UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2008

or

¨ TRANSITION REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from __________ to ____________.

Commission file number 000-30248

JACKSONVILLE BANCORP, INC.

(Exact name of registrant as specified in its charter)

| Florida | | 59-3472981 |

| (State or other jurisdiction of | | (IRS Employer |

| incorporation or organization) | | Identification No.) |

100 North Laura Street, Suite 1000, Jacksonville, Florida 32202

(Address of principal executive offices)

(904) 421-3040

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class | Name of Each Exchange on which Registered |

| Common Stock, $.01 par value | The Nasdaq Stock Market (Nasdaq Global Market) |

Securities registered under Section 12(g) of the Exchange Act: None.

Indicate by check mark if the registrant is a well-known seasoned issuer as defined in Rule 405 of the Securities Act.

Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ¨ | Accelerated filer | ¨ |

| Non-accelerated filer | x | Smaller reporting company | ¨ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act).

Yes ¨ No x

The aggregate market value of the registrant’s voting stock held by non-affiliates of the registrant (based upon the per share closing sale price of $15.90 on June 30, 2008) was approximately $27,805,904.

There were 1,748,799 outstanding shares of common stock as of March 18, 2009.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s Definitive Proxy Statement for the 2009 Annual Meeting of

Shareholders are incorporated by reference in Part III of this Annual Report.

TABLE OF CONTENTS

| Description | | | | Page |

| | | | | |

| | | Forward-Looking Statements | | 3 |

| PART I | | | | |

| Item 1. | | Business | | 3 |

| | | General | | 3 |

| | | Market Area and Competition | | 4 |

| | | Deposits | | 4 |

| | | Lending Activities | | 4 |

| | | Investments | | 6 |

| | | Employees | | 6 |

| | | Data Processing | | 6 |

| | | Regulation and Supervision | | 6 |

| | | | | |

| Item 1A. | | Risk Factors | | 9 |

| | | | | |

| Item 1B. | | Unresolved Staff Comments | | 13 |

| | | | | |

| Item 2. | | Properties | | 13 |

| | | | | |

| Item 3. | | Legal Proceedings | | 14 |

| | | | | |

| Item 4. | | Submission of Matters to a Vote of Security Holders | | 14 |

| | | | | |

| PART II | | | | |

| Item 5. | | Market for Registrant’s Common Equity and Related Stockholder Matters and Issuer Purchases of Equity Securities | | 14 |

| | | | | |

| Item 6. | | Selected Financial Data | | 16 |

| | | | | |

| Item 7. | | Management’s Discussion and Analysis of Financial Condition and Results of Operations | | 17 |

| | | | | |

| Item 7A. | | Quantitative and Qualitative Disclosures about Market Risk | | 33 |

| | | | | |

| Item 8. | | Financial Statements and Supplementary Data | | 35 |

| | | | | |

| Item 9. | | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | | 36 |

| | | | | |

| Item 9A. | | Controls and Procedures | | 36 |

| | | | | |

| Item 9B. | | Other Information | | 37 |

| | | | | |

| PART III | | | | |

| Item 10. | | Directors, Executive Officers and Corporate Governance | | 37 |

| | | | | |

| Item 11. | | Executive Compensation | | 39 |

| | | | | |

| Item 12. | | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | | 39 |

| | | | | |

| Item 13. | | Certain Relationships and Related Transactions, and Director Independence | | 40 |

| | | | | |

| Item 14. | | Principal Accounting Fees and Services | | 40 |

| | | | | |

| PART IV | | | | |

| Item 15. | | Exhibits, Financial Statement Schedules | | 40 |

| | | | | |

| | | Signatures | | 42 |

Notice Regarding Forward-Looking Statements

This Annual Report on Form 10-K contains certain forward-looking statements. Assumptions relating to forward-looking statements involve judgments with respect to, among other things, future economic, competitive, and market conditions, and future business decisions, all of which are difficult or impossible to predict accurately and many of which are beyond our control. When used in this report, the words “estimate,” “project,” “anticipate,” “intend,” “believe,” “expect” and similar expressions are intended to identify forward-looking statements. Although we believe that assumptions underlying the forward-looking statements are reasonable, any of the assumptions could prove inaccurate, and we may not realize the results contemplated by these statements. Management decisions are subjective in many respects and susceptible to interpretations and periodic revisions based on actual experience and business developments, the impact of which may cause us to alter our business strategy or capital expenditure plans and may, in turn, affect our results of operations. In light of the significant uncertainties inherent in the forward-looking information included in this report, you should not regard the inclusion of such information as our representation that we will achieve any strategy, objectives or other plans. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date hereof. The Company does not undertake any obligation to publicly release any revisions to these forward-looking statements to reflect events or circumstances after the date hereof or to reflect the occurrence of unanticipated events.

PART I

Unless the context requires otherwise, references in this report to “the Company,” “we,” “us,” or “our” refer to Jacksonville Bancorp, Inc., its wholly owned subsidiary, The Jacksonville Bank, and the Bank’s wholly owned subsidiary, Fountain Financial, Inc., on a consolidated basis. References to “Bancorp” denote Jacksonville Bancorp, Inc., and The Jacksonville Bank is referred to as the “Bank.”

ITEM 1. BUSINESS

General

Bancorp was incorporated under the laws of the State of Florida on October 24, 1997 for the purpose of organizing the Bank. Bancorp is a one-bank holding company owning 100% of the outstanding shares of the Bank. Bancorp’s only business is the ownership and operation of the Bank. The Bank is a Florida state-chartered commercial bank, and its deposits are insured by the Federal Deposit Insurance Corporation (“FDIC”). The Bank opened for business on May 28, 1999 and currently provides a variety of community banking services to businesses and individuals through its five offices in Jacksonville, Duval County, Florida.

We offer a variety of competitive commercial and retail banking services. In order to compete with the financial institutions in the market, we use our independent status to the fullest extent. This includes an emphasis on specialized services for small business owners with a particular focus on the medical and legal sectors. Additionally, we rely on the professional and personal relationships of our officers, directors and employees. Loan participations are arranged for customers whose loan demands exceed legal lending limits. Our product lines include personal and business online banking and sweep accounts tied to Goldman Sachs proprietary funds, in addition to our traditional banking products. Furthermore, through the Bank’s subsidiary, Fountain Financial, Inc., and our marketing agreement with New England Financial (an affiliate of MetLife), we are able to meet the investment and insurance needs of our customers.

Substantial consolidation of the Florida banking market has occurred since the early 1980’s. As more out-of-state bank holding companies enter the Florida market, we believe that the number of depository institutions headquartered and operating in Florida will continue to decline. Our marketing programs focus on the advantages of local ownership and management, personal service and customer relationships. Particular emphasis is placed on building personal face-to-face relationships. Our management and business development teams have extensive experience with individuals and companies within our targeted market segments in the Jacksonville area. Based on our experience, we believe that we have been and will continue to be effective in gaining market share. The Bank now has five full-service branches in Jacksonville, currently employing 58 bankers. We are focused on small business, professionals and commercial real estate. Over the past three years, the Company’s Board of Directors (also referred to herein as the “Board”) has granted every employee (excluding executive officers) of the Company restricted stock.

Market Area and Competition

Our primary market area is all of Duval County (primarily in the Southside, Westside, Arlington, Mandarin, Beaches and Downtown areas of Jacksonville). Jacksonville is the largest city in the United States covering 841 square miles and is a leading financial and insurance center. Jacksonville is home to the Jacksonville Jaguars and is the corporate headquarters to a number of regional and national companies. Duval County has a strong commercial and industrial base, which has been steadily expanding in recent years.

Financial institutions primarily compete with one another for deposits. In turn, a bank’s deposit base directly affects such bank’s loan activities and general growth. Primary competitive factors include interest rates on deposits and loans, service charges on deposit accounts, the availability of unique financial services products, a high level of personal service, and personal relationships between our officers and customers. We compete with financial institutions that have greater resources, and that may be able to offer more services, unique services, or possibly better terms to their customers. We believe, however, that we will be able to continue to attract sufficient loans and deposits to effectively compete with other area financial institutions.

We are in competition with existing area financial institutions, including commercial banks and savings institutions, insurance companies, consumer finance companies, brokerage houses, mortgage banking companies, credit unions, and other business entities which target traditional banking markets. We face increased competition due to the Gramm-Leach-Bliley Act (the “GLB Act”), discussed under Regulation and Supervision, which allows insurance firms, securities firms, and other non-traditional financial companies to provide traditional banking services. Due to the growth of the Jacksonville area, we anticipate that significant competition will continue from existing financial services providers, as well as new entrants to the market. There are 28 separate financial institutions located in Duval County, of which seven are considered community banks with their headquarters located in Northeast Florida.

Funding Sources

Deposits

We offer a wide range of deposit accounts, including commercial and retail checking, money market, individual retirement and statement savings accounts, and certificates of deposit with fixed rates and a range of maturity options. Our sources of deposits are primarily residents, businesses, and employees of businesses within our market areas, obtained through personal solicitation by our officers and directors, direct mail solicitation, and advertisements published in the local media. We also have the ability to obtain deposits from the “national and brokered CD markets” as an additional source of funding. We pay competitive interest rates on interest-bearing deposits. In addition, our service charge schedule is competitive with other area financial institutions, covering such matters as maintenance and per item processing fees on deposit accounts and special handling charges. We are also part of the Star, Cirrus, Presto and Plus ATM networks, and a member of VISA.

Borrowings

Additional sources of funds are available to the Bank by borrowing from the Federal Home Loan Bank (“FHLB”) and Federal Reserve Bank (“FRB”). Our lending capacity with these institutions provides credit availability based on qualifying collateral from the investment and loan portfolios. See “Note 5-Deposits” and “Note 6-Short-term borrowings and Federal Home Loan Bank Advances” of the Notes to the Consolidated Financial Statements for further information on our funding sources.

Lending Activities

Our Board has adopted certain policies and procedures to guide individual loan officers in carrying out lending functions. The Board has formed a Directors’ Loan Committee and appointed six directors to provide the following oversight:

| | · | ensure compliance with loan policy, procedures and guidelines as well as appropriate regulatory requirements; |

| | · | approve secured loans above an aggregate amount of $500,000 and unsecured loans above an aggregate amount of $100,000 to any entity and/or related interests; |

| | · | monitor overall loan quality through review of information relative to all new loans; |

| | · | approve lending authority for individual officers; |

| | · | monitor our loan review systems; |

| | · | review the adequacy of the loan loss reserve; and |

| | · | approve any additional advances to any borrower whose loan or line of credit has been adversely classified Substandard. |

The Board realizes that occasionally loans need to be made which fall outside the typical policy guidelines. Consequently, the Chief Executive Officer and Chief Lending Officer have the authority to make certain policy exceptions on secured loans up to $500,000 and unsecured loans up to $100,000. Policy exceptions on secured and unsecured loans greater than $500,000 and $100,000, respectively, must be approved by the Directors’ Loan Committee, and the full Board reviews reports of all loans and policy exceptions at its regular meetings. Additionally, the Bank has an independent company that also evaluates the quality of loans and determines if loans are originated in accordance with the guidelines established by the Board.

We recognize that credit losses will be experienced and the risk of loss will vary with, among other things, the type of loan being made, the creditworthiness of the borrower over the term of the loan and, in the case of a collateralized loan, the quality of the collateral, as well as general economic conditions. We intend to maintain an adequate allowance for loan losses based on, among other things, industry standards, management’s experience, historical loan loss experience, evaluation of economic conditions, and regular reviews of delinquencies and loan portfolio quality. We follow a conservative lending policy, but one which permits prudent risks to assist businesses and consumers primarily in our principal market areas. Interest rates vary depending on our cost of funds, the loan maturity, the degree of risk and other loan terms. As appropriate, some interest rates are adjustable with fluctuations in the “prime” rate.

Loan Portfolio Composition

The composition of the Bank’s loan portfolio at December 31, 2008 and 2007 is indicated below, along with the growth from the prior year.

| (dollars in thousands) | | Total Loans December 31, 2008 | | | % of Total Loans | | | Total Loans December 31, 2007 | | | % of Total Loans | | | % Increase (Decrease) from December 31, 2007 to 2008 | |

| Real estate mortgage loans: | | | | | | | | | | | | | | | |

| Commercial | | $ | 224,677 | | | | 59.1 | % | | $ | 210,614 | | | | 61.4 | % | | | 6.7 | % |

| Residential | | | 81,152 | | | | 21.3 | % | | | 75,141 | | | | 21.9 | % | | | 8.0 | % |

| Construction | | | 41,759 | | | | 11.0 | % | | | 29,737 | | | | 8.7 | % | | | 40.4 | % |

| Farmland | | | — | | | | — | | | | 2,325 | | | | 0.7 | % | | | (100.0 | )% |

| Commercial loans | | | 28,445 | | | | 7.5 | % | | | 20,291 | | | | 5.9 | % | | | 40.2 | % |

| Consumer loans | | | 4,070 | | | | 1.1 | % | | | 4,631 | | | | 1.4 | % | | | (12.1 | )% |

| TOTAL | | $ | 380,103 | | | | 100.0 | % | | $ | 342,739 | | | | 100.0 | % | | | 10.9 | % |

Our nonperforming loans as a percentage of gross loans increased from 0.20% at December 31, 2007 to 3.27% at December 31, 2008.

Commercial Real Estate

Commercial real estate loans are typically segmented into three categories: owner occupied commercial properties, properties used by non-profit organizations (i.e., churches and schools) and commercial properties leased to third parties for investment purposes. Commercial real estate loans are secured by the subject property and are underwritten based upon standards set forth in the policy as approved by the Board. Such standards include, among other factors, loan to value limits, cash flow coverage and general creditworthiness of the obligors.

Residential Real Estate

Residential real estate loans include loans secured by first or second mortgages and home equity loans on one-to-four family residential properties. Loans in the residential real estate portfolio are underwritten in accordance with policies set forth and approved by the Board, including repayment capacity and source, value of the underlying property, credit history and stability.

Construction Loans

The Bank provides construction permanent loans to borrowers to finance the construction of owner occupied and lease properties. These loans are categorized as construction loans during the construction period, later converting to commercial or residential real estate loans after the construction is complete and amortization of the loan begins. Real estate development and construction loans are approved based on an analysis of the borrower and guarantor, the viability of the project and are also based on an acceptable percentage of the appraised value of the property securing the loan. Real estate development and construction loan funds are disbursed periodically based on the percentage of construction completed. The Bank carefully monitors these loans with on-site inspections and requires the receipt of lien waivers on funds advanced. Development and construction loans are typically secured by the properties under development or construction, and personal guarantees are typically obtained. Further, to assure that reliance is not placed solely on the value of the underlying property, the Bank considers the market conditions and feasibility of proposed projects, the financial condition and reputation of the borrower and guarantors, the amount of the borrower’s equity in the project, independent appraisals, costs estimates and pre-construction sale information.

Commercial Loans

Commercial loans are primarily underwritten on the basis of the borrowers’ ability to service such debt from income. As a general practice, we take as collateral a security interest in any available real estate, equipment, or other chattel, although loans may also be made on an unsecured basis. Collateralized working capital loans typically are secured by short-term assets whereas long-term loans are primarily secured by long-term assets.

Other

Consumer loans are extended for various purposes, including purchases of automobiles, recreational vehicles, and boats. We also offer home improvement loans, lines of credit, personal loans, and deposit account collateralized loans. Loans to consumers are extended after a credit evaluation, including the creditworthiness of the borrower(s), the purpose of the credit, and the secondary source of repayment. Consumer loans are made at fixed and variable interest rates and may be made on terms of up to ten years.

Loan Referral Programs

The Bank entered into a loan referral agreement with a third party lender whereby we could offer an unsecured line of credit up to $100,000 to small business customers. The product, which was branded by the Bank, was underwritten and closed by a third party. During 2008, the third party lender made a decision to exit this line of business; as a result, the Bank ceased offering this product in August 2008.

Investments

The primary objective of the investment portfolio is to develop a mixture of investments with maturities and compositions so as to earn an acceptable rate of return while meeting liquidity requirements. We invest primarily in obligations guaranteed by the U.S. government and government-sponsored agencies. We also enter into federal funds transactions through our principal correspondent banks. Investments with maturities in excess of one year are generally readily salable on the open market.

Employees

As of February 27, 2009, the Bank had 58 employees. Except for certain officers of the Bank who presently serve as officers of the Company, the Company does not have any employees. Management believes Company relations with its employees have been good.

Data Processing

We currently have an agreement with Metavante Corporation, formerly known as M & I Data Services, to provide our core processing and support certain customer products and delivery systems. We believe that Metavante Corporation will continue to be able to provide state of the art data processing and customer service related processing at a competitive price to support our future growth.

Regulation and Supervision

We operate in a highly regulated environment, where statutes, regulations, and administrative policies govern our business activities. We are supervised by, examined by, and submit reports to, a number of regulatory agencies, including the Federal Reserve Board, the FDIC, and the Florida Department of Financial Services.

We are regulated by the Federal Reserve Board under the Federal Bank Holding Company Act (“BHC Act”), which requires every bank holding company to obtain the prior approval of the Federal Reserve Board before acquiring more than 5% of the voting shares of any bank or all or substantially all of the assets of a bank, and before merging or consolidating with another bank holding company. The Federal Reserve Board, under its regulations and published policy statements, has maintained that a bank holding company must serve as a source of financial strength to its subsidiary bank(s). In adhering to the Federal Reserve Board policy, Bancorp may be required to provide financial support for the Bank at a time when, absent such policy, Bancorp may not otherwise deem it advisable to provide such assistance.

At one time, a bank holding company was generally prohibited from acquiring control of any company which was not a bank and from engaging in any business other than the business of banking or managing and controlling banks. In April 1997, the Federal Reserve Board revised and expanded the list of permissible non-banking activities in which a bank holding company could engage; however, limitations continue to exist under certain laws and regulations. The GLB Act repeals certain regulations pertaining to bank holding companies and eliminates many of the previous prohibitions. Specifically, Title I of the GLB Act repeals Sections 20 and 32 of the Glass-Steagall Act and is intended to facilitate affiliations among banks, securities firms, insurance firms, and other financial companies. To further this goal, the GLB Act amends Section 4 of the BHC Act to authorize bank holding companies that qualify as “financial holding companies” to engage in securities, insurance and other activities that are financial in nature or incidental to a financial activity. The activities of bank holding companies that are not financial holding companies continue to be limited to activities authorized under the BHC Act, such as activities that the Federal Reserve Board previously has determined to be closely related to banking and permissible for bank holding companies.

With respect to expansion, we may establish branch offices anywhere within the State of Florida with regulatory approval. We are also subject to the Florida banking and usury laws limiting the amount of interest that can be charged when making loans or other extensions of credit. In addition, the Bank, as a subsidiary of Bancorp, is subject to restrictions under federal law in dealing with Bancorp and other affiliates. These restrictions apply to extensions of credit to an affiliate, investments in the securities of an affiliate, and the purchase of assets from an affiliate.

The primary source of Bancorp’s income is expected to be dividends from the Bank. A Florida state-chartered commercial bank may not pay cash dividends that would cause the bank’s capital to fall below the minimum amount required by federal or state law. Accordingly, commercial banks may only pay dividends out of the total of current net profits plus retained net profits of the preceding two years to the extent it deems expedient, except as follows. No bank may pay a dividend at any time that the total of net income for the current year when combined with retained net income from the preceding two years produces a loss. The future ability of the Bank to pay dividends to Bancorp will also depend in part on the FDIC capital requirements in effect at such time and our ability to comply with such requirements.

Loans and extensions of credit by all banks are subject to legal lending limitations. Under state law, a state bank may generally grant unsecured loans and extensions of credit in an amount up to 15% of its unimpaired capital and surplus to any person. In addition, a state bank may grant additional loans and extensions of credit to the same person of up to 10% of its unimpaired capital and surplus, provided that the transactions are fully secured. This 10% limitation is separate from, and in addition to, the 15% limitation for unsecured loans. Loans and extensions of credit may exceed these general lending limits only if they qualify under one of several exceptions.

We are subject to regulatory capital requirements imposed by the Federal Reserve Board and the FDIC. Both the Federal Reserve Board and the FDIC have established risk-based capital guidelines for bank holding companies and banks which make regulatory capital requirements more sensitive to differences in risk profiles of various banking organizations. The capital adequacy guidelines issued by the Federal Reserve Board are applied to bank holding companies on a consolidated basis with the banks owned by the holding company. The FDIC’s risk-based capital guidelines apply directly to state banks regardless of whether they are a subsidiary of a bank holding company. Both agencies’ requirements (which are substantially similar) provide that banking organizations must have minimum capital equivalent to 8% of risk-weighted assets to be considered adequately capitalized. The risk weights assigned to assets are based primarily on the perceived levels of risk to capital. For example, securities with an unconditional guarantee by the United States government are assigned the lowest risk weighting. A risk weight of 50% is assigned to loans secured by owner-occupied one-to-four family residential properties. The aggregate amount of assets assigned to each risk category is multiplied by the risk weight assigned to that category to determine the weighted values, which are added together to determine total risk weighted assets.

The Federal Deposit Insurance Corporation Improvement Act of 1991 (“FDICIA”) created and defined five capital categories (well capitalized, adequately capitalized, undercapitalized, significantly undercapitalized, and critically undercapitalized), which are used to determine the nature of any corrective action the appropriate regulator may take in the event an institution reaches a given level of undercapitalization. For example, an institution which becomes undercapitalized must submit a capital restoration plan to the appropriate regulator outlining the steps it will take to become adequately capitalized. Upon approving the plan, the regulator will monitor the institution’s compliance. Before a capital restoration plan will be approved, an entity controlling a bank (i.e., the holding company) must guarantee compliance with the plan until the institution has been adequately capitalized for four consecutive calendar quarters. The liability of the holding company is limited to the lesser of 5% of the institution’s total assets at the time it became undercapitalized or the amount necessary to bring the institution into compliance with all capital standards. Further, in the event of the bankruptcy of the parent holding company, such guarantee would take priority over the parent’s general unsecured creditors. Undercapitalized institutions also will be restricted from paying management fees, dividends, and other capital distributions, will be subject to certain asset growth restrictions, and will be required to obtain prior approval from the appropriate regulator to open new branches or expand into new lines of business. As an institution drops to lower capital levels, the extent of action to be taken by the appropriate regulator increases, restricting the types of transactions in which the institution may engage and ultimately providing for the appointment of a receiver for certain institutions deemed to be critically undercapitalized.

The FDICIA also requires each federal banking agency to prescribe, and the Federal Reserve Board and the FDIC have adopted, for all insured depository institutions and their holding companies, safety and soundness standards relating to such items as: internal controls, information and audit systems, asset quality, loan documentation, classified assets, credit underwriting, interest-rate risk exposure, asset growth, earnings, compensation, fees and benefits, valuation of publicly traded shares, and such other operational and managerial standards as the agency deems appropriate. Finally, each federal banking agency was required to prescribe standards for employment contracts and other compensation arrangements with executive officers, employees, directors, and principal shareholders of insured depository institutions that would prohibit compensation and benefits and other arrangements that are excessive or that could lead to a material financial loss. If an insured depository institution or its holding company fails to meet any of the standards described above, it will be required to submit to the appropriate federal banking agency a plan specifying the steps that will be taken to cure the deficiency. If an institution fails to submit an acceptable plan or fails to implement a plan, the appropriate federal banking agency will require the institution or holding company to correct the deficiency and, until corrected, may impose further restrictions on the institution or holding company, including any of the restrictions applicable under the prompt corrective action provisions of the FDICIA. Both the capital standards and the safety and soundness standards that the FDICIA implements were designed to bolster and protect the deposit insurance fund.

In response to the directives issued under the FDICIA, the regulators have adopted regulations that, among other things, prescribe the capital thresholds for each of five established capital categories. The following table reflects these capital thresholds:

| | | Total Risk-Based Capital Ratio | | | Tier 1 Risk-Based

Capital Ratio | | | | |

Well capitalized (1) | | | 10% | | | | 6% | | | 5% | |

Adequately capitalized (1) | | | 8% | | | | 4% | | | 4%(2) | |

Undercapitalized (3) | | Less than 8% | | | Less than 4% | | | Less than 4% | |

| Significantly undercapitalized | | Less than 6% | | | Less than 3% | | | Less than 3% | |

| Critically undercapitalized | | | — | | | | — | | | Less than 2% | |

| (1) | An institution must meet all three minimums. |

| (2) | 3% for CAMELS composite 1 rated institutions, subject to appropriate federal banking agency guidelines. |

| (3) | An institution falls into this category if it is below the adequately capitalized level for any of the three capital measures. |

Under these capital categories, the Company is classified as well capitalized. At December 31, 2008, the Company’s total risk-based capital and Tier 1 risk-based capital ratios were 11.93% and 9.23%, respectively. The Tier 1 leverage ratio was 8.26% as of the same date. In addition to maintaining all capital levels at or above well-capitalized levels, the Company is committed to maintaining a Tier 1 leverage ratio above 8% at all times.

Under federal law and regulations and subject to certain exceptions, the addition or replacement of any director, or the employment, dismissal, or reassignment of a senior executive officer at any time that the Bank is not in compliance with applicable minimum capital requirements, or otherwise in a troubled condition, or when the FDIC has determined that such prior notice is appropriate, is subject to prior notice to, and potential disapproval by, the FDIC.

Proposals to change the laws and regulations governing the banking industry are frequently introduced in Congress, in the state legislatures and by the various bank regulatory agencies. Accordingly, the scope of regulation and permissible activities of Bancorp and the Bank are subject to change by future federal and state legislation or regulation.

Substantially all of our revenues from external customers, long-lived assets, long-term customer relationships, mortgage and other servicing rights, deferred policy acquisition costs, and deferred tax assets are attributed to the United States.

For Additional Information

We are required to comply with the informational requirements of the Securities Exchange Act of 1934, as amended, and, accordingly, we file annual reports, quarterly reports, current reports, proxy statements and other information with the SEC. You may read or obtain a copy of these reports at the SEC’s public reference room at 100 F. Street, N.E., Room 1580, Washington, D.C. 20549. You may obtain information on the operation of the public reference room and their copy charges by calling the SEC at 1-800-SEC-0330. The SEC maintains a website that contains registration statements, reports, proxy information statements and other information regarding registrants that file electronically with the SEC. The address of the website is http://www.sec.gov.

ITEM 1A. RISK FACTORS

An investment in our common stock involves a number of risks. Before making an investment decision, you should carefully consider all of the risks. If any of the events contemplated by the risk factors discussed below actually impact us, our business, financial condition and results of operations could be materially adversely affected. If this were to occur, the trading price of our common stock could decline.

RISKS RELATED TO OUR BUSINESS

Since we commenced operations in 1999, we have had a relatively short history of experiencing profits.

We rely on the profitability of the Bank to provide funding for our operations. We cannot assure you that we will consistently operate profitably in the future. While we project that the Bank will be profitable in all future periods, we are unable to assure you that we will earn profits as projected, that we will be able to maintain profitability, or that the Bank will be able to consistently fund our ongoing operations.

We are not certain that our capital will be adequate to continue to support the current rate of growth.

Future capital requirements depend on many factors, including the ability to successfully attract new customers and provide additional services, the timing of opening new branch locations, and our profitability levels. If adequate capital is not available, we will be subject to an increased level of regulatory supervision, we may not be able to expand our operations, and our business operating results and financial condition could be adversely affected.

We may require additional capital in the future, which could result in dilution of your ownership interest.

Any capital that is likely to be generated by our operations over the next several years is expected to be needed to continue expanding our operations. Additionally, our board of directors may determine from time to time that, in order to support our strategic objectives, there is a need to obtain additional capital through the issuance of additional shares of our common stock or other securities. These issuances would dilute the ownership interest of current shareholders in the Company and may dilute the per share book value of our common stock.

Our business may face risks with respect to future expansion.

We may acquire other financial institutions or parts of financial institutions in the future and we may engage in additional de novo branch expansion. Acquisitions and mergers involve a number of risks, including:

| | · | the time and costs associated with identifying and evaluating potential acquisitions and merger partners; |

| | · | the estimates and judgments used to evaluate credit, operations, management and market risks with respect to the target institution may not be accurate; |

| | · | the time and costs of evaluating new markets, hiring experienced local management and opening new offices, and the time lags between these activities and the generation of sufficient assets and deposits to support the costs of the expansion; |

| | · | our ability to finance an acquisition and possible dilution to our existing shareholders; |

| | · | the diversion of our management’s attention to the negotiation of a transaction, and the integration of the operations and personnel of the combining businesses; |

| | · | entry into new markets where we lack experience; |

| | · | the introduction of new products and services into our business; |

| | · | the incurrence and possible impairment of goodwill associated with an acquisition and possible adverse short-term effects on our results of operations; and |

| | · | the risk of loss of key employees and customers. |

We may incur substantial costs to expand and can give no assurance such expansion will result in the levels of profits we would expect. There can be no assurance that integration efforts for future mergers or acquisitions will be successful. We may issue equity securities, including common stock, in connection with future acquisitions, which could cause ownership and economic dilution to our shareholders. There is no assurance that, following any future mergers or acquisitions, our integration efforts will be successful or, after giving effect to the acquisition, that we will achieve profits comparable to, or better than, our historical experience.

Customers may not repay their loans, which could have a material adverse effect on our profitability.

The risk that customers may fail to repay their loans is inherent in any bank lending relationship. If our loans are not repaid in accordance with the loan terms, it could have a material adverse effect on our earnings and overall financial condition as well as the value of our common stock. We focus our lending activity in commercial, commercial real estate, residential, home equity and consumer loans.

Our management attempts to minimize credit exposure by carefully monitoring the concentration of loans within specific industries and through loan application and approval procedures. However, we are unable to assure you that such monitoring and procedures will reduce lending risks. Credit losses can cause insolvency and failure of a financial institution and, in such event, shareholders could lose their entire investment.

Our business focus in the Jacksonville area of Florida could make us vulnerable to adverse economic conditions in the area.

Our operations are materially affected by and sensitive to the economy of our market areas in northeastern Florida, and are particularly impacted by the economic conditions in Duval County and the Jacksonville metropolitan area. Because our business is focused in the Jacksonville area, we could be more affected by a weakening of the Jacksonville area economy than banking institutions with operations in diverse geographical areas.

Current economic conditions and industry developments may adversely affect our business and financial results.

If the current U.S. recession continues for a long period of time or the economy and industry experience further deterioration, there can be no assurance that our business, our industry or results of operations will not be significantly adversely impacted. We may have further increases in loan losses, deterioration of capital or limitations on our access to funding or capital. A prolonged recession could also cause further deterioration in real estate values which could drive foreclosures and higher losses than we have historically experienced.

Our location on the east coast of Florida makes us susceptible to weather-related problems.

We rely on our ongoing operations to sustain profitability. Although we have a disaster recovery plan in place, we cannot ensure that severe weather conditions will not have a material adverse effect on our financial condition, results of operations, or cash flows.

We are subject to government regulation and monetary policies that could constrain our growth and profitability.

Bank regulators have imposed various conditions on us. The conditions include, among other things, that: (1) we would not assume additional debt without prior approval by the Federal Reserve Board; (2) we will remain well-capitalized at all times; (3) we will make appropriate filings with the regulatory agencies; and (4) the Bank will meet all regulatory requirements. The regulatory capital requirements imposed on the Bank could have the effect of constraining growth.

We are subject to extensive state and federal government supervision and regulations that impose substantial limitations with respect to loans, purchase of securities, payment of dividends, and many other aspects of the banking business. Regulators include the Board of Governors of the Federal Reserve System (the "Federal Reserve Board"), the FDIC, and the Florida Department of Banking and Finance (the "Florida DBF"). Applicable laws, regulations, interpretations, assessments and enforcement policies have been subject to significant and sometimes retroactively applied changes and may be subject to significant future changes. Regulatory agencies are funded, in part, by assessments imposed upon banks. The FDIC Board of Directors has approved a new system for risk-based assessments effective January 1, 2007 which resulted in additional cost to the Bank in support of a designated reserve ratio. Additional assessments could occur in the future which could impact our financial condition. Many of these regulations are intended to protect depositors, the public, and the FDIC, not shareholders. Future legislation or government policy could adversely affect the banking industry, our operations, or our shareholders. The burden imposed by federal and state regulations may place banks, in general, and us, specifically, at a competitive disadvantage compared to less regulated competitors. Federal economic and monetary policy may affect our ability to attract deposits, make loans, and achieve satisfactory operating results.

We could be negatively impacted by changes in interest rates and economic conditions.

Our results of operations may be materially and adversely affected by changes in prevailing economic conditions, including declines in real estate market values, rapid changes in interest rates, and the monetary and fiscal policies of the federal government. Our profitability is partly a function of the spread between the interest rates earned on investments and loans and those paid on deposits and other liabilities. As with most banking institutions, our net interest spread is affected by general economic conditions and other factors that influence market interest rates. Changes in interest rates may negatively affect our earnings and the value of our assets. Changes in interest rates may affect our level of interest income, the primary component of our gross revenue, as well as the level of our interest expense, our largest recurring expenditure. In a period of rising interest rates, our interest expense could increase in different amounts and at different rates while the interest that we earn on our assets may not change in the same amounts or at the same rates. Accordingly, increases in interest rates could decrease our net interest income. At any given time, our assets and liabilities may be affected differently by a given change in interest rates. As a result, an increase or decrease in rates could have a material adverse effect on our net income, capital and liquidity. While we take measures to reduce interest-rate risk, these measures may not adequately minimize exposure to interest-rate risk.

Bancorp is dependent on the operating performance of the Bank to provide Bancorp with operating funds.

Bancorp is a bank holding company and is dependent upon dividends from the Bank for funds to pay expenses and any cash dividends to shareholders. The Bank is subject to regulatory limitations regarding the payment of dividends. Therefore, the Bank may not be able to provide us with adequate funds to conduct our ongoing operations.

We face competition from a variety of competitors.

We face competition for deposits, loans and other financial services from other community banks, regional banks, out-of-state and in-state national banks, savings banks, thrifts, credit unions and other financial institutions as well as other entities that provide financial services, including consumer finance companies, securities brokerage firms, mortgage brokers, insurance companies, mutual funds, and other lending sources and alternative investment providers. Some of these financial institutions and financial services organizations are not subject to the same degree of regulation as we are. We face increased competition due to the GLB Act which allows insurance firms, securities firms, and other non-traditional financial companies to provide traditional banking services. Due to the growth of the Jacksonville area, it can be expected that significant competition will continue from existing financial services providers, as well as new entrants to the market. Many of these competitors have been in business for many years, have established customers, are larger, have substantially higher lending limits than we do, and are able to offer certain services that we do not provide, such as certain loan products and international banking services. In addition, many of these entities have greater capital resources than we have, which among other things may allow them to price their services at levels more favorable to the customer or to provide larger credit facilities. If we are unable to attract and retain customers with personal services, attractive product offerings and competitive rates, our business, results of operations, future growth and operational results will be adversely affected.

Our lending limit restricts our ability to compete with larger financial institutions.

Our per customer lending limit is approximately $9.0 million, subject to further reduction based on regulatory criteria relevant to any particular loan. Accordingly, the size of loans which we can offer to potential customers is less than the size that many of our competitors with larger lending limits are able to offer. This limit has affected and will continue to affect our ability to seek relationships with larger businesses in the market. We accommodate loans in excess of our lending limit through the sale of portions of such loans to other banks. However, we may not be successful in attracting or maintaining customers seeking larger loans or in selling portions of such larger loans on terms that are favorable to us.

We may need to spend significant money to keep up with technology so we can remain competitive.

The banking industry continues to undergo rapid technological changes with frequent introduction of new technology-driven products and services. In addition to providing better service to customers, the effective use of technology increases efficiency and enables us to reduce costs. Our future success depends in part upon our ability to address the needs of our customers by using technology to provide products and services that will satisfy customer demands for convenience as well as to create additional operating efficiencies. Many of our competitors have substantially greater resources to invest in technological improvements. Such technology may permit competitors to perform certain functions at a lower cost than we can. We may not be able to effectively implement new technology-driven products and services or be successful in marketing these to our customers.

We are dependent on the experience and expertise of our current management and their departure may impair our operations.

Bancorp and the Bank are primarily dependent upon the services of Gilbert J. Pomar, III, Chief Executive Officer and President; Valerie A. Kendall, Executive Vice President and Chief Financial Officer; and Scott M. Hall, Executive Vice President and Chief Lending Officer. If the services of these individuals were to become unavailable for any reason, or if we were unable to hire highly qualified and experienced personnel to replace them, our operating results could be adversely affected. While we have an employment agreement with each of Mr. Pomar and Mr. Hall, we do not have an agreement with Ms. Kendall.

RISKS RELATED TO OUR COMMON STOCK

Our common stock is thinly traded and, therefore, you may have difficulty selling shares.

Our common stock is traded on the NASDAQ Global Market; however, we are unable to provide assurance that an active market will exist in the future or that shares can be liquidated without delay. The average daily trading volume in Bancorp stock was 1,774 in 2008.

We do not anticipate paying dividends for the foreseeable future.

We do not anticipate that dividends will be paid on our common stock for the foreseeable future. It is the policy of our Board to reinvest earnings for such period of time as is necessary to ensure our successful operations. There are no current plans to initiate payment of cash dividends, and future dividend policy will depend on our earnings, capital and regulatory requirements, financial conditions and other factors considered relevant by our Board. Bancorp is largely dependent upon dividends paid by the Bank to provide funds to pay cash dividends if and when the Board may declare such dividends. No assurance can be given that future earnings will be sufficient to satisfy regulatory requirements and permit the legal payment of dividends to shareholders at any time in the future. Even if we could legally declare dividends, the amount and timing of such dividends would be at the discretion of our Board. The Board may in its sole discretion decide not to declare dividends.

The market price of our common stock may be volatile.

The market price of our common stock is subject to fluctuations as a result of a variety of factors, including the following:

| | · | quarterly variations in our operating results or those of other banking institutions; |

| | · | changes in national and regional economic conditions, financial markets or the banking industry; and |

| | · | other developments affecting us or other financial institutions. |

The trading volume of our common stock is limited, which may increase the volatility of the market price for our stock. In addition, the stock market has experienced significant price and volume fluctuations in recent years. This volatility has had a significant effect on the market prices of securities issued by many companies for reasons not necessarily related to the operating performance of these companies.

Our articles of incorporation and bylaws, and certain laws that we are subject to, contain provisions that may delay or prevent a change of control.

Sections 607.0901 through 607.0908 of the Florida Business Corporation Act (the "FBCA") provide for supermajority voting and impose other requirements on certain business combinations with interested shareholders and limit voting rights of certain acquirers of control shares. Federal law requires the approval of the Federal Reserve Board before acquisition or "control" of a bank holding company. Our articles of incorporation provide that the FBCA's control shares statute applies to acquisitions of our shares unless the acquirer has acquired the shares (1) for others in good faith and not to circumvent the control shares statute and requires instruction from others to vote the shares, or (2) through a distribution conducted by us in a private or public offering or under a warrant, option or employee benefit plan, under the laws of descent and distribution, from a donee of a lifetime gift, through a transfer between immediate family members or through satisfaction of a pledge or security interest.

Our articles of incorporation also (1) provide for a board of directors that is divided into three classes of directors; (2) require the shareholders to take action at a duly called meeting and not by written consent; (3) limit the Board's ability to increase the number of directors; (4) require the affirmative vote of holders of two-thirds of our voting stock for certain affiliated transactions such as mergers, consolidations, sales, leases, pledges, transfers, dissolutions, reclassifications with or loans to shareholders owning more than 10% of our shares or their affiliates unless the transaction is approved by the disinterested directors and certain other conditions are met; (5) require the Board to consider a variety of factors when evaluating any proposal involving a potential tender or exchange offer, merger, sale or business combination, including the social and economic impact of such a proposal on customers, employees, and the communities in which we operate or are located, and on our ability to fulfill our corporate objectives and perform under applicable statutes and regulations; and (6) require the affirmative vote of holders of at least 66% of the voting stock to change any provisions of the articles of incorporation relating to the right of shareholders to act by consent, the classification of the board, affiliated transactions or control share acquisitions. These provisions may have the effect of delaying or preventing a change in control. As a result, these provisions could adversely affect the price of our common stock by reducing the gain which could potentially be realized by a shareholder in a change of control.

ITEM 1B. UNRESOLVED STAFF COMMENTS

None.

ITEM 2. PROPERTIES

| Property Location | | Year Location Established | | Approximate Square Footage | | Owned / Leased |

Headquarters (1) 100 North Laura Street | | 2004 | | | 14,815 | | Leased |

| | | | | | | | |

Branch Office 10325 San Jose Boulevard | | 1998 | | | 3,567 | | Owned |

| | | | | | | | |

Branch Office 12740-200 Atlantic Boulevard | | 2000 | | | 3,080 | | Owned |

| | | | | | | | |

Branch Office (2) 4343 Roosevelt Boulevard | | 2005 | | | 3,127 | | Leased |

| | | | | | | | |

Branch Office (3) 7880 Gate Parkway | | 2006 | | | 9,372 | | Leased |

| | (1) | The Bank has a 10-year lease that expires September 30, 2014 for our headquarters location which specifies rent of $20.00 per square foot and is subject to annual increases of $0.50 per square foot on October 1st of each year through September 30, 2014. The Bank has five renewal options, each to extend the term of the lease for five years, the first option term commencing on October 1, 2014, and the last option term ending on September 30, 2039. |

| | (2) | The Bank took occupancy of this branch on November 1, 2005 and opened for business on February 6, 2006. The Bank has a 10-year lease that expires November 1, 2015 for this branch, which specifies rent of $90,000 per annum and is subject to annual increases of 3% on November 1 of each year through November 1, 2015. The Bank has four renewal options, each to extend the term of the lease for five years, the first option term commencing on November 1, 2015, and the last option term ending on November 1, 2035. |

| | (3) | The Bank took occupancy of this branch on January 13, 2006 and opened for business on June 9, 2006. The Bank has a 10-year lease that expires January 13, 2016 for this branch, which specifies rent of $210,870 per annum and is subject to annual increases on the anniversary date to the extent of any percentage change that occurs in the consumer price index for all urban consumers. The Bank has two renewal options, each to extend the term of the lease for five years, the first option term commencing on January 13, 2016, and the last option term ending on January 13, 2026. |

ITEM 3. LEGAL PROCEEDINGS

From time to time, as a normal incident of the nature and kind of business in which we are engaged, various claims or charges are asserted against us and/or our directors, officers or affiliates. In the ordinary course of business, the Company is also subject to regulatory examinations, information gathering requests, inquiries and investigations. Other than ordinary routine litigation incidental to our business, management believes after consultation with legal counsel that there are no pending legal proceedings against Bancorp or the Bank that will, individually or in the aggregate, have a material adverse effect on the consolidated results of operations or financial condition of the Company.

ITEM 4. SUBMISSION OF MATTERS TO A VOTE OF SECURITY HOLDERS

There were no matters submitted to a vote of security holders during the fourth quarter of 2008.

PART II

| ITEM 5. | MARKET FOR REGISTRANT’S COMMON EQUITY AND RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES |

Our common stock is traded on NASDAQ under the symbol JAXB. The following table shows the high and low sale prices of our common stock for each quarter of 2007 and 2008.

| Year | | Quarter | | High | | | Low | |

| 2007 | | First | | $ | 35.99 | | | $ | 31.16 | |

| | | Second | | $ | 35.93 | | | $ | 26.95 | |

| | | Third | | $ | 32.21 | | | $ | 27.00 | |

| | | Fourth | | $ | 27.95 | | | $ | 18.29 | |

| 2008 | | First | | $ | 27.54 | | | $ | 18.50 | |

| | | Second | | $ | 24.50 | | | $ | 15.75 | |

| | | Third | | $ | 16.07 | | | $ | 11.60 | |

| | | Fourth | | $ | 13.00 | | | $ | 10.92 | |

As of March 18, 2009, Bancorp had 1,748,799 outstanding shares of common stock, par value $.01 per share, held by approximately 155 registered shareholders of record.

It is the policy of our board of directors to reinvest earnings for such period of time as is necessary to ensure our successful operations. There are no current plans to initiate payment of cash dividends, and future dividend policy will depend on our earnings, capital and regulatory requirements, financial condition, and other factors considered relevant by our board of directors. For more information regarding Bancorp’s ability to pay dividends, please refer to the section captioned “Regulation and Supervision” under Item 1 of this Annual Report on Form 10-K, which information is hereby incorporated by reference.

Equity Compensation Plans Information

The following table sets forth information about the Jacksonville Bancorp, Inc. Stock Option Plan, as amended, and the 2008 Amendment and Restatement of the Jacksonville Bancorp, Inc. 2006 Stock Incentive Plan, as of December 31, 2008:

| Plan Category | | Number of securities to be issued upon exercise of outstanding options, warrants and rights | | | Weighted average exercise price of

outstanding options, warrants and rights | | | Number of securities remaining available for future issuance | |

| Equity compensation plans approved by security holders | | | 158,942 | | | $ | 14.62 | | | | 68,233 | |

| Equity compensation plans not approved by security holders | | | — | | | | — | | | | — | |

| Total | | | 158,942 | | | $ | 14.62 | | | | 68,233 | |

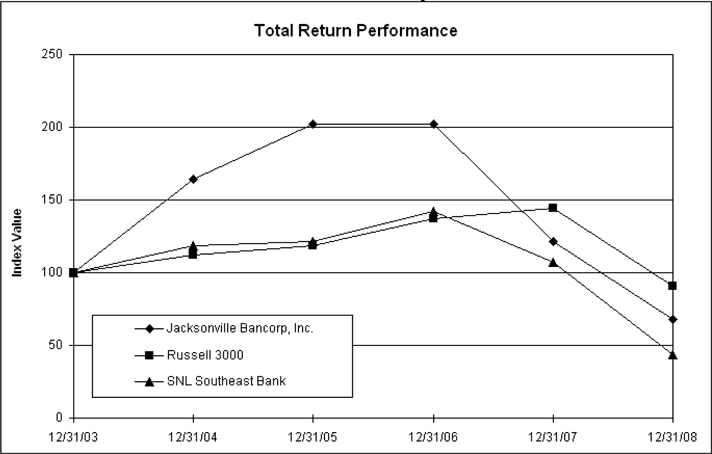

Shareholder Return Performance

A five-year comparison of shareholder return performance of the Company with the Russell 3000 Index and the SNL Southeast Bank Index is shown on the graph below. This graph assumes that $100 was invested on December 31, 2002 and all dividends were reinvested in the Company and other indices. The Russell 3000 index is a broad equity market index which measures the performance of the largest 3,000 U.S. companies representing approximately 98% of the U.S. equity market. The SNL Southeast Bank Index is a published industry index which represents publicly-traded banks and bank holding companies located in the southeastern United States.

Jacksonville Bancorp, Inc.

| | | Period Ending | |

| Index | | 12/31/03 | | | 12/31/04 | | | 12/31/05 | | | 12/31/06 | | | 12/31/07 | | | 12/31/08 | |

| Jacksonville Bancorp, Inc. | | | 100.00 | | | | 164.35 | | | | 202.13 | | | | 201.83 | | | | 121.34 | | | | 67.68 | |

| Russell 3000 | | | 100.00 | | | | 111.95 | | | | 118.80 | | | | 137.47 | | | | 144.54 | | | | 90.61 | |

| SNL Southeast Bank | | | 100.00 | | | | 118.59 | | | | 121.39 | | | | 142.34 | | | | 107.23 | | | | 43.41 | |

COMPANY PURCHASES OF EQUITY SECURITIES

Following approval by the shareholders at the 2003 Annual Meeting, the Company established the Directors’ Stock Purchase Plan for nonemployee directors. Under this plan, directors may elect to receive shares of the Company’s common stock as an alternative to the equivalent of cash for directors’ fees. All transactions executed under the Director’s Stock Purchase Plan were open-market purchases and were accounted for as treasury stock on the date of purchase. The Company repurchased an aggregate of 1,379 shares of its common stock during the last quarter for issuance under this Plan.

| Period | | Total number of shares purchased | | | Average price paid per share | | | Total number of shares purchased as part of publicly announced plans or programs | | | Maximum number (or approximate dollar value) of shares that may yet be purchased under the plans or programs | |

| October 1 – October 31, 2008 | | | 1,179 | | | $ | 12.10 | | | | — | | | | — | |

| November 1 – November 30, 2008 | | | — | | | | — | | | | — | | | | — | |

| December 1 – December 31, 2008 | | | 200 | | | $ | 11.72 | | | | — | | | | — | |

| Total | | | 1,379 | | | | — | | | | — | | | | — | |

ITEM 6. SELECTED FINANCIAL DATA

The selected consolidated financial data presented below as of and for the years ended December 31, 2008, 2007, 2006, 2005 and 2004 have been derived from our Consolidated Financial Statements. The ratios and other data are unaudited and have been derived from our records. The information presented below should be read in conjunction with the Consolidated Financial Statements and related notes and “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

At or for the Year Ended December 31,

(Dollars in thousands, except per share figures)

| | 2008 | | | 2007 | | | 2006 | | | 2005 | | | 2004 | |

| Cash and cash equivalents | | $ | 10,148 | | | $ | 6,035 | | | $ | 4,478 | | | $ | 4,767 | | | $ | 6,735 | |

| Securities, available for sale and held to maturity | | | 29,734 | | | | 29,777 | | | | 26,109 | | | | 24,261 | | | | 23,175 | |

| Loans, net | | | 374,993 | | | | 339,265 | | | | 281,006 | | | | 232,031 | | | | 188,137 | |

| All other assets | | | 19,124 | | | | 16,885 | | | | 13,982 | | | | 11,985 | | | | 5,697 | |

| | | | | | | | | | | | | | | | | | | | | |

| Total assets | | $ | 433,999 | | | $ | 391,962 | | | $ | 325,575 | | | $ | 273,044 | | | $ | 223,744 | |

| | | | | | | | | | | | | | | | | | | | | |

| Deposit accounts | | | 345,544 | | | | 288,893 | | | | 282,626 | | | | 234,211 | | | | 201,188 | |

| Other borrowings | | | 60,550 | | | | 74,830 | | | | 18,832 | | | | 17,650 | | | | 4,000 | |

| All other liabilities | | | 1,060 | | | | 1,610 | | | | 979 | | | | 1,337 | | | | 752 | |

| Shareholders' equity | | | 26,845 | | | | 26,629 | | | | 23,138 | | | | 19,846 | | | | 17,804 | |

| | | | | | | | | | | | | | | | | | | | | |

| Total liabilities and shareholders' equity | | $ | 433,999 | | | $ | 391,962 | | | $ | 325,575 | | | $ | 273,044 | | | $ | 223,744 | |

| | | | | | | | | | | | | | | | | | | | | |

| Operations Data: | | 2008 | | | 2007 | | | 2006 | | | 2005 | | | 2004 | |

| Total interest income | | $ | 25,563 | | | $ | 26,808 | | | $ | 22,017 | | | $ | 15,748 | | | $ | 10,858 | |

| Total interest expense | | | 13,560 | | | | 14,419 | | | | 10,945 | | | | 6,529 | | | | 3,928 | |

| | | | | | | | | | | | | | | | | | | | | |

| Net interest income | | | 12,003 | | | | 12,389 | | | | 11,072 | | | | 9,219 | | | | 6,930 | |

| Provision for loan losses | | | 3,570 | | | | 542 | | | | 546 | | | | 481 | | | | 282 | |

| | | | | | | | | | | | | | | | | | | | | |

| Net interest income after provision for loan losses | | | 8,433 | | | | 11,847 | | | | 10,526 | | | | 8,738 | | | | 6,648 | |

| | | | | | | | | | | | | | | | | | | | | |

| Noninterest income | | | 1,178 | | | | 1,184 | | | | 1,047 | | | | 964 | | | | 767 | |

| Noninterest expenses | | | 9,805 | | | | 8,485 | | | | 7,573 | | | | 6,287 | | | | 5,274 | |

| | | | | | | | | | | | | | | | | | | | | |

| Income before income taxes | | | (194 | ) | | | 4,546 | | | | 4,000 | | | | 3,415 | | | | 2,141 | |

| Income taxes | | | (229 | ) | | | 1,588 | | | | 1,477 | | | | 1,242 | | | | 806 | |

| | | | | | | | | | | | | | | | | | | | | |

| Net income | | $ | 35 | | | $ | 2,958 | | | $ | 2,523 | | | $ | 2,173 | | | $ | 1,335 | |

| | | | | | | | | | | | | | | | | | | | | |

| Per Share Data: | | | | | | | | | | | | | | | | | | | | |

| Basic earnings per share | | $ | .02 | | | $ | 1.70 | | | $ | 1.46 | | | $ | 1.27 | | | $ | .86 | |

| Diluted earnings per share | | | .02 | | | | 1.63 | | | | 1.39 | | | | 1.21 | | | | .79 | |

| Dividends declared per share | | | — | | | | — | | | | — | | | | — | | | | — | |

| Total shares outstanding at end of year | | | 1,748,599 | | | | 1,746,331 | | | | 1,741,688 | | | | 1,714,716 | | | | 1,708,366 | |

| | | | | | | | | | | | | | | | | | | | | |

| Ratios and Other Data: | | | | | | | | | | | | | | | | | | | | |

| Book value per share at end of year | | $ | 15.35 | | | $ | 15.25 | | | $ | 13.28 | | | $ | 11.57 | | | $ | 10.42 | |

| Return on average assets | | | 0.01 | % | | | 0.82 | % | | | 0.83 | % | | | 0.88 | % | | | 0.66 | % |

| Return on average equity | | | 0.13 | % | | | 12.08 | % | | | 11.92 | % | | | 11.69 | % | | | 8.84 | % |

| Average equity to average assets | | | 6.40 | % | | | 6.76 | % | | | 6.95 | % | | | 7.49 | % | | | 7.46 | % |

| Interest rate spread during the period | | | 2.46 | % | | | 2.90 | % | | | 3.15 | % | | | 3.27 | % | | | 3.14 | % |

| Net yield on average interest-earning assets | | | 2.97 | % | | | 3.56 | % | | | 3.81 | % | | | 3.88 | % | | | 3.53 | % |

| Noninterest expenses to average assets | | | 2.33 | % | | | 2.34 | % | | | 2.49 | % | | | 2.53 | % | | | 2.60 | % |

| Average interest-earning assets to average interest-bearing liabilities | | | 1.15 | | | | 1.16 | | | | 1.17 | | | | 1.22 | | | | 1.19 | |

| Nonperforming loans and foreclosed assets as a percentage of total assets at end of year | | | 2.89 | % | | | 0.18 | % | | | 0.26 | % | | | 0.28 | % | | | 0.29 | % |

| Allowance for loan losses as a percentage of total loans at end of year | | | 1.24 | % | | | 0.91 | % | | | 0.92 | % | | | 0.94 | % | | | 0.97 | % |

Total number of banking offices1 | | | 5 | | | | 5 | | | | 5 | | | | 3 | | | | 3 | |

(1) Amount represents banking offices operating at December 31 of each year. The Bank currently has five operating offices.

ITEM 7.

MANAGEMENT'S DISCUSSION AND ANALYSIS

OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

Years Ended December 31, 2008, 2007 and 2006

General

Jacksonville Bancorp, Inc. (“Bancorp”) was incorporated on October 24, 1997 and was organized to conduct the operations of The Jacksonville Bank (the “Bank”). The Bank is a Florida state-chartered commercial bank that opened for business on May 28, 1999, and its deposits are insured by the Federal Deposit Insurance Corporation. The Bank provides a variety of community banking services to businesses and individuals in Duval County, Florida. During 2000, the Bank formed Fountain Financial, Inc., a wholly owned subsidiary. The primary business activities of Fountain Financial, Inc. consist of the referral of our customers to third parties for the sale of insurance and investment products.

Business Strategy

Our primary business segment is community banking and consists of attracting deposits from the general public and using such deposits and other sources of funds to originate commercial business loans, commercial real estate loans, residential mortgage loans and a variety of consumer loans. We also invest in mortgage-backed securities and securities backed by the United States Government, and agencies thereof, as well as other securities.

Our goal is to sustain profitable, controlled growth by focusing on increasing our loan and deposit market share in the Northeast Florida market by developing new financial products, services and delivery channels; closely managing yields on earning assets and rates on interest-bearing liabilities; focusing on noninterest income opportunities, controlling the growth of noninterest expenses and maintaining strong asset quality. Our current strategy is to grow organically and through acquisition if price, culture and market fit within our strategies.

On January 28, 2008, Bancorp entered into an Agreement and Plan of Merger (the “Merger Agreement”) with Heritage Bancshares, Inc. (“Heritage”) pursuant to which, subject to the satisfaction or waiver of the conditions contained therein, Heritage would merge with and into Bancorp (the “Merger”), with Bancorp remaining as the surviving entity.

On June 24, 2008, Bancorp announced that, through mutual agreement, the Merger Agreement with Heritage had been terminated. Both companies attributed the amicable termination of the deal to the current economic climate in the banking industry which changed the benefits of the merger for their respective shareholders.

2008 Executive Overview

The following were significant factors related to 2008 results as compared to 2007. The 2008 performance is reflective of the successful execution of our strategy to focus on organic growth within the Northeast Florida market. During 2008, we recorded growth in commercial real estate, construction and commercial loans. During the year, commercial real estate loans increased by $14.1 million, or 6.7%, construction loans increased by $12.0 million, or 40.4%, and commercial loans increased by $8.2 million, or 40.2%. Total loans increased by $37.4 million, or 10.9%.

Total deposits increased by $57.7 million, or 19.6%, during 2008. The following are changes in the deposit categories:

| | o | Noninterest-bearing deposits increased $5.5 million, or 15.5%. |

| | o | Money market savings and NOW deposits decreased by $28.4 million, or 24.5%. The decline was due to the run-off in one money market product which is tied to the prime lending rate (which declined rapidly during 2008). The Bank adjusted the spread on this product to be more competitive in October 2008 which slowed this run-off substantially. |

| | o | The certificate of deposit portfolio increased by $79.6 million, or 58.0%. The Company’s management pursued local deposits more aggressively by offering competitive deposit products in an effort to attract core deposits and utilized the National and Brokered CD markets as an additional source of funding the asset growth. |

| | o | Borrowed funds, consisting of Federal Home Loan Bank (FHLB) advances¸ Federal Reserve borrowings, and subordinated debentures, totaled $60.6 million at year end 2008 compared to $74.8 million at the end of 2007. During 2008, we decreased our FHLB advances by $47.8 million, increased our borrowing by $26.0 million from the Federal Reserve and increased subordinated debentures by $7.6 million as a result of a private placement offering of trust preferred securities. |

Total shareholders’ equity increased $216,000, or 0.8%, during 2008. Management remains committed to retaining sufficient equity to protect shareholders and depositors, provide for reasonable growth and fully comply with regulatory requirements.

The allowance for loan loss as a percentage of total loans outstanding was 1.24% at December 31, 2008, compared to 0.91% at December 31, 2007. During 2008, the Company had charge-offs of $2.1 million, recoveries of $114,000 and recorded a provision for loan loss of $3.6 million, compared to charge-offs of $71,000, recoveries of $24,000 and provision for loan losses of $542,000 in 2007.

Our net income was $35,000 in 2008 as compared to $3.0 million in 2007. Our diluted earnings per share were $0.02 in 2008 as compared to $1.63 in 2007. Return on average assets and return on average equity were 0.01% and 0.13%, respectively, in 2008 compared to 0.82% and 12.08%, respectively, in 2007.

Interest income was $25.6 million in 2008 as compared to $26.8 million in 2007, a decrease of $1.2 million, or 4.6%, primarily as a result of the ongoing reduction in short-term rates by the Federal Reserve in 2008 as well as $12.4 million added to nonperforming assets offset by an average earnings asset growth of $55.4 million.

Basic average shares outstanding increased to 1,748,295 in 2008 from 1,744,512 in 2007. The diluted weighted average shares outstanding decreased to 1,791,342 from 1,816,149 in the same periods.

Noninterest income remained flat at $1.2 million for 2008 and 2007. In 2008, there was a reduction in mortgage origination referral income due to the slow real estate market, partially offset by income earned on an additional $3.5 million BOLI contract entered into by the Bank during the second quarter.

Critical Accounting Policies

A critical accounting policy is one that is both very important to the portrayal of the Company's financial condition and requires management's most difficult, subjective or complex judgments. The circumstances that make these judgments difficult, subjective or complex have to do with the need to make estimates about the effect of matters that are inherently uncertain. Based on this definition, the Company's primary critical accounting policy is the establishment and maintenance of an allowance for loan loss.

The allowance for loan loss is established through a provision for loan loss charged to expense. Loans are charged against the allowance for loan loss when management believes that the collectability of the principal is unlikely. The allowance is an amount that management believes will be adequate to absorb probable incurred losses on existing loans that may become uncollectible based on evaluations of the collectability of the loans. The evaluations take into consideration such objective factors as changes in the nature and volume of the loan portfolio and historical loss experience. The evaluation also considers certain subjective factors such as overall portfolio quality, review of specific problem loans and current economic conditions that may affect the borrowers' ability to pay. The level of the allowance for loan loss is also impacted by increases and decreases in loans outstanding, because either more or less allowance is required as the amount of the Company's credit exposure changes. To the extent actual loan losses differ materially from management's estimate of these subjective factors, loan growth/run-off accelerates, or the mix of loan types changes, the level of the provision for loan loss, and related allowance can, and will, fluctuate.

Recent Accounting Pronouncements

Please refer to Note 1 to the accompanying Consolidated Financial Statements for information related to the adoption of new accounting standards and the effect of newly issued but not yet effective accounting standards.

FDIC Insurance Assessments

The FDIC is an independent federal agency established originally to insure the deposits, up to prescribed statutory limits, of federally insured banks and to preserve the safety and soundness of the banking industry. The FDIC has adopted a risk-based assessment system for insured depository institutions that takes into account the risks attributable to different categories and concentrations of assets and liabilities.