Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2006

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number 0-27512

CSG SYSTEMS INTERNATIONAL, INC.

(Exact name of registrant as specified in its charter)

| Delaware | 47-0783182 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

9555 Maroon Circle

Englewood, Colorado 80112

(Address of principal executive offices, including zip code)

(303) 200-2000

(Registrant’s telephone number, including area code)

Securities Registered Pursuant to Section 12(b) of the Act:

Common Stock, Par Value $0.01 Per Share

Securities Registered Pursuant to Section 12(g) of the Act: None.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by a check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to the Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act.

Large accelerated filer x Accelerated filer ¨ Non-accelerated filer ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No x

The aggregate market value of the voting and non-voting common equity held by non-affiliates of the registrant, computed by reference to the last sales price of such stock, as of the close of trading on June 30, 2006 was $1,041,037,528.

Shares of common stock outstanding at February 26, 2007: 45,350,947

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Registrant’s Proxy Statement for its 2007 Annual Meeting of Stockholders to be filed on or prior to April 30, 2007, are incorporated by reference into Part III of the Form 10-K.

Table of Contents

CSG SYSTEMS INTERNATIONAL, INC.

2006 FORM 10-K

| Page | ||||

PART I | ||||

Item 1. | 3 | |||

Item 1A. | 8 | |||

Item IB. | 11 | |||

Item 2. | 12 | |||

Item 3. | 12 | |||

Item 4. | 12 | |||

Item 5. | 16 | |||

Item 6. | 19 | |||

Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | 21 | ||

Item 7A. | 40 | |||

Item 8. | 42 | |||

Item 9. | Changes in and Disagreements With Accountants on Accounting and Financial Disclosure | 77 | ||

Item 9A. | 77 | |||

Item 9B. | 77 | |||

Item 10. | 78 | |||

Item 11. | 78 | |||

Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 78 | ||

Item 13. | Certain Relationships and Related Transactions, and Director Independence | 78 | ||

Item 14. | 78 | |||

Item 15. | 78 | |||

| 79 | ||||

2

Table of Contents

| Item 1. | Business |

Overview

CSG Systems International, Inc. (the “Company”, “CSG”, or forms of the pronoun “we”) was formed in October 1994 and acquired all of the outstanding stock of CSG Systems, Inc. (formerly Cable Services Group, Inc.) from First Data Corporation (“FDC”) in November 1994. CSG Systems, Inc. had been a subsidiary or division of FDC from 1982 until this acquisition.

We are a leading provider of outsourced billing, customer care and print and mail solutions and services supporting the North American cable and direct broadcast satellite (“DBS”) markets. Our solutions support some of the world’s largest and most innovative providers of bundled multi-channel video, Internet, voice and IP-based services. Our unique combination of solutions, services and expertise ensure that cable and satellite operators can continue to rapidly launch new service offerings, improve operational efficiencies and deliver a high-quality customer experience in a competitive and ever-changing marketplace.

Our principal executive offices are located at 9555 Maroon Circle, Englewood, Colorado 80112, and the telephone number at that address is (303) 200-2000. Our common stock is listed on the Nasdaq Stock Market LLC under the symbol “CSGS”. We are a S&P Midcap 400 company.

General Development of Business

Comcast Business Relationship.In September 1997, we entered into a 15-year exclusive contract (the “Master Subscriber Agreement”) with Tele-Communications, Inc. (“TCI”) to consolidate all TCI customers onto our customer care and billing systems. At the same time, we acquired a non-operational billing system from TCI for $105 million. This transaction allowed our company to substantially increase the number of customers processed on our systems, and at the time, was one of the catalysts to the growth of our domestic broadband business.

In 1999 and 2000, respectively, AT&T completed its mergers with TCI and MediaOne Group, Inc. (“MediaOne”), and consolidated the merged operations into AT&T Broadband (“AT&T”), and we continued to service the merged operations under the terms of the Master Subscriber Agreement. On November 18, 2002, Comcast Corporation (“Comcast”) completed its merger with AT&T, and assumed the Master Subscriber Agreement. Comcast is our largest client, making up approximately 24% of our total revenues in 2006.

During 2002 and 2003, we were involved in various legal proceedings with Comcast, consisting principally of arbitration proceedings related to the Master Subscriber Agreement. In October 2003, we received an unfavorable ruling in the arbitration proceedings. The Comcast arbitration ruling included an award of $119.6 million to be paid by us to Comcast. The award was based on the arbitrator’s determination that we had violated the most favored nations (“MFN”) clause of the Master Subscriber Agreement. We recorded the full impact from the arbitration ruling in the third quarter of 2003 as a charge to revenues. In addition, the arbitration ruling also required that we invoice Comcast for lower fees under the MFN clause of the Master Subscriber Agreement beginning in October 2003. This had the effect of reducing quarterly revenues from Comcast by approximately $13-14 million ($52-56 million annually), when compared to amounts prior to the arbitration ruling. In March 2004, we signed a new contract with Comcast (the “Comcast Contract”). The Comcast Contract superseded the former Master Subscriber Agreement that was set to expire at the end of 2012. Under the new agreement, we expect to continue to provide services to Comcast at least through December 31, 2008. The pricing inherent in the Comcast Contract was consistent with that of the arbitration ruling in October 2003. See Management’s Discussion and Analysis of Financial Condition and Results of Operations (“MD&A”) for additional discussion of our business relationship with Comcast.

Purchase and Sale of the GSS Business. In February 2002, we acquired the billing and customer care assets of Lucent Technologies (“Lucent”). Lucent’s billing and customer care business consisted primarily of: (i) software products and related consulting services acquired by Lucent when it purchased Kenan Systems Corporation in February 1999; (ii) BILLDATS Data Manager mediation software; and (iii) elements of Lucent’s client support, product support, and sales and marketing organizations (collectively, the “Kenan Business”). This acquisition allowed us to expand our customer care and billing product and service offerings into international markets. On December 9, 2005, we sold our Global Software Services (“GSS”)

3

Table of Contents

business (“GSS Business”), which consisted principally of the acquired Kenan Business, to Comverse, Inc., a division of Comverse Technology, Inc. (“Comverse”). As a result of our sale of the GSS Business, we no longer provide customer care and billing products or services outside of North America. The decision to sell the GSS Business is consistent with our decision to intensify our focus on our core competencies in the cable and DBS markets utilizing our Advanced Convergent Platform (“ACP”) product and related services. See Note 2 to our Consolidated Financial Statements and MD&A for additional discussion of the sale of the GSS Business.

Financial Information About Our Company and Business Segment

In addition to the sale of the GSS Business noted above, we also sold our plaNet Consulting business to a group of private investors led by the plaNet management team on December 30, 2005. As a result, the results of operations for the GSS and plaNet businesses have been reflected as discontinued operations for all periods presented in the accompanying Consolidated Statements of Income. The remainder of the “Business” section of this Form 10-K is focused on our continuing operations. See Notes 2 and 5 to our Consolidated Financial Statements and MD&A for additional discussion of our reporting of discontinued operations, and the impact these sales had on our reporting of segment and related information.

Industry Overview

Background.We provide customer care and billing services primarily to the North American converged broadband and DBS markets. Customer care and billing systems coordinate many aspects of the customer’s interaction with a service provider, from the initial set-up and activation of customer accounts, to the support of various service activities, through the monitoring of customer invoicing and accounts receivable management, and the presentment of customer invoices. These systems enable service providers to manage the lifecycle of their customer interactions.

Market Conditions of Communications Industry. The North American communications industry has experienced significant consolidation and increased competition among communications providers, and there is the possibility of further consolidation. Market consolidation results in a fewer number of service providers who have massive scale and can deliver a total communications package. The significant plant upgrades and network rationalizations that have taken place have allowed service providers to focus their attention on new revenue and growth opportunities. In addition, new competitors, new technologies and unique partnerships are forcing service providers to be more creative in their approaches for rolling out new products and services and enhancing their customers’ experiences. These factors, in combination with the improving financial condition of service providers, are resulting in a more positive outlook for the demand for scalable, flexible and cost efficient customer care and billing solutions, which we believe will provide us with new revenue opportunities.

However, another facet of this market consolidation poses certain risks to our company. The consolidation of service providers decreases the potential number of buyers for our products and services, and carries the inherent risk that the consolidators may choose to move their purchased customers to a competitor’s system. Should this consolidation result in a concentration of customer accounts being owned by companies with whom we do not have a relationship, or with whom competitors are entrenched, it could negatively affect our ability to maintain or expand our market share, thereby having a material adverse effect to our results of operations. In addition, service providers at times have chosen to use their size and scale to exert more pressure on pricing negotiations.

In addition, it is widely anticipated that communication service providers will continue their aggressive pursuit of providing convergent services. Traditional wireline and wireless telephone providers have recently entered the residential video market, a market dominated by our clients. Should these traditional telephone service providers be successful in their video strategy, it could threaten our clients’ market share, and thus our processing revenues, as generally speaking, these companies do not currently use our products and services.

Business Strategy

Our business strategy is designed to achieve revenue and profit growth. The key elements of our business strategy include:

Expand Core Processing Business. We will continue to leverage our investment and expertise in high-volume transaction processing to expand our processing business. Our processing business provides highly predictable, recurring revenues

4

Table of Contents

through multi-year contracts with a client base that includes leading communications service providers. We increased the number of customers processed on our systems from 18 million as of December 31, 1995 to 45.4 million as of December 31, 2006. We provide a full suite of customer care and billing products and services that combine the reliability and high volume transaction processing capabilities of a mainframe platform with the flexibility of client/server architecture.

Increase the Penetration of Ancillary Products/Services.We provide a complete suite of customer care and billing products and services that enable and automate various activities for service providers, ranging from the call center, to the field technicians, to the end consumer. As our clients’ businesses consolidate and become much more complex, we have seen an increase in the use of ancillary products and services.

Evolve Our Products and Services to Meet the Changing Needs of Our Clients.In 1995, we offered customer care and billing solutions to providers of analog cable video. Since then, our solution has evolved and expanded to satellite, digital, high-speed Internet (“HSI”) and digital voice. Our clients continue to look to add more services to their product bundle, including advanced IP and wireless services, as well as services to commercial customers. Our continued investment in our solution set is designed to enable our clients to grow their product offerings, and thereby, grow our revenues.

Enhance Growth Through Focused Acquisitions. We follow a disciplined approach in acquiring assets and businesses which provide the technology and technical personnel to expedite our product development efforts, provide complementary products and services, increase market share, and/or provide access to new markets and clients.

Continue Technology Leadership. We believe that our technology in customer care and billing solutions gives communications service providers a competitive advantage. Our continuing investment in research and development (“R&D”) is designed to position us to meet the growing and evolving needs of existing and potential clients. Over the last five years, we have invested approximately $175 million, or approximately 10% of our total revenues, into R&D.

Narrative Description of Business

General Description.Our operations consist of our processing operations and the provision of related software products. We generate a substantial percentage of our revenues by providing outsourced customer care and billing services to the North American cable television and satellite industries. Our full suite of processing, software, and professional services allows clients to automate their customer interaction management and billing functions. These functions include such things as set-up and activation of customer accounts, sales support, order processing, invoice calculation, production and mailing of invoices, management reporting, electronic presentment and payment of invoices, and deployment and management of the client’s field technicians.

Clients. We work with the leading cable and satellite providers located in the U.S. and Canada. A partial list of those service providers as of December 31, 2006 is included below:

Charter Communications (“Charter”) | EchoStar Communications Corporation (“EchoStar”) | |

Comcast Corporation (“Comcast”) | Mediacom Communications | |

Cox Communications | Time Warner Inc. (“Time Warner”) |

As discussed above, the North American communications industry has experienced significant consolidation over the last few years, resulting in a large percentage of the market being served by a limited number of service providers with greater size and scale. Consistent with this market concentration, a large percentage of our historical revenues have been generated from a limited number of clients, with approximately 70% of our revenues being generated from our four largest clients, which include Comcast, EchoStar, Time Warner, and Charter. Revenues from these clients represented the following percentages of our total revenues for 2006 and 2005:

| 2006 | 2005 | |||||

Comcast | 24 | % | 22 | % | ||

EchoStar | 19 | % | 21 | % | ||

Time Warner | 12 | % | 10 | % | ||

Charter | 11 | % | 10 | % |

5

Table of Contents

CCS Architectural Upgrade and Migration.During 2004, we completed a significant architectural upgrade to our primary product, CCS, and related services and software products. This enhancement to CCS, called ACP, has enhanced our ability to support convergent broadband services including cross-service bundling, convergent order entry and advanced service provisioning capabilities for video, HSI, and Voice over Internet Protocol (“VoIP”). This advanced convergent solution for broadband service providers will facilitate our clients’ offering of combinations of video, voice and data services (commonly referred to in the industry as the “triple-play” service offering). The ACP project was initiated in 2002 and is our next generation product offering. As of December 31, 2006, approximately 90% of the cable customer accounts processed on our systems have successfully migrated to our ACP solution, and we expect the remaining cable customer accounts to be migrated to ACP by the end of 2007.

Products and Services. Our primary product offerings include our core service bureau processing product, ACP, and related services and software products. A background in high-volume transaction processing, complemented with world-class applications software, allows us to offer one of the most comprehensive, pre-integrated products and services solutions to the communications market, serving video, data and voice providers and handling many aspects of the customer lifecycle. We believe this pre-integrated approach has allowed communications service providers to get to market quickly as well as reduce the total cost of ownership for their solution.

We license our software products (e.g., ACSR, Workforce Express, etc.) and provide our professional services principally to our existing base of processing clients to enhance the core functionality of our service bureau processing application, increase the efficiency and productivity of the clients’ operations, and allow clients to effectively roll out new products and services to new and existing markets, such as HSI and telephony to residential and commercial customers.

Historically, a substantial percentage of our total revenues have been generated from ACP processing services and related software products. These products and services are expected to provide a substantial percentage of our total revenues in the foreseeable future as well.

FDC Data Processing Facility.We outsource to FDC the data processing and related computer services required for the operation of our processing services. Our ACP proprietary software is run in FDC’s facility to obtain the necessary mainframe computer capacity and other computer support services without us having to make the substantial capital and infrastructure investments that would be necessary for us to provide these services internally. Our clients are connected to the FDC facility through a combination of private and commercially-provided networks. Our service agreement with FDC expires June 30, 2010, and is cancelable only for cause, as defined in the agreement. We believe we could obtain mainframe data processing services from alternative sources, if necessary. We have a business continuity plan as part of our agreement with FDC should the FDC data processing center suffer an extended business interruption or outage. This plan is tested on an annual basis.

Client and Product Support. Our clients typically rely on us for ongoing support and training needs related to our products. We have a multi-level support environment for our clients. We have strategic business units (“SBUs”) to support the business, operational, and functional requirements of each client. These dedicated account management teams help clients resolve strategic and business issues and are supported by our Product Support Center (“PSC”), which operates 24 hours a day, seven days a week. Clients call an 800 number, and through an automated voice response unit, have their calls directed to the appropriate PSC personnel to answer their questions. We have a full-time training staff and conduct ongoing training sessions both in the field and at our training facilities.

Sales and Marketing.We organize our sales efforts to existing clients within our SBUs, with senior level account managers who are responsible for new revenues and renewal of existing contracts within a client account. The SBUs are supported by sales support personnel who are experienced in the various products and services that we provide. In addition, we have dedicated staff engaged in selling our products and services to prospective clients.

Competition. The market for customer care and billing products and services in the converging communications industry in North America is highly competitive. We compete with both independent outsourced providers and in-house developers of customer management systems. We believe that our most significant competitors are Amdocs Limited, Convergys Corporation, and in-house systems. Some of our actual and potential competitors have substantially greater financial, marketing and technological resources than us.

6

Table of Contents

We believe service providers in our industry use the following criteria when selecting a vendor to provide customer care and billing products and services: (i) functionality, scalability, flexibility and architecture of the billing system; (ii) the breadth and depth of pre-integrated product solutions: (iii) product quality, client service and support; (iv) quality of R&D efforts; and (v) price. We believe that our products and services allow us to compete effectively in these areas.

Proprietary Rights and Licenses

We rely on a combination of trade secret and copyright laws, nondisclosure agreements, and other contractual and technical measures to protect our proprietary rights in our products. While we hold a limited number of patents on some of our newer products, we do not rely upon patents as a primary means of protecting our rights in our intellectual property. There can be no assurance that these provisions will be adequate to protect our proprietary rights. Although we believe that our intellectual property rights do not infringe upon the proprietary rights of third parties, there can be no assurance that third parties will not assert infringement claims against us or our clients.

We continually assess whether there is any risk to our intellectual property rights. Should these risks be improperly assessed, or if for any reason should our right to develop, produce and distribute our products be successfully challenged or be significantly curtailed, it could have a material adverse impact on our financial condition and results of operations.

Research and Development

Our product development efforts are focused on developing new products and improving our existing products. We believe that the timely development of new applications and enhancements to existing applications is essential to maintaining our competitive position in the marketplace. Our most recent development efforts have been focused primarily on enhancements to ACP and related software products, to include the integration of the Telution COMX product with ACP (see Note 4 to our Consolidated Financial Statements for a discussion of our Telution acquisition), targeted to increase the functionalities and features of the products, including those necessary to service new and expanded product offerings provided by our clients (e.g., VoIP commercial services, etc.).

Our total R&D expenses were $46.2 million and $33.9 million, respectively, for 2006 and 2005, or approximately 12% and 9% of total revenues. Over the last five years, we have invested approximately 10% of our total revenues into R&D. We expect our future R&D efforts to continue to focus on enhancements to ACP and related products and services, and we expect that over time, our investment in R&D will approximate our historical investment rate of 10-12% of our total revenues. However, consistent with the fourth quarter of 2006 (which reflected R&D expense as a percentage of total revenues of approximately 14%), we expect this percentage to be at or above the top end of this range in the near term.

There are certain inherent risks associated with significant technological innovations. Some of these risks are described in this report in our Risk Factors section below.

Employees

As of December 31, 2006, we had a total of 1,685 employees, an increase of 145 from December 31, 2005. The increase in number of employees is due to an expected increase in our R&D and support function costs to address the opportunities we see within our clients’ changing business needs, to include the personnel that came over in the Telution acquisition. Our success is dependent upon our ability to attract and retain qualified employees. None of our employees are subject to a collective bargaining agreement. We believe that our relations with our employees are good.

Available Information

Our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, proxy materials, and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act are available free of charge on our website at www.csgsystems.com. Additionally, these reports are available at the SEC’s Public Reference Room at 100 F Street, N.E., Washington, D.C. 20549 or on the SEC’s website at www.sec.gov. Information on the operation of the Public Reference Room can be obtained by calling the SEC at 1-800-SEC-0330.

7

Table of Contents

Code of Business Conduct and Ethics

A copy of our Code of Business Conduct and Ethics (the “Code of Conduct”) is maintained on our website. Any future amendment to the Code of Conduct, or any future waiver of a provision of our Code of Conduct, will be timely posted to our website upon their occurrence. Historically, we have had minimal changes to our Code of Conduct, and have had no waivers of a provision of our Code of Conduct.

| Item 1A. | Risk Factors |

We or our representatives from time-to-time may make or may have made certain forward-looking statements, whether orally or in writing, including without limitation, any such statements made or to be made in MD&A contained in our various SEC filings or orally in conferences or teleconferences. We wish to ensure that such statements are accompanied by meaningful cautionary statements, so as to ensure, to the fullest extent possible, the protections of the safe harbor established in the Private Securities Litigation Reform Act of 1995.

Accordingly, the forward-looking statements are qualified in their entirety by reference to and are accompanied by the following meaningful cautionary statements identifying certain important risk factors that could cause actual results to differ materially from those in such forward-looking statements. This list of risk factors is likely not exhaustive. We operate in a rapidly changing and evolving market involving the North American communications industry (e.g., bundled multi-channel video, Internet, voice and IP-based services), and new risk factors will likely emerge. Management cannot predict all of the important risk factors, nor can it assess the impact, if any, of such risk factors on our business or the extent to which any risk factor, or combination of risk factors, may cause actual results to differ materially from those in any forward-looking statements. Accordingly, there can be no assurance that forward-looking statements will be accurate indicators of future actual results, and it is likely that actual results will differ from results projected in forward-looking statements and that such differences may be material.

We Derive a Significant Portion of Our Revenues From a Limited Number of Clients, and the Loss of the Business of a Significant Client Would Materially Adversely Affect Our Financial Condition and Results of Operations.The North American communications industry has experienced significant consolidation over the last few years, resulting in a large percentage of the market being served by a limited number of service providers with greater size and scale. Consistent with this market concentration, a large percentage of our revenues are generated from a limited number of clients, with approximately 70% of our revenues being generated from our four largest clients, which are (in order of size) Comcast, EchoStar, Time Warner, and Charter. See MD&A for a brief summary of our business relationship with each of these clients.

There are inherent risks whenever a large percentage of total revenues are concentrated with a limited number of clients. One such risk is that, should a significant client: (i) terminate or fail to renew their contracts with us, in whole or in part for any reason; (ii) significantly reduce the number of customer accounts processed on our systems, the price paid for our services, or the scope of services that we provide; or (iii) experience significant financial or operating difficulties, it could have a material adverse effect on our financial condition and results of operations (including possible impairment, or significant acceleration of the amortization of intangible assets).

Our industry is highly competitive, and the possibility that a major client may move all or a portion of its customers to a competitor has increased. While our clients may incur some costs in switching to our competitors, they may do so for a variety of reasons, including if we do not maintain favorable relationships, do not provide satisfactory services and products, or for reasons associated with price.

A Reduction in Demand for Our Key Customer Care and Billing Products and Services Could Have a Material Adverse Effect on Our Financial Condition and Results of Operations. Historically, a substantial percentage of our total revenues have been generated from our core outsourced processing product, ACP, and related services. These products and services are expected to continue to provide a large percentage of our total revenues in the foreseeable future. Any significant reduction in demand for ACP and related services could have a material adverse effect on our financial condition and results of operations, including possible impairment to intangible assets.

8

Table of Contents

We May Not Be Able to Respond to the Rapid Technological Changes in Our Industry.The market for customer care and billing systems is characterized by rapid changes in technology and is highly competitive with respect to the need for timely product innovations and new product introductions. As a result, we believe that our future success in sustaining and growing our revenues depends upon the continued market acceptance of our products, especially ACP, and our ability to continuously adapt, modify, maintain, and operate our products to address the increasingly complex and evolving needs of our clients, without sacrificing the reliability or quality of the products. In addition, the market is demanding that our products have greater architectural flexibility and are more easily integrated with other computer systems, and that we are able to meet the demands for technological advancements to our products and services at a greater pace. Attempts to meet these demands subjects our R&D efforts to greater risks.

As a result, substantial R&D will be required to maintain the competitiveness of our products and services in the market. Technical problems may arise in developing, maintaining and operating our products and services as the complexities are increased. Development projects can be lengthy and costly, and may be subject to changing requirements, programming difficulties, a shortage of qualified personnel, and/or unforeseen factors which can result in delays. In addition, we may be responsible for the implementation of new products and/or the migration of clients to new products, and depending upon the specific product, we may also be responsible for operations of the product.

There is an inherent risk in the successful development, implementation, migration, and operations of our products and services as the technological complexities, and the pace at which we must deliver these products and services to market, continues to increase. The risk of making an error that causes significant operational disruption to a client increases proportionately with the frequency and complexity of changes to our products and services. There can be no assurance:

| • | of continued market acceptance of our products and services; |

| • | that we will be successful in the development of product enhancements or new products that respond to technological advances or changing client needs at the pace the market demands; or |

| • | that we will be successful in supporting the implementation, migration and/or operations of product enhancements or new products. |

Our Business is Dependent on the North American Communications Industry.We generate our revenues by providing products and services to the U.S. and Canadian communication industries. A decrease in the number of customers served by our clients, loss of business due to non-renewal of client contracts, industry and client consolidations, an adverse change in the economic condition of these industries, movement of customers from our systems to a competitor’s system as a result of regionalization strategies by our clients, and/or changing consumer demand for services could have a material adverse effect on our results of operations. Additionally, our current clients’ distribution methods could be disrupted by new entrants into the communications industry. There can be no assurance that new entrants into the communications market will become our clients. Also, there can be no assurance that communication providers will be successful in expanding into other segments of the converging communications industry. Even if major forays into new markets are successful, we may be unable to meet the special billing and customer care needs of that market.

The Consolidation of the North American Communications Industry May Have a Material Adverse Effect on Our Results of Operations. The North American communications industry is undergoing significant ownership changes at an accelerated pace. One facet of these changes is that communications service providers are consolidating, decreasing the potential number of buyers for our products and services. Such client consolidations carry with them the inherent risk that the consolidators may choose to move their purchased customers to a competitor’s system. Should this consolidation result in a concentration of customer accounts being owned by companies with whom we do not have a relationship, or with whom competitors are entrenched, it could negatively affect our ability to maintain or expand our market share, thereby having a material adverse effect on our results of operations. In addition, service providers may choose to use their size and scale to exercise more severe pressure on pricing negotiations.

In addition, it is widely anticipated that communication service providers will continue their aggressive pursuit of providing convergent services. Traditional wireline and wireless telephone providers have recently entered the residential

9

Table of Contents

video market, a market dominated by our clients. Should these traditional telephone service providers be successful in their video strategy, it could threaten our clients’ market share, and thus our processing revenues, as generally speaking, these companies do not currently use our products and services.

We Face Significant Competition in Our Industry.The market for our products and services is highly competitive. We directly compete with both independent providers of products and services and in-house systems developed by existing and potential clients. In addition, some independent providers are entering into strategic alliances with other independent providers, resulting in either new competitors, or competitors with greater resources. Many of our current and potential competitors have significantly greater financial, marketing, technical, and other competitive resources than our company, many with significant and well-established domestic and international operations. There can be no assurance that we will be able to compete successfully with our existing competitors or with new competitors.

Client Bankruptcies Could Adversely Affect Our Business, and Any Accounting Reserves We Have Established May Not Be Sufficient.In the past, certain of our clients have filed for bankruptcy protection. Companies involved in bankruptcy proceedings pose greater financial risks to us, consisting principally of possible claims of preferential payments for certain amounts paid to us prior to the bankruptcy filing date, as well as increased collectibility risk for accounts receivable, particularly those accounts receivable that relate to periods prior to the bankruptcy filing date. We consider such risks in assessing our revenue recognition and the collectibility of accounts receivable related to our clients that have filed for bankruptcy protection, and for those clients that are seriously threatened with a possible bankruptcy filing. We establish accounting reserves for our estimated exposure on these items. However, there can be no assurance that our accounting reserves related to this exposure will be adequate. Should any of the factors considered in determining the adequacy of the overall reserves change adversely, an adjustment to the accounting reserves may be necessary. Because of the potential significance of this exposure, such an adjustment could be material.

We May Incur Additional Material Restructuring Charges in the Future. Since the third quarter of 2002, we have recorded restructuring charges related to involuntary employee terminations, various facility abandonments, and various other restructuring activities. The accounting for facility abandonments requires highly subjective judgments in determining the proper accounting treatment for such matters. We continually evaluate our assumptions, and adjust the related restructuring reserves based on the revised assumptions at that time. Moreover, we continually evaluate ways to reduce our operating expenses through new restructuring opportunities, including more effective utilization of our assets, workforce and operating facilities. As a result, there is a reasonable likelihood that we may incur additional material restructuring charges in the future.

Failure to Attract and Retain Our Key Management and Other Highly Skilled Personnel Could Have a Material Adverse Effect on Our Business. Our future success depends in large part on the continued service of our key management, sales, product development, and operational personnel. We believe that our future success also depends on our ability to attract and retain highly skilled technical, managerial, operational, and marketing personnel, including, in particular, personnel in the areas of R&D and technical support. Competition for qualified personnel at times can be intense, particularly in the areas of R&D, conversions, software implementations, and technical support, especially now that market conditions are improved and the demand for such talent has increased. For these reasons, we may not be successful in attracting and retaining the personnel we require, which could have a material adverse effect on our ability to meet our commitments and new product delivery objectives.

We May Not Be Successful in the Integration of Our Acquisitions. As part of our growth strategy, we seek to acquire assets, technology, and businesses which will provide the technology and technical personnel to expedite our product development efforts, provide complementary products or services, or provide access to new markets and clients.

Acquisitions involve a number of risks and difficulties, including: (i) expansion into new markets and business ventures; (ii) the requirement to understand local business practices; (iii) the diversion of management’s attention to the assimilation of acquired operations and personnel; and (iv) potential adverse effects on a company’s operating results for various reasons, including, but not limited to, the following items: (a) the inability to achieve revenue targets; (b) the inability to achieve certain operating synergies; (c) charges related to purchased in-process R&D projects; (d) costs incurred to exit current or acquired contracts or activities; (e) costs incurred to service any acquisition debt; and (f) the amortization or impairment of intangible assets.

10

Table of Contents

Due to the multiple risks and difficulties associated with any acquisition, there can be no assurance that we will be successful in achieving our expected strategic, operating, and financial goals for any such acquisition.

Failure to Protect Our Proprietary Intellectual Property Rights Could Have a Material Adverse Effect on Our Financial Condition and Results of Operations. We rely on a combination of trade secret and copyright laws, nondisclosure agreements, and other contractual and technical measures to protect our proprietary rights in our products. We also hold a limited number of patents on some of our newer products, but do not rely upon patents as a primary means of protecting our rights in our intellectual property. There can be no assurance that these provisions will be adequate to protect our proprietary rights. Although we believe that our intellectual property rights do not infringe upon the proprietary rights of third parties, there can be no assurance that third parties will not assert infringement claims against us or our clients.

We continually assess whether there are any risks to our intellectual property rights. Should these risks be improperly assessed or if for any reason should our right to develop, produce and distribute our products be successfully challenged or be significantly curtailed, it could have a material adverse effect on our financial condition and results of operations.

The Delivery of Our Products and Services is Dependent on a Variety of Computing Environments and Communications Networks, Which May Not Be Available or May Be Subject to Security Attacks.Our products and services are generally delivered through a variety of computing environments operated by us, which we will collectively refer to herein as “Systems.” We provide such computing environments through both out-sourced arrangements, such as our data processing arrangement with FDC, as well as internally operating numerous distributed servers in geographically dispersed environments. The end users are connected to our Systems through a variety of public and private communications networks, which we will collectively refer to herein as “Networks.” Our products and services are generally considered to be mission critical customer management systems by our clients. As a result, our clients are highly dependent upon the continuous availability and uncompromised security of our Networks and Systems to conduct their business operations.

Our Networks and Systems are subject to the risk of an extended interruption or outage due to many factors such as: (i) planned changes to our Systems and Networks for such things as scheduled maintenance and technology upgrades, or migrations to other technologies, service providers, or physical location of hardware; (ii) human and machine error; (iii) acts of nature; and (iv) intentional, unauthorized attacks from computer “hackers.” In addition, we continue to expand our use of the Internet with our product offerings thereby permitting, for example, our clients’ customers to use the Internet to review account balances, order services or execute similar account management functions. Allowing access to our Networks and Systems via the Internet increases their vulnerability to unauthorized access and corruption, as well as increasing the dependency of our Systems’ reliability on the availability and performance of the Internet’s infrastructure.

As a means to mitigate certain risks in this area of our business, we have done the following: (i) established policies and procedures related to planned changes to our Systems and Networks; (ii) implemented a business continuity plan, and test certain aspects of this plan on a periodic basis; and (iii) implemented a security and data privacy program (utilizing ISO 17799 as a guideline) designed to mitigate the risk of an unauthorized access to the Networks and Systems primarily through the use of network firewalls, procedural controls, intrusion detection systems and antivirus applications. In addition, we undergo periodic security reviews of certain aspects of our Networks and Systems by independent parties.

The method, manner, cause and timing of an extended interruption or outage in our Networks or Systems are impossible to predict. As a result, there can be no assurances that our Networks and Systems will not fail, or that our business continuity plans will adequately mitigate all damages incurred as a consequence. Should our Networks or Systems: (i) experience an extended interruption or outage, (ii) have their security breached, or (iii) have their data lost, corrupted or otherwise compromised, it would impede our ability to meet product and service delivery obligations, and likely have an immediate impact to the business operations of our clients. This would most likely result in an immediate loss to us of revenue or increase in expense, as well as damaging our reputation. Any of these events could have both an immediate, negative impact upon our financial condition and our short-term revenue and profit expectations, as well as our long-term ability to attract and retain new clients.

| Item 1B. | Unresolved Staff Comments |

None.

11

Table of Contents

| Item 2. | Properties |

As of December 31, 2006, we were operating from six leased sites in the U.S., representing approximately 493,000 square feet. This amount excludes approximately 68,000 square feet of leased space that we have abandoned.

We lease office facilities totaling approximately 100,000 square feet in Denver, Colorado and surrounding communities. We utilize these office facilities primarily for: (i) corporate headquarters; (ii) sales and marketing activities; (iii) product and operations support; and (iv) R&D activities. The leases for these office facilities expire in the years 2008 through 2015.

We lease office facilities totaling approximately 201,000 square feet in Omaha, Nebraska. We utilize these facilities primarily for (i) client services, training and product support; (ii) systems and programming activities; (iii) R&D activities; and (iv) general and administrative functions. The leases for these facilities expire in the years 2009 through 2012.

We lease an office facility totaling approximately 16,000 square feet in Chicago, Illinois. We utilize this facility primarily for: (i) R&D activities; (ii) client services; and (iii) professional services staff. The lease for this office facility expires in 2009.

We lease statement production and mailing facilities totaling approximately 176,000 square feet in Omaha, Nebraska and Wakulla County, Florida. The leases for these facilities expire in the years 2011 and 2013, respectively.

| Item 3. | Legal Proceedings |

From time-to-time, we are involved in litigation relating to claims arising out of our operations in the normal course of business. In the opinion of our management, we are not presently a party to any material pending or threatened legal proceedings.

| Item 4. | Submission of Matters to a Vote of Security Holders |

None.

Executive Officers of the Registrant

As of December 31, 2006, our executive officers were Edward C. Nafus (Chief Executive Officer and President), Randy R. Wiese (Executive Vice President and Chief Financial Officer), Peter E. Kalan (Executive Vice President of Business and Corporate Development), Robert M. (“Mike”) Scott (Executive Vice President and Chief Operating Officer) and Joseph T. Ruble (Executive Vice President, General Counsel and Corporate Secretary). We have employment agreements with each of the executive officers.

Edward C. Nafus

Chief Executive Officer and President

Mr. Nafus, 66, joined CSG in August 1998 as Executive Vice President and became the President of our Broadband Services Division in January 2002. In March 2005, he was added to our Board of Directors. Effective April 1, 2005, Mr. Nafus assumed the position of Chief Executive Officer and President of CSG. From 1978 to 1998, Mr. Nafus held numerous management positions within FDC. From 1992 to 1998, he served as Executive Vice President of FDC; from 1989 to 1992, he served as President of First Data International; and Executive Vice President of First Data Resources from 1984 to 1989. From 1971 to 1978, Mr. Nafus worked in sales management, training and sales for Xerox Corporation. From 1966 to 1971, Mr. Nafus was a pilot and division officer in the United States Navy.Mr. Nafus holds a BS degree from Jamestown College.

Peter E. Kalan

Executive Vice President of Business and Corporate Development

Mr. Kalan, 47, joined CSG in January 1997 and was named Chief Financial Officer in October 2000. In April 2006, he was named Executive Vice President of Business and Corporate Development. Prior to joining CSG, Mr. Kalan was Chief Financial

12

Table of Contents

Officer at Bank One, Chicago, and he also held various other financial management positions with Bank One in Texas and Illinois from 1985 through 1996. Mr. Kalan holds a BA degree in Business Administration from the University of Texas at Arlington.

Robert M. Scott

Executive Vice President and Chief Operating Officer

Mr. Scott, 56, joined CSG in September 1999 as Vice President of the Broadband Services Division and served as Senior Vice President of that division from 2001 to 2004. In December 2004, Mr. Scott was named Executive Vice President, and became the head of the Broadband Services Division in March 2005. In July 2006, he was named Chief Operating Officer. Prior to joining CSG, he served for 21 years in a variety of management positions, both domestically and internationally, with First Data Corporation. Mr. Scott holds a BA degree in Social Studies from Florida Atlantic University.

Randy R. Wiese

Executive Vice President and Chief Financial Officer

Mr. Wiese, 47, joined CSG in 1995 as Controller and later served as Chief Accounting Officer. He was named Executive Vice President and Chief Financial Officer in April 2006. Prior to joining CSG, he was manager of audit and business advisory services and held other accounting-related positions at Arthur Andersen & Co. Mr. Wiese is a member of the AICPA and the Nebraska Society of Certified Public Accountants. He holds a BS degree in Accounting from the University of Nebraska-Omaha.

Joseph T. Ruble

Executive Vice President, General Counsel & Corporate Secretary

Mr. Ruble, 46, joined CSG in 1997 as Vice President and General Counsel. In November 2000 he was appointed Senior Vice President of Corporate Development, General Counsel & Corporate Secretary. In February 2007, he was named Executive Vice President. Prior to joining CSG, Mr. Ruble served from 1991 to 1997 as Vice President, General Counsel & Corporate Secretary for Intersolv, Inc., and as counsel to Pansophic Systems, Inc. for its international operations from 1988 to 1991. Prior to that, he represented the software industry in Washington, D.C. on legislative matters. Mr. Ruble holds a JD from Catholic University of America and a BS degree from Ohio University.

Board of Directors of the Registrant

Effective November 16, 2006, our Board of Directors increased the number of directors of our company from seven to eight by adding a Class II director and elected Mr. Ronald Cooper to fill such additional director position.

Information related to our Board of Directors is provided below.

Bernard W. Reznicek

Consultant

The Premier Group

Mr. Reznicek, 70, was elected to the Board in January 1997 and presently serves as the Company’s non-executive Chairman of the Board. He currently provides consulting services through Premier Enterprises. Mr. Reznicek previously was an Executive with Central States Indemnity Company of Omaha, a Berkshire Hathaway company, from 1997 to 2003. He has 40 years of experience in the electric utility industry, having served as Chairman, President and Chief Executive Officer of Boston Edison Company and President and Chief Executive Officer of Omaha Public Power District. Mr. Reznicek currently is a director of Pulte Homes, Inc. (NYSE) and infoUSA Inc. (NASDAQ).

Edward C. Nafus

Chief Executive Officer and President

CSG Systems International, Inc.

Mr. Nafus’ biographical information in included in “Executive Officers of the Registrant” section shown directly above.

13

Table of Contents

Ronald Cooper

Former President and Chief Operating Officer

Adelphia Communications

Mr. Cooper, 49, was elected to the Board in November 2006. He has spent nearly 25 years in the cable and telecommunications industry, most recently at Adelphia Communications where he served as President and Chief Operating Officer from 2003 to 2006. Prior to Adelphia, Mr. Cooper held a series of executive positions at AT&T Broadband, RELERA Data Centers & Solutions, and MediaOne and its predecessor Continental Cablevision, Inc. He has held various board and committee seats with the National Cable Television Association, California Cable & Telecommunications Association, Cable Television Association for Marketing and the New England Cable Television Association. In addition, Mr. Cooper is either a director or trustee at the Denver Art Museum, Colorado Public Radio and the Cable Center at the University of Denver.

Janice I. Obuchowski

President

Freedom Technologies, Inc.

Ms. Obuchowski, 55, was elected to the Board in November 1997. She has been President of Freedom Technologies, Inc., a public policy and corporate strategy consulting firm specializing in telecommunications, since 1992. In 2003, Ms. Obuchowski was appointed by President George W. Bush to serve as Ambassador and Head of the U.S. Delegation to the World Radio Communication Conference. She has served as Assistant Secretary for Communications and Information at the Department of Commerce and as Administrator for the National Telecommunications and Information Administration. Ms. Obuchowski currently is a director of Orbital Sciences Corporation and Stratos Global Corporation.

Donald B. Reed

Former Chief Executive Officer

Global Cable & Wireless

Mr. Reed, 62, was elected to the Board in May 2005. He currently is retired, having served as Chief Executive Officer of Cable & Wireless Global from May 2000 to January 2003. Cable & Wireless Global, Cable & Wireless plc’s wholly owned operations in the United States, United Kingdom, Europe and Japan, is a provider of internet protocol (IP) and data services to business customers. From June 1998 until May 2000, Mr. Reed served Cable & Wireless in various other executive positions. Mr. Reed’s career includes 30 years at NYNEX Corporation (now part of Verizon), a regional telephone operating company. From 1995 to 1997 Mr. Reed served NYNEX Corporation as President and Group Executive with responsibility for directing the company’s regional, national and international government affairs, public policy initiatives, legislative and regulatory matters, and public relations. Mr. Reed currently is a director of Intervoice, Inc., St. Lawrence Cement (TSX), Idearc Media (formerly Verizon Yellow Pages) (NYSE) and Aggregate Industries in London, England, a wholly owned subsidiary of Holcim Group located in Switzerland.

Frank V. Sica

Managing Partner

Tailwind Capital

Mr. Sica, 56, has served as a director of the Company since its formation in 1994. He is currently a Managing Partner of Tailwind Capital. From 2004 to 2005, Mr. Sica was a Senior Advisor to Soros Private Funds Management. From 2000 until 2003, he was President of Soros Private Funds Management which oversaw the direct real estate and private equity investment activities of Soros. In 1998, he joined Soros Fund Management where he was a Managing Director responsible for Soros’ private equity investments. From 1988 to 1998, Mr. Sica was a Managing Director at Morgan Stanley and its private equity affiliate, Morgan Stanley Capital Partners. Prior to 1988, Mr. Sica was a Managing Director in Morgan Stanley’s mergers and acquisitions department. From 1974 to 1977, Mr. Sica was an officer in the U.S. Air Force. Mr. Sica currently is a director of JetBlue Airways, Kohl’s Corporation, NorthStar Realty Finance Corporation and Onvoy, Inc.

14

Table of Contents

Donald V. Smith

Senior Managing Director

Houlihan Lokey Howard & Zukin, Inc.

Mr. Smith, 64, was elected to the Board in January 2002. He presently serves as Senior Managing Director of Houlihan Lokey Howard & Zukin, Inc., an international investment banking firm with whom he has been associated since 1988. Mr. Smith currently is in charge of the firm’s New York office and serves on the board of directors of the firm. From 1978 to 1988, he was employed by Morgan Stanley & Co. Incorporated, where he headed the valuation and reorganization services within that firm’s corporate finance group. Mr. Smith is director of the Princeton (NJ) Health Care Foundation and of Business Executives for National Security.

James A. Unruh

Managing Principal

Alerion Capital Group

Mr. Unruh, 66, was elected to the Board in June 2005. He became a founding principal of Alerion Capital Group, LLC (a private equity investment company) in 1998 and currently holds such position. Mr. Unruh was an executive with Unisys Corporation from 1987 to 1997 and served as its Chairman and Chief Executive Officer from 1990 to 1997. From 1982 to 1987, Mr. Unruh held various executive positions, including Senior Vice President, Finance, with Burroughs Corporation, a predecessor of Unisys Corporation. Mr. Unruh currently is a director of Prudential Financial, Inc., Tenet Healthcare Corporation, and Qwest Communications International Inc.

15

Table of Contents

| Item 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities |

Our common stock is listed on the Nasdaq Stock Market LLC (“NASDAQ/NMS”) under the symbol “CSGS”. The following table sets forth, for the fiscal quarters indicated, the high and low sale prices of our common stock as reported by NASDAQ/NMS.

| High | Low | |||||

2006 | ||||||

First quarter | $ | 23.29 | $ | 20.82 | ||

Second quarter | 26.21 | 22.87 | ||||

Third quarter | 27.48 | 23.18 | ||||

Fourth quarter | 28.45 | 26.11 | ||||

| High | Low | |||||

2005 | ||||||

First quarter | $ | 18.93 | $ | 15.88 | ||

Second quarter | 19.75 | 15.74 | ||||

Third quarter | 21.82 | 16.15 | ||||

Fourth quarter | 24.76 | 21.06 | ||||

On February 26, 2007, the last sale price of our common stock as reported by NASDAQ/NMS was $25.35 per share. On January 31, 2007, the number of holders of record of common stock was 242.

Dividends

We have not declared or paid cash dividends on our common stock since our incorporation. We did, however, complete a two-for-one stock split, effected in the form of a stock dividend, in March 1999. We intend to retain any earnings to finance the growth and development of our business, and at this time, we do not plan to pay cash dividends in the foreseeable future.

Our revolving credit facility contains certain restrictions on the payment of dividends. In addition, the payment of dividends has certain impacts to our Convertible Debt Securities. See Note 7 to our Consolidated Financial Statements for additional discussion of our revolving credit facility and Convertible Debt Securities, and the impact the payment of dividends may have on these items.

16

Table of Contents

Stock Price Performance

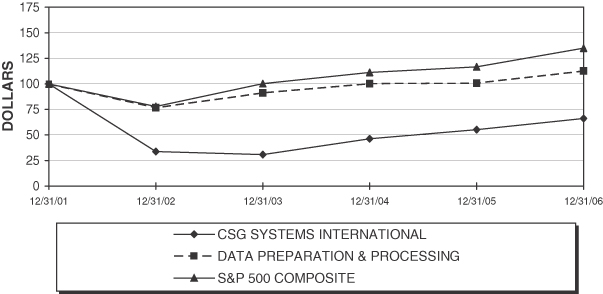

The following graph compares the cumulative total stockholder return on our common stock, the S&P 500 Index, and our Standard Industrial Classification (“SIC”) Code Index: Computer Processing and Data Preparation and Processing Services during the indicated five-year period. The graph assumes that $100 was invested on December 31, 2001, in our common stock and in each of the two indexes and that all dividends, if any, were reinvested.

| 12/31/01 | 12/31/02 | 12/31/03 | 12/31/04 | 12/31/05 | 12/31/06 | |||||||

CSG Systems International Inc. | 100.00 | 33.75 | 30.88 | 46.23 | 55.18 | 66.08 | ||||||

Data Preparation & Processing Services | 100.00 | 76.63 | 91.21 | 100.18 | 100.68 | 112.54 | ||||||

S&P 500 Index | 100.00 | 77.90 | 100.25 | 111.15 | 116.61 | 135.03 |

Equity Compensation Plan Information

The following table summarizes certain information about our equity compensation plans as of December 31, 2006:

Plan Category | Number of securities to be issued upon exercise of outstanding options, warrants, and rights | Weighted-average exercise price of outstanding options, warrants, and rights | Number of securities remaining available for future issuance | ||||

Equity compensation plans approved by security holders | 438,301 | $ | 29.51 | 12,224,515 | |||

Equity compensation plan not approved by security holders | 121,455 | 20.09 | 58,790 | ||||

Total | 559,756 | $ | 27.47 | 12,283,305 | |||

Of the total number of securities remaining available for future issuance, 11,900,790 shares can be used for various types of stock-based awards, as specified in the individual plans, with the remaining 382,515 shares to be used for our employee stock purchase plan. See Note 13 to our Consolidated Financial Statements for additional discussion of our equity compensation plans.

17

Table of Contents

Issuer Repurchases of Equity Securities

The following table presents information with respect to purchases of company common stock made during the three months ended December 31, 2006 by CSG Systems International, Inc. or any “affiliated purchaser” of CSG Systems International, Inc., as defined in Rule 10b-18(a)(3) under the Exchange Act.

Period | Total Number of Shares Purchased2 | Average Price Paid Per Share | Total Number of Shares Purchased as Part of Publicly Announced Plans or Programs | Maximum Number of Shares that May Yet Be Purchased Under the Plan or Programs1 | |||||

October 1 - October 31 | 150,000 | $ | 26.82 | 150,000 | 14,990,908 | ||||

November 1 - November 30 | 343,370 | 27.40 | 343,370 | 14,647,538 | |||||

December 1 - December 31 | 319,677 | 26.91 | 262,872 | 14,384,666 | |||||

Total | 813,047 | $ | 27.10 | 756,242 | |||||

1 | Effective July 12, 2006, our Board of Directors approved a 10 million share increase in the number of shares we are authorized to repurchase under the Stock Repurchase Program, bringing the total number of authorized shares to 30 million. The Stock Repurchase Program does not have an expiration date. |

2 | The total number of shares purchased that are not part of the Stock Repurchase Program represents shares purchased and cancelled in connection with stock incentive plans. |

18

Table of Contents

Item 6. Selected Financial Data

The following selected financial data have been derived from our audited financial statements. The selected financial data presented below should be read in conjunction with, and is qualified by reference to, our MD&A and our Consolidated Financial Statements. The information below is not necessarily indicative of the results of future operations.

| Year Ended December 31, | ||||||||||||||||||||

| 2006 | 2005 | 2004 | 2003 | 2002 | ||||||||||||||||

| (in thousands, except per share amounts) | ||||||||||||||||||||

Statement of Operations Data: | ||||||||||||||||||||

Revenues: | ||||||||||||||||||||

Processing and related services (2) | $ | 351,764 | $ | 346,463 | $ | 326,556 | $ | 341,628 | $ | 372,426 | ||||||||||

Software, maintenance and services (2) | 31,342 | 30,854 | 24,845 | 25,766 | 48,623 | |||||||||||||||

| 383,106 | 377,317 | 351,401 | 367,394 | 421,049 | ||||||||||||||||

Charge for arbitration ruling attributable to periods prior to July 1, 2003 (2) | — | — | — | (105,679 | ) | — | ||||||||||||||

Total revenues, net | 383,106 | 377,317 | 351,401 | 261,715 | 421,049 | |||||||||||||||

Cost of revenues (5): | ||||||||||||||||||||

Processing and related services | 173,536 | 170,344 | 146,837 | 140,475 | 138,452 | |||||||||||||||

Software, maintenance and services | 20,975 | 19,720 | 25,047 | 30,359 | 26,696 | |||||||||||||||

Total cost of revenues | 194,511 | 190,064 | 171,884 | 170,834 | 165,148 | |||||||||||||||

Gross margin (exclusive of depreciation) | 188,595 | 187,253 | 179,517 | 90,881 | 255,901 | |||||||||||||||

Operating expenses (5): | ||||||||||||||||||||

Research and development | 46,191 | 33,932 | 31,887 | 30,398 | 32,764 | |||||||||||||||

Selling, general and administrative | 43,127 | 52,492 | 39,453 | 50,041 | 40,864 | |||||||||||||||

Depreciation | 10,438 | 9,862 | 10,412 | 12,701 | 14,751 | |||||||||||||||

Restructuring charges (4) | 2,368 | 14,534 | 1,292 | 2,149 | 2,256 | |||||||||||||||

Total operating expenses | 102,124 | 110,820 | 83,044 | 95,289 | 90,635 | |||||||||||||||

Operating income (loss) | 86,471 | 76,433 | 96,473 | (4,408 | ) | 165,266 | ||||||||||||||

Other income (expense): | ||||||||||||||||||||

Interest expense | (7,465 | ) | (7,537 | ) | (10,261 | ) | (14,296 | ) | (13,817 | ) | ||||||||||

Write-off of deferred financing costs (6) | — | — | (6,569 | ) | — | — | ||||||||||||||

Interest and investment income, net (1) | 21,984 | 4,059 | 975 | 920 | 1,729 | |||||||||||||||

Other, net | (21 | ) | 6 | (303 | ) | (85 | ) | 833 | ||||||||||||

Total other | 14,498 | (3,472 | ) | (16,158 | ) | (13,461 | ) | (11,255 | ) | |||||||||||

Income (loss) from continuing operations before income taxes | 100,969 | 72,961 | 80,315 | (17,869 | ) | 154,011 | ||||||||||||||

Income tax (provision) benefit (2) | (38,408 | ) | (26,219 | ) | (29,317 | ) | 12,703 | (55,960 | ) | |||||||||||

Income (loss) from continuing operations | 62,561 | 46,742 | 50,998 | (5,166 | ) | 98,051 | ||||||||||||||

Discontinued operations (1): | ||||||||||||||||||||

Loss from discontinued operations (5) | (6,555 | ) | (5,685 | ) | (11,109 | ) | (30,591 | ) | (66,468 | ) | ||||||||||

Income tax benefit | 3,764 | 12,172 | 7,295 | 9,480 | 13,035 | |||||||||||||||

Discontinued operations, net of tax | (2,791 | ) | 6,487 | (3,814 | ) | (21,111 | ) | (53,433 | ) | |||||||||||

Net income (loss) | $ | 59,770 | $ | 53,229 | $ | 47,184 | $ | (26,277 | ) | $ | 44,618 | |||||||||

Diluted net income (loss) per common share: | ||||||||||||||||||||

Income (loss) from continuing operations | $ | 1.33 | $ | 0.96 | $ | 0.99 | $ | (0.10 | ) | $ | 1.87 | |||||||||

Discontinued operations, net of tax | (0.06 | ) | 0.13 | (0.07 | ) | (0.41 | ) | (1.02 | ) | |||||||||||

Net income (loss) | $ | 1.27 | $ | 1.09 | $ | 0.92 | $ | (0.51 | ) | $ | 0.85 | |||||||||

Weighted-average diluted shares outstanding (3) | 47,102 | 48,571 | 51,223 | 51,432 | 52,525 | |||||||||||||||

Other Data (at Period End): | ||||||||||||||||||||

Number of clients' customers processed (2) | 45,354 | 45,228 | 43,472 | 44,148 | 45,816 | |||||||||||||||

Balance Sheet Data (at Period End): | ||||||||||||||||||||

Cash, cash equivalents and short-term investments (1)(7) | $ | 415,490 | $ | 392,224 | $ | 149,436 | $ | 105,397 | $ | 95,437 | ||||||||||

Working Capital (2)(7) | 454,117 | 444,738 | 172,675 | 69,642 | 119,782 | |||||||||||||||

Total assets | 653,496 | 638,376 | 710,407 | 724,775 | 731,317 | |||||||||||||||

Total debt (6) | 230,000 | 230,000 | 230,000 | 228,925 | 270,000 | |||||||||||||||

Total treasury stock (3) | 360,259 | 296,976 | 224,008 | 171,111 | 186,045 | |||||||||||||||

Stockholders' equity | 317,734 | 298,330 | 308,070 | 290,785 | 282,105 | |||||||||||||||

19

Table of Contents

| (1) | We sold our GSS and plaNet businesses in 2005. As a result, the results of operations for the GSS and plaNet businesses have been reflected as discontinued operations for all periods presented in our Consolidated Statements of Income. We recorded a net pretax gain (loss) on the disposal of these businesses of $(6.0) million and $10.9 million, respectively, in 2006 and 2005. We received approximately $233 million in net cash proceeds from the sale of these businesses, which is the primary reason for the significant increase in cash, cash equivalents, and short-term investments between 2004 and 2005. See Note 2 to our Consolidated Financial Statements and MD&A for additional discussion. |

| (2) | During 2003, we recorded a $119.6 million charge to revenue related to the Comcast arbitration ruling award. The award was segregated such that $105.7 million was attributable to periods prior to July 1, 2003, and $13.9 million was attributable to the third quarter of 2003. Of the $13.9 million attributable to the third quarter, we attributed $13.5 million to processing revenues, and the remaining $0.4 million to software maintenance revenues. The arbitration ruling also required us to begin invoicing Comcast lower monthly processing fees beginning in October 2003, which had the effect of reducing quarterly revenues from Comcast by approximately $13-$14 million ($52-$56 million annually), when compared to amounts prior to the arbitration ruling. As a result of the Comcast arbitration award, we were in a net operating loss position for the year, and recorded an income tax benefit of $12.7 million. During the fourth quarter of 2003, we paid Comcast $94.4 million of the arbitration award and in January 2004, we paid the remaining $25.2 million. Additionally, as a result of the arbitration ruling, Comcast customer accounts began being measured differently in October 2003, which resulted in a reduction in the total number of clients’ customers processed. |

| (3) | In August 1999, our Board of Directors approved our Stock Repurchase Program which authorized us to purchase shares of our common stock from time-to-time as business conditions warrant. During 2006, 2005, 2004, 2003, and 2002, we repurchased 2.5 million, 3.8 million, 3.0 million, zero, and 1.6 million shares, respectively. As of December 31, 2006, 14.4 million shares of the 30.0 million shares authorized under the Stock Repurchase Program remain available for repurchase. See Note 12 to our Consolidated Financial Statements and MD&A for additional discussion of the Stock Repurchase Program. |

| (4) | Beginning in the third quarter of 2002 and continuing through 2006, we made several changes to our business operations and implemented several cost reduction initiatives that resulted in restructuring charges of $2.4 million, $14.5 million, $1.3 million, $2.1 million, and $2.3 million, respectively, for 2006, 2005, 2004, 2003, and 2002. See Note 8 to our Consolidated Financial Statements and MD&A for additional discussion of the restructuring charges. |

| (5) | In 2003, we adopted the fair value method of accounting for our stock-based awards. In addition, we completed our exchange of certain stock options for restricted stock (also referred to by us as our “tender offer”) in December 2003. As a result, our stock-based compensation expense is significantly higher in 2006, 2005, and 2004 when compared to previous years. Additionally, in 2005, certain equity awards held by key members of our management team included a change in control provision that was triggered upon the closing of the sale of the GSS Business. The change in control provision resulted in accelerated vesting as of December 9, 2005 for the equity awards impacted, and thus, stock-based compensation expense of $4.7 million related to the accelerated vesting of these equity awards was recorded as stock-based compensation expense in the fourth quarter of 2005, of which $0.9 million was included in discontinued operations, and $3.8 million was included in continuing operations as part of restructuring charges. Total stock-based compensation expense recognized during 2006, 2005, 2004, 2003, and 2002 was $12.2 million, $20.4 million, $14.9 million, $5.6 million, and $1.4 million, respectively. Of these amounts, $12.2 million, $17.0 million, $10.6 million, $5.0 million, and $1.3 million are reflected in continuing operations for 2006, 2005, 2004, 2003, and 2002, respectively, with the remaining amounts reflected in discontinued operations for the respective periods. See Notes 3 and 13 to our Consolidated Financial Statements for additional discussion of these matters. |

| (6) | In February 2002, we entered into a $300 million term credit facility to finance the acquisition of the Kenan Business (which became part of our GSS Business). In June 2004, we completed an offering of $230 million of Convertible Debt Securities and used the proceeds, along with available cash, cash equivalents and short-term investments to: (i) repay the outstanding balance of the term credit facility; (ii) repurchase 2.1 million of shares of our common stock; and (iii) pay debt issuance costs of $7.2 million. As a result, we wrote off unamortized deferred financing costs attributable to the term credit facility of $6.6 million. See Note 7 to our Consolidated Financial Statements for additional discussion of our long-term debt. |

| (7) | As a result of the sale of the GSS and plaNet businesses, our December 31, 2006 and 2005 Consolidated Balance Sheets no longer include any amounts related to these sold businesses. To provide for consistent comparisons, the December 31, 2004 Consolidated Balance Sheet was restated to reflect the components of the sold GSS and plaNet businesses as assets and liabilities related to discontinued operations. Thus, the 2006, 2005, and 2004 cash, cash equivalents and short-term investments and working capital amounts in the above table are presented on a different basis, as the 2003 and 2002 amounts have not been restated and still include amounts related to the GSS and plaNet businesses. |

20

Table of Contents

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operation |

Forward-Looking Statements

This report contains a number of forward-looking statements relative to our future plans and our expectations concerning the North American customer care and billing industry, as well as the converging communications industry it serves, and similar matters. These forward-looking statements are based on assumptions about a number of important factors, and involve risks and uncertainties that could cause actual results to differ materially from estimates contained in the forward-looking statements. Some of the risks that are foreseen by management are outlined above within Item 1A., “Risk Factors”. Item 1A. constitutes an integral part of this report, and readers are strongly encouraged to review this section closely in conjunction with MD&A.

Management Overview

Our Company. We are a leading provider of outsourced billing, customer care and print and mail solutions and services supporting the North American communications market. Our solutions support some of the world’s largest and most innovative providers of bundled multi-channel video, Internet, and IP-based services. Our unique combination of solutions, services and expertise ensures that communication providers can continue to rapidly launch new service offerings, improve operational efficiencies and deliver a high-quality customer experience in a competitive and ever-changing marketplace.

As noted above, the North American communications industry has experienced significant consolidation over the last few years, resulting in a large percentage of the market being served by a fewer number of service providers with greater size and scale. Consistent with this market concentration, a large percentage of our revenues from continuing operations are generated from a limited number of clients, with approximately 70% of our revenues for 2006 being generated from our four largest clients, which are Comcast, EchoStar, Time Warner, and Charter.