Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-08510

Matthews International Funds

(Exact name of registrant as specified in charter)

Four Embarcadero Center, Suite 550

San Francisco, CA 94111

(Address of principal executive offices) (Zip code)

James Cooper Abbott, President

Four Embarcadero Center, Suite 550

San Francisco, CA 94111

(Name and address of agent for service)

Registrant’s telephone number, including area code: 415-788-7553

Date of fiscal year end: December 31

Date of reporting period: December 31, 2022

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Table of Contents

| Item 1. | Reports to Stockholders. |

| (a) | The Reports to Shareholders are attached herewith. |

Table of Contents

Matthews Asia Funds | Annual Report

December 31, 2022 | matthewsasia.com

GLOBAL EMERGING MARKETS STRATEGIES

Matthews Emerging Markets Equity Fund

Matthews Emerging Markets Sustainable Future Fund

Matthews Emerging Markets Small Companies Fund

ASIA GROWTH STRATEGIES

Matthews Asia Growth Fund

Matthews Pacific Tiger Fund

Matthews Asia Innovators Fund

Matthews China Fund

Matthews China Small Companies Fund

Matthews India Fund

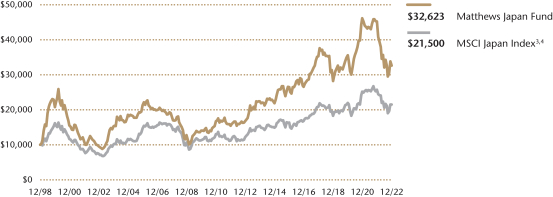

Matthews Japan Fund

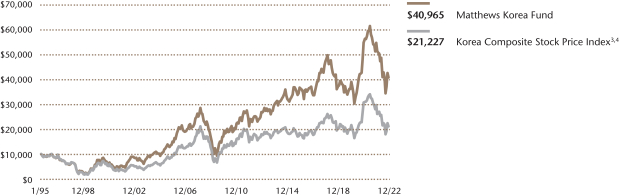

Matthews Korea Fund

ASIA GROWTH AND INCOME STRATEGIES

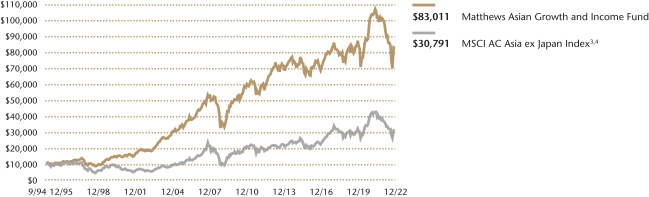

Matthews Asian Growth and Income Fund

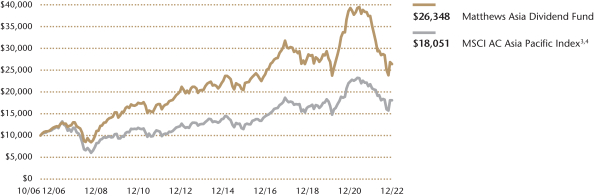

Matthews Asia Dividend Fund

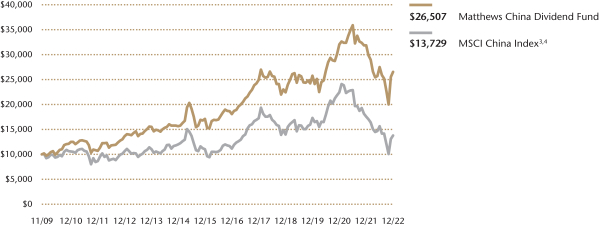

Matthews China Dividend Fund

ASIA FIXED INCOME STRATEGIES

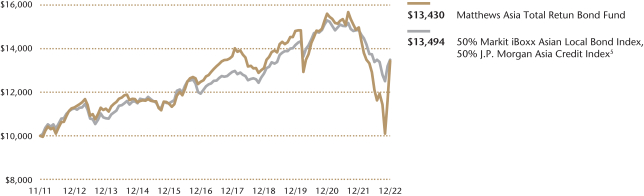

Matthews Asia Total Return Bond Fund

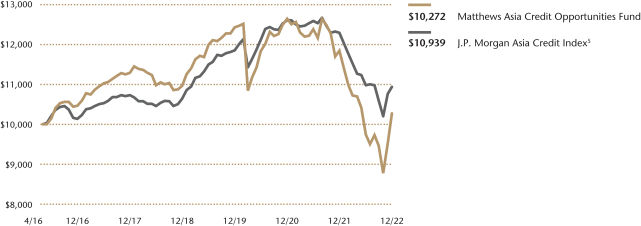

Matthews Asia Credit Opportunities Fund

Paper copies of the Funds’ annual and semi-annual shareholder reports are no longer being sent by mail, unless you specifically request paper copies of the reports. Instead, the reports will be made available on the Funds’ website matthewsasia.com, and you will be notified by mail each time a report is posted and provided with a website link to access the report. You may elect to receive paper copies of shareholder reports and other communications from the Funds anytime by contacting your financial intermediary (such as a broker-dealer or bank) or, if you are a direct investor, by calling 800.789.ASIA (2742).

Your election to receive reports in paper will apply to all Funds held in your account if you invest through your financial intermediary or all Funds held directly with Matthews Asia Funds.

Table of Contents

Investor Class Performance and Expense Ratios (December 31, 2022) (unaudited)

|

| Average Annual Total Return† | Inception | 2022 Annual Operating Expense Ratios* | 2022 Annual Operating Expense Ratios after Fee Waiver and Expense Reim- bursement** | Prospectus Expense Ratios‡‡ | Prospectus Expense Ratios after Fee Waiver and Expense Reim- bursement‡‡ | ||||||||||||||||||||||||||||||

| Investor Class | 1 year | 5 years | 10 years | Since Inception | ||||||||||||||||||||||||||||||||

GLOBAL EMERGING MARKETS STRATEGIES | ||||||||||||||||||||||||||||||||||||

Emerging Markets Equity Fund (MEGMX) | -20.94% | n.a. | n.a. | 9.26% | 4/30/20 | 1.58% | 1.09% | 1 | 1.52% | 1.13% | 1 | |||||||||||||||||||||||||

Emerging Markets Sustainable Future Fund (MASGX)§ | -14.38% | 6.79% | n.a. | 7.15% | 4/30/15 | 1.24% | 1.30% | 3,4 | 1.35% | 1.35% | 3,4 | |||||||||||||||||||||||||

Emerging Markets Small Companies Fund (MSMLX) | -16.84% | 7.02% | 6.93% | 10.57% | 9/15/08 | 1.49% | 1.37% | 3 | 1.51% | 1.35% | 3 | |||||||||||||||||||||||||

ASIA GROWTH STRATEGIES | ||||||||||||||||||||||||||||||||||||

Asia Growth Fund (MPACX) | -33.12% | -2.41% | 4.19% | 6.76% | 10/31/03 | 1.13% | 1.13% | 1.07% | 1.07% | |||||||||||||||||||||||||||

Pacific Tiger Fund (MAPTX) | -20.73% | -0.80% | 4.38% | 7.46% | 9/12/94 | 1.10% | 1.09% | 2 | 1.06% | 1.03% | 2 | |||||||||||||||||||||||||

Asia Innovators Fund (MATFX) | -24.80% | 5.17% | 10.72% | 4.47% | 12/27/99 | 1.18% | 1.18% | 1.09% | 1.09% | |||||||||||||||||||||||||||

China Fund (MCHFX) | -24.40% | 0.07% | 4.72% | 8.45% | 2/19/98 | 1.12% | 1.12% | 1.06% | 1.06% | |||||||||||||||||||||||||||

China Small Companies Fund (MCSMX) | -31.26% | 6.16% | 10.14% | 6.38% | 5/31/11 | 1.55% | 1.41% | 3 | 1.48% | 1.43% | 3 | |||||||||||||||||||||||||

India Fund (MINDX) | -9.92% | 2.00% | 8.70% | 9.57% | 10/31/05 | 1.15% | 1.15% | 1.10% | 1.10% | |||||||||||||||||||||||||||

Japan Fund (MJFOX) | -27.85% | -1.56% | 6.90% | 5.05% | 12/31/98 | 1.05% | 1.05% | 0.95% | 0.95% | |||||||||||||||||||||||||||

Korea Fund (MAKOX) | -25.42% | -3.31% | 3.65% | 5.17% | 1/3/95 | 1.22% | 1.22% | 1.13% | 1.13% | |||||||||||||||||||||||||||

ASIA GROWTH AND INCOME STRATEGIES | ||||||||||||||||||||||||||||||||||||

Asian Growth and Income Fund (MACSX) | -18.43% | -0.23% | 1.96% | 7.76% | 9/12/94 | 1.13% | 1.13% | 1.07% | 1.07% | |||||||||||||||||||||||||||

Asia Dividend Fund (MAPIX) | -29.57% | -2.71% | 3.48% | 6.18% | �� | 10/31/06 | 1.10% | 1.10% | 1.03% | 1.02% | ||||||||||||||||||||||||||

China Dividend Fund (MCDFX) | -16.75% | 1.27% | 6.87% | 7.73% | 11/30/09 | 1.20% | 1.20% | 1.12% | 1.12% | |||||||||||||||||||||||||||

ASIA FIXED INCOME STRATEGIES | ||||||||||||||||||||||||||||||||||||

Asia Total Return Bond Fund (MAINX)5 | -10.25% | -0.33% | 1.74% | 2.70% | 11/30/11 | 1.23% | 1.08% | 1 | 1.05% | 1.05% | 1 | |||||||||||||||||||||||||

Asia Credit Opportunities Fund (MCRDX)5 | -13.28% | -1.87% | n.a. | 0.40% | 4/29/16 | 1.45% | 1.11% | 1 | 1.07% | 1.07% | 1 | |||||||||||||||||||||||||

| † | Annualized performance for periods of at least one year, otherwise cumulative. |

| * | Before fee waivers and expense reimbursement. |

| ** | Expense ratio represents the actual expense ratio a shareholder would have paid if they had been invested the entire year. |

| ‡‡ | These figures are from the Funds’ prospectus dated as of April 28, 2022, and may differ from the actual expense ratios for fiscal year 2022, as shown in the financial highlights section of this report. |

| § | The Fund’s name changed from Matthews Asia ESG Fund to Matthews Emerging Markets Sustainable Future Fund on July 29, 2022. |

| 1 | Matthews has contractually agreed (i) to waive fees and reimburse expenses to the extent needed to limit Total Annual Fund Operating Expenses (excluding Rule 12b-1 fees, taxes, interest, brokerage commissions, short sale dividend expenses, expenses incurred in connection with any merger or reorganization or extraordinary expenses such as litigation) of the Institutional Class to 0.90% first by waiving class specific expenses (i.e., shareholder service fees specific to a particular class) of the Institutional Class and then, to the extent necessary, by waiving non-class specific expenses (e.g., custody fees) of the Institutional Class, and (ii) if any Fund-wide expenses (i.e., expenses that apply to both the Institutional Class and the Investor Class) are waived for the Institutional Class to maintain the 0.90% expense limitation, to waive an equal amount (in annual percentage terms) of those same expenses for the Investor Class. The Total Annual Fund Operating Expenses After Fee Waiver and Expense Reimbursement for the Investor Class may vary from year to year and will in some years exceed 0.90%. Pursuant to this agreement, any amount waived for prior fiscal years with respect to the Matthews Asia Total Return Bond Fund and the Matthews Asia Credit Opportunities Fund is not subject to recoupment. For the Matthews Emerging Markets Equity Fund, if the operating expenses fall below the expense limitation within three years after Matthews has made a waiver or reimbursement, the Fund may reimburse Matthews up to an amount that does not cause the expenses for that year to exceed the lesser of (i) the expense limitation applicable at the time of that fee waiver and/or expense reimbursement or (ii) the expense limitation in effect at the time of recoupment. This agreement will remain in place until April 30, 2023 and may be terminated at any time by the Board of Trustees on behalf of the Fund on 60 days’ written notice to Matthews. Matthews may decline to renew this agreement by written notice to the Trust at least 30 days before its annual expiration date. |

| 2 | Matthews has contractually agreed to waive a portion of its advisory fee and administrative and shareholder services fee if the Fund’s average daily net assets are over $3 billion, as follows: for every $2.5 billion average daily net assets of the Fund that are over $3 billion, the advisory fee rate and the administrative and shareholder services fee rate for the Fund with respect to such excess average daily net assets will be each reduced by 0.01%, in each case without reducing such fee rate below 0.00%. Any amount waived by Matthews pursuant to this agreement may not be recouped by Matthews. This agreement will remain in place until April 30, 2023 and may be terminated (i) at any time by the Board of Trustees upon 60 days’ prior written notice to Matthews; or (ii) by Matthews at the annual expiration date of the agreement upon 60 days’ prior written notice to the Trust, in each case without payment of any penalty. |

| 3 | Matthews has contractually agreed (i) to waive fees and reimburse expenses to the extent needed to limit Total Annual Fund Operating Expenses (excluding Rule 12b-1 fees, taxes, interest, brokerage commissions, short sale dividend expenses, expenses incurred in connection with any merger or reorganization or extraordinary expenses such as litigation) of the Institutional Class to 1.20% (except for the Matthews Emerging Markets Sustainable Future Fund and the Matthews Emerging Markets Small Companies Fund, which have an expense limitation of 1.15% for the Institutional Class) first by waiving class specific expenses (i.e., shareholder service fees specific to a particular class) of the Institutional Class and then, to the extent necessary, by waiving non-class specific expenses (e.g., custody fees) of the Institutional Class, and (ii) if any Fund-wide expenses (i.e., expenses that apply to both the Institutional Class and the Investor Class) are waived for the Institutional Class to maintain the 1.20% expense limitation (or 1.15% for the Matthews Emerging Markets Sustainable Future Fund and the Matthews Emerging Markets Small Companies Fund), to waive an equal amount (in annual percentage terms) of those same expenses for the Investor Class. The Total Annual Fund Operating Expenses After Fee Waiver and Expense Reimbursement for the Investor Class may vary from year to year and will in some years exceed 1.20% (or 1.15% for the Matthews Emerging Markets Sustainable Future Fund and the Matthews Emerging Markets Small Companies Fund). If the operating expenses fall below the expense limitation within three years after Matthews has made a waiver or reimbursement, the Fund may reimburse Matthews up to an amount that does not cause the expenses for that year to exceed the lesser of (i) the expense limitation applicable at the time of that fee waiver and/or expense reimbursement or (ii) the expense limitation in effect at the time of recoupment. This agreement will remain in place until April 30, 2023 and may be terminated at any time by the Board of Trustees on behalf of the Fund on 60 days’ written notice to Matthews. Matthews may decline to renew this agreement by written notice to the Trust at least 30 days before its annual expiration date. |

| 4 | Expense ratios are from the Fund’s prospectus dated as of July 29, 2022. |

| 5 | Please refer to “Subsequent Events” in the Notes to the Financial Statements relating to the closure and liquidation of these Funds. |

| 2 | MATTHEWS ASIA FUNDS |

Table of Contents

Institutional Class Performance and Expense Ratios (December 31, 2022) (unaudited)

|

| Average Annual Total Return† |

| 2022 Annual Operating Expense Ratios* | 2022 Annual Operating Expense Ratios after Fee Waiver and Expense Reim- bursement** | Prospectus Expense Ratios‡‡ | Prospectus after Fee | ||||||||||||||||||||||||||||||

| Institutional Class | 1 year | 5 years | 10 years | Since Inception | Inception Date | |||||||||||||||||||||||||||||||

GLOBAL EMERGING MARKETS STRATEGIES | ||||||||||||||||||||||||||||||||||||

Emerging Markets Equity Fund (MIEFX) | -20.81% | n.a. | n.a. | 9.49% | 4/30/20 | 1.47% | 0.90% | 1 | 1.38% | 0.90% | 1 | |||||||||||||||||||||||||

Emerging Markets Sustainable Future Fund (MISFX)§ | -14.32% | 6.97% | n.a. | 7.36% | 4/30/15 | 1.11% | 1.17% | 3,4 | 1.15% | 1.15% | 3,4 | |||||||||||||||||||||||||

Emerging Markets Small Companies Fund (MISMX) | -16.66% | 7.24% | n.a. | 6.63% | 4/30/13 | 1.37% | 1.15% | 3 | 1.38% | 1.15% | 3 | |||||||||||||||||||||||||

ASIA GROWTH STRATEGIES | ||||||||||||||||||||||||||||||||||||

Asia Growth Fund (MIAPX) | -32.99% | -2.25% | 4.38% | 4.05% | 10/29/10 | 0.98% | 0.98% | 0.92% | 0.92% | |||||||||||||||||||||||||||

Pacific Tiger Fund (MIPTX) | -20.62% | -0.65% | 4.54% | 4.40% | 10/29/10 | 0.97% | 0.96% | 2 | 0.92% | 0.90% | 2 | |||||||||||||||||||||||||

Asia Innovators Fund (MITEX) | -24.73% | 5.33% | n.a. | 10.35% | 4/30/13 | 1.04% | 1.04% | 0.93% | 0.93% | |||||||||||||||||||||||||||

China Fund (MICFX) | -24.31% | 0.23% | 4.88% | 3.07% | 10/29/10 | 0.98% | 0.98% | 0.91% | 0.91% | |||||||||||||||||||||||||||

China Small Companies Fund (MICHX) | -31.08% | 6.40% | n.a. | 7.56% | 11/30/17 | 1.38% | 1.20% | 3 | 1.31% | 1.20% | 3 | |||||||||||||||||||||||||

India Fund (MIDNX)# | -9.83% | 2.15% | 8.88% | 5.52% | 10/29/10 | 1.01% | 1.01% | 0.96% | 0.96% | |||||||||||||||||||||||||||

Japan Fund (MIJFX) | -27.84% | -1.50% | 6.99% | 6.65% | 10/29/10 | 0.97% | 0.97% | 0.89% | 0.89% | |||||||||||||||||||||||||||

Korea Fund (MIKOX) | -25.39% | -3.22% | 3.76% | 5.09% | 10/29/10 | 1.08% | 1.08% | 0.98% | 0.98% | |||||||||||||||||||||||||||

ASIA GROWTH AND INCOME STRATEGIES | ||||||||||||||||||||||||||||||||||||

Asian Growth and Income Fund (MICSX) | -18.31% | -0.08% | 2.11% | 3.02% | 10/29/10 | 1.01% | 1.01% | 0.94% | 0.94% | |||||||||||||||||||||||||||

Asia Dividend Fund (MIPIX) | -29.55% | -2.62% | 3.60% | 3.97% | 10/29/10 | 0.99% | 0.99% | 0.92% | 0.91% | |||||||||||||||||||||||||||

China Dividend Fund (MICDX) | -16.59% | 1.42% | 7.05% | 6.90% | 10/29/10 | 1.06% | 1.06% | 0.97% | 0.97% | |||||||||||||||||||||||||||

ASIA FIXED INCOME STRATEGIES | ||||||||||||||||||||||||||||||||||||

Asia Total Return Bond Fund (MINCX)5 | -10.11% | -0.13% | 1.96% | 2.90% | 11/30/11 | 1.11% | 0.90% | 1 | 0.91% | 0.90% | 1 | |||||||||||||||||||||||||

Asia Credit Opportunities Fund (MICPX)5 | -13.02% | -1.65% | n.a. | 0.63% | 4/29/16 | 1.31% | 0.90% | 1 | 0.93% | 0.90% | 1 | |||||||||||||||||||||||||

| † | Annualized performance for periods of at least one year, otherwise cumulative. |

| ‡‡ | These figures are from the Funds’ prospectus dated as of April 28, 2022, and may differ from the actual expense ratios for fiscal year 2022, as shown in the financial highlights section of this report. |

| * | Before fee waivers and expense reimbursement. |

| ** | Expense ratio represents the actual expense ratio a shareholder would have paid if they had been invested the entire year. |

| § | The Fund’s name changed from Matthews Asia ESG Fund to Matthews Emerging Markets Sustainable Future Fund on July 29, 2022. |

| # | Performance results include adjustments made for financial reporting purposes in accordance with U.S. generally accepted accounting principles. |

| 1 | Matthews has contractually agreed to waive fees and reimburse expenses to the extent needed to limit Total Annual Fund Operating Expenses (excluding Rule 12b-1 fees, taxes, interest, brokerage commissions, short sale dividend expenses, expenses incurred in connection with any merger or reorganization or extraordinary expenses such as litigation) of the Institutional Class to 0.90%. Pursuant to this agreement, any amount waived for prior fiscal years with respect to the Matthews Asia Total Return Bond Fund and the Matthews Asia Credit Opportunities Fund is not subject to recoupment. For the Matthews Emerging Markets Equity Fund, if the operating expenses fall below the expense limitation within three years after Matthews has made a waiver or reimbursement, the Fund may reimburse Matthews up to an amount that does not cause the expenses for that year to exceed the lesser of (i) the expense limitation applicable at the time of that fee waiver and/or expense reimbursement or (ii) the expense limitation in effect at the time of recoupment. This agreement will remain in place until April 30, 2023 and may be terminated at any time by the Board of Trustees on behalf of the Fund on 60 days’ written notice to Matthews. Matthews may decline to renew this agreement by written notice to the Trust at least 30 days before its annual expiration date. |

| 2 | Matthews has contractually agreed to waive a portion of its advisory fee and administrative and shareholder services fee if the Fund’s average daily net assets are over $3 billion, as follows: for every $2.5 billion average daily net assets of the Fund that are over $3 billion, the advisory fee rate and the administrative and shareholder services fee rate for the Fund with respect to such excess average daily net assets will be each reduced by 0.01%, in each case without reducing such fee rate below 0.00%. Any amount waived by Matthews pursuant to this agreement may not be recouped by Matthews. This agreement will remain in place until April 30, 2023 and may be terminated (i) at any time by the Board of Trustees upon 60 days’ prior written notice to Matthews; or (ii) by Matthews at the annual expiration date of the agreement upon 60 days’ prior written notice to the Trust, in each case without payment of any penalty. |

| 3 | Matthews has contractually agreed to waive fees and reimburse expenses to the extent needed to limit Total Annual Fund Operating Expenses (excluding Rule 12b-1 fees, taxes, interest, brokerage commissions, short sale dividend expenses, expenses incurred in connection with any merger or reorganization or extraordinary expenses such as litigation) of the Institutional Class to 1.20% (except for the Matthews Emerging Markets Sustainable Future Fund and the Matthews Emerging Markets Small Companies Fund, which have an expense limitation of 1.15% for the Institutional Class). If the operating expenses fall below the expense limitation within three years after Matthews has made a waiver or reimbursement, the Fund may reimburse Matthews up to an amount that does not cause the expenses for that year to exceed the lesser of (i) the expense limitation applicable at the time of that fee waiver and/or expense reimbursement or (ii) the expense limitation in effect at the time of recoupment. This agreement will remain in place until April 30, 2023 and may be terminated at any time by the Board of Trustees on behalf of the Fund on 60 days’ written notice to Matthews. Matthews may decline to renew this agreement by written notice to the Trust at least 30 days before its annual expiration date. |

| 4 | Expense ratios are from the Fund’s prospectus dated as of July 29, 2022. |

| 5 | Please refer to “Subsequent Events” in the Notes to the Financial Statements relating to the closure and liquidation of these Funds. |

Past Performance: All performance quoted in this report is past performance and is no guarantee of future results. Investment return and principal value will fluctuate with changing market conditions so that when redeemed, shares may be worth more or less than their original cost. Current performance may be lower or higher than the returns quoted. If certain of the Funds’ fees and expenses had not been waived, returns would have been lower. For the Funds’ most recent month-end performance, please call 800.789.ASIA (2742) or visit matthewsasia.com.

| matthewsasia.com | 800.789.ASIA | 3 |

Table of Contents

Cover photo: Looking out to brighter and greener pastures (Chiang Mai, Thailand)

This report has been prepared for Matthews International Funds (d/b/a Matthews Asia Funds) shareholders. It is not authorized for distribution to prospective investors unless accompanied or preceded by a current Matthews Asia Funds prospectus, which contains more complete information about the Funds’ investment objectives, risks and expenses. Additional copies of the prospectus or summary prospectus may be obtained at matthewsasia.com. Please read the prospectus carefully before you invest or send money.

The views and opinions in this report were current as of December 31, 2022. They are not guarantees of performance or investment results and should not be taken as investment advice. Investment decisions reflect a variety of factors, and the managers reserve the right to change their views about individual stocks, sectors and the markets at any time. As a result, the views expressed should not be relied upon as a forecast of a Fund’s future investment intent. Current and future portfolio holdings are subject to risk.

Statements of fact are from sources considered reliable, but neither the Funds nor the Investment Advisor makes any representation or guarantee as to their completeness or accuracy.

| 4 | MATTHEWS ASIA FUNDS |

Table of Contents

* The Fund’s name changed from Matthews Asia ESG Fund to Matthews Emerging Markets Sustainable Future Fund on July 29, 2022.

† Please refer to “Subsequent Events” in the Notes to the Financial Statements relating to the closure and liquidation of these Funds.

Investment Risk: Mutual fund shares are not deposits or obligations of, or guaranteed by, any depositary institution. Shares are not insured by the FDIC, Federal Reserve Board or any government agency and are subject to investment risks, including possible loss of principal amount invested. Investing in international and emerging markets may involve additional risks, such as social and political instability, market illiquidity, exchange-rate fluctuations, a high level of volatility and limited regulation. Fixed income investments are subject to additional risks, including, but not limited to, interest rate, credit and inflation risks. In addition, single-country and sector funds may be subject to a higher degree of market risk than diversified funds because of a concentration in a specific industry, sector or geographic location. Investing in small and mid-size companies is more risky than investing in large companies as they may be more volatile and less liquid than larger companies. Please see the Funds’ Prospectuses and Statement of Additional Information for more risk disclosure.

| matthewsasia.com | 800.789.ASIA | 5 |

Table of Contents

Message to Shareholders from the President of Your Funds

Dear Fellow Shareholder,

I believe in the opportunity of Emerging Markets, Asia and China—and that these markets can offer investors important opportunity sets for return and diversification.

While 2022 was a volatile year for broad equity and fixed income markets around the world, the importance of Matthews as an experienced and trusted guide remained paramount. Inflation and weakening economic growth expectations were exacerbated by the war in Ukraine and China’s zero-COVID policy, while geopolitical ‘tensions’ between the U.S. and China negatively affected investor sentiment. Most investments suffered in this difficult environment, including Developed Market, Emerging Market and Asia Market equities. The short term was challenging, but Matthews’ longer-term performance and insights remain strong.

Emerging Markets & Sustainability

Emerging Markets and Asia represent a broad investment opportunity, and a unique one for Sustainable investing. Emerging Markets remain at the forefront tackling critical sustainability issues including reducing carbon emissions, alleviating poverty, providing access to affordable health care and housing, and facilitating greater financial inclusion. Emerging Markets—and we all—can benefit from companies that adopt more sustainable and responsible practices. We believe that it is critical for ESG (environmental, social, and governance) and sustainability-focused investors to gain exposure to Emerging Markets. With this in mind, we reorganized the Matthews Asia ESG Fund into the Matthews Emerging Markets Sustainable Future Fund, expanding the investment universe to provide more geographically diverse opportunities for the strategy.

Following this reorganization, we are pleased to offer three distinctive Emerging Markets strategies to help our shareholders gain exposure to this increasingly important parts of investment universe: Matthews Emerging Markets Equity Fund, Matthews Emerging Markets Sustainable Future Fund and Emerging Markets Small Companies Fund. Each of these is founded in fundamental investment research, including sustainability considerations to address risk and offer opportunities.

Matthews’ Active ETFs and the Power of Choice

Based on our history of providing investors with unique access to Emerging Markets, Asia and China, we have launched our first actively managed exchange-traded funds (ETFs) focused on these regions. These active, research-based new vehicles incorporate experienced insights and our deep research to offer a range of investment opportunity in a new way with the aim of building differentiated portfolios, providing investors the ‘power of choice’ for investing in these dynamic markets.

Privilege to Serve and Looking Forward

On a personal note, I am honored to have joined Matthews and to serve as the firm’s CEO, and as a Trustee and President of the Matthews Asia Funds in 2022. I have long admired the firm’s unique value proposition, with deep investment expertise in the Emerging Markets, strong fundamental research capabilities and commitment to delivering outstanding client service.

Looking forward, we will continue to maintain a thoughtful and opportunistic approach to identifying the most attractive long-term investment opportunities and we remain steadfast in our research-based investment approach.

We take seriously the stewardship of your assets and thank you for being a valued shareholder during what has been a tumultuous and challenging year. We look forward to the opportunities to come in the Lunar Year of the Rabbit.

Cooper Abbott, CFA

President, Matthews Asia Funds

Chief Executive Officer, Matthews International Capital Management, LLC

| 6 | MATTHEWS ASIA FUNDS |

Table of Contents

This page intentionally left blank.

| matthewsasia.com | 800.789.ASIA | 7 |

Table of Contents

Message to Shareholders from the

Investment Advisor

Dear Valued Shareholder,

2022 was the year of inflation. It seems like for a while it was all we talked about. Of course, there were other terrible things happening, like the war in Ukraine and China’s zero-COVID policy. And there was growing disagreement between the world’s two superpowers. Still, nothing screws up growth equity markets quite like a sudden burst of inflation, coupled with rising bond yields, and horror stories about the seventies and oil price shocks. Naturally, the hope is that 2023 will be the year when all these things get resolved and the markets spring back to rampant optimism. Hmmmmmm…. Maybe. But I’m a little more interested in the possibility of a real investment cycle and what that means for long-term sustainable demand.

And there are some good signs. The oil price shock, shockingly for the doomsayers, turned out to be a mere shocklet, barely an adolescent. Gas prices have retreated from highs and, outside of Europe, they were never that high in wage-adjusted terms. The war on Europe’s doorstep is likely to keep prices high there and push economies into a recession. The U.S. meanwhile seems impervious to a lot of these pressures. Core inflation is now by some measures, running at the Federal Reserve’s 2% target. There are more ways of calculating core inflation these days than there are of dressing a burger but by all accounts, the surge in inflation had a significant supply-side element. The Federal Reserve seems remarkably close to achieving a deceleration in inflation from 9% to 2% without provoking a recession.

Trade and reopening

Then we had China’s zero-COVID policy. The abandonment of the policy at the tail end of the year surprised me. I thought the government would wait out the winter. But popular protest was too much and so they made an about turn. That tells us a couple of things. Ultimately, the Chinese government is pragmatic. In addition, the rather simplistic division of the world into ‘democracy’ and ‘dictatorship’ is about as nuanced and thought-provoking as a sledgehammer. Some democracies can show a cavalier disregard for half their population; some authoritarian states can show a rapid response to popular opinion. Even in the sphere of U.S.—China relations there seems to be a hint of rapprochement—the kind of global warming we can all embrace.

For most of the year, of course, U.S.—China relations, like China’s zero-COVID policy, were also a negative on markets. Aside from Taiwan there were tensions over China’s role in global trade and that generated rhetoric over whether we would see China retreat from the global stage. We don’t believe this will happen and right now China’s share of world exports is higher than ever. Its domestic economy continues to grow and while exports as a share of its own economy may decrease that would only be natural in a country that is transitioning to a middle class and ultimately to higher value-added businesses, innovation, and ultimately higher incomes. It suggests neither lack of growth nor lack of productivity, and no desire to isolate from the world.

Staying on trade, in 2022 we heard a lot about ‘friend-shoring’ and the division of the world between multi-party and single-party states. But beneath it all, the process of building out supply chains and manufacturing bases in order to cut costs and raise productivity continues unabated. Undoubtedly, reorganizing supply chains on political grounds may entail extra costs. But someone’s extra cost might be another person’s extra income. Latin America, for example, could benefit from friend-shoring or, as it is sometimes called, near-shoring. Brazil and Mexico, particularly, could see inflows of capital from U.S. and, ironically, Chinese companies, seeking to avoid the political issues around trade and supply chains. I can see auto sectors, textiles, even pharmaceuticals, benefiting from these trends.

India would also seem to have similar opportunities. Here, the issue is that equity valuations are high. They are not perhaps as high as they have reached in the recent past, but they certainly seem quite expensive relative to other markets. But it is my experience that valuations play out only over the very long-term and while this may put a dampener on long-term returns other things can also create long-term tailwinds. The Indian government, for example, is targeting growth in the manufacturing export sector as this will raise both labor productivity and help the domestic economy to retain a high savings rate

| 8 | MATTHEWS ASIA FUNDS |

Table of Contents

to fuel further investment. It’s the virtuous circle of savings-productivity-exports-wage growth-savings that has helped propel some of the Asian tigers of the past. If India is successful, then valuations relative to history may be a poor indicator of relative cheapness.

The fears around inflation and Federal Reserve interest rate rises also sent shivers through the currency markets. The strength of the U.S. dollar was particularly noticeable against the yen, where the Japanese currency fell to levels with the potential to render some Japanese international businesses super competitive. It offers not only opportunities in Japan but also raises the potential for developing countries to upgrade their capital stocks and manufacturing processes, and perhaps an opportunity for Southeast Asia to try and build a manufacturing base.

Looking ahead, if a global recession were to take hold, then enthusiasm for export markets would be dampened. However, at the same time it may lower the cost of capital and make longer-term investments more profitable, particularly given the fact that international trade has in fact continued to grow. In addition, the diversification of supply chains due to economic tensions and an aging population and increased wages in China will also spur cross-border investments. Any global recession may also be mitigated by what appears to be a continually buoyant U.S. labor market and by a recovery in post-COVID China.

A new investment cycle

To put it all together, I think we are entering a world with a more realistic view of the cost of capital and consequently, returns on capital ought to be driven higher, too. I don’t see a return to rampant optimism. I think realism will be the watchword. And if this is the case it will undeniably be a good thing, at least for the way I think about emerging markets investing.

In recent years, I think we had an investment cycle that was abrupt, short-term and focused on listed securities. Real interest rates were driven so low that stocks began to trade on narratives of companies’ future values, on stories of what they might become. Track records, cash flows, dividends, all of the real things that companies produce for investors started to matter less and less. The far future became less anchored to any history of the company or any achievements in the present.

As we awake from our COVID slumber, emerging markets seem to have preconditions for a long-term, real, economic investment cycle. Not a financial cycle. Not a stock-market boom and bust. But countries and corporates cooperating to build more efficient and sustainable economic relationships given the new environment in which they find themselves. The logic of cross-border investments and rising productivity and wages continues.

In order to take advantage of a continued globalization as well as the increasing political tensions between the West and East, we believe in the need to focus on domestic businesses in the countries we invest in. Global trade increases efficiencies and this tends to raise wages at home. And while much of the supply chain is concentrated in businesses with fine margins and strong competitive pressures, domestic businesses can have more opportunities to shelter themselves from these pressures through attributes like brand, technological prowess, intellectual property, consumer tastes, logistical infrastructure, and owning of real estate. If political tensions increase and the world moves into more regional structures, domestic businesses are also likely to be somewhat protected.

And then there is also the fact that even as global trade grows, domestic economies may grow even faster. Twenty years ago or so, export businesses were the parts of economies that were considered modern. Now, services industries have caught up and become just as much areas of productivity gains as manufacturing sectors. Therefore, a lot of the innovation and growth that we see in emerging markets lies in sectors that are inherently more domestic in nature. Emerging market companies continue to be a good place to invest for the long term.

The economic and financial climate is undoubtedly difficult, but these are the times when opportunities arise. Our research-based investment team continues to comb our investment universe for these opportunities.

Robert Horrocks, PhD

Chief Investment Officer

Matthews International Capital Management, LLC

| matthewsasia.com | 800.789.ASIA | 9 |

Table of Contents

| PORTFOLIO MANAGERS | ||||

| John Paul Lech | ||||

Lead Manager | ||||

| Alex Zarechnak | ||||

Co-Manager | ||||

| FUND FACTS | ||||

| Investor | Institutional | |||

Ticker | MEGMX | MIEFX | ||

CUSIP | 577130651 | 577130644 | ||

Inception | 4/30/20 | 4/30/20 | ||

NAV | $11.14 | $11.13 | ||

Initial Investment | $2,500 | $100,000 | ||

Gross Expense Ratio1 | 1.58% | 1.47% | ||

After fee waiver and Reimbursement2 | 1.08% | 0.90% | ||

Portfolio Statistics | ||||

Total # of Positions | 59 | |||

Net Assets | $33.5 million | |||

Weighted Average Market Cap | $90.5 billion | |||

Portfolio Turnover3 | 63.25% | |||

Benchmark | ||||

MSCI Emerging Markets Index | ||||

OBJECTIVE

Long-term capital appreciation.

STRATEGY

Under normal circumstances, the Fund seeks to achieve its investment objective by investing at least 80% of its net assets, which include borrowings for investment purposes, in the common and preferred stocks of companies located in emerging market countries. Emerging market countries generally include every country in the world except the United States, Australia, Canada, Hong Kong, Israel, Japan, New Zealand, Singapore and most of the countries in Western Europe.

Matthews Emerging Markets Equity Fund

Portfolio Manager Commentary (unaudited)

For the year ending December 31, 2022, the Matthews Emerging Markets Equity Fund returned –20.94% (Investor Class) and –20.81% (Institutional Class), while its benchmark, the MSCI Emerging Markets Index, returned –19.74% over the same period. For the fourth quarter, the Fund returned 11.69% (Investor Class) and 11.66% (Institutional Class), while the benchmark returned 9.79%.

Market Environment

Markets around the world were weak in 2022. U.S. markets had their worst year since the global financial crisis of 2008 and their fourth-worst year since the 1930s. The MSCI Emerging Markets Index was also down more than in any year since 2008 and had its second-worst year since 2000. Many concerns contributed to the weakness in markets including: persistent inflation in many regions and rising interest rates; Russia’s invasion of Ukraine which contributed to both inflation and recession risks globally; rising tensions between China and the U.S.; and President Xi’s moves to consolidate political and economic power in China. In addition, high starting valuations and the post-pandemic normalization of consumer spending patterns contributed to dramatic declines in many high-growth stocks. Conversely, high raw material prices and strong company fundamentals helped many commodity stocks in 2022. Consequently, Latin American countries performed relatively well, with Brazil leading the pack.

In the fourth quarter, markets rebounded and emerging markets outperformed developed markets in December as investors worried about a hawkish U.S. Federal Reserve and inflation fell or stabilized in many emerging markets. By year end, the U.S. dollar had weakened from its peak in September. A weaker greenback often reflects optimism about global growth relative to the U.S. Markets also began to anticipate a re-opening of the Chinese economy after the abrupt abandonment of the zero-COVID policy.

Performance contributors and detractors

At the regional level, Russia was by far the biggest detractor to relative performance in 2022 as we held four Russian stocks at the time of the Ukraine invasion. We draw two lessons from the episode. One is to be wary of undemocratic regimes in which decision-makers aren’t constrained by civil society and the second is that a so-called “fortress balance sheet” at the country level can embolden aggressive leaders to make poor decisions. These conclusions inform our cautious approach to certain other markets, such as Saudi Arabia, even as we appreciate the social and market reforms being undertaken there. Our stock selection in India was another detractor from performance in 2022 as was our underweight in United Arab Emirates and our lack of exposure to Kuwait, Saudi Arabia and South Africa. On the other hand, our overweight in Mexico and Brazil were among the biggest contributors to performance. Our underweight and stock selection in South Korea, our underweight to Taiwan and our overweight to Vietnam were also top contributors.

At the sector level, real estate was the top contributor. Stock selection in information technology was the biggest contributor but was offset by our overweight position. Stock selection in materials and our underweight in communication services were

(continued)

| 1 | Actual 2022 expense ratios. |

| 2 | Matthews has contractually agreed (i) to waive fees and reimburse expenses to the extent needed to limit Total Annual Fund Operating Expenses (excluding Rule 12b-1 fees, taxes, interest, brokerage commissions, short sale dividend expenses, expenses incurred in connection with any merger or reorganization or extraordinary expenses such as litigation) of the Institutional Class to 0.90% first by waiving class specific expenses (i.e., shareholder service fees specific to a particular class) of the Institutional Class and then, to the extent necessary, by waiving non-class specific expenses (e.g., custody fees) of the Institutional Class, and (ii) if any Fund-wide expenses (i.e., expenses that apply to both the Institutional Class and the Investor Class) are waived for the Institutional Class to maintain the 0.90% expense limitation, to waive an equal amount (in annual percentage terms) of those same expenses for the Investor Class. The Total Annual Fund Operating Expenses After Fee Waiver and Expense Reimbursement for the Investor Class may vary from year to year and will in some years exceed 0.90%. If the operating expenses fall below the expense limitation within three years after Matthews has made a waiver or reimbursement, the Fund may reimburse Matthews up to an amount that does not cause the expenses for that year to exceed the lesser of (i) the expense limitation applicable at the time of that fee waiver and/or expense reimbursement or (ii) the expense limitation in effect at the time of recoupment. This agreement will remain in place until April 30, 2023 and may be terminated at any time by the Board of Trustees on behalf of the Fund on 60 days’ written notice to Matthews. Matthews may decline to renew this agreement by written notice to the Trust at least 30 days before its annual expiration date. |

| 3 | The lesser of fiscal year 2022 long-term purchase costs or sales proceeds divided by the average monthly market value of long-term securities. |

| 10 | MATTHEWS ASIA FUNDS |

Table of Contents

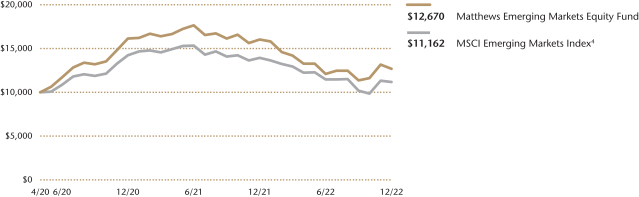

| PERFORMANCE AS OF DECEMBER 31, 2022 | ||||||||||||||||

| 3 Months | 1 Year | Since Inception | Inception date | |||||||||||||

| Investor Class (MEGMX) | 11.69% | -20.94% | 9.26% | 04/30/20 | ||||||||||||

| Institutional Class (MIEFX) | 11.66% | -20.81% | 9.49% | 04/30/20 | ||||||||||||

| MSCI Emerging Markets Index4 | 9.79% | -19.74% | 4.20% | |||||||||||||

Performance assumes reinvestment of all dividends and/or distributions before taxes. All performance quoted represents past performance and is no guarantee of future results. Investment return and principal value will fluctuate with market conditions so that when redeemed, shares may be worth more or less than their original cost. Current performance may be lower or higher than the return figures quoted. Returns would have been lower if certain of the Fund’s fees and expenses had not been waived. For the Fund’s most recent month-end performance visit matthewsasia.com.

GROWTH OF A HYPOTHETICAL $10,000 INVESTMENT SINCE INCEPTION—INVESTOR CLASS

Plotted monthly. The performance data and graph do not reflect the deduction of taxes that a shareholder would pay on dividends, capital gains distributions or redemption of Fund shares. Values are in US$.

| 4 | It is not possible to invest directly in an index. Source: Index data from Morgan Stanley Capital International and Bloomberg; total return calculations performed by BNY Mellon Investment Servicing (US) Inc. Please see page 87 for index definition. |

| TOP TEN HOLDINGS5 | ||||||||

| Name | Sector | Country | % Net Assets | |||||

| Taiwan Semiconductor Manufacturing Co., Ltd. | Information Technology | Taiwan | 5.7% | |||||

| Samsung Electronics Co., Ltd., Pfd. | Information Technology | South Korea | 5.3% | |||||

| Tencent Holdings, Ltd. | Communication Services | China/Hong Kong | 4.8% | |||||

| FPT Corp. | Information Technology | Vietnam | 4.3% | |||||

| HDFC Bank, Ltd. | Financials | India | 3.4% | |||||

| Prudential PLC | Financials | United Kingdom | 2.8% | |||||

| Woodside Energy Group, Ltd. | Energy | Australia | 2.8% | |||||

| AIA Group, Ltd. | Financials | China/Hong Kong | 2.8% | |||||

| Prologis Property Mexico SA de CV REIT | Real Estate | Mexico | 2.8% | |||||

| ICICI Bank, Ltd. | Financials | India | 2.6% | |||||

| % OF ASSETS IN TOP 10 | 37.3% | |||||||

| 5 | Holdings may combine more than one security from same issuer and related depositary receipts. |

| matthewsasia.com | 800.789.ASIA | 11 |

Table of Contents

| COUNTRY ALLOCATION (%)6,7 | ||||

| China/Hong Kong | 19.6 | |||

| India | 14.0 | |||

| Mexico | 8.5 | |||

| Brazil | 8.4 | |||

| South Korea | 6.8 | |||

| Vietnam | 6.7 | |||

| Taiwan | 5.7 | |||

| Singapore | 3.3 | |||

| United States | 2.8 | |||

| United Kingdom | 2.8 | |||

| Australia | 2.8 | |||

| Indonesia | 2.7 | |||

| Canada | 2.6 | |||

| Philippines | 2.5 | |||

| France | 2.4 | |||

| Poland | 1.5 | |||

| Qatar | 1.4 | |||

| Argentina | 1.4 | |||

| Kazakhstan | 1.1 | |||

| United Arab Emirates | 1.0 | |||

| Turkey | 0.7 | |||

| Cash and Other Assets, Less Liabilities | 1.3 | |||

| SECTOR ALLOCATION (%)7 | ||||

| Financials | 25.4 | |||

| Information Technology | 22.0 | |||

| Consumer Discretionary | 10.5 | |||

| Materials | 9.8 | |||

| Industrials | 6.4 | |||

| Energy | 6.2 | |||

| Real Estate | 5.6 | |||

| Consumer Staples | 5.0 | |||

| Communication Services | 4.8 | |||

| Health Care | 2.9 | |||

| Cash and Other Assets, Less Liabilities | 1.3 | |||

| MARKET CAP EXPOSURE (%)7 | ||||

| Mega Cap (over $25B) | 50.4 | |||

| Large Cap ($10B-$25B) | 16.9 | |||

| Mid Cap ($3B-10B) | 18.1 | |||

| Small Cap (under $3B) | 13.3 | |||

| Cash and Other Assets, Less Liabilities | 1.3 | |||

| 6 | Not all countries where the Fund may invest are included in the benchmark index. |

| 7 | Source: FactSet Research Systems. Percentage values in data are rounded to the nearest tenth of one percent, so the values may not sum to 100% due to rounding. Country allocations and percentage values may be derived from different data sources and may not be consistent with other Fund literature. |

Matthews Emerging Markets Equity Fund

Portfolio Manager Commentary (unaudited) (continued)

also positive contributors. Conversely, stock selection in energy was the biggest detractor and financials and health care were also detractors.

At the holdings level, a number of Brazilian stocks were among the top contributors, including Petrobras, the oil and gas conglomerate, and Vale, the metals and mining group, which both benefited from high commodity prices. Banco BTG Pactual also performed well as the Brazilian economy strengthened. On the flip side, Russian stocks including energy companies Lukoil and Novatek, and banking financial group Sberbank, were among the worst performers as their values crashed after Russia’s invasion of Ukraine.

Notable portfolio changes

In the fourth quarter, we added a handful of stocks and exited a handful of positions leaving the name count unchanged at 59. After visiting Brazil in November following the election, we started a position in Weg, an industrial motors producer which has translated its success in Brazil to China and other countries. We also added two China-related companies—Hong Kong Exchanges and Clearing and CSPC Pharmaceutical Group—and increased the number of China/HK stocks in the portfolio to 11. We also added United Arab Emirates-based Fertiglobe, a fertilizer company which is a leader in managing costs—a key attribute for maintaining annual crop yields. In the semiconductor space, our sale of LAM Research to buy Applied Materials was driven by a desire to reduce exposure to memory in favor of foundry while also realizing a tax loss to minimize shareholder distributions.

Outlook

Looking to the year ahead we see two positive developments driving optimism about emerging markets. Firstly, inflation is falling in much of the world and secondly, China’s abandonment of its zero-COVID policy should quickly lead to a re-opening of its economy. Companies we speak to are aware of recession risks and are challenged by rising costs but few are noticing dramatic declines in demand for their products and services or facing meaningful financial or operating stresses.

Our focus remains on good companies—those which can succeed in a variety of macroeconomic and political environments. Many of our portfolio companies reacted rationally to the turbulent events of recent years by strengthening their balance sheets, reducing costs, and improving their competitive positions. Some commodity businesses, for example, have seen the disruption in energy and mining production, as well as the growing needs for certain materials in the energy transition, as reasons to move forward with important projects. Many companies we have exposure to have managed through a number of volatile cycles in the past and emerged stronger. As the world looks beyond the most disruptive consequences of the pandemic, we believe our holdings are positioned to emerge stronger still.

| 12 | MATTHEWS ASIA FUNDS |

Table of Contents

Matthews Emerging Markets Equity Fund

December 31, 2022

Schedule of Investmentsa

COMMON EQUITIES: 93.4%

| Shares | Value | |||||||

| CHINA/HONG KONG: 19.6% | ||||||||

Tencent Holdings, Ltd. | 37,600 | $1,594,254 | ||||||

AIA Group, Ltd. | 85,200 | 940,897 | ||||||

H World Group, Ltd. ADR | 14,627 | 620,477 | ||||||

JD.com, Inc. A Shares | 20,352 | 568,159 | ||||||

Yum China Holdings, Inc. | 10,084 | 551,091 | ||||||

Midea Group Co., Ltd. A Shares | 65,700 | 491,670 | ||||||

Hong Kong Exchanges & Clearing, Ltd. | 10,200 | 438,297 | ||||||

NARI Technology Co., Ltd. A Shares | 113,820 | 399,559 | ||||||

ESR Group, Ltd.b,c | 158,800 | 331,979 | ||||||

Techtronic Industries Co., Ltd. | 29,000 | 322,098 | ||||||

CSPC Pharmaceutical Group, Ltd. | 286,000 | 297,747 | ||||||

|

| |||||||

Total China/Hong Kong | 6,556,228 | |||||||

|

| |||||||

| INDIA: 14.0% | ||||||||

HDFC Bank, Ltd. ADR | 16,636 | 1,138,069 | ||||||

ICICI Bank, Ltd. ADR | 39,641 | 867,741 | ||||||

Infosys, Ltd. ADR | 45,361 | 816,952 | ||||||

Kotak Mahindra Bank, Ltd. | 24,793 | 545,478 | ||||||

Dabur India, Ltd. | 68,765 | 465,892 | ||||||

Restaurant Brands Asia, Ltd.d | 321,392 | 433,295 | ||||||

PI Industries, Ltd. | 9,767 | 403,366 | ||||||

|

| |||||||

Total India | 4,670,793 | |||||||

|

| |||||||

| MEXICO: 8.5% | ||||||||

Prologis Property Mexico SA de CV REIT | 322,698 | 924,549 | ||||||

Grupo Financiero Banorte SAB de CV Class O | 77,300 | 555,002 | ||||||

Grupo Aeroportuario del Sureste SAB de CV ADR | 2,109 | 491,376 | ||||||

Becle SAB de CV | 201,900 | 438,996 | ||||||

GCC SAB de CV | 64,000 | 428,276 | ||||||

|

| |||||||

Total Mexico | 2,838,199 | |||||||

|

| |||||||

| BRAZIL: 8.4% | ||||||||

Banco BTG Pactual SA | 134,600 | 608,858 | ||||||

Vinci Partners Investments, Ltd. Class A | 57,009 | 515,362 | ||||||

Vale SA ADR | 28,864 | 489,822 | ||||||

Hapvida Participacoes e Investimentos SAb,c,d | 367,400 | 354,039 | ||||||

Hypera SA | 37,500 | 321,554 | ||||||

Petroleo Brasileiro SA ADR | 25,363 | 270,116 | ||||||

WEG SA | 35,300 | 256,429 | ||||||

|

| |||||||

Total Brazil | 2,816,180 | |||||||

|

| |||||||

| VIETNAM: 6.7% | ||||||||

FPT Corp. | 443,017 | 1,443,069 | ||||||

Military Commercial Joint Stock Bankd | 464,376 | 336,696 | ||||||

Sai Gon Cargo Service Corp. | 98,695 | 313,814 | ||||||

HDBankd | 203,175 | 137,618 | ||||||

|

| |||||||

Total Vietnam | 2,231,197 | |||||||

|

| |||||||

| TAIWAN: 5.7% | ||||||||

Taiwan Semiconductor Manufacturing Co., Ltd. | 131,000 | 1,902,574 | ||||||

|

| |||||||

Total Taiwan | 1,902,574 | |||||||

|

| |||||||

| UNITED STATES: 4.2% | ||||||||

Applied Materials, Inc. | 4,987 | 485,634 | ||||||

Globant SAd | 2,793 | 469,671 | ||||||

Excelerate Energy, Inc. Class A | 18,007 | 451,075 | ||||||

|

| |||||||

Total United States | 1,406,380 | |||||||

|

| |||||||

| Shares | Value | |||||||

| SINGAPORE: 3.3% | ||||||||

Capitaland Investment, Ltd. | 223,200 | $616,856 | ||||||

TDCX, Inc. ADRd | 40,389 | 500,016 | ||||||

|

| |||||||

Total Singapore | 1,116,872 | |||||||

|

| |||||||

| UNITED KINGDOM: 2.8% | ||||||||

Prudential PLC | 69,369 | 945,867 | ||||||

|

| |||||||

Total United Kingdom | 945,867 | |||||||

|

| |||||||

| AUSTRALIA: 2.8% | ||||||||

Woodside Energy Group, Ltd. | 38,983 | 944,098 | ||||||

|

| |||||||

Total Australia | 944,098 | |||||||

|

| |||||||

| INDONESIA: 2.7% | ||||||||

PT Bank Rakyat Indonesia Persero Tbk | 2,028,900 | 643,263 | ||||||

PT Avia Avian Tbk | 6,602,800 | 267,208 | ||||||

|

| |||||||

Total Indonesia | 910,471 | |||||||

|

| |||||||

| ZAMBIA: 2.6% | ||||||||

First Quantum Minerals, Ltd. | 41,500 | 867,086 | ||||||

|

| |||||||

Total Zambia | 867,086 | |||||||

|

| |||||||

| PHILIPPINES: 2.5% | ||||||||

Wilcon Depot, Inc. | 895,800 | 474,887 | ||||||

Ayala Corp. | 29,360 | 367,503 | ||||||

|

| |||||||

Total Philippines | 842,390 | |||||||

|

| |||||||

| FRANCE: 2.4% | ||||||||

TotalEnergies SE ADR | 6,774 | 420,530 | ||||||

LVMH Moet Hennessy Louis Vuitton SE | 521 | 379,128 | ||||||

|

| |||||||

Total France | 799,658 | |||||||

|

| |||||||

| POLAND: 1.5% | ||||||||

Dino Polska SAb,c,d | 6,026 | 517,539 | ||||||

|

| |||||||

Total Poland | 517,539 | |||||||

|

| |||||||

| SOUTH KOREA: 1.5% | ||||||||

LG Chem Ltd. | 1,067 | 509,524 | ||||||

|

| |||||||

Total South Korea | 509,524 | |||||||

|

| |||||||

| QATAR: 1.4% | ||||||||

Qatar National Bank QPSC | 91,663 | 454,358 | ||||||

|

| |||||||

Total Qatar | 454,358 | |||||||

|

| |||||||

| KAZAKHSTAN: 1.1% | ||||||||

Kaspi.KZ JSC GDRc | 5,097 | 366,087 | ||||||

|

| |||||||

Total Kazakhstan | 366,087 | |||||||

|

| |||||||

| UNITED ARAB EMIRATES: 1.0% | ||||||||

Fertiglobe PLC | 278,189 | 319,765 | ||||||

|

| |||||||

Total United Arab Emirates | 319,765 | |||||||

|

| |||||||

| TURKEY: 0.7% | ||||||||

BIM Birlesik Magazalar AS | 33,543 | 245,127 | ||||||

|

| |||||||

Total Turkey | 245,127 | |||||||

|

| |||||||

| matthewsasia.com | 800.789.ASIA | 13 |

Table of Contents

Matthews Emerging Markets Equity Fund

December 31, 2022

Schedule of Investmentsa (continued)

COMMON EQUITIES (continued)

| Shares | Value | |||||||

| RUSSIA: 0.0% | ||||||||

Sberbank of Russia PJSCd,e | 128,308 | $1,740 | ||||||

LUKOIL PJSC ADRe | 18,010 | 360 | ||||||

TCS Group Holding PLC GDRc,d,e | 3,865 | 77 | ||||||

|

| |||||||

Total Russia | 2,177 | |||||||

|

| |||||||

| TOTAL COMMON EQUITIES | 31,262,570 | |||||||

|

| |||||||

(Cost $35,331,884) | ||||||||

PREFERRED EQUITIES: 5.3% | ||||||||

| SOUTH KOREA: 5.3% | ||||||||

Samsung Electronics Co., Ltd., Pfd. | 43,849 | 1,757,177 | ||||||

|

| |||||||

Total South Korea | 1,757,177 | |||||||

|

| |||||||

| TOTAL PREFERRED EQUITIES | 1,757,177 | |||||||

|

| |||||||

(Cost $2,545,709) | ||||||||

| TOTAL INVESTMENTS: 98.7% |

| 33,019,747 | ||||||

(Cost $37,877,593) | ||||||||

| CASH AND OTHER ASSETS, LESS LIABILITIES: 1.3% | 445,021 | |||||||

|

| |||||||

NET ASSETS: 100.0% |

| $33,464,768 | ||||||

|

| |||||||

| a | Certain securities were fair valued under the valuation policies approved by the Board of Trustees (Note 2-A). |

| b | Security exempt from registration under Rule 144A of the Securities Act of 1933, as amended. The security may be resold in transactions exempt from registration normally to qualified institutional buyers. The security has been determined to be liquid in accordance with procedures adopted by the Funds’ Board of Trustees. At December 31, 2022, the aggregate value is $1,203,557, which is 3.60% of net assets. |

| c | The securities may be resold to qualified foreign investors and foreign institutional buyers under Regulation S of the Securities Act of 1933. |

| d | Non-income producing security. |

| e | Security is valued using significant unobservable inputs and is classified as Level 3 in the fair value hierarchy. The aggregate value of Level 3 security is $2,177 and 0.01% of net assets. |

| ADR | American Depositary Receipt |

| GDR | Global Depositary Receipt |

| JSC | Joint Stock Co. |

| Pfd. | Preferred |

| PJSC | Public Joint Stock Co. |

| QPSC | Qatari Public Shareholding Co. |

| REIT | Real Estate Investment Trust |

See accompanying notes to financial statements.

| 14 | MATTHEWS ASIA FUNDS |

Table of Contents

| PORTFOLIO MANAGER | ||||

| Vivek Tanneeru | ||||

Lead Manager | ||||

| FUND FACTS | ||||

| Investor | Institutional | |||

Ticker | MASGX | MISFX | ||

CUSIP | 577130727 | 577130719 | ||

Inception | 4/30/15 | 4/30/15 | ||

NAV | $12.51 | $12.51 | ||

Initial Investment | $2,500 | $100,000 | ||

Gross Expense Ratio1 | 1.24% | 1.11% | ||

After Fee Waiver and Reimbursement2 | 1.30% | 1.17% | ||

Portfolio Statistics | ||||

Total # of Positions | 55 | |||

Net Assets | $172.3 million | |||

Weighted Average | $19.6 billion | |||

Portfolio Turnover3 | 31.53% | |||

Benchmark | ||||

MSCI Emerging Markets Index | ||||

OBJECTIVE

Long-term capital appreciation.

STRATEGY

Under normal circumstances, the Fund seeks to achieve its investment objective by investing at least 80% of its net assets, which include borrowings for investment purposes, in the common and preferred stocks of companies of any market capitalization located in emerging market countries that satisfy one or more of the Fund’s environmental, social and governance (“ESG”) standards. Emerging market countries generally include every country in the world except the United States, Australia, Canada, Hong Kong, Israel, Japan, New Zealand, Singapore and most of the countries in Western Europe.

Matthews Emerging Markets Sustainable Future Fund*

Portfolio Manager Commentary (unaudited)

For the year ending December 31, 2022, the Matthews Emerging Markets Sustainable Future Fund returned –14.38% (Investor Class) and –14.32% (Institutional Class), while its benchmark, the MSCI Emerging Markets Index, returned –19.74% over the same period. For the fourth quarter, the Fund returned 11.90% (Investor Class) and 11.87% (Institutional Class), while the benchmark returned 9.79%.

Market Environment

In 2022, the U.S. and many other parts of the developed world saw high rates of inflation that they hadn’t experienced since the 1980s. The U.S. Federal Reserve increased the Fed funds rate seven times last year after guiding for a transitory inflation for much of 2021. This led to strong U.S. dollar performance that peaked around the end of the third quarter. Inflation was less of a challenge in key emerging markets like China, partly because of suppressed economic activity resulting from China’s zero-COVID policy which was in place for much of 2022, and because where inflation was elevated, a number of central banks proactively addressed it by sharply increasing rates.

Nonetheless, emerging markets currencies were not completely immune to the impact of a very strong greenback. Among Latin American currencies, the Brazilian real, Mexican peso and Peruvian sol gained over 5% against the dollar in 2022, while the Argentine peso and Turkish lira were the worst performers as a result of runaway inflation. For perspective, some major developed market currencies, such as the Japanese yen, British pound and the euro, fared worse than some emerging-market currencies.

For the year, Turkey was the best performing emerging market, followed by Chile and Brazil. Asian markets like South Korea, Taiwan and China were among the worst-performing emerging markets alongside Eastern European markets including Hungary and Poland. Many of the poor performers for the full year turned in robust performances in the fourth quarter as markets in Asia particularly were aided by China’s lifting of its pandemic restrictions.

Performance Contributors and Detractors

On a country basis, our stock selection and overweight in both China and India were the biggest contributors to relative performance during the year, followed by our stock selection and underweight to Taiwan. On the other hand, our underweight to Brazil and stock selection in Indonesia detracted from performance.

From a sector perspective, stock selection in consumer discretionary was the biggest contributor to relative performance during the year. Our stock selection in health care and allocation to industrials also contributed positively. On the flip side, our stock selection in financials was the biggest detractor from relative performance.

At the stock level, as China’s zero-COVID policy was lifted toward the end of 2022, our Chinese portfolio holdings in general and holdings in JD Health and Full Truck Alliance, in particular, rebounded strongly and contributed positively to relative performance. JD Health, an internet health-care platform, was the top performer as it benefited from a surge in demand for health-care products and services during the latest wave of COVID and also on expectations of favorable

(continued)

| * | The Fund’s name changed from Matthews Asia ESG Fund to Matthews Emerging Markets Sustainable Future Fund on July 29, 2022. |

| 1 | Actual 2022 expense ratios. |

| 2 | Matthews has contractually agreed (i) to waive fees and reimburse expenses to the extent needed to limit Total Annual Fund Operating Expenses (excluding Rule 12b-1 fees, taxes, interest, brokerage commissions, short sale dividend expenses, expenses incurred in connection with any merger or reorganization or extraordinary expenses such as litigation) of the Institutional Class to 1.15% first by waiving class specific expenses (i.e., shareholder service fees specific to a particular class) of the Institutional Class and then, to the extent necessary, by waiving non-class specific expenses (e.g., custody fees) of the Institutional Class, and (ii) if any Fund-wide expenses (i.e., expenses that apply to both the Institutional Class and the Investor Class) are waived for the Institutional Class to maintain the 1.15% expense limitation, to waive an equal amount (in annual percentage terms) of those same expenses for the Investor Class. The Total Annual Fund Operating Expenses After Fee Waiver and Expense Reimbursement for the Investor Class may vary from year to year and will in some years exceed 1.15%. If the operating expenses fall below the expense limitation within three years after Matthews has made a waiver or reimbursement, the Fund may reimburse Matthews up to an amount that does not cause the expenses for that year to exceed the lesser of (i) the expense limitation applicable at the time of that fee waiver and/or expense reimbursement or (ii) the expense limitation in effect at the time of recoupment. This agreement will remain in place until April 30, 2023 and may be terminated at any time by the Board of Trustees on behalf of the Fund on 60 days’ written notice to Matthews. Matthews may decline to renew this agreement by written notice to the Trust at least 30 days before its annual expiration date. |

| 3 | The lesser of fiscal year 2022 long-term purchase costs or sales proceeds divided by the average monthly market value of long-term securities. |

| matthewsasia.com | 800.789.ASIA | 15 |

Table of Contents

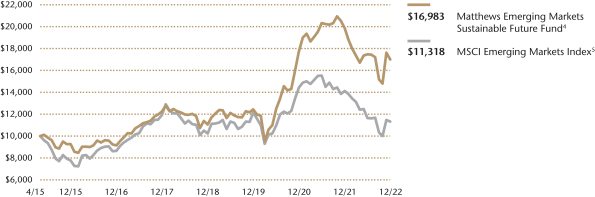

| PERFORMANCE AS OF DECEMBER 31, 2022 | ||||||||||||||||||||||||

|

|

|

| Average Annual Total Returns |

| ||||||||||||||||||||

| 3 Months | 1 Year | 3 years | 5 years | Since Inception | Inception Date | |||||||||||||||||||

| Investor Class (MASGX)4 | 11.90% | -14.38% | 10.99% | 6.79% | 7.15% | 4/30/15 | ||||||||||||||||||

| Institutional Class (MISFX)4 | 11.87% | -14.32% | 11.15% | 6.97% | 7.36% | 4/30/15 | ||||||||||||||||||

| MSCI Emerging Markets Index5 | 9.79% | -19.74% | -2.34% | -1.03% | 1.63% | |||||||||||||||||||

| MSCI All Country Asia ex Japan Index5 | 11.43% | -19.36% | -1.15% | -0.34% | 2.36% | |||||||||||||||||||

Performance assumes reinvestment of all dividends and/or distributions before taxes. All performance quoted represents past performance and is no guarantee of future results. Investment return and principal value will fluctuate with market conditions so that when redeemed, shares may be worth more or less than their original cost. Current performance may be lower or higher than the return figures quoted. Returns would have been lower if certain of the Fund’s fees and expenses had not been waived. For the Fund’s most recent month-end performance visit matthewsasia.com.

GROWTH OF A HYPOTHETICAL $10,000 INVESTMENT SINCE INCEPTION—INVESTOR CLASS

Plotted Monthly. The performance data and graph do not reflect the deduction of taxes that a shareholder would pay on dividends, capital gain distributions or redemption of Fund shares. Values are in US$.

| 4 | Before July 29, 2022, the Fund was managed with a slightly different investment strategy and may have achieved different performance results under its current investment strategy from the performance shown for periods before that date. |

| 5 | Effective July 29, 2022, in connection with changes to the Fund’s name and principal investment strategies, the primary benchmark changed from the MSCI All Country Asia ex Japan Index to the MSCI Emerging Markets Index. It is not possible to invest directly in an index. Source: Index data from Morgan Stanley Capital International; total return calculations performed by BNY Mellon Investment Servicing (US) Inc. Please see page 86 for index definition. |

| TOP TEN HOLDINGS6 | ||||||||

| Name | Sector | Country | % Net Assets | |||||

| Full Truck Alliance Co., Ltd. | Industrials | China/Hong Kong | 6.9% | |||||

| JD Health International, Inc. | Consumer Discretionary | China/Hong Kong | 6.0% | |||||

| Shriram Finance, Ltd. | Financials | India | 5.2% | |||||

| Legend Biotech Corp. | Health Care | United States | 5.0% | |||||

| Bandhan Bank, Ltd. | Financials | India | 4.9% | |||||

| Hong Kong Exchanges & Clearing, Ltd. | Financials | China/Hong Kong | 4.4% | |||||

| Samsung SDI Co., Ltd., Pfd. | Information Technology | South Korea | 3.9% | |||||

| Meituan | Consumer Discretionary | China/Hong Kong | 3.3% | |||||

| Phoenix Mills, Ltd. | Real Estate | India | 3.1% | |||||

| Marico, Ltd. | Consumer Staples | India | 2.9% | |||||

% OF ASSETS IN TOP 10 | 45.6% | |||||||

| 6 | Holdings may combine more than one security from same issuer and related depositary receipts. |

| 16 | MATTHEWS ASIA FUNDS |

Table of Contents

Matthews Emerging Markets Sustainable Future Fund

Portfolio Manager Commentary (unaudited) (continued)

regulatory changes. Full Truck Alliance, an online freight platform, gained as a result of China reopening expectations and a rebound in economic activity that would be beneficial to its revenue growth and also on expectations of movement restrictions that constrained the trucking industry being lifted. Our Indian holdings also benefited from the normalization of economic activity in the country. Phoenix Mills, a retail mall operator, and Lemon Tree Hotels were among top contributors amid stronger pricing and/or higher sales in these consumer segments compared with pre-pandemic levels. Conversely, electric vehicle (EV) supply-chain names underperformed toward the end of 2022 on worries about developed world economic growth potentially softening in 2023 at a time when the EV industry is rapidly increasing production capacity. South Korean EV component company Solus Advanced Materials, which has manufacturing operations in Europe, was one of the biggest detractors for the year amid concerns about its cost competitiveness given a significant increase in energy prices in Europe. We retain a positive view on the long-term demand trends for the EV industry and the competitiveness of Asian battery cell makers within it.

Notable Portfolio Changes

In 2022, we initiated a position in Brazilian education services and technology provider YDUQS. The company has higher-education offerings in an on-campus setting as well as digital learning. YDUQS is among leading players in the distance-learning programs in Brazil which makes education possible for students from lower-income households and students who work. YDUQS has strong governance, and a good track record of social and community engagement and environmental stewardship, in our view. It also stands to benefit if the Lula administration decides to support the education sector through increased funding. During the fourth quarter, we exited a position in MTR Corp., a Hong Kong mass transit operator, and redeployed the capital elsewhere.

Outlook

The Fed’s interest rate strategy and the market’s expectation of its evolution continue to be the most important variables impacting the near-term regional, sector and currency performance in emerging markets. We expect the impact of the Fed’s actions in 2023 to be less than it was in 2022 as the tightening cycle enters late stages. In addition, we are also wary of the cumulative impact of the Fed’s interest rate hikes on U.S. and developed world economic activity.

Our other key focus in 2022 was the evolution of China’s zero-COVID policy and its impact on economic activity in the country. This has largely been resolved given the unexpected lifting of most COVID restrictions in China in late 2022. Elsewhere, Russia’s invasion of Ukraine and its effect on energy prices—alongside OPEC’s efforts to keep the prices high—needs careful watching, especially as Chinese economic activity is likely to pick up as 2023 progresses.

Over the coming years, we expect the emerging markets gross domestic product (GDP) growth-differential with developed markets to improve from a 23-year low reached in 2022. This development, alongside relatively attractive valuations, should potentially lend support to better equity performance against developed markets compared with the last decade.

Companies that address critical challenges, such as climate change and inclusive development, will continue to thrive, in our view. And for investors interested in sustainability themes, including reducing carbon emissions, alleviating poverty and creating greater financial inclusion in the developing world, emerging markets remains a key investment destination. To tackle sustainable themes globally, we believe we need to include the world’s most populous economies, many of which lie in emerging markets. As the post-COVID global economic recovery matures and markets contend with macro headwinds and volatility, we believe there are attractive opportunities for alpha generation throughout our large, diverse, sustainable investment universe.

| COUNTRY ALLOCATION (%)7,8 | ||||

| China/Hong Kong | 40.3 | |||

| India | 22.1 | |||

| Taiwan | 7.6 | |||

| South Korea | 7.2 | |||

| United States | 6.3 | |||

| Brazil | 2.8 | |||

| Portugal | 2.1 | |||

| Indonesia | 2.0 | |||

| Netherlands | 1.6 | |||

| Vietnam | 1.6 | |||

| Saudi Arabia | 1.3 | |||

| Romania | 1.2 | |||

| United Kingdom | 1.1 | |||

| Bangladesh | 1.1 | |||

| Estonia | 0.8 | |||

| Cash and Other Assets, Less Liabilities | 1.0 | |||

| SECTOR ALLOCATION (%)8 | ||||

| Industrials | 25.0 | |||

| Financials | 20.4 | |||

| Consumer Discretionary | 16.4 | |||

| Information Technology | 12.3 | |||

| Health Care | 11.2 | |||

| Real Estate | 6.0 | |||

| Consumer Staples | 5.0 | |||

| Communication Services | 2.0 | |||

| Utilities | 0.8 | |||

| Cash and Other Assets, Less Liabilities | 1.0 | |||

| MARKET CAP EXPOSURE (%)8 | ||||

| Mega Cap (over $25B) | 22.9 | |||

| Large Cap ($10B-$25B) | 8.0 | |||

| Mid Cap ($3B-10B) | 48.6 | |||

| Small Cap (under $3B) | 19.5 | |||

| Cash and Other Assets, Less Liabilities | 1.0 | |||

| 7 | Not all countries are included in the benchmark index. |

| 8 | Source: FactSet Research Systems. Percentage values in data are rounded to the nearest tenth of one percent, so the values may not sum to 100% due to rounding. Country allocations and percentage values may be derived from different data sources and may not be consistent with other Fund literature. |

| matthewsasia.com | 800.789.ASIA | 17 |

Table of Contents

Matthews Emerging Markets Sustainable Future Fund

December 31, 2022

Schedule of Investmentsa

COMMON EQUITIES: 95.0%

| Shares | Value | |||||||

| CHINA/HONG KONG: 40.3% | ||||||||

Full Truck Alliance Co., Ltd. ADRb | 1,486,997 | $11,895,976 | ||||||

JD Health International, Inc.b,c,d | 1,143,700 | 10,327,670 | ||||||

Hong Kong Exchanges & Clearing, Ltd. | 177,700 | 7,635,814 | ||||||

Meituan B Sharesb,c,d | 259,900 | 5,758,302 | ||||||

Airtac International Group | 156,000 | 4,709,867 | ||||||

Contemporary Amperex Technology Co., Ltd. A Shares | 76,000 | 4,301,619 | ||||||

Ginlong Technologies Co., Ltd. A Sharesb | 153,300 | 3,992,488 | ||||||

Medlive Technology Co., Ltd.c,d | 2,189,500 | 2,375,043 | ||||||

China Conch Venture Holdings, Ltd. | 1,090,500 | 2,365,653 | ||||||

Centre Testing International Group Co., Ltd. A Shares | 655,100 | 2,114,513 | ||||||

Xinyi Glass Holdings, Ltd. | 1,099,000 | 2,030,485 | ||||||

Wuxi Biologics Cayman, Inc.b,c,d | 240,000 | 1,817,739 | ||||||

CSPC Pharmaceutical Group, Ltd. | 1,634,960 | 1,702,114 | ||||||

Flat Glass Group Co., Ltd. H Shares | 678,000 | 1,630,513 | ||||||

Innovent Biologics, Inc.b,c,d | 378,500 | 1,610,936 | ||||||

OPT Machine Vision Tech Co., Ltd. A Shares | 83,485 | 1,592,033 | ||||||

Hangzhou Tigermed Consulting Co., Ltd. A Shares | 88,476 | 1,335,398 | ||||||

Morimatsu International Holdings Co., Ltd.b,d | 1,084,000 | 1,196,807 | ||||||

Zhejiang HangKe Technology, Inc., Co. A Shares | 127,664 | 809,685 | ||||||

China Conch Environment Protection Holdings, Ltd.b | 733,500 | 295,371 | ||||||

|

| |||||||

Total China/Hong Kong | 69,498,026 | |||||||

|

| |||||||

| INDIA: 22.1% | ||||||||

Shriram Finance, Ltd. | 541,070 | 8,981,895 | ||||||

Bandhan Bank, Ltd.b,c,d | 2,982,606 | 8,417,741 | ||||||

Phoenix Mills, Ltd. | 308,254 | 5,294,086 | ||||||

Marico, Ltd. | 810,916 | 4,990,137 | ||||||

Mahindra & Mahindra, Ltd. | 238,338 | 3,588,116 | ||||||

Indus Towers, Ltd. | 1,224,949 | 2,812,489 | ||||||

Lemon Tree Hotels, Ltd.b,c,d | 2,420,831 | 2,503,496 | ||||||

UNO Minda, Ltd. | 136,156 | 856,628 | ||||||

NBCC India, Ltd. | 1,278,019 | 598,310 | ||||||

|

| |||||||

Total India | 38,042,898 | |||||||

|

| |||||||

| TAIWAN: 7.6% | ||||||||

Andes Technology Corp. | 281,000 | 4,522,281 | ||||||

Poya International Co., Ltd. | 237,477 | 3,844,934 | ||||||

M31 Technology Corp. | 153,000 | 2,267,388 | ||||||

Sporton International, Inc. | 233,448 | 1,590,967 | ||||||

Formosa Sumco Technology Corp. | 182,000 | 801,710 | ||||||

|

| |||||||

Total Taiwan | 13,027,280 | |||||||

|

| |||||||

| UNITED STATES: 6.2% | ||||||||

Legend Biotech Corp. ADRb | 172,279 | 8,600,168 | ||||||

Micron Technology, Inc. | 43,500 | 2,174,130 | ||||||

|

| |||||||

Total United States | 10,774,298 | |||||||

|

| |||||||