UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

_______________________

FORM 10-Q

_______________________

| þ | Quarterly report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. | |

| For the quarterly period ended June 30, 2008 |

| o | Transition report under Section 13 or 15(d) of the Exchange Act of 1934. |

Commission file number 000-1326205

INDIA GLOBALIZATION CAPITAL, INC.

(Exact name of small business issuer in its charter)

Maryland (State or other jurisdiction of incorporation or organization) | 20-2760393 (I.R.S. Employer Identification No.) |

4336 Montgomery Ave. Bethesda, Maryland 20814

(Address of principal executive offices)

(301) 983-0998

(Issuer’s telephone number)

Securities registered under Section 12(b) of the Exchange Act:

| Title of Each Class | Name of exchange on which registered |

| Units, each consisting of one share of Common Stock | American Stock Exchange |

| and two Warrants | |

| Common Stock | American Stock Exchange |

| Common Stock Purchase Warrants | American Stock Exchange |

Check whether the issuer: (1) filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act during the past 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. þ Yes o No

Indicate by check mark whether the registrant is a large accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

Large Accelerated Filer o Accelerated Filer o Non-Accelerated Filer þ

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). o Yes þ No

Indicate the number of shares outstanding for each of the issuer’s classes of common equity as of the latest practicable date.

Class Shares Outstanding as of July 15, 2008

Common Stock, $.0001 Par Value 8,570,107

India Globalization Capital

QUARTERLY REPORT ON FORM 10-Q

FOR THE QUARTERLY PERIOD ENDED JUNE 30, 2008

Table of Contents

| Page | ||||

| PART I – FINANCIAL INFORMATION | ||||

| Item 1. | 3 | |||

| 3 | ||||

| 4 | ||||

| 5 | ||||

| 6 | ||||

| 7 | ||||

| Item 2. | 13 | |||

| Item 3. | 18 | |||

| Item 4. | 18 | |||

| PART II – OTHER INFORMATION | ||||

| Item 1. | 19 | |||

| Item 2. | 19 | |||

| Item 3. | 19 | |||

| Item 4. | 19 | |||

| Item 5. | 19 | |||

| Item 6. | 19 | |||

| 19 | ||||

| 20 | ||||

PART I - Financial Information

Item 1. Financial Statements

India Globalization Capital, Inc.

CONSOLIDATED STATEMENTS OF OPERATIONS

(unaudited)

| Three Months | Three Months | Combined Predecessor Three Months | ||||||||||

| Ended | Ended | Ended | ||||||||||

| June 30, 2008 | June 30, 2007 | June 30, 2007 | ||||||||||

| Revenues: | $ | 17,928,381 | $ | $ | 3,311,309 | |||||||

| Cost of revenues: | (13,155,698 | ) | (2,747,235 | ) | ||||||||

| Gross Profit | 4,772,683 | 564,074 | ||||||||||

| Selling, General and Administrative | (947,506 | ) | (429,601 | ) | ||||||||

| Depreciation | (231,583 | ) | (193,565 | ) | ||||||||

| One Time Legal and start up costs | (179,844 | ) | ||||||||||

| Total operating expenses | (1,179,089 | ) | (179,844 | ) | (623,166 | ) | ||||||

| Operating income (loss) | 3,593,594 | (179,844 | ) | (59,093 | ) | |||||||

| Other income (expense): | ||||||||||||

| Interest income | 128,879 | 694,918 | 87,561 | |||||||||

| Interest expense | (474,310 | ) | (459,878 | ) | (251,761 | ) | ||||||

| Total other income (expense) | (345,431 | ) | 235,040 | (164,200 | ) | |||||||

| Income (loss) before provision for income taxes | 3,248,163 | 55,196 | (223,293 | ) | ||||||||

| (Provision) benefit for income taxes | (1,089,090 | ) | (18,913 | ) | (216,721 | ) | ||||||

| Income (loss) after provision for income tax | 2,159,073 | 36,283 | (440,013 | ) | ||||||||

| Provision for Dividend on Preference Stock and its Tax | (25,904 | ) | ||||||||||

| Minority interest | (872,255 | ) | ||||||||||

| Net income (loss) | $ | 1,286,818 | $ | 36,283 | $ | (465,917 | ) | |||||

| Weighted average number of shares outstanding: | ||||||||||||

| Basic | 8,570,107 | 13,974,500 | ||||||||||

| Diluted | 8,885,618 | 13,974,500 | ||||||||||

| Net income per share: | ||||||||||||

| Basis | $ | 0.15 | $ | .03 | ||||||||

| Diluted | $ | 0.14 | $ | .03 | ||||||||

The accompanying notes should be read in connection with the financial statements

India Globalization Capital, Inc.

CONSOLIDATED BALANCE SHEETS

June 30, 2008 (unaudited) | March 31, 2008 (audited) | |||||||

| ASSETS | ||||||||

| Current Assets: | ||||||||

| Cash and cash equivalents | $ | 1,549,528 | $ | 8,397,441 | ||||

| Accounts Receivable | 12,653,106 | 8,708,861 | ||||||

| Unbilled Receivables | 4,883,994 | 5,208,722 | ||||||

| Inventories | 1,763,712 | 1,550,080 | ||||||

| Interest Receivable - Convertible Debenture | 337,479 | 277,479 | ||||||

| Convertible debenture in MBL | 3,000,000 | 3,000,000 | ||||||

| Prepaid taxes | 50,038 | 49,289 | ||||||

| Restricted cash | 625 | 6,257 | ||||||

| Short term investments | 3,372,057 | 671 | ||||||

| Prepaid expenses and other current assets | 1,216,991 | 4,324,201 | ||||||

| Due from related parties | 321,261 | 1,373,447 | ||||||

| Total Current Assets | $ | 29,148,791 | $ | 32,896,447 | ||||

| Property and equipment, net | 8,185,108 | 7,337,361 | ||||||

| Build, Operate and Transfer (BOT under Progress) | 3,281,365 | 3,519,965 | ||||||

| Goodwill | 17,483,501 | 17,483,501 | ||||||

| Investment | 1,763,506 | 1,688,303 | ||||||

| Deposits towards acquisitions | 187,500 | 187,500 | ||||||

| Restricted cash, non-current | 1,974,241 | 2,124,160 | ||||||

| Deferred tax assets - Federal and State, net of valuation allowance | 982,200 | 1,013,611 | ||||||

| Other Assets | 2,796,767 | 1,376,126 | ||||||

| Total Assets | $ | 65,802,979 | $ | 67,626,973 | ||||

| LIABILITIES AND STOCKHOLDERS’ EQUITY | ||||||||

| Current Liabilities: | ||||||||

| Short-term borrowings and current portion of long-term debt | $ | 7,772,429 | $ | 5,635,408 | ||||

| Trade payables | 2,627,966 | 1,771,151 | ||||||

| Advance from Customers | 594,958 | 931,092 | ||||||

| Accrued expenses | 820,183 | 1,368,219 | ||||||

| Taxes payable | 71,259 | 58,590 | ||||||

| Notes Payable to Oliveira Capital, LLC | 3,000,000 | 3,000,000 | ||||||

| Due to related parties | 2,661,171 | 1,330,291 | ||||||

| Other current liabilities | 3,418,352 | 3,289,307 | ||||||

| Total current liabilities | $ | 20,966,318 | $ | 17,384,058 | ||||

| Long-term debt, net of current portion | 1,456,422 | 1,212,841 | ||||||

| Advance from Customers | 832,717 | |||||||

| Deferred taxes on income | 669,503 | 608,535 | ||||||

| Other liabilities | 2,424,115 | 6,717,109 | ||||||

| Total Liabilities | 25,516,358 | 26,755,261 | ||||||

| Minority Interest | 14,417,912 | 13,545,656 | ||||||

| STOCKHOLDERS’ EQUITY | ||||||||

| Common stock — $.0001 par value; 75,000,000 shares authorized; 8,570,107 issued and outstanding at June 30, 2008 and March 31, 2008 | 857 | 857 | ||||||

| Additional paid-in capital | 31,470,133 | 31,470,134 | ||||||

| Money received pending allotment | ||||||||

| Retained Earnings (Deficit) | (2,854,295 | ) | (4,141,113 | ) | ||||

| Accumulated other comprehensive (loss) income | (2,747,986 | ) | (3,822 | ) | ||||

| Total stockholders’ equity | 25,868,709 | 27,326,056 | ||||||

| Total liabilities and stockholders’ equity | $ | 65,802,979 | $ | 67,626,973 | ||||

The accompanying notes should be read in connection with the financial statements.

India Globalization Capital, Inc.

CONSOLIDATED STATEMENT OF STOCKHOLDERS’ EQUITY

(unaudited)

| Common Stock | Additional Paid-in | Earnings | Accumulated Other Comprehensive Income | Total Stockholders' | ||||||||||||||||||||

| Shares | Amount | Capital | (Deficit) | / Loss | Equity | |||||||||||||||||||

| Balance at March 31, 2008 | 8,570,107 | $ | 857 | $ | 31,470,134 | $ | (4,141,113 | ) | $ | (3,822 | ) | $ | 27,326,056 | |||||||||||

| Net Income (Loss) | - | - | - | 1,286,818 | (2,744,164 | ) | (1,457,347 | ) | ||||||||||||||||

| Balance at June 30, 2008 | 8,570,107 | $ | 857 | $ | 31,470,134 | $ | (2,854,295 | ) | $ | (2,747,986 | ) | $ | 25,868,709 | |||||||||||

The accompanying notes should be read in connection with the financial statements.

India Globalization Capital, Inc.

CONSOLIDATED STATEMENT OF CASH FLOWS

(unaudited)

| Three months ended | ||||||||

| June 30, 2008 | June 30, 2007 | |||||||

| Cash flows from operating activities: | ||||||||

| Net income | $ | 1,286,818 | $ | 36,283 | ||||

| Adjustment to reconcile net income to net cash used in operating activities: | ||||||||

| Interest earned on Treasury Bills | (721,805 | ) | ||||||

| Non-cash compensation expense | ||||||||

| Deferred taxes | 129,517 | (348,236 | ) | |||||

| Depreciation | 231,583 | |||||||

| Loss/(Gain) on sale of property, plant and equipment | (33,740 | ) | ||||||

| Amortization of debt discount on Oliveira debt | 386,850 | |||||||

| Changes in: | ||||||||

| Accounts receivable | (4,685,180 | ) | ||||||

| Unbilled Receivable | (29,286 | ) | ||||||

| Inventories | (329,288 | ) | ||||||

| Prepaid expenses and other current assets | 3,284,246 | 38,340 | ||||||

| Interest receivable - convertible debenture | (60,000 | ) | (60,000 | ) | ||||

| Deferred interest liability | 95,268 | |||||||

| Accrued expenses | (563,535 | ) | 111,367 | |||||

| Taxes payable | 11,920 | 12,149 | ||||||

| Trade Payable | 1,009,317 | |||||||

| Other Current Liabilities | 2,690 | |||||||

| Advance from Customers | (1,084,142 | ) | ||||||

| Non current assets | (1,564,201 | ) | ||||||

| Other non-current liabilities | (3,965,110 | ) | ||||||

| Minority Interest | 872,255 | |||||||

| Net cash used in operating activities | (5,486,136 | ) | (449,784 | ) | ||||

| Cash flows from investing activities: | ||||||||

| Purchase of treasury bills | (132,811,913 | ) | ||||||

| Maturity of treasury bills | 133,166,157 | |||||||

| Decrease (increase) in cash held in trust | 486 | |||||||

| Purchase of property and equipment | (1,646,738 | ) | ||||||

| Proceeds from sale of property and equipment | 59,085 | |||||||

| Purchase of short term investments | (3,483,283 | ) | ||||||

| Non Current Investments | (195,944 | ) | ||||||

| Restricted Cash | 11,386 | |||||||

| Deposit to CWEL | (250,000 | ) | ||||||

| Payment of deferred acquisition costs | (77,333 | ) | ||||||

| Net cash provided used in investing activities | (5,255,494 | ) | 27,397 | |||||

| Cash flows from financing activities: | ||||||||

| Net movement in cash credit and bank overdraft | 2,414,063 | |||||||

| Proceeds from other short-term borrowings | 1,699,083 | |||||||

| Repayment of long-term borrowings | (1,173,852 | ) | ||||||

| Due to related parties | 1,213,865 | |||||||

| Proceeds from notes payable to stockholders | 275,000 | |||||||

| Repayment of notes payable to stockholder | (600,000 | ) | ||||||

| Net cash provided by financing activities | 4,153,159 | (325,000 | ) | |||||

| Effect of exchange rate changes on cash and cash equivalents | (259,442 | ) | ||||||

| Net increase in cash and cash equivalent | (6,847,913 | ) | (747,387 | ) | ||||

| Cash and cash equivalent at the beginning of the period | 8,397,441 | 1,169,422 | ||||||

| Cash and cash equivalent at the end of the period | $ | 1,549,528 | $ | 422,035 | ||||

The accompanying notes should be read in connection with the financial statements.

Predecessor cash flow statements for the three month ended period June 30, 2007 are not available, and not included with the Consolidated Cash Flow Report.

Background of India Globalization Capital, Inc. (IGC)

Notes to Consolidated Financial Statements (unaudited)

Note 1 - Nature of Operations and Basis of Presentation

IGC operates through two infrastructure companies in India, Sricon Infrastructure Private Limited (“Sricon”) and Techni Bharathi, Limited (“TBL”). IGC owns sixty-three percent of Sricon and seventy-seven percent of TBL. IGC through its subsidiaries has three core businesses: 1) highway and other heavy construction, 2) mining & quarrying and 3) civil construction and engineering of high temperature plants. The Company’s medium term plans are to expand each of these lines of business.

The Company’s operations are subject to certain risks and uncertainties, including among others, dependency on India’s economy and government policies, seasonal business factors, competitively priced raw materials, dependence upon key members of the management team and increased competition from existing and new entrants.

India Globalization Capital, Inc.

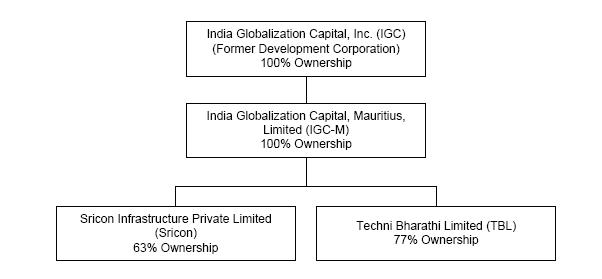

IGC, a Maryland corporation, was organized on April 29, 2005 as a blank check company formed for the purpose of acquiring one or more businesses with operations primarily in India through a merger, capital stock exchange, asset acquisition or other similar business combination or acquisition. On March 8, 2006, the company completed an initial public offering. On February 19, 2007, the Company incorporated India Globalization Capital, Mauritius, Limited (IGC-M), a wholly owned subsidiary, under the laws of Mauritius.

Merger and Accounting Treatment

On March 7, 2008, the Company consummated the acquisition of 63% of the equity of Sricon Infrastructure Private Limited (Sricon) and 77% of the equity of Techni Bharathi Limited (TBL). The shares of the two Indian companies, Sricon and TBL, are held by IGC-M. Most of the shares of Sricon and TBL acquired by IGC were purchased directly from the companies. IGC purchased a portion of the shares from the existing owners of the companies. The founders and management of Sricon own 37% of Sricon and the founders and management of TBL own 23% of TBL. Prior to the acquisitions of Sricon and TBL, IGC had no operations and was considered a developmental stage enterprise.

The acquisitions were accounted for under the purchase method of accounting. Under this method of accounting, for accounting and financial purposes, IGC-M, Limited was treated as the acquiring entity and Sricon and TBL as the acquired entities. The consolidated financial statements provided here and going forward are the consolidated statements of IGC, which include IGC-M following the date of formation of IGC-M and Sricon and TBL following the date of the Company’s acquisition of the interests in Sricon and TBL. The consolidated financial statements do not reflect the operating results of Sricon and TBL prior to the acquisition. However, for comparative purposes, the combined statement of operations for the two acquired companies are presented as the “Combined Predecessors” for the three month period ended June 30, 2007.

Unless the context requires otherwise, all references in this report to the “Company”, “IGC”, “we”, “our”, and “us” refer to India Globalization Capital, Inc, together with its wholly owned subsidiary IGC-M, and its direct and indirect subsidiaries (Sricon and TBL). Ownership in these two companies is reflected in the financial statements as “Minority Interest”. The following represents our corporate structure after the acquisitions:

Securities

We have three securities listed on the American Stock Exchange: (1) common stock, $.0001 par value (ticker symbol: IGC), (2) redeemable warrants to purchase common stock (ticker symbol: IGC.WS) and (3) units consisting of one share of common stock and two redeemable warrants to purchase common stock (ticker symbol: IGC.U). On March 8, 2006, we sold 11,304,500 units in our initial public offering. These 11,304,500 units include 9,830,000 units sold to the public and the over-allotment option of 1,474,500 units exercised by the underwriters of the public offering. The units were separated into common stock and warrants on April 13, 2006. Each warrant entitles the holder to purchase one share of common stock at an exercise price of $5.00. The warrants expire on March 3, 2011, or earlier upon redemption. The registration statement for initial public offering was declared effective on March 2, 2006. The warrants are currently not exercisable pending the effectiveness of a registration statement relating to the warrants. When the warrants become exercisable, they may be exercised by contacting the Company or the transfer agent Continental Stock Transfer & Trust Company. We have a right to call the warrants, provided the common stock has traded at a closing price of at least $8.50 per share for any 20 trading days within a 30 trading day period ending on the third business day prior to the date on which notice of redemption is given. If we call the warrants, the holder will either have to redeem the warrants by purchasing the common stock from us for $5.00 or the warrants will expire.

On March 7, 2008, we bought and redeemed a total of 6,159,346 shares. As a result, on June 30, 2008, we had 8,570,107 shares outstanding (including shares sold to our founders in a private placement prior to the public offering) and 24,874,000 shares of common stock were reserved for issuance upon exercise of redeemable warrants and underwriters’ purchase option.

Unaudited Interim Financial Statements

The unaudited consolidated balance sheet as of June 30, 2008, consolidated statements of operations and cash flows for the three months ended June 30, 2008 and 2007 and consolidated statements of stockholders’ equity (deficit) for the three months ended June 30, 2008 include the accounts of the Company and its subsidiaries. The unaudited financial statements include all adjustments (consisting of normal recurring adjustments) which are, in the opinion of management, necessary for a fair presentation of such financial statements. Operating results for the interim periods presented are not necessarily indicative of the

results to be expected for a full fiscal year.

Pro Forma Results of Operations

The accompanying unaudited consolidated statements of operations only reflect the operating results of companies acquired following the date of acquisition and do not reflect the operating results prior to the acquisitions. The following are pro forma unaudited results of operations for the Company for the three months ended June 30, 2008 and 2007 with the results for the Company alone for the three months ended June 30, 2007 included for comparative purposes. The results in the column labeled “Pro Forma Three Months Ended June 30, 2007” assume the Sricon and TBL acquisitions occurred on April 1, 2007. The unaudited pro forma results of operations are not necessarily indicative of results of operations that may have actually occurred had the acquisitions taken place on the dates noted, or the future financial position or operating results of the Company. The pro forma adjustments are based upon available information and assumptions that the Company believes are reasonable. The pro forma adjustments include adjustments for interest expense, start up costs, increased depreciation and amortization expense as a result of the application of the purchase method of accounting based on the fair values of the tangible and intangible assets.

PRO FORMA CONSOLIDATED STATEMENTS OF OPERATIONS

(unaudited)

| Three Months | Three Months | Pro forma Three Months | ||||||||||

| Ended | Ended | Ended | ||||||||||

| June 30, 2008 | June 30, 2007 | June 30, 2007 | ||||||||||

| Revenues: | $ | 17,928,381 | $ | $ | 3,311,309 | |||||||

| Cost of revenues: | (13,155,698 | ) | (2,747,235 | ) | ||||||||

| Gross Profit | 4,772,683 | 564,074 | ||||||||||

| Selling, general and administrative | (947,506 | ) | (429,601 | ) | ||||||||

| Depreciation | (231,583 | ) | (193,565 | ) | ||||||||

| One Time Legal and other start up costs | (179,844 | ) | (179,844 | ) | ||||||||

| Total operating expenses | (1,179,089 | ) | (179,844 | ) | (803,010 | ) | ||||||

| Operating income (loss) | 3,593,594 | (179,844 | ) | (238,936 | ) | |||||||

| Other income (expense): | ||||||||||||

| Interest income | 128,879 | 694,918 | 87,561 | |||||||||

| Interest expense | (474,310 | ) | (459,878 | ) | (711,639 | ) | ||||||

| Total other income (expense) | (345,431 | ) | 235,040 | (624,078 | ) | |||||||

| Income (loss) before provision for income taxes | 3,248,163 | 55,196 | (863,014 | ) | ||||||||

| (Provision) benefit for income taxes | (1,089,090 | ) | (18,913 | ) | 2,481 | |||||||

| Income (loss) after provision for income tax | 2,159,073 | 36,283 | (860,533 | ) | ||||||||

| Provision for Dividend on Preference Stock and its Tax | (25,904 | ) | ||||||||||

| Minority interest | (872,255 | ) | 64,091 | |||||||||

| Net income (loss) | $ | 1,286,818 | $ | 36,283 | $ | (822,346 | ) | |||||

| Weighted average number of shares outstanding: | ||||||||||||

| Basic | 8,570,107 | 13,974,500 | ||||||||||

| Diluted | 8,885,618 | 13,974,500 | ||||||||||

| Net income per share: | ||||||||||||

| Basis | $ | 0.15 | $ | .03 | ||||||||

| Diluted | $ | 0.14 | $ | .03 | ||||||||

Note 2 - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Principles of Consolidation:

The consolidated financial statements include the accounts of the Company and its subsidiaries. All material intercompany balances and transactions have been eliminated.

Reclassifications

Certain prior year balances have been reclassified to the presentation of the current year. Sales and services include adjustments made towards liquidated damages, price variation and charges paid for discounting of receivables arising from construction/project contracts on a non-recourse basis, wherever applicable.

Revenue Recognition

The majority of the revenue recognized for the three month period ended June 30, 2008 was derived from the Company’s subsidiaries and as follows:

Revenue is recognized based on the nature of activity when consideration can be reasonably measured and there exists reasonable certainty of its recovery.

Revenue from sale of goods is recognized when substantial risks and rewards of ownership are transferred to the buyer under the terms of the contract.

Revenue from construction/project related activity and contracts for supply/commissioning of complex plant and equipment is recognized as follows:

| a) | Cost plus contracts: Contract revenue is determined by adding the aggregate cost plus proportionate margin as agreed with the customer and expected to be realized. | ||

| b) | Fixed price contracts: Contract revenue is recognized using the percentage completion method. Percentage of completion is determined as a proportion of cost incurred-to-date to the total estimated contract cost. Changes in estimates for revenues, costs to complete and profit margins are recognized in the period in which they are reasonably determinable | ||

Full provision is made for any loss in the period in which it is foreseen.

Revenue from property development activity is recognized when all significant risks and rewards of ownership in the land and/or building are transferred to the customer and a reasonable expectation of collection of the sale consideration from the customer exists.

Revenue from service related activities and miscellaneous other contracts are recognized when the service is rendered using the proportionate completion method or completed service contract method.

Policy for Goodwill / Impairment

Goodwill represents the excess cost of an acquisition over the fair value of the Group's share of net identifiable assets of the acquired subsidiary at the date of acquisition. Goodwill on acquisition of subsidiaries is disclosed separately. Goodwill is stated at cost less accumulated amortization and impairment losses, if any.

The company adopted provisions of FAS No. 142, "Goodwill and Other Intangible Assets" ('FAS 142') which sets forth the accounting for goodwill and intangible assets subsequent to their acquisition. FAS 142 requires that goodwill and indefinite-lived intangible assets be allocated to the reporting unit level, which the Group defines as each circle.

FAS 142 also prohibits the amortization of goodwill and indefinite-lived intangible assets upon adoption, but requires that they be tested for impairment at least annually, or more frequently as warranted, at the reporting unit level.

The goodwill impairment test under FAS 142 is performed in two phases. The first step of the impairment test, used to identify potential impairment, compares the fair value of the reporting unit with its carrying amount, including goodwill. If the carrying amount of the reporting unit exceeds its fair value, goodwill of the reporting unit is considered impaired, and step two of the impairment test must be performed. The second step of the impairment test quantifies the amount of the impairment loss by comparing the carrying amount of goodwill to the implied fair value. An impairment loss is recorded to the extent the carrying amount of goodwill exceeds its implied fair value.

Impairment of long – lived assets and intangible assets

The company reviews its long-lived assets, including identifiable intangible assets with finite lives, for impairment whenever events or changes in business circumstances indicate that the carrying amount of assets may not be fully recoverable. Such circumstances include, though are not limited to, significant or sustained declines in revenues or earnings and material adverse changes in the economic climate. For assets that the company intends to hold for use, if the total of the expected future undiscounted cash flows produced by the assets or subsidiary company is less than the carrying amount of the assets, a loss is recognized for the difference between the fair value and carrying value of the assets. For assets the company intends to dispose of by sale, a loss is recognized for the amount by which the estimated fair value less cost to sell is less than the carrying value of the assets. Fair value is determined based on quoted market prices, if available, or other valuation techniques including discounted future net cash flows.

Income per common share:

Basic earnings per share is computed by dividing net income (loss) applicable to common stockholders by the weighted average number of common shares outstanding for the period. Diluted earnings per share reflect the additional dilution for all potentially dilutive securities such as stock warrants and options. The effect of the 23,374,000 warrants have been included in the diluted weighted average shares.

For June 30, 2008, the basis shares include shares sold in the IPO, founder’s shares and shares sold in the private placement, and shares awarded to the Bridge Investors, and shares redeemed by the company. The fully diluted shares include basic shares plus the following: shares arising from the exercise of warrants sold as part of the units in the offering plus shares arising from the exercise of warrants issued to Oliveira Capital. The UPO issued to the underwriters (1,500,000 shares) is not considered in this calculation as the strike price for the UPO is “out of the money” at $6.50 per share. The historical weighted average per share, for our shares, for the three month period ended June 30, 2008, was applied using the treasury method of calculating the fully diluted shares. The calculation for fully diluted shares includes 378,511 shares and excludes 22,999,489 shares from the EPS computations.

Use of estimates:

The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenue and expenses during the reporting period. Actual results could differ from those estimates.

Income taxes:

Deferred income taxes are provided for the differences between the bases of assets and liabilities for financial reporting and income tax purposes. A valuation allowance is established when necessary to reduce deferred tax assets to the amount expected to be realized.

Cash and Cash Equivalents:

For financial statement purposes, the Company considers all highly liquid debt instruments with maturity of three months or less when purchased to be cash equivalents. The company maintains its cash in bank accounts in the United States of America and Mauritius, which at times may exceed applicable insurance limits. The Company has not experienced any losses in such accounts. The Company believes it is not exposed to any significant credit risk on cash and cash equivalent. The company does not invest its cash in securities that have an exposure to U.S. mortgages.

Recent Pronouncements:

The Company adopted FASB Interpretation No. 48, “Accounting for Uncertainty in Income Taxes,” an interpretation of FASB Statement No. 109 (“FIN 48”) on April 1, 2007. FIN 48 clarifies the criteria for the recognition, measurement, presentation and disclosure of uncertain tax positions. A tax benefit from an uncertain position may be recognized only if it is “more likely than not” that the position is sustainable based on its technical merits. FIN 48 also provides guidance on de-recognition, classification, interest and penalties, accounting in interim periods, disclosure, and transition. In May 2007, the FASB issued Staff Position, FIN 48-1, “Definition of Settlement in FASB Interpretation No. 48” (FSP FIN 48-1) which provides guidance on how an enterprise should determine whether a tax position is effectively settled for the purpose of recognizing previously unrecognized tax benefits. FSP FIN 48-1 was effective with the initial adoption of FIN 48. The adoption of FIN 48 or FSP FIN 48-1 did not have a material effect on the Company’s financial condition or results of operations.

In December 2007, the Financial Accounting Standards Board released SFAS 160 “Non-controlling Interests in Consolidated Financial Statements” that is effective for annual periods beginning December 15, 2008. The pronouncement resulted from a joint project between the FASB and the International Accounting Standards Board and continues the movement toward the greater use of fair values in financial reporting. Upon adoption of SFAS 160, the Company will re-classify any non-controlling interests as a component of equity.

Management does not believe that any other recently issued, but not yet effective, accounting standards if currently adopted would have a material effect on the accompanying financial statements.

Note 3 – SHORT TERM BORROWINGS & CURRENT PORTION OF LONG-TERM DEBT

(Amounts in Thousand US Dollars)

Short term debt for the consolidated companies consists of the following:

| As of | As of | |||||||

| June 30, 2008 | March 31, 2008 | |||||||

| Secured | $ | 6,578 | $ | 4,556 | ||||

| Unsecured | 3,316 | 3,306 | ||||||

| Total | 9,894 | 7,862 | ||||||

| Add: | ||||||||

| Current portion of long term debt | 878 | 773 | ||||||

| Total | $ | 10,772 | $ | 8,635 | ||||

The above debt is secured by hypothecation of materials/stock of spares, Work in Progress, receivables and property & equipment in addition to personal guarantee of three directors & collaterally secured by mortgage of company’s land & other immovable properties of directors and their relatives.

Note 4 - LONG TERM DEBT COMPRIMISES:

(Amounts in Thousand US Dollars)

Long term debt for the consolidated companies consists of the following:

| As of | As of | |||||||

| June 30, 2008 | March 31, 2008 | |||||||

| Secured | $ | $ | ||||||

| Term loans | - | 632 | ||||||

| Loan for assets purchased under capital lease | 2,335 | 1,354 | ||||||

| Total | 2,335 | 1,982 | ||||||

| Less: Current portion (Payable within 1 year) | 878 | 773 | ||||||

| Total | $ | 1,456 | $ | 1,213 | ||||

The secured loans were collateralized by:

| · | Unencumbered Net Asset Block of the Company |

| · | Equitable mortgage of properties owned by promoter directors/ guarantors |

| · | Term Deposits |

| · | Hypothecation of receivables, assignment of toll rights, machineries and vehicles and collaterally secured by deposit of title deeds of land |

| · | First charge on Debt-Service Reserve Account |

NOTE 5 - RELATED PARTY TRANSACTIONS

For the three month period ended June 30, 2008, $10,000 was paid to SJS Associates for Mr. Selvaraj’s consulting services.

The Company had agreed to pay Integrated Global Network, LLC (“IGN, LLC”), an affiliate of our Chief Executive Officer, Mr. Mukunda, an administrative fee of $4,000 per month for office space and general and administrative services. A total $12,000 was paid to IGN, LLC including a $4,000 payment for the prior period. The Company and IGN, LLC have agreed to continue the agreement on a month-to-month basis.

In April 2008 R.L. Srivastava, Chairman of Sricon, made an unsecured loan of $1,953,157 to Sricon which is due in 6 months from the date of the loan, which due date is extendable after the 6 month period by mutual consent. The loan’s interest rate is 2% annually.

NOTE 6 -COMMITMENTS AND CONTINGENCY

The Founders will be entitled to registration rights with respect to their shares of common stock acquired prior to the Public Offering and the shares of common stock they purchased in the Private Placement pursuant to an agreement executed on March 3, 2006. The holders of the majority of these shares are entitled to make up to two demands that the Company register these shares at any time after the date on which the lock-up period expires. In addition, the Founders have certain “piggy-back” registration rights on registration statements filed subsequent to the anniversary of the effective date of the Public Offering. In addition, the holders of certain shares of common stock of the Company and warrants to purchase Common Stock of the Company purchased from the Company in private placements are entitled to demand and “piggy back” registration rights.

In connection with our proposed acquisition of a wind energy farm from Chiranjjeevi Wind Energy Limited ("CWEL"), we have agreed to pay a finder’s fee of 0.25% of the purchase price to Master Aerospace Consultants (Pvt) Ltd, a consulting firm located in India. The fee is contingent on the consummation of the transaction.

NOTE 7 - INVESTMENT ACTIVITIES

Contract Agreement between IGC, CWEL, AMTL and MAIL

As previously disclosed in our Form 8-K dated May 2, 2007 and Form 10-QSB for the quarterly period ended June 30, 2007, on April 29, 2007, the Company entered into a Contract Agreement Dated April 29, 2007 (“CWEL Purchase Agreement”) with CWEL, Arul Mariamman Textiles Limited (AMTL), and Marudhavel Industries Limited (MAIL), collectively CWEL. Pursuant to the CWEL Purchase Agreement, the Company or its subsidiary in Mauritius will acquire 100% of a 24-mega watt wind energy farm, consisting of 96 250-kilowatt wind turbines, located in Karnataka, India to be manufactured by CWEL.

CWEL is a manufacturer and supplier of wind operated electricity generators, towers and turnkey implementers of wind energy farms. On May 22, 2007, the Company made a down payment of approximately $250,000 to CWEL. Pursuant to the First Amendment dated August 20, 2007 (as previously disclosed in the Company’s Form 8-K dated August 22, 2007), if the Company does not consummate the transaction with CWEL, approximately $187,500 will be returned to the Company.

The Company is contemplating pursuing this opportunity, or a similar one if it is able to obtain adequate funding from the exercise of warrants, debt or other means.

NOTE 8 - COMMON STOCK

On August 24, 2005, the Company’s Board of Directors authorized a reverse stock split of one share of common stock for each two outstanding shares of common stock and approved an amendment to the Company’s Certificate of Incorporation to decrease the number of authorized shares of common stock to 75,000,000. All references in the accompanying financial statements to the number of shares of stock have been retroactively restated to reflect these transactions. On March 7, 2008 we redeemed and bought a total of 6,159,346 shares at $5.94 per share. At June 30, 2008 and 2007 we had 8,570,107 and 13,974,500 shares of common stock issued and outstanding respectively. At June 30, 2008 and 2007, 24,874,000 shares of common stock, were reserved for issuance upon exercise of redeemable warrants, underwriters’ purchase option and warrants issued to Oliveira Capital, LLC.

NOTE 9 - BUSINESS COMBINATIONS

As previously disclosed in our Form 8-K dated September 21, 2007 and Form 10-QSB for the quarterly period ended June 30, 2007, on September 21, 2007, the Company entered into a Share Subscription cum Purchase Agreement (the “Sricon Subscription Agreement”) dated as of September 15, 2007 with Sricon Infrastructure Private Limited (“Sricon”) and certain individuals (collectively, the “Sricon Promoters”), pursuant to which the Company or its subsidiary in Mauritius (IGC-M) will acquire (the “Sricon Acquisition”) 4,041,676 newly-issued equity shares (the “New Sricon Shares”) directly from Sricon for approximately $26 million and 351,840 equity shares from Mr. R. L. Srivastava for approximately $3 million (both based on an exchange rate of INR 40 per USD) so that at the conclusion of the transactions contemplated by the Sricon Subscription Agreement the Company would own approximately 63% of the outstanding equity shares of Sricon. The Sricon Acquisition was consummated on March 7, 2008.

As previously disclosed in our Form 8-K dated September 21, 2007 and Form 10-QSB for the quarterly period ended June 30, 2007, on September 21, 2007, the Company entered into a Share Subscription Agreement (the “TBL Subscription Agreement”) dated as of September 16, 2007 with Techni Bharathi Limited (“TBL”) and certain individuals (collectively, the “TBL Promoters”), pursuant to which the Company through its subsidiary in Mauritius (IGC-M) acquired (the “TBL Acquisition”) 7,150,000 newly-issued company stock for approximately $6.9 million, 1,250,000 newly-issued convertible preference shares for approximately $3.13 million (both at an exchange rate of INR 40 per USD; collectively, the “New Shares”) directly from TBL and 5,000,000 convertible preference shares from Odeon, a Singapore based holder of TBL securities, for approximately $2 million. With the conclusion of this transaction, on March 7, 2008 the Company owns approximately 77%, of the outstanding equity shares of TBL.

No acquisitions or mergers transactions occurred during the three month period ended June 30, 2008. Details of the Sricon and TBL acquisitions can be found in the Company’s 10-KSB filed for year end March 31, 2008.

NOTE 10 - SUBSEQUENT EVENTS

On August 6, 2008, we received $3,000,000 plus interest from an investment in MBL Infrastructures Limited and subsequently on August 6, 2008 repaid $3,000,000 principal and accrued interest to Oliveira Capital and is negotiating the issuance of an additional 425,000 warrants. It will be reflected in the financial results for quarter end September 30, 2008.

Item 2. Management’s Discussion and Analysis

The following discussion and analysis of our financial condition and results of operations should be read in conjunction with our unaudited condensed financial statements and related notes that appear elsewhere in this Quarterly Report on Form 10-Q. In addition to historical consolidated financial information, the following discussion contains forward-looking statements that reflect our plans, estimates and beliefs. Our actual results could differ materially from those discussed in the forward-looking statements. Factors that could cause or contribute to these differences include those discussed below and elsewhere in this Quarterly Report on Form 10-Q, as well as in our Annual Report on Form 10-KSB filed on July 16, 2008.

Overview

In response to India’s rapidly expanding economy, our primary focus is to execute infrastructure projects through our subsidiaries such as constructing interstate highways, rural roads, mining and quarrying, and construction of high temperature cement and steel plants.

The 2008 share of infrastructure investment in India is expected to increase to 9 per cent of GDP, which is an increase from 5 per cent in 2006-07. This forecast is based on The Indian Planning Commission’s annual publication surmised that for the Eleventh Plan period (2007-12), a large investment of approximately $494 Billion would be required for Infrastructure build and modernization. The infrastructure development industry is the largest employer in India – the construction industry alone employs more than 30 million people. According to the Business Monitor International (BMI), by 2012, the construction industry’s contribution to India’s GDP is forecasted to be 16.98%. The sector is riding on a high growth wave powered by the large expenditures committed to infrastructure programs – evidenced all over the country in the form of new highways, dams, power plants and pipelines. The sectors contributing to the high growth rates are power, transport, petroleum and urban infrastructure.

Our operations are subject to certain risks and uncertainties, including among others, dependency on India’s economy and government policies, competitively priced raw materials, dependence upon key members of the management team and increased competition from existing and new entrants.

Sricon Infrastructure Private Limited

Sricon Infrastructure Private Limited (“Sricon”) was incorporated as a private limited company on March 3, 1997 in Nagpur, India. Sricon is an engineering and construction company that is engaged in three business areas: 1) civil construction of highways and other heavy construction, 2) mining and quarrying and 3) the construction and maintenance of high temperature cement and steel plants. Sricon has a pan-India focus and is accredited with ISO 9001:2000 certification and its present and past clients include various Indian government organizations. Sricon employs approximately 250 skilled employees and over 800 unskilled labor contractors. It currently has the capacity and prior experience to bid on contracts that are priced at a maximum of about $116 million. Sricon recently won a $103 million contract as disclosed in a press release, a contract to build about 150 miles of rural roads including one major and 32 minor bridges.

Techni Bharathi Limited

Techni Bharathi Limited (“TBL”) was incorporated as a public (but not listed on the stock market) limited company on June 19, 1982 in Cochin, India. TBL is an engineering and construction company engaged in the execution of civil construction and structural engineering projects. TBL has a focus in the Indian states of Andhra Pradesh, Karnataka, Assam and Tamil Nadu. Its present and past clients include various Indian government organizations.

Core Business Areas

Our core business areas include the following:

Highway and heavy construction:

The Indian government has articulated a plan to build and modernize Indian infrastructure. The government’s plan, which calls for spending over $475 billion over the next five years, includes the construction of rural roads, major highways and townships among other infrastructure. As of August 2008, we have approximately $243 million worth of contracts in our order book including a $103 million contract to build 150 miles of rural roads including 33 bridges in the state of Madhya Pradesh, and contracts for the building of highways in Assam, Maharashtra and Madhya Pradesh totaling around $108 million. In addition, we have smaller construction contracts amounting for about $32 million, including a construction contract for a township in Nagpur.

Mining and Quarrying

As Indian infrastructure modernizes, the demand for raw materials like stone aggregate, coal, ore and similar resources is projected to increase. In 2006, according to the Freedonia Group, India was the fourth largest stone aggregate market in the world with demand of up to 1.1 billion metric tons. Sricon has five site licenses with two installed crushers and produces approximately 600,000 metric tons of aggregate annually. The aggregate reserves in Sricon’s five quarries have a projected value of around $50 million. India is the third largest producer of coal and fourth largest producer of ore. Ten percent of the world’s coal reserves are in India. As of August 2008, we have a multiyear contract valued around $78 million for the removal of overburden from open pit coal mines and extraction of limestone. Overburden is the layers of rock and dirt covering the coal seam.

Construction and maintenance of high temperature plants

Sricon has an expertise in the civil engineering, construction and maintenance of high temperature plants. For example, we construct cement and steel plants. This requires specialized skills to build and maintain the high temperature chimneys and kilns. As of August 2008, we have a multiyear contract valued around $60 million for civil engineering and maintenance of high temperature cement plants.

Customers

Over the past 10 years, Sricon has qualified in all states in India and has worked in several, including Maharashtra, Gujarat, Orissa and Madhya Pradesh. The National Highway Authority of India (NHAI) awards interstate highway contracts on a national level, while intra-state contracts are awarded by state agencies. The National Thermal Power Corporation (NTPC) awards contacts for civil work associated with power plants. The National Coal Limited (NCL) awards large mining contracts. Our customers include, or have included, NHAI, NTPC, and various state public works departments. Sricon is registered across India and is qualified to bid on contracts anywhere in India.

Foreign Currency Translation

The financial statements are reported in U.S. dollars. The Indian rupee is the functional currency for the Sricon and TBL. The translation of the functional currencies into U.S. dollars is performed for assets and liabilities using the exchange rates in effect at the balance sheet date and for revenues, costs and expenses using average exchange rates prevailing during the reporting periods. Adjustments resulting from the translation of functional currency financial statements to reporting currency are accumulated and reported as other comprehensive income/(loss), a separate component of shareholders’ equity.

Transactions in foreign currency are recorded at the exchange rate prevailing on the date of the transaction. Monetary assets and liabilities denominated in foreign currencies are expressed in the functional currency at the exchange rates in effect at the balance sheet date. Revenues, costs and expenses are recorded using exchange rates prevailing on the date of transaction. Gains or losses resulting from foreign currency transactions are included in the statement of income.

The exchange rate between the Indian Rupee and the U.S. dollars are as follows:

| Quarter ending | Average rate used for translating operations. INR to one U.S.D. | Rate used for translating Balance Sheet. INR to one U.S.D. |

| June 30, 2007 | 41.05 | 40.58 |

| March 31, 2008 | 39.73 | 40.02 |

| June 30, 2008 | 41.55 | 42.93 |

Critical Accounting Policies and Estimates

The discussion and analysis of our financial condition and results of operations are based upon our consolidated financial statements, which have been prepared in accordance with accounting principles generally accepted in the United States of America. The preparation of these financial statements requires us to make significant estimates and judgments that affect the reported amounts of assets, liabilities, revenues and expenses, and related disclosure of contingent assets and liabilities. These items are regularly monitored and analyzed by management for changes in facts and circumstances, and material changes in these estimates could occur in the future. These estimates include, among others, our revenue recognition policies related to the proportional performance and percentage of completion methodologies of revenue recognition of contracts and assessing our goodwill for impairment annually. Changes in estimates are recorded in the period in which they become known. We base our estimates on historical experience and various other assumptions that we believe are reasonable under the circumstances. Actual results will differ and may differ materially from the estimates if past experience or other assumptions do not turn out to be substantially accurate.

Our significant accounting policies are presented within Note 2 to our consolidated financial statements and the following summaries should be read in conjunction with the unaudited consolidated financial statements and the related notes included in this Report. While all accounting policies impact the financial statements, certain policies may be viewed as critical. Critical accounting policies are those that are both most important to the portrayal of financial condition and results of operations and that require management’s most subjective or complex judgments and estimates. Our management believes the policies that fall within this category are the policies on revenue recognition, accounting for stock-based compensation, goodwill and income taxes.

Revenue Recognition

The majority of the revenue recognized for three month period ended June 30, 2008 was derived from the Company’s subsidiaries and as accordingly:

Revenue is recognized based on the nature of activity when consideration can be reasonably measured and there exists reasonable certainty of its recovery.

Revenue from sale of goods is recognized when substantial risks and rewards of ownership are transferred to the buyer under the terms of the contract.

Revenue from construction/project related activity and contracts for supply/commissioning of complex plant and equipment is recognized as follows:

| a) | Cost plus contracts: Contract revenue is determined by adding the aggregate cost plus proportionate margin as agreed with the customer and expected to be realized. | ||

| b) | Fixed price contracts: Contract revenue is recognized using the percentage completion method. Percentage of completion is determined as a proportion of cost incurred-to-date to the total estimated contract cost. Changes in estimates for revenues, costs to complete and profit margins are recognized in the period in which they are reasonably determinable | ||

Full provision is made for any loss in the period in which it is foreseen.

Revenue from property development activity is recognized when all significant risks and rewards of ownership in the land and/or building are transferred to the customer and a reasonable expectation of collection of the sale consideration from the customer exists.

Revenue from service related activities and miscellaneous other contracts are recognized when the service is rendered using the proportionate completion method or completed service contract method.

Accounting for Stock-Based Compensation

As of June 30, 2008, we had not granted any stock options under our Employee Stock Plan.

Goodwill

We account for goodwill in accordance with SFAS No. 142, “Goodwill and Other Intangible Assets” (“SFAS No. 142”). SFAS No. 142 requires the use of a non-amortization approach to account for purchased goodwill and certain intangibles. Under the non-amortization approach, goodwill and certain intangibles are not amortized into results of operations, but instead are reviewed for impairment at least annually and written down and charged to operations only in the periods in which the recorded value of goodwill and certain intangibles exceeds its fair value. We have elected to perform our annual impairment test in November of each calendar year. An interim goodwill impairment test would be performed if an event occurs or circumstances change between annual tests that would more likely than not reduce the fair value of a reporting unit below its carrying amount. For purposes of performing the goodwill impairment test, we concluded there is one reporting unit. During November 2007,we completed the required annual test, which indicated there was no impairment.

Accounting for Income Taxes

In connection with preparing our financial statements, we are required to estimate our income taxes in each of the jurisdictions in which we operate. This process involves the assessment of our net operating loss carry forwards and credits, as well as estimating the actual current tax liability together with assessing temporary differences resulting from differing treatment of items, such as reserves and accrued liabilities, for tax and accounting purposes. We then assess the likelihood that deferred tax assets will be recovered from future taxable income, and to the extent we believe that recovery is not likely, we must establish a valuation allowance. Based on historical results, we believe that it is more likely than not that we will not realize the value of our deferred tax assets and therefore have provided a full valuation allowance against our net deferred tax assets.

Results of Operations

Three Months Ended June 30, 2008 Compared to Three Months Ended June 30, 2007

The following results of operations discussion compares our consolidated company results for the three months ended June 30, 2008 to the Combined Predecessor Results of Operations for the three months ended June 30, 2007. We believe this is a better measure of performance than comparing the consolidated company results to pre-acquisition results because there were no significant operating results before acquiring Sricon and TBL companies.

Revenue - Total revenues increased 441% to $17.9 million for the three months ended June 30, 2008, as compared to $3,311,309 for the three months ended June 30, 2007. Our revenue increased due to the increase in the number of new and active contracts in our contract backlog.

Operating Income (loss) - In the three month period ending June 30, 2008, operating margin is 3.7 million, compared to a loss of $59 thousand for the combined predecessor companies for the three month period ending June 30, 2007. Our operating margin increased due to the increase in the number of new and active contracts in our contract backlog.

Total Costs of Revenues and operating expenses - Our total cost of revenues and operating expenses principally consist of construction materials, employee compensation and benefits, depreciation and amortization, startup costs, and general and administrative expense. In the three month period ending June 30, 2008, total cost of revenue and operating expenses increased by $11 million or 325%, compared to the three month period ending June 30, 2007.

Costs of Revenues - Costs of revenues consists primarily of compensation and related fringe benefits for project-related personnel, department management and all other dedicated project related costs and indirect costs. Cost of Revenue increased by $10.4 million or 379%, compared to the three month period ending June 30, 2007. The increase was due to higher contract revenue during the year.

Selling, General and Administrative - Consist primarily of employee-related expenses, professional fees, other corporate expenses and allocated overhead. We expect that in the future, selling, general and administrative expenses will increase as we add personnel and incur additional professional fees and insurance costs related to being a publicly held company. Selling, general and administrative expenses increased by $0.5 million or 121%, compared to the three month period ending June 30, 2007, due to higher scale of operations resulting from acquisitions.

Net Interest Income (Expense) – Net interest (expense) increased by $0.2 million or 110% compared to the three month period ending June 30, 2007. The increase was due to higher utilization of debt and an increase in interest rates.

Net Income (loss) – Net income increased 246% to $1.3 million for the three months ended June 30, 2008, as compared a loss of $0.5 million for the three months ended June 30, 2007. Our net income increased due to the increase in the number of new and active contracts in our contract backlog.

Off-Balance Sheet Arrangements

We do not have any off-balance sheet arrangements as defined in Item 303(a) (4) (ii) of Regulation S-K promulgated under the Securities Exchange Act of 1934.

Liquidity and Capital Resources

This liquidity and capital resources discussion compares the consolidated company results for three months period ended June 30, 2008 and 2007. The Predecessor cash flow statements for the three month ended period June 30, 2007 are not available.

Cash used for operating activities from continuing operations is our net loss adjusted for certain non-cash items and changes in operating assets and liabilities. During the first three months of 2008, cash used for operating activities was $5.5 million compared to cash used for operating activities of $0.4 million during the first three months of 2007. The uses of cash in the first three months of 2008 relates primarily to the payment of general operating expenses of our subsidiary companies.

During the first three months of 2008, investing activities from continuing operations used $ 5.2 million of cash as compared to $27 thousand used during the comparable period in 2007. In the first quarter of 2008, we paid $1.6 million for equipment purchases and $3.5 million for short term investments.

Financing cash flows from continuing operations consist primarily of transactions related to our debt and equity structure. In the first three months of 2008 there was financing cash provided of approximately $4.2 million, compared to cash used of approximately $325 thousand for the first three months of 2007. The cash provided in 2008 was primarily due to use of bank credit lines. The cash used in 2007 was primarily due to repayment of long-term notes to stockholders.

Our future liquidity needs will depend on, among other factors, stability of construction costs, interest rates, and a continued increase in infrastructure contracts in India. We believe that our current cash balances and anticipated operating cash flow, will be sufficient to fund our normal operating requirements for at least the next 12 months. However, we may seek to secure additional capital to fund further growth of our business in the near term.

Commitments

1) Capital commitments

The estimated amount of contracts remaining to be executed on capital account not provided for as on June 30, 2008 are USD zero.

2) Guarantees

The Company had outstanding financial / performance bank guarantees of approximately USD 4 million as of June 30, 2008.

| a) | The Sricon was awarded a contract from National Highway Authority of India (‘NHAI’) in 2004-05, for restoring the Jaipur – Gurgaon National Highway 8. The total contract value was USD 5.10 million to be completed in 9 months. The entire stretch of the site was handed over on piecemeal basis without any defined schedule in contravention with contractual provisions and approved construction program and methodology. This has resulted in additional costs due to additional deployment of resources for prolonged period. Thus, Sricon invoked the escalation clause of the contract and filed a claim of USD 8.16 million. The dispute has been referred to arbitration. The Company has not recognized the claimed amounts on its books. | ||

| b) | Sricon was awarded a contract from National Highway Authority of India (‘NHAI’) in 2001-02 for construction of a four lane highway on the Namkkal bypass on National Highway 7, in the state of Tamilnadu. The total contract value was USD 4 million and the construction was to have been completed by November 30, 2002. The escalation and variation claim of USD 5.27 million is pending with NHAI. An arbitration process was initiated on July 3, 2007. The company has not recognized the claim amounts on its books. | ||

| c) | TBL is contingently liable to pay four-thousand dollars towards interest and penalty towards Provident Dues as per the orders of the competent authorities. | ||

Forward-Looking Statements

This report contains forward-looking statements, including, among others, (a) our expectations about possible business combinations, (b) our growth strategies, (c) our future financing plans, and (d) our anticipated needs for working capital. Forward-looking statements, which involve assumptions and describe our future plans, strategies, and expectations, are generally identifiable by use of the words “may,” “should,” “expect,” “anticipate,” “approximate,” “estimate,” “believe,” “intend,” “plan,” or “project,” or the negative of these words or other variations on these words or comparable terminology. This information may involve known and unknown risks, uncertainties, and other factors that may cause our actual results, performance, or achievements to be materially different from the future results, performance, or achievements expressed or implied by any forward-looking statements. These statements may be found in this report. Actual events or results may differ materially from those discussed in forward-looking statements as a result of various factors, including, without limitation, the risks outlined under our “Description of Business” and matters described in this report generally. In light of these risks and uncertainties, the events anticipated in the forward-looking statements may or may not occur. These statements are based on current expectations and speak only as of the date of such statements. We undertake no obligation to publicly update or revise any forward-looking statement, whether as a result of future events, new information or otherwise.

The information contained in this report identifies important factors that could adversely affect actual results and performance. All forward-looking statements attributable to us are expressly qualified in their entirety by the foregoing cautionary statements.

Item 3. Quantitative and Qualitative Disclosures About Market Risk

The primary objective of the following information is to provide forward-looking quantitative and qualitative information about our potential exposure to market risks. Market risk is the sensitivity of income to changes in interest rates, foreign exchanges, commodity prices, equity prices, and other market-driven rates or prices. The disclosures are not meant to be precise indicators of expected future losses, but rather, indicators of reasonably possible losses. This forward-looking information provides indicators of how we view and manage our ongoing market risk exposures.

Item 4. Controls and Procedures

The Company maintains disclosure controls and procedures that are designed to ensure that information requiring disclosure in our reports filed pursuant to the Securities Exchange Act of 1934, as amended, is recorded, processed, summarized and reported within the time periods specified in the SEC’s rules, regulations and related forms, and that such information is accumulated and communicated to our principal executive officer and principal financial officer, as appropriate, to allow timely decisions regarding required disclosure.

The Company, under the supervision of our principal executive officer and principal financial officer, carried out an evaluation of the effectiveness of the design and operation of its disclosure controls and procedures as defined in Rules 13a-15(e) and 15d-15(e) under the Securities Exchange Act of 1934, as of June 30, 2008. Based upon that evaluation, management, including our principal executive officer and principal financial officer, concluded that the Company’s disclosure controls and procedures were effective in alerting it in a timely manner to information relating to the Company required to be disclosed in this report other than with respect to our procedures for including the required auditor consents.

In connection with the preparation of our Form 10-KSB for our fiscal year ended March 31, 2008, we failed to request one of the consents from our auditors in a timely manner. This deficiency in our controls caused us to file our Form 10-KSB for fiscal the year ended March 31, 2008 one day late. We determined that this control deficiency did not result, however, in a material misstatement or lack of disclosure within the Form 10-KSB.

Based on the changes and improvements made since July 16, 2008 (the date we filed our Form 10-KSB), our management, including our principal executive officer and principal financial officer, believes that we have designed and implemented a new controls environment to address the weakness described above. Such remediation activities involved assigning the principal financial officer with the responsibility of requesting consents from our auditors, allocating additional personnel to the disclosure process, adopting written disclosure controls and procedures, forming a disclosure controls committee that will consider the materiality of information and determine disclosure obligations on a timely basis and engaging outside counsel to review to future SEC filings.

With these programs in place, we believe our control procedures sufficiently effective to ensure that information requiring inclusion or disclosure in our reports filed pursuant to the Securities Exchange Act of 1934, as amended, is recorded, processed, summarized and reported within the time periods specified in the SEC’s rules, regulations and related forms, and that such information is accumulated and communicated to our principal executive officer and principal financial officer, as appropriate, to allow timely decisions regarding required disclosure.

No change in the Company's internal control over financial reporting occurred during the year ended June 30, 2008, that materially affected, or is reasonably likely to materially affect, the Company's internal control over financial reporting.

PART II – OTHER INFORMATION

Item 1. | Legal Proceedings |

The Company is not a party to any pending legal proceeding other than routine litigation that is incidental to our business.

Item 2. Unregistered Sales of Equity Securities and Use of Proceeds.

No unregistered sales of securities were made during the quarter that were not previously reported on a Current Report on Form 8-K.

Item 3. | Defaults Upon Senior Securities |

None

| Item 4. | Submission of Matters to a Vote of Security Holders |

On or about June 25, 2008, we distributed our Definitive Proxy Statement to each stockholder of record as of June 18, 2008, for our Special Meeting of Stockholders held on July 15, 2008 at 10:00 a.m. local time (the “Special Meeting”). At the Special Meeting, the stockholders were asked to consider a proposal to amend the Company’s 2008 Omnibus Incentive Plan (the “Plan”) to increase the number of shares authorized for issuance under the Plan from 300,000 to 1,300,000, to reduce the base number of outstanding shares used to calculate adjustments to the shares under the Plan from 13,974,500 to 8,570,107 and to make additional clarifying changes to the Plan. The voting results were:

| For: | 4,847,067 | ||

| Against: | 90,374 | ||

| Abstain: | 3,120 | ||

| Broker Non-Votes: | 0 |

Item 5. Other Information

None.

Item 6. Exhibits

The following exhibits are filed as part of, or are incorporated by reference into, this report:

(a) Financial Statements

Our financial statements as set forth in the Index to Financial Statements attached hereto commencing on page F-1 are hereby incorporated by reference.

(b) Exhibits.

In accordance with Section 13 or 15(d) of the Exchange Act, the registrant caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

| INDIA GLOBALIZATION CAPITAL, INC. | |||

| Date: August 18, 2008 | By: | /s/ Ram Mukunda | |

| Ram Mukunda | |||

| Chief Executive Officer and President (Principal Executive Officer) | |||

| Date: August 18, 2008 | By: | /s/ John B. Selvaraj | |

| John B. Selvaraj | |||

| Treasurer, Principal Financial and Accounting Officer | |||