Exhibit 99.3

1 Conference Call Second Quarter July 15, 2008

2 Investment Portfolio As of June 30, 2008

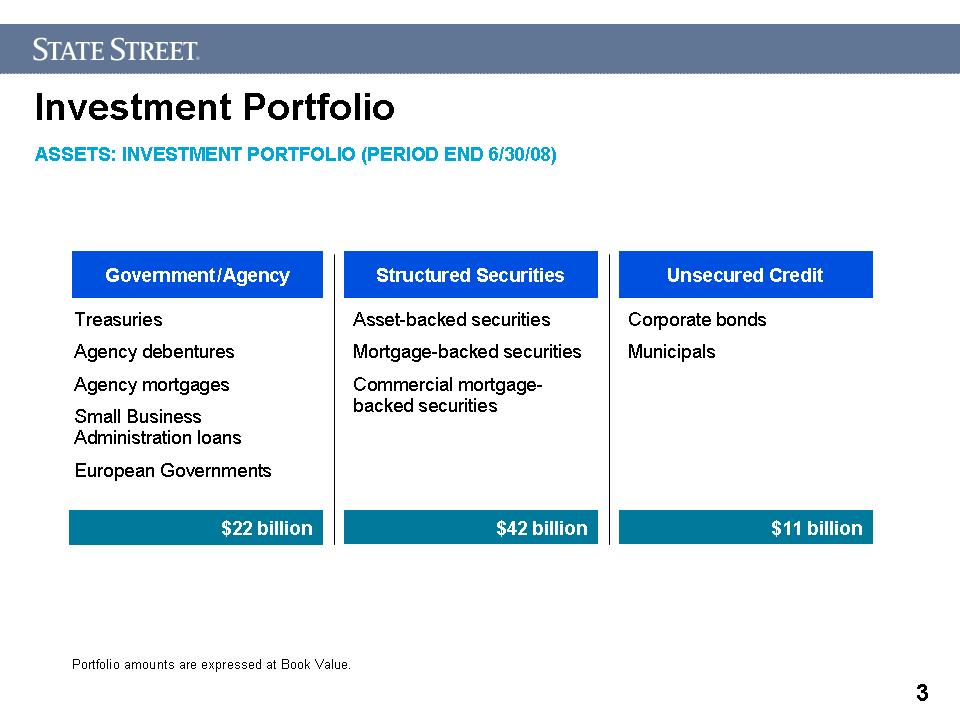

3 Asset-backed securities Mortgage-backed securities Commercial mortgage-backed securities $25 billion $42 billion $11 billion Corporate bonds Municipals Treasuries Agency debentures Agency mortgages Small Business Administration loans European Governments Investment Portfolio Government / Agency Structured Securities Unsecured Credit Portfolio amounts are expressed at Book Value. ASSETS: INVESTMENT PORTFOLIO (PERIOD END 6/30/08) $22 billion

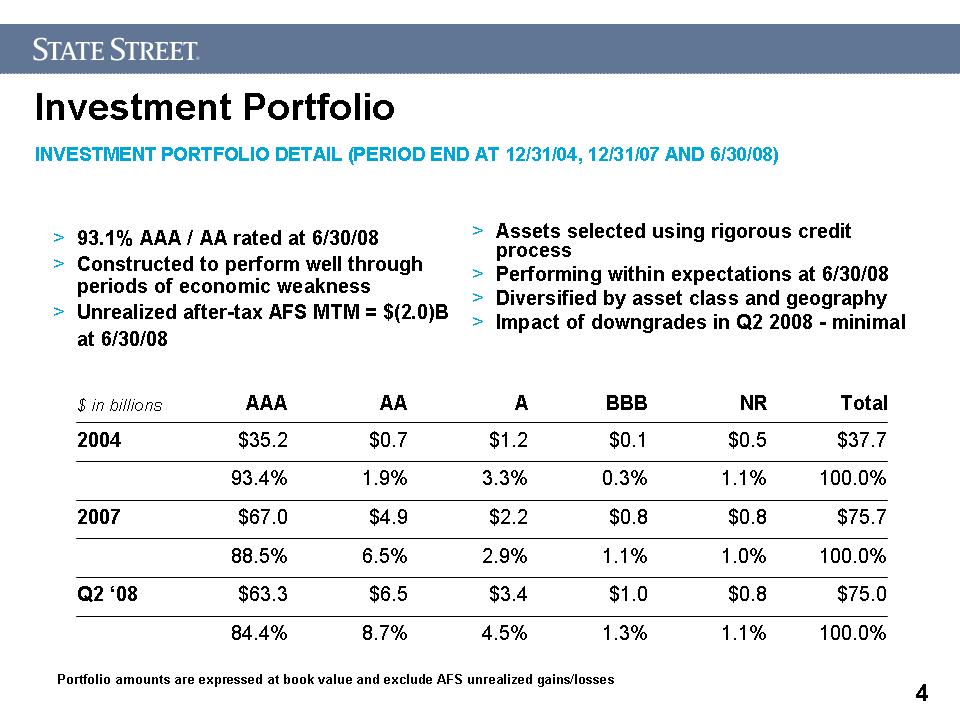

4 Assets selected using rigorous credit process Performing within expectations at 6/30/08 Diversified by asset class and geography Impact of downgrades in Q2 2008 - minimal 93.1% AAA / AA rated at 6/30/08 Constructed to perform well through periods of economic weakness Unrealized after-tax AFS MTM = $(2.0)B at 6/30/08 INVESTMENT PORTFOLIO DETAIL (PERIOD END AT 12/31/04, 12/31/07 AND 6/30/08) Portfolio amounts are expressed at book value and exclude AFS unrealized gains/losses Investment Portfolio

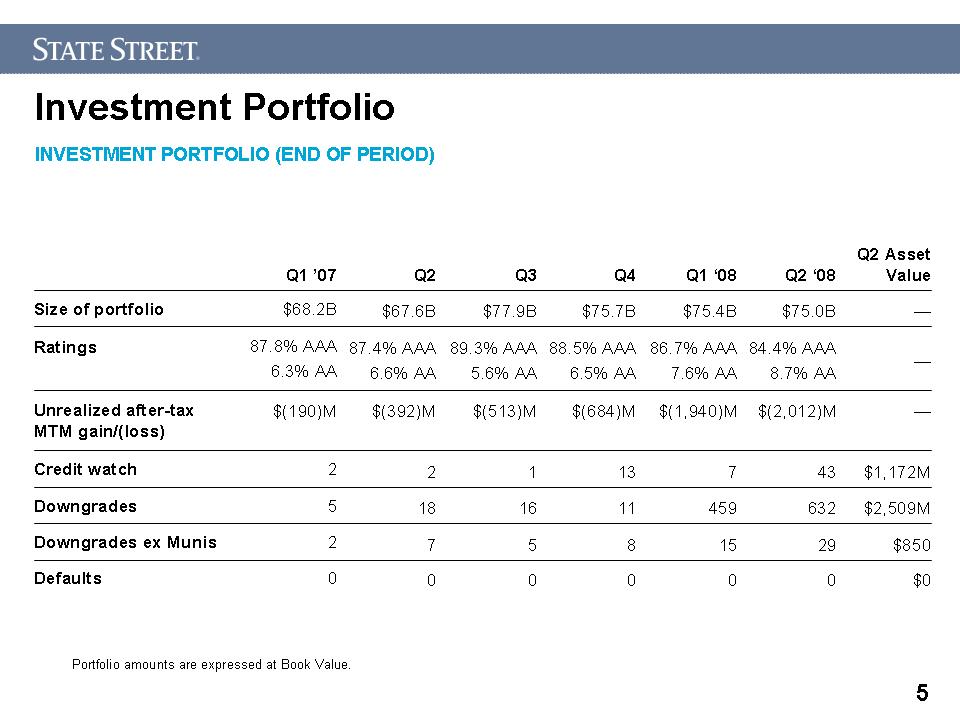

5 Investment Portfolio Portfolio amounts are expressed at Book Value. INVESTMENT PORTFOLIO (END OF PERIOD)

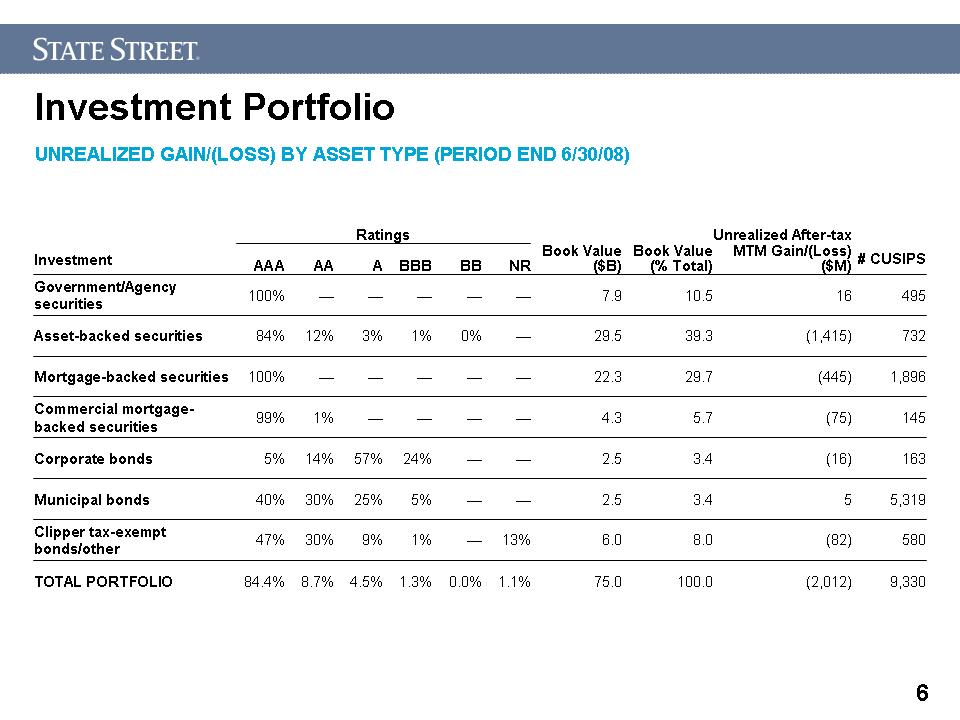

6 Investment Portfolio UNREALIZED GAIN/(LOSS) BY ASSET TYPE (PERIOD END 6/30/08)

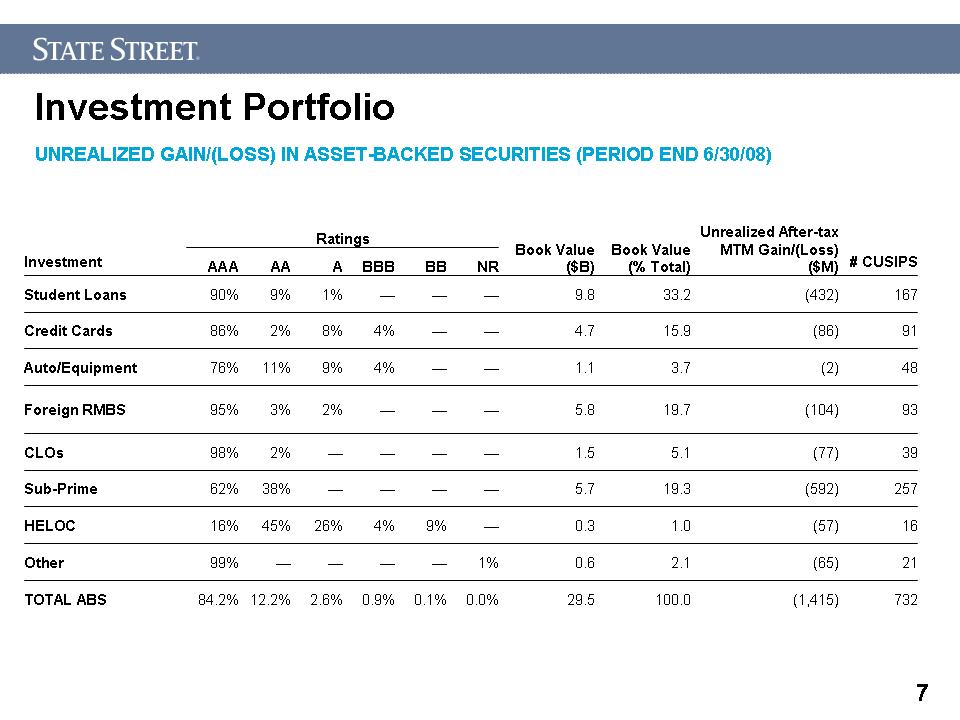

7 Investment Portfolio UNREALIZED GAIN/(LOSS) IN ASSET-BACKED SECURITIES (PERIOD END 6/30/08)

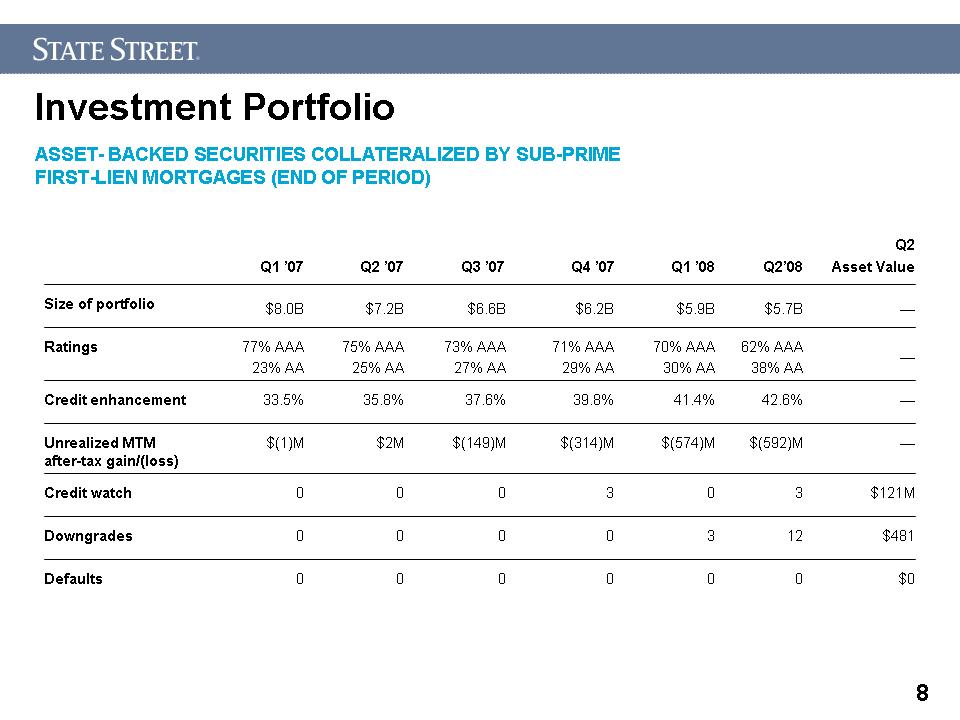

8 Investment Portfolio ASSET- BACKED SECURITIES COLLATERALIZED BY SUB-PRIME FIRST-LIEN MORTGAGES (END OF PERIOD)

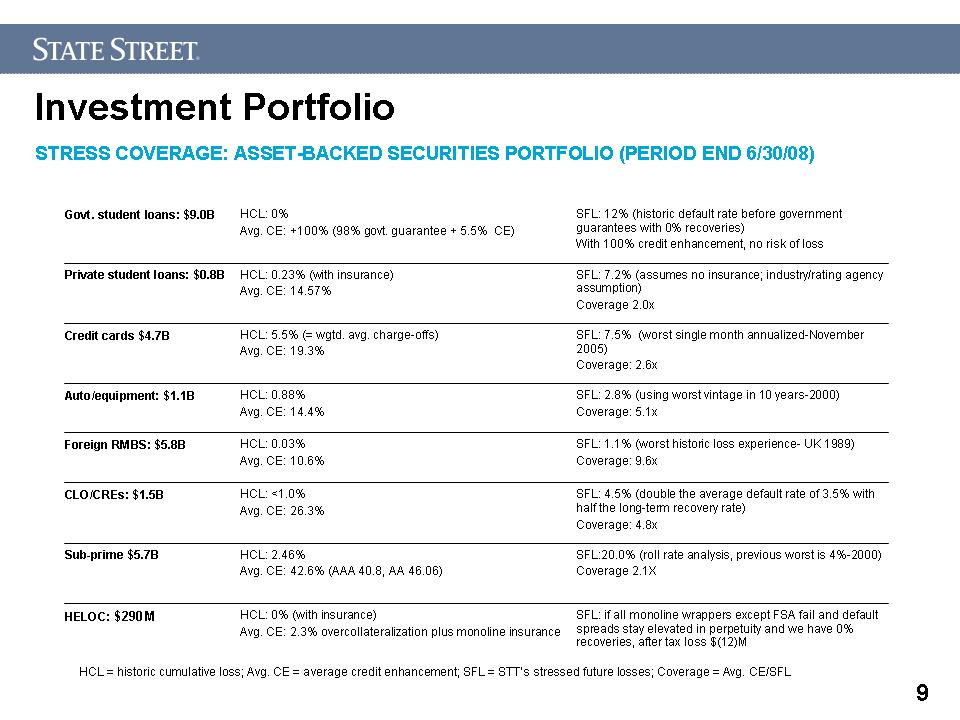

9 Investment Portfolio HCL = historic cumulative loss; Avg. CE = average credit enhancement; SFL = STT’s stressed future losses; Coverage = Avg. CE/SFL STRESS COVERAGE: ASSET-BACKED SECURITIES PORTFOLIO (PERIOD END 6/30/08)

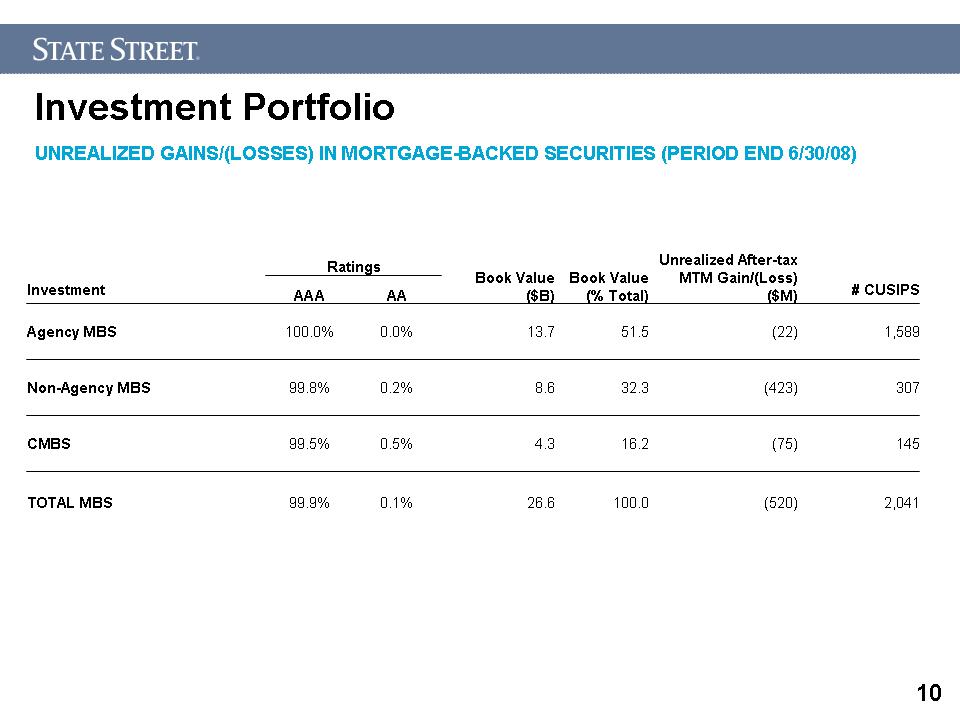

10 Investment Portfolio UNREALIZED GAINS/(LOSSES) IN MORTGAGE-BACKED SECURITIES (PERIOD END 6/30/08)

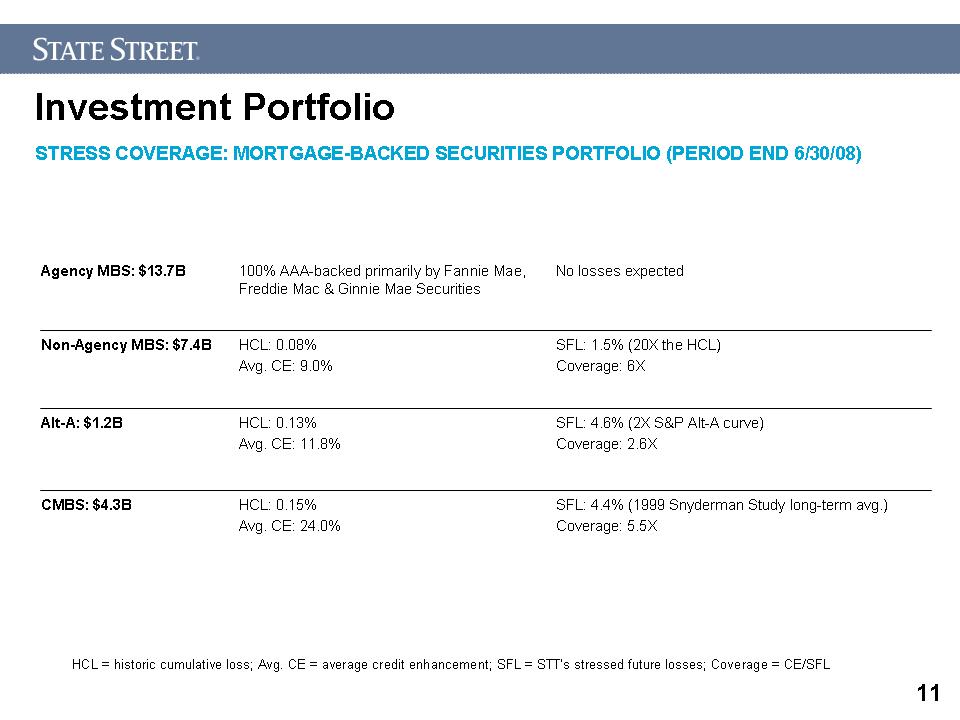

11 Investment Portfolio STRESS COVERAGE: MORTGAGE-BACKED SECURITIES PORTFOLIO (PERIOD END 6/30/08) HCL = historic cumulative loss; Avg. CE = average credit enhancement; SFL = STT’s stressed future losses; Coverage = CE/SFL

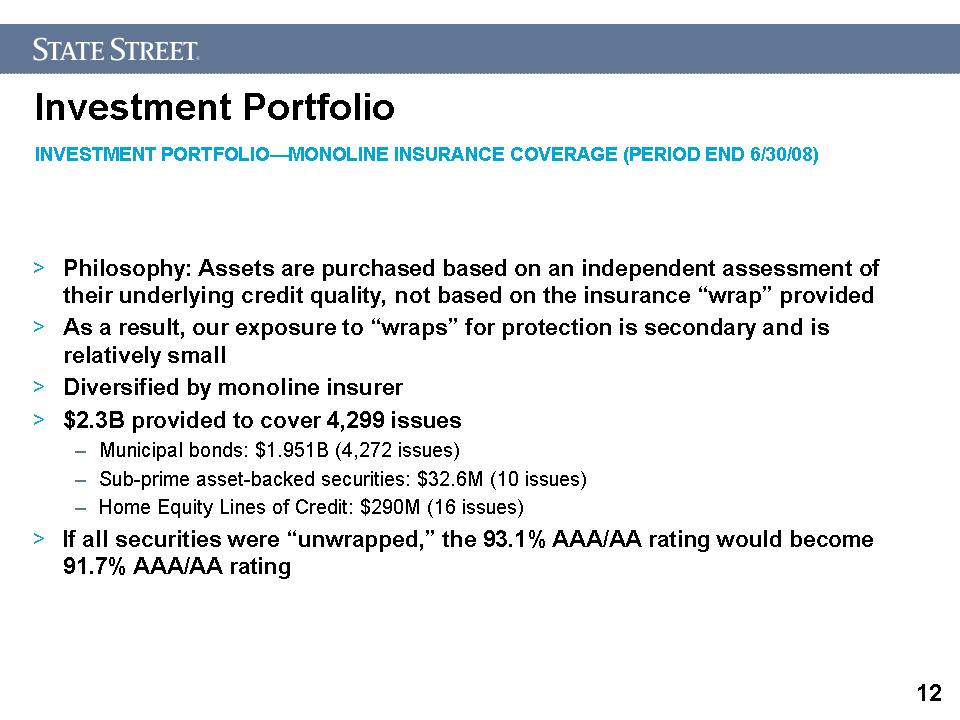

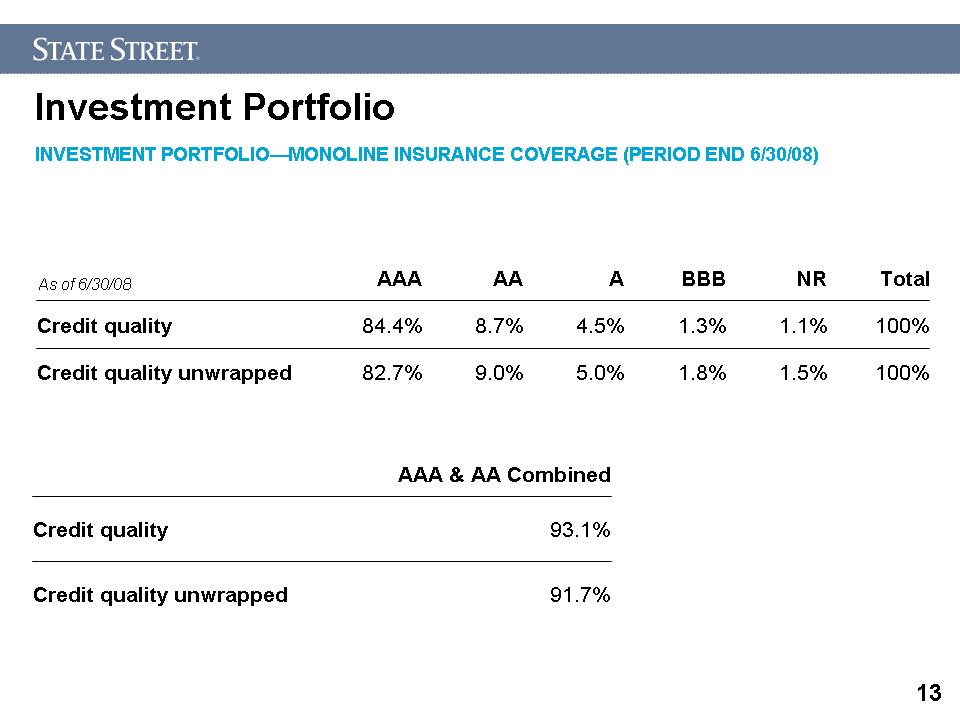

12 Investment Portfolio Philosophy: Assets are purchased based on an independent assessment of their underlying credit quality, not based on the insurance “wrap” provided As a result, our exposure to “wraps” for protection is secondary and is relatively small Diversified by monoline insurer $2.3B provided to cover 4,299 issues Municipal bonds: $1.951B (4,272 issues) Sub-prime asset-backed securities: $32.6M (10 issues) Home Equity Lines of Credit: $290M (16 issues) If all securities were “unwrapped,” the 93.1% AAA/AA rating would become 91.7% AAA/AA rating INVESTMENT PORTFOLIO—MONOLINE INSURANCE COVERAGE (PERIOD END 6/30/08)

13 Investment Portfolio As of 6/30/08 INVESTMENT PORTFOLIO—MONOLINE INSURANCE COVERAGE (PERIOD END 6/30/08)

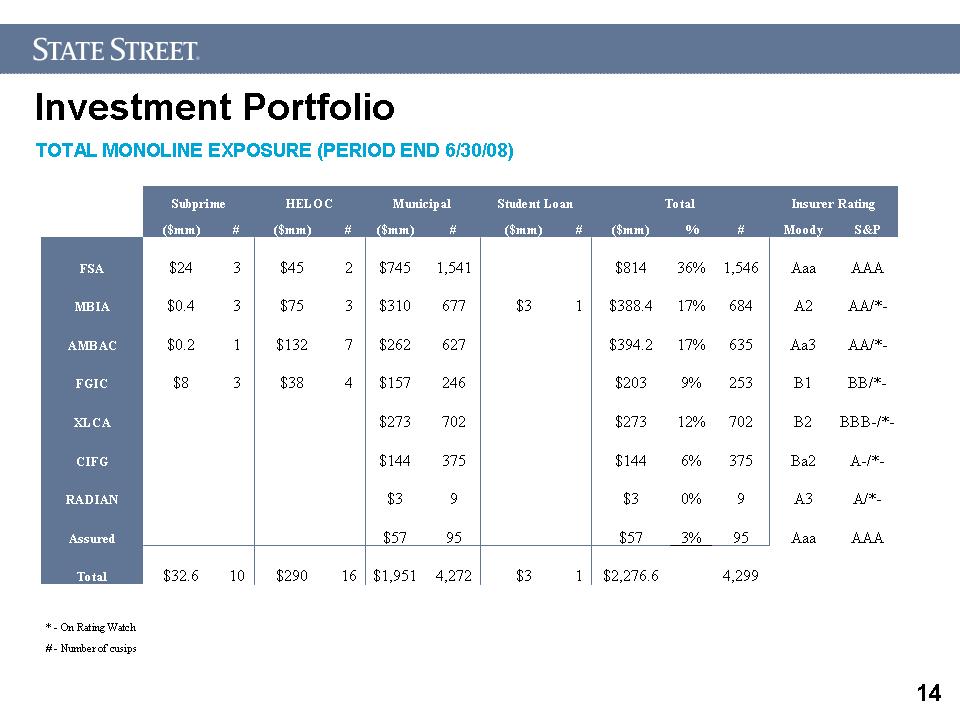

14 Investment Portfolio TOTAL MONOLINE EXPOSURE (PERIOD END 6/30/08)