Exhibit 99.3

MANAGEMENT’S DISCUSSION AND ANALYSIS

FOR THE YEAR ENDED

DECEMBER 31, 2018

March 6, 2019

TABLE OF CONTENTS

1 | |

2 | |

3 | |

4 | |

10 | |

11 | |

12 | |

17 | |

25 | |

30 | |

35 | |

36 | |

39 | |

Off Balance Sheet Arrangements and Related Party Transactions | 44 |

45 | |

46 | |

Disclosure Controls and Procedures and Internal Control over Financial Reporting | 46 |

49 |

MANAGEMENT’S DISCUSSION AND ANALYSIS

This Management’s Discussion and Analysis (this “MD&A”) provides a review of the results of operations, financial condition and cash flows for The Stars Group Inc. on a consolidated basis for the quarter and year ended December 31, 2018. References to “The Stars Group” or the “Corporation” in this MD&A refer to The Stars Group Inc. and its subsidiaries or any one or more of them, unless the context requires otherwise. This document should be read in conjunction with the information contained in the Corporation’s audited consolidated financial statements and related notes for the year ended December 31, 2018 (the “2018 Annual Financial Statements”), and the Corporation’s annual information form for the year ended December 31, 2018 (the “2018 Annual Information Form” and together with this MD&A and the 2018 Annual Financial Statements, the “2018 Annual Reports”). These documents and additional information regarding the business of the Corporation are available on the System for Electronic Document Analysis and Retrieval (“SEDAR”) at www.sedar.com, the Electronic Data Gathering, Analysis, and Retrieval system (“EDGAR”) at www.sec.gov, and the Corporation’s website at www.starsgroup.com.

For reporting purposes, the Corporation prepared the 2018 Annual Financial Statements in U.S. dollars and, unless otherwise indicated, in conformity with International Financial Reporting Standards (“IFRS”) as issued by the International Accounting Standards Board (“IASB”). The financial information contained in this MD&A was derived from the 2018 Annual Financial Statements. Unless otherwise indicated, all references to “USD” and “$” are to U.S. dollars, “EUR” or “€” are to European Euros, “GBP” or “£” are to British pound sterling, “CDN” or “CDN $” are to Canadian dollars and “AUD” or “AUD $” are to Australian dollars. Unless otherwise indicated, all references to a specific “note” refer to the notes to the 2018 Annual Financial Statements.

As at December 31, 2018, the Corporation had three reporting segments, “International”, “United Kingdom” and “Australia”, each with certain major lines of operations, and a “Corporate” cost center, all as further described below. The International segment currently includes the business operations of Stars Interactive Group, the United Kingdom segment currently includes the business operations of Sky Betting & Gaming, and the Australia segment currently includes the business operations of BetEasy (each as defined below). Prior quarterly and annual segmental results and information presented in this MD&A have been recast to be presented in a manner consistent with these reporting segments. See “Segment Results of Operations” below and note 7 of the 2018 Annual Financial Statements for additional information on the Corporation’s reporting segments.

As at December 31, 2018, the Corporation had up to four major lines of operations within each of its reporting segments, as applicable: real-money online poker (“Poker”), real-money online betting (“Betting”), real-money online casino and, where applicable, bingo (collectively, “Gaming”), and other gaming-related revenue, including revenue from social and play-money gaming, live poker events, branded poker rooms, Oddschecker and other nominal sources of revenue (collectively, “Other”). As it relates to these lines of operation, online revenue includes revenue generated through the Corporation’s online, mobile and desktop client platforms, as applicable.

For purposes of this MD&A: (i) the term “gaming license” refers collectively to all the different licenses, consents, permits, authorizations, and other regulatory approvals that are necessary to be obtained in order for the recipient to lawfully conduct (or be associated with) gaming in a particular jurisdiction; and (ii) unless the context requires otherwise or otherwise defined (particularly as it relates to the Gaming line of operation as used in this MD&A and the 2018 Annual Financial Statements, which currently only includes real-money online casino and, where applicable, bingo revenue), all references in this MD&A to “gaming” include all online gaming (e.g., poker, casino and bingo) and betting.

Unless otherwise stated, in preparing this MD&A the Corporation has considered information available to it up to March 6, 2019, the date the Corporation’s board of directors (the “Board”) approved the 2018 Annual Reports, including this MD&A.

1

CAUTION REGARDING FORWARD-LOOKING STATEMENTS

The 2018 Annual Reports, including this MD&A, contain certain information that may constitute forward-looking information and statements (collectively, “forward-looking statements”) within the meaning of the Private Securities Litigation Reform Act of 1995 and applicable securities laws, including financial and operational expectations and projections. These statements, other than statements of historical fact, are based on management’s current expectations and are subject to a number of risks, uncertainties, and assumptions, including market and economic conditions, business prospects or opportunities, future plans and strategies, projections, technological developments, anticipated events and trends and regulatory changes that affect the Corporation, its subsidiaries and their respective customers and industries. Although the Corporation and management believe the expectations reflected in such forward-looking statements are reasonable and are based on reasonable assumptions and estimates as at the date hereof, there can be no assurance that these assumptions or estimates are accurate or that any of these expectations will prove accurate. Forward-looking statements are inherently subject to significant business, regulatory, economic and competitive risks, uncertainties and contingencies that could cause actual events to differ materially from those expressed or implied in such statements. Forward-looking statements are often, but not always, identified by the use of words such as “seek”, “anticipate”, “plan”, “continue”, “estimate”, “expect”, “may”, “will”, “project”, “predict”, “potential”, “targeting”, “intend”, “could”, “might”, “would”, “should”, “believe”, “objective”, “ongoing”, “imply” or the negative of these words or other variations or synonyms of these words or comparable terminology and similar expressions. For example, see “Non-IFRS Measures, Key Metrics and Other Data”, “Overview and Outlook”, “Liquidity and Capital Resources” and “Recent Accounting Pronouncements”.

Specific factors and assumptions include the following: the heavily regulated industry in which the Corporation carries on its business; risks associated with interactive entertainment and online and mobile gaming generally; current and future laws or regulations and new interpretations of existing laws or regulations, or potential prohibitions, with respect to interactive entertainment or online gaming or activities related to or necessary for the operation and offering of online gaming; potential changes to the gaming regulatory framework; legal and regulatory requirements; ability to obtain, maintain and comply with all applicable and required licenses, permits and certifications to offer, operate, and market its product offerings, including difficulties or delays in the same; significant barriers to entry; competition and the competitive environment within addressable markets and industries; impact of inability to complete future or announced acquisitions or to integrate businesses successfully, including Sky Betting & Gaming and BetEasy; the Corporation’s substantial indebtedness requires that it use a significant portion of its cash flow to make debt service payments; the Corporation’s secured credit facilities contain covenants and other restrictions that may limit the Corporation’s flexibility in operating its business; risks associated with advancements in technology, including artificial intelligence; ability to develop and enhance existing product offerings and new commercially viable product offerings; ability to mitigate foreign exchange and currency risks; ability to mitigate tax risks and adverse tax consequences, including changes in tax laws or administrative policies relating to tax and the imposition of new or additional taxes, such as value-added (“VAT”) and point of consumption taxes, and gaming duties; the Corporation’s exposure to greater than anticipated tax liability; risks of foreign operations generally; protection of proprietary technology and intellectual property rights; ability to recruit and retain management and other qualified personnel, including key technical, sales and marketing personnel; defects in product offerings; losses due to fraudulent activities; management of growth; contract awards; potential financial opportunities in addressable markets and with respect to individual contracts; ability of technology infrastructure to meet applicable demand and reliance on online and mobile telecommunications operators; systems, networks, telecommunications or service disruptions or failures or cyber-attacks and failure to protect customer data, including personal and financial information; regulations and laws that may be adopted with respect to the Internet and electronic commerce or that may otherwise impact the Corporation in the jurisdictions where it is currently doing business or intends to do business, particularly those related to online gaming or that could impact the ability to provide online product offerings, including as it relates to payment processing; ability to obtain additional financing or to complete any refinancing on reasonable terms or at all; customer and operator preferences and changes in the economy; dependency on customers’ acceptance of its product offerings; consolidation within the gaming industry; litigation costs and outcomes; expansion within existing and into new markets; relationships with vendors and distributors; natural events; contractual relationships of SBG (as defined below) or the Corporation with Sky plc and/or its subsidiaries; counterparty risks; failure of systems and controls of the Corporation to restrict access to its products; reliance on scheduling and live broadcasting of major sporting events; macroeconomic conditions and trends in the gaming industry; bookmaking risks; an ability to realize projected financial increases attributable to acquisitions and the Corporation’s business strategies; and an ability to realize all or any of the Corporation’s estimated synergies and cost savings in connection with acquisitions, including the SBG Acquisition and Australian Acquisitions (each as defined below). These factors are not intended to represent a complete list of the factors that could affect the Corporation; however, these factors, as well as those risk factors presented under the heading “Risk Factors and Uncertainties” in the 2018 Annual Information Form, elsewhere in this

2

MD&A and the 2018 Annual Reports and in other filings that The Stars Group has made and may make in the future with applicable securities authorities, should be considered carefully.

The foregoing list of important factors and assumptions may not contain all the material factors and assumptions that are important to shareholders and investors. Shareholders and investors should not place undue reliance on forward-looking statements as the plans, assumptions, intentions or expectations upon which they are based might not occur. The forward-looking statements contained in this MD&A are expressly qualified by this cautionary statement. Unless otherwise indicated by the Corporation, forward-looking statements in this MD&A describe the Corporation’s expectations as at March 6, 2019, and, accordingly, are subject to change after such date. The Corporation does not undertake to update or revise any forward-looking statements to reflect events and circumstances after the date hereof or to reflect the occurrence of unanticipated events, except in accordance with applicable securities laws.

RISK FACTORS AND UNCERTAINTIES

Certain factors may have a material adverse effect on the Corporation’s business, financial condition and results of operations. Current and prospective investors should carefully consider the risks and uncertainties and other information contained in this MD&A and the 2018 Annual Reports, particularly under the heading “Risk Factors and Uncertainties” in the 2018 Annual Information Form, and in other filings that the Corporation has made and may make in the future with applicable securities authorities, including those available on SEDAR at www.sedar.com, EDGAR at www.sec.gov or The Stars Group’s website at www.starsgroup.com. The risks and uncertainties described herein and therein are not the only ones the Corporation may face. Additional risks and uncertainties that the Corporation is unaware of, or that the Corporation currently believes are not material, may also become important factors that could adversely affect the Corporation’s business. If any of such risks actually occur, the Corporation’s business, financial condition, results of operations, and future prospects could be materially and adversely affected. In that event, the trading price of the common shares of the Corporation (the “Common Shares”) (or the value of any other securities of the Corporation) could decline, and the Corporation’s securityholders could lose part or all of their investment.

3

NON-IFRS MEASURES, KEY METRICS AND OTHER DATA

This MD&A references non-IFRS financial measures and key metric operational performance measures, including those under the headings “Consolidated Results of Operations and Cash Flows”, “Segment Results of Operations”, and “Reconciliations” below. The Corporation believes these measures and metrics will provide investors with useful supplemental information about the financial and operational performance of its business, enable comparison of financial results between periods where certain items may vary independent of business performance, and allow for greater transparency with respect to key metrics used by management in operating its business, identifying and evaluating trends, and making decisions. The Corporation believes that such non-IFRS financial measures provide useful information about its underlying, core operating results and trends, enhance the overall understanding of its past performance and future prospects and allow for greater transparency with respect to metrics and measures used by management in its financial and operational decision-making.

Although management believes these non-IFRS financial measures and key metrics are important in evaluating the Corporation, they are not intended to be considered in isolation or as a substitute for, or superior to, financial information prepared and presented in accordance with IFRS. They are not recognized measures under IFRS and do not have standardized meanings prescribed by IFRS. These measures may be different from non-IFRS financial measures and key metrics used by other companies and may not be comparable to similar meanings prescribed by other companies, limiting their usefulness for comparison purposes. Moreover, presentation of certain of these measures is provided for period-over-period comparison purposes, and investors should be cautioned that the effect of the adjustments thereto provided herein have an actual effect on the Corporation’s operating results.

Non-IFRS Measures

The Corporation presents the following non-IFRS measures in this MD&A, reconciliations of which to their nearest IFRS measures are provided, as applicable, under “Reconciliations” below:

Adjusted EBITDA

The Corporation defines Adjusted EBITDA as net earnings before financial expenses, income taxes expense (recovery), depreciation and amortization, stock-based compensation, restructuring, net earnings (loss) on associate and certain other items as set out in the reconciliation tables under “Reconciliations” below.

The Corporation believes Adjusted EBITDA is a useful performance measure as it provides information regarding the Corporation’s ongoing core operating activities, and trends in underlying performance and growth, and is used by management primarily to forecast and budget the allocation of applicable resources, particularly in light of its current strategic initiatives, including its geographic and product expansion strategy.

Adjusted EBITDA Margin

The Corporation defines Adjusted EBITDA Margin as Adjusted EBITDA as a proportion of total revenue.

The Corporation believes Adjusted EBITDA Margin is a useful performance measure as it is representative of the Corporation’s ongoing core business activities and assists management in monitoring the impact of any significant change in revenue generation (e.g., as a result of geographic or product changes, sporting results, or seasonality) or costs (e.g., a change in gaming duty rates or gaming regulatory fees or costs) on the Corporation’s operating performance.

Adjusted Net Earnings

The Corporation defines Adjusted Net Earnings as net earnings before interest accretion, amortization of intangible assets resulting from purchase price allocations following acquisitions, stock-based compensation, restructuring, net earnings (loss) on associate, and certain other items. In addition, as previously disclosed, the Corporation makes adjustments for (i) the re-measurement of contingent consideration, which was previously included in, and adjusted for through, interest accretion, but starting with the Corporation’s interim condensed consolidated financial statements and related notes for the three and nine months ended September 30, 2018 (the “Q3 2018 Financial Statements”), it is a separate line item, (ii) the re-measurement of embedded derivatives and ineffectiveness on cash flow hedges, each of which were new line items in the Q3 2018 Financial Statements, and (iii) certain non-recurring tax adjustments and settlements. Each adjustment to net earnings is then adjusted for the tax impact, where applicable, in the respective

4

jurisdiction to which the adjustment relates. Adjusted Net Earnings and any other non-IFRS measures used by the Corporation that relies on or otherwise incorporates Adjusted Net Earnings that was reported for previous periods have not been restated under the updated definition on the basis that the Corporation believes that the impact of the change to those periods would not be material.

The Corporation believes Adjusted Net Earnings is also a useful performance measure as, similar to Adjusted EBITDA, it provides meaningful information relating to the Corporation’s trends in underlying performance and growth, but it also takes into account the Corporation’s current capital structure, the impact of its geographic diversity on taxes and the Corporation’s historical investments in technology.

Adjusted Diluted Net Earnings per Share

The Corporation defines Adjusted Diluted Net Earnings per Share as Adjusted Net Earnings attributable to the Shareholders of The Stars Group Inc. divided by Diluted Shares. Diluted Shares means the weighted average number of Common Shares on a fully diluted basis, including options, other equity-based awards such as warrants and any convertible preferred shares of the Corporation then outstanding. The effects of anti-dilutive potential Common Shares are ignored in calculating Diluted Shares. Diluted Shares used in the calculation of diluted earnings per share may differ from diluted shares used in the calculation of Adjusted Diluted Net Earnings per Share where the dilutive effects of the potential Common Shares differ. See note 10 in the 2018 Annual Financial Statements. For the quarter and year ended December 31, 2018, Diluted Shares used for the calculation of Adjusted Diluted Net Earnings per Share equalled 273,294,532 and 242,768,766, respectively, compared with 206,807,485 and 203,707,589 for the same periods in 2017, respectively.

The Corporation believes Adjusted Diluted Net Earnings per Share is a useful measure for the same reasons as Adjusted Net Earnings as well as providing a per share measure that factors in the dilutive effect of the Corporation’s outstanding equity and equity-based awards and instruments.

Constant Currency Revenue

The Corporation defines Constant Currency Revenue as IFRS reported revenue for the relevant period calculated using the prior year’s monthly average exchange rates for its local currencies other than the U.S. dollar. Currently, the Corporation provides Constant Currency Revenue for the International segment and its applicable lines of operations. It does not currently provide Constant Currency Revenue for the United Kingdom and Australia segments because the Corporation does not have comparative periods for these segments.

The Corporation believes providing Constant Currency Revenue for the International segment is useful because it helps show the foreign exchange impact due to translation and purchasing power, and it facilitates comparison to its historical performance mainly because the U.S. dollar is the primary currency of gameplay on the International segment’s product offerings and the majority of the segment’s customers are from European Union jurisdictions. The Corporation is also exposed to foreign exchange risk as a result of the Acquisitions (as defined below), primarily when translating the functional currencies of the United Kingdom segment (i.e., GBP) and Australia segment (i.e., AUD) into U.S. dollars for financial reporting purposes. The Corporation intends to provide information on the impact of foreign exchange for these segments either individually or on a consolidated basis when applicable reported comparative period information is available.

Free Cash Flow

The Corporation defines Free Cash Flow as net cash flows from operating activities after adding back customer deposit liability movements, and after capital expenditures and debt servicing cash flows (excluding voluntary prepayments).

The Corporation believes that Free Cash Flow is a useful liquidity measure because it believes that removing movements in customer deposit liabilities provides a meaningful understanding of its underlying cash flows as customer deposits are not available funds that the Corporation can use for financial or operational purposes, and removing capital expenditures and debt servicing costs shows cash potentially available for voluntary debt repayments and other financial or operational purposes including to pursue strategic initiatives.

5

The Corporation currently considers the below noted key metrics in this MD&A for its reporting segments, as applicable. The Corporation does not currently provide consolidated key metrics because management analyzes these metrics primarily on a segment-by-segment basis due to differences in the nature of the applicable segment’s market, customer base and product offerings. Notwithstanding and unless the context otherwise requires, the Corporation believes that readers should consider the applicable metrics together for each segment (but not on a consolidated basis) as customer growth and monetization trends reflected in such metrics are key factors that affect the Corporation’s revenue for the applicable segment. The Corporation is also in the process of integrating its recent acquisitions, as applicable, and implementing its recently changed operating and reporting segments, and once complete, the Corporation may revise or remove currently presented key metrics or report certain additional or other measures in the future.

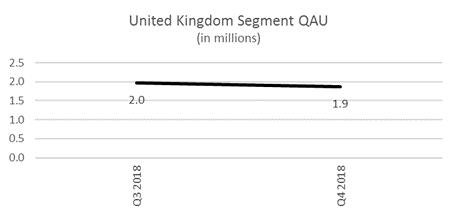

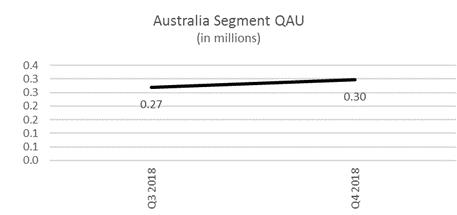

Quarterly Real-Money Active Uniques (QAUs)

The Corporation defines QAUs for the International and Australia reporting segments as active unique customers (online, mobile and desktop client) who (i) made a deposit or transferred funds into their real-money account with the Corporation at any time, and (ii) generated real-money online rake or placed a real-money online bet or wager on during the applicable quarterly period. The Corporation defines “active unique customer” as a customer who played or used one of its real-money offerings at least once during the period, and excludes duplicate counting, even if that customer is active across multiple lines of operation (Poker, Gaming and/or Betting, as applicable) within the applicable reporting segment. The definition of QAUs excludes customer activity from certain low-stakes, non-raked real-money poker games, but includes real-money activity by customers using funds (cash and cash equivalents) deposited by the Corporation into such customers’ previously funded accounts as promotions to increase their lifetime value.

The Corporation currently defines QAUs for the United Kingdom reporting segment (which currently includes the SBG business operations only) as active unique customers (online and mobile) who have settled a Stake (as defined below) or made a wager on any betting or gaming product within the applicable quarterly period. The Corporation defines active unique customer for the United Kingdom reporting segment as a customer who played at least once on one of its real-money offerings during the period, and excludes duplicate counting, even if that customer is active across more than one line of operation. For the quarter ended September 30, 2018, QAUs for the United Kingdom reporting segment also include the applicable pre-acquisition period of July 1, 2018 through July 9, 2018.

QAUs are a measure of the player liquidity on the Corporation’s real-money poker product offerings and level of usage on all its real-money product offerings, collectively. Trends in QAUs affect revenue and financial results by influencing the volume of activity, the Corporation’s product offerings, and its expenses and capital expenditures.

The Corporation has faced and may continue to face challenges in increasing the size of its active customer base within its reporting segments, as applicable, due to, among other things, competition from alternative products and services for all verticals, as well as regulatory changes, payment processing or other restrictions that may impact customer acquisition or the ability of customers to make a deposit or play certain products, high-volume, net-withdrawing customers who detract from the overall poker ecosystem and discourage recreational customers, the use of certain sophisticated technology that may provide an artificial competitive advantage for certain online poker customers over others, and past and potential future weakness in certain global currencies against the U.S. dollar, which decreases the purchasing power of the Corporation’s customer base as the U.S. dollar is the primary currency of gameplay on many of its International segment product offerings. Notwithstanding, the Corporation intends to retain and grow its reporting segments’ customer bases and reactivate dormant users by, as applicable, continuing to improve the poker ecosystem to benefit recreational players, continuing to introduce new and innovative product offerings, features and enhancements for all verticals, improving the user interfaces, platforms and user experience across its lines of operations, investing in customer relationship management (“CRM”) initiatives, improving the effectiveness of its marketing and promotional efforts, and expanding the availability of its offerings geographically, including through potential acquisitions and strategic transactions, among other things. To the extent the growth of the customer base of a reporting segment of the Corporation continues to decline, that segment’s revenue growth will become increasingly dependent on its ability to increase levels of customer engagement and monetization.

6

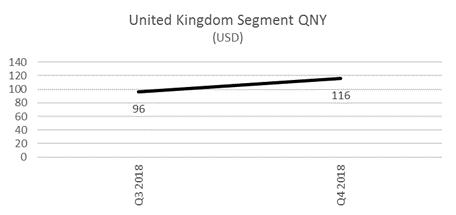

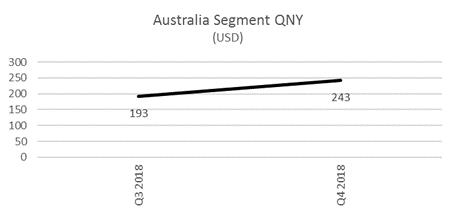

Quarterly Net Yield (QNY)

The Corporation defines QNY as combined revenue for its lines of operation (i.e., Poker, Gaming and/or Betting, as applicable) for each reporting segment, excluding Other revenue, as reported during the applicable quarterly period (or as adjusted to the extent any accounting reallocations are made in later periods) divided by the total QAUs during the same period. For the quarter ended September 30, 2018, QNY for the United Kingdom reporting segment also includes the applicable pre-acquisition period of July 1, 2018 through July 9, 2018. The numerator of QNY is a non-IFRS measure.

Trends in QNY are a measure of growth as the Corporation continues to expand its applicable core real-money online product offerings. In addition, the trends in the Corporation’s ability to generate revenue on a per customer basis across its real-money online product offerings are reflected in QNY and are key factors that affect the Corporation’s revenue. The Corporation also provides QNY using Constant Currency Revenue for the International reporting segment.

Many variables can impact a reporting segment’s QNY, including, as applicable, the rake and fees charged in real-money online poker, the applicable margin of online casino games, Stakes and Betting Net Win Margin, the amount of time customers play on its product offerings, offsets to gross revenue for loyalty program rebates, rewards, bonuses, and promotions, VAT and similar taxes in certain jurisdictions, and the amount the applicable reporting segment spends on advertising and other similar expenses. The Corporation currently intends to increase QNY for its reporting segments in future periods by, among other things, and as applicable, (i) continuing to introduce new and innovative product offerings and other initiatives to enhance the customer experience and increase customer engagement, including through CRM initiatives to attract and retain high-value customers, (ii) capitalizing on its existing online poker platforms and offerings, which provides customers with the highest level of player liquidity globally, (iii) cross-selling its online offerings to both existing and new customers, and (iv) continuing to expand and improve its online gaming offerings.

Net Deposits

The Corporation defines Net Deposits for the International segment as the aggregate of gross deposits or transfer of funds made by customers into their real-money online accounts less withdrawals or transfer of funds by such customers from such accounts, in each case during the applicable quarterly period. Gross deposits exclude (i) any deposits, transfers or other payments made by such customers into the Corporation’s play-money and social gaming offerings, and (ii) any real-money funds (cash and cash equivalents) deposited by the Corporation into such customers’ previously funded accounts as promotions to increase their lifetime value.

Net Deposits are representative of the money the Corporation’s customers hold in their accounts to potentially play with. Net Deposits are correlated to the International segment’s reported revenue, as some, all or none of such deposits may eventually be used and become revenue. Trends in Net Deposits are used by management to gauge expected revenue performance across the International segment’s applicable lines of operations and are considered by management when making decisions with respect to applicable product offering changes, including the recent and continuing changes to the Corporation’s online poker ecosystem to benefit and attract high-value, net-depositing customers (primarily recreational players).

Net Deposits are not, and should not be considered, representative of revenue bookings or deferred revenue. Many variables impact the International segment’s Net Deposits, most of which are substantially similar to those noted above impacting the monetization of a product offering as evidenced through QNY. In addition, certain factors have impacted, and may in the future impact, Net Deposits that are not indicative of the performance or underlying health of that segment’s business. For example, as it relates to online poker and following the implementation of certain previously disclosed changes to the poker ecosystem, the movement in customer real-money account balances (i.e., customer deposits on the consolidated statements of financial position) by high-volume, net-withdrawing customers has reduced, and may in the future reduce, Net Deposits as a result of increased withdrawals by such customers, but the Corporation believes that such movements will ultimately create a more attractive environment and experience for recreational players, which in turn may lead to increased Net Deposits. The Corporation believes that the funds in the accounts of the high-volume, net-withdrawing customers are generally not additive to the overall poker ecosystem or to the Corporation’s revenue as such customers generally use only a small portion of them to bet or wager. As the Corporation continues to adjust and improve its product offerings, it expects that such customers may continue to

7

withdraw at greater rates and amounts immediately following such adjustments and improvements, which would impact Net Deposits accordingly.

Stakes and Betting Net Win Margin

The Corporation defines Stakes as betting amounts wagered on the Corporation’s applicable online betting product offerings, and is also an industry term that represents the aggregate amount of funds wagered by customers within the Betting line of operation for the period specified. Betting Net Win Margin is calculated as Betting revenue as a proportion of Stakes. The Corporation uses Stakes and Betting Net Win Margin as measures of the scale of its operations, the engagement of its customers and performance of its operations across its product offerings and geographic regions. Trends in Stakes are a measure of growth in the Corporation’s Betting line of operations as the Corporation continues to expand its applicable core real-money online betting offerings. Trends in Betting Net Win Margin are primarily a measure of the favorability of the outcomes of sporting and other events and the impact of promotional offerings related to the Corporation’s betting offerings.

Many variables impact a reporting segment’s Stakes, including, as applicable, that segment’s QAUs, the seasonality of sporting events throughout the year (such as timing of European football (or soccer) including English Premier League, horse races, rugby seasons, tennis, and others) and major tournaments, such as the 2018 FIFA World Cup (“World Cup”) and UEFA European Championships. For example, the World Cup, and other major sporting events provide a unique opportunity to drive both customer acquisition and engagement. Furthermore, the amount of external marketing and CRM promotions including free bets and offers and the Corporation’s pricing strategy can lead to positive or negative “recycling of winnings”. Similarly, betting outcomes can also lead to positive or negative “recycling of winnings”. Recycling of winnings refers to customer winnings earned from prior bets that are subsequently used to place additional bets or play other products. The mix of products and markets is also an important driver of total Stakes.

Like Stakes, many variables also impact a reporting segment’s Betting Net Win Margin, including client management and bet limits, sporting results, the mix of Stakes and bet types, and the use of offers, promotions and pricing strategy. For example, the International segment’s Betting Net Win Margin is less exposed to the English Premier League and UK horse racing, and as such, is generally not impacted to the same extent by the operator-unfavorable (or customer-favorable) results seen within the United Kingdom segment as a whole. Betting Net Win Margin can vary significantly from quarter to quarter depending on the variables noted above; however, over the long term, the Corporation believes these margins tend to become more predictable.

Limitations of Non-IFRS Measures, Key Metrics and Other Data

There are a number of limitations related to the use of such non-IFRS measures as opposed to their nearest IFRS equivalent. Some of these limitations are:

| • | these non-IFRS financial measures exclude or are otherwise adjusted for the applicable items listed in the reconciliation tables under “Reconciliations” below and as set forth in the definitions of such measures; and |

| • | the income or expenses that the Corporation excludes in its calculation of these non-IFRS financial measures may differ from the income or expenses that its peer companies may exclude from similarly-titled non-IFRS measures that they report. In addition, although certain excluded income or expenses may have been incurred in the past or may be expected to recur in the future, management believes it is appropriate to exclude such income or expenses at this time as it does not consider them as on-going core operating income or expenses of the Corporation. Moreover, certain integration and related costs of the Acquisitions are or will be excluded as being more similar to acquisition-related costs rather than on-going core operating expenses. Management currently believes that, subject to unanticipated events or impacts of anticipated events, over time it should have fewer adjustments or the amounts of such adjustments should decrease, except for acquisition-related or integration costs, which the Corporation may incur in the future based on the Corporation’s strategic initiatives. |

While management may have provided other non-IFRS financial measures and key metrics in the past, it continues to review and assess the importance, completeness and accuracy of such measures as it relates to its evaluation of the Corporation’s business, performance and trends affecting the same. This includes customer engagement, gameplay,

8

depositing activity and various other customer trends, particularly following the introduction of certain previously announced improvements in the poker ecosystem to benefit and attract recreational customers and reduce incentives for high-volume, net-withdrawing customers, the introduction of certain customer acquisition initiatives, and the Corporation’s expansion in real-money online casino and sportsbook. As such, management may determine that particular measures that it may have presented in the past are no longer helpful or relevant to understanding the Corporation’s current and future business, performance or trends affecting the same, and as a result it may remove or redefine any such measures, or introduce new or alternative measures. For each applicable period, management intends to provide such metrics and measures that it believes may be the most helpful and relevant to an understanding of the Corporation’s business and performance, including on a consolidated and segmental basis and normalized measures of the same, and trends affecting the foregoing.

The numbers for the Corporation’s key metrics and related information are calculated using internal company data based on the activity of customer accounts. While these numbers are based on what the Corporation believes to be reasonable judgments and estimates of its customer base for the applicable period of measurement, there are certain challenges and limitations in measuring the usage of its product offerings across its customer base. Such challenges and limitations may also affect the Corporation’s understanding of certain details of its business. In addition, the Corporation’s key metrics and related estimates, including the definitions and calculations of the same, may differ among reporting segments, from estimates published by third parties or from similarly-titled metrics of its competitors due to differences in operations, product offerings, methodology and access to information. The Corporation continually seeks to improve its estimates of its active customer base and the level of customer activity, and such estimates may change due to improvements or changes in the Corporation’s methodology.

For example, the methodologies used to measure the Corporation’s customer metrics may be susceptible to algorithm, calculation or other technical or human errors, including how certain metrics may be defined (and the assumptions and considerations made and included in, or excluded from, such definitions) and how certain data may be, among other things, integrated, analyzed and reported after the Corporation completes an acquisition or strategic transaction. Moreover, the Corporation’s business intelligence tools may experience glitches or fail on a particular data backup or upload, which could lead to certain customer activity not being properly included in the calculation of a particular key metrics. Another challenge with respect to certain key metrics is that customers could create multiple real-money accounts with the Corporation (in nearly all instances such account creation would violate the Corporation’s applicable terms and conditions of use), and customers could take advantage of certain customer acquisition incentives to register and interact with the Corporation’s product offerings without actually depositing or transferring funds into their real-money accounts. Furthermore, customers may have more than one account across the Corporation’s brands that currently do not have common or shared account structure, which could lead to such customers being counted more than once for a particular key metric. Although the Corporation typically addresses and corrects any such failures, duplications and inaccuracies relatively quickly, its metrics are still susceptible to the same and its estimations of such metrics may be lower or higher than the actual numbers.

The Corporation regularly reviews its processes for calculating and defining these metrics, and from time to time it may make adjustments to improve their accuracy that may result in the recalculation or replacement of historical metrics or introduction of new metrics. These changes may also include adjustments to underlying data, such as changes to historical figures as a result of accounting adjustments and revisions to definitions in an effort to provide what management believes may be the most helpful and relevant data. These changes may arise as a result of, among other things, the Corporation implementing new technology, software or accounting methods, engaging third-party advisors or consultants, or acquiring or integrating new assets, businesses or business units. The Corporation also continuously seeks to improve its ability to identify irregularities and inaccuracies (and suspend any customer accounts that violate its terms and conditions of use and limit or eliminate promotional incentives that are susceptible to abuse), and its key metrics or estimates of key metrics may change due to improvements or changes in its methodology. Notwithstanding, the Corporation believes that any such irregularities, inaccuracies or adjustments are immaterial unless otherwise stated.

9

Business Overview and Background

The Stars Group is a global leader in the online and mobile gaming and interactive entertainment industries, entertaining millions of customers across its online real- and play-money poker, gaming and betting product offerings, which are delivered through mobile, web and desktop applications. The Stars Group offers these products directly or indirectly under several ultimately owned or licensed gaming and related consumer businesses and brands, including, among others, PokerStars, PokerStars Casino, BetStars, Full Tilt, BetEasy, Sky Bet, Sky Vegas, Sky Casino, Sky Bingo, Sky Poker, and Oddschecker, as well as live poker tour and events brands, including the PokerStars Players No Limit Hold’em Championship, European Poker Tour, PokerStars Caribbean Adventure, Latin American Poker Tour, Asia Pacific Poker Tour, PokerStars Festival and PokerStars MEGASTACK. The Stars Group is one of the world’s most licensed online gaming operators with its subsidiaries collectively holding licenses or approvals in 21 jurisdictions throughout the world, including in Europe, Australia, and the Americas. The Stars Group’s vision is to become the world’s favorite iGaming destination and its mission is to provide its customers with winning moments.

The Stars Group’s primary business and source of revenue is its online gaming and betting businesses. These currently consist of the operations of Stars Interactive Holdings (IOM) Limited and its subsidiaries and affiliates (collectively, “Stars Interactive Group”), which it acquired in August 2014 (the ‘‘Stars Interactive Group Acquisition’’), the operations of Cyan Blue Topco Limited and its subsidiaries and affiliates (collectively, “Sky Betting & Gaming” or “SBG”), which it acquired in July 2018 (the “SBG Acquisition”), and the operations of TSG Australia Pty Ltd (formerly CrownBet Holdings Pty Limited) and its subsidiaries and affiliates, including TSGA Holdco Pty Limited (formerly William Hill Australia Holdings Pty Ltd) and its subsidiaries and affiliates (“TSGA” and where the context requires, collectively, “BetEasy”), which it acquired an 80% equity interest in between February 2018 and April 2018 (BetEasy acquired TSGA in April 2018) (collectively, the “Australian Acquisitions”). The Stars Interactive Group is headquartered in the Isle of Man and Malta and operates globally, with certain exceptions; SBG is headquartered in and primarily operates in the United Kingdom; and BetEasy is headquartered in and primarily operates in Australia.

For additional information about The Stars Group, including a detailed overview of the business, current strategies and a discussion of the competitive landscape affecting The Stars Group, see the disclosure and discussion elsewhere in this MD&A and the 2018 Annual Reports, particularly in the 2018 Annual Information Form. For risks and uncertainties relating to, among other things, The Stars Group, its business, its customers, its regulatory and tax environment and the industries and geographies in which it operates or where its customers are located, see “Risk Factors and Uncertainties” above and in the 2018 Annual Information Form as well as the risks and uncertainties contained elsewhere herein, the 2018 Annual Reports and in other filings that The Stars Group has made and may make in the future with applicable securities authorities. For information about The Stars Group’s outlook, see the 2018 Annual Reports, particularly in the 2018 Annual Information Form, including under the headings “Business of the Corporation—Business Strategy of the Corporation” and “—Markets and Customers”.

Recent Corporate and Other Developments

Below is a general summary of certain recent corporate and other developments from the beginning of the fourth quarter of 2018 through the date hereof. For additional corporate and other developments and highlights, see the 2018 Annual Reports, particularly the 2018 Annual Information Form, and “Further Information” below.

UK CMA Clearance of SBG Acquisition

On October 11, 2018, the UK Competition and Markets Authority cleared the SBG Acquisition following its Phase 1 review under the Enterprise Act 2002, which permitted the Corporation to begin executing on its integration plans.

Eldorado Market Access Agreement

On November 26, 2018, the Corporation announced it entered into an

agreement with Eldorado Resorts, Inc. (Nasdaq: ERI) (“Eldorado”) that grants the Corporation the option to operate online betting and gaming in the states where Eldorado currently or in the future owns or operates casino properties. The agreement currently covers 11 states (Colorado, Florida, Illinois, Indiana, Iowa, Louisiana, Mississippi, Missouri, Nevada, Ohio and West Virginia) which, when combined with the Corporation’s existing market access deals in New

10

Jersey and Pennsylvania, gives the Corporation potential access to 13 states. The agreement grants the Corporation the option to own, operate and brand real-money online sports betting, poker and casino offerings in each of the applicable states subject to license availability, state law and regulatory approvals. As it relates to sports betting, the Corporation’s options will provide first skin access in states where Eldorado owns or operates more than one casino property and second skin access in all other applicable states.

Under the terms of the agreement, Eldorado will receive a revenue share from the operation of the applicable offerings by the Corporation, and the Corporation issued Eldorado 1,076,658 Common Shares at a contractual price of $23.22 per share for a value of $25 million and the Corporation will issue an additional $5 million of Common Shares upon the Corporation’s exercise of the first option and following the satisfaction of certain conditions. Further, Eldorado would be entitled to additional Common Shares at a price of $23.22 per share beginning in five years. The number of additional shares potentially issuable to Eldorado would be solely based on the success of the Corporation’s online gaming offerings in applicable states as measured by net gaming revenue generated in each applicable state.

On December 21, 2018, the Kentucky Court of Appeals ruled in The Stars Group’s favor and reversed in its entirety the $870 million judgment issued against it by a trial court judge in December 2015 under a centuries old statute and relating to alleged losses by Kentucky residents who played real-money online poker on PokerStars’ website during a period between 2006 and 2011. The Supreme Court of Kentucky is currently considering whether to hear the Commonwealth’s appeal of the reversal and The Stars Group intends to vigorously dispute any and all liability in the event the Kentucky Supreme Court grants review and hears the appeal. For additional information regarding the Kentucky proceeding, see the 2018 Annual Information Form, particularly under the heading “Legal Proceedings and Regulatory Actions”, and note 28 to the 2018 Annual Financial Statements.

Prepayment of First Lien Term Loans

On February 22, 2019, the Corporation prepaid $100.0 million of its USD First Lien Term Loan (as defined below), including accrued and unpaid interest, using cash on its balance sheet. For additional information, see “Liquidity and Capital Resources” below.

SELECTED FINANCIAL INFORMATION

Selected financial information of the Corporation for the three months ended December 31, 2018 and 2017, and for the years ended December 31, 2018, 2017 and 2016 is set forth below.

|

| Quarter ended December 31 |

|

|

| Year ended December 31, |

| ||||||||||||||

In thousands of U.S. Dollars, except per share amounts |

| 2018 |

|

| 2017 |

|

|

| 2018 |

|

| 2017 |

|

| 2016 |

| |||||

Revenue |

|

| 652,852 |

|

|

| 360,250 |

|

|

|

| 2,029,238 |

|

|

| 1,312,315 |

|

|

| 1,155,247 |

|

Net (loss) earnings |

|

| (38,173 | ) |

|

| 47,175 |

|

|

|

| (108,906 | ) |

|

| 259,285 |

|

|

| 135,550 |

|

Basic net (loss) earnings per Common Share |

| $ | (0.14 | ) |

| $ | 0.32 |

|

|

| $ | (0.49 | ) |

| $ | 1.77 |

|

| $ | 0.96 |

|

Diluted net (loss) earnings per Common Share |

| $ | (0.14 | ) |

| $ | 0.23 |

|

|

| $ | (0.49 | ) |

| $ | 1.27 |

|

| $ | 0.70 |

|

Total assets (as at) |

|

| 11,265,538 |

|

|

| 5,415,126 |

|

|

|

| 11,265,538 |

|

|

| 5,415,126 |

|

|

| 5,462,475 |

|

Total long-term liabilities (as at) |

|

| 6,100,164 |

|

|

| 2,509,221 |

|

|

|

| 6,100,164 |

|

|

| 2,509,221 |

|

|

| 2,412,579 |

|

Revenue increased in both the quarter and year ended December 31, 2018 as compared to the applicable prior year periods and as compared to the year ended December 31, 2016 primarily as a result of the SBG Acquisition and Australian Acquisitions (collectively, the “Acquisitions”) as well as growth of the Corporation’s online Poker, Gaming and Betting and product offerings. For additional variance analysis on revenue, see “Consolidated Results of Operations and Cash Flows”, and “Segment Results of Operations” below.

The increase in the Corporation’s total assets as at December 31, 2018 compared to December 31, 2017 and 2016 was primarily the result of an increase in goodwill and intangible assets following the Acquisitions. The increase in outstanding long-term liabilities as at December 31, 2018 compared to December 31, 2017 and 2016 was primarily to

11

the result of an increase to long-term debt resulting from the SBG Financing. For additional variance analysis on total assets and non-current liabilities, see “Consolidated Results of Operations and Cash Flows” below.

CONSOLIDATED RESULTS OF OPERATIONS AND CASH FLOWS

Summary consolidated results of the Corporation’s operations, cash flows and certain other items for the quarters and years ended December 31, 2018 and 2017 are set forth below:

|

| Quarter Ended December 31, |

|

| Year Ended December 31, |

| ||||||||||||||||||

In thousands of U.S. Dollars (except otherwise noted) |

| 2018 |

|

| 2017 |

|

| % Change |

|

| 2018 |

|

| 2017 |

|

| % Change |

| ||||||

Revenue |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Poker |

|

| 213,985 |

|

|

| 234,350 |

|

|

| (8.7 | %) |

|

| 892,557 |

|

|

| 877,296 |

|

|

| 1.7 | % |

Gaming |

|

| 196,275 |

|

|

| 90,822 |

|

|

| 116.1 | % |

|

| 585,846 |

|

|

| 334,781 |

|

|

| 75.0 | % |

Betting |

|

| 224,040 |

|

|

| 21,690 |

|

|

| 932.9 | % |

|

| 491,139 |

|

|

| 49,231 |

|

|

| 897.6 | % |

Other |

|

| 18,552 |

|

|

| 13,388 |

|

|

| 38.6 | % |

|

| 59,696 |

|

|

| 51,007 |

|

|

| 17.0 | % |

Total revenue |

|

| 652,852 |

|

|

| 360,250 |

|

|

| 81.2 | % |

|

| 2,029,238 |

|

|

| 1,312,315 |

|

|

| 54.6 | % |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Gross profit (excluding depreciation and amortization) |

|

| 486,815 |

|

|

| 290,358 |

|

|

| 67.7 | % |

|

| 1,570,074 |

|

|

| 1,064,818 |

|

|

| 47.4 | % |

Gross profit margin (%) |

|

| 74.6 | % |

|

| 80.6 | % |

|

| (7.5 | %) |

|

| 77.4 | % |

|

| 81.1 | % |

|

| (4.6 | %) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Operating expenses |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

General and administrative |

|

| 312,638 |

|

|

| 115,542 |

|

|

| 170.6 | % |

|

| 984,194 |

|

|

| 437,886 |

|

|

| 124.8 | % |

Sales and marketing |

|

| 96,115 |

|

|

| 55,883 |

|

|

| 72.0 | % |

|

| 292,963 |

|

|

| 154,358 |

|

|

| 89.8 | % |

Research and development |

|

| 10,972 |

|

|

| 6,667 |

|

|

| 64.6 | % |

|

| 39,995 |

|

|

| 25,180 |

|

|

| 58.8 | % |

Operating income |

|

| 67,090 |

|

|

| 112,266 |

|

|

| (40.2 | %) |

|

| 252,922 |

|

|

| 447,394 |

|

|

| (43.5 | %) |

Net (earnings) loss from associates |

|

| — |

|

|

| — |

|

|

| — |

|

|

| (1,068 | ) |

|

| 2,569 |

|

|

| (141.6 | %) |

Net financing charges |

|

| 90,813 |

|

|

| 38,739 |

|

|

| 134.4 | % |

|

| 363,884 |

|

|

| 158,332 |

|

|

| 129.8 | % |

Income tax expense (recovery) |

|

| 14,450 |

|

|

| 26,352 |

|

|

| (45.2 | %) |

|

| (988 | ) |

|

| 27,208 |

|

|

| (103.6 | %) |

Net (loss) earnings |

|

| (38,173 | ) |

|

| 47,175 |

|

|

| (180.9 | %) |

|

| (108,906 | ) |

|

| 259,285 |

|

|

| (142.0 | %) |

Adjusted Net Earnings ¹ |

|

| 144,663 |

|

|

| 111,951 |

|

|

| 29.2 | % |

|

| 533,948 |

|

|

| 458,940 |

|

|

| 16.3 | % |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Adjusted EBITDA ¹ |

|

| 239,404 |

|

|

| 147,002 |

|

|

| 62.9 | % |

|

| 780,949 |

|

|

| 600,306 |

|

|

| 30.1 | % |

Adjusted EBITDA Margin ¹ |

|

| 36.7 | % |

|

| 40.8 | % |

|

| (10.1 | %) |

|

| 38.5 | % |

|

| 45.7 | % |

|

| (15.9 | %) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(Loss) earnings per share |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Basic ($/Share) |

|

| (0.14 | ) |

|

| 0.32 |

|

|

| (145.1 | %) |

|

| (0.49 | ) |

|

| 1.77 |

|

|

| (127.9 | %) |

Diluted ($/Share) |

|

| (0.14 | ) |

|

| 0.23 |

|

|

| (162.8 | %) |

|

| (0.49 | ) |

|

| 1.27 |

|

|

| (138.7 | %) |

Adjusted Diluted Net Earnings per Share ($/Share) ¹ |

|

| 0.52 |

|

|

| 0.54 |

|

|

| (4.2 | %) |

|

| 2.19 |

|

|

| 2.25 |

|

|

| (2.9 | %) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net cash inflows from operating activities |

|

| 190,537 |

|

|

| 123,757 |

|

|

| 54.0 | % |

|

| 559,844 |

|

|

| 494,600 |

|

|

| 13.2 | % |

Net cash (outflows) inflows from investing activities |

|

| (54,703 | ) |

|

| 184,958 |

|

|

| (129.6 | %) |

|

| (1,934,173 | ) |

|

| 174,850 |

|

|

| (1206.2 | %) |

Net cash (outflows) inflows from financing activities |

|

| (166,214 | ) |

|

| (28,275 | ) |

|

| (487.8 | %) |

|

| 1,592,579 |

|

|

| (443,802 | ) |

|

| 458.8 | % |

Free Cash Flow ¹ |

|

| 82,558 |

|

|

| 84,854 |

|

|

| (2.7 | %) |

|

| 222,950 |

|

|

| 339,882 |

|

|

| (34.4 | %) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

As at |

| December 31, 2018 |

|

| December 31, 2017 |

|

| % Change |

| |||||||||||||||

Total assets |

|

|

|

|

|

| 11,265,538 |

|

|

|

|

|

|

| 5,415,126 |

|

|

|

|

|

|

| 108.0 | % |

Total non-current liabilities |

|

|

|

|

|

| 6,100,164 |

|

|

|

|

|

|

| 2,509,221 |

|

|

|

|

|

|

| 143.1 | % |

¹ Non-IFRS measure. A reconciliation to its nearest IFRS measure is provided under “Reconciliations” below.

The discussion below sets forth a summary of the results, trends and variances of the Corporation on a consolidated basis. For further discussion and detail of the individual segment results, trends and variances, including details of

12

separate trends in revenue by individual line of operation for each segment, as applicable, and the Corporate cost center, see the section “Segment Results of Operations”.

Revenue

Revenue for the quarter and year ended December 31, 2018 increased $292.6 million, or 81.2% and $716.9 million, or 54.6%, respectively, compared to the applicable prior year period. The increase for both periods was primarily driven by the Acquisitions, which added $298.1 million and $591.1 million to revenue for the respective periods. With respect to the International segment, revenue increased in all lines of operation for the year but decreased in Poker for the quarter, which was partially offset by increased revenue across Gaming and Betting, in each case primarily driven by those factors set forth under “Segment Results of Operations—International—Revenue”.

With respect to Canada, the jurisdiction where its registered office is located, and based solely on calculations derived from internal records, the Corporation estimates that revenue derived from customers in Canada, which currently relates only to peer-to-peer Poker, represented less than 3% of its total consolidated revenue for the quarter and year ended December 31, 2018 and less than 5% for the applicable prior year periods. These estimations are neither itemized nor otherwise separated from the revenue the Corporation reports under IFRS or otherwise, and as such, they cannot be reconciled to a reported IFRS measure.

Foreign Exchange Impact on Revenue

The U.S. dollar, which is the primary currency of gameplay for the International segment, was stronger during the quarter ended December 31, 2018 and weaker during the year ended December 31, 2018, against certain foreign currencies, particularly the Euro, which is the primary depositing currency of the International segment’s customers. This impact to customer purchasing power and translation of foreign currency gameplay, had a negative impact on revenue across all lines of operations during the quarter and had a positive impact on revenue across all lines of operations during the year. By including Constant Currency Revenue for the International segment in the consolidated results of operations for the quarter and year ended December 31, 2018, revenue would have been $672.9 million and $2.01 billion, respectively, and would have increased by 86.8% and 53.5%, as opposed to 81.2% and 54.6%, respectively, compared to the applicable prior year period. For discussion of Constant Currency Revenue for the International segment, see discussion under “Segment Results of Operations—International—Revenue”.

Gross Profit (Excluding Depreciation and Amortization) and Gross Profit Margin

Gross profit for the quarter and year ended December 31, 2018 increased $196.5 million, or 67.7%, and $505.3 million, or 47.4%, respectively, compared to the applicable prior year period. The increase in both periods was primarily driven by the Acquisitions, which added $201.6 million and $412.5 million to gross profit for the respective periods, and solely related to the full year period, the increase in revenue within the International segment.

Gross profit margin for the quarter ended December 31, 2018 was 74.6%, a decrease of 7.5% compared to the prior year period. Gross profit margin for the year ended December 31, 2018 was 77.4%, a decrease of 4.6% compared to the prior year period. The decrease in both periods was primarily driven by the change in revenue mix among and across geographies and lines of operations. For instance, revenue in locally regulated or taxed geographies, which generally impose higher rates of taxes, gaming duties, levies and fees represented 76% of revenue in the quarter ended December 31, 2018, compared to 54% of revenue in the prior year period. In addition, Betting and Gaming revenue as a result of the Acquisitions, which generally have lower gross profit margins than Poker, represented 64.4% of revenue in the quarter ended December 31, 2018, compared to 31.2% of revenue in the prior year period.

Operating Expenses

General and Administrative

General and administrative expenses for the quarter and year ended December 31, 2018 increased $197.1 million, or 170.6%, and $546.3 million, or 124.8%, respectively, compared to the applicable prior year period. The increase in both periods was primarily the result of (i) additional general and administrative expenses resulting from the Acquisitions, which added $168.3 million and $357.5 million to general and administrative expenses for the respective periods, (ii) increased salary and wages of $11.2 million and $27.3 million within the International segment and Corporate cost center for the respective periods as the result of investment in additional headcount, (iii) increased information technology and software costs within the International segment driven by increased cloud storage space

13

and additional leased data center spaces, and (iv) solely in respect of the full year period, acquisition-related costs and deal contingent forwards in relation to the Acquisitions of $115.7 million within the Corporate cost center.

Sales and Marketing

Sales and marketing expenses for the quarter and year ended December 31, 2018 increased $40.2 million, or 72.0%, and $138.6 million, or 89.8%, respectively, compared to the applicable prior year period. The increase in both periods was primarily the result of (i) additional sales and marketing expenses resulting from the Acquisitions, which added $51.3 million and $129.0 million to sales and marketing expenses for the respective periods, and (ii) timing of certain advertising costs and other marketing initiatives during the year related to certain sporting events, including an increase in advertising costs during the second and third quarter related to the World Cup, and the launch of some or all lines of operations in certain new markets, as applicable.

Research and Development

Research and development expenses for the quarter and year ended December 31, 2018 increased $4.3 million, or 64.6%, and $14.8 million, 58.8%, respectively, compared to the applicable prior year period. The increase in both periods was primarily the result of (i) additional research and development expenses resulting from the Acquisitions, which added $6.1 million and $12.1 million to research and development expenses for the respective periods, (ii) increased salary and wages within the International segment as a result of investment in additional headcount and (iii) increased costs in relation to investment in technology including new product development, mainly in PokerStars and PokerStars Casino.

Foreign Exchange Impact on Operating Expenses

The Corporation’s expenses are impacted by currency fluctuations. Almost all of its expenses are incurred in either the Euro, British Pound Sterling, U.S. dollar, Canadian dollar or Australian dollar. There are some natural hedges as a result of customer deposits and revenue made in such currencies; however, the Corporation also enters into certain economic hedges to mitigate the impact of foreign currency fluctuations as it deems necessary. See “Liquidity and Capital Resources—Market Risk—Foreign Currency Exchange Risk” for further information on foreign currency risk.

Net Financing Charges

Net financing charges for the quarter and year ended December 31, 2018 increased $52.1 million, or 134.4%, and $205.6 million, or 129.8% compared to the applicable prior year period. The increase in both periods was primarily the result of (i) increased interest expense primarily related to the First Lien Term Loans and Senior Notes (each as defined below) after the effects of hedging activities, and (ii) solely in respect of the full year period, losses on extinguishment of $147.0 million recorded in respect of the amendment and extension and the subsequent early repayment of debt in connection with the Acquisitions.

Income Taxes

Income tax expense for the quarter ended December 31, 2018 was $14.5 million and income tax recovery for the year ended December 31, 2018 was $(1.0) million (quarter and year ended December 31, 2017, income tax expense of $26.4 million and $27.2 million, respectively), which resulted in effective tax rates for those periods of (60.9%) and 0.9%, respectively (quarter and year ended December 31, 2017, 35.8% and 9.5%, respectively). The income tax expense and recovery for the quarter and year ended December 31, 2018, respectively, includes $12.9 million and $27.3 million, respectively (quarter and year ended December 31, 2017, $nil) in relation to the income tax recovery on the amortization expense of acquired intangible assets from the Acquisitions.

The Corporation’s income taxes for the current period were impacted by the tax recovery on amortization as noted above and the mix of taxable earnings among and across geographies, with an increase in taxable earnings following the Acquisitions in geographies with higher statutory corporate tax rates. The Corporation expects the mix of taxable earnings to continue to impact income tax expense in future periods as the acquired businesses operate primarily in

14

Australia and the United Kingdom, where statutory corporate income tax rates are higher than those in the Isle of Man and Malta, where the Corporation primarily operated from prior to the Acquisitions.

Net (Loss) Earnings

Net loss for the quarter ended December 31, 2018 was $38.2 million, a decrease of 180.9%, compared to net earnings of $47.2 million in the prior year period. Net loss for the year ended December 31, 2018 was $108.9 million, a decrease of 142.0%, compared to net earnings of $259.3 million in the prior year period. The losses in both periods were primarily the result of (i) increased amortization of acquisition intangibles due to the Acquisitions of $55.6 million and $117.4 million, respectively, and (ii) solely in relation to the full year, the above noted losses on extinguishment, acquisition-related costs, deal contingent forwards, and integration costs, each in connection with the Acquisitions and recorded through general and administrative expenses.

Basic and Diluted Net (Loss) Earnings per Share

Basic net loss per share for the quarter ended December 31, 2018 was $(0.14), a decrease of 145.1%, compared to basic net earnings per share of $0.32 for the prior year period, based on weighted average Common Shares outstanding of 272,636,266 and 147,678,824, respectively. Basic net loss per share for the year ended December 31, 2018 was $(0.49), a decrease of 127.9%, compared to basic net earnings per share of $1.77 for the prior year period, based on weighted average Common Shares outstanding of 208,269,905 and 146,818,764, respectively. The decreases in both periods were due to the net losses incurred as noted above and were partially offset by increases in the weighted average Common Shares outstanding, which was primarily the result of the issuance of Common Shares in connection with the Equity Offering (as defined below), the Corporation’s mandatory conversion of its preferred shares and the Acquisitions.

Diluted net loss per share for the quarter ended December 31, 2018 was $(0.14), a decrease of 162.8%, compared to diluted net earnings per share of $0.23 for the prior year period, based on weighted average Common Shares outstanding of 272,636,266 and 206,807,485, respectively. Diluted net loss per share for the year ended December 31, 2018 was $(0.49), a decrease of 138.7%, compared to diluted net earnings per share of $1.27 for the prior year period, based on weighted average Common Shares outstanding of 208,269,905 and 203,707,589, respectively. The decreases in both periods were due to the net losses incurred as noted above. The decreases were further negatively impacted as all potentially dilutive securities of the Corporation (i.e., securities exercisable or convertible into Common Shares or equity-based awards that can be settled into Common Shares), were not included in the weighted average diluted Common Share amount above used to calculate diluted loss per share because the exercise, conversion or settlement of such securities would be anti-dilutive. This compares to the same period in 2017 where dilutive securities were primarily impacted by dilutive impact of its then outstanding preferred shares.

Adjusted EBITDA, Adjusted Net Earnings, and Adjusted Diluted Net Earnings per Share

For additional information regarding Adjusted EBITDA, Adjusted Net Earnings and Adjusted Diluted Net Earnings per Share, including applicable definitions and explanations of the relative usefulness of such measures, see “Non-IFRS Measures, Key Metrics and Other Data—Non-IFRS Measures” above. For quantitative reconciliations of such measures to their nearest IFRS measures, see “Reconciliations” below.

The primary adjustment from operating income to Adjusted EBITDA for the applicable quarterly and full year periods was depreciation and amortization, which increased by $61.8 million and $135.6 million for the quarter and year ended December 31, 2018, respectively, primarily as a result of the Acquisitions. In addition to depreciation and amortization, total adjustments and reconciling items also collectively increased by $75.8 million and $239.5 million for the quarter and year ended December 31, 2018, respectively, compared to the applicable prior year period primarily driven by (i) acquisition-related costs and deal contingent forwards incurred in connection with the Acquisitions of $3.1 million and $115.6 million, respectively, (ii) integration-related costs also in connection with the Acquisitions of $17.0 million and $45.6 million, respectively, and (iii) costs incurred in respect of the market access agreement with Eldorado of $20.7 million.

As it relates to Adjusted Net Earnings and Adjusted Diluted Net Earnings per Share for the applicable quarterly and full year periods, the primary adjustments from net (loss) earnings and diluted net (loss) earnings per share were the amortization of acquisition intangibles and acquisition- and integration-related costs, together with the losses on debt extinguishment for the applicable periods, all as noted above. Adjusted Diluted Net Earnings per Share for the quarter and the year were also impacted by the increase in Common Shares issued and outstanding primarily as a result of the

15

Equity Offering and the Acquisitions, which included the issuance of a total 59,924,398 Common Shares. In addition, all potentially dilutive securities of the Corporation were not included in the weighted average diluted Common Share amount used to calculate the nearest IFRS measure because the exercise, conversion or settlement of such securities would be anti-dilutive, as noted above. However, these dilutive securities, and in particular the then-outstanding convertible preferred shares of the Corporation, were included in the weighted average Common Share amount used in the calculation of Adjusted Diluted Net Earnings per Share.

Cash Flows by Activity

Cash from Operating Activities

Cash from operating activities for the year ended December 31, 2018 increased $65.2 million, or 13.2%, compared to the prior year period. The increase in the year was primarily the result of (i) the above noted increase in revenue and gross profit generated from the underlying operations of the Corporation, including the impacts of the Acquisitions, and (ii) movements in customer deposit liabilities relative to the prior year period. This was partially offset by increased general and administrative expenses and sales and marketing costs, as described above and in particular resulting from acquisition-related costs and integration costs incurred in respect of the Acquisitions.

Cash used in Investing Activities

The Corporation’s cash outflows from investing activities during the year ended December 31, 2018 were primarily the result of (i) $1.87 billion in aggregate cash consideration (net of cash acquired) paid in connection with the SBG Acquisition and the acquisition of a 62% equity interest in BetEasy, and (ii) capital expenditures, primarily consisting of investments in online gaming development, in each case partially offset by the inflow of cash from the sale of certain investments made with customer deposits.

Cash from (used in) Financing Activities