Exhibit 15.3

A focused strategy for a lifetime of learning Annual report and accounts 2022

We are the world’s leading learning company |  |

Strategic report | ||||||||

| 2 | ||||||||

| 6 | ||||||||

| 7 | ||||||||

| 10 | ||||||||

| 12 | ||||||||

| 16 | ||||||||

| 18 | ||||||||

| 20 | ||||||||

| 26 | ||||||||

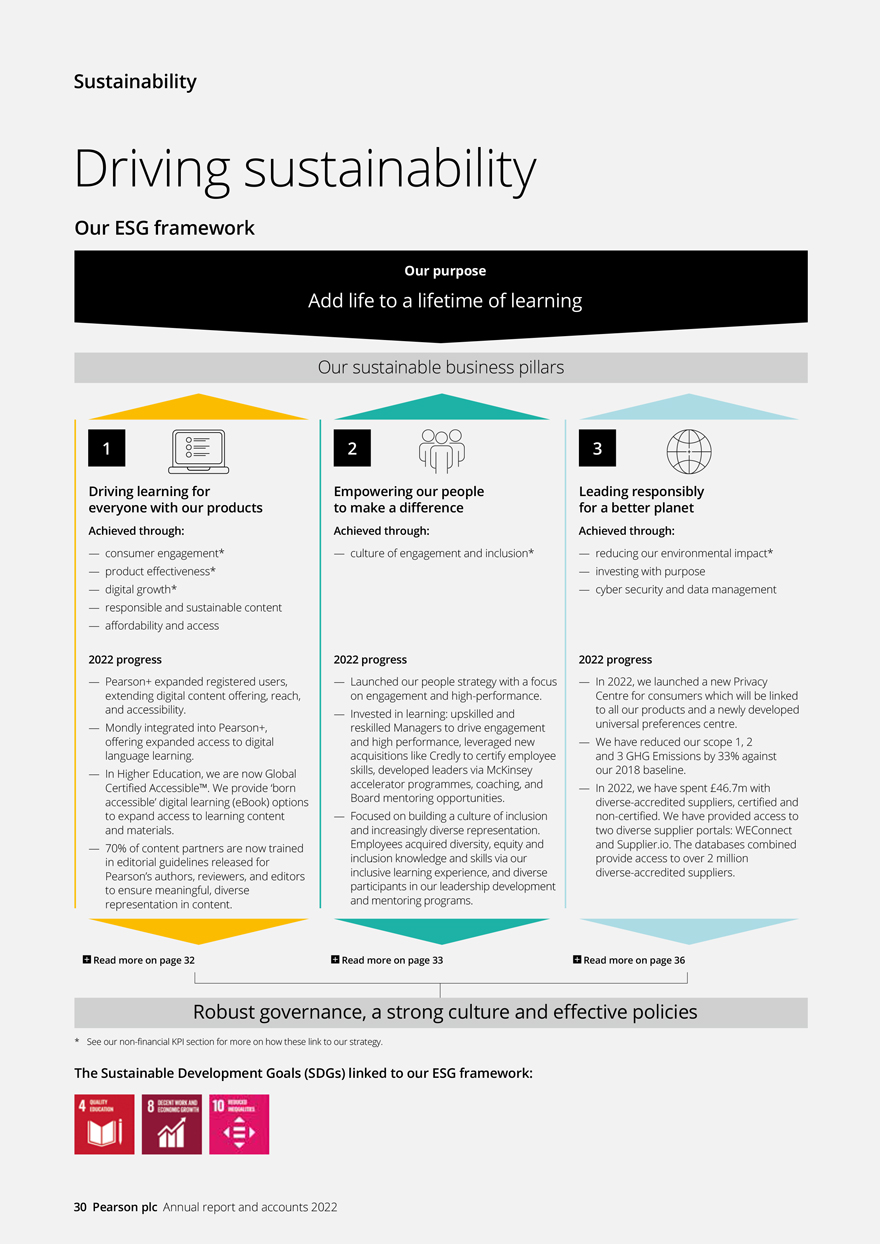

| 30 | ||||||||

| 43 | ||||||||

Governance report | ||||||||

| 53 | ||||||||

| 88 | ||||||||

| 120 | ||||||||

Independent auditor’s report to the members of Pearson plc | 126 | |||||||

| 134 | ||||||||

Company financial statements | 202 | |||||||

Other information | ||||||||

| 213 | ||||||||

| 215 | ||||||||

| 220 | ||||||||

| 221 | ||||||||

The strategic report, up to and including page 52, was approved for issue by the Board on 15 March 2023 and signed on its behalf by:

Sally Johnson

Chief Financial Officer

| Use this QR code to visit our Pearson plc website where you can find the online version of this report.  https://plc.pearson.com/en-GB/ investors/2022-annual-report-accounts | |

| We have a focused strategy for a lifetime of learning |  | ||||

Andy Bird, Chief Executive | ||||||

“At Pearson, we’re connecting our different products and brands to support people in their learning journey and create real-life impact. We’re forming an exciting lifelong digital learning ecosystem that provides people with affordable learning throughout their lifetime. By increasing our scale and customer reach, investing in new opportunities and expanding the interconnectedness between our divisions, we’re uncovering great things. The possibilities are vast for Pearson as we embrace the future of learning.” |

At a glance Our purpose is to add life to a lifetime of learning. Because learning isn’t just what we do – it’s who we are. Our vision We want everyone to realise the life they imagine through learning.. Our mission Create vibrant and enriching learning experiences designed for real-life impact. Our values begin with ‘we’ because they apply to all of us. They help guide how we show up every day for our customers, each other, and the communities we serve. 1. We ask ‘why’? We challenge the status quo by challenging ourselves. 2. We ask ‘what if’? We spark curiosity to innovate new possibilities for everyone. 3. We earn trust. We build credibility by acting with integrity every day. 4. We deliver quality. We hold our customers and consumers in the highest regard, and our work to the highest standards. 5. We make our mark. We execute with speed and agility to leave a lasting impact on everyone we serve. “We’ve redefined our purpose to meet this moment in our world where learning is becoming more fluid and exists inside and outside of formal education.” Lynne Frank, Chief Marketing Officer and

Co-President,

Direct-to-Consumer

Our strategy

Our strategy is to create trusted relationships with consumers throughout their lifelong learning journeys. We want to empower them to realise their goals and potential, by developing their skills across multiple stages of their learning lifetime, encompassing not only formal primary, secondary and higher education, but also, increasingly, the world of work.

Our strategy places consumers at the heart of everything we do, and we are integrating our products to create a learning ecosystem that reaches our consumers across all their life stages.

Annual report and accounts 2022 Pearson plc 3 |

At a glance continued | ||||||||||

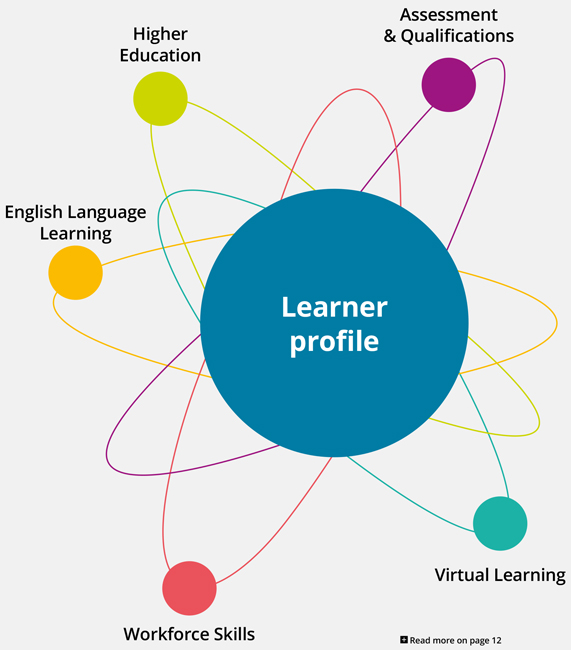

Our interconnected divisions | Assessment & Qualifications We provide the assessments, qualifications, certifications and licences that enable people to demonstrate their knowledge, skills and aptitude across a lifetime of learning – from school to professional careers. We play an integral role in a host of technology certifications, in areas such as cloud computing and cyber security, that power growth and innovation across the global economy. We deliver numerous medical certification and licensing examinations around the world, giving governments and the public the assurance that their providers have met the standards for care. Exam delivery volumes in the Information Technology sector increased by 12% from 2021 to 2022. Our growth will be fuelled by our unrivalled breadth of offering and global scale across both physical and digital assessment, combined with the growing market need for accreditation and certification in the professional market, more effective formative and summative assessment in the school market, and increased demand and spend across the education landscape in mental health and wellbeing. | Higher Education We provide around 18 million higher education students every year with vibrant digital content, assessments and enriching experiences, leading to positive learning outcomes. We provide a significant entry point for a lifetime of learning in the Pearson ecosystem. We intend to remain the Higher Education content market leader by deepening our relationships with students beyond instructor and faculty required course materials. By enhancing product features and investments into Pearson+, we enable students to succeed in achieving their goals across disciplines and academic paths. We will drive growth through increasing market share and recapture of the secondary market, particularly through enhancements to our suite of digital products including Pearson+, MyLabs, Mastering and Revel. In addition, we will invest in growth in the large international higher education market and capitalise on increased demand in Inclusive Access. | ||||||||

2022 Revenue |  |  | ||||||||

2022 Highlights | — Pearson VUE test volumes grew 16% to 19.4m with particularly strong growth in the IT and healthcare segments. VUE also won major contracts across its portfolio and expanded its presence in the US federal market. — Announced the intention to acquire Personnel Decisions Research Institutes (PDRI) which has significant expertise in providing assessment solutions to the US federal government, one of the largest employers in the US with more than 4 million employees. — Clinical Assessment had a strong performance due to good government funding and continued focus on health and wellbeing. — UK and International Qualifications 2022 revenue was driven by the return to full testing and growth in qualifications and assessment contracts internationally. — US Student Assessment had strong revenue growth with a full testing cycle in 2022 and new contract wins.  | — Inclusive Access sales to not-for-profit — A three-fold increase compared to prior year Fall semester in Pearson+ paid subscriptions, expanding our reach through US college bookstores: — Pearson+ paid subscriptions compared to prior year Fall semester up 205% to 406k (2021: 133k) — Pearson+ registered users compared to prior year Fall semester increased 3% to 2.83m (2021: 2.75m) — Launched Pearson+ Channels (with 18 study channels) in Autumn 2022 to help students understand complex concepts and prepare for exams in the toughest college courses, whether they are using a Pearson eTextbook or not. This increases the total addressable market for Pearson+. | ||||||||

4 Pearson plc | ||||||||||

Virtual Learning We offer highly effective online learning for every age and stage of education. Our users can learn where, when, and how they learn best, in a way that is tailored to their needs and propels them forward in their lives and careers. Our vision in Virtual Schools is to provide a holistic, academic, and innovative learning experience to our students, while being a trusted best-in-class partner for our schools and families. We will grow by continuing to focus on the core learning experience, including individualised learning and curriculum transformation, while innovating and adapting to both industry and market changes to stay ahead of the competition. Our career readiness solutions will fuel growth by providing pathways for students beyond high school, be it in the job market or further study. We will also capitalise on increased awareness and openness to virtual learning and the demand for alternative education mediums driven by parents’ new hybrid and remote working schedules. Our Online Program Management (OPM) business is currently under strategic review. | English Language Learning There are 1.4 billion English language learners across the globe. We have the courseware and assessments to help them achieve their goals, including digital and blended English solutions for educational institutions and the flagship Pearson Test of English, in over 150 countries. Our vision is to become the world’s leading destination for committed learners to build and prove their proficiency in English. We are growing through creating an interconnected suite of personalised products across direct to consumer, institutional, enterprise language learning and assessments, and online language learning through Mondly. This will allow us to expand our addressable market, increase market penetration, and create more repeatable, personal relationships with language learners, capturing more of their lifetime spend. We are also capitalising on a consistent market need for English proficiency in global employment and education, a growing demand for online language learning, and renewed global mobility. | Workforce Skills We’re building a world where everyone is prepared for the future of work and people are recognised for what they know and what they can do. Our newly launched talent investment platform uses workforce analysis and assessment to realise untapped potential, mobilise talent, and help enterprises and individuals close the workforce skills gap, helping everyone find the right work for them. We will grow by connecting consumers, enterprises, recruiters, and learning partners to a marketplace for verified skills. We can also capitalise on employers’ increasing need to reskill and develop their workforce to protect against shifts in both growing and shrinking markets and in response to the high speed of economic and technology change. We need to respond to and enable the accelerating convergence between previously disconnected parts of the HR technology market, particularly Learning and Development, Recruitment, and Talent Management. | ||||||||||

|  |  | ||||||||||

— Increased retention rates and Net Promoter Score, now +67, for Virtual Schools, which will drive enrolment growth. — Opened our first virtual school in Virginia focusing on grades 6-10 students, expanding to gradesK-10 in 2023.— Helped enact new legislation in Missouri, facilitating easier access to publicly funded virtual learning, leading to a doubling of our virtual school enrolments within that State. | — Pearson Test of English (PTE) test volumes up 90% and underlying revenue up 72%, particularly driven by border reopenings and gaining market share in India, where investment in our agent network and successful market campaigns have helped to drive growth. — Completed the acquisition of Mondly and entered the Online Self-Study language learning space. See our Strategy in Action for more detail on how Mondly is helping us to grow. — Transformed our institutional business through initiatives such as Pearson English Connected Learning, which creates personalised, connected solutions including courseware, assessment and certification to fast-track learning. — Enhanced our user experience to ensure that our courseware is the most engaging and effective on the market, leveraging our partnerships with major corporations including Disney and the BBC. | — Acquired Credly, a leading digital credentials business, giving us a strong foothold and user base in the workplace credentials space. — Developed our talent investment platform which provides accurate, real-time access to employee skills. — Integrated Faethm and Credly into the Workforce Skills division, creating single enterprise go-to-market — We launched Skills Accelerator, a suite of peer-supported, project-based learning courses that help people complete business-critical projects while developing future skills. | ||||||||||

| | | ||||||||||

Annual report and accounts 2022 Pearson plc 5 | ||||||||||||

2022 highlights

A year of

strategic and

operational

progress

| Achieved underlying sales growth of 5% and adjusted operating profit growth of 11% on an underlying basis, ahead of expectations | |

| Acquired Mondly and Credly to support the growth strategy across the Pearson ecosystem | |

| Announced £ 120m | |

6 Pearson plc | ||

Launched our people strategy with a focus on engagement and high-performance Launched 18 study channels on Pearson+ Enterprise Learning reaching c.2000 enterprise clients across Workforce Skills and Pearson VUE Completed the disposal international local courseware publishing businesses |  | |

Chair’s note

| I believe we are well- positioned to continue to grow profitably and to deliver long-term success, creating value for all our stakeholders. | |

Omid Kordestani, Chair | ||

2022 dividend growth 5% | “What drew me to this fantastic company was the incredible opportunity to be globally consequential and the important role we can play in improving society through lifelong learning.” | |||

Return on capital in 2022 8.7% | ||||

| Annual report and accounts 2022 Pearson plc 7 |

Chair’s note

continued

Overview

I’m delighted to be writing my first letter to you as Chair of Pearson. It’s a privilege to join Pearson at this exciting time. What drew me to this fantastic company was the incredible opportunity to be globally consequential and the important role we can play in improving society through lifelong learning. We have a tremendous opportunity to capitalise on this, benefiting all our stakeholders, particularly with the significant potential in digital learning. It is also exciting to see that we are delivering particularly on enterprise learning, in ways we never have before, as the workplace becomes the new heart of many people’s learning journey.

2022 has been a year of strategic and operational development as we continue to create a digital learning ecosystem, fit for the future of learning. We have made considerable progress in executing our direct to consumer, lifelong learning strategy as we reshape our portfolio for profitable growth, adding capabilities and increasing interconnectivity between divisions.

Financial and operational highlights

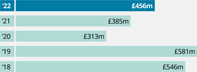

We delivered a strong performance in 2022 with sales increasing on an underlying basis by 5% and our adjusted operating profit margin increased from 11% to 12%. This resulted in our adjusted operating profit increasing to £456m.

We have also made good strategic and operational progress as we build further lifelong learning potential. We’ve been disciplined in right sizing the company to our strategic direction. We have taken bold actions to make Pearson a more efficient, focused company and through this we will accelerate our improved margin expectations to 2023 from 2025.

We have also retained a strong balance sheet and liquidity position that will enable us to continue to invest in our comprehensive growth strategy.

As a result of the strong performance in 2022, the Board recommends a final dividend of 14.9 pence per share. The final dividend will be paid on 5 May 2023 to shareholders on the register on 24 March 2023.

Environmental, social and governance

Pearson has a clear purpose adding life to a lifetime of learning that links naturally to our potential to make a significant positive impact on our society and our planet. Our products and services enable more engaging and stimulating learning experiences. They are accessible to more people, and with a smaller carbon footprint. We continue to make good progress against our ambitious climate targets, and we recognise the role that top talent plays in driving our long-term growth. This year, we also launched a people strategy focused on employee engagement as a driver of performance. We also ensure that we continue to operate as a responsible business and will always act in the best interests of our customers.

Our people make Pearson’s success

Our people are fundamental to our success and strong performance. I would like to take this opportunity to thank everybody for their commitment. I appreciate their incredible work, operational discipline, and focus over 2022. We cannot underestimate how this difficult environment has affected our people, I’m very proud of them all. Taking care of our employees, and ensuring we keep our positive culture is vital. Their efforts have, and will, continue to underpin the company’s performance as we take advantage of the significant growth opportunities ahead.

I also want to thank all our customers for their continued support. We will continue to provide them with engaging ways of learning that reflect today’s world, as we look to deliver the needs of both employers and employees.

| Pearson has an opportunity to educate the world and be a good citizen, as a business that acts responsibly and sets the right tone. |

Leading for the future We have a strong performance culture at Pearson, with a high level of execution and operational excellence. We also have a wonderfully diverse Board in terms of both experience and backgrounds. Ensuring we continue to have a diverse set of views and perspectives at Board and leadership level is key to our success. We need different types of leadership and operational talent to execute against our strategy. We will keep monitoring this as Pearson continues to transform so we have the right skill sets for our future, as well as managing succession planning for any upcoming departures. On the Board, we will miss Linda Lorimer, who steps down at Pearson’s upcoming Annual General Meeting (AGM) after serving nearly ten years on the Board. Linda has been an amazing force throughout her tenure, most recently as Chair of our Reputation & Responsibility Committee. At the executive level, we saw new leaders join the leadership team with Marykay Wells being elevated internally to Chief Information Officer. Marykay is working with the Board and leadership team to build a technology strategy that supports a coordinated, cross functional approach to data, content delivery, and product development. Sulaekha (Sue) Kolloru Barger also joined us to become our new Chief Strategy Officer. Since joining, Sue has been focused on driving strategic planning across the company and charting the course for future growth. | Engagement is fundamental As a Board and leadership team, it is critical we engage frequently with all our stakeholders. We want to ensure that our strategy is clear, that the way we’re operating is well understood, and to identify any gaps in our approach. This enables a constructive and positive relationship and helps us understand the views and perspectives of our stakeholders. It also ensures our team is focused on the right approaches, policies, and activities. This year, we undertook a comprehensive review of Pearson’s executive remuneration framework, with the proposed new Directors’ remuneration policy detailed on page 112. The Remuneration Committee and the Board have spent significant time rigorously reviewing the policy and its implementation to ensure it remains fit for purpose. This review considered Pearson’s renewed strategy, the recent strong performance of the business, and the views and expectations of our shareholders, their advisers, and other stakeholders. I believe the proposed policy is the best way to continue to drive a strong pay for performance culture. It also responds to the needs of the global talent market for digital innovators, whilst remaining mindful of the UK governance environment and the views of our shareholders. Confident in our potential In March, the company announced that the Board had received and rejected, in total, three unsolicited, preliminary, and highly conditional takeover approaches from investment firm Apollo. Under Sidney Taurel as Chair, the Board considered the right response for Pearson and our shareholders. While the Board deliberated the approaches with all due focus and attention, our confidence in the strategy that Andy and the leadership team are pursuing led us to unanimously vote against the approaches. We believe they all significantly undervalued the company and its future prospects. I would like to thank our shareholders for their support for the Board’s position. Outlook We start 2023 in a challenging macro environment, but we have a clear focus on execution. I have every confidence in our ability to deliver as we continue to transform because: 1. The company is confident of its strategy. 2. We have a strong executive team that has been established to execute on that strategy, and 3. The company will be very disciplined in measuring how to achieve success and to deliver results for shareholders. Pearson has an opportunity to educate the world and be a good citizen, as a business that acts responsibly and sets the right tone. We take our duties seriously and drive a level of execution that brings us closer to our promise of lifelong Learning: our ‘North Star’. I believe we are well positioned to continue to grow profitably and to deliver long-term success, creating value for all our stakeholders. Omid Kordestani Chair |

| Annual report and accounts 2022 Pearson plc 9 |

Chief Executive’s review

| | Another year of significant strategic, operational and financial progress. | |

Andy Bird, Chief Executive | ||

Underlying sales growth in 2022 5% | “Over the last year, a new Pearson has emerged -streamlined, interconnected, and more agile. This new Pearson is expanding our market opportunities, driving value for our stakeholders and making a positive impact on our world.” | |||

Underlying adjusted operating profit growth in 2022 11% | ||||

10 Pearson plc |

Dear shareholders,

I am pleased to report to you on another year of significant strategic, operational, and financial progress, one that has strengthened our foundations for a future of increasing sustainable growth.

Over the last year, a new Pearson has emerged - streamlined, interconnected, and more agile. This new Pearson is expanding our market opportunities, driving value for our stakeholders, and making a positive impact on our world.

Our 2022 financial results demonstrate the strong momentum we’ve been building. For a second consecutive year, our financial performance was ahead of our expectations, with underlying sales growing by 5% and underlying adjusted operating profits increasing by 11% to £456m. This reflects excellent progress across the Group, driven by our strategic initiatives.

Delivering on our strategy

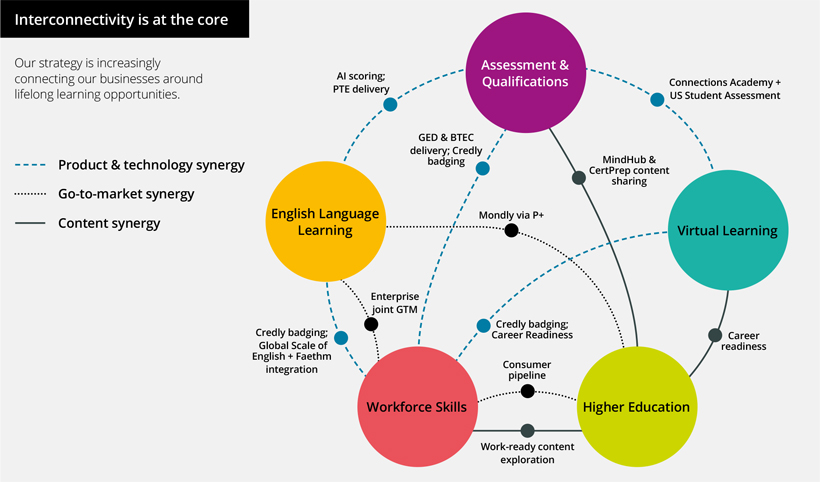

Our strategy focuses on a lifetime of learning and building a company that is digital-first, puts the consumer at its heart, and delivers high quality learning products at scale. A major focus this year has been enhancing the interconnectivity between our divisions, making more parts of Pearson more relevant to each other while driving financial and operational benefits. Because of this, our business model is moving from standalone products and services to connected learning applications, centered around our trusted relationships with consumers.

At the start of 2022, I identified four clear priorities for Pearson:

| — | Deliver sales and profit growth |

| — | Increase our focus on execution, quality, and trust |

| — | Embed customer and consumer insights across the company |

| — | Scale and grow Pearson+ |

We delivered on those priorities and much more, including significantly evolving our overall proposition and ourstrategies. Critically, we remain on track to deliver approximately £120m of cost efficiencies in 2023, accelerating our improved margin expectations to 2023 from 2025. We reshaped our portfolio with the acquisitions of Credly and Mondly, and announced the intention to acquire Personnel Decisions Research Institutes (PDRI), to drive growth. In addition, we completed the sale of our international courseware local publishing businesses and initiated the strategic review of our Online Programme Management (OPM) business. We saw strong growth in Pearson+ paid subscribers, launched the new Pearson+ Channels feature, and integrated Mondly into the service. As we do all of this, we are growing our universe of consumer relationships. In 2022, our products and services impacted the lives of around 160 million global users.

go-to-market

A future focused on a lifetime of learning

While we continue to work with the full spectrum of learning institutions, the workplace is now the heart of many people’s learning journey. Enterprise learning has long been foundational to our business but 2022 saw us scale that in new ways. Credly added about 70,000 new users each week, for the past 12 months, a strong signal of the need for individual upskilling. We now have more than 2000 enterprise learning clients. This part of our business is, and will continue to be, the subject of strategic investment. We have been hard at work developing our new Workforce Skills talent investment platform, a combination of Credly and Faethm capabilities that aims to help enterprises solve their talent planning, upskilling, and recruiting challenges. As it goes to market in 2023 and beyond, this new product has the potential to greatly accelerate the growth of our Workforce Skills division. In addition, we continue to expand our Pearson VUE offerings, and we are capitalising on the demand for English learning as a gateway to employment.

Beyond our workforce offerings, the progress of Pearson+ continues to point to an exciting future. In the calendar year 2022, our first full year in the market, Pearson+ had c.600,000 paid subscribers and 4.8 million registered users. We now have more than 1,800

e-textbook

titles in Pearson+ and we have introduced 18 study Channels to provide students with supplemental video and learning content. In the Fall of 2022, students viewed nearly 2 million minutes of Channels video content and utilised 1 million practice problems-impressive engagement activity. Between new content, the integration of Mondly, and broadened distribution through college bookstores, we continue to expand our total addressable market and prove the product market fit of Pearson+. We still see Pearson+ as the springboard for our Higher Education business and our bigger ambitions across a lifetime of learning. In our broader Higher Education business, we’re making excellent progress building the tools to return that division to top line growth. This effort centres on going to market more effectively and ensuring we have engaging products that faculty and students love to use.As we’ve demonstrated throughout the year, the cross over between our businesses is accelerating, which is creating synergies and forming the foundations of our digital learning ecosystem. We are at a critical moment where we can combine our capabilities to benefit a vast number of people. We believe there is enormous power in an ecosystem that brings our products together, with a consumer profile at its heart. As we move into 2023 and beyond, you will see us push further into a business model that connects consumer led learning into one Pearson experience.

Looking forward with confidence

As we turn this concept into reality, we continue to work hard every day to deliver what consumers demand: vibrant, impactful, frictionless learning solutions that will help them progress in their lives. As we deepen relationships with our consumers, they can move with ease between our products as their learning needs evolve. That creates lifetime value for learners, for Pearson, and for all our stakeholders.

We are delivering on what we have promised to our stakeholders, and we will continue to do that. The level of activity around the business is unprecedented. But it is also focused and better executed, resulting in better delivery of our strategic goals. I’d like to take this opportunity to thank each and every Pearson employee for their unwavering dedication to our purpose and our strategy. Led by their drive, determination, and unparalleled expertise, we are in a strong position to capture the opportunities in front of us.

Andy Bird

Chief Executive

| Annual report and accounts 2022 Pearson plc 11 |

Our strategy

An integrated strategy

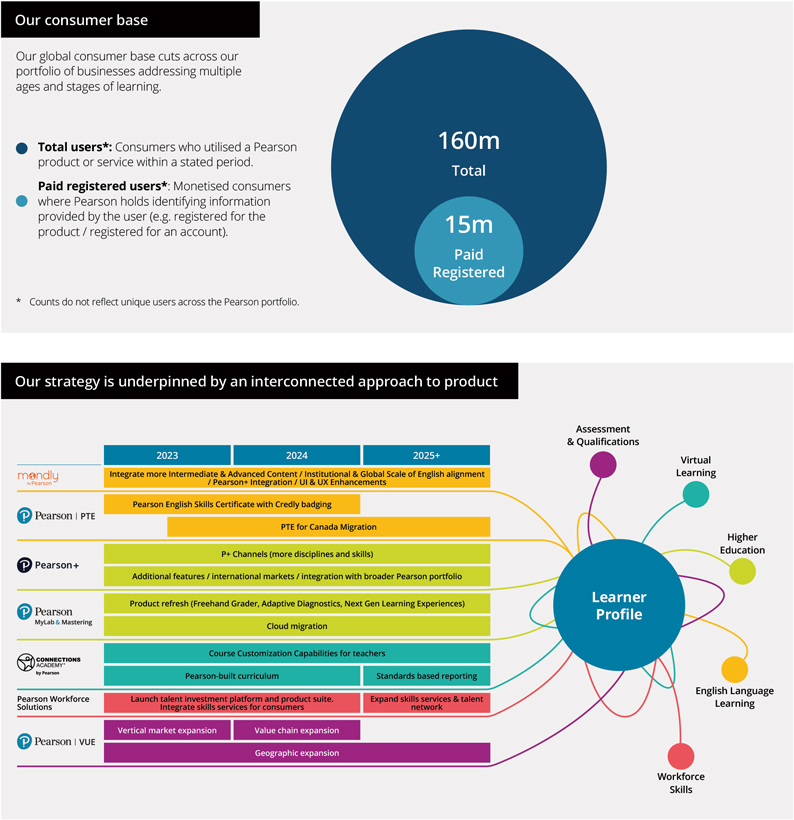

| In 2022, our products and services reached more than 160 million users around the world. |

Our strategy is to grow both by increasing our scale and customer reach. We are deepening our investment in opportunities across our divisions, and are expanding the interconnectedness between our divisions, to uncover and capitalise on further potential. We are confident that there are vast possibilities to expand our reach by linking our different learning capabilities into one experience as we move from standalone to connected learning applications.

We have a well-diversified global consumer base, coming from direct individual customers and institutional, enterprise and government relationships. Of our 160 million users, 15 million are registered with us. It is incumbent upon us to make every interaction with our consumers more meaningful by building relationships. We aim to provide all our audiences with the ability to move between our products as their learning needs evolve.

12 Pearson plc |

| | We are driving successful change through targeted investment, acquisitions, and disposals. |  | ||||

Sulaekha (Sue) Kolloru Barger, Chief Strategy Officer | ||||||

Strategic progress in 2022

Pearson has evolved from a matrixed holding company to the focusedlearning company we are today, as we integrate our businesses and products to form a lifelong digital learning ecosystem. As we better understand our consumers, we are embedding our insights to unlock synergies, build relationships and provide more relevant and inspiring products.

end-to-end

We are reshaping our product portfolio to meet increasing demand from consumers. Their needs are evolving to place a higher importance on skills and continuous learning, and they are consequently turning to their employers for support in upskilling and reskilling to ensure their relevancy in a dynamic workplace. More employers are investing in talent and we are working with them to provide the training and upskilling for their employees to help them progress.

Our 2022 results are evidence that our strategy is delivering results for our consumers and shareholders alike. We made good progress in 2022 both strategically and operationally, which is reflected in our strong financial performance: underlying sales growth was up 5% and underlying adjusted operating profit up 11%. Our new operating model has enabled us to identify approximately £120m of efficiencies in 2022, which we will deliver in 2023 and beyond. In turn, this will help us deliver our improved

mid-teens

margin target in 2023 - two years earlier than expected.Our strong progress in the face of macroeconomic headwinds demonstrates the benefits of our well-diversified business, coupled with the fundamental lifelong need to learn.

We are driving successful change by regularly reviewing and refining our portfolio through:

Significant organic investment, bringing new capabilities

| — | We have invested in new capabilities for Pearson+, including Channels functionality. |

| — | Expanded the reach of our VUE remote proctoring solution to include an in-country China solution |

| — | Workforce Skills launched Skills Accelerator, a suite of peer-supported, project-based learning courses that help people complete business-critical projects while developing future skills |

| — | Developed our MondlyWORKS capabilities and go-to-market |

| — | Virtual Learning began building an enhanced career readiness solution for K-12 students expected to launch later in 2023 |

Acquisitions to bolster our capabilities and enter new markets

| — | Recent acquisitions include Credly (Workforce Skills), Mondly (English Language Learning), Navvy (Assessment & Qualifications), and ClutchPrep (Higher Education), and we have signed an agreement to acquire PDRI (Assessment & Qualifications). |

Strategic disposals to refine our portfolio

| — | We completed the strategic review of our international courseware local publishing business, resulting in successful exits of our Europe, French Canadian, South Africa and Hong Kong local K12 publishing businesses. |

| Annual report and accounts 2022 Pearson plc 13 |

Our strategy

continued

Strategy in action | ||

Enterprise / Workforce Skills Our opportunity Our ambition is to enable a world where people and organisations can achieve their full potential in the new skills economy. We believe that is no longer just about what you’ve done, but what you can do. Our objective is to provide solutions that help employees thrive and empower employers to maximise the value of their most important asset: their people. The £200bn global Workforce Skills market is comprised of several different sub-markets including employee learning and development, talent management, andpre-hire recruitment services. This market is in the midst of widespread disruption, driven by seismic change in the workplace. The World Economic Forum estimates that over 1 billion people will need reskilling by 2030.Organisations are struggling to navigate this change because they lack a comprehensive understanding of the skills their employees have, or the skills they need, to achieve their commercial goals. And without this understanding, their investments into current learning and development services are not delivering the results that they should be. Progress so far We have built integrated product and engineering teams, re-engineered our product portfolio and tech stack, developed a new product roadmap, launched new products, created a single global sales team and built astate-of-the-art We have reshaped our Workforce Skills portfolio to serve an expanding remit, building on Pearson’s existing strong foundation with Enterprise consumers (c.16% of Group sales). To focus on the needs of our different customer segments, we have organised our | Workforce Skills division into two parts: Vocational Qualifications and Workforce Solutions. Vocational Qualifications offers high quality vocational qualifications that allow learners to build the knowledge, skills and behaviours they need for career success. Whether it’s a Higher National Diploma in Computing, a BTEC in Health and Social Care, or training as part of the TQ Construction Academy, these provide the skills and qualifications that our economy needs now and in the future. Workforce Solutions is our enterprise and consumer-focused business. It brings together our two recent acquisitions – Credly and Faethm – with our existing portfolio of products and capabilities in GED, Talentlens and Accelerated Pathways. We have moved quickly this year to restructure and integrate these businesses into a single global entity. Workforce Solutions’ portfolio of services has been specifically designed to meet the needs of enterprises and institutional customers, but with a core focus on the needs of the individual consumers upon which the success of any organisation depends. Throughout 2022, we continued to grow our revenue, including our SaaS subscriptions, expanding our customer base by 133%, and accelerating our reach by adding 4.7m new users to our Credly platform. We firmly fit into Pearson’s wider strategy, with products that can interconnect with others across the Pearson ecosystem, supporting and accelerating Pearson’s lifelong learning ambition. For example, we have a library of certified preparation content and courses for IT professionals in Professional Learning and Development which is relevant for learners in the workplace. English is the globally recognised language of business, so we have added English to Faethm’s skills framework, as well as offering Credly badges for Pearson’s range of English assessment products. | |

English Language Learning Our opportunity We operate in a c.£6 billion addressable market, which integrates three key market segments: 1. Institutional English Language Learning: an addressable market of approximately £3 billion. We offer digital and blended courseware solutions to academic institutions, private language schools and enterprises across the globe. 2. Online self-study language learning, an addressable market of c.£2 billion with double-digit growth, which we have entered through our acquisition of Mondly. 3. High Stakes Assessments: an addressable market of c.£900 million. Our flagship product PTE is a verified, secure certification of English proficiency for international migrants and students. A substantial element of our Institutional business is in K-12, which is generally government funded and backed, making it stable in a variety of macro-economic environments. For PTE, we believe that there will be a strong desire for people to invest in their education and to study in our key destination markets. We aim to acquire more new and existing language learners, and capture more of their lifetime spend on language learning, through cross-selling English Language Learning solutions. We are dedicated to growing the business through improving customer experience, which has already been successful in 2022, with a 24% increase in underlying revenue and 33% increase in underlying profit, and with the potential to gain further share over the next few years. | a. Our institutional business plays an important strategic role. It provides the potential to form relationships with millions of institutional learners as well as corporate learners, and it lends invaluable reputation and credibility in the language space to our entire product portfolio It is also a large lead-generator for our suite of assessment products and Mondly, both of which are complementary products that enhance the student experience. b. Mondly gives us more opportunities to reach more committed learners: a foothold in the fast-growing direct to consumer online language learning market, and the MondlyWORKS platform for enterprise language learning. c. PTE and Mondly give us more direct relationships with consumers, which is strategically important to the division and our ability to cross-sell within Pearson. Progress so far In 2022, we developed the Pearson English Skills Certificate, a new mid-stakes English exam which will complement the PTE to capture more of the English assessments market, and which will launch in 2023. We prioritised aligning Pearson products to the Global Scale of English (GSE), our proprietary scale that allows more granular understanding of English ability, furthermore, working to align Workforce Skills’ Faethm product, laying the ground for future collaboration. Finally, in addition to finding ways to use our institutional content to bolster Mondly material, particularly in the intermediate and advanced levels, we integrated Mondly with Pearson+, welcoming over 10,000 new users through this route. | |

14 Pearson plc |

This allows consumers to prove their language proficiency to employers. The connection between students and work is an obvious collaboration point with Pearson+ and there are fantastic opportunities to connect our services with Pearson VUE, to maximise the value that Pearson can bring to our enterprise customers and consumers.  Mike Howells, President, Workforce Skills | Pearson+ Our opportunity We are a leader in the Higher Education courseware market, with millions of students enrolled in courses using Pearson eTextbooks. We want to leverage this market dynamic in two phases: 1. Shift eTextbook consumption for students directly to Pearson+, and improve monetisation 2. Engage and retain students with relevant and valuable services beyond eTextbooks, and maximise consumer lifetime value Pearson+ is currently monetised through paid access to eTextbooks by students where faculty adopt Pearson content in their courses. Our existing Higher Education business provides a large, efficient customer acquisition funnel for Pearson+. Additional content beyond eTextbooks, such as Pearson+ Channels, will encourage further use of the application. Over time, Pearson+ users can be further monetised through cross-selling other relevant Pearson products and services. Progress so far In 2022, we started to scale users and expand product features. During the fall back-to-school  Tim Bozik, Chief Product Officer | |||||||||

Spotlight on Credly — Credly is an end-to-end — It adds an established, well-known credentialing service to our workforce analytics, learning & assessment capabilities — It has a network of 3,000 certification and badge issuers — It generates 70,000 new users every week — It has issued more than 50 million credentials | ||||||||||

Giovanni Giovannelli, President, English Language Learning | ||||||||||

Spotlight on Mondly — Global language learning app — 100m+ downloads — 446k paid subscriptions — Highly-rated app both on mobile and VR — 41 languages offered, with more than 1,300 possible language pairs (learners can learn a target language from any other language) | ||||||||||

| Annual report and accounts 2022 Pearson plc 15 |

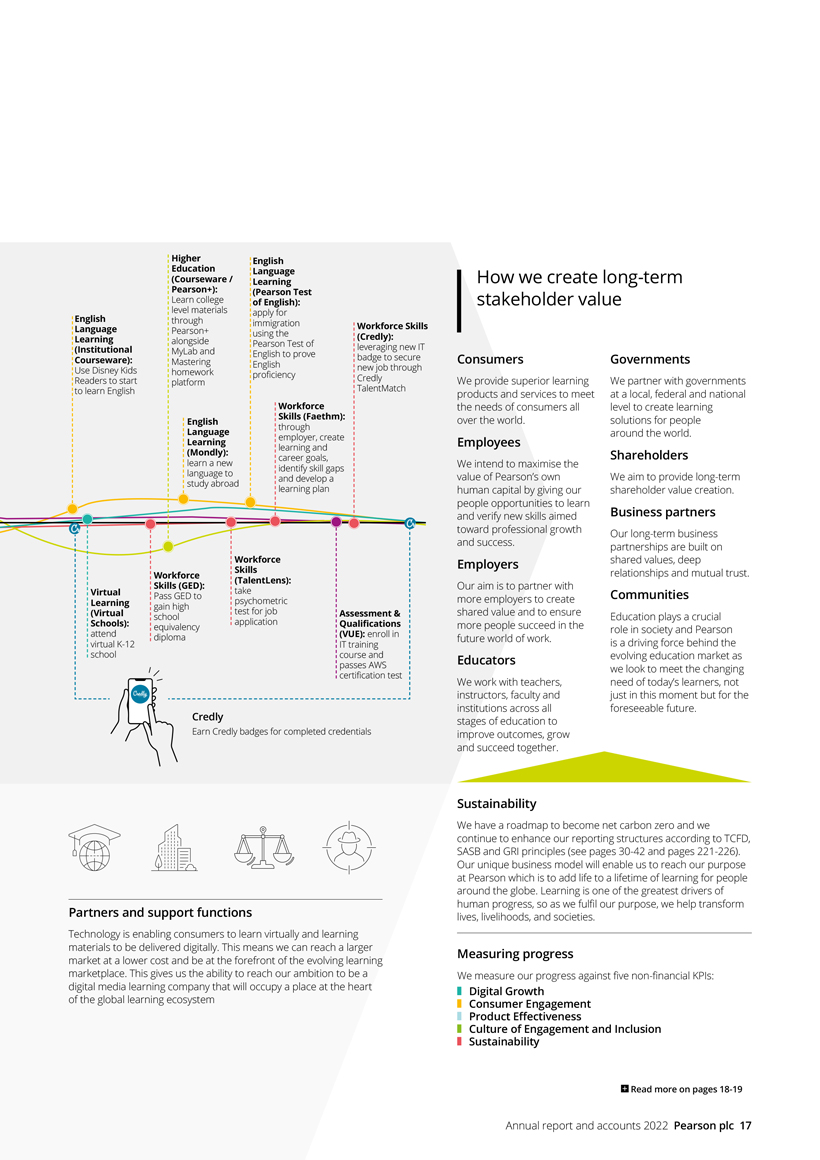

Our business model

Creating value

Our foundations An integrated business to support customers through their learning journey Committed people and partners Assessment Virtual From our brilliant and dedicated employees to our fantastic authors, we are the Learning & Qualifications home for the best talent. We have a broad range of partners across our business who we expect to share our Pearson values. Our relationships with governments, customers, non-governmental organisations (NGOs) and other global organisations help us to increase our impact on consumers around the world. Higher R&D and product innovation Education Our product team, with expertise in learning science, has a focus on learning outcomes. Through ongoing innovation and Research and Development (R&D) we are committed to creating learning products which offer a great user Learner experience and that demonstrate measurable learning progress. profile Financial assets Our shareholders entrust us with their capital in order to invest on their behalf for the long term. Our physical footprint English Language Learning Our products and services are available in most countries and territories around the world and are focusing on simplifying our property portfolio to enable digital and flexible ways of working. Data and insight As we move to a direct to consumer business we are able to know our customers Workforce Skills better – and serve them more effectively – through the effective and responsible use of data. We are also building out our capabilities in data analytics and AI See overleaf for examples of how our businesses through acquisitions including Faethm, which enable us to use data insights to support customers through their learner journeys help identify skills gaps and provide compelling solutions to workforce challenges. Strong market fundamentals Direct-to-Consumer We are well placed to benefit from structural tailwinds in the global learning Increasing Direct to Consumer products and services market including three big market opportunities: is an important initiative that spans all our divisions. For example, we are growing Pearson+, our digital learning service in Higher Education, alongside our 1 2 3 acquisition of Direct to Consumer language learning platform Mondly. Both of these services will be an Online and digital Solutions to Academic and important customer acquisition tool underpinning tools for schools evaluate and professional skills our Direct-to-Consumer offerings across the Group. and education address workforce accreditation and skills gaps certification Our Direct-to-Consumer strategy also means that our business model needs to evolve. We now go directly to consumers as well as through our existing models whereby we reach the consumer via an educational institution, employer or other partner.

Partners and support functions Technology is enabling consumers to learn virtually and learning materials to be delivered digitally. This means we can reach a larger market at a lower cost and be at the forefront of the evolving learning marketplace. This gives us the ability to reach our ambition to be a digital media learning company that will occupy a place at the heart of the global learning ecosystem How we create long-term stakeholder value Consumers We provide superior learning products and services to meet the needs of consumers all over the world. Employees We intend to maximise the value of Pearson’s own human capital by giving our people opportunities to learn and verify new skills aimed toward professional growth and success. Employers Our aim is to partner with more employers to create shared value and to ensure more people succeed in the future world of work. Educators We work with teachers, instructors, faculty and institutions across all stages of education to improve outcomes, grow and succeed together. Governments We partner with governments at a local, federal and national level to create learning solutions for people around the world. Shareholders We aim to provide long-term shareholder value creation. Business partners Our long-term business partnerships are built on shared values, deep relationships and mutual trust. Communities Education plays a crucial role in society and Pearson is a driving force behind the evolving education market as we look to meet the changing need of today’s learners, not just in this moment but for the foreseeable future. Sustainability We have a roadmap to become net carbon zero and we continue to enhance our reporting structures according to TCFD, SASB and GRI principles (see pages

30-42

and pages221-226).

Our unique business model will enable us to reach our purpose at Pearson which is to add life to a lifetime of learning for people around the globe. Learning is one of the greatest drivers of human progress, so as we fulfil our purpose, we help transform lives, livelihoods, and societies. Measuring progress We measure our progress against fivenon-financial

KPIs: Digital Growth Consumer Engagement Product Effectiveness Culture of Engagement and Inclusion SustainabilityKey performance indicators

Monitoring progress

Non-financial measures |

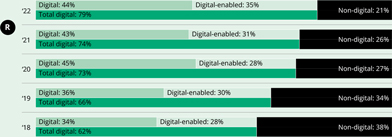

Digital Growth Objective: Drive digital revenue growth | Digital sales* Underlying Growth in group digital and digital-enabled sales +9% (2021: +9%) |  | ||||||||

Virtual Schools US enrolments 106k (2021: 111k) | OPM student enrolments 270k (2021: 275k) | OnVUE volumes 3.0m (2021: 3.0m) | PTE volume 827k (2021: 436k) | Higher Education US digital registrations 9.9m (2021: 11.1m a ) | ||||||

Consumer Engagement Objective: Create engaging and personalised consumer experiences | NPS for Connections Academy +67 (2021: +62) | NPS for PTE +52 (2021: +56) | Mondly paid subscriptions 446K (2021: n/a) | Workforce Skills registered users c 4.7m (2021: n/a) | Pearson+ registered users b 2.83m (2021: 2.75m) | |||||

Product Effectiveness Objective: Improve the effectiveness of our products to deliver better outcomes | PTE speed of score return 1.3 days (2021: 1.2 days) | VUE Test volumes d 19.4m (2021: 16.8m) | VUE partner retention e 99.9% (2021: 99%) | Workforce Skills number of enterprise customers f 1,503 (2021 : 645) | Workforce Skills enterprise customer net retention rate 74% (2021: n/a) | Higher Education Product usage - text units 4.8m (2021: 5.4m) | ||||||

Culture of Engagement and Inclusion Objective: Build an inclusive culture and increase diverse representation | Employee Engagement Pearson uses the Gallup Q 12 ® surveyto measure engagement, annually 3.96 grand mean on a 5 point Likert scale (2021: n/a) | Investing in diverse talent The % of responses who agree or strongly agree to Gallup Q 12 ® surveyquestions In the last six months, someone at work has talked to me about my progress 67% (2021: n/a) This last year, I have had opportunities at work to learn and grow 72% (2021: n/a) | Culture of inclusion index The grand mean of 3 Gallup Q 12 ® survey questions — At work, I am treated with respect — My company is committed to building the strengths of each employee — If I raised a concern about ethics and integrity, I am confident my employer would do what is right 4.12 grand mean on a 5 point Likert scale (2021: n/a) | Increasing diverse talent % of people in leadership development and mentoring programmes who are diverse. 75% (2021: n/a) % of people in succession plans for leadership who are diverse |   | |||||||

Women People of Colour/BAME 52% 26% (2021: 72%) (2021: 24%) | ||||||||||||

Sustainability  Strategy | Progress against achieving net zero carbon by 2030, as measured through percentage carbon reduction | |||||||||||

Objective: Achieve net zero carbon by 2030 | Reduction in total tCO 2 in 2022 | Reduction in total tCO 2 in 2021 | ||||||||||

33% | 31% | |||||||||||

vs 2018 g | vs 2018 g | |||||||||||

| a. | 2021 US digital registrations restated from 11.4m to 11.1m due to recategorising 0.3m of registrations from US to International. |

| b. | Pearson+ registered users represents the number of unique user accounts added over an academic year. |

| c. | Workforce Skills registered users represents the number of net new user accounts on a trailing 12-month basis and includes net new user accounts from Credly pre-acquisition. |

| d. | VUE test volumes include GED tests. |

| e. | VUE Partner retention is based on revenue mix. |

| f. | Workforce Skills number of enterprise customers represent the number of customers at period end. |

| g. | Net zero carbon figures have been restated in 2021 to reflect acquisitions, disposals and data improvements. The net zero carbon figures have been assured by an independent third-party, Corporate Citizenship. |

| * | Historical figures restated to exclude Wall Street English and US K-12 Courseware (sold in 2018, and 2019 respectively). |

Please find further details on our Strategic KPIs here https://plc.pearson.com |  | See how this aligns strategy to management reward: pages 98 & 99 |

18 Pearson plc |

| Financial measures |

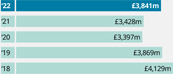

Sales b |  | Adjusted operating profit a |  | Net debt a | ||||

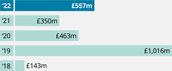

£3,841m | £456m | £557m | ||||||

|  |  | ||||||

| This is our revenue as reported in our income statement. | A non-GAAP financial measure that enables management to consistently track the underlying operational performance of the Group. | This is a non-GAAP financial measure and is used by management to assess the Group’s cash position. | ||||||

Adjusted earnings per share a |  | Operating profit b | Basic earnings per share b | |||||

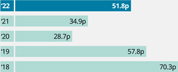

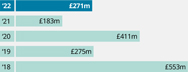

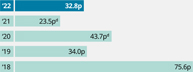

51.8p | £271m | 32.8p | ||||||

|  |  | ||||||

A non-GAAP financial measure used to evaluate performance. | This is our operating profit as reported in our income statement. | A measure of the amount of profit that can be allocated to one share of our common stock. | ||||||

Operating cash flow and cash conversion a | | Net cash generated from operations b | Dividend per share | |||||

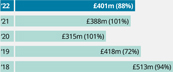

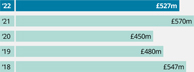

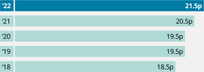

£401m (88%) | £527m | 21.5p | ||||||

|  |  | ||||||

| Operating cash flow is an adjusted measure and is presented in order to align the cash flows with corresponding adjusted operating profit measures. | This is our net cash generated from operations as reported in our cash flow statement. | This is the proposed full year dividend. Our dividend policy is to be progressive and sustainable. | ||||||

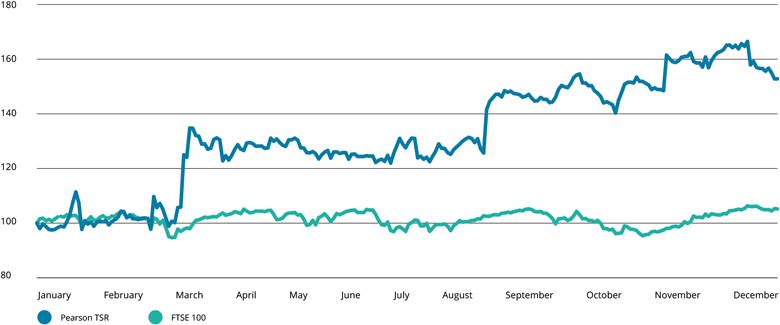

Total shareholder returns c 57.16%  This is a measure of financial performance of shares over time. |  | Return on Capital a 8.7%  A non-GAAP measure of how efficiently we are generating returns from our asset base. |  | a. See page 215 for an explanation of these alternative performance measures. b. Statutory measure. c. Source: Bloomberg. d. Comparative amounts have been restated, see note 1 of the financial statements for further details. Note: See page 215 for full reconciliation of the alternative performance measures to the equivalent statutory measure. | ||||

| See how this aligns strategy to management reward: pages 98 & 99 |

For more information on our KPI measures, including why and how we measure them, please refer to the glossary on our website.

| Annual report and accounts 2022 Pearson plc 19 |

Financial review

| We saw continuing momentum in 2022, with 5% underlying sales growth and adjusted operating profit of £456 million. | |

Sally Johnson, Chief Financial Officer | ||

| Financial summary | ||||||||||||||||||||

Business performance | ||||||||||||||||||||

| £ millions | 2022 | 2021 | Headline growth | CER growth | Underlying growth | |||||||||||||||

| Sales | 3,841 | 3,428 | 12% | 3% | 5% | |||||||||||||||

| Adjusted operating profit | 456 | 385 | 18% | 6% | 11% | |||||||||||||||

| Operating cash flow | 401 | 388 | ||||||||||||||||||

| Adjusted earnings per share | 51.8p | 34.9p | ||||||||||||||||||

| Net debt | (557) | (350 | ) | |||||||||||||||||

Statutory results | ||||||||||||||||||||

| £ millions | 2022 | 2021 | Headline growth | |||||||||||||||||

| Sales | 3,841 | 3,428 | 12% | |||||||||||||||||

| Operating profit | 271 | 183 | ||||||||||||||||||

| Profit for the year | 244 | 178 | * | |||||||||||||||||

| Cash generated from operations | 527 | 570 | ||||||||||||||||||

| Basic earnings per share | 32.8p | 23.5p | * | |||||||||||||||||

| Dividend per share | 21.5p | 20.5p | ||||||||||||||||||

Throughout this section: a) Growth rates are on an underlying basis unless otherwise stated. Underlying growth rates exclude currency movements and portfolio changes; b) The ‘business performance’ measures are non-GAAP measures, and reconciliations to the equivalent statutory heading under IFRS are included in the financial key performance indicators section on pages 215-219; c) Constant exchange rates are calculated by assuming the average FX in the prior year prevailed through the current year.

| * | Comparative amounts have been restated, see note 1b to the financial statements for further details. |

20 Pearson plc |

Financial expectations | ||||||||||||||||||||||||

| Segment | 2022 revenue (£m) | Margins 2022* | 2023 expectations Revenue | 2023 expectations Margins* | Underlying revenue 3-year CAGR 2022 to 2025 | Margins 2025* | ||||||||||||||||||

Assessment & Qualifications | 1,444 | 18% | Low to mid-single digit | Increase | Low to mid-single digit | Increase | ||||||||||||||||||

Virtual Learning | 820 | 9% | ||||||||||||||||||||||

| Virtual Schools | 519 | | Mid-single digit decline | | Increase | Low-single digit | Increase | |||||||||||||||||

| OPM | 301 | – – – – – – – – – – – – Under strategic review – – – – – – – – – – – – | ||||||||||||||||||||||

Higher Education | 898 | 10% | Low-single digit decline | Increase | | Low to mid-single digit | | Increase | ||||||||||||||||

English Language Learning | 321 | 8% | High-single digit | Increase | High-single digit | Increase | ||||||||||||||||||

Workforce Skills | 204 | (1)% | Double-digits | Improve | Greater than 20% | Increase | ||||||||||||||||||

Strategic review | 154 | 10% | ||||||||||||||||||||||

Group | 3,841 | 12% | | Excluding OPM and Strategic review: Low to mid-single digit | | Mid-teens | | Mid-single digit | | | Upper end of mid-teens | | ||||||||||||

| * | Adjusted operating profit margins. |

Operating results

Sales increased on a headline basis by £413m or 12% from £3,428m in 2021 to £3,841m in 2022 and adjusted operating profit increased by £71m or 18% from £385m in 2021 to £456m in 2022 (for a reconciliation of this measure see note 2 to the consolidated financial statements).

The headline basis simply compares the reported results for 2022 with those for 2021. We also present sales and profits on an underlying basis which exclude the effects of exchange, the effect of portfolio changes arising from acquisitions and disposals and the impact of adopting new accounting standards that are not retrospectively applied. Our portfolio change is calculated by excluding sales and profits made by businesses disposed in either 2021 or 2022 and by ensuring the contribution from acquisitions is comparable year on year. Portfolio changes mainly relate to the disposals of our international courseware local publishing businesses in Europe, French-speaking Canada, South Africa and Hong Kong in 2022, the sale of the Sistemas business in Brazil in 2021 and the acquisitions of Credly and Mondly in 2022 and of Faethm in 2021.

| All figures in £ millions | 2022 | 2021 | ||||||

| Operating profit | 271 | 183 | ||||||

| Add back: Cost of major restructuring | 150 | 214 | ||||||

| Add back: Intangible charges | 56 | 51 | ||||||

| Add back: UK pension discretionary increases | 3 | – | ||||||

| Add back: Other net gains and losses | (24 | ) | (63) | |||||

Adjusted operating profit | 456 | 385 | ||||||

On an underlying basis, sales increased by 5% in 2022 compared to 2021 and adjusted operating profit increased by 11%. Currency movements increased sales by £296m and increased adjusted operating profit by £46m. Portfolio changes decreased sales by £37m and decreased adjusted operating profit by £13m. There were no new accounting standards adopted in 2022 that impacted sales or operating profits.

Adjusted operating profit includes the results from discontinued operations when relevant but excludes charges for intangible amortisation and impairment, acquisition related costs, gains and losses arising from disposals, the cost of major restructuring and one off-costs related to the UK pension scheme. A summary of these adjustments is included below and in more detail in note 2 to the consolidated financial statements.

In August 2022, the Group announced a major restructuring programme to run in 2022. The programme includes efficiencies in product and content, support costs, technology and corporate property.

The restructuring costs in 2022 of £150m mainly relate to staff redundancies and impairment of right-of-use property assets. In 2021, restructuring costs of £214m mainly related to the impairment of right-of-use property assets, the write-down of product development assets and staff redundancies. The 2022 charge includes the impact of updated assumptions related to the recoverability of right-of-use assets made in 2021.

Intangible amortisation charges in 2022 were £56m compared to a charge of £51m in 2021. This is due to increased amortisation from recent acquisitions partially offset by a reduction in amortisation from intangible assets at the end of their useful life and recent disposals.

UK pension discretionary increases in 2022 relate to one-off pension increases awarded to certain cohorts of pensioners in response to the cost of living crisis.

2023 outlook

We are confident of further group underlying sales growth of low to mid-single digit, excluding OPM and the strategic review businesses, with adjusted operating profit and tax in line with current market expectations

1

. Our interest charge is expected to be c.£35m.| — | Assessment & Qualifications revenue growth of low to mid-single digit with increased margins. |

| — | In Virtual Learning, Virtual Schools revenue to decline by mid-single digit impacted by the COVID-19 cohort unwind in the 2022/23 academic year, as well as the loss of a major school. We expect margins to increase. We remain confident in the long-term performance of this division and will launch Career Academies aimed at supporting teenagers who wish to gain career education and experience. Four Career Academies will operate in the 2023-24 school year in four states and enrolment is underway. OPM continues to be under strategic review. |

| — | Higher Education revenue to decline, by low-single digit, with increased margins. |

| — | English Language Learning revenue growth of high-single digit with increased margins. |

| — | Double-digits revenue growth in Workforce Skills, underpinned by our talent investment platform, with improved margins. |

2025 ambition

We continue to expect the Group to achieve mid-single digit underlying revenue 3-year CAGR from 2022 to 2025 and for margins to be mid-teens in the near term, as we invest to drive growth, improving by 2025.

| 1. | 2023 consensus on the Pearson website as at 28 th November 2022; median adjusted operating profit of £585m at £:$ 1.14, tax rate 24%. |

Annual report and accounts 2022

Pearson plc 21

Financial review

continued

Other net gains and losses in 2022 relate to the gains on the disposal of our international courseware local publishing businesses in Europe, French-speaking Canada and Hong Kong and a gain arising on a decrease in the deferred consideration payable on prior year acquisitions, offset by a loss on disposal of our international courseware local publishing businesses in South Africa due to recycled currency translation adjustments and costs related to disposals and acquisitions. Other net gains and losses in 2021 largely related to the disposal of PIHE and the disposal of the K12 Sistemas business in Brazil offset by costs related to the acquisition of Faethm and the wind down of certain strategic review businesses.

The reported operating profit of £271m in 2022 compares to a profit of £183m in 2021. The increase in 2022 was driven by operating leverage on revenue growth, property cost savings and a lower restructuring charge, partially offset by inflation and a reduction in other net gains and losses from business acquisitions and disposals.

Divisional results

| £ millions | 2022 | 2021 | Headline growth | CER Growth | Underlying growth | |||||||||||||||

| Sales | ||||||||||||||||||||

| Assessment & Qualifications | 1,444 | 1,238± | 17% | 8% | 8% | |||||||||||||||

| Virtual Learning | 820 | 713 | 15% | 4% | 4% | |||||||||||||||

| Higher Education | 898 | 849 | 6% | (4)% | (4)% | |||||||||||||||

| English Language Learning | 321 | 238 | 35% | 28% | 24% | |||||||||||||||

| Workforce Skills | 204 | 172 | 19% | 16% | 7% | |||||||||||||||

| Strategic review | 154 | 218± | (29)% | (30)% | (16)% | |||||||||||||||

| Total | 3,841 | 3,428 | 12% | 3% | 5% | |||||||||||||||

| Adjusted operating profit | ||||||||||||||||||||

| Assessment & Qualifications | 258 | 219± | 18% | 6% | 6% | |||||||||||||||

| Virtual Learning | 70 | 32 | 119% | 88% | 88% | |||||||||||||||

| Higher Education | 91 | 73 | 25% | 12% | 12% | |||||||||||||||

| English Language Learning | 25 | 15 | 67% | 47% | 33% | |||||||||||||||

| Workforce Skills | (3) | 27 | (111)% | (104)% | (67)% | |||||||||||||||

| Strategic review | 15 | 19± | (21)% | (26)% | 0% | |||||||||||||||

| Total adjusted operating profit | 456 | 385 | 18% | 6% | 11% | |||||||||||||||

± Comparative amounts have been restated to reflect the move between operating segments.

Assessment & Qualifications

In Assessment & Qualifications, sales increased 8% on an underlying basis and 17% on a headline basis. Adjusted operating profit increased 6% in underlying terms due to operating leverage on revenue growth partially offset by inflation and 18% in headline terms due to this and currency movements.

Pearson VUE sales were flat in underlying terms with test volumes increasing 16% to 19.4m with particularly strong growth in the IT and healthcare segments, offset by the known headwind resulting from the DVSA contract change, as previously announced in 2021. Within VUE test volumes, we still capture the volume for all three DVSA regions, given we provide the central platform for test delivery. We retained all our major contracts that were up for renewal and increased our contract renewal rate to 99.9% across the business.

In US Student Assessment, sales increased 17% in underlying terms due to a combination of the commencement of new contracts, which were won in 2020 and 2021, a return of volumes with full state testing commencing post COVID-19, and the addition of new services to existing contracts.

In Clinical Assessment, sales increased 7% in underlying terms due to good government funding and continued focus on health and wellbeing.

In UK and International Qualifications, sales increased 16% in underlying terms as exams resumed following COVID-19.

Virtual Learning

In Virtual Learning, sales increased 4% on an underlying basis and 15% on a headline basis. Adjusted operating profit grew 88% in underlying terms due to operating leverage on revenue growth and efficiency improvements in Virtual Schools and OPM, more than offsetting the investment in our Virtual Schools’ platform and teaching costs, and increased 119% in headline terms due to this and currency movements.

Virtual Schools sales were up 4%, driven by firm retention rates in the 2021/22 academic year and favourable revenue mix, partially offset by a 5% decline in enrolments for the 2022/23 academic year and lower district partnership renewals. We opened new full-time online partner schools in Colorado, Missouri and Virginia which partially offset the planned exits of partner schools in Washington, Colorado, Missouri and one of two schools in Tennessee. As at December 2022, this brings the 2022/2023 total number of partner schools to 46 in 31 states.

In OPM, sales were up 4% driven by enrolment growth in our UK and Australia programs, which were offset by an enrolment decline in our North America programs.

Higher Education

In Higher Education, sales declined 4% for the full year on an underlying basis and increased 6% on a headline basis due to currency movements. Adjusted operating profit increased 12% in underlying terms driven primarily by cost savings, partially offset by trading performance, and increased 25% in headline terms due to this and currency movements.

In the US, we saw a decline in enrolments and a loss of adoptions to non-mainstream publishers, including open educational resources, partially offset by improved pricing. There was continued momentum in Inclusive Access with 9% sales growth to not-for-profit institutions and the total number of institutions increasing to 1,040. Pearson+ performed well in the Fall semester with 2.83m registered users and 406k paid subscriptions, representing a threefold increase compared to the prior year Fall semester.

English Language Learning

In English Language Learning, sales were up 24% on an underlying basis and 35% on a headline basis. Adjusted operating profit increased by 33% in underlying terms due to increased revenue partially offset by increased investment and increased 67% in headline terms due to this and currency movements.

PTE volumes were up 90% driven by border re-openings, as well as market share gain in India. Within Institutional, there was strong growth in Latin America and the Middle East, offset by the impact of government reforms in China.

Workforce Skills

In Workforce Skills, sales were up 7% on an underlying and 19% on a headline basis. Adjusted operating profit declined by 67% in underlying terms due to investment in the business across Faethm, Credly and our talent investment platform and decreased 111% in headline terms due to this, currency movements and portfolio changes.

Revenue growth was driven by growth in BTEC and Apprenticeships, GED and TalentLens. The Vocational Qualifications business (previously known as the Performance business) grew by 5% in underlying terms. The Workforce Solutions business (previously known as the Transformation business) grew by 12% in underlying terms. Pearson has 1,503 enterprise clients in its Workforce Skills portfolio, up 133% on last year, with the acquisition of Credly underpinning this growth.

22 Pearson plc |

Strategic review

Sales in our international courseware local publishing businesses under strategic review declined 16% on an underlying basis and were down 29% on a headline basis for the full year. Following the announcement of the sale of our international courseware local publishing businesses in Europe, French speaking Canada, Hong Kong and South Africa, these financials are no longer included in our underlying performance measures.

Net finance costs

Net interest payable reflected in adjusted earnings in 2022 was £1m, compared to £57m in 2021. The difference is primarily due to the release of £35m of interest recorded in respect of provisions for uncertain tax positions where the related interest was recognised in this line in the income statement. In addition, interest charges have reduced due to the reduction in gross bond debt and increased interest income on cash balances given interest rate rises.

Net finance income relating to retirement benefits has been excluded from our adjusted earnings as we believe the income statement presentation does not reflect the economic substance of the underlying assets and liabilities. Also included in the net finance costs (but not in our adjusted measure) are interest costs relating to acquisition or disposal transactions, fair value movements on investments classified as fair value through profit and loss, foreign exchange and other gains and losses on derivatives. Interest relating to acquisition or disposal transactions is excluded from adjusted earnings as it is considered part of the acquisition cost or disposal proceeds rather than being reflective of the underlying financing costs of the Group. Foreign exchange, fair value movements and other gains and losses are excluded from adjusted earnings as they represent short-term fluctuations in market value and are subject to significant volatility. Other gains and losses may not be realised in due course as it is normally the intention to hold the related instruments to maturity. Interest on certain tax provisions is excluded from our adjusted measure in order to mirror the treatment of the underlying tax item.

In 2022, the total of these items excluded from adjusted earnings was income of £53m compared to income of £51m in 2021. Net finance income in respect of retirement benefits increased from £4m in 2021 to £9m in 2022 reflecting the comparative funding position of the plans at the beginning of each year and higher prevailing discount rates. Interest costs in respect of deferred and contingent consideration are £5m in 2022 due to recent acquisitions. In 2022, there were no finance charges relating to the revaluation of the K12 disposal proceeds compared to income of £6m in 2021 as the outstanding amount has been fully repaid. Fair value gains on investments in unlisted securities are £28m in 2022 compared to £20m in 2021. In addition, there were similar gains year on year on long-term interest rate hedges and an interest charge on tax provisions of £5m has been recognised in 2022 in relation to the State Aid matter.

| £ millions | 2022 | 2021 | ||||||

| Net interest payable | (1 | ) | (57 | ) | ||||

| Finance income in respect of retirement benefits | 9 | 4 | ||||||

| Fair value remeasurement of investments held at FVTPL | 28 | 20 | * | |||||

| Other net finance costs | 16 | 27 | ||||||

Net finance costs | 52 | (6 | )* | |||||

| * | Comparative amounts have been restated, see note 1b to the |

financial statements for further details. |

Taxation

The reported tax charge on a statutory basis in 2022 was a charge of £79m (24.5%) compared to a credit of £1m* (0.6%) in 2021. The tax charge for the period has been impacted principally by two items:

| — | The release of tax risk provisions totalling £72m following the expiry of the statute of limitations for certain periods in the US. This release impacts both statutory and adjusted earnings with a £37m credit to adjusted earnings and the remainder only impacting statutory results. |

| — | As previously disclosed, the European Commission determined that the United Kingdom controlled foreign company group financing partial exemption partially constituted State Aid. This decision was appealed by the UK Government and other parties. On 8 June 2022, the EU General Court dismissed the appeal. Following the EU General Court’s negative decision, the UK Government and other parties have submitted appeals to the European the Court of Justice. At 31 December 2021, the potential risk associated with this issue was disclosed as a contingent liability, however, following the dismissal of the first appeal the prospects of successfully challenging the European Commission’s decision are now considered to be such that a provision is required. |

| — | On that basis a tax provision of £63m plus £5m of associated interest has been recorded. The provision represents an estimate of the expected value which has been calculated by considering a range of possible outcomes and applying a probability to each, resulting in a weighted average outcome. The possible outcomes considered range from no liability through to the full exposure (£105m excluding interest). Due to the large and unusual nature of the provision and the specific one-off nature of the issue, the provision is excluded from adjusted earnings. There is no cash impact in 2022 as a payment on account was made during 2021. The provision of £63m has been offset on the balance sheet against the payments previously made. As the provision is less than the payments made there is a remaining non-current tax receivable of £41m disclosed on the balance sheet. |

The tax on adjusted earnings in 2022 was a charge of £71m (2021: £64m), corresponding to an effective tax rate on adjusted profit before tax of 15.6% (2021: 19.5%). The decrease in the effective rate is primarily due to the release of tax risk provisions following the expiry of the statute of limitations in the US. For a reconciliation of the adjusted measure see note 7 to the consolidated financial statements.

In 2022, there was a net tax payment of £109m (2021: £177m). The overall amount decreased primarily due to the 2021 payment of £97m related to the ongoing EU Commission investigation which is non-recurring. Excluding this payment, tax payments increased primarily due to increased operating profits and legislative changes in the US.

A net deferred tax asset of £20m is recognised in 2022 compared to a net £17m deferred tax asset in 2021. The current tax creditor principally consists of provisions for tax uncertainties. There are contingent liabilities in relation to tax as outlined in note 34 to the consolidated financial statements.

Earnings per share

Adjusted earnings includes adjusted operating profit and adjusted finance and tax charges. The reconciling items between the statutory inputs to earnings per share and the adjusted inputs are discussed in the previous sections.

Adjusted earnings per share is 51.8p in 2022 compared to 34.9p in 2021. The increase is primarily driven by an increase in adjusted operating profit, a reduction in net finance costs, a reduction in the adjusted effective tax rate and a decrease in the number of shares following the share buy back.

Basic earnings per share is 32.8p in 2022 compared to 23.5p* in 2021. The increase in 2022 is mainly due to increased operating profits, reduced interest charges and a decrease in the number of shares following the share buy back, partially offset by increased tax charges.

| Annual report and accounts 2022 Pearson plc 23 |

Financial review

continued

Other comprehensive income

Included in other comprehensive income are the net exchange differences on translation of foreign operations. The gain on translation of £330m in 2022 compares to a loss in 2021 of £6m. The gain in 2022 arises from an overall strengthening of the currencies to which the Group is exposed and in particular the relative strength of the US dollar. A significant proportion of the Group’s operations are based in the US and the US dollar strengthened in 2022 from an opening rate of £1:$1.35 to a closing rate at the end of 2022 of £1:$1.21. At the end of 2021, the US dollar had strengthened from an opening rate of £1:$1.37 to a closing rate of £1:$1.35. The loss in 2021 was driven by this movement in the US dollar, offset by the weakening of other currencies used by the Group.

Also included in other comprehensive income in 2022 is an actuarial gain of £54m in relation to the retirement benefit obligations of the Group. The gain arises largely from a decrease in liabilities driven by higher discount rates and changes to demographic assumptions, partially offset by losses on associated matching assets and experience losses. The actuarial gain in 2022 of £54m compares to an actuarial gain in 2021 of £149m.

Fair value gains of £18m have been recognised in other comprehensive income and relate to movements in the value of investments in unlisted securities held at FVOCI. In 2021, fair value gains of £4m* were recognised.

In 2022, a loss of £5m (2021: £4m gain) was recycled from the currency translation reserve to the income statement in relation to businesses disposed.

Cash flow and working capital

Our operating cash flow measure is an adjusted measure used to align cash flows with our adjusted profit measures. Operating cash inflow increased on a headline basis by £13m from £388m in 2021 to £401m in 2022. The increase is largely explained by the drop-through of increased operating profits offset by unfavourable working capital movements driven by the timing of the disposals of the international courseware local publishing businesses and an increase in capitalised product development.

The equivalent statutory measure, net cash generated from operations, was £527m in 2022 compared to £570m in 2021. Compared to operating cash flow, this measure includes restructuring costs but does not include regular dividends from associates. It also excludes capital expenditure on property, plant, equipment and software, and additions to right-of-use assets as well as disposal proceeds from the sale of property, plant, equipment and right-of-use assets (including the impacts of transfers to/from investment in finance lease receivable). In 2022, restructuring cash outflow was £35m compared to £24m in 2021.