UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

ý Annual Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the fiscal year ended December 31, 2017.

o Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the Transition Period From _____________________ to __________________.

Commission file number 001-32265 (American Campus Communities, Inc.)

Commission file number 333-181102-01 (American Campus Communities Operating Partnership, L.P.)

AMERICAN CAMPUS COMMUNITIES, INC.

AMERICAN CAMPUS COMMUNITIES OPERATING PARTNERSHIP, L.P.

(Exact name of registrant as specified in its charter)

|

| | |

Maryland (American Campus Communities, Inc.) Maryland (American Campus Communities Operating Partnership, L.P.) | | 76-0753089 (American Campus Communities, Inc.) 56-2473181 (American Campus Communities Operating Partnership, L.P.) |

(State or Other Jurisdiction of Incorporation or Organization) | | (IRS Employer Identification No.) |

12700 Hill Country Blvd., Suite T-200 Austin, TX (Address of Principal Executive Offices) | | 78738 (Zip Code) |

(512) 732-1000

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

|

| | |

| (Title of Each Class) | | (Name of Each Exchange on Which Registered) |

| | | |

| Common Stock, $.01 par value | | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

|

| | | |

| American Campus Communities, Inc. | Yes x | No o | |

| American Campus Communities Operating Partnership, L.P. | Yes o | No x | |

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

|

| | | |

| American Campus Communities, Inc. | Yes o | No x | |

| American Campus Communities Operating Partnership, L.P. | Yes o | No x | |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15 (d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

|

| | | |

| American Campus Communities, Inc. | Yes x | No o | |

| American Campus Communities Operating Partnership, L.P. | Yes x | No o | |

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

|

| | | |

| American Campus Communities, Inc. | Yes x | No o | |

| American Campus Communities Operating Partnership, L.P. | Yes x | No o | |

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K.

|

| | | |

| American Campus Communities, Inc. | o | | |

| American Campus Communities Operating Partnership, L.P. | o | | |

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer”, “accelerated filer”, “smaller reporting company”, and “emerging growth company” in Rule 12b-2 of the Exchange Act.

American Campus Communities, Inc.

|

| | |

Large accelerated filer x | Accelerated Filer o | |

Non-accelerated filer o (Do not check if a smaller reporting company) | Smaller reporting company o | |

| | Emerging growth company o | |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

American Campus Communities Operating Partnership, L.P. |

| | |

Large accelerated filer o | Accelerated Filer o | |

Non-accelerated filer x (Do not check if a smaller reporting company) | Smaller reporting company o | |

| | Emerging growth company o | |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act).

|

| | | |

| American Campus Communities, Inc. | Yes o | No x | |

| American Campus Communities Operating Partnership, L.P. | Yes o | No x | |

The aggregate market value of voting and non-voting common equity held by non-affiliates of the registrant was $5,450,514,562 based on the last sale price of the common equity on June 30, 2017 which is the last business day of the Company’s most recently completed second quarter.

There were 136,494,954 shares of the Company’s common stock with a par value of $0.01 per share outstanding as of the close of business on February 23, 2018.

DOCUMENTS INCORPORATED BY REFERENCE

Part III of this report incorporates information by reference from the definitive Proxy Statement for the 2018 Annual Meeting of Stockholders.

EXPLANATORY NOTE

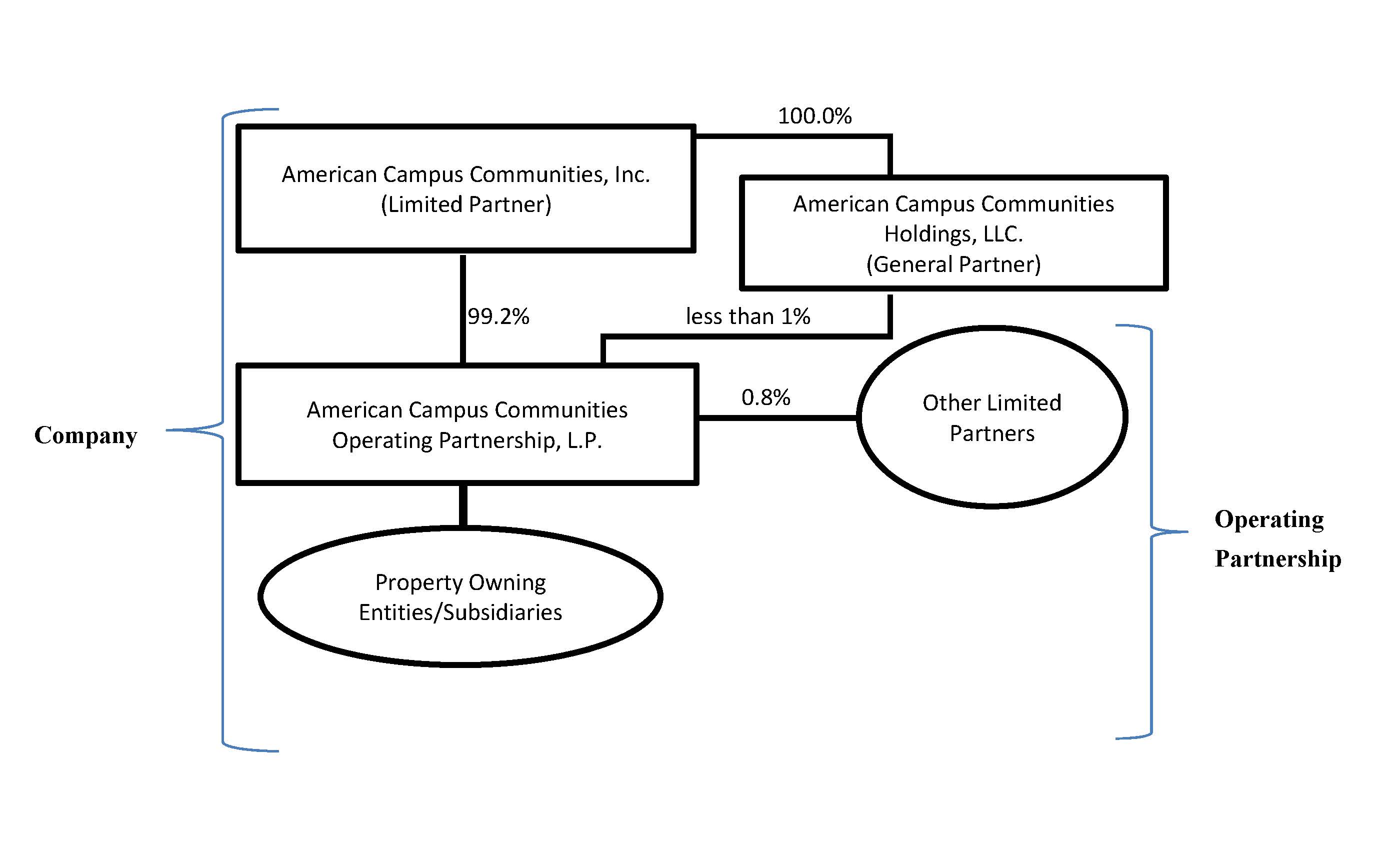

This report combines the annual reports on Form 10-K for the year ended December 31, 2017 of American Campus Communities, Inc. and American Campus Communities Operating Partnership, L.P. Unless stated otherwise or the context otherwise requires, references to “ACC” mean American Campus Communities, Inc. a Maryland corporation that has elected to be treated as a real estate investment trust (“REIT”) under the Internal Revenue Code, and references to “ACCOP” mean American Campus Communities Operating Partnership, L.P., a Maryland limited partnership. References to the “Company,” “we,” “us” or “our” mean collectively ACC, ACCOP and those entities/subsidiaries owned or controlled by ACC and/or ACCOP. References to the “Operating Partnership” mean collectively ACCOP and those entities/subsidiaries owned or controlled by ACCOP. The following chart illustrates the Company’s and the Operating Partnership’s corporate structure:

The general partner of ACCOP is American Campus Communities Holdings, LLC (“ACC Holdings”), an entity that is wholly-owned by ACC. As of December 31, 2017, ACC Holdings held an ownership interest in ACCOP of less than 1%. The limited partners of ACCOP are ACC and other limited partners consisting of current and former members of management and nonaffiliated third parties. As of December 31, 2017, ACC owned an approximate 99.2% limited partnership interest in ACCOP. As the sole member of the general partner of ACCOP, ACC has exclusive control of ACCOP’s day-to-day management. Management operates the Company and the Operating Partnership as one business. The management of ACC consists of the same members as the management of ACCOP. The Company is structured as an umbrella partnership REIT (“UPREIT”) and ACC contributes all net proceeds from its various equity offerings to the Operating Partnership. In return for those contributions, ACC receives a number of units of ACCOP (“OP Units,” see definition below) equal to the number of common shares it has issued in the equity offering. Contributions of properties to the Company can be structured as tax-deferred transactions through the issuance of OP Units in ACCOP. Based on the terms of ACCOP’s partnership agreement, OP Units can be exchanged for ACC’s common shares on a one-for-one basis. The Company maintains a one-for-one relationship between the OP Units of ACCOP issued to ACC and ACC Holdings and the common shares issued to the public. The Company believes that combining the reports on Form 10-K of the Company and the Operating Partnership into this single report provides the following benefits:

| |

| • | enhances investors’ understanding of the Company and the Operating Partnership by enabling investors to view the business as a whole in the same manner as management views and operates the business; |

| |

| • | eliminates duplicative disclosure and provides a more streamlined and readable presentation since a substantial portion of the disclosure applies to both the Company and the Operating Partnership; and |

| |

| • | creates time and cost efficiencies through the preparation of one combined report instead of two separate reports. |

ACC consolidates ACCOP for financial reporting purposes, and ACC essentially has no assets or liabilities other than its investment in ACCOP. Therefore, the assets and liabilities of the Company and the Operating Partnership are the same on their respective financial statements. However, the Company believes it is important to understand the few differences between the Company and the Operating Partnership in the context of how the entities operate as a consolidated company. All of the Company’s property ownership, development and related business operations are conducted through the Operating Partnership. ACC also issues public equity from time to time and guarantees certain debt of ACCOP. ACC does not have any indebtedness, as all debt is incurred by the Operating Partnership. The Operating Partnership holds substantially all of the assets of the Company, including the Company’s ownership interests in its joint ventures. The Operating Partnership conducts the operations of the business and is structured as a partnership with no publicly traded equity. Except for the net proceeds from ACC’s equity offerings, which are contributed to the capital of ACCOP in exchange for OP Units on a one-for-one common share per OP Unit basis, the Operating Partnership generates all remaining capital required by the Company’s business. These sources include, but are not limited to, the Operating Partnership’s working capital, net cash provided by operating activities, borrowings under its credit facility, the issuance of unsecured notes, and proceeds received from the disposition of certain properties. Noncontrolling interests, stockholders’ equity, and partners’ capital are the main areas of difference between the consolidated financial statements of the Company and those of the Operating Partnership. The noncontrolling interests in the Operating Partnership’s financial statements consist of the interests of unaffiliated partners in various consolidated joint ventures. The noncontrolling interests in the Company’s financial statements include the same noncontrolling interests at the Operating Partnership level and OP Unit holders of ACCOP. The differences between stockholders’ equity and partners’ capital result from differences in the type of equity issued at the Company and Operating Partnership levels.

To help investors understand the significant differences between the Company and the Operating Partnership, this report provides separate consolidated financial statements for the Company and the Operating Partnership. A single set of consolidated notes to such financial statements is presented that includes separate discussions for the Company and the Operating Partnership when applicable (for example, noncontrolling interests, stockholders’ equity or partners’ capital, earnings per share or unit, etc.). A combined Management’s Discussion and Analysis of Financial Condition and Results of Operations section is also included that presents discrete information related to each entity, as applicable. This report also includes separate Part II, Item 9A Controls and Procedures sections and separate Exhibits 31 and 32 certifications for each of the Company and the Operating Partnership in order to establish that the requisite certifications have been made and that the Company and the Operating Partnership are compliant with Rule 13a-15 or Rule 15d-15 of the Securities Exchange Act of 1934 and 18 U.S.C. §1350.

In order to highlight the differences between the Company and the Operating Partnership, the separate sections in this report for the Company and the Operating Partnership specifically refer to the Company and the Operating Partnership. In the sections that combine disclosure of the Company and the Operating Partnership, this report refers to actions or holdings as being actions or holdings of the Company. Although the Operating Partnership is generally the entity that directly or indirectly enters into contracts and joint ventures and holds assets and debt, reference to the Company is appropriate because the Company operates its business through the Operating Partnership. The separate discussions of the Company and the Operating Partnership in this report should be read in conjunction with each other to understand the results of the Company on a consolidated basis and how management operates the Company.

FORM 10-K

FOR THE YEAR ENDED DECEMBER 31, 2017

TABLE OF CONTENTS

|

| | |

| | | PAGE NO. |

PART I. | | |

| Item 1. | Business | |

| Item 1A. | Risk Factors | |

| Item 1B. | Unresolved Staff Comments | |

| Item 2. | Properties | |

| Item 3. | Legal Proceedings | |

| Item 4. | Mine Safety Disclosures | |

| | | |

PART II. | | |

| Item 5. | Market for Registrant’s Common Equity and Related Stockholder Matters | |

| Item 6. | Selected Financial Data | |

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | |

| Item 7A. | Quantitative and Qualitative Disclosures About Market Risk | |

| Item 8. | Financial Statements and Supplementary Data | |

| Item 9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | |

| Item 9A. | Controls and Procedures | |

| | | |

| PART III. | | |

| Item 10. | Directors, Executive Officers and Corporate Governance | |

| Item 11. | Executive Compensation | |

| Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | |

| Item 13. | Certain Relationships, Related Transactions and Director Independence | |

| Item 14. | Principal Accountant Fees and Services | |

| | | |

| PART IV. | | |

| Item 15. | Exhibits and Financial Statement Schedules | |

| | | |

| SIGNATURES | | |

PART I

Item 1. Business

Overview

American Campus Communities, Inc. (“ACC”) is a real estate investment trust (“REIT”) that commenced operations effective with the completion of an initial public offering (“IPO”) on August 17, 2004. Through ACC’s controlling interest in American Campus Communities Operating Partnership, L.P. (“ACCOP”), ACC is one of the largest owners, managers and developers of high quality student housing properties in the United States in terms of beds owned and under management. ACC is a fully integrated, self-managed and self-administered equity REIT with expertise in the acquisition, design, financing, development, construction management, leasing and management of student housing properties. ACC’s common stock is publicly traded on the New York Stock Exchange (“NYSE”) under the ticker symbol “ACC.”

The general partner of ACCOP is American Campus Communities Holdings, LLC (“ACC Holdings”), an entity that is wholly-owned by ACC. As of December 31, 2017, ACC Holdings held an ownership interest in ACCOP of less than 1%. The limited partners of ACCOP are ACC and other limited partners consisting of current and former members of management and nonaffiliated third parties. As of December 31, 2017, ACC owned an approximate 99.2% limited partnership interest in ACCOP. As the sole member of the general partner of ACCOP, ACC has exclusive control of ACCOP’s day-to-day management. Management operates ACC and ACCOP as one business. The management of ACC consists of the same members as the management of ACCOP. ACC consolidates ACCOP for financial reporting purposes, and ACC does not have significant assets other than its investment in ACCOP. Therefore, the assets and liabilities of ACC and ACCOP are the same on their respective financial statements. References to the “Company,” “we,” “us” or “our” mean collectively ACC, ACCOP and those entities/subsidiaries owned or controlled by ACC and/or ACCOP. References to the “Operating Partnership” mean collectively ACCOP and those entities/subsidiaries owned or controlled by ACCOP.

As of December 31, 2017, our total owned and third-party managed portfolio included 206 properties with approximately 134,100 beds.

Business Objectives, Investment Strategies, and Operating Segments

Business Objectives

Our primary business objectives are to create long-term stockholder value by deploying capital to develop, redevelop, acquire and operate student housing communities, and to sell communities when they no longer meet our long-term investment strategy and when market conditions are favorable. We believe we can achieve these objectives by continuing to implement our investment strategies and successfully manage our operating segments, which are described in more detail below.

Investment Strategies

We seek to own high quality, well designed and well located student housing properties. We seek to acquire or develop properties in markets that have stable or increasing student populations, are in submarkets with barriers to entry and provide opportunities for economic growth as a result of their product position and/or differentiated design and close proximity to campuses, or through our superior operational capabilities. We believe that our reputation and established relationships with universities give us an advantage in sourcing acquisitions and developments and obtaining municipal approvals and community support for our development projects.

Acquisitions and Joint Venture Investments: As discussed in more detail in Note 5 in the accompanying Notes to Consolidated Financial Statements contained in Item 8, in 2017 we executed an agreement to acquire a portfolio of seven student housing properties from affiliates of Core Spaces and DRW Real Estate Investments (the “Core Transaction”). The transaction included the purchase of 100% of the ownership interests in two operating properties, the purchase of partial ownership interests in two operating properties through a joint venture arrangement, and the purchase of partial ownership interests in three in-process development properties through a joint venture arrangement. In total, the Core Transaction properties contain 3,776 beds and the initial investment made at closing was $306.0 million. Including the initial investment, the Company expects to invest a total of $590.6 million through a phased purchase of 100% of the ownership interest in all seven properties.

Additionally in 2017, the Company acquired three wholly-owned properties containing 1,240 beds for approximately $222.9 million. Refer to Note 5 in the accompanying Notes to Consolidated Financial Statements contained in Item 8 for a more detailed discussion of our recent acquisition activity.

We believe our relationships with university systems and individual educational institutions, our knowledge of the student housing market and our prominence as the first publicly-traded REIT focused exclusively on student housing in the United States will afford us a competitive advantage in acquiring additional student housing properties.

Development: In August 2017, the final stages of construction were completed on three on-campus ACE properties and seven owned off-campus properties. These properties are summarized in the following table:

|

| | | | | | | | | | | | | | |

Project | | Location | | Primary University Served | | Project Type | | Beds | | Total Project Cost | | Opened for Occupancy |

| | | | | | | | | | | | | |

| Tooker House | | Tempe, AZ | | Arizona State University | | ACE | | 1,594 | | $ | 105,500 |

| | August 2017 |

| Sky View | | Flagstaff, AZ | | Northern Arizona University | | ACE | | 626 | | 58,200 |

| | August 2017 |

| University Square | | Prairie View, TX | | Prairie View A&M University | | ACE | | 466 | | 25,900 |

| | August 2017 |

| U Centre on Turner | | Columbia, MO | | University of Missouri | | Off-campus | | 718 | | 69,600 |

| | August 2017 |

| U Pointe on Speight | | Waco, TX | | Baylor University | | Off-campus | | 700 | | 51,800 |

| | August 2017 |

| 21Hundred @ Overton Park | | Lubbock, TX | | Texas Tech University | | Off-campus | | 1,204 | | 82,700 |

| | August 2017 |

| Suites at 3rd | | Champaign, IL | | University of Illinois | | Off-campus | | 251 | | 25,200 |

| | August 2017 |

| U Club Binghamton Phase II | | Binghamton, NY | | SUNY Binghamton University | | Off-campus | | 562 | | 56,900 |

| | August 2017 |

| Callaway House Apartments | | Norman, OK | | University of Oklahoma | | Off-campus | | 915 | | 90,700 |

| | August 2017 |

| U Centre on College | | Clemson, SC | | Clemson University | | Off-campus | | 418 | | 42,700 |

| | August 2017 |

| TOTAL – 2017 DELIVERIES | | 7,454 | | $ | 609,200 |

| | |

At December 31, 2017, we were in the process of constructing seven on-campus ACE properties, and six owned off-campus properties. These properties are summarized in the tables below:

Owned Development Projects Under Construction:

|

| | | | | | | | | | | | | | | | | | |

Project | | Location | | Primary University Served | | Project Type | | Beds | | Estimated Project Cost | | Total Costs Incurred | | Scheduled Completion |

| | | | | | | | | | | | | | | |

| Gladding Residence Center | | Richmond, VA | | Virginia Commonwealth University | | ACE | | 1,524 | | $ | 95,700 |

| | $ | 74,764 |

| | August 2018 |

| Irvington House | | Indianapolis, IN | | Butler University | | ACE | | 648 | | 38,900 |

| | 22,922 |

| | August 2018 |

| Greek Leadership Village | | Tempe, AZ | | Arizona State University | | ACE | | 957 | | 69,600 |

| | 31,461 |

| | August 2018 |

| David Blackwell Hall | | Berkeley, CA | | University of California, Berkeley | | ACE | | 781 | | 98,700 |

| | 60,234 |

| | August 2018 |

| NAU Honors College | | Flagstaff, AZ | | Northern Arizona University | | ACE | | 636 | | 43,400 |

| | 24,880 |

| | August 2018 |

| U Club Townhomes | | Oxford, MS | | University of Mississippi | | Off-campus | | 528 | | 44,300 |

| | 26,181 |

| | August 2018 |

| SUBTOTAL – 2018 DELIVERIES | | 5,074 | | $ | 390,600 |

| | $ | 240,442 |

| | |

| | | | | | | | | | | | | | | |

| 191 College | | Auburn, AL | | Auburn University | | Off-campus | | 495 | | 59,300 |

| | 15,874 |

| | July 2019 |

| University of Arizona Honors College | | Tucson, AZ | | University of Arizona | | ACE | | 1,056 | | 84,700 |

| | 13,348 |

| | August 2019 |

| Columbus Avenue Student Apts. | | Boston, MA | | Northeastern University | | ACE | | 825 | | 153,400 |

| | 42,096 |

| | August 2019 |

| SUBTOTAL – 2019 DELIVERIES | | 2,376 | | $ | 297,400 |

| | $ | 71,318 |

| | |

| | | | | | | | | | | | | | | |

| TOTAL – ALL PROJECTS | | 7,450 | | $ | 688,000 |

| | $ | 311,760 |

| | |

| | | | | | | | | | | | | | | |

Presale Development Projects Under Construction:

Under the terms of a presale transaction, the Company is obligated to purchase the property as long as certain construction completion deadlines and other closing conditions are met. The Company is responsible for leasing, management, and initial operations of the project while the third-party developer retains development risk during the construction period. In accordance with accounting guidance, the Company includes presale properties in its consolidated financial statements upon execution of the presale agreement with the developer.

|

| | | | | | | | | | | | | | | | | | |

Project | | Location | | Primary University Served | | Project Type | | Beds | | Purchase Price | | Amount Funded as of December 31, 2017 | | Scheduled Completion |

| | | | | | | | | | | | | | | |

| The Edge - Stadium Centre | | Tallahassee, FL | | Florida State University | | Off-campus | | 412 | | $ | 42,600 |

| | $ | 400 |

| | August 2018 |

Core Spaces / DRW Portfolio (1) | | | | | | | | | | | | | | |

| Hub Ann Arbor | | Ann Arbor, MI | | University of Michigan | | Off-campus | | | | | | | | September 2018 |

| Hub Flagstaff | | Flagstaff, AZ | | Northern Arizona University | | Off-campus | | | | | | | | September 2018 |

| Hub West Lafayette | | West Lafayette, IN | | Purdue University | | Off-campus | | | | | | | | September 2018 |

| | | | | | | | | 1,500 | | $ | 240,000 |

| | $ | 24,208 |

| | |

| TOTAL – 2018 DELIVERIES | | 1,912 | | $ | 282,600 |

| | $ | 24,608 |

| | |

| | | | | | | | | | | | | | | |

| |

(1) | We funded an initial investment of $24.2 million through a joint venture with Core Spaces/DRW Real Estate Investments in August 2017. Including the initial investment, we expect to invest a total of $240.0 million over a two year period. See Note 5 in the accompanying Notes to Consolidated Financial Statements contained in Item 8 for further discussion. |

Our experienced development staff intends to continue to identify and acquire land parcels in close proximity to colleges and universities that offer location advantages or that allow for the development of unique products that offer a competitive advantage. We expect to continue to benefit from opportunities derived from our extensive network with colleges and universities as well as our relationship with certain developers with whom we have previously developed student housing properties.

Operating Segments

We define business segments by their distinct customer base and service provided. We have identified four reportable segments: Owned Properties, On-Campus Participating Properties, Development Services and Property Management Services. For a detailed financial analysis of our segments’ results of operations and financial position, please refer to Note 17 in the accompanying Notes to Consolidated Financial Statements contained in Item 8.

Property Operations

Unique Leasing Characteristics: Student housing properties are typically leased by the bed on an individual lease liability basis, unlike multifamily housing where leasing is by the unit. Individual lease liability limits each resident’s liability to his or her own rent without liability for a roommate’s rent. A parent or guardian is generally required to execute each lease as a guarantor unless the resident provides adequate proof of income or financial aid. The number of lease contracts that we administer is therefore approximately equivalent to the number of beds occupied and not the number of units. Leases at our off-campus properties typically require 12 monthly rent payments, whereas leases for our residence hall properties typically correspond to the university’s academic year and require 10 monthly rent payments. (Please refer to the property table contained in Item 2 – Properties for a listing of the typical rent payment terms at our properties.) As an example, in the case of our typical off-campus leases, the commencement date coincides with the commencement of the respective university’s Fall academic term and the termination date is the last day of the subsequent summer school session. As such, we must re-lease each property in its entirety each year.

Management Philosophy: Our management philosophy is based upon meeting the following objectives:

| |

| • | Satisfying the specialized needs of residents by providing the highest levels of customer service; |

| |

| • | Developing and maintaining an academically oriented environment via a premier residence life/student development program; |

| |

| • | Maintaining each project’s physical plant in top condition; |

| |

| • | Maximizing revenue through the development and implementation of a strategic annual marketing plan and leasing administration program; and |

| |

| • | Maximizing cash flow through maximizing revenue coupled with prudent control of expenses. |

LAMS: We believe we have developed the industry’s only specialized, fully integrated leasing administration and marketing software program, which we call LAMS. We utilize LAMS to maximize our revenue and improve the efficiency and effectiveness of our marketing and lease administration process. Through LAMS, each of our properties’ ongoing marketing and leasing efforts are supervised at the corporate office on a real time basis. Among other things, LAMS provides:

| |

| • | a fully integrated prospect tracking and follow-up system; |

| |

| • | a built-in marketing effectiveness program to measure the success of our marketing efforts on a real time basis; |

| |

| • | a real-time monitor of lease closings and leasing terms; |

| |

| • | an automated lease generation system; |

| |

| • | the generation of future period rent rolls to aid in budgeting and forecasting; and |

| |

| • | a customized report writer. |

Owned Properties: Off-campus properties are generally located in close proximity to the school campus, generally with pedestrian, bicycle, or university shuttle access. Off-campus housing tends to offer more relaxed rules and regulations than on-campus housing, resulting in off-campus housing being generally more appealing to upper-classmen. We believe that the support of colleges and universities can be beneficial to the success of our owned properties. We actively seek to have these institutions recommend our facilities to their students or to provide us with mailing lists so that we may directly market to students and parents. In some cases, the institutions actually promote our off-campus facilities in their recruiting and admissions literature. In cases where the educational institutions do not provide mailing lists or recommendations for off-campus housing, most provide comprehensive lists of suitable properties to their students, and we continually work to ensure that our properties are on these lists in each of the markets that we serve.

Off-campus housing is subject to competition for tenants with on-campus housing owned by colleges and universities, and vice versa. Colleges and universities can generally avoid real estate taxes and borrow funds at lower interest rates than us (and other private sector operators), thereby decreasing their operating costs. Residence halls owned and operated by the primary colleges and universities in the markets of our off-campus properties may charge lower rental rates, but typically offer fewer amenities than we offer at our properties. Additionally, most universities are only able to house a small percentage of their overall enrollment, and are therefore highly dependent upon the off-campus market to provide housing for their students. High-quality, well run off-campus student housing can be a critical component to an institution’s ability to attract and retain students. Therefore, developing and maintaining good relationships with educational institutions can result in a privately owned off-campus facility becoming, in effect, an extension of the institution’s housing program, with the institution providing highly valued references and recommendations to students and parents.

This segment also competes with national and regional owner-operators of off-campus student housing in a number of markets as well as with smaller local owner-operators. Therefore, the performance of this segment could be affected by the construction of new on-campus or off-campus residences, increases or decreases in the general levels of rents for housing in competing communities, increases or decreases in the number of students enrolled at one or more of the colleges or universities in the market of a property, and other general economic conditions.

American Campus Equity (ACE): Included in our owned properties segment and branded and marketed to colleges and universities as the ACE program, this transaction structure provides us with what we believe is a lower-risk opportunity compared to other off-campus projects, as our ACE projects have premier on-campus locations with marketing and operational assistance from the university. The subject university substantially benefits by increasing its housing capacity with modern, well-amenitized student housing with no or minimal impacts to its own credit ratios, preserving the university’s credit capacity to fund academic and research facilities.

On-Campus Participating Properties: Our On-Campus Participating Properties segment includes five on-campus properties that are operated under long-term ground/facility leases with three university systems. Under our ground/facility leases, we receive an annual distribution representing 50% of these properties’ net cash flows, as defined in the ground/facility lease agreements. We also manage these properties under long-term management agreements and are paid management fees equal to a percentage of defined gross receipts. Refer to Note 8 in the accompanying Notes to Consolidated Financial Statements contained in Item 8 herein for a more detailed description of these properties.

Our on-campus participating properties are susceptible to some of the same risks as our owned properties, including: (i) seasonality in rents; (ii) annual re-leasing that is highly dependent on marketing and university admission policies; and (iii) competition for tenants from other on-campus housing operated by educational institutions or other off-campus properties.

Third-Party Services

Our third-party services consist of development services and management services and are typically provided to university and college clients. Many of our third-party management services are provided to clients for whom we also provide development services. While management evaluates the operational performance of our third-party services based on the distinct segments identified below, at times we also evaluate these segments on a combined basis.

Development Services: Our Development Services segment consists of development and construction management services that we provide through one of our taxable REIT subsidiaries (“TRSs”) for third-party owners. These services range from short-term consulting projects to long-term full-scale development and construction projects. We typically provide these services to colleges

and universities seeking to modernize their on-campus student housing properties. They look to us to bring our student housing experience and expertise to ensure they develop marketable, functional and financially sustainable facilities. Educational institutions usually seek to build housing that will enhance their recruitment and retention of students while facilitating their academic objectives. Most of these development service contracts are awarded via a competitive request for proposal (“RFP”) process that qualifies developers based on their overall capability to provide specialized student housing design, development, construction management, financial structuring and property management services. Our development services typically include pre-development, design and financial structuring services. Our pre-development services typically include feasibility studies for third-party owners and design services. Feasibility studies include an initial feasibility analysis, review of conceptual design and assistance with master planning. Some of the documents produced in this process include the conceptual design documents, preliminary development and operating budgets, cash flow projections and a preliminary market assessment. Our design services include coordination with the architect and other members of the design team, review of construction plans and assistance with project due diligence and project budgets.

Construction management services typically consist of hiring of project professionals and a general contractor, coordinating and supervising the construction, equipping and furnishing the property, site visits, and full coordination and administration of all activities necessary for project completion in accordance with plans and specifications and with verification of adequate insurance.

Our Development Services activities benefit our primary goal of owning and operating student housing properties in a number of ways. By providing these services to others, we are able to expand and refine our unit plan and community design, the operational efficiency of our material specifications and our ability to determine market acceptance of unit and community amenities. Our development and construction management personnel enable us to establish relationships with general contractors, architects and project professionals throughout the nation. Through these services, we gain experience and expertise in residential and commercial construction methodologies under various labor conditions, including right-to-work labor markets, markets subject to prevailing wage requirements and fully unionized environments. This segment is subject to competition from other specialized student housing development companies as well as from national real estate development companies.

Property Management Services: Our Property Management Services segment, conducted by one of our TRSs, includes revenues generated from third-party management contracts in which we are typically responsible for all aspects of operations, including marketing, leasing administration, facilities maintenance, business administration, accounts payable, accounts receivable, financial reporting, capital projects and residence life student development. We provide these services pursuant to management agreements that have initial terms that range from one to five years.

There are several housing options that compete with our third-party managed properties including, but not limited to, multifamily housing, for-rent single family dwellings, other off-campus specialized student housing and the aforementioned on-campus participating properties. We also compete with other regional and national providers of third-party management services.

Americans with Disabilities Act and Federal Fair Housing Act

Many laws and governmental regulations are applicable to our properties and changes in the laws and regulations, or their interpretation by agencies and the courts, occur frequently. Our properties must comply with Title III of the Americans with Disabilities Act, or ADA, to the extent that such properties are “public accommodations” as defined by the ADA. The ADA may require removal of structural barriers to access by persons with disabilities in certain public areas of our properties where such removal is readily achievable. We believe that the existing properties are in substantial compliance with the ADA and that we will not be required to make substantial capital expenditures to address the requirements of the ADA. However, noncompliance with the ADA could result in imposition of fines or an award of damages to private litigants. The obligation to make readily achievable accommodations is an ongoing one, and we intend to continue to assess our properties and to make alterations as appropriate in this respect.

Under the federal and state fair housing laws, discrimination on the basis of certain protected classes is prohibited. Violation of these laws can result in significant damage awards to victims.

Environmental Matters

Under various laws and regulations relating to the protection of the environment, an owner of real estate may be held liable for the costs of removal or remediation of certain hazardous or toxic substances located on or in its property. These laws often impose liability without regard to whether the owner was responsible for, or even knew of, the presence of such substances. The presence of such substances may adversely affect the owner’s ability to rent or sell the property or use the property as collateral. Independent environmental consultants conducted environmental site assessments on all acquired or developed owned properties and on-campus participating properties in our existing portfolio. We are not aware of any environmental conditions that management

believes would have a material adverse effect on the Company. There is no assurance, however, that environmental site assessments or other investigations would reveal all environmental conditions or that environmental conditions not known to us may exist now or in the future which would result in liability to the Company for remediation or fines, either under existing laws and regulations or future changes to such requirements.

From time to time, the United States Environmental Protection Agency, or EPA, designates certain sites affected by hazardous substances as “Superfund” sites pursuant to CERCLA. Superfund sites can cover large areas, affecting many different parcels of land. Although CERCLA imposes joint and several liability for contamination on property owners and operators regardless of fault, the EPA may choose to pursue potentially responsible parties (“PRPs”) based on their actual contribution to the contamination. PRPs are liable for the costs of responding to the hazardous substances. Each of Villas on Apache (disposed of in April 2011), The Village on University (disposed of in December 2006) and University Village at San Bernardino (disposed of in January 2005) are located within federal Superfund sites. The EPA designated these areas as Superfund sites because groundwater underneath these areas is contaminated. We have not been named, and do not expect to be named, as a PRP with respect to these sites. However, there can be no assurance regarding potential future developments concerning such sites.

Insurance

Our primary lines of insurance coverage are property, liability and workers’ compensation. We believe that our insurance coverages are of the type and amount customarily obtained on real property assets. We intend to obtain similar coverage for properties we acquire in the future. However, there are certain types of losses, generally of a catastrophic nature, such as losses from floods or earthquakes, which may be subject to limitations in certain areas. When not otherwise contractually stipulated, we exercise our judgment in determining amounts, coverage limits and deductibles, in an effort to maintain appropriate levels of insurance on our investments. If we suffer a substantial loss, our insurance coverage may not be sufficient due to market conditions at the time or other unforeseen factors. Inflation, changes in building codes and ordinances, environmental considerations and other factors also might make it infeasible to use insurance proceeds to replace a property after it has been damaged or destroyed.

Employees

As of December 31, 2017, we had approximately 3,183 employees, consisting of:

| |

| • | approximately 1,805 on-site employees in our owned properties segment, including 696 Resident Assistants; |

| |

| • | approximately 107 on-site employees in our on-campus participating properties segment, including 46 Resident Assistants; |

| |

| • | approximately 1,086 employees in our property management services segment, including 908 on-site employees and 178 corporate office employees; |

| |

| • | approximately 58 corporate office employees in our development services segment; and |

| |

| • | approximately 127 executive, corporate administration and financial personnel. |

Our employees are not currently represented by a labor union.

Offices and Website

Our principal executive offices are located at 12700 Hill Country Boulevard, Suite T-200 Austin, TX 78738. Our telephone number at that location is (512) 732-1000.

We file our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and other reports required by Sections 13(a) and 15(d) of the Securities Exchange Act of 1934. You may read and copy any materials we file with the SEC at the SEC’s Public Reference Room at 100 F Street, NE, Washington, DC 20549. You may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. The SEC maintains an internet site that contains reports, proxy and information statements and other information regarding issuers that file electronically with the SEC. The address of that site is www.sec.gov.

Our website is located at www.americancampus.com. We make available free of charge through our website our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to these reports filed or furnished pursuant to Sections 13(a) or 15(d) of the Securities Act of 1934, as amended, as soon as reasonably practicable after we electronically file such material with, or furnish it to, the SEC. Our website also contains copies of our Corporate Governance Guidelines and Code of Business Ethics as well as the charters of our Nominating and Corporate Governance, Audit, Compensation and Risk committees. The information on our website is not part of this filing.

Forward-looking Statements

This report contains forward-looking statements within the meaning of the federal securities laws. We caution investors that any forward-looking statements presented in this report, or which management may make orally or in writing from time to time, are based on management’s beliefs and assumptions made by, and information currently available to, management. When used, the words “anticipate,” “believe,” “expect,” “intend,” “may,” “might,” “plan,” “estimate,” “project,” “should,” “will,” “result” and similar expressions, do not relate solely to historical matters and are intended to identify forward-looking statements. Such statements are subject to risks, uncertainties and assumptions and may be affected by known and unknown risks, trends, uncertainties and factors that are beyond our control. Should one or more of these risks or uncertainties materialize, or should underlying assumptions prove incorrect, actual results may vary materially from those anticipated, estimated or projected. We caution you that forward-looking statements are not guarantees of future performance and will be impacted by actual events when they occur after we make such statements. We expressly disclaim any responsibility to update forward-looking statements, whether as a result of new information, future events or otherwise. Accordingly, investors should use caution in relying on past forward-looking statements, which are based on results and trends at the time they were made, to anticipate future results or trends.

Some of the risks and uncertainties that may cause our actual results, performance or achievements to differ materially from those expressed or implied by forward-looking statements include, among others, the following: general risks affecting the real estate industry; risks associated with changes in University admission or housing policies; risks associated with the availability and terms of financing and the use of debt to fund acquisitions and developments; failure to manage effectively our growth and expansion into new markets or to integrate acquisitions successfully; risks and uncertainties affecting property development and construction; risks associated with downturns in the national and local economies, volatility in capital and credit markets, increases in interest rates, and volatility in the securities markets; costs of compliance with the Americans with Disabilities Act and other similar laws; potential liability for uninsured losses and environmental contamination; risks associated with our Company’s potential failure to qualify as a REIT under the Internal Revenue Code of 1986 (the “Code”), as amended, and possible adverse changes in tax and environmental laws; and the other factors discussed in the “Risk Factors” contained in Item 1A of this report.

Item 1A. Risk Factors

The following risk factors may contain defined terms that are different from those used in other sections of this report. Unless otherwise indicated, when used in this section, the terms “we” and “us” refer to American Campus Communities, Inc. and its subsidiaries, including American Campus Communities Operating Partnership, L.P., our Operating Partnership, and the term “securities” refers to shares of common stock of American Campus Communities, Inc. and units of limited partnership interest in our Operating Partnership.

The factors described below represent our principal risks. Other factors may exist that we do not consider being significant based on information that is currently available or that we are not currently able to anticipate.

Risks Related to Our Properties, Our Business and the Real Estate Industry

Our results of operations are subject to risks inherent in the student housing industry, including a concentrated lease-up period and seasonal cash flows.

Leases at our off-campus properties typically require 12 monthly lease payments, whereas leases at our residence hall properties typically correspond to the university’s academic year and require 10 monthly rent payments. As a result, we may experience significantly reduced cash flows during the summer months at our residence hall properties. Furthermore, all of our properties must be entirely re-leased each year during a limited leasing season. We are therefore highly dependent on the effectiveness of our marketing and leasing efforts and personnel during this season, exposing us to significant leasing risk. In addition, we are subject to increased leasing risk on our properties under construction and future acquired properties based on our lack of experience leasing those properties and unfamiliarity with their leasing cycles. If we are unable to lease a substantial portion of our properties, or if the rental rates upon such leasing are significantly lower than expected rates, our cash flow from operations and our ability to make distributions to stockholders and service indebtedness could be adversely affected.

Additionally, prior to the commencement of each new lease period, generally during the first two weeks of August, we prepare the units for new incoming residents. During this period (referred to as “turn”), we incur significant expenses making our units ready for occupancy, which we recognize as incurred. We therefore experience seasonally decreased operating results and cash flows during the third quarter of each year as a result of expenses we incur during turn as well as lower revenue at our residence hall properties.

We rely on our relationships with universities, and changes in university personnel and/or policies could adversely affect our operating results.

In some cases, we rely on our relationships with colleges and universities for referrals of prospective student-tenants or for mailing lists of prospective student-tenants and their parents. Many of these colleges and universities own and operate their own competing on-campus facilities. Any failure to maintain good relationships with these colleges and universities could therefore have a material adverse effect on us. If colleges and universities refuse to make their lists of prospective student-tenants and their parents available to us or increase the costs of these lists, there could be a material adverse effect on us.

Changes in university admission policies could adversely affect us. For example, if a university reduces the number of student admissions or requires that a certain class of students, such as freshmen, live in a university-owned facility, the demand for our properties may be reduced and our occupancy rates may decline. While we may engage in marketing efforts to compensate for such change in admission policy, we may not be able to affect such marketing efforts prior to the commencement of the annual lease-up period or at all.

A decrease in enrollment at the Universities at which our properties are located could adversely affect our financial results.

University enrollment can be affected by a number of factors including, but not limited to, the current macroeconomic environment, students’ ability to afford tuition and/or the availability of student loans, competition for international students, the impact of visa requirements for international students, higher demand for distance education, and budget constraints that could limit a University’s ability to attract and retain students. If a University’s enrollment were to significantly decline as a result of these or other factors, our ability to achieve our leasing targets and thus our properties’ financial performance could be adversely affected.

We face significant competition from university-owned student housing and from other private student housing communities located within close proximity to universities.

On-campus student housing traditionally has certain inherent advantages over off-campus student housing because of, among other factors, closer physical proximity to the university campus and integration of on-campus facilities into the academic community. Colleges and universities can generally avoid real estate taxes, while we and other private sector owners are subject to full real estate tax rates. Also, colleges and universities may be able to borrow funds at lower interest rates than those available to us and other private sector owners. As a result, universities may be able to offer more convenient and/or less expensive student housing than we can, which may adversely affect our occupancy and rental rates.

We also compete with other national and regional owner-operators of off-campus student housing in a number of markets as well as with smaller local owner-operators. There are a number of purpose-built student housing properties that compete directly with us located near or in the same general vicinity of many of our student housing communities. Such competing student housing communities may be newer than our student housing communities, located closer to campus, charge less rent, possess more attractive amenities, or offer more services, shorter lease terms or more flexible leases. The construction of competing properties or decreases in the general levels of rents for housing at competing properties could adversely affect our rental income.

We have recently seen a number of large new entrants in the student housing business and there may be additional new entrants with substantial financial and marketing resources. The entry of these companies has increased and may continue to increase competition for students and for the acquisition, development and management of other student housing properties.

We may be unable to successfully complete and operate our properties or our third-party developed properties.

We intend to continue to develop and construct student housing. These activities include a number of risks, which may include the following:

| |

| • | we may be unable to obtain financing on favorable terms or at all; |

| |

| • | we may not complete development projects on schedule, within budgeted amounts or in conformity with building plans and specifications; |

| |

| • | we may encounter delays or refusals in obtaining all necessary zoning, land use, building, occupancy and other required governmental permits and authorizations; |

| |

| • | occupancy and rental rates at newly developed or renovated properties may fluctuate depending on a number of factors, including market and economic conditions, and may reduce or eliminate our return on investment; |

| |

| • | we may become liable for injuries and accidents occurring during the construction process and for environmental liabilities, including off-site disposal of construction materials; |

| |

| • | we may decide to abandon our development efforts if we determine that continuing the project would not be in our best interests; and |

| |

| • | we may encounter strikes, weather, government regulations and other conditions beyond our control. |

Our newly developed properties will be subject to risks associated with managing new properties, including lease-up and integration risks. In addition, new development activities, regardless of whether or not they are ultimately successful, typically will require a substantial portion of the time and attention of our development and management personnel. Newly developed properties may not perform as expected.

We anticipate that we will, from time to time, elect not to proceed with ongoing development projects. If we elect not to proceed with a development project, the development costs associated therewith will ordinarily be charged against income for the then-current period. Any such charge could have a material adverse effect on our results of operations in the period in which the charge is taken.

We may in the future develop properties nationally, internationally or in geographic regions other than those in which we currently operate. We do not possess the same level of familiarity with development and related regulations in these new markets, which could adversely affect our ability to develop such properties successfully or at all or to achieve expected performance. Future development opportunities may not be available to us on terms that meet our investment criteria or we may be unsuccessful in capitalizing on such opportunities.

We typically provide guarantees of timely completion of projects that we develop for third parties. In certain cases, our contingent liability under these guarantees may exceed our development fee from the project. Although we seek to mitigate this risk by, among other things, obtaining similar guarantees from the project contractor, we could sustain significant losses if development

of a project were to be delayed or stopped and we were unable to cover our guarantee exposure with the guarantee received from the project contractor.

We may be unable to successfully acquire properties on favorable terms.

Our future growth will be in part dependent upon our ability to successfully acquire new properties on favorable terms. With respect to recently acquired properties, and as we acquire additional properties, we will continue to be subject to risks associated with managing new properties, including lease-up and integration risks. Acquired properties may not perform as expected and may have characteristics or deficiencies unknown to us at the time of acquisition. Future acquisition opportunities may not be available to us on terms that meet our investment criteria or we may be unsuccessful in capitalizing on such opportunities.

Our ability to acquire properties on favorable terms and successfully operate them involves the following significant risks:

| |

| • | our potential inability to acquire a desired property may be caused by competition from other real estate investors; |

| |

| • | competition from other potential acquirers may significantly increase the purchase price and decrease expected yields; |

| |

| • | we may be unable to finance an acquisition on favorable terms or at all; |

| |

| • | we may have to incur significant unexpected capital expenditures to improve or renovate acquired properties; |

| |

| • | we may be unable to quickly and efficiently integrate new acquisitions, particularly acquisitions of portfolios of properties, into our existing operations; |

| |

| • | market conditions may result in higher than expected costs and vacancy rates and lower than expected rental rates; and |

| |

| • | we may acquire properties subject to liabilities but without any recourse, or with only limited recourse, to the sellers, or with liabilities that are unknown to us, such as liabilities for clean-up of undisclosed environmental contamination, claims by tenants, vendors or other persons dealing with the former owners of our properties and claims for indemnification by members, directors, officers and others indemnified by the former owners of our properties. |

Our failure to acquire or finance property acquisitions on favorable terms, or operate acquired properties to meet our financial expectations, could adversely affect us.

Difficulties of selling real estate could limit our flexibility.

We intend to evaluate the potential disposition of assets that may no longer meet our investment objectives. When we decide to sell an asset, we may encounter difficulty in finding buyers in a timely manner as real estate investments generally cannot be disposed of quickly, especially when market conditions are poor. This may limit our ability to vary our portfolio promptly in response to changes in economic or other conditions. In some cases, we may also determine that we will not recover the carrying value of the property upon disposition and might recognize an impairment charge. In addition, in order to maintain our status as a REIT, the Internal Revenue Code imposes restrictions on our ability to sell properties held fewer than two years, which may cause us to incur losses thereby reducing our cash flows and adversely impacting distributions to equity holders.

Our ownership of properties through ground leases may expose us to the loss of such properties upon the exercise by the lessors of purchase options or the breach or termination of the ground leases.

We have acquired an interest in certain of our properties by acquiring a leasehold interest in the property on which the building is located (or under development), and we may acquire additional properties in the future through the purchase of interests in ground leases. We could lose our interests in a property if the ground lease is terminated, if a purchase option is exercised by the lessor or if we breach the ground lease, which could adversely affect our financial condition or results of operations.

We face risks associated with land holdings.

We hold land for future development and may in the future acquire additional land holdings. The risks inherent in owning or purchasing and developing land increase as demand for student housing, or rental rates, decrease. As a result, we hold certain land and may in the future acquire additional land in our development pipeline at a cost we may not be able to recover fully or on which we cannot build and develop into a profitable student housing project. Also, real estate markets are highly uncertain and, as a result, the value of undeveloped land has fluctuated significantly and may continue to fluctuate as a result of changing market conditions. In addition, carrying costs can be significant and can result in losses or reduced margins in a poorly performing project. If there are subsequent changes in the fair value of our land holdings that we determine is less than the carrying basis of our land holdings reflected in our financial statements plus estimated costs to sell, we may be required to take future impairment charges, which would reduce our net income.

We may not be able to recover pre-development costs for third-party university developments.

University systems and educational institutions typically award us development services contracts on the basis of a competitive award process, but such contracts are typically executed following the formal approval of the transaction by the institution’s governing body. In the intervening period, we may incur significant pre-development and other costs in the expectation that the development services contract will be executed. If an institution’s governing body does not ultimately approve our selection and the terms of the pending development contract, we may not be able to recoup these costs from the institution and the resulting losses could be substantial.

Our awarded projects may not be successfully structured or financed and may delay our recognition of revenues.

The recognition and timing of revenues from our awarded development services projects will, among other things, be contingent upon successfully structuring and closing project financing as well as the timing of construction. The development projects that we have been awarded have at times been delayed beyond the originally scheduled construction commencement date. If such delays were to occur with our current awarded projects, our recognition of expected revenues and receipt of expected fees from these projects would be delayed.

We may encounter delays in completion or experience cost overruns with respect to our properties under construction.

As of December 31, 2017, we were in the process of constructing 13 owned properties. These properties are subject to the various risks relating to properties that are under construction referred to elsewhere in these risk factors, including the risks that we may encounter delays in completion and that any such project may experience cost overruns or may not be completed on time. Additionally, if we do not complete the construction of properties on schedule, we may be required to provide alternative housing to the students with whom we have signed leases, which would result in our incurring significant expenses, and may result in students attempting to terminate their leases, which may adversely affect occupancy at such properties for the applicable academic year.

Our guarantees could result in liabilities in excess of our development fees.

In third-party developments, we typically provide guarantees of the obligations of the developer, including development budgets and timely project completion. These guarantees include, among other things, the cost of providing alternate housing for students in the event we do not timely complete a development project. These guarantees typically exclude delays resulting from force majeure and also, in third-party transactions, are typically limited in amount to the amount of our development fees from the project. In certain cases, however, our contingent liability under these guarantees has exceeded our development fee from the project and we may agree to such arrangements in the future. Our obligations under alternative housing guarantees typically expire five days after construction is complete. Project cost guarantees are normally satisfied within one year after completion of the project.

Tax laws have recently changed and may continue to change at any time, and any such legislative or other actions could have a negative effect on us.

The Tax Cut and Jobs Act was signed into law on December 22, 2017. The law includes significant changes to the U.S. corporate income tax system, including a Federal corporate rate reduction from 35% to 21% for non-REIT “C” corporations, which may cause investors to perceive investments in REITs to be less attractive than investments in the stock of non-REIT “C” corporations. The law also includes limitations on the deductibility of executive compensation and interest expense, which may result in our being required to pay higher dividends to continue to qualify as a REIT at a time and in an amount that otherwise may not be in our and our stockholders’ best interests.

In addition, tax laws remain under constant review by persons involved in the legislative process, at the Internal Revenue Service and the U.S. Department of the Treasury, and by various state and local tax authorities. Changes to tax laws, regulations, or administrative interpretations, which may be applied retroactively, could adversely affect us in a number of additional ways, including making it more difficult or more costly for us to qualify as a REIT or decreasing real estate values generally.

We cannot predict the full impact of the Tax Cut and Jobs Act or whether, when, in what forms, or with what effective dates, the tax laws, regulations, and administrative interpretations applicable to us or our shareholders may be further changed. Any of these matters may significantly affect our liquidity and results of operations, as well as the value of our shares.

We are subject to numerous other laws and regulations, changes to which could increase our costs and individually or in the aggregate adversely affect our business.

In addition to tax laws, we are subject to laws and regulations affecting our operations in a number of areas. Changes in these laws and regulations, including, among others, additional healthcare reform, employment law reform such as the enactment of federal overtime exemption regulations, and financial and disclosure reform such as revisions to the Dodd-Frank Act and related SEC rulemaking, or the enactment of new laws or regulations, may increase our costs. Also, compliance with these laws, regulations and similar requirements may be onerous and expensive, and they may be inconsistent from jurisdiction to jurisdiction, which may further increase the cost of compliance and doing business.

We cannot predict whether, when, in what forms, or with what effective dates, laws, regulations, and administrative interpretations applicable to us or our stockholders may be changed. Any such change may significantly affect our liquidity and results of operations, as well as the value of our shares.

We may be adversely impacted by new accounting pronouncements.

Accounting policies are fundamental to how we record and report our financial condition and results of operations. From time to time, the Financial Accounting Standards Board (“FASB”) and the U.S. Securities and Exchange Commission, entities that create and interpret accounting standards, may issue new accounting pronouncements or change their interpretation and application of these standards that govern the preparation of our financial statements. These changes could have a material impact on our reported financial condition and results of operations, and could also affect the comparability of our financial results to previous periods. In some cases, we could be required to apply a new or revised standard retroactively, resulting in restating prior period financial statements. The adoption of new accounting pronouncements could also affect the calculation of our debt covenants, and we cannot be assured that we will be able to work with our lenders to amend our debt covenants in response to such.

A cybersecurity incident and other technology disruptions could negatively impact our business, our relationships and our reputation.

We use computers in substantially all aspects of our business operations. We also use mobile devices, social networking and other online activities to connect with our employees, suppliers and our residents. Such uses give rise to cybersecurity risks, including security breach, espionage, system disruption, theft and inadvertent release of information. Our business involves the storage and transmission of numerous classes of sensitive and/or confidential information and intellectual property, including residents’ and suppliers’ personal information, private information about employees, and financial and strategic information about us. Further, as we pursue our strategy to grow through development and acquisitions and to pursue new initiatives to improve our operations, we are also expanding our information technologies, resulting in a larger technological presence and corresponding exposure to cybersecurity risk. As our reliance on technology has increased, so have the risks posed to our systems, both internal and those we have outsourced to third party service providers. In addition, information security risks have generally increased in recent years due to the rise in new technologies and the increased sophistication and activities of perpetrators of cyber attacks. The theft, destruction, loss, misappropriation or release of sensitive and/or confidential information or intellectual property, or interference with our information technology systems or the technology systems of third-parties on which we rely, could result in business disruption, negative publicity, brand damage, violation of privacy laws, loss of residents, potential liability and competitive disadvantage, any of which could result in a material adverse effect on financial condition or results of operations.

A degradation of a university’s reputation due to negative publicity or other events may adversely impact our communities.

It is important that the universities from which our communities draw residents maintain good reputations and are able to attract the desired number of incoming students. Any degradation in a university’s reputation could inhibit its ability to attract students and reduce the demand for our communities.

Federal and state laws require universities to publish and distribute reports of on-campus crime statistics, which may result in negative publicity and media coverage associated with crimes occurring in the vicinity of, or on the premises of, our on-campus communities. Reports of crime or other negative publicity regarding the safety of the students residing on, or near, our communities may have an adverse effect on both our on-campus and off-campus communities.

Joint venture investments could be adversely affected by our lack of sole decision-making authority, our reliance on co-venturers’ financial condition and disputes between our co-venturers and us.

We have co-invested, and may continue in the future to co-invest, with third parties through partnerships, joint ventures or other entities, acquiring non-controlling interests in or sharing responsibility for managing the affairs of a property, partnership, joint

venture or other entity. In connection with joint venture investments, we do not have sole decision-making control regarding the property, partnership, joint venture or other entity. Investments in partnerships, joint ventures or other entities may, under certain circumstances, involve risks not present were a third-party not involved, including the possibility that our partners or co-venturers might become bankrupt or fail to fund their share of required capital contributions. Our partners or co-venturers also may have economic or other business interests or goals that are inconsistent with our business interests or goals, and may be in a position to take actions contrary to our preferences, policies or objectives. Such investments also will have the potential risk of impasses on decisions, such as a sale, because neither we nor our partners or co-venturers would have full control over the partnership or joint venture. Disputes between us and our partners or co-venturers may result in litigation or arbitration that would increase our expenses and prevent our officers and/or directors from focusing their time and effort exclusively on our business. Consequently, actions by or disputes with our partners or co-venturers might result in subjecting properties owned by the partnership, joint venture or other entity to additional risk. In addition, we may in certain circumstances be liable for the actions of our partners or co-venturers.

Litigation risks could affect our business.

As a publicly traded owner of properties, we have become and in the future may become involved in legal proceedings, including consumer, employment, tort or commercial litigation, that if decided adversely to or settled by us, and not adequately covered by insurance, could result in liability that is material to our financial condition or results of operations.

Our performance and value are subject to risks associated with real estate assets and with the real estate industry.

Our ability to satisfy our financial obligations and make expected distributions to our security holders depends on our ability to generate cash revenues in excess of expenses and capital expenditure requirements. Events and conditions generally applicable to owners and operators of real property that are beyond our control may decrease cash available for distribution and the value of our properties. These events include:

| |

| • | general economic conditions; |

| |

| • | rising level of interest rates; |

| |

| • | local oversupply, increased competition or reduction in demand for student housing; |

| |

| • | inability to collect rent from tenants; |

| |

| • | vacancies or our inability to rent beds on favorable terms; |

| |

| • | inability to finance property development and acquisitions on favorable terms; |

| |

| • | increased operating costs, including insurance premiums, utilities, and real estate taxes; |

| |

| • | costs of complying with changes in governmental regulations; |

| |

| • | the relative illiquidity of real estate investments; |

| |

| • | decreases in student enrollment at particular colleges and universities; |

| |

| • | changes in university policies related to admissions and housing; and |

| |

| • | changing student demographics. |

In addition, periods of economic slowdown or recession, rising interest rates or declining demand for real estate, or the public perception that any of these events may occur, could result in a general decline in rents or an increased incidence of defaults under existing leases, which would adversely affect us.

Potential losses may not be covered by insurance.