SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 8-K

CURRENT REPORT

Pursuant to Section 13 or 15(d) of

the Securities Exchange Act of 1934

Date of Report (Date of earliest event reported): May 5, 2003

IBERIABANK CORPORATION

(Exact name of Registrant as Specified in Charter)

Louisiana (State or Other Jurisdiction of Incorporation) | 0-25756 (Commission File Number) | 72-1280718 (I.R.S. Employer Identification No.) |

200 West Congress Street, Lafayette, Louisiana 70501

(Address of Principal Executive Offices)

(337) 521-4003

Registrant’s telephone number, including area code

Not Applicable

(Former name or former address, if changed since last report)

Item 9. Regulation FD Disclosure

Presentation by management of the Registrant to Gulf South Conference, May 5, 2003.

Investor Presentation

Gulf South Conference

May 5, 2003

Presentation Outline

• Pathways To Growth

• Our Current Paths

• A Path of Lower Risk

• Investment Perspective

• Comparatives

Forward Looking Statements

Safe Harbor

Statements contained in this presentation which are not historical facts and which pertain to future operating results of IBERIABANK Corporation and its subsidiaries constitute "forward-looking statements" within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements involve significant risks and uncertainties. Actual results may differ materially from the results discussed in these forward-looking statements. Factors that might cause such a difference include, but are not limited to, those discussed in the Company's periodic filings with the SEC.

Pathways

To Growth

Pathways To Growth

Brief History

One Of Oldest Banks In LA - March 12, 1887

Mutual Thrift Until IPO In 1995

Converted To Bank Charter In 1997

Acquired Branches From FCOM in 1998

New Leadership Team In Place In Late 1999

New Strategic Direction Set 3 Years Ago

Focus On Core earnings And Performance

Pathways To Growth

Our Current Position

• $2 Billion One-Bank Holding Company

• 3rd Largest Independent BHC In Louisiana

• Market Capitalization Of Over $300 Million

• 30 Offices Serving Acadiana, New Orleans, and Northeast Louisiana

• Excellent Geographic Diversification

• Commercial Bank With A Relationship Focus

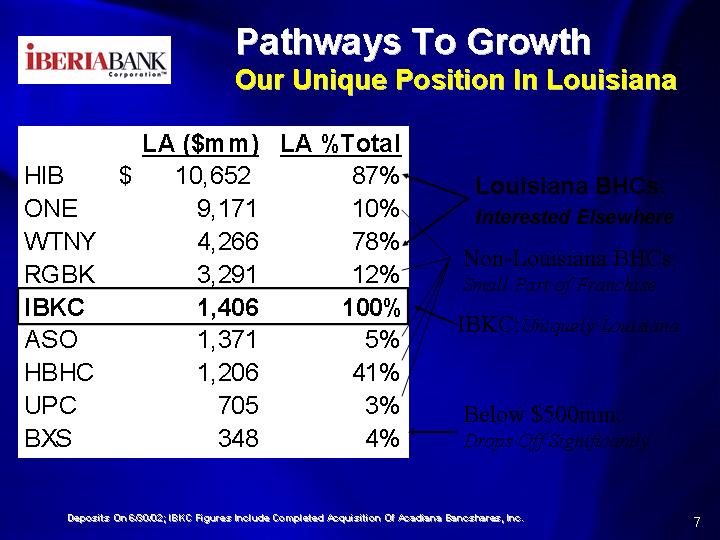

Pathways to Growth

Our Unique Position In Louisiana

| LA % Total | ||

| HIB | $ 10,652 | 87% |

| ONE | 9,171 | 10% |

| WTNY | 4,266 | 78% |

| RGBK | 3,291 | 12% |

| IBKC | 1,406 | 100% |

| ASO | 1,371 | 5% |

| HBHC | 1,206 | 41% |

| UPC | 705 | 3% |

| BXS | 348 | 4% |

Deposits On 6/30/2002; IBKC Figures Include Completed Acquisition of Acadiana Bancshares, Inc.

Pathways To Growth

Underlying Focus

Belief In The Power Of Progression

Shareholder Returns

Predictability - Clients, Associates And Shareholders

Remain Disciplined And Conservative

Critical Issues:

Focus On People And Relationships, Less On Facilities And Products

Make The Right Kind Of Investments

Continuous Improvement - A Way Of Life

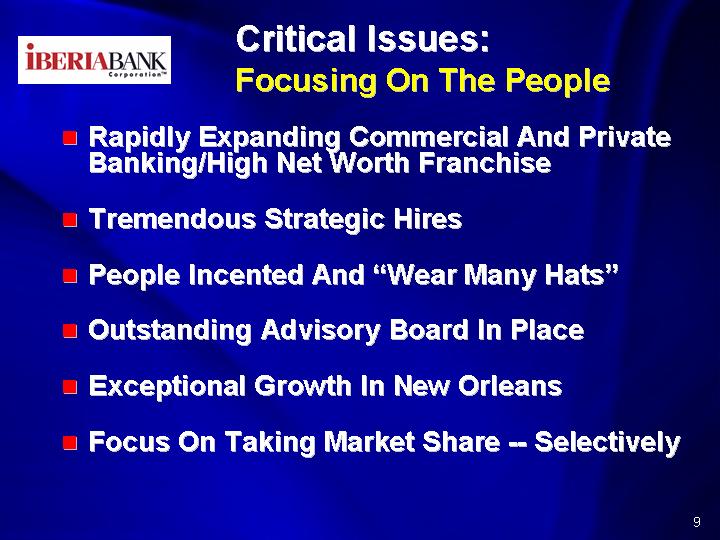

Critical Issues:

Focusing On The People

Rapidly Expanding Commercial And Private Banking/High Net Worth Franchise

Tremendous Strategic Hires

People Incented and "Wear Many Hats"

Outstanding Advisory Board In Place

Exceptional Growth In New Orleans

Focus On Taking Market Share - Selectively

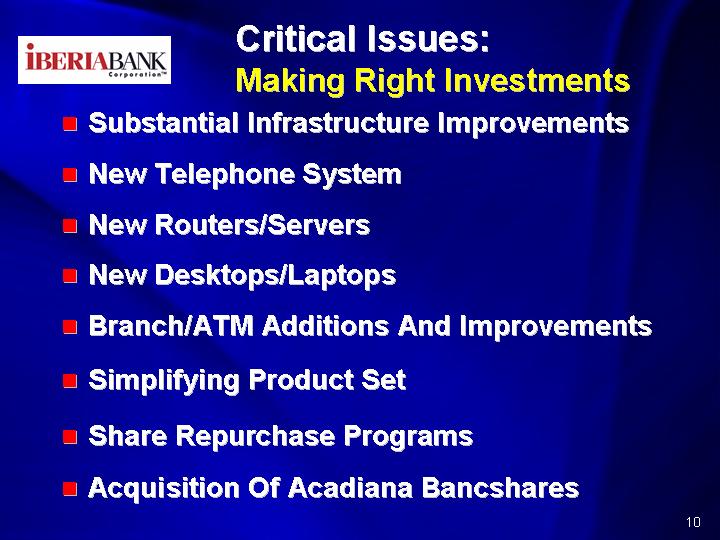

Critical Issues:

Making Right Investments

Substantial Infrastructure Improvements

New Telephone System

New Routers/Servers

New Desktops/Laptops

Branch/ATM Additions And Improvements

Simplifying Product Set

Share Repurchase Programs

Acquisition Of Acadiana Bancshares

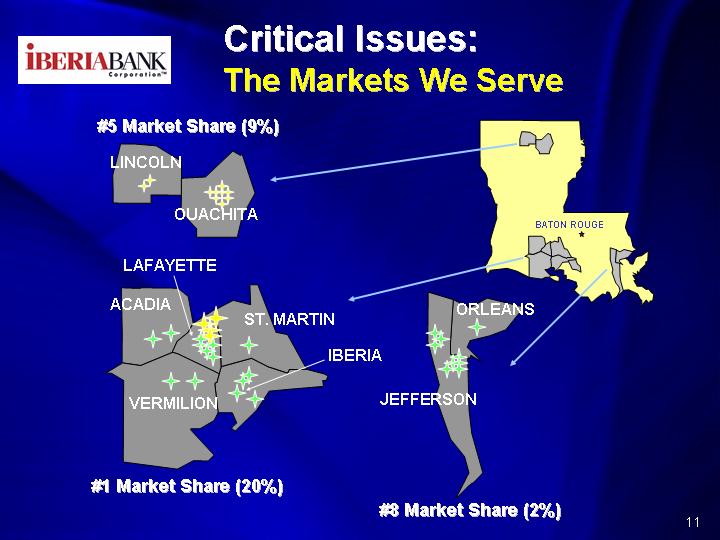

Critical Issues:

The Markets We Serve

Our Current Paths

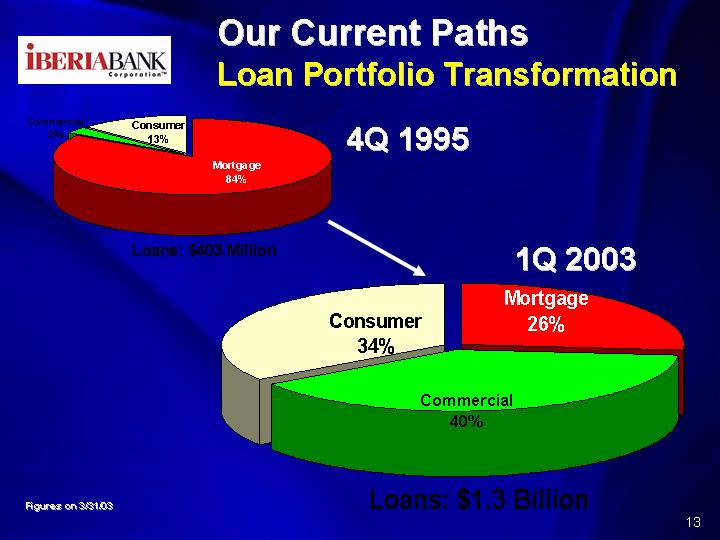

Our Current Paths

Loan Portfolio Transformation

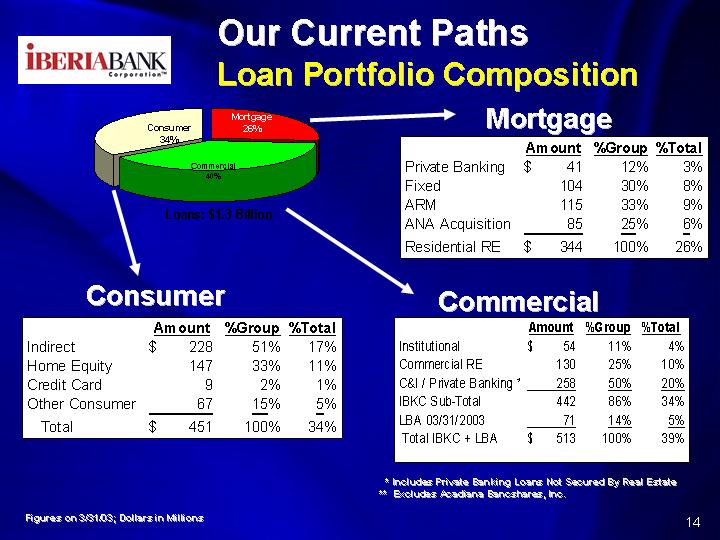

Our Current Paths

Loan Portfolio Composition

Consumer

| Indirect | $228 | 51% | 17% |

| Home Equity | 147 | 33% | 11% |

| Credit Card | 9 | 2% | 1% |

| Other Consumer | 67 | 15% | 5% |

| Total | $451 | 100% | 34% |

Mortgage

| Private Banking | $41 | 12% | 3% |

| Fixed | 104 | 30% | 8% |

| ARM | 115 | 33% | 9% |

| ANA Acquisition | 85 | 25% | 6% |

| Residential RE | $344 | 100% | 26% |

Commercial

| Institutional | $54 | 11% | 4% |

| Commercial RE | 130 | 25% | 10% |

| C&I/Private Banking* | 258 | 50% | 20% |

| IBKC Sub-Total | 442 | 86% | 34% |

| LBA 03/31/2003 | 71 | 14% | 5% |

| Total IBKC + LBA | $513 | 100% | 39% |

* Includes Private Banking Loans Not Secured By Real Estate

**Excludes Acadiana Bancshares, Inc.

Figures on 3/31/03; Dollars in Millions

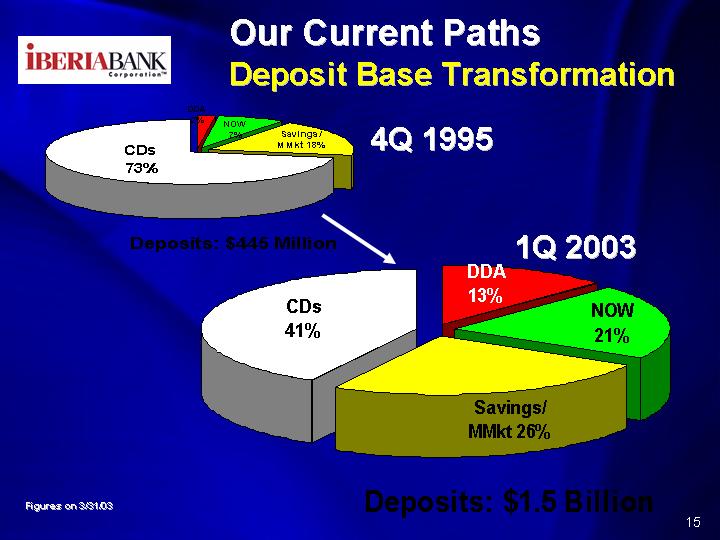

Our Current Paths

Deposit Base Transformation

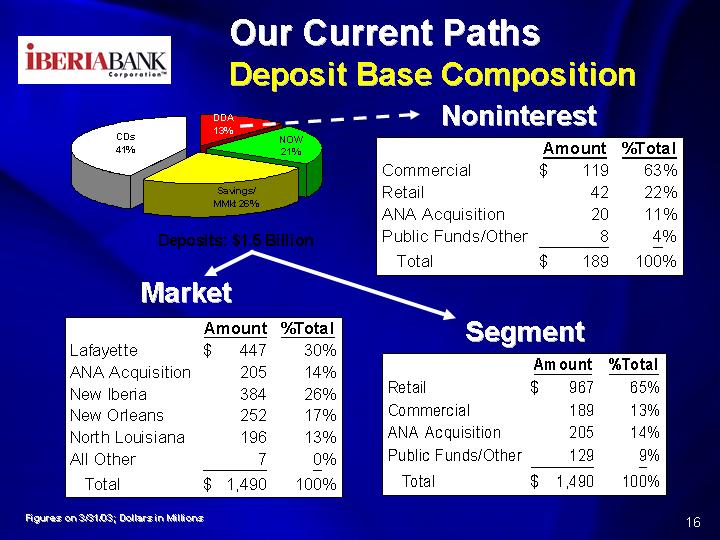

Our Current Paths

Deposit Base Composition

Noninterest

| Commercial | $119 | 63% |

| Retail | 42 | 22% |

| ANA Acquisition | 20 | 11% |

| Public Funds/Other | 8 | 4% |

| Total | $189 | 100% |

Market

| Lafayette | $447 | 30% |

| ANA Acquisition | 205 | 14% |

| New Iberia | 384 | 26% |

| New Orleans | 252 | 17% |

| North Louisiana | 196 | 13% |

| All Other | 7 | 0% |

| Total | $1,490 | 100% |

Segment

| Retail | $967 | 65% |

| Commercial | 189 | 13% |

| ANA Acquisition | 205 | 14% |

| Public Funds/Other | 129 | 9% |

| Total | $1,490 | 100% |

Figures on 3/31/03; Dollars in Millions

Continuous

Improvement

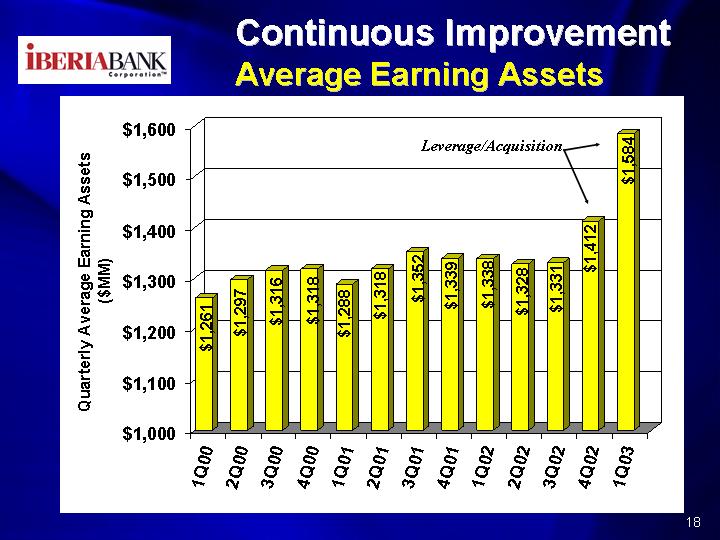

Continuous Improvement

Average Earning Assets

Continuous Improvement

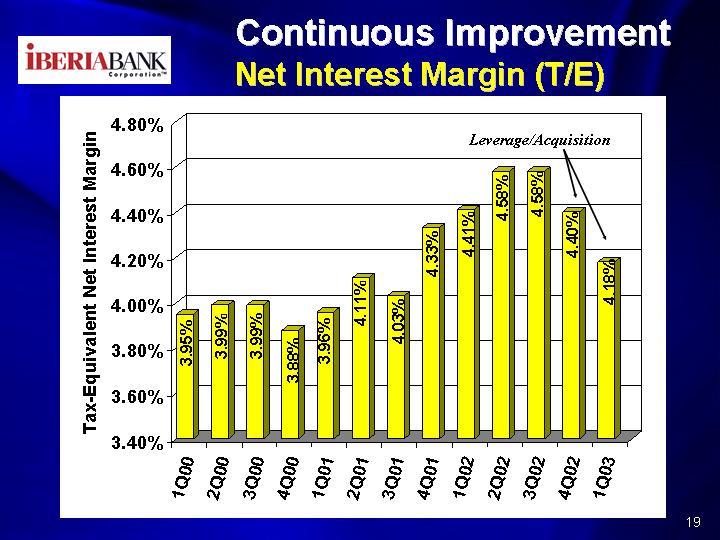

Net Interest Margin (T/E)

Continuous Improvement

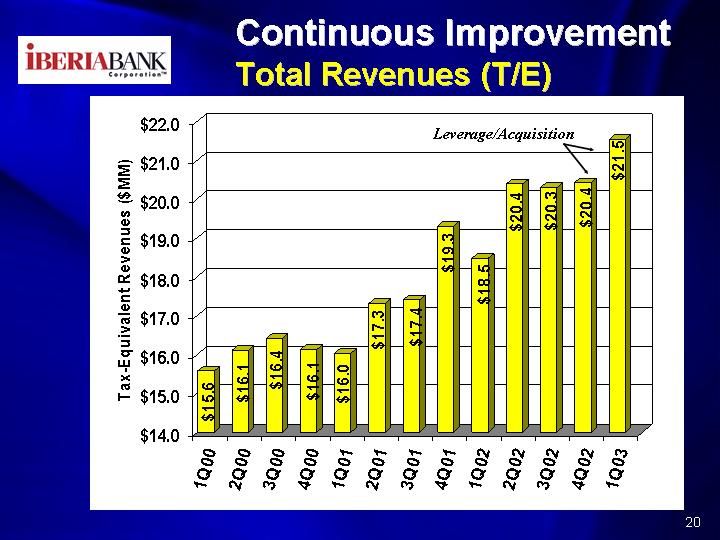

Total Revenues (T/E)

Continuous Improvement

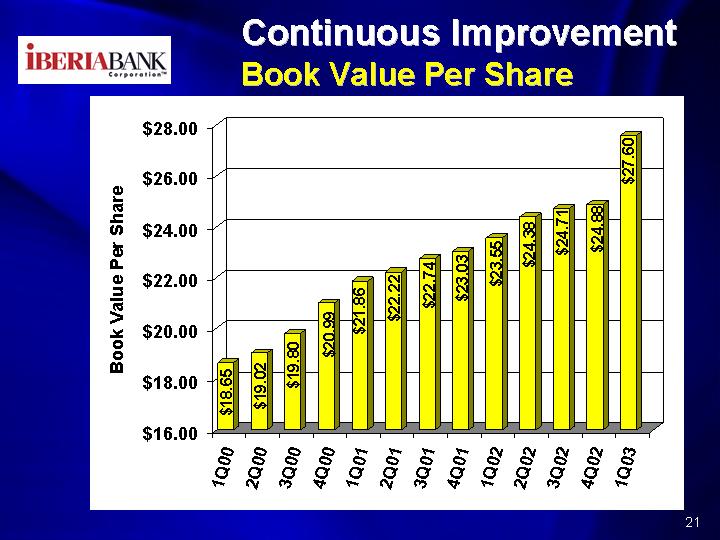

Book Value Per Share

Continuous Improvement

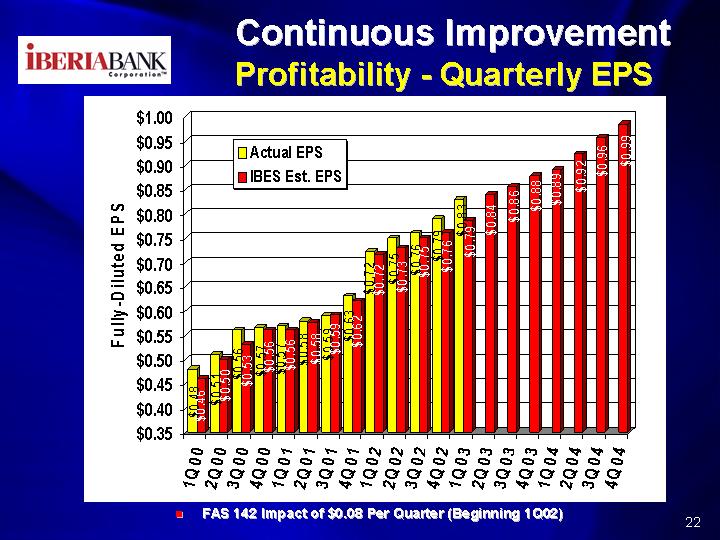

Profitability - Quarterly EPS

Continuous Improvement

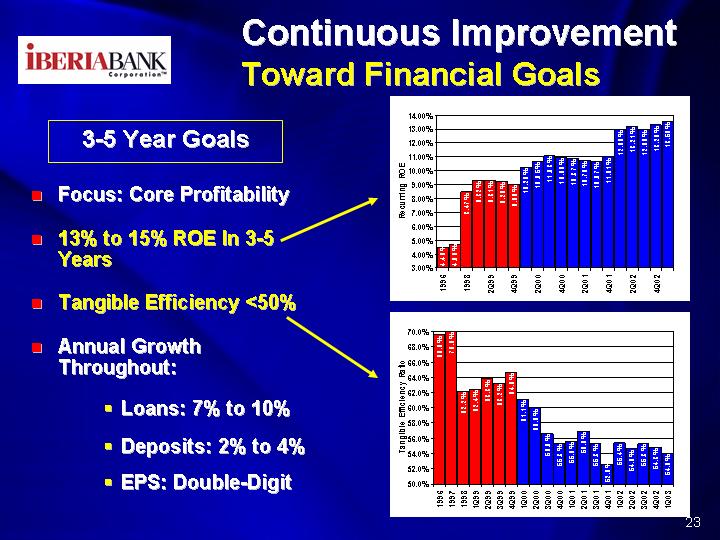

Toward Financial Goals

3-5 Year Goals

Focus: Core Profitability

13% to 15% ROE In 3-5 Years

Tangible Efficiency (less than)50%

Annual Growth

Throughout:

Loans: 7% to 10%

Deposits: 2% to 4%

EPS: Double-Digit

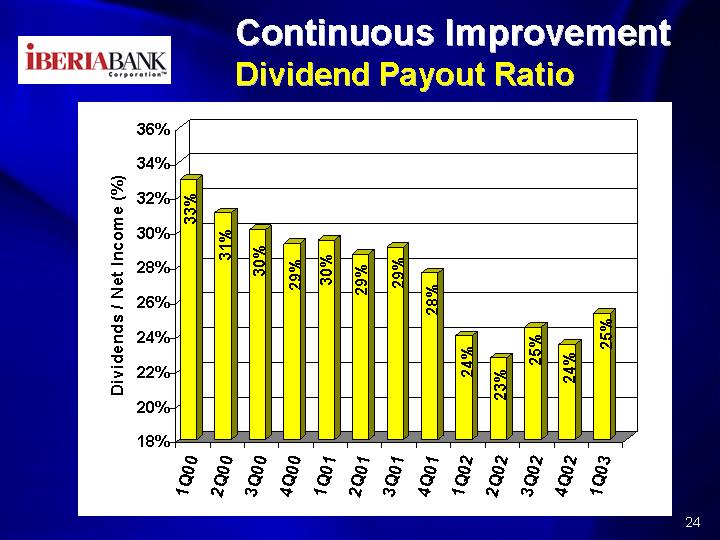

Continuous Improvement

Dividend Payout Ratio

A Path Of

Lower Risk

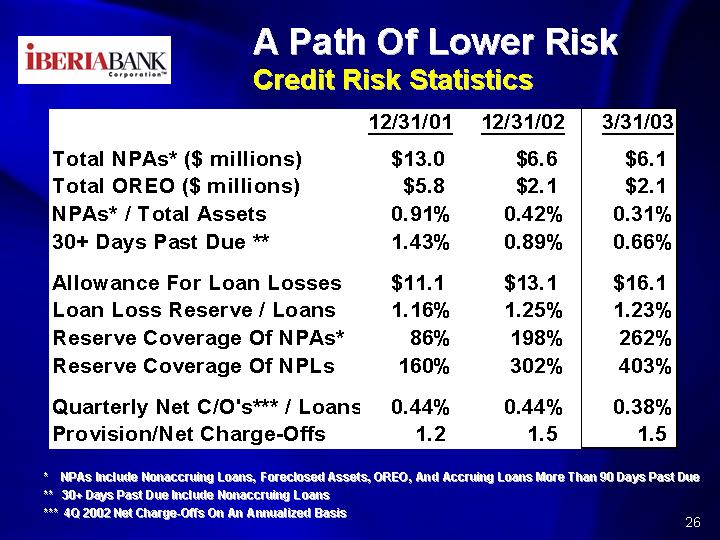

A Path of Lower Risk

Credit Risk Statistics

| 12/31/01 | 12/31/02 | 3/31/03 | |

| Total NPAs* ($ millions) | $13.0 | $6.6 | $6.1 |

| Total OREO ($ millions) | $5.8 | $2.1 | $2.1 |

| NPAs*/Total Assets | 0.91% | 0.42% | 0.31% |

| 30+ Days Past Due ** | 1.43% | 0.89% | 0.66% |

| Allowance For Loan Losses | $11.1 | $13.1 | $16.1 |

| Loan Loss Reserve / Loans | 1.16% | 1.25% | 1.23% |

| Reserve Coverage Of NPAs* | 86% | 198% | 262% |

| Reserve Coverage Of NPLs | 160% | 302% | 403% |

| Quarterly Net C/O's *** / Loans | 0.44% | 0.44% | 0.38% |

| Provision/Net Charge-Offs | 1.2 | 1.5 | 1.5 |

* NPAs Include Nonaccruing Loans, Foreclosed Assets, OREO, And Accruing

Loans More Than 90 Days Past Due

** 30+ Days Past Due Include Nonaccruing Loans

*** 4Q 2002 Net Charge-Offs On An Annualized Basis

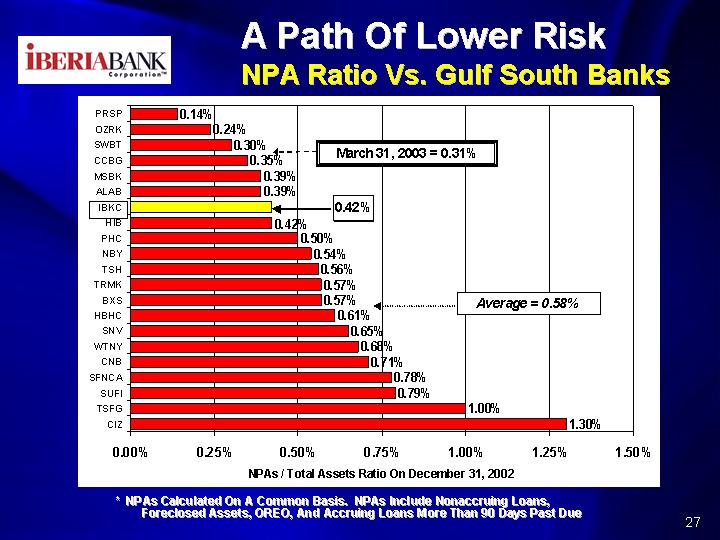

A Path Of Lower Risk

NPA Ratio Vs. Gulf South Banks

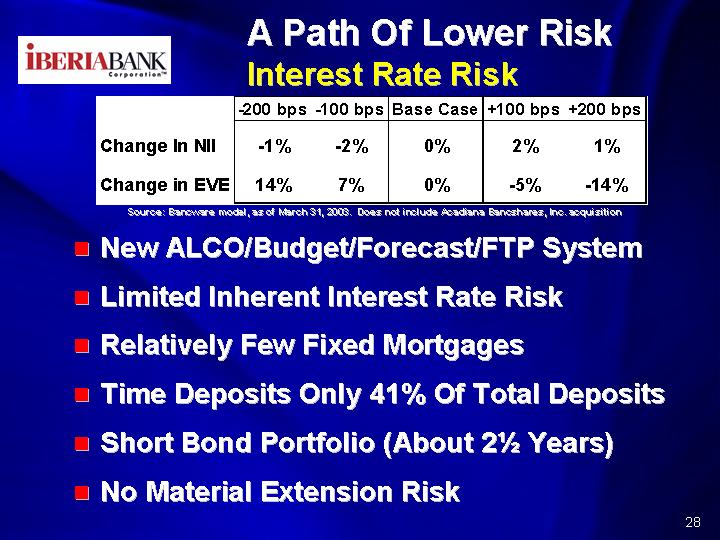

A Path Of Lower Risk

Interest Rate Risk

| Change In NII | |||||

| Change in EVE |

Source: Bancware model, as of March 31, 2003. Does not include Acadiana Bancshares, Inc. acquisition

New ALCO/Budget/Forecast/FTP System

Limited Inherent Interest Rate Risk

Relatively Few Fixed Mortgages

Time Deposits Only 41% Of Total Deposits

Short Bond Portfolio (About 2 1/2 Years)

No Material Extension Risk

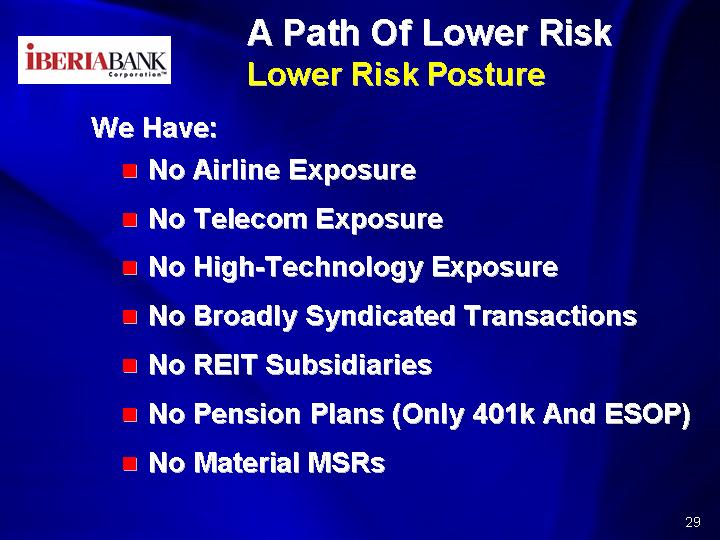

A Path Of Lower Risk

Lower Risk Posture

We Have:

No Airline Exposure

No Telecom Exposure

No High-Technology Exposure

No Broadly Syndicated Transactions

No REIT Subsidiaries

No Pension Plans (Only 401k And ESOP)

No Material MSRs

Investment

Perspective

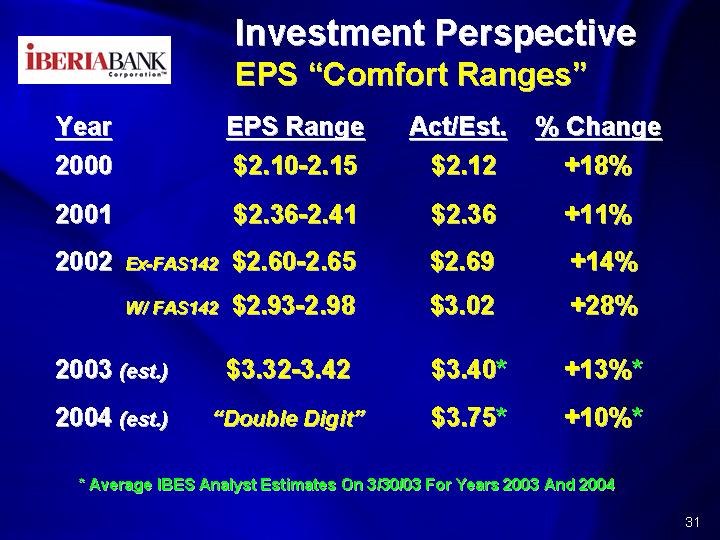

Investment Perspective

EPS "Comfort Ranges"

% Change | |||

| 2000 | |||

| 2001 | |||

| 2002 Ex-FAS142 | |||

| W/FAS142 | |||

| 2003 (est.) | |||

| 2004 (est.) |

*Average IBES Analyst Estimates On 3/30/03 For Years 2003 and 2004

Investment Perspective

Stock Price

Investment Perspective

Price-To-Earnings Ratio

Investment Perspective

Market-To-Book Ratio

Investment Perspective

Institutional Holders

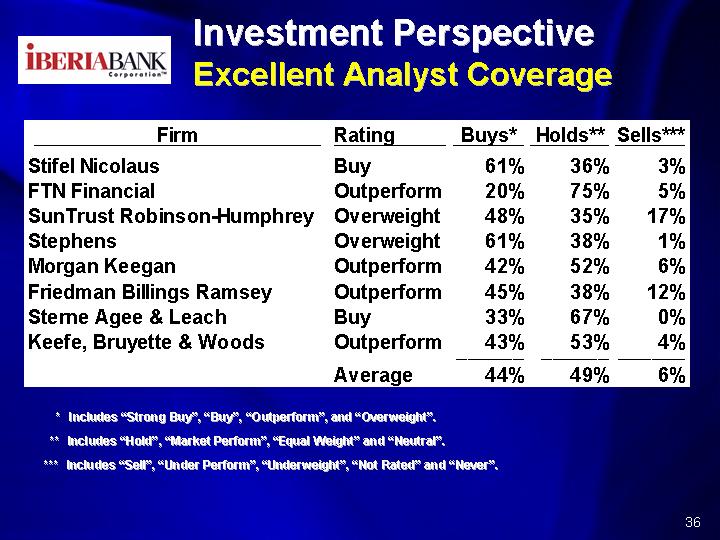

Investment Perspective

Excellent Analyst Coverage

Comparatives

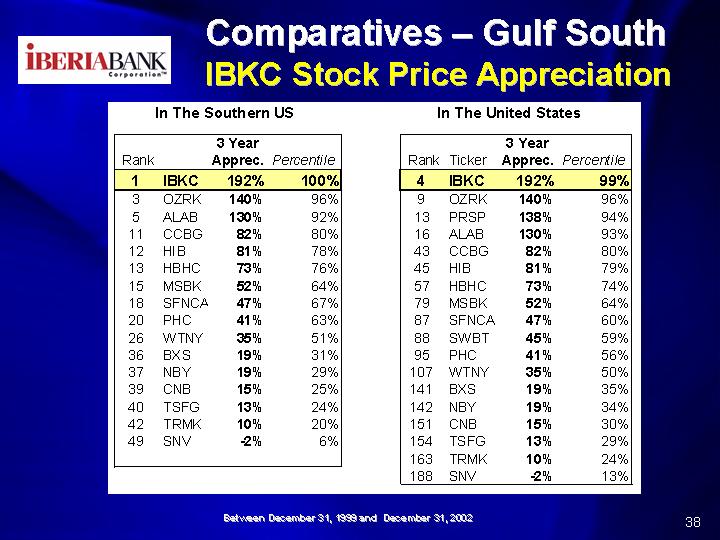

Comparatives - Gulf South

IBKC Stock Price Appreciation

Comparatives - Gulf South

Analyst Recommendations

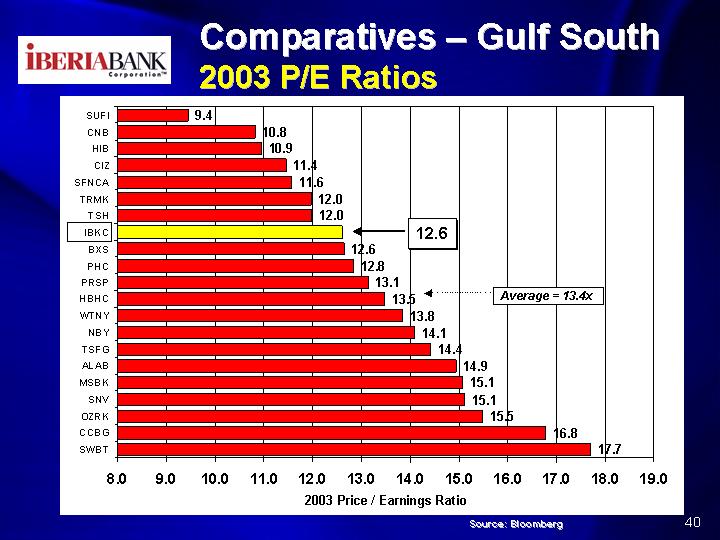

Comparatives - Gulf South

2003 P/E Ratios

Comparatives - Gulf South

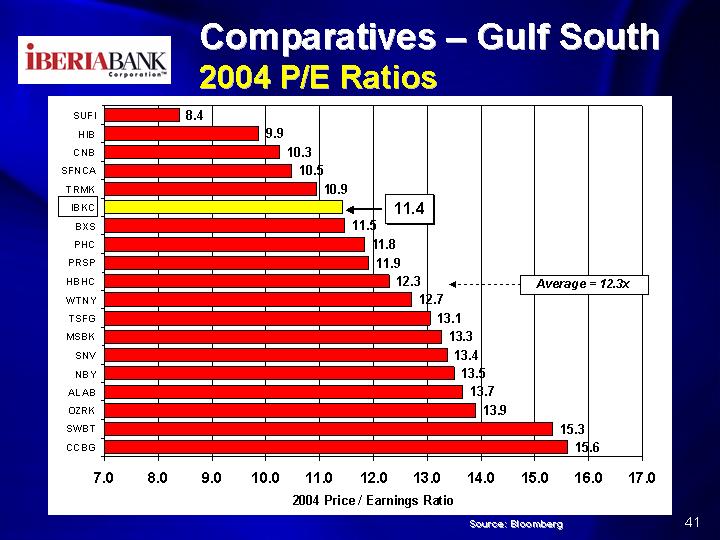

2004 P/E Ratios

Comparatives - Gulf South

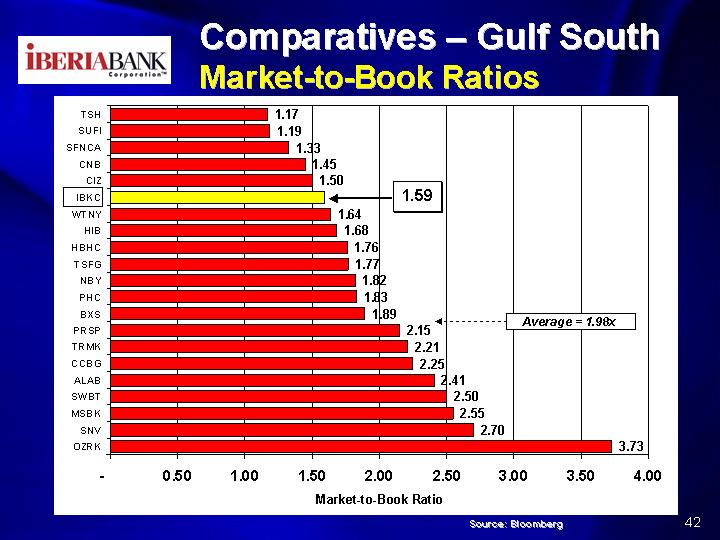

Market-to-Book Ratios

Comparatives - Gulf South

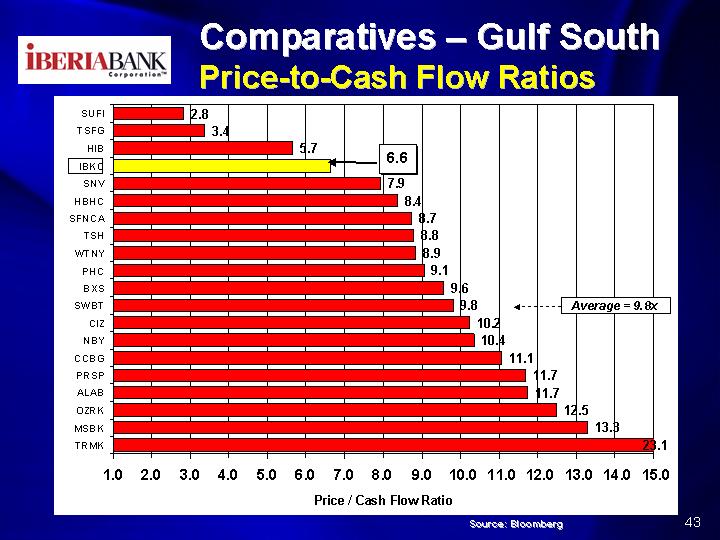

Price-to-Cash Flow Ratios

Comparatives - Gulf South

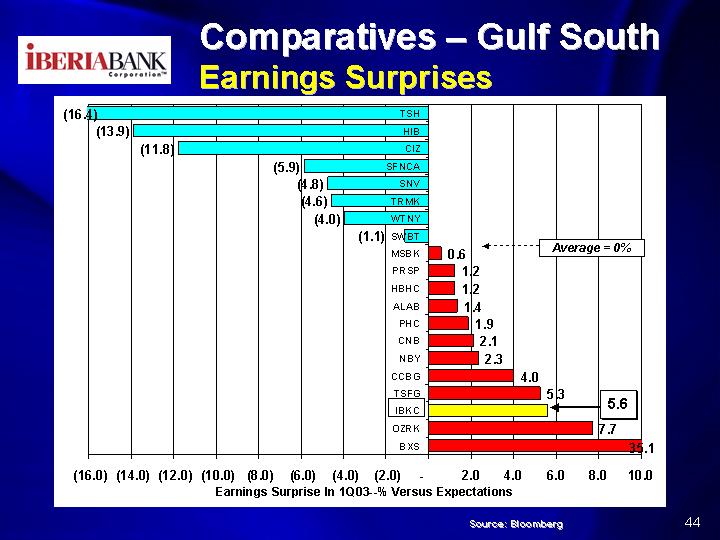

Earnings Surprises

Summary Of IBKC

Large Bank Resources & Small Bank Agility

People And Relationship Focused

Emphasis On Taking Market Share

Turnaround; Now Showing Growth Results

EPS/Stock Price Linkage - Shareholder Focus

Reducing Risk Posture In Many Ways

Building A Solid Platform For Future Growth

Tremendous Expansion Opportunities

Appendix A

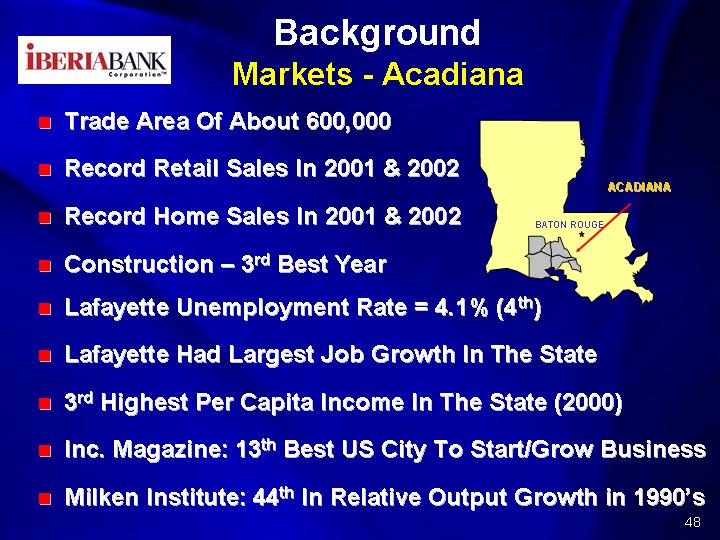

Background

Markets - Acadiana

- Trade Area of About 600,000

- Record Retail Sales In 2001 & 2002

- Record Home Sales In 2001 & 2002

- Construction - 3rd Best Year

- Lafayette Unemployment Rate = 4.1% (4th)

- Lafayette Had Largest Job Growth In The State

- 3rd Highest Per Capita Income In The State (2000)

- Inc. Magazine: 13th Best US City To Start/Grow Business

- Milken Institute: 44th In Relative Output Growth in 1990's

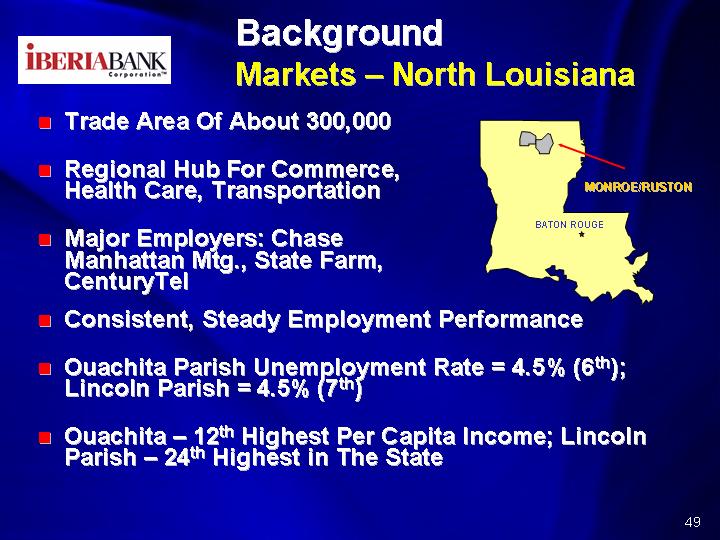

Background

Markets - North Louisiana

Trade Area Of About 300,000

Regional Hub For Commerce, Health Care, Transportation

Major Employers: Chase Manhattan Mtg., State Farm, CenturyTel

Consistent, Steady Employment Performance

Ouachita Parish Unemployment Rate = 4.5% (6th); Lincoln Parish = 4.5% (7th)

Ouachita - 12th Highest Per Capita Income; Lincoln Parish - 24th Highest in The State

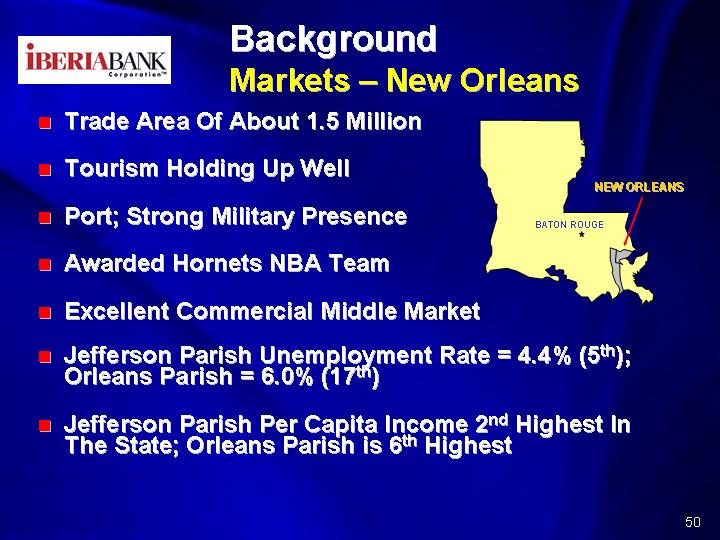

Background

Markets - New Orleans

Trade Area of About 1.5 Million

Tourism Holding Up Well

Port; Strong Military Presence

Awarded Hornets NBA Team

Excellent Commercial Middle Market

Jefferson Parish Unemployment Rate = 4.4% (5th); Orleans Parish = 6.0% (17th)

Jefferson Parish Per Capita Income 2nd Highest In The State; Orleans Parish is 6th Highest

Appendix B

Recent Merger

Acadiana Bancshares, Inc.

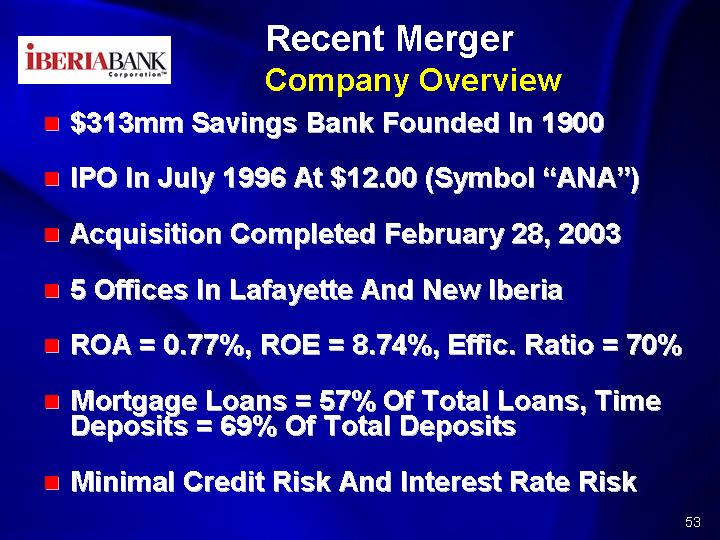

Recent Merger

Company Overview

$313mm Savings Bank Founded in 1900

IPO in July 1996 At $12.00 (Symbol "ANA")

Acquisition Completed February 28, 2003

5 Offices In Lafayette And New Iberia

ROA = 0.77%, ROE = 8.74%, Effic. Ratio = 70%

Mortgage Loans = 57% Of Total Loans, Time Deposits = 69% Of Total Deposits

Minimal Credit Risk And Interest Rate Risk

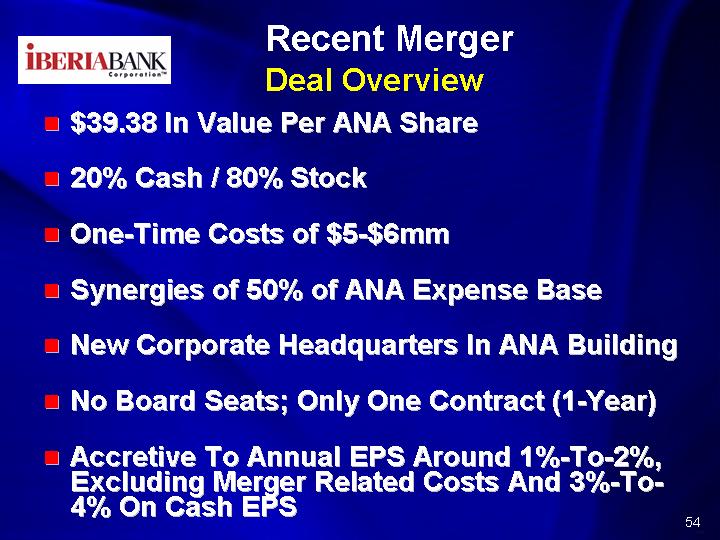

Recent Merger

Deal Overview

$39.38 In Value Per ANA Share20% Cash / 80% StockOne-Time Costs of $5-$6mmSynergies of 50% of ANA Expense BaseNew Corporate Headquarters In ANA BuildingNo Board Seats; Only One Contract (1-Year)Accretive To Annual EPS Around 1%-To-2%, Excluding Merger Related Costs

And 3%-To-4% On Cash EPS

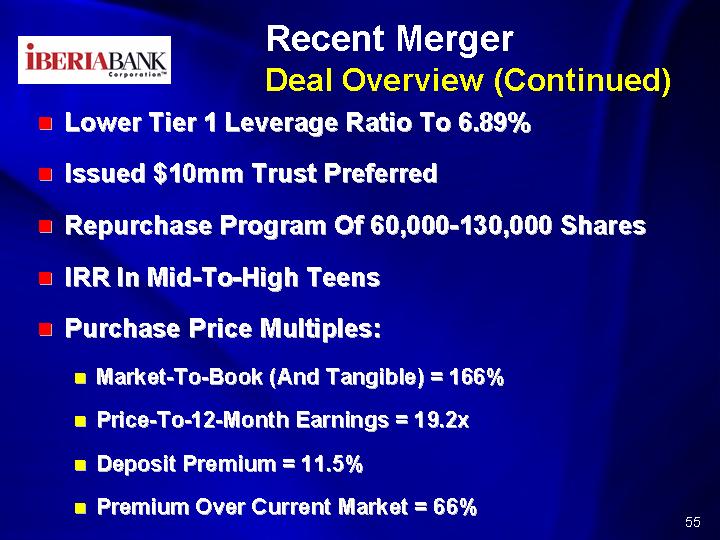

Recent Merger

Deal Overview (Continued)

Lower Tier 1 Leverage Ratio To 6.89%

Issued $10mm Trust Preferred

Repurchase Program Of 60,000-130,000 Shares

IRR In Mid-To-High Teens

Purchase Price Multiples:

Market-To-Book (And Tangible) = 166%

Price-To-12-Month Earnings = 19.2x

Deposit Premium = 11.5%

Premium Over Current Market = 66%

Recent Merger

Summary Of Merger

Compelling Synergies--Cross-town HQs

#1 Market Share With Excellent Distribution System

Excellent Returns For Shareholders Of Both Companies

Provides Diversity--Retail Shareholders

Excellent Asset Quality; Relatively Low Interest Rate Risk

Our View Of The Deal: Low Risk & Good Return

Appendix C

DARYL BYRD

President & Chief Executive Officer

1981 Trust Company Bank, Atlanta

Banking Officer, Corporate Banking

1983 First National Bank of South Carolina

Vice President, Commercial Lending Officer

1984 BB&T (North Carolina)

Vice President, Business Services Manager

Commercial Lending Officer

1985 FNB-Lafayette (First Commerce Corp.)

Executive Vice President, Corporate Banking Manager

1990 Rapides Bank & Trust (First Commerce Corp.)

President & CEO

1992 First National Bank of Commerce, New Orleans

Executive Vice President in charge of the commercial bank and mortgage banking groups.

Managed the strategic development for multiple businesses and had responsibility for other business lines and support functions.

1998 Bank One Louisiana

President and CEO New Orleans Region

MICHAEL BROWN

New Orleans President; Chief Credit Officer

1987 Wachovia Bank

Treasury Services Representative and Assistant Vice President

Vice President and Relationship Manager - Managed all aspects of bank relationships with Fortune 500 clients in

Texas and Louisiana.

Loan Administration Manager - Managed the loan administration and credit policy functions for the Midwest and Chicago credit portfolios.

1996 First Commerce Corporation, New Orleans

Senior Vice President, Manager of Credit and Client Services - Re-engineered and managed consumer and commercial credit

processes.

1998 Bank One Louisiana

Chief Credit Officer for the Commercial Line of Business in Louisiana

Capital Markets Specialist - Responsible for the sale of capital market products and served as corporate finance advisor to the bank's

client base.

Chartered Financial Analyst (CFA)

JOHN DAVIS

Finance And Retail Strategy

1983 BB&T (NC)

Senior Vice President and Manager of the Financial Planning Department

Responsible for mergers and acquisitions, strategic planning, and budgeting.

1993 First Commerce Corporation, New Orleans

Senior Vice President

Responsibilities included mergers and acquisitions, corporate finance, and President of Marquis Insurance Agency.

1997 Crestar Financial Corporation (VA)

Corporate Senior Vice President

Responsibilities included strategic planning, forecasting, and budgeting for the corporation.

Chartered Financial Analyst (CFA)

MARILYN BURCH

Executive Vice President &

Chief Financial Officer

1973 First Commerce Corporation, New Orleans

Accounting Supervisor

1978 Reamco, Lafayette

Manager of Accounting

1980 American Bank, Lafayette

Vice President and Controller

1985 FNB-Lafayette (First Commerce Corp.)

Senior Vice President and Controller

1999 IBERIABANK

Senior Vice President and Controller

Certified Public Accountant (CPA)

GEORGE BECKER

Secretary; Technology & Operations

1973 First National Bank of Commerce, New Orleans

Vice President and Controller - Managed the bank's accounting, budgeting, planning, systems, and asset/liability management activities.

1983 First National Bank of Lafayette

Executive Vice President and Chief Financial Officer

Managed all financial and administrative areas, as well as Investments, Brokerage Services and Private Banking area.

1989 Rapides Bank & Trust Company

Executive Vice President - Managed all financial and administrative areas, Investments, Brokerage Services, Private Banking,

as well as the Mortgage and Retail areas.

1991 First Commerce Corporation, New Orleans

Senior Vice President - Strategic Management Information Systems and Automation activities state-wide.

1997 Bank One Louisiana

Worked on various special acquisition related projects.

Certified Public Accountant (CPA)

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the Registrant has duly caused this report to be signed on its behalf by the undersigned hereunto duly authorized.

IBERIABANK CORPORATION | ||||

DATE:May 5, 2003 | By: | /s/ Daryl G. Byrd | ||

Daryl G. Byrd | ||||

President and Chief Executive | ||||

Officer | ||||