Table of Contents

As filed with the Securities and Exchange Commission on March 9, 2012

Registration No. 333-172237

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 5 to

Form S-11

FOR REGISTRATION UNDER THE SECURITIES ACT OF 1933

OF SECURITIES OF CERTAIN REAL ESTATE COMPANIES

RETAIL PROPERTIES OF AMERICA, INC.

(Exact Name of Registrant as Specified in its Governing Instruments)

2901 Butterfield Road

Oak Brook, Illinois 60523

(630) 218-8000

(Address, Including Zip Code, and Telephone Number, including Area Code, of Registrant’s Principal Executive Offices)

Steven P. Grimes

Chief Executive Officer

Retail Properties of America, Inc.

2901 Butterfield Road

Oak Brook, Illinois 60523

(630) 218-8000

(Name, Address, Including Zip Code, and Telephone Number, Including Area Code, of Agent for Service)

Copies to:

Gilbert G. Menna Daniel P. Adams Goodwin Procter LLP Exchange Place, 53 State Street Boston, MA 02109 (617) 570-1000 | Dennis K. Holland General Counsel and Secretary Retail Properties of America, Inc. 2901 Butterfield Road Oak Brook, Illinois 60523 (630) 218-8000 | David W. Bonser David P. Slotkin Hogan Lovells US LLP 555 Thirteenth Street, NW Washington, DC 20004 (202) 637-5600 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after this registration statement becomes effective.

If any of the securities being registered on this form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ¨

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If delivery of the prospectus is expected to be made pursuant to Rule 434, check the following box. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer | ¨ | Accelerated filer | ¨ | |||||

| Non-accelerated filer | x (Do not check if a smaller reporting company) | Smaller reporting company | ¨ | |||||

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to Section 8(a), may determine.

Table of Contents

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and we are not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED MARCH 9, 2012

PROSPECTUS

Shares

RETAIL PROPERTIES OF AMERICA, INC.

Class A Common Stock

Retail Properties of America, Inc. is a fully integrated, self administered and self-managed real estate company that owns and operates high quality, strategically located shopping centers across 35 states. We are one of the largest owners and operators of shopping centers in the United States.

We are offering shares of our Class A Common Stock as described in this prospectus. All of the shares of Class A Common Stock offered by this prospectus are being sold by us. We currently expect the public offering price to be between $ and $ per share. We have applied to have our Class A Common Stock listed on the New York Stock Exchange, or the NYSE, under the symbol “RPAI”. Currently, our Class A Common Stock is not traded on a national securities exchange, and this will be our first listed public offering.

We are a Maryland corporation, and we have elected to qualify as a real estate investment trust, or REIT, for U.S. federal income tax purposes. Shares of our Class A Common Stock are subject to ownership limitations that are primarily intended to assist us in maintaining our qualification as a REIT. Our charter contains certain restrictions relating to the ownership and transfer of our Class A Common Stock, including, subject to certain exceptions, a 9.8% ownership limit of common stock by value or number of shares, whichever is more restrictive. See “Description of Capital Stock—Restrictions on Ownership and Transfer” beginning on page 143 of this prospectus.

Investing in our Class A Common Stock involves risk. See “Risk Factors” beginning on page 16 of this prospectus.

| Per Share | Total | |||||||

Public offering price | $ | $ | ||||||

Underwriting discount | $ | $ | ||||||

Proceeds, before expenses, to us | $ | $ | ||||||

We have granted the underwriters the option to purchase an additional shares of our Class A Common Stock on the same terms and conditions set forth above within 30 days after the date of this prospectus solely to cover overallotments, if any.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The underwriters expect to deliver the shares of our Class A Common Stock on or about , 2012.

| J.P. Morgan | Citigroup | Deutsche Bank Securities | KeyBanc Capital Markets |

The date of this prospectus is , 2012.

Table of Contents

[PICTURE, TEXT AND/OR GRAPHICS FOR INSIDE COVER]

i

Table of Contents

| Page | ||||

| 1 | ||||

| 16 | ||||

| 42 | ||||

| 44 | ||||

| 45 | ||||

| 46 | ||||

| 48 | ||||

| 49 | ||||

| 50 | ||||

Management’s discussion and analysis of financial condition and results of operations | 56 | |||

| 86 | ||||

| 92 | ||||

| 114 | ||||

| 133 | ||||

| 135 | ||||

| 139 | ||||

| 142 | ||||

Certain provisions of Maryland law and of our charter and bylaws | 147 | |||

| 154 | ||||

| 158 | ||||

| 178 | ||||

| 181 | ||||

| 186 | ||||

| 186 | ||||

| 187 | ||||

| F-1 | ||||

You should rely only upon the information contained in this prospectus, or in any free writing prospectus prepared by us or information to which we have referred you. No dealer, salesperson or other person is authorized to give any information or to represent anything not contained in this prospectus. You must not rely on any unauthorized information or representations. This prospectus is an offer to sell only the shares offered hereby, but only under circumstances and in jurisdictions where it is lawful to do so. The information contained in this prospectus is current only as of its date, regardless of the time of delivery of this prospectus or of any sale of our Class A Common Stock. Our business, financial condition, liquidity, results of operations and prospects may have changed since those dates. We will update this prospectus as required by law.

We use market data throughout this prospectus. We have obtained the information under “Prospectus Summary—Industry Overview” and “Industry Overview” from the market study prepared for us by Rosen Consulting Group, or Rosen, a nationally recognized real estate consulting firm, and such information is included in this prospectus in reliance on Rosen’s authority as an expert in such matters. See “Experts.” In addition, we have obtained certain market data from publicly available information and industry publications. These sources generally state that the information they provide has been obtained from sources believed to be reliable, but the accuracy and completeness of the information are not guaranteed. The forecasts and projections are based on industry surveys and the preparers’ experience in the industry, and there is no assurance that any of the projections or forecasts will be achieved. We believe that the surveys and market research others have performed are reliable, but we have not independently verified this information.

ii

Table of Contents

On February 24, 2011, our shareholders approved an amendment and restatement of our charter that is intended to facilitate the listing of our Class A Common Stock on the NYSE. The amendment and restatement of our charter will become effective upon the filing of the amendment and restatement of our charter with the Maryland State Department of Assessments and Taxation. We expect to file the proposed amendment and restatement of our charter prior to the completion of this offering. Unless otherwise indicated, the information contained in this prospectus assumes that the amendment and restatement of our charter has become effective.

Recapitalization

Prior to the completion of this offering, we intend to declare a stock dividend pursuant to which each then outstanding share of our common stock will receive:

| • | one share of our Class B-1 Common Stock; plus |

| • | one share of our Class B-2 Common Stock; plus |

| • | one share of our Class B-3 Common Stock. |

In connection with this stock dividend, we intend to redesignate our then outstanding common stock as “Class A Common Stock.” Prior to the declaration of the stock dividend, we intend to effectuate a ten to one reverse stock split of our common stock outstanding.

In this prospectus, we refer to these transactions as the “Recapitalization,” we refer to Class B-1 Common Stock, Class B-2 Common Stock and Class B-3 Common Stock collectively as our “Class B Common Stock,” and we refer to Class A and Class B Common Stock collectively as our “common stock.” We are offering our Class A Common Stock in this offering, and we intend to list our Class A Common Stock on the NYSE. Our Class B Common Stock will be identical to our Class A Common Stock except that (i) we do not intend to list our Class B Common Stock on a national securities exchange and (ii) shares of our Class B Common Stock will convert automatically into shares of our Class A Common Stock at specified times. Subject to the provisions of our charter, shares of our Class B-1, Class B-2 and Class B-3 Common Stock will convert automatically into shares of our Class A Common Stock six months following the Listing, 12 months following the Listing and 18 months following the Listing, respectively. On the 18 month anniversary of the listing of our Class A Common Stock on the NYSE (the “Listing”), all shares of our Class B Common Stock will have converted into our Class A Common Stock. The terms of our Class A and Class B Common Stock are described more fully under “Description of Capital Stock” in this prospectus.

The Recapitalization also will have the effect of reducing the total number of outstanding shares of our common stock. As of March 2, 2012, without giving effect to the Recapitalization, we had approximately 485.5 million shares of common stock outstanding. As of March 2, 2012, after giving effect to the Recapitalization, we would have had an aggregate of approximately 194.2 million shares of our Class A and Class B Common Stock outstanding, divided equally among our Class A, Class B-1, Class B-2 and Class B-3 Common Stock.

The Recapitalization will be effected prior to the completion of this offering. Unless otherwise indicated, all information in this prospectus gives effect to, and all share and per share amounts have been retroactively adjusted to give effect to, the Recapitalization. Unless otherwise indicated, share and per share amounts have not been adjusted to give effect to any exercise by the underwriters of their option to purchase up to shares of our Class A Common Stock solely to cover overallotments, if any.

In this prospectus:

| • | “annualized base rent” as of a specified date means monthly base rent as of the specified date, before abatements, under leases which have commenced as of the specified date multiplied by 12. Annualized base rent (i) does not include tenant reimbursements or expenses borne by the tenants in triple net or modified gross leases, such as the expenses for real estate taxes and insurance and common area and |

iii

Table of Contents

other operating expenses, (ii) does not reflect amounts due per percentage rent lease terms, where applicable, and (iii) is calculated on a cash basis and differs from how we calculate rent in accordance with generally accepted accounting principles in the United States of America, or GAAP, for purposes of our financial statements; |

| • | “community center” means a shopping center that we believe meets the International Council of Shopping Centers’s, or ICSC’s, definition of community center. ICSC, generally, defines a community center as a shopping center similar to a neighborhood center, defined below, but which offers a wider range of apparel and other soft goods than a neighborhood center. Community centers are usually configured as a strip, or may be laid out in an L or U shape, and are commonly anchored by supermarkets, super drugstores and discount department stores; |

| • | “lifestyle center” means a shopping center that we believe meets ICSC’s definition of lifestyle center. ICSC, generally, defines a lifestyle center as a shopping center that is most often located near affluent residential neighborhoods and caters to the retail needs and “lifestyle” pursuits of consumers in its trading area. Lifestyle centers typically have open-air configurations, include at least 50,000 square feet of retail space occupied by upscale national chain specialty stores and include other elements serving its role as a multi-purpose leisure-time destination, such as restaurants and entertainment; |

| • | “neighborhood center” means a shopping center that we believe meets ICSC’s definition of neighborhood center. ICSC, generally, defines a neighborhood center as a shopping center designed to provide convenience shopping for the day-to-day needs of consumers in the immediate neighborhood, which is usually configured as a straight-line strip with parking in the front and no enclosed walkway or mall area. Neighborhood centers are frequently anchored by a grocer or drug store and supported by stores offering drugs, sundries, snacks and personal services; |

| • | “power center” means a shopping center that we believe meets ICSC’s definition of power center. ICSC, generally, defines a power center as a shopping center dominated by several large anchors, including discount department stores, off-price stores, warehouse clubs, or “category killers,” i.e., stores that offer tremendous selection in a particular merchandise category at low prices. Power centers typically consist of several anchors, some of which may be freestanding (unconnected) and only a minimum amount of small specialty tenants; and |

| • | “shadow anchors” means one or more retailers situated on parcels that are owned by unrelated third parties but, due to their location within or immediately adjacent to our shopping center, to the consumer appear as another retail tenant of the shopping center and, as a result, attract additional customer traffic to the center. |

Unless otherwise indicated, references in this prospectus to our properties or portfolio include information with respect to properties held by us on a consolidated basis as of December 31, 2011. Information with respect to our operating properties excludes non-stabilized operating properties, which are properties that have not achieved 90% or greater occupancy since their development and have been operational for less than one year.

iv

Table of Contents

This summary highlights some of the information in this prospectus. It does not contain all of the information that you should consider before investing in our Class A Common Stock. You should read carefully the more detailed information set forth under the heading “Risk Factors” and the other information included in this prospectus. Except where the context suggests otherwise, the terms “our company,” “we,” “us” and “our” refer to Retail Properties of America, Inc., a Maryland corporation, together with its consolidated subsidiaries. Unless otherwise indicated, the information contained in this prospectus assumes that the Class A Common Stock to be sold in the offering is sold at $ per share, the midpoint of the pricing range set forth on the cover page of this prospectus, and that the underwriters do not exercise their option to purchase up to an additional shares solely to cover overallotments, if any. Unless otherwise indicated, all property information contained in this prospectus is for our retail operating properties as of December 31, 2011 excluding seasonal leases.

Company Overview

We are one of the largest owners and operators of shopping centers in the United States. As of December 31, 2011, our retail operating portfolio consisted of 259 properties with 34.6 million square feet of gross leasable area, or GLA. Our retail operating portfolio is geographically diversified across 35 states and includes power centers, community centers, neighborhood centers and lifestyle centers, as well as single-user retail properties. Our retail properties are primarily located in retail districts within densely populated areas in highly visible locations with convenient access to interstates and major thoroughfares. Our retail properties have a weighted average age, based on annualized base rent, of approximately 9.8 years since the initial construction or most recent major renovation. As of December 31, 2011, our retail operating portfolio was 90.4% leased, including leases signed but not commenced. In addition to our retail operating portfolio, as of December 31, 2011, we also held interests in 12 office properties, three industrial properties, one non-stabilized retail operating property, 24 retail operating properties held by three unconsolidated joint ventures and three retail properties under development.

As of December 31, 2011, over 90% of our shopping centers, based on GLA, were anchored or shadow anchored by a grocer, discount department store, wholesale club or retailer that sells basic household goods or clothing. Overall, we have a broad and highly diversified retail tenant base that includes approximately 1,500 tenants with no one tenant representing more than 3.3% of the total annualized base rent generated from our retail operating properties, or our retail annualized base rent.

We are a client-focused organization, maintaining very active relationships with our key tenants. We have 19 property management offices strategically located across the country and over 180 employees primarily dedicated to our leasing, asset management and property management activities. Our senior management team applies a hands-on approach to leasing our portfolio and is supported by over 80 property managers and senior leasing agents who have an average of 15 years of experience in the industry. We believe that the size and scale of our property management and leasing organization, the breadth of our tenant relationships and the scale of our retail portfolio provides us with a competitive advantage in dealing with national and large regional grocers and retailers. Through the efforts of our leasing team since the beginning of 2009, we have renewed approximately 78% of our expiring leases based on GLA at aggregate base rental rates that reflected modest increases from the base rental rates of the expiring leases and have signed 575 new leases for 4.7 million square feet of GLA, representing approximately 14% of the total GLA in our retail operating portfolio.

1

Table of Contents

Competitive Strengths

We believe that we distinguish ourselves from other owners and operators of shopping centers through the following competitive strengths:

Large, Diversified, High Quality Retail Portfolio

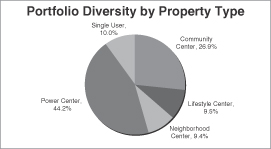

We own a national portfolio of high quality retail properties that is well diversified both geographically and by property type. We have retail operating properties in 35 states with no one metropolitan statistical area, or MSA, accounting for more than 4.6% of our retail annualized base rent, other than the Dallas-Fort Worth-Arlington area, which accounts for 15.0% of our retail annualized base rent. Our retail operating portfolio is also well diversified by type, including 63 power centers with 15.3 million square feet of GLA, 60 community centers with 9.3 million square feet of GLA, 43 neighborhood centers with 3.3 million square feet of GLA and seven lifestyle shopping centers with 3.3 million square feet of GLA, as well as 86 single-user retail properties with 3.5 million square feet of GLA. We believe the scale of our retail portfolio gives us an advantage in working with national and large regional grocers and retailers, as we offer many potential locations within a selected area from which to choose and can address multiple needs for space in different geographic areas for tenants with multiple locations.

Our shopping centers are well located within strong retail districts in densely populated areas. They have high quality anchors and shadow anchors that consistently drive traffic to our centers and make them more attractive to other potential tenants. Consistent with our entire retail operating portfolio, our shopping centers are also generally recently constructed, which makes them more appealing to shoppers and potential tenants and reduces redevelopment and renovation costs. As of December 31, 2011, 67.2% of our shopping centers, based on annualized base rent, were located in the 50 largest MSAs. These shopping centers are positioned in highly attractive markets with favorable demographics, including a weighted average population of 92,274, expected population growth of 7.5% per year and household income of approximately $83,545 within a three-mile radius, based on information derived and interpreted by us as a result of our own analysis from data provided by The Nielsen Company. We believe our shopping centers located in markets outside of the 50 largest MSAs are among the most attractive shopping centers in each of the markets in which they are located based on location, age and overall quality. As of December 31, 2011, approximately 89.5% of these shopping centers, based on annualized base rent, were anchored or shadow anchored by either Best Buy (13 locations), Target (11 locations), Home Depot (ten locations), Kohl’s (ten locations), Wal-Mart (five locations), Lowe’s (two locations), or a national or regional grocer, such as Publix (nine locations), Stop & Shop (three locations), Kroger (four locations) and Giant Foods (one location).

Diversified Base of Value-Oriented Retail Tenants

Our retail portfolio has a broad and highly diversified tenant base that primarily consists of grocers, drug stores, discount retailers and other retailers that provide basic household goods or services. As of December 31, 2011, our total retail tenant base included approximately 1,500 tenants with approximately 3,200 leases at our retail properties, and our largest shopping center tenants include Best Buy, TJX Companies, Stop & Shop, Bed Bath & Beyond, Home Depot, PetSmart, Ross Dress for Less, Kohl’s, Wal-Mart and Publix. As of December 31, 2011, no single retail tenant represented more than 3.3% of our retail annualized base rent, and our top 20 retail tenants, with 389 locations across our portfolio, represented an aggregate of 36.9% of our retail annualized base rent. We believe that maintaining a diversified tenant base with a value-oriented focus limits the impact of economic cycles and our exposure to any single tenant.

We generally have long-term leases with our tenants. As of December 31, 2011, the weighted average lease term of our existing retail leases, based on annualized base rent, was 6.1 years, with leases constituting less than 17.9% of our retail annualized base rent expiring before 2014. We believe the limited near-term expirations of

2

Table of Contents

our existing retail leases will allow us to more aggressively pursue leasing of space that is currently vacant and provide for more stable cash flows from operations.

Demonstrated Leasing and Property Management Platform

We believe that our national leasing platform overseen by our focused executive team dedicated to leasing provides us with a distinct competitive advantage. Our executive team applies a hands-on approach and capitalizes upon a network of relationships to aggressively lease-up vacant space, maintain high tenant retention rates and creatively address the needs of our retail properties. Since the beginning of 2009, we have demonstrated our leasing capabilities through our success in addressing a significant portion of the 3.2 million square feet of vacant space in our portfolio created by the bankruptcies of Mervyns, Linens ‘n Things and Circuit City in 2008. Primarily as a result of these vacancies, the percentage of our retail operating portfolio that was leased decreased from 96.8% as of December 31, 2007. However, as a result of our strong leasing platform, as of December 31, 2011, we have been able to lease approximately 2.3 million square feet of this vacant space, primarily to existing tenants, and in total we have leased, sold or are in negotiations for 2.7 million square feet, or 82.5%, of the 3.2 million square feet of GLA that was vacated as a result of these bankruptcies.

As a large, national owner of retail properties, we believe that we offer national and large regional grocers and retailers a greater level of service and credibility with respect to property management than our smaller competitors. We believe that tenants value our commitment to consistently maintain the high standards of our retail properties through our in-house handling of property management and day-to-day operational functions, which has translated into tenant retention rates of approximately 78%, based on expiring GLA, since the beginning of 2009.

Capital Structure Positioned for Growth

Upon completion of this offering, our aggregate indebtedness will consist primarily of fixed rate debt, which will have staggered maturities and a weighted average maturity of approximately years based on balances as of December 31, 2011, as adjusted for our recently amended and restated credit agreement and the completion of this offering and the application of proceeds from both. We also will have a conservative leverage structure with less than $ million of debt maturing in any one year, a weighted average interest rate of % per annum and $ million of availability under our $350.0 million senior unsecured revolving line of credit. Overall, we believe our capital structure will provide us with significant financial flexibility to fund future growth.

Experienced Management Team with a Proven Track Record

Our senior management team has on average over 22 years of real estate industry experience through several real estate, credit and retail cycles. They have proven themselves by successfully managing our large, geographically diverse portfolio through the severe economic recession that began in December 2007. Since the beginning of 2009, without accessing the public equity markets, we refinanced or repaid $3.0 billion of mortgage indebtedness, excluding indebtedness assumed through asset dispositions. This equates to the refinancing or repayment of greater than 63% of our total indebtedness at the beginning of 2009, which was accomplished in severely constrained credit markets, and in the process we reduced our total indebtedness by over $1.1 billion. Our senior management team also has significant transactional experience, having acquired, disposed of, contributed to joint ventures and developed billions of dollars of real estate throughout their careers. We believe that our senior management team’s property management, leasing and operating expertise, combined with their acquisition and financing experience, provide us with a distinct competitive advantage.

3

Table of Contents

Business and Growth Strategies

Our primary objective is to provide attractive risk-adjusted returns for our shareholders by executing on internal and external business and growth initiatives, which include:

Maximizing Net Operating Income (“NOI”) through Internal Growth

We believe that we will be able to generate same store NOI growth through the leasing of currently vacant space in our retail operating portfolio. As of December 31, 2011, our retail operating portfolio was 90.4% leased, including leases signed but not commenced, and had 3.3 million square feet of available space. The 843,000 square feet of GLA of signed leases that had not commenced as of December 31, 2011 represented approximately $9.9 million in contractually obligated annualized base rent, which we expect to begin realizing over the next 18 months. As of December 31, 2011, our remaining available space was comprised of 1.7 million square feet of available small shop space (under 10,000 square feet) and 1.6 million square feet of available anchor space (over 10,000 square feet), the re-leasing of which would increase our NOI. Additionally, as of December 31, 2011, 42.8% of the leases in our retail operating portfolio, based on annualized base rent, have remaining contractual rent increases, which is expected to increase our future NOI.

Preserving and Strengthening Our Portfolio through Active Property Management and Leasing

We actively manage our portfolio through 19 property management offices across the country, concentrating primarily on leasing opportunities, but also on redevelopment, expansion and remerchandising opportunities. We focus on increasing operating income and cash flows, active risk mitigation and tenant retention as well as other value enhancing strategies including cost reductions, long-term capital planning and asset sustainability initiatives. Examples of how we execute these strategies include Gurnee Town Center, where we completed a series of transactions designed to stabilize the asset following a period of disruption related to bankruptcy activity and downsizing requests by certain tenants, and Tollgate Marketplace, where we were able to anticipate that an existing grocery store tenant would not renew its lease due to the expected opening of a new Wal-Mart Supercenter in the area and re-lease the vacated space within nine months to Ashley Furniture for more than double the base rent per square foot that the grocer had been paying.

Recycling Capital through Dispositions of Non-Core and Non-Strategic Assets

We believe that one of our primary strengths is the effective and efficient operation of multi-tenant retail assets. Accordingly, we plan to pursue opportunistic dispositions of non-core assets, which include our non-retail properties and our free-standing triple net retail properties, as well as select multi-tenant retail properties that we view as non-strategic in nature. We view non-strategic assets as those assets that are in markets where we do not have a significant presence or where we do not anticipate building a significant presence over time, or assets in markets identified as strategic, but where management believes that long-term demographic trends within the individual asset’s submarket no longer justify continued investment. For example, in addition to our retail operating portfolio, as of December 31, 2011, we held interests in 12 office properties and three industrial properties, which had a total of 4.7 million square feet of GLA and represented 9.6% of our operating portfolio based on annualized based rent. From the end of 2007 through December 31, 2011, we have sold 31 non-core and non-strategic properties for an aggregate sales price of $857.8 million. We anticipate using the proceeds from future dispositions to further improve our balance sheet, reinvest in our existing asset base, and selectively acquire multi-tenant retail properties that meet our underwriting criteria.

Acquiring High Quality, Multi-Tenant Retail Properties

Although we anticipate remaining a net seller of assets for the next 12 months, we intend to pursue a disciplined and targeted acquisition program focusing on high quality, multi-tenant retail properties. In evaluating potential acquisitions, we will focus on, among other things, projected returns on investment, geographic location, submarket demographics, anchor tenant type and credit-worthiness, and other identified asset specific attributes. Management has an extensive relationship with tenants and public and private owners of real estate and intends to utilize this network to source attractive opportunities going forward.

4

Table of Contents

Pursuing Strategic Joint Ventures to Leverage Management Platform

We intend to leverage our leasing and property management platform through the formation, capitalization and management of joint ventures. In the past, we have partnered with strong institutional investors to supplement our capital base in a manner accretive to our shareholders. For example, in 2010, we formed a joint venture with a wholly-owned subsidiary of RioCan Real Estate Investment Trust, or RioCan, a real estate investment trust based in Canada. The RioCan joint venture has purchased nine properties from us since its formation for a total purchase price of $280.0 million, including $9.7 million in post-closing earnout proceeds, and also has purchased four multi-tenant retail properties from third parties for a combined purchase price of $246.0 million. We earn property management, asset management and other customary fees from the RioCan joint venture and a separate joint venture with a large state pension fund, which totaled $1.8 million and $1.3 million in 2011 and 2010, respectively. We remain active in evaluating opportunities to further grow and enhance our existing joint ventures and believe that we are well positioned to strategically pursue additional joint ventures with high quality capital partners going forward.

Our Properties

The following table sets forth summary information regarding our operating portfolio as of December 31, 2011. Dollars (other than per square foot information) and square feet of GLA are presented in thousands in the table. This information is grouped into geographic regions based on the manner in which we have structured our property management and leasing operations.

Property Type/Region | Number of Properties | GLA | Percent of Total GLA(1) | Percent Leased(2) | ABR(3) | Percent of ABR(1) | ABR Per Leased Sq. Ft.(4) | |||||||||||||||||||||

Consolidated: | ||||||||||||||||||||||||||||

Retail: | ||||||||||||||||||||||||||||

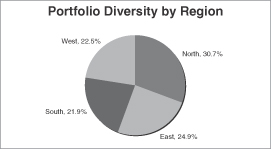

North | 83 | 10,626 | 30.7 | % | 90.5 | % | $ | 136,163 | 31.6 | % | $ | 14.16 | ||||||||||||||||

East | 68 | 8,628 | 24.9 | % | 90.5 | % | 101,404 | 23.6 | % | 12.98 | ||||||||||||||||||

West | 50 | 7,806 | 22.5 | % | 83.2 | % | 91,276 | 21.2 | % | 14.06 | ||||||||||||||||||

South | 58 | 7,589 | 21.9 | % | 86.4 | % | 101,572 | 23.6 | % | 15.50 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||

Total—Retail(5) | 259 | 34,649 | 100.0 | % | 87.9 | % | $ | 430,415 | 100.0 | % | $ | 14.13 | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||

Total—Retail including leases signed but not commenced(6) | 259 | 34,649 | 90.4 | % | $ | 440,353 | $ | 14.06 | ||||||||||||||||||||

Office | 12 | 3,335 | 96.5 | % | $ | 39,081 | $ | 12.15 | ||||||||||||||||||||

Industrial | 3 | 1,323 | 100.0 | % | 6,844 | 5.17 | ||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

Total—Office and Industrial | 15 | 4,658 | 97.5 | % | $ | 45,925 | $ | 10.12 | ||||||||||||||||||||

Total—Consolidated Operating Portfolio | 274 | 39,307 | 89.1 | % | $ | 476,340 | $ | 13.61 | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

Total—Unconsolidated Operating Portfolio(7) | 24 | 4,508 | 91.4 | % | $ | 63,874 | $ | 15.50 | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

| (1) | Percentages are only provided for our retail operating portfolio. |

| (2) | Except as otherwise noted, based on leases commenced as of December 31, 2011, and calculated as leased GLA divided by total GLA. |

| (3) | Excludes $1.4 million of annualized base rent from our consolidated development properties. Rental abatements for leases commenced as of December 31, 2011, which are excluded, were $0.1 million for our retail operating portfolio for the 12 months ending December 31, 2012. Annualized base rent does not reflect scheduled lease expirations for the 12 months ending December 31, 2012. The portion of the annualized base rent of our consolidated operating portfolio attributable to leases scheduled to expire during the 12 months ending December 31, 2012, including month-to-month leases, is approximately $33.6 million. |

5

Table of Contents

| (4) | Represents annualized base rent divided by leased GLA. |

| (5) | Includes (i) 55 properties with 6.5 million square feet of GLA representing $84.1 million of annualized base rent held in one joint venture in which we have a 77% interest. Regarding the 55 properties held in the joint venture in which we have a 77% interest, we currently anticipate using a portion of the net proceeds from this offering to exercise our option to repurchase the 23% interest held by others. As a result, following this offering we anticipate that we will own 100% of those properties. Excludes one non-stabilized operating property. |

| (6) | Includes leases signed but not commenced as of December 31, 2011 for approximately 843,000 square feet of GLA representing $9.9 million of annualized base rent as of lease commencement. |

| (7) | Includes 20 properties with 4.3 million square feet of GLA representing $62.5 million of annualized base rent held in two separate joint ventures in which we have a 20% interest and four properties with 0.2 million square feet of GLA representing $1.4 million of annualized base rent held in one joint venture in which we have a 95.9% interest. |

Industry Overview

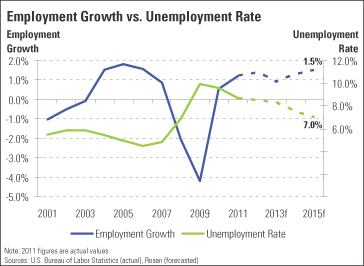

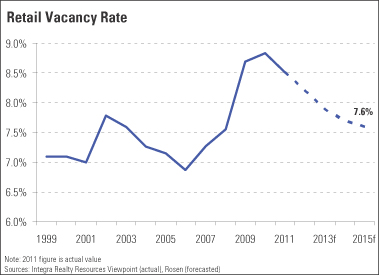

Rosen believes that positive job growth combined with higher consumer confidence will continue to improve retail market conditions in 2012. Rosen forecasts that this growth in employment and consumer confidence is expected to boost retail demand, leading to increased retail sales. As demand increases, retailers are expected to absorb new space, and landlords should be able to increase rents at an accelerating pace because of the limited new supply entering the market. Rosen forecasts these factors to cause the national retail occupancy rate to continue to improve through 2015.

Since bottoming in February 2010, the economy has added more than 3.4 million jobs in the private sector through December 31, 2011. According to a January 2012 survey by Challenger Gray & Christmas, the number of hirings anticipated by surveyed firms totaled approximately 237,000 in the fourth quarter of 2011, up from about 161,000 anticipated hirings when surveyed one year earlier, highlighting businesses’ higher confidence in the economic recovery. Rosen expects the annual rate of job creation to increase to 1.4% in 2012, followed by 0.9%, 1.3% and 1.5% growth in 2013, 2014 and 2015, respectively. In total, Rosen expects 6.85 million new jobs to be created between 2012 and 2015. Accordingly, the unemployment rate is forecasted to decline from 8.7% in 2011 to 7.0% in 2015.

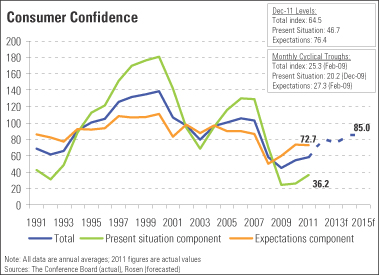

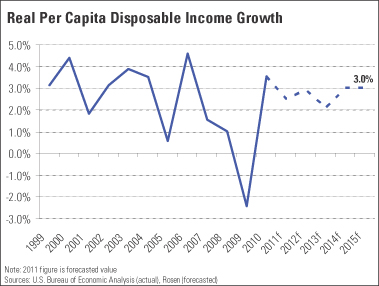

Consumer confidence levels have increased from recessionary lows, even as uncertainty stemming from the European debt crisis and U.S. credit downgrade prevented the indices from improving more significantly in 2011. Consumers at year-end 2011 were much more positive regarding future economic conditions than about their current situations, as evidenced by the consumer confidence index measured by The Conference Board. The consumer expectation component of the index has increased significantly from its low of 27.3 in February 2009 to 76.4 in December 2011. Further, Rosen expects real per capita disposable income, a key metric for the retail industry, to grow by 2.8% annually between 2012 and 2015, compared with an estimated 3.0% average annual increase in 2010 and 2011.

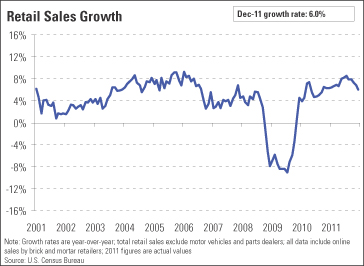

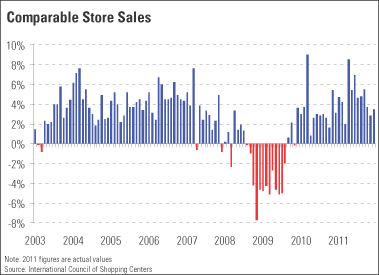

Retail sales continued to recover in 2011, increasing at an average annual rate of 7.3% per month, bolstered by a strong 2011 holiday season. Although sales growth is unlikely to return to peak rates, Rosen believes that annual retail sales growth (including online sales made by brick and mortar retailers) will average 2.8% during the next four years, bringing total fourth-quarter sales in 2015 to more than $1.1 trillion, an increase of more than $115 billion from the fourth quarter of 2011. Moreover, Rosen believes that the recession caused a lasting shift in consumer behavior, providing a boost to value-oriented grocers, discount retailers and other retailers that provide basic household goods and/or clothing. Therefore, Rosen expects sales at these grocers and retailers to remain strong going forward.

6

Table of Contents

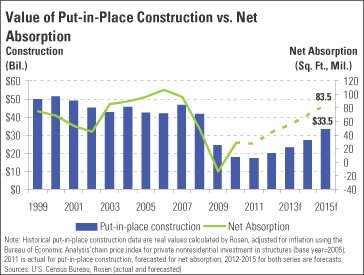

Even as the economy recovered, retail construction activity, as measured by the value of construction put-in-place, remained very low in 2011 because of the high vacancy rate and a lack of available construction financing. In the fourth quarter of 2011, the value of put-in-place construction totaled a seasonally adjusted annual rate of $17.5 billion, compared with fourth-quarter averages of $42.2 billion between 2002 and 2008. As demand rebounds, tenant competition for existing space is expected to increase due to the limited new supply entering the market. Rosen forecasts the value of inflation-adjusted, put-in-place construction to increase slightly to $20.0 billion in 2012, and continue to remain well below the recent peak of $46.8 billion in 2007.

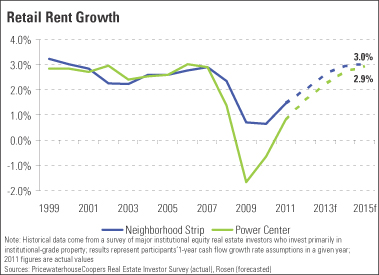

As job growth and higher consumer confidence levels boost demand, Rosen expects retail market conditions to continue to improve in 2012. Rosen forecasts the national retail vacancy rate to continue to improve through 2015, and as vacant space is absorbed, landlords should be able to increase rents at an accelerating pace.

Summary Risk Factors

An investment in shares of our Class A Common Stock involves various risks. You should consider carefully the risks discussed below and under the heading “Risk Factors” beginning on page 16 of this prospectus before purchasing our Class A Common Stock. If any of these risks occur, our business, prospects, financial condition, liquidity, results of operations and ability to make distributions to our shareholders could be materially and adversely affected. In that case, the trading price of our Class A Common Stock could decline and you could lose some or all of your investment.

| • | Real estate investments are subject to various risks and fluctuations and cycles in value and demand, many of which are beyond our control. Our financial performance and the value of our properties can be affected by many of these factors, including, among others, the following: |

| • | adverse changes in financial conditions of buyers, sellers and tenants of our properties, including bankruptcies, financial difficulties, or lease defaults by our tenants; |

| • | the national, regional and local economy, which may be negatively impacted by concerns about inflation, deflation and government deficits, including the European sovereign debt crisis, high unemployment rates, decreased consumer confidence, industry slowdowns, reduced corporate profits, liquidity concerns in our markets and other adverse business concerns; |

| • | local real estate conditions, such as an oversupply of, or a reduction in demand for, retail space or retail goods, and the availability and creditworthiness of current and prospective tenants; |

| • | vacancies or ability to rent space on favorable terms, including possible market pressures to offer tenants rent abatements, tenant improvements, early termination rights or below-market renewal options; |

| • | changes in operating costs and expenses, including, without limitation, increasing labor and material costs, insurance costs, energy prices, environmental restrictions, real estate taxes, and costs of compliance with laws, regulations and government policies, which we may be restricted from passing on to our tenants; |

| • | fluctuations in interest rates, which could adversely affect our ability, or the ability of buyers and tenants of properties, to obtain financing on favorable terms or at all; and |

| • | competition from other real estate investors with significant capital, including other real estate operating companies, publicly traded REITs and institutional investment funds. |

| • | We may be unable to complete acquisitions and even if acquisitions are completed, we may fail to successfully operate acquired properties. |

7

Table of Contents

| • | We may be unable to sell a property at the time we desire and on favorable terms or at all, which could inhibit our ability to utilize our capital to make strategic acquisitions and could adversely affect our results of operations, financial condition and ability to make distributions to our shareholders. |

| • | We have experienced aggregate net losses attributable to Company shareholders for the years ended December 31, 2011, 2010 and 2009, and we may experience future losses. |

| • | Our development and construction activities have inherent risks, which could adversely impact our results of operations and cash flow. |

| • | We had approximately $3.5 billion of consolidated indebtedness outstanding as of December 31, 2011, which could adversely affect our financial health and operating flexibility. |

| • | We have a high concentration of properties in the Dallas-Fort Worth-Arlington area, and adverse economic and other developments in that area could have a material adverse effect on us. |

| • | Our financial condition and ability to make distributions to our shareholders could be adversely affected by financial and other covenants and other provisions under the credit agreement governing our senior unsecured revolving line of credit and unsecured term loan or other debt agreements. |

| • | We depend on external sources of capital that are outside of our control, which may affect our ability to seize strategic opportunities, satisfy our debt obligations and make distributions to our shareholders. |

| • | Certain provisions of Maryland law could inhibit changes in control of us, which could lower the value of our Class A Common Stock. |

| • | Failure to qualify as a REIT would cause us to be taxed as a regular corporation, which would substantially reduce funds available for distributions to our shareholders and materially and adversely affect our financial condition and results of operations. |

| • | Complying with REIT requirements may cause us to forego otherwise attractive opportunities or to liquidate otherwise attractive investments. |

| • | Because we have a large number of shareholders and our shares have not been listed on a national securities exchange prior to this offering, there may be significant pent-up demand to sell our shares. Significant sales of our Class A Common Stock, or the perception that significant sales of such shares could occur, may cause the price of our Class A Common Stock to decline significantly. |

Recapitalization

Prior to the completion of this offering, we intend to declare a stock dividend pursuant to which each then outstanding share of our common stock will receive:

| • | one share of our Class B-1 Common Stock; plus |

| • | one share of our Class B-2 Common Stock; plus |

| • | one share of our Class B-3 Common Stock. |

In connection with this stock dividend, we intend to redesignate our then outstanding common stock as “Class A Common Stock.” Prior to the declaration of the stock dividend, we intend to effectuate a ten to one reverse stock split of our common stock.

Subject to the provisions of our charter, shares of our Class B-1, B-2 and B-3 Common Stock will convert automatically into shares of our Class A Common Stock six months following the Listing, 12 months following the Listing and 18 months following the Listing, respectively. In addition, if they have not otherwise converted, all shares of our Class B Common Stock will convert automatically into shares of our Class A Common Stock on the date that is 18 months following the Listing.

8

Table of Contents

Our Class B Common Stock will be identical to our Class A Common Stock except that (i) we do not intend to list our Class B Common Stock on a national securities exchange and (ii) shares of our Class B Common Stock will convert automatically into shares of our Class A Common Stock at specified times. As of March 2, 2012, without giving effect to the Recapitalization, we had approximately 485.5 million shares of common stock outstanding. As of March 2, 2012, the aggregate number of shares of our common stock outstanding (including all shares of our Class A and Class B Common Stock) immediately following the Recapitalization will be approximately 194.2 million, all of which (except for certain shares described in “Shares Eligible for Future Sale”) will be freely tradable upon the completion of this offering except as otherwise provided in the restrictions on ownership and transfer of stock set forth in our charter. Of this amount, approximately 48.55 million shares of our Class A Common Stock will be outstanding and approximately 145.65 million shares of our Class B Common Stock, representing 75% of our total outstanding common stock, will be outstanding.

Distribution Policy

The Internal Revenue Code of 1986, as amended, or the Code, generally requires that a REIT distribute annually at least 90% of its REIT taxable income, determined without regard to the deduction for dividends paid and excluding net capital gains, and imposes tax on any taxable income retained by a REIT, including capital gains. To satisfy the requirements for qualification as a REIT and generally not be subject to U.S. federal income and excise tax, we intend to make regular quarterly distributions of all or substantially all of our REIT taxable income to holders of our common stock out of assets legally available for such purposes. Our future distributions will be at the sole discretion of our board of directors.

Our senior unsecured revolving line of credit and unsecured term loan limit our distributions to the greater of 95% of funds from operations, or FFO, as defined in the credit agreement (which equals FFO, as set forth in “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Funds from Operations,” excluding gains or losses from extraordinary items, impairment charges not already excluded from FFO and other non-cash charges) or the amount necessary for us to maintain our qualification as a REIT. To the extent these limits prevent us from distributing 100% of our REIT taxable income, we will be subject to income tax, and potentially excise tax, on the retained amounts. If our operations do not generate sufficient cash flow to allow us to satisfy the REIT distribution requirements, we may be required to fund distributions from working capital, borrow funds, sell assets or reduce such distributions. Our distribution policy enables us to review the alternative funding sources available to us from time to time.

Our REIT Status

We have elected to be taxed as a REIT under Sections 856 through 860 of the Code. We believe that we have been organized, owned and operated in conformity with the requirements for qualification and taxation as a REIT under the Code beginning with our taxable year ended December 31, 2003, and that our intended manner of ownership and operation will enable us to continue to meet the requirements for qualification and taxation as a REIT for federal income tax purposes. To maintain our qualification as a REIT, we must meet a number of organizational and operational requirements, including a requirement that we annually distribute at least 90% of our REIT taxable income to our shareholders, determined without regard to the deduction for dividends paid and excluding net capital gains. As a REIT, we generally are not subject to U.S. federal income tax on the taxable income we currently distribute to our shareholders. If we fail to qualify as a REIT in any taxable year, we will be subject to U.S. federal income tax at regular corporate rates. Even if we qualify for taxation as a REIT, we may be subject to some U.S. federal, state and local taxes on our income or property, and the taxable income of our taxable REIT subsidiaries, or TRSs, will be subject to taxation at regular corporate rates.

Restrictions on Ownership of Our Common Stock

To assist us in complying with the limitations on the concentration of ownership of a REIT imposed by the Code, among other purposes, our charter generally prohibits, with certain exceptions, any shareholder from

9

Table of Contents

beneficially or constructively owning, applying certain attribution rules under the Code, more than 9.8% by value or number of shares, whichever is more restrictive, of the outstanding shares of our common stock, or 9.8% by value of the outstanding shares of our capital stock. Our board of directors may, in its sole discretion, waive (prospectively or retroactively) the 9.8% ownership limits with respect to a particular shareholder if it receives certain representations and undertakings required by our charter and is presented with evidence satisfactory to it that such ownership will not then or in the future cause us to fail to qualify as a REIT. See “Description of Capital Stock—Restrictions on Ownership and Transfer.”

Certain Relationships and Related Transactions

The Inland Group and its affiliates were our initial sponsor, and Daniel L. Goodwin, who has not been one of our directors but beneficially owns approximately 5.0% of our common stock prior to this offering, Brenda G. Gujral, one of our current directors, and Robert D. Parks, one of our former directors, are significant shareholders and/or principals of the Inland Group and/or hold directorships and are executive officers of affiliates of the Inland Group.

We have ongoing agreements with affiliates of the Inland Group, including an office sublease for our corporate headquarters and various service agreements. With the exception of the sublease, the majority of these service agreements are non-exclusive and cancellable by providing not less than 180 days prior written notice and specifying the effective date of said termination. These service agreements are generally for administrative services. We primarily use these service agreements in situations where it is more efficient for us to obtain services from an outside party than it would be for us to obtain the dedicated internal resources necessary to provide similar quality services. During the year ended December 31, 2011, we paid a total of $5.9 million to Inland Group affiliates under these arrangements, of which $4.1 million was generally for the reimbursement of our portion of shared administrative costs and $1.0 million was for amounts payable pursuant to our office sublease.

In addition, in 2009, in connection with a $625 million debt refinancing transaction, we raised additional capital of $50 million from an affiliate of the Inland Group in exchange for a 23% noncontrolling interest in a newly formed joint venture to which we contributed 55 of our properties. We currently anticipate using a portion of the net proceeds from this offering to exercise our option to repurchase this noncontrolling interest for , as a result of which we would again own 100% of these properties. In 2009, we also sold three single-user office buildings to Inland American Real Estate Trust, Inc., or IARETI, with an aggregate sales price of $161.6 million, which resulted in net sales proceeds of $52.6 million and a gain on sale of $9.3 million. IARETI is externally managed by an affiliate of the Inland Group.

All related person transactions must be approved or ratified by a majority of the disinterested directors on our board of directors, and we continue to monitor our ongoing agreements with affiliates of the Inland Group to ensure that it is in the best interests of our shareholders to maintain these agreements. See “Certain Relationships and Related Transactions.”

Background and Corporate Information

We are a Maryland corporation formed in March 2003, and we have been publicly held and subject to Securities and Exchange Commission, or SEC, reporting obligations since the completion of our first public offering in 2003. We were initially formed as Inland Western Retail Real Estate Trust, Inc. and were sponsored by The Inland Group, Inc. and its affiliates, but we have not been affiliated with The Inland Group, Inc. since the internalization of our management in November 2007. On March 8, 2012, we filed Articles of Amendment to our Fifth Articles of Amendment and Restatement with the Maryland State Department of Assessments and Taxation effecting a change of our name from Inland Western Retail Real Estate Trust, Inc. to Retail Properties of America, Inc. Our principal executive office is located at 2901 Butterfield Road, Oak Brook, Illinois 60523, and our telephone number is (630) 218-8000. We maintain an internet website at www.inland-western.com that contains information concerning us. The information included or referenced to on, or otherwise accessible through, our website is not intended to form a part of or be incorporated by reference into this prospectus.

10

Table of Contents

The Offering

Class A Common Stock offered by us | shares (plus up to shares that we may issue if the underwriters exercise their overallotment option in full) |

Common stock to be outstanding after this offering:

Class A Common Stock | shares(1) |

Class B-1 Common Stock | 48,549,461 shares(2) |

Class B-2 Common Stock | 48,549,461 shares(2) |

Class B-3 Common Stock | 48,549,461 shares(2) |

Conversion rights | Subject to the provisions of our charter, shares of our Class B-1, B-2 and B-3 Common Stock will convert automatically into shares of our Class A Common Stock six months following the Listing, 12 months following the Listing and 18 months following the Listing, respectively. |

Dividend rights | Our Class A Common Stock and our Class B Common Stock will share equally in any distributions authorized by our board of directors and declared by us. |

Voting rights | Each share of our Class A Common Stock and each share of our Class B Common Stock will entitle its holder to one vote per share. |

Use of proceeds | We intend to use approximately $ million of net proceeds received from this offering to repay amounts outstanding under our senior unsecured revolving line of credit, $ million of net proceeds to repurchase Inland Equity Investors, LLC’s, or Inland Equity’s, interest in IW JV 2009, LLC, or IW JV, and the remaining net proceeds for general corporate and working capital purposes. |

Proposed NYSE symbol | We have applied to have our Class A Common Stock listed on the NYSE under the symbol “RPAI”. |

| (1) | Excludes shares of Class A Common Stock issuable upon exercise of the underwriters’ overallotment option, 1,016,597 shares of Class A Common Stock available for future issuance under our incentive award plans and 17,350 shares of Class A Common Stock underlying options granted under our incentive award plans as of March 2, 2012. |

| (2) | Excludes 3,049,790 shares of Class B-1, B-2, and B-3 Common Stock available for future issuance under our incentive award plans and 52,050 shares of Class B-1, B-2 and B-3 Common Stock underlying options granted under our incentive awards plans as of March 2, 2012. |

11

Table of Contents

Summary Consolidated Financial and Operating Data

The summary consolidated financial data set forth below as of December 31, 2011 and 2010 and for the years ended December 31, 2011, 2010 and 2009 have been derived from our audited consolidated financial statements included elsewhere in this prospectus. The audited consolidated financial statements as of December 31, 2011 and 2010 and for the years ended December 31, 2011, 2010 and 2009 have been audited by Deloitte & Touche LLP, an independent registered public accounting firm. The selected consolidated financial and operating data set forth below as of December 31, 2009 has been derived from our audited consolidated financial statements not included in this prospectus. Certain amounts presented for the years ended December 31, 2010 and 2009 have been reclassified to conform to our presentation of discontinued operations in our audited consolidated financial statements as of and for the year ended December 31, 2011.

Because the information presented below is only a summary and does not provide all of the information contained in our historical consolidated financial statements, including the related notes, you should read it in conjunction with “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our historical consolidated financial statements, including the related notes, included elsewhere in this prospectus. The amounts in the table are dollars in thousands except for share and per share information. The share and per share information set forth below gives effect to the Recapitalization.

12

Table of Contents

| Year Ended December 31, | ||||||||||||

| 2011 | 2010 | 2009 | ||||||||||

(in thousands except for per share data) | ||||||||||||

Statements of Operations Data: | ||||||||||||

Rental income | $ | 485,783 | $ | 500,636 | $ | 508,012 | ||||||

Tenant recovery income | 109,745 | 113,326 | 119,805 | |||||||||

Other property income | 10,155 | 15,471 | 18,520 | |||||||||

Insurance captive income | — | 2,996 | 2,261 | |||||||||

|

|

|

|

|

| |||||||

Total revenues | 605,683 | 632,429 | 648,598 | |||||||||

|

|

|

|

|

| |||||||

Property operating expenses | $ | 102,373 | $ | 104,413 | $ | 120,370 | ||||||

Real estate taxes | 79,543 | 84,330 | 91,844 | |||||||||

Depreciation and amortization | 235,598 | 240,720 | 243,571 | |||||||||

Provision for impairment of investment properties | 38,023 | 11,030 | 27,600 | |||||||||

Loss on lease terminations | 8,712 | 13,812 | 13,681 | |||||||||

Insurance captive expenses | — | 3,392 | 3,655 | |||||||||

General and administrative expenses | 20,605 | 18,119 | 21,191 | |||||||||

|

|

|

|

|

| |||||||

Total expenses | 484,854 | 475,816 | 521,912 | |||||||||

|

|

|

|

|

| |||||||

Operating income | $ | 120,829 | $ | 156,613 | $ | 126,686 | ||||||

Dividend income | 2,538 | 3,472 | 10,132 | |||||||||

Interest income | 663 | 740 | 1,483 | |||||||||

Gain on extinguishment of debt, net | 16,705 | — | — | |||||||||

Equity in (loss) income of unconsolidated joint ventures, net | (6,437 | ) | 2,025 | (11,299 | ) | |||||||

Interest expense | (232,400 | ) | (257,208 | ) | (228,271 | ) | ||||||

Co-venture obligation expense | (7,167 | ) | (7,167 | ) | (597 | ) | ||||||

Recognized gain on marketable securities, net | 277 | 4,007 | 18,039 | |||||||||

Impairment of notes receivable | — | — | (17,322 | ) | ||||||||

Gain on interest rate locks | — | — | 3,989 | |||||||||

Other income (expense), net | 1,861 | (4,302 | ) | (10,370 | ) | |||||||

|

|

|

|

|

| |||||||

Loss from continuing operations | (103,131 | ) | (101,820 | ) | (107,530 | ) | ||||||

Income (loss) from discontinued operations | 24,647 | 7,113 | (7,879 | ) | ||||||||

Gain on sales of investment properties | 5,906 | — | — | |||||||||

|

|

|

|

|

| |||||||

Net loss | (72,578 | ) | (94,707 | ) | (115,409 | ) | ||||||

Net (income) loss attributable to noncontrolling interests | (31 | ) | (1,136 | ) | 3,074 | |||||||

|

|

|

|

|

| |||||||

Net loss attributable to Company shareholders | $ | (72,609 | ) | $ | (95,843 | ) | $ | (112,335 | ) | |||

|

|

|

|

|

| |||||||

(Loss) earnings per common share—basic and diluted: | ||||||||||||

Continuing operations | $ | (0.51 | ) | $ | (0.53 | ) | $ | (0.54 | ) | |||

Discontinued operations | 0.13 | 0.03 | (0.04 | ) | ||||||||

|

|

|

|

|

| |||||||

Net loss per common share attributable to Company shareholders | $ | (0.38 | ) | $ | (0.50 | ) | $ | (0.58 | ) | |||

|

|

|

|

|

| |||||||

Comprehensive loss | $ | (75,130 | ) | $ | (83,725 | ) | $ | (96,158 | ) | |||

Comprehensive (income) loss attributable to noncontrolling interests | (31 | ) | (1,136 | ) | 3,074 | |||||||

|

|

|

|

|

| |||||||

Comprehensive loss attributable to Company shareholders | $ | (75,161 | ) | $ | (84,861 | ) | $ | (93,084 | ) | |||

|

|

|

|

|

| |||||||

13

Table of Contents

| December 31, 2011 | December 31, | |||||||||||||

| As Adjusted(1) | Actual | 2010 | 2009 | |||||||||||

| (in thousands except for share and per share data) | ||||||||||||||

Selected Balance Sheet Data: | ||||||||||||||

Net investment properties less accumulated depreciation | $ | 5,260,788 | $ | 5,686,473 | $ | 6,103,782 | ||||||||

Total assets | $ | 5,941,894 | $ | 6,386,836 | $ | 6,928,365 | ||||||||

Mortgages and notes payable | $ | 2,926,218 | $ | 3,602,890 | $ | 4,003,985 | ||||||||

Total liabilities | $ | 3,804,851 | $ | 4,090,244 | $ | 4,482,119 | ||||||||

Common stock and additional paid-in-capital | $ | 4,428,171 | $ | 4,383,758 | $ | 4,350,966 | ||||||||

Total shareholders’ equity | $ | 2,135,024 | $ | 2,294,902 | $ | 2,441,550 | ||||||||

Ratio Data: | ||||||||||||||

Total net debt to Adjusted EBITDA(2)(6) | 8.3x | 8.4x | 9.1x | |||||||||||

Combined net debt to combined Adjusted EBITDA(2)(6) |

| 8.3x |

| 8.5x | 8.9x | |||||||||

| Year Ended December 31, | ||||||||||||

| 2011 | 2010 | 2009 | ||||||||||

(in thousands except for number of | ||||||||||||

Other Data: | ||||||||||||

Number of consolidated operating properties | 274 | (3) | 284 | 299 | ||||||||

Total GLA (in thousands) | 39,307 | 42,491 | 44,496 | |||||||||

Distributions declared per common share | $ | 0.63 | $ | 0.49 | $ | 0.39 | ||||||

Funds from operations(4) | $ | 195,105 | $ | 168,390 | $ | 216,567 | ||||||

Total net operating income(5) | $ | 425,499 | $ | 435,785 | $ | 431,420 | ||||||

Combined net operating income(5) | $ | 435,060 | $ | 441,274 | $ | 435,206 | ||||||

Adjusted EBITDA(6) | $ | 400,646 | $ | 429,734 | $ | 438,891 | ||||||

Combined Adjusted EBITDA(6) | $ | 415,614 | $ | 436,164 | $ | 456,578 | ||||||

Cash flows provided by (used in): | ||||||||||||

Operating activities | $ | 174,607 | $ | 184,072 | $ | 249,837 | ||||||

Investing activities | $ | 107,471 | $ | 154,400 | $ | 193,706 | ||||||

Financing activities | $ | (276,282 | ) | $ | (321,747 | ) | $ | (438,806 | ) | |||

| (1) | Presents historical information as of December 31, 2011 as adjusted to give effect to (i) the amendment and restatement of our existing credit agreement to provide for a senior unsecured credit facility in the aggregate amount of $650.0 million, without adjusting the December 31, 2011 balance of the senior unsecured credit facility, and (ii) this offering and the use of the net proceeds from this offering as set forth in “Use of Proceeds.” |

| (2) | Total net debt to Adjusted EBITDA represents (i) our total debt less cash and cash equivalents divided by (ii) Adjusted EBITDA for the prior 12 months. Combined net debt to combined Adjusted EBITDA represents (i) the sum of (A) our total debt less cash and cash equivalents plus (B) our pro rata share of our investment property unconsolidated joint ventures’ total debt less our pro rata share of these joint ventures’ cash and cash equivalents divided by (ii) combined Adjusted EBITDA for the prior 12 months. For a reconciliation of total net debt to Adjusted EBITDA and combined net debt to combined Adjusted EBITDA and a statement disclosing the reasons why our management believes that presentation of these ratios provides useful information to investors and, to the extent material, any additional purposes for which our management uses these ratios, see “Selected Consolidated Financial Operating Data.” |

| (3) | Excludes one non-stabilized operating property. |

14

Table of Contents

| (4) | For a definition and reconciliation of FFO and a statement disclosing the reasons why our management believes that presentation of FFO provides useful information to investors and, to the extent material, any additional purposes for which our management uses FFO, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Funds from Operations.” |

| (5) | Total NOI represents operating revenues (rental income, tenant recovery income, other property income, excluding straight-line rental income and amortization of acquired above and below market lease intangibles) less property operating expenses (real estate tax expense and property operating expense, excluding straight-line ground rent expense and straight-line bad debt expense). Combined NOI, represents NOI plus our pro rata share of NOI from our investment property unconsolidated joint ventures. For a reconciliation of total net operating income, or NOI, and a statement disclosing the reasons why our management believes that presentation of NOI provides useful information to investors and, to the extent material, any additional purposes for which our management uses NOI, which is also applicable to combined NOI, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Results of Operations.” For a reconciliation of combined NOI, see “Selected Consolidated Financial Operating Data.” |

| (6) | Adjusted EBITDA represents net income (loss) before interest, income taxes, depreciation and amortization, as further adjusted to eliminate the impact of certain items that we do not consider indicative of our ongoing operating performance. Combined Adjusted EBITDA represents Adjusted EBITDA plus our pro rata share of the EBITDA adjustments from our investment property unconsolidated joint ventures. For a reconciliation of Adjusted EBITDA and combined Adjusted EBITDA and a statement disclosing the reasons why our management believes that presentation of Adjusted EBITDA and combined Adjusted EBITDA provides useful information to investors and, to the extent material, any additional purposes for which our management uses Adjusted EBITDA and combined Adjusted EBITDA, see “Selected Consolidated Financial Operating Data.” |

15

Table of Contents

An investment in our Class A Common Stock involves a high degree of risk. Before making an investment decision, you should carefully consider the following risk factors, which address the material risks concerning our business and an investment in our Class A Common Stock, together with the other information contained in this prospectus. If any of the risks discussed in this prospectus occur, our business, prospects, financial condition, results of operations and our ability to make distributions to our shareholders could be materially and adversely affected. In that case, the trading price of our Class A Common Stock could decline significantly and you could lose all or a part of your investment. Some statements in this prospectus, including statements in the following risk factors constitute forward-looking statements. Please refer to the section entitled “Forward-Looking Statements.”

RISKS RELATING TO OUR BUSINESS AND OUR PROPERTIES

There are inherent risks associated with real estate investments and with the real estate industry, each of which could have an adverse impact on our financial performance and the value of our retail properties.

Real estate investments are subject to various risks and fluctuations and cycles in value and demand, many of which are beyond our control. Our financial performance and the value of our properties can be affected by many of these factors, including the following:

| • | adverse changes in financial conditions of buyers, sellers and tenants of our properties, including bankruptcies, financial difficulties, or lease defaults by our tenants; |

| • | the national, regional and local economy, which may be negatively impacted by concerns about inflation, deflation and government deficits (including the European sovereign debt crisis), high unemployment rates, decreased consumer confidence, industry slowdowns, reduced corporate profits, liquidity concerns in our markets and other adverse business concerns; |

| • | local real estate conditions, such as an oversupply of, or a reduction in demand for, retail space or retail goods, and the availability and creditworthiness of current and prospective tenants; |

| • | vacancies or ability to rent space on favorable terms, including possible market pressures to offer tenants rent abatements, tenant improvements, early termination rights or below-market renewal options; |

| • | changes in operating costs and expenses, including, without limitation, increasing labor and material costs, insurance costs, energy prices, environmental restrictions, real estate taxes, and costs of compliance with laws, regulations and government policies, which we may be restricted from passing on to our tenants; |

| • | fluctuations in interest rates, which could adversely affect our ability, or the ability of buyers and tenants of properties, to obtain financing on favorable terms or at all; |

| • | competition from other real estate investors with significant capital, including other real estate operating companies, publicly traded REITs and institutional investment funds; |

| • | the convenience and quality of competing retail properties and other retailing options such as the Internet; |

| • | perceptions by retailers or shoppers of the safety, convenience and attractiveness of the retail property; |

| • | inability to collect rent from tenants; |

| • | our ability to secure adequate insurance; |

| • | our ability to provide adequate management services and to maintain our properties; |

16

Table of Contents

| • | changes in, and changes in enforcement of, laws, regulations and governmental policies, including, without limitation, health, safety, environmental, zoning and tax laws, government fiscal policies and the Americans with Disabilities Act of 1990, or the ADA; and |

| • | civil unrest, acts of war, terrorist attacks and natural disasters, including earthquakes and floods, which may result in uninsured and underinsured losses. |

In addition, because the yields available from equity investments in real estate depend in large part on the amount of rental income earned, as well as property operating expenses and other costs incurred, a period of economic slowdown or recession, declining demand for real estate, or the public perception that any of these events may occur, could result in a general decline in rents or an increased incidence of defaults among our existing leases, and, consequently, our properties, including those held by joint ventures, may fail to generate revenues sufficient to meet operating, debt service and other expenses. As a result, we may have to borrow amounts to cover fixed costs, and our financial condition, results of operations, cash flow, per share trading price of our Class A Common Stock and our ability to satisfy our principal and interest obligations and to make distributions to our shareholders may be adversely affected.

Continued economic weakness from the severe economic recession that the U.S. economy recently experienced may materially and adversely affect our financial condition and results of operations.