UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-Q

x Quarterly Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the quarterly period ended March 31, 2013.

o Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the Transition Period From ______________________ to _________________________

Commission file number 001-32265 (American Campus Communities, Inc.)

Commission file number 333-181102-01 (American Campus Communities Operating Partnership, L.P.)

AMERICAN CAMPUS COMMUNITIES, INC.

AMERICAN CAMPUS COMMUNITIES OPERATING PARTNERSHIP, L.P.

(Exact name of registrant as specified in its charter)

Maryland (American Campus Communities, Inc.) Maryland (American Campus Communities Operating Partnership, L.P.) | 76-0753089 (American Campus Communities, Inc.) 56-2473181 (American Campus Communities Operating Partnership, L.P.) | |

(State or Other Jurisdiction of Incorporation or Organization) | (IRS Employer Identification No.) | |

12700 Hill Country Blvd., Suite T-200 Austin, TX (Address of Principal Executive Offices) | 78738 (Zip Code) |

(512) 732-1000

Registrant’s telephone number, including area code

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15 (d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

| American Campus Communities, Inc. | Yes x No o | |

| American Campus Communities Operating Partnership, L.P. | Yes x No o |

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

| American Campus Communities, Inc. | Yes x No o | |

| American Campus Communities Operating Partnership, L.P. | Yes x No o |

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

American Campus Communities, Inc.

| Large accelerated filer x | Accelerated Filer o | |

| Non-accelerated filer o (Do not check if a smaller reporting company) | Smaller reporting company o |

American Campus Communities Operating Partnership, L.P.

| Large accelerated filer o | Accelerated Filer o | |

| Non-accelerated filer x (Do not check if a smaller reporting company) | Smaller reporting company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act)

| American Campus Communities, Inc. | Yes o No x | |

| American Campus Communities Operating Partnership, L.P. | Yes o No x |

There were 104,776,745 shares of the American Campus Communities, Inc.’s common stock with a par value of $0.01 per share outstanding as of the close of business on May 3, 2013.

EXPLANATORY NOTE

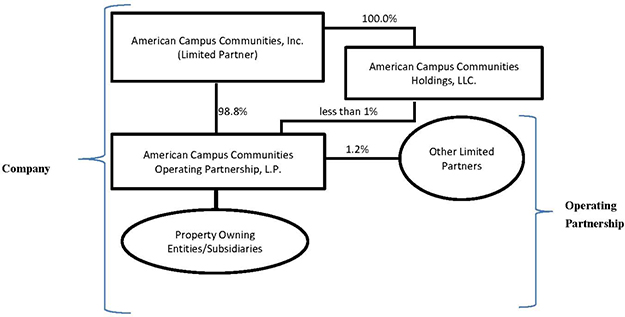

This report combines the reports on Form 10-Q for the quarterly period ended March 31, 2013 of American Campus Communities, Inc. and American Campus Communities Operating Partnership, L.P.. Unless stated otherwise or the context otherwise requires, references to “ACC” mean American Campus Communities, Inc. a Maryland real estate investment trust (“REIT”), and references to “ACCOP” mean American Campus Communities Operating Partnership, L.P., a Maryland limited partnership. References to the “Company,” “we,” “us” or “our” mean collectively ACC, ACCOP and those entities/subsidiaries owned or controlled by ACC and/or ACCOP. References to the “Operating Partnership” mean collectively ACCOP and those entities/subsidiaries owned or controlled by ACCOP. The following chart illustrates the Company’s and the Operating Partnership’s corporate structure:

The general partner of ACCOP is American Campus Communities Holdings, LLC (“ACC Holdings”), an entity that is wholly-owned by ACC. As of March 31, 2013, ACC Holdings held an ownership interest in ACCOP of less than 1%. The limited partners of ACCOP are ACC and other limited partners consisting of current and former members of management and nonaffiliated third parties. As of March 31, 2013, ACC owned an approximate 98.8% limited partnership interest in ACCOP. As the sole member of the general partner of ACCOP, ACC has exclusive control of ACCOP’s day-to-day management. Management operates the Company and the Operating Partnership as one business. The management of ACC consists of the same members as the management of ACCOP. The Company is structured as an umbrella partnership REIT (“UPREIT”) and ACC contributes all net proceeds from its various equity offerings to the Operating Partnership. In return for those contributions, ACC receives a number of units of the Operating Partnership (“OP Units,” see definition below) equal to the number of common shares it has issued in the equity offering. Contributions of properties to the Company can be structured as tax-deferred transactions through the issuance of OP Units in the Operating Partnership. Based on the terms of ACCOP’s partnership agreement, OP Units can be exchanged for ACC’s common shares on a one-for-one basis. The Company maintains a one-for-one relationship between the OP Units of the Operating Partnership issued to ACC and ACC Holdings and the common shares issued to the public. The Company believes that combining the reports on Form 10-Q of ACC and ACCOP into this single report provides the following benefits:

(1) | enhances investors’ understanding of the Company and the Operating Partnership by enabling investors to view the business as a whole in the same manner as management views and operates the business; | |

(2) | eliminates duplicative disclosure and provides a more streamlined and readable presentation since a substantial portion of the disclosure applies to both the Company and the Operating Partnership; and | |

(3) | creates time and cost efficiencies through the preparation of one combined report instead of two separate reports. |

ACC consolidates ACCOP for financial reporting purposes, and ACC essentially has no assets or liabilities other than its investment in ACCOP. Therefore, the assets and liabilities of the Company and the Operating Partnership are the same on their respective financial statements. However, the Company believes it is important to understand the few differences between the Company and the Operating Partnership in the context of how the entities operate as a consolidated company. All of the Company’s property ownership, development and related business operations are conducted through the Operating Partnership. ACC also issues public equity from time to time and guarantees certain debt of ACCOP, as disclosed in this report. ACC does not have any indebtedness, as all debt is incurred by the Operating Partnership. The Operating Partnership holds substantially all of the assets of the Company, including the Company’s ownership interests in its joint ventures. The Operating Partnership conducts the operations of the business and is structured as a partnership with no publicly traded equity. Except for the net proceeds from ACC’s equity offerings, which are contributed to the capital of ACCOP in exchange for OP Units on a one-for-one common share per OP Unit basis, the Operating Partnership generates all remaining capital required by the Company’s business. These sources include, but are not limited to, the Operating Partnership’s working capital, net cash provided by operating activities, borrowings under its credit facility, and proceeds received from the disposition of certain properties. Noncontrolling interests, stockholders’ equity, and partners’ capital are the main areas of difference between the consolidated financial statements of the Company and those of the Operating Partnership. The noncontrolling interests in the Operating Partnership’s financial statements consist of the interests of unaffiliated partners in various consolidated joint ventures. The noncontrolling interests in the Company’s financial statements include the same noncontrolling interests at the Operating Partnership level and OP Unit holders of the Operating Partnership. The differences between stockholders’ equity and partners’ capital result from differences in the equity issued at the Company and Operating Partnership levels.

To help investors understand the significant differences between the Company and the Operating Partnership, this report provides separate consolidated financial statements for the Company and the Operating Partnership. A single set of consolidated notes to such financial statements is presented that includes separate discussions for the Company and the Operating Partnership when applicable (for example, noncontrolling interests, stockholders’ equity or partners’ capital, earnings per share or unit, etc.). A combined Management’s Discussion and Analysis of Financial Condition and Results of Operations section is also included that presents discrete information related to each entity, as applicable. This report also includes separate Part I, Item 4 Controls and Procedures sections and separate Exhibits 31 and 32 certifications for each of the Company and the Operating Partnership in order to establish that the requisite certifications have been made and that the Company and the Operating Partnership are compliant with Rule 13a-15 or Rule 15d-15 of the Securities Exchange Act of 1934 and 18 U.S.C. §1350.

In order to highlight the differences between the Company and the Operating Partnership, the separate sections in this report for the Company and the Operating Partnership specifically refer to the Company and the Operating Partnership. In the sections that combine disclosure of the Company and the Operating Partnership, this report refers to actions or holdings as being actions or holdings of the Company. Although the Operating Partnership is generally the entity that directly or indirectly enters into contracts and joint ventures and holds assets and debt, reference to the Company is appropriate because the Company operates its business through the Operating Partnership. The separate discussions of the Company and the Operating Partnership in this report should be read in conjunction with each other to understand the results of the Company on a consolidated basis and how management operates the Company.

FORM 10-Q

FOR THE QUARTER ENDED MARCH 31, 2013

TABLE OF CONTENTS

| PAGE NO. | |||

| PART I. | |||

| Item 1. | Consolidated Financial Statements of American Campus Communities, Inc. and Subsidiaries: | ||

| 1 | |||

| 2 | |||

| 3 | |||

| 4 | |||

| Consolidated Financial Statements of American Campus Communities Operating Partnership, L.P. and Subsidiaries: | |||

| 5 | |||

| 6 | |||

| 7 | |||

| 8 | |||

| 9 | |||

| 27 | |||

| 39 | |||

| 40 | |||

| Item 1. | 41 | ||

| Item 1A. | 41 | ||

| Unregistered Sales of Equity Securities and Use of Proceeds | 41 | ||

| Item 3. | Defaults Upon Senior Securities | 41 | |

| Item 4. | Mine Safety Disclosures | 41 | |

| Item 5. | Other Information | 41 | |

| 42 | |||

| 43 | |||

AMERICAN CAMPUS COMMUNITIES, INC. AND SUBSIDIARIES

(in thousands, except share data)

| March 31, 2013 | December 31, 2012 | |||||||

| (Unaudited) | ||||||||

| Assets | ||||||||

| Investments in real estate: | ||||||||

| Wholly-owned properties, net | $ | 4,840,091 | $ | 4,871,376 | ||||

| Wholly-owned properties held for sale | 87,304 | - | ||||||

| On-campus participating properties, net | 56,508 | 57,346 | ||||||

| Investments in real estate, net | 4,983,903 | 4,928,722 | ||||||

| Cash and cash equivalents | 15,033 | 21,454 | ||||||

| Restricted cash | 38,817 | 36,790 | ||||||

| Student contracts receivable, net | 6,475 | 14,122 | ||||||

| Other assets | 115,913 | 117,874 | ||||||

| Total assets | $ | 5,160,141 | $ | 5,118,962 | ||||

| Liabilities and equity | ||||||||

| Liabilities: | ||||||||

| Secured mortgage, construction and bond debt | $ | 1,516,407 | $ | 1,509,105 | ||||

| Unsecured term loan | 350,000 | 350,000 | ||||||

| Unsecured revolving credit facility | 321,000 | 258,000 | ||||||

| Secured agency facility | 104,000 | 104,000 | ||||||

| Accounts payable and accrued expenses | 44,690 | 56,046 | ||||||

| Other liabilities | 104,294 | 107,223 | ||||||

| Total liabilities | 2,440,391 | 2,384,374 | ||||||

| Commitments and contingencies (Note 13) | ||||||||

| Redeemable noncontrolling interests | 56,736 | 57,534 | ||||||

| Equity: | ||||||||

American Campus Communities, Inc. stockholders’ equity: | ||||||||

| Common stock, $.01 par value, 800,000,000 shares authorized, 104,776,745 and 104,665,212 shares issued and outstanding at March 31, 2013 and December 31, 2012, respectively | 1,043 | 1,043 | ||||||

| Additional paid in capital | 3,000,617 | 3,001,520 | ||||||

| Accumulated earnings and distributions | (361,575 | ) | (347,521 | ) | ||||

| Accumulated other comprehensive loss | (5,848 | ) | (6,661 | ) | ||||

| Total American Campus Communities, Inc. stockholders’ equity | 2,634,237 | 2,648,381 | ||||||

| Noncontrolling interests - partially owned properties | 28,777 | 28,673 | ||||||

| Total equity | 2,663,014 | 2,677,054 | ||||||

| Total liabilities and equity | $ | 5,160,141 | $ | 5,118,962 | ||||

See accompanying notes to consolidated financial statements.

1

AMERICAN CAMPUS COMMUNITIES, INC. AND SUBSIDIARIES

(unaudited, in thousands, except share and per share data)

| Three Months Ended March 31, | ||||||||

| 2013 | 2012 | |||||||

| Revenues | ||||||||

| Wholly-owned properties | $ | 154,756 | $ | 94,819 | ||||

| On-campus participating properties | 8,102 | 7,967 | ||||||

| Third-party development services | 479 | 2,094 | ||||||

| Third-party management services | 1,709 | 1,758 | ||||||

| Resident services | 597 | 343 | ||||||

| Total revenues | 165,643 | 106,981 | ||||||

| Operating expenses | ||||||||

| Wholly-owned properties | 67,143 | 42,058 | ||||||

| On-campus participating properties | 2,504 | 2,495 | ||||||

| Third-party development and management services | 2,306 | 2,785 | ||||||

| General and administrative | 3,806 | 3,540 | ||||||

| Depreciation and amortization | 46,143 | 23,399 | ||||||

| Ground/facility leases | 1,203 | 964 | ||||||

| Total operating expenses | 123,105 | 75,241 | ||||||

| Operating income | 42,538 | 31,740 | ||||||

| Nonoperating income and (expenses) | ||||||||

| Interest income | 427 | 516 | ||||||

| Interest expense | (17,641 | ) | (12,845 | ) | ||||

| Amortization of deferred financing costs | (1,314 | ) | (986 | ) | ||||

| Income from unconsolidated joint ventures | - | 444 | ||||||

| Other nonoperating expense | (2,800 | ) | (122 | ) | ||||

| Total nonoperating expenses | (21,328 | ) | (12,993 | ) | ||||

| Income before income taxes and discontinued operations | 21,210 | 18,747 | ||||||

| Income tax provision | (255 | ) | (156 | ) | ||||

| Income from continuing operations | 20,955 | 18,591 | ||||||

| Income attributable to discontinued operations | 1,426 | 2,214 | ||||||

| Net income | 22,381 | 20,805 | ||||||

| Net income attributable to noncontrolling interests | ||||||||

| Redeemable noncontrolling interests | (279 | ) | (287 | ) | ||||

| Partially owned properties | (512 | ) | (492 | ) | ||||

| Net income attributable to noncontrolling interests | (791 | ) | (779 | ) | ||||

| Net income attributable to common shareholders | $ | 21,590 | $ | 20,026 | ||||

| Other comprehensive income | ||||||||

| Change in fair value of interest rate swaps | 813 | 3,404 | ||||||

| Comprehensive income | $ | 22,403 | $ | 23,430 | ||||

| Income per share attributable to common shareholders - basic | ||||||||

| Income from continuing operations per share | $ | 0.19 | $ | 0.24 | ||||

| Net income per share | $ | 0.20 | $ | 0.27 | ||||

| Income per share attributable to common shareholders - diluted | ||||||||

| Income from continuing operations per share | $ | 0.19 | $ | 0.23 | ||||

| Net income per share | $ | 0.20 | $ | 0.26 | ||||

| Weighted-average common shares outstanding | ||||||||

| Basic | 104,697,433 | 74,216,854 | ||||||

| Diluted | 105,364,769 | 74,864,447 | ||||||

| Distributions declared per common share | $ | 0.3375 | $ | 0.3375 | ||||

See accompanying notes to consolidated financial statements.

2

AMERICAN CAMPUS COMMUNITIES, INC. AND SUBSIDIARIES

(unaudited, in thousands, except share data)

Common Shares | Par Value of Common Shares | Additional Paid in Capital | Accumulated Earnings and Distributions | Accumulated Other Comprehensive Loss | Noncontrolling Interests – partially owned properties | Total | ||||||||||||||||||||||

| Equity, December 31, 2012 | 104,665,212 | $ | 1,043 | $ | 3,001,520 | $ | (347,521 | ) | $ | (6,661 | ) | $ | 28,673 | $ | 2,677,054 | |||||||||||||

Adjustments to reflect redeemable noncontrolling interests at fair value | - | - | 649 | - | - | - | 649 | |||||||||||||||||||||

| Amortization of restricted stock awards | - | - | 1,578 | - | - | - | 1,578 | |||||||||||||||||||||

| Vesting of restricted stock awards | 111,533 | - | (3,130 | ) | - | - | - | (3,130 | ) | |||||||||||||||||||

| Distributions to common and restricted stockholders | - | - | - | (35,644 | ) | - | - | (35,644 | ) | |||||||||||||||||||

| Distributions to noncontrolling joint venture partners | - | - | - | - | - | (408 | ) | (408 | ) | |||||||||||||||||||

| Change in fair value of interest rate swaps | - | - | - | - | 813 | - | 813 | |||||||||||||||||||||

| Net income | - | - | - | 21,590 | - | 512 | 22,102 | |||||||||||||||||||||

| Equity, March 31, 2013 | 104,776,745 | $ | 1,043 | $ | 3,000,617 | $ | (361,575 | ) | $ | (5,848 | ) | $ | 28,777 | $ | 2,663,014 | |||||||||||||

See accompanying notes to consolidated financial statements.

3

AMERICAN CAMPUS COMMUNITIES, INC. AND SUBSIDIARIES

(unaudited, in thousands)

| Three Months Ended March 31, | ||||||||

| 2013 | 2012 | |||||||

| Operating activities | ||||||||

| Net income | $ | 22,381 | $ | 20,805 | ||||

| Adjustments to reconcile net income to net cash provided by operating activities: | ||||||||

| Non-cash litigation settlement expense | 2,800 | - | ||||||

| Loss on remeasurement of equity method investment | - | 122 | ||||||

| Depreciation and amortization | 46,971 | 24,399 | ||||||

| Amortization of deferred financing costs and debt premiums/discounts | (2,284 | ) | 706 | |||||

| Share-based compensation | 1,578 | 1,297 | ||||||

| Income from unconsolidated joint ventures | - | (444 | ) | |||||

| Income tax provision | 255 | 156 | ||||||

| Changes in operating assets and liabilities: | ||||||||

| Restricted cash | (922 | ) | 3,298 | |||||

| Student contracts receivable, net | 7,647 | 2,250 | ||||||

| Other assets | (1,661 | ) | 5,979 | |||||

| Accounts payable and accrued expenses | (17,541 | ) | (9,800 | ) | ||||

| Other liabilities | (2,064 | ) | 788 | |||||

| Net cash provided by operating activities | 57,160 | 49,556 | ||||||

| Investing activities | ||||||||

| Cash paid for property acquisitions | (263 | ) | (14,319 | ) | ||||

| Cash paid for land acquisitions | (138 | ) | (7,770 | ) | ||||

| Capital expenditures for wholly-owned properties | (12,348 | ) | (2,977 | ) | ||||

| Investments in wholly-owned properties under development | (87,226 | ) | (93,217 | ) | ||||

| Capital expenditures for on-campus participating properties | (335 | ) | (145 | ) | ||||

| Investment in loan receivable | - | (7,211 | ) | |||||

| Repayment of mezzanine loan | - | 4,000 | ||||||

| Increase in escrow deposits | - | (850 | ) | |||||

| Change in restricted cash related to capital reserves | (486 | ) | (81 | ) | ||||

| Purchase of corporate furniture, fixtures and equipment | (743 | ) | (579 | ) | ||||

| Net cash used in investing activities | (101,539 | ) | (123,149 | ) | ||||

| Financing activities | ||||||||

| Proceeds from sale of common stock | - | 75,000 | ||||||

| Offering costs | - | (1,196 | ) | |||||

| Pay-off of mortgage loans | - | (16,180 | ) | |||||

| Proceeds from unsecured term loan | - | 150,000 | ||||||

| Proceeds from credit facilities | 63,000 | 64,000 | ||||||

| Pay downs of credit facilities | - | (187,000 | ) | |||||

| Proceeds from construction loans | 14,544 | 31,243 | ||||||

| Principal payments on debt | (4,252 | ) | (2,666 | ) | ||||

| Change in construction accounts payable | 2,142 | 14 | ||||||

| Debt issuance and assumption costs | (996 | ) | (3,169 | ) | ||||

| Distributions to common and restricted stockholders | (35,644 | ) | (25,423 | ) | ||||

| Distributions to noncontrolling partners | (836 | ) | (837 | ) | ||||

| Net cash provided by financing activities | 37,958 | 83,786 | ||||||

| Net change in cash and cash equivalents | (6,421 | ) | 10,193 | |||||

| Cash and cash equivalents at beginning of period | 21,454 | 22,399 | ||||||

| Cash and cash equivalents at end of period | $ | 15,033 | $ | 32,592 | ||||

| Supplemental disclosure of non-cash investing and financing activities | ||||||||

| Change in fair value of derivative instruments, net | $ | 813 | $ | 3,404 | ||||

| Supplemental disclosure of cash flow information | ||||||||

| Interest paid | $ | 24,497 | $ | 16,226 | ||||

See accompanying notes to consolidated financial statements.

4

AMERICAN CAMPUS COMMUNITIES OPERATING PARTNERSHIP, L.P. AND SUBSIDIARIES

(in thousands, except unit data)

| March 31, 2013 | December 31, 2012 | |||||||

| (Unaudited) | ||||||||

| Assets | ||||||||

| Investments in real estate: | ||||||||

| Wholly-owned properties, net | $ | 4,840,091 | $ | 4,871,376 | ||||

| Wholly-owned properties held for sale | 87,304 | - | ||||||

| On-campus participating properties, net | 56,508 | 57,346 | ||||||

| Investments in real estate, net | 4,983,903 | 4,928,722 | ||||||

| Cash and cash equivalents | 15,033 | 21,454 | ||||||

| Restricted cash | 38,817 | 36,790 | ||||||

| Student contracts receivable, net | 6,475 | 14,122 | ||||||

| Other assets | 115,913 | 117,874 | ||||||

| Total assets | $ | 5,160,141 | $ | 5,118,962 | ||||

| Liabilities and capital | ||||||||

| Liabilities: | ||||||||

| Secured mortgage, construction and bond debt | $ | 1,516,407 | $ | 1,509,105 | ||||

| Unsecured term loan | 350,000 | 350,000 | ||||||

| Unsecured revolving credit facility | 321,000 | 258,000 | ||||||

| Secured agency facility | 104,000 | 104,000 | ||||||

| Accounts payable and accrued expenses | 44,690 | 56,046 | ||||||

| Other liabilities | 104,294 | 107,223 | ||||||

| Total liabilities | 2,440,391 | 2,384,374 | ||||||

| Commitments and contingencies (Note 13) | ||||||||

| Redeemable limited partners | 56,736 | 57,534 | ||||||

| Capital: | ||||||||

Partners’ capital: | ||||||||

| General partner – 12,222 OP units outstanding at both March 31, 2013 and December 31, 2012 | 114 | 116 | ||||||

| Limited partner – 104,764,523 and 104,652,990 OP units outstanding at March 31, 2013 and December 31, 2012, respectively | 2,639,971 | 2,654,926 | ||||||

| Accumulated other comprehensive loss | (5,848 | ) | (6,661 | ) | ||||

| Total partners’ capital | 2,634,237 | 2,648,381 | ||||||

| Noncontrolling interests - partially owned properties | 28,777 | 28,673 | ||||||

| Total capital | 2,663,014 | 2,677,054 | ||||||

| Total liabilities and capital | $ | 5,160,141 | $ | 5,118,962 | ||||

See accompanying notes to consolidated financial statements.

5

AMERICAN CAMPUS COMMUNITIES OPERATING PARTNERSHIP, L.P. AND SUBSIDIARIES

(unaudited, in thousands, except unit and per unit data)

| Three Months Ended March 31, | ||||||||

| 2013 | 2012 | |||||||

| Revenues | ||||||||

| Wholly-owned properties | $ | 154,756 | $ | 94,819 | ||||

| On-campus participating properties | 8,102 | 7,967 | ||||||

| Third-party development services | 479 | 2,094 | ||||||

| Third-party management services | 1,709 | 1,758 | ||||||

| Resident services | 597 | 343 | ||||||

| Total revenues | 165,643 | 106,981 | ||||||

| Operating expenses | ||||||||

| Wholly-owned properties | 67,143 | 42,058 | ||||||

| On-campus participating properties | 2,504 | 2,495 | ||||||

| Third-party development and management services | 2,306 | 2,785 | ||||||

| General and administrative | 3,806 | 3,540 | ||||||

| Depreciation and amortization | 46,143 | 23,399 | ||||||

| Ground/facility leases | 1,203 | 964 | ||||||

| Total operating expenses | 123,105 | 75,241 | ||||||

| Operating income | 42,538 | 31,740 | ||||||

| Nonoperating income and (expenses) | ||||||||

| Interest income | 427 | 516 | ||||||

| Interest expense | (17,641 | ) | (12,845 | ) | ||||

| Amortization of deferred financing costs | (1,314 | ) | (986 | ) | ||||

| Income from unconsolidated joint ventures | - | 444 | ||||||

| Other nonoperating expense | (2,800 | ) | (122 | ) | ||||

| Total nonoperating expenses | (21,328 | ) | (12,993 | ) | ||||

| Income before income taxes and discontinued operations | 21,210 | 18,747 | ||||||

| Income tax provision | (255 | ) | (156 | ) | ||||

| Income from continuing operations | 20,955 | 18,591 | ||||||

| Income attributable to discontinued operations | 1,426 | 2,214 | ||||||

| Net income | 22,381 | 20,805 | ||||||

| Net income attributable to noncontrolling interests – partially owned properties | (512 | ) | (492 | ) | ||||

| Net income attributable to American Campus Communities Operating Partnership, L.P. | 21,869 | 20,313 | ||||||

| Series A preferred unit distributions | (46 | ) | (46 | ) | ||||

| Net income available to common unitholders | $ | 21,823 | $ | 20,267 | ||||

| Other comprehensive income | ||||||||

| Change in fair value of interest rate swaps | 813 | 3,404 | ||||||

| Comprehensive income | $ | 22,636 | $ | 23,671 | ||||

| Income per unit attributable to common unitholders – basic | ||||||||

| Income from continuing operations per unit | $ | 0.19 | $ | 0.24 | ||||

| Net income per unit | $ | 0.20 | $ | 0.27 | ||||

| Income per unit attributable to common unitholders – diluted | ||||||||

| Income from continuing operations per unit | $ | 0.19 | $ | 0.23 | ||||

| Net income per unit | $ | 0.20 | $ | 0.26 | ||||

| Weighted-average common units outstanding | ||||||||

| Basic | 105,830,509 | 75,116,289 | ||||||

| Diluted | 106,497,845 | 75,763,882 | ||||||

| Distributions declared per common unit | $ | 0.3375 | $ | 0.3375 | ||||

See accompanying notes to consolidated financial statements.

6

AMERICAN CAMPUS COMMUNITIES OPERATING PARTNERSHIP, L.P. AND SUBSIDIARIES

(unaudited, in thousands, except unit data)

| Accumulated | Noncontrolling | |||||||||||||||||||||||||||

| General Partner | Limited Partner | Other | Interests - | |||||||||||||||||||||||||

| Comprehensive | Partially Owned | |||||||||||||||||||||||||||

| Units | Amount | Units | Amount | Loss | Properties | Total | ||||||||||||||||||||||

| Capital as of December 31, 2012 | 12,222 | $ | 116 | 104,652,990 | $ | 2,654,926 | $ | (6,661 | ) | $ | 28,673 | $ | 2,677,054 | |||||||||||||||

Adjustments to reflect redeemable limited partners’ interest at fair value | - | - | - | 649 | - | - | 649 | |||||||||||||||||||||

| Amortization of restricted stock awards | - | - | - | 1,578 | - | - | 1,578 | |||||||||||||||||||||

| Vesting of restricted stock awards | - | - | 111,533 | (3,130 | ) | - | - | (3,130 | ) | |||||||||||||||||||

| Distributions | - | (4 | ) | - | (35,640 | ) | - | - | (35,644 | ) | ||||||||||||||||||

| Distributions to noncontrolling joint venture partners | - | - | - | - | - | (408 | ) | (408 | ) | |||||||||||||||||||

| Change in fair value of interest rate swaps | - | - | - | - | 813 | - | 813 | |||||||||||||||||||||

| Net income | - | 2 | - | 21,588 | - | 512 | 22,102 | |||||||||||||||||||||

| Capital as of March 31, 2013 | 12,222 | $ | 114 | 104,764,523 | $ | 2,639,971 | $ | (5,848 | ) | $ | 28,777 | $ | 2,663,014 | |||||||||||||||

See accompanying notes to consolidated financial statements.

7

AMERICAN CAMPUS COMMUNITIES OPERATING PARTNERSHIP, L.P. AND SUBSIDIARIES

(unaudited, in thousands)

| Three Months Ended March 31, | ||||||||

| 2013 | 2012 | |||||||

| Operating activities | ||||||||

| Net income | $ | 22,381 | $ | 20,805 | ||||

| Adjustments to reconcile net income to net cash provided by operating activities: | ||||||||

| Non-cash litigation settlement expense | 2,800 | - | ||||||

| Loss on remeasurement of equity method investment | - | 122 | ||||||

| Depreciation and amortization | 46,971 | 24,399 | ||||||

| Amortization of deferred financing costs and debt premiums/discounts | (2,284 | ) | 706 | |||||

| Share-based compensation | 1,578 | 1,297 | ||||||

| Income from unconsolidated joint ventures | - | (444 | ) | |||||

| Income tax provision | 255 | 156 | ||||||

| Changes in operating assets and liabilities: | ||||||||

| Restricted cash | (922 | ) | 3,298 | |||||

| Student contracts receivable, net | 7,647 | 2,250 | ||||||

| Other assets | (1,661 | ) | 5,979 | |||||

| Accounts payable and accrued expenses | (17,541 | ) | (9,800 | ) | ||||

| Other liabilities | (2,064 | ) | 788 | |||||

| Net cash provided by operating activities | 57,160 | 49,556 | ||||||

| Investing activities | ||||||||

| Cash paid for property acquisitions | (263 | ) | (14,319 | ) | ||||

| Cash paid for land acquisitions | (138 | ) | (7,770 | ) | ||||

| Capital expenditures for wholly-owned properties | (12,348 | ) | (2,977 | ) | ||||

| Investments in wholly-owned properties under development | (87,226 | ) | (93,217 | ) | ||||

| Capital expenditures for on-campus participating properties | (335 | ) | (145 | ) | ||||

| Investment in loan receivable | - | (7,211 | ) | |||||

| Repayment of mezzanine loan | - | 4,000 | ||||||

| Increase in escrow deposits | - | (850 | ) | |||||

| Change in restricted cash related to capital reserves | (486 | ) | (81 | ) | ||||

| Purchase of corporate furniture, fixtures and equipment | (743 | ) | (579 | ) | ||||

| Net cash used in investing activities | (101,539 | ) | (123,149 | ) | ||||

| Financing activities | ||||||||

| Proceeds from issuance of common units in exchange for contributions, net | - | 73,804 | ||||||

| Pay-off of mortgage loans | - | (16,180 | ) | |||||

| Proceeds from unsecured term loan | - | 150,000 | ||||||

| Proceeds from credit facilities | 63,000 | 64,000 | ||||||

| Paydowns of credit facilities | - | (187,000 | ) | |||||

| Proceeds from construction loans | 14,544 | 31,243 | ||||||

| Principal payments on debt | (4,252 | ) | (2,666 | ) | ||||

| Change in construction accounts payable | 2,142 | 14 | ||||||

| Debt issuance and assumption costs | (996 | ) | (3,169 | ) | ||||

| Distributions paid on unvested restricted stock awards | (272 | ) | (258 | ) | ||||

| Distributions paid on common units | (35,754 | ) | (25,468 | ) | ||||

| Distributions paid on preferred units | (46 | ) | (46 | ) | ||||

| Distributions paid to noncontrolling partners - partially owned properties | (408 | ) | (488 | ) | ||||

| Net cash provided by financing activities | 37,958 | 83,786 | ||||||

| Net change in cash and cash equivalents | (6,421 | ) | 10,193 | |||||

| Cash and cash equivalents at beginning of period | 21,454 | 22,399 | ||||||

| Cash and cash equivalents at end of period | $ | 15,033 | $ | 32,592 | ||||

| Supplemental disclosure of non-cash investing and financing activities | ||||||||

| Change in fair value of derivative instruments, net | $ | 813 | $ | 3,404 | ||||

| Supplemental disclosure of cash flow information | ||||||||

| Interest paid | $ | 24,497 | $ | 16,226 | ||||

See accompanying notes to consolidated financial statements.

8

AMERICAN CAMPUS COMMUNITIES, INC. AND SUBSIDIARIES

AMERICAN CAMPUS COMMUNITIES OPERATING PARTNERSHIP, L.P. AND SUBSIDIARIES

(unaudited)

| 1. | Organization and Description of Business |

American Campus Communities, Inc. (“ACC”) is a real estate investment trust (“REIT”) that commenced operations effective with the completion of an initial public offering (“IPO”) on August 17, 2004. Through ACC’s controlling interest in American Campus Communities Operating Partnership, L.P. (“ACCOP”), ACC is one of the largest owners, managers and developers of high quality student housing properties in the United States in terms of beds owned and under management. ACC is a fully integrated, self-managed and self-administered equity REIT with expertise in the acquisition, design, financing, development, construction management, leasing and management of student housing properties. ACC’s common stock is publicly traded on the New York Stock Exchange (“NYSE”) under the ticker symbol “ACC.”

The general partner of ACCOP is American Campus Communities Holdings, LLC (“ACC Holdings”), an entity that is wholly-owned by ACC. As of March 31, 2013, ACC Holdings held an ownership interest in ACCOP of less than 1%. The limited partners of ACCOP are ACC and other limited partners consisting of current and former members of management and nonaffiliated third parties. As of March 31, 2013, ACC owned an approximate 98.8% limited partnership interest in ACCOP. As the sole member of the general partner of ACCOP, ACC has exclusive control of ACCOP’s day-to-day management. Management operates ACC and ACCOP as one business. The management of ACC consists of the same members as the management of ACCOP. ACC consolidates ACCOP for financial reporting purposes, and ACC does not have significant assets other than its investment in ACCOP. Therefore, the assets and liabilities of ACC and ACCOP are the same on their respective financial statements. References to the “Company,” “we,” “us” or “our” mean collectively ACC, ACCOP and those entities/subsidiaries owned or controlled by ACC and/or ACCOP. References to the “Operating Partnership” mean collectively ACCOP and those entities/subsidiaries owned or controlled by ACCOP. Unless otherwise indicated, the accompanying Notes to the Consolidated Financial Statements apply to both the Company and the Operating Partnership.

As of March 31, 2013, our property portfolio contained 160 properties with approximately 98,900 beds in approximately 31,900 apartment units. Our property portfolio consisted of 143 owned off-campus student housing properties that are in close proximity to colleges and universities, 13 American Campus Equity (“ACE®”) properties operated under ground/facility leases with six university systems and four on-campus participating properties operated under ground/facility leases with the related university systems. Of the 160 properties, nine were under development as well as an additional phase under development at an existing property as of March 31, 2013, and when completed will consist of a total of approximately 6,200 beds in approximately 1,700 units. Our communities contain modern housing units and are supported by a resident assistant system and other student-oriented programming, with many offering resort-style amenities.

Through one of ACC’s taxable REIT subsidiaries (“TRSs”), we also provide construction management and development services, primarily for student housing properties owned by colleges and universities, charitable foundations, and others. As of March 31, 2013, also through one of ACC’s TRSs, we provided third-party management and leasing services for 30 properties that represented approximately 23,700 beds in approximately 9,400 units. Third-party management and leasing services are typically provided pursuant to management contracts that have initial terms that range from one to five years. As of March 31, 2013, our total owned and third-party managed portfolio included 190 properties with approximately 122,600 beds in approximately 41,300 units.

2. Summary of Significant Accounting Policies

Basis of Presentation

The accompanying consolidated financial statements, presented in U.S. dollars, are prepared in accordance with U.S. generally accepted accounting principles (“GAAP”). GAAP requires us to make estimates and assumptions that affect the reported amounts of assets and liabilities, disclosure of contingent assets and liabilities as of the date of the financial statements, and revenue and expenses during the reporting periods. Our actual results could differ from those estimates and assumptions. All material intercompany transactions among consolidated entities have been eliminated. All dollar amounts in the tables herein, except share, per share, unit and per unit amounts, are stated in thousands unless otherwise indicated. Certain prior period amounts have been reclassified to conform to the current period presentation.

9

AMERICAN CAMPUS COMMUNITIES, INC. AND SUBSIDIARIES

AMERICAN CAMPUS COMMUNITIES OPERATING PARTNERSHIP, L.P. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(unaudited)

Interim Financial Statements

The accompanying interim financial statements are unaudited, but have been prepared in accordance with GAAP for interim financial information and in conjunction with the rules and regulations of the Securities and Exchange Commission. Accordingly, they do not include all disclosures required by GAAP for complete financial statements. In the opinion of management, all adjustments (consisting solely of normal recurring matters) necessary for a fair presentation of the financial statements of the Company for these interim periods have been included. Because of the seasonal nature of the Company’s operations, the results of operations and cash flows for any interim period are not necessarily indicative of results for other interim periods or for the full year. These financial statements should be read in conjunction with the financial statements and the notes thereto included in the Company’s Annual Report on Form 10-K for the year ended December 31, 2012.

Use of Estimates

The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities, disclosures of contingent assets and liabilities at the date of the financial statements, and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates.

Investments in Real Estate

Investments in real estate are recorded at historical cost. Major improvements that extend the life of an asset are capitalized and depreciated over the remaining useful life of the asset. The cost of ordinary repairs and maintenance are charged to expense when incurred. Depreciation and amortization are recorded on a straight-line basis over the estimated useful lives of the assets as follows:

| Buildings and improvements | 7-40 years | |

Leasehold interest - on-campus participating properties | 25-34 years (shorter of useful life or respective lease term) | |

| Furniture, fixtures and equipment | 3-7 years |

Project costs directly associated with the development and construction of an owned real estate project, which include interest, property taxes, and amortization of deferred finance costs, are capitalized as construction in progress. Upon completion of the project, costs are transferred into the applicable asset category and depreciation commences. Interest totaling approximately $2.3 million and $2.5 million was capitalized during the three months ended March 31, 2013 and March 31, 2012, respectively. Amortization of deferred financing costs totaling approximately $0.1 million was capitalized as construction in progress during both three month periods ended March 31, 2013 and March 31, 2012, respectively.

Management assesses whether there has been an impairment in the value of the Company’s investments in real estate whenever events or changes in circumstances indicate that the carrying amount of an asset may not be recoverable. Impairment is recognized when estimated expected future undiscounted cash flows are less than the carrying value of the property. The estimation of expected future net cash flows is inherently uncertain and relies on assumptions regarding current and future economics and market conditions. If such conditions change, then an adjustment to the carrying value of the Company’s long-lived assets could occur in the future period in which the conditions change. To the extent that a property is impaired, the excess of the carrying amount of the property over its estimated fair value is charged to earnings. The Company believes that there were no impairments of the carrying values of its investments in real estate as of March 31, 2013.

10

AMERICAN CAMPUS COMMUNITIES, INC. AND SUBSIDIARIES

AMERICAN CAMPUS COMMUNITIES OPERATING PARTNERSHIP, L.P. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(unaudited)

The Company allocates the purchase price of acquired properties to net tangible and identified intangible assets based on relative fair values. Fair value estimates are based on information obtained from a number of sources, including independent appraisals that may be obtained in connection with the acquisition or financing of the respective property, our own analysis of recently acquired and existing comparable properties in our portfolio, and other market data. Information obtained about each property as a result of due diligence, marketing and leasing activities is also considered. The value allocated to land is generally based on the actual purchase price adjusted to fair value (as necessary) if acquired separately, or market research / comparables if acquired as part of an existing operating property. The value allocated to building is based on the fair value determined on an “as-if vacant” basis, which is estimated using an income, or discounted cash flow, approach that relies upon internally determined assumptions that we believe are consistent with current market conditions for similar properties. The value allocated to furniture, fixtures, and equipment is based on an estimate of the fair value of the appliances and fixtures inside the units.

Long-Lived Assets–Held for Sale

Long-lived assets to be disposed of are classified as held for sale in the period in which all of the following criteria are met:

| a. | Management, having the authority to approve the action, commits to a plan to sell the asset. |

| b. | The asset is available for immediate sale in its present condition subject only to terms that are usual and customary for sales of such assets. |

| c. | An active program to locate a buyer and other actions required to complete the plan to sell the asset have been initiated. |

| d. | The sale of the asset is probable, and transfer of the asset is expected to qualify for recognition as a completed sale, within one year. |

| e. | The asset is being actively marketed for sale at a price that is reasonable in relation to its current fair value. |

| f. | Actions required to complete the plan indicate that it is unlikely that significant changes to the plan will be made or that the plan will be withdrawn. |

Concurrent with this classification, the asset is recorded at the lower of cost or fair value less estimated selling costs, and depreciation ceases.

Intangible Assets

A portion of the purchase price of acquired properties is allocated to the value of in-place leases for both student and commercial tenants, which is based on the difference between (i) the property valued with existing in-place leases adjusted to market rental rates and (ii) the property valued “as-if” vacant. As lease terms for student leases are typically one year or less, rates on in-place leases generally approximate market rental rates. Factors considered in the valuation of in-place leases include an estimate of the carrying costs during the expected lease-up period considering current market conditions, nature of the tenancy, and costs to execute similar leases. Carrying costs include estimates of lost rentals at market rates during the expected lease-up period, as well as marketing and other operating expenses. The value of in-place leases is amortized over the remaining initial term of the respective leases. The purchase price of property acquisitions is not expected to be allocated to student tenant relationships, considering the terms of the leases and the expected levels of renewals.

Amortization expense related to in-place leases was approximately $5.5 million and $0.9 million for the three months ended March 31, 2013 and 2012, respectively. Accumulated amortization at March 31, 2013 and December 31, 2012 was approximately $17.6 million and $12.4 million, respectively. Intangible assets, net of amortization, are included in other assets on the accompanying consolidated balance sheets and the amortization of intangible assets is included in depreciation and amortization expense in the accompanying consolidated statements of comprehensive income.

11

AMERICAN CAMPUS COMMUNITIES, INC. AND SUBSIDIARIES

AMERICAN CAMPUS COMMUNITIES OPERATING PARTNERSHIP, L.P. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(unaudited)

Debt Premiums and Discounts

Debt premiums and discounts represent fair value adjustments to account for the difference between the stated rates and market rates of debt assumed in connection with the Company’s property acquisitions. The debt premiums and discounts are amortized to interest expense over the term of the related loans using the effective-interest method. The amortization of debt premiums and discounts resulted in a net decrease to interest expense of approximately $3.6 million and $0.3 million for the three months ended March 31, 2013 and 2012, respectively. As of March 31, 2013 and December 31, 2012, net unamortized debt premiums were approximately $86.1 million and $90.1 million, respectively, and net unamortized debt discounts were approximately $3.1 million and $3.5 million, respectively. Debt premiums and discounts are included in secured mortgage, construction and bond debt on the accompanying consolidated balance sheets and amortization of debt premiums and discounts is included in interest expense on the accompanying consolidated statements of comprehensive income.

Redeemable Noncontrolling Interests – Operating Partnership / Redeemable Limited Partners

The Company classifies Redeemable Noncontrolling Interests – Operating Partnership / Redeemable Limited Partners in the mezzanine section of the accompanying consolidated balance sheets for the portion of common and preferred Operating Partnership units (“OP Units”) that the Operating Partnership is required, either by contract or securities law, to deliver registered common shares of ACC to the exchanging OP unit holder. The redeemable noncontrolling interest units / redeemable limited partner units are adjusted to the greater of carrying value or fair market value based on the common share price of ACC at the end of each respective reporting period.

Third-Party Development Services Revenue and Costs

Pre-development expenditures such as architectural fees, permits and deposits associated with the pursuit of third-party and owned development projects are expensed as incurred, until such time that management believes it is probable that the contract will be executed and/or construction will commence. Because the Company frequently incurs these pre-development expenditures before a financing commitment and/or required permits and authorizations have been obtained, the Company bears the risk of loss of these pre-development expenditures if financing cannot ultimately be arranged on acceptable terms or the Company is unable to successfully obtain the required permits and authorizations. As such, management evaluates the status of third-party and owned projects that have not yet commenced construction on a periodic basis and expenses any deferred costs related to projects whose current status indicates the commencement of construction is unlikely and/or the costs may not provide future value to the Company in the form of revenues. Such write-offs are included in third-party development and management services expenses (in the case of third-party development projects) or general and administrative expenses (in the case of owned development projects) on the accompanying consolidated statements of comprehensive income. As of March 31, 2013, the Company has deferred approximately $3.3 million in pre-development costs related to third-party and owned development projects that have not yet commenced construction. Such costs are included in other assets on the accompanying consolidated balance sheets.

Earnings per Share – Company

Basic earnings per share is computed using net income attributable to common shareholders and the weighted average number of shares of the Company’s common stock outstanding during the period. Diluted earnings per share reflect common shares issuable from the assumed conversion of OP Units and common share awards granted. Only those items having a dilutive impact on basic earnings per share are included in diluted earnings per share.

12

AMERICAN CAMPUS COMMUNITIES, INC. AND SUBSIDIARIES

AMERICAN CAMPUS COMMUNITIES OPERATING PARTNERSHIP, L.P. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(unaudited)

The following potentially dilutive securities were outstanding for the three months ended March 31, 2013 and 2012, but were not included in the computation of diluted earnings per share because the effects of their inclusion would be anti-dilutive.

| Three Months Ended March 31, | ||||||||

| 2013 | 2012 | |||||||

| Common OP Units (Note 9) | 1,133,076 | 899,435 | ||||||

| Preferred OP Units (Note 9) | 114,128 | 114,128 | ||||||

| Total potentially dilutive securities | 1,247,204 | 1,013,563 | ||||||

The following is a summary of the elements used in calculating basic earnings per share:

| Three Months Ended March 31, | ||||||||

| 2013 | 2012 | |||||||

| Basic earnings per share calculation: | ||||||||

| Income from continuing operations | $ | 20,955 | $ | 18,591 | ||||

| Income from continuing operations attributable to noncontrolling interests | (775 | ) | (749 | ) | ||||

| Income from continuing operations attributable to common shareholders | 20,180 | 17,842 | ||||||

| Amount allocated to participating securities | (272 | ) | (258 | ) | ||||

| Income from continuing operations attributable to common shareholders, net of amount allocated to participating securities | 19,908 | 17,584 | ||||||

| Income from discontinued operations | 1,426 | 2,214 | ||||||

| Income from discontinued operations attributable to noncontrolling interests | (16 | ) | (30 | ) | ||||

| Income from discontinued operations attributable to common shareholders | 1,410 | 2,184 | ||||||

| Net income attributable to common shareholders, as adjusted – basic | $ | 21,318 | $ | 19,768 | ||||

| Income from continuing operations attributable to common shareholders, as adjusted – per share | $ | 0.19 | $ | 0.24 | ||||

| Income from discontinued operations attributable to common shareholders – per share | $ | 0.01 | $ | 0.03 | ||||

| Net income attributable to common shareholders, as adjusted – per share | $ | 0.20 | $ | 0.27 | ||||

| Basic weighted average common shares outstanding | 104,697,433 | 74,216,854 | ||||||

| Diluted earnings per share calculation: | ||||||||

| Income from continuing operations attributable to common shareholders, net of amount allocated to participating securities | $ | 19,908 | $ | 17,584 | ||||

| Income from discontinued operations attributable to common shareholders | 1,410 | 2,184 | ||||||

Net income attributable to common shareholders, as adjusted – diluted | $ | 21,318 | $ | 19,768 | ||||

| Income from continuing operations attributable to common shareholders, net of amount allocated to participating securities – per share | $ | 0.19 | $ | 0.23 | ||||

| Income from discontinued operations attributable to common shareholders – per share | $ | 0.01 | $ | 0.03 | ||||

13

AMERICAN CAMPUS COMMUNITIES, INC. AND SUBSIDIARIES

AMERICAN CAMPUS COMMUNITIES OPERATING PARTNERSHIP, L.P. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(unaudited)

| Three Months Ended March 31, | ||||||||

| 2013 | 2012 | |||||||

Net income attributable to common shareholders-per share | $ | 0.20 | $ | 0.26 | ||||

| Basic weighted average common shares outstanding | 104,697,433 | 74,216,854 | ||||||

| Restricted Stock Awards (Note 10) | 667,336 | 647,593 | ||||||

| Diluted weighted average common shares outstanding | 105,364,769 | 74,864,447 | ||||||

Earnings per Unit – Operating Partnership

Basic earnings per OP Unit is computed using net income attributable to common unitholders and the weighted average number of common units outstanding during the period. Diluted earnings per OP Unit reflects the potential dilution that could occur if securities or other contracts to issue OP Units were exercised or converted into OP Units or resulted in the issuance of OP Units and then shared in the earnings of the Operating Partnership.

The following is a summary of the elements used in calculating basic earnings per unit:

| Three Months Ended March 31, | ||||||||

| 2013 | 2012 | |||||||

| Basic earnings per unit calculation: | ||||||||

| Income from continuing operations | $ | 20,955 | $ | 18,591 | ||||

| Income from continuing operations attributable to noncontrolling interests – partially owned properties | (512 | ) | (492 | ) | ||||

| Income from continuing operations attributable to Series A preferred units | (45 | ) | (43 | ) | ||||

| Amount allocated to participating securities | (272 | ) | (258 | ) | ||||

| Income from continuing operations attributable to common unitholders, net of amount allocated to participating securities | 20,126 | 17,798 | ||||||

| Income from discontinued operations | 1,426 | 2,214 | ||||||

| Income from discontinued operations attributable to Series A preferred unit distributions | (1 | ) | (3 | ) | ||||

| Income from discontinued operations attributable to common unitholders | 1,425 | 2,211 | ||||||

| Net income attributable to common unitholders, as adjusted – basic | $ | 21,551 | $ | 20,009 | ||||

| Income from continuing operations attributable to common unitholders, as adjusted – per unit | $ | 0.19 | $ | 0.24 | ||||

| Income from discontinued operations attributable to common unitholders – per unit | $ | 0.01 | $ | 0.03 | ||||

| Net income attributable to common unitholders, as adjusted – per unit | $ | 0.20 | $ | 0.27 | ||||

| Basic weighted average common units outstanding | 105,830,509 | 75,116,289 | ||||||

14

AMERICAN CAMPUS COMMUNITIES, INC. AND SUBSIDIARIES

AMERICAN CAMPUS COMMUNITIES OPERATING PARTNERSHIP, L.P. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(unaudited)

| Three Months Ended March 31, | ||||||||

| 2013 | 2012 | |||||||

| Diluted earnings per unit calculation: | ||||||||

| Income from continuing operations attributable to common unitholders, net of amount allocated to participating securities | $ | 20,126 | $ | 17,798 | ||||

| Income from discontinued operations attributable to common unitholders | 1,425 | 2,211 | ||||||

Net income attributable to common unitholders, as adjusted | $ | 21,551 | $ | 20,009 | ||||

| Income from continuing operations attributable to common unitholders, net of amount allocated to participating securities – per unit | $ | 0.19 | $ | 0.23 | ||||

| Income from discontinued operations attributable to common unitholders – per unit | $ | 0.01 | $ | 0.03 | ||||

Net income attributable to common unitholders- per unit | $ | 0.20 | $ | 0.26 | ||||

| Basic weighted average common units outstanding | 105,830,509 | 75,116,289 | ||||||

| Restricted Stock Awards (Note 10) | 667,336 | 647,593 | ||||||

| Diluted weighted average common units outstanding | 106,497,845 | 75,763,882 | ||||||

3. Property Dispositions and Discontinued Operations

As of March 31, 2013, four owned off-campus properties were classified as Held for Sale on the accompanying consolidated balance sheet. These four properties are The Village at Blacksburg, State College Park, University Mills and University Pines. Concurrent with this classification, these properties were recorded at the lower of cost or fair value less estimated selling costs. The net income attributable to these properties is included in discontinued operations on the accompanying consolidated statements of comprehensive income for all periods presented.

In 2012, the Company sold three owned off-campus properties, located in Wilmington, North Carolina (Brookstone Village and Campus Walk) and Greenville, North Carolina (Pirates Cove) containing 1,584 beds for a combined sales price of approximately $54.1 million. The net income attributable to these properties is included in discontinued operations on the accompanying consolidated statements of comprehensive income for the three months ended March 31, 2012.

The properties discussed above are included in the wholly-owned properties segment (see Note 14). Below is a summary of the results of operations for the properties discussed above:

| Three Months Ended March 31, | ||||||||

| 2013 | 2012 | |||||||

| Total revenues | $ | 3,959 | $ | 5,924 | ||||

| Total operating expenses | (1,425 | ) | (2,258 | ) | ||||

| Depreciation and amortization | (828 | ) | (1,000 | ) | ||||

| Operating income | 1,706 | 2,666 | ||||||

| Total nonoperating expenses | (280 | ) | (452 | ) | ||||

Net income | $ | 1,426 | $ | 2,214 | ||||

15

AMERICAN CAMPUS COMMUNITIES, INC. AND SUBSIDIARIES

AMERICAN CAMPUS COMMUNITIES OPERATING PARTNERSHIP, L.P. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(unaudited)

4. Investments in Wholly-Owned Properties

Wholly-owned properties consisted of the following:

| March 31, 2013 | December 31, 2012 | |||||||

Land (1) (2) (3) | $ | 539,713 | $ | 550,274 | ||||

| Buildings and improvements | 4,268,527 | 4,351,239 | ||||||

Furniture, fixtures and equipment (2) | 225,638 | 227,409 | ||||||

Construction in progress (2) (3) | 222,716 | 138,923 | ||||||

| 5,256,594 | 5,267,845 | |||||||

| Less accumulated depreciation | (416,503 | ) | (396,469 | ) | ||||

Wholly-owned properties, net (4) | $ | 4,840,091 | $ | 4,871,376 | ||||

| (1) | The land balance above includes undeveloped land parcels with book values of approximately $30.7 million as of both March 31, 2013 and December 31, 2012. Also includes land totaling approximately $41.6 million as of both March 31, 2013 and December 31, 2012, related to properties under development. |

| (2) | Land, furniture, fixtures and equipment and construction in progress as of March 31, 2013 include $7.7 million, $0.6 million and $14.8 million, respectively, related to the Townhomes at Newtown Crossing property located in Lexington, Kentucky, that will serve students attending the University of Kentucky. In July 2012, the Company entered into a purchase and contribution agreement with a private developer whereby the Company is obligated to purchase the property as long as the developer meets certain construction completion deadlines and other closing conditions. The development of the property is anticipated to be completed in August 2013. The entity that owns Townhomes at Newtown Crossing is deemed to be a variable interest entity (“VIE”), and the Company is determined to be the primary beneficiary of the VIE. As such, the assets and liabilities of the entity owning the property are included in the Company’s and the Operating Partnership’s consolidated financial statements. |

| (3) | Land and construction in progress as of March 31, 2013 include $3.3 million and $12.0 million, respectively, related to an additional phase currently under development at The Lodges of East Lansing located in East Lansing, Michigan that will serve students attending Michigan State University. Concurrent with the purchase of the Kayne Anderson Portfolio on November 30, 2012, the Company entered into a purchase and sale agreement whereby the Company is obligated to purchase this additional phase as long as the developer meets certain construction completion deadlines and other closing conditions. The development of the additional phase is anticipated to be completed in September 2013. The entity that owns The Lodges of East Lansing Phase II is deemed to be a variable interest entity (“VIE”), and the Company is determined to be the primary beneficiary of the VIE. As such, the assets and liabilities of the entity owning the property are included in the Company’s and the Operating Partnership’s consolidated financial statements. |

| (4) | The balances above exclude the net book value of four properties, The Village at Blacksburg, State College Park, University Mills and University Pines which were classified as wholly-owned properties held for sale in the accompanying consolidated balance sheet as of March 31, 2013. |

16

AMERICAN CAMPUS COMMUNITIES, INC. AND SUBSIDIARIES

AMERICAN CAMPUS COMMUNITIES OPERATING PARTNERSHIP, L.P. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(unaudited)

5. On-Campus Participating Properties

On-campus participating properties are as follows:

| Historical Cost | ||||||||||||

| Lessor/University | Lease Commencement | Required Debt Repayment (1) | March 31, 2013 | December 31, 2012 | ||||||||

Texas A&M University System / Prairie View A&M University (2) | 2/1/96 | 9/1/23 | $ | 41,587 | $ | 41,485 | ||||||

Texas A&M University System / Texas A&M International | 2/1/96 | 9/1/23 | 6,663 | 6,651 | ||||||||

Texas A&M University System / Prairie View A&M University (3) | 10/1/99 | 8/31/25/ 8/31/28 | 25,937 | 25,766 | ||||||||

University of Houston System / University of Houston (4) | 9/27/00 | 8/31/35 | 35,986 | 35,936 | ||||||||

| 110,173 | 109,838 | |||||||||||

| Less accumulated amortization | (53,665 | ) | (52,492 | ) | ||||||||

| On-campus participating properties, net | $ | 56,508 | $ | 57,346 | ||||||||

| (1) | Represents the effective lease termination date. The Leases terminate upon the earlier to occur of the final repayment of the related debt or the end of the contractual lease term. |

| (2) | Consists of three phases placed in service between 1996 and 1998. |

| (3) | Consists of two phases placed in service in 2000 and 2003. |

| (4) | Consists of two phases placed in service in 2001 and 2005. |

6. Investments in Unconsolidated Joint Ventures

As of March 31, 2013, the Company owned a noncontrolling interest in one unconsolidated joint venture that is accounted for utilizing the equity method of accounting. The investment consists of a noncontrolling equity interest in a joint venture with the United States Navy that owns military housing privatization projects located on naval bases in Norfolk and Newport News, Virginia. In 2010, the Company discontinued applying the equity method in regards to its investment in this joint venture as a result of the Company’s share of losses exceeding its investment in the joint venture. Because the Company has not guaranteed any obligations of the investee and is not otherwise committed to provide further financial support to the investee, it therefore suspended recording its share of losses once the investment was reduced to zero. We also earn fees for providing management services to this joint venture, which totaled approximately $0.4 million for each of the three month periods ended March 31, 2013 and 2012.

17

AMERICAN CAMPUS COMMUNITIES, INC. AND SUBSIDIARIES

AMERICAN CAMPUS COMMUNITIES OPERATING PARTNERSHIP, L.P. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(unaudited)

7. Debt

A summary of the Company’s outstanding consolidated indebtedness, including unamortized debt premiums and discounts, is as follows:

| March 31, 2013 | December 31, 2012 | |||||||

| Debt secured by wholly-owned properties: | ||||||||

| Mortgage loans payable | $ | 1,284,965 | $ | 1,288,482 | ||||

Construction loans payable (1) | 71,899 | 57,355 | ||||||

| 1,356,864 | 1,345,837 | |||||||

| Debt secured by on-campus participating properties: | ||||||||

| Mortgage loan payable | 31,652 | 31,768 | ||||||

| Bonds payable | 44,915 | 44,915 | ||||||

| 76,567 | 76,683 | |||||||

| Unsecured revolving credit facility | 321,000 | 258,000 | ||||||

| Unsecured term loan | 350,000 | 350,000 | ||||||

| Secured agency facility | 104,000 | 104,000 | ||||||

| Unamortized debt premiums | 86,118 | 90,091 | ||||||

| Unamortized debt discounts | (3,142 | ) | (3,506 | ) | ||||

| Total debt | $ | 2,291,407 | $ | 2,221,105 | ||||

| (1) | Construction loans payable as of March 31, 2013 and December 31, 2012 includes $27.3 million and $12.7 million, respectively, related to two constructions loans that are financing the development and construction of Townhomes at Newtown Crossing and The Lodges of East Lansing Phase II, both VIEs the Company is including in its consolidated financial statements (see Note 4). The creditors of these construction loans do not have recourse to the assets of the Company. |

Unsecured Credit Facility

The Company has an aggregate Credit Facility of $800 million, which is composed of a $350 million unsecured term loan and a $450 million unsecured revolving credit facility, and may be expanded by up to an additional $100 million upon the satisfaction of certain conditions. The maturity dates of the unsecured term loan and unsecured revolving credit facility are January 10, 2017 and January 10, 2016, respectively. The maturity date of the unsecured revolving credit facility can be extended for an additional 12 months to January 10, 2017, subject to the satisfaction of certain conditions.

Each loan bears interest at a variable rate, at the Company’s option, based upon a base rate or one-, two-, three- or six-month LIBOR, plus, in each case, a spread based upon the Company's investment grade rating from either Moody’s Investor Services, Inc. or Standard & Poor’s Rating Group. The Company has entered into multiple interest rate swaps with notional amounts totaling $350 million that effectively fix the interest rate to 2.54% (0.89% + 1.65% spread) on the outstanding balance of the unsecured term loan (see Note 11 for more details).

Availability under the revolving credit facility is limited to an "aggregate borrowing base amount" equal to 60% of the value of the Company’s unencumbered properties, calculated as set forth in the Credit Facility. Additionally, the Company is required to pay a facility fee of 0.30% per annum on the $450 million revolving credit facility. As of March 31, 2013, the revolving credit facility bore interest at a weighted average annual rate of 1.96% (inclusive of the facility fee discussed above), and availability under the revolving credit facility totaled $129.0 million.

The terms of the Credit Facility include certain restrictions and covenants, which limit, among other items, the incurrence of additional indebtedness, liens, and the disposition of assets. The facility contains customary affirmative and negative covenants and also contains financial covenants that, among other things, require the Company to maintain certain minimum ratios of "EBITDA" (earnings before interest, taxes, depreciation and amortization) to fixed charges and total indebtedness. The Company may not pay distributions that exceed a specified percentage of funds from operations, as adjusted, for any four consecutive quarters. The financial covenants also include consolidated net worth and leverage ratio tests. As of March 31, 2013, the Company was in compliance with all such covenants.

18

AMERICAN CAMPUS COMMUNITIES, INC. AND SUBSIDIARIES

AMERICAN CAMPUS COMMUNITIES OPERATING PARTNERSHIP, L.P. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(unaudited)

Secured Agency Facility

The Company has a $125 million secured revolving credit facility with a Freddie Mac lender. The facility has a five-year term and is currently secured by 10 properties referred to as the “Collateral Pool.” The facility bears interest at one- or three-month LIBOR plus a spread that varies based on the debt service ratio of the Collateral Pool. Additionally, the Company is required to pay an unused commitment fee of 1.0% per annum. As of March 31, 2013, the secured agency facility bore interest at a weighted average annual rate of 2.25%. The secured agency facility includes some, but not all, of the same financial covenants as the unsecured credit facility, described above. As of March 31, 2013, the Company was in compliance with all such covenants.

8. Stockholders’ Equity / Partners’ Capital

In March 2013, the Company established a new at-the-market share offering program (the “ATM Equity Program”) through which the Company may issue and sell, from time to time, shares of common stock having an aggregate offering price of up to $500 million. Actual sales under the program will depend on a variety of factors, including, but not limited to, market conditions, the trading price of the Company’s common stock and determinations of the appropriate sources of funding for the Company. The Company has not sold any shares under the ATM Equity Program and has $500.0 million available for issuance under this program as of March 31, 2013.

9. Noncontrolling Interests

Operating Partnership

Partially-owned properties: As of March 31, 2013, the Operating Partnership consolidates four joint ventures that own and operate The Varsity, University Village at Sweet Home, University Centre and Villas at Chestnut Ridge owned-off campus properties. The portion of net assets attributable to the third-party partners in these joint ventures is classified as “noncontrolling interests - partially owned properties” within capital on the accompanying consolidated balance sheets of the Operating Partnership. Accordingly, the third-party partners’ share of the income or loss of the joint ventures is reported on the consolidated statements of comprehensive income of the Operating Partnership as “net income attributable to noncontrolling interests – partially owned properties.”

OP Units: For the portion of OP Units that the Operating Partnership is required, either by contract or securities law, to deliver registered common shares of ACC to the exchanging OP unit holder, or for which the Operating Partnership has the intent or history of exchanging such units for cash, we classify the units as “redeemable limited partners” in the mezzanine section of the consolidated balance sheets of the Operating Partnership and “redeemable noncontrolling interests” in the mezzanine section of the consolidated balance sheets of ACC. The units classified as such include Series A preferred units as well as common units that are not held by ACC or ACC Holdings. The value of redeemable limited partners/redeemable noncontrolling interests on the consolidated balance sheets is reported at the greater of fair value or historical cost at the end of each reporting period. Changes in the value from period to period are charged to limited partner’s capital on the consolidated statement of changes in capital of the Operating Partnership and to additional paid in capital on the consolidated statement of changes in equity of ACC. Below is a table summarizing the activity of redeemable limited partners/redeemable noncontrolling interests for the three months ended March 31, 2013:

| Balance, December 31, 2012 | $ | 57,534 | ||

| Net income | 279 | |||

| Distributions | (428 | ) | ||

| Adjustments to reflect redeemable limited partner units at fair value | (649 | ) | ||

| Balance, March 31, 2013 | $ | 56,736 |

19

AMERICAN CAMPUS COMMUNITIES, INC. AND SUBSIDIARIES

AMERICAN CAMPUS COMMUNITIES OPERATING PARTNERSHIP, L.P. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(unaudited)

During the year ended December 31, 2012, 88,457 common OP units were converted into an equal number of shares of ACC’s common stock and none were converted during the three months ended March 31, 2013. As of March 31, 2013 and December 31, 2012, approximately 1.2% of the equity interests of the Operating Partnership were held by owners of common OP Units and Series A preferred units not held by ACC or ACC Holdings.

Company

The noncontrolling interests of the Company include the third-party equity interests in partially-owned properties, as discussed above, which are presented as a component of equity in the Company’s consolidated balance sheets. The Company’s noncontrolling interests also include the redeemable limited partners presented in the consolidated balance sheets of the Operating Partnership, which are referred to as “redeemable noncontrolling interests” in the mezzanine section of the Company’s consolidated balance sheets. Noncontrolling interests on the Company’s consolidated statements of comprehensive income include the income/loss attributable to third-party equity interests in partially-owned properties, as well as the income/loss attributable to redeemable noncontrolling interests (i.e. OP Units not held by ACC or ACC Holdings.)

10. Incentive Award Plan

Restricted Stock Awards (“RSAs”)

A summary of ACC’s RSAs under the Plan as of March 31, 2013 and activity during the three months then ended, is presented below:

Number of RSAs | ||||

| Nonvested balance at December 31, 2012 | 575,668 | |||

| Granted | 230,800 | |||

| Vested | (111,533 | ) | ||

| Forfeited | (75,581 | ) | ||

| Nonvested balance at March 31, 2013 | 619,354 | |||

The fair value of RSA’s is calculated based on the closing market value of ACC’s common stock on the date of grant. The fair value of these awards is amortized to expense over the vesting periods, which amounted to approximately $1.6 million and $1.3 million for the three months ended March 31, 2013 and 2012, respectively.

11. Derivative Instruments and Hedging Activities

The Company is exposed to certain risk arising from both its business operations and economic conditions. The Company principally manages its exposures to a wide variety of business and operational risks through management of its core business activities. The Company manages economic risks, including interest rate, liquidity, and credit risk primarily by managing the amount, sources, and duration of its debt funding and the use of derivative financial instruments. Specifically, the Company enters into derivative financial instruments to manage exposures that arise from business activities that result in the receipt or payment of future known and uncertain cash amounts, the value of which are determined by interest rates. The Company’s derivative financial instruments are used to manage differences in the amount, timing, and duration of the Company’s known or expected cash receipts and its known or expected cash payments principally related to the Company’s investments and borrowings.

Cash Flow Hedges of Interest Rate Risk

The Company’s objectives in using interest rate derivatives are to add stability to interest expense and to manage its exposure to interest rate movements. To accomplish this objective, the Company primarily uses interest rate swaps as part of its interest rate risk management strategy. Interest rate swaps designated as cash flow hedges involve the receipt of variable-rate amounts from a counterparty in exchange for the Company making fixed-rate payments over the life of the agreements without exchange of the underlying notional amount. The effective portion of changes in the fair value of derivatives designated and that qualify as cash flow hedges is recorded in Accumulated Other Comprehensive Loss and is subsequently reclassified into earnings in the period that the hedged forecasted transaction affects earnings. No portion of designated hedges was ineffective during the three months ended March 31, 2013 and 2012.

20

AMERICAN CAMPUS COMMUNITIES, INC. AND SUBSIDIARIES

AMERICAN CAMPUS COMMUNITIES OPERATING PARTNERSHIP, L.P. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(unaudited)