Our business depends on the creditworthiness of our customers and their ability to fulfill their obligations to us. We maintain a consolidated allowance for loan losses on finance receivables that reflects management’s judgment of losses inherent in the portfolio. We regularly review our consolidated allowance for adequacy considering economic conditions and trends, collateral values, and credit quality indicators, including past charge-off experience and levels of past due loans, past due loan migration trends, and non-performing assets. Our credit losses were significantly more severe from 2007 to 2009 than in prior economic downturns, due to a significant decline in real estate values, an increase in the proportion of cash flow loans versus asset based loans in our corporate finance segment, the limited ability of borrowers to restructure their liabilities or their business, and reduced values of the collateral underlying the loans.

While our portfolio credit quality improved since mid-2010, the economic environment is dynamic, and our portfolio credit quality could decline in the future. Our allowance for loan losses may not keep pace with changes in the credit-worthiness of our customers or in collateral values. If the credit quality of our customer base declines, if the risk profile of a market, industry, or group of customers changes significantly, or if the markets for accounts receivable, equipment, real estate, or other collateral deteriorates significantly, our allowance for loan losses may prove inadequate, which could have a material adverse effect on our business, results of operations, and financial condition.

In addition to customer credit risk associated with loans and leases, we are exposed to other forms of credit risk, including counterparties to our derivative transactions, loan sales, syndications and equipment purchases. These counterparties include other financial institutions, manufacturers, and our customers. If our credit underwriting processes or credit risk judgments fail to adequately identify or assess such risks, or if the credit quality of our derivative counterparties, customers, manufacturers, or other parties with which we conduct business materially deteriorates, we may be exposed to credit risk related losses that may negatively impact our financial condition, results of operations or cash flows.

Our business depends upon our customers believing that we will be able to provide them with funding on a timely basis through a wide range of products. Many of our customers rely upon our funding to provide them with the working capital necessary to operate their business or to fund capital improvements that allow them to maintain or expand their business. In many instances, these funding requirements are time sensitive. If our customers are uncertain as to our ability to continue to provide them with funding on a timely basis or to provide the same breadth and quality of products, we may be unable to attract new customers and we may experience lower business volume or a loss of business with our existing customers.

As part of our strategy and business plan, we may consider a number of measures designed to manage our business, the products and services we offer, and our asset levels, credit exposures, or liquidity position, including potential business or asset acquisitions or sales. There can be no assurance that we will be successful in completing all or any of these transactions.

If CIT engages in business acquisitions, it may be necessary to pay a premium over book and market values to complete the transaction, which may result in some dilution of our tangible book value and net income per common share. If CIT uses substantial cash or other liquid assets or incurs substantial debt to acquire a business or assets, we could become more susceptible to economic downturns and competitive pressures. Inherent uncertainties exist when integrating the operations of an acquired entity. CIT may not be able to fully achieve its strategic objectives and planned operating efficiencies in an acquisition. CIT may also be exposed to other risks inherent in an acquisition, including potential exposure to unknown or contingent liabilities, exposure to potential asset quality issues, potential disruption of our existing business and diversion of management’s time and attention, possible loss of key employees or customers of the acquired business, potential risk that certain items were not accounted for properly by the seller in accordance with financial accounting and reporting standards. Failure to realize the expected revenue increases, cost savings, increases in geographic or product presence, and/or other projected benefits from an acquisition could have a material adverse effect on our business, financial condition, and results of operations.

As a result of economic cycles and other factors, the value of certain asset classes may fluctuate and decline below their historic cost. If CIT is holding such businesses or asset classes, we may not recover our carrying value if we sell such businesses or assets. In addition, potential purchasers may be unwilling to pay an amount equal to the face value of a loan or lease if the purchaser is concerned about the quality of the Company’s credit underwriting. There is no assurance that we will receive adequate consideration for any dispositions. These transactions, if completed, may reduce the size of our business and we may not be able to replace the volume associated with these businesses. As a result, our future disposition of assets could have a material adverse effect on our business, financial condition and results of operations.

Under the terms of the Written Agreement, we are restricted from declaring dividends on our common stock or repurchasing our common stock without prior written approval of the FRBNY. We are not currently paying dividends on our common stock and have not repurchased any common stock since our emergence from bankruptcy. Even when the Written Agreement is

CIT ANNUAL REPORT 2012 23

terminated, we may still require regulatory approval to pay dividends on our common stock or repurchase our common stock, and we cannot determine when, if ever, we will be permitted to do so. Although we recently submitted our 2013 capital plan to the Federal Reserve, which included a modest return of capital, we cannot determine whether the Federal Reserve will object to such capital return.

Uncertainties related to our business may create a distraction for employees and may otherwise materially adversely affect our ability to retain existing employees and/or attract new employees.

Our future results of operations will depend in part upon our ability to retain existing highly skilled and qualified employees and to attract new and retain qualified executive officers and management, financial, technical, marketing, sales, and support employees. Competition for qualified executive officers and employees is intense, and CIT cannot ensure success in attracting or retaining such individuals. If we fail to attract and retain qualified executive officers and employees, it could materially adversely affect our ability to compete and it could have a material adverse effect on our ability to successfully operate our business or to meet our operations, risk management, compliance, regulatory, funding and financial reporting requirements.

We may not be able to realize our entire investment in the equipment we lease to our customers.

The realization of equipment values (residual values) during the life and at the end of the term of a lease is an important element in the leasing business. At the inception of each lease, we record a residual value for the leased equipment based on our estimate of the future value of the equipment at the expected disposition date. Internal equipment management specialists, as well as external consultants, determine residual values.

If the market value of leased equipment decreases at a rate greater than we projected, whether due to rapid technological or economic obsolescence, unusual wear and tear on the equipment, excessive use of the equipment, recession or other adverse economic conditions, or other factors, it would adversely affect the current values or the residual values of such equipment.

Further, certain equipment residual values, including commercial aerospace residuals, are dependent on the manufacturers’ or vendors’ warranties, reputation, and other factors, including market liquidity. In addition, we may not realize the full market value of equipment if we are required to sell it to meet liquidity needs or for other reasons outside of the ordinary course of business. Consequently, there can be no assurance that we will realize our estimated residual values for equipment.

The degree of residual realization risk varies by transaction type. Capital leases bear the least risk because contractual payments cover approximately 90% of the equipment’s cost at the inception of the lease. Operating leases have a higher degree of risk because a smaller percentage of the equipment’s value is covered by contractual cash flows over the term of the lease. Leveraged leases bear the highest level of risk as third parties have a priority claim on equipment cash flows. A significant portion of our leasing portfolios are comprised of operating leases, and a small portion is comprised of leveraged leases, both of which increase our residual realization risk.

We are currently involved, and may from time to time in the future be involved, in a number of judicial, regulatory, and arbitration proceedings related to the conduct of our business, the results of which could have a material adverse effect on our business, financial condition, or results of operation.

We are currently involved, and from time to time in the future may be involved, in a number of judicial, regulatory, and arbitration proceedings relating to matters that arise in connection with the conduct of our business (collectively, “Litigation”). It is inherently difficult to predict the outcome of Litigation matters, particularly when such matters are in their early stages or where the claimants seek indeterminate damages. We cannot state with certainty what the eventual outcome of the pending Litigation will be, what the timing of the ultimate resolution of these matters will be, or what the eventual loss, fines, or penalties related to each pending matter will be, if any. Although we have established reserves for certain matters, the actual results of resolving such matters may be substantially higher than the amounts reserved, or judgments may be rendered, or fines or penalties assessed in matters for which we have no reserves. Adverse judgments, fines or penalties in one or more Litigation matters could have a material adverse effect on our business, financial condition, or results of operation.

We and our subsidiaries are party to various financing arrangements, commercial contracts and other arrangements that under certain circumstances give, or in some cases may give, the counterparty the ability to exercise rights and remedies under such arrangements which, if exercised, may have material adverse consequences.

We and our subsidiaries are party to various financing arrangements, commercial contracts and other arrangements, such as securitization transactions, derivatives transactions, funding facilities, and agreements for the purchase or sale of assets, that give, or in some cases may give, the counterparty the ability to exercise rights and remedies upon the occurrence of certain events. Such events may include a material adverse effect or material adverse change (or similar event), a breach of representations or warranties, a failure to disclose material information, a breach of covenants, certain insolvency events, a default under certain specified other obligations, or a failure to comply with certain financial covenants. The counterparty could have the ability, depending on the arrangement, to, among other things, require early repayment of amounts owed by us or our subsidiaries and in some cases payment of penalty amounts, or require the repurchase of assets previously sold to the counterparty. Additionally, a default under financing arrangements or derivatives transactions that exceed a certain size threshold in the aggregate may also cause a cross-default under instruments governing our other financing arrangements or derivatives transactions. If the ability of any counterparty to exercise such rights and remedies is triggered and we are unsuccessful in avoiding or minimizing the adverse consequences discussed above, such consequences could have a material adverse effect on our business, results of operations, and financial condition.

For example, in 2008, we entered into a purchase agreement (the “Purchase Agreement”) to sell our home lending business, including the related residential mortgage loan portfolio and mortgage backed securities, to a company created by a private

Item 1A: Risk Factors

24 CIT ANNUAL REPORT 2012

equity fund for the purpose of entering into the Purchase Agreement (the “Purchaser”). Prior to the sale of our home lending business to the Purchaser, we periodically had securitized a portion of the residential mortgage loans that we originated, and we sold residential mortgage loans or residential mortgage backed securities to Government Sponsored Entities, monoline home lenders, and investors. Pursuant to the Purchase Agreement with the Purchaser, we made certain representations and warranties regarding the business and portfolio, nearly all of which have since expired. In addition, the Purchaser agreed to assume all repurchase obligations for residential mortgage loans under the securitization and loan sale agreements entered into prior to the Purchase Agreement and scheduled as part of the Purchase Agreement.

The Purchaser has not given any indication that it has been subject to significant repurchase obligations or that it does not intend to honor its agreement to assume such repurchase obligations. However, if the Purchaser is subject to repurchase obligations and is unable or unwilling to accept responsibility for such repurchase obligations, and particularly if the Purchaser does not have sufficient capital to address such repurchase obligations, then we may become subject to claims under such repurchase obligations. If we become responsible for such repurchase obligations to third parties, it may have a material adverse effect on our results of operations and financial condition.

Adverse or volatile market conditions could continue to negatively impact fees and other income.

A portion of our revenue base is generated through loan syndication fees and participation income, advisory fees, servicing fees, and other types of fee income, which are recorded in other income. In addition, we also generate significant fee income from our factoring business. These revenue streams are dependent on market conditions and the confidence of clients, customers, and syndication partners in our ability to perform our obligations, and, therefore, are more volatile than interest payments on loans and rentals on leased equipment. Current market conditions, including lower liquidity levels in the syndication market, have significantly reduced our syndication activity, and have resulted in significantly lower fee income. In addition, if our clients, customers, or syndication partners become concerned about our ability to meet our obligations on a transaction, it may become more difficult for us to originate new transactions, to syndicate transactions that we originate, or to participate in syndicated transactions originated by others, which could further negatively impact our fee income and have a material adverse effect on our business. If we are unable to sell or syndicate a transaction after it is originated, we will end up holding a larger portion of the transaction and assume greater underwriting risk than we originally intended, which could increase our capital and liquidity requirements to support our business or expose us to the risk of valuation allowances for assets held for sale. If the capital markets are disrupted or if we otherwise fail to produce increased fees and other income, it could adversely affect our financial condition and results of operations.

Investment in and revenues from our foreign operations are subject to various risks and requirements associated with transacting business in foreign countries.

An economic recession or downturn, increased competition, or business disruption associated with the political or regulatory environments in the international markets in which we operate could adversely affect us.

In addition, our foreign operations generally conduct business in foreign currencies, which subject us to foreign currency exchange rate fluctuations. These exposures, if not effectively hedged could have a material adverse effect on our investment in international operations and the level of international revenues that we generate from international financing and leasing transactions. Reported results from our operations in foreign countries may fluctuate from period to period due to exchange rate movements in relation to the U.S. dollar, particularly exchange rate movements in the Canadian dollar, which is our largest non-U.S. exposure.

Foreign countries have various compliance requirements for financial statement audits and tax filings, which are required in order to obtain and maintain licenses to transact business. If we are unable to properly complete and file our statutory audit reports or tax filings, regulators or tax authorities in the applicable jurisdiction may restrict our ability to do business.

Furthermore, our international operations could expose us to trade and economic sanctions or other restrictions imposed by the United States or other governments or organizations. The U.S. Department of Justice (“DOJ”) and other federal agencies and authorities have a broad range of civil and criminal penalties they may seek to impose against corporations and individuals for violations of trade sanctions laws, the Foreign Corrupt Practices Act (“FCPA”) and other federal statutes. Under trade sanctions laws, the government may seek to impose modifications to business practices, including cessation of business activities in sanctioned countries, and modifications to compliance programs, which may increase compliance costs, and may subject us to fines, penalties and other sanctions. If any of the risks described above materialize, it could adversely impact our operating results and financial condition.

These laws also prohibit improper payments or offers of payments to foreign governments and their officials and political parties for the purpose of obtaining or retaining business. We have operations, deal with government entities and have contracts in countries known to experience corruption. Our activities in these countries create the risk of unauthorized payments or offers of payments by one of our employees, consultants, sales agents, or associates that could be in violation of various laws, including the FCPA, even though these parties are not always subject to our control. Our existing safeguards and procedures may prove to be less than fully effective, and our employees, consultants, sales agents, or associates may engage in conduct for which we may be held responsible. Violations of the FCPA may result in severe criminal or civil sanctions, and we may be subject to other liabilities, which could negatively affect our business, operating results, and financial condition.

CIT ANNUAL REPORT 2012 25

We may be adversely affected by significant changes in interest rates.

In addition to our equity capital, we rely on borrowed money from unsecured debt, secured debt, and deposits to fund our business. We derive the bulk of our income from net finance revenue, which is the difference between interest and rental income on our financing and leasing assets and interest expense on deposits and other borrowing and depreciation on our operating lease equipment. Prevailing economic conditions, the trade, fiscal, and monetary policies of the federal government and the policies of various regulatory agencies all affect market rates of interest and the availability and cost of credit, which in turn significantly affects our net finance revenue. Volatility in interest rates can also result in disintermediation, which is the flow of funds away from financial institutions into direct investments, such as federal government and corporate securities and other investment vehicles, which, because of the absence of federal insurance premiums and reserve requirements, generally pay higher rates of return than financial institutions.

Although interest rates are currently lower than usual, as interest rates rise and fall over time, any significant decrease in market interest rates may result in a change in net interest margins. A substantial portion of our loans and other financing products, as well as our deposits and other borrowings, bear interest at floating interest rates. If interest rates increase, monthly interest obligations owed by our customers to us will also increase, as will our own interest expense. Demand for our loans or other financing products may decrease as interest rates rise or if interest rates are expected to rise in the future. In addition, if prevailing interest rates increase, some of our customers may not be able to make the increased interest payments or refinance their balloon and bullet payment transactions, resulting in payment defaults and loan impairments. Conversely, if interest rates remain low, our interest expense may decrease, but our customers may refinance the loans they have with us at lower interest rates, or with others, leading to lower revenues. As interest rates rise and fall over time, any significant change in market rates may result in a decrease in net finance revenue, particularly if the interest rates we pay on our deposits and other borrowings and the interest rates we charge our customers do not change in unison, which may have a material adverse effect on our business, operating results, and financial condition.

We may be adversely affected by deterioration in economic conditions that is general in scope or affects specific industries, products or geographic areas.

Prolonged economic weakness, or other adverse economic or financial developments in the U.S. or global economies in general, or affecting specific industries, geographic locations and/or products, would likely impact credit quality as borrowers may fail to meet their debt payment obligations, particularly customers with highly leveraged loans. Adverse economic conditions have in the past and could in the future result in declines in collateral values, which also decreases our ability to fund against collateral. Accordingly, higher credit and collateral related losses could impact our financial position or operating results.

In addition, a downturn in certain industries may result in reduced demand for products that we finance in that industry or negatively impact collection and asset recovery efforts. Decreased demand for the products of various manufacturing customers due to recession may adversely affect their ability to repay their loans and leases with us. Similarly, a decrease in the level of airline passenger traffic or a decline in railroad shipping volumes due to reduced demand for certain raw materials or bulk products may adversely affect our aerospace or rail businesses, the value of our aircraft and rail assets, and the ability of our lessees to make lease payments.

We are also affected by the economic and other policies adopted by various governmental authorities in the U.S. and other jurisdictions in reaction to economic conditions. Changes in monetary policies of the Federal Reserve and non-U.S. central banking authorities directly impact our cost of funds for lending, capital raising, and investment activities, and may impact the value of financial instruments we hold. In addition, such changes may affect the credit quality of our customers. Changes in domestic and international monetary policies are beyond our control and difficult to predict.

Competition from both traditional competitors and new market entrants may adversely affect our market share, profitability, and returns.

Our markets are highly competitive and are characterized by competitive factors that vary based upon product and geographic region. We have a wide variety of competitors that include captive and independent finance companies, commercial banks and thrift institutions, industrial banks, community banks, leasing companies, hedge funds, insurance companies, mortgage companies, manufacturers and vendors.

We compete primarily on the basis of pricing, terms and structure. If we are unable to match our competitors’ terms, we could lose market share. Should we match competitors’ terms, it is possible that we could experience lower returns and/or increased losses.

We rely on our systems, employees, and certain third party vendors and service providers in conducting our operations, and certain failures, including internal or external fraud, operational errors, systems malfunctions, or cybersecurity incidents, could materially adversely affect our operations.

We are exposed to many types of operational risk, including the risk of fraud by employees and outsiders, clerical and recordkeeping errors, and computer or telecommunications systems malfunctions. Our businesses depend on our ability to process a large number of increasingly complex transactions. If any of our operational, accounting, or other data processing systems fail or have other significant shortcomings, we could be materially adversely affected. We are similarly dependent on our employees. We could be materially adversely affected if one of our employees causes a significant operational break-down or failure, either as a result of human error or intentional sabotage or fraudulent manipulation of our operations or systems. Third parties with which we do business, including vendors that provide services or security solutions for our operations, could also be sources of operational and information security risk to us, including from breakdowns, failures, or capacity constraints of their own systems or employees. Any of these occurrences could diminish our ability to operate one or more of our businesses, or cause financial loss, potential liability to clients, inability to secure

Item 1A: Risk Factors

26 CIT ANNUAL REPORT 2012

insurance, reputational damage, or regulatory intervention, which could materially adversely affect us.

We may also be subject to disruptions of our operating systems arising from events that are wholly or partially beyond our control, which may include, for example, electrical or telecommunications outages, natural or man-made disasters, such as earthquakes, hurricanes, floods, or tornados, disease pandemics, or events arising from local or regional politics, including terrorist acts. Such disruptions may give rise to losses in service to clients and loss or liability to us. In addition, there is the risk that our controls and procedures as well as business continuity and data security systems prove to be inadequate. The computer systems and network systems we and others use could be vulnerable to unforeseen problems. These problems may arise in both our internally developed systems and the systems of third-party service providers. In addition, our computer systems and network infrastructure present security risks, and could be susceptible to hacking, computer viruses, or identity theft. Any such failure could affect our operations and could materially adversely affect our results of operations by requiring us to expend significant resources to correct the defect, as well as by exposing us to litigation or losses not covered by insurance. Although we have business continuity plans and other safeguards in place, our business operations may be adversely affected by significant and widespread disruption to our physical infrastructure or operating systems that support our businesses and customers.

Information security risks for large financial institutions such as CIT have generally increased in recent years in part because of the proliferation of new technologies, the use of the Internet and telecommunications technologies to conduct financial transactions, and the increased sophistication and activities of organized crime, hackers, terrorists, activists, and other external parties. Our operations rely on the secure processing, transmission and storage of confidential information in our computer systems and networks. Our businesses rely on our digital technologies, computer and email systems, software, and networks to conduct their operations. Although we believe we have robust information security procedures and controls, our technologies, systems, networks, and our customers’ devices may become the target of cyber attacks or information security breaches that could result in the unauthorized release, gathering, monitoring, misuse, loss or destruction of CIT’s or our customers’ confidential, proprietary and other information, or otherwise disrupt CIT’s or its customers’ or other third parties’ business operations.

Since January 1, 2010, we have not experienced any material information security breaches involving either proprietary or customer information. However, in two instances, data on consumer accounts serviced by a third party provider, including certain customers of the Company, were taken by insiders of the third party provider without authorization. In both instances, the suspects were identified, the data was recovered, and there was no damage to either the Company or the customers. Although to date neither the Company nor our customers has experienced any material losses relating to cyber attacks or other information security breaches, there can be no assurance that we will not suffer such losses in the future. Our risk and exposure to these matters remains heightened because of, among other things, the evolving nature of these threats, the prominent size and scale of CIT and its role in the financial services industry, our plans to continue to implement our online banking channel strategies and develop additional remote connectivity solutions to serve our customers when and how they want to be served, our expanded geographic footprint and international presence, the outsourcing of some of our business operations, and the continued uncertain global economic environment. As a result, cyber security and the continued development and enhancement of our controls, processes and practices designed to protect our systems, computers, software, data and networks from attack, damage or unauthorized access remain a priority for CIT. As cyber threats continue to evolve, we may be required to expend significant additional resources to continue to modify or enhance our protective measures or to investigate and remediate any information security vulnerabilities.

Disruptions or failures in the physical infrastructure or operating systems that support our businesses and customers, or cyber attacks or security breaches of the networks, systems or devices that our customers use to access our products and services could result in customer attrition, regulatory fines, penalties or intervention, reputational damage, reimbursement or other compensation costs, and/or additional compliance costs, any of which could materially adversely affect our results of operations or financial condition.

Item 1B. Unresolved Staff CommentsThere are no unresolved SEC staff comments.

CIT operates in the United States, Canada, Europe, Latin America, and Asia. CIT occupies approximately 1.4 million square feet of office space, the majority of which is leased.

CIT ANNUAL REPORT 2012 27

Item 3. Legal ProceedingsCIT is currently involved, and from time to time in the future may be involved, in a number of judicial, regulatory, and arbitration proceedings relating to matters that arise in connection with the conduct of its business (collectively, “Litigation”), certain of which Litigation matters are described inNote 20 — Contingencies ofItem 8. Financial Statements and Supplementary Data. In view of the inherent difficulty of predicting the outcome of Litigation matters, particularly when such matters are in their early stages or where the claimants seek indeterminate damages, CIT cannot state with confidence what the eventual outcome of the pending Litigation will be, what the timing of the ultimate resolution of these matters will be, or what the eventual loss, fines, or penalties related to each pending matter may be, if any. In accordance with applicable accounting guidance, CIT establishes reserves for Litigation when those matters present loss contingencies as to which it is both probable that a loss will occur and the amount of such loss can be reasonably estimated. Based on currently available information, CIT believes that the results of Litigation that is currently pending, taken together, will not have a material adverse effect on the Company’s financial condition, but may be material to the Company’s operating results or cash flows for any particular period, depending in part on its operating results for that period. The actual results of resolving such matters may be substantially higher than the amounts reserved.

For more information about pending legal proceedings, including an estimate of certain reasonably possible losses in excess of reserved amounts, seeNote 20 — Contingencies ofItem 8. Financial Statements and Supplementary Data.

Item 4. Mine Safety DisclosuresNot applicable.

Item 3: Legal Proceedings

28 CIT ANNUAL REPORT 2012

PART TWO

Item 5. Market for Registrant’s Common Equity and Related Stockholder Matters and Issuer Purchases of Equity SecuritiesMarket Information – CIT’s common stock trades on the New York Stock Exchange (“NYSE”) under the symbol “CIT.”

The following tables set forth the high and low reported closing prices for CIT’s common stock.

Common Stock

| | | | 2012

| | 2011

| |

|---|

| | | | High

| | Low

| | High

| | Low

|

|---|

| | | | $ | 43.19 | | | $ | 34.84 | | | $ | 49.01 | | | $ | 41.82 | |

| | | | $ | 41.60 | | | $ | 32.57 | | | $ | 44.33 | | | $ | 39.60 | |

| | | | $ | 41.38 | | | $ | 34.20 | | | $ | 44.74 | | | $ | 30.27 | |

| | | | $ | 40.81 | | | $ | 36.12 | | | $ | 36.60 | | | $ | 29.12 | |

Holders of Common Stock – As of February 11, 2013, there were 110,598 beneficial owners of common stock.

Dividends – We have not declared nor paid any common stock dividends on the shares of common stock during 2011 and 2012.

Issuer Purchases of Equity Securities – There were no purchases of equity securities made during 2012 and there are no repurchase plans or programs under which shares may be purchased.

Return of Capital – We have requested from the Federal Reserve permission for a modest return of capital during 2013.

Securities Authorized for Issuance Under Equity Compensation Plans – Our equity compensation plans in effect following the Effective Date were approved by the Court and do not require shareholder approval. Equity awards associated with these plans are presented in the following table.

| | | | Number of Securities

to be Issued

Upon Exercise of

Outstanding Options

| | Weighted-Average

Exercise Price of

Outstanding Options

| | Number of Securities

Remaining Available for

Future Issuance Under

Equity Compensation Plans

|

|---|

Equity compensation plan

approved by the Court | | | | | 60,295 | | | $ | 31.16 | | | | 7,267,663 | * |

* Excludes the number of securities to be issued upon exercise of outstanding options and 1,997,412 shares underlying outstanding awards granted to employees and/or directors that are unvested and/or unsettled.

During 2012, we had no equity compensation plans that were not approved by the Court or by shareholders. For further information on our equity compensation plans, including the weighted average exercise price, seeItem 8. Financial Statements and Supplementary Data, Note 18 – Retirement, Other Postretirement and Other Benefit Plans.

Unregistered Sales of Equity Securities – There were no sales of common stock during 2012, however, there were issuances of common stock under equity compensation plans and an employee stock purchase plan.

On December 10, 2009, the effective date of our plan of reorganization, we provided for 600,000,000 shares of authorized common stock, par value $0.01 per share, of which 200,000,000 shares were issued, and 100,000,000 shares of authorized new preferred stock, par value $0.01 per share, of which no shares were issued. We reserved 10,526,316 shares of common stock for future issuance under the Amended and Restated CIT Group Inc. Long-Term Incentive Plan.

Based on the Confirmation Order, the Company relied on Section 1145(a)(1) of the United States Bankruptcy Code to exempt from the registration requirements of the Securities Act of 1933, as amended, the issuance of the new securities.

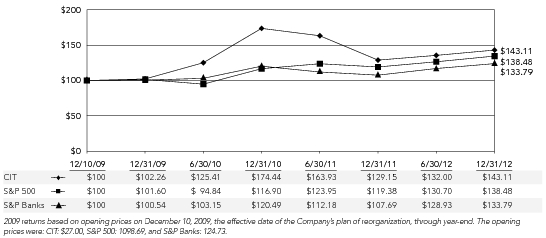

Shareholder Return – The following graph shows the semi-annual cumulative total shareholder return for common stock during the period from December 10, 2009 to December 31, 2012. Five year historical data is not presented since we emerged from bankruptcy on December 10, 2009 and the stock performance of CIT’s common stock is not comparable to the performance of pre-bankruptcy CIT’s common stock. The chart also shows the cumulative returns of the S&P 500 Index and S&P Banks Index for the same period. The comparison assumes $100 was invested on December 10, 2009 (the date our new common stock began trading on the NYSE). Each of the indices shown assumes that all dividends paid were reinvested.

CIT ANNUAL REPORT 2012 29

CIT STOCK PERFORMANCE DATA

Item 5: Market for Registrant’s Common Equity

30 CIT ANNUAL REPORT 2012

Item 6. Selected Financial DataThe following table sets forth selected consolidated financial information regarding our results of operations, balance sheets and certain ratios.

The Company has revised its total assets and total liabilities on its Balance Sheets at December 31, 2011 and 2010, and the respective quarters in 2012 and 2011, from the results released in the Company’s January 29, 2013 Earnings Release and Current Report on Form 8-K filing. The subsequent revisions reduced other assets and other liabilities and did not have any impact on tangible book value per common share for those periods or any line items in the Statement of Operations. SeeNote 27 – Selected Quarterly Financial Data inItem 8. Financial Statements and Supplementary Data.

As detailed inItem 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations, upon emergence from bankruptcy on December 10, 2009, CIT adopted fresh start accounting effective December 31, 2009, which resulted in data subsequent to adoption not being comparable to data in periods prior to emergence. Therefore, balance sheet information for CIT at December 31, 2012, 2011, 2010 and 2009 and statement of operations information for the years ended December 31, 2012, 2011 and 2010 are presented separately. Data for the years ended December 2009 and 2008 and at December 2008 represent amounts for Predecessor CIT. Predecessor CIT presents the operations of the home lending business as a discontinued operation.

The data presented below is explained further in, and should be read in conjunction with,Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations andItem 7A. Quantitative and Qualitative Disclosures about Market Risk andItem 8. Financial Statements and Supplementary Data.

Select Data (dollars in millions)

| | | | At or for the Years Ended December 31,

| |

|---|

| | | | CIT

| | Predecessor CIT

| |

|---|

| | | | 2012

| | 2011

| | 2010

| | 2009

| | 2009

| | 2008

|

|---|

Select Statement of Operations Data | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | $ | (1,328.3 | ) | | $ | (565.7 | ) | | $ | 639.3 | | | $ | – | | | $ | (308.1 | ) | | $ | 499.1 | |

Provision for credit losses | | | | | (51.6 | ) | | | (269.7 | ) | | | (820.3 | ) | | | – | | | | (2,660.8 | ) | | | (1,049.2 | ) |

Total non-interest income | | | | | 2,437.7 | | | | 2,620.3 | | | | 2,653.3 | | | | – | | | | 1,560.2 | | | | 2,460.3 | |

| | | | | (1,512.6 | ) | | | (1,606.5 | ) | | | (1,700.9 | ) | | | – | | | | (2,795.7 | ) | | | (2,986.5 | ) |

Reorganization items and fresh start adjustments | | | | | – | | | | – | | | | – | | | | – | | | | 4,240.2 | | | | – | |

| | | | | (592.3 | ) | | | 14.8 | | | | 521.3 | | | | – | | | | (3.8 | ) | | | (2,864.2 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | | |

Diluted income (loss) per common share | | | | $ | (2.95 | ) | | $ | 0.07 | | | $ | 2.60 | | | $ | – | | | $ | (0.01 | ) | | $ | (2.69 | ) |

Book value per common share | | | | $ | 41.49 | | | $ | 44.27 | | | $ | 44.54 | | | $ | 41.99 | | | $ | – | | | $ | 13.22 | |

Tangible book value per common share | | | | $ | 39.61 | | | $ | 42.23 | | | $ | 42.17 | | | $ | 39.06 | | | $ | – | | | $ | 11.78 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | |

Return on average common stockholders’ equity | | | | | (7.0 | )% | | | 0.2 | % �� | | | 6.0 | % | | | – | | | | N/M | | | | (11.0 | )% |

Net finance revenue as a percentage of average earning assets | | | | | (0.24 | )% | | | 1.53 | % | | | 3.95 | % | | | – | | | | 0.75 | % | | | 2.05 | % |

Return on average total assets | | | | | (1.34 | )% | | | 0.03 | % | | | 0.93 | % | | | – | | | | N/M | | | | (0.85 | )% |

Total ending equity to total ending assets | | | | | 18.9 | % | | | 19.6 | % | | | 17.3 | % | | | 13.9 | % | | | – | | | | 10.1 | % |

| | | | | | | | | | | | | | | | | | | | | | | | | | |

Loans including receivables pledged | | | | $ | 20,847.6 | | | $ | 19,905.9 | | | $ | 24,648.4 | | | $ | 35,185.1 | | | $ | – | | | $ | 53,126.6 | |

Allowance for loan losses | | | | | (379.3 | ) | | | (407.8 | ) | | | (416.2 | ) | | | – | | | | – | | | | (1,096.2 | ) |

Operating lease equipment, net | | | | | 12,411.7 | | | | 12,006.4 | | | | 11,155.0 | | | | 10,927.5 | | | | – | | | | 12,706.4 | |

Goodwill and intangible assets, net | | | | | 377.8 | | | | 409.5 | | | | 474.7 | | | | 586.6 | | | | – | | | | 698.6 | |

Total cash and short-term investments | | | | | 7,571.6 | | | | 8,374.0 | | | | 11,205.4 | | | | 9,826.2 | | | | – | | | | 8,365.8 | |

| | | | | 44,012.0 | | | | 45,263.4 | | | | 51,453.4 | | | | 60,561.5 | | | | – | | | | 80,448.9 | |

| | | | | 9,684.5 | | | | 6,193.7 | | | | 4,536.2 | | | | 5,177.7 | | | | – | | | | 2,626.8 | |

Total long-term borrowings | | | | | 21,961.8 | | | | 26,307.7 | | | | 34,049.3 | | | | 43,333.1 | | | | – | | | | 63,750.7 | |

Total common stockholders’ equity | | | | | 8,334.8 | | | | 8,883.6 | | | | 8,929.1 | | | | 8,400.0 | | | | – | | | | 5,138.0 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | |

Non-accrual loans as a percentage of finance receivables | | | | | 1.59 | % | | | 3.53 | % | | | 6.57 | % | | | 4.47 | % | | | 6.86 | % | | | 2.66 | % |

Net charge-offs as a percentage of average finance receivables | | | | | 0.37 | % | | | 1.16 | % | | | 1.53 | % | | | – | | | | 4.04 | % | | | 0.90 | % |

Allowance for loan losses as a percentage of finance receivables | | | | | 1.82 | % | | | 2.05 | % | | | 1.69 | % | | | – | | | | 4.33 | % | | | 2.06 | % |

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | 16.3 | % | | | 18.8 | % | | | 19.0 | % | | | 14.2 | % | | | – | | | | 9.4 | % |

| | | | | 17.0 | % | | | 19.7 | % | | | 19.9 | % | | | 14.2 | % | | | – | | | | 13.1 | % |

CIT ANNUAL REPORT 2012 31

The following table presents CIT’s individual components of net interest revenue and operating lease margins.

Average Balances(1)and Associated Income for the year ended: (dollars in millions)

| | | | December 31, 2012

| | December 31, 2011

| | December 31, 2010

| |

|---|

| | | | Average

Balance

| | Interest

| | Average

Rate (%)

| | Average

Balance

| | Interest

| | Average

Rate (%)

| | Average

Balance

| | Interest

| | Average

Rate (%)

|

|---|

Interest bearing deposits | | | | $ | 6,612.2 | | | $ | 21.8 | | | | 0.33 | % | | $ | 7,032.1 | | | $ | 24.2 | | | | 0.34 | % | | $ | 9,382.0 | | | $ | 19.6 | | | | 0.21 | % |

| | | | | 1,320.9 | | | | 10.5 | | | | 0.79 | % | | | 1,962.3 | | | | 10.6 | | | | 0.54 | % | | | 397.2 | | | | 12.1 | | | | 3.05 | % |

Loans (including held for sale)(2)(3) | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | 17,190.7 | | | | 1,131.7 | | | | 7.07 | % | | | 19,452.5 | | | | 1,608.3 | | | | 8.76 | % | | | 24,561.1 | | | | 2,732.9 | | | | 11.55 | % |

| | | | | 4,029.1 | | | | 405.1 | | | | 10.06 | % | | | 4,566.2 | | | | 585.6 | | | | 12.83 | % | | | 6,280.0 | | | | 954.4 | | | | 15.22 | % |

| | | | | 21,219.8 | | | | 1,536.8 | | | | 7.67 | % | | | 24,018.7 | | | | 2,193.9 | | | | 9.57 | % | | | 30,841.1 | | | | 3,687.3 | | | | 12.32 | % |

Total interest earning assets / interest income(2)(3) | | | | | 29,152.9 | | | | 1,569.1 | | | | 5.61 | % | | | 33,013.1 | | | | 2,228.7 | | | | 6.98 | % | | | 40,620.3 | | | | 3,719.0 | | | | 9.37 | % |

Operating lease equipment, net (including held for sale)(4) | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | 6,139.0 | | | | 596.9 | | | | 9.72 | % | | | 5,186.7 | | | | 428.1 | | | | 8.25 | % | | | 4,922.1 | | | | 383.9 | | | | 7.80 | % |

| | | | | 6,299.0 | | | | 654.5 | | | | 10.39 | % | | | 6,220.0 | | | | 664.3 | | | | 10.68 | % | | | 6,062.7 | | | | 588.7 | | | | 9.71 | % |

Total operating lease equipment, net(4) | | | | | 12,438.0 | | | | 1,251.4 | | | | 10.06 | % | | | 11,406.7 | | | | 1,092.4 | | | | 9.58 | % | | | 10,984.8 | | | | 972.6 | | | | 8.85 | % |

| | | | | 41,590.9 | | | $ | 2,820.5 | | | | 6.98 | % | | | 44,419.8 | | | $ | 3,321.1 | | | | 7.67 | % | | | 51,605.1 | | | $ | 4,691.6 | | | | 9.25 | % |

Non interest earning assets | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | 435.4 | | | | | | | | | | | | 938.8 | | | | | | | | | | | | 1,039.1 | | | | | | | | | |

Allowance for loan losses | | | | | (405.1 | ) | | | | | | | | | | | (412.0 | ) | | | | | | | | | | | (288.3 | ) | | | | | | | | |

All other non-interest earning assets | | | | | 2,671.1 | | | | | | | | | | | | 3,094.0 | | | | | | | | | | | | 3,557.1 | | | | | | | | | |

| | | | $ | 44,292.3 | | | | | | | | | | | $ | 48,040.6 | | | | | | | | | | | $ | 55,913.0 | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | $ | 7,707.9 | | | $ | 152.5 | | | | 1.98 | % | | $ | 4,796.6 | | | $ | 111.2 | | | | 2.32 | % | | $ | 4,780.1 | | | $ | 87.4 | | | | 1.83 | % |

| | | | | 24,235.5 | | | | 2,744.9 | | | | 11.33 | % | | | 30,351.5 | | | | 2,683.2 | | | | 8.84 | % | | | 38,769.3 | | | | 2,992.3 | | | | 7.72 | % |

Total interest-bearing liabilities | | | | | 31,943.4 | | | $ | 2,897.4 | | | | 9.07 | % | | | 35,148.1 | | | $ | 2,794.4 | | | | 7.95 | % | | | 43,549.4 | | | $ | 3,079.7 | | | | 7.07 | % |

Credit balances of factoring clients | | | | | 1,194.4 | | | | | | | | | | | | 1,098.1 | | | | | | | | | | | | 910.5 | | | | | | | | | |

Other non-interest bearing liabilities | | | | | 2,665.5 | | | | | | | | | | | | 2,834.1 | | | | | | | | | | | | 2,763.1 | | | | | | | | | |

| | | | | 5.0 | | | | | | | | | | | | 1.1 | | | | | | | | | | | | (3.5 | ) | | | | | | | | |

| | | | | 8,484.0 | | | | | | | | | | | | 8,959.2 | | | | | | | | | | | | 8,693.5 | | | | | | | | | |

Total Average Liabilities and Stockholders’ Equity | | | | $ | 44,292.3 | | | | | | | | | | | $ | 48,040.6 | | | | | | | | | | | $ | 55,913.0 | | | | | | | | | |

| | | | | | | | | | | | | (2.09 | )% | | | | | | | | | | | (0.28 | )% | | | | | | | | | | | 2.18 | % |

Impact of non-interest bearing sources | | | | | | | | | | | | | 1.90 | % | | | | | | | | | | | 1.50 | % | | | | | | | | | | | 1.00 | % |

Net revenue/yield on earning assets(2) | | | | | | | | $ | (76.9 | ) | | | (0.19 | )% | | | | | | $ | 526.7 | | | | (1.22 | )% | | | | | | $ | 1,611.9 | | | | 3.18 | % |

(1) | | The average balances presented are derived based on month end balances during the year. Tax exempt income was not significant in any of the years presented. Average rates are impacted by FSA accretion and amortization. |

(2) | | The rate presented is calculated net of average credit balances for factoring clients. |

(3) | | Non-accrual loans and related income are included in the respective categories. |

(4) | | Operating lease rental income is a significant source of revenue; therefore, we have presented the rental revenues net of depreciation. |

(5) | | Interest and average rates include FSA accretion, including amounts accelerated due to redemptions or extinguishments, prepayment penalties, and accelerated original issue discount on debt extinguishment related to the GSI facility. |

Item 6: Selected Financial Data

32 CIT ANNUAL REPORT 2012

The table below disaggregates CIT’s year-over-year changes (2012 versus 2011 and 2011 versus 2010) in net interest revenue and operating lease margins as presented in the preceding tables between volume (level of lending or borrowing) and rate (rates charged customers or incurred on borrowings). See‘Net Finance Revenue’ section for further discussion.

Changes in Net Finance Revenue (dollars in millions)

| | | | 2012 Compared to 2011

| | 2011 Compared to 2010

| |

|---|

| | | | Increase (decrease)

due to change in:

| | | | Increase (decrease)

due to change in:

| |

|---|

| | | | Volume

| | Rate

| | Net

| | Volume

| | Rate

| | Net

|

|---|

| | | | | | | | | | | | | | | | | | | | | | | | | | |

Loans (including held for sale) | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | $ | (160.0 | ) | | $ | (316.5 | ) | | $ | (476.5 | ) | | $ | (447.6 | ) | | $ | (677.0 | ) | | $ | (1,124.6 | ) |

| | | | | (54.0 | ) | | | (126.6 | ) | | | (180.6 | ) | | | (219.9 | ) | | | (148.9 | ) | | | (368.8 | ) |

| | | | | (214.0 | ) | | | (443.1 | ) | | | (657.1 | ) | | | (667.5 | ) | | | (825.9 | ) | | | (1,493.4 | ) |

Interest bearing deposits | | | | | (1.4 | ) | | | (1.0 | ) | | | (2.4 | ) | | | (8.1 | ) | | | 12.7 | | | | 4.6 | |

| | | | | (5.1 | ) | | | 5.0 | | | | (0.1 | ) | | | 8.5 | | | | (10.0 | ) | | | (1.5 | ) |

| | | | | (220.5 | ) | | | (439.1 | ) | | | (659.6 | ) | | | (667.1 | ) | | | (823.2 | ) | | | (1,490.3 | ) |

Operating lease equipment, net (including held for sale)(1) | | | | | 100.8 | | | | 58.2 | | | | 159.0 | | | | 38.6 | | | | 81.2 | | | | 119.8 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | 57.6 | | | | (16.3 | ) | | | 41.3 | | | | 0.4 | | | | 23.4 | | | | 23.8 | |

Interest on long-term borrowings(2) | | | | | (692.7 | ) | | | 754.4 | | | | 61.7 | | | | (744.2 | ) | | | 435.1 | | | | (309.1 | ) |

| | | | | (635.1 | ) | | | 738.1 | | | | 103.0 | | | | (743.8 | ) | | | 458.5 | | | | (285.3 | ) |

| | | | $ | 515.4 | | | $ | (1,119.0 | ) | | $ | (603.6 | ) | | $ | 115.3 | | | $ | (1,200.5 | ) | | $ | (1,085.2 | ) |

(1) | | Operating lease rental income is a significant source of revenue; therefore, we have presented the net revenues. |

(2) | | Includes acceleration of FSA accretion resulting from redemptions or extinguishments, prepayment penalties, and accelerated original issue discount on debt extinguishment related to the GSI facility. |

The average long-term borrowings balances presented below, both quarterly and for the full year, were derived based on daily balances and the average rates are based on a 30 days per month day count convention. The average rates include FSA accretion, including amounts accelerated due to redemptions or extinguishments and prepayment costs. The debt coupon rates at December 31, 2012, were as follows: Senior Unsecured Notes – 4.90%, Series C Notes (other) – 5.37%, Other Debt – 6.02% (pre-FSA basis), Secured Borrowings – 2.30% (pre-FSA basis), and Revolving Credit Facility – 2.71%. The aggregate long-term borrowing weighted average rate at December 31, 2012 was 3.81%, 5.12% at December 31, 2011 and 5.54% at December 31, 2010.

Average Daily Long-term Borrowings Balances and Rates (dollars in millions)

| | | | Quarters Ended

| |

|---|

| | | | December 31, 2012

| | September 30, 2012

| | June 30, 2012

| | March 31, 2012

| |

|---|

| | | | Average

Balance

| | Interest

| | Average

Rate

| | Average

Balance

| | Interest

| | Average

Rate

| | Average

Balance

| | Interest

| | Average

Rate

| | Average

Balance

| | Interest

| | Average

Rate

|

|---|

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Revolving Credit Facility | | | | $ | 113.6 | | | $ | 1.0 | | | | 3.45 | % | | $ | 354.6 | | | $ | 2.7 | | | | 3.00 | % | | $ | 457.5 | | | $ | 3.4 | | | | 2.95 | % | | $ | 210.8 | | | $ | 1.7 | | | | 3.22 | % |

| | | | | 6,500.0 | | | | 82.7 | | | | 5.09 | % | | | 5,435.5 | | | | 68.9 | | | | 5.07 | % | | | 2,766.7 | | | | 36.9 | | | | 5.34 | % | | | 266.7 | | | | 3.5 | | | | 5.25 | % |

Series C Notes (Exchanged)(1) | | | | | – | | | | – | | | | – | | | | 2,936.3 | | | | 532.9 | | | | 72.59 | % | | | 5,906.4 | | | | 410.0 | | | | 27.77 | % | | | 7,982.4 | | | | 189.6 | | | | 9.50 | % |

| | | | | 5,250.0 | | | | 70.5 | | | | 5.37 | % | | | 5,250.0 | | | | 72.3 | | | | 5.51 | % | | | 5,250.0 | | | | 72.3 | | | | 5.51 | % | | | 3,942.5 | | | | 55.4 | | | | 5.62 | % |

| | | | | 84.0 | | | | 10.7 | | | | 50.99 | % | | | 85.4 | | | | 2.7 | | | | 12.67 | % | | | 86.5 | | | | 2.6 | | | | 12.08 | % | | | 86.4 | | | | 2.7 | | | | 12.42 | % |

| | | | | 11,947.6 | | | | 164.9 | | | | 5.52 | % | | | 14,061.8 | | | | 679.5 | | | | 19.33 | % | | | 14,467.1 | | | | 525.2 | | | | 14.52 | % | | | 12,488.8 | | | | 252.9 | | | | 8.10 | % |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | 10,284.8 | | | | 159.2 | | | | 6.19 | % | | | 10,544.7 | | | | 98.1 | | | | 3.72 | % | | | 10,243.4 | | | | 73.7 | | | | 2.88 | % | | | 10,347.8 | | | | 107.6 | | | | 4.16 | % |

| | | | | – | | | | – | | | | – | | | | – | | | | – | | | | – | | | | – | | | | – | | | | – | | | | 3,424.8 | | | | 683.8 | | | | 79.86 | % |

| | | | | 10,284.8 | | | | 159.2 | | | | 6.19 | % | | | 10,544.7 | | | | 98.1 | | | | 3.72 | % | | | 10,243.4 | | | | 73.7 | | | | 2.88 | % | | | 13,772.6 | | | | 791.4 | | | | 22.99 | % |

Total Long-term Borrowings | | | | $ | 22,232.4 | | | $ | 324.1 | | | | 5.83 | % | | $ | 24,606.5 | | | $ | 777.6 | | | | 12.64 | % | | $ | 24,710.5 | | | $ | 598.9 | | | | 9.69 | % | | $ | 26,261.4 | | | $ | 1,044.3 | | | | 15.91 | % |

(1) | | See footnote 1 on next table. |

CIT ANNUAL REPORT 2012 33

Average Daily Long-term Borrowings Balances and Rates (dollars in millions)

| | | | Years Ended

| |

|---|

| | | | December 31, 2012

| | December 31, 2011

| | December 31, 2010

| |

|---|

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Revolving Credit Facility | | | | $ | 284.1 | | | $ | 8.8 | | | | 3.07 | % | | $ | – | | | $ | – | | | | – | | | $ | – | | | $ | – | | | | – | |

| | | | | 3,742.2 | | | | 192.0 | | | | 5.13 | % | | | – | | | | – | | | | – | | | | – | | | | – | | | | – | |

Series C Notes (Exchanged)(1) | | | | | 4,206.3 | | | | 1,132.5 | | | | 26.92 | % | | | – | | | | – | | | | – | | | | – | | | | – | | | | – | |

| | | | | 4,923.1 | | | | 270.5 | | | | 5.49 | % | | | – | | | | – | | | | – | | | | – | | | | – | | | | – | |

| | | | | 85.6 | | | | 18.7 | | | | 21.86 | % | | | – | | | | – | | | | – | | | | – | | | | – | | | | – | |

| | | | | 13,241.3 | | | | 1,622.5 | | | | 12.25 | % | | | – | | | | – | | | | – | | | | – | | | | – | | | | – | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | 10,355.1 | | | | 438.6 | | | | 4.24 | % | | | 10,022.3 | | | | 563.3 | | | | 5.62 | % | | | 13,006.6 | | | | 526.1 | | | | 4.04 | % |

First Lien Term Facility(1) | | | | | – | | | | – | | | | – | | | | 1,916.3 | | | | 42.9 | | | | 2.24 | % | | | 4,907.4 | | | | 455.9 | | | | 9.29 | % |

Revolving Credit Facility | | | | | – | | | | – | | | | – | | | | 479.3 | | | | 14.9 | | | | 3.11 | % | | | – | | | | – | | | | – | |

| | | | | 856.2 | | | | 683.8 | | | | 79.86 | % | | | 11,970.8 | | | | 1,538.0 | | | | 12.85 | % | | | 18,915.0 | | | | 1,779.2 | | | | 9.41 | % |

| | | | | – | | | | – | | | | – | | | | 6.3 | | | | 2.1 | | | | 16.03 | % | | | 1,944.3 | | | | 209.1 | | | | 10.75 | % |

Series C Notes (Exchanged)(1) | | | | | – | | | | – | | | | – | | | | 4,282.3 | | | | 415.3 | | | | 9.70 | % | | | – | | | | – | | | | – | |

| | | | | – | | | | – | | | | – | | | | 1,505.5 | | | | 91.1 | | | | 6.05 | % | | | – | | | | – | | | | – | |

| | | | | – | | | | – | | | | – | | | | 127.9 | | | | 15.6 | | | | 12.19 | % | | | 206.8 | | | | 22.0 | | | | 10.64 | % |

| | | | | 11,211.3 | | | | 1,122.4 | | | | 10.01 | % | | | 30,310.7 | | | | 2,683.2 | | | | 8.85 | % | | | 38,980.1 | | | | 2,992.3 | | | | 7.68 | % |

Total Long-term Borrowings | | | | $ | 24,452.6 | | | $ | 2,744.9 | | | | 11.22 | % | | $ | 30,310.7 | | | $ | 2,683.2 | | | | 8.85 | % | | $ | 38,980.1 | | | $ | 2,992.3 | | | | 7.68 | % |

(1) | | Interest expense includes accelerated FSA accretion (amortization), prepayment penalties, and accelerated original issue discount on debt extinguishment related to the GSI facility, as presented in the following table. |

| | | | Quarters Ended

| | Years Ended December 31,

| |

|---|

| | | | December 31,

2012

| | September 30,

2012

| | June 30,

2012

| | March 31,

2012

| | 2012

| | 2011

| | 2010

|

|---|

Series C Notes – (Exchanged) – accelerated FSA | | | | $ | – | | | $ | 453.9 | | | $ | 264.9 | | | $ | – | | | $ | 718.8 | | | $ | – | | | $ | – | |

Series A Notes – accelerated FSA | | | | | – | | | | – | | | | – | | | | 596.9 | | | | 596.9 | | | | 289.7 | | | | – | |

Series A Notes – prepayment penalty | | | | | – | | | | – | | | | – | | | | – | | | | – | | | | 99.2 | | | | – | |

Secured Borrowings – student lending facility – accelerated FSA | | | | | 121.5 | | | | – | | | | – | | | | – | | | | 121.5 | | | | 88.0 | | | | – | |

Secured Borrowings – student lending facility – accelerated original issue discount on debt extinguishments related to the GSI facility | | | | | (45.7 | ) | | | – | | | | – | | | | – | | | | (45.7 | ) | | | – | | | | – | |

Secured Borrowings – Transportation Finance – accelerated original issue discount on debt extinguishments related to the GSI facility | | | | | (6.9 | ) | | | – | | | | – | | | | – | | | | (6.9 | ) | | | – | | | | – | |

Other Secured Borrowings – accelerated FSA | | | | | 13.7 | | | | – | | | | – | | | | – | | | | 13.7 | | | | – | | | | – | |

First Lien Term Facility – accelerated FSA | | | | | – | | | | – | | | | – | | | | – | | | | – | | | | (85.0 | ) | | | (56.8 | ) |

First Lien Term Facility – prepayment penalty | | | | | – | | | | – | | | | – | | | | – | | | | – | | | | – | | | | 89.0 | |

Series B Notes – accelerated FSA | | | | | – | | | | – | | | | – | | | | – | | | | – | | | | (13.5 | ) | | | (29.0 | ) |

Series B Notes – prepayment penalty | | | | | – | | | | – | | | | – | | | | – | | | | – | | | | 15.0 | | | | 48.9 | |

| | | | $ | 82.6 | | | $ | 453.9 | | | $ | 264.9 | | | $ | 596.9 | | | $ | 1,398.3 | | | $ | 393.4 | | | $ | 52.1 | |

| |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Item 6: Selected Financial Data

34 CIT ANNUAL REPORT 2012

Item 7: Management’s Discussion and Analysis of Financial Condition and Results of Operations andItem 7A. Quantitative and Qualitative Disclosures about Market Risk

CIT Group Inc., together with its subsidiaries (“we”, “our”, “CIT” or the “Company”) has provided financial solutions to its clients since its formation in 1908. CIT became a bank holding company (“BHC”) in December 2008, and is regulated by the Board of Governors of the Federal Reserve System (“FRS”) and the Federal Reserve Bank of New York (“FRBNY”) under the U.S. Bank Holding Company Act of 1956 (“BHC Act”). CIT Bank, a wholly-owned subsidiary, is a state chartered bank located in Salt Lake City, Utah, that offers commercial financing and leasing products as well as deposit products, such as certificates of deposits (“CDs”) and savings accounts.

We operate primarily in North America, with locations in Europe, South America and Asia. We are a commercial lender and lessor, providing financial solutions to small businesses and middle market companies. Our clients operate in over 20 countries and in over 30 industries, including transportation, particularly aerospace and rail, manufacturing and retail. We originated over $9 billion of funded new business volume during 2012 and have nearly $34 billion of financing and leasing assets at December 31, 2012.

“Management’s Discussion and Analysis of Financial Condition and Results of Operations” and“Quantitative and Qualitative Disclosures about Market Risk” contain financial terms that are relevant to our business and a glossary of key terms used is included in Part IItem 1. Business Section.

Management uses certain non-GAAP financial measures in its analysis of the financial condition and results of operations of the Company. See “Non-GAAP Financial Measurements” for a reconciliation of these to comparable GAAP measures.

2012 PRIORITIES AND COMMENTARY

Our 2012 priorities were developed to further advance our broader strategic initiatives and were centered on improving our financial condition, enhancing our business model, and further improving our approach to risk management and control functions. During the year, we reached an important strategic milestone as we completed the refinancing and/or repayment of all of the nearly $31 billion of debt that was issued in the 2009 restructuring. The following highlights some of our accomplishments:

| 1. | | Accelerate Growth and Business Development Initiatives |

| - | | Increased commercial assets. Commercial financing and leasing assets increased each quarter throughout 2012 and 8%, or $2.3 billion, for the year to $30.2 billion, driven by growth in Corporate Finance and Vendor Finance, and expansion of our air and rail leasing portfolios. We also agreed to acquire $1.3 billion of commercial loan commitments (of which approximately $800 million was outstanding) on December 31, 2012, the purchase of which should be substantially completed during the first quarter of 2013. |

| - | | Increased new business activity. We funded new business volume of $9.6 billion during 2012, a 23% increase over 2011 on strong Corporate Finance activity. Committed volume, which totaled $11.3 billion, was up 20%. |

| 2. | | Improve Profitability While Maintaining Financial Strength |

| - | | We reported a net loss of $592 million and pre-tax loss of $455 million for 2012, which were driven by debt redemption charges. The pre-tax loss compared to pre-tax income of $178 million for 2011 and $771 million for 2010. However, pre-tax income excluding debt redemption charges and accelerated original issue discount (“OID”) on debt extinguishment related to the GSI facility(3) improved to $1.0 billion from $707 million in 2011 and $824 million in 2010, on a comparable basis. |

| - | | Lowered funding costs. The weighted average coupon rates of outstanding deposits and long-term borrowings declined to 3.18% at December 31, 2012 from 4.69% and 5.30% at December 31, 2011 and 2010, respectively. |

| - | | Increased proportion of funding provided by deposits. As of December 31, 2012, total CIT deposits were $9.7 billion and comprised 31% of total CIT funding, compared to 19% and 12% at December 31, 2011 and 2010, respectively. |

| - | | Maintained strong capital position. Tier 1 and Total Capital ratios at December 31, 2012 were 16.3% and 17.0%, respectively, well above regulatory requirements. |

| - | | Maintained strong liquidity. Liquidity to total assets was 22% at December 31, 2012, down slightly from 23% at December 31, 2011. Liquidity includes cash and short-term investments and the unused portion of the Revolving Credit Facility. |

(3) | | Pre-tax income excluding debt redemption charges and accelerated OID on debt extinguishment related to the GSI facility is a non-GAAP measure. Debt redemption charges include accelerated fresh start accounting debt discount amortization, loss on debt extinguishments and prepayment costs. See “Non-GAAP Financial Measurements” for components and for reconciliation of non-GAAP to GAAP financial information. |

CIT ANNUAL REPORT 2012 35

| 3. | | Expand CIT Bank Assets and Funding |

| - | | Increased bank assets. Total assets at CIT Bank increased to $12.2 billion at December 31, 2012, from $9.0 billion and $7.1 billion at December 31, 2011 and 2010, respectively, reflecting growth in commercial financing and leasing assets. |

| - | | Increased asset origination activity. Funded new business volume totaled $6.0 billion, which represents over 90% of total U.S. volume in 2012, up from 72% in 2011. Committed loan volume rose to $7.6 billion from $4.4 billion for 2011. |

| - | | Diversified deposit sources. Placed approximately $4.5 billion of deposits since launching online banking platform in the 2011 fourth quarter. CIT Bank began offering on-line savings accounts in March 2012 to supplement the suite of CD offerings. |

2012 FINANCIAL OVERVIEW

Our 2012 operating results reflected increased commercial business activity and debt redemption and refinancing activities. We achieved our goal of refinancing or redeeming all the approximately $31 billion of debt incurred in the 2009 restructuring, including over $15 billion in 2012, which caused acceleration of FSA debt discount accretion.

Net loss for 2012 totaled $592 million, $2.95 per diluted share, and was largely influenced by debt redemption charges. The net loss compares to net income of $15 million for 2011, or $0.07 per diluted share and $521 million for 2010, $2.60 per diluted share. The 2012 amounts included $1.5 billion of debt redemption charges, while the prior periods included debt redemption charges of $528 million and $52 million for 2011 and 2010, respectively.

Pre-tax loss totaled $455 million for 2012 compared to pre-tax income of $178 million for 2011 and $771 million in 2010. Although down on a GAAP basis, pre-tax income excluding debt redemption charges, net FSA accretion/amortization and accelerated OID on debt extinguishment related to the GSI facility(4) for 2012 was nearly $640 million, up from $292 million in 2011 and a pre-tax loss of $581 million in 2010, driven by lower funding costs and lower credit costs. 2012 included net FSA costs of $1.1 billion, primarily due to the acceleration of interest expense related to the redemption of over $15 billion of high cost debt, while 2011 and 2010 included net FSA benefits of $135 million and $1.5 billion, respectively.

The following table presents pre-tax results adjusted for debt redemption charges, net FSA accretion / amortization and accelerated OID on debt extinguishment related to the GSI facility. This is a non-GAAP measurement.

Impacts of FSA Accretion and Debt Refinancing Costs on Pre-tax Income (Loss) (dollars in millions)

| | | | Years Ended December 31,

| |

|---|

| | | | 2012

| | 2011

| | 2010

|

|---|

Pre-tax income/(loss) – reported | | | | $ | (454.8 | ) | | $ | 178.4 | | | $ | 771.4 | |

Accelerated FSA net discount/(premium) on debt extinguishments and repurchases | | | | | 1,450.9 | | | | 279.2 | | | | (85.8 | ) |

Debt related – loss on debt extinguishments | | | | | 61.2 | | | | 134.8 | | | | – | |

Accelerated OID on debt extinguishments related to the GSI facility | | | | | (52.6 | ) | | | – | | | | – | |

Debt related – prepayment costs | | | | | – | | | | 114.2 | | | | 137.9 | |

Total debt redemption charges and OID acceleration | | | | | 1,459.5 | | | | 528.2 | | | | 52.1 | |

Pre-tax income – excluding debt redemption charges and OID acceleration | | | | | 1,004.7 | | | | 706.6 | | | | 823.5 | |

Net FSA accretion (excluding debt related acceleration) | | | | | (365.2 | ) | | | (414.4 | ) | | | (1,404.7 | ) |

Pre-tax income (loss) – excluding debt redemption charges, FSA net accretion and OID acceleration | | | | $ | 639.5 | | | $ | 292.2 | | | $ | (581.2 | ) |

Net finance revenue(5) (“NFR”) continued to be impacted by accelerated interest expense related to the redemption of high cost debt during 2012. The negative NFR for 2012 was driven by the FSA discount accretion resulting from repayments of over $15 billion of high cost debt. NFR was $527 million for 2011 and $1.6 billion for 2010. Average earning assets(5) (“AEA”) were $32.5 billion in 2012, down $1.8 billion from 2011 and $8.3 billion from 2010, primarily due to student loan sales. Average commercial earning assets increased during 2012 to $27.6 billion in 2012, from $26.7 billion 2011 but was down from $31.9 billion in 2010. NFR as a percentage of AEA (“net finance margin” or “NFM”) was negative and below 2011 and 2010 reflecting debt redemption costs. Excluding net FSA accretion, debt redemption charges and accelerated OID on debt extinguishment related to the GSI facility, net finance margin was 2.95% for 2012, improved from 1.60% in 2011 and 0.74% in 2010, driven by lower funding costs and the reduction of low yielding assets. Net operating lease revenue increased compared to 2011 and 2010 on higher assets. While other institutions may use net interest margin (“NIM”), defined as interest income less interest expense, we discuss NFR, which includes operating lease rental revenue and depreciation expense, due to their significant impact on revenue and expense.

Provision for credit losses for 2012 was $52 million, down from $270 million last year and $820 million in 2010. The 2010 provision included $416 million for the establishment of loan loss reserves post the adoption of FSA. The lower trend in provisions reflects a reduction in specific reserves and the overall improvements in credit metrics, including lower net charge-offs and non-accrual balances.

(4) | | Pre-tax income excluding debt redemption charges, net FSA accretion/amortization and accelerated OID on debt extinguishment related to the GSI facility is a non-GAAP measure. See “Non-GAAP Financial Measurements” for reconciliation of non-GAAP financial information. |

(5) | | Net finance revenue and average earning assets are non-GAAP measures; see “Non-GAAP Financial Measurements” for a reconciliation of non-GAAP to GAAP financial information. |

Item 7: Management’s Discussion and Analysis

36 CIT ANNUAL REPORT 2012

Other income of $653 million decreased from $953 million in 2011 and $1.0 billion in 2010, largely due to reduced gains on assets sold and fewer recoveries of loans charged off pre-emergence and loans charged off prior to transfer to held for sale. Factoring commissions of $127 million were down from 2011 and 2010, reflecting lower factoring volume.

Operating expenses were $918 million, up from $897 million in 2011, as higher compensation and benefit costs along with costs related to raising deposits offset lower professional fees, and down from $1.0 billion in 2010 on lower compensation and benefit costs and professional fees. Headcount at December 31, 2012, 2011 and 2010 was approximately 3,560, 3,530, and 3,780, respectively.

Provision for income taxes was $134 million for 2012, compared to $159 million for 2011 and $246 million for 2010. The tax provision predominantly reflects provisions for taxable income generated by our international operations and no income tax benefit on our U.S. losses.

Total assets at December 31, 2012 were $44.0 billion, down from $45.3 billion and $51.5 billion at December 31, 2011 and 2010, respectively, as growth in commercial financing and leasing assets was offset by sales and runoff of over $4 billion of government-guaranteed student loans since 2010. Commercial financing and leasing assets increased to $30.2 billion, up $2.3 billion from a year-ago and $1.5 billion from December 31, 2010. Cash and short-term investments totaled $7.6 billion, down from $8.4 billion and $11.2 billion at December 31, 2011 and 2010, respectively.

Funded new business volume of $9.6 billion during 2012 increased 23% from 2011 on strong Corporate Finance activity, while committed new business volume of $11.3 billion increased 20%. Both metrics were significantly above 2010 levels. Trade Finance factoring volume of $25.1 billion decreased 3% from 2011 and 6% from 2010.

Credit metrics reflected favorable trends. Net charge-offs of $74 million declined from $265 million in 2011 and $465 million in 2010, essentially due to improvements in Corporate Finance and Vendor Finance. Net charge-offs in the commercial segments were 0.46%, down significantly from 1.68% in 2011 and 2.04% in 2010. Non-accrual balances declined over 50% to $332 million at December 31, 2012 from $702 million a year ago and down significantly from $1.6 billion at December 31, 2010.

PRIOR PERIOD REVISIONS

In preparing its quarterly financial statements for the first three quarters of 2012, the Company discovered, corrected and disclosed the larger amounts in those quarters immaterial errors that impacted prior periods. Additional out-of-period errors were identified in the fourth quarter. These additional out-of-period errors were individually and in the aggregate not material to the fourth quarter results but, when combined with the other out-of-period errors previously identified this year, were determined by management to be material to the full year 2012 results.

The cumulative effect of these revisions was to increase tangible book value (“TBV”) by $8 million, as accumulated deficit decreased by $9 million, accumulated other comprehensive loss decreased by $14 million and goodwill increased by $15 million. As a result of these revisions, the net loss for the quarters ended September 30 and March 31, 2012 was decreased by approximately $6 million and $20 million, respectively, and the net loss for the quarter ended June 30, 2012 was increased by $2 million, from our previously reported amounts. As a result of these revisions, the net income for the years ended December 31, 2011 and 2010 decreased by $12 million and $3 million, respectively, from previously reported amounts. As a result of our adoption of fresh start accounting, the recognition of amounts relating to periods prior to 2010 resulted in a corresponding $15 million increase to goodwill.

Management will revise in subsequent quarterly filings on Form 10-Q and has revised in Item 8 Financial Data and Supplementary Data, Note 27 – Select Quarterly Data, its previously reported financial statements for 2012, 2011 and 2010. All prior period data reflects the revised balances.

2013 PRIORITIES

During 2013, we will focus on continued progress toward profitability targets by growing earning assets, managing expenses and growing CIT Bank assets and deposits. Enhancing internal control functions and our relationships with our regulators will also remain a focus for 2013.

Specific business objectives established for 2013 include:

| - | | Prudently Grow Assets – We plan to grow earning assets, either organically or through portfolio acquisitions, by focusing on existing products and markets as well as newer initiatives, including equipment finance, real estate finance, and maritime finance. |

| - | | Execute on Expense Initiatives – In order to achieve and maintain our target pre-tax return on average earning assets of between 2.0% and 2.5%, we plan to reduce the quarterly run rate of operating expenses by $15 million to $20 million from third quarter 2012 levels. These improvements will be phased in over 2013 through improved operating efficiencies and expense reductions. |

| - | | Continue to Expand CIT Bank – CIT Bank will continue to fund virtually all of our U.S. lending and leasing volume, expand on-line deposit offerings and begin to implement a thin branch network. |

| - | | Continue Progress Towards Profitability Targets – We will focus on managing towards our return on asset targets in order to improve profitability and grow book value. |

CIT ANNUAL REPORT 2012 37

The following chart reflects key performance indicators evaluated by management and used throughout this management discussion and analysis:

| | | | |

Asset Generation – to originate new business and build earning assets. | | | | -Origination volumes; and

-Financing and leasing assets balances. |

Revenue Generation – lend money at rates in excess of cost of borrowing, earn rentals on the equipment we lease commensurate with the risk, and generate other revenue streams. | | | | -Net finance revenue and other income;

-Asset yields and funding costs;

-Net finance revenue as a percentage of average earning assets (AEA); and

-Operating lease revenue as a percentage of average operating lease equipment (AOL). |