Exhibit 99.3

1 Investment Portfolio As of March 31. 2008

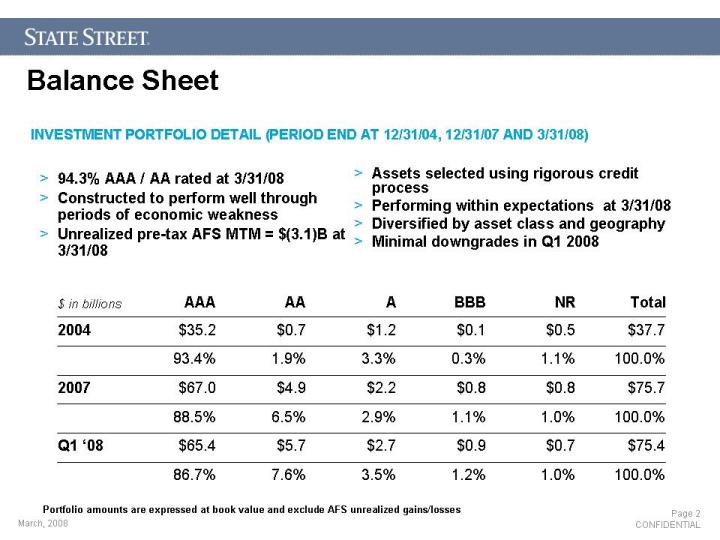

2 94.3% AAA / AA rated at 3/31/08 Constructed to perform well through periods of economic weakness Unrealized pre-tax AFS MTM = $(3.1)B at 3/31/08 Assets selected using rigorous credit process Performing within expectations at 3/31/08 Diversified by asset class and geography Minimal downgrades in Q1 2008 INVESTMENT PORTFOLIO DETAIL (PERIOD END AT 12/31/04, 12/31/07 AND 3/31/08) Portfolio amounts are expressed at book value and exclude AFS unrealized gains/losses Balance Sheet

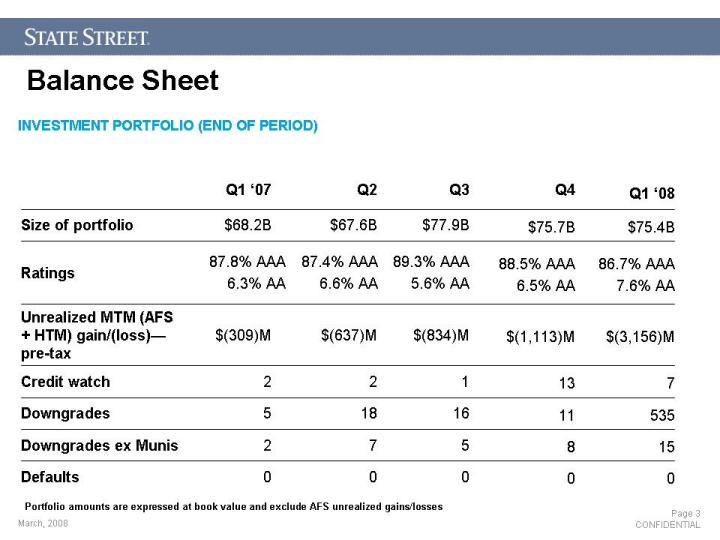

3 INVESTMENT PORTFOLIO (END OF PERIOD) Portfolio amounts are expressed at book value and exclude AFS unrealized gains/losses Balance Sheet

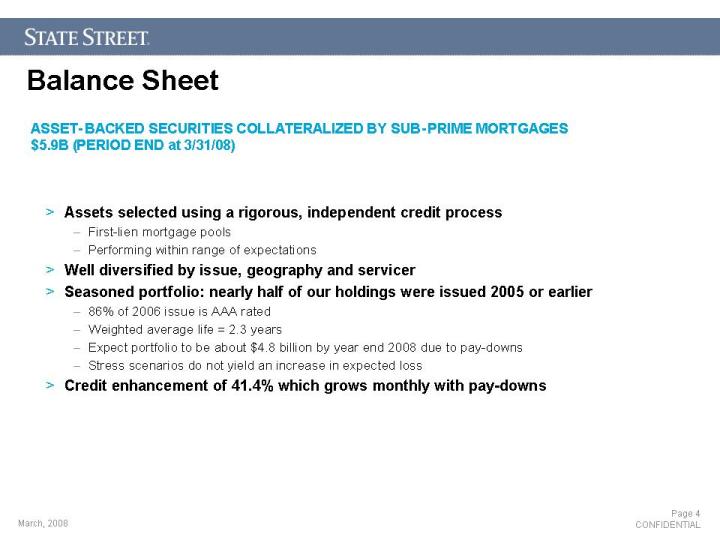

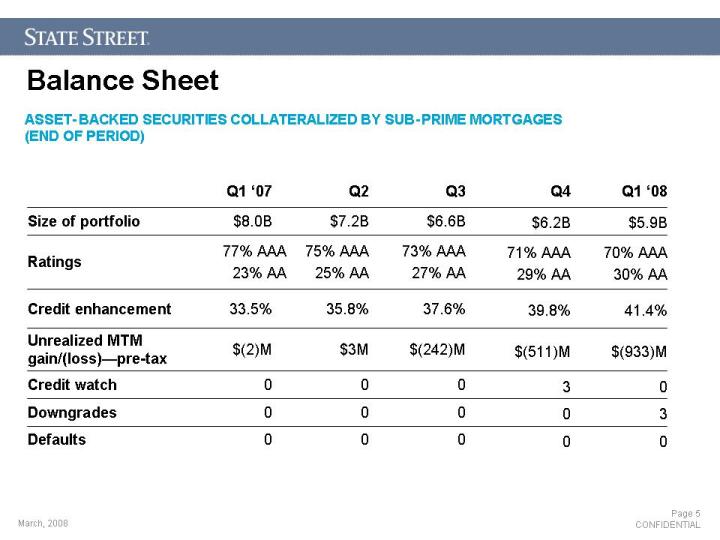

4 Balance Sheet Assets selected using a rigorous, independent credit process First-lien mortgage pools Performing within range of expectations Well diversified by issue, geography and servicer Seasoned portfolio: nearly half of our holdings were issued 2005 or earlier 86% of 2006 issue is AAA rated Weighted average life = 2.3 years Expect portfolio to be about $4.8 billion by year end 2008 due to pay-downs Stress scenarios do not yield an increase in expected loss Credit enhancement of 41.4% which grows monthly with pay-downs ASSET- BACKED SECURITIES COLLATERALIZED BY SUB - PRIME MORTGAGES $5.9B (PERIOD END at 3/31/08)

5 Balance Sheet ASSET- BACKED SECURITIES COLLATERALIZED BY SUB - PRIME MORTGAGES (END OF PERIOD)

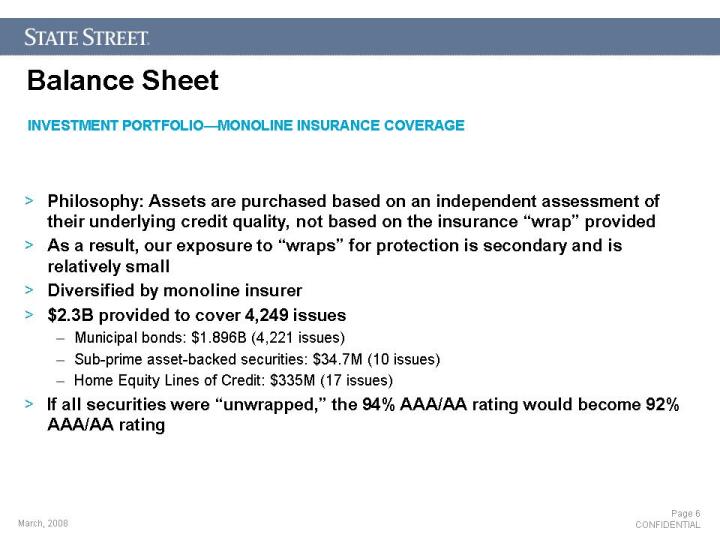

6 Balance Sheet Philosophy: Assets are purchased based on an independent assessment of their underlying credit quality, not based on the insurance “wrap” provided As a result, our exposure to “wraps” for protection is secondary and is relatively small Diversified by monoline insurer $2.3B provided to cover 4,249 issues Municipal bonds: $1.896B (4,221 issues) Sub-prime asset-backed securities: $34.7M (10 issues) Home Equity Lines of Credit: $335M (17 issues) If all securities were “unwrapped,” the 94% AAA/AA rating would become 92% AAA/AA rating INVESTMENT PORTFOLIO—MONOLINE INSURANCE COVERAGE

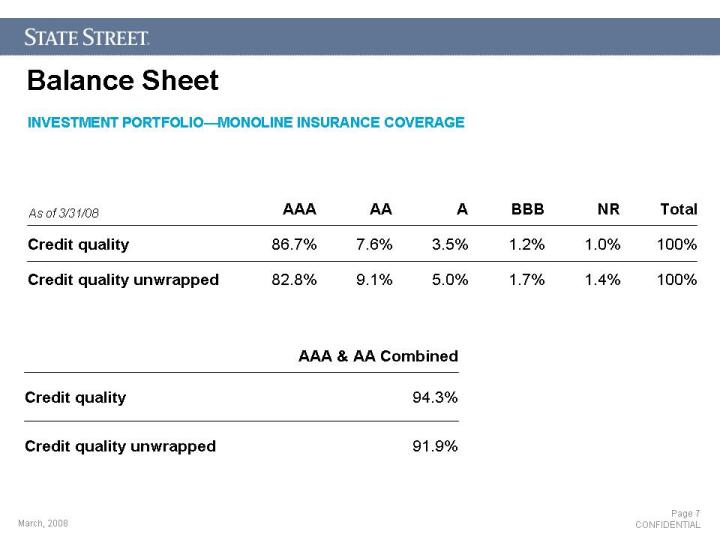

7 Balance Sheet As of 3/31/08 INVESTMENT PORTFOLIO—MONOLINE INSURANCE COVERAGE

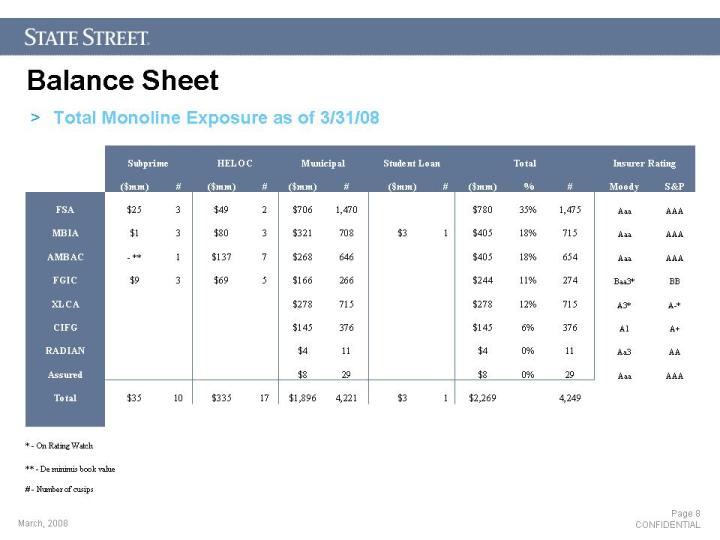

8 Balance Sheet Total Monoline Exposure as of 3/31/08