UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM 10-Q

| ☑ | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | ||||

| for the quarterly period ended March 31, 2024 | |||||

| OR | |||||

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | ||||

COMMISSION FILE NUMBER: 001-37590

AVALO THERAPEUTICS, INC.

(Exact name of registrant as specified in its charter)

Delaware (State of incorporation) | 45-0705648 (I.R.S. Employer Identification No.) | ||||

540 Gaither Road, Suite 400 Rockville, Maryland 20850 (Address of principal executive offices) | (410) 522-8707 (Registrant’s telephone number, including area code) | ||||

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol | Name of each exchange on which registered | ||||||

Common Stock, $0.001 par value | AVTX | Nasdaq Capital Market | ||||||

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☑ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☑ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b‑2 of the Exchange Act.

Large accelerated filer ☐ | Accelerated filer ☐ | |||||||

| Non-accelerated filer ☑ | Smaller reporting company ☑ | |||||||

| Emerging growth company ☐ | ||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b‑2 of the Exchange Act). Yes ☐ No ☑

As of May 8, 2024, the registrant had 1,034,130 shares of common stock outstanding.

AVALO THERAPEUTICS, INC.

FORM 10-Q

For the Quarter Ended March 31, 2024

TABLE OF CONTENTS

| Page | |||||||||||||||||

| a) | |||||||||||||||||

| b) | |||||||||||||||||

| c) | |||||||||||||||||

| d) | |||||||||||||||||

| e) | |||||||||||||||||

2

PART I - FINANCIAL INFORMATION

Item 1. Financial Statements.

AVALO THERAPEUTICS, INC. and SUBSIDIARIES

Condensed Consolidated Balance Sheets

(In thousands, except share and per share data)

3

| March 31, 2024 | December 31, 2023 | |||||||||||||

| (unaudited) | ||||||||||||||

| Assets | ||||||||||||||

| Current assets: | ||||||||||||||

| Cash and cash equivalents | $ | 110,177 | $ | 7,415 | ||||||||||

| Other receivables | 35 | 136 | ||||||||||||

| Prepaid expenses and other current assets | 997 | 843 | ||||||||||||

| Restricted cash, current portion | 4 | 1 | ||||||||||||

| Total current assets | 111,213 | 8,395 | ||||||||||||

| Property and equipment, net | 1,882 | 1,965 | ||||||||||||

| Goodwill | 10,502 | 10,502 | ||||||||||||

| Restricted cash, net of current portion | 131 | 131 | ||||||||||||

| Total assets | $ | 123,728 | $ | 20,993 | ||||||||||

| Liabilities, mezzanine equity and stockholders’ (deficit) equity | ||||||||||||||

| Current liabilities: | ||||||||||||||

| Accounts payable | $ | 916 | $ | 446 | ||||||||||

| Accrued expenses and other current liabilities | 7,383 | 4,172 | ||||||||||||

| Warrant liability | 194,901 | — | ||||||||||||

| Contingent consideration | 12,500 | — | ||||||||||||

| Total current liabilities | 215,700 | 4,618 | ||||||||||||

| Royalty obligation | 2,000 | 2,000 | ||||||||||||

| Deferred tax liability, net | 162 | 155 | ||||||||||||

| Derivative liability | 5,670 | 5,550 | ||||||||||||

| Other long-term liabilities | 1,281 | 1,366 | ||||||||||||

| Total liabilities | 224,813 | 13,689 | ||||||||||||

| Mezzanine equity: | ||||||||||||||

| Series C Preferred Stock—$0.001 par value; 34,326 and 0 shares of Series C Preferred Stock authorized at March 31, 2024 and December 31, 2023, respectively; 22,358 and 0 shares of Series C Preferred Stock issued and outstanding at March 31, 2024 and December 31, 2023, respectively | 11,457 | — | ||||||||||||

| Series D Preferred Stock—$0.001 par value; 1 and 0 shares of Series D Preferred Stock authorized at March 31, 2024 and December 31, 2023, respectively; 1 and 0 shares of Series D Preferred Stock issued and outstanding at March 31, 2024 and December 31, 2023, respectively | — | — | ||||||||||||

| Series E Preferred Stock—$0.001 par value; 1 and 0 shares of Series E Preferred Stock authorized at March 31, 2024 and December 31, 2023, respectively; 1 and 0 shares of Series E Preferred Stock issued and outstanding at March 31, 2024 and December 31, 2023, respectively | — | — | ||||||||||||

| Stockholders’ (deficit) equity: | ||||||||||||||

| Common stock—$0.001 par value; 200,000,000 shares authorized at March 31, 2024 and December 31, 2023; 1,034,130 and 801,746 shares issued and outstanding at March 31, 2024 and December 31, 2023, respectively | 1 | 1 | ||||||||||||

| Additional paid-in capital | 343,881 | 342,437 | ||||||||||||

| Accumulated deficit | (456,424) | (335,134) | ||||||||||||

| Total stockholders’ (deficit) equity | (112,542) | 7,304 | ||||||||||||

| Total liabilities, mezzanine equity and stockholders’ (deficit) equity | $ | 123,728 | $ | 20,993 | ||||||||||

See accompanying notes to the unaudited condensed consolidated financial statements.

4

AVALO THERAPEUTICS, INC. and SUBSIDIARIES

Condensed Consolidated Statements of Operations and Comprehensive Loss (Unaudited)

(In thousands, except per share data)

| Three Months Ended | ||||||||||||||

| March 31, | ||||||||||||||

| 2024 | 2023 | |||||||||||||

| Revenues: | ||||||||||||||

| Product revenue, net | $ | — | $ | 475 | ||||||||||

| Total revenues, net | — | 475 | ||||||||||||

| Operating expenses: | ||||||||||||||

| Cost of product sales | (80) | 551 | ||||||||||||

| Research and development | 2,116 | 6,008 | ||||||||||||

| Acquired in-process research and development | 27,538 | — | ||||||||||||

| General and administrative | 3,193 | 2,708 | ||||||||||||

| Total operating expenses | 32,767 | 9,267 | ||||||||||||

| (32,767) | (8,792) | |||||||||||||

| Other expense: | ||||||||||||||

| Excess of warrant fair value over private placement proceeds | (79,276) | — | ||||||||||||

| Private placement transaction costs | (9,220) | — | ||||||||||||

| Change in fair value of derivative liability | (120) | (180) | ||||||||||||

| Interest income, net | 100 | (949) | ||||||||||||

| Other expense, net | — | (26) | ||||||||||||

| Total other expense, net | (88,516) | (1,155) | ||||||||||||

| Loss before taxes | (121,283) | (9,947) | ||||||||||||

| Income tax expense | 7 | 8 | ||||||||||||

| Net loss and comprehensive loss | $ | (121,290) | $ | (9,955) | ||||||||||

Net loss per share of common stock, basic and diluted1 | $ | (141) | $ | (204) | ||||||||||

1 Amounts for prior periods presented have been retroactively adjusted to reflect the 1-for-240 reverse stock split effected on December 28, 2023. See Note 1 for details.

See accompanying notes to the unaudited condensed consolidated financial statements.

5

AVALO THERAPEUTICS, INC. and SUBSIDIARIES

Condensed Consolidated Statements of Preferred Stock and Changes in Stockholders’ (Deficit) Equity (Unaudited)

(In thousands, except share amounts)

| Preferred Stock | Common stock | Additional paid-in | Accumulated | Total stockholders’ | |||||||||||||||||||||||||||||||||||||||||||||||||

| Shares | Amount | Shares | Amount | capital | deficit | (deficit) equity | |||||||||||||||||||||||||||||||||||||||||||||||

| Three Months Ended March 31, 2024 | |||||||||||||||||||||||||||||||||||||||||||||||||||||

| Balance, December 31, 2023 | — | — | 801,746 | $ | 1 | $ | 342,437 | $ | (335,134) | $ | 7,304 | ||||||||||||||||||||||||||||||||||||||||||

| Impact of reverse split fractional share round-up | — | — | 60,779 | — | — | — | — | ||||||||||||||||||||||||||||||||||||||||||||||

| Issuance of common stock pursuant to Almata Transaction | — | — | 171,605 | — | 815 | — | 815 | ||||||||||||||||||||||||||||||||||||||||||||||

| Issuance of Series C Preferred Stock pursuant to Almata Transaction | 2,412 | 11,457 | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||||||||||||

| Issuance of Series C Preferred Stock in private placement | 19,946 | — | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||||||||||||

| Issuance of Series D Preferred Stock in private placement | 1 | — | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Issuance of Series E Preferred Stock in private placement | 1 | — | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Stock-based compensation | — | — | — | — | 629 | — | 629 | ||||||||||||||||||||||||||||||||||||||||||||||

| Net loss | — | — | — | — | — | (121,290) | (121,290) | ||||||||||||||||||||||||||||||||||||||||||||||

| Balance, March 31, 2024 | 22,360 | $ | 11,457 | 1,034,130 | $ | 1 | $ | 343,881 | $ | (456,424) | $ | (112,542) | |||||||||||||||||||||||||||||||||||||||||

| Preferred Stock | Common stock | Additional paid-in | Accumulated | Total stockholders’ | |||||||||||||||||||||||||||||||||||||||||||||||||

| Shares | Amount | Shares1 | Amount1 | capital1 | deficit | deficit | |||||||||||||||||||||||||||||||||||||||||||||||

| Three Months Ended March 31, 2023 | |||||||||||||||||||||||||||||||||||||||||||||||||||||

| Balance, December 31, 2022 | — | — | 39,294 | $ | — | $ | 292,909 | $ | (303,824) | $ | (10,915) | ||||||||||||||||||||||||||||||||||||||||||

| Issuance of shares of common stock and warrants in underwritten public offering, net | — | — | 15,709 | — | 13,748 | — | 13,748 | ||||||||||||||||||||||||||||||||||||||||||||||

| Stock-based compensation | — | — | — | — | 855 | — | 855 | ||||||||||||||||||||||||||||||||||||||||||||||

| Net loss | — | — | — | — | — | (9,955) | (9,955) | ||||||||||||||||||||||||||||||||||||||||||||||

| Balance, March 31, 2023 | — | $ | — | 55,003 | $ | — | $ | 307,512 | $ | (313,779) | $ | (6,267) | |||||||||||||||||||||||||||||||||||||||||

1 Amounts for prior periods presented have been retroactively adjusted to reflect the 1-for-240 reverse stock split effected on December 28, 2023. See Note 1 for details.

See accompanying notes to the unaudited condensed consolidated financial statements.

6

AVALO THERAPEUTICS, INC. and SUBSIDIARIES

Condensed Consolidated Statements of Cash Flows (Unaudited)

(Amounts in thousands)

| Three Months Ended March 31, | ||||||||||||||

| 2024 | 2023 | |||||||||||||

| Operating activities | ||||||||||||||

| Net loss | $ | (121,290) | $ | (9,955) | ||||||||||

| Adjustments to reconcile net loss used in operating activities: | ||||||||||||||

| Depreciation and amortization | 34 | 33 | ||||||||||||

| Stock-based compensation | 629 | 855 | ||||||||||||

| Acquired in-process research and development | 27,538 | — | ||||||||||||

| Excess of warrant fair value over private placement proceeds | 79,276 | — | ||||||||||||

| Transaction costs paid pursuant to private placement | 7,013 | — | ||||||||||||

| Transaction costs payable upon exercise of warrants issued in private placement | 1,734 | — | ||||||||||||

| Change in fair value of derivative liability | 120 | 180 | ||||||||||||

| Accretion of debt discount | — | 350 | ||||||||||||

| Deferred taxes | 7 | 8 | ||||||||||||

| Changes in assets and liabilities: | ||||||||||||||

| Other receivables | 101 | 1,062 | ||||||||||||

| Inventory, net | — | 1 | ||||||||||||

| Prepaid expenses and other assets | (154) | (337) | ||||||||||||

| Lease incentive | 158 | — | ||||||||||||

| Accounts payable | 470 | 2,683 | ||||||||||||

| Deferred revenue | — | 22 | ||||||||||||

| Accrued expenses and other liabilities | (1,652) | (4,941) | ||||||||||||

| Lease liability, net | (186) | (13) | ||||||||||||

| Net cash used in operating activities | (6,202) | (10,052) | ||||||||||||

| Investing activities | ||||||||||||||

| Cash assumed from Almata Transaction | 356 | — | ||||||||||||

| Leasehold improvements | — | (158) | ||||||||||||

| Disposal of property and equipment | — | 25 | ||||||||||||

| Net cash provided by (used in) investing activities | 356 | (133) | ||||||||||||

| Financing activities | ||||||||||||||

| Proceeds from private placement investment, gross | 115,625 | — | ||||||||||||

| Transaction costs paid pursuant to private placement | (7,013) | — | ||||||||||||

| Proceeds from issuance of common stock and pre-funded warrants in underwritten public offering, net | — | 13,748 | ||||||||||||

| Net cash provided by financing activities | 108,612 | 13,748 | ||||||||||||

| Increase in cash, cash equivalents and restricted cash | 102,766 | 3,563 | ||||||||||||

| Cash, cash equivalents, and restricted cash at beginning of period | 7,546 | 13,318 | ||||||||||||

| Cash, cash equivalents, and restricted cash at end of period | $ | 110,312 | $ | 16,881 | ||||||||||

| Supplemental disclosures of cash flow information | ||||||||||||||

| Cash paid for interest | $ | — | $ | 704 | ||||||||||

| Supplemental disclosures of non-cash activities | ||||||||||||||

| Issuance of common stock and Series C Preferred Stock pursuant to Almata Transaction | $ | 12,727 | $ | — | ||||||||||

The following table provides a reconciliation of cash, cash equivalents and restricted cash reported within the condensed consolidated balance sheets that sum to the total of the same such amounts shown in the condensed consolidated statements of cash flows (in thousands):

| March 31, | ||||||||||||||

| 2024 | 2023 | |||||||||||||

| Cash and cash equivalents | $ | 110,177 | $ | 16,687 | ||||||||||

| Restricted cash, current | 4 | 63 | ||||||||||||

| Restricted cash, non-current | 131 | 131 | ||||||||||||

| Total cash, cash equivalents and restricted cash | $ | 110,312 | 16,881 | |||||||||||

7

See accompanying notes to the unaudited condensed consolidated financial statements.

8

AVALO THERAPEUTICS, INC. and SUBSIDIARIES

Notes to Unaudited Condensed Consolidated Financial Statements

1. Business

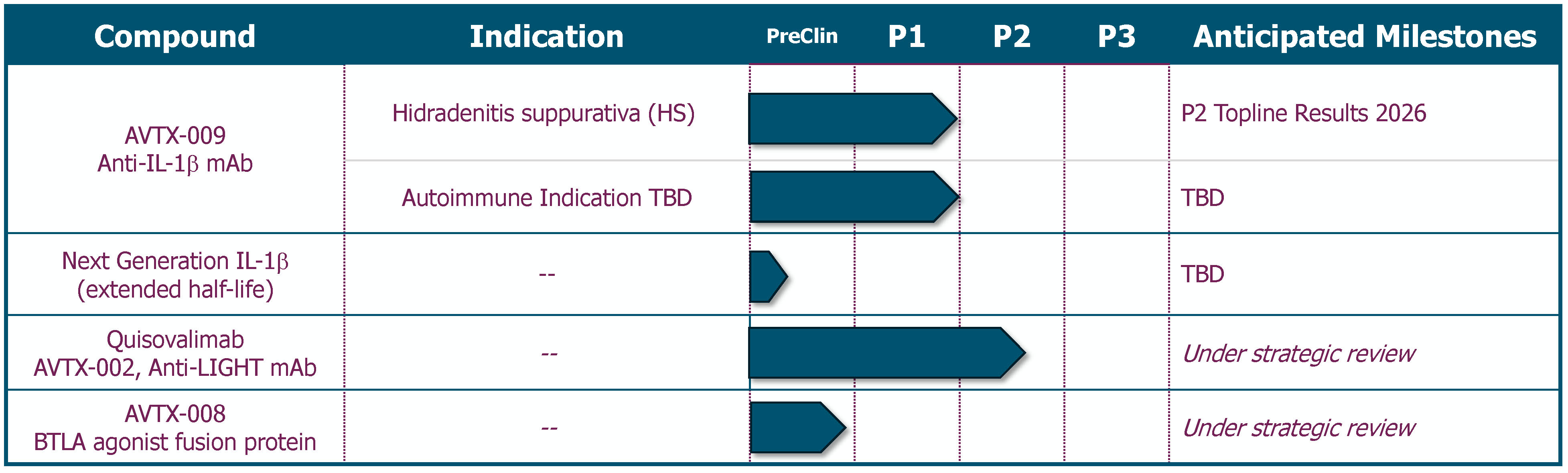

Avalo Therapeutics, Inc. (the “Company,” “Avalo” or “we”) is a clinical stage biotechnology company focused on the treatment of immune dysregulation. Avalo’s lead asset is AVTX-009, an anti-IL-1β monoclonal antibody (“mAb”), targeting inflammatory diseases. Avalo’s pipeline also includes quisovalimab (anti-LIGHT mAb) and AVTX-008 (BTLA agonist fusion protein).

Avalo was incorporated in Delaware and commenced operation in 2011, and completed its initial public offering in October 2015.

On March 27, 2024, the Company acquired AVTX-009, a Phase 2-ready anti-IL-1β mAb, through a merger with AlmataBio, Inc. (“AlmataBio”) with and into its wholly owned subsidiary (the “Almata Transaction”). Additionally, on March 28, 2024, the Company closed a private placement investment for up to $185 million in gross proceeds, including initial upfront gross investment of $115.6 million. The upfront net proceeds were approximately $108.1 million after deducting transaction costs. The Company could receive up to an additional $69.4 million of gross proceeds upon the exercise of warrants issued in the financing.

Liquidity

Since inception, we have incurred significant operating and cash losses from operations. We have primarily funded our operations to date through sales of equity securities, out-licensing transactions and sales of assets.

For the three months ended March 31, 2024, Avalo generated a net loss of $121.3 million and negative cash flows from operations of $6.2 million. As of March 31, 2024, Avalo had $110.2 million in cash and cash equivalents. In March 2024, the Company closed a private placement investment for up to $185 million in gross proceeds, including an initial upfront gross investment of $115.6 million. Net proceeds were $108.1 million after deducting transaction costs. The Company could receive up to an additional $69.4 million of gross proceeds upon the exercise of warrants issued in the financing.

Based on our current operating plans, we expect that our existing cash and cash equivalents are sufficient to fund operations for at least twelve months from the filing date of this Quarterly Report on Form 10-Q and we expect current cash on hand to fund operations into 2027. The Company closely monitors its cash and cash equivalents and seeks to balance the level of cash and cash equivalents with our projected needs to allow us to withstand periods of uncertainty relative to the availability of funding on favorable terms. We may need to satisfy our future cash needs through sales of equity securities under the Company’s ATM program or otherwise, out-licensing transactions, strategic alliances/collaborations, sale of programs, and/or mergers and acquisitions. There can be no assurance that any financing or business development initiatives can be realized by the Company, or if realized, what the terms may be. Further, if the Company raises additional funds through collaborations, strategic alliances or licensing arrangements with third parties, the Company might have to relinquish valuable rights to its technologies, future revenue streams, research programs or product candidates. To the extent that we raise capital through the sale of equity, the ownership interest of our existing stockholders will be diluted, and the terms may include liquidation or other preferences that adversely affect the rights of our stockholders.

2. Basis of Presentation and Significant Accounting Policies

Basis of Presentation

9

The Company’s unaudited condensed consolidated financial statements have been prepared in accordance with U.S. generally accepted accounting principles (“GAAP”). Any reference in these notes to applicable guidance is meant to refer to the authoritative GAAP as found in the Accounting Standards Codification (“ASC”) and Accounting Standards Updates (“ASU”) of the Financial Accounting Standards Board (“FASB”).

In the opinion of management, the accompanying unaudited condensed consolidated financial statements include all adjustments, consisting of normal recurring adjustments, which are necessary to present fairly the Company’s financial position, results of operations, and cash flows. The condensed consolidated balance sheet at December 31, 2023 has been derived from audited financial statements at that date. The interim results of operations are not necessarily indicative of the results that may occur for the full fiscal year. Certain information and footnote disclosure normally included in the financial statements prepared in accordance with GAAP have been condensed or omitted pursuant to instructions, rules, and regulations prescribed by the United States Securities and Exchange Commission (“SEC”).

The Company believes that the disclosures provided herein are adequate to make the information presented not misleading when these unaudited condensed consolidated financial statements are read in conjunction with the December 31, 2023 audited consolidated financial statements.

On December 28, 2023, Avalo effected a 1-for-240 reverse stock split of the outstanding shares of the Company’s common stock and began trading on a split-adjusted basis on December 29, 2023. The Company retroactively applied the reverse stock split to common share and per share amounts for periods prior to December 28, 2023, including the unaudited consolidated financial statements for the quarter ended March 31, 2023. Additionally, pursuant to their terms, a proportionate adjustment was made to the per share exercise price and number of shares issuable under all of the Company’s outstanding options and warrants, and the number of shares authorized for issuance pursuant to the Company’s equity incentive plans have been reduced proportionately. Avalo retroactively applied such adjustments in the notes to consolidated financial statements for periods presented prior to December 28, 2023, including the quarter ended March 31, 2023. The reverse stock split did not reduce the number of authorized shares of common and preferred stock and did not alter the par value.

Unless otherwise indicated, all amounts in the following tables are in thousands except share and per share amounts.

Significant Accounting Policies

During the three months ended March 31, 2024, there were no significant changes to the Company’s summary of significant accounting policies contained in the Company’s Annual Report on Form 10-K for the year ended December 31, 2023, as filed with the SEC on March 29, 2024, except for the policies related to asset acquisitions and warrant liability as described below.

Asset Acquisitions

The Company evaluates acquisitions of assets and other similar transactions to assess whether the transaction should be accounted for as a business combination or asset acquisition by first applying a screen test to determine if substantially all of the fair value of the gross assets acquired is concentrated in a single identifiable asset or group of similar identifiable assets. If the screen test is met, the transaction is accounted for as an asset acquisition. If the screen test is not met, further determination is required as to whether the Company has acquired inputs and processes that have the ability to create outputs which would meet the definition of a business. Significant judgment is required in the application of the screen test to determine whether an acquisition is a business combination or an acquisition of assets.

Warrant Liability

10

The Company accounts for warrants as either equity-classified or liability-classified instruments based on an assessment of the warrant’s specific terms and applicable authoritative guidance in ASC 480, Distinguishing Liabilities from Equity and ASC 815, Derivatives and Hedging. Warrants classified as equity are recorded at fair value as of the date of issuance on the Company’s consolidated balance sheets and no further adjustments to their valuation are made. Warrants classified as derivative liabilities that require separate accounting as liabilities are recorded on the Company’s consolidated balance sheets at their fair value on the date of issuance and are revalued on each subsequent balance sheet date until such instruments are exercised or expire, with any changes in the fair value between reporting periods recorded on the consolidated statement of operations. The assessment of whether the warrants are accounted for as equity-classified or liability-classified instruments is re-evaluated on a periodic basis.

3. Asset Acquisition

Almata Transaction

On March 27, 2024, the Company acquired AVTX-009, a Phase 2-ready anti-IL-1β mAb, through a merger with AlmataBio with and into its wholly owned subsidiary. The Company’s acquisition of AlmataBio was structured as a stock-for-stock transaction whereby all outstanding equity interests in AlmataBio were exchanged in a merger for a combination of the Company’s common stock and shares of the Company’s Series C Preferred Stock, resulting in the issuance of 171,605 shares of Company common stock and 2,412 shares of Series C Preferred Stock. Subject to Company stockholder approval, each share of Company Series C Preferred Stock (i) issued to former AlmataBio stockholders and ii) pursuant to the private placement investment will automatically convert to 1,000 shares of common stock, subject to certain beneficial ownership limitations. The Series C Preferred Stock holds no voting rights.

In addition to the shares issued, a cash payment of $7.5 million was due to the former AlmataBio stockholders upon the closing of a private placement investment. The private placement closed on March 28, 2024 and the Company paid the $7.5 million in April 2024. The Company is also required to pay potential development milestone payments to the former AlmataBio stockholders, including $5.0 million due upon the first patient dosed in a Phase 2 trial in patients with HS for AVTX-009 and $15.0 million due upon the first patient dosed in a Phase 3 trial for AVTX-009, both of which are payable in cash, Avalo stock, or a combination thereof at the election of the former AlmataBio stockholders, subject to the terms and conditions of the definitive merger agreement.

The Company has been determined to be the acquiring company for accounting purposes. In connection with the Almata Transaction, substantially all of the consideration paid is allocable to the fair value of acquired in-process research and development (“IPR&D”), specifically AVTX-009, and as such the acquisition is treated as an asset acquisition. The Company initially recognized AlmataBio’s assets and liabilities by allocating the accumulated cost of the acquisition based on their relative fair values, as estimated by management. The net assets acquired as of the transaction date have been combined with the assets, liabilities, and results of operations of the Company on consummation of the Almata Transaction. In accordance with ASC 730, Research and Development, the portion of the consideration allocated to the acquired IPR&D, specifically AVTX-009, based on its relative fair value, is included as an operating expense as there is no alternative future use.

Below is a summary of the total consideration, assets acquired and the liabilities assumed in connection with the Almata Transaction (in thousands):

11

| Three Months Ended March 31, 2024 | ||||||||||||||

Stock consideration1 | $ | 12,272 | ||||||||||||

Milestone payment due upon close of private placement investment2 | 7,500 | |||||||||||||

Milestone payment due upon first patient dosed in a Phase 2 trial2 | 5,000 | |||||||||||||

| Transaction costs | 2,402 | |||||||||||||

| Total GAAP Purchase Price at Close | $ | 27,174 | ||||||||||||

| Acquired IPR&D | $ | 27,538 | ||||||||||||

| Cash | 356 | |||||||||||||

| Accrued expenses and other current liabilities | (720) | |||||||||||||

| Total net assets acquired and liabilities assumed | $ | 27,174 | ||||||||||||

1 Equal to the aggregate common shares issued of 171,605 and the aggregate preferred shares issued of 2,412 (as-converted to 2,412,000 shares of common stock), multiplied by the Company’s closing stock price of $4.75 on March 27, 2024.

2 Avalo deemed these milestones probable and estimable as of the transaction close date and therefore included them as part of the GAAP purchase price at close. The first milestone payment due upon the close of the private placement investment was met on March 28, 2024 and was paid on April 1, 2024.

The cost to acquire the IPR&D asset related to AVTX-009 was expensed on the date of the Almata Transaction as it was determined to have no future alternative use. Accordingly, costs associated with the Almata Transaction to acquire the asset were expensed as incurred in acquired IPR&D.

4. Revenue

The Company’s license and supply agreement for Millipred®, an oral prednisolone indicated across a wide variety of inflammatory conditions, ended on September 30, 2023, and therefore there was no net product revenues for the three months ended March 31, 2024. Avalo considered Millipred® a non-core asset. Historically, the Company sold Millipred® in the United States primarily through wholesale distributors, who accounted for substantially all of the Company’s net product revenues and trade receivables. For the three months ended March 31, 2023, the Company recognized net product revenue of $0.5 million.

The Company will continue to monitor estimates for commercial liabilities, such as sales returns. As additional information becomes available, the Company could recognize expense (or a benefit) for differences between actuals or updated estimates to the reserves previously recognized. Pursuant the Millipred® license and supply agreement, Avalo was required to pay the supplier fifty percent of the net profit of the Millipred® product following each calendar quarter, subject to a $0.5 million quarterly minimum payment dependent on Avalo reaching certain net profit amounts as stipulated in the agreement. The profit share commenced on July 1, 2021 and ended on September 30, 2023. Within twenty-five months of September 30, 2023, the net profit share is subject to a reconciliation process where estimated deductions to arrive at net profit will be trued-up to actuals and could result in Avalo owing additional amounts to the supplier or vice versa, which would be recognized in cost of product sales.

12

Aytu BioScience, Inc. (“Aytu”), to which the Company sold its rights, title, and interests in assets relating to certain commercialized products in 2019 (the “Aytu Transaction”), managed Millipred® commercial operations until August 31, 2021 pursuant to transition service agreements, which included managing the third-party logistics provider. As a result, Aytu collected cash on behalf of Avalo for revenue generated by sales of Millipred® from the second quarter of 2020 through the third quarter of 2021. The transition services agreement allows Aytu to withhold up to $1.0 million until December of 2024. In the second quarter of 2022, Avalo fully reserved the receivable as a result of Aytu’s conclusion within its Quarterly Report on Form 10-Q for the quarter ended June 30, 2022 that substantial doubt existed with respect to its ability to continue as a going concern within one year after the date those financial statements were issued. As of March 31, 2024, the total receivable balance was approximately $0.6 million and remains fully reserved as of March 31, 2024. We will continue to reassess its collectability each reporting period.

5. Net Loss Per Share

The Company had two classes of stock outstanding during the three months ended March 31, 2024, common stock and preferred stock, and had only common stock outstanding during the three months ended March 31, 2023. The Company computes net loss per share using the two-class method, as the Series C Preferred Stock participates in distributions with the Company’s common stock. The two-class method of computing net loss per share is an earnings allocation formula that determines net loss for common stock and any participating securities according to dividends declared and participation rights in undistributed earnings. As the Company is in a net loss position for the three months ended March 31, 2024, the two-class method of computing net loss per share results in no allocation of undistributed losses to participating securities.

Basic net loss per share for common stock is computed by dividing the sum of distributed earnings by the weighted average number of shares outstanding for the period. The weighted average number of common shares outstanding as of March 31, 2023 includes the weighted average effect of pre-funded warrants, the exercise of which required nominal consideration for the delivery of the shares of common stock. There were no pre-funded warrants outstanding as of March 31, 2024.

Diluted net loss per share may include the potential dilutive effect of common stock equivalents as if such securities were converted or exercised during the period, when the effect is dilutive. Common stock equivalents include: (i) outstanding stock options and restricted stock units, which are included under the “treasury stock method” when dilutive; (ii) common stock to be issued upon the exercise of outstanding warrants, which are included under the “treasury stock method” when dilutive, and (iii) preferred stock under the if-converted method. Because the impact of these items is anti-dilutive during periods of net loss, there is no difference between basic and diluted loss per common share for periods with net losses.

The following tables set forth the computation of basic and diluted net loss per share of common stock for the three months ended March 31, 2024 and March 31, 2023 (in thousands, except share and per share amounts):

| Three Months Ended March 31, 2024 | ||||||||||||||

| Common stock | ||||||||||||||

| Net loss | $ | (121,290) | ||||||||||||

| Weighted average shares | 859,381 | |||||||||||||

| Basic and diluted net loss per share | $ | (141) | ||||||||||||

As the Company is in a net loss position as of March 31, 2024, the two-class method of computing net loss per share results in no allocation of undistributed losses to participating securities. As such, there is no allocation of undistributed losses to the Series C Preferred Stock outstanding for the three months ended March 31, 2024, and therefore the preferred stock is not reflected in the above table.

13

| Three Months Ended March 31, 2023 | ||||||||

| Common stock | ||||||||

| Net loss | $ | (9,955) | ||||||

| Weighted average shares | 48,845 | |||||||

| Basic and diluted net loss per share | $ | (204) | ||||||

The following outstanding securities have been excluded from the computation of diluted weighted shares outstanding for the three months ended March 31, 2024 and 2023, as they could have been anti-dilutive:

| Three Months Ended | ||||||||||||||

| March 31, | ||||||||||||||

| 2024 | 2023 | |||||||||||||

| Stock options | 7,543 | 7,558 | ||||||||||||

Warrants on common stock1 | 11,969,063 | 17,254 | ||||||||||||

Series C Preferred Stock (as-converted to common stock)2 | 22,357,897 | — | ||||||||||||

1 The weighted average number of common shares outstanding for the three months ended March 31, 2023 includes the weighted average outstanding pre-funded warrants for the period because their exercise price was nominal. There were no pre-funded warrants outstanding as of March 31, 2024.

2 Subject to stockholder approval, each share of the Company’s Series C Preferred Stock will automatically convert to 1,000 shares of common stock, subject to certain beneficial ownership limitations.

6. Fair Value Measurements

ASC 820, Fair Value Measurements and Disclosures (“ASC 820”) defines fair value as the price that would be received to sell an asset, or paid to transfer a liability, in the principal or most advantageous market in an orderly transaction between market participants on the measurement date. The fair value standard also establishes a three‑level hierarchy, which requires an entity to maximize the use of observable inputs and minimize the use of unobservable inputs when measuring fair value. The valuation hierarchy is based upon the transparency of inputs to the valuation of an asset or liability on the measurement date. The three levels are defined as follows:

•Level 1—inputs to the valuation methodology are quoted prices (unadjusted) for an identical asset or liability in an active market.

•Level 2—inputs to the valuation methodology include quoted prices for a similar asset or liability in an active market or model‑derived valuations in which all significant inputs are observable for substantially the full term of the asset or liability.

•Level 3—inputs to the valuation methodology are unobservable and significant to the fair value measurement of the asset or liability.

The following table presents, for each of the fair value hierarchy levels required under ASC 820, the Company’s assets and liabilities that are measured at fair value on a recurring basis (in thousands):

14

| March 31, 2024 | ||||||||||||||||||||

| Fair Value Measurements Using | ||||||||||||||||||||

| Quoted prices in active markets for identical assets | Significant other observable inputs | Significant unobservable inputs | ||||||||||||||||||

| (Level 1) | (Level 2) | (Level 3) | ||||||||||||||||||

| Assets | ||||||||||||||||||||

| Investments in money market funds* | $ | 104,776 | $ | — | $ | — | ||||||||||||||

| Liabilities | ||||||||||||||||||||

| Derivative liability | $ | — | $ | — | $ | 5,670 | ||||||||||||||

| Warrant liability | $ | — | $ | — | 194,901 | |||||||||||||||

| December 31, 2023 | ||||||||||||||||||||

| Fair Value Measurements Using | ||||||||||||||||||||

| Quoted prices in active markets for identical assets | Significant other observable inputs | Significant unobservable inputs | ||||||||||||||||||

| (Level 1) | (Level 2) | (Level 3) | ||||||||||||||||||

| Assets | ||||||||||||||||||||

| Investments in money market funds* | $ | 7,077 | $ | — | $ | — | ||||||||||||||

| Liabilities | ||||||||||||||||||||

| Derivative liability | $ | — | $ | — | $ | 5,550 | ||||||||||||||

*Investments in money market funds are reflected in cash and cash equivalents on the accompanying unaudited condensed consolidated balance sheets.

As of March 31, 2024, the Company’s financial instruments included cash and cash equivalents, restricted cash, other receivables, prepaid and other current assets, accounts payable, accrued expenses and other current liabilities, derivative liability, and warrant liability. As of December 31, 2023, the Company’s financial instruments included cash and cash equivalents, restricted cash, accounts receivable, other receivables, prepaid and other current assets, accounts payable, accrued expenses and other current liabilities, and derivative liability.

The carrying amounts reported in the accompanying unaudited condensed consolidated financial statements for cash and cash equivalents, restricted cash, accounts receivable, other receivables, prepaid and other current assets, accounts payable, and accrued expenses and other current liabilities approximate their respective fair values because of the short-term nature of these accounts.

Level 3 Valuation

The table presented below is a summary of changes in the fair value of the Company’s Level 3 valuations for the warrant liability and derivative liability for the three months ended March 31, 2024:

| Warrant liability | Derivative liability | Total | ||||||||||||||||||

| Balance at December 31, 2023 | $ | — | $ | 5,550 | $ | 5,550 | ||||||||||||||

| Initial valuation of warrant liability | 194,901 | — | 194,901 | |||||||||||||||||

| Change in fair value | — | 120 | 120 | |||||||||||||||||

| Balance at March 31, 2024 | $ | 194,901 | $ | 5,670 | $ | 200,571 | ||||||||||||||

15

| Warrant liability | Derivative liability | Total | ||||||||||||||||||

| Balance at December 31, 2022 | $ | — | $ | 4,830 | $ | 4,830 | ||||||||||||||

| Initial valuation of warrant liability | — | — | — | |||||||||||||||||

| Change in fair value | — | 180 | 180 | |||||||||||||||||

| Balance at March 31, 2023 | $ | — | $ | 5,010 | $ | 5,010 | ||||||||||||||

Warrant liability

On March 28, 2024, the Company closed a private placement investment with institutional investors in which the investors received (i) 19,946 shares of non-voting convertible preferred stock (the “Series C Preferred Stock”) and (ii) warrants to purchase up to an aggregate of 11,967,526 shares of Avalo’s common stock (or a number of shares of Series C Preferred Stock convertible into the number of shares of common stock the warrant is then exercisable into). Refer to Note 10 - Capital Structure and sub-header “Q1 2024 Financing” for more information regarding the warrants.

The Company determined that the warrants do not satisfy the conditions to be accounted for as equity instruments. As the warrants do not meet the equity contract scope exception, the Company classified the warrants as a derivative liability upon issuance.

The Company’s warrant liability is measured at fair value each reporting period utilizing the Black-Scholes option pricing model, which requires assumptions including the value of the stock on the measurement date, exercise price, expected term, expected volatility, and the risk-free interest rate. Certain assumptions, including the expected term and expected volatility, are subjective and require judgment to develop. As a result, if factors or expected outcomes change and we use significantly different assumptions or estimates, our warrant liability could be materially different.

The closing stock price of Avalo’s common stock on March 28, 2024, which was the date the transaction closed, as well as the last trading day of the first quarter of 2024, was the main driver of the fair value of the warrant liability. Future increases or decreases to the stock price at each reporting period will drive increases or decreases, respectively, to the fair value of the warrant liability. The expected term was estimated based on when the Company expects the first patient dosed in a Phase 2 trial of AVTX-009 in hidradenitis suppurativa (the “Dosing Date”), to occur. If the Dosing Date occurs earlier or later than expected, then the expected term will decrease or increase, respectively, which may decrease or increase, respectively, the value of the warrant liability. Expected volatility is based on a blend between the Company’s historical volatility and the volatility of comparable peer companies. The risk-free interest rate was based on the implied yield available on U.S. treasury securities with a maturity equivalent to the expected term. The warrant liability was classified as a Level 3 instrument as its value was based on unobservable market inputs. The inputs utilized include the following:

| As of March 31, 2024 | ||||||||

| Common stock price | $ | 21.75 | ||||||

| Expected term (in years) | 0.5 | |||||||

| Expected volatility | 109 | % | ||||||

| Risk-free rate | 5.35 | % | ||||||

| Exercise price | $ | 5.796933 | ||||||

| Dividend yield rate | — | % | ||||||

The initial measurement of the warrant liability of $194.9 million exceeded the proceeds received from the private placement investment of $115.6 million, which resulted in a $79.3 million loss recognized in other expense, net. Subsequently, the warrants are carried at fair value with changes in fair value recognized in the Company’s consolidated statements of operations and comprehensive loss until either exercised or expired.

16

Derivative liability

In the fourth quarter of 2022, Avalo sold its economic rights to future milestone and royalty payments for previously out-licensed assets AVTX-501, AVTX-007, and AVTX-611 to ES Therapeutics, LLC (“ES”), an affiliate of Armistice, in exchange for $5.0 million (the “ES Transaction”). At the time of the transaction, Armistice was a significant stockholder of the Company and whose chief investment officer, Steven Boyd, and managing director, Keith Maher, served on Avalo’s Board until August 8, 2022. The ES Transaction was approved in accordance with Avalo’s related party transaction policy.

The economic rights sold include (a) rights to a milestone payment of $20.0 million upon the filing and acceptance of an NDA for AVTX-501 pursuant to an agreement with Janssen Pharmaceutics, Inc., (the “AVTX-501 Milestone”) and (b) rights to any future milestone payments and royalties relating to AVTX-007 under a license agreement with Apollo AP43 Limited, including up to $6.25 million of development milestones, up to $67.5 million in sales-based milestones, and royalty payments of a low single digit percentage of annual net sales (which percentage increases to another low single digit percentage if annual net sales exceed a specified threshold) (the “AVTX-007 Milestones and Royalties”). In addition, Avalo waived all its rights to AVTX-611 sales-based payments of up to $20.0 million that were payable by ES.

The exchange of the economic rights of the AVTX-501 Milestone and AVTX-007 Milestones and Royalties for cash meets the definition of a derivative instrument. The fair value of the derivative liability is determined using a combination of a scenario-based method and an option pricing method (implemented using a Monte Carlo simulation). The significant inputs including probabilities of success, expected timing, and forecasted sales as well as market-based inputs for volatility, risk-adjusted discount rates and allowance for counterparty credit risk are unobservable and based on the best information available to Avalo. Certain information used in the valuation is inherently limited in nature and could differ from Janssen and Apollo’s internal estimates.

The fair value of the derivative liability as of the transaction date was approximately $4.8 million, of which $3.5 million was attributable to the AVTX-501 Milestone and $1.3 million was attributable to the AVTX-007 Milestones and Royalties. Subsequent to the transaction date, at each reporting period, the derivative liability is remeasured at fair value. As of March 31, 2024, the fair value of the derivative liability was $5.7 million, of which $3.8 million was attributable to the AVTX-501 Milestone and $1.9 million was attributable to the AVTX-007 Milestones and Royalties. For the three months ended March 31, 2024, the $0.1 million change in fair value was recognized in other expense, net in the accompanying unaudited condensed consolidated statements of operations and comprehensive loss.

The fair value of the AVTX-501 Milestone was primarily driven by an approximate 23% probability of success to reach the milestone in approximately 3.6 years. The fair value of AVTX-007 Milestones and Royalties was primarily driven by an approximate 17% probability of success, time to commercialization of approximately 4.6 years, and sales forecasts with peak annual net sales reaching $300 million. As discussed above, these unobservable inputs were estimated by Avalo based on limited publicly available information and therefore could differ from Janssen and Apollo’s internal development plans. Any changes to these inputs may result in significant changes to the fair value measurement. Notably, the probability of success is the largest driver of the fair value and therefore changes to such input would likely result in significant changes to such fair value.

In the event that Janssen and/or Apollo are required to make payment(s) to ES Therapeutics pursuant to the underlying agreements, Avalo will recognize revenue under its existing contracts with those customers for that amount when it is no longer probable there would be a significant revenue reversal with any differences between the fair value of the derivative liability related to that payment immediately prior to the revenue recognition and revenue recognized to be recorded as other expense. However, given Avalo is no longer entitled to collect these payments, the potential ultimate settlement of the payments in the future from Janssen and/or Apollo to ES Therapeutics (and the future mark-to-market activity each reporting period) will not impact Avalo’s future cash flows.

17

No changes in valuation techniques or inputs occurred during the three months ended March 31, 2024 and 2023. No transfers of assets between Level 1 and Level 2 of the fair value measurement hierarchy occurred during the three months ended March 31, 2024 and 2023.

7. Leases

Avalo currently occupies two leased properties, both of which serve as administrative office space. The Company determined that both of these leases are operating leases based on the lease classification test performed at lease commencement.

The annual base rent for the Company’s office located in Rockville, Maryland is $0.2 million, subject to annual 2.5% increases over the term of the lease. The applicable lease provided for a rent abatement for a period of 12 months following the Company’s date of occupancy. The lease has an initial term of 10 years from the date the Company made its first annual fixed rent payment, which occurred in January 2020. The Company has the option to extend the lease two times, each for a period of five years, and may terminate the lease as of the sixth anniversary of the first annual fixed rent payment, upon the payment of a termination fee.

The initial annual base rent for the Company’s office located in Chesterbrook, Pennsylvania is $0.2 million and the annual operating expenses are approximately $0.1 million. The annual base rent is subject to periodic increases of approximately 2.4% over the term of the lease. The lease has an initial term of 5.25 years from the lease commencement on December 1, 2021.

The weighted average remaining term of the operating leases at March 31, 2024 was 4.4 years.

Supplemental balance sheet information related to the leased properties include (in thousands):

| As of | ||||||||||||||

| March 31, 2024 | December 31, 2023 | |||||||||||||

| Property and equipment, net | $ | 1,280 | $ | 1,329 | ||||||||||

| Accrued expenses and other current liabilities | $ | 545 | $ | 537 | ||||||||||

| Other long-term liabilities | 1,281 | 1,366 | ||||||||||||

| Total operating lease liabilities | $ | 1,826 | $ | 1,903 | ||||||||||

The operating lease right-of-use (“ROU”) assets are included in property and equipment, net and the lease liabilities are included in accrued expenses and other current liabilities and other long-term liabilities in our unaudited condensed consolidated balance sheets. The Company utilized a weighted average discount rate of 9.1% to determine the present value of the lease payments.

The components of lease expense for the three months ended March 31, 2024 and 2023 were as follows (in thousands):

| Three Months Ended March 31, | ||||||||||||||

| 2024 | 2023 | |||||||||||||

| Operating lease cost* | $ | 108 | $ | 120 | ||||||||||

*Includes short-term leases, which are immaterial.

The following table shows a maturity analysis of the operating lease liabilities as of March 31, 2024 (in thousands):

18

| Undiscounted Cash Flows | ||||||||

| April 1, 2024 through December 31, 2024 | $ | 407 | ||||||

| 2025 | 553 | |||||||

| 2026 | 563 | |||||||

| 2027 | 259 | |||||||

| 2028 | 201 | |||||||

| 2029 | 207 | |||||||

| Thereafter | 17 | |||||||

| Total lease payments | $ | 2,207 | ||||||

| Less implied interest | (381) | |||||||

| Total | $ | 1,826 | ||||||

8. Accrued Expenses and Other Current Liabilities

Accrued expenses and other current liabilities as of March 31, 2024 and December 31, 2023 consisted of the following (in thousands):

| As of | ||||||||||||||

| March 31, 2024 | December 31, 2023 | |||||||||||||

| Research and development | $ | 329 | $ | 352 | ||||||||||

| Compensation and benefits | 752 | 580 | ||||||||||||

| General and administrative (including asset acquisition related transaction costs) | 1,934 | 830 | ||||||||||||

| Private placement investment transaction costs | 2,034 | — | ||||||||||||

| Commercial operations | 1,789 | 1,873 | ||||||||||||

| Lease liability, current | 545 | 537 | ||||||||||||

| Total accrued expenses and other current liabilities | $ | 7,383 | $ | 4,172 | ||||||||||

9. Notes Payable

On June 4, 2021, the Company entered into a $35.0 million venture loan and security agreement (the “Loan Agreement”) with Horizon Technology Finance Corporation (“Horizon”) and Powerscourt Investments XXV, LP (“Powerscourt”, and together with Horizon, the “Lenders”). Between June and September of 2021, the Company borrowed the full $35.0 million (the “Note”) available under the Loan Agreement.

In the second quarter of 2022, the Company, as collectively agreed upon with the Lenders, prepaid $15.0 million of principal and accrued interest. In June of 2023, the Company, as collectively agreed upon with the Lenders, prepaid $6.0 million of principal. On September 22, 2023, the Company and the Lenders entered into a Payoff Letter (the “Payoff Letter”), pursuant to which the Company repaid all outstanding principal, inclusive of the final payment fee, and interest under the Loan Agreement in the aggregate amount of $14.3 million. As a result of the payment, all obligations of the parties under the Loan Agreement were deemed satisfied and terminated.

19

On June 4, 2021, pursuant to the Loan Agreement, the Company issued warrants to the Lenders to purchase 148 shares of the Company’s common stock with an exercise price of $7,488 per share (the “Warrants”). The Warrants are exercisable for ten years from the date of issuance. Pursuant to the Payoff Letter, Avalo’s obligations under the Warrants shall survive pursuant to the original terms at issuance. The Warrants, which met equity classification, were recognized as a component of permanent stockholders’ (deficit) equity within additional paid-in-capital and were recorded at the issuance date using a relative fair value allocation method. The Company recognized debt issuance costs and the amount allocated to the warrants as a debt discount on the date of issuance and amortized these costs to interest expense using the effective interest method over the original term of the loan. As a result of the payoff in the third quarter of 2023, the Company accelerated the remaining $0.9 million amortization of the debt discount, which was recognized as interest expense in the third quarter of 2023.

10. Capital Structure

Pursuant to the Company’s amended and restated certificate of incorporation, the Company is authorized to issue two classes of stock, common stock and preferred stock. At March 31, 2024, the total number of shares of capital stock the Company was authorized to issue was 205,000,000, of which 200,000,000 was common stock and 5,000,000 was preferred stock. All shares of common and preferred stock have a par value of $0.001 per share.

Almata Transaction

On March 27, 2024, the Company acquired AlmataBio in which the former AlmataBio stockholders received (i) 171,605 shares of the Company’s common stock and (ii) 2,412 shares of the Company’s Series C Preferred Stock. Subject to the Requisite Stockholder Approval, the date Company shareholders approve the issuance of common stock for conversion of Series C Preferred Stock and for exercise of warrants, each share of the Series C Preferred Stock issued to former AlmataBio stockholders will automatically convert to 1,000 shares of common stock, subject to certain beneficial ownership limitations. The Series C Preferred Stock holds no voting rights. Refer to Note 3 - Asset Acquisition for more information regarding the acquisition and refer to sub-header “Series C Preferred Stock” within the “Q1 2024 Financing” section below for more information regarding the Series C Preferred Stock issued pursuant to the Almata Transaction.

Q1 2024 Financing

On March 28, 2024, the Company closed a private placement investment with institutional investors in which the investors received (i) 19,946 shares of non-voting convertible preferred stock, the Series C Preferred Stock, and (ii) warrants to purchase up to an aggregate of 11,967,526 shares of Avalo’s common stock (or a number of shares of Series C Preferred Stock convertible into the number of shares of common stock the warrant is then exercisable into), resulting in upfront gross proceeds of $115.6 million. Net proceeds were $108.1 million after deducting transaction costs. The Company could receive up to an additional $69.4 million of gross proceeds upon the exercise of the warrants.

Warrants on common stock or Series C Preferred Stock issued in Q1 2024 Financing

The warrants are exercisable via gross physical settlement for $5.796933 per underlying share of common stock (or a number of shares of Series C Preferred Stock convertible into the number of shares of common stock the warrant is then exercisable into). The warrants will become exercisable on (i) March 28, 2024, if exercised for shares of Series C Preferred Stock, or (ii) upon receipt of Requisite Stockholder Approval if exercised for shares of common stock. The warrants will expire on the earlier of (y) the fifth anniversary of the date of issuance or (z) the Dosing Date (as defined in Note 6 - Fair Value Measurements), provided that if the Requisite Stockholder Approval has not been received by the Dosing Date, then the warrants will expire on the earlier of the (A) the fifth anniversary of the date of issuance or (B) thirty-first day following receipt of the Requisite Stockholder Approval. The warrants include anti-dilution protection provisions.

20

The Company determined that the warrants do not satisfy the conditions to be accounted for as equity instruments. As the warrants do not meet the equity contract scope exception, the Company classified the warrants as a derivative liability upon issuance. The initial measurement of the warrant at fair value exceeded the proceeds received such that the difference between the initial fair value of the warrants and net upfront cash proceeds is recognized in the income statement as a loss. Subsequently, the warrants are carried at fair value with changes in fair value recognized in the Company’s unaudited consolidated statements of operations and comprehensive loss until either exercised or expired. The valuation of the warrants is considered under Level 3 of the fair value hierarchy due to the need to use assumptions in the valuation that are both significant to the fair value measurement and unobservable. See Note 6 - Fair Value Measurement for a description of the warrant’s valuation methodology.

No warrants were exercised for the quarterly period ended on March 31, 2024.

Upon exercise of the warrants, the Company will pay an additional amount of transaction costs to a third-party financial institution, based on 2.5% gross proceeds received from the exercise. As the warrants are in the money as of the quarterly period ended March 31, 2024, the Company has recognized $1.7 million for transaction costs within other expense, net. The Company also incurred an additional $7.5 million of transaction costs related to the private placement investment which were expensed within other expense, net.

Series C Preferred Stock issued in the Almata Transaction and Q1 2024 Financing

As of March 31, 2024, the Company had 5,000,000 shares of Preferred Stock authorized, of which 34,326 have been designated as Series C Preferred Stock. As of March 31, 2024, there were 22,358 shares of Series C Preferred Stock outstanding, with a par value of $0.001 per share. The Series C Preferred Stock have no voting rights, no liquidation preference, and are not redeemable. In the event of any liquidation, dissolution or winding up of the Company, Series C Preferred Stock are entitled to be paid out of the assets with the Company legally available for distribution to its stockholders on an as-converted and pari-passu basis with common stock. The Series C Preferred Stock is subject to broad-based weighted average anti-dilution protection for certain issuances of common stock and securities convertible into common stock. The Series C Preferred Stock are entitled to receive dividends equal to and in the same form, and in the same manner, based on the then-current conversion ratio as dividends actually paid on shares of the common stock, when, as and if such dividends are paid on shares of the common stock. Upon Requisite Stockholder Approval, each share of Series C Preferred Stock (i) issued to the former AlmataBio stockholders (as discussed above) and (ii) pursuant to the private placement investment will automatically convert to 1,000 shares of common stock, subject to certain beneficial ownership limitations.

The Series C Preferred Stock is contingently redeemable outside the control of the Company such that the Series C Preferred Stock is recognized outside of permanent equity. The carrying value of Series C Preferred Stock issued to the former AlmataBio stockholders pursuant to the Almata Transaction of $11.5 million is recognized outside of stockholder’s (deficit) equity on the Company’s unaudited consolidated balance sheet. No amounts were allocated to the Series C Preferred Stock issued pursuant to the Q1 2024 Financing because the initial fair value of the warrants exceeded gross proceeds received for the issuance of the private placement bundle that included both Series C Preferred Stock and warrants. The Series C Preferred Stock is not remeasured to redemption value until the shares are probable of becoming redeemable for cash. As of March 31, 2024, the Company expects to have sufficient authorized and unissued shares to settle the Series C Preferred Stock upon Requisite Stockholder Approval, and therefore it is not probable that the Series C Preferred Stock would be redeemable for cash as of the balance sheet date.

As of March 31, 2024, no Series C Preferred Stock were converted to common stock.

Series D and Series E Preferred Stock issued in the Q1 2024 Financing

21

As a condition to the Q1 2024 Financing, a single Series D Preferred Stock and a single Series E Preferred Stock were issued to two institutional investors that participated in the private placement. Both the Series D and the Series E Preferred Stock have a par value and liquidation preference of $0.001 per share. The Series D and Series E Preferred Stock do not have voting rights, are not entitled to dividends, and are not convertible into common stock. The holders of the Series D and Series E Preferred Stock have the option to require the Company to redeem their shares at a price equal to the par value at any time. The Company retains the right to redeem the Series D and Series E Preferred Stock at a price equal to the par value if the holder owns less than a certain threshold of the Company’s outstanding common stock. While the Series D and Series E Preferred Stock do not provide the holders with substantive economics, the Series D and Series E Preferred Stock were issued solely to allow for the institutional investors to appoint a director to the Company’s board of directors.

Common Stock Warrants

At March 31, 2024, the following common stock warrants were outstanding:

| Number of common shares | Exercise price | Expiration | ||||||||||||

| underlying warrants | per share | date | ||||||||||||

| 1,389 | $ | 36,000 | June 2024 | |||||||||||

| 148 | $ | 7,488 | June 2031 | |||||||||||

| 11,967,526 | $ | 5.80 | (1) | (1) | ||||||||||

| 11,969,063 | ||||||||||||||

(1) The warrants will become exercisable (i) on March 28, 2024, if exercised for shares of Series C Preferred Stock, or (ii) upon receipt of Requisite Stockholder Approval, the date Company shareholders approve the issuance of common stock for conversion of Series C Preferred Stock and for exercise of warrants, if exercised for shares of common stock. The warrants will expire on the earlier of (y) the fifth anniversary of the date of issuance or (z) the thirty-first day following the Dosing Date, provided that if the Requisite Stockholder Approval has not been received by the Dosing Date, then the warrants will expire on the earlier of the (A) the fifth anniversary of the date of issuance or (B) thirty-first day following receipt of the Requisite Stockholder Approval. The warrants include anti-dilution protection provisions.

11. Stock-Based Compensation

2016 Equity Incentive Plan

In April 2016, our board of directors adopted the 2016 Equity Incentive Plan, which was approved by our stockholders in May 2016 and which was subsequently amended and restated in May 2018 and August 2019 with the approval of our board of directors and our stockholders (the “2016 Third Amended Plan”). During the term of the 2016 Third Amended Plan, the share reserve will automatically increase on the first trading day in January of each calendar year ending on (and including) January 1, 2026, by an amount equal to 4% of the total number of outstanding shares of common stock of the Company on the last trading day in December of the prior calendar year. On January 1, 2024, pursuant to the terms of the 2016 Third Amended Plan, an additional 32,070 shares were made available for issuance. As of March 31, 2024, there were 32,520 shares available for future issuance under the 2016 Third Amended Plan.

Option grants expire after ten years. Employee options typically vest over four years. Employees typically receive a new hire option grant, as well as an annual grant in the first or second quarter of each year. Options granted to directors typically vest either immediately or over a period of one or three years. Directors may elect to receive stock options in lieu of board compensation, which vest immediately. For stock options granted to employees and non-employee directors, the estimated grant date fair market value of the Company’s stock-based awards is amortized ratably over the individuals’ service periods, which is the period in which the awards vest. Stock-based compensation expense includes expense related to stock options and employee stock purchase plan shares. The amount of stock-based compensation expense recognized for the three months ended March 31, 2024 and 2023 was as follows (in thousands):

22

| Three Months Ended March 31, | ||||||||||||||||||||||||||

| 2024 | 2023 | |||||||||||||||||||||||||

| Research and development | $ | 269 | $ | 326 | ||||||||||||||||||||||

| General and administrative | 360 | 529 | ||||||||||||||||||||||||

| Total stock-based compensation | $ | 629 | $ | 855 | ||||||||||||||||||||||

Stock options with service-based vesting conditions

The Company has granted options that contain service-based vesting conditions. The compensation cost for these options is recognized on a straight-line basis over the vesting periods. A summary of option activity for the three months ended March 31, 2024 is as follows:

| Options Outstanding | ||||||||||||||||||||||||||

| Number of shares | Weighted average exercise price per share | Weighted average grant date fair value per share | Weighted average remaining contractual term (in years) | |||||||||||||||||||||||

| Balance at December 31, 2023 | 7,211 | $ | 3,192 | $ | 1,930 | 8.3 | ||||||||||||||||||||

| Granted | — | $ | — | $ | — | |||||||||||||||||||||

| Forfeited | (13) | $ | 660 | $ | 473 | |||||||||||||||||||||

| Expired | (3) | $ | 11,232 | $ | 6,444 | |||||||||||||||||||||

| Balance at March 31, 2024 | 7,195 | $ | 3,192 | $ | 1,936 | 8.0 | ||||||||||||||||||||

| Exercisable at March 31, 2024 | 4,058 | $ | 4,791 | $ | 2,803 | 7.4 | ||||||||||||||||||||

The aggregate intrinsic value of stock options is calculated as the difference between the exercise price of the stock options and the fair value of the Company’s common stock for those stock options that had exercise prices lower than the fair value of the Company’s common stock. As of March 31, 2024, the aggregate intrinsic value of options outstanding was minimal. There were 545 options that vested during the three months ended March 31, 2024 with a weighted average exercise price of $1,598 per share. The total grant date fair value of shares which vested during the three months ended March 31, 2024 was $0.6 million.

The Company recognized stock-based compensation expense of $0.6 million related to stock options with service-based vesting conditions for the three months ended March 31, 2024. At March 31, 2024, there was $2.2 million of total unrecognized compensation cost related to unvested service-based vesting condition awards. The unrecognized compensation cost is expected to be recognized over a weighted-average period of 1.4 years.

Stock-based compensation assumptions

There were no stock options granted in the three months ended March 31, 2024.

Stock options with market-based vesting conditions

As of March 31, 2024, there were 348 exercisable stock options that contained market-based vesting conditions (that had been previously satisfied). The options have a weighted average share price per share of $9,488 and a weighted average remaining contractual term of 0.2 years. There were no stock options with market-based vesting conditions granted, exercised, or forfeited for the three months ended March 31, 2024.

Employee Stock Purchase Plan

23

On April 5, 2016, the Company’s board of directors approved the 2016 Employee Stock Purchase Plan (the “ESPP”). The ESPP was approved by the Company’s stockholders and became effective on May 18, 2016 (the “ESPP Effective Date”).

Under the ESPP, eligible employees can purchase common stock through accumulated payroll deductions at such times as are established by the administrator. The ESPP is administered by the compensation committee of the Company’s board of directors. Under the ESPP, eligible employees may purchase stock at 85% of the lower of the fair market value of a share of the Company’s common stock (i) on the first day of an offering period or (ii) on the purchase date. Eligible employees may contribute up to 15% of their earnings during the offering period. The Company’s board of directors may establish a maximum number of shares of the Company’s common stock that may be purchased by any participant, or all participants in the aggregate, during each offering or offering period. Under the ESPP, a participant may not accrue rights to purchase more than $25,000 of the fair market value of the Company’s common stock for each calendar year in which such right is outstanding.

The Company initially reserved and authorized up to 174 shares of common stock for issuance under the ESPP. On January 1 of each calendar year, the aggregate number of shares that may be issued under the ESPP automatically increases by a number equal to the lesser of (i) 1% of the total number of shares of the Company’s capital stock outstanding on December 31 of the preceding calendar year, (ii) 174 shares of the Company’s common stock, or (iii) a number of shares of the Company’s common stock as determined by the Company’s board of directors or compensation committee. On January 1, 2024, the number of shares available for issuance under the ESPP increased by 174. As of March 31, 2024, 958 shares remained available for issuance.

In accordance with the guidance in ASC 718-50, Employee Share Purchase Plans, the ability to purchase shares of the Company’s common stock at the lower of the offering date price or the purchase date price represents an option and, therefore, the ESPP is a compensatory plan under this guidance. Accordingly, stock-based compensation expense is determined based on the option’s grant-date fair value and is recognized over the requisite service period of the option. The Company used the Black-Scholes valuation model and recognized minimal stock-based compensation expense for the three months ended March 31, 2024.

12. Income Taxes

The Company recognized minimal income tax expense for the three months ended March 31, 2024 and 2023 due to the significant valuation allowance against the Company’s deferred tax assets and the current and prior period losses.

13. Commitments and Contingencies

Litigation

Litigation - General

The Company may become party to various contractual disputes, litigation, and potential claims arising in the ordinary course of business. Reserves are established in connection with such matters when a loss is probable and the amount of such loss can be reasonably estimated. The Company currently does not believe that the resolution of such matters will have a material adverse effect on its financial position or results of operations except as otherwise disclosed in this report.

Dispute Notice Settlement

24

On August 14, 2023, the Company received a notice from Apollo AP43 Limited alleging that the Company was in breach of the license agreement between them dated July 29, 2022 by virtue of owing $0.8 million to a service provider under the terms of that license. On January 25, 2024, the Company and Apollo entered into a settlement and release agreement, pursuant to which Avalo agreed to pay Apollo $0.2 million to settle the dispute and Apollo released Avalo from any and all liabilities or claims relating to the dispute that Apollo may have against Avalo from the date of the license agreement through the date of the settlement and release agreement. The Company recognized the $0.2 million settlement within accrued expenses and other current liabilities as of December 2023 and made the $0.2 million settlement payment in the first quarter of 2024.

Possible Future Milestone Payments for In-Licensed Compounds

General

Avalo is a party to license and development agreements with various third parties, which contain future payment obligations such as royalties and milestone payments. The Company recognizes a liability (and related expense) for each milestone if and when such milestone is probable and can be reasonably estimated. As typical in the biotechnology industry, each milestone has unique risks that the Company evaluates when determining the probability of achieving each milestone and the probability of success evolves over time as the programs progress and additional information is obtained. The Company considers numerous factors when evaluating whether a given milestone is probable including (but not limited to) the regulatory pathway, development plan, ability to dedicate sufficient funding to reach a given milestone and the probability of success.

AVTX-009 Agreements

On March 27, 2024, Avalo obtained the rights to an anti-IL-1β mAb (AVTX-009), including the world-wide exclusive license from Eli Lilly and Company (the “Lilly License Agreement”), pursuant to its acquisition of AlmataBio. AlmataBio had previously purchased the rights, title and interest in the asset from Leap Therapeutics, Inc. (“Leap”) in 2023.

Avalo is required to pay up to $70 million based on the achievement of specified development and regulatory milestones. Upon commercialization, the Company is required to pay sales-based milestones aggregating up to $720 million. Additionally, Avalo is required to pay royalties during a country-by-country royalty term equal to a mid-single digit-to-low double digit of Avalo or its sublicensees’ annual net sales.

No expense related to these AVTX-009 agreements was recognized in the three months ended March 31, 2024. There has been no cumulative expense recognized as of March 31, 2024 related to the milestones under these AVTX-009 agreements. The Company will continue to monitor the milestones at each reporting period.

Refer to the sub-header below entitled “Acquisition Related and Other Contingent Liabilities” for information regarding future development milestones that are payable to the former AlmataBio stockholders.

AVTX-002 KKC License Agreement

On March 25, 2021, the Company entered into a license agreement with Kyowa Kirin Co., Ltd. (“KKC”) for exclusive worldwide rights to develop, manufacture and commercialize AVTX-002, KKC’s first-in-class fully human anti-LIGHT (TNFSF14) monoclonal antibody for all indications (the “KKC License Agreement”). The KKC License Agreement replaced the Amended and Restated Clinical Development and Option Agreement between the Company and KKC dated May 28, 2020.

25

Under the KKC License Agreement, the Company paid KKC an upfront license fee of $10.0 million, which we recognized within research and development expenses in 2021. The Company is also required to pay KKC up to an aggregate of $112.5 million based on the achievement of specified development and regulatory milestones. Upon commercialization, the Company is required to pay KKC sales-based milestones aggregating up to $75.0 million tied to the achievement of annual net sales targets.

Additionally, the Company is required to pay KKC royalties during a country-by-country royalty term equal to a mid-teen percentage of annual net sales. The Company is required to pay KKC a double-digit percentage (less than 30%) of the payments that the Company receives from any sublicensing of its rights under the KKC License Agreement, subject to certain exclusions. Avalo is responsible for the development and commercialization of AVTX-002 in all indications worldwide (other than the option in the KKC License Agreement that, upon exercise by KKC, allows KKC to develop, manufacture and commercialize AVTX-002 in Japan). In addition to the KKC License Agreement, Avalo is subject to additional royalties upon commercialization of up to an amount of less than 10% of net sales.

No expense related to the KKC License Agreement was recognized in the three months ended March 31, 2024. There has been no cumulative expense recognized as of March 31, 2024 related to the milestones under the KKC License Agreement. The Company will continue to monitor the milestones at each reporting period.

AVTX-008 Sanford Burnham Prebys License Agreement

On June 22, 2021, the Company entered into an Exclusive Patent License Agreement with Sanford Burnham Prebys Medical Discovery Institute (the “Sanford Burnham Prebys License Agreement”) under which the Company obtained an exclusive license to a portfolio of issued patents and patent applications covering an immune checkpoint program (AVTX-008).