| | | | | |

| PROSPECTUS SUPPLEMENT NO. 7 | Filed pursuant to Rule 424(b)(3) |

| (To prospectus dated July 9, 2024) | Registration No. 333-280341 |

TALEN ENERGY CORPORATION

36,825,683 SHARES OF COMMON STOCK

This prospectus supplement is being filed to update and supplement the information contained in the prospectus dated July 9, 2024, as supplemented by Prospectus Supplement No. 1, dated August 13, 2024, Prospectus Supplement No. 2, dated November 14, 2024, Prospectus Supplement No. 3, dated December 13, 2024, Prospectus Supplement No. 4, dated December 20, 2024, Prospectus Supplement No. 5, dated January 7, 2025, and Prospectus Supplement No. 6, dated January 11, 2025 (as so supplemented, the “Prospectus”), with the information contained in our Annual Report on Form 10-K, filed with the Securities and Exchange Commission (the “SEC”) on February 27, 2025 (the “Annual Report”). Accordingly, we have attached the Annual Report to this prospectus supplement.

The Prospectus and this prospectus supplement relate to the resale from time to time of up to 36,825,683 shares of our common stock, par value $0.001 per share (the “Common Stock”), by the selling stockholders named in the Prospectus or their permitted transferees.

This prospectus supplement updates and supplements the information in the Prospectus and is not complete without, and may not be delivered or utilized except in combination with, the Prospectus, including any other amendments or supplements thereto. This prospectus supplement should be read in conjunction with the Prospectus, and if there is any inconsistency between the information in the Prospectus and this prospectus supplement, you should rely on the information in this prospectus supplement. The information in this prospectus supplement modifies and supersedes, in part, the information in the Prospectus. Any information in the Prospectus that is modified or superseded shall not be deemed to constitute a part of the Prospectus except as modified or superseded by this prospectus supplement.

You should not assume that the information provided in this prospectus supplement or the Prospectus is accurate as of any date other than their respective dates. Neither the delivery of this prospectus supplement and Prospectus, nor any sale made hereunder, shall under any circumstances create any implication that there has been no change in our affairs since the date of this prospectus supplement or that the information contained in this prospectus supplement or the Prospectus is correct as of any time after the date of that information.

The Common Stock is listed on The Nasdaq Global Select Market (“Nasdaq”) under the symbol “TLN”. On February 27, 2025, the last sale price of the Common Stock as reported on Nasdaq was $201.82 per share.

Investing in our securities involves certain risks, including those that are described in the sections entitled “Risk Factors” beginning on page 19 of the Prospectus, as updated and supplemented by the section entitled “Risk Factors” beginning on page 12 of the Annual Report (which is attached to this prospectus supplement).

Neither the SEC nor any state securities commission has approved or disapproved of the securities to be issued under the Prospectus or determined if the Prospectus or this prospectus supplement is truthful or complete. Any representation to the contrary is a criminal offense.

The date of this prospectus supplement is February 28, 2025.

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| | | | | |

| ☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2024

OR

| | | | | |

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from __________ to __________

Commission File Number: 001-37388

Talen Energy Corporation

(Exact name of registrant as specified in its charter)

| | | | | |

| Delaware | 47-1197305 |

| (State or other jurisdiction of incorporation or organization) | (IRS Employer Identification No.) |

2929 Allen Pkwy, Suite 2200, Houston, TX 77019

(Address of principal executive offices) (Zip Code)

(888) 211-6011

(Registrant’s telephone number, including area code)

Not applicable

(Former name, former address and former fiscal year, if changed since last report)

Securities registered pursuant to Section 12(b) of the Act:

| | | | | | | | | | | | | | |

| Title of each class | | Trading Symbol(s) | | Name of each exchange on which registered |

| Common stock, par value $0.001 per share | | TLN | | The Nasdaq Global Select Market |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| ☒ | Large accelerated filer | ☐ | Accelerated filer | ☐ | Non-accelerated filer | ☐ | Smaller reporting company | ☐ | Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☐

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant's executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court. Yes ☐ No ☒

The aggregate market value of the voting and non-voting common equity held by non-affiliates of the registrant was approximately 5.9 billion as of June 28, 2024, the last business day of the registrant’s most recently completed second fiscal quarter, based on 53254954 shares then outstanding at the OTCQX closing price of 111 per share.

As of February 27, 2025, the registrant had 45,961,910 shares outstanding of common stock, par value $0.001 per share (“common stock”).

Documents Incorporated by Reference

The information required pursuant to Part III of this Form 10-K will be set forth in, and incorporated by reference from, the registrant’s definitive proxy statement for the 2025 annual meeting of stockholders (the “2025 Proxy Statement”), which will be filed with the Securities and Exchange Commission not later than 120 days after the end of the fiscal year ended December 31, 2024.

TALEN ENERGY CORPORATION

ANNUAL REPORT ON FORM 10-K

Capitalized terms and abbreviations used but not defined in this Annual Report on Form 10-K are defined in the glossary.

CAUTIONARY NOTE REGARDING FORWARD-LOOKING INFORMATION

This Annual Report (this “Report”) contains forward-looking statements concerning expectations, beliefs, plans, objectives, goals, strategies, and (or) future performance or other events, as well as underlying assumptions and other statements, that are not statements of historical fact. These statements often include words such as “believe,” “expect,” “anticipate,” “intend,” “plan,” “estimate,” “target,” “project,” “forecast,” “seek,” “will,” “may,” “should,” “could,” “would,” or similar expressions. Although we believe that the expectations and assumptions reflected in these forward-looking statements are reasonable, there can be no assurance that these expectations and assumptions will prove to be correct. Forward-looking statements are subject to many risks and uncertainties. The results, events, or circumstances reflected in forward-looking statements may not be achieved or occur, and actual results, events, or circumstances may differ materially from those discussed in forward-looking statements.

The risks, uncertainties, and other factors that could cause actual results to differ materially from the forward-looking statements made by us include those discussed in this Report, including but not limited to “Item 1A. Risk Factors.” Moreover, we operate in a very competitive and rapidly changing environment. New risks and uncertainties emerge from time to time, and it is not possible for us to predict all risks and uncertainties that could have an impact on the forward-looking statements contained in this Report.

You should not rely on forward-looking statements as predictions of future events. We have based the forward-looking statements contained in this Report primarily on our current expectations and assumptions about future events. Furthermore, statements such as “we believe” and similar statements reflect our beliefs and opinions on the relevant subject. These statements are based on information available to us as of the date of this Report. While we believe such information provides a reasonable basis for these statements, such information may be limited or incomplete, and there can be no assurance that any expectations, assumptions, beliefs, or opinions will prove to be correct. Our statements should not be read to indicate that we have conducted an exhaustive inquiry into, or review of, all relevant information. These statements are inherently uncertain, and readers are cautioned not to unduly rely on these statements.

The forward-looking statements made in this Report relate only to events as of the date on which the statements are made. We undertake no obligation to update any forward-looking statements made in this Report to reflect events or circumstances after the date of this Report or to reflect new information, actual results, revised expectations, or the occurrence of unanticipated events, except as required by law. We may not actually achieve the plans, intentions, or expectations described in our forward-looking statements, and you should not place undue reliance on our forward-looking statements. Our forward-looking statements do not reflect the potential impact of any future acquisitions, mergers, dispositions, joint ventures, or investments.

MARKET AND INDUSTRY DATA

This Report includes estimates regarding market and industry data. Unless otherwise indicated, information concerning our industry and the markets in which we operate, including our general expectations, market position, market opportunity, and market size, are based on our management’s knowledge and experience in the markets in which we operate, together with currently available information obtained from various sources, including publicly available information, industry reports and publications, surveys, our customers, trade and business organizations, and other contacts in the markets in which we operate. Certain information is based on management estimates, which have been derived from third-party sources, as well as data from our internal research.

In presenting this information, we have made certain assumptions that we believe to be reasonable based on such data and other similar sources and on our knowledge of, and our experience to date in, the markets in which we operate. While we believe the estimated market and industry data included in this Report is generally reliable, such information is inherently uncertain and imprecise. Market and industry data is subject to change and may be limited by the availability of raw data, the voluntary nature of the data gathering process, and other limitations inherent in any statistical survey of such data. In addition, projections, assumptions, and estimates of the future performance of the markets in which we operate are necessarily subject to uncertainty and risk due to a variety of factors, including those described in “Cautionary Note Regarding Forward-Looking Information” and “Item 1A. Risk Factors.” These and other factors could cause results to differ materially from those expressed in the estimates made by third parties and by us. Accordingly, you are cautioned not to place undue reliance on such market and industry data or any other such estimates.

PART I.

ITEM 1. BUSINESS

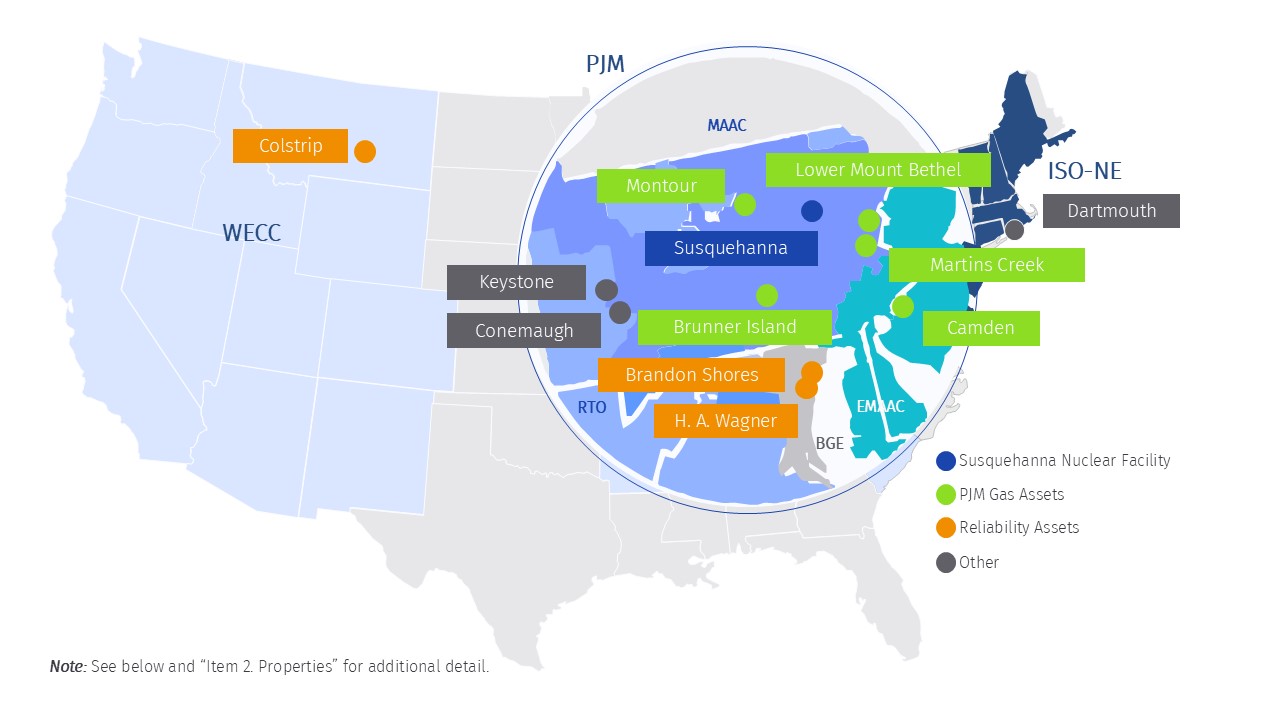

Talen is a leading independent power producer and energy infrastructure company dedicated to powering the future. We own and operate approximately 10.7 gigawatts of power infrastructure in the United States, including 2.2 gigawatts of nuclear power and a significant dispatchable generation fleet. We produce and sell electricity, capacity, and ancillary services into wholesale U.S. power markets, with our generation fleet principally located in the Mid-Atlantic and Montana. Our team is committed to generating power safely and reliably, delivering the most value per megawatt produced and driving the energy transition. Talen is also powering the digital infrastructure revolution. We are well-positioned to capture this significant growth opportunity, as data centers serving artificial intelligence increasingly demand more reliable, clean power.

Our Operations

Our Fleet

The following discussion provides a brief overview of our fleet. See “Item 2. Properties” for additional information on each of our facilities.

Baseload, carbon-free nuclear facility. We operate, and own a 90 interest in, the 2.5 GW Susquehanna facility, the sixth largest nuclear-powered generation facility in the U.S. Susquehanna typically comprises approximately half of our total annual generation. In 2024, Talen produced over 18 GWh of reliable, zero-carbon power from Susquehanna at a low all-in cost of less than $24 per MWh, while also maintaining excellent safety and operational performance (when measured by standards adopted by the nuclear industry). Susquehanna’s efficient cost structure is supported in part by a portfolio of supply contracts for all stages of the nuclear fuel cycle. See “—Fuel Supply—Nuclear” for additional information. Susquehanna’s two units are currently licensed through 2042 and 2044, respectively (with up to 20-year extensions possible with regulatory approval).

Susquehanna has historically generated revenues primarily from energy sales into the PJM wholesale market, PJM capacity sales, and strategic hedging. As part of the AWS Data Campus Sale in 2024, Susquehanna and AWS have contracted under the AWS PPA for the long-term, fixed-price supply of power directly from Susquehanna to the adjacent AWS Data Campus. See Note 20 to the Annual Financial Statements for additional information on the AWS Data Campus Sale and “—Our Key Markets and Revenue Streams—Contracted Revenues—AWS PPA” for additional information on the AWS PPA. Susquehanna also benefits from the Nuclear PTC included under the Inflation Reduction Act, which runs through 2032 and provides a tax credit of up to 44 per MW (indexed to inflation) for power produced from a nuclear generation source. See “—Our Key Markets and Revenue Streams—Nuclear PTC” for additional information on the Nuclear PTC.

Dispatchable natural gas and oil intermediate and peaking units. Our 6.3 GW natural gas and oil fleet (of which 3.2 GW is from Brunner Island, Montour, and H.A Wagner Unit 3 after conversion, as discussed below) includes seven technologically diverse natural gas and oil generation facilities across the generation stack (including intermediate and peaking dispatch). Certain units are capable of utilizing multiple fuel sources, providing meaningful operational flexibility. These strategically located assets include significant generation in attractive wholesale markets (primarily PJM), allowing them to generate predictable revenues on cleared capacity while also benefiting from varying market dynamics. See “Item 2. Properties” for additional information on each of these facilities.

Reliability assets and carbon deleveraging. Our coal-fired generation assets continue to be impacted by changing environmental regulations and power market economics. We have already completed the conversion of approximately 3.2 GW of our legacy coal fleet to lower-carbon fuels, including our Brunner Island and Montour facilities, which together represent over 25 of our total generation capacity, and Unit 3 of our H.A Wagner facility. We previously requested deactivation of both H.A Wagner and our wholly-owned 1.3 GW Brandon Shores facility in mid-2025. However, PJM subsequently notified us that both H.A Wagner and Brandon Shores are needed past their previously planned retirement dates to maintain reliability in PJM. In January 2025, we reached a settlement (which remains subject to FERC approval) with key stakeholders to continue running both facilities through May 2029 under an RMR arrangement. See “—Our Key Markets and Revenue Streams—Contracted Revenues—Brandon Shores and H.A Wagner RMR Arrangements” and Note 10 to the Annual Financial Statements for additional information on the RMR proceedings and settlement. We also own minority interests, totaling approximately 800 MW, in three coal-fired generation facilities in PJM and WECC, and we are exploring ways to maximize the value of these assets in the context of changing market conditions. See “Item 2. Properties” for additional information on each of these facilities.

Our Key Markets and Revenue Streams

Our operating revenues have historically consisted primarily of capacity revenues, energy/ancillary services revenues, and unrealized gain (loss) on hedging instruments. As further discussed below, we sell capacity and energy through a combination of forward auctions, bilateral contracts, and spot market sales (as applicable). See “—Our Strategies—Optimize risk management program and hedging” for a discussion of our commercial optimization strategy. Beginning in mid-2025, we expect our Brandon Shores and H.A. Wagner facilities to begin operating as reliability resources under an RMR agreement that will provide fixed payments to Talen in addition to reimbursement for certain costs and expenses. In addition, our Susquehanna facility is party to the AWS PPA for the supply of power from Susquehanna to AWS through long-term, fixed-price power commitments that increase over time. See “—Contracted Revenues” for additional information on both the RMR arrangements and the AWS PPA. We continue to evaluate business opportunities resulting from industrial load growth. See “—Demand Growth from Multiple Sources” for additional information. We also benefit from the Nuclear PTC under the Inflation Reduction Act. See “—Nuclear PTC” for additional information.

Wholesale Markets

The substantial majority of our generation capacity is located in, and accordingly the majority of our revenues are derived from, PJM. Specifically, a majority of our generation capacity (over 10 GW) is located in the MAAC (Mid-Atlantic Area Council) and BGE (Baltimore Gas and Electric) regions of PJM. The remainder of our generation capacity is in ISO-NE and WECC. See “Item 2. Properties” for additional information on the market location of each of our facilities.

PJM. PJM is an RTO responsible for the operation of wholesale electric markets and for centrally dispatching electric systems in all or parts of 13 states and the District of Columbia. It coordinates the dispatch of approximately 180000 MW of generating capacity to more than 65 million people and operates wholesale electricity markets with approximately 1090 members. Generators in PJM may earn revenues from sales of capacity, energy, and (or) ancillary services.

The PJM Reliability Pricing Model is intended to ensure that resources are available when needed for grid reliability. Under this model, PJM conducts a series of forward capacity auctions, which establish a long-term market for capacity. We sell capacity through PJM Base Residual Auctions and, to the extent we are unable to sell capacity through the PJM BRAs, we may sell uncleared capacity through PJM Incremental Auctions or bilateral capacity transactions. PJM BRAs are typically conducted three years prior to the start of the applicable capacity year (which runs from June 1–May 31), but FERC has recently accepted requests by PJM to delay certain PJM BRAs in order to propose additional changes to the PJM Reliability Pricing Model. See “Item 1A. Risk Factors—Regulatory, Environmental, and Legal Risks—We could be impacted by changes in, or state interference with, the structure or operation of the markets in which we operate, including ongoing market restructuring in PJM.” and Note 12 to the Annual Financial Statements for additional information on ongoing market reforms in PJM and related auction delays. PJM also operates day-ahead and real-time markets into which generators can bid to provide energy and ancillary services. We sell energy/ancillary services into these markets. We also enter into bilateral transactions for the sale of energy directly to power purchasers.

ISO-NE. ISO-NE is an ISO that manages the flow of electricity from approximately 30000 MW of generation capacity to approximately 15 million people in all or part of six states in New England. ISO-NE conducts forward capacity auctions and operates day-ahead and real-time energy/ancillary services markets. In ISO-NE, we both earn capacity revenues and sell energy/ancillary services into the spot markets from our Dartmouth generating facility.

WECC. WECC is a non-profit corporation that promotes a reliable and secure bulk electric system in the Western Interconnection, covering all or parts of Montana, 13 other U.S. States, Canada, and Mexico. WECC does not operate energy or capacity markets. The Colstrip facility in Montana operates within NorthWestern’s Balancing Authority within WECC. We enter into bilateral transactions for the direct sale of energy from our portion of the generation from Colstrip.

Contracted Revenues

Brandon Shores and H.A Wagner RMR Arrangements. In 2023, we notified PJM of our intent to deactivate electric generation at both our Brandon Shores and H.A. Wagner facilities on June 1, 2025. However, PJM subsequently notified us that both Brandon Shores and H.A Wagner are needed past their previously planned retirement dates to maintain reliability in PJM. In January 2025, we reached a settlement (which remains subject to FERC approval) with key stakeholders on the terms of an RMR arrangement and filed with FERC the resulting Joint Offers of Settlement regarding both facilities’ RMR Continuing Operations Rates Schedules (the “CORS”). If approved, the proposed RMR arrangements will extend the operating life of these plants through May 31, 2029, or until such time as the necessary transmission upgrades are placed into service. Beginning June 1, 2025, the CORS will provide a monthly fixed-cost payment of 12083333 (312/MW-day) for Brandon Shores and 2916667 (137/MW-day) for H.A Wagner, which includes a performance “hold back” of 416667 per month for Brandon Shores and 208333 per month for H.A Wagner, each to be paid out based on unit performance. We will also receive separate reimbursement for variable costs and approved project investments. See Note 10 to the Annual Financial Statements for additional information on the RMR proceedings and settlement.

AWS PPA. In connection with the AWS Data Campus Sale in 2024, we and AWS entered into the AWS PPA, pursuant to which we agreed to supply long-term, carbon-free power from Susquehanna to the AWS Data Campus through fixed-price power commitments. Under the AWS PPA, AWS has minimum contractual power commitments that increase in 120 MW increments annually (or earlier, at AWS’s option), with a one-time option to either cap commitments at 480 MW or otherwise purchase, in continuing annual steps, up to 960 MW. Each step up in capacity commitment has a fixed price for an initial 10-year term, after which AWS has the option to renew each step at a price that includes a fixed margin above then-applicable PJM energy and capacity prices. The initial term of the AWS PPA is 18 years, with two 10-year extensions at AWS’s option. Under a separate agreement, we will receive additional revenue from AWS related to the sales of carbon-free energy to the grid. We expect to begin receiving initial revenues from power sales in 2025. See Note 20 to the Annual Financial Statements for additional information on the AWS Data Campus Sale.

In November 2024, FERC issued an order denying the Susquehanna ISA Amendment between PJM, PPL Corporation, and Susquehanna that would permit Susquehanna to decrease the amount of power supply it would otherwise provide to the power grid. Such order does not have an impact on the existing ISA permitting 300 MW of co-located load at Susquehanna to supply power for the first phases of the AWS Data Campus. In December 2024, FERC issued an order stating that it would address our request for rehearing in a future order, which FERC has not yet issued. Due to FERC’s decision not to address the merits of our motion for rehearing, we have filed an appeal in the U.S. Court of Appeals for the Fifth Circuit. Delivery “behind-the-meter” of more than 300 MW of power under the AWS PPA requires that FERC approve an amended ISA between Susquehanna, PPL, and PJM. Without an amendment we will be unable to deliver the full amount of contract volume under the AWS PPA on a behind-the-meter basis, which may require a contract renegotiation to deliver the additional power “in-front-of-the-meter.” We are evaluating our commercial and legal options to provide the most efficient path to full development of the AWS Data Campus. Such options include, but are not limited to, potential submission of a revised form of Susquehanna ISA Amendment or alternative contract structures with AWS. See “Item 3. Legal Proceedings” and “Item 1A. Risk Factors—Regulatory, Environmental, and Legal Risks—Our business is subject to extensive energy-related regulation and oversight.” for additional information on the Susquehanna ISA Amendment.

Demand Growth from Multiple Sources

Power demand forecasts continue to rise over time in PJM compared to previous expectations. In January 2025, PJM released updated long-term load forecasts which point to RTO-wide load in summer 2030 and 2035 that is approximately 10 and 17 higher, respectively, than 2024 expectations. Fundamental demand growth in PJM is expected to come from multiple sources, most notably high-performance computing and data center demand, continued re-shoring in the wake of the COVID-19 pandemic and associated supply chain disruptions, and continued electrification of the U.S. economy. This demand growth is not currently well matched with increases in supply, as the PJM queue for new-build generation is predominately intermittent rather than dispatchable in nature. In addition, continued PJM coal plant retirements are expected through the end of the decade. These drivers of demand have had, and could continue to have, direct impacts on the overall supply/demand balance and resulting energy and capacity prices in the markets in which we operate, the profitability, value, and growth prospects of our business, and the regulatory framework under which we operate.

Nuclear PTC

The Inflation Reduction Act was signed into law in August 2022. Among the Act’s provisions are amendments to the Internal Revenue Code to create a nuclear production tax credit program. The Nuclear PTC program provides qualified nuclear power generation facilities with a transferable tax credit for electricity produced and sold to an unrelated party during each tax year. The credit provides support beginning when annual gross receipts decline below an equivalent 44/MWh, increases ratably up to $3/MWh when annual gross receipts are equivalent to 25/MWh, and is subject to potential adjustments including inflation escalators and a five-times increase in value (up to $15/MWh) for meeting prevailing wage requirements (which we expect to meet). Electricity produced and sold by Susquehanna to third parties from December 31, 2023 through December 31, 2032 will be eligible for the credit. This program serves as an important tool for mitigating power price exposure, effectively creating a minimum price that Susquehanna is expected to receive for its generation. We can monetize the credit by reducing our income taxes payable or selling the credits to a third-party. See Notes 6 and 7 to the Annual Financial Statements for additional information on Nuclear PTC revenue recognized and the Inflation Reduction Act.

Fuel Supply

Our power generation assets are advantaged by significant fuel diversity, including nuclear, natural gas, coal, oil, and various dual-fuel capabilities. Further, our natural gas generation assets are situated near the Marcellus shale region of Pennsylvania, which provides access to fuel from one of the largest producing natural gas regions in the U.S. See “Item 2. Properties” for additional information on the fuel capabilities of each of our facilities.

Nuclear. Susquehanna has a portfolio of supply contracts for raw uranium, conversion, enrichment, and fabrication. Our nuclear fuel cycle is fully contracted through the 2027 fuel load, almost entirely contracted through 2028, and over 70 contracted through 2029. We have no current fuel exposure to any Russian-affiliated counterparties. Susquehanna has an on-site dry-cask spent fuel storage facility that, together with its spent fuel pools, accommodates discharged SNF. We expect to continue expanding this storage facility in phases to accommodate additional SNF and, assuming receipt of appropriate approvals, we expect such expansion to accommodate all of the SNF discharged by Susquehanna through 2044, the current license life of unit 2. Federal law requires the U.S. government to provide for the permanent disposal of commercial SNF, but the government has not yet done so. Consequently, under a related settlement agreement, the government is required to reimburse Susquehanna for certain SNF storage costs through 2025. See Note 12 to the Annual Financial Statements for additional information on this arrangement.

Natural Gas and Oil. We manage our natural gas and oil supply utilizing a combination of contracted purchases, spot market purchases, and on-site storage for the commodities and pipeline capacity. The amount and duration of contracted purchases vary due to factors including fuel availability, economic considerations, and generation facility location on the pipeline grid. A significant portion of our natural gas need is satisfied through short-term transactions on a spot basis. Oil is generally supplied from on-site inventory and replenished through purchases on the spot market. The price risk associated with these transactions is managed via financial hedges.

Coal. We actively manage our coal requirements by purchasing coal from central and northern Appalachia for our PJM facilities and from a mine adjacent to Colstrip for that facility. Reliability of coal deliveries can be affected from time to time by a number of factors, including fluctuations in demand, coal mine production issues, and other supplier or transporter operating difficulties. We maintain coal inventory at levels estimated to be necessary to avoid operational disruptions at our coal-fired units. Short- and long-term supply contracts support adequate coal inventory levels and are augmented with spot market purchases as needed.

Seasonality/Scheduled Maintenance

The demand for and market prices of electricity and natural gas are affected considerably by weather and, as a result, our operating results may fluctuate significantly on a seasonal basis. In general, below-average temperatures in the winter and above-average temperatures in the summer tend to increase electricity demand, energy prices, and revenues. Alternatively, moderate temperatures tend to decrease electricity demand and may adversely affect resulting energy margins, particularly in PJM. In addition, our operating expenses typically fluctuate geographically on a seasonal basis, with peak power generation and expenses during the winter in the Mid-Atlantic. We ordinarily perform planned facility maintenance during milder non-peak demand periods in the spring and fall to ensure reliability during peak periods. The pattern of fluctuations in our operating results varies depending on the type and location of the facilities being serviced, the capacity markets served, the maintenance requirements of our facilities, and the terms of bilateral contracts to purchase or sell electricity. Our largest recurring maintenance project is the annual spring refueling outage at Susquehanna. We serve our fossil generation fleet through a combination of self-service and contracted maintenance activity (including long-term service agreements at certain facilities). See also “Item 1A. Risk Factors—Industry and Market Risks—Our business is subject to physical, market, economic, and regulatory risks relating to weather conditions and extreme weather events.”

Competition

Increased competition in U.S. energy markets exists in part due to federal and state competitive market initiatives. The power generation business is regionally varied in industry structure and fundamentals. PJM, the primary market in which we operate, is a competitive market and has from time-to-time considered new market rules, while some states have considered re-regulation measures that could result in more limited opportunities for competitive energy suppliers. See Note 12 to the Annual Financial Statements for additional information on ongoing market reforms in PJM. We face competition in wholesale markets from other suppliers of available energy, capacity, and ancillary services, which may include operators of various competing generation technologies, such as natural gas-fired, coal-fired, and nuclear generation, as well renewable and other alternative energy sources. Competition is affected by electricity and fuel prices, grid congestion, government subsidies for new and certain existing generation facilities (including some which might otherwise retire), new market entrants, construction of new generation assets, technological advances in power generation, environmental and regulatory matters, and various other factors. Competitors in wholesale power markets include other non-utility generators, regulated utilities and their competitive subsidiaries, industrial companies, financial institutions, and other energy marketers. See also “Item 1A. Risk Factors—Industry and Market Risks—We face intense competition in the competitive power generation market.” and “Item 1A. Risk Factors—Regulatory, Environmental, and Legal Risks—We could be impacted by changes in, or state interference with, the structure or operation of the markets in which we operate, including ongoing market restructuring in PJM.”

Insurance

Power generation involves hazardous activities, which could expose our assets, employees, contractors, customers, and the general public to various risks inherent in the nature of our operations. Various hazards, including but not limited to accidents or natural disasters, can cause damage or destruction of our assets or other property and equipment, personal injury or loss of life, pollution or environmental damage, and (or) suspension of operations. We maintain a portfolio of general liability, property, business interruption, pollution liability, workers’ compensation, nuclear, cybersecurity, financial lines, and other insurance policies (as applicable) with varying limits, deductibles, and self-insurance that we believe are reasonable and prudent under the circumstances to cover our operations and assets; however, we cannot provide any assurance that our insurance program will be sufficient or effective under all circumstances and against all hazards or liabilities to which we may be subject, or that insurance coverage will continue to be available at economic rates or at all. We will continue to periodically evaluate our policy limits and retentions as they relate to the overall cost and scope of our insurance program. See also “Item 1A. Risk Factors—Industry and Market Risks—Operation of power generation facilities involves significant risks and hazards customary to the power industry, which we cannot assure our insurance will be adequate to cover.,” “Item 1C. Cybersecurity,” and Note 12 to the Annual Financial Statements.

Our Strategies

We believe we are well-positioned to achieve our business objectives through the following strategies:

Focus and maintain our core generation fleet that provides stable earnings and cash flows. Our core fleet, anchored by our Susquehanna nuclear facility, generates stable earnings from cleared capacity and cash flows backed by multiple sources. Our integrated generation, wholesale marketing, and commercial capabilities enable us to produce significant recurring cash flow, and our commercial and risk management strategies provide cash flow stability while balancing operational, price, and liquidity risk through physical and financial commodity transactions. In today’s robust but volatile energy markets, our team has been able to capture high realized pricing through both reliable generation and strategic risk management. Capacity revenue is a key indicator of the important role that nuclear, natural gas, and peaking generation all play in PJM grid reliability. In 2024, our PJM fleet generated significant capacity revenues. See “Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations—Results of Operations” for additional information on our energy and capacity revenues. We are now also poised to benefit from long-term, stable cash flows from both contractual revenues under the Brandon Shores and H.A. Wagner RMR arrangements and fixed-price power sales under the AWS PPA. See “—Our Key Markets and Revenue Streams—Contracted Revenues” for additional information on both the RMR arrangements and the AWS PPA. We now also have substantive federal support for nuclear generation, which is accretive to our portfolio, in the form of the Nuclear PTC. See “—Our Key Markets and Revenue Streams—Nuclear PTC” for additional information on the Nuclear PTC.

Continue our operational excellence, with focus on continued efficiencies. The foundation of our platform is safe, disciplined operational and commercial performance. We drive operational excellence by maximizing the safety, reliability, and efficiency of our core assets. While we will continue to evaluate ways to find the highest and best use of our assets and capital, we are committed to maintaining best-in-class operations at our core generation facilities, including a disciplined cost structure across all categories. To sustain our robust performance, our leadership team focuses on, among other priorities, maximizing reliability through carefully planned and periodic maintenance and upgrades of our equipment, retaining experienced facility managers and employees and positioning them on-site to address emerging issues quickly, capitalizing on procurement efficiencies across our platform, and implementing redundancy in our generation facility design. While prioritizing operational safety and excellence, we intend to continue evaluating and executing on available opportunities for additional cost efficiencies.

Optimize risk management program and hedging. We are focused on maintaining appropriate risk management policies in the context of a right-sized balance sheet and the cash flow stability provided by the Nuclear PTC. We maintain both an internal risk management committee, comprised of members of senior management from across the organization, and a Board-level risk oversight committee, comprised of members of our Board of Directors with extensive trading and risk backgrounds. Our commercial optimization strategy is focused on hedging commodity price volatility within appropriate risk tolerances while providing stable cash flow generation and preserving forward margin. We employ a variety of physical and financial instruments to manage risk and optimize the value of our assets. In some cases, we use a portfolio approach to manage risks, such as those associated with capacity and ancillary offerings. We target a hedge range of 60-80% of our expected generation for the prompt 12 months and ratably scale the hedge percentage down further out in time to align with our financial objectives. Our strong balance sheet provides ample capacity and counterparty appetite for lien-based hedging, which limits the use of margin posting requirements. We intend to continue employing a disciplined strategy focused on first-lien hedging while minimizing exchange-based hedging and the associated margin requirements. Importantly, we now have lower overall hedging needs given the cash-flow stability afforded by the Nuclear PTC (which provides a built-in hedging apparatus through the tax credit) and significantly reduced debt service requirements following the Restructuring and subsequent refinancing transactions.

Maintain disciplined financial policy and capital allocation. We actively manage our capital structure, future capital commitments, and asset base by following disciplined capital allocation principles focused on generating cash flow, maintaining reasonable leverage, and reducing our cost of capital. We have a strong balance sheet underpinned by modest leverage, robust liquidity, and no significant debt maturities until 2030. Our strong balance sheet also provides ample capacity and counterparty appetite for lien-based hedging, which does not require cash collateral posting, and we intend to prioritize balance sheet efficiency through the active preservation of liquidity, targeting a modest leverage profile with a go-forward net leverage ratio of 3.5x or less, depending on seasonal dynamics. In furtherance of our disciplined capital allocation strategy, we are targeting the return of 70% of our adjusted free cash flow to shareholders through the share repurchase program authorized by our Board of Directors. See “Item 5. Market for Registrant’s Common Equity, Related Shareholder Matters and Issuer Purchases of Equity Securities—Issuer Purchases of Equity Securities” and Note 18 to the Annual Financial Statements for additional information on the SRP and other share repurchases.

Maximize the value of our platform opportunities in a capital efficient manner. We believe there is significant value embedded in our platform, and that we have the flexibility to explore both organic and inorganic growth options. In addition to optimizing our core operations, we have unlocked previously unrecognized value from our existing assets and believe we have more opportunities to do so. Within our generation portfolio, we remain focused on delivering the most value per megawatt produced, including through long-term power sales to computing, industrial, or other end users, whether from our reliable, zero-carbon nuclear facility - Susquehanna - or our dispatchable fossil fleet. We expect to evolve our asset base both by continuing to evaluate opportunities to drive value uplift for our existing assets and by pursuing opportunistic acquisitions and divestitures in order to drive cash flow generation and investor returns, all in keeping with our commitment to appropriate leverage levels and a thoughtful capital allocation framework. We will continue exploring strategic opportunities if economically favorable, but any strategic investment will require a sound basis and an attractive returns profile when compared to other uses of capital.

Legal, Regulatory, and Environmental Matters

Legal Matters

We are involved in various legal and administrative proceedings, investigations, claims, and litigation from time to time in the course of our business. Such matters may include, but are not limited to, those relating to employment and benefits, commercial disputes, personal injury, property damage, regulatory matters, environmental matters, and various other claims for injuries and (or) damages. While we believe we have meritorious positions and will continue to appropriately respond to all legal matters, because of the inherently unpredictable nature of legal proceedings, there is a wide range of potential outcomes for any such matter. See “Item 1A. Risk Factors—Regulatory, Environmental, and Legal Risks” for additional information on legal risks related to our business. See “Item 3. Legal Proceedings” and Note 12 to the Annual Financial Statements for additional information on specific legal matters.

Energy Regulation

We are subject to regulation by federal and state agencies and other bodies that exercise regulatory authority in the various regions where we conduct business, including but not limited to FERC; the Department of Energy; the NRC; NERC; the Federal Communications Commission; and state public utility commissions. In addition, the RTOs and ISOs in the regions in which we conduct business inherently have complex rules that are intended to balance the interests of market stakeholders. See “Item 1A. Risk Factors—Regulatory, Environmental, and Legal Risks” for additional information on regulatory risks related to our business. The following discussion provides an overview of certain key regulatory matters applicable to our business. See Note 12 to the Annual Financial Statements for additional information on these and other regulatory topics.

FERC. Our subsidiaries that own or control electric generation facilities are defined as public utilities under the Federal Power Act and are subject to FERC’s exclusive ratemaking jurisdiction over wholesale sales of electricity and the transmission of electricity in interstate commerce. FERC has the authority to grant or deny market-based rate authority for wholesale sales of energy, capacity, and ancillary services to ensure that such sales are just and reasonable and not unduly discriminatory, and to suspend market-based rate authority and set cost-based rates if it finds that its previous grant of market-based rate authority is no longer just and reasonable. Other matters subject to FERC’s jurisdiction include, but are not limited to: review of certain public utility dispositions of jurisdictional facilities, mergers, acquisitions of other public utility securities, or acquisitions of existing generation facilities; review of certain holding company acquisitions of securities of, or mergers with, a public utility or other holding company; third-party financings; affiliate transactions; intercompany financings and cash management arrangements; and certain internal corporate reorganizations.

RTOs and ISOs. RTOs and ISOs are FERC-regulated entities that exist in several regions to provide transmission service across multiple transmission systems. FERC has approved PJM, MISO, ISO-NE, and SPP as RTOs and CAISO and NYISO as ISOs. These entities are responsible for regional planning, managing transmission congestion, developing wholesale markets for energy and capacity, maintaining reliability, market monitoring, the scheduling of physical power sales brokered through ICE and NYMEX, and managing transmission charges across multiple systems. With the exception of Colstrip in Montana, all of our generation facilities currently participate in wholesale electricity markets administered by PJM and ISO-NE. See “—Our Operations—Our Key Markets and Revenue Streams—Wholesale Markets” for additional information on the RTOs and ISOs in which we operate.

Nuclear. Under the Atomic Energy Act of 1954, as amended (the “Atomic Energy Act”), our operation and 90 ownership of Susquehanna are subject to regulation by the NRC, including requirements pertaining to, among other matters: licensing, inspection, and enforcement; testing, evaluation, and modification of all aspects of nuclear reactor power generation facility design and operation; environmental and safety performance; handling and storage of SNF; technical and financial qualifications; decommissioning funding assurance; and transfer and foreign ownership restrictions. The NRC may modify, suspend, or revoke operating licenses and impose civil or criminal penalties for failure to comply with the Atomic Energy Act or the terms of nuclear operating licenses. In addition, new or amended NRC safety and regulatory requirements may give rise to additional operation and maintenance costs and capital expenditures. The current facility operating licenses for our two units at Susquehanna expire in 2042 and 2044. See Note 9 to the Annual Financial Statements for additional information on the NDT. See “—Our Operations—Fuel Supply—Nuclear” for additional information on SNF.

Other Regulation. In addition to federal regulation, our operations are subject to various state and local laws and regulations. These include oversight of siting, permitting, and environmental compliance for our facilities, as well as participation in state-specific energy markets and programs. Our operations are also subject to compliance with reliability standards developed and enforced by NERC and its regional entities. Compliance with these standards is critical to maintaining the reliability of the bulk electric system and avoiding penalties for violations. See “—Environmental Regulation” for additional information on environmental regulation of our business.

Environmental Regulation

Our business is subject to extensive federal, state, and local environmental laws, regulations, and requirements, including but not limited to those related to air emissions, water discharges, hazardous substances, and solid waste management. These requirements have become more stringent over time and impose, among other things: (i) permitting requirements for regulated activities; (ii) costs to limit or prevent pollution or other contamination; and (iii) substantial liabilities and remedial obligations for pollution or contamination. Accordingly, in the ordinary course of our business, we may: (i) incur significant costs to comply with environmental requirements; (ii) be required to modify, curtail, replace, or cease certain operations for environmental reasons; (iii) be required to perform environmental remediation work; or (iv) become involved in other environmental matters, including government enforcement actions and citizen’s suit litigation. In addition, environmental requirements are rapidly evolving, and we may become subject to new or revised environmental laws, regulations, or requirements. Legal challenges to environmental regulations, rules, and requirements add to the uncertainty of estimating future compliance and remedial costs. In addition, in January 2025, President Trump issued executive orders directing the heads of all federal agencies to identify and begin the processes to suspend, revise, or rescind all agency actions, including existing regulations, that are unduly burdensome on the identification, development, or use of domestic energy resources. Consequently, future implementation and enforcement of these rules remains uncertain at this time.

See “Item 1A. Risk Factors—Regulatory, Environmental, and Legal Risks” for additional information on environmental risks related to our business. The following discussion provides an overview of certain key environmental matters. See Note 12 to the Annual Financial Statements for additional information on these and other environmental topics.

Air. Under the Clean Air Act, as well as comparable state laws and local ordinances, our plants are subject to extensive emission control, emission allowance, emission monitoring, and air reporting obligations. Compliance with these requirements impacts the operation of our plants as well as their operating costs. In addition, new or modified obligations could significantly impact how we produce electricity and the life of certain plants (in some cases resulting in premature unit retirements) and could impede strategic planning. Key air matters currently affecting our business include, but are not limited to, nitrogen oxides requirements (including potential implementation of the EPA’s Good Neighbor Plan or similar requirements) as well as the revised EPA MATS and GHG Rules, both of which could significantly impact certain facilities, including our Colstrip facility, and are being legally challenged by us and others.

Hazardous Substances and Waste Handling. Our business is subject to a range of waste laws and regulations at the federal, state, and local levels. These rules are designed to manage and mitigate the potential environmental and health impacts of waste generated by power plants during the production of electricity, and they put controls in place on waste disposal, management, transportation, and storage. The Comprehensive Environmental Response, Compensation, and Liability Act (“CERCLA”), also known as the “Superfund” law, and comparable state laws impose liability, without regard to fault or the legality of the original conduct, on certain classes of persons that are considered to have contributed to the release of a “hazardous substance” into the environment. These persons include the current and past owners or operators of the site where the release occurred and companies that transported or disposed, or arranged for the transport or disposal, of the hazardous substances at the site where the release occurred. Most states have also enacted statutes that contain provisions substantially similar to CERCLA. We generate materials in the course of our operations that may be regulated as hazardous substances based on their characteristics under CERCLA and analogous state laws.

The EPA’s regulation of CCRs under the Resource Conservation and Recovery Act is a currently evolving regulatory program under which we may incur significant costs impacting AROs. We have joined several parties to legally challenge the EPA’s new requirements for legacy CCR surface impoundments under the EPA CCR Rule, while also following the Rule’s timeline to assess applicability and define cost impacts to our business.

Water. Various statutes and regulations at the federal, state, regional, and local levels govern water use, discharge, protection, and influence and add challenge and uncertainty to our business. The Federal Water Pollution Control Act, known as the Clean Water Act (“CWA”), and comparable state laws impose restrictions and strict controls regarding the discharge of pollutants into federal and state waters. The discharge of pollutants into regulated waters is prohibited except in accordance with the terms of a permit issued by the EPA or a state equivalent agency. Compliance with existing and future requirements may increase costs, affect operations, and impede strategic planning. One of the most impactful CWA programs currently affecting our business is the EPA ELG Rule, under which certain of our generation facilities have incurred operating restrictions and committed to prematurely end the use of certain fuels. In the future, new permit conditions could be established to meet the EPA’s most recent revisions to the EPA ELG Rule, which will be defined following negotiations with state permitting authorities. We and other parties are legally challenging the EPA’s latest revisions to the EPA ELG Rule. Until litigation is complete and permit conditions are established, full cost impacts remain uncertain.

Health and Safety. We are also subject to the requirements of the federal Occupational Safety and Health Act and comparable state laws that regulate the protection of the health and safety of employees. In addition, the Occupational Health and Safety Administration's (“OSHA”) hazard communication standard, the Emergency Planning and Community Right to Know Act and implementing regulations and similar state statutes and regulations require us to maintain information about hazardous materials used or produced in our operations, and this information is required to be provided to employees, state and local government authorities, and citizens.

Corporate Responsibility

Through our core values of Excellence, No Harm, Integrity, and Continuous Improvement, we are committed to operating thoughtfully and ethically as we strive to consider impacts to our stakeholders, including communities, employees, customers, suppliers, investors, and the environment. Our approach to corporate responsibility, with oversight from our Board of Directors, is a key to the long-term success of our business.

Environmental

Our emission profile is firmly anchored by Susquehanna, which enabled us to generate over half of our electricity output carbon-free in 2024, and our natural gas portfolio also includes a number of energy-efficient assets with low heat rates, which provide a lower carbon intensity than traditional fossil fuel sources. We have reduced our environmental footprint over the past several years, investing heavily in environmental controls and switching to cleaner fuels in response to market and other conditions. We have already completed the conversion of our Brunner Island, Montour, and H.A. Wagner plants to lower-carbon fuels. See “—Our Fleet—Reliability assets and carbon deleveraging” for additional information.

As of December 31, 2024, we have reduced our annual carbon dioxide emissions by approximately 65 when compared to 2010 levels. We expect to continue reducing our carbon footprint through the recently-completed conversions of our legacy coal fleet discussed above and the eventual retirement of certain other legacy coal assets. See Note 10 to the Annual Financial Statements for additional information on ongoing RMR proceedings and a pending settlement related to our Brandon Shores and H.A. Wagner facilities. As we retire older, economically nonviable conventional power generation assets, we are continuing to explore opportunities to repurpose these sites to advance our carbon deleveraging while also extending the life and increasing the value of our legacy assets.

We are an innovator in the movement to power critical infrastructure and industry with carbon-free nuclear generation. Prior to its sale to AWS, we initially developed the data center campus adjacent to our Susquehanna facility, the world’s first 24x7 carbon-free, direct-connect data center campus, to provide digital infrastructure powered by generation from Susquehanna. We are well-positioned to continue leading the energy transition by responsibly providing zero- and low-carbon power to meet growing demand from energy consumers in a variety of sectors, many of whom have sustainability requirements.

Community Engagement

We generally focus our community engagement and philanthropic efforts in the local communities we serve and where our employees live and work. We believe that a decentralized approach to engagement and giving allows us to more effectively identify areas of need and have a greater local impact. Across our fleet and our corporate offices, our facilities and their employees, often in conjunction with charitable organizations such as United Way, Salvation Army, and local food banks, we strive to participate regularly in events supplying holiday toys, school supplies, food, winter coats, volunteer work, and monetary donations. For instance, to date, events hosted by Susquehanna have raised over $1.1 million for the Berwick Area United Way. Our plants also provide community education through both on-site and off-site programs and events with first responders, professional organizations, students, interns, scouts, and other groups. The majority of our operating facilities also provide nature preserves or other recreational sites that allow for community activities such as golf, fishing and boating, walking and hiking, outdoor education, sports, and other events.

Our business also provides significant support to the communities in which we operate in the form of critical services, high-quality jobs, economic development, and tax dollars. We have adopted a Supplier Code of Conduct (available on our website) to promote safe, ethical, and socially-conscious behavior among our suppliers. Throughout 2024, we worked with all stakeholders to reach an arrangement for the continued operation of our Brandon Shores and H.A. Wagner facilities past their initially planned retirement dates to support grid reliability in the greater Baltimore area. In January 2025, we reached a settlement (which remains subject to FERC approval) with key stakeholders to continue running both facilities through May 2029 under an RMR arrangement. The continued operation of these facilities maintains critical infrastructure, facilitates reliable electricity in Baltimore, and protects Maryland consumer electricity rates. See “—Our Key Markets and Revenue Streams—Contracted Revenues—Brandon Shores and H.A Wagner RMR Arrangements” and Note 10 to the Annual Financial Statements for additional information on the RMR proceedings and settlement.

We believe the emerging data economy and the growing importance of artificial intelligence and continued re-shoring will require an all-of-the-above approach to generating the electricity necessary to power load in a responsible and efficient manner. Our AWS PPA is an example of how we are powering the future in partnership with data center and artificial intelligence enterprises and, in the case of the AWS PPA, doing so with large volumes of clean, carbon-free energy. We are actively engaged in the policy discussions taking place between generators, PJM, political leaders, and consumer advocates to solve burgeoning resource adequacy issues and seek to ensure the availability of affordable and reliable power in the regions we serve.

Human Capital

We strive to maintain a culture that empowers our employees to influence operational decisions and to trust and rely on each other, while driving safety, operational excellence, and strong financial performance. We believe our people are a valuable asset. As key stakeholders in our business, we invest in our employees by prioritizing their safety, presenting numerous training and development opportunities, carefully considering employee feedback, offering competitive compensation that includes our employees in the success of our business, providing comprehensive health and wellness benefits, and fostering an inclusive and respectful workplace.

Safety. At Talen, safety is a core value. We strive for a “No Harm” culture for all our employees, suppliers, guests, and communities, and we strive to continuously improve our systems, processes, and communications to support the safe operation of our business. Our safety management system focuses on four key components: Safety Policy, Risk Management, Safety Assurance, and Promotion. Within our safety management framework, we take a decentralized approach to health and safety coupled with centralized reporting, information sharing, and oversight. This empowers our business units and operating plants to determine the most appropriate health and safety procedures, training, engagement, and incident resolution at their sites while facilitating knowledge sharing, enabling continuous improvement, and fostering a “No Harm” culture across our organization.

We track and (or) externally report OSHA recordable incidents, lost time injuries, and near miss incidents to enhance knowledge sharing and organizational learning. In 2024, we had seven OSHA recordable incidents and an OSHA Total Recordable Incident Rate (“TRIR”) of 0. Our overall safety performance is a result of an enhanced health and safety framework and training, increased leadership visibility and accountability, and a greater focus on incident reporting, including near misses and good catches. Our safety team reviews several proactive metrics to mitigate risks before they become safety incidents. All employees and contractors are required to immediately report all safety-related incidents and have a responsibility to stop work when there is a safety concern. Once a “stop work” situation has been identified, a corrective plan must be developed and the safety team determines a path to continue work. Prior to resumption of work, a supervisor or manager that is “one step removed” must review and concur with the plan to continue work. Susquehanna has an additional corrective action Employee Concerns Program that establishes procedures for reporting and resolving nuclear safety and general work environment concerns.

We continuously work to improve safety. In 2022, we implemented an annual Safety Assessment Program, under which safety professionals from across the organization inspect plants with a focus on workplace inspections, work observations, and regulatory compliance. Other recent safety enhancements have included improvements to our overall safety management system, as well as the addition of a company-wide safety summit, a strain/sprain program, a supervisor safety assessment program, and a human performance management program. We believe these initiatives will continue to support our strong safety culture. Our safety management system allows frequent analysis of all aspects of safety for continuous monitoring and improvement, and has been key to our safety performance in 2024.

Training, Development, and Feedback. We recognize that our success depends on our ability to attract, retain, motivate, and develop qualified personnel, and we strive to provide our employees with the tools they need to succeed personally and professionally. We provide training programs covering a wide range of relevant job- and Company-specific topics for employees in all positions, including continuing education resources for professional licenses, and we also regularly promote and train interested employees into new roles. To train the next generation of professionals, we offer apprenticeship programs, internships, and educational assistance. To further develop promising leadership across our organization, we offer programs such as the Talen Leadership Academy and the Union Leader Academy, which are seminars covering a variety of business, operational, leadership, and interpersonal skills.

Formal and informal feedback at Talen runs in all directions. In addition to this feedback, non-union employees annually receive a formal review to discuss their performance, development, and goals. Coaching and performance improvement plans are used when appropriate. We strive to thoughtfully consider and respond to ideas and feedback from all employees, including plant management teams, asset managers, and frontline workers, and we provide a variety of avenues for employee feedback, including through performance review dialogue, appropriate escalation of informal feedback, and various identifiable and anonymous formal reporting channels. In 2024, we conducted an anonymous employee engagement survey and, after reviewing the results, reported key themes and next steps to employees. We have already implemented a number of specific employee recommendations.

Compensation, Benefits, and Wellness. We are committed to maintaining a highly competitive compensation structure. We maintain short-term and long-term cash incentive programs for many employees, as well as a long-term equity compensation program that aligns the interests of key team members with our strategy and the interests of our stockholders. Starting in 2025, we also offer an employee stock purchase program, under which eligible employees can purchase our common stock at a discount through payroll deductions. Full- and part-time employees also qualify for our 401(k) plan, under which we make fixed, matching, and (or) additional discretionary contributions (depending on employment specifics).

We maintain a comprehensive benefits program, under which eligible employees and their dependents are offered healthcare coverage, life and accident insurance, short- and long-term disability, maternity and parental leave, and (or) identity theft protection. To further support employee wellness, we also offer virtual health screenings, diabetes management programs, and reduced pricing on specialty medications. All employees are also eligible for our employee assistance program, which provides mental and physical health resources and discounts on essentials such as childcare, education, and insurance, among other things.

Collective Bargaining Agreements. As of December 31, 2024, we had 1894 full-time employees, approximately 43 of which were represented by labor unions. Our collective bargaining agreements (“CBAs”) include: (i) a CBA with IBEW Local 1638, covering 193 Talen Montana employees, which is in effect until April 2026; (ii) a CBA with Teamsters Local 190, covering six Talen Montana employees, which is in effect until August 2027; and (iii) a CBA with IBEW Local 1600, covering 626 Pennsylvania employees, which is in effect until August 2025. We maintain generally constructive relationships with our labor unions.

Governance

We are committed to maintaining corporate governance policies and practices that support the interests of all our stakeholders. Our values of Excellence, No Harm, Integrity, and Continuous Improvement help foster a culture of robust governance from the Board of Directors and officers to each employee. Additional information about our corporate governance will be set forth in the 2025 Proxy Statement.

Emergence from Restructuring

Increased collateral posting requirements caused by rapid and sustained increases to wholesale natural gas and power prices in mid-2021 resulted in lower available cash and liquidity to operate our business. As a result, TES and 71 of its subsidiaries commenced the Restructuring in May 2022 and TEC joined the Restructuring in December 2022. The Company emerged from the Restructuring in May 2023 with a significantly deleveraged balance sheet. See Notes 3 and 4 to the Annual Financial Statements for additional information on the Restructuring.

Corporate and Other Available Information

We are a Delaware corporation with our principal executive office located at 2929 Allen Parkway, Suite 2200, Houston, TX 77019. The telephone number for our principal executive office is (888) 211-6011. We maintain a website at www.talenenergy.com. Information contained on or accessible from our website is not, and shall not be deemed to be, incorporated by reference into this Report or any other filings with the Securities and Exchange Commission (the “SEC”).

We file our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and any amendments to those reports with the SEC. You may obtain copies of these documents, free of charge, on the SEC's website at www.sec.gov. In addition, as soon as reasonably practicable after such materials are filed or furnished with the SEC, we make copies available free of charge on the “Investor Relations” section of our website at https://ir.talenenergy.com. We also post important information, including press releases, investor presentations, and notices of upcoming events on our website, and utilize it as a channel for distributions to public investors and for disclosing material non-public information in compliance with Regulation FD. Investors may be notified of postings to our website by signing up for email alerts under the “Resources” tab on the “Investor Relations” section of our website.

ITEM 1A. RISK FACTORS

You should carefully read and consider all the risks and uncertainties described below, as well as the other information included in this Report, including the Annual Financial Statements. Although we believe the following discussion includes the key risks affecting our business, new risks and uncertainties emerge from time to time, and it is not possible for us to predict all risks and uncertainties that could have an impact on our business. The occurrence of any of the following risks, or additional risks and uncertainties not presently known to us or that we currently believe to be immaterial, could materially and adversely affect our business, financial condition, results of operations, cash flows, and (or) liquidity.

Industry and Market Risks

We may be adversely impacted by changes in the market prices, availability, and transmission of electricity, fuel, and other commodities.

Market prices for electricity, capacity, ancillary services, natural gas, uranium, coal, and fuel oil are unpredictable and fluctuate substantially over relatively short periods. Market prices for electricity are particularly volatile due to the inability to store electricity in large quantities (requiring it to be used as it is produced), which can result in significant price fluctuations based on supply and demand imbalances in the day-ahead and real-time markets. Because natural gas facilities often serve as the marginal, price-setting generating units, there is a strong positive correlation between the price of natural gas and the wholesale market price of electricity in the competitive power markets in which we operate. In recent years, the market price of natural gas has experienced substantial volatility, while prices for other fuels have also varied. Our energy margin is influenced by the relationship between the prices of electricity and natural gas and, to a lesser extent, other fuels like coal and uranium. A decline, or significant volatility, in the price of natural gas or other fuels could negatively impact energy margin and energy revenues.

Additionally, we purchase some of our fuel and other consumables such as water, lime, limestone, and other chemicals and sorbents on a short-term or spot market basis. Delivery of these products to our facilities depends on available transportation infrastructure and available shipping capacity. In certain market conditions, transportation costs to our facilities may be significant and fluctuate substantially. Accordingly, as the prices for our fuels, other consumables, and transportation fluctuate, the price we can obtain for the sale of electricity may not rise similarly or at all to match any increase in our costs. Any inability to obtain supply or delivery of necessary fuel or other products could impair our ability to operate our facilities profitably or at all.

Our business is subject to physical, market, economic, and regulatory risks relating to weather conditions and extreme weather events.

Because weather can influence actual and expected electricity demand, as well as current and future prices of electricity and fuel, mild or unexpected weather conditions could have an adverse effect on our business. Our operations are substantially concentrated in PJM, where sustained cold weather during the winter and sustained hot weather during the summer generally result in increased market demand and higher prices for electricity. Conversely, mild winter or summer temperatures in the Mid-Atlantic tend to suppress electric demand and may result in lower overall settled prices that reduce our energy margin. Additionally, extreme weather events or sustained mild weather could result in market conditions that generate substantial gains or losses. For example, certain market and operating conditions may require us to purchase electricity in the wholesale market during periods of unusually high prices to meet our supply obligations or to sell electricity in the wholesale market during periods of low prices.

The effects of storms, floods, and other climatic events could disrupt our operations and cause us to incur significant costs in preparing for or responding to these effects. These or other meteorological changes could lead to increased operating costs, capital expenses, or power purchase costs. Such climatic events could also affect the availability of a secure and economical water supply in some locations, which is essential for the continued operation of our generation facilities.

Furthermore, under PJM’s Capacity Performance model, we may be (and have in the past been) subject to substantial monetary penalties for failing to meet the Capacity Performance requirements set forth by PJM in certain emergency events, including extreme weather events. See also “—Commercial and Operational Risks—We may experience unplanned interruptions or periods of reduced output, which could result in lower energy margin, lost opportunities, monetary penalties, contractual damages, and (or) other losses.” Extreme weather events could also result (and in the past have resulted) in governmental investigations and changes in applicable laws and regulations, reliability requirements, and market rules, including efforts to reform PJM. See also “—Regulatory, Environmental, and Legal Risks—We could be impacted by changes in, or state interference with, the structure or operation of the markets in which we operate, including ongoing market restructuring in PJM.” and “—Regulatory, Environmental, and Legal Risks—We may be affected by changes in applicable laws and regulations.”