UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2016

|

| | | | |

Commission File Number | | Exact name of registrant as specified in its charter, address of principal executive office and registrant's telephone number | | IRS Employer Identification Number |

| 1-36518 | | NEXTERA ENERGY PARTNERS, LP | | 30-0818558

|

| | | 700 Universe Boulevard Juno Beach, Florida 33408 (561) 694-4000 | | |

State or other jurisdiction of incorporation or organization: Delaware

|

| | |

| | Name of exchange on which registered |

| Securities registered pursuant to Section 12(b) of the Act: | |

| | Common Units | New York Stock Exchange |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act of 1933. Yes þ No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Securities Exchange Act of 1934. Yes o No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months, and (2) has been subject to such filing requirements for the past 90 days. Yes þ No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months. Yes þ No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. þ

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Securities Exchange Act of 1934.

|

| | | | |

Large Accelerated Filer þ | Accelerated Filer o | Non-Accelerated Filer o | Smaller Reporting Company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Securities Exchange Act of 1934). Yes o No þ

Aggregate market value of the voting and non-voting common equity of NextEra Energy Partners, LP held by non-affiliates as of June 30, 2016 (based on the closing market price on the Composite Tape on June 30, 2016) was $1,274,972,073.

Number of NextEra Energy Partners, LP common units outstanding as of January 31, 2017: 54,236,995

DEFINITIONS

Acronyms and defined terms used in the text include the following:

|

| |

| Term | Meaning |

| ASA | administrative services agreements |

| Bcf | billion cubic feet |

| BLM | U.S. Bureau of Land Management |

| Bluewater | wind project located in Huron County, Ontario, Canada, that is held by the Bluewater Project Entity |

| Bluewater Project Entity | Prior to the consummation of NEP’s IPO in 2014, refers to Varna Wind, Inc. and, after the consummation of NEP’s IPO, refers to Varna Wind, LP |

| Canadian Project Entities | Conestogo Project Entity, Summerhaven Project Entity, Bluewater Project Entity, Sombra Project Entity, Moore Project Entity and Jericho Wind, LP, collectively |

| Canyon Wind | Canyon Wind, LLC, which is the borrower under the credit agreement under which financing is provided to Perrin Ranch and Tuscola Bay |

| Cedar Bluff Wind | wind project located in Ellis, Ness, Rush and Trego counties, Kansas |

| CITC | convertible investment tax credit |

| COD | commercial operation date |

| Code | U.S. Internal Revenue Code of 1986, as amended |

| Conestogo | wind project located in Wellington County, Ontario, Canada, that is held by the Conestogo Project Entity |

| Conestogo Project Entity | Conestogo Wind, LP |

| CSCS agreement | cash sweep and credit support agreement |

| Desert Sunlight Investment | NEP's indirect 24% ownership interest in Desert Sunlight |

| Desert Sunlight | Desert Sunlight Investment Holdings, LLC, which owns a solar generation plant located in Riverside County, California |

| Elk City | wind project located in Roger Mills and Beckham counties, Oklahoma, that is held by Elk City Wind, LLC |

| FCPA | Foreign Corrupt Practices Act of 1977, as amended |

| FERC | U.S. Federal Energy Regulatory Commission |

| FIT | Feed-in-Tariff |

| FPA | U.S. Federal Power Act |

| Genesis | solar project held by Genesis Solar, LLC, which project is composed of Genesis Unit 1 and Genesis Unit 2 |

| Genesis Unit 1 | Genesis Unit 1 universal solar generating facility located in Riverside County, California |

| Genesis Unit 2 | Genesis Unit 2 universal solar generating facility located in Riverside County, California |

| Golden Hills Wind | wind project located in Alameda County, California |

| GWh | gigawatt-hour(s) |

| IESO | Independent Electricity System Operator |

| IPO | initial public offering |

| IPP | independent power producer |

| ITC | investment tax credit |

| kWh | kilowatt-hour(s) |

| Logan Wind | Logan Wind Energy, LLC, an indirect wholly owned subsidiary of NEE and the owner of a wind-powered energy production facility near Peetz, Colorado, that shares certain facilities owned by Peetz Table with Northern Colorado |

| Mammoth Plains | wind project located in Dewey and Blaine counties, Oklahoma |

| management sub-contract | management services subcontract between NEE Management and NEER |

| Management's Discussion | Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations |

| Moore | solar project located in Lambton County, Ontario, Canada, that is held by the Moore Project Entity |

| Moore Project Entity | Prior to the consummation of NEP’s IPO in 2014, refers to Moore Solar, Inc. and, after the consummation of NEP’s IPO, refers to Moore Solar, LP, a limited partnership formed under the laws of the Province of Ontario |

| Mountain Prairie | Mountain Prairie Wind, LLC, the issuer of notes that provide financing to Elk City and Northern Colorado |

| MSA | Management Services Agreement among NEP, NEE Management, NEP OpCo and NEP OpCo GP |

| MW | megawatt(s) |

| NECIP | NextEra Canadian IP, Inc., an indirect wholly owned subsidiary of NEE |

| NECOS | NextEra Energy Canadian Operating Services, Inc., an indirect wholly owned subsidiary of NEE |

| NEE | NextEra Energy, Inc. |

| NEEC | Prior to the consummation of NEP’s IPO in 2014, refers to NextEra Energy Canada, ULC, an indirect wholly owned subsidiary of NEE, and after the consummation of NEP’s IPO, refers to NextEra Energy Canada Partners Holdings, ULC, a direct wholly owned subsidiary of NEP OpCo |

| NEECH | NextEra Energy Capital Holdings, Inc. |

| NEE Equity | NextEra Energy Equity Partners, LP |

| NEE Management | NextEra Energy Management Partners, LP |

| NEER | NextEra Energy Resources, LLC |

| NEER ROFO projects | certain projects owned by NEER in which NEP has a right of first offer should NEER decide to sell them |

| NEOS | NextEra Energy Operating Services, LLC, an indirect wholly owned subsidiary of NEE |

| NEP | NextEra Energy Partners, LP |

| NEP GP | NextEra Energy Partners GP, Inc. |

| NEP OpCo | NextEra Energy Operating Partners, LP |

|

| |

| Term | Meaning |

| NEP OpCo GP | NextEra Energy Operating Partners GP, LLC |

| NERC | North American Electric Reliability Corporation |

| NOLs | net operating losses |

| Northern Colorado | wind project located in Logan County, Colorado, that is held by Northern Colorado Wind Energy, LLC |

| Note __ | Note __ to consolidated financial statements |

| NYSE | New York Stock Exchange |

| O&M | operations and maintenance |

| Palo Duro | wind project located in Hansford and Ochiltree counties, Texas |

| Peetz Table | Peetz Table Wind Energy, LLC, an indirect wholly owned subsidiary of NEE and the owner of certain facilities shared by Logan Wind, Northern Colorado and PLI |

| Pemex | Petróleos Mexicanos |

| Perrin Ranch | wind project located in Coconino County, Arizona, that is held by Perrin Ranch Wind, LLC |

| PLI | Peetz Logan Interconnect, LLC, an indirect wholly owned subsidiary of NEE and the owner of the transmission line used by Northern Colorado to deliver energy output to the interconnection point |

| PPA | power purchase agreement, which could include contracts under a FIT or RESOP |

| PTC | production tax credit |

| renewable energy project entities | U.S. Project Entities together with the Canadian Project Entities |

| RESOP | Renewable Energy Standard Offer Program |

| RPS | renewable portfolio standards |

| SEC | U.S. Securities and Exchange Commission |

| Seiling Wind | wind project located in Dewey County, Oklahoma |

| Seiling Wind II | wind project located in Dewey and Woodward counties, Oklahoma |

| Shafter | solar project located in Shafter, California |

| Sombra | solar project located in Lambton County, Ontario, Canada, that is held by the Sombra Project Entity |

| Sombra Project Entity | Prior to the consummation of NEP’s IPO in 2014, refers to Sombra Solar, Inc. and, after the consummation of NEP’s IPO, refers to Sombra Solar, LP |

| St. Clair Holding | Prior to the consummation of NEP’s IPO in 2014, refers to St. Clair Holding, Inc. and, after the consummation of NEP’s IPO, refers to St. Clair Holding, ULC, a co-issuer of notes that provide financing to Moore and Sombra |

| St. Clair LP | St. Clair Solar, LP, a co-issuer of notes that provide financing to Moore and Sombra |

| St. Clair entities | St. Clair Holding and St. Clair LP, collectively |

| Summerhaven | wind project located in Haldimand County, Ontario, Canada, that is held by the Summerhaven Project Entity |

| Summerhaven Project Entity | Summerhaven Wind, LP |

| Texas pipelines | natural gas pipeline assets located in Texas |

| Texas pipelines acquisition | acquisition of NET Holdings Management, LLC (the Texas pipeline business) |

| Texas pipeline entities | the subsidiaries of NEP that directly own the Texas pipelines |

| Trillium | Trillium Windpower, LP, the issuer of notes that provides financing to Conestogo and Summerhaven |

| Tuscola Bay | wind project located in Tuscola, Bay and Saginaw counties, Michigan, that is held by Tuscola Bay Wind, LLC |

| U.S. | United States of America |

| U.S. Project Entities | U.S. Wind Project Entities together with the U.S. Solar Project Entities and the Desert Sunlight Investment |

| U.S. Solar Project Entities | Genesis Solar LLC, Shafter Solar, LLC, Adelanto Solar, LLC, Adelanto Solar II, LLC and McCoy Solar, LLC, each of which is a limited liability company formed under the laws of the State of Delaware |

| U.S. Wind Project Entities | Elk City Wind, LLC, Northern Colorado Wind Energy, LLC, Perrin Ranch Wind, LLC, Tuscola Bay Wind, LLC, Palo Duro Wind Energy, LLC, FPL Energy Vansycle L.L.C. (Stateline), Ashtabula Wind III, LLC, Baldwin Wind, LLC, Mammoth Plains Wind Project, LLC, Seiling Wind, Seiling Wind II, Golden Hills Wind and Cedar Bluff Wind, each of which is a limited liability company formed under the laws of the State of Delaware |

Each of NEP and NEP OpCo has subsidiaries and affiliates with names that may include NextEra Energy, NextEra Energy Partners and similar references. For convenience and simplicity, in this report, the terms NEP and NEP OpCo are sometimes used as abbreviated references to specific subsidiaries, affiliates or groups of subsidiaries or affiliates. The precise meaning depends on the context. Discussions of NEP's ownership of subsidiaries and projects refers to its controlling interest in the general partner of NEP OpCo and NEP's indirect interest in and control over the subsidiaries of NEP OpCo. See Note 1 for a description of the non-controlling interest in NEP OpCo.

TABLE OF CONTENTS

|

| | |

| | | Page No. |

| | |

| |

| | PART I | |

| Business | |

| Risk Factors | |

| Unresolved Staff Comments | |

| Properties | |

| Legal Proceedings | |

| Mine Safety Disclosures | |

| | PART II | |

| Market for Registrant's Common Equity, Related Unitholder Matters and Issuer Purchases of Equity Securities | |

| Selected Financial Data | |

| Management's Discussion and Analysis of Financial Condition and Results of Operations | |

| Quantitative and Qualitative Disclosures About Market Risk | |

| Financial Statements and Supplementary Data | |

| Changes in and Disagreements With Accountants on Accounting and Financial Disclosure | |

| Controls and Procedures | |

| Other Information | |

| | PART III | |

| Directors, Executive Officers and Corporate Governance | |

| Executive Compensation | |

| Security Ownership of Certain Beneficial Owners and Management and Related Unitholder Matters | |

| Certain Relationships and Related Transactions, and Director Independence | |

| Principal Accounting Fees and Services | |

| | PART IV | |

| Exhibits, Financial Statement Schedules | |

| | |

| | |

FORWARD-LOOKING STATEMENTS

This report includes forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. Any statements that express, or involve discussions as to, expectations, beliefs, plans, objectives, assumptions, strategies, future events or performance (often, but not always, through the use of words or phrases such as result, are expected to, will continue, anticipate, aim, believe, will, could, should, would, estimated, may, plan, potential, future, projection, goals, target, predict and intend or words of similar meaning) are not statements of historical facts and may be forward looking. Forward-looking statements involve estimates, assumptions and uncertainties. Accordingly, any such statements are qualified in their entirety by reference to, and are accompanied by important factors included in Part I, Item 1A. Risk Factors (in addition to any assumptions and other factors referred to specifically in connection with such forward-looking statements) that could have a significant impact on NEP's operations and financial results, and could cause NEP's actual results to differ materially from those contained or implied in forward-looking statements made by or on behalf of NEP in this Form 10-K, in presentations, on its website, in response to questions or otherwise.

Any forward-looking statement speaks only as of the date on which such statement is made, and NEP undertakes no obligation to update any forward-looking statement to reflect events or circumstances, including, but not limited to, unanticipated events, after the date on which such statement is made, unless otherwise required by law. New factors emerge from time to time and it is not possible for management to predict all of such factors, nor can it assess the impact of each such factor on the business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained or implied in any forward-looking statement.

PART I

Item 1. Business

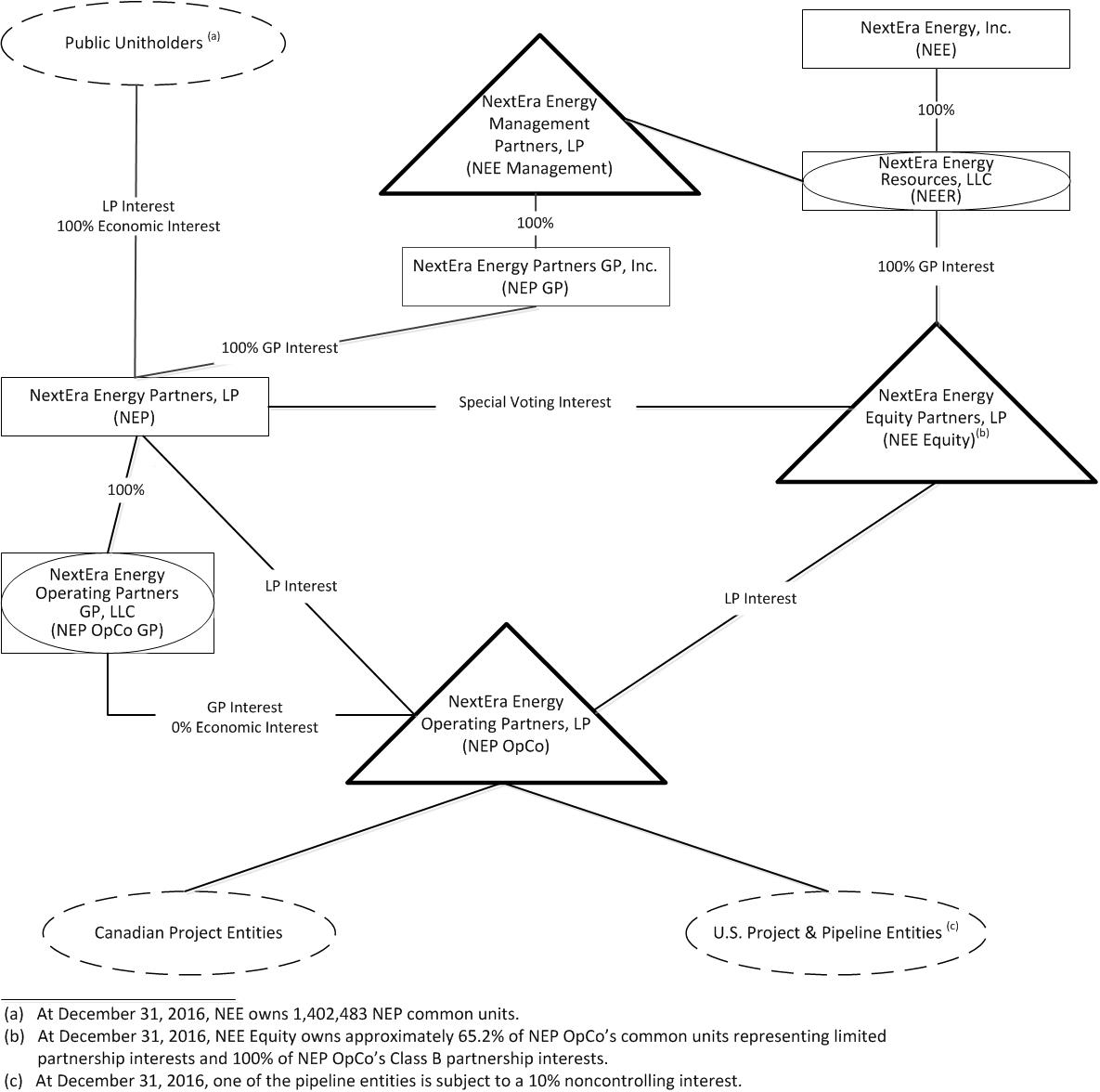

NEP is a growth-oriented limited partnership formed by NEE to acquire, manage and own contracted clean energy projects with stable long-term cash flows. At December 31, 2016, NEP owns a controlling, non-economic general partner interest and a 34.8% limited partner interest in NEP OpCo. Through NEP OpCo, NEP owns a portfolio of contracted renewable generation assets consisting of wind and solar projects, as well as seven contracted natural gas pipeline assets.

NEP expects to take advantage of trends in the North American energy industry, including the addition of clean energy projects as aging or uneconomic generation facilities are phased out, increased demand from utilities for renewable energy to meet state RPS requirements, improving competitiveness of energy generated from wind and solar projects relative to energy generated using other fuels and increased demand for natural gas transportation. NEP plans to focus on high-quality, long-lived projects operating under long-term contracts with creditworthy counterparties that are expected to produce stable long-term cash flows. NEP believes its cash flow profile, geographic, technological and resource diversity, cost-efficient business model and relationship with NEE provide NEP with a significant competitive advantage and enable NEP to execute its business strategy.

NEP was formed as a Delaware limited partnership in March 2014 as an indirect wholly owned subsidiary of NEE. On July 1, 2014, NEP completed its IPO by issuing 18,687,500 common units at a price to the public of $25 per unit. The proceeds from the IPO, net of underwriting discounts, commissions and structuring fees, were approximately $438 million, of which NEP used approximately $288 million to purchase 12,291,593 common units of NEP OpCo from NEE Equity and approximately $150 million to purchase 6,395,907 NEP OpCo common units from NEP OpCo. Subsequent to the IPO, NEP issued a total of 35,549,495 additional common units and purchased an additional 35,549,495 NEP OpCo common units.

The following diagram depicts NEP's simplified ownership structure at December 31, 2016:

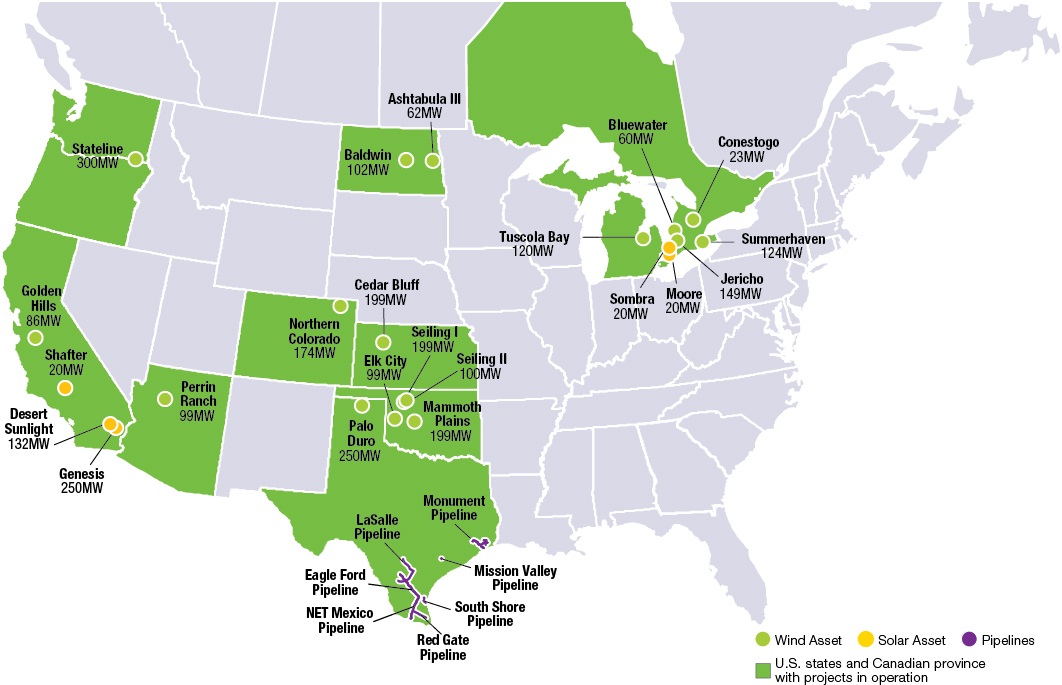

At December 31, 2016, NEP owns interests in the following portfolio of clean, contracted renewable energy projects located in ten states in the U.S. and one province in Canada:

|

| | | | | | | | |

| Project | | Resource | | MW | | Contract Expiration | | NEP Acquisition / Investment Date |

Genesis(a) | | Solar | | 250 | | 2039 | | July 2014 |

Northern Colorado(a) | | Wind | | 174 | | 2029 (22 MW) 2034 (152 MW) | | July 2014 |

Summerhaven(a) | | Wind | | 124 | | 2033 | | July 2014 |

Tuscola Bay(a) | | Wind | | 120 | | 2032 | | July 2014 |

Elk City(a) | | Wind | | 99 | | 2030 | | July 2014 |

Perrin Ranch(a) | | Wind | | 99 | | 2037 | | July 2014 |

Bluewater(a) | | Wind | | 60 | | 2034 | | July 2014 |

Conestogo(a) | | Wind | | 23 | | 2032 | | July 2014 |

Moore(a) | | Solar | | 20 | | 2032 | | July 2014 |

Sombra(a) | | Solar | | 20 | | 2032 | | July 2014 |

Palo Duro(b) | | Wind | | 250 | | 2034 | | January 2015 |

Shafter(a) | | Solar | | 20 | | 2035 | | February 2015 |

Stateline(a) | | Wind | | 300 | | 2026 | | May 2015 |

Mammoth Plains(b) | | Wind | | 199 | | 2034 | | May 2015 |

Baldwin Wind(a) | | Wind | | 102 | | 2041 | | May 2015 |

Ashtabula Wind III(a) | | Wind | | 62 | | 2038 | | May 2015 |

Jericho(a) | | Wind | | 149 | | 2034 | | October 2015 |

Seiling Wind(b) | | Wind | | 199 | | 2035 | | March 2016 |

Seiling Wind II(b) | | Wind | | 100 | | 2034 | | March 2016 |

Cedar Bluff Wind(b) | | Wind | | 199 | | 2035 | | July 2016 |

Golden Hills Wind(b) | | Wind | | 86 | | 2035 | | July 2016 |

Investment in Desert Sunlight(a)(c) | | Solar | | 132 | | 2035 (60 MW) 2039 (72 MW) | | October 2016 |

| | | | | 2,787 | | | | |

| Non-Economic Ownership Interests: | | | | | | | | |

Adelanto I and II(a)(d) | | Solar | | 14 | | 2035 | | April 2015 |

McCoy(a)(d) | | Solar | | 125 | | 2036 | | April 2015 |

| Total | | | | 2,926 | | | | |

____________________

| |

| (a) | These projects are encumbered by liens against their assets securing various financings. |

| |

| (b) | NEP owns these wind projects together with third-party investors with differential membership interests. See Note 2 - Sale of Differential Membership Interests and Note 8. |

| |

| (c) | NEP owns an indirect 24% equity method investment in Desert Sunlight and the MWs reflect the net ownership interest in plant capacity. See Note 2 - Investments in Unconsolidated Entities. |

| |

| (d) | NEP owns an approximately 50% non-economic ownership interest in each of these solar projects and the MWs reflect the net ownership interest in plant capacity. All equity in earnings of these non-economic ownership interests is allocated to net income attributable to noncontrolling interest. See Note 2 - Investments in Unconsolidated Entities. |

At December 31, 2016, NEP owns interests in the following contracted natural gas pipeline assets located in Texas:

|

| | | | | | | | | | | | | | |

Pipeline(a) | | Miles of Pipeline | | Diameter (inches) | | Capacity per day | | Contracted Capacity per day | | Contract Expiration | | In Service Date | | NEP Acquisition Date(b) |

NET Mexico(c) | | 120 | | 42" / 48" | | 2.30 Bcf | | 2.15 Bcf | | 2034 - 2035 | | December 2014 | | October 2015 |

| Eagle Ford | | 158 | | 16" / 24" - 30" | | 1.10 Bcf | | 0.45 Bcf | | 2018 - 2024 | | September 2011 / June 2013 | | October 2015 |

| Monument | | 156 | | 16" | | 0.25 Bcf | | 0.20 Bcf | | 2017 - 2030 | | Built in the 1950s - 2000s | | October 2015 |

| Other | | 108 | | 8" - 16" | | 0.40 Bcf | | 0.28 Bcf | | 2016 - 2035 | | Built in the 1960s - 1980s; upgraded in 2001 / others placed in service in 2002 - 2015 | | October 2015 |

____________________

| |

| (a) | All of the pipelines are encumbered by liens against their assets securing various financings. |

| |

| (b) | See Note 3 for a description of the Texas pipelines acquisition. |

| |

| (c) | A subsidiary of Pemex owns a 10% interest in the NET Mexico pipeline. |

At December 31, 2016, NEP's clean energy projects and pipelines, excluding its non-economic ownership interests, are as follows:

Each of the renewable energy projects sells substantially all of its output and related renewable energy attributes pursuant to long-term, fixed price PPAs to various counterparties. The pipelines primarily operate under long-term firm transportation contracts where counterparties pay for a fixed amount of capacity that is reserved by the counterparties and also generate revenues based on the volume of natural gas transported on the pipelines. During 2016, NEP derived approximately 19%, 18% and 16% of its consolidated revenues from its contracts with Pacific Gas and Electric Company, Mex Gas Supply S.L. and the IESO, respectively. In 2016, 2015 and 2014, approximately $136 million, $136 million and $95 million, respectively, of NEP's consolidated revenues were attributable to its Canadian operations. In addition, NEP's 2016 and 2015 revenues included approximately $129 million and $18 million, respectively, of revenues attributable to its contract with a subsidiary of Pemex. At December 31, 2016, 2015 and 2014, NEP's total net long-lived assets, including construction work in progress, located in Canada amounted to approximately $881 million, $879 million and $1,075 million, respectively. See Item 1A for a discussion of risks related to NEP's operations in Canada and NEP's business relationship with Pemex.

In connection with the IPO, NEP entered into a ROFO agreement with NEER and NEP OpCo that, among other things, provides NEP OpCo with a right of first offer to acquire the NEER ROFO projects, if NEER should seek to sell any of these projects. NEP believes that the NEER ROFO projects have many of the characteristics of the renewable energy projects in its current portfolio, including long-term contracts with creditworthy counterparties and recently constructed, long-lived facilities that NEP believes will generate stable cash flows. Under the ROFO agreement, however, NEER is not obligated to offer to sell any of the NEER ROFO projects. In addition, in the event that NEER elects to sell any of the NEER ROFO projects, NEER is not required to accept any offer NEP OpCo makes to acquire any NEER ROFO project and, following the completion of good faith negotiations, may choose to sell the project to third parties or not to sell the project at all. NEER is not obligated to offer NEP OpCo the NEER ROFO projects at prices or on terms that are consistent with NEP's business strategy. The NEER ROFO projects as of December 31, 2016 include contracted wind and solar projects in the U.S. and Canada with a combined capacity of approximately 1,076 MW.

Effective July 2014, NEP and certain subsidiaries of NEP entered into the MSA with an indirect wholly owned subsidiary of NEE, under which operational, management and administrative services are provided to NEP, including managing NEP’s day-to-day affairs and providing individuals to act as NEP GP’s executive officers and directors, in addition to those services that are provided under O&M agreements and ASAs between NEER subsidiaries and NEP subsidiaries. NEP OpCo pays NEE an annual management fee and makes certain payments to NEE based on the achievement by NEP OpCo of certain target quarterly distribution levels to its unitholders (incentive distribution rights fees, or IDRs). See Note 11 - Management Services Agreement.

In addition, effective October 2015, subsidiaries of NEP entered into transportation agreements and a fuel management agreement with a subsidiary of NEE. See Note 11 - Transportation and Fuel Management Agreements.

INDUSTRY OVERVIEW

U.S. Renewable Energy Industry

Growth in renewable energy is largely attributable to the increasing cost competitiveness of renewable energy driven primarily by government incentives, RPS, improving technology and declining installation costs and the impact of increasingly stringent environmental rules and regulations on fossil-fired generation.

U.S. federal, state and local governments have established various incentives to support the development of renewable energy. These incentives make the development of renewable energy projects more competitive by providing accelerated depreciation, tax credits or grants for a portion of the development costs, decreasing the costs associated with developing such projects or creating demand for renewable energy assets through RPS programs. In addition, RPS provide incentives to utilities to contract for energy generated from renewable energy providers.

Renewable energy technology has improved and installation costs have declined meaningfully in recent years. Wind technology is improving as a result of taller towers, longer blades and more efficient energy conversion equipment, which allow wind projects to more efficiently capture wind resource and produce more energy. Solar technology is also improving as solar cell efficiencies improve and solar equipment costs decline.

Fossil-fired plants emit greenhouse gases (GHG) and other pollutants. A number of U.S. Environmental Protection Agency (EPA) rules have been proposed that are expected to impact many coal-fired plants in the U.S. While there is some uncertainty as to the timing and requirements that will ultimately be imposed by these proposed rules (see discussion of the Clean Power Plan in Environmental Matters - Regulation of GHG emissions below), NEP expects that the owners of some of the smaller, older or less efficient coal-fired plants will choose to decommission these facilities rather than make the significant investments that will be necessary to comply with environmental rules and regulations. In addition, NEP expects the current relatively low natural gas prices will affect the decision whether to make such investments.

Canadian Renewable Energy Industry

Canada is a world leader in the production and use of clean energy as a percentage of its total energy needs. Capacity additions are expected to be required throughout Canada in order to replace aging projects and meet growing demand. While a majority of Canada’s electricity is generated by hydro energy plants, non-hydro renewable energy is providing an increasing portion of Canada’s energy.

The Canadian energy industry is also benefiting from the increased competitiveness of renewable energy, due in part to improving technology and declining installation costs. Furthermore, government targets and incentives at the provincial level continue to drive the growth of renewable energy in Canada. Ontario, in particular, has been a leader in supporting the development of renewable energy in Canada.

U.S. Natural Gas Pipeline Transportation Industry

The increase in natural gas production in the U.S. has led to opportunities to construct new gas pipelines to transport natural gas from areas of strong production to areas of strong natural gas demand. Over the next several years, NEP expects electricity generators to continue to demand higher volumes of natural gas due to prices being near historic lows and the emergence of GHG emissions standards. NEP expects these factors to continue to support a growing natural gas transportation industry.

Policy Incentives

Policy incentives in the U.S. and Canada have the effect of making the development of renewable energy projects more competitive by providing credits for a portion of the development costs or by providing favorable contract prices. A loss of or reduction in such incentives could decrease the attractiveness of renewable energy projects to developers, including NEE, which could reduce NEP's future acquisition opportunities. Such a loss or reduction could also reduce NEP's willingness to pursue or develop certain renewable energy projects due to higher operating costs or decreased revenues under its PPAs.

U.S. federal, state and local governments have established various incentives to support the development of renewable energy projects. These incentives include accelerated tax depreciation, PTCs, ITCs, cash grants, tax abatements and RPS programs. Wind and solar projects qualify as 5-year property that is eligible to be depreciated under the U.S. federal Modified Accelerated Cost Recovery System (MACRS). Pursuant to MACRS, wind and solar projects are fully depreciated for tax purposes over a five-year period even though the useful life of such projects is generally much longer than five years.

Owners of utility-scale wind facilities are eligible to claim an income tax credit (the PTC, or an ITC in lieu of the PTC) upon initially achieving commercial operation. The PTC is determined based on the amount of electricity produced by the wind facility during the first ten years of commercial operation. This incentive was created under the Energy Policy Act of 1992 and has been extended several times. Alternatively, an ITC equal to 30% of the cost of a wind facility may be claimed in lieu of the PTC. In December 2015, the PTC (and ITC in lieu of the PTC) for wind facilities was extended for five years, subject to the phase-down schedule in the table

below. In order to qualify for the PTC (or ITC in lieu of the PTC), construction of a wind facility must begin before a specified date. The Internal Revenue Service (IRS) previously issued guidance setting forth two alternatives pursuant to which a taxpayer may begin construction on a wind facility and providing that the taxpayer must maintain a continuous program of construction or continuous efforts to advance the project to completion. In May 2016, the IRS issued additional guidance relating to the December 2015 extension and phase-down of the PTC and ITC for wind facilities. In general, this guidance modifies and extends the safe harbor for the continuous efforts and continuous construction requirements to four years compared to two years under the previous guidance. The safe harbor will generally be satisfied if the facility is placed in service no more than four calendar years after the calendar year in which construction of the facility began. The IRS also confirmed that retrofitted wind facilities may re-qualify for PTCs or ITCs pursuant to the 5% safe harbor for the begin construction requirement, as long as the cost basis of the new investment is at least 80% of the facility’s total fair value.

Owners of solar projects are eligible to claim a 30% ITC for new solar projects, or can elect to receive an equivalent cash payment from the U.S. Department of Treasury for the value of the 30% ITC for qualifying solar projects where construction began before the end of 2011 and the projects are placed in service before 2017. In December 2015, the 30% ITC for new solar projects was extended, subject to the following phase-down schedule.

|

| | | | | | | | | | | | | | | | | | | | | | | |

| | Year construction of project begins |

| | 2015 | | 2016 | | 2017 | | 2018 | | 2019 | | 2020 | | 2021 | | 2022 |

PTC(a) | 100 | % | | 100 | % | | 80 | % | | 60 | % | | 40 | % | | - |

| | - |

| | - |

|

| Wind ITC | 30 | % | | 30 | % | | 24 | % | | 18 | % | | 12 | % | | - |

| | - |

| | - |

|

Solar ITC(b) | 30 | % | | 30 | % | | 30 | % | | 30 | % | | 30 | % | | 26 | % | | 22 | % | | 10 | % |

______________________

| |

| (a) | Percentage of the full PTC available for wind projects that begin construction during the applicable year. |

| |

| (b) | ITC is limited to 10% for projects not placed in service before January 1, 2024. |

RPS, currently in place in certain states and territories, require electricity providers in the state or territory to meet a certain percentage of their retail sales with energy from renewable sources. Additionally, other states in the U.S. have set renewable energy goals to reduce GHG emissions from historic levels. NEP believes that these standards and goals will create incremental demand for renewable energy in the future. See Environmental Matters - Regulation of GHG Emissions below for a further discussion.

Government incentives at the provincial level continue to drive the growth of renewable energy in Canada. Provincial governments have been supportive of renewable energy in general, and wind energy in particular, through renewable energy targets and incentive plans.

BUSINESS STRATEGY

NEP's primary business objective is to invest in contracted clean energy projects that allow it to increase its cash distributions to the holders of its common units over time. To achieve this objective, NEP intends to execute the following business strategy:

| |

| • | Focus on contracted clean energy projects. NEP intends to focus on long-term contracted clean energy projects with newer and more reliable technology, lower operating costs and relatively stable cash flows, subject to seasonal variances, consistent with the characteristics of its portfolio. |

| |

| • | Focus on the U.S. and Canada. NEP intends to focus its investments in the U.S. and Canada, where it believes industry trends present significant opportunities to acquire contracted clean energy projects in diverse regions and favorable locations. By focusing on the U.S. and Canada, NEP believes it will be able to take advantage of NEE’s long-standing industry relationships, knowledge and experience. |

| |

| • | Maintain a sound capital structure and financial flexibility. NEP and its subsidiaries have various financing structures in place including limited recourse project-level financings, financings through the sale of differential membership interests, term loans and revolving credit facilities. NEP believes its cash flow profile, the long-term nature of its contracts and its ability to raise capital provide flexibility for optimizing its capital structure and increasing distributions. NEP intends to continually evaluate opportunities to finance future acquisitions or refinance its existing debt and seeks to limit recourse, optimize leverage, hedge exposure, extend maturities and increase cash distributions to unitholders over the long term. |

| |

| • | Take advantage of NEER’s operational excellence to maintain the value of the projects in its portfolio. NEER provides O&M, administrative and management services to NEP's projects pursuant to the MSA and other agreements. Through these agreements, NEP benefits from the operational expertise that NEER currently provides across its entire portfolio. NEP expects that these services will maximize the operational efficiencies of its portfolio. |

| |

| • | Grow NEP's business and cash distributions through selective acquisitions of operating projects or projects under construction. NEP believes the ROFO agreement and its relationship with NEE provide it with opportunities for growth through the acquisition of projects that have similar characteristics to the renewable energy projects in its portfolio. NEER has granted NEP OpCo a right of first offer on any proposed sale of the NEER ROFO projects through mid-2020. NEP intends to focus on acquiring projects in operation, maintaining a disciplined investment approach and taking advantage of opportunities to acquire additional projects from NEER and third parties in the future, which it believes will allow it to increase cash distributions to its unitholders over the long term. NEER is not required, however, to offer NEP OpCo the opportunity to purchase any of its projects, including the NEER ROFO projects. |

COMPETITION

Wholesale power generation is a capital-intensive, commodity-driven business with numerous industry participants. While NEP's renewable energy projects are currently fully contracted, NEP may compete in the future primarily on the basis of price, but also believes the green attributes of NEP's renewable energy generation assets and relationship with NEE, among other advantages discussed below, are competitive advantages. Wholesale power generation is a regional business that is highly fragmented relative to many other commodity industries and diverse in terms of industry structure. As such, there is a wide variation in terms of the capabilities, resources, nature and identity of the companies NEP competes with depending on the market. In wholesale markets, customers' needs are met through a variety of means, including long-term bilateral contracts, standardized bilateral products such as full requirements service and customized supply and risk management services.

In addition, NEP competes with other companies to acquire well-developed projects with projected stable cash flows. NEP believes its primary competitors for opportunities in North America are regulated utilities, developers, IPPs, pension funds and private equity funds.

NEP's pipeline projects face competition with respect to retaining and obtaining firm transportation contracts and compete with other pipeline companies based on location, capacity, price and reliability. The market for supply of natural gas is highly competitive, and new pipelines, storage facilities, treating facilities and facilities for related services are currently being built to serve the growing demand for natural gas.

NEP believes that it is well-positioned to execute its strategy and increase cash distributions to its unitholders over the long term based on the following competitive strengths:

Relationship with NEE. NEP believes that its relationship with NEE provides it with the following significant benefits:

| |

| • | NEE Management and Operational Expertise. NEP believes it benefits from NEE’s experience, operational excellence, cost-efficient operations and reliability. Through the MSA and other agreements with NEE, NEP's projects will receive the same benefits and expertise that NEE currently provides across its entire portfolio. |

| |

| • | NEE Project Development Track Record and Pipeline. NEP believes that NEE’s long history of developing, owning and operating renewable energy projects provides NEP with a competitive advantage in North America. |

Contracted projects with stable cash flows. The contracted nature of NEP's portfolio supports expected stable long-term cash flows. NEP's portfolio is composed of renewable energy projects with approximately 2,926 MW of capacity and pipeline projects with approximately 3 Bcf per day of capacity under firm transportation contracts. The renewable energy projects are fully contracted under long-term contracts that generally provide for fixed price payments subject to annual escalation over the contract term. Revenues from the pipeline projects are primarily generated from firm transportation contracts based on the fixed amount of capacity reserved by the counterparties. The renewable energy projects and pipeline projects have a total weighted average remaining contract term, based on forecasted contributions to earnings, of approximately 18 years as of December 31, 2016.

New, well-maintained portfolio. NEP's portfolio includes renewable energy projects that have on average, based on contributions to earnings, been operating for fewer than five years. Additionally, approximately 85% of NEP's pipeline projects (on a capacity-weighted basis) have been operating for fewer than five years. Because NEP's renewable energy portfolio is relatively new and uses what NEP believes is industry-leading technology, NEP believes that it will achieve the expected levels of availability and performance without incurring unexpected operating and maintenance costs.

Geographic and resource diversification. NEP's portfolio is geographically diverse across the U.S. and Canada. In addition, NEP's portfolio includes both wind and solar electric generating facilities, as well as natural gas pipeline operations. A diverse portfolio tends to reduce the magnitude of individual project or regional deviations from historical resource conditions, providing a more stable stream of cash flows over the long term than a non-diversified portfolio. In addition, NEP believes the geographic diversity of the portfolio helps minimize the impact of adverse regulatory conditions in any one jurisdiction.

Competitiveness of renewable energy. Renewable energy technology has improved and installation costs have declined meaningfully in recent years. Wind technology has improved as a result of taller towers, longer blades and more efficient energy conversion equipment, which allow wind projects to more efficiently capture wind resource and produce more energy. Solar technology is also improving as solar cell efficiencies improve and installation costs decline.

REGULATION

NEP's operations are subject to regulation by a number of U.S. federal, state and other organizations, including, but not limited to, the following:

| |

| • | the FERC, which oversees the acquisition and disposition of generation, transmission and other facilities, transmission of electricity and natural gas in interstate commerce and wholesale purchases and sales of electric energy, among other things; |

| |

| • | the NERC, which, through its regional entities, establishes and enforces mandatory reliability standards, subject to approval by the FERC, to ensure the reliability of the U.S. electric transmission and generation system and to prevent major system blackouts; |

| |

| • | the EPA, which has the responsibility to maintain and enforce national standards under a variety of environmental laws. The EPA also works with industries and all levels of government, including federal and state governments, in a wide variety of voluntary pollution prevention programs and energy conservation efforts; |

| |

| • | various agencies in Texas, which oversee safety, environmental and certain aspects of rates and transportation related to the pipeline projects; and |

| |

| • | the Pipeline and Hazardous Material Safety Administration and Texas Railroad Commission's Pipeline Safety Division, which, among other things, oversee the safety of natural gas pipelines. |

NEP and its affiliates are also subject to federal and provincial or regional regulations in Canada related to energy operations, energy markets and environmental standards. In Canada, activities related to owning and operating wind and solar projects and participating in wholesale and retail energy markets are regulated at the provincial level. In Ontario, for example, electricity generation facilities must be licensed by the Ontario Energy Board and may also be required to complete registrations and maintain market participant status with the IESO, in which case they must agree to be bound by and comply with the provisions of the market rules for the Ontario electricity market as well as the mandatory reliability standards of the NERC.

NEP is subject to environmental laws and regulations, and is affected by the issues described in the Environmental Matters section below.

ENVIRONMENTAL MATTERS

NEP's operations are required to comply with various environmental, health and safety laws and regulations in each of the jurisdictions in which it operates. These existing and future laws and regulations may impact existing and new projects and may require NEP to obtain and maintain permits and approvals, comply with all environmental laws and regulations applicable within each jurisdiction and implement environmental, health and safety programs and procedures to monitor and control risks associated with the construction, operation and decommissioning of regulated or permitted energy assets, all of which involve a significant investment of time and resources. The following is a discussion of certain existing initiatives and rules, some of which could potentially have a material effect (either positive or negative) on NEP and its subsidiaries.

Avian/Bat Regulations and Wind Turbine Siting Guidelines. NEP is subject to numerous environmental regulations and guidelines related to threatened and endangered species and their habitats, as well as avian and bat species, for the ongoing operations of its facilities. The environmental laws in the U.S., including, among others, the Endangered Species Act, the Migratory Bird Treaty Act, and the Bald and Golden Eagle Protection Act and similar environmental laws in Canada (the Species at Risk Act, the Migratory Birds Convention Act and the Endangered Species Act of 2007) provide for the protection of migratory birds, eagles and bats and endangered species of birds and bats and their habitats. Regulations have been adopted under some of these laws that contain provisions that allow the owner/operator of a facility to apply for a permit to undertake specific activities, including those associated with certain siting decisions, construction activities and operations. In addition to regulations, voluntary wind turbine siting guidelines established by the U.S. Fish and Wildlife Service set forth siting, monitoring and coordination protocols that are designed to support wind development in the U.S. while also protecting both birds and bats and their habitats. These guidelines include provisions for specific monitoring and study conditions which need to be met in order for projects to be in adherence with these voluntary guidelines. Complying with these environmental regulations and adhering to the provisions set forth in the voluntary wind turbine siting guidelines could result in additional costs or reduced revenues at existing and new wind and solar facilities and transmission and distribution facilities at NEP and, in the case of environmental regulations, failure to comply could result in fines and penalties.

Regulation of GHG Emissions. The U.S. Congress and certain states and regions, as well as the Government of Canada and its provinces, have taken and continue to take certain actions, such as proposing and finalizing regulation or setting targets and goals, regarding the reduction of GHG emissions and the increase of renewable energy generation. In 2015, the EPA's final rule under Section 111(d) of the Clean Air Act (Clean Power Plan) to reduce carbon emissions from existing fossil fuel-fired electric generation units became effective. Numerous parties challenged the Clean Power Plan and, in February 2016, the U.S. Supreme Court issued an order staying implementation of the Clean Power Plan pending resolution of legal challenges to the rule. The U.S. Court of Appeals for the District of Columbia Circuit heard oral arguments in September 2016 and a decision is pending. The timing and ultimate outcome of the Clean Power Plan are uncertain at this time. Other GHG reduction initiatives including, among others, the Regional Greenhouse Gas Initiative and the California Greenhouse Gas Regulation, aim to reduce emissions through a variety of programs currently in place and periodically undergo review and revision.

EMPLOYEES

NEP does not have any officers or employees and relies solely on officers and employees of NEP GP and NEP GP's affiliates, including NEE and NEER. See further discussion of the MSA and other payments to NEE in Note 11.

WEBSITE ACCESS TO SEC FILINGS

NEP makes its SEC filings, including the annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and any amendments to those reports, available free of charge on NEP's internet website, www.nexteraenergypartners.com, as soon as reasonably practicable after those documents are electronically filed with or furnished to the SEC. The information and materials available on NEP's website are not incorporated by reference into this Form 10-K. The SEC maintains an internet website that contains reports, proxy and information statements, and other information regarding registrants that file electronically with the SEC at www.sec.gov.

Item 1A. Risk Factors

Limited partnership interests are inherently different from shares of capital stock of a corporation, although many of the business risks to which NEP is subject are similar to those that would be faced by a corporation engaged in similar businesses and NEP has elected to be treated as a corporation for U.S. federal income tax purposes. If any of the following risks were to occur, NEP's business, financial condition, results of operations and ability to make cash distributions to its unitholders could be materially and adversely affected. In that case, it may not be able to pay distributions to its unitholders, the trading price of its common units could decline and investors could lose all or part of their investment in NEP.

Operational Risks

NEP has a limited operating history and its projects include renewable energy projects that have a limited operating history. Such projects may not perform as expected.

NEP's portfolio includes renewable energy projects that have, on average, been operating for fewer than five years. In addition, NEP expects that many of the renewable energy projects that it may acquire, including, but not limited to, NEER ROFO projects, will not have commenced operations, will have recently commenced operations or otherwise will have a limited operating history. As a result, the assumptions and estimates regarding the performance of these projects are and will be made without the benefit of a meaningful operating history. The ability of NEP's projects that have a limited operating history to perform as expected will also be subject to risks inherent in newly constructed energy projects, including, but not limited to, equipment performance below NEP's expectations, unexpected component failures and product defects, and generation and transmission system failures and outages. The failure of some or all of the projects to perform as expected could have a material adverse effect on NEP's business, financial condition, results of operations and ability to make cash distributions to its unitholders.

NEP's ability to make cash distributions to its unitholders is affected by wind and solar conditions at its renewable energy projects.

The amount of energy that a wind project can produce depends on wind speeds, air density, weather and equipment, among other factors. If wind speeds are too low, NEP's wind projects may not perform as expected or may not be able to generate energy at all and, if wind speeds are too high, the wind projects may have to shut down to avoid damage. As a result, the output from NEP's wind projects can vary greatly as local wind speeds and other conditions vary. Similarly, the amount of energy that a solar project is able to produce depends on several factors, including, but not limited to, the amount of solar energy that reaches its solar panels. Wind turbine or solar panel placement, interference from nearby wind projects or other structures and the effects of vegetation, snow, ice, land use and terrain also affect the amount of energy that NEP's wind and solar projects generate. If wind, solar, meteorological, topographical or other conditions at NEP's wind or solar projects are less conducive to energy production, NEP's projects may not produce the amount of energy NEP expects. The failure of some or all of NEP's projects to perform according to NEP's expectations could have a material adverse effect on its business, financial condition, results of operations and ability to make cash distributions to its unitholders.

NEP's business, financial condition, results of operations and prospects can be materially adversely affected by weather conditions, including, but not limited to, the impact of severe weather.

Weather conditions directly influence the demand for electricity, natural gas and other fuels and affect the price of energy and energy-related commodities. In addition, severe weather and natural disasters, such as hurricanes, tornadoes, floods, icing events and earthquakes, can be destructive and cause power outages and property damage, reduce revenue, affect the availability of water, and require NEP to incur additional costs. Furthermore, NEP's physical plants could be placed at greater risk of damage should changes in the global climate produce unusual variations in temperature and weather patterns, resulting in more intense, frequent and extreme weather events and abnormal levels of precipitation. A disruption or failure of electric generation, transmission or distribution systems or natural gas production, transmission, storage or distribution systems in the event of a hurricane, tornado or other severe weather event, or otherwise, could prevent NEP from operating its business in the normal course and could result in

any of the adverse consequences described above. Any of the foregoing could have a material adverse effect on NEP's business, financial condition, results of operations and ability to make cash distributions to its unitholders.

Severe weather, natural disasters or meteorological conditions could damage or require NEP to shut down its turbines, solar panels, pipelines or other equipment or facilities (including, but not limited to, generation transmission tie lines). Such damage or a shutdown could impede NEP's ability to operate its projects, or decrease its energy production levels, pipeline transportation capability and revenues. To the extent these conditions equate to a force majeure event under NEP's PPAs, the renewable energy contract counterparty may terminate such PPAs if such a force majeure event continues for a period ranging from 12 months to 36 months, as specified in the applicable PPA. These conditions could also damage or reduce the useful life of interconnection and transmission facilities of a project or of third parties relied upon by NEP's projects and increase maintenance costs. For example, certain NEP projects are located in an area of California that has experienced substantial seismic activity, the reoccurrence of which could cause significant physical damage to facilities and the surrounding energy transmission infrastructure. Replacement and spare parts for solar panels, wind turbines and key pieces of equipment may be difficult or costly to acquire or may be unavailable. In certain instances, NEP's renewable energy projects would be unable to sell energy until a replacement part is installed. If NEP experiences a prolonged interruption at one of its renewable energy projects or pipelines, energy production or gas transportation capability would decrease. Production of less energy than expected, or the ability to transport natural gas at less than expected levels due to these or other conditions, could reduce NEP's revenues, which could have a material adverse effect on its business, financial condition, results of operations and ability to make cash distributions to its unitholders.

Changes in weather can also affect the production of electricity at NEP's power generating facilities. For example, the level of wind resource affects the revenue produced by wind generating facilities. Because the levels of wind and solar resources are variable and difficult to predict, NEP’s results of operations for individual wind and solar facilities specifically, and NEP's results of operations generally, may vary significantly from period to period, depending on the level of available resources. To the extent that resources are not available at planned levels, the financial results from these facilities may be less than expected.

NEP may fail to realize expected profitability or growth, and may incur unanticipated liabilities, as a result of the Texas pipelines acquisition.

There are a number of risks and uncertainties relating to the Texas pipelines acquisition, including, but not limited to, the failure to realize expected profitability or growth; the incurrence of liabilities or other compliance costs related to environmental or regulatory matters, including potential liabilities that may be imposed without regard to fault or the legality of conduct; and the incurrence of unanticipated liabilities and costs for which insurance or indemnification is unavailable or inadequate. If these risks or other unanticipated liabilities were to materialize, any desired benefits of the Texas pipelines acquisition may not be fully realized, if at all, and the Texas pipelines acquisition could accordingly have a material adverse effect on NEP's ability to grow its business and make cash distributions to its unitholders.

NEP is pursuing the expansion of natural gas pipelines in its portfolio that will require up-front capital expenditures and expose NEP to project development risks.

NEP is pursuing the expansion of natural gas pipelines in its portfolio. The development of pipeline expansion projects involves numerous regulatory, environmental, construction, safety, political and legal uncertainties and may require the expenditure of significant amounts of capital. These projects may not be completed on schedule, at the budgeted cost or at all. There may be cost overruns and construction difficulties. In addition, NEP may agree to pay liquidated damages to committed shippers if an expansion project does not achieve commercial operations before a specified date that the parties may agree to in advance. Any cost overruns NEP experiences or liquidated damages NEP pays could have a material adverse effect on NEP's business, financial condition, results of operations and ability to make cash distributions to its unitholders. In addition, NEP may choose to finance all or a portion of the development costs of any expansion project through the sale of additional common units, which could result in dilution to NEP’s unitholders. Moreover, NEP's revenues may not increase immediately upon the expenditure of funds on a significant expansion project, or at all. If NEP undertakes an expansion of one of the pipelines in the portfolio, the construction may occur over an extended period of time and NEP will not receive material increases in revenues until the project is placed in service. Accordingly, if NEP pursues expansion projects, NEP's efforts may not result in additional long-term contracted revenue streams that increase the amount of cash available to execute NEP's business plan and make cash distributions to its unitholders.

NEP's ability to maximize the productivity of the Texas pipeline business and to complete potential pipeline expansion projects is dependent on the continued availability of natural gas production in the Texas pipelines’ areas of operation.

The natural gas pipelines in NEP's portfolio have more capacity available than is under long-term firm transport contracts. Low prices for natural gas could adversely affect development of additional natural gas reserves and production that is accessible by the Texas pipelines’ assets. Production from existing wells and natural gas supply basins with access to the Texas pipelines’ transmission systems will naturally decline over time. The amount of natural gas reserves underlying these wells may also be less than anticipated, and the rate at which production from these reserves declines may be greater than anticipated. Additionally, the competition for natural gas supplies to serve other markets could reduce the amount of natural gas supply for its customers or low natural gas prices could cause producers to determine in the future that drilling activities in areas outside of the current areas of operation of the Texas pipelines are strategically more attractive to them. A reduction in the natural gas volumes supplied by producers could make it more challenging to increase the amount of the Texas pipelines’ capacity that is under long-term firm transport contracts

or that shippers otherwise pay to use or have access to the pipeline capacity, and it may decrease the likelihood that NEP will continue to pursue some or all of the potential pipeline expansion projects NEP is pursuing. Any of these events could have a material adverse effect on NEP's business, financial condition, results of operations and ability to make cash distributions to its unitholders.

Operation and maintenance of renewable energy projects involve significant risks that could result in unplanned power outages, reduced output, personal injury or loss of life.

There are risks associated with the operation of NEP's renewable energy projects. These risks include:

| |

| • | breakdown or failure of, or damage to, turbines, blades, blade attachments, solar panels, mirrors and other equipment, which could reduce a project’s energy output or result in personal injury or loss of life; |

| |

| • | catastrophic events, such as fires, earthquakes, severe weather, tornadoes, ice or hail storms,other meteorological conditions, landslides and other similar events beyond NEP's control, which could severely damage or destroy all or a part of a project, reduce its energy output or result in personal injury or loss of life; |

| |

| • | technical performance below expected levels, including, but not limited to, the failure of wind turbines, solar panels, mirrors and other equipment to produce energy as expected due to incorrect measures of expected performance provided by equipment suppliers; |

| |

| • | increases in the cost of operating the projects, including, but not limited to, costs relating to labor, equipment, insurance and real estate taxes; |

| |

| • | operator or contractor error or failure to perform; |

| |

| • | serial design or manufacturing defects, which may not be covered by warranty; |

| |

| • | extended events, including, but not limited to, force majeure, under certain PPAs that may give rise to a termination right of the customer under such a PPA (renewable energy counterparty); |

| |

| • | failure to comply with permits and the inability to renew or replace permits that have expired or terminated; |

| |

| • | the inability to operate within limitations that may be imposed by current or future governmental permits; |

| |

| • | replacements for failed equipment, which may need to meet new interconnection standards or require system impact studies and compliance that may be difficult or expensive to achieve; |

| |

| • | land use, environmental or other regulatory requirements; |

| |

| • | disputes with the BLM, other owners of land on which NEP's projects are located or adjacent landowners; |

| |

| • | changes in law, including, but not limited to, changes in governmental permit requirements, corporate income tax laws, regulations and policies and international trade laws, regulations, agreements, treaties and policies of the U.S. or other countries; |

| |

| • | government or utility exercise of eminent domain power or similar events; and |

| |

| • | existence of liens, encumbrances and other imperfections in title affecting real estate interests. |

These and other factors could require NEP to shut down its wind or solar projects. These factors could also degrade equipment, reduce the useful life of interconnection and transmission facilities and materially increase maintenance and other costs. Unanticipated capital expenditures associated with maintaining or repairing NEP's projects may reduce profitability.

In addition, replacement and spare parts for solar panels, wind turbines and other key equipment may be difficult or costly to acquire or may be unavailable. Each solar and wind project may require a specific design for certain critical equipment and, if it does not have acceptable spare equipment available, the project would need to order replacements with potentially lengthy order lead times.

Such events or actions could significantly decrease or eliminate the revenues of a project, significantly increase its operating costs, cause a default under NEP's financing agreements or give rise to damages or penalties to a renewable energy contract counterparty, another contractual counterparty, a governmental authority or other third parties or cause defaults under related contracts or permits. Any of these events could have a material adverse effect on NEP's business, financial condition, results of operations and ability to make cash distributions to its unitholders.

Portions of NEP’s pipeline systems have been in service for several decades. There could be unknown events or conditions or increased maintenance or repair expenses and downtime associated with NEP's pipelines that could have a material adverse effect on NEP's business, financial condition, results of operations, liquidity and ability to make distributions.

Portions of NEP’s transmission system and its gathering system have been in service for several decades. The age and condition of NEP’s systems could result in increased maintenance or repair expenditures, and any downtime associated with increased maintenance and repair activities could materially reduce NEP’s revenue. Any significant increase in maintenance and repair expenditures or loss of revenue due to the age or condition of NEP’s systems could adversely affect NEP's business, financial condition, results of operations, liquidity and NEP's ability to make cash distributions to its unitholders.

Natural gas gathering and transmission activities involve numerous risks that may result in accidents or otherwise affect the Texas pipelines’ operations.

There are a variety of hazards and operating risks inherent in natural gas gathering and transmission activities, such as leaks, explosions, mechanical problems, activities of third parties, including, but not limited to, the possibility of terrorist acts, and damage

to pipelines, facilities and equipment caused by hurricanes, tornadoes, floods, fires and other natural disasters, that could cause substantial financial losses. In addition, these risks could result in significant injury, loss of life, significant damage to property, environmental pollution and impairment of operations, any of which could result in substantial losses. For pipeline assets located near populated areas, including, but not limited to, residential areas, commercial business centers, industrial sites and other public gathering areas, the level of damage resulting from these risks could be greater. Therefore, should any of these risks materialize, it could have a material adverse effect on NEP's business, financial condition, results of operations and ability to make cash distributions to its unitholders.

The wind turbines at some of NEP's projects and some of NEER's ROFO projects are not generating the amount of energy estimated by their manufacturers’ original power curves, and the manufacturers may not be able to restore energy capacity at the affected turbines.

Wind turbine generators for certain of NEP's projects are not generating the amount of energy they should be according to the turbine manufacturer’s original power curves. In addition, NEP has been advised that the wind turbine generators of certain NEER ROFO projects are not generating the amount of energy they should be according to the turbine manufacturer’s original power curves. NEP expects that the turbine manufacturer will undertake a combination of modifications to improve the electricity generation to within the manufacturer's guaranteed levels with respect to certain affected turbines. NEP does not expect that the energy generation with respect to the remaining affected turbines will be able to be restored to within guaranteed levels, although NEP expects some incremental improvements.

Although NEP's projections assume that these efforts will restore or incrementally improve the energy generation of the affected turbines as described above, the proposed efforts may fail to restore the energy generation as expected, if at all, or these or other turbines may experience additional energy generation deficiencies. The occurrence of any of these events could have a material adverse effect on NEP's business, financial condition, results of operations and ability to make cash distributions to its unitholders.

NEP depends on the Texas pipelines and certain of the renewable energy projects in its portfolio for a substantial portion of its anticipated cash flows.

NEP depends on the Texas pipelines and certain of the renewable energy projects in its portfolio for a substantial portion of its anticipated cash flows. For example, in the most recently completed fiscal year, the Texas pipelines and Genesis provided a significant portion of NEP’s net income plus interest expense, income tax expense and depreciation and amortization expense. Consequently, the impairment or loss of any one or more of those projects or pipelines could materially and, depending on the relative size of the affected projects or pipelines, disproportionately reduce NEP’s cash flows and, as a result, have a material adverse effect on NEP's business, financial condition, results of operations and ability to make cash distributions to its unitholders.

Terrorist or similar attacks could impact NEP's projects, pipelines or surrounding areas and adversely affect its business.

Terrorists have attacked energy assets such as substations and related infrastructure in the past and may attack them in the future. Any attacks on NEP’s projects, pipelines or the facilities of third parties on which its projects or pipelines rely could severely damage such projects or pipelines, disrupt business operations, result in loss of service to customers and require significant time and expense to repair. Additionally, energy-related facilities, such as substations and related infrastructure, are protected by limited security measures, in most cases only perimeter fencing. Projects and pipelines in NEP's portfolio, as well as projects or pipelines it may acquire and the transmission and other facilities of third parties on which NEP's projects rely, may also be targets of terrorist acts and affected by responses to terrorist acts, each of which could fully or partially disrupt the ability of NEP's projects or pipelines to operate.

Cyber-attacks, including, but not limited to, those targeting information systems or electronic control systems used to operate NEP's energy projects (including, but not limited to, generation transmission tie lines) and the transmission and other facilities of third parties on which NEP's projects rely, could severely disrupt business operations and result in loss of service to customers and significant expense to repair security breaches or system damage. As cyber incidents continue to evolve, NEP may be required to expend additional resources to continue to modify or enhance NEP's protective measures or to investigate and remediate any vulnerability to cyber incidents.

To the extent terrorist attacks or other similar acts equate to a force majeure event under NEP's PPAs, the renewable energy counterparty may terminate such PPAs if such a force majeure event continues for a period ranging from 12 months to 36 months, as specified in the applicable agreement. As a result, a terrorist act or similar attack could significantly decrease revenues or result in significant reconstruction or remediation costs, any of which could have a material adverse effect on NEP's business, financial condition, results of operations and ability to make cash distributions to its unitholders.

The ability of NEP to obtain insurance and the terms of any available insurance coverage could be materially adversely affected by international, national, state or local events and company-specific events, as well as the financial condition of insurers. NEP's insurance coverage does not insure against all potential risks and it may become subject to higher insurance premiums.

NEP is exposed to numerous risks inherent in the operation of wind and solar projects and natural gas pipelines, including, but not limited to, equipment failure, manufacturing defects, natural disasters, terrorist attacks, sabotage, vandalism and environmental risks. The occurrence of any one of these events may result in NEP being named as a defendant in lawsuits asserting claims for substantial damages, including, but not limited to, environmental cleanup costs, personal injury, property damage, fines and penalties. Further, with respect to any future acquisitions of any projects that are under construction or development, NEP is, or will be, exposed to risks inherent in the construction or development of these projects.

NEP shares insurance coverage with NEE and its affiliates, for which NEP reimburses NEE. NEE currently maintains liability insurance coverage for itself and its affiliates, including NEP, which covers legal and contractual liabilities arising out of bodily injury, personal injury or property damage, including, but not limited to, resulting loss of use, to third parties. NEE also maintains coverage for itself and its affiliates, including NEP, for physical damage to assets and resulting business interruption, including, but not limited to, damage caused by terrorist acts. However, such policies do not cover all potential losses and coverage is not always available in the insurance market on commercially reasonable terms. To the extent NEE or any of its affiliates experiences covered losses under the insurance policies, the limit of NEP's coverage for potential losses may be decreased.

NEE may also reduce or eliminate such coverage at any time. NEP may not be able to maintain or obtain insurance of the type and amount NEP desires at reasonable rates and NEP may elect to self-insure some of its wind and solar projects and natural gas pipelines. The insurance coverage NEP does obtain may contain large deductibles or fail to cover certain risks or all potential losses. In addition, insurance coverage may not continue to be available or may not be available at rates or on terms similar to those presently available to NEE. NEE’s insurance policies are subject to annual review by its insurers and may not be renewed on similar or favorable terms, including, but not limited to, coverage, deductibles or premiums, or at all. The ability of NEE to obtain insurance and the terms of any available insurance coverage could be materially adversely affected by international, national, state or local events and company-specific events, as well as the financial condition of insurers. If insurance coverage is not available or obtainable on acceptable terms, NEP may be required to pay costs associated with adverse future events. A loss for which NEP is not fully insured could have a material adverse effect on NEP's business, financial condition, results of operations and ability to make cash distributions to its unitholders.

Warranties provided by the suppliers of equipment for NEP's projects may be limited by the ability of a supplier to satisfy its warranty obligations, or by the terms of the warranty, so the warranties may be insufficient to compensate NEP for its losses.

NEP expects to benefit from various warranties, including, but not limited to, product quality and performance warranties, provided by suppliers in connection with the purchase of equipment necessary to operate its projects. NEP's suppliers may fail to fulfill their warranty obligations. Even if a supplier fulfills its obligations, the warranty may not be sufficient to compensate NEP for all of its losses. In addition, these warranties generally expire within two to five years after the date each equipment item is delivered or commissioned and are subject to liability limits. If installation is delayed, NEP may lose all or a portion of the benefit of a warranty. If NEP seeks warranty protection and a supplier is unable or unwilling to perform its warranty obligations, whether as a result of its financial condition or otherwise, or if the term of the warranty has expired or a liability limit has been reached, there may be a reduction or loss of warranty protection for the affected equipment, which could have a material adverse effect on NEP's business, financial condition, results of operations and ability to make cash distributions to its unitholders.

Supplier concentration at certain of NEP's projects may expose it to significant credit or performance risks.