QuickLinks -- Click here to rapidly navigate through this document

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

ý |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2012 |

or |

o |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to |

Commission File Number: 001-35358

TC PipeLines, LP

(Exact name of registrant as specified in its charter)

Delaware

(State or other jurisdiction

of incorporation or organization) | | 52-2135448

(I.R.S. Employer

Identification No.) |

717 Texas Street, Suite 2400

Houston, Texas

(Address of principal executive offices) |

|

77002-2761

(Zip code) |

877-290-2772

(Registrant's telephone number, including area code) |

Securities registered pursuant to Section 12(b) of the Act: |

Common units representing limited partner interests |

|

New York Stock Exchange |

| (Title of each class) | | (Name of each exchange on which registered) |

Securities registered pursuant to Section 12(g) of the Act:

None |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ý No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ý No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ý

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "small reporting company" in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ý | | Accelerated filer o | | Non-accelerated filer o

(Do not check if a small reporting company) | | Small Reporting Company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No ý

The aggregate market value of the common units of the registrant held by non-affiliates as of June 30, 2012 was approximately $1.6 billion.

As of February 28, 2013, there were 53,472,766 common units of the registrant outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

None

TC PIPELINES, LP

TABLE OF CONTENTS

| | | | | Page No. |

|

| PART I | | |

| Item 1. | | Business | | 8 |

| Item 1A. | | Risk Factors | | 17 |

| Item 1B. | | Unresolved Staff Comments | | 27 |

| Item 2. | | Properties | | 27 |

| Item 3. | | Legal Proceedings | | 28 |

| Item 4. | | Mine Safety Disclosure | | 29 |

PART II |

|

|

|

|

| Item 5. | | Market for Registrant's Common Equity, Related Stockholder Matters and Issuer | | |

| | | Purchases of Equity Securities | | 29 |

| Item 6. | | Selected Financial Data | | 30 |

| Item 7. | | Management's Discussion and Analysis of Financial Condition and Results of Operations | | 30 |

| Item 7A. | | Quantitative and Qualitative Disclosures About Market Risk | | 45 |

| Item 8. | | Financial Statements and Supplementary Data | | 47 |

| Item 9. | | Changes in and Disagreements With Accountants on Accounting and Financial Disclosure | | 47 |

| Item 9A. | | Controls and Procedures | | 47 |

| Item 9B. | | Other Information | | 48 |

PART III |

|

|

|

|

| Item 10. | | Directors, Executive Officers and Corporate Governance | | 48 |

| Item 11. | | Executive Compensation | | 52 |

| Item 12. | | Security Ownership of Certain Beneficial Owners and Management and Related | | |

| | | Stockholder Matters | | 55 |

| Item 13. | | Certain Relationships and Related Transactions, and Director Independence | | 57 |

| Item 14. | | Principal Accountant Fees and Services | | 61 |

PART IV |

|

|

|

|

| Item 15. | | Exhibits and Financial Statement Schedules | | 61 |

Signatures |

|

|

|

67 |

All amounts are stated in United States dollars unless otherwise indicated.

4 TC PIPELINES, LP

Definitions

The abbreviations, acronyms, and industry terminology used in this annual report are defined as follows:

| 2011 Credit Agreement | | $200 million amended and restated revolving Credit Agreement for Northern Border |

Acquisitions |

|

The acquisition from subsidiaries of TransCanada of a 25 percent membership interest in each of GTN and Bison |

AFUDC |

|

Allowance for funds used during construction |

ASC |

|

Accounting Standards Codification |

Bison |

|

Bison Pipeline LLC |

Delaware Act |

|

Delaware Revised Uniform Limited Partnership Act |

DOT |

|

U.S. Department of Transportation |

DSUs |

|

Deferred Share Units |

EPA |

|

U.S. Environmental Protection Agency |

FERC |

|

Federal Energy Regulatory Commission |

Fracking |

|

Horizontal drilling in combination with multi-stage hydraulic fractoring |

GAAP |

|

U.S. generally accepted accounting principles |

General Partner |

|

TC PipeLines GP, Inc. |

GHG |

|

Greenhouse Gas |

Great Lakes |

|

Great Lakes Gas Transmission Limited Partnership |

GTN |

|

Gas Transmission Northwest LLC |

GTN Settlement |

|

Stipulation and Agreement of Settlement for GTN regarding its rates and terms and conditions of service |

HCAs |

|

High consequence areas |

IDRs |

|

Incentive Distribution Rights |

IRS |

|

Internal Revenue Service |

KPMG |

|

KPMG LLP |

LDCs |

|

Local Distribution Companies |

LIBOR |

|

London Interbank Offered Rate |

LNG |

|

Liquefied Natural Gas |

Mainline |

|

TransCanada's Mainline, a natural gas transmission system extending from the Alberta/Saskatchewan border east to Quebec |

MBT |

|

Michigan Business Tax |

MDth/d |

|

Thousand dekatherms per day |

NGA |

|

Natural Gas Act of 1938 |

North Baja |

|

North Baja Pipeline, LLC |

Northern Border |

|

Northern Border Pipeline Company |

Northern Border Settlement |

|

Stipulation and Agreement of Settlement for Northern Border regarding its rates and conditions of service |

NYSE |

|

New York Stock Exchange |

Other Pipes |

|

North Baja and Tuscarora |

Our pipeline systems/our pipelines |

|

Our ownership interests in Great Lakes, Northern Border, GTN, Bison, North Baja and Tuscarora |

Partnership |

|

TC PipeLines, LP and its subsidiaries |

2012 ANNUAL REPORT5

Partnership Agreement |

|

Second Amended and Restated Agreement of Limited Partnership |

PHMSA |

|

U.S. Department of Transportation Pipeline and Hazardous Materials Safety Administration |

SEC |

|

Securities and Exchange Commission |

Senior Credit Facility |

|

TC PipeLines, LP's revolving credit and term loan agreement |

TransCanada |

|

TransCanada Corporation and its subsidiaries |

Tuscarora |

|

Tuscarora Gas Transmission Company |

Tuscarora Settlement |

|

Stipulation and Agreement of Settlement for Tuscarora regarding its rates and terms and conditions of service |

U.S. |

|

United States of America |

WCSB |

|

Western Canada Sedimentary Basin |

Unless the context clearly indicates otherwise, TC PipeLines, LP, its subsidiaries and equity investees are collectively referred to in this annual report as "we," "us," "our" and "the Partnership." We use "our pipeline systems" and "our pipelines" when referring to the Partnership's ownership interests in Great Lakes Gas Transmission Limited Partnership (Great Lakes), Northern Border Pipeline Company (Northern Border), Gas Transmission Northwest LLC (GTN), Bison Pipeline LLC (Bison), North Baja Pipeline, LLC (North Baja) and Tuscarora Gas Transmission Company (Tuscarora).

6 TC PIPELINES, LP

PART I

FORWARD-LOOKING STATEMENTS AND CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING INFORMATION

This report includes certain forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. Forward-looking statements are identified by words and phrases such as: "anticipate," "estimate," "expect," "project," "intend," "plan," "believe," "forecast," "should," "predict," "could," "will," "may," and other terms and expressions of similar meaning. The absence of these words, however, does not mean that the statements are not forward-looking. These statements are based on management's beliefs and assumptions and on currently available information and include, but are not limited to, statements regarding anticipated financial performance, future capital expenditures, liquidity, market or competitive conditions, regulations, organic or strategic growth opportunities, contract renewals and ability to market open capacity, business prospects, outcome of regulatory proceedings and cash distributions to unitholders.

Forward-looking statements involve risks and uncertainties that may cause actual results to differ materially from the results predicted. Factors that could cause actual results to differ materially from those contemplated in forward-looking statements include, but are not limited to:

- •

- the ability to grow distributions through accretive expansions or acquisitions;

- •

- the ability of our pipeline systems to sell available capacity on favorable terms and renew expiring contracts which are affected by, among other factors:

- •

- demand for natural gas;

- •

- changes in relative cost structures and production levels of natural gas producing basins;

- •

- natural gas prices and regional differences;

- •

- weather conditions;

- •

- availability and location of natural gas supplies in Canada and United States of America (U.S.);

- •

- competition from other pipeline systems;

- •

- natural gas storage levels;

- •

- the level of production of natural gas liquids and the subsequent impact on relative competitiveness of natural gas producing basins; and

- •

- rates and terms of service;

- •

- increases in operational or compliance costs resulting from changes in laws and governmental regulations affecting our pipeline systems, particularly regulations issued by the Federal Energy Regulatory Commission (FERC), the U.S. Environmental Protection Agency (EPA), U.S. Department of Transportation (DOT) and U.S. DOT Pipeline and Hazardous Materials Safety Administration (PHMSA);

- •

- the outcome and frequency of rate proceedings on our pipeline systems;

- •

- our ability to identify and complete expansion projects and other accretive growth opportunities;

- •

- the performance by the shippers of their contractual obligations on our pipeline systems;

- •

- changes in the taxation of master limited partnership investments by states or the federal government such as the elimination of pass-through taxation or tax deferred distributions;

- •

- potential conflicts of interest between TC PipeLines GP, Inc., our general partner (General Partner) its affiliates and us;

- •

- the ability to maintain secure operation of our information technology;

- •

- the impact of any impairment charges;

- •

- operating hazards, casualty losses and other matters beyond our control; and

- •

- unfavorable economic conditions and the impact on capital markets.

2012 ANNUAL REPORT7

These and other risks are described in greater detail in Part II, Item 1A. "Risk Factors." All forward-looking statements attributable to us or persons acting on our behalf are expressly qualified in their entirety by these factors. All forward-looking statements are made only as of the date made and except as required by applicable law, we undertake no obligation to update any forward-looking statements to reflect new information, subsequent events or other changes.

Item 1. Business

NARRATIVE DESCRIPTION OF BUSINESS

General

We are a publicly traded Delaware master limited partnership, formed by TransCanada Corporation and its subsidiaries (TransCanada) in 1998, to acquire, own and participate in the management of energy infrastructure businesses in North America. Our pipeline systems transport natural gas in the U.S. Our common units are traded on the New York Stock Exchange (NYSE) under the symbol TCP.

We are managed by our General Partner, which is an indirect, wholly-owned subsidiary of TransCanada. Through its subsidiaries, TransCanada owns an approximate 33.3 percent equity interest in us, including a 31.3 percent limited partner interest and an effective two percent general partner interest held by our General Partner. See Part II, Item 5. "Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities" for more information regarding TransCanada's ownership in us.

Recent Business Developments

Cash Distributions – In July 2012, we increased our quarterly cash distribution by 1.3 percent to $0.78 per common unit and during fiscal year 2012, we paid cash distributions of $3.10 per common unit. On February 14, 2013, we paid a cash distribution of $0.78 per common unit for the fourth quarter of 2012.

Great Lakes – On October 31, 2012, a number of long-haul capacity contracts expired on the Great Lakes system. Great Lakes re-contracted a portion of this capacity on a shorter-term, short-haul basis. These contracts are indicative of the current industry trend towards short-term contract renewals and the changing dynamics for the Great Lakes pipeline system from a west to east conduit pipeline to a more regional pipeline.

Northern Border Rate Settlement – In January 2013, FERC gave final approval for Northern Border's settlement with shippers on transportation rates and other terms of service (Northern Border Settlement) effective January 1, 2013. See "Government Regulation – Rate Proceedings" for more information.

Tuscarora Rate Settlement – On March 9, 2012, Tuscarora received FERC approval of its settlement regarding its rates and terms and conditions of service (Tuscarora Settlement) effective January 1, 2012. See "Government Regulation – Rate Proceedings" for more information.

Business Strategies

- •

- Our strategic approach is to invest in long-life critical energy infrastructure that provides reliable delivery of energy to customers.

- •

- Our investment approach is to develop or acquire assets that provide stable cash distributions and opportunities for new capital additions, while maintaining a low-risk profile. We are opportunistic and disciplined in our approach when identifying new investments.

- •

- Our goal is to maximize revenue opportunities over the long-term through efficient utilization of our pipeline systems and appropriate business strategies, while maintaining a commitment to safe and reliable operations.

8 TC PIPELINES, LP

Understanding the Natural Gas Pipelines Business

Natural gas pipelines move natural gas from major sources of supply to locations or markets that use natural gas to meet their energy needs. Pipeline systems include meter stations that record how much natural gas comes on to the network and how much comes off at the delivery locations; compressor stations that act like pumps to move the large volumes of natural gas along the pipeline; and the pipelines themselves that transport natural gas under high pressure.

Regulation, rates and cost recovery

Interstate natural gas pipelines are regulated by FERC. FERC approves the construction of new pipeline facilities and regulates certain aspects of ongoing operations including the maximum rates that are allowed to be charged. Maximum rates are based on operating costs, which include allowances for operating and maintenance costs, income and property taxes, interest on debt, depreciation expense to recover invested capital and a return on the capital invested. Although FERC regulates maximum rates for services, interstate natural gas pipelines frequently face competition and therefore may choose to discount their services in order to compete.

Because FERC rate reviews are periodic and not annual, actual revenues and costs typically vary from those projected during the rate case. If revenues no longer provide a reasonable opportunity to recover costs, a pipeline can file with FERC for a determination of new rates, subject to any moratoriums in effect. FERC also has the authority to initiate a review to determine whether a pipeline's rates of return are just and reasonable. Sometimes a settlement or agreement with the pipeline shippers is achieved for rates, which may include mutually beneficial performance incentives. The regulator must approve the components of any settlement.

Contracting

New pipeline projects are typically supported by long-term contracts. The term (in years) of contracts required by a developer for a new pipeline is dependent on the individual developer's appetite for risk and is a function of expected rates of return and stability or certainty of returns. Transportation contracts expire at varying times and underpin varying amounts of capacity. As existing contracts approach their expiration dates, efforts are made to extend and/or renew the contracts. If market conditions are not favorable at the time of renewal, transportation capacity may remain uncontracted, contracted at lower rates or contracted on a shorter-term basis. Unsold capacity may be recontracted if and when market conditions become more favorable. The ability to extend and/or renew expiring contracts and the terms of such subsequent contracts will depend upon the overall commercial environment, including factors such as:

- •

- demand for natural gas;

- •

- cost structures and production levels of natural gas producing basins;

- •

- natural gas prices and regional differences in natural gas prices;

- •

- weather conditions; and

- •

- availability and location of natural gas supplies.

Business environment

The North American natural gas pipeline network has been developed to connect supply to market. Use and growth of this infrastructure is affected by changes in the location and relative cost of natural gas supply and changing demand levels.

Supply

Natural gas is primarily transported from producing regions and, in limited circumstances, from liquefied natural gas (LNG) import facilities to market hubs or interconnects for distribution to natural gas consumers. Significant producing regions in North America include the Gulf of Mexico, Western Canada Sedimentary Basin (WCSB), Mid-Continent, Rockies, Appalachian Basin, Permian Basin and San Juan Basin. Recent increases in the development of shale and other unconventional gas reserves have resulted in increases in overall North American natural gas production and increased reserves.

2012 ANNUAL REPORT9

There has been an increase in the number of significant supply basins to serve the North American market. The development of shale gas reserves that are located close to traditional existing markets, particularly in the Northeastern U.S., has led to an increase in the number of supply choices and is changing traditional natural gas pipeline flow patterns.

The supply of natural gas in North America is expected to increase significantly over the next decade and to continue to increase over the long-term for a number of reasons, including the following:

- •

- use of technology, including horizontal drilling in combination with multi-stage hydraulic fracturing (fracking), is allowing companies to access unconventional resources economically. This has increased the technically accessible resource base of existing basins and is opening up new producing regions; and

- •

- these technologies are also being applied to existing oil fields where further recovery of the existing resource is now possible. High oil prices, particularly compared to natural gas prices, has resulted in an increase in exploration and production of liquid-rich hydrocarbon basins. There are often incremental supplies of natural gas associated with these resources which, when produced, increases the overall natural gas supply for North America.

Other factors that can influence the overall level of natural gas supply in North America include:

- •

- the price of natural gas – the current low prices in North America may slow drilling activities that in turn diminishes production levels, particularly in dry natural gas fields where the extra revenue generated from the entrained liquids is not available;

- •

- producer portfolio diversification – large producers often diversify their portfolios by developing several basins but this is influenced by actual costs to develop the resource as well as economic access to markets and cost of pipeline transportation services. Basin on basin competition impacts the extent and timing of a resource development that, in turn, drives changing dynamics for pipeline capacity demand; and

- •

- regulatory and public scrutiny – changes in regulations that apply to fracking could impact the cost and pace of development of natural gas in these large shale and unconventional basins.

Demand

The natural gas pipeline business ultimately depends on a shipper's demand for pipeline capacity and the price paid for that capacity. Demand for pipeline capacity is influenced by, among other things, supply and market competition, economic activity, weather conditions, natural gas pipeline and storage competition and the price of alternative fuels.

The growing supply of natural gas has resulted in relatively low natural gas prices in North America which has supported increased demand for natural gas particularly in the following areas:

- •

- natural gas fired power generation;

- •

- petrochemical and industrial facilities;

- •

- the production of Alberta oil sands;

- •

- exports to Mexico to fuel electric power generation facilities; and

- •

- exports from North America to global markets through a number of proposed LNG export facilities.

This trend is expected to continue.

Competition

Competition among natural gas pipelines is based primarily on transportation rates and proximity to natural gas supply areas and consuming markets. Changes in supply and demand have resulted in growing pipeline infrastructure and increased competition for transportation service throughout North America. More pipeline capacity was added to the continental pipeline network between 2008 and 2011 than in any comparable period in history, and natural gas supply areas that were once constrained, like the U.S. Rockies and east Texas, now have several paths to reach markets. The increase in capacity from new pipeline infrastructure has caused regional basis differentials, which is the difference in market prices paid for natural gas between different natural gas receipt and delivery points, to shrink. Basis differentials

10 TC PIPELINES, LP

have generally declined in the U.S. over the past few years which indicates the value of pipeline transportation has also, generally, decreased. Construction of new pipeline infrastructure has slowed and is currently focused on regional debottlenecking.

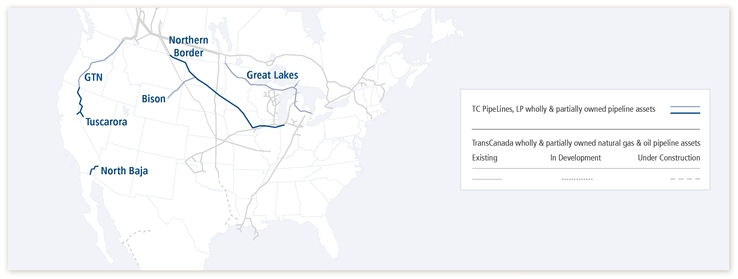

Our Pipeline Systems

We have equity ownership interests in four natural gas interstate pipeline systems that are accounted for on an equity basis and two wholly-owned pipelines that are accounted for on a consolidated basis. Collectively, they are designed to transport approximately 8.9 billion cubic feet per day of natural gas from producing regions and import facilities to market hubs and consuming markets primarily in the Western and Midwestern U.S. and Central Canada. All of our pipeline systems are operated by subsidiaries of TransCanada.

Our pipeline systems include:

Pipeline

| | Length

| | Description

| | Ownership

|

|

|---|

|

| Great Lakes | | 2,115 miles | | Connects with the TransCanada Mainline at the Canadian border near Emerson, Manitoba, Canada and St. Clair, Michigan, near Detroit. Great Lakes is a bi-directional pipeline that can receive and deliver natural gas at multiple points along its system. TransCanada owns the remaining 53.55 percent of Great Lakes. | | 46.45% | |

Northern Border |

|

1,408 miles |

|

Extends between the Canadian border near Port of Morgan, Montana to a terminus near North Hayden, Indiana, south of Chicago. Northern Border is capable of receiving natural gas from Canada, the Williston Basin and Rockies Basin. ONEOK Partners, L.P. owns the remaining 50 percent of Northern Border. |

|

50% |

|

GTN |

|

1,353 miles |

|

Extends between an interconnection near Kingsgate, British Columbia, Canada at the Canadian Border to a point near Malin, Oregon at the California border. TransCanada owns the remaining 75 percent of GTN. |

|

25% |

|

Bison |

|

303 miles |

|

Extends from a location near Gillette, Wyoming to Northern Border's pipeline system in North Dakota. Bison was placed into service in January 2011 to transport natural gas from the Powder River Basin to Midwest markets. TransCanada owns the remaining 75 percent of Bison. |

|

25% |

|

North Baja |

|

86 miles |

|

Extends between an interconnection with the El Paso Natural Gas Company pipeline near Ehrenberg, Arizona to an interconnection with a natural gas pipeline near Ogilby, California on the Mexican border. North Baja is a bi-directional pipeline. |

|

100% |

|

Tuscarora |

|

305 miles |

|

Extends between GTN near Malin, Oregon to its terminus near Reno, Nevada and delivers natural gas in northeastern California and northwestern Nevada. |

|

100% |

|

2012 ANNUAL REPORT11

The map below shows the location of our pipeline systems.

Customers, Contracting and Demand

Our customers are generally large utilities, local distribution companies (LDCs) and major natural gas marketers and producing companies. Our pipelines generate revenue by charging rates for transporting natural gas. Natural gas transportation service is provided pursuant to long-term and short-term contracts. The majority of our pipeline systems' natural gas transportation services are provided through firm service transportation contracts with a reservation or demand charge that reserves pipeline capacity, regardless of use, for the term of the contract. The revenues associated with capacity reserved under firm service transportation contracts are not subject to fluctuations caused by changing supply and demand conditions, competition or customers. Customers with interruptible service transportation agreements may utilize available capacity after firm service transportation requests are satisfied.

Our pipeline systems actively market their available capacity and work closely with customers, including natural gas producers and end users, to ensure our pipelines are offering attractive services and competitive rates.

Great Lakes – The composition of Great Lakes' revenue has substantially shifted to shorter-term, short-haul and bidirectional transportation. This shift reflects ongoing changes in supply, particularly growth of supply in Great Lakes' traditional market area, demand and infrastructure fundamentals across the North American natural gas market and the expiration of long-term, long-haul contracts. Therefore, Great Lakes' revenues are not substantially supported by long-term contracts. Great Lakes' ability to sell its available and future capacity will depend on future market conditions which are impacted by a number of factors including weather in 2013, levels of natural gas in storage and the price of natural gas liquids and the associated impact to North American natural gas production. Demand for Great Lakes' services is usually highest in the summer, when the vast storage complexes in Ontario and Michigan are typically being filled in advance of the upcoming winter season. During the winter, Great Lakes serves peak heating requirements for customers in Minnesota, Wisconsin and Michigan.

Northern Border – Northern Border's revenues are substantially supported by firm transportation contracts through March 2014. As contracts expired in 2012, market conditions allowed Northern Border to negotiate contract extensions that are typically for terms of three years or longer. Its uncontracted capacity is subject to seasonal demand for transportation services which has traditionally been strongest during peak winter months to serve heating demand and peak spring/summer months to serve electric cooling demand and storage injection. Northern Border's tariff has a seasonal rate structure providing for higher rates during traditional peak months.

GTN – GTN's revenues are substantially supported by long-term contracts. Contracts expiring prior to 2023 are primarily held by LDCs. GTN's rates were established primarily based on its current contracted long-term capacity. As a result,

12 TC PIPELINES, LP

GTN's revenues will be subject to positive variation as a result of capacity sold at levels above its current contracted amount.

Other Pipelines – Bison, North Baja and Tuscarora revenues are substantially supported by long-term contracts through 2020.

For the year ended December 31, 2012, no single customer accounted for more than ten percent of our proportionate share of our pipeline systems' operating revenues.

Competition

Four of our pipeline systems, Great Lakes, Northern Border, GTN and Tuscarora, compete with each other for WCSB natural gas supply as well as with other pipelines, including TransCanada's Mainline system, the Alliance pipeline and the Westcoast pipeline. Great Lakes, Northern Border and Tuscarora compete in their respective market areas for natural gas supplies from other basins as well, such as the Rocky Mountain, Mid-Continent, Gulf Coast, Appalachian and Marcellus Basins. GTN primarily competes with pipelines supplying natural gas into California and Pacific Northwest markets.

Bison competes for deliveries with other pipelines that transport natural gas supplies within, and away from, the Rocky Mountain basin.

North Baja's southbound pipeline capacity competes with deliveries of LNG received at the Costa Azul terminal in Mexico. When LNG shipments are received at Costa Azul, North Baja's northbound capacity competes with pipelines that deliver Rocky Mountain, Permian and San Juan basin natural gas into the Southern California area.

Tuscarora competes for deliveries primarily into the northern Nevada natural gas market with natural gas from the Rockies Basin.

To the extent our pipeline systems are contracted, they are less vulnerable to competitive factors such as those discussed above. When their contracts expire, the value of their transportation services will be impacted by competitive pressures.

Relationship with TransCanada

TransCanada is the indirect parent of our General Partner and owns, through its subsidiaries, an approximate 33.3 percent equity interest in the Partnership. TransCanada is a major energy infrastructure company, listed on the Toronto Stock Exchange and NYSE, with more than 60 years of experience in the responsible development and reliable operation of energy infrastructure in North America. TransCanada is primarily focused on natural gas and oil transmission and power generation services. TransCanada owns approximately $48 billion in total assets, including 35,500 miles of wholly-owned natural gas pipelines, interests in an additional 7,000 miles of natural gas pipelines, 2,154 miles of wholly-owned oil pipelines and approximately 407 billion cubic feet of storage capacity. TransCanada also owns, controls or is developing over 11,800 megawatts of power generation.

TransCanada operates our pipeline systems and, in some cases, contracts for pipeline capacity. We have purchased assets from TransCanada and jointly participated with TransCanada in acquiring assets from third parties, including acquisitions that we would have been unable to pursue on our own. We may have similar opportunities going forward. TransCanada, however, is under no obligation to allow us to participate in any of its pipeline or energy infrastructure acquisitions, nor is TransCanada required to offer any of its assets to us.

See Part II, Item 13. "Certain Relationships and Related Transactions, and Director Independence" for more information on our relationship with TransCanada.

2012 ANNUAL REPORT13

Government Regulation

Federal Energy Regulatory Commission

All of our pipeline systems are regulated by FERC under the Natural Gas Act of 1938 (NGA) and Energy Policy Act of 2005, which give FERC jurisdiction to regulate virtually all aspects of our business, including:

- •

- transportation of natural gas in interstate commerce;

- •

- rates and charges;

- •

- terms of service and service contracts with customers, including creditworthiness requirements;

- •

- certification and construction of new facilities;

- •

- extension or abandonment of service and facilities;

- •

- accounts and records;

- •

- depreciation and amortization policies;

- •

- acquisition and disposition of facilities;

- •

- initiation and discontinuation of services; and

- •

- standards of conduct for business relations with certain affiliates.

Our pipeline systems' operating revenues are determined based on rate options stated in our tariffs which are approved by FERC. Tariffs specify the general terms and conditions for pipeline transportation service including the rates that may be charged. FERC, either through hearing a rate case or as a result of approving a negotiated settlement, approves the maximum rates permissible for transportation service on a pipeline system which are designed to recover the pipeline's cost-based investment, operating expenses and a reasonable return for its investors. Once maximum rates are set, a pipeline system is not permitted to adjust the maximum rates to reflect changes in costs or contract demand until new rates are approved by FERC. Pipelines are permitted to charge rates lower than the maximum tariff rates in order to compete. As a result, earnings and cash flows of each pipeline system depend on a number of factors including costs incurred, contracted capacity and transportation path, the volume of natural gas transported, and rates charged.

Rate Proceedings

Great Lakes – Great Lakes has a FERC-approved rate settlement in place. It can file for new rates at any time, but must file no later than November 2013.

Northern Border – In January 2013, FERC gave final approval for Northern Border's settlement with shippers on transportation rates and other terms of service. With this approval, Northern Border's transportation rates were reduced by approximately 11 percent effective January 1, 2013. In addition, the composite depreciation rate was reduced to 2.19 percent from 2.40 percent. The Northern Border Settlement also includes a three-year moratorium on filing rate cases and requires Northern Border to file for new rates no later than January 1, 2018.

GTN – GTN has a FERC-approved settlement agreement for transportation rates that was effective January 2012, and these rates will remain in effect, subject to certain actions, until December 31, 2015. GTN is required to file for new rates to go into effect on January 1, 2016.

Bison – Bison continues to operate under the rates approved by FERC in connection with Bison's initial construction and has no requirements to file a new rate proceeding.

North Baja – North Baja continues to operate under the rates approved by FERC in 2004 in connection with North Baja's initial construction and has no requirements to file a new rate proceeding.

Tuscarora – Tuscarora received approval from FERC on March 9, 2012 of its settlement agreement with shippers. The settlement includes three-year contract extensions to the term of a number of contracts with Tuscarora's largest

14 TC PIPELINES, LP

customer, provided for new rates effective January 1, 2012, and a moratorium on the filing of future rate proceedings until December 31, 2014.

Environmental

Our pipelines are subject to stringent and complex federal, state and local laws and regulations governing environmental protection, including air emissions, water quality, wastewater discharges and solid waste management. Such laws and regulations generally require natural gas pipelines to obtain and comply with a wide variety of environmental registrations, licenses, permits and other approvals. Failure to comply with these laws and regulations may result in the assessment of administrative, civil and/or criminal penalties, the imposition of remedial requirements and/or the issuance of orders enjoining future operations.

The following is a discussion of some of the applicable environmental laws and regulations that relate to our business.

- •

- Waste and Hazardous Substance Statutes – The operations of our pipeline systems generate hazardous waste that are subject to the Resource Conservation and Recovery Act and comparable state statutes. Additionally, federal and state regulators have adopted strict disposal standards for non-hazardous industrial waste and hazardous substances, such as the Solid Waste Disposal Act and the Comprehensive Response, Compensation and Liability Act. These requirements are subject to rigorous waste management and disposal practices to ensure compliance.

- •

- The Clean Air Act (CAA) – The CAA and comparable state laws regulate emissions of air pollutants from various industrial sources, including compressor stations, and impose various monitoring, reporting, and in some cases, control requirements. Such laws and regulations may require pre-approval for the construction or modification of certain facilities expected to produce air emissions or result in an increase of existing air emissions. Such facilities must also comply with air permits containing various emission and operational limitations, or requiring the use of emission control or abatement technologies.

- •

- Toxic Substances Control Act (TSCA) – The TSCA addresses the production, importation, use, and disposal of specific chemicals and provides the EPA with authority to require reporting, record-keeping and testing requirements, and restrictions relating to chemical substances and mixtures. These include polychlorinated biphenyls, asbestos, radon and lead-based paint.

- •

- The Clean Water Act (CWA) – The CWA and comparable state laws impose strict controls with respect to the discharge of pollutants, including spills and leaks of oil and other substances, into or adjacent to waters of the U.S. The discharge of pollutants into regulated waters is generally prohibited, except in accordance with the terms of a permit issued by the EPA or a delegated state or federal agency. The CWA and regulations implemented also prohibit the discharge of dredge and fill material into regulated waters, including wetlands, unless authorized by an appropriately issued permit.

- •

- National Environmental Policy Act (NEPA) – Natural gas transportation activities can be subject to review under NEPA, or analogous federal or state requirements. NEPA requires federal agencies, including the Department of the Interior or FERC, to evaluate governmental agency actions having the potential to significantly impact the environment. In the course of such evaluations, an agency will prepare an Environmental Assessment that addresses the potential direct, indirect and cumulative impacts of a proposed project and, if necessary, will prepare a more detailed Environmental Impact Statement that may be made available for public review and comment. The current activities of our pipeline systems, as well as any proposed plans for future activities, on federal lands are subject to the requirements of NEPA in connection with any new approval that is required for construction, operation or the use of federal lands.

- •

- The Endangered Species Act (ESA) – The ESA restricted activities that may affect endangered or threatened species or their habitats. The designation of previously unidentified or threatened species could cause us to incur additional costs or become subject to operating restrictions or bans in the affected states.

2012 ANNUAL REPORT15

We have not incurred and do not anticipate incurring material costs to comply with existing environmental laws and regulations. We have not accrued for any environmental liabilities. We believe that we are in substantial compliance with all environmental laws and regulations.

Emissions Regulation

Substantial uncertainty exists regarding the impact of new and proposed greenhouse gas (GHG) laws and regulations. In California, the Assembly Bill 32 Cap and Trade Program took effect on January 1, 2013. Our facilities do not meet the GHG emission threshold and are excluded from the program. We cannot estimate the effect of proposed legislation on our future financial position, results of operations or cash flow. However, such legislation could materially increase our operating costs, including our cost of environmental compliance. Because of the uncertainty of policy and regulatory schemes, the future effects on our pipeline systems cannot be predicted.

Safety

Our pipeline systems are affected by existing and proposed pipeline safety regulations administered by PHMSA with respect to pipeline design, installation, testing, construction, operation, replacement and integrity management.

The Pipeline Safety Improvement Act of 2002, as amended, (Pipeline Safety Act) requires pipeline companies to perform baseline integrity assessments on pipeline segments that traverse densely populated areas or near sites that are specifically designated as high consequence areas (HCAs). On December 29, 2006, the Pipeline Inspection, Protection, Enforcement, and Safety Act of 2006, referred to as PIPES of 2006, was enacted, which further amended the Pipeline Safety Act. Pipeline companies are required to perform the baseline integrity assessments within ten years of the date of enactment and perform reassessments on a seven-year cycle. HCAs make up a small percentage of our pipeline systems in which we are fully compliant with the Pipeline Safety Act. In addition to complying with the Pipeline Safety Act, our Integrity Management Program (IMP) is applied annually to our pipelines.

On January 3, 2012, the Pipeline Safety, Regulatory Certainty, and Job Creation Act of 2011 (2011 Pipeline Act) was enacted. The 2011 Pipeline Act reauthorized and amended the previous PIPES Act of 2006 and Pipeline Safety Act. The 2011 Pipeline Act reauthorizes the PHMSA federal pipeline safety programs through fiscal year 2015 and includes a number of additional provisions affecting pipeline owners and operators. Items that may have a material effect on pipeline owners and operators include increases to the cap on civil penalties for violators of pipeline regulations and additional civil penalties for obstructing investigations; a directive for PHMSA to develop regulations requiring the installation of automatic or remote control shut off valves for new or replaced transmission pipelines; a directive for PHMSA to establish requirements for natural gas transmission pipeline operators to confirm the physical and operational characteristics and their maximum allowable operating pressure (MAOP) for pipelines in more populated areas (class 3 and 4 locations) and HCAs; a directive that PHMSA issue regulations requiring natural gas transmission pipeline operators to report to PHMSA any pipeline segments with insufficient MAOP records; and a requirement that PHMSA issue regulations on testing of grandfathered or previously untested natural gas transmission pipelines.

PHMSA and the Comptroller General are also required by the 2011 Pipeline Act to conduct several studies and develop several reports by 2013, some of which are a necessary prelude to additional rulemaking. These studies include a study on expanding IMP requirements outside of HCAs, and possibly eliminating class location requirements, as well as a report to Congress on using risk based Assessment Intervals for IMP. These studies are in progress and may result in regulatory changes. No regulatory changes are expected prior to 2014 as a result of these studies.

In addition, there are various other ongoing legislative and regulatory measures proposed at the federal and state levels to increase pipeline safety. These legislative and regulatory policies, if enacted, may impact our pipeline systems, as well as other pipelines in the industry. While we believe that our pipeline systems are in substantial compliance with current applicable requirements, due to the possibility of enactment of these new or amended laws and regulations, there can be no assurance that future compliance with the requirements will not have a material adverse effect on our pipeline systems and the Partnership's financial position, results of operations and cash flows.

16 TC PIPELINES, LP

EMPLOYEES

We do not have any employees. We are managed by our General Partner. Subsidiaries of TransCanada operate our pipeline systems pursuant to operating agreements.

AVAILABLE INFORMATION

We make available free of charge on or through our website (www.tcpipelineslp.com) our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and any amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act, as soon as reasonably practicable after we electronically file the material with, or furnish it to, the Securities and Exchange Commission (SEC). Copies of our Code of Business Conduct and Ethics, Corporate Governance Guidelines and the Audit Committee Charter of our General Partner are also available on our website under "Corporate Governance." We will also provide copies of these documents at no charge upon request. The information contained on our website is not part of this report.

Item 1A. Risk Factors

Limited partner interests are inherently different from the capital stock of a corporation, although many of the business risks to which we are subject are similar to those that would be faced by a corporation engaged in a similar business. Realization of any of the risks described below could have a material adverse effect on our business, financial condition, including valuation of our equity investments, results of operations and cash flows, including our ability to make distributions to our unitholders. Investors should review and carefully consider all of the information contained in this report, including the following discussion of risks when making investment decisions relating to our Partnership.

RISKS RELATED TO OUR PIPELINE SYSTEMS

Our pipeline systems may not be able to renew or replace expiring transportation contracts or do so at favorable rates or for a long term.

The value of our transportation services depends on a shipper's demand for pipeline capacity and the price paid for that capacity. Excess pipeline capacity may lead to an inability of our pipelines to charge maximum rates, and may drive customers' decisions with respect to contracting for capacity.

Our primary exposure to market risk and competitive pressure occurs at the time existing shipper contracts expire and are subject to renegotiation and renewal. The inability of our pipelines to extend or replace expiring contracts on comparable terms could have a material adverse effect on our business, financial condition, results of operations and our ability to make cash distributions. Our ability to extend and replace expiring contracts, particularly long-term firm contracts, on terms comparable to prior contracts or on any terms depends on many factors including:

- •

- the availability and supply of natural gas in Canada and the U.S.;

- •

- competition from alternative sources of supply;

- •

- competition from other existing or proposed pipelines;

- •

- contract expirations and capacity on competing pipelines;

- •

- changes in rates upstream or downstream of our pipeline systems, which can affect our pipeline systems' relative competitiveness;

- •

- basis differentials between the market location and location of natural gas supplies;

- •

- the liquidity and willingness of shippers to contract for transportation services; and

- •

- regulatory developments.

2012 ANNUAL REPORT17

Great Lakes has been negatively impacted by the factors described above, particularly by the growth of supply in Great Lakes' traditional market area. Great Lakes has a considerable portion of its available capacity unsold and its contract portfolio has transitioned from being comprised primarily of long-term, long-haul contracts to now being comprised primarily of shorter-term, short-haul contracts. Although our other pipelines generally have longer-term contract portfolios, over the medium to long term, they are also subject to the factors described above.

The long-term financial condition of Great Lakes, Northern Border and GTN is largely dependent on the continued availability of and demand for natural gas from the WCSB.

As the long-term contracts on our pipeline systems expire, the demand for transportation service on some of our pipeline systems will depend in large part on the availability of supply of natural gas available for export from the WCSB. Natural gas available for export from the WCSB depends on numerous factors, including the demand for natural gas within Western Canada, WCSB natural gas production, the availability of storage and natural gas prices. Western Canadian demand for natural gas is expected to continue to increase primarily as a result of oil sands development and natural gas fired electric power generation. In addition, there are a number of pipelines and related LNG export terminal proposals along the British Columbia, Canada west coast that, if constructed, would source natural gas from the WCSB beginning in the latter half of the decade. Unless there is a corresponding increase in the amount of natural gas production in the WCSB to meet this growing demand, there could be diminished natural gas volumes available for export from the WCSB.

Rates and other terms of service of our pipeline systems are subject to approval and potential adjustment by FERC, which could limit their ability to recover all costs of operations and negatively impact their rate of return, results of operations and cash available for distribution.

Our pipeline systems are subject to extensive regulation over nearly every aspect of their business, including the rates that they can charge to shippers. Under the NGA, our rates must be just, reasonable and not unduly discriminatory. Actions by FERC could adversely affect the ability of our pipeline systems to recover all of their current or future costs and negatively impact their rate of return, results of operations and cash available for distribution.

If our pipeline systems do not make additional capital expenditures sufficient to offset depreciation expense, our rate base will decline and our earnings and cash flow will decrease over time.

Our pipeline systems are allowed to collect from their customers a return on their assets or "rate base" as reflected in their financial records, as well as recover a portion of that rate base over time through depreciation. In the absence of additions to the rate base through capital expenditures, the rate base will decline over time and revenue and cash flows associated with return on the rate base will likely decline.

We are exposed to credit risk when a shipper fails to perform its contractual obligations.

Although no one customer represents greater than ten percent of our revenues, our pipeline systems are subject to a risk of loss resulting from the nonperformance by a customer of its contractual obligations. Our exposure generally relates to receivables for services provided and future performance over the remaining contract terms under firm transportation contracts. Our tariffs allow us to require limited credit support in the event that our customers are unable to pay for our services. If a significant customer has credit or financial problems which result in a delay or failure to pay for services provided by us or contracted for with us, it could have a material adverse effect on our business and results of operations. In addition, as contracts expire, the failure of any of our customers could also result in the non-renewal of contracted capacity, which could have a material adverse effect on our business and results of operations.

Our pipeline systems are subject to operational hazards and unforeseeable interruptions that may not be covered by insurance or force majeure provisions.

Our pipeline systems are subject to inherent risks including earthquakes, adverse weather conditions and other natural disasters; terrorist activity or acts of aggression; and damage to a pipeline by a third party; explosions, pipeline failures, and safety failures. Each of these risks could result in damage to one of our pipeline systems, business interruptions, release of pollution or contaminants into the environment and other environmental hazards, or injuries to persons and property. These risks could cause us to suffer a substantial loss of revenue and incur significant costs to the extent they

18 TC PIPELINES, LP

are not covered by insurance or considered a force majeure event under our shipper contracts, as applicable. In addition, if one of our pipeline systems was to experience a serious pipeline failure, a regulator could require our pipelines to conduct testing of the pipeline system or upgrade segments of a pipeline unrelated to the failure which costs may not be covered by insurance or recoverable through rate increases.

Our pipeline systems may experience significant costs and liabilities related to pipeline integrity testing programs and any necessary pipeline repairs, or preventative or remedial measures may cause significant costs and liabilities.

The DOT and PHMSA have adopted regulations that require pipeline operators to develop integrity management programs to comprehensively evaluate their pipelines and take measures to protect pipeline segments located in HCAs where a leak or rupture could do the most harm. The regulations require operators to perform ongoing assessments of pipeline integrity, identify applicable threats to pipeline segments that could affect HCAs, improve data collection and analysis, repair and remediate the pipeline as necessary and implement preventative and mitigating actions.

The results of the integrity management programs could cause our pipeline systems to incur significant and unanticipated capital and operating expenditures for repairs or upgrades deemed necessary to ensure their continued safe and reliable operation. Additionally, any failure to comply with the DOT and PHMSA regulations could subject our pipeline systems to penalties and fines.

To the extent not recoverable through rates, the cost of additional integrity management requirements to our pipeline systems could have a material adverse effect on our results of operations or financial position and our ability to maintain current distribution levels.

Our pipeline systems are regulated by federal, state and local laws and regulations that could impose costs for compliance with environmental protection.

Each of our pipeline systems are subject to federal, state and local environmental laws, regulations and enforcement policies and potential liabilities, may arise related to protection of the environment and natural resources.

Under certain environmental laws and regulations, we may be exposed to substantial liabilities for pollution or contamination that arise in connection with our operations. For instance, we may be required to obtain and maintain permits and approvals issued by various federal, state and local governmental authorities, and to limit or prevent releases of materials from our operations in accordance with these permits and approvals, or install pollution control equipment. In addition, various legislative and regulatory reforms associated with pipeline safety and integrity issues have been proposed, including reforms that would require increased periodic inspections. It is uncertain which proposed laws, regulations or reforms, if any, will be adopted and what impact they might ultimately have on our operations or financial results. Moreover, new environmental laws, regulations or enforcement policies could be implemented that significantly increase our pipeline systems' compliance costs or the cost of any remediation of environmental contamination which may not be recoverable under their rates.

Emissions Regulation legislation or regulations restricting emissions of GHG could result in increased operating costs.

There have been a number of legislative initiatives to regulate GHG emissions, however, substantial uncertainty exists regarding the impact of new and proposed GHG laws and regulations. We cannot estimate the effect of proposed legislation on our future financial position, results of operations or cash flow. However, such legislation could materially increase our operating costs, including our cost of environmental compliance. Given the uncertainty of policy and regulatory schemes, the future effects on our pipeline cannot be predicted.

Our pipeline systems are subject to pipeline safety laws and regulations, compliance with which can require significant expenditures, may increase our cost of operations and may affect or limit our business plans.

Our pipeline systems are subject to pipeline safety regulations administered by PHMSA. These laws and regulations require our pipeline systems to comply with design, construction, maintenance and operation requirements, including monitoring and maintaining their integrity. Pipeline failures or failure to comply with applicable regulations could result

2012 ANNUAL REPORT19

in the interruption of operations or in the reduction of allowable operating pressures which would reduce available capacity on our pipeline systems.

Should any of these risks materialize, it could have a material adverse effect on our operations, financial condition, results of operations and cash flows.

Our pipeline systems' indebtedness may limit their ability to borrow additional funds, make distributions to us or capitalize on business opportunities.

As of December 31, 2012, Great Lakes, Northern Border, GTN and Tuscarora had $354 million, $473 million, $325 and $27 million of debt outstanding, respectively. Of the debt outstanding, Great Lakes and Tuscarora have $19 million and $3 million of debt maturing in 2013, respectively. Our pipeline systems' respective debt levels could have negative consequences to each of them, including the following:

- •

- their ability to obtain additional financing, if necessary, for working capital, capital expenditures, acquisitions or other purposes may be impaired or such financing may not be available on favorable terms;

- •

- their need for cash to fund interest payments on the debt; reduces the funds that would otherwise be available for operations, future business opportunities and distributions to us;

- •

- their debt level may make them more vulnerable to competitive pressures or a downturn in their business or the economy generally; and

- •

- their debt level may limit their flexibility in responding to changing business and economic conditions.

Our pipeline systems' ability to service their respective debt will depend upon, among other things, future financial and operating performance which will be affected by prevailing economic conditions and financial, business, regulatory and other factors, some of which are beyond their control.

In addition, under the terms of these financing arrangements, our pipeline systems are prohibited from making cash distributions during an event of default under their debt instruments. Under Great Lakes' debt instruments, Great Lakes has limitations on the level of indebtedness and has other restrictions, including a general prohibition against liens on pipeline facilities. Provisions in Northern Border's debt instruments limit its ability to incur indebtedness and engage in specific transactions. This could reduce its ability to capitalize on business opportunities that arise in the course of its business. GTN's debt provisions contain limitations on debt secured by liens and sale-leaseback transactions, as well as restrictions on GTN's debt to capitalization ratio. Under Tuscarora's debt instruments, Tuscarora is granted a security interest in its transportation contracts which is available to noteholders upon an event of default.

Our pipeline systems do not own all of the land on which their pipelines and facilities are located, which could impact their operations.

Our pipeline systems do not own all of the land on which their pipelines and facilities are located and they are, therefore, subject to the risk of increased costs to maintain necessary land use. They must either obtain the right from landowners or exercise the power of eminent domain in order to use most of the land on which they are constructed and operated. The loss of these rights, through their inability to renew right-of-way contracts or increased costs to renew such rights, could have a material adverse effect on our financial condition, results of operations and cash flows.

Our pipeline systems' business systems could be negatively impacted by security threats, including cyber security threats, and related disruptions.

We depend on the secure operation of our information technology to process, transmit and store electronic information, including information we use to safely operate our pipeline systems. Security breaches could expose our business to a risk of loss, misuse or interruption of critical information and functions that affect the pipeline operations. Such losses could result in operational impacts, damage to our assets, safety incidents, damage to the environment, reputational harm, competitive disadvantage, regulatory enforcement actions, litigation and a potential material adverse effect on our operations, financial position and results of operations.

20 TC PIPELINES, LP

RISKS RELATED TO THE PARTNERSHIP

Our indebtedness may limit our ability to obtain additional financing, make distributions or pursue business opportunities.

As of December 31, 2012, the Partnership had $688 million of debt outstanding, including the revolving credit facility and Senior Notes. This level of debt could have negative consequences to the Partnership including the following:

- •

- our ability to obtain additional financing, if necessary, for working capital, acquisitions, payment of distributions or other purposes may be impaired or such financing may not be available on favorable terms;

- •

- our need for cash to fund interest payments on the debt reduces the funds that would otherwise be available for operations, future business opportunities and distributions to our unitholders; and

- •

- our flexibility in responding to changing business and economic conditions may be limited.

Our ability to service our debt will depend upon, among other things, the future financial and operating performance of our pipeline systems, which will be affected by prevailing economic conditions and financial, business, regulatory and other factors, some of which are beyond our control. In addition, the Partnership's third party credit facility requires us to maintain certain financial ratios and contains restrictions on incurring additional debt and making distributions to unitholders.

An impairment of our equity investment, long-lived assets or goodwill could reduce our earnings or negatively impact the value of our common units.

We are required by GAAP to evaluate our equity investments, long-lived assets and goodwill for impairment on an annual basis or whenever events or circumstances indicate that the carrying value may not be recoverable. Long-lived assets, including intangible assets with finite useful lives, are reviewed for impairment whenever events or changes in circumstances indicate that the carrying amount may not be recoverable. For the investments we account for under the equity method, the impairment test considers whether the fair value of the equity investment as a whole, not the underlying net assets, has declined and whether that decline is other than temporary. If we determine that an impairment is indicated, we would be required to take an immediate noncash charge to earnings with a correlative effect on equity and balance sheet leverage as measured by debt to total capitalization.

As of December 31, 2012, we determined that the fair values of our equity investments, long-lived assets and goodwill were higher than their carrying values. As the composition of Great Lakes' revenue has shifted from long-term contracts to shorter-term and short-haul transportation, there is an increased risk that adverse changes in key assumptions could result in a future impairment of our equity investment in Great Lakes.

Our ability to make cash distributions is dependent primarily on our cash flow, financial reserves and working capital borrowings.

Cash distributions are not dependent solely on our profitability. Therefore, we may make cash distributions during periods when losses are reported and may not make cash distributions during periods when we report profits.

Factors that affect the actual amount of cash that we will have available for distribution to our unitholders include the following:

- •

- the amount of cash set aside and the adjustment in reserves made by our General Partner in its sole discretion;

- •

- the amount of cash distributed to us by our pipeline systems;

- •

- the level of capital expenditures made by our pipeline systems;

- •

- the required principal and interest payments on our debt, retirement of debt and other liabilities, including cost of acquisitions;

- •

- our ability to borrow funds and access capital markets, including the issuance of debt and equity securities; and

- •

- restrictions on distributions contained in debt agreements.

2012 ANNUAL REPORT21

We do not own a controlling interest in Great Lakes, Northern Border, GTN or Bison, which limits our ability to control these assets.

We do not own a controlling interest in Great Lakes, Northern Border, GTN or Bison and are therefore unable to cause certain actions to occur without the agreement of the other owners. As a result, we may be unable to control the amount of cash distributions received from these assets or the cash contributions required to fund our share of their operations. The organizational documents of these assets require distribution of their available cash to their owners on a quarterly basis; however, in each case, available cash is reduced, in part, by appropriate reserves. Any disagreements with the other owners of these assets could adversely affect our ability to respond to changing economic or industry conditions, which could have a material adverse effect on our business, results of operations, financial condition and ability to make cash distributions to unitholders.

If we do not successfully identify and complete expansion projects or make and integrate acquisitions that are accretive, we may not be able to continue to grow.

Our strategy is to continue to grow the cash distributions on our common units by expanding our business. Our ability to grow depends on our ability to undertake acquisitions and organic growth projects, and the ability of our pipeline systems to complete expansion projects and make and integrate acquisitions that result in an increase in cash per common unit generated from operations. Our ability to complete successful, accretive expansion projects or acquisitions is dependent upon many factors, including our ability to secure necessary rights-of-way or regulatory approvals, our ability to finance such expansion projects or acquisitions on economically acceptable terms and the degree to which our assumptions about volumes, reserves, revenues, costs and customer commitments materialize.

In addition, we face competition for acquisitions from investment funds, strategic buyers and commercial finance companies. These companies may have higher risk tolerances or different risk assessments that we may be unwilling to match.

Expansion projects or future acquisitions that appear to be accretive may nevertheless reduce our cash from operations on a per unit basis.

Even if we complete expansion projects or make acquisitions that we believe will be accretive, these expansion projects or acquisitions may nevertheless reduce our cash from operations on a per-unit basis. Any expansion project or acquisition involves potential risks, including:

- •

- an inability to complete expansion projects on schedule or within the budgeted cost due to, among other factors, the unavailability of required construction personnel, equipment or materials, and the risk of cost overruns resulting from inflation or increased costs of materials, labor and equipment;

- •

- a decrease in our liquidity as a result of using a significant portion of our available cash or borrowing capacity to finance the project or acquisition;

- •

- an inability to receive cash flows from a newly built or acquired asset until it is operational; and

- •

- unforeseen difficulties operating in new business areas or new geographic areas.

As a result, our new facilities may not achieve expected investment returns, which could adversely affect our results of operations, financial position or cash flows. If any completed expansion projects or acquisitions reduce our cash from operations on a per unit basis, our ability to make distributions may be reduced.

Exposure to variable interest rates and general volatility in the financial markets and economy could adversely affect our business, our common unit price, results of operations, cash flows and financial condition.

As of December 31, 2012, $312 million of our total $688 million consolidated debt was subject to variable interest rates. As a result, our results of operations, cash flows and financial condition could be materially adversely affected by significant increases in interest rates. From time to time, we may enter into interest rate swap arrangements which may increase or decrease our exposure to variable interest rates but there is no assurance that these will be sufficient to offset rising interest rates.

22 TC PIPELINES, LP

For more information about our interest rate risk, see Item 7A "Quantitative and Qualitative Disclosures About Market Risk – Market Risk."

We do not have the same flexibility as corporations to accumulate cash and equity to protect against illiquidity in the future.

As a limited partnership, we are required by our Partnership Agreement to make quarterly distributions to our unitholders of all available cash, reduced by any amounts of reserves for commitments and contingencies, including capital and operating costs and debt service requirements. The value of our units and other limited partner interests may decrease in direct correlation with decreases in the amount we distribute per common unit. Accordingly, if we experience a liquidity shortfall in the future, we may not be able to recapitalize by issuing more equity.

Unitholders have limited voting rights and are not entitled to elect our General Partner or its board of directors.

The General Partner is our manager and operator. Unlike the stockholders in a corporation, holders of our common units have only limited voting rights on matters affecting our business. Unitholders have no right to elect our General Partner or its board of directors. The members of the board of directors of our General Partner, including the independent directors, are appointed by its parent company and not by the unitholders.

Unitholders cannot remove our General Partner without its consent.

Our General Partner may not be removed except by the vote of the holders of at least 662/3 percent of the outstanding common units. These required votes would include the votes of common units owned by our General Partner and its affiliates. The ownership of an aggregate of approximately 31 percent of the outstanding common units by our General Partner and its affiliates has the practical effect of making removal of our General Partner difficult.

In addition, the Partnership Agreement contains some provisions that may have the effect of discouraging a person or group from attempting to remove our General Partner or otherwise change our management. If our General Partner is removed as our general partner under circumstances where cause does not exist and common units held by our General Partner and its affiliates are not voted in favor of that removal:

- •

- any existing arrearages in the payment of the minimum quarterly distributions on the common units will be extinguished; and

- •

- our General Partner will have the right to convert its general partner interests and its incentive distribution rights into common units or to receive cash in exchange for those interests.

Our Partnership Agreement restricts voting and other rights of unitholders owning 20 percent or more of our common units.

The Partnership Agreement contains provisions limiting the ability of unitholders to call meetings of unitholders or to acquire information about our operations, as well as other provisions limiting the unitholders' ability to influence the manner or direction of management. Further, if any person or group other than our General Partner or its affiliates or a direct transferee of our General Partner or its affiliates acquires beneficial ownership of 20 percent or more of any class of common units then outstanding, that person or group will lose voting rights with respect to all of its common units. As a result, unitholders will have limited influence on matters affecting our operations, and third parties may find it difficult to attempt to gain control of us or influence our activities.

We may issue additional common units without unitholder approval, which would dilute the existing unitholders' ownership interests. In addition, issuance of additional common units may increase the risk that we will be unable to maintain the quarterly distribution payment at current levels.

Subject to certain limitations, we may issue additional common units and limited partner interests of any type, without the approval of unitholders.

Based on the circumstances of each case, the issuance of additional common units or securities ranking senior to, or on parity with, the common units may dilute the value of the interests of the then-existing holders of common units in the net assets of the Partnership. In addition, the issuance of additional common units may increase the risk that we will be unable to maintain the quarterly distribution payment at current levels.

2012 ANNUAL REPORT23

Unitholders may not have limited liability in some circumstances.

A general partner generally has unlimited liability for the obligations of a limited partnership, except for those contractual obligations of the partnership that are expressly made without recourse to the general partner. We are organized under Delaware law and conduct business in a number of other states. The limitations on the liability of holders of limited partner interests for the obligations of a limited partnership have not been clearly established in some states. Our unitholders could be liable for any and all of our obligations as if our unitholders were a general partner if a court or government agency determined that:

- •

- the Partnership had been conducting business in any state without compliance with the applicable limited partnership statute; or

- •