Use these links to rapidly review the document

TABLE OF CONTENTS

INDEX TO FINANCIAL STATEMENTS

As filed with the Securities and Exchange Commission on November 8, 2010

Registration No. 333-170074

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 1 to

FORM S-11

FOR REGISTRATION UNDER THE SECURITIES ACT OF 1933

OF SECURITIES OF CERTAIN REAL ESTATE COMPANIES

The Howard Hughes Corporation

(formerly Spinco, Inc.)

(Exact name of registrant as specified in governing instruments)

110 N. Wacker Drive

Chicago, IL 60606

(312) 960-5000

(Address, including Zip Code and Telephone Number,

including Area Code, of Registrant's Principal Executive Offices)

Thomas Nolan, Jr.

President and Chief Operating Officer

The Howard Hughes Corporation

110 N. Wacker Drive

Chicago, IL 60606

(312) 960-5000

(Name, Address, Including Zip Code, and Telephone Number, Including Area Code, of Agent For Service)

Copies to:

Matthew D. Bloch, Esq.

Heather L. Emmel, Esq.

Weil, Gotshal & Manges LLP

767 Fifth Avenue

New York, New York

(212) 310-8000 (Phone)

(212) 310-8007 (Fax)

Approximate date of commencement of proposed sale to the public:

As soon as practicable after the effective date of this Registration Statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ý

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

(Continued on following page)

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

| Large accelerated filer o | Accelerated filer o | Non-accelerated filer ý (Do not check if a smaller reporting company) | Smaller reporting company o |

CALCULATION OF REGISTRATION FEE

Title of securities to be registered | Amount to be Registered(1) | Proposed maximum offering price per unit | Proposed maximum aggregate offering price(2) | Amount of registration fee | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

Common stock, $0.01 par value per share(3) | 12,946,424 | N/A | $ | 616,508,710 | (4) | $ | 43,957.07 | |||||||

Common stock warrants(5) | 6,083,333 | N/A | — | — | ||||||||||

Common stock issuable upon the exercise of common stock warrants(6) | 6,083,333 | — | $ | 304,166,650 | $ | 21,687.08 | ||||||||

Common stock issuable upon the exercise of options to acquire common stock(7) | 180,057 | N/A | 8,574,314 | $ | 611.35 | |||||||||

Total | $ | 66,255.50 | ||||||||||||

- (1)

- Pursuant to Rule 416, the securities being registered hereunder include such indeterminate number of additional shares of common stock as may be issuable as a result of stock splits, stock dividends, recapitalizations, anti-dilution adjustments or similar transactions.

- (2)

- Estimated solely for purposes of calculating the registration fee in accordance with Rule 457(o) promulgated under the Securities Act of 1933, as amended (the "Securities Act").

- (3)

- Represents (a) 4,037,691 shares of our common stock to be issued to (i) Brookfield Retail Holdings LLC (formerly known as REP Investments LLC), an affiliate of Brookfield Asset Management Inc. (and its designees, as applicable, "Brookfield Investor"), (ii) Pershing Square Capital Management, L.P. on behalf of Pershing Square, L.P., Pershing Square II, L.P., Pershing Square International, Ltd. and Pershing Square International V, Ltd. (collectively, "Pershing Square") and (iii) Blackstone Real Estate Partners VI, L.P. ("Blackstone") and its permitted assigns (together with Blackstone, the "Blackstone Investors") pursuant to the investment agreements and designation described in this registration statement and (b) 8,908,733 shares of common stock to be issued to Pershing Square and General Trust Company in connection with the distribution of our common stock in connection with the Separation of the Company from General Growth Properties, Inc. as described in this registration statement.

- (4)

- The proposed maximum aggregate offering price for the common stock is the product of (x) 12,946,424 (the number of shares of common stock being registered hereby) and (y) $47.62 (the price at which the Plan Sponsors and Blackstone have agreed to purchase the shares of our common stock pursuant to the investment agreements and designation).

- (5)

- Represents warrants to acquire 6,083,333 shares of our common stock to be issued to Brookfield Investor, Pershing Square and the Blackstone Investors pursuant to the investment agreements and designation described in the registration statement. Pursuant to Rule 457(g) promulgated under the Securities Act, no separate registration fee is required for the warrants being offered hereby because the warrants are being registered on the same registration statement as the common stock underlying the warrants.

- (6)

- Includes 6,083,333 shares of our common stock issuable upon the exercise of warrants to be issued to Brookfield Investor, Pershing Square and the Blackstone Investors pursuant to the investment agreements described in this registration statement. Pursuant to Rule 457(g) promulgated under the Securities Act, the maximum aggregate offering price is based on the $50.00 exercise price of the warrants.

- (7)

- Includes 180,057 shares of our common stock issuable upon the exercise of stock options to acquire our common stock held by certain of the selling stockholders named in this registration statement. The proposed maximum aggregate offering price is based upon $47.62 per share (the price at which the Plan Sponsors and Blackstone have agreed to purchase the shares of our common stock pursuant to the investment agreements and designation).

The Registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the registration statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

The information in this prospectus is not complete and may be changed. The selling stockholders may not sell these securities until the registration statement filed with the Securities and Exchange Commission relating to these securities is effective. This prospectus is not an offer to sell these securities and it is not a solicitation of an offer to buy these securities in any jurisdiction where such offer, solicitation or sale is not permitted.

SUBJECT TO COMPLETION, DATED NOVEMBER 8, 2010

Preliminary Prospectus

THE HOWARD HUGHES CORPORATION

19,209,814 shares of Common Stock

Warrants to purchase up to 6,083,333 shares of Common Stock

This prospectus relates solely to the resale by the selling stockholders identified in this prospectus of up to an aggregate of (i) 19,209,814 shares of common stock of The Howard Hughes Corporation ("THHC"), $0.01 par value per share, consisting of 4,037,691 shares of common stock issued pursuant to the investment agreements described herein, 8,908,733 shares of common stock issued in connection with the separation and distribution described herein, 6,083,333 shares of common stock issuable upon exercise of the warrants described herein and 180,057 shares of common stock issuable upon exercise of certain outstanding stock options and (ii) 6,083,333 warrants to acquire common stock of THHC.

The selling stockholders identified in this prospectus (which term as used herein includes their pledgees, donees, transferees or other successors-in-interest) may offer the shares or warrants from time to time as they may determine through public transactions or through other means and at varying prices as determined by the prevailing market price for shares or in negotiated transactions as described in the section entitled "Plan of Distribution" beginning on page 123.

We do not know when or in what amount the selling stockholders may offer the shares or warrants for sale. We expect that the offering price for our common stock will be based on the prevailing market price of our common stock at the time of sale. Our common stock has been approved for listing, subject to official notice of issuance, on the New York Stock Exchange (the "NYSE") under the symbol "HHC." We do not intend to list the warrants on any exchange; accordingly, there will not be an established market price for the warrants. There is currently no established market price for the warrants. We expect that the offering price for the warrants will be based on the relationship between the exercise price of the warrants and the prevailing market price for our common stock at the time of sale. The closing price for our common stock on the "when-issued" market of the NYSE on November 5, 2010 was $38.00.

We will not receive any of the proceeds from the sale of these shares of our common stock or the warrants by the selling stockholders.

Investing in shares of our common stock or the warrants involves risks. See "Risk Factors" beginning on page 17 to read about factors you should consider before buying shares of our common stock or the warrants.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

This prospectus is dated , 2010.

EXPLANATORY NOTE | iii | |

USE OF NON-GAAP MEASURES | iii | |

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS | v | |

PROSPECTUS SUMMARY | 1 | |

RISK FACTORS | 17 | |

USE OF PROCEEDS | 33 | |

DIVIDEND POLICY | 33 | |

MARKET FOR OUR COMMON STOCK | 34 | |

SELECTED HISTORICAL COMBINED FINANCIAL DATA | 36 | |

UNAUDITED PRO FORMA CONDENSED COMBINED FINANCIAL INFORMATION | 38 | |

MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 45 | |

BUSINESS | 69 | |

MANAGEMENT | 98 | |

EXECUTIVE COMPENSATION | 105 | |

DIRECTOR COMPENSATION | 109 | |

SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT | 110 | |

CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS, AND DIRECTOR INDEPENDENCE | 113 | |

SELLING STOCKHOLDERS | 116 | |

DESCRIPTION OF CAPITAL STOCK | 118 | |

PLAN OF DISTRIBUTION | 124 | |

UNITED STATES FEDERAL INCOME TAX CONSIDERATIONS | 128 | |

LEGAL MATTERS | 134 | |

EXPERTS | 134 | |

WHERE YOU CAN FIND MORE INFORMATION | 134 | |

INDEX TO FINANCIAL STATEMENTS | F-i |

This prospectus is part of a registration statement on Form S-11 that we filed with the Securities and Exchange Commission (the "SEC"). You should rely only on the information contained in this prospectus (as supplemented and amended). We have not authorized anyone to provide you with different information. This document may only be used where it is legal to sell these securities. You should not assume that the information contained in this prospectus is accurate as of any date other than its date regardless of the time of delivery of the prospectus or any sale of our common stock. We will from time to time supplement the information contained in this prospectus in a prospectus supplement.

ii

This registration statement is being filed by The Howard Hughes Corporation, formerly known as Spinco, Inc. ("THHC"), in order to register its common stock and warrants for resale pursuant to Section 415(a)(1)(i) under the Securities Act of 1933, as amended (the "Securities Act") pursuant to certain investment agreements described herein. THHC is a newly formed Delaware corporation that was created to hold certain assets and liabilities of General Growth Properties, Inc. ("GGP") and its subsidiaries (collectively, the "Predecessors"). In conjunction with a plan of reorganization filed by GGP and certain of its subsidiaries under Chapter 11 of title 11 of the United States Code (as the same may be amended, modified or supplemented from time to time, the "Plan"), THHC will receive certain of the assets and liabilities of the Predecessors (the "Separation"), which we refer to as our business. We expect the reorganization to be completed during the fourth quarter of 2010 (such time of completion is referred to herein as the "Effective Date"). Pursuant to the Plan, on or prior to the Effective Date, approximately 32,500,000 shares of common stock of THHC (0.098344 shares of THHC common stock for each share of GGP common stock which is based upon a maximum number of THHC shares and options and warrants to acquire THHC common stock), will be distributed or issued to the common and preferred unit holders of GGP Limited Partnership ("GGPLP"), which includes GGP, and then GGP will distribute its portion of such shares to holders of GGP common stock (the "Distribution") and the Plan Sponsors (as defined herein) and certain designees if applicable, (as further described herein), will purchase $250.0 million of our common stock. GGP will not retain any ownership interest in THHC. Unless otherwise noted, all information contained in this registration statement relates to THHC after the Effective Date. THHC's common stock has been approved for listing, subject to official notice of issuance, on the New York Stock Exchange (the "NYSE") under the symbol "HHC."

The shares of THHC common stock and warrants that are the subject of this registration statement will only be issued, and offerings of such securities under this registration statement will only be made, if the Plan is confirmed and the closing of the transactions contemplated by the Plan, including the Separation, are completed. Accordingly, the information presented in the prospectus contained in this registration statement is presented, to the extent possible, as if the closing of the transactions described above, including GGP's emergence from bankruptcy and the Separation, have occurred. Any material changes to the Plan or these transactions will be reflected in a subsequent amendment to the registration statement.

We present EBITDA and Adjusted EBITDA, each as defined below, in this prospectus as supplemental measures of our performance that are not required by, or presented in accordance with, accounting principles generally accepted in the United States of America ("GAAP"). They are not measures of our financial performance under GAAP and should not be considered as alternatives to any other performance measures derived in accordance with GAAP or as alternatives to cash flow from operating activities as measures of our liquidity.

EBITDA is defined as net income (loss) attributable to controlling interests (currently, GGP), plus interest expense net of interest income, income tax provision (benefit), depreciation and amortization. We calculate Adjusted EBITDA by adjusting EBITDA for the following items: (a) costs incurred with respect to reorganization items following GGP's filing for bankruptcy protection, including gains on liabilities subject to compromise, interest income, U.S. Trustee fees and other restructuring items; (b) our 2009 and 2008 strategic initiatives, which consist of GGP's pre-bankruptcy filing restructuring costs; and (c) provisions for impairment. We present EBITDA and Adjusted EBITDA because we believe certain investors use them as additional measures of a company's historical operating performance and its ability to service and incur debt. We believe that the inclusion of supplementary adjustments to EBITDA applied in presenting Adjusted EBITDA is appropriate to provide additional

iii

information to investors because Adjusted EBITDA excludes certain non-recurring and/or non-cash items, including bankruptcy and restructuring costs, which we believe are not indicative of our core operating performance and which are not excluded in the calculation of EBITDA. In addition, we present EBITDA and Adjusted EBITDA of our properties that we own jointly with independent joint venture partners under the proportionate share method. Under the proportionate share method, our share of revenues and expenses of such properties are aggregated with the revenues and expenses of our combined properties.

EBITDA and Adjusted EBITDA should not be considered as alternatives to GAAP net income (loss) attributable to controlling interests, and you should not consider them in isolation, or as substitutes for analysis of our results as reported under GAAP. Some of the limitations inherent in these non-GAAP measures are that:

- •

- they do not reflect our cash expenditures, or future requirements for capital expenditures or contractual commitments;

- •

- they do not reflect changes in, or cash requirements for, our working capital needs;

- •

- they do not reflect the cash requirements necessary to service interest or principal payments on our debt;

- •

- they do not reflect any cash income taxes that we may be required to pay;

- •

- assets are depreciated or amortized over differing estimated useful lives and often have to be replaced in the future, and these measures do not reflect any cash requirements for such replacements;

- •

- they do not adjust for all non-cash income or expense items that are reflected in our statements of cash flows;

- •

- they do not reflect the impact of earnings or charges resulting from matters we consider not to be indicative of our ongoing operations;

- •

- they do not reflect the value of our non-income producing assets;

- •

- they may not be calculated in the same manner as research analysts calculate EBITDA or Adjusted EBITDA or in the same manner as may be required by any current or future indebtedness;

- •

- they do not reflect limitations on, or costs related to, transferring earnings from our subsidiaries and unconsolidated joint ventures to us; and

- •

- other companies in our industry may calculate these measures differently than we do, limiting their usefulness as comparative measures.

For a reconciliation of Adjusted EBITDA and EBITDA to net income (loss) attributable to controlling interests, see "Summary Historical Combined Financial Data."

iv

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This prospectus contains forward-looking statements that are subject to risks and uncertainties. All statements other than statements of historical fact included in this prospectus are forward-looking statements. Forward-looking statements give our current expectations relating to our financial condition, results of operations, plans, objectives, future performance and business. You can identify forward-looking statements by the fact that they do not relate strictly to current or historical facts. These statements may include words such as "anticipate," "estimate," "expect," "project," "forecast," "plan," "intend," "believe," "may," "should," "would," "likely," and other words of similar expression.

Forward-looking statements should not be unduly relied upon. They give our expectations about the future and are not guarantees. These statements involve known and unknown risks, uncertainties and other factors that may cause our actual results, performance and achievements to materially differ from any future results, performance and achievements expressed or implied by such forward-looking statements. We caution you, therefore, not to rely on these forward-looking statements.

In this prospectus, for example, we make forward-looking statements discussing our expectations about:

- •

- capital required for our operations and development opportunities for the properties in our Strategic Development segment following the Distribution;

- •

- expected performance of our Master Planned Communities segment and other current income producing properties;

- •

- future management;

- •

- future liquidity;

- •

- future development opportunities;

- •

- expenses we expect to incur as a stand-alone entity;

- •

- future development spending; and

- •

- future management plans.

Factors that could cause actual results to differ materially from those expressed or implied by the forward-looking statements include:

- •

- our history of losses;

- •

- our lack of operating history as an independent company;

- •

- our reliance on an interim management company;

- •

- our inability to obtain operating and development capital;

- •

- our inability to establish our own financial, administrative and other support functions to operate as a stand-alone business and loss of operational efficiency we had as a part of GGP;

- •

- our new directors and officers may change our long-range plans;

- •

- our new directors may be involved or have interests in other businesses, including, without limitation, real estate activities and investments;

- •

- a prolonged recession in the national economy and adverse economic conditions in the retail sector;

- •

- our inability to compete effectively;

v

- •

- potential conflicts arising with GGP after the Distribution from agreements with GGP with respect to certain of our assets;

- •

- our inability to control certain of our properties due to the joint ownership of such property and our inability to successfully attract desirable strategic partners;

- •

- risks associated with the Distribution not qualifying as a tax-free distribution for U.S. federal income tax purposes;

- •

- the Plan Sponsors (as subsequently defined) having influence over us, whose interests may be adverse to ours or yours; and

- •

- the other risks described in "Risk Factors."

These forward-looking statements present our estimates and assumptions only as of the date of this prospectus. Except as may be required by law, we undertake no obligation to modify or revise any forward-looking statements to reflect events or circumstances occurring after the date of this prospectus.

vi

We are a newly formed Delaware corporation that was created to hold certain assets and liabilities of General Growth Properties, Inc. ("GGP") and its subsidiaries (collectively, the "Predecessors"). In conjunction with the third amended plan of reorganization, as modified, filed by GGP and certain of its subsidiaries under Chapter 11 of title 11 of the United States Code (the "Plan"), we received certain of the assets and liabilities of the Predecessors and substantially all of our common stock was distributed to the holders of GGP's common stock (the "Distribution"). GGP does not retain any ownership interest in us.

We refer to the "Effective Date" as the date on which the reorganization of GGP and certain of its subsidiaries was completed, at which time the Predecessors transferred to us the Predecessors' properties and related assets and liabilities described herein (the "Separation"), which we refer to as our business. The description of our business is presented herein as if the transferred business was our business for all historical periods described. Unless the context otherwise requires, references to "we," "us" and "our" refer to The Howard Hughes Corporation and its subsidiaries and joint venture interests after giving effect to the Separation and the Distribution.

The items in the following summary are described in more detail later in this prospectus. This summary provides an overview of selected information and does not contain all the information you should consider before making a future investment decision with respect to our securities. Therefore, you should also read the more detailed information set out in this prospectus, including the risk factors, the combined financial statements and the notes thereto, and the other documents to which this prospectus refers before making an investment decision.

On April 16, 2009 and April 22, 2009 (collectively, the "Petition Date"), GGP and certain of its subsidiaries filed voluntary petitions for relief (the "Chapter 11 Cases") in the Bankruptcy Court for the Southern District of New York (the "Bankruptcy Court") under Chapter 11 of title 11 of the United States Code (the "Bankruptcy Code"). On August 27, 2010, GGP filed with the Bankruptcy Court its third amended Plan (as supplemented on September 30, 2010 and further modified on October 21, 2010) and the related disclosure statement (the "Disclosure Statement") for the debtors remaining in the Chapter 11 Cases (the "TopCo Debtors"). On October 21, 2010, the Bankruptcy Court confirmed the Plan and on the Effective Date, the Plan became effective, the TopCo Debtors emerged from bankruptcy, and the Separation and the Distribution were completed. The Plan set forth the structure of GGP and the TopCo Debtors following the Effective Date. We refer to the public company successor to GGP following the Effective Date as "reorganized GGP." See "Business—Bankruptcy Proceedings."

We are a real estate company created to specialize in the development of master planned communities and other strategic real estate development opportunities across the United States. Our goal is to create sustainable, long-term growth and value for our stockholders. We own a diverse portfolio of properties with a relatively small amount of debt (an amount equal to 11.7% of our total assets as of June 30, 2010) and with near, medium and long-term development opportunities, including our master planned communities, mall development projects and a series of mixed-use development opportunities in premier locations. As operated by the Predecessors, our master planned communities have won numerous awards for, among other things, design and community contribution. We expect the competitive position and desirable location of certain of our assets (which collectively comprise millions of square feet and thousands of acres of developable land), combined with their operations and long-term opportunity through entitlements, land and home site sales and project developments, to drive our income and growth. We expect to pursue development opportunities for a number of our assets that were postponed by the Predecessors due to lack of liquidity resulting from deteriorating economic conditions, the credit market collapse and certain of the Predecessors' bankruptcy filings in

1

April 2009, and to develop plans for other assets for which no plans had been developed. We expect to assess the opportunities for these assets, which are currently in various stages of completion, to determine how to finance their completion and how to maximize their long-term value potential, which may include entering into joint venture arrangements.

For the year ended December 31, 2009, our net loss attributable to controlling interests and Adjusted EBITDA were $703.6 million and $21.5 million, respectively, and for the six months ended June 30, 2010, our net loss attributable to controlling interests and Adjusted EBITDA were $48.6 million and $10.7 million, respectively. As of June 30, 2010, our combined debt was $340.5 million and our share of the debt of our Real Estate Affiliates (as defined below) was $196.2 million and we had $2.9 billion of total assets. As a newly formed company with no operating history as a stand alone company and on a combined, carve-out basis, a history of losses and negative cash flow from operations, there are significant risks to investing in our securities. See "Risk Factors" and "Management's Discussion and Analysis of Financial Condition and Results of Operations—Liquidity and Capital Resources."

We operate our business in two lines of business: Master Planned Communities and Strategic Development.

Master Planned Communities. Our Master Planned Communities segment consists of the development and sale of residential and commercial land, primarily in large-scale projects. We currently own four master planned communities (including four separate communities in Maryland that are commonly, and collectively, referred to as the "Maryland communities") with over 14,000 acres of land remaining to be sold in desirable locations, which in some cases have no land suitable for large-scale residential development nearby. Residential sales, which are made primarily to home builders, include standard, custom and high density (i.e., condominium, town homes and apartments) parcels. Standard residential lots are designated for detached and attached single- and multi-family homes, ranging from entry-level to luxury homes. Commercial sales include parcels designated for retail, office, services and other for-profit activities, as well as those parcels designated for use by government, schools and other not-for-profit entities.

Strategic Development. Our Strategic Development segment is made up of near, medium and long-term real estate properties and development projects, some of which we believe have the potential to create meaningful value. For example, the Hawaii Community Development Authority ("HCDA") approved a 15-plus year master plan that will permit us to transform 60 acres of land at our Ward Centers project in Honolulu, Hawaii into a vibrant and diverse neighborhood of residences, shops, entertainment and offices.

To better understand the nature of our strategic development opportunities and our current expectations for the type of development we may ultimately pursue, we present our development opportunities in this registration statement in the following four categories: nine mixed-use development opportunities, four mall development projects, seven redevelopment projects and eleven other property interests, including ownership of various land parcels and certain profit interests. At present all of these assets generally share the fundamental characteristic of requiring substantial future development to achieve their highest and best use. However, as discussed elsewhere in this registration statement, following the Separation, our new board of directors and management are expected to reevaluate the Predecessor's plans and ideas for these assets based on market conditions and availability of capital. In order to be able to realize a development plan for any of these assets, in addition to the permitting and approval process attendant to almost all large-scale real estate development of this nature, we will need to obtain financing either through joint venture equity or construction, bridge or long-term financing, none of which is assured. See "Risk Factors—We may face potential difficulties in obtaining operating and development capital" and "Our business model includes entering into joint venture arrangements with strategic partners. This model may not be successful and

2

our business could be adversely affected if we are not able to successfully attract desirable strategic partners or complete agreements with strategic partners." As a result of these shared attributes, management evaluates and manages the strategic development assets as a single operating unit, with the employees responsible for individual projects reporting up to a single executive responsible for this segment.

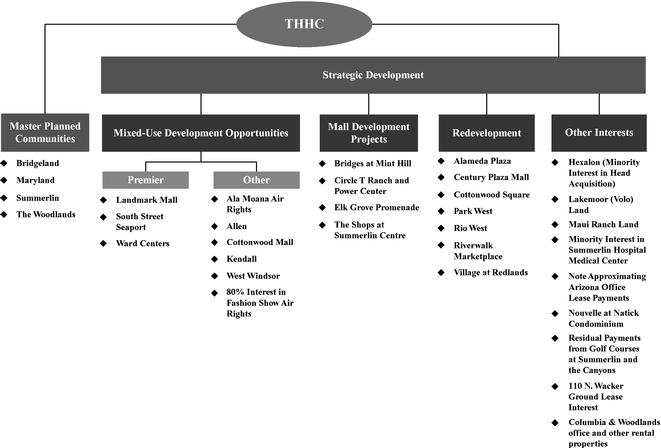

The chart below presents our assets by reportable segment and, with respect to our strategic development business, by the potential type of development opportunity:

We own non-controlling investments and interests in The Woodlands Partnerships and Circle T, which we account for using the equity method, and the cost method for non-ownership rights in certain real estate assets. We collectively refer to these investments as our "Real Estate Affiliates." See "Note 3 Real Estate Affiliates" of our audited combined financial statements and "Note 5 Real Estate Affiliates" of our unaudited combined financial statements each included elsewhere in this prospectus.

3

The table below sets forth certain financial information for our two segments as of June 30, 2010 and as of December 31, 2009, or, as applicable, for the six months ended June 30, 2010 and for the year ended December 31, 2009.

| | As of or For the Six Months Ended June 30, 2010 | As of or For the Year Ended December 31, 2009 | |||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | Master Planned Communities | Strategic Development | Total | Master Planned Communities | Strategic Development | Total | |||||||||||||

| | (dollars in thousands) | (dollars in thousands) | |||||||||||||||||

Adjusted EBITDA—Segment basis | $ | (1,259 | ) | $ | 11,924 | $ | 10,665 | $ | 1,243 | $ | 20,280 | $ | 21,523 | ||||||

Net Book Value of Assets | 1,762,679 | 836,347 | 2,599,026 | 1,741,878 | 945,378 | 2,687,256 | |||||||||||||

Combined Mortgages, notes and loans payable(*) | 80,223 | 260,272 | 340,495 | 82,011 | 260,822 | 342,833 | |||||||||||||

- (*)

- In addition, our share of our Real Estate Affiliates debt was $196.2 million at June 30, 2010.

We believe that we will distinguish ourselves through the following competitive strengths:

Award Winning Master Planned Communities. We believe that we are a leader in the master planned communities business. As operated by the Predecessors, the master planned communities in our portfolio have won numerous awards for, among other things, design and community contribution. In 2009, Bridgeland was awarded the "Master Planned Community of the Year" by the National Association of Home Builders. Our communities represent over 78,000 total acres and we have over 14,000 acres of land remaining to be sold in desirable locations. These communities are located in areas of the country that feature strong demographic fundamentals, such as high income and population growth rates. We believe that it would be difficult for other real estate development companies to acquire significant parcels of land in areas with similar demographics. While the economic downturn and housing recession has slowed land and home site sales across the nation, we believe that the long-term value of these communities remains strong given their competitive positioning and our expertise in long-range land use planning and entitlements for communities such as these.

Development Opportunities in Premier Locations. We will have the opportunity to develop mixed-use properties in some of the highest quality and most desirable economic and demographic regions of the United States, including Ward Centers in Honolulu, Hawaii; Landmark Mall in Alexandria, Virginia; and South Street Seaport in Manhattan, New York. Ward Centers is situated along prime Hawaiian oceanfront property located within one mile of downtown Honolulu and within walking distance of the Ala Moana Center, one of the highest traffic and sales volume regional malls in the world. At our Landmark Mall, we have certain limited entitlements to construct buildings as tall as 25 stories on some parcels, which could be used for retail, residential and commercial development, subject to acquisition of the 30 acres of adjacent lands from the anchor store owners and demolition of the existing mall structures. In addition, the South Street Seaport property is located in downtown Manhattan on the waterfront adjacent to the financial center of Wall Street.

Experienced Management Team. The Predecessors' existing experienced master planned community operational management team joined us on the Effective Date. We intend to hire industry-leading senior executives with master planned community and other real estate development expertise to complement this existing operational management team. Utilizing their significant experience managing our master planned community assets, the existing operational management team will maintain its current focus on our properties for the benefit of us and our stockholders. In addition, until our

4

permanent senior executives have been selected, Brookfield Asset Management and its affiliates ("Brookfield Advisors") will provide certain management services to THHC pursuant to an interim management agreement (the "Management Agreement"). Brookfield Advisors is a pre-eminent global real estate company. Brookfield Advisors will apply its considerable expertise in developing and operating premier real estate assets and experience in successfully managing our business by providing us with interim executive officers and commercial, technical, administrative and strategic services until our permanent executive management team can be identified and assume their roles. The Management Agreement has an initial term of six months subject to extension for up to an additional six months at our option, subject to good faith negotiation with respect to certain terms.

We will seek to maximize what we believe is the significant long-term value potential of our assets and create a leading real estate development company, while providing our stockholders with appropriate long-term returns commensurate with development risk. Given the makeup of our assets, particularly the undeveloped land in our Master Planned Communities segment, we have elected not to be treated as a real estate investment trust, or REIT, for U.S. federal income tax purposes; however, one of our subsidiaries, Victoria Ward, Limited, is and will continue to be treated as a REIT. Given the capital and operational differences between our two business segments, we intend to follow specific strategies in each business segment to maximize the value of our assets. Our strategies for each segment are detailed below.

Master Planned Communities Segment. In our Master Planned Communities segment, we plan to grow long-term value for our stockholders through continued improvements, entitlements and land development. We believe we have the potential to generate high cash flow in this segment because we expect our capital investment in properties to generally coincide with anticipated sales. With expertise in large-scale, long-range land use planning, residential and commercial real estate development, sales and other special skills, we intend to leverage our operational management team to oversee our operations. One of our primary strategies is to develop and sell land in a manner that increases the value of the remaining land to be developed and to provide current cash flows. To implement our strategy, we intend to build upon the experienced operational professionals who joined us from the Predecessors and, on an interim basis, we have engaged Brookfield Advisors to provide certain executive-level services.

Strategic Development Segment. Our portfolio of strategic development assets represents a diverse mix of near, medium and long-term real estate properties and development projects. We expect to pursue development opportunities for a number of our assets that were postponed by the Predecessors due to lack of liquidity resulting from deteriorating economic conditions, the credit market collapse and certain of the Predecessors' bankruptcy filings in April 2009. We expect to assess the opportunities for these assets, which are currently in various stages of completion, and determine how to finance their completion and how to maximize their long-term value potential. Any such development will require resources which may be significant in some cases. Real estate development is a capital intensive business with multi-year time frames for each project that will require higher leverage than our master planned communities segment will require. While the cash generated from land sales in our Master Planned Communities segment, cash flows from operations and the proceeds from the $250 million investment by the Plan Sponsors and the Blackstone Investors (each as subsequently defined) is expected to fund our ordinary course operating expenses and existing contractual obligations, we expect to fund our development projects with a mix of construction, bridge and long-term financing, as well as joint venture equity. We would expect to contribute the land and development expertise and planning to projects and form strategic and institutional partnerships to operate and finance these projects. We have not yet obtained any construction, bridge or long-term financing or identified any potential lenders or joint venture equity partners for any of our strategic development projects and cannot assure

5

you that such financing or joint venture arrangements will be available to us. We also do not intend to be a general contractor or property manager for most of our assets in this segment, and therefore will consider outsourcing the majority of property management, design and construction responsibilities to third parties.

Master Planned Communities

Our Master Planned Communities segment consists of the development and sale of residential and commercial land, primarily in large-scale projects in and around Columbia, Maryland; Houston, Texas; and Las Vegas, Nevada.

Revenues are derived primarily from the sale of finished lots, including infrastructure and amenities, and undeveloped property to both residential and commercial developers. Additional revenues are earned through participations with builders in their sales of finished homes to homebuyers. Revenues and Adjusted EBITDA are affected by factors such as the availability to purchasers of construction and permanent mortgage financing at acceptable interest rates, consumer and business confidence, regional economic conditions in the areas surrounding the projects, employment levels, levels of homebuilder inventory, other factors generally affecting the homebuilder business and sales of residential properties, availability of saleable land for particular uses and our decisions to sell, develop or retain land. For our more mature communities such as in Columbia, Maryland, we are also creating new design plans to increase density and add additional neighborhoods.

Master planned communities in the United States have suffered due to continued weak demand in the residential real estate market following the sharp decline in 2007. As a business venture, development of master planned communities requires expertise in large-scale, long-range land use planning, residential and commercial real estate development, sales and other special skills. The development of these communities requires decades of investment and a continual focus on the changing market dynamics surrounding these communities. In recent periods, the economic downturn has slowed land and home site sales, requiring the development and growth of these communities to be delayed. We believe that the long-term value of our communities remains strong given their competitive positioning and our expertise in long-range land use planning and entitlements for communities such as these.

6

The following table summarizes our master planned communities as of June 30, 2010:

| | | | | People Living in community (Approx. No.) | | | | | | |||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | | | | Remaining Saleable Acres(b) | | Projected Community Sell-Out Date | ||||||||||||||||||||||

| | | | Total/Gross Acres(a) | Redevelopment Acres(e) | ||||||||||||||||||||||||

Community | Location | Ownership (%) | Residential(c) | Commercial(d) | Total | |||||||||||||||||||||||

Bridgeland | Houston, TX | 100.0 | 11,400 | 3,250 | 3,981 | 1,246 | 5,227 | — | 2036 | |||||||||||||||||||

Summerlin | Las Vegas, NV | 100.0 | 22,500 | 100,000 | 6,559 | 625 | 7,184 | — | 2039 | |||||||||||||||||||

The Woodlands | Houston, TX | 52.5 | (f) | 28,400 | 94,000 | 1,063 | 1,018 | 2,081 | — | 2017 | ||||||||||||||||||

Maryland Communities | ||||||||||||||||||||||||||||

Columbia | Howard County, MD | 100.0 | 14,200 | 100,000 | — | — | — | 136 | 2035 | (g) | ||||||||||||||||||

Gateway | Howard County, MD | 100.0 | 630 | — | — | 121 | 121 | — | 2013 | |||||||||||||||||||

Emerson | Howard County, MD | 100.0 | 520 | 2,000 | 12 | 68 | 80 | — | 2013 | |||||||||||||||||||

Fairwood | Prince George's County, MD | 100.0 | 1,100 | 2,300 | — | 11 | 11 | — | 2013 | |||||||||||||||||||

Total | 78,750 | 301,550 | 11,615 | 3,089 | 14,704 | 136 | ||||||||||||||||||||||

- (a)

- Encompasses all of the land located within the borders of the master planned community, including parcels already sold, saleable parcels and non-saleable areas, such as roads, parks and recreation and conservation areas.

- (b)

- Includes only parcels that are intended for sale. The mix of intended use, as well as the amount of remaining saleable acres, are primarily based on assumptions regarding entitlements and zoning of the remaining project and are likely to change over time as the master plan is refined.

- (c)

- Includes standard, custom and high density residential land parcels. Standard residential lots are designated for detached and attached single- and multi-family homes, of a broad range, from entry-level to luxury homes. At Summerlin, we have designated certain residential parcels as custom lots as their premium price reflects their larger size and other distinguishing features—such as being within a gated community, having golf course access, or being located at higher elevations. High density residential includes townhomes, apartments and condominiums.

- (d)

- Designated for retail, office, services and other for-profit activities, as well as those parcels allocated for use by government, schools, houses of worship and other not-for-profit entities.

- (e)

- Reflects the number of acres we expect to redevelop.

- (f)

- Reflects our economic interest. Our ownership interest is 42.5% and we jointly make decisions with our joint venture partner.

- (g)

- Reflects the projected redevelopment completion date.

On May 10, 2010, certain of the TopCo Debtors entered into purchase agreements with two proposed purchasers, Richmond American Homes of Nevada, Inc. ("Richmond") and PN II, Inc., dba Pulte Homes of Nevada ("Pulte"), for the sale of certain lots in our Summerlin master planned community. The purchase agreement with Richmond is for parcels comprising 115 and 117 lots representing 32 acres in the aggregate for purchase prices of $8,510,000 and $9,477,000, respectively. The purchase agreement with Pulte is for parcels comprising 109 and 162 lots representing 31.5 acres in the aggregate for purchase prices of $7,739,000 and $12,231,000, respectively. As of October 4, 2010, the applicable TopCo Debtors have closed on the sale of 50 finished lots to Pulte and 20 finished lots to Richmond with gross purchase prices of $4,219,000 and $2,133,000, respectively. Both purchase agreements provide for closings of the remaining lots in stages through 2011.

7

Strategic Development

Our Strategic Development segment is made up of near, medium and long-term real estate properties and development projects. Our Strategic Development segment includes the following assets:

Mixed-Use Development Opportunities. We have the opportunity to create mixed-use development projects on nine properties in attractive locations, including the following premier opportunities:

- •

- South Street Seaport, located in the downtown financial and insurance districts of New York City, is within walking distance of lower Manhattan's many tourist attractions, such as the World Financial Center, Tribeca, the Brooklyn Bridge, City Hall and the NYSE. South Street Seaport currently contains approximately 285,000 square feet of retail, restaurant and exhibition space. South Street Seaport is easily accessible via subway, bus, car or water taxi. We believe that South Street Seaport represents a unique development opportunity which, subject to the approval of the City of New York, our ground lessor, could potentially include new shops, restaurants, hotels and residences.

- •

- The city council of Alexandria, Virginia unanimously approved a small area plan in February 2009 that authorized up to 5.5 million square feet of mixed-use development on the site currently occupied by our Landmark Mall. This site is located just nine miles west of Washington, D.C. and the Pentagon, and is within approximately one mile of public rail service on D.C.'s metro blue line. We have certain limited entitlements to construct buildings as tall as 25 stories on some parcels, subject to acquisition of the 30 acres of adjacent lands from the anchor store owners and demolition of their existing structures. Although plans continuously evolve as market conditions change, it is illustrative that our entitlements envision about 800,000 square feet of retail and other commercial space, 500 hotel rooms and 1.2 million square feet of residences. These could be developed by us or sold to others for development.

- •

- Ward Centers is situated along Ala Moana Beach Park and is within one mile of Waikiki and downtown Honolulu. The Ward Neighborhood is the site of Ward Centers, a chic shopping district of six specialty centers with over 135 unique shops (many found only there) and 22 restaurants. In January 2009, the HCDA approved a 15-plus year master plan by Victoria Ward, Limited to transform the 60-acre site into a vibrant and diverse neighborhood of residences, shops, entertainment and offices. We believe that the land's value increased significantly with the HCDA's approval of entitlements and we have the opportunity to undertake an oceanfront development project to add up to 10 million square feet of retail, residential, office and industrial use.

8

The following table summarizes our mixed-use development opportunities as of June 30, 2010:

ASSET | LOCATION | EXISTING GROSS LEASABLE AREA ("GLA") | SIZE (ACRES) | NET BOOK VALUE ($ MILLIONS) | ACQUISITION DATE | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

South Street Seaport | New York, NY | 285,849 | 11 | 2.9 | 11/04 | (1) | ||||||||||

Landmark Mall | Alexandria, VA | 859,710 | 22 | 48.3 | 11/04 | (1) | ||||||||||

Ward Centers | Honolulu, HI | 1,151,912 | (2) | 60 | 319.1 | 05/02 | ||||||||||

Ala Moana Tower Air Rights | Honolulu, HI | — | — | 22.8 | — | |||||||||||

Fashion Show Air Rights | Las Vegas, NV | — | — | — | — | |||||||||||

West Windsor | Princeton, NJ | — | 653 | 20.5 | 11/04 | (1) | ||||||||||

Allen | Dallas, TX | — | 238 | 26.0 | 03/06 | |||||||||||

Kendall | Miami, FL | — | 91 | 13.7 | 11/04 | (1) | ||||||||||

Cottonwood Mall | Holladay, UT | 220,954 | 54 | 20.3 | 07/02 | |||||||||||

Total | 2,518,425 | 1,129 | 473.6 | |||||||||||||

- (1)

- Acquired in 2004 as part of the Predecessors' acquisition of The Rouse Company.

- (2)

- Includes 642,165 of mall and freestanding GLA and other anchor store or other locations within the project.

Mall Development Projects. We own four mall development projects in desirable demographic regions. Examples include:

- •

- The Shops at Summerlin Centre, located in Las Vegas, Nevada, consists of an approximately 100-acre parcel that is part of a larger 1,300-acre mixed-use village located at the western rim of the Las Vegas valley in the heart of our Summerlin master planned community. The Shops at Summerlin Centre is surrounded by in-place residential and commercial development. The 100-acre parcel has the potential to be developed with office, retail, hotel and conference facilities, and residences. In 2009, Summerlin Town Centre's trade area encompassed approximately 672,000 people and 257,000 households. From 2009 to 2014, the trade area population is expected to grow at a rate that is almost three times the national average. By 2014, Nielsen™ estimates this trade area will grow by more than 100,000 people. The 2009 average household income within five miles of the site is $93,600, which is approximately 35% higher than the estimated 2009 average household income for all U.S. households of approximately $69,400.

- •

- Elk Grove Promenade is a partially constructed open air regional mall, which when completed is envisioned to be 1.1 million square feet, located on 100 acres in the community of Elk Grove, California. The project is approximately 17 miles southeast of downtown Sacramento and we believe that it has the potential to become a retail destination of choice in this community. In 2009, Elk Grove Promenade's trade area encompassed approximately 583,000 people and 194,000 households. From 2009 to 2014, the trade area population is expected to grow at a rate that is twice the national average. By 2014, Nielsen™ estimates there will be approximately 647,000 people within this trade area. The 2009 average household income within five miles of the site exceeds $100,000, which is approximately 44% higher than the estimated 2009 average household income for all U.S. households.

9

The following table summarizes our mall development projects as of June 30, 2010:

ASSET | LOCATION | SIZE (ACRES) | NET BOOK VALUE ($ MILLIONS) | ACQUISITION DATE | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

The Shops at Summerlin Centre | Summerlin, NV | 106 | 37.2 | 11/04 | (a) | ||||||||

Elk Grove Promenade | Elk Grove, CA | 100 | 10.9 | 11/03 | |||||||||

Circle T Ranch and Power Center(b) | Dallas/Ft. Worth, TX | 279 | 9.0 | 10/05 | |||||||||

Bridges at Mint Hill | Charlotte, NC | 162 | 12.2 | 10/06 - 01/07 | |||||||||

Total | 647 | 69.3 | |||||||||||

- (a)

- Acquired in 2004 as part of the Predecessors' acquisition of The Rouse Company.

- (b)

- Represents our 50% interest in these two development projects.

Redevelopment Projects. We own seven operating properties that we consider to be redevelopment projects. These properties today comprise approximately 1 million total square feet of GLA (as defined below) in the aggregate. These assets have the potential for future growth by means of an improved tenant mix, additional GLA, re-positioning of the asset or alternative uses. Our future development plans may include office, retail or residential space, shopping centers, movie theaters, parking complexes and open space. Any future redevelopment will require the receipt of permits, licenses, consents and waivers from various parties.

The following table summarizes our redevelopment projects as of June 30, 2010:

ASSET | LOCATION | MALL SHOP(a) GLA | SIZE (ACRES) | NET BOOK VALUE ($ MILLIONS) | ACQUISITION DATE | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

Alameda Plaza | Pocatello, ID | 190,341 | 5 | 2.4 | 07/02 | |||||||||||

Village at Redlands/Redlands Promenade | Redlands, CA | 79,248 | (b) | 15 | 9.8 | 01/04 | ||||||||||

Century Plaza | Birmingham, AL | 16,706 | (c) | 63 | 17.4 | 05/97 | ||||||||||

Rio West Mall | Gallup, NM | 332,447 | 50 | 11.4 | 1981 | (d) | ||||||||||

Riverwalk Marketplace | New Orleans, LA | 194,228 | 11 | 79.7 | 11/04 | (e) | ||||||||||

Park West | Peoria, AZ | 102,171 | 48 | 83.8 | 10/06 | |||||||||||

Cottonwood Square | Salt Lake City, UT | 77,079 | 6 | 5.3 | 07/02 | |||||||||||

Total | 992,220 | 198 | 209.8 | |||||||||||||

- (a)

- Mall shop GLA is gross leasable area for spaces less than 30,000 feet.

- (b)

- Scheduled to close all but 38,069 square feet of Mall shop GLA on September 30, 2010.

- (c)

- Only includes operating tenant space.

- (d)

- Reflects the date that the Rio West Mall opened.

- (e)

- Acquired in 2004 as part of the Predecessors' acquisition of The Rouse Company.

Other Interests. We also own or have interests in a variety of other assets. Some of our other interests include unsold condos in a luxury condominium community, a profit interest in two golf courses in Nevada and other land parcels. These assets had an aggregate net book value of less than $100 million as of June 30, 2010.

10

Risks Associated with our Business

You should carefully consider the matters discussed in the "Risk Factors" section beginning on page 17 of this prospectus prior to deciding whether to invest in our securities. Some of these risks include:

- •

- our history of losses and lack of operating history as an independent company;

- •

- our reliance on an interim management company;

- •

- our inability to obtain operating and development capital;

- •

- our inability to establish our own financial, administrative and other support functions to operate as a stand-alone business; and

- •

- risks associated with the ownership, development and expansion of properties.

In order to fund a portion of the Plan, GGP entered into investment agreements (the "Investment Agreements") with each of (i) REP Investments LLC (now known as Brookfield Retail Holdings LLC), an affiliate of Brookfield Asset Management Inc. (and its designees, as applicable, the "Brookfield Investor"), (ii) The Fairholme Fund and Fairholme Focused Income Fund (collectively, "Fairholme") and (iii) Pershing Square Capital Management, L.P. on behalf of Pershing Square, L.P., Pershing Square II, L.P., Pershing Square International, Ltd. and Pershing Square International V, Ltd. (collectively, together with their permitted assigns, including PSRH, Inc., "Pershing Square" and, together with Brookfield Investor and Fairholme, the "Plan Sponsors"). The Plan Sponsors entered into agreements with Blackstone Real Estate Partners VI, L.P. ("Blackstone" and together with its permitted assigns, the "Blackstone Investors") whereby Blackstone subscribed for approximately 7.6% of the shares of reorganized GGP's and our common stock issued to each of the Plan Sponsors under the Investment Agreements on the Effective Date and, in connection therewith, received an allocation of each of the Plan Sponsor's warrants described below to acquire our common stock (collectively, the "Blackstone Designation"). At the Effective Date, the Plan Sponsors and the Blackstone Investors purchased $6.3 billion of common stock of reorganized GGP and $250 million of our common stock at $47.619048 per share.

Upon consummation of the Plan and after giving effect to the Blackstone Designation, we issued to Brookfield Investor, Pershing Square, Fairholme and the Blackstone Investors 2,424,618, 1,212,309, 1,212,309 and 400,764 shares of our common stock, respectively, pursuant to the Investment Agreements and the Blackstone Designation. Of the Plan Sponsors and the Blackstone Investors, only Pershing Square will receive shares of our common stock pursuant to the Distribution in the amount of 2,355,709 shares, as a result of its ownership of shares of common stock of GGP prior to the Effective Date.

Upon consummation of the Plan, we issued to Brookfield Investor warrants to purchase approximately 3.83 million shares of our common stock, to each of Fairholme and Pershing Square warrants to purchase approximately 1.92 million shares of our common stock and to the Blackstone Investors warrants to purchase approximately 0.33 million shares of our common stock, in each case, with an initial exercise price of $50.00 per share. The per share exercise price has been adjusted from the originally contemplated exercise price to reflect a reduction in the number of warrants that will be issued for the same aggregate consideration upon exercise of the warrants. See "Certain Relationships and Related Transactions, and Director Independence."

At the Effective Date, Brookfield Investor, Fairholme, Pershing Square and the Blackstone Investors beneficially owned 6.4%, 3.2%, 9.5%, and 1.1%, respectively, of our common stock (excluding shares issuable upon exercise of the warrants) or 13.7%, 6.8%, 12.0% and 1.6%, respectively, of our

11

common stock (assuming exercise of all outstanding warrants, including shares issuable upon the exercise of warrants held by Fairholme, which are only exercisable upon 90 days' notice).

Each of the Plan Sponsors has participation rights in future public and private equity issuances by us, to allow them to maintain their respective percentage ownership on a fully diluted basis. These participation rights terminate when the applicable Plan Sponsor's beneficial ownership (together with its affiliates' beneficial ownership) is less than 5% on a fully diluted basis.

We were incorporated in Delaware on July 1, 2010. Our principal executive offices are located at 110 N. Wacker Drive, Chicago, Illinois 60606. Our main telephone number is (312) 960-5000.

12

Issuer | The Howard Hughes Corporation | |

Securities offered by the selling stockholders | 19,209,814 shares of our common stock. | |

Warrants to acquire 6,083,333 shares of our common stock. | ||

Securities outstanding after this offering | 37,718,326 shares of our common stock (not including shares underlying the warrants and shares underlying previously granted stock options pursuant to the Plan). | |

Warrants to acquire 6,083,333 shares of our common stock. | ||

Use of proceeds | We will not receive any proceeds from the resale of our common stock or warrants by the selling stockholders pursuant to this offering. | |

Listing | Our common stock has been approved for listing on the NYSE, subject to official notice of issuance, under the symbol "HHC." | |

Risk factors | Investing in our common stock and warrants involves a high degree of risk. See "Risk Factors" beginning on page 17 of this prospectus for a discussion of factors you should carefully consider before investing in our common stock or the warrants. |

13

Summary Historical Combined Financial Data

The following table sets forth the summary historical combined financial and other data of our business, which was carved-out from the financial information of GGP, as described below. We were formed for the purpose of holding certain assets and assuming certain liabilities of the Predecessors pursuant to the Plan. Prior to the Effective Date and the completion of the Separation and the Distribution, we did not conduct any business and did not have any material assets or liabilities. The operating data for the fiscal years ended December 31, 2009, 2008 and 2007 and the balance sheet data as of December 2009 and 2008 has been derived from our audited combined financial statements included elsewhere in this prospectus. The financial data as of and for the six months ended June 30, 2010 and 2009 has been derived from our unaudited interim combined financial statements included elsewhere in this prospectus, each of which have been prepared on a basis consistent with our audited financial statements. Such financial data is presented on a combined basis as all of the assets pertaining to such data are controlled by GGP. In the opinion of management, our unaudited interim combined financial statements as of and for the six months ended June 30, 2010 and 2009, include all adjustments, consisting only of normal, recurring adjustments, necessary to present fairly our financial position and results of operations for these periods. The interim results of operations are not necessarily indicative of operations for a full fiscal year.

Our combined financial statements were carved-out from the financial information of GGP. Our historical financial results reflect allocations for certain corporate expenses which include, but are not limited to, costs related to property management, human resources, security, payroll and benefits, legal, corporate communications, information services and restructuring and reorganization. Costs of the services that were allocated or charged to us were based on either actual costs incurred or a proportion of costs estimated to be applicable to us based on a number of factors, most significantly, our percentage of GGP's adjusted revenue and assets and the number of properties. We believe these allocations are reasonable; however, these results do not reflect what our expenses would have been had we been operating as a separate stand-alone public company. The years ended December 31, 2009, 2008 and 2007 include corporate cost allocations of $28.6 million, $20.4 million and $24.5 million, respectively. The six months ended June 30, 2010 and 2009 include corporate cost allocations of $33.8 million and $15.0 million, respectively. The historical combined financial information presented is not indicative of the results of operations, financial position or cash flows that would have been obtained if we had been an independent, stand-alone entity during the periods shown or of our future performance as an independent, stand-alone entity. See "Management's Discussion and Analysis of Financial Condition and Results of Operations—Overview—Basis of Presentation."

14

The historical results set forth below do not indicate results expected for any future periods. The summary historical combined financial information should be read in conjunction with "Management's Discussion and Analysis of Financial Condition and Results of Operations" and the unaudited and audited combined financial statements and notes thereto included elsewhere in this prospectus.

| | Six Months Ended June 30, | Year Ended December 31, | |||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | 2010 | 2009 | 2009 | 2008 | 2007 | ||||||||||||

| | (In thousands) | ||||||||||||||||

Operating Data: | |||||||||||||||||

Revenues | $ | 59,419 | $ | 75,120 | $ | 136,348 | $ | 172,507 | $ | 260,498 | |||||||

Depreciation and amortization | (8,425 | ) | (10,787 | ) | (19,841 | ) | (18,421 | ) | (22,995 | ) | |||||||

Provisions for impairment | (486 | ) | (140,180 | ) | (680,349 | ) | (52,511 | ) | (125,879 | ) | |||||||

Other operating expenses | (58,463 | ) | (72,201 | ) | (128,833 | ) | (141,392 | ) | (196,121 | ) | |||||||

Interest (expense) income, net | (1,148 | ) | (250 | ) | 712 | 1,105 | 1,504 | ||||||||||

Reorganization items | (26,614 | ) | (2,017 | ) | (6,674 | ) | — | — | |||||||||

Benefit from (provision for) income taxes | (17,953 | ) | 2,913 | 23,969 | (2,703 | ) | 10,643 | ||||||||||

Equity in income (loss) of Real Estate Affiliates | 5,172 | 4,121 | (28,209 | ) | 23,506 | 68,451 | |||||||||||

Loss from continuing operations | (48,498 | ) | (143,281 | ) | (702,877 | ) | (17,909 | ) | (3,899 | ) | |||||||

Discontinued operations—loss on dispositions | — | — | (939 | ) | — | — | |||||||||||

Allocation to noncontrolling interests | (73 | ) | (65 | ) | 204 | (100 | ) | (101 | ) | ||||||||

Net loss attributable to GGP | $ | (48,571 | ) | $ | (143,346 | ) | $ | (703,612 | ) | $ | (18,009 | ) | $ | (4,000 | ) | ||

Cash Flow Data: | |||||||||||||||||

Operating activities | $ | (51,162 | ) | $ | (9,166 | ) | $ | (17,870 | ) | $ | (50,699 | ) | $ | (52,041 | ) | ||

Investing activities | (37,118 | ) | (13,441 | ) | (21,432 | ) | (300,201 | ) | (146,208 | ) | |||||||

Financing activities | 88,058 | 32,434 | 37,543 | 348,424 | 183,073 | ||||||||||||

Other Financial Data: | |||||||||||||||||

EBITDA(*) | $ | (16,435 | ) | $ | (131,848 | ) | $ | (701,469 | ) | $ | 11,384 | $ | 14,121 | ||||

Adjusted EBITDA(*) | 10,665 | 15,472 | 21,523 | 65,391 | 98,643 | ||||||||||||

Balance Sheet Data:

| | As of June 30, | As of December 31, | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| | 2010 | 2009 | 2008 | |||||||

| | (In thousands) | |||||||||

Investments in real estate—cost | $ | 2,836,316 | $ | 2,827,814 | $ | 3,376,321 | ||||

Total assets | 2,906,150 | 2,905,227 | 3,443,956 | |||||||

Total debt | 340,495 | 342,833 | 358,467 | |||||||

Total equity | 1,520,638 | 1,503,520 | 1,985,815 | |||||||

- (*)

- We have presented EBITDA and Adjusted EBITDA because we believe that they are useful to investors. For our definitions of EBITDA and Adjusted EBITDA as well as an important discussion of their uses and limitations, see "Use of Non-GAAP Measures."

15

The following is a reconciliation of Segment basis Adjusted EBITDA and EBITDA to GAAP net loss attributable to GGP on a combined basis for the periods presented below. The Segment basis results are based on the proportionate share method. Under the proportionate share method, our share of the revenues and expenses of the Real Estate Affiliates are combined with the revenues and expenses of the combined properties.

| | Six Months Ended June 30, | Year Ended December 31, | ||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | 2010 | 2009 | 2009 | 2008 | 2007 | |||||||||||

| | (In thousands) | |||||||||||||||

Adjusted EBITDA | $ | 10,665 | $ | 15,472 | $ | 21,523 | $ | 65,391 | $ | 98,643 | ||||||

Strategic initiatives(a) | — | (5,114 | ) | (5,380 | ) | (1,496 | ) | — | ||||||||

Provisions for impairment(b) | (486 | ) | (140,180 | ) | (709,990 | ) | (52,511 | ) | (125,879 | ) | ||||||

Debt extinguishment costs | — | (9 | ) | (9 | ) | — | (618 | ) | ||||||||

Reorganization items(c) | (26,614 | ) | (2,017 | ) | (6,674 | ) | — | — | ||||||||

Discontinued operations—gains (losses) on dispositions | — | — | (939 | ) | — | 41,975 | ||||||||||

EBITDA | (16,435 | ) | (131,848 | ) | (701,469 | ) | 11,384 | 14,121 | ||||||||

Depreciation and amortization | (10,421 | ) | (12,805 | ) | (25,110 | ) | (22,470 | ) | (25,690 | ) | ||||||

Amortization of deferred finance costs | (305 | ) | (552 | ) | (916 | ) | (720 | ) | (1,194 | ) | ||||||

Interest income | 762 | 516 | 2,353 | 2,341 | 2,304 | |||||||||||

Interest expense | (3,549 | ) | (1,437 | ) | (2,999 | ) | (4,914 | ) | (957 | ) | ||||||

(Provision for) benefit from income taxes | (18,550 | ) | 2,845 | 24,325 | (3,530 | ) | 7,517 | |||||||||

Allocation to noncontrolling interests | (73 | ) | (65 | ) | 204 | (100 | ) | (101 | ) | |||||||

Net loss attributable to GGP | $ | (48,571 | ) | $ | (143,346 | ) | $ | (703,612 | ) | $ | (18,009 | ) | $ | (4,000 | ) | |

- (a)

- Our strategic initiatives include expenses related to the restructuring efforts of our Predecessors who were subject to bankruptcy proceedings prior to such bankruptcy filings.

- (b)

- For a discussion on provisions for impairment, see Note 2—Summary of Significant Accounting Policies to the December 31, 2009 combined financial statements and Note 1—Organization—Impairment to the June 30, 2010 combined financial statements contained elsewhere in this prospectus.

- (c)

- Reorganization items reflect bankruptcy-related activity, including gains on liabilities subject to compromise, interest income, U.S. Trustee fees, and other restructuring costs, incurred after the Predecessors filed for protection under the Bankruptcy Code on April 16, 2009.

16

An investment in our common stock or warrants involves a high degree of risk. You should carefully consider the following material risks, as well as the other information contained in this prospectus, before making an investment in our company. If any of the following risks actually occur, our business, financial condition and/or results of operations could be materially and adversely affected. In such an event, the trading price of our common stock and warrants could decline and you could lose part or all of your investment.

Risks Related to our Business

We have a history of losses and may not be profitable in the future.

Our historical combined financial data was carved-out from the financial information of GGP and shows that had we been a stand-alone company, we would have had a history of losses, and we cannot assure you that we will achieve sustained profitability going forward. For the six months ended June 30, 2010 and the years ended December 31, 2009, 2008 and 2007, we would have incurred losses from continuing operations of $48.5 million, $702.9 million, $17.9 million and $3.9 million, respectively. In addition, for the six months ended June 30, 2010 and the years ended December 31, 2009, 2008 and 2007, net cash used in operating activities was $51.2 million, $17.9 million, $50.7 million and $52.0 million, respectively. If we cannot improve our profitability or generate positive cash from operating activities, the trading value of our common stock may decline.

We have no operating history as an independent company upon which you can evaluate our performance, and accordingly, our prospects must be considered in light of the risks that any newly independent company encounters.

We have no experience operating as an independent company and performing various corporate functions, including human resources, tax administration, legal (including compliance with the Sarbanes-Oxley Act of 2002 (the "Sarbanes-Oxley Act") and with the periodic reporting obligations of the Securities Exchange Act of 1934 (the "Exchange Act")), treasury administration, investor relations, internal audit, insurance, information technology and telecommunications services, as well as the accounting for items such as equity compensation and income taxes. Our business will be subject to the substantial risks inherent in the commencement of a new business enterprise in an intensely competitive industry. Our prospects must be considered in light of the risks, expenses and difficulties encountered by companies in the early stages of independent business operations, particularly companies that are heavily affected by economic conditions and operate in highly competitive environments.

We depend on an interim management company to assist us in operating our business.

We intend to hire permanent executives with development and master planned community expertise to complement our existing strong operational management team in our Master Planned Communities segment. Our financial results and ability to compete as a stand-alone entity will suffer if we are unable to attract, integrate or retain qualified executives to serve as our permanent executive management team. In the interim, we have entered into the Management Agreement with Brookfield Advisors to provide us with interim executive officers and leadership and oversight for our business until our permanent executive management team can be identified and assume their roles. During this interim period, we will be heavily reliant on Brookfield Advisors, who will have significant discretion as to the implementation and execution of our business strategies and risk management practices. Our operational success and ability to execute our business strategy will depend significantly upon the satisfactory performance of these services by Brookfield Advisors until permanent management is in place. See "Certain Relationships and Related Transactions, and Director Independence—Interim Management Agreement."

17

We may face potential difficulties in obtaining operating and development capital.

The successful execution of our business strategy will require the availability of substantial amounts of operating and development capital both initially and over time. Sources of such capital could include operating cash flow, bank borrowings, public and private offerings of debt or equity, sale of certain assets and joint ventures with one or more other parties. In recent periods, it has been difficult for companies with substantial profitable operating history to source capital for real estate development and acquisition projects, as well as basic working capital needs. As we have no operating history as a stand-alone company or permanent executive management team in place, we may find it difficult or impossible to acquire cost-effective capital to implement our business strategy from any source.

We expect to continue making investments in real estate development, which will require still more capital. We cannot assure you that financing for future expenditures will be available on favorable terms or at all, due to instability in the credit markets, our lack of operating history as a stand-alone company and a variety of other factors. As a result, we may be unable to operate our business as currently planned, take advantage of future development opportunities or respond to competitive pressures.

Our ability to operate our business effectively may suffer if we do not establish our own financial, administrative and other support functions to operate as a stand-alone company.

Historically, we have relied on the financial, administrative and other support functions of GGP to operate our business and we will continue to rely on reorganized GGP for these and other vital services on a transitional basis pursuant to a transition services agreement that we entered into with GGP and certain of its subsidiaries (the "Transition Services Agreement"). See "Business—Our Relationship with Reorganized GGP following the Separation—Transition Services Agreement." These services may not be sufficient to meet our needs and, after this agreement expires, we may not be able to replace these services at all or obtain these services at acceptable prices and terms.