UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act File Number 811-08614

Brandes Investment Trust

(Exact name of registrant as specified in charter)

4275 Executive Square, Suite 500

La Jolla, California 92037

(Address of principal executive offices) (Zip code)

Lea Anne Copenhefer

Morgan, Lewis & Bockius LLP

One Federal Street

Boston, MA 02110-1726

(Name and address of agent for service)

(858) 755-0239

Registrant’s telephone number, including area code

Date of fiscal year end: September 30

Date of reporting period: September 30, 2022

Item 1. Reports to Stockholders.

(a) The following are copies of the reports transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940 (the “Act”) (17 CFR 270.30e-1):

1

| Letter to Shareholders and Performance Graphs | 2 | |||

| 2 | ||||

| 7 | ||||

| 14 | ||||

| 21 | ||||

| 28 | ||||

| 36 | ||||

| 42 | ||||

| 49 | ||||

| Expense Example | 57 | |||

| Schedule of Investments | 60 | |||

| 60 | ||||

| 63 | ||||

| 66 | ||||

| 70 | ||||

| 75 | ||||

| 78 | ||||

| 81 | ||||

| Statements of Assets and Liabilities | 86 | |||

| Statements of Operations | 88 | |||

| Statements of Changes in Net Assets | 90 | |||

| Financial Highlights | 94 | |||

| Notes to Financial Statements | 108 | |||

| Report of Independent Registered Public Accounting Firm | 134 | |||

| Additional Information | 136 | |||

| Trustees and Officers Information | 142 |

1

From our beginnings, Brandes has been a reflective investment manager, constantly renewing our bond with our founding principles and periodically reviewing our past communications with the dual goals of staying focused and thinking forward.

Recently, we’ve taken stock of Brandes Letters from the past several years, the messages affirming our core principles woven throughout them, and the client reactions to them. We think our championing of value investing has passed the twin tests of critical scrutiny and time.

In our experience, it takes commitment to invest consistently through a repeatable process. Brandes has upheld its value investing convictions and has consistently delivered exposure to what we consider value portfolios. In our opinion, being purpose-built for value is what makes us distinctive. It’s the reason why our investment decisions are not driven by the composition of the benchmarks. We have not diluted our approach, though it’s more adaptable than often perceived, nor have we renounced what we stand for to ourselves or to our clients.

Key value investing principles can get lost in translation. While value principles are straightforward in concept, they can be difficult to execute. In this Letter, we will elaborate on why we endeavor not to deviate from a value approach. We will also offer insights into behavioral biases that can undermine disciplined, long-term investing and will discuss in depth the changing market/economic factors that we interpret as favorable to investing with a genuine value orientation. And, finally, we will explain why this could be an ideal time to review your allocation to value investing.

Staying True to Our “Constitution”

Let us begin with the origins of Brandes as an investing organization and how and why we have committed ourselves to the search for value.

Our “constitution” as a firm is Benjamin Graham and David Dodd’s 1934 classic, Security Analysis, as well as Graham’s 1949 follow-on, The Intelligent Investor. Graham and Dodd insisted that there is a profound difference between deliberate investing based on careful analysis of business fundamentals and mere speculation. For us, this remains a bedrock truth, and the books established the mindset we regard as the most trustworthy approach to investing.

In our opinion, Security Analysis and The Intelligent Investor are among those rare texts that continue to speak to audiences long after their publication because they have withstood the challenge of change. Our founder, Charles Brandes, was convinced by the clarity of the arguments about the importance of examining long-term fundamentals and having a “margin of safety” (the discount of a security’s market price to an estimate of the security’s intrinsic value) especially after he met with the “brilliant…gracious …very formal” author in the early 1970s. At Graham’s California home, they conversed about their mutual understanding of what really counts (no pun

2

intended) in investing. Graham later sent a congratulatory letter to Charles on his starting the firm in 1974.

As a value manager, Brandes undertakes analytical examination of the companies we buy and concentrates on identifying solid financial fundamentals that markets may overlook or ignore. Value investing is not—and has never been—about a search only for low price-to-book stocks to us. It’s not about being a contrarian for the sake of being a contrarian. It is about avoiding competing priorities that can distort sound stock selection.

Around the time Brandes began operating, the “Nifty Fifty” (50 NYSE-listed large-cap stocks dominant in the ’60s and ’70s) captured the imagination of institutional investors—a situation strikingly similar to the so-called FAANGs (i.e., the large American technology companies Meta [formerly Facebook], Amazon, Apple, Netflix and Alphabet [formerly Google] over the past several years). Applying value principles, Charles Brandes rejected buying the Nifty Fifty, and today we continue to rebuff what we consider overpriced market offerings.

We acknowledge that some of these can be great companies, but we will not pay more for them than we think they are worth. In a similar and related way, we’re also vigilant for and strive to overcome the psychological and behavioral biases that inhibit discerning investing and will discuss them in depth in the next section.

Given that value investing has been out of favor during most of the past decade, the pressure and temptation to ‘flex’ the definition of value has been intense. However, we have worked hard to embed our self-defining standards into our culture and have committed training resources to impart them to the newcomers and future leaders of our firm. This includes, for example, periodically offering a “Graham Course” to all members of our firm in order to share the wisdom conveyed by Ben Graham in The Intelligent Investor and its application by Charles Brandes. We do this to ensure that the style fidelity we seek to preserve lives long into the future and want existing and future clients to have full confidence in Brandes’ commitment to being a true value manager.

Seeking to Understand Investor Psychology, Behavior

We are convinced that understanding investor psychology and behavior are important—maybe the most important—elements in successful long-term investing. This applies to our own self-awareness in our selection and decision-making processes, as well as to the direction of educational content we create for our clients. We therefore work to counter emotion-centered biases that might creep into investment decisions, as well as other errors in judgment that can erode rational investing.

Behavioral finance expert and MarketPsych co-founder, Dr. Frank Murtha, with whom the Brandes Institute has worked on various educational initiatives, described other known biases in a March 2019 paper for the Institute: Five Wealth-Destroying Biases: Where They Strike in the Investment Process and How to Address Them. These include anchoring, availability, framing, extrapolation (which fits under Prospect Theory) and planning fallacy. It’s beyond the scope or focus of this Letter to explore each, let alone others in detail, but we trust you can appreciate that bias can interfere with making an accurate assessment of an investment’s inherent worth and a valid case for acquisition or divestment. An important step to dealing with biases is to recognize

3

them. At Brandes and the Brandes Institute, we’ve done a lot of work studying biases and thinking about how to mitigate them.

In our view, investing based on innate but potentially misleading cognitive biases is an adversary of patient, discipline value investing. Without the diligent process of undertaking fundamental analysis and searching for intrinsic value, it will be hard, in our opinion, to remain committed to the long term when excessive optimism (or “irrational exuberance” as former Federal Reserve Chair Alan Greenspan called it in 1996), heightened uncertainty or unconscious predispositions dominate the markets—as they have many times in the past. Accordingly, we will continue to remind ourselves and our clients about the potential consequences that emotions and biases can bring to any investment approach.

What hasn’t Changed? What has? Why does it Matter?

Fundamental, bottom-up investing based on time-tested principles typically does not materially differ from one period to another. Brandes has not departed from them or sought to water down how we apply them. However, our approach is not absolutely rigid: we have adapted our understanding and application of our value-seeking process by deploying intelligent flexibility, as we think Graham would advise.

For example, we have seen a meaningful shift in how value is created over the past 20-plus years, where capital invested in intangible assets, like intellectual property, brands or research and development, has become more prominent. Intangible assets may not always be accurately captured on the balance sheet under current generally accepted accounting principles, and therefore, possibly not reflected in the stated book value of a company.

In today’s global economy, stated book value’s efficacy as a measure of value has become less useful, especially for a large subset of the investible universe. It is not a metric that we have abandoned completely, but one that is more relevant for our analysis of capital-intensive industries.

For knowledge-intensive industries, we either have to make thoughtful adjustments to book value to reflect economic reality or rely on other metrics that are more indicative of value in those industries.

Technological and competitive disruption has always been a part of value investing, but there is a legitimate argument that the speed and intensity of disruption has increased. The internet has facilitated competitive transparency, the cloud has reduced some start-up costs and moats, and network effects have changed the competitive landscape of a number of industries.

So, no, it’s not different this time as far as our emphasis on seeking out undervalued companies offering a margin of safety is concerned. However, the circumstances in which that occurs can change—and have evolved. Accordingly, we can and will evolve our approach.

In recent years, we’ve seen a significant rise of passive or index-replicating funds. Passive investing does not necessarily align allocations with business fundamentals: sometimes capital will flow toward certain companies merely because of their weight in an index. To us, this disconnect from fundamentals can increase the potential for financial bubbles. Most significantly, from our perspective, index investing

4

does not focus on the margin of safety that is at the heart of value investing. We argue that index-weighted passive investing effectively decouples investing from purposeful choice—money flows to a company not because of fundamentals. We further argue that in such situations, money is “directed” as opposed to “invested.” Directed investing can result in speculation and we are very mindful that Ben Graham dedicated the first chapter of The Intelligent Investor to a discussion on the difference between speculation and investing.

Passive investing alone does not account for the sky-high valuations of recent years. Following the Great Financial Crisis, Quantitative Easing (QE) led to record low interest rates being offered as a stimulus to revive economic activity. The sustained low interest rates have helped skew perceptions about risk, reshape financial conduct and reset expectations.

More recently, a global pandemic caused central banks to keep the money taps open to help economies function. However, COVID-19 followed by the Russian invasion of Ukraine, have also reintroduced an awareness of risk, prompting genuine fears and a renewed interest in downside protection. Ubiquitous global supply challenges stemming from the pandemic and aggravated by the prolonged conflict in Eastern Europe have contributed to inflation levels not seen in most national economies in decades and has also resulted in a resurgence in stock market volatility. Some pundits are talking about “stagflation,” a condition in which prices rise but employment and gross domestic product growth decline.

As the headline of our August 2019 Letter stated: Interest Rates—Lower for Longer Not Lower Forever. At the time, we observed that the record-low rates were likely unsustainable. And now with central banks weighing higher interest rates to help cool down inflation, pervasive geopolitical and economic unease, and accelerating anxieties about the effects of climate change, it’s clear to many investors that risks abound. The rise in inflation, specifically, may require a readjustment in thinking because it effectively touches everyone. When you stand in a grocery line expecting to pay much more to keep your family fed or fill your gas tank and shudder, the price-to-value relationship is starkly obvious. It forces you to look for the best deals, i.e., to search for authentic value.

The situation today and for the foreseeable future may inspire some investors to rethink where they place their investible assets. We would argue for investing with a long-term perspective, one that regards sound fundamentals and a margin of safety as essential today as they have ever been.

Owning “Companies for All Seasons”

In a particularly volatile period of turbulent change and unpleasant disruption, we believe investors may benefit from owning a portfolio of “companies for all seasons,” i.e., those that demonstrate enduring value under a variety of economic and market conditions. And that they should consider avoiding the pricey performers that generate headlines and whose value appears fully recognized (and then some) by the markets. Rather, it is times like we are experiencing when companies the market has seemingly discounted for a variety of reasons may deserve a closer look.

In presenting this line of argument, we make no predictions about future results because forecasts of this nature cannot be made with certainty. At the same time, we

5

cannot ignore recent macroeconomic data that speaks to us loudly and fairly clearly. Nobody knows the future direction of the markets, especially given current circumstances, but that is all the more reason for a value investing style—with its emphasis on identifying underestimated resilience and hidden potential in individual companies. It is why the search for value has defined Brandes from its beginnings: as we’ve said, we’re purpose-built for it.

Our responsibility—and our pledge to our clients—therefore, is to stay the course in our detailed, bottom-up research practices and style fidelity, even when it is not “trendy” to do so.

Your opportunity—toward pursuing your long-term financial goals—is to re-explore value in light of the economic/financial conditions we’ve described in this Letter. Is your allocation to value—that is, to true value—where you want it to be?

Ultimately, we ask you to reconsider the value-seeking journey. The conditions are promising because we expect the external drivers described in this letter—high inflation and the potential for higher interest rates to combat it—will likely persist for some time. The indicators are robust and compelling.

Thank you,

Brandes Investment Partners

Price/Book: Price per share divided by book value per share.

Price/Earnings: Price per share divided by earnings per share.

Past performance is not a guarantee of future results. One cannot invest directly in an index.

This material is intended for informational purposes only. The information provided in this material should not be considered a recommendation to purchase or sell any particular security.

It should not be assumed that any security transactions, holdings or sectors discussed were or will be profitable, or that the investment recommendations or decisions we make in the future will be profitable or will equal the investment performance discussed herein. Strategies discussed are subject to change at any time by the investment manager in its discretion due to market conditions or opportunities. Market conditions may impact performance. The performance results presented were achieved in particular market conditions which may not be repeated. Moreover, the current market volatility and uncertain regulatory environment may have a negative impact on future performance. The Brandes investment approach tends to result in portfolios that are materially different than their benchmarks with regard to characteristics such as risk, volatility, diversification, and concentration. Diversification does not assure a profit or protect against a loss in a declining market. International and emerging markets investing is subject to certain risks such as currency fluctuation and social and political changes; such risks may result in greater share price volatility.

The foregoing reflects the thoughts and opinions of Brandes Investment Partners® exclusively and is subject to change without notice.

Brandes Investment Partners® is a registered trademark of Brandes Investment Partners, L.P. in the United States and Canada.

6

Brandes International Equity Fund

Dear Fellow Investor,

The net asset value of the Brandes International Equity Fund (Class I Shares) declined 24.83% in the year ended September 30, 2022. During the same period, the MSCI EAFE Index declined 25.13%.

From a country perspective, holdings in Brazil and Canada helped performance. Energy firms Petrobras (Brazil) and Cameco Corporation (Canada) were top performers in the Fund, both experiencing meaningful share price appreciation over the trailing twelve-month period. U.K.-based energy equipment & services company TechnipFMC also contributed materially, while certain other U.K. holdings held up well in the declining market environment (e.g., tobacco firm Imperial Brands and household products business Reckitt Benckiser Group).

From an industry perspective, Fund holdings in commercial services & supplies (e.g., Societe BIC) and chemicals (e.g., BASF) aided returns. Other contributors included Brazil-based beverage company Ambev and diversified telecommunication services firm Telefonica Brasil, as well as Spanish oil & gas firm Repsol.

The most significant detractors were holdings in Russia (Mobile TeleSystems and Surgutneftegas). Our thoughts continue to be with the people of Ukraine, as well as those in Russia that are advocating for peace. Other performance detractors included Japanese automaker Honda Motor, Spanish biotechnology firm Grifols, and German health care company Fresenius.

Select Portfolio Activity

The investment committee initiated positions in several companies over the year, including Germany-based software company SAP, Dutch health care equipment company Philips, Austria-domiciled bank Erste Group, and U.K.-based industrial company Rolls-Royce. Other major activity included the full sales of Spain-based oil firm Repsol and U.K. household products company Reckitt Benckiser. Both holdings appreciated to our estimates of intrinsic value, and we decided to reallocate the capital to what we consider better investment opportunities.

SAP is a leader in enterprise resource planning (ERP) software, which includes applications for payroll, procurement, finance, manufacturing, and operations. We believe enterprise software is an attractive industry with high switching cost, low capital intensity and robust returns on equity. SAP has historically traded at a premium relative to the broad market, largely due to its dominant position in an appealing growth industry, and the scarcity of technology-related investment opportunities in Europe relative to the United States. However, because SAP’s ERP software was heavily customized and difficult to upgrade, its growth rate lagged that of many of its peers, leading the company to turn to acquisitions for growth.

Past performance is not a guarantee of future results.

7

Brandes International Equity Fund

SAP has delivered disappointing earnings as it tried to balance integrating its acquisitions with moving its applications to the cloud, both of which have proven challenging for the company. As a result, its share price has dropped near a five-year low, making the company more attractive to us.

Although SAP may continue to deliver subdued financial results in the short term, we believe its business strategy, combined with its recent record of execution, positions it well for the long term, which is the investment horizon for us. Its strong focus on cloud migration corresponds well with enterprise customers’ urgent need to improve the flexibility and agility of their enterprise application software as they grappled with the pandemic-triggered disruptions and uncertainties over the past two years. SAP’s effort to offer a fully integrated technology solution should serve well as the foundation for both its organically developed software and its acquired software. This, in turn, should enable SAP to revive its organic growth rate as it will be easier for customers to buy and implement additional software modules, which was not the case with on-premise software. Even though its short-term financial results may be depressed due to frontloaded expenses associated with both efforts (integration and cloud migration), we believe these projects will help SAP achieve organic growth that should benefit its operating leverage and profitability over the longer term. We have seen this happen with other enterprise software firms that have gone through a similar multi-year transitional period. As such, at its current valuation, SAP represents a compelling long-term risk/reward tradeoff to us.

Rolls-Royce is a U.K.-based conglomerate with a focus on the aerospace and defense industry. The company primarily designs, manufactures and services engines and turbines used in aircraft, ships, and power generators.

Rolls-Royce has struggled for several years, despite what has been a robust civilian aviation market pre-pandemic. The company appears to have made a strategic misstep in exiting the narrow-body engine market in 2012, a market that proved to be more stable and better growing than the wide-body market it strategically focused on. Additionally, Rolls-Royce’s newly designed Trent 1000 engine experienced premature wear, forcing the company to spend significant capital to fix the issue in 2017.

Rolls-Royce seemed to have overcome these challenges in 2019 when its revenue and profitability improved. However, the impact of COVID-19 the following year severely hit Rolls-Royce’s business. Lower utilization of aircraft weighed on demand and uncharacteristically caused a steep fall in the company’s maintenance business, which tended to be more profitable than its manufacturing business. Cash-flow burn in 2020 forced Roll-Royce to issue over $2 billion in equity and divest some non-core businesses. More recently, lingering pandemic concerns, high fuel prices and the risk of a recession in major economies have further hurt investor sentiment. The combination of strategic missteps, the unfortunate timing of a pandemic-triggered moratorium on travel and a potentially weak economic environment led Roll-Royce’s share price to drop to less than one-tenth of its 2019-high.

8

Brandes International Equity Fund

While we acknowledge the near-term future appears bleak for Rolls-Royce, we believe there are reasons for longer-term optimism. In our opinion, cash-flow characteristics in the next downturn should be better as the company can release working capital to cushion any slowdown in orders. We also think that the service business should continue to recover as pandemic restrictions ease and aircraft utilization increases. Even a recessionary level of activity in the service business would be an improvement over the past couple of years. When activity potentially picks up again, Rolls-Royce is poised, in our view, to resume its duopoly position in an industry with high barriers to entry and should benefit from the next aerospace cycle. Overall, Rolls-Royce’s current market valuations are attractive enough for us to take the near-term cyclical risk and initiate a measured allocation to the company.

Looking Forward

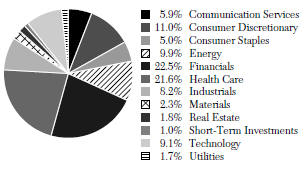

As of September 30, 2022, the Brandes International Equity Fund held its key overweights to communication services, health care and consumer staples, while maintaining significantly lower allocations to technology and industrials than the benchmark. Geographically, we continued to have overweight positions in France and emerging markets, and underweight positions in Australia and Japan. We believe the differences between the Fund’s portfolio and the benchmark continue to make it an attractive complement to index-tracking or growth-oriented alternatives.

A variety of headwinds face international stocks today, ranging from elevated inflation, slowing economic growth and recession concerns to energy risk and political as well as regulatory uncertainties. While our overall positioning is driven by a bottom-up stock selection with a focus on the long term, we do consider many of these concerns when we analyze an investment opportunity, determining how they can impact the fundamentals of a business and comparing our intrinsic value estimate against what is currently being priced in by the market. We believe the Fund’s current positioning offers an attractive opportunity for long-term investors. Compared to the benchmark, the Fund generally has less cyclical or what we consider expensive growth exposure, as seen through our underweights to technology, industrials, and materials. In contrast, the Fund provides more defensive exposure, as highlighted by our overweights to consumer staples and health care. Additionally, our allocation to companies in the energy and financials sectors, in which we also hold overweight positions, may benefit from rising energy prices and interest rates.

As of September 30, 2022, the overall international equity market (MSCI EAFE) traded among its largest discount ever relative to the U.S. market (MSCI USA) based on valuation metrics such as price/cash flow, forward price/earnings and EV/sales, while offering exposure to many well positioned global and domestic oriented companies. Although the strong U.S. dollar has been a headwind for international stocks for the last decade, and particularly so this past year or two, it is reaching levels only seen twice in the last 50 years. Both times boded well for the subsequent returns of international

9

Brandes International Equity Fund

stocks as companies operating in cheaper currencies were better positioned with a lower cost basis and an eventual recovery in growth.

In addition to international stocks trading at historically large discounts to U.S. stocks, international value stocks are trading at even more attractive levels. MSCI EAFE Value continues to trade at near record level discounts to MSCI EAFE Growth on a variety of valuation metrics. Large discount levels, such as the ones we see today, have historically portended attractive returns over a long-term time horizon for value stocks, and the Fund has tended to do well when value stocks did well. Moreover, the current margin of safety exhibited by the Fund’s portfolio is among the highest we have observed in the last 15 or so years, outside of the peaks seen during the most dramatic crises.

We remain optimistic about the prospects of the Brandes International Equity Fund and appreciate your continued trust.

Sincerely yours,

The Brandes International Large-Cap Investment Committee

Brandes Investment Trust

Cash Flow: The amount of cash generated minus the amount of cash used by a company in a given period.

EV/Sales: Compares the enterprise value of a company to its annual sales.

Forward Price/Earnings: Price per share divided by expected earnings per share.

Price/Book: Price per share divided by book value per share.

Price/Cash Flow: Price per share divided by cash flow per share.

Margin of Safety: The discount of a security’s market price to what the firm believes is the intrinsic value of that security.

Working Capital: Current assets minus current liabilities; a measure of a company’s efficiency and short-term financial health.

Past performance is not a guarantee of future results.

Diversification does not assure a profit or protect against a loss.

Because the values of the Fund’s investments will fluctuate with market conditions, so will the value of your investment in the Fund. You could lose money on your investment in the Fund, or the Fund could underperform other investments. The values of the Fund’s investments fluctuate in response to the activities of individual companies and general stock market and economic conditions. In addition, the performance of foreign securities depends on the political and economic environments and other overall economic conditions in the countries where the Fund invests. Emerging country markets involve greater risk and volatility than more developed markets. Some emerging markets countries may have fixed or managed currencies that are not free-floating against the U.S. dollar. Certain of these currencies have experienced, and may experience in the future, substantial fluctuations or a steady devaluation relative to

10

Brandes International Equity Fund

the U.S. dollar. Value stocks typically are less volatile than growth stocks; however, issues of value stocks typically have a lower expected growth rate in earnings and sales than issues of growth stocks.

Please refer to the Schedule of Investments in the report for complete holdings information. Fund holdings, geographic allocations and/or sector allocations are subject to change at any time and are not considered a recommendation to buy or sell any security.

The foregoing reflects the thoughts and opinions of Brandes Investment Partners® exclusively and is subject to change without notice.

Brandes Investment Partners® is a registered trademark of Brandes Investment Partners, L.P. in the United States and Canada.

Must be preceded or accompanied by a prospectus.

Index Guide

The MSCI EAFE Index with net dividends captures large and mid cap representation of developed market countries excluding the U.S. and Canada.

The MSCI EAFE Value Index with net dividends captures large and mid cap securities across developed market countries, excluding the United States and Canada, exhibiting value style characteristics, defined using book value to price, 12-month forward earnings to price, and dividend yield.

The MSCI EAFE Growth Index with net dividends captures large and mid cap securities across developed market countries, excluding the United States and Canada, exhibiting growth style characteristics, defined using long-term forward earnings per share (EPS) growth rate, short-term forward EPS growth rate, current internal growth rate, long-term historical EPS growth trend, and long-term historical sales per share growth trend.

The MSCI USA Index with gross dividends measures the performance of the large and mid cap segments of the U.S. equity market.

MSCI has not approved, reviewed or produced this report, makes no express or implied warranties or representations and is not liable whatsoever for any data in the report. You may not redistribute the MSCI data or use it as a basis for other indices or investment products.

One cannot invest directly in an index.

The Brandes International Equity Fund is distributed by ALPS Distributors, Inc.

11

Brandes International Equity Fund

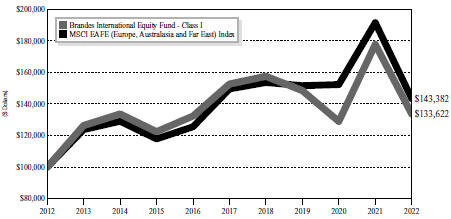

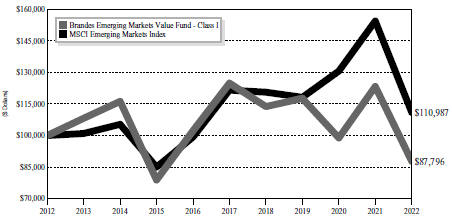

The following chart compares the value of a hypothetical $100,000 investment in the Brandes International Equity Fund – Class I from September 30, 2012 to September 30, 2022 with the value of such an investment in the MSCI EAFE (Europe, Australasia and Far East) Index for the same period.

Value of $100,000 Investment vs MSCI

EAFE (Europe, Australasia and Far East) Index (Unaudited)

| Average Annual Total Return Periods Ended September 30, 2022 | ||||||||||||||||||||

| One Year | Three Years | Five Years | Ten Years | Since Inception(1) | ||||||||||||||||

Brandes International Equity Fund | ||||||||||||||||||||

Class A(2) | -25.05 | % | -3.72 | % | -2.87 | % | 2.71 | % | 5.79% | |||||||||||

Class A (2) (with maximum sales charge) | -29.37 | % | -5.60 | % | -4.02 | % | 2.10 | % | 5.55% | |||||||||||

Class C(3) | -25.64 | % | -4.36 | % | -3.55 | % | 2.11 | % | N/A | |||||||||||

Class C (3) (with maximum sales charge) | -26.36 | % | -4.36 | % | -3.55 | % | 2.11 | % | N/A | |||||||||||

Class I | -24.83 | % | -3.44 | % | -2.63 | % | 2.94 | % | 6.03% | |||||||||||

Class R6(4) | -24.76 | % | -3.36 | % | -2.51 | % | 3.05 | % | 6.10% | |||||||||||

MSCI EAFE (Europe, Australasia and Far East) Index | -25.13 | % | -1.83 | % | -0.84 | % | 3.67 | % | 3.83% | |||||||||||

| (1) | The inception date is January 2, 1997. |

| (2) | Performance shown prior to January 31, 2011 for Class A shares reflects the performance of Class I shares adjusted to reflect Class A expenses. |

| (3) | Performance shown prior to January 31, 2013 for Class C shares reflects the performance of Class I shares adjusted to reflect Class C expenses. The Class C shares’ average annual total return for the 10-year period assumes that Class C shares automatically converted to Class A shares 8 years after the start of the period. |

12

Brandes International Equity Fund

The Class C shares’ average annual total return for the since inception period cannot be calculated as the Class A shares did not yet exist 8 years after the Fund’s inception date.

| (4) | Performance shown prior to February 1, 2016 for Class R6 shares reflects the performance of Class I shares adjusted to reflect Class R6 expenses. |

Performance data quoted represents past performance; past performance does not indicate future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 800-331-2979.

The returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Brandes Investment Partners, L.P., the Advisor, has a fee waiver arrangement in place to limit the Fund’s annual operating expenses.

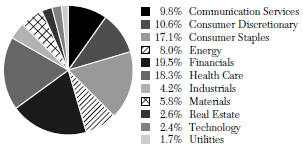

Sector Allocation as a Percentage of Total Investments as of

September 30, 2022 (Unaudited)

The sector classifications represented in the graph above are in accordance with Global Industry Classification Standard (GICS®), which was developed by and/or is the exclusive property of MSCI, Inc. and Standard & Poor’s Financial Services LLC.

13

Dear Fellow Investor,

The net asset value of the Brandes Global Equity Fund (Class I Shares) declined 18.08% in the twelve months ended September 30, 2022. During the same period, the MSCI World Index declined 19.63%.

The Fund’s performance was helped by solid contributions from holdings in health care providers and services (e.g., McKesson, Cigna, Cardinal Health) and pharmaceuticals (e.g., Merck, Pfizer, Euroapi). Additionally, a continued rise in energy prices benefited our oil-related holdings, such as Shell, BP, and Total Energies. Other contributors included U.K. based tobacco manufacturer Imperial Brands, U.S. food products company Ingredion, and energy equipment & services giant Halliburton, which all held up well during the declining market environment.

A variety of concerns led to market declines in the period, from geopolitical risks to inflation, as well as concerns around future economic growth. As a result, certain cyclically oriented companies were some of the weakest performers, along with technology-related companies, which continued to see their valuations compress amid rising interest rates.

The Fund’s most significant detractors were holdings in banks (e.g., Erste Group Bank, Citigroup, Bank of America) and media (e.g., Comcast, WPP, Publicis Groupe), along with Brazilian regional jet manufacturer Embraer and South Korean technology company Samsung Electronics. China-based internet company Alibaba was also a notable detractor. The company continued to deal with market concerns about China’s regulatory environment and the extension of the country’s zero-tolerance COVID policy, which has dampened consumer demand.

Lastly, Spain-based blood plasma company Grifols saw its shares decline after announcing weaker-than-expected short-term earnings as it continues to deal with effects from COVID-19 on its recovery. Grifols has been materially affected by COVID-19 as initial shelter-in place orders and government financial support led to a significant drop in plasma collection in 2020 and 2021. While plasma collections have recovered, the resulting impact in Grifols’ financial results won’t likely be seen until next year because plasma-derived products require a six-month quarantine. Additionally, in anticipation of an increase in long-term demand for blood plasma-derived products, Grifols has been ramping up its spending to build more collection centers, which has hurt its short-term results and increased its balance sheet leverage. Longer-term, we believe Grifols offers an attractive opportunity given the likelihood of blood-plasma supply recovery and the potential improvement of the company’s margins and earnings from today’s depressed levels.

Past performance is not a guarantee of future results.

14

Brandes Global Equity Fund

Select Portfolio Activity

The global large-cap investment committee initiated positions in several companies, including software company SAP and semiconductor equipment company Applied Materials, as well as industrial company Rolls-Royce.

SAP is a leader in enterprise resource planning (ERP) software, which includes applications for payroll, procurement, finance, manufacturing, and operations. We believe enterprise software is an attractive industry with high switching cost, low capital intensity and robust returns on equity. SAP has historically traded at a premium relative to the broad market, largely due to its dominant position in an appealing growth industry, and the scarcity of technology-related investment opportunities in Europe relative to the United States. However, because SAP’s ERP software was heavily customized and difficult to upgrade, its growth rate lagged that of many of its peers, leading the company to turn to acquisitions for growth. SAP has delivered disappointing earnings as it tried to balance integrating its acquisitions with moving its applications to the cloud, both of which have proven challenging for the company. As a result, its share price recently dropped near a five-year low, making the company more attractive to us.

Although SAP may still deliver subdued financial results in the short term, we believe its business strategy, combined with its recent record of execution, positions it well for the long term, which is the investment horizon for us.Its strong focus on cloud migration corresponds well with enterprise customers’ urgent need to improve the flexibility and agility of their enterprise application software as they grappled with the pandemic-triggered disruptions and uncertainties over the past two years. Its effort to offer a fully integrated technology solution should serve well as the foundation for both SAP’s organically developed software and acquired software. This, in turn, should enable SAP to revive its organic growth rate as it will be easier for customers to buy and implement additional software modules, which was the not the case with on-premise software. Even though its short-term financial results may be depressed due to frontloaded expenses associated with both efforts (integration and cloud migration), we believe these projects will help SAP achieve organic growth that should benefit its operating leverage and profitability over the longer term. We have seen this happen with other enterprise software firms that have gone through similar multi-year transitional periods. As such, at its current valuation, SAP represents a compelling long-term risk/reward tradeoff to us.

Rolls-Royce is a U.K.-based conglomerate with a focus on the aerospace and defense industry. The company primarily designs, manufactures and services engines and turbines used in aircraft, ships, and power generators.

Rolls-Royce has struggled for several years, despite what has been a robust civilian aviation market pre-pandemic. The company appears to have made a strategic misstep in exiting the narrow-body engine market in 2012, a market that proved to be more

15

Brandes Global Equity Fund

stable and better growing than the wide-body market it strategically focused on. Additionally, Rolls-Royce’s newly designed Trent 1000 engine experienced premature wear, forcing the company to spend significant capital to fix the issue in 2017.

Rolls-Royce seemed to have overcome these challenges in 2019 when its revenue and profitability improved. However, the impact of COVID-19 the following year severely hit Rolls-Royce’s business. Lower utilization of aircraft weighed on demand and uncharacteristically caused a steep fall in the company’s maintenance business, which tended to be more profitable than its manufacturing business. Cash-flow burn in 2020 forced Roll-Royce to issue over $2 billion in equity and divest some non-core businesses. More recently, lingering pandemic concerns, high fuel prices and the risk of a recession in major economies have further hurt investor sentiment. The combination of strategic missteps, the unfortunate timing of a pandemic-triggered moratorium on travel and a potentially weak economic environment led Roll-Royce’s share price to drop to less than one-tenth of its 2019-high.

While we acknowledge the near-term future appears bleak for Rolls-Royce, we believe there are reasons for longer-term optimism. In our opinion, cash-flow characteristics in the next downturn should be better as the company can release working capital to cushion any slowdown in orders. We also think that the service business should continue to recover as pandemic restrictions ease and aircraft utilization increases. Even a recessionary level of activity in the service business would be an improvement over the past couple of years. When activity potentially picks up again, Rolls-Royce is poised, in our view, to resume its duopoly position in an industry with high barriers to entry and should benefit from the next aerospace cycle. Overall, Rolls-Royce’s current market valuations are attractive enough for us to take the near-term cyclical risk and initiate a measured allocation to the company.

Beyond these new purchases, other major fund activity included the full sales of Mexico-based Fomento Economico Mexicano (FEMSA) and American food products company Ingredion.

The investment committee bought Ingredion during the market downturn of early 2020. The company’s share price came under pressure due to concerns around global trade, as well as the risk of a significant recession as COVID-19 began to spread globally. However, we thought Ingredion offered an attractive long-term opportunity as it had exposure to the growing specialty ingredients market and at its valuation, it also offered a significant margin of safety. Over our holding period, the company has executed well and its share price climbed significantly. When it reached our estimate of its intrinsic value, we divested.

Looking Forward

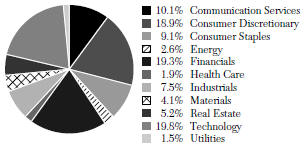

As of September 30, 2022, the Brandes Global Equity Fund held its key positions in the economically sensitive financials and energy sectors, and the more defensive health care sector. Our overall weight to the health care sector hasn’t changed materially this

16

Brandes Global Equity Fund

year. However, our relative overweight decreased as our holdings performed well, and we pared some of our exposure, even while health care became a larger part of the benchmark. Our energy overweight also did well, and while we have slightly reduced our exposure to some oil and gas companies, our relative overweight has also narrowed given the sector’s strong performance in the benchmark. Financials haven’t performed well overall but remain our largest overweight as we believe our holdings are well capitalized, trade at attractive valuation levels and should benefit from a rising interest rate environment.

Our most significant underweight remains in the technology sector. However, that gap has narrowed somewhat as we have added to a number of our holdings and initiated a position in SAP as mentioned above, while the underperformance of the sector has led to it being a smaller part of the index. The decline in market valuations globally has helped expand our opportunity set as some companies within the technology sector or other cyclically oriented areas are starting to look more attractive.

Geographically, we remained overweight in the United Kingdom, France and emerging markets, while underweight in the United States and Japan. We believe the differences between our portfolio and the broader market continue to make the Fund an intelligent complement to index-tracking or growth-oriented alternatives.

Looking ahead, we remain optimistic about the prospects for the Global Equity Fund given the current valuation discounts of value stocks to the market in general and the Fund’s history of outperforming the MSCI World Value Index during periods of strong value performance.

Thank you for the trust you have placed in us.

Sincerely yours, The Brandes Global Large-Cap Investment Committee

Brandes Investment Trust

Cyclically Oriented Companies: Those following the cycles of an economy through expansion, peak, recession and recovery, including companies that sell items that consumers buy more during a booming economy but spend less on during a recession.

Intrinsic Value: The actual value of a company or an asset based on an underlying perception of its true value by the investment committee.

Margin of Safety: The discount of a security’s market price to what the firm believes is the intrinsic value of that security.

Working Capital: Current assets minus current liabilities; a measure of a company’s efficiency and short-term financial health.

Past performance is not a guarantee of future results.

Diversification does not assure a profit or protect against a loss.

Because the values of the Fund’s investments will fluctuate with market conditions, so will the value of your investment in the Fund. You could lose money on your investment

17

Brandes Global Equity Fund

in the Fund, or the Fund could underperform other investments. The values of the Fund’s investments fluctuate in response to the activities of individual companies and general stock market and economic conditions. In addition, the performance of foreign securities depends on the political and economic environments and other overall economic conditions in the countries where the Fund invests. Emerging country markets involve greater risk and volatility than more developed markets. Some emerging markets countries may have fixed or managed currencies that are not free-floating against the U.S. dollar. Certain of these currencies have experienced, and may experience in the future, substantial fluctuations or a steady devaluation relative to the U.S. dollar. Value stocks typically are less volatile than growth stocks; however, issues of value stocks typically have a lower expected growth rate in earnings and sales than issues of growth stocks.

Please refer to the Schedule of Investments in the report for complete holdings information. Fund holdings, geographic allocations and/or sector allocations are subject to change at any time and are not considered a recommendation to buy or sell any security.

The foregoing reflects the thoughts and opinions of Brandes Investment Partners® exclusively and is subject to change without notice.

Brandes Investment Partners® is a registered trademark of Brandes Investment Partners, L.P. in the United States and Canada.

Must be preceded or accompanied by a prospectus.

Index Guide

The MSCI World Index with net dividends captures large and mid cap representation of developed markets.

The MSCI World Value Index with net dividends captures large and mid cap securities across developed market countries exhibiting value style characteristics, defined using book value to price, 12-month forward earnings to price, and dividend yield.

MSCI has not approved, reviewed or produced this report, makes no express or implied warranties or representations and is not liable whatsoever for any data in the report. You may not redistribute the MSCI data or use it as a basis for other indices or investment products.

One cannot invest directly in an index.

The Brandes Global Equity Fund is distributed by ALPS Distributors, Inc.

18

Brandes Global Equity Fund

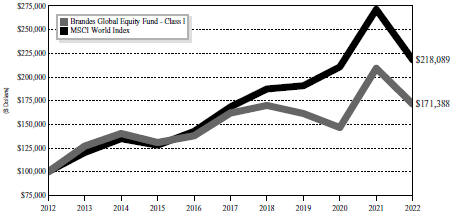

The following chart compares the value of a hypothetical $100,000 investment in the Brandes Global Equity Fund – Class I from September 30, 2012 to September 30, 2022 with the value of such an investment in the MSCI World Index for the same period.

Value of $100,000 Investment vs MSCI

World Index (Unaudited)

| Average Annual Total Return Periods Ended September 30, 2022 | ||||||||||||||||||||

| One Year | Three Years | Five Years | Ten Years | Since Inception(1) | ||||||||||||||||

Brandes Global Equity Fund | ||||||||||||||||||||

Class A(2) | -18.30 | % | 1.74 | % | 0.88 | % | 5.27 | % | 5.09% | |||||||||||

Class A (2) (with maximum sales charge) | -23.00 | % | -0.25 | % | -0.30 | % | 4.65 | % | 4.64% | |||||||||||

Class C(3) | -18.91 | % | 0.98 | % | 0.13 | % | 4.65 | % | 4.62% | |||||||||||

Class C (3) (with maximum sales charge) | -19.67 | % | 0.98 | % | 0.13 | % | 4.65 | % | 4.62% | |||||||||||

Class I | -18.08 | % | 2.01 | % | 1.14 | % | 5.54 | % | 5.33% | |||||||||||

MSCI World Index | -19.63 | % | 4.56 | % | 5.30 | % | 8.11 | % | 7.95% | |||||||||||

| (1) | The inception date is October 6, 2008. |

| (2) | Performance shown prior to January 31, 2011 for Class A shares reflects the performance of Class I shares adjusted to reflect Class A expenses. |

| (3) | Performance shown prior to January 31, 2013 for Class C shares reflects the performance of Class I shares adjusted to reflect Class C expenses. The Class C shares’ average annual total return for the 10-year and since inception periods assumes that Class C shares automatically converted to Class A shares 8 years after the start of the period. |

Performance data quoted represents past performance; past performance does not indicate future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than

19

Brandes Global Equity Fund

their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 800-331-2979.

The returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Brandes Investment Partners, L.P., the Advisor, has a fee waiver arrangement in place to limit the Fund’s annual operating expenses.

Sector Allocation as a Percentage of Total Investments as of

September 30, 2022 (Unaudited)

The sector classifications represented in the graph above are in accordance with Global Industry Classification Standard (GICS®), which was developed by and/or is the exclusive property of MSCI, Inc. and Standard & Poor’s Financial Services LLC.

20

Brandes Emerging Markets Value Fund

Dear Fellow Investor,

The net asset value of the Brandes Emerging Markets Value Fund (Class I Shares) declined 28.79% in the year ended September 30, 2022. During the same period, the MSCI Emerging Markets Index declined 28.11%.

A variety of headwinds face emerging market stocks today, ranging from elevated inflation, slowing economic growth/recession concerns and COVID lockdowns to energy risk and political as well as regulatory uncertainties. Within the Brandes Emerging Markets Value Fund, holdings in Russia were the most significant detractors over the trailing twelve-month (TTM) period. Our thoughts continue to be with the people of Ukraine, as well as those in Russia that are advocating for peace.

Meanwhile, select holdings in China also declined, although our underweight and stock selection in the country helped returns relative to the benchmark.

Engines manufacturer Weichai Power issued a warning in September 2022 that its subsidiary KION, an automated logistics solutions provider, would record a material loss from ongoing inefficiencies due to supply issues and rising input costs. This, coupled with a continued downcycle in its heavy-duty truck segment, has contributed to the company’s share price decline.

Internet company Alibaba hurt returns as market concerns persisted around the regulatory environment in China and the uncertain future of its listing in the U.S., as well as the continuation of China’s zero-Covid policy and its effect on consumer demand.

Besides Weichai and Alibaba, Chinasoft International, China Education Group and Ping An Insurance also weighed on performance.

Our underweights to India and Saudi Arabia detracted from relative returns. From an industry perspective, several technology-related holdings weighed on performance, notably Samsung Electronics, Taiwan Semiconductor Manufacturing Company, and SK Hynix.

Strong performers in the Fund included select Brazilian holdings such as oil and gas firm Petrobras and diversified telecommunications company Telefonica Brasil. Additionally, China’s Wens Foodstuffs Group and Galaxy Entertainment Group Limited, as well as U.K.-based Vivo Energy saw their share prices rise. The Fund’s positions in Greece (e.g., Hellenic Telecommunications) and Czech Republic (e.g., O2 Czech Republic) also held up relatively well in a declining market.

Select Portfolio Activity

During the period, the emerging markets investment committee initiated positions in several businesses including Kimberly-Clark de Mexico, IndusInd Bank, Millicom International Cellular, and LG Household & Healthcare.

Past performance is not a guarantee of future results.

21

Brandes Emerging Markets Value Fund

Kimberly-Clark de Mexico (KCM) is the leading producer of tissue and fiber-based personal care products in Mexico, where it holds 60% market share. The company derives over 90% of its revenue from baby diapers and tissue products, with feminine care products making up the rest. Historically, KCM has boasted solid operating margins of more than 20% due to its strong position in Mexico’s brand-conscious consumer products market. However, despite the high margins, KCM’s profitability has recently fluctuated as the company has had trouble passing inflationary raw material costs on to end consumers. Approximately two-thirds of KCM’s manufacturing costs (paper and pulp products and oil derivatives) are in U.S. dollars, so inflation and currency fluctuations present challenges, especially considering that the Mexican consumer sector is not particularly strong. In the past year as a result of these dynamics, KCM’s EBITDA margin declined to its lowest level since 2005. Management has been pushing through price increases, resulting in lost market share as its competitors were slower to react. We believe the market has overly punished KCM due to the near-term margin pressure, creating a buying opportunity. This is not the first time KCM has dealt with raw material cost headwinds, and the company has a history of overcoming such challenges over time as pricing and volumes eventually offset short-term cost pressures. Furthermore, pulp is a raw material for which pricing has been elevated lately and tends to be cyclical. With new capacity coming to market over the next few years, we expect pulp input costs to fall.

Founded in 1994, Mumbai-based IndusInd Bank (IIB) is the fifth-largest private bank in India by market share (based on assets). Over the past several years, IIB has faced a variety of internal and external issues. Between 2018 and 2020, the bank came under pressure following the defaults of several corporate and infrastructure finance companies it had exposure to. During the pandemic, IIB struggled to manage its vehicle and microfinance loans, which require more high-touch, in-person access to customers. Additionally, the company experienced some government deposit outflows driven by risk aversion toward mid-sized private sector banks.

We believe IndusInd is now on an underappreciated recovery path, having taken the following actions:

Weighing its recovery potential in a credit growth cycle against its past challenges, we believe IIB represents an attractive investment opportunity.

Headquartered in Luxembourg, Millicom provides wireless and fixed-line services to 49 million customers across nine countries in Latin America (LatAm). Millicom differs from its LatAm peers in its focus on smaller countries, either by early entry or by acquisition, a strategy that has helped it gain top market share positions in most of the countries in which it operates. Given the low adoption rates of wireless data services across a population of nearly 120 million, meaningful growth opportunities persist across Millicom’s geographic markets.

22

Brandes Emerging Markets Value Fund

Although we have followed Millicom for more than 15 years, this was the first time we purchased its shares. The company underwent a large rights offering that increased its shares outstanding by 70%. This, combined with general market malaise, has put Millicom’s shares under significant pressure.

In our view, Millicom is among the most attractively valued LatAm telecommunications services providers. Its operations are concentrated in countries that have relatively low competition (many are duopolies), lenient regulation and manageable foreign-exchange risk, while offering a favorable macroeconomic outlook. There are several potential catalysts that can unlock the value we see in Millicom, including:

We believe Millicom’s positive attributes outweigh the potential risks, and the share-price decline has created a compelling entry point for an investment in a company with a strong market position and appealing growth opportunity.

LG Household & Health Care (LGHH) is a diversified consumer goods company based in South Korea. The company has enjoyed consistent growth, with revenues growing at a 10-year compounded rate of 13% annually (pre-pandemic) and operating profit at 18%, leading it to become South Korea’s top player in all three of its divisions: Beauty (cosmetic products), Health (health care and household products) and Refreshment (beverages). LGHH’s flagship luxury cosmetics brand, The History of Whoo, has steadily been gaining share in the Chinese beauty market (its main market) as it benefited from the shift in consumer preferences from value to premium products, a trend that is expected to continue in the foreseeable future. However, sales have slowed, mainly due to the strict lockdowns in China and the related decline in the duty-free sales channel. We believe the market is applying an overly harsh scenario of permanently slower sales growth of LGHH’s cosmetic products, providing us with an opportunity to invest in a company with a solid market presence at appealing valuations. In our opinion, LGHH remains well positioned to benefit from the premiumization of China’s beauty market and from a rebound in sales as mobility restrictions ease in its main markets.

During the period, the investment committee sold various positions from the Fund including China-based Wens Foodstuffs, Argentina’s YPF and O2 Czech Republic, as well as Greece’s Hellenic Telecommunications. We exited these positions as the shares appreciated toward our estimates of their intrinsic values.

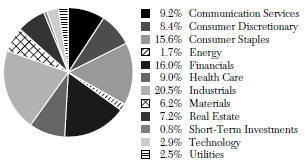

Looking Forward

As of September 30, 2022, the Fund continued to have its largest sector overweights in consumer discretionary and real estate (note that we do not own any real estate holdings in China), while maintaining key underweights in materials, financials, and energy. Mexico and Indonesia were the largest overweights from a country perspective, while India, Taiwan, Saudi Arabia, and China represented our key underweight positions.

We believe the Brandes Emerging Markets Value Fund continues to offer a diversified portfolio with exposure to post-COVID economic reopening (e.g., through holdings in

23

Brandes Emerging Markets Value Fund

air travel, casino, luxury retail), inflation (e.g., holdings in financials may benefit from a rising interest rate environment), and long-term growth drivers in emerging markets (e.g., consumer-related holdings such as e-commerce, food products, apparel, appliances, education). Furthermore, even though the Fund’s portfolio has always stayed true to its value investing style, our value exposure is different than that of a quantitative or factor approach. Emerging markets value stocks (MSCI EM Value) have performed relatively well compared to the broad market (MSCI EM), partly due to classic cyclicals in the energy and materials sectors that benefited from higher commodity prices. We believe valuations in these sectors were already indicative of above mid-cycle profitability prior to the invasion of Ukraine, and they have become even more elevated since then. In our opinion, economically sensitive sectors levered to a potential post-pandemic rebound, such as consumer discretionary (where we hold an overweight relative to the benchmark and the value index), represent a more appealing opportunity today than classic cyclical sectors such as energy and materials.

We believe the Fund’s positioning, combined with its overall attractive valuation levels, bodes well for its returns in the long term. As always, we appreciate your continued trust and remain optimistic about the long-term prospects of the Brandes Emerging Markets Value Fund.

Sincerely yours,

The Brandes Emerging Markets Investment Committee

Brandes Investment Trust

EBITDA: Earnings before interest, taxes, depreciation and amortization.

EBITDA Margin: EBITDA divided by total sales.

Free Cash Flow: Total cash flow from operations less capital expenditures.

Operating Profit: Earnings before interests and taxes.

Operating Margin: Operating income divided by net sales; used to measure a company’s operating efficiency.

Rights Offering: A company’s offer to its existing shareholders to purchase additional shares in proportion to their existing stakes.

Share Buyback: A company’s re-acquisition of its own stock.

Past performance is not a guarantee of future results.

Diversification does not assure a profit or protect against a loss.

Because the values of the Fund’s investments will fluctuate with market conditions, so will the value of your investment in the Fund. You could lose money on your investment in the Fund, or the Fund could underperform other investments. The values of the Fund’s investments fluctuate in response to the activities of individual companies and general stock market and economic conditions. In addition, the performance of foreign securities depends on the political and economic environments and other overall

24

Brandes Emerging Markets Value Fund

economic conditions in the countries where the Fund invests. Emerging markets involve greater risk and volatility than more developed markets. Some emerging markets may have fixed or managed currencies that are not free-floating against the U.S. dollar. Certain of these currencies have experienced, and may experience in the future, substantial fluctuations or a steady devaluation relative to the U.S. dollar. Investments in small and medium capitalization companies tend to have limited liquidity and greater price volatility than investments in larger capitalization companies. Value stocks typically are less volatile than growth stocks; however, issues of value stocks typically have a lower expected growth rate in earnings and sales than issues of growth stocks.

Please refer to the Schedule of Investments in the report for complete holdings information. Fund holdings, geographic allocations and/or sector allocations are subject to change at any time and are not considered a recommendation to buy or sell any security.

The foregoing reflects the thoughts and opinions of Brandes Investment Partners® exclusively and is subject to change without notice.

Brandes Investment Partners® is a registered trademark of Brandes Investment Partners, L.P. in the United States and Canada.

Must be preceded or accompanied by a prospectus.

Index Guide

The MSCI Emerging Markets Index with net dividends captures large and mid cap representation of emerging market countries.

The MSCI Emerging Markets Value Index with net dividends captures large and mid cap securities exhibiting value style characteristics, defined using book value to price, 12-month forward earnings to price, and dividend yield.

MSCI has not approved, reviewed or produced this report, makes no express or implied warranties or representations and is not liable whatsoever for any data in the report. You may not redistribute the MSCI data or use it as a basis for other indices or investment products.

One cannot invest directly in an index.

The Brandes Emerging Markets Value Fund is distributed by ALPS Distributors, Inc.

25

Brandes Emerging Markets Value Fund

The following chart compares the value of a hypothetical $100,000 investment in the Brandes Emerging Markets Value Fund – Class I from September 30, 2012 to September 30, 2022 with the value of such an investment in the MSCI Emerging Markets Index for the same period.

Value of $100,000 Investment vs MSCI

Emerging Markets Index (Unaudited)

| Average Annual Total Return Periods Ended September 30, 2022(1) | ||||||||||||||||||||

| One Year | Three Years | Five Years | Ten Years | Since Inception(2) | ||||||||||||||||

Brandes Emerging Markets Value Fund | ||||||||||||||||||||

Class A | -28.99 | % | -9.50 | % | -7.02 | % | -1.52 | % | 4.87% | |||||||||||

Class A (with maximum sales charge) | -33.08 | % | -11.27 | % | -8.11 | % | -2.10 | % | 4.64% | |||||||||||

Class C(3) | -29.54 | % | -10.03 | % | -7.62 | % | -2.11 | % | N/A | |||||||||||

Class C (3) (with maximum sales charge) | -30.22 | % | -10.03 | % | -7.62 | % | -2.11 | % | N/A | |||||||||||

Class I | -28.79 | % | -9.29 | % | -6.81 | % | -1.29 | % | 5.10% | |||||||||||

Class R6(4) | -28.75 | % | -9.19 | % | -6.70 | % | -1.19 | % | 5.18% | |||||||||||

MSCI Emerging Markets Index | -28.11 | % | -2.07 | % | -1.81 | % | 1.05 | % | 4.83% | |||||||||||

| (1) | Prior to January 31, 2011, the Advisor managed a private investment fund with an investment objective, investment policies and strategies that were, in all material respects, equivalent to those of the Brandes Emerging Markets Value Fund. The performance information shown for the Class I shares for periods before January 31, 2011 is that of the private investment fund and reflects the net expenses of the private investment fund. The performance of the private investment fund prior to January 31, 2011 is based on a calculation method that is different from the standardized calculation method prescribed by the SEC. The performance information shown for the Class A shares has been adjusted to reflect the differences in |

26

Brandes Emerging Markets Value Fund

the net expense ratios between the Class I and A shares. The private investment fund was not registered under the Investment Company Act of 1940 (“1940 Act”) and was not subject to certain investment limitations, diversification requirements, and other restrictions imposed by the 1940 Act and the Internal Revenue Code of 1986, which, if applicable, may have adversely affected its performance.

| (2) | The inception date is August 20, 1996. |

| (3) | Performance shown prior to January 31, 2013 for Class C shares reflects the performance of Class I shares adjusted to reflect Class C expenses. The Class C shares’ average annual total return for the 10-year period assumes that Class C shares automatically converted to Class A shares 8 years after the start of the period. The Class C shares’ average annual total return for the since inception period cannot be calculated as the Class A shares did not yet exist 8 years after the Fund’s inception date. |

| (4) | Performance shown prior to July 11, 2016 for Class R6 shares reflects the performance of Class I shares adjusted to reflect Class R6 expenses. |

Performance data quoted represents past performance; past performance does not indicate future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 800-331-2979.

The returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Brandes Investment Partners, L.P., the Advisor, has a fee waiver arrangement in place to limit the Fund’s annual operating expenses.

Sector Allocation as a Percentage of Total Investments as of

September 30, 2022 (Unaudited)

The sector classifications represented in the graph above are in accordance with Global Industry Classification Standard (GICS®), which was developed by and/or is the exclusive property of MSCI, Inc. and Standard & Poor’s Financial Services LLC.

27

Brandes International Small Cap Equity Fund

Dear Fellow Investor,

The net asset value of the Brandes International Small Cap Equity Fund (Class I Shares) declined 28.04% in the year ended September 30, 2022. During the same period, the S&P Developed Ex-U.S. SmallCap Index declined 33.01%.

A variety of headwinds face international stocks today, ranging from elevated inflation, slowing economic growth and recession concerns to energy risk and political as well as regulatory uncertainties. While our overall positioning in the Fund is driven by bottom-up stock selection with a focus on the long term, we do consider many of these concerns when we analyze an investment opportunity, determining how they can impact the fundamentals of a business and comparing our intrinsic value estimate against what is currently being priced in by the market. Compared to the benchmark, the Brandes International Small Cap Equity Fund generally has less cyclical (or what we currently consider more expensive growth) exposure, as seen through our underweights to technology and materials. In contrast, the Fund provides more defensive exposure, as evidenced by our overweights to the consumer staples and communication services sectors. Additionally, our allocation to companies in the financials sector, in which we also have an overweight position, may benefit from a rising interest rate environment.

Against this backdrop, the Fund’s trailing twelve-month (TTM) performance was helped by holdings in energy equipment & services (e.g., TechnipFMC) and oil gas & consumable fuels (e.g., Cameco Corporation). TechnipFMC’s share price appreciated significantly as oil prices rose and the market has generally become more optimistic about a recovery in oil services activities. Canada-based Cameco, one of the largest uranium producers globally, has recently benefited from a surge in commodity prices. Additionally, Fund returns were helped by allocations to Italian aerospace & defense company Leonardo and Canadian communications equipment firm Sierra Wireless.

Performance detractors in the TTM period included holdings in consumer staples, notably U.K. retailers Marks and Spencer and J Sainsbury, food products companies Greencore Group (Ireland) and Binggrae (South Korea), and Ireland-based beverage firm C&C Group. The weak macroeconomic outlook, particularly in Europe, was a headwind to these companies. However, we believe market sentiment is overly negative, especially given the defensive nature of these businesses.

Other detractors included Brazilian aerospace & defense manufacturer Embraer and German-based health care equipment & supplies company Draegerwerk.

Select Portfolio Activity

The small-cap investment committee initiated a variety of positions during the period, including Ireland-based food products company Greencore Group, Japanese

Past performance is not a guarantee of future results.

28

Brandes International Small Cap Equity Fund

entertainment business DeNA, U.K.-domiciled energy equipment company TechnipFMC and defense technology firm QinetiQ, as well as Hong Kong-based Yue Yuen.

Founded in 1988, Yue Yuen is the world’s largest manufacturer of branded athletic and casual footwear, producing nearly 250 million pairs of shoes in the fiscal year 2020 as an original equipment manufacturer for major brands such as Nike and Adidas, which together account for almost two-thirds of Yue Yuen’s sales, as well as Reebok, Asics, New Balance, and Puma. The company also has a majority stake in sportswear (athletic shoes and apparel) retailer Pou Sheng.

We see significant value potential in Yue Yuen. While volume growth has been muted in recent years as key customers have been working to reduce inventories and demanding shorter lead times, Yue Yuen has maintained a strong pricing power which is attributable to increased popularity of athletic shoes and a style shift toward more complex designs. Provided COVID-related conditions continue to improve, the industry is expected to grow at mid-single digits. Furthermore, we believe Yue Yuen is well positioned to expand its operating margins, which have been negatively affected by forced factory closures and occupancy reductions (for social distancing). Although the timing of the recovery is impossible to predict, it is our opinion that Yue Yuen’s current share price is overly discounted, providing us with what we consider a compelling entry point for an investment.

Based in Ireland, Greencore Group is the leading provider of private-label fresh prepared foods in the United Kingdom, selling fresh sandwiches, salads, sushi and other ready-to-eat meals. Greencore works with grocery retailers to develop their private-label offerings, with nearly half of its revenues coming from strategic partnerships with the U.K.’s Big Four (Tesco, J Sainsbury, Asda and Wm Morrison). The company also caters to what we consider better-growing channels, such as convenience stores.

Prior to COVID-19, the U.K. food-to-go market was growing above global GDP (gross domestic product) amid many structural changes in consumer behavior and expectations by supermarkets. While the pandemic has altered the trajectory of the industry, Greencore has navigated the environment better than expected. Revenue growth and profitability in 2021 exceeded expectations, and the near-term and medium-term outlook for the company is favorable. However, this progress has not been reflected in the company’s share price. New COVID-19 variants and consumer mobility restrictions have weighed on investor sentiment, along with supply-chain and labor challenges, as well as the recent departure of Greencore’s chief executive officer. We believe the market has overreacted to these concerns, creating a buying opportunity in a company with improving fundamentals, a positive growth outlook and an undemanding valuation.

29

Brandes International Small Cap Equity Fund

TechnipFMC (FTI) is the product of a 2016 merger between Technip, a leading engineering, procurement and construction company (EPC), and FMC, a leading provider of subsea production and processing equipment. The rationale of the merger was to combine equipment manufacturing with engineering and construction of subsea oilfields. More recently, the company completed a long-planned separation of its onshore EPC business, making it purely focused on offshore oilfield exploration and development.

With an over 40% market share, FTI is the industry leader in subsea systems, highly engineered capital goods that reside on the seabed producing and processing hydrocarbons. The subsea industry has been in a multi-year slump following a decade of high oil prices. Capital expenditures (capex) among upstream oil and gas companies (FTI’s customer base) reached highs in 2014 and were estimated to be less than half of the peak levels in 2021. In addition to the collapse in capex, there has been a shift of investment to unconventional opportunities on land. The overall effect has been a sustained period of low manufacturing utilization, high price competition and distressed profitability for the subsea industry.