, combined with revenue growth, offset by declines in ARPM, resulted in the carrier charges improvement noted. None of the cost benefits of the recent CRTC decision (Telecom Decision CRTC 2005-6) on CDN services rates is reflected in 2004 results.

2004 Carrier Charges & Gross Profit

| | | | For the 12 months ended December 31 | |

| (in millions Canadian $) | | 2004 | | 2003 | | Change | | % Change | |

| Carrier charges | | | 400.6 | | | 409.9 | | | (9.3 | ) | | (2.3 | )% |

| | % of revenue | | | 48.9 | % | | 50.9 | % | | (2.0 | )% | | | |

| Gross profit | | | 418.0 | | | 395.4 | | | 22.6 | | | 5.7 | % |

| | Gross profit margin | | | 51.1 | % | | 49.1 | % | | 2.0 | % | | | |

The reduction in carrier charges translated into an increased gross profit and a higher gross margin. Gross profit was up by $22.6 million, $9.3 million of which came from a net reduction in carrier charges and $13.3 million of which came from revenue growth. On a consolidated basis, our profit margin from long distance services was unchanged from 2003, while there were gross margin increases in local, data and wireless services. The underlying profitability of our non-long distance services continues to improve as we gain economies of scale in local service, and as we make more effective use of the benefits of our hybrid network, leasing when appropriate and building when the economics warrant.

| Call-Net Enterprises Inc. | Page 15 | 2004 & Q4 Managements Discussion & Analysis |

OPERATING COSTS

Overall, in 2004 operating costs were $313.1 million, up $13.8 million from $299.3 million in 2003. Operating costs as a percentage of revenue were 38 per cent in 2004, as compared to 37 per cent of revenue in 2003. The increase in operating costs reflects investments in sales and customer care in both consumer and business services. The changes in consumer, business and carrier operating costs was discussed earlier.

2004 Operating Costs

| | | | For the 12 months ended December 31 | |

| (in millions Canadian $) | | 2004 | | 2003 | | Change | | % Change | |

| Consumer services | | | 119.3 | | | 98.3 | | | 21.0 | | | 21.4 | % |

| Business services | | | 78.2 | | | 63.2 | | | 15.0 | | | 23.7 | % |

| Carrier services | | | 9.7 | | | 6.9 | | | 2.8 | | | 40.6 | % |

| Network operations & corporate | | | 105.9 | | | 130.9 | | | (25.0 | ) | | (19.1 | )% |

| Total operating costs | | | 313.1 | | | 299.3 | | | 13.8 | | | 4.6 | % |

| | % of revenue | | | 38.2 | % | | 37.2 | % | | 1.0 | % | | | |

NETWORK OPERATIONS AND CORPORATE COSTS

Network operations and corporate costs in 2004 were $105.9 million, down from $130.9 million in 2003. Approximately $15.7 million of this reduction related to the movement of our provisioning operations from network operations to consumer and business services. The remaining reduction in costs is attributed to human resource costs, due in part to the organizational realignment and to lower incentive payments.

OPERATING PROFIT (LOSS)

EBITDA

Primarily as a result of the previously mentioned increase in gross profit, together with decreases in operating costs, EBITDA for 2004 was $104.9 million, an increase of $8.8 million or nine per cent from 2003.

2004 EBITDA & Operating Profit (Loss)

| | | For the 12 months ended December 31 | |

| (in millions $) | | 2004 | | 2003 | | Change | | % Change | |

Operating profit (loss) | | | (42.9 | ) | | (68.2 | ) | | 25.3 | | | (37.1 | )% |

| Depreciation & amortization | | | 146.6 | | | 157.3 | | | (10.7 | ) | | (6.8 | )% |

| Realignment & other charges | | | 1.2 | | | 7.0 | | | (5.8 | ) | | (82.9 | )% |

EBITDA | | | 104.9 | | | 96.1 | | | 8.8 | | | 9.2 | % |

Depreciation and amortization charges totaled $146.6 million, a seven per cent decrease from 2003. Depreciation and amortization has generally been falling as our ongoing capital spending program has declined.

We recorded a net expense of $1.2 million in the year for realignment and other charges. This expense was the result of a $7.8 million realignment charge reflecting the severance costs of employees directly affected by the realignment, offset by a $6.6 million gain resulting from the reversal of the provision taken in 2003, for maintenance costs associated with certain dark fibre. During 2004, we came to an agreement with the owner of the fibre whereby we abandoned these routes and allowed this party to abandon certain other routes on which we were collecting maintenance fees.

As a consequence of the above factors, operating loss was $42.9 million for the year, an improvement of $25.3 million, or 37 per cent from last year.

| Call-Net Enterprises Inc. | Page 16 | 2004 & Q4 Managements Discussion & Analysis |

OTHER EXPENSES

2004 Other Expenses

| | | For the 12 months ended December 31 | |

| (in millions Canadian $) | | 2004 | | 2003 | | Change | | % Change | |

| Loss on repurchase of long-term debt | | | (4.0 | ) | | - | | | (4.0 | ) | | - | |

| Reversal of change in control provision | | | 4.7 | | | - | | | 4.7 | | | - | |

| Net loss on the sale of capital assets | | | (0.9 | ) | | - | | | (0.9 | ) | | - | |

Sub-total | | | (0.2 | ) | | - | | | (0.2 | ) | | - | |

In 2004, we recorded several items that are non-recurring by nature. In the first quarter of 2004, we made market purchases for cancellation of approximately U.S.$76.4 million of long term debt ($100.8 million), recording a loss on repurchase of $4.0 million. The repurchases served to reduce our interest expense on long term debt by U.S.$8.1 million per year.

In the first quarter, we also recorded a gain of $4.7 million in connection with the elimination of a reserve established in connection with the application brought by Montreal Trust Company of Canada (now Compushare Investor Services), discussed in note 12 of the audited consolidated financial statements. Both the initial decision and subsequent appeal were ruled in our favour and the plaintiffs in the case did not seek leave to appeal further.

In the second quarter, we recorded a loss on the sale of assets. Capital equipment with a book value of $1.3 million was sold for proceeds of $0.4 million, resulting in a $0.9 million loss.

2004 Interest Expense, Other Income and Foreign Exchange Gains & Losses

| | | | For the 12 months ended December 31 | |

| (in millions Canadian $) | | 2004 | | 2003 | | Change | | % Change | |

| Interest expense | | | (32.7 | ) | | (43.2 | ) | | 10.5 | | | (24.3 | )% |

| Interest income & other expense | | | (13.4 | ) | | (5.7 | ) | | (7.7 | ) | | 135.1 | % |

| | Foreign exchange gain (loss) | | | 17.1 | | | 85.9 | | | (68.8 | ) | | (80.1 | )% |

Interest expense on long-term debt in the year was $32.7 million, down from $43.2 million in 2003. This $10.5 million reduction was a result of two factors: 1) the market purchase of U.S.$76.4 million (approximately $100.8 million) of senior secured notes in March 2004 and the consequent elimination of $8.8 million in interest costs associated with the repurchased notes; and 2) fluctuations in the Canadian dollar exchange rate, which resulted in $1.7 million less in Canadian dollar interest payments on our senior secured notes as these notes are denominated in U.S. dollars.

As a result of our accounts receivable securitization program, certain of our gains and losses related to bad debt are classified as gains or losses on securitization and appear as an ‘other’ expense. In 2004 these losses totaled $9.8 million, and comprised 73 per cent of the $13.4 million of net other expenses. Other expenses also grew in 2004 reflecting the first full year impact of the accounts receivable securitization program.

In 2004, we recorded a foreign exchange gain of $17.1 million as the result of the appreciation in the Canadian dollar against the U.S. dollar. Of this gain, $17.8 million related to a change in the principal amount of our long-term debt and the remaining $(0.7) million represented a net loss, during the year, on the foreign exchange related component of our operations. While the foreign exchange gain in 2004 is significant, it was much less than the $85.9 million gain recorded in 2003, itself the result of the strong Canadian dollar favourably impacting both operations and our balance sheet.

A one cent change in the value of the Canadian dollar against the U.S. dollar changes the principal amount of our long-term debt by approximately $3.3 million.

NET INCOME (LOSS)

As a consequence of the above factors, we recorded a net loss in the year of $78.4 million, or $2.20 per share, compared with a net loss of $37.5 million, or $1.36 per share in 2003. A 109 per cent increase in net loss translated into a 62 per cent increase in net loss per share as a consequence of an increase in the weighted average number of shares outstanding in 2004.

| Call-Net Enterprises Inc. | Page 17 | 2004 & Q4 Managements Discussion & Analysis |

2004 Net Income (Loss)

| | | For the 12 months ended December 31 | |

| (in millions Canadian $) | | 2004 | | 2003 | | Change | | % Change | |

Net income (loss) | | | (78.4 | ) | | (37.5 | ) | | (40.9 | ) | | 109.1 | % |

| Earnings per share - basic | | | (2.20 | ) | | (1.36 | ) | | (0.84 | ) | | 61.8 | % |

LIQUIDITY AND CAPITAL RESOURCES

Our plan is to remain cash flow positive, meaning that we will generate more than enough EBITDA to cover interest and other financing costs, capital expenditures and cash taxes. This should leave our cash balance relatively intact and allow us to keep these cash resources for general corporate purposes, opportunistic investments or acquisitions, or to further reduce our debt levels.

Cash, cash equivalents and short-term investments are generally invested in liquid Canadian and U.S. dollar denominated securities with maturities no greater than one year and having one of the two highest ratings by either the Standard and Poor’s Rating Group or Moody’s Investor Service, Inc.

CASH FLOW

CASH FLOW FROM OPERATING ACTIVITIES

Operating activities before changes in non-cash working capital provided $59.0 million of cash in 2004 compared with $41.2 million in 2003. This $17.8 million, or 43 per cent increase in operating cash flow was assisted by higher EBITDA of $8.8 million, and lower interest payments of $10.5 million, consistent with our strategy of growing profitability and giving us greater opportunities to re-invest in our business. Cash flow from operating activities grew relative to the last year as changes in non-cash working capital provided $25.3 million of cash. Over the past two years, changes in non-cash working capital have provided $30.3 million of cash. This change has resulted from a number of activities including proceeds from the sale of accounts receivable partly offset by the effect of normalizing our payment relationships with carrier suppliers to reduce the overall level of carrier disputes.

2004 Cash Flow from Operating Activities

| | | | For the 12 months ended December 31 | |

| (in millions Canadian $) | | 2004 | | 2003 | | Change | | % Change | |

| Net income (loss) | | | (78.4 | ) | | (37.5 | ) | | (40.9 | ) | | 109.1 | % |

| | Depreciation & amortization | | | 146.6 | | | 157.3 | | | (10.7 | ) | | (6.8 | )% |

| | Foreign exchange gain (loss) | | | (17.8 | ) | | (85.9 | ) | | 68.1 | | | (79.3 | )% |

| | Reversal of provisions | | | (4.7 | ) | | - | | | (4.7 | ) | | - | |

| | Loss on repurchase of debt | | | 4.0 | | | - | | | 4.0 | | | - | |

| | Future income taxes | | | 3.9 | | | 4.3 | | | (0.4 | ) | | (9.3 | )% |

| | Interest income & other expense | | | 2.7 | | | 3.0 | | | (0.3 | ) | | (10.0 | )% |

| | Loss on sale of assets | | | 0.9 | | | - | | | 0.9 | | | - | |

| | Realignment & other charges | | | 1.2 | | | - | | | 1.2 | | | - | |

| Operating cash flow | | | 58.4 | | | 41.2 | | | 17.2 | | | 41.8 | % |

| | Change in non-cash working capital | | | 28.4 | | | 2.5 | | | 25.9 | | | 1,036.0 | % |

| Cash flow from operating activities | | | 86.8 | | | 43.7 | | | 43.1 | | | 98.6 | % |

| | Per share - basic | | $ | 2.43 | | $ | 1.59 | | $ | 0.84 | | | 52.8 | % |

CASH FLOW FROM INVESTING ACTIVITIES

Overall, investment activities in 2004 generated $2.8 million of cash compared with a use of cash of $59.7 million in 2003. However, we have combined capital expenditures, acquisitions, dispositions, and changes in deferred costs, long-term assets and other, into investing cash flow. This measure reflects the net change in operating assets of the business, assets on which we expect to make operating returns. In total we spent slightly less in 2004 on operating assets than in 2003 ($56.0 million in 2004, as compared to $57.0 million in 2003). In order for us to meet our cash flow self sufficiency goals, we intend to keep this investment in operating assets in the range of seven to eight per cent of revenue.

| Call-Net Enterprises Inc. | Page 18 | 2004 & Q4 Managements Discussion & Analysis |

Capital investments of $55.4 million were made in 2004 to expand local services, improve existing systems, enhance cost efficiency, and accommodate new products. The increase of $11.3 million from 2003 reflects principally the increased scale of our local operations.

2004 Cash Flow from Investing Activities

| | | | For the 12 ended December 31 | |

| (in millions Canadian $) | | 2004 | | 2003 | | Change | | % Change | |

| Acquisition of capital assets | | | (55.4 | ) | | (44.1 | ) | | (11.3 | ) | | 25.6 | % |

| Change in deferred costs & other | | | (0.3 | ) | | (1.0 | ) | | 0.7 | | | (70.0 | )% |

| Increase in long term assets | | | (0.2 | ) | | - | | | (0.2 | ) | | - | |

| Net proceeds from disposals | | | 0.4 | | | 7.8 | | | (7.4 | ) | | (94.9 | )% |

| Acquisitions | | | (0.5 | ) | | (19.7 | ) | | 19.2 | | | (97.5 | )% |

| Investing cash flow | | | (56.0 | ) | | (57.0 | ) | | 1.0 | | | (1.8 | )% |

| | % of revenue | | | (6.8 | )% | | (7.1 | )% | | 0.3 | % | | | |

| Change in short-term investments | | | 58.8 | | | (2.7 | ) | | 61.5 | | | (2,277.8 | )% |

| Cash flow from investing activities | | | 2.8 | | | (59.7 | ) | | 62.5 | | | (104.7 | )% |

Most of the $62.5 million change in cash flow from investing activities between 2003 and 2004 is from changes in short-term investments which provided $61.5 million more cash in 2004 than in the prior year.

CASH FLOW FROM FINANCING ACTIVITIES

Financing activities consumed $107.2 million in 2004. This compares to 2003 when financing activities generated $38.4 million of cash. In 2004, financing activities were dominated by the repurchase of long term debt for $104.8 million, while in 2003 activities were dominated by the issuance of equity in the amount of $40.6 million. The combined effect of these two events was a $145.4 million swing between the two years. Excluding the effects of the equity issuance, and the debt repurchase cash flow from financing activities has been stable and limited to the costs incurred in connection with the retirement of the right-of-way liability.

2004 Cash Flow from Financing Activities

| | | For the 12 months ended December 31 | |

| (in millions Canadian $) | | 2004 | | 2003 | | Change | | % Change | |

| Change in right-of-way liability | | | (2.4 | ) | | (2.2 | ) | | (0.2 | ) | | 9.1 | % |

| Repurchase of long term debt | | | (104.8 | ) | | - | | | (104.8 | ) | | - | |

| Issuance of class B shares | | | - | | | 40.6 | | | (40.6 | ) | | (100.0 | )% |

Cash flow from financing activities | | | (107.2 | ) | | 38.4 | | | (145.6 | ) | | (379.2 | )% |

FREE CASH FLOW

In 2004, we had free cash flow of $10.8 million, which is $1.2 million, or 10 per cent, lower than 2003. Consistent with our strategy of reinvestment to the extent of discretionary cash flow availability, all of the $8.8 million improvement in EBITDA and the $7.4 million improvement in financing costs was reinvested in capital expenditures, which grew by $18.7 million.

| Call-Net Enterprises Inc. | Page 19 | 2004 & Q4 Managements Discussion & Analysis |

2004 Free Cash Flow

| | | | For the 12 months ended December 31 | |

| (in millions Canadian $) | | 2004 | | 2003 | | Change | | % Change | |

| EBITDA | | | 104.9 | | | 96.1 | | | 8.8 | | | 9.2 | % |

| Financing costs | | | (37.4 | ) | | (44.8 | ) | | 7.4 | | | (16.5 | )% |

| Cash income taxes paid | | | (1.4 | ) | | (2.0 | ) | | 0.6 | | | (30.0 | )% |

| Net capital expenditures | | | (55.0 | ) | | (36.3 | ) | | (18.7 | ) | | 51.5 | % |

| Cash component of change in deferred costs | | | (0.3 | ) | | (1.0 | ) | | 0.7 | | | (70.0 | )% |

| Free cash flow | | | 10.8 | | | 12.0 | | | (1.2 | ) | | (10.0 | )% |

| Change in non-cash working capital & other | | | 20.7 | | | (5.6 | ) | | 26.3 | | | (469.6 | )% |

| Acquisitions | | | (0.5 | ) | | (19.7 | ) | | 19.2 | | | (97.5 | )% |

| Increase in long-term investments | | | (0.2 | ) | | - | | | (0.2 | ) | | - | |

| Change in right-of-way liability | | | (2.4 | ) | | (2.2 | ) | | (0.2 | ) | | 9.1 | % |

| Repurchase of long-term debt | | | (104.8 | ) | | - | | | (104.8 | ) | | - | |

| Issuance of equity | | | - | | | 40.6 | | | (40.6 | ) | | (100.0 | %) |

| Change in cash, cash equivalents & short-term investments | | | (76.4 | ) | | 25.1 | | | (101.5 | ) | | (404.4 | )% |

| Increase (decrease) in short-term investments | | | 58.8 | | | (2.7 | ) | | 61.5 | | | (2,277.8 | )% |

| Change in cash & cash equivalents | | | (17.6 | ) | | 22.4 | | | (40.0 | ) | | (178.6 | )% |

FINANCIAL POSITION

At December 31, 2004, we had current assets of $126.7 million and current liabilities of $149.7 million. Net working capital was a negative $23.0 million, a decline from the positive $92.3 million at December 31, 2003. This $115.3 million change primarily reflects our decision to use $104.8 million of cash to repurchase notes in 2004.

2004 Working Capital Changes

| | | | For the 12 months ended December 31 | |

| (in millions Canadian $) | | 2004 | | 2003 | | Change | | % Change | |

| Accounts receivable & other current assets | | | 126.7 | | | 241.7 | | | (115.0 | ) | | (47.6 | )% |

| Accounts payable & accrued liabilities | | | 149.7 | | | 149.4 | | | 0.3 | | | 0.2 | % |

| Net working capital | | | (23.0 | ) | | 92.3 | | | (115.3 | ) | | (124.9 | )% |

| | Current ratio | | | 0.9 | | | 1.6 | | | (0.7 | ) | | (43.8 | )% |

| | Accounts receivable days sales outstanding | | | 32 | | | 32 | | | 0 | | | | |

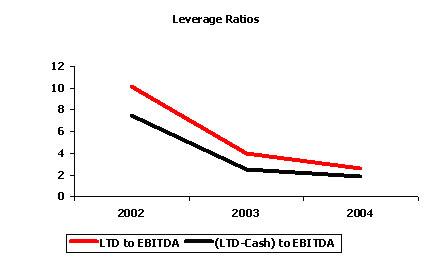

In 2004, long-term debt (LTD) decreased by $118.6 million to $268.5 million resulting from positive effects of the repurchase of senior secured notes, which accounted for $100.8 million, and the strong Canadian dollar, which accounted for $17.8 million.

| Call-Net Enterprises Inc. | Page 20 | 2004 & Q4 Managements Discussion & Analysis |

Other long-term liabilities, which include the right-of-way liability, the long-term portion of Bell/360 acquisition account payable, lease exit costs and asset retirement obligations, have increased by $4.2 million to $53.3 million. Apart from the Bell/360 acquisition related changes, factors contributing to the year over year change include the accretion of the asset retirement obligation, offset partly by the reversal of the dark fibre maintenance charge, and the continuing amortization of our right-of-way liability.

2004 Capital Structure

| | | | For the 12 months ended December 31 | |

| (in millions Canadian $) | | 2004 | | 2003 | | Change | | % Change | |

| Long-term debt | | | 268.5 | | | 387.1 | | | (118.6 | ) | | (30.6 | )% |

| Right-of-way liability | | | 38.3 | | | 37.0 | | | 1.3 | | | 3.5 | % |

| Less: | | | | | | | | | | | | | |

| | Cash & short-term investments | | | 73.7 | | | 150.1 | | | (76.4 | ) | | (50.9 | )% |

| | Prepaid right-of-way | | | 5.9 | | | 6.9 | | | (1.0 | ) | | (14.5 | )% |

| Total net debt | | | 227.2 | | | 267.1 | | | (39.9 | ) | | (14.9 | )% |

| Total shareholders’ equity | | | 177.4 | | | 253.5 | | | (76.1 | ) | | (30.0 | )% |

| Total capitalization | | | 404.6 | | | 502.6 | | | (98.0 | ) | | (19.5 | )% |

| | Net debt to capitalization | | | 56.2 | % | | 53.1 | % | | 3.1 | % | | 5.8 | % |

| | Common & class B shares outstanding at end of period | | | 35.8 | | | 35.6 | | | 0.2 | | | 0.6 | % |

| | Options outstanding at end of period | | | 1.7 | | | 1.4 | | | 0.3 | | | 21.4 | % |

Our net debt to net capitalization ratio stood at 56 per cent at the end of the fourth quarter, as compared to 53 per cent at the end of 2003. The increase is because net debt declined by 15 per cent, while capitalization declined by 19 per cent. The increased decline in capitalization is the result of a decline in shareholders’ equity, driven primarily by our net loss of $78.4 million during 2004.

LIQUIDITY

LONG-TERM CONTRACTUAL OBLIGATIONS

2004 Long Term Contractual Obligations

| (in millions Canadian $) | | Total | | <1 Year | | 1-3 Years | | 4-5 years | | > 5 years | |

| Long-term debt | | | 268.5 | | | - | | | - | | | 268.5 | | | - | |

| | Interest payments on debt (1) | | | 114.1 | | | 28.5 | | | 57.1 | | | 28.5 | | | - | |

| Right-of-way liability | | | 77.6 | | | 5.3 | | | 10.3 | | | 10.8 | | | 51.2 | |

| Operating leases | | | 41.9 | | | 14.3 | | | 19.0 | | | 5.1 | | | 3.5 | |

| Network facilities | | | 62.6 | | | 21.2 | | | 26.9 | | | 14.3 | | | 0.2 | |

| Other long-term obligations | | | 125.8 | | | 36.7 | | | 37.4 | | | 14.8 | | | 35.4 | |

| | Total contractual obligations | | | 690.5 | | | 106.0 | | | 150.7 | | | 342.0 | | | 90.3 | |

| (1) | Converted to Canadian dollars at the year-end exchange rate of $1.2036 |

CAPITAL RESOURCES

We have certain commitments to capital expenditures and to payments in respect of acquisitions. In the normal course of business we make commitments to purchase capital equipment that will be invoiced in future periods. At year-end 2004, our commitments to purchase capital equipment that had not yet been received totaled $1.6 million. These commitments are expected to be realized in the first quarter of 2005.

On November 20, 2004, we purchased the Eastern Canadian business customers of 360networks from Bell Canada. Excluding transaction costs, the purchase price of this acquisition is expected to total $16.7 million and will be paid in four installments. Two of these installments, totaling $6.7 million, or 40 per cent of the purchase price, will be paid in 2005, while the remaining two installments, totaling $10 million, will be paid in 2006.

| Call-Net Enterprises Inc. | Page 21 | 2004 & Q4 Managements Discussion & Analysis |

OFF BALANCE SHEET ARRANGEMENTS

In 2003, we entered into a five-year accounts receivable securitization program whereby we sell, on an on-going basis, an undivided co-ownership interest in certain of our trade receivables to a securitization trust to a maximum of $55.0 million. At December 31, 2004, the program was fully utilized. We are exposed to certain risks of default on the amount of the receivables under securitization. We retain ongoing servicing responsibilities, and have a retained interest in the securitized receivables and rights to future excess cash flows generated by the trust. The sales are on a fully-serviced basis and we do not receive any fees for our on-going servicing responsibilities. In the event of a failure of debtors to pay when due, the trust and its investors have recourse to the retained interest of the trust, but have no recourse to our other assets.

During the year ended December 31, 2004, we recognized a loss of $9.8 million on the securitization of receivables. We measure the loss on securitization by applying the same methodology used to estimate our allowance for doubtful accounts. The result is a provision for anticipated credit losses of approximately one per cent of the accounts receivable balance.

RELATED PARTY TRANSACTIONS

We engage in significant sales and purchases of telecommunication services with Sprint, which maintains an approximate 6.6 per cent equity interest in our company. These transactions are made at market prices under normal trade terms and conditions. In addition, a royalty payment based on revenues is paid to Sprint, see note 11 of consolidated financial statements. Revenue, carrier charges and royalty costs transactions with Sprint and its affiliates for each of the periods in the three years ended December 31 are as follows:

2004 Transactions with Sprint

| (in millions $) | | 2004 | | 2003 | | Change | | % Change | |

| Revenue | | | 30.4 | | | 27.0 | | | 3.4 | | | 12.6 | % |

| Carrier charges | | | 42.4 | | | 44.0 | | | (1.6 | ) | | (3.6 | )% |

| Royalty costs | | | 19.7 | | | 19.5 | | | 0.2 | | | 1.0 | % |

We also engage in sales of telecommunication services with a company in which we maintain an approximate 7.5% equity interest and have a right to two board seats. These transactions were made at market prices under normal trade terms and conditions. Revenue derived from this company was $3.5 million in 2004 and $3.2 million in 2003.

Furthermore, we engage in sales of telecommunication services with companies to which various members of our company’s board of directors are related. These transactions were made at market prices under normal trade terms and conditions, and total less than $1.5 million.

OUTSTANDING SHARE DATA

Our authorized share capital consists of an unlimited number of common shares, class B non-voting shares and preferred shares.

The holders of the common shares are entitled to one vote for each share held at any meeting of our shareholders. The common shares are convertible, at the option of the common shareholders, at any time into class B non-voting shares on a share-for-share basis.

In certain circumstances, the class B non-voting shares are convertible, at the option of the class B shareholders, into common shares on a share-for-share basis.

The common shares and class B non-voting shares rankpari passu on a per share basis with respect to payment of dividends and the right to participate in a distribution of assets on winding up, dissolution or otherwise.

We are authorized to issue an unlimited number of the preferred shares. We issued Sprint one preferred share (of a value of $1.00) as part of the consideration for entering into a commercial agreement with us. The preferred shares are generally non-voting and have no right to dividends, but do entitle the holder to nominate and elect two directors to our board. The preferred shares also have a priority right over all other classes of shares to receive a return of capital equal to $1.00 per preferred share on winding up, dissolution or otherwise.

| | Outstanding as at | |

Authorized Share Capital | Dec 31 2004 | |

| Common shares | | | 4,302,011 | |

| Class B non-voting shares | | | 31,462,025 | |

Total | | | 35,764,036 | |

Preferred shares | | | 1 | |

| Call-Net Enterprises Inc. | Page 22 | 2004 & Q4 Managements Discussion & Analysis |

RISKS AND UNCERTAINTIES

FINANCING

We are cash flow self sufficient, and have been for several years. However, our debt level relative to our EBITDA and our book capitalization is high in comparison to many Canadian telecommunications firms, although not higher than the Canadian universe of communications companies in general such as cable and broadcast media. While this leverage has given us access to important capital that we have used to build our business, we must manage our business so that this long term debt can be repaid or refinanced on or before maturity.

TECHNOLOGY CHANGES