Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D. C. 20549

FORM 10-K

(Mark One)

| þ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2008

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to .

Commission File Number 0-23827

PC CONNECTION, INC.

(Exact name of registrant as specified in its charter)

| Delaware | 02-0513618 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

730 Milford Road Merrimack, New Hampshire | 03054 | |

| (Address of principal executive offices) | (Zip Code) | |

Registrant’s telephone number, including area code (603) 683-2000

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Name of each exchange on which registered | |

| Common Stock, $.01 par value | Nasdaq Global Select Market |

Securities registered pursuant to Section 12(g) of the Act:

None

(Title of Class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

YES ¨ NO þ

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

YES ¨ NO þ

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

YES þ NO ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer ¨ | Accelerated filer þ | Non-accelerated filer ¨ | Smaller reporting company ¨ | |||

| (Do not check if a smaller reporting company) |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act).

YES ¨ NO þ

The aggregate market value of the registrant’s voting shares of common stock held by non-affiliates of the registrant on June 30, 2008, based on $9.31 per share, the last reported sale price on the Nasdaq Global Select Market on that date, was $88,664,139.

The number of shares outstanding of each of the registrant’s classes of common stock, as of March 4, 2009:

Class | Number of Shares | |

| Common Stock, $.01 par value | 27,012,729 |

The following documents are incorporated by reference into the Annual Report on Form 10-K: Portions of the registrant’s definitive Proxy Statement for its 2009 Annual Meeting of Stockholders are incorporated by reference into Part III of this Report.

Table of Contents

| Page | ||||

| PART I | ||||

ITEM 1. | 1 | |||

ITEM 1A. | 10 | |||

ITEM 1B. | 16 | |||

ITEM 2. | 16 | |||

ITEM 3. | 17 | |||

ITEM 4. | 17 | |||

| PART II | ||||

ITEM 5. | 18 | |||

ITEM 6. | 21 | |||

ITEM 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | 23 | ||

ITEM 7A. | 40 | |||

ITEM 8. | 40 | |||

ITEM 9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | 40 | ||

ITEM 9A. | 40 | |||

ITEM 9B. | 43 | |||

| PART III | ||||

ITEM 10. | 44 | |||

ITEM 11. | 44 | |||

ITEM 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 44 | ||

ITEM 13. | Certain Relationships and Related Transactions, and Director Independence | 44 | ||

ITEM 14. | 44 | |||

| PART IV | ||||

ITEM 15. | 45 | |||

| 52 | ||||

Table of Contents

PART I

| Item 1. | Business |

GENERAL

We are a leading direct marketer of a wide range of information technology, or IT, products and services, including computer systems, software and peripheral equipment, networking communications, and other products and accessories that we purchase from manufacturers, distributors, and other suppliers. We also offer a growing range of installation, configuration, repair, and other services performed by our personnel and third-party providers. We operate through three primary business segments: (1) consumers and small- to medium-sized businesses, or SMB, through our PC Connection Sales subsidiaries, (2) large enterprise customers, or Large Account, through our MoreDirect subsidiary, and (3) federal, state, and local government and educational institutions, or Public Sector, through our GovConnection subsidiary. Our principal customers are SMBs (comprised of 20 to 1,000 employees), medium-to-large corporate accounts, and government and educational institutions. We generate sales through (i) outbound telemarketing and field sales contacts by sales representatives focused on the business, education, and government markets, (ii) our websites, and (iii) inbound calls from customers responding to our catalogs and other advertising media. We offer a broad selection of over 150,000 products targeted for business use at competitive prices, including products from Acer, Apple, Cisco Systems, Hewlett-Packard, IBM, Lenovo, Microsoft, Sony, Symantec, and Toshiba. Our most frequently ordered products are carried in inventory and are typically shipped to customers the same day the order is received.

Since our founding in 1982, we have consistently served our customers’ needs by providing innovative, reliable, and timely service and technical support, and by offering an extensive assortment of branded products through knowledgeable, well-trained sales and support teams. Our strategy’s effectiveness is reflected in the recognition we have received, including being named to the Fortune 1000 and the VARBusiness 500 for each of the last eight years. In 2008, we were awarded first place by InformationWeek in the Supply Chain Innovation and Retail Industry categories and were ranked #8 overall among the nation’s most innovative companies by InformationWeek.

We believe that our consistent customer focus has also resulted in strong brand name recognition and a broad and loyal customer base. Approximately 91% of our net sales in the year ended December 31, 2008 were made to customers who had previously purchased products from us. We believe we also have strong relationships with vendors, resulting in favorable product allocations and marketing assistance.

Our marketing efforts are targeted at SMBs, government and educational institutions, and medium-to-large corporate accounts. As of December 31, 2008, we employed 712 sales representatives, including 186 new sales representatives with less than 12 months of outbound telemarketing experience with us. Sales representatives are responsible for managing corporate and public sector accounts and focus on outbound sales calls to prospective customers. We believe that increasing our sales representatives’ productivity is important to our future success, and we have increased our investments in this area accordingly.

We market our products and services through our websites: www.pcconnection.com, www.macconnection.com, www.moredirect.com, and www.govconnection.com. Our websites provide customers and prospective customers with product information and enable customers to place electronic orders for products. For the fiscal year 2008, Internet sales processed directly online were $515.7 million, or 29.4% of net sales, compared to 29.6% in 2007.

We publish several catalogs, including PC Connection®, focusing on PCs and compatible products, and MacConnection®, focusing on Apple personal computers and compatible products. We also issue, from time to time, specialty catalogs, including GovConnection catalogs directed to government and educational institutions. With concise product descriptions, relevant technical information, and illustrations, along with toll-free telephone numbers for ordering, our catalogs are recognized as a leading source for personal computer hardware, software, and other related products. We distributed approximately 12 million catalogs in 2008.

1

Table of Contents

Additional financial information regarding our business segments and geographic data about our customers and assets is contained in Management’s Discussion and Analysis of Financial Condition and Results of Operations in Item 7 of Part II, and Note 15 to our Consolidated Financial Statements included in Item 8 of Part II of this Annual Report on Form 10-K.

We are subject to the informational requirements of the Securities Exchange Act of 1934, as amended, or the Exchange Act, and accordingly, we file reports, proxy and information statements, and other information with the Securities and Exchange Commission, or the SEC. Such reports and information can be read and copied at the public reference facilities maintained by the SEC at the Public Reference Room, 100 F Street, NE, Washington, D.C. 20549. Information regarding the operation of the Public Reference Room may be obtained by calling the SEC at 1-800-SEC-0330. The SEC maintains a website (http://www.sec.gov) that contains such reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC. We maintain a website with the address www.pcconnection.com. We are not including the information contained in our website as part of, or incorporating by reference into, this annual report on Form 10-K. We make available free of charge through our website our annual reports on Form 10-K, quarterly reports on Form 10-Q, and current reports on Form 8-K, and amendments to these reports, as soon as reasonably practicable after we electronically file these materials with, or otherwise furnish them to, the SEC.

MARKET AND COMPETITION

We generate approximately 52% of our sales from the SMB market, 27% from medium-to-large corporate accounts (Fortune 1000), and 21% from government agencies and educational organizations. The overall U.S. IT market that we serve is estimated to be in excess of $200 billion.

The largest segment of this market is served by local and regional “value added resellers,” or VARs, many of whom we believe are transitioning from the hardware and software business to IT services, which generally have higher margins. We have transitioned from an end-user or desktop-centric computing supplier to a network or enterprise-wide computing supplier. We have also partnered with third-party technology and telecommunications service providers. We now offer our customers access to the same services and technical expertise as local and regional VARs, but with more extensive product selection at lower prices.

Intense competition for customers has led manufacturers of PCs and related products to use all available channels, including direct marketers, to distribute products. Certain manufacturers who have traditionally used resellers to distribute their products have established their own direct marketing operations, including sales through the Internet. Nonetheless, we believe that these manufacturers of PCs and related products will continue to provide us and other third-party direct marketers favorable product allocations and marketing support.

We believe new entrants to the direct marketing channel must overcome a number of obstacles, including:

| • | the substantial time and resources required to build a customer base of meaningful size and profitability for cost-effective operation; |

| • | the high costs of developing the information and operating infrastructure required by direct marketers; |

| • | the advantages enjoyed by larger and more established competitors in terms of purchasing and operating efficiencies; |

| • | the difficulty of building relationships with manufacturers to achieve favorable product allocations and attractive pricing terms; and |

| • | the difficulty of identifying and recruiting management personnel with significant direct marketing experience in the industry. |

2

Table of Contents

BUSINESS STRATEGIES

Our objective is to become the principal supplier of IT products and solutions, including personal computers and related products and services, to our customers. The key elements of our business strategies include:

| • | Providing consistent customer service before, during, and after the sale. We believe that we have earned a reputation for providing superior customer service by consistently focusing on our customers’ needs. We deliver value to our customers through high-quality service and technical support provided by our knowledgeable, well-trained personnel. We also have efficient delivery programs and offer our customers reasonable return policies. |

| • | Offering a broad product selection at competitive prices. We offer a wide assortment of IT products and solutions, including personal computers and related products and networking products, at competitive prices. Our merchandising programs feature products that provide customers with aggressive price and performance and the convenience of one-stop shopping for their personal computer and related needs. |

| • | Simplifying technology products procurement for corporate customers.We offer Internet-based procurement options that simplify the process and lower the cost of procurement for our customers. Our Large Account subsidiary, MoreDirect, specializes in Internet-based solutions and provides electronic integration with its customers and suppliers. |

| • | Maintaining a strong brand name and customer awareness. Since our founding in 1982, we have built a strong brand name and customer awareness. We have been named to the Fortune 1000 and the VARBusiness 500 for each of the last eight years, and in 2007 Forbes Magazine acknowledged us as one of America’s most trustworthy companies. Our mailing list includes more than 4,200,000 names, of which approximately 370,000 have purchased products from us during the last 12 months. |

| • | Maintaining long-standing vendor relationships. We have a history of strong relationships with vendors, and were among the first direct marketers qualified by manufacturers to market computer systems to end users. We provide our vendors with both information concerning customer preferences and an efficient channel for the advertising and distribution of their products. |

GROWTH STRATEGIES

Our growth strategies are to increase revenues derived from broader product and service offerings, increased penetration of our existing customers, and expanded customer base. The key elements of our growth strategies include:

| • | Expanding product, solution, and service offerings. We offer our customers an extensive range of IT products, solutions, and services, and continually evaluate and add new products and services, as they become available or in response to customer demand. We work closely with vendors to identify and source first-to-market product offerings at aggressive prices. We offer a growing range of installation, configuration, repair, and other services performed by our personnel and third-party providers, and seek to become a total IT solution provider to our customers. |

| • | Targeting customer segments. Through targeted marketing, we seek to expand the number of our active customers and generate additional sales from existing customers. We have developed specialty catalogs featuring product offerings designed to address the needs of specific customer populations, including new product inserts targeted to purchasers of graphics, server, and networking products. We also utilize internet marketing campaigns that focus on select markets. |

| • | Pursuing strategic acquisitions and alliances. We seek acquisitions and alliances that add new customers, strengthen our product offerings, add management talent, and produce operating results which are accretive to our core business earnings. |

| • | Increasing productivity of our sales representatives. We believe that higher sales productivity is the key to leveraging our expense structure and driving future profitability improvements. We invest |

3

Table of Contents

significant resources in training new sales representatives, and provide ongoing training to experienced personnel. Our training and evaluation programs are focused towards assisting our sales personnel in understanding and anticipating clients’ IT needs, with the goal of fostering loyal client relationships. We are currently undertaking a major modification and upgrade of our sales order and customer management system that are expected to improve sales productivity beginning in the second half of 2009. Significant sales growth over the long term will also likely require us to add sales representatives in the future. |

SERVICE AND SUPPORT

Since our founding in 1982, our primary objective has been to provide products that meet the demands and needs of customers and to supplement those products with up-to-date product information and excellent customer service and support. We believe that offering our customers superior value, through a combination of product knowledge, consistent and reliable service, and leading products at competitive prices, differentiates us from other direct marketers and provides the foundation for developing a broad and loyal customer base.

We invest in training programs for our service and support personnel, with an emphasis on putting customer needs and service first. We provide toll-free technical support from 9:00 a.m. through 5:30 p.m. Eastern Time, Monday through Friday. Product support technicians assist callers with questions concerning compatibility, installation, determination of defects, and more difficult questions relating to product use. The product support technicians authorize customers to return defective or incompatible products to either the manufacturer or to us for warranty service. In-house technicians perform both warranty and non-warranty repair on most major systems and hardware products.

Using our customized information system, we send our customer orders either to our distribution center or to our drop-ship suppliers, depending on product availability, for processing immediately after a customer receives a credit approval. At our distribution center, we also perform custom configuration of computer systems as requested by our customers, which typically consists of the installation of memory, accessories, and/or software purchased. Our customers may select the method of delivery that best meets their needs and is most cost effective, ranging from expedited overnight delivery for urgently-needed items to ground freight, generally used for heavier, more bulky items. Through our Everything Overnight® service, orders accepted up to 7:00 p.m. Eastern Time can be shipped for overnight delivery.

Our inventory stocking levels are based on three primary criteria. First, we stock and maintain a large quantity of products that sell through quickly (such as notebook and desktop systems, printers, and monitors). Second, we stock products obtained through opportunistic purchases (including first-to-market and end-of-life special promotions, and popular products with limited availability). Third, we stock products in common demand, such as components we use to configure systems prior to shipping, for which we want to avoid shortages. Inventory stocking decisions are made generally independent of the level of shipping service, as expedited shipping, including overnight delivery, is available through the majority of our drop-ship suppliers as well as through our warehouse.

MARKETING AND SALES

We sell our products through our direct marketing channels to SMBs, government and educational institutions, and medium-to-large corporate accounts. We strive to be the primary supplier of IT products and solutions, including personal computers and related products, to our existing customers and to our expanding customer base. We use multiple marketing approaches to reach existing and prospective customers, including:

| • | outbound telemarketing and field sales; |

| • | Web and print media advertising; |

| • | marketing programs targeted to specific customer populations; and |

4

Table of Contents

| • | catalogs and inbound telesales. |

All of our marketing approaches emphasize our broad product offerings, fast delivery, customer support, competitive pricing, and our increasing range of service solutions.

We believe that our ability to establish and maintain long-term customer relationships and to encourage repeat purchases is largely dependent on the strength of our sales personnel and programs. Because our customers’ primary contact with us is through our sales representatives, we are committed to maintaining a qualified, knowledgeable, and motivated sales staff with its principal focus on customer service.

Sales Channels.The following table sets forth our percentage of net sales by sales channel:

| Years Ended December 31, | |||||||||

| 2008 | 2007 | 2006 | |||||||

Sales Channel | |||||||||

Outbound Telemarketing and Field Sales | 69 | % | 68 | % | 66 | % | |||

Online Internet | 29 | 30 | 31 | ||||||

Inbound Telesales | 2 | 2 | 3 | ||||||

Total | 100 | % | 100 | % | 100 | % | |||

Outbound Telemarketing and Field Sales. We seek to build loyal relationships with potential high-volume customers by assigning them to individual account managers. We believe that customers respond favorably to one-on-one relationships with personalized, well-trained account managers. Once established, these one-on-one relationships are maintained and enhanced through frequent telecommunications and targeted catalogs and other marketing materials designed to meet each customer’s specific IT needs. We pay most of our account managers a base annual salary plus incentive compensation. Incentive compensation is tied to gross profit dollars produced by the individual account manager. Account managers historically have significantly increased productivity after approximately twelve months of training and experience. At December 31, 2008, we employed 712 sales representatives, including 186 with less than twelve months of outbound telemarketing experience with us.

Online Internet. (www.pcconnection.com, www.macconnection.com, www.moredirect.com, and www.govconnection.com) We provide product descriptions and prices of generally all products online. Our PC Connection website also provides updated information for more than 140,000 items and on-screen images for more than 100,000 items. We offer, and continuously update, selected product offerings and other special buys. We believe our websites are an important sales source and communication tool for improving customer service.

Our MoreDirect subsidiary’s business process and operations are primarily Web based. During 2008, approximately two-thirds of MoreDirect’s orders were received via the Internet. Most of its corporate customers utilize a customized Web page to quickly search, source, and track IT products. MoreDirect’s website aggregates the current available inventories of its largest IT suppliers into a single on-line source for its corporate customers. Its custom designed Internet-based system, TRAXX™, provides corporate buyers with comparative pricing from several suppliers as well as special pricing arranged through the manufacturer.

The Internet supports three key business initiatives for us:

| • | Customer choice—We have built our business on the premise that our customers should be able to choose how they interact with us, be it by telephone, over the Internet, e-mail, fax, or mail. |

| • | Lowering transactions costs—Our website tools include robust product search features and Internet Business Accounts (customized Web pages), which allow customers to quickly and |

5

Table of Contents

easily find information about products of interest to them. If customers still have questions, they may call into our Telesales Representatives or Account Managers. Such phone calls are typically shorter and have higher close rates than calls from customers who have not first visited our websites. |

| • | Leveraging the time of experienced sales representatives—Our investments in technology-based sales and service programs allow our sales representatives more time to build and maintain relationships with our customers and help them to solve their business problems. |

Inbound Telesales. Our inbound sales representatives answer customer telephone calls generated by our catalogs and other advertising programs. These representatives also assist customers in making purchasing decisions, process product orders, and respond to customer inquiries on order status, product pricing, and availability. Using our proprietary information systems, sales representatives can quickly access customer records which detail purchase history and billing and shipping information, expediting the ordering process. Our inbound sales have decreased in recent years reflecting our focus on more diverse marketing strategies and programs designed to reach our business customers, as well as increased Internet usage by our customers.

Business Segments. We conduct our business operations through three primary business segments: (1) SMB, (2) Large Account, and (3) Public Sector.

SMB Segment. Our principal target customers in this segment are small-to-medium-sized business customers with 20 to 1,000 employees, although we continue to sell to consumers. Our primary means of marketing to this segment incorporate all three sales channels—outbound telemarketing, primarily to our business customers; inbound telesales, particularly to our consumer group and very small business customers; and online Internet sales to both consumer and business customers.

Large Account Segment. Through our MoreDirect subsidiary’s custom designed Web-based system, we are able to offer our larger corporate customers an efficient and effective method of sourcing, evaluating, purchasing, and tracking a wide variety of IT products and services. MoreDirect’s strategy is to be the primary single source procurement portal for its large corporate customers. MoreDirect’s sales representatives typically have ten to twenty years of experience and are located strategically across the United States. This allows them to work directly with customers, often on site. MoreDirect generally places its product orders with manufacturers and/or distribution companies for drop shipment directly to its customers.

Public Sector Segment. We use a combination of outbound telemarketing, including some on-site sales solicitation by field sales account managers, and online Internet sales through Internet Business Accounts, to reach these customers. Through our GovConnection subsidiary, we target each of the four distinct market sectors within this segment—federal government, higher educational institutions, school grades K-12, and state and local governments.

The following table sets forth the relative distribution of our net sales by business segment:

| Years Ended December 31, | |||||||||

| 2008 | 2007 | 2006 | |||||||

Business Segment | |||||||||

SMB | 52 | % | 54 | % | 54 | % | |||

Large Account | 27 | 29 | 30 | ||||||

Public Sector | 21 | 17 | 16 | ||||||

Total | 100 | % | 100 | % | 100 | % | |||

Catalog Distribution. Our two principal catalogs are PC Connection® for the PC market and MacConnection® for the Apple market. In 2008, we published twelve editions of each. We distribute catalogs to purchasers on our in-house mailing list as well as to other prospective customers. In addition, we

6

Table of Contents

distribute specialty catalogs to educational and government customers and prospects on a periodic basis. We also distribute our monthly catalogs customized with special covers and inserts, offering a wide assortment of special offers on products in specific areas such as graphics, server/netcom, and mobile computing, or for specific customers, such as developers.

Specialty Marketing. Our specialty marketing activities include direct mail, other inbound and outbound telemarketing services, bulletin board services, package inserts, fax broadcasts, and electronic mail. We also market call-answering and fulfillment services to certain product vendors.

Customers. We maintain an extensive database of customers and prospects currently aggregating more than 4,200,000 names. Approximately 91% of our net sales in the year ended December 31, 2008 were made to customers who had previously purchased products from us. Except for sales to the federal government, which accounted for approximately 8% of consolidated revenues, no single customer accounted for more than 2% of our consolidated revenue in 2008. The loss of any single customer will not have a material adverse effect on any of our business segments. In addition, we do not have individual orders in our backlog that are material to our business. We typically ship products within hours of receipt of orders.

PRODUCTS AND MERCHANDISING

We continuously focus on expanding the breadth of our product offerings. We currently offer our customers over 150,000 information technology products designed for business applications from more than 1,400 manufacturers, including hardware and peripherals, accessories, networking products, and software. We select the products we sell based upon their technology and effectiveness, market demand, product features, quality, price, margins, and warranties. As part of our merchandising strategy, we also offer products related to PCs, such as digital cameras and digital media players.

The following table sets forth our percentage of net sales (in dollars) of notebooks and personal digital assistants, or PDAs, video, imaging and sound, desktops and servers, software, and other major product categories:

| PERCENTAGE OF NET SALES | |||||||||

| Years Ended December 31, | |||||||||

| 2008 | 2007 | 2006 | |||||||

Notebooks and PDAs | 15 | % | 16 | % | 17 | % | |||

Video, Imaging and Sound | 15 | 14 | 13 | ||||||

Desktops/Servers | 13 | 14 | 14 | ||||||

Software | 13 | 13 | 13 | ||||||

Net/Com Products | 10 | 8 | 8 | ||||||

Printers and Printer Supplies | 9 | 10 | 10 | ||||||

Storage Devices | 9 | 9 | 9 | ||||||

Memory and System Enhancements | 4 | 5 | 5 | ||||||

Accessories/Other | 12 | 11 | 11 | ||||||

Total | 100 | % | 100 | % | 100 | % | |||

We offer a 30-day right of return generally limited to defective merchandise. Returns of non-defective products are subject to restocking fees. Substantially all of the products marketed by us are warranted by the manufacturer. We generally accept returns directly from the customer and then either credit the customer’s account or ship the customer a similar product from our inventory.

PURCHASING AND VENDOR RELATIONS

During the year ended December 31, 2008, we shipped approximately half of our purchases directly to our distribution facility in Wilmington, Ohio. For the years ended December 31, 2008, 2007, and 2006, product purchases from Ingram Micro, Inc., our largest vendor, accounted for 24%, 24%, and 27%, respectively, of our total product purchases. Purchases from Tech Data Corporation comprised 17% of our total product purchases in

7

Table of Contents

each of the years ended December 31, 2008, 2007, and 2006. Purchases from Hewlett Packard, or HP, constituted 12%, 14%, and 15% of our total product purchases in 2008, 2007, and 2006, respectively. No other vendor accounted for more than 10% of our total product purchases in the years ended December 31, 2008, 2007, and 2006. We believe that, while we may experience some short-term disruption, alternative sources for products obtained from Ingram Micro, Tech Data, and HP are available to us.

Many product suppliers reimburse us for advertisements or other cooperative marketing programs in our catalogs and other marketing vehicles. Reimbursements may be in the form of discounts, advertising allowances, and/or rebates. We also receive allowances from certain vendors based upon the volume of purchases or sales of the vendors’ products by us.

Some of our vendors offer limited price protection in the form of rebates or credits against future purchases. We may also participate in end-of-life product and other special purchases which may not be eligible for price protection.

We believe that we have excellent relationships with our vendors. We generally pay vendors within stated terms, or earlier when favorable discounts are offered. We believe that because of our volume purchases we are able to obtain product pricing and terms that are competitive with those available to other major direct marketers. Although brand names and individual product offerings are important to our business, we believe that competitive products are available in substantially all of the merchandise categories offered by us.

DISTRIBUTION

We fulfill orders from customers both from products we hold in inventory and through drop shipping arrangements with manufacturers and distributors. At our approximately 205,000 square foot distribution and fulfillment complex in Wilmington, Ohio, we receive and ship inventory, configure computer systems, and process returned products. Orders are transmitted electronically from our various sales facilities to our Wilmington distribution center after credit approval, where packing documentation is printed automatically and order fulfillment takes place. Our customers are given several shipping options, ranging from expedited overnight delivery through our Everything Overnight® service to normal ground freight service. Through our Everything Overnight® service, orders accepted up until 7:00 p.m. Eastern Time, are generally shipped for overnight delivery via United Parcel Service (“UPS”) or FedEx Corporation. Upon request, orders may also be shipped by other common carriers. Given the significant reduction in shipping services by DHL in 2008, UPS has become our primary shipping provider.

We also place product orders directly with manufacturers and/or distribution companies for drop shipment by those manufacturers and/or suppliers directly to customers. Our MoreDirect subsidiary generally utilizes drop shipping for all product orders. Order status with distributors is tracked online, and in all circumstances, a confirmation of shipment from manufacturers and/or distribution companies is received prior to initial recording of the transaction. At the end of each financial reporting period, revenue is adjusted pursuant to Staff Accounting Bulletin No. 104, “Revenue Recognition,” (“SAB 104”) to reflect the anticipated receipt of products by the customers in the period. Products drop shipped by suppliers were 55% of net sales in 2008 and 51% of net sales in 2007. In future years, we expect that products drop shipped from suppliers will continue to increase, both in dollars and as a percentage of net sales, as we seek to lower our overall inventory and distribution costs while maintaining excellent customer service.

Certain of our larger customers occasionally request special staged delivery arrangements under which either we or our distribution partners set aside and temporarily hold inventory on our customer’s behalf. Such orders are firm delivery orders, and customers generally pay under normal credit terms, regardless of delivery. Revenue on such transactions is not recorded until shipment to their final destination as requested by the customer. Inventory held for such staged delivery requests aggregated $11.0 million at December 31, 2008.

We maintain inventories of fast moving products to meet customer demand, representing products that account for a high percentage of our ongoing product sales transactions and sales dollars. We may also, from

8

Table of Contents

time to time, make large inventory purchases of certain first-to-market products or end-of-life products to obtain favorable purchasing discounts. We also maintain sufficient inventory levels of common-demand components and accessories used for configuration services.

MANAGEMENT INFORMATION SYSTEMS

All of our subsidiaries, except for MoreDirect, utilize centralized management information systems principally comprised of applications software running on IBM i5 and p5 computers and Microsoft Windows 2003-based servers, which we have customized for our use. These systems permit centralized management of key functions, including order taking and processing, inventory and accounts receivable management, purchasing, sales, and distribution, and the preparation of daily operating control reports on key aspects of the business. We also operate advanced telecommunications equipment to support our sales and customer service operations. Key elements of the telecommunications systems are integrated with our computer systems to provide timely customer information to sales and service representatives, and to facilitate the preparation of operating and performance data.

MoreDirect has developed a custom designed Internet-based system, TRAXX™, which comprises applications software running on Linux servers. This system is an integrated application of sales order processing, integrated supply chain visibility, and full EDI links with major manufacturers’ distribution partners for product information, availability, pricing, ordering, delivery, and tracking, including related accounting functions.

We believe our customized information systems enable us to improve our productivity, ship customer orders on a same-day basis, respond quickly to changes in our industry, and provide high levels of customer service.

Our success is dependent in large part on the accuracy and proper use of our information systems, including our telephone systems, to manage our inventory and accounts receivable collections, to purchase, sell, and ship our products efficiently and on a timely basis, and to maintain cost-efficient operations. We have undertaken a significant upgrade of our sales processing systems, which is expected to be completed in the second half of 2009. We expect to continually upgrade our information systems in the future to more effectively manage our operations and customer database.

COMPETITION

The direct marketing and sale of information technology products, including personal computers and related products, is highly competitive. We compete with other direct marketers of IT products, including CDW Corporation and Insight Enterprises, Inc., who are much larger than we are. We also compete with:

| • | certain product manufacturers that sell directly to customers, such as Dell Inc., as well as some of our own suppliers, such as HP, Lenovo, and Apple; |

| • | distributors that sell directly to certain customers; |

| • | local and regional VARs; |

| • | various franchisers, office supply superstores, and national computer retailers; and |

| • | companies with more extensive websites and commercial online networks. |

Additional competition may arise if other new methods of distribution, such as broadband electronic software distribution, emerge in the future. We compete not only for customers, but also for favorable product allocations and cooperative advertising support from product manufacturers. Several of our competitors are larger and have substantially greater financial resources than we do.

We believe that price, product selection and availability, and service and support are the most important competitive factors in our industry.

9

Table of Contents

INTELLECTUAL PROPERTY RIGHTS

Our trademarks include PC Connection®, GovConnection®, MacConnection®, and MoreDirect®, and their related logos; Everything Overnight®, The Connection®, Raccoon Character®, Service Connection®, HealthConnection™, ProConnection™, TRAXX™, Graphics Connection®, Education Connection®, Get Connected®, Connect®, and Your Brands, Your Way, Next Day®. We intend to use and protect these and our other marks, as we deem necessary. We believe our trademarks have significant value and are an important factor in the marketing of our products. We do not maintain a traditional research and development group, but we work closely with computer product manufacturers and other technology developers to stay abreast of the latest developments in computer technology, with respect to the products we both sell and use.

WORK FORCE

As of December 31, 2008, we employed 1,625 persons, of whom 878 (including 166 management and support personnel) were engaged in sales related activities, 120 were engaged in providing IT services and customer service and support, 308 were engaged in purchasing, marketing, and distribution related activities, 105 were engaged in the operation and development of management information systems, and 214 were engaged in administrative and finance functions. We consider our employee relations to be good. Our employees are not represented by a labor union, and we have never experienced a labor related work stoppage.

| Item 1A. | Risk Factors |

Statements contained or incorporated by reference in this Annual Report on Form 10-K that are not based on historical fact are “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995, Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Exchange Act. These forward-looking statements regarding future events and our future results are based on current expectations, estimates, forecasts, and projections and the beliefs and assumptions of management including, without limitation, our expectations with regard to the industry’s rapid technological change and exposure to inventory obsolescence, availability and allocations of goods, reliance on vendor support and relationships, competitive risks, pricing risks, and the overall level of economic activity and the level of business investment in information technology products. Forward-looking statements may be identified by the use of forward-looking terminology such as “may,” “could,” “will,” “expect,” “estimate,” “anticipate,” “continue,” or similar terms, variations of such terms or the negative of those terms.

We cannot assure investors that our assumptions and expectations will prove to have been correct. Important factors could cause our actual results to differ materially from those indicated or implied by forward-looking statements. Such factors that could cause or contribute to such differences include those factors discussed below. We undertake no intention or obligation to update or revise any forward-looking statements, whether as a result of new information, future events, or otherwise. If any of the following risks actually occur, our business, financial condition, or results of operations would likely suffer.

We have experienced variability in sales, and there is no assurance that we will be able to maintain profitable operations.

Several factors have caused our sales and results of operations to fluctuate and we expect these fluctuations to continue on a quarterly basis. Causes of these fluctuations include:

| • | changes in the overall level of economic activity; |

| • | the condition of the personal computer industry in general; |

| • | changes in the level of business investment in information technology products; |

| • | shifts in customer demand for hardware and software products; |

| • | variations in levels of competition; |

10

Table of Contents

| • | industry shipments of new products or upgrades; |

| • | the timing of new merchandise and catalog offerings; |

| • | fluctuations in response rates; |

| • | fluctuations in postage, paper, shipping, and printing costs and in merchandise returns; |

| • | adverse weather conditions that affect response, distribution, or shipping; |

| • | changes in our product offerings; and |

| • | changes in vendor distribution of products. |

Our results also may vary based on our ability to hire and retain sales representatives and other essential personnel, as well as our success in integrating acquisitions into our business, and their relative costs.

We base our operating expenditures on sales forecasts. If our revenues do not meet anticipated levels in the future, we may not be able to reduce our staffing levels and operating expenses in a timely manner to avoid significant losses from operations.

Should our financial performance not meet expectations and our stock price continue to trade at current levels, we may be required to record an additional significant charge to earnings for impairment of goodwill and other intangibles.

In accordance with Statement of Financial Accounting Standards, (“SFAS”) 142, “Goodwill and Other Intangibles,” we test goodwill for impairment on an annual basis, and more frequently if potential impairment indicators arise. We determined that the fair values of our SMB and Public Sector segments’ goodwill were lower than the carrying values as of December 31, 2008, and accordingly the carrying values of those segments’ goodwill were written off, resulting in a significant non-cash charge to earnings. Although we determined that the fair value of our Large Account segment’s goodwill exceeded its carrying value, should this segment’s financial performance not meet expectations, we would likely adjust downward expected future operating results. Such adjustment may result in a determination that our carrying values for goodwill and other non-amortizing intangibles for that segment exceed fair values. This determination may in turn require that we record an additional significant non-cash charge to earnings to reduce the $50.2 million aggregate carrying amount of goodwill and other intangibles in the Large Account operating segment, resulting in a negative effect on our results of operations.

The current volatility in economic conditions and the financial markets may adversely affect our access to capital and credit markets.

The current volatility and disruption to the capital and credit markets has reached nearly unprecedented levels and has significantly adversely impacted economic conditions, resulting in additional significant recessionary pressures and further declines in consumer confidence and economic growth.

These conditions have also resulted in a substantial tightening of the credit markets, including lending by financial institutions which is a source of capital for our borrowing and liquidity. This tightening of the credit markets has increased the cost of capital and reduced the availability of credit. It is difficult to predict how long the current economic and capital and credit market conditions will continue, the extent to which they will continue to deteriorate, and to which our business may be adversely affected. However, if current levels of economic and capital and credit market disruption and volatility worsen, we are likely to experience an adverse impact, which may be material, on our business, the cost of and access to capital and credit markets, and our results of operations.

11

Table of Contents

We may experience a reduction in the incentive programs offered to us by our vendors.

Some product manufacturers and distributors provide us with incentives such as supplier reimbursements, payment discounts, price protection, rebates, and other similar arrangements. The increasingly competitive computer hardware market has already resulted in the following:

| • | reduction or elimination of some of these incentive programs; |

| • | more restrictive price protection and other terms; and |

| • | reduced advertising allowances and incentives, in some cases. |

Many product suppliers provide us with advertising allowances, and in exchange, we feature their products in our catalogs and other marketing vehicles. These vendor allowances, to the extent that they represent specific reimbursements of incremental and identifiable costs, are offset against selling, general, and administrative, or SG&A, expenses. Advertising allowances that cannot be associated with a specific program funded by an individual vendor or that exceed the fair value of advertising expense associated with that program are classified as offsets to cost of sales or inventory. In the past, we have experienced a decrease in the level of vendor consideration available to us from certain manufacturers. The level of such consideration we receive from some manufacturers may decline in the future. Such a decline could decrease our gross margin and have a material adverse effect on our earnings and cash flows.

We face many competitive risks.

The direct marketing industry and the computer products retail business, in particular, are highly competitive. We compete with consumer electronics and computer retail stores, including superstores. We also compete with other direct marketers of hardware and software and computer related products, including CDW Corporation, Insight Enterprises, Inc., and Dell Inc., who are much larger than we are. Certain hardware and software vendors, such as HP, Lenovo, and Apple, who provide products to us, are also selling their products directly to end users through their own catalogs, stores, and via the Internet. We compete not only for customers, but also for advertising support from personal computer product manufacturers. Some of our competitors have larger catalog circulations and customer bases and greater financial, marketing, and other resources. In addition, some of our competitors offer a wider range of products and services than we do and may be able to respond more quickly to new or changing opportunities, technologies, and customer requirements. Many current and potential competitors also have greater name recognition, engage in more extensive promotional activities, and adopt pricing policies that are more aggressive than ours. We expect competition to increase as retailers and direct marketers who have not traditionally sold computers and related products enter the industry.

In addition, product resellers and direct marketers are combining operations or acquiring or merging with other resellers and direct marketers to increase efficiency. Moreover, current and potential competitors have established or may establish cooperative relationships among themselves or with third parties to enhance their products and services. Accordingly, it is possible that new competitors or alliances among competitors may emerge and acquire significant market share.

We cannot provide assurance that we can continue to compete effectively against our current or future competitors. If we encounter new competition or fail to compete effectively against our competitors, our business may be harmed.

We face and will continue to face significant price competition.

Generally, pricing is very aggressive in the personal computer industry, particularly in this current economic environment, and we expect pricing pressures to escalate if economic conditions worsen. An increase in price competition could result in a reduction of our profit margins. There can be no assurance that we will be able to offset the effects of price reductions with an increase in the number of customers, higher sales, cost reductions, or otherwise. Also, our sales of personal computer hardware products are generally producing lower profit margins

12

Table of Contents

than those associated with software products. Such pricing pressures could result in an erosion of our market share, reduced sales, and reduced operating margins, any of which could have a material adverse effect on our business.

The failure to comply with our public sector contracts could result in, among other things, fines or liabilities.

Revenues from the public sector segment are derived from sales to federal, state, and local government departments and agencies, as well as to educational institutions, through various contracts and open market sales. Government contracting is a highly regulated area. Noncompliance with government procurement regulations or contract provisions could result in civil, criminal, and administrative liability, including substantial monetary fines or damages, termination of government contracts, and suspension, debarment, or ineligibility from doing business with the government. Our current arrangements with these government agencies allow them to cancel orders with little or no notice and do not require them to purchase products from us in the future. The effect of any of these possible actions by any government department or agency could adversely affect our financial position, results of operations, and cash flows.

We are exposed to inventory obsolescence due to the rapid technological changes occurring in the personal computer industry.

The market for personal computer products is characterized by rapid technological change and the frequent introduction of new products and product enhancements. Our success depends in large part on our ability to identify and market products that meet the needs of customers in that marketplace. In order to satisfy customer demand and to obtain favorable purchasing discounts, we have and may continue to carry increased inventory levels of certain products. By so doing, we are subject to the increased risk of inventory obsolescence. Also, in order to implement our business strategy, we intend to continue, among other things, placing larger than typical inventory stocking orders of selected products and increasing our participation in first-to-market purchase opportunities. We may also, from time to time, make large inventory purchases of certain end-of-life products and market products on a private-label basis, which would increase the risk of inventory obsolescence. In addition, we sometimes acquire special purchase products without return privileges. There can be no assurance that we will be able to avoid losses related to obsolete inventory. In addition, manufacturers are limiting return rights and are taking steps to reduce their inventory exposure by supporting “configure-to-order” programs authorizing distributors and resellers to assemble computer hardware under the manufacturers’ brands. These trends reduce the costs to manufacturers and shift the burden of inventory risk to resellers like us, which could negatively impact our business.

We acquire products for resale from a limited number of vendors. The loss of any one of these vendors could have a material adverse effect on our business.

We acquire products for resale both directly from manufacturers and indirectly through distributors and other sources. The five vendors supplying the greatest amount of goods to us constituted 70%, 74%, and 70% of our total product purchases in the years ended December 31, 2008, 2007, and 2006, respectively. Among these five vendors, purchases from Ingram represented 24%, 24%, and 27% of our total product purchases in the years ended December 31, 2008, 2007, and 2006, respectively. Purchases from Tech Data comprised 17% of our total product purchases in each of the years ended December 31, 2008, 2007, and 2006. Purchases from HP represented 12%, 14%, and 15% of our total product purchases in the years ended December 31, 2008, 2007, and 2006, respectively. No other vendor supplied more than 10% of our total product purchases in the years ended December 31, 2008, 2007, and 2006. If we were unable to acquire products from Ingram, HP, or Tech Data, we could experience a short-term disruption in the availability of products, and such disruption could have a material adverse effect on our results of operations and cash flows.

Substantially all of our contracts and arrangements with our vendors that supply significant quantities of products are terminable by such vendors or us without notice or upon short notice. Most of our product vendors provide us with trade credit, of which the net amount outstanding at December 31, 2008 was $101.8 million.

13

Table of Contents

Termination, interruption, or contraction of relationships with our vendors, including a reduction in the level of trade credit provided to us, could have a material adverse effect on our financial position.

Some product manufacturers either do not permit us to sell the full line of their products or limit the number of product units available to direct marketers such as us. An element of our business strategy is to continue increasing our participation in first-to-market purchase opportunities. The availability of certain desired products, especially in the direct marketing channel, has been constrained in the past. We could experience a material adverse effect to our business if we are unable to source first-to-market purchase or similar opportunities, or if we face the reemergence of significant availability constraints.

We could experience system failures which would interfere with our ability to process orders.

We depend on the accuracy and proper use of our management information systems, including our telephone system. Many of our key functions depend on the quality and effective utilization of the information generated by our management information systems, including:

| • | our ability to manage inventory and accounts receivable collection; |

| • | our ability to purchase, sell, and ship products efficiently and on a timely basis; and |

| • | our ability to maintain operations. |

Our management information systems require continual upgrades to most effectively manage our operations and customer database. Although we maintain some redundant systems, with full data backup, a substantial interruption in management information systems or in telephone communication systems, including those resulting from natural disasters as well as power loss, telecommunications failure, or similar events, would substantially hinder our ability to process customer orders and thus could have a material adverse effect on our business.

We are dependent on key personnel.

Our future performance will depend to a significant extent upon the efforts and abilities of our senior executives. The competition for qualified management personnel in the computer products industry is very intense, and the loss of service of one or more of these persons could have an adverse effect on our business. Our success and plans for future growth will also depend on our ability to hire, train, and retain skilled personnel in all areas of our business, including sales representatives and technical support personnel. There can be no assurance that we will be able to attract, train, and retain sufficient qualified personnel to achieve our business objectives.

The methods of distributing personal computers and related products are changing, and such changes may negatively impact us and our business.

The manner in which personal computers and related products are distributed and sold is changing, and new methods of distribution and sale, such as online shopping services, have emerged. Hardware and software manufacturers have sold, and may intensify their efforts to sell, their products directly to end users. From time to time, certain manufacturers have instituted programs for the direct sales of large order quantities of hardware and software to certain major corporate accounts. These types of programs may continue to be developed and used by various manufacturers. Some of our vendors, including Apple, HP, and Lenovo, currently sell some of their products directly to end users and have stated their intentions to increase the level of such direct sales. In addition, manufacturers may attempt to increase the volume of software products distributed electronically to end users. An increase in the volume of products sold through or used by consumers of any of these competitive programs or distributed electronically to end users could have a material adverse effect on our results of operations.

We depend heavily on third-party shippers to deliver our products to customers.

Many of our customers elect to have their purchases shipped by an interstate common carrier, such as UPS or FedEx Corporation. A strike or other interruption in service by these shippers could adversely affect our ability to market or deliver products to customers on a timely basis.

14

Table of Contents

We may experience potential increases in shipping, paper, and postage costs, which may adversely affect our business if we are not able to pass such increases on to our customers.

Shipping costs are a significant expense in the operation of our business. Increases in postal or shipping rates and paper costs could significantly impact the cost of producing and mailing our catalogs and shipping customer orders. Postage prices and shipping rates increase periodically, and we have no control over future increases. We have a long-term contract with UPS, and believe that we have negotiated favorable shipping rates with our carriers. We generally invoice customers for shipping and handling charges. There can be no assurance that we will be able to pass on to our customers the full cost, including any future increases in the cost, of commercial delivery services.

We also incur substantial paper and postage costs related to our marketing activities, including producing and mailing our catalogs. Paper prices historically have been cyclical, and we have experienced substantial increases in the past. Significant increases in postal or shipping rates and paper costs could adversely impact our business, financial condition, and results of operations, particularly if we cannot pass on such increases to our customers or offset such increases by reducing other costs.

We rely on the continued development of electronic commerce and Internet infrastructure development.

We have had an increasing level of sales made via the Internet in part because of the growing use and acceptance of the Internet by end users. Sales of computer products via the Internet represent a significant and increasing portion of overall computer product sales. Growth of our Internet sales is dependent on potential customers using the Internet in addition to traditional means of commerce to purchase products. We cannot accurately predict the rate at which they will do so.

Our success in growing our Internet business will depend in large part upon the development of an increasingly sophisticated infrastructure for providing Internet access and services. If the number of Internet users or their use of Internet resources continues to grow rapidly, such growth may overwhelm the existing Internet infrastructure. Our ability to increase the speed with which we provide services to customers and to increase the scope of such services ultimately is limited by, and reliant upon, the sophistication, speed, reliability, and cost-effectiveness of the networks operated by third parties, and these networks may not continue to be developed or be available at prices consistent with our required business model.

We face many uncertainties relating to the collection of state sales and use tax.

We collect and remit sales and use taxes in states in which we have either voluntarily registered or have a physical presence. Various states have sought to impose on direct marketers the burden of collecting state sales and use taxes on the sales of products shipped to their residents. In 1992, the United States Supreme Court affirmed its position that it is unconstitutional for a state to impose sales or use tax collection obligations on an out-of-state mail-order company whose only contacts with the state are limited to the distribution of catalogs and other advertising materials through the mail and the subsequent delivery of purchased goods by United States mail or by interstate common carrier. However, legislation that would expand the ability of states to impose sales and use tax collection obligations on direct marketers has been introduced in Congress on many occasions. Additionally, certain states have adopted rules that require companies and their affiliates to register in those states as a condition of doing business with those state agencies.

Moreover, due to our presence on various forms of electronic media and other operational factors, our contacts with many states may exceed the limited contacts involved in the Supreme Court case. We cannot predict the level of contacts that is sufficient to permit a state to impose on us a sales or use tax collection obligation. Two of our competitors have elected to collect sales and use taxes in all states. If the Supreme Court changes its position, or if legislation is passed to overturn the Supreme Court’s decision, or if a court were to determine that our contacts with a state exceed the constitutionally permitted contacts, the expansion of a sales or use tax collection obligation on us in states to which we ship products would result in additional administrative expenses to us, could result in tax liability for past sales as well as price increases to our customers, and could reduce future sales.

15

Table of Contents

Privacy concerns with respect to list development and maintenance may materially adversely affect our business.

We mail catalogs and send electronic messages to names in our proprietary customer database and to potential customers whose names we obtain from rented or exchanged mailing lists. World-wide public concern regarding personal privacy has subjected the rental and use of customer mailing lists and other customer information to increased scrutiny. Any domestic or foreign legislation enacted limiting or prohibiting these practices could negatively affect our business.

We are controlled by two principal stockholders.

Patricia Gallup and David Hall, our two principal stockholders, beneficially own or control, in the aggregate, approximately 64% of the outstanding shares of our common stock. Because of their beneficial stock ownership, these stockholders can continue to elect the members of the Board of Directors and decide all matters requiring stockholder approval at a meeting or by a written consent in lieu of a meeting. Similarly, such stockholders can control decisions to adopt, amend, or repeal our charter and our bylaws, or take other actions requiring the vote or consent of our stockholders and prevent a takeover of us by one or more third parties, or sell or otherwise transfer their stock to a third party, which could deprive our stockholders of a control premium that might otherwise be realized by them in connection with an acquisition of our Company. Such control may result in decisions that are not in the best interest of our public stockholders. In connection with our initial public offering, the principal stockholders placed substantially all shares of common stock beneficially owned by them into a voting trust, pursuant to which they are required to agree as to the manner of voting such shares in order for the shares to be voted. Such provisions could discourage bids for our common stock at a premium as well as have a negative impact on the market price of our common stock.

| Item 1B. | Unresolved Staff Comments |

None.

| Item 2. | Properties |

In November 1997 we entered into a fifteen year lease for our corporate headquarters and telemarketing center located at 730 Milford Road, Merrimack, New Hampshire 03054-4631, with an affiliated entity, G&H Post, which is related to us through common ownership. The total lease is valued at approximately $7.0 million, based upon an independent property appraisal obtained at the date of lease, and interest is calculated at an annual rate of 11%. The lease, as amended, requires us to pay our proportionate share of real estate taxes and common area maintenance charges as either additional rent or directly to third-parties and also to pay insurance premiums for the leased property. We have the option to renew the lease for two additional terms of five years each. The lease has been recorded as a capital lease in the financial statements.

In August 2008, our subsidiary Merrimack Services Corporation entered into a lease agreement with G&H Post, which is related to us through common ownership, for an office facility adjacent to our corporate headquarters. The lease has a term of ten years and provides Merrimack Services Corporation an option to renew the lease for two additional two-year terms, at the then comparable market rate. The lease requires us to pay our proportionate share of real estate taxes and common area maintenance charges as either additional rent or directly to third-parties and also to pay insurance premiums for the leased property. The lease has been recorded as an operating lease in the financial statements.

We also lease 205,000 square feet in two facilities in Wilmington, Ohio, which houses our distribution and order fulfillment operations. The leases governing these two facilities expire in the fourth quarter of 2009 and the first quarter of 2010 and contain provisions to renew for additional terms. We also operate sales and support offices in Keene and Portsmouth, New Hampshire; Marlborough, Massachusetts; Rockville, Maryland; Fairfield, Connecticut; Sioux City, South Dakota; Addison, Texas; and Boca Raton, Florida, and lease facilities at these

16

Table of Contents

locations. Leasehold improvements associated with these properties are amortized over the terms of the leases or their useful lives, whichever is shorter. We believe that existing or otherwise available distribution facilities in Wilmington, Ohio will be sufficient to support our anticipated needs through the next twelve months and beyond.

| Item 3. | Legal Proceedings |

We are subject to audits by states on sales and income taxes, unclaimed property, and other assessments. A comprehensive multi-state unclaimed property audit is in progress, and total accruals for unclaimed property aggregated $2.5 million at December 31, 2008. While management believes that known and estimated liabilities have been adequately provided for, it is too early to determine the ultimate outcome of such audits. Such outcome could have a material negative impact on our financial position, results of operations, and cash flows.

We are subject to various legal proceedings and claims which have arisen during the ordinary course of business. In the opinion of management, the outcome of such matters is not expected to have a material effect on our financial position, results of operations, and cash flows.

| Item 4. | Submission of Matters to a Vote of Security Holders |

There were no matters submitted during the fourth quarter of 2008 to a vote of security holders.

Executive Officers of PC Connection

Our executive officers and their ages as of March 4, 2009 are as follows:

Name | Age | Position | ||

| Patricia Gallup | 54 | Chairman and Chief Executive Officer | ||

| Jack Ferguson | 70 | Executive Vice President, Treasurer, and Chief Financial Officer | ||

| Timothy McGrath | 50 | Executive Vice President, PC Connection Enterprises | ||

| Bradley Mousseau | 57 | Senior Vice President, Human Resources |

Patricia Gallup is a co-founder of PC Connection and has served as Chief Executive Officer and Chairman of the Board since September 2002. Ms. Gallup also assumed the role of President upon the resignation of our president in March 2003. Ms. Gallup served as Chairman from June 2001 to August 2002. Ms. Gallup has served as a member of our executive management team since its inception in 1982.

Jack Fergusonhas served as Executive Vice President since May 2007, as Chief Financial Officer since December 2005, and as Treasurer since November 1997. Mr. Ferguson served as Senior Vice President from April 2006 to May 2007 and as Vice President from December 2005 to April 2006. Mr. Ferguson served as Interim Chief Financial Officer from October 2004 to December 2005 and as Director of Finance from December 1992 to November 1997. Prior to joining our company, Mr. Ferguson was a partner with Deloitte & Touche LLP, an international accounting firm.

Timothy McGrath has served as Executive Vice President, PC Connection Enterprises since May 2007. Mr. McGrath served as Senior Vice President, PC Connection Enterprises from December 2006 to May 2007 and as President of PC Connection Sales Corporation, our largest sales subsidiary, from August 2005 to December 2006. Prior to joining our company, Mr. McGrath served from 2002 to 2005 in a variety of senior management positions at Insight Enterprises, Inc. Initially he served as President of Comark, a division of Insight, and later as Executive Vice President of Sales. Mr. McGrath served in various executive sales positions at Comark Inc. from 1999 to 2002, which was purchased by Insight Enterprises, Inc. in April 2002.

Bradley Mousseau has served as Senior Vice President, Human Resources since April 2006. Mr. Mousseau served as Vice President, Human Resources from January 2000 to April 2006. Prior to joining our company, Mr. Mousseau served as Vice President of Global Workforce Strategies for Systems & Computer Technology Corporation from April 1997 to January 2000.

17

Table of Contents

PART II

| Item 5. | Market for the Registrant’s Common Equity, Related Stockholder Matters, and Issuer Purchases of Equity Securities |

Market Information

Our common stock commenced trading on March 3, 1998, on the Nasdaq Global Select Market under the symbol “PCCC.” As of March 4, 2009, there were 27,012,729 shares outstanding of our common stock held by approximately 100 stockholders of record and 2,050 beneficial holders.

The following table sets forth for the fiscal periods indicated the range of high and low sales prices for our common stock on the Nasdaq Global Select Market.

2008 | High | Low | ||||

Quarter Ended: | ||||||

December 31 | $ | 6.73 | $ | 3.10 | ||

September 30 | 9.64 | 6.04 | ||||

June 30 | 12.07 | 6.60 | ||||

March 31 | 13.19 | 7.85 | ||||

2007 | High | Low | ||||

Quarter Ended: | ||||||

December 31 | $ | 16.09 | $ | 11.18 | ||

September 30 | 15.52 | 11.16 | ||||

June 30 | 15.44 | 10.85 | ||||

March 31 | 18.80 | 12.97 | ||||

We have never declared or paid cash dividends on our capital stock. We anticipate that we will generally retain future earnings, if any, to fund the development and growth of our business, and we have no current plans to pay cash dividends on our common stock in the foreseeable future. Our secured credit agreement contains restrictions that may limit our ability to pay dividends in the future.

Share Repurchase Authorization

On March 28, 2001, our Board of Directors authorized the spending of up to $15.0 million to repurchase our common stock. Share purchases will be made in the open market from time to time depending on market conditions. Our current bank line of credit, however, limits repurchases made after June 2005 to $10.0 million without bank approval of higher amounts.

During the year ended December 31, 2008, we repurchased an aggregate of 195,994 shares for $1.4 million. As of December 31, 2008, we had repurchased an aggregate of 558,411 shares for $3.7 million. The maximum approximate dollar value of shares that may yet be purchased under the program without further bank approval is $8.6 million. We have issued nonvested shares from treasury stock and have reflected upon vesting the net remaining balance of treasury stock on the consolidated balance sheet. In addition, we withheld 14,852 shares, having an aggregate fair value of $0.1 million, upon the vesting of stock awards to satisfy related employee tax obligations during the year ended December 31, 2008. Such transactions were recognized as a repurchase of common stock and returned to treasury but do not apply against authorized repurchase limits under our bank line agreement and Board of Directors’ authorization.

18

Table of Contents

The following table provides information about our purchases during the quarter ended December 31, 2008, of equity securities that we registered pursuant to Section 12 of the Exchange Act:

ISSUER PURCHASES OF EQUITY SECURITIES

Period | Total Number of Shares Purchased (1) | Average Price Paid per Share | Total Number of Shares Purchased as Part of Publicly Announced Plans or Programs | Maximum Approximate Dollar Value of Shares that May Yet Be Purchased Under the Program(2) | |||||

10/01/08 – 10/31/08 | — | — | — | $ | 11,569,537 | ||||

11/01/08 – 11/30/08 | 50,031 | 3.76 | 50,031 | $ | 11,381,321 | ||||

12/01/08 – 12/31/08 | 32,824 | 4.45 | 26,211 | $ | 11,265,683 | ||||

Total | 82,855 | 4.08 | 76,242 | $ | 11,265,683 | ||||

| (1) | In December 2008, an employee withheld 6,613 shares from his nonvested stock award to satisfy income tax obligations due upon the vesting of the award. |

| (2) | On March 28, 2001, our Board of Directors announced approval of a share repurchase program of our common stock having an aggregate value of up to $15.0 million. Share purchases are made in open market transactions from time to time depending on market conditions. The Program does not have a fixed expiration date. |

19

Table of Contents

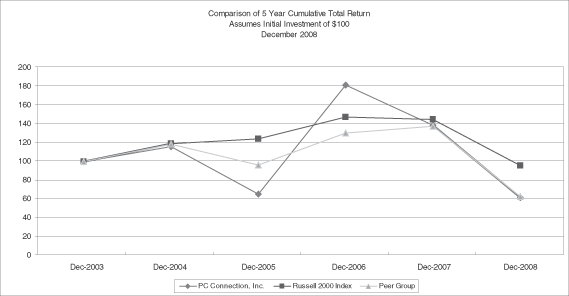

Stock Performance Graph

The following performance graph and related information shall not be deemed “soliciting material” or to be “filed” with the SEC, nor shall such information be incorporated by reference into any future filing under the Securities Act of 1933 or the Exchange Act, each as amended, except to the extent that we specifically incorporate it by reference into such filing.