UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

______________________________________

FORM 10-K

______________________________________

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2016

Commission File Number 1-11921

________________________________

E TRADE Financial Corporation

TRADE Financial Corporation (Exact Name of Registrant as Specified in its Charter)

______________________________________________

|

| | |

| Delaware | | 94-2844166 |

(State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification Number) |

1271 Avenue of the Americas, 14th Floor, New York, New York 10020

(Address of principal executive offices and Zip Code)

(646) 521-4300

(Registrant’s telephone number, including area code)

Securities Registered Pursuant to Section 12(b) of the act:

|

| | |

| Title of Each Class | | Name of Each Exchange on Which Registered |

| Common Stock, par value $0.01 per share | | The NASDAQ Stock Market LLC NASDAQ Global Select Market |

Securities Registered Pursuant to Section 12(g) of the Act: None

_____________________________________

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendments to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act. |

| | | |

Large accelerated filer x | Accelerated filer | | ¨ |

Non-accelerated filer ¨ (Do not check if a smaller reporting company) | Smaller reporting company | | ¨ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

At June 30, 2016, the aggregate market value of voting stock held by non-affiliates of the registrant was approximately $4.3 billion (based upon the closing price per share of the registrant's common stock as reported by the NASDAQ Global Select Market on that date). Shares of common stock held by each officer, director and holder of 5% or more of the outstanding common stock have been excluded in that such persons may be deemed to be affiliates. This determination of affiliates' status is not necessarily a conclusive determination for other purposes.

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of the latest practicable date:

As of February 17, 2017, there were 274,678,179 shares of common stock outstanding.

Documents Incorporated by Reference: Certain portions of the definitive Proxy Statement related to the Company’s 2017 Annual Meeting of Stockholders, to be filed hereafter (incorporated into Part III hereof).

E*TRADE FINANCIAL CORPORATION

FORM 10-K ANNUAL REPORT

For the Year Ended December 31, 2016

TABLE OF CONTENTS |

| | |

| PART I | | |

| | | |

| Item 1. | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| Item 1A. | | |

| Item 1B. | | |

| Item 2. | | |

| Item 3. | | |

| Item 4. | | |

| | | |

| PART II | | |

| Item 5. | | |

| Item 6. | | |

| Item 7. | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| Item 7A. | | |

| | | |

| Item 8. | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

|

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| Item 9. | | |

| Item 9A. | | |

| Item 9B. | | |

| | | |

| PART III |

| Item 10. | | |

| Item 11. | | |

| Item 12. | | |

| Item 13. | | |

| Item 14. | | |

| | | |

| PART IV |

| Item 15. | | |

| Item 16. | | |

| | | |

Unless otherwise indicated, references to "the Company," "we," "us," "our," "E*TRADE" and "E*TRADE Financial" mean E*TRADE Financial Corporation and its subsidiaries, and references to the parent company mean E*TRADE Financial Corporation but not its subsidiaries.

E*TRADE, E*TRADE Financial, E*TRADE Bank, the Converging Arrows logo and OptionsHouse are registered trademarks of E*TRADE Financial Corporation in the United States and in other countries.

PART I

FORWARD-LOOKING STATEMENTS

This report contains forward-looking statements, within the meaning of the Private Securities Litigation Reform Act of 1995, that involve risks and uncertainties. These statements discuss, among other things, our future plans, objectives, outlook, strategies, expectations and intentions relating to our business and future financial and operating results and the assumptions that underlie these matters and include statements regarding our capital plan initiatives and expected balance sheet size, the payment of dividends from our subsidiaries to our parent company, the management of our legacy loan portfolio, our ability to utilize deferred tax assets, the expected implementation and applicability of government regulation and our ability to comply with these regulations, continued repurchases of our common stock, payment of dividends on our preferred stock, our ability to meet upcoming debt obligations, the integration and related restructuring costs of past and any future acquisitions, the expected outcome of existing or new litigation, our ability to execute our business plans and manage risk, the potential decline of fees and service charges, the future sources of revenue, expense and liquidity and any other statement that is not historical in nature. These statements may be identified by the use of words such as "assume," "expect," "believe," "may," "will," "should," "anticipate," "intend," "plan," "estimate," "continue" and similar expressions. We caution that actual results could differ materially from those discussed in these forward-looking statements. Important factors that could contribute to our actual results differing materially from any forward-looking statements include, but are not limited to, changes in business, economic or political condition, performance, volume and volatility in the equity and capital markets, performance of the residential real estate and credit markets, changes in interest rates or interest rate volatility, credit and counterparty risk, customer demand for financial products and services, our ability to continue to compete effectively, cyber security threats, reliance on technology infrastructure, our ability to participate in consolidation opportunities in our industry, our ability to service our corporate debt, changes in government regulation or actions by our regulators, our ability to move capital to our parent company from our subsidiaries, adverse developments in litigation, and other factors discussed under Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations; Item 1A. Risk Factors of this Form 10-K; and elsewhere in this report and in other reports we file with the Securities and Exchange Commission (SEC). By their nature forward-looking statements are not guarantees of future performance or results and are subject to risks, uncertainties and assumptions that are difficult to predict or quantify. Actual future results may vary materially from expectations expressed or implied in this report or any of our prior communications. The forward-looking statements contained in this report reflect our expectations only as of the date of this report. Investors should not place undue reliance on forward-looking statements, as we do not undertake to update or revise forward-looking statements to reflect the impact of circumstances or events that arise after the date the forward-looking statements were made, except as required by law.

ITEM 1. BUSINESS

OVERVIEW

We are a financial services company that provides online brokerage and related products and services primarily to individual retail investors. Founded on the principle of innovation, we aim to enhance the financial independence of traders and investors through a powerful digital experience that includes tools and educational material, supported by professional guidance, to help individual investors and traders meet their near- and long-term investing goals. We provide these services to customers through our digital platforms and network of industry-licensed customer service representatives and Financial Consultants, over the phone and by email at two national branches and in-person at 30 regional branches across the United States. We operate federally chartered savings banks with the primary purpose of maximizing the value of deposits generated through our brokerage business.

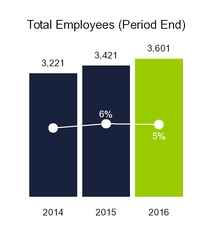

Our corporate offices are located at 1271 Avenue of the Americas, 14th Floor, New York, New York 10020. We were incorporated in California in 1982 and reincorporated in Delaware in July 1996. We had approximately 3,600 employees at December 31, 2016. We operate directly and through several subsidiaries, many of which are overseen by governmental and self-regulatory organizations. Substantially all of our revenues for the years ended December 31, 2016, 2015 and 2014 were derived from our operations in the United States. Our most important subsidiaries are described below:

| |

| • | E*TRADE Securities LLC (E*TRADE Securities) is a registered broker-dealer that clears and settles securities transactions for its customers. Our legacy clearing firm, E*TRADE Clearing LLC (E*TRADE Clearing), was merged into E*TRADE Securities effective October 1, 2016. |

| |

| • | Aperture, LLC (dba OptionsHouse) is a registered broker-dealer acquired on September 12, 2016 that provides brokerage products and services primarily to active traders through its derivatives platform. |

| |

| • | E*TRADE Bank and its subsidiary E*TRADE Savings Bank are federally chartered savings banks which provide our customers with Federal Deposit Insurance Corporation (FDIC) insurance on qualifying amounts of customer deposits and other banking and cash management capabilities. We utilize our bank structure to effectively monetize the value of brokerage deposits. |

| |

| • | E*TRADE Financial Corporate Services is a provider of software and services for managing equity compensation plans to our corporate clients. |

Delivering a powerful digital offering to our customers is a core pillar of our business strategy. We believe our focus on being a digital leader in the financial services industry is a competitive advantage. Our hybrid service delivery model is available through the following award-winning digital platforms, which include both E*TRADE and OptionsHouse products:

|

| |

| Web |

| Our leading-edge sites for customers and our primary channel to interact with prospects |

| |

• Access to a broad range of trading solutions • Actionable ideas and information • Research and knowledge for decision making |

| |

| Mobile |

| Powerful trading applications for smartphones, tablets and watches |

| |

• Award-winning mobile apps • Platform to manage accounts on the move • Stock and portfolio alerts |

| | |

| Active Trading Platform |

| Powerful software-based trading application |

| |

• Sophisticated trading tools • Idea generation and analysis • Advanced portfolio and market tracking |

These digital platforms are complemented by our offline channels, which include our network of customer service representatives and financial consultants and our 24/7 customer service available via phone, email and online at our two national branches and in person through our 30 regional branches.

STRATEGY

Our business strategy is centered on two key objectives: accelerating the growth of our core brokerage business to improve market share, and generating robust earnings growth and healthy returns on capital to deliver long-term value for our stockholders.

Accelerate Growth of Core Brokerage Business

| |

| • | Enhance overall customer experience |

We are focused on delivering cutting-edge trading solutions while improving our market position in investing products. Through these offerings, we aim to continue growing our customer base while deepening engagement with our existing customers.

| |

| • | Capitalize on value of corporate services channel |

We leverage our industry-leading position in corporate stock plan administration to improve client acquisition and engage with plan participants to bolster awareness of our full suite of offerings. Our corporate services channel is a strategically important driver of brokerage account and asset growth.

Generate Robust Earnings Growth and Healthy Returns on Capital

| |

| • | Utilize balance sheet to enhance returns |

We utilize our bank structure to effectively monetize brokerage relationships by investing stable, low-cost deposits primarily in agency mortgage-backed securities. Meanwhile, we continue to manage down the size and risk associated with our legacy loan portfolio.

| |

| • | Put capital to work for shareholders |

As we continue to deliver on our capital plan initiatives, we are focused on generating and effectively deploying excess capital for the benefit of our shareholders.

PRODUCTS AND SERVICES

We offer a broad range of products and services to our customers. Our core brokerage business is organized into three product areas: Trading, Investing, and Corporate Services. Additionally, we offer banking and cash management capabilities, including FDIC-insured deposit accounts, which are fully integrated into customer brokerage accounts. Among other features, customers have access to debit cards with ATM fee refunds, online and mobile bill pay, mobile check deposits and Apple Pay.

Trading

Trading products deliver automated trade order placement and execution services. We offer our customers a full range of investment vehicles including U.S. equities, exchange-traded funds (ETFs), options, bonds, futures, American depositary receipts (ADRs), and non-proprietary mutual funds. Margin accounts are also available to qualified customers, enabling them to borrow against their securities. We provide margin solutions, including calculators and requirement lookup and analysis tools, helping customers strategize, plan, and execute margin trades efficiently and effectively.

The Company markets trading products and services to self-directed investors and active traders. Products and services are delivered through web, desktop, and mobile digital channels. Trading and investing tools are supported by guidance, including fixed income, options, and futures specialists available on-call for customers. Other tools and resources include independent research and analytics, live and on-demand education, and strategies, trading ideas, and screeners for major asset classes.

Investing

Investing products help investors build wealth and address their long-term investing needs. Products and services include individual retirement accounts (IRAs), including Roth IRAs, virtual advice through our Adaptive Portfolio product, managed investment portfolios, unified managed accounts, and separately managed accounts. Investors are provided a full breadth of digital tools through web and mobile channels to address their investing needs. These include resource centers, allocation tools, educational, and editorial content.

The Company also offers guidance through a team of licensed Financial Consultants and Chartered Retirement Planning CounselorsSM at our 30 regional branches across the country, and through our two national branches by phone and email. Customers can receive complimentary portfolio reviews and personalized investment recommendations.

Corporate Services

The Corporate Services channel provides stock plan administration services for both public and private companies. Through its industry-leading platform, Equity Edge Online™, the Company offers management of employee stock option plans, employee stock purchase plans, and restricted stock plans with fully-automated stock plan administration, as well as accounting, reporting, and scenario modeling tools. The integrated stock plan solutions include multi-currency settlement and delivery, disbursement in international countries, and streamlined tax calculation. Additionally, corporate clients are offered 10b5-1 plan design and implementation, and SEC filing assistance. The Company's digital platforms allow participants in corporate client stock plans to view and manage their holdings. Additionally, participants have access to educational tools, restricted stock sales support, and dedicated stock plan service representatives. The Corporate Services channel is an important driver of brokerage account and asset growth, serving as an introductory channel for the Company's core brokerage business, with approximately 1.5 million individual stock plan accounts across approximately 1,000 corporate clients that represent approximately 20% of S&P 500 companies.

Equity Edge Online™ recordkeeping and reporting was rated #1 in Loyalty and Overall Satisfaction for the fifth year in a row by Group Five, an independent consulting and research firm, in its 2016 Stock Plan Administration Study Industry Report.

SALES AND CUSTOMER SERVICE

We believe providing superior sales and customer service is fundamental to our business. We strive to maintain a high standard of customer service by staffing the customer support team with appropriately trained personnel who are equipped to handle customer inquiries in a prompt and thorough manner. Our customer service representatives utilize our proprietary web-based platform that enables our team to reduce the number of touch-points required to answer customer inquiries. We also have specialized customer service programs that are tailored to the needs of each core customer group. We provide sales and customer support through the following channels of our registered broker-dealer and investment advisory subsidiaries:

|

| |

| Online |

| Our Online Service Center serves as a portal where customers can request services on their accounts and obtain answers to frequently asked questions. The online service center also provides customers with the ability to send a secure message and/or engage in live chat with one of our customer service representatives. In addition, we offer our Investor Education Center, providing customers with access to a variety of live and on-demand educational content and courses. |

| |

| Phone |

| We have a toll free number that connects customers to the appropriate department where a financial consultant or customer service representative can assist with the customer's inquiry. |

| | |

| Branches |

| We have 30 branches located across the U.S. where retail investors can get face-to-face support and guidance. Financial consultants are available on-site to help customers assess their current asset allocation and develop plans to help them achieve their investment goals. Customers can also contact our financial consultants via phone or e-mail if they cannot visit the branches. |

COMPETITION

The online financial services industry continues to evolve and remains highly competitive. Our core brokerage business competes with full service brokerage firms, Registered Investment Advisers (RIAs), discount brokerage firms, online brokerage firms, personal finance start-ups, internet banks and traditional "brick & mortar" retail banks and thrifts. Some of these competitors provide online trading and banking services, investment advisor services, robo-advice capabilities, touchtone telephone and voice response banking services, electronic bill payment services and a host of other financial products. We also compete with all users of market liquidity, including the types of competitors listed above, in order to obtain the least expensive source of funding.

Competition in the financial services industry continues to intensify, particularly amidst continued consolidation and declines in pricing over time. The proliferation of emerging financial technology start-ups further evidences the continued shift to digital advice. Our future success will rely upon our ability to keep providing digitally compelling and easy to use products and solutions to retail customers.

We also face competition in attracting and retaining qualified employees. Our ability to compete effectively in financial services will depend upon our ability to attract new employees, and retain and motivate our existing employees while efficiently managing compensation-related costs.

REGULATION

Our business is subject to regulation, primarily by U.S. federal and state regulatory agencies and certain self-regulatory organizations (SROs), such as central banks and securities exchanges, that have been charged with the protection of the financial markets and the interests of those participating in those markets. We, along with other larger institutions, have been subject to a broad range of rules and regulations and a climate of heightened regulatory scrutiny, particularly with respect to compliance with laws and regulations, including controls and business processes. This scrutiny and related rule-making has resulted in part from the enactment of the Dodd-Frank Wall Street Reform and Consumer Protection Act (Dodd-Frank Act) in 2010. The Dodd-Frank Act contains various provisions designed to enhance financial stability and to reduce the likelihood of another financial crisis and significantly changed the bank regulatory structure of our Company and its thrift subsidiaries. While the substance and full impact of the Dodd-Frank Act and other laws and regulations to which we are subject may be affected by changes in the U.S. political landscape and may not be fully known for months or years, we expect to continue to incur costs to implement the new requirements and monitor for continued compliance.

Regulators

Our primary regulators include, among others, the Securities and Exchange Commission (SEC), the Financial Industry Regulatory Authority (FINRA), the NASDAQ Stock Market (NASDAQ), the Commodity Futures Trading Commission (CFTC), the National Futures Association (NFA), the FDIC, the Board of Governors of the Federal Reserve System (Federal Reserve), the Municipal Securities Rulemaking Board, the Office of the Comptroller of the Currency (OCC) and the Consumer Financial Protection Bureau (CFPB).

Financial Services Regulation

Our regulators and regulatory examiners are increasingly focused on ensuring that our customer privacy, data protection, information security and cyber security-related policies and practices are adequate to inform consumers of our data collection, use, sharing and/or security practices, to provide them with choices, if required, about how we use and share their information, and to safeguard their personal information. We maintain systems designed to comply with these privacy, data protection, information security and cyber security requirements, including procedures designed to securely process, transmit and store confidential information and protect against unauthorized access to such information.

Our brokerage and banking entities are also required to disclose their privacy policies and practices related to sharing customer information with affiliates and non-affiliates by the Gramm-Leach-Bliley Act of 1999. These rules give customers the ability to "opt out" of having non-public information disclosed to third parties or receiving marketing solicitations from affiliates and non-affiliates based on non-public information received from our brokerage and banking entities.

As well, our brokerage and banking entities are subject to the Bank Secrecy Act, as amended by the USA PATRIOT ACT of 2001 (BSA/USA PATRIOT Act), which requires financial institutions to develop anti-money laundering (AML) programs to assist in the prevention and detection of money laundering and combating terrorism. In order to comply with the BSA/USA PATRIOT Act, we have an AML department that is responsible for developing and implementing our enterprise-wide programs for compliance with the various anti-money laundering and counter-terrorist financing laws and regulations. Our brokerage and banking entities are also subject to U.S. sanctions laws administered by the Office of Foreign Assets Control and we have policies and procedures in place to comply with these laws.

Brokerage Regulation

Our U.S. broker-dealers are registered with the SEC and are subject to regulation by the SEC and by SROs, such as FINRA and the securities exchanges of which each is a member, as well as various state regulators. In addition, they are registered with the CFTC as futures commission merchants (FCMs) and are members of the NFA. Such regulation covers various aspects of these broker-dealers, including for example, client protection, net capital requirements, required books and records, safekeeping of funds and securities, trading, prohibited transactions, public offerings, margin lending, customer qualifications for

margin and options transactions, registration of personnel and transactions with affiliates. Our international broker-dealer is regulated by the Hong Kong Securities & Futures Commission.

In April 2016, the U.S. Department of Labor published its final fiduciary regulations under the Employee Retirement Income Security Act of 1974 and the Internal Revenue Code of 1986. While currently scheduled to take effect in 2017, it is possible that implementation may be delayed. These regulations will subject certain persons, such as broker-dealers and other financial services providers that provide investment advice to individual retirement accounts and other qualified retirement plans and accounts, to fiduciary duties and prohibited transaction restrictions for a wider range of customer interactions. The Company is in the process of implementing the regulations, which has resulted in additional internal costs and expenses. Implementation of the regulations will have an impact on how advice is provided to our customers' tax-qualified retirement accounts and benefit plans and, in their current form, may diminish our profitability and will increase potential liabilities with respect to these accounts and plans.

Banking Regulation

Our banking entities are subject to regulation, supervision and examination for safety and soundness by the Federal Reserve, OCC, FDIC and CFPB for compliance with federal banking and consumer finance laws. Such regulation covers all aspects of the banking business, including lending practices, safeguarding deposits, customer privacy and information security, capital structure, transactions with affiliates and conduct and qualifications of personnel.

The Federal Reserve has primary jurisdiction for the supervision and regulation of savings and loan holding companies, including the Company. We are required to file periodic reports with the Federal Reserve and are subject to examination and supervision by it. The Federal Reserve has issued guidance aligning the supervisory and regulatory standards of savings and loan holding companies more closely with the standards applicable to bank holding companies on such matters as liquidity risk management, securitizations, operational risk management, internal controls and audit systems, business continuity and compensation and other employee benefits.

E*TRADE Bank is a federally chartered savings association and therefore is subject to regulation, supervision and examination by the OCC, which is its primary regulator, and by the CFPB. In addition, because E*TRADE Bank is an insured depository institution, it is subject to supervision by the FDIC.

Under the Dodd-Frank Act, all companies, including savings and loan holding companies, that directly or indirectly control an insured depository institution are required to serve as a source of strength for the institution.

Regulatory Capital Requirements

The Dodd-Frank Act also imposed new banking regulatory capital requirements at the Company, effective January 1, 2015. Previously, only E*TRADE Bank was subject to bank regulatory capital requirements.

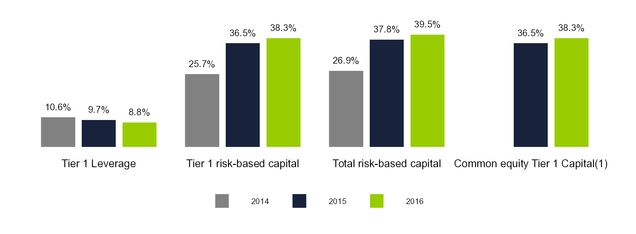

In July 2013, the U.S. federal banking agencies finalized a rule to implement Basel III in the U.S., which provides the framework for the calculation of a banking organization’s regulatory capital and risk-weighted assets. The rule became effective for us and for E*TRADE Bank on January 1, 2015, subject to a phase-in period for certain requirements over several years. The Basel III rule established Common Equity Tier 1 capital as a new tier of capital, raised the minimum thresholds for required capital, increased minimum required risk-based capital ratios, narrowed the eligibility criteria for regulatory capital instruments, provided for new regulatory capital deductions and adjustments, and modified methods for calculating risk-weighted assets (the denominator of risk-based capital ratios) by, among other things, strengthening counterparty credit risk capital requirements.

The Basel III final rule also introduces a capital conservation buffer that limits a banking organization’s ability to make capital distributions and discretionary bonus payments to executive officers if a banking organization fails to maintain a Common Equity Tier 1 capital conservation buffer of at least 2.5%, on a fully phased-in basis, of total risk-weighted assets above each of the following minimum risk-based capital ratio requirements: Common Equity Tier 1 (4.5%), Tier 1 (6.0%), and total risk-based capital (8.0%). This requirement was effective beginning on January 1, 2016, and will be fully phased-in by 2019. In addition, certain new deductions from and adjustments to regulatory capital are subject to a phase-in period over a

four year period that began at 40% in 2015 and will be fully implemented at 100% in 2018. We expect to remain compliant with the Basel III framework as it is phased-in.

In addition, in certain circumstances each of our banking entities may be subject to restrictions on their ability to declare dividends or make capital distributions and may be required to submit applications or requests for non-objection from the OCC or the Federal Reserve in connection with a planned capital distribution. A federal savings association, such as E*TRADE Bank, must file an application with the OCC if, among other things, the association would not be at least “adequately capitalized” following the distribution. Where no application or non-objection is required, a federal savings association is still required to provide the OCC with notice of the proposed distribution. Federal savings associations that are subsidiaries of savings and loan holding companies may also be required to obtain the non-objection of or provide notice of a proposed dividend to the Federal Reserve. If the association is not otherwise required to file an application or notice with the OCC, it must provide the OCC with a copy of the notice at the same time that it is filed with the Federal Reserve. A savings and loan holding company, such as the Company, is also required to notify and consult with the Federal Reserve in advance of taking capital actions when, among other things, doing so could create safety and soundness concerns or the savings and loan holding company is experiencing financial weakness.

The FDIC Improvement Act of 1991 requires the appropriate federal banking regulator to take "prompt corrective action" with respect to a depository institution if that institution does not meet certain capital adequacy standards. While these regulations apply only to banks, such as E*TRADE Bank, the Federal Reserve is authorized to take appropriate action against the parent savings and loan holding company, such as the Company, based on the undercapitalized status of any bank subsidiary. In certain instances, we would be required to guarantee the performance of a capital restoration plan if our bank subsidiary were undercapitalized.

Deposit Insurance Assessments

Each of our banking entities has deposits insured by the FDIC and pays quarterly assessments to the Deposit Insurance Fund (DIF), maintained by the FDIC, for this insurance coverage. On March 25, 2016, the FDIC published its final rule to add a surcharge to the regular DIF assessments of banks with $10 billion or more in assets, which includes E*TRADE Bank. Under the final rule, E*TRADE Bank is subject to an additional surcharge applied to its assessment base, which took effect for the assessment period beginning on July 1, 2016. Surcharges at an annual rate of 4.5 basis points will be assessed until the sooner of (1) the DIF attaining the minimum reserve ratio of 1.35 percent of insured deposits or (2) the fourth quarter of 2018. The FDIC anticipates eight quarters of "surcharge assessments." There may be a one-time “shortfall assessment” in the first quarter of 2019 to bring the fund immediately to 1.35 percent if needed. The surcharge has not had, and is not expected to have, a material impact on our financial condition, results of operations or cash flows.

Home Owners' Loan Act

Under the Home Owners’ Loan Act (HOLA), the OCC requires E*TRADE Bank to comply with the qualified thrift lender (QTL) test. Under the QTL test, E*TRADE Bank is required to maintain at least 65% of its “portfolio assets” in certain “qualified thrift investments” (primarily residential mortgages and related investments, including certain mortgage-backed securities, credit card loans, student loans and small business loans) in at least nine months of the most recent 12-month period. E*TRADE Bank currently meets that test. A savings association that fails to meet the QTL test is subject to certain operating restrictions and may be required to convert to a national bank charter.

Derivatives

Title VII of the Dodd-Frank Act subjects derivatives that we enter into for hedging, risk management and other purposes to a comprehensive regulatory regime. This regime requires central clearing and execution on designated markets or execution facilities for certain standardized derivatives and imposes or will impose margin, documentation, trade reporting and other new requirements. We are currently in compliance with these requirements as they apply to our activities.

Volcker Rule

In December 2013, the Federal Reserve, OCC, FDIC, SEC and CFTC issued final rules to implement section 619 of the Dodd-Frank Act (these rules collectively known as the "Volcker Rule"). The Volcker Rule imposes prohibitions and restrictions on the ability of banking entities and nonbank financial companies to engage in proprietary trading, and to have certain interests in, or relationships with, hedge funds or private equity funds. Banking entities were required to bring all of their activities and investments into conformance with the Volcker Rule by July 21, 2015, subject to certain extensions. In addition, the Volcker Rule requires banking entities to have comprehensive compliance programs reasonably designed to ensure and monitor compliance with the Volcker Rule. We are currently in compliance with all Volcker Rule requirements applicable to our operations.

Stress Testing

In October 2012, federal banking regulators issued final rules implementing provisions of the Dodd-Frank Act that require banking organizations with total consolidated assets of more than $10 billion but less than $50 billion to conduct annual company-run stress tests, report the results to their primary federal regulator and the Federal Reserve and publish a summary of the results. Under the rules, stress tests must be conducted using certain scenarios (baseline, adverse and severely adverse), which the Federal Reserve publishes by February 15 of each year.

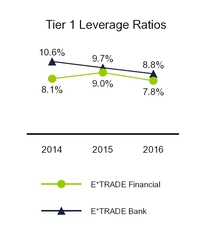

E*TRADE Bank is required to publish certain results of its annual stress test between October 15 and October 31 each year. In October 2016, E*TRADE Bank publicly disclosed a summary of its stress test results under the severely adverse scenario prescribed by the Federal Reserve and OCC based upon a nine-quarter period beginning on January 1, 2016 and ending on March 31, 2018. In the summary, E*TRADE Bank reported that its Tier 1 leverage ratio of 9.7% at the beginning of the forecast period declined to 8.5% at the end of the nine-quarter forecast horizon, which is well in excess of required minimum capital levels.

The Company will be required to conduct its first annual stress test using financial statement data as of December 31, 2016, report the results of the stress test to the Federal Reserve on or before July 31, 2017, and disclose a summary of the stress test results in October 2017.

For additional regulatory information on our brokerage and banking regulations, see Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations—Liquidity and Capital Resources and Item 8. Financial Statements and Supplementary Data—Note 19—Regulatory Requirements.

Regulatory Developments

The Company is currently not subject to certain regulatory requirements that apply to banking organizations with $50 billion or more in total consolidated assets as defined by each applicable regulation. Fifty billion dollars in total consolidated assets, which is measured in accordance with each applicable regulation, but generally on the basis of the average of the four most recent quarters, is a meaningful regulatory threshold, as U.S. banking organizations become subject to a number of additional, and in some cases more stringent, regulatory requirements once they reach that size. The Company expects these regulations, not all of which have been finalized, to become applicable as it surpassed $50 billion in total consolidated assets in the first quarter of 2017 and expects to surpass $50 billion on a four quarter average later this year. The Company has begun implementing policies, procedures, systems and governance structures that are designed to comply with the anticipated requirements. Additionally, while savings and loan holding companies are currently excluded from the scope of certain regulations that apply to bank holding companies, the Company expects it will ultimately be subject to these requirements.

Comprehensive Capital Adequacy Review

The Company is currently not subject to the annual Comprehensive Capital Analysis and Review (CCAR) process, which requires certain financial institutions to submit annual capital plans to the Federal Reserve. Through the CCAR process, the Federal Reserve may object to a banking organization's planned capital actions for the coming year. When the Federal Reserve objects to a capital plan, the banking organization may not make any capital distributions unless expressly permitted by the Federal Reserve. When the Federal Reserve does not object to a capital plan, the banking organization must request prior approval for any capital distributions that will exceed the amount described in the capital plan. The Company expects the

CCAR process, which currently only applies to bank holding companies with total consolidated assets of greater than or equal to $50 billion on a four quarter average, will be applicable to the Company in the future and will continue to monitor related regulatory updates and developments.

Resolution and Recovery Plans

In October 2011, the Federal Reserve and the FDIC issued a final rule requiring bank holding companies with total consolidated assets of $50 billion or more, based on the average of the four most recent quarters, to submit resolution plans and requiring each plan to describe the company’s strategy for rapid and orderly resolution in bankruptcy during times of financial distress. The Company is not currently subject to this rule as savings and loan holding companies are currently excluded from its scope.

In January 2012, the FDIC issued interim final rules requiring insured depository institutions, such as E*TRADE Bank, with total assets of $50 billion or more, based on the average of the four most recent quarters, to submit to the FDIC periodic plans providing for their resolution by the FDIC in the event of failure (resolution plans or living wills) under the receivership and liquidation provisions of the Federal Deposit Insurance Act. E*TRADE Bank is currently not subject to these rules, but if it were to exceed the asset threshold, it would be required to file with the FDIC an annual resolution plan demonstrating how it could be resolved in an orderly and timely manner in the event of receivership such that the FDIC would be able to ensure the bank's depositors receive access to their deposits within one business day, to maximize the net present value of the bank's assets when disposed of, and to minimize losses incurred by the bank's creditors.

In September 2016, the OCC published final guidelines that establish standards for recovery planning by insured national banks, federal savings associations, and federal branches of foreign banks with average total consolidated assets of $50 billion or more, based on the average of the four most recent quarters. E*TRADE Bank is currently not subject to these guidelines, but if it were to exceed the asset threshold, it would be required to develop and maintain a recovery plan for identifying and responding rapidly to significant stress events that could affect its financial condition and threaten its viability. The recovery plan would need to identify triggers for escalation of information to senior management and the board of directors, identify a wide range of credible options that E*TRADE Bank could undertake in response to severe stress, and be integrated into E*TRADE Bank’s risk governance function.

Liquidity Requirements

In September 2014, federal banking agencies issued a final inter-agency rule that imposes a quantitative liquidity coverage ratio (LCR) requirement on large banking institutions. The purpose of the LCR is to require banking organizations to hold minimum amounts of high-quality liquid assets (HQLA) based on a percentage of their net cash outflows over a 30-day period. Banking organizations with $250 billion or more in total consolidated assets or foreign exposures of $10 billion or more must hold HQLA in an amount equal to at least 100% of their projected net cash outflows over a 30-day period. Bank and savings and loan holding companies with total consolidated assets of $50 billion or more, based on the average of the four most recent quarters, are subject to a modified LCR requiring them to hold HQLA in an amount equal to at least 70% of their projected net cash outflows over a 30-day period. The Company believes the LCR is an important measure of liquidity and has been managing against it in preparation for the applicability of these requirements. Based on anticipated balance sheet growth the Company expects to be subject to these requirements beginning April 1, 2018.

In May 2016, federal banking agencies issued a proposed inter-agency rule that would impose a net stable funding requirement, the net stable funding ratio (NSFR), for large banking organizations with $50 billion or more in total consolidated assets. The proposed NSFR requirement would require a banking organization subject to the rule to maintain a sufficient level of stable funding relative to a measure based on the liquidity, maturity, quality and other characteristics of the organization’s assets and certain off-balance sheet exposures. The proposed NSFR requirement is designed to reduce the likelihood that disruptions to a banking organization’s regular sources of funding will compromise its liquidity position, as well as to promote improvements in the measurement and management of liquidity risk. The proposed NSFR requirement would apply to the same banking organizations that are subject to the LCR, and, also like the LCR, includes a modified version of the requirement for bank and savings and loan holding companies with total consolidated assets of $50 billion or more and less than $250 billion, based on the average of the four most recent quarters. Banking organizations subject to the modified NSFR would be required to maintain a

lower stable funding amount and have additional time to comply once they become subject to the requirements. The proposal contemplates that the NSFR would go into effect on January 1, 2018.

AVAILABLE INFORMATION

We make our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports, available free of charge at our website as soon as reasonably practicable after they have been filed with the SEC. Our website address is www.etrade.com. Information on our website is not part of this report.

The public may read and copy any materials we file with the SEC at the SEC’s Public Reference Room at 100 F Street, NE, Washington, DC 20549. The public may obtain information of the Public Reference Room by calling the SEC at 1-800-SEC-0330. The SEC maintains a website that contains the materials we file with the SEC at www.sec.gov.

ITEM 1A. RISK FACTORS

The following discussion sets forth the risk factors which could materially and adversely affect our business, financial condition and results of operations, and should be carefully considered in addition to the other information set forth in this report. Additional risks and uncertainties not currently known to us or that we currently do not deem to be material may also adversely affect our business, financial condition and results of operations.

Risks Relating to the Nature and Operation of Our Business

Changes in business, economic, or political conditions that negatively impact global financial markets could reduce trading volumes and margin lending, resulting in lower revenues.

Digital investing services to the retail customer, including trading, margin lending and sweep deposits, account for a significant portion of our revenues. Changes in business, economic or political conditions could cause a downturn in the global financial markets. Such a downturn could decrease volume and price levels of securities transactions which may, in turn, result in lower transactions revenue. A decrease in trading activity or securities prices would also typically be expected to result in a decrease in margin lending, which would reduce the revenue that we generate from interest charged on margin receivables and increase our credit risk because the value of the collateral could fall below the amount of indebtedness it secures.

We may be unsuccessful in managing the effects of changes in interest rates on our business.

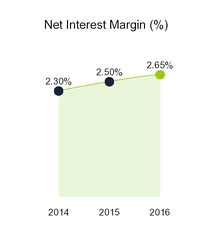

Net interest income is our most significant source of revenue. Our results of operations depend, in part, on our level of net interest income and our effective management of the impact of changing interest rates and varying asset and liability maturities. Our ability to manage interest rate risk could impact our financial condition. We use derivatives as hedging instruments to reduce the potential effects of changes in interest rates on our results of operations. However, the derivatives we utilize may not be effective at managing this risk and changes in market interest rates and the yield curve could reduce the value of our financial assets and reduce our net interest income.

Net interest margin may fluctuate based on the size and mix of the balance sheet, as well as the impact from the interest rate environment.

We rely on third party service providers to perform certain key functions and any failure to perform those functions as a result of operational or technological failure, including cybersecurity attacks on our third party service providers could result in the interruption of our operations and systems and could result in significant costs and reputational damage to us.

We rely on third party service providers for certain technology, processing, servicing and support functions. These third party service providers are also susceptible to operational and technology vulnerabilities, which may impact our business. In addition, these third party service providers may rely on other parties (sub-contractors), to provide services to us which also face similar risks. For example, external content providers provide us with financial information, market news, quotes, research reports and other fundamental data that we offer to clients. Also, we do not directly service any of our loans and, as a result, we rely on third party vendors and servicers to provide information on our loan portfolio.

As part of our enterprise risk management program build-out, we have invested in our third party oversight capabilities which included enhanced processes to evaluate third party providers, designed to verify that the third party service providers can support the stability of our operations and systems. However, these efforts may be insufficient and we cannot assure that we will not experience a failure as a result of a third party service provider. Any significant failures or security breaches by or of our third party service providers or their sub-contractors, including any actual or perceived cybersecurity attacks, security breaches, fraud, phishing attacks, acts of vandalism, information security breaches and computer viruses which could result in unauthorized access, misuse, loss or destruction of data, an interruption in service or other similar events could interrupt our business, cause us to incur losses, subject us to fines or litigation and harm our reputation. An interruption in or the cessation of service by any third party service provider and our inability to make alternative arrangements in a timely manner could have a material impact on our ability to offer certain products and services and cause us to incur losses. We cannot assure that any of these third party service providers or their sub-contractors will be able to continue to provide their products and services in an efficient, cost effective manner, if at all, or that they will be able to adequately expand their services to meet our needs and those of our customers. We may incur significant additional costs to implement enhanced protective measures and technology, to investigate and remediate vulnerabilities or other exposures or to make required notifications.

We expect that our regulators will hold us responsible for any deficiencies in our oversight and control of our third party relationships and for the performance of such third parties. If there were deficiencies in the oversight and control of our third party relationships, and if our regulators held us responsible for those deficiencies, our business, reputation, and results of operations could be adversely affected.

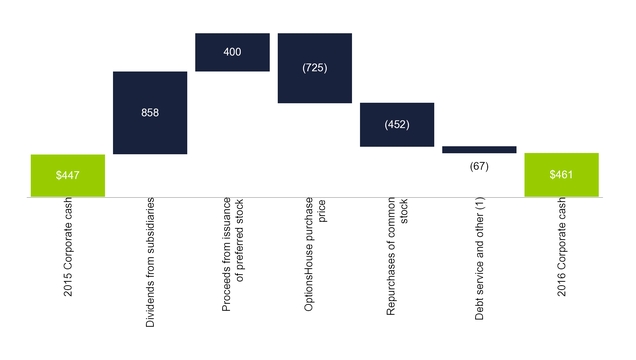

We conduct all of our operations through subsidiaries and rely on dividends from our subsidiaries for a substantial amount of our cash flows.

We depend on dividends, distributions and other payments from our subsidiaries to fund payments on our obligations, including our debt obligations. Regulatory and other legal restrictions limit our ability to transfer funds to or from certain subsidiaries. In addition, many of our subsidiaries are subject to laws and regulations that authorize regulatory bodies to block or reduce the flow of funds to us, or that prohibit such transfers altogether in certain circumstances. These laws and regulations may hinder our ability to access funds that we may need to make payments on our obligations, including our debt obligations, and otherwise conduct our business.

In particular, a savings association that is part of a savings and loan holding company structure, such as E*TRADE Bank, must file a notice of a declaration of a dividend with the Federal Reserve at least 30 days before the proposed dividend declaration by the bank’s board of directors. OCC regulations set forth the circumstances under which a federal savings association is required to submit an application or notice before it may make a capital distribution. See Item 1. Business—Regulation for additional information.

As of December 31, 2016, much of our capital was invested in our banking subsidiary, E*TRADE Bank. The Federal Reserve may object to a proposed capital distribution if, among other things, E*TRADE Bank is, or as a result of such dividend or distribution would be, undercapitalized or it has safety and soundness concerns. We cannot be certain, however, that we will receive regulatory approval for such contemplated dividends at the requested levels or at all. As we expect to use excess capital generated by E*TRADE Bank

to grow our balance sheet, we do not expect to distribute dividends from E*TRADE Bank to the parent until 2018.

Under the OCC stress test regulations, E*TRADE Bank is required to conduct stress-testing using the prescribed stress-testing methodologies. The final OCC regulations require E*TRADE Bank to conduct its stress test using financial statement data as of December 31 of each year, and to submit the results prior to July 31 of the following year. E*TRADE Bank is also required to publish summary results of its annual stress test between October 15 and October 31 each year. In 2016, E*TRADE Bank submitted and published the results of its second annual stress test, as required. The OCC analyzes and provides feedback on the quality of E*TRADE Bank's stress test process and results. While there is no formal mechanism for the OCC to "pass" or "fail" E*TRADE Bank's stress test processes and results, it will likely consider these processes and results in evaluating proposed actions that may affect our bank's capital, including but not limited to redemption or repurchase of regulatory capital instruments, dividends and mergers and acquisitions. If the OCC were to object to any such proposed action, our business prospects, results of operations and financial condition could be adversely affected.

We operate in a highly competitive industry where many of our competitors have greater financial, technical, marketing and other resources.

The financial services industry is highly competitive, with multiple industry participants competing for the same customers. Many of our competitors have longer operating histories and greater resources than we have and offer a wider range of financial products and services. Other of our competitors offer a more narrow range of financial products and services and have not been as susceptible to the disruptions in the credit markets that have impacted us, and therefore have not suffered the losses we have. The impact of competitors with superior name recognition, greater market acceptance, larger customer bases or stronger capital positions could adversely affect our revenue growth and customer retention. Our competitors may also be able to respond more quickly to new or changing opportunities and demands and withstand changing market conditions better than we can. Competitors may conduct extensive promotional activities, offering better terms, lower prices, or different products and services that could attract current and prospective E*TRADE customers and potentially result in intensified price competition within the industry. We may not be able to match the marketing efforts or prices of our competitors. Some of our competitors may also benefit from established relationships among themselves or with third parties that enhance their products and services.

In addition, we compete in a technology-intensive industry characterized by rapid innovation. We may be unable to effectively use new technologies, adapt our services to emerging industry standards or develop, introduce and market enhanced or new products and services. If we are not able to update or adapt our products and services to take advantage of the latest technologies and standards, or are otherwise unable to tailor the delivery of our services to the latest personal and mobile computing devices preferred by our retail customers, our business and financial performance could suffer.

Our ability to compete successfully in the financial services industry depends on a number of factors, including, among other things:

| |

| • | Maintaining and expanding our market position |

| |

| • | Attracting and retaining customers |

| |

| • | Providing easy to use and innovative financial products and services |

| |

| • | Our reputation and the market perception of our brand and overall value |

| |

| • | Maintaining competitive pricing |

| |

| • | Competing in a concentrated competitive landscape |

| |

| • | The quality of our technology (including cybersecurity defenses), products and services |

| |

| • | Deploying a secure and scalable technology and back office platform |

| |

| • | Innovating effectively in launching new or enhanced products |

| |

| • | The differences in regulatory oversight regimes to which we and our competitors are subject |

| |

| • | Attracting new employees and retaining our existing employees |

| |

| • | General economic and industry trends |

Our competitive position within the industry could be adversely affected if we are unable to adequately address these factors, which could have a material adverse effect on our business and financial condition.

If we do not successfully participate in consolidation opportunities, we could be at a competitive disadvantage.

There has been significant consolidation in the financial services industry and this consolidation may continue in the future. If we fail to take advantage of viable consolidation opportunities, our competitors may be able to capitalize on those opportunities and take advantage of greater scale and cost efficiencies to our detriment.

For example, on September 12, 2016, we completed the acquisition of Aperture New Holdings, Inc., the ultimate parent company of OptionsHouse, an online brokerage, for $725 million in cash. The acquisition subjects us to a number of risks, uncertainties, and potential costs, including that:

| |

| • | We may experience significant attrition in the acquired accounts or experience other issues that would prevent us from achieving synergies consistent with the expected amounts or within the anticipated timeframe. |

| |

| • | Our retention of customers’ assets may be impacted by our ability to successfully integrate the acquired operations, products (including pricing) and personnel. |

| |

| • | Attempts to retain key personnel may not succeed. |

| |

| • | We could be subject to undisclosed liabilities that could be material or become subject to litigation or regulatory risks as a result of the acquisition. |

| |

| • | Management’s attention may be diverted from other business initiatives. |

| |

| • | Unanticipated restructuring costs may be incurred. |

| |

| • | There may be negative changes in general economic conditions in the regions or the industries in which the combined businesses operate. |

| |

| • | We will have less cash available for other purposes, including for use in acquisitions or the development of other technologies or products. |

Any future acquisitions could involve these and additional risks. Our ability to pursue additional strategic transactions may also be limited by our corporate debt, including our senior secured credit facility. Future acquisitions may also be funded through the issuance of additional debt or preferred stock.

Any of these risks, whether with respect to the current or any future acquisitions, could have a material adverse effect on our business and results of operations.

We rely heavily on technology, which can be subject to interruption and instability due to operational and technological failures, both internal and external.

We rely on technology, particularly the Internet and mobile services, to conduct much of our business activity and allow our customers to conduct financial transactions. Our systems and operations, including our primary and disaster recovery data center operations, are vulnerable to disruptions from human error, natural disasters, power outages, computer and telecommunications failures, software bugs, computer viruses or other malicious software, distributed denial of service (DDoS) attacks, spam attacks, security breaches and other similar events. In addition, extraordinary trading volumes or site usage could cause our computer systems to operate at an unacceptably slow speed or even fail. Disruptions to, instability of or other failure to effectively maintain our information technology systems or external technology that allows

our customers to use our products and services could harm our business and our reputation. Should our technology operations be disrupted, we may have to make significant investments to upgrade, repair or replace our technology infrastructure and may not be able to make such investments on a timely basis. While we have made significant investments designed to enhance the reliability and scalability of our operations, we cannot assure that we will be able to maintain, expand and upgrade our systems and infrastructure to meet future requirements and mitigate future risks on a timely basis or that we will be able to retain skilled information technology employees. Disruptions in service and slower system response times could result in substantial losses, decreased client service and satisfaction, customer attrition and harm to our reputation. In addition, technology systems, including our own proprietary systems and the systems of third parties on whom we rely to conduct portions of our operations, are potentially vulnerable to security breaches and unauthorized usage. An actual or perceived breach of the security of our technology could harm our business and our reputation. Further, any actual or perceived breach or cybersecurity attack directed at other financial institutions or financial services companies, whether or not we are impacted, could lead to a general loss of customer confidence in the use of technology to conduct financial transactions, which could negatively impact us, including the market perception of the effectiveness of our security measures and technology infrastructure. The occurrence of any of these events may have a material adverse effect on our business or results of operations.

Further, because our business model relies heavily on our customers’ use of their own personal computers, mobile devices and the Internet, our business and reputation could be harmed by security breaches of our customers and third parties. Computer viruses and other attacks on our customers’ personal computer systems, home networks and mobile devices or against the third-party networks and systems of internet and mobile service providers could create losses for our customers even without any breach in the security of our systems, and could thereby harm our business and our reputation. As part of our E*TRADE Complete Protection Guarantee, we reimburse our customers for losses caused by a breach of security of our customers’ own personal systems. Such reimbursements may not be covered by applicable insurance and could have a material impact on our financial performance and results of operations.

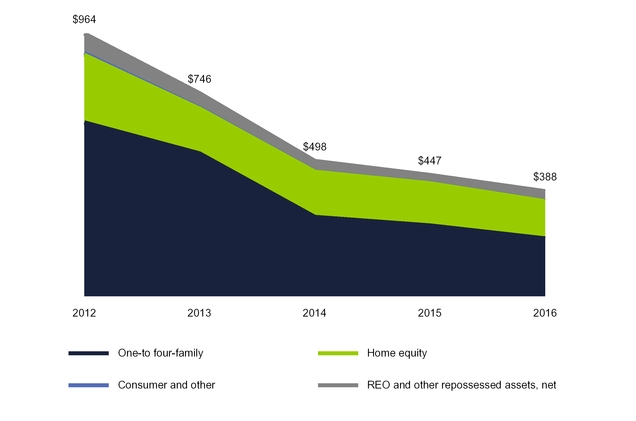

We may continue to experience losses in our mortgage loan portfolio.

At December 31, 2016, the principal balance of our one-to four-family loan portfolio was $2.0 billion and the allowance for loan losses for this portfolio was $45 million. At December 31, 2016, the principal balance of our home equity loan portfolio was $1.6 billion and the allowance for loan losses for this portfolio was $171 million. Although the provision for loan losses has declined in recent periods and we recognized a benefit for loan losses of $149 million during the year ended December 31, 2016, performance is subject to variability in any given quarter and we cannot state with certainty that the declining loan loss trend will continue. Due to the complexity and judgment required by management about the effect of matters that are inherently uncertain, there can be no assurance that our allowance for loan losses will be adequate. In the normal course of conducting examinations, our banking regulators, the OCC and Federal Reserve, continue to review our policies and procedures. This process is dynamic and ongoing and we cannot be certain that additional changes or actions to our policies and procedures will not result from their continuing review. We may be required under such circumstances to further increase the allowance for loan losses, which could have an adverse effect on our regulatory capital position and our results of operations in future periods.

Certain characteristics of our mortgage loan portfolio indicate an additional risk of loss. For example, at December 31, 2016:

| |

| • | Approximately 12% and 29% of the one- to four-family and home equity loan portfolios, respectively, had a current loan-to-value (LTV)/combined loan-to-value (CLTV) of greater than 100%. |

| |

| • | Borrowers with current Fair Isaac Credit Organization (FICO) scores less than 700 consisted of approximately 33% and 40% of the one- to four-family and home equity loan portfolios, respectively. |

| |

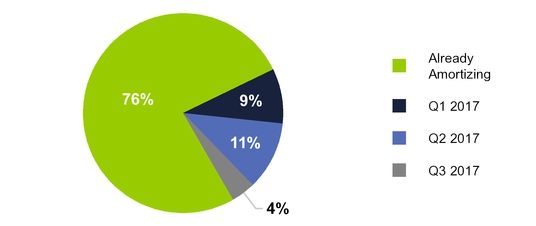

| • | Approximately 24% and 15% of the one- to four-family and home equity loan portfolios, respectively, were not yet amortizing. |

The foregoing factors are among the key items we track to predict and monitor credit risk in our mortgage portfolio, together with loan type, housing prices, loan vintage and geographic location of the underlying property. We believe the relative importance of these factors varies, depending upon economic conditions.

Home equity loans have certain characteristics that result in higher risk than first lien, amortizing one- to four-family loans. For example, at December 31, 2016:

| |

| • | Approximately 87% of the home equity loan portfolio are second lien loans on residential real estate properties. |

| |

| • | We hold both the first and second lien positions in less than 1% of the home equity loan portfolio. |

| |

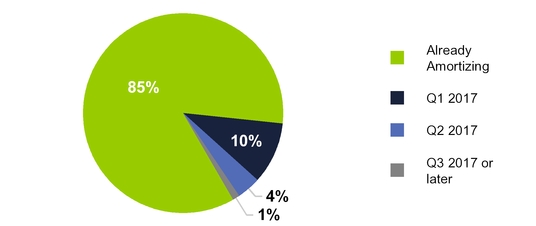

| • | The majority of home equity lines of credit (HELOCs) convert to amortizing loans at the end of the draw period, which typically ranges from five to ten years. At December 31, 2016, 85% of the home equity line of credit portfolio had converted to amortizing. Less than 1% of this portfolio will require the borrowers to repay the loan in full at the end of the draw period, commonly referred to as "balloon loans." |

Second lien loans carry higher credit risk because the holder of the first lien mortgage has priority in right of payment. Therefore, downturns in real estate markets may result in the value of the collateral being insufficient to cover the second lien positions. In addition, in loans for which we do not hold the first lien positions, we are exposed to risk associated with the actions and inactions of the first lien holder. The average estimated current CLTV on our home equity loan portfolio was 87% as of December 31, 2016.

We monitor our borrowers by refreshing FICO scores and CLTV information on a quarterly basis. We do not have access to complete data on the first lien positions of second lien home equity loans. Actual loan defaults and delinquencies of amortizing HELOCs that exceed our current expectations could negatively impact our financial performance.

Unauthorized disclosure of customer data, whether through a breach of our computer systems or those of our customers or third parties, may subject us to significant liability and reputational harm.

We are dependent on information technology to securely process, transmit and store electronic information and to communicate among our locations and with our clients and third party service providers. As the breadth and complexity of this infrastructure continue to grow, the potential risk of breach of security and cybersecurity attacks increases. As a financial services company, we are continuously subject to cybersecurity attacks by third parties. Such breaches could lead to shutdowns or disruptions of our systems and potential unauthorized disclosure of customer data. In addition, vulnerabilities of our external service providers and other third parties could pose security risks to client information.

As part of our business, we are required to collect, use and store customer, employee and third party data, including personally identifiable information (PII). This may include, among other information, names, addresses, phone numbers, email addresses, contact preferences, tax identification numbers and account information. We maintain systems and procedures designed to securely process, transmit and store confidential information (including PII) and to protect against unauthorized access to such information. We also require our third party service providers to have adequate security if they have access to PII. However, risks associated with the management, use and storage of sensitive data have grown in recent years due to increased sophistication and activities of organized crime, hackers, terrorists and other external parties. For example, we, and other financial institutions, experienced a cyber-incident in 2013 which resulted in certain customer contact information being compromised and potentially accessed by unauthorized third parties. As of the date of this Annual Report, we are unaware of any financial fraud or other misuse of customer data resulting from this incident. We are cooperating with government agencies in connection with their investigation.

We have continued to invest in our technology, including advanced security measures, but, despite these investments, we, our customers and our third party service providers may be vulnerable to security breaches, phishing attacks, acts of vandalism, computer viruses or other cybersecurity attacks which could result in unauthorized access, misuse, loss or destruction of data, an interruption in service or other similar events. In addition, because the methods and techniques employed by organized crime, hackers, terrorists and other external parties are increasingly sophisticated and often are not fully recognized or understood until after they have been launched, we may be unable to anticipate, detect or implement effective preventative measures against cybersecurity attacks, which could result in substantial exposure of either employee or customer PII. Any breach of security, real or perceived, involving the misappropriation, loss or

other unauthorized disclosure of PII, whether by us, our customers or our third party service providers, could severely damage our reputation, expose us to the risk of litigation and liability, disrupt our operations and have a materially adverse effect on our business. In addition, although we maintain insurance coverage that we believe is reasonable, prudent and adequate for the purpose of our business, it may be insufficient to protect us against all losses and costs stemming from breaches of security, cyber-attacks and other types of unlawful activity, or any resulting disruptions from such events.

In providing services to clients, we manage, utilize and store sensitive and confidential client data, including personal data. As a result, we are subject to numerous laws and regulations designed to protect this information, such as U.S. federal and state laws and foreign regulations governing the protection of PII and other customer data. These laws and regulations are increasing in complexity and number, change frequently and sometimes conflict. If any person, including any of our employees, negligently disregards or intentionally breaches our established controls with respect to client data, or otherwise mismanages or misappropriates that data, we could be subject to significant monetary damages, regulatory enforcement actions, fines and/or criminal prosecution in one or more jurisdictions.

We may suffer losses due to credit risk associated with margin lending, securities loaned transactions or financial transactions with counterparties.

We permit certain customers to purchase securities on margin. A downturn in securities markets may impact the value of collateral held in connection with margin receivables and may reduce its value below the amount borrowed, potentially creating collections issues with our margin receivables. In addition, we frequently borrow securities from and lend securities to other broker-dealers. Under regulatory guidelines, when we borrow or lend securities, we must simultaneously disburse or receive cash deposits. A sharp change in security market values may result in losses if counterparties to the borrowing and lending transactions default on their obligations. We also engage in financial transactions with counterparties, including repurchase agreements, that expose us to credit losses in the event counterparties cannot meet their obligations. See Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations—Risk Management for additional information.

Advisory services subject us to additional risks.

We provide advisory services to investors to aid them in their decision making. Investment recommendations and suggestions are based on publicly available documents and communications with investors regarding investment preferences and risk tolerances. Publicly available documents may be inaccurate and misleading, resulting in recommendations or transactions that are inconsistent with investors’ intended results. In addition, advisors may not understand investor needs or risk tolerances, which may result in the recommendation or purchase of a portfolio of assets that may not be suitable for the investor. Risks associated with advisory services also include those arising from possible conflicts of interest, inadequate due diligence, inadequate disclosure, human error and fraud. To the extent that we fail to know our customers or improperly advise them, we could be found liable for losses suffered by such customers, which could harm our reputation and business.

Our risk management practices may leave us exposed to unidentified or unanticipated risk.

As a financial services company, our business exposes us to certain risks. We seek to monitor and manage our significant risk exposures through a set of board approved limits as well as Key Risk Indicators (KRIs) or metrics. We have adopted a governance framework which includes reporting of these metrics and other significant risks and exposures to management and the Board of Directors. However, our risk management methods may not predict future risk exposures effectively and may not be effective in identifying and mitigating our key risks. In addition, some of our risk management methods are based on an evaluation of information regarding markets, customers and other matters that are based on assumptions that may not be accurate. A failure to manage our risk effectively could materially and adversely affect our business, results of operations and financial condition.

Our corporate debt may restrict how we conduct our business and failure to comply with the terms of our corporate debt could adversely affect our financial condition and results of operations.

As of December 31, 2016, we have $1 billion of corporate debt and have the capacity to incur $250 million in additional indebtedness under our senior secured revolving credit facility, subject to certain covenant requirements. Our expected annual debt service interest payment is approximately $50 million. The degree to which we are leveraged could have important consequences, including:

| |

| • | A portion of our cash flow from operations is dedicated to the payment of principal and interest on our indebtedness, thereby reducing the funds available for other purposes. |

| |

| • | Our ability to obtain additional financing for working capital, capital expenditures, acquisitions and other corporate needs may be limited. |

| |

| • | Our leverage may affect our ability to adjust rapidly to changing market conditions and make us more vulnerable in the event of a downturn in general economic conditions or our business. |

Our senior secured revolving credit facility and the indentures governing our corporate debt contain various covenants and restrictions that place limitations on our ability and certain of our subsidiaries’ ability to, among other things:

| |

| • | Incur additional indebtedness |

| |

| • | Pay dividends, make distributions or other payments |

| |

| • | Repurchase or redeem capital stock |

| |

| • | Make investments or other restricted payments |

| |

| • | Merge, consolidate or transfer substantially all of our assets |

| |

| • | Enter into transactions with our shareholders or affiliates |