UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year endedDecember 31, 2006

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

COMMISSION FILE NUMBER 001-12307

ZIONS BANCORPORATION

(Exact name of Registrant as specified in its charter)

| | |

UTAH

| | 87-0227400

|

(State or other jurisdiction of incorporation or organization) | | (Internal Revenue Service Employer Identification Number) |

| |

ONE SOUTH MAIN, 15TH FLOOR SALT LAKE CITY, UTAH

| | 84111

|

| (Address of principal executive offices) | | (Zip Code) |

Registrant’s telephone number, including area code: (801) 524-4787

Securities registered pursuant to Section 12(b) of the Act:

| | |

Title of Each Class

| | Name of Each Exchange on Which Registered

|

Guarantee related to 8.00% Capital Securities of Zions Capital Trust B | | New York Stock Exchange |

6% Subordinated Notes due September 15, 2015 | | New York Stock Exchange |

Depositary Shares each representing a 1/40th ownership interest in a share of Series A Floating-Rate Non-Cumulative Perpetual Preferred Stock | | New York Stock Exchange |

Common Stock, without par value | | The NASDAQ Stock Market LLC |

Securities registered pursuant to Section 12(g) of the Act:None.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes x No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (Section 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K.

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer x Accelerated filer ¨ Non-accelerated filer ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes ¨ No x

| | | |

Aggregate Market Value of Common Stock Held by Non-affiliates at June 30, 2006 | | $ | 7,939,764,713 |

| |

Number of Common Shares Outstanding at February 16, 2007 | | | 109,997,378 shares |

Documents Incorporated by Reference:

Portions of the Company’s Proxy Statement (to be dated approximately March 16, 2007) for the Annual Meeting of Shareholders to be held May 4, 2007 – Incorporated into Part III

FORM 10-K TABLE OF CONTENTS

2

PART I

FORWARD-LOOKING INFORMATION

Statements in this Annual Report on Form 10-K that are based on other than historical data are forward-looking within the meaning of the Private Securities Litigation Reform Act of 1995. Forward-looking statements provide current expectations or forecasts of future events and include, among others:

| • | | statements with respect to the beliefs, plans, objectives, goals, guidelines, expectations, anticipations, and future financial condition, results of operations and performance of Zions Bancorporation and its subsidiaries (collectively “the Company”); |

| • | | statements preceded by, followed by or that include the words “may,” “could,” “should,” “would,” “believe,” “anticipate,” “estimate,” “expect,” “intend,” “plan,” “projects,” or similar expressions. |

These forward-looking statements are not guarantees of future performance, nor should they be relied upon as representing management’s views as of any subsequent date. Forward-looking statements involve significant risks and uncertainties and actual results may differ materially from those presented, either expressed or implied, in this Annual Report on Form 10-K, including, but not limited to, those presented in the Management’s Discussion and Analysis. Factors that might cause such differences include, but are not limited to:

| • | | the Company’s ability to successfully execute its business plans, manage its risks, and achieve its objectives; |

| • | | changes in political and economic conditions, including the economic effects of terrorist attacks against the United States and related events; |

| • | | changes in financial market conditions, either nationally or locally in areas in which the Company conducts its operations, including without limitation, reduced rates of business formation and growth, commercial real estate development and real estate prices; |

| • | | fluctuations in the equity and fixed-income markets; |

| • | | changes in interest rates, the quality and composition of the loan and securities portfolios, demand for loan products, deposit flows and competition; |

| • | | acquisitions and integration of acquired businesses; |

| • | | increases in the levels of losses, customer bankruptcies, claims and assessments; |

| • | | changes in fiscal, monetary, regulatory, trade and tax policies and laws, including policies of the U.S. Treasury and the Federal Reserve Board; |

| • | | continuing consolidation in the financial services industry; |

| • | | new litigation or changes in existing litigation; |

| • | | success in gaining regulatory approvals, when required; |

| • | | changes in consumer spending and savings habits; |

| • | | increased competitive challenges and expanding product and pricing pressures among financial institutions; |

| • | | demand for financial services in the Company’s market areas; |

| • | | inflation and deflation; |

| • | | technological changes and the Company’s implementation of new technologies; |

| • | | the Company’s ability to develop and maintain secure and reliable information technology systems; |

3

| • | | legislation or regulatory changes which adversely affect the Company’s operations or business; |

| • | | the Company’s ability to comply with applicable laws and regulations; and |

| • | | changes in accounting policies or procedures as may be required by the Financial Accounting Standards Board or regulatory agencies. |

The Company specifically disclaims any obligation to update any factors or to publicly announce the result of revisions to any of the forward-looking statements included herein to reflect future events or developments.

AVAILABILITY OF INFORMATION

We also make available free of charge on our website,www.zionsbancorporation.com, annual reports on Form 10-K, quarterly reports on Form 10-Q, and current reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as well as proxy statements, as soon as reasonably practicable after we electronically file such material with, or furnish it to, the U.S. Securities and Exchange Commission.

DESCRIPTION OF BUSINESS

Zions Bancorporation (“the Parent”) is a financial holding company organized under the laws of the State of Utah in 1955, and registered under the Bank Holding Company Act of 1956, as amended (the “BHC Act”). The Parent and its subsidiaries (collectively “the Company”) own and operate eight commercial banks with a total of 470 offices at year-end 2006. The Company provides a full range of banking and related services through its banking and other subsidiaries, primarily in Utah, California, Texas, Arizona, Nevada, Colorado, Idaho, Washington, and Oregon. Full-time equivalent employees totaled 10,618 at year-end 2006. For further information about the Company’s industry segments, see “Business Segment Results” in Management’s Discussion and Analysis (“MD&A”) and Note 22 of the Notes to Consolidated Financial Statements. For information about the Company’s foreign operations, see “Foreign Operations” in MD&A. The “Executive Summary” in MD&A provides further information about the Company.

PRODUCTS AND SERVICES

The Company focuses on maintaining community-minded banking services by continuously strengthening its core business lines of 1) small, medium-sized business and corporate banking; 2) commercial and residential development, construction and term lending; 3) retail banking; 4) treasury cash management and related products and services; 5) residential mortgage; and 6) investment activities. It operates eight different banks in ten Western and Southwestern states with each bank operating under a different name and each having its own board of directors, chief executive officer, and management team. The banks provide a wide variety of commercial and retail banking and mortgage lending products and services. They also provide a wide range of personal banking services to individuals, including home mortgages, bankcard, student and other installment loans, home equity lines of credit, checking accounts, savings accounts, time certificates of various types and maturities, trust services, safe deposit facilities, direct deposit, and 24-hour ATM access. In addition, certain banking subsidiaries provide services to key market segments through their Women’s Financial, Private Client Services, and Executive Banking Groups. We also offer wealth management services through a subsidiary, Contango Capital Advisors, Inc., (“Contango”) that was launched in 2004.

4

In addition to these core businesses, the Company has built specialized lines of business in capital markets, public finance, and certain financial technologies, and is also a leader in U.S. Small Business Administration (“SBA”) lending. Through its eight banking subsidiaries, the Company provides SBA 7(a) loans to small businesses throughout the United States and is also one of the largest providers of SBA 504 financing in the nation. The Company owns an equity interest in the Federal Agricultural Mortgage Corporation (“Farmer Mac”) and is the nation’s top originator of secondary market agricultural real estate mortgage loans through Farmer Mac. The Company is a leader in municipal finance advisory and underwriting services. The Company also controls four venture capital funds that provide early-stage capital primarily for start-up companies located in the Western United States. Finally, the Company’s NetDeposit, Inc. (“NetDeposit”) and P5, Inc. (“P5”) subsidiaries are national leaders in the provision of check imaging and clearing software and of web-based medical claims tracking and cash management services, respectively.

COMPETITION

The Company operates in a highly competitive environment. The Company’s most direct competition for loans and deposits comes from other commercial banks, thrifts, and credit unions, including institutions that do not have a physical presence in our market footprint but solicit via the Internet and other means. In addition, the Company competes with finance companies, mutual funds, brokerage firms, securities dealers, investment banking companies, financial technology firms, and a variety of other types of companies. Many of these companies have fewer regulatory constraints and some have lower cost structures.

The primary factors in competing for business include pricing, convenience of office locations and other delivery methods, range of products offered, and the level of service delivered. The Company must compete effectively along all of these parameters to remain successful.

SUPERVISION AND REGULATION

The Gramm-Leach-Bliley Act of 1999 (“the GLB Act”) provides a regulatory framework for financial holding companies, which have as their umbrella regulator the Federal Reserve Board (“FRB”). The functional regulation of the separately regulated subsidiaries of a holding company is conducted by each subsidiary’s primary functional regulator. To qualify for and maintain status as a financial holding company, a company must satisfy certain ongoing criteria.

The GLB Act also provides federal regulations dealing with privacy for nonpublic personal information of individual customers, with which the Company must comply. In addition, the Company is subject to various other federal and state laws that deal with the use and disclosure of nonpublic personal information.

The Parent is a financial holding company and, as such, is subject to the BHC Act. The BHC Act requires the prior approval of the FRB for a financial holding company to acquire or hold more than 5% voting interest in any bank. The BHC Act allows, subject to certain limitations, interstate bank acquisitions and interstate branching by acquisition anywhere in the country.

The BHC Act restricts the Company’s nonbanking activities to those that are permitted for financial holding companies or that have been determined by the FRB to be financial in nature, incidental to financial activities, or complementary to a financial activity. The BHC Act does not place territorial restrictions on the activities of nonbank subsidiaries of financial holding companies.

5

The Company’s banking subsidiaries are also subject to various requirements and restrictions contained in both the laws of the United States and the states in which the banks operate. These include restrictions on:

| • | | transactions with affiliates; |

| • | | the amount of loans to a borrower and its affiliates; |

| • | | the nature and amount of any investments; |

| • | | their ability to act as an underwriter of securities; |

| • | | the opening of branches; and |

| • | | the acquisition of other financial entities. |

In addition, the Company’s subsidiary banks are subject to the provisions of the National Bank Act or the banking laws of their respective states, as well as the rules and regulations of the Office of the Comptroller of the Currency (“OCC”), the FRB, and the Federal Deposit Insurance Corporation (“FDIC”). They are also under the supervision of, and are subject to periodic examination by, the OCC or their respective state banking departments, the FRB, and the FDIC.

The FRB has established capital guidelines for financial holding companies. The OCC, the FDIC, and the FRB have also issued regulations establishing capital requirements for banks. Failure to meet capital requirements could subject the Company and its subsidiary banks to a variety of restrictions and enforcement remedies. See Note 19 of the Notes to Consolidated Financial Statements for information regarding capital requirements.

The U.S. federal bank regulatory agencies’ risk-based capital guidelines are based upon the 1988 capital accord (“Basel I”) of the Basel Committee on Banking Supervision (the “BCBS”). The BCBS is a committee of central banks and bank supervisors/regulators from the major industrialized countries that develops broad policy guidelines that each country’s supervisors can use to determine the supervisory policies they apply. The BCBS has been working for a number of years on revisions to Basel I and in June 2004 released the final version of its proposed new capital framework with an update in November 2005 (“Basel II”). Basel II provides two approaches for setting capital standards for credit risk – an internal ratings-based approach tailored to individual institutions’ circumstances (which for many asset classes is itself broken into a “foundation” approach and an “advanced” or “A-IRB” approach, the availability of which is subject to additional restrictions) and a standardized approach that bases risk weightings on external credit assessments to a much greater extent than permitted in existing risk-based capital guidelines. Basel II also would set capital requirements for operational risk and refine the existing capital requirements for market risk exposures. However, U.S. regulatory authorities consistently have taken the position that U.S. banks would not be permitted to utilize the “foundation” approach. Operational risk is defined by the proposal to mean the risk of direct or indirect loss resulting from inadequate or failed internal processes, people and systems, or from external events. Basel I does not include separate capital requirements for operational risk.

In September 2006, the U.S. banking and thrift agencies issued an interagency Advance Notice of Proposed Rulemaking (“NPR”) setting forth a definitive proposal for implementing Basel II in the United States that would apply only to internationally active banking organizations – defined as those with consolidated total assets of $250 billion or more or consolidated on-balance sheet

6

foreign exposures of $10 billion or more – but that other U.S. banking organizations could elect, but would not be required to apply. We do not currently expect to be an early “opt in” bank holding company, as the Company does not have in place the data collection and analytical capabilities necessary to adopt Basel II. However, we believe that the competitive advantages afforded to companies that do adopt the framework will make it necessary for the Company to elect to “opt in” at some point, and we have begun investing in the required capabilities.

Also, in December 2006, the agencies issued another NPR for modifications to the Basel I framework for those banks not adopting Basel II, called Basel IA. The Basel IA NPR will allow non-Basel II banking organizations the choice of adopting all of the revisions suggested in the proposed NPR or continuing the use of existing risk-based capital rules. The agencies have indicated their intent to have the A-IRB provisions for internationally active U.S. banking organizations first become effective in March 2009 and that those provisions and the Basel IA provisions for others will be implemented on similar time frames.

Dividends payable by the subsidiary banks to the Parent are subject to various legal and regulatory restrictions. These restrictions and the amount available for the payment of dividends at year-end are summarized in Note 19 of the Notes to Consolidated Financial Statements.

The Financial Institutions Reform, Recovery, and Enforcement Act of 1989 provides that the Company’s bank subsidiaries are liable for any loss incurred by the FDIC in connection with the failure of an affiliated insured bank.

The Federal Deposit Insurance Corporation Improvement Act of 1991 prescribes standards for the safety and soundness of insured banks. These standards relate to internal controls, information systems, internal audit systems, loan documentation, credit underwriting, interest rate exposure, asset growth, and compensation, as well as other operational and management standards deemed appropriate by the federal banking regulatory agencies.

The Community Reinvestment Act (“CRA”) requires banks to help serve the credit needs in their communities, including credit to low and moderate income individuals. Should the Company or its subsidiaries fail to adequately serve their communities, penalties may be imposed including denials of applications to add branches, relocate, add subsidiaries and affiliates, and merge with or purchase other financial institutions. The GLB Act requires “satisfactory” or higher CRA compliance for insured depository institutions and their financial holding companies for them to engage in new financial activities. If one of the Company’s banks should receive a CRA rating of less than satisfactory, the Company could lose its status as a financial holding company.

On October 26, 2001, the President signed into law comprehensive anti-terrorism legislation known as the USA PATRIOT Act of 2001 (the “USA Patriot Act”). Title III of the USA Patriot Act substantially broadens the scope of U.S. anti-money laundering laws and regulations by imposing significant new compliance and due diligence obligations, defining new crimes and related penalties, and expanding the extra-territorial jurisdiction of the United States. The U.S. Treasury Department has issued a number of implementing regulations, which apply various requirements of the USA Patriot Act to financial institutions. The Company’s bank and broker-dealer subsidiaries and mutual funds and private investment companies advised or sponsored by the Company’s subsidiaries must comply with these regulations. These regulations also impose new obligations on financial institutions to maintain appropriate policies, procedures and controls to detect, prevent and report money laundering and terrorist financing.

7

The Company has adopted appropriate policies, procedures and controls to address compliance with the requirements of these acts and will continue to make appropriate revisions to reflect any changes required.

Regulators, Congress, and state legislatures continue to enact rules, laws, and policies to regulate the financial services industry and to protect consumers. The nature of these laws and regulations and the effect of such policies on future business and earnings of the Company cannot be predicted.

On July 30, 2002, the Senate and the House of Representatives of the United States (Congress) enacted the Sarbanes-Oxley Act of 2002, a law that addresses, among other issues, corporate governance, auditing and accounting, executive compensation, and enhanced and timely disclosure of corporate information. The Nasdaq has also adopted corporate governance rules, which are intended to allow shareholders and investors to more easily and efficiently monitor the performance of companies and their directors.

The Board of Directors of the Parent has implemented a system of strong corporate governance practices. This system includes Corporate Governance Guidelines, a Code of Business Conduct and Ethics for Employees, a Directors Code of Conduct, and charters for the Audit, Credit Review, Executive Compensation, and Nominating and Corporate Governance Committees. More information on the Company’s corporate governance practices is available on the Company’s website atwww.zionsbancorporation.com. (The Company’s website is not part of this Annual Report on Form 10-K.)

GOVERNMENT MONETARY POLICIES

The earnings and business of the Company are affected not only by general economic conditions, but also by fiscal and other policies adopted by various governmental authorities. The Company is particularly affected by the monetary policies of the FRB, which affect short-term interest rates and the national supply of bank credit. The methods of monetary policy available to the FRB include:

| • | | open-market operations in U.S. government securities; |

| • | | adjustment of the discount rates or cost of bank borrowings from the FRB; and |

| • | | imposing or changing reserve requirements against bank deposits. |

These methods are used in varying combinations to influence the overall growth or contraction of bank loans, investments and deposits, and the interest rates charged on loans or paid for deposits.

In view of the changing conditions in the economy and the effect of the FRB’s monetary policies, it is difficult to predict future changes in loan demand, deposit levels and interest rates, or their effect on the business and earnings of the Company. FRB monetary policies have had a significant effect on the operating results of commercial banks in the past and are expected to continue to do so in the future.

8

ITEM 1A. RISK FACTORS

The following list describes several risk factors which are significant to the Company:

| • | | Credit risk is one of our most significant risks. Over the last three years we have experienced historically high levels of credit quality. We do not see any indications that credit quality will deteriorate significantly, but it is unlikely that we will be able to maintain credit quality at these levels indefinitely. Economic conditions in the high growth geographical areas in which our banks operate have been strong, but events could result in weaker economic conditions including deterioration of property values that could significantly increase the Company’s credit risk. |

| • | | Net interest income is the largest component of the Company’s revenue. The management of interest rate risk for the Company and all bank subsidiaries is centralized and overseen by an Asset Liability Management Committee appointed by the Company’s Board of Directors. The Company has been successful in its interest rate risk management as evidenced by its achieving a relatively stable interest rate margin over the last several years when interest rates have been volatile and the rate environment challenging. Factors beyond the Company’s control can significantly influence the interest rate environment and increase the Company’s risk. These factors include competitive pricing pressures for our loans and deposits and volatile market interest rates subject to general economic conditions and the polices of governmental and regulatory agencies, in particular the FRB. |

| • | | The Company is exposed to accounting, financial reporting, and regulatory/compliance risk. The Company provides to its customers a number of complex financial products and services. Estimates, judgments and interpretations of complex and changing accounting and regulatory policies are required in order to provide and account for these products and services. Identification, interpretation and implementation of complex and changing accounting standards as well as compliance with regulatory requirements therefore pose an ongoing risk. |

| • | | A failure in our internal controls could have a significant negative impact not only on our earnings, but also on the perception that customers, regulators and investors may have of the Company. We continue to devote a significant amount of effort, time and resources to improving our controls and ensuring compliance with complex accounting standards and regulations. |

| • | | We have a number of business initiatives that, while we believe they will ultimately produce profits for our shareholders, currently generate expenses in excess of revenues. Two significant initiatives are Contango, a wealth management business started in 2004, and NetDeposit, a subsidiary that provides electronic check processing systems. Our management of these businesses takes into account the development of revenues and control of expenses so that results of operations are not adverse to an extent that is not warranted by the expected opportunities these businesses provide. |

| • | | As noted previously, U.S. and international regulators have proposed new capital standards commonly known as Basel II. These standards would apply to a number of our largest competitors and potentially give them a significant competitive advantage over |

9

| | banks that do not adopt these standards. Sophisticated systems and data are required to adopt Basel II standards; the Company does not yet have these systems and data. While the Company is developing some of the systems, data, and analytical capabilities required to adopt Basel II, adoption is difficult and the Company has not yet decided that it will or can adopt Basel II. More recently, U.S. banking regulators issued another NPR which might reduce competitive inequities for modifications to the Basel I framework for those banks not adopting Basel II, called Basel IA. The Basel IA NPR will allow non-Basel II banking organizations the choice of adopting all of the revisions suggested in the proposed NPR or continuing the use of existing risk-based capital rules. However, our initial analysis indicates that a significant risk of competitive inequity would persist between banks operating under Basel IA and those using Basel II by potentially allowing Basel II banks to operate with lower levels of capital for certain lines of business. |

| • | | From time to time the Company makes acquisitions. The success of any acquisition depends, in part, on our ability to realize the projected cost savings from the merger and on the continued growth and profitability of the acquisition target. We have been successful with most prior mergers, but it is possible that the merger and integration process with an acquisition target could result in the loss of key employees, disruptions in controls, procedures and policies, or other factors that could affect our ability to realize the projected savings and successfully retain and grow the target’s customer base. |

The Company’s Board of Directors has established an Enterprise-Wide Risk Management policy and appointed an Enterprise Risk Management Committee to oversee and implement the policy. In addition to credit and interest rate risk, the Committee also oversees and monitors the following risk areas: market risk, liquidity risk, operational risk, information technology risk, strategic risk, and reputation risk.

| ITEM 1B. | UNRESOLVED STAFF COMMENTS |

None.

At year-end 2006, the Company operated 470 domestic branches, of which 225 are owned and 245 are on leased premises. The Company also leases its headquarter offices in Salt Lake City, Utah. Other operations facilities are either owned or leased. The annual rentals under long-term leases for leased premises are determined under various formulas and factors, including operating costs, maintenance, and taxes. For additional information regarding leases and rental payments, see Note 18 of the Notes to Consolidated Financial Statements.

The information contained in Note 18 of the Notes to Consolidated Financial Statements is incorporated by reference herein.

| ITEM 4. | SUBMISSION OF MATTERS TO A VOTE OF SECURITY HOLDERS |

None.

10

PART II

| ITEM 5. | MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES |

MARKET INFORMATION

The Company’s common stock is traded on the Nasdaq Global Select Market under the symbol “ZION.” The last reported sale price of the common stock on Nasdaq on February 16, 2007 was $87.56 per share.

The following table sets forth, for the periods indicated, the high and low sale prices of the Company’s common stock, as quoted on Nasdaq:

| | | | | | | | | |

| | | 2006

| | 2005

|

| | | High

| | Low

| | High

| | Low

|

1st Quarter | | $ | 85.25 | | 75.13 | | 70.45 | | 63.33 |

2nd Quarter | | | 84.18 | | 76.28 | | 75.17 | | 66.25 |

3rd Quarter | | | 84.09 | | 75.25 | | 74.00 | | 68.45 |

4th Quarter | | | 83.15 | | 77.37 | | 77.67 | | 66.67 |

As of February 16, 2007, there were 6,982 holders of record of the Company’s common stock.

DIVIDENDS

The frequency and amount of common stock dividends paid during the last two years are as follows:

| | | | | | | | | |

| | | 1st Quarter

| | 2nd Quarter

| | 3rd Quarter

| | 4th Quarter

|

2006 | | $ | 0.36 | | 0.36 | | 0.36 | | 0.39 |

2005 | | | 0.36 | | 0.36 | | 0.36 | | 0.36 |

On January 26, 2007, the Company’s Board of Directors approved a dividend of $0.39 per common share payable on February 21, 2007 to shareholders of record on February 7, 2007. The Company expects to continue its policy of paying regular cash dividends on a quarterly basis, although there is no assurance as to future dividends because they depend on future earnings, capital requirements, and financial condition.

On December 7, 2006, we issued 240,000 shares of our Series A Floating-Rate Non-Cumulative Perpetual Preferred Stock with an aggregate liquidation preference of $240 million, or $1,000 per share. The preferred stock was offered in the form of 9,600,000 depositary shares with each depositary share representing a 1/40th ownership interest in a share of the preferred stock. In general, preferred shareholders are entitled to receive asset distributions before common shareholders; however, preferred shareholders have no preemptive or conversion rights, and only limited voting rights pertaining generally to amendments to the terms of the preferred stock or the issuance of senior preferred stock as well as the right to elect two directors in the event of certain defaults. The preferred stock is not redeemable prior to December 15, 2011, but will be redeemable subsequent to that date at the Company’s option at the liquidation preference value plus any declared but unpaid dividends. The preferred stock dividend reduces earnings available

11

to common shareholders and is computed at an annual rate equal to the greater of three-month LIBOR plus 0.52%, or 4.0%. Dividend payments are made quarterly in arrears on the 15th day of March, June, September, and December, commencing on March 15, 2007.

Under the terms of the preferred stock agreements, in December 2006 the Company was required to declare the full quarterly dividend of $3.8 million and set aside the funds before it could resume the repurchase of its common shares.

SECURITIES AUTHORIZED FOR ISSUANCE UNDER EQUITY COMPENSATION PLANS

The information contained in Item 12 of this Form 10-K is incorporated by reference herein.

SHARE REPURCHASES

The following table summarizes the Company’s share repurchases for the fourth quarter of 2006:

| | | | | | | | | | |

Period

| | Total number of shares

repurchased (1)

| | Average

price paid

per share

| | Total number of shares purchased

as part of publicly

announced plans

or programs

| | Approximate dollar value of shares that may yet be purchased

under the

plan (2)

|

October | | 1,057 | | $ | 80.68 | | – | | $ | 59,253,657 |

November | | 365 | | | 79.27 | | – | | | 59,253,657 |

December | | 311,987 | | | 81.06 | | 308,359 | | | 375,006,404 |

| | |

| | | | |

| | | |

Fourth quarter | | 313,409 | | | 81.05 | | 308,359 | | | |

| | |

| | | | |

| | | |

| (1) | Includes 4,435 shares tendered for exercise of stock options and 615 shares to cover payroll taxes on the vesting of restricted stock. |

| (2) | On December 11, 2006, the Company’s Board of Directors authorized the repurchase of up to $400 million of its common stock and the Company thus resumed the repurchase of its common stock. Prior to December, the Company had suspended the repurchase of its shares since July 2005 in conjunction with the acquisition of Amegy Bancorporation, Inc. |

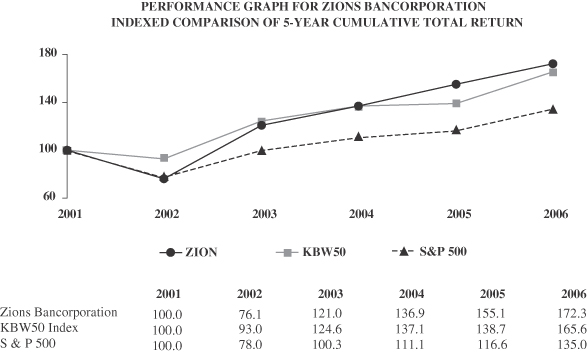

PERFORMANCE GRAPH

The following stock performance graph compares the five-year cumulative total return of Zions Bancorporation’s common stock with the Standard & Poor’s 500 Index and the KBW50 Index. The KBW50 Index is a market-capitalization weighted bank stock index developed and published by Keefe, Bruyette & Woods, Inc., a national recognized brokerage and investment banking firm specializing in bank stocks. The index is composed of 50 of the nation’s largest banking companies. The stock performance graph is based upon an initial investment of $100 on December 31, 2001 and assumes reinvestment of dividends.

12

13

| ITEM 6. | SELECTED FINANCIAL DATA |

FINANCIAL HIGHLIGHTS

| | | | | | | | | | | | | |

| (In millions, except per share amounts) | | 2006/2005

CHANGE

| | 2006

| | 2005 (3)

| | 2004

| | 2003

| | 2002

|

FOR THE YEAR | | | | | | | | | | | | | |

Net interest income | | +30% | | $ | 1,764.7 | | 1,361.4 | | 1,160.8 | | 1,084.9 | | 1,025.7 |

Noninterest income | | +26% | | | 551.2 | | 436.9 | | 431.5 | | 500.7 | | 386.2 |

Total revenue | | +29% | | | 2,315.9 | | 1,798.3 | | 1,592.3 | | 1,585.6 | | 1,411.9 |

Provision for loan losses | | +69% | | | 72.6 | | 43.0 | | 44.1 | | 69.9 | | 71.9 |

Noninterest expense | | +31% | | | 1,330.4 | | 1,012.8 | | 923.2 | | 893.9 | | 858.9 |

Impairment loss on goodwill | | -100% | | | – | | 0.6 | | 0.6 | | 75.6 | | – |

Income from continuing operations before income taxes and minority interest | | +23% | | | 912.9 | | 741.9 | | 624.4 | | 546.2 | | 481.1 |

Income taxes | | +21% | | | 318.0 | | 263.4 | | 220.1 | | 213.8 | | 167.7 |

Minority interest | | +817% | | | 11.8 | | (1.6) | | (1.7) | | (7.2) | | (3.7) |

Income from continuing operations | | +21% | | | 583.1 | | 480.1 | | 406.0 | | 339.6 | | 317.1 |

Loss on discontinued operations | | – | | | – | | – | | – | | (1.8) | | (28.4) |

Cumulative effect adjustment | | – | | | – | | – | | – | | – | | (32.4) |

Net income | | +21% | | | 583.1 | | 480.1 | | 406.0 | | 337.8 | | 256.3 |

Net earnings applicable to common shareholders | | +21% | | | 579.3 | | 480.1 | | 406.0 | | 337.8 | | 256.3 |

| | | | | | |

PER COMMON SHARE | | | | | | | | | | | | | |

Earnings from continuing operations – diluted | | +4% | | | 5.36 | | 5.16 | | 4.47 | | 3.74 | | 3.44 |

Net earnings – diluted | | +4% | | | 5.36 | | 5.16 | | 4.47 | | 3.72 | | 2.78 |

Net earnings – basic | | +4% | | | 5.46 | | 5.27 | | 4.53 | | 3.75 | | 2.80 |

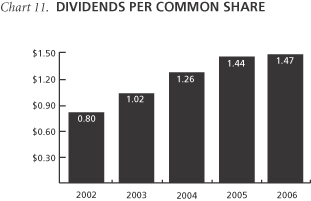

Dividends declared | | +2% | | | 1.47 | | 1.44 | | 1.26 | | 1.02 | | 0.80 |

Book value (1) | | +10% | | | 44.48 | | 40.30 | | 31.06 | | 28.27 | | 26.17 |

Market price – end | | | | | 82.44 | | 75.56 | | 68.03 | | 61.34 | | 39.35 |

Market price – high | | | | | 85.25 | | 77.67 | | 69.29 | | 63.86 | | 59.65 |

Market price – low | | | | | 75.13 | | 63.33 | | 54.08 | | 39.31 | | 34.14 |

| | | | | | |

AT YEAR-END | | | | | | | | | | | | | |

Assets | | +10% | | | 46,970 | | 42,780 | | 31,470 | | 28,558 | | 26,566 |

Net loans and leases | | +15% | | | 34,668 | | 30,127 | | 22,627 | | 19,920 | | 19,040 |

Loans sold being serviced (2) | | -24% | | | 2,586 | | 3,383 | | 3,066 | | 2,782 | | 2,476 |

Deposits | | +7% | | | 34,982 | | 32,642 | | 23,292 | | 20,897 | | 20,132 |

Long-term borrowings | | -9% | | | 2,495 | | 2,746 | | 1,919 | | 1,843 | | 1,310 |

Shareholders’ equity | | +18% | | | 4,987 | | 4,237 | | 2,790 | | 2,540 | | 2,374 |

| | | | | | |

PERFORMANCE RATIOS | | | | | | | | | | | | | |

Return on average assets | | | | | 1.32% | | 1.43% | | 1.31% | | 1.20% | | 0.97% |

Return on average common equity | | | | | 12.89% | | 15.86% | | 15.27% | | 13.69% | | 10.95% |

Efficiency ratio | | | | | 56.85% | | 55.67% | | 57.22% | | 55.65% | | 63.40% |

Net interest margin | | | | | 4.63% | | 4.58% | | 4.27% | | 4.41% | | 4.52% |

| | | | | | |

CAPITAL RATIOS (1) | | | | | | | | | | | | | |

Equity to assets | | | | | 10.62% | | 9.90% | | 8.87% | | 8.89% | | 8.94% |

Tier 1 leverage | | | | | 7.86% | | 8.16% | | 8.31% | | 8.06% | | 7.56% |

Tier 1 risk-based capital | | | | | 7.98% | | 7.52% | | 9.35% | | 9.42% | | 9.26% |

Total risk-based capital | | | | | 12.29% | | 12.23% | | 14.05% | | 13.52% | | 12.94% |

| | | | | | |

SELECTED INFORMATION | | | | | | | | | | | | | |

Average common and common-equivalent shares (in thousands) | | | | | 108,028 | | 92,994 | | 90,882 | | 90,734 | | 92,079 |

Common dividend payout ratio | | | | | 27.10% | | 27.14% | | 28.23% | | 27.20% | | 28.58% |

Full-time equivalent employees | | | | | 10,618 | | 10,102 | | 8,026 | | 7,896 | | 8,073 |

Commercial banking offices | | | | | 470 | | 473 | | 386 | | 412 | | 415 |

ATMs | | | | | 578 | | 600 | | 475 | | 553 | | 588 |

| (2) | Amount represents the outstanding balance of loans sold and being serviced by the Company, excluding conforming first mortgage residential real estate loans. |

| (3) | Amounts for 2005 include Amegy Corporation at December 31, 2005 and for the month of December 2005. Amegy was acquired on December 3, 2005. |

14

| ITEM 7. | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

MANAGEMENT’S DISCUSSION AND ANALYSIS

EXECUTIVE SUMMARY

Company Overview

Zions Bancorporation (“the Parent”) and subsidiaries (collectively “the Company,” “Zions,” “we,” “our,” “us”) together comprise a $47 billion financial holding company headquartered in Salt Lake City, Utah. The Company is the twenty-second largest domestic bank in terms of deposits, operating banking businesses through 470 offices and 578 ATMs in ten Western and Southwestern states: Arizona, California, Colorado, Idaho, Nevada, New Mexico, Oregon, Texas, Utah, and Washington. Our banking businesses include: Zions First National Bank (“Zions Bank”), in Utah and Idaho; California Bank & Trust (“CB&T”); Amegy Corporation (“Amegy”) and its subsidiary, Amegy Bank, in Texas; National Bank of Arizona (“NBA”); Nevada State Bank (“NSB”); Vectra Bank Colorado (“Vectra”), in Colorado and New Mexico; The Commerce Bank of Washington (“TCBW”); and The Commerce Bank of Oregon (“TCBO”).

The Company also operates a number of specialty financial services and financial technology businesses that conduct business on a regional or national scale. The Company is a national leader in Small Business Administration (“SBA”) lending, public finance advisory services, and software sales and cash management services related to “Check 21 Act” electronic imaging and clearing of checks. In addition, Zions is included in the S&P 500 and NASDAQ Financial 100 indices.

In operating its banking businesses, the Company seeks to combine the advantages that it believes can result from decentralized organization and branding, with those that can come from centralized risk management, capital management and operations. In its specialty financial services and technology businesses, the Company seeks to develop a competitive advantage in a particular product, customer, or technology niche.

Banking Businesses

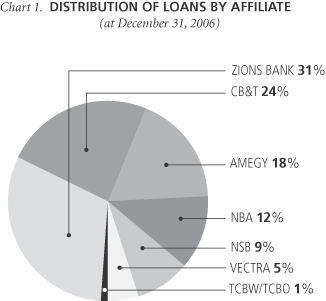

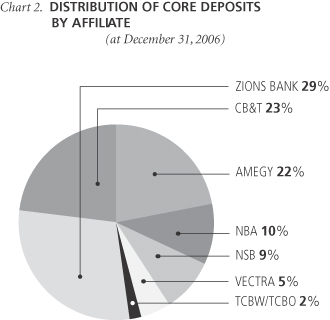

As shown in Charts 1 and 2 the Company’s loans and core deposits are widely diversified among the banking franchises the Company operates.

15

We believe that the Company distinguishes itself by having a strategy for growth in its banking businesses that is unique for a bank holding company of its size. This growth strategy is driven by three key factors: (1) focus on high growth markets; (2) keep decisions about customers local; and (3) centralize technology and operations to achieve economies of scale.

16

Focus on High Growth Markets

Each of the states in which the Company conducts its banking businesses has experienced relatively high levels of historical economic growth and each ranks among the top one-third of the fastest growing states as projected by the U.S. Census Bureau. In addition, in the recent past these states have experienced relatively high levels of population growth compared to the rest of the country.

SCHEDULE 1

DEMOGRAPHIC PROFILE

BY STATE

| | | | | | | | | | | | | | | | | | | | |

(Dollar amounts in thousands) | | Number of branches

12/31/2006

| | Deposits in

market at

12/31/2006 (1)

| | Percent of

Zions’

deposit base

| | Estimated

2006 total

population (2)

| | Estimated

population

% change

2000-2006 (2)

| | Projected

population

% change

2006-2011 (2)

| | Estimated

median

household

income

2006 (2)

| | Estimated

household

income % change

2000-2006 (2)

| | Projected

household

income % change

2006-2011 (2)

|

Utah | | 112 | | $ | 9,531,472 | | 27.25% | | 2,551,534 | | 14.26% | | 12.43% | | $ | 56.4 | | 23.38% | | 18.39% |

California | | 91 | | | 8,351,369 | | 23.87 | | 37,236,136 | | 9.93 | | 8.00 | | | 57.8 | | 21.32 | | 16.95 |

Texas | | 77 | | | 7,329,258 | | 20.95 | | 23,786,899 | | 14.08 | | 10.96 | | | 49.3 | | 23.35 | | 17.56 |

Arizona | | 53 | | | 3,675,458 | | 10.51 | | 6,135,872 | | 19.59 | | 16.09 | | | 51.3 | | 26.44 | | 21.27 |

Nevada | | 72 | | | 3,378,945 | | 9.66 | | 2,575,444 | | 28.88 | | 22.95 | | | 55.1 | | 23.42 | | 18.06 |

Colorado | | 38 | | | 1,665,988 | | 4.76 | | 4,821,136 | | 12.09 | | 9.08 | | | 58.5 | | 23.82 | | 18.03 |

Idaho | | 24 | | | 519,211 | | 1.48 | | 1,475,700 | | 14.05 | | 11.75 | | | 46.6 | | 23.59 | | 17.88 |

Washington | | 1 | | | 504,918 | | 1.44 | | 6,396,653 | | 8.53 | | 6.36 | | | 56.5 | | 23.38 | | 18.35 |

New Mexico | | 1 | | | 16,385 | | 0.05 | | 1,956,417 | | 7.55 | | 6.07 | | | 41.5 | | 21.56 | | 16.62 |

Oregon | | 1 | | | 8,742 | | 0.03 | | 3,694,335 | | 7.98 | | 6.28 | | | 50.1 | | 22.23 | | 17.56 |

| | | | | | | | | |

Zions’ weighted average | | | | | | | | | | | 15.12 | | 12.33 | | | 54.7 | | 23.28 | | 18.21 |

Aggregate national | | | | | | | | | 303,582,361 | | 7.87 | | 6.66 | | | 51.5 | | 22.25 | | 17.77 |

| (1) | Excludes intercompany deposits. |

| (2) | Data Source: SNL Financial Database |

The Company seeks to grow both organically and through acquisitions in these banking markets. In 2005 we acquired Amegy Bank in Texas, which continued to enjoy very strong organic growth through 2006. In September 2006, we announced the pending acquisition of The Stockmen’s Bancorp, Inc. (“Stockmen’s”), a bank holding company with $1.2 billion in assets headquartered in Kingman, Arizona. On January 17, 2007, this acquisition was completed and Stockmen’s banking subsidiary, The Stockmen’s Bank, was merged into our NBA affiliate bank.

Within each of the states that the Company operates, we focus on the market segments that we believe present the best opportunities for us. We believe that these states have experienced higher rates of growth, business formation, and expansion than other states. We also believe that these states will continue to experience higher rates of commercial real estate development as local businesses strive to provide housing, shopping, business facilities, and other amenities for their growing populations. As a result, a common focus of all of Zions’ subsidiary banks is small and middle market business banking (including the personal banking needs of the executives and employees of those businesses) and commercial real estate development. In many cases, the Company’s relationship with its customers is primarily driven by the goal to satisfy their needs for credit to finance their expanding business opportunities. In addition to our commercial business, we also provide a broad base of consumer financial products in selected markets, including home mortgages, home equity lines, auto loans, and credit cards. This mix of business often leads to loan balances growing faster than internally generated deposits. In addition, it has important implications for the Company’s management of certain risks, including interest rate and liquidity risks, which are discussed further in later sections of this document.

17

Keep Decisions About Customers Local

The Company operates eight different community/regional banks, each under a different name, each with its own charter, and each with its own chief executive officer and management team. This structure helps to ensure that decisions related to customers are made at a local level. In addition, each bank controls, among other things, all decisions related to its branding, market strategies, customer relationships, product pricing, and credit decisions (within the limits of established corporate policy). In this way we are able to differentiate our banks from much larger, “mass market” banking competitors that operate regional or national franchises under a common brand and often around “vertical” product silos. We believe that this approach allows us to attract and retain exceptional management, and that it also results in providing service of the highest quality to our targeted customers. In addition, we believe that over time this strategy generates superior growth in our banking businesses.

Centralize Technology and Operations to Achieve Economies of Scale

We seek to differentiate the Company from smaller banks in two ways. First, we use the combined scale of all of the banking operations to create a broad product offering without the fragmentation of systems and operations that would typically drive up costs. Second, for certain products for which economies of scale are believed to be important, the Company “manufactures” the product centrally, or outsources it from a third party. Examples include cash management, credit card administration, mortgage servicing and deposit operations. In this way the Company seeks to create and maintain efficiencies while generating superior growth.

Specialty Financial Services and Technology Businesses

In addition to its community and regional banking businesses, the Company operates a number of specialized businesses that in many cases are national in scope. These include a number of businesses in which the Company believes it ranks in the top ten institutions nationally such as SBA 7(a) loan originations, SBA 504 lending, public finance advisory and underwriting services, software and cash management services related to the electronic imaging of checks pursuant to the Check 21 Act, and the origination of farm mortgages sold to Farmer Mac.

High growth market opportunities are not always geographically defined. The Company continues to invest in several expanded or new initiatives that we believe present unusual opportunities for us, including the following:

National Real Estate Lending

This business consists of making SBA 504 and similar low loan-to-value, primarily owner-occupied, first mortgage small business commercial loans. During both 2006 and 2005, the Company originated directly and purchased from correspondents approximately $1.2 billion of these loans. During 2005 we securitized $707 million of these loans; no securitization was completed during 2006. A qualifying special-purpose entity (“QSPE”), Lockhart Funding, LLC (“Lockhart”), purchases the resultant securities after credit enhancement and funds them through the issuance of commercial paper.

18

NetDeposit and Related Services

NetDeposit, Inc. (“NetDeposit”) is a subsidiary of the Parent that was created to develop and sell software and processes that facilitate electronic check clearing. With the implementation of the Check 21 Act late in 2004, this company and its products are well positioned to take advantage of the revolution in check processing now underway in America. During 2006, NetDeposit reduced earnings by $0.07 per diluted share, compared to $0.08 per share in 2005. Revenues for 2006 increased almost 90% from 2005 and we have continued to increase our investment in this business.

The Company generates revenues in several ways from this business. First, NetDeposit licenses software, sells consulting services, and resells scanners to other banks and processors. Newly announced customers since January 1, 2006 include BOK Financial Corporation, Deutsche Bank, First National Bank of Arizona, and National City Bank. These activities initially generate revenue from scanner sales, consulting, and licensing fees. Deployment-related fees related to work station site licenses and check processing follow, but have been slower to increase than expected as deployment throughout the industry has been slower than expected.

Second, NetDeposit has licensed its software to the Company’s banks, which use the capabilities of the software to provide state-of-the art cash management services to business customers and to correspondent banks. At year-end, over 4,500 Zions affiliate bank cash management customers were using NetDeposit, and we processed over $8.5 billion of imaged checks from our cash management customers in the month of December.

Third, Zions Bank uses NetDeposit software to provide check-clearing services to correspondent banks. Zions Bank has contracts and co-marketing agreements with a number of bank processors and resellers, both domestically and abroad.

NetDeposit seeks to protect its intellectual property in business methods related to the electronic processing and clearing of checks. It has applied for several patents and was recently notified by the United States Patent and Trademark Office that it has been granted two patents.

Treasury Management

With the acquisition of Amegy Bank, Zions’ cash, or treasury, management capabilities were significantly enhanced. Zions believes that it has a significant opportunity to increase its treasury management penetration of commercial customers in its geographic territory, and increased its investment in these capabilities in 2006. An increased level of investment in treasury management, both in technology and service and in sales, is expected to continue in 2007.

In addition to enhancing its general treasury management capabilities, Zions has made significant investments specifically in creating enhanced capabilities in services related to claims processing and reconciliation for medical providers. Included among these investments was the acquisition of the remaining minority interests in P5, Inc. (“P5”); Zions had for several years owned a majority interest in this start-up provider of web-based claims reconciliation services. At year-end 2006, P5 provided these services to over 800 medical practitioners, mostly pharmacy outlets. The Company is in the process of integrating P5’s services and other payment processing services into its more traditional treasury management products and services for the medical provider industry.

19

Wealth Management

We have extensive relationships with small and middle-market businesses and business owners that we believe present an unusual opportunity to offer wealth management services. As a result, the Company established a wealth management business, Contango Capital Advisors, Inc. (“Contango”), and launched the business in the latter half of 2004. The business offers financial and tax planning, trust and inheritance services, over-the-counter, exchange-traded and synthetic derivative and hedging strategies, quantitative asset allocation and risk management and a global array of investment strategies from equities and bonds through alternative and private equity investments. At year-end Contango had over $885 million of client assets under management and a strong pipeline of referrals from our affiliate banks as compared to over $170 million at December 31, 2005. At December 31, 2006, the Company had total discretionary assets under management of $2.1 billion, including assets managed by Contango, Amegy, and Western National Trust Company, a wholly owned subsidiary of Zions Bank. During 2006, Contango generated net losses of $0.07 per diluted share, unchanged from 2005. We expect that net losses will decline in 2007 and that the business will approach break-even late in 2007 or in 2008.

Employee Stock Option Appreciation Rights

In December 2004, the Financial Accounting Standards Board (“FASB”) issued Statement of Financial Accounting Standards (“SFAS”) No. 123R,Share-Based Payment, which is a revision of SFAS No. 123,Accounting for Stock-Based Compensation. We have developed a market-based method for the valuation of employee stock options for SFAS 123R purposes. This method uses an online auction to price a tracking instrument that measures the fair value of the option grant. On January 25, 2007, we received notice from the Office of the Chief Accountant of the Securities and Exchange Commission (“SEC”) that they concur with our view that our tracking instrument, with modifications described in the notification, is sufficiently designed to be used for SFAS 123R. Zions did not use this method to value its 2006 grant; however we intend to use the method to value our 2007 option grant. We also intend to market this method as a service to other SEC registrants.

MANAGEMENT’S OVERVIEW OF 2006 PERFORMANCE

The Company’s primary or “core” business consists of providing community and regional banking services to both individuals and businesses in ten Western and Southwestern states. We believe that this core banking business performed well during 2006. The Company experienced strong organic loan growth of over 15%, continued to experience excellent credit quality, and maintained a high and stable net interest margin in a difficult rate environment.

On December 3, 2005 we completed our acquisition of Amegy Bancorporation, Inc. The merger was accounted for under the purchase method of accounting and, accordingly, results of operations for 2005 include the results of Amegy only for the month of December. All comparisons to 2005 and prior periods reflect the impact of the acquisition. In May 2006 the conversion of Amegy’s major systems to the Zions technology and operations platform was completed.

20

In September 2006 the Company announced the acquisition of The Stockmen’s Bancorp, Inc. headquartered in Kingman, Arizona. This acquisition was completed on January 17, 2007; consequently 2006 results were not impacted by the acquisition of Stockmen’s, but the acquisition will increase loans, deposits, revenue and expenses in 2007. As previously announced, the Company expects this acquisition to be about $0.03 dilutive to earnings per share in 2007, excluding merger related costs.

The Company reported record earnings for 2006 of $579.3 million or $5.36 per diluted common share. This compares with $480.1 million or $5.16 per diluted share for 2005 and $406.0 million or $4.47 per share for 2004. Return on average common equity was 12.89% and return on average assets was 1.32% in 2006, compared with 15.86% and 1.43% in 2005 and 15.27% and 1.31% in 2004.

The key drivers of the Company’s performance during 2006 were as follows:

SCHEDULE 2

KEY DRIVERS OF PERFORMANCE

2006 COMPARED TO 2005

| | | | | | | |

Driver

| | 2006

| | 2005

| | Change

|

| | | (in billions) | | |

Average net loans and leases | | $ | 32.4 | | 24.0 | | 35% |

Average total noninterest-bearing deposits | | | 9.5 | | 7.4 | | 28% |

Average total deposits | | | 32.8 | | 24.9 | | 32% |

| | |

| | | (in millions) | | |

Net interest income | | $ | 1,764.7 | | 1,361.4 | | 30% |

Provision for loan losses | | | 72.6 | | 43.0 | | 69% |

Net interest margin | | | 4.63% | | 4.58% | | 5bp |

Nonperforming assets as a percentage of net loans and leases and other real estate owned | | | 0.24% | | 0.30% | | (6)bp |

Efficiency ratio | | | 56.85% | | 55.67% | | 118bp |

As illustrated by the previous schedule, the Company’s earnings growth in 2006 compared to 2005 reflected the following:

| • | | The acquisition of Amegy, which closed in December 2005, and resulted in significant increases in most balance sheet and income statement line items, and improvement in Amegys’ pre-acquisition efficiency ratio; |

| • | | Strong organic loan growth; |

| • | | Lagging organic deposit growth, resulting in a greater dependence on market rate funds; |

| • | | A stable net interest margin in a difficult interest rate environment, and pricing pressure on both loans and funding costs; |

| • | | An increased provision for loan losses mainly attributable to strong loan growth, but a continued high level of credit quality; and |

| • | | A higher ratio of expenses to revenue (“efficiency ratio”), which increased as a result of the Amegy acquisition, but declined through the year as integration efficiencies were attained. |

21

We believe that the performance the Company experienced in 2006 was a direct result of our focusing on five primary objectives: 1) organic loan and deposit growth, 2) maintaining credit quality at high levels, 3) managing interest rate risk, 4) completing the conversion of Amegy onto Zions’ systems, and 5) controlling expenses.

Organic Loan and Deposit Growth

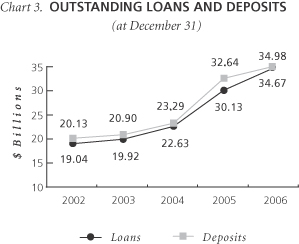

Since 2002, the Company has experienced steady and strong loan growth and moderate deposit growth, augmented in 2005 and 2006 by the Amegy acquisition. We consider this performance to be a direct result of steadily improving economic conditions throughout most of our geographical footprint, and of effectively executing our operating strategies. Chart 3 depicts this growth.

The Company experienced strong loan growth in all of its markets early in 2006, however, declining rates of residential housing development and construction in the West resulted in significantly slower rates of loan growth in its CB&T, NBA, and NSB subsidiaries in the latter half of the year. In fact, total loans outstanding in CB&T and NSB actually declined in the fourth quarter compared to the third quarter of 2006. The Company expects that the slower rate of residential development and construction lending will continue to result in much slower or no net loan growth in CB&T, NBA, and NSB in at least the first half of 2007. However, commercial lending strengthened during 2006 particularly in Zions Bank and Amegy, but also in our Vectra and TCBW bank subsidiaries, and remained very strong in the latter half of the year. The result was net loan growth of $4.5 billion, or 15.1%, from year-end 2006 compared to year-end 2005, and a mix shift away from commercial real estate and towards commercial lending sectors in new loan originations.

Reflecting trends throughout the banking industry, the Company’s deposit growth in 2006 slowed significantly. Core deposits grew only $552 million from year-end 2005, a rate of 1.8% – significantly lagging the growth rate of loans. In addition, noninterest-bearing

22

demand deposits only increased by $56 million from year-end 2005. Thus, the Company increased its reliance on more costly sources of funding during the year.

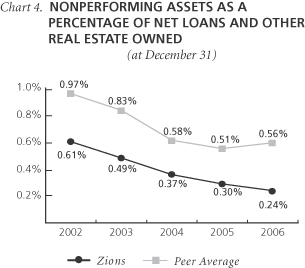

Maintaining Credit Quality at High Levels

The ratio of nonperforming assets to net loans and other real estate owned improved to 0.24% at year-end, compared to 0.30% at the end of 2005. Net loan charge-offs for 2006 were $46 million, compared to $25 million for 2005. The provision for loan losses during 2006 significantly increased relative to 2005, driven in significant part by strong loan growth and the Amegy acquisition. The Company believes that it is unlikely that credit quality will improve further from these year-end levels; however, it also sees little sign of significant deterioration in credit quality.

Note: Peer group is defined as bank holding companies with assets > $10 billion.

Peer data source: SNL Financial Database

Peer information for 2006 is from 3rd quarter 2006.

Managing Interest Rate Risk

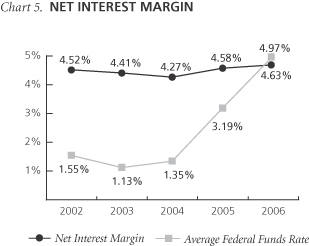

Our focus in managing interest rate risk is not to take positions based upon management’s forecasts of interest rates, but rather to maintain a position of slight “asset-sensitivity.” This means that our assets tend to reprice slightly more quickly than our liabilities. The Company makes extensive use of interest rate swaps to hedge interest rate risk in order to seek to achieve this desired position. This practice has enabled us to achieve a relatively stable net interest margin during periods of volatile interest rates, which is depicted in Chart 5.

Taxable-equivalent net interest income in 2006 increased 29.4% over 2005. Excluding Amegy from 2006 and December 2005, taxable-equivalent net interest income increased 9.1%. The net interest margin increased to 4.63% for 2006, up from 4.58% for 2005. The Company was able to achieve this performance despite the challenges of a flat-to-inverted yield curve, and significant pressures on both loan pricing and funding costs that resulted in fairly steady compression of the net interest spread (the difference between the average yield on all interest-earning assets and the average cost of all interest-bearing funding sources).

23

See the section “Interest Rate Risk” on page 87 for more information regarding the Company’s asset-liability management (“ALM”) philosophy and practice and our interest rate risk management.

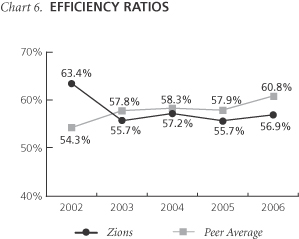

Controlling Expenses

During 2006 the Company’s efficiency ratio increased to 56.9% compared to 55.7% for 2005. The efficiency ratio is the relationship between noninterest expense and total taxable-equivalent revenue. The efficiency ratio deteriorated following the close of the Amegy acquisition, both due to Amegy’s higher pre-merger efficiency ratio relative to Zions and due to acquisition and integration related costs. However, after peaking in the first quarter, the efficiency ratio improved as cost synergies were realized.

Note: Peer group is defined as bank holding companies with assets > $10 billion.

Peer data source: SNL Financial Database

Peer information for 2006 is from 3rd quarter 2006.

24

Capital and Return on Capital

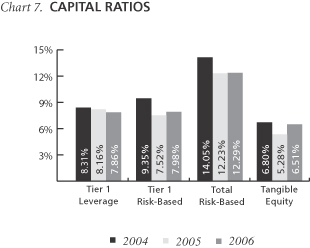

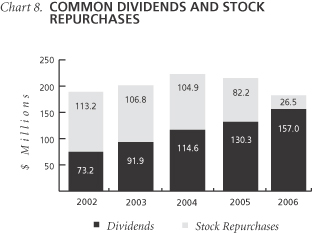

As regulated financial institutions, the Parent and its subsidiary banks are required to maintain adequate levels of capital as measured by several regulatory capital ratios. One of our goals is to maintain capital levels that are at least “well capitalized” under regulatory standards. The Company and each of its banking subsidiaries met the “well capitalized” guidelines at December 31, 2006. In addition, the Parent and certain of its banking subsidiaries have issued various debt securities that have been rated by the principal rating agencies. As a result, another goal is to maintain capital at levels consistent with an “investment grade” rating for these debt securities. The Company has maintained its “investment grade” debt ratings, as have those of its bank subsidiaries that have ratings. At year-end 2006 the Company’s tangible common equity ratio increased to 5.98% compared to 5.28% at the end of 2005. In December 2006 the Company issued $240 million of non-cumulative perpetual preferred stock; this additional capital raised the Company’s tangible equity ratio to 6.51% at year-end. The Company announced in the fourth quarter that it would target a tangible equity ratio of 6.25 - 6.50%, replacing the previously announced tangible common equity ratio target at the same level. In conjunction with these actions, the Company’s Board of Directors authorized a $400 million common stock buyback program, and the Company repurchased $25.0 million of its common stock in December 2006.

The Company continues to believe that capital in excess of that required to support the risks of the business in which it engages should be returned to the shareholders. In addition to dividends, the Company currently expects to use the remaining $375 million stock buyback authorization during 2007.

25

In addition, we believe that the Company should engage or invest in business activities that provide attractive returns on equity. Chart 9 illustrates that as a result of earnings improvement, the exit of underperforming businesses and returning unneeded capital to the shareholders, the Company’s return on average common equity has improved in recent years. The decline in 2006 is due to the additional common equity held due to additional intangible assets (primarily goodwill and core deposit intangibles) that resulted from the premium paid to acquire Amegy.

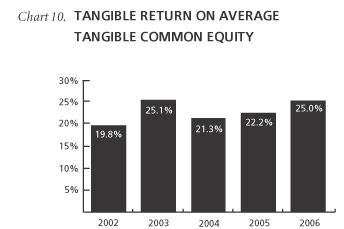

As depicted in Chart 10, tangible return on average tangible common equity further improved in 2006 as the Company continued to improve its core operating results.

26

Note: Tangible return is net earnings applicable to common

shareholders plus after-tax amortization of core deposit and

other intangibles and impairment losses on goodwill.

Challenges to Operations

As detailed in Schedule 2 on page 21, several factors combined to improve the Company’s performance in 2006 from 2005. The Company continued to experience strong loan growth, but deposit growth lagged. The improving economic conditions that began in 2004 continued through 2005 and 2006, and spread to include essentially all of our markets during the past year. However, as noted, growth in residential real estate development and construction slowed considerably in the second half of 2006 in Arizona, Southern California, and Southern Nevada. Credit quality remained exceptional during the year as nonperforming assets and net charge-off percentages remained at historically low levels. The Company was able to slightly improve its net interest margin year over year during a period when other financial institutions were experiencing significant margin compression due to the challenging interest rate environment.

As we enter 2007, we see several significant challenges to improving performance.

We expect that commercial real estate loans, which declined in CB&T and NSB in the fourth quarter, may continue to decline in our Southwestern markets throughout the first half of 2007. However, commercial loan growth has been accelerating, particularly in Zions Bank, Amegy and Vectra, which has kept aggregate loan growth robust.

Over the last two years, the Company has experienced historically high levels of credit quality. While we do not see any indications that loan quality will deteriorate significantly, it is unlikely we will be able to maintain credit quality at these levels for an indefinite period of time. The 2006 annual provision for loan losses was $73 million, an increase from 2005 of $30 million, and we expect that loan loss provisions may continue in 2007 at levels similar to 2006 if loan growth remains strong.

During 2006 we saw increased pressure on the pricing of both loans and deposits as the economy continued to expand and competition for good business increased. In particular, deposit rates repriced upward at an increasing rate in the latter half of 2005 and first half of 2006, the Federal Reserve continued to raise short-term interest rates, and the competition for deposits intensified.

27

We expect these pressures to continue in 2007, although perhaps not as severely if the Federal Reserve does not raise interest rates further. For more information on our asset-liability management processes, see “Interest Rate and Market Risk Management” on page 86.

We anticipate that economic conditions will continue to be strong in our geographic footprint during 2007, with weakness in residential real estate as previously discussed. However, any number of unforeseen events could result in a weaker economy that in turn could negatively impact loan growth and credit quality.

Excluding the impact of the Stockmen’s acquisition, we expect to see moderate growth in both revenues and expenses during 2007, and believe that controlling operating expenses will continue to be an important factor in improving our overall performance. We will continue to see increased expense levels during 2007 for systems conversions at Stockmen’s and CB&T, but we expect these conversions to result in ongoing expense savings when completed. We are also investing in creating systems, data and processes that may enable us to qualify for the proposed Basel II capital requirements.

Compliance with regulatory requirements pose an ongoing challenge. A failure in our internal controls could have a significant negative impact not only on our earnings but also on the perception that customers, regulators and investors may have of the Company. We continue to devote a significant amount of effort, time and resources to improving our controls and ensuring compliance with these complex regulations.

We have a number of business initiatives that, while we believe they will ultimately produce profits for our shareholders, currently generate expenses in excess of revenues. Three significant initiatives are Contango, a wealth management business started in 2004, NetDeposit, our subsidiary that provides electronic check processing systems, and the increased investments in treasury management and medical claims capabilities discussed in the Executive Summary. We will need to manage these businesses carefully to ensure that expenses and revenues develop in a planned way and that profits are not impaired to an extent that is not warranted by the opportunities these businesses provide.

Finally, competition from credit unions continues to pose a significant challenge. The aggressive expansion of some credit unions, far beyond the traditional concept of a common bond, presents a competitive threat to Zions and many other banking companies. While this is an issue in all of our markets, it is especially acute in Utah where two of the five largest financial institutions (measured by local deposits) are credit unions that are exempt from all state and federal income tax.

CRITICAL ACCOUNTING POLICIES AND SIGNIFICANT ESTIMATES

The Notes to Consolidated Financial Statements contain a summary of the Company’s significant accounting policies. We believe that an understanding of certain of these policies, along with the related estimates that we are required to make in recording the financial transactions of the Company, is important in order to have a complete picture of the Company’s financial condition. In

28

addition, in arriving at these estimates, we are required to make complex and subjective judgments, many of which include a high degree of uncertainty. The following is a discussion of these critical accounting policies and significant estimates related to these policies. We have discussed each of these accounting policies and the related estimates with the Audit Committee of the Board of Directors.

We have included sensitivity schedules and other examples to demonstrate the impact of the changes in estimates made for various financial transactions. The sensitivities in these schedules and examples are hypothetical and should be viewed with caution. Changes in estimates are based on variations in assumptions and are not subject to simple extrapolation, as the relationship of the change in the assumption to the change in the amount of the estimate may not be linear. In addition, the effect of a variation in one assumption is in reality likely to cause changes in other assumptions, which could potentially magnify or counteract the sensitivities.

Securitization Transactions

The Company from time to time enters into securitization transactions that involve transfers of loans or other receivables to off-balance-sheet QSPEs. In most instances, we provide the servicing on these loans as a condition of the sale. In addition, as part of these transactions, the Company may retain a cash reserve account, an interest-only strip, or in some cases a subordinated tranche, all of which are considered to be retained interests in the securitized assets.

Whenever we initiate a securitization, the first determination that we must make in connection with the transaction is whether the transfer of the assets constitutes a sale under U.S. generally accepted accounting principles. If it does, the assets are removed from the Company’s consolidated balance sheet with a gain or loss recognized. Otherwise, the transfer is considered a financing, resulting in no gain or loss being recognized and the recording of a liability on the Company’s consolidated balance sheet. The financing treatment could have unfavorable financial implications including an adverse effect on Zions’ results of operations and capital ratios. However, all of the Company’s securitizations have been structured to meet the existing criteria for sale treatment.

Another determination that must be made is whether the special-purpose entity involved in the securitization is independent from the Company or whether it should be included in its consolidated financial statements. If the entity’s activities meet certain criteria for it to be considered a QSPE, no consolidation is required. Since all of the Company’s securitizations have been with entities that have met the requirements to be treated as QSPEs, they have met the existing accounting criteria for nonconsolidation.

Finally, we must make assumptions to determine the amount of gain or loss resulting from the securitization transaction as well as the subsequent carrying amount for the retained interests. In determining the gain or loss, we use assumptions that are based on the facts surrounding each securitization. Using alternatives to these assumptions could affect the amount of gain or loss recognized on the transaction and, in turn, the Company’s results of operations. In valuing the retained interests, since quoted market prices of these interests are generally not available, we must estimate their value based on the present value of the future cash flows associated with the securitizations. These value estimations require the Company to make a number of assumptions including:

| • | | the method to use in computing the prepayments of the securitized loans; |

29

| • | | the annualized prepayment speed of the securitized loans; |

| • | | the weighted average life of the loans in the securitization; |

| • | | the expected annual net credit loss rate; and |

| • | | the discount rate for the residual cash flows. |

Quarterly, the Company reviews its valuation assumptions for retained beneficial interests under the rules contained in Emerging Issues Task Force Issue No. 99-20,Recognition of Interest Income and Impairment on Purchased and Retained Beneficial Interests in Securitized Financial Assets, (“EITF 99-20”). These rules require the Company to periodically update its assumptions used to compute estimated cash flows for its retained beneficial interests and compare the net present value of these cash flows to the carrying value. The Company complies with EITF 99-20 by quarterly evaluating and updating its assumptions including the default assumption as compared to the historical credit losses and the credit loss expectation of the portfolio, and its prepayment speed assumption as compared to the historical prepayment speeds and prepayment rate expectation. Changes in certain 2006 assumptions from 2005 for securizations were made in accordance with this process.

Schedule 3 summarizes the key economic assumptions that we used for measuring the values of the retained interests at the date of sale for securitizations during 2006, 2005, and 2004.

30

SCHEDULE 3

KEY ECONOMIC ASSUMPTIONS USED TO VALUE

RETAINED INTERESTS

| | | | |

| | | Home

equity

loans

| | Small business loans

|