UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

[X] ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934

FOR THE FISCAL YEAR ENDED DECEMBER 31, 2014

or

[ ] TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934

FOR THE TRANSITION PERIOD FROM TO

COMMISSION FILE NUMBER 1-4825

WEYERHAEUSER COMPANY

A WASHINGTON CORPORATION

91-0470860

(IRS EMPLOYER IDENTIFICATION NO.)

33663 WEYERHAEUSER WAY SOUTH, FEDERAL WAY, WASHINGTON 98063-9777 TELEPHONE (253) 924-2345

SECURITIES REGISTERED PURSUANT TO SECTION 12(B) OF THE ACT:

|

| | |

| TITLE OF EACH CLASS | | NAME OF EACH EXCHANGE ON WHICH REGISTERED: |

| Common Shares ($1.25 par value) | | Chicago Stock Exchange |

| | | New York Stock Exchange |

| 6.375% Mandatory Convertible Preference Shares, Series A ($1.00 par value) | | New York Stock Exchange |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. [X] Yes [ ] No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. [ ] Yes [X] No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. [X] Yes [ ] No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). [X] Yes [ ] No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer [X] Accelerated filer [ ] Non-accelerated filer [ ] Smaller reporting company [ ]

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). [ ] Yes [X] No

As of June 30, 2014, the aggregate market value of the registrant’s common stock held by non-affiliates of the registrant was $19.1 billion based on the closing sale price as reported on the New York Stock Exchange Composite Price Transactions.

As of January 30, 2015, 524,997,504 shares of the registrant’s common stock ($1.25 par value) were outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Notice of 2015 Annual Meeting of Shareholders and Proxy Statement for the company’s Annual Meeting of Shareholders to be held May 22, 2015, are incorporated by reference into Part II and III.

WEYERHAEUSER COMPANY > 2014 ANNUAL REPORT AND FORM 10-K

TABLE OF CONTENTS |

| | |

| PART I | | |

| ITEM 1. | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | EXECUTIVE OFFICERS OF THE REGISTRANT | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| ITEM 1A. | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | • STRATEGIC INITIATIVES | |

| | | |

| | | |

| | | |

| | | |

| | • PEOPLE | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| ITEM 1B. | | |

| ITEM 2. | | |

| ITEM 3. | | |

| ITEM 4. | MINE SAFETY DISCLOSURES — NOT APPLICABLE | |

|

| | | |

| PART II | | |

| ITEM 5. | | |

|

| ITEM 6. | | |

|

| ITEM 7. | | |

|

| | | |

|

| | | |

|

| | | |

|

| | | |

|

| | | |

|

| | | |

|

| | | |

|

| | | |

|

| | | |

|

| | | |

|

| | | |

|

| | | |

|

| | | |

|

| | | |

|

| | | |

|

| | | |

|

| | | |

|

| | | |

|

| | | |

|

| | | |

|

| ITEM 7A. | | |

|

| | | |

|

| ITEM 8. | | |

|

| | | |

|

| | | |

|

| | | |

|

| | | |

|

| | | |

|

| | | |

|

| | | |

|

| | | |

|

| ITEM 9. | | |

|

| ITEM 9A. | | |

|

| | | |

|

| | | |

|

| | | |

|

| | | |

|

| ITEM 9B. | OTHER INFORMATION — NOT APPLICABLE | |

| | | |

| PART III | | |

| ITEM 10. | | |

|

| ITEM 11. | | |

|

| ITEM 12. | | |

|

| ITEM 13. | | |

|

| ITEM 14. | | |

|

| | | |

| PART IV | | |

| ITEM 15. | | |

|

| | | |

|

| | | |

|

| | | |

| | CERTIFICATIONS | 105 |

|

OUR BUSINESS

We are one of the world's largest private owners of timberlands. We own or control nearly 7 million acres of timberlands, primarily in the U.S., and manage additional timberlands under long-term licenses in Canada. We manage these timberlands on a sustainable basis in compliance with internationally recognized forestry standards. We are also one of the largest manufacturers of wood and specialty cellulose fibers products. Our company is a real estate investment trust (REIT).

We are committed to operate as a sustainable company and are listed on the Dow Jones World Sustainability Index. We focus on increasing energy and resource efficiency, reducing greenhouse gas emissions, reducing water consumption, conserving natural resources, and offering products that meet human needs with superior sustainability attributes. We operate with world class safety results, understand and address the needs of the communities in which we operate, and present ourselves transparently.

In 2014, we generated $7.4 billion in net sales and employed approximately 12,800 people who serve customers worldwide.

This portion of our Annual Report and Form 10-K provides detailed information about who we are, what we do and where we are headed. Unless otherwise specified, current information reported in this Form 10-K is as of the fiscal year ended December 31, 2014.

We break out financial information such as revenues, earnings and assets by the business segments that form our company. We also discuss the development of our company and the geographic areas where we do business.

Throughout this Form 10-K, unless specified otherwise, references to “we,” “our,” “us” and “the company” refer to the consolidated company.

AVAILABLE INFORMATION

We meet the information-reporting requirements of the Securities Exchange Act of 1934 by filing periodic reports, proxy statements and other information with the Securities and Exchange Commission (SEC). These reports and statements — information about our company’s business, financial results and other matters — are available at:

| |

| • | the SEC website — www.sec.gov; |

| |

| • | the SEC’s Public Conference Room, 100 F St. N.E., Washington, D.C., 20549, (800) SEC-0330; and |

| |

| • | our website — www.weyerhaeuser.com. |

When we file the information electronically with the SEC, it also is added to our website.

We started out as Weyerhaeuser Timber Company, incorporated in the state of Washington in January 1900, when Frederick Weyerhaeuser and 15 partners bought 900,000 acres of timberland. Today, we are working to grow a truly great company for our shareholders, customers and employees. We grow and harvest trees and manufacture and sell products made from trees.

REAL ESTATE INVESTMENT TRUST (REIT) ELECTION

Starting with our 2010 fiscal year, we elected to be taxed as a REIT. We expect to derive most of our REIT income from investments in timberlands, including the sale of standing timber through pay-as-cut sales contracts. REIT income can be distributed to shareholders without first paying corporate level tax, substantially eliminating the double taxation on income. A significant portion of our timberland segment earnings receives this favorable tax treatment. We are, however, subject to corporate taxes on built-in-gains (the excess of fair market value over tax basis at January 1, 2010) on sales of real property (other than standing timber) held by the REIT during the first 10 years following the REIT conversion. We continue to be required to pay federal corporate income taxes on earnings of our Taxable REIT Subsidiary (TRS), which includes our manufacturing businesses and the portion of our Timberlands segment income included in the TRS.

OUR BUSINESS SEGMENTS

EFFECT OF MARKET CONDITIONS

The health of the U.S. housing market strongly affects our Wood Products and Timberlands segments. Wood Products primarily sells into the new residential building and repair and remodel markets. Demand for logs from our Timberlands segment is affected by the production of wood-based building products as well as export demand. Cellulose Fibers is primarily affected by global demand and the relative strength of the U.S. dollar.

WEYERHAEUSER COMPANY > 2014 ANNUAL REPORT AND FORM 10-K 1

COMPETITION IN OUR MARKETS

We operate in highly competitive domestic and foreign markets, with numerous companies selling similar products. Many of our products also face competition from substitutes for wood and wood-fiber products. We compete in our markets primarily through price, product quality and service levels. We are relentlessly focused on improving operational excellence to ensure a competitive cost structure and producing quality products customers want and are wiling to pay for.

Our business segments’ competitive strategies are as follows:

| |

| • | Timberlands — Extract maximum value from each acre we own or manage. |

| |

| • | Wood Products — Deliver high-quality lumber, structural panels, engineered wood products and complementary building products for residential, multi-family, industrial and light commercial applications at competitive costs. |

| |

| • | Cellulose Fibers — Concentrate on value-added pulp products and low cost manufacturing assets. |

SALES OUTSIDE THE U.S.

In 2014, $2.5 billion — 34 percent — of our total consolidated sales from continuing operations were to customers outside the U.S. The table below shows sales outside the U.S. for the last three years.

|

| | | | | | | | | |

| SALES OUTSIDE THE U.S. IN MILLIONS OF DOLLARS |

| 2014 |

| 2013 |

| 2012 |

|

| Exports from the U.S. | $ | 1,892 |

| $ | 1,891 |

| $ | 1,682 |

|

| Canadian export and domestic sales | 472 |

| 488 |

| 348 |

|

| Other foreign sales | 150 |

| 114 |

| 92 |

|

| Total | $ | 2,514 |

| $ | 2,493 |

| $ | 2,122 |

|

| Percent of total sales | 34 | % | 29 | % | 30 | % |

OUR EMPLOYEES

We have approximately 12,800 employees. This number includes:

| |

| • | 11,930 employed in North America and |

| |

| • | 870 employed by our operations outside of North America. |

This section provides information about how we:

| |

| • | grow and harvest trees and |

| |

| • | manufacture and sell products made from them. |

For each of our business segments, we provide details about what we do, where we do it, how much we sell and where we are headed.

TIMBERLANDS

Our Timberlands segment manages 6.9 million acres of private commercial timberlands worldwide. We own 6.2 million of those acres and have long-term leases on the other 0.7 million acres. In addition, we have renewable, long-term licenses on Canadian timberlands. The tables presented in this section include data from this segment's business units as of the end of 2014.

WHAT WE DO

Forestry Management

Our Timberlands segment:

| |

| • | grows and harvests trees to be converted into lumber, other wood and building products and pulp and paper; |

| |

| • | exports logs to other countries where they are made into products; |

| |

| • | plants seedlings to reforest harvested areas using the most effective regeneration method for the site and species (in parts of Canada natural regeneration is employed); |

| |

| • | monitors and cares for the planted trees as they grow to maturity; and |

| |

| • | strives to sustain and maximize the timber supply from our timberlands while keeping the health of our environment a key priority. |

Our goal is to maximize returns by selling logs and stumpage to internal and external customers. We focus on solid wood and use intensive silviculture to improve forest productivity and returns while managing our forests on a sustainable basis to meet customer and public expectations.

Sustainable Forestry Practices

We are committed to responsible environmental stewardship wherever we operate, managing forests to produce financially mature timber while protecting the ecosystem services they provide. Our working forests include places with unique environmental, cultural, historical or recreational value. To protect their unique qualities, we follow regulatory requirements, voluntary standards and implement the Sustainable Forestry Initiative® (SFI) standard. Independent auditing of all of the forests we own or manage in the United States and Canada certifies that we meet the SFI standard. Our timberlands in Uruguay are certified under the Forest Stewardship Council (FSC) standard or the Uruguayan national forestry management standard which is endorsed by the Program for the Endorsement of Forest Certification (PEFC).

WEYERHAEUSER COMPANY > 2014 ANNUAL REPORT AND FORM 10-K 2

Canadian Forestry Operations

In Canada, we manage timberlands under long-term licenses that provide raw material for our manufacturing facilities in various provinces. When we harvest trees, we pay the provinces at stumpage rates set by the government, which generally are based on prevailing market prices. We transfer logs to our manufacturing facilities at cost, and do not generate any profit in the Timberlands segment from the harvest of timber from the licensed acres in Canada.

Other Values From Our Timberlands

In the United States, we actively manage mineral, oil and gas leases on our land and use geologic databases to identify and market opportunities for commercial mineral and geothermal development. We recognize leasing revenue over the terms of agreements with customers. Revenue primarily comes from:

| |

| • | royalty payments on oil and gas production; |

| |

| • | upfront bonus payments from oil and gas leasing and exploration activity; |

| |

| • | royalty payments on hard minerals (rock, sand and gravel); |

| |

| • | geothermal lease and option revenues; and |

| |

| • | the sale of mineral assets. |

In managing mineral resources, we generate revenue related to our ownership of the minerals and, separately, related to our ownership of the surface. The ownership of mineral rights and surface acres may be held by two separate parties. Materials that can be mined from the surface, and whose value comes from factors other than their chemical composition, typically belong to the surface owner. Examples of surface materials include rock, sand, gravel, dirt and topsoil. The mineral owner holds the title to commodities that derive value from their unique chemical composition. Examples of mineral rights include oil, gas, coal (even if mined at the surface) and precious metals. If the two types of rights conflict, then mineral rights generally are superior to surface rights. A third type of land right is geothermal, which can belong to either the surface or mineral owner. We routinely reserve mineral and geothermal rights when selling surface timberlands acreage.

Timberlands Products

|

| |

| PRODUCTS | HOW THEY’RE USED |

| Logs | Logs are made into lumber, other wood and building products and pulp and paper products. |

| Timberlands | Timberland tracts are sold or exchanged to improve our timberland portfolio. |

| Timber | Standing timber is sold to third parties. |

| Minerals, oil and gas | Minerals, oil and gas are sold into construction and energy markets. |

| Other products | Other products includes seed and seedlings, recreational leases, as well as plywood produced by our international operations in Uruguay. |

HOW WE MEASURE OUR PRODUCT

We report Timberlands data in cubic meters. Cubic meters measure the total volume of wood fiber in a tree or log that we can sell. Cubic meter volume is determined from the large and small-end diameters and length and provides a more consistent and comparative measure of timber and log volume among operating regions, species, size and seasons of the year than other units of measure.

We also use multiple units of measure when transacting business including:

| |

| • | Thousand board feet (MBF) — used in the West to measure the expected lumber recovery from a tree or log. This measure does not include taper or recovery of non-lumber residual products. |

| |

| • | Hundred cubic feet (CCF) — used in the West to measure the volume of a log. The measure does not include any calculation for expected lumber recovery. |

| |

| • | Green tons (GT) — used in the South to measure weight, but factors used for conversion to product volume can vary by species, size, location and season. |

WHERE WE DO IT

Our timberlands assets are located primarily in North America. In the U.S. we own and manage sustainable timberlands in nine states for use in wood products and pulp and paper manufacturing. We own or lease:

| |

| • | 4.0 million acres in the southern U.S. (Alabama, Arkansas, Louisiana, Mississippi, North Carolina, Oklahoma and Texas); and |

| |

| • | 2.6 million acres in the Pacific Northwest (Oregon and Washington). |

We also own and operate nurseries and seed orchards in Washington, Oregon, South Carolina and Georgia.

Our international operations are located in Uruguay, where we own 298,000 acres and have long-term leases on 25,000 acres. In Canada, we manage timberlands under long-term licenses that provide raw material for our manufacturing facilities. These licenses are in Alberta, British Columbia, Ontario (license is managed by partnership) and Saskatchewan.

Our total timber inventory — including timber on owned and leased land in our U.S. and international operations — is approximately 345 million cubic meters. The amount of timber inventory does not translate into an amount of lumber or panel products because the quantity of end products:

| |

| • | varies according to the species, size and quality of the timber; and |

| |

| • | will change through time as the mix of these variables adjust. |

The species, size and grade of the trees affects the relative value of our timberlands.

We maintain our timber inventory in an integrated resource inventory and geographic information system (“GIS”). The resource inventory component of the system is proprietary and is largely based on internally developed technologies, including growth and yield models developed by our research and development organization. The GIS component is based on GIS software that is viewed as the standard in our industry.

WEYERHAEUSER COMPANY > 2014 ANNUAL REPORT AND FORM 10-K 3

Timber inventory data collection and verification techniques include the use of industry standard field sampling procedures as well as proprietary remote sensing technologies in some geographies where they generate improved estimates. The data is collected and maintained at the timber stand level.

DISCUSSION OF OPERATIONS BY GEOGRAPHY

Summary of 2014 United States Standing Timber Inventory

|

| | |

| GEOGRAPHIC AREA | MILLIONS OF CUBIC METERS AT

DECEMBER 31, 2014 |

|

| TOTAL INVENTORY(1) |

|

| West: | |

| Douglas fir/Cedar | 153 |

|

| Whitewood | 31 |

|

| Other conifer | 1 |

|

| Hardwood | 11 |

|

| | 196 |

|

| South: | |

| Southern yellow pine | 110 |

|

| Hardwood | 29 |

|

| | 139 |

|

| Total U.S. | 335 |

|

| (1) Inventory includes all conservation and set aside areas. |

Summary of 2014 United States Timberland Locations

|

| | | | | | |

| GEOGRAPHIC AREA | THOUSANDS OF ACRES AT

DECEMBER 31, 2014 | |

| FEE OWNERSHIP |

| LONG- TERM LEASES |

| TOTAL ACRES(1) |

|

| U.S.: | | | |

| West | 2,594 |

| — |

| 2,594 |

|

| South | 3,398 |

| 642 |

| 4,040 |

|

| Total U.S. | 5,992 |

| 642 |

| 6,634 |

|

| (1) Acres include all conservation and set aside areas. |

We provide a constant year round flow of logs to internal and third-party customers. We sell grade logs to mills that manufacture a diverse range of products including lumber, plywood and veneer. We also sell chips and fiber logs to pulp, paper and oriented strand board mills. Our timberlands are well located to take advantage of road, logging and transportation systems for efficient delivery of logs to these customers.

Western United States

Our Western acres are well situated to serve the wood product markets in Oregon and Washington. In addition, our location on the West Coast provides access to higher-value export markets for Douglas fir and whitewood logs in Japan, China and Korea. The size and quality of our Western timberlands, coupled with their proximity to several deep-water port facilities, positions us to meet the needs of Pacific Rim log markets.

Our lands are composed primarily of Douglas fir, a species highly valued for its structural strength. Our coastal lands also contain whitewood and have a higher proportion of whitewood than our interior holdings. Our management systems range from research and forestry, to technical planning models, mechanized harvesting, and marketing and logistics. They provide us a competitive operating advantage.

On July 23, 2013, we purchased 100 percent of the equity interests in Longview Timber LLC (Longview Timber) for $1.58 billion cash and assumed debt of $1.07 billion, for an aggregate purchase price of $2.65 billion. Longview Timber was a privately-held Delaware limited liability company engaged in the ownership and management of approximately 645,000 acres of timberlands in Oregon and Washington. More information on this transaction can be found in Note 4: Longview Timber Purchase in the Notes to Consolidated Financial Statements. WEYERHAEUSER COMPANY > 2014 ANNUAL REPORT AND FORM 10-K 4

2014 Western U.S. Inventory by Species

2014 Western U.S. Inventory by Age / Species

The average age of timber harvested in 2014 was 52 years. Most of our U.S. timberland is intensively managed for timber production, but some areas are conserved for environmental, historical, recreational or cultural reasons. Some of our older trees are protected in acreage set aside for conservation, and some are not yet logged due to harvest rate regulations. While over the long term our average harvest age will decrease in accordance with our sustainable forestry practices, we harvest generally 2 percent of our Western acreage each year.

Southern United States

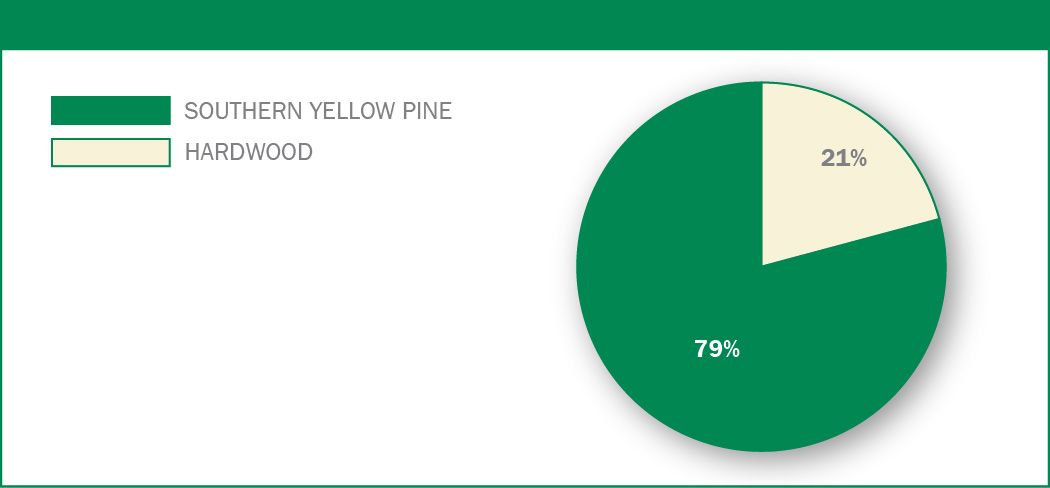

Our Southern acres predominantly contain southern yellow pine and encompass timberlands in seven states.

We intensively manage our timber plantations using forestry research and planning systems to optimize grade log production. We also actively manage our land to capture revenues from our oil, gas and hard minerals resources. We do this while providing quality habitat for a range of animals and birds. We lease more than 93 percent of our acres to the public and state wildlife agencies for recreational purposes.

2014 Southern U.S. Inventory by Species

WEYERHAEUSER COMPANY > 2014 ANNUAL REPORT AND FORM 10-K 5

2014 Southern U.S. Inventory by Age / Species

The average age of timber harvested in 2014 was 31 years for southern yellow pine. In accordance with our sustainable forestry practices, we harvest generally 3 percent of our acreage each year in the South.

International

Summary of 2014 International Standing Timber Inventory

|

| | |

| GEOGRAPHIC AREA | MILLIONS OF CUBIC METERS AT

DECEMBER 31, 2014 |

|

| TOTAL INVENTORY |

|

| Uruguay: | |

| Pine | 7 |

|

| Eucalyptus | 3 |

|

| Total International | 10 |

|

Summary of 2014 International Timberland Locations

|

| | | | | | |

| GEOGRAPHIC AREA | THOUSANDS OF ACRES AT

DECEMBER 31, 2014 | |

| | FEE OWNERSHIP |

| LONG-TERM LEASES |

| TOTAL ACRES |

|

| Uruguay | 298 |

| 25 |

| 323 |

|

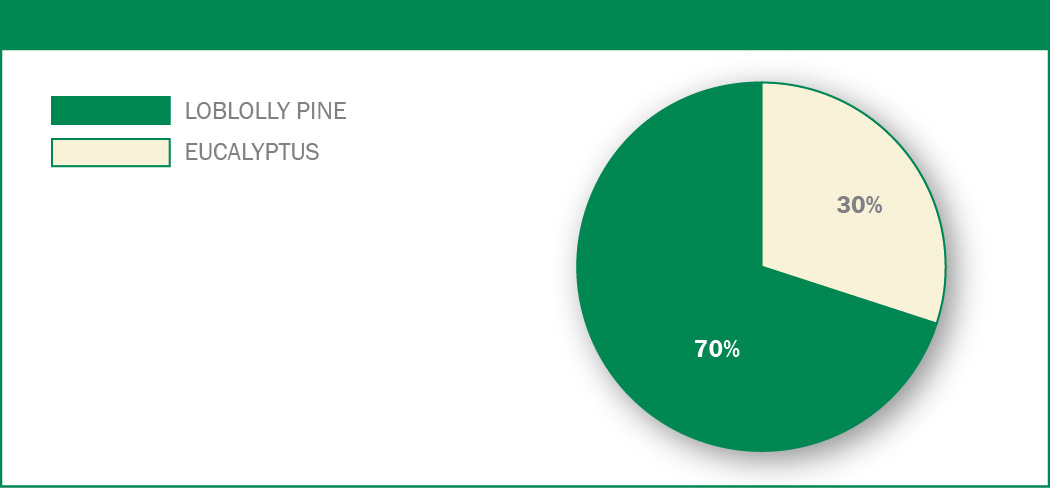

Our timberland acres in Uruguay are split approximately 50 percent loblolly pine and 50 percent eucalyptus. Loblolly pine comprises more of our timber inventory due to its older age. On average, the timber in Uruguay is in the second third of its rotation age. It is entering into that part of the growth rotation when we will see increased volume accretion. About 96 percent of the area to be planted has been afforested to date.

2014 International Inventory by Species (Uruguay)

In Uruguay, the target rotation ages are 21 to 22 years for pine and 14 to 17 years for eucalyptus. We manage both species to a grade (appearance) regime.

We also operate a plywood mill in Uruguay with a production capacity of 250,000 cubic meters. Production volume reached 216,000 cubic meters in 2014.

In Brazil, we were a managing partner in a joint venture that operated a hardwood sawmill. We sold our interest in this joint venture during 2014.

WEYERHAEUSER COMPANY > 2014 ANNUAL REPORT AND FORM 10-K 6

Canada — Licensed Timberlands

We manage timberlands under long-term licenses in Canada from the provincial government to secure the volume for our manufacturing facilities in various provinces. The provincial governments regulate the volume of timber that may be harvested each year through the Annual Allowable Cut (AAC) allotment, which is updated every 10 years. As of December 31, 2014, our AAC allotment was:

| |

| • | Alberta — 3,917 thousand cubic meters, |

| |

| • | British Columbia — 682 thousand cubic meters, |

| |

| • | Ontario — 146 thousand cubic meters and |

| |

| • | Saskatchewan — 755 thousand cubic meters. |

When the volume is harvested, we pay the province at stumpage rates set by the government and generally based on prevailing market prices. The harvested logs are transferred to our manufacturing facilities at cost (stumpage plus harvest, haul and overhead costs less any margin on selling logs to third parties). Any profit from harvesting the log through to converting it to a finished product is recognized at the respective mill in either the Cellulose Fibers or Wood Products segment.

|

| | |

| GEOGRAPHIC AREA | THOUSANDS OF ACRES AT

DECEMBER 31, 2014 |

|

| TOTAL LICENSE ARRANGEMENTS |

|

| Canada: | |

| Alberta | 5,306 |

|

| British Columbia | 1,012 |

|

Ontario(1) | 2,573 |

|

| Saskatchewan | 4,970 |

|

| Total Canada | 13,861 |

|

| (1) License is managed by partnership. |

Five-Year Summary of Timberlands Fee Harvest Volumes

|

| | | | | | | | | | |

| FEE HARVEST VOLUMES IN THOUSANDS |

| 2014 |

| 2013 |

| 2012 |

| 2011 |

| 2010 |

|

| Fee harvest volume – cubic meters: | |

| | | | |

| West | 11,173 |

| 8,907 |

| 7,170 |

| 6,595 |

| 5,569 |

|

| South | 11,676 |

| 11,596 |

| 11,488 |

| 9,738 |

| 8,197 |

|

| International | 990 |

| 818 |

| 763 |

| 854 |

| 349 |

|

| Total | 23,839 |

| 21,321 |

| 19,421 |

| 17,187 |

| 14,115 |

|

Our Timberlands annual fee harvest volumes represents the depletion of the timber assets we own. Depletion is a method of expensing the cost of establishing the fee timber asset base over the harvest or timber sales volume. The increase in fee harvest volumes from 2010 through 2014 reflects improving market conditions. The increase in fee harvest volumes in the West in 2013 and 2014 also reflects the purchase of Longview Timber.

Our fee harvest volumes are managed sustainably across all regions to ensure the preservation of long-term economic value of the timber and to capture maximum value from the markets. This is accomplished by ensuring annual harvest schedules target financially mature timber and reforestation activities align with the growing of timber through its life cycle to financial maturity.

Five-Year Summary of Timberlands Fee Harvest Volumes - Percentage of Grade and Fiber

|

| | | | | | | | | | | |

| PERCENTAGE OF GRADE AND FIBER |

| | 2014 |

| 2013 |

| 2012 |

| 2011 |

| 2010 |

|

| West | Grade | 89 | % | 90 | % | 90 | % | 90 | % | 92 | % |

| Fiber | 11 | % | 10 | % | 10 | % | 10 | % | 8 | % |

| South | Grade | 59 | % | 57 | % | 59 | % | 58 | % | 55 | % |

| Fiber | 41 | % | 43 | % | 41 | % | 42 | % | 45 | % |

| International | Grade | 63 | % | 60 | % | 67 | % | 55 | % | 65 | % |

| Fiber | 37 | % | 40 | % | 33 | % | 45 | % | 35 | % |

| Total | Grade | 73 | % | 69 | % | 71 | % | 70 | % | 70 | % |

| Fiber | 27 | % | 31 | % | 29 | % | 30 | % | 30 | % |

WEYERHAEUSER COMPANY > 2014 ANNUAL REPORT AND FORM 10-K 7

HOW MUCH WE SELL

Our net sales to unaffiliated customers over the last two years were:

| |

| • | $1.5 billion in 2014 — up 11 percent from 2013; and |

Our intersegment sales over the last two years were:

| |

| • | $867 million in 2014 — up 9 percent from 2013; and |

Five-Year Summary of Net Sales for Timberlands

|

| | | | | | | | | | | | | | | |

| NET SALES IN MILLIONS OF DOLLARS |

| 2014 |

| 2013 |

| 2012 |

| 2011 |

| 2010 |

|

| To unaffiliated customers: | | | | | |

| Logs: | | | | | |

| West | $ | 972 |

| $ | 828 |

| $ | 559 |

| $ | 545 |

| $ | 414 |

|

| South | 257 |

| 256 |

| 233 |

| 196 |

| 145 |

|

| Canada | 22 |

| 19 |

| 19 |

| 17 |

| 17 |

|

| Total | 1,251 |

| 1,103 |

| 811 |

| 758 |

| 576 |

|

| Chip sales | 12 |

| 9 |

| 18 |

| 19 |

| 16 |

|

Timberlands sales and exchanges(1) | 52 |

| 65 |

| 59 |

| 77 |

| 109 |

|

Higher and better use land sales(1) | 19 |

| 19 |

| 22 |

| 25 |

| 22 |

|

| Minerals, oil and gas | 32 |

| 32 |

| 31 |

| 53 |

| 60 |

|

Products from international operations(2) | 96 |

| 90 |

| 106 |

| 86 |

| 65 |

|

| Other products | 35 |

| 25 |

| 30 |

| 26 |

| 26 |

|

| Subtotal sales to unaffiliated customers | 1,497 |

| 1,343 |

| 1,077 |

| 1,044 |

| 874 |

|

| Intersegment sales: | | | | | |

| United States | 576 |

| 518 |

| 447 |

| 424 |

| 409 |

|

| Other | 291 |

| 281 |

| 236 |

| 222 |

| 194 |

|

| Subtotal intersegment sales | 867 |

| 799 |

| 683 |

| 646 |

| 603 |

|

| Total | $ | 2,364 |

| $ | 2,142 |

| $ | 1,760 |

| $ | 1,690 |

| $ | 1,477 |

|

(1) Significant dispositions of higher and better use timberland and some non-strategic timberlands are made through subsidiaries. (2) Products include logs, plywood and hardwood lumber harvested or produced by our international operations. Includes sales of our operations in Uruguay, Brazil (sold in 2014) and China (sold in 2012). |

Five-Year Trend for Total Net Sales in Timberlands

WEYERHAEUSER COMPANY > 2014 ANNUAL REPORT AND FORM 10-K 8

Percentage of 2014 Sales Dollars to Unaffiliated Customers

Log Sales Volumes

Logs sold to unaffiliated customers in 2014 increased 1.4 million cubic meters — 10 percent — from 2013.

| |

| • | Sales volumes in the West increased 1.3 million cubic meters — 17 percent — primarily due to strong export and domestic demand and the purchase of Longview Timber. Our western sales to unaffiliated customers generally are higher-grade logs sold into the export market and domestic-grade logs sold to West Coast sawmills. |

| |

| • | Sales to unaffiliated customers in the South decreased 210 thousand cubic meters — 4 percent — primarily due to a shift to stumpage sales. |

| |

| • | Sales volumes from Canada increased 81 thousand cubic meters — 16 percent — in 2014. The increase in volume to unaffiliated customers primarily was due to increased internal mill demand. |

| |

| • | Sales volumes from our international operations increased 247 thousand cubic meters — 69 percent — in 2014. The increase in volume was primarily due to increased fiber log sales in Uruguay. |

We sell three grades of logs — domestic grade, domestic fiber and export. Factors that may affect log sales in each of these categories include:

| |

| • | domestic grade log sales — lumber usage, primarily for housing starts and repair and remodel activity, the needs of our own mills and the availability of logs from both outside markets and our own timberlands; |

| |

| • | domestic fiber log sales — demand for chips by pulp, containerboard mills, and OSB mills; and |

| |

| • | export log sales — the level of housing starts in Japan and construction in China. |

Our sales volumes include logs purchased in the open market and all our domestic and export logs that are sold to unaffiliated customers or transferred at market prices to our internal mills by the sales and marketing staff within our Timberlands business units.

Five-Year Summary of Log Sales Volumes to Unaffiliated Customers for Timberlands

|

| | | | | | | | | | |

| SALES VOLUMES IN THOUSANDS |

| 2014 |

| 2013 |

| 2012 |

| 2011 |

| 2010 |

|

Logs – cubic meters: | | | | | |

| West | 8,980 |

| 7,708 |

| 5,898 |

| 5,267 |

| 4,476 |

|

| South | 5,678 |

| 5,888 |

| 5,575 |

| 4,879 |

| 3,357 |

|

| Canada | 592 |

| 511 |

| 531 |

| 479 |

| 507 |

|

| International | 604 |

| 357 |

| 343 |

| 314 |

| 283 |

|

| Total | 15,854 |

| 14,464 |

| 12,347 |

| 10,939 |

| 8,623 |

|

WEYERHAEUSER COMPANY > 2014 ANNUAL REPORT AND FORM 10-K 9

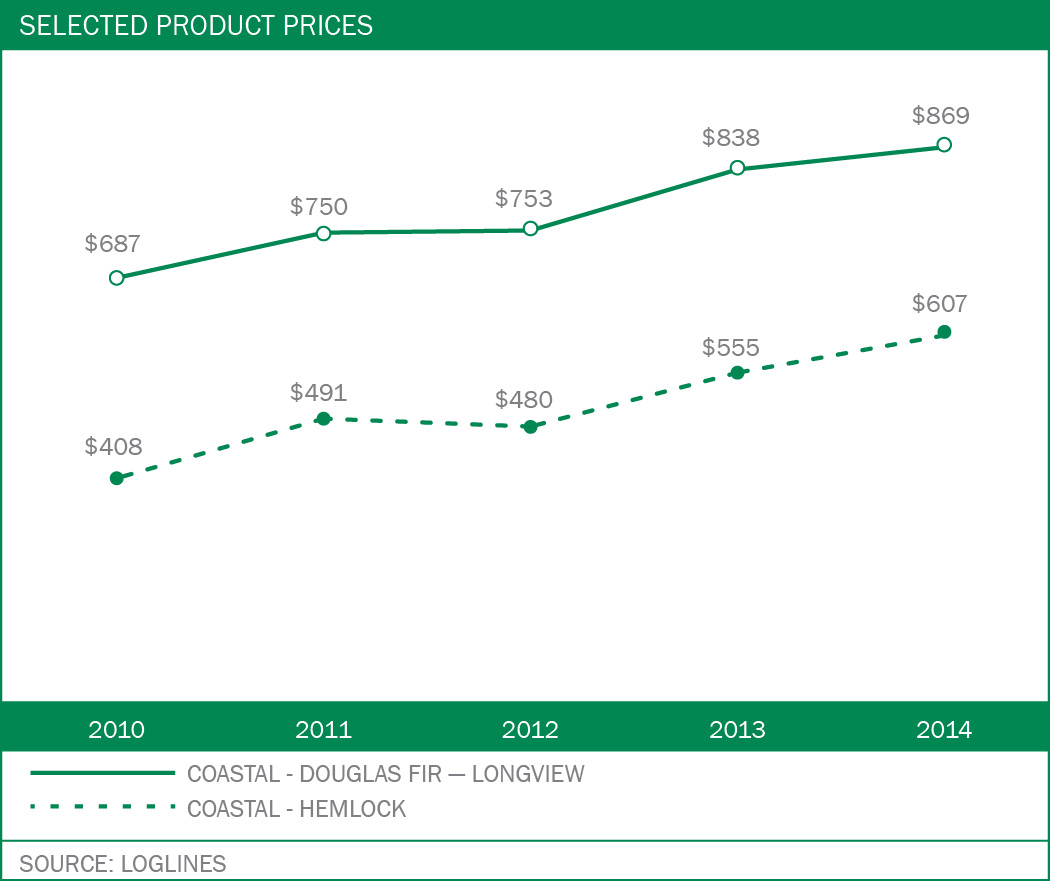

Log Prices

The majority of our log sales to unaffiliated customers involve sales to domestic sawmills and the export market. Log prices in the following tables are on a delivered (mill) basis:

Five-Year Summary of Published Domestic Log Prices (#2 Sawlog Bark On — $/MBF)

Five-Year Summary of Export Log Prices (#2 Sawlog Bark On — $/MBF)

Our log prices are affected by the supply of and demand for grade and fiber logs and are influenced by the same factors that affect log sales. Export log prices are particularly affected by the Japanese housing market.

Our average 2014 log realizations in the West increased from 2013 — primarily due to stronger demand for logs in the domestic market. Our average 2014 log realizations in the South increased from 2013 — primarily due to strengthening market conditions in the South.

Minerals and Energy Products

Mineral revenue was down slightly in 2014 as royalty revenue from natural gas and construction aggregates declined.

WHERE WE’RE HEADED

Our competitive strategies include:

| |

| • | continuing to capitalize on our scale operations, silviculture expertise and sustainability practices; |

| |

| • | maximizing cash flow through operational excellence initiatives such as merchandising for value, harvest and transportation efficiencies, and flexing harvest to seasonal and short term opportunities; |

| |

| • | sustaining our export and domestic market access, infrastructure and strong customer relationships; and |

| |

| • | increasing non-timber revenue streams. |

WEYERHAEUSER COMPANY > 2014 ANNUAL REPORT AND FORM 10-K 10

WOOD PRODUCTS

We are a large manufacturer and distributor of wood products primarily in North America and Asia.

WHAT WE DO

Our wood products segment:

| |

| • | provides a family of high-quality softwood lumber, engineered wood products, structural panels and other specialty products to the residential, multi-family, industrial, light commercial and repair and remodel markets; |

| |

| • | distributes our products as well as complementary building products that we purchase from other manufacturers; and |

| |

| • | exports our softwood lumber, oriented strand board (OSB) and engineered wood products primarily to Asia. |

Wood Products

|

| |

| PRODUCTS | HOW THEY’RE USED |

| Structural lumber | Structural framing for new residential, repair and remodel, treated applications, industrial and commercial structures |

Engineered wood products • Solid section • I-joists | Floor and roof joists, and headers and beams for residential, multi-family and commercial structures |

Structural panels • OSB • Softwood plywood | Structural sheathing, subflooring and stair tread for residential, multi-family and commercial structures |

| Other products | Complementary building products such as cedar, decking, siding, insulation and rebar sold in our distribution facilities |

WHERE WE DO IT

We operate manufacturing facilities in the United States and Canada. We distribute through a combination of Weyerhaeuser and third-party locations. Information about the locations, capacities and actual production of our manufacturing facilities is included below.

Principal Manufacturing Locations

Locations of our principal manufacturing facilities as of December 31, 2014, by major product group were:

– U.S. — Alabama, Arkansas, Louisiana, Mississippi, North Carolina, Oklahoma, Oregon and Washington

– Canada — Alberta and British Columbia

| |

| • | Engineered wood products |

– U.S. — Alabama, Louisiana, Oregon and West Virginia

– Canada — British Columbia and Ontario

– U.S. — Louisiana, Michigan, North Carolina and West Virginia

– Canada — Alberta and Saskatchewan

– U.S. — Arkansas and Louisiana

We also own or lease 21 distribution centers in the U.S. where our major products and complementary building products are sold.

Summary of Wood Products Capacities as of December 31, 2014

|

| | | | |

| CAPACITIES IN MILLIONS |

| PRODUCTION CAPACITY |

| NUMBER OF FACILITIES |

|

| Structural lumber – board feet | 4,690 |

| 18 |

|

Engineered solid section – cubic feet(1) | 43 |

| 6 |

|

| Oriented strand board – square feet (3/8”) | 3,035 |

| 6 |

|

| Softwood plywood – square feet (3/8”) | 460 |

| 2 |

|

| (1) Three engineered wood products facilities also produce engineered I-Joists to meet market demand. 2014 production of I-Joists was 182 million lineal feet. |

Production capacities listed represent annual production volume under normal operating conditions and producing a normal product mix for each individual facility. Production capacities do not include any capacity for facilities that were sold or permanently closed as of the end of 2014. We also operate a facility in Foster, Oregon that produces veneer, primarily for use in our engineered wood products facilities.

During 2013, we decided to permanently close our Colbert, Georgia engineered wood products facility. In 2014, we decided to reopen our Evergreen, Alabama engineered wood products facility. Both facilities were previously indefinitely closed.

WEYERHAEUSER COMPANY > 2014 ANNUAL REPORT AND FORM 10-K 11

Five-Year Summary of Wood Products Production

|

| | | | | | | | | | |

| PRODUCTION IN MILLIONS |

| 2014 |

| 2013 |

| 2012 |

| 2011 |

| 2010 |

|

| Structural lumber – board feet | 4,152 |

| 4,084 |

| 3,846 |

| 3,528 |

| 3,289 |

|

Engineered solid section – cubic feet(1) | 20.4 |

| 18.0 |

| 15.4 |

| 13.4 |

| 14.5 |

|

Engineered I-joists – lineal feet(1) | 182 |

| 168 |

| 147 |

| 122 |

| 133 |

|

| Oriented strand board – square feet (3/8”) | 2,749 |

| 2,723 |

| 2,511 |

| 2,127 |

| 1,721 |

|

Softwood plywood – square feet (3/8”)(2) | 252 |

| 241 |

| 214 |

| 197 |

| 212 |

|

(1) Weyerhaeuser engineered I-joist facilities also may produce engineered solid section. (2) All Weyerhaeuser plywood facilities also produce veneer. |

HOW MUCH WE SELL

Revenues of our Wood Products segment come from sales to wood products dealers, do-it-yourself retailers, builders and industrial users. Wood Products net sales were $4.0 billion in 2014 and 2013.

Five-Year Summary of Net Sales for Wood Products

|

| | | | | | | | | | | | | | | |

| NET SALES IN MILLIONS OF DOLLARS |

| 2014 |

| 2013 |

| 2012 |

| 2011 |

| 2010 |

|

| Structural lumber | $ | 1,901 |

| $ | 1,873 |

| $ | 1,400 |

| $ | 1,087 |

| $ | 1,044 |

|

| Engineered solid section | 402 |

| 353 |

| 279 |

| 235 |

| 246 |

|

| Engineered I-joists | 277 |

| 247 |

| 190 |

| 161 |

| 171 |

|

| Oriented strand board | 610 |

| 809 |

| 612 |

| 354 |

| 319 |

|

| Softwood plywood | 143 |

| 144 |

| 115 |

| 66 |

| 65 |

|

| Other products produced | 176 |

| 171 |

| 167 |

| 142 |

| 125 |

|

| Complementary building products | 461 |

| 412 |

| 295 |

| 231 |

| 254 |

|

| Total | $ | 3,970 |

| $ | 4,009 |

| $ | 3,058 |

| $ | 2,276 |

| $ | 2,224 |

|

Five-Year Trend for Total Net Sales in Wood Products

Percentage of 2014 Net Sales Dollars in Wood Products

WEYERHAEUSER COMPANY > 2014 ANNUAL REPORT AND FORM 10-K 12

Wood Products Volume

The volume of structural lumber, OSB, and engineered wood products sold in 2014 increased from 2013 due to increased demand.

Five-Year Summary of Sales Volume for Wood Products

|

| | | | | | | | | | |

| SALES VOLUMES IN MILLIONS |

| 2014 |

| 2013 |

| 2012 |

| 2011 |

| 2010 |

|

| Structural lumber – board feet | 4,463 |

| 4,436 |

| 4,031 |

| 3,586 |

| 3,356 |

|

| Engineered solid section – cubic feet | 20.0 |

| 18.2 |

| 15.4 |

| 12.3 |

| 13.1 |

|

| Engineered I-joists – lineal feet | 184 |

| 177 |

| 152 |

| 128 |

| 145 |

|

| Oriented strand board – square feet (3/8”) | 2,788 |

| 2,772 |

| 2,508 |

| 1,977 |

| 1,547 |

|

| Softwood Plywood – square feet (3/8”) | 395 |

| 402 |

| 340 |

| 249 |

| 237 |

|

| Sales volumes include sales of internally produced products and complementary building products primarily through our distribution business. |

Wood Products Prices

Prices for commodity wood products — Structural lumber and Plywood — increased in 2014 from 2013 while OSB decreased.

In general, the following factors influence prices for wood products:

| |

| • | Demand for wood products used in residential and multi-family construction and the repair and remodel of existing homes affects prices. Residential construction is influenced by factors such as population growth and other demographics, the level of employment, consumer confidence, consumer income, availability of financing and interest rate levels, and the supply and pricing of existing homes on the market. Repair and remodel activity is affected by the size and age of existing housing inventory and access to home equity financing and other credit. |

| |

| • | The availability of supply of commodity building products such as structural lumber, OSB and plywood affects prices. A number of factors can influence supply, including changes in production capacity and utilization rates, weather, raw material supply and availability of transportation. |

The North American housing market continued to show sustained improvement in 2014. This improvement led to increased demand and resulted in improved pricing for commodity wood products, excluding OSB, in 2014. The following graphs reflect product price trends for the past five years.

Five-Year Summary of Published Lumber Prices — $/MBF

Five-Year Summary of Published Oriented Strand Board Prices — $/MSF

WEYERHAEUSER COMPANY > 2014 ANNUAL REPORT AND FORM 10-K 13

WHERE WE’RE HEADED

Our competitive strategies include:

| |

| • | reduce controllable manufacturing costs through operational excellence and capital execution; |

| |

| • | maintain a value-added product mix; |

| |

| • | leverage our brand and reputation as the preferred provider of quality building products; and |

| |

| • | pursue disciplined, profitable sales growth. |

CELLULOSE FIBERS

Our cellulose fibers segment is one of the world’s largest producers of absorbent fluff pulp used in products such as diapers. We also manufacture liquid packaging board and other pulp products. We have a 50 percent interest in North Pacific Paper Corporation (NORPAC) — a joint venture with Nippon Paper Industries that produces primarily high-brightness publication papers and newsprint.

WHAT WE DO

Our cellulose fibers segment:

| |

| • | provides cellulose fibers for absorbent products in markets around the world; |

| |

| • | works closely with our customers to develop unique or specialized applications; |

| |

| • | manufactures liquid packaging board used primarily for the production of containers for liquid products; and |

| |

| • | is largely energy self sufficient, with over 80 percent of its energy derived from black liquor produced at the mills and biomass. |

Cellulose Fibers Products

|

| |

| PRODUCTS | HOW THEY’RE USED |

Pulp • Fluff pulp (Southern softwood kraft fiber) • Softwood papergrade pulp • Specialty chemical cellulose pulp | • Used in sanitary disposable products that require bulk, softness and absorbency • Used in products that include printing and writing papers and tissue • Used in textiles, absorbent products, specialty packaging, specialty applications and proprietary high-bulking fibers |

| Liquid packaging board | Converted into containers to hold liquids such as milk, juice and tea |

Other products • Slush pulp • Wet lap pulp | Used in the manufacture of paper products |

WHERE WE DO IT

Our cellulose fibers products are distributed globally through a direct sales network. Locations of our principal manufacturing facilities by major product group are:

– U.S. — Georgia (2), Mississippi and North Carolina

– Canada — Alberta

– U.S. — Mississippi

– Poland

– U.S. — Washington

Summary of Cellulose Fibers Capacities as of December 31, 2014

|

| | | | |

| CAPACITIES IN THOUSANDS |

| PRODUCTION CAPACITY |

| NUMBER OF FACILITIES |

|

| Pulp – air-dry metric tons | 1,870 |

| 5 |

|

| Liquid packaging board – tons | 350 |

| 1 |

|

Production capacities listed represent annual production volume under normal operating conditions and producing a normal product mix for each individual facility.

Five-Year Summary of Cellulose Fibers Production

|

| | | | | | | | | | |

| PRODUCTION IN THOUSANDS |

| 2014 |

| 2013 |

| 2012 |

| 2011 |

| 2010 |

|

| Pulp – air-dry metric tons | 1,859 |

| 1,815 |

| 1,773 |

| 1,769 |

| 1,774 |

|

| Liquid packaging board – tons | 292 |

| 307 |

| 292 |

| 307 |

| 316 |

|

Liquid packaging board production decreased in 2014 primarily due to a scheduled machine rebuild.

WEYERHAEUSER COMPANY > 2014 ANNUAL REPORT AND FORM 10-K 14

HOW MUCH WE SELL

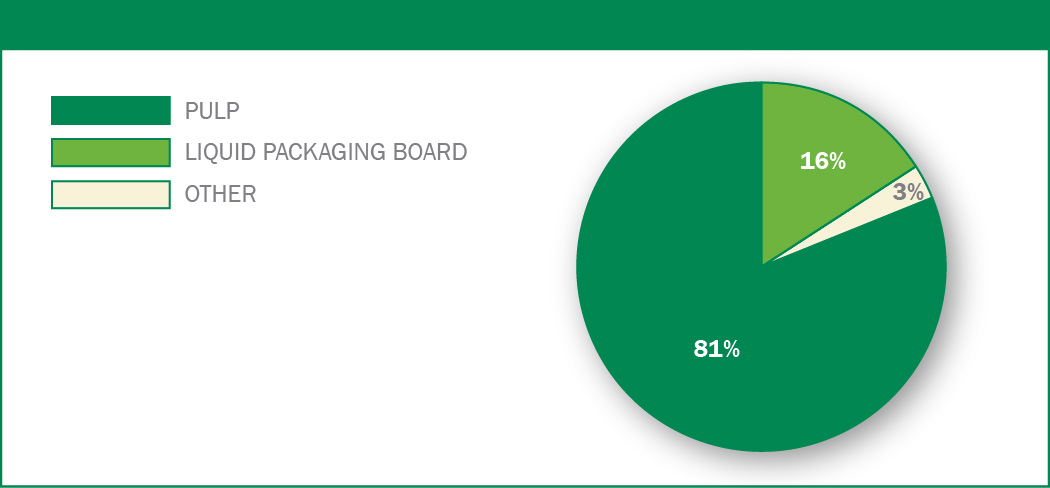

Revenues of our Cellulose Fibers segment come from sales to customers who use the products for further manufacturing or distribution and for direct use. Our net sales were $1.9 billion in 2014, comparable to $1.9 billion in 2013.

Five-Year Summary of Net Sales for Cellulose Fibers

|

| | | | | | | | | | | | | | | |

| NET SALES IN MILLIONS OF DOLLARS |

| 2014 |

| 2013 |

| 2012 |

| 2011 |

| 2010 |

|

| Pulp | $ | 1,559 |

| $ | 1,501 |

| $ | 1,433 |

| $ | 1,617 |

| $ | 1,489 |

|

| Liquid packaging board | 310 |

| 326 |

| 332 |

| 346 |

| 337 |

|

| Other products | 67 |

| 75 |

| 89 |

| 95 |

| 85 |

|

| Total | $ | 1,936 |

| $ | 1,902 |

| $ | 1,854 |

| $ | 2,058 |

| $ | 1,911 |

|

Five-Year Trend for Total Net Sales in Cellulose Fibers

Percentage of 2014 Net Sales Dollars in Cellulose Fibers

Pulp Volumes

Our sales volumes of cellulose fiber products were 1.8 million tons in 2014 and 1.9 million tons in 2013.

Factors that affect sales volumes for cellulose fiber products include:

| |

| • | growth of the world gross domestic product, |

| |

| • | demand for absorbent hygiene products and paper and |

| |

| • | relative strength of the U.S. dollar. |

Five-Year Summary of Sales Volume for Cellulose Fibers

|

| | | | | | | | | | |

| SALES VOLUMES IN THOUSANDS |

| 2014 |

| 2013 |

| 2012 |

| 2011 |

| 2010 |

|

| Pulp – air-dry metric tons | 1,826 |

| 1,866 |

| 1,762 |

| 1,756 |

| 1,714 |

|

| Liquid packaging board – tons | 274 |

| 305 |

| 289 |

| 297 |

| 311 |

|

Liquid packaging board sales volume decreased in 2014 primarily due to lower production.

WEYERHAEUSER COMPANY > 2014 ANNUAL REPORT AND FORM 10-K 15

Pulp Prices

Our average pulp prices in 2014 increased compared with 2013 due to improvement in the market demand and supply balance.

Five-Year Summary of Published NBSK Pulp Prices — $/ADMT

WHERE WE’RE HEADED

Our competitive strategies include:

| |

| • | continued execution of operational excellence initiatives such as manufacturing reliability, predictive, preventive maintenance practices, and liquid packaging board cost and quality improvement; |

| |

| • | profitably growing with long-term strategic customers; and |

| |

| • | focusing capital investments on cost reduction, green energy opportunities and product quality. |

|

|

| EXECUTIVE OFFICERS OF THE REGISTRANT |

Patricia M. Bedient, 61, has been executive vice president and chief financial officer since 2007. She was senior vice president, Finance and Strategic Planning from February 2006 to 2007. She served as vice president, Strategic Planning from 2003, when she joined the company, to 2006. Prior to joining the company, she was a partner with Arthur Andersen LLP (Independent Accountant) from 1987 to 2002 and served as the managing partner for the Seattle office and as the partner in charge of the firm’s forest products practice from 1999 to 2002. She is on the Board of Directors for Alaska Air Group and Oregon State University and also serves as Treasurer and a Board member of Overlake Hospital Medical Center. She is a CPA and member of the American Institute of CPAs.

Adrian M. Blocker, 58, was appointed senior vice president, Wood Products effective January 1, 2015. He has served as senior vice president, Lumber since August 2013. He joined the company in May 2013 as vice president, Lumber. Prior to joining the company, he served as CEO of the Wood Products Council and Chairman. He has held numerous leadership positions in the industry focused on forest management, fiber procurement, consumer packaging, strategic planning, business development and manufacturing, including at West Fraser, International Paper and Champion International.

Rhonda D. Hunter, 52, has been senior vice president, Timberlands, since January 2014. Previously, she was vice president, Southern Timberlands from 2010 to 2014. She held a number of leadership positions in the Southern Timberlands organization and has experience in inventory and planning, regional timberlands management, environmental and work systems, finance and land acquisition. She joined Weyerhaeuser in 1987 as an accountant.

Denise M. Merle, 51, has been senior vice president, Human Resources and Investor Relations since August 2014. She served as senior vice president, Human Resources beginning February 2014. Prior to that, she was director, Finance and Human Resources for the Lumber business from 2013, director, Compliance & Enterprise Planning from 2009 to 2013, and director of Internal Audit from 2004 to 2009. She has held various roles in the company’s paper and packaging businesses, including finance, capital planning and analysis, and business development. She joined the company in 1981. She is a licensed CPA in the state of Washington.

Doyle R. Simons, 51, has been president and chief executive officer since August 2013 and a director of the company since June 2012. He was appointed chief executive officer-elect and an executive officer of the company on June 17, 2013. Prior to joining the company, he served as chairman and chief executive officer of Temple-Inland, Inc. (forest products) from 2008 until February 2012 when it was acquired by International Paper Company. He held various management positions with Temple-Inland, including executive vice president from 2005 through 2007 and chief administrative officer from 2003 to 2005. Prior to joining Temple-Inland in 1992, he practiced real estate and banking law with Hutcheson and Grundy, L.L.P. He also serves on the Board of Fiserv, Inc.

Catherine I. Slater, 51, was appointed senior vice president, Cellulose Fibers effective January 1, 2015. She has served as senior vice president, Engineered Products and Distribution since August 2013 and vice president, OSB from 2011 to 2013. Prior to that role, she held a number of other leadership positions in the company’s Wood Products business, including vice president for both engineered wood products manufacturing and veneer technologies. Before joining the Wood Products team, she held positions in Cellulose Fibers business, including leadership roles at Flint River and Port Wentworth pulp mills, and leadership oversight for the company’s operations in Alberta, Canada, which included pulp, timberlands, OSB, lumber, and engineered wood products. Prior to joining the company in 1992, she held several leadership roles at Procter and Gamble.

Devin W. Stockfish, 41, was appointed senior vice president, general counsel and corporate secretary in July 2014. He leads the company's Law & Corporate Affairs department, with responsibility for global Legal, Compliance, Government Affairs, Real Estate Services, Land Title, and Environmental, Health and Safety functions. He joined the company in March 2013 as corporate secretary and assistant general counsel. Before joining the company, he was vice president & associate general counsel at Univar Inc. where he focused on mergers and acquisitions, corporate governance and securities law. Previously, he was an attorney in the law department at Starbucks Corporation and practiced corporate law at K&L Gates LLP. Before he began practicing law, Mr. Stockfish was an engineer with the Boeing Company.

WEYERHAEUSER COMPANY > 2014 ANNUAL REPORT AND FORM 10-K 16

|

|

| NATURAL RESOURCE AND ENVIRONMENTAL MATTERS |

We are subject to a multitude of laws and regulations in the operation of our businesses. We also participate in voluntary certification of our timberlands to assure that we sustain their values including the protection of wildlife and water quality. Changes in law and regulation, or certification standards, can significantly affect our business.

REGULATIONS AFFECTING FORESTRY PRACTICES

In the United States, regulations established by federal, state and local government agencies to protect water quality and wetlands could affect future harvests and forest management practices on some of our timberlands. Forest practice laws and regulations that affect present or future harvest and forest management activities in certain states include:

| |

| • | limits on the size of clearcuts, |

| |

| • | requirements that some timber be left unharvested to protect water quality and fish and wildlife habitat, |

| |

| • | regulations regarding construction and maintenance of forest roads, |

| |

| • | rules requiring reforestation following timber harvest, and |

| |

| • | various related permit programs. |

Each state in which we own timberlands has developed best management practices to reduce the effects of forest practices on water quality and aquatic habitats. Additional and more stringent regulations may be adopted by various state and local governments to achieve water-quality standards under the federal Clean Water Act, protect fish and wildlife habitats, or achieve other public policy objectives.

In Canada, our forest operations are carried out on public timberlands under forest licenses with the provinces. All forest operations are subject to:

| |

| • | forest practices and environmental regulations, and |

| |

| • | license requirements established by contract between us and the relevant province designed to: |

- protect environmental values, and

- encourage other stewardship values.

In Canada, 21 member companies of the Forest Products Association of Canada (FPAC), including Weyerhaeuser’s Canadian subsidiary, announced in May 2010 the signing of a Canadian Boreal Forest Agreement (CBFA) with nine environmental organizations. The CBFA applies to approximately 72 million hectares of public forests licensed to FPAC members and, when fully implemented, is expected to lead to the conservation of significant areas of Canada’s boreal forest and protection of boreal species at risk, in particular woodland caribou. CBFA signatories continue to work on management plans with provincial governments, and seek the participation of aboriginal and local communities in advancing the goals of the CBFA. Progress under the CBFA is measured and reported on by an independent auditor.

ENDANGERED SPECIES PROTECTIONS

In the United States, a number of fish and wildlife species that inhabit geographic areas near or within our timberlands have been listed as threatened or endangered under the federal Endangered Species Act (ESA) or similar state laws, such as:

| |

| • | the northern spotted owl, the marbled murrelet, a number of salmon species, bull trout and steelhead trout in the Pacific Northwest, |

| |

| • | several freshwater mussel and sturgeon species, and |

| |

| • | the red-cockaded woodpecker, gopher tortoise, gopher frog and American burying beetle in the South or Southeast. |

Additional species or populations may be listed as threatened or endangered as a result of pending or future citizen petitions or petitions initiated by federal or state agencies. In addition, significant citizen litigation seeks to compel the federal agencies to designate "critical habitat" for ESA-listed species, and many cases have resulted in settlements under which designations will be implemented over time. Such designations may adversely affect some management activities and options. Restrictions on timber harvests can result from:

| |

| • | federal and state requirements to protect habitat for threatened and endangered species, |

| |

| • | regulatory actions by federal or state agencies to protect these species and their habitat, and |

| |

| • | citizen suits under the ESA. |

Such actions could increase our operating costs and affect timber supply and prices in general. To date, we do not believe that these measures have had, and we do not believe that in 2015 they will have, a significant effect on our harvesting operations. We anticipate that likely future actions will not disproportionately affect Weyerhaeuser as compared with comparable operations of U.S. competitors.

In Canada:

| |

| • | The federal Species at Risk Act (SARA) requires protective measures for species identified as being at risk and for critical habitat, pursuant to SARA, Environment Canada continues to identify and assess species deemed to be at risk and their critical habitat, and |

| |

| • | in October 2012, the Canadian Minister of the Environment released a strategy for the recovery of the boreal population of woodland caribou under the SARA. The population and distribution objectives for boreal caribou across Canada are to (1) maintain the current status of existing, self-sustaining local caribou populations and (2) stabilize and achieve self-sustaining status for non-self-sustaining local caribou populations. Critical habitat for boreal caribou is identified for all boreal caribou ranges, except for northern Saskatchewan’s Boreal Shield range (SK1) where additional information is required for that population. Species assessment and recovery plans are developed in consultation with aboriginal communities and stakeholders. |

The identification and protection of habitat and the implementation of range plans and land use action plans may, over time, result in additional restrictions on timber harvests and other forest management practices that could increase operating costs for operators of timberlands in Canada. To date, we do not believe that these Canadian measures have had, and we do not believe that in 2015 they will have, a significant effect on our harvesting operations. We anticipate that likely future measures will not disproportionately affect Weyerhaeuser as compared with similar operations of Canadian competitors.

WEYERHAEUSER COMPANY > 2014 ANNUAL REPORT AND FORM 10-K 17

FOREST CERTIFICATION STANDARDS

We operate in North America under the Sustainable Forestry Initiative (SFI®). This is a certification standard designed to supplement government regulatory programs with voluntary landowner initiatives to further protect certain public resources and values. SFI® is an independent standard, overseen by a governing board consisting of:

| |

| • | conservation organizations, |

| |

| • | the forest industry, and |

| |

| • | large and small forest landowners. |

Ongoing compliance with SFI® may result in some increases in our operating costs and curtailment of our timber harvests in some areas. There also is competition from other private certification systems, primarily the Forest Stewardship Council (FSC), coupled with efforts by supporters to further those systems by persuading customers of forest products to require products certified to their preferred system. Certain features of the FSC system could impose additional operating costs on timberland management. Because of the considerable variation in FSC standards, and variability in how those standards are interpreted and applied, if sufficient marketplace demand develops for products made from raw materials sourced from other than SFI-certified forests, we could incur substantial additional costs for operations and be required to reduce harvest levels.

WHAT THESE REGULATIONS AND CERTIFICATION PROGRAMS MEAN TO US

The regulatory and nonregulatory forest management programs described above have:

| |

| • | increased our operating costs, |

| |

| • | resulted in changes in the value of timber and logs from our timberlands, |

| |

| • | contributed to increases in the prices paid for wood products and wood chips during periods of high demand, |

| |

| • | sometimes made it more difficult for us to respond to rapid changes in markets, extreme weather or other unexpected circumstances, and |

| |

| • | potentially encouraged further reductions in the use of, or substitution of other products for, lumber, oriented strand board, and plywood. |

We believe that these kinds of programs have not had, and in 2015 will not have, a significant effect on the total harvest of timber in the United States or Canada. However, these kinds of programs may have such an effect in the future. We expect we will not be disproportionately affected by these programs as compared with typical owners of comparable timberlands. We also expect that these programs will not significantly disrupt our planned operations over large areas or for extended periods.

CANADIAN ABORIGINAL RIGHTS

Many of the Canadian timberlands are subject to the constitutionally protected treaty or common-law rights of aboriginal peoples of Canada. Most of British Columbia (B.C.) is not covered by treaties, and as a result the claims of B.C.’s aboriginal peoples relating to forest resources have been largely unresolved. On June 26, 2014 the Supreme Court of Canada ruled that the Tsilhqot’in Nation holds aboriginal title to approximately 1,900 square kilometers in B.C. This was the first time that the court has declared title to exist based on historical occupation by aboriginal peoples. Many aboriginal groups continue to be engaged in treaty discussions with the governments of B.C., other provinces and Canada.

Final or interim resolution of claims brought by aboriginal groups can be expected to result in:

| |

| • | additional restrictions on the sale or harvest of timber, |

| |

| • | potential increase in operating costs, and |

| |

| • | impact to timber supply and prices in Canada. |

We believe that such claims will not have a significant effect on our total harvest of timber or production of forest products in 2015, although they may have such an effect in the future. In 2008, FPAC, of which we are a member, signed a Memorandum of Understanding with the Assembly of First Nations, under which the parties agree to work together to strengthen Canada’s forest sector through economic-development initiatives and business investments, strong environmental stewardship and the creation of skill-development opportunities particularly targeted to aboriginal youth.

POLLUTION-CONTROL REGULATIONS

Our operations are subject to various laws and regulations, including:

| |

| • | local pollution controls. |

These laws and regulations, as well as market demands, impose controls with regard to:

| |

| • | solid and hazardous waste management, |

| |

| • | remediation of contaminated sites, and |

| |

| • | the chemical content of some of our products. |

Compliance with these laws, regulations and demands usually involves capital expenditures as well as additional operating costs. We cannot easily quantify the future amounts of capital expenditures we might have to make to comply with these laws, regulations and demands or the effects on our operating costs because in some instances compliance standards have not been developed or have not become final or definitive. In addition, it is difficult to isolate the environmental component of most manufacturing capital projects.

WEYERHAEUSER COMPANY > 2014 ANNUAL REPORT AND FORM 10-K 18

Our capital projects typically are designed to:

| |

| • | extend the life of a facility, |

| |

| • | facilitate raw material changes and handling requirements, |

| |

| • | increase the economic value of assets or products, and |

| |

| • | comply with regulatory standards. |

We had no material capital expenditures relating primarily to environmental compliance in 2014. Based on our understanding of current regulatory requirements in the U.S. and Canada, we expect approximately $23 million of capital expenditures relating primarily to environmental compliance in 2015.

ENVIRONMENTAL CLEANUP

We are involved in the environmental investigation or remediation of numerous sites. Of these sites:

| |

| • | we may have the sole obligation to remediate, |

| |

| • | we may share that obligation with one or more parties, |

| |

| • | several parties may have joint and several obligations to remediate, or |

| |

| • | we may have been named as a potentially responsible party for sites designated as U.S. Superfund sites. |

Our liability with respect to these various sites ranges from insignificant to substantial. The amount of liability depends on:

| |

| • | the quantity, toxicity and nature of materials at the site, and |

| |

| • | the number and economic viability of the other responsible parties. |

We spent approximately $5 million in 2014 and expect to spend approximately $7 million in 2015 on environmental remediation of these sites.

It is our policy to accrue for environmental-remediation costs when we:

| |

| • | determine it is probable that such an obligation exists, and |

| |

| • | can reasonably estimate the amount of the obligation. |

We currently believe it is reasonably possible that our costs to remediate all the identified sites may exceed our current accruals of $29 million. The excess amounts required may be insignificant or could range, in the aggregate, up to $138 million over several years. This estimate of the upper end of the range of reasonably possible additional costs is much less certain than the estimates we currently are using to determine how much to accrue. The estimate of the upper range also uses assumptions less favorable to us among the range of reasonably possible outcomes.

REGULATION OF AIR EMISSIONS IN THE U.S.

The United States Environmental Protection Agency (EPA) has promulgated regulations for air emissions from:

| |

| • | pulp and paper manufacturing facilities, |

| |

| • | wood products facilities, and |

These regulations cover:

| |

| • | hazardous air pollutants that require use of maximum achievable control technology (MACT); and |

| |

| • | controls for pollutants that contribute to smog, haze and more recently, greenhouse gases. |

In 2011 and 2013 EPA issued new MACT standards for industrial boilers and process heaters. In 2012 EPA completed a technology and residual risk review for MACT standards applicable to pulping and bleaching operations at pulp and paper manufacturing facilities. In 2014 EPA issued a revised New Source Performance Standard for kraft pulp mills. These latter two rules apply on a project specific basis when certain thresholds are exceeded; as a result, we cannot predict whether or when those rules may have a material impact on future projects. Regarding other recent final actions by the EPA, we expect to spend $23 million in 2015 to comply with MACT standards.

The EPA must still promulgate:

| |

| • | technology and residual risk review standards for additional operations at pulp and paper manufacturing facilities and |

| |

| • | supplemental MACT standards for plywood, lumber and composite wood products facilities. |

We cannot currently quantify the amount of capital we will need in the future to comply with new regulations being developed by the EPA because final rules have not been promulgated.

In 2010 EPA issued a final greenhouse gas rule limiting the growth of emissions from new projects meeting certain thresholds. On June 23, 2014, the US Supreme Court issued a decision that removed potential applicability of the underlying 2010 regulations based solely on greenhouse gas emissions and limited application of the rule’s technology requirements to larger emission sources as a result of new emissions from non-greenhouse gas pollutants. As a result of this Supreme Court ruling, EPA is expected to issue new guidance to set thresholds for when the greenhouse gas technology requirements apply if the non-greenhouse gas emissions trigger the rule in the first instance. The impact of the Supreme Court ruling is to end the potential applicability of the technology requirements for our smaller manufacturing operations and limit the applicability for our other operations.

In June 2014 EPA proposed an extensive regulatory program for existing electric utility generating units to scale back emissions of greenhouse gas carbon dioxide (CO2) arising from fossil fuel use to generate electricity. This regulatory program potentially will have indirect impacts on our operations, such as from rising purchased electricity prices or from secondary regulation of cogeneration units that we operate. We are evaluating the proposal but are not able to predict whether the regulations, when final and implemented, will have a material impact on our operations.

We use significant biomass for energy production at our mills. EPA is currently working on rules regarding regulation of biomass emissions.

The impact of these greenhouse gas and biomass rules, as well as recent court decisions, on our operations remains uncertain.

WEYERHAEUSER COMPANY > 2014 ANNUAL REPORT AND FORM 10-K 19

To address concerns about greenhouse gases as a pollutant, we:

| |

| • | closely monitor legislative, regulatory and scientific developments pertaining to climate change; |

| |

| • | adopted in 2006, as part of the Company's sustainability program, a goal of reducing greenhouse gas emissions by 40 percent by 2020 compared with our emissions in 2000, assuming a comparable portfolio and regulations; |

| |

| • | determined to achieve this goal by increasing energy efficiency and using more greenhouse gas-neutral, biomass fuels instead of fossil fuels; and |

| |

| • | reduced greenhouse gas emissions by approximately 28 percent considering changes in the asset portfolio according to 2012 data, compared to our 2000 baseline. |

Additional factors that could affect greenhouse gas emissions in the future include:

| |

| • | policy proposals by state governments regarding regulation of greenhouse gas emissions, |

| |

| • | Congressional legislation regulating greenhouse gas emissions within the next several years and |

| |

| • | establishment of a multistate or federal greenhouse gas emissions reduction trading systems with potentially significant implications for all U.S. businesses. |

We believe these developments have not had, and in 2015 will not have, a significant effect on our operations. Although these measures could have a material adverse effect on our operations in the future, we expect that we will not be disproportionately affected by these measures as compared with owners of comparable operations. We maintain an active forestry research program to track and understand any potential effect from actual climate change related parameters that could affect the forests we own and manage and do not anticipate any disruptions to our planned operations.

REGULATION OF AIR EMISSIONS IN CANADA

In addition to existing provincial air quality regulations, the Canadian federal government has proposed an air quality management system (AQMS) as a comprehensive national approach for improving air quality in Canada. The federal proposed AQMS includes:

| |

| • | ambient air quality standards for outdoor air quality management across the country, |

| |

| • | a framework for air zone air management within provinces and territories that targets specific sources of air emissions, |

| |

| • | regional airsheds that facilitate coordinated action across borders, |

| |

| • | industrial sector based emission requirements that set a national base level of performance for major industries in Canada, and |

| |