UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

| (Mark one) | ||

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

FOR THE FISCAL YEAR ENDED DECEMBER 31, 2010

OR

| o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

COMMISSION FILE NUMBER 000-50129

HUDSON HIGHLAND GROUP, INC.

(Exact Name of Registrant as Specified in its Charter)

| Delaware | 59-3547281 | |

| (State or Other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification Number) |

560 Lexington Avenue, New York, New York 10022

(Address of Principal Executive Offices)

(212) 351-7300

(Registrant’s telephone number, including area code)

Securities Registered Pursuant to Section 12(b) of the Act:

| Title of Each Class | Name of Each Exchange on Which Registered | |

| Common Stock, $0.001 par value | The NASDAQ Stock Market LLC | |

| Preferred Share Purchase Rights | The NASDAQ Stock Market LLC |

Securities Registered Pursuant to Section 12(g) of the Act:None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yeso Nox

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Act. Yeso Nox

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. Yesx Noo

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit to post such flies). Yeso Noo

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K.o

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definition of “large accelerated filer”, “accelerated filer”, and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filero | Accelerated filerx | Non-accelerated filero | Smaller reporting companyo |

Indicate by checkmark whether the Registrant is a shell company (as defined in Exchange Act Rule 12b-2). Yeso Nox

The aggregate market value of the voting common stock held by non-affiliates of the Registrant was approximately $138,860,000 based on the closing price of the Common Stock on the NASDAQ Global Market on June 30, 2010.

The number of shares of Common Stock, $.001 par value, outstanding as of January 31, 2011 was 32,166,474

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Proxy Statement for the 2011 Annual Meeting of Stockholders are incorporated by reference into Part III.

HUDSON HIGHLAND GROUP, INC.

Table of Contents

| Page | ||||

| PART I | ||||

ITEM 1. BUSINESS | 1 | |||

ITEM 1A. RISK FACTORS | 3 | |||

ITEM 1B. UNRESOLVED STAFF COMMENTS | 8 | |||

ITEM 2. PROPERTIES | 9 | |||

ITEM 3. LEGAL PROCEEDINGS | 9 | |||

ITEM 4. REMOVED AND RESERVED | 9 | |||

EXECUTIVE OFFICERS OF THE REGISTRANT | 10 | |||

| PART II | ||||

ITEM 5. MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES | 12 | |||

ITEM 6. SELECTED FINANCIAL DATA | 14 | |||

ITEM 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 16 | |||

ITEM 7A. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK | 44 | |||

ITEM 8. FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA | 45 | |||

ITEM 9. CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURE | 81 | |||

ITEM 9A. CONTROLS AND PROCEDURES | 81 | |||

ITEM 9B. OTHER INFORMATION | 81 | |||

| PART III | ||||

ITEM 10. DIRECTORS, EXECUTIVE OFFICERS AND CORPORATE GOVERNANCE | 82 | |||

ITEM 11. EXECUTIVE COMPENSATION | 82 | |||

ITEM 12. SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT AND RELATED STOCKHOLDER MATTERS | 82 | |||

ITEM 13. CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS, AND DIRECTOR INDEPENDENCE | 83 | |||

ITEM 14. PRINCIPAL ACCOUNTING FEES AND SERVICES | 83 | |||

| PART IV | ||||

ITEM 15. EXHIBITS, FINANCIAL STATEMENT SCHEDULES | 84 | |||

| SIGNATURES | 90 | |||

| EXHIBIT INDEX | 91 | |||

i

PART I

ITEM 1. BUSINESS

Hudson Highland Group, Inc. (the “Company” or “Hudson”, “we”, “us” and “our”) is one of the world’s largest specialized professional staffing and talent management solutions providers. The Company provides professional staffing services on a permanent and contract consulting basis and a range of talent management services to businesses operating in many industries. The Company helps its clients in recruiting and developing employees for professional-level functional and managerial positions.

The Company is organized into four reportable segments: Hudson Europe, Hudson Australia and New Zealand (“ANZ”), Hudson Americas and Hudson Asia. These reportable segments constituted approximately 46%, 30%, 13% and 11% of the Company’s gross margin, respectively, for the year ended December 31, 2010. The Hudson regional businesses were historically the combination of 67 acquisitions made between 1999 and 2001, which became the eResourcing division of Monster Worldwide, Inc. (“Monster”), formerly TMP Worldwide, Inc. Some of the Company’s constituent businesses have operated for more than 20 years. On March 31, 2003, Monster distributed all of the outstanding shares of the Company to its stockholders of record on March 14, 2003 (the “Distribution”). Since the Distribution, the Company has operated as an independent publicly held company.

Hudson’s four regional businesses provide professional contract consultants and permanent recruitment services to a wide range of clients. With respect to temporary and contract personnel, Hudson focuses on providing candidates with specialized functional skills and competencies, such as accounting and finance, legal and information technology. The length of a contract assignment varies. With respect to permanent recruitment, Hudson focuses on mid-level professionals typically earning between $50,000 and $150,000 annually and possessing the professional skills and/or profile required by clients. Hudson provides permanent recruitment services on both a retained and contingent basis. In larger markets, Hudson’s sales strategy focuses on both clients operating in particular industry sectors, such as financial services or technology, and candidates possessing particular professional skills, such as accounting and finance, information technology, legal and human resources. Hudson uses both traditional and interactive methods to select potential candidates for its clients.

Hudson regional businesses also provide candidate assessment, competency modeling, leadership development, performance management, and career transition through their talent management units. These services enable Hudson to offer clients a comprehensive set of management services, across the entire employment life-cycle from attracting, assessing and selecting best-fit employees to engaging and developing those individuals to help build a high-performance organization.

Hudson Europe operates from 38 offices in 13 countries, with 48% of its 2010 gross margin generated in the United Kingdom. Hudson ANZ operates from 12 offices in Australia and New Zealand, with 88% of its 2010 gross margin generated in Australia. Hudson Americas operates from 26 offices in the United States and Canada, with 97% of its 2010 gross margin generated in the United States. Hudson Asia operates from 5 offices in Mainland China, Hong Kong and Singapore, with 45% of its 2010 gross margin generated in Mainland China.

Corporate expenses are reported separately from the four reportable segments and pertain to certain functions, such as executive management, corporate governance, human resources, accounting, administration, tax and treasury, the majority of which are attributable and have been allocated to the reportable segments.

DISCONTINUED OPERATIONS

In the first half of 2009, the Company exited Italy and Japan. The operations in Italy were part of the Hudson Europe reportable segment and the operations in Japan were part of the Hudson Asia reportable segment.

In the second quarter of 2008, the Company sold substantially all of the assets of Balance Public Management B.V. (“BPM”), a division of Balance Ervaring op Projectbasis, B.V. (“Balance”), a subsidiary of the Company, which was part of the Hudson Europe reportable segment. In the first quarter of 2008, the Company sold substantially all of the assets of its Hudson Americas energy, engineering and technical staffing division (“ETS”), which was part of the Hudson Americas reportable segment.

1

In the fourth quarter of 2006, the Company sold its Highland Partners (“Highland”) executive search business, which was a separate reportable segment of the Company.

In accordance with the provisions of Financial Accounting Standards Board (“FASB”) Accounting Standards Codification Topic (“ASC”) 205-20-45 “Reporting Discontinued Operations”, the assets, liabilities, and results of operations of the Company’s discontinued operations above were reclassified as discontinued operations for all the periods presented. The gain or loss on sale and results of operations of the disposed businesses were reported in discontinued operations in the relevant periods.

SALES AND MARKETING

Each of Hudson’s regional businesses maintains sales personnel aligned along functional practice areas or industry sector groups as appropriate for the market. From time to time, sales people receive incentives for cross-selling services with other practices and business units as the client need arises. In addition, each region has the capability to identify and develop international sales opportunities that arise from clients with global needs.

The Company’s global marketing and communications function is responsible for brand and marketing strategy, client and candidate lead generation campaigns, public relations and corporate/employee communications. This team closely coordinates with the local operations to generate leads, support sales efforts and build a strong brand reputation — both in the external market and within the organization.

We use three principal channels for marketing our services and promoting our brand: (1) in the United Kingdom, Australia, New Zealand, and other countries where it is an accepted practice, we use client-paid and Company-paid advertising for vacant positions; (2) public relations to promote our experts and offerings, and original research on business management and human capital issues of particular relevance to senior business managers; and (3) the Internet, both for promoting the Company’s services to clients and attracting, assisting and managing candidates.

CLIENTS

The Company’s clients include small to large-sized corporations and government agencies. At December 31, 2010, there were approximately 3,600 Hudson Europe clients, 1,187 Hudson ANZ clients, 316 Hudson Americas clients, and 833 Hudson Asia clients. The business of the Company is not dependent upon either a single client or a limited number of clients.

COMPETITION

The markets for the Company’s services and products are highly competitive. There are few barriers to entry, so new entrants occur frequently, resulting in considerable market fragmentation. Companies in this industry compete on price, service quality, new capabilities and technologies, client attraction methods, and speed of completing assignments.

EMPLOYEES

The Company employs approximately 2,200 people worldwide. In most jurisdictions, our employees are not represented by a labor union or a collective bargaining agreement. The Company regards its relationships with its employees as satisfactory.

SEGMENT AND GEOGRAPHIC DATA

Financial information concerning the Company’s reportable segments and geographic areas of operation is included in Note 15 in the Notes to Consolidated Financial Statements contained in Item 8 of this Form 10-K.

AVAILABLE INFORMATION

We maintain a Web site with the address www.hudson.com. We are not including the information contained on our Web site as part of, or incorporating it by reference into, this report. Through our Web site, we make available free of charge (other than an investor’s own Internet access charges) our annual reports on Form 10-K, quarterly reports on Form 10-Q and current reports on Form 8-K, and amendments to these reports in a timely manner after we provide them to the Securities and Exchange Commission.

2

ITEM 1A. RISK FACTORS

The following risk factors and other information included in this Annual Report on Form 10-K should be carefully considered. The risks and uncertainties described below are not the only ones we face. Additional risks and uncertainties not presently known to us or that we currently deem immaterial also may impair our business operations. If any of the following risks occur, our business, financial condition, results of operations, and cash flows could be materially adversely affected.

Our operations will be affected by global economic fluctuations, including the global economic conditions prevailing during 2010.

Demand for our services fluctuates with changes in economic conditions in the markets in which we operate. Those conditions include slower employment growth or reductions in employment. We have limited flexibility to reduce expenses during economic downturns due to some overhead costs which are fixed in the short-term. Furthermore, we may face increased pricing pressures during economic downturns. During the 2009 economic downturn, many employers in our operating regions reduced their overall workforce to reflect the reduced demand for their products and services. This contributed to an operating loss for our company in 2009. While conditions improved during 2010, weakness persisted in some economies. As a result, we reported a net loss for 2010. During 2010, many governments also announced reductions in public sector spending. This may have an ongoing impact on our businesses in certain markets. Despite indications of improving economic conditions, the economic recovery has been slower than in previous business cycles and may result in lower operating results than expected.

Our operating results fluctuate from quarter to quarter and therefore quarterly results cannot be used to predict future periods’ results.

Our operating results fluctuate quarter to quarter primarily due to the vacation periods during the first quarter in the ANZ region and the third quarter in the Americas and Europe regions. Demand for our services is typically lower during traditional national vacation periods when clients are on vacation.

Our revenue can vary because our clients can terminate their relationship with us at any time with limited or no penalty.

We provide professional mid-market staffing services on a temporary assignment-by-assignment basis, which clients can generally terminate at any time or reduce their level of use when compared to prior periods. Our professional recruitment business is also significantly affected by our clients’ hiring needs and their views of their future prospects. Clients may, on very short notice, reduce or postpone their recruiting assignments with us and, therefore, affect demand for our services. This could have a material adverse effect on our business, financial condition and results of operations.

Our markets are highly competitive.

The markets for our services are highly competitive. Our markets are characterized by pressures to reduce prices, provide high levels of service, incorporate new capabilities and technologies and accelerate job completion schedules. Furthermore, we face competition from a number of sources. These sources include other executive search firms and professional search, staffing and consulting firms. Several of our competitors have greater financial and marketing resources than we do. Due to competition, we may experience reduced margins on our services, loss of market share and our customers. If we are not able to compete effectively with current or future competitors as a result of these and other factors, our business, financial condition and results of operations could be materially adversely affected.

We have no significant proprietary technology that would preclude or inhibit competitors from entering the mid-market professional staffing contract and consulting markets. We cannot provide assurance that existing or future competitors will not develop or offer services that provide significant performance, price, creative or other advantages over our services. In addition, we believe that, with continuing development and increased availability of information technology, the industries in which we compete may attract new competitors. Specifically, the increased use of the Internet may attract technology-oriented companies to the professional staffing industry. We cannot provide assurance that we will be able to continue to compete effectively against existing or future competitors. Any of these events could have a material adverse effect on our business, financial condition and results of operations.

3

Our investment strategy subjects us to risks.

From time to time, we make investments, including acquisitions, as part of our growth plans. Investments may not perform as expected because they are dependent on a variety of factors, including our ability to effectively integrate new personnel and operations, our ability to sell new services, and our ability to retain existing or gain new clients. Furthermore, we may need to borrow more money from lenders or sell equity or debt securities to the public to finance future investments and the terms of these financings may be adverse to us.

We face risks related to our international operations.

We conduct operations in nineteen countries and face both translation and transaction risks related to foreign currency exchange. For the year ended December 31, 2010, approximately 87% of our gross margin was earned outside of the United States. Our financial results could be materially affected by a number of factors particular to international operations. These include, but are not limited to, difficulties in staffing and managing international operations, operational issues such as longer customer payment cycles and greater difficulties in collecting accounts receivable, changes in tax laws or other regulatory requirements, issues relating to uncertainties of laws and enforcement relating to the regulation and protection of intellectual property, and currency fluctuation. If we are forced to discontinue any of our international operations, we could incur material costs to close down such operations.

Regarding the foreign currency risk inherent in international operations, the results of our local operations are reported in the applicable foreign currencies and then translated into U.S. dollars at the applicable foreign currency exchange rates for inclusion in our financial statements. In addition, we generally pay operating expenses in the corresponding local currency. Because of devaluations and fluctuations in currency exchange rates or the imposition of limitations on conversion of foreign currencies into U.S. dollars, we are subject to currency translation exposure on the revenue and income of our operations in addition to economic exposure. Our consolidated U.S. dollar cash balance could be lower because a significant amount of cash is generated outside of the United States. This risk could have a material adverse effect on our business, financial condition and results of operations.

We depend on our key management personnel.

Our continued success will depend to a significant extent on our senior management team. The loss of the services of one or more key senior management team member could have a material adverse effect on our business. On February 22, 2011, our Board of Directors removed Jon F. Chait as chairman and chief executive officer (“CEO”) of the company and appointed Mary Jane Raymond, the company’s executive vice president and chief financial officer, to serve as interim CEO until the search process of the successor is completed. Our inability to attract a suitable successor to replace Mr. Chait could have a material adverse effect on our business, financial condition and results of operations. In addition, if one or more key employees join a competitor or form a competing company, the resulting loss of existing or potential clients could have a material adverse effect on our business, financial condition and results of operations.

If we fail to attract and retain qualified personnel, it may negatively impact our business, financial condition and results of operations.

Our success also depends upon our ability to attract and retain highly-skilled professionals who possess the skills and experience necessary to meet the staffing requirements of our clients. We must continually evaluate and upgrade our base of available qualified personnel to keep pace with changing client needs and emerging technologies. Furthermore, a substantial number of our contractors during any given year may terminate their employment with us and accept regular staff employment with our clients. Competition for qualified professionals with proven skills is intense, and demand for these individuals is expected to remain strong for the foreseeable future. There can be no assurance that qualified personnel will continue to be available to us in sufficient numbers. If we are unable to attract the necessary qualified personnel for our clients, it may have a negative impact on our business, financial condition and results of operations.

4

We face risks in collecting our accounts receivable.

In virtually all of our businesses, we invoice customers after providing services, which creates accounts receivable. Delays or defaults in payments owed to us could have a significant adverse impact on our business, financial condition and results of operations. Factors that could cause a delay or default include, but are not limited to, business failures, turmoil in the financial and credit markets, and global economic conditions.

We have had periods of negative cash flows and operating losses that may reoccur in the future.

We have experienced negative cash flows and reported operating and net losses in the past. For example, our cash flows from operations were negative during 2010 and 2009 and we had operating and net losses for the years ended December 31, 2010, 2009 and 2008, which included impairment charges related to goodwill of $64.5 million in 2008. We cannot provide any assurance that we will have positive cash flows or operating profitability in the future, particularly to the extent the global economy continues to recover slowly from the global economic downturn. If our revenue declines or if operating expenses exceed our expectations, we may not be profitable and may not generate positive operating cash flows.

Our credit facilities restrict our operating flexibility.

Our credit facilities contain various restrictions and covenants that restrict our operating flexibility including:

| • | borrowings limited to eligible receivables; |

| • | lenders’ ability to impose restrictions, such as payroll or other reserves; |

| • | limitations on payments of dividends; |

| • | restrictions on our ability to make additional borrowings, or to consolidate, merge or otherwise fundamentally change our ownership; |

| • | limitations on capital expenditures, investments, dispositions of assets, guarantees of indebtedness, permitted acquisitions and repurchases of stock; and |

| • | limitations on certain intercompany payments of expenses, interest and dividends. |

These restrictions and covenants could have adverse consequences for investors, including the need to use a portion of our cash flow from operations for debt service rather than for our operations, restrictions on our ability to incur additional debt financing for future working capital or capital expenditures, a lesser ability to take advantage of significant business opportunities, such as acquisition opportunities, the potential need to undertake equity transactions which may dilute the ownership of existing investors, and inability to react to market conditions by selling lesser-performing assets.

In addition, a default, amendment or waiver to our credit facilities to avoid a default may result in higher rates of interest and could impact our ability to obtain additional borrowings. Finally, debt incurred under our credit facilities bear interest at variable rates. Any increase in interest expense could reduce the funds available for operations.

If we are unable to achieve anticipated cost savings through our cost reduction initiatives, including outsourcing, our ability to compete could be adversely impacted and our regional operations could be disrupted.

We have undertaken a series of cost reduction initiatives. In 2009, we initiated a number of structural cost reduction and productivity improvement initiatives in our operations to reduce costs and improve profitability. The impact of these cost reduction actions may be influenced by several factors’ including our ability to maintain the level of cost savings currently being realized as a result of these initiatives.

In the first quarter of 2009, we outsourced certain back-office processes performed in our Hudson ANZ regional business to a company located in India. The processes that were outsourced are invoicing, accounts payable, accounts receivable and transactional accounting. The efficient operation of that regional business is dependent on, among other things, the stability of the Indian political environment. Substantially all of the

5

specially-trained employees at the Indian company are Indian nationals. Because substantially all of the named operations have been transferred, it may not be possible to replace the Indian-based employees in another location, should operations at this Indian company be disrupted. This could impact adversely the operational efficiency of that regional business.

We rely on our information systems, and if we lose that technology or fail to further develop our technology, our business could be harmed.

Our success depends in large part upon our ability to store, retrieve, process, and manage substantial amounts of information, including our client and candidate databases. To achieve our strategic objectives and to remain competitive, we must continue to develop and enhance our information systems. This may require the acquisition of equipment and software and the development, either internally or through independent consultants, of new proprietary software. Our inability to design, develop, implement and utilize, in a cost-effective manner, information systems that provide the capabilities necessary for us to compete effectively, or any interruption or loss of our information processing capabilities, for any reason, could harm our business, financial condition and results of operations.

Our business depends on uninterrupted service to clients.

Our operations depend on our ability to protect our facilities, computer and telecommunication equipment and software systems against damage or interruption from fire, power loss, cyber attacks, sabotage, telecommunications interruption, weather conditions, natural disasters and other similar events. Additionally, severe weather can cause our employees or contractors to miss work and interrupt delivery of our service, resulting in a loss of revenue. While interruptions of these types that have occurred in the past have not caused material disruption, it is not possible to predict the type, severity or frequency of interruptions in the future or their impact on our business.

We may be exposed to employment-related claims, legal liability and costs from clients, employers and regulatory authorities that could adversely affect our business, financial condition or results of operations, and our insurance coverage may not cover all of our potential liability.

We are in the business of employing people and placing them in the workplaces of other businesses. Risks relating to these activities include:

| • | claims of misconduct or negligence on the part of our employees; |

| • | claims by our employees of discrimination or harassment directed at them, including claims relating to actions of our clients; |

| • | claims related to the employment of illegal aliens or unlicensed personnel; |

| • | claims for payment of workers’ compensation and other similar claims; |

| • | claims for violations of wage and hour requirements; |

| • | claims for retroactive entitlement to employee benefits; |

| • | claims of errors and omissions of our temporary employees; |

| • | claims by taxing authorities related to our independent contractors and the risk that such contractors could be considered employees for tax purposes; |

| • | claims related to our non-compliance with data protection laws, which require the consent of a candidate to transfer resumes and other data; and |

| • | claims by our clients relating to our employees’ misuse of client proprietary information, misappropriation of funds, other misconduct, criminal activity or similar claims. |

We are exposed to potential claims with respect to the recruitment process. A client could assert a claim for matters such as breach of a blocking arrangement or recommending a candidate who subsequently proves to be unsuitable for the position filled. Similarly, a client could assert a claim for deceptive trade practices on the grounds that we failed to disclose certain referral information about the candidate or misrepresented

6

material information about the candidate. Further, the current employer of a candidate whom we place could file a claim against us alleging interference with an employment contract. In addition, a candidate could assert an action against us for failure to maintain the confidentiality of the candidate’s employment search or for alleged discrimination or other violations of employment law by one of our clients.

We may incur fines and other losses or negative publicity with respect to these problems. In addition, some or all of these claims may give rise to litigation, which could be time-consuming to our management team, costly and could have a negative effect on our business. In some cases, we have agreed to indemnify our clients against some or all of these types of liabilities. We cannot assure that we will not experience these problems in the future, that our insurance will cover all claims, or that our insurance coverage will continue to be available at economically-feasible rates.

From time to time, we may continue to incur liabilities associated with certain pre-spin off activities with Monster. Under the terms of our Distribution Agreement with Monster, these liabilities generally will continue to be retained by us. If these liabilities are significant, the retained liabilities could have a material adverse effect on our business, financial condition and results of operations. However, in some circumstance, we may have claims against Monster, and we will make a determination on a case by case basis

Our ability to utilize net operating loss carry-forwards may be limited.

The Company has U.S. net operating loss carry-forwards that expire through 2030. Section 382 of the Internal Revenue Code imposes an annual limitation on a corporation’s ability to utilize NOLs if it experiences an “ownership change.” In general terms, an ownership change may result from transactions increasing the ownership of certain stockholders in the stock of a corporation by more than 50% over a three-year period. Future changes in our stock ownership, some of which are outside of our control, could result in an ownership change. The imposition of a limitation on our ability to use our NOLs to offset future taxable income could cause U.S. federal income taxes to be paid earlier than otherwise would be paid if such limitation were not in effect and could cause such NOLs to expire unused, reducing or eliminating the benefit of such NOLs.

There may be volatility in our stock price.

The market price for our common stock has fluctuated in the past and could fluctuate substantially in the future. For example, during 2010, the market price of our common stock reported on the NASDAQ Global Market ranged from a high of $6.02 to a low of $2.93. Factors such as general macroeconomic conditions adverse to workforce expansion, the announcement of variations in our quarterly financial results or changes in our expected financial results could cause the market price of our common stock to fluctuate significantly. Further, due to the volatility of the stock market generally, the price of our common stock could fluctuate for reasons unrelated to our operating performance.

Government regulations may result in the prohibition, regulation or restriction of certain types of employment services we offer, the imposition of additional licensing or tax requirements, or increases in compliance audits may reduce our future earnings.

In many jurisdictions in which we operate, the contract staffing industry is heavily regulated. For example, governmental regulations can restrict the length of contracts of contract employees and the industries in which they may be used. In some countries, special taxes, fees or costs are imposed in connection with the use of contract workers.

The countries in which we operate may:

| • | create additional regulations that prohibit or restrict the types of employment services that we currently provide; |

| • | impose new or additional benefit requirements; |

| • | require us to obtain additional licensing to provide staffing services; |

| • | impose new or additional visa restrictions on movements between countries; |

| • | increase taxes, such as sales or value-added taxes, payable by the providers of staffing services; or |

7

| • | increase the number of various tax and compliance audits relating to a variety of regulations, including wage and hour laws, unemployment taxes, workers’ compensation, immigration, and income, value-added and sales taxes. |

Any future regulations that make it more difficult or expensive for us to continue to provide our staffing services may have a material adverse effect on our business, financial condition and results of operations.

Provisions in our organizational documents and Delaware law will make it more difficult for someone to acquire control of us.

Our certificate of incorporation and by-laws and the Delaware General Corporation Law contain several provisions that make more difficult an acquisition of control of us in a transaction not approved by our Board of Directors, including transactions in which stockholders might otherwise receive a premium for their shares over then current prices, and that may limit the ability of stockholders to approve transactions that they may deem to be in their best interests. Our certificate of incorporation and by-laws include provisions:

| • | dividing our Board of Directors into three classes to be elected on a staggered basis, one class each year; |

| • | authorizing our Board of Directors to issue shares of our preferred stock in one or more series without further authorization of our stockholders; |

| • | requiring that stockholders provide advance notice of any stockholder nomination of directors or any proposal of new business to be considered at any meeting of stockholders; |

| • | permitting removal of directors only for cause by a super-majority vote; |

| • | providing that vacancies on our Board of Directors will be filled by the remaining directors then in office; |

| • | requiring that a super-majority vote be obtained to amend or repeal specified provisions of our certificate of incorporation or by-laws; and |

| • | eliminating the right of stockholders to call a special meeting of stockholders or take action by written consent without a meeting of stockholders. |

In addition, Section 203 of the Delaware General Corporation Law generally provides that a corporation may not engage in any business combination with any interested stockholder during the three-year period following the time that the stockholder becomes an interested stockholder, unless a majority of the directors then in office approve either the business combination or the transaction that results in the stockholder becoming an interested stockholder or specified stockholder approval requirements are met.

In February 2005, our Board of Directors declared a dividend of one preferred share purchase right (a “Right”) for each outstanding share of our common stock payable upon the close of business on February 28, 2005 to the stockholders of record on that date. Each Right entitles the registered holder to purchase from us one one-hundredth (1/100th) of a share of our Series A Junior Participating Preferred Stock (“Preferred Shares”) at a price of $60 per one one-hundredth of a Preferred Share, subject to adjustment. These Rights may make the cost of acquiring us more expensive and, therefore, make an acquisition more difficult.

ITEM 1B. UNRESOLVED STAFF COMMENTS

The Company has not received a closing letter related to an SEC Division of Corporation Finance comment letter received by the Company in July 2009. The letter provided comments about (1) whether the factors driving the Company’s 2008 goodwill impairment were reflected in the relevant trend commentary, and (2) how the Company accounted for the sales tax matters disclosed in the Company’s May 13, 2009 Form 8-K. The Company responded in August 2009.

8

ITEM 2. PROPERTIES

All of the Company’s operating offices are located in leased premises. Our principal executive office is currently located at 560 Lexington Avenue, New York, New York, where we occupy space under a lease expiring in March 2017.

Hudson Europe operates from 38 leased locations with approximately 298,000 aggregate square feet. Hudson ANZ operates from 12 leased locations with approximately 148,000 aggregate square feet. Hudson Americas operates from 31 leased locations with approximately 170,000 aggregate square feet, which includes 2 leased locations with space of approximately 60,000 aggregate square feet, which are shared between the Hudson Americas and corporate functions. Hudson Asia operates from 6 leased locations with approximately 51,000 aggregate square feet. All leased space is considered to be adequate for the operation of its business, and no difficulties are foreseen in meeting any future space requirements.

ITEM 3. LEGAL PROCEEDINGS

In January 2011, the Company reached a settlement with the SEC regarding a previously disclosed investigation of sales tax issues in its North American subsidiary. The Company neither admitted nor denied the findings of the SEC order, but agreed to pay a $200,000 penalty in conjunction with the settlement. The SEC order found that the Company failed to maintain adequate books and records and internal accounting controls to accurately track, calculate and remit amounts due for U.S. state sales tax obligations for a number of years up to 2007. These issues date back prior to the Company’s 2003 spin off from Monster. The Company settled all sales tax claims, and by the beginning of 2009, paid all related state sales tax due. The staff of the SEC previously advised in August 2010 that it did not intend to recommend that the Commission take action in this matter against the Company’s chief financial officer.

The Company is involved in various legal proceedings that are incidental to the conduct of its business. The Company is not involved in any pending or threatened legal proceedings that it believes could reasonably be expected to have a material adverse effect on its financial condition or results of operations.

ITEM 4. REMOVED AND RESERVED

9

EXECUTIVE OFFICERS OF THE REGISTRANT

The following table sets forth certain information, as of February 23, 2011, regarding the executive officers of Hudson Highland Group, Inc.:

| Name | Age | Title | ||

| Mary Jane Raymond | 50 | Interim Chief Executive Officer and Executive Vice President and Chief Financial Officer | ||

| Margaretta R. Noonan | 53 | Senior Human Resources Officer | ||

| Richard S. Gray | 54 | Senior Vice President, Marketing and Communications | ||

| Latham Williams | 58 | Senior Vice President, Legal Affairs and Administration, Corporate Secretary | ||

| Frank P. Lanuto | 48 | Senior Vice President and Corporate Controller | ||

| Neil J. Funk | 59 | Vice President, Internal Audit |

The following biographies describe the business experience of our executive officers:

Mary Jane Raymond was appointed to serve as Interim Chief Executive Officer on February 23, 2011. She continues to also serve as the Executive Vice President and Chief Financial Officer, which position she has held since joining the Company in December 2005. Prior to that, Ms. Raymond was the Chief Risk Officer of The Dun & Bradstreet Corporation during 2005. From 2002 to 2005, Ms. Raymond served as the Vice President and Corporate Controller of the Dun & Bradstreet Corporation. Ms. Raymond served as the Merger Integration Vice President of Lucent Technologies, Inc. from 1998 to 2002 and as Financial Vice President in International from 1997 to 1998. From 1988 to 1997, Ms. Raymond served in various positions with Cummins, Inc.

Margaretta R. Noonan has served as Senior Human Resources Officer since March 3, 2009. Prior to that, Ms. Noonan served as Executive Vice President and Chief Administrative Officer since February 2005. Prior to that Ms. Noonan served as Executive Vice President, Human Resources since she joined the Company in April 2003. Prior to joining the Company, Ms. Noonan served as Senior Vice President, Global Human Resources and corporate officer of Monster Worldwide, Inc. Prior to joining Monster in 1998, Ms. Noonan was Vice President, Human Resources — Stores, for the Lord & Taylor division of May Department Stores Company, a large retail department store, from February 1997 to May 1998 and was Vice President, Human Resources, of Kohl’s Corporation, a large retail department store, from November 1992 to February 1997.

Richard S. Gray has served as Senior Vice President, Marketing and Communications since February 2005. Prior to that, Mr. Gray served as Vice President, Marketing and Communications since joining the Company in May 2003. Prior to joining the Company, Mr. Gray was Senior Vice President for Ogilvy Public Relations Worldwide, a large public relations firm, in Chicago, Illinois from September 2002 until May 2003. Before joining Ogilvy Public Relations Worldwide, Mr. Gray was Vice President, Marketing and Communications for Lante Corporation, an internet consulting boutique, in Chicago, Illinois from November 1998 until November 2001.

Latham Williams has served as Senior Vice President, Legal Affairs and Administration, Corporate Secretary since February 2007. Prior to that, Mr. Williams served as Vice President, Legal Affairs and Administration, Corporate Secretary since joining the Company in April 2003. Prior to joining the Company, Mr. Williams was a Partner, Leader Diversity Practice Group and Co-Leader Global Legal Practice in Monster’s executive search division. Prior to joining Monster in 2001, Mr. Williams was an equity partner with the international law firm of Sidley Austin LLP from 1993 to 2000, specializing in health care joint ventures, mergers and acquisitions. Before joining Sidley Austin, Mr. Williams was an equity partner in the Chicago-based law firm of Gardner, Carton & Douglas (now, Drinker Biddle) and was with the firm from 1981 to 1993.

10

Frank P. Lanuto has served as Senior Vice President and Corporate Controller since November 9, 2009. Prior to that, Mr. Lanuto served as Vice President and Corporate Controller since he joined the Company in June 2008. Prior to joining the Company, Mr. Lanuto served as Executive Vice President and Chief Financial Officer of Initiative Media Worldwide, a subsidiary of The Interpublic Group of Companies. Inc., from September 2005 to March 2008. Prior to that, Mr. Lanuto served as Chief Financial Officer of Publicis Healthcare Communications, from April 2003 to August 2005. Prior to that, he served as Executive Vice President, Corporate Finance of Bcom3 Group, Inc. from December 2001 to March 2003 and Senior Vice President and Director, Group Financial Reporting of Bcom3 Group from May 2000 to November 2001. Mr. Lanuto served in various positions for Omnicom Group Inc. from 1993 to 2000, including Chief Operating Officer and Chief Financial Officer of its Rapp Collins Worldwide (New York office) business.

Neil J. Funk has served as Vice President, Internal Audit since joining the Company in August 2003. Prior to joining the Company, Mr. Funk was a Senior Manager at Deloitte & Touche LLP, a multi-national auditing and consulting firm, from September 2000 until July 2003. Before joining Deloitte & Touche, Mr. Funk was with Prudential Financial, Inc., a large insurance company, specializing in personal financial planning from March 2000 until August 2000. Before joining Prudential Financial, Inc., Mr. Funk was District Audit Manager for PRG-Schultz, Inc., a recovery audit company, based in Atlanta, Georgia from September 1997 until February 2000.

Executive officers are elected by, and serve at the discretion of, the Board of Directors. There are no family relationships between any of our directors or executive officers.

11

PART II

| ITEM 5. | MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES |

MARKET FOR COMMON STOCK

The Company’s common stock was listed for trading on the NASDAQ Global Market under the symbol “HHGP” in 2010. Effective January 3, 2011, the Company’s common stock is listed for trading on the NASDAQ Global Select Market under the symbol “HHGP” because NASDAQ determined that the Company meets the initial listing requirement of the NASDAQ Global Select Market. On December 31, 2010, there were approximately 969 holders of record of the Company’s common stock.

The following is a list by fiscal quarter of the market prices of the Company’s common stock.

| Market Price | ||||||||

| High | Low | |||||||

| 2010 | ||||||||

| Fourth quarter | $ | 6.01 | $ | 3.30 | ||||

| Third quarter | $ | 4.81 | $ | 2.93 | ||||

| Second quarter | $ | 6.02 | $ | 4.30 | ||||

| First quarter | $ | 5.56 | $ | 4.00 | ||||

| 2009 | ||||||||

| Fourth quarter | $ | 5.19 | $ | 2.99 | ||||

| Third quarter | $ | 4.04 | $ | 1.70 | ||||

| Second quarter | $ | 2.63 | $ | 1.09 | ||||

| First quarter | $ | 3.67 | $ | 0.68 | ||||

We have never declared or paid cash dividends on our common stock, and we currently do not intend to declare or pay cash dividends on our common stock. Any payment of cash dividends will depend upon our financial condition, capital requirements, earnings and other factors deemed relevant by our Board of Directors. In addition, the terms of our credit agreement prohibit us from paying dividends and making other distributions.

ISSUER PURCHASES OF EQUITY SECURITIES

The Company’s purchases of its common stock during the fourth quarter of fiscal 2010 were as follows:

| Period | Total Number of Shares Purchased | Average Price Paid per Share | Total Number of Shares Purchased as Part of Publicly Announced Plans or Programs | Approximate Dollar Value of Shares that May Yet Be Purchased Under the Plans or Programs(a) | ||||||||||||

| October 1, 2010 – October 31, 2010 | — | $ | — | — | $ | 6,792,000 | ||||||||||

| November 1, 2010 – November 30, 2010(b) | 368 | $ | 3.65 | — | $ | 6,792,000 | ||||||||||

| December 1, 2010 – December 31, 2010 | — | $ | — | — | $ | 6,792,000 | ||||||||||

| Total | 368 | $ | 3.65 | — | $ | 6,792,000 | ||||||||||

| (a) | On February 4, 2008, the Company announced that its Board of Directors authorized the repurchase of a maximum of $15 million of the Company’s common stock. The Company has repurchased 1,491,772 shares for a total cost of approximately $8.2 million under this authorization. Repurchases of common stock are restricted under the Company’s revolver agreement entered into on August 5, 2010. |

| (b) | Consisted of shares of restricted stock withheld from employees upon the vesting of such shares to satisfy employees’ income tax withholding requirements. |

The following information in this Item 5 of this Annual Report on Form 10-K is not deemed to be “soliciting material” or to be “filed” with the SEC or subject to Regulation 14A or 14C under the Securities Exchange Act of 1934 or to the liabilities of Section 18 of the Securities Exchange Act of 1934, and will not

12

be deemed to be incorporated by reference into any filing under the Securities Act of 1933 or the Securities Exchange Act of 1934, except to the extent we specifically incorporate it by reference into such a filing.

PERFORMANCE INFORMATION

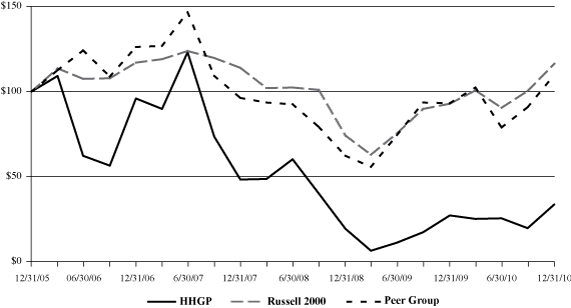

The following graph compares on a cumulative basis changes since December 31, 2005 in (a) the total stockholder return on the Company’s common stock with (b) the total return on the Russell 2000 Index and (c) the total return on the companies in a peer group selected in good faith by the Company, in each case assuming reinvestment of dividends. Such changes have been measured by dividing (a) the difference between the price per share at the end of and the beginning of the measurement period by (b) the price per share at the beginning of the measurement period. The graph assumes $100 was invested on December 31, 2005 in the Company’s common stock, the Russell 2000 Index and the peer group consisting of Kforce Inc., Manpower, Inc., Spherion Corporation, CDI Corp. and Robert Half International Inc. The returns of each component company in the peer group have been weighted based on each company’s relative market capitalization on December 31, 2010.

| December 31, | ||||||||||||||||||||||||

| 2010 | 2009 | 2008 | 2007 | 2006 | 2005 | |||||||||||||||||||

| HHGP | $ | 33.58 | $ | 27.36 | $ | 19.30 | $ | 48.44 | $ | 96.08 | $ | 100.00 | ||||||||||||

| PEER GROUP | $ | 109.75 | $ | 93.06 | $ | 62.32 | $ | 96.35 | $ | 126.33 | $ | 100.00 | ||||||||||||

| RUSSELL 2000 INDEX | $ | 116.40 | $ | 92.90 | $ | 74.19 | $ | 113.79 | $ | 117.00 | $ | 100.00 | ||||||||||||

13

ITEM 6. SELECTED FINANCIAL DATA

The following table shows selected financial data of the Company that has been adjusted to reflect the classification of certain businesses as discontinued operations. The data has been derived from, and should be read together with, the Consolidated Financial Statements and corresponding notes and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” included in Items 7 and 8 of this Form 10-K.

| Year ended December 31, | ||||||||||||||||||||

| 2010 | 2009 | 2008 | 2007 | 2006 | ||||||||||||||||

| (dollars in thousands, except per share data) | ||||||||||||||||||||

| SUMMARY OF OPERATIONS: | ||||||||||||||||||||

| Revenue | $ | 794,542 | $ | 691,149 | $ | 1,079,085 | $ | 1,170,061 | $ | 1,146,794 | ||||||||||

| Gross margin | $ | 298,573 | $ | 260,453 | $ | 454,986 | $ | 496,440 | $ | 444,213 | ||||||||||

| Business reorganization and integration expense | $ | 1,694 | $ | 18,180 | $ | 11,217 | $ | 3,575 | $ | 6,046 | ||||||||||

| Goodwill and other impairment charges(a) | $ | — | $ | 1,549 | $ | 67,087 | $ | — | $ | 1,300 | ||||||||||

| Depreciation and amortization | $ | 8,184 | $ | 12,543 | $ | 14,662 | $ | 14,377 | $ | 18,196 | ||||||||||

| Operating (loss) income | $ | (5,618 | ) | $ | (49,453 | ) | $ | (70,783 | ) | $ | 18,995 | $ | (5,826 | ) | ||||||

| (Loss) income from continuing operations | $ | (4,441 | ) | $ | (42,953 | ) | $ | (73,096 | ) | $ | 5,528 | $ | (8,855 | ) | ||||||

| (Loss) income from discontinued operations, net of income taxes | $ | (244 | ) | $ | 2,344 | $ | (1,222 | ) | $ | 9,453 | $ | 29,283 | ||||||||

| Net (loss) income | $ | (4,685 | ) | $ | (40,609 | ) | $ | (74,318 | ) | $ | 14,981 | $ | 20,428 | |||||||

| Basic (loss) income per share from continuing operations | $ | (0.15 | ) | $ | (1.65 | ) | $ | (2.90 | ) | $ | 0.22 | $ | (0.36 | ) | ||||||

| Basic net (loss) income per share | $ | (0.16 | ) | $ | (1.56 | ) | $ | (2.95 | ) | $ | 0.59 | $ | 0.83 | |||||||

| Diluted (loss) income per share from continuing operations | $ | (0.15 | ) | $ | (1.65 | ) | $ | (2.90 | ) | $ | 0.21 | $ | (0.36 | ) | ||||||

| Diluted net (loss) income per share | $ | (0.16 | ) | $ | (1.56 | ) | $ | (2.95 | ) | $ | 0.58 | $ | 0.83 | |||||||

| OTHER FINANCIAL DATA: | ||||||||||||||||||||

| Net cash (used in) provided by operating activities | $ | (14,461 | ) | $ | (26,988 | ) | $ | 11,860 | $ | 37,741 | $ | 35,867 | ||||||||

| Net cash (used in) provided by investing activities | $ | (57 | ) | $ | 6,804 | $ | 4,196 | $ | (50,837 | ) | $ | 1,881 | ||||||||

| Net cash provided by (used in) financing activities | $ | 7,578 | $ | 4,371 | $ | (646 | ) | $ | 4,864 | $ | (28,803 | ) | ||||||||

| BALANCE SHEET DATA: | ||||||||||||||||||||

| Current assets | $ | 172,087 | $ | 148,366 | $ | 194,149 | $ | 259,075 | $ | 280,107 | ||||||||||

| Total assets | $ | 205,834 | $ | 181,944 | $ | 230,953 | $ | 374,206 | $ | 352,182 | ||||||||||

| Current liabilities | $ | 93,760 | $ | 86,154 | $ | 104,581 | $ | 152,426 | $ | 167,289 | ||||||||||

| Long-term debt, less current portion | $ | — | $ | — | $ | — | $ | — | $ | 235 | ||||||||||

| Total stockholders’ equity | $ | 93,278 | $ | 76,260 | $ | 107,992 | $ | 200,115 | $ | 171,324 | ||||||||||

| OTHER DATA: | ||||||||||||||||||||

| EBITDA (loss)(b) | $ | 6,503 | $ | (35,466 | ) | $ | (52,852 | ) | $ | 36,795 | $ | 13,959 | ||||||||

| (a) | The results for the year ended December 31, 2009 included an impairment charge of $1,669 related to goodwill associated with the Tong Zhi (Beijing) Consulting Service Ltd. and Guangzhou Dong Li Consulting Service Ltd. (collectively, “TKA”) acquisition. The results for the year ended December 31, 2008 included impairment charges related to goodwill of $64,495, a write down of long-term assets of |

14

| $2,224 and impairment charges related to intangible assets of $368. The results for the year ended December 31, 2006 included an impairment charge of $1,300 related to goodwill associated with the Alder Novo acquisition. |

| (b) | SEC Regulation S-K 229.10(e)1(ii)(A) defines EBITDA as earnings before interest, taxes, depreciation and amortization. EBITDA is presented to provide additional information to investors about the Company’s operations on a basis consistent with the measures that the Company uses to manage its operations and evaluate its performance. Management also uses this measurement to evaluate working capital requirements. EBITDA should not be considered in isolation or as a substitute for operating income and net income prepared in accordance with generally accepted accounting principles or as a measure of the Company’s profitability. See Note 15 to the Consolidated Financial Statements for further EBITDA segment and reconciliation information. |

15

| ITEM 7. | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

This Management’s Discussion and Analysis of Financial Condition and Results of Operations (“MD&A”) should be read in conjunction with the Consolidated Financial Statements and the notes thereto, included in Item 8 of this Form 10-K. This MD&A contains forward-looking statements. Please see note “Regarding Forward-Looking Statements” for a discussion of the uncertainties, risks and assumptions associated with these statements. This MD&A also uses the non-GAAP measure of earnings before interest, taxes, depreciation and amortization (“EBITDA”). See Note 15 to the Consolidated Financial Statements for EBITDA segment reconciliation information.

Executive Overview

Hudson Highland Group, Inc. (the “Company” or “Hudson,” “we,” “us” and “our”) has operated as an independent publicly traded company since April 1, 2003, when we were spun-off from Monster Worldwide, Inc. Our businesses are specialized professional staffing services for permanent and contract and talent management services to businesses operating in many industries and in 19 countries around the world. Our largest operations are in the United Kingdom (“U.K.”), Australia, and the U.S. We are organized into four reportable segments: Hudson Europe, Hudson Australia and New Zealand (“ANZ”), Hudson Americas and Hudson Asia. These segments contributed approximately 46%, 30%, 13% and 11% of the Company’s gross margin, respectively, for the year ended December 31, 2010. Our management’s primary focus since the spin-off has been to move the Company to profitability, particularly at the level most in the control of the country level operating leaders. We have focused on specialized professional recruitment through our staffing, project solutions and talent management businesses. In doing so, we have sold or discontinued non-core businesses, taken actions to streamline support operations to match the business focus and reduced costs to increase our long-term profitability. We have measured our improvements at the level of gross margin, less selling, general and administrative expenses, and depreciation and amortization.

Prevailing Economic Conditions

During 2010, the Company continued to experience improving economic conditions first seen in the fourth quarter of 2009. Conditions generally improved throughout the year, though rates of improvement varied from market to market in both overall magnitude and momentum. The improvement was led by increases in permanent placement activities, followed by increases in temporary contracting, which were more evident in the second half of the year.

As the year progressed, growth in the recovery leading markets of the U.K. and Asia began to level off, while markets in North America, Continental Europe and ANZ began to pick up. Unemployment rates, traditionally a lagging economic indicator, remained generally elevated in North America and the Europe, at high single digit levels. Unemployment rates in Asia and ANZ, which were less affected by the global economic downturn in 2009, continued to improve.

We believe the economic growth outlook for 2011 is positive. Growth rates for developing markets, particularly those in Asia, are generally expected to continue to outpace developed economies. However, the strength of the global economic recovery and related job creation could be moderated by several factors, including expansion of the sovereign debt crisis in Europe, mounting governmental budget deficits, and a continued weak housing market in the U.S. While we are unable to accurately predict changes in general economic conditions and their effect on the levels of new hiring, we do not expect a return to significantly negative conditions in any market, even though companies are likely to remain cautious on hiring.

16

Financial Performance

As discussed in more detail in this MD&A, the following financial data present an overview of our financial performance for 2010, 2009 and 2008:

| Year Ended December 31, | Changes 2010 vs. 2009 | Changes 2009 vs. 2008 | ||||||||||||||||||

| $ in thousands | 2010 | 2009 | 2008 | Amount | Amount | |||||||||||||||

| Revenue | $ | 794,542 | $ | 691,149 | $ | 1,079,085 | $ | 103,393 | $ | (387,936 | ) | |||||||||

| Gross margin | 298,573 | 260,453 | 454,986 | 38,120 | (194,533 | ) | ||||||||||||||

| Selling, general and administrative expenses(a) | 302,497 | 290,177 | 447,465 | 12,320 | (157,288 | ) | ||||||||||||||

| Business reorganization and integration expenses | 1,694 | 18,180 | 11,217 | (16,486 | ) | 6,963 | ||||||||||||||

| Goodwill and other impairment charges | — | 1,549 | 67,087 | (1,549 | ) | (65,538 | ) | |||||||||||||

| Operating loss | (5,618 | ) | (49,453 | ) | (70,783 | ) | 43,835 | 21,330 | ||||||||||||

| Loss from continuing operations | (4,441 | ) | (42,953 | ) | (73,096 | ) | 38,512 | 30,143 | ||||||||||||

| Net loss | $ | (4,685 | ) | $ | (40,609 | ) | $ | (74,318 | ) | $ | 35,924 | $ | 33,709 | |||||||

| (a) | Selling, general and administrative expenses include depreciation and amortization expense of $8.2 million, $12.5 million and $14.7 million, respectively, for the years ended December 31, 2010, 2009 and 2008. |

| • | Revenue was $794.5 million for the year ended December 31, 2010, compared to $691.1 million for 2009, an increase of $103.4 million, or 15.0%. Of this increase, $63.5 million, or a 12.2% increase compared to 2009, was in contracting and $42.5 million, or a 37% increase compared to 2009, was in permanent recruitment revenue. The increase was partially offset by a $2.8 million, or 5.8%, decline in talent management revenue compared to 2009 primarily from counter-cyclical outplacement services. |

| • | Revenue was $691.1 million for the year ended December 31, 2009, compared to $1,079.1 million for 2008, a decrease of $388 million, or 36%. Of this decrease, $244 million, or a 32% decrease compared to 2008, was in contracting and $122 million, or a 51% decrease compared to 2008, was in permanent recruitment revenue. |

| • | Gross margin was $298.6 million for the year ended December 31, 2010, compared to $260.5 million for 2009, an increase of $38.1 million, or 14.6%. Of this increase, $41.3 million, or a 36.4% increase compared to 2009, was in permanent recruitment gross margin and $0.4 million, or a 0.3% increase compared to 2009, was in contracting gross margin. The increase was partially offset by a $3 million, or 7.3%, decline in talent management gross margin compared to 2009. |

| • | Gross margin was $260.5 million for the year ended December 31, 2009, compared to $455 million for 2008, a decrease of $194.5 million, or 42.8%. Of this decrease, $120.8 million, or a 51.4% decrease compared to 2008, was in permanent recruitment gross margin and $60.2 million, or a 36.9% decrease compared to 2008, was in contracting gross margin. |

| • | Selling, general and administrative expenses were $302.5 million for the year ended December 31, 2010, as compared to $290.2 million for 2009, an increase of $12.3 million, or 4.2%. The increase was primarily due to increased staff compensation as a result of the increase in gross margin, partially offset by reductions in costs resulting from the restructuring program completed in 2009. |

| • | Selling, general and administrative expenses were $290.2 million for the year ended December 31, 2009, as compared to $447.5 million for 2008, a decrease of $157.3 million, or 35.2%. The decrease was primarily due to decreased staff compensation as a result of the decline in gross margin, and reductions in costs resulting from the restructuring programs completed in 2009 and 2008. |

| • | There were no goodwill and other impairment charges in 2010. Goodwill and other impairment charges of $1.7 million were included in the results for the year ended December 31, 2009, as compared to $67.1 million for 2008. |

17

Goodwill and Other Impairment Charges

Under the Financial Accounting Standards Board (“FASB”) Accounting Standards Codification Topic (“ASC”) 350-20-35“Intangibles — Goodwill and Other, Goodwill Subsequent Measurement”, the Company is required to test goodwill and indefinite-lived intangible assets for impairment on an annual basis as of October 1, or more frequently if circumstances indicate that its carrying value might exceed its current fair value.

By the fourth quarter of 2008, virtually all of our markets were affected by weakening economic conditions. These conditions negatively impacted both the Company’s stock price and its outlook for operating results. The Company’s stock price declined approximately fifty percent as of December 31, 2008 compared to the stock price as of October 1, 2008. As a result, the Company’s market capitalization declined below its book value, an indication that the aggregate fair value of its reporting units could potentially be less than their carrying value. Accordingly, management updated its impairment testing from October 1 (annual assessment date), through December 31, 2008 with the assistance of a third-party valuation firm utilizing both an income and market based approach.

At the conclusion of the impairment testing, the Company determined that goodwill was impaired at all of its reporting units and recorded an impairment charge of $64.5 million in 2008. It also recorded an additional impairment charge on intangible assets of $2.6 million. The total charges of $67.1 million for 2008 were recorded under the caption of “Goodwill and other impairment charges” in the Company’s Consolidated Statements of Operations included in the Company’s 2008 Annual Report on Form 10-K. The primary drivers that resulted in the goodwill impairment charge were the anticipated significant reduction in 2009 revenue, earnings and cash flows with modest expected recovery in 2010 and a reduction in the market price of the Company’s stock.

During the first half of 2009, the Company experienced a continued deterioration in market conditions. Over the course of the first six months of the 2009, the Company’s stock price declined approximately thirty-five percent as of June 30, 2009 as compared to December 31, 2008. As a result, management performed an interim test for impairment of the $1.7 million additional purchase price payment for its Tong Zhi (Beijing) Consulting Service Ltd and Guangzhou Dong Li Consulting Service Ltd (collectively, “TKA”) acquisition, which was recorded as goodwill at June 30, 2009. The Company concluded that the entire amount of recorded goodwill was impaired and recorded an impairment charge of $1.7 million at the same reporting unit.

In 2010, the Company’s financial results continued the improvement which began in the latter half of 2009, particularly in Asia. However, business and economic conditions remained mixed. As a result, the Company performed an interim test for impairment of the $1.9 million final purchase price payment for its TKA acquisition, which was recorded as goodwill at June 30, 2010. At the conclusion of its testing, the Company determined that no impairment of goodwill existed at June 30, 2010. Management updated its testing for impairment as of October 1 (annual impairment date) and confirmed its earlier determination that no impairment of goodwill existed as of October 1, 2010.

Strategic Actions

Our management’s primary focus has been on specialized professional recruitment through our recruitment, staffing, project solutions and talent management businesses. Our long-term financial goal is to reach 7 – 10% EBITDA margins, with EBITDA being the measure most within the control of our operating leaders. We continue to execute this strategy through a combination of delivery of higher margin services, efficient delivery of services, investments, cost management, acquisitions and divestitures. In doing so, we continue to focus on retaining and maintaining key clients, retaining high performing revenue earning employees, integrating businesses to achieve synergies, discontinuing non-core businesses, streamlining support operations and reducing costs to achieve the Company’s long-term profitability goals. We expect to continue our review of opportunities to expand our operations in specialized professional recruitment.

18

Discontinued Operations

In the first half of 2009, the Company exited Italy and Japan. The operations in Italy were part of the Hudson Europe reportable segment and the operations of Japan were part of the Hudson Asia reportable segment.

In the second quarter of 2008, the Company sold substantially all of the assets of Balance Public Management B.V. (“BPM”), a division of Balance Ervaring op Projectbasis, B.V. (“Balance”), a subsidiary of the Company, which was part of the Hudson Europe reportable segment. In the first quarter of 2008, the Company sold substantially all of the assets of its Hudson Americas energy, engineering and technical staffing division (“ETS”), which was part of the Hudson Americas reportable segment.

In the fourth quarter of 2006, the Company sold its Highland Partners (“Highland”) executive search business, which was a separate reportable segment of the Company.

In accordance with the provisions of ASC 205-20-45 “Reporting Discontinued Operations”, the assets, liabilities, and results of operations of the Company’s discontinued operations above were reclassified as discontinued operations for all the periods presented. The gain or loss on sale and results of operations of the disposed businesses were reported in discontinued operations in the relevant periods

Use of EBITDA

Management believes EBITDA is a meaningful indicator of the Company’s performance that provides useful information to investors regarding the Company’s financial condition and results of operations. EBITDA is also considered by management as the best indicator of operating performance and most comparable measure across our regions. Management also uses this measurement to evaluate capital needs and working capital requirements. EBITDA should not be considered in isolation or as a substitute for operating income, or net income prepared in accordance with generally accepted accounting principles in the United States of America (“US GAAP”) or as a measure of the Company’s profitability. EBITDA is derived from net income (loss) adjusted for (benefit from) provision for income taxes, interest expense (income), and depreciation and amortization. The reconciliation of EBITDA to the most directly comparable US GAAP financial measure is provided in the table below:

| Year Ended December 31, | ||||||||||||

| $ in thousands | 2010 | 2009 | 2008 | |||||||||

| Net loss | $ | (4,685 | ) | $ | (40,609 | ) | $ | (74,318 | ) | |||

| Adjusted for (loss) income from discontinued operations, net of income taxes | (244 | ) | 2,344 | (1,222 | ) | |||||||

| Loss from continuing operations | (4,441 | ) | (42,953 | ) | (73,096 | ) | ||||||

| Adjustments to loss from continuing operations | ||||||||||||

| Provision for (benefit from) income taxes | 1,482 | (5,750 | ) | 6,681 | ||||||||

| Interest expense (income), net | 1,278 | 694 | (1,099 | ) | ||||||||

| Depreciation and amortization | 8,184 | 12,543 | 14,662 | |||||||||

| Total adjustments from loss from continuing operations to EBITDA (loss) | 10,944 | 7,487 | 20,244 | |||||||||

| EBITDA (loss) | $ | 6,503 | $ | (35,466 | ) | $ | (52,852 | ) | ||||

Critical Accounting Policies

Our discussion and analysis of our financial condition and results of operations are based upon our Consolidated Financial Statements, which have been prepared in accordance with US GAAP. The preparation of financial statements in accordance with US GAAP requires our management to make estimates and assumptions that affect the reported amounts of assets, liabilities, revenues and expenses, and the disclosure of contingent assets and liabilities. US GAAP provides the framework from which to make these estimates, assumptions and disclosures. We choose accounting policies within US GAAP that our management believes are appropriate to accurately and fairly report our operating results and financial position in a consistent manner. Our management regularly assesses these policies in light of current and forecasted economic

19

conditions. Our accounting policies are stated in Note 2 to our Consolidated Financial Statements included in Item 8. We believe the following accounting policies are critical to understanding our results of operations and affect the more significant judgments and estimates used in the preparation of our Consolidated Financial Statements that are inherently uncertain:

Revenue Recognition

The Company recognizes revenue for temporary services at the time services are provided and revenue is recorded on a time and materials basis. Temporary contracting revenue is reported on a gross basis when the Company acts as the principal in the transaction and is at risk for collection in accordance with ASC 605-45, “Overall Considerations of Reporting Revenue Gross as a Principal versus Net as an Agent”.The Company’s revenues are derived from its gross billings, which are based on (i) the payroll cost of its worksite employees; and (ii) a markup computed as a percentage of the payroll cost.

The Company recognizes revenue for permanent placements based on the nature of the fee arrangement. Revenue generated when the Company permanently places an individual with a client on a contingent basis is recorded at the time of acceptance of employment, net of an allowance for estimated fee reversals. Revenue generated when the Company permanently places an individual with a client on a retained basis is recorded ratably over the period services are rendered, net of an allowance for estimated fee reversals.

ASC 605-45-50-3 and ASC 605-45-50-4, “Taxes Collected from Customers and Remitted to Governmental Authorities” provide that the presentation of taxes on either a gross or net basis is an accounting policy decision. The Company collects various taxes assessed by governmental authorities and records these amounts on a net basis.

Accounts Receivable

The Company’s accounts receivable balances are composed of trade and unbilled receivables. The Company maintains an allowance for doubtful accounts and makes ongoing estimates as to the collectability of the various receivables. If the Company determines that the allowance for doubtful accounts is not adequate to cover estimated losses, an expense to provide for doubtful accounts is recorded in selling, general and administrative expenses. If an account is determined to be uncollectible, it is written off against the allowance for doubtful accounts. Management’s assessment and judgment are vital requirements in assessing the ultimate realization of these receivables, including the current credit-worthiness, financial stability and effect of market conditions on each customer.

Income Taxes

We account for income taxes using the asset and liability method in accordance with ASC 740, “Income Taxes”. This standard establishes financial accounting and reporting standards for the effects of income taxes that result from an enterprise’s activities during the current and preceding years. It requires an asset and liability approach for financial accounting and reporting of income taxes.

The calculation of net deferred tax assets assumes sufficient future earnings for the realization of such assets as well as the continued application of currently anticipated tax rates. Included in net deferred tax assets is a valuation allowance for deferred tax assets where management believes it is more likely than not that the deferred tax assets will not be realized in the relevant jurisdiction. If we determine that a deferred tax asset will not be realizable, an adjustment to the deferred tax asset will result in a reduction of earnings at that time. See Note 10 to the Consolidated Financial Statements for further information regarding deferred tax assets and valuation allowance.

ASC 740-10-55-3 “Recognition and Measurement of Tax Positions — a Two Step Process” provides implementation guidance related to the accounting for uncertainty in income taxes recognized in an enterprise’s financial statements and prescribes a two-step evaluation process for a tax position taken or expected to be taken in a tax return. The first step is recognition and the second is measurement. ASC 740 also provides guidance on derecognition, measurement, classification, disclosures, transition and accounting for interim periods. In addition, ASC 740-10-25-9 provides guidance on how to determine whether a tax position is effectively settled for the purpose of recognizing previously unrecognized tax benefits.

20

The Company’s unrecognized tax benefits, if recognized in the future, would affect the annual effective income tax rate. See Note 10 to the Consolidated Financial Statements for further information regarding unrecognized tax benefits. We elected to continue our historical practice of classifying applicable interest and penalties as a component of the provision for income taxes.