Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington D.C. 20549

FORM 10-K

Annual Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 For the Fiscal Year Ended December 31, 2007

Commission File No.: 001-13581

Noble International, Ltd.

(Exact name of registrant as specified in its charter)

| Delaware | 38-3139487 | |

| (State of incorporation) | (I.R.S. Employer Identification No.) | |

840 W. Long Lake Rd., Suite 601 Troy, Michigan | 48098 | |

| (Address of principal executive offices) | (Zip Code) |

Registrant’s telephone number, including area code: (248) 519-0700

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Name of each exchange on which registered | |

| Common Stock, $.00067 par value | NASDAQ Global Select Market |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large Accelerated Filer ¨ Accelerated Filer x Non-Accelerated Filer ¨ Smaller Reporting Company ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

The aggregate market value of the shares of common stock, $.00067 par value (“Common Stock”) held by non-affiliates of the registrant as of June 30, 2007 was approximately $245.7 million based upon the closing price for the Common Stock on the NASDAQ Global Select Market on such date.

The number of shares of the registrant’s Common Stock outstanding as of March 11, 2008 was 23,601,224.

DOCUMENTS INCORPORATED BY REFERENCE

Part III of this Annual Report on Form 10-K (“Report”) incorporates by reference information (to the extent specific sections are referred to herein) from the Registrant’s Proxy Statement for its 2008 Annual Meeting (the “2008 Proxy Statement”).

Table of Contents

| Page | ||||

| 3 | ||||

| Item 1. | 3 | |||

| Item 1A. | 9 | |||

| Item 1B. | 15 | |||

| Item 2. | 15 | |||

| Item 3. | Legal Proceedings | 15 | ||

| Item 4. | Submission of Matters to a Vote of Security Holders | 15 | ||

| 16 | ||||

| Item 5. | 16 | |||

| Item 6. | 18 | |||

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | 19 | ||

| Item 7A. | 28 | |||

| Item 8. | 30 | |||

| Item 9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | 78 | ||

| Item 9A. | 78 | |||

| Item 9B. | 81 | |||

| 82 | ||||

| Item 10. | 82 | |||

| Item 11. | 82 | |||

| Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 82 | ||

| Item 13. | Certain Relationships and Related Transactions, and Director Independence | 82 | ||

| Item 14. | 82 | |||

| 83 | ||||

| Item 15. | Exhibits, Financial Statement Schedules | 83 | ||

* * *

The matters discussed in this Annual Report (“Report”) contain certain forward-looking statements. For this purpose, any statements contained in this Report that are not statements of historical fact may be deemed to be forward-looking statements. Without limiting the foregoing, words such as “may,” “expect,” “believe,” “anticipate,” “estimate,” or “continue,” the negative or other variations thereof, or comparable terminology, are intended to identify forward-looking statements. These statements by their nature involve substantial risks and uncertainties, and actual results may differ materially depending on a variety of factors, including continued market demand for the types of products and services produced and sold by the Company, change in worldwide economic and political conditions and associated impact on interest and foreign exchange rates, the level of sales by original equipment manufacturers of vehicles for which the Company supplies parts, the successful integration of companies acquired by the Company, and changes in consumer debt levels.

2

Table of Contents

| Item 1. | Business |

GENERAL

Noble International, Ltd. (“we,” “us,” “our,” “Noble” or the “Company”), through its subsidiaries, is a full-service provider of21st Century Auto Body Solutions® primarily to the automotive industry. We utilize laser-welding, roll-forming, and other technologies to produce flat, tubular, shaped and enclosed formed structures used by original equipment manufacturers (“OEMs”) or their suppliers in automobile applications including doors, fenders, body side panels, pillars, bumpers, door beams, load floors, windshield headers, door tracks, door frames, and glass channels.

We operate twenty-four production facilities worldwide, including two joint ventures in China and one in India. Thirteen of our facilities are located in North America and the remaining eleven facilities are located primarily in Western Europe. Our executive offices are located at 840 W. Long Lake Rd., Suite 601, Troy, MI 48098, tel. (248) 519-0700. Our common stock is traded on the NASDAQ Global Select Market under the symbol NOBL and our website iswww.nobleintl.com. Our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and amendments to those reports filed or furnished pursuant to section 13(a) or 15(d) of the Exchange Act are available free of charge through our website as soon as reasonably practicable after they are electronically filed with, or furnished to, the Securities and Exchange Commission (“SEC”). Except as otherwise stated in these reports, the information contained on our website or available by hyperlink from our website is not incorporated into this Report or other documents we file with, or furnish to, the SEC.

We were incorporated on October 3, 1993 in the State of Michigan. On June 29, 1999, we reincorporated in the State of Delaware. Since our formation in 1993, we have completed numerous significant acquisitions and divestitures. As used in this Report, each of the terms “we,” “us,” “our,” “Noble” and the “Company” refers to Noble International, Ltd. and its subsidiaries and their combined operations after consummation of all such acquisitions and divestitures. Our fiscal year is the calendar year. Any reference to a fiscal year in this Report should be understood to mean the period from January 1 to December 31 of that year.

RECENT ACQUISITIONS

Tailored Laser-Welded Blank Business of Arcelor S.A.

In August 2007, we completed the purchase of Arcelor’s Tailored Laser-Welded Blank operations (the “Arcelor Transaction”). Arcelor S.A. (“Arcelor”), a Luxembourg corporation, is a member of the ArcelorMittal group, the world’s largest steel company. The ArcelorMittal group, with 330,000 employees in more than 60 countries, has an industrial presence in 27 countries across Europe, the Americas, Asia and Africa and is a steel provider to numerous industrial sectors such as automotive, construction, household appliances and packaging.

The total value of the Arcelor Transaction was approximately $300 million, with Arcelor receiving 9.375 million shares of our common stock with the balance in the form of cash, assumption of certain obligations and a subordinated note. As part of the Arcelor Transaction, we acquired eight production facilities, including one facility in the United States, plus interests in two joint ventures in Asia (the “Arcelor Business”.) The remaining facilities are located in Belgium, France, Germany, Spain, Slovakia and the United Kingdom.

The Arcelor Transaction provides us with considerable customer and geographic diversification. Our post-transaction customer concentration improved dramatically, with the largest customer only accounting for approximately 18% of our total net sales. Products manufactured outside of North America will account for approximately 53% of our total net sales. The acquisition also provides us with important new customers including Renault and Peugeot, as well as the European operations of Ford, General Motors and Volkswagen.

3

Table of Contents

We entered into a three year transition services agreement and a five year steel supply and services agreement with ArcelorMittal to support our European operations. We also have access to ArcelorMittal’s automotive-related research and development efforts, and we intend to work together to develop new products and applications for the automotive industry.

Post-Closing Developments Relating to the Arcelor Transaction

On March 19, 2008, we entered into a Securities Purchase Agreement (the “Securities Purchase Agreement”) with ArcelorMittal pursuant to which ArcelorMittal agreed to provide subordinated debt financing to us in the form of a convertible subordinated note with a principal amount of $50 million. The convertible subordinated note was issued on March 20, 2008, bears interest at the rate of 6% per annum and matures on March 20, 2013. The conversion price is subject to reset and adjustment. For more information on the terms of the convertible note, see “Item 8. Financial Statements and Supplementary Data; Note 2—Earnings (Loss) Per Share and Note 20—Subsequent Events.”

Pursuant to the Securities Purchase Agreement, we have agreed: (a) at our next annual meeting of stockholders, to submit for approval a proposal to allow the issuance of the shares upon conversion in accordance with NASDAQ Marketplace Rule 4350(i), to use our best efforts to solicit our stockholders’ approval of such issuance and to cause our board of directors to recommend to the stockholders that they approve such proposal; (b) to avail ourselves of the “controlled company” exemption regarding corporate governance requirements under the NASDAQ listing requirements at any time that ArcelorMittal’s beneficial ownership (including shares held by ArcelorMittal’s affiliates) exceeds 50% of the outstanding shares of our common stock; and (c) promptly following (i) the closing under the Securities Purchase Agreement and (ii) the designation by ArcelorMittal of nominees to serve on our board of directors and board committees (the “Nominees”), to use our best efforts to cause the Nominees to be duly elected to fill vacancies on the board of directors in accordance with the standstill and stockholder agreement described above, as amended by the Agreement and Waiver (as hereinafter defined).

In connection with the closing under the Securities Purchase Agreement, we entered into an agreement and waiver with ArcelorMittal and our former chairman of the board, Mr. Robert Skandalaris (the “Agreement and Waiver”), which waives the applicability to ArcelorMittal of the standstill provisions and other provisions of the standstill and stockholders agreement. We also entered into the first amendment to the registration rights agreement with ArcelorMittal and Mr. Skandalaris, which amended the registration rights agreement to provide that the convertible note and the shares issuable upon its conversion are included as “registrable securities” that ArcelorMittal may require us to register.

Pullman Industries, Inc.

In October 2006, we completed the acquisition of all outstanding common stock of Pullman Industries, Inc. (“Pullman”) for approximately $122.1 million, including cash of $90.7 million, the assumption of long-term debt of $22.0 million, and contingent consideration of approximately $14.0 million offset by cash acquired of $4.6 million. The contingent consideration is payable upon our receipt of amounts owed by certain customers, subject to any rights of offset available to us, and has been recorded as Contingent consideration in our financial statements. For additional information on this liability, see “Item 8. Financial Statements and Supplementary Data, Note 8—Acquisitions.”

Pullman operated four facilities in the United States and two facilities in Mexico. Pullman’s product line consisted primarily of structural, impact and trim roll-formed components for automotive and furniture applications. Pullman’s expertise as an “enabling technology” allows us to create more advanced tubular, shaped and enclosed formed structures to meet the future demands of the automotive industry. Combining roll-forming and laser-welding allows us to create more complex, finished impact and structural products, improving safety in more parts of the vehicle. This combination is particularly important as the need to produce safer and lighter vehicles is a focus of the industry. Both laser-welding and roll-forming offer similar advantages over costly,

4

Table of Contents

traditional stamping methods, including more efficient processing, better material utilization and lower total cost. The combination significantly reinforces our21st Century Auto Body Solutions® strategy.

Operations in Silao, Mexico

In January 2005, we completed the acquisition of the assets of Oxford Automotive Inc.’s steel processing facility in Silao, Mexico for $5.7 million in cash and the assumption of $1.1 million in operating liabilities. The facility supplies component blanks on a toll processing basis to the Mexican automotive industry. In the fourth quarter 2005, we entered into an agreement with Sumitomo Corporation and its affiliates (“Sumitomo”) to sell a 49% interest in the Silao facility for consideration of approximately $5.5 million in cash and assumption of a portion of the entity’s debt. We continue to consolidate results of operations from the Silao facility in our financial statements.

For additional information on the above acquisitions, see “Item 8. Financial Statements and Supplementary Data, Note 8—Acquisitions.”

INDUSTRY

The process of laser-welding involves the concentration of a beam of light, producing energy densities of 16 to 20 million watts per square inch at the point where two metal pieces are to be joined. Laser-welding allows rapid weld speeds with low heat input, thus minimizing topical distortion of the metal and resulting in ductile and formable welds that have mechanical properties comparable to, or in some cases superior to, the metal being welded. Laser welds provide improved performance as well as visual aesthetics and allow significant automation of the welding process.

The integration of the Pullman roll-forming andP-Tech® hot forming technology with our laser- welding technology further enhances our21st Century Auto Body Solutions®strategy. Roll-forming is a continuous, rapid, low-scrap forming method that improves upon the production cost and tooling burden of traditional metal stamping. Parts are formed into final shape by progressively passing through sets of roller dies. As an additional competitive advantage, this forming method can be used with ultra high strength steels that cannot be stamped, furthering our ability to supply parts for advancing vehicle structures. Roll-formed components are applied to the vehicle in the trim, base structure, and impact system areas. With ourP-Tech® hot forming technology, low-cost, heat treatable steel is formed into highly complex and efficient engineered structures, and then heat treated to form the strongest of steels: martensite. This unique combination of formability and strength enables our engineers to provide impact structure to the automakers with aluminum-like strength to weight performance while maintaining the cost advantages of steel. Combined with roll-forming, the proprietaryP-Tech® hot forming technology places us at the forefront of impact structure and energy management design and production. Both roll-forming andP-Tech® add up to 15 unique product applications to our portfolio, but more importantly, they complement most of the existing product applications by adding additional cost, weight and strength efficiencies.

The combination of laser-welding, roll-forming andP-Tech® technologies offers significant advantages over other welding and forming technologies, including cost, weight and safety benefits. We have developed a technology and production process that we believe permits us to produce products more quickly and with higher quality and tolerance levels than our competitors. The Ultra Light Steel Auto Body Consortium, a worldwide industry association of steel producers, commissioned a study which concluded that laser-welded blanks and tubes will play a significant role in car manufacturing in the next decade as the automotive industry is further challenged to produce lighter cars for better fuel economy with enhanced safety features and lower manufacturing costs. The study identified 19 potential applications for laser-welding blanks per vehicle. We have identified nine additional potential applications. In addition, we have identified 17 potential applications for laser-welded tubular structures.

We market our products to automakers by promoting the integrated benefits of laser-welding and roll-formed products. We have quantified the benefits of incorporating our products into customer vehicles, which may include lower total cost, lower vehicle weight, improved crash performance and reductions in steel usage.

5

Table of Contents

Our sales force actively markets our products to automaker engineers as well as to management to drive penetration of our products into more vehicles.

Our customers include automotive original equipment manufacturers (“OEM”) such as General Motors, Chrysler, Ford, Honda, Volkswagen, Nissan, Renault and Peugeot, as well as other companies that are suppliers to OEMs (“Tier I” suppliers). We, as a Tier I and a supplier to Tier I companies (“Tier II”) provide prototype, design, engineering, laser welded blanks and tubes, roll-formed products and other automotive component services.

Our manufacturing facilities in Warren, Michigan; South Haven, Michigan (2 facilities); Butler, Indiana; Shelbyville, Kentucky; Brantford, Canada; Queretaro, Mexico and Puebla, Mexico have been awarded ISO 14001 and TS16949 certifications. Our facility in Silao, Mexico has been awarded TS16949 certification. All of our European manufacturing facilities are certified by ISO/TS 16949, with the exception of our facility in Slovakia, which is in the process of obtaining the certification. In addition, our facilities in Warren, Michigan; Shelbyville, Kentucky; and Butler, Indiana have been awarded Q1 certification from Ford.

DESIGNAND ENGINEERING

The development of new automobile models or the redesign of existing models generally begins two to five years prior to the marketing of such models to the public. Our engineering staff typically work with the OEM and Tier I engineers of our customers early in the development phase to design specific automotive body components for the new or redesigned models. We also provide other value-added services, such as prototyping, to our customers.

Our engineering and research staff design and integrate proprietary laser-welding and roll-formed systems using the latest design techniques. These systems are for our exclusive use and are not marketed or sold to third parties. Continued strategic investment in process technology is essential for us to remain competitive in the markets we serve, and we plan to continue to make research and development expenditures. During the years ended December 31, 2007, 2006 and 2005, we expensed $0.5 million, $0.7 million and $0.2 million, respectively, on research and development.

Noble Advanced Technologies (“NAT”) is an organization within Noble that is completely dedicated to product and process research and development activities. The NAT product application engineers enter early into the automaker’s design process to gain better access to component sales. Several new processes are under development to enhance market competitiveness and scope for the auto structures. Research spans laser-welding, roll-forming, and metallurgical transformation processes and includes supporting design and simulation techniques. NAT is responsible for our intellectual property development and protection.

In conjunction with the Arcelor Transaction, we entered into a five-year steel supply and services agreement with Arcelor Auto, a subsidiary of ArcelorMittal. As part of this agreement, Arcelor Auto provides research and development services to our European operations. All research and development plans will be jointly agreed to by Arcelor Auto and us. Arcelor Auto will pay approximately the first €2.0 million of research and development cost each year, and we will pay any cost in excess of €2.0 million. Arcelor Auto will grant us a license to use the intellectual property that is developed on the same terms as provided in the intellectual property licensing agreement.

MARKETING

Our sales and engineering staff are located in direct proximity to our major customers. Typically, OEMs and Tier I suppliers conduct a competitive bid process to select suppliers for the parts that are to be included in end products. Our direct sales force, marketing and technical personnel work closely with OEM and Tier I engineers to satisfy their specific requirements. In addition, our technical personnel spend a significant amount of time assisting OEM and Tier I engineers in product planning and integration of our products in future automotive models.

6

Table of Contents

In addition, the five-year steel supply and services agreement with Arcelor Auto stipulates that certain marketing, technical support, sales, credit risk, invoicing, collections, and consulting services be provided by Arcelor Auto to our European operations.

RAW MATERIALS

The raw materials required for our products include rolled steel, coated steel, and gases including helium, carbon dioxide and argon. We obtain our raw materials and purchased parts from a variety of suppliers. We do not believe that we are dependent upon any one of our suppliers, despite concentration of purchasing of certain materials from a few sources, as other suppliers of the same or similar materials are readily available. We typically purchase our raw materials on a purchase order basis as needed and have generally been able to obtain adequate supplies of raw materials for our operations.

In North America, the majority of the steel used in our operations is purchased through OEMs’ steel buying programs. Under these programs we purchase the steel from specific suppliers at the steel price the customer negotiated with the steel suppliers. We take ownership and the attendant risks of ownership of the steel, and the price at which the steel is purchased has historically been fixed for the duration of each program. However, certain OEM’s have made mid-program changes to steel prices. Furthermore, a portion of the automotive operations involves the toll processing of materials supplied by another Tier I supplier, typically a steel manufacturer or processor. Under these toll processing arrangements, we charge a specified fee for operations performed without acquiring ownership of the steel.

Under the five-year steel supply and services agreement, Arcelor Auto supplies all flat-rolled carbon steel products needed by our European production facilities. Arcelor Auto has agreed to provide us with the most favorable pricing contemporaneously provided by Arcelor Auto, with respect to similar volumes and on the same terms and conditions, to any of our European welded-blanks competitors.

PATENTSAND TRADEMARKS

We own numerous patents and patents pending and certain trademarks related to our products and methods of manufacturing. It is our belief that the loss of any single patent or group of patents would not have a material adverse effect on our business. We also have proprietary technology and equipment that constitute trade secrets, which we have chosen not to register to avoid public disclosure thereof. We rely upon patent and trademark law, trade secret protection and confidentiality or license agreements with our employees, customers and third parties to protect our proprietary rights.

SEASONALITY

Our operations are largely dependent upon the automotive industry, which is highly cyclical and is dependent upon consumer spending. In addition, the automotive component supply industry is somewhat seasonal. Increased net sales and operating profit are generally experienced during the second calendar quarter as a result of the automotive industry’s spring selling season, the peak sales and production period of the year. Net sales and operating profit generally decrease during July and December of each year as a result of changeovers in production lines for new model years as well as scheduled OEM plant shutdowns for vacations and holidays. For more information on this topic, see “Item 1A. Risk Factors; Our business could be adversely affected by the cyclicality and seasonality of the automotive industry.”

CUSTOMERS

Automotive industry customers account for substantially all of our consolidated net sales. Certain customers accounted for significant percentages (greater than 10%) of our consolidated net sales as follows:

7

Table of Contents

| Year Ended December 31, | |||||||||

| 2007 | 2006 | 2005 | |||||||

Chrysler | 26 | % | 40 | % | 37 | % | |||

General Motors | 25 | % | 24 | % | 21 | % | |||

Ford Motor Company | 15 | % | 20 | % | 28 | % | |||

For more information on the concentrated nature of our significant customers, see “Item 1A. Risk Factors; The loss of any significant customer or the failure of any significant customer to pay amounts due to us could have a material adverse effect on our business.”

COMPETITION

The automotive component supply and tooling component industries are highly competitive. Our primary competitors across various markets are TWB Company, Shiloh Industries, Powerlasers, Shape Corporation, Magna International, Global Automotive Systems, Flex-N-Gate, Thyssen Krupp Steel, Voest Alpine, Gestamp and Saltzgitter, among others. In addition, some OEMs produce some of the products we provide in-house. Competition is based on many factors, including engineering, product design, process capability, quality, cost, delivery and responsiveness. We believe that our performance record places us in a strong competitive position although there can be no assurance that we can continue to compete successfully against existing or future competitors in each of the markets in which we compete. For more information on this topic, see “Item 1A. Risk Factors; Our business faces substantial competition.”

ENVIRONMENTAL MATTERS

We are subject to environmental laws and regulations concerning emissions to the air, discharges to waterways, and generation, handling, storage, transportation, treatment and disposal of waste materials. We are also subject to other federal and state laws and regulations regarding health and safety matters. We believe that we are currently in compliance with applicable environmental and health and safety laws and regulations. For more information on this topic, see “Item 1A. Risk Factors; We are subject to the requirements of federal, state, local and foreign environmental and occupational health and safety laws and regulations.”

EMPLOYEES

As of December 31, 2007, we employed approximately 3,000 associates including approximately 2,300 production employees and 700 managerial, engineering, research and administrative personnel. Approximately 1,300 associates are employed in the United States. For additional information about our employees, see “Item 1A. Risk Factors; Our business could be adversely affected by labor interruptions.”

FINANCIAL INFORMATION ABOUT SEGMENTSAND GEOGRAPHIC AREAS

Prior to the closing of the Arcelor Transaction on August 31, 2007, we had historically classified our operations into one industry segment operating in the automotive industry. As a result of the Arcelor Transaction and subsequent reorganization of our business, we identified the following two operating segments as of December 31, 2007, which are based upon geographical areas (region of production):

| • | North America, which includes our operations in the United States, Canada and Mexico |

| • | Europe and Rest of World, which includes our operations in Europe, Australia and Asia |

Both segments perform laser-welding and metal processing activities for the automotive industry.

International operations are subject to certain additional risks inherent in conducting business outside the United States such as changes in currency exchange rates, price and currency exchange controls, import restrictions, nationalization, expropriation and other governmental action.

8

Table of Contents

For additional information about segments and geographic areas, see “Item 8. Financial Statements and Supplementary Data, Note 18—Segment Information.”

| Item 1A. | Risk Factors |

The following factors are important and should be considered carefully in connection with any evaluation of our business, financial condition, results of operations and prospects. Additionally, the following factors could cause our actual results to differ materially from those reflected in any forward-looking statements.

Our business is subject to all of the risks associated with substantial leverage, including that available cash may not be adequate to make required payments, and we may not comply with our credit facilities. To finance our operations, including costs related to various acquisitions, we have incurred indebtedness. Our credit facilities are subject to customary financial and other covenants including, but not limited to, limitations on debt, consolidations, mergers, sales of assets, and bank approval on certain acquisitions. Our credit facilities are also secured by the equity interests of our subsidiaries and substantially all of our assets. Our ability to satisfy outstanding debt obligations from cash flow is dependent upon our future performance and is subject to financial, business and other factors, many of which may be beyond our control. In the event that we do not have sufficient cash resources to satisfy our repayment obligations, we would be in default under the agreements pursuant to which such obligations were incurred, which would have a material adverse effect on our business. To the extent that we are required to use cash resources to satisfy interest payments to the holders of outstanding debt obligations, we will have fewer resources available for other purposes. We may increase our leverage in the future, whether as a result of operational or financial performance, acquisition or otherwise.

We are subject to certain financial and other restrictive covenants pursuant to our credit facilities.We may not be able to meet all the covenants under each of our credit agreements and, if we do not meet a covenant obligation, we may be subject to a notice of default under such agreement. The credit agreements governing our credit facilities contain a number of restrictive covenants, the violation of which could result in a notice of default under such agreements. When we have not been able to meet our covenant obligations, we have been able to obtain waivers of such covenant requirements or amendments to the credit agreements. In the future, however, we may not be able to obtain a waiver or consent in the event of a default. We can give no assurance that we will be able to amend or obtain a permanent waiver of the covenants in the event that we are unable to meet the requirements of such covenants. If we are unable to amend or obtain a permanent waiver from compliance with the covenants by the date stated in such agreement, the lenders could exercise their remedies against us, which would have a material adverse effect on our results of operations and financial condition.

As of December 31, 2007, we were not in compliance with all of our covenants under the European Credit Facility (as hereinafter defined), but we subsequently received a waiver from the syndicate of commercial banks with respect to any defaults based on such non-compliance. This waiver is effective until May 2, 2008, at which date we would be in default unless the covenants are formally amended. This waiver is contingent upon us making a €20.0 million prepayment on the European Term Loan (as hereinafter defined). Such prepayment amount shall be funded by the proceeds of subordinated debt provided to us by ArcelorMittal or a mutually agreed upon alternative solution. We are in discussions with the lenders under the European Credit Facility regarding an amendment or permanent waiver to avoid potential future covenant defaults.

If we do not make our periodic filings with the SEC in a timely manner, our stock may be delisted. On April 3, 2008, we received a letter from the Nasdaq Stock Market (“Nasdaq”) notifying us that Nasdaq did not receive our Form 10-K for the period ended December 31, 2007 as required by applicable Nasdaq marketplace rules, and that, accordingly, subject to our right to request an appeal, trading of our common stock will be suspended at the opening of business on April 14, 2008 and our securities will be removed from listing and registration on the Nasdaq Global Select Market. Subsequent to our receipt of this letter, we filed an appeal with Nasdaq, which has resulted in a stay of the trading suspension and the delisting of our common stock, pending the outcome of the appeal. If the outcome of the appeal is not resolved in our favor, and if the trading of our common stock is suspended for a material amount of time and/or if we are delisted, an investor would find it

9

Table of Contents

difficult to dispose of, or to obtain quotations as to the price of, our common stock. Delisting of our common stock could also result in lower prices per share of our common stock than would otherwise prevail, which might also materially affect our ability to raise capital and, thus, affect our business.

Our business could be adversely affected by the cyclicality and seasonality of the automotive industry.The automotive industry is highly cyclical and dependent on consumer spending. Economic factors adversely affecting automotive production and consumer spending could adversely impact our business. In addition, the automotive component supply industry is somewhat seasonal. Our need for continued significant expenditures for capital equipment purchases, equipment development and ongoing manufacturing improvement and support, among other factors, makes it difficult for us to reduce operating expenses in a particular period if our net sales forecasts for such period are not met because a substantial component of our operating expenses are fixed. Generally, net sales and operating profit increase during the second calendar quarter of each year as a result of the automotive industry’s spring selling season, which is the peak sales and production period of the year. Net sales and operating profit generally decrease during July and December of each year as a result of changeovers in production lines for new model years as well as scheduled OEM plant shutdowns for vacations and holidays.

Our historical results of operations have generally not reflected typical cyclical or seasonal fluctuations in net sales and operating profit. The acquisitions and divestitures completed by us and new product sales growth have resulted in a growth trend through successive periods, which has masked the effect of typical seasonal fluctuations. We may not continue our historical growth trend, return to profitability, or conform to industry norms for seasonality in future periods.

The loss of any significant customer or the failure of any significant customer to pay amounts due to us could have a material adverse effect on our business.Sales to the automotive industry accounted for substantially all of our net sales in 2007. In addition, our automotive sales are highly concentrated among a few major OEMs and Tier I suppliers. As is typical in the automotive supply industry, we generally do not have long-term contracts with our customers. Our customers provide annual estimates of their requirements; however, sales are made on a short-term purchase order basis. There is substantial and continuing pressure from the major OEMs and Tier I suppliers to reduce costs, including the cost of products purchased from outside suppliers. If in the future we are unable to generate sufficient production cost savings to offset price reductions, our operating profit could be adversely affected.

Acquisitions could materially and adversely affect our financial performance. The automotive component supply industry is undergoing consolidation as OEMs seek to reduce both their costs and their supplier base. Future acquisitions may be made to enable us to expand into new geographic markets, add new customers, provide new products, expand manufacturing and service capabilities and increase automotive model market penetration with existing customers. We may not be successful in identifying appropriate acquisition candidates or in combining operations with such candidates if they are identified. It should be noted that any acquisitions could involve the dilutive issuance of equity securities or the incurrence of debt. In addition, acquisitions involve numerous other risks, including difficulties in assimilation of the acquired company’s operations following consummation of the acquisition, the diversion of management’s attention from other business concerns, risks of producing products we have limited experience with, the potential loss of key customers of the acquired company, and the inability of pre-acquisition due diligence to identify all possible issues that may arise with respect to products of the acquired company. Our ability to successfully integrate the operations acquired in the Arcelor Transaction involves numerous risks, including designing and implementing internal controls over financial reporting at those locations. We may not be able to ensure that all such internal controls over financial reporting are operating effectively.

We may be unable to remediate our material weaknesses in audit committee composition and sufficiency of accounting personnel at our roll-forming business headquarters location. This failure and any failure in the future to achieve and maintain effective internal controls over financial reporting and otherwise comply with the requirements of Section 404 of the Sarbanes-Oxley Act of 2002 could have a material adverse effect on our business. Such noncompliance could result in perceptions of our business among customers, suppliers, lenders, investors, securities analysts and others being adversely affected. We may not be able to

10

Table of Contents

complete our remediation plans designed to address the identified material weaknesses in our internal controls over financial reporting and continue to attract additional qualified accountants to assist in completing such plans and maintaining compliance programs. The failure to successfully complete our remediation plans could adversely affect our business. For additional information see “Item 9A. Controls and Procedures.”

Our business may be adversely affected by the failure to obtain business on new and redesigned model introductions. Our automotive product lines are subject to change as our customers, including both OEMs and Tier I suppliers, introduce new or redesigned products. We compete for new business both at the beginning of the development phase of new vehicle models, which generally begins two to five years prior to the marketing of such models to the public, and upon the redesign of existing models. Our net sales would be adversely affected if we fail to obtain business on new models, fail to retain or increase business on redesigned existing models, if our customers do not successfully introduce new products incorporating our products, or if market demand for these new products does not develop as anticipated.

Our business faces substantial competition. Markets for all of our products are extremely competitive. We compete based upon a variety of factors, including engineering, product design, process capability, quality, cost, delivery and responsiveness. In addition, with respect to certain of our products, we face competition from divisions of our OEM customers. Our business may be adversely affected by competition, and we may not be able to maintain our profitability if the competitive environment changes.

We are dependent upon the continuous improvement of our production technologies.Our ability to continue to meet customer demands within our automotive operations with respect to performance, cost, quality and service will depend, in part, upon our ability to remain technologically competitive with our production processes. New automotive products are increasingly complex, require increased welding precision, use of various materials and have to be run at higher production speeds and with lower scrap ratios to reduce costs. The investment of significant additional capital or other resources may be required to meet this continuing challenge. If we are unable to improve our production technologies, we may lose business and our business could be adversely affected.

Our up-front dedication of design and engineering resources may have a material adverse effect on our financial condition, cash flow or results of operations.Within the automotive industry, OEMs and Tier I suppliers require their suppliers to provide design and engineering input during the product development process. The direct costs of design and engineering are generally borne by our customers. However, we bear the indirect cost associated with the allocation of design and engineering resources to such product development projects. Despite our up-front dedication of design and engineering resources, our customers are under no obligation to order the subject components or systems from us following their development. In addition, when we deem it strategically advisable, we may also bear the direct up-front design and engineering costs as well.

We are subject to U.S. and global economic risks and uncertainties. Demand in the automotive industry is significantly dependent on the U.S. and the global economies, and our business and profitability are exposed to current and future uncertainties. Demand in the automotive industry fluctuates in response to overall economic conditions and is particularly sensitive to changes in interest rate levels, consumer confidence and fuel costs. The threat or act of terrorism and war, higher energy costs, the housing and mortgage crisis, and other recent developments have adversely affected consumer confidence throughout the U.S. and much of the world, and exacerbated the uncertainty in our markets. The future impact resulting from changes in economic conditions is difficult to predict. Our results of operations would be harmed by any sustained weakness in demand or continued downturn in the economy.

Our net sales are impacted by automotive retail inventory levels and production schedules. In recent years, OEM customers have significantly reduced their production and inventory levels due to the uncertain economic environment. It is extremely difficult to predict future production rates and inventory levels for such OEM customers. Any additional decline in production rates or inventory levels would adversely affect our operating results.

11

Table of Contents

We are under pressure from our customers to reduce prices. We and other suppliers to the automotive markets face continued price reduction pressure from our customers. The U.S.-based OEMs, in particular, have experienced significant market share erosion to non-U.S.-based OEMs over the past few years, thereby putting pressure on their profitability. The U.S.-based OEMs respond by pressuring their suppliers, including us, to reduce the prices of products sold. To the extent this trend continues, the price reduction pressures experienced will be ongoing. While we constantly strive to sustain and improve our margins through a variety of efforts, we may not be able to maintain or improve our operating results in the face of such price reduction pressures.

Our business could be adversely affected by labor interruptions.Within the automotive supply industry, substantially all of the hourly employees of the OEMs and many Tier I suppliers are represented by labor unions and work pursuant to collective bargaining agreements. The failure of any of our significant customers to reach agreement with a labor union on a timely basis, resulting in either a work stoppage or strike, could have a material adverse effect on our business. We have collective bargaining agreements with several unions, including: the United Auto Workers, the International Brotherhood of Teamsters, the Confederation of Mexican Workers and the Confederation of Workers & Farm Laborers in Mexico. In addition, the majority of our European employees are members of industrial trade union organizations and confederations within their respective countries. Although no facility has been subject to a strike, lockout or other major work stoppage, any such incident would have a material adverse effect on our operating profit.

We may incur losses as a result of product liability exposure. As a supplier to the automotive market, we face an inherent business risk of exposure to product liability claims if the failure of one of our products results in personal injury or death. Material product liability losses may occur in the future. In addition, if any of our products prove to be defective, we may be required to participate in a recall involving such products. We maintain insurance against product liability claims, but there can be no assurance that such coverage may be adequate or may continue to be available to us on acceptable terms or at all. A successful claim brought against us in excess of available insurance coverage or a requirement to participate in any product recall could have a material adverse effect on our business.

We are subject to the requirements of federal, state, local and foreign environmental and occupational health and safety laws and regulations. Although we have made and will continue to make expenditures to comply with environmental and health and safety requirements, these requirements are constantly evolving, and it is impossible to predict whether compliance with these laws and regulations may have a material adverse effect on us in the future. If a release of hazardous substances occurs on or from our properties or from any of our disposals at offsite disposal locations, or if contamination is discovered at any of our current or former properties, we may be held liable, and the amount of such liability could be material.

Our ability to operate efficiently may be impaired if we lose key personnel.Our operations and the integration of our new European operations are dependent upon our ability to attract and retain qualified employees in the areas of finance, accounting, engineering, operations and management, and are greatly influenced by the efforts and abilities of our executive officers. We have employment agreements with several executive officers. We do not maintain key-person life insurance coverage on our executives.

Certain key personnel have the opportunity to return to ArcelorMittal for up to two years after the closing of the Arcelor Transaction. If a significant number of these individuals exercise this right, our ability to operate our European business could be significantly impaired. The operation of our new European business and the integration of this business with other operations depends significantly upon our ability to attract and retain qualified employees in the areas of finance, accounting, engineering, operations and management. Each key employee of our European business, as well as approximately 29 other employees, will have the opportunity to return to ArcelorMittal following the closing of the Arcelor Transaction for up to two years. ArcelorMittal has agreed not to solicit our employees, but we cannot prevent these 34 employees from returning to ArcelorMittal. If a significant number of these executives elect to return to ArcelorMittal, our ability to operate the European business and to integrate its operations with our other operations could be significantly impaired. We will be dependent on management in the various countries where the European facilities are located for their

12

Table of Contents

customer contacts and their knowledge and experience, including their knowledge about local regulations and business customs. Loss of these executives could adversely affect our revenues in these countries.

Our European business is dependent upon ArcelorMittal for various support functions including contract manufacturing, invoicing, collections, payroll, and other human resources functions. In addition, we are dependent upon ArcelorMittal for information technology support for up to four years after theclosing of the Arcelor Transaction. The operations of our European business could be disrupted if there are problems in the provision of these support services.Because our European business has not been operated as a stand-alone business, we have entered into a number of agreements with ArcelorMittal providing for ArcelorMittal to provide support services to the European business for up to three years after closing of the Arcelor Transaction and four years for certain information technology products and services. ArcelorMittal provides payroll, human resources, administration, information technology, purchasing and other support services. We believe that these arrangements will facilitate the integration of the European business by allowing us to transition these various functions away from ArcelorMittal over a period of time. Currently, we do not have the personnel or other resources to perform all of these functions internally. If ArcelorMittal experiences problems in providing these support services or materially defaults under these agreements, we would be required to make alternative arrangements. Our net sales could be adversely affected, and our expenses could increase if we are required to assume these support functions earlier than projected.

We are exposed to risks related to our reliance on our business relationship with ArcelorMittal. ArcelorMittal has granted us a royalty-free, perpetual exclusive license to certain patents and intellectual property used in our European business. The exclusivity of this license will lapse, and the license will continue on a non-exclusive basis, upon the latter of: (1) the fifth anniversary of the closing of the Arcelor Transaction; and (2) the date ArcelorMittal and its affiliates own fewer than 4,687,500 shares of our common stock. Both the limited time of exclusivity and any sale of ArcelorMittal’s shares are outside of our control. The loss of this exclusivity could result in competitors obtaining licenses from ArcelorMittal that could enable them to compete more effectively with us and result in a reduction in our net sales.

Under a steel supply and services agreement, ArcelorMittal provides us, among other things, marketing, sales, after sales, credit risk, invoicing, collection and consulting services. We have only a small sales force in Europe. Under this agreement, Arcelor Auto serves as Noble’s sales representative and will promote the interests of our European business along with the interests of Arcelor Auto. If ArcelorMittal materially defaults on this agreement or otherwise fails to successfully sell our products, our net sales may be adversely affected.

We are heavily dependent upon ArcelorMittal meeting our quantity and quality demands with regard to flat-rolled carbon steel in Europe. If ArcelorMittal’s production of steel should be disrupted or should ArcelorMittal’s production processes generate greater than usual defective products, we could face difficulties in delivering our products on time, which could adversely affect our results of operations.

A change of control cannot occur unless ArcelorMittal transfers a significant portion of its shares of our common stock to third parties.As of the date of this Report, ArcelorMittal owns approximately 49.95% of the outstanding shares of our common stock, which gives ArcelorMittal substantial voting control to accept or reject a change in control proposal. The increase in ownership by ArcelorMittal is attributable to the fact that ArcelorMittal and our former chairman of the board and current director, Mr. Robert Skandalaris, executed and closed a sale option exercise agreement dated March 12, 2008 (“Exercise Agreement”), pursuant to which ArcelorMittal purchased 2,439,055 shares of our common stock held by Mr. Skandalaris. Moreover, as part of the Exercise Agreement, ArcelorMittal also has an option to purchase Mr. Skandalaris’ remaining 41,902 shares of our common stock. Unless ArcelorMittal transfers a significant portion of our common stock owned by it, it is not possible to effect a change of control without ArcelorMittal’s participation or approval, even if a change of control, such as a business combination at a premium to the trading price of our common stock, is in the best interests of our other stockholders. In addition, if ArcelorMittal were to convert the entire principal amount outstanding under the $50 million convertible subordinated note, ArcelorMittal would acquire up to an additional 19.9% of the outstanding shares of our common stock.

13

Table of Contents

The significant blocks of our common stock owned by ArcelorMittal could adversely affect the market price of our common stock.ArcelorMittal has registration rights pursuant to which they may require us to register their shares of our common stock for resale under the Securities Act of 1933. See “Item 1. Business: Post-Closing Developments Related to the Arcelor Transaction” and “Item 8. Financial Statements and Supplementary Data, Note 20—Subsequent Events.” Sales from time to time under the registration statements that we must file under the registration rights agreement could adversely affect the market price of our common stock. Moreover, the mere possibility of these sales could create an “overhang” that could adversely affect the market price of our common stock.

Certain provisions of our Certificate of Incorporation and Bylaws may inhibit changes in control not approved by the board of directors. These anti-takeover provisions include: (i) a prohibition on stockholder action through written consents; (ii) a requirement that special meetings of stockholders be called only by the board of directors; (iii) advance notice requirements for stockholder proposals and nominations and; (iv) limitations on the ability of stockholders to amend, alter or repeal the Bylaws. We are also afforded the protections of Section 203 of the Delaware General Corporation Law, which could have similar effects.

The inability to effectively manage risks associated with international operations could adversely affect our business.We operate international production facilities in Canada, Mexico, Europe, and Australia and joint ventures in China and India. Our business strategy may include the further continued expansion of international operations. As we expand our international operations, we will increasingly be subject to the risks associated with such operations, including: (i) fluctuations in currency exchange rates; (ii) compliance with local laws and other regulatory requirements; (iii) restrictions on the repatriation of funds; (iv) inflationary conditions; (v) political and economic instability; (vi) war or other hostilities; (vii) overlap of tax structures; and (viii) expropriation or nationalization of assets. The realization of any one or more of these risks could adversely affect our results of operations.

We cannot predict the effect that future sales of our common stock will have on the market price of our common stock. Sales of substantial amounts of our common stock, or the perception that such sales could occur, could adversely affect the market price of our common stock. Approximately 49.95% of the shares of common stock currently issued and outstanding are “restricted securities” as that term is defined under Rule 144 under the Securities Act of 1933, as amended (“Rule 144”) or “control securities” (as that term is used in Rule 144), and may not be sold unless they are registered or unless an exemption from registration, such as the exemption provided by Rule 144, is available. All of these restricted or control securities are currently eligible for resale pursuant to Rule 144, subject in most cases to the volume and manner of sale limitations prescribed by Rule 144.

Trading price volatility may adversely affect the market price of our common stock.The trading price of our common stock could be subject to significant fluctuations in response to, among other factors, variations in operating results, developments in the automotive industry, general economic conditions, fluctuations in interest rates and changes in securities analysts’ recommendations regarding our securities.

The failure of SET Enterprises, Inc. (“SET”) could have a material adverse affect on our financial condition. We currently hold $10.0 million face value of SET preferred stock and 4% of the issued and outstanding shares of SET common stock. The carrying values of our investments in SET’s preferred stock and common stock are zero as of December 31, 2007. In addition, we provide a $3.0 million guarantee of SET’s senior debt. This guarantee is reduced $0.5 million on a quarterly basis beginning in the first quarter 2008 if SET is in compliance with its debt covenants. The failure of SET’s business could materially adversely affect our financial condition if it resulted in SET’s inability to pay dividends or repay its senior debt resulting in our requirement to perform under the guarantee. In addition, our relationship with SET provides minority content in product sold to certain OEMs. These OEMs use a supplier’s percentage of minority content as a consideration when awarding new business. To the extent that we could not replace minority content provided by SET with content from another minority business enterprise, the failure of SET could affect the future award of new business.

14

Table of Contents

| Item 1B. | Unresolved Staff Comments |

None.

| Item 2. | Properties |

We operate production facilities worldwide which are used for multiple purposes and range in size from 23,000 square feet to 524,000 square feet, with an aggregate of 2.7 million square feet. Our corporate headquarters are located in Troy, Michigan. None of our facilities, with the exception of the former Pullman headquarters that we are currently seeking to sublease, are materially underutilized. We believe that all of our property and equipment, owned or leased, is in good, working condition, is well maintained and provides sufficient capacity to meet our current and expected manufacturing and distribution needs.

The following table presents the locations of our facilities and the operating segments that use such facilities:

Property Location | ||

Corporate Headquarters, Troy, Michigan | Leased | |

Former Pullman Headquarters, Troy, Michigan | Leased | |

North America Segment | ||

Brantford, Ontario Canada | Leased | |

Butler, Indiana | Leased | |

Holt, Michigan | Owned | |

Queretaro, Mexico | Owned | |

Puebla, Mexico | Leased | |

Shelbyville, Kentucky | Leased | |

Silao, Mexico | Owned | |

South Haven, Michigan (East) | Leased | |

South Haven, Michigan (West) | Leased | |

Spring Lake, Michigan | Owned | |

Stow, Ohio | Leased | |

Tonawanda, New York | Leased | |

Warren, Michigan | Leased | |

Europe and Rest of World Segment | ||

Adelaide, Australia | Leased | |

Birmingham, United Kingdom | Leased | |

Bremen, Germany | Owned | |

Genk, Belgium | Leased | |

Gent, Belgium | Owned | |

European Headquarters, Merelbeke, Belgium | Leased | |

Lorraine, France | Leased | |

European Sales Office, St. Denis, France | Leased | |

Senica, Slovakia | Leased | |

Zaragoza, Spain | Owned | |

| Item 3. | Legal Proceedings |

We are a party to several routine litigation proceedings incidental to our business, none of which would have a material adverse effect on our financial condition, business or operations.

| Item 4. | Submission of Matters to a Vote of Security Holders |

No matter was submitted to a vote of security holders during the fourth quarter of the fiscal year covered by this Report.

15

Table of Contents

| Item 5. | Market for the Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities |

Market Information

Our common stock is traded on the NASDAQ Global Select Market under the symbol NOBL. The following table sets forth the range of high and low closing prices, as adjusted for the three-for-two stock split effective on February 3, 2006, for our common stock for each period indicated:

| Price Range of Common Stock | ||||||

| High | Low | |||||

Year Ended December 31, 2007 | ||||||

Fourth Quarter | $ | 21.74 | $ | 14.64 | ||

Third Quarter | 22.60 | 17.70 | ||||

Second Quarter | 20.52 | 16.29 | ||||

First Quarter | 20.12 | 16.67 | ||||

Year Ended December 31, 2006 | ||||||

Fourth Quarter | $ | 20.37 | $ | 12.56 | ||

Third Quarter | 15.61 | 12.16 | ||||

Second Quarter | 16.80 | 13.31 | ||||

First Quarter | 17.62 | 12.74 | ||||

As of March 11, 2008, there were approximately 51 record holders and approximately 1,463 beneficial owners of our common stock.

Dividends

During the years ended December 31, 2007 and 2006, we paid dividends on a quarterly basis in the annual aggregate amount of $6.0 million and $4.3 million, respectively. In May 2006, our Board of Directors approved a resolution to increase the quarterly cash dividend to $0.08 per share. There are no restrictions that currently limit our ability to pay, or that we believe are likely to limit the future payment of, ordinary dividends to our equity holders. On a periodic basis, we will reassess our dividend policy depending upon our financial condition and liquidity needs.

Performance Graph

Notwithstanding anything to the contrary set forth in any of our previous filings with the SEC that might incorporate future filings or this Report, the following performance graph and accompanying data shall not be deemed to be incorporated by reference into any such filings. In addition, such information shall not be deemed to be “soliciting material” or “filed” with the SEC.

16

Table of Contents

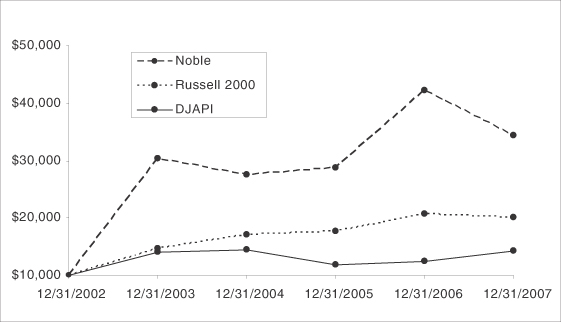

The following graph demonstrates the cumulative total return, on an indexed basis, to the holders of our common stock in comparison with the Russell 2000 Index and the Dow Jones Auto Part Index (“DJAPI”). We selected the DJAPI because the companies included therein are engaged in either the manufacturing of motor vehicles or related parts and accessories.

The graph assumes $10,000 invested on December 31, 2002 in our common stock, in the Russell 2000 Index and the DJAPI. The historical performance shown on the graph is not necessarily indicative of future price performance.

Total Shareholder Return

| 12/31/2002 | 12/31/2003 | 12/31/2004 | 12/31/2005 | 12/31/2006 | 12/31/2007 | |||||||||||||

Noble | $ | 10,000 | $ | 30,336 | $ | 27,500 | $ | 28,613 | $ | 42,122 | $ | 34,265 | ||||||

Russell 2000 | $ | 10,000 | $ | 14,537 | $ | 17,008 | $ | 17,573 | $ | 20,561 | $ | 19,996 | ||||||

DJAPI | $ | 10,000 | $ | 13,948 | $ | 14,411 | $ | 11,899 | $ | 12,496 | $ | 14,129 | ||||||

Securities Authorized for Issuance Under Equity Compensation Plans

For information regarding our equity compensation plans see “Item 12. Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters.”

Sales of Unregistered Securities

For information regarding the sale of unregistered shares of our securities, see “Item 1. Business” and “Item 8. Financial Statements and Supplementary Data; Note 2—Earnings (Loss) Per Share”; and “Note 20—Subsequent Events.”

17

Table of Contents

| Item 6. | Selected Financial Data |

The following selected financial data as of and for each of the five fiscal years in the period ended December 31, 2007 is derived from our audited financial statements and should be read in conjunction with the consolidated financial statements and notes thereto included elsewhere herein or in prior filings. See “Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

| Year Ended December 31, | ||||||||||||||||

| 2007 | 2006 | 2005 | 2004 | 2003 | ||||||||||||

| (in thousands, except per share data) | ||||||||||||||||

Consolidated Statements of Operations | ||||||||||||||||

Net sales | $ | 872,096 | $ | 441,372 | $ | 363,820 | $ | 332,611 | $ | 183,759 | ||||||

(Loss) income from continuing operations | (6,860 | ) | 7,779 | 5,093 | 15,351 | 9,135 | ||||||||||

(Loss) income per common share from continuing operations | (0.40 | ) | 0.55 | 0.37 | 1.05 | 0.78 | ||||||||||

Consolidated Balance Sheets | ||||||||||||||||

Total assets | 803,691 | 387,148 | 209,319 | 182,478 | 142,983 | |||||||||||

Total debt | 291,701 | 143,679 | 41,280 | 38,625 | 52,999 | |||||||||||

Dividends declared and paid per share | 0.32 | 0.31 | 0.27 | 0.27 | 0.21 | |||||||||||

Non-GAAP Financial Measures

This information is not and should not be viewed as a substitute for financial measures determined under accounting principles generally accepted in the United States (“GAAP”). Other companies may calculate these non-GAAP financial measures differently. The metric of earnings from continuing operations before income taxes, depreciation and amortization (“EBITDA”) adjusted for other non-cash items (“Adjusted EBITDA”) is not presented as, and should not be considered, an alternative measure of operating results or cash flows from operations (as determined in accordance with GAAP), but is presented because it is a widely accepted financial indicator of a company’s operating performance. While commonly used, however, EBITDA is not identically calculated by companies presenting EBITDA and is, therefore, not necessarily an accurate means of comparison, and may not be comparable to similarly titled measures disclosed by our competitors. We believe that Adjusted EBITDA is useful to both management and investors in their analysis of our operating performance. Furthermore, we use Adjusted EBITDA for planning and forecasting in future periods. The reconciliation of Adjusted EBITDA to (loss) income from continuing operations before income taxes, minority interest and equity loss is as follows:

| Year Ended December 31, | ||||||||||||||||||

| 2007 | 2006 | 2005 | 2004 | 2003 | ||||||||||||||

| (in thousands) | ||||||||||||||||||

(Loss) income from continuing operations before income taxes, minority interest and equity loss | $ | (7,196 | ) | $ | 12,775 | $ | 10,645 | $ | 21,669 | $ | 13,807 | |||||||

Depreciation expense | 27,312 | 11,781 | 10,063 | 9,366 | 6,987 | |||||||||||||

Amortization expense | 3,346 | 660 | 255 | 338 | 200 | |||||||||||||

Net interest expense | 15,971 | 4,498 | 2,234 | 3,196 | 1,823 | |||||||||||||

Stock compensation expense | 607 | 333 | 367 | 228 | 427 | |||||||||||||

Net loss (gain) on derivative instruments | 3,047 | 600 | — | (2,458 | ) | — | ||||||||||||

Loss on extinguishment of debt | 3,285 | — | — | — | — | |||||||||||||

Impairment (recovery) charges | — | (1,000 | ) | 10,140 | 129 | — | ||||||||||||

Adjusted EBITDA | $ | 46,372 | $ | 29,647 | $ | 33,704 | $ | 32,468 | $ | 23,244 | ||||||||

18

Table of Contents

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations |

The following management’s discussion and analysis of financial condition and results of operations should be read in conjunction with our consolidated financial statements and notes thereto, and the other information included in this Report. See “Item 8. Financial Statements and Supplementary Data.”

General

We are a full-service provider of21st Century Auto Body Solutions® primarily to the automotive industry. Our fiscal year is the calendar year. Customers include OEMs, such as General Motors, Chrysler, Ford, Honda, Volkswagen, Nissan, Renault and Peugeot, as well as other OEMs and companies which are suppliers to OEMs. We, as a Tier I and Tier II supplier, provide prototype, design, engineering, laser welded blanks and tubes, roll-formed products and other automotive component services.

Results of Operations

Fiscal 2007 vs. Fiscal 2006

Net Sales. Net sales increased $430.7 million, or 97.6%, to $872.1 million for the year ended December 31, 2007 from $441.4 million for the year ended December 31, 2006. This $430.7 million increase in net sales was driven primarily by the Pullman acquisition in the fourth quarter of 2006 and the Arcelor Business acquisition in the third quarter of 2007. Incremental 2007 net sales from the Pullman and Arcelor Business acquisitions were $218.3 million and $190.3 million, respectively. The remaining $22.1 million increase in 2007 net sales was driven primarily by $25.0 million of increased steel pass-through pricing for several laser-welding programs. The $2.9 million decrease in non-steel net sales was driven by lower North American light vehicle production (1.4% decline) and lower sales at our Shelbyville, KY facility driven by the discontinuation of the Saturn Ion vehicle by General Motors and the transfer of production of the Saturn Vue vehicle by General Motors to another supplier in Mexico. This decrease in net sales was offset by new programs including the Ford Edge program in our Stow, OH and Tonawanda, NY facilities, the full year volume impact of the GM Holden Commodore program in our Australia facility and the launch of the Dodge Grand Caravan program in our Stow, OH facility.

Cost of Sales. Cost of sales increased $411.7 million, or 102.2%, to $814.7 million for the year ended December 31, 2007 from $402.9 million for the year ended December 31, 2006. This $411.7 million increase in cost of sales was driven primarily by the Pullman acquisition in the fourth quarter of 2006 and the Arcelor Business acquisition in the third quarter of 2007. Incremental 2007 cost of sales from the Pullman and Arcelor Business acquisitions were $208.2 million and $178.8 million, respectively. The remaining $24.7 million increase in 2007 cost of sales was driven primarily by an increase in the cost of steel due to the increased steel pass-through pricing for several laser-welding programs. As a percentage of net sales, cost of sales increased to 93.4% in fiscal 2007 from 91.3% in 2006. This increase in cost of sales as a percentage of sales in 2007 was driven primarily by approximately $13.0 million in costs pursuant to the launch of several new roll-forming programs including the Buick Enclave program in our South Haven (East), MI facility.

Gross Margin. Gross margin increased $19.0 million, or 49.4%, to $57.4 million for the year ended December 31, 2007 from $38.4 million for the year ended December 31, 2006. This $19.0 million increase in gross margin was driven primarily by the Pullman acquisition in the fourth quarter of 2006 and the Arcelor Business acquisition in the third quarter of 2007. Incremental 2007 gross margin from the Pullman and Arcelor Business acquisitions was $10.2 million and $11.5 million, respectively. The remaining $2.7 million decline in gross margin was driven primarily by the $2.9 million decrease in non-steel net sales from 2006 to 2007. As a percentage of net sales, gross margin declined to 6.6% in fiscal 2007 compared to 8.7% in 2006.

Selling, General and Administrative Expenses. Selling, general and administrative expenses (“SG&A”) increased $22.2 million, or 100.7%, to $44.3 million for the year ended December 31, 2007 from $22.1 million for the year ended December 31, 2006. This $22.2 million increase in SG&A was driven primarily by the

19

Table of Contents

Pullman acquisition in the fourth quarter of 2006 and the Arcelor Business acquisition in the third quarter of 2007. Incremental 2007 SG&A from the Pullman and Arcelor Business acquisitions were $9.7 million and $9.2 million, respectively. The remaining $3.3 million increase in SG&A was driven primarily by additional headcount to support our growth ($2.2 million), incremental audit, tax and legal fees to support our larger organization ($0.8 million), and fees associated with the bank covenant waiver process for our U.S. and Canadian Credit Facility ($0.3 million). As a percentage of sales, SG&A increased to 5.1% in fiscal 2007 from 5.0% in fiscal 2006.

Operating Profit. As a result of the foregoing factors, operating profit decreased $3.2 million, or 19.9%, to $13.1 million for the year ended December 31, 2007 from $16.3 million for the year ended December 31, 2006. As a percentage of sales, operating profit decreased to 1.5% in fiscal year 2007 from 3.7% in fiscal year 2006.

Interest Income. Interest income decreased $0.8 million to $0.4 million for the year ended December 31, 2007 from $1.2 million for the year ended December 31, 2006. Interest income in 2006 was driven by cash invested in the first three quarters of 2006. In the fourth quarter of 2006, this cash was used to consummate the Pullman acquisition. Interest income in 2007 primarily relates to cash invested by our non-U.S. facilities.

Interest Expense. Interest expense increased $10.6 million to $16.3 million for the year ended December 31, 2007 from $5.7 million for the year ended December 31, 2006. The higher interest expense was primarily driven by incremental interest costs related to additional debt incurred pursuant to the Pullman acquisition ($9.2 million) and the Arcelor Business acquisition ($3.0 million) offset by lower amortization of fees and a debt discount in 2007 on the convertible subordinated notes ($1.6 million).

Net Loss on Derivative Instruments. During 2007, we entered into two derivative transactions which were contingent upon the Arcelor Business acquisition. We determined that while our contingent derivative instruments provided significant economic hedges, they did not qualify for hedge accounting treatment. Accordingly, we recorded a net loss on these derivative instruments of $3.0 million for the year ended December 31, 2007. In October 2006, pursuant to Statement of Financial Accounting Standards No. 133, “Accounting for Derivative Instruments and Hedging Activities,” (“SFAS 133”) and based upon provisions included in the $32.5 million convertible subordinated notes, we bifurcated a conversion option and established the fair value of an embedded derivative separate from the debt instrument and recorded it as a derivative liability. At issuance, the initial fair value of the embedded derivative liability was $5.6 million, which was recorded as a discount to the convertible subordinated notes. This derivative liability was adjusted for changes in fair value from the date of the amendment in October 2006 to December 31, 2006, and we recognized a net loss on derivative instruments of $0.6 million.

Loss on Extinguishment of Debt. We recognized a loss on extinguishment of debt of $3.3 million for the year ended December 31, 2007 related to an amendment of our $32.5 million convertible subordinated notes.

Impairment Recovery (Charges). Impairment recovery (charges) in 2006 include the reversal of a $1.0 million credit reserve on the Logistics Notes established in 2005 due to the full collection of amounts owed in 2006.

Other, Net. Other income increased $1.5 million to $2.0 million for the year ended December 31, 2007 from $0.5 million for the year ended December 31, 2006. Other income for the year ended December 31, 2007 primarily included dividend income and management fees from SET ($2.8 million), commission income from our joint venture in Shanghai, China ($0.3 million) offset by foreign currency losses ($1.1 million). Other income for the year ended December 31, 2006 was comprised primarily of a $0.5 million gain from the reversal of a potential liability favorably resolved at our Mexican operations.

Income Tax (Benefit) Expense. Income tax benefit was $3.4 million for the year ended December 31, 2007. Income tax expense was $3.9 million for the year ended December 31, 2006. The effective tax rate implicit in the

20

Table of Contents