Cash Flow from Investing Activities. Net cash used for investing activities, excluding net cash used to purchase time deposits, for the nine-months ended September 30, 2022 was $20.2 million, primarily consisting of $18.4 million purchase of property and equipment, $4.2 million purchase of long term investment (Note 14), $1 million investments in affiliates (Note 14), and $1.1 million purchase of intangible assets, offset by $4.5 million in proceeds from selling trading securities (Note 15).

Cash Flow from Financing Activities. Net cash provided by financing for the nine-months ended September 30, 2022 was $36.8 million, primarily consisting of $35.7 million net proceeds from short and long-term borrowings, and $1.2 million in proceeds from the exercise of stock options.

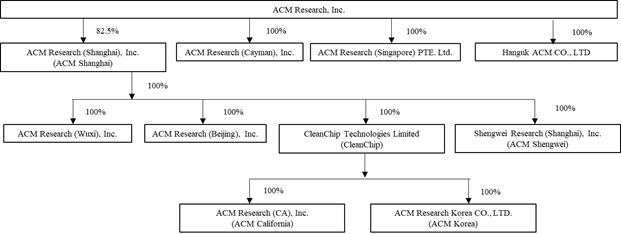

ACM Shanghai, together with its subsidiaries, has short-term and long-term borrowings with five banks, as follows:

| Lender | | Agreement Date | | Maturity Date | | Annual Interest Rate | | | Maximum Borrowing

Amount(1) | | | Amount

Outstanding at September 30, 2022 | |

| | | | | | | | | | (in thousands) | |

| China Everbright Bank | | July 2021 | | September 2023 | | 3.40%~3.60% | | | RMB150,000 | | | RMB120,000 | |

| | | | | | | | | | $ | 21,120 | | | $ | 16,896 | |

| Bank of Communications | | August 2022 | | September 2023 | | 3.50%~3.60% | | | RMB100,000 | | | RMB100,000 | |

| | | | | | | | | | $ | 14,080 | | | $ | 14,080 | |

| Bank of China | | August 2022 | | August 2023 | | | 3.15 | % | | RMB40,000 | | | RMB40,000 | |

| | | | | | | | | | | $ | 5,632 | | | $ | 5,632 | |

| China Merchants Bank | | October 2021 | | October 2022 | | | 3.50 | % | | RMB100,000 | | | RMB100,000 | |

| | | | | | | | | | | $ | 14,080 | | | | 14,080.00 | |

| China Merchants Bank | | November 2020 | | Repayable by

installments and the last installments repayable in November 2030 | | | 3.95 | % | | RMB128,500 | | | RMB109,149 | |

| | | | | | | | | | | $ | 18,093 | | | $ | 15,368 | |

| Bank of China | | June 2021 | | Repayable by installments and the last installments repayable in June 2024 | | | 2.60 | % | | RMB10,000 | | | RMB9,000 | |

| | | | | | | | | | | $ | 1,408 | | | $ | 1,267 | |

| Bank of China | | September, 2021 | | Repayable by installments and the last installments repayable in September 2021 | | | 2.60 | % | | RMB35,000 | | | RMB31,500 | |

| | | | | | | | | | | $ | 4,928 | | | $ | 4,435 | |

| | | | | | | | | | | $ | 79,341 | | | $ | 71,758 | |

| (1) | Converted from RMB to dollars as of September 30, 2022. All of the amounts owing under the line of credit with Bank of Shanghai Pudong Branch are guaranteed by CleanChip Technologies LTD, a wholly-owned subsidiary of ACM Shanghai. The loan from China Merchants Bank is secured by a pledge of the property of ACM Shengwei and guaranteed by ACM Shanghai, as described above under “—Contractual Obligations.” |

Effect of exchange rate changes on cash, cash equivalents and restricted cash. The value of our cash, and cash equivalents declined $42.6 million during the first nine months of 2022. The impact of fluctuations of the RMB to U.S. dollar currency exchange rate on a significant balance of these items held in RMB-denominated accounts (Note 2) contributed to the change.

Contractual Obligations

Grant Contract for State-owned Construction Land Use Right in Shanghai City

In 2020 ACM Shanghai, through its wholly-owned subsidiary ACM Shengwei, entered into a Grant Contract for State-owned Construction Land Use Right in Shanghai City (Category of R&D Headquarters and Industrial Projects), or the Grant Agreement, with the China (Shanghai) Pilot Free Trade Zone Lin-gang Special Area Administration, or the Grantor. ACM Shengwei obtained rights to use approximately 43,000 square meters (10.6 acres) of land in the Lingang Heavy Equipment Industrial Zone of Lin-gang Special Area of China (Shanghai) Pilot Free Trade Zone, or the Land Use Right, for a period of fifty years, commencing on the date of delivery of the land in July 2020, which we refer to as the Delivery Date.

In exchange for its land use rights, ACM Shengwei paid aggregate grant fees of RMB 61.7 million ($9.5 million), or the Grant Fees, and a performance deposit of RMB 12.3 million ($1.9 million), which is equal to 20% of the aggregate grant fees, to secure its achievement of the following performance milestones:

| • | the start of construction within 6 months after the Delivery Date (60% of the performance deposit), or Construction Start Milestone; |

| • | the completion of construction within 30 months after the Delivery Date (20% of the performance deposit), or Construction Completion Milestone; and |

| • | the start of production within 42 months after the Delivery Date (20% of the performance deposit), or Production Start Milestone. |

Upon satisfaction of a milestone, the portion of the performance deposit attributable to that milestone will be repayable to ACM Shengwei within ten business days. If the achievement of any of the above milestones is delayed or abandoned, ACM Shengwei may be subject to additional penalties and may lose its rights to both the use of the granted land and any partially completed facilities on that land.

The status of the performance milestones for the period ended September 30, 2022 is as follows:

| • | ACM Shengwei achieved the Construction Start Milestone and 60% of the performance deposit was refunded to ACM Shanghai in 2020. |

| • | The Construction Completion Milestone is required to be met prior to January 9, 2023. Although this date has not yet been reached, due to COVID-19 related restrictions, ACM Shengwei has experienced delays and does not expect to meet the milestone, and plans to file a request for an extension in December 2022. We cannot guarantee the extension will be met or that ACM Shengwei will be refunded this 20% portion of the performance deposit. |

Contractual penalties in the case of a delay of Construction Completion Milestone:

| o | If ACM Shengwei fails to complete the construction pursuant to the date agreed under the Grant Agreement or any extended completion date approved by the Grantor, ACM Shengwei shall pay 50% of the deposit for timely completion of construction as liquidated damages; |

| o | If the ACM Shengwei delays the completion for more than six months beyond the date agreed under the Grant Agreement, or beyond any extended completion date approved by the Grantor, it shall pay the total deposit for timely completion of construction as liquidated damages. |

| o | If the delay is more than one year, the Grantor is entitled to terminate the Grant Agreement and take back the Land Use Right. In such case, the Grantor shall refund the Grant Fees for the remaining land use term after deducting the deposit agreed under the Grant Agreement and refund the deposit for timely commencement of production and relevant bank interests in full to ACM Shengwei. |

| • | The Production Start Milestone is required to be met prior to January 9, 2024. Although this date has not yet been reached, ACM Shengwei plans to also file a request for an extension of this milestone due to COVID-related delays. We cannot guarantee the extension will be met or that ACM Shengwei will be refunded this 20% portion of the performance deposit. |

Contractual penalties in the case of a delay of Production Start Milestone:

| o | If ACM Shengwei fails to commence production pursuant to the date agreed under the Grant Agreement or any extended commencement date approved by the Grantor, ACM Shengwei shall pay the total deposit for timely commencement of production as liquidated damages; |

| o | If ACM Shengwei fails to commence production pursuant to the extended commencement of production date, the Grantor is entitled to terminate the Grant Agreement and take back the Land Use Right. In such case, the Grantor shall refund the Grant Fees for the remaining land use term after deducting the deposit agreed under the Grant Agreement to ACM Shengwei. |

In addition to the milestones, covenants in the Grant Agreement require that, among other things, ACM Shengwei will be required to pay liquidated damages in the event that:

(a) it does not make a total investment (including the costs of construction, fixtures, equipment and grant fees) of at least RMB 450.0 million ($63.4 million). ACM Shengwei shall pay the liquidated damages equal to the same proportion of the Grant Fees as the proportion of the actual shortfall amount of investment in the total agreed investment amount or the investment intensity.

(b) within six years after the Delivery Date, or prior to July 9, 2026, it does not (i) generate a minimum specified amount of annual sales of products manufactured on the granted land or (ii) pay to the PRC at least RMB 157.6 million ($22.2 million) in annual total taxes (including value-added taxes, corporate income tax, personal income taxes, urban maintenance and construction taxes, education surcharges, stamp taxes, and vehicle and shipping taxes) as a result of operations in connection with the granted land.

If the total tax revenue of the project fails to reach but is no less than 80% of the standard agreed under the Grant Agreement, ACM Shengwei shall pay 20% of the actual shortfall amount of the tax revenue as liquidated damages. If the total tax revenue of the project fails to reach 80% of the standard agreed under the Grant Agreement within 1 month after the agreed date of reaching target production, the Grantor is entitled to terminate this Contract, take back the Land Use Right, and shall refund the Grant Fees for the remaining Land Use Term to ACM Shengwei.

If the Grant Agreement is terminated because of breach of any terms above, the Grantor shall take back the buildings, fixtures and auxiliary facilities on the land area and provide ACM Shengwei with corresponding compensation according to the residual value of the buildings, fixtures and auxiliary facilities when they are taken back. The total cumulative investment of land, buildings and construction in progress related to ACM Shengwei amounted to $23.1 million and $13.3 million at September 30, 2022 and December 31, 2021, respectively.

Loan and Mortgage Contract for Lingang, Shanghai Housing Units

In connection with its financing the purchase of housing units in Lingang, Shanghai, or the Property, in November 2020 ACM Shengwei entered into a Loan and Mortgage Contract, or the Loan Agreement, with China Merchants Bank Co., Ltd., Shanghai Pilot Free Trade Zone Lin-Gang Special Area Sub-branch, or the Lender, pursuant to which ACM Shengwei obtained a loan in the aggregate amount of $19.6 million. The loan under the Loan Agreement is secured by a pledge of the Property, which ACM Shangwei’s subsidiary received ownership of in January 2022, and is guaranteed by ACM Shanghai. Under the Loan Agreement, ACM Shengwei must deliver the right certificate of the Property within sixty days of the execution of the Loan Agreement or the Lender has the right to, among other things, declare a breach of contract and enforce its remedies under the Loan Agreement, which remedies include the ability to declare any borrowings outstanding, together with accrued and unpaid interest and fees, to be immediately due and payable. As of the date of this report, ACM Shengwei and its developer have been unable to obtain the required right certificate of the Property due to administrative difficulties related to the COVID 19 pandemic and, as a result, the procedures of the formal pledge registration by the Lender have not been completed. The Lender delivered an updated letter to ACM Shengwei on October 21, 2022 confirming that it is aware of the cause of the delay in ACM Shengwei’s delivery of the right certificate of the Property and as of the date of this report has not taken any action to date as a result of the delay. The Lender could, however, assert at any time that the delay is a breach of contract and, among other remedies, could seek to declare the amounts owing under the Loan Agreement to be due and payable. The Shanghai Lingang Industrial Zone Public Rental Housing Construction and Operation Management Co., Ltd., or the Developer, delivered a letter to ACM Shengwei on August 4, 2022, citing a force majeure delay due to the COVID-19-related restrictions in Shanghai for the delay of the initial registration of the housing ownership, and that it expected to complete the initial registration of housing ownership by the end of August 2022. ACM Shanghai has confirmed the Developer has completed the initial registration of the housing ownership with local PRC authorities, and, as of the date of this filing, expects to receive the right certificate before December 31, 2022. See “Risks Related to International Aspects of Our Business—As the result of administrative delays in the PRC related to the COVID-19 pandemic, ACM Research’s indirect subsidiary ACM Shengwei has not been able to obtain the right certificate of property in Lingang, Shanghai as required by its Loan and Mortgage Contract, and our liquidity, financial position and business would be adversely affected if the lender bank were to assert successfully that the failure to obtain the right certificate is a breach of the Loan and Mortgage Contract” in Item 1A. Risk Factors of Part II of our Quarterly Report on Form 10-Q for the quarter ended June 30, 2022.

How We Evaluate Our Operations

We present information below with respect to four measures of financial performance:

| ● | We define “shipments” of tools to include (a) a “repeat” delivery to a customer of a type of tool that the customer has previously accepted, for which we recognize revenue upon delivery, and (b) a “first-time” delivery of a “first tool” to a customer on an approval basis, for which we may recognize revenue in the future if contractual conditions are met, or if a purchase order is received. |

| ● | We define “adjusted EBITDA” as net income excluding interest expense (net), income tax benefit (expense), depreciation and amortization, unrealized (gain) loss on trading securities, and stock-based compensation. We define adjusted EBITDA to also exclude restructuring costs, although we have not incurred any such costs to date. |

| ● | We define “free cash flow” as net cash provided by operating activities less purchases of property and equipment (net of proceeds from disposals). |

| ● | We define “adjusted operating income (loss)” as our income (loss) from operations excluding stock-based compensation. |

These financial measures are not based on any standardized methodologies prescribed by accounting principles generally accepted in the United States, or GAAP, and are not necessarily comparable to similarly titled measures presented by other companies.

We have presented shipments, adjusted EBITDA, free cash flow and adjusted operating income (loss) because they are key measures used by our management and board of directors to understand and evaluate our operating performance, to establish budgets and to develop operational goals for managing our business. We believe that these financial measures help identify underlying trends in our business that could otherwise be masked by the effect of the expenses that we exclude. In particular, we believe that the exclusion of the expenses eliminated in calculating adjusted EBITDA and adjusted operating income (loss) can provide useful measures for period-to-period comparisons of our core operating performance and that the exclusion of property and equipment purchases from operating cash flow can provide a usual means to gauge our capability to generate cash. Accordingly, we believe that these financial measures provide useful information to investors and others in understanding and evaluating our operating results, enhancing the overall understanding of our past performance and future prospects, and allowing for greater transparency with respect to key financial metrics used by our management in its financial and operational decision-making.

Shipments, adjusted EBITDA, free cash flow and adjusted operating income (loss) are not prepared in accordance with GAAP, and should not be considered in isolation of, or as an alternative to, measures prepared in accordance with GAAP.

Shipments

We consider shipments a key operating metric as it reflects the total value of products delivered to customers and prospective customers by our productive assets.

Shipments consist of two components:

| ● | a shipment to a customer of a type of tool that the customer has previously accepted, for which we recognize revenue when the tool is delivered; and |

| ● | a shipment to a customer of a type of tool that the customer is receiving and evaluating for the first time, in each case a “first tool,” for which we may recognize revenue at a later date, subject to the customer’s acceptance of the tool upon the tool’s satisfaction of applicable contractual requirements or subject to the costumer’s subsequent discretionary commitment to purchase the tool. |

“First tool” shipments can be made to either an existing customer that has not previously accepted that specific type of tool in the past ─ for example, a delivery of a SAPS V tool to a customer that previously had received only SAPS II tools ─ or to a new customer that has never purchased any tool from us.

Shipments in the three and nine months ended September 30, 2022 totaled $163 million and $342 million, as compared to $99 million and $255 million for the same periods in 2021. Repeat tool shipments in the three and nine months ended September 30, 2022 totaled $112 million and $209 million, as compared to $58 million and $145 million for the same periods in 2021. First tool shipments in the three- and nine-months ended September 30, 2022 totaled $51 million and $133 million, as compared to $41 million and $110 million for the same periods in 2021.

The dollar amount attributed to a “first tool” shipment is equal to the consideration we expect to receive if any and all contractual requirements are satisfied and the customer accepts the tool, or if the customer subsequently determines in its discretion to purchase the tool. There are a number of limitations related to the use of shipments in evaluating our business, including that customers have significant, or in some cases total, discretion in determining whether to accept or purchase our tools after evaluation and their decision not to accept or purchase delivered tools is likely to result in our inability to recognize revenue from the delivered tools. “First tool” shipments reflect the value of incremental new products under evaluation delivered to our customers or prospective customers for a given period and is used as an internal key metric to reflect future potential revenue opportunity. The cumulative cost of “first tool” shipments under evaluation at customers which have not been accepted by the customer is carried at cost and reflected in finished goods inventory (see note 5 to the condensed consolidated financial statements included in this report). “First tool” shipments exclude deliveries to customers for which ACM does not have a basis to expect future revenue.

Adjusted EBITDA

There are a number of limitations related to the use of adjusted EBITDA rather than net income (loss), which is the nearest GAAP equivalent. Some of these limitations are:

| ● | adjusted EBITDA excludes depreciation and amortization and, although these are non-cash expenses, the assets being depreciated or amortized may have to be replaced in the future; |

| ● | we exclude stock-based compensation expense from adjusted EBITDA and adjusted operating income (loss), although (a) it has been, and will continue to be for the foreseeable future, a significant recurring expense for our business and an important part of our compensation strategy and (b) if we did not pay out a portion of our compensation in the form of stock-based compensation, the cash salary expense included in operating expenses would be higher, which would affect our cash position; |

| ● | the expenses and other items that we exclude in our calculation of adjusted EBITDA may differ from the expenses and other items, if any, that other companies may exclude from adjusted EBITDA when they report their operating results; |

| ● | adjusted EBITDA does not reflect changes in, or cash requirements for, working capital needs; |

| ● | adjusted EBITDA does not reflect interest expense, or the requirements necessary to service interest or principal payments on debt; |

| ● | adjusted EBITDA does not reflect income tax expense (benefit) or the cash requirements to pay taxes; |

| ● | adjusted EBITDA does not reflect historical cash expenditures or future requirements for capital expenditures or contractual commitments; |

| ● | although depreciation and amortization charges are non-cash charges, the assets being depreciated and amortized will often have to be replaced in the future, and adjusted EBITDA does not reflect any cash requirements for such replacements; and |

| ● | adjusted EBITDA includes expense reductions and non-operating other income attributable to PRC governmental grants, which may mask the effect of underlying developments in net income, including trends in current expenses and interest expense, and free cash flow includes the PRC governmental grants, the amount and timing of which can be difficult to predict and are outside our control. |

The following table reconciles net income, the most directly comparable GAAP financial measure, to adjusted EBITDA:

| | | Nine Months Ended September 30, | | | % Change

2022 v 2021 | |

| Absolute Change 2022 v 2021 | |

| | | 2022 | | | 2021 | | |

| | | (in thousands) | | | | | | | |

| Adjusted EBITDA Data: | | | | | | | | | | | | |

| Net Income | | $ | 36,381 | | | $ | 24,306 | | | | 49.7 | % | | $ | 12,075 | |

| Interest expense (income), net | | | (4,979 | ) | | | 461 | | | | -1180.0 | % | | | (5,440 | ) |

| Income tax expense (benefit) | | | 14,138 | | | | (3,021 | ) | | | -568.0 | % | | | 17,159 | |

| Depreciation and amortization | | | 4,104 | | | | 1,597 | | | | 157.0 | % | | | 2,507 | |

| Stock based compensation | | | 5,236 | | | | 3,823 | | | | 37.0 | % | | | 1,413 | |

| Unrealized (gain) loss on trading securities | | | 9,562 | | | | (1,817 | ) | | | -626.3 | % | | | 11,379 | |

| Adjusted EBITDA | | $ | 64,442 | | | $ | 25,349 | | | | 154.2 | % | | $ | 39,093 | |

The $39.1 million increase in adjusted EBITDA for the nine months ended September 30, 2022 as compared to the same period in 2021 reflected a $17.2 million impact from a change in income tax benefit (expense), a $12.1 million increase in net income, an $11.4 million increase in unrealized (gain) loss on trading securities, a $1.4 million increase in stock based compensation, and a $2.5 million increase in depreciation and amortization, partly offset by a $5.4 million impact from an increase in interest income, net.

We do not exclude from adjusted EBITDA expense reductions and non-operating other income attributable to PRC governmental grants because we consider and incorporate the expected amounts and timing of those grants in incurring expenses and capital expenditures. If we did not receive the grants, our cash expenses therefore would be lower, and our cash position would not be affected, to the extent we have accurately anticipated the amounts of the grants. For additional information regarding our PRC grants, please see “—Key Components of Results of Operations—PRC Government Research and Development Funding.”

Free Cash Flow

The following table reconciles net cash provided by (used in) operating activities, the most directly comparable GAAP financial measure, to free cash flow:

| | | Nine Months Ended September 30, | | | % Change

2022 v 2021 | | | Absolute Change 2022 v 2021 | |

| | | 2022 | | | 2021 | | |

| | | (in thousands) | | | | | | | |

| Free Cash Flow Data: | | | | | | | | | | | | |

| Net cash used in operating activities | | $ | (63,530 | ) | | $ | (3,822 | ) | | | 1562.2 | % | | $ | (59,708 | ) |

| Purchase of property and equipment | | | (18,417 | ) | | | (5,059 | ) | | | 264.0 | % | | | (13,358 | ) |

| Free cash flow | | $ | (81,947 | ) | | $ | (8,881 | ) | | | 822.7 | % | | $ | (73,066 | ) |

The $73.1 million decrease in free cash flow for the nine months ended September 30, 2022 as compared to the same period in 2021 reflected the factors driving net cash used in operating activities, an increase of purchases of property and equipment, and an increase of purchase of intangible assets. Consistent with our methodology for calculating adjusted EBITDA, we do not adjust free cash flow for the effects of PRC government subsidies, because we take those subsidies into account in incurring expenses and capital expenditures. We do not adjust free cash flow for the effects of time-deposits, which for our internal purposes are considered as largely similar to cash.

Adjusted Operating Income

Adjusted operating income excludes stock-based compensation from income from operations. Although stock-based compensation is an important aspect of the compensation of our employees and executives, determining the fair value of certain of the stock-based instruments we utilize involves a high degree of judgment and estimation and the expense recorded may bear little resemblance to the actual value realized upon the vesting or future exercise of the related stock-based awards. Furthermore, unlike cash compensation, the value of stock options, which is an element of our ongoing stock-based compensation expense, is determined using a complex formula that incorporates factors, such as market volatility, that are beyond our control. Management believes it is useful to exclude stock-based compensation in order to better understand the long-term performance of our core business and to facilitate comparison of our results to those of peer companies. The use of non-GAAP financial measures excluding stock-based compensation has limitations, however. If we did not pay out a portion of our compensation in the form of stock-based compensation, the cash salary expense included in operating expenses would be higher and our cash holdings would be less. The following tables reflect the exclusion of stock-based compensation, or SBC, from line items comprising income from operations:

| | | Nine Months Ended September 30, | |

| | | 2022 | | | 2021 | |

| | | Actual

(GAAP) | | | SBC | | | Adjusted

(Non- GAAP) | | | Actual

(GAAP) | | | SBC | | | Adjusted

(Non-GAAP) | |

| | | (in thousands) | |

| Revenue | | $ | 280,290 | | | $ | - | | | $ | 280,290 | | | $ | 164,609 | | | $ | - | | | $ | 164,609 | |

| Cost of revenue | | | (150,480 | ) | | | (383 | ) | | | (150,097 | ) | | | (95,199 | ) | | | (289 | ) | | | (94,910 | ) |

| Gross profit | | | 129,810 | | | | (383 | ) | | | 130,193 | | | | 69,410 | | | | (289 | ) | | | 69,699 | |

| Operating expenses: | | | | | | | | | | | | | | | | | | | | | | | | |

| Sales and marketing | | | (27,494 | ) | | | (1,277 | ) | | | (26,217 | ) | | | (17,460 | ) | | | (1,400 | ) | | | (16,060 | ) |

| Research and development | | | (44,391 | ) | | | (1,733 | ) | | | (42,658 | ) | | | (21,293 | ) | | | (801 | ) | | | (20,492 | ) |

| General and administrative | | | (15,560 | ) | | | (1,843 | ) | | | (13,717 | ) | | | (11,081 | ) | | | (1,333 | ) | | | (9,748 | ) |

| Income (loss) from operations | | | 42,365 | | | | (5,236 | ) | | | 47,601 | | | | 19,576 | | | | (3,823 | ) | | | 23,399 | |

Adjusted operating income for the nine months ended September 30, 2022 increased by $24.2 million, as compared with the same period in 2021, due to a $22.8 million increase in income from operations and a $1.4 million increase in stock-based compensation expense.

| | Three Months Ended September 30, | |

| | | 2022 | | | 2021 | |

| | | Actual

(GAAP) | | | SBC | | | Adjusted

(Non- GAAP) | | | Actual

(GAAP) | | | SBC | | | Adjusted

(Non-GAAP) | |

| | | (in thousands) | |

| Revenue | | $ | 133,709 | | | $ | - | | | $ | 133,709 | | | $ | 67,013 | | | $ | - | | | $ | 67,013 | |

| Cost of revenue | | | (67,742 | ) | | | (130 | ) | | | (67,612 | ) | | | (37,328 | ) | | | (108 | ) | | | (37,220 | ) |

| Gross profit | | | 65,967 | | | | (130 | ) | | | 66,097 | | | | 29,685 | | | | (108 | ) | | | 29,793 | |

| Operating expenses: | | | | | | | | | | | | | | | | | | | | | | | | |

| Sales and marketing | | | (13,133 | ) | | | (349 | ) | | | (12,784 | ) | | | (6,363 | ) | | | (417 | ) | | | (5,946 | ) |

| Research and development | | | (15,678 | ) | | | (666 | ) | | | (15,012 | ) | | | (7,856 | ) | | | (293 | ) | | | (7,563 | ) |

| General and administrative | | | (5,520 | ) | | | (748 | ) | | | (4,772 | ) | | | (3,671 | ) | | | (460 | ) | | | (3,211 | ) |

| Income (loss) from operations | | | 31,636 | | | | (1,893 | ) | | | 33,529 | | | | 11,795 | | | | (1,278 | ) | | | 13,073 | |

Adjusted operating income for the three months ended September 30, 2022 increased by $20.5 million, as compared with the same period in 2021, due to a $19.8 million increase in income from operations, offset by a $0.6 million increase in stock-based compensation expense.

| Item 3. | Quantitative and Qualitative Disclosures About Market Risks |

Our market risks and the ways we manage them are summarized in the section captioned “Part II, Item 7A. Quantitative and Qualitative Disclosures About Market Risk” in our Annual Report. There have been no material changes in the first nine months of 2022 to our market risks or to our management of such risks.

| Item 4. | Controls and Procedures |

Evaluation of Disclosure Controls and Procedures

Our management, with the participation of our Chief Executive Officer and Chief Financial Officer, evaluated the effectiveness of our company’s disclosure controls and procedures pursuant to Rule 13a-15 under the Securities Exchange Act of 1934, or the Exchange Act, as of September 30, 2022. The evaluation included certain internal control areas in which we have made and are continuing to make changes to improve and enhance controls. In designing and evaluating the disclosure controls and procedures, management recognized that any controls and procedures, no matter how well designed and operated, can provide only reasonable assurance of achieving the desired control objectives. In addition, the design of disclosure controls and procedures must reflect the fact that there are resource constraints and that management is required to apply its judgment in evaluating the benefits of possible controls and procedures relative to their costs. The effectiveness of the disclosure controls and procedures is also necessarily limited by the staff and other resources available to management and the geographic diversity of our company’s operations. As a result of the COVID-19 pandemic, beginning in 2020 we have faced additional challenges in operating and monitoring our disclosure controls and procedures as a result of employees working remotely and management travel being limited. In addition, we face potential heightened cybersecurity risks as our level of dependence on our IT networks and related systems increases, stemming from employees working remotely, and the number of malware campaigns and phishing attacks preying on the uncertainties surrounding COVID‑19 increases.

Based on that evaluation, our Chief Executive Officer and Chief Financial Officer concluded that, as of September 30, 2022, our company’s disclosure controls and procedures were effective to provide reasonable assurance that information we are required to disclose in reports that we file or submit under the Exchange Act is recorded, processed, summarized and reported within the time periods specified in Securities and Exchange Commission rules and forms, and that such information is accumulated and communicated to our management, including our Chief Executive Officer and Chief Financial Officer, as appropriate, to allow timely decisions regarding required disclosure.

Changes in Internal Control over Financial Reporting and Remediation Efforts

There were no changes in our internal control over financial reporting during the nine months ended September 30, 2022 that have materially affected, or are reasonably likely to materially affect, our internal control over financial reporting. We will continue to review and document our disclosure controls and procedures, including our internal control over financial reporting and may from time to time make changes to enhance their effectiveness and ensure that our systems evolve with our business.

PART II. OTHER INFORMATION

From time to time, we may become involved in other legal proceedings or may be subject to claims arising in the ordinary course of our business. Although the results of these proceedings and claims cannot be predicted with certainty, we currently believe that the final outcome of these ordinary course matters will not have a material adverse effect on our business, operating results, financial condition or cash flows. Regardless of the outcome, litigation can have an adverse impact on us because of defense and settlement costs, diversion of management resources and other factors.

Except as set forth below, there were no material changes to the risk factors discussed in Item 1A. “Risk Factors” of Part I in our Annual Report and in Item 1A. “Risk Factors” of Part II in our Quarterly Report on Form 10-Q for the quarter ended June 30, 2022. In addition to the other information set forth in this report, you should carefully consider those risk factors, which could materially affect our business, financial condition and future operating results. Those risk factors are not the only risks facing our company. Additional risks and uncertainties not currently known to us or that we currently deem to be immaterial also may have a material adverse effect on our business, financial condition and operating results.

Risks Related to International Aspects of Our Business

We could be adversely affected if we are unable to comply with recent and proposed legislation and regulations regarding improved access to audit and other information and audit inspections of accounting firms, including registered public accounting firms, such as our audit firm since our initial public offering in 2017, operating in the PRC.

We are one of the companies named in the SEC’s “Conclusive list of issuers identified under the HFCAA.” BDO China had been our independent registered public accounting firm in recent years, including for the year ended December 31, 2021, and is not inspected by the PCAOB.

The HFCA Act, which became law in December 2020, includes requirements for the SEC to identify issuers whose audit work is performed by auditors that the PCAOB is unable to inspect or investigate completely because of a restriction imposed by a non-U.S. authority in the auditor’s local jurisdiction. The HFCA Act also requires that, to the extent that the PCAOB has been unable to inspect an issuer’s auditor for three consecutive years since 2021, the SEC shall prohibit the issuer’s securities registered in the United States from being traded on any national securities exchange or over-the-counter market in the United States.

| • | On March 24, 2021, the SEC adopted interim final amendments to implement congressionally mandated submission and disclosure required of the HFCA Act, and on December 2, 2021, the SEC adopted final amendments to finalize rules implementing the submission and disclosures in the HFCA Act. These final amendments apply to registrants that the SEC identifies as having filed an Annual Report on Form 10-K (or certain other forms) with an audit report issued by a registered public accounting firm that is located in a foreign jurisdiction and that the PCAOB has determined it is unable to inspect or investigate completely because of a position taken by an authority in that jurisdiction. Any such identified registrant will be required to submit documentation to the SEC establishing that it is not owned or controlled by a governmental entity in that foreign jurisdiction, and will also require disclosure in the registrant’s annual report regarding the audit arrangements of, and governmental influence on, such a registrant. |

| • | Furthermore, on June 22, 2021, the U.S. Senate passed the Accelerating Holding Foreign Companies Accountable Act, which, if enacted, would amend the HFCA Act to require the SEC to prohibit an issuer’s securities from trading on any national securities exchange or over-the-counter market in the United States if the PCAOB has been unable to inspect an issuer’s auditor for two, rather than three, consecutive years. On September 22, 2021, the PCAOB adopted a final rule implementing the HFCA Act, which provides a framework for the PCAOB to use when determining, as contemplated under the HFCA Act, whether the PCAOB is unable to inspect or investigate completely registered public accounting firms located in a foreign jurisdiction because of a position taken by one or more authorities in that jurisdiction. |

| • | On December 16, 2021, the PCAOB designated China and Hong Kong as jurisdictions where the PCAOB is not allowed to conduct full and complete audit inspections and has identified firms registered in such jurisdictions, including BDO China. Pursuant to each annual determination by the PCAOB, the SEC will, on an annual basis, identify issuers that have used non-inspected audit firms. |

| • | On March 8, 2022, the SEC published its first “Provisional list of issuers identified under the HFCAA.” Our company was identified on the SEC’s provisional list after we filed the Annual Report, which included an audit report issued by BDO China. According to current SEC guidelines, a trading prohibition on our Class A common stock could be invoked as early as 2024. |

| • | On March 30, 2022, our company was transferred to the SEC’s “Conclusive list of issuers identified under the HFCAA.” |

| • | On August 26, 2022, the PCAOB signed a Statement of Protocol, or SOP, Agreement with the CSRC and China’s Ministry of Finance. The SOP, together with two protocol agreements governing inspections and investigation, establishes a specific, accountable framework to make possible complete inspections and investigations by the PCAOB of audit firms based in China and Hong Kong, as required under U.S. law. Pursuant to the fact sheet with respect to the SOP disclosed by the SEC, the PCAOB has sole discretion to select the audit firms, engagements and potential violations that it inspects or investigates and has the ability to transfer information to the SEC in the normal course. PCAOB inspectors and investigators can view all audit documentation without redaction, and the PCAOB can retain any audit information it reviews as needed to support the findings of its inspections and investigations. In addition, the SOP allows the PCAOB to interview and take testimony of personnel associated with the audits that the PCAOB inspects or investigates. However, uncertainties still exist as to whether and how the SOP will be implemented and whether the PCAOB can make a determination that it is able to inspect and investigate completely audit firms based in mainland China and Hong Kong. When the PCAOB reassesses its determinations by the end of 2022, it could determine that it is still unable to inspect and investigate completely audit firms based in mainland China and Hong Kong. |

Per current regulations, if ACM Research were to appear three consecutive times on the “Conclusive list of issuers identified under the HFCAA”, which could occur should our independent auditor that signs our 2022 and 2023 annual report be located in a jurisdiction that does not allow for PCAOB inspections, the value of our securities may significantly decline or become worthless, and our securities may eventually be delisted. If enacted, the Accelerating Holding Foreign Companies Accountable Act could reduce the threshold to two consecutive appearances on the “Conclusive List of issuers identified under the HFCAA”, and thus could trigger a de-listing should our independent auditor that signs our 2022 annual report be located in a jurisdiction that does not allow for PCAOB inspections.

Our independent registered public accounting firm for the year ended December 31, 2022 is Armanino LLP, which is registered with the PCAOB. On June 30, 2022, stockholders of ACM Research ratified the appointment of Armanino LLP as our independent auditor for the fiscal year ending December 31, 2022. Armanino LLP is neither headquartered in the PRC or Hong Kong nor is it subject to the determinations announced by the PCAOB.

It remains unclear what further actions the SEC, the PCAOB or Nasdaq may take to address these issues and what impact those actions will have on U.S. companies, such as ours, that have significant operations in the PRC and have securities listed on a U.S. stock exchange. Any such actions could materially affect our operations and stock price, including by resulting in our being de-listed from Nasdaq or being required to engage a new audit firm, which would require significant expense and management time.

If any PRC central government authority were to determine that existing PRC laws or regulations require that ACM Shanghai obtain the authority’s permission or approval to continue the listing of ACM Research’s Class A common stock in the United States or if those existing PRC laws and regulations, or interpretations thereof, were to change to require such permission or approval, or if we inadvertently conclude that permissions or approvals are not required, ACM Shanghai may be unable to obtain the required permission or approval or may only be able to obtain such permission or approval on terms and conditions that impose material new restrictions and limitations on operation of ACM Shanghai, either of which could have a material adverse effect on our business, financial condition, results of operations, reputation and prospects and on the trading price of ACM Research Class A common stock, which could decline in value or become worthless.

PRC central government authorities have taken steps to preclude, or significantly discourage, certain PRC companies from listing on U.S. and other exchanges outside the PRC. Investments activities in the PRC by non-PRC investors are principally governed by the Encouraged Industries Catalog for Foreign Investment (2020 version) and the Special Administrative Measures for Foreign Investment Access (Negative List 2021), both of which were promulgated by the PRC’s Ministry of Commerce, or MOFCOM, and National Development and Reform Commission. These regulations set forth the industries in which foreign investments are encouraged, restricted and prohibited.

Industries that are not listed in any of these three categories are generally open to foreign investment unless otherwise specifically restricted by other PRC rules and regulations. We believe that our operations do not fall within any industry that is restricted or prohibited under these regulations and that the regulations therefore do not apply to us.

PRC-based companies that seek to list their shares in the United States but are subject to PRC restrictions on investments by non-PRC investors sometimes use a special purpose vehicle known as a variable interest entity, or VIE, created in an off-shore jurisdiction such as the Cayman Islands. In these structures, a VIE enters into a series of contractual arrangements with the PRC-based operating company and its PRC-based shareholders that afford those shareholders, rather than the shareholders of the VIE, effective control over the finances and operations of the operating company. The VIE, effectively a shell company, issues shares that are listed for trading on a U.S. exchange, but the enterprise is controlled by the legacy PRC-based shareholders and is subject to PRC laws and regulations. ACM Research is not a VIE or other special purpose, or shell, company, and its relationship with ACM Shanghai does not involve the types of contractual arrangements existing between a VIE and a PRC-based operating company. ACM Research is a Delaware corporation founded in California in 1998 that formed ACM Shanghai to conduct business operations in the PRC. ACM Research controls the operations of ACM Shanghai through its direct ownership of ACM Shanghai shares, and it also conducts sales and marketing activities focused on sales of ACM Shanghai products in North America, Europe and certain regions in Asia outside mainland China.

We do not believe that our corporate structure or any other matters relating to our business operations currently require that ACM Shanghai obtain any permissions or approvals from the China Securities Regulatory Commission, or CSRC, or any other PRC central government authority in connection with ACM’s listing, or offering for sale in the future, shares of our Class A common stock in the United States. We, including ACM Shanghai, therefore have never solicited any permission or approval from any PRC central government authority in connection with ACM Research’s seeking and maintaining the listing of our Class A common stock in the United States. In the event that we inadvertently conclude that permissions or approvals are not required, or either the CSRC or another PRC central government authority were to determine that existing PRC laws or regulations require that ACM Shanghai obtain the authority’s permission or approval to continue ACM Research’s listing of Class A common stock in the United States or if those existing PRC laws and regulations, or interpretations thereof, were to change to require such permission or approval, ACM Shanghai could be unable to obtain any such permission or approval or could be able to obtain such permission or approval only on terms and conditions that impose material new operating or other restrictions and limitations on ACM Shanghai. In such circumstances, it would materially and adversely affect the value of our Class A common stock, which may decline in value or become worthless. In addition, ACM Shanghai could face sanctions by the CSRC or other PRC central government authorities or pressure from the PRC government in various business matters for failure to obtain such permission or approval. Such potential sanctions or pressure may include fines and penalties on ACM Shanghai’s operations in the PRC, limitations on its operating privileges in the PRC, delays in or restrictions on the transfer of proceeds from a public offering of ACM Research securities in the United States to ACM Shanghai, restrictions on or prohibition of the payments or remittance of dividends by ACM Shanghai to ACM Research, or other actions that could have a material and adverse effect on our business, financial condition, results of operations, reputation and prospects, as well as the trading price of ACM Research Class A common stock, which could decline in value or become worthless.

PRC central government authorities may intervene in, or influence, ACM Shanghai’s PRC-based operations at any time, and those authorities’ rules and regulations in the PRC can change quickly with little or no advance notice.

The business of ACM Shanghai is subject to complex laws and regulations in the PRC that can change quickly with little or no advance notice. To date, beyond the COVID-19-related restrictions in 2022, we have not experienced such intervention or influence by PRC central government authorities or a change in those authorities’ rules and regulations that have had a material impact of ACM Shanghai or ACM Research. We cannot assure you, however, that future changes in PRC laws and regulations will not materially and adversely affect our PRC-based operations. For example:

| • | Intellectual Property. Our commercial success depends in part on our ability to obtain and maintain patent and trade secret protection for our intellectual property, including our SAPS, TEBO, Tahoe, ECP, furnace and other technologies and the design of our Ultra C equipment. See “Risks Related to Our Intellectual Property and Data Security¾Our success depends on our ability to protect our intellectual property, including our SAPS, TEBO, Tahoe, ECP, furnace and other technologies.” in Item 1A, “Risk Factors” of Part I of our Annual Report. The significant majority of our intellectual property has been developed in the PRC and is owned by ACM Shanghai. Implementation and enforcement of intellectual property-related laws in the PRC has historically been lacking due primarily to ambiguities in PRC intellectual property law. See “Risks Related to Our Intellectual Property and Data Security¾We may not be able to protect our intellectual property rights throughout the world, including the PRC, which could materially, negatively affect our business.” in Item 1A, “Risk Factors” of Part I of our Annual Report. In the event PRC central government authorities were to significantly revise or revamp the current scope and structure of intellectual property protection in the PRC, our ability to protect and enforce our intellectual property rights for our key proprietary technologies may be adversely impacted and competitors may be able to match our technologies and tools in order to compete with us. |

| • | Title Defect in Leased Premises. We conduct research and development, service support operations, and a portion of our manufacturing at ACM Shanghai’s headquarters located in the Zhangjiang Hi Tech Park in Shanghai, which ACM Shanghai leases from Zhangjiang Group. Zhangjiang Group has not obtained a certificate of property title for the premises, although it has represented to ACM Shanghai that it has the right to rent the premises to ACM Shanghai. If any adjustment in local regional overall planning of Shanghai, or any other reason, results in the demolition of such premises, the premises could not continue to be leased to ACM Shanghai and the day-to-day production and operation of ACM Shanghai would be materially and adversely affected. See Item 2, “Properties” of Part I of our Annual Report. |

| • | COVID-19 Pandemic. We conduct substantially all of our product development, manufacturing, support and services in the PRC, and those activities have been directly impacted by COVID-19 and related restrictions on transportation and public appearances, including implementation by PRC government authorities of “spot” and full-city quarantines in the city of Shanghai, where substantially all of our operations are located. Furthermore, a number of our key customers have substantial operations based in operations areas of the PRC, including in the City of Shanghai, which required us to defer, in the first quarter of 2022, shipments of finished products to those customers. Protective measures taken by PRC government authorities in upcoming months could result in closures or reductions of PRC operations or production, whether of ACM Shanghai or of some of its key customers, or other business interruptions, any of which could materially adversely affect our operations. See “Substantially all of our operations, as well as significant operations of a number of our key customers, are located in areas of the PRC impacted by the COVID‑19 pandemic, and our operations have been, and may continue to be, adversely affected by the effects of PRC restrictions imposed as the result of COVID‑19.” in Item 1A, “Risk Factors” of Part II of this report. |

| • | Data Security. The Standing Committee of the National People’s Congress, or the Standing Committee, has promulgated the Cyber Security Law, which imposes requirements on entities who build and operate the PRC’s internet architecture or provide services in the PRC over the internet, and the Data Security Law, which imposes data security and privacy obligations on entities and individuals carrying out data activities. The Data Security Law also provides for a national security review procedure for data activities that may affect national security and imposes export restrictions on certain data an information. ACM Shanghai is not subject to the existing restrictions imposed by the Cyber Security Law or the Data Security Law, in part because its business operations do not involve the collection, processing or use of data or information involving personal privacy or private information of customers. In addition, ACM Shanghai is subject to oversight by the Cyberspace Administration of China, or the CAC, regarding data security. ACM Shanghai does not collect or maintain personal information except for routine personal information necessary to process payroll payments and other benefits and emergency contact information, and as a result, ACM Shanghai is not currently subject to significant restrictions or limitations in addressing and managing data security issues and complying with CAC regulations. To date, ACM Shanghai has not been involved in any investigations on cybersecurity review initiated by the CAC or any related PRC central government authority and has not received any inquiry, notice, warning, or sanction in such respect. However, cybersecurity is increasingly a focus of the PRC central government. If the CAC or other PRC central government authorities should in the future require ACM Shanghai to comply with these or additional, or more restrictive, PRC cybersecurity regulations, it could require ACM Shanghai to make changes to its operations, and any failure to satisfy or delay in meeting such requirements may subject ACM Shanghai to restrictions and penalties imposed by the CAC or other PRC regulatory authorities, which may include regulatory actions, fines and penalties on our operations in the PRC, which could materially harm our business, financial condition, results of operations, reputation and prospects. |

| • | Anti-Monopoly. A number of PRC laws and regulations have established procedures and requirements that could make merger and acquisition activities in China by foreign investors more time consuming and complex. These laws and regulations, which include the Anti-Monopoly Law and the Rules of the Ministry of Commerce on Implementation of Security Review System of Mergers and Acquisitions of Domestic Enterprises by Foreign Investors, impose requirements that in some instances that MOFCOM be notified in advance of, for example, any change-of-control transaction in which a foreign investor takes control of a PRC domestic enterprise. In addition, such Rules specify that mergers and acquisitions by foreign investors that raise “national defense and security” concerns and mergers and acquisitions through which foreign investors may acquire de facto control over domestic enterprises that raise “national security” concerns are subject to strict review by MOFCOM. In February 2021, the Anti-Monopoly Committee of the State Council published the Anti-Monopoly Guidelines for the Internet Platform Economy Sector, which stipulate that any concentration of undertakings involving VIEs is subject to anti-monopoly review. Those Guidelines provide more stringent rules for Internet platform operators, including regulations on the use of data and algorithms, technology and platform to commit abusive acts. The Measures for the Security Review for Foreign Investment, which was promulgated jointly by National Development and Reform Commission and MOFCOM effective January 18, 2021, and the Standing Committee on Amending the Anti-Monopoly Law of the People’s Republic of China, which was promulgated by the Standing Committee effective August 1, 2022, delineated provisions concerning the security review procedures on foreign investment, including the types of investments subject to review and the scopes and procedures of the review. ACM Shanghai does not have the concentration of business operators stipulated in the Anti-Monopoly Law, and our operations and activities to date have not otherwise subjected us to restrictive provisions or limitations set forth in applicable PRC laws and regulations govern merger and acquisition activities. Among other things, ACM Shanghai’s business operations do not constitute identified “national defense and security” concerns associated with the arms industry, any industry ancillary to the arms industry, or any other field related to national defense security. We cannot assure you, however, that future changes in PRC laws and regulations governing mergers and acquisitions, including activities in the PRC by foreign investors, will not extend or otherwise modify existing requirements, which could materially and adversely affect our PRC-based operations or our ability to expand by investments or acquisitions. |

| • | Permits. In the ordinary course of business, ACM Shanghai has obtained all of the permits and licenses it believes are necessary for it to operate in the PRC. ACM Shanghai may be adversely affected, however, by the complexity, uncertainties and changes in PRC laws and regulations applicable to, or otherwise affecting, the semiconductor equipment industry and related businesses, and any lack of requisite approvals, licenses or permits applicable to ACM Shanghai’s business may have a material adverse effect on its business and results of operations. |

| • | Trade Policies. Since 2018, general trade tensions between the United States and the PRC have escalated. See “Regulatory Risks —Changes in government trade policies could limit the demand for our tools and increase the cost of our tools.” in Item 1A, “Risk Factors” of Part I of our Annual Report. The imposition of tariffs by the U.S. and PRC governments and the surrounding economic uncertainty may negatively impact the semiconductor industry, including reducing the demand of fabricators for capital equipment such as our tools. Further changes in trade policy, tariffs, additional taxes, restrictions on exports or other trade barriers, or restrictions on supplies, equipment, and raw materials including rare earth minerals, may limit the ability of our customers to manufacture or sell semiconductors or to make the manufacture or sale of semiconductors more expensive and less profitable, which could lead those customers to fabricate fewer semiconductors and to invest less in capital equipment such as our tools. In addition, if the PRC were to impose additional tariffs on raw materials, subsystems or other supplies that we source from the United States, our cost for those supplies would increase. As a result of any of the foregoing events, the imposition or new or additional tariffs may limit our ability to manufacture tools, increase our selling and/or manufacturing costs, decrease margins, or inhibit our ability to sell tools or to purchase necessary equipment and supplies, which could have a material adverse effect on our business, results of operations, or financial conditions. |

Moreover, by imposing industrial policies and other economic measures, such as control of foreign exchange, taxation and foreign investment, the PRC central government exerts considerable direct and indirect influence on the development of the PRC economy. Other political, economic and social factors may also lead to further legal and regulatory changes and reforms, which may adversely affect our operations and business development.

Regulatory Risks

Our ability to sell our tools to Chinese customers may be restricted by regulatory actions.

ACM Shanghai utilizes certain items subject to export controls under the U.S. Export Administration Regulations (EAR) in manufacturing its products. The EAR applies to exports of commodities, software and technology from the U.S. (including for use in manufacturing products outside the U.S.), as well as to certain products manufactured outside the U.S. that incorporate, or are based on, designated U.S. content, software or technology. The Bureau of Industry and Security of the U.S. Department of Commerce (BIS), which administers the EAR, recently imposed and may continue to impose additional restrictions under the EAR on certain exports to the PRC, including through licensing requirements with a presumption of denial. These types of restrictions may impact the operations of ACM Shanghai.

The restrictions include the designation of additional PRC companies on certain restricted party lists under the EAR, such as the Entity List and the Unverified List. These designations result in the imposition of special requirements in connection with the supply of products to such companies. In addition, more recently, BIS imposed a series of new restrictions on exports of designated products and exports for designated uses and users in connection with the supercomputer, artificial intelligence, integrated circuit (IC) and semiconductor manufacturing sectors in the PRC. These new restrictions may have some impacts on the procurement by ACM Shanghai of certain items from the U.S. for use in manufacturing its products and the ongoing feasibility of supplying ACM Shanghai products to certain end users and for certain end uses in the PRC.

For example, BIS has added a number of PRC entities to the Entity List under the EAR. Any items subject to the EAR, including certain foreign produced products with specified U.S. content, now require a BIS export license for supply to the newly listed PRC entities. Along with other companies, in December 2020, SMIC, one of the largest chip manufacturers in the PRC, was added to the Entity List. Challenges faced by SMIC and its key suppliers as a result of the listing could indirectly impact SMIC’s demand for, or ACM Shanghai’s ability to supply, ACM Shanghai products. As part of the recent October 2022 actions, Yangtze Memory Technologies Co., Ltd. (YMTC), a leading PRC memory chip company was added to the Unverified List of the EAR alongside a number of other Chinese entities. The Unverified List identifies parties for whom BIS has been unable to confirm their bona fides (i.e., legitimacy and reliability about the end-use and end-user of items subject to the EAR). Entities listed on the Unverified List are ineligible to receive items subject to the EAR by means of a license exception if a U.S. export license is required. Challenges faced by YMTC and its key suppliers as a result of the listing could indirectly impact YMTC’s demand for, or ACM Shanghai’s ability to supply, ACM Shanghai products.

Also in October 2022, BIS announced new rules that significantly expand U.S. export controls as applied to advanced IC products, related manufacturing equipment and technology, and supercomputers, where the destination or ultimate end user is based in China. In the case of semiconductor manufacturing equipment, the new rules require an export license with a presumption of denial for the export from the U.S. to the PRC of additional types of semiconductor manufacturing equipment and of items for use in manufacturing designated types of semiconductor manufacturing equipment in the PRC, as well as for the supply of semiconductor manufacturing equipment to certain IC manufacturing and development facilities in the PRC. In addition, U.S. persons are effectively barred from engaging in certain activities related to the development and production of certain semiconductors in China, even if no items subject to the EAR are involved.

We are evaluating the potential direct impact of the rules, including any necessary modifications to our business policies and practices in China, and any expected changes in the capital spending plans of our customer base. We cannot be certain what additional actions the U.S. government may take with respect to PRC entities, and whether such actions will impact our relationships with our PRC-based customers, including by virtue of changes to the Entity List or Unverified List, other export regulations, tariffs or other trade restrictions. We also cannot know whether the PRC government may take any actions in response to the various U.S. government actions that may adversely affect our ability to do business with our PRC-based customers. Even in the absence of further restrictions, tariffs or trade actions imposed by the U.S. or PRC governments, our PRC-based customers could take actions to reduce dependence on the supply of products subject to potential U.S. trade regulations (including potentially our tools). This could have a material adverse effect on our operating results. We are unable to predict the duration of the restrictions imposed by the U.S. government or the effects of any future governmental actions that may impact our relationships with our PRC-based customers, any of which could have a long-term adverse effect on our business, operating results and financial condition.

| Item 2. | Unregistered Sales of Equity Securities and Use of Proceeds |

Recent Sales of Unregistered Equity Securities

In the three months ended September 30, 2022, ACM Research issued, pursuant to the exercise of stock options at a per share exercise prices ranging from $0.25 to $0.50 per share, an aggregate of 131,884 shares of Class A common stock that were not registered under the Securities Act of 1933. We believe the offer and sale of those shares were exempt from registration under the Securities Act of 1933 by virtue of Section 4(a)(2) thereof (or Regulation D promulgated thereunder) because they did not involve a public offering. The recipients of the shares acquired the securities for investment only and not with a view to or for sale in connection with any distribution thereof, and appropriate legends were recorded with respect to the shares. The recipients of the shares were accredited investors under Rule 501 of Regulation D.

| Sale Date | | Excercised Shares (Net) | |

| July 1, 2022 | | | 39,407 | |

| August 4, 2022 | | | 19,421 | |

| August 8, 2022 | | | 36,519 | |

| August 15, 2022 | | | 36,537 | |

| Total | | | 131,884 | |

The following exhibits are filed as part of this report:

Exhibit No. | | Description |

| | | |

| | Certification of Principal Executive Officer Pursuant to Rules 13a-14(a) and 15d-14(a) under the Securities Exchange Act of 1934, as Adopted Pursuant to Section 302 of the Sarbanes-Oxley Act of 2002 |

| | Certification of Principal Financial Officer Pursuant to Rules 13a-14(a) and 15d-14(a) under the Securities Exchange Act of 1934, as Adopted Pursuant to Section 302 of the Sarbanes-Oxley Act of 2002 |

| | Certification of Principal Executive Officer and Principal Financial Officer Pursuant to 18 U.S.C. Section 1350, as Adopted Pursuant to Section 906 of the Sarbanes-Oxley Act of 2002 |

| 101.INS | | Inline XBRL Instance Document (the instance document does not appear in the Interactive Data File because its XBRL tags are embedded within the Inline XBRL document) |

| 101.SCH | | Inline XBRL Taxonomy Extension Schema Document |

| 101.CAL | | Inline XBRL Taxonomy Extension Calculation Linkbase Document |

| 101.DEF | | Inline XBRL Taxonomy Extension Definition Linkbase Document |

| 101.LAB | | Inline XBRL Taxonomy Extension Label Linkbase Document |

| 101.PRE | | Inline XBRL Taxonomy Extension Presentation Linkbase Document |

| 104 | | Cover Page Interactive Data File (formatted as inline XBRL and contained in exhibit 101) |

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

| | ACM RESEARCH, INC. |

| Date: November 8, 2022 | By: | /s/ Mark McKechnie | |

| | | Mark McKechnie | |

| | | Chief Financial Officer, Executive Vice President and Treasurer (Principal Financial Officer) |

79