United States

Securities and Exchange Commission

Washington, D.C. 20549

FORM 6-K

Report of Foreign Private Issuer

Pursuant to Rule 13a-16 or 15d-16

of the

Securities Exchange Act of 1934

For the month of

May 2021

Vale S.A.

Praia de Botafogo nº 186, 18º andar, Botafogo

22250-145 Rio de Janeiro, RJ, Brazil

(Address of principal executive office)

(Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F.)

(Check One) Form 20-F X Form 40-F ___

(Indicate by check mark if the registrant is submitting the Form 6-K in paper

as permitted by Regulation S-T Rule 101(b)(1))

(Check One) Yes No X

(Indicate by check mark if the registrant is submitting the Form 6-K in paper

as permitted by Regulation S-T Rule 101(b)(7))

(Check One) Yes No X

(Indicate by check mark whether the registrant by furnishing the information contained in this Form is also thereby furnishing information to the Commission pursuant to Rule 12g3-2(b) under the Securities Exchange Act of 1934.)

(Check One) Yes No X

(If “Yes” is marked, indicate below the file number assigned to the registrant in connection with Rule 12g3-2(b). 82- .)

| No. 02 Tax Transparency 2020 Annual Report vale.com |

| Tax Tr anspar enc y |A nnual Rep or t 2020 Contents p a g e p a g e p a g e 03 Our purpose 04 Foreword 05 Introduction p a g e 08 p a g e 09 p a g e 11 Global key figures for 2020 Key figures for Brazil 2020 Vale’s tax contribution p a g e 25 p a g e 29 p a g e 32 Payments breakdown Our Value Chain Our approach to tax p a g e 39 p a g e 40 Adjusted effective tax rate Independent auditors’ report Appendix 1 – The basis on which this report was prepared Appendix 2 – Glossary Appendix 3 – List of our Companies |

| FIG 01 Ponta da Madeira Maritime Terminal, North Port. In the photo: Luana Ferreira in the area of pelletizing. Our Purpose We exist to improve life and transform the future. Together. Values 1. Life matters most. 2. Act with integrity. 3. Value the people who built our company. 4. Make it happen. 5. Respect our planet and communities. Key Behaviours 1. Obsession with safety and risk management. 2. Open and transparent dialogue. 3. Empowerment with accountability. 4. Ownership for the whole. 5. Active listening and engagement with society. Ambitions We want to be a great company recognized by society for being: 1. A safety reference. 2. The best operator and the most reliable. 3. A talent-oriented organization. 4. A leader in low-carbon mining. 5. A reference in value creation and sharing. Picture: Ricardo Teles 3 B3ack to Contents |

| Tax Tr anspar enc y | A nnual Rep or t 2020 Message from our Executive Vice President Legal and Tax We are proud to publish our second Tax Transparency Report. This report is designed to share details of the taxes we pay and the economic contributions we make in the places we work. We believe it is a small but important part of our new pact with society – a journey compliance. It means our business decisions are guided not by our tax liability but by creating shared long-term value for our communities and partners. And it means we increasingly look for new and better ways to share this information with our stakeholders. to better engage our stakeholders and understand one another. It follows the important lessons we needed to learn as a company in the aftermath of the collapse of Dam I at the Córrego do Feijão Mine in January 2019. This desire to build a more positive economic, social and environment legacy is at the heart of our response to COVID-19. I am incredibly proud of the response of the Vale family to this crisis. We allocated early a US$ 115 million war chest to fund better protection for our employees, support our suppliers, and help the communities we are a part of. I am also proud that in this difficult time we managed to not only protect jobs but increase the number of employees and outsourced workers. At heart of this initiative is a commitment to transparency. We want to be as open about the taxes we pay as possible and build more positive relationships with the people, communities and governments where we operate. We know through our operations, investments and taxes, we make an important contribution to the growth of the local, national and global economy. It is why I am delighted this report adds more detail, including publishing our contribution per project, and strives harder to explain how, when and why we pay taxes. Alex D’Ambrosio Executive Vice President Legal and Tax For example, we used our logistics structure in China to buy and transport 30 million items of personal protective equipment and five million rapid test kits to Brazil. We provided US$ 2 million in funding to help Mozambique. And we worked with our partners in Oman to open a COVID-19 quarantine center. We engage with and consider guidance from global industry forums, such as the principles recommended by the International Council on Mining & Metals (ICMM) and the terms of the Extractive Industries Transparency Initiative (EITI). Information on our payments to governments are publicly available and disclosed through the compliance with the Canadian Extractive Sector Transparency Measures Act (“ESTMA”) and our participation in the EITI reports in jurisdictions including Indonesia and Mozambique, where we operate mines. Last year, Vale paid US$ 5.7 billion in taxes and royalties globally – meeting our legal obligations in full. This forms part of a total economic contribution of US$ 28.3 billion, which captures the amounts we also paid to suppliers; as reinvestments; in dividends and in salaries to our employees. The vast majority of our taxes and royalties were paid in Brazil, which reflects our greater operational presence in the country. We remain steadfastly committed to continuing this support. We hope this year’s report gives you a greater insight into our business and the contributions we make in the places where we work. We believe in a principles-led approach to taxation – one rooted in transparency, compliance, a long-term view, collaboration with tax authorities, and risk management. It means we respect local tax laws and build effective internal processes to ensure full We, of course, welcome your feedback. 4 B4ack to Contents |

| Tax Tr anspar enc y | A nnual Rep or t 2020 Introduction Vale’s second tax transparency report aims to create a better understanding amongst our stakeholders of our businesses, our operations and the taxes we pay. Vale is one of the world’s largest iron ore and nickel producers. Ores and minerals extracted from our mines are used around the globe to manufacture essential products from cell phones to airplanes, building structures to coins. With operations in more than 20 jurisdictions on five continents, the company also produces manganese, ferro-alloys, copper, metals of the platinum group metals, gold, silver, cobalt, and metallurgical and thermal coals. Producing this variety of raw materials requires an infrastructure that includes mineral exploration, administrative offices and operational units connected by modern integrated logistics systems, comprising railroads, maritime terminals and ports. Octavio Bulcão Vale is committed to integrating sustainability into its business by building a strong and positive economic, social and environmental legacy and mitigating the impacts of its operations. The taxes we collect and pay represent one of the ways in which we embrace this responsibility. Global Tax Director This report is intended to be concise, understandable and accessible to all our stakeholders. Our logistics structure also carries third-party cargo and offers two passenger train lines in Brazil – the Vitória-Minas Railroad and Carajás Railroad. 5 Back to Contents of the global economy. contribution to the growth we make an impor tant investments and taxes, Through our operations, |

| Ta x Tr a n s p a r e n c y | A n n u a l R e p o r t 2 0 2 0 G F Main Global Operations Brazil A Argentina E B A Chile C D Paraguay D Peru E C B USA F Canada G 6 Back to Contents Headquarter Join Venture Operation Exploration Office |

| Ta x Tr a n s p a r e n c y | A n n u a l R e p o r t 2 0 2 0 H I J U T M L N O Q P K R S Main Global Operations United Kingdom H Indonesia I Q J Mozambique K Oman L U.A.E M India N Malaysia O 7 Back to Contents Headquarter Join Venture Operation Exploration Office Netherlands Switzerland P R S T U Singapore Australia New Caledonia China Japan |

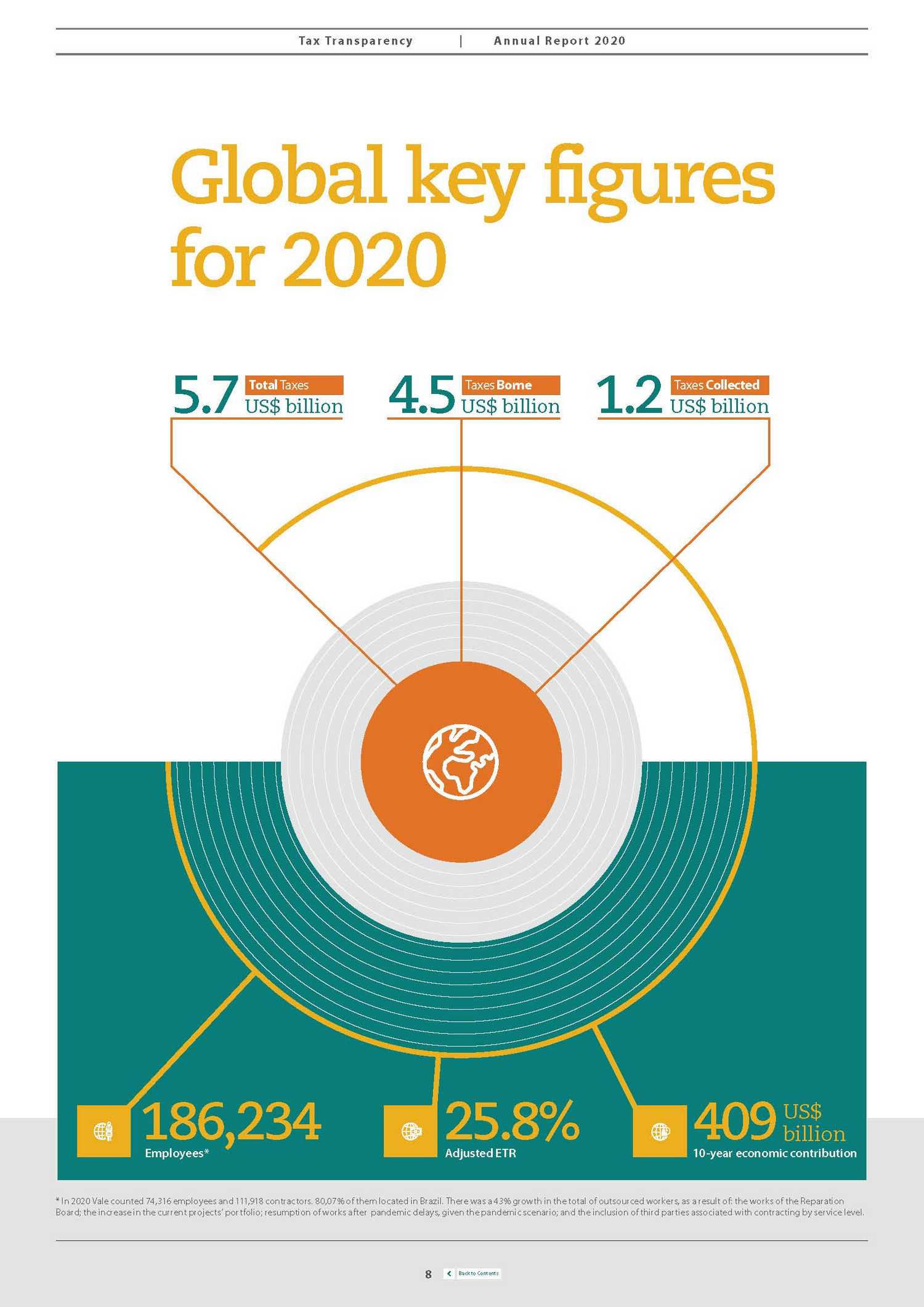

| Tax Tr anspar enc y | A nnual Rep or t 2020 Global key figures for 2020 5.7US$ billion 4.5US$ billion 1.2 US$ billion billion 10-year economic contribution Employees* Adjusted ETR * In 2020 Vale counted 74,316 employees and 111,918 contractors. 80,07% of them located in Brazil. There was a 43% growth in the total of outsourced workers, as a result of: the works of the Reparation Board; the increase in the current projects’ portfolio; resumption of works after pandemic delays, given the pandemic scenario; and the inclusion of third parties associated with contracting by service level. 8 Back to Contents 186,234 25.8% 409 US$ Taxes Borne Taxes Collected Total Taxes |

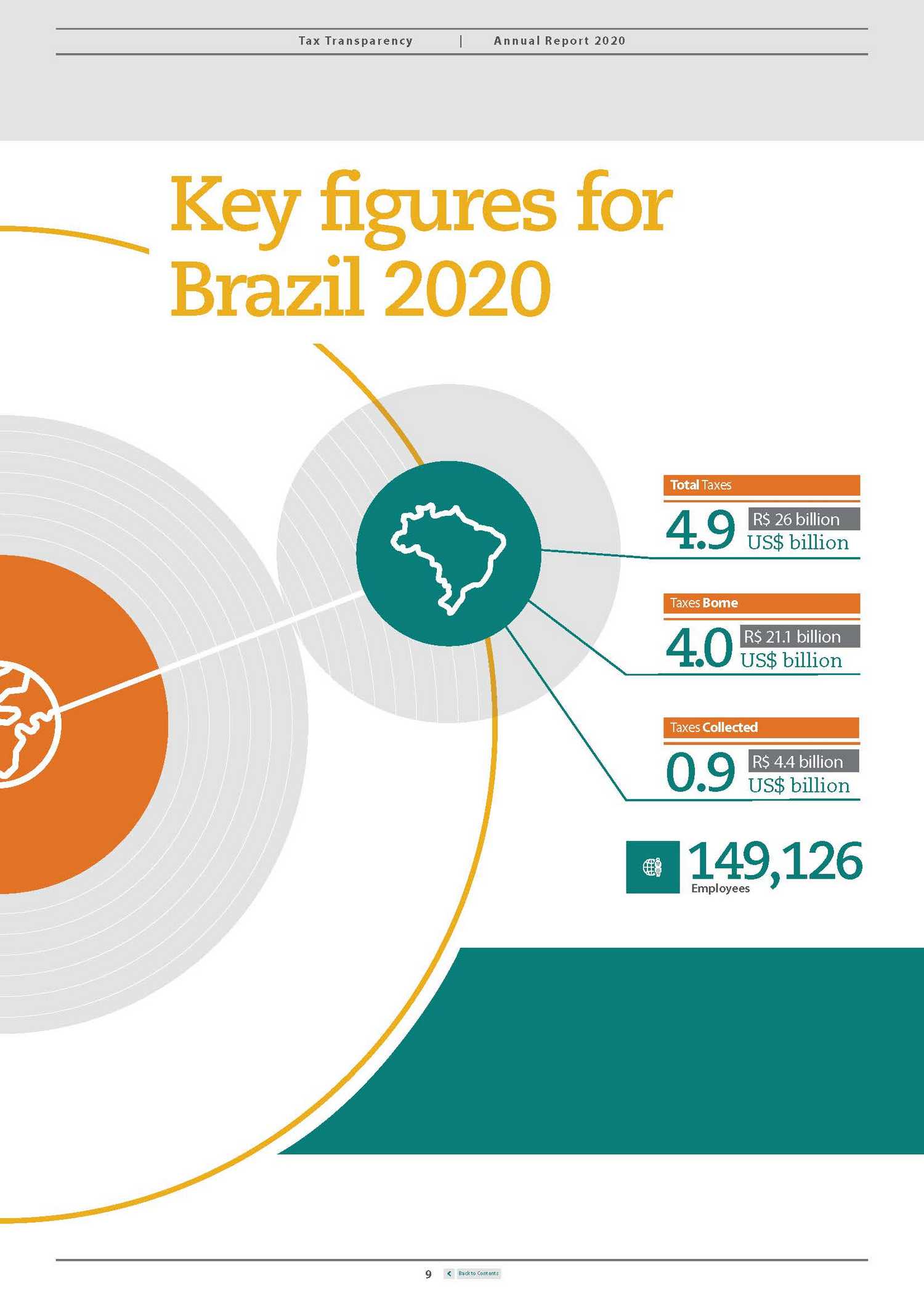

| Tax Tr anspar enc y | A nnual Rep or t 2020 Key figures for Brazil 2020 4.9 US$ billion 4.0 US$ billion 0.9 US$ billion 149,126 Employees 9 Back to Contents R$ 4.4 billion Taxes Collected R$ 21.1 billion Taxes Borne R$ 26 billion Total Taxes |

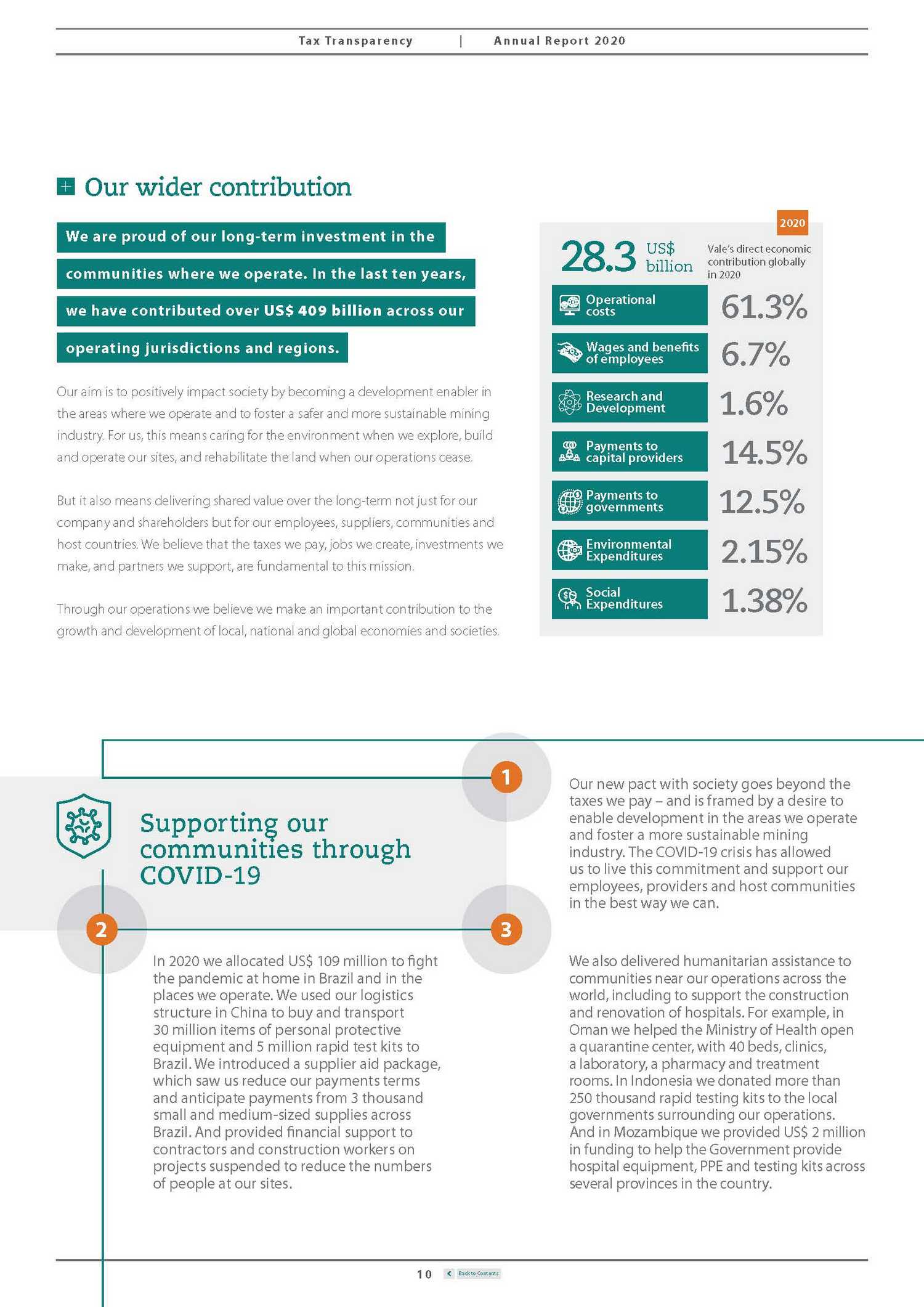

| Tax Tr anspar enc y | A nnual Rep or t 2020 Our wider contribution 2020 US$ Vale’s direct economic in 2020 we have contributed o ver US$ 409 billion across our costs opera ting jurisdictions and r egions. of employees Our aim is to positively impact society by becoming a development enabler in the areas where we operate and to foster a safer and more sustainable mining industry. For us, this means caring for the environment when we explore, build and operate our sites, and rehabilitate the land when our operations cease. capital provi But it also means delivering shared value over the long-term not just for our company and shareholders but for our employees, suppliers, communities and host countries. We believe that the taxes we pay, jobs we create, investments we make, and partners we support, are fundamental to this mission. governments Expenditures Through our operations we believe we make an important contribution to the growth and development of local, national and global economies and societies. 1 Our new pact with society goes beyond the taxes we pay – and is framed by a desire to enable development in the areas we operate and foster a more sustainable mining industry. The COVID-19 crisis has allowed Supporting our communities through employees, providers and host communities 2 3 COVID-19 us to live this commitment and support our in the best way we can. We also delivered humanitarian assistance to communities near our operations across the world, including to support the construction and renovation of hospitals. For example, in Oman we helped the Ministry of Health open a quarantine center, with 40 beds, clinics, a laboratory, a pharmacy and treatment rooms. In Indonesia we donated more than 250 thousand rapid testing kits to the local governments surrounding our operations. And in Mozambique we provided US$ 2 million in funding to help the Government provide hospital equipment, PPE and testing kits across several provinces in the country. In 2020 we allocated US$ 109 million to fight the pandemic at home in Brazil and in the places we operate. We used our logistics structure in China to buy and transport 30 million items of personal protective equipment and 5 million rapid test kits to Brazil. We introduced a supplier aid package, which saw us reduce our payments terms and anticipate payments from 3 thousand small and medium-sized supplies across Brazil. And provided financial support to contractors and construction workers on projects suspended to reduce the numbers of people at our sites. 10 Back to Contents communities where we operate. In the last ten years, We are proud of our long-term investment in the 28.3 billion contribution globally 61.3% 6.7% 1.6% 14.5% 12.5% 2.15% 1.38% Social Expenditures Environmental Payments to Payments toders Research and Development Wages and benefits Operational |

| Tax Tr anspar enc y | A nnual Rep or t 2020 FIG 02 Picture shows Vale’s passengers train that connects Cariacica (ES) to Belo Horizonte (MG). Picture: Gabriel Lordêllo Vale’s tax contribution Vale is a leading participant in the global mining sector. Vale is a leading participant in the global mining sector. We recognize that this brings significant social and economic responsibilities in the jurisdictions where we operate. Vale strives to provide employment, strategic and sustainable development, significant community investment to pays taxes and royalties to governments in full as required by local legislation. It presents Vale’s total tax contribution by jurisdiction, by level of government and by project. This report also provides further detailed information on Vale’s tax contributions in the following jurisdictions where its mining operations are located: • Brazil • Indonesia • Canada • New Caledonia • Mozambique This report details taxes and royalties paid in jurisdictions where Vale has a presence. Vale´s total tax contribution in the year. As a result of these changes, 2020 data is not comparable with the previous year. We welcome feedback from our stakeholders on how further we can improve this reporting. 11 Back to Contents In 2020, we adopted new definitions for reporting tax payments and refunds, to provide a more complete view of ! |

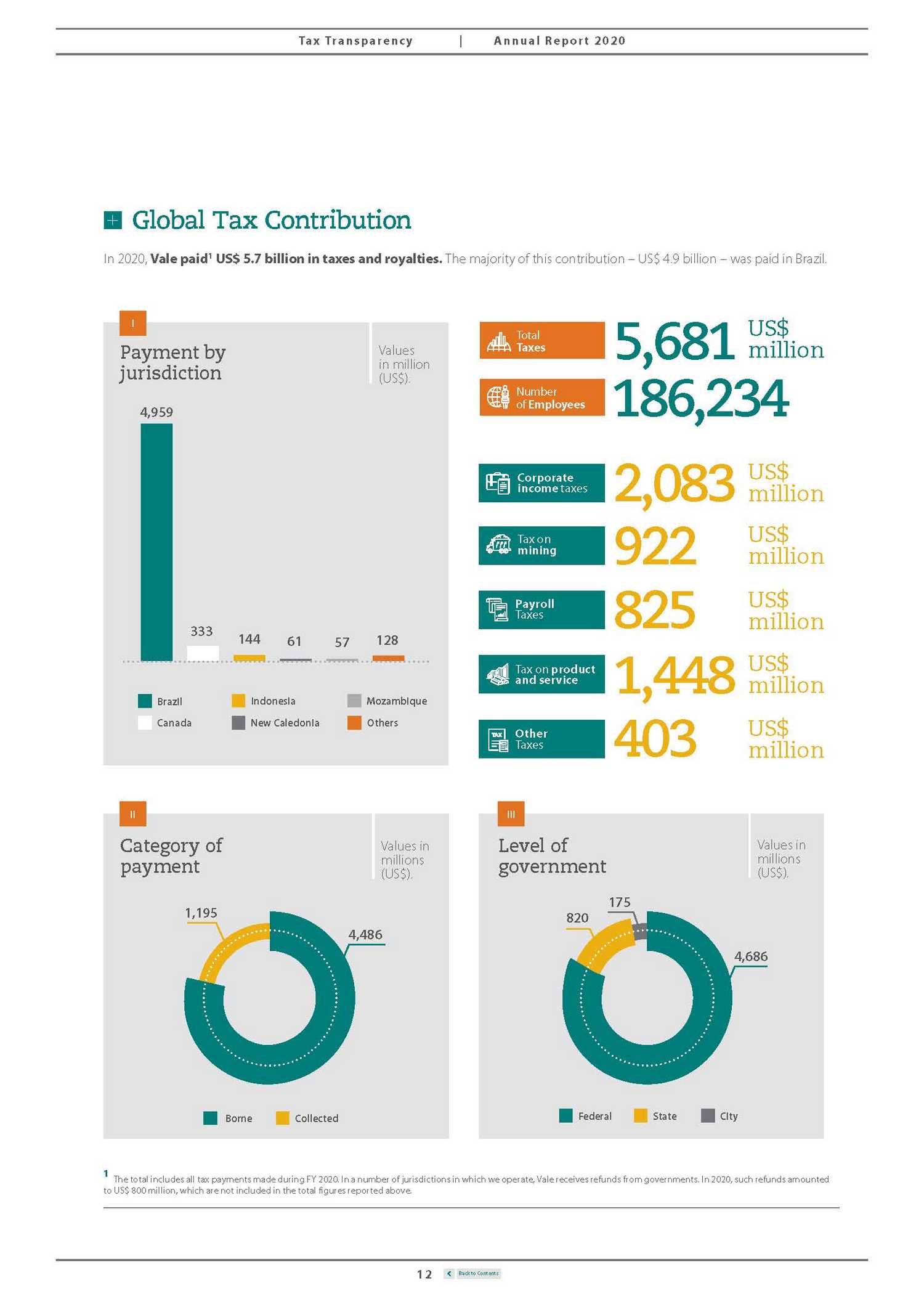

| Tax Tr anspar enc y | A nnual Rep or t 2020 Global Tax Contribution In 2020, Vale paid1 US$ 5.7 billion in taxes and royalties. The majority of this contribution – US$ 4.9 billion – was paid in Brazil. I 5,681 US$ million jurisdiction 186,234 of Employees 2,083 922 825 1,448 403 US$ million US$ million US$ million US$ million US$ million 57 II III government 820 1 The total includes all tax payments made during FY 2020. In a number of jurisdictions in which we operate, Vale receives refunds from governments. In 2020, such refunds amounted to US$ 800 million, which are not included in the total figures reported above. 12 Back to Contents Values in millions (US$). Level of 175 4,686 Federal StateCity Values in millions (US$). Category of payment 1,195 4,486 Borne Collected Other Taxes Tax on product and service Payroll Taxes Tax on mining Corporate income taxes Number Total Taxes Values in million (US$). Payment by 4,959 61 Brazil Indonesia Mozambique CanadaNew Caledonia Others 333144128 |

| Tax Tr anspar enc y | A nnual Rep or t 2020 IV and services financial year (for example tax over property tax or financial transactions). More V and services 13 Back to Contents Values in millions (US$). Tax on mining Payroll taxes Tax on products Other taxes Tax Collected 435433 1 326 Values in millions (US$). Corporate income taxes Tax on mining Payroll taxes Tax on products Other taxes Tax Borne 2,083 ”Other taxes” refers to fees and discretionary contributions made during the details can be found in “Appendix 1 – The basis on which this report was prepared”. 9211,015 390 77 |

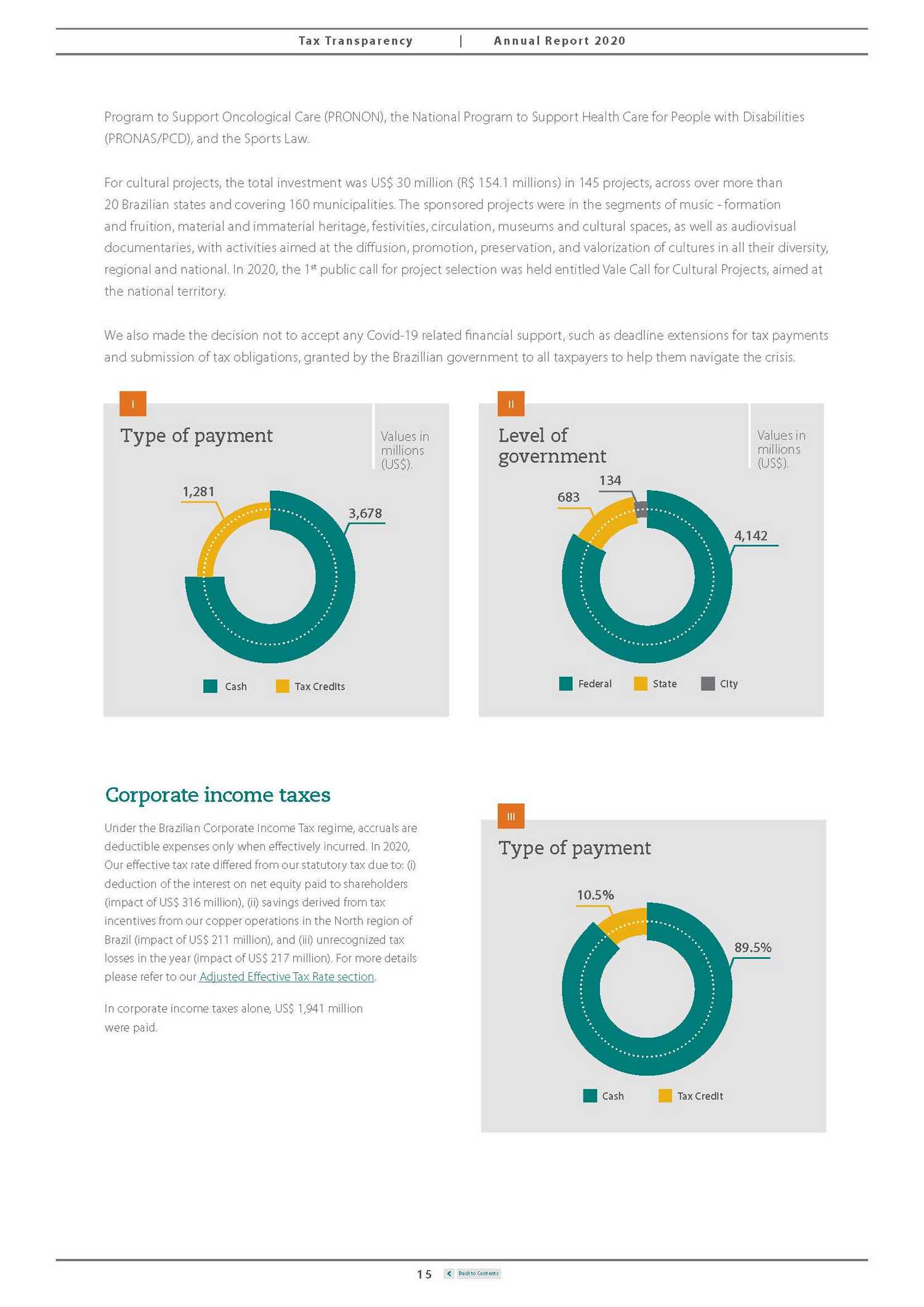

| Tax Tr anspar enc y | A nnual Rep or t 2020 FIG 03 Aerial view of wagons loaded with iron ore in Paraupebas, Pará. Picture: Ricardo Teles 4,959 US$ million Contribution in Brazil In Brazil, Vale’s primary commodities are iron ore and base metals, principally copper. Vale also extracts other raw materials, such as manganese and ferroalloys. Vale’s operations in Brazil benefit from pre-existing logistics infrastructure, which was originally built to transport iron ore. Vale is working closely with public and private sector partners to invest in technology and infrastructure to continuously improve the efficiency and sustainability of its operations, from extraction to delivery to customers. 149,126 1,941 871 511 1,297 339 US$ million US$ million US$ million US$ million US$ million In 2020 we paid US$ 4.9 billion in taxes in Brazil. This translates to a BRL total taxes paid figure in 2020 of R$ 26 billion. Approximately 26% of the total was paid through available tax credits2. We employ nearly 150 thousand people in Brazil. Guided by a broad vision of sustainability, Vale invests in initiatives that produce a positive legacy in the areas of culture, defense of the rights of the elderly, children and adolescents, health, and sports, through incentive funds. Through federal incentive laws, Vale supports initiatives that strengthen public policies, leveraging its commitment to make a positive contribution to society. 2 Brazilian legislation allows the offset of federal taxes or contributions with other federal credits to companies that follow a process set out by the Brazilian Federal Revenue (RFB) Service called PER/ DCOMP. The main credits used by Vale are: • Overpayment of federal taxes and/or contributions. • Social integration plan (“PIS”) and social welfare (“COFINS”) taxes . • Tax Losses of Corporate Income Tax (“IRPJ”) and Social contributions (“CSLL”). In 2020, Vale’s investments from tax incentives totaled US$ 54 million (R$ 274.5 millions) through the Federal Law for Cultural Incentives, the Fund for Childhood and Adolescence, the Senior Citizens Fund, the National 14 Back to Contents Other Taxes Tax on product and service Payroll Taxes Tax on mining Corporate income taxes Number of Employees Total Taxes |

| Tax Tr anspar enc y | A nnual Rep or t 2020 Program to Support Oncological Care (PRONON), the National Program to Support Health Care for People with Disabilities (PRONAS/PCD), and the Sports Law. For cultural projects, the total investment was US$ 30 million (R$ 154.1 millions) in 145 projects, across over more than 20 Brazilian states and covering 160 municipalities. The sponsored projects were in the segments of music - formation and fruition, material and immaterial heritage, festivities, circulation, museums and cultural spaces, as well as audiovisual documentaries, with activities aimed at the diffusion, promotion, preservation, and valorization of cultures in all their diversity, regional and national. In 2020, the 1st public call for project selection was held entitled Vale Call for Cultural Projects, aimed at the national territory. We also made the decision not to accept any Covid-19 related financial support, such as deadline extensions for tax payments and submission of tax obligations, granted by the Brazillian government to all taxpayers to help them navigate the crisis. I II government 683 Corporate income taxes Under the Brazilian Corporate Income Tax regime, accruals are deductible expenses only when effectively incurred. In 2020, Our effective tax rate differed from our statutory tax due to: (i) deduction of the interest on net equity paid to shareholders (impact of US$ 316 million), (ii) savings derived from tax incentives from our copper operations in the North region of Brazil (impact of US$ 211 million), and (iii) unrecognized tax losses in the year (impact of US$ 217 million). For more details please refer to our Adjusted Effective Tax Rate section. In corporate income taxes alone, US$ 1,941 million were paid. 15 Back to Contents III Type of payment 10.5% 89.5% CashTax Credit Values in millions (US$). Level of 134 4,142 Federal StateCity Values in millions (US$). Type of payment 1,281 3,678 CashTax Credits |

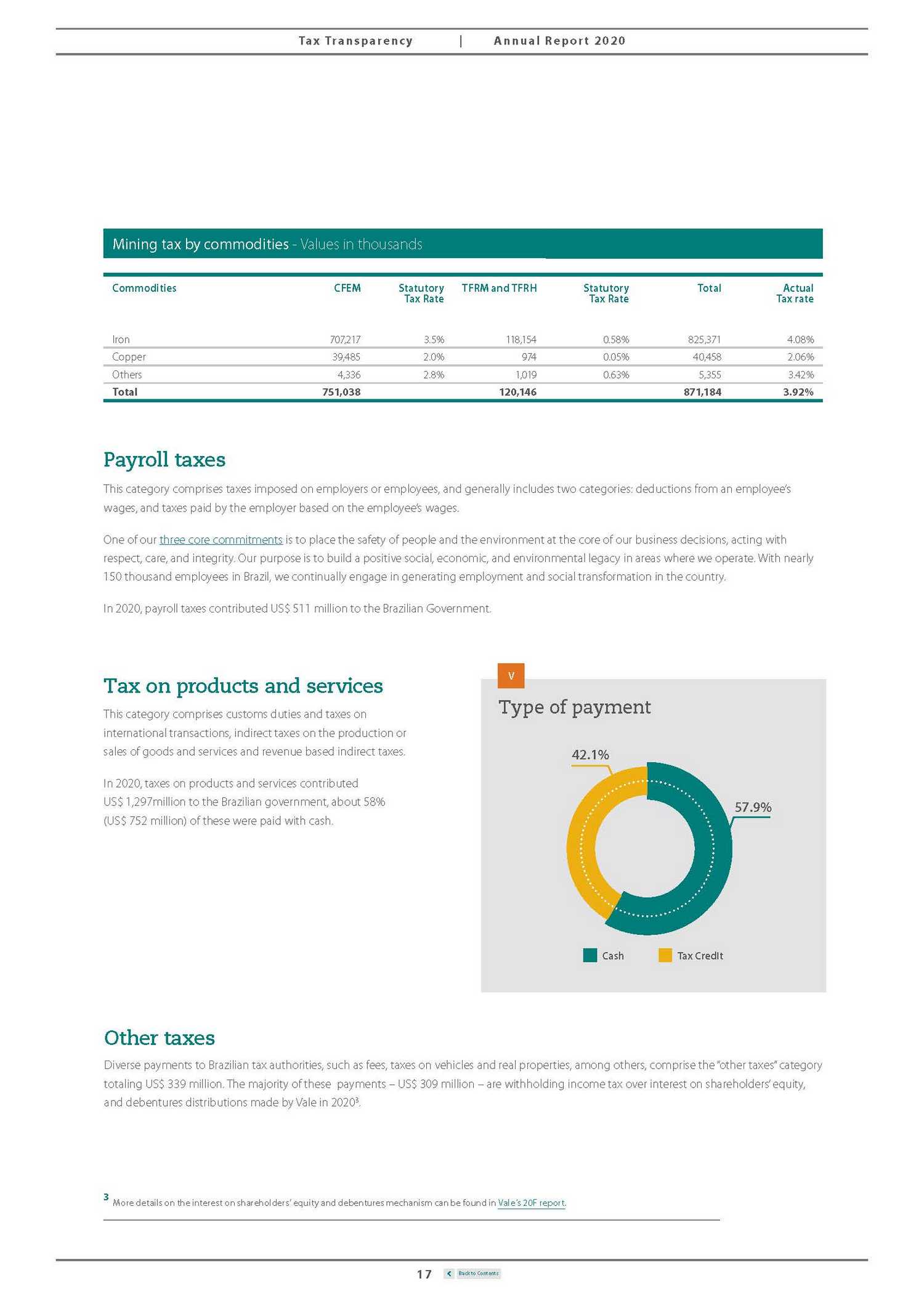

| Tax Tr anspar enc y | A nnual Rep or t 2020 Tax on mining In Brazil, mining companies are subject to contributions due to the exploration of public mineral resources. Rates vary from 0.2% to 3.5%, according to the type of mining operation. Payments are made to the National Mining Agency, which is responsible for distributing proceeds to states and municipalities, according to where the mining activity occurs. Furthermore, some states have enacted specific charges over mining and related activities. Payments include: • Financial Compensation for the Exploration of Mineral Resources (“CFEM” in Portuguese). According to the Brazilian Federal Constitution, this compensation must be calculated over the value derived from the mining activity. Following constitutional requirements, not all of them adequately reflected in infraconstitutional laws, the compensation must be calculated over: (i) net revenues, when mineral resources are subject to third-party sale; (ii) costs of mining, when mineral resources are subject to internal consumption; and (iii) net revenues according to transfer pricing rules (PECEX), when mineral resources are subjected to intra-group international sales. Vale strictly follows all constitutional rules regarding the matter. • State taxes on mineral production (“TFRM” in Portuguese). • Tax for control, monitoring and surveillance of water resources exploitation and utilization activities (“TFRH” in Portuguese). For mining taxes in Brazil, Vale has paid an average tax rate on revenue of 3.9%. In 2020, this corresponded to US$ 871 million payable to the Brazilian tax authorities. See additional details in the table below. III IV (US$). 565 16 Back to Contents Values in millions Commodities 540 826 Iron OreCopperOthers Values in millions (US$). Distribution by level of government 75 231 Federal StateCity ! |

| Tax Tr anspar enc y | A nnual Rep or t 2020 Commodities CFEM Statutory Tax Rate TFRM and TFRH Statutory Tax Rate Total Actual Tax rate Iron 707,217 3.5% 118,154 0.58% 825,371 4.08% Copper 39,485 2.0% 974 0.05% 40,458 2.06% Others 4,336 2.8% 1,019 0.63% 5,355 3.42% Total 751,038 120,146 871,184 3.92% Payroll taxes This category comprises taxes imposed on employers or employees, and generally includes two categories: deductions from an employee’s wages, and taxes paid by the employer based on the employee’s wages. One of our three core commitments is to place the safety of people and the environment at the core of our business decisions, acting with respect, care, and integrity. Our purpose is to build a positive social, economic, and environmental legacy in areas where we operate. With nearly 150 thousand employees in Brazil, we continually engage in generating employment and social transformation in the country. In 2020, payroll taxes contributed US$ 511 million to the Brazilian Government. Tax on products and services This category comprises customs duties and taxes on international transactions, indirect taxes on the production or sales of goods and services and revenue based indirect taxes. In 2020, taxes on products and services contributed US$ 1,297million to the Brazilian government, about 58% (US$ 752 million) of these were paid with cash. Other taxes Diverse payments to Brazilian tax authorities, such as fees, taxes on vehicles and real properties, among others, comprise the “other taxes” category totaling US$ 339 million. The majority of these payments – US$ 309 million – are withholding income tax over interest on shareholders’ equity, and debentures distributions made by Vale in 20203. 3 More details on the interest on shareholders’ equity and debentures mechanism can be found in Vale´s 20F report. 17 Back to Contents V Type of payment 42.1% 57.9% CashTax Credit Mining tax by commodities - Values in thousands |

| Tax Tr anspar enc y | A nnual Rep or t 2020 FIG 04 Nickel Processing Plant facilities, in Sorowako, Sulawesi Island, Indonesia. Picture: Marcelo Coelho 144 US$ million Contribution in Indonesia In Indonesia, Vale produces 75 thousand tons of nickel-in-matte per year, supplying 5% of the world’s nickel demand. Vale signed a Contract of Work with the Government of Indonesia in 1968 to explore, mine and process nickel ore, and has been contributing to the economy there ever since. 9,581 33 22 7 55 27 US$ million US$ million US$ million US$ million US$ million Through our operations in Indonesia, we employ more than 9 thousand people. In 2020, we paid over US$144 million in taxes across corporate income taxes, payroll taxes, taxes on products and services and other taxes. Vale also undertakes significant environmental programs in Indonesia, including reforestation efforts and a revegetation program to provide the opportunity to reintroduce native plant species. Vale’s Indonesian operations are also investing in greenhouse gas emissions reduction initiatives and working to align with the policies and frameworks of the International Council on Mining and Metals (ICMM). 18 Back to Contents Other Taxes Tax on product and service Payroll Taxes Tax on mining Corporate income taxes Number of Employees Total Taxes |

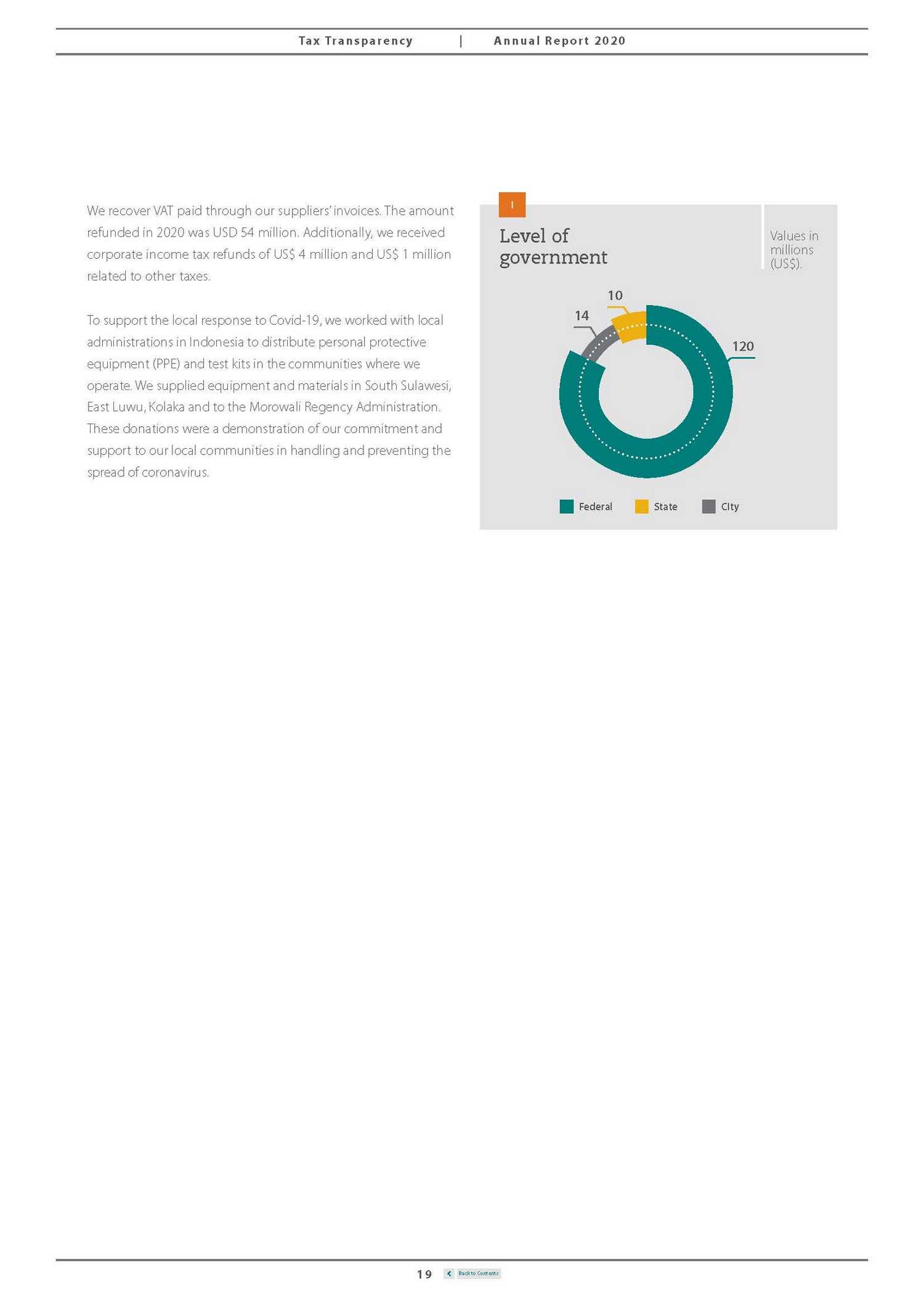

| Tax Tr anspar enc y | A nnual Rep or t 2020 We recover VAT paid through our suppliers’ invoices. The amount refunded in 2020 was USD 54 million. Additionally, we received corporate income tax refunds of US$ 4 million and US$ 1 million related to other taxes. To support the local response to Covid-19, we worked with local administrations in Indonesia to distribute personal protective equipment (PPE) and test kits in the communities where we operate. We supplied equipment and materials in South Sulawesi, East Luwu, Kolaka and to the Morowali Regency Administration. These donations were a demonstration of our commitment and support to our local communities in handling and preventing the spread of coronavirus. 19 Back to Contents I Values in millions (US$). Level of government 10 14 120 Federal StateCity |

| Kiruna truck inside Coleman Mine, in Sudbury (Ontario), Canada. FIG 05 Picture: Marcelo Coelho 333 US$ million Contribution in Canada In Canada, Vale produces high quality nickel, one of the most versatile metals in existence known for its use in batteries and metal coatings. We also produce copper, cobalt, platinum group metals and precious metals at three separate operations in Canada: five mines and processing facilities in Ontario; a mine and mill in Manitoba; and mine and processing facilities in Newfoundland and Labrador. 10,783 2 25 217 69 20 US$ million US$ million US$ million US$ million US$ million In 2020, Vale employed over 10,750 people (an increase of over 800 relative to 2019) across Canada with the bulk of employees residing in the various rural communities where our mining operations are located. In Canada, Vale works to operate in alignment with the goals and objectives of both the International Council on Mining and Metals as well as the Towards Sustainable Mining Initiative (TSM) of the Mining Association of Canada. Vale’s environmental work includes reforestation and 20 Back to Contents Other Taxes Tax on product and service Payroll Taxes Tax on mining Corporate income taxes Number of Employees Total Taxes |

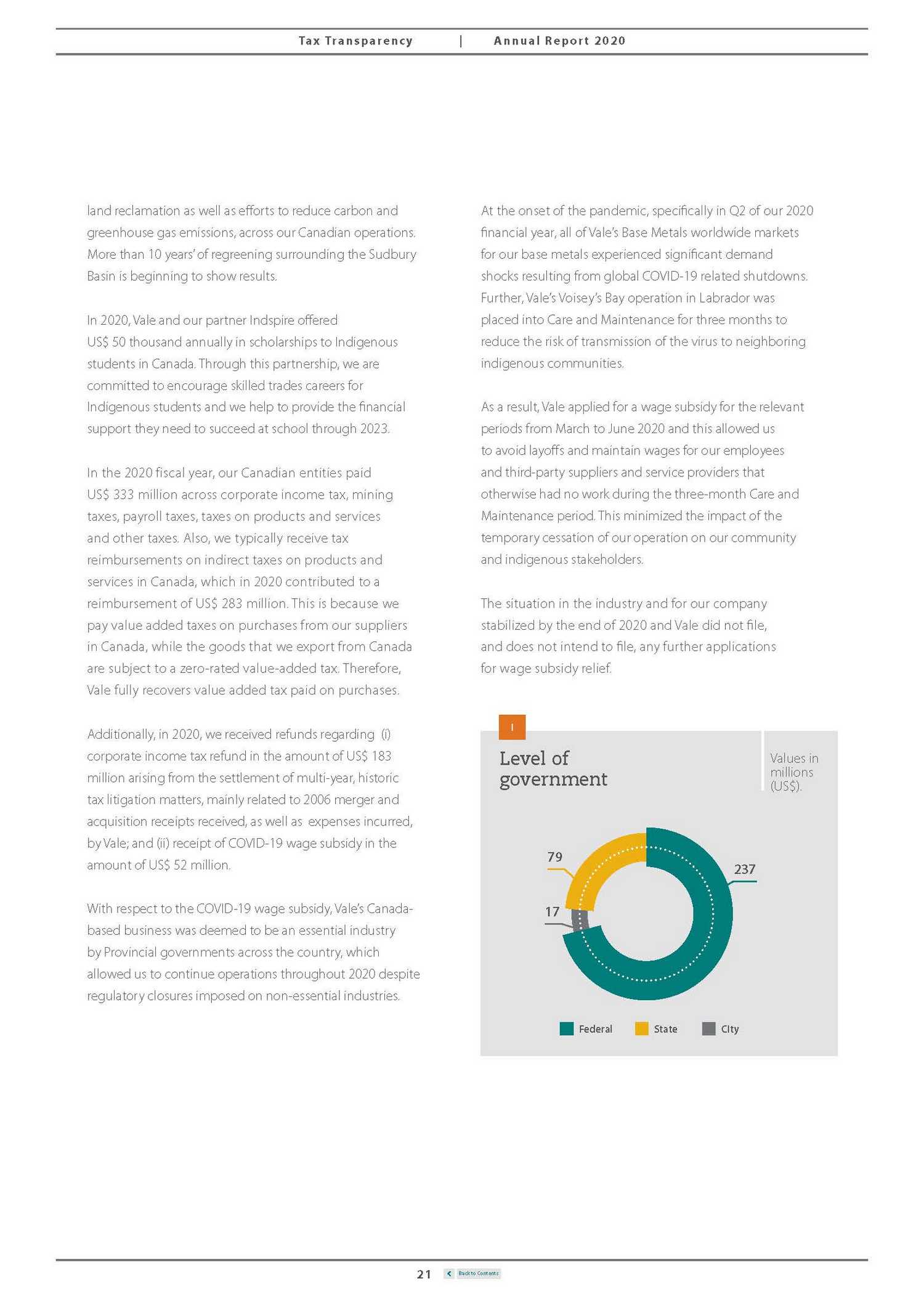

| Tax Tr anspar enc y | A nnual Rep or t 2020 land reclamation as well as efforts to reduce carbon and greenhouse gas emissions, across our Canadian operations. More than 10 years’ of regreening surrounding the Sudbury Basin is beginning to show results. At the onset of the pandemic, specifically in Q2 of our 2020 financial year, all of Vale’s Base Metals worldwide markets for our base metals experienced significant demand shocks resulting from global COVID-19 related shutdowns. Further, Vale’s Voisey’s Bay operation in Labrador was placed into Care and Maintenance for three months to reduce the risk of transmission of the virus to neighboring indigenous communities. In 2020, Vale and our partner Indspire offered US$ 50 thousand annually in scholarships to Indigenous students in Canada. Through this partnership, we are committed to encourage skilled trades careers for Indigenous students and we help to provide the financial support they need to succeed at school through 2023. As a result, Vale applied for a wage subsidy for the relevant periods from March to June 2020 and this allowed us to avoid layoffs and maintain wages for our employees and third-party suppliers and service providers that otherwise had no work during the three-month Care and Maintenance period. This minimized the impact of the temporary cessation of our operation on our community and indigenous stakeholders. In the 2020 fiscal year, our Canadian entities paid US$ 333 million across corporate income tax, mining taxes, payroll taxes, taxes on products and services and other taxes. Also, we typically receive tax reimbursements on indirect taxes on products and services in Canada, which in 2020 contributed to a reimbursement of US$ 283 million. This is because we pay value added taxes on purchases from our suppliers in Canada, while the goods that we export from Canada are subject to a zero-rated value-added tax. Therefore, Vale fully recovers value added tax paid on purchases. The situation in the industry and for our company stabilized by the end of 2020 and Vale did not file, and does not intend to file, any further applications for wage subsidy relief. Additionally, in 2020, we received refunds regarding (i) corporate income tax refund in the amount of US$ 183 million arising from the settlement of multi-year, historic tax litigation matters, mainly related to 2006 merger and acquisition receipts received, as well as expenses incurred, by Vale; and (ii) receipt of COVID-19 wage subsidy in the amount of US$ 52 million. With respect to the COVID-19 wage subsidy, Vale’s Canada-based business was deemed to be an essential industry by Provincial governments across the country, which allowed us to continue operations throughout 2020 despite regulatory closures imposed on non-essential industries. 21 Back to Contents I Values in millions (US$). Level of government 79237 17 Federal StateCity |

| Tax Tr anspar enc y | A nnual Rep or t 2020 FIG 06 New Caledonia Valley - VNC. Usine du Grand Sud - overview of the Nickel Processing Plant facilities. Picture: Marcelo Coelho 61 US$ million Contribution in New Caledonia 1,447 In New Caledonia, Vale produces nickel and cobalt, and is responsible for extracting laterites and saprolites. We operate in the Goro plateau and our operations consist of a mine, a port and a power plant. In 2020, we paid over US$ 61 million in taxes in New Caledonia. In line with one of our five strategic environmental, social and governance (ESG pillars), to keep on track with the transformation of the Base Metals business unit, in March 2021 Vale completed the sale of Vale New Caledonia to the Prony Resources New Caledonia consortium. Vale’s intention from the beginning of the divestment process was to withdraw from New Caledonia in an orderly and responsible manner and this transaction meets that premise. All payments were made on a federal level. < 0.1 2 36 16 7 US$ million US$ million US$ million US$ million US$ million 22 Back to Contents Other Taxes Tax on product and service Payroll Taxes Tax on mining Corporate income taxes Number of Employees Total Taxes |

| Tax Tr anspar enc y | A nnual Rep or t 2020 FIG 07 Maritime Terminal receives coal mined by Vale in the Moatize area (Tete). Picture: Marcelo Coelho 57 US$ million Contribution in Mozambique 11,714 Vale has operated in Mozambique since 2011, extracting metallurgical and thermal coal from the Moatize Mine in the north-west region of the country. The Moatize Mine has an estimated production capacity of 22 million tons, and serves markets across Asia, Africa, Europe and the Americas. Metallurgical coal is used to transform iron ore into steel, one of the most versatile and widely used materials in the world. Thermal coal is used for electricity generation. 1 20 32 4 US$ million US$ million US$ million US$ million Vale’s operations generate more than 11 thousand jobs in Mozambique in its mining and logistics operation. In 2020, we paid US$ 57 million in taxes in Mozambique across corporate income tax, payroll taxes, taxes on mining, taxes on products and services and other taxes. Through a joint venture we have invested significantly in improving local infrastructure – for example the 912km Nacala Corridor Railroad connecting the 23 Back to Contents Other Taxes Tax on product and service Payroll Taxes Tax on mining Number of Employees Total Taxes |

| Tax Tr anspar enc y | A nnual Rep or t 2020 Moatize Mine to the deep-water port of Nacala, benefiting the whole north of Mozambique with cargo and passenger trains, connecting people and markets. According VAT local regulations all mining and oil & gas entities in Mozambique exporting 75% of their production do not have to pay input VAT related to domestic purchases. Therefore, the VAT paid by Vale in Mozambique in 2020 corresponds to VAT on imports, which is, in principle, recoverable due to the fact that coal exported is subject to a zero-rated VAT. The amount refunded in 2020 from previous period was US$ 29 million. Vale has a consistent social investment portfolio, with more than US$ 7 million invested yearly, benefiting more than 10k families included in social programs ranging from agriculture, school feeding for 25 thousand primary school students daily, fishing and capacity building initiatives. On the environmental side, sustainability training, marine preservation and mangrove restoration area are our primary focus. We have also stood side-by-side with Mozambique throughout the COVID-19 crisis, including providing US$ 2 million in funding to help the Government provide hospital equipment, PPE and testing kits across several provinces in the country. In January 2021, we signed a Heads of Agreement (“HOA”) with Mistui as a first step on the process of divesting its participation in the coal business, which will be guided by the preservation of the operational continuity of the Moatize mine and the Nacala corridor through the search of a third party interested in those assets. 24 Back to Contents I Values in millions (US$). Level of government 15 42 Federal State |

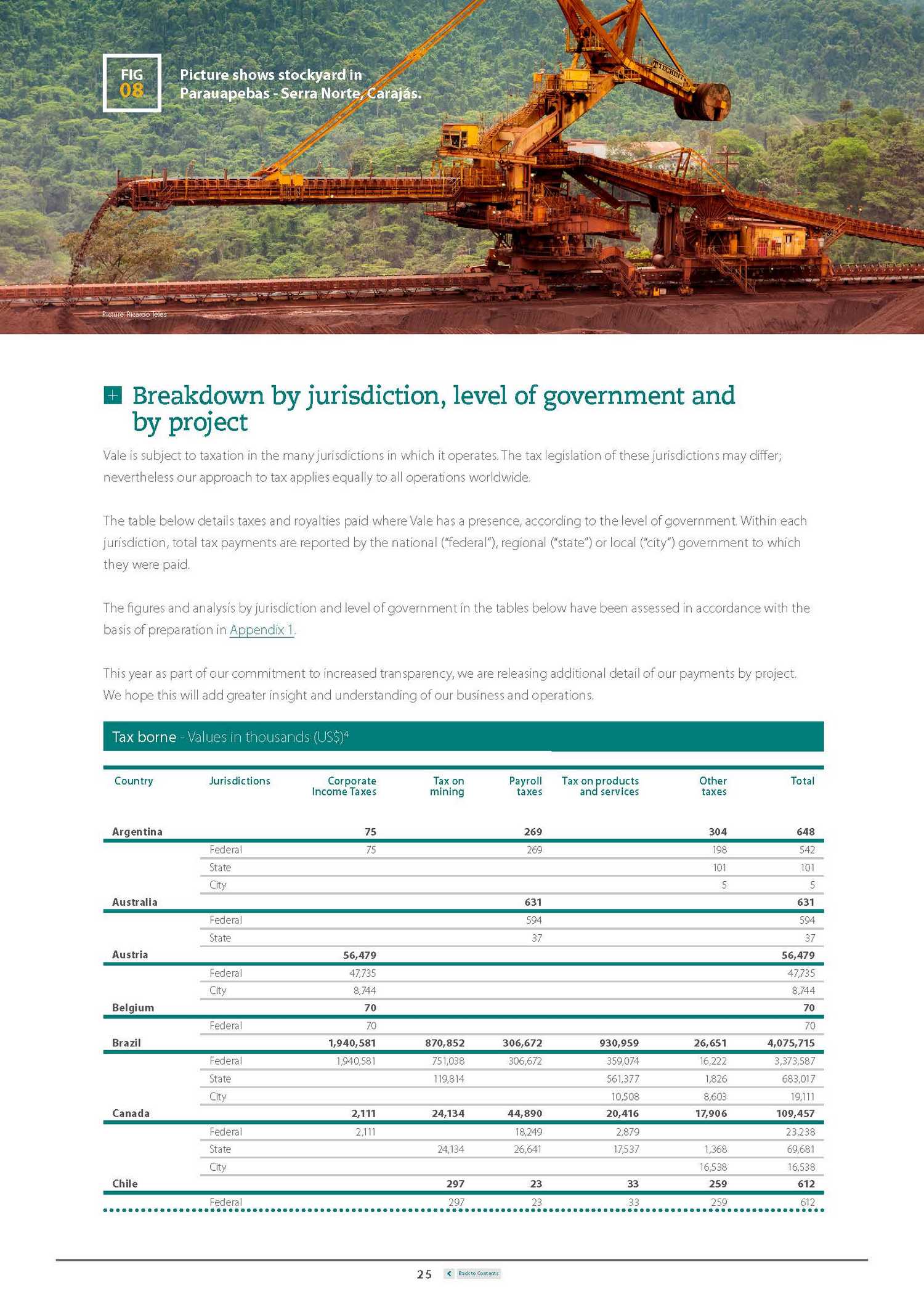

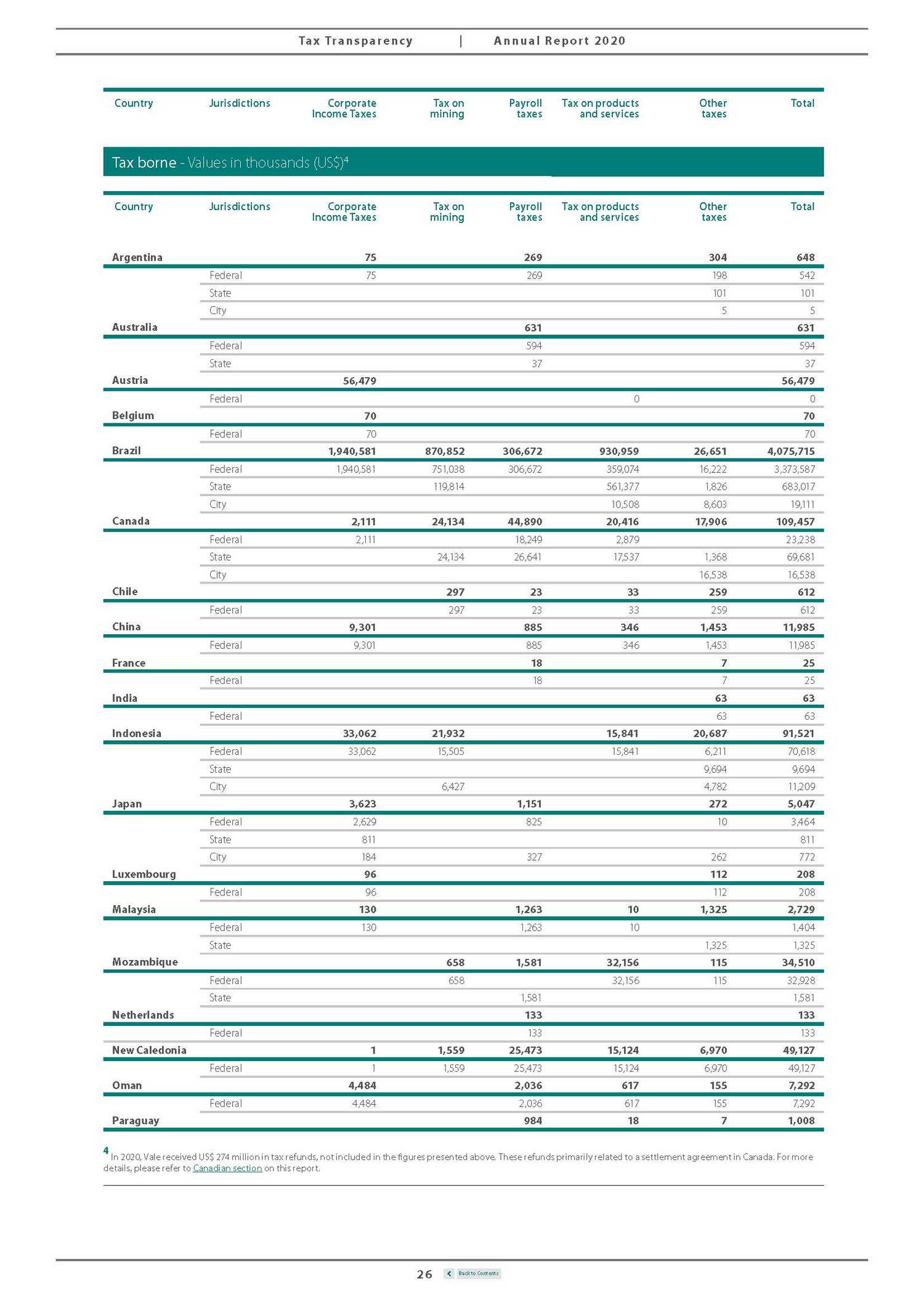

| Tax Tr anspar enc y | A nnual Rep or t 2020 Parauapebas - Serra Norte, Carajás. Picture: Ricardo Teles Breakdown by jurisdiction, level of government and by project Vale is subject to taxation in the many jurisdictions in which it operates. The tax legislation of these jurisdictions may differ; nevertheless our approach to tax applies equally to all operations worldwide. The table below details taxes and royalties paid where Vale has a presence, according to the level of government. Within each jurisdiction, total tax payments are reported by the national (“federal”), regional (“state”) or local (“city”) government to which they were paid. The figures and analysis by jurisdiction and level of government in the tables below have been assessed in accordance with the basis of preparation in Appendix 1. This year as part of our commitment to increased transparency, we are releasing additional detail of our payments by project. We hope this will add greater insight and understanding of our business and operations. Country Jurisdictions Corporate Income Taxes Tax on mining Payroll taxes Tax on products and services Other taxes Total Argentina 75 269 304 648 Federal 75 269 198 542 State 101 101 City 5 5 Australia 631 631 Federal 594 594 State 37 37 Austria 56,479 56,479 Federal 47,735 47,735 City 8,744 8,744 Belgium 70 70 Federal 70 70 Brazil 1,940,581 870,852 306,672 930,959 26,651 4,075,715 Federal 1,940,581 751,038 306,672 359,074 16,222 3,373,587 State 119,814 561,377 1,826 683,017 City 10,508 8,603 19,111 Canada 2,111 24,134 44,890 20,416 17,906 109,457 Federal 2,111 18,249 2,879 23,238 State 24,134 26,641 17,537 1,368 69,681 City 16,538 16,538 Chile 297 23 33 259 612 Federal 297 23 33 259 612 25 Back to Contents Tax borne - Values in thousands (US$)4 FIG 08 Picture shows stockyard in |

| Tax Tr anspar enc y | A nnual Rep or t 2020 Country Jurisdictions Corporate Income Taxes Tax on mining Payroll taxes Tax on products and services Other taxes Total Country Jurisdictions Corporate Income Taxes Tax on mining Payroll taxes Tax on products and services Other taxes Total Argentina 75 269 304 648 Federal 75 269 198 542 State 101 101 City 5 5 Australia 631 631 Federal 594 594 State 37 37 Austria 56,479 56,479 Federal 0 0 Belgium 70 70 Federal 70 70 Brazil 1,940,581 870,852 306,672 930,959 26,651 4,075,715 Federal 1,940,581 751,038 306,672 359,074 16,222 3,373,587 State 119,814 561,377 1,826 683,017 City 10,508 8,603 19,111 Canada 2,111 24,134 44,890 20,416 17,906 109,457 Federal 2,111 18,249 2,879 23,238 State 24,134 26,641 17,537 1,368 69,681 City 16,538 16,538 Chile 297 23 33 259 612 Federal 297 23 33 259 612 China 9,301 885 346 1,453 11,985 Federal 9,301 885 346 1,453 11,985 France 18 7 25 Federal 18 7 25 India 63 63 Federal 63 63 Indonesia 33,062 21,932 15,841 20,687 91,521 Federal 33,062 15,505 15,841 6,211 70,618 State 9,694 9,694 City 6,427 4,782 11,209 Japan 3,623 1,151 272 5,047 Federal 2,629 825 10 3,464 State 811 811 City 184 327 262 772 Luxembourg 96 112 208 Federal 96 112 208 Malaysia 130 1,263 10 1,325 2,729 Federal 130 1,263 10 1,404 State 1,325 1,325 Mozambique 658 1,581 32,156 115 34,510 Federal 658 32,156 115 32,928 State 1,581 1,581 Netherlands 133 133 Federal 133 133 New Caledonia 1 1,559 25,473 15,124 6,970 49,127 Federal 1 1,559 25,473 15,124 6,970 49,127 Oman 4,484 2,036 617 155 7,292 Federal 4,484 2,036 617 155 7,292 Paraguay 984 18 7 1,008 4 In 2020, Vale received US$ 274 million in tax refunds, not included in the figures presented above. These refunds primarily related to a settlement agreement in Canada. For more details, please refer to Canadian section on this report. 26 Back to Contents Tax borne - Values in thousands (US$)4 |

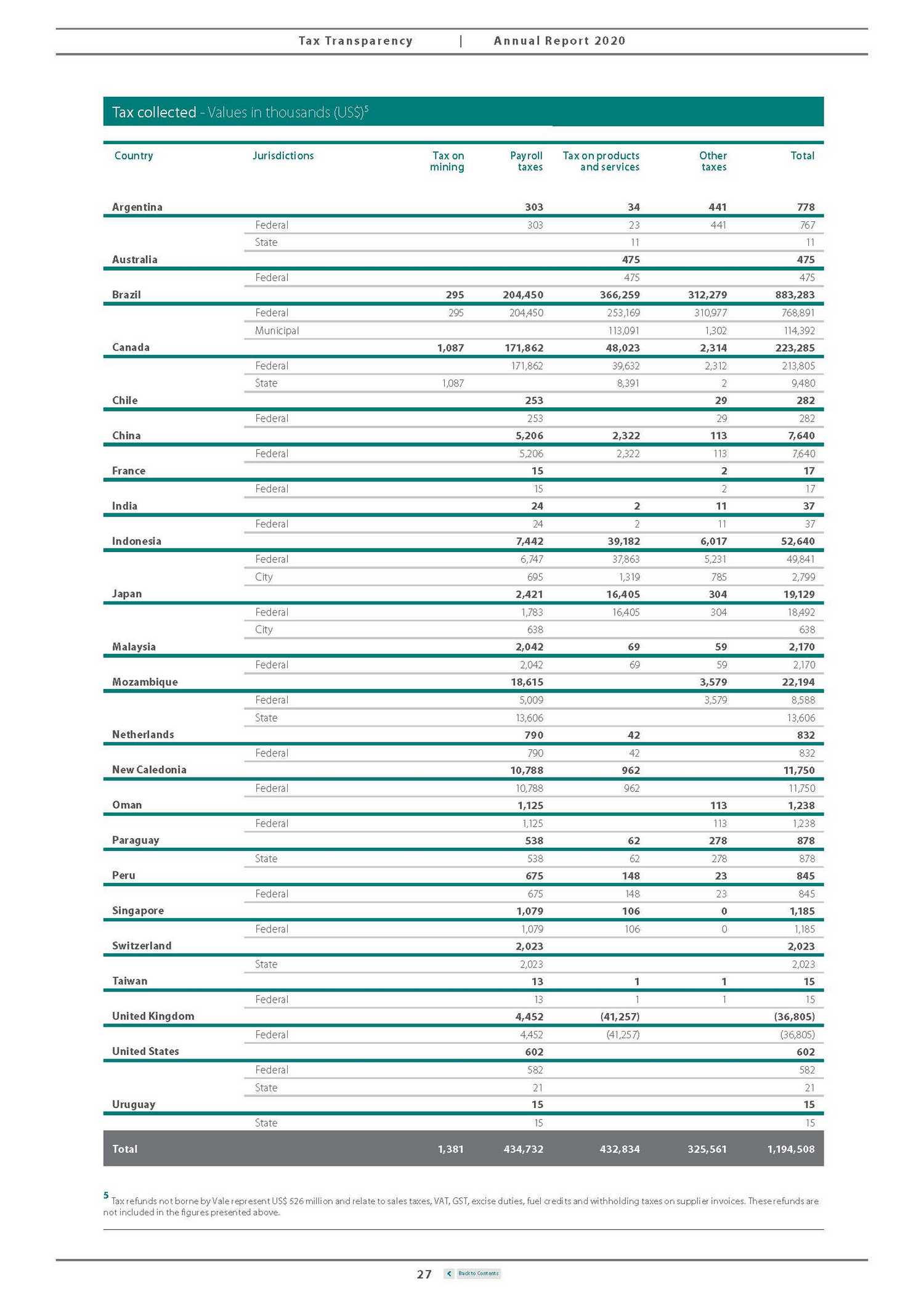

| Tax Tr anspar enc y | A nnual Rep or t 2020 Country Jurisdictions Tax on mining Payroll taxes Tax on products and services Other taxes Total Argentina 303 34 441 778 Federal 303 23 441 767 State 11 11 Australia 475 475 Federal 475 475 Brazil 295 204,450 366,259 312,279 883,283 Federal 295 204,450 253,169 310,977 768,891 Municipal 113,091 1,302 114,392 Canada 1,087 171,862 48,023 2,314 223,285 Federal 171,862 39,632 2,312 213,805 State 1,087 8,391 2 9,480 Chile 253 29 282 Federal 253 29 282 China 5,206 2,322 113 7,640 Federal 5,206 2,322 113 7,640 France 15 2 17 Federal 15 2 17 India 24 2 11 37 Federal 24 2 11 37 Indonesia 7,442 39,182 6,017 52,640 Federal 6,747 37,863 5,231 49,841 City 695 1,319 785 2,799 Japan 2,421 16,405 304 19,129 Federal 1,783 16,405 304 18,492 City 638 638 Malaysia 2,042 69 59 2,170 Federal 2,042 69 59 2,170 Mozambique 18,615 3,579 22,194 Federal 5,009 3,579 8,588 State 13,606 13,606 Netherlands 790 42 832 Federal 790 42 832 New Caledonia 10,788 962 11,750 Federal 10,788 962 11,750 Oman 1,125 113 1,238 Federal 1,125 113 1,238 Paraguay 538 62 278 878 State 538 62 278 878 Peru 675 148 23 845 Federal 675 148 23 845 Singapore 1,079 106 0 1,185 Federal 1,079 106 0 1,185 Switzerland 2,023 2,023 State 2,023 2,023 Taiwan 13 1 1 15 Federal 13 1 1 15 United Kingdom 4,452 (41,257) (36,805) Federal 4,452 (41,257) (36,805) United States 602 602 Federal 582 582 State 21 21 Uruguay 15 15 State 15 15 5 Tax refunds not borne by Vale represent US$ 526 million and relate to sales taxes, VAT, GST, excise duties, fuel credits and withholding taxes on supplier invoices. These refunds are not included in the figures presented above. 27 Back to Contents Total 1,381434,732432,834325,5611,194,508 Tax collected - Values in thousands (US$)5 |

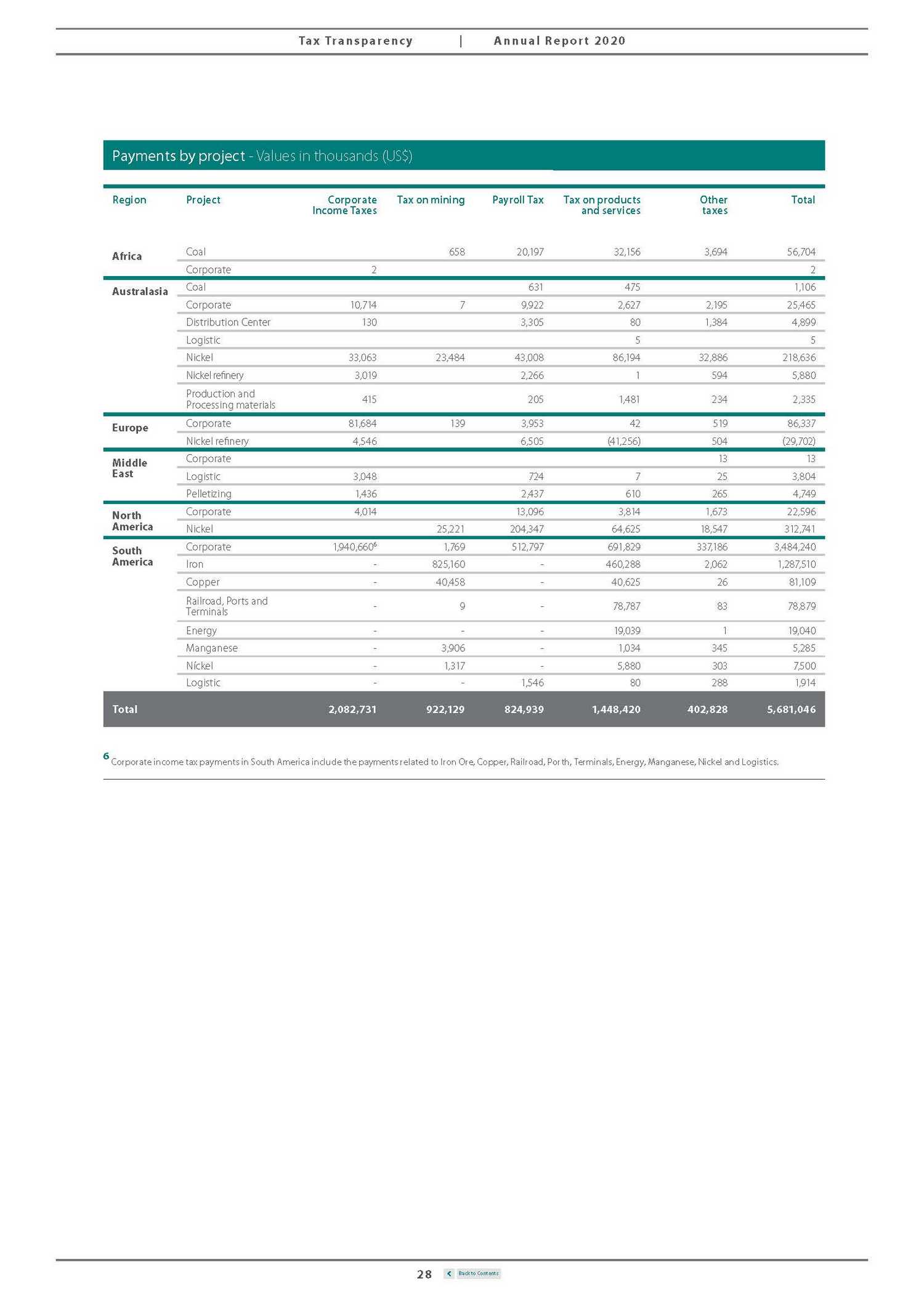

| Tax Tr anspar enc y | A nnual Rep or t 2020 Region Project Corporate Income Taxes Tax on mining Payroll Tax Tax on products and services Other taxes Total Coal 658 20,197 32,156 3,694 56,704 Africa Corporate 2 2 Coal 631 475 1,106 Australasia Corporate 10,714 7 9,922 2,627 2,195 25,465 Distribution Center 130 3,305 80 1,384 4,899 Logistic 5 5 Nickel 33,063 23,484 43,008 86,194 32,886 218,636 Nickel refinery 3,019 2,266 1 594 5,880 Production and Processing materials 415 205 1,481 234 2,335 Corporate 81,684 139 3,953 42 519 86,337 Europe Nickel refinery 4,546 6,505 (41,256) 504 (29,702) Corporate 13 13 Middle East Logistic 3,048 724 7 25 3,804 Pelletizing 1,436 2,437 610 265 4,749 Corporate 4,014 13,096 3,814 1,673 22,596 North America Nickel 25,221 204,347 64,625 18,547 312,741 Corporate 1,940,6606 1,769 512,797 691,829 337,186 3,484,240 South America Iron - 825,160 - 460,288 2,062 1,287,510 Copper - 40,458 - 40,625 26 81,109 Railroad, Ports and Terminals - 9 - 78,787 83 78,879 Energy - - - 19,039 1 19,040 Manganese - 3,906 - 1,034 345 5,285 Níckel - 1,317 - 5,880 303 7,500 Logistic - - 1,546 80 288 1,914 6 Corporate income tax payments in South America include the payments related to Iron Ore, Copper, Railroad, Porth, Terminals, Energy, Manganese, Nickel and Logistics. 28 Back to Contents Total2,082,731922,129824,939 1,448,420402,8285,681,046 Payments by project - Values in thousands (US$) |

| Tax Tr anspar enc y | A nnual Rep or t 2020 FIG 08 Worker in Sorowako, Indonesia. Picture: Marcelo Coelho Our value chain Through our operations we make important contributions to the places where we work. The taxes and royalties we pay, people we employ, local businesses we support, and social development projects we fund improve our communities. Our projects are long-term investments and the amount we contribute depends on where in the project life cycle it is. Our objective is to create long-term, win-win and sustainable value not just for our shareholders but our employees, our suppliers, our local communities and the regions and countries where we operate. The below graphic is our attempt to demonstrate how we contribute, financially, socially and sustainably to the communities and areas we work in at the different stages of our projects. Mineral Exploration Development and Construction Mine and Process Commercial and Distribution Decommission and Rehabilitation 29 Back to Contents |

| Tax Tr anspar enc y | A nnual Rep or t 2020 fees normally paid on third party this stage. related (wages and taxes) rural or urban vehicles) to suppliers and contractors to suppliers and related contractors • Property taxes to suppliers, rural or urban vehicles) • Taxes on real communities taxes on payments contractors taxes related contributions on third party (taxes for owning properties and to suppliers, estate transfers contribution to 30 Back to Contents We operate our mines and process minerals and metals safely to generate value Our contribution Extraction and processing of commodities is at the core of this operating life phase. At this stage royalty payments start and corporate income taxes begin. This phase also involves logistics, including the moving, handling, warehousing and distribution of materials throughout the supply chain. • Royalties• Withholding • Corporate income to suppliers and • Employment• Social contribution (wages and taxes)contractors • Indirect taxes • Property taxes • Payments rural or urban contractorsvehicles) • Long-term • Taxes on real communities Mine and Process We build to create future value Our contribution This stage involves heavy investment in people and infrastructure as we construct facilities and supporting networks. In some cases, it also involves the construction of towns and social amenities, like schools and parks, as well rail lines like the Vitória-Minas and Carajás Railroad. This period of development creates jobs, both through construction and through local business who supply materials, equipment and services to our sites and workforce. Alongside this significant capital investment and payments to supplies, our economic contribution also includes indirect taxes, such as employment taxes, and excises taxes on materials and equipment. • Significant capital • Withholding expenditure taxes on payments • Employmentcontractors contributions • Social contribution (wages and taxes)on third party • Indirect taxes • Payments (taxes for owning contractorsproperties and • Contribution to estate transfers Development and Construction We invest in technical and feasibility studies to understand potential value Our contribution The first stage is mineral exploration, which means assessing and quantifying reserves. It involves early excavation and analysis by highly-skilled employees and contractors, including geologists and experts in sustainability. Our contribution at this stage is limited to permits and license fees, as well as employment taxes and costs associated with construction – recognizing the huge upfront investment needed for exploration. • Licenses, permits, • Social contribution to governments at contractors • Property taxes • Employment(taxes for owning contributions properties and • Payments • Taxes on real to suppliers, estate transfers contractors • Withholding taxes on payments Mineral Exploration |

| Tax Tr anspar enc y | A nnual Rep or t 2020 on third party related rural or urban vehicles) to suppliers, • Taxes on real to suppliers and contractors 31 Back to Contents We create sustainable value after we finish our operations Our contribution This phase involves the closure of operations and the sustainable rehabilitation of the land. The multiple legal, environmental and social attributes, as well as economic aspects are all considered. Integrated and systemic planning is essential to the sustainability of the territories to promote the reintegration of the mined territories to physical, biotic and socioeconomic environments, contributing to the sustainable development of these locations • Employment• Social relatedcontribution contributions on third party (wages and taxes)contractors • Payments • Property taxes to suppliers, (taxes for owning contractorsrural or urban properties and • Support tovehicles) communities • Taxes on real • Withholding estate transfers taxes on payments to suppliers and Decommission and Rehabilitation We commercialize and transport our products to maximize value Our contribution Products are sold and transported to our customers to maximize value and minimize market risk through core commercial activities. This phase in particular supports our suppliers and local and international business partners. It constitutes with no doubt a substantial logistic effort with significant payments to suppliers with their corresponding economic contribution in terms of indirect taxes and others. • Corporate• Social income taxes contribution • Employmentcontractors contributions • Property taxes (wages and taxes)(taxes for owning • Indirect taxes properties and • Payments contractorsestate transfers • Withholding taxes on payments contractors Commercial and Distribution |

| Tax Tr anspar enc y | A nnual Rep or t 2020 Our approach to tax Our tax principles Vale’s tax affairs are managed by a global team of professionals who abide by the following principles in their day-to-day work: I II III IV V We have robust internal risk management procedures in place to manage the diverse and complex tax transactions carried out across our business. While uncertainty in relation to tax matters is an element that cannot be fully excluded in our business, all potential tax risks are regularly identified and monitored. Where material uncertainties are identified, they are properly assessed and discussed with external advisors, before the company’s position is agreed by the Compliance Business Risks Executive Committee; the Executive Board; and the Board of Directors. We have a responsibility to consider tax as part of normal operations but the primary motivation of our business is to generate shared and sustainable value for our stakeholders and not reduce our tax liabilities. 1 The guidelines and guidance for the corporate risk management strategy are set out in Vale’s Risk Management Policy. http://www.vale.com/en/investors/corporate-governance/policies/pages/default.aspx 32 Back to Contents ! Risk management and control Effective risk management and control In every aspect of our business, we work to provide certainty and manage risk. In terms of tax, this means that we have effective frameworks in place to monitor, identify, control and manage of our tax commitments, and to ensure we are correctly meeting our obligations1. Engagement Proactive and open engagement with authorities We seek to develop open, collaborative relationships with tax authorities, acting with integrity in the jurisdictions in which we operate. We engage in proactive discussions in relation to tax matters, business operations and investments. Compliance Excellence in compliance We target excellence in relation to tax compliance. We fully respect applicable local tax laws and tax reporting obligations in every jurisdiction where we operate. We do not engage in aggressive tax planning. Long-term value Creation of long-term value Our vision is to create long-term value for all who are involved in our business activities. Our investment in our mines is often a multi-decade commitment to a community, and where we can share value, we create a stronger sustainable business. Transparency Transparency about our taxes Being transparent about the taxes and royalties we pay is an opportunity to share how we contribute to the economic vitality of the jurisdictions and communities where we operate. By adopting a transparent approach, we aim to build trust with our local, national and international stakeholders over time. |

| Tax Tr anspar enc y | A nnual Rep or t 2020 Tax compliance As a company with global footprint, we are subject to numerous statutory reporting obligations. For this reason, we count on expert professionals with a deep knowledge of local and international taxation. Our companies meet their compliance requirements on a local, regional or worldwide basis by means of consistent, timely and efficient processes. Tax planning We do not engage in aggressive tax planning nor artificial arrangements and tax considerations do not influence our business operations. It is our company’s policy to always operate in strict compliance with all relevant local legislation. In case of uncertainty or doubt when interpreting the law, we seek independent external advice to fulfill our tax obligations. taxes paid abroad can be deducted from the Brazilian tax payable. These rules result in the effective curtailment of any tax planning benefits that could arise from international structures. Second, Brazilian CFC rules apply in coordination with very strict transfer pricing rules, which hamper any transfer of profits to foreign affiliates. Considering the nature of Vale’s products, the PECEX method applies. This is a specific methodology in Brazil and under this, when Vale promotes sales to related parties abroad, the value is of its revenues is determined according to quoted prices in internationally recognized commodities exchanges, subjected to adjustments regarding timing, location, intermediation costs and others. Apart from CIT, PECEX is also employed regarding royalties (CFEM). Vale is subject to various legal controls, especially under Brazilian tax legislation, which assure payment of taxes regardless of the international nature of its operations. First, under Brazilian legislation, Vale is subject to Controlled Foreign Corporation (“CFC”) rules, as the ultimate parent of the group’s various enterprises around the world. Brazilian CFC rules are among the strictest in the world, as they comprise the profits of all foreign subsidiaries and affiliates, even if there is no direct shareholding, regardless of the international entity being located in a low-tax jurisdiction. All such profits are subject to corporate income tax in Brazil, whose statutory rate is 34%, also among the highest in the world. Corporate income Third, these rules also apply in coordination with very severe thin-capitalization rules, which hinder any attempt to erode the Brazilian tax base with interest payments to related parties or financial institutions located in tax havens, which is a conduct that Vale does not engage in. These three levels of overlying controls, coupled with Vale’s strict compliance with tax rules, ensure that no aggressive tax planning is undertaken by the company. 33 Back to Contents compliance procedures. that analyzes how we meet tax filing and and have a robust internal audit process regard to our tax compliance obligations We focus on quality and control with |

| Tax Tr anspar enc y | A nnual Rep or t 2020 Engagement with tax authorities Vale values and maintains a transparent, collaborative, and good faith relationship with tax authorities, in compliance with our Code of Conduct, global anti-corruption rules, and the legislation in force in the jurisdictions where we operate. Due to the complexity of the activities that we are engaged in and that of various legal systems, contentious points in tax and royalty legislation do arise from time to time. Where disputes occur, Vale is committed to engaging transparently and in good faith with administrative and judicial proceedings in accordance with local laws. We conduct all disputes consistently on a technical and legal basis. No tax liability is ever purposefully disregarded. Whenever there are tax assessments in conflict with the company’s technical position, strictly legal means of defense are always employed and all guarantees demanded by the legislation are provided. All tax liabilities currently under dispute in Brazil are either not chargeable or subjected to adequate guarantees. Vale seeks to comply with all fiscal regularity certifications provided by the Brazilian government, according to applicable rules. In the few circumstances where the company’s position is not confirmed by the Judiciary, the tax liability is promptly paid. Intra-group transactions Due to the nature of our business, we carry out transactions with affiliates, subsidiaries, and jointly controlled companies with third parties, to integrate activities across our production and commercial operations. Our main intra-group transactions are with our Swiss-based entity, Vale International, which manages our interface with our customers, many of whom are in Europe and Asia. Vale International specializes in fulfilling customer requirements, managing freight from production assets to customers, managing inventories in export sales, and arranging processing operations abroad in order to find the best markets and prices for our products. This entity manages risk and uncertainty in the global market. The geographical location and time zone, mid-way between our production location and our markets, enables us to serve our customers effectively. Our export operations are carried out in compliance with Brazilian transfer pricing rules2, which aim to prevent artificial shifts of profit to foreign subsidiaries. Compliance with these rules is measured using the “Commodity Exchange Export Price Method (“PECEX” in Portuguese). Any adjustment identified under this methodology must be included in CFEM3 calculation basis and Corporate Income Tax. The Brazilian Federal Revenue Service regularly monitors transfer prices for compliance with PECEX. made to create a feasible comparability between the transfer price and the average quoted price. These adjustments are related to the quality of the commodity exported and to the terms and conditions in which the exports are made, such as the freight; payment deadline; amount in negotiation; climate’s effects on the commodity exported; intermediation costs in connection with assets employed, the risks assumed, the functions performed by entities involved and handling fees. 2 Law nº 9,430 / 96 and IN RFB nº 1,312 / 12 3 Financial Compensation for the Exploration of Mineral Resources. 34 Back to Contents The PECEX transfer pricing methodology uses the average commodity exchange price (the “average quoted price”) as a benchmark to assess outbound transactions of commodities, for example, ores. Positive and negative adjustments may be ! |

| Tax Tr anspar enc y | A nnual Rep or t 2020 Products originating outside of Brazil – primarily in our nickel operations, as well as intercompany transactions – are priced in a manner that complies with the “arm’s length” principle which holds that transactions should be valued as if they had been carried out between unrelated parties, each acting in its own best interest. To demonstrate compliance with this principle, Vale prepares and lodges transfer pricing documentation annually according with OECD transfer pricing guidelines and relevant local requirements. We comply with the OECD’s Country-by-Country Reporting (“CbCR”) requirements, which were implemented in Brazil by the Normative Ruling nº 1,681/2016. The CbCR document is lodged in July annually, as part of our ultimate parent company’s corporate income tax return (ECF in Portuguese) in Brazil. The report contains the required information on taxes, financial elements, employment and the company´s functional profile, and is provided to the tax authorities. Low-tax jurisdictions We regularly monitor international developments to understand how individual jurisdictions are assessed against various measures of transparency and cooperation. Sources include the EU list of non-cooperative jurisdictions for tax purposes (as published in February 2020), the EU Watch List and Brazilian regulations on favorable jurisdictions4. Brazilian authorities apply a broader definition of low-tax jurisdictions than the EU, such that Brazilian transfer pricing rules also apply to third-party transactions between Vale (and other Vale Brazilian Affiliates) with third party organizations located in favorable jurisdictions as defined by Brazilian tax regulations. We have certain operational entities, notably in Oman, where we operate two iron ore pelletizing plants together with a distribution center and in the United Kingdom5 where one of our nickel refineries is located, as well as Special Purpose Vehicles and holding companies located in low-tax jurisdictions, mainly for historical reasons and as a result of acquisitions. The profit of the entities located in low-tax jurisdictions6 did not exceed US$ 190 million in total in 2020, computed according to Brazilian CFC rules. In all cases, the profits of Vale entities located in low-tax jurisdictions are ultimately taxed in Brazil under CFC regulations and therefore there is no income tax benefit derived from entities in those jurisdictions. To simplify and rationalize our structure and operations, we carry out regular reviews of all entities through our Legal Entities Reduction (LER) program. Where the program identifies them as not required, we endeavor to close them. Tax incentives Vale obtains tax incentives in some of the jurisdictions in which we operate, due to the contribution of our operations in the local economy, such as employment and economic activity in our wider supply chain. None of the regimes under which Vale has been granted incentives are noted by the OECD as being a harmful tax practice. 4 Normative Instruction nº 1,037 / 10 and Law nº 12,973 / 14 5 Unlike most other low-tax jurisdictions lists, the United Kingdom is included under the broader Brazilian list because one of the conditions of being included in the Brazilian list is that jurisdictions where corporate income tax rates are lower than 20% are deemed to be considered low tax jurisdictions from a Brazilian perspective. 6 As defined by the broader Brazilian regulations. 35 Back to Contents |

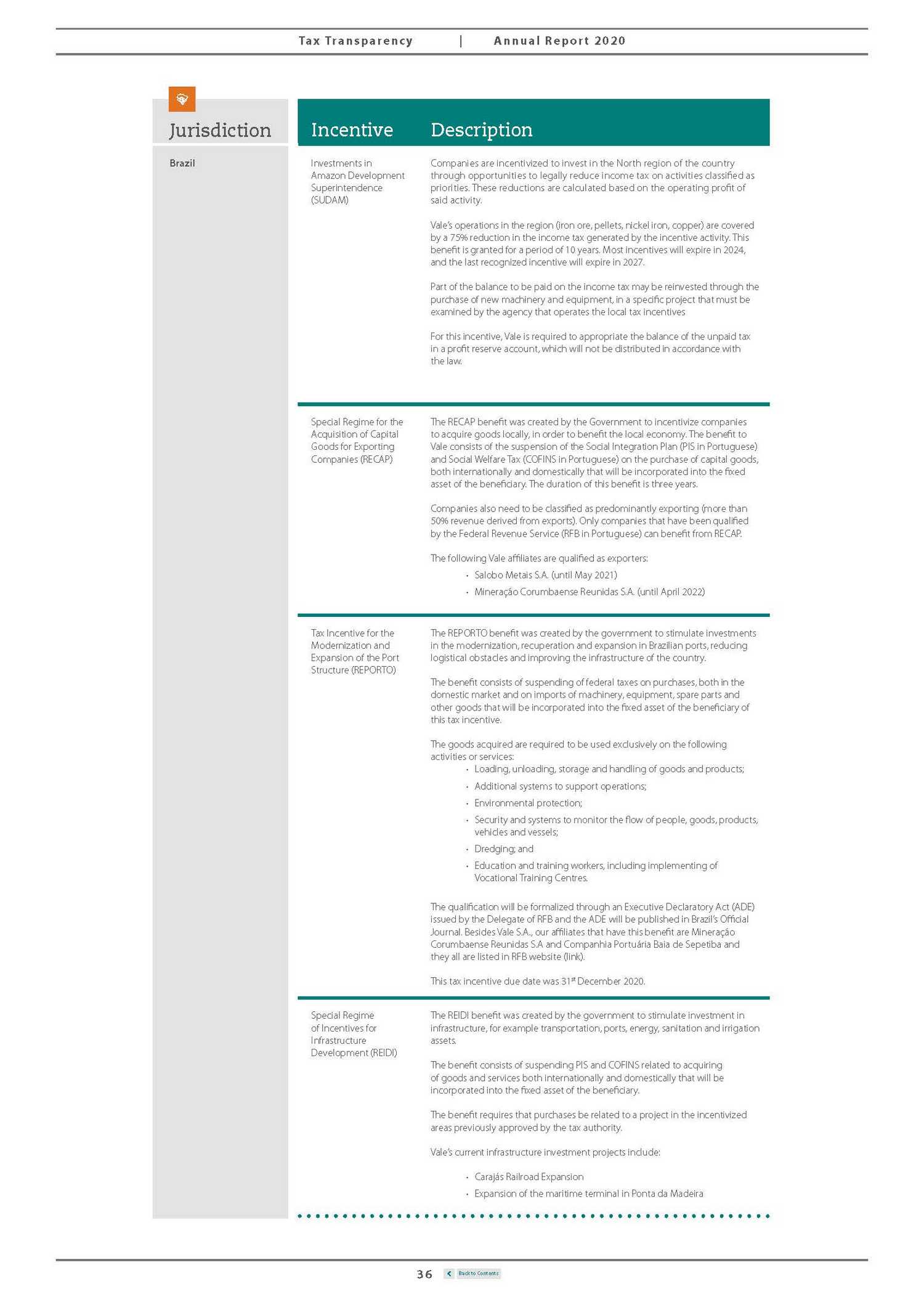

| Tax Tr anspar enc y | A nnual Rep or t 2020 36 Back to Contents IncentiveDescription Jurisdiction Brazil Investments inCompanies are incentivized to invest in the North region of the country Amazon Developmentthrough opportunities to legally reduce income tax on activities classified as Superintendencepriorities. These reductions are calculated based on the operating profit of (SUDAM)said activity. Vale’s operations in the region (iron ore, pellets, nickel iron, copper) are covered by a 75% reduction in the income tax generated by the incentive activity. This benefit is granted for a period of 10 years. Most incentives will expire in 2024, and the last recognized incentive will expire in 2027. Part of the balance to be paid on the income tax may be reinvested through the purchase of new machinery and equipment, in a specific project that must be examined by the agency that operates the local tax incentives For this incentive, Vale is required to appropriate the balance of the unpaid tax in a profit reserve account, which will not be distributed in accordance with the law. Special Regime for theThe RECAP benefit was created by the Government to incentivize companies Acquisition of Capital to acquire goods locally, in order to benefit the local economy. The benefit to Goods for ExportingVale consists of the suspension of the Social Integration Plan (PIS in Portuguese) Companies (RECAP)and Social Welfare Tax (COFINS in Portuguese) on the purchase of capital goods, both internationally and domestically that will be incorporated into the fixed asset of the beneficiary. The duration of this benefit is three years. Companies also need to be classified as predominantly exporting (more than 50% revenue derived from exports). Only companies that have been qualified by the Federal Revenue Service (RFB in Portuguese) can benefit from RECAP. The following Vale affiliates are qualified as exporters: • Salobo Metais S.A. (until May 2021) • Mineração Corumbaense Reunidas S.A. (until April 2022) Tax Incentive for theThe REPORTO benefit was created by the government to stimulate investments Modernization andin the modernization, recuperation and expansion in Brazilian ports, reducing Expansion of the Port logistical obstacles and improving the infrastructure of the country. Structure (REPORTO) The benefit consists of suspending of federal taxes on purchases, both in the domestic market and on imports of machinery, equipment, spare parts and other goods that will be incorporated into the fixed asset of the beneficiary of this tax incentive. The goods acquired are required to be used exclusively on the following activities or services: • Loading, unloading, storage and handling of goods and products; • Additional systems to support operations; • Environmental protection; • Security and systems to monitor the flow of people, goods, products, vehicles and vessels; • Dredging; and • Education and training workers, including implementing of Vocational Training Centres. The qualification will be formalized through an Executive Declaratory Act (ADE) issued by the Delegate of RFB and the ADE will be published in Brazil’s Official Journal. Besides Vale S.A., our affiliates that have this benefit are Mineração Corumbaense Reunidas S.A and Companhia Portuária Baia de Sepetiba and they all are listed in RFB website (link). This tax incentive due date was 31st December 2020. Special RegimeThe REIDI benefit was created by the government to stimulate investment in of Incentives forinfrastructure, for example transportation, ports, energy, sanitation and irrigation Infrastructure assets. Development (REIDI) The benefit consists of suspending PIS and COFINS related to acquiring of goods and services both internationally and domestically that will be incorporated into the fixed asset of the beneficiary. The benefit requires that purchases be related to a project in the incentivized areas previously approved by the tax authority. Vale’s current infrastructure investment projects include: • Carajás Railroad Expansion • Expansion of the maritime terminal in Ponta da Madeira |

| Tax Tr anspar enc y | A nnual Rep or t 2020 In addition to the incentives listed above, Vale also receives tax incentives in other jurisdictions where it operates. 7 Law nº 8,313 / 1991 8 Law nº 11,438 / 2006 9 Law nº 8,069 / 1990 37 Back to Contents IncentiveDescription Jurisdiction Singapore Corporate income taxWe benefit from a corporate income tax incentive in Singapore. Such benefit incentiveis legislated and open to all entities demonstrating contribution to the local economy and meeting criteria set by the Singaporean Government. Oman Custom Duty We benefit from customs duty exemption on the imports of raw material and equipment in Oman, such exemption is legislated and open to all taxpayers if certain conditions are satisfied. IncentiveDescription Jurisdiction Brazil Research andThe tax incentives associated with technological innovation were instituted in development (GoodBrazil, through the “Good Law”, to encourage investment in the development of Law – Lei do Bem innational technology. Portuguese) Vale supports several research, development and Innovation (P&D in Portuguese) projects in the areas of mining (iron ore, manganese, coal, pellets, and base metals), logistics, steel and energy. The expenditures on labour, materials and services for projects linked to this law are deductible from the company’s income tax basis, according to Law nº. 11,196/05. In 2008, Vale Technological Institute (ITV in Portuguese) was created and it has more than 1 thousand patents in 61 countries. Since that year, Vale has used the tax incentives associated with Good Law, thus contributing to promote a culture of research, development and technological innovation. Vale identifies and evaluates P&DI initiatives and projects annually, ranking the projects that qualify for the concept of technological innovation described in the legislation. In 2020, more than 500 projects and initiatives with the potential to capture tax benefits via the Good Law were evaluated. Sponsorships andThe Brazilian government incentivizes companies to support social projects donationsrelated to culture7, sports8, childhood and adolescence9 and seniors and health programs. Payments made towards these programs can be deducted directly from the organization’s Corporate income tax bill for the year, up to a limit of 4%. In 2020, Vale invested over US$ 54 million in more than 190 qualifying projects in Brazil. Guided by a broad vision of sustainability, investments are made either through its own resources or via incentivized resources. Through incentive laws, the company has the opportunity to strengthen public policies in the country, a vision that is in line with Vale’s commitment to contribute positively to society. Prospective applications are assessed according to set criteria, such as alignment with Vale’s values. In addition, projects need to be located in areas where the company operates. |

| Tax Tr anspar enc y | A nnual Rep or t 2020 Brazilian CFC legislation. Under the CFC rules, there is no overall corporate income tax reduction because of these benefits. 38 Back to Contents The statutory profit of all concerned legal entities remains fully taxable in Brazil under the ! IncentiveDescription Jurisdiction Malaysia Income taxWe were granted with 100% income tax exemption on statutory income until 2024 to carry out Regional Distribution activities. Custom DutyExemption regarding import duty on raw materials, machinery and equipment, until 2027 provided specific requirements are met and subject to prevailing regulations. New Caledonia Income Tax andVale has tax incentives related to the production of nickel and cobalt. These Indirect taxesincentives include the exemption of income tax during the construction phase of the project, and also for a period of 15 years beginning in the first year of commercial production (i.e., 2016), as defined by applicable law, followed by a 5-year 50% exemption of income tax. Vale is subject to a branch profit tax on its profits (after deducting available tax losses) starting in the first year that commercial production is reached. To date, there has been no net taxable income realized in New Caledonia. In addition, Vale benefits from indirect tax incentives; notably on customs duties, property tax and other local taxes. Mozambique Custom dutyVale benefits from customs duty exemption related to a certain category of goods. This exemption is also legislated and open to all importers. |

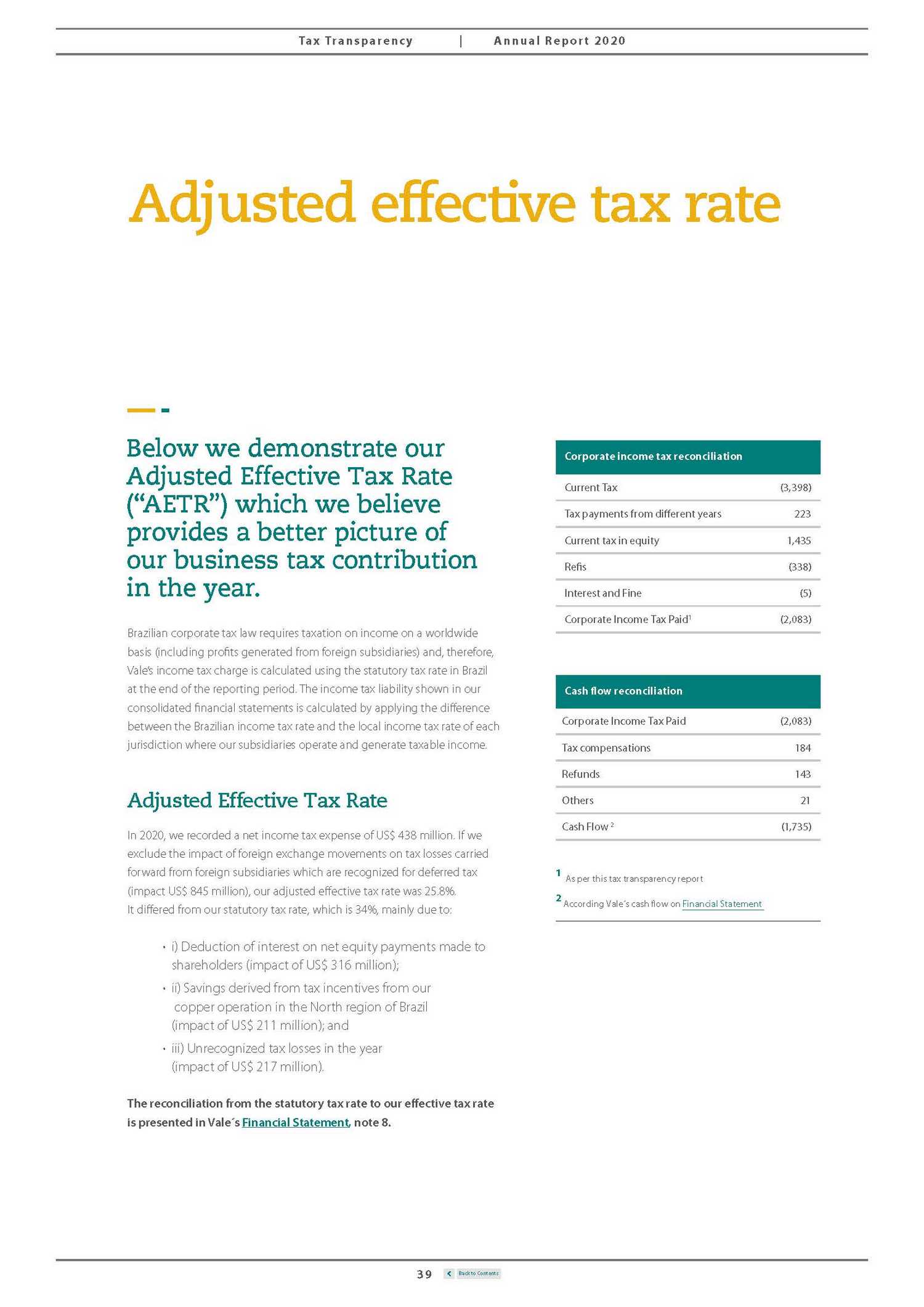

| Tax Tr anspar enc y | A nnual Rep or t 2020 Adjusted effective tax rate Below we demonstrate our Adjusted Effective Tax Rate (“AETR”) which we believe provides a better picture of our business tax contribution in the year. Brazilian corporate tax law requires taxation on income on a worldwide basis (including profits generated from foreign subsidiaries) and, therefore, Vale’s income tax charge is calculated using the statutory tax rate in Brazil at the end of the reporting period. The income tax liability shown in our consolidated financial statements is calculated by applying the difference between the Brazilian income tax rate and the local income tax rate of each jurisdiction where our subsidiaries operate and generate taxable income. Current Tax (3,398) Tax payments from different years 223 Current tax in equity 1,435 Refis (338) Interest and Fine (5) Corporate Income Tax Paid1 (2,083) Corporate Income Tax Paid (2,083) Tax compensations 184 Refunds 143 Adjusted Effective Tax Rate In 2020, we recorded a net income tax expense of US$ 438 million. If we exclude the impact of foreign exchange movements on tax losses carried forward from foreign subsidiaries which are recognized for deferred tax (impact US$ 845 million), our adjusted effective tax rate was 25.8%. It differed from our statutory tax rate, which is 34%, mainly due to: Others 21 Cash Flow 2 (1,735) 1 As per this tax transparency report 2 According Vale´s cash flow on Financial Statement • i) Deduction of interest on net equity payments made to shareholders (impact of US$ 316 million); • ii) Savings derived from tax incentives from our copper operation in the North region of Brazil (impact of US$ 211 million); and • iii) Unrecognized tax losses in the year (impact of US$ 217 million). The reconciliation from the statutory tax rate to our effective tax rate is presented in Vale´s Financial Statement, note 8. 39 Back to Contents Cash flow reconciliation Corporate income tax reconciliation |

| Tax Tr anspar enc y | A nnual Rep or t 2020 Independent auditor's report To the Board of Directors and Shareholders Vale S.A. Rio de Janeiro - RJ Opinion We have audited the accompanying Selected Information, which comprises the amounts in the tables entitled "Tax borne" and "Tax collected", included in the section "Breakdown by jurisdiction, level of government and by project" of the Tax Transparency Report (the "Report") of Vale S.A. and its subsidiaries (the "Company") for the year ended December 31, 2020. In our opinion, the Selected Information referred to above has been properly prepared, in all material respects, in accordance with the basis of preparation in Appendix 1 to the Report. Basis for opinion We conducted our audit in accordance with Brazilian and International Standards on Auditing. Our responsibilities under those standards are further described in the Auditor's Responsibilities for the Audit of the Selected Information included within the Report. We are independent of the Company and its subsidiaries in accordance with the ethical requirements established in the Code of Professional Ethics and in the Professional Standards issued by the Brazilian Federal Accounting Council, and we have fulfilled our other ethical responsibilities in accordance with these requirements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion. Emphasis of matter - basis of preparation of the selected information to the report We draw attention to Appendix 1 to the Report, which describes the basis of preparation of the Selected Information. The Report is prepared in accordance with a special purpose framework for providing reasonable assurance over total taxes paid by the Company in 2020. As a result, the Report may not be suitable for another purpose. The Report does not comprise a full set of financial statements, prepared in accordance with accounting practices adopted in Brazil and with the International Financial Reporting Standards (IFRS) as issued by the International Accounting Standards Board (IASB). Our opinion is not qualified in respect of this matter. PricewaterhouseCoopers, Rua do Russel 804, 6º e 7º, Edifício Manchete, Rio de Janeiro, RJ, Brasil, 22210-907, T: +55 (21) 3232 6112, www.pwc.com.br 40 Back to Contents |

| Tax Tr anspar enc y | A nnual Rep or t 2020 Vale S.A. Responsibilities of management and those charged with governance for the Selected Information to the Report Management is responsible for the preparation of the Selected Information in accordance with the basis of preparation in Appendix 1 to the Report and for determining that the basis of preparation is acceptable in the circumstances. Management is also responsible for such internal control as they determine is necessary to enable the preparation of the Selected Information that is free from material misstatement, whether due to fraud or error. Those charged with governance are responsible for overseeing the financial reporting process of the Company and its subsidiaries. Auditor's responsibilities for the Selected Information to the Report Our objectives are to obtain reasonable assurance about whether the Selected Information is free from material misstatement, whether due to fraud or error, and to issue an auditor's report that includes our opinion. Reasonable assurance is a high level of assurance, but is not a guarantee that an audit conducted in accordance with Brazilian and International Standards on Auditing will always detect a material misstatement when it exists. Misstatements can arise from fraud or error and are considered material if, individually or in the aggregate, they could reasonably be expected to influence the economic decisions of users taken on the basis of the Selected Information. As part of an audit in accordance with Brazilian and International Standards on Auditing, we exercise professional judgment and maintain professional skepticism throughout the audit. We also: . Identify and assess the risks of material misstatement of the Selected Information, whether due to fraud or error, design and perform audit procedures responsive to those risks, and obtain audit evidence that is sufficient and appropriate to provide a basis for our opinion. The risk of not detecting a material misstatement resulting from fraud is higher than for one resulting from error, as fraud may involve collusion, forgery, intentional omissions, misrepresentations, or the override of internal control. . Obtain an understanding of internal control relevant to the audit in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the internal control of the Company and its subsidiaries. . Evaluate the appropriateness of accounting policies used and the reasonableness of accounting estimates and related disclosures made by management. . Conclude on the appropriateness of management's use of the going concern basis of accounting and, based on the audit evidence obtained, whether a material uncertainty exists related to events or conditions that may cast significant doubt on the ability of the Company to continue as a going concern. If we conclude that a material uncertainty exists, we are required to draw attention in our auditor's 41 Back to Contents |

| Tax Tr anspar enc y | A nnual Rep or t 2020 Vale S.A. report to the related disclosures of the Selected Information or, if such disclosures are inadequate, to modify our opinion. Our conclusions are based on the audit evidence obtained up to the date of our auditor's report. However, future events or conditions may cause the Company to cease to continue as a going concern. We communicate with those charged with governance regarding, among other matters, the planned scope and timing of the audit and significant audit findings, including any significant deficiencies in internal control that we identify during our audit. We also provide those charged with governance, in connection with the audit of the financial statements of the Company as at and for the year ended December 31, 2020, with a statement that we have complied with relevant ethical requirements regarding independence, and to communicate with them all relationships and other matters that may reasonably be thought to bear on our independence, and where applicable, related safeguards. Rio de Janeiro, May 31, 2021 PricewaterhouseCoopers Auditores Independentes CRC 2SP000160/O-5 Patricio Marques Roche Contador CRC 1RJ081115/O-4 42 Back to Contents |