June 16, 2011 Investor Presentation Investor Presentation Exhibit 99.1 |

2 Forward Looking Statements Forward Looking Statements This presentation contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act giving Capital One’s expectations or predictions of future financial or business performance or conditions. Such forward- looking statements include, but are not limited to, statements about the projected impact and benefits of the transaction involving Capital One and ING Direct, including future financial and operating results, the company’s plans, objectives, expectations and intentions and other statements that are not historical facts. These forward-looking statements are subject to numerous assumptions, risks and uncertainties which change over time. Forward-looking statements speak only as of the date they are made, and Capital One assumes no duty to update forward-looking statements. In addition to factors previously disclosed in our filings with the U.S. Securities and Exchange Commission and those identified elsewhere in this presentation, the following factors, among others, could cause actual results to differ materially from forward-looking statements or historical performance: the possibility that regulatory and other approvals and conditions to the transaction are not received or satisfied on a timely basis or at all; the possibility that modifications to the terms of the transactions may be required in order to obtain or satisfy such approvals or conditions; changes in the anticipated timing for closing the transaction; difficulties and delays in integrating Capital One’s and ING Direct’s businesses or fully realizing projected cost savings and other projected benefits of the transaction; business disruption during the pendency of or following the transaction; the inability to sustain revenue and earnings growth; changes in interest rates and capital markets; diversion of management time on transaction-related issues; reputational risks and the reaction of customers and counterparties to the transaction; and changes in asset quality and credit risk as a result of the transaction. Annualized, pro forma, projected and estimated numbers are used for illustrative purposes only, are not forecasts and may not reflect actual results. |

3 • Transaction summary and strategic rationale • Financial overview |

4 Transaction Summary Transaction Summary Transaction Value Form of Consideration to Approvals Expected Closing $9.0 Billion 1 Fixed Number of Capital One shares of approximately 55.9 million (9.9% COF pro forma ownership) Approved by both Boards No Capital One or ING shareholder approval necessary Federal Reserve Board and Dutch Central Bank and certain other regulatory approvals will be necessary Late Q4 2011 / Early Q1 2012 Source of Funds Planned market equity raise prior to closing of approximately $2.0 billion to fund a portion of the cash payment to ING Group Shareholder Agreement One ING Group representative added to Capital One Board ING Group not permitted to sell Capital One shares before the later of 180 days after market equity raise and 90 days after closing Footnotes: 1) Share consideration valued at COF 10-day average closing price of $50.07 for the period ending June 15, 2011. 2) If ING’s stock ownership would exceed 9.9% at closing, the excess will be paid in cash Additional sources of cash consideration: $0.5B financed through cash $3.7B financed through planned issuance of Capital One senior debt ING 1 Fixed cash amount of approximately $6.2 billion 2 |

5 The ING Direct acquisition delivers attractive The ING Direct acquisition delivers attractive financial results and long-term strategic value financial results and long-term strategic value • Accretive to EPS in 2012 • Mid-single digit EPS accretion in 2013 • Accretive to tangible book value per share • ROIC > cost of capital in 2013 • IRR > 20% • Buying without significant premium reduces risks Compelling Strategic Value Attractive Deal Economics • Industry-leading direct banking franchise with national reach • 7 million young, high- income, loyal customers • $80 billion of low cost, stable deposits • Accretive to long-term growth, returns, and capital generation Note: see “Financial Assumptions” in this presentation for underlying assumptions |

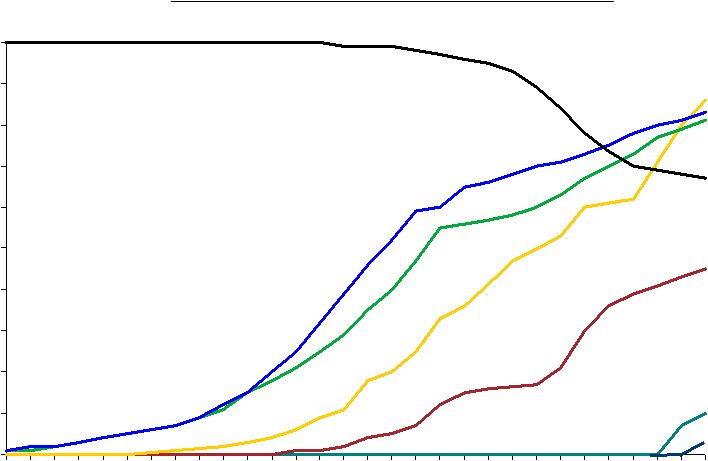

6 $0 $10 $20 $30 $40 $50 $60 $70 $80 $90 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 Savings/ MMDA ING Direct Deposits B Source: SNL Financial (FDIC), Company reports Electric Orange Checking Time ING ING Direct Direct has has grown grown rapidly rapidly to to become become the the nation’s nation’s 15 th largest bank, and by far the largest direct banking franchise largest bank, and by far the largest direct banking franchise 16.2 71.8 60.6 47.2 77.7 75.0 40.0 28.8 9.3 2.9 .7 |

7 Mortgages and investment securities are ING Direct’s Mortgages and investment securities are ING Direct’s predominant assets predominant assets • $29.6B outstanding as of 3/31/11 – $28.7B Fair Value – $0.9B HFI • Majority are mortgage related – $15.0B US Agency backed MBS – $3.7B US Non-Agency MBS – $8.4B US Treasuries and TLGP-backed debt – $1.3B ABS/CMBS – $1.2B European government-backed and supranationals • ~88% rated AAA • $40.7B outstanding as of 3/31/2011 • 62% of portfolio is 2008 or newer vintages • Average original LTV 66% • 30-179 day delinquency rate of 1.2% • Mostly 5 and 7 year ARMs • Weighted average FICO – Original = 755 – Current = 746 • Gross estimated credit mark of $1.7B (~4% of loans) Investment Securities Mortgage Loans |

8 Capital synergy Deposit synergies Opportunity to swap higher-yield Capital One loans for ING assets Achievable cost synergies Capital One can build on ING Direct’s franchise to realize Capital One can build on ING Direct’s franchise to realize greater value for customers, associates and shareholders greater value for customers, associates and shareholders Opportunity to expand and deepen relationships with large and loyal customer base |

9 Capital One has been a successful player in Capital One has been a successful player in direct banking for over a decade direct banking for over a decade $6 $8 $9 $12 $14 $14 $14 $15 $21 $22 $27 $29 $0 $5 $10 $15 $20 $25 $30 $35 Capital One Direct Bank Deposit Balances $B |

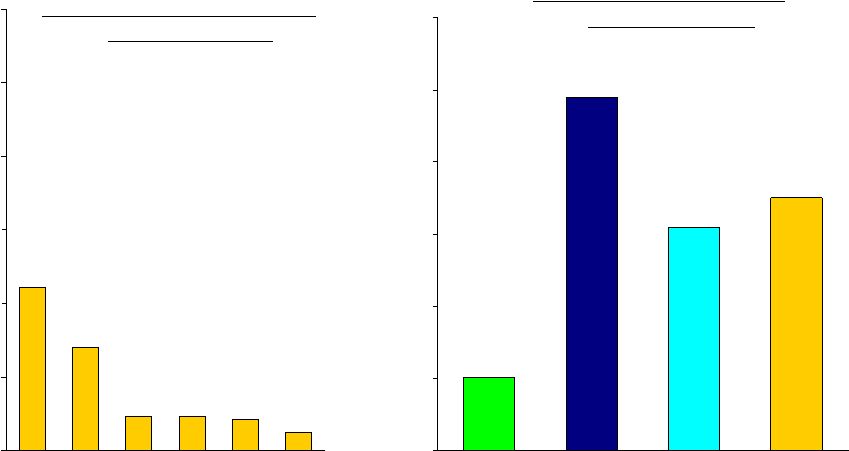

10 ING Direct’s all-in cost of deposits is competitive due ING Direct’s all-in cost of deposits is competitive due in large part to much lower non-interest expense in large part to much lower non-interest expense Interest Expense for Liquid Deposits* (2010) 0.12% 1.11% 0.70% 0.21% 0.23% 0.23% 0.0% 0.5% 1.0% 1.5% 2.0% 2.5% 3.0% ING DirectCapital One PNC USBank BofA JPMChase 0.51% 2.45% 1.75% 1.55% 0.0% 0.5% 1.0% 1.5% 2.0% 2.5% 3.0% ING Direct Typical Large Bank Average Typical Large Bank net of fees Typical Large Bank net of fees and Durbin Non Interest Expense for Liquid Deposits* 1 2 2 2 Source: Company Reports; *Liquid deposits includes non-interest deposits, NOW deposits, money market and savings 1 – Includes operating expenses and marketing for ING Direct, excludes mortgage and ShareBuilder. Data as of YE 2010. 2 - Based on BCG analysis |

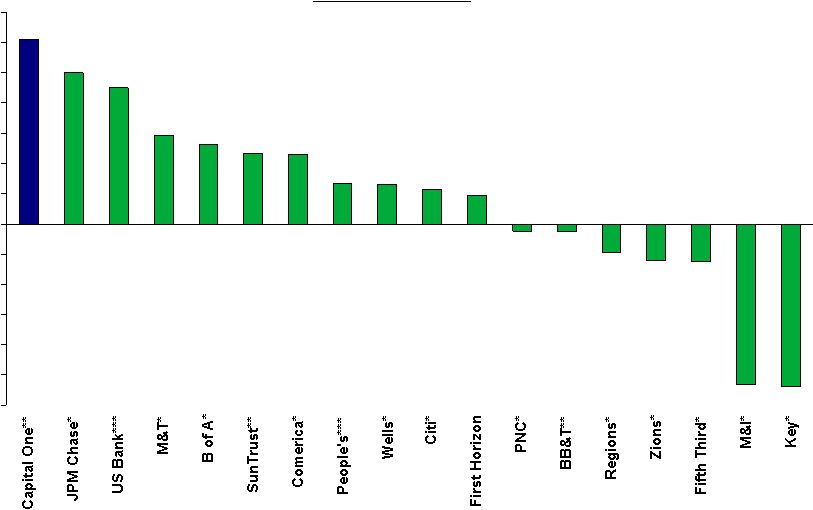

11 We are a leader in deposit growth We are a leader in deposit growth Deposit Growth Q1 2010 – Q1 2011 * Excludes foreign deposits ** Excludes brokered deposits. *** Excludes impact from acquisitions. Additional notes: B of A also excludes “negotiable CDs, public funds, and other time deposits” category. SunTrust excludes both foreign and brokered deposits. Source: Company reports. 10.0% 9.0% 5.9% 5.3% 4.7% 4.6% 2.7% 2.6% 2.3% 1.9% (0.5%)(0.5%) (1.9%) (2.4%) (10.8%) (2.5%) (10.7%) 12.2% -12% -10% -8% -6% -4% -2% 0% 2% 4% 6% 8% 10% 12% 14% |

12 ING Direct deposit customers are exceptionally ING Direct deposit customers are exceptionally loyal loyal ING Direct Annual Customer Attrition 3% 3% 4% 3% 2% 2% 6% 5% 5% 5% 0% 2% 4% 6% 8% 10% 12% 14% 16% 18% 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 5.8% 4.0% 16.2% 0% 2% 4% 6% 8% 10% 12% 14% 16% 18% National average (savings/MMA) ING Direct Capital One National Direct Bank Source: ING Direct; BAI Deposit Performance Benchmarking (May 2010) Annual Customer Attrition 2007-2009 Average average |

13 50% 60% 70% 80% 90% 100% 110% 120% 130% 140% 1 2 3 4 5 6 ING Direct customers maintain and grow ING Direct customers maintain and grow balances over time balances over time *Includes certificate of deposit bookings Source: ING Direct; BAI Deposit Performance Benchmarking (May 2010) 2005 2006 2007 2008 2009 ING Direct Balance View by Cohort* |

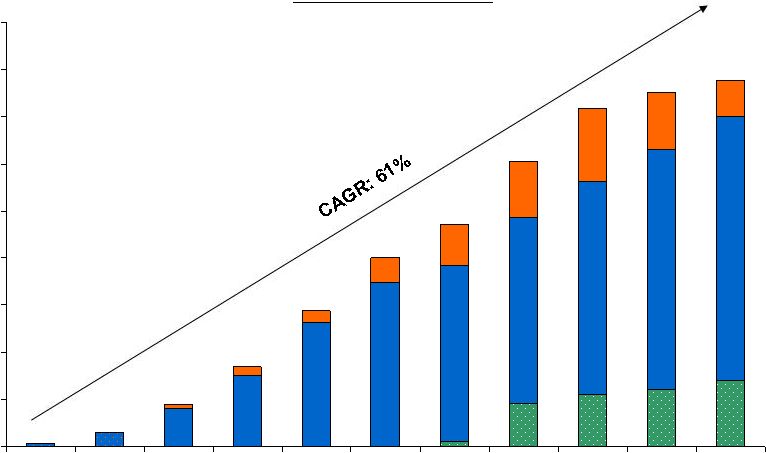

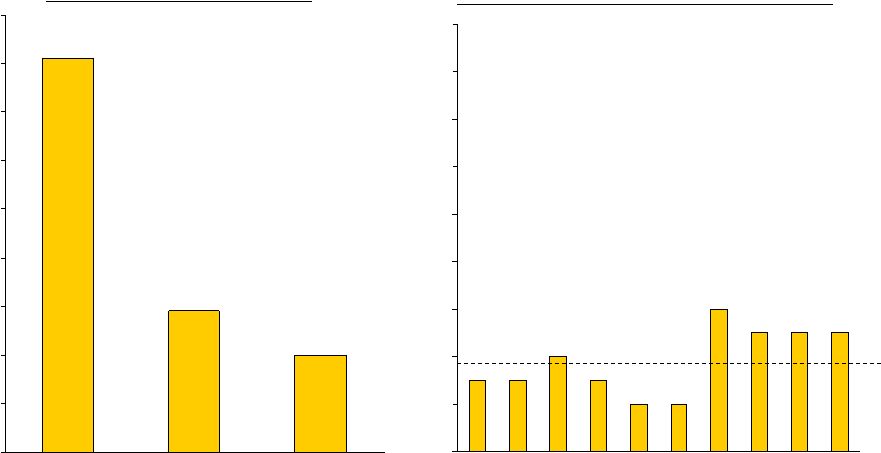

14 A handful of banks are breaking away from the pack A handful of banks are breaking away from the pack to build very large customer bases to build very large customer bases 3 3 3 5 6 7 7 7 8 8 9 9 17 33 37 47 70 76 88 106 0 20 40 60 80 100 120 M Number of Customer Accounts 12/31/2010 Data is U.S. Only for firms with large International presence (Citi, ING, TD Bank); May include account overlap both between segmented silos and within silos due to multiproduct relationships Source: Company reports, Nilson |

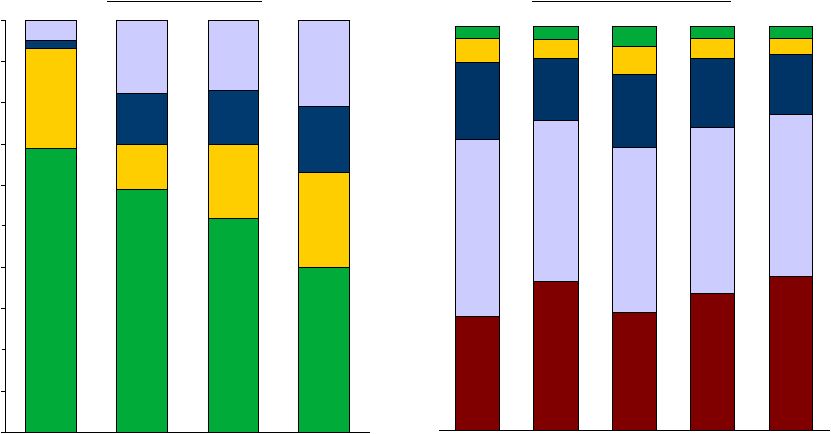

15 ING Direct’s customers are young and have ING Direct’s customers are young and have attractive income and potential attractive income and potential Notes: US households segmented by year of birth of primary head; Age breakdown is based on those responding each institution was his or her “Primary Bank or Credit Union” Source: MacroMonitor 69% 59% 52% 40% 24% 11% 18% 23% 2% 12% 13% 16% 5% 18% 17% 21% 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100% ING Direct Capital One Bank Chase BofA <47 48-56 57-64 65+ Household Age 28% 36% 29% 34% 38% 44% 39% 41% 41% 40% 19% 15% 18% 17% 15% 6% 5% 7% 5% 4% 3% 3% 5% 3% 3% ING Direct BofA Savings Capital One Savings Chase Savings Wells Fargo Savings Income Distribution <$50k $50k-$99k $150-$199k $200k+ $100-$149k Source: Lightspeed (Panel size 174,925) |

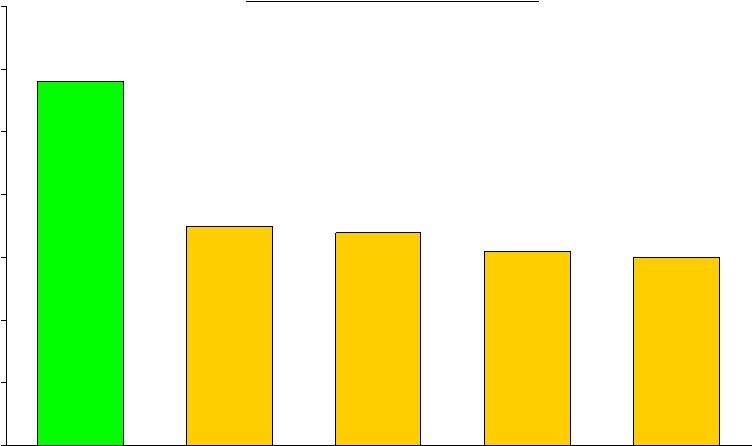

16 ING Direct customers are avid supporters of the ING Direct customers are avid supporters of the franchise franchise 58% 35% 34% 31% 30% 0% 10% 20% 30% 40% 50% 60% 70% ING Direct Wells Chase BofA Citi 1 When asked if the customer would recommend their bank, NPS is defined as % scored 9 or 10 less % 1 to 6, scores out of 10 Source: NPS Benchmarking Study Results: Consumer Insights and Analytics (October 2010) Net Promoter Score (“NPS”) 1 2010 Q3 |

17 Banking is increasingly moving to digital Banking is increasingly moving to digital channels channels 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100% 1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 Branch Banking (at least once in last 12 months) Mobile Banking ATM Direct Deposit Debit Cards Remote Deposit Capture Source: Federal Reserve, FRB Boston, FRB Philadelphia, SRI Consulting, University of Michigan, Mintel, Celent, Bank of America, comScore, Nielsen Mobile, Wall Street Journal, Mercatus Analytics Online Banking (% of U.S. banking households) Consumer Distribution Channel Penetration Percent of U.S. Households, 1980-2009 |

18 ING Direct complements our advantaged access ING Direct complements our advantaged access to assets and local-scale banking with national to assets and local-scale banking with national reach reach • Commercial • Small Business • Consumer National banking reach Local-scale banking in attractive markets • Industry-leading direct banking franchise • Direct brokerage Advantaged access to assets • Credit Card • Auto Finance • Other Consumer Lending Powerful national brand Very large national customer base |

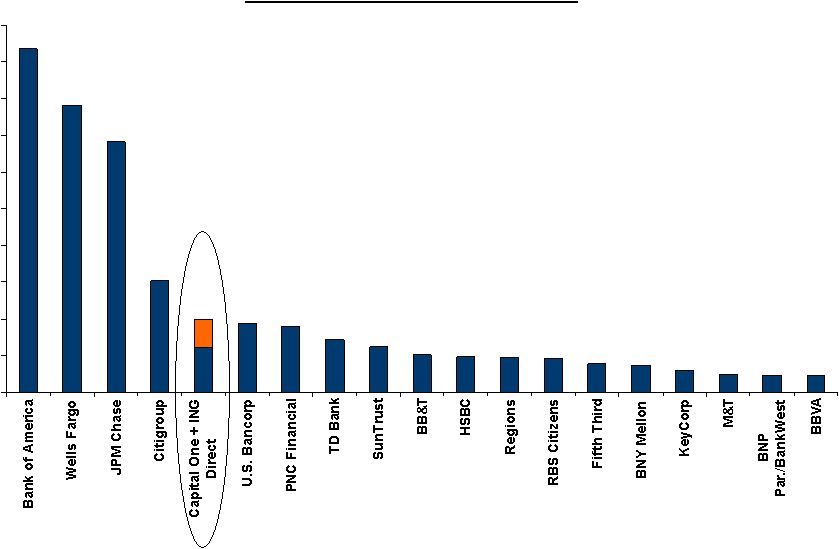

19 $0 $100 $200 $300 $400 $500 $600 $700 $800 $900 $1,000 Total U.S. Domestic Deposits As of 12/31/2010 Source: SNL Financial $B With ING Direct we become the With ING Direct we become the 5 th largest U.S. largest U.S. bank bank |

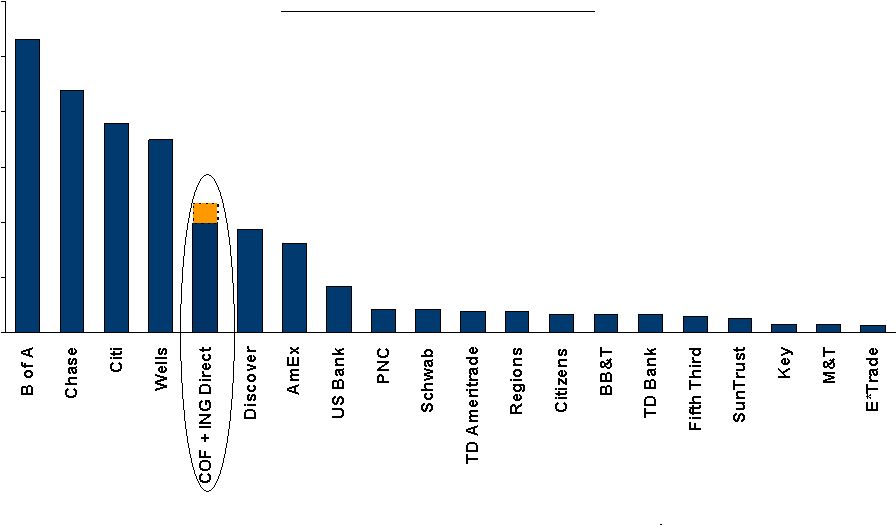

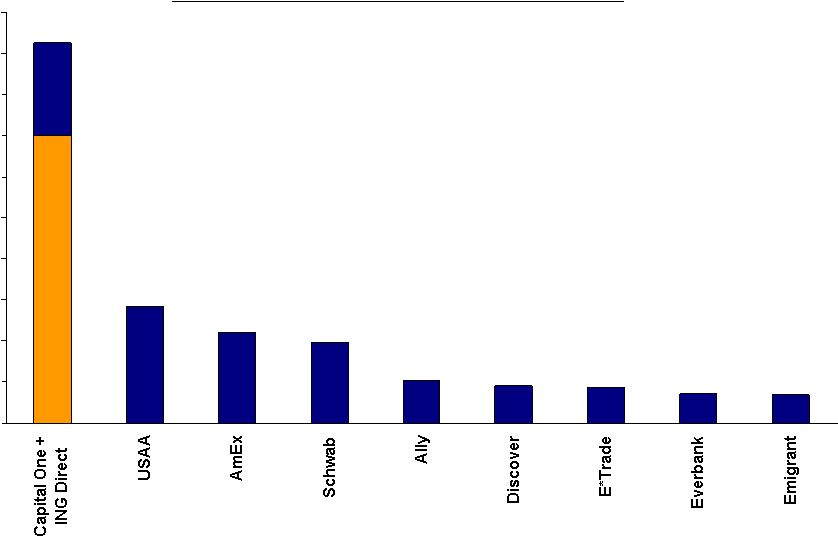

20 $93 $7 $7 $9 $9 $10 $20 $22 $28 $0 $10 $20 $30 $40 $50 $60 $70 $80 $90 $100 With ING Direct we become the largest direct With ING Direct we become the largest direct bank bank Direct U.S. Banks: Liquid Domestic Deposits As of 12/31/2010 Source: SNL Financial, Company reports $B |

21 Acquiring fully marked balance sheet without paying significant premium Demonstrated capability to effectively mark and manage mortgage loans Modest cost reduction targets Transaction risks are low Transaction risks are low Strong cultural alignment |

22 • Transaction summary and strategic rationale • Financial overview |

23 Transaction Summary Transaction Summary Transaction Value Form of Consideration to ING 1 Approvals Expected Closing $9.0 Billion 1 Fixed Number of Capital One shares of approximately 55.9 million (9.9% COF pro forma ownership) Fixed cash amount of approximately $6.2 billion 2 Approved by both Boards No Capital One or ING shareholder approval necessary Federal Reserve and Dutch Central Bank regulatory and certain other approvals will be necessary Late Q4 2011 / Early Q1 2012 Source of Funds Planned market equity raise prior to closing of approximately $2.0 billion to fund a portion of the cash payment to ING Group Shareholder Agreement One ING Group representative added to Capital One Board ING Group not permitted to sell Capital One shares before the later of 180 days after market equity raise and 90 days after closing Footnotes: Additional sources of cash consideration: $0.5B financed through cash $3.7B financed through planned issuance of Capital One senior debt 1) Share consideration valued at COF 10-day average closing price of $50.07 for the period ending June 15, 2011. 2) If ING’s stock ownership would exceed 9.9% at closing, the excess will be paid in cash |

24 Financial Assumptions Financial Assumptions Earnings 1 Intangibles + Goodwill 3 Restructuring charges and transaction costs Dividends COF: IBES EPS estimates through 2013 ING Direct: Baseline annual earnings of $630MM 1 Goodwill of $975MM Core deposit intangibles of $455MM Other identifiable intangibles of $240MM $210MM Capital One current dividend level maintained, subject to Capital One board review Synergies Base case includes cost and modest funding synergies Upside potential from balance sheet repositioning, cross-sell, and additional funding synergies See next page Gross Credit Mark 2 Gross credit mark of $1.7B (~4.2% of loans) Footnotes: 1) Estimated $630MM adjusted pre-provision NIAT for the 12 months ended March 31, 2011 excludes loss on debt extinguishment, AFS securities sales, OTTI, and incorporates Capital One’s tax rate. 2) At 3/31/11. 3) Estimated at 12/31/11 transaction close. Equity Planned market equity raise prior to closing of approximately $2.0B |

25 We believe there is upside potential from our modeled We believe there is upside potential from our modeled synergies synergies Cost Savings Cross-Sell Deposit / Funding Optimization Balance Sheet Repositioning • Consolidation of direct banking and mortgage platform • Infrastructure / data center savings • Corporate systems rationalization • Staff function consolidation • ShareBuilder online brokerage • Capital One Venture card • Volume / deposit mix opportunities in combined portfolio • Replace planned ING Direct assets with additional card, auto, and commercial assets 2013 Modeled Impact Long-Term Potential Run-Rate $90MM (~12% of ING Direct’s costs) $90MM None Included $50-70MM 10 bps $200MM 15-25 bps $300MM to $450MM None Included $75-140MM Pre-Tax Annual Synergies |

26 Attractive Financial Transaction Attractive Financial Transaction Strong Pro Forma Capital Generation Accretive Transaction Attractive Shareholder Returns 1 EPS accretive in 2012 Mid-single digit EPS accretion in 2013 Accretive to tangible book value per share at closing IRR in excess of 20% Return on Invested Capital exceeds cost of capital by 2013 Pro forma Tier 1 Common ratio of approximately 9% at estimated closing of 12/31/2011 Accretive to Tier 1 Common capital generation in 2013 Positive ROE Impact Accretive to ROE in 2012 Attractive Valuation Price to tangible book multiple of 1.0x Premium to core deposits of 0.4% Note: See “Financial Assumptions” in this presentation for underlying assumptions; IRR and ROIC calculations based on 6% TCE. |

27 Combines valuable ING Direct deposit franchise with Capital One’s advantaged access to assets Accelerates winning banking strategy positioned where the markets are going Strengthens our customer franchise and brand Provides significant financial and strategic upside with low risk ING Direct is a game-changing acquisition that delivers ING Direct is a game-changing acquisition that delivers compelling financial results immediately and over the compelling financial results immediately and over the long-term long-term Compelling deal economics and long-term value creation |