Under Sarbanes-Oxley Section 404, as implemented by the SEC and PCAOB, we were required to provide an initial management assessment on our internal control over financial reporting for fiscal 2007 and we have complied with that requirement in this Form 10-K.

Under current rules, we will be required to provide an auditors’ attestation on our internal controls for fiscal 2008. However, the SEC has recently proposed extending the deadline for that requirement so that, as long as we are a non-accelerated filer measured at June 30, 2008, we would not be required to comply with the auditor’s attestation requirement until fiscal 2009. We cannot assure you that, in the course of completing the work to satisfy the auditors’ attestation requirement, we or our auditors will not detect a material weakness in our internal control over financial reporting or that we can satisfactorily comply with the attestation requirement.

Schools and clinicians that use our products frequently use students’ names to register them in our products and enter into our database academic, diagnostic and/or demographic information about the students. In addition, the results of student use of our products are uploaded to our database. We have designed our system to safeguard this personally-identifiable information, but the protection of such information is an area of increasing public concern and significant government regulation, including but not limited to the Children’s Online Privacy Protection Act. If our privacy protection measures prove to be ineffective, we could be subject to liability claims for unauthorized access to or misuses of personally-identifiable information stored in our database. We may also face additional expenses to analyze and comply with increasing regulation in this area.

United States public schools are funded primarily through state and local tax revenues, which are devoted primarily to school building costs, teacher salaries and general operating expenses. Public schools also receive funding from the federal government through a variety of federal programs, many of which target children who are poor and/or are struggling academically. Federal funds typically are restricted to specified uses.

We believe that the funding for a substantial portion of our K-12 sales comes from federal funding, in particular IDEA (special education) and Title One funding. The current federal budget deficit and competing federal priorities may impact the availability of federal education funding. A cutback in federal education funding could have a materially adverse impact on our revenue.

State and local school funding can be significantly impacted by fluctuations in tax revenues due to changing economic conditions. States are forecasting shortfalls in their tax revenues for fiscal 2009, because of the existing housing slump and a potential recession in the nationwide economy. While education spending remains an important priority for states, it faces competition from demands for relief for homeowners, transportation spending and rising health care costs. An economic downturn leading to a significant reduction in state tax revenues could have a materially adverse impact on our revenue.

The availability of funding for instructional products like ours can also be affected by unpredictable events, such as increases in energy costs or damage due to severe weather. We believe that severe storms and spiking energy costs adversely impacted our sales in 2005. Unpredictable events of similar magnitude could adversely impact our revenue in the future.

The market in which we operate is very competitive. While our products are highly differentiated by their neuroscience basis and their focus on improving brain processing efficiency and developing cognitive skills, we nevertheless compete vigorously for the funding available to schools. We compete not only against other software-based reading intervention products but also against print and service-based offerings from other companies and against traditional methods of teaching language and reading. Many of the companies providing these competitive offerings are much larger than we are, are more established in the school market than we are, offer a broader range

of products to schools, and have greater financial, technical, marketing and distribution resources than we do. Encouraged by the No Child Left Behind Act, new competitors may enter our market segment and offer actual or claimed results similar to those achieved by our products. In addition, although traditional approaches to language and reading are fundamentally different from our approach, the traditional methods are more widely known and accepted and, therefore, represent significant competition for available funds.

If we lose key personnel or are unable to hire additional qualified personnel as necessary, we may not be able to achieve our business goals, which could materially and adversely affect our financial results and share price.

We depend on the performance of our senior management, sales, marketing, development, research, educational, finance and other administrative personnel with extensive experience in our industry and with our Company. The loss of key personnel could harm our ability to execute our business strategy, which could adversely affect our financial results and share price. In addition, we believe that our future success will depend in large part on our continued ability to identify, hire, retain and motivate highly skilled employees who are in great demand. We cannot assure you that we will be able to do so.

Our current liquidity resources may not be sufficient to meet our needs.

We believe that cash flow from operations will be our primary source of funding for our operations during 2008 and the next several years. In 2007 and 2006, we generated $6.1 million and $4.3 million, respectively, in cash from operating activities. We ended 2007 with $21.2 million in cash and cash equivalents. We expended $10.7 million in cash in connection with the acquisition of the Reading Assistant product line.

In addition, we have a line of credit with Comerica Bank totaling $5.0 million, which expires on December 30, 2008. At December 31, 2007 no borrowings were outstanding and we were in compliance with the covenants of that line.

Funding our liquidity needs out of cash flow from operations will require us to achieve certain levels of booked sales and expenses. If we are unable to achieve sufficient levels of cash flow from operations, or are unable to obtain waivers or amendments from Comerica in the event we do not comply with our covenants, we would be required either to obtain debt or equity financing from other sources, or to reduce expenses. Reducing our expenses could adversely affect our operations by reducing the resources available for sales, marketing, research or development efforts. We cannot assure you that we will be able to secure additional debt or equity financing on acceptable terms, if at all.

If we are unable to maintain our access to the intellectual property rights that we license from third parties, our sales and net income will be materially and adversely affected.

Our most important products are based on licensed inventions owned by the University of California and Rutgers, the State University of New Jersey. In 2007, we generated approximately 78% of our booked sales from products that use this licensed technology. If we were to lose our rights under these licenses (whether through expiration of our exclusive license period, expiration of the underlying patent’s exclusivity, invalidity or unenforceability of the underlying patents, a breach by us of the terms of the license agreements or otherwise), such a loss of these licensed rights or a requirement that we must re-negotiate these licenses could materially harm our booked sales, our revenue and our net income.

If we are unable to adequately protect our intellectual property rights or if we infringe on the rights of others, we could become subject to significant liabilities, need to seek licenses or lose our rights to sell our products.

Our ability to compete effectively depends in part on whether we are able to maintain the proprietary aspects of our technology and to operate without infringing on the proprietary rights of others. It is possible that our issued patents will not offer sufficient protection against competitors with similar technology, that our trademarks will be challenged or infringed by competitors, or that our pending patent applications will not result in the issuance of patents. Issued patents can prove to be invalid or unenforceable as a result of a variety of reasons, including deficiencies in prosecution. As a result of potential deficiencies during the prosecution of certain patents to which we have rights, it is possible that these patents may be subject to a claim of unenforceability or invalidity. If others are able to develop similar products due to the expiration, unenforceability or invalidity of the underlying patents, the resulting competition could materially harm our booked sales, revenue and net income. The Company

Page 25

historically has not registered its copyrights in the United States, which may make it difficult to collect damages from a third party that may be infringing a Company copyright. The degree of future protection for our proprietary rights is also uncertain for products or product improvements in early-stage development, because it is difficult to predict from early-stage development efforts which product(s) will ultimately be marketed or what form the ultimately marketed product(s) will take.

In addition, we could become party to patent or trademark infringement claims, litigation or interference proceedings. These proceedings could result from claims that we are violating the rights of others or may be necessary to enforce our own rights. Any such proceedings would result in substantial expense and significant diversion of management effort, and the outcome of any such proceedings cannot be accurately predicted. An adverse determination in such proceedings could subject us to significant liabilities or require us to seek licenses from third parties, which may not be available on commercially reasonable terms or at all. In addition, competitors may design around our technology or develop competing technologies. Intellectual property rights may also be unavailable or limited in some foreign countries, which could make it easier for competitors to capture or increase their market share with respect to related technologies.

We generally require the execution of a written licensing agreement, which restricts the use and copying of our software products. However, if unauthorized copying or misuse were to occur to a substantial degree, our sales could be adversely affected.

Our common stock is thinly traded and its price is volatile.

Our common stock presently trades on the Nasdaq Global Market, and our trading volume is low. For example, for the last three months of 2007, our average daily trading volume was approximately 43,000 shares. The market price of our common stock has been highly volatile since we became publicly traded and could continue to be subject to wide fluctuations.

The ownership of our common stock is concentrated.

At December 31, 2007, Trigran Investments owned approximately 24% of our outstanding stock, and our executive officers and directors held approximately 15% of the outstanding stock. As a result, these stockholders are able to exercise significant influence over all matters requiring stockholder approval, including the election of directors and approval of significant corporate transactions, and may have interests that diverge from those of other stockholders. This concentration of ownership may also delay, prevent or deter a change in control of our company.

| |

ITEM 1B. | UNRESOLVED STAFF COMMENTS |

Not applicable

We lease approximately 30,500 square feet of office space in Oakland, California for our headquarters under a lease that expires in December 2013. The lease includes two five-year options to extend the term of the lease. We also lease approximately 2,500 square feet of office space in Tucson, Arizona for our support center under a lease that expires in 2009. In early 2008, we entered into a new lease for our Reading Assistant operations in Waltham, Massachusetts for approximately 6,000 square feet that expires in September 2011. We are currently evaluating our space requirements in Tucson, Arizona and may lease additional space in that area. We believe our other facilities are sufficient for our operations currently and should be adequate to meet our needs for at least the next two years.

Litigation with Former Sales Representative

On January 23, 2008, Robert G. (Jerry) Smith, a former account manager in Florida, filed a complaint against us in US District Court for the Middle District of Florida. The lawsuit claims breach of contract for unpaid wages of approximately $423,000. Smith alleges that he is owed additional commission relating to large sale transaction in the second quarter of 2007. We are in the early stages of this proceeding. Discovery has not yet started.

Page 26

Litigation with School District Customer

On October 22, 2007, we were sued by the Christina School District (the “District”) in the US District Court for the District of Delaware. The District had previously been sued by investors who are the assignees of the lessor under a Master Lease Purchase Agreement (the “Lease Agreement”) entered into by the District in 2003. The District ceased making payments under the Lease Agreement and the investors have claimed that the District breached the Lease Agreement. The District filed a third party complaint against us, claiming that we must refund amounts paid to us by the District for training and consulting under our contracts with the District. Because the District decided not to use our products, it did not therefore use all of the services specified in the contract. The third party complaint alleges unjust enrichment against us. The District states that the amount it is seeking is approximately $220,000. We have filed a motion to dismiss the complaint, which has not yet been decided.

We believe that these claims are not meritorious and that we do not have any significant liability to these claimants.. We therefore do not believe that the resolution of these matters will have a material adverse effect on our financial position or results of operations.

| |

ITEM 4 | SUBMISSION OF MATTERS TO A VOTE OF SECURITY HOLDERS |

None

Page 27

EXECUTIVE OFFICERS

The following table sets forth various information concerning our executive officers, as of March 10, 2008:

| | | | |

NAME | | AGE | | POSITION |

| |

| |

|

|

Robert C. Bowen | | 66 | | Chairman and Chief Executive Officer |

| | | | |

D. Andrew Myers | | 36 | | President and Chief Operating Officer |

| | | | |

Linda L. Carloni | | 54 | | Vice President, General Counsel and Corporate Secretary |

| | | | |

Glenn G. Chapin | | 52 | | Vice President, Sales |

| | | | |

Jane A. Freeman | | 54 | | Executive Vice President, Chief Financial Officer, and Treasurer |

| | | | |

| | | | |

Dr. William M. Jenkins | | 57 | | Sr. Vice President, Product Development |

| | | | |

Jessica Lindl | | 34 | | Vice President, Marketing |

| | | | |

Gillian A. McCormack | | 52 | | Vice President, Operations |

Robert C. Bowen joined us as Chairman and Chief Executive Officer in June 2002. From 1989 to 2001, he served as a senior executive and officer of National Computer Systems, a provider of educational assessment and administrative software and services. His last assignment there, from 1995 to 2001, was as President of NCS Education, a leading provider of enterprise software for K-12 school districts. NCS was acquired by Pearson, PLC, in 2000. After retiring from NCS in 2001, Mr. Bowen consulted for various businesses in education until joining us. Previously, Mr. Bowen held senior executive positions with other leading education and publishing companies, including seventeen years with McGraw-Hill. Early in his career, Mr. Bowen was a high school math teacher, a coach, and a school district administrator. Mr. Bowen received his bachelor’s and master’s degrees from the University of Tennessee, Chattanooga.

D. Andrew Myers joined us as President and Chief Operating Officer in January 2008. Prior to joining us, Mr. Myers worked at Pearson Education since 1997. His last position was as Senior Vice President, Digital Product Development for Pearson Curriculum, where he was responsible for integrating the technology teams from six preceding business units into a digital development group of 275 employees. From August 2004 to March 2007, Mr. Myers was the Chief Operations Officer for Pearson Digital Learning, where he was responsible for setting product, financial, technical and operational strategies for that 580-employee business unit. From 2002 to 2004, Mr. Myers served as Vice President Sales for Pearson Digital Learning. Mr. Myers started with Pearson as a sales representative in 1996. Pearson Education is the education division of Pearson PLC, an international media company. Mr. Myers holds an MBA from the Haas School of Business at the University of California Berkeley and a BA in finance from the University of Utah.

Linda L. Carloni joined the Company as General Counsel in October 1999, became our Secretary in March 2000 and was appointed Vice President in June 2000. Before joining us, Ms. Carloni was a founder and Vice President of Alere Medical Incorporated, a healthcare services start-up. Earlier in her career, Ms. Carloni worked in technology transfer for the University of California, was the general counsel of Nellcor Incorporated, a medical device company, and was an associate and a partner at the Cooley Godward law firm. She received her bachelor’s degree in political science from Case Western Reserve University and her law degree from Boalt Hall School of Law at the University of California, Berkeley.

Glenn G. Chapin joined the Company in April 2001 as Vice President of K-12 Sales. Mr. Chapin brings to his role with us more than 25 years experience working with schools to implement technology based curriculum and management systems that impact teaching and student learning. From 1995 to 2001, Mr. Chapin held sales executive positions at CompassLearning, completing his service there as the Southern Region Vice President. Prior to his post at CompassLearning, Mr. Chapin held sales executive positions at National Computer Systems, where he held positions of increasing responsibility over a 15 year period, from serving as the Midwest territory sales representative and rising

Page 28

to Southern Region Sales VP prior to his departure. Mr. Chapin is a graduate of St. John Fischer College in Rochester, New York where he received his Bachelor of Science degree in Business Administration.

Jane A. Freeman joined us as Vice President, Finance and Treasurer in August 1999 and was named Chief Financial Officer in January 2000. She was appointed Senior Vice President in January 2004 and Executive Vice President in December 2007. She also served as our Vice President Business Development from August 1999 until June 2000. Prior to joining us, Ms. Freeman spent 20 years in the investment business. From 1988 through 1998, she was employed by Rockefeller & Co., a global investment firm, where she led the global asset allocation process, managed the US Small Cap equity product and served on the Management Committee of the firm. She is a director of four mutual funds managed by Harding Loevner LLP. Ms. Freeman holds a B.A. in mathematics and chemistry and an M.B.A. (with distinction) from Cornell University and a License in Applied Economics from the University of Louvain in Belgium.

Dr. William M. Jenkins was appointed Senior Vice President, Product Development in November 2000. Dr. Jenkins is a founder and served as our Vice President, Product Development from June 1997 until November 2000. From March 1996 to June 1997, Dr. Jenkins was our Vice President, Research and Development. From 1990 to 1996, Dr. Jenkins was an Adjunct Associate Professor at the University of California, San Francisco. Dr. Jenkins is the principal developer of our current software products. Dr. Jenkins holds a B.S. in Psychology, an M.A. in Psychobiology and a Ph.D. in Psychobiology from Florida State University, with additional post-doctoral training from UCSF.

Jessica Lindl joined us as Vice President of Marketing in March 2007. Prior to joining us, Ms. Lindl served as Vice President of Marketing and Product Management for Riverdeep, a leading developer of educational software. Ms. Lindl held marketing management positions of increasing responsibility at Riverdeep and The Learning Company, which was acquired by Riverdeep, from 2001 through 2006. Prior to her tenure at Riverdeep, Ms. Lindl served as the Director of Product Management for Simplexis, an e-procurement provider for the K-12 market, in 2000 and 2001 and as part of the sales management team for AT&T in San Francisco from 1995 to 1998. Ms. Lindl holds a bachelor’s degree in economics and international studies from Miami University in Oxford, Ohio and an MBA from the Haas School of Business at the University of California, Berkeley.

Gillian A. McCormack joined us as Vice President, Operations in October 2002. Prior to joining us, Ms. McCormack had served as vice president of professional and technical services for NCS Learn (Pearson Education) beginning in 2000. From 1994 through 2000, she was the vice president of customer support for NovaNET, an E-learning company. Earlier in her career, Ms. McCormack worked in management and field positions at Jostens Learning, an educational software company. Ms. McCormack began her career as an elementary and middle school teacher and was a master of teacher training in Tucson, Arizona. She holds a bachelor of science in elementary education and a bachelor of science in special education and learning disabled K-12 from the University of Arizona.

Page 29

ITEM 5. MARKET FOR THE REGISTRANT’S COMMON EQUITY AND RELATED STOCKHOLDER MATTERS

(a) Market Information. Our common stock currently is, and during all of 2006 and 2007 was, traded on the NASDAQ Global Market under the symbol “SCIL”. (In 2006, the name of the market was changed from the NASDAQ National Market to the NASDAQ Global Market.)

The following table sets forth, for the periods indicated, the closing high and low sales prices per share of our common stock as reported on the NASDAQ Global Market.

| | | | | | | |

2006 | | High | | Low | |

First Quarter | | $ | 5.96 | | $ | 4.28 | |

Second Quarter | | $ | 5.20 | | $ | 3.91 | |

Third Quarter | | $ | 5.25 | | $ | 3.82 | |

Fourth Quarter | | $ | 6.09 | | $ | 4.44 | |

| | | | | | | |

2007 | | High | | Low | |

First Quarter | | | 7.72 | | | 5.28 | |

Second Quarter | | | 7.71 | | | 6.23 | |

Third Quarter | | | 7.95 | | | 5.19 | |

Fourth Quarter | | | 6.49 | | | 4.98 | |

Holders. As of January 31, 2008, the approximate number of stockholders of record of our common stock was 112.

Dividend Policy. We have never declared or paid cash dividends on our common stock, and we do not anticipate paying any cash dividends in the foreseeable future. Our current Loan and Security Agreement with Comerica Bank provides that we may not pay any dividends other than stock dividends during the term of the Agreement.

Securities Authorized for Issuance under Equity Compensation Plans. For information regarding securities authorized for issuance under equity compensation plans, see Item 12.

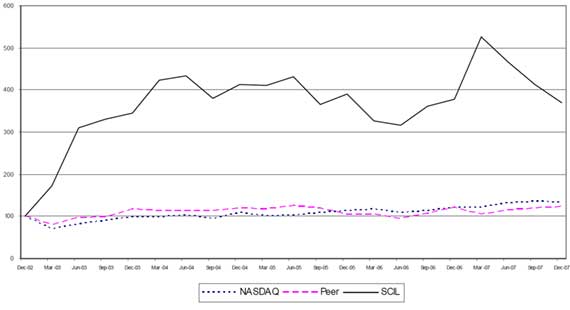

Performance Measurement Comparison.

The following chart compares the cumulative total stockholder return of Scientific Learning Common Stock for the five years ended December 31, 2007 with the cumulative total return during the same period of (i) the NASDAQ Composite Market Index and (ii) a Scientific Learning constructed peer group index. The companies in the peer group index were selected on the basis of similarity in the nature of their business. At December 31, 2007, the peer group included Plato Learning, Inc., Princeton Review, Renaissance Learning Inc., and Scholastic Corporation.

Over the last five years, the peer group has changed from time to time because of acquisitions, changes in business, and other changes affecting peer group companies. This table shows these changes:

| | |

Members of Peer Group | | Tenure in Peer Group |

| |

|

Excelligence | | Removed from peer group after September 30, 2006 after it stopped trading. |

| | |

Lightspan, Inc. | | Removed from peer group during 2003 upon its acquisition |

| | |

Riverdeep | | Removed from peer group during 2002 because its stock was moved from the Nasdaq to the Irish Stock Exchange |

| | |

Smart Force | | Removed from peer group during 2002 upon its acquisition |

| | |

Student Advantage | | Removed from peer group during 2002 when in the process of negotiating its sale |

| | |

Sylvan Learning Systems, Inc. | | Removed from peer group during 2003 because it changed the nature of its business. |

Page 30

The comparison assumes $100 was invested on December 31, 2002 in Scientific Learning Common Stock and in each of the foregoing indices. It also assumes reinvestment of dividends. The stock price performance shown in the graph below should not be considered indicative of potential future stock price performance.

Recent Sales of Unregistered Securities; Use of Proceeds from Registered Securities. Not applicable

(b) Not applicable

(c) Not applicable

Page 31

| |

ITEM 6. | SELECTED FINANCIAL DATA |

In thousands, except per share amounts

| | | | | | | | | | | | | | | | |

| | Year Ended December 31, | |

| | 2007 | | 2006 | | 2005 | | 2004 | | 2003 | |

| |

| |

| |

| |

| |

| |

Statement of Operations Data: | | | | | | | | | | | | | | | | |

Revenues: | | | | | | | | | | | | | | | | |

Products | | $ | 31,023 | | $ | 29,966 | | $ | 30,263 | | $ | 22,802 | | $ | 24,491 | |

Service and support | | | 15,030 | | | 11,032 | | | 10,056 | | | 8,174 | | | 5,425 | |

| |

|

| |

|

| |

|

| |

|

| |

|

| |

Total revenues | | | 46,053 | | | 40,998 | | | 40,319 | | | 30,976 | | | 29,916 | |

Cost of revenues: | | | | | | | | | | | | | | | | |

Products | | | 1,680 | | | 1,638 | | | 2,018 | | | 1,775 | | | 2,127 | |

Service and support | | | 8,539 | | | 7,897 | | | 5,637 | | | 4,981 | | | 3,872 | |

| |

|

| |

|

| |

|

| |

|

| |

|

| |

Total cost of revenues | | | 10,219 | | | 9,535 | | | 7,655 | | | 6,756 | | | 5,999 | |

| |

|

| |

|

| |

|

| |

|

| |

|

| |

Gross profit | | | 35,834 | | | 31,463 | | | 32,664 | | | 24,220 | | | 23,917 | |

| | | | | | | | | | | | | | | | |

Operating expenses: | | | | | | | | | | | | | | | | |

Sales and marketing | | | 24,868 | | | 21,073 | | | 17,619 | | | 16,087 | | | 12,961 | |

Research and development | | | 4,500 | | | 4,129 | | | 3,896 | | | 3,555 | | | 3,500 | |

General and administrative | | | 7,660 | | | 6,643 | | | 5,841 | | | 5,313 | | | 4,529 | |

Restructuring | | | — | | | — | | | — | | | — | | | (7 | ) |

| |

|

| |

|

| |

|

| |

|

| |

|

| |

Total operating expenses | | | 37,028 | | | 31,845 | | | 27,356 | | | 24,955 | | | 20,983 | |

| |

|

| |

|

| |

|

| |

|

| |

|

| |

Operating income (loss) | | | (1,194 | ) | | (382 | ) | | 5,308 | | | (735 | ) | | 2,934 | |

Other income from related party | | | 247 | | | 150 | | | 50 | | | 99 | | | 448 | |

Interest income (expense), net | | | 1,019 | | | 643 | | | 421 | | | (100 | ) | | (1,209 | ) |

| |

|

| |

|

| |

|

| |

|

| |

|

| |

| | | | | | | | | | | | | | | | |

Net income (loss) before income tax | | | 72 | | | 411 | | | 5,779 | | | (736 | ) | | 2,173 | |

Income tax provision (benefit) | | | (1,082 | ) | | 203 | | | 182 | | | (43 | ) | | 43 | |

| |

|

| |

|

| |

|

| |

|

| |

|

| |

Net income (loss) | | $ | 1,154 | | $ | 208 | | $ | 5,597 | | $ | (693 | ) | $ | 2,130 | |

| |

|

| |

|

| |

|

| |

|

| |

|

| |

| | | | | | | | | | | | | | | | |

Basic net income (loss) per share | | $ | 0.07 | | $ | 0.01 | | $ | 0.33 | | $ | (0.04 | ) | $ | 0.13 | |

| |

|

| |

|

| |

|

| |

|

| |

|

| |

| | | | | | | | | | | | | | | | |

Shares used in computing basic net income (loss) per share | | | 17,161 | | | 16,846 | | | 16,715 | | | 16,408 | | | 16,007 | |

| |

|

| |

|

| |

|

| |

|

| |

|

| |

Diluted net income (loss) per share | | $ | 0.06 | | $ | 0.01 | | $ | 0.31 | | $ | (0.04 | ) | $ | 0.13 | |

| |

|

| |

|

| |

|

| |

|

| |

|

| |

Shares used in computing diluted net income (loss) per share | | | 18,297 | | | 17,740 | | | 18,023 | | | 16,408 | | | 16,908 | |

| |

|

| |

|

| |

|

| |

|

| |

|

| |

| | | | | | | | | | | | | | | | |

Balance Sheet Data: | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

Cash and cash equivalents | | $ | 21,179 | | $ | 16,364 | | $ | 9,022 | | $ | 10,281 | | $ | 3,648 | |

Short-term investments | | | — | | | — | | | 3,043 | | | — | | | — | |

Working capital | | | 7,862 | | | 3,951 | | | 2,842 | | | (3,986 | ) | | (11,331 | ) |

Total assets | | | 33,803 | | | 26,283 | | | 18,734 | | | 22,958 | | | 15,597 | |

Stockholders’ equity (deficit) (1) | | | 5,820 | | | 1,017 | | | (1,835 | ) | | (8,111 | ) | | (8,544 | ) |

| |

(1) | We have paid no cash dividends since our inception. |

Page 32

ITEM 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITIONS AND RESULTS OF OPERATIONS

Overview

We develop and distribute the Fast ForWord family of software. Our patented products build learning capacity by rigorously and systematically applying neuroscience-based learning principles to improve the fundamental cognitive skills required to read and learn. Extensive outcomes research by independent researchers, our founding scientists, school districts and our company demonstrates the rapid and lasting gains achieved through Fast ForWord participation. Our products are marketed primarily to K-12 schools in the US, to whom we sell through a direct sales force. To facilitate the use of our products, we offer a variety of on-site and remote professional and technical services, as well as phone, email and web-based support. Since our inception, learners have used our Fast ForWord products over one million times and approximately 5,200 schools have purchased at least $10,000 of our Fast ForWord product licenses and services. As of December 31, 2007 we had 215 full-time equivalent employees, compared to 197 at December 31, 2006.

On January 7, 2008, we completed the acquisition of substantially all of the assets of Soliloquy Learning, including the Reading Assistant product, for $10.7 million in cash. The Scientific Learning Reading Assistant combines advanced speech recognition technology with scientifically based courseware to help students strengthen fluency, vocabulary and comprehension to become proficient life-long readers.

Business Highlights

We market our Fast ForWord products primarily as a reading intervention solution for struggling, at-risk, English Language Learners, and special education students. Approximately 70% of the estimated 55 million public and private school K-12 students in the United States test as not proficient in reading. While our installed base is growing, the approximately 5,200 schools that have purchased at least $10,000 of our product licenses and services represent a small fraction of the approximately 125,000 K-12 schools in the US.

Federal education funds are a critical resource in helping school districts address the needs of the most challenged learners. We believe that a significant proportion of our sales are funded by federal sources, particularly Title One and IDEA (special education) grants. In fiscal 2008, these programs are projected to total $25.4 billion. States are forecasting shortfalls in their taxation revenues for fiscal 2009 because of the existing housing slump and a potential recession in the nationwide economy. Such shortfalls would have an impact on education spending, although it is likely that education would remain among the top priorities.

Sales of our products are included in the growing supplemental education materials segment of the overall education materials market. Simba Information’s Publishing for the PreK-12 Market 2007 – 2008 (April 2007) estimates that:

| | |

| Ø | The total market for K-12 instructional materials is $8.58 billion, growing at 4.2% |

| | |

| Ø | The supplemental materials segment of that market is $4.29 billion |

| | |

| Ø | The fastest growing supplemental market, technology based electronic courseware, is $856 million and expected to grow 9.4% |

Company Highlights

In 2007 total revenue increased by 12% compared to 2006. This compares to an increase of 2% in 2006 compared to 2005. We attribute our revenue increase primarily to:

| | |

| • | Our improved sales capacity resulting from additional sales representatives hired in 2006 who became productive in 2007. |

| | |

| • | A continued focus within our sales organization on quickly closing transactions over $100,000, and on increasing the size of these transactions. |

Booked sales increased 16% in 2007 compared to 2006. Revenue increased at a slower rate than booked sales because in 2007 our sales mix contained a greater proportion of multiple year service and support offerings, where a significant amount of revenue is to be recognized in future periods, as compared to previous years. (For more explanation of booked sales, see Booked Sales and Selling Activity, below.)

We also experienced continued growth in our international sales, which increased 62% in 2007 compared to 2006, following an increase of 112% in 2006 compared to 2005. In 2007, international sales comprised approximately 2%

Page 33

of total sales, compared to 1.5% in 2006. We conduct our international business through value-added representatives (“VARs”). At December 31, 2007 we had 24 VARs selling in 42 countries.

We reported net income of $1.2 million in 2007, compared to net income of $0.2 million in 2006. The increase in net income is primarily due to an income tax benefit of approximately $1.2 million arising from the reduction of a portion of our deferred taxation valuation allowance.

During 2007 we introduced our Reading Progress Indicator service. While we are pleased with the initial results, the incremental revenue from this additional offering was not significant in 2007.

We ended 2007 with $21.2 million in cash and cash equivalents, and had no outstanding debt. We did not make use of our credit line during 2007. Net cash generated from operating activities was $6.1 million.

In January 2008 we completed the acquisition of the Soliloquy Reading Assistant product line and substantially all of the other assets of the Soliloquy Learning business, based in Waltham, Massachusetts, for cash consideration of $10.7 million. We estimate that as a direct result of this acquisition our revenue and our operating expenses in 2008 will increase.

Results of Operations

Revenues

| | | | | | | | | | | | | | | | |

| | Year Ended December 31, | |

| |

|

(dollars in thousands) | | 2007 | | Change | | 2006 | | Change | | 2005 | |

|

|

|

|

|

|

|

|

|

|

|

|

Products | | $ | 31,023 | | 4 | % | | $ | 29,966 | | -1 | % | | $ | 30,263 | |

Service and support | | | 15,030 | | 36 | % | | | 11,032 | | 10 | % | | | 10,056 | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total revenues | | $ | 46,053 | | 12 | % | | $ | 40,998 | | 2 | % | | $ | 40,319 | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2007 revenue compared to 2006: Product revenues, which comprise the majority of our revenue, increased modestly in 2007 compared to 2006. The growth in product revenues was slower than total revenues due to lower than expected product sales, and an increase in multiple year service and support packages which include a lower proportion of product revenue. In 2007 one customer accounted for more than 10% of our total revenue. On average 48% of booked sales in 2007 were recognized into revenue in the quarter in which the sale occurred.

Our service and support revenue increased significantly in 2007 compared to 2006 due to more services delivered and a higher number of schools on support. At December 31, 2007 we had approximately 32% more schools on support than at December 31, 2006. The increase in schools on support is mainly due to our success in selling renewals to our growing installed base.

2006 revenue compared to 2005: Product revenue declined in 2006 compared to 2005 because we recognized approximately $6.5 million less revenue from sales made in prior periods. This decrease was almost offset by increased revenue recognized on sales booked in 2006. On average 52% of booked sales in 2006 were recognized into revenue in the quarter in which the sale occurred.

Service and support revenue increased in 2006 by 10%, primarily due to stronger sales of on-site services, partially offset by a lower level of revenue recognized from sales made in prior years. Service and support revenue also reflected the increase in the number of schools purchasing ongoing Progress Tracker access and support contracts. We had 26% more customers on support at December 31, 2006 than at December 31, 2005.

Booked sales and selling activity: Booked sales is a non-GAAP financial measure that management uses to evaluate current selling activity. We believe that booked sales is a useful metric for investors as well as management because it is the most direct measure of current demand for our products and services. Booked sales equals the total value (net of allowances) of software, services and support invoiced in the period. Revenue on a GAAP basis is recorded for booked sales when all four of the requirements for revenue recognition have been met; if any of the requirements to recognize revenue are not met, the sale is booked to deferred revenue. We use booked sales information for resource allocation, planning, compensation and other management purposes. We believe that revenue is the most comparable GAAP measure to booked sales. However, booked sales should not be considered in isolation from revenue, and is not intended to represent a substitute measure of revenue or any other performance measure calculated under GAAP.

Page 34

The following reconciliation table sets forth our booked sales, revenues and change in deferred revenue for the twelve months ended December 31, 2007, 2006 and 2005:

| | | | | | | | | | | | | | | | |

| | Year Ended December 31, | |

(dollars in thousands) | | 2007 | | Change | | 2006 | | Change | | 2005 | |

|

Booked sales | | $ | 49,849 | | 16 | % | | $ | 43,154 | | 37 | % | | $ | 31,538 | |

Less revenue | | | 46,053 | | 12 | % | | | 40,998 | | 2 | % | | | 40,319 | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net increase/(decrease) in deferred revenue | | | 3,796 | | | | | | 2,156 | | | | | | (8,781 | ) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total deferred revenue end of period | | $ | 22,955 | | 20 | % | | $ | 19,159 | | 13 | % | | $ | 17,003 | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Booked sales in the K-12 sector, which accounted for over 91% of booked sales in 2007, increased 14% to $45.6 million compared to $40.2 million in 2006. Booked sales in the K-12 sector were $28.4 million in 2005.

We believe that the principal reasons for the increase in 2007 booked sales are:

| | |

| • | Our improved sales capacity resulting from additional sales representatives hired in 2006 who became productive in 2007. We had an average of 49 quota bearing sales representatives in 2007, compared to 42 in 2006. |

| | |

| • | A continued focus within our sales organization on quickly closing transactions over $100,000, and on increasing the size of these transactions. Our 2007 sales included one transaction for approximately $7.4 million. |

The increase in booked sales in 2007 was smaller than the increase that we experienced in 2006. The large increase in 2006 was mainly because sales in 2005 in several key states had been depressed due to severe weather conditions, spiking energy prices, and other factors that contributed to general funding uncertainty.

We believe large booked sales are an important indicator of mainstream education industry acceptance and an important factor in reaching our goal of increasing sales force productivity. In 2007 we continued to focus our sales force on multi-site sales, and we closed 90 transactions in excess of $100,000 compared to 102 in 2006 and 59 in 2005. Although we closed fewer large deals in 2007 than in 2006, the average size of these transactions increased substantially, from approximately $285,000 in 2006 to approximately $349,000 in 2007. The increase in average transaction size was mainly due to the impact of one transaction for approximately $7.4 million. For the year ended December 31, 2007, 69% of our K-12 booked sales were realized from sales over $100,000. For the comparable periods ending December 31, 2006 and 2005, large booked sales accounted for 67% and 59% of booked sales respectively.

Large booked sales include volume discounts but the percentage discount applicable to any given transaction will vary and the relative percentage of large sales and smaller sales in a given quarter may fluctuate. Because we discount product license fees but do not discount service and support fees, product booked sales and revenue are disproportionately affected by discounting. We cannot predict the size, number and timing of large transactions in the future.

Booked sales outside the K-12 market (primarily to the adult corrections market, private practice clinicians and international customers) increased by 40% in 2007 compared to 2006, mainly due to the impact of a large corrections sale. International sales increased by 62% in 2007 compared to 2006. Non K-12 sales in 2006 were flat relative to 2005.

Although federal, state and local budget pressures make for an uncertain funding environment for our customers, we are optimistic about our growth prospects in the K-12 market. However, achieving our booked sales growth objectives will depend on increasing customer acceptance of our products, which requires us to continue to focus on improving our products’ ease of use, their fit with school requirements, and our connection with classroom teachers and administrators. Our K-12 growth prospects are also influenced by factors outside our control including the overall level, certainty and allocation of state, local and federal funding. For a discussion of some of the other important factors that affect our results, see Risk Factors. In addition, the revenue recognized from our booked sales can be unpredictable. Our various license and service packages have substantially differing revenue recognition periods, and it is often difficult to predict which license package a customer will purchase, even when the amount and timing of a sale can be reasonably projected. See Management’s Discussion and Analysis – Application of

Page 35

Critical Accounting Policies for a discussion of our revenue recognition policy. In addition, the timing of a single large order or its implementation can significantly impact the level of booked sales and revenue at any given time.

Gross Profit and Cost of Revenues

| | | | | | | | | | |

| | Year Ended December 31, | |

(dollars in thousands) | | 2007 | | 2006 | | 2005 | |

|

Gross profit on products | | $ | 29,343 | | $ | 28,328 | | $ | 28,245 | |

Gross profit margin on products | | | 95 | % | | 95 | % | | 93 | % |

Gross profit on service and support | | | 6,491 | | | 3,135 | | | 4,419 | |

Gross profit margin on services and support | | | 43 | % | | 28 | % | | 44 | % |

|

|

|

|

|

|

|

|

|

|

|

Total gross profit | | $ | 35,834 | | $ | 31,463 | | $ | 32,664 | |

Total gross profit margin | | | 78 | % | | 77 | % | | 81 | % |

|

|

|

|

|

|

|

|

|

|

|

The overall gross profit margin improved slightly in 2007 compared to 2006. The increase in gross margin was driven primarily by increased service and support margins, partially offset by a reduction in the proportion of higher margin product revenue. Service and support revenue growth of 36%, combined with an 8% increase in service and support costs, resulted in an increase in the service and support gross margin from 28% to 43%. The main reasons for the increase in service and support gross margin were higher staff utilization and leverage from our new Tucson support center. Higher margin product revenues comprised 67% of total revenues in 2007 compared to 73% in 2006.

The overall gross profit margin declined in 2006 compared to 2005, as a small improvement in product margin was more than offset by a substantial decrease in services and support margin. Product margins improved primarily because capitalized software amortization, which was charged to product cost of revenue, ceased in June 2006. We also reduced costs by limiting the quantity of electronic media that we send to customers. Service and support margins declined from 2005 to 2006 primarily due to our investment in a new support center in Tucson, Arizona, which replaced an outside vendor. We also hired additional service staff in anticipation of increased service sales.

Operating Expenses

| | | | | | | | | | | | | | | | |

| | Year Ended December 31, | |

(dollars in thousands) | | 2007 | | Change | | 2006 | | Change | | 2005 | |

|

Sales and marketing | | $ | 24,868 | | 18 | % | | $ | 21,073 | | 20 | % | | $ | 17,619 | |

Research and development | | | 4,500 | | 9 | % | | | 4,129 | | 6 | % | | | 3,896 | |

General and administrative | | | 7,660 | | 15 | % | | | 6,643 | | 14 | % | | | 5,841 | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total operating expenses | | $ | 37,028 | | 16 | % | | $ | 31,845 | | 16 | % | | $ | 27,356 | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Sales and Marketing: Sales and marketing expenses consist principally of salaries and incentive compensation paid to employees engaged in sales and marketing activities, travel costs, tradeshows, conferences, and marketing and promotional materials. The increase in sales and marketing costs in 2007 compared to 2006 is mostly due to higher employee costs, as headcount has increased by 11% year over year, and also to increased spending on marketing initiatives such as trade shows and the use of marketing consultants, partially offset by reduced incentive compensation costs. In 2006, our sales and marketing expenses increased over 2005, primarily due to increased sales and marketing staff, more marketing activities and higher commissions reflecting higher booked sales. Commissions in 2006 were $1.3 million higher than in 2005. At December 31, 2007, we had 51 field-based quota-bearing sales personnel selling to public schools, compared to 44 and 36 at December 31, 2006 and 2005 respectively. We expect our sales and marketing expenses to increase at a low double digit rate in 2008.

Research and Development: Research and development expenses principally consist of compensation paid to employees and consultants engaged in research and product development activities and product testing, together with software and equipment costs. The increased costs for 2007 compared to 2006 are primarily due to higher outsourced development costs. Research and development expenses increased by 6% in 2006 due primarily to stock compensation expenses and patent acquisition legal fees. We expect research and development expenses to almost double in 2008 due to the addition of the Reading Assistant employees and the amortization of the acquired intangible assets.

Page 36

General and Administrative: General and administrative expenses principally consist of salaries and compensation paid to our executives, accounting staff and other support personnel, as well as travel expenses for these employees, and outside legal and accounting fees. The increase in 2007 expenses compared to 2006 is mostly due to the legal, accounting, printing and travel costs of approximately $688,000 related to our secondary stock offering. Stock compensation expense was also higher in 2007 than in 2006. These costs were partially offset by lower expenses for management incentive compensation. General and administrative expenses increased by 14% in 2006 due primarily to stock compensation expenses and incentive compensation expenses, partially offset by a reduction in accounting and legal fees relating to the restatement of financial results that were expensed in 2005. Accounting and legal fees associated with the restatement that were expensed in 2005 totaled approximately $380,000. We expect general and administrative expenses to increase modestly in 2008.

Other Income from Related Party

In September 2003, we signed an agreement with Posit Science Corporation (“PSC”), transferring our patented technology to PSC for use in the health field. During the twelve months ended December 31, 2007, 2006 and 2005 we recorded $247,000, $150,000, and $50,000 respectively, for royalties received and services provided to PSC. Amounts received to date and any future receipts are being reported as other income as we do not consider these royalties to be part of our recurring operations.

Interest and Other Income (Expense), net

| | | | | | | | | | | | | | | | |

| | Year Ended December 31, | |

(dollars in thousands) | | 2007 | | Change | | 2006 | | Change | | 2005 | |

|

Interest on invested cash | | | 680 | | 38 | % | | | 494 | | 104 | % | | | 242 | |

Reclassification of service revenue | | | 332 | | 132 | % | | | 143 | | NA | | | | — | |

Miscellaneous | | | 7 | | 17 | % | | | 6 | | -97 | % | | | 179 | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Interest and other income (expense), net | | $ | 1,019 | | 58 | % | | $ | 643 | | 53 | % | | $ | 421 | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

In 2007, interest and other income (expense), net, consisted primarily of interest earned on our invested cash of $680,000 and a reclassification of $332,000 of service and support revenue relating to two customers for whom we are no longer performing services. For 2006, interest and other income (expense), net, consisted primarily of interest earned of $494,000 and a reclassification of $143,000 of service and support revenue relating to the same two customers. In 2005, interest and other income (expense), net, comprised mainly interest earned on our invested cash of $242,000 and interest on officer loans of $170,000. All officer loans were repaid in full by March 31, 2006.

Income Tax Provision (Benefit)

During the fourth quarter of 2007, we recorded an income tax benefit of approximately $1.1 million. This benefit included a $1.2 million reduction in our deferred tax asset valuation allowance related to a portion of our deferred tax assets that will more likely than not be realized, based on future projected taxable income for fiscal 2008. Prior to the fourth quarter of 2007, we recorded a full valuation allowance against our deferred tax assets. These projections were based on one year of projected future taxable income.

As of December 31, 2007, we have U.S. federal and state net operating loss carryforwards of approximately $61.2 million and $46.5 million, respectively. The U.S. federal net operating loss carryforwards will expire at various dates beginning in 2018 through 2027 if not utilized. State net operating loss carryforwards will expire at various dates beginning in 2012 through 2017.

As of December 31, 2007, we had U.S. federal and state tax credit carryforwards of approximately $1.2 million and $0.9 million, respectively. The federal credit will expire at various dates beginning in 2011 through 2027, if not utilized. California state research and development credits can be carried forward indefinitely.

Net operating loss carryforwards and credit carryforwards reflected above are limited due to ownership changes as provided in the Internal Revenue Code and similar state provisions.

Page 37

Liquidity and Capital Resources

Our cash and cash equivalents and short-term investments were $21.2 million at December 31, 2007 compared to $16.4 million at December 31, 2006 and $12.1 million at December 31, 2005. At December 31, 2007 there were no borrowings outstanding under our credit line. In January 2008 we expended $9.7 million of our cash for the acquisition of the assets of Soliloquy Learning.

Net cash provided by operations in 2007 was $6.1 million, compared to cash provided by operations of $4.3 million in 2006 and $2.1 million used in operations in 2005. Overall, our receivable collection experience has remained strong throughout 2007. We collected $51.7 million of receivables in 2007, compared to $40.3 million of receivables in 2006 and $34.1 million in 2005.

Net cash used in investing activities in 2007 was $2.4 million, consisting of net purchases of property and equipment of $1.1 million, a loan to JTT Holdings of $1.0 million in connection with the January 2008 acquisition of Soliloquy Learning, and acquisition costs incurred of $319,000.

During the year ended December 31, 2006, we purchased an enterprise-wide customer relationship management system. As of December 31, 2007 and 2006, a net book value of $1.4 million and $463,000, respectively, related to the purchase and subsequent implementation of this system was included in property and equipment. These costs will be depreciated over the initial estimated useful life of five years.

Net cash generated by investing activities in 2006 was $2.4 million, consisting of the maturity of short-term investments of $3.0 million and officer loan repayments of $0.2 million, partially offset by property and equipment purchases of $0.8 million.

Net cash generated by investing activities in 2005 was $0.4 million, consisting of the purchase of $3.0 million of short-term investments and the purchase of hardware and software for $0.2 million, which were more than offset by the repayment of $3.6 million of officer loans.

Net cash generated by financing activities in 2007, 2006 and 2005 was $1.2 million, $0.6 million, and $0.5 million respectively. Net cash generated by financing activities in all three years resulted from the sale of stock upon option exercises and through purchases of stock through the employee stock purchase plan. There was no borrowing on our credit line in 2007 or 2006.

Because our booked sales tend to be seasonal, we may have negative cash flows in particular quarters, particularly the first quarter, when booked sales tend to be substantially lower than in other quarters.

On June 5, 2007 we amended our existing revolving line of credit agreement with Comerica Bank. The maximum that can be borrowed under the agreement is $5.0 million. The line expires on December 2, 2008. Borrowing under the line of credit bears interest at a floating prime rate, or a fixed rate of LIBOR plus 2.5%. To secure the line we granted Comerica a security interest in all of our assets other than our intellectual property. We also agreed with Comerica that we will not grant a security interest in our intellectual property to any third party. Borrowings under the line are subject to various covenants. The agreement includes a letter of credit sublimit not to exceed $1.0 million. At December 31, 2007, we have an outstanding letter of credit for $206,000. There were no borrowings outstanding on the line of credit at December 31, 2007 and we were in compliance with all our covenants.

We expect that cash flow from operations will continue to be our primary source of funds for the next several years. Again, this will require us to achieve certain levels of booked sales. If we are unable to achieve sufficient levels of cash flow from operations, we may seek other sources of debt or equity financing, or may be required to reduce expenses. Reducing our expenses could adversely affect our operations by reducing the resources available for sales, marketing, research or development efforts. We cannot assure you that we will be able to secure additional debt or equity financing on acceptable terms.

Off-Balance Sheet Arrangements

We have no off-balance sheet arrangements.

Page 38

Contractual Obligations and Commitments

We have a non-cancelable lease agreement for our corporate office facilities. The minimum lease payment is approximately $78,000 per month through 2008. After 2008 the base lease payment increases at a compound annual rate of approximately 5%. The lease expires in December 2013. We also have a lease agreement for our Tucson, Arizona office through April 2009 at an average rent of approximately $4,500 per month for the period subsequent to January 1, 2007. In early 2008, we entered into a new lease for our Reading Assistant operations in Waltham, Massachusetts for approximately 6,000 square feet that expires in September 2011. This lease, as well as the existing Waltham lease that expires on March 31, 2008, is included in the table under “operating lease obligations”.

We also make royalty payments to the institutions who participated in the original research that produced our initial products. Our minimum royalty payments are $150,000 per year.

The following table summarizes our obligations at December 31, 2007 and the effects such obligations are expected to have on our liquidity and cash flow in future periods.

| | | | | | | | | | | | | | | | | | | | | |

(dollars in thousands) | | 2008 | | 2009 | | 2010 | | 2011 | | 2012 and

thereafter | | Total | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Contractual Obligations: | | | | | | | | | | | | | | | | | | | |

Operating lease obligations | | $ | 1,143 | | $ | 1,142 | | $ | 1,171 | | $ | 1,183 | | | $ | 2,312 | | | $ | 6,951 | |

Purchase obligations | | | 150 | | | 150 | | | 150 | | | 150 | | | | 450 | | | $ | 1,050 | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total | | $ | 1,293 | | $ | 1,292 | | $ | 1,321 | | $ | 1,333 | | | $ | 2,762 | | | $ | 8,001 | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Our purchase order commitments at December 31, 2007 are not material

Effective January 1, 2007, we adopted the provisions of FASB Interpretation No. 48, “Accounting for Uncertainty in Income Taxes — an interpretation of FASB Statement No. 109.” At December 31, 2007, we had a liability for unrecognized tax benefits and an accrual for the payment of related interest totaling $25,000, of which approximately $3,000 is expected to be paid within one year. For the remaining liability, due to the uncertainties related to these tax matters, we are unable to make a reasonably reliable estimate when cash settlement with a taxing authority will occur. Refer to Note 10 to the Financial Statements for additional discussion on unrecognized tax benefits.

Loans to Current and Former Officers

In March 2001 we made full recourse loans to certain of our officers, in amounts totaling $3.1 million. In 2002 some of these officers left our Company. The notes were secured by shares of our Common Stock owned by the current and former officers. The loans bore interest at 4.94%. Principal and interest were due December 31, 2005. During the twelve months ended December 31, 2005 we received $3.6 million in loan repayments, including interest. At December 31, 2005 there was a remaining balance due of $297,000. This represented principal and interest from one of the former officers. During the first quarter of 2006 we received the balance due in the form of cash and stock.

Application of Critical Accounting Policies

Our financial statements are prepared in accordance with accounting principles generally accepted in the United States (“GAAP”). These accounting principles require us to make certain estimates, assumptions and judgments. We believe that the estimates, assumptions and judgments upon which we rely are reasonable based upon information available to us at the time. The estimates, assumptions and judgments that we make can affect the reported amounts of assets and liabilities as of the date of the financial statements, as well as the reported amounts of revenues and expenses during the periods presented. To the extent there are material differences between these estimates and actual results, our financial statements would be affected.

We believe that the estimates, assumptions and judgments pertaining to revenue recognition and allowance for doubtful accounts are the most critical assumptions to understand in order to evaluate our reported financial results. A detailed discussion of our use of estimates, assumptions and judgments as they relate to these polices is presented below. We have discussed the application of these critical accounting policies with the Audit Committee of the Board of Directors.

Page 39

Revenue Recognition

We derive revenue from the sale of licenses to our software and from service and support fees. Software license revenue is recognized in accordance with AICPA Statement of Position 97-2, “Software Revenue Recognition,” as amended by Statement of Position 98-9 (SOP 97-2). SOP 97-2 provides specific industry guidance and four basic criteria, which must be met to recognize revenue. These are: 1) persuasive evidence of an arrangement exists; 2) delivery of the product has occurred; 3) a fixed or determinable fee; and 4) the probability that the fee will be collected. The application of SOP 97-2 requires us to exercise significant judgment related to our specific transactions and transaction types.

Sales to our school customers typically include multiple elements (e.g., Fast ForWord software licenses, Progress Tracker, our Internet-based participant tracking service, support, training, implementation management, and other services). We recognize revenue using the residual method, whereby the difference between the total arrangement fee and the total “vendor specific objective evidence”(“VSOE”) of fair value of the undelivered elements is recognized as revenue relating to the delivered elements. VSOE of fair value for each element of an arrangement is based upon the normal pricing and discounting practices for those products and services when sold separately and, for support services, is also measured by the renewal price. We are required to exercise judgment in determining whether VSOE exists for each undelivered element based on whether our pricing for these elements is sufficiently consistent.

The value of software licenses, services and support invoiced during a particular period is recorded as deferred revenue until recognized. All revenue from transactions that include new products that have not yet been delivered is deferred until the delivery of all products. Deferred revenue is recognized as revenue as discussed below.

Multiple contracts with the same customer are generally accounted for as separate arrangements except in cases where contracts are so closely related that they are effectively part of a single arrangement.

Product revenue

Product revenue is primarily derived from the licensing of software and is recognized as follows:

| |

• | Perpetual licenses – software licensed on a perpetual basis. Revenue is recognized at the later of product delivery date or contract start date using the residual method. If VSOE does not exist for all the undelivered elements, all revenue is deferred and recognized ratably over the service period if the undelivered element is services or when all elements have been delivered. |

| |

• | Term licenses – software licensed for a specific time period, generally three to twelve months. Revenue is recognized ratably over the license term. |

| |

• | Individual participant licenses – software licensed for a single participant. Revenue is recognized over the average period of use, typically six weeks. |

Service and support revenue

Service and support revenue is derived from a combination of training, implementation, technical and professional services, online services and customer support. Training, technical and other professional services are typically sold on a per day basis. If VSOE exists for all elements of an arrangement or all elements except software licenses, services revenue is recognized as performed. If VSOE does not exist for all the elements in an arrangement except software licenses, service revenue is recognized over the longest contractual period in an arrangement. Revenue from services sold alone or with support is recognized as performed.

Allowance for Doubtful Accounts

We maintain an allowance for doubtful accounts for estimated losses due to the inability of customers to make payments. We adjust this allowance periodically based on our historical experience of bad debt write offs, which have been low in recent years. Cancellations and refunds are allowed in limited circumstances, and such amounts have not been significant.

Page 40

Income Taxes

We account for income taxes using the liability method, which requires the recognition of deferred tax assets or liabilities for the tax-effected temporary differences between the financial reporting and tax bases of our assets and liabilities, and for net operating loss and tax credit carryforwards. Prior to the fourth quarter of 2007, we recorded a full valuation allowance to reserve for the benefit of our deferred tax assets due to the uncertainty surrounding our ability to realize these assets.

During the fourth quarter of 2007, we recorded an income tax benefit of $1.1 million. This benefit included a $1.2 million reduction in the valuation allowance related to a portion of our deferred tax assets that will more likely than not be realized. This determination was primarily based on projected taxable income. In evaluating our ability to realize our deferred tax assets we consider all available positive and negative evidence including our past operating results and our forecast of future taxable income. In determining future taxable income, we make assumptions to forecast federal and state operating income, the reversal of temporary differences, and the implementation of any feasible and prudent tax planning strategies. These assumptions require significant judgment regarding the forecasts of future taxable income, and are consistent with the forecasts used to manage our business. We intend to maintain the remaining valuation allowance until sufficient further positive evidence exists to support further reversals of the valuation allowance. Our income tax expense recorded in the future will be reduced to the extent of offsetting decreases in our valuation allowance.

Stock-Based Compensation

Under the fair value recognition provisions of SFAS No. 123R, we use the Black-Scholes option valuation model to estimate stock-based compensation expense at the grant date based on the fair value of the award and recognize the expense ratably over the requisite service period of the award. Determining the appropriate fair value model and assumptions used in calculating the fair value of stock-based awards requires judgment, including estimating stock price volatility, forfeiture rates and expected life.

The estimated expected stock price volatility decreased from 80% in 2006 to 49% in 2007. Our expected stock price volatility is based upon our historical experience over the expected life of the options, and this decrease occurred as a result of historical periods beyond the expected life of the options containing highly volatile prices being eliminated from the fiscal 2007 volatility calculation.

In the fourth quarter of 2007 we changed our estimate of the forfeiture rate from 11% to 3.5%, based on our experience of actual forfeiture rates. This resulted in incremental stock compensation expense of approximately $316,000 in the fourth quarter. Stock compensation expense may be adjusted in the future if actual forfeiture rates differ significantly from our current estimates.

| |

ITEM 7A. | QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK |

Interest Rate Risk

Our exposure to market risk for changes in interest rates relates primarily to the rate of interest that we earn on our cash and cash equivalents. We did not hold any marketable debt securities at December 31, 2007. A hypothetical increase or decrease in market interest rates by 10% from the market interest rates at December 31, 2007 would not have a material affect on our results of operations.

Page 41

| |

ITEM 8. | FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA |

| |

| Report of Ernst & Young LLP, Independent Registered Public Accounting Firm |

The Board of Directors and Stockholders

Scientific Learning Corporation

We have audited the accompanying balance sheets of Scientific Learning Corporation as of December 31, 2007 and 2006 and the related statements of income, stockholders equity (deficit), and cash flows for each of the three years in the period ended December 31, 2007. Our audits also included the financial statement schedule listed in the index at Item 15(a)(2). These financial statements and schedule are the responsibility of the Company’s management. Our responsibility is to express an opinion on these financial statements and schedule based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. We were not engaged to perform an audit of the Company’s internal control over financial reporting. Our audits included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Company’s internal control over financial reporting. Accordingly, we express no such opinion. An audit also includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements referred to above present fairly, in all material respects, the financial position of Scientific Learning Corporation as of December 31, 2007 and 2006, and the results of its operations and its cash flows for each of the three years in the period ended December 31, 2007, in conformity with U.S. generally accepted accounting principles. Also, in our opinion, the related financial statement schedule, when considered in relation to the basic financial statements taken as a whole, presents fairly in all material respects the information set forth therein.

As discussed in Notes 1 and 10 to the financial statements, Scientific Learning Corporation changed its method of accounting for share based payments as of January 1, 2006 and its method of accounting for uncertain tax positions as of January 1, 2007.

/s/ ERNST & YOUNG LLP

San Francisco, California

March 10, 2008

Page 42

Scientific Learning Corporation

Balance Sheets

(In thousands, except share and per share amounts)

| | | | | | | | | | | |

| | December 31,

2007 | | December 31,

2006 | |

| |

| |

| |

Assets | | | | | | | |

Current assets: | | | | | | | |

Cash and cash equivalents | | | $ | 21,179 | | | | $ | 16,364 | | |

Accounts receivable, net of allowance for doubtful accounts of $96 and $99 at December 31, 2007 and 2006, respectively | | | | 6,155 | | | | | 7,098 | | |

Deferred income taxes | | | | 1,191 | | | | | — | | |

Prepaid expenses and other current assets | | | | 1,291 | | | | | 971 | | |

| | |

|

| | | |

|

| | |

| | | | | | | | | | | |

Total current assets | | | | 29,816 | | | | | 24,433 | | |

| | | | | | | | | | | |

Property and equipment, net | | | | 1,742 | | | | | 941 | | |

Loan to JTT Holdings | | | | 1,000 | | | | | — | | |

Deferred acquisition costs | | | | 319 | | | | | — | | |

Other assets | | | | 926 | | | | | 909 | | |

| | |

|

| | | |

|

| | |

|

Total assets | | | $ | 33,803 | | | | $ | 26,283 | | |

| | |

|

| | | |

|

| | |

| | | | | | | | | | | |

Liabilities and stockholders’ equity | | | | | | | | | | | |

Current liabilities: | | | | | | | | | | | |

Accounts payable | | | $ | 716 | | | | $ | 607 | | |

Accrued liabilities | | | | 3,859 | | | | | 5,089 | | |

Deferred revenue | | | | 17,379 | | | | | 14,786 | | |

| | |

|

| | | |

|

| | |

| | | | | | | | | | | |

Total current liabilities | | | | 21,954 | | | | | 20,482 | | |

Deferred revenue, long-term | | | | 5,576 | | | | | 4,373 | | |

Other liabilities | | | | 453 | | | | | 411 | | |

| | |

|

| | | |

|

| | |

| | | | | | | | | | | |

Total liabilities | | | | 27,983 | | | | | 25,266 | | |

| | | | | | | | | | | |

Commitments and contingencies | | | | | | | | | | | |

| | | | | | | | | | | |

Stockholders’ equity: | | | | | | | | | | | |

Preferred stock, $0.01 par value; 1,000,000 shares authorized,

no shares issued or outstanding | | | | — | | | | | — | | |

Common stock, $0.01 par value; 40,000,000 authorized,17,315,886 and 16,972,333 shares issued and outstanding at December 31, 2007 and 2006, respectively, and additional paid-in capital | | | | 82,558 | | | | | 78,909 | | |

Accumulated deficit | | | | (76,738 | ) | | | | (77,892 | ) | |

| | |

|

| | | |

|

| | |

| | | | | | | | | | | |

Total stockholders’ equity | | | | 5,820 | | | | | 1,017 | | |

| | |

|

| | | |

|

| | |

| | | | | | | | | | | |

Total liabilities and stockholders’ equity | | | $ | 33,803 | | | | $ | 26,283 | | |

| | |

|

| | | |

|

| | |

See accompanying notes.

Page 43

Scientific Learning Corporation

Statements of Income

(In thousands, except per share amounts)

| | | | | | | | | | |

| | Year Ended December 31, | |

| |

| |

| | 2007 | | 2006 | | 2005 | |

| |

| |

| |

| |

| | | | | | | | | | |

Revenues: | | | | | | | | | | |

Products | | $ | 31,023 | | $ | 29,966 | | $ | 30,263 | |

Service and support | | | 15,030 | | | 11,032 | | | 10,056 | |

| |

|

| |

|

| |

|

| |

Total revenues | | | 46,053 | | | 40,998 | | | 40,319 | |

| | | | | | | | | | |

Cost of revenues: | | | | | | | | | | |

Cost of products | | | 1,680 | | | 1,638 | | | 2,018 | |

Cost of service and support | | | 8,539 | | | 7,897 | | | 5,637 | |

| |

|

| |

|

| |

|

| |

Total cost of revenues | | | 10,219 | | | 9,535 | | | 7,655 | |

| |

|

| |

|

| |

|

| |

| | | | | | | | | | |

Gross profit | | | 35,834 | | | 31,463 | | | 32,664 | |

| | | | | | | | | | |

Operating expenses: | | | | | | | | | | |

Sales and marketing | | | 24,868 | | | 21,073 | | | 17,619 | |

Research and development | | | 4,500 | | | 4,129 | | | 3,896 | |

General and administrative | | | 7,660 | | | 6,643 | | | 5,841 | |

| |

|

| |

|

| |

|

| |

| | | | | | | | | | |

Total operating expenses | | | 37,028 | | | 31,845 | | | 27,356 | |

| |

|

| |

|